UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSRS

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-02781

Templeton Funds

(Exact name of registrant as specified in charter)

300 S.E. 2nd Street, Fort Lauderdale, FL 33301-1923

(Address of principal executive offices) (Zip code)

Craig S. Tyle, One Franklin Parkway, San Mateo, CA 94403-1906

(Name and address of agent for service)

Registrant's telephone number, including area code: (954) 527-7500_

Date of fiscal year end: _8/31__

Date of reporting period: 2/28/14_

Item 1. Reports to Stockholders.

| | | | | |

| | Contents | | | |

| Shareholder Letter | 1 | Semiannual Report | | Financial Statements | 28 |

| | | Templeton World Fund. | 4 | Notes to Financial Statements | 32 |

| | | Performance Summary | 14 | Shareholder Information | 45 |

| | | Your Fund’s Expenses | 17 | | |

| | | Financial Highlights and Statement of | | | |

| | | Investments | 19 | | |

Semiannual Report

Templeton World Fund

Your Fund’s Goal and Main Investments: Templeton World Fund seeks long-term capital growth. Under normal market conditions, the Fund invests primarily in equity securities of companies located anywhere in the world, including emerging markets. Under normal circumstances, the Fund will invest in issuers located in at least three different countries (including the U.S.).

|

| Performance data represent past |

| performance, which does not |

| guarantee future results. |

| Investment return and principal |

| value will fluctuate, and you may |

| have a gain or loss when you sell |

| your shares. Current performance |

| may differ from figures shown. |

| Please visit franklintempleton.com |

| or call (800) 342-5236 for most |

| recent month-end performance. |

This semiannual report for Templeton World Fund covers the period ended February 28, 2014.

Performance Overview

Templeton World Fund – Class A delivered a +14.33% cumulative total return for the six months under review. In comparison, the MSCI World Index, which measures stock market performance in global developed markets, posted a +14.92% total return.1, 2 The Fund’s long-term results are shown in the Performance Summary beginning on page 14. For the 10-year period ended February 28, 2014, Templeton World Fund – Class A delivered a +104.99% cumulative total return, compared with the MSCI World Index’s +102.81% cumulative total return for the same period.1, 2 Please note index performance information is provided for reference and we do not attempt to track the index but rather undertake investments on the basis of fundamental research. You can find more performance data in the Performance Summary.

Economic and Market Overview

The six months under review were characterized by continued economic recovery in most developed countries, and many central banks reaffirmed their accommodative monetary stances. In contrast, growth in emerging market economies generally tended to slow, and central banks in many emerging markets raised interest rates as they sought to control inflation and currency depreciation.

In the U.S., economic data were generally positive. Manufacturing activity expanded during the review period and unemployment declined. In October 2013, the federal government temporarily shut down after Congress reached

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 23.

4 | Semiannual Report

a budget impasse. However, Congress passed a spending bill in January to fund the federal government through September 2014. Congress then approved suspension of the debt ceiling until March 2015. Encouraged by positive economic and employment reports, the Federal Reserve Board (Fed) in January 2014 began reducing its bond purchases by $10 billion a month and committed to keeping interest rates low. The new Fed Chair, Janet Yellen, confirmed that the Fed would continue to reduce its asset purchases, although it would reconsider its plan if the economic outlook changed significantly.

Outside the U.S., the U.K. enjoyed strong growth, driven by easing credit conditions and stronger consumer confidence. Elsewhere, economic activity in the eurozone and Japan showed signs of improvement. Although technically out of its recession, the eurozone experienced weak employment trends and deflationary risks. However, German Chancellor Angela Merkel’s reelection and the European Central Bank’s rate cut to a record low helped partly restore investor confidence. In Japan, improving business sentiment, personal consumption and higher exports resulting from a weaker yen supported the economy, and the unemployment rate reached its lowest level in six years. The Bank of Japan announced it would provide additional monetary stimulus, if required. Political turmoil in Ukraine surfaced in November 2013 when its government avoided firming up trade links with the European Union, raising fears of a sovereign default and investor concerns over the country’s relationship with Russia.

Growth in many emerging market economies moderated based on lower domestic demand, falling exports and weakening commodity prices. However, select emerging market economies such as those of China, Malaysia, South Korea, Poland and Hungary improved in 2013’s second half. Monetary policies tightened in several emerging market countries, including Brazil, India, Turkey and South Africa, as their central banks raised interest rates to curb inflation and support their currencies.

Stocks in Europe helped developed market equities advance for most of the period despite a January 2014 decline. Led by Asian equities, emerging market equities also gained, although weak economic data, especially in China, weighed on markets in January. Several emerging market currencies depreciated against the U.S. dollar during the period. Gold prices declined for the period despite a rally in early 2014, and international oil prices rose amid supply concerns related to political unrest and adverse U.S. weather.

Semiannual Report | 5

| | |

| Top 10 Sectors/Industries | | |

| Based on Equity Securities | | |

| 2/28/14 | | |

| % of Total | |

| Net Assets | |

| Banks | 14.1 | % |

| Pharmaceuticals | 10.7 | % |

| Oil, Gas & Consumable Fuels | 8.8 | % |

| Insurance | 5.3 | % |

| Energy Equipment & Services | 5.2 | % |

| Capital Markets | 4.5 | % |

| Diversified Telecommunication Services | 3.7 | % |

| Food & Staples Retailing | 3.2 | % |

| Media | 3.0 | % |

| Specialty Retail | 2.8 | % |

Investment Strategy

Our investment strategy employs a bottom-up, value-oriented, long-term approach. We focus on the market price of a company’s securities relative to our evaluation of the company’s long-term earnings, asset value and cash flow potential. As we look worldwide, we consider specific companies, rather than sectors or countries, while doing in-depth research to construct a bargain list from which we buy. Before we make a purchase, we look at the company’s price/earnings ratio, price/cash flow ratio, profit margins and liquidation value.

Manager’s Discussion

Many of the positive economic trends we discussed in the 2013 annual shareholder report persisted during the six-month review period, and the Fund performed well, supported by the market environment. Although the Fund’s performance slightly trailed that of the benchmark MSCI World Index for the period, all of the Fund’s major sectors and regions delivered absolute gains. The Fund’s Class A shares outperformed the benchmark for the one-, five- and 10-year annual periods ended February 28, 2014. Even so, the Fund traded at a significant valuation discount relative to the benchmark index. Positive trends included moderate global economic growth and ongoing policy support from developed market central banks. Stabilizing market conditions allowed investors to refocus on business fundamentals, creating an environment that seemed to us to reward disciplined stock picking and helped drive further value recognition for Fund positions.

Value investing generally was pressured during the global financial crisis as investors seemed to grow more concerned with overall market stability than with the relationship between stock prices and business fundamentals. However, the rise in investor confidence since Europe’s recovery from its debt crisis laid the groundwork for the resurgence of value investing, a strategy that has historically delivered compelling performance. Many of the sectors and regions most punished during the 2008–2009 global crisis and 2010–2011 European crisis have since had a dramatic recovery. As Sir John Templeton wrote, “For those properly prepared in advance, a bear market in stocks is not a calamity, but an opportunity.”

6 | Semiannual Report

|

| What is return on equity? |

| Return on equity is an amount, |

| expressed as a percentage, earned on |

| a company’s common stock investment |

| for a given period. Return on equity tells |

| common shareholders how effectually |

| their money is being employed. |

| Comparing percentages for current and |

| prior periods also reveals trends, and |

| comparison with industry composites |

| reveals how well a company is holding |

| its own against its competitors. |

The strong performance of Europe, and particularly European financials, during the review period seemed to us the latest validation of Sir John Templeton’s words.3 As the European sovereign debt crisis escalated during 2010 and 2011, investor sentiment turned largely pessimistic, with many investors anticipating the breakup of the European Monetary Union. Reflective of the negative investor sentiment for Europe, the forward price-to-earnings ratio of the EuroStoxx 50 Index, an index of European blue chips with diverse global revenue streams, fell in 2011 to the same level as its estimated dividend yield. As recently as 2012, the entire market capitalization of the eurozone banking system was worth less than one U.S. stock, Apple. At the market bottom, European banks were trading at a 60% to 70% discount to their tangible book values, a level that major global financial institutions had not reached since U.S. banks did during the Great Depression. We believed this was a classic Templeton opportunity. However, investment decisions can be very difficult in a challenging environment. As Sir John Templeton pointed out, “It is not easy to act contrary to popular opinion.” As disciplined investors, we tried to ignore the crowd and adhere to our time-tested process. Our decision to substantially increase exposure to Europe and the banking sector during this tumultuous period served our clients well, and record inflows into European stocks during the review period further accelerated regional gains.

