UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811- 02753

SBL Fund

(Exact name of registrant as specified in charter)

805 King Farm Boulevard, Suite 600

Rockville, Maryland 20850

(Address of principal executive offices) (Zip code)

Donald C. Cacciapaglia

SBL Fund

805 King Farm Boulevard, Suite 600

Rockville, Maryland 20850

(Name and address of agent for service)

Registrant's telephone number, including area code: 1-301-296-5100

Date of fiscal year end: December 31

Date of reporting period: December 31, 2013

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. §3507.

Item 1. Reports to Stockholders.

SERIES A (STYLEPLUS–LARGE CORE SERIES)

| (Formerly, Large Cap Core Series) | |

| SERIES B (LARGE CAP VALUE SERIES) | |

| SERIES C (MONEY MARKET SERIES) | |

| SERIES D (WORLD EQUITY INCOME SERIES) | |

| (Formerly, MSCI EAFE Equal Weight Series) | |

| SERIES E (TOTAL RETURN BOND SERIES) | |

| (Formerly, U.S. Intermediate Bond Series) | |

| SERIES F (FLOATING RATE STRATEGIES SERIES) | |

| SERIES J (STYLEPLUS–MID GROWTH SERIES) | |

| (Formerly, Mid Cap Growth Series) | |

| SERIES M (MACRO OPPORTUNITIES SERIES) | |

| SERIES N (MANAGED ASSET ALLOCATION SERIES) | |

| SERIES O (ALL CAP VALUE SERIES) | |

| SERIES P (HIGH YIELD SERIES) | |

| SERIES Q (SMALL CAP VALUE SERIES) | |

| SERIES V (MID CAP VALUE SERIES) | |

| SERIES X (STYLEPLUS–SMALL GROWTH SERIES) | |

| (Formerly, Small Cap Growth Series) | |

| SERIES Y (STYLEPLUS–LARGE GROWTH SERIES) | |

| (Formerly, Large Cap Concentrated Growth Series) | |

| SERIES Z (ALPHA OPPORTUNITY SERIES) | 460425800 |

This report and the financial statements contained herein are submitted for the general information of our shareholders. The report is not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus.

Distributed by Guggenheim Distributors, LLC.

| TABLE OF CONTENTS |

| The GUGGENHEIM FUNDS annual report | 1 |

| December 31, 2013 |

Security Investors, LLC and Guggenheim Partners Investment Management (the “Investment Advisers”) is pleased to present the annual shareholder report for 16 of our variable insurance funds. This report covers performance of the Funds for the annual period ended December 31, 2013. Series F (Floating Rate Strategies Series) and M (Macro Opportunities Series) were both launched on April 24, 2013.

The Investment Advisers is a part of Guggenheim Investments, which represents the investment management businesses of Guggenheim Partners, LLC, a global, diversified financial services firm.

Guggenheim Distributors, LLC is the distributor of the Funds. Guggenheim Distributors, LLC is affiliated with Guggenheim Partners, LLC and Security Investors, LLC.

We encourage you to read the Economic and Market Overview section of the report, which follows this letter, and then the Manager’s Commentary for each Fund.

We are committed to providing innovative investment solutions and appreciate the trust you place in us.

Sincerely,

Donald C. Cacciapaglia

President

January 31, 2014

Read a prospectus and summary prospectus (if available) carefully before investing. It contains the investment objectives, risks, charges, expenses and other information, which should be considered carefully before investing. Obtain a prospectus and summary prospectus (if available) at guggenheiminvestments.com or call 800.820.0888.

The Series StylePlus Funds may not be suitable for all investors. Investments in large capitalization stocks may underperform other segments of the equity market or the equity market as a whole. • Investments in small-sized company securities may present additional risks such as less predictable earnings, higher volatility and less liquidity than larger, more established companies. • Growth stocks may be more volatile than other stocks because they are more sensitive to investor perceptions regarding the growth potential of the issuing companies. • The Funds may invest in derivative instruments, which may be more volatile and less liquid, increasing the risk of loss when compared to traditional securities. Certain of the derivative instruments are also subject to the risks of counterparty default and adverse tax treatment. • The Funds’ use of leverage, through borrowings or instruments such as derivatives, may cause the Funds to be more volatile than if it had not been leveraged. • The Funds’ investments in other investment vehicles subject the Funds to those risks and expenses affecting the investment vehicle. • The Funds may invest in foreign securities which carry additional risks when compared to U.S. securities, due to the impact of diplomatic, political or economic developments in the country in question (investments in emerging markets securities are generally subject to an even greater level of risks). • The Funds may invest in fixed income securities whose market value will change in response to interest rate changes and market conditions among other factors. In general, bond prices rise when interest rates fall and vice versa. • The Fund’s exposure to high yield securities may subject the Fund to greater volatility. • The Funds may invest in bank loans and asset-backed securities, including mortgage backed, which involve special types of risks. • The Funds may invest in restricted securities which may involve financial and liquidity risk. • You may have a gain or loss when you sell your shares. • It is important to note that the Funds are not guaranteed by the U.S. government. • Please read the prospectus for more detailed information regarding these and other risks.

The Series Value Funds may not be suitable for all investors. • An investment in the Funds will fluctuate and is subject to investment risks, which means investors could lose money. The intrinsic value of the underlying stocks may never be realized or the stocks may decline in value. Investments in small- and/ or mid-sized company securities may present additional risks such as less predictable earnings, higher volatility and less liquidity than larger, more established companies. Please read the prospectus for more detailed information regarding these and other risks.

| 2 | the GUGGENHEIM FUNDS annual report |

| December 31, 2013 |

The Series C (Money Market Series) may not be suitable for all investors. • An investment in the Fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency. • It is possible to lose money by investing in the Fund. The principal risks of investing in the Fund are listed below. • The Fund could lose money if the issuer of a bond is unable to repay interest and principal on time or defaults. • The issuer of a bond could also suffer a decrease in quality rating, which would affect the volatility and liquidity of the bond. • Investments in fixed-income securities are subject to the possibility that interest rates could rise sharply, causing the value of the Fund’s securities and share price to decline. • Fixed income securities with longer durations are subject to more volatility than those with shorter durations. • Regulations of money market funds are evolving. • New regulations may affect negatively the Fund’s performance, yield and cost.

The Series D (World Equity Income Series) may not be suitable for all investors. • Investments in securities in general are subject to market risks that may cause their prices to fluctuate over time. • The Fund’s investments in foreign securities carry additional risks when compared to U.S. securities, due to the impact of diplomatic, political or economic developments in the country in question (investments in emerging markets are generally subject to an even greater level of risks). Additionally, the Fund’s exposure to foreign currencies subjects the Fund to the risk that those currencies will decline in value relative to the U.S. Dollar. • The Fund’s investments in derivatives may pose risks in addition to those associated with investing directly in securities or other investments, including illiquidity of the derivatives, imperfect correlations with underlying investments or the Fund’s other portfolio holdings, lack of availability and counterparty risk. • The Fund’s use of leverage, through instruments such as derivatives, may cause the fund to be more volatile than if it had not been leveraged. • The Fund’s investments in other investment vehicles subject the Fund to those risks and expenses affecting the investment vehicle. • The Fund may have significant exposure to securities in a particular capitalization range e.g., large-, mid- or small-cap securities. As a result, the Fund may be subject to the risk that the pre-denominate capitalization range may underperform other segments of the equity market or the equity market as a whole. • Please read the prospectus for more detailed information regarding these and other risks.

The Series E (Total Return Bond Series) may not be suitable for all investors. • The Fund’s market value will change in response to interest rate changes and market conditions among other factors. In general, bond prices rise when interest rates fall and vice versa. • The Fund’s exposure to high yield securities may subject the Fund to greater volatility. • When market conditions are deemed appropriate, the Fund will leverage to the full extent permitted by its investment policies and restrictions and applicable law. Leveraging will exaggerate the effect on net asset value of any increase or decrease in the market value of the Fund’s portfolio. • The Fund may invest in derivative instruments, which may be more volatile and less liquid, increasing the risk of loss when compared to traditional securities. Certain of the derivative instruments are also subject to the risks of counterparty default and adverse tax treatment. • Instruments and strategies (such as borrowing transactions and reverse repurchase agreements) may provide leveraged exposure to a particular investment, which will magnify any gains or losses on those investments. • Investments in reverse repurchase agreements expose the Fund to the many of the same risks as investments in derivatives. • The Fund’s investments in other investment vehicles subject the Fund to those risks and expenses affecting the investment vehicle. • The Fund’s investments in foreign securities carry additional risks when compared to U.S. securities, due to the impact of diplomatic, political or economic developments in the country in question (investments in emerging markets securities are generally subject to an even greater level of risks). • Investments in syndicated bank loans generally offer a floating interest rate and involve special types of risks. • The Fund’s investments in municipal securities can be affected by events that affect the municipal bond market. • The Fund’s investments in real estate securities subject the Fund to the same risks as direct investments in real estate, which is particularly sensitive to economic downturns. • The Fund’s investments in restricted securities may involve financial and liquidity risk. • You may have a gain or loss when you sell your shares. • It is important to note that the Fund is not guaranteed by the U.S. government. • Please read the prospectus for more detailed information regarding these and other risks.

