UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-23703 |

| MassMutual Advantage Funds | |

| (Exact name of registrant as specified in charter) | |

| 1295 State Street, Springfield, MA | 01111 |

| (Address of principal executive offices) | (Zip code) |

| Andrea Anastasio |

| 1295 State Street, Springfield, MA 01111 |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (413) 744-1000 |

| Date of fiscal year end: | 9/30/2023 | �� |

| Date of reporting period: | 9/30/2023 |

Item 1. Reports to Stockholders.

| (a) | The Report to Stockholders is attached herewith. |

Table of Contents | |

This material must be preceded or accompanied by a current prospectus (or summary prospectus, if available) for the applicable MassMutual Funds. Investors should consider a Fund’s investment objective, risks, and charges and expenses carefully before investing. This and other information about the investment company is available in the prospectus (or summary prospectus, if available). Read it carefully before investing.

[THIS PAGE INTENTIONALLY LEFT BLANK]

MassMutual Funds Annual Report – Economic and Market Overview (Unaudited) |

September 30, 2023

Global markets continue to reward retirement investors

During the fiscal year ended September 30, 2023, U.S. stocks were up over 21%, in a market environment where the U.S. Federal Reserve (the “Fed”) raised interest rates by nearly 3% in an effort to combat heightened inflation by curtailing economic activity. Stocks in foreign developed markets and emerging markets also experienced significant gains during the fiscal year, aided by a weaker U.S. dollar. Global stock gains during the period were driven by a resilient consumer, surprisingly strong economic activity, strong suggestions of a generative artificial intelligence (“AI”) revolution, and investors’ improving earnings expectations. U.S. bond investors experienced slightly positive returns in the rising interest rate environment, fueled by aggressive interest rate hikes by the Fed that were aimed at reducing demand-driven inflationary pressures.

Market highlights

● | For the reporting period from October 1, 2022 through September 30, 2023, U.S. stocks were up over 21%, in a market environment where economic activity remained strong, despite the Fed continuing to raise interest rates in an effort to combat high inflation. |

● | In the fourth quarter of 2022, investors experienced a stock market rally, as fears generally lessened regarding high inflation, high interest rates, high energy prices, and a global recession. |

● | The first quarter of 2023 was a continuation of the prior quarter, aided by the excitement around generative AI. Investors remained generally enthusiastic, notwithstanding a relatively unexpected banking crisis in March, which resulted in the takeover of certain U.S. regional banks by U.S. regulators and the bailout of Credit Suisse Group by the Swiss government. |

● | In the second quarter of 2023, global stocks exhibited strength thanks in part to a resilient U.S. economy, receding inflationary pressures, banking sector stability, and the resolution of the debt ceiling crisis. |

● | The third quarter of 2023 was difficult for global stocks and bonds, as investors grew increasingly concerned over inflation, a possible U.S. government shutdown, and higher prolonged interest rates from the Fed. |

● | Foreign stocks in developed markets and emerging markets also experienced strong gains in the fiscal year, aided by falling energy costs, a resilient consumer, and the weakening of the U.S. dollar. |

● | U.S. bond investors experienced slightly positive returns in the rising interest rate environment, fueled by aggressive Fed interest rate hikes aimed at reducing demand-driven inflationary pressures. |

Market environment

For the fiscal year beginning on October 1, 2022, global stock investors experienced significant gains. During this period, U.S. stock prices rose sharply in response, with the S&P 500 Index® (“S&P 500”)1 entering bull market territory after rising more than 20% from its previous highs. Investors breathed a sigh of relief as the possibility of a recession lessened in the face of robust economic activity and falling inflation during the period. Consumer sentiment rose sharply, up 19.4% in the period,2 aided by lower inflation, low unemployment, and positive wage growth. In MassMutual’s view, the strong economic growth may be unsustainable, as more Americans are borrowing to make ends meet, resulting in consumer loan levels at record highs, having increased by 5.8% year-over-year.3

1 The S&P 500 Index measures the performance of 500 widely held stocks in the U.S. equity market. Standard and Poor’s chooses member companies for the Index based on market size, liquidity, and industry group representation. Included are the stocks of industrial, financial, utility, and transportation companies. Since mid-1989, this composition has been more flexible and the number of issues in each sector has varied. The Index is market capitalization-weighted. The Index does not reflect any deduction for fees, expenses, or taxes and cannot be purchased directly by investors.

2 August 2023, University of Michigan: Consumer Sentiment (UMCSENT), retrieved from FRED, Federal Reserve Bank of St. Louis;

https://fred.stlouisfed.org/series/UMCSENT, October 5, 2023.

3 August 2023, Board of Governors of the Federal Reserve System (US), Consumer Loans, All Commercial Banks [CONSUMER], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/CONSUMER, October 5, 2023.

1

MassMutual Funds Annual Report – Economic and Market Overview (Unaudited) (Continued) |

As a result, the broad-market S&P 500 rose 21.62% for the period. The technology-heavy NASDAQ Composite Index4 performed even better, rising 26.11% for the period. The more economically sensitive Dow Jones Industrial AverageSM5 was up 19.18% for the period. During the reporting period, small-cap stocks underperformed their larger-cap peers, while growth stocks outperformed their value brethren. The information technology and communication services sectors were each up by 35% or more for the period. The utilities sector was the weakest performer for the fiscal year, down 7.02% over the period, hurt by the sharp rise in interest rates that made the stock dividend yields less attractive. The real estate sector also ended the period in the red, declining 1.84%.

Developed international markets, as measured by the MSCI EAFE® Index,6 outperformed their domestic peers, ending the fiscal year up 25.65%. Emerging-market stocks, as measured by the MSCI Emerging Markets Index,7 also rose sharply, ending up 11.70% for the period. Investors shifted back into developed international and emerging-market stocks during the period in response to lower-than-expected energy costs, a more resilient consumer, and stronger-than-expected economic activity.

Bond yields rose sharply during the fiscal year, with the 10-year U.S. Treasury bond yield rising from 3.83% on October 1, 2022 to close the period at 4.59%. During the period, rising yields produced falling bond prices, and bond index returns suffered. The Bloomberg U.S. Aggregate Bond Index8 ended the period up 0.64%. Investment-grade corporate bonds fared better. The Bloomberg U.S. Corporate Bond Index,9 which tracks investment-grade corporate bonds, ended the period with a 3.65% gain. The Bloomberg U.S. Corporate High-Yield Bond Index10 also ended the period higher, rising 10.28%.

Review and maintain your strategy

At MassMutual, looking out for each other isn’t just a nice idea; it’s how we’ve done business for more than 170 years. Since 1851, we’ve had a single purpose: to help people secure their future and protect the ones they love. While the current market volatility, including the reality of market sell-offs, can test an investor’s mettle, we’d like to remind you that, as a retirement investor, it’s important to maintain perspective and have realistic expectations about the future performance of your investment accounts. As described in this report, financial markets can reverse suddenly, with little or no notice. That’s why we continue to believe that retirement investors should create and maintain a plan that focuses on their goals, how long they have to invest, and

4 The NASDAQ Composite Index measures the performance of all domestic and international based common type stocks listed on the NASDAQ Stock Market. It includes common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests, and tracking stocks. The Index is market capitalization-weighted. The Index does not reflect any deduction for fees, expenses, or taxes and cannot be purchased directly by investors.

5 The Dow Jones Industrial Average Index measures the performance of stocks of 30 U.S. blue-chip companies covering all industries with the exception of transportation and utilities. It is price-weighted. The Index does not reflect any deduction for fees, expenses, or taxes and cannot be purchased directly by investors.

6 The MSCI EAFE Index measures the performance of the large- and mid-cap segments of developed markets, excluding the U.S. and Canada equity securities. It is free float-adjusted market-capitalization weighted. The Index does not reflect any deduction for fees or expenses and cannot be purchased directly by investors.

7 The MSCI Emerging Markets Index measures the performance of the large- and mid-cap segments of emerging market equity securities. It is free float-adjusted market-capitalization weighted. The Index does not reflect any deduction for fees or expenses and cannot be purchased directly by investors.

8 The Bloomberg U.S. Aggregate Bond Index measures the performance of investment grade, U.S. dollar-denominated, fixed-rate taxable bond market securities, including Treasuries, government-related and corporate securities, mortgage-backed securities (MBS) (agency fixed-rate and hybrid ARM pass-throughs), asset-backed securities (ABS), and commercial mortgage-backed securities (CMBS). It rolls up into other Bloomberg flagship indexes, such as the multi-currency Global Aggregate Index and the U.S. Universal Index, which includes high yield and emerging markets debt. The Index does not reflect any deduction for fees, expenses, or taxes and cannot be purchased directly by investors.

9 The Bloomberg U.S. Corporate Bond Index measures the performance of the investment grade, U.S. dollar-denominated, fixed-rate, taxable corporate bond market. It includes U.S. dollar-denominated securities publicly issued by U.S. and non-U.S. industrial, utility, and financial issuers that meet specified maturity, liquidity, and quality requirements. The Index does not reflect any deduction for fees, expenses, or taxes and cannot be purchased directly by investors.

10 The Bloomberg U.S. Corporate High-Yield Bond Index measures the performance of U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bonds, including corporate bonds, fixed-rate bullet, putable, and callable bonds, SEC Rule 144A securities, original issue zeros, pay-in-kind bonds, fixed-rate and fixed-to-floating capital securities. The Index does not reflect any deduction for fees, expenses, or taxes and cannot be purchased directly by investors.

2

MassMutual Funds Annual Report – Economic and Market Overview (Unaudited) (Continued) |

how comfortable they are with market volatility. Our multi-managed and sub-advised mutual funds tap into the deep expertise of seasoned asset managers who are committed to helping long-term investors prepare for retirement – in all market conditions. As always, we recommend that you work with a personal financial professional, who can help you define an investment strategy that aligns with your comfort level with respect to market volatility, how long you have to save and invest, and your specific financial goals. Thank you for your confidence in MassMutual.

