CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-00248 -------------------------------------------------------------------------

THE ADAMS EXPRESS COMPANY ------------------------------------------------------------------------- (Exact name of registrant as specified in charter)

7 Saint Paul Street, Suite 1140, Baltimore, Maryland 21202 ------------------------------------------------------------------------- (Address of principal executive offices)

Lawrence L. Hooper, Jr. The Adams Express Company 7 Saint Paul Street, Suite 1140 Baltimore, Maryland 21202 ------------------------------------------------------------------------- (Name and address of agent for service)

Registrant's telephone number, including area code: (410) 752-5900 Date of fiscal year end: December 31 Date of reporting period: December 31, 2013

Item 1. Reports to Stockholders.

2013ATA GLANCE

The Fund

Ÿ

a closed-end equity investment company

Ÿ

objectives: preservation of capital

reasonable income

opportunity for capital gain

Ÿ

internally-managed

Ÿ

annual distribution rate of at least 6%

Stock Data (12/31/13)

NYSE Symbol ........... ADX

Market Price ............. $13.07

52-Week Range ........ $10.72– $13.32

Discount .................... 13.4%

Shares Outstanding .... 94,223,617

Summary Financial Information

Year Ended December 31,

2013

2012

Net asset value per share

$

15.09

$

12.43

Total net assets

1,421,550,920

1,155,997,037

Unrealized appreciation on investments

393,843,628

143,061,370

Net investment income

18,656,769

17,547,510

Net realized gain

57,371,366

47,997,411

Total return (based on market price)

31.8%

16.9%

Total return (based on net asset value)

29.7%

14.7%

Ratio of expenses to average net assets

0.69%

0.65%

Annual distribution rate

7.1%

6.3%

2013 Dividends and Distributions

Paid

Amount (per share)

Type

March 1, 2013

$

0.01

Long-term capital gain

March 1, 2013

0.01

Short-term capital gain

March 1, 2013

0.03

Investment income

June 3, 2013

0.05

Investment income

September 3, 2013

0.05

Investment income

December 27, 2013

0.44

Long-term capital gain

December 27, 2013

0.16

Short-term capital gain

December 27, 2013

0.09

Investment income

$

0.84

2014 Annual Meeting of Shareholders

Location: Four Seasons Hotel, Baltimore, Maryland

Date: April 10, 2014

Time: 9:00 a.m.

PORTFOLIO REVIEW

December 31, 2013

(unaudited)

Ten Largest Equity Portfolio Holdings

Market Value

% of Net Assets

Petroleum & Resources Corp.*

$

59,873,872

4.2

%

Apple Inc.

55,157,113

3.9

JPMorgan Chase & Co.

35,088,000

2.5

Pfizer Inc.

32,274,831

2.3

Gilead Sciences, Inc.

31,112,100

2.2

Citigroup Inc.

30,744,900

2.1

Wells Fargo & Co.

30,418,000

2.1

Chevron Corp.

29,353,850

2.1

Walt Disney Co.

28,848,640

2.0

Google Inc. (Class A)

28,578,105

2.0

$

361,449,411

25.4

%

* Non-controlled affiliated closed-end fund

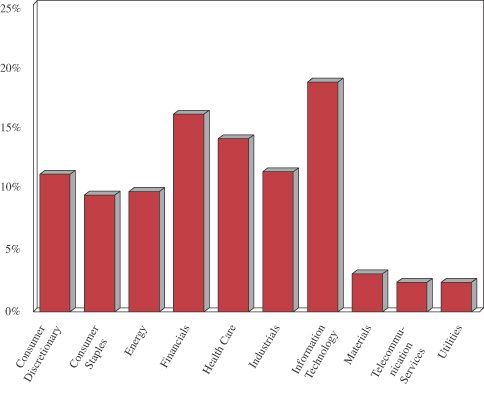

Sector Weightings

1

LETTERTO SHAREHOLDERS

Dear Fellow Shareholders,

By any measure, 2013 was a banner year for the U.S. stock market. Few would have expected such a robust stock market in the face of the many things that transpired during 2013. Markets experienced a strong start to 2013 as the “fiscal cliff” and the potential consequences of federal spending cuts and tax increases were averted. Concerns of a weakening U.S. economy subsided with the flow of solid corporate earnings growth and a modest economic recovery. High unemployment rates and low inflation reinforced the Federal Reserve’s (Fed) resolve to continue accommodative monetary policy, keeping a lid on interest rates. Stabilization in Europe and a managed slowdown in China fostered optimism for investors.

The rally was sustained in February, but at a significantly reduced rate. Investor enthusiasm was tempered as retailers expressed caution, economic growth slowed in China, and many European countries were in a recession. However, slow but positive growth in the U.S. was sufficient to offset sequestration cuts and the Fed’s meeting minutes that revealed discussions of winding down asset purchases. The S&P 500 gained 10.6% through the first quarter as cash flowed back into the equity markets.

The second quarter presented a different story. Despite weakened labor markets, slowing retail sales, and an easing in manufacturing growth, investor sentiment remained bullish through April. The market’s exuberance started to diminish as China’s growth rate continued to contract. Investors balanced economic news with a myopic focus on the Fed’s stimulus program. Comments in May suggesting an end to the stimulus program roiled markets. By the end of the second quarter, dovish comments by the Fed had calmed investor uncertainty.

U.S. equities hit record highs in July as positive earnings reports by companies coincided with improving economic indicators. The unemployment rate fell to the lowest level in five years and interest rates remained low. The S&P 500 exited July with a 19.6% year-to-date gain.

Turbulence quickly followed as investors struggled to balance Fed comments, economic news, and escalating worldwide geopolitical tensions. Volatility stemmed from civil war in Syria and violence in Egypt following a military coup. Rising geopolitical instability in the Middle East/North Africa region put upward pressure on oil prices, creating a headwind for global economic growth. By late September, violence in Egypt subsided and Syria’s risks diminished, supporting a recovery in U.S. markets back to July levels. Europe showed evidence of an upturn, China’s growth stabilized, and the Fed’s tapering was delayed.

The fall also brought the roll-out of the Affordable Care Act (ACA). Rarely has a law been as divisive as the ACA. While the problems with the online exchange grabbed most of the headlines, the reimbursement cuts and additional fees mandated by the ACA had a larger impact on health care companies. Specifically, the Managed Care companies suffered, at least initially, as these new costs were not offset by the promised increase in individuals covered.

A 16-day shutdown by the U.S. Government in early October and concerns of a budget resolution did little to slow the rise of the markets for the remainder of the year. Stocks hit a new high as government funding was restored. Key economic data, corporate earnings, and labor market results buoyed investors’ sentiment. Reflected in the equity market gains was approval of Janet Yellen’s nomination to head the Fed. As a Bernanke loyalist, she makes continuity at the Fed likely in 2014. The passing by Congress of a two-year budget deal near year-end enhanced the outlook, contributing to the full year gain of 32.4% for the S&P 500.

Against this backdrop, Adams Express had a good 2013, distributing 7.1% to shareholders and generating a total return on market price of 31.8%. The Lipper Large-Cap Core Mutual Fund Average, our peer group, returned 31.4%. The Adams Express total return on net asset value was 29.7%.

The two best performing sectors in the Fund were Health Care and Industrials. Increased investor appetite for biotechnology stocks powered the Health Care sector again in 2013, rising 46.2%. Our overweight in the Aerospace and Defense industry group within Industrials paced the Fund’s holdings in that sector, with additional help from our Electrical Equipment holdings, allowing that sector to advance 45.1%. While Utilities underperformed the S&P 500, our holdings outperformed the sector and contributed positively to the Fund’s performance. A conscious decision to have more of a mid-cap focus with our Utilities stock selection served the Fund well as those holdings were up 19.0% for the year.