The Series F (Floating Rate Strategies Series) may not be suitable for all investors. • Investments in floating rate senior secured syndicated bank loans and other floating rate securities involve special types of risks, including credit rate risk, interest rate risk, liquidity risk and prepayment risk. • The Fund’s market value will change in response to interest rate changes and market conditions among other factors. In general, bond prices rise when interest rates fall and vice versa. • The Fund’s exposure to high yield securities may subject the Fund to greater volatility. • When market conditions are deemed appropriate, the Fund will leverage to the full extent permitted by its investment policies and restrictions and applicable law. Leveraging will exaggerate the effect on net asset value of any increase or decrease in the market value of the Fund’s portfolio. • The Fund may invest in derivative instruments, which may be more volatile and less liquid, increasing the risk of loss when compared to traditional securities. Certain of the derivative instruments are also subject to the risks of counterparty default and adverse tax treatment. • Instruments and strategies (such as borrowing transactions and reverse repurchase agreements) may provide leveraged exposure to a particular investment, which will magnify any gains or losses on those investments. • Investments in reverse repurchase agreements and synthetic instruments (such as synthetic collateralized debt obligations) expose the Fund to the many of the same risks as investments in derivatives. • The Fund’s investments in other investment vehicles subject the Fund to those risks and expenses affecting the investment vehicle. • The Fund’s investments in foreign securities carry additional risks when compared to U.S. securities, due to the impact of diplomatic, political or economic developments in the country in question (investments in emerging markets securities are generally subject to an even greater level of risks). • The Fund’s investments in real estate securities subject the Fund to the same risks as direct investments in real estate, which is particularly sensitive to economic downturns. • The Fund’s investments in restricted securities may involve financial and liquidity risk. • The Fund is subject to active trading risks that may increase volatility and impact its ability to achieve its investment objective. • You may have a gain or loss when you sell your shares. • It is important to note that the Fund is not guaranteed by the U.S. government. • Please read the prospectus for more detailed information regarding these and other risks.

The Series M (Macro Opportunities Series) may not be suitable for all investors. • The Fund’s market value will change in response to interest rate changes and market conditions among other factors. In general, bond prices rise when interest rates fall and vice versa. • The Fund’s exposure to high yield securities may subject the Fund to greater volatility. • The intrinsic value of the underlying stocks in which the Fund invests may never be realized or the stock may decline in value. • When market conditions are deemed appropriate, the Fund will leverage to the full extent permitted by its investment policies and restrictions and applicable law. Leveraging will exaggerate the effect on net asset value of any increase or decrease in the market value of the Fund’s portfolio. • The use of short selling involves increased risks and costs. You risk paying more for a security than you received from its sale. Theoretically, stocks sold short have the risk of unlimited losses. • The Fund may invest in derivative instruments, which may be more volatile and less liquid, increasing the risk of loss when compared to traditional securities. Certain of the derivative instruments are also subject to the risks of counterparty default and adverse tax treatment. • Instruments and strategies (such as borrowing transactions and reverse repurchase agreements) may provide leveraged exposure to a particular investment, which will magnify any gains or losses on those investments. • Investments in reverse repurchase agreements expose the Fund to the many of the same risks as investments in derivatives. • The Fund’s investments in other investment vehicles subject the Fund to those risks and expenses affecting the investment vehicle. • The Fund’s

| the GUGGENHEIM FUNDS annual report | 3 |

| December 31, 2013 |

investments in foreign securities carry additional risks when compared to U.S. securities, due to the impact of diplomatic, political or economic developments in the country in question (investments in emerging markets securities are generally subject to an even greater level of risks). • Investments in syndicated bank loans generally offer a floating interest rate and involve special types of risks. • A highly liquid secondary market may not exist for the commodity-linked structured notes the Fund invests in, and there can be no assurance that a highly liquid secondary market will develop. • The Fund’s exposure to the commodity markets may subject the Fund to greater volatility as commodity-linked investments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity. • The Fund’s investments in municipal securities can be affected by events that affect the municipal bond market. • The Fund’s investments in real estate securities subject the Fund to the same risks as direct investments in real estate, which is particularly sensitive to economic downturns. • The Fund’s investments in restricted securities may involve financial and liquidity risk. • You may have a gain or loss when you sell your shares. • It is important to note that the Fund is not guaranteed by the U.S. government. • Please read the prospectus for more detailed information regarding these and other risks.

The Series N (Managed Asset Allocation Series) may not be suitable for all investors. • The value of an investment in the Fund will fluctuate and is subject to investment risks, which means investors could lose money. • The Fund could lose money if the issuer of a bond or a counterparty to a derivatives transaction or other transaction is unable to repay interest and principal on time or defaults. • The issuer of a bond could also suffer a decrease in quality rating, which would affect the volatility and liquidity of the bond. • Derivatives may pose risks in addition to those associated with investing directly in securities or other investments, including the risk that the Fund will be unable to sell, unwind or value the derivative because of an illiquid market, the risk that the derivative is not well correlated with underlying investments or the Fund’s other portfolio holdings, and the risk that the counterparty is unwilling or unable to meet its obligation. • The use of derivatives by the Fund to hedge risk may reduce the opportunity for gain by offsetting the positive effect of favorable price movements. • Furthermore, if the Investment Manager is incorrect about its expectations of market conditions, the use of derivatives could result in a loss, which in some cases may be unlimited. • Foreign securities carry additional risks when compared to U.S. securities, including currency fluctuations, adverse political and economic developments, unreliable or untimely information, less liquidity, limited legal recourse and higher transactional costs. • The Investment Manager may not be able to cause certain of the underlying funds’ performance to match or correlate to that of the underlying funds’ respective underlying index or benchmark, either on a daily or aggregate basis. • Factors such as underlying fund expenses, imperfect correlation between an underlying fund’s investments and those of its underlying index or underlying benchmark, rounding of share prices, changes to the composition of the underlying index or underlying benchmark, regulatory policies, high portfolio turnover rate, and the use of leverage all contribute to tracking error. • Tracking error may cause an underlying fund’s and, thus the Fund’s, performance to be less than you expect. • Please read the prospectus for more detailed information regarding these and other risks.

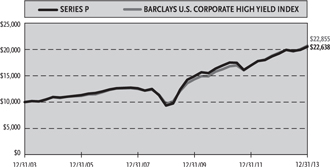

The Series P (High Yield Series) may not be suitable for all investors. • The Fund’s market value will change in response to interest rate changes and market conditions among other factors. In general, bond prices rise when interest rates fall and vice versa. • The Fund’s exposure to high yield securities may subject the Fund to greater volatility. • The Fund may invest in derivative instruments, which may be more volatile and less liquid, increasing the risk of loss when compared to traditional securities. Certain of the derivative instruments are also subject to the risks of counterparty default and adverse tax treatment. • The Fund’s use of leverage, through borrowings or instruments such as derivatives, may cause the Fund to be more volatile than if it had not been leveraged. • Instruments and strategies (such as borrowing transactions and reverse repurchase agreements) may provide leveraged exposure to a particular investment, which will magnify any gains or losses on those investments. • The Fund may invest in foreign securities which carry additional risks when compared to U.S. securities, due to the impact of diplomatic, political or economic developments in the country in question (investments in emerging markets securities are generally subject to an even greater level of risks). • Investments in syndicated bank loans generally offer a floating interest rate and involve special types of risks. • The Fund’s investments in other investment vehicles subject the Fund to those risks and expenses affecting the investment vehicle. • The Fund’s investments in restricted securities may involve financial and liquidity risk. • You may have a gain or loss when you sell your shares. • It is important to note that the Fund is not guaranteed by the U.S. government. • Please read the prospectus for more detailed information regarding these and other risks.

The Series Z (Alpha Opportunity Series) may not be suitable for all investors. • Value stocks are subject to the risk that the intrinsic value of the stock may never be realized by the market, or that the stock’s price will decline in value. • Growth stocks may be more volatile than other stocks because they are more sensitive to investor perceptions regarding the growth potential of the issuing company. Please read the prospectus for more detailed information regarding these and other risks.

| 4 | the GUGGENHEIM FUNDS annual report |

| Economic and Market Overview (Unaudited) | December 31, 2013 |

The year ended December 31, 2013 wound down with a series of stronger-than-expected economic data releases. ISM manufacturing data (historically indicative of expansion or contraction) rose to its highest levels in over two years, consumer confidence rebounded following the government shutdown, housing starts surged, and the job market strengthened. Citing improved labor market conditions and a sustainable economic expansion, the U.S. Federal Reserve (the “Fed”) announced in December that it would reduce its monthly bond purchases by $10 billion, to $75 billion, starting in January 2014. Yet, at the same time, the Fed lengthened the time frame before which it will raise rates by promising to keep the Fed funds target rate at 0-0.25% at least as long as the unemployment rate remains above 6.5% and perhaps “well past” the time this target is reached. For the first time, the Fed also added a lower-bound target for inflation of 2%–lengthening the expected time frame before rates rise.

As the U.S. economy slowly strengthens, we may return to an environment where taking credit risk is not just a consequence of staying within duration targets or reaching for yield, but rather a proactive choice driven by a positive outlook on the economy. To sustain optimism, the Fed will need to monitor the unintended consequences of tapering and avoid negative economic repercussions, as happened in the summer of 2013 when a spike in 10-year Treasury yields dampened home sales. For markets, the Fed must convince investors that the economy is strong enough to withstand steady reductions of its asset purchases. These will likely be Janet Yellen’s top priorities as she takes over the helm of the Fed.

Last January, the global economy faced myriad headwinds, choppiness lay ahead, and we expected plenty of volatility in 2013. Nevertheless, we believed at that point that risk assets were the best choice for investors. Now, the headwinds of 2013 have largely dissipated, and the outlook appears benign for risk assets for the first three to six months of 2014, if not longer.

Many pundits may have underestimated the strength of the U.S. economy, with both third quarter and fourth quarter economic growth beating expectations. The final three months of 2013 were exceptionally good for U.S. equities, which produced a wealth effect that probably boosted holiday sales. All of this bodes well for the first quarter of 2014.

Market conditions could be even stronger in Europe. Economic data from the euro area’s periphery is improving faster than from the core, where inflation is also rising at a faster pace, giving the peripheral nations a competitive advantage. In Asia, markets have priced for a more negative scenario that now appears less likely. With the U.S. and Europe now out of recession, they are ready to underpin a recovery in export growth in the Asian region. As a synchronous global expansion gets under way, investors may become more comfortable with taking risk, and this should be reflected in asset prices in many regions around the globe.

