Exhibit 99.2

Public Accounts 2022-23 Volume 1 Summary Financial Statements

2022-23 Public Accounts of Saskatchewan

Volume 1

Contents

| 3 | Letters of Transmittal | |

| 4 | Introduction to the Public Accounts | |

| Financial Statement Discussion and Analysis | ||

| 7 | Highlights | |

| 13 | Assessment of Fiscal Health | |

| 18 | Details | |

| 38 | Risks and Uncertainties | |

| Summary Financial Statements | ||

| 41 | Responsibility for the Summary Financial Statements | |

| 43 | Independent Auditor’s Report | |

| 47 | Statement of Financial Position | |

| 48 | Statement of Operations | |

| 49 | Statement of Accumulated Operating Deficit | |

| 49 | Statement of Accumulated Remeasurement Gains and Losses | |

| 50 | Statement of Change in Net Debt | |

| 51 | Statement of Cash Flow | |

| 52 | Notes to the Financial Statements | |

| Schedules to the Financial Statements | ||

| 68 | Accounts Receivable | |

| 69 | Loans Receivable | |

| 70 | Investment in Government Business Enterprises | |

| 72 | Sinking Fund Investments | |

| 74 | Portfolio Investments | |

| 75 | Accounts Payable and Accrued Liabilities | |

| 76 | Unearned Revenue | |

| 77 | Pension Liabilities | |

| 78 | Public Debt | |

| 80 | Obligations Under Long-Term Financing Arrangements | |

| 81 | Other Liabilities | |

| 82 | Tangible Capital Assets | |

| 83 | Inventories Held for Consumption | |

| 84 | Revenue | |

| 85 | Expense by Object | |

| 85 | Financing Charges | |

| 86 | Segmented Reporting | |

| 88 | Supplemental Cash Flow Information | |

| 89 | Government Reporting Entity | |

| 92 | Glossary of Terms | |

Letters of Transmittal

Regina, Saskatchewan

June 2023

To His Honour

The Honourable Russell B. Mirasty

Lieutenant Governor of Saskatchewan

Your Honour:

I have the honour to submit Volume 1 of the Public Accounts of the Government of Saskatchewan for the fiscal year ended March 31, 2023.

Respectfully submitted,

DONNA HARPAUER

Deputy Premier and

Minister of Finance

Regina, Saskatchewan

June 2023

The Honourable Donna Harpauer

Deputy Premier and

Minister of Finance

We have the honour to present Volume 1 of the Public Accounts of the Government of Saskatchewan for the fiscal year ended March 31, 2023.

Respectfully submitted,

|  | |

| MAX HENDRICKS | CHRIS BAYDA | |

| Deputy Minister of Finance | Provincial Comptroller |

| Government of Saskatchewan Public Accounts 2022-23 | 3 | |

Introduction to the Public Accounts

Introduction to the Public Accounts

The 2022-23 Public Accounts of the Government of Saskatchewan (the Government) are prepared in accordance with the Financial Administration Act, 1993 and consist of two volumes. The Government is responsible for the integrity and objectivity of the information presented in these two volumes.

Volume 1

Financial Statement Discussion and Analysis provides users of the Government’s Summary Financial Statements with an overview of the Government’s performance by presenting comparative financial highlights and variance analysis. The information in the financial statement discussion and analysis should be read in conjunction with the Summary Financial Statements.

Summary Financial Statements provide an accounting of the full nature and extent of the financial affairs and resources of the Government. This includes the financial results of the General Revenue Fund, Crown corporations, boards and other entities controlled by the Government. A listing of all entities controlled by the Government, collectively referred to as the government reporting entity, is provided in schedule 19 of the Summary Financial Statements.

Volume 2

Volume 2 contains the following unaudited financial information:

| • | General Revenue Fund schedules and details; |

| • | General Revenue Fund capital asset acquisitions schedule and details; |

| • | revolving fund expenditure details; |

| • | summary listing of payees who provided goods and services and capital assets of $50,000 or more to the General Revenue Fund and revolving funds during the fiscal year; |

| • | assets, liabilities and residual balances of pension plans and trust funds administered by the Government; |

| • | remissions of taxes and fees; and |

| • | road-use fuel tax accountability revenues and expenditures. |

The Public Accounts, including the Compendiums, are available on the Government of Saskatchewan’s website.

The Compendium of Financial Statements contains the financial statements of various government agencies, boards, commissions, pension plans, special purpose funds and institutions, as well as Crown corporations which are accountable to Treasury Board.

The Compendium of Payee Details contains the payee details of all Summary Financial Statement entities, except Crown Investments Corporation of Saskatchewan and its subsidiaries.

In addition, the financial statements and payee details of Crown corporations and wholly-owned subsidiaries that are accountable to the Crown Investments Corporation of Saskatchewan (CIC) Board can be found on CIC’s website.

| 4 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Financial Statement Discussion and Analysis

Financial Statement Discussion and Analysis

Highlights

Introduction

The Financial Statement Discussion and Analysis (FSD&A) provides an overview of the Government’s financial performance and information to report on the Government’s accountability for the resources entrusted to it. The FSD&A is intended to assist users of the Summary Financial Statements (SFS) in their assessment of the Government’s fiscal health. The Government is responsible for the integrity and objectivity of this discussion and analysis.

This information should be read in conjunction with the SFS which include the financial activities of all government-controlled entities, collectively referred to as the government reporting entity. A complete listing of the public sector entities included in the government reporting entity is provided in schedule 19 of the SFS.

Financial Results

In 2022-23, the Government reports an operating surplus of $1.58 billion, a $3.05 billion improvement from the operating deficit reported in the prior year and a $2.04 billion improvement from the budgeted deficit. Significant increases in non-renewable resources revenue and continued post-COVID economic recovery combined with lower crop insurance payments when compared to the prior year help contribute to the Government’s improved fiscal results for the year.

Overall revenue is greater than both the prior year and budget with a $2.46 billion and $3.44 billion increase over the prior year and budget respectively. The most notable increases are in non-renewable resources and taxation revenues resulting primarily from global increases in commodity prices and post-COVID economic recovery. These revenue increases are partially offset by a decrease in net income from Government Business Enterprises (GBEs) primarily due to significantly increased costs for power generation and a decline in investment returns.

Total expenses for the year are $591 million lower than the prior year and $1.39 billion higher than budget. Agriculture expense saw the most notable impact as drought conditions significantly improved in parts of the province resulting in crop insurance payouts lower than the prior year but greater than budget. Additionally, economic development expense increased as a result of the Saskatchewan Affordability Tax Credit payments made to residents in recognition of rising costs from inflation.

The Government continues to invest in the Province’s infrastructure, with significant investment in electricity generation, transmission and distribution assets, communication networks and other investments through the Saskatchewan Capital Plan. The $2.66 billion capital investment during 2023 will continue to be used to replace aging infrastructure and invest in capital projects to meet the demand for growth and improve safety.

The Government’s overall financial position as at March 31, 2023 is an accumulated deficit of $1.60 billion.

| Government of Saskatchewan Public Accounts 2022-23 | 7 | |

Financial Statement Discussion and Analysis

Highlights

At a Glance

Financial Results

(millions of dollars)

| Increase (Decrease) | ||||||||||||||||||||

| 2023 | 2022 | from | ||||||||||||||||||

| Budget | Actual | Actual | Budget | 2022 Actual | ||||||||||||||||

Revenue | 17,158 | 20,595 | 18,136 | 3,437 | 2,458 | |||||||||||||||

Expense | 17,621 | 19,014 | 19,604 | 1,393 | (591 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operating Surplus (Deficit) | (463 | ) | 1,581 | (1,468 | ) | 2,044 | 3,049 | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net Debt | (16,748 | ) | (14,598 | ) | (15,488 | ) | (2,150 | ) | (890 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Accumulated Deficit1 | (3,453 | ) | (1,604 | ) | (2,832 | ) | (1,849 | ) | (1,228 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

1 Comprised of: | ||||||||||||||||||||

Accumulated operating deficit | (3,453 | ) | (1,771 | ) | (2,832 | ) | (1,682 | ) | (1,061 | ) | ||||||||||

Accumulated remeasurement gains | — | 167 | — | 167 | 167 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Accumulated Deficit | (3,453 | ) | (1,604 | ) | (2,832 | ) | (1,849 | ) | (1,228 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Totals may not add due to rounding.

| 8 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Highlights

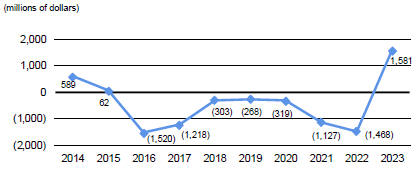

Operating Surplus (Deficit)

The operating surplus (deficit) represents the amount by which revenue exceeds expense (expense exceeds revenue) for the fiscal period.