The Fund’s Consumer Discretionary holdings were up 35.4% during the year but trailed their sector peer group. Good calls in Lowe’s Companies and Dollar General Corporation helped limit the relative shortfall. Our holding in The Walt Disney Company, advancing 55.3%, was also helpful in the Media industry group that had a remarkable year. Although advancing 30.3% and 23.7%, respectfully, our holdings in Financials and Information Technology trailed the market.

2

LETTERTO SHAREHOLDERS (CONTINUED)

Portfolio holdings in Diversified Financials and Capital Markets disappointed, while our Insurance names offset some of the disappointing stock selection. Difficulty in Software & Services and Semiconductors contributed to our underperformance in Information Technology. A bright spot was the Fund’s position in MasterCard Incorporated within IT Services.

Looking Forward to 2014

As we look forward to 2014, there are several themes in the portfolio to keep an eye on. First, we remain convinced that the earnings growth in biotechnology is real and that we should have an overweight in that Health Care industry group. As of this writing, Gilead Sciences, Inc., Celgene Corp. and Biogen Idec Inc. remain compelling opportunities for us. Each addresses complex issues, with Gilead a leader in Hepatitis C, Celgene in multiple myeloma, and Biogen in multiple sclerosis. It is very difficult to find the kind of revenue and earnings growth within Health Care that biotechnology offers. Despite strong gains recently, we believe the market continues to underappreciate the opportunities these stocks provide. As we look out over the horizon, another area that appears promising is the immuno-oncology arena. We are intrigued with the breakthrough in cancer treatment that this opportunity suggests and will look for attractive investments in this arena.

Within Industrials, we benefited during 2013 by an overweight in Aerospace and Defense and believe that theme continues to be warranted. The Boeing Company again will play a meaningful role in our Industrials exposure. Boeing has many years of increasing free cash flow growth in front of it and also continues to enjoy a record production backlog. New growth in emerging markets and established market replacement demand gives us comfort that Boeing has a long runway of opportunity.

Although the Consumer Discretionary sector has enjoyed an unprecedented four-year run of outperformance, we believe there are a few areas that should continue to be a positive source of excess return. One such area is home improvement. Our investment in Lowe’s Companies addresses this thought. The home improvement market remains quite good as the housing market continues to move in a positive direction. Our belief is that Lowe’s has a number of drivers for increased margins and, with a commitment to increased service levels and merchandising, they could deliver strong earnings growth in 2014. Building on this theme is our recent investment in Whirlpool Corporation. We expect a powerful household appliance replacement cycle in North America as well as in international markets. With the supportive fundamentals, we believe Whirlpool will deliver strong free cash flow and earnings beyond what investors are expecting.

Financials is a sector that has gotten a great deal of scrutiny and bears watching as more reforms make their way to reality. A good bit has been made of the work that JP Morgan Chase & Co. has done to put its legal issues behind it. We think this is very positive and positions the nation’s largest bank well for 2014. The global depth and breadth of its businesses gives us comfort that the bank will continue to execute and drive earnings per share growth in the coming year. In addition to JP Morgan, we see a compelling investment opportunity in the Life Insurance industry group within Financials. We believe these stocks will benefit from the upward pressure on interest rates resulting from continued tapering by the Fed.

The Fund was active in repurchasing its shares in 2013 and repurchased a total of 948,339 shares. The Board of Directors has approved the repurchase of up to 5% of the outstanding shares for 2014.

Our investment philosophy and process is very focused on free cash flow generation, earnings growth, valuation, and being properly paid for the risks we are taking. Within this framework, we strive to identify high quality companies we can own for an extended period of time. With that said, we also look for opportunities to take advantage of market anomalies for the benefit of our shareholders. We are encouraged by the increasing strength in the economy, both home and abroad, and remain optimistic about what that will mean for the Fund in 2014.

Open written option contracts* at value (proceeds $7,300)

29,320

Accrued pension liabilities

2,733,408

Accrued expenses and other liabilities

1,902,201

Total Liabilities

9,262,760

Net Assets

$

1,421,550,920

Net Assets

Common Stock at par value $0.001 per share, authorized 150,000,000 shares; issued and outstanding 94,223,617 shares (includes 159,401 nonvested restricted shares, 18,000 nonvested or deferred restricted stock units, and 17,964 deferred stock units) (note 6)

$

94,224

Additional capital surplus

1,029,332,121

Accumulated other comprehensive income (note 5)

(1,535,718

)

Undistributed net investment income

734,051

Undistributed net realized gain on investments

(917,386

)

Unrealized appreciation on investments

393,843,628

Net Assets Applicable to Common Stock

$

1,421,550,920

Net Asset Value Per Share of Common Stock

$15.09

*See Schedule of Investments on page 14 and Schedule of Outstanding Written Option Contracts on page 17.

The accompanying notes are an integral part of the financial statements.

4

STATEMENTOF OPERATIONS

Year Ended December 31, 2013

Investment Income

Income:

Dividends:

From unaffiliated issuers (net of $46,048 in foreign taxes)

$

25,502,274

From non-controlled affiliate

1,246,462

Other income

781,225

Total income

27,529,961

Expenses:

Investment research

4,617,083

Administration and operations

1,949,761

Travel, training, and other office expenses

589,829

Directors’ fees

379,030

Transfer agent, registrar, and custodian

321,712

Reports and shareholder communications

279,177

Investment data services

216,676

Occupancy

155,017

Audit and accounting services

128,763

Insurance

107,563

Legal services

94,010

Other

34,571

Total expenses

8,873,192

Net Investment Income

18,656,769

Realized Gain and Change in Unrealized Appreciation on Investments

Net realized gain on security transactions

53,717,544

Net realized gain distributed by regulated investment company (non-controlled affiliate)

2,864,674

Net realized gain on written option contracts

789,148

Change in unrealized appreciation on securities

251,052,425

Change in unrealized appreciation on written option contracts

(270,167

)

Net Gain on Investments

308,153,624

Other Comprehensive Income (note 5)

Defined benefit pension plans:

Net actuarial gain arising during period

345,260

Amortization of net loss

260,068

Effect of settlement (non-recurring)

740,825

Other Comprehensive Income

1,346,153

Change in Net Assets Resulting from Operations

$

328,156,546

The accompanying notes are an integral part of the financial statements.

5

STATEMENTSOF CHANGESIN NET ASSETS

For the Year Ended December 31,

2013

2012

From Operations:

Net investment income

$

18,656,769

$

17,547,510

Net realized gain on investments

57,371,366

47,997,411

Change in unrealized appreciation on investments

250,782,258

80,550,174

Change in accumulated other comprehensive income (note 5)

1,346,153

(243,338

)

Increase in net assets resulting from operations

328,156,546

145,851,757

Distributions to Shareholders from:

Net investment income

(20,354,079

)

(16,392,876

)

Net realized gain from investment transactions

(57,121,286

)

(44,625,641

)

Decrease in net assets from distributions

(77,475,365

)

(61,018,517

)

From Capital Share Transactions:

Value of shares issued in payment of distributions (note 4)

26,419,945

20,118,651

Cost of shares purchased (note 4)

(11,659,522

)

—

Deferred compensation (notes 4, 6)

112,279

311,468

Increase in net assets from capital share transactions

14,872,702

20,430,119

Total Increase in Net Assets

265,553,883

105,263,359

Net Assets:

Beginning of year

1,155,997,037

1,050,733,678

End of year (including undistributed net investment income of $734,051 and $2,836,318, respectively)

$

1,421,550,920

$

1,155,997,037

The accompanying notes are an integral part of the financial statements.

6

NOTES TO FINANCIAL STATEMENTS

1. Significant Accounting Policies

The Adams Express Company (the Fund) is registered under the Investment Company Act of 1940 as a diversified investment company. The Fund is an internally-managed closed-end fund whose investment objectives are preservation of capital, the attainment of reasonable income from investments, and an opportunity for capital appreciation.