For 2014, investors should bear in mind that the Fed will continue injecting liquidity into financial markets even as it tapers its asset purchases. Assuming that the Fed continues the same pace of reductions at each Federal Open Market Committee meeting, it would still purchase more than $500 billion of bonds in 2014–nearly the size of the Fed’s QE2 from November 2010 to June 2011. This should help support credit spreads. An accelerated pace of tapering from the Fed would signal faster-than-expected economic growth and spark higher demand for risk assets. On balance, we expect the impact of tapering to be neutral. Barring economic weakness, we expect relatively benign market conditions with no major spike in volatility.

For the year ended December 31, 2013, the Standard & Poor’s 500® (“S&P 500”) Index* returned 32.39%. Foreign markets were also strong: the Morgan Stanley Capital International (“MSCI”) Europe-Australasia-Far East (“EAFE”) Index* returned 22.78%. The return of the MSCI Emerging Markets Index* was -2.60%.

In the bond market, the Barclays U.S. Aggregate Bond Index* posted a -2.02% return for the period, while the Barclays U.S. Corporate High Yield Index* returned 7.44%. The return of the Bank of America Merrill Lynch 3-Month U.S. Treasury Bill Index* was 0.07% for the 12-month period.

The opinions and forecasts expressed may not actually come to pass. This information is subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security or strategy.

| the GUGGENHEIM FUNDS annual report | 5 |

| Economic and Market Overview (Unaudited) (concluded) | December 31, 2013 |

*Index Definitions:

The following indices are referenced throughout this report. Indices are unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees, or expenses.

Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar denominated, fixed-rate taxable bond market, including U.S. Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS.

Barclays U.S. Corporate High Yield Index measures the market of USD-denominated, non-investment grade, fixed-rate, taxable corporate bonds. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below.

Barclays U.S. Intermediate Government/Credit Bond Index measures the performance of U.S. Dollar denominated U.S. Treasuries, government-related and investment grade U.S. corporate securities that have a remaining maturity of greater than one year and less than ten years.

Bank of America Merrill Lynch 3-Month U.S. Treasury Bill Index is an unmanaged market index of U.S. Treasury securities maturing in 90 days that assumes reinvestment of all income.

Credit Suisse Leveraged Loan Index is designed to mirror the investable universe of the U.S. dollar-denominated leveraged loan market.

MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. & Canada.

MSCI Emerging Markets Index is a free float-adjusted market capitalization weighted index that is designed to measure equity market performance in the global emerging markets.

MSCI EAFE Equal Weighted Index equally weights the issuers in the MSCI EAFE Index, which is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The MSCI EAFE Equal Weighted Index is rebalanced quarterly so that each issuer has the same weight on each rebalancing date. The MSCI EAFE Index consists of the following 22 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom.

MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets.

S&P 500® Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad economy, representing all major industries and is considered a representation of the U.S. stock market.

Russell 3000® Value Index measures the performance of the broad value segment of the U.S. equity value universe. It includes those Russell 3000 companies with lower price-to-book ratios and lower forecasted growth values.

Russell 2500® Value Index measures the performance of the small- to mid-cap value segment of the U.S. equity universe. It includes those Russell 2500 companies with lower price-to-book ratios and lower forecasted growth values.

Russell 2000® Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values.

Russell 2000® Value Index measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values.

Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth value.

Russell 1000® Value Index measures the performance for the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected growth values.

Russell Midcap® Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap Index companies with higher price-to-book ratios and higher forecasted growth values.

| 6 | the GUGGENHEIM FUNDS annual report |

| ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited) |

All mutual funds have operating expenses and it is important for our shareholders to understand the impact of costs on their investments. Shareholders of a Fund incur two types of costs: (i) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; and exchange fees; and (ii) ongoing costs, including management fees, administrative services, and shareholder reports, among others. These ongoing costs, or operating expenses, are deducted from a fund’s gross income and reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets, which is known as the expense ratio. The following examples are intended to help investors understand the ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 made at the beginning of the period and held for the entire six-month period beginning June 30, 2013 and ending December 31, 2013.

The following tables illustrate a Fund’s costs in two ways:

Table 1. Based on actual Fund return. This section helps investors estimate the actual expenses paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the fourth column shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. Investors may use the information here, together with the amount invested, to estimate the expenses paid over the period. Simply divide the Fund’s account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number provided under the heading “Expenses Paid During Period.”

Table 2. Based on hypothetical 5% return. This section is intended to help investors compare a Fund’s cost with those of other mutual funds. The table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses paid during the period. The example is useful in making comparisons because the U.S. Securities and Exchange Commission (the “SEC”) requires all mutual funds to calculate expenses based on the 5% return. Investors can assess a Fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

The calculations illustrated above assume no shares were bought or sold during the period. Actual costs may have been higher or lower, depending on the amount of investment and the timing of any purchases or redemptions.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) on purchase payments, and contingent deferred sales charges (“CDSC”) on redemptions, if any. Therefore, the second table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

More information about a Fund’s expenses, including annual expense ratios for the past five years, can be found in the Financial Highlights section of this report. For additional information on operating expenses and other shareholder costs, please refer to the appropriate Fund prospectus.

| the GUGGENHEIM FUNDS annual report | 7 |

| ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited) (concluded) |

| Beginning | Ending | Expenses | ||||||||||||||||||

| Expense | Fund | Account Value | Account Value | Paid During | ||||||||||||||||

| Ratio1,4 | Return | June 30, 2013 | December 31, 2013 | Period2 | ||||||||||||||||

| Table 1. Based on actual Fund return3 | ||||||||||||||||||||

| Series A (StylePlus–Large Core Series) | 0.98 | % | 16.78 | % | $1,000.00 | $1,167.80 | $ 5.35 | |||||||||||||

| Series B (Large Cap Value Series) | 0.84 | % | 14.29 | % | 1,000.00 | 1,142.90 | 4.54 | |||||||||||||

| Series C (Money Market Series) | 0.57 | % | (0.23 | %) | 1,000.00 | 997.70 | 2.87 | |||||||||||||

| Series D (World Equity Income Series) | 1.12 | % | 13.96 | % | 1,000.00 | 1,139.60 | 6.04 | |||||||||||||

| Series E (Total Return Bond Series) | 0.91 | % | 2.37 | % | 1,000.00 | 1,023.70 | 4.64 | |||||||||||||

| Series F (Floating Rate Strategies Series) | 1.19 | % | 3.10 | % | 1,000.00 | 1,031.00 | 6.09 | |||||||||||||

| Series J (StylePlus–Mid Growth Series) | 1.02 | % | 19.37 | % | 1,000.00 | 1,193.70 | 5.64 | |||||||||||||

| Series M (Macro Opportunities Series) | 1.53 | % | 3.49 | % | 1,000.00 | 1,034.90 | 7.85 | |||||||||||||

| Series N (Managed Asset Allocation Series) | 1.05 | % | 10.20 | % | 1,000.00 | 1,102.00 | 5.56 | |||||||||||||

| Series O (All Cap Value Series) | 0.92 | % | 14.94 | % | 1,000.00 | 1,149.40 | 4.98 | |||||||||||||

| Series P (High Yield Series) | 1.11 | % | 4.53 | % | 1,000.00 | 1,045.30 | 5.72 | |||||||||||||

| Series Q (Small Cap Value Series) | 1.18 | % | 18.82 | % | 1,000.00 | 1,188.20 | 6.51 | |||||||||||||

| Series V (Mid Cap Value Series) | 0.95 | % | 15.44 | % | 1,000.00 | 1,154.40 | 5.16 | |||||||||||||

| Series X (StylePlus–Small Growth Series) | 1.33 | % | 22.48 | % | 1,000.00 | 1,224.80 | 7.46 | |||||||||||||

| Series Y (StylePlus–Large Growth Series) | 1.18 | % | 19.65 | % | 1,000.00 | 1,196.50 | 6.53 | |||||||||||||

| Series Z (Alpha Opportunity Series) | 2.43 | % | 16.23 | % | 1,000.00 | 1,162.30 | 13.24 | |||||||||||||

| Table 2. Based on hypothetical 5% return (before expenses) | ||||||||||||||||||||

| Series A (StylePlus–Large Core Series) | 0.98 | % | 5.00 | % | $1,000.00 | $1,020.27 | $ 4.99 | |||||||||||||

| Series B (Large Cap Value Series) | 0.84 | % | 5.00 | % | 1,000.00 | 1,020.97 | 4.28 | |||||||||||||

| Series C (Money Market Series) | 0.57 | % | 5.00 | % | 1,000.00 | 1,022.33 | 2.91 | |||||||||||||

| Series D (World Equity Income Series) | 1.12 | % | 5.00 | % | 1,000.00 | 1,019.56 | 5.70 | |||||||||||||

| Series E (Total Return Bond Series) | 0.91 | % | 5.00 | % | 1,000.00 | 1,020.62 | 4.63 | |||||||||||||

| Series F (Floating Rate Strategies Series) | 1.19 | % | 5.00 | % | 1,000.00 | 1,019.21 | 6.06 | |||||||||||||

| Series J (StylePlus–Mid Growth Series) | 1.02 | % | 5.00 | % | 1,000.00 | 1,020.06 | 5.19 | |||||||||||||

| Series M (Macro Opportunities Series) | 1.53 | % | 5.00 | % | 1,000.00 | 1,017.49 | 7.78 | |||||||||||||

| Series N (Managed Asset Allocation Series) | 1.05 | % | 5.00 | % | 1,000.00 | 1,019.91 | 5.35 | |||||||||||||

| Series O (All Cap Value Series) | 0.92 | % | 5.00 | % | 1,000.00 | 1,020.57 | 4.69 | |||||||||||||

