UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSRS

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-02781

Templeton Funds

(Exact name of registrant as specified in charter)

300 S.E. 2nd Street, Fort Lauderdale, FL 33301-1923

(Address of principal executive offices) (Zip code)

Craig S. Tyle, One Franklin Parkway, San Mateo, CA 94403-1906

(Name and address of agent for service)

Registrant’s telephone number, including area code: (954) 527-7500

Date of fiscal year end: 8/31

Date of reporting period: 2/28/18

| Item 1. | Reports to Stockholders. |

[INSERT SEMIANNUAL REPORT]

| | | | |

| | | | Semiannual Report and Shareholder Letter February 28, 2018 |

Sign up for electronic delivery at franklintempleton.com/edelivery

Franklin Templeton Investments

Why choose Franklin Templeton Investments?

Successful investing begins with ambition. And achievement only comes when you reach for it. That’s why we continually strive to deliver better outcomes for investors. No matter what your goals are, our deep, global investment expertise allows us to offer solutions that can help.

During our more than 70 years of experience, we’ve managed through all kinds of markets—up, down and those in between. We’re always preparing for what may come next. It’s because of this, combined with our strength as one of the world’s largest asset managers that we’ve earned the trust of millions of investors around the world.

Dear Shareholder:

During the six months ended February 28, 2018, mostly upbeat global economic data, improved corporate earnings and generally supportive monetary policies benefited global securities markets. The European Central Bank (ECB) and the Bank of Japan (BOJ) kept their benchmark interest rates unchanged, while the US Federal Reserve (Fed) raised the target range for the federal funds rate at its December 2017 meeting amid signs of a growing US economy. The BOJ maintained its quantitative easing measures during the period, while the ECB began to reduce its bond purchases in January 2018. The Fed also began a gradual reduction in its balance sheet during the period as part of its ongoing plan to normalize US monetary policy. However, investors expressed concerns about the pace of central bankers’ monetary policy tightening amid an improving economic outlook. In this environment, stocks in global developed and emerging markets excluding the US generated strong returns, as measured by the MSCI All Country World Index ex USA Index.

We are committed to our long-term perspective and disciplined investment approach as we conduct a rigorous, fundamental analysis of securities with a regular emphasis on investment risk management.

Historically, patient investors have achieved rewarding results by evaluating their goals, diversifying their assets globally and maintaining a disciplined investment program, all hallmarks of the Templeton investment philosophy developed more than 60 years ago. We continue to recommend investors consult

their financial advisors and review their portfolios to design a long-term strategy and portfolio allocation that meet their individual needs, goals and risk tolerance.

Templeton Foreign Fund’s semiannual report includes more detail about prevailing conditions and a discussion about investment decisions during the period. Please remember all securities markets fluctuate, as do mutual fund share prices.

We thank you for investing with Franklin Templeton, welcome your questions and comments, and look forward to serving your investment needs in the years ahead.

Sincerely,

Norman J. Boersma, CFA

President and Chief Executive Officer –

Investment Management

Templeton Funds

This letter reflects our analysis and opinions as of February 28, 2018, unless otherwise indicated. The information is not a complete analysis of every aspect of any market, country, industry, security or fund. Statements of fact are from sources considered reliable.

CFA® is a trademark owned by CFA Institute.

| | |

| | Not FDIC Insured | May Lose Value | No Bank Guarantee |

| | | | |

| | | |

| franklintempleton.com | | Not part of the semiannual report | | 1 |

Contents

Visit franklintempleton.com for fund updates, to access your account, or to find helpful financial planning tools.

| | | | |

| | | |

2 | | Semiannual Report | | franklintempleton.com |

Semiannual Report

Templeton Foreign Fund

This semiannual report for Templeton Foreign Fund covers the period ended February 28, 2018.

Your Fund’s Goal and Main Investments

The Fund seeks long-term capital growth. Under normal market conditions, the Fund invests at least 80% of its net assets in “foreign securities,” as described in the prospectus. These securities are predominantly equity securities of companies located outside the US, including developing markets.

Performance Overview

The Fund’s Class A shares delivered a +3.10% cumulative total return for the six months under review. In comparison, the Fund’s benchmark, the MSCI All Country World Index (ACWI) ex USA Index, which measures stock performance in global developed and emerging markets excluding the US, generated a +7.71% total return.1 For the 10-year period ended February 28, 2018, the Fund’s Class A shares generated a +36.34% cumulative total return, compared with the MSCI ACWI ex USA Index’s +36.00% cumulative total return for the same period.1 Please note index performance information is provided for reference and we do not attempt to track the index but rather undertake investments on the basis of fundamental research. You can find more performance data in the Performance Summary beginning on page 9.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

Economic and Market Overview

The global economy expanded during the six-month period under review amid generally upbeat economic data across regions. In this environment, global developed and emerging market stocks generated a +9.29% total return, as measured by

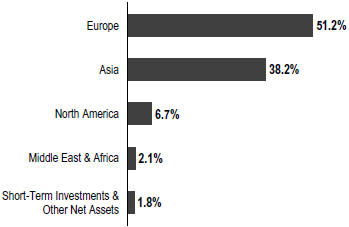

Geographic Composition

Based on Total Net Assets as of 2/28/18

the MSCI ACWI.1 Global markets were also aided by price gains in oil and other commodities, the European Central Bank’s (ECB’s) extension of its monetary easing program, encouraging corporate earnings reports and the passage of the US tax reform bill.

However, global markets reflected investor concerns about geopolitical tensions in the Korean peninsula, expectations that key central bankers around the world may potentially raise interest rates amid an improving economic outlook, and political uncertainties in the US and the European Union (EU). In early February, global markets experienced significant volatility amid concerns about stronger inflation and rising long-term interest rates in the US.

The US economy expanded in 2017’s fourth quarter, though at a slower pace compared to the third quarter as lower inventory investment and higher imports partially offset the positive contributions of growth in consumer spending, business and housing investment, exports, and government spending. The unemployment rate declined from 4.4% in August 2017 to 4.1% at period-end.2 Annual inflation, as measured by the Consumer Price Index, increased from 1.9% in August 2017 to 2.2% at period-end.2 The US Federal Reserve (Fed) began reducing its balance sheet in October and raised its target range

1. Source: Morningstar. As of 2/28/18, the Fund’s Class A 10-year average annual total return not including the maximum sales charge was +3.15%, compared with the MSCI ACWI ex USA Index’s 10-year average annual total return of +3.12%.

The index is unmanaged and includes reinvestment of any income or distributions. It does not reflect any fees, expenses or sales charges. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

2. Source: US Bureau of Labor Statistics.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI).

The SOI begins on page 17.

| | | | |

| | | |

| franklintempleton.com | | Semiannual Report | | 3 |

TEMPLETON FOREIGN FUND

for the federal funds rate 0.25% to 1.25%–1.50% in December. The Fed left its target rate for the federal funds rate unchanged at its January 2018 meeting, but expressed that it anticipated inflation to rise in 2018 and stabilize around the 2% target over the medium term.

In Europe, the UK’s economic growth moderated in 2017’s fourth quarter over the previous quarter, due to slower growth in production output, household spending and business investment. In November, the Bank of England raised its key policy rate for the first time in a decade. The eurozone’s growth moderated in 2017’s fourth quarter over the previous quarter. The bloc’s annual inflation rate ended the period lower than in August 2017. The ECB kept its benchmark interest rate unchanged during the period. However, at its October meeting, the ECB extended the time frame for its massive bond-buying program from December 2017 to at least September 2018, while reducing the amount of monthly bond purchases in half beginning in January 2018.

In Asia, Japan’s gross domestic product (GDP) growth slowed in 2017’s fourth quarter compared to the third quarter, as a slowdown in business spending and contractions in private residential investment offset a recovery in private consumption. The Bank of Japan left its benchmark interest rate unchanged during the period and continued its monetary stimulus measures.

In emerging markets, Brazil’s quarterly GDP grew in 2017’s fourth quarter, although at a slower pace compared to the previous quarter. The country’s central bank cut its benchmark interest rate several times during the period to spur economic growth. Russia’s GDP grew in 2017’s fourth quarter compared to the prior-year period, amid the Bank of Russia’s continued policy support. China’s GDP grew at a stable rate in 2017’s fourth quarter compared to the prior-year period. The People’s Bank of China left its benchmark interest rate unchanged during the period. Overall, emerging market stocks, as measured by the MSCI Emerging Markets Index, rose substantially during the period.