Operating Surplus (Deficit)

The 2023 SFS report an operating surplus of $1.58 billion, a $3.05 billion improvement over the $1.47 billion deficit reported in the previous year. The year-over-year improvement in operating results is mainly attributable to a significant increase in overall revenue and a decrease in overall expenses. Notable increases in revenue include non-renewable resources and taxation, partially offset by decreases in net income from GBEs, other own-source and transfers from the federal government. The overall decrease in expenses is largely the result of a notable decrease in the agriculture theme, partially offset by increases in most other themes.

Compared to the budget, the operating surplus is $2.04 billion greater than expected. The improvement over budget is mainly attributable to higher-than-budgeted revenue offset partially by higher-than-budgeted expenses. All revenue categories are greater-than-budget except for net income from GBEs. All expense themes exceed budget except for social services and assistance, general government, environment and natural resources and education.

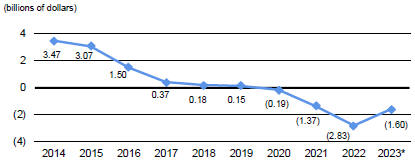

Accumulated (Deficit) Surplus

An accumulated (deficit) surplus represents a government’s reported net economic (shortfall) resources. An accumulated (deficit) surplus indicates that a government (requires) has additional resources to provide future services.

Accumulated (Deficit) Surplus

| * | Beginning in 2023, accumulated (deficit) surplus includes accumulated remeasurement gains (losses). |

At March 31, 2023, the Government reported an accumulated deficit of $1.60 billion, an improvement of $1.23 billion over the previous year’s accumulated deficit and a $1.85 billion improvement over budget. These improvements are mainly due to the $1.58 billion operating surplus.

| Government of Saskatchewan Public Accounts 2022-23 | 9 | |

Financial Statement Discussion and Analysis

Highlights

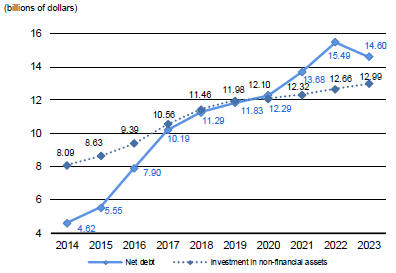

Net Debt

Net debt provides a measure of the future revenue that is required to pay for past transactions and events.

Net Debt

The net debt at March 31, 2023 is $14.60 billion, an improvement of $890 million over the prior year. The year-over-year improvement is primarily due to the operating surplus, partially offset by the net acquisition of tangible capital assets and the one-time impact of the adoption of new accounting standards.

Net debt is a $2.15 billion improvement over budget, primarily due to the greater-than-expected operating surplus.

The net debt of the SFS is:

| • | the accumulated (deficit) surplus, representing the extent to which past (expenses) revenues have exceeded past (revenue) expenses; and |

| • | the investment in non-financial assets, primarily representing the Government’s investment in highways and health care and educational facilities. |

Net Debt Components

(millions of dollars)

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |||||||||||||||||||||||||||||||

Accumulated (deficit) surplus | 3,469 | 3,074 | 1,495 | 372 | 176 | 155 | (191 | ) | (1,368 | ) | (2,832 | ) | (1,604 | ) | ||||||||||||||||||||||||||

Investment in non-financial assets | (8,085 | ) | (8,626 | ) | (9,394 | ) | (10,564 | ) | (11,464 | ) | (11,984 | ) | (12,098 | ) | (12,315 | ) | (12,656 | ) | (12,994 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Net Debt | (4,615 | ) | (5,552 | ) | (7,899 | ) | (10,192 | ) | (11,288 | ) | (11,829 | ) | (12,289 | ) | (13,683 | ) | (15,488 | ) | (14,598 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Totals may not add due to rounding

| 10 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Highlights

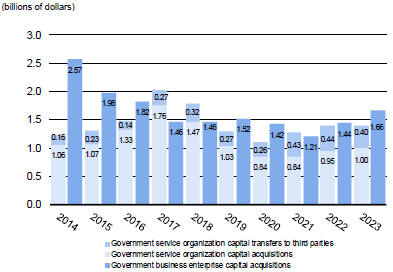

Investment in Infrastructure

The Government invests in infrastructure by:

| • | investing in government-owned capital; and |

| • | providing transfers to third parties, including municipalities and universities, for capital purposes. |

Investment in Infrastructure

During 2022-23, the Government invested $2.66 billion in government-owned infrastructure: $1.66 billion for GBEs to build new and maintain existing infrastructure; and $999 million to meet the capital requirements of government service organizations (GSOs). In addition, $398 million is provided to third parties to fund their capital needs.

Investment in government-owned infrastructure is down from the average of the previous nine years of $2.80 billion and is $345 million less than budget.

Credit Rating

Credit Ratings – March 2023

Rating Agency1 | ||||||

Jurisdiction | Moody’s Investors Service Inc. | Standard & Poor’s | DBRS Morningstar | |||

British Columbia | Aaa | AA+ | AA (high) | |||

Alberta | Aa2 | A+ | AA (low) (pos) | |||

Saskatchewan | Aa1 | AA | AA (low) | |||

Manitoba | Aa2 | A+ | A (high) | |||

Ontario | Aa3 | A+ | AA (low) | |||

Quebec | Aa2 | AA- | AA (low) | |||

New Brunswick | Aa2 (pos) | A+ | A (high) | |||

Nova Scotia | Aa2 | AA- | A (high) | |||

Prince Edward Island | Aa2 | A | A | |||

Newfoundland & Labrador | A1 | A | A (low) (pos) | |||

Ratings reflect the latest credit ratings available at March 31, 2023.

| 1 | The rating agencies assign letter ratings to borrowers. The major A bracket categories, in descending order of credit quality, are: AAA/Aaa; AA/Aa; A. The ‘1’, ‘2’, ‘3’, ‘high’, ‘low’, ‘-’, and ‘+’ modifiers show relative standing within the major categories with (pos)/(neg) representing a positive/negative outlook or trend. For example, AAA exceeds AA, Aa1 exceeds Aa2 and AA exceeds AA-. |

Province obtains a credit rating from the three major credit rating agencies: Moody’s Investors Service Inc.; Standard & Poor’s; and the DBRS Morningstar. Overall, Saskatchewan’s credit rating from the three major credit rating agencies ranks second highest among the Canadian provinces.

| Government of Saskatchewan Public Accounts 2022-23 | 11 | |

Financial Statement Discussion and Analysis

Highlights

Accounting Changes

During 2022-23 the Government adopted new accounting standards, including the introduction of fair value measurement for certain financial instruments. The introduction of fair value measurement results in a new component of accumulated (deficit) surplus, called accumulated remeasurement gains and losses. Unrealized changes in fair value are recorded as remeasurement gains and losses.

Changes have been made to the presentation of public debt. Public debt is no longer reported net of sinking fund investments. In all years represented in the FSD&A, sinking fund investments are presented as financial assets, and public debt has been presented at its value gross of sinking fund investments.

| 12 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Assessment of Fiscal Health

A government’s fiscal management can be gauged through an assessment of its fiscal health in the context of the overall economic and financial environment. Fiscal health describes a government’s ability to meet its existing financial obligations, both with respect to its service commitments to the public and its financial commitments to creditors, employees and others. The assessment of the Government’s fiscal health considers the three elements of sustainability, flexibility and vulnerability on the basis of the following indicators:

Sustainability

| • | Accumulated (deficit) surplus to the Province’s GDP |

| • | Net debt to the Province’s GDP |

| • | Net debt to total revenue |

| • | Net debt per capita |

Flexibility

| • | Financing charges to total revenue |

| • | Own-source revenue to the Province’s GDP |

Vulnerability

| • | Non-renewable resources revenue to total expense |

| • | Transfers from the federal government to total revenue |

| • | Foreign currency debt to net debt |

Sustainability

Sustainability is the degree to which a government can maintain its existing level of spending and meet its existing debt obligations.

Accumulated (Deficit) Surplus to the Province’s GDP

The accumulated (deficit) surplus measures the sum of all current and prior years’ operating results. Gross domestic product (GDP) is a measure of the value of the goods and services produced during a year, indicating the size of the provincial economy. GDP reflects the latest figures available for the current and prior years based on the data produced by Statistics Canada. The indicator takes a long-term view of government finances. The trend of accumulated (deficit) surplus as a percentage of GDP indicates whether the accumulated (deficit) surplus is changing faster or slower than the growth or decline in the economy and provides insight into the Government’s fiscal strategy in the context of the economy.