Dutch financial services firm ING Groep was among the top contributors to performance. We established our position in ING at what we believed were distressed valuations. Our analysis indicated that the firm, which accepted a bailout from the Dutch government in 2008, could successfully restructure and reemerge as a well-capitalized European bank earning double-digit returns on equity. The company was nearing completion of its European Union-imposed bailout commitments following more than 35 disposals that raised roughly 23 billion euros, and recent results highlighted the operational gains achieved at ING’s banking business as the company cut costs and improved margins. Other financials holdings contributing to relative performance included U.S. financial services firm Morgan Stanley, U.K. insurer Aviva and lenders BNP Paribas (France) and UniCredit (Italy). Our analysis did not suggest that European banks were soon likely to return to the book value multiples enjoyed before the European sovereign debt crisis. However, we believe these companies remain undervalued relative to their global peers and could continue to improve profitability and capital ratios as economic conditions normalize.

Semiannual Report | 7

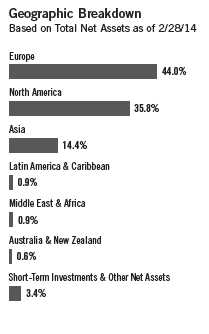

| | |

| Top 10 Countries | | |

| Based on Equity Securities | | |

| 2/28/14 | | |

| | % of Total | |

| | Net Assets | |

| U.S. | 34.0 | % |

| U.K. | 15.9 | % |

| France | 8.1 | % |

| Switzerland | 5.9 | % |

| South Korea | 5.0 | % |

| Japan | 3.7 | % |

| Germany | 2.9 | % |

| Netherlands | 2.7 | % |

| Italy | 2.6 | % |

| Singapore | 2.3 | % |

The cyclical European industrials sector also experienced significant pressure in recent years.4 European airlines were hit particularly hard. Financial sector cutbacks and private sector belt-tightening led to a steep reduction in air traffic volume, and internal labor demands and competition from low-cost carriers further pressured profit margins. In 2009 and 2011, European airlines fell to record-low price-to-book levels that averaged a 50% discount to book value. Although the airline industry has always been a challenging business in our view, it was not one that we believed could disappear. Our analysis indicated that the industry required significant restructuring and that it would need to shed a great deal of capacity but that there would be winners and losers. We decided to focus on the companies that we believed could be the long-term survivors of this industry shake-up. For example, International Consolidated Airlines Group (IAG) was a company we viewed as having a strong foothold at Heathrow Airport and attractive position in the lucrative transatlantic market. The share price of British Airways’ parent company rose to a six-year high after quarterly operating profits more than doubled and management raised its 2015 profit target. Although we remained positive given the stock’s continued discount to our projection of IAG’s long-term business value, we reduced exposure to realize significant gains after the stock more than tripled in value over the past 18 months. Stock selection in the industrials sector bolstered relative performance.

Other sector contributors to relative performance included the Fund’s underweighting and stock selection in consumer staples.5 Consumer staples stocks have offered a scarcity of bargains in recent years based on our analysis, and we believed conditions remained unfavorable for wider value creation. Unlike other sectors, consumer staples has a perceived combination of non-discretionary products and high emerging markets exposure with a defensive growth profile for which some investors were willing to pay a premium.

We also found few bargains in the materials sector in recent years, where a legacy of poor capital discipline in the mining industry resulted in overca-pacity that continued to pressure profitability.6 Buoyed by stock selection in the chemicals industry, the Fund’s materials sector holdings outperformed during the period. Although most of our materials sector investment prospects have been limited to deeper value business segments, emerging market volatility and investor pessimism could create opportunities for us in the mining industry, and we monitored the industry for new bargains.

8 | Semiannual Report

| | |

| Top 10 Equity Holdings | | |

| 2/28/14 | | |

| |

| Company | % of Total | |

| Sector/Industry, Country | Net Assets | |

| BNP Paribas SA | 2.6 | % |

| Banks, France | | |

| Roche Holding AG | 2.4 | % |

| Pharmaceuticals, Switzerland | | |

| Morgan Stanley | 2.3 | % |

| Capital Markets, U.S. | | |

| Baker Hughes Inc. | 2.2 | % |

| Energy Equipment & Services, U.S. | | |

| Total SA, B | 2.0 | % |

| Oil, Gas & Consumable Fuels, France | |

| Citigroup Inc. | 2.0 | % |

| Banks, U.S. | | |

| Microsoft Corp. | 2.0 | % |

| Software, U.S. | | |

| Credit Suisse Group AG | 2.0 | % |

| Capital Markets, Switzerland | | |

| Samsung Electronics Co. Ltd. | 2.0 | % |

| Semiconductors & Semiconductor | | |

| Equipment, South Korea | | |

| Medtronic Inc. | 1.9 | % |

| Health Care Equipment & Supplies, U.S. | |

Among defensive stocks, we favored opportunities in the telecommunication services sector.7 The Fund’s stake in Vodafone Group (U.K.), one of the world’s largest mobile telephone operators, helped relative performance after the firm announced it was selling its stake in U.S. mobile telephone operator Verizon Wireless for $130 billion.

Conversely, the Fund’s stock selection in the information technology (IT) sector pressured relative returns.8 Relative weakness was primarily attributable to losses at U.S. networking equipment firm Cisco Systems, which reported its first sales decline in four years. The stock price was relatively close to the same level as when we initiated our position in 2008 and continued to look cheap to us based on many valuation measures. From our perspective, management has made solid progress implementing a sensible restructuring plan in recent years. However, industry headwinds and new risks surfaced, including low-cost competition from emerging markets, weak corporate networking spending and a lower-than-expected correlation between Internet traffic growth and demand growth for Cisco’s routers. Overall, recent IT gains have made bargain hunting in the sector somewhat challenging for us, although we continued to search for companies whose long-term growth prospects seemed to us materially undervalued.

The health care sector was largely undervalued over the past decade, based on our analysis.9 We began increasing exposure to the sector about a decade ago. At the time, investor sentiment was hampered by fears that impending patent expirations, compounded by declining research and development productivity and rising generic competition, could depress the profitability of major pharmaceuticals manufacturers. Based on our analysis, top-tier pharmaceuticals and biotechnology companies were being valued at levels that assigned no credit for future drug development or earnings recovery. Although many investors saw an industry in decline, our analysis identified what we believed were cheap stocks with underappreciated recovery potential. Rising health care spending in the developing world represented a long-term growth catalyst, and we also identified potential for cost cutting and consolidation in a capital intensive industry. These investments took time to reward us, but with the patent cliff past and margin recovery ongoing, returns for the Fund’s overweighting in health care provided positive momentum during the period. Swiss biotechnology firm Roche Holding was one of the leading performers during the period. However, muted gains from major European drugmakers Sanofi (France) and GlaxoSmithKline (U.K.), as well as U.S. biotechnology firm Amgen, resulted in modest underperformance relative to the benchmark for our overall health care holdings.

Semiannual Report | 9

Stock selection in consumer discretionary and an overweighting in energy also weighed on relative performance, despite absolute gains for these sectors.10 In the consumer discretionary sector, Japanese car maker Nissan Motor’s share price retreated after the company attributed a profit warning to weaker emerging market volume, higher-than-expected recall costs and unfavorable currency moves. Even after we lowered our near-term earnings estimates to reflect these short-term headwinds, the stock’s long-term investment case remained attractive to us, given what we viewed as Nissan’s proven cost-cutting capability, popular new model pipeline and excellent management track record. Elsewhere in the consumer discretionary sector, we reduced exposure as soaring valuations allowed us to realize gains on contrarian investments made in periods of extreme investor pessimism. Instead, we were overweighted in the energy sector, where investor concerns about heavy capital expenditures and stagnant production growth depressed the share prices of many major oil companies to what we viewed as bargain levels. We believed some of these companies could ultimately benefit from their heavy capital expenditures as innovation accelerates and major new projects begin producing. As we wait for this to occur, the industry has provided a roughly 3% average dividend yield. We also found attractive opportunities in the oil services industry, which directly benefits from increasing demand for technology and specialization in the oil extraction process. The share price of U.S.-listed deep-water drilling contractor Noble declined based on concerns about continued oversupply in the industry. However, long-term valuations and industry dynamics remained favorable in our view.

Regionally, the Fund’s European holdings outperformed owing to a large regional overweighting and stock selection. Specifically, stock selection in the U.K. and the Netherlands and an overweighting in Ireland bolstered relative performance. Stock selection in the U.S. and an underweighting and stock selection in Australia also contributed to relative performance. In contrast, allocations to off-benchmark countries South Korea and Brazil, along with an overweighting in Singapore, hampered relative results.