Investment Strategy

Our investment strategy employs a bottom-up, value-oriented, long-term approach. We focus on the market price of a company’s securities relative to our evaluation of the company’s long-term earnings, asset value and cash flow

potential. We also consider the company’s price/earnings ratio, price/cash flow ratio, profit margins and liquidation value.

Manager’s Discussion

International equities carried positive momentum into the semiannual review period, rising every month until February, when volatility resurfaced as concerns about the pace of central bank policy tightening sparked a sharp sell-off in risk assets. In this environment, the Fund delivered absolute gains, but it underperformed its benchmark, the MSCI ACWI ex USA Index. Despite relative headwinds, we were encouraged by a number of market transitions that we believe align well with our strategy going forward. After years of official stimulus, central bankers—led by the Fed—are tightening policies. After years of tranquility, volatility is awakening. After a long period of low inflation, low global growth and ultra-low interest rates, inflationary forces are stirring, growth is accelerating and bond yields are rising. As these key underpinnings of global financial markets change, so too will the characteristics and leadership of those markets. The leaders of the last cycle—US equities, growth stocks, and consumer and internet stocks—have become priced at levels that dramatically increase the likelihood of sub-par future returns, in our view. However, we believe shifting conditions may facilitate the passing of the performance baton to the last cycle’s laggards: international equities and value stocks across a range of out-of-favor sectors such as health care, telecommunication services, energy and financials.

At Templeton, we have maintained our valuation discipline and adhered to our time-tested investment process throughout this challenging period. These strategies have led to a number of encouraging performance developments during the six months under review, such as the outperformance of overweighted energy stocks as oil prices rebounded and financials stocks as interest rates rose, but also some continued challenges.3 Notable among challenges was the continued weakness of the Fund’s overweighted health care holdings.4 Concerns about generic competition, regulatory scrutiny and a consolidating payor sector all remained headwinds for health care stocks during the review period. At the stock level, French drugmaker Sanofi was the sector’s largest detractor, declining amid concerns that the company was overpaying for acquisitions to stem a decline in revenues from existing operations. Although Sanofi has its challenges, including an admittedly poor track

3. The energy sector comprises energy equipment and services and oil, gas and consumable fuels in the SOI. The financials sector comprises banks, capital markets and insurance in the SOI.

4. The health care sector comprises biotechnology, health care equipment and supplies, health care providers and services, life sciences tools and services, and pharmaceuticals in the SOI.

| | | | |

| | | |

4 | | Semiannual Report | | franklintempleton.com |

TEMPLETON FOREIGN FUND

record of capital allocation, we believe the stock’s price has been too low. In our analysis, Sanofi’s recent share price represents a modest valuation multiple on low earnings, which could give us a significant margin of safety and considerable upside potential as the company addresses its issues and benefits from its diverse business portfolio over the long term.

We remain positive on the health care sector more generally. We believe pricing pressures and generic competition are best addressed through innovation, and innovation is fueled by research and development, which has doubled in the pharmaceuticals industry in the past 30 years. Furthermore, despite the political controversy surrounding drug pricing, prescription drug costs account for less than 15% of health care spending in the US and the EU. Given the efficacy of these drugs and their ability to reduce costs elsewhere in the health care system, we believe they likely represent good value for the money. Overall, the pharmaceuticals industry is not often cheap based on free cash flow multiples, and we are finding the best values among innovative firms that in our analysis are capable of commanding pricing power by successfully addressing unmet medical needs. It is rare to find highly cash-generative, innovative businesses with attractive growth potential trading in what we consider deep value territory, but we believe select biotechnology and pharmaceuticals firms offer just such a proposition.

Industrials stocks also detracted, led lower by UK-based professional services firm Capita (not held by period-end).5 Its stock declined sharply during the period after management announced plans to halt dividends and sell shares to raise capital. The recent bankruptcy of a competing UK outsourcing firm further compounded investor concerns about the magnitude of Capita’s woes. The emergence of new information requires a reassessment of the investment thesis, and our analysis suggests that the risk profile of Capita has increased significantly. The combination of equity issuance decreasing existing shareholders’ ownership percentages and new guidance for negative free cash flows in 2018 suggests to us that the firm’s finances are more impaired than initially portrayed by outgoing management. With fundamentals deteriorating, valuations no longer appear supportive to us. Although we remain underweighted in industrials, we are finding select opportunities in the sector, particularly among companies benefiting from restructuring or exposure to end

Top 10 Sectors/Industries

2/28/18

| | | | |

| | | % of Total

Net Assets | |

| Banks | | | 14.4% | |

| Oil, Gas & Consumable Fuels | | | 11.0% | |

| Pharmaceuticals | | | 8.7% | |

| Insurance | | | 5.4% | |

| Technology Hardware, Storage & Peripherals | | | 4.5% | |

| Metals & Mining | | | 4.4% | |

| Wireless Telecommunication Services | | | 4.1% | |

| Internet Software & Services | | | 4.0% | |

| Life Sciences Tools & Services | | | 3.6% | |

| Diversified Telecommunication Services | | | 3.1% | |

markets with better growth prospects. We have tried to avoid what we consider expensive companies that fail to reflect the maturity of their business cycles, as well as those discounting excessive optimism with regard to sustainable growth rates and returns.

Stock selection in materials also detracted, pressured by a handful of precious metals stocks.6 Canadian gold miners Alamos Gold and Barrick Gold both finished among the biggest detractors, as did Wheaton Precious Metals, a Canadian firm that finances mining activities in return for a “stream” of precious metals by-products. Although the price of gold has remained firm amid US dollar weakness and geopolitical uncertainties, mining stocks declined as gold stayed range-bound. History suggests that a modest exposure to gold and silver miners can help optimize risk-adjusted returns over time, and we view these investments as attractive portfolio hedges at a time when global debt has reached an all-time high and economic and market cycles look increasingly mature. With valuations across the precious metals industry looking cheap to us, we have maintained select investments in a handful of companies that in our analysis have resilient balance sheets, low cost positions and identifiable value catalysts.

Information technology (IT) was another relative laggard during the period.7 Although the Fund’s IT holdings delivered solid gains, they failed to keep pace with the benchmark’s IT components, and relative performance was also hindered by our underweighting in the sector. We continue to find select value in the IT sector more broadly, though not enough to justify an

5. The industrials sector comprises aerospace and defense, construction and engineering, industrial conglomerates, machinery, and trading companies and distributors in the SOI.

6. The materials sector comprises chemicals, construction materials, and metals and mining in the SOI.

7. The IT sector comprises electronic equipment, instruments and components; internet software and services; semiconductors and semiconductor equipment; software; and technology hardware, storage and peripherals in the SOI.

| | | | |

| | | |

| franklintempleton.com | | Semiannual Report | | 5 |

TEMPLETON FOREIGN FUND

even-weighted allocation relative to the index, as some pockets of the IT sector look unsustainably expensive to us. With every major tier in the tech “stack” disrupted by new technologies, our approach is to identify mature companies we believe have the ability to adapt to change, as well as new entrants we feel are likely to emerge as winners. Although we have some exposure to the dominant internet and consumer technology firms that have performed well recently, we have avoided a number of these stocks due to valuation concerns.

An overweighting in telecommunication services and an underweighting in consumer discretionary also detracted, as did stock-specific weakness.8 In the telecommunication services sector, China Telecom and China Mobile declined as investors worried about data pricing competition and the high capital expenditure forecasts associated with the buildout of China’s 5G network. Yet, data pricing in the industry has so far been rational, in our assessment, and the high levels of investment are required to create scalability and are at least partially offset by the fact that Chinese telecommunication services companies do not have to pay for access to parts of the radio frequency spectrum. Although the market continues to focus on the perceived negatives, we see companies trading at modest valuations that are growing earnings and dividends and are investing to gain scale and share in a secular growth market. In the consumer discretionary sector, shares of Luxembourg-based satellite provider SES declined after management delivered disappointing results, citing one-off headwinds and delayed revenues attributable to a changing business model. Recent adversities have caused the stock to decline and its price-to-book value to become much lower than the company’s industry peers. Our analysis implies SES has recently been trading at replacement cost for a business with very high barriers to entry and valuable orbital satellite slots that cannot be replicated. Additionally, the company’s high single-digit dividend and free cash flow yields, as well as a contract backlog equivalent to four years of revenue, lead us to believe its shares remain undervalued.