The information provided is the opinion of MML Investment Advisers, LLC (“MML Advisers”) and is subject to change without notice. It is not to be construed as tax, legal, or investment advice. Of course, past performance does not guarantee future results.

Underwriter: MML Distributors, LLC (MMLD), Member FINRA and SIPC (www.FINRA.org and www.SIPC.org), 1295 State Street, Springfield, MA 01111-0001. Investment advisory services are provided to the Funds by MML Advisers. MMLD and MML Advisers are subsidiaries of MassMutual.

©2023 Massachusetts Mutual Life Insurance Company (MassMutual®), Springfield, MA 01111-0001. All rights reserved. www.MassMutual.com.

3

MassMutual Global Floating Rate Fund – Portfolio Manager Report (Unaudited) |

What is the investment approach of MassMutual Global Floating Rate Fund, and who is the Fund’s subadviser?

This Fund seeks a high level of current income with preservation of capital as a secondary goal. Under normal circumstances, the Fund invests at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in income-producing floating rate debt securities, consisting of floating rate loans, bonds, and notes, issued primarily by North American and Western European companies. The Fund’s subadviser is Barings LLC (Barings). In addition, Baring International Investment Limited serves as a sub-subadviser for the Fund.

How did the Fund perform during the 12 months ended September 30, 2023?

The Fund’s Class I shares returned 13.74%, outperforming the 12.47% return of the Credit Suisse Leveraged Loan Index* (the “benchmark”), which is designed to mirror the investable universe of the U.S. dollar-denominated leveraged loan market. The Fund underperformed the 16.44% return of the Credit Suisse Western European Leveraged Loan Index, which is designed to mirror the investable universe of the Western European leveraged loan market, with loans denominated in U.S. and Western European currencies. Finally, the Fund outperformed the 13.35% return of the Custom Global Loan Index, which comprises the market-capitalization weighted average of the Credit Suisse Leveraged Loan Index and the Credit Suisse Western European Leveraged Loan Index.

* Effective February 1, 2023, the Credit Suisse Leveraged Loan Index became the Fund’s primary performance benchmark index because it is an appropriate broad-based securities market index. Information is also provided for the Credit Suisse Western European Leveraged Loan Index and the Custom Global Loan Index, which MML Advisers believes may provide a more useful comparison.

For a discussion on the economic and market environment during the 12-month period ended September 30, 2023, please see the Economic and Market Overview, beginning on page 1.

Subadviser discussion of factors that contributed to the Fund’s performance

For the fiscal year ended September 30, 2023, a combination of modest price appreciation and the return from interest income was the primary driver of performance for the Fund and the benchmark. Since the Fund primarily invests in senior secured loans that have a floating-rate coupon, the return from interest income materially increased during the reporting period, compared to recent fiscal years, due to the increase in short-term base rates. As such, interest income was a primary driver of the elevated total return. Sentiment in the secondary market was generally positive for the asset class, as there was only one month during the reporting period in which the Fund had a negative monthly total return. Though the Fund and the loan market were not immune to the negative sentiment caused by the uncertainty in the regional banking sector during the reporting period, the Fund and the loan market did not have direct exposure to the affected companies, and therefore trading weakness in that respect was limited in the loan market.

To provide some context to relative performance, the Fund’s holdings across rating categories outperformed during the period, with the highest positive impact to relative performance coming from the single-B rating category, as that was the category the Fund had the largest exposure to during the period. Within industry sectors, most of the outperformance was the result of outperformance by the Fund’s holdings within sectors rather than relative sector positioning. Though spread across a wider range of sectors, outperforming sectors included the information technology, health care, and leisure sectors, which included areas of the market that underperformed the prior fiscal year when sentiment was weaker. Partially detracting from relative results was underperformance within the diversified media and manufacturing sectors, as well as the Fund’s cash allocation, given the strong performance for the market during the period. Finally, the Fund typically invests across the North American and European senior secured loan markets. During the period, the Fund’s North American holdings led the outperformance.

At a Fund holdings level, the Fund’s top contributors to total return were Asurion, a provider of technology protection services; Virgin Media, a broadband services provider; and Quest Software, an enterprise software solutions provider. The Fund’s top detractors from total return were CWT, a business travel company; Technicolor, a creative and technology provider for the media industry; and Team Health, a provider of outsourced physician staffing and administrative services.

4

MassMutual Global Floating Rate Fund – Portfolio Manager Report (Unaudited) (Continued) |

Derivatives are securities that derive their value from the performance of one or more other investments and take the form of a contract between two or more parties. Derivatives can be used for hedging, speculation, or both. During the reporting period, the Fund’s derivative usage was limited to currency forwards used to passively hedge currency exposure for non-U.S. dollar-denominated debt back to the Fund’s base currency, which is the U.S. dollar, and did not have a material impact on the Fund’s performance.

Subadviser outlook

Barings observes that the senior secured loan market has been a beneficiary of the increases in short-term interest rates in recent years by exhibiting less price sensitivity to rate increases than fixed-rate markets and a higher contribution to total return from the elevated coupon levels. This provided positive performance for the asset class over the past year. However, in Fund management’s view, it is also supportive of the relative value for the senior secured loan market into the new year, as yield levels remain elevated driven by the higher coupons.

From a fundamental perspective, default activity during the reporting period increased from the prior period, as companies navigated the impacts from higher inflation and financing costs. However, in Fund management’s view, default rates in the coming fiscal year are expected to remain manageable and near longer-term averages, as many borrowers from the market have been focused on proactively addressing their capital needs and utilizing a supportive primary market to refinance their debt and push out maturities. As a result, Barings continues to view relative value for the market as compelling through a combination of elevated yields and manageable defaults, although as some uncertainty remains, a credit-intensive approach will, in Fund management’s opinion, be critical in the months ahead.

MassMutual Global Floating Rate Fund | |

Bank Loans | 87.7% |

Corporate Debt | 3.9% |

Common Stock | 1.0% |

Warrants | 0.0% |

Total Long-Term Investments | 92.6% |

Short-Term Investments and Other Assets and Liabilities | 7.4% |

Net Assets | 100.0% |

5

MassMutual Global Floating Rate Fund – Portfolio Manager Report (Unaudited) (Continued) |

GROWTH OF $10,000 INVESTMENT - Class I

The graph above illustrates a representative class of the Fund’s historical performance+ for the past 10 fiscal years or since inception (for Funds lacking 10-year records) in comparison to its benchmark index, as well as one or more additional indexes, if applicable. The performance of other share classes will be greater than or less than the class depicted above.

Average Annual Total Returns+ (for the periods ended 09/30/2023) | ||||

| Inception Date | 1 Year | 5 Years | 10 Years |

Class I | 9/16/2013 | 13.74% | 3.92% | 4.08% |

Class Y | 9/16/2013 | 13.73% | 3.90% | 4.06% |

Class L | 9/16/2013 | 13.61% | 3.65% | 3.79% |

Class L (sales load deducted)* | 9/16/2013 | 9.23% | 3.02% | 3.48% |

Class C | 9/16/2013 | 12.77% | 2.89% | 3.04% |

Class C (CDSC fees deducted)* | 9/16/2013 | 11.77% | 2.89% | 3.04% |

Credit Suisse Leveraged Loan Index# | 12.47% | 4.31% | 4.33% | |

Credit Suisse Western European Leveraged Loan Index | 16.44% | 5.41% | 5.26% | |

Custom Global Loan Index | 13.35% | 4.55% | 4.51% | |

# Benchmark

* Class L (sales load deducted) returns include the 3.00% maximum sales charge and Class C (CDSC fees deducted) returns include the 1.00% maximum contingent deferred sales charge for the first 12 months shown.

+ The Fund is the successor to the Barings Global Floating Rate Fund (the “Predecessor Fund”), a mutual fund with substantially similar investment objectives, policies, and restrictions, as a result of the reorganization of the Predecessor Fund into the Fund on December 13, 2021. The performance provided is that of the Predecessor Fund prior to December 13, 2021, and is that of the Fund after December 13, 2021. Performance shown for Class L shares prior to December 13, 2021 reflects the performance of Class A shares of the Predecessor Fund.

Generally accepted accounting principles require adjustments to be made to the net assets of the Fund at period end for financial reporting purposes only, and as such, the total return based on the unadjusted net asset value per share may differ from the total return reported in the financial highlights.

Performance results in the graph and table are shown both with and without the imposition of the maximum applicable sales charge (if applicable) and reflect the percentage change in net asset value, including reinvestment of dividends and capital gains distributions. Investors should note that the Fund is a professionally managed mutual fund, while the index or indexes shown above are unmanaged, cannot be purchased directly, and, with the exception of any peer group index, do not incur expenses.

Performance data quoted in the graph and table represents past performance; past performance is not predictive of future results. The investment return and principal value of shares of the Fund fluctuate, so your shares, when sold, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. The performance shown does not reflect the deduction of taxes, if any, that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data current to the most recent month end may be obtained by calling 1-888-309-3539.

Investors should read the Fund’s prospectus with regard to the Fund’s investment objectives, risks, and charges and expenses in conjunction with these financial statements. Employee retirement benefit plans that invest plan assets in the Separate Investment Accounts (SIAs) may be subject to certain charges as set forth in their respective Plan Documents. Total return figures would be lower for the periods presented if they reflected these charges.

6

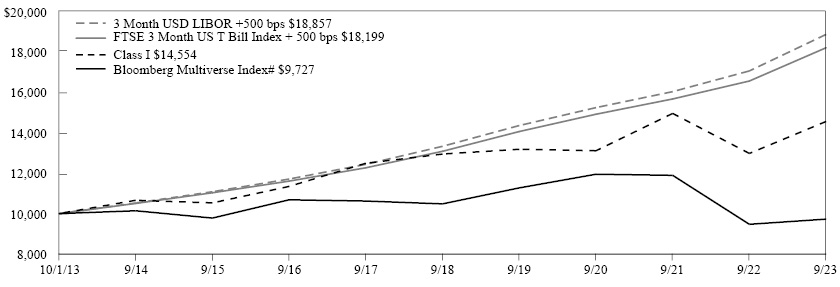

MassMutual Global Credit Income Opportunities Fund – Portfolio Manager Report (Unaudited) |

What is the investment approach of MassMutual Global Credit Income Opportunities Fund, and who is the Fund’s subadviser?

