CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-00248 -------------------------------------------------------------------------

THE ADAMS EXPRESS COMPANY ------------------------------------------------------------------------- (Exact name of registrant as specified in charter)

7 Saint Paul Street, Suite 1140, Baltimore, Maryland 21202 ------------------------------------------------------------------------- (Address of principal executive offices)

Lawrence L. Hooper, Jr. The Adams Express Company 7 Saint Paul Street, Suite 1140 Baltimore, Maryland 21202 ------------------------------------------------------------------------- (Name and address of agent for service)

Registrant's telephone number, including area code: (410) 752-5900 Date of fiscal year end: December 31 Date of reporting period: December 31, 2012

Item 1. Reports to Stockholders.

GENERATION AFTER GENERATION – WE GROW WITH YOU.™

ANNUAL REPORT 2012

ADAMS

EXPRESS

COMPANY

2012ATA GLANCE

The Fund

Ÿ

a closed-end equity investment company

Ÿ

objectives:

preservation of capital

reasonable income

opportunity for capital gain

Ÿ

internally-managed

Ÿ

annual distribution rate of at least 6%

Ÿ

low turnover

Stock Data (12/31/12)

NYSE Symbol

ADX

Market Price

$10.59

52-Week Range

$9.75 – $11.57

Discount

14.8%

Shares Outstanding

93,029,724

Summary Financial Information

Year Ended December 31,

2012

2011

Net asset value per share

$

12.43

$

11.54

Total net assets

1,155,997,037

1,050,733,678

Unrealized appreciation

143,061,370

62,511,196

Net investment income

17,547,510

13,858,578

Net realized gain

47,997,411

45,998,641

Total return (based on market price)

16.9%

(4.2)%

Total return (based on net asset value)

14.7%

(2.8)%

Ratio of expenses to average net assets

0.65%

0.55%

Annual distribution rate

6.3%

6.1%

2012 Dividends and Distributions

Paid

Amount (per share)

Type

March 1, 2012

$

0.01

Long-term capital gain

March 1, 2012

0.01

Short-term capital gain

March 1, 2012

0.03

Investment income

June 1, 2012

0.05

Investment income

September 1, 2012

0.05

Investment income

December 27, 2012

0.38

Long-term capital gain

December 27, 2012

0.09

Short-term capital gain

December 27, 2012

0.05

Investment income

$

0.67

2013 Annual Meeting of Shareholders

Location: Maryland Club, Baltimore, Maryland

Date: March 19, 2013

Time: 10:00 a.m.

PORTFOLIO REVIEW

December 31, 2012

(unaudited)

Ten Largest Equity Portfolio Holdings

Market Value

% of Net Assets

Petroleum & Resources Corp.*

$

52,307,634

4.5

%

Apple Inc.

49,571,790

4.3

JPMorgan Chase & Co.

26,382,000

2.3

QUALCOMM Inc.

24,808,000

2.2

Lowe’s Companies, Inc.

21,312,000

1.8

International Business Machines Corp.

20,112,750

1.7

Wells Fargo & Co.

19,140,800

1.7

Microsoft Corp.

18,711,000

1.6

AT&T Corp.

18,540,500

1.6

Google Inc. (Class A)

18,443,620

1.6

$

269,330,094

23.3

%

* Non-controlled affiliated closed-end fund

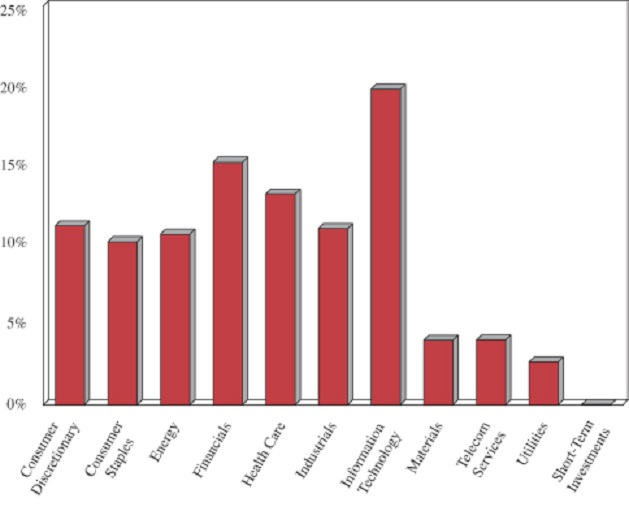

Sector Weightings

1

LETTERTO SHAREHOLDERS

The Year in Review

Equity markets produced a solid return in 2012 led by a renewed interest in the financial and consumer sectors. A strong start to the year was built upon an improving U.S. economy and the anticipation that Europe would find a way to avoid economic disaster. The upward trajectory of the market paused in the spring as tensions escalated in the Middle East and again in the fall as the presidential election and fiscal cliff drew investors’ attention. The S&P 500 Index ended the year at its highest point, producing a total return of 16.0%. Adams Express enjoyed a very good 2012 with a total return on net asset value of 14.7%. The Lipper Large-Cap Core Mutual Fund Average, our peer group, returned 15.0%. The Adams Express total return on market value was 16.9%, reflecting a narrowing of the discount during the year.

Our view at the onset of 2012 was for 2.5% GDP growth in the U.S. and global growth of 3.5%, led by China and held back by Europe. Closing out 2012, the U.S. growth was about 2.3%, not straying too far from expectations. A U.S. economy in search of stability was helped by a recovering housing market and gradual job improvement, only to face generally weak capital investment, a severe drought, the uncertainty surrounding the presidential election, and a looming fiscal cliff. China disappointed modestly and served to drag global growth expectations lower. The outlook for China’s GDP waned as the year progressed, driven by concerns over a decelerating economy. China is challenged by a shift toward an economy driven by domestic consumption from one based on investment and exports. Further, sharply rising wages and production costs have eroded the once prevalent low-cost manufacturing advantage long enjoyed by China. Brazil experienced a severe drought that left output far short of expectations, highlighting the country’s dependence on agriculture. In India, underinvestment in infrastructure led to widespread blackouts during the summer. The country continues to face political and economic challenges that will likely leave output below potential. European growth was weak, as expected, as the European Union dealt with a fractured financial system and worked through concerns over dissolution. Globally, many of the same issues affecting 2012 will continue to serve as the backdrop for the economy in 2013.

Earnings for the S&P 500 Index only grew about 3%-4% in 2012 following 15% growth in 2011. A low level of economic expansion and corporations struggling to achieve additional cost savings produced only modest earnings growth in 2012. However, equities rose sharply as valuations expanded to reflect the removal of some uncertainty in the outlook. Throughout the year, several economic indicators inched higher, led by stronger housing construction and improved manufacturing activity. Similar to 2011, the year began with a strong surge by equity markets. Europe agreed to bail out Greece again, removing a major hurdle in the global outlook. The spring brought about additional concerns as unrest grew in the Middle East. In the U.S., summer brought a severe drought, leading to a sharp rise in commodity prices, including record corn prices. Late in the year, attention shifted to the election and the fiscal cliff of tax increases and spending cuts set to take effect in 2013.

Our portfolio performed well in 2012. Consumer discretionary and financials were the Fund’s best performing sectors, up 29.6% and 25.4% for the year, respectively. The consumer discretionary sector was led by companies with exposure to a recovering housing market. Financials drew the attention of investors as the economy appeared to be stabilizing and regulatory uncertainty waned. The health care sector rose 19.1%, with very strong performance in biotechnology. Telecommunications holdings rose 18.2%, fueled by an increased appetite for dividends. Industrial holdings benefited from a recovering economy and rose 16.9% as the cyclically-sensitive machinery companies and housing-exposed names performed very well. Our holdings in technology companies lagged the broader market and were up only 11.8% as capital spending plans, in general, fell short of expectations. Holdings in consumer staples and utilities, typically viewed as defensive, rose by only mid-single digits for the year as investors shifted toward more cyclical areas of the market. Fund holdings in the energy and materials sectors were up 3.1% and 7.2%, respectively, due to uncertainty about global growth, particularly in China, and relatively flat energy and commodity prices. Overall, our Fund had a solid year and is positioned well for 2013 and beyond.