| Series P (High Yield Series) | 1.11 | % | 5.00 | % | 1,000.00 | 1,019.61 | 5.65 | |||||||||||||

| Series Q (Small Cap Value Series) | 1.18 | % | 5.00 | % | 1,000.00 | 1,019.26 | 6.01 | |||||||||||||

| Series V (Mid Cap Value Series) | 0.95 | % | 5.00 | % | 1,000.00 | 1,020.42 | 4.84 | |||||||||||||

| Series X (StylePlus–Small Growth Series) | 1.33 | % | 5.00 | % | 1,000.00 | 1,018.50 | 6.77 | |||||||||||||

| Series Y (StylePlus–Large Growth Series) | 1.18 | % | 5.00 | % | 1,000.00 | 1,019.26 | 6.01 | |||||||||||||

| Series Z (Alpha Opportunity Series) | 2.43 | % | 5.00 | % | 1,000.00 | 1,012.96 | 12.33 | |||||||||||||

| 1 | Annualized and excludes expenses of the underlying funds in which the Fund invests. |

| 2 | Expenses are equal to the Fund’s annualized expense ratio, net of any applicable fee waivers, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). Expenses shown do not include fees charged by insurance companies. |

| 3 | Actual cumulative return at net asset value for the period June 30, 2013 to December 31, 2013. |

| 4 | This ratio represents annualized net expenses which includes extraordinary expenses. Excluding these expenses, the operating expense ratios would be 0.55% for Series C (Money Market Series), 0.81% for Series E (Total Return Bond Series), 1.16% for Series F (Floating Rate Strategies Series), 1.47% for Series M (Macro Opportunities Series) and 2.35% for Series Z (Alpha Opportunity Series). |

| 8 | the GUGGENHEIM FUNDS annual report |

| Manager’S Commentary (Unaudited) | December 31, 2013 |

To Our Shareholders:

The Series A (StylePlus–Large Core Series, formerly Large Cap Core Series) is managed by a team of seasoned professionals, including B. Scott Minerd, Global Chief Investment Officer; Farhan Sharaff, Senior Managing Director and Assistant Chief Investment Officer, Equities; Jayson Flowers, Senior Managing Director and Head of Equity and Derivative Strategies; and Scott Hammond, Managing Director and Portfolio Manager. In the following paragraphs, the investment team discusses performance and changes to the Fund that occurred during the fiscal year ended December 31, 2013.

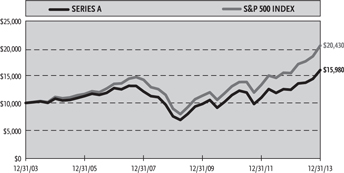

For the fiscal year ended December 31, 2013, the Series A (StylePlus–Large Core Series, formerly Large Cap Core Series) returned 28.87%. The benchmark, the S&P 500® Index, returned 32.39%.

The Fund’s Board of Directors approved the following changes, which became effective on April 30, 2013: a new Fund name, new principal investment strategies and new portfolio management team.

The Fund’s investment objective is to deliver long-term growth of capital in excess of that produced by the total return of the S&P 500 Index. The Fund seeks to add alpha above the target index by leveraging Guggenheim’s competencies in fixed income and systematic stock selection. To accomplish this, the StylePlus strategy allocates to quantitative selection models when stock picking opportunities in the market are high. When stock selection opportunities are less attractive, the Fund invests in derivatives based on the target index, backed by a diversified portfolio of fixed income instruments. In this way, the Fund believes it will deliver the target index return plus an alpha component commensurate with the yield achieved on the active fixed income portfolio.

The Fund’s underperformance for the 12 months came predominantly during the four months it was being managed according to the legacy strategy. Specifically—from January 1, 2013 through April 30, 2013—the Fund underperformed the benchmark by almost four percentage points, largely due to poor stock selection in the Information Technology. The Fund’s cash position was also a drag on performance. A sector overweight and stock selection in Consumer Discretionary contributed most to the Fund’s performance.

For the time the Fund was being managed according to the new strategy, the eight months from April 30, 2013 through December 31, 2013, the Fund performed slightly better than the benchmark. During much of this period, the Fund maintained an approximate allocation of 20% to systematic equity selection, 80% allocated to the passive equity position, which was maintained with swap agreements and futures contracts and 53% allocated to fixed income investments (excluding short term). Beginning in December 2013, due to a more favorable outlook for active stock selection, the equity sleeve was increased to 25%, with 74% allocated to the passive equity position.

The equity sleeve was additive over the period, delivering the strongest returns during the months of May, June and December.

The fixed income allocation also contributed to performance over the eight months, after detracting from performance during the substantial debt selloff that began at the end of May and lasted in to June. The swap agreements also contributed to performance.

Performance displayed represents past performance, which is no guarantee of future results.

The opinions and forecast expressed may not actually come to pass. This information is subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security or strategy.

| The Guggenheim Funds annual REPORT | 9 |

| performance report and FUND PROFILE (Unaudited) | December 31, 2013 |

SERIES A (STYLEPLUS–LARGE CORE SERIES)

OBJECTIVE: Seeks long-term growth of capital.

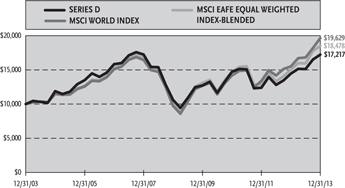

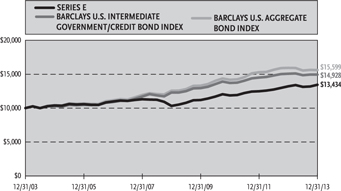

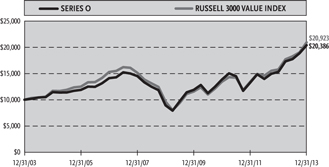

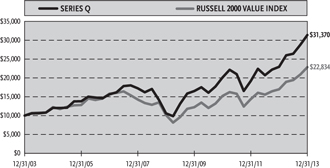

Cumulative Fund Performance*,†

Average Annual Returns*

Periods Ended December 31, 2013†

| 1 Year | 5 Year | 10 Year | ||||||||||

| Series A (StylePlus–Large Core Series) | 28.87 | % | 16.14 | % | 4.80 | % | ||||||

| S&P 500 Index | 32.39 | % | 17.94 | % | 7.41 | % | ||||||

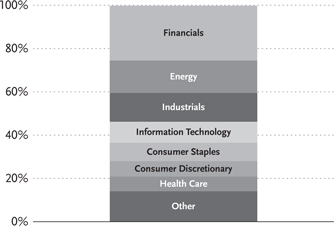

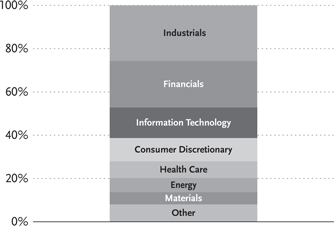

Ten Largest Holdings (% of Total Net Assets)

| Dreyfus Treasury Prime Cash Management Fund | 6.8 | % | ||

| U.S. Treasury Bill | 3.0 | % | ||

| Guggenheim BulletShares 2016 High Yield Corporate Bond ETF | 2.0 | % | ||

| Guggenheim BulletShares 2015 High Yield Corporate Bond ETF | 2.0 | % | ||

| Guggenheim BulletShares 2014 High Yield Corporate Bond ETF | 1.9 | % | ||

| Floating Rate Strategies Fund Institutional Class | 1.7 | % | ||

| Macro Opportunities Fund Institutional Class | 1.7 | % | ||

| New York City Water & Sewer System Revenue Bonds | 1.3 | % | ||

| Duane Street CLO IV Ltd. — Class A1T | 1.3 | % | ||

| HSI Asset Securitization Corporation Trust 2007-WF1 — Class 2A3 | 1.2 | % | ||

| Top Ten Total | 22.9 | % |

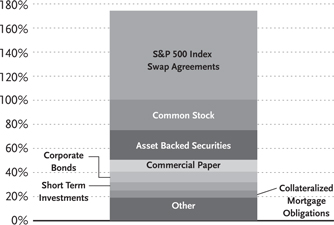

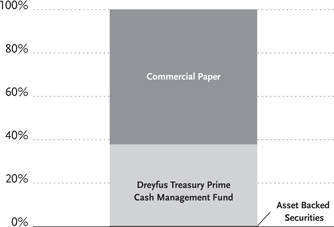

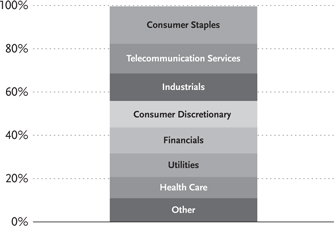

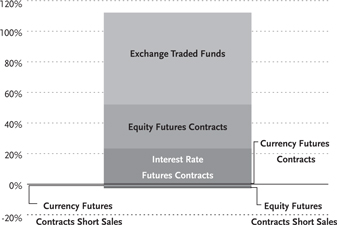

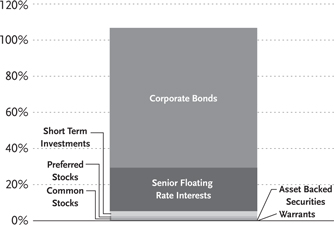

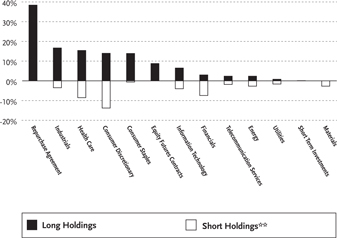

Holdings Diversification (Market Exposure as % of Net Assets)

