UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-2884

Salomon Brothers Opportunity Fund Inc.

(Exact name of registrant as specified in charter)

| | |

| 125 Broad Street, New York, | | NY 10004 |

| |

| (Address of principal executive offices) | | (Zip code) |

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

300 First Stamford Place,4th Fl.

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 725-6666

Date of fiscal year end: August 31

Date of reporting period: August 31, 2006

ITEM 1. REPORT TO STOCKHOLDERS.

The Annual Report to Stockholders is filed herewith.

ANNUAL REPORT

AUGUST 31, 2006

Salomon Brothers

Opportunity Fund Inc.

INVESTMENT PRODUCTS: NOT FDIC INSURED Ÿ NO BANK GUARANTEE Ÿ MAY LOSE VALUE

Salomon Brothers

Opportunity Fund Inc.

Annual Report • August 31, 2006

What’s

Inside

Fund Objective

The Fund seeks to achieve above average long-term capital appreciation. Current income is a secondary objective. The Fund invests primarily in common stocks and securities convertible into or exchangeable for common stock such as convertible preferred stock or convertible debt securities.

“Smith Barney”, “Salomon Brothers” and “Citi” are service marks of Citigroup, licensed for use by Legg Mason as the names of funds and investment managers. Legg Mason and its affiliates, as well as the Fund’s investment manager, are not affiliated with Citigroup.

Letter from the Chairperson

Dear Shareholder,

We are pleased to provide this annual report of the Salomon Brothers Opportunity Fund Inc (the “Fund”) for the period ended August 31, 2006.

I urge you to read carefully the Manager’s Overview and the accompanying financial statements. Also included is a detailed summary of the Fund’s performance and other pertinent information, which I hope you find useful.

Special Shareholder Notices

The Fund’s Board of Directors has approved Barrett Associates, Inc. (“Barrett Associates”) as the new investment manager for the Fund to replace the Fund’s current investment manager, ClearBridge Asset Management Inc. (“ClearBridge”) (formerly known as Salomon Brothers Asset Management Inc). Barrett Associates and ClearBridge are affiliates of Legg Mason, Inc. (“Legg Mason”).

Under the new management agreement, which is substantially similar to the Fund’s current management agreement with ClearBridge, Barrett Associates will provide advisory services to the Fund and will be responsible for the Fund’s overall investment strategy and its implementation. The management fee rate under the new management agreement with Barrett Associates will be the same as the fee rate under the current management agreement with ClearBridge. Under the Investment Company of Act of 1940, as amended, the management agreement with Barrett Associates is subject to shareholder approval, and the Board has authorized seeking such approval. Proxy materials describing Barrett Associates and the new management agreement are expected to be mailed in October 2006. If shareholder approval is obtained, Barrett Associates is expected to replace ClearBridge as the Fund’s investment manager on or about December 1, 2006. Effective December 1, 2006, the Fund will change its name to “Barrett Opportunity Fund, Inc.” Starting December 1, 2006, Amy LaGuardia and Robert J. Milnamow of Barrett Associates will be responsible for the day-to-day management of the Fund. If shareholder approval of the new management agreement with Barrett Associates is not obtained by December 1, 2006, Ms. LaGuardia and Mr. Milnamow will manage the Fund as employees of ClearBridge.

On December 1, 2006, it is expected that certain changes to the Fund’s investment strategies that have been approved by the Fund’s Board of Directors will be implemented. First, the Fund’s stock selection criteria will be revised to focus on companies whose securities are undervalued based on the investment manager’s judgment of the company’s sustainable earnings growth in addition to the company’s intrinsic value. Second, the Fund will no longer pursue a strategy of retaining unrealized long-term capital gains to avoid the

Salomon Brothers Opportunity Fund Inc. I

tax impact of realizing those gains. In managing the Fund’s portfolio, Barrett Associates expects that some portion of the Fund’s built-in long-term capital gains will be realized gradually over time. This may result in an increase in the Fund’s annual distributions of net capital gains, and, accordingly, an increase in taxable distributions to shareholders. These changes to the Fund’s investment strategies do not require shareholder approval and will be implemented regardless of whether shareholder approval of the new management agreement with Barrett Associates is obtained.

Information About Your Fund

As you may be aware, several issues in the mutual fund industry have come under the scrutiny of federal and state regulators. Affiliates of the Fund’s Manager have, in recent years, received requests for information from various government regulators regarding market timing, late trading, fees, and other mutual fund issues in connection with various investigations. The regulators appear to be examining, among other things, the Fund’s response to market timing and shareholder exchange activity, including compliance with prospectus disclosure related to these subjects. The Fund is not in a position to predict the outcome of these requests and investigations.

Important information with regard to recent regulatory developments that may affect the Fund is contained in the Notes to Financial Statements included in this report.

On behalf of the Directors and officers of the Fund, I also want to thank you for your ongoing confidence in the Fund.

Sincerely,

Rosalind A. Kochman

Chairperson

October 1, 2006

II Salomon Brothers Opportunity Fund Inc.

Manager Overview

Q. What were the overall market conditions during the Fund’s reporting period?

A. Ongoing economic expansion and solid corporate profits helped the U.S. equity market to generate positive returns over the period. That said, the market experienced periods of volatility during the reporting period—often triggered by the Federal Reserve Board (“Fed”)i and changing expectations whether or not it would end its two year tightening campaign. The Fed did pause from raising rates in August, which led to a strong rally at the end of the period.

Performance Review

For the 12 months ended August 31, 2006, the Salomon Brothers Opportunity Fund Inc returned 14.79%. The Fund’s unmanaged benchmark, the S&P 500 Indexii, returned 8.87% for the same period. The Lipper Multi-Cap Value Funds Category Average1 increased 9.75% over the same time frame.

| | | | |

| Performance Snapshot as of August 31, 2006 (unaudited) | | |

| | |

| | | 6 Months | | 12 Months |

Salomon Brothers Opportunity Fund Inc. | | 7.55% | | 14.79% |

| |

S&P 500 Index | | 2.79% | | 8.87% |

| |

Lipper Multi-Cap Value Funds Category Average | | 3.26% | | 9.75% |

| |

| The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value and investment returns will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost. |

| Fund returns assume the reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Fund expenses. |

| Performance figures reflect reimbursements and/or fee waivers, without which the performance would have been lower. |

| Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the period ended August 31, 2006, including the reinvestment of distributions, including returns of capital, if any, calculated among the 508 funds for the six-month period and among the 488 funds for the 12-month period in the Fund’s Lipper category and excluding sales charges. |

Q. What were the most significant factors affecting Fund performance?

What were the leading contributors to performance?

A. The Fund significantly outperformed its benchmark over the period. This was due, in part, to the strong performance of the Fund’s holdings in the financials sector. Both the Fund’s overweight position, as well as stock selection in the sector, was beneficial to results. In particular, the Fund’s holdings in Forest City Enterprises Inc., a real estate

| 1 | | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 12-month period ended August 31, 2006, including the reinvestment of distributions, including returns of capital, if any, calculated among the 488 funds in the Fund’s Lipper category and excluding sales charges. |

Salomon Brothers Opportunity Fund Inc. 2006 Annual Report 1

development company, insurance company Chubb Corp. and the Bank of New York were leading contributors to performance. Elsewhere, Phillips Electronics, one of the world’s largest electronics companies, enhanced results over the period.

What were the leading detractors from performance?

A. The largest detractor from results over the period was Popular Inc. This Puerto Rico-based bank, with operations in the U.S., performed poorly over the last 12 months. Elsewhere, Murphy Oil Corp., an oil and gas exploration and production company, TRC Companies Inc., a consulting, engineering and construction management firm, and Tecumseh Products Co., a global manufacturer of hermetic compressors for residential and commercial refrigerators, detracted from results.