Douglas G. Ober

Chairman and Chief

Executive Officer

David D. Weaver

President

2

LETTERTO SHAREHOLDERS (CONTINUED)

Investment Results

At the end of 2012, our net assets were $1,155,997,037 or $12.43 per share on 93,029,724 shares outstanding. This compares with $1,050,733,678 or $11.54 per share on 91,073,899 shares outstanding a year earlier. Net investment income for 2012 was $17,547,510 compared to $13,858,578 for 2011. These earnings are equal to $0.19 and $0.16 per share, respectively, on the average number of shares outstanding throughout each year. Our expense ratio (total expenses to average net assets) for 2012 was 0.65%. Net realized gains amounted to $47,997,411 during the year, while the unrealized appreciation on investments increased from $62,511,196 at December 31, 2011 to $143,061,370 at the end of 2012.

Dividends and Distributions

The total dividends and distributions paid in 2012 were $0.67 per share, producing a 6.3% annual distribution rate for the year, compared to $0.65 and an annual distribution rate of 6.1% in 2011 and, in both years, exceeding our 6% minimum distribution rate commitment. The table on page 21 shows the history of our dividends and distributions over the past fifteen years, including the annual distribution rate to shareholders.

The total distributions made in 2012 included a year-end distribution of $0.52 per share, as announced on November 8, 2012, consisting of investment income of $0.05 and capital gains of $0.47, paid on December 27, 2012 and taxable to shareholders in 2012. On January 10, 2013, a distribution of $0.05 per share was declared to shareholders of record February 15, 2013, payable March 1, 2013, representing the balance of undistributed net investment income and capital gains earned during 2012, all taxable to shareholders in 2013.

Outlook for 2013

Global economic growth in 2012 was modest. Some progress was made, but many challenges remain. We expect global GDP growth in 2013 to approximate 2.5%-3.0%, slightly below 2012. The U.S. economy is gradually improving on the backs of the consumer and a recovering housing market, but the swelling budget deficit remains the greatest challenge. U.S. GDP should expand by 2.5% in 2013, a slight uptick from the 2012 rate of 2.3%. We believe Europe is likely to grow slightly despite forecasts for economic contraction. Europe appears to be avoiding disaster by pulling together to address the result of years of overspending and structural deficiencies. Deleveraging and austerity may serve to boost confidence over the next year. Significant work remains, but the intent seems genuine. As mentioned earlier, China is going through a transformation. The country has significant potential and will remain one of the most influential economies in the world. China’s demand for the world’s commodities and materials is a key factor in the outlook. The extent to which it is able to shift toward a consumer-based economy without upsetting the global marketplace will shape the world economy in the coming years.

The stock market jumped nicely to start 2013 as the U.S. passed legislation to avoid going over the fiscal cliff. Another reason for the early strength may be in fund money flows. Money has flowed into equity funds to start the year at a pace not seen in a long time. Following years of money flowing out of equities, a reversal of that trend could be significant for the markets, but it is too early to draw any conclusions. Despite early strength, many issues will continue to weigh on the equity markets in the short term as investors focus on the debt ceiling and the impact of higher taxes on consumers’ spending habits. Our long-term focus helps us find opportunities during periods of uncertainty. The changes we made to the portfolio in 2012, and those being made today, are designed to position the Fund for solid long-term performance. In the fourth quarter of 2012, most of the additions to the portfolio were in higher-growth areas such as technology, consumer discretionary, and financials. We also shifted some of our health care holdings toward better growth opportunities within the same sector. Throughout our investment process, we keep a sharp eye on maintaining a high-quality, diversified portfolio. The turnover of the Fund has increased as we have strived to be more nimble in responding to market opportunities. We believe the changes made serve to position the Fund for long-term success.

By order of the Board of Directors,

Douglas G. Ober

David D. Weaver

Chairman and Chief Executive Officer

President

January 25, 2013

3

LETTERTO SHAREHOLDERS (CONTINUED)

Douglas G. Ober, our long-time CEO and Chairman of the Board, is retiring on March 31, 2013. After joining the Fund in 1980, he became the CEO and lead portfolio manager in 1990 and Board Chairman in 1991. He has been the driving force behind the Fund’s performance over that time. His investment acumen and steady management style have come to define the Fund and have guided us through the many challenges that we have faced over the past 23 years. He has also served as our resident historian and has worked tirelessly to preserve our fascinating corporate history.

Mr. Ober also will be stepping down as the Chairman of the Board after this year’s Annual Meeting, but will continue as a consultant to the Fund to assist with the transition to our new CEO. Mr. Ober has built and leaves behind an outstanding team that will continue to build on the Fund’s 83-year track record of investment performance for our shareholders. We want to express our profound admiration and appreciation for everything that he has accomplished over the past 32 years and wish him all the best in his well-deserved retirement.

Mark E. Stoeckle has been selected as the Fund’s next CEO and will begin his tenure on February 11, 2013. He will also be joining the Board of Directors. Mr. Stoeckle has had a distinguished 30-year career in financial services and asset management, and brings a wealth of investment and business experience to the role. He comes to the Fund from the global investment management firm BNP Paribas Investment Partners, in Boston, where he has served since 2004 as Chief Investment Officer, U.S. Equities and Global Sector Funds. With his outstanding record of achievement, his leadership ability and experience are ideally suited to lead our portfolio management team and the Fund.

Daniel E. Emerson, the Fund’s Lead Director and a member of the Board of Directors since 1982, has decided not to stand for reelection to the Board at the Annual Meeting. He has been a tremendous asset to the Fund over his tenure and has played an instrumental role in its success. He has served as the Chair of all of our Board Committees at one time or another and has helped to define the role of Lead Director that has served the Fund so well. Mr. Emerson is greatly admired by us all and we are so thankful for his keen insights and enthusiastic dedication to our mission. He will be missed.

Open written option contracts* at value (proceeds $522,721)

274,574

Obligations to return securities lending collateral

17,166,879

Accrued pension liabilities

3,349,453

Accrued expenses and other liabilities

1,710,379

Total Liabilities

22,501,285

Net Assets

$

1,155,997,037

Net Assets

Common Stock at par value $0.001 per share, authorized 150,000,000 shares; issued and outstanding 93,029,724 shares (includes 138,648 restricted shares, 18,000 nonvested or deferred restricted stock units, and 13,551 deferred stock units) (note 6)

$

93,030

Additional capital surplus

1,014,055,656

Accumulated other comprehensive income (note 5)

(2,881,871

)

Undistributed net investment income

2,836,318

Undistributed net realized gain on investments

(1,167,466

)

Unrealized appreciation on investments

143,061,370

Net Assets Applicable to Common Stock

$

1,155,997,037

Net Asset Value Per Share of Common Stock

$12.43

*See Schedule of Investments on page 15 and Schedule of Outstanding Written Option Contracts on page 14.

The accompanying notes are an integral part of the financial statements.

5

STATEMENTOF OPERATIONS

Year Ended December 31, 2012

Investment Income

Income:

Dividends:

From unaffiliated issuers (net of $90,127 in foreign taxes)

$

23,539,092

From non-controlled affiliate

940,313

Other income

459,822

Total income

24,939,227

Expenses:

Investment research

3,588,753

Administration and operations

1,513,672

Directors’ fees

490,310

Travel, training, and other office expenses

389,659

Transfer agent, registrar, and custodian

332,751

Investment data services

265,318

Reports and shareholder communications

255,509

Occupancy

160,964

Audit and accounting services

122,900

Insurance

102,548

Legal services

82,116

Other

87,217

Total expenses

7,391,717

Net Investment Income

17,547,510

Realized Gain and Change in Unrealized Appreciation on Investments

Net realized gain on security transactions

43,793,406

Net realized gain distributed by regulated investment company (non-controlled affiliate)

2,558,526

Net realized gain on written option contracts

1,645,479

Change in unrealized appreciation on securities

80,656,064

Change in unrealized appreciation on written option contracts

(105,890

)

Net Gain on Investments

128,547,585

Other Comprehensive Income (note 5)

Defined benefit pension plans:

Net actuarial loss arising during period

(699,409

)

Amortization of net loss

268,331

Effect of settlement (non-recurring)

187,740

Other Comprehensive Income

(243,338

)

Change in Net Assets Resulting from Operations

$

145,851,757

The accompanying notes are an integral part of the financial statements.

