| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-255934-04 | ||

| Dated January 12, 2023 | BMO 2023-C4 |

Structural and Collateral Term Sheet | ||

BMO 2023-C4 Mortgage Trust | ||

$785,102,870 (Approximate Mortgage Pool Balance) | ||

$[ ] (Approximate Offered Certificates) | ||

BMO Commercial Mortgage Securities LLC Depositor | ||

Commercial Mortgage Pass-Through Certificates, Series 2023-C4 | ||

Bank of Montreal Citi Real Estate Funding Inc. LMF Commercial, LLC Argentic Real Estate Finance LLC 3650 Real Estate Investment Trust 2 LLC Natixis Real Estate Capital LLC Oceanview Commercial Mortgage Finance, LLC Greystone Commercial Mortgage Capital LLC Starwood Mortgage Capital LLC Sponsors and Mortgage Loan Sellers | ||

| BMO Capital Markets | Natixis | Citigroup |

| Co-Lead Managers and Joint Bookrunners | ||

| Bancroft Capital, LLC Co-Manager | Drexel Hamilton Co-Manager | |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| Dated January 12, 2023 | BMO 2023-C4 |

This material is for your information, and none of BMO Capital Markets Corp., Citigroup Global Markets Inc., Natixis Securities Americas LLC, Bancroft Capital, LLC and Drexel Hamilton, LLC (the “Underwriters”) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-255934) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or BMO Capital Markets Corp., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling 1-866-864-7760. The Offered Certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more Classes of Certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these Certificates, a contract of sale will come into being no sooner than the date on which the relevant Class has been priced and we have verified the allocation of Certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time. The information should be reviewed only in conjunction with the entire offering document relating to the Commercial Mortgage Pass-Through Certificates, Series 2023-C4 (the “Offering Document”). All of the information contained herein is subject to the same limitations and qualifications contained in the Offering Document. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described elsewhere in the Offering Document. The information contained herein will be more fully described elsewhere in the Offering Document. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Offering Document its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this free writing prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This document has been prepared by the Underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Regulation (EU) 2017/1129 (as amended or superseded) and/or Part VI of the Financial Services and Markets Act 2000 (as amended) or other offering document.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these Certificates. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the Certificates may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of the Underwriters or any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the Certificates. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This document contains forward-looking statements. If and when included in this document, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in consumer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this document are made as of the date hereof. We have no obligation to update or revise any forward-looking statement.

BMO Capital Markets is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A. (member FDIC), Bank of Montreal Europe p.l.c, and Bank of Montreal (China) Co. Ltd, the institutional broker dealer business of BMO Capital Markets Corp. (Member FINRA and SIPC) and the agency broker dealer business of Clearpool Execution Services, LLC (Member FINRA and SIPC) in the U.S., and the institutional broker dealer businesses of BMO Nesbitt Burns Inc. (Member Investment Industry Regulatory Organization of Canada and Member Canadian Investor Protection Fund) in Canada and Asia, Bank of Montreal Europe p.l.c. (authorized and regulated by the Central Bank of Ireland) in Europe and BMO Capital Markets Limited (authorized and regulated by the Financial Conduct Authority) in the UK and Australia.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this document is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE CERTIFICATES REFERRED TO IN THESE MATERIALS ARE SUBJECT TO MODIFICATION OR REVISION (INCLUDING THE POSSIBILITY THAT ONE OR MORE CLASSES OF CERTIFICATES MAY BE SPLIT, COMBINED OR ELIMINATED AT ANY TIME PRIOR TO ISSUANCE OR AVAILABILITY OF A FINAL PROSPECTUS) AND ARE OFFERED ON A “WHEN, AS AND IF ISSUED” BASIS.

THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 2 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| Collateral Characteristics | ||

Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate | % of IPB |

| BMO | 20 | 47 | $379,932,162 | 48.4% |

| CREFI | 4 | 13 | $82,501,292 | 10.5% |

| LMF | 5 | 16 | $77,200,000 | 9.8% |

| AREF | 2 | 2 | $51,000,000 | 6.5% |

| 3650 REIT | 3 | 16 | $47,650,000 | 6.1% |

| Natixis | 2 | 3 | $46,560,897 | 5.9% |

| Oceanview | 5 | 5 | $46,062,500 | 5.9% |

| GCMC | 3 | 5 | $42,000,000 | 5.3% |

| SMC | 2 | 2 | $12,196,019 | 1.6% |

| Total: | 46 | 109 | $785,102,870 | 100.0% |

| Loan Pool | ||

| Initial Pool Balance (“IPB”): | $785,102,870 | |

| Number of Mortgage Loans: | 46 | |

| Number of Mortgaged Properties: | 109 | |

| Average Cut-off Date Balance per Mortgage Loan: | $17,067,454 | |

| Weighted Average Current Mortgage Rate: | 5.89592% | |

| 10 Largest Mortgage Loans as % of IPB: | 36.5% | |

| Weighted Average Remaining Term to Maturity: | 103 months | |

| Weighted Average Seasoning: | 4 months | |

| Credit Statistics | ||

| Weighted Average UW NCF Debt Service Coverage Ratio (“DSCR”): | 1.94x | |

| Weighted Average UW NOI Debt Yield (“DY”): | 12.2% | |

| Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”): | 53.0% | |

| Weighted Average Maturity Date/ARD LTV: | 51.7% | |

| Other Statistics | ||

| % of Mortgage Loans with Additional Debt: | 17.7% | |

| % of Mortgage Loans with Single Tenants: | 25.8% | |

| % of Mortgage Loans secured by Multiple Properties: | 28.6% | |

| Amortization | ||

| Weighted Average Original Amortization Term: | 353 months | |

| Weighted Average Remaining Amortization Term: | 352 months | |

| % of Mortgage Loans with Interest-Only: | 72.1% | |

| % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 21.4% | |

| % of Mortgage Loans with Amortizing Balloon: | 6.5% | |

| Lockboxes | ||

| % of Mortgage Loans with Hard Lockboxes: | 52.0% | |

| % of Mortgage Loans with Springing Lockboxes: | 36.8% | |

| % of Mortgage Loans with Soft Lockboxes: | 6.9% | |

| % of Mortgage Loans with Soft (Residential); Hard (Commercial) Lockboxes: | 4.4% | |

| Reserves | ||

| % of Mortgage Loans Requiring Monthly Tax Reserves: | 65.3% | |

| % of Mortgage Loans Requiring Monthly Insurance Reserves: | 42.7% | |

| % of Mortgage Loans Requiring Monthly CapEx Reserves: | 66.1% | |

| % of Mortgage Loans Requiring Monthly TI/LC Reserves: | 38.7% | |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 3 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| Collateral Characteristics | ||

| Ten Largest Mortgage Loans |

| No. | Loan Name | City, State | Mortgage Loan Seller | No. of Prop. | Cut-off Date Balance | % of IPB | Square Feet / Rooms / Units | Property Type | UW NCF DSCR | UW NOI DY | Cut-off Date LTV | Maturity Date/ARD LTV |

| 1 | 70 Hudson Street | Jersey City, NJ | Natixis | 1 | $36,000,000 | 4.6% | 431,281 | Office | 4.10x | 13.3% | 40.5% | 40.5% |

| 2 | Rialto Industrial | Rialto, CA | AREF | 1 | $35,000,000 | 4.5% | 1,106,124 | Industrial | 1.23x | 9.7% | 51.7% | 51.7% |

| 3 | Gilardian NYC Portfolio | New York, NY | BMO | 2 | $28,000,000 | 3.6% | 153 | Multifamily | 2.61x | 11.5% | 39.5% | 39.5% |

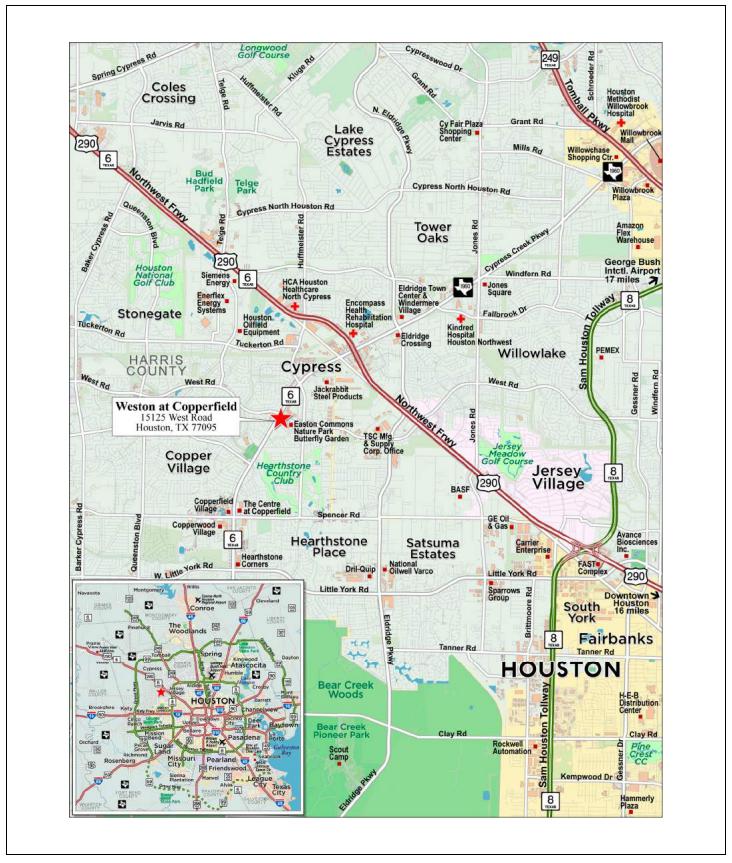

| 4 | Weston at Copperfield | Houston, TX | BMO | 1 | $28,000,000 | 3.6% | 330 | Multifamily | 1.79x | 8.1% | 42.3% | 42.3% |

| 5 | IPG Portfolio | Various, Various | CREFI | 8 | $28,000,000 | 3.6% | 1,791,714 | Industrial | 1.64x | 11.1% | 52.3% | 52.3% |