It is important to recognize the effect of currency movements on the Fund’s performance. In general, if the value of the U.S. dollar goes up compared with a foreign currency, an investment traded in that foreign currency will go down in value because it will be worth fewer U.S. dollars. This can have a negative effect on Fund performance. Conversely, when the U.S. dollar weakens in relation to a foreign currency, an investment traded in that foreign currency will increase in value, which can contribute to Fund performance. For the six

10 | Semiannual Report

months ended February 28, 2014, the U.S. dollar declined in value relative to most currencies. As a result, the Fund’s performance was positively affected by the portfolio’s substantial investment in securities with non-U.S. currency exposure. However, one cannot expect the same result in future periods.

Market momentum remained positive in early 2014, although concerns persisted about emerging market volatility and the sustainability of the global economic recovery. Following a strong recovery from the post-financial crisis trough and accompanying rising valuations, some value-minded investors have expressed concerns about the sustainability of the ongoing market rally. We do not know where the market is going. However, as investors with a long-term perspective, we note that on a trailing 10-year basis, recent annualized global equity returns of slightly above 6% remained meaningfully below the nearly 9% average annualized 10-year returns for the asset class going back to 1835.11 Long-term stock returns have historically reverted to the average, so although we do not know what will happen in the near term, we believe potential remains for continued stock strength over our long-term investment horizon. Furthermore, while some parts of the market seemed to grow more expensive, other parts of the market remained decidedly cheap, in our assessment. Europe continued to trade at multi-decade low valuations relative to the U.S. based on cyclically adjusted earnings multiples, and depressed profit margins in the region could improve if companies with high operating leverage benefit from Europe’s economic recovery. Emerging markets have offered what appeared to us as a number of selective opportunities for long-term bargain hunters amid recent turmoil. With economic and policy conditions diverging around the world and correlations between markets and asset classes declining, we believe bottom-up stock pickers with a proven process, like Templeton, remained well positioned to help investors navigate an uncertain future.

Semiannual Report | 11

Thank you for your continued participation in Templeton World Fund.

We look forward to serving your future investment needs.

The foregoing information reflects our analysis, opinions and portfolio holdings as of February 28, 2014, the end

of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings

may change depending on factors such as market and economic conditions. These opinions may not be relied upon

as investment advice or an offer for a particular security. The information is not a complete analysis of every

aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered

reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy.

Although historical performance is no guarantee of future results, these insights may help you understand our

investment management philosophy.

12 | Semiannual Report

|

| Heather Arnold assumed portfolio manager responsibilities for the Fund in January 2014. |

| Ms. Arnold is the director of research for the Templeton Global Equity Group, as well as a |

| portfolio manager and research analyst. Ms. Arnold manages institutional and retail equity |

| portfolios and has research responsibilities for Japan and Russia. Prior to joining Franklin |

| Templeton in 1997, she was a managing director for Goldman Sachs Asset Management, |

| head of European equities and portfolio manager for European, international and global |

| institutional and retail client portfolios. In 2001, Ms. Arnold left to start her own company |

| and returned to Franklin Templeton in 2008. |

The index is unmanaged and includes reinvested dividends. One cannot invest directly in an index, and an index is not

representative of the Fund’s portfolio.

1. Source: © 2014 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar

and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or

timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of

this information. As of 2/28/14, the Fund’s Class A 10-year average annual total return not including the maximum

sales charge was +7.44%, compared with the MSCI World Index’s 10-year average annual total return of +7.33%.

2. Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoev-

er with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis

for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

3. The financials sector comprises banks, capital markets, diversified financial services and insurance in the SOI.

4. The industrials sector comprises aerospace and defense, air freight and logistics, airlines, commercial services

and supplies, construction and engineering, electrical equipment, industrial conglomerates, machinery, and trading

companies and distributors in the SOI.

5. The consumer staples sector comprises food and staples retailing in the SOI.

6. The materials sector comprises chemicals, construction materials, and metals and mining in the SOI.

7. The telecommunication services sector comprises diversified telecommunication services and wireless telecom-

munication services in the SOI.

8. The information technology sector comprises communications equipment; electronic equipment, instruments and

components; IT services; semiconductors and semiconductor equipment; software; and technology hardware, storage

and peripherals in the SOI.

9. The health care sector comprises biotechnology, health care equipment and supplies, and pharmaceuticals in

the SOI.

10. The consumer discretionary sector comprises automobiles, household durables, media and specialty retail in the

SOI. The energy sector comprises energy equipment and services; and oil, gas and consumable fuels in the SOI.

11. Source: Stifel Equity Strategist Barry B. Bannister, In the Spring There Will be Growth, presentation on March 1,

2010. Data as of 12/31/13.

Semiannual Report | 13

Performance Summary as of 2/28/14

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

| | | | | | | | |

| Price and Distribution Information | | | | | | |

| |

| Class A (Symbol: TEMWX) | | | | Change | | 2/28/14 | | 8/31/13 |

| Net Asset Value (NAV) | | | +$ | 1.54 | $ | 19.56 | $ | 18.02 |

| Distributions (9/1/13–2/28/14) | | | | | | | | |

| Dividend Income | $ | 0.1860 | | | | | | |

| Short-Term Capital Gain | $ | 0.1371 | | | | | | |

| Long-Term Capital Gain | $ | 0.6902 | | | | | | |

| Total | $ | 1.0133 | | | | | | |

| Class C (Symbol: TEWTX) | | | | Change | | 2/28/14 | | 8/31/13 |

| Net Asset Value (NAV) | | | +$ | 1.52 | $ | 18.92 | $ | 17.40 |

| Distributions (9/1/13–2/28/14) | | | | | | | | |

| Dividend Income | $ | 0.0556 | | | | | | |

| Short-Term Capital Gain | $ | 0.1371 | | | | | | |

| Long-Term Capital Gain | $ | 0.6902 | | | | | | |

| Total | $ | 0.8829 | | | | | | |

| Class R6 (Symbol: FTWRX) | | | | Change | | 2/28/14 | | 8/31/13 |

| Net Asset Value (NAV) | | | +$ | 1.51 | $ | 19.53 | $ | 18.02 |

| Distributions (9/1/13–2/28/14) | | | | | | | | |

| Dividend Income | $ | 0.2473 | | | | | | |

| Short-Term Capital Gain | $ | 0.1371 | | | | | | |

| Long-Term Capital Gain | $ | 0.6902 | | | | | | |

| Total | $ | 1.0746 | | | | | | |

| Advisor Class (Symbol: TWDAX) | | | | Change | | 2/28/14 | | 8/31/13 |

| Net Asset Value (NAV) | | | +$ | 1.53 | $ | 19.54 | $ | 18.01 |

| Distributions (9/1/13–2/28/14) | | | | | | | | |

| Dividend Income | $ | 0.2294 | | | | | | |

| Short-Term Capital Gain | $ | 0.1371 | | | | | | |

| Long-Term Capital Gain | $ | 0.6902 | | | | | | |

| Total | $ | 1.0567 | | | | | | |

14 | Semiannual Report

Performance Summary (continued)

Performance

Cumulative total return excludes sales charges. Aggregate and average annual total returns and value of $10,000 investment include maximum sales charges. Class A: 5.75% maximum initial sales charge; Class C: 1% contingent deferred sales charge in first year only; Class R6/Advisor Class: no sales charges.