The decrease in this ratio from 2014 to 2017 was mainly a result of market-driven variables, such as low oil prices. The return to relatively stable ratios from 2018 to 2020 reflects the revenue stability and cost control measures introduced in the 2017-18 budget. A decline in this ratio in 2021 and 2022 was primarily due to the adverse effect of the COVID-19 pandemic on government operations and the economy. In 2022, record drought-related crop insurance claim payouts further adversely impacted the accumulated deficit. An improvement in the ratio in 2023 is the combination of growth in the GDP due to a strengthening provincial economy and a significant decrease in the accumulated deficit. The decrease in the accumulated deficit is largely due to the operating surplus.

| Government of Saskatchewan Public Accounts 2022-23 | 13 | |

Financial Statement Discussion and Analysis

Assessment of Fiscal Health

Sustainability (continued)

Net Debt to the Province’s GDP

Net debt is the difference between a government’s financial assets and liabilities and represents the future revenue that is required to pay for past transactions and events. Net debt as a percentage of the Province’s GDP provides a measure of the level of financial demands placed on the economy by the Government’s spending and taxation policies. A lower net debt to GDP ratio is desired and indicates higher sustainability.

The rise in this ratio from 2014 to 2017 is mainly a result of market-driven variables, such as low oil prices, together with the Government’s continued investment in infrastructure. The return to relatively stable ratios from 2018 to 2020 reflects the revenue stability measures introduced in the 2017-18 budget and a strengthening provincial economy over this period of time. A rise in this ratio in 2021 was primarily due to the adverse effect of the COVID-19 pandemic on government operations and the economy. The ratio stabilized in 2022 as an overall improvement in the economy and a corresponding growth in GDP was offset by an increase in net debt. A decline in the ratio in 2023 is a result of a continued strengthening of the economy, corresponding GDP growth and a reduction in net debt. The reduction in net debt is primarily due to the current year operating surplus.

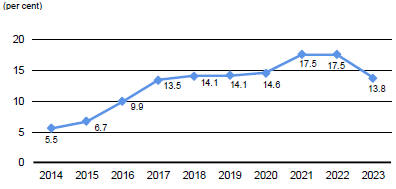

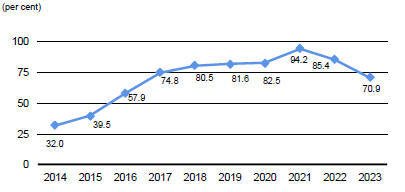

Net Debt to Total Revenue

Another measure of a government’s sustainability is net debt as a percentage of total revenue. Net debt provides a measure of the future revenue that is required to pay for past transactions and events. A lower net debt to revenue ratio indicates higher sustainability, as less time is required to eliminate net debt.

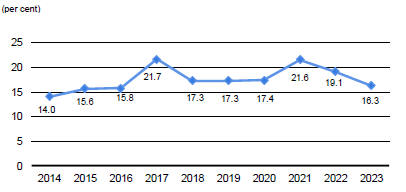

Over the last ten years, the Government’s net debt as a percentage of total revenue has increased from 32.0 per cent in 2014 to 70.9 per cent in 2023. The fall in revenue, tied to low oil and potash prices in 2016 and 2017, increased this upward trend; however, responsible spending, efforts to reduce reliance on non-renewable resource revenues as well as more favourable non-renewable resource revenues slowed this upward trend from 2018 to 2020. A rise in this ratio in 2021 was primarily due the adverse effect of the COVID-19 pandemic on government operations and the economy, negatively impacting both net debt and total revenues. A decrease in this ratio in 2022 and 2023 is primarily due to an overall improvement in the economy resulting in an increase in total revenue that exceeded the overall increase in net debt over the same period.

| 14 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Assessment of Fiscal Health

Sustainability (continued)

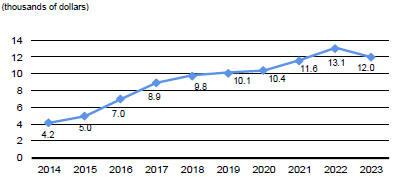

Net Debt per Capita

Figures are based on Statistics Canada first quarter estimates representing the population at January 1 of each year.

Net debt per capita represents the net debt attributable to each Saskatchewan resident. A rise in this ratio indicates the debt burden per resident has grown.

The overall increase in this ratio over the previous ten years is a result of an increase in net debt that exceeds the growth in the Province’s population over the same period. The increase over the period between 2014 and 2017 was mainly a result of market-driven variables, such as low oil prices, together with the Government’s investment in infrastructure. The return to relatively stable ratios from 2018 to 2020 reflects the revenue stability measures introduced in the 2017-18 budget and a strengthening provincial economy over much of this period. A rise in this ratio in 2021 was primarily due to the adverse effect of the COVID-19 pandemic on government operations and the economy. A further increase in this ratio in 2022 primarily reflects the record drought-related crop insurance claims. A decrease in the ratio in 2023 is due to a decrease in net debt resulting from a continued strengthening of the economy, with increases in non-renewable resources and taxation revenues and a decrease from the prior year record high crop insurance payouts.

Flexibility

Flexibility is the extent to which a government has room to maneuver in terms of increasing its debt or tax burden on the economy.

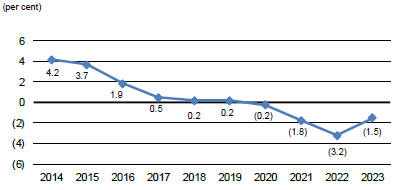

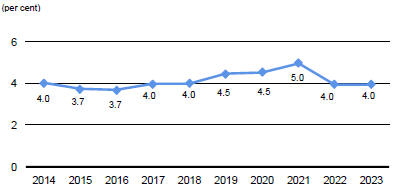

Financing Charges to Total Revenue

A financing charges to total revenue ratio, often referred to as the interest bite, indicates the proportion of provincial revenue that is required to pay interest charges on general debt and therefore is not available to pay for essential public services and programs. A lower ratio means that there is more money available to provide government services.

Between 2014 and 2020 this ratio was relatively consistent. A rise in this ratio in 2021 was due to both an increase in interest costs tied to COVID-related borrowing and a decrease in total revenue tied to the adverse impact of the COVID-19 pandemic on the provincial economy. In 2022 and 2023, this ratio returned to pre-pandemic levels with an increase in total revenue relative to the increase in interest costs on general debt. In 2023, the Government spent approximately 4.0 cents of each dollar of revenue on financing charges on general debt.

| Government of Saskatchewan Public Accounts 2022-23 | 15 | |

Financial Statement Discussion and Analysis

Assessment of Fiscal Health

Flexibility (continued)

Own-Source Revenue to the Province’s GDP

This ratio measures the extent to which the Government is taking income out of the provincial economy, through taxation, non-renewable resources revenue or user fees. An increase in this ratio indicates that the Government’s own-source revenue is growing faster than the economy, reducing the Government’s flexibility to increase revenue without slowing the growth of the provincial economy.

Own-source revenue as a percentage of GDP remained relatively constant between 2014 and 2021 indicating that the Government had not significantly changed its demands on the provincial economy over this time. This constant ratio indicated that the Government’s flexibility was relatively unchanged over that period. In 2022, the significant increase in own-source revenue, largely from insurance, relative to the Province’s GDP growth pushed this ratio up, decreasing the Government’s flexibility to increase own-source revenue without impacting the economy. In 2023, the ratio remains constant as increases in own-source revenue, primarily from non-renewable resources and taxation sources are matched by the continued growth in the Province’s GDP.

Vulnerability

Vulnerability is the extent to which a government is dependent on, or exposed to, risks associated with sources of funding outside its control.

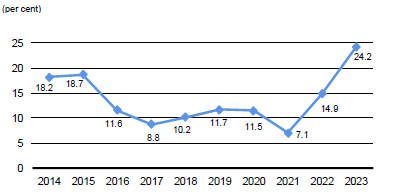

Non-Renewable Resources Revenue to Total Expense

Non-renewable resources revenue is affected by price and sales factors which are beyond a government’s direct control. Non-renewable resources revenue as a percentage of total expense is therefore an indicator of how vulnerable the Province is as a result of its dependence on non-renewable resources revenue to fund its expenses.

In Saskatchewan, non-renewable resources revenue is an important but volatile source of revenue.

A decline in this ratio in 2021 was primarily due to the adverse effect of the COVID-19 pandemic on the economy and government operations. In 2022 and 2023, this ratio increased significantly due to an overall improvement in the economy and a corresponding increase in all categories of non-renewable resources revenue, with the largest increases in potash, oil and gas and resource surcharges. In 2023, this is an indicator of non-renewable resources available to fund expenses.

| 16 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Assessment of Fiscal Health

Vulnerability (continued)

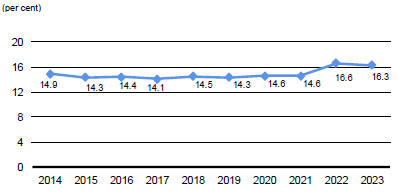

Transfers from the Federal Government to Total Revenue

The Government does not control the amount of federal transfers that it receives each year. Transfers from the federal government as a percentage of total revenue is therefore an indicator of the degree of vulnerability the Government has as a result of reliance on the federal government for revenue. Generally, a decreasing ratio indicates that a government is less reliant on federal transfers to fund its programs, making it less vulnerable.