Turning to contributors, stock selection in the financials sector notably contributed, led by Dutch market-maker Flow Traders. Its shares surged late in the period as higher volatility boosted trading volumes, leading to record monthly income. We remain positive on the stock at these levels. After an unusually quiet period, we expect higher volatility going forward as central banks wind down bond purchases and raise interest rates. The firm could also potentially benefit from structural growth

Top 10 Holdings

2/28/18

| | | | |

Company Sector/Industry, Country | | % of Total

Net Assets | |

| |

Samsung Electronics Co. Ltd. Technology Hardware, Storage & Peripherals, South Korea | | | 3.3% | |

| |

Baidu Inc. Internet Software & Services, China | | | 3.1% | |

| |

BP PLC Oil, Gas & Consumable Fuels, UK | | | 2.7% | |

| |

Standard Chartered PLC Banks, UK | | | 2.6% | |

| |

Royal Dutch Shell PLC Oil, Gas & Consumable Fuels, UK | | | 2.5% | |

| |

SoftBank Group Corp. Wireless Telecommunication Services, Japan | | | 2.4% | |

| |

Aegon NV Insurance, Netherlands | | | 2.3% | |

| |

Teva Pharmaceutical Industries Ltd. Pharmaceuticals, Israel | | | 2.1% | |

| |

BNP Paribas SA Banks, France | | | 2.1% | |

| |

Roche Holding AG Pharmaceuticals, Switzerland | | | 2.0% | |

opportunities as the market for exchange-traded funds (ETFs) matures and Flow Traders develops its business in the US and Asia. Finally, we believe new European regulations that require all ETF trading volume to be conducted on transparent exchanges should further increase volumes for Flow Traders, which has a reputation for best-in-class trade executions. The Fund also benefited from investments in Asian lenders, such as South Korea-based KB Financial Group and Thailand-based Bangkok Bank. We continue to find attractive opportunities among modestly valued financials holdings in Asia, where prospects for improving corporate governance and political stability have combined with rising interest rates and genuine economic growth to benefit the regional banking sector.

The Fund’s energy holdings also benefited from stock selection and an overweighted allocation. UK oil major BP was one of the Fund’s top energy contributors. Its stock rallied after the firm reported an encouraging increase in profits and cash flow. Furthermore, the company announced plans to buy back shares in a sign it had put past incidents behind it and emerged stronger from an industry-wide downturn. BP’s potential free cash flow generation should continue to rise as costs remain muted and production comes online over the medium term,

8. The telecommunication services sector comprises diversified telecommunication services and wireless telecommunication services in the SOI. The consumer discretionary sector comprises auto components, automobiles, household durables, media, multiline retail and specialty retail in the SOI.

| | | | |

| | | |

6 | | Semiannual Report | | franklintempleton.com |

TEMPLETON FOREIGN FUND

offering additional upside from current levels in our view. More generally, a rising oil price and strong sector performance have largely rewarded our decision to stay the course despite price volatility that accompanied fears of a supply glut earlier in 2017. We expected that oil price would climb toward US$60 per barrel, beyond which it could remain range-bound as swing producers in the North American shale fields bring supply back on line. Barring any external shocks, we expected renewed supply above US$60, which will likely cap further significant price appreciation, and we have been selectively reducing exposure at this point in the cycle.

The Fund also benefited from stock selection and underweighted allocations in the consumer staples and utilities sectors.9 We continue to find only limited opportunities in these defensive sectors, which we consider to be expensive. The consumer staples sector remains more richly valued than both the broader market and its own history, a premium that we believe is unwarranted given the sector’s generally weak profit margins and scarce growth opportunities. Utilities also appear richly valued considering the potential impacts of weaker economic growth and increasing regulatory interference on power demand and industry pricing. Concerns about oversupply in developed markets also persist, further clouding the sector’s outlook.

From a regional standpoint, stock selection and an overweighting in Europe detracted from relative performance, while in Asia, stock selection offset the benefit of an overweighting. Stock selection in Canada also detracted.

It is important to recognize the effect of currency movements on the Fund’s performance. In general, if the value of the US dollar goes up compared with a foreign currency, an investment traded in that foreign currency will go down in value because it will be worth fewer US dollars. This can have a negative effect on Fund performance. Conversely, when the US dollar weakens in relation to a foreign currency, an investment traded in that foreign currency will increase in value, which can contribute to Fund performance. For the six months ended February 28, 2018, the US dollar declined in value relative to many currencies in which the Fund’s investments were traded. As a result, the Fund’s performance was positively affected by the portfolio’s investment predominantly in securities with non-US currency exposure. However, one cannot expect the same result in future periods.

Top 10 Countries

2/28/18

| | | | |

| | | % of Total

Net Assets | |

| UK | | | 20.0% | |

| Japan | | | 12.2% | |

| China | | | 10.7% | |

| France | | | 7.3% | |

| Germany | | | 6.8% | |

| Netherlands | | | 6.8% | |

| South Korea | | | 6.7% | |

| Canada | | | 5.0% | |

| Switzerland | | | 3.9% | |

| Italy | | | 2.8% | |

At Templeton, we continue to favor international markets over the US due to our view of their discounted valuations, better structural growth prospects and earlier stage economic and policy cycles. Ultimately, we remain committed to buying what we consider undervalued and mispriced stocks wherever we find them. Admittedly, this value-oriented approach has faced some headwinds. After outperforming growth in 2016, value lagged growth in 2017, with global growth outperforming value in the past 10 years. We believe value’s headwinds stem largely from unconventional monetary policies, which have depressed interest rates and sent investors out the risk curve in search of growth and yield. We believe these policies are unsustainable for three reasons. First, they increase social inequality, which has political consequences; second, they inflate asset prices, which creates stability risks; and third, rising inflation pressure and falling unemployment give data-dependent central bankers reasons to begin reversing such policies. We believe this mature cycle will eventually change, and with it the conditions that have been unfavorable to value. Against this backdrop, we have positioned the portfolio somewhat more defensively in recent quarters, taking gains among pro-cyclical stocks and reinvesting in what we consider cheaper, under-owned areas of the market. Despite some clear areas of what we deem as excessive enthusiasm and overvaluation, our bottom-up, fundamentals-oriented research has continued to uncover cheap stocks in regions and sectors around the world, and we remain constructive about the Fund’s prospects for capital appreciation and preservation over a long-term investment horizon.

9. The consumer staples sector comprises beverages, food and staples retailing, and food products in the SOI. The utilities sector comprises electric utilities and multi-utilities in the SOI.

See www.franklintempletondatasources.com for additional data provider information.

| | | | |

| | | |

| franklintempleton.com | | Semiannual Report | | 7 |

TEMPLETON FOREIGN FUND

Thank you for your continued participation in Templeton Foreign Fund. We look forward to serving your future investment needs.

| | |

| |  |

| | Tucker Scott, CFA |

| |  |

| | Norman J. Boersma, CFA |

| | James Harper, CFA |

| | Heather Arnold, CFA |

| | Christopher James Peel, CFA |

| | Herbert J. Arnett, Jr. |

| | Portfolio Management Team |

The foregoing information reflects our analysis, opinions and portfolio holdings as of February 28, 2018, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

|

Christopher James Peel is a vice president, research analyst and portfolio manager for the Templeton Global Equity Group. Mr. Peel has global research responsibility for software, IT services and consulting, and integrated oils. Mr. Peel is group coordinator for the energy sector. Prior to joining Franklin Templeton in 2007, he was a commercial analyst at Lloyds TSB Group. Mr. Peel holds a B.Sc. in computer science from the University of Nottingham, UK, and is a Chartered Financial Analyst (CFA) charterholder. |

|

Herbert J. Arnett, Jr. is a senior vice president, portfolio manager and research analyst for the Templeton Global Equity Group. Mr. Arnett has global research responsibilities for large-cap and small-cap media, internet software and services, as well US telecommunication companies. He serves as coordinator for the telecommunication sector team, and previously served as coordinator for the consumer sector team. Previously, Mr. Arnett was the lead hedge fund trader with Templeton’s Global Equity Trading Group, where he traded European and North American markets. Prior to joining Franklin Templeton in 1996, Mr. Arnett worked at Union Bancarie Privee, Nassau, Bahamas, in international private banking, specializing in money market, foreign exchange and derivative instruments. Mr. Arnett holds a B.A. in Finance and an M.B.A. from the University of Miami. |

| | | | |

| | | |

8 | | Semiannual Report | | franklintempleton.com |

TEMPLETON FOREIGN FUND

Performance Summary as of February 28, 2018

The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses. Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities.