This Fund seeks an absolute return, primarily through current income and secondarily through capital appreciation. Under normal circumstances, the Fund invests at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in debt instruments (consisting of loans, bonds, and notes). The Fund may invest in a wide range of debt instruments of issuers based in U.S. and non-U.S. markets, including emerging markets, as well as over-the-counter and exchange-traded derivatives. The Fund’s subadviser is Barings LLC (Barings). In addition, Baring International Investment Limited serves as a sub-subadviser for the Fund.

How did the Fund perform during the 12 months ended September 30, 2023?

The Fund’s Class I shares returned 12.17%, outperforming, by a wide margin, the 2.69% return of the Bloomberg Multiverse Index* (the “benchmark”), which measures the performance of bonds in the global fixed-income bond market. It represents the union of the Global Aggregate Index and the Global High-Yield Index and captures investment grade and high yield securities in all eligible currencies. The Fund outperformed, by a wide margin, the 10.58% return** of the 3 Month USD LIBOR (London Interbank Offered Rate), which measures the performance of the U.S. dollar-denominated ICE LIBOR rate with a maturity of 3 months. LIBOR indicates the interest rate that banks pay when they borrow from each other on an unsecured basis. It is used to determine payments made under derivatives by a wide range of counterparties including small businesses, large financial institutions, and public authorities. The Fund outperformed, by a wide margin, the 9.94% return*** of the FTSE 3 Month US T Bill Index****, which measures the performance of the last three 3-month Treasury bill month-end rates.

* Effective July 1, 2023, the Bloomberg Multiverse Index became the Fund’s performance benchmark index rather than the 3 Month USD LIBOR plus 500 basis points (5.00%) because LIBOR expired on June 30, 2023 and the Bloomberg Multiverse Index represents an appropriate broad-based securities market index for the Fund.

** Return shown for the 3 Month USD LIBOR reflects the Index’s return for the reporting period, plus 500 basis points (5.00%). From July 1, 2023-September 30, 2023, the 3 Month USD LIBOR was calculated using the Synthetic 3 Month USD LIBOR of CME Term Secured Overnight Financing Rate plus the International Swaps and Derivatives Association/Alternative Reference Rates Committee Spread Adjustment of 26 basis points.

*** Return shown for the FTSE 3 Month US T Bill Index reflects the Index’s return for the reporting period, plus 500 basis points (5.00%).

**** Effective July 1, 2023, the FTSE 3 Month US T Bill Index plus 500 basis points (5.00%) became the Fund’s performance supplemental index because the FTSE 3 Month US T Bill Index plus 500 basis points (5.00%) closely represents the Fund’s investment strategy.

For a discussion on the economic and market environment during the 12-month period ended September 30, 2023, please see the Economic and Market Overview, beginning on page 1.

Subadviser discussion of factors that contributed to the Fund’s performance

For the fiscal year ended September 30, 2023, a combination of modest price appreciation and the return from interest income was the primary driver of performance for the Fund. The Fund held a meaningful exposure to floating-rate assets, including senior secured loans and collateralized loan obligations (CLOs). As these asset classes have floating-rate coupons, the return from interest income materially increased during the reporting period, compared to recent fiscal years, due to the increase in short-term base rates. As a result, holdings in these markets outperformed the Fund’s holdings in the fixed-rate high yield bond market overall.

The top-performing asset class for the Fund was its CLO holdings, although as the Fund had a smaller allocation to this market during the reporting period, its senior secured loan holdings had a larger contribution to total return.

7

MassMutual Global Credit Income Opportunities Fund – Portfolio Manager Report (Unaudited) (Continued) |

By region, the Fund’s North American senior secured loan holdings outperformed its loan holdings in Europe. Within high yield bonds, the Fund’s European high yield bond holdings outperformed their counterparts in North America and both outperformed holdings in hard currency corporate credits in Asia due to underperformance in the housing sector in China. Despite the detraction from that sector in China, for the Fund as a whole, the housing sector was a marginally positive contributor to total return, with other credits offsetting the detraction.

Looking elsewhere, most sectors in which the Fund was invested during the period finished the period with a positive total return. Top-contributing sectors included the information technology, health care, and energy sectors, with each including some areas of the sector or credits also experiencing some price recovery in addition to income. Finally, given the positive total return across the markets that the Fund invested in, the Fund’s cash exposure was a modest detractor from relative performance.

At the Fund holdings level, the Fund’s top contributors to total return were Global Aircraft Leasing, a global aircraft lessor; Quest Software, an enterprise software solutions provider; and Tullow Oil, a United Kingdom-based exploration and production company. The Fund’s top detractors from total return were Shimao Group Holdings, a China-based real estate development company; Vue Cinemas, a European cinema chain; and Technicolor, a creative and technology provider for the media industry.

Derivatives are securities that derive their value from the performance of one or more other investments and take the form of a contract between two or more parties. Derivatives can be used for hedging, speculation, or both. During the reporting period, derivative usage was primarily limited to currency forwards used to passively hedge currency exposure for non-U.S. dollar-denominated debt back to the Fund’s base currency, which is the U.S. dollar, and did not have a material impact on the Fund’s performance. Other derivative usage was limited to a small position in a put option for hedging purposes and did not have a material impact on the Fund’s performance during the period.

Subadviser outlook

Barings notes that the aftermath of central bank rate hikes over and before the reporting period includes, but is not limited to, elevated yields across credit markets. For fixed-rate markets, such as high yield bonds, the increase in yields has been driven by discounted trading levels, whereas for floating-rate markets, such as senior secured loans and CLOs, it has been the increase in floating-rate coupons. Though high yield credit markets in general performed well during the reporting period, the elevated yields, in Fund management’s view, provide a compelling argument for relative value into the new year. From a fundamental perspective, default activity during the reporting period has increased from the prior period, with slightly higher activity in the senior secured loan market versus the high yield bond market due to the higher rating profile of the high yield bond market and fixed financing costs. However, in Fund management’s view, the volume of defaults in both markets is expected to remain manageable, as high yield borrowers have been focused on proactively addressing their capital needs and utilizing a supportive primary market to refinance their debt to push out maturities. Therefore, while there remains some uncertainty across global economies, Barings believes the relative value remains attractive through a combination of higher yields and manageable defaults, though Fund management views a credit-intensive approach as being critical to navigating the months ahead.

MassMutual Global Credit Income | |

Corporate Debt | 41.5% |

Bank Loans | 41.0% |

Non-U.S. Government Agency Obligations | 9.4% |

Common Stock | 0.5% |

Warrants | 0.0% |

Total Long-Term Investments | 92.4% |

Short-Term Investments and Other Assets and Liabilities | 7.6% |

Net Assets | 100.0% |

8

MassMutual Global Credit Income Opportunities Fund – Portfolio Manager Report (Unaudited) (Continued) |

GROWTH OF $10,000 INVESTMENT - Class I

The graph above illustrates a representative class of the Fund’s historical performance+ for the past 10 fiscal years or since inception (for Funds lacking 10-year records) in comparison to its benchmark index, as well as one or more additional indexes, if applicable. The performance of other share classes will be greater than or less than the class depicted above.

Average Annual Total Returns+ (for the periods ended 09/30/2023) | ||||

| Inception Date | 1 Year | 5 Years | 10 Years |

Class I | 9/16/2013 | 12.17% | 2.37% | 3.82% |

Class Y | 9/16/2013 | 12.12% | 2.35% | 3.81% |

Class L | 9/16/2013 | 11.82% | 2.10% | 3.56% |

Class L (sales load deducted)* | 9/16/2013 | 6.39% | 1.27% | 3.16% |

Class C | 9/16/2013 | 10.95% | 1.34% | 2.78% |

Class C (CDSC fees deducted)* | 9/16/2013 | 9.95% | 1.34% | 2.78% |

Bloomberg Multiverse Index# | 2.69% | -1.48% | -0.28% | |

3 Month USD LIBOR +500 bps | 10.58% | 7.19% | 6.55% | |

FTSE 3 Month US T Bill Index + 500 bps | 9.94% | 6.83% | 6.17% | |

# Benchmark

* Class L (sales load deducted) returns include the 4.00% maximum sales charge and Class C (CDSC fees deducted) returns include the 1.00% maximum contingent deferred sales charge for the first 12 months shown.

+ The Fund is the successor to the Barings Global Credit Income Opportunities Fund (the “Predecessor Fund”), a mutual fund with substantially similar investment objectives, policies, and restrictions, as a result of the reorganization of the Predecessor Fund into the Fund on December 13, 2021. The performance provided is that of the Predecessor Fund prior to December 13, 2021, and is that of the Fund after December 13, 2021. Performance shown for Class L shares prior to December 13, 2021 reflects the performance of Class A shares of the Predecessor Fund.

Generally accepted accounting principles require adjustments to be made to the net assets of the Fund at period end for financial reporting purposes only, and as such, the total return based on the unadjusted net asset value per share may differ from the total return reported in the financial highlights.

Performance results in the graph and table are shown both with and without the imposition of the maximum applicable sales charge (if applicable) and reflect the percentage change in net asset value, including reinvestment of dividends and capital gains distributions. Investors should note that the Fund is a professionally managed mutual fund, while the index or indexes shown above are unmanaged, cannot be purchased directly, and, with the exception of any peer group index, do not incur expenses.

Performance data quoted in the graph and table represents past performance; past performance is not predictive of future results. The investment return and principal value of shares of the Fund fluctuate, so your shares, when sold, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. The performance shown does not reflect the deduction of taxes, if any, that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data current to the most recent month end may be obtained by calling 1-888-309-3539.

Investors should read the Fund’s prospectus with regard to the Fund’s investment objectives, risks, and charges and expenses in conjunction with these financial statements. Employee retirement benefit plans that invest plan assets in the Separate Investment Accounts (SIAs) may be subject to certain charges as set forth in their respective Plan Documents. Total return figures would be lower for the periods presented if they reflected these charges.