Inception Date: May 1, 1979

| Portfolio Composition by Quality Rating** |

| Rating |

| Fixed Income Instruments | ||||

| AAA | 10.8 | % | ||

| AA | 3.9 | % | ||

| A | 7.4 | % | ||

| BBB | 21.9 | % | ||

| BB | 3.0 | % | ||

| B | 4.6 | % | ||

| CCC | 5.2 | % | ||

| NR | 2.1 | % | ||

| Other Instruments | ||||

| Common Stock | 25.3 | % | ||

| Short Term Investments | 6.8 | % | ||

| Exchange Traded Funds | 5.9 | % | ||

| Mutual Funds | 3.4 | % | ||

| Total Investments | 100.3 | % |

The chart above reflects percentages of the value of total investments.

| * | The performance data above represents past performance that is not predictive of future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Returns are historical and include changes in principal and reinvested dividends and capital gains and do not reflect the effect of taxes. The S&P 500 Index is an unmanaged index and, unlike the Fund, has no management fees or operating expenses to reduce its reported return. |

| ** | Source: Factset. Credit quality ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest). All rated securities have been rated by Moody’s, Standard & Poor’s (“S&P”), or Fitch, which are all a Nationally Recognized Statistical Rating Organization (“NRSRO”). For purposes of this presentation, when ratings are available from more than one agency, the highest rating is used. Guggenheim Investments has converted Moody’s and Fitch ratings to the equivalent S&P rating. Unrated securities do not necessarily indicate low credit quality. Security ratings are determined at the time of purchase and may change thereafter. |

| † | Performance figures do not reflect fees and expenses associated with an investment in variable insurance products. If returns had taken into account these fees and expenses, performance would have been lower. Shares of a series of SBL Fund are available only through the purchase of such products. |