Q. Were there any significant changes to the Fund during the reporting period?

A. There were no major changes to the Fund over the reporting period.

Thank you for your investment in the Salomon Brothers Opportunity Fund Inc. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

| | |

| |  |

| George J. Williamson | | Patrick Hughes |

Vice President and

Investment Officer | | Vice President and

Investment Officer |

October 1, 2006

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

RISKS: Investments in small- and medium capitalization companies may involve a higher degree of risk and volatility than investments in larger, more established companies. The Fund may invest in high yield and foreign securities, including those in emerging markets, which involve risks beyond those inherent in higher-rated and domestic investments. As interest rates rise, bond prices fall, reducing the value of the Fund’s share price. High yield bonds involve greater credit and liquidity risks than investment grade bonds. Investing in foreign securities is subject to certain risks not associated with domestic investing, such as currency fluctuations and changes in political and economic conditions. These risk are magnified in emerging or developing markets. The Fund may use derivatives, such as options or futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on fund performance.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| ii | | The S&P 500 Index is an unmanaged Index of 500 stocks that is generally representative of the performance of larger companies in the U.S. |

2 Salomon Brothers Opportunity Fund Inc. 2006 Annual Report

Fund at a Glance (unaudited)

Salomon Brothers Opportunity Fund Inc. 2006 Annual Report 3

Fund Expenses (unaudited)

Example

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs; and (2) ongoing costs, including management fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on March 1, 2006 and held for the six months ended August 31, 2006.

Actual Expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

| | | | | | | | | | | | | | |

| Based on Actual Total Return(1) | | | | | | |

| | | | | |

| | | Actual

Total Return(2) | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratio | | | Expenses

Paid During

the Period(3) |

Salomon Brothers Opportunity Fund Inc. | | 7.55% | | $ | 1,000.00 | | $ | 1,075.50 | | 1.04 | % | | $ | 5.44 |

| |

| (1) | | For the six months ended August 31, 2006. |

| (2) | | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Performance figures may reflect fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. |

| (3) | | Expenses (net of fee waivers and/or expense reimbursements) are equal to the Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. |

4 Salomon Brothers Opportunity Fund Inc. 2006 Annual Report

Fund Expenses (unaudited) (continued)

Hypothetical Example for Comparison Purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | |

| Based on Hypothetical Total Return(1) | | | | | | |

| | | | | |

| | | Hypothetical

Annualized

Total Return | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratio | | | Expenses

Paid During

the Period(2) |

Salomon Brothers Opportunity

Fund Inc. | | 5.00% | | $ | 1,000.00 | | $ | 1,019.96 | | 1.04 | % | | $ | 5.30 |

| |

| (1) | | For the six months ended August 31, 2006. |

| (2) | | Expenses (net of fee waivers and/or expense reimbursements) are equal to the Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. |

Salomon Brothers Opportunity Fund Inc. 2006 Annual Report 5

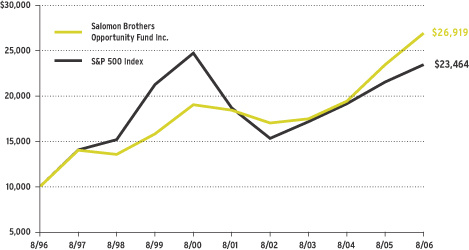

Historical Performance (unaudited)

Value of $10,000 Invested in Salomon Brothers Opportunity Fund Inc vs.

the S&P 500 Index† (August 1996 – August 2006)

| † | | Hypothetical illustration of $10,000 invested in the Fund on August 31, 1996 assuming the reinvestment of all distributions, including returns of capital, if any, at net asset value through August 31, 2006. The S&P 500 Index is a broad-based unmanaged index of widely held common stocks. The index is unmanaged and it is not subject to the same management and trading expenses of a mutual fund. Please note that an investor cannot invest directly in an index. |

All figures represent past performance and are not a guarantee of future results. Investments return and principal value will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower.

6 Salomon Brothers Opportunity Fund Inc. 2006 Annual Report

Schedule of Investments (August 31, 2006)

SALOMON BROTHERS OPPORTUNITY FUND INC.

| | | | | | |

| | |

| Shares | | Security | | Value | |

| | | | | | |

| COMMON STOCKS — 90.5% | |

| CONSUMER DISCRETIONARY — 7.3% | |

| Household Durables — 6.8% | |

| 306,010 | | Koninklijke Philips Electronics NV, New York Registered Shares | | $ | 10,502,263 | |

| | Liberty Homes Inc.: | | | | |

| 14,850 | | Class A Shares (a) | | | 88,729 | |

| 22,050 | | Class B Shares (a) | | | 140,569 | |

| | |

| | Total Household Durables | | | 10,731,561 | |

| | |

| Media — 0.5% | |

| 19,400 | | News Corp., Class A Shares | | | 369,182 | |

| 28,700 | | Time Warner Inc. | | | 476,994 | |

| | |

| | Total Media | | | 846,176 | |

| | |

| | TOTAL CONSUMER DISCRETIONARY | | | 11,577,737 | |

| | |

| CONSUMER STAPLES — 0.3% | |

| Food & Staples Retailing — 0.3% | |

| 96,000 | | FHC Delaware Inc. (a)(b)* | | | 456,000 | |

| | |

| ENERGY — 15.4% | |

| Energy Equipment & Services — 0.7% | |

| 14,200 | | Diamond Offshore Drilling Inc. | | | 1,029,216 | |

| | |

| Oil, Gas & Consumable Fuels — 14.7% | |

| 10,876 | | EnCana Corp. | | | 573,600 | |

| 112,500 | | Murphy Oil Corp. | | | 5,502,375 | |

| 20,900 | | Overseas Shipholding Group Inc. | | | 1,394,030 | |

| 228,600 | | Royal Dutch Shell PLC, ADR, Class A Shares | | | 15,759,684 | |

| | |

| | Total Oil, Gas & Consumable Fuels | | | 23,229,689 | |

| | |

| | TOTAL ENERGY | | | 24,258,905 | |

| | |

| FINANCIALS — 47.8% | |

| Capital Markets — 9.1% | |

| 425,876 | | Bank of New York Co. Inc. | | | 14,373,315 | |

| | |

| Commercial Banks — 2.9% | |

| 237,400 | | Popular Inc. | | | 4,522,470 | |

| | |

| Diversified Financial Services — 2.3% | |

| 139,900 | | Leucadia National Corp. | | | 3,599,627 | |

| | |

| Insurance — 14.1% | |

| 308,600 | | Chubb Corp. | | | 15,479,376 | |

| 81,900 | | CNA Financial Corp. * | | | 2,839,473 | |

| 26,400 | | Loews Corp. | | | 1,015,872 | |

| 40,000 | | Merchants Group Inc. (a) | | | 1,195,200 | |

| 82,500 | | Old Republic International Corp. | | | 1,724,250 | |

| | |

| | Total Insurance | | | 22,254,171 | |

| | |

| Real Estate Investment Trusts (REITs) — 1.8% | |

| 70,490 | | Rayonier Inc. | | | 2,784,355 | |

| | |

See Notes to Financial Statements.

Salomon Brothers Opportunity Fund Inc. 2006 Annual Report 7

Schedule of Investments (August 31, 2006) (continued)

| | | | | | |

| | |

| Shares | | Security | | Value | |

| | | | | | |

| Real Estate Management & Development — 16.1% | |

| | Forest City Enterprises Inc.: | | | | |

| 299,200 | | Class A Shares | | $ | 16,090,976 | |

| 173,300 | | Class B Shares (c) | | | 9,257,686 | |

| 5,500 | | Harbor Global Co., Ltd. (a) | | | 60,775 | |

| | |

| | Total Real Estate Management & Development | | | 25,409,437 | |

| | |

| Thrifts & Mortgage Finance — 1.5% | |

| 38,300 | | Freddie Mac | | | 2,435,880 | |

| | |

| | TOTAL FINANCIALS | | | 75,379,255 | |

| | |

| HEALTH CARE — 5.6% | |

| Health Care Equipment & Supplies — 0.1% | |

| 3,500 | | Stryker Corp. | | | 168,105 | |

| | |

| Health Care Providers & Services — 4.5% | |

| 10,600 | | Health Net Inc. * | | | 443,186 | |

| 23,900 | | Humana Inc. * | | | 1,456,227 | |

| 67,208 | | WellPoint Inc. * | | | 5,202,571 | |

| | |

| | Total Health Care Providers & Services | | | 7,101,984 | |

| | |

| Pharmaceuticals — 1.0% | |

| 55,864 | | Pfizer Inc. | | | 1,539,612 | |

| | |

| | TOTAL HEALTH CARE | | | 8,809,701 | |

| | |

| INDUSTRIALS — 11.2% | |

| Aerospace & Defense — 5.4% | |

| 112,200 | | General Dynamics Corp. | | | 7,579,110 | |

| 10,600 | | Lockheed Martin Corp. | | | 875,560 | |

| | |

| | Total Aerospace & Defense | | | 8,454,670 | |

| | |

| Air Freight & Logistics — 0.2% | |

| 64,300 | | ABX Air Inc. * | | | 356,865 | |

| | |

| Airlines — 0.7% | |

| 52,100 | | AMR Corp. * | | | 1,075,865 | |

| | |

| Building Products — 1.9% | |

| 43,500 | | Ameron International Corp. | | | 3,051,090 | |

| | |

| Commercial Services & Supplies — 0.6% | |

| 103,550 | | TRC Cos. Inc. * | | | 978,548 | |

| | |

| Industrial Conglomerates — 1.1% | |

| 44,100 | | General Electric Co. | | | 1,502,046 | |

| 8,303 | | Tyco International Ltd. | | | 217,123 | |

| | |

| | Total Industrial Conglomerates | | | 1,719,169 | |

| | |

| Machinery — 0.6% | |

| | Tecumseh Products Co.: | | | | |

| 35,300 | | Class A Shares * | | | 524,205 | |

| 36,000 | | Class B Shares * | | | 502,200 | |

| | |

| | Total Machinery | | | 1,026,405 | |

| | |

See Notes to Financial Statements.