6

STATEMENTSOF CHANGESIN NET ASSETS

For the Year Ended December 31,

2012

2011

From Operations:

Net investment income

$

17,547,510

$

13,858,578

Net realized gain on investments

47,997,411

45,998,641

Change in unrealized appreciation on investments

80,550,174

(96,710,494

)

Change in accumulated other comprehensive income (note 5)

(243,338

)

(602,411

)

Change in net assets resulting from operations

145,851,757

(37,455,686

)

Distributions to Shareholders From:

Net investment income

(16,392,876

)

(13,335,356

)

Net realized gain from investment transactions

(44,625,641

)

(44,457,396

)

Decrease in net assets from distributions

(61,018,517

)

(57,792,752

)

From Capital Share Transactions:

Value of shares issued in payment of distributions (note 4)

20,118,651

20,946,619

Deferred compensation (notes 4, 6)

311,468

363,531

Increase in net assets from capital share transactions

20,430,119

21,310,150

Total Change in Net Assets

105,263,359

(73,938,288

)

Net Assets:

Beginning of year

1,050,733,678

1,124,671,966

End of year (including undistributed net investment income of $2,836,318 and $1,943,560, respectively)

$

1,155,997,037

$

1,050,733,678

The accompanying notes are an integral part of the financial statements.

NOTES TO FINANCIAL STATEMENTS

1. Significant Accounting Policies

The Adams Express Company (the Fund) is registered under the Investment Company Act of 1940 as a diversified investment company. The Fund is an internally-managed closed-end fund whose investment objectives are preservation of capital, the attainment of reasonable income from investments, and an opportunity for capital appreciation.

The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America, which require the use of estimates made by Fund management. Management believes that estimates and security valuations are appropriate; however, actual results may differ from those estimates, and the security valuations reflected in the financial statements may differ from the value the Fund ultimately realizes upon sale of the securities.

Affiliated Companies — Investments in companies 5% or more of whose outstanding voting securities are held by the Fund are defined as “Affiliated Companies” in Section 2(a)(3) of the Investment Company Act of 1940.

Expenses — The Fund shares certain costs for investment research and data services, administration and operations, travel, training, office expenses, occupancy, accounting and legal services, insurance, and other miscellaneous items with its non-controlled affiliate, Petroleum & Resources Corporation. Shared expenses that are not solely attributable to one fund are allocated to each fund based on relative net asset values or, in the case of investment research staff and related costs,

7

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

relative market values of portfolio securities in the particular sector of coverage. Changes in expense allocations are updated quarterly, as appropriate, except for those related to payroll, which are updated annually.

Security Transactions and Investment Income — Investment transactions are accounted for on the trade date. Gain or loss on sales of securities and options is determined on the basis of specific identification. Dividend income and distributions to shareholders are recognized on the ex-dividend date, and interest income is recognized on the accrual basis.

Security Valuation — The Fund’s investments are reported at fair value as defined under accounting principles generally accepted in the United States of America. Investments in securities traded on national security exchanges are valued at the last reported sale price on the day of valuation. Over-the-counter and listed securities for which a sale price is not available are valued at the last quoted bid price. Short-term investments (excluding purchased options and money market funds) are valued at amortized cost, which approximates fair value. Purchased and written options are valued at the last quoted bid and asked price, respectively. Money market funds are valued at net asset value on the day of valuation.

Various inputs are used to determine the fair value of the Fund’s investments. These inputs are summarized in the following three levels:

•

Level 1 — fair value is determined based on market data obtained from independent sources; for example, quoted prices in active markets for identical investments,

•

Level 2 — fair value is determined using other assumptions obtained from independent sources; for example, quoted prices for similar investments,

•

Level 3 — fair value is determined using the Fund’s own assumptions, developed based on the best information available in the circumstances.

The Fund’s investments at December 31, 2012 were classified as follows:

Level 1

Level 2

Level 3

Total

Common stocks

$

1,153,761,081

$

—

$

—

$

1,153,761,081

Short-term investments

585,046

—

—

585,046

Securities lending collateral

17,166,879

—

—

17,166,879

Total investments

$

1,171,513,006

$

—

$

—

$

1,171,513,006

Written options

$

(274,574

)

$

—

$

—

$

(274,574

)

There were no transfers into or from Level 1 or Level 2 during the year ended December 31, 2012.

2. Federal Income Taxes

No federal income tax provision is required since the Fund’s policy is to qualify as a regulated investment company under the Internal Revenue Code and to distribute substantially all of its taxable income to its shareholders. Additionally, management has analyzed and concluded that tax positions included in federal income tax returns from the previous three years that remain subject to examination do not require any provision. Any income tax-related interest or penalties would be recognized as income tax expense. As of December 31, 2012, the identified cost of securities for federal income tax purposes was $1,031,216,276 and net unrealized appreciation aggregated $140,296,730, consisting of gross unrealized appreciation of $227,536,069 and gross unrealized depreciation of $87,239,339.

Distributions are determined in accordance with our 6% minimum distribution rate commitment, based on the Fund’s average market price, and income tax regulations, which may differ from generally accepted accounting principles. Such differences are primarily related to the Fund’s retirement plans, equity-based compensation, and loss deferrals for wash sales. Differences that are permanent, while not material for the year ended December 31, 2012, are reclassified in the capital accounts of the Fund’s financial statements and have no impact on net assets. For tax purposes, distributions paid by the Fund during the years ended December 31, 2012 and December 31, 2011 were classified as ordinary income of $25,489,925 and $19,552,826, respectively, and as long-term capital gain of $35,504,402 and $38,214,991, respectively. The tax basis of distributable earnings at December 31, 2012 was $3,616,709 of undistributed ordinary income and $407,546 of undistributed long-term capital gain.

3. Investment Transactions

The Fund’s investment decisions are made by a committee of management, and recommendations to that committee are made by the research staff. Purchases and sales of portfolio securities, other than options and short-term investments, during the year ended December 31, 2012 were $326,867,754 and $300,241,389, respectively.

The Fund is subject to changes in the value of equity securities held (“equity price risk”) in the normal course of pursuing its investment objectives. The Fund may purchase and write option contracts to increase or decrease its equity price risk exposure or may write

8

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

option contracts to generate additional income. Option contracts generally entail risks associated with counterparty credit, liquidity, and unfavorable equity price movements. The Fund has mitigated counterparty credit and liquidity risks by trading its options through an exchange. The risk of unfavorable equity price movements is limited for purchased options to the premium paid and for written options by writing only covered call or collateralized put option contracts, which require the Fund to segregate certain securities or cash at its custodian when the option is written. A schedule of outstanding option contracts as of December 31, 2012 can be found on page 14.

When the Fund writes (purchases) an option, an amount equal to the premium received (paid) by the Fund is recorded as a liability (asset) and is subsequently marked to market daily in the Statement of Assets and Liabilities, with any related change recorded as an unrealized gain or loss in the Statement of Operations. Premiums received (paid) from unexercised options are treated as realized gains (losses) on the expiration date and are separately identified in the Statement of Operations. Upon the exercise of written put (purchased call) option contracts, premiums received (paid) are deducted from (added to) the cost basis of the underlying securities purchased. Upon the exercise of written call (purchased put) option contracts, premiums received (paid) are added to (deducted from) the proceeds from the sale of underlying securities in determining whether there is a realized gain or loss.

Transactions in written covered call and collateralized put options during the year ended December 31, 2012 were as follows:

Covered Calls

Collateralized Puts

Contracts

Premiums

Contracts

Premiums

Options outstanding, December 31, 2011

676

$

116,650

1,259

$

327,066

Options written

9,805

1,240,218

11,110

1,727,880

Options terminated in closing purchase transactions

(1,737

)

(240,806

)

(731

)

(203,631

)

Options expired

(6,719

)

(876,752

)

(8,532

)

(1,383,386

)

Options exercised

(250

)

(27,049

)

(1,160

)

(157,469

)

Options outstanding, December 31, 2012

1,775

$

212,261

1,946

$

310,460

4. Capital Stock

The Fund has 10,000,000 authorized and unissued preferred shares, $0.001 par value.