Performance as of 2/28/181

Cumulative total return excludes sales charges. Average annual total return includes maximum sales charges. Sales charges will vary depending on the size of the investment and the class of share purchased. The maximum is 5.75% and the minimum is 0%. Class A: 5.75% maximum initial sales charge; Advisor Class: no sales charges. For other share classes, visit franklintempleton.com.

| | | | | | | | |

| Share Class | | Cumulative Total Return2 | | | Average Annual Total Return3 | |

A | | | | | | | | |

| 6-Month | | | +3.10% | | | | -2.87% | |

| 1-Year | | | +10.75% | | | | +4.43% | |

| 5-Year | | | +33.20% | | | | +4.64% | |

| 10-Year | | | +36.34% | | | | +2.54% | |

Advisor | | | | | | | | |

| 6-Month | | | +3.33% | | | | +3.33% | |

| 1-Year | | | +11.13% | | | | +11.13% | |

| 5-Year | | | +34.90% | | | | +6.17% | |

| 10-Year | | | +39.84% | | | | +3.41% | |

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

See page 10 for Performance Summary footnotes.

| | | | |

| | | |

| franklintempleton.com | | Semiannual Report | | 9 |

TEMPLETON FOREIGN FUND

PERFORMANCE SUMMARY

Distributions (9/1/17–2/28/18)

| | | | |

| Share Class | | Net Investment Income | |

| A | | | $0.1125 | |

| C | | | $0.0524 | |

| R | | | $0.0993 | |

| R6 | | | $0.1534 | |

| Advisor | | | $0.1374 | |

Total Annual Operating Expenses4

| | | | | | |

| Share Class | | With Waiver | | Without Waiver | |

| A | | 1.10% | | | 1.19% | |

| Advisor | | 0.85% | | | 0.94% | |

Each class of shares is available to certain eligible investors and has different annual fees and expenses, as described in the prospectus.

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in developing markets involve heightened risks related to the same factors. Currency rates may fluctuate significantly over short periods of time, and can reduce returns. Because the Fund may invest its assets in companies in a specific region, including Europe, it is subject to greater risks of adverse developments in that region and/or the surrounding regions than a fund that is more broadly diversified geographically. Current political and financial uncertainty surrounding the European Union may increase market volatility and the economic risk of investing in companies in Europe. Derivatives, including currency management strategies, involve costs and can create economic leverage in the portfolio which may result in significant volatility and cause the Fund to participate in losses (as well as enable gains) on an amount that exceeds the Fund’s initial investment. The Fund may not achieve the anticipated benefits, and may realize losses when a counterparty fails to perform as promised. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

1. The Fund has an expense reduction contractually guaranteed through 12/31/19. Fund investment results reflect the expense reduction; without this reduction, the results would have been lower.

2. Cumulative total return represents the change in value of an investment over the periods indicated.

3. Average annual total return represents the average annual change in value of an investment over the periods indicated. Return for less than one year, if any, has not been annualized.

4. Figures are as stated in the Fund’s current prospectus and may differ from the expense ratios disclosed in the Your Fund’s Expenses and Financial Highlights sections in this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

| | | | |

| | | |

10 | | Semiannual Report | | franklintempleton.com |

TEMPLETON FOREIGN FUND

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs: (1) transaction costs, including sales charges (loads) on Fund purchases and redemptions; and (2) ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The table below shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The table below provides information about actual account values and actual expenses in the columns under the heading “Actual.” In these columns the Fund’s actual return, which includes the effect of Fund expenses, is used to calculate the “Ending Account Value” for each class of shares. You can estimate the expenses you paid during the period by following these steps (of course, your account value and expenses will differ from those in this illustration): Divide your account value by $1,000 (if your account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6). Then multiply the result by the number in the row for your class of shares under the headings “Actual” and “Expenses Paid During Period” (if Actual Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50). In this illustration, the actual expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Under the heading “Hypothetical” in the table, information is provided about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. This information may not be used to estimate the actual ending account balance or expenses you paid for the period, but it can help you compare ongoing costs of investing in the Fund with those of other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transactional costs. Therefore, information under the heading “Hypothetical” is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transactional costs were included, your total costs would have been higher.

| | | | | | | | | | | | | | | | | | |

| | | | | | | Actual | | | | Hypothetical | | | | |

| | | | | | | (actual return after expenses) | | | | (5% annual return before expenses) | | | | |

| | | | | | | | | Expenses | | | | | | Expenses | | | | Net |

| | | Beginning | | | | Ending | | Paid During | | | | Ending | | Paid During | | | | Annualized |

| Share | | Account | | | | Account | | Period | | | | Account | | Period | | | | Expense |

| Class | | Value 9/1/17 | | | | Value 2/28/18 | | 9/1/17–2/28/181,2 | | | | Value 2/28/18 | | 9/1/17–2/28/181,2 | | | | Ratio2 |

A | | $1,000 | | | | $1,031.00 | | $5.89 | | | | $1,018.99 | | $5.86 | | | | 1.17% |

C | | $1,000 | | | | $1,027.90 | | $9.65 | | | | $1,015.27 | | $9.59 | | | | 1.92% |

R | | $1,000 | | | | $1,029.90 | | $7.15 | | | | $1,017.75 | | $7.10 | | | | 1.42% |

R6 | | $1,000 | | | | $1,032.80 | | $3.58 | | | | $1,021.27 | | $3.56 | | | | 0.71% |

Advisor | | $1,000 | | | | $1,033.30 | | $4.64 | | | | $1,020.23 | | $4.61 | | | | 0.92% |

1. Expenses are equal to the annualized expense ratio for the six-month period as indicated above—in the far right column—multiplied by the simple average account value over the period indicated, and then multiplied by 181/365 to reflect the one-half year period.

2. Reflects expenses after fee waivers and expense reimbursements. Does not include acquired fund fees and expenses.

| | | | |

| | | |

| franklintempleton.com | | Semiannual Report | | 11 |

TEMPLETON FUNDS

Financial Highlights

Templeton Foreign Fund

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Six Months Ended | | | | | | | | | | | | | | | | |

| | | February 28, 2018 | | | Year Ended August 31, | |

| | | (unaudited) | | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 | |

| | | | | | |

Class A | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Per share operating performance | | | | | | | | | | | | | | | | | | | | | | | | |

(for a share outstanding throughout the period) | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net asset value, beginning of period | | | $ 7.81 | | | | $ 6.87 | | | | $ 6.74 | | | | $ 8.58 | | | | $ 7.67 | | | | $ 6.26 | |

| | | | | | |

Income from investment operationsa: | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net investment incomeb | | | 0.02 | | | | 0.11 | | | | 0.11 | | | | 0.12 | | | | 0.20 | c | | | 0.12 | |

| | | | | | |

Net realized and unrealized gains (losses) | | | 0.22 | | | | 0.96 | | | | 0.11 | | | | (1.52 | ) | | | 1.12 | | | | 1.44 | |

| | | | | | |

Total from investment operations | | | 0.24 | | | | 1.07 | | | | 0.22 | | | | (1.40 | ) | | | 1.32 | | | | 1.56 | |

| | | | | | |

Less distributions from: | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net investment income | | | (0.11 | ) | | | (0.13 | ) | | | (0.09 | ) | | | (0.21 | ) | | | (0.11 | ) | | | (0.15 | ) |

| | | | | | |

Net realized gains | | | — | | | | — | | | | (— | )d | | | (0.23 | ) | | | (0.30 | ) | | | — | |

| | | | | | |

Total distributions | | | (0.11 | ) | | | (0.13 | ) | | | (0.09 | ) | | | (0.44 | ) | | | (0.41 | ) | | | (0.15 | ) |

| | | | | | |

Net asset value, end of period | | | $ 7.94 | | | | $ 7.81 | | | | $ 6.87 | | | | $ 6.74 | | | | $ 8.58 | | | | $ 7.67 | |

| | | | | | |

Total returne | | | 3.10% | | | | 15.83% | | | | 3.46% | | | | (16.46)% | | | | 17.61% | | | | 25.17% | |

| | | | | | |

Ratios to average net assetsf | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses before waiver and payments by affiliates | | | 1.19% | | | | 1.21% | | | | 1.22% | | | | 1.18% | | | | 1.16% | | | | 1.19% | |

| | | | | | |

Expenses net of waiver and payments by affiliates | | | 1.17% | g | | | 1.21% | g,h | | | 1.22% | g,h | | | 1.18% | h | | | 1.16% | | | | 1.19% | g |

| | | | | | |

Net investment income | | | 0.46% | | | | 1.55% | | | | 1.66% | | | | 1.54% | | | | 2.39% | c | | | 1.72% | |

| | | | | | |

Supplemental data | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net assets, end of period (000’s) | | | $3,225,414 | | | | $3,287,394 | | | | $3,644,336 | | | | $4,165,454 | | | | $4,524,854 | | | | $3,904,719 | |

| | | | | | |

Portfolio turnover rate | | | 11.81% | | | | 42.56% | | | | 22.89% | | | | 29.12% | | | | 30.82% | | | | 32.05% | |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income share includes approximately $0.07 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.57%.