| | | | | | | | | | | | |

| Class A | | 6-Month | | | 1-Year | | | 5-Year | | | 10-Year | |

| Cumulative Total Return1 | + | 14.33 | % | + | 25.24 | % | + | 153.59 | % | + | 104.99 | % |

| Average Annual Total Return2 | + | 7.75 | % | + | 18.07 | % | + | 19.03 | % | + | 6.81 | % |

| Value of $10,000 Investment3 | $ | 10,775 | | $ | 11,807 | | $ | 23,891 | | $ | 19,318 | |

| Avg. Ann. Total Return (3/31/14)4 | | | | + | 17.32 | % | + | 17.29 | % | + | 7.03 | % |

| Total Annual Operating Expenses5 | | | | | 1.05 | % | | | | | | |

| Class C | | 6-Month | | | 1-Year | | | 5-Year | | | 10-Year | |

| Cumulative Total Return1 | + | 13.95 | % | + | 24.31 | % | + | 144.43 | % | + | 90.15 | % |

| Average Annual Total Return2 | + | 12.95 | % | + | 23.31 | % | + | 19.57 | % | + | 6.64 | % |

| Value of $10,000 Investment3 | $ | 11,295 | | $ | 12,331 | | $ | 24,443 | | $ | 19,015 | |

| Avg. Ann. Total Return (3/31/14)4 | | | | + | 22.58 | % | + | 17.80 | % | + | 6.85 | % |

| Total Annual Operating Expenses5 | | | | | 1.81 | % | | | | | | |

| Class R6 | | | | | | | | 6-Month | | | Inception (5/1/13) | |

| Cumulative Total Return1 | | | | | | | + | 14.59 | % | + | 20.19 | % |

| Aggregate Total Return6 | | | | | | | + | 14.59 | % | + | 20.19 | % |

| Value of $10,000 Investment3 | | | | | | | $ | 11,459 | | $ | 12,019 | |

| Aggregate Total Return (3/31/14)4, 6 | | | | | | | | | | + | 20.87 | % |

| Total Annual Operating Expenses5 | | | | | 0.72 | % | | | | | | |

| Advisor Class7 | | 6-Month | | | 1-Year | | | 5-Year | | | 10-Year | |

| Cumulative Total Return1 | + | 14.54 | % | + | 25.55 | % | + | 156.76 | % | + | 109.05 | % |

| Average Annual Total Return2 | + | 14.54 | % | + | 25.55 | % | + | 20.76 | % | + | 7.65 | % |

| Value of $10,000 Investment3 | $ | 11,454 | | $ | 12,555 | | $ | 25,676 | | $ | 20,905 | |

| Avg. Ann. Total Return (3/31/14)4 | | | | + | 24.82 | % | + | 18.98 | % | + | 7.87 | % |

| Total Annual Operating Expenses5 | | | | | 0.81 | % | | | | | | |

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

Semiannual Report | 15

Performance Summary (continued)

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. To the extent the Fund focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a fund that invests in a wider variety of countries, regions, industries, sectors or investments. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

Class C: These shares have higher annual fees and expenses than Class A shares.

Class R6: Shares are available to certain eligible investors as described in the prospectus.

Advisor Class: Shares are available to certain eligible investors as described in the prospectus.

1. Cumulative total return represents the change in value of an investment over the periods indicated.

2. Average annual total return represents the average annual change in value of an investment over the periods indicated. Six-month return has not

been annualized.

3. These figures represent the value of a hypothetical $10,000 investment in the Fund over the periods indicated.

4. In accordance with SEC rules, we provide standardized average annual total return information through the latest calendar quarter.

5. Figures are as stated in the Fund’s current prospectus. In periods of market volatility, assets may decline significantly, causing total annual Fund

operating expenses to become higher than the figures shown.

6. Aggregate total return represents the change in value of an investment for the period indicated. Since Class R6 shares have existed for less than

one year, average annual total return is not available.

7. Effective 5/15/06, the Fund began offering Advisor Class shares, which do not have sales charges or a Rule 12b-1 plan. Performance quotations

for this class reflect the following methods of calculation: (a) For periods prior to 5/15/06, a restated figure is used based upon the Fund’s Class A

performance, excluding the effect of Class A’s maximum initial sales charge, but reflecting the effect of the Class A Rule 12b-1 fees; and (b) for

periods after 5/15/06, actual Advisor Class performance is used reflecting all charges and fees applicable to that class. Since 5/15/06 (commence-

ment of sales), the cumulative and average annual total returns of Advisor Class shares were +56.64% and +5.93%.

16 | Semiannual Report

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases; and

- Ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

| 1. | Divide your account value by $1,000. |

| | If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6. |

| 2. | Multiply the result by the number under the heading “Expenses Paid During Period.” |

| | If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50. |

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

Semiannual Report | 17

Your Fund’s Expenses (continued)

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

| | | | | | |

| | | Beginning Account | | Ending Account | | Expenses Paid During |

| Class A | | Value 9/1/13 | | Value 2/28/14 | | Period* 9/1/13–2/28/14 |

| Actual | $ | 1,000 | $ | 1,143.30 | $ | 5.63 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,019.54 | $ | 5.31 |

| Class C | | | | | | |

| Actual | $ | 1,000 | $ | 1,139.50 | $ | 9.60 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,015.82 | $ | 9.05 |

| Class R6 | | | | | | |

| Actual | $ | 1,000 | $ | 1,145.90 | $ | 3.83 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,021.22 | $ | 3.61 |

| Advisor Class | | | | | | |

| Actual | $ | 1,000 | $ | 1,145.40 | $ | 4.31 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,020.78 | $ | 4.06 |

*Expenses are calculated using the most recent six-month expense ratio, annualized for each class (A: 1.06%; C: 1.81%; R6: 0.72%; and Advisor: 0.81%), multiplied by the average account value over the period, multiplied by 181/365 to reflect the one-half year period.

18 | Semiannual Report

Templeton World Fund

Financial Highlights

| | | | | | | | | | | | | | | | | | |

| | | �� Six Months Ended | | | | | | | | | | | | | |

| | | February 28, 2014 | | | | | | Year Ended August 31, | | | | |

| Class A | | (unaudited) | | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | |

| Per share operating performance | | | | | | | | | | | | | | | | | | |

| (for a share outstanding throughout | | | | | | | | | | | | | | | | | | |

| the period) | | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of period | $ | 18.02 | | $ | 15.06 | | $ | 14.21 | | $ | 12.74 | | $ | 12.80 | | $ | 15.78 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.21 | c | | 0.25 | | | 0.29 | | | 0.24 | | | 0.21 | | | 0.24 | |

| Net realized and unrealized | | | | | | | | | | | | | | | | | | |

| gains (losses) | | 2.35 | | | 3.38 | | | 0.84 | | | 1.47 | | | (0.01 | ) | | (2.59 | ) |

| Total from investment operations | | 2.56 | | | 3.63 | | | 1.13 | | | 1.71 | | | 0.20 | | | (2.35 | ) |

| Less distributions from: | | | | | | | | | | | | | | | | | | |

| Net investment income | | (0.19 | ) | | (0.42 | ) | | (0.28 | ) | | (0.24 | ) | | (0.26 | ) | | (0.30 | ) |

| Net realized gains | | (0.83 | ) | | (0.25 | ) | | — | | | — | | | — | | | (0.33 | ) |

| Total distributions | | (1.02 | ) | | (0.67 | ) | | (0.28 | ) | | (0.24 | ) | | (0.26 | ) | | (0.63 | ) |

| Net asset value, end of period | $ | 19.56 | | $ | 18.02 | | $ | 15.06 | | $ | 14.21 | | $ | 12.74 | | $ | 12.80 | |

| |

| Total returnd | | 14.33 | % | | 24.71 | % | | 8.18 | % | | 13.45 | % | | 1.32 | % | | (14.04 | )% |

| |

| Ratios to average net assetse | | | | | | | | | | | | | | | | | | |

| Expenses | | 1.06 | % | | 1.05 | %f | | 1.09 | % | | 1.07 | %f | | 1.09 | %f | | 1.10 | %f |

| Net investment income | | 1.60 | %c | | 1.49 | % | | 1.99 | % | | 1.62 | % | | 1.54 | % | | 2.15 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000’s) | $ | 5,905,511 | | $ | 5,278,292 | | $ | 4,857,469 | | $ | 5,067,228 | | $ | 5,029,053 | | $ | 5,431,882 | |

| Portfolio turnover rate | | 9.12 | % | | 17.57 | % | | 18.77 | % | | 16.11 | % | | 16.77 | % | | 17.66 | % |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of

the Fund shares in relation to income earned and/or fluctuating market value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.12 per share received in the form of a special dividend paid in connection with certain Fund’s holdings. Excluding this

amount, the ratio of net investment income to average net assets would have been 1.00%.

dTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable, and is not annualized for periods less than one year.

eRatios are annualized for periods less than one year.

fBenefit of expense reduction rounds to less than 0.01%.