On December 27, 2012, the Fund issued 1,923,171 shares of its Common Stock at a price of $10.455 per share (the average market price on December 10, 2012) to shareholders of record November 19, 2012 who elected to take stock in payment of the distribution from 2012 capital gain and investment income. During 2012, 1,125 shares were issued at a weighted average price of $10.53 per share as dividend equivalents to holders of deferred stock units and restricted stock units under the 2005 Equity Incentive Compensation Plan.

On December 27, 2011, the Fund issued 2,147,935 shares of its Common Stock at a price of $9.745 per share (the average market price on December 7, 2011) to shareholders of record November 21, 2011 who elected to take stock in payment of the distribution from 2011 capital gain and investment income. During 2011, 1,435 shares were issued at a weighted average price of $10.43 per share as dividend equivalents to holders of deferred stock units and restricted stock units under the 2005 Equity Incentive Compensation Plan.

The Fund may purchase shares of its Common Stock from time to time at such prices and amounts as the Board of Directors may deem advisable. Transactions in Common Stock for 2012 and 2011 were as follows:

Shares

Amount

2012

2011

2012

2011

Shares issued in payment of distributions

1,924,296

2,149,370

$

20,118,651

$

20,946,619

Net activity under the 2005 Equity Incentive Compensation Plan

31,529

39,343

311,468

363,531

Net change

1,955,825

2,188,713

$

20,430,119

$

21,310,150

5. Retirement Plans

Defined Contribution Plans — The Fund sponsors a qualified defined contribution plan for all employees with at least six months of service and a nonqualified defined contribution plan for eligible employees to supplement the qualified plan. The Fund expensed contributions to the plans in the amount of $320,389, a portion thereof based on company performance, for the year ended December 31, 2012. The Fund does not provide postretirement medical benefits.

Defined Benefit Plans — On October 1, 2009, the Fund froze its non-contributory qualified and nonqualified defined benefit pension plans. Benefits are based on length of service and compensation during the last five years of employment through September 30, 2009, with no additional benefits being accrued beyond that date.

The funded status of the plans is recognized as an asset (overfunded plan) or a liability (underfunded plan) in

9

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

the Statement of Assets and Liabilities. Changes in the prior service costs and accumulated actuarial gains and losses are recognized as accumulated other comprehensive income, a component of net assets, in the year in which the changes occur and are subsequently amortized into net periodic pension cost. Non-recurring settlement costs are recognized in net periodic pension cost when a plan participant receives a lump-sum benefit payment and includes the amount of which is in excess of the present value of the projected benefit and any unamortized actuarial losses attributable to the portion of the projected benefit obligation being satisfied.

The Fund’s policy is to contribute annually to the plans those amounts that can be deducted for federal income tax purposes, plus additional amounts as the Fund deems appropriate in order to provide assets sufficient to meet benefits to be paid to plan participants. The Fund contributed $1,225,000 to the qualified plan and $227,424 to the nonqualified plan in 2012 and anticipates making aggregate contributions of up to $525,000 in 2013.

The Fund uses a December 31 measurement date for its plans. Details in aggregate for the plans were as follows:

2012

2011

Change in benefit obligation

Benefit obligation at beginning of year

$

10,207,237

$

9,417,968

Interest cost

359,366

389,980

Actuarial loss

1,029,954

604,445

Benefits paid

(177,079

)

(205,156

)

Effect of settlement (non-recurring)

(554,067

)

—

Benefit obligation at end of year

$

10,865,411

$

10,207,237

Change in qualified plan assets

Fair value of qualified plan assets at beginning of year

$

8,148,262

$

8,058,143

Actual return on plan assets

615,406

247,851

Employer contributions

1,225,000

—

Benefits paid

(129,655

)

(157,732

)

Settlement (non-recurring)

(554,067

)

—

Fair value of qualified plan assets at end of year

$

9,304,946

$

8,148,262

Funded status

$

(1,560,465

)

$

(2,058,975

)

The accumulated benefit obligation for all defined benefit pension plans was $10,865,411 and $10,207,237 at December 31, 2012 and 2011, respectively.

The primary investment objectives of the Fund’s qualified pension plan assets are to provide capital appreciation, income, and preservation of capital. The plan’s objectives are achieved through a diversified portfolio including common stock of the Company and pooled separate accounts (“PSA”). PSAs are made up of a wide variety of underlying investments in equity and fixed income securities. The Fund’s targeted asset allocation for 2013 is to maintain approximately 80% of plan assets invested in fixed income securities, approximately 15% of plan assets invested in equity securities, and approximately 5% in cash and short-term securities. The investment in the Fund’s common stock represented 8% of plan assets at December 31, 2012.

The net asset value of a PSA is based on the fair value of its underlying investments. The fair value of the plan assets is determined using various inputs, summarized into the three levels described in footnote 1. The plan assets at December 31, 2012 were classified as follows:

Level 1

Level 2

Level 3

Total

Equity PSAs

$

—

$

638,844

$

—

$

638,844

Fixed Income PSAs

—

5,620,998

—

5,620,998

Money Market PSA’s

—

2,345,036

—

2,345,036

Regulated Investment Companies

700,068

—

—

700,068

Total

$

700,068

$

8,604,878

$

—

$

9,304,946

Items impacting the Fund’s net investment income and accumulated other comprehensive income were:

2012

2011

Components of net periodic pension cost

Interest cost

$

359,366

$

389,980

Expected return on plan assets

(278,506

)

(436,909

)

Net loss component

268,331

191,093

Effect of settlement (non-recurring)

187,740

—

Net periodic pension cost

$

536,931

$

144,164

2012

2011

Accumulated other comprehensive income

Defined benefit pension plans:

Balance at beginning of year

$

(2,638,533

)

$

(2,036,122

)

Current period other comprehensive income

(243,338

)

(602,411

)

Balance at end of year

$

(2,881,871

)

$

(2,638,533

)

Accumulated other comprehensive income was comprised of net actuarial losses of $(2,881,871) and $(2,638,533) at December 31, 2012 and 2011, respectively. In 2013, the Fund estimates that $252,062 of net losses will be amortized from accumulated other comprehensive income into net periodic pension cost.

Assumptions used to determine benefit obligations were:

2012

2011

Discount rate

3.75%

4.42%

Rate of compensation increase

—

—

The assumptions used to determine net periodic pension cost were:

2012

2011

Discount rate

4.20%

5.18%

Expected long-term return on plan assets

4.00%

6.00%

Rate of compensation increase

—

—

10

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

The assumption used to determine expected long-term return on plan assets was based on historical and future expected returns of multiple asset classes in order to develop a risk-free real rate of return and risk premiums for each asset class. The overall rate for each asset class was developed by combining a long-term inflation component, the risk-free real rate of return, and the associated risk premium. A weighted average rate was developed based on those overall rates and the target asset allocation of the plan.

The following benefit payments are eligible to be paid in the years indicated:

Pension Benefits

2013

$

3,760,000

2014

679,000

2015

321,000

2016

311,000

2017

920,000

Years 2018-2022

1,850,000

6. Equity-Based Compensation

The 2005 Equity Incentive Compensation Plan (“2005 Plan”), adopted at the 2005 Annual Meeting and re-approved at the 2010 Annual Meeting, permits the grant of restricted stock awards (both performance and nonperformance-based), as well as stock options and other stock incentives, to key employees and all non-employee directors. Performance-based restricted stock awards vest at the end of a specified three year period, with the ultimate number of shares earned contingent on achieving certain performance targets. If performance targets are not achieved, all or a portion of the performance-based restricted shares are forfeited and become available for future grants. Nonperformance-based restricted stock awards typically vest ratably over a three year period and nonperformance-based restricted stock units (granted to non-employee directors) vest over a one year period. Payment of awards may be deferred, if elected. It is the current intention that annual employee grants will be performance-based. The 2005 Plan provides for accelerated vesting in the event of death or retirement. Non-employee directors also may elect to defer a portion of their cash compensation, with such deferred amount to be paid by delivery of deferred stock units. Outstanding awards are granted at fair market value on grant date. The 2005 Plan provides for the issuance of up to 3,413,131 shares of the Fund’s Common Stock, of which 3,108,908 remain available for future grants at December 31, 2012.