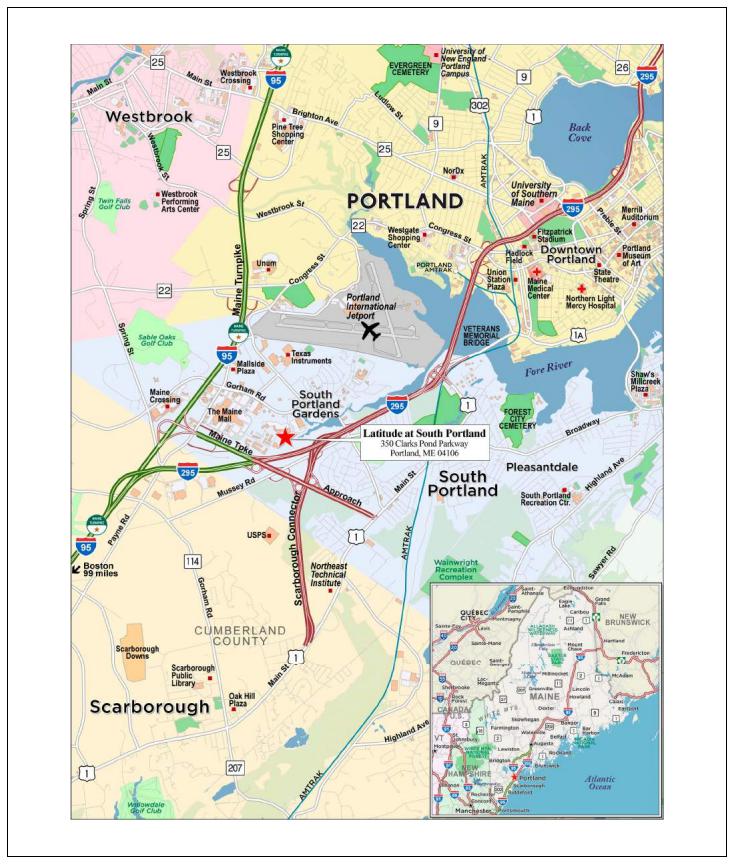

| 6 | Latitude at South Portland | Portland, ME | BMO | 1 | $27,000,000 | 3.4% | 256 | Multifamily | 1.58x | 8.0% | 63.9% | 63.9% |

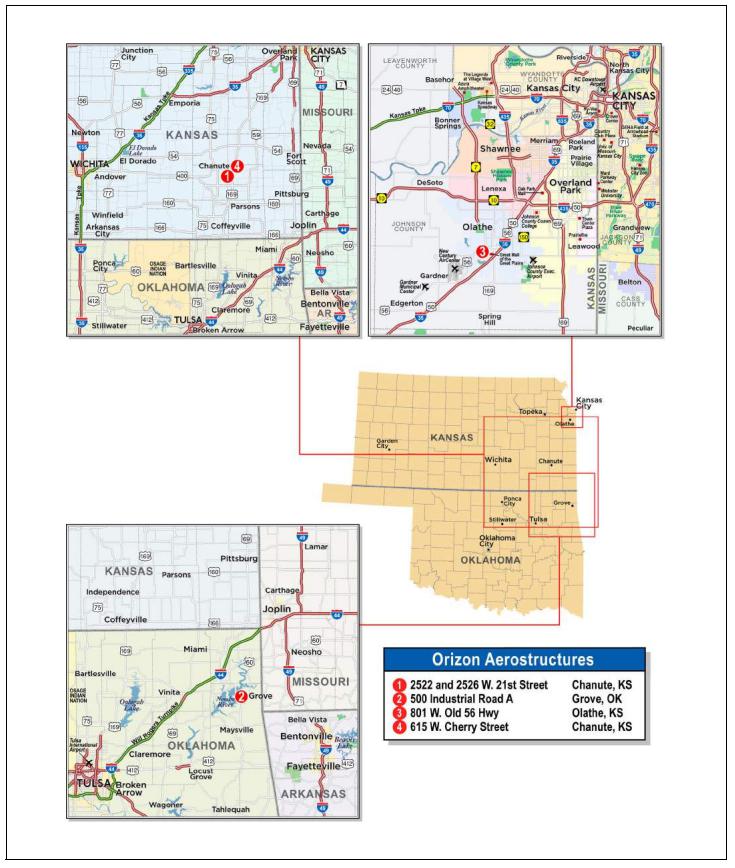

| 7 | Orizon Aerostructures | Various, Various | BMO | 4 | $27,000,000 | 3.4% | 785,000 | Industrial | 1.83x | 12.6% | 48.9% | 48.9% |

| 8 | Park West Village | New York, NY | BMO | 1 | $26,000,000 | 3.3% | 850 | Multifamily | 2.60x | 12.3% | 32.6% | 32.6% |

| 9 | Green Acres | Valley Stream, NY | BMO | 1 | $26,000,000 | 3.3% | 2,081,286 | Retail | 2.10x | 13.0% | 54.5% | 54.5% |

| 10 | 575 Broadway | New York, NY | CREFI | 1 | $25,951,292 | 3.3% | 176,648 | Mixed Use | 1.38x | 12.6% | 59.1% | 54.7% |

| Top 3 Total/Weighted Average | 4 | $99,000,000 | 12.6% | 2.66x | 11.5% | 44.2% | 44.2% | |||||

| Top 5 Total/Weighted Average | 13 | $155,000,000 | 19.7% | 2.32x | 10.8% | 45.3% | 45.3% | |||||

| Top 10 Total/Weighted Average | 21 | $286,951,292 | 36.5% | 2.13x | 11.2% | 48.3% | 47.9% | |||||

| Non-Top 10 Total/Weighted Average | 88 | $498,151,578 | 63.5% | 1.84x | 12.7% | 55.8% | 53.9% | |||||

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 4 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| Collateral Characteristics | ||

| Pari Passu Companion Loan Summary |

No. | Loan Name | Mortgage Loan Seller | Trust Cut-off Date Balance | Aggregate Pari Passu Loan Cut-off Date Balance | Controlling Pooling/Trust & Servicing Agreement | Master Servicer | Special Servicer | Related Pari Passu Loan(s) Securitizations | Related Pari Passu Loan(s) Original Balance |

| 1 | 70 Hudson Street | Natixis | $36,000,000 | $84,000,000 | BBCMS 2022-C18 | Midland | Rialto | BBCMS 2022-C16 BBCMS 2022-C18 | $48,000,000 $36,000,000 |

| 2 | Rialto Industrial | AREF | $35,000,000 | $146,000,000 | BBCMS 2022-C18(1) | Midland(1) | Rialto(1) | BBCMS 2022-C18 Future Securitization(s) | $68,000,000 $78,000,000 |

| 3 | Gilardian NYC Portfolio | BMO | $28,000,000 | $27,750,000 | BMO 2023-C4(2) | Midland(2) | LNR(2) | Future Securitization(s) | $27,750,000 |

| 5 | IPG Portfolio | CREFI | $28,000,000 | $75,000,000 | BMARK 2022-B37 | Midland | Rialto | Benchmark 2022-B37 3650R 2022-PF2 | $60,000,000 $15,000,000 |

| 6 | Latitude at South Portland | BMO | $27,000,000 | $28,192,000 | BMO 2023-C4(2) | Midland(2) | LNR(2) | Future Securitization(s) | $28,192,000 |

| 7 | Orizon Aerostructures | BMO | $27,000,000 | $34,095,000 | BMO 2023-C4(2) | Midland(2) | LNR(2) | Future Securitization(s) | $34,095,000 |

| 8 | Park West Village | BMO | $26,000,000 | $161,500,000 | BBCMS 2022-C17 | KeyBank | KeyBank | BBCMS 2022-C17 BBCMS 2022-C18 BMO 2022-C3 Benchmark 2022-B37 Future Securitization(s) | $47,500,000 $7,500,000 $37,500,000 $62,500,000 $6,500,000 |

| 9 | Green Acres | BMO | $26,000,000 | $344,000,000 | BMO 2023-C4(2) | Midland(2) | LNR(2) | Future Securitization(s) | $344,000,000 |

| 10 | 575 Broadway | CREFI | $25,951,292 | $101,210,038 | BMO 2023-C4(2) | Midland(2) | LNR(2) | Future Securitization(s) | $101,400,000 |

| 12 | Great Lakes Crossing Outlets | BMO | $25,750,000 | $154,250,000 | BMO 2023-C4(2) | Midland(2) | LNR(2) | Future Securitization(s) | $154,250,000 |

| 15 | WRS Retail Portfolio | LMF | $24,000,000 | $60,000,000 | BBCMS 2022-C18 | Midland | Rialto | BBCMS 2022-C18 | $60,000,000 |

| 21 | Triple Net Portfolio | 3650 REIT | $20,000,000 | $73,500,000 | 3650R 2022-PF2 | Midland | 3650 REIT Loan Servicing LLC | 3650R 2022-PF2 Future Securitization(s) | $53,500,000 $20,000,000 |

| 22 | Stoney Creek Hotel Portfolio | BMO | $17,000,000 | $13,900,000 | BMO 2023-C4 | Midland | LNR | Future Securitization(s) | $13,900,000 |

| 26 | 800 Cesar Chavez | 3650 REIT | $15,000,000 | $23,000,000 | 3650R 2022-PF2 | Midland | 3650 REIT Loan Servicing LLC | 3650R 2022-PF2 Future Securitization(s) | $13,000,000 $10,000,000 |

| 28 | Kingston Square Apartments | BMO | $14,000,000 | $37,000,000 | BMO 2022-C3 | Midland | Midland | BMO 2022-C3 | $37,000,000 |

| 30 | PetSmart HQ | 3650 REIT | $12,650,000 | $55,350,000 | 3650R 2021-PF1 | Midland | 3650 REIT Loan Servicing LLC | 3650R 2021-PF1 3650R 2022-PF2 Future Securitization(s) | $23,000,000 $10,000,000 $22,350,000 |

| 33 | Oak Ridge Office Park | Natixis | $10,560,897 | $15,841,346 | BBCMS 2022-C16 | Midland | LNR | BBCMS 2022-C16 | $16,200,000 |

| (1) | Until the securitization of the related controlling pari passu companion loan, the related whole loan will be serviced and administered pursuant to the pooling and servicing agreement for the BBCMS 2022-C18 securitization transaction by the parties thereto. Upon the securitization of the related controlling pari-passu companion loan, servicing of the related whole loan will shift to the servicers under the servicing agreement with respect to such future securitization transaction. |

| (2) | Until the securitization of the related controlling pari passu companion loan, the related whole loan will be serviced and administered pursuant to the pooling and servicing agreement for the BMO 2023-C4 securitization transaction by the parties thereto. Upon the securitization of the related controlling pari-passu companion loan, servicing of the related whole loan will shift to the servicers under the servicing agreement with respect to such future securitization transaction. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 5 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Type |