In 2023, 16.3 per cent of the Government’s revenue came from transfers from the federal government with the remainder coming from Saskatchewan sources. Between 2014 and 2020, the Government’s ability to fund essential programs and services from own-source revenue remained fairly stable with the exception of significant one-time infrastructure transfers from the federal government received during 2017. An increase in this ratio in 2021 was primarily due to the adverse impact of the COVID-19 pandemic on the economy and the resulting support received from the federal government. In 2022 and 2023, the decrease in this ratio is primarily due to increases in own-source revenue, mainly from non-renewable resources and taxation outpacing increases in transfers from the federal government. In 2023, the ratio returned to pre-pandemic levels.

Foreign Currency Debt to Net Debt

The ratio of foreign currency debt to net debt is an indicator of the degree of vulnerability a government has to currency rate fluctuations. Where the Government holds debt that is issued in foreign currencies it uses cross-currency swaps, a hedging strategy, to effectively convert this debt to Canadian dollar debt. At March 31, 2023, this ratio is nil due to the Government’s hedging strategies. Over the last ten years, exposure to currency rate fluctuations on foreign currency debt has been minimal. Decreasing this exposure through the use of hedging activities mitigates the risk of debt and financing charges changing due to changes in foreign currency rates.

| Government of Saskatchewan Public Accounts 2022-23 | 17 | |

Financial Statement Discussion and Analysis

Details

Revenue

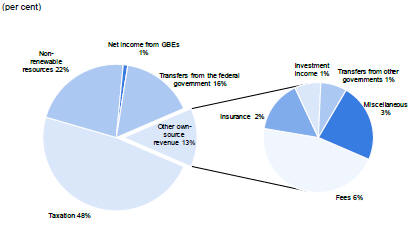

Total revenue is $20.59 billion in 2023, 16.3 per cent of which represents transfers from the federal government and the remaining 83.7 per cent own-source revenue.

Revenue by Source – 2023 ($20.59 billion)

| ||||||

Revenue by Source – Percentage of Total Revenue

| ||||||

* In 2023, key components of “other own-source revenue” include fees (6%), insurance (2%), investment income (1%), and transfers from other governments (1%). | ||||||

| 18 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Details

Revenue (continued)

Revenue by Source – Comparison to Budget and Prior Year

| * | In 2023 Actual, key components of “other own-source revenue” include fees ($1.31 billion), insurance ($487 million), investment income ($165 million), and transfers from other governments ($81 million). |

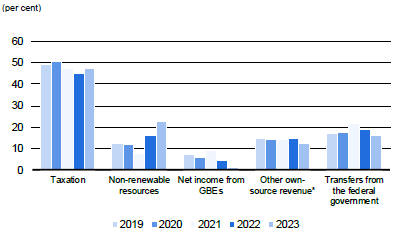

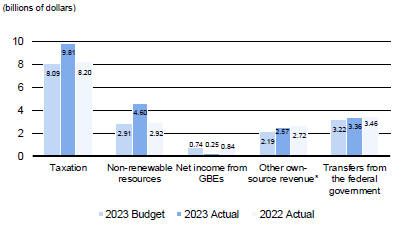

Total revenue of $20.59 billion in 2023 represents a year-over-year and an actual-to-budget increase of $2.46 billion, or 13.6 per cent, and $3.44 billion, or 20.0 per cent, respectively. This increase over prior year and budget results from increases in non-renewable resources and taxation revenues, partially offset by decrease in net income from GBEs.

| Government of Saskatchewan Public Accounts 2022-23 | 19 | |

Financial Statement Discussion and Analysis

Details

Revenue (continued)

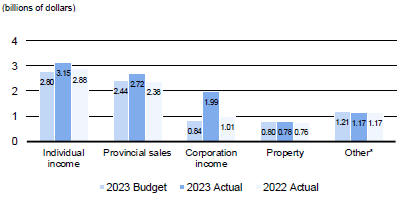

Taxation Revenue – Comparison to Budget and Prior Year

| * | In 2023 Actual, key components of “other” include fuel ($474 million) and tobacco ($164 million). |

Taxation revenue is $9.81 billion in 2023, an increase of $1.61 billion, or 19.6 per cent, over 2022 and $1.72 billion, or 21.2 per cent, over budget. The increases over prior year and budget are largely due to year-over-year and higher-than-expected increases in corporation, individual income and provincial sales taxes.

Individual income tax

The year-over-year and actual-to-budget increases are primarily due to:

| • | an unbudgeted increase in taxable income due to high compensation growth; and |

| • | an unbudgeted large positive prior-year adjustment due to favourable 2021 taxpayer assessments. |

Provincial sales tax

The year-over-year and actual-to-budget increases are primarily due to:

| • | a continuation of growth in the Saskatchewan economy and corresponding improvement in the sales tax base, reflecting GDP and retail sales growth. |

This increase is partially offset by:

| • | Saskatchewan Low Income Tax Credit payments that are higher than the previous year but lower than budget. |

Corporation income tax

The year-over-year and actual-to-budget increases are primarily due to:

| • | a continuation of the post-COVID economic recovery which resulted in a substantial improvement in the federal tax base forecast. |

Actual-to-budget increases were also impacted by:

| • | greater-than-expected 2021 taxpayer assessments resulting in a positive prior year adjustment; partially offset by: |

| • | a one-year extension of the small business rate reduction. |

Property tax

The year-over-year increase is primarily due to:

| • | an increase in mill rates and normal base growth as new construction occurs. |

The actual-to-budget decrease is primarily due to:

| • | lower-than-budget assessment growth for commercial, resource and residential property classes. |

| 20 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Details

Revenue (continued)

Other tax (including fuel, tobacco and other miscellaneous tax)

The year-over-year and actual-to-budget changes are primarily due to:

| • | an unbudgeted increase in Insurance Premiums Tax, primarily due to an increase in insurance product sales; |

| • | an unbudgeted decrease in fuel tax, primarily due to a decrease in gasoline consumption and an increase in Gasoline Competition Assistance Program rebates, partially offset by an increase in diesel consumption; and |

| • | an unbudgeted decrease in tobacco tax as a result of reduced consumption, partially offset by lower-than-budget First Nations rebates. |

Additionally, the year-over-year increase was also due to:

| • | an increase in Corporation Capital Tax, primarily reflecting strong results from both financial institutions and Crown Corporations. |

The decrease-over-budget was partially offset by:

| • | an increase in vapor products and liquor consumption taxes due to greater-than-budget consumption. |

| Government of Saskatchewan Public Accounts 2022-23 | 21 | |

Financial Statement Discussion and Analysis

Details

Revenue (continued)

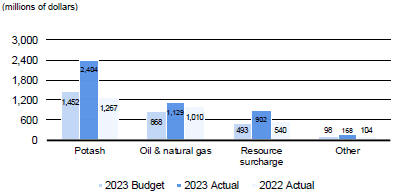

| Non-Renewable Resources Revenue – Comparison to Budget and Prior Year |

In 2023, non-renewable resources revenue is $4.60 billion, an increase of $1.68 billion, or 57.6 per cent, over 2022 and a $1.69 billion, or 58.2 per cent, increase when compared to budget. There is a year-over-year and actual-to-budget increase in all non-renewable resources revenue categories with the most significant increases in potash, resource surcharge and oil and natural gas.

Potash

The year-over-year and actual-to-budget increases are primarily due to:

| • | the average mine netback price increasing from $683 per K2O tonne in 2022 and $833 per K2O tonne at budget to $1,205 per K2O tonne in 2023; |

| • | an increase in sales volume from 13.8 million K2O tonnes in the prior year and 13.7 million K2O tonnes at budget to 13.9 million K2O tonnes in 2023; and |

| • | an unbudgeted decline in the average exchange rate. |

These increases are partially offset by:

| • | an unbudgeted increase in capital spending deductions and natural gas and operating costs. |

In addition:

| • | the year-over-year increase is partially offset by a decrease in assessments. |

Oil & natural gas

The year-over-year and actual-to-budget increases are primarily due to:

| • | a higher average Canadian dollar well-head oil price in Saskatchewan of $91.26 per barrel in 2023, compared to $77.54 per barrel in the prior year and $74.19 at budget. These increases in the average Canadian dollar well-head oil price are due to: |

| • | a higher average U.S. dollar West Texas Intermediate (WTI) oil price; and |

| • | a lower average exchange rate; partially offset by |

| • | a higher-than-budget light-heavy oil blend differential. |

| • | an increase in oil production compared to the prior year and budget. |

Resource surcharge

The year-over-year and actual-to-budget increases is primarily due to:

| • | an increase in the oil and gas, potash and uranium sectors, primarily due to higher average prices. |

Other non-renewable resources

The year-over-year and actual-to-budget increases are primarily due to:

| • | an increase in uranium revenue primarily due to higher prices and increased sales; and |

| • | an increase in crown land sales due to subsurface mineral rights sales; and |

| • | an increase in crown land sales due to an increase in oil and gas land sales |

In addition, there is:

| • | a year-over-year increase in crown land sales due to an increase in oil and gas land sales. |

| 22 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Details

Revenue (continued)

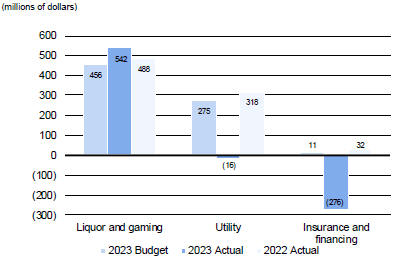

Net Income from GBEs – Comparison to Budget and Prior Year

Net income from GBEs is $250 million in 2023, a decrease of $587 million from 2022 and $492 million from budget. The decreases from both prior year and budget are due to decreases in the insurance and financing and utility sectors, offset partially by an increase in the liquor and gaming sector.