The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America, which require the use of estimates made by Fund management. Management believes that estimates and security valuations are appropriate; however, actual results may differ from those estimates, and the security valuations reflected in the financial statements may differ from the value the Fund ultimately realizes upon sale of the securities.

Affiliated Companies — Investments in companies 5% or more of whose outstanding voting securities are held by the Fund are defined as “Affiliated Companies” in Section 2(a)(3) of the Investment Company Act of 1940.

Expenses — The Fund shares certain costs for investment research and data services, administration and operations, travel, training, office expenses, occupancy, accounting and legal services, insurance, and other miscellaneous items with its non-controlled affiliate, Petroleum & Resources Corporation. Shared expenses that are not solely attributable to one fund are allocated to each fund based on relative net asset values or, in the case of investment research staff and related costs, relative market values of portfolio securities in the particular sector of coverage. Changes in expense allocations are updated quarterly, as appropriate, except for those related to payroll, which are updated annually.

Security Transactions and Investment Income — Investment transactions are accounted for on the trade date. Gain or loss on sales of securities and options is determined on the basis of specific identification. Dividend income and distributions to shareholders are recognized on the ex-dividend date, and interest income is recognized on the accrual basis.

Security Valuation — The Fund’s investments are reported at fair value as defined under accounting principles generally accepted in the United States of America. Investments in securities traded on national security exchanges are valued at the last reported sale price on the day of valuation. Over-the-counter and listed securities for which a sale price is not available are valued at the last quoted bid price. Short-term investments (excluding purchased options and money market funds) are valued at amortized cost, which approximates fair value. Purchased and written options are valued at the last quoted bid and asked price, respectively. Money market funds are valued at net asset value on the day of valuation.

Various inputs are used to determine the fair value of the Fund’s investments. These inputs are summarized in the following three levels:

•

Level 1 — fair value is determined based on market data obtained from independent sources; for example, quoted prices in active markets for identical investments,

•

Level 2 — fair value is determined using other assumptions obtained from independent sources; for example, quoted prices for similar investments,

•

Level 3 — fair value is determined using the Fund’s own assumptions, developed based on the best information available in the circumstances.

The Fund’s investments at December 31, 2013 were classified as follows:

Level 1

Level 2

Level 3

Total

Common stocks

$

1,413,334,011

$

—

$

—

$

1,413,334,011

Short-term investments

9,819,486

—

—

9,819,486

Total investments

$

1,423,153,497

$

—

$

—

$

1,423,153,497

Written options

$

(29,320

)

$

—

$

—

$

(29,320

)

There were no transfers into or from Level 1 or Level 2 during the year ended December 31, 2013.

New Accounting Pronouncements — In February 2013, the Financial Accounting Standards Board issued new guidance, effective for annual and interim periods beginning after December 15, 2012, requiring disclosure of items reclassified out of accumulated other comprehensive income. Adoption of this guidance had no effect on Fund net assets or results of operations and no material impact on the financial statements.

7

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

2. Federal Income Taxes

No federal income tax provision is required since the Fund’s policy is to qualify as a regulated investment company under the Internal Revenue Code and to distribute substantially all of its taxable income to its shareholders. Additionally, management has analyzed and concluded that tax positions included in federal income tax returns from the previous three years that remain subject to examination do not require any provision. Any income tax-related interest or penalties would be recognized as income tax expense. As of December 31, 2013, the identified cost of securities for federal income tax purposes was $1,031,804,342 and net unrealized appreciation aggregated $391,349,155, consisting of gross unrealized appreciation of $397,654,046 and gross unrealized depreciation of $6,304,891.

Distributions are determined in accordance with our annual 6% minimum distribution rate commitment, based on the Fund’s average market price, and income tax regulations, which may differ from generally accepted accounting principles. Such differences are primarily related to the Fund’s retirement plans, equity-based compensation, and loss deferrals for wash sales. Differences that are permanent, while not material for the year ended December 31, 2013, are reclassified in the capital accounts of the Fund’s financial statements and have no impact on net assets. For tax purposes, distributions paid by the Fund during the years ended December 31, 2013 and December 31, 2012 were classified as ordinary income of $36,005,425 and $25,489,925, respectively, and as long-term capital gain of $41,470,068 and $35,504,402, respectively. The tax basis of distributable earnings at December 31, 2013 was $1,404,905 of undistributed ordinary income and $1,405,220 of undistributed long-term capital gain.

3. Investment Transactions

The Fund’s investment decisions are made by the portfolio management team with recommendations from the research staff. Purchases and sales of portfolio securities, other than options and short-term investments, during the year ended December 31, 2013 were $720,527,760 and $765,212,378, respectively.

The Fund is subject to changes in the value of equity securities held (“equity price risk”) in the normal course of pursuing its investment objectives. The Fund may purchase and write option contracts to increase or decrease its equity price risk exposure or may write option contracts to generate additional income. Option contracts generally entail risks associated with counterparty credit, liquidity, and unfavorable equity price movements. The Fund has mitigated counterparty credit and liquidity risks by trading its options through an exchange. The risk of unfavorable equity price movements is limited for purchased options to the premium paid and for written options by writing only covered call or collateralized put option contracts, which require the Fund to segregate certain securities or cash at its custodian when the option is written. A schedule of outstanding option contracts as of December 31, 2013 can be found on page 17.

When the Fund writes (purchases) an option, an amount equal to the premium received (paid) by the Fund is recorded as a liability (asset) and is subsequently marked to market daily in the Statement of Assets and Liabilities, with any related change recorded as an unrealized gain or loss in the Statement of Operations. Premiums received (paid) from unexercised options are treated as realized gains (losses) on the expiration date and are separately identified in the Statement of Operations. Upon the exercise of written put (purchased call) option contracts, premiums received (paid) are deducted from (added to) the cost basis of the underlying securities purchased. Upon the exercise of written call (purchased put) option contracts, premiums received (paid) are added to (deducted from) the proceeds from the sale of underlying securities in determining whether there is a realized gain or loss.

Transactions in written covered call and collateralized put options during the year ended December 31, 2013 were as follows:

Covered Calls

Collateralized Puts

Contracts

Premiums

Contracts

Premiums

Options outstanding, December 31, 2012

1,775

$

212,261

1,946

$

310,460

Options written

4,217

342,499

3,755

471,526

Options terminated in closing purchase transactions

(1,905

)

(157,740

)

—

—

Options expired

(3,704

)

(369,221

)

(5,561

)

(765,796

)

Options exercised

(343

)

(25,239

)

(100

)

(11,450

)

Options outstanding, December 31, 2013

40

$

2,560

40

$

4,740

8

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

4. Capital Stock

The Fund has 10,000,000 authorized and unissued preferred shares, $0.001 par value.

On December 27, 2013, the Fund issued 2,093,644 shares of its Common Stock at a price of $12.61 per share (the average market price on December 9, 2013) to shareholders of record November 25, 2013 who elected to take stock in payment of the distribution from 2013 capital gain and investment income. During 2013, 1,567 shares were issued at a weighted average price of $12.15 per share as dividend equivalents to holders of deferred stock units and restricted stock units under the 2005 Equity Incentive Compensation Plan.

On December 27, 2012, the Fund issued 1,923,171 shares of its Common Stock at a price of $10.455 per share (the average market price on December 10, 2012) to shareholders of record November 19, 2012 who elected to take stock in payment of the distribution from 2012 capital gain and investment income. During 2012, 1,125 shares were issued at a weighted average price of $10.53 per share as dividend equivalents to holders of deferred stock units and restricted stock units under the 2005 Equity Incentive Compensation Plan.