9

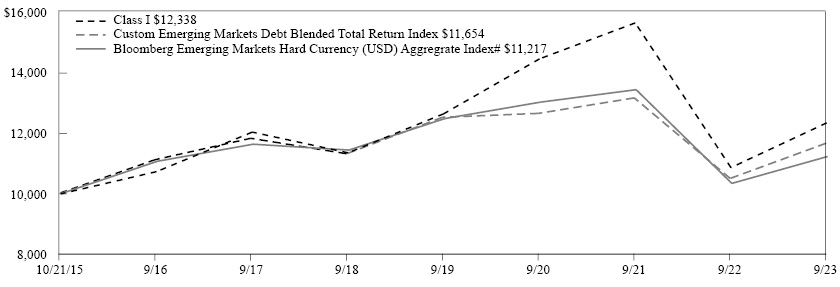

MassMutual Emerging Markets Debt Blended Total Return Fund – Portfolio Manager Report (Unaudited) |

What is the investment approach of MassMutual Emerging Markets Debt Blended Total Return Fund, and who is the Fund’s subadviser?

This Fund seeks to achieve maximum total return, consistent with preservation of capital and prudent investment management, through high current income generation and, where appropriate, capital appreciation. The Fund invests in debt securities, derivatives, and other instruments that are economically tied to emerging market countries or countries with relatively low gross national product per capita and with the potential for rapid economic growth. Under normal circumstances, the Fund will invest at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in (i) securities denominated in currencies of the emerging market countries, (ii) fixed income securities or debt instruments issued by emerging market entities or sovereign nations, and/or (iii) debt instruments denominated in or based on the currencies, interest rates, or issues of emerging market countries. The Fund focuses its investments in Asia, Africa, the Middle East, Latin America, and the developing countries of Europe. The Fund’s subadviser is Barings LLC (Barings). In addition, Baring International Investment Limited serves as a sub-subadviser for the Fund.

How did the Fund perform during the 12 months ended September 30, 2023?

The Fund’s Class I shares returned 13.57%, outperforming the 8.57% return of the Bloomberg Emerging Markets Hard Currency (USD) Aggregate Index* (the “benchmark”), which measures the performance of USD, EUR, and GBP-denominated debt from sovereign, quasi-sovereign, and corporate Emerging Markets issuers. Country eligibility and classification as Emerging Markets is rules-based and reviewed annually using the World Bank income group and International Monetary Fund country classifications. The Fund outperformed the 11.06% return of the Custom Emerging Markets Debt Blended Total Return Index, which is a blend of 50% JPMorgan Government Bond Index – Emerging Markets Global Diversified (GBI-EMGD), 30% JPMorgan EMBI Global Diversified, and 20% JPMorgan CEMBI Broad Diversified.

* Effective February 1, 2023, the Bloomberg Emerging Markets Hard Currency (USD) Aggregate Index became the Fund’s performance benchmark index rather than the Custom Emerging Markets Debt Blended Total Return Index because the Bloomberg Emerging Markets Hard Currency (USD) Aggregate Index is an appropriate broad-based securities market index and is well aligned with the Fund’s investment strategy.

For a discussion on the economic and market environment during the 12-month period ended September 30, 2023, please see the Economic and Market Overview, beginning on page 1.

Subadviser discussion of factors that contributed to the Fund’s performance

During the fiscal year ended September 30, 2023, broader emerging-market (EM) debt asset classes experienced strong returns for different reasons. In the EM local space, strong returns were led by interest rates, as many emerging-market central banks were starting their monetary easing during the reporting period. Currencies were also additive, though less so against a slightly weaker U.S. dollar compared to the prior fiscal year. In the hard currency space, sovereign and corporate returns were led by spread tightening, while a significant rise in U.S. Treasury yields put pressure on the asset class, causing some detractions. High yield significantly outperformed investment-grade during the reporting period.

The Fund’s local interest rate exposure was additive during the fiscal year, as the Fund was positioned well for the end of the EM central bank tightening cycle and subsequent easing that started in calendar year 2023, given generally well-behaved inflation in many EM economies. Sovereign and corporate hard currency positions were also additive, given the rally seen in both asset classes during the reporting period. The Fund performed well there, given the bias towards high yield credits, specifically in the BB space. On the other hand, currency exposures were a drag on performance. Though the Fund has historically had a long EM foreign exchange trading bias, the individual currency exposures in the Fund did not translate into positive returns during the reporting period.

Derivatives are securities that derive their value from the performance of one or more other investments and take the form of a contract between two or more parties. Derivatives can be used for hedging, speculation, or both. The Fund typically does use derivative instruments in managing its portfolio, both from a hedging perspective as well as for speculation to gain credit risk, local interest rate risk and currency risk. Currency derivatives (primarily currency forwards) were detractors from performance during the reporting period, while interest rate derivatives (U.S. Treasury futures and interest rate swaps) and credit derivatives (short credit default swaps) contributed to performance.

10

MassMutual Emerging Markets Debt Blended Total Return Fund – Portfolio Manager Report (Unaudited) (Continued) |

Subadviser outlook

Barings observes that, looking ahead, risks abound in the form of uncertainty over U.S. Federal Reserve policy, emerging drivers of inflation, and growing political uncertainty. But Fund management observes that it is worth noting that these headwinds are mainly macro-driven, rather than credit risks or default concerns for EM sovereigns and corporates. In particular, Fund management observes that, as of the end of the reporting period, EM credit continues to benefit from relatively healthy fundamentals, especially for higher-quality issuers. As of the end of the reporting period, a number of EM countries were experiencing declining inflation, which in some cases, was allowing central banks to cut rates. This has led Fund management to be more constructive on local interest rates, specifically in countries like Korea, Peru, and the Czech Republic. However, if the U.S. economy remains strong, particularly in the face of weakness in China and Europe, Fund management believes that EM currencies could face headwinds, which could, in turn, limit further rate cutting.

MassMutual Emerging Markets | |

Sovereign Debt Obligations | 58.9% |

Corporate Debt | 34.8% |

Purchased Options | 0.1% |

Total Long-Term Investments | 93.8% |

Short-Term Investments and Other Assets and Liabilities | 6.2% |

Net Assets | 100.0% |

11

MassMutual Emerging Markets Debt Blended Total Return Fund – Portfolio Manager Report (Unaudited) (Continued) |

GROWTH OF $10,000 INVESTMENT - Class I

The graph above illustrates a representative class of the Fund’s historical performance+ for the past 10 fiscal years or since inception (for Funds lacking 10-year records) in comparison to its benchmark index, as well as one or more additional indexes, if applicable. The performance of other share classes will be greater than or less than the class depicted above.

Average Annual Total Returns+ (for the periods ended 09/30/2023) | ||||

| Inception Date | 1 Year | 5 Years | Since |

Class I | 10/21/2015 | 13.57% | 1.68% | 2.68% |

Class Y | 10/21/2015 | 13.58% | 1.64% | 2.66% |

Class L | 10/21/2015 | 13.12% | 1.40% | 2.40% |

Class L (sales load deducted)* | 10/21/2015 | 7.64% | 0.57% | 1.88% |

Class C | 10/21/2015 | 12.29% | 0.65% | 1.65% |

Class C (CDSC fees deducted)* | 10/21/2015 | 11.29% | 0.65% | 1.65% |

Bloomberg Emerging Markets Hard Currency (USD) Aggregrate Index# | 8.57% | -0.37% | 1.46% | |

Custom Emerging Markets Debt Blended Total Return Index | 11.06% | 0.60% | 1.94% | |

# Benchmark

* Class L (sales load deducted) returns include the 4.00% maximum sales charge and Class C (CDSC fees deducted) returns include the 1.00% maximum contingent deferred sales charge for the first 12 months shown.

+ The Fund is the successor to the Barings Emerging Markets Debt Blended Total Return Fund (the “Predecessor Fund”), a mutual fund with substantially similar investment objectives, policies, and restrictions, as a result of the reorganization of the Predecessor Fund into the Fund on December 13, 2021. The performance provided is that of the Predecessor Fund prior to December 13, 2021, and is that of the Fund after December 13, 2021. Performance shown for Class L shares prior to December 13, 2021 reflects the performance of Class A shares of the Predecessor Fund.

Generally accepted accounting principles require adjustments to be made to the net assets of the Fund at period end for financial reporting purposes only, and as such, the total return based on the unadjusted net asset value per share may differ from the total return reported in the financial highlights.

Performance results in the graph and table are shown both with and without the imposition of the maximum applicable sales charge (if applicable) and reflect the percentage change in net asset value, including reinvestment of dividends and capital gains distributions. Investors should note that the Fund is a professionally managed mutual fund, while the index or indexes shown above are unmanaged, cannot be purchased directly, and, with the exception of any peer group index, do not incur expenses.

Performance data quoted in the graph and table represents past performance; past performance is not predictive of future results. The investment return and principal value of shares of the Fund fluctuate, so your shares, when sold, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. The performance shown does not reflect the deduction of taxes, if any, that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data current to the most recent month end may be obtained by calling 1-888-309-3539.

Investors should read the Fund’s prospectus with regard to the Fund’s investment objectives, risks, and charges and expenses in conjunction with these financial statements. Employee retirement benefit plans that invest plan assets in the Separate Investment Accounts (SIAs) may be subject to certain charges as set forth in their respective Plan Documents. Total return figures would be lower for the periods presented if they reflected these charges.

12

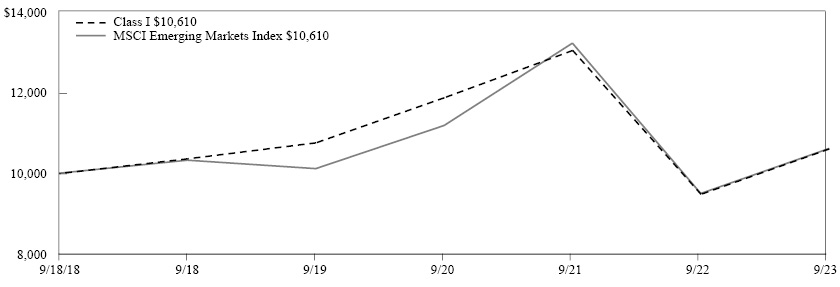

MassMutual Global Emerging Markets Equity Fund – Portfolio Manager Report (Unaudited) |

What is the investment approach of MassMutual Global Emerging Markets Equity Fund, and who is the Fund’s subadviser?

