UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-23483

Axonic Funds

(exact name of registrant as specified in charter)

520 Madison Avenue, 42nd Floor

New York, NY 10022

(Address of Principal Office)

Clayton DeGiacinto, President

c/o Axonic Capital LLC

520 Madison Avenue, 42nd Floor

New York, New York 10022

(Name and Address of Agent for Service)

Copies of information to:

Jeffrey Skinner

Kilpatrick Townsend & Stockton LLP

1001 West Fourth Street

Winston-Salem, NC 27101

Registrant’s telephone number, including area code: (212) 259-0430

Date of fiscal year end: October 31

Date of reporting period: October 31, 2023

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-1090. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Report to Stockholders.

AXONIC STRATEGIC INCOME FUND

ANNUAL REPORT

October 31, 2023

TABLE OF CONTENTS

| Shareholder Letter | 1 |

| Portfolio Update | 2 |

| Disclosure of Fund Expenses | 4 |

| Consolidated Schedule of Investments | 5 |

| Consolidated Statement of Assets and Liabilities | 17 |

| Consolidated Statement of Operations | 18 |

| Consolidated Statement of Changes in Net Assets | 19 |

| Consolidated Financial Highlights | 20 |

| Notes to Consolidated Financial Statements | 22 |

| Report of Independent Registered Public Accounting Firm | 30 |

| Additional Information | 31 |

| Trustees and Officers | 32 |

| Privacy Policy | 34 |

Axonic Strategic Income Fund | Shareholder Letter |

| | October 31, 2023 (Unaudited) |

In our outlook for 2023, we suggested financial markets would remain volatile. Indeed, the early part of the year saw a rates shock that led to the failure of a handful of regional banks. While rates’ volatility persisted, an all-but-explicit blanket deposit bailout in March marked the dénouement for equity market volatility. Since then, the dispersion in volatility between rates and equities has endured, but most financial stocks and many small cap equities have not recovered. High yield corporate credit spreads have retreated significantly from wides but remain elevated at about 400bps. Rates markets – both through implied swaptions volatility and yield curve inversion – seem to recognize the risks we foresee. On the other hand, Magnificent 7 dominated large cap equities seem to see a different world. To some, the regional banking crisis no longer seems like it was a crisis at all. Yet, banks continue to copiously use the BTFP (Bank Term Funding Program), which expires in March 2024. It will likely need extension.

This time has, in fact, been somewhat different. The distortions and unintended consequences from pandemic-era stimulus were not limited to inflation. They also extended the ‘long and variable’ lags with which monetary policy typically works - albeit not remarkably beyond historical ranges relative to the initial yield curve inversion. Direct stimulus deposits and other policies like ERC (Employee Retention Credits) enabled consumers and small business owners to repair credit scores, increase credit lines, delay rents and student loan payments, and create a massive excess savings cushion. The benefits from this fiscal largesse have now expired. After almost two years of contraction, real wage growth, which only recently turned positive, just won’t be strong enough to compensate. We are already beginning to see the bouts of disinflation in commodities and goods we predicted in last year’s review. The collapse in the money supply (M2) that began at the end of 2023 suggested it was coming; M2 continues to contract. It's the bouts of disinflation following inflationary episodes that are often the most difficult for companies, and its showing in survey data (regional Fed surveys, PMIs, and ISMs). Fiscal policy’s counteraction of monetary policy has delayed, rather prevented, the historical consequences from monetary policy tightening.

Importantly, because rates could go no lower than the zero bound, the highly accommodative ZIRP regime that followed the Great Financial Crisis marked the end of a four-decade secular bull market for Treasury bonds. Indeed, yields have risen in fits and starts ever since. The end of this bond bull market has profound implications for the way investors will need to think about generating returns. No longer will passive, equity beta strategies generate satisfactory returns above the rate of inflation. With the S&P 500 dividend yield below the real 5-year treasury yield and the S&P 500 earnings risk premium now negative, history suggests that forward equity returns will suffer greatly. While not all excesses have been washed from the markets, the impacts of higher rates in the frothiest corners of private equity and venture capital are stark. This new regime opens the door wide for fundamentally driven credit strategies in alternative assets classes.

Axonic’s funds have been benefitting from structured credit markets whose yields are better compensating investors for risk. Relative to equities and corporate credit markets, structured credit assets are providing superior risk-adjusted returns. Owning hard real estate assets, senior non-agency RMBS, select CMBS, and front pay ABS bonds will continue to provide a margin of safety and risk-adjusted return profile available in few other asset classes. In October, as 10-year yields approached five percent, we started becoming comfortable with modestly extending portfolio duration. We continue to run the portfolio without the use of leverage and hold a healthy cash position which allows us to be nimble in shifting portfolio positioning to take advantage of future dislocations across the structured credit market.

The Axonic Strategic Income Fund, I shares, (“the Fund”) was up +5.82% for the fiscal year ended October 31, 2023, on a price per share performance basis that compares to the Fund's benchmark, the Bloomberg U.S. Aggregate Bond Index (the Agg), returned +0.36% for the year to date ended October 31, 2023. The Fund returned positive performance on a relative dollar basis of approximately +$82,169,030.

While we are cautious in the deployment of capital in the current market, we remain convinced that this environment is well suited to our investment style and asset class expertise. In particular, we continue to remain constructive on multifamily workforce housing assets. While interest rates have likely peaked, housing remains unaffordable and in short supply. Consequently, we believe multifamily rents will continue to remain strong. We also like front pay consumer ABS bonds and feel stress in ABS markets will eventually provide opportunity in subordinated tranches. As more vulnerable parts of the capital markets continue to suffer, this may create opportunity for us to acquire cash flowing assets at even more attractive valuations.

We continue to believe the Fund will represent an attractive solution for income-oriented investors in a challenging environment for traditional fixed income and equity strategies.

Thank you for your continued support.

Clayton DeGiacinto

Managing Partner, Chief Investment Officer

Axonic Capital LLC

An investor should consider the investment objectives, risks, charges, and expenses of the Fund carefully before investing. To obtain a prospectus containing this and other information, please call (212) 259-0430 or download the file from www.AxonicFunds.com. Please read the prospectus carefully before you invest.

| Annual Report | October 31, 2023 | 1 |

| Axonic Strategic Income Fund | Portfolio Update |

| | October 31, 2023 (Unaudited) |

Average Annual Total Returns (as of October 31, 2023)

| | 1 Month | Quarter | 6 Month | 1 Year | 3 Year | Since Inception* |

| Axonic Strategic Income Fund – A – NAV | 0.09% | 1.25% | 2.89% | 5.25% | 2.44% | 2.89% |

| Axonic Strategic Income Fund – A – LOAD | -2.16% | -1.03% | 0.57% | 2.90% | 1.68% | 2.18% |

| Axonic Strategic Income Fund – I – NAV | 0.21% | 1.48% | 3.24% | 5.82% | 2.93% | 1.72% |

| Bloomberg US Aggregate Bond Index(a) | -1.58% | -4.69% | -6.13% | 0.36% | -5.57% | -2.86% |

Past performance does not guarantee future results. Investment returns, and principal value of the Fund will fluctuate so that shares may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted above. For current performance information, please call 1-833-429-6642. Total annual fund operating expense (as reported in the February 28, 2023 Prospectus) for the I shares is 1.02% gross and 1.02% net and for the A shares is 1.52% gross and 1.52% net. The Fund’s investment adviser, Axonic Capital LLC (the “Adviser”) has entered into an Expense Limitation Agreement with the Fund under which it has contractually agreed to waive Advisory Fees and to assume other expenses of the Fund, if necessary, in an amount that limits annual operating expenses to not more than 1.10% of average daily net assets. The Expense Limitation Agreement is currently in effect until December 31, 2023. Class A (Maximum Offering Price) performance reflects the Fund's maximum sales charge of 2.25%.

| * | Class A has an inception date of July 16, 2020. Class I has an inception date of December 30, 2019. |

| (a) | The Bloomberg US Aggregate Bond Index is an unmanaged index which represents the U.S. investment-grade fixed-rate bond market (including government and corporate securities, mortgage pass-through securities and asset-backed securities). Investors cannot invest directly in an index or benchmark. |

Excludes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value and total return for shareholder transactions reported to the market may differ from the net asset value for financial reporting purposes.

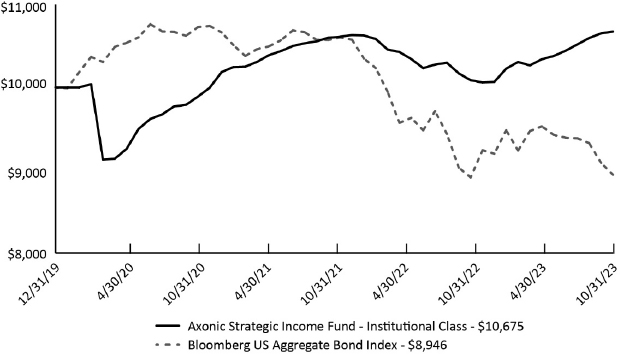

Performance of $10,000 Initial Investment (as of October 31, 2023)

The graph shown above represents historical performance of a hypothetical investment of $10,000 in the Institutional Class since inception. Past performance does not guarantee future results. All returns reflect reinvested dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the repurchase of Fund shares.

Performance data quoted represents past performance, which is not a guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and investment return of an investment will fluctuate so that your shares, if repurchased, may be worth more or less than their original cost. Total return measures net investment income and capital gain or loss from portfolio investments. All performance shown assumes reinvestment of dividends and capital gains distributions. For the most current month-end performance please call 1-833-429-6642 (833-4Axonic) or visit at www.axonicfunds.com.

Axonic Strategic Income Fund | Portfolio Update |

| | October 31, 2023 (Unaudited) |

| Top Ten Holdings (as a % of Net Assets)* | |

| U.S. Treasury Bond | 4.80% |

| MFA Financial, Inc. | 1.57% |

| LHOME Mortgage Trust, Series 2023-RTL3, Class A1 | 1.48% |

| Hertz Vehicle Financing III LP, Series 2021-2A, Class D | 1.36% |

| Roc Mortgage Trust, Series 2021-RTL1, Class A1 | 1.33% |

| MFA , Series 2023-RTL2, Class A1 | 1.33% |

| BAMLL Commercial Mortgage Securities Trust, Series 2019-AHT, Class E | 1.31% |

| BCRR , Series 2016-FRR3, Class E | 1.21% |

| JP Morgan Chase Commercial Mortgage Securities Trust, Series2016-NINE, Class A | 1.15% |

| MTK Mortgage Trust, Series 2021-GRNY, Class B | 1.13% |

| Top Ten Holdings | 16.67% |

| Sector Allocation (as a % of Net Assets)* | |

| Mortgage Securities | 51.87% |

| Asset Backed Securities | 17.95% |

| Financials | 7.56% |

| Government | 4.80% |

| Other Securities | 0.02% |

| Cash, Cash Equivalents, & Other Net Assets | 17.80% |

| | 100.00% |

| * | Holdings are subject to change, and may not reflect the current or future position of the portfolio. Tables present indicative values only. |

| Annual Report | October 31, 2023 | 3 |

| Axonic Strategic Income Fund | Disclosure of Fund Expenses |

| | October 31, 2023 |

As a shareholder of the Axonic Strategic Income Fund (the "Fund"), you will incur two types of costs: (1) transaction costs, including any applicable redemption fees; and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees (if applicable) and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on May 1, 2023 and held through October 31, 2023.