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 19

| | | | | | | | | | | | | | | | | | |

| Templeton World Fund | | | | | | | | | | | | | | | | |

| |

| Financial Highlights (continued) | | | | | | | | | | | | | | | | | | |

| |

| | | Six Months Ended | | | | | | | | | | | | | | | | |

| | | February 28, 2014 | | | Year Ended August 31, | | | | |

| Class C | | (unaudited) | | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | |

| Per share operating performance | | | | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the period) | | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of period | $ | 17.40 | | $ | 14.53 | | $ | 13.69 | | $ | 12.28 | | $ | 12.39 | | $ | 15.23 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.14 | c | | 0.12 | | | 0.17 | | | 0.13 | | | 0.10 | | | 0.15 | |

| Net realized and unrealized gains (losses) | | 2.27 | | | 3.26 | | | 0.83 | | | 1.41 | | | (0.01 | ) | | (2.49 | ) |

| Total from investment operations | | 2.41 | | | 3.38 | | | 1.00 | | | 1.54 | | | 0.09 | | | (2.34 | ) |

| Less distributions from: | | | | | | | | | | | | | | | | | | |

| Net investment income | | (0.06 | ) | | (0.26 | ) | | (0.16 | ) | | (0.13 | ) | | (0.20 | ) | | (0.17 | ) |

| Net realized gains | | (0.83 | ) | | (0.25 | ) | | — | | | — | | | — | | | (0.33 | ) |

| Total distributions | | (0.89 | ) | | (0.51 | ) | | (0.16 | ) | | (0.13 | ) | | (0.20 | ) | | (0.50 | ) |

| Net asset value, end of period | $ | 18.92 | | $ | 17.40 | | $ | 14.53 | | $ | 13.69 | | $ | 12.28 | | $ | 12.39 | |

| |

| Total returnd | | 13.95 | % | | 23.76 | % | | 7.41 | % | | 12.50 | % | | 0.60 | % | | (14.65 | )% |

| |

| Ratios to average net assetse | | | | | | | | | | | | | | | | | | |

| Expenses | | 1.81 | % | | 1.81 | %f | | 1.84 | % | | 1.82 | %f | | 1.84 | %f | | 1.85 | %f |

| Net investment income | | 0.85 | %c | | 0.73 | % | | 1.24 | % | | 0.87 | % | | 0.79 | % | | 1.40 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000’s) | $ | 238,495 | | $ | 210,256 | | $ | 186,483 | | $ | 201,956 | | $ | 208,330 | | $ | 233,637 | |

| Portfolio turnover rate | | 9.12 | % | | 17.57 | % | | 18.77 | % | | 16.11 | % | | 16.77 | % | | 17.66 | % |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of

the Fund shares in relation to income earned and/or fluctuating market value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.12 per share received in the form of a special dividend paid in connection with certain Fund’s holdings. Excluding this

amount, the ratio of net investment income to average net assets would have been 0.25%.

dTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable, and is not annualized for periods less than one year.

eRatios are annualized for periods less than one year.

fBenefit of expense reduction rounds to less than 0.01%.

20 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

| | | | | | |

| Templeton World Fund | | | | | | |

| |

| Financial Highlights (continued) | | | | | | |

| |

| | | Six Months Ended | | | Period Ended | |

| | | February 28, 2014 | | | August 31, | |

| Class R6 | | (unaudited) | | | 2013 | a |

| Per share operating performance | | | | | | |

| (for a share outstanding throughout the period) | | | | | | |

| Net asset value, beginning of period | $ | 18.02 | | $ | 17.17 | |

| Income from investment operationsb: | | | | | | |

| Net investment incomec | | 0.27 | d | | 0.12 | |

| Net realized and unrealized gains (losses) | | 2.32 | | | 0.73 | |

| Total from investment operations | | 2.59 | | | 0.85 | |

| Less distributions from: | | | | | | |

| Net investment income | | (0.25 | ) | | — | |

| Net realized gains | | (0.83 | ) | | — | |

| Total distributions | | (1.08 | ) | | — | |

| Net asset value, end of period | $ | 19.53 | | $ | 18.02 | |

| |

| Total returne | | 14.59 | % | | 4.95 | % |

| |

| Ratios to average net assetsf | | | | | | |

| Expenses | | 0.72 | % | | 0.72 | %g |

| Net investment income | | 1.94 | %d | | 1.82 | % |

| |

| Supplemental data | | | | | | |

| Net assets, end of period (000’s) | $ | 54,022 | | $ | 24,306 | |

| Portfolio turnover rate | | 9.12 | % | | 17.57 | % |

aFor the period May 1, 2013 (effective date) to August 31, 2013.

bThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of

the Fund shares in relation to income earned and/or fluctuating market value of the investments of the Fund.

cBased on average daily shares outstanding.

dNet investment income per share includes approximately $0.12 per share received in the form of a special dividend paid in connection with certain Fund’s holdings. Excluding this

amount, the ratio of net investment income to average net assets would have been 1.34%.

eTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable, and is not annualized for periods less than one year.

fRatios are annualized for periods less than one year.

gBenefit of expense reduction rounds to less than 0.01%.

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 21

| | | | | | | | | | | | | | | | | | |

| Templeton World Fund | | | | | | | | | | | | | | | | |

| |

| Financial Highlights (continued) | | | | | | | | | | | | | | | | | | |

| |

| | | Six Months Ended | | | | | | | | | | | | | | | | |

| | | February 28, 2014 | | | Year Ended August 31, | | | | |

| Advisor Class | | (unaudited) | | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | |

| Per share operating performance | | | | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the period) | | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of period | $ | 18.01 | | $ | 15.07 | | $ | 14.22 | | $ | 12.75 | | $ | 12.80 | | $ | 15.79 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.24 | c | | 0.30 | | | 0.33 | | | 0.29 | | | 0.24 | | | 0.28 | |

| Net realized and unrealized gains (losses) | | 2.35 | | | 3.36 | | | 0.84 | | | 1.46 | | | (0.02 | ) | | (2.60 | ) |

| Total from investment operations | | 2.59 | | | 3.66 | | | 1.17 | | | 1.75 | | | 0.22 | | | (2.32 | ) |

| Less distributions from: | | | | | | | | | | | | | | | | | | |

| Net investment income | | (0.23 | ) | | (0.47 | ) | | (0.32 | ) | | (0.28 | ) | | (0.27 | ) | | (0.34 | ) |

| Net realized gains | | (0.83 | ) | | (0.25 | ) | | — | | | — | | | — | | | (0.33 | ) |

| Total distributions | | (1.06 | ) | | (0.72 | ) | | (0.32 | ) | | (0.28 | ) | | (0.27 | ) | | (0.67 | ) |

| Net asset value, end of period | $ | 19.54 | | $ | 18.01 | | $ | 15.07 | | $ | 14.22 | | $ | 12.75 | | $ | 12.80 | |

| |

| Total returnd | | 14.54 | % | | 24.97 | % | | 8.51 | % | | 13.63 | % | | 1.61 | % | | (13.79 | )% |

| |

| Ratios to average net assetse | | | | | | | | | | | | | | | | | | |

| Expenses | | 0.81 | % | | 0.81 | %f | | 0.84 | % | | 0.82 | %f | | 0.84 | %f | | 0.86 | %f |

| Net investment income | | 1.85 | %c | | 1.73 | % | | 2.24 | % | | 1.87 | % | | 1.79 | % | | 2.39 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000’s) | $ | 251,087 | | $ | 216,767 | | $ | 232,104 | | $ | 191,488 | | $ | 170,328 | | $ | 166,706 | |

| Portfolio turnover rate | | 9.12 | % | | 17.57 | % | | 18.77 | % | | 16.11 | % | | 16.77 | % | | 17.66 | % |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of

the Fund shares in relation to income earned and/or fluctuating market value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.12 per share received in the form of a special dividend paid in connection with certain Fund’s holdings. Excluding this

amount, the ratio of net investment income to average net assets would have been 1.25%.

dTotal return is not annualized for periods less than one year.

eRatios are annualized for periods less than one year.

fBenefit of expense reduction rounds to less than 0.01%.

22 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

| | | | |

| Templeton World Fund | | | |

| |

| Statement of Investments, February 28, 2014 (unaudited) | | | |

| |

| |

| | Industry | Shares | | Value |

| Common Stocks 95.1% | | | | |

| Australia 0.6% | | | | |

| a Qantas Airways Ltd. | Airlines | 39,258,599 | $ | 40,801,323 |

| |

| Austria 0.4% | | | | |

| UNIQA Insurance Group AG | Insurance | 212,000 | | 2,779,320 |

| b UNIQA Insurance Group AG, 144A | Insurance | 1,891,099 | | 24,792,307 |

| | | | | 27,571,627 |

| |

| Canada 1.8% | | | | |

| Suncor Energy Inc. | Oil, Gas & Consumable Fuels | 1,244,777 | | 41,087,651 |

| Talisman Energy Inc. | Oil, Gas & Consumable Fuels | 6,001,970 | | 61,825,660 |

| Trican Well Service Ltd. | Energy Equipment & Services | 869,300 | | 10,988,983 |

| | | | | 113,902,294 |

| |

| China 0.8% | | | | |

| Digital China Holdings Ltd. | Electronic Equipment, Instruments & Components | 25,078,000 | | 24,818,185 |

| Dongfang Electric Corp. Ltd., H | Electrical Equipment | 9,202,319 | | 14,703,978 |