| 10 | the GUGGENHEIM FUNDS annual report |

| Schedule of Investments | December 31, 2013 |

| Series A (styleplus–large Core Series) |

| Shares | Value | |||||||

| COMMON STOCKS† - 25.3% | ||||||||

| Information Technology - 5.1% | ||||||||

| Apple, Inc. | 2,910 | $ | 1,632,830 | |||||

| International Business Machines Corp. | 6,919 | 1,297,796 | ||||||

| Microsoft Corp. | 26,620 | 996,387 | ||||||

| Cisco Systems, Inc. | 40,904 | 918,295 | ||||||

| Hewlett-Packard Co. | 27,970 | 782,601 | ||||||

| Oracle Corp. | 20,381 | 779,777 | ||||||

| EMC Corp. | 30,566 | 768,735 | ||||||

| Corning, Inc. | 38,511 | 686,266 | ||||||

| TE Connectivity Ltd. | 11,910 | 656,360 | ||||||

| Google, Inc. — Class A* | 463 | 518,889 | ||||||

| Western Digital Corp. | 6,059 | 508,350 | ||||||

| Texas Instruments, Inc. | 10,466 | 459,562 | ||||||

| Intel Corp. | 15,873 | 412,063 | ||||||

| QUALCOMM, Inc. | 5,511 | 409,192 | ||||||

| Seagate Technology plc | 6,603 | 370,824 | ||||||

| Accenture plc — Class A | 3,703 | 304,461 | ||||||

| Symantec Corp. | 7,786 | 183,594 | ||||||

| Total Information Technology | 11,685,982 | |||||||

| Health Care - 5.0% | ||||||||

| Pfizer, Inc. | 43,814 | 1,342,023 | ||||||

| Merck & Company, Inc. | 21,016 | 1,051,851 | ||||||

| Johnson & Johnson | 10,139 | 928,631 | ||||||

| Express Scripts Holding Co.* | 11,410 | 801,438 | ||||||

| Abbott Laboratories | 20,581 | 788,869 | ||||||

| Medtronic, Inc. | 13,298 | 763,172 | ||||||

| UnitedHealth Group, Inc. | 9,606 | 723,331 | ||||||

| Covidien plc | 9,695 | 660,230 | ||||||

| Cardinal Health, Inc. | 9,856 | 658,480 | ||||||

| Eli Lilly & Co. | 12,011 | 612,561 | ||||||

| WellPoint, Inc. | 5,930 | 547,873 | ||||||

| Aetna, Inc. | 7,790 | 534,316 | ||||||

| McKesson Corp. | 3,083 | 497,596 | ||||||

| Cigna Corp. | 5,349 | 467,931 | ||||||

| Amgen, Inc. | 3,457 | 394,651 | ||||||

| Thermo Fisher Scientific, Inc. | 3,212 | 357,656 | ||||||

| Stryker Corp. | 2,904 | 218,207 | ||||||

| Becton Dickinson and Co. | 1,591 | 175,790 | ||||||

| Total Health Care | 11,524,606 | |||||||

| Industrials - 4.7% | ||||||||

| General Electric Co. | 57,642 | 1,615,705 | ||||||

| United Technologies Corp. | 8,270 | 941,126 | ||||||

| United Parcel Service, Inc. — Class B | 8,127 | 853,985 | ||||||

| Caterpillar, Inc. | 8,832 | 802,034 | ||||||

| FedEx Corp. | 5,208 | 748,754 | ||||||

| General Dynamics Corp. | 7,354 | 702,675 | ||||||

| Waste Management, Inc. | 15,541 | 697,325 | ||||||

| Northrop Grumman Corp. | 6,002 | 687,889 | ||||||

| CSX Corp. | 23,771 | 683,892 | ||||||

| Boeing Co. | 4,802 | 655,425 | ||||||

| Delta Air Lines, Inc. | 19,092 | 524,457 | ||||||

| Emerson Electric Co. | 6,606 | 463,609 | ||||||

| Raytheon Co. | 3,707 | 336,225 | ||||||

| Union Pacific Corp. | 1,851 | 310,968 | ||||||

| Lockheed Martin Corp. | 1,372 | 203,962 | ||||||

| Norfolk Southern Corp. | 2,040 | 189,373 | ||||||

| Republic Services, Inc. — Class A | 5,236 | 173,835 | ||||||

| Stanley Black & Decker, Inc. | 2,144 | 172,999 | ||||||

| Total Industrials | 10,764,238 | |||||||

| Energy - 3.3% | ||||||||

| Exxon Mobil Corp. | 12,009 | 1,215,311 | ||||||

| ConocoPhillips | 11,007 | 777,644 | ||||||

| Anadarko Petroleum Corp. | 9,067 | 719,194 | ||||||

| Marathon Oil Corp. | 19,224 | 678,607 | ||||||

| Phillips 66 | 8,153 | 628,841 | ||||||

| Occidental Petroleum Corp. | 6,466 | 614,917 | ||||||

| Baker Hughes, Inc. | 10,811 | 597,416 | ||||||

| Chevron Corp. | 4,732 | 591,074 | ||||||

| Apache Corp. | 4,847 | 416,551 | ||||||

| EOG Resources, Inc. | 2,289 | 384,186 | ||||||

| Valero Energy Corp. | 7,410 | 373,464 | ||||||

| Devon Energy Corp. | 4,406 | 272,599 | ||||||

| Nabors Industries Ltd. | 10,848 | 184,308 | ||||||

| Kinder Morgan, Inc. | 4,964 | 178,704 | ||||||

| Total Energy | 7,632,816 | |||||||

| Consumer Staples - 3.2% | ||||||||

| Wal-Mart Stores, Inc. | 14,272 | 1,123,064 | ||||||

| CVS Caremark Corp. | 14,062 | 1,006,418 | ||||||

| PepsiCo, Inc. | 9,349 | 775,406 | ||||||

| Walgreen Co. | 13,175 | 756,772 | ||||||

| Kimberly-Clark Corp. | 6,797 | 710,014 | ||||||

| General Mills, Inc. | 13,782 | 687,859 | ||||||

| Procter & Gamble Co. | 6,453 | 525,339 | ||||||

| Mondelez International, Inc. — Class A | 14,836 | 523,711 | ||||||

| Philip Morris International, Inc. | 4,908 | 427,634 | ||||||

| Kroger Co. | 8,881 | 351,066 | ||||||

| Archer-Daniels-Midland Co. | 7,531 | 326,845 | ||||||

| Kellogg Co. | 3,199 | 195,363 | ||||||

| Total Consumer Staples | 7,409,491 | |||||||

| Financials - 1.8% | ||||||||

| Citigroup, Inc. | 20,145 | 1,049,757 | ||||||

| JPMorgan Chase & Co. | 15,353 | 897,843 | ||||||

| Wells Fargo & Co. | 9,245 | 419,723 | ||||||

| MetLife, Inc. | 7,484 | 403,537 | ||||||

| Berkshire Hathaway, Inc. — Class B* | 2,882 | 341,690 | ||||||

| American International Group, Inc. | 5,993 | 305,943 | ||||||

| Regions Financial Corp. | 23,982 | 237,182 | ||||||

| Capital One Financial Corp. | 2,551 | 195,432 | ||||||

| Aflac, Inc. | 2,864 | 191,315 | ||||||

| Allstate Corp. | 3,391 | 184,945 | ||||||

| Total Financials | 4,227,367 | |||||||

| Consumer Discretionary - 1.6% | ||||||||

| Comcast Corp. — Class A | 20,780 | 1,079,832 | ||||||

| Time Warner, Inc. | 11,801 | 822,766 | ||||||

| Target Corp. | 11,314 | 715,837 | ||||||

| Ford Motor Co. | 34,291 | 529,110 | ||||||

| Macy’s, Inc. | 6,057 | 323,444 | ||||||

| The Gap, Inc. | 4,476 | 174,922 | ||||||

| Time Warner Cable, Inc. | 1,035 | 140,243 | ||||||

| Total Consumer Discretionary | 3,786,154 | |||||||

| See Notes to Financial Statements. | The GUGGENHEIM FUNDS annual report | 11 |

| Schedule of Investments (continued) | December 31, 2013 |

| Series A (styleplus–large Core Series) |

| Shares | Value | |||||||

| Utilities - 0.4% | ||||||||

| Exelon Corp. | 22,205 | $ | 608,195 | |||||

| American Electric Power Company, Inc. | 4,997 | 233,560 | ||||||

| Total Utilities | 841,755 | |||||||

| Telecommunication Services - 0.2% | ||||||||

| CenturyLink, Inc. | 15,772 | 502,338 | ||||||

| Total Common Stocks | ||||||||

| (Cost $53,671,807) | 58,374,747 | |||||||

| EXCHANGE TRADED FUNDS†,4 - 5.9% | ||||||||

| Guggenheim BulletShares 2016 | ||||||||

| High Yield Corporate Bond ETF | 169,000 | 4,566,380 | ||||||

| Guggenheim BulletShares 2015 | ||||||||

| High Yield Corporate Bond ETF | 168,800 | 4,520,464 | ||||||

| Guggenheim BulletShares 2014 | ||||||||

| High Yield Corporate Bond ETF | 169,100 | 4,509,897 | ||||||

| Total Exchange Traded Funds | ||||||||

| (Cost $13,569,434) | 13,596,741 | |||||||

| MUTUAL FUNDS†,5 - 3.4% | ||||||||

| Floating Rate Strategies Fund | ||||||||

| Institutional Class | 150,653 | 4,029,967 | ||||||

| Macro Opportunities Fund | ||||||||

| Institutional Class | 146,257 | 3,910,920 | ||||||

| Total Mutual Funds | ||||||||

| (Cost $8,137,283) | 7,940,887 | |||||||

| SHORT TERM INVESTMENTS† - 6.8% | ||||||||

| Dreyfus Treasury Prime Cash | ||||||||

| Management Fund | 15,627,652 | 15,627,652 | ||||||

| Total Short Term Investments | ||||||||

| (Cost $15,627,652) | 15,627,652 | |||||||

| Face | ||||||||

| Amount | ||||||||

| ASSET BACKED SECURITIES†† - 24.6% | ||||||||

| Duane Street CLO IV Ltd. | ||||||||

| 2007-4A, 0.47% due 11/14/211,2 | $ | 3,109,214 | 3,047,652 | |||||

| HSI Asset Securitization | ||||||||

| Corporation Trust | ||||||||

| 2007-WF1, 0.33% due 05/25/371 | 3,100,693 | 2,848,173 | ||||||

| JP Morgan Mortgage Acquisition Trust | ||||||||

| 2006-CH2, 0.26% due 10/25/361 | 2,752,754 | 2,702,813 | ||||||

| Garrison Funding 2013-2 Ltd. | ||||||||