A summary of the status of the Fund’s awards granted under the 2005 Plan as of December 31, 2012, and changes during the year then ended, is presented below:

Awards

Shares/Units

Weighted Average Grant-Date Fair Value

Balance at December 31, 2011

158,237

$

9.96

Granted:

Restricted stock

55,494

10.15

Restricted stock units

6,000

10.98

Deferred stock units

821

10.51

Vested & issued

(29,715

)

8.83

Forfeited

(20,638

)

8.41

Balance at December 31, 2012 (includes 134,912 performance-based awards and 35,287 nonperformance-based awards)

170,199

$

10.57

Compensation cost resulting from awards granted under the 2005 Plan are based on the fair value of the award on grant date (determined by the average of the high and low price on grant date) and recognized on a straight-line basis over the requisite service period. For those awards with performance conditions, compensation cost is based on the most probable outcome and, if such goals are not met, compensation cost is not recognized and any previously recognized compensation cost is reversed. The total compensation cost for restricted stock granted to employees for the year ended December 31, 2012 was $339,383. The total compensation cost for restricted stock units granted to non-employee directors for the year ended December 31, 2012 was $66,059. As of December 31, 2012, there was total unrecognized compensation cost of $541,772, a component of additional capital surplus, related to nonvested equity-based compensation arrangements granted under the 2005 Plan. That cost is expected to be recognized over a weighted average period of 1.61 years. The total fair value of shares and units vested during the year ended December 31, 2012 was $302,117.

The Stock Option Plan of 1985 (“1985 Plan”) has been discontinued and, as of December 31, 2012, there are no remaining grants of stock options and stock appreciation rights outstanding.

A summary of option activity under the 1985 Plan as of December 31, 2012, and changes during the year then ended, is presented below:

Options

Weighted- Average Exercise Price

Weighted- Average Remaining Life (Years)

Aggregate Intrinsic Value

Outstanding at December 31, 2011

24,857

$

8.70

0.16

Exercised

(24,857

)

8.70

—

$

40,049

Outstanding at December 31, 2012

—

$

—

—

$

—

11

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

Compensation cost resulting from stock options and stock appreciation rights granted under the 1985 Plan is based on the intrinsic value of the award, recognized over the award’s vesting period, and remeasured at each reporting date through the date of settlement. The total compensation cost recognized for the year ended December 31, 2012 was $16,919.

7. Officer and Director Compensation

The aggregate remuneration paid during the year ended December 31, 2012 to officers and directors amounted to $2,904,541, of which $472,468 was paid to directors who were not officers. These amounts represent the taxable income to the Fund’s officers and directors and therefore differ from the amounts reported in the accompanying Statement of Operations that are recorded and expensed in accordance with generally accepted accounting principles.

8. Portfolio Securities Loaned

The Fund makes loans of securities to approved brokers to earn additional income. It receives as collateral cash deposits, U.S. Government securities, or bank letters of credit valued at 102% of the value of the securities on loan. The market value of the loaned securities is calculated based upon the most recent closing prices and any additional required collateral is delivered to the Fund on the next business day. Cash deposits are placed in a registered money market fund. The Fund accounts for securities lending transactions as secured financing and receives compensation in the form of fees or retains a portion of interest on the investment of any cash received as collateral. The Fund also continues to receive interest or dividends on the securities loaned. Gain or loss in the fair value of the securities loaned that may occur during the term of the loan will be for the account of the Fund. At December 31, 2012, the Fund had securities on loan of $17,279,889 and held cash collateral of $17,166,879; additional collateral was delivered the next business day in accordance with the procedure described above. The Fund is indemnified by the Custodian, serving as lending agent, for loss of loaned securities and has the right under the lending agreement to recover the securities from the borrower on demand.

9. Operating Lease Commitments

The Fund leases office space and equipment under operating lease agreements expiring at various dates through the year 2016. The Fund recognized rental expense of $147,967 in 2012, and its minimum rental commitments are as follows:

2013

$

158,100

2014

158,558

2015

158,836

2016

76,736

Total

$

552,230

12

FINANCIAL HIGHLIGHTS

Year Ended December 31,

2012

2011

2010

2009

2008

Per Share Operating Performance

Net asset value, beginning of year

$11.54

$12.65

$11.95

$9.61

$15.72

Net investment income

0.19

0.16

0.15

0.13

0.25

Net realized gains and increase (decrease) in unrealized appreciation

1.41

(0.56)

1.10

2.64

(5.68)

Change in accumulated other comprehensive income (note 5)

0.00

(0.01)

0.00

0.04

(0.05)

Total from investment operations

1.60

(0.41)

1.25

2.81

(5.48)

Less distributions

Dividends from net investment income

(0.18)

(0.15)

(0.14)

(0.15)

(0.26)

Distributions from net realized gains

(0.49)

(0.50)

(0.37)

(0.30)

(0.38)

Total distributions

(0.67)

(0.65)

(0.51)

(0.45)

(0.64)

Capital share repurchases

0.00

0.00

0.00

0.02

0.05

Reinvestment of distributions

(0.04)

(0.05)

(0.04)

(0.04)

(0.04)

Total capital share transactions

(0.04)

(0.05)

(0.04)

(0.02)

0.01

Net asset value, end of year

$12.43

$11.54

$12.65

$11.95

$9.61

Market price, end of year

$10.59

$ 9.64

$10.72

$10.10

$8.03

Total Investment Return

Based on market price

16.9%

(4.2)%

11.5%

32.1%

(38.9)%

Based on net asset value

14.7%

(2.8)%

11.2%

30.6%

(34.4)%

Ratios/Supplemental Data

Net assets, end of year (in 000’s)

$1,155,997

$1,050,734

$1,124,672

$1,045,027

$840,012

Ratio of expenses to average net assets*

0.65%

0.55%

0.58%

0.90%

0.48%

Ratio of net investment income to average net assets*

1.54%

1.25%

1.29%

1.30%

1.82%

Portfolio turnover

27.40%

21.50%

16.15%

15.05%

18.09%

Number of shares outstanding at end of year (in 000’s)

93,030

91,074

88,885

87,415

87,406

*

For 2009, the ratios of expenses and net investment income to average net assets were 0.76% and 1.44%, respectively, after adjusting for non-recurring pension expenses. For 2012, the adjusted ratios were 0.63% and 1.56%, respectively.

13

SCHEDULEOF OUTSTANDING WRITTEN OPTION CONTRACTS

December 31, 2012

Contracts

(100 shares

each)

Security

Strike

Price

Contract

Expiration

Value

COVERED CALLS

200

Boeing Co.

$ 85

May 13

$

22,800

100

BorgWarner, Inc.

82.50

Jan 13

1,000

100

Caterpillar Inc.

100

Jan 13

600

76

CF Industries Holdings, Inc.

250

Jan 13

1,672

76

CF Industries Holdings, Inc.

240

Feb 13

8,132

14

CF Industries Holdings, Inc.

245

May 13

4,060

195

Cliffs Natural Resources Inc.

55

Jan 13

390

207

Freeport-McMoRan Copper & Gold Inc.

36

Feb 13

15,111

300

Halliburton Co.

35

Jan 13

23,400

129

National Oilwell Varco, Inc.

90

Jan 13

387

135

Praxair, Inc.

115

Apr 13

23,625

143

Teck Resources Ltd. (Class B)

36

Jan 13

17,589

100

Terex Corp.

30

Jan 13

5,000

1,775

123,766

COLLATERALIZED PUTS

100

Boeing Co.

62.50

Feb 13

2,700

200

Boeing Co.

62.50

May 13

21,000

100

BorgWarner, Inc.

55

Jan 13

2,000

100

BorgWarner, Inc.

57.50

Apr 13

12,000

100

Caterpillar Inc.

72.50

Jan 13

1,100

100

Caterpillar Inc.

77.50

Jan 13

1,800

100

Caterpillar Inc.

70

Feb 13

2,700

76

CF Industries Holdings, Inc.

165

Jan 13

1,520

7

CF Industries Holdings, Inc.

165

Feb 13

903

76

CF Industries Holdings, Inc.

165

May 13

31,920

100

Eaton Corp. plc

37.50

Jan 13

500

100

FedEx Corp.

75

Jan 13

700

200

MEDNAX, Inc.

75

Jan 13

8,000

100

National Oilwell Varco, Inc.