8 Salomon Brothers Opportunity Fund Inc. 2006 Annual Report

Schedule of Investments (August 31, 2006) (continued)

| | | | | | |

| | |

| Shares | | Security | | Value | |

| | | | | | |

| Marine — 0.7% | |

| 25,000 | | Alexander & Baldwin Inc. | | $ | 1,096,500 | |

| | |

| | TOTAL INDUSTRIALS | | | 17,759,112 | |

| | |

| INFORMATION TECHNOLOGY — 1.7% | |

| Computers & Peripherals — 0.7% | |

| 13,300 | | International Business Machines Corp. | | | 1,076,901 | |

| | |

| IT Services — 0.1% | |

| 8,134 | | Sabre Holdings Corp., Class A Shares | | | 178,297 | |

| | |

| Semiconductors & Semiconductor Equipment — 0.3% | |

| 21,000 | | National Semiconductor Corp. | | | 510,090 | |

| | |

| Software — 0.6% | |

| 35,200 | | Microsoft Corp. | | | 904,288 | |

| | |

| | TOTAL INFORMATION TECHNOLOGY | | | 2,669,576 | |

| | |

| MATERIALS — 1.1% | |

| Chemicals — 0.9% | |

| 6,320 | | Kronos Worldwide Inc. | | | 192,128 | |

| 22,242 | | Monsanto Co. | | | 1,055,161 | |

| 11,400 | | NL Industries Inc. | | | 117,990 | |

| | |

| | Total Chemicals | | | 1,365,279 | |

| | |

| Metals & Mining — 0.2% | |

| 7,177 | | Newmont Mining Corp. | | | 367,821 | |

| | |

| | TOTAL MATERIALS | | | 1,733,100 | |

| | |

| TELECOMMUNICATION SERVICES — 0.1% | |

| Diversified Telecommunication Services — 0.1% | |

| 5,500 | | Verizon Communications Inc. | | | 193,490 | |

| | |

| | TOTAL INVESTMENTS BEFORE SHORT-TERM INVESTMENTS

(Cost — $23,958,216) | | | 142,836,876 | |

| | |

See Notes to Financial Statements.

Salomon Brothers Opportunity Fund Inc. 2006 Annual Report 9

Schedule of Investments (August 31, 2006) (continued)

| | | | | | |

| | |

Face

Amount | | Security | | Value |

| | SHORT-TERM INVESTMENTS(d) — 3.3% |

| | Commercial Paper — 3.3% |

| $ | 2,255,000 | | Norddeutsche Landesbank, 5.272% due 9/15/06 (e) | | | 2,250,387 |

| | 2,919,000 | | Rabobank USA Financial Corp., 5.271% due 9/1/06 | | | 2,919,000 |

| | |

| | | TOTAL SHORT-TERM INVESTMENTS

(Cost — $5,169,387) | | | 5,169,387 |

| | |

| | | TOTAL INVESTMENTS — 93.8% (Cost — $29,127,603#) | | | 148,006,263 |

| | | Other Assets in Excess of Liabilities — 6.2% | | | 9,750,532 |

| | |

| | | TOTAL NET ASSETS — 100.0% | | $ | 157,756,795 |

| | |

| * | | Non-income producing security. |

| (b) | | Security is valued in good faith at fair value by or under the direction of the Board of Directors (See Note 1). |

| (c) | | Convertible into Forest City Enterprises Inc., Class A Shares. |

| (d) | | Rate shown represents yield-to-maturity on date of purchase. |

| (e) | | Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Directors, unless otherwise noted. |

| # | | Aggregate cost for federal income tax purposes is $29,247,418. |

|

Abbreviation used in this schedule: |

ADR — American Depositary Receipt |

See Notes to Financial Statements.

10 Salomon Brothers Opportunity Fund Inc. 2006 Annual Report

Statement of Assets and Liabilities (August 31, 2006)

| | | |

| ASSETS: | | | |

Investments, at value (Cost — $29,127,603) | | $ | 148,006,263 |

Cash | | | 642 |

Receivable for Fund shares sold | | | 9,983,448 |

Dividends receivable | | | 229,895 |

Prepaid expenses | | | 14,528 |

| |

Total Assets | | | 158,234,776 |

| |

| LIABILITIES: | | | |

Payable for Fund shares repurchased | | | 252,494 |

Investment management fee payable | | | 92,622 |

Directors’ fees payable | | | 12,712 |

Accrued expenses | | | 120,153 |

| |

Total Liabilities | | | 477,981 |

| |

Total Net Assets | | $ | 157,756,795 |

| |

| NET ASSETS: | | | |

Par value (Note 4) | | $ | 27,819 |

Paid-in capital in excess of par value | | | 33,823,277 |

Undistributed net investment income | | | 414,974 |

Accumulated net realized gain on investments | | | 4,612,065 |

Net unrealized appreciation on investments | | | 118,878,660 |

| |

Total Net Assets | | $ | 157,756,795 |

| |

Shares Outstanding | | | 2,781,880 |

| |

Net Asset Value | | | $56.71 |

| |

See Notes to Financial Statements.

Salomon Brothers Opportunity Fund Inc. 2006 Annual Report 11

Statement of Operations (For the year ended August 31, 2006)

| | | | |

| INVESTMENT INCOME: | | | | |

Dividends | | $ | 2,356,688 | |

Interest | | | 138,123 | |

Income from securities lending | | | 4,912 | |

Less: Foreign taxes withheld | | | (122,397 | ) |

| | |

Total Investment Income | | | 2,377,326 | |

| | |

| EXPENSES: | | | | |

Investment management fee (Note 2) | | | 1,046,442 | |

Legal fees | | | 167,195 | |

Shareholder reports | | | 74,270 | |

Directors’ fees | | | 57,945 | |

Audit and tax | | | 34,600 | |

Transfer agent fees | | | 29,890 | |

Registration fees | | | 27,710 | |

Custody fees | | | 7,342 | |

Insurance | | | 3,394 | |

Miscellaneous expenses | | | 7,605 | |

| | |

Total Expenses | | | 1,456,393 | |

Less: Fee waivers and/or expense reimbursements (Note 2) | | | (2,988 | ) |

| | |

Net Expenses | | | 1,453,405 | |

| | |

Net Investment Income | | | 923,921 | |

| | |

| REALIZED AND UNREALIZED GAIN ON INVESTMENTS (NOTES 1, 3 AND 5): | | | | |

Net Realized Gain From Investment Transactions | | | 6,471,248 | |

Change in Net Unrealized Appreciation/Depreciation From Investments | | | 11,969,845 | |

| | |

Net Gain on Investments | | | 18,441,093 | |

| | |

Increase in Net Assets From Operations | | $ | 19,365,014 | |

| | |

See Notes to Financial Statements.