dAmount rounds to less than $0.01 per share.

eTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable, and is not annualized for periods less than one year.

fRatios are annualized for periods less than one year.

gBenefit of expense reduction rounds to less than 0.01%.

hBenefit of waiver and payments by affiliates rounds to less than 0.01%.

| | | | |

| | | |

12 | | Semiannual Report | The accompanying notes are an integral part of these financial statements. | | franklintempleton.com |

TEMPLETON FUNDS

FINANCIAL HIGHLIGHTS

Templeton Foreign Fund (continued)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Six Months Ended | | | | | | | | | | | | | | | | |

| | | February 28, 2018 | | | Year Ended August 31, | |

| | | (unaudited) | | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 | |

| | | | | | |

Class C | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Per share operating performance | | | | | | | | | | | | | | | | | | | | | | | | |

(for a share outstanding throughout the period) | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net asset value, beginning of period | | | $ 7.60 | | | | $ 6.69 | | | | $ 6.56 | | | | $ 8.35 | | | | $ 7.48 | | | | $ 6.11 | |

| | | | | | |

Income from investment operationsa: | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net investment income (loss)b | | | (0.01 | ) | | | 0.05 | | | | 0.06 | | | | 0.05 | | | | 0.13 | c | | | 0.07 | |

| | | | | | |

Net realized and unrealized gains (losses) | | | 0.22 | | | | 0.94 | | | | 0.11 | | | | (1.46 | ) | | | 1.10 | | | | 1.40 | |

| | | | | | |

Total from investment operations | | | 0.21 | | | | 0.99 | | | | 0.17 | | | | (1.41 | ) | | | 1.23 | | | | 1.47 | |

| | | | | | |

Less distributions from: | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net investment income | | | (0.05 | ) | | | (0.08 | ) | | | (0.04 | ) | | | (0.15 | ) | | | (0.06 | ) | | | (0.10 | ) |

| | | | | | |

Net realized gains | | | — | | | | — | | | | (— | )d | | | (0.23 | ) | | | (0.30 | ) | | | — | |

| | | | | | |

Total distributions | | | (0.05 | ) | | | (0.08 | ) | | | (0.04 | ) | | | (0.38 | ) | | | (0.36 | ) | | | (0.10 | ) |

| | | | | | |

Net asset value, end of period | | | $ 7.76 | | | | $ 7.60 | | | | $ 6.69 | | | | $ 6.56 | | | | $ 8.35 | | | | $ 7.48 | |

| | | | | | |

Total returne | | | 2.79% | | | | 14.92% | | | | 2.64% | | | | (17.04)% | | | | 16.72% | | | | 24.21% | |

| | | | | | |

Ratios to average net assetsf | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Expenses before waiver and payments by affiliates | | | 1.94% | | | | 1.96% | | | | 1.97% | | | | 1.93% | | | | 1.91% | | | | 1.94% | |

| | | | | | |

Expenses net of waiver and payments by affiliates | | | 1.92% | g | | | 1.96% | g,h | | | 1.97% | g,h | | | 1.93% | h | | | 1.91% | | | | 1.94% | g |

| | | | | | |

Net investment income (loss) | | | (0.29 | )% | | | 0.80% | | | | 0.91% | | | | 0.79% | | | | 1.64% | c | | | 0.97% | |

| | | | | | |

Supplemental data | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net assets, end of period (000’s) | | | $339,981 | | | | $346,032 | | | | $397,512 | | | | $468,128 | | | | $617,421 | | | | $517,468 | |

| | | | | | |

Portfolio turnover rate | | | 11.81% | | | | 42.56% | | | | 22.89% | | | | 29.12% | | | | 30.82% | | | | 32.05% | |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.07 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been (0.82)%.

dAmount rounds to less than $0.01 per share.

eTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable, and is not annualized for periods less than one year.

fRatios are annualized for periods less than one year.

gBenefit of expense reduction rounds to less than 0.01%.

hBenefit of waiver and payments by affiliates rounds to less than 0.01%.

| | | | |

| | | |

| franklintempleton.com | | The accompanying notes are an integral part of these financial statements. | Semiannual Report | | 13 |

TEMPLETON FUNDS

FINANCIAL HIGHLIGHTS

Templeton Foreign Fund (continued)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | Six Months Ended | | | | | | | | | | | | | | | | |

| | | February 28, 2018 | | | Year Ended August 31, | |

| | | (unaudited) | | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 | |

| | | | | | |

Class R | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Per share operating performance | | | | | | | | | | | | | | | | | | | | | | | | |

(for a share outstanding throughout the period) | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net asset value, beginning of period | | | $ 7.65 | | | | $ 6.73 | | | | $ 6.61 | | | | $ 8.42 | | | | $ 7.54 | | | | $ 6.16 | |

| | | | | | |

Income from investment operationsa: | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net investment incomeb | | | 0.01 | | | | 0.09 | | | | 0.09 | | | | 0.09 | | | | 0.18 | c | | | 0.10 | |

| | | | | | |

Net realized and unrealized gains (losses) | | | 0.22 | | | | 0.94 | | | | 0.10 | | | | (1.48 | ) | | | 1.09 | | | | 1.41 | |

| | | | | | |

Total from investment operations | | | 0.23 | | | | 1.03 | | | | 0.19 | | | | (1.39 | ) | | | 1.27 | | | | 1.51 | |

| | | | | | |

Less distributions from: | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net investment income | | | (0.10 | ) | | | (0.11 | ) | | | (0.07 | ) | | | (0.19 | ) | | | (0.09 | ) | | | (0.13 | ) |

| | | | | | |

Net realized gains | | | — | | | | — | | | | (— | )d | | | (0.23 | ) | | | (0.30 | ) | | | — | |

| | | | | | |

Total distributions | | | (0.10 | ) | | | (0.11 | ) | | | (0.07 | ) | | | (0.42 | ) | | | (0.39 | ) | | | (0.13 | ) |

| | | | | | |

Net asset value, end of period | | | $ 7.78 | | | | $ 7.65 | | | | $ 6.73 | | | | $ 6.61 | | | | $ 8.42 | | | | $ 7.54 | |

| | | | | | |

Total returne | | | 2.99% | | | | 15.57% | | | | 3.10% | | | | (16.63)% | | | | 17.22% | | | | 24.81% | |

| | | | | | |

Ratios to average net assetsf | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Expenses before waiver and payments by affiliates | | | 1.44% | | | | 1.46% | | | | 1.47% | | | | 1.43% | | | | 1.41% | | | | 1.44% | |

| | | | | | |

Expenses net of waiver and payments by affiliates | | | 1.42% | g | | | 1.46% | g,h | | | 1.47% | g,h | | | 1.43% | h | | | 1.41% | | | | 1.44% | g |

| | | | | | |

Net investment income | | | 0.21% | | | | 1.30% | | | | 1.41% | | | | 1.29% | | | | 2.14% | c | | | 1.47% | |

| | | | | | |

Supplemental data | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net assets, end of period (000’s) | | | $153,567 | | | | $153,516 | | | | $159,802 | | | | $174,865 | | | | $207,738 | | | | $172,393 | |

| | | | | | |

Portfolio turnover rate | | | 11.81% | | | | 42.56% | | | | 22.89% | | | | 29.12% | | | | 30.82% | | | | 32.05% | |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.07 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.32%.

dAmount rounds to less than $0.01 per share.

eTotal return is not annualized for periods less than one year.

fRatios are annualized for periods less than one year.

gBenefit of expense reduction rounds to less than 0.01%.

hBenefit of waiver and payments by affiliates rounds to less than 0.01%.

| | | | |

| | | |

14 | | Semiannual Report | The accompanying notes are an integral part of these financial statements. | | franklintempleton.com |

TEMPLETON FUNDS

FINANCIAL HIGHLIGHTS

Templeton Foreign Fund (continued)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Six Months Ended | | | | | | | | | | | | | | | | |

| | | February 28, 2018 | | | Year Ended August 31, | |

| | | (unaudited) | | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013a | |

| | | | | | |

Class R6 | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Per share operating performance | | | | | | | | | | | | | | | | | | | | | | | | |