65

May 13

40,500

100

Peabody Energy Corp.

23

Jan 13

1,700

67

Praxair, Inc.

90

Jan 13

1,005

120

Schlumberger Ltd.

60

Apr 13

18,360

100

Terex Corp.

15

Jan 13

500

100

United Technologies Corp.

72.50

Jan 13

1,900

1,946

150,808

Total Option Liability (Unrealized Gain of $248,147)

$

274,574

14

SCHEDULEOF INVESTMENTS

December 31, 2012

Shares

Value (A)

Common Stocks — 99.8%

Consumer Discretionary — 10.9%

Bed Bath & Beyond Inc. (C)

130,000

$

7,268,300

BorgWarner, Inc. (C) (F)

110,000

7,878,200

Coach, Inc.

100,000

5,551,000

Columbia Sportswear Co. (B)

200,000

10,672,000

Lowe’s Companies, Inc.

600,000

21,312,000

Marriott International Inc. (Class A)

300,000

11,181,000

McDonald's Corp.

180,000

15,877,800

Newell Rubbermaid Inc.

400,000

8,908,000

Ryland Group, Inc.

333,500

12,172,750

Target Corp.

120,000

7,100,400

Walt Disney Co.

360,000

17,924,400

125,845,850

Consumer Staples — 10.0%

Avon Products, Inc.

359,600

5,163,856

Bunge Ltd.

100,000

7,269,000

Coca-Cola Co.

300,000

10,875,000

CVS/Caremark Corp.

295,000

14,263,250

Diageo plc ADR

50,000

5,829,000

General Mills, Inc.

230,000

9,294,300

PepsiCo, Inc. (G)

250,000

17,107,500

Philip Morris International Inc.

160,000

13,382,400

Procter & Gamble Co.

175,000

11,880,750

Safeway Inc. (B)

340,000

6,150,600

Senomyx, Inc. (B) (C)

1,284,400

2,157,792

Unilever plc ADR

325,000

12,584,000

115,957,448

Energy — 10.4%

Anadarko Petroleum Corp.

50,000

3,715,500

Chevron Corp.

156,000

16,869,840

CONSOL Energy Inc.

73,700

2,365,770

Exxon Mobil Corp. (G)

105,000

9,087,750

Halliburton Co. (F)

150,000

5,203,500

Kinder Morgan Inc.

170,000

6,006,100

National Oilwell Varco, Inc. (F)

100,000

6,835,000

Noble Corp. (C)

120,000

4,178,400

Peabody Energy Corp.

38,560

1,026,082

Petroleum & Resources Corp. (D)

2,186,774

52,307,634

Schlumberger Ltd.

120,000

8,314,800

Seadrill Ltd.

40,000

1,472,000

Spectra Energy Corp.

107,580

2,945,540

120,327,916

Financials — 14.9%

Banks — 4.2%

Fifth Third Bancorp

630,000

9,569,700

Hancock Holding Co.

160,000

5,078,400

PNC Financial Services Group, Inc.

250,000

14,577,500

Wells Fargo & Co.

560,000

19,140,800

48,366,400

15

SCHEDULEOF INVESTMENTS (CONTINUED)

December 31, 2012

Shares

Value (A)

Diversified Financials — 6.4%

Affiliated Managers Group, Inc. (C)

40,000

$

5,206,000

Bank of America Corp.

930,000

10,788,000

Bank of New York Mellon Corp.

403,775

10,377,017

Capital One Financial Corp.

225,000

13,034,250

JPMorgan Chase & Co.

600,000

26,382,000

T. Rowe Price Group, Inc.

135,000

8,792,550

74,579,817

Insurance — 3.0%

ACE Ltd. (C)

165,000

13,167,000

AXIS Capital Holdings, Ltd.

220,000

7,620,800

MetLife Inc.

435,000

14,328,900

35,116,700

Real Estate — 1.3%

American Campus Communities, Inc.

90,000

4,151,700

Digital Realty Trust, Inc.

70,000

4,752,300

HCP, Inc.

125,000

5,647,500

14,551,500

Health Care — 13.0%

Bristol-Myers Squibb Co.

159,061

5,183,798

Catamaran Corp. (C)

180,000

8,479,800

Celgene Corp. (C)

120,000

9,446,400

Covidien plc

120,000

6,928,800

Express Scripts Holding Co. (C)

215,000

11,610,000

Gilead Sciences, Inc. (C)

170,000

12,486,500

Hologic, Inc. (C)

420,000

8,412,600

Intuitive Surgical, Inc. (C)

7,500

3,677,775

Johnson & Johnson

170,000

11,917,000

McKesson Corp.

116,000

11,247,360

MEDNAX, Inc. (C)

70,000

5,566,400

Medtronic, Inc.

130,000

5,332,600

Pfizer Inc.

690,000

17,305,200

Teva Pharmaceutical Industries Ltd. ADR

220,000

8,214,800

UnitedHealth Group Inc.

287,500

15,594,000

WellCare Health Plans, Inc. (C)

14,000

681,660

Zimmer Holdings, Inc.

115,000

7,665,900

149,750,593

Industrials — 10.8%

Boeing Co. (F)

150,000

11,304,000

Caterpillar Inc. (F)

120,000

10,749,600

Eaton Corp. plc

205,000

11,111,000

Emerson Electric Co.

110,000

5,825,600

FedEx Corp.

75,000

6,879,000

General Electric Co.

730,000

15,322,700

Honeywell International Inc.

255,000

16,184,850

Kansas City Southern

75,000

6,261,000

Masco Corp.

725,000

12,078,500

Norfolk Southern Corp.

35,000

2,164,400

Spirit AeroSystems Holdings, Inc. (Class A) (C)

500,000

8,485,000

Terex Corp. (C) (F)

285,000

8,011,350

United Technologies Corp.

127,500

10,456,275

124,833,275

Information Technology — 19.3%

Semiconductors — 1.3%

Broadcom Corp. (Class A) (C)

100,000

3,321,000

Intel Corp.

570,000

11,759,100

15,080,100

16

SCHEDULEOF INVESTMENTS (CONTINUED)

December 31, 2012

Principal/ Shares

Value (A)

Software & Services — 9.7%

Automatic Data Processing, Inc.

200,000

$

11,402,000

Cognizant Technology Solutions Group (Class A) (C)

Cash, receivables, prepaid expenses and other assets, less liabilities — (1.3)%

(15,515,969

)

Net Assets — 100.0%

$

1,155,997,037

Notes:

(A)

Common stocks are listed on the New York Stock Exchange or the NASDAQ and are valued at the last reported sale price on the day of valuation. See note 1 to financial statements.

(B)

A portion of shares held are on loan. See note 8 to financial statements.

(C)

Presently non-dividend paying.

(D)

Non-controlled affiliate, a closed-end sector fund, registered as an investment company under the Investment Company Act of 1940.

(E)

Rate presented is as of period-end and represents the annualized yield earned over the previous seven days.

(F)

All or a portion of this security is pledged to cover open written call option contracts. Aggregate market value of such pledged securities is $12,152,411.

(G)

All or a portion of this security is pledged to collateralize open written put option contracts with an aggregate value to deliver upon exercise of $13,526,500.

REPORTOF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Shareholders of The Adams Express Company:

In our opinion, the accompanying statement of assets and liabilities, including the schedule of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of The Adams Express Company (the “Fund”) at December 31, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the auditing standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at December 31, 2012 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Baltimore, Maryland

February 15, 2013

18

CHANGESIN PORTFOLIO SECURITIES

During the Three Months Ended December 31, 2012

(unaudited)

Shares

Additions

Reductions

Held Dec. 31, 2012

Apple Inc.

7,000

2,000

93,000

Bed Bath & Beyond Inc.

130,000

130,000

Calpine Corp.

300,000

300,000

Catamaran Corp.

120,000

180,000

Coach, Inc.

10,000

100,000

Covidien plc

120,000

120,000

Digital Realty Trust, Inc.

25,000

70,000

Eaton Corp. plc

205,000

(1)

205,000

Fifth Third Bancorp.

180,000

630,000

General Mills, Inc.

50,000

230,000

Google Inc. (Class A)

3,600

26,000

HCP, Inc.