Liquor and gaming

The year-over-year and actual-to-budget increases are primarily a result of:

| • | the first full year of casino and video lottery (VLT) operations since COVID-related public health measures were lifted part way through the prior year. |

These increases are partially offset by:

| • | an unbudgeted loss related to discontinuing retail liquor operations. |

Utility

The year-over-year decrease is primarily due to:

| • | a decreased margin on electricity sales resulting from: |

| • | an increase in fuel and purchased power costs due to a change in fuel mix moving to more expensive zero-emission supply sources, higher natural gas and coal prices and higher demand; partially offset by |

| • | an increase in electricity sales revenue due to increased commercial demand, a |

September 2022 rate increase and export sales volume increases sold at higher prices to Alberta and Southwest Power Pool markets; |

| • | a decreased margin on natural gas sales resulting from: |

| • | unfavourable year-over-year market value adjustments; partially offset by |

| • | an in-year rate increase to address increasing market prices; |

| • | additional asset optimization opportunities resulting from increased market volatility; and |

| • | increased demand due to both a colder winter and additional customers; |

| • | greater operating and maintenance expenses primarily due to increased costs for power generation facility overhauls, storm-related emergency power grid infrastructure maintenance and increased spending on information technology initiatives; |

| • | a decrease in funding for power grid renewal; |

| • | litigation settlements where: |

| • | an unfavourable arbitration ruling resulting in an in-year cash settlement for SaskPower; and |

| • | litigation resolved in favour of SaskEnergy in the prior year; |

| • | an increase in the estimated decommissioning cost to remediate SaskPower owned sites; and |

| Government of Saskatchewan Public Accounts 2022-23 | 23 | |

Financial Statement Discussion and Analysis

Details

Revenue (continued)

Utility (continued)

| • | increased financing charges primarily due to higher interest rates as well as additional borrowing for capital investment. |

These year-over-year decreases are partially offset by:

| • | an increase in natural gas transportation revenue, primarily due to increased demand coupled with an April 2022 rate increase; and |

| • | an increase in natural gas delivery revenue, primarily due to a colder winter, a mid-year rate increase and additional customers. |

The decrease over budget is primarily due to:

| • | a lower-than-budget margin on electricity sales, where the unexpected rise in fuel and purchased power costs far exceeded the expected increase in electricity sales revenue; |

| • | unexpected operating and maintenance costs due to emergency maintenance and overhaul activity on the power grid; |

| • | unbudgeted increases in the cost of decommissioning and legal settlements; and |

| • | higher-than-expected financing charges where the cost of borrowing is higher-than-budget and sinking fund earnings lower-than-budget. |

These decreases from budget are partially offset by:

| • | a small improvement over the budgeted margin on natural gas sales, where significant increases in both natural gas sales revenue and natural gas sales expenses, both due to significantly higher-than-budget market prices, mostly offset each other. |

Insurance and financing

The decrease over prior year is primarily due to:

| • | a continued decline in investment returns as a result of market volatility primarily associated with rising interest rates; |

| • | costs associated with corporate transformation at Saskatchewan Government Insurance and Saskatchewan Auto Fund; and |

| • | a reduction in auto and property insurance underwriting results where an overall growth in premium revenue is more than offset by an increase in claim costs. There were many factors that contributed to the increase in claims costs, including: |

| • | an increase in the number of catastrophic events for which, unlike the prior year, none were eligible for reinsurance; |

| • | a continued increase in claim frequency associated with a post-COVID return to the roads; |

| • | an increase in the average cost per claim related to high levels of inflation and supply chain issues; and |

| • | an increase in an actuarially determined premium deficiency. |

These year-over-year decreases are partially offset by:

| • | a large recovery related to an actuarially determined reduction in the workers’ compensation benefit liability primarily resulting from an increase in the valuation discount rate; and |

| • | a rebate paid to the motoring public of Saskatchewan in the prior year with no rebate in the current year. |

The decrease over budget is primarily due to:

| • | lower-than-anticipated investment returns, primarily due to a higher-than-anticipated increase in interest rates; and |

| • | poorer-than-expected auto and property underwriting results mainly due to higher than anticipated summer storm activity, an unbudgeted premium deficiency and unbudgeted inflationary and supply chain pressures on repair costs. These pressures on claims costs were partially offset by higher-than-budget growth in policies written. |

These budget-to-actual decreases are partially offset by:

| • | a larger-than-budget decrease in the workers’ compensation benefit liability resulting from a higher valuation discount rate than anticipated. |

| 24 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Details

Revenue (continued)

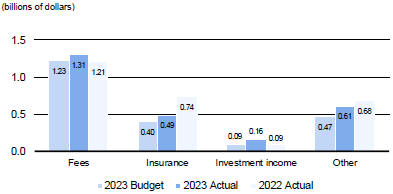

Other Own-Source Revenue – Comparison to Budget and Prior Year

Other own-source revenue is $2.57 billion in 2023, a decrease of $144 million, or 5.3 per cent, from 2022 and an increase of $380 million, or 17.4 per cent, when compared to budget. A significant portion of the year-over-year decrease is due to reinsurance recoveries on drought-related crop insurance claims in the prior year. The actual-to-budget increase is primarily due to: greater-than-expected crop insurance premiums, mainly the result of increased insured acres and higher prices; and greater-than-expected donations of COVID-related inventory received in the current year.

Fees

The year-over-year and actual-to-budget increases are due to:

| • | an unbudgeted first-time charge of compliance fees for excess carbon emissions; |

| • | an increase over budget and the prior year in tuition and other education-related fees as COVID-related restrictions ease and students utilize more services; and |

| • | an increase over budget and the prior year in healthcare fees due to higher rates and service volumes. |

These year-over-year increases are partially offset by:

| • | a decrease in fees from transportation partnership agreements where the magnitude of prior year projects exceeded that of the current year; and |

| • | a decrease in forest-related license and permit revenue. |

Additionally, the actual-to-budget increase is impacted by greater-than-budget fees for:

| • | Treaty Land Entitlement mineral rights; |

| • | agricultural land lease revenues; and |

| • | fire support services to other provincial jurisdictions. |

Insurance

The year-over-year decrease is due to:

| • | a decrease in reinsurance recovery due to greater crop insurance losses related to drought-related claims in the prior year, partially offset by an increase in crop insurance premiums, mainly the result of increased insured acres and higher prices. |

The actual-to-budget increase is due to:

| • | greater-than-budget crop insurance premiums, mainly the result of increased insured acres and higher prices. |

Investment Income

The year-over-year and actual-to-budget increase are due to:

| • | an increase in returns on investments, student loans and other financial instruments primarily due to increasing interest rates, partially offset by lower sinking fund earnings. |

| Government of Saskatchewan Public Accounts 2022-23 | 25 | |

Financial Statement Discussion and Analysis

Details

Revenue (continued)

Other (including transfers from other governments and miscellaneous)

The year-over-year decrease is mainly due to:

| • | a decrease in donations of COVID-19 test kits and personal protective equipment. |

This decrease is partially offset by:

| • | proceeds from a sale of land related to the new canola crush facility; and |

| • | an increase in miscellaneous revenue at various Boards of Education. |

The actual-to-budget increase is mainly due to:

| • | greater-than-expected donations of COVID-19 test kits and personal protective equipment; |

| • | an unbudgeted cash recovery of prior year expenses; |

| • | greater-than-expected proceeds from a sale of land related to the new canola crush facility; and |

| • | greater-than-expected lottery sales. |

| 26 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Details

Revenue (continued)

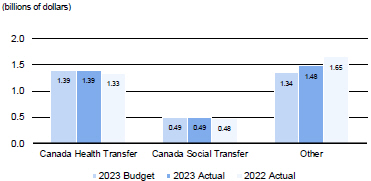

Transfers from the Federal Government – Comparison to Budget and Prior Year

Federal transfers are $3.36 billion in 2023, a decrease of $103 million, or 3.0 per cent, compared to 2022 and increases of $137 million, or 4.3 per cent, when compared to budget. The year-over-year decrease is mainly due to a decrease in COVID-related funding and one-time Drought Response Initiative funding in the prior year, partially offset by an increase in crop insurance contributions. The actual-to-budget increase is primarily due to greater-than-expected federal contributions to crop insurance and one-time funding in the current year to address medical backlogs.