(for a share outstanding throughout the period) | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net asset value, beginning of period | | | $ 7.70 | | | | $ 6.78 | | | | $ 6.66 | | | | $ 8.49 | | | | $ 7.59 | | | | $ 7.16 | |

| | | | | | |

Income from investment operationsb: | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net investment incomec | | | 0.04 | | | | 0.16 | | | | 0.14 | | | | 0.15 | | | | 0.25 | d | | | 0.08 | |

| | | | | | |

Net realized and unrealized gains (losses) | | | 0.22 | | | | 0.93 | | | | 0.11 | | | | (1.50 | ) | | | 1.10 | | | | 0.35 | |

| | | | | | |

Total from investment operations | | | 0.26 | | | | 1.09 | | | | 0.25 | | | | (1.35 | ) | | | 1.35 | | | | 0.43 | |

| | | | | | |

Less distributions from: | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net investment income | | | (0.15 | ) | | | (0.17 | ) | | | (0.13 | ) | | | (0.25 | ) | | | (0.15 | ) | | | — | |

| | | | | | |

Net realized gains | | | — | | | | — | | | | (— | )e | | | (0.23 | ) | | | (0.30 | ) | | | — | |

| | | | | | |

Total distributions | | | (0.15 | ) | | | (0.17 | ) | | | (0.13 | ) | | | (0.48 | ) | | | (0.45 | ) | | | — | |

| | | | | | |

Net asset value, end of period | | | $ 7.81 | | | | $ 7.70 | | | | $ 6.78 | | | | $ 6.66 | | | | $ 8.49 | | | | $ 7.59 | |

| | | | | | |

Total returnf | | | 3.28% | | | | 16.52% | | | | 3.92% | | | | (16.08)% | | | | 18.16% | | | | 6.01% | |

| | | | | | |

Ratios to average net assetsg | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Expenses before waiver and payments by affiliates | | | 0.73% | | | | 0.74% | | | | 0.72% | | | | 0.72% | | | | 0.72% | | | | 0.74% | |

| | | | | | |

Expenses net of waiver and payments by affiliates | | | 0.71% | h | | | 0.73% | h | | | 0.72% | h,i | | | 0.72% | i | | | 0.72% | | | | 0.74% | h |

| | | | | | |

Net investment income | | | 0.93% | | | | 2.03% | | | | 2.16% | | | | 2.00% | | | | 2.83% | d | | | 2.17% | |

| | | | | | |

Supplemental data | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net assets, end of period (000’s) | | | $1,694,801 | | | | $1,757,902 | | | | $880,092 | | | | $816,746 | | | | $666,249 | | | | $366,042 | |

| | | | | | |

Portfolio turnover rate | | | 11.81% | | | | 42.56% | | | | 22.89% | | | | 29.12% | | | | 30.82% | | | | 32.05% | |

aFor the period May 1, 2013 (effective date) to August 31, 2013.

bThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

cBased on average daily shares outstanding.

dNet investment income per share includes approximately $0.07 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 2.01%.

eAmount rounds to less than $0.01 per share.

fTotal return is not annualized for periods less than one year.

gRatios are annualized for periods less than one year.

hBenefit of expense reduction rounds to less than 0.01%.

iBenefit of waiver and payments by affiliates rounds to less than 0.01%.

| | | | |

| | | |

| franklintempleton.com | | The accompanying notes are an integral part of these financial statements. | Semiannual Report | | 15 |

TEMPLETON FUNDS

FINANCIAL HIGHLIGHTS

Templeton Foreign Fund (continued)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Six Months Ended | | | | | | | | | | | | | | | | |

| | | February 28, 2018 | | | Year Ended August 31, | |

| | | (unaudited) | | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 | |

| | | | | | |

Advisor Class | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Per share operating performance | | | | | | | | | | | | | | | | | | | | | | | | |

(for a share outstanding throughout the period) | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net asset value, beginning of period | | | $ 7.70 | | | | $ 6.78 | | | | $ 6.66 | | | | $ 8.49 | | | | $ 7.59 | | | | $ 6.20 | |

| | | | | | |

Income from investment operationsa: | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net investment incomeb | | | 0.03 | | | | 0.13 | | | | 0.12 | | | | 0.13 | | | | 0.22 | c | | | 0.13 | |

| | | | | | |

Net realized and unrealized gains (losses) | | | 0.23 | | | | 0.94 | | | | 0.11 | | | | (1.50 | ) | | | 1.11 | | | | 1.43 | |

| | | | | | |

Total from investment operations | | | 0.26 | | | | 1.07 | | | | 0.23 | | | | (1.37 | ) | | | 1.33 | | | | 1.56 | |

| | | | | | |

Less distributions from: | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net investment income | | | (0.14 | ) | | | (0.15 | ) | | | (0.11 | ) | | | (0.23 | ) | | | (0.13 | ) | | | (0.17 | ) |

| | | | | | |

Net realized gains | | | — | | | | — | | | | (— | )d | | | (0.23 | ) | | | (0.30 | ) | | | — | |

| | | | | | |

Total distributions | | | (0.14 | ) | | | (0.15 | ) | | | (0.11 | ) | | | (0.46 | ) | | | (0.43 | ) | | | (0.17 | ) |

| | | | | | |

Net asset value, end of period | | | $ 7.82 | | | | $ 7.70 | | | | $ 6.78 | | | | $ 6.66 | | | | $ 8.49 | | | | $ 7.59 | |

| | | | | | |

Total returne | | | 3.33% | | | | 16.10% | | | | 3.65% | | | | (16.25 | )% | | | 17.93% | | | | 25.39% | |

| | | | | | |

Ratios to average net assetsf | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Expenses before waiver and payments by affiliates | | | 0.94% | | | | 0.96% | | | | 0.97% | | | | 0.93% | | | | 0.91% | | | | 0.94% | |

| | | | | | |

Expenses net of waiver and payments by affiliates | | | 0.92% | g | | | 0.96% | g,h | | | 0.97% | g,h | | | 0.93% | h | | | 0.91% | | | | 0.94% | g |

| | | | | | |

Net investment income | | | 0.71% | | | | 1.80% | | | | 1.91% | | | | 1.79% | | | | 2.64% | c | | | 1.97% | |

| | | | | | |

Supplemental data | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net assets, end of period (000’s) | | | $1,667,369 | | | | $1,717,937 | | | | $1,125,431 | | | | $1,206,146 | | | | $1,727,057 | | | | $1,340,444 | |

| | | | | | |

Portfolio turnover rate | | | 11.81% | | | | 42.56% | | | | 22.89% | | | | 29.12% | | | | 30.82% | | | | 32.05% | |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.07 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.82%.

dAmount rounds to less than $0.01 per share.

eTotal return is not annualized for periods less than one year.

fRatios are annualized for periods less than one year.

gBenefit of expense reduction rounds to less than 0.01%.

hBenefit of waiver and payments by affiliates rounds to less than 0.01%.

| | | | |

| | | |

16 | | Semiannual Report | The accompanying notes are an integral part of these financial statements. | | franklintempleton.com |

TEMPLETON FUNDS

Statement of Investments, February 28, 2018 (unaudited)

Templeton Foreign Fund

| | | | | | | | | | | | |

| | | Industry | | | Shares | | | Value | |

| | | |

Common Stocks 98.2% | | | | | | | | | | | | |

Canada 5.0% | | | | | | | | | | | | |

Alamos Gold Inc., A | | | Metals & Mining | | | | 13,968,340 | | | $ | 70,959,167 | |

Barrick Gold Corp. | | | Metals & Mining | | | | 3,818,380 | | | | 43,987,738 | |

Cenovus Energy Inc. | | | Oil, Gas & Consumable Fuels | | | | 6,587,142 | | | | 47,945,687 | |

a Husky Energy Inc. | | | Oil, Gas & Consumable Fuels | | | | 3,829,620 | | | | 50,556,237 | |

Wheaton Precious Metals Corp. | | | Metals & Mining | | | | 7,307,912 | | | | 139,472,229 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 352,921,058 | |

| | | | | | | | | | | | |

China 10.7% | | | | | | | | | | | | |

a Baidu Inc., ADR | | | Internet Software & Services | | | | 872,000 | | | | 220,040,480 | |

China Life Insurance Co. Ltd., H | | | Insurance | | | | 18,831,800 | | | | 55,947,118 | |