| Kunlun Energy Co. Ltd. | Oil, Gas & Consumable Fuels | 594,800 | | 1,059,241 |

| Weichai Power Co. Ltd., H | Machinery | 2,171,400 | | 8,226,272 |

| | | | | 48,807,676 |

| |

| France 8.1% | | | | |

| Alstom SA | Electrical Equipment | 1,196,140 | | 32,278,914 |

| AXA SA | Insurance | 2,231,490 | | 58,324,899 |

| BNP Paribas SA | Banks | 2,071,960 | | 170,014,259 |

| Sanofi | Pharmaceuticals | 1,089,710 | | 113,281,236 |

| Technip SA | Energy Equipment & Services | 213,030 | | 20,928,535 |

| Total SA, B | Oil, Gas & Consumable Fuels | 2,016,820 | | 130,894,438 |

| | | | | 525,722,281 |

| |

| Germany 2.9% | | | | |

| a Commerzbank AG | Banks | 1,012,200 | | 18,354,425 |

| Deutsche Boerse AG | Diversified Financial Services | 18,570 | | 1,523,245 |

| Merck KGaA | Pharmaceuticals | 288,600 | | 50,580,035 |

| Metro AG | Food & Staples Retailing | 757,708 | | 31,416,164 |

| a Osram Licht AG | Electrical Equipment | 2 | | 136 |

| SAP AG | Software | 162,344 | | 13,110,511 |

| Siemens AG | Industrial Conglomerates | 546,680 | | 72,997,522 |

| | | | | 187,982,038 |

| |

| Hong Kong 0.4% | | | | |

| Hutchison Whampoa Ltd. | Industrial Conglomerates | 1,541,583 | | 20,778,514 |

| Noble Group Ltd. | Trading Companies & Distributors | 7,586,400 | | 6,164,399 |

| | | | | 26,942,913 |

| |

| India 0.4% | | | | |

| Reliance Industries Ltd. | Oil, Gas & Consumable Fuels | 1,756,441 | | 22,734,178 |

Semiannual Report | 23

| | | | |

| Templeton World Fund | | | |

| |

| Statement of Investments, February 28, 2014 (unaudited) (continued) | | | |

| |

| |

| | Industry | Shares | | Value |

| Common Stocks (continued) | | | | |

| Ireland 1.3% | | | | |

| CRH PLC | Construction Materials | 2,944,063 | $ | 87,147,207 |

| |

| Israel 0.9% | | | | |

| Teva Pharmaceutical Industries Ltd., ADR | Pharmaceuticals | 1,155,484 | | 57,647,097 |

| |

| Italy 2.6% | | | | |

| Eni SpA | Oil, Gas & Consumable Fuels | 2,505,453 | | 60,437,538 |

| Saipem SpA | Energy Equipment & Services | 535,009 | | 12,580,843 |

| UniCredit SpA | Banks | 11,762,737 | | 93,580,804 |

| | | | | 166,599,185 |

| |

| Japan 3.7% | | | | |

| ITOCHU Corp. | Trading Companies & Distributors | 4,437,211 | | 55,094,643 |

| Nikon Corp. | Household Durables | 500,200 | | 9,153,955 |

| Nissan Motor Co. Ltd. | Automobiles | 11,268,900 | | 100,844,478 |

| Toyota Motor Corp. | Automobiles | 1,268,925 | | 72,782,447 |

| | | | | 237,875,523 |

| |

| Netherlands 2.7% | | | | |

| Akzo Nobel NV | Chemicals | 374,860 | | 31,043,580 |

| Fugro NV, IDR | Energy Equipment & Services | 463,519 | | 26,935,923 |

| a ING Groep NV, IDR | Diversified Financial Services | 8,074,698 | | 117,782,387 |

| | | | | 175,761,890 |

| |

| Norway 1.2% | | | | |

| Telenor ASA | Diversified Telecommunication Services | 3,470,220 | | 76,684,194 |

| |

| Portugal 0.8% | | | | |

| Galp Energia SGPS SA, B | Oil, Gas & Consumable Fuels | 2,902,130 | | 48,780,161 |

| |

| Russia 0.8% | | | | |

| Gazprom OAO, ADR | Oil, Gas & Consumable Fuels | 934,572 | | 7,195,270 |

| Mining and Metallurgical Co. | | | | |

| Norilsk Nickel OJSC, ADR | Metals & Mining | 2,289,558 | | 38,870,971 |

| Mobile TeleSystems, ADR | Wireless Telecommunication Services | 165,226 | | 2,845,192 |

| | | | | 48,911,433 |

| |

| Singapore 2.3% | | | | |

| DBS Group Holdings Ltd. | Banks | 3,301,396 | | 43,025,451 |

| a Flextronics International Ltd. | Electronic Equipment, Instruments & Components | 4,973,635 | | 44,514,034 |

| Singapore Telecommunications Ltd. | Diversified Telecommunication Services | 22,487,261 | | 63,864,105 |

| | | | | 151,403,590 |

| |

| South Korea 5.0% | | | | |

| Hana Financial Group Inc. | Banks | 1,154,470 | | 45,160,363 |

| KB Financial Group Inc. | Banks | 1,876,166 | | 70,223,566 |

| POSCO | Metals & Mining | 293,882 | | 78,294,282 |

| Samsung Electronics Co. Ltd. | Semiconductors & Semiconductor Equipment | 100,633 | | 127,347,696 |

| | | | | 321,025,907 |

| |

| 24 | Semiannual Report | | | | |

Templeton World Fund

Statement of Investments, February 28, 2014 (unaudited) (continued)

| | | | |

| | Industry | Shares | | Value |

| Common Stocks (continued) | | | | |

| Spain 0.9% | | | | |

| Telefonica SA | Diversified Telecommunication Services | 3,802,046 | $ | 58,292,207 |

| |

| Switzerland 5.9% | | | | |

| ABB Ltd. | Electrical Equipment | 1,080,030 | | 27,614,682 |

| Credit Suisse Group AG | Capital Markets | 4,053,632 | | 127,655,305 |

| Roche Holding AG | Pharmaceuticals | 500,372 | | 154,389,451 |

| Swiss Re AG | Insurance | 762,200 | | 71,228,786 |

| | | | | 380,888,224 |

| |

| Taiwan 1.4% | | | | |

| Compal Electronics Inc. | Technology Hardware, Storage & Peripherals | 34,584,086 | | 23,395,385 |

| Taiwan Semiconductor Manufacturing Co. | | | | |

| Ltd. | Semiconductors & Semiconductor Equipment | 7,501,690 | | 26,735,168 |

| Tripod Technology Corp. | Electronic Equipment, Instruments & Components | 20,588,000 | | 39,404,171 |

| | | | | 89,534,724 |

| |

| Turkey 0.4% | | | | |

| a Turkcell Iletisim Hizmetleri AS | Wireless Telecommunication Services | 5,561,571 | | 29,009,009 |

| |

| United Kingdom 15.9% | | | | |

| Aviva PLC | Insurance | 13,300,126 | | 105,449,074 |

| BAE Systems PLC | Aerospace & Defense | 8,784,320 | | 60,426,384 |

| BP PLC | Oil, Gas & Consumable Fuels | 6,798,278 | | 57,393,197 |

| Carillion PLC | Construction & Engineering | 7,144,390 | | 45,366,442 |

| GlaxoSmithKline PLC | Pharmaceuticals | 4,294,493 | | 120,174,606 |

| HSBC Holdings PLC | Banks | 7,758,970 | | 81,790,285 |

| a International Consolidated Airlines | | | | |

| Group SA | Airlines | 11,829,900 | | 86,544,938 |

| Kingfisher PLC | Specialty Retail | 17,216,830 | | 113,562,253 |

| a Lloyds Banking Group PLC | Banks | 57,898,630 | | 79,990,041 |

| Man Group PLC | Capital Markets | 7,953,365 | | 13,812,379 |

| Royal Dutch Shell PLC, A (EUR Traded) | Oil, Gas & Consumable Fuels | 128,452 | | 4,689,513 |

| Royal Dutch Shell PLC, A (GBP Traded) | Oil, Gas & Consumable Fuels | 5,923 | | 215,913 |

| Royal Dutch Shell PLC, B | Oil, Gas & Consumable Fuels | 1,461,012 | | 56,921,056 |

| Serco Group PLC | Commercial Services & Supplies | 4,993,940 | | 38,499,012 |

| Tesco PLC | Food & Staples Retailing | 16,476,424 | | 90,806,768 |

| Vodafone Group PLC | Wireless Telecommunication Services | 16,287,079 | | 67,891,535 |