Weighted Average | ||||||||

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | UW NCF DSCR | UW NOI DY | Cut-off Date LTV | Maturity Date/ARD LTV |

| Multifamily | Garden | 6 | $74,564,000 | 9.5% | 1.54x | 8.9% | 56.6% | 54.1% |

| High Rise | 3 | 54,000,000 | 6.9 | 2.61x | 11.9% | 36.2% | 36.2% | |

| Mid Rise | 2 | 41,189,000 | 5.2 | 1.52x | 8.3% | 61.8% | 61.8% | |

| Low Rise | 1 | 4,000,000 | 0.5 | 1.48x | 9.0% | 55.6% | 55.6% | |

| Subtotal: | 12 | $173,753,000 | 22.1% | 1.86x | 9.7% | 51.4% | 50.4% | |

| Industrial | Warehouse/Distribution | 25 | $80,267,156 | 10.2% | 1.64x | 11.2% | 50.9% | 50.9% |

| Manufacturing | 16 | 50,594,063 | 6.4 | 1.76x | 11.4% | 52.5% | 52.5% | |

| Flex | 3 | 26,268,793 | 3.3 | 2.25x | 14.1% | 52.1% | 52.1% | |

| Warehouse | 1 | 15,000,000 | 1.9 | 2.00x | 8.4% | 53.7% | 53.7% | |

| Subtotal: | 45 | $172,130,011 | 21.9% | 1.80x | 11.4% | 51.8% | 51.8% | |

| Retail | Regional Mall | 2 | $51,750,000 | 6.6% | 2.30x | 15.2% | 49.8% | 49.8% |

| Anchored | 3 | 33,550,000 | 4.3 | 1.99x | 13.5% | 56.0% | 56.0% | |

| Shadow Anchored | 14 | 31,450,000 | 4.0 | 1.49x | 11.2% | 58.9% | 57.9% | |

| Unanchored | 2 | 27,596,019 | 3.5 | 1.55x | 11.1% | 50.8% | 49.2% | |

| Subtotal: | 21 | $144,346,019 | 18.4% | 1.91x | 13.2% | 53.4% | 52.9% | |

| Hospitality | Limited Service | 11 | $58,350,662 | 7.4% | 2.18x | 19.1% | 56.0% | 51.0% |

| Extended Stay | 2 | 29,100,000 | 3.7 | 1.88x | 15.4% | 56.8% | 54.0% | |

| Full Service | 1 | 22,000,000 | 2.8 | 1.69x | 14.4% | 58.7% | 55.5% | |

| Subtotal: | 14 | $109,450,662 | 13.9% | 2.00x | 17.2% | 56.7% | 52.7% | |

| Mixed Use | Retail/Office | 2 | $47,951,292 | 6.1% | 1.32x | 11.4% | 60.1% | 56.0% |

| Office/Retail | 1 | 25,000,000 | 3.2 | 1.43x | 9.6% | 51.2% | 51.2% | |

| Retail/Multifamily | 1 | 8,250,000 | 1.1 | 1.58x | 8.3% | 64.0% | 64.0% | |

| Subtotal: | 4 | $81,201,292 | 10.3% | 1.38x | 10.5% | 57.8% | 55.4% | |

| Office | CBD | 2 | $48,650,000 | 6.2% | 3.62x | 12.6% | 46.2% | 46.2% |

| Suburban | 4 | 28,209,386 | 3.6 | 1.80x | 11.9% | 57.1% | 52.1% | |

| Subtotal: | 6 | $76,859,386 | 9.8% | 2.95x | 12.3% | 50.2% | 48.4% | |

| Self Storage | Self Storage | 5 | $19,362,500 | 2.5% | 2.40x | 12.2% | 49.1% | 49.1% |

| Manufactured Housing | Manufactured Housing | 2 | $8,000,000 | 1.0% | 1.37x | 9.7% | 45.6% | 45.6% |

| Total / Weighted Average: | 109 | $785,102,870 | 100.0% | 1.94x | 12.2% | 53.0% | 51.7% | |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 6 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

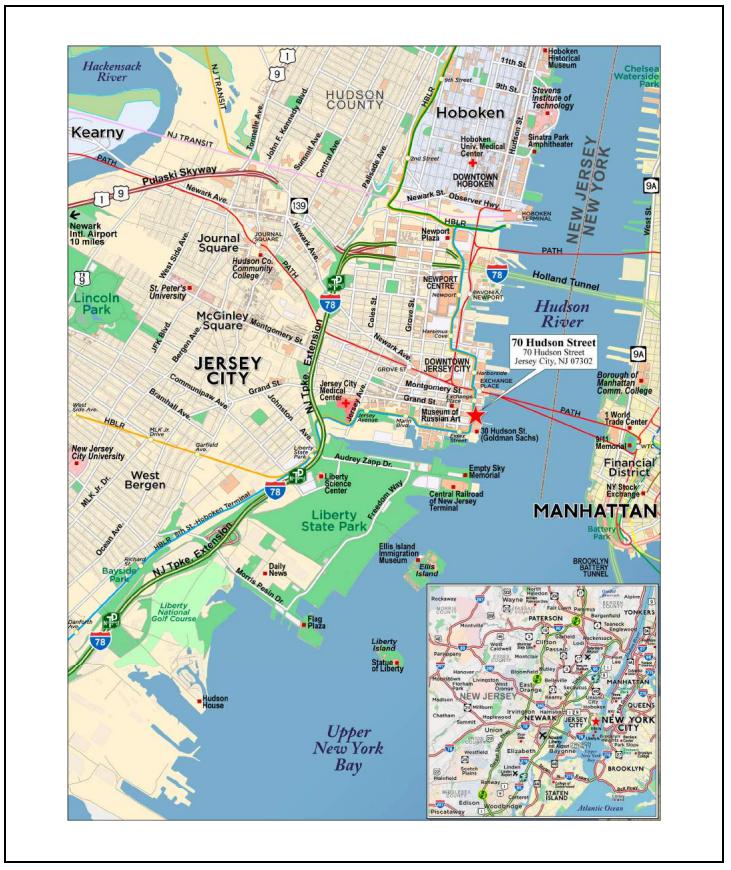

| No. 1 – 70 Hudson Street | ||

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 7 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 1 – 70 Hudson Street | ||

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 8 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 1 – 70 Hudson Street | ||

| Mortgage Loan Information | Property Information | |||

| Mortgage Loan Seller: | Natixis | Single Asset / Portfolio: | Single Asset | |

| Original Principal Balance(1): | $36,000,000 | Title: | Fee | |

| Cut-off Date Principal Balance(1): | $36,000,000 | Property Type – Subtype: | Office – CBD | |

| % of IPB: | 4.6% | Net Rentable Area (SF): | 431,281 | |

| Loan Purpose: | Acquisition | Location: | Jersey City, NJ | |

| Borrower: | 70 Hudson LLC | Year Built / Renovated: | 2002 / 2018 | |

| Borrower Sponsor: | NAP | Occupancy: | 94.1% | |

| Interest Rate: | 3.19200% | Occupancy Date: | 9/30/2022 | |

| Note Date: | 2/11/2022 | 4th Most Recent NOI (As of)(4): | $1,587,874 (12/31/2019) | |

| Maturity Date: | 3/8/2027 | 3rd Most Recent NOI (As of)(4): | $6,836,402 (12/31/2020) | |

| Interest-only Period: | 60 months | 2nd Most Recent NOI (As of)(4): | $14,298,336 (12/31/2021) | |

| Original Term: | 60 months | Most Recent NOI (As of)(5): | $15,425,668 (T-6 Annualized 9/30/2022) | |

| Original Amortization Term: | None | UW Economic Occupancy: | 94.0% | |

| Amortization Type: | Interest Only | UW Revenues: | $22,465,058 | |

| Call Protection(2): | YM1(35),DorYM1(18),O(7) | UW Expenses: | $6,481,062 | |

| Lockbox / Cash Management: | Hard / Springing | UW NOI: | $15,983,997 | |

| Additional Debt(1): | Yes | UW NCF: | $15,919,304 | |

| Additional Debt Balance(1): | $84,000,000 / $76,950,000 | Appraised Value / Per SF: | $296,000,000 / $686 | |

| Additional Debt Type(1): | Pari Passu / Subordinate | Appraisal Date: | 10/19/2022 | |

| Escrows and Reserves(3) | Financial Information(1) | ||||||

| Initial | Monthly | Initial Cap | Senior Notes | Whole Loan | |||

| Taxes: | $263,338 | $131,669 | N/A | Cut-off Date Loan / SF: | $278 | $457 | |

| Insurance: | $313,920 | $26,160 | N/A | Maturity Date Loan / SF: | $278 | $457 | |

| Replacement Reserves: | $0 | $5,391 | N/A | Cut-off Date LTV: | 40.5% | 66.5% | |

| TI/LC Reserve: | $0 | $0 | N/A | Maturity Date LTV: | 40.5% | 66.5% | |

| Other: | $306,422 | $0 | N/A | UW NCF DSCR: | 4.10x | 2.50x | |

| UW NOI Debt Yield: | 13.3% | 8.1% | |||||

| Sources and Uses | ||||||||

| Sources | Proceeds | % of Total | Uses | Proceeds | % of Total | |||

| Senior Loan(1) | $120,000,000 | 38.9 | % | Purchase Price | $300,000,000 | 97.3 | % | |

| Subordinate Loan(1) | 76,950,000 | 24.9 | Closing Costs | 7,587,304 | 2.5 | |||

| Borrower Sponsor Equity | 111,520,984 | 36.2 | Upfront Reserve | 883,680 | 0.3 | |||

| Total Sources | $308,470,984 | 100.0 | % | Total Uses | $308,470,984 | 100.0 | % | |

| (1) | The 70 Hudson Street Mortgage Loan (as defined below) is part of a whole loan evidenced by six senior pari passu notes totaling $120.0 million and one subordinate companion note of $76.95 million, with an aggregate outstanding principal balance as of the Cut-off Date of $196.95 million (the “70 Hudson Street Whole Loan”). The Financial Information in the chart above reflects the Cut-off Date Balance and Maturity Date Balance of the 70 Hudson Street Senior Notes (as defined below) and the 70 Hudson Street Whole Loan. |

| (2) | The borrower has the option to prepay (with the payment of a yield maintenance premium) the 70 Hudson Street Whole Loan at any time prior to the open prepayment period. In addition, the borrower has the option to defease the 70 Hudson Street Whole Loan in full, but not in part, on and after the first payment date following the earlier to occur of (i) two years after the closing date of the securitization that includes the last note to be securitized and (ii) February 11, 2026. |

| (3) | For a full description of Escrows and Reserves, please refer to “Escrows and Reserves” below. |

| (4) | The increase in NOI from 2019 to 2021 was driven by an increase in occupancy. |

| (5) | The 70 Hudson Street Property (as defined below) was acquired in February 2022. Therefore, the Most Recent NOI is based on the annualized six-month period through September 2022. |

