UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSRS

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-02781

Templeton Funds

(Exact name of registrant as specified in charter)

300 S.E. 2nd Street, Fort Lauderdale, FL 33301-1923

(Address of principal executive offices) (Zip code)

Craig S. Tyle, One Franklin Parkway, San Mateo, CA 94403-1906

(Name and address of agent for service)

Registrant's telephone number, including area code: (954) 527-7500_

Date of fiscal year end: _8/31__

Date of reporting period: 2/29/16_

Item 1. Reports to Stockholders.

Semiannual Report

and Shareholder Letter

February 29, 2016

Templeton World Fund

A SERIES OF TEMPLETON FUNDS

Sign up for electronic delivery at franklintempleton.com/edelivery

| |

| Contents | |

| Semiannual Report | |

| Templeton World Fund | 3 |

| Performance Summary | 8 |

| Your Fund’s Expenses | 11 |

| Financial Highlights and Statement of Investments | 13 |

| Financial Statements | 21 |

| Notes to Financial Statements | 25 |

| Shareholder Information | 34 |

Visit franklintempleton.com for fund updates, to access your account, or to find helpful financial planning tools.

2 Semiannual Report

franklintempleton.com

Semiannual Report

Templeton World Fund

This semiannual report for Templeton World Fund covers the period ended February 29, 2016.

Your Fund’s Goal and Main Investments

The Fund seeks long-term capital growth. Under normal market conditions, the Fund invests primarily in equity securities of companies located anywhere in the world, including developing markets. Under normal circumstances, the Fund will invest in issuers located in at least three different countries (including the U.S.).

Performance Overview

The Fund’s Class A shares had a -12.00% cumulative total return for the six months under review. In comparison, the MSCI World Index, which measures stock market performance in global developed markets, had a -4.94% total return.1 The Fund’s long-term relative results are shown in the Performance Summary beginning on page 8. For the 10-year period ended February 29, 2016, the Fund’s Class A shares delivered a +30.75% cumulative total return, compared with the MSCI World Index’s +53.76% cumulative total return for the same period.1 Please note index performance information is provided for reference and we do not attempt to track the index but rather undertake investments on the basis of fundamental research. You can find more performance data in the Performance Summary.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

Economic and Market Overview

The global economy expanded moderately during the six months under review. For global stocks, concerns about China’s slowing economy and tumbling stock market, declining commodity prices, tensions between Russia and Turkey, and uncertainty about the U.S. Federal Reserve’s (Fed’s) timing for raising interest rates contributed to market volatility. Toward

period-end, equity markets regained some ground after the Fed’s decision to increase its target interest rate alleviated some worries about a change in U.S. monetary policy. Also bolstering stocks were hopes of additional stimulus measures from key global central banks and the Bank of Japan’s (BOJ’s) decision to cut interest rates. Oil prices declined sharply amid strong global supply that exceeded demand. Gold prices fell for most of the period but recovered toward period-end. The U.S. dollar appreciated against most currencies, which reduced returns of many foreign assets in U.S. dollar terms. In this environment, global developed market stocks overall, as measured by the MSCI World Index, declined during the period.

The U.S. economy grew moderately in the third and fourth quarters of 2015 amid healthy consumer spending, slower export growth, and reduced state and local government spending. At its December 2015 meeting, the Fed raised its target range for the federal funds rate to 0.25%–0.50%, as poli-cymakers cited the labor market’s considerable improvement and were reasonably confident that inflation would move back to the Fed’s 2% medium-term objective. The Fed kept its interest rate unchanged at its January meeting and indicated that given increased uncertainty arising from declining oil prices and slowing growth in China, it would monitor global economic

1. Source: Morningstar. As of 2/29/16, the Fund’s Class A 10-year average annual total return not including the maximum sales charge was +2.72%, compared with the MSCI

World Index’s 10-year average annual total return of +4.40%.

The index is unmanaged and includes reinvestment of any income or distributions. One cannot invest directly in an index, and an index is not representative of the

Fund’s portfolio.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI

begins on page 17.

franklintempleton.com

Semiannual Report 3

TEMPLETON WORLD FUND

and financial developments and their implications on the U.S. labor market and inflation.

In Europe, U.K. fourth-quarter economic growth gained momentum from the services sector. The eurozone grew modestly during the period and generally benefited from lower oil prices, a weaker euro that supported exports, the European Central Bank’s (ECB’s) accommodative policy and expectations of further ECB stimulus. The eurozone’s annual inflation rate rose for most of the period but declined toward period-end due to a fall in energy prices. The ECB maintained its benchmark interest rates, although it reduced its bank deposit rate in December to boost the region’s slowing growth.

Japan’s economy contracted in the fourth quarter after expanding in the third quarter, as private consumption and housing investment declined. The BOJ took several actions during the period, including lowering its inflation forecasts, and reorganizing its stimulus program to increase exposure to long-term government bonds and exchange-traded funds. In January, the BOJ introduced a negative interest rate on excess reserves kept by financial institutions with the central bank, in an effort to boost lending and support inflation.

In emerging markets, economic growth generally moderated. China’s economy grew in the fourth quarter at an annual rate that was largely in line with the government’s target. Russia’s 2015 economic growth contracted because of declining oil prices and a weakening Russian ruble, while Brazil’s economy shrank amid weakness in the mining and services sectors. Central bank actions varied across emerging markets during the six months under review, as some banks raised interest rates in response to rising inflation and weakening currencies, while others lowered interest rates to promote economic growth. In the recent global environment, emerging market stocks overall, as measured by the MSCI Emerging Markets Index, fell for the six-month period.

Investment Strategy

Our investment strategy employs a bottom-up, value-oriented, long-term approach. We focus on the market price of a company’s securities relative to our evaluation of the company’s long-term earnings, asset value and cash flow potential. As we look worldwide, we consider specific companies, rather than sectors or countries, while doing in-depth research to construct a bargain list from which we buy. Before we make a purchase, we look at the company’s price/earnings ratio, price/cash flow ratio, profit margins and liquidation value.

Manager’s Discussion

Market headwinds intensified during the six months under review as concerns about debt, deflation and growth weighed on global share prices. Cyclical sectors such as energy, materials and financials bore the brunt of the downturn, as did emerging markets and Europe. Our strategy of fundamentally oriented, long-term value investing remained out of favor during much of the period, although promising signs of a recovery did emerge toward period-end. However, performance was led primarily by stocks offering either strong growth momentum or counter-cyclical defensive characteristics. Given the rising demand for such attributes and their relative scarcity, the valuations of stocks fitting this description have become unusually expensive, in our analysis. By contrast, the value-oriented stocks that we favor as patient and disciplined investors have become the cheapest since the tech bubble frenzy at the turn of the century. The result was a distinctly two-tiered market characterized by expensive and popular stocks on one end, and cheap and unloved stocks on the other.

In our opinion, this two-tiered market is in many ways the inverse of the tech bubble period. Back then, it was investor greed that propelled growth stocks to such extreme heights, and all it took was a little bit of bad news to topple those securities. In the recent environment, we believed it was investor fear that was propping up growth and perceived “safe” stocks as investors paid for the perception of certainty in a very uncertain environment. Once again, value stocks were left behind, and discounted such pessimism so that we think the mere absence of bad news could be all it takes to spark a value recovery. With value stocks trading at more than two standard deviations below their long-term average multiples—in many cases cheaper than during the depths of the global financial crisis—the current environment for bargain hunters appeared attractive to us.

Yet, the reality has been anything but favorable for value investors in recent quarters, and our positive view remained in the minority. This experience has been largely reminiscent of the late 1990s when our avoidance of what we deemed irrationally expensive “new economy” sectors in preference of cyclically depressed “old economy” stocks resulted in sustained performance challenges until reality finally set in and the market eventually rebalanced. Indeed, during the period under review, our overweighted positions in cyclically depressed, unloved sectors such as financials and energy (where we found what we considered abundant value) and an underweighted position in the expensive and defensive consumer staples sector (where

4 Semiannual Report

franklintempleton.com

TEMPLETON WORLD FUND

| | |

| Top 10 Sectors/Industries | | |

| 2/29/16 | | |

| | % of Total | |

| | Net Assets | |

| Banks | 16.2 | % |

| Pharmaceuticals | 10.2 | % |

| Oil, Gas & Consumable Fuels | 9.3 | % |

| Insurance | 6.1 | % |

| Technology Hardware, Storage & Peripherals | 4.8 | % |

| Automobiles | 4.3 | % |

| Energy Equipment & Services | 4.1 | % |

| Software | 3.9 | % |

| Biotechnology | 3.5 | % |

| Media | 3.4 | % |

value appeared limited to us) all notably detracted from relative performance.2

The financials sector was a major laggard, delivering the bulk of absolute and relative losses and accounting for several of the Fund’s biggest detractors. Swiss financial services firm Credit Suisse Group was a significant detractor in the sector, declining after the firm scrapped profitability targets and announced a multi-billion dollar equity raise to bolster capital levels and fund its strategic restructuring. Although we believed Credit Suisse could have closed its capital deficit over time, the equity raise effectively allowed the company to implement its cost-saving and growth strategies immediately. The long-term benefits unlocked by Credit Suisse’s restructuring—including increased focus on its growth-oriented wealth management franchise, an optimization of its investment banking profit center and additional investment in its fast-growing Asia-Pacific business—were not properly reflected in its share price, and we remained positive on the company and its strategic direction under new management. Across the European financials sector, banks traded at record low valuations amid a confluence of stock-specific and macroeconomic fears. Overall, we think such concerns were overdone given the relatively low exposure of European loan books to commodities and energy, the incrementally better economic data coming out of Europe, and the continued and willing support of the ECB for the regional financial system.