This Fund seeks to achieve long-term capital growth. Under normal market conditions, the Fund will invest at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in equity and equity-related securities, including convertible securities, preferred stocks, options, and warrants, of issuers that are economically tied to one or more emerging market countries. The Fund may invest in fixed income securities or debt instruments issued by emerging market entities or sovereign nations. The Fund’s subadviser is Barings LLC (Barings). In addition, Baring International Investment Limited serves as a sub-subadviser for the Fund.

How did the Fund perform during the 12 months ended September 30, 2023?

The Fund’s Class I shares returned 11.84%, outperforming the 11.70% return of the MSCI Emerging Markets Index (the “benchmark”), which measures the performance of the large- and mid-cap segments of emerging market equity securities. It is free float-adjusted market-capitalization weighted.

For a discussion on the economic and market environment during the 12-month period ended September 30, 2023, please see the Economic and Market Overview, beginning on page 1.

Subadviser discussion of factors that contributed to the Fund’s performance

For the fiscal year ended September 30, 2023, in absolute terms, the Fund’s performance was strongest during the first half of the reporting period, reflecting hopes of a strong rebound for the Chinese economy after policymakers relaxed COVID-19 restrictions at the end of calendar year 2022. During this time, markets also reacted positively to signs that interest rates across the U.S. and Europe were potentially reaching a peak, as inflation showed signs of cooling. Emerging markets were weaker throughout the latter six months of the reporting period, as China’s economic recovery showed signs of faltering. However, this was not enough to offset the Fund’s strong returns earlier in the period.

In absolute terms, the Fund’s holdings in the information technology sector were some of the best performers, with the share prices of some companies benefiting from the opportunities presented by generative artificial intelligence. Holdings in the utilities and consumer staples sector declined on an absolute basis. The Fund’s top-performing holdings on a relative basis were Korean multinational Samsung Electronics, South African gold miner AngloGold, and Korean commercial bank Hana Financial. The largest detractors were wind power company China Longyuan Power and ecommerce sites JD.com and Meituan, all of which are listed in Hong Kong.

Value-style equities outperformed their growth counterparts over the reporting period. While this proved to be a meaningful headwind for the Fund’s “growth at a reasonable price” approach, the Fund still managed to outperform relative to the benchmark.

Subadviser outlook

In the short term, Barings believes that global markets are likely to remain volatile as investors weigh up a potential peak in monetary tightening later this year by the U.S. Federal Reserve against a backdrop of deteriorating corporate earnings. In Fund management’s view, the outlook for emerging markets is more constructive, as the policy cycle has also already peaked in many countries and in some is already easing. Barings observes that China’s reopening and policy stimulus would likely help lift economic activity domestically, but also in broader emerging markets, which could support a recovery in corporate earnings in the remainder of 2023 and beyond.

The recent reversal in the U.S. dollar is also an important tailwind for the asset class, which Fund management believes has the potential to continue, as economic activity and inflationary pressures potentially ease in the U.S.

13

MassMutual Global Emerging Markets Equity Fund – Portfolio Manager Report (Unaudited) (Continued) |

MassMutual Global Emerging | |

Taiwan Semiconductor Manufacturing Co. Ltd. | 8.7% |

Samsung Electronics Co. Ltd. | 7.7% |

Tencent Holdings Ltd. | 5.8% |

Alibaba Group Holding Ltd. | 4.3% |

HDFC Bank Ltd. ADR | 3.5% |

Reliance Industries Ltd. GDR | 3.5% |

Axis Bank Ltd. GDR | 2.7% |

Hana Financial Group, Inc. | 2.6% |

Hyundai Motor Co. | 2.1% |

Ping An Insurance Group Co. of China Ltd. Class H | 2.0% |

42.9% | |

MassMutual Global Emerging | |

Financial | 29.1% |

Technology | 21.2% |

Communications | 17.2% |

Consumer, Cyclical | 12.2% |

Industrial | 6.1% |

Basic Materials | 5.0% |

Energy | 3.5% |

Consumer, Non-cyclical | 2.5% |

Utilities | 2.0% |

Total Long-Term Investments | 98.8% |

Short-Term Investments and Other Assets and Liabilities | 1.2% |

Net Assets | 100.0% |

14

MassMutual Global Emerging Markets Equity Fund – Portfolio Manager Report (Unaudited) (Continued) |

GROWTH OF $10,000 INVESTMENT - Class I

The graph above illustrates a representative class of the Fund’s historical performance+ for the past 10 fiscal years or since inception (for Funds lacking 10-year records) in comparison to its benchmark index, as well as one or more additional indexes, if applicable. The performance of other share classes will be greater than or less than the class depicted above.

Average Annual Total Returns+ (for the periods ended 09/30/2023) | ||||

| Inception Date | 1 Year | 5 Years | Since Inception |

Class I | 9/18/2018 | 11.84% | 0.47% | 1.18% |

Class Y | 9/18/2018 | 11.83% | 0.47% | 1.18% |

Class L | 9/18/2018 | 11.63% | 0.23% | 0.94% |

Class L (sales load deducted)* | 9/18/2018 | 6.20% | -0.59% | 0.12% |

Class C | 9/18/2018 | 10.74% | -0.53% | 0.17% |

Class C (CDSC fees deducted)* | 9/18/2018 | 9.74% | -0.53% | 0.17% |

MSCI Emerging Markets Index | 11.70% | 0.55% | 1.18% | |

* Class L (sales load deducted) returns include the 4.00% maximum sales charge and Class C (CDSC fees deducted) returns include the 1.00% maximum contingent deferred sales charge for the first 12 months shown.

+ The Fund is the successor to the Barings Global Emerging Markets Equity Fund (the “Predecessor Fund”), a mutual fund with substantially similar investment objectives, policies, and restrictions, as a result of the reorganization of the Predecessor Fund into the Fund on December 13, 2021. The performance provided is that of the Predecessor Fund prior to December 13, 2021, and is that of the Fund after December 13, 2021. Performance shown for Class L shares prior to December 13, 2021 reflects the performance of Class A shares of the Predecessor Fund.

Generally accepted accounting principles require adjustments to be made to the net assets of the Fund at period end for financial reporting purposes only, and as such, the total return based on the unadjusted net asset value per share may differ from the total return reported in the financial highlights.

Performance results in the graph and table are shown both with and without the imposition of the maximum applicable sales charge (if applicable) and reflect the percentage change in net asset value, including reinvestment of dividends and capital gains distributions. Investors should note that the Fund is a professionally managed mutual fund, while the index or indexes shown above are unmanaged, cannot be purchased directly, and, with the exception of any peer group index, do not incur expenses.

Performance data quoted in the graph and table represents past performance; past performance is not predictive of future results. The investment return and principal value of shares of the Fund fluctuate, so your shares, when sold, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. The performance shown does not reflect the deduction of taxes, if any, that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance data current to the most recent month end may be obtained by calling 1-888-309-3539.

Investors should read the Fund’s prospectus with regard to the Fund’s investment objectives, risks, and charges and expenses in conjunction with these financial statements. Employee retirement benefit plans that invest plan assets in the Separate Investment Accounts (SIAs) may be subject to certain charges as set forth in their respective Plan Documents. Total return figures would be lower for the periods presented if they reflected these charges.

15

MassMutual Global Floating Rate Fund – Portfolio of Investments |

September 30, 2023 |

Number of | Value | |||||||

EQUITIES — 1.0% | ||||||||

COMMON STOCK — 1.0% | ||||||||

Communications — 0.2% | ||||||||

Media — 0.2% | ||||||||

Learfield Communications, Inc. (a) (b) | 9,599 | $ | 364,762 | |||||

Telecommunications — 0.0% | ||||||||

Vantiva SA (a) (c) | 88,751 | 14,438 | ||||||

| 379,200 | ||||||||

Consumer, Cyclical — 0.2% | ||||||||

Entertainment — 0.0% | ||||||||

Technicolor Creative Studios SA (Acquired 6/08/23, Cost $158,820) (a) (d) | 29,944 | 51,550 | ||||||

Home Furnishing — 0.2% | ||||||||

Serta Simmons, Inc. (a) (b) | 22,009 | 330,135 | ||||||

| 381,685 | ||||||||

Consumer, Non-cyclical — 0.4% | ||||||||

Food — 0.3% | ||||||||

CTI Foods Holding Co. LLC (a) (b) (e) | 4,657 | 516,135 | ||||||

Health Care – Services — 0.1% | ||||||||

Don Jersey Topco Ltd. (Acquired 8/03/20-6/23/23, Cost $234,326) (a) (b) (d) (e) | 353,106 | 150,789 | ||||||

| 666,924 | ||||||||

Energy — 0.2% | ||||||||

Oil & Gas Services — 0.2% | ||||||||

KCA Deutag International Ltd. (a) | 7,834 | 438,704 | ||||||

Financial — 0.0% | ||||||||

Diversified Financial Services — 0.0% | ||||||||

Campfire Topco Ltd. (a) (b) (e) | 1,484,798 | — | ||||||

Travelex Topco Ltd. (a) (b) (e) | 3,602 | — | ||||||

| — | ||||||||

Investment Companies — 0.0% | ||||||||

Jubilee Topco Ltd. (a) (b) (e) | 689,952 | — | ||||||

| — | ||||||||

Industrial — 0.0% | ||||||||

Transportation — 0.0% | ||||||||

Bahia De Las Isletas SL, Class A2 (a) (b) (e) | 688 | — | ||||||

Bahia De Las Isletas SL, Class A3 (a) (b) (e) | 98 | — | ||||||

Bahia De Las Isletas SL, Class B2 (a) (b) (e) | 876 | — | ||||||

Bahia De Las Isletas SL, Class B3 (a) (b) (e) | 125 | — | ||||||

| — | ||||||||

| — | ||||||||

Number of | Value | |||||||

TOTAL COMMON STOCK (Cost $1,904,142) | $ | 1,866,513 | ||||||

TOTAL EQUITIES (Cost $1,904,142) | 1,866,513 | |||||||

Principal | ||||||||

BONDS & NOTES — 91.6% | ||||||||

BANK LOANS — 87.7% | ||||||||

Advertising — 1.0% | ||||||||

Clear Channel Outdoor Holdings, Inc., Term Loan B, 1 mo. USD Term SOFR + 3.500%, 3 mo. USD Term SOFR + 3.500% | ||||||||