Actual Expenses

The first line under each class of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period May 1, 2023 – October 31, 2023” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line under each class of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and to other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees, if any. Therefore, the second line under each class of the table below is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | Beginning Account Value May 1, 2023 | Ending Account Value October 31, 2023 | Expense Ratio(a) | Expenses Paid During Period May 1, 2023 - October 31, 2023(a) |

| Axonic Strategic Income Fund | | | | |

| Class A | | | | |

| Actual | $ 1,000.00 | $ 1,028.90 | 1.40% | $ 7.16 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,018.15 | 1.40% | $ 7.12 |

| Institutional | | | | |

| Actual | $ 1,000.00 | $ 1,032.40 | 1.00% | $ 5.12 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,020.16 | 1.00% | $ 5.09 |

| (a) | Annualized, based on the Fund's most recent fiscal half year expenses. |

| (a) | Expenses are equal to the Fund's annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (184), divided by 365. |

| See Notes to Consolidated Financial Statements. | |

| 4 | www.axonicfunds.com |

| Axonic Strategic Income Fund | Consolidated Schedule of Investments |

| | October 31, 2023 |

| Description | | | | | | | | Shares | | | Value | |

| COMMON STOCKS (0.10%) | | | | | | | | | | | | | | | | |

| Financials (0.10%) | | | | | | | | | | | | | | | | |

| ACRES Commercial Realty Corp. REIT | | | | | | | | | | | 91,094 | | | $ | 660,431 | |

| PennyMac Financial Services, Inc. REIT | | | | | | | | | | | 6,390 | | | | 429,408 | |

| Redwood Trust, Inc. REIT | | | | | | | | | | | 44,220 | | | | 277,701 | |

| Rithm Capital Corp. REIT | | | | | | | | | | | 12,466 | | | | 116,308 | |

| TPG RE Finance Trust, Inc. REIT | | | | | | | | | | | 77,880 | | | | 429,119 | |

| | | | | | | | | | | | | | | | 1,912,967 | |

| TOTAL COMMON STOCKS | | | | | | | | | | | | | | | | |

| (Cost $3,276,313) | | | | | | | | | | | | | | | 1,912,967 | |

| | | | | Rate | | Shares | | | Value | |

| PREFERRED STOCKS (1.31%) | | | | | | | | | | | | |

| Financials (1.31%) | | | | | | | | | | | | |

| ACRES Commercial Realty Corp., Series D, (a) | | | | 7.88% | | | 200,000 | | | $ | 3,820,000 | |

| Arbor Realty Trust, Series F, | | | | 6.25% | | | 200,000 | | | | 3,494,000 | |

| Arbor Realty Trust, Series D, | | | | 6.38% | | | 170,454 | | | | 2,735,787 | |

| Granite Point Mortgage Trust, Inc., Series A, (a)(b) | | | | 1D US SOFR + 5.83% | | | 257,360 | | | | 4,140,922 | |

| KKR Real Estate Finance Trust, Inc., Series A, (a) | | | | 6.50% | | | 113,712 | | | | 1,853,506 | |

| New Residential, Series A, (a)(b) | | | | 7.50% | | | 5,470 | | | | 123,567 | |

| New York Mortgage Trust, Inc., Series F, (a)(b) | | | | 6.88% | | | 173,386 | | | | 3,171,230 | |

| Ready Capital Corp., Series E, (a) | | | | 6.50% | | | 12,474 | | | | 216,673 | |

| Rithm Capital Corp., Series D, (a)(b) | | | | 7.00% | | | 166,420 | | | | 3,325,072 | |

| TPG RE Finance Trust, Inc., Series C, (a) | | | | 6.25% | | | 160,000 | | | | 2,230,400 | |

| | | | | | | | | | | | 25,111,157 | |

| TOTAL PREFERRED STOCKS | | | | | | | | | | | | |

| (Cost $36,442,025) | | | | | | | | | | | 25,111,157 | |

| | | Rate | | Maturity Date | | Principal Amount | | | Value | |

| ASSET-BACKED SECURITIES (17.95%) | | | | | | | | | | | | |

| Achieve Mortgage, Series 2023-HE2, Class A(b)(c) | | 7.50% | | 10/25/38 | | $ | 16,000,000 | | | $ | 15,812,520 | |

| Achieve Personal Loan Master Pass-Through Trust Series 2023- PT1, Series 2023-1, Class PT(b)(c) | | 21.11% | | 09/15/53 | | | 9,872,180 | | | | 9,975,838 | |

| Achieve Personal Loan Master Pass-Through Trust Series 2023- PT2, Series 2023-2, Class PT(b)(c) | | 20.60% | | 10/15/53 | | | 4,258,656 | | | | 4,334,034 | |

| ACM Auto Trust 2023-2, Series 2023-2A, Class A(c) | | 7.97% | | 11/20/24 | | | 10,201,962 | | | | 10,197,881 | |

| Affirm Asset Securitization Trust, Series 2022-Z1, Class A(c) | | 4.55% | | 06/15/27 | | | 21,112,908 | | | | 20,789,880 | |

| Arivo Acceptance Auto Loan Receivables Trust 2021-1, Series 2021-1A, Class A(c) | | 1.19% | | 01/15/27 | | | 662,357 | | | | 647,785 | |

| Asset Backed Securities Corp. Home Equity Loan Trust Series NC, Series 2006-HE2, Class A3(b) | | 1M CME TERM SOFR + 0.49% | | 03/25/36 | | | 743,513 | | | | 733,663 | |

| Avant Credit Card Master Trust, Series 2021-1A, Class D(c) | | 4.28% | | 10/15/24 | | | 3,500,000 | | | | 3,248,000 | |

| Castlelake Aircraft Securitization Trust, Series 2018-1, Class B(c) | | 5.30% | | 06/15/25 | | | 4,334,216 | | | | 3,223,573 | |

| Castlelake Aircraft Structured Trust, Series 2017-1R, Class C(c) | | 6.50% | | 08/15/25 | | | 14,232,380 | | | | 6,831,543 | |

| Castlelake Aircraft Structured Trust, Series 2019-1A, Class A(c) | | 3.97% | | 04/15/26 | | | 5,177,266 | | | | 4,586,022 | |

| Castlelake Aircraft Structured Trust, Series 2019-1A, Class B(c) | | 5.10% | | 04/15/26 | | | 2,422,091 | | | | 1,556,194 | |

| Castlelake Aircraft Structured Trust, Series 2021-1A, Class B(c) | | 6.66% | | 07/15/27 | | | 2,215,762 | | | | 1,850,161 | |

| Castlelake Aircraft Structured Trust, Series 2021-1A, Class C(c) | | 7.00% | | 10/15/26 | | | 10,634,667 | | | | 7,550,614 | |

| Clsec Holdings 22t LLC, Series 2021-1, Class C(c) | | 6.17% | | 11/10/28 | | | 6,940,122 | | | | 5,274,493 | |

| Cologix Data Centers US Issuer LLC, Series 2021-1A, Class C(c) | | 5.99% | | 12/28/26 | | | 3,700,000 | | | | 3,011,060 | |

| DT Auto Owner Trust 2022-1, Series 2022-1A, Class E(c) | | 5.53% | | 11/17/25 | | | 3,170,000 | | | | 2,963,633 | |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | October 31, 2023 | 5 |

Axonic Strategic Income Fund | Consolidated Schedule of Investments |

| | October 31, 2023 |

| | | Rate | | Maturity Date | | Principal Amount | | | Value | |

| Falcon Aerospace, Ltd., Series 2019-1, Class A(c) | | 3.60% | | 09/15/26 | | $ | 1,852,157 | | | $ | 1,654,902 | |

| Falcon Aerospace, Ltd., Series 2019-1, Class B(c) | | 4.79% | | 09/15/26 | | | 3,389,332 | | | | 2,516,579 | |

| FAT Brands Fazoli's Native I LLC, Series 2021-1, Class B2(c) | | 8.00% | | 01/25/25 | | | 2,000,000 | | | | 1,875,400 | |

| FAT Brands GFG Royalty I LLC, Series 2021-1A, Class A2(c) | | 6.00% | | 07/25/51 | | | 8,553,000 | | | | 7,598,485 | |

| FAT Brands GFG Royalty I LLC, Series 2021-1A, Class B2(c) | | 7.00% | | 07/25/51 | | | 12,000,000 | | | | 10,641,600 | |

| FAT Brands Twin Peaks I LLC, Series 2021-1A, Class A2(c) | | 7.00% | | 01/25/25 | | | 9,038,000 | | | | 8,572,543 | |

| FAT Brands Twin Peaks I LLC, Series 2021-1A, Class B2(c) | | 9.00% | | 01/25/25 | | | 3,000,000 | | | | 2,747,400 | |

| First Investors Auto Owner Trust, Series 2021-1A, Class F(c) | | 5.37% | | 02/15/25 | | | 1,270,000 | | | | 1,178,179 | |

| Flexential Issuer 2021-1, Series 2021-1A, Class C(c) | | 6.93% | | 11/25/26 | | | 8,000,000 | | | | 6,815,200 | |

| GAIA Aviation, Ltd., Series 2019-1, Class B(c)(e) | | 5.19% | | 12/15/26 | | | 13,426,043 | | | | 11,110,050 | |

| Hertz Vehicle Financing III LP, Series 2021-2A, Class D(c) | | 4.34% | | 12/25/26 | | | 30,000,000 | | | | 26,103,000 | |

| Horizon Aircraft Finance I, Ltd., Series 2018-1, Class A(c) | | 4.46% | | 12/15/25 | | | 5,022,849 | | | | 4,317,641 | |

| Horizon Aircraft Finance I, Ltd., Series 2018-1, Class B(c) | | 5.27% | | 12/15/25 | | | 1,080,960 | | | | 678,302 | |

| Horizon Aircraft Finance II, Ltd., Series 2019-1, Class A(c) | | 3.72% | | 07/15/26 | | | 1,602,642 | | | | 1,385,484 | |

| Horizon Aircraft Finance II, Ltd., Series 2019-1, Class B(c) | | 4.70% | | 07/15/26 | | | 2,483,333 | | | | 1,583,125 | |

| Horizon Aircraft Finance III, Ltd., Series 2019-2, Class A(c) | | 3.43% | | 11/15/26 | | | 5,542,618 | | | | 4,385,874 | |

| Horizon Aircraft Finance III, Ltd., Series 2019-2, Class B(c) | | 4.46% | | 11/15/26 | | | 4,880,953 | | | | 2,306,250 | |

| JOL Air, Ltd., Series 2019-1, Class B(c) | | 4.95% | | 04/15/26 | | | 15,805,372 | | | | 12,051,596 | |

| JP Morgan Chase Bank NA - Chase Auto Credit Linked Notes, Series 2021-2, Class G(c) | | 8.48% | | 07/25/25 | | | 2,350,000 | | | | 2,278,795 | |

| Lendingpoint Asset Securitization Trust, Series 2021-B, Class D(c) | | 6.12% | | 12/16/24 | | | 3,000,000 | | | | 2,505,300 | |

| Lunar Structured Aircraft Portfolio Notes, Series 2021-1, Class C(c) | | 5.68% | | 09/15/28 | | | 7,363,093 | | | | 6,074,552 | |

| LUNAR AIRCRAFT, Ltd., Series 2020-1A, Class B(c) | | 4.34% | | 02/15/27 | | | 5,476,292 | | | | 3,997,693 | |