12 Salomon Brothers Opportunity Fund Inc. 2006 Annual Report

Statements of Changes in Net Assets (For the years ended August 31,)

| | | | | | | | |

| | |

| | | 2006 | | | 2005 | |

| OPERATIONS: | | | | | | | | |

Net investment income | | $ | 923,921 | | | $ | 1,397,595 | |

Net realized gain | | | 6,471,248 | | | | 7,792,806 | |

Change in net unrealized appreciation/depreciation | | | 11,969,845 | | | | 15,694,793 | |

| | |

Increase in Net Assets From Operations | | | 19,365,014 | | | | 24,885,194 | |

| | |

| DISTRIBUTIONS TO SHAREHOLDERS FROM (NOTES 1 AND 6): | | | | | | | | |

Net investment income | | | (1,199,486 | ) | | | (1,600,228 | ) |

Net realized gains | | | (3,070,462 | ) | | | (639,003 | ) |

| | |

Decrease in Net Assets From Distributions to Shareholders | | | (4,269,948 | ) | | | (2,239,231 | ) |

| | |

| FUND SHARE TRANSACTIONS (NOTES 4 AND 5): | | | | | | | | |

Net proceeds from sale of shares | | | 12,287,794 | | | | 737,875 | |

Reinvestment of distributions | | | 2,092,345 | | | | 1,075,977 | |

Cost of shares repurchased | | | (8,557,079 | ) | | | (18,346,019 | ) |

| | |

Increase (Decrease) in Net Assets From Fund Share Transactions | | | 5,823,060 | | | | (16,532,167 | ) |

| | |

Increase in Net Assets | | | 20,918,126 | | | | 6,113,796 | |

| NET ASSETS: | | | | | | | | |

Beginning of year | | | 136,838,669 | | | | 130,724,873 | |

| | |

End of year* | | $ | 157,756,795 | | | $ | 136,838,669 | |

| | |

*Includes undistributed net investment income of: | | | $414,974 | | | | $759,619 | |

| | |

See Notes to Financial Statements.

Salomon Brothers Opportunity Fund Inc. 2006 Annual Report 13

Financial Highlights

For a share of capital stock outstanding throughout each year ended August 31:

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

| | | 2006 | | | 2005 | | | 2004 | | | 2003 | | | 2002 | |

Net Asset Value, Beginning of Year | | $ | 50.98 | | | $ | 42.92 | | | $ | 41.34 | | | $ | 41.86 | | | $ | 48.72 | |

| | |

Income (Loss) From Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.32 | | | | 0.53 | | | | 0.49 | | | | 0.33 | | | | 0.28 | |

Net realized and unrealized gain (loss) | | | 7.04 | | | | 8.31 | | | | 3.99 | | | | 0.61 | | | | (3.74 | ) |

| | |

Total Income (Loss) From Operations | | | 7.36 | | | | 8.84 | | | | 4.48 | | | | 0.94 | | | | (3.46 | ) |

| | |

Less Distributions From: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.46 | ) | | | (0.56 | ) | | | (0.37 | ) | | | (0.19 | ) | | | (0.64 | ) |

Net realized gains | | | (1.17 | ) | | | (0.22 | ) | | | (2.53 | ) | | | (1.27 | ) | | | (2.76 | ) |

| | |

Total Distributions | | | (1.63 | ) | | | (0.78 | ) | | | (2.90 | ) | | | (1.46 | ) | | | (3.40 | ) |

| | |

Net Asset Value, End of Year | | $ | 56.71 | | | $ | 50.98 | | | $ | 42.92 | | | $ | 41.34 | | | $ | 41.86 | |

| | |

Total Return(1) | | | 14.79 | % | | | 20.77 | % | | | 11.09 | % | | | 2.57 | % | | | (7.65 | )% |

| | |

Net Assets, End of Year (millions) | | | $158 | | | | $137 | | | | $131 | | | | $146 | | | | $160 | |

| | |

Ratios to Average Net Assets: | | | | | | | | | | | | | | | | | | | | |

Gross expenses | | | 1.04 | % | | | 0.96 | % | | | 1.06 | % | | | 1.12 | % | | | 1.11 | % |

Net expenses | | | 1.04 | (2) | | | 0.96 | | | | 1.06 | | | | 1.12 | | | | 1.11 | |

Net investment income | | | 0.66 | | | | 1.06 | | | | 1.04 | | | | 0.82 | | | | 0.64 | |

| | |

Portfolio Turnover Rate | | | 0 | %(3)(4) | | | 1 | %(3) | | | 1 | %(3) | | | 5 | % | | | 1 | % |

| | |

| (1) | | Performance figures may reflect fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. |

| (2) | | Reflects fee waivers and/or expense reimbursements. |

| (3) | | Excludes the value of portfolio securities delivered as a result of in-kind redemptions of the Fund’s capital shares. |

| (4) | | Amount represents less than 1%. |

See Notes to Financial Statements.

14 Salomon Brothers Opportunity Fund Inc. 2006 Annual Report

Notes to Financial Statements

| 1. | Organization and Significant Accounting Policies |

The Salomon Brothers Opportunity Fund Inc. (the “Fund”) is registered as a non-diversified, open-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”).

The following are significant accounting policies consistently followed by the Fund and are in conformity with U.S. generally accepted accounting principles (“GAAP”). Estimates and assumptions are required to be made regarding assets, liabilities and changes in net assets resulting from operations when financial statements are prepared. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ.

(a) Investment Valuation. Equity securities for which market quotations are available are valued at the last sale price or official closing price on the primary market or exchange on which they trade. Debt securities are valued at the mean between the bid and ask prices provided by an independent pricing service that are based on transactions in debt obligations, quotations from bond dealers, market transactions in comparable securities and various other relationships between securities. When prices are not readily available, or are determined not to reflect fair value, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded, but before the Fund calculates its net asset value, the Fund may value these investments at fair value as determined in accordance with the procedures approved by the Fund’s Board of Directors. Short-term obligations with maturities of 60 days or less are valued at amortized cost, which approximates market value.

(b) Lending of Portfolio Securities. The Fund has an agreement with its custodian whereby the custodian may lend securities owned by the Funds to brokers, dealers and other financial organizations. In exchange for lending securities under the terms of the agreement with their custodian, the Fund receives a lender’s fee. Fees earned by the Fund on securities lending are recorded as securities lending income. Loans of securities by the Fund are collateralized by cash, U.S. government securities or high quality money market instruments that are maintained at all times in an amount at least equal to the current market value of the loaned securities, plus a margin which varies depending on the type of securities loaned. The custodian establishes and maintains the collateral in a segregated account. The Fund has the right under the lending agreement to recover the securities from the borrower on demand.

The Fund maintains the risk of any loss on the securities on loan as well as the potential loss on investments purchased with cash collateral received from securities lending.

(c) Security Transactions and Investment Income. Security transactions are accounted for on a trade date basis. Interest income, adjusted for amortization of premium and accretion of discount, is recorded on the accrual basis. Dividend income is recorded on the ex-dividend date. Foreign dividend income is recorded on the ex-dividend date or as soon as practical after the Fund determines the existence of a dividend declaration after exercising reasonable due diligence. The cost of investments sold is determined by use of the specific identification method. To the extent any issuer defaults on an expected interest payment, the Fund’s policy is to generally halt any additional interest income accruals and consider the realizability of interest accrued up to the date of default.

Salomon Brothers Opportunity Fund Inc. 2006 Annual Report 15

Notes to Financial Statements (continued)

(d) Distributions to Shareholders. Distributions from net investment income and distributions of net realized gains, if any, are declared at least annually. Distributions to shareholders of the Fund are recorded on the ex-dividend date and are determined in accordance with income tax regulations, which may differ from GAAP.

(e) REIT Distributions. The character of distributions received from Real Estate Investment Trusts (“REITs”) held by the Fund is generally comprised of net investment income, capital gains, and return of capital. It is the policy of the Fund to estimate the character of distributions received from underlying REITs based on historical data provided by the REITs. After each calendar year end, REITs report the true tax character of these distributions. Differences between the estimated and actual amounts reported by the REITs are reflected in the Fund’s records in the year in which they are reported by the REITs.

(f) Federal and Other Taxes. It is the Fund’s policy to comply with the federal income and excise tax requirements of the Internal Revenue Code of 1986, as amended, applicable to regulated investment companies. Accordingly, the Fund intends to distribute substantially all of its income and net realized gains on investments, if any, to shareholders each year. Therefore, no federal income tax provision is required in the Fund’s financial statements. Under the applicable foreign tax laws, a withholding tax may be imposed on interest, dividends and capital gains at various rates.