8.818% - 9.131% VRN 8/21/26 | $ | 990,009 | 959,893 | |||||

Summer (BC) Holdco B Sarl, USD Term Loan B1, 3 mo. USD Term SOFR + 5.000% | ||||||||

10.661% VRN 12/04/26 | 997,409 | 963,747 | ||||||

| 1,923,640 | ||||||||

Aerospace & Defense — 0.4% | ||||||||

TransDigm, Inc., 2023 Term Loan I, 3 mo. USD Term SOFR + 3.250% | ||||||||

8.640% VRN 8/24/28 | 854,627 | 854,491 | ||||||

Airlines — 2.2% | ||||||||

Air Canada, 2021 Term Loan B, 3 mo. USD Term SOFR + 3.500% | ||||||||

9.128% VRN 8/11/28 | 766,464 | 766,303 | ||||||

American Airlines, Inc. | ||||||||

2023 Term Loan B, 3 mo. USD Term SOFR + 2.750% | ||||||||

8.543% VRN 2/15/28 | 874,776 | 867,621 | ||||||

2021 Term Loan, 3 mo. USD Term SOFR + 4.750% | ||||||||

10.338% VRN 4/20/28 | 962,373 | 990,282 | ||||||

Kestrel Bidco, Inc., Term Loan B, 3 mo. USD Term SOFR + 3.000% | ||||||||

8.420% VRN 12/11/26 | 556,782 | 544,488 | ||||||

United Airlines, Inc., 2021 Term Loan B, 1 mo. USD Term SOFR + 3.750% | ||||||||

9.182% VRN 4/21/28 | 930,492 | 930,706 | ||||||

| 4,099,400 | ||||||||

Apparel — 0.5% | ||||||||

Crocs, Inc. ., 2023 Term Loan B, 1 mo. USD Term SOFR + 3.000%, 3 mo. USD Term SOFR + 3.000% | ||||||||

8.318% - 8.540% VRN 2/20/29 | 658,516 | 659,563 | ||||||

The accompanying notes are an integral part of the financial statements.

16

MassMutual Global Floating Rate Fund – Portfolio of Investments (Continued) |

Principal | Value | |||||||

Hanesbrands, Inc., 2023 Term Loan B, 1 mo. USD Term SOFR + 3.750% | ||||||||

9.066% VRN 3/08/30 | $ | 118,638 | $ | 115,969 | ||||

Samsonite International SA, 2023 Term Loan, 1 mo. USD Term SOFR + 2.750% | ||||||||

8.066% VRN 6/21/30 | 238,524 | 238,674 | ||||||

| 1,014,206 | ||||||||

Auto Parts & Equipment — 0.3% | ||||||||

DexKo Global, Inc., 2021 USD Term Loan B, | ||||||||

0.000% 10/04/28 (f) | 518,673 | 504,881 | ||||||

Banks — 0.4% | ||||||||

AqGen Ascensus, Inc., 2021 2nd Lien Term Loan, 3 mo. USD Term SOFR + 6.500% | ||||||||

12.030% VRN 8/02/29 | 250,358 | 236,746 | ||||||

AqGen Island Holdings, Inc., Term Loan, | ||||||||

0.000% 8/02/28 (f) | 485,030 | 479,273 | ||||||

| 716,019 | ||||||||

Beverages — 0.3% | ||||||||

Amphora Finance Ltd., 2018 GBP Term Loan B, 6 mo. SONIA + 4.750% | ||||||||

9.378% VRN 5/23/25 GBP (g) | 500,000 | 228,006 | ||||||

Triton Water Holdings, Inc., Term Loan, 3 mo. USD Term SOFR + 3.250% | ||||||||

8.902% VRN 3/31/28 | 368,222 | 358,402 | ||||||

| 586,408 | ||||||||

Biotechnology — 0.6% | ||||||||

Advanz Pharma Corp., 2021 EUR Term Loan B, 1 mo. EUR EURIBOR + 4.500% | ||||||||

8.358% VRN 6/01/28 EUR (g) | 1,000,000 | 1,049,321 | ||||||

Building Materials — 0.8% | ||||||||

CP Atlas Buyer, Inc., 2021 Term Loan B, 1 mo. USD Term SOFR + 3.750% | ||||||||

9.166% VRN 11/23/27 | 231,773 | 218,108 | ||||||

Emrld Borrower LP, Term Loan B, 3 mo. USD Term SOFR + 3.000%, | ||||||||

8.316% VRN 5/31/30 (f) | 445,161 | 444,329 | ||||||

LSF10 XL Bidco SCA, 2021 EUR Term Loan B4, 3 mo. EUR EURIBOR + 3.925% | ||||||||

8.147% VRN 4/12/28 EUR (g) | 853,470 | 773,921 | ||||||

| 1,436,358 | ||||||||

Principal | Value | |||||||

Chemicals — 4.7% | ||||||||

Ascend Performance Materials Operations LLC, 2021 Term Loan B, 3 mo. USD Term SOFR + 4.750% | ||||||||

10.317% VRN 8/27/26 | $ | 746,173 | $ | 728,683 | ||||

Consolidated Energy Finance SA, Term Loan B, 3 mo. USD Term SOFR + 2.500% | ||||||||

7.916% VRN 5/07/25 | 36,747 | 36,342 | ||||||

CPC Acquisition Corp., Term Loan, 3 mo. USD Term SOFR + 3.750% | ||||||||

9.150% VRN 12/29/27 | 1,520,192 | 1,251,437 | ||||||

Cyanco Intermediate 2 Corp., 2023 Term Loan B, 1 mo. USD Term SOFR + 4.750% | ||||||||

10.066% VRN 7/10/28 | 1,242,714 | 1,243,099 | ||||||

Flint Group Packaging INKS North America Holdings LLC | ||||||||

EUR PIK 2nd lien Holdco Term Loan, 3 mo. EUR EURIBOR + 0.100% | ||||||||

3.793% VRN 12/31/27 EUR (g) | 233,177 | 49,305 | ||||||

EUR PIK Holdco Term Loan, 3 mo. EUR EURIBOR + 0.100% | ||||||||

3.794% VRN 12/31/27 EUR (g) | 174,854 | 129,714 | ||||||

EUR Opco Term Loan, 3 mo. EUR EURIBOR + 4.250% | ||||||||

7.944% VRN 12/31/26 EUR (g) | 369,226 | 361,867 | ||||||

Kraton Corp., 2022 USD Term Loan, 3 mo. USD Term SOFR + 3.250% | ||||||||

8.921% VRN 3/15/29 | 395,129 | 389,573 | ||||||

LSF11 A5 Holdco LLC, Term Loan, 1 mo. USD Term SOFR + 3.500% | ||||||||

8.810% VRN 10/15/28 | 679,692 | 662,870 | ||||||

New Arclin US Holding Corp., 2021 Term Loan, 1 mo. USD Term SOFR + 3.750% | ||||||||

9.166% VRN 9/30/28 | 871,966 | 860,387 | ||||||

Olympus Water US Holding Corporation, 2021 USD Term Loan B, 3 mo. USD Term SOFR + 3.750% | ||||||||

9.402% VRN 11/09/28 | 915,710 | 902,304 | ||||||

PMHC II, Inc., 2022 Term Loan B, 3 mo. USD Term SOFR + 4.250% | ||||||||

9.698% VRN 4/23/29 | 786,909 | 740,945 | ||||||

Polar US Borrower LLC, 2018 1st Lien Term Loan, 3 mo. USD Term SOFR + 4.750% | ||||||||

9.721% - 10.151% VRN 10/15/25 | 1,214,853 | 970,364 | ||||||

The accompanying notes are an integral part of the financial statements.

17

MassMutual Global Floating Rate Fund – Portfolio of Investments (Continued) |

Principal | Value | |||||||

Starfruit Finco BV, 2023 Term Loan B, 3 mo. USD Term SOFR + 4.000% | ||||||||

9.347% VRN 4/03/28 | $ | 218,112 | $ | 215,205 | ||||

Trinseo Materials Operating S.C.A, 2021 Term Loan B2, 1 mo. USD Term SOFR + 2.500% | ||||||||

7.931% VRN 5/03/28 | 474,483 | 397,109 | ||||||

| 8,939,204 | ||||||||

Commercial Services — 8.0% | ||||||||

APX Group, Inc., 2021 Term Loan B, 3 mo. USD LIBOR + 3.250%, 3 mo. U.S. (Fed) Prime Rate + 2.250% | ||||||||

0.087% - 11.750% VRN 7/10/28 | 706,167 | 705,185 | ||||||

AVSC Holding Corp., 2020 Term Loan B1, 1 mo. USD Term SOFR + 3.250% | ||||||||

8.568% VRN 3/03/25 | 644,122 | 619,014 | ||||||

BCP V Modular Services Holdings IV Ltd., EUR Term Loan B, 3 mo. EUR EURIBOR + 4.425% | ||||||||