| MAPS 2021-1 Trust, Series 2021-1A, Class C(c) | | 5.44% | | 06/15/28 | | | 5,314,447 | | | | 3,773,257 | |

| New Residential Mortgage Loan Trust, Series 2022-SFR1, Class G(c) | | 5.00% | | 02/17/27 | | | 5,000,000 | | | | 4,201,312 | |

| Pagaya AI Debt Selection Trust, Series 2021-3, Class B(c) | | 1.74% | | 05/15/29 | | | 4,159,774 | | | | 4,078,658 | |

| Pagaya AI Debt Selection Trust, Series 2022-5, Class A(c) | | 8.10% | | 06/17/30 | | | 4,910,909 | | | | 4,950,687 | |

| Pagaya AI Debt Selection Trust, Series 2023-5, Class A(c) | | 7.18% | | 04/15/31 | | | 6,662,774 | | | | 6,665,439 | |

| Pioneer Aircraft Finance, Ltd., Series 2019-1, Class A(c) | | 3.97% | | 06/15/26 | | | 2,444,666 | | | | 2,116,347 | |

| Pioneer Aircraft Finance, Ltd., Series 2019-1, Class B(c) | | 4.95% | | 06/15/26 | | | 1,656,250 | | | | 1,192,500 | |

| Prosper Marketplace Issuance Trust Series 2023-1, Series 2023-1A, Class A(c) | | 7.06% | | 06/15/25 | | | 9,331,680 | | | | 9,328,881 | |

| Prosper Marketplace Issuance Trust Series 2023-1, Series 2023-1A, Class B(c) | | 7.48% | | 11/15/25 | | | 2,300,000 | | | | 2,303,220 | |

| RAMP, Series 2007-RS1, Class A4(b) | | 1M CME TERM SOFR + 0.67% | | 02/25/37 | | | 17,244,743 | | | | 3,925,549 | |

| Reach ABS Trust 2023-1, Series 2023-1A, Class A(c) | | 7.05% | | 02/18/31 | | | 7,492,552 | | | | 7,471,573 | |

| RMF Buyout Issuance Trust, Series 2021-HB1, Class M4(b)(c) | | 4.70% | | 11/25/31 | | | 3,250,000 | | | | 2,740,075 | |

| Saluda Grade Alternative Mortgage Trust, Series 2022-SEQ2, Class A1(b)(c) | | 3.50% | | 05/25/55 | | | 10,665,037 | | | | 10,090,428 | |

| Santander Consumer Auto Receivables Trust, Series 2021-AA, Class F(c) | | 5.79% | | 07/15/25 | | | 1,370,000 | | | | 1,240,535 | |

| Sapphire Aviation Finance II, Ltd., Series 2020-1A, Class C(c) | | 6.78% | | 03/15/27 | | | 2,854,229 | | | | 662,467 | |

| Start II, Ltd., Series 2019-1, Class B(c) | | 5.10% | | 03/15/26 | | | 2,079,592 | | | | 1,705,265 | |

| Stellar Jay Ireland DAC, Series 2021-1, Class B(c) | | 5.93% | | 03/15/28 | | | 4,220,577 | | | | 3,387,013 | |

| Stonepeak 2021-1 ABS, Series 2021-1A, Class C(c) | | 5.93% | | 05/15/28 | | | 8,537,721 | | | | 6,488,668 | |

| Theorem Funding Trust 2021-1, Series 2021-1A, Class B(c) | | 1.84% | | 12/15/27 | | | 2,735,688 | | | | 2,696,568 | |

| Thunderbolt III Aircraft Lease, Ltd., Series 2019-1, Class B(c) | | 4.75% | | 11/15/26 | | | 10,868,487 | | | | 6,140,695 | |

| Towd Point HE Trust 2021- HE1, Series 2021-HE1, Class A1(b)(c) | | 0.92% | | 10/25/24 | | | 10,150,465 | | | | 9,544,278 | |

| Upstart Securitization Trust, Series 2023-2, Class A(c) | | 6.77% | | 01/20/26 | | | 12,857,492 | | | | 12,825,349 | |

| See Notes to Consolidated Financial Statements. | |

| 6 | www.axonicfunds.com |

| Axonic Strategic Income Fund | Consolidated Schedule of Investments |

| | October 31, 2023 |

| | | Rate | | Maturity Date | | Principal Amount | | | Value | |

| Veros Auto Receivables Trust, Series 2022-1, Class B(c) | | 4.39% | | 10/15/24 | | $ | 2,114,000 | | | $ | 2,063,475 | |

| WAVE LLC, Series 2019-1, Class B(c) | | 4.58% | | 09/15/27 | | | 6,963,966 | | | | 4,021,690 | |

| Westlake Automobile Receivables Trust 2021-1, Series 2021-1A, Class C(c) | | 0.95% | | 03/16/26 | | | 5,684,791 | | | | 5,604,636 | |

| | | | | | | | | | | | | |

| TOTAL ASSET-BACKED SECURITIES | | | | | | | | | | | | |

| (Cost $391,074,443) | | | | | | | | | | | 344,183,409 | |

| | | | | | | | | | | | | |

| BANK LOANS (1.05%) | | | | | | | | | | | | |

| BRE Select Service(f) | | 3M US L + 13.61% | | 12/31/49 | | | 11,555,014 | | | | 11,521,881 | |

| Copper Hill Sportsmans RT | | 4.25% | | 02/01/27 | | | 7,082,719 | | | | 6,555,003 | |

| UTEX-DEFEASED(f) | | 1M US L + 6.35% | | 12/31/49 | | | 2,113,859 | | | | 2,101,598 | |

| | | | | | | | | | | | | |

| TOTAL BANK LOANS | | | | | | | | | | | | |

| (Cost $20,049,289) | | | | | | | | | | | 20,178,482 | |

| | | | | | | | | | | | | |

| COMMERCIAL MORTGAGE-BACKED SECURITIES (24.48%) | | | | | | | | | | | | |

| BAMLL Commercial Mortgage Securities Trust, Series 2019-AHT, Class E(b)(c) | | 1M CME TERM SOFR + 3.25% | | 03/15/34 | | | 25,835,000 | | | | 25,217,543 | |

| BAMLL Commercial Mortgage Securities Trust, Series 2022-DKLX, Class E(b)(c) | | 1M CME TERM SOFR + 4.13% | | 01/15/24 | | | 2,000,000 | | | | 1,919,800 | |

| BBCMS Mortgage Trust, Series 2018-TALL, Class C(b)(c) | | 1M CME TERM SOFR + 1.32% | | 03/15/37 | | | 3,312,000 | | | | 2,672,453 | |

| BBCMS Mortgage Trust, Series 2018-TALL, Class E(b)(c) | | 1M US L + 2.44% | | 03/15/37 | | | 14,615,000 | | | | 8,869,843 | |

| BBCMS Mortgage Trust, Series 2022-C17, Class E(c) | | 2.50% | | 08/15/32 | | | 5,223,000 | | | | 2,433,396 | |

| BCP Trust, Series 2021-330N, Class E(b)(c) | | 1M US L + 3.64% | | 06/15/38 | | | 15,300,000 | | | | 13,000,410 | |

| BCP Trust, Series 2021-330N, Class F(b)(c) | | 1M US L + 4.63% | | 06/15/38 | | | 8,500,000 | | | | 6,626,600 | |

| BCRR , Series 2016-FRR3, Class E(b)(c) | | 18.46% - 30D US SOFR% | | 05/26/26 | | | 24,057,599 | | | | 23,251,670 | |

| Benchmark Mortgage Trust, Series 2023-V3, Class XA(b)(g) | | 0.81% | | 03/15/28 | | | 76,610,789 | | | | 2,543,478 | |

| BMO Mortgage Trust, Series 2023-5C1, Class C(b) | | 7.12% | | 08/15/28 | | | 1,000,000 | | | | 919,900 | |

| BMO Mortgage Trust, Series 2023-5C1, Class XA(b)(g) | | 0.58% | | 07/15/28 | | | 134,095,153 | | | | 3,218,284 | |

| BX Mortgage Trust, Series 2022-MVRK, Class G(b)(c) | | 1M US SOFR + 5.61% | | 03/15/27 | | | 13,844,079 | | | | 13,308,313 | |

| BX Trust, Series 2019-ATL, Class B(b)(c) | | 1M CME TERM SOFR + 1.50% | | 10/15/36 | | | 1,200,000 | | | | 1,159,800 | |

| BX Trust, Series 2019-ATL, Class G(b)(c) | | 1M US L + 3.49% | | 10/15/36 | | | 8,242,707 | | | | 7,737,429 | |

| BX Trust, Series 2021-RISE, Class D(b)(c) | | 1M CME TERM SOFR + 1.86% | | 11/15/23 | | | 2,751,100 | | | | 2,665,541 | |

| Cantor Commercial Real Estate Lending, Series 2019-CF1, Class 65D(b)(c) | | 4.66% | | 04/15/24 | | | 4,600,000 | | | | 3,128,000 | |

| Cantor Commercial Real Estate Lending, Series 2019-CF2, Class SWD(c) | | 4.52% | | 09/15/29 | | | 4,988,052 | | | | 3,642,276 | |

| Cascade Funding Mortgage Trust, Series 2021-FRR1, Class CK58(c)(d) | | 0.00% | | 09/29/29 | | | 24,870,000 | | | | 18,441,105 | |

| COLT Mortgage Loan Trust, Series 2020-3, Class A1(b)(c) | | 1.51% | | 04/27/65 | | | 2,555,179 | | | | 2,328,715 | |

| Countrywide Alternative Loan, Series 2007-17CB | | 5.01% | | 08/25/37 | | | 6,742,962 | | | | 3,268,806 | |

| Credit Suisse Mortgage Capital Certificates, Series 2010-6R, Class 2A7(c) | | 6.25% | | 05/26/48 | | | 2,945,132 | | | | 2,246,065 | |

| Credit Suisse Mortgage Capital Certificates, Series 2021-980M, Class G(b)(c) | | 3.54% | | 07/15/26 | | | 6,311,003 | | | | 5,252,017 | |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | October 31, 2023 | 7 |

| Axonic Strategic Income Fund | Consolidated Schedule of Investments |

| | October 31, 2023 |

| | | Rate | | Maturity Date | | Principal Amount | | | Value | |

| Credit Suisse Mortgage Capital Certificates, Series 2020-FACT, Class F(b)(c) | | 1M US L + 6.16% | | 10/15/25 | | $ | 10,500,000 | | | $ | 9,403,800 | |

| CSMC, Series 2021-980M, Class A(c) | | 2.39% | | 07/15/26 | | | 3,900,000 | | | | 3,425,760 | |

| CSMC, Series 2021-980M, Class D(b)(c) | | 3.54% | | 07/15/26 | | | 3,000,000 | | | | 2,568,600 | |

| CSMC, Series 2021-980M, Class E(b)(c) | | 3.54% | | 07/15/26 | | | 2,000,000 | | | | 1,699,600 | |

| CSMC, Series 2021-980M, Class F(b)(c) | | 3.54% | | 07/15/26 | | | 11,700,000 | | | | 9,858,420 | |

| Extended Stay America Trust, Series 2021-ESH, Class C(b)(c) | | 1M CME TERM SOFR + 1.81% | | 07/15/26 | | | 11,680,824 | | | | 11,433,191 | |