Elsewhere among beaten-down cyclical sectors, an overweighted position in energy notably detracted. Shares of U.S. natural gas producer Chesapeake Energy led the sector lower due to slumping gas prices, an overleveraged balance sheet and

legacy operational issues. The firm mounted an ambitious turnaround under new management and we were encouraged by the progress being made deleveraging, lowering costs, increasing efficiencies and improving Chesapeake’s long-term production growth profile. This holding is one of the more leveraged in our energy portfolio as we tend to favor firms with strong balance sheets capable of weathering lower-for-longer commodity price cycles. However, at what we deemed severely depressed valuations and with apparent catalysts under new management, we believed the risk versus reward proposition for Chesapeake remained compelling.

More generally, although the recent oil price decline was painful for our overweighted energy position, we believe such price levels could accelerate the supply adjustment process required to stabilize the market. The huge market for oil contracts tends to exacerbate price swings, and this has certainly felt to us like a situation where financial speculation caused prices to overshoot fundamentals. Virtually no production outside the Middle East is profitable below US$30 per barrel, and even in the Middle East and elsewhere in the Organization of the Petroleum Exporting Countries cartel, oil-dependent national budgets experienced severe strains at these price levels. We do not know if oil prices have definitively bottomed, but we believe that the recent situation is unsustainable for corporate and national oil producers, and we continue to find compelling bargains in the energy sector in this environment.

We found fewer opportunities in consumer staples, which has become the most expensive in at least a decade by nearly all major measures, including earnings, book value and cash flow multiples, while yielding the lowest dividend since the global financial crisis. Despite the sector’s stable earnings and balance sheet profile, we do not favor richly valued companies in an ultra-competitive industry selling commoditized products at single-digit profit margins. The few bargains we found in the consumer staples sector were mostly in special situations or restructuring stories, and our underweighting and stock selection hurt relative performance.

We found selectively better opportunities in telecommunication services, another relative detractor due to stock selection, although not necessarily among the more stable and defensive firms that have propped up the sector.3 As Sir John Templeton once wrote, “To get a bargain price, you have to look where the public is most frightened and pessimistic.” Within the telecommunications sector, Spanish mobile phone company Telefonica is a great example. Economic weakness in Spain and

2. The financials sector comprises banks, capital markets, consumer finance, diversified financial services and insurance in the SOI. The energy sector comprises energy

equipment and services; and oil, gas and consumable fuels in the SOI. The consumer staples sector comprises food and staples retailing in the SOI.

3. The telecommunication services sector comprises diversified telecommunication services and wireless telecommunication services in the SOI.

franklintempleton.com

Semiannual Report 5

| | |

| T E M P L E T O N W O R L D F U N D | | |

| |

| |

| |

| Top 10 Holdings | | |

| 2/29/16 | | |

| Company | % of Total | |

| Sector/Industry, Country | Net Assets | |

| Samsung Electronics Co. Ltd. | 3.5 | % |

| Technology Hardware, Storage & Peripherals, | | |

| South Korea | | |

| Microsoft Corp. | 2.7 | % |

| Software, U.S. | | |

| Amgen Inc. | 2.6 | % |

| Biotechnology, U.S. | | |

| Citigroup Inc. | 2.2 | % |

| Banks, U.S. | | |

| BNP Paribas SA | 2.1 | % |

| Banks, France | | |

| JPMorgan Chase & Co. | 2.0 | % |

| Banks, U.S. | | |

| Nissan Motor Co. Ltd. | 2.0 | % |

| Automobiles, Japan | | |

| Roche Holding AG | 1.9 | % |

| Pharmaceuticals, Switzerland | | |

| Sanofi | 1.9 | % |

| Pharmaceuticals, France | | |

| Teva Pharmaceutical Industries Ltd., ADR | 1.8 | % |

| Pharmaceuticals, Israel | | |

a deepening malaise in Brazil, Telefonica’s two main markets, have depressed sentiment, driving shares to 12-year lows. Although Telefonica’s management acknowledged recent difficulties in its end-markets, it also confirmed solid operational progress and an improving competitive positioning, suggesting that strategic initiatives are producing the desired results. Tele-fonica took major steps to streamline and focus its operations where it has the best growth opportunities, exiting minor Euro-pean markets and using cash to pay down debt and improve its market position in Brazil, Spain and Germany. With Spain exiting recession and the commercial environment in Brazil likely to improve over our investment horizon, Telefonica appears well positioned for positive long-term performance, in our analysis.

Turning to contributors, stock selection also supported the relative performance of the Fund’s information technology holdings.4 U.S. software developer Microsoft was among the Fund’s top contributors, underscoring CEO Satya Nadella’s positive progress repositioning the firm to compete in mobile and cloud computing. We expect that the continued migration

to cloud computing could allow Microsoft to post strong growth and capture revenue and market share opportunities from other parts of the technology sector. Elsewhere in technology, the IT hardware environment has been more challenging, with traditional personal computer and printing companies coming under heavy pressure and strong growth trends in tablets and smart-phones moderating. In our analysis, profit margins may improve as costs are reduced, but revenue growth is likely to remain elusive and bargains limited. The semiconductor industry was negatively impacted by the slowdown in hardware end-markets as well as by intensifying pricing pressures. We believe value opportunities may remain limited as industry participants will have to navigate a weak demand environment, elevated inventory levels, slowing mergers and acquisitions activity and unattractive equity valuations.

Stock selection in consumer discretionary and materials also helped relative performance.5 From the former sector, shares of U.S. fashion retailer Michael Kors Holdings rebounded during the review period after sales rose the most in almost four years due to better-than-expected holiday results. Despite continued investor pessimism, the progress we anticipated because of an accessories revamp and a strengthened e-commerce platform appeared to be coming to fruition, allowing the firm to bolster growth during a holiday period that was mediocre for many other retailers. Michael Kors maintains a healthy balance sheet and solid cash-generating capabilities, and we continued to monitor the company and industry closely to assess the firm’s medium-term growth prospects. From the materials sector, a new position in Switzerland-based commodities trader and diversified miner Glencore stood out, regaining ground following acute weakness. In our opinion, a general misunderstanding of the firm’s trading business and funding model, combined with existential fears surrounding the balance sheet in an environment of falling commodity prices, had weighed heavily on the stock, driving shares far below the firm’s 2011 initial public offering price. Glencore has since responded decisively to market concerns by selling assets, cutting debt, improving liquidity and gaining efficiencies across its industrial and trading businesses. Although the stock may remain volatile in the near term, we believed the recent share price understates the long-term advantages of Glencore’s diversified model.

It is important to recognize the effect of currency movements on the Fund’s performance. In general, if the value of the U.S. dollar goes up compared with a foreign currency, an investment

4. The information technology sector comprises communications equipment; electronic equipment, instruments and components; IT services; semiconductors and semi-

conductor equipment; software; and technology hardware, storage and peripherals in the SOI.

5. The consumer discretionary sector comprises automobiles; media; specialty retail; and textiles, apparel and luxury goods in the SOI. The materials sector comprises chem-

icals, construction materials, and metals and mining in the SOI.

See www.franklintempletondatasources.com for additional data provider information.