The Fund may purchase shares of its Common Stock from time to time at such prices and amounts as the Board of Directors may deem advisable. In 2013, the Fund purchased 948,339 shares of its Common Stock, including 66,191 shares from the Fund’s defined benefit plan trust and 26,271 shares from Petroleum & Resources Corporation’s defined benefit plan trust. The cost of the shares purchased from the trusts was $1,163,172, based on the closing market price on the date of the transaction. Transactions in Common Stock for 2013 and 2012 were as follows:

Shares

Amount

2013

2012

2013

2012

Shares issued in payment of distributions

2,095,211

1,924,296

$26,419,945

$20,118,651

Shares purchased (at a weighted average discount from net asset value of 13.6%)

(948,339

)

—

(11,659,522

)

—

Net activity under the 2005 Equity Incentive Compensation Plan

47,021

31,529

112,279

311,468

Net change

1,193,893

1,955,825

$14,872,702

$20,430,119

5. Retirement Plans

Defined Contribution Plans — The Fund sponsors a qualified defined contribution plan for all employees with at least six months of service and a nonqualified defined contribution plan for eligible employees to supplement the qualified plan. The Fund expensed contributions to the plans in the amount of $252,260, a portion thereof based on company performance, for the year ended December 31, 2013. The Fund does not provide postretirement medical benefits.

Defined Benefit Plans — On October 1, 2009, the Fund froze its non-contributory qualified and nonqualified defined benefit pension plans. Benefits are based on length of service and compensation during the last five years of employment through September 30, 2009, with no additional benefits being accrued beyond that date. The process of terminating the plans will begin in 2014. Upon receiving the required regulatory approvals, all benefits under the plans will be paid out and all related pension liabilities will be relieved.

The funded status of the plans is recognized as an asset (overfunded plan) or a liability (underfunded plan) in the Statement of Assets and Liabilities. Changes in the prior service costs and accumulated actuarial gains and losses are recognized as accumulated other comprehensive income, a component of net assets, in the year in which the changes occur and are subsequently amortized into net periodic pension cost. Non-recurring settlement costs are recognized in net periodic pension cost when a plan participant receives a lump-sum benefit payment and includes the amount of which is in excess of the present value of the projected benefit and any unamortized actuarial losses attributable to the portion of the projected benefit obligation being satisfied.

The Fund’s policy is to contribute annually to the plans those amounts that can be deducted for federal income tax purposes, plus additional amounts as the Fund deems appropriate in order to provide assets sufficient to meet benefits to be paid to plan participants. The Fund contributed $0 to the qualified plan and $85,167 to the nonqualified plan in 2013 and anticipates making contributions of $198,394 to the nonqualified plan in 2014.

9

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

The Fund uses a December 31 measurement date for its plans. Details in aggregate for the plans were as follows:

2013

2012

Change in benefit obligation

Benefit obligation at beginning of year

$

10,865,411

$

10,207,237

Interest cost

319,801

359,366

Actuarial (gain) loss

(430,184

)

1,029,954

Benefits paid

(200,120

)

(177,079

)

Effect of settlement (non-recurring)

(2,276,773

)

(554,067

)

Benefit obligation at end of year

$

8,278,135

$

10,865,411

Change in qualified plan assets

Fair value of qualified plan assets at beginning of year

$

9,304,946

$

8,148,262

Actual return on plan assets

246,307

615,406

Employer contributions

—

1,225,000

Benefits paid

(114,953

)

(129,655

)

Settlement (non-recurring)

(2,276,773

)

(554,067

)

Fair value of qualified plan assets at end of year

$

7,159,527

$

9,304,946

Funded status

$

(1,118,608

)

$

(1,560,465

)

The accumulated benefit obligation for all defined benefit pension plans was $8,278,135 and $10,865,411 at December 31, 2013 and 2012, respectively.

The primary investment objective of the Fund’s qualified pension plan assets is capital preservation, achieved through a portfolio of mutual funds and pooled separate accounts (“PSA”). PSAs, like mutual funds, are made up of a wide variety of underlying investments in securities. The Fund’s targeted asset allocation for 2014 is to maintain approximately 60% of plan assets invested in short-term fixed income securities and approximately 40% of plan assets invested in cash and money market securities.

The net asset value of mutual funds and PSAs are based on the fair value of its underlying investments. The fair value of the plan assets is determined using various inputs, summarized into the three levels described in footnote 1. The plan assets at December 31, 2013 were classified as follows:

Level 1

Level 2

Level 3

Total

Fixed income securities

$

—

$

4,185,736

$

—

$

4,185,736

Money market securities

2,964,212

9,579

—

2,973,791

Total

$

2,964,212

$

4,195,315

$

—

$

7,159,527

Items impacting the Fund’s net investment income and accumulated other comprehensive income were:

2013

2012

Components of net periodic pension cost

Interest cost

$

319,801

$

359,366

Expected return on plan assets

(323,274

)

(278,506

)

Net loss component

260,068

268,331

Effect of settlement (non-recurring)

740,825

187,740

Net periodic pension cost

$

997,420

$

536,931

2013

2012

Accumulated other comprehensive income

Defined benefit pension plans:

Balance at beginning of year

$

(2,881,871

)

$

(2,638,533

)

Net actuarial gain/(loss) arising during period

345,260

(699,409

)

Reclassifications to net periodic pension cost:

Amortization of net loss

260,068

268,331

Effect of settlement (non-recurring)

740,825

187,740

Balance at end of year

$

(1,535,718

)

$

(2,881,871

)

Accumulated other comprehensive income was comprised of net actuarial losses of $(1,535,718) and $(2,881,871) at December 31, 2013 and 2012, respectively. In 2014, the Fund estimates that $151,830 of net losses will be amortized from accumulated other comprehensive income into net periodic pension cost. Any remaining net losses will be recognized upon termination of the plans.

Assumptions used to determine benefit obligations were:

2013

2012

Discount rate

4.25%

3.75%

Rate of compensation increase

—

—

The assumptions used to determine net periodic pension cost were:

2013

2012

Discount rate

3.58%

4.20%

Expected long-term return on plan assets

4.00%

4.00%

Rate of compensation increase

—

—

The assumption used to determine expected long-term return on plan assets was based on historical and future expected returns of multiple asset classes in order to develop a risk-free real rate of return and risk premiums for each asset class. The overall rate for each asset class was developed by combining a long-term inflation component, the risk-free real rate of return, and the associated risk premium. A weighted average rate was developed based on those overall rates and the target asset allocation of the plan.

10

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

The following benefit payments are eligible to be paid in the years indicated:

Pension Benefits

2014

$

960,000

2015

990,000

2016

320,000

2017

1,240,000

2018

690,000

Years 2019-2023

1,590,000

6. Equity-Based Compensation

The 2005 Equity Incentive Compensation Plan (“2005 Plan”), adopted at the 2005 Annual Meeting and re-approved at the 2010 Annual Meeting, permits the grant of restricted stock awards (both performance and nonperformance-based), as well as stock options and other stock incentives, to all employees and non-employee directors. Performance-based restricted stock awards vest at the end of a specified three year period, with the ultimate number of shares earned contingent on achieving certain performance targets. If performance targets are not achieved, all or a portion of the performance-based restricted shares are forfeited and become available for future grants. Nonperformance-based restricted stock awards typically vest ratably over a three year period and nonperformance-based restricted stock units (granted to non-employee directors) vest over a one year period. Payment of awards may be deferred, if elected. The 2005 Plan provides for accelerated vesting in the event of death or retirement. Non-employee directors also may elect to defer a portion of their cash compensation, with such deferred amount to be paid by delivery of deferred stock units. Outstanding awards are granted at fair market value on grant date. The 2005 Plan provides for the issuance of up to 3,413,131 shares of the Fund’s Common Stock, of which 3,060,320 remain available for future grants at December 31, 2013.