10,000

125,000

Hologic Inc.

420,000

420,000

IDACORP, Inc.

13,000

125,000

International Business Machines Corp.

15,000

105,000

Intuitive Surgical, Inc.

2,500

7,500

Kansas City Southern

25,000

75,000

Kinder Morgan Inc.

30,000

170,000

LyondellBasell Industries N.V. (Class A)

40,000

40,000

MasterCard, Inc.

15,000

15,000

MEDNAX, Inc.

70,000

70,000

MetLife Inc.

150,000

435,000

Philip Morris International Inc.

10,000

160,000

PNC Financial Services Group, Inc.

15,000

250,000

QUALCOMM Inc.

100,000

400,000

UnitedHealth Group Inc.

40,000

287,500

WellCare Health Plans, Inc.

14,000

14,000

ADTRAN, Inc.

135,000

—

Air Products & Chemicals, Inc.

30,000

—

Amerigroup Corp.

115,000

—

Bunge Ltd.

30,000

100,000

Cisco Systems, Inc.

150,000

700,000

Eaton Corp.

205,000

(1)

—

Emerson Electric Co.

60,000

110,000

FedEx Corp.

40,000

75,000

Gilead Sciences, Inc.

45,000

170,000

Life Technologies Corp.

125,000

—

McDonald’s Corp.

60,000

180,000

MDU Resources Group, Inc.

274,600

—

Medtronic, Inc.

220,000

130,000

NetApp, Inc.

90,000

35,000

Norfolk Southern Corp.

40,000

35,000

Pfizer Inc.

110,000

690,000

Procter & Gamble Co.

105,000

175,000

Prudential Financial, Inc.

100,000

—

Spectra Energy Corp.

40,000

107,580

Wells Fargo & Co.

50,000

560,000

(1)

Received one share of Eaton Corp. plc for each share of Eaton Corp. surrendered in merger.

19

THE ADAMS EXPRESS COMPANY

(unaudited)

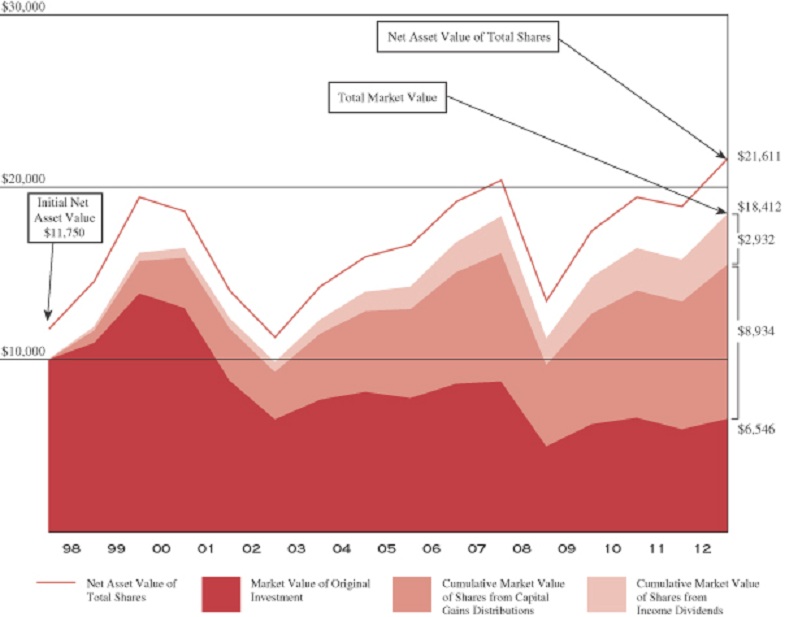

Calendar year- end

Market value of original investment

Cumulative market value of shares from capital gains distributions

Cumulative market value of shares from income dividends

Total market value

Net asset value of total shares

1998

$

10,971

$

715

$

194

$

11,880

$

14,518

1999

13,830

1,885

444

16,159

19,391

2000

12,980

2,900

554

16,434

18,562

2001

8,769

3,046

543

12,378

13,971

2002

6,533

2,747

542

9,822

11,263

2003

7,670

3,819

801

12,290

14,222

2004

8,109

4,685

1,110

13,904

15,939

2005

7,757

5,157

1,286

14,200

16,644

2006

8,573

6,450

1,712

16,735

19,137

2007

8,727

7,443

2,126

18,296

20,370

2008

4,963

4,722

1,486

11,171

13,369

2009

6,243

6,410

2,095

14,748

17,448

2010

6,626

7,366

2,445

16,437

19,396

2011

5,958

7,387

2,404

15,749

18,853

2012

6,546

8,934

2,932

18,412

21,611

Illustration of an assumed

15 year investment of $10,000

Investment income dividends and capital gains distributions are taken in additional shares. This chart covers the years 1998–2012. Fees for the reinvestment of interim dividends are assumed as 2% of the amount reinvested (maximum of $2.50) and commissions of $0.05 per share. There is no charge for reinvestment of year-end distributions. No adjustment has been made for any income taxes payable by shareholders on income dividends or on capital gains distributions, or the sale of any shares. These results should not be considered representative of the dividend income or capital gain or loss which may be realized in the future.

20

HISTORICAL FINANCIAL STATISTICS

(unaudited)

Dec. 31

Value of Net Assets

Shares Outstanding*

Net Asset Value Per Share*

Market Value Per Share*

Income Dividends Per Share*

Capital Gains Distributions Per Share*

Total Dividends and Distributions Per Share*

Annual Distribution Rate**

1998

$

1,688,080,336

77,814,977

$

21.69

$

17.75

$

.30

$

1.10

$

1.40

8.2

%

1999

2,170,801,875

80,842,241

26.85

22.38

.26

1.37

1.63

8.5

2000

1,951,562,978

82,292,262

23.72

21.00

.22

1.63

1.85

7.8

2001

1,368,366,316

85,233,262

16.05

14.22

.26

1.39

1.65

9.6

2002

1,024,810,092

84,536,250

12.12

10.57

.19

.57

.76

6.2

2003

1,218,862,456

84,886,412

14.36

12.41

.17

.61

.78

6.8

2004

1,295,548,900

86,135,292

15.04

13.12

.24

.66

.90

7.1

2005

1,266,728,652

86,099,607

14.71

12.55

.22

.64

.86

6.7

2006

1,377,418,310

86,838,223

15.86

13.87

.23

.67

.90

6.8

2007

1,378,479,527

87,668,847

15.72

14.12

.32

.71

1.03

7.1

2008

840,012,143

87,406,443

9.61

8.03

.26

.38

.64

5.7

2009

1,045,027,339

87,415,193

11.95

10.10

.15

.30

.45

5.2

2010

1,124,671,966

88,885,186

12.65

10.72

.14

.37

.51

5.1

2011

1,050,733,678

91,073,899

11.54

9.64

.15

.50

.65

6.1

2012

1,155,997,037

93,029,724

12.43

10.59

.18

.49

.67

6.3

*

Adjusted to reflect the 3-for-2 stock split effected in October 2000.

**

The annual distribution rate is the total dividends and capital gain distributions during the year divided by the average month-end market price of the Fund’s Common Stock for the calendar year in years prior to 2011 and for the twelve months ended October 31 beginning in 2011, which is consistent with the calculation to determine the minimum distribution rate commitment announced in September 2011.

This report, including the financial statements herein, is transmitted to the shareholders of The Adams Express Company for their information. It is not a prospectus, circular or representation intended for use in the purchase or sale of shares of the Fund’s or of any securities mentioned in the report. The rates of return will vary and the principal value of an investment will fluctuate. Shares, if sold, may be worth more or less than their original cost. Past performance is no guarantee of future investment results.

21

BOARDOF DIRECTORS

Personal Information

Position

held with

the fund

Term

of

office

Length

of time

served

Principal Occupations

Number of portfolios in fund complex overseen by director

Other directorships

Independent Directors

Enrique R. Arzac, Ph.D. 7 St. Paul Street, Suite 1140 Baltimore, MD 21202 Age 71

Director

One Year

Since 1983

Professor of Finance and Economics at the Graduate School of Business, Columbia University, formerly Vice Dean of Academic Affairs.