| Freddie Mac Multifamily Structured Credit Risk, Series 2023-MN7, Class M2(b)(c) | | 30D US SOFR + 5.70% | | 04/25/33 | | | 2,300,000 | | | | 2,302,300 | |

| Freddie Mac Multifamily Structured Pass Through Certificates, Series 2023-153, Class X3(b)(g) | | 4.68% | | 01/25/33 | | | 19,488,345 | | | | 5,655,518 | |

| Freddie Mac Multifamily Structured Pass Through Certificates, Series 2023-154, Class X3(b)(g) | | 5.10% | | 01/25/33 | | | 11,437,000 | | | | 3,633,535 | |

| Freddie Mac Multifamily Structured Pass Through Certificates, Series 2022-151, Class X3(b)(g) | | 4.38% | | 11/25/32 | | | 6,840,000 | | | | 1,835,172 | |

| Freddie Mac Multifamily Structured Pass Through Certificates, Series 2018-Q008, Class X(b)(g) | | 1.47% | | 12/25/24 | | | 20,752,626 | | | | 255,257 | |

| FREMF Mortgage Trust, Series 2016-KF24, Class B(b)(c) | | 30D US SOFR + 5.11% | | 10/25/26 | | | 3,152,937 | | | | 3,105,959 | |

| FREMF Mortgage Trust, Series 2018-KF49, Class B(b)(c) | | 30D US SOFR + 2.01% | | 06/25/25 | | | 4,849,698 | | | | 4,661,530 | |

| FREMF Mortgage Trust, Series 2018-KF49, Class C(b)(c) | | 30D US SOFR + 6.11% | | 06/25/25 | | | 20,662,824 | | | | 20,441,731 | |

| FRESB Mortgage Trust, Series 2019-SB66, Class X1(b)(g) | | 0.86% | | 07/25/29 | | | 32,419,167 | | | | 817,968 | |

| FRESB Mortgage Trust, Series 2020-SB74, Class X1(b)(g) | | 1.10% | | 03/25/30 | | | 26,852,304 | | | | 859,274 | |

| FRESB Mortgage Trust, Series 2020-SB76, Class X1(b)(g) | | 1.17% | | 05/25/30 | | | 12,715,779 | | | | 429,158 | |

| FRESB Mortgage Trust, Series 2020-SB77, Class X1(b)(g) | | 0.88% | | 06/25/27 | | | 17,248,203 | | | | 459,916 | |

| FRESB Mortgage Trust, Series 2020-SB78, Class X1(b)(g) | | 1.14% | | 06/25/30 | | | 28,559,352 | | | | 1,057,887 | |

| FRESB Mortgage Trust, Series 2020-SB79, Class X1(b)(g) | | 1.09% | | 07/25/40 | | | 15,528,688 | | | | 583,818 | |

| FRESB Mortgage Trust, Series 2020-SB80, Class X1(b)(g) | | 1.12% | | 09/25/30 | | | 56,678,113 | | | | 2,275,190 | |

| FRESB Mortgage Trust, Series 2020-SB81, Class X1(b)(g) | | 1.04% | | 10/25/30 | | | 19,017,252 | | | | 721,263 | |

| FRESB Mortgage Trust, Series 2021-SB82, Class X1(b)(g) | | 1.06% | | 10/25/40 | | | 45,893,510 | | | | 1,527,781 | |

| FRESB Mortgage Trust, Series 2021-SB83, Class X1(b)(g) | | 0.87% | | 01/25/41 | | | 28,855,382 | | | | 952,112 | |

| FRESB Mortgage Trust, Series 2021-SB84, Class X1(b)(g) | | 0.50% | | 01/25/31 | | | 27,838,959 | | | | 562,386 | |

| FRESB Mortgage Trust, Series 2022-SB95, Class X1(b)(g) | | 0.00% | | 11/25/31 | | | 118,412,909 | | | | 1,218,102 | |

| GAM RE-REMIC Trust, Series 2022-FRR3, Class EK41(c)(d) | | 0.00% | | 10/27/47 | | | 2,445,000 | | | | 2,198,544 | |

| Government National Mortgage Association, Series 2018-16, Class IO(b)(g) | | 0.58% | | 03/16/59 | | | 72,681,648 | | | | 2,645,612 | |

| Great Wolf Trust 2019-WOLF, Class C(b)(c) | | 1M CME TERM SOFR + 1.75% | | 12/15/24 | | | 10,695,000 | | | | 10,559,174 | |

| Hudsons Bay Simon JV Trust, Series 2015-HB7, Class A7(c) | | 3.91% | | 08/05/34 | | | 12,896,000 | | | | 11,588,346 | |

| Hudsons Bay Simon JV Trust, Series 2015-HBFL, Class AFL(b)(c) | | 1M CME TERM SOFR + 1.94% | | 08/05/34 | | | 11,274,447 | | | | 11,032,046 | |

| Hudsons Bay Simon JV Trust 2015-HBS, Series 2015-HB10, Class A10(c) | | 4.15% | | 08/05/25 | | | 2,214,207 | | | | 2,004,079 | |

| JP Morgan Chase Commercial Mortgage Securities Trust, Series 2007-LD12, Class AJ(b) | | 6.50% | | 02/15/51 | | | 5,222,610 | | | | 4,997,515 | |

| JP Morgan Chase Commercial Mortgage Securities Trust, Series 2008-C2, Class AM(b) | | 6.83% | | 02/12/51 | | | 3,705,455 | | | | 1,959,815 | |

| See Notes to Consolidated Financial Statements. | |

| 8 | www.axonicfunds.com |

| Axonic Strategic Income Fund | Consolidated Schedule of Investments |

| | October 31, 2023 |

| | | Rate | | Maturity Date | | Principal Amount | | | Value | |

| JP Morgan Chase Commercial Mortgage Securities Trust, Series 2016-NINE, Class A(b)(c) | | 2.85% | | 09/06/26 | | $ | 25,000,000 | | | $ | 22,050,000 | |

| JP Morgan Chase Commercial Mortgage Securities Trust, Series 2022-NLP, Class B(b)(c) | | 1M CME TERM SOFR + 1.11% | | 04/15/27 | | | 19,525,591 | | | | 17,161,042 | |

| JP Morgan Chase Commercial Mortgage Securities Trust, Series 2022-NLP, Class G(b)(c) | | 1M US SOFR + 4.27% | | 04/15/27 | | | 7,400,199 | | | | 6,284,249 | |

| MRCD 2019-MARK Mortgage Trust, Series 2019-PARK, Class G(c) | | 2.72% | | 12/15/24 | | | 8,311,000 | | | | 6,193,726 | |

| MTK Mortgage Trust, Series 2021-GRNY, Class F(b)(c) | | 1M CME TERM SOFR + 5.91% | | 12/15/23 | | | 2,600,000 | | | | 2,454,140 | |

| MTK Mortgage Trust, Series 2021-GRNY, Class B(b)(c) | | 1M CME TERM SOFR + 2.76% | | 12/15/23 | | | 22,648,900 | | | | 21,704,441 | |

| MTN Commercial Mortgage Trust, Series 2022-LPFL, Class F(b)(c) | | 1M US SOFR + 5.29% | | 03/15/27 | | | 10,000,000 | | | | 9,207,000 | |

| NCMF Trust, Series 2022-MFP, Class G(b)(c) | | 1M CME TERM SOFR + 5.13% | | 03/15/27 | | | 12,600,000 | | | | 11,758,320 | |

| SB Multifamily Repack Trust, Series 2020-FRR1, Class A(c) | | 5.60% | | 05/27/26 | | | 16,123,490 | | | | 15,886,474 | |

| Series RR , Series 2014-1, Class A(c)(d) | | 0.00% | | 04/25/24 | | | 700,000 | | | | 679,560 | |

| SFAVE Commercial Mortgage Securities Trust, Series 2015-5AVE, Class A2B(b)(c) | | 4.14% | | 01/05/35 | | | 7,000,000 | | | | 4,526,200 | |

| SFAVE Commercial Mortgage Securities Trust, Series 2015-5AVE, Class B(b)(c) | | 4.39% | | 01/05/35 | | | 3,692,000 | | | | 2,167,573 | |

| SFAVE Commercial Mortgage Securities Trust, Series 2015-5AVE, Class C(b)(c) | | 4.39% | | 01/05/35 | | | 3,179,000 | | | | 1,712,845 | |

| SLG Office Trust, Series 2021-OVA, Class E(c) | | 2.85% | | 07/15/31 | | | 13,600,000 | | | | 9,242,560 | |

| SMR Mortgage Trust, Series 2022-IND, Class E(b)(c) | | 1M CME TERM SOFR + 5.00% | | 02/15/24 | | | 10,483,290 | | | | 9,586,969 | |

| Velocity Commercial Capital Loan Trust, Series 2019-2, Class M5(b)(c) | | 4.93% | | 03/25/27 | | | 285,177 | | | | 239,393 | |

| Velocity Commercial Capital Loan Trust, Series 2019-2, Class M6(b)(c) | | 6.30% | | 02/25/28 | | | 339,022 | | | | 265,261 | |

| Velocity Commercial Capital Loan Trust, Series 2019-1, Class M6(b)(c) | | 6.79% | | 10/29/29 | | | 1,446,067 | | | | 1,070,588 | |

| Velocity Commercial Capital Loan Trust, Series 2019-3, Class M5(b)(c) | | 4.73% | | 08/25/28 | | | 311,071 | | | | 246,326 | |

| Velocity Commercial Capital Loan Trust, Series 2020-1, Class M6(b)(c) | | 5.69% | | 02/25/50 | | | 1,010,338 | | | | 694,876 | |

| Velocity Commercial Capital Loan Trust, Series 2021-1, Class M6(b)(c) | | 5.03% | | 03/25/31 | | | 1,979,181 | | | | 1,153,218 | |

| Velocity Commercial Capital Loan Trust, Series 2021-3, Class M6(b)(c) | | 5.03% | | 11/25/31 | | | 687,886 | | | | 453,392 | |

| Velocity Commercial Capital Loan Trust, Series 2022-1, Class M5(b)(c) | | 5.82% | | 06/25/32 | | | 3,857,986 | | | | 2,974,871 | |

| Velocity Commercial Capital Loan Trust, Series 2022-1, Class M6(b)(c) | | 5.82% | | 08/25/33 | | | 2,281,768 | | | | 1,735,693 | |

| Velocity Commercial Capital Loan Trust, Series 2022-2, Class M5(b)(c) | | 5.84% | | 04/25/52 | | | 3,750,383 | | | | 2,803,037 | |

| VMC Finance LLC, Series 2021-HT1, Class B(b)(c) | | 1M CME TERM SOFR + 4.61% | | 01/18/37 | | | 20,580,000 | | | | 19,606,566 | |

| Wells Fargo Commercial Mortgage Trust, Series 2020-SDAL, Class E(b)(c) | | 1M CME TERM SOFR + 2.85% | | 02/15/25 | | | 3,742,000 | | | | 3,672,399 | |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | October 31, 2023 | 9 |