6 Semiannual Report

franklintempleton.com

TEMPLETON WORLD FUND

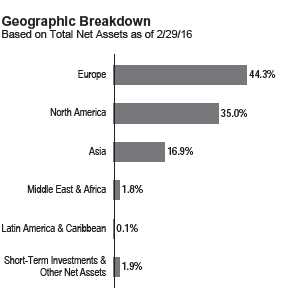

| | |

| Top 10 Countries | | |

| 2/29/16 | | |

| | % of Total | |

| | Net Assets | |

| U.S. | 33.8 | % |

| U.K. | 16.2 | % |

| France | 7.1 | % |

| South Korea | 7.1 | % |

| Switzerland | 5.7 | % |

| Germany | 4.7 | % |

| Japan | 4.2 | % |

| Netherlands | 3.3 | % |

| Italy | 2.4 | % |

| Singapore | 2.2 | % |

traded in that foreign currency will go down in value because it will be worth fewer U.S. dollars. This can have a negative effect on Fund performance. Conversely, when the U.S. dollar weakens in relation to a foreign currency, an investment traded in that foreign currency will increase in value, which can contribute to Fund performance. For the six months ended February 29, 2016, the U.S. dollar rose in value relative to most currencies. As a result, the Fund’s performance was negatively affected by the portfolio’s substantial investment in securities with non-U.S. currency exposure.

A critical lesson that we have learned through six decades of investing in global equity markets is that returns seem to accrue to value intermittently. Our style of investing has historically provided positive performance over a long-term investment horizon. But, it has rarely been a steady appreciation. At Tem-pleton, we buy on pessimism, and the market can remain at odds with our portfolios for a considerable stretch. However, empirical evidence shows that when the value cycle turns, it does so swiftly and abruptly. We believe being properly positioned for these turns is essential to capturing the long-term benefits of the value investment discipline. We have been witnessing historic extremes in the discount afforded to value relative to the rest of the market. Although this environment has been, and may remain, painful for some time, we believe the eventual normalization of these extremes represents the most compelling opportunity in equity markets today, and we have sought to position our portfolio accordingly.

Thank you for your continued participation in Templeton World Fund. We look forward to serving your future investment needs.

The foregoing information reflects our analysis, opinions and portfolio

holdings as of February 29, 2016, the end of the reporting period. The

way we implement our main investment strategies and the resulting

portfolio holdings may change depending on factors such as market

and economic conditions. These opinions may not be relied upon as

investment advice or an offer for a particular security. The information

is not a complete analysis of every aspect of any market, country,

industry, security or the Fund. Statements of fact are from sources

considered reliable, but the investment manager makes no representa-

tion or warranty as to their completeness or accuracy. Although

historical performance is no guarantee of future results, these insights

may help you understand our investment management philosophy.

franklintempleton.com

Semiannual Report 7

TEMPLETON WORLD FUND

Performance Summary as of February 29, 2016

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

| | | | | | |

| Net Asset Value | | | | | | |

| |

| Share Class (Symbol) | | 2/29/16 | | 8/31/15 | | Change |

| A (TEMWX) | $ | 13.50 | $ | 16.51 | -$ | 3.01 |

| C (TEWTX) | $ | 13.00 | $ | 15.86 | -$ | 2.86 |

| R6 (FTWRX) | $ | 13.46 | $ | 16.50 | -$ | 3.04 |

| Advisor (TWDAX) | $ | 13.47 | $ | 16.50 | -$ | 3.03 |

| |

| |

| Distributions1 (9/1/15–2/29/16) | | | | | | |

| |

| | | Dividend | | Long-Term | | |

| Share Class | | Income | | Capital Gain | | Total |

| A | $ | 0.2800 | $ | 0.8489 | $ | 1.1289 |

| C | $ | 0.1507 | $ | 0.8489 | $ | 0.9996 |

| R6 | $ | 0.3414 | $ | 0.8489 | $ | 1.1903 |

| Advisor | $ | 0.3216 | $ | 0.8489 | $ | 1.1705 |

See page 10 for Performance Summary footnotes.

8 Semiannual Report

franklintempleton.com

TEMPLETON WORLD FUND

PERFORMANCE SUMMARY

Performance as of 2/29/162

Cumulative total return excludes sales charges. Average annual total returns and value of $10,000 investment include maximum sales charges. Class A: 5.75% maximum initial sales charge; Class C: 1% contingent deferred sales charge in first year only; Class R6/Advisor Class: no sales charges.

| | | | | | | | | | |

| | | | | | | | | | Total Annual | |

| | Cumulative | | Average Annual | | | Value of $10,000 | Average Annual | | Operating | |

| Share Class | Total Return3 | | Total Return4 | | | Investment5 | Total Return (3/31/16)6 | | Expenses7 | |

| A | | | | | | | | | 1.06 | % |

| 6-Month | -12.00 | % | -17.08 | % | $ | 8,292 | | | | |

| 1-Year | -17.87 | % | -22.60 | % | $ | 7,740 | -15.58 | % | | |

| 5-Year | +13.40 | % | +1.34 | % | $ | 10,687 | +2.95 | % | | |

| 10-Year | +30.75 | % | +2.11 | % | $ | 12,322 | +2.76 | % | | |

| C | | | | | | | | | 1.81 | % |

| 6-Month | -12.30 | % | -13.12 | % | $ | 8,688 | | | | |

| 1-Year | -18.47 | % | -19.23 | % | $ | 8,077 | -11.92 | % | | |

| 5-Year | +9.23 | % | +1.78 | % | $ | 10,923 | +3.40 | % | | |

| 10-Year | +21.28 | % | +1.95 | % | $ | 12,128 | +2.59 | % | | |

| R6 | | | | | | | | | 0.72 | % |

| 6-Month | -11.85 | % | -11.85 | % | $ | 8,815 | | | | |

| 1-Year | -17.59 | % | -17.59 | % | $ | 8,241 | -10.02 | % | | |

| Since Inception (5/1/13) | -1.80 | % | -0.64 | % | $ | 9,820 | +2.02 | % | | |

| Advisor8 | | | | | | | | | 0.81 | % |

| 6-Month | -11.90 | % | -11.90 | % | $ | 8,810 | | | | |

| 1-Year | -17.69 | % | -17.69 | % | $ | 8,231 | -10.13 | % | | |

| 5-Year | +14.78 | % | +2.80 | % | $ | 11,478 | +4.45 | % | | |

| 10-Year | +33.95 | % | +2.97 | % | $ | 13,395 | +3.63 | % | | |

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

See page 10 for Performance Summary footnotes.

franklintempleton.com

Semiannual Report 9

TEMPLETON WORLD FUND

PERFORMANCE SUMMARY

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. In addition, smaller company stocks have historically experienced more price volatility than larger company stocks, especially over the short term. To the extent the Fund focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a fund that invests in a wider variety of countries, regions, industries, sectors or investments. Derivatives, including currency management strategies, involve costs and can create economic leverage in the portfolio, which may result in significant volatility and cause the Fund to participate in losses (as well as enable gains) on an amount that exceeds the Fund’s initial investment. The Fund may not achieve the anticipated benefits, and may realize losses when a counterparty fails to perform as promised. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

Class C: These shares have higher annual fees and expenses than Class A shares.

Class R6: Shares are available to certain eligible investors as described in the prospectus.

Advisor Class: Shares are available to certain eligible investors as described in the prospectus.

1. The distribution amount is the sum of the dividend payments to shareholders for the period shown and includes only estimated tax-basis net investment income and

capital gain.

2. The Fund has a fee waiver associated with any investment in a Franklin Templeton money fund, contractually guaranteed through at least its current fiscal year-end. Fund

investment results reflect the fee waiver, to the extent applicable; without this reduction, the results would have been lower.

3. Cumulative total return represents the change in value of an investment over the periods indicated.

4. Average annual total return represents the average annual change in value of an investment over the periods indicated. Return for less than one year, if any, has not

been annualized.

5. These figures represent the value of a hypothetical $10,000 investment in the Fund over the periods indicated.

6. In accordance with SEC rules, we provide standardized average annual total return information through the latest calendar quarter.

7. Figures are as stated in the Fund’s current prospectus. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to

become higher than the figures shown.

8. Effective 5/15/06, the Fund began offering Advisor Class shares, which do not have sales charges or a Rule 12b-1 plan. Performance quotations for this class reflect the

following methods of calculation: (a) For periods prior to 5/15/06, a restated figure is used based upon the Fund’s Class A performance, excluding the effect of Class A’s

maximum initial sales charge, but reflecting the effect of the Class A Rule 12b-1 fees; and (b) for periods after 5/15/06, actual Advisor Class performance is used reflecting all

charges and fees applicable to that class. Since 5/15/06 (commencement of sales), the cumulative and average annual total returns of Advisor Class shares were +27.73%

and +2.53%.

10 Semiannual Report

franklintempleton.com

TEMPLETON WORLD FUND

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases; and

- Ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

1. Divide your account value by $1,000.

If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6.

2. Multiply the result by the number under the heading “Expenses Paid During Period.”

If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50.