The Loan. The largest mortgage loan (the “70 Hudson Street Mortgage Loan”) is part of a whole loan with an aggregate outstanding principal balance as of the Cut-off Date of $196.95 million consisting of six pari passu senior notes with an aggregate outstanding principal balance as of the Cut-off Date of $120.0 million (the “70 Hudson Street Senior Notes”) and one subordinate companion note with an outstanding principal balance as of the Cut-off Date of $76.95 million (the “70 Hudson Street Subordinate Companion Note”). The 70 Hudson Street Whole Loan was originated by Natixis Real Estate Capital LLC on February 11, 2022. The 70 Hudson Street Whole Loan is secured by the borrower’s fee interest in a 431,281 square foot, Class A office property located in Jersey City, New Jersey (the “70 Hudson Street Property”). Notes A-A-3, A-A-4, A-A-5 and A-A-6 with an outstanding principal balance as of the Cut-off Date of $36.0 million, will be included in the

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 9 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 1 – 70 Hudson Street | ||

BMO 2023-C4 trust. The 70 Hudson Street Whole Loan has a five-year term, is interest-only for the full term of the loan and accrues interest at a rate of 3.19200% per annum on an Actual/360 basis. Note A-B is the controlling note for the 70 Hudson Street Whole Loan. Upon the occurrence of a control appraisal period, Note A-A-1 will be the controlling note. The 70 Hudson Street Whole Loan is serviced under the BBCMS 2022-C18 pooling and servicing agreement. See “Description of the Mortgage Pool—The Whole Loans—The 70 Hudson Street Pari Passu-AB Whole Loan” and “The Pooling and Servicing Agreement—Servicing of the Outside Serviced Mortgage Loans” in the Preliminary Prospectus.

| Whole Loan Summary | |||||

| Note | Original Balance | Cut-off Date Balance | Note Holder | Lead Servicer for Whole Loan | Controlling Piece |

| A-A-1 | $36,000,000 | $36,000,000 | BBCMS 2022-C18 | Yes | No |

| A-A-2 | $48,000,000 | $48,000,000 | BBCMS 2022-C16 | No | No |

| A-A-3 | $12,000,000 | $12,000,000 | BMO 2023-C4 | No | No |

| A-A-4 | $12,000,000 | $12,000,000 | BMO 2023-C4 | No | No |

| A-A-5 | $6,000,000 | $6,000,000 | BMO 2023-C4 | No | No |

| A-A-6 | $6,000,000 | $6,000,000 | BMO 2023-C4 | No | No |

| Total Senior Notes | $120,000,000 | $120,000,000 | |||

| A-B | $76,950,000 | $76,950,000 | John Hancock Life Insurance Company (U.S.A.) | No | Yes(1) |

| Whole Loan | $196,950,000 | $196,950,000 | |||

| (1) | Note A-B is the controlling note for the 70 Hudson Street Whole Loan. Upon the occurrence of a control appraisal period, Note A-A-1 will be controlling note. The 70 Hudson Street Whole Loan will be serviced under the BBCMS 2022-C18 pooling and servicing agreement. |

The Property. The 70 Hudson Street Property is a Class A, 12-story office building totaling 431,281 square feet located in Jersey City, New Jersey, situated within Jersey City’s waterfront district along New Jersey’s Gold Coast with views of Manhattan and the Statue of Liberty. The 70 Hudson Street Property was built in 2002 and most recently renovated in 2018, including a new atrium lobby, upgraded/renovated parking garage, roof replacement and upgraded common corridor and retail entryways. Tenants at the 70 Hudson Street Property have access to a dedicated parking structure, which has 226 parking spaces (approximately 0.5 spaces per 1,000 square feet). The 70 Hudson Street Property has access to Manhattan through multiple public transportation options (PATH, NY Waterway Ferry and NJ Transit Bus & Rail Services) offering direct access into Midtown and Downtown Manhattan. The 70 Hudson Street Property is 94.1% occupied by seven tenants with a weighted average remaining lease term of approximately 10.0 years as of the Cut-off Date with three tenants (78.5% of NRA) having a weighted average remaining lease term of approximately 10 years as of the Cut-off Date.

COVID-19 Update. As of November 2, 2022, 70 Hudson Street is open and operating. As of the date of this term sheet, the 70 Hudson Street Mortgage Loan is not subject to any modification or forbearance requests.

Major Tenants. The three largest tenants based on net rentable area are TD Ameritrade, Fidessa Corporation and Federal Home Loan Bank of New York.

TD Ameritrade (208,396 square feet; 48.3% of NRA; 51.9% of underwritten base rent; Moody’s/S&P/Fitch: A2/A/A). TD Ameritrade, a subsidiary of Charles Schwab, is an online brokerage that provides services to both individuals and institutions that invest online. The company hosts over 11 million customer accounts from across the world. Investors use the company’s electronic trading platforms to buy and sell securities such as stocks, ETFs, mutual funds, options, futures, foreign exchange, and fixed-income investments. Customers can trade these financial securities on their computer or via mobile phone applications. In October 2020, TD Ameritrade was acquired by The Charles Schwab Corporation. The two companies, as of February 2022, have a combined $7.69 trillion in client assets, 33.4 million brokerage accounts, and 6.6 million daily average trades. TD Ameritrade spent approximately $40.3 million ($193.34 per square foot) on tenant improvements to its occupied space. TD Ameritrade has been in occupancy since March 2019. TD Ameritrade has no termination option and has one, seven- or ten-year renewal option remaining.

Fidessa Corporation (78,000 square feet; 18.1% of NRA; 18.0% of underwritten base rent; Moody’s/S&P/Fitch: NR/NR/NR). Fidessa Corporation (“Fidessa”) is a British based financial software company offering financial consulting, investment, trading, and advising services. Fidessa offers both buy-side solutions and sell-side solutions, global connectivity services and solutions, market data services, and investment infrastructure to customers around the globe. Buy-side products and services include compliance, decision support, order and execution management, trading, and portfolio management. Sell-side products and services include order management, advanced trading tools, smart order routing, high frequency trading, compliance, and business intelligence. Fidessa offers both enterprise solutions, and a SaaS platform to help connect

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 10 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 1 – 70 Hudson Street | ||

customers around the globe. Fidessa spent approximately $15.0 million ($192.78 per square foot) on tenant improvements to its occupied space. Fidessa has been in occupancy since March 2017. Fidessa has no termination option and has one, ten-year renewal option remaining.

Federal Home Loan Bank of New York (52,041 square feet; 12.1% of NRA; 12.6% of underwritten base rent; Moody’s/S&P/Fitch: Aaa/AA+/NR). The Federal Home Loan Bank of New York is part of the congressionally chartered, nationwide Federal Home Loan Bank System, which was created in 1932 to provide a flexible credit liquidity source for member community lenders engaged in home mortgage and neighborhood lending. The Federal Home Loan Bank of New York helps community lenders in New Jersey, New York, Puerto Rico and the U.S. Virgin Islands advance housing and community growth. The Federal Home Loan Bank of New York increases the availability of mortgages and home financing to families of all income levels by offering high-value correspondent and cash management services to assist their members, more effectively serve their neighborhoods and meet their Community Reinvestment Act responsibilities. The Federal Home Loan Bank of New York spent approximately $21.2 million ($407.28 per square foot) on tenant improvements to its occupied space. The Federal Home Loan Bank of New York has been in occupancy since February 2018. The Federal Home Loan Bank of New York has no termination or appropriation option and has one, five-year renewal option remaining.

Environmental. According to a Phase I environmental assessment dated October 24, 2022, there was no evidence of any recognized environmental conditions at the 70 Hudson Street Property.