(g) Reclassification. GAAP requires that certain components of net assets be adjusted to reflect permanent differences between financial and tax reporting. These reclassifications have no effect on net assets or net asset values per share. During the current year, the following reclassifications have been made:

| | | | | | | | | |

| | | |

| | | Undistributed

Net Investment

Income | | Accumulated Net

Realized Gain | | Paid-in Capital |

| (a) | | $ | (277) | | $ | (1,302,944) | | $ | 1,303,221 |

| (b) | | | (68,803) | | | 68,803 | | | — |

| |

| (a) | Reclassifications are primarily due to tax adjustments associated with securities involved in an in-kind distribution and book/tax differences in the treatment of an in-kind distribution of securities. |

| (b) | Reclassifications are primarily due to book/tax differences in the treatment of distributions from real estate investment trusts and book/tax differences in the treatment of various items. |

Additionally, during the current period, Undistributed Realized Gains and Cost of Investments have each been reduced by $49,363 as a result of return of capital distributions paid by REITs. These adjustments have no effect on net assets or net asset values per share.

| 2. | Investment Management Agreement and Other Transactions with Affiliates |

On December 1, 2005, Citigroup Inc. (“Citigroup”) completed the sale of substantially all of its asset management business, to Legg Mason, Inc. (“Legg Mason”). As a result, the Fund’s investment manager, ClearBridge Asset Management Inc. (“ClearBridge”) (formerly known as Salomon Brothers Asset Management Inc (“SBAM”)), previously an indirect wholly-owned subsidiary of Citigroup, became a wholly-owned subsidiary of Legg Mason. Completion of the sale caused the Fund’s then existing investment management contract to

16 Salomon Brothers Opportunity Fund Inc. 2006 Annual Report

Notes to Financial Statements (continued)

terminate. The Fund’s shareholders approved a new investment management contract between the Fund and ClearBridge, which became effective on December 1, 2005.

Prior to October 1, 2005, the Fund paid ClearBridge an investment management fee calculated at an annual rate of 0.75% of the Fund’s average daily net assets. These fees were calculated daily and paid monthly.

Effective October 1, 2005, and continuing under the new investment management agreement, which became effective December 1, 2005, the Fund paid ClearBridge a management fee calculated daily and payable monthly, at the annual rate of the Fund’s average daily net assets in accordance with the following break point schedule:

| | | |

| |

| Average Daily Net Assets | | Annual

Rate | |

First $1 billion | | 0.750 | % |

Next $1 billion | | 0.725 | |

Next $3 billion | | 0.700 | |

Next $5 billion | | 0.675 | |

Over $10 billion | | 0.650 | |

| | |

During the year ended August 31, 2006, ClearBridge waived a portion of its fee in the amount of $2,988.

The Fund’s Board has appointed Citigroup Global Markets Inc. (“CGM”), a subsidiary of Citigroup, and Legg Mason Investor Services, LLC (“LMIS”), a wholly-owned broker-dealer subsidiary of Legg Mason, as co-distributors of the Fund. CGM and other broker-dealers, financial intermediaries and financial institutions (each called a “Service Agent”) that currently offer Fund shares will continue to make the Fund’s shares available to their clients. Additional Service Agents may offer Fund shares in the future.

The Fund has a concentration of several shareholders who may be related parties, holding a significant percentage of shares outstanding. Investment activities of these shareholders could have a material impact on the Fund.

Certain officers of the Fund are employees of Legg Mason or its affiliates and do not receive compensation from the Fund.

During the year ended August 31, 2006, the aggregate cost of purchases and proceeds from sales of investments (excluding short-term investments and redemption in-kind transactions) were as follows:

| | | |

Purchases | | $ | 144,833 |

| |

Sales | | | 6,759,111 |

| |

Salomon Brothers Opportunity Fund Inc. 2006 Annual Report 17

Notes to Financial Statements (continued)

At August 31, 2006, the aggregate gross unrealized appreciation and depreciation of investments for federal income tax purposes were as follows:

| | | | |

Gross unrealized appreciation | | $ | 121,064,242 | |

Gross unrealized depreciation | | | (2,305,397 | ) |

| | |

Net unrealized appreciation | | $ | 118,758,845 | |

| | |

At August 31, 2006, the Fund had 15,000,000 shares of capital stock authorized with a par value of $0.01 per share.

Transactions in shares of the Fund were as follows:

| | | | | | |

| | | Year Ended

August 31, 2006 | | | Year Ended

August 31, 2005 | |

Shares sold | | 218,940 | | | 15,857 | |

Shares issued on reinvestment | | 40,890 | | | 23,085 | |

Shares repurchased | | (162,328 | ) | | (400,224 | ) |

| | |

Net Increase (Decrease) | | 97,502 | | | (361,282 | ) |

| | |

The Fund may make payment for Fund shares redeemed wholly or in part by distributing portfolio securities to the shareholders. For the year ended August 31, 2006, the Fund had redemptions-in-kind with total proceeds in the amount of $1,689,456. The net realized gains on these redemptions-in-kind amounted to $1,305,603, which will not be realized for tax purposes.

6. Income Tax Information and Distributions to Shareholders

The tax character of distributions paid during the fiscal years ended August 31, were as follows:

| | | | | | |

| | |

| | | 2006 | | 2005 |

Distributions paid from: | | | | | | |

Ordinary Income | | $ | 1,218,448 | | $ | 1,611,685 |

Net Long-term Capital Gains | | | 3,051,500 | | | 627,546 |

| |

Total Distributions Paid | | $ | 4,269,948 | | $ | 2,239,231 |

| |

As of August 31, 2006, the components of accumulated earnings on a tax basis were as follows:

| | | |

Undistributed ordinary income — net | | $ | 414,974 |

Undistributed long-term capital gains — net | | | 4,731,880 |

| |

Total undistributed earnings | | $ | 5,146,854 |

Unrealized appreciation/(depreciation)(a) | | | 118,758,845 |

| |

Total accumulated earnings/(losses) — net | | $ | 123,905,699 |

| |

| (a) | The difference between book-basis and tax-basis unrealized appreciation/(depreciation) is attributable primarily to the tax deferral of losses on wash sales, book/tax differences in the treatment of corporate actions and other book/tax basis adjustments. |

18 Salomon Brothers Opportunity Fund Inc. 2006 Annual Report

Notes to Financial Statements (continued)

On May 31, 2005, the U.S. Securities and Exchange Commission (“SEC”) issued an order in connection with the settlement of an administrative proceeding against Smith Barney Fund Management Inc. (“SBFM”) and CGM relating to the appointment of an affiliated transfer agent for the Smith Barney family of mutual funds (the “Affected Funds”).

The SEC order finds that SBFM and CGM willfully violated Section 206(1) of the Investment Advisers Act of 1940 (“Advisers Act”). Specifically, the order finds that SBFM and CGM knowingly or recklessly failed to disclose to the boards of the Affected Funds in 1999 when proposing a new transfer agent arrangement with an affiliated transfer agent that: First Data Investors Services Group (“First Data”), the Affected Funds’ then-existing transfer agent, had offered to continue as transfer agent and do the same work for substantially less money than before; and that Citigroup Asset Management (“CAM”), the Citigroup business unit that, at the time, included the Affected Fund’s investment manager and other investment advisory companies, had entered into a side letter with First Data under which CAM agreed to recommend the appointment of First Data as sub-transfer agent to the affiliated transfer agent in exchange for, among other things, a guarantee by First Data of specified amounts of asset management and investment banking fees to CAM and CGM. The order also finds that SBFM and CGM willfully violated Section 206(2) of the Advisers Act by virtue of the omissions discussed above and other misrepresentations and omissions in the materials provided to the Affected Funds’ boards, including the failure to make clear that the affiliated transfer agent would earn a high profit for performing limited functions while First Data continued to perform almost all of the transfer agent functions, and the suggestion that the proposed arrangement was in the Affected Funds’ best interests and that no viable alternatives existed. SBFM and CGM do not admit or deny any wrongdoing or liability. The settlement does not establish wrongdoing or liability for purposes of any other proceeding.