China Mobile Ltd. | | | Wireless Telecommunication Services | | | | 7,794,180 | | | | 73,102,027 | |

China Telecom Corp. Ltd., H | | | Diversified Telecommunication Services | | | | 219,339,292 | | | | 96,693,764 | |

Kunlun Energy Co. Ltd. | | | Oil, Gas & Consumable Fuels | | | | 40,057,050 | | | | 37,672,089 | |

NetEase Inc., ADR | | | Internet Software & Services | | | | 209,470 | | | | 61,448,025 | |

Shandong Weigao Group Medical Polymer Co. Ltd., H | | | Health Care Equipment & Supplies | | | | 42,940,060 | | | | 29,354,816 | |

Shanghai Pharmaceuticals Holding Co. Ltd., H | | | Health Care Providers & Services | | | | 22,098,290 | | | | 55,683,754 | |

Sinopec Engineering Group Co. Ltd. | | | Construction & Engineering | | | | 61,868,670 | | | | 59,924,293 | |

Sinopharm Group Co. Ltd., H | | | Health Care Providers & Services | | | | 15,295,130 | | | | 67,524,932 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 757,391,298 | |

| | | | | | | | | | | | |

Denmark 0.5% | | | | | | | | | | | | |

Orsted AS | | | Electric Utilities | | | | 591,391 | | | | 36,905,620 | |

| | | | | | | | | | | | |

France 7.3% | | | | | | | | | | | | |

AXA SA | | | Insurance | | | | 3,085,182 | | | | 97,335,028 | |

BNP Paribas SA | | | Banks | | | | 1,840,973 | | | | 146,820,180 | |

Cie Generale des Etablissements Michelin SCA | | | Auto Components | | | | 294,680 | | | | 45,549,868 | |

Sanofi | | | Pharmaceuticals | | | | 1,133,075 | | | | 89,894,321 | |

Total SA | | | Oil, Gas & Consumable Fuels | | | | 1,201,950 | | | | 68,875,824 | |

Veolia Environnement SA | | | Multi-Utilities | | | | 2,861,260 | | | | 69,710,025 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 518,185,246 | |

| | | | | | | | | | | | |

Germany 6.8% | | | | | | | | | | | | |

Bayer AG | | | Pharmaceuticals | | | | 704,920 | | | | 82,758,034 | |

Gerresheimer AG | | | Life Sciences Tools & Services | | | | 769,760 | | | | 59,257,667 | |

innogy SE | | | Multi-Utilities | | | | 1,720,370 | | | | 68,863,317 | |

Merck KGaA | | | Pharmaceuticals | | | | 650,094 | | | | 65,209,891 | |

a MorphoSys AG | | | Life Sciences Tools & Services | | | | 906,960 | | | | 90,898,256 | |

Siemens AG | | | Industrial Conglomerates | | | | 531,282 | | | | 70,286,911 | |

Telefonica Deutschland Holding AG | | | Diversified Telecommunication Services | | | | 9,400,530 | | | | 43,466,172 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 480,740,248 | |

| | | | | | | | | | | | |

Hong Kong 1.9% | | | | | | | | | | | | |

CK Hutchison Holdings Ltd. | | | Industrial Conglomerates | | | | 8,707,000 | | | | 109,032,897 | |

Value Partners Group Ltd. | | | Capital Markets | | | | 26,572,000 | | | | 25,193,649 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 134,226,546 | |

| | | | | | | | | | | | |

India 0.8% | | | | | | | | | | | | |

Hero Motocorp Ltd. | | | Automobiles | | | | 634,530 | | | | 34,997,915 | |

Jain Irrigation Systems Ltd. | | | Machinery | | | | 11,859,610 | | | | 21,269,459 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 56,267,374 | |

| | | | | | | | | | | | |

Ireland 1.2% | | | | | | | | | | | | |

a Bank of Ireland Group PLC | | | Banks | | | | 4,912,886 | | | | 46,151,653 | |

CRH PLC | | | Construction Materials | | | | 1,273,950 | | | | 42,383,554 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 88,535,207 | |

| | | | | | | | | | | | |

| | | | |

| | | |

| franklintempleton.com | | Semiannual Report | | 17 |

TEMPLETON FUNDS

STATEMENT OF INVESTMENTS (UNAUDITED)

Templeton Foreign Fund (continued)

| | | | | | | | | | | | |

| | | Industry | | | Shares | | | Value | |

| | | |

Common Stocks (continued) | | | | | | | | | | | | |

Israel 2.1% | | | | | | | | | | | | |

Teva Pharmaceutical Industries Ltd., ADR | | | Pharmaceuticals | | | | 7,864,800 | | | $ | 147,229,056 | |

| | | | | | | | | | | | |

Italy 2.8% | | | | | | | | | | | | |

Eni SpA | | | Oil, Gas & Consumable Fuels | | | | 7,552,934 | | | | 126,368,748 | |

Tenaris SA | | | Energy Equipment & Services | | | | 4,160,710 | | | | 72,080,143 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 198,448,891 | |

| | | | | | | | | | | | |

Japan 12.2% | | | | | | | | | | | | |

Astellas Pharma Inc. | | | Pharmaceuticals | | | | 6,345,940 | | | | 93,995,203 | |

Ezaki Glico Co. Ltd. | | | Food Products | | | | 358,400 | | | | 17,566,487 | |

INPEX Corp. | | | Oil, Gas & Consumable Fuels | | | | 6,339,780 | | | | 77,921,573 | |

Kirin Holdings Co. Ltd. | | | Beverages | | | | 2,966,090 | | | | 77,234,254 | |

Panasonic Corp. | | | Household Durables | | | | 2,738,300 | | | | 43,048,576 | |

Ryohin Keikaku Co. Ltd. | | | Multiline Retail | | | | 234,530 | | | | 80,554,093 | |

Seven & i Holdings Co. Ltd. | | | Food & Staples Retailing | | | | 899,100 | | | | 37,588,539 | |

SoftBank Group Corp. | | | Wireless Telecommunication Services | | | | 2,028,670 | | | | 169,111,285 | |

Sumitomo Metal Mining Co. Ltd. | | | Metals & Mining | | | | 1,118,470 | | | | 52,744,867 | |

Sumitomo Rubber Industries Ltd. | | | Auto Components | | | | 3,966,520 | | | | 76,501,553 | |

Suntory Beverage & Food Ltd. | | | Beverages | | | | 1,415,900 | | | | 66,081,083 | |

Taiheiyo Cement Corp. | | | Construction Materials | | | | 1,876,841 | | | | 70,356,253 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 862,703,766 | |

| | | | | | | | | | | | |

Luxembourg 1.3% | | | | | | | | | | | | |

SES SA, IDR | | | Media | | | | 5,579,580 | | | | 89,377,063 | |

| | | | | | | | | | | | |

Netherlands 6.8% | | | | | | | | | | | | |

Aegon NV | | | Insurance | | | | 22,983,505 | | | | 160,724,576 | |

Flow Traders | | | Capital Markets | | | | 1,703,977 | | | | 70,015,736 | |

ING Groep NV | | | Banks | | | | 2,456,418 | | | | 43,388,106 | |

a QIAGEN NV | | | Life Sciences Tools & Services | | | | 3,140,291 | | | | 106,122,998 | |

SBM Offshore NV | | | Energy Equipment & Services | | | | 5,872,711 | | | | 100,162,613 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 480,414,029 | |

| | | | | | | | | | | | |

Singapore 1.9% | | | | | | | | | | | | |

Singapore Telecommunications Ltd. | | | Diversified Telecommunication Services | | | | 30,793,240 | | | | 78,569,602 | |

Singapore Telecommunications Ltd., ADR | | | Diversified Telecommunication Services | | | | 33,000 | | | | 837,705 | |

United Overseas Bank Ltd. | | | Banks | | | | 2,591,590 | | | | 54,562,878 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 133,970,185 | |

| | | | | | | | | | | | |

South Korea 6.7% | | | | | | | | | | | | |

DB Insurance Co. Ltd. | | | Insurance | | | | 183,810 | | | | 11,775,741 | |

Hana Financial Group Inc. | | | Banks | | | | 2,203,300 | | | | 99,823,195 | |

KB Financial Group Inc. | | | Banks | | | | 1,968,477 | | | | 116,130,054 | |

Posco Daewoo Corp. | | | Trading Companies & Distributors | | | | 1,036,900 | | | | 19,307,345 | |