The following table presents certain information relating to the historical and current occupancy of the 70 Hudson Street Property. The seller of the 70 Hudson Street Property acquired it vacant in 2016 and has since invested over $21.0 million towards capital improvements and leasing up the 70 Hudson Street Property.

| Historical and Current Occupancy(1) | ||||

| 2018 | 2019 | 2020 | 2021 | Current(2) |

| 31.5% | 71.3% | 94.0% | 94.1% | 94.1% |

| (1) | Historical occupancies are as of December 31 of each respective year. |

| (2) | Current occupancy is as of September 30, 2022 |

The following table presents certain information relating to the largest tenants based on net rentable area of the 70 Hudson Street Property:

| Top Tenant Summary(1) | |||||||||||

| Tenant | Ratings Moody’s/S&P/Fitch(2) | Net Rentable Area (SF) | % of Total NRA | UW Base Rent PSF(3) | UW Base Rent(3) | % of Total UW Base Rent(3) | Lease Expiration Date | ||||

| TD Ameritrade | A2/A/A | 208,396 | 48.3 | % | $48.91 | $10,193,424 | 51.9 | % | 6/30/2033 | ||

| Fidessa Corporation | NR/NR/NR | 78,000 | 18.1 | $45.27 | 3,530,850 | 18.0 | 12/31/2032 | ||||

| Federal Home Loan Bank of New York | Aaa/AA+/NR | 52,041 | 12.1 | $47.62 | 2,478,225 | 12.6 | 12/31/2033 | ||||

| Gucci America, Inc. | NR/A/NR | 51,824 | 12.0 | $50.58 | 2,621,067 | 13.3 | 12/31/2029 | ||||

| New Jersey CVS Pharmacy, LLC | Baa2/BBB/NR | 11,659 | 2.7 | $60.00 | 699,540 | 3.6 | 10/31/2038 | ||||

| Top Five Tenants | 401,920 | 93.2 | % | $48.57 | $19,523,108 | 99.4 | % | ||||

| Other Tenants(4) | 3,713 | 0.9 | % | $32.29 | $119,910 | 0.6 | % | ||||

| Occupied Collateral Total / Wtd. Avg. | 405,633 | 94.1 | % | $48.43 | $19,643,018 | 100.0 | % | ||||

| Vacant Space | 25,648 | 5.9 | % | ||||||||

| Collateral Total | 431,281 | 100.0 | % | ||||||||

| (1) | Based on the underwritten rent roll dated September 30, 2022. |

| (2) | In certain instances, ratings provided are those of the parent company of the entity shown, whether or not the parent company guarantees the lease. |

| (3) | UW Base Rent, UW Base Rent PSF and % of Total UW Base Rent are inclusive of approximately $558,355 of contractual rent steps through December 1, 2023 and approximately $385,165 of straight line rent. |

| (4) | Maman NJ City, LLC leases 2,000 square feet with a rent commencement date of November 25, 2021. The first-year rent was 10% of gross sales of the tenant, the second-year base rent will be $45.00 PSF, the third-year base rent will be $60.00 PSF and 2.75% rent steps annually thereafter. Given unknown gross sales of the tenant, the UW Base Rent is $0 for Maman NJ City, LLC. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 11 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 1 – 70 Hudson Street | ||

The following table presents certain information relating to the tenant lease expirations of the 70 Hudson Street Property:

Lease Rollover Schedule(1) | ||||||||||||||

| Year | Number of Leases Expiring | Net Rentable Area Expiring | % of NRA Expiring | UW Base Rent Expiring(2)(3) | % of UW Base Rent Expiring | Cumulative Net Rentable Area Expiring | Cumulative % of NRA Expiring | Cumulative UW Base Rent Expiring(2) | Cumulative % of UW Base Rent Expiring | |||||

| Vacant | NAP | 25,648 | 5.9 | % | NAP | NAP | 25,648 | 5.9% | NAP | NAP | ||||

| 2022 & MTM | 0 | 0 | 0.0 | $0 | 0.0 | % | 25,648 | 5.9% | $0 | 0.0% | ||||

| 2023 | 0 | 0 | 0.0 | 0 | 0.0 | 25,648 | 5.9% | $0 | 0.0% | |||||

| 2024 | 0 | 0 | 0.0 | 0 | 0.0 | 25,648 | 5.9% | $0 | 0.0% | |||||

| 2025 | 0 | 0 | 0.0 | 0 | 0.0 | 25,648 | 5.9% | $0 | 0.0% | |||||

| 2026 | 0 | 0 | 0.0 | 0 | 0.0 | 25,648 | 5.9% | $0 | 0.0% | |||||

| 2027 | 0 | 0 | 0.0 | 0 | 0.0 | 25,648 | 5.9% | $0 | 0.0% | |||||

| 2028 | 0 | 0 | 0.0 | 0 | 0.0 | 25,648 | 5.9% | $0 | 0.0% | |||||

| 2029 | 1 | 51,824 | 12.0 | 2,621,067 | 13.3 | 77,472 | 18.0% | $2,621,067 | 13.3% | |||||

| 2030 | 1 | 1,713 | 0.4 | 119,910 | 0.6 | 79,185 | 18.4% | $2,740,977 | 14.0% | |||||

| 2031 | 1 | 2,000 | 0.5 | 0 | 0.0 | 81,185 | 18.8% | $2,740,977 | 14.0% | |||||

| 2032 | 1 | 78,000 | 18.1 | 3,530,850 | 18.0 | 159,185 | 36.9% | $6,271,828 | 31.9% | |||||

| 2033 & Beyond | 3 | 272,096 | 63.1 | 13,371,190 | 68.1 | 431,281 | 100.0% | $19,643,018 | 100.0% | |||||

| Total | 7 | 431,281 | 100.0 | % | $19,643,018 | 100.0 | % | |||||||

| (1) | Based on the underwritten rent roll dated September 30, 2022. |

| (2) | UW Base Rent Expiring and Cumulative UW Base Rent Expiring are inclusive of approximately $558,355 of contractual rent steps through December 1, 2023 and approximately $385,165 of straight line rent. |

| (3) | Maman NJ City, LLC leases 2,000 square feet with a rent commencement date of November 25, 2021. The first-year rent was 10% of gross sales of the tenant, the second-year base rent will be $45.00 PSF, the third-year base rent will be $60.00 PSF and 2.75% rent steps annually thereafter. Given unknown gross sales of the tenant, the UW Base Rent is $0 for Maman NJ City, LLC. |

The following table presents certain information relating to the operating history and underwritten cash flows of the 70 Hudson Street Property:

| Operating History and Underwriting Net Cash Flow | |||||||||

| 2019 | 2020 | 2021 | TTM(1) | Underwritten | Per Square Foot | %(2) | |||

| Base Rent(3) | $5,535,328 | $9,834,710 | $17,445,367 | $19,010,898 | $18,699,497 | $43.36 | 78.2 | % | |

| Rent Steps(4) | 0 | 0 | 0 | 0 | 558,355 | 1.29 | 2.3 | ||

| Straight-Line Rent | 0 | 0 | 0 | 0 | 385,165 | 0.89 | 1.6 | ||

| Vacant Income | 0 | 0 | 0 | 0 | 1,102,864 | 2.56 | 4.6 | ||

| Gross Potential Rent | $5,535,328 | $9,834,710 | $17,445,367 | $19,010,898 | $20,745,882 | $48.10 | 86.8 | % | |

| Total Reimbursements | 531,016 | 665,556 | 921,565 | 1,431,220 | 1,798,717 | 4.17 | 7.5 | ||

| Total Other Income | 1,164,511 | 1,518,118 | 1,340,257 | 1,351,198 | 1,354,400 | 3.14 | 5.7 | ||

| Net Rental Income | $7,230,855 | $12,018,384 | $19,707,189 | $21,793,316 | $23,898,998 | $55.41 | 100.0 | % | |

| (Vacancy/Credit Loss) | 0 | 0 | 0 | 0 | (1,433,940) | (3.32) | (6.0 | ) | |

| Effective Gross Income | $7,230,855 | $12,018,384 | $19,707,189 | $21,793,316 | $22,465,058 | $52.09 | 94.0 | % | |

| Total Expenses | 5,642,981 | 5,181,982 | 5,408,854 | 6,367,648 | 6,481,062 | 15.03 | 28.8 | ||

| Net Operating Income | $1,587,874 | $6,836,402 | $14,298,335 | $15,425,668 | $15,983,997 | $37.06 | 71.2 | % | |

| Total TI/LC, Capex/RR | 0 | 0 | 0 | 0 | 64,692 | 0.15 | 0.3 | ||

| Net Cash Flow | $1,587,874 | $6,836,402 | $14,298,335 | $15,425,668 | $15,919,304 | $36.91 | 70.9 | % | |

| (1) | TTM is based on the trailing six months annualized ending on September 30, 2022. |

| (2) | % column represents percent of Net Rental Income for all revenue lines and represents percent of Effective Gross Income for the remainder of the fields. |

| (3) | Base Rent is based on the underwritten rent roll as of September 30, 2022. The increase in UW Base Rent from 2021 Base Rent is associated with the expiration of a free rent period. |

| (4) | Rent Steps totaling approximately $558,355 are taken through December 1, 2023. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 12 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 1 – 70 Hudson Street | ||

The Market. The 70 Hudson Street Property is situated within the Hudson Waterfront office submarket of Jersey City. The Hudson Waterfront office submarket has established itself as a long-standing institutional market for both investors and tenants. The Hudson Waterfront office submarket has attracted tenants such as JP Morgan, Goldman Sachs, AIG, Mizuho, Bank of NY, RBC, Pearson Education, Marsh & McLennan, BNP Paribas, Merck, New York Life, and Ernst & Young. There has been significant residential growth in the area with over 13,000 rental units throughout 38 buildings constructed since 2010. In addition, 3,410 units are under construction and 19,500 units are approved. The 70 Hudson Street Property is located at the Exchange Place PATH Station, near Metro-Area mass transit system services (PATH, NJ Transit-Hudson-Bergen Line Light Rail, NY Waterway Ferry and NJ Transit Bus & Rail Services).

According to a third-party report, as of December 13, 2022, the Hudson Waterfront office submarket had an inventory of approximately 31.5 million square feet, overall vacancy in the market of approximately 13.9% and average asking rents of $42.35 per square foot. According to a third-party market report, the estimated 2021 population within a one-, three- and five-mile radius of the 70 Hudson Street Property is 67,445, 879,441 and 1,892,770, respectively. The estimated 2021 average household income within the same radii is $205,471, $167,096 and $168,161, respectively.