| | | | | 1,023,533,396 |

| |

| United States 33.9% | | | | |

| Abercrombie & Fitch Co., A | Specialty Retail | 121,310 | | 4,807,515 |

| Accenture PLC, A | IT Services | 164,571 | | 13,716,993 |

| American International Group Inc. | Insurance | 1,283,575 | | 63,883,528 |

| Amgen Inc. | Biotechnology | 924,300 | | 114,631,686 |

| Baker Hughes Inc. | Energy Equipment & Services | 2,245,350 | | 142,085,748 |

| a Brocade Communications Systems Inc. | Communications Equipment | 2,439,605 | | 23,347,020 |

| Chevron Corp. | Oil, Gas & Consumable Fuels | 169,276 | | 19,522,601 |

| Cisco Systems Inc. | Communications Equipment | 4,452,390 | | 97,062,102 |

| Citigroup Inc. | Banks | 2,663,930 | | 129,546,916 |

Semiannual Report | 25

| | | | |

| Templeton World Fund | | | |

| |

| Statement of Investments, February 28, 2014 (unaudited) (continued) | | | |

| |

| |

| | Industry | Shares | | Value |

| Common Stocks (continued) | | | | |

| United States (continued) | | | | |

| Comcast Corp., Special A | Media | 1,259,099 | $ | 62,822,745 |

| CVS Caremark Corp. | Food & Staples Retailing | 1,130,850 | | 82,710,369 |

| FedEx Corp. | Air Freight & Logistics | 262,667 | | 35,021,391 |

| Foot Locker Inc. | Specialty Retail | 1,476,200 | | 61,572,302 |

| Halliburton Co. | Energy Equipment & Services | 1,006,589 | | 57,375,573 |

| The Hartford Financial Services Group Inc. | Insurance | 386,300 | | 13,593,897 |

| Hewlett-Packard Co. | Technology Hardware, Storage & Peripherals | 3,459,430 | | 103,367,768 |

| ING U.S. Inc. | Diversified Financial Services | 176,020 | | 6,313,837 |

| JPMorgan Chase & Co. | Banks | 1,809,934 | | 102,840,450 |

| KBR Inc. | Construction & Engineering | 589,580 | | 16,284,200 |

| LyondellBasell Industries NV, A | Chemicals | 186,550 | | 16,431,324 |

| Medtronic Inc. | Health Care Equipment & Supplies | 2,059,090 | | 122,021,673 |

| Merck & Co. Inc. | Pharmaceuticals | 1,337,900 | | 76,246,921 |

| Microsoft Corp. | Software | 3,363,450 | | 128,853,769 |

| Morgan Stanley | Capital Markets | 4,752,350 | | 146,372,380 |

| a Navistar International Corp. | Machinery | 1,144,790 | | 42,929,625 |

| a News Corp., A | Media | 1,918,833 | | 35,172,209 |

| Noble Corp. PLC | Energy Equipment & Services | 2,107,874 | | 65,449,488 |

| Oracle Corp. | Software | 466,951 | | 18,262,454 |

| Pfizer Inc. | Pharmaceuticals | 3,659,230 | | 117,497,875 |

| PNC Financial Services Group Inc. | Banks | 160,070 | | 13,090,525 |

| a Sprint Corp. | Wireless Telecommunication Services | 2,001,967 | | 17,497,191 |

| SunTrust Banks Inc. | Banks | 1,710,680 | | 64,458,422 |

| a,c Swift Energy Co. | Oil, Gas & Consumable Fuels | 1,736,740 | | 17,367,400 |

| Time Warner Cable Inc. | Media | 315,199 | | 44,238,180 |

| Twenty-First Century Fox Inc., A | Media | 1,479,852 | | 49,634,236 |

| United Parcel Service Inc., B | Air Freight & Logistics | 257,279 | | 24,639,610 |

| Verizon Communications Inc. | Diversified Telecommunication Services | 785,312 | | 37,255,185 |

| | | | | 2,187,925,108 |

| |

| Total Common Stocks | | | | |

| (Cost $4,481,349,148) | | | | 6,135,483,185 |

| |

| Preferred Stocks 0.9% | | | | |

| Brazil 0.9% | | | | |

| Petroleo Brasileiro SA, ADR, pfd. | Oil, Gas & Consumable Fuels | 2,943,702 | | 34,323,565 |

| Vale SA, ADR, pfd., A | Metals & Mining | 2,037,464 | | 25,447,926 |

| |

| Total Preferred Stocks | | | | |

| (Cost $66,626,664) | | | | 59,771,491 |

| |

| Non-Registered Mutual Funds | | | | |

| (Cost $27,904,400) 0.5% | | | | |

| China 0.5% | | | | |

| a,d,e,f Templeton China Opportunities Fund, Ltd., | | | | |

| Reg D | Diversified Financial Services | 2,792,110 | | 30,126,869 |

26 | Semiannual Report

Templeton World Fund

Statement of Investments, February 28, 2014 (unaudited) (continued)

| | | | | |

| | | Principal Amount* | | Value | |

| Mortgage-Backed Securities (Cost $2,178,270) 0.1% | | | | | |

| United States 0.1% | | | | | |

| FHLMC Gold 30 Year, 5.50%, 12/01/35 | $ | 2,210,040 | $ | 2,438,162 | |

| |

| Total Investments before Short Term Investments | | | | | |

| (Cost $4,578,058,482) | | | | 6,227,819,707 | |

| |

| Short Term Investments 3.6% | | | | | |

| Time Deposits 3.4% | | | | | |

| Canada 3.4% | | | | | |

| Bank of Montreal, 0.04%, 3/03/14 | | 150,000,000 | | 150,000,000 | |

| Royal Bank of Canada, 0.03%, 3/03/14 | | 70,000,000 | | 70,000,000 | |

| |

| Total Time Deposits (Cost $220,000,000) | | | | 220,000,000 | |

| |

| Total Investments before Money Market Funds | | | | | |

| (Cost $4,798,058,482) | | | | 6,447,819,707 | |

| |

| | | Shares | | | |

| g Investments from Cash Collateral Received for Loaned Securities | | | | | |

| (Cost $14,532,450) 0.2% | | | | | |

| Money Market Funds 0.2% | | | | | |

| United States 0.2% | | | | | |

| h BNY Mellon Overnight Government Fund, 0.032% | | 14,532,450 | | 14,532,450 | |

| |

| Total Investments (Cost $4,812,590,932) 100.2% | | | | 6,462,352,157 | |

| Other Assets, less Liabilities (0.2)% | | | | (13,236,228 | ) |

| |

| Net Assets 100.0% | | | $ | 6,449,115,929 | |

See Abbreviations on page 44.

*The principal amount is stated in U.S. dollars unless otherwise indicated.

aNon-income producing.

bSecurity was purchased pursuant to Rule 144A under the Securities Act of 1933 and may be sold in transactions exempt from registration only to qualified institutional buyers

or in a public offering registered under the Securities Act of 1933. This security has been deemed liquid under guidelines approved by the Trust’s Board of Trustees. At February 28,

2014, the aggregate value of this security was $24,792,307, representing 0.38% of net assets.

cA portion or all of the security is on loan at February 28, 2014. See Note 1(e).

dSee Note 1(d) regarding investment in Templeton China Opportunities Fund, Ltd.

eSee Note 8 regarding restricted securities.

fSee Note 9 regarding holdings of 5% voting securities.

gSee Note 1(e) regarding securities on loan.

hThe rate shown is the annualized seven-day yield at period end.