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

franklintempleton.com

Semiannual Report 11

TEMPLETON WORLD FUND

YOUR FUND’S EXPENSES

| | | | | | |

| | | Beginning Account | | Ending Account | | Expenses Paid During |

| Share Class | | Value 9/1/15 | | Value 2/29/16 | | Period* 9/1/15–2/29/16 |

| A | | | | | | |

| Actual | $ | 1,000 | $ | 880.00 | $ | 4.95 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,019.59 | $ | 5.32 |

| C | | | | | | |

| Actual | $ | 1,000 | $ | 877.00 | $ | 8.45 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,015.86 | $ | 9.07 |

| R6 | | | | | | |

| Actual | $ | 1,000 | $ | 881.50 | $ | 3.37 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,021.28 | $ | 3.62 |

| Advisor | | | | | | |

| Actual | $ | 1,000 | $ | 881.00 | $ | 3.79 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,020.84 | $ | 4.07 |

*Expenses are calculated using the most recent six-month expense ratio, annualized for each class (A: 1.06%; C: 1.81%; R6: 0.72%; and Advi-

sor: 0.81%), multiplied by the average account value over the period, multiplied by 182/366 to reflect the one-half year period.

12 Semiannual Report

franklintempleton.com

TEMPLETON WORLD FUND

| | | | | | | | | | | | | | | | | | |

| Financial Highlights | | | | | | | | | | | | | | | | | | |

| | | Six Months Ended | | | | | | Year Ended August 31, | | | | |

| | | February 29, 2016 | | | | | | | | | | | | | | | | |

| | | (unaudited) | | | 2015 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| Class A | | | | | | | | | | | | | | | | | | |

| Per share operating performance | | | | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the period) | | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of period | $ | 16.51 | | $ | 20.18 | | $ | 18.02 | | $ | 15.06 | | $ | 14.21 | | $ | 12.74 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.08 | | | 0.29 | | | 0.43 | c | | 0.25 | | | 0.29 | | | 0.24 | |

| Net realized and unrealized gains (losses) | | (1.96 | ) | | (2.35 | ) | | 2.75 | | | 3.38 | | | 0.84 | | | 1.47 | |

| Total from investment operations | | (1.88 | ) | | (2.06 | ) | | 3.18 | | | 3.63 | | | 1.13 | | | 1.71 | |

| Less distributions from: | | | | | | | | | | | | | | | | | | |

| Net investment income | | (0.28 | ) | | (0.52 | ) | | (0.19 | ) | | (0.42 | ) | | (0.28 | ) | | (0.24 | ) |

| Net realized gains | | (0.85 | ) | | (1.09 | ) | | (0.83 | ) | | (0.25 | ) | | — | | | — | |

| Total distributions | | (1.13 | ) | | (1.61 | ) | | (1.02 | ) | | (0.67 | ) | | (0.28 | ) | | (0.24 | ) |

| Net asset value, end of period | $ | 13.50 | | $ | 16.51 | | $ | 20.18 | | $ | 18.02 | | $ | 15.06 | | $ | 14.21 | |

| |

| Total returnd | | (12.00 | )% | | (10.59 | )% | | 17.96 | % | | 24.71 | % | | 8.18 | % | | 13.45 | % |

| |

| Ratios to average net assetse | | | | | | | | | | | | | | | | | | |

| Expenses | | 1.06 | %f | | 1.06 | %f | | 1.05 | % | | 1.05 | %g | | 1.09 | % | | 1.07 | %g |

| Net investment income | | 1.03 | % | | 1.61 | % | | 2.20 | %c | | 1.49 | % | | 1.99 | % | | 1.62 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000’s) | $ | 3,967,753 | | $ | 4,791,792 | | $ | 5,917,398 | | $ | 5,278,292 | | $ | 4,857,469 | | $ | 5,067,228 | |

| Portfolio turnover rate | | 8.76 | % | | 15.73 | % | | 18.56 | % | | 17.57 | % | | 18.77 | % | | 16.11 | % |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases

of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.18 per share related to income received in the form of special dividends in connection with certain Fund holdings.

Excluding this amount, the ratio of net investment income to average net assets would have been 1.30%.

dTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable, and is not annualized for periods less than one year.

eRatios are annualized for periods less than one year.

fBenefit of waiver and payments by affiliates rounds to less than 0.01%.

gBenefit of expense reduction rounds to less than 0.01%.

franklintempleton.com The accompanying notes are an integral part of these financial statements. | Semiannual Report 13

TEMPLETON WORLD FUND

FINANCIAL H IGHLIGHTS

| | | | | | | | | | | | | | | | | | |

| | | Six Months Ended | | | | | | Year Ended August 31, | | | | |

| | | February 29, 2016 | | | | | | | | | | | | | | | | |

| | | (unaudited) | | | 2015 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| Class C | | | | | | | | | | | | | | | | | | |

| Per share operating performance | | | | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the period) | | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of period | $ | 15.86 | | $ | 19.44 | | $ | 17.40 | | $ | 14.53 | | $ | 13.69 | | $ | 12.28 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.02 | | | 0.15 | | | 0.27 | c | | 0.12 | | | 0.17 | | | 0.13 | |

| Net realized and unrealized gains (losses) | | (1.88 | ) | | (2.26 | ) | | 2.66 | | | 3.26 | | | 0.83 | | | 1.41 | |

| Total from investment operations | | (1.86 | ) | | (2.11 | ) | | 2.93 | | | 3.38 | | | 1.00 | | | 1.54 | |

| Less distributions from: | | | | | | | | | | | | | | | | | | |

| Net investment income | | (0.15 | ) | | (0.38 | ) | | (0.06 | ) | | (0.26 | ) | | (0.16 | ) | | (0.13 | ) |

| Net realized gains | | (0.85 | ) | | (1.09 | ) | | (0.83 | ) | | (0.25 | ) | | — | | | — | |

| Total distributions | | (1.00 | ) | | (1.47 | ) | | (0.89 | ) | | (0.51 | ) | | (0.16 | ) | | (0.13 | ) |

| Net asset value, end of period | $ | 13.00 | | $ | 15.86 | | $ | 19.44 | | $ | 17.40 | | $ | 14.53 | | $ | 13.69 | |

| |

| Total returnd | | (12.30 | )% | | (11.27 | )% | | 17.08 | % | | 23.76 | % | | 7.41 | % | | 12.50 | % |

| |

| Ratios to average net assetse | | | | | | | | | | | | | | | | | | |

| Expenses | | 1.81 | %f | | 1.81 | %f | | 1.80 | % | | 1.81 | %g | | 1.84 | % | | 1.82 | %g |

| Net investment income | | 0.28 | % | | 0.86 | % | | 1.45 | %c | | 0.73 | % | | 1.24 | % | | 0.87 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000’s) | $ | 154,613 | | $ | 193,309 | | $ | 241,635 | | $ | 210,256 | | $ | 186,483 | | $ | 201,956 | |

| Portfolio turnover rate | | 8.76 | % | | 15.73 | % | | 18.56 | % | | 17.57 | % | | 18.77 | % | | 16.11 | % |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases

of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.18 per share related to income received in the form of special dividends in connection with certain Fund holdings.

Excluding this amount, the ratio of net investment income to average net assets would have been 0.55%.

dTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable, and is not annualized for periods less than one year.

eRatios are annualized for periods less than one year.

fBenefit of waiver and payments by affiliates rounds to less than 0.01%.

gBenefit of expense reduction rounds to less than 0.01%.