The following table presents certain information relating to comparable office leases for the 70 Hudson Street Property:

| Comparable Office Leases(1) | |||||||||

| Property / Location | Tenant SF | Year Built / Renovated | Tenant | Rent PSF | Lease Date | Lease Term | Structure | ||

70 Hudson Street Jersey City, NJ | 388,944(2) | 2002 / 2018 | Various | $48.33(2) | Various(2) | Various(2) | Modified Gross | ||

Exchange Place Center 10 Exchange Place Jersey City, NJ | 5,932 9,920 78,709 | 1988 / 2019 | Nagarro, Inc. Zim America Integrated Shipping Ace | $44.50 $42.50 $43.00 | Sep-2022 May-2022 Feb-2021 |

| 5.3 Yrs. 10.8 Yrs. 8.9 Yrs. |

| Modified Gross |

Evertrust Plaza 1 Evertrust Plaza Jersey City, NJ | 6,989 2,532 | 1986 / NAP | Celltrion Inc. Staci Flex Made Logistics | $36.00 $36.50 | Aug-2022 Aug-2022 |

| 5.2 Yrs. 3.2 Yrs. |

| Modified Gross |

Goldman Sachs 30 Hudson Street Jersey City, NJ | 111,416 227,852 | 2004 / NAP | Merck & Company AIG | $46.00 $45.00 | Sep-2020 Jun-2020 |

| 10.4 Yrs. 15.0 Yrs. |

| Modified Gross |

Harborside Financial Center 3 210 Hudson Street Jersey City, NJ | 4,491 | 1928 / 1986 | Flipt | $45.00 | Sep-2020 | 5.3 Yrs. | Modified Gross | ||

Colgate Center 101 Hudson Street Jersey City, NJ | 6,694 6,923 10,525 13,588 | 1992 / NAP | Trend Micro Insight Catastrophe Insurance NJ Institute of Technology DealCloud | $46.00 $45.00 $47.00 $46.00 | Jul-2021 Jul-2021 Jul-2020 Jun-2020 |

| 5.3 Yrs. 10.8 Yrs. 5.3 Yrs. 3.1 Yrs. |

| Modified Gross |

Newport Tower 525 Washington Boulevard Jersey City, NJ | 183,087 4,672 23,204 | 1992 / NAP | BNP Super Micro Computer Temco Service Industries, Inc. | $39.25 $46.00 $43.00 | Jun-2020 May-2020 Nov-2019 |

| 20.0 Yrs. 1.5 Yrs. 11.0 Yrs. |

| Modified Gross |

Office Property 15 Exchange Place Jersey City, NJ | 5,274 14,073 | 1920 / 2017 | Claro Enterprise Drivewealth Holdings | $38.00 $41.00 | Sep-2021 Aug-2021 |

| 3.0 Yrs. 7.0 Yrs. |

| Modified Gross |

International Financial Tower 95 Christopher Columbus Drive Jersey City, NJ | 310,137 | 1989 / NAP | Pershing | $37.50 |

Jul-2021 |

| 16.0 Yrs. | Modified Gross | |

| (1) | Source: Appraisal unless otherwise indicated. |

| (2) | Tenant SF, Rent PSF, Lease Date and Lease Term for the 70 Hudson Street Property is based on underwritten rent from the underwritten rent roll dated September 30, 2022. Tenant SF represents office space occupied by tenants with modified gross lease structure. Rent PSF is inclusive of (i) contractual rent steps on office tenants through December 1, 2023 in the amount of approximately $557,846 and (ii) straight line rent on office tenants in the amount of approximately $384,604. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 13 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 1 – 70 Hudson Street | ||

The following table presents certain information relating to comparable sales for the 70 Hudson Street Property:

| Comparable Sales(1) | |||||||

| Property Location | Sale Date | Total NRA (SF) | Total Occupancy | Sale Price | Sale Price PSF | Adjusted Sales Price PSF | |

70 Hudson Street Jersey City, NJ | 431,281(2) | 94.1% | (2) | NAP | NAP | NAP | |

Colgate Center 101 Hudson Street Jersey City, NJ | Oct-2022 | 1,347,712 | 74.0% | $346,000,000 | $257 | $257 | |

Key West Corporate Center 9713, 9715, 9717 Key West Avenue Rockville, MD | Jun-2022 | 298,300 | 100.0% | $148,000,000 | $496 | $496 | |

15 Exchange Place Jersey City, NJ | Feb-2022 | 136,000 | 71.0% | $48,000,000 | $353 | $353 | |

Warren Corporate Center 100 and 200 Everest Way Warren, NJ | Jun-2021 | 315,494 | 100.0% | $150,250,000 | $476 | $476 | |

Two Washingtonian Center 9737 Washingtonian Boulevard Gaithersburg, MD | Sep-2021 | 274,805 | 100.0% | $119,000,000 | $433 | $433 | |

Newport Office Center 545 Washington Boulevard Jersey City, NJ | Jan-2020 | 866,706 | 95.0% | $372,800,000 | $430 | $430 | |

179 Lincoln on the Greenway 179 Lincoln Street Boston, MA | Jan-2020 | 221,474 | 85.0% | $155,650,000 | $703 | $703 | |

| (1) | Source: Appraisal unless otherwise indicated. |

| (2) | Based on the underwritten rent roll dated September 30, 2022. |

The Borrower. The borrower is 70 Hudson LLC, a Delaware limited liability company. The borrower is structured as a single purpose bankruptcy-remote entity, with two independent directors. Legal counsel to the borrower delivered a non-consolidation opinion in connection with the origination of the 70 Hudson Street Whole Loan. There is no non-recourse carveout guarantor or separate environmental indemnitor with respect to the 70 Hudson Street Whole Loan. The 70 Hudson Street Whole Loan is recourse to the borrower.

The Borrower Sponsor. The borrower sponsor is Hana Alternative Asset Management Co., Ltd. (“Hana”), which is an investment management firm affiliated with HANA Financial Group, specializing in alternative investments. Hana was founded in 2006 as the first asset management company to specialize in commercial real estate in Korea. As of November 2022, Hana had approximately $7.35 billion USD of assets under management of which 66.8% are investments in real estate.

Property Management. The 70 Hudson Street Property is managed by CBRE, Inc.

Escrows and Reserves. At origination, the borrower deposited into escrow (i) approximately $263,338 for real estate taxes, (ii) approximately $313,920 for insurance premiums, (iii) $200,000 for the rent abatement reserve and (iv) approximately $106,422 for the Maman reserve for outstanding approved leasing expense.

Tax Escrows – On a monthly basis, the borrower is required to escrow 1/12th of the annual estimated real estate taxes, which currently equates to approximately $131,669.

Insurance Escrows – On a monthly basis, the borrower is required to escrow 1/12th of the annual estimated insurance premiums, which currently equates to approximately $26,160.

Replacement Reserve – On a monthly basis, the borrower is required to escrow $5,391 for replacement reserves.

Lockbox / Cash Management. The 70 Hudson Street Whole Loan is structured with a hard lockbox and springing cash management upon the occurrence and continuance of a Cash Management Period (as defined below). The borrower is required to cause each tenant at the 70 Hudson Street Property to deposit rents directly into a lender-controlled lockbox account. In addition, the borrower is required to cause all rents received by the borrower or property manager with respect to the 70 Hudson Street Property to be deposited into such lockbox account within one business day. During the continuance of a Cash Management Period, all funds in the lockbox account are required to be swept daily to a lender-controlled cash management account and disbursed in accordance with the 70 Hudson Street Whole Loan documents, and excess funds on deposit in the cash management account (after payments of required monthly reserve deposits, debt service payment on the 70 Hudson Street Whole Loan, operating expenses and cash management bank fees) will be applied as follows: (a)

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 14 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 1 – 70 Hudson Street | ||

if a Significant Tenant Trigger Event (as defined below) has occurred and is continuing (and no other Cash Management Period is then continuing), to a Significant Tenant (as defined below) reserve subaccount, (b) if a Cash Management Period (other than a Cash Management Period solely due to a Significant Tenant Trigger Event) has occurred and is continuing, to an excess cash flow reserve account or (c) if no Cash Management Period has occurred and is continuing, to the borrower.

A “Cash Management Period” means a period commencing upon the occurrence of (i) an event of default under the 70 Hudson Street Whole Loan, (ii) at the end of a calendar quarter, the debt yield on the 70 Hudson Street Whole Loan is less than 6.50%, or (iii) the occurrence of a Significant Tenant Trigger Event; and will end (x) with respect to clause (i) above, if the lender has accepted a cure of such event of default; (y) with respect to clause (ii) above, the debt yield on the 70 Hudson Street Whole Loan is at least equal to 6.75% for two consecutive calendar quarters; and (z) with respect to clause (iii) above, the cure of such Significant Tenant Trigger Event.

A “Significant Tenant Trigger Event” will commence upon the earliest to occur of (i) any Significant Tenant is in default of any monetary or material non-monetary term of its Significant Tenant lease, (ii) any Significant Tenant (a) terminates its lease or (b) notifies the borrower or manager, in writing, that it intends to terminate its Significant Tenant lease, or (iii) any Significant Tenant becomes insolvent or a debtor in any bankruptcy action.

A “Significant Tenant” means TD Ameritrade and thereafter, any acceptable significant replacement tenant.

Subordinate Debt. The 70 Hudson Street Property also secures the 70 Hudson Street Subordinate Companion Note, which has an outstanding Cut-off Date principal balance of $76,950,000. The 70 Hudson Street Subordinate Companion Note accrues interest at a rate of 3.19200% per annum. The 70 Hudson Street Senior Notes are senior in right of payment to the 70 Hudson Street Subordinate Companion Note. The 70 Hudson Street Whole Loan has a Cut-off Date LTV Ratio, UW NCF DSCR and UW NOI Debt Yield of 66.5%, 2.50x and 8.1%, respectively.

Mezzanine Debt. None.

Partial Release. Not permitted.