A summary of the status of the Fund’s awards granted under the 2005 Plan as of December 31, 2013, and changes during the year then ended, is presented below:

Awards

Shares/Units

Weighted Average Grant-Date Fair Value

Balance at December 31, 2012

170,199

$

10.57

Granted:

Restricted stock

136,418

11.51

Restricted stock units

5,250

11.67

Deferred stock units

6,020

11.87

Vested & issued

(31,003

)

10.58

Forfeited

(91,519

)

10.57

Balance at December 31, 2013 (includes 71,531 performance-based awards and 123,834 nonperformance-based awards)

195,365

$

11.27

Compensation cost resulting from awards granted under the 2005 Plan are based on the fair value of the award on grant date (determined by the average of the high and low price on grant date) and recognized on a straight-line basis over the requisite service period. For those awards with performance conditions, compensation cost is based on the most probable outcome and, if such goals are not met, compensation cost is not recognized and any previously recognized compensation cost is reversed. The total compensation cost for restricted stock granted to employees for the year ended December 31, 2013 was $83,019. The total compensation cost for restricted stock units granted to non-employee directors for the year ended December 31, 2013 was $62,030. As of December 31, 2013, there was total unrecognized compensation cost of $1,060,650, a component of additional capital surplus, related to nonvested equity-based compensation arrangements granted under the 2005 Plan. That cost is expected to be recognized over a weighted average period of 1.63 years. The total fair value of shares and units vested during the year ended December 31, 2013 was $349,076.

7. Officer and Director Compensation

The aggregate remuneration paid during the year ended December 31, 2013 to officers and directors amounted to $3,619,501, of which $337,752 was paid to directors who were not officers. These amounts represent the taxable compensation to the Fund’s officers and directors and therefore differ from the amounts reported in the accompanying Statement of Operations that are recorded and expensed in accordance with generally accepted accounting principles.

8. Portfolio Securities Loaned

The Fund makes loans of securities to approved brokers to earn additional income. It receives as collateral cash deposits, U.S. Government securities, or bank letters of credit valued at 102% of the value of the securities on loan. The market value of the loaned securities is calculated based upon the most recent closing prices and any additional required collateral is delivered to the Fund on the next business day. Cash deposits are placed in a registered money market fund. The Fund accounts for securities lending transactions as secured financing and receives compensation in the form of fees or retains a portion of interest on the investment of any cash received as collateral. The

11

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

Fund also continues to receive interest or dividends on the securities loaned. Gain or loss in the fair value of the securities loaned that may occur during the term of the loan will be for the account of the Fund. At December 31, 2013, the Fund had no securities on loan. The Fund is indemnified by the Custodian, serving as lending agent, for loss of loaned securities and has the right under the lending agreement to recover the securities from the borrower on demand.

9. Operating Lease Commitments

The Fund leases office space and equipment under operating lease agreements expiring at various dates through the year 2019. The Fund recognized rental expense of $160,317 in 2013, and its minimum rental commitments are as follows:

2014

$

215,365

2015

222,165

2016

140,434

2017

64,157

2018 & 2019

71,398

Total

$

713,519

12

FINANCIAL HIGHLIGHTS

Year Ended December 31,

2013

2012

2011

2010

2009

Per Share Operating Performance

Net asset value, beginning of year

$12.43

$11.54

$12.65

$11.95

$9.61

Net investment income

0.20

0.19

0.16

0.15

0.13

Net realized gains and increase (decrease) in unrealized appreciation

3.32

1.41

(0.56)

1.10

2.64

Change in accumulated other comprehensive income (note 5)

0.01

—

(0.01)

—

0.04

Total from investment operations

3.53

1.60

(0.41)

1.25

2.81

Less distributions

Dividends from net investment income

(0.22)

(0.18)

(0.15)

(0.14)

(0.15)

Distributions from net realized gains

(0.62)

(0.49)

(0.50)

(0.37)

(0.30)

Total distributions

(0.84)

(0.67)

(0.65)

(0.51)

(0.45)

Capital share repurchases

0.02

—

—

—

0.02

Reinvestment of distributions

(0.05)

(0.04)

(0.05)

(0.04)

(0.04)

Total capital share transactions

(0.03)

(0.04)

(0.05)

(0.04)

(0.02)

Net asset value, end of year

$15.09

$12.43

$11.54

$12.65

$11.95

Market price, end of year

$13.07

$10.59

$ 9.64

$10.72

$10.10

Total Investment Return

Based on market price

31.8%

16.9%

(4.2)%

11.5%

32.1%

Based on net asset value

29.7%

14.7%

(2.8)%

11.2%

30.6%

Ratios/Supplemental Data

Net assets, end of year (in 000’s)

$1,421,551

$1,155,997

$1,050,734

$1,124,672

$1,045,027

Ratio of expenses to average net assets*

0.69%

0.65%

0.55%

0.58%

0.90%

Ratio of net investment income to average net assets**

1.44%

1.54%

1.25%

1.29%

1.30%

Portfolio turnover

55.9%

27.4%

21.5%

16.2%

15.1%

Number of shares outstanding at end of year (in 000’s)

94,224

93,030

91,074

88,885

87,415

*

The ratios of expenses to average net assets were 0.63%, 0.63%, and 0.76% in 2013, 2012, and 2009, respectively, after adjusting for non-recurring pension expenses as described in footnote 5.

**

The ratios of net investment income to average net assets were 1.50%, 1.56%, and 1.44% in 2013, 2012, and 2009, respectively, after adjusting for non-recurring pension expenses as described in footnote 5.

RBC U.S. Government Money Market (Institutional Class I), 0.01% (D)

10,000

10,000

Vanguard Federal Money Market, 0.01% (D)

10,000

10,000

Western Asset Institutional Government Reserves (Institutional Class), 0.04% (D)

10,000

10,000

130,000

Total Short-Term Investments (Cost $9,819,486)

9,819,486

Total Investments — 100.1% (Cost $1,029,287,849)

1,423,153,497

Cash, receivables, prepaid expenses and other assets, less liabilities – (0.1)%

(1,602,577

)

Net Assets — 100.0%

$

1,421,550,920

Notes:

(A)

Common stocks are listed on the New York Stock Exchange or the NASDAQ and are valued at the last reported sale price on the day of valuation. See note 1 to financial statements.

(B)

Presently non-dividend paying.

(C)

Non-controlled affiliate, a closed-end sector fund, registered as an investment company under the Investment Company Act of 1940.

(D)

Rate presented is as of period-end and represents the annualized yield earned over the previous seven days.

(E)

All or a portion of this security is pledged to cover open written call option contracts. Aggregate market value of such pledged securities is $404,800.

(F)

A portion of this security or cash is pledged to collateralize open written put option contracts with an aggregate value to deliver upon exercise of $300,000.

CHANGESIN PORTFOLIO SECURITIES

The unaudited list of quarterly changes in the Fund’s portfolio securities can be found on the Fund’s website at www.adamsexpress.com under “Investment Information”.

16

SCHEDULEOF OUTSTANDING WRITTEN OPTION CONTRACTS

December 31, 2013

Contracts

(100 shares

each)

Security

Strike

Price

Contract

Expiration Date

Value

COVERED CALLS

40

Exxon Mobil Corp.

$

95

Apr 14

$

28,800

COLLATERALIZED PUTS

40

Exxon Mobil Corp.