Canadian Health Transfer

The year-over-year increase is primarily due to:

| • | a legislated annual increase in the national allocation equal to the greater of 3 per cent and the three-year moving average of the Canadian nominal GDP growth rate with an adjustment for changes in Saskatchewan’s share of the national population. |

The decrease from budget is nominal.

Canadian Social Transfer

The year-over-year increase is primarily due to:

| • | a legislated 3 per cent annual increase in the national allocation with an adjustment made for changes in Saskatchewan’s share of the national population. |

The decrease from budget is nominal.

Other transfers from the federal government

The year-over-year and actual-to-budget changes are primarily due to:

| • | a budgeted decrease in funding for COVID-related health, safety and financial support measures; |

| • | a budgeted decrease related to one-time funding received in the prior year for the Drought Response Initiative to compensate livestock producers; |

| • | a budgeted decrease in funding for the Accelerated Site Closure Program related to a planned decrease in activity in the reclamation of inactive oil wells; |

| • | federal funding for disaster assistance which is less than the prior year but greater than budgeted; |

| • | an unbudgeted increase in federal contributions to crop insurance premiums, mainly the result of increased insured acres and higher prices; |

| • | funding for Saskatchewan’s share of the Early Learning and Child Care agreements for which increased funding, tied to increased spending over the prior year, is slightly less-than-budget; |

| • | a one-time unbudgeted Canada Health Transfer top-up to reduce surgical and other medical procedures backlogs; |

| • | federal reimbursements through the Investing in Canada Infrastructure Program which are greater than the prior year but less than budgeted; and |

| • | an unbudgeted increase in claims for the Wildlife Damage Compensation Program due to higher crop prices and an activity related unbudgeted increase in the Farm and Ranch Water Infrastructure Program. |

| Government of Saskatchewan Public Accounts 2022-23 | 27 | |

Financial Statement Discussion and Analysis

Details

Expense

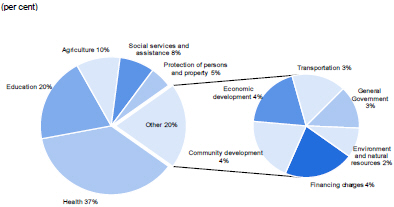

Total expense was $19.01 billion in 2023, 56.8 per cent of which represents spending in the health and education sectors. The SFS report expense by theme and by object, or major type of expense such as salaries and benefits, transfers and operating costs.

Expense by Theme – 2023 ($19.01 billion)

|

Expense by Theme – Percentage of Total Expense

| ||

* In 2023, key components of “other” include financing charges (4%), community development (4%), economic development (4%), transportation (3%), general government (3%) and environment and natural resources (2%). | ||

| 28 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Details

Expense (continued)

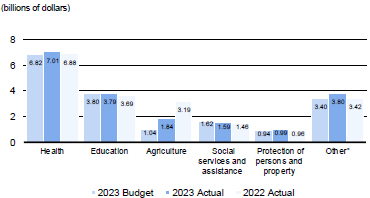

Expense by Theme – Comparison to Budget and Prior Year

| * | In 2023 Actual, key components of “other” include financing charges ($816 million), community development ($758 million), economic development ($734 million), transportation ($627 million), general government ($512 million) and environment and natural resources ($353 million). |

Total expenses are $19.01 billion in 2023. This represents a decrease of $591 million, or 3.0 per cent, from the prior year and an increase of $1.39 billion, or 7.9 per cent, over budget. The agriculture theme saw the most notable impact as drought conditions significantly improved in parts of the province resulting in crop insurance payouts lower than the prior year but greater than budget. Additionally, there is a significant increase in the economic development theme, both year-over-year and from budget, for Saskatchewan Affordability Tax Credit payments made to Saskatchewan residents.

Health

The year-over-year increase is primarily due to:

| • | a general increase in the cost of delivering healthcare primarily due to inflationary pressures and increased demand for services as evidenced by higher surgical volumes; |

| • | increased investment in the health care information system and supporting infrastructure, modernization and security; and |

| • | increases in utilization for medical services and medical education programs, including out-of-province medical services, as well as the Senior Citizens’ Ambulance Assistance, Saskatchewan Aids to Independent Living and the Supplementary Health programs. |

These increases are partially offset by:

| • | a reduction in COVID-related expenses including immunization clinics, contact tracing and the distribution of federally donated COVID test kits. |

The increase from budget is mainly attributed to:

| • | higher-than-budget costs for delivering healthcare primarily due to inflationary pressures, greater-than-budgeted demand for services, increased overtime costs and contracted positions, partially offset by savings from an increase in the number of vacant positions; |

| • | greater-than-expected utilization and inflationary pressures, leading to increased costs for medical supplies and drug usage; |

| • | higher-than-budget utilization and distribution of federally donated COVID test kits; |

| • | greater-than-budget building repairs and maintenance due to COVID-related delays in prior years; and |

| • | higher-than-budget utilization in the Saskatchewan Prescription Drug, Supplementary Health, Senior Citizens’ Ambulance Assistance and Air Ambulance programs. |

| Government of Saskatchewan Public Accounts 2022-23 | 29 | |

Financial Statement Discussion and Analysis

Details

Expense (continued)

Education

The year-over-year increase is primarily due to:

| • | increased costs in boards of education related to a negotiated salary increase in 2022, inflationary pressures, increased enrollment and continuing COVID-related spending mainly for staff absenteeism; and |

| • | increased spending related to the Canada-wide Early Learning and Child Care agreements. |

These increases are partially offset by:

| • | a decrease in pension costs for the Teacher’s Superannuation Plan (TSP) primarily due to fully amortized prior year losses, new gains arising from plan experience differences and changes in actuarial assumptions for inflation and salary; and |

| • | reduced costs related to the wind-down of the Provincial Training Allowance program. |

The decrease from budget is mainly attributed to:

| • | lower-than-expected pension costs for TSP primarily due to gains for the change in the interest rate assumption being higher-than-estimated; and |

| • | lower-than-anticipated spending related to the Canada-wide Early Learning and Child Care agreements. |

These decreases are partially offset by:

| • | higher-than-anticipated costs in boards of education due to increased spending on K-12 initiatives, preventative maintenance and renewal, staffing to address increased enrollment and inflationary pressures. |

Agriculture

The year-over-year decrease is primarily due to:

| • | drought conditions that were widespread in the prior year but limited to western areas of the province in 2022-23, resulting in a significant decrease in crop insurance indemnities paid to producers; and |

| • | prior year relief payments to livestock producers under the federal-provincial Drought Response Initiative, a one-year program offered in 2022. |

The increase over budget is mainly attributed to:

| • | drought conditions in the western part of the province during 2022-23, resulting in higher-than-budget crop insurance indemnities paid to producers; |

| • | higher-than-budget payments under the Wildlife Damage Compensation program due to higher crop prices; |

| • | greater-than-anticipated AgriStability indemnities; and |

| • | an increase over the budgeted program activity under the Farm and Ranch Water Infrastructure program. |

Social services and assistance

The year-over-year increase is primarily due to:

| • | increased utilization of the Saskatchewan Income Support and the Saskatchewan Assured Income for Disability programs; |

| • | increased spending in various disability and child and family programs to address utilization pressures, to increase funding to community-based organizations and for expansion and enhancement of existing services; and |

| • | increased social housing maintenance and renovation costs. |

The decrease from budget is primarily due to:

| • | lower-than-anticipated utilization of the Saskatchewan Income Support program which was partially offset by higher-than-anticipated utilization of the Saskatchewan Assured Income for Disability and Saskatchewan Rental Housing Supplement programs. |

| 30 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Details

Expense (continued)

Protection of persons and property

The year-over-year and budget-to-actual changes are primarily due to:

| • | increased Provincial Disaster Assistance claims, resulting from extreme weather events; partially offset by |

| • | the costs associated with fire and emergency response activities that were lower than the prior year but higher than budget. |

In addition, there is:

| • | a year-over-year increase for the establishment of Provincial Protective Services, which integrates Saskatchewan’s enforcement services under a single organizational structure; and |

| • | an increase over budget in correctional facilities due to higher-than-anticipated inmate counts. |

Other expense themes (including financing charges, community development, economic development, transportation, general government, and environment and natural resources)

The year-over-year increase is primarily due to:

| • | the $500 Saskatchewan Affordability Tax Credit payments made to Saskatchewan residents during the year; |

| • | an increase in financing charges primarily related to increased debt and interest rates; |

| • | increased payments to First Nations and Métis organizations as gaming profits returned to normal post-COVID, partially offset by a fall off of pandemic support payments; |

| • | increased costs related to information technology management, coordination and transformation initiatives; |

| • | increased infrastructure funding to municipalities through the Investing in Canada Infrastructure program; |

| • | increased grants provided for investment in film and television production; |

| • | increased input costs for highways winter maintenance and surface preservation; |

| • | increased payments to municipalities as a result of federal transit and housing supports; and |

| • | increased pension related financing charges primarily due to higher interest rates and a lower return on TSP assets, offset by declining pension obligation balances. |