14 Semiannual Report | The accompanying notes are an integral part of these financial statements. franklintempleton.com

TEMPLETON WORLD FUND

FINANCIAL H IGHLIGHTS

| | | | | | | | | | | | |

| | | Six Months Ended | | | Year Ended August 31, | |

| | | February 29, 2016 | | | | | | | | | | |

| | | (unaudited) | | | 2015 | | | 2014 | | | 2013 | a |

| Class R6 | | | | | | | | | | | | |

| Per share operating performance | | | | | | | | | | | | |

| (for a share outstanding throughout the period) | | | | | | | | | | | | |

| Net asset value, beginning of period | $ | 16.50 | | $ | 20.18 | | $ | 18.02 | | $ | 17.17 | |

| Income from investment operationsb: | | | | | | | | | | | | |

| Net investment incomec | | 0.10 | | | 0.35 | | | 0.57 | d | | 0.12 | |

| Net realized and unrealized gains (losses) | | (1.95 | ) | | (2.35 | ) | | 2.67 | | | 0.73 | |

| Total from investment operations | | (1.85 | ) | | (2.00 | ) | | 3.24 | | | 0.85 | |

| Less distributions from: | | | | | | | | | | | | |

| Net investment income | | (0.34 | ) | | (0.59 | ) | | (0.25 | ) | | — | |

| Net realized gains | | (0.85 | ) | | (1.09 | ) | | (0.83 | ) | | — | |

| Total distributions | | (1.19 | ) | | (1.68 | ) | | (1.08 | ) | | — | |

| Net asset value, end of period | $ | 13.46 | | $ | 16.50 | | $ | 20.18 | | $ | 18.02 | |

| |

| Total returne | | (11.85 | )% | | (10.30 | )% | | 18.40 | % | | 4.95 | % |

| |

| Ratios to average net assetsf | | | | | | | | | | | | |

| Expenses | | 0.72 | %g | | 0.72 | %g | | 0.72 | % | | 0.72 | %h |

| Net investment income | | 1.37 | % | | 1.95 | % | | 2.53 | %d | | 1.82 | % |

| |

| Supplemental data | | | | | | | | | | | | |

| Net assets, end of period (000’s) | $ | 51,475 | | $ | 51,733 | | $ | 55,175 | | $ | 24,306 | |

| Portfolio turnover rate | | 8.76 | % | | 15.73 | % | | 18.56 | % | | 17.57 | % |

aFor the period May 1, 2013 (effective date) to August 31, 2013.

bThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases

of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

cBased on average daily shares outstanding.

dNet investment income per share includes approximately $0.18 per share related to income received in the form of special dividends in connection with certain Fund holdings.

Excluding this amount, the ratio of net investment income to average net assets would have been 1.63%.

eTotal return is not annualized for periods less than one year.

fRatios are annualized for periods less than one year.

gBenefit of waiver and payments by affiliates rounds to less than 0.01%.

hBenefit of expense reduction rounds to less than 0.01%.

franklintempleton.com The accompanying notes are an integral part of these financial statements. | Semiannual Report 15

TEMPLETON WORLD FUND

FINANCIAL H IGHLIGHTS

| | | | | | | | | | | | | | | | | | |

| | | Six Months Ended | | | | | | Year Ended August 31, | | | | |

| | | February 29, 2016 | | | | | | | | | | | | | | | | |

| | | (unaudited) | | | 2015 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| Advisor Class | | | | | | | | | | | | | | | | | | |

| Per share operating performance | | | | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the period) | | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of period | $ | 16.50 | | $ | 20.18 | | $ | 18.01 | | $ | 15.07 | | $ | 14.22 | | $ | 12.75 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.10 | | | 0.33 | | | 0.48 | c | | 0.30 | | | 0.33 | | | 0.29 | |

| Net realized and unrealized gains (losses) | | (1.96 | ) | | (2.35 | ) | | 2.75 | | | 3.36 | | | 0.84 | | | 1.46 | |

| Total from investment operations | | (1.86 | ) | | (2.02 | ) | | 3.23 | | | 3.66 | | | 1.17 | | | 1.75 | |

| Less distributions from: | | | | | | | | | | | | | | | | | | |

| Net investment income | | (0.32 | ) | | (0.57 | ) | | (0.23 | ) | | (0.47 | ) | | (0.32 | ) | | (0.28 | ) |

| Net realized gains | | (0.85 | ) | | (1.09 | ) | | (0.83 | ) | | (0.25 | ) | | — | | | — | |

| Total distributions | | (1.17 | ) | | (1.66 | ) | | (1.06 | ) | | (0.72 | ) | | (0.32 | ) | | (0.28 | ) |

| Net asset value, end of period | $ | 13.47 | | $ | 16.50 | | $ | 20.18 | | $ | 18.01 | | $ | 15.07 | | $ | 14.22 | |

| |

| Total returnd | | (11.90 | )% | | (10.38 | )% | | 18.29 | % | | 24.97 | % | | 8.51 | % | | 13.63 | % |

| |

| Ratios to average net assetse | | | | | | | | | | | | | | | | | | |

| Expenses | | 0.81 | %f | | 0.81 | %f | | 0.80 | % | | 0.81 | %g | | 0.84 | % | | 0.82 | %g |

| Net investment income | | 1.28 | % | | 1.86 | % | | 2.45 | %c | | 1.73 | % | | 2.24 | % | | 1.87 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000’s) | $ | 134,137 | | $ | 181,661 | | $ | 273,478 | | $ | 216,767 | | $ | 232,104 | | $ | 191,488 | |

| Portfolio turnover rate | | 8.76 | % | | 15.73 | % | | 18.56 | % | | 17.57 | % | | 18.77 | % | | 16.11 | % |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases

of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.18 per share related to income received in the form of special dividends in connection with certain Fund holdings.

Excluding this amount, the ratio of net investment income to average net assets would have been 1.55%.

dTotal return is not annualized for periods less than one year.

eRatios are annualized for periods less than one year.

fBenefit of waiver and payments by affiliates rounds to less than 0.01%.

gBenefit of expense reduction rounds to less than 0.01%.

16 Semiannual Report | The accompanying notes are an integral part of these financial statements. franklintempleton.com

TEMPLETON WORLD FUND

| | | | | |

| Statement of Investments, February 29, 2016 (Unaudited) | | | | |

| | Industry | Shares | | | Value |

| Common Stocks 98.0% | | | | | |

| Austria 0.3% | | | | | |

| UNIQA Insurance Group AG | Insurance | 2,200,557 | $ | 13,375,264 |

| Belgium 0.3% | | | | | |

| UCB SA | Pharmaceuticals | 198,590 | | 14,793,232 |

| Canada 1.2% | | | | | |

| Silver Wheaton Corp | Metals & Mining | 1,532,800 | | 24,166,939 |

| Suncor Energy Inc | Oil, Gas & Consumable Fuels | 1,157,014 | | 28,277,815 |

| | | | | 52,444,754 |

| China 1.7% | | | | | |

| China Life Insurance Co. Ltd., H | Insurance | 11,080,000 | | 24,103,680 |

| GCL-Poly Energy Holdings Ltd | Semiconductors & Semiconductor Equipment | 130,941,600 | | 19,192,242 |

| Kunlun Energy Co. Ltd | Oil, Gas & Consumable Fuels | 34,333,100 | | 24,543,192 |

| Weichai Power Co. Ltd., H | Machinery | 6,584,000 | | 6,010,234 |

| | | | | 73,849,348 |

| France 7.1% | | | | | |

| AXA SA | Insurance | 1,965,270 | | 43,399,036 |

| BNP Paribas SA | Banks | 1,975,640 | | 92,436,835 |

| Compagnie de Saint-Gobain | Building Products | 130,095 | | 5,063,471 |

| Sanofi | Pharmaceuticals | 1,004,300 | | 79,980,481 |

| Technip SA | Energy Equipment & Services | 486,060 | | 24,198,990 |

| Total SA, B | Oil, Gas & Consumable Fuels | 1,377,280 | | 62,005,333 |

| | | | | 307,084,146 |

| Germany 4.7% | | | | | |

| Deutsche Boerse AG | Diversified Financial Services | 277,060 | | 22,962,892 |

| a Deutsche Lufthansa AG | Airlines | 3,583,050 | | 53,743,808 |

| Merck KGaA | Pharmaceuticals | 523,150 | | 44,634,069 |

| Metro AG | Food & Staples Retailing | 981,551 | | 24,238,841 |

| SAP SE | Software | 78,040 | | 5,938,978 |

| Siemens AG | Industrial Conglomerates | 546,680 | | 50,835,240 |

| | | | | 202,353,828 |

| Hong Kong 0.2% | | | | | |

| CK Hutchison Holdings Ltd | Industrial Conglomerates | 570,170 | | 6,898,223 |

| India 0.4% | | | | | |

| Reliance Industries Ltd | Oil, Gas & Consumable Fuels | 1,171,931 | | 16,609,444 |

| Ireland 1.2% | | | | | |

| CRH PLC | Construction Materials | 1,977,216 | | 50,988,386 |

| Israel 1.8% | | | | | |

| Teva Pharmaceutical Industries Ltd., ADR | Pharmaceuticals | 1,352,304 | | 75,188,102 |

| Italy 2.4% | | | | | |

| Eni SpA | Oil, Gas & Consumable Fuels | 3,695,594 | | 52,074,226 |

| UniCredit SpA | Banks | 13,855,955 | | 51,803,418 |

| | | | | 103,877,644 |

| Japan 4.2% | | | | | |

| ITOCHU Corp | Trading Companies & Distributors | 1,283,897 | | 15,148,539 |

| Nissan Motor Co. Ltd | Automobiles | 9,407,800 | | 85,472,364 |

| SoftBank Group Corp | Wireless Telecommunication Services | 1,141,600 | | 56,429,552 |