75

Apr 14

520

Total Option Liability (Unrealized Loss of $22,020)

$

29,320

17

REPORTOF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Shareholders of The Adams Express Company:

In our opinion, the accompanying statement of assets and liabilities, including the schedule of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of The Adams Express Company (the “Fund”) at December 31, 2013, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the auditing standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at December 31, 2013 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Baltimore, Maryland

February 14, 2014

18

HISTORICAL FINANCIAL STATISTICS

(unaudited)

Year

Value of Net Assets

Shares Outstanding*

Net Asset Value Per Share*

Market Value Per Share*

Income Dividends Per Share*

Capital Gains Distributions Per Share*

Total Dividends and Distributions Per Share*

Annual Distribution Rate**

1999

$

2,170,801,875

80,842,241

$

26.85

$

22.38

$

.26

$

1.37

$

1.63

8.5

%

2000

1,951,562,978

82,292,262

23.72

21.00

.22

1.63

1.85

7.8

2001

1,368,366,316

85,233,262

16.05

14.22

.26

1.39

1.65

9.6

2002

1,024,810,092

84,536,250

12.12

10.57

.19

.57

.76

6.2

2003

1,218,862,456

84,886,412

14.36

12.41

.17

.61

.78

6.8

2004

1,295,548,900

86,135,292

15.04

13.12

.24

.66

.90

7.1

2005

1,266,728,652

86,099,607

14.71

12.55

.22

.64

.86

6.7

2006

1,377,418,310

86,838,223

15.86

13.87

.23

.67

.90

6.8

2007

1,378,479,527

87,668,847

15.72

14.12

.32

.71

1.03

7.1

2008

840,012,143

87,406,443

9.61

8.03

.26

.38

.64

5.7

2009

1,045,027,339

87,415,193

11.95

10.10

.15

.30

.45

5.2

2010

1,124,671,966

88,885,186

12.65

10.72

.14

.37

.51

5.1

2011

1,050,733,678

91,073,899

11.54

9.64

.15

.50

.65

6.1

2012

1,155,997,037

93,029,724

12.43

10.59

.18

.49

.67

6.3

2013

1,421,550,920

94,223,617

15.09

13.07

.22

.62

.84

7.1

*

Adjusted to reflect the 3-for-2 stock split effected in October 2000.

**

The annual distribution rate is the total dividends and capital gain distributions during the year divided by the average month-end market price of the Fund’s Common Stock for the calendar year in years prior to 2011 and for the twelve months ended October 31 beginning in 2011, which is consistent with the calculation to determine the annual minimum distribution rate commitment announced in September 2011.

19

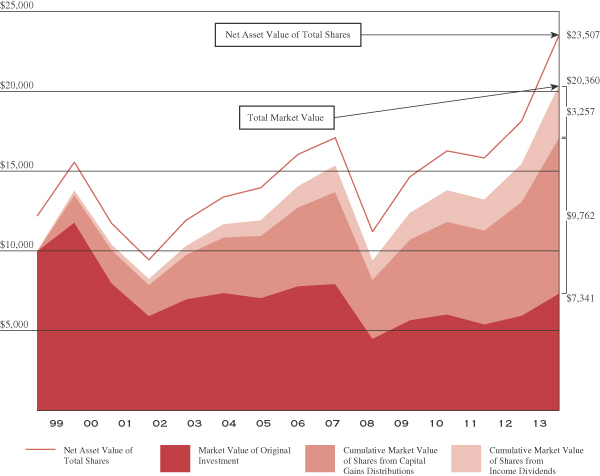

THE ADAMS EXPRESS COMPANY

(unaudited)

Calendar year- end

Market value of original investment

Cumulative market value of shares from capital gains distributions

Cumulative market value of shares from income dividends

Total market value

Net asset value of total shares

1999

$

12,567

$

825

$

167

$

13,559

$

16,272

2000

11,795

1,723

272

13,790

15,576

2001

7,987

2,075

325

10,387

11,724

2002

5,937

1,948

358

8,243

9,451

2003

6,970

2,785

559

10,314

11,935

2004

7,369

3,487

811

11,667

13,375

2005

7,049

3,903

964

11,916

13,967

2006

7,790

4,944

1,310

14,044

16,058

2007

7,931

5,768

1,655

15,354

17,093

2008

4,510

3,691

1,173

9,374

11,219

2009

5,673

5,037

1,665

12,375

14,642

2010

6,021

5,819

1,954

13,794

16,276

2011

5,414

5,873

1,929

13,216

15,820

2012

5,948

7,139

2,363

15,450

18,135

2013

7,341

9,762

3,257

20,360

23,507

Illustration of an assumed

15 year investment of $10,000

Investment income dividends and capital gains distributions are taken in additional shares. This chart covers the years 1999–2013. Fees for the reinvestment of interim dividends are assumed as 2% of the amount reinvested (maximum of $2.50) and commissions of $0.05 per share. There is no charge for reinvestment of year-end distributions. No adjustment has been made for any income taxes payable by shareholders on income dividends, capital gains distributions, or the sale of any shares. These results should not be considered representative of the dividend income or capital gain or loss which may be realized in the future.

20

SHAREHOLDER INFORMATIONAND SERVICES

DIVIDEND PAYMENT SCHEDULE

The Fund presently pays dividends four times a year, as follows: (a) three interim distributions on or about March 1, June 1, and September 1, and (b) a “year-end” distribution, payable in late December, consisting of the estimated balance of the net investment income for the year and the net realized capital gain earned through October 31 and, if applicable, a return of capital. Shareholders may elect to receive the year-end distribution in stock or cash. In connection with this distribution, all shareholders of record are sent a dividend announcement notice and an election card in mid-November. Shareholders holding shares in “street” or brokerage accounts may make their election by notifying their brokerage house representative.

INVESTORS CHOICE

INVESTORS CHOICE is a direct stock purchase and sale plan, as well as a dividend reinvestment plan, sponsored and administered by our transfer agent, American Stock Transfer & Trust Corporation (AST). The Plan provides registered shareholders and interested first time investors an affordable alternative for buying, selling, and reinvesting in Fund shares. A brochure which further details the benefits and features of INVESTORS CHOICE as well as an enrollment form may be obtained by contacting AST.

The costs to participants in administrative service fees and brokerage commissions for each type of transaction are listed below. Fees are subject to change at any time.

Fees:

Initial Enrollment and Optional Cash Investments:

Service Fee $2.50 per investment

Brokerage Commission $0.05 per share

Reinvestment of Dividends*:

Service Fee 2% of amount invested

(maximum of $2.50 per investment)

Brokerage Commission $0.05 per share

Sale of Shares:

Service Fee $10.00

Brokerage Commission $0.05 per share

Deposit of Certificates for safekeeping $7.50

(waived if sold)

Book to Book Transfers Included

To transfer shares to another participant or to a new participant

* The year-end dividend and capital gain distribution will usually be made in newly issued shares of Common Stock. There are no fees or commissions in connection with this dividend and capital gain distribution when made in newly issued shares.

For shareholders whose stock is held by a broker in “street” name, the AST INVESTORS CHOICE Direct Stock Purchase and Sale Plan remains available through many registered investment security dealers. If your shares are currently held in a “street” name or brokerage account, please contact your broker for details about how you can participate in AST’s Plan or contact AST.

ELECTRONIC DELIVERY OF SHAREHOLDER REPORTS

The Fund offers shareholders the benefits and convenience of viewing Quarterly and Annual Reports and other shareholder materials on-line. With your consent, paper copies of these documents will cease with the next mailing and will be provided via e-mail. Reduce paper mailed to your home and help lower the Fund’s printing and mailing costs. To enroll, please visit the following websites:

Registered shareholders with AST: www.amstock.com/main

Shareholders using brokerage accounts: http://enroll.icsdelivery.com/ADX

21

BOARDOF DIRECTORS

Personal Information

Position

Held with

the Fund

Term

of

Office

Length

of Time

Served

Principal Occupations

Number of Portfolios in Fund Complex Overseen by Director

Other Directorships

Independent Directors

Enrique R. Arzac, Ph.D. 7 St. Paul Street, Suite 1140 Baltimore, MD 21202 Age 72

Director

One Year

Since 1983

Professor of Finance and Economics at the Graduate School of Business, Columbia University, formerly Vice Dean of Academic Affairs.