These increases over prior year are partially offset by:

| • | the completion of the Saskatchewan Economic Recovery Rebate program which subsidized power bills in the prior year; |

| • | decreased funding to communities through the federal Canada Community-Building Fund related to a one-time pandemic recovery top-up in the prior year; |

| • | decreased capital funding for utilities related to power grid renewal in the prior year; |

| • | decreased spending related to the completion of the Accelerated Site Closure Program; |

| • | decreased expenses in the environment and transportation themes related to the transfer of conservation and highway patrol officers to the newly established Provincial Protective Services, which is reflected in the increased expenses in the protection of persons and property theme; and |

| • | decreased payments under the Small Business Emergency Payment program. |

The increase from budget is primarily due to:

| • | unbudgeted $500 Saskatchewan Affordability Tax Credit payments made to Saskatchewan residents; |

| • | higher-than-budget post-COVID gaming profits resulting in higher-than-expected payments to First Nations and Metis organizations; |

| • | greater-than-expected weather-related highway winter maintenance costs; |

| • | unbudgeted payments to municipalities as a result of federal transit and housing supports; and |

| • | higher-than-expected pension-related financing charges primarily due to greater-than-budget interest rates. |

These increases from budget are partially offset by:

| • | lower-than-anticipated funding to municipalities through the Investing in Canada Infrastructure program; |

| • | lower-than-anticipated activity for the Accelerated Site Closure program; |

| • | unbudgeted changes in public employee benefit plans’ insurance provisions; |

| • | deferred costs for information technology project implementation; |

| • | lower-than-anticipated spending on northern water and sewer projects due to unexpected delays; and |

| • | lower-than-budget financing charges primarily due to lower-than-expected overall borrowing, partially offset by greater-than-budget interest rates. |

| Government of Saskatchewan Public Accounts 2022-23 | 31 |

Financial Statement Discussion and Analysis

Details

Expense (continued)

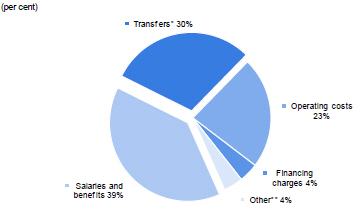

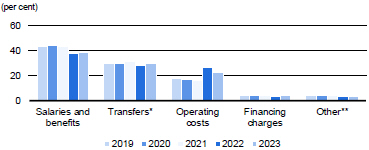

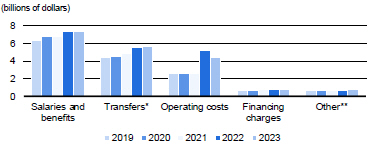

Expense by Object – 2023 ($19.01 billion)

|

| * | Transfers are provided to third parties for salaries, capital and other costs. |

| ** | The key component of “other” is amortization of capital assets. |

Expense by Object – Percentage of Total Expense

|

| * | Transfers are provided to third parties for salaries, capital and other costs. |

| ** | The key component of “other” is amortization of capital assets. |

Expense by Object

| The most significant change is a $929 million decrease in operating costs, primarily due to record crop insurance claims in the prior year resulting from drought conditions experienced across the province. |

| * | Transfers are provided to third parties for salaries, capital and other costs. |

| ** | The key component of “other” is amortization of capital assets. |

| 32 | Government of Saskatchewan Public Accounts 2022-23 |

Financial Statement Discussion and Analysis

Details

Expense (continued)

Financing Charges

| * | In 2016, the inclusion of an additional three months of operations of certain GBEs contributed approximately $120 million to GBE financing charges. |

The Statement of Operations reports financing charges that the Government incurs related to its general debt, unfunded pension liability and obligations under long-term financing arrangements (P3 obligations) but does not include government business enterprise (GBE) financing charges. GBE financing charges are included in the net income from GBEs reported on the Statement of Operations and disclosed in schedule 3 of the SFS. For general debt, financing charges are determined by the amount of general debt and the interest rate attached to that debt.

Financing charges have increased in recent years mainly due to an increase in debt financing for the replacement of aging infrastructure as well as for the building of new capacity to meet the demands of the Province’s growing population.

The average effective interest rate on gross debt during 2023 was 3.2 per cent (2022 - 3.1 per cent). Pension interest expense is a function of the unfunded pension liability and the interest costs that are based on the Government’s borrowing rates. The average effective interest rate on the unfunded pension liability during 2023 was 2.9 per cent (2022 - 2.6 per cent). Interest on P3 obligations, ranging from 3.1 to 3.5 per cent, reflects the Government’s cost of borrowing at the date the P3 contract was signed.

| Government of Saskatchewan Public Accounts 2022-23 | 33 | |

Financial Statement Discussion and Analysis

Details

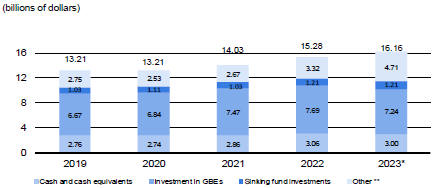

Financial Assets

Financial assets represent the amount of resources available to the Government that can be converted to cash to meet obligations or fund operations.

Financial Assets

| * | Beginning in 2023, sinking fund investments are reported as financial assets with prior year balances reclassified to conform with this presentation. In addition, beginning in 2023, portfolio investments include amounts reclassified from cash and cash equivalents and the fair value remeasurement of certain portfolio investments. |

| ** | At March 31, 2023, primarily accounts receivable ($2.19 billion), portfolio investments ($1.46 billion) and loans receivable ($994 million). |

From 2019 to 2023, financial assets increased by $2.95 billion. This was primarily a result of an $998 million increase in portfolio investments and $577 million increase in investment in GBEs.

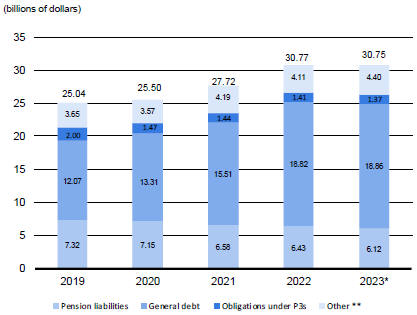

Liabilities

Liabilities represent the obligations the Government has to others arising from past transactions or events.

Liabilities

| * | Beginning in 2023, general debt is no longer reported net of sinking fund investments. Prior year balances have been reclassified to conform with this presentation. |

| ** | At March 31, 2023, primarily accounts payable and accrued liabilities ($3.47 billion). |

From 2019 to 2023, liabilities increased by $5.71 billion. This was primarily a result of a $6.79 billion increase in general debt.

| 34 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Details

Liabilities (continued)

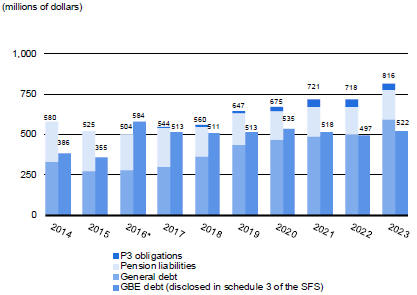

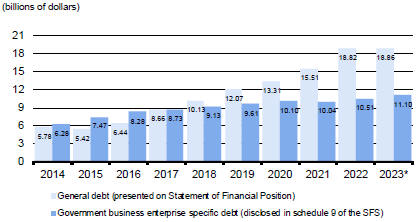

Public Debt

| * | Beginning in 2023, public debt is no longer reported net of sinking fund investments. Prior year balances have been reclassified to conform with this presentation. |

Public debt consists of:

| • | general debt, which is: |

| • | debt issued by the General Revenue Fund (GRF) and other government service organizations (GSOs); and |

| • | debt issued by the GRF and subsequently loaned to GBEs; and |

| • | GBE specific debt, which is debt issued by GBEs or debt issued by the GRF specifically on behalf of GBEs where the Government expects to realize the receivables from the GBEs and settle the external debt simultaneously. |

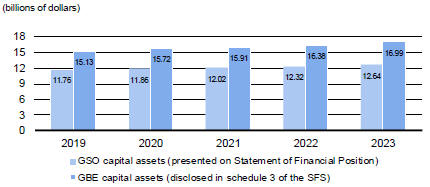

The general debt on the Statement of Financial Position does not include GBE specific debt. GBE specific debt is included in the Investment in GBEs reported on the Statement of Financial Position and disclosed in schedule 9 of the SFS.

At March 31, 2023, the SFS report general debt of $18.86 billion and GBE specific debt of $11.10 billion. General debt, after several years of little change, has increased over the past eight years. Until 2021, these increases helped to finance the replacement of aging infrastructure as well as build new capacity to meet the demands of a growing population in the Province. The increase since 2021 is primarily a combination of COVID-related economic stimulus spending on infrastructure and borrowing to cover COVID-related revenue shortfalls and incremental expenses.