| a Toshiba Corp | Industrial Conglomerates | 5,350,500 | | 8,293,951 |

| Toyota Motor Corp | Automobiles | 264,225 | | 13,817,539 |

| | | | | 179,161,945 |

| |

| |

| |

| franklintempleton.com | | Semiannual Report | 17 |

TEMPLETON WORLD FUND

STATEMENT O F INVESTMENTS

| | | | |

| | Industry | Shares | | Value |

| Common Stocks (continued) | | | | |

| Netherlands 3.3% | | | | |

| Aegon NV | Insurance | 7,465,582 | $ | 37,594,630 |

| Akzo Nobel NV | Chemicals | 281,760 | | 16,629,065 |

| ING Groep NV, IDR | Banks | 4,012,942 | | 47,572,822 |

| a QIAGEN NV | Life Sciences Tools & Services | 1,170,061 | | 25,068,193 |

| a SBM Offshore NV | Energy Equipment & Services | 1,306,962 | | 16,610,190 |

| | | | | 143,474,900 |

| Norway 0.9% | | | | |

| Telenor ASA | Diversified Telecommunication Services | 2,656,020 | | 39,795,134 |

| Portugal 0.6% | | | | |

| Galp Energia SGPS SA, B | Oil, Gas & Consumable Fuels | 2,464,100 | | 27,106,802 |

| Russia 0.3% | | | | |

| LUKOIL PJSC, ADR | | | | |

| (London Stock Exchange) | Oil, Gas & Consumable Fuels | 61,774 | | 2,192,977 |

| MMC Norilsk Nickel PJSC, ADR | Metals & Mining | 773,066 | | 9,354,099 |

| | | | | 11,547,076 |

| Singapore 2.2% | | | | |

| DBS Group Holdings Ltd | Banks | 3,301,396 | | 31,883,482 |

| a Flextronics International Ltd | Electronic Equipment, Instruments & Components | 1,760,632 | | 19,120,463 |

| Singapore Telecommunications Ltd | Diversified Telecommunication Services | 15,862,261 | | 42,076,758 |

| | | | | 93,080,703 |

| South Korea 7.1% | | | | |

| Hana Financial Group Inc | Banks | 1,857,147 | | 31,238,365 |

| Hyundai Motor Co | Automobiles | 446,466 | | 53,127,131 |

| KB Financial Group Inc | Banks | 1,876,166 | | 44,953,515 |

| POSCO | Metals & Mining | 137,511 | | 22,020,841 |

| Samsung Electronics Co. Ltd | Technology Hardware, Storage & Peripherals | 160,895 | | 152,905,740 |

| | | | | 304,245,592 |

| Spain 0.9% | | | | |

| Telefonica SA | Diversified Telecommunication Services | 4,019,156 | | 40,426,263 |

| Switzerland 5.7% | | | | |

| ABB Ltd | Electrical Equipment | 1,244,840 | | 22,309,407 |

| Credit Suisse Group AG | Capital Markets | 4,892,487 | | 65,834,026 |

| Glencore PLC | Metals & Mining | 21,418,990 | | 39,731,654 |

| Roche Holding AG | Pharmaceuticals | 324,842 | | 83,584,696 |

| Swiss Re AG | Insurance | 396,920 | | 35,308,712 |

| | | | | 246,768,495 |

| Taiwan 1.1% | | | | |

| Taiwan Semiconductor Manufacturing | | | | |

| Co. Ltd | Semiconductors & Semiconductor Equipment | 2,423,578 | | 10,862,832 |

| Tripod Technology Corp | Electronic Equipment, Instruments & Components | 20,588,000 | | 36,415,919 |

| | | | | 47,278,751 |

| Turkey 0.4% | | | | |

| Turkcell Iletisim Hizmetleri AS | Wireless Telecommunication Services | 4,097,336 | | 15,309,654 |

| United Kingdom 16.2% | | | | |

| Aviva PLC | Insurance | 8,118,486 | | 49,524,244 |

| BAE Systems PLC | Aerospace & Defense | 9,078,149 | | 64,831,356 |

18 Semiannual Report

franklintempleton.com

TEMPLETON WORLD FUND

STATEMENT O F INVESTMENTS

| | | | |

| | Industry | Shares | | Value |

| Common Stocks (continued) | | | | |

| United Kingdom (continued) | | | | |

| Barclays PLC | Banks | 12,246,142 | $ | 29,330,833 |

| BP PLC | Oil, Gas & Consumable Fuels | 7,633,066 | | 37,345,046 |

| Carillion PLC | Construction & Engineering | 7,084,170 | | 27,139,875 |

| GlaxoSmithKline PLC | Pharmaceuticals | 1,830,076 | | 35,654,345 |

| HSBC Holdings PLC | Banks | 9,610,740 | | 61,497,084 |

| International Consolidated Airlines Group SA | Airlines | 580,880 | | 4,439,450 |

| Kingfisher PLC | Specialty Retail | 8,748,399 | | 40,713,214 |

| Lloyds Banking Group PLC | Banks | 31,861,170 | | 32,112,249 |

| Petrofac Ltd | Energy Equipment & Services | 2,175,180 | | 27,419,156 |

| Royal Dutch Shell PLC, A | Oil, Gas & Consumable Fuels | 82,455 | | 1,891,093 |

| Royal Dutch Shell PLC, B | Oil, Gas & Consumable Fuels | 2,915,047 | | 66,754,708 |

| a Serco Group PLC | Commercial Services & Supplies | 7,428,920 | | 9,669,583 |

| Sky PLC | Media | 2,576,294 | | 37,406,766 |

| Standard Chartered PLC | Banks | 6,478,396 | | 38,820,456 |

| a Subsea 7 SA | Energy Equipment & Services | 2,803,140 | | 17,778,901 |

| a Tesco PLC | Food & Staples Retailing | 24,754,912 | | 62,168,209 |

| Vodafone Group PLC | Wireless Telecommunication Services | 17,315,179 | | 52,957,500 |

| | | | | 697,454,068 |

| United States 33.8% | | | | |

| Accenture PLC, A | IT Services | 63,681 | | 6,384,657 |

| a Allergan PLC | Pharmaceuticals | 63,000 | | 18,276,930 |

| a Ally Financial Inc | Consumer Finance | 793,660 | | 13,952,543 |

| a Alphabet Inc., A | Internet Software & Services | 65,530 | | 46,999,427 |

| American International Group Inc | Insurance | 1,180,295 | | 59,250,809 |

| Amgen Inc | Biotechnology | 791,390 | | 112,598,969 |

| Apache Corp | Oil, Gas & Consumable Fuels | 692,430 | | 26,506,220 |

| Baker Hughes Inc | Energy Equipment & Services | 774,878 | | 33,219,020 |

| Best Buy Co. Inc | Specialty Retail | 456,800 | | 14,795,752 |

| Capital One Financial Corp | Consumer Finance | 220,430 | | 14,488,864 |

| Chesapeake Energy Corp | Oil, Gas & Consumable Fuels | 5,183,580 | | 13,529,144 |

| Chevron Corp | Oil, Gas & Consumable Fuels | 219,566 | | 18,320,587 |

| Cisco Systems Inc | Communications Equipment | 972,592 | | 25,462,459 |

| Citigroup Inc | Banks | 2,407,060 | | 93,514,281 |

| Comcast Corp., Special A | Media | 1,044,439 | | 60,295,463 |

| CVS Health Corp | Food & Staples Retailing | 229,842 | | 22,333,747 |

| Devon Energy Corp | Oil, Gas & Consumable Fuels | 756,330 | | 14,884,574 |

| Eli Lilly & Co | Pharmaceuticals | 240,510 | | 17,316,720 |

| Foot Locker Inc | Specialty Retail | 238,610 | | 14,913,125 |

| General Motors Co | Automobiles | 1,165,770 | | 34,320,269 |

| Gilead Sciences Inc | Biotechnology | 429,740 | | 37,494,815 |

| Halliburton Co | Energy Equipment & Services | 1,777,430 | | 57,375,440 |

| Hewlett Packard Enterprise Co | Technology Hardware, Storage & Peripherals | 2,312,330 | | 30,684,619 |

| HP Inc | Technology Hardware, Storage & Peripherals | 2,312,330 | | 24,718,808 |

| JPMorgan Chase & Co | Banks | 1,531,634 | | 86,230,994 |

| a,b Knowles Corp | Electronic Equipment, Instruments & Components | 2,785,470 | | 31,698,649 |

| Medtronic PLC | Health Care Equipment & Supplies | 952,550 | | 73,717,844 |

| Merck & Co. Inc | Pharmaceuticals | 559,434 | | 28,089,181 |

| a Michael Kors Holdings Ltd | Textiles, Apparel & Luxury Goods | 560,690 | | 31,763,089 |