Two

Director of Petroleum & Resources Corporation (investment company), Aberdeen Asset Management Funds (6 funds) (investment companies), Credit Suisse Asset Management Funds (“CSAM”) (9 funds) (investment companies), Epoch Holdings Corporation (asset management), and Mirae Asset Discovery Funds (6 funds) (investment companies). In addition to the CSAM funds referred to above, Dr. Arzac served as a director of 8 other funds at CSAM and as a director of Starcomms Plc (telecommunications) within the past five years.

Phyllis O. Bonanno

7 St. Paul Street,

Suite 1140 Baltimore, MD 21202

Age 69

Director

One Year

Since 2003

Retired President & CEO of International Trade Solutions, Inc. (consultants). Formerly, President of Columbia College, Columbia, South Carolina, and Vice President of Warnaco Inc. (apparel).

Two

Director of Petroleum & Resources Corporation (investment company), Borg-Warner Inc. (industrial), and Mohawk Industries, Inc. (carpets and flooring).

Kenneth J. Dale

7 St. Paul Street,

Suite 1140 Baltimore, MD 21202

Age 56

Director

One Year

Since 2008

Senior Vice President and Chief Financial Officer of The Associated Press.

Two

Director of Petroleum & Resources Corporation (investment company).

Daniel E. Emerson

7 St. Paul Street,

Suite 1140 Baltimore, MD 21202

Age 88

Director

One Year

Since 1982

Retired Executive Vice President of NYNEX Corp. (communications), retired Chairman of the Board of both NYNEX Information Resources Co. and NYNEX Mobile Communications Co. Previously, Executive Vice President and Director of New York Telephone Company.

Two

Director of Petroleum & Resources Corporation (investment company).

Frederic A. Escherich

7 St. Paul Street,

Suite 1140

Baltimore, MD 21202

Age 60

Director

One Year

Since 2006

Private Investor. Formerly, Managing Director and head of Mergers and Acquisitions Research and the Financial Advisory Department with JPMorgan.

Two

Director of Petroleum & Resources Corporation (investment company).

Roger W. Gale, Ph.D.

7 St. Paul Street,

Suite 1140

Baltimore, MD 21202

Age 66

Director

One Year

Since 2005

President & CEO of GF Energy, LLC (consultants to electric power companies). Formerly, member of management group of PA Consulting Group (energy consultants).

Two

Director of Petroleum & Resources Corporation (investment company) and during the past five years also served as a director of Ormat Technologies, Inc. (geothermal and renewable energy).

22

BOARDOF DIRECTORS (CONTINUED)

Personal Information

Position

held with

the fund

Term

of

office

Length

of time

served

Principal Occupations

Number of portfolios in fund complex overseen by director

Other directorships

Independent Directors (continued)

Kathleen T. McGahran,

Ph.D., J.D., C.P.A.

7 St. Paul Street,

Suite 1140

Baltimore, MD 21202

Age 62

Director

One Year

Since 2003

President & CEO of Pelham Associates, Inc. (executive education), and Adjunct Associate Professor, Stern School of Business, New York University. Formerly, Associate Dean and Director of Executive Education and Associate Professor, Columbia University.

Two

Director of Petroleum & Resources Corporation (investment company).

Craig R. Smith, M.D.

7 St. Paul Street,

Suite 1140

Baltimore, MD 21202

Age 66

Director

One Year

Since 2005

Chief Operating Officer and Manager of Algenol LLC (ethanol manufacturing). Formerly, President, Williston Consulting LLC (consultants to pharmaceutical and biotechnology industries) and Chairman, President & CEO of Guilford Pharmaceuticals (pharmaceuticals & biotechnology).

Two

Director of Petroleum & Resources Corporation (investment company), Depomed, Inc. (specialty pharmaceuticals), and during the past five years also served as a director of LaJolla Pharmaceutical Company and Algenol Biofuels, Inc. (ethanol manufacturing).

Interested Director

Douglas G. Ober

7 St. Paul Street,

Suite 1140

Baltimore, MD 21202

Age 66

Director, Chairman and CEO

One Year

Director Since 1989; Chairman of the Board Since 1991

Chairman and CEO of the Fund and Chairman and CEO of Petroleum & Resources Corporation.

Two

Director of Petroleum & Resources Corporation (investment company).

SHAREHOLDER INFORMATIONAND SERVICES

DIVIDEND PAYMENT SCHEDULE

The Fund presently pays dividends four times a year, as follows: (a) three interim distributions on or about March 1, June 1, and September 1, and (b) a “year-end” distribution, payable in late December, consisting of the estimated balance of the net investment income for the year and the net realized capital gain earned through October 31 and, if applicable, a return of capital. Shareholders may elect to receive the year-end distribution in stock or cash. In connection with this distribution, all shareholders of record are sent a dividend announcement notice and an election card in mid-November. Shareholders holding shares in “street” or brokerage accounts may make their election by notifying their brokerage house representative.

ELECTRONIC DELIVERY OF SHAREHOLDER REPORTS

The Fund offers shareholders the benefits and convenience of viewing Quarterly and Annual Reports and other shareholder materials on-line. With your consent, paper copies of these documents will cease with the next mailing and will be provided via e-mail. Reduce paper mailed to your home and help lower the Fund’s printing and mailing costs. To enroll, please visit the following websites:

Registered shareholders with AST: www.amstock.com/main

Shareholders using brokerage accounts: http://enroll.icsdelivery.com/ADX

23

OTHER INFORMATION

Statement on Quarterly Filing of Complete Portfolio Schedule

In addition to publishing its complete schedule of portfolio holdings in the First and Third Quarter Reports to stockholders, the Fund also files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the Commission’s website at www.sec.gov. The Company’s Forms N-Q may be reviewed and copied at the Commission’s Public Reference Room, and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330. The Fund also posts a link to its Forms N-Q on its website at www.adamsexpress.com, under the headings “Investment Information”, “Financial Reports” and then “SEC Filings”.

Annual Certification

The Fund’s CEO has submitted to the New York Stock Exchange the annual CEO certification as required by Section 303A.12(a) of the NYSE Listed Company Manual.

Proxy Voting Policies and Record

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities owned by the Fund and the Fund’s proxy voting record for the 12-month period ended June 30, 2012 are available (i) without charge, upon request, by calling the Fund’s toll free number at (800) 638-2479; (ii) on the Fund’s website at www.adamsexpress.com under the headings “About Adams Express” and “Corporate Information” and (iii) on the Securities and Exchange Commission’s website at www.sec.gov.

Forward-Looking Statements

This report contains “forward-looking statements” within the meaning of the Securities Act of 1933 and the Securities Exchange Act of 1934. By their nature, all forward-looking statements involve risks and uncertainties, and actual results could differ materially from those contemplated by the forward-looking statements. Several factors that could materially affect the Fund’s actual results are the performance of the portfolio of stocks held by the Fund, the conditions in the U.S. and international financial markets, the price at which shares of the Fund will trade in the public markets, and other factors discussed in the Fund’s periodic filings with the Securities and Exchange Commission.

Privacy Policy

In order to conduct its business, the Fund, through its transfer agent, currently American Stock Transfer & Trust Company, collects and maintains certain nonpublic personal information about our shareholders of record with respect to their transactions in shares of our securities. This information includes the shareholder’s address, tax identification or Social Security number, share balances, and dividend elections. We do not collect or maintain personal information about shareholders whose shares of our securities are held in “street name” by a financial institution such as a bank or broker.

We do not disclose any nonpublic personal information about you, our other shareholders or our former shareholders to third parties unless necessary to process a transaction, service an account or as otherwise permitted by law.

To protect your personal information internally, we restrict access to nonpublic personal information about our shareholders to those employees who need to know that information to provide services to our shareholders. We also maintain certain other safeguards to protect your nonpublic personal information.

24

THE ADAMS EXPRESS COMPANY

Board Of Directors

Enrique R. Arzac 2,3

Phyllis O. Bonanno 1,3,5

Kenneth J. Dale 2,4

Daniel E. Emerson 1,3,5

Frederic A. Escherich 1,4,5

Roger W. Gale 2,4

Kathleen T. McGahran 2,3

Douglas G. Ober 1

Craig R. Smith 1,3,5

1. Member of Executive Committee

2. Member of Audit Committee

3. Member of Compensation Committee