| 2013-2A, 2.13% due 09/25/231,2 | 2,400,000 | 2,390,400 | ||||||

| Argent Securities Incorporated | ||||||||

| Asset-Backed Pass-Through | ||||||||

| Certificates Series | ||||||||

| 2005-W3, 0.50% due 11/25/351 | 2,281,357 | 2,138,025 | ||||||

| JP Morgan Mortgage | ||||||||

| Acquisition Trust | ||||||||

| 2007-CH3, 0.31% due 03/25/371 | 2,135,248 | 2,031,578 | ||||||

| Brentwood CLO Corp. | ||||||||

| 2006-1A, 0.51% due 02/01/221,2 | 1,511,565 | 1,479,822 | ||||||

| 2006-1A, 1.06% due 02/01/221,2 | 600,000 | 531,780 | ||||||

| Foothill CLO Ltd. | ||||||||

| 2007-1A, 0.48% due 02/22/211,2 | 1,890,230 | 1,853,371 | ||||||

| Cornerstone CLO Ltd. | ||||||||

| 2007-1A, 0.46% due 07/15/211,2 | 1,850,000 | 1,803,750 | ||||||

| NewStar Commercial Loan Trust | ||||||||

| 2006-1A, 0.63% due 03/30/221,2 | 1,100,000 | 1,073,490 | ||||||

| 2006-1A, 0.52% due 03/30/221,2 | 739,436 | 728,344 | ||||||

| Goldman Sachs Asset Management CLO plc | ||||||||

| 2007-1A, 2.99% due 08/01/221,2 | 1,800,000 | 1,726,380 | ||||||

| Salus CLO 2012-1 Ltd. | ||||||||

| 2013-1AN, 2.49% due 03/05/211,2 | 1,700,000 | 1,700,000 | ||||||

| Halcyon Structured Asset Management | ||||||||

| Long Secured/Short Unsecured 2007-2 Ltd. | ||||||||

| 2007-2A, 3.99% due 10/29/211,2 | 1,700,000 | 1,683,510 | ||||||

| Cerberus Onshore II CLO LLC | ||||||||

| 2014-1A, 2.94% due 10/15/231,2 | 1,350,000 | 1,338,120 | ||||||

| 2014-1A, 2.24% due 10/15/231,2 | 250,000 | 250,200 | ||||||

| Lehman XS Trust | ||||||||

| 2007-9, 0.28% due 06/25/371 | 1,818,997 | 1,579,777 | ||||||

| Central Park CLO Ltd. | ||||||||

| 2011-1A, 3.44% due 07/23/221,2 | 1,580,000 | 1,527,544 | ||||||

| Aegis Asset Backed Securities Trust | ||||||||

| 2005-3, 0.63% due 08/25/351 | 1,600,000 | 1,522,638 | ||||||

| N-Star REL CDO VIII Ltd. | ||||||||

| 2006-8A, 0.46% due 02/01/411,2 | 1,487,458 | 1,355,818 | ||||||

| Wells Fargo Home Equity Asset-Backed | ||||||||

| Securities 2006-2 Trust | ||||||||

| 2006-3, 0.31% due 01/25/371 | 1,487,672 | 1,345,766 | ||||||

| KKR Financial CLO Corp. | ||||||||

| 2007-1A, 2.49% due 05/15/211,2 | 1,400,000 | 1,318,240 | ||||||

| Black Diamond CLO Delaware Corp. | ||||||||

| 2005-1A, 2.15% due 06/20/171,2 | 1,350,000 | 1,299,240 | ||||||

| Newcastle CDO Ltd. | ||||||||

| 2007-9A, 0.42% due 05/25/52 | 1,317,869 | 1,287,031 | ||||||

| West Coast Funding Ltd. | ||||||||

| 2006-1A, 0.39% due 11/02/411,2 | 1,308,657 | 1,262,069 | ||||||

| GreenPoint Mortgage Funding Trust | ||||||||

| 2005-HE4, 0.87% due 07/25/301 | 1,400,000 | 1,246,123 | ||||||

| Symphony CLO VII Ltd. | ||||||||

| 2011-7A, 3.44% due 07/28/211,2 | 1,250,000 | 1,239,500 | ||||||

| Popular ABS Mortgage | ||||||||

| Pass-Through Trust | ||||||||

| 2005-A, 0.59% due 06/25/351 | 1,248,943 | 1,189,674 | ||||||

| FM Leveraged Capital Fund II | ||||||||

| 2006-2A, 1.84% due 11/15/201,2 | 1,180,000 | 1,165,604 | ||||||

| GSC Group CDO Fund VIII Ltd. | ||||||||

| 2007-8A, 0.62% due 04/17/211,2 | 1,250,000 | 1,158,125 | ||||||

| Global Leveraged Capital | ||||||||

| Credit Opportunity Fund | ||||||||

| 2006-1A, 0.54% due 12/20/181,2 | 1,054,234 | 1,042,215 | ||||||

| California Republic Auto Receivables Trust | ||||||||

| 2013-2, 1.23% due 03/15/19 | 1,000,000 | 999,249 | ||||||

| TICC CLO LLC | ||||||||

| 2011-1A, 2.49% due 07/25/211,2 | 1,000,000 | 995,400 | ||||||

| Black Diamond CLO 2006-1 Luxembourg S.A. | ||||||||

| 2007-1A, 0.63% due 04/29/191,2 | 1,000,000 | 912,400 | ||||||

| Northwoods Capital VII Ltd. | ||||||||

| 2006-7A, 1.79% due 10/22/211,2 | 960,000 | 902,592 | ||||||

| Golub Capital Partners Fundings Ltd. | ||||||||

| 2007-1A, 0.49% due 03/15/221,2 | 683,761 | 671,658 | ||||||

| ACS 2007-1 Pass Through Trust | ||||||||

| 2007-1A, 0.48% due 06/14/371,2 | 645,125 | 599,966 | ||||||

| Ares XVI CLO Ltd. | ||||||||

| 2011-16A, 3.54% due 05/17/211,2 | 500,000 | 497,500 | ||||||

| 12 | the GUGGENHEIM FUNDS annual report | See Notes to Financial Statements. |

| Schedule of Investments (continued) | December 31, 2013 |

| Series A (styleplus–large Core Series) |

| Face | ||||||||

| Amount | Value | |||||||

| Race Point IV CLO Ltd. | ||||||||

| 2007-4A, 0.99% due 08/01/211,2 | $ | 500,000 | $ | 470,500 | ||||

| NewStar Commercial Loan Trust 2007-1 | ||||||||

| 2007-1A, 1.54% due 09/30/221,2 | 500,000 | 459,200 | ||||||

| Riverside Park CLO Ltd. | ||||||||

| 2011-1A, 3.00% due 09/27/211,2 | 450,000 | 450,000 | ||||||

| Accredited Mortgage Loan Trust | ||||||||

| 2007-1, 0.29% due 02/25/371 | 477,329 | 441,165 | ||||||

| DIVCORE CLO Ltd. | ||||||||

| 2013-1A B, 4.10% due 11/15/32 | 400,000 | 398,800 | ||||||

| Legg Mason Real Estate CDO I Ltd. | ||||||||

| 2006-1A, 0.45% due 03/25/381,2 | 186,381 | 183,809 | ||||||

| Total Asset Backed Securities | ||||||||

| (Cost $56,951,385) | 56,849,011 | |||||||

| CORPORATE BONDS†† - 8.9% | ||||||||

| Financials - 3.6% | ||||||||

| Icahn Enterprises Limited Partnership / | ||||||||

| Icahn Enterprises Finance Corp. | ||||||||

| 8.00% due 01/15/18 | 1,220,000 | 1,268,800 | ||||||

| 7.75% due 01/15/16 | 620,000 | 632,400 | ||||||

| Ford Motor Credit Company LLC | ||||||||

| 7.00% due 04/15/15 | 1,630,000 | 1,754,478 | ||||||

| Citigroup, Inc. | ||||||||

| 1.20% due 07/25/161 | 1,510,000 | 1,525,692 | ||||||

| International Lease Finance Corp. | ||||||||

| 2.19% due 06/15/161 | 1,100,000 | 1,105,500 | ||||||

| Nationstar Mortgage LLC / | ||||||||

| Nationstar Capital Corp. | ||||||||

| 6.50% due 08/01/18 | 700,000 | 712,250 | ||||||

| Mack-Cali Realty, LP | ||||||||

| 5.13% due 02/15/14 | 680,000 | 682,998 | ||||||

| WEA Finance LLC / WT Finance Aust Pty Ltd. | ||||||||

| 5.75% due 09/02/152 | 450,000 | 485,381 | ||||||

| Emigrant Bancorp, Inc. | ||||||||

| 6.25% due 06/15/142 | 400,000 | 405,371 | ||||||

| Total Financials | 8,572,870 | |||||||

| Materials - 1.9% | ||||||||

| Glencore Funding LLC | ||||||||

| 1.40% due 05/27/161,2 | 2,210,000 | 2,199,659 | ||||||

| Rio Tinto Finance USA plc | ||||||||

| 1.08% due 06/17/161 | 1,570,000 | 1,581,139 | ||||||

| Anglo American Capital plc | ||||||||

| 9.38% due 04/08/142 | 700,000 | 715,518 | ||||||

| Total Materials | 4,496,316 | |||||||

| Telecommunication Services - 1.3% | ||||||||

| Level 3 Financing, Inc. | ||||||||

| 3.85% due 01/15/181,2 | 1,700,000 | 1,710,625 | ||||||

| WPP Finance UK | ||||||||

| 8.00% due 09/15/14 | 1,200,000 | 1,259,713 | ||||||

| Total Telecommunication Services | 2,970,338 | |||||||

| Energy - 1.2% | ||||||||

| Ras Laffan Liquefied Natural | ||||||||

| Gas Company Limited III | ||||||||

| 5.83% due 09/30/162 | 1,902,560 | 2,021,470 | ||||||

| Petroleos Mexicanos | ||||||||

| 2.27% due 07/18/181 | 660,000 | 679,800 | ||||||

| Total Energy | 2,701,270 | |||||||

| Consumer Staples - 0.3% | ||||||||

| Harbinger Group, Inc. | ||||||||

| 7.88% due 07/15/192 | 590,000 | 633,513 | ||||||

| Consumer Discretionary - 0.3% | ||||||||

| Vail Resorts, Inc. | ||||||||

| 6.50% due 05/01/19 | 300,000 | 318,000 | ||||||

| Sabre, Inc. | ||||||||

| 8.50% due 05/15/192 | 240,000 | 266,400 | ||||||

| Total Consumer Discretionary | 584,400 | |||||||

| Information Technology - 0.2% | ||||||||

| iGATE Corp. | ||||||||

| 9.00% due 05/01/16 | 340,000 | 361,250 | ||||||

| Industrials - 0.1% | ||||||||

| Victor Technologies Group, Inc. | ||||||||

| 9.00% due 12/15/17 | 180,000 | 192,600 | ||||||

| Total Corporate Bonds | ||||||||

| (Cost $20,480,021) | 20,512,557 | |||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS†† - 5.1% | ||||||||