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 27

| | |

| Templeton World Fund | | |

| |

| Financial Statements | | |

| |

| |

| Statement of Assets and Liabilities | | |

| February 28, 2014 (unaudited) | | |

| |

| Assets: | | |

| Investments in securities: | | |

| Cost - Unaffiliated issuers | $ | 4,784,686,532 |

| Cost - Non-controlled affiliated issuers (Note 9) | | 27,904,400 |

| Total cost of investments | $ | 4,812,590,932 |

| Value - Unaffiliated issuers | $ | 6,432,225,288 |

| Value - Non-controlled affiliated issuers (Note 9) | | 30,126,869 |

| Total value of investments (includes securities loaned in the amount of $14,178,000) | | 6,462,352,157 |

| Cash | | 942,234 |

| Receivables: | | |

| Investment securities sold | | 2,153,650 |

| Capital shares sold | | 5,276,504 |

| Dividends and interest | | 26,850,026 |

| Other assets | | 4,404 |

| Total assets | | 6,497,578,975 |

| Liabilities: | | |

| Payables: | | |

| Investment securities purchased | | 21,575,254 |

| Capital shares redeemed | | 6,273,602 |

| Management fees | | 2,963,797 |

| Administrative fees | | 382,330 |

| Distribution fees | | 1,274,693 |

| Transfer agent fees | | 932,798 |

| Payable upon return of securities loaned | | 14,532,450 |

| Accrued expenses and other liabilities | | 528,122 |

| Total liabilities | | 48,463,046 |

| Net assets, at value | $ | 6,449,115,929 |

| Net assets consist of: | | |

| Paid-in capital | $ | 4,634,921,171 |

| Undistributed net investment income | | 64,881,376 |

| Net unrealized appreciation (depreciation) | | 1,649,993,025 |

| Accumulated net realized gain (loss) | | 99,320,357 |

| Net assets, at value | $ | 6,449,115,929 |

28 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

| | | |

| Templeton World Fund | | | |

| |

| Financial Statements (continued) | | | |

| |

| |

| Statement of Assets and Liabilities (continued) | | | |

| February 28, 2014 (unaudited) | | | |

| |

| Class A: | | | |

| Net assets, at value | $ | | 5,905,511,164 |

| Shares outstanding | | | 301,853,936 |

| Net asset value per sharea | | $ | 19.56 |

| Maximum offering price per share (net asset value per share ÷ 94.25%) | | $ | 20.75 |

| Class C: | | | |

| Net assets, at value | $ | | 238,495,084 |

| Shares outstanding | | | 12,604,365 |

| Net asset value and maximum offering price per sharea | | $ | 18.92 |

| Class R6: | | | |

| Net assets, at value | $ | | 54,022,425 |

| Shares outstanding | | | 2,766,029 |

| Net asset value and maximum offering price per share | | $ | 19.53 |

| Advisor Class: | | | |

| Net assets, at value | $ | | 251,087,256 |

| Shares outstanding | | | 12,850,843 |

| Net asset value and maximum offering price per share | | $ | 19.54 |

| |

| |

| aRedemption price is equal to net asset value less contingent deferred sales charges, if applicable. | | | |

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 29

| | |

| Templeton World Fund | | |

| |

| Financial Statements (continued) | | |

| |

| |

| Statement of Operations | | |

| for the six months ended February 28, 2014 (unaudited) | | |

| |

| Investment income: | | |

| Dividends (net of foreign taxes of $2,783,148) | $ | 100,345,542 |

| Interest | | 97,280 |

| Paydown gain | | 12,508 |

| Income from securities loaned | | 5,965 |

| Total investment income | | 100,461,295 |

| Expenses: | | |

| Management fees (Note 3a) | | 18,970,503 |

| Administrative fees (Note 3b) | | 2,448,926 |

| Distribution fees: (Note 3c) | | |

| Class A | | 7,125,921 |

| Class C | | 1,139,785 |

| Transfer agent fees: (Note 3e) | | |

| Class A | | 2,416,256 |

| Class C | | 96,871 |

| Class R6 | | 140 |

| Advisor Class | | 99,906 |

| Custodian fees (Note 4) | | 324,203 |

| Reports to shareholders | | 154,983 |

| Registration and filing fees | | 76,271 |

| Professional fees | | 81,500 |

| Trustees’ fees and expenses | | 53,617 |

| Other | | 49,453 |

| Total expenses | | 33,038,335 |

| Net investment income | | 67,422,960 |

| Realized and unrealized gains (losses): | | |

| Net realized gain (loss) from: | | |

| Investments | | 119,531,234 |

| Written options | | 198,000 |

| Foreign currency transactions | | 757,532 |

| Net realized gain (loss) | | 120,486,766 |

| Net change in unrealized appreciation (depreciation) on: | | |

| Investments | | 629,627,956 |

| Translation of other assets and liabilities denominated in foreign currencies | | 209,795 |

| Net change in unrealized appreciation (depreciation) | | 629,837,751 |

| Net realized and unrealized gain (loss) | | 750,324,517 |

| Net increase (decrease) in net assets resulting from operations | $ | 817,747,477 |

30 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

| | | | | | |

| Templeton World Fund | | | | | | |

| |

| Financial Statements (continued) | | | | | | |

| |

| |

| Statements of Changes in Net Assets | | | | | | |

| |

| |

| |

| | | Six Months Ended | | | | |

| | | February 28, 2014 | | | Year Ended | |

| | | (unaudited) | | | August 31, 2013 | |

| Increase (decrease) in net assets: | | | | | | |

| Operations: | | | | | | |

| Net investment income | $ | 67,422,960 | | $ | 81,403,846 | |

| Net realized gain (loss) from investments, written options and foreign currency | | | | | | |

| transactions | | 120,486,766 | | | 268,907,233 | |

| Net change in unrealized appreciation (depreciation) on investments and translation of | | | | | | |

| other assets and liabilities denominated in foreign currencies and deferred taxes | | 629,837,751 | | | 861,074,243 | |

| Net increase (decrease) in net assets resulting from operations | | 817,747,477 | | | 1,211,385,322 | |

| Distributions to shareholders from: | | | | | | |

| Net investment income: | | | | | | |

| Class A | | (53,927,369 | ) | | (125,749,470 | ) |

| Class C | | (671,577 | ) | | (3,213,854 | ) |

| Class R6 | | (321,643 | ) | | — | |

| Advisor Class | | (2,783,214 | ) | | (6,995,392 | ) |

| Net realized gains: | | | | | | |

| Class A | | (239,843,544 | ) | | (76,399,449 | ) |

| Class B | | — | | | (16,935 | ) |

| Class C | | (9,992,724 | ) | | (3,102,423 | ) |

| Class R6 | | (1,076,002 | ) | | — | |

| Advisor Class | | (10,037,283 | ) | | (3,774,084 | ) |

| Total distributions to shareholders | | (318,653,356 | ) | | (219,251,607 | ) |

| Capital share transactions: (Note 2) | | | | | | |

| Class A | | 167,765,690 | | | (490,498,402 | ) |

| Class B | | — | | | (2,160,569 | ) |

| Class C | | 9,663,146 | | | (11,906,897 | ) |

| Class R6 | | 27,246,841 | | | 24,666,179 | |

| Advisor Class | | 15,725,982 | | | (60,679,854 | ) |

| Total capital share transactions | | 220,401,659 | | | (540,579,543 | ) |

| Net increase (decrease) in net assets | | 719,495,780 | | | 451,554,172 | |

| Net assets: | | | | | | |

| Beginning of period | | 5,729,620,149 | | | 5,278,065,977 | |

| End of period | $ | 6,449,115,929 | | $ | 5,729,620,149 | |

| Undistributed net investment income included in net assets: | | | | | | |

| End of period | $ | 64,881,376 | | $ | 55,162,219 | |

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 31

Templeton World Fund

Notes to Financial Statements (unaudited)

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Templeton Funds (Trust) is registered under the Investment Company Act of 1940, as amended, (1940 Act) as an open-end investment company, consisting of two separate funds. The Templeton World Fund (Fund) is included in this report. The financial statements of the remaining fund in the Trust are presented separately. The Fund offers four classes of shares: Class A, Class C, Class R6, and Advisor Class. Each class of shares differs by its initial sales load, contingent deferred sales charges, voting rights on matters affecting a single class, its exchange privilege and fees primarily due to differing arrangements for distribution and transfer agent fees.

The following summarizes the Fund’s significant accounting policies.

a. Financial Instrument Valuation

The Fund’s investments in financial instruments are carried at fair value daily. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants on the measurement date. The Fund calculates the net asset value (NAV) per share at the close of the New York Stock Exchange (NYSE), generally at 4 p.m. Eastern time (NYSE close) on each day the NYSE is open for trading. Under procedures approved by the Trust’s Board of Trustees (the Board), the Fund’s administrator, investment manager and other affiliates have formed the Valuation and Liquidity Oversight Committee (VLOC). The VLOC provides administration and oversight of the Fund’s valuation policies and procedures, which are approved annually by the Board. Among other things, these procedures allow the Fund to utilize independent pricing services, quotations from securities and financial instrument dealers, and other market sources to determine fair value.

Equity securities and derivative financial instruments (derivatives) listed on an exchange or on the NASDAQ National Market System are valued at the last quoted sale price or the official closing price of the day, respectively. Foreign equity securities are valued as of the close of trading on the foreign stock exchange on which the security is primarily traded, or the NYSE, whichever is earlier. The value is then converted into its U.S. dollar equivalent at the foreign exchange rate in effect at the close of the NYSE on the day that the value of the security is determined. Over-the-counter (OTC) securities are valued within the range of the most recent quoted bid and ask prices. Securities that trade in multiple markets or on multiple exchanges are valued according to the broadest and most representative market. Certain equity securities are valued based upon fundamental characteristics or relationships to similar securities. Investments in non-registered funds are valued at the closing net asset value.