| Microsoft Corp | Software | 2,298,840 | | 116,964,979 |

| Morgan Stanley | Capital Markets | 2,170,130 | | 53,602,211 |

| a Navistar International Corp | Machinery | 1,933,970 | | 16,264,688 |

| News Corp., A | Media | 810,759 | | 8,772,412 |

| Noble Corp. PLC | Energy Equipment & Services | 234,605 | | 1,954,260 |

franklintempleton.com

Semiannual Report 19

TEMPLETON WORLD FUND

STATEMENT O F INVESTMENTS

| | | | | |

| | | Industry | Shares | | Value |

| | Common Stocks (continued) | | | | |

| | United States (continued) | | | | |

| | Oracle Corp | Software | 1,262,581 | $ | 46,437,729 |

| | Pfizer Inc | Pharmaceuticals | 1,395,449 | | 41,402,972 |

| | SunTrust Banks Inc | Banks | 1,692,580 | | 56,159,804 |

| | Twenty-First Century Fox Inc., A | Media | 1,411,332 | | 38,134,191 |

| | United Parcel Service Inc., B | Air Freight & Logistics | 56,299 | | 5,435,668 |

| | Verizon Communications Inc | Diversified Telecommunication Services | 168,634 | | 8,554,803 |

| | | | | | 1,456,820,716 |

| | Total Common Stocks | | | | |

| | (Cost $4,263,137,956) | | | | 4,219,932,470 |

| | Preferred Stocks (Cost $41,548,819) 0.1% | | | | |

| | Brazil 0.1% | | | | |

| a Petroleo Brasileiro SA, ADR, pfd | Oil, Gas & Consumable Fuels | 2,589,090 | | 6,550,398 |

| |

| | | | Principal | | |

| | | | Amount | | |

| | Mortgage-Backed Securities | | | | |

| | (Cost $1,187,515) 0.0%† | | | | |

| | United States 0.0%† | | | | |

| | FHLMC, 5.50%, 12/01/35 | | 1,204,835 | | 1,349,678 |

| | Total Investments before Short Term | | | | |

| | Investments (Cost $4,305,874,290) | | | | 4,227,832,546 |

| | Short Term Investments 1.9% | | | | |

| | Time Deposits 1.5% | | | | |

| | Australia 0.5% | | | | |

| | National Australia Bank, 0.25%, 3/01/16 | | 20,000,000 | | 20,000,000 |

| | Canada 1.0% | | | | |

| | Bank of Montreal, 0.27%, 3/01/16 | | 29,000,000 | | 29,000,000 |

| | Royal Bank of Canada, 0.20%, 3/01/16 | | 15,600,000 | | 15,600,000 |

| | | | | | 44,600,000 |

| | Total Time Deposits (Cost $64,600,000) | | | | 64,600,000 |

| | Total Investments before Money Market | | | | |

| | Funds (Cost $4,370,474,290) | | | | 4,292,432,546 |

| |

| | | | Shares | | |

| c Investments from Cash Collateral Received for | | | | |

| | Loaned Securities (Cost $14,100,000) 0.4% | | | | |

| | Money Market Funds 0.4% | | | | |

| | United States 0.4% | | | | |

| a,d Institutional Fiduciary Trust Money Market Portfolio | | 14,100,000 | | 14,100,000 |

| | Total Investments | | | | |

| | (Cost $4,384,574,290) 100.0% | | | | 4,306,532,546 |

| | Other Assets, less Liabilities 0.0%† | | | | 1,445,622 |

| | Net Assets 100.0% | | | $ | 4,307,978,168 |

| |

| See Abbreviations on page 33. | | | | |

| |

| †Rounds to less than 0.1% of net assets. | | | | |

| aNon-income producing. | | | | |

| bA portion or all of the security is on loan at February 29, 2016. See Note 1(d). | | | | |

| cSee Note 1(d) regarding securities on loan. | | | | |

| dSee Note 3(f) regarding investments in affiliated management investment companies. | | | |

| |

| |

| 20 | Semiannual Report | The accompanying notes are an integral part of these financial statements. | franklintempleton.com |

TEMPLETON WORLD FUND

| | | |

| Financial Statements | | | |

| |

| Statement of Assets and Liabilities | | | |

| February 29, 2016 (unaudited) | | | |

| |

| Assets: | | | |

| Investments in securities: | | | |

| Cost - Unaffiliated issuers | $ | 4,370,474,290 | |

| Cost - Non-controlled affiliates (Note 3f) | | 14,100,000 | |

| Total cost of investments | $ | 4,384,574,290 | |

| Value - Unaffiliated issuers | $ | 4,292,432,546 | |

| Value - Non-controlled affiliates (Note 3f) | | 14,100,000 | |

| Total value of investments (includes securities loaned in the amount of $13,656,000) | | 4,306,532,546 | |

| Cash | | 1,093,000 | |

| Foreign currency, at value (cost $3,999,340) | | 3,979,044 | |

| Receivables: | | | |

| Investment securities sold | | 2,155,072 | |

| Capital shares sold | | 2,119,609 | |

| Dividends and interest | | 14,449,726 | |

| European Union tax reclaims | | 261,248 | |

| Other assets | | 3,216 | |

| Total assets | | 4,330,593,461 | |

| Liabilities: | | | |

| Payables: | | | |

| Investment securities purchased | | 95,488 | |

| Capital shares redeemed | | 4,026,666 | |

| Management fees | | 2,350,085 | |

| Distribution fees | | 901,526 | |

| Transfer agent fees | | 710,465 | |

| Payable upon return of securities loaned | | 14,100,000 | |

| Accrued expenses and other liabilities | | 431,063 | |

| Total liabilities | | 22,615,293 | |

| Net assets, at value | $ | 4,307,978,168 | |

| Net assets consist of: | | | |

| Paid-in capital | $ | 4,394,464,836 | |

| Undistributed net investment income | | 11,808,502 | |

| Net unrealized appreciation (depreciation) | | (78,482,004 | ) |

| Accumulated net realized gain (loss) | | (19,813,166 | ) |

| Net assets, at value | $ | 4,307,978,168 | |

franklintempleton.com The accompanying notes are an integral part of these financial statements. | Semiannual Report 21

TEMPLETON WORLD FUND

FINANCIAL STATEMENTS

| | |

| Statement of Assets and Liabilities (continued) | | |

| February 29, 2016 (unaudited) | | |

| |

| Class A: | | |

| Net assets, at value | $ | 3,967,753,406 |

| Shares outstanding | | 293,973,712 |

| Net asset value per sharea | $ | 13.50 |

| Maximum offering price per share (net asset value per share ÷ 94.25%) | $ | 14.32 |

| Class C: | | |

| Net assets, at value | $ | 154,612,996 |

| Shares outstanding | | 11,896,740 |

| Net asset value and maximum offering price per sharea | $ | 13.00 |

| Class R6: | | |

| Net assets, at value | $ | 51,474,822 |

| Shares outstanding | | 3,824,844 |

| Net asset value and maximum offering price per share | $ | 13.46 |

| Advisor Class: | | |

| Net assets, at value | $ | 134,136,944 |

| Shares outstanding | | 9,958,360 |

| Net asset value and maximum offering price per share | $ | 13.47 |

| |

| aRedemption price is equal to net asset value less contingent deferred sales charges, if applicable. | | |

22 Semiannual Report | The accompanying notes are an integral part of these financial statements.

franklintempleton.com

TEMPLETON WORLD FUND

FINANCIAL STATEMENTS

| | | |

| Statement of Operations | | | |

| for the six months ended February 29, 2016 (unaudited) | | | |

| |

| Investment income: | | | |

| Dividends (net of foreign taxes of $3,896,906) | $ | 50,265,880 | |

| Interest | | 329,267 | |

| Income from securities loaned (net of fees and rebates) | | 94,742 | |

| Total investment income | | 50,689,889 | |

| Expenses: | | | |

| Management fees (Note 3a) | | 16,799,681 | |

| Distribution fees: (Note 3c) | | | |

| Class A | | 5,577,616 | |

| Class C | | 886,303 | |

| Transfer agent fees: (Note 3e) | | | |

| Class A | | 2,065,064 | |

| Class C | | 82,035 | |

| Class R6 | | 446 | |

| Advisor Class | | 74,102 | |

| Custodian fees (Note 4) | | 223,781 | |

| Reports to shareholders | | 134,807 | |

| Registration and filing fees | | 92,488 | |

| Professional fees | | 76,531 | |

| Trustees’ fees and expenses | | 52,503 | |

| Other | | 49,499 | |

| Total expenses | | 26,114,856 | |

| Expenses waived/paid by affiliates (Note 3f) | | (6,458 | ) |

| Net expenses | | 26,108,398 | |

| Net investment income | | 24,581,491 | |

| Realized and unrealized gains (losses): | | | |

| Net realized gain (loss) from: | | | |

| Investments | | 18,182,731 | |

| Written options | | 143,077 | |

| Foreign currency transactions | | (1,175,279 | ) |

| Net realized gain (loss) | | 17,150,529 | |

| Net change in unrealized appreciation (depreciation) on: | | | |

| Investments | | (642,000,934 | ) |

| Translation of other assets and liabilities denominated in foreign currencies | | (144,649 | ) |

| Net change in unrealized appreciation (depreciation) | | (642,145,583 | ) |

| Net realized and unrealized gain (loss) | | (624,995,054 | ) |

| Net increase (decrease) in net assets resulting from operations | $ | (600,413,563 | ) |

franklintempleton.com The accompanying notes are an integral part of these financial statements. | Semiannual Report 23