Ground Lease. None.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 15 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

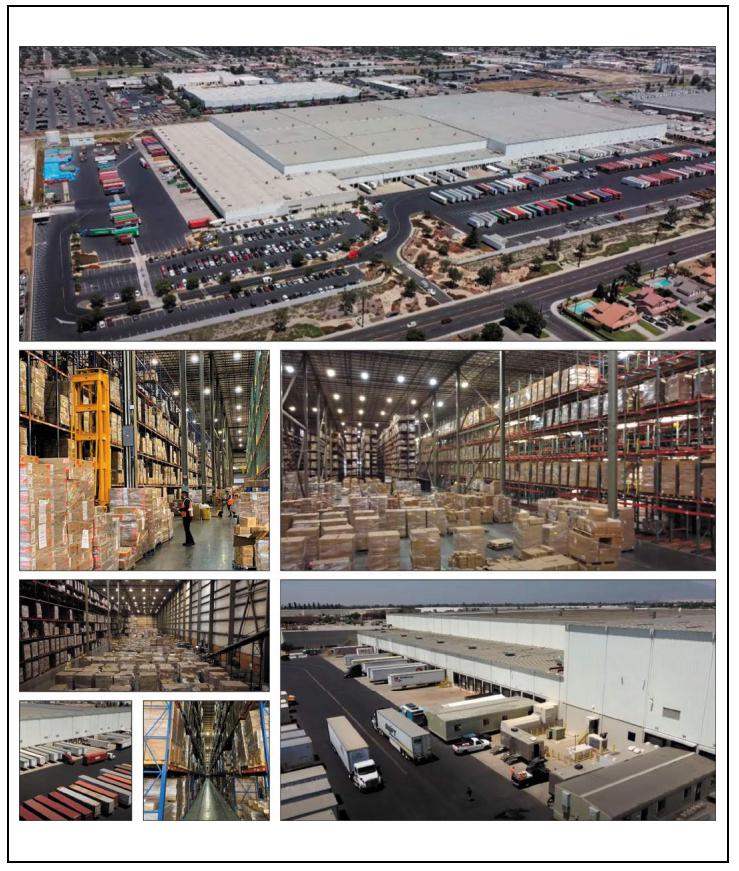

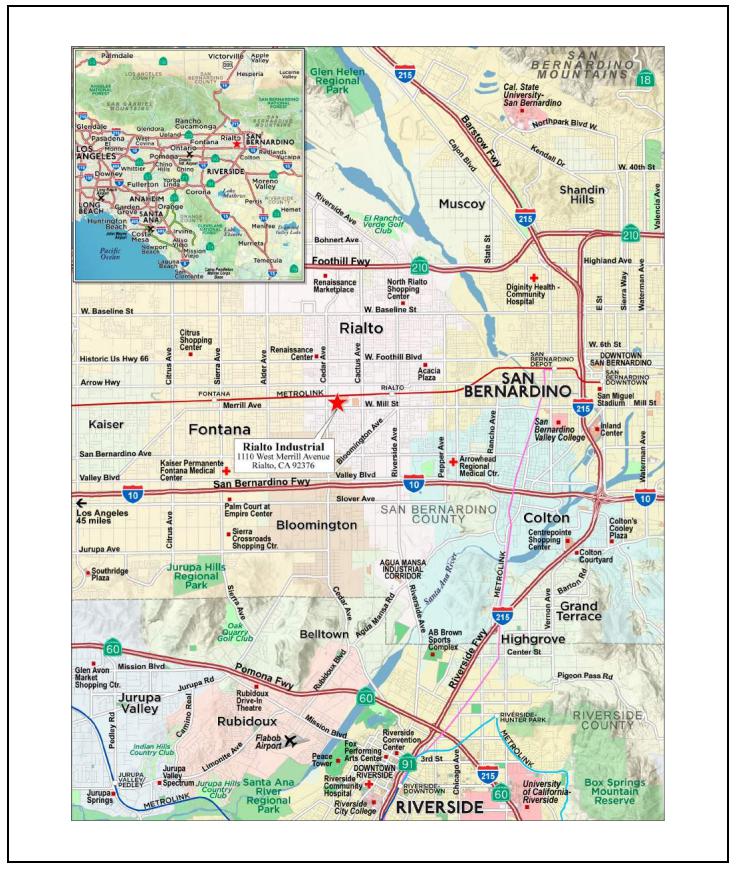

| No. 2 – Rialto Industrial | ||

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 16 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 2 – Rialto Industrial | ||

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 17 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 2 – Rialto Industrial | ||

| Mortgage Loan Information | Property Information | |||

| Mortgage Loan Seller: | AREF | Single Asset / Portfolio: | Single Asset | |

| Original Principal Balance(1): | $35,000,000 | Title: | Fee | |

| Cut-off Date Principal Balance(1): | $35,000,000 | Property Type – Subtype: | Industrial – Warehouse/ | |

| % of IPB: | 4.5% | Distribution | ||

| Loan Purpose: | Refinance | Net Rentable Area (SF): | 1,106,124 | |

| Borrower: | Rialto Merrill Holdings LLC | Location: | Rialto, CA | |

| Borrower Sponsors: | Ezra Danziger, Paul Reisz and | Year Built / Renovated: | 1989 / 2020 | |

| Solomon Weber | Occupancy: | 100.0% | ||

| Interest Rate: | 7.61000% | Occupancy Date: | 2/6/2023 | |

| Note Date: | 11/10/2022 | 4th Most Recent NOI (As of)(4): | NAV | |

| Maturity Date: | 12/6/2032 | 3rd Most Recent NOI (As of)(4): | NAV | |

| Interest-only Period: | 120 months | 2nd Most Recent NOI (As of)(4): | NAV | |

| Original Term: | 120 months | Most Recent NOI (As of)(4): | NAV | |

| Original Amortization Term: | None | UW Economic Occupancy: | 95.0% | |

| Amortization Type: | Interest Only | UW Revenues: | $22,349,341 | |

| Call Protection(2): | L(26),D(90),O(4) | UW Expenses: | $4,721,514 | |

| Lockbox / Cash Management: | Hard / Springing | UW NOI: | $17,627,827 | |

| Additional Debt(1): | Yes | UW NCF: | $17,185,377 | |

| Additional Debt Balance(1): | $146,000,000 | Appraised Value / Per SF(5): | $350,000,000 / $316 | |

| Additional Debt Type(1): | Pari Passu | Appraisal Date: | 10/12/2022 | |

| Escrows and Reserves(3) | Financial Information(1) | |||||

| Initial | Monthly | Initial Cap | Cut-off Date Loan / SF: | $164 | ||

| Taxes: | $514,722 | $128,681 | N/A | Maturity Date Loan / SF: | $164 | |

| Insurance: | $122,072 | $61,036 | N/A | Cut-off Date LTV: | 51.7% | |

| Replacement Reserves: | $0 | $9,218 | N/A | Maturity Date LTV: | 51.7% | |

| Immediate Repairs: | $8,125 | $0 | N/A | UW NCF DSCR: | 1.23x | |

| Rent Abatement Reserve: | $9,402,054 | $0 | N/A | UW NOI Debt Yield: | 9.7% | |

| Litigation Reserve | $50,000 | Springing | $50,000 | |||

| Sources and Uses | |||||||

| Sources | Proceeds | % of Total | Uses | Proceeds | % of Total | ||

| Whole Loan(1) | $181,000,000 | 100.0% | Loan Payoff | $130,724,472 | 72.2 | % | |

| Closing Costs(6) | 24,015,699 | 13.3 | |||||

| Return of Equity | 16,162,856 | 8.9 | |||||

| Upfront Reserves | 10,096,973 | 5.6 | |||||

| Total Sources | $181,000,000 | 100.0% | Total Uses | $181,000,000 | 100.0 | % | |

| (1) | The Rialto Industrial Mortgage Loan (as defined below) is part of a whole loan evidenced by eight pari passu notes with an aggregate outstanding principal balance as of the Cut-off Date of $181.0 million (the “Rialto Industrial Whole Loan”). The Financial Information in the chart above reflects the Rialto Industrial Whole Loan. |

| (2) | The lockout period will be at least 26 months beginning with and including the first payment date on January 6, 2023. Defeasance of the Rialto Industrial Whole Loan is permitted after the date that is the earlier of (i) two years from the closing date of the securitization that includes the last note to be securitized and (ii) November 10, 2025. The assumed lockout period of 26 payments is based on the anticipated closing date of the BMO 2023-C4 securitization trust in February 2023. The actual lockout period may be longer. |

| (3) | For a full description of Escrows and Reserves, please refer to “Escrows and Reserves” below. |

| (4) | Operating history is not available as the Rialto Industrial Property (as defined below) has been occupied under a triple net lease from March 2020 and was vacant from 2018 to March 2020. |

| (5) | The appraisal also concluded to a “go-dark” value of $303,000,000 and land value of $242,000,000. |

| (6) | Closing Costs include approximately $15.0 million in payment to third-party contractors for the cost of the TI Project (as defined below). |

The Loan. The second largest mortgage loan (the “Rialto Industrial Mortgage Loan”) is part of a fixed rate whole loan secured by the borrower’s fee interest in an industrial warehouse/distribution facility in Rialto, California (the “Rialto Industrial Property”). The Rialto Industrial Whole Loan is evidenced by eight pari passu notes and accrues interest at a rate of 7.61000% per annum. The Rialto Industrial Whole Loan has a 10-year term and is interest only for the entire term. The non-controlling Note A-2 and Note A-6, with an aggregate original principal balance of $35,000,000, will be included in the BMO 2023-C4 securitization trust. The Rialto Industrial Whole Loan will be serviced pursuant to the pooling and servicing agreement for the BBCMS 2022-C18 trust until the controlling Note A-4 is securitized, whereupon the Rialto Industrial Whole

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 18 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 2 – Rialto Industrial | ||

Loan will be serviced pursuant to the pooling and servicing agreement for such future securitization. See “Description of the Mortgage Pool—The Whole Loans—The Outside Serviced Pari Passu Whole Loans” and “The Pooling and Servicing Agreement—Servicing of the Outside Serviced Mortgage Loans” in the Preliminary Prospectus.

| Whole Loan Summary | ||||

| Note | Original Balance | Cut-off Date Balance | Note Holder | Controlling Piece |

| A-1 | $65,000,000 | $65,000,000 | BBCMS 2022-C18 | No |

| A-2 | $30,000,000 | $30,000,000 | BMO 2023-C4 | No |

| A-3(1) | $30,000,000 | $30,000,000 | AREF or an affiliate | No |

| A-4(1) | $25,000,000 | $25,000,000 | AREF or an affiliate | Yes |

| A-5(1) | $20,000,000 | $20,000,000 | AREF or an affiliate | No |

| A-6 | $5,000,000 | $5,000,000 | BMO 2023-C4 | No |

| A-7(1) | $3,000,000 | $3,000,000 | AREF or an affiliate | No |

| A-8 | $3,000,000 | $3,000,000 | BBCMS 2022-C18 | No |

| Whole Loan | $181,000,000 | $181,000,000 | ||

| (1) | Expected to be contributed to one or more future securitization(s). |

The Property. The Rialto Industrial Property is a 1,106,124 square foot industrial warehouse/distribution facility in the Inland Empire industrial market in Rialto, California approximately seven miles west of downtown San Bernardino. Situated on 55.57 acres, the Rialto Industrial Property features a single-story building constructed in 1989 and renovated in 2020. The Rialto Industrial Property includes 1,089,119 square feet of warehouse space and 17,005 square feet of office space (1.5% of net rentable area). The majority clear height of the improvements is 53 to 58 feet with approximately 5% of the building at the west end having a lower clear component of approximately 21 feet. Additionally, approximately 100,000 square feet of the mezzanine area is utilized for storage and materials handling and sorting along the south end of the building that is not included in the 1,106,124 million square feet of net rentable area. The Rialto Industrial Property also contains an on-site fueling station, truck maintenance building (currently being converted into a fitness center as an amenity for the employees), a grade level overhead door, 132 dock high overhead doors, 12 rail doors to the BNSF (freight railroad) spur at the north side of the building and includes 8,000 amps of power. The Rialto Industrial Property has above standard yard functionality on both the south and west sides with 317 striped excess trailer spaces. The Rialto Industrial Property is currently 100.0% occupied by Rialto Distribution LLC (“Rialto Distribution” or the “Tenant”), an affiliate of the borrower sponsor, under a new 20-year lease that expires in October 2042. The Rialto Industrial Property serves as the west coast headquarters for Rialto Distribution and its operating affiliate, All-Ways Pacific LLC, who is the lease guarantor. A true lease opinion was obtained at loan closing.