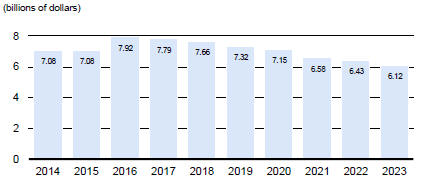

Pension Liabilities

Pension liabilities represent the future obligations for the Government’s defined benefit pension plans. The pension liability fluctuates with changes in actuarial assumptions such as interest rates and life expectancy. The Government limited its pension exposure over 40 years ago when it closed the main defined benefit plans to new members and introduced defined contribution plans. There is no liability exposure for the Government under defined contribution plans.

At March 31, 2023, the SFS report pension liabilities of $6.12 billion, a decrease of $96 million since 2014. Pension liability increases up to 2016 represent the amount by which pension costs, including interest on the pension liabilities and actuarial adjustments, exceeded payments to the pension plans and retirees. This was primarily a result of a decline in interest rates over the same period of time, where small fluctuations in interest rates had a significant impact on the pension liability. Since 2016, the pension liability has decreased by $1.80 billion as payments have begun to exceed the pension costs.

| Government of Saskatchewan Public Accounts 2022-23 | 35 | |

Financial Statement Discussion and Analysis

Details

Liabilities (continued)

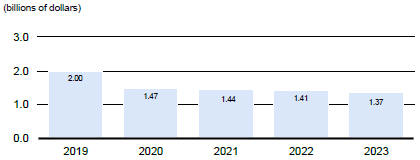

Obligations under Long-Term Financing Arrangements

Obligations under long-term financing arrangements represent the Government’s liability for public private partnerships (P3s). P3 obligations increase as the related assets are built (percentage of completion basis), and are reduced as payments are made to the P3 partner.

The Government is party to four P3 arrangements (as disclosed in schedule 10 of the SFS). All four P3 projects have been operational since 2020.

Non-Financial Assets

Non-financial assets typically represent resources that the Government can use to provide services in the future. Non-financial assets primarily consist of capital assets but also include inventories held for consumption and prepaid expenses.

Net Book Value of Capital Assets

The Statement of Financial Position reports a net book value of capital assets recognized by government service organizations (GSOs) and does not include the capital assets recognized by GBEs. Capital assets recognized by GBEs are included in the investment in GBEs reported on the Statement of Financial Position and disclosed in schedule 3 of the SFS. The net book value represents the original cost of capital assets net of accumulated amortization, disposals and write-downs in value.

The net book value of capital assets recognized by the Government has steadily increased over the last five years indicating that the Government has been acquiring new, or replacing existing, capital assets.

Acquisition of capital assets in 2023 was $2.66 billion, $1.66 billion acquired by GBEs and $999 million by GSOs. The investment in capital assets made by GSOs is primarily in the transportation, health and education sectors mainly for road, bridge and water management assets ($434 million) and land, buildings and improvements ($345 million). The GBEs continued to replace aging infrastructure and invest in capital projects to meet the demand for growth and improve safety.

| 36 | Government of Saskatchewan Public Accounts 2022-23 | |

Financial Statement Discussion and Analysis

Details

Cash Flow

The Statement of Cash Flow reports on the sources and uses of cash and cash equivalents during the year During the year, the Government’s overall cash position decreased by $55 million, from $3.05 billion in 2022 to $3.00 billion in 2023.

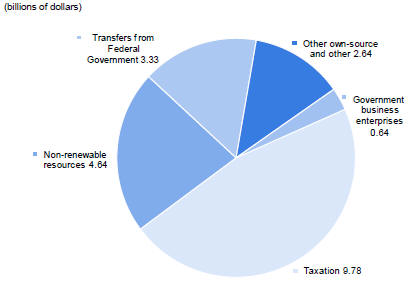

Sources of Cash

The primary source of cash is $9.78 billion from taxation. Other significant sources of cash are $4.64 billion from non-renewable resources and $3.33 billion from transfers from Federal Government.

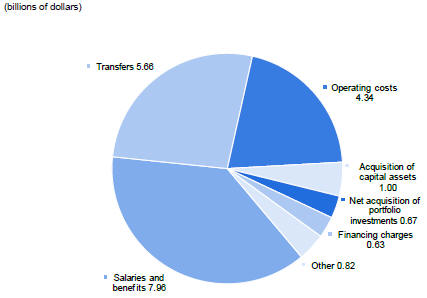

Uses of Cash

The most significant use of cash is $7.96 billion for salaries and benefits largely for frontline service providers in the health and education sectors. Another significant use of cash is $5.66 billion for transfers mainly in the health, social services and assistance, and education themes.

| Government of Saskatchewan Public Accounts 2022-23 | 37 | |

Financial Statement Discussion and Analysis

Risks and Uncertainties

The Government is subject to risks and uncertainties that arise from variables which the Government cannot directly control. These risks and uncertainties include:

| • | changes in economic factors such as economic growth or decline, commodity and non-renewable resource prices, inflation, interest rates, marketplace competition, trade barriers, population change, personal income and retail sales; |

| • | exposure to interest rate risk, foreign exchange rate risk, price risk, credit risk and liquidity risk (see note 4 of the SFS); |

| • | changes in transfers from the federal government; |

| • | utilization of government services, such as insurance, health care and social services; |

| • | volatility in the pension liability due to external factors such as interest rates and actuarially determined assumptions of future events; |

| • | other unforeseen developments including unusual weather patterns and natural and other disasters; |

| • | criminal or malicious attacks, both cyber and physical in nature, potentially resulting in business interruption, privacy breach and loss of, or damage to, information, facilities and equipment; |

| • | identification and quantification of environmental liabilities; |

| • | supply chain disruptions and other factors that could hinder the safe delivery of products and services; |

| • | outcomes from litigation, arbitration and negotiations with third parties; |

| • | changes in reported results where actual experience may differ from initial estimates as discussed in note 3 of the SFS; and |

| • | changes in accounting standards. |

Recognizing that Saskatchewan is reliant on the revenue from non-renewable resources and that the Province’s financial results can be influenced by other external factors, the Government takes a prudent approach in developing its budget assumptions for macroeconomic variables and non-renewable resources prices. The Government uses a number of forecasts from national forecasting agencies and banks, private industry and private sector analysts when developing the underlying assumptions for fiscal forecasts both on budget day and throughout the fiscal year.

The fiscal impact of changes in the underlying economic assumptions, including non-renewable resources prices, are estimated on a regular basis to quantify the risk associated with each forecast assumption. By understanding the size of the risk inherent in the fiscal projections, the Government is better able to make sound financial decisions.

Finally, for the Government to meet its challenges of growth and remain competitive where it operates in a competitive environment, attention is directed towards maintaining and investing in the Province’s infrastructure to support the steady growth the Province has been experiencing and to allow for continued growth in the future.

| 38 | Government of Saskatchewan Public Accounts 2022-23 | |

Summary Financial Statements

Summary Financial Statements

Responsibility for the Summary Financial Statements

The Government is responsible for the Summary Financial Statements. The Government maintains a system of accounting and administrative controls to ensure that accurate and reliable financial statements are prepared and to obtain reasonable assurance that transactions are authorized, assets are safeguarded, and financial records are maintained.

The Provincial Comptroller prepares these statements in accordance with generally accepted accounting principles for the public sector, using the Government’s best estimates and judgement when appropriate. He uses information from the accounts of the General Revenue Fund, Crown corporations and other government organizations to prepare these statements.

The Provincial Auditor expresses an independent opinion on these statements. Her report, which appears on the following page, provides the scope of her audit and states her opinion.

Treasury Board approves the Summary Financial Statements. The statements are tabled in the Legislative Assembly as part of the Public Accounts and referred to the Standing Committee on Public Accounts for review.

On behalf of the Government of the Province of Saskatchewan.

DONNA HARPAUER

Deputy Premier and

Minister of Finance

MAX HENDRICKS

Deputy Minister of Finance

CHRIS BAYDA

Provincial Comptroller

Regina, Saskatchewan

June 2023

| Government of Saskatchewan Public Accounts 2022-23 | 41 |

Summary Financial Statements

Independent Auditor’s Report

To the Members of the Legislative Assembly of Saskatchewan

Opinion

We have audited the consolidated financial statements of the Government of Saskatchewan, which comprise the consolidated Statement of Financial Position as at March 31, 2023, and the consolidated Statements of Operations, Accumulated Operating Deficit, Accumulated Remeasurement Gains and Losses, Change in Net Debt, and Cash Flow for the year then ended, and notes to the consolidated financial statements, including a summary of significant accounting policies.

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the consolidated financial position of the Government of Saskatchewan as at March 31, 2023, and the consolidated results of its operations, accumulated remeasurement gains and losses, changes in net debt, and cash flows for the year then ended in accordance with Canadian public sector accounting standards.

Basis for Opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Consolidated Financial Statements section of our report. We are independent of the Government of Saskatchewan in accordance with the ethical requirements that are relevant to our audit of the consolidated financial statements in Canada, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Key Audit Matters