8.397% VRN 12/15/28 EUR (g) | 1,000,000 | 990,812 | ||||||

CoreLogic, Inc. | ||||||||

Term Loan, 1 mo. USD Term SOFR + 3.500% | ||||||||

8.931% VRN 6/02/28 | 559,537 | 515,938 | ||||||

2nd Lien Term Loan, 1 mo. USD Term SOFR + 6.500% | ||||||||

11.931% VRN 6/04/29 | 532,670 | 446,554 | ||||||

Eagle Bidco Ltd., 2021 GBP Term Loan B, 1 mo. SONIA + 4.750% | ||||||||

9.718% VRN 3/20/28 GBP (g) | 500,000 | 582,677 | ||||||

Ensono LP, 2021 Term Loan, 1 mo. USD Term SOFR + 4.000% | ||||||||

9.431% VRN 5/26/28 | 635,747 | 610,793 | ||||||

Fugue Finance BV, EUR Term Loan, 2 mo. EUR EURIBOR + 4.750% | ||||||||

8.114% VRN 1/31/28 EUR (g) | 1,000,000 | 1,056,817 | ||||||

Lernen Bidco Ltd., 2023 EUR Extended Term Loan B, 3 mo. EUR EURIBOR + 4.750% | ||||||||

8.482% VRN 4/25/29 EUR (g) | 2,000,000 | 2,104,583 | ||||||

Mavis Tire Express Services Corp., 2021 Term Loan B, 1 mo. USD Term SOFR + 4.000% | ||||||||

9.431% VRN 5/04/28 | 746,183 | 743,572 | ||||||

Neptune Bidco US, Inc., 2022 USD Term Loan B, 3 mo. USD Term SOFR + 5.000% | ||||||||

10.398% VRN 4/11/29 | 996,255 | 894,557 | ||||||

Principal | Value | |||||||

OMNIA Partners LLC, Term Loan B, 3 mo. USD Term SOFR + 4.250% | ||||||||

9.601% VRN 7/25/30 | $ | 252,899 | $ | 252,952 | ||||

PECF USS Intermediate Holding III Corp., Term Loan B, 1 mo. USD Term SOFR + 4.250% | ||||||||

9.568% VRN 12/15/28 (f) | 673,734 | 538,084 | ||||||

Prometric Holdings, Inc., 1st Lien Term Loan, 3 mo. USD Term SOFR + 3.000% | ||||||||

8.684% VRN 1/29/25 | 972,010 | 960,832 | ||||||

Sabre GLBL, Inc. | ||||||||

2021 Term Loan B2, 1 mo. USD Term SOFR + 3.500% | ||||||||

8.931% VRN 12/17/27 | 465,931 | 406,525 | ||||||

2021 Term Loan B1, 1 mo. USD Term SOFR + 3.500% | ||||||||

8.931% VRN 12/17/27 | 298,172 | 260,155 | ||||||

Spin Holdco, Inc., 2021 Term Loan, 3 mo. USD Term SOFR + 4.000% | ||||||||

9.664% VRN 3/04/28 | 646,684 | 557,564 | ||||||

Techem Verwaltungsgesellschaft 675 mbH, EUR Term Loan B4, 6 mo. EUR EURIBOR + 2.375% | ||||||||

6.275% VRN 7/15/25 EUR (g) | 1,000,000 | 1,053,899 | ||||||

Verisure Holding AB, 2021 EUR Term Loan, 3 mo. EUR EURIBOR + 3.000% | ||||||||

6.972% VRN 3/27/28 EUR (g) | 1,375,000 | 1,435,940 | ||||||

Wand NewCo 3, Inc., 2020 Term Loan, 1 mo. USD Term SOFR + 2.750% | ||||||||

8.166% VRN 2/05/26 | 483,568 | 480,323 | ||||||

| 15,216,776 | ||||||||

Computers — 2.5% | ||||||||

Ahead DB Holdings LLC, 2021 Term Loan B, 3 mo. USD Term SOFR + 3.750% | ||||||||

9.240% VRN 10/18/27 | 419,814 | 415,616 | ||||||

Magenta Buyer LLC, 2021 USD 1st Lien Term Loan, 3 mo. USD Term SOFR + 5.000% | ||||||||

10.631% VRN 7/27/28 | 671,350 | 497,545 | ||||||

McAfee LLC, 2022 USD Term Loan B, 1 mo. USD Term SOFR + 3.750% | ||||||||

9.180% VRN 3/01/29 | 766,439 | 747,516 | ||||||

Peraton Corp., Term Loan B, 1 mo. USD Term SOFR + 3.750% | ||||||||

9.166% VRN 2/01/28 | 706,626 | 704,421 | ||||||

The accompanying notes are an integral part of the financial statements.

18

MassMutual Global Floating Rate Fund – Portfolio of Investments (Continued) |

Principal | Value | |||||||

Redstone Holdco 2 LP, 2021 Term Loan, 1 mo. USD Term SOFR + 4.750% | ||||||||

10.184% VRN 4/27/28 | $ | 299,265 | $ | 254,938 | ||||

SITEL Worldwide Corp., 2021 USD Term Loan, 1 mo. USD Term SOFR + 3.750% | ||||||||

9.181% VRN 8/28/28 | 1,045,050 | 1,017,293 | ||||||

Vision Solutions, Inc. | ||||||||

2021 Incremental Term Loan, 1 mo. USD Term SOFR + 4.000% | ||||||||

9.613% VRN 4/24/28 | 415,889 | 402,285 | ||||||

2021 2nd Lien Term Loan, 1 mo. USD Term SOFR + 7.250% | ||||||||

12.863% VRN 4/23/29 | 770,186 | 689,594 | ||||||

| 4,729,208 | ||||||||

Cosmetics & Personal Care — 0.5% | ||||||||

Journey Personal Care Corp., 2021 Term Loan B, 6 mo. USD LIBOR + 4.250% | ||||||||

9.981% VRN 3/01/28 | 1,036,472 | 974,284 | ||||||

Distribution & Wholesale — 0.4% | ||||||||

Fluid-Flow Products, Inc., Term Loan, 3 mo. USD Term SOFR + 3.750%, | ||||||||

9.855% VRN 3/31/28 | 717,431 | 710,034 | ||||||

Diversified Financial Services — 3.6% | ||||||||

Advisor Group, Inc., 2023 Term Loan B, 3 mo. USD Term SOFR + 4.500% | ||||||||

9.816% VRN 8/17/28 (f) | 294,310 | 293,851 | ||||||

AllSpring Buyer LLC, Term Loan B, 3 mo. USD Term SOFR + 3.250% | ||||||||

8.650% VRN 11/01/28 | 797,982 | 789,252 | ||||||

Campfire Bidco Ltd. | ||||||||

USD Opco Term Loan, 3 mo. USD Term SOFR + 4.250% | ||||||||

9.856% VRN 12/31/26 | 2,192,840 | 2,037,982 | ||||||

EUR Super Senior Term Loan, 3 mo. EUR EURIBOR + 8.000% | ||||||||

11.770% VRN 6/30/26 EUR (g) | 335,910 | 356,139 | ||||||

Campfire TopCo Ltd. | ||||||||

USD First Lien HoldCo Facility, 3 mo. USD Term SOFR + 0.100% | ||||||||

5.706% VRN 12/31/27 | 1,038,461 | 732,115 | ||||||

USD Second Lien HoldCo Facility, 3 mo. USD Term SOFR + 0.100% | ||||||||

5.706% VRN 12/31/27 | 1,384,843 | 279,281 | ||||||

Principal | Value | |||||||

Castlelake Aviation Ltd., Term Loan B, 3 mo. USD Term SOFR + 2.750% | ||||||||

8.421% VRN 10/22/26 | $ | 1,123,778 | $ | 1,121,227 | ||||

Deerfield Dakota Holding LLC, 2021 USD 2nd Lien Term Loan, 1 mo. USD Term SOFR + 6.750% | ||||||||

12.402% VRN 4/07/28 | 857,143 | 805,714 | ||||||

VFH Parent LLC, 2022 Term Loan B, 1 mo. USD Term SOFR + 3.000% | ||||||||

8.418% VRN 1/13/29 | 518,809 | 514,161 | ||||||

| 6,929,722 | ||||||||

Electric — 0.9% | ||||||||

Arvos BidCo Sarl | ||||||||

EUR 1st Lien Term Loan B1 (Acquired 8/31/23, Cost $1,027,918), 3 mo. EUR EURIBOR + 5.500% | ||||||||

9.283% VRN 8/29/24 EUR (d) (g) | 889,475 | 423,179 | ||||||

USD 1st Lien Term Loan B1 (Acquired 7/31/23, Cost $126,658), 3 mo. USD LIBOR + 5.761% | ||||||||

11.131% VRN 8/29/24 (d) | 126,765 | 50,706 | ||||||

USD 1st Lien Term Loan B2 (Acquired 7/31/23, Cost $126,659), 3 mo. USD LIBOR + 5.761% | ||||||||

11.131% VRN 8/29/24 (d) | 126,765 | 50,706 | ||||||

Calpine Construction Finance Co. LP, 2023 Refinancing Term Loan B, 1 mo. USD Term SOFR + 2.250% | ||||||||

7.566% VRN 7/31/30 | 461,509 | 458,708 | ||||||

Edgewater Generation LLC, Term Loan, 1 mo. USD Term SOFR + 3.750% | ||||||||

9.181% VRN 12/13/25 | 572,532 | 555,465 | ||||||

EFS Cogen Holdings I LLC, 2020 Term Loan B, | ||||||||

0.000% 10/01/27 (f) | 149,644 | 148,667 | ||||||

| 1,687,431 | ||||||||

Electrical Components & Equipment — 0.5% | ||||||||

CEP IV Investment 16 Sarl, EUR Term Loan B, 3 mo. EUR EURIBOR + 4.750% | ||||||||

8.545% VRN 10/03/26 EUR (g) | 500,000 | 486,113 | ||||||

SGB-SMIT Management GmbH, EUR Term Loan B, 1 mo. EUR EURIBOR + 4.500% | ||||||||

8.214% VRN 4/18/28 EUR (g) | 458,692 | 452,824 | ||||||

| 938,937 | ||||||||

The accompanying notes are an integral part of the financial statements.