TEMPLETON WORLD FUND

FINANCIAL STATEMENTS

| | | | | | |

| Statements of Changes in Net Assets | | | | | | |

| |

| | | Six Months Ended | | | | |

| | | February 29, 2016 | | | Year Ended | |

| | | (unaudited) | | | August 31, 2015 | |

| Increase (decrease) in net assets: | | | | | | |

| Operations: | | | | | | |

| Net investment income | $ | 24,581,491 | | $ | 93,634,345 | |

| Net realized gain (loss) | | 17,150,529 | | | 285,239,137 | |

| Net change in unrealized appreciation (depreciation) | | (642,145,583 | ) | | (1,032,149,917 | ) |

| Net increase (decrease) in net assets resulting from operations | | (600,413,563 | ) | | (653,276,435 | ) |

| Distributions to shareholders from: | | | | | | |

| Net investment income: | | | | | | |

| Class A | | (78,902,555 | ) | | (148,302,524 | ) |

| Class C | | (1,757,658 | ) | | (4,547,565 | ) |

| Class R6 | | (1,218,271 | ) | | (1,601,276 | ) |

| Advisor Class | | (3,143,320 | ) | | (7,396,095 | ) |

| Net realized gains: | | | | | | |

| Class A | | (239,212,776 | ) | | (310,296,789 | ) |

| Class C | | (9,900,748 | ) | | (13,123,838 | ) |

| Class R6 | | (3,029,263 | ) | | (2,965,913 | ) |

| Advisor Class | | (8,297,152 | ) | | (14,074,841 | ) |

| Total distributions to shareholders | | (345,461,743 | ) | | (502,308,841 | ) |

| Capital share transactions: (Note 2) | | | | | | |

| Class A | | 45,994,738 | | | (69,471,771 | ) |

| Class C | | (4,458,915 | ) | | (4,668,310 | ) |

| Class R6 | | 11,136,388 | | | 6,893,427 | |

| Advisor Class | | (17,313,328 | ) | | (46,359,007 | ) |

| Total capital share transactions | | 35,358,883 | | | (113,605,661 | ) |

| Net increase (decrease) in net assets | | (910,516,423 | ) | | (1,269,190,937 | ) |

| Net assets: | | | | | | |

| Beginning of period | | 5,218,494,591 | | | 6,487,685,528 | |

| End of period | $ | 4,307,978,168 | | $ | 5,218,494,591 | |

| Undistributed net investment income included in net assets: | | | | | | |

| End of period | $ | 11,808,502 | | $ | 72,248,815 | |

24 Semiannual Report | The accompanying notes are an integral part of these financial statements. franklintempleton.com

TEMPLETON WORLD FUND

Notes to Financial Statements (unaudited)

1. Organization and Significant Accounting Policies

Templeton Funds (Trust) is registered under the Investment Company Act of 1940 (1940 Act) as an open-end management investment company, consisting of two separate funds and applies the specialized accounting and reporting guidance in U.S. Generally Accepted Accounting Principles (U.S. GAAP). Templeton World Fund (Fund) is included in this report. The financial statements of the remaining fund in the Trust are presented separately. The Fund offers four classes of shares: Class A, Class C, Class R6, and Advisor Class. Each class of shares differs by its initial sales load, contingent deferred sales charges, voting rights on matters affecting a single class, its exchange privilege and fees primarily due to differing arrangements for distribution and transfer agent fees.

The following summarizes the Fund’s significant accounting policies.

a. Financial Instrument Valuation

The Fund’s investments in financial instruments are carried at fair value daily. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants on the measurement date. The Fund calculates the net asset value (NAV) per share as of 4 p.m. Eastern time each day the New York Stock Exchange (NYSE) is open for trading. Under compliance policies and procedures approved by the Trust’s Board of Trustees (the Board), the Fund’s administrator has responsibility for oversight of valuation, including leading the cross-functional Valuation and Liquidity Oversight Committee (VLOC). The VLOC provides administration and oversight of the Fund’s valuation policies and procedures, which are approved annually by the Board. Among other things, these procedures allow the Fund to utilize independent pricing services, quotations from securities and financial instrument dealers, and other market sources to determine fair value.

Equity securities and derivative financial instruments (derivatives) listed on an exchange or on the NASDAQ National Market System are valued at the last quoted sale price or the official closing price of the day, respectively. Foreign equity securities are valued as of the close of trading on the foreign stock exchange on which the security is primarily traded or as of 4 p.m. Eastern time whichever is earlier. The value is then converted into its U.S. dollar equivalent at the foreign exchange rate in effect at 4 p.m. Eastern time on the day that the value of the security is determined. Over-the-counter (OTC)

securities are valued within the range of the most recent quoted bid and ask prices. Securities that trade in multiple markets or on multiple exchanges are valued according to the broadest and most representative market. Certain equity securities are valued based upon fundamental characteristics or relationships to similar securities.

Debt securities generally trade in the OTC market rather than on a securities exchange. The Fund’s pricing services use multiple valuation techniques to determine fair value. In instances where sufficient market activity exists, the pricing services may utilize a market-based approach through which quotes from market makers are used to determine fair value. In instances where sufficient market activity may not exist or is limited, the pricing services also utilize proprietary valuation models which may consider market characteristics such as benchmark yield curves, credit spreads, estimated default rates, anticipated market interest rate volatility, coupon rates, anticipated timing of principal repayments, underlying collateral, and other unique security features in order to estimate the relevant cash flows, which are then discounted to calculate the fair value.

Investments in open-end mutual funds are valued at the closing NAV. Time deposits are valued at cost, which approximates fair value.

The Fund has procedures to determine the fair value of financial instruments for which market prices are not reliable or readily available. Under these procedures, the VLOC convenes on a regular basis to review such financial instruments and considers a number of factors, including significant unobservable valuation inputs, when arriving at fair value. The VLOC primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information for the investment to determine the fair value of the investment. An income-based valuation approach may also be used in which the anticipated future cash flows of the investment are discounted to calculate fair value. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. Due to the inherent uncertainty of valuations of such investments, the fair values may differ significantly from the values that would have been used had an active market existed. The VLOC employs various methods for calibrating these valuation approaches including a regular review of key inputs and assumptions, transactional back-testing or disposition analysis, and reviews of any related market activity.

franklintempleton.com

Semiannual Report 25

TEMPLETON WORLD FUND

NOTES TO FINANCIAL STATEMENTS (UNAUDITED)

1. Organization and Significant Accounting

Policies (continued)

a. Financial Instrument Valuation (continued)

Trading in securities on foreign securities stock exchanges and OTC markets may be completed before 4 p.m. Eastern time. In addition, trading in certain foreign markets may not take place on every NYSE business day. Occasionally, events occur between the time at which trading in a foreign security is completed and the close of the NYSE that might call into question the reliability of the value of a portfolio security held by the Fund. As a result, differences may arise between the value of the Fund’s portfolio securities as determined at the foreign market close and the latest indications of value at the close of the NYSE. In order to minimize the potential for these differences, the VLOC monitors price movements following the close of trading in foreign stock markets through a series of country specific market proxies (such as baskets of American Depositary Receipts, futures contracts and exchange traded funds). These price movements are measured against established trigger thresholds for each specific market proxy to assist in determining if an event has occurred that may call into question the reliability of the values of the foreign securities held by the Fund. If such an event occurs, the securities may be valued using fair value procedures, which may include the use of independent pricing services.

When the last day of the reporting period is a non-business day, certain foreign markets may be open on those days that the NYSE is closed, which could result in differences between the value of the Fund’s portfolio securities on the last business day and the last calendar day of the reporting period. Any significant security valuation changes due to an open foreign market are adjusted and reflected by the Fund for financial reporting purposes.

b. Foreign Currency Translation