Axonic Strategic Income Fund | Consolidated Schedule of Investments |

| | October 31, 2023 |

| | | Rate | | Maturity Date | | Principal Amount | | | Value | |

| Wells Fargo Commercial Mortgage Trust, Series 2020-SDAL, Class F(b)(c) | | 1M CME TERM SOFR + 3.61% | | 02/15/25 | | $ | 1,469,000 | | | $ | 1,426,399 | |

| | | | | | | | | | | | | |

| TOTAL COMMERCIAL MORTGAGE-BACKED SECURITIES | | | | | | | | | | | | |

| (Cost $519,162,774) | | | | | | | | | | | 469,538,921 | |

| | | | | | | | | | | | | |

| CONVERTIBLE CORPORATE BONDS (3.72%) | | | | | | | | | | | | |

| MFA Financial, Inc. | | 6.25% | | 06/15/24 | | | 30,730,000 | | | | 30,066,232 | |

| PennyMac Corp. | | 5.50% | | 11/01/24 | | | 5,000,000 | | | | 4,873,000 | |

| PennyMac Corp. | | 5.50% | | 03/15/26 | | | 10,682,000 | | | | 9,600,981 | |

| Redwood Trust, Inc. | | 5.63% | | 07/15/24 | | | 8,763,000 | | | | 8,578,101 | |

| RWT Holdings, Inc. | | 5.75% | | 10/01/25 | | | 19,800,000 | | | | 18,318,960 | |

| | | | | | | | | | | | | |

| TOTAL CONVERTIBLE CORPORATE BONDS | | | | | | | | | | | | |

| (Cost $72,961,585) | | | | | | | | | | | 71,437,274 | |

| | | | | | | | | | | | | |

| CORPORATE BONDS (1.38%) | | | | | | | | | | | | |

| Ambac Assurance Corp.(c) | | 5.10% | | 12/31/99 | | | 2,079,758 | | | | 2,984,452 | |

| Apollo Commercial Real Estate Finance, Inc.(c) | | 4.63% | | 06/15/29 | | | 5,000,000 | | | | 3,862,500 | |

| GKN Subordinated CTL Pass-Through Trust/Auburn MI(b)(c)(d) | | 0.00% | | 03/15/30 | | | 7,076,849 | | | | 3,560,363 | |

| Rithm Capital Corp.(c) | | 6.25% | | 10/15/25 | | | 16,839,000 | | | | 16,039,148 | |

| | | | | | | | | | | | | |

| TOTAL CORPORATE BONDS | | | | | | | | | | | | |

| (Cost $28,283,831) | | | | | | | | | | | 26,446,463 | |

| | | | | | | | | | | | | |

| GOVERNMENT BOND (4.80%) | | | | | | | | | | | | |

| U.S. Treasury Bond | | 3.88% | | 08/15/33 | | | 100,000,000 | | | | 92,054,688 | |

| | | | | | | | | | | | | |

| TOTAL GOVERNMENT BOND | | | | | | | | | | | | |

| (Cost $92,426,281) | | | | | | | | | | | 92,054,688 | |

| | | | | | | | | | | | | |

| RESIDENTIAL MORTGAGE-BACKED SECURITIES (27.39%) | | | | | | | | | | | | |

| A&D Mortgage Trust, Series 2023-NQM4, Class A3(c)(e) | | 8.10% | | 10/25/27 | | | 1,000,000 | | | | 1,000,943 | |

| A&D Mortgage Trust, Series 2023-NQM4, Class A2(c)(e) | | 7.82% | | 10/25/27 | | | 4,170,000 | | | | 4,175,945 | |

| AlphaFlow Transitional Mortgage Trust, Series 2021-WL1, Class A2(c)(e) | | 5.61% | | 01/25/26 | | | 573,701 | | | | 472,450 | |

| Alternative Loan Trust, Series 2006-14CB, Class A5(b) | | 1M CME TERM SOFR + 0.81% | | 06/25/36 | | | 2,223,130 | | | | 1,108,972 | |

| Alternative Loan Trust, Series 2006-18CB, Class A5(b) | | 1M CME TERM SOFR + 0.46% | | 07/25/36 | | | 2,001,388 | | | | 923,849 | |

| Alternative Loan Trust, Series 2006-18CB, Class A1(b) | | 1M CME TERM SOFR + 0.58% | | 07/25/36 | | | 9,385,700 | | | | 4,404,377 | |

| Alternative Loan Trust, Series 2006-18CB, Class A7(b) | | 1M CME TERM SOFR + 0.46% | | 07/25/36 | | | 24,846,094 | | | | 11,469,056 | |

| Alternative Loan Trust, Series 2006-20CB, Class A4(b) | | 1M CME TERM SOFR + 0.46% | | 07/25/36 | | | 4,951,168 | | | | 1,863,289 | |

| Alternative Loan Trust, Series 2006-20CB, Class A6(b) | | 1M CME TERM SOFR + 0.61% | | 07/25/36 | | | 1,884,659 | | | | 727,342 | |

| Alternative Loan Trust, Series 2006-24CB, Class A5(b) | | 1M CME TERM SOFR + 0.71% | | 08/25/36 | | | 5,371,579 | | | | 2,680,946 | |

| Alternative Loan Trust, Series 2006-24CB, Class A19(b) | | 1M CME TERM SOFR + 0.61% | | 08/25/36 | | | 2,478,672 | | | | 1,218,894 | |

| See Notes to Consolidated Financial Statements. | |

| 10 | www.axonicfunds.com |

| Axonic Strategic Income Fund | Consolidated Schedule of Investments |

| | October 31, 2023 |

| | | Rate | | Maturity Date | | Principal Amount | | | Value | |

| Alternative Loan Trust, Series 2006-40T1, Class 1A3(b) | | 1M CME TERM SOFR + 0.66% | | 01/25/37 | | $ | 4,587,653 | | | $ | 2,694,705 | |

| Alternative Loan Trust, Series 2006-41CB, Class 2A8(b) | | 1M CME TERM SOFR + 0.76% | | 01/25/37 | | | 3,203,755 | | | | 1,560,868 | |

| Alternative Loan Trust, Series 2006-41CB, Class 2A7(b) | | 1M CME TERM SOFR + 0.71% | | 01/25/37 | | | 3,057,287 | | | | 1,479,791 | |

| Alternative Loan Trust, Series 2006-42, Class 1A1(b) | | 1M CME TERM SOFR + 0.71% | | 01/25/47 | | | 6,411,341 | | | | 3,169,435 | |

| Alternative Loan Trust, Series 2006-6CB, Class 2A13(b) | | 1M CME TERM SOFR + 0.51% | | 05/25/36 | | | 3,954,804 | | | | 1,381,824 | |

| Alternative Loan Trust, Series 2007-2CB, Class 1A12(b) | | 1M CME TERM SOFR + 0.61% | | 03/25/37 | | | 1,632,782 | | | | 810,891 | |

| Alternative Loan Trust, Series 2007-5CB, Class 1A19(b) | | 1M CME TERM SOFR + 0.56% | | 04/25/37 | | | 13,075,397 | | | | 6,186,408 | |

| Alternative Loan Trust, Series 2007-5CB, Class 1A21(b) | | 1M CME TERM SOFR + 0.65% | | 04/25/37 | | | 2,094,606 | | | | 1,002,320 | |

| AMSR, Series 2021-SFR3, Class G(c) | �� | 3.80% | | 10/17/26 | | | 7,000,000 | | | | 5,882,218 | |

| Angel Oak Mortgage Trust, Series 2020-R1, Class A1(b)(c) | | 0.99% | | 12/25/24 | | | 665,588 | | | | 593,404 | |

| Angel Oak Mortgage Trust, Series 2022-1, Class B2(b)(c) | | 4.02% | | 01/25/26 | | | 1,185,369 | | | | 660,545 | |

| Angel Oak Mortgage Trust I LLC, Series 2019-1, Class M1(b)(c) | | 4.50% | | 11/25/48 | | | 3,880,848 | | | | 3,795,693 | |

| ANTLR Mortgage Trust, Series 2021-RTL1, Class A1(c)(e) | | 3.12% | | 11/25/24 | | | 3,158,458 | | | | 3,145,855 | |

| Bear Stearns Asset Backed Securities I Trust, Series 2007-AC5, Class A2 | | 6.00% | | 07/25/37 | | | 4,492,876 | | | | 1,474,447 | |

| Bear Stearns Asset Backed Securities I Trust, Series 2007-HE3, Class 1A4(b) | | 1M CME TERM SOFR + 0.46% | | 04/25/37 | | | 511,918 | | | | 463,138 | |

| Bear Stearns Asset Backed Securities I Trust, Series 2007-HE3, Class 1A3(b) | | 1M CME TERM SOFR + 0.36% | | 04/25/37 | | | 579,516 | | | | 729,218 | |

| Bear Stearns Asset Backed Securities I Trust, Series 2007-HE7, Class M1(b) | | 1M CME TERM SOFR + 0.51% | | 10/25/37 | | | 3,986,727 | | | | 2,830,090 | |

| Bear Stearns Mortgage Funding Trust, Series 2006-AR3, Class 1A2A(b) | | 1M CME TERM SOFR + 0.35% | | 10/25/36 | | | 332,969 | | | | 330,973 | |

| Bear Stearns Mortgage Funding Trust, Series 2006-AR3, Class 1A2G(b) | | 1M CME TERM SOFR + 0.35% | | 10/25/36 | | | 2,661,425 | | | | 2,645,473 | |

| Bear Stearns Mortgage Funding Trust, Series 2007-AR2, Class A2(b) | | 1M CME TERM SOFR + 0.51% | | 03/25/37 | | | 6,264,738 | | | | 5,547,498 | |

| Bear Stearns Mortgage Funding Trust, Series 2007-AR4, Class G2AB(b) | | 1M CME TERM SOFR + 0.35% | | 04/25/37 | | | 5,689,353 | | | | 5,087,102 | |

| Bear Stearns Mortgage Funding Trust, Series 2007-AR5, Class 1A2G(b) | | 1M CME TERM SOFR + 0.55% | | 06/25/37 | | | 834,421 | | | | 717,881 | |

| Bear Stearns Mortgage Funding Trust, Series 2007-AR5, Class 2A2(b) | | 1M CME TERM SOFR + 0.34% | | 06/25/37 | | | 2,160,451 | | | | 1,924,427 | |

| Boston Lending Trust, Series 2022-1, Class M2(b)(c) | | 2.75% | | 02/25/27 | | | 2,621,501 | | | | 1,854,450 | |

| BRAVO Residential Funding Trust, Series 2021-NQM1, Class A1(b)(c) | | 0.94% | | 02/25/49 | | | 3,236,507 | | | | 2,796,604 | |

| BRAVO Residential Funding Trust, Series 2021-NQM1, Class A3(b)(c) | | 1.33% | | 02/25/49 | | | 1,032,534 | | | | 883,384 | |

| BRAVO Residential Funding Trust, Series 2021-NQM3, Class A1(b)(c) | | 1.70% | | 04/25/60 | | | 7,207,726 | | | | 6,272,455 | |

| CHL Mortgage Pass-Through Trust, Series 2007-4, Class 1A51(b) | | 1M CME TERM SOFR + 0.71% | | 05/25/37 | | | 2,261,388 | | | | 894,594 | |

| CHNGE Mortgage Trust, Series 2023-3, Class A1(c)(e) | | 7.10% | | 06/25/27 | | | 4,693,258 | | | | 4,636,937 | |

| CHNGE Mortgage Trust, Series 2023-4, Class A1(b)(c)(e) | | 7.57% | | 09/25/58 | | | 7,671,948 | | | | 7,645,094 | |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | October 31, 2023 | 11 |

| Axonic Strategic Income Fund | Consolidated Schedule of Investments |

| | October 31, 2023 |

| | | Rate | | Maturity Date | | Principal Amount | | | Value | |

| CitiMortgage Alternative Loan Trust, Series 2007-A2, Class 1A1(b) | | 1M CME TERM SOFR + 0.71% | | 02/25/37 | | $ | 1,319,938 | | | $ | 1,091,712 | |