Samsung Electronics Co. Ltd. | | | Technology Hardware, Storage & Peripherals | | | | 106,154 | | | | 230,246,269 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 477,282,604 | |

| | | | | | | | | | | | |

Sweden 0.6% | | | | | | | | | | | | |

Getinge AB, B | | | Health Care Equipment & Supplies | | | | 3,489,111 | | | | 44,046,031 | |

| | | | | | | | | | | | |

Switzerland 3.9% | | | | | | | | | | | | |

a Landis+Gyr Group AG | | | Electronic Equipment, Instruments & Components | | | | 355,630 | | | | 27,306,900 | |

Roche Holding AG | | | Pharmaceuticals | | | | 615,590 | | | | 142,977,004 | |

UBS Group AG | | | Capital Markets | | | | 5,530,030 | | | | 105,833,131 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 276,117,035 | |

| | | | | | | | | | | | |

| | | | |

| | | |

18 | | Semiannual Report | | franklintempleton.com |

TEMPLETON FUNDS

STATEMENT OF INVESTMENTS (UNAUDITED)

Templeton Foreign Fund (continued)

| | | | | | | | | | | | |

| | | Industry | | | Shares | | | Value | |

| | | |

Common Stocks (continued) | | | | | | | | | | | | |

Taiwan 2.2% | | | | | | | | | | | | |

Catcher Technology Co. Ltd. | | | Technology Hardware, Storage & Peripherals | | | | 3,961,120 | | | $ | 46,756,777 | |

Quanta Computer Inc. | | | Technology Hardware, Storage & Peripherals | | | | 20,220,680 | | | | 40,774,170 | |

Taiwan Semiconductor Manufacturing Co. Ltd. | | | Semiconductors & Semiconductor Equipment | | | | 7,980,000 | | | | 65,920,610 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 153,451,557 | |

| | | | | | | | | | | | |

Thailand 1.8% | | | | | | | | | | | | |

Bangkok Bank PCL, fgn | | | Banks | | | | 2,448,000 | | | | 17,874,286 | |

Bangkok Bank PCL, NVDR | | | Banks | | | | 9,123,830 | | | | 61,115,179 | |

Kasikornbank PCL, fgn | | | Banks | | | | 1,695,300 | | | | 12,486,019 | |

Kasikornbank PCL, NVDR | | | Banks | | | | 4,442,200 | | | | 32,717,155 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 124,192,639 | |

| | | | | | | | | | | | |

United Kingdom 20.0% | | | | | | | | | | | | |

Aviva PLC | | | Insurance | | | | 7,557,114 | | | | 52,611,563 | |

BAE Systems PLC | | | Aerospace & Defense | | | | 11,438,470 | | | | 91,256,664 | |

Barclays PLC | | | Banks | | | | 29,338,430 | | | | 86,248,770 | |

BP PLC | | | Oil, Gas & Consumable Fuels | | | | 28,917,960 | | | | 189,198,002 | |

a Cobham PLC | | | Aerospace & Defense | | | | 22,941,809 | | | | 35,838,541 | |

HSBC Holdings PLC (GBP Traded) | | | Banks | | | | 11,683,650 | | | | 115,365,625 | |

HSBC Holdings PLC (HKD Traded) | | | Banks | | | | 989,600 | | | | 9,863,186 | |

Johnson Matthey PLC | | | Chemicals | | | | 2,214,526 | | | | 95,595,289 | |

Kingfisher PLC | | | Specialty Retail | | | | 23,879,104 | | | | 117,678,706 | |

Rolls-Royce Holdings PLC | | | Aerospace & Defense | | | | 5,040,818 | | | | 58,276,251 | |

Royal Dutch Shell PLC, B | | | Oil, Gas & Consumable Fuels | | | | 5,550,600 | | | | 177,391,674 | |

Shire PLC | | | Biotechnology | | | | 1,367,760 | | | | 58,552,950 | |

SIG PLC | | | Trading Companies & Distributors | | | | 26,088,083 | | | | 52,086,878 | |

a Standard Chartered PLC | | | Banks | | | | 16,424,505 | | | | 183,368,271 | |

Travis Perkins PLC | | | Trading Companies & Distributors | | | | 2,675,920 | | | | 47,347,212 | |

Vodafone Group PLC | | | Wireless Telecommunication Services | | | | 16,907,095 | | | | 47,433,456 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,418,113,038 | |

| | | | | | | | | | | | |

United States 1.7% | | | | | | | | | | | | |

Oracle Corp. | | | Software | | | | 2,352,910 | | | | 119,221,950 | |

| | | | | | | | | | | | |

| | | |

Total Common Stocks

(Cost $5,904,639,395) | | | | | | | | | | | 6,949,740,441 | |

| | | | | | | | | | | | |

| | | | |

| | | |

| franklintempleton.com | | Semiannual Report | | 19 |

TEMPLETON FUNDS

STATEMENT OF INVESTMENTS (UNAUDITED)

Templeton Foreign Fund (continued)

| | | | | | | | |

| | | Principal | | | | |

| | | Amount | | | Value | |

| | |

Short Term Investments 1.4% | | | | | | | | |

| | |

Time Deposits 1.4% | | | | | | | | |

United States 1.4% | | | | | | | | |

National Australia Bank Ltd., 1.32%, 3/01/18 | | $ | 49,000,000 | | | $ | 49,000,000 | |

Royal Bank of Canada, 1.37%, 3/01/18 | | | 50,600,000 | | | | 50,600,000 | |

| | | | | | | | |

Total Time Deposits (Cost $99,600,000) | | | | | | | 99,600,000 | |

| | | | | | | | |

Total Investments (Cost $6,004,239,395) 99.6% | | | | | | | 7,049,340,441 | |

Other Assets, less Liabilities 0.4% | | | | | | | 31,792,478 | |

| | | | | | | | |

| | |

Net Assets 100.0% | | | | | | $ | 7,081,132,919 | |

| | | | | | | | |

See Abbreviations on page 32.

aNon-income producing.

| | | | |

| | | |

20 | | Semiannual Report | The accompanying notes are an integral part of these financial statements. | | franklintempleton.com |

TEMPLETON FUNDS

Financial Statements

Statement of Assets and Liabilities

February 28, 2018 (unaudited)

Templeton Foreign Fund

| | | | |

Assets: | | | | |

Investments in securities: | | | | |

Cost - Unaffiliated issuers | | | $6,004,239,395 | |

| | | | |

| |

Value - Unaffiliated issuers | | | $7,049,340,441 | |

Cash | | | 141,222 | |

Receivables: | | | | |

Investment securities sold | | | 18,955,475 | |

Capital shares sold | | | 9,600,254 | |

Dividends | | | 35,606,415 | |

European Union tax reclaims | | | 6,485,224 | |

Other assets | | | 7,662 | |

| | | | |

Total assets | | | 7,120,136,693 | |

| | | | |

Liabilities: | | | | |

Payables: | | | | |

Investment securities purchased | | | 18,019,798 | |

Capital shares redeemed | | | 13,270,350 | |

Management fees | | | 3,347,586 | |

Distribution fees | | | 948,336 | |

Transfer agent fees | | | 2,529,054 | |

Accrued expenses and other liabilities | | | 888,650 | |

| | | | |

Total liabilities | | | 39,003,774 | |

| | | | |

| |

Net assets, at value | | | $7,081,132,919 | |

| | | | |

| |

Net assets consist of: | | | | |

Paid-in capital | | | $6,554,544,194 | |

Distributions in excess of net investment income | | | (88,738 | ) |

Net unrealized appreciation (depreciation) | | | 1,045,922,677 | |

Accumulated net realized gain (loss) | | | (519,245,214 | ) |

| | | | |

| |

Net assets, at value | | | $7,081,132,919 | |

| | | | |

| | | | | | |

| | | |

| franklintempleton.com | | The accompanying notes are an integral part of these financial statements. | Semiannual Report | | 21 |

TEMPLETON FUNDS

FINANCIAL STATEMENTS

Statement of Assets and Liabilities (continued)

February 28, 2018 (unaudited)

Templeton Foreign Fund

| | | | |

Class A: | | | | |

Net assets, at value | | | $3,225,414,383 | |

| | | | |

Shares outstanding | | | 406,263,246 | |

| | | | |

Net asset value per sharea | | | $7.94 | |

| | | | |

Maximum offering price per share (net asset value per share ÷ 94.25%) | | | $8.42 | |

| | | | |

Class C: | | | | |

Net assets, at value | | | $ 339,981,134 | |

| | | | |