The Rialto Industrial Property previously served as a national distribution facility for Toys “R” Us until they filed bankruptcy and vacated in 2018. In March 2020, Rialto Distribution entered into a lease with prior ownership along with an option agreement to purchase the Rialto Industrial Property for approximately $123.35 million ($112 per square foot). Between 2020 and 2021, the Tenant completed renovations that include the installation of Early Suppression Fire Response (“ESFR”) sprinkler systems throughout approximately 600,000 square feet of the facility with the remainder of the facility’s sprinkler system comprising in-rack sprinklers. This modernization project allowed the Tenant to make full use of the minimum 53 feet clear heights by stacking to 50 feet. In August 2021, Rialto Distribution exercised the purchase option and subsequently entered into a new, owner-occupied affiliated lease as part of the acquisition financing. Additional capital expenditures were completed through September 2022 including the renovation of over 17,000 square feet of office space, installation of an in-floor laser guidance system for forklifts, restroom additions/upgrades, capital repairs and maintenance to the entire facility, and removal of obsolete systems and equipment such as conveyer belt systems left behind by prior ownership to increase the usability of the facility. Total tenant improvements and capital expenditure invested by the Tenant into the Rialto Industrial Property totaled approximately $8.0 million. Furthermore, approximately $4.5 million was invested in warehouse relocation expenses, equipment rentals, and capital repairs / maintenance. By increasing the usable clear heights of the Rialto Industrial Property significantly through converting approximately 600,000 square feet of space to ESFR sprinkler systems and removing obsolete systems and equipment to free up space and improve efficiencies, the Tenant increased its maximum pallet capacity from 44,000 pallets to 100,000 pallets and its actual pallet utilization from 45,810 pallets in July 2020 to 123,593 pallets as of October 2022 (170% increase). At the origination of the Rialto Industrial Whole Loan, the

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 19 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 2 – Rialto Industrial | ||

Tenant entered into a newly amended 20-year lease at a starting rent of $17.00 per square foot triple net with 3.00% annual increases. The appraisal concluded to a market rent of $17.40 per square foot for the space.

According to the appraisal, the purchase price under the option agreement was predicated on the then “as is” condition of the Rialto Industrial Property, which required a substantial amount of work and based on the lease date and option date the price reflects pre-COVID pricing since which time the Inland Empire industrial market experienced rapid growth in rents and compression in cap rates (see “The Market” below), with rents effectively doubling during this time on top of cap rate compression throughout. Furthermore, the Rialto Industrial Property is located in an opportunity zone which holds various tax benefits from long-term ownership and property improvements. In August 2022, the borrower sponsors received an unsolicited offer to purchase the Rialto Industrial Property for $350 million based on a 10-year leaseback at $17.40 per square foot triple-net with 3.5% annual increase or $325 million for delivery of a vacant building.

The Tenant is currently performing further upgrades to the Rialto Industrial Property which are estimated to cost no more than approximately $15 million ($13.56 per square foot) (the “TI Project”), with the contractors being responsible for any expenses over $15 million. The TI Project includes the removal of the existing conveyer modules, installation of new racking systems, and replacement of the existing sprinkler system on one side of the building comprising an estimated 500,000 square feet with ESFR sprinklers. The TI Project is expected to increase the pallet racking capacity of the entire 1.1 million square foot facility by 40%, which the Tenant projects will generate an additional $19 million in annual revenue with no additional underlying real estate costs. Rialto Distribution expects the TI Project to be complete by August 2023. In the event that the TI Project is not completed by June 30, 2024, a Cash Management Period (as defined below) commences.

Sole Tenant. Rialto Distribution (1,106,124 square feet; 100.0% of NRA; 100.0% of underwritten base rent): Rialto Distribution was formed in 2020 as an operating affiliate of All-Ways Pacific LLC, which was formed in 2013 as a third-party warehousing and distribution provider. The Rialto Distribution lease is guaranteed by the operating affiliate All-Ways Pacific LLC. Rialto Distribution and All-Ways Pacific LLC report financials on a combined basis. For the trailing 12-month period ending July 2022, All-Ways Pacific and Rialto Distribution reported a combined revenue of $89.4 million and an adjusted EBITDAR of approximately $40.2 million. Rialto Distribution has been a tenant at the Rialto Industrial Property since July 2020 and in 2022 extended its lease term to expire in October 2042. The lease is structured as triple net with Rialto Distribution also being responsible for all capital expenditure costs. Rialto Distribution has no renewal options and no termination options.

Rialto Distribution plans to sublease 100,000 square feet (9.0% of NRA) of its space to I World, LLC. The sublease is expected to commence in the first quarter of 2023 and will have a lease expiration in December 2032. The rent under the sublease will be $19.20 per square foot, increasing by 4.0% annually, plus $2.40 per square foot in estimated expense reimbursement. I World, LLC is one of Rialto Distribution’s top corporate accounts on the West Coast. Under the terms of the Rialto Industrial Whole Loan documents, the borrower is permitted to allow future subleases which in the aggregate do not account for greater than 20% of NRA at the Rialto Industrial Property. A sublease comprising less than 5% of NRA does not require lender approval so long as the sublease rent and terms are equal to or superior to the Rialto Distribution lease. Any future sublease comprising 5% or greater of NRA requires lender approval.

Environmental. According to the Phase I environmental assessment dated October 24, 2022, there was no evidence of any recognized environmental conditions at the Rialto Industrial Property.

The following table presents certain information relating to the historical and current occupancy of the Rialto Industrial Property:

| Historical and Current Occupancy | ||

| 2020(1) | 2021(1) | Current(2) |

| 100.0% | 100.0% | 100.0% |

| (1) | Rialto Distribution signed a lease in March 2020 to occupy the entire Rialto Industrial Property. The Rialto Industrial Property had previously been owned and occupied by Toys “R” Us, who filed for bankruptcy in 2018 and subsequently sold and vacated the Rialto Industrial Property. |

| (2) | Current Occupancy is as of February 6, 2023. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 20 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 2 – Rialto Industrial | ||

The following table presents certain information relating to the sole tenant for the Rialto Industrial Property:

| Tenant Summary(1) | |||||||

| Tenant | Ratings Moody’s/S&P/Fitch | Net Rentable Area (SF) | % of Total NRA | UW Base Rent PSF | UW Base Rent | % of Total UW Base Rent | Lease Expiration Date |

| Rialto Distribution LLC(2) | NR/NR/NR | 1,106,124 | 100.0% | $17.00 | $18,804,108 | 100.0% | 10/31/2042 |

| Occupied Collateral Total / Wtd. Avg. | 1,106,124 | 100.0% | $17.00 | $18,804,108 | 100.0% | ||

| Vacant Space | 0 | 0.0% | |||||

| Collateral Total | 1,106,124 | 100.0% | |||||

| (1) | Based on the underwritten rent roll. |

| (2) | Rialto Distribution plans to sublease 100,000 square feet of its space to I World, LLC at $19.20 per square foot. The sublease is expected to commence in the first quarter of 2023. |

The following table presents certain information relating to the tenant lease expiration dates of the Rialto Industrial Property:

| Lease Rollover Schedule(1) | |||||||||||||||

| Year | Number of Leases Expiring | Net Rentable Area Expiring | % of NRA Expiring | UW Base Rent Expiring | % of UW Base Rent Expiring | Cumulative Net Rentable Area Expiring | Cumulative % of NRA Expiring | Cumulative UW Base Rent Expiring | Cumulative % of UW Base Rent Expiring | ||||||

| Vacant | NAP | 0 | 0.0 | % | NAP | NAP | 0 | 0.0% | NAP | NAP | |||||

| 2022 & MTM | 0 | 0 | 0.0 | $0 | 0.0 | % | 0 | 0.0% | $0 | 0.0% | |||||

| 2023 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | ||||||

| 2024 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | ||||||

| 2025 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | ||||||

| 2026 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | ||||||

| 2027 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | ||||||

| 2028 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | ||||||

| 2029 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | ||||||

| 2030 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | ||||||

| 2031 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | ||||||

| 2032 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | ||||||

| 2033 & Beyond | 1 | 1,106,124 | 100.0 | 18,804,108 | 100.0 | 1,106,124 | 100.0% | $18,804,108 | 100.0% | ||||||

| Total | 1 | 1,106,124 | 100.0 | % | $18,804,108 | 100.0 | % | ||||||||

| (1) | Based on the underwritten rent roll. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 21 | ||

| Structural and Collateral Term Sheet | BMO 2023-C4 | |

| No. 2 – Rialto Industrial | ||

The following table presents certain information relating to the operating history and underwritten cash flows at the Rialto Industrial Property:

| Operating History and Underwritten Net Cash Flow(1) | ||||

| Underwritten | Per Square Foot | %(2) | ||

| Rents in Place | $18,804,108 | $17.00 | 79.9 | % |

| Vacant Income | 0 | 0.00 | 0.0 | |

| Contractual Rent Steps | 0 | 0.00 | 0.0 | |

| Gross Potential Rent | $18,804,108 | $17.00 | 79.9 | % |

| Total Reimbursements | 4,721,514 | 4.27 | 20.1 | |