The SEC censured SBFM and CGM and ordered them to cease and desist from violations of Sections 206(1) and 206(2) of the Advisers Act. The order requires Citigroup to pay $208.1 million, including $109 million in disgorgement of profits, $19.1 million in interest, and a civil money penalty of $80 million. Approximately $24.4 million has already been paid to the Affected Funds, primarily through fee waivers. The remaining $183.7 million, including the penalty, has been paid to the U.S. Treasury and will be distributed pursuant to a plan submitted for the approval of the SEC. At this time, there is no certainty as to how the above-described proceeds of the settlement will be distributed, to whom such distributions will be made, the methodology by which such distributions will be allocated, and when such distributions will be made. The order also required that transfer agency fees received from the Affected Funds since December 1, 2004, less certain expenses, be placed in escrow and provided that a portion of such fees might be subsequently distributed in accordance with the terms of the order. On April 3, 2006, an aggregate amount of approximately $9 million was distributed to the Affected Funds.

The order required SBFM to recommend a new transfer agent contract to the Affected Fund boards within 180 days of the entry of the order; if a Citigroup affiliate submitted a proposal to serve as transfer agent or sub-transfer agent, SBFM and CGM would have

Salomon Brothers Opportunity Fund Inc. 2006 Annual Report 19

Notes to Financial Statements (continued)

been required, at their expense, to engage an independent monitor to oversee a competitive bidding process. On November 21, 2005, and within the specified timeframe, the Affected Funds’ Boards selected a new transfer agent for the Affected Funds. No Citigroup affiliate submitted a proposal to serve as transfer agent. Under the order, SBFM also must comply with an amended version of a vendor policy that Citigroup instituted in August 2004.

Although there can be no assurance, the Fund’s manager does not believe that this matter will have a material adverse effect on the Affected Fund.

This Fund is not one of the Affected Funds and therefore did not implement the transfer agent arrangement described above and therefore has not received and will not receive any portion of the distributions.

On December 1, 2005, Citigroup completed the sale of substantially all of its global asset management business, including SBFM, to Legg Mason.

Beginning in August 2005, five class action lawsuits alleging violations of federal securities laws and state law were filed against CGM and SBFM (collectively, the “Defendants”), based on the May 31, 2005 settlement order issued against the Defendants by the SEC described in Note 7. The complaints seek injunctive relief and compensatory and punitive damages, removal of SBFM as the investment manager for the Smith Barney family of funds, rescission of the Funds’ management and other contracts with SBFM, recovery of all fees paid to SBFM pursuant to such contracts, and an award of attorneys’ fees and litigation expenses.

On October 5, 2005, a motion to consolidate the five actions and any subsequently filed, related action was filed. That motion contemplates that a consolidated amended complaint alleging substantially similar causes of action will be filed in the future.

As of the date of this report, the Fund’s manager believes that resolution of the pending lawsuit will not have a material effect on the financial position or results of operations of the Fund or the ability of the Fund’s investment manager and its affiliates to continue to render services to the Fund under their respective contracts.

* * *

Beginning in June 2004, class action lawsuits alleging violations of the federal securities laws were filed against CGM and a number of its then-affiliates, including SBFM and SBAM, which were then investment adviser or manager to certain of the Funds (the “Managers”), substantially all of the mutual funds then managed by the Managers (the “Defendant Funds”), and Board members of the Defendant Funds (collectively, the “Defendants”). The complaints alleged, among other things, that CGM created various undisclosed incentives for its brokers to sell Smith Barney and Salomon Brothers funds. In addition, according to the complaints, the Managers caused the Defendant Funds to pay excessive brokerage commissions to CGM for steering clients towards proprietary funds. The complaints also alleged that the defendants breached their fiduciary duty to the Defendant Funds by improperly charging Rule 12b-1 fees and by drawing on fund assets to make undisclosed payments of soft dollars and excessive brokerage commissions. The complaints also alleged that the Defendant Funds failed to adequately disclose certain of

20 Salomon Brothers Opportunity Fund Inc. 2006 Annual Report

Notes to Financial Statements (continued)

the allegedly wrongful conduct. The complaints sought injunctive relief and compensatory and punitive damages, rescission of the Defendant Funds’ contracts with the Managers, recovery of all fees paid to the Managers pursuant to such contracts and an award of attorneys��� fees and litigation expenses.

On December 15, 2004, a consolidated amended complaint (the “Complaint”) was filed alleging substantially similar causes of action. On May 27, 2005, all of the Defendants filed motions to dismiss the Complaint. On July 26, 2006, the court issued a decision and order (1) finding that plaintiffs lacked standing to sue on behalf of the shareholders of the Funds in which none of the plaintiffs had invested (including Salomon Brothers Opportunity Fund Inc. (the “Fund”)) and dismissing those Funds from the case (although stating that they could be brought back into the case if standing as to them could be established), and (2) other than one stayed claim, dismissing all of the causes of action against the remaining Defendants, with prejudice, except for the cause of action under Section 36(b) of the Investment Company Act, which the court granted plaintiffs leave to repeal as a derivative claim.

On October 16, 2006, plaintiffs filed their Second Consolidated Amended Complaint (“Second Amended Complaint”) which alleges derivative claims on behalf of nine funds identified in the Second Amended Complaint, under Section 36(b) of the 1940 Act, against Citigroup Asset Management, Salomon Brothers Asset Management Inc, SBFM and CGM as investment advisers to the identified funds, as well as CGM as a distributor for the identified funds (collectively, the “Second Amended Complaint Defendants”). The Fund was not identified in the Second Amended Complaint. The Second Amended Complaint alleges no claims against any of the Funds or any of their Board Members. Under Section 36(b), the Second Amended Complaint alleges similar facts and seeks similar relief against the Second Amended Complaint Defendants as the Complaint.

Additional lawsuits arising out of these circumstances and presenting similar allegations and requests for relief may be filed in the future.

On September 16, 2005, the staff of the SEC informed SBFM and SBAM that the staff is considering recommending that the SEC institute administrative proceedings against SBFM and SBAM for alleged violations of Section 19(a) and 34(b) of the Investment Company Act (and related Rule 19a-1). The notification is a result of an industry wide inspection by the SEC and is based upon alleged deficiencies in disclosures regarding dividends and distributions paid to shareholders of certain funds. Section 19(a) and related Rule 19a-1 of the Investment Company Act generally require funds that are making dividend and distribution payments to provide shareholders with a written statement disclosing the source of the dividends and distributions, and, in particular, the portion of the payments made from each of net investment income, undistributed net profits and/or paid-in capital. In connection with the contemplated proceedings, the staff may seek a cease and desist order and/or monetary damages from SBFM or SBAM.

Although there can be no assurance, the Fund’s manager believes that this matter is not likely to have a material adverse effect on the Fund.

Salomon Brothers Opportunity Fund Inc. 2006 Annual Report 21

Notes to Financial Statements (continued)

Effective, September 20, 2006, Fund’s Board of Directors has approved Barrett Associates, Inc. (“Barrett Associates”) as the new investment manager for the Fund to replace the Fund’s current investment manager, ClearBridge. Barrett Associates and ClearBridge are wholly-owned subsidiaries of Legg Mason.

Under the new management agreement, which is substantially similar to the Fund’s current management agreement with ClearBridge, Barrett Associates will provide advisory services to the Fund and will be responsible for the Fund’s overall investment strategy and its implementation. The management fee rate under the new management agreement with Barrett Associates will be the same as the fee rate under the current management agreement with ClearBridge. Under the 1940 Act, the management agreement with Barrett Associates is subject to shareholder approval, and the Board has authorized seeking such approval. Proxy materials describing Barrett Associates and the new management agreement are expected to be mailed in October 2006. If shareholder approval is obtained, Barrett Associates is expected to replace ClearBridge as the Fund’s investment manager on or about December 1, 2006. Effective December 1, 2006, the Fund will change its name to “Barrett Opportunity Fund, Inc.”

Effective December 1, 2006, Amy LaGuardia and Robert J. Milnamow of Barrett Associates will be responsible for the day-to-day management of the Fund. If shareholder approval of the new management agreement with Barrett Associates is not obtained by December 1, 2006, Ms. LaGuardia and Mr. Milnamow will manage the Fund as employees of ClearBridge.

On December 1, 2006, it is expected that certain changes to the Fund’s investment strategies that have been approved by the Fund’s Board of Directors will be implemented. First, the Fund’s stock selection criteria will be revised to focus on companies whose securities are undervalued based on the investment manager’s judgment of the company’s sustainable earnings growth in addition to the company’s intrinsic value. Second, the Fund will no longer pursue a strategy of retaining unrealized long-term capital gains to avoid the tax impact of realizing those gains. In managing the Fund’s portfolio, Barrett Associates expects that some portion of the Fund’s built-in long- term capital gains will be realized gradually over time. This may result in an increase in the Fund’s annual distributions of net capital gains and, accordingly, an increase in taxable distributions to shareholders. These changes to the Fund’s investment strategies do not require shareholder approval and will be implemented regardless of whether shareholder approval of the new management agreement with Barrett Associates is obtained.