| Boca Hotel Portfolio Trust | ||||||||

| 2013-BOCA, 3.22% due 08/15/261,2 | 1,900,000 | 1,902,276 | ||||||

| Hilton USA Trust | ||||||||

| 2013-HLF, 2.92% due 11/05/301,2 | 1,700,000 | 1,700,122 | ||||||

| Wachovia Bank Commercial Mortgage | ||||||||

| Trust Series 2007-WHALE 8 | ||||||||

| 2007-WHL8, 0.25% due 06/15/201,2 | 1,421,546 | 1,407,186 | ||||||

| SRERS-2011 Funding Ltd. | ||||||||

| 2011-RS, 0.42% due 05/09/461,2 | 1,505,762 | 1,364,823 | ||||||

| COMM 2007-FL14 Mortgage Trust | ||||||||

| 2007-FL14, 0.92% due 06/15/221,2 | 1,340,253 | 1,322,788 | ||||||

| HarborView Mortgage Loan Trust | ||||||||

| 2006-12, 0.36% due 01/19/381 | 1,368,628 | 1,112,696 | ||||||

| Banc of America Merrill Lynch | ||||||||

| Commercial Mortgage, Inc. | ||||||||

| 2005-6, 6.13% due 09/10/471,2 | 1,075,200 | 1,109,172 | ||||||

| GCCFC Commercial Mortgage Trust | ||||||||

| 2006-FL4A C, 0.40% due 11/05/21 | 1,000,000 | 985,223 | ||||||

| Banc of America Large Loan Trust | ||||||||

| 2007-BMB1, 1.27% due 08/15/291,2 | 950,000 | 942,567 | ||||||

| Total Collateralized Mortgage Obligations | ||||||||

| (Cost $11,781,296) | 11,846,853 | |||||||

| SENIOR FLOATING RATE INTERESTS††,1 - 3.9% | ||||||||

| Industrials - 1.1% | ||||||||

| Travelport Holdings Ltd. | ||||||||

| 6.25% due 06/26/19 | 1,880,550 | 1,926,002 | ||||||

| Thermasys Corp. | ||||||||

| 5.26% due 05/03/19 | 765,188 | 752,432 | ||||||

| Total Industrials | 2,678,434 | |||||||

| Financials - 1.0% | ||||||||

| National Financial Partners | ||||||||

| 5.25% due 07/01/20 | 1,512,400 | 1,526,268 | ||||||

| Knight/Getco | ||||||||

| 5.75% due 11/30/17 | 603,972 | 604,727 | ||||||

| First Data Corp. | ||||||||

| 4.16% due 03/23/18 | 150,000 | 150,104 | ||||||

| See Notes to Financial Statements. | The GUGGENHEIM FUNDS annual report | 13 |

| Schedule of Investments (concluded) | December 31, 2013 |

| Series A (styleplus–large Core Series) | |

| Face | ||||||||

| Amount | Value | |||||||

| Cunningham Lindsey U.S., Inc. | ||||||||

| 5.00% due 12/10/19 | $ | 138,947 | $ | 138,774 | ||||

| Total Financials | 2,419,873 | |||||||

Energy - 0.7% | ||||||||

| Pacific Drilling 4.50% due 05/18/18 | 776,100 | 784,350 | ||||||

| Ocean Rig ASA 5.50% due 07/15/16 | 748,125 | 757,791 | ||||||

| Total Energy | 1,542,141 | |||||||

| Consumer Discretionary - 0.6% | ||||||||

| Pinnacle Entertainment, Inc. | ||||||||

| 3.75% due 08/15/16 | 646,518 | 650,966 | ||||||

| Go Daddy Operating Company LLC | ||||||||

| 4.00% due 12/16/18 | 285,268 | 285,328 | ||||||

| Sears Holdings Corp. | ||||||||

| 5.50% due 06/30/18 | 240,000 | 241,318 | ||||||

| Laureate Education, Inc. | ||||||||

| 5.00% due 06/16/18 | 124,366 | 124,911 | ||||||

| Total Consumer Discretionary | 1,302,523 | |||||||

| Information Technology - 0.4% | ||||||||

| Blue Coat Systems, Inc. | ||||||||

| 4.50% due 05/31/19 | 887,775 | 889,719 | ||||||

| Health Care - 0.1% | ||||||||

| Apria Healthcare Group, Inc. | ||||||||

| 6.75% due 04/06/20 | 179,100 | 179,473 | ||||||

| Total Senior Floating Rate Interests | ||||||||

| (Cost $8,875,794) | 9,012,163 | |||||||

| U.S. TREASURY BILLS† - 3.0% | ||||||||

| U.S. Treasury Bill6 | ||||||||

| due 02/20/14 | 7,000,000 | 6,999,783 | ||||||

| Total U.S. Treasury Bills | ||||||||

| (Cost $6,999,810) | 6,999,783 | |||||||

| MUNICIPAL BONDS†† - 2.7% | ||||||||

| New York - 2.5% | ||||||||

| New York City Water & Sewer | ||||||||

| System Revenue Bonds | ||||||||

| 0.30% due 06/15/331 | 3,120,000 | 3,120,000 | ||||||

| City of New York New York | ||||||||

| General Obligation Unlimited | ||||||||

| 0.30% due 04/01/351 | 1,550,000 | 1,550,000 | ||||||

| 0.30% due 11/01/261 | 1,220,000 | 1,220,000 | ||||||

| Total New York | 5,890,000 | |||||||

| Michigan - 0.2% | ||||||||

| Michigan Finance Authority | ||||||||

| Revenue Notes | ||||||||

| 4.38% due 08/20/14 | 375,000 | 378,911 | ||||||

| Total Municipal Bonds | ||||||||

| (Cost $6,265,000) | 6,268,911 | |||||||

| MORTGAGE BACKED SECURITIES†† - 0.8% | ||||||||

| Resource Capital Corporation | ||||||||

| CRE Notes 2013 Ltd. | ||||||||

| 3.02% due 12/15/281,2 | 1,900,000 | 1,901,520 | ||||||

| Total Mortgage Backed Securities | ||||||||

| (Cost $1,900,000) | 1,901,520 | |||||||

| COMMERCIAL PAPER†† - 9.9% | ||||||||

| Centrica plc | ||||||||

| 0.22% due 01/03/14 | 2,200,000 | 2,199,968 | ||||||

| FMC Technologies Inc. | ||||||||

| 0.23% due 01/14/14 | 2,000,000 | 1,999,835 | ||||||

| Diageo Capital plc | ||||||||

| 0.08% due 01/02/14 | 1,700,000 | 1,699,992 | ||||||

| Tesco Treasury Services plc | ||||||||

| 0.13% due 01/06/142 | 1,700,000 | 1,699,965 | ||||||

| Kellogg Co. | ||||||||

| 0.12% due 01/08/14 | 1,700,000 | 1,699,957 | ||||||

| Northeast Utilities | ||||||||

| 0.18% due 01/08/14 | 1,700,000 | 1,699,941 | ||||||

| Kinder Morgan Energy Partners, LP | ||||||||

| 0.23% due 01/07/142 | 1,700,000 | 1,699,935 | ||||||

| VW Credit, Inc. | ||||||||

| 0.22% due 01/13/142 | 1,700,000 | 1,699,875 | ||||||

| Ryder System, Inc. | ||||||||

| 0.20% due 01/15/14 | 1,700,000 | 1,699,868 | ||||||

| BAT International Finance | ||||||||

| 0.25% due 01/13/14 | 1,700,000 | 1,699,858 | ||||||

| Potomac Electric Power Co. | ||||||||

| 0.25% due 01/13/14 | 1,700,000 | 1,699,858 | ||||||

| Nissan Motor Acceptance | ||||||||

| 0.30% due 01/13/14 | 1,700,000 | 1,699,830 | ||||||

| CBS Corp. | ||||||||

| 0.24% due 01/24/142 | 1,700,000 | 1,699,739 | ||||||

| Total Commercial Paper | ||||||||

| (Cost $22,898,621) | 22,898,621 | |||||||

| Total Investments - 100.3% | ||||||||

| (Cost $227,158,103) | $ | 231,829,446 | ||||||

| Other Assets & Liabilities, net - (0.3)% | (635,348 | ) | ||||||

| Total Net Assets - 100.0% | $ | 231,194,098 | ||||||

| Unrealized | ||||||||

| Units | Gain | |||||||

| OTC EQUITY INDEX SWAP AGREEMENTS†† | ||||||||

| Morgan Stanley Capital Services, Inc. | ||||||||

| February 2014 S&P 500 Index Swap, | ||||||||

| Terminating 02/03/143 | ||||||||

| (Notional Value $170,799,554) | 92,406 | $ | — | |||||

| * | Non-income producing security. |

| † | Value determined based on Level 1 inputs — See Note 4. |

| †† | Value determined based on Level 2 inputs — See Note 4. |

| 1 | Variable rate security. Rate indicated is rate effective at December 31, 2013. |

| 2 | Security is a 144A or Section 4(a)(2) security. The total market value of 144A or Section 4(a)(2) securities is $64,006,104 (cost $64,052,387), or 27.7% of total net assets. |

| 3 | Total Return based on S&P 500 Index +/- financing at a variable rate. |

| 4 | Investment in a product that pays a management fee to a party related to the advisor. |

| 5 | Affiliated funds. |

| 6 | Zero coupon rate security. |

| plc — Public Limited Company |

| 14 | the GUGGENHEIM FUNDS annual report | See Notes to Financial Statements. |

| Series A (styleplus–large Core Series) |

| STATEMENT OF ASSETS |

| AND LIABILITIES |

December 31, 2013

| Assets: | ||||

| Investments in unaffiliated issuers, at value | ||||

| (cost $219,020,820) | $ | 223,888,559 | ||

| Investments in affiliated issuers, at value | ||||

| (cost $8,137,283) | 7,940,887 | |||

| Total investments | ||||

| (cost $227,158,103) | 231,829,446 | |||

| Receivable for swap settlement | 4,671,296 | |||

| Cash | 95,002 | |||

| Prepaid expenses | 18,823 | |||

| Receivables: | ||||

| Interest | 432,128 | |||

| Securities sold | 320,800 | |||

| Dividends | 202,375 | |||

| Fund shares sold | 3,940 | |||

| Foreign taxes reclaim | 115 | |||

| Total assets | 237,573,925 | |||

| Liabilities: | ||||

| Due to broker | 4,039,162 | |||

| Payable for: | ||||

| Securities purchased | 1,907,263 | |||

| Fund shares redeemed | 203,402 | |||

| Management fees | 144,960 | |||

| Fund accounting/administration fees | 18,361 | |||

| Transfer agent/maintenance fees | 3,698 | |||

| Directors’ fees* | 2,111 | |||

| Miscellaneous | 60,870 | |||

| Total liabilities | 6,379,827 | |||

| Net assets | $ | 231,194,098 | ||

| Net assets consist of: | ||||

| Paid in capital | $ | 200,600,696 | ||

| Undistributed net investment income | 1,196,673 | |||

| Accumulated net realized gain on investments | 24,725,386 | |||

| Net unrealized appreciation on investments | 4,671,343 | |||

| Net assets | $ | 231,194,098 | ||

| Capital shares outstanding | 7,113,720 | |||

| Net asset value per share | $ | 32.50 |

| STATEMENT OF |

| OPERATIONS |

Year Ended December 31, 2013

| Investment Income: | ||||

| Dividends from securities of unaffiliated issuers | $ | 1,936,841 | ||

| Interest | 1,090,682 | |||

| Dividends from securities of affiliated issuers | 264,423 | |||

| Total investment income | 3,291,946 | |||

| Expenses: | ||||

| Management fees | 1,623,772 | |||

| Transfer agent/maintenance fees | 25,455 | |||

| Fund accounting/administration fees | 206,448 | |||

| Directors’ fees* | 22,227 | |||

| Custodian fees | 15,049 | |||

| Tax expense | 6 | |||

| Miscellaneous | 175,888 | |||

| Total expenses | 2,068,845 | |||

| Net investment income | 1,223,101 | |||

| Net Realized and Unrealized Gain (Loss): | ||||

| Net realized gain (loss) on: | ||||

| Investments in unaffiliated issuers | 42,552,123 | |||

| Investments in affiliated issuers | 3,744 | |||

| Swap agreements | 26,517,485 | |||

| Futures contracts | 371,912 | |||

| Net realized gain | 69,445,264 | |||

| Net change in unrealized appreciation (depreciation) on: | ||||

| Investments in unaffiliated issuers | (15,664,656 | ) | ||

| Investments in affiliated issuers | (196,396 | ) | ||

| Net change in unrealized appreciation (depreciation) | (15,861,052 | ) | ||

| Net realized and unrealized gain | 53,584,212 | |||

| Net increase in net assets resulting from operations | $ | 54,807,313 |

| * | Relates to Directors not deemed “interested persons” within the meaning of Section 2(a)(19) of the 1940 Act. |

| See Notes to Financial Statements. | The GUGGENHEIM FUNDS annual report | 15 |

| Series A (styleplus–large Core Series) |

| STATEMENTS OF CHANGES IN NET ASSETS |

| Year Ended | Year Ended | |||||||

| December 31, | December 31, | |||||||

| 2013 | 2012 | |||||||

| Increase (Decrease) In Net Assets From Operations: | ||||||||

| Net investment income | $ | 1,223,101 | $ | 1,952,226 | ||||

| Net realized gain on investments | 69,445,264 | 13,722,503 | ||||||

| Net change in unrealized appreciation (depreciation) on investments | (15,861,052 | ) | 10,476,312 | |||||

| Net increase in net assets resulting from operations | 54,807,313 | 26,151,041 | ||||||

| Capital share transactions: | ||||||||

| Proceeds from sale of shares | 13,501,310 | 8,284,929 | ||||||

| Cost of shares redeemed | (35,729,632 | ) | (42,815,935 | ) | ||||

| Net decrease from capital share transactions | (22,228,322 | ) | (34,531,006 | ) | ||||

| Net increase (decrease) in net assets | 32,578,991 | (8,379,965 | ) | |||||

| Net assets: | ||||||||

| Beginning of year | 198,615,107 | 206,995,072 | ||||||

| End of year | $ | 231,194,098 | $ | 198,615,107 | ||||

| Undistributed net investment income at end of year | $ | 1,196,673 | $ | 1,952,226 | ||||

| Capital share activity: | ||||||||

| Shares sold | 476,713 | 335,217 | ||||||

| Shares redeemed | (1,236,898 | ) | (1,738,927 | ) | ||||

| Net decrease in shares | (760,185 | ) | (1,403,710 | ) | ||||

| 16 | the GUGGENHEIM FUNDS annual report | See Notes to Financial Statements. |

| Series A (styleplus–large Core Series) |

| FINANCIAL HIGHLIGHTS |

This table is presented to show selected data for a share outstanding throughout each period and to assist shareholders in evaluating a Fund’s performance for the periods presented.

| Year Ended | Year Ended | Year Ended | Year Ended | Year Ended | ||||||||||||||||

| December 31, | December 31, | December 31, | December 31, | December 31, | ||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| Per Share Data | ||||||||||||||||||||

| Net asset value, beginning of period | $ | 25.22 | $ | 22.31 | $ | 23.24 | $ | 19.97 | $ | 15.38 | ||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment incomea | .16 | .23 | .13 | .18 | .11 | |||||||||||||||

| Net gain (loss) on investments (realized and unrealized) | 7.12 | 2.68 | (1.06 | ) | 3.09 | 4.48 | ||||||||||||||

| Total from investment operations | 7.28 | 2.91 | (.93 | ) | 3.27 | 4.59 | ||||||||||||||