| COLTMortgage Pass-Through Certificates, Series 2021-1R, Class A3(b)(c) | | 1.42% | | 05/25/65 | | | 3,222,548 | | | | 2,624,309 | |

| COLT Mortgage Loan Trust, Series 2022-1, Class B2(b)(c) | | 4.11% | | 12/27/66 | | | 1,000,000 | | | | 645,918 | |

| COLT Mortgage Loan Trust, Series 2023-3, Class A3(c)(e) | | 7.58% | | 09/25/68 | | | 2,288,000 | | | | 2,283,100 | |

| CoreVest American Finance Ltd, Series 2022-RTL1, Class A1(e) | | 4.25% | | 05/28/29 | | | 1,280,000 | | | | 1,223,187 | |

| Credit Suisse Mortgage Capital Certificates, Series 2021-NQM3, Class B2(b)(c) | | 4.13% | | 04/25/66 | | | 800,000 | | | | 428,264 | |

| Deephaven Residential Mortgage Trust, Series 2021-3, Class B2(b)(c) | | 4.13% | | 09/25/25 | | | 2,800,000 | | | | 1,528,224 | |

| Deephaven Residential Mortgage Trust, Series 2022-1, Class B2(b)(c) | | 4.28% | | 01/25/26 | | | 2,628,000 | | | | 1,488,116 | |

| Dominion Mortgage Trust, Series 2021-RTL1, Class A1(c)(e) | | 2.49% | | 02/25/25 | | | 20,000,000 | | | | 18,677,304 | |

| Dominion Mortgage Trust, Series 2021-RTL1, Class M(c)(e) | | 5.73% | | 02/25/25 | | | 3,500,000 | | | | 2,874,120 | |

| Ellington Financial Mortgage Trust 2017-1, Series 2021-1, Class A1(b)(c) | | 0.80% | | 02/25/66 | | | 2,442,256 | | | | 1,947,443 | |

| GCAT, Series 2021-NQM4, Class A1(b)(c) | | 1.09% | | 08/25/25 | | | 5,009,967 | | | | 3,666,909 | |

| GS Mortgage-Backed Securities Trust, Series 2021-NQM1, Class B2(b)(c) | | 4.21% | | 07/25/61 | | | 1,000,000 | | | | 596,097 | |

| Home Partners of America, Series 2021-2, Class G(c) | | 4.51% | | 12/17/26 | | | 5,775,901 | | | | 4,917,025 | |

| Imperial Fund Mortgage Trust, Series 2021-NQM1, Class A3(b)(c) | | 1.62% | | 06/25/56 | | | 6,027,906 | | | | 4,835,265 | |

| Imperial Fund Mortgage Trust, Series 2021-NQM1, Class B2(b)(c) | | 4.36% | | 06/25/56 | | | 2,785,000 | | | | 1,604,083 | |

| Imperial Fund Mortgage Trust, Series 2021-NQM1, Class A2(b)(c) | | 1.21% | | 06/25/56 | | | 5,525,581 | | | | 4,416,676 | |

| Lehman Mortgage Trust, Series 2005-2, Class 3A1(b) | | 1M CME TERM SOFR + 0.86% | | 12/25/35 | | | 1,373,952 | | | | 716,617 | |

| Lehman Mortgage Trust, Series 2005-2, Class 2A1(b) | | 1M CME TERM SOFR + 0.79% | | 12/25/35 | | | 4,918,486 | | | | 2,798,495 | |

| Lehman Mortgage Trust, Series 2006-9, Class 1A5(b) | | 1M CME TERM SOFR + 0.71% | | 01/25/37 | | | 1,687,015 | | | | 967,610 | |

| Lehman Mortgage Trust, Series 2008-3, Class A1(b) | | 1M CME TERM SOFR + 0.48% | | 02/25/37 | | | 7,825,658 | | | | 2,109,391 | |

| Lehman XS Trust, Series 2007-6, Class 3A32(b) | | 1M CME TERM SOFR + 0.61% | | 05/25/37 | | | 6,824,711 | | | | 5,861,986 | |

| Lehman XS Trust, Series 2007-6, Class 3A31(e) | | 4.27% | | 05/25/37 | | | 3,217,628 | | | | 2,755,509 | |

| LHOME Mortgage Trust, Series 2022-RTL1, Class A1(c) | | 3.97% | | 02/25/27 | | | 17,000,000 | | | | 16,490,554 | |

| LHOME Mortgage Trust, Series 2022-RTL2, Class M(c)(e) | | 8.00% | | 04/25/27 | | | 4,413,000 | | | | 4,101,565 | |

| LHOME Mortgage Trust, Series 2021-RTL1, Class A1(b)(c) | | 3.09% | | 02/25/26 | | | 643,614 | | | | 641,414 | |

| LHOME Mortgage Trust, Series 2021-RTL2, Class M(c)(e) | | 4.61% | | 01/25/24 | | | 4,750,000 | | | | 4,322,728 | |

| LHOME Mortgage Trust, Series 2021-RTL3, Class M(c)(e) | | 5.19% | | 05/25/25 | | | 9,000,000 | | | | 8,151,445 | |

| LHOME Mortgage Trust, Series 2023-RTL1, Class A1(c)(e) | | 7.87% | | 01/25/28 | | | 11,000,000 | | | | 10,959,578 | |

| LHOME Mortgage Trust, Series 2023-RTL2, Class A1(b)(c)(e) | | 8.00% | | 06/25/28 | | | 15,000,000 | | | | 14,968,920 | |

| LHOME Mortgage Trust, Series 2023-RTL3, Class A1(b)(c)(e) | | 8.00% | | 08/25/28 | | | 28,498,000 | | | | 28,434,757 | |

| LHOME Mortgage Trust, Series 2023-RTL3, Class A2(b)(c)(e) | | 9.00% | | 08/25/28 | | | 3,000,000 | | | | 2,949,032 | |

| MASTR Alternative Loan Trust, Series 2007-1, Class 2A15(b) | | 1M CME TERM SOFR + 0.48% | | 10/25/36 | | | 924,970 | | | | 241,082 | |

| MFA , Series 2021-INV1, Class A2(b)(c) | | 1.06% | | 01/25/56 | | | 568,357 | | | | 509,766 | |

| MFA , Series 2022-RTL1, Class A2(c)(e) | | 6.41% | | 03/25/24 | | | 13,000,000 | | | | 12,191,882 | |

| MFA 2023-NQM3 Trust, Series 2023-RTL1, Class A1(c)(e) | | 7.58% | | 08/25/27 | | | 7,500,000 | | | | 7,422,324 | |

| MFA , Series 2023-RTL2, Class A1(c)(e) | | 8.50% | | 04/25/26 | | | 25,486,000 | | | | 25,497,193 | |

| Morgan Stanley Resecuritization Trust, Series 2015-R4, Class 4B2(b)(c) | | 4.19% | | 08/26/47 | | | 1,753,165 | | | | 1,195,650 | |

| See Notes to Consolidated Financial Statements. | |

| 12 | www.axonicfunds.com |

| Axonic Strategic Income Fund | Consolidated Schedule of Investments |

| | October 31, 2023 |

| | | Rate | | Maturity Date | | Principal Amount | | | Value | |

| Morgan Stanley Residential Mortgage Loan Trust, Series 2023-3, Class A2(b)(c) | | 6.00% | | 09/25/53 | | $ | 7,000,000 | | | $ | 6,702,500 | |

| Morgan Stanley Residential Mortgage Loan Trust, Series 2023- NQM1, Class A1(c)(e) | | 7.28% | | 10/25/27 | | | 10,000,000 | | | | 10,007,478 | |

| New Residential Mortgage Loan Trust, Series 2022-NQM2, Class B1(b)(c) | | 3.87% | | 02/25/26 | | | 3,087,000 | | | | 1,695,769 | |

| NYMT Loan Trust, Series 2022-BPL1, Class A1(c)(e) | | 3.97% | | 11/25/27 | | | 7,545,000 | | | | 7,292,528 | |

| OBX , Series 2021-NQM1, Class A1(b)(c) | | 1.07% | | 03/25/25 | | | 7,031,890 | | | | 5,530,736 | |

| OBX , Series 2021-NQM2, Class A1(b)(c) | | 1.10% | | 05/25/61 | | | 6,199,993 | | | | 4,493,382 | |

| Point Securitization Trust, Series 2021-1, Class A2(b)(c)(g) | | 5.56% | | 02/25/52 | | | 14,000,001 | | | | 11,517,421 | |

| Progress Residential , Series 2021-SFR10, Class G(c) | | 4.86% | | 12/17/28 | | | 3,980,603 | | | | 3,168,372 | |

| Progress Residential , Series 2022-SFR1, Class G(c) | | 5.52% | | 02/17/29 | | | 2,000,000 | | | | 1,596,479 | |

| PRPM , Series 2023-NQM2, Class A2(c)(e) | | 7.00% | | 09/25/27 | | | 8,370,000 | | | | 8,306,616 | |

| RAAC, Series 2007-SP1, Class M3(b) | | 1M CME TERM SOFR + 1.61% | | 03/25/37 | | | 3,219,351 | | | | 2,359,717 | |

| RALI, Series 2006-QS2, Class 1A10(b) | | 1M CME TERM SOFR + 0.61% | | 02/25/36 | | | 1,202,316 | | | | 907,763 | |

| RALI, Series 2006-QS8, Class A4(b) | | 1M CME TERM SOFR + 0.56% | | 08/25/36 | | | 1,027,400 | | | | 742,939 | |

| RALI, Series 2007-QO5, Class A(b) | | 12M US FED + 3.12% | | 08/25/47 | | | 9,462,102 | | | | 1,603,024 | |

| Residential Asset Securitization Trust, Series 2006-R1, Class A2(b) | | 1M CME TERM SOFR + 0.51% | | 01/25/46 | | | 9,989,869 | | | | 3,651,772 | |

| Residential Asset Securitization Trust, Series 2007-A1, Class A1 | | 6.00% | | 03/25/37 | | | 3,524,933 | | | | 1,080,216 | |

| Residential Mortgage Loan Trust, Series 2020-1, Class A3(b)(c) | | 2.68% | | 01/26/60 | | | 915,153 | | | | 862,781 | |

| RMF Proprietary Issuance Trust, Series 2022-1, Class M2(b)(c) | | 3.00% | | 01/25/28 | | | 5,000,000 | | | | 3,782,000 | |

| Roc Mortgage Trust, Series 2021-RTL1, Class A1(b)(c) | | 2.49% | | 03/25/24 | | | 25,957,740 | | | | 25,566,415 | |

| Roc Mortgage Trust, Series 2021-RTL1, Class M(b)(c) | | 5.68% | | 03/25/24 | | | 6,745,000 | | | | 5,971,833 | |

| Saxon Asset Securities Trust, Series 2005-1, Class M4(b) | | 1M US L + 1.13% | | 03/25/35 | | | 730,404 | | | | 422,614 | |

| SG Residential Mortgage Trust, Series 2019-3, Class A2(b)(c) | | 2.88% | | 09/25/59 | | | 651,001 | | | | 627,135 | |

| SG Residential Mortgage Trust, Series 2019-3, Class A3(b)(c) | | 3.08% | | 09/25/59 | | | 550,297 | | | | 530,241 | |