19

MassMutual Global Floating Rate Fund – Portfolio of Investments (Continued) |

Principal | Value | |||||||

Engineering & Construction — 0.6% | ||||||||

DG Investment Intermediate Holdings 2, Inc., 2021 Term Loan, 1 mo. USD Term SOFR + 3.750% | ||||||||

9.181% VRN 3/31/28 | $ | 715,275 | $ | 702,014 | ||||

US Anesthesia Partners, Inc., 2021 Term Loan, 1 mo. USD Term SOFR + 3.500% | ||||||||

8.931% VRN 5/12/28 | 433,904 | 426,311 | ||||||

| 1,128,325 | ||||||||

Entertainment — 3.2% | ||||||||

Bally’s Corp., 2021 Term Loan B, 3 mo. USD Term SOFR + 3.250% | ||||||||

8.838% VRN 10/02/28 | 748,101 | 732,062 | ||||||

International Park Holdings BV, 2023 EUR Term Loan B, 6 mo. EUR EURIBOR + 5.000% | ||||||||

8.794% VRN 12/14/26 EUR (g) | 500,000 | 528,128 | ||||||

Motion Finco Sarl, EUR Term Loan B, 3 mo. EUR EURIBOR + 3.000% | ||||||||

6.972% VRN 11/12/26 EUR (g) | 1,000,000 | 1,049,765 | ||||||

Scientific Games Holdings LP, 2022 USD Term Loan B, 3 mo. USD Term SOFR + 3.500% | ||||||||

8.768% VRN 4/04/29 | 982,718 | 976,164 | ||||||

Technicolor Creative Studios | ||||||||

2023 EUR PIK Term Loan (Acquired 6/08/23, Cost $8,442), 3 mo. EUR EURIBOR + 0.500% | ||||||||

0.500% VRN 6/08/33 EUR (b) (d) (e) (g) | 246,435 | — | ||||||

2023 EUR PIK Term Loan (Acquired 4/03/23, Cost $109,571), 3 mo. EUR EURIBOR + 0.5000% | ||||||||

4.215% VRN 7/31/26 EUR (d) (g) | 105,348 | 104,140 | ||||||

2023 EUR PIK Reinstated Term Loan B (Acquired 6/08/23, Cost $488,305), 6 mo. EUR EURIBOR + 0.500% | ||||||||

4.294% VRN 9/15/26 EUR (d) (g) | 610,076 | 334,479 | ||||||

2023 EUR PIK Reinstated Term Loan B (Acquired 4/03/23, Cost $111,279), 6 mo. EUR EURIBOR + 0.500% | ||||||||

15.335% VRN 7/31/26 EUR (d) (g) | 115,320 | 113,998 | ||||||

Vue International Bidco PLC | ||||||||

2023 EUR PIK Term Loan, 6 mo. EUR EURIBOR + 2.000% | ||||||||

4.859% VRN 12/31/27 EUR (g) | 698,672 | 341,022 | ||||||

2022 EUR Term Loan, 6 mo. EUR EURIBOR + 8.000% | ||||||||

12.072% VRN 6/30/27 EUR (g) | 145,796 | 148,362 | ||||||

Principal | Value | |||||||

William Morris Endeavor Entertainment LLC, 2018 1st Lien Term Loan, 1 mo. USD Term SOFR + 2.750% | ||||||||

8.181% VRN 5/18/25 | $ | 1,193,349 | $ | 1,190,198 | ||||

WMG Acquisition Corp., 2021 Term Loan G, 1 mo. USD Term SOFR + 2.125% | ||||||||

7.556% VRN 1/20/28 | 518,991 | 518,488 | ||||||

| 6,036,806 | ||||||||

Environmental Controls — 0.9% | ||||||||

Gopher Resource LLC, 1st Lien Term Loan, 3 mo. USD LIBOR + 3.250% | ||||||||

8.981% VRN 3/06/25 | 1,042,374 | 870,382 | ||||||

Madison IAQ LLC, Term Loan, 1 mo. USD Term SOFR + 3.250% | ||||||||

8.689% VRN 6/21/28 | 805,224 | 790,931 | ||||||

| 1,661,313 | ||||||||

Food — 1.2% | ||||||||

BCPE North Star US HoldCo 2, Inc., Term Loan, 3 mo. USD LIBOR + 4.000% | ||||||||

9.652% VRN 6/09/28 | 301,520 | 268,353 | ||||||

CHG PPC Parent LLC, 2021 Term Loan, 1 mo. USD Term SOFR + 3.000% | ||||||||

8.318% VRN 12/08/28 | 492,467 | 488,158 | ||||||

CTI Foods Holding Co. LLC | ||||||||

First Out Term Loan, 3 mo. USD Term SOFR + 7.000% | ||||||||

12.861% VRN 5/03/24 | 308,326 | 308,034 | ||||||

Second Out Term Loan, 3 mo. USD Term SOFR + 9.000% | ||||||||

14.861% VRN 5/03/24 | 204,535 | 194,114 | ||||||

Deoleo Financial, Ltd., EUR Senior Term Loan (Acquired 6/24/20, Cost $62,999), 3 mo. EUR EURIBOR + 5.500% | ||||||||

9.441% VRN 6/24/25 EUR (b) (d) (g) | 55,872 | 56,117 | ||||||

Froneri International Ltd., 2020 EUR Term Loan B1, 6 mo. EUR EURIBOR + 2.125% | ||||||||

6.097% VRN 1/29/27 EUR (g) | 1,000,000 | 1,039,457 | ||||||

| 2,354,233 | ||||||||

Health Care – Products — 2.8% | ||||||||

Auris Luxembourg III Sarl, EUR Term Loan B1A, 6 mo. EUR EURIBOR + 4.000% | ||||||||

7.781% VRN 2/27/26 EUR (g) | 1,000,000 | 1,027,340 | ||||||

The accompanying notes are an integral part of the financial statements.

20

MassMutual Global Floating Rate Fund – Portfolio of Investments (Continued) |

Principal | Value | |||||||

Embecta Corp., Term Loan B, 6 mo. USD Term SOFR + 3.000% | ||||||||

8.337% VRN 3/30/29 | $ | 362,179 | $ | 354,313 | ||||

Iris BidCo GmbH, EUR Term Loan B, 3 mo. EUR EURIBOR + 5.000% | ||||||||

8.714% VRN 6/29/28 EUR (g) | 650,000 | 669,654 | ||||||

Lifescan Global Corp., 2023 Term Loan, 3 mo. USD Term SOFR + 6.500% | ||||||||

11.747% VRN 12/31/26 | 943,480 | 743,774 | ||||||

Medline Borrower LP, USD Term Loan B, 1 mo. USD Term SOFR + 3.250% | ||||||||

8.681% VRN 10/23/28 | 2,462,500 | 2,454,374 | ||||||

| 5,249,455 | ||||||||

Health Care – Services — 4.7% | ||||||||

Aveanna Healthcare LLC, 2021 2nd Lien Term Loan, 3 mo. USD Term SOFR + 7.000% | ||||||||

12.572% VRN 12/10/29 | 1,497,326 | 973,262 | ||||||

Envision Healthcare Corp. | ||||||||

2022 Third Out Term Loan, 3 mo. USD Term SOFR + 3.750% | ||||||||

8.992% VRN 3/31/27 | 367,879 | 552 | ||||||

2022 First Out Term Loan, 3 mo. USD Term SOFR + 7.875% | ||||||||

13.275% VRN 3/31/27 | 145,176 | 169,613 | ||||||

ICON Luxembourg Sarl, LUX Term Loan, 3 mo. USD Term SOFR + 2.250% | ||||||||

7.902% VRN 7/03/28 | 557,811 | 557,365 | ||||||

Medical Solutions Holdings, Inc., 2021 2nd Lien Term Loan, 3 mo. USD Term SOFR + 7.000% | ||||||||

12.522% VRN 11/01/29 | 294,737 | 263,053 | ||||||

Midwest Physician Administrative Services LLC, 2021 Term Loan, 3 mo. USD LIBOR + 3.250% | ||||||||

8.902% VRN 3/12/28 | 992,366 | 928,964 | ||||||

NAPA Management Services Corp., Term Loan B, 1 mo. USD Term SOFR + 5.250% | ||||||||

10.666% VRN 2/23/29 | 822,352 | 659,938 | ||||||

Radiology Partners, Inc., 2018 1st Lien Term Loan B, 1 mo. USD Term SOFR + 4.250% | ||||||||

10.179% VRN 7/09/25 | 1,746,310 | 1,308,545 | ||||||

RegionalCare Hospital Partners Holdings, Inc., 2018 Term Loan B, 3 mo. USD Term SOFR + 3.750% | ||||||||

9.072% VRN 11/16/25 | 1,165,152 | 1,161,272 | ||||||

Principal | Value | |||||||

Select Medical Corp., 2023 Term Loan B1, 1 mo. USD Term SOFR + 3.000% | ||||||||

8.316% VRN 3/06/27 | $ | 997,500 | $ | 993,759 | ||||

Team Health Holdings, Inc., 2022 Term Loan B, 1 mo. USD Term SOFR + 5.250% | ||||||||

10.566% VRN 3/02/27 | 521,841 | 393,990 | ||||||

Tunstall Group Holdings Limited | ||||||||

2023 EUR Reinstated Term Loan B (Acquired 6/23/23, Cost $314,153), 3 mo. EUR EURIBOR + 0.100% | ||||||||

3.894% VRN 12/20/27 EUR (b) (d) (e) (g) | 321,190 | 305,620 | ||||||

2023 EUR Super Senior Term Loan (Acquired 6/23/23, Cost $107,052), 3 mo. EUR EURIBOR + 3.000% | ||||||||

6.794% VRN 12/18/26 EUR (b) (d) (e) (g) | 104,512 | 103,865 | ||||||

US Anesthesia Partners, Inc., 2021 Term Loan, 1 mo. USD Term SOFR + 4.250% | ||||||||

9.694% VRN 10/01/28 | 722,639 | 661,728 | ||||||

US Radiology Specialists, Inc., 2020 Term Loan, 1 mo. USD Term SOFR + 5.250% | ||||||||

10.740% VRN 12/15/27 | 525,721 | 508,898 | ||||||

| 8,990,424 | ||||||||