The Fund’s Board of Directors has also approved Legg Mason Partners Fund Advisor, LLC (“LMPFA”), a wholly-owned subsidiary of Legg Mason, as a new sub-administrator for the Fund to provide certain administrative services for the Fund pursuant to a sub-administration agreement between Barrett Associates and LMPFA. The effectiveness of the sub-administration agreement is contingent on shareholder approval being obtained for the new management agreement with Barrett Associates. If such approval is obtained, the sub-administration agreement will take effect on the same date as the new management agreement.

22 Salomon Brothers Opportunity Fund Inc. 2006 Annual Report

Notes to Financial Statements (continued)

In addition, the Fund’s Board of Directors has approved the standardization of the Fund’s current fundamental investment restrictions with those of certain other Legg Mason-affiliated open-end funds to the extent practicable to simplify compliance monitoring and to provide additional portfolio management flexibility for the Fund. Also, the Board has determined that certain existing restrictions should be removed or revised due to the development of new practices or changes in applicable law. The Board has authorized seeking shareholder approval for these changes. If shareholder approval is obtained, these matters are expected to go into effect as soon as practicable.

| 11. | Recent Accounting Pronouncements |

During June 2006, the Financial Accounting Standards Board (“FASB”) issued FASB Interpretation 48 (“FIN 48” or the “Interpretation”), Accounting for Uncertainty in Income Taxes — an interpretation of FASB Statement 109. FIN 48 supplements FASB Statement 109, Accounting for Income Taxes, by defining the confidence level that a tax position must meet in order to be recognized in the financial statements. FIN 48 prescribes a comprehensive model for how a fund should recognize, measure, present, and disclose in its financial statements uncertain tax positions that the fund has taken or expects to take on a tax return. FIN 48 requires that the tax effects of a position be recognized only if it is “more likely than not” to be sustained based solely on its technical merits. Management must be able to conclude that the tax law, regulations, case law, and other objective information regarding the technical merits sufficiently support the position’s sustainability with a likelihood of more than 50 percent. FIN 48 is effective for fiscal periods beginning after December 15, 2006, which for this Fund will be September 1, 2007. At adoption, the financial statements must be adjusted to reflect only those tax positions that are more likely than not to be sustained as of the adoption date. Management of the Fund is currently evaluating the impact that FIN 48 will have on the financial statements.

* * *

On September 20, 2006, FASB released Statement of Financial Accounting Standards No. 157 “Fair Value Measurements” (“FAS 157”). FAS 157 establishes an authoritative definition of fair value, sets out a framework for measuring fair value, and requires additional disclosures about fair value measurements. The application of FAS 157 is required for fiscal years beginning after November 15, 2007 and interim periods within those fiscal years. At this time, management is evaluating the implications of FAS 157 and its impact on the financial statements has not yet been determined.

Salomon Brothers Opportunity Fund Inc. 2006 Annual Report 23

Report of Independent Registered Public Accounting Firm

The Board of Directors and Shareholders

Salomon Brothers Opportunity Fund Inc:

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Salomon Brothers Opportunity Fund Inc, as of August 31, 2006, and the related statement of operations for the year then ended, the statements of changes in net assets and financial highlights for each of the years in the two-year period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. The financial highlights for each of the years in the three-year period then ended August 31, 2004 were audited by other independent registered public accountants whose report thereon, dated October 22, 2004, expressed an unqualified opinion on those financial highlights.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). These standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of August 31, 2006, by correspondence with the custodian and brokers or by other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Salomon Brothers Opportunity Fund Inc, as of August 31, 2006, and the results of its operations for the year then ended, the changes in its net assets and the financial highlights for each of the years in the two-year period then ended, in conformity with U.S. generally accepted accounting principles.

New York, New York

October 26, 2006

24 Salomon Brothers Opportunity Fund Inc. 2006 Annual Report

Additional Information (unaudited)

Information about Directors and Officers

The business and affairs of Salomon Brothers Opportunity Fund Inc (“Fund”) are managed under the direction of its Board of Directors. Information pertaining to the Directors and certain officers of the Fund is set forth below.

| | | | | | | | | | |

| | | | | |

| Name, Address and Birth Year | | Position(s)

Held with

Fund | | Term of

Office and

Length

of Time

Served | | Principal

Occupation(s)

During Past

5 Years | | Number of

Portfolios

in Fund

Complex

Overseen by

Director | | Other Board

Memberships

Held by

Director |

| Non-Interested Directors: | | | | | | | | |

Barry Handel, CPA 893 Lakeside Drive Woodmere, NY 11598 Birth Year: 1951 | | Director | | Since 2005 | | Partner, Falk & Handel LLP (accounting firm) | | 1 | | None |

| | | | | |

Rosalind A. Kochman 35 Prospect Park West, Apt. 15B Brooklyn, NY 11215 Birth Year: 1937 | | Director Chairperson | | Since

1990 Since

2005 | | Health care consultant and retired attorney, prior to 2002, Chief Executive Officer, Brooklyn Eye Surgery Center, and Administrator, Kochman, Lebowitz & Mobil, MDs | | 1 | | None |

| | | | | |

William Morris, Jr., CPA 22 Stonegate Drive Silver Spring, MD 20905 Birth Year: 1948 | | Director | | Since 2005 | | President, William Morris & Associates P.C. (accounting firm) (since 2001); formerly, President, Reese & Morris P.A. (accounting firm) (1980-2001) | | 1 | | None |

| | | | | |

Irving Sonnenschein Sonnenschein, Sherman & Deutsch 888 7th Avenue New York, NY 10106 Birth Year: 1920 | | Director | | Since

1994 | | Partner in the law firm of Sonnenschein, Sherman & Deutsch | | 1 | | None |

| Interested Director: | | | | | | | | |

Irving Brilliant* 35 Prospect Park West, Apt. 11B Brooklyn, NY 11215 Birth Year: 1918 | | Director | | Since

1978 | | Retired; prior to April 2003, Director of SBAM and Citigroup Global Markets Inc. (“CGM”) and portfolio manager of the Fund | | 1 | | None |

Salomon Brothers Opportunity Fund Inc. 25

Additional Information (unaudited) (continued)

| | | | | | | | | | |

| | | | | |

| Name, Address and Birth Year | | Position(s)

Held with

Fund | | Term of

Office* and

Length

of Time

Served | | Principal

Occupation(s)

During Past

5 Years | | Number of

Portfolios

in Fund

Complex

Overseen by

Director | | Other Board

Memberships

Held by

Director |

| Officers: | | | | | | | | |

R. Jay Gerken, CFA Legg Mason & Co., LLC (“Legg Mason”) 399 Park Avenue, 4th Floor New York, NY 10022 Birth Year: 1951 | | Executive Vice President | | Since 2002 | | Managing Director of Legg Mason; President and Chief Executive Officer of Legg Mason Partners Fund Advisors, LLC (“LMPFA”) (Since 2006); President and Chief Executive Officer of Smith Barney Fund Management LLC (“SBFM”) and Citi Fund Management Inc. (“CFM”); President and Chief Executive Officer of certain mutual funds associated with Legg Mason; Formerly Chairman of SBFM and CFM (2002 to 2006); Formerly, Chairman, President and Chief Executive Officer of Travelers Investment Adviser Inc. (from 2002 to 2005) | | 167 | | Trustee Consulting Group Capital Markets Fund |

| | | | | |

Frances M. Guggino Legg Mason 125 Broad Street 10th Floor New York, NY 10004 Birth Year: 1957 | | Chief Financial Officer and Treasurer Controller | | Since

2004 2002-

2004 | | Director of Legg Mason; Chief Financial Officer and Treasurer of certain mutual funds associated with Legg Mason Formerly Controller of certain mutual funds associated with Legg Mason (from 1999 to 2004) | | N/A | | N/A |

| | | | | |

George J. Williamson Legg Mason 399 Park Avenue 4th Floor New York, NY 10022 Birth Year: 1933 | | Vice President and Investment Officer President | | Since 2002 2000-