Two

Director of Petroleum & Resources Corporation (closed-end fund), Aberdeen Asset Management Funds (6 closed-end funds), Credit Suisse Asset Management Funds (2 closed-end funds and 9 open-end funds), and Mirae Asset Discovery Funds (6 open-end funds). In addition, within the past five years, Dr. Arzac served as a director of Epoch Holdings Corporation (an investment management and investment advisory services company) and Starcomms Plc (telecommunications company).

Phyllis O. Bonanno

7 St. Paul Street,

Suite 1140 Baltimore, MD 21202

Age 70

Director

One Year

Since 2003

Retired President & CEO of International Trade Solutions, Inc. (consultants). Formerly, President of Columbia College, Columbia, South Carolina, and Corporate Vice President of Warnaco, Inc. (apparel).

Two

Director of Petroleum & Resources Corporation (closed-end fund) and Borg-Warner Inc. (industrial). In addition, within the past five years, Ms. Bonanno served as Director of Mohawk Industries, Inc. (carpets and flooring).

Kenneth J. Dale

7 St. Paul Street,

Suite 1140 Baltimore, MD 21202

Age 57

Director

One Year

Since 2008

Senior Vice President and Chief Financial Officer of The Associated Press. Formerly, Vice President, J.P. Morgan Chase & Co. Inc.

Two

Director of Petroleum & Resources Corporation (closed-end fund).

Frederic A. Escherich

7 St. Paul Street,

Suite 1140

Baltimore, MD 21202

Age 61

Director

One Year

Since 2006

Private Investor. Formerly, Managing Director and head of Mergers and Acquisitions Research and the Financial Advisory Department with JPMorgan & Co. Inc.

Two

Director of Petroleum & Resources Corporation (closed-end fund).

Roger W. Gale, Ph.D.

7 St. Paul Street,

Suite 1140

Baltimore, MD 21202

Age 67

Director

One Year

Since 2005

President & CEO of GF Energy, LLC (consultants to electric power companies). Formerly, member of management group of PA Consulting Group (energy consultants).

Two

Director of Petroleum & Resources Corporation (closed-end fund) and during the past five years also served as a director of Ormat Technologies, Inc. (geothermal and renewable energy).

22

BOARDOF DIRECTORS (CONTINUED)

Personal Information

Position

Held with

the Fund

Term

of

Office

Length

of Time

Served

Principal Occupations

Number of Portfolios in Fund Complex Overseen by Director

Other Directorships

Independent Directors (continued)

Kathleen T. McGahran,

Ph.D., J.D., CPA

7 St. Paul Street,

Suite 1140

Baltimore, MD 21202

Age 63

Director, Chair of the Board

One Year

Since 2003

President & CEO of Pelham Associates, Inc. (an executive education provider) and Senior Lecturer at Yale University’s School of Management. Formerly, Associate Dean and Director of Executive Education and Associate Professor, Columbia University, and Adjunct Associate Professor, Stern School of Business, New York University and Tuck School of Business, Dartmouth College.

Two

Director of Petroleum & Resources Corporation (closed-end fund).

Craig R. Smith, M.D.

7 St. Paul Street,

Suite 1140

Baltimore, MD 21202

Age 67

Director

One Year

Since 2005

Chief Operating Officer and Manager of Algenol LLC (ethanol manufacturing). Formerly, President, Williston Consulting LLC (consultants to pharmaceutical and biotechnology industries) and Chairman, President & CEO of Guilford Pharmaceuticals (pharmaceuticals & biotechnology).

Two

Director of Petroleum & Resources Corporation (closed-end fund) and during the past five years also served as a director of LaJolla Pharmaceutical Company, Depomed, Inc. (specialty pharmaceuticals), and Algenol Biofuels, Inc. (ethanol manufacturing).

Interested Director

Mark E. Stoeckle

7 St. Paul Street,

Suite 1140

Baltimore, MD 21202

Age 57

Director and CEO

One Year

Since 2013

CEO of the Fund and CEO of Petroleum & Resources Corporation.

Two

Director of Petroleum & Resources Corporation (closed-end fund).

This report, including the financial statements herein, is transmitted to the shareholders of The Adams Express Company for their information. It is not a prospectus, circular or representation intended for use in the purchase or sale of shares of the Fund’s or of any securities mentioned in the report. The rates of return will vary and the principal value of an investment will fluctuate. Shares, if sold, may be worth more or less than their original cost. Past performance is no guarantee of future investment results.

23

OTHER INFORMATION

Statement on Quarterly Filing of Complete Portfolio Schedule

In addition to publishing its complete schedule of portfolio holdings in the First and Third Quarter Reports to shareholders, the Fund also files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the Commission’s website at www.sec.gov. The Company’s Forms N-Q may be reviewed and copied at the Commission’s Public Reference Room, and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330. The Fund also posts a link to its Forms N-Q on its website: www.adamsexpress.com under the headings “Investment Information”, “Financial Reports” and then “SEC Filings”.

Annual Certification

The Fund’s CEO has submitted to the New York Stock Exchange the annual CEO certification as required by Section 303A.12(a) of the NYSE Listed Company Manual.

Proxy Voting Policies and Record

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities owned by the Fund and the Fund’s proxy voting record for the 12-month period ended June 30, 2013 are available (i) without charge, upon request, by calling the Fund’s toll free number at (800) 638-2479; (ii) on the Fund’s website: www.adamsexpress.com under the headings “About Adams Express” and “Corporate Information”; and (iii) on the Securities and Exchange Commission’s website: www.sec.gov.

Forward-Looking Statements

This report contains “forward-looking statements” within the meaning of the Securities Act of 1933 and the Securities Exchange Act of 1934. By their nature, all forward-looking statements involve risks and uncertainties, and actual results could differ materially from those contemplated by the forward-looking statements. Several factors that could materially affect the Fund’s actual results are the performance of the portfolio of stocks held by the Fund, the conditions in the U.S. and international financial markets, the price at which shares of the Fund will trade in the public markets, and other factors discussed in the Fund’s periodic filings with the Securities and Exchange Commission.

Privacy Policy

In order to conduct its business, the Fund, through its transfer agent, American Stock Transfer & Trust Company, collects and maintains certain nonpublic personal information about our shareholders of record with respect to their transactions in shares of our securities. This information includes the shareholder’s address, tax identification or Social Security number, share balances, and dividend elections. We do not collect or maintain personal information about shareholders whose shares of our securities are held in “street name” by a financial institution such as a bank or broker.

We do not disclose any nonpublic personal information about you, our other shareholders or our former shareholders to third parties unless necessary to process a transaction, service an account or as otherwise permitted by law.

To protect your personal information internally, we restrict access to nonpublic personal information about our shareholders to those employees who need to know that information to provide services to our shareholders. We also maintain certain other safeguards to protect your nonpublic personal information.

24

THE ADAMS EXPRESS COMPANY

Board Of Directors

Enrique R. Arzac 1,3,5

Phyllis O. Bonanno 1,3,5

Kenneth J. Dale 2,4

Frederic A. Escherich 1,4,5

Roger W. Gale 2,4

Kathleen T. McGahran 1,2,3,5,6

Craig R. Smith 3,5

Mark E. Stoeckle 1

1. Member of Executive Committee

2. Member of Audit Committee

3. Member of Compensation Committee

4. Member of Retirement Benefits Committee

5. Member of Nominating and Governance Committee

6. Chair of the Board

Officers

Mark E. Stoeckle

Chief Executive Officer

James P. Haynie, CFA

President

Nancy J.F. Prue, CFA

Executive Vice President

Brian S. Hook, CFA, CPA

Vice President, Chief Financial Officer and Treasurer

Lawrence L. Hooper, Jr.