| Specialty Underwriting & Residential Finance, Series 2005-BC1, Class B1(b) | | 1M CME TERM SOFR + 1.91% | | 12/25/35 | | | 1,986,367 | | | | 1,613,112 | |

| Spruce Hill Mortgage Loan Trust, Series 2020-SH2, Class M1(b)(c) | | 4.33% | | 06/25/55 | | | 3,520,221 | | | | 3,427,481 | |

| STAR , Series 2021-1, Class A1(b)(c) | | 1.22% | | 05/25/65 | | | 1,124,827 | | | | 963,897 | |

| Starwood Mortgage Residential Trust, Series 2019-INV1, Class A3(b)(c) | | 2.92% | | 09/27/49 | | | 9,421,834 | | | | 8,907,623 | |

| Starwood Mortgage Residential Trust, Series 2021-2, Class A2(b)(c) | | 1.17% | | 05/25/65 | | | 982,844 | | | | 869,784 | |

| Starwood Mortgage Residential Trust, Series 2021-2, Class A3(b)(c) | | 1.43% | | 05/25/65 | | | 1,198,590 | | | | 1,047,571 | |

| Starwood Mortgage Residential Trust, Series 2021-4, Class B2(b)(c) | | 4.14% | | 08/25/56 | | | 3,700,000 | | | | 2,131,422 | |

| Starwood Mortgage Residential Trust, Series 2021-4, Class A1(b)(c) | | 1.16% | | 08/25/56 | | | 8,534,420 | | | | 6,739,705 | |

| Structured Asset Mortgage Investments II Trust, Series 2007-AR1, Class 2A2(b) | | 1M CME TERM SOFR + 0.32% | | 01/25/37 | | | 1,549,988 | | | | 1,477,550 | |

| Structured Asset Mortgage Investments II Trust, Series 2007-AR2, Class 1A2(b) | | 1M CME TERM SOFR + 0.49% | | 02/25/37 | | | 4,888,531 | | | | 5,120,666 | |

| Toorak Mortgage Corp., Ltd., Series 2021-1, Class A1(c)(e) | | 2.24% | | 06/25/24 | | | 1,461,047 | | | | 1,413,493 | |

| Toorak Mortgage Corp., Ltd., Series 2021-1, Class M1(c)(e) | | 5.80% | | 06/25/24 | | | 9,500,000 | | | | 8,882,933 | |

| Toorak Mortgage Trust, Series 2022-1, Class A1(c)(e) | | 3.97% | | 03/25/29 | | | 6,506,000 | | | | 6,195,134 | |

| TVC Mortgage Trust, Series 2023-RTL1, Class A1(c)(e) | | 8.25% | | 11/25/27 | | | 12,000,000 | | | | 12,024,649 | |

| Velocity Commercial Capital Loan Trust, Series 2023-RTL1, Class A1(c)(e) | | 8.00% | | 01/25/26 | | | 2,903,000 | | | | 2,860,795 | |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | October 31, 2023 | 13 |

| Axonic Strategic Income Fund | Consolidated Schedule of Investments |

| | October 31, 2023 |

| | | Rate | | Maturity Date | | Principal Amount | | | Value | |

| Verus Securitization Trust, Series 2021-3 | | 1.05% | | 06/25/66 | | $ | 8,858,969 | | | $ | 7,005,552 | |

| Verus Securitization Trust, Series 2021-R1, Class A1(b)(c) | | 0.82% | | 10/25/63 | | | 2,238,418 | | | | 2,007,236 | |

| Verus Securitization Trust, Series 2021-R1, Class A2(b)(c) | | 1.06% | | 10/25/63 | | | 1,661,418 | | | | 1,492,107 | |

| Verus Securitization Trust, Series 2021-R1, Class A3(b)(c) | | 1.26% | | 10/25/63 | | | 3,978,617 | | | | 3,571,532 | |

| Verus Securitization Trust, Series 2021-R3, Class B2(b)(c) | | 4.07% | | 04/25/64 | | | 3,000,000 | | | | 1,875,101 | |

| Verus Securitization Trust, Series 2023-6, Class A3(c)(e) | | 7.09% | | 09/25/27 | | | 2,589,000 | | | | 2,569,043 | |

| Verus Securitization Trust, Series 2023-7, Class A3(c)(e) | | 7.42% | | 10/25/68 | | | 4,388,000 | | | | 4,386,216 | |

| Verus Securitization Trust, Series 2023-7, Class A2(c)(e) | | 7.27% | | 10/25/68 | | | 12,000,000 | | | | 11,995,324 | |

| Washington Mutual Mortgage Pass-Through Certificates, Series 2005-3, Class 1CB3(b) | | 1M CME TERM SOFR + 0.56% | | 05/25/35 | | | 1,172,555 | | | | 951,852 | |

| | | | | | | | | | | | | |

| TOTAL RESIDENTIAL MORTGAGE-BACKED SECURITIES | | | | | | | | | | | | |

| (Cost $566,257,652) | | | | | | | | | | | 525,228,544 | |

| | | | | 7-Day Yield | | Shares | | | Value | |

| SHORT TERM INVESTMENTS - COMMON SHARES (17.80%) | | | | | | | | | | | | |

| First American Government Obligations Fund | | | | 5.27% | | | 341,423,670 | | | | 341,423,670 | |

| | | | | | | | | | | | | |

| TOTAL SHORT TERM INVESTMENTS | | | | | | | | | | | | |

| (Cost $341,423,670) | | | | | | | | | | | 341,423,670 | |

| | | | | | | | | | | | | |

| TOTAL INVESTMENTS (99.98%) | | | | | | | | | | | | |

| (Cost $2,071,357,863) | | | | | | | | | | $ | 1,917,515,575 | |

| | | | | | | | | | | | | |

| Other Assets In Excess Of Liabilities (0.02%) | | | | | | | | | | | 307,796 | |

| NET ASSETS (100.00%) | | | | | | | | | | $ | 1,917,823,371 | |

| (b) | Floating or variable rate security. The Reference Rates are described below. Interest rate shown reflects the rate in effect at October 31, 2023. For securities based on a published reference rate and spread, the reference rate and spread are indicated in the description above. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

| (c) | Security exempt from registration under Rule 144A of the Securities Act of 1933. Such securities may normally be sold to qualified institutional buyers in transactions exempt from registration. The total value of Rule 144A securities amounts to $1,208,310,203, which represents 63.26% of net assets as of October 31, 2023. |

| (d) | Issued with a zero coupon. Income is recognized through the accretion of discount. |

| (e) | Step bond. Coupon changes periodically based upon a predetermined schedule. Interest rate disclosed is that which is in effect at October 31, 2023. |

| (f) | The Fund’s interest in this loan is held through a wholly-owned LLC of the Fund. |

| (g) | Interest only securities. |

Investment Abbreviations:

LIBOR - London Interbank Offered Rate

REIT - Real Estate Investment Trust

SOFR - Secured Overnight Financing Rate

FED - Federal Funds Rate

Reference Rates:

1M US L - 1 Month LIBOR as of October 31, 2023 was 5.43%

3M US L - 3 Month LIBOR as of October 31, 2023 was 5.64%

1M CME Term SOFR - 1 Month CME SOFR as of October 31, 2023 was 5.34%

| See Notes to Consolidated Financial Statements. | |

| 14 | www.axonicfunds.com |

Axonic Strategic Income Fund | Consolidated Schedule of Investments |

| | October 31, 2023 |

12M US FED - 12 Month US FED as of October 31, 2023 was 5.33%

1D US SOFR - 1 Day US SOFR as of October 31, 2023 was 5.35%

1M US SOFR - 1 Month US SOFR as of October 31, 2023 was 5.31%

30D US SOFR - 30 Day US SOFR as of October 31, 2023 was 5.31%

| See Notes to Consolidated Financial Statements. | |

| Annual Report | October 31, 2023 | 15 |

| Axonic Strategic Income Fund | Consolidated Schedule of Investments |

| | October 31, 2023 |

INTEREST RATE SWAP CONTRACTS (CENTRALLY CLEARED)

| Pay/Receive Floating Rate* | | Clearing House | | Floating Rate | | Expiration Date | | Notional Amount** | | | Currency | | Fixed Rate | | Fair Value | | | Unrealized Appreciation / (Depreciation) | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 04/07/2027 | | | 4,000,000 | | | USD | | 2.46% | | $ | 273,619 | | | $ | 273,619 | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 04/07/2024 | | | 13,000,000 | | | USD | | 2.45% | | | 173,110 | | | | 173,110 | |

| Receive | | Goldman Sachs & Co. LLC | | 3M US SOFR | | 05/25/2026 | | | 20,000,000 | | | USD | | 0.91% | | | 1,977,219 | | | | 1,977,219 | |

| Receive | | Goldman Sachs & Co. LLC | | 3M US SOFR | | 12/17/2023 | | | 50,000,000 | | | USD | | 0.87% | | | 314,415 | | | | 314,414 | |

| Receive | | Goldman Sachs & Co. LLC | | 3M US SOFR | | 08/05/2026 | | | 50,000,000 | | | USD | | 0.73% | | | 5,469,098 | | | | 5,469,098 | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 07/07/2027 | | | 5,000,000 | | | USD | | 2.54% | | | 347,482 | | | | 347,482 | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 08/05/2024 | | | 2,000,000 | | | USD | | 3.04% | | | 36,306 | | | | 36,306 | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 08/05/2025 | | | 2,000,000 | | | USD | | 2.82% | | | 74,563 | | | | 74,563 | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 04/11/2025 | | | 2,800,000 | | | USD | | 2.51% | | | 104,014 | | | | 104,014 | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 03/21/2026 | | | 9,000,000 | | | USD | | 1.99% | | | 573,561 | | | | 573,561 | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 04/19/2026 | | | 2,000,000 | | | USD | | 2.50% | | | 106,645 | | | | 106,645 | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 07/08/2024 | | | 2,000,000 | | | USD | | 2.87% | | | 35,280 | | | | 35,280 | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 08/05/2024 | | | 2,000,000 | | | USD | | 3.10% | | | 35,367 | | | | 35,367 | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 08/05/2025 | | | 2,000,000 | | | USD | | 2.87% | | | 72,934 | | | | 72,934 | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 04/14/2025 | | | 3,000,000 | | | USD | | 2.43% | | | 115,224 | | | | 115,224 | |

| Receive | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 05/13/2026 | | | 3,837,000 | | | USD | | 2.69% | | | 191,577 | | | | 191,577 | |

| | | | | | | | | | | | | | | | | $ | 9,900,413 | | | $ | 9,900,413 | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Pay | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 10/03/2033 | | | 50,000,000 | | | USD | | 4.27% | | $ | (992,898 | ) | | $ | (992,898 | ) |

| Pay | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 10/04/2033 | | | 50,000,000 | | | USD | | 4.39% | | | (521,303 | ) | | | (521,303 | ) |

| Pay | | Goldman Sachs & Co. LLC | | 1D US SOFR | | 10/16/2033 | | | 50,000,000 | | | USD | | 4.39% | | | (500,344 | ) | | | (500,344 | ) |

| Pay | | Goldman Sachs & Co. LLC | | 1M US SOFR | | 04/24/2033 | | | 35,542,920 | | | USD | | 3.78% | | | (3,402,803 | ) | | | (3,402,803 | ) |

| Pay | | Goldman Sachs & Co. LLC | | 1M US SOFR | | 04/03/2033 | | | 34,745,115 | | | USD | | 3.39% | | | (3,265,521 | ) | | | (3,265,521 | ) |