2002 | | Director of ClearBridge Asset Management Inc. (“ClearBridge”) and Legg Mason & Co. | | N/A | | N/A |

| | | | | |

Patrick Hughes Legg Mason 399 Park Avenue 4th Floor New York, NY 10022 Birth Year: 1964 | | Vice President and Investment Officer | | Since

2005 | | Vice President of ClearBridge | | | | |

26 Salomon Brothers Opportunity Fund Inc.

Additional Information (unaudited) (continued)

| | | | | | | | | | |

| | | | | |

| Name, Address and Birth Year | | Position(s)

Held with

Fund | | Term of

Office* and

Length

of Time

Served | | Principal

Occupation(s)

During Past

5 Years | | Number of

Portfolios

in Fund

Complex

Overseen by

Director | | Other Board

Memberships

Held by

Director |

Ted Becker Legg Mason 399 Park Avenue 4th Floor New York, NY 10022 Birth Year: 1951 | | Chief Compliance Officer | | Since

2006 | | Chief Compliance Officer of LMPFA (since 2006); Managing Director of Compliance at Legg Mason (2005-Present); Chief Compliance Officer with certain mutual funds associated with Legg Mason (since 2006), Managing Director of Compliance at Legg Mason or its predecessor (2002-2005); Prior to 2002, Managing Director — Internal Audit & Risk Review at Citigroup, Inc. | | N/A | | N/A |

| | | | | |

John Chiota Legg Mason 300 First Stamford Place 4th Floor Stamford, CT 06902 Birth Year: 1968 | | Chief Anti-Money Laundering Compliance Officer | | Since

2006 | | Vice President of Legg Mason or its predecessors (since 2004); Chief Anti-Money Laundering Compliance Officer with certain mutual funds associated with Legg Mason (since 2006); Prior to August 2004, Chief AML Compliance Officer with TD Waterhouse | | N/A | | N/A |

| | | | | |

Wendy S. Setnicka Legg Mason 125 Broad Street, 10th Floor New York, NY 10004 Birth Year: 1964 | | Controller | | Since

2004 | | Vice President of Legg Mason (since 2003); Controller of certain mutual funds associated with Legg Mason; Formerly, Assistant Controller of Legg Mason (from 2002 to 2004); Accounting Manager of Legg Mason (from 1998 to 2002) | | N/A | | N/A |

| | | | | |

Robert I. Frenkel Legg Mason 300 First Stamford Place 4th Floor Stamford, CT 06902 Birth Year: 1954 | | Secretary and Chief Legal Officer | | Since

2003 | | Managing Director and General Counsel of Global Mutual Funds for Legg Mason and its predecessors (since 1994); Secretary and Chief Legal Officer of mutual funds associated with Legg Mason & Co.; Formerly, Secretary of CFM (from 2001 to 2004) | | N/A | | N/A |

| * | Mr. Brilliant is an “Interested Director” by virtue of his ownership of Citigroup Inc. securities. |

Salomon Brothers Opportunity Fund Inc. 27

Important Tax Information (unaudited)

The following information is provided with respect to the distributions paid during the taxable year ended August 31, 2006.

| | | | |

Record Date: | | | 12/8/2005 | |

Payable Date: | | | 12/9/2005 | |

| | |

Ordinary Income: | | | | |

Qualified Dividend Income for Individuals | | | 100.00 | % |

| | |

Dividends Qualifying for the Dividends | | | | |

Received Deduction for Corporations | | | 100.00 | % |

| | |

Ordinary Income Dividends (including short-term gains) | | $ | 0.465676 | |

| | |

Long-Term Capital Gain Dividend | | $ | 1.166144 | |

| | |

Please retain this information for your records.

28 Salomon Brothers Opportunity Fund Inc.

Salomon Brothers Opportunity Fund Inc.

| | |

DIRECTORS Irving G. Brilliant Barry Handel, CPA Rosalind A. Kochman Chairperson William Morris, Jr., CPA Irving Sonnenschein | | INVESTMENT MANAGER ClearBridge Asset

Management Inc. DISTRIBUTORS Citigroup Global Markets Inc. Legg Mason Investor Services, LLC CUSTODIAN State Street Bank and Trust Company TRANSFER AGENT PFPC Inc.

4400 Computer Drive

Westborough, Massachusetts 01581 INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM KPMG LLP

345 Park Avenue

New York, NY 10154 |

This report is transmitted to the shareholders of Salomon Brothers Opportunity Fund Inc for their information. This is not a prospectus, circular or representation intended for use in the purchase of shares of the Fund or any securities mentioned in this report.

This report must be preceded or accompanied by a free prospectus. Investors should consider the Fund’s investment objectives, risks, charges and expenses carefully before investing. The prospectus contains this and other important information about the Fund. Please read the prospectus carefully before investing.

www.leggmason.com/InvestorServices

©2006 Legg Mason Investor Services, LLC

Member NASD, SIPC

Salomon Brothers

Opportunity Fund Inc.

125 Broad Street

10th Floor, MF-2

New York, New York 10004

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the SEC’s website at www.sec.gov. The Fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C., and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330. To obtain information on Form N-Q from the Fund, shareholders can call 1-800-446-1013.

Information on how the Fund voted proxies relating to portfolio securities during the prior 12-month period ended June 30th of each year, and a description of the policies and procedures that the Fund uses to determine how to vote proxies related to portfolio transactions is available (1) without charge, upon request, by calling 1-800-446-1013, (2) on the Fund’s website at www.leggmason.com/InvestorServices and (3) on the SEC’s website at www.sec.gov.

ITEM 2. CODE OF ETHICS.

The registrant has adopted a code of ethics that applies to the registrant’s principal executive officer, principal financial officer, principal accounting officer or controller.

| ITEM 3. | AUDIT COMMITTEE FINANCIAL EXPERT. |

The Board of Directors of the registrant has determined that Mr. Barry Handel possesses the technical attributes identified in Instruction 2(b) of Item 3 to Form N-CSR to qualify as an “audit committee financial expert,” and has designated Mr. Handel as the Audit Committee’s financial expert. Mr. Handel is an “independent” Director pursuant to paragraph (a)(2) of Item 3 to Form N-CSR.

| ITEM 4. | PRINCIPAL ACCOUNTANT FEES AND SERVICES. |

a) Audit Fees. Effective June 17, 2005, PricewaterhouseCoopers LLP (“PwC”) resigned as the Registrant’s principal accountant (the “Auditor”). The Registrant’s audit committee approved the engagement of KPMG LLP (“KPMG”) as the Registrant’s new principal accountant for the fiscal year ended August 31, 2006. The aggregate fees billed in the last two fiscal years ending August 31, 2005 and August 31, 2006 (the “Reporting Periods”) for professional services rendered for the audit of the Registrant’s annual financial statements, or services that are normally provided by the Auditor in connection with the statutory and regulatory filings or engagements for the Reporting Periods, were $42,000 in 2005 and $32,000 in 2006.

b) Audit-Related Fees. The aggregate fees billed in the Reporting Periods for assurance and related services by PwC or KPMG that are reasonably related to the performance of the audit of the Registrant’s financial statements and are not reported under paragraph (a) of this Item 4 were $0 in 2005 and $4,912 in 2006. These services consisted of procedures performed in connections with the Annual Registration Statement filed on Form N-1A on behalf of the Salomon Brothers Opportunity Fund Inc.

In addition, there were no Audit-Related Fees billed in the Reporting Period for assurance and related services by the Auditor to the Registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by or under common control with the investment adviser that provides ongoing services to the Salomon Brothers Opportunity Fund Inc. (“service affiliates”), that were reasonably related to the performance of the annual audit of the service affiliates. Accordingly, there were no such fees that required pre-approval by the Audit Committee for the Reporting Periods (prior to May 6, 2003 services provided by the Auditor were not required to be pre-approved).

(c) Tax Fees. The aggregate fees billed in the Reporting Periods for professional services rendered by PwC for tax compliance, tax advice and tax planning (“Tax Services”) were $0 in 2005 and $3,713 in

2006. These services consisted of (i) review or preparation of U.S. federal, state, local and excise tax returns; (ii) U.S. federal, state and local tax planning, advice and assistance regarding statutory, regulatory or administrative developments, and (iii) tax advice regarding tax qualification matters and/or treatment of various financial instruments held or proposed to be acquired or held. As of August 31, 2006, KPMG has not billed the Registrant for any Tax Services rendered.