Vice President, General Counsel and Secretary

David R. Schiminger, CFA

Vice President — Research

D. Cotton Swindell, CFA

Vice President — Research

Christine M. Sloan, CPA

Assistant Treasurer

The Adams Express Company

Seven St. Paul Street, Suite 1140, Baltimore, MD 21202

(410) 752-5900 (800) 638-2479

Website: www.adamsexpress.com

E-mail: contact@adamsexpress.com

Counsel: Chadbourne & Parke LLP

Independent Registered Public Accounting Firm: PricewaterhouseCoopers LLP

Custodian of Securities: Brown Brothers Harriman & Co.

Transfer Agent & Registrar: American Stock Transfer & Trust Company, LLC

Stockholder Relations Department

6201 15th Avenue

Brooklyn, NY 11219

(877) 260-8188

Website: www.amstock.com

E-mail: info@amstock.com

amsexpress.com

Item 2. Code of Ethics.

On June 12, 2003, the Board of Directors adopted a code of ethics that applies to the registrant's principal executive officer and principal financial officer. The code of ethics is available on the registrant's website at: www.adamsexpress.com. Since the code of ethics was adopted, there have been no amendments to it nor have any waivers from any of its provisions been granted.

Item 3. Audit Committee Financial Expert.

The Board of Directors has determined that at least one of the members of the registrant's audit committee meets the definition of audit committee financial expert as that term is defined by the Securities and Exchange Commission. The directors on the registrant's audit committee whom the Board of Directors has determined meet such definition are Kenneth J. Dale and Kathleen T. McGahran, who are independent pursuant to paragraph (a)(2) of this Item.

Item 4. Principal Accountant Fees and Services.

(a) Audit Fees. The aggregate fees for professional services rendered by the registrant's independent registered public accounting firm, PricewaterhouseCoopers LLP, for the audit of the registrant's annual financial statements and review of the registrant's semi-annual financial statements for 2013 and 2012 were $73,967 and $71,167, respectively.

(b) Audit-Related Fees. There were no audit-related fees in 2013 and 2012.

(c) Tax Fees. The aggregate fees for professional services rendered to the registrant by PricewaterhouseCoopers LLP for the review of the registrant's excise tax calculations and preparations of federal, state, and excise tax returns for 2013 and 2012 were $8,581 and $7,521, respectively.

(d) All Other Fees. The aggregate fees for services rendered to the registrant by PricewaterhouseCoopers LLP, other than for the services referenced above, for 2013 and 2012 were $5,477 and $6,617, respectively, which related to the review of the registrant's procedures for calculating the amounts to be paid or granted to the registrant's officers in accordance with the registrant's cash incentive plan and the 2005 Equity Incentive Compensation Plan, review of the registrant's calculations related to those plans, and preparation of a related report to the registrant's Compensation Committee. Services in 2012 also included the review of the documentation relating to compliance by the registrant's employees and directors with the requirements of the registrant's Code of Ethics pertaining to personal stock trading, and presentation of a related report to the Chief Executive Officer.

(e)

(1)

The audit committee's policy is to pre-approve all audit and permissible non-audit services provided by the independent accountants. In assessing requests for services by the independent accountants, the audit committee considers whether such services are consistent with the auditor's independence; whether the independent accountants are likely to provide the most effective and efficient service based upon their familiarity with the registrant; and whether the service could enhance the registrant's ability to manage or control risk or improve financial statement audit and review quality. The audit committee may delegate pre-approval authority to its Chair. Any pre-approvals by the Chair under this delegation are to be reported to the audit committee at its next scheduled meeting. All services performed in 2013 were pre-approved by the audit committee.

(2)

Not applicable.

(f) Not applicable.

(g) The aggregate fees for non-audit professional services rendered by PricewaterhouseCoopers LLP to the registrant for 2013 and 2012 were $14,058 and $14,138, respectively.

(h) The registrant's audit committee has considered the provision by PricewaterhouseCoopers LLP of the non-audit services described above and found that they are compatible with maintaining PricewaterhouseCoopers LLP's independence.

Item 5. Audit Committee of Listed Registrants.

(a) The registrant has a standing audit committee established in accordance with Section 3(a)(58)(A) of the Securities Exchange Act of 1934. The members of the Audit Committee are: Kenneth J. Dale, Chair, Roger W. Gale, Kathleen T. McGahran, and Craig R. Smith.

(b) Not applicable.

Item 6. Investments.

(a) This schedule is included as part of the Report to Stockholders filed under Item 1 of this form.

(b) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

PROXY VOTING GUIDELINES

The Adams Express Company ("Adams") follows long-standing general guidelines for the voting of portfolio company proxies and takes very seriously its responsibility to vote all such proxies. The portfolio company proxies are evaluated by our research staff and voted by our portfolio management team, and we annually provide the Board of Directors with a report on how proxies were voted during the previous year. We do not use an outside service to assist us in voting our proxies.

As an internally-managed investment company, Adams uses its own staff of research analysts and portfolio managers. In making the decision to invest in a company for the portfolio, among the factors the research team analyses is the integrity and competency of the company's management. We must be satisfied that the companies we invest in are run by managers with integrity. Therefore, having evaluated this aspect of our portfolio companies' managements, we give significant weight to the recommendations of the company's management in voting on proxy issues.

We vote proxies on a case-by-case basis according to what we deem to be the best long-term interests of our shareholders. The key over-riding principle in any proxy vote is that stockholders be treated fairly and equitably by the portfolio company's management. In general, on the election of directors and on routine issues that we do not believe present the possibility of an adverse impact upon our investment, after reviewing whether applicable corporate governance requirements as to board and committee composition have been met, we will vote in accordance with the recommendations of the company's management. When we believe that the management's recommendation is not in the best interests of our stockholders, we will vote against that recommendation.

Our general guidelines for when we will vote contrary to the recommendation of the portfolio company management's recommendation are:

Stock Options

Our general guideline is to vote against stock option plans that we believe are unduly dilutive of our stock holdings in the company. We use a general guideline that we will vote against any stock option plan that results in dilution in shares outstanding exceeding 4%. Most stock option plans are established to motivate and retain key employees and to reward them for their achievement. An analysis of a stock option plan cannot be made in a vacuum but must be made in the context of the company's overall compensation scheme. In voting on stock option plans, we give consideration to whether the stock option plan is broad-based in the number of employees who are eligible to receive grants under the plan. We generally vote against plans that permit re-pricing of grants or the issuance of options with exercise prices below the grant date value of the company's stock.

Corporate Control/Governance Issues

Unless we conclude that the proposal is favorable to our interests as a long-term shareholder in the company, we have a long-standing policy of voting against proposals to create a staggered board of directors. In conformance with that policy, we will generally vote in favor of shareholder proposals to eliminate the staggered election of directors.

Unless we conclude that the proposal is favorable to our interests as a long-term shareholder in the company, our general policy is to vote against amendments to a company's charter that can be characterized as blatant anti-takeover provisions.

With respect to so-called golden parachutes and other severance packages, it is our general policy to vote against proposals relating to future employment contracts that provide that compensation will be paid to any director, officer or employee that is contingent upon a merger or acquisition of the company.

We generally vote for proposals to require that the majority of a board of directors consist of independent directors and vote against proposals to establish a retirement plan for non-employee directors.

We have found that most stockholder proposals relating to social issues focus on very narrow issues that either fall within the authority of the company's management, under the oversight of its board of directors, to manage the day-to- day operations of the company or concern matters that are more appropriate for global solutions rather than company- specific ones. We consider these proposals on a case-by-case basis but usually are persuaded management's position is reasonable and vote in accordance with management's recommendation on these types of proposals.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

(a)