| | | | | | | | | | | | | | | | | $ | (8,682,869 | ) | | $ | (8,682,869 | ) |

| | | | | | | | | | | | | | | | | $ | 1,217,544 | | | $ | 1,217,544 | |

| * | The swap contracts with the floating rates of 1D US SOFR pay and receive interest amounts annually, while 1M US SOFR pay amounts semiannually and receive amounts quarterly, and while 3M US SOFR pay amounts monthly and receive amounts semiannually. |

| ** | The notional amount of each interest rate swap contract is stated in the currency in which the derivative is denominated. |

| See Notes to Consolidated Financial Statements. | |

| 16 | www.axonicfunds.com |

| Axonic Strategic Income Fund | Consolidated Statement of Assets and Liabilities |

| | October 31, 2023 |

| ASSETS: | | | |

| Investments, at fair value (Cost $2,071,357,863) | | $ | 1,917,515,575 | |

| Unrealized appreciation on interest rate swap contracts | | | 1,217,544 | |

| Receivable for investment securities sold | | | 313,001 | |

| Dividend receivable | | | 75,373 | |

| Interest receivable | | | 8,870,003 | |

| Receivable for shares sold | | | 8,725,904 | |

| Deposit held with broker for interest rate swap contracts | | | 10,270,674 | |

| Prepaid expenses and other assets | | | 18,500 | |

| Total Assets | | | 1,947,006,574 | |

| | | | | |

| LIABILITIES: | | | | |

| Payable for investments purchased | | | 20,032,531 | |

| Income distribution payable | | | 2,416,586 | |

| Capital shares payable | | | 4,810,640 | |

| Accrued legal and audit fees payable | | | 80,455 | |

| Due to Adviser | | | 1,321,141 | |

| Accrued fund accounting and administration fees payable | | | 329,405 | |

| Distribution and shareholder service fees payable | | | 28,115 | |

| Accrued Chief Compliance Officer fee payable | | | 4,167 | |

| Other payables and accrued expenses | | | 160,163 | |

| Total Liabilities | | | 29,183,203 | |

| Net Assets | | $ | 1,917,823,371 | |

| | | | | |

| COMPOSITION OF NET ASSETS: | | | | |

| Paid-in capital | | $ | 2,050,808,149 | |

| Total distributable earnings (accumulated deficit) | | | (132,984,778 | ) |

| Net Assets | | $ | 1,917,823,371 | |

| | | | | |

| PRICING OF SHARES: | | | | |

| Class A | | | | |

| Net Assets | | $ | 62,414,847 | |

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common share authorized) | | | 7,196,036 | |

| Net Asset Value and redemption price per share | | $ | 8.67 | |

| Institutional Class | | | | |

| Net Assets | | $ | 1,855,408,524 | |

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common share authorized) | | | 211,105,129 | |

| Net Asset Value and redemption price per share | | $ | 8.79 | |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | October 31, 2023 | 17 |

| Axonic Strategic Income Fund | Consolidated Statement of Operations |

| | For the Year Ended October 31, 2023 |

| INVESTMENT INCOME: | | | |

| Dividends | | $ | 19,389,888 | |

| Interest | | | 104,761,379 | |

| Total Investment Income | | | 124,151,267 | |

| | | | | |

| EXPENSES: | | | | |

| Advisory fees (Note 4) | | | 12,647,168 | |

| Audit and tax fees | | | 55,375 | |

| Chief Compliance Officer fee (Note 4) | | | 50,000 | |

| Custodian fees | | | 141,834 | |

| Distribution fees | | | | |

| Class A | | | 131,553 | |

| Fund accounting and administration fees (Note 4) | | | 1,033,026 | |

| Insurance expenses | | | 61,099 | |

| Interest Expense | | | 291,605 | |

| Legal fees | | | 164,314 | |

| Printing expenses | | | 119,313 | |

| Registration expenses | | | 113,391 | |

| Shareholder service fees | | | | |

| Class A | | | 78,932 | |

| Transfer agent fees (Note 4) | | | 230,319 | |

| Trustees' fees and expenses (Note 4) | | | 169,702 | |

| Other expenses | | | 99,887 | |

| Recoupment of previously waived fees (Note 4) | | | 14,304 | |

| Total expenses before waiver/reimbursement/recoupment (Note 4) | | | 15,401,822 | |

| Net expenses | | | 15,401,822 | |

| Net Investment Income | | | 108,749,445 | |

| | | | | |

| REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS: | | | | |

| Net realized loss on investments | | | (10,990,794 | ) |

| Net realized gain on interest rate swap contracts | | | 16,119,492 | |

| Net change in unrealized (depreciation) on investments | | | (10,070,358 | ) |

| Net change in unrealized (depreciation) on interest rate swap contracts | | | (21,638,755 | ) |

| Net Realized and Unrealized Loss on Investments | | | (26,580,415 | ) |

| | | | | |

| Net Increase in Net Assets from Operations | | $ | 82,169,030 | |

| See Notes to Consolidated Financial Statements. | |

| 18 | www.axonicfunds.com |

| Axonic Strategic Income Fund | Consolidated Statement of Changes in Net Assets |

| | | For the Year Ended October 31, 2023 | | | For the Year Ended October 31, 2022 | |

| FROM OPERATIONS: | | | | | | | | |

| Net investment income | | $ | 108,749,445 | | | $ | 62,500,128 | |

| Net realized gain | | | 5,128,698 | | | | 4,225,865 | |

| Net change in unrealized (depreciation) | | | (31,709,113 | ) | | | (137,005,903 | ) |

| Net Increase/(Decrease) in Net Assets from Operations | | | 82,169,030 | | | | (70,279,910 | ) |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS: | | | | | | | | |

| From distributable earnings | | | | | | | | |

| Class A | | | (3,336,744 | ) | | | (2,998,205 | ) |

| Institutional Class | | | (92,176,627 | ) | | | (95,860,121 | ) |

| Decrease in Net Assets from Distributions to Shareholders | | | (95,513,371 | ) | | | (98,858,326 | ) |

| | | | | | | | | |

| CAPITAL SHARE TRANSACTIONS: | | | | | | | | |

| Class A | | | | | | | | |

| Proceeds from sale of shares of beneficial interest | | | 37,021,653 | | | | 34,255,131 | |

| Distributions reinvested | | | 3,053,488 | | | | 2,672,358 | |

| Disbursements for redemption of shares of beneficial interest | | | (21,606,067 | ) | | | (27,285,729 | ) |

| Institutional Class | | | | | | | | |

| Proceeds from sale of shares of beneficial interest | | | 1,115,039,459 | | | | 722,865,452 | |

| Distributions reinvested | | | 67,278,841 | | | | 68,313,060 | |

| Disbursements for redemption of shares of beneficial interest | | | (627,928,046 | ) | | | (620,328,268 | ) |

| Net Increase from Capital Share Transactions | | | 572,859,328 | | | | 180,492,004 | |

| Net Increase in Net Assets | | | 559,514,987 | | | | 11,353,768 | |

| | | | | | | | | |

| NET ASSETS: | | | | | | | | |

| Beginning of period | | | 1,358,308,384 | | | | 1,346,954,616 | |

| End of period | | $ | 1,917,823,371 | | | $ | 1,358,308,384 | |

| | | | | | | | | |

| OTHER INFORMATION: | | | | | | | | |

| CAPITAL SHARE TRANSACTIONS: | | | | | | | | |

| Class A | | | | | | | | |

| Beginning shares | | | 5,072,634 | | | | 4,067,120 | |

| Issued | | | 4,257,979 | | | | 3,679,860 | |

| Distributions reinvested | | | 351,474 | | | | 285,277 | |

| Redeemed | | | (2,486,051 | ) | | | (2,959,623 | ) |

| Institutional Class | | | | | | | | |

| Beginning shares | | | 148,201,874 | | | | 130,781,627 | |

| Issued | | | 126,750,994 | | | | 76,296,995 | |

| Distributions reinvested | | | 7,657,616 | | | | 7,217,982 | |

| Redeemed | | | (71,505,355 | ) | | | (66,094,730 | ) |

| Net increase in capital shares | | | 65,026,657 | | | | 18,425,761 | |

| Ending shares | | | 218,301,165 | | | | 153,274,508 | |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | October 31, 2023 | 19 |

| Axonic Strategic Income Fund Class A | Consolidated Financial Highlights |

| | For a Share Outstanding Throughout the Period Presented |

| | | For the Year Ended October 31, 2023 | | | For the Year Ended October 31, 2022 | | | For the Year Ended October 31, 2021 | | | For the Period July 17, 2020 (Commencement of Operations) to October 31, 2020 | |

| OPERATING PERFORMANCE: | | | | | | | | | | | | | | | | |

| Net asset value - beginning of period | | $ | 8.78 | | | $ | 9.94 | | | $ | 9.68 | | | $ | 9.55 | |

| INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | | | | | | | | | | | | | | | | |

| Net investment income(a) | | | 0.60 | | | | 0.37 | | | | 0.44 | | | | 0.06 | |

| Net realized and unrealized gain/(loss) on investments | | | (0.16 | ) | | | (0.90 | ) | | | 0.30 | (b) | | | 0.15 | (b) |

| Total Income/(Loss) from Investment Operations | | | 0.44 | | | | (0.53 | ) | | | 0.74 | | | | 0.21 | |

| | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS: | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.53 | ) | | | (0.43 | ) | | | (0.43 | ) | | | (0.08 | ) |

| From net realized gains | | | (0.02 | ) | | | (0.20 | ) | | | (0.05 | ) | | | – | |

| Total Distributions to Shareholders | | | (0.55 | ) | | | (0.63 | ) | | | (0.48 | ) | | | (0.08 | ) |

| | | | | | | | | | | | | | | | | |

| Net asset value - end of period | | $ | 8.67 | | | $ | 8.78 | | | $ | 9.94 | | | $ | 9.68 | |

| | | | | | | | | | | | | | | | | |

| Total Investment Return - Net Asset Value(c) | | | 5.25 | %(d) | | | (5.29 | %)(d) | | | 7.85 | %(d) | | | 2.17 | %(d)(e) |

| | | | | | | | | | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA: | | | | | | | | | | | | | | | | |

| Net assets end of period (000s) | | $ | 62,415 | | | $ | 44,534 | | | $ | 40,414 | | | $ | 22,495 | |

| Ratio of expenses to average net assets excluding reimbursement/recoupment(f) | | | 1.42 | % | | | 1.39 | % | | | 1.60 | % | | | 1.84 | %(g) |

| Ratio of expenses to average net assets including reimbursement/recoupment(f) | | | 1.44 | % | | | 1.50 | % | | | 1.50 | % | | | 1.50 | %(g) |

| Ratio of net investment income to average net assets(f) | | | 6.90 | % | | | 3.93 | % | | | 4.40 | % | | | 2.28 | %(g) |

| Portfolio turnover rate | | | 38 | % | | | 32 | % | | | 66 | % | | | 54 | %(e) |

| (a) | Calculated using average shares method. |

| (b) | Realized and unrealized gains and losses per share in this caption are balancing amounts necessary to reconcile the change in net asset value per share for the period and may not reconcile with the aggregate gains and losses in the Consolidated Statement of Operations due to share transactions for the period. |

| (c) | During periods in which certain expenses were reimbursed, total returns would have been lower. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns shown exclude applicable sales charges. |

| (d) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and, consequently, the net asset values for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |