AUXIER FOCUS FUND

Annual Report

June 30, 2019

Fund Adviser:

Auxier Asset Management LLC

15668 NE Eilers Road

Aurora, Oregon 97002

Toll Free: (877) 3AUXIER or (877) 328-9437

AUXIER FOCUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

JUNE 30, 2019

Market Commentary

The US economy, while slowing, is still benefiting from a strong labor market, a stable service sector and robust consumer spending. Conversely big ticket “goods” producers are suffering from tariffs, a strong dollar and turmoil in the international markets. 39% of S&P 500 earnings in 2018 came from foreign countries (S&P Dow Jones Indices). Consumer facing franchises are generally seeing an improvement in sales trends and pricing. These include leaders in fast-food restaurants, coffee, snacks, beverages, skincare and other necessities. These businesses are reworking product offerings and utilizing technology to speed up service while enhancing the customer experience. Low fuel prices are helping to stimulate travel. This is particularly impactful for millennials who tend to value and spend on “experiences.” We continue to see strong fundamentals for businesses involved with the digital transformation of the economy, although prices for many of these businesses are getting prohibitively expensive.

Housing

The decline in the 30-year mortgage rate to 3.75% has stimulated refinancing activity. However high-end housing across the country has been softer partly due to the pull back of Chinese investment along with the limits on tax deductibility of mortgages over $750,000 and property taxes over $10,000, depending on your tax filing status. The dollar volume of homes purchased by foreigners for the 12 months ending in March was down 36%. First time buyers have been struggling to come up with down payments. Student loan debts nearing $1.6 trillion are impeding the growth of the entry level housing market.

New Technology Can Lead to Pricing

New technology disrupters garner excitement and often nosebleed valuations. A good example is the comparison of two transportation companies Uber and UPS. After 112 years UPS recently had their best quarterly performance in the history of the company. It operates in 220 countries and moves 3% of the global GDP of goods and 6% of US GDP. With profits exceeding $6.5 billion and a well-compensated workforce, it trades for a lower valuation than ride-sharing Uber which is losing $3 billion a year with a temporary workforce of drivers. FedEx is trading at ten times earnings, 40% lower than their historical valuation, over fears that Amazon will overtake them. We estimate it would cost a startup over $110 billion to get up to speed with FedEx which has been diligent in leadership through state-of-the-art logistics technology. In the late 1990s companies with great stories and no cash flow were the rage. E-toys, Webvan food delivery and Pets.com all enjoyed great momentum and sky-high valuations until reality set in and they crashed and burned. Investing comes down to the cash an investment generates not just a story. We aggressively follow industry cycles and those with the most euphoria that are going parabolic tend to be late cycle. Excitement amid a merger frenzy marked the peak in commodities in 2011 after a 118-month boom. Commodities may have finally reached bottom after a painful eight-year correction. At the peak many commodities reached prices over double their cost of production. In farming it is so tough just to cover the cost of production. Today most of the farm sector is in a deep decline with farm incomes down over 50% from their peak while many commodities are trading for less than the cost of production. The odds favor food shortages in the next few years.

Companies in Secular Decline

While we always like a bargain price many companies can appear to be statistically cheap but are actually in secular decline. Take Eastman Kodak, once a dominant blue chip. It totally missed the digital transformation in photographs. We now take over two trillion pictures a year. That is why an investor needs to be a dedicated, investigative researcher to seek out potential technological disruption that can interrupt the compounding of returns. The power of compounded knowledge is also important to surviving and thriving over the long term.

AUXIER FOCUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

JUNE 30, 2019

Healthcare

Numerous health care stocks have lagged the market advance in 2019. Recurring adversarial headlines out of Washington DC have depressed valuations. The negative headlines drown out the exciting innovation that we see taking place that has the potential to cure many chronic diseases. Abbot is making great strides in diabetes and heart valves. Medtronic is combining data analytics and artificial intelligence. Both Alphabet and Apple are making meaningful advances. Merck’s cancer fighting drug Keytruda is making excellent progress with sales gaining over 50% this past quarter. More competition and improved efficiency via technology is needed to drive costs lower. A total government takeover of healthcare could cost $32 trillion (Committee for a Responsible Federal Budget). Socialism means less competition and higher prices. Venezuela’s state-run economic model now has inflation exceeding 10 million percent (CNBC). So much for “safe” sovereign debt. Venezuela was the number one ranked economy in Latin America in 2000.

Central Bank Distortion Negative Interest Rates

Nearly $13 trillion face amount of bonds from outside the US are priced to yield negative interest rates. If you deposit money in a savings account in a German bank you pay the bank interest. It is a form of competitive currency devaluation that gives an export advantage in the global markets. A risk is a prolonged trade/currency war. It is a man-made (central banks) distortion that leads to the misallocation of investments. It is killing European banks. Germany’s largest bank, Deutsche Bank recently dropped to less than one third of book value. Europe has relied heavily on monetary policy and has failed to make the tough policy decisions needed to restructure in order to unleash the potential of a market-based economy.

Hemp as a New Disrupter

The outlawing of hemp in 1937 (due to its relationship with its sister cannabis plant, marijuana) froze the development of the nation’s ability to understand the crop. However, with the passage of the 2018 Farm Bill, hemp was federally legalized. Through recent research, CBD effects on the body are being explored at greater lengths and scientists are finding beneficial uses across a vast array of medical applications. CBD has entered the market rapidly in accordance with recent deregulation and has created an unprecedented number of opportunities for development and investment. Due to the explosion of the hemp industry in a relatively short period of time, the supply chain has proven to be challenging. These bottlenecks are where investments could prove to be the most advantageous. CBD is positioned to eventually overshadow traditional over-the-counter pain relief (such as acetaminophen or ibuprofen). The health and wellness, beauty products, beverage and pet health industry have all championed this emerging hemp market and have benefited from this major introduction. The industrial side of hemp poses a similar number of disruptions as there is an incredible number of products that could soon be replaced by the hemp crop including certain textiles, plastics, building materials and insulation. Levi’s now makes a hemp shirt. Oregon State University, in our back yard, has some of the best research in the country allowing us to gather unrivaled data and insights for identifying attractive investments.

AUXIER FOCUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

JUNE 30, 2019

Performance Update

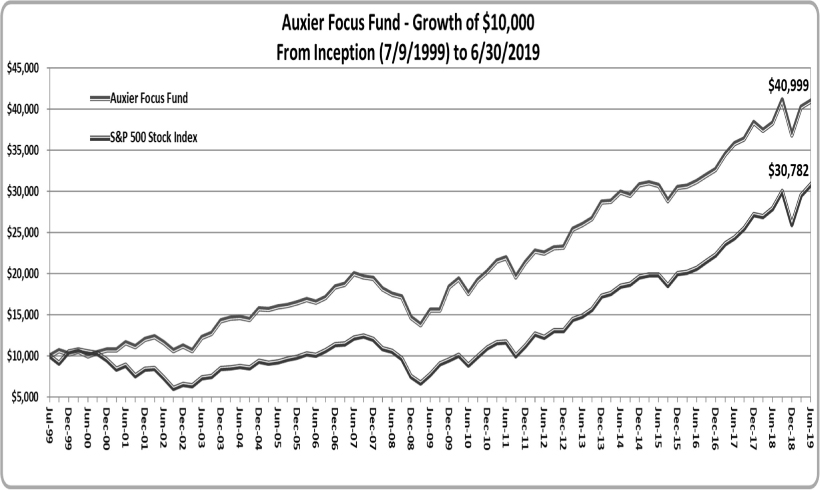

Auxier Focus Fund’s (the “Fund”) Investor Class returned 1.92% in the second quarter vs. 4.30% for the S&P 500 Index and 3.21% for the DJIA. Stocks in the Fund comprised 95% and gained 2.24%. The equity breakdown was 81% domestic and 14% foreign. Health care stocks hurt performance for the year. A hypothetical $10,000 investment in the Fund since inception in July 1999 to June 30, 2019, is now worth $40,999 vs. $30,782 for the S&P 500. The equities in the Auxier Focus Fund have returned over 450% since inception. This was achieved with an average exposure to the market of less than 79% over the entire period.

Contributors to the period: Our outlook on a cross section of portfolio positions with a positive return for the period ended 06/30/2019.

Visa

Visa Inc. saw strong performance in revenues and earnings for the quarter led by continued growth in payments volume, cross-border volume and processed transactions. During the quarter, the company repurchased 14 million shares of common stock using $2 billion of cash on hand. They have $8.3 billion of authorized funds available for further stock repurchases. Management expects revenue growth for the full-year 2019 to be in the low double-digits. Visa recently partnered with Razer to allow their 60 million users to make payments wherever Visa is accepted. This partnership will increase Visa’s reach in Southeast Asia, a region which has a large underserved population of over 438 million. Visa also launched their payment | Auxier Focus Fund – Investor Class Average Annual Total Returns (06/30/2019) Since Inception (07/09/1999) 7.32% 10-year 10.14% 5-year 6.48% 1-year 7.08% 3-month 1.92%

Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than original cost. As stated in the current prospectus, the Fund’s Investor Class Share’s annual operating expense ratio (gross) is 1.10%. The Fund’s adviser has contractually agreed to waive a portion of its fee and/or reimburse Fund expenses to limit total annual operating expenses at 0.98%, which is in effect until October 31, 2019. Other share classes may vary. The Fund charges a 2.0% redemption fee on shares redeemed within 180 days of purchase. For the most recent month-end performance, please call (877) 328-9437 or visit the Adviser’s website at www.auxierasset.com. The recent growth rate in the stock market has helped to produce short-term returns that are not typical and may not continue in the future. |

AUXIER FOCUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

JUNE 30, 2019

| Top Holdings on 06/30/2019 | % Assets |

| Mastercard, Inc., Class A | 5.4% |

| UnitedHealth Group, Inc. | 4.2% |

| PepsiCo., Inc. | 3.6% |

| Medtronic PLC | 3.6% |

| Microsoft Corp. | 3.4% |

| Bank of New York Mellon Corp. | 3.3% |

| Johnson & Johnson | 3.1% |

| Philip Morris International | 2.9% |

| Merk & Co., Inc. | 2.7% |

| BP PLC, ADR | 2.6% |

system called Visa B2B Connect to offer seamless and secure cross-border payment processing for businesses.

PepsiCo Inc. (PEP)

PepsiCo is showing strong performance in their snacking and international segments. Shares have increased by 20.0% in the past six months, outperforming the S&P’s increase of 17.2%. The company’s growing snack business has largely offset slight dips in the beverage industry. PepsiCo has instituted a cost savings program that could achieve $1 billion in annual savings through 2023. They expect to generate cash flows of about $9B and return $8B to shareholders in the form of dividends and share repurchases. PepsiCo has cemented itself as one of the best dividend stocks on the market with 47 consecutive years of dividend hikes.

Microsoft Corporation (MSFT)

Microsoft’s revenue increased by 14% for the quarter while earnings increased by 19%. Revenue growth was led by increased demand for Microsoft’s Azure cloud offerings. Microsoft plans to increase their investment in cloud-based systems to continue to shrink the gap between them and Amazon in the cloud service segment. Microsoft has almost doubled its market share in the public cloud infrastructure industry over the last few years. They are now #2 in the cloud industry and well ahead of other competitors. Management is very optimistic about the continued growth of the company providing guidance of double-digit revenue and operating income growth over the next year. Microsoft’s debt is dwarfed by its near $1 trillion market cap. This should give the company the flexibility to continue investments in more growth-oriented projects.

Mastercard Inc. (MA)

Mastercard, the largest holding in the fund, continued its strong performance with another quarter of solid growth. Revenues were up 9% and net earnings were up 25% for the quarter. Revenue was boosted by a 12% increase in global gross dollar volume. Mastercard returned over $2 billion to shareholders in the form of share repurchases and dividends during the quarter. Year-to-date, Mastercard stock has increased by 40% versus a 17% increase in the S&P 500. Mastercard’s underlying infrastructure means that they can continue to increase the number of total transactions they can handle with only a minimal increase in expenses. Mastercard seems likely to benefit from the continued growth in the e-commerce industry which is currently growing five-times as fast as face-to-face transactions (eMarketer).

Detractors to the period: Our outlook on a cross section of portfolio positions with a negative return for the period ended 06/30/19:

Bank of New York Mellon Corp. (BK)

After coming over from Visa in July of 2017, CEO Charles Scharf has worked to transform Bank of New York Mellon just as he did with Visa. Under Scharf Visa nearly tripled in price due particularly to his focus on improving their technology infrastructure and diversifying the company through international expansion. At Bank of New York Mellon Scharf has also focused on diversification and technology. While the diversification has hurt margins in the short-term and the investments in technology have lowered current earnings, we believe that the improvements Scharf has made will pay off in the long run. In the short-term Bank of New York Mellon continues to return capital to their shareholders with a recent 11% dividend increase and a nearly $4 billion share repurchase authorization.

Kroger Co. (KR)

In the second year of their Restock Kroger program, Kroger is continuing to invest in their technology and infrastructure to make good on their goal to “deliver anything, anytime, anywhere.” The results from Kroger’s investments can already be seen as their total sales, excluding fuel and the effect of their sale of their convenience store business, were up 2%. They have a long history of success and are trading at a steep discount of around nine times earnings. Kroger used their $1.4 billion in free cash flow in the quarter to invest in their business and reduce their debt.

AUXIER FOCUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

JUNE 30, 2019

Philip Morris International (PM)

Philip Morris has been facing extreme currency pressure due to the strength of the US dollar. Despite the foreign exchange headwinds, they continue to dominate the international tobacco market with total market share increasing by a point to 28.4%. Their in-market sales were up 1.7% led by strong growth from their IQOS heated tobacco devices which grew by nearly 35%. IQOS has taken off in Japan and is starting to pick up steam across the rest of the globe with the EU and Russia both seeing double-digit growth. Philip Morris has marketed the IQOS devices as a substitute to traditional cigarettes that releases fewer chemicals since the tobacco is not burned. The rapid growth of IQOS is only projected to increase as local governments push this alternative.

Zimmer Biomet Holdings (ZBH)

Zimmer Biomet has faced some fixable issues with their supply chain hampering current operating results. However, they are a low-cost provider with a strong history in hip and knee replacements. Their rapidly growing S.E.T (surgical, sports medicine, extremities and trauma) and Spine & CMF (craniomaxillofacial) divisions leave them well positioned to take advantage of the growing demand for medical devices. The peak demand for hips and knees is 68 years old—just about the average age of the baby boomer today. Zimmer Biomet is planning on using their strong free cash flow generation to further reduce their debt in 2019.

Our primary focus is to take advantage of the power of compounding with businesses and management teams that appear likely to successfully navigate through the most challenging environments. We search for solid businesses and managements, priced right, that can pursue compelling returns over long periods. The explosion of data has contributed to the power of networks and platforms. With network effects businesses can leverage their users with the potential to grow returns with greater scale. By utilizing data analytics and artificial intelligence they are better able to identify customer needs. This is especially true in digital advertising, Facebook, Google Search and YouTube are a few examples. As users increase, the value of the experience or product can increase exponentially.

Shortage of Shares

Supply and demand is still favorable for publicly traded US stocks as buybacks are running close to $950 billion annualized (Standard & Poor’s). Private equity demand has exploded with over 8000 firms armed with over $2 trillion in buying power (Bain & Co.). We favor businesses with high free cash flow yields which private equity buyers seek. Industry mergers are common as well. With investors fear of volatility in public auction markets together with disclosure and regulation we think some of the best odds for success come when dealing with smaller sums of money in the markets where investors can take advantage of the periodic waves of irrational behavior to score bargains not available in the private markets.

Other misperceptions of risk include the safety of utilities and big companies. Recently the largest utility in the country, Pacific Gas and Electric, declared bankruptcy over wildfire liabilities in California. In 2007 Texas Utilities went bankrupt. In 2001 Enron was the largest bankruptcy in history, a year after Fortune magazine featured them as having industry best practices. In 2000 CFO magazine named Enron’s Andrew Fastow CFO of the year. Enron had acquired our local utility Portland General Electric and we saw the rapid buildup of off-balance sheet debt and sold the stock at $80 before it dropped to zero. Overpaying and overborrowing are the recurring sins of capital allocation.

We appreciate your trust.

Jeff Auxier

Fund returns (i) assume the reinvestment of all dividends and capital gain distributions and (ii) would have been lower during the period if certain fees and expenses had not been waived. Performance shown is for the Fund’s Investor Class shares; returns for other share classes will vary. Performance for Investor Class shares for periods prior to December 10, 2004 reflects performance of the applicable share class of Auxier Focus Fund, a series of Unified Series Trust (the “Predecessor Fund”). Prior to January 3, 2003, the Predecessor Fund was a series of Ameriprime Funds. The performance of the Fund’s Investor Class shares for the period prior to December 10, 2004 reflects the expenses of the Predecessor Fund.

The Fund may invest in value and/or growth stocks. Investments in value stocks are subject to risk that their intrinsic value may never be realized and investments in growth stocks may be susceptible to rapid price swings, especially during periods of economic uncertainty. In addition, the Fund may invest in mid-sized companies which generally carry greater risk than is customarily associated with larger companies. Moreover, if the Fund’s portfolio is overweighted in a sector, any negative development affecting

AUXIER FOCUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

JUNE 30, 2019

that sector will have a greater impact on the Fund than a fund that is not overweighted in that sector. An increase in interest rates typically causes a fall in the value of a debt security (Fixed-Income Securities Risk) with corresponding changes to the Fund’s value.

The S&P 500 Index is a broad-based, unmanaged measurement of changes in stock market conditions based on 500 widely held common stocks. One cannot invest directly in an index or average.

The views in this shareholder letter were those of the Fund Manager as of the letter’s publication date and may not reflect his views on the date this letter is first distributed or anytime thereafter. These views are intended to assist readers in understanding the Fund’s investment methodology and do not constitute investment advice.

AUXIER FOCUS FUND

PERFORMANCE CHART AND ANALYSIS (Unaudited)

JUNE 30, 2019

The following chart reflects the change in the value of a hypothetical $10,000 investment in Investor Shares, including reinvested dividends and distributions, in the Auxier Focus Fund (the “Fund”) compared with the performance of the benchmark, the S&P 500 Index (“S&P 500”), over the past ten fiscal years. The S&P 500 is a broad-based measurement of the U.S. stock market based on the performance of 500 widely held large capitalization common stocks. The total return of the Fund's classes includes the maximum sales charge of 5.75% (A Shares only) and operating expenses that reduce returns, while the total return of the S&P 500 does not include the effect of sales charges and expenses. A Shares are subject to a 1.00% contingent deferred sales charge on shares purchased without an initial sales charge and redeemed less than one year after purchase. The total return of the index includes the reinvestment of dividends and income. The total return of the Fund includes operating expenses that reduce returns, while the total return of the index does not include expenses. The Fund is professionally managed, while the index is unmanaged and is not available for investment.

Comparison of Change in Value of a $10,000 Investment

Investor Shares vs. S&P 500 Index

| Average Annual Total Returns Periods Ended June 30, 2019 | One Year | Five Years | Ten Years | Since Inception(1) | ||||

| Investor Shares | 7.08% | 6.48% | 10.14% | 7.32% | ||||

| S&P 500® Index (Since July 9, 1999) | 10.42% | 10.71% | 14.70% | 5.79% | ||||

| A Shares (with sales charge)(2)(3) | 0.66% | 5.03% | 9.38% | 6.95% | ||||

| Institutional Shares(3) | 7.24% | 6.67% | 10.29% | 7.39% |

| (1) | Institutional, A Shares and Investor Shares commenced operations on May 9, 2012, July 8, 2005 and July 9, 1999, respectively. |

| (2) | Due to shareholder redemptions on August 21, 2005, net assets of the class were zero from the close of business on that date until September 22, 2005. Financial information presented for the period August 21, 2005 to September 22, 2005 reflects performance of Investor Shares of the Fund. |

| (3) | For Institutional Shares, performance for the 10-year and since inception periods are blended average annual returns which include the returns of the Investor Shares prior to commencement of operations of the Institutional Shares. For A Shares, performance for the since inception period is a blended average annual return which includes the return of the Investor Shares prior to commencement of operations of the A Shares. |

Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than original cost. As stated in the Fund’s prospectus, the annual operating expense ratios (gross) for Investor Shares, A Shares and Institutional Shares are 1.10%, 1.44% and 1.10%, respectively. However, the Fund’s Adviser has contractually agreed to waive its fee and/or reimburse Fund expenses to limit Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement (excluding all taxes, interest, portfolio transaction expenses, dividend expenses on short sales, and extraordinary expenses) to 0.98%, 1.25% and 0.80% of the Investor Shares, A Shares and Institutional Shares, respectively, through October 31, 2019 (the “Expense Cap”). The Expense Cap may be raised or eliminated only with the consent of the Board of Trustees. The Adviser may be reimbursed by the Fund for fees waived and expenses reimbursed by the Adviser pursuant to the Expense Cap if such payment is made within three years of the fee waiver or expense reimbursement and does not cause the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement to exceed the lesser of (i) the then-current Expense Cap and (ii) the Expense Cap in place at the time the fees/expenses were waived/reimbursed. Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement will increase if exclusions from the Expense Cap apply. Shares redeemed or exchanged within 180 days of purchase will be charged a 2.00% redemption fee. The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns greater than one year are annualized. For the most recent month-end performance, please call (877) 328-9437 or visit www.auxierasset.com.

Performance for Investor Shares for periods prior to December 10, 2004, reflects performance and expenses of Auxier Focus Fund, a series of Unified Series Trust (the “Predecessor Fund”). Prior to January 3, 2003, the Predecessor Fund was a series of Ameriprime Funds.

AUXIER FOCUS FUND

SCHEDULE OF INVESTMENTS

JUNE 30, 2019

| Shares | Security Description | Value | ||||||

| Equity Securities - 95.1% | ||||||||

| Common Stock - 95.1% | ||||||||

| Communication Services - 1.9% | ||||||||

| 197,175 | America Movil SAB de CV, ADR | $ | 2,870,868 | |||||

| 1,719 | Cisco Systems, Inc. | 94,081 | ||||||

| 162,738 | Telefonica SA, ADR | 1,349,098 | ||||||

| 6,845 | Viacom, Inc., Class B | 204,460 | ||||||

| 4,518,507 | ||||||||

| Consumer Cyclicals - 1.3% | ||||||||

| 1,241 | Booking Holdings, Inc. (a) | 2,326,515 | ||||||

| 13,675 | DR Horton, Inc. | 589,803 | ||||||

| 2,916,318 | ||||||||

| Consumer Discretionary - 6.7% | ||||||||

| 91,179 | Arcos Dorados Holdings, Inc., Class A | 663,783 | ||||||

| 34,000 | Becle SAB de CV | 53,380 | ||||||

| 51,460 | Comcast Corp., Class A | 2,175,729 | ||||||

| 12,465 | CVS Health Corp. | 679,218 | ||||||

| 112,077 | Discovery, Inc., Class A (a) | 3,440,764 | ||||||

| 4,641 | Discovery, Inc., Class C (a) | 132,036 | ||||||

| 16,250 | General Motors Co. | 626,112 | ||||||

| 169,545 | Lincoln Educational Services Corp. (a) | 391,649 | ||||||

| 18,550 | Lowe's Cos., Inc. | 1,871,880 | ||||||

| 5,756 | McDonald's Corp. | 1,195,291 | ||||||

| 52,302 | Sally Beauty Holdings, Inc. (a) | 697,709 | ||||||

| 1,176 | The Andersons, Inc. | 32,034 | ||||||

| 4,725 | The Home Depot, Inc. | 982,658 | ||||||

| 12,850 | Walmart, Inc. | 1,419,797 | ||||||

| 7,050 | Yum China Holdings, Inc. | 325,710 | ||||||

| 7,050 | Yum! Brands, Inc. | 780,224 | ||||||

| 15,467,974 | ||||||||

| Consumer Staples - 16.7% | ||||||||

| 65,455 | Altria Group, Inc. | 3,099,294 | ||||||

| 34,055 | British American Tobacco PLC, ADR | 1,187,498 | ||||||

| 13,200 | Coca-Cola HBC AG, ADR (a) | 498,960 | ||||||

| 4,135 | Diageo PLC, ADR | 712,543 | ||||||

| 2,214 | Lamb Weston Holdings, Inc. | 140,279 | ||||||

| 50,327 | Molson Coors Brewing Co., Class B | 2,818,312 | ||||||

| 34,800 | Monster Beverage Corp. (a) | 2,221,284 | ||||||

| 63,820 | PepsiCo., Inc. | 8,368,717 | ||||||

| 84,525 | Philip Morris International, Inc. | 6,637,748 | ||||||

| 92,280 | Tesco PLC, ADR | 803,750 | ||||||

| 51,300 | The Coca-Cola Co. | 2,612,196 | ||||||

| 2,845 | The J.M. Smucker Co. | 327,716 | ||||||

| 203,368 | The Kroger Co. | 4,415,119 | ||||||

| 9,025 | The Procter & Gamble Co. | 989,591 | ||||||

| 63,421 | Unilever NV, ADR | 3,850,923 | ||||||

| 38,683,930 | ||||||||

| Energy - 4.2% | ||||||||

| 144,810 | BP PLC, ADR | 6,038,577 | ||||||

| 7,430 | Chevron Corp. | 924,589 | ||||||

| 13,600 | ConocoPhillips | 829,600 | ||||||

| 7,800 | Phillips 66 | 729,612 | ||||||

| 14,415 | Valero Energy Corp. | 1,234,068 | ||||||

| 9,756,446 | ||||||||

| Financials - 23.4% | ||||||||

| 53,260 | Aflac, Inc. | 2,919,181 | ||||||

| 49,445 | American International Group, Inc. | 2,634,430 | ||||||

| 2,480 | Ameriprise Financial, Inc. | 359,997 | ||||||

| 201,699 | Bank of America Corp. | 5,849,271 | ||||||

| 16,545 | Berkshire Hathaway, Inc., Class B (a) | 3,526,898 | ||||||

| 67,374 | Central Pacific Financial Corp. | 2,018,525 | ||||||

| 25,975 | Citigroup, Inc. | 1,819,029 | ||||||

| 5,616 | Colliers International Group, Inc. | 402,218 | ||||||

| 132,268 | Credit Suisse Group AG, ADR | 1,583,248 | ||||||

| Shares | Security Description | Value | ||||||

| Financials - 23.4% (continued) | ||||||||

| 5,616 | FirstService Corp. | $ | 538,687 | |||||

| 63,668 | Franklin Resources, Inc. | 2,215,646 | ||||||

| 3,625 | Legg Mason, Inc. | 138,765 | ||||||

| 2,025 | Marsh & McLennan Cos., Inc. | 201,994 | ||||||

| 47,550 | Mastercard, Inc., Class A | 12,578,401 | ||||||

| 1,100 | PayPal Holdings, Inc. (a) | 125,906 | ||||||

| 171,625 | The Bank of New York Mellon Corp. | 7,577,244 | ||||||

| 18,918 | The Travelers Cos., Inc. | 2,828,619 | ||||||

| 7,350 | U.S. Bancorp | 385,140 | ||||||

| 15,249 | Unum Group | 511,604 | ||||||

| 31,600 | Visa, Inc., Class A | 5,484,180 | ||||||

| 14,350 | Waddell & Reed Financial, Inc., Class A | 239,214 | ||||||

| 4,400 | Wells Fargo & Co. | 208,208 | ||||||

| 54,146,405 | ||||||||

| Health Care - 24.7% | ||||||||

| 44,051 | Abbott Laboratories | 3,704,689 | ||||||

| 2,900 | Alkermes PLC (a) | 65,366 | ||||||

| 4,230 | Allergan PLC | 708,229 | ||||||

| 740 | Amgen, Inc. | 136,367 | ||||||

| 18,731 | Anthem, Inc. | 5,286,076 | ||||||

| 12,200 | Becton Dickinson and Co. | 3,074,522 | ||||||

| 12,190 | Biogen, Inc. (a) | 2,850,875 | ||||||

| 13,490 | Cigna Corp. | 2,125,349 | ||||||

| 51,240 | Johnson & Johnson | 7,136,707 | ||||||

| 84,318 | Medtronic PLC | 8,211,730 | ||||||

| 74,249 | Merck & Co., Inc. | 6,225,779 | ||||||

| 7,282 | Pfizer, Inc. | 315,456 | ||||||

| 22,337 | Quest Diagnostics, Inc. | 2,274,130 | ||||||

| 39,676 | UnitedHealth Group, Inc. | 9,681,341 | ||||||

| 45,400 | Zimmer Biomet Holdings, Inc. | 5,345,396 | ||||||

| 57,142,012 | ||||||||

| Industrials - 4.2% | ||||||||

| 1,240 | Caterpillar, Inc. | 169,000 | ||||||

| 122,841 | Corning, Inc. | 4,082,006 | ||||||

| 3,695 | FedEx Corp. | 606,682 | ||||||

| 18,157 | Gates Industrial Corp. PLC (a) | 207,171 | ||||||

| 88,671 | Manitex International, Inc. (a) | 541,780 | ||||||

| 11,500 | Raytheon Co. | 1,999,620 | ||||||

| 2,780 | The Boeing Co. | 1,011,948 | ||||||

| 11,595 | United Parcel Service, Inc., Class B | 1,197,416 | ||||||

| 9,815,623 | ||||||||

| Information Technology - 8.0% | ||||||||

| 1,742 | Alphabet, Inc., Class A (a) | 1,886,238 | ||||||

| 35,910 | Cerner Corp. | 2,632,203 | ||||||

| 16,675 | Cognizant Technology Solutions Corp., Class A | 1,057,028 | ||||||

| 3,155 | Facebook, Inc., Class A (a) | 608,915 | ||||||

| 57,887 | Microsoft Corp. | 7,754,543 | ||||||

| 82,320 | Oracle Corp. | 4,689,770 | ||||||

| 18,628,697 | ||||||||

| Materials - 3.6% | ||||||||

| 14,225 | Celanese Corp., Class A | 1,533,455 | ||||||

| 28,458 | Corteva, Inc. (a) | 841,503 | ||||||

| 28,458 | Dow, Inc. | 1,403,264 | ||||||

| 28,458 | DuPont de Nemours, Inc. | 2,136,342 | ||||||

| 26,505 | LyondellBasell Industries NV, Class A | 2,282,876 | ||||||

| 4,980 | The Mosaic Co. | 124,649 | ||||||

| 8,322,089 | ||||||||

| Telecommunications - 0.1% | ||||||||

| 22,075 | CenturyLink, Inc. | 259,602 | ||||||

See Notes to Financial Statements.

AUXIER FOCUS FUND

SCHEDULE OF INVESTMENTS

JUNE 30, 2019

| Shares | Security Description | Value | ||||||

| Transportation - 0.3% | ||||||||

| 2,550 | Delta Air Lines, Inc. | $ | 144,713 | |||||

| 3,110 | Union Pacific Corp. | 525,932 | ||||||

| 670,645 | ||||||||

| Total Common Stock (Cost $116,677,416) | 220,328,248 | |||||||

| Total Equity Securities (Cost $116,677,416) | 220,328,248 | |||||||

| Principal | Security Description | Rate | Maturity | Value | |||||||||

| Fixed Income Securities - 3.9% | |||||||||||||

| Corporate Non-Convertible Bonds - 0.8% | |||||||||||||

| Financials - 0.6% | |||||||||||||

| $ | 500,000 | JPMorgan Chase & Co. (callable at 100) (b)(c) | 4.63% | 11/01/22 | 485,135 | ||||||||

| 400,000 | SunTrust Banks, Inc. (callable at 100) (b)(c) | 5.13 | 12/15/27 | 392,880 | |||||||||

| 500,000 | The Goldman Sachs Group, Inc. (callable at 100) (b)(c) | 5.00 | 11/10/22 | 480,760 | |||||||||

| 1,358,775 | |||||||||||||

| Industrials - 0.2% | |||||||||||||

| 450,000 | General Electric Co. (callable at 100) (b)(c) | 5.00 | 01/21/21 | 432,351 | |||||||||

| Total Corporate Non-Convertible Bonds (Cost $1,815,432) | 1,791,126 | ||||||||||||

| U.S. Government & Agency Obligations - 3.1% | |||||||||||||

| U.S. Treasury Securities - 3.1% | |||||||||||||

| 2,000,000 | U.S. Treasury Bill (d) | 2.15 | 07/09/19 | 1,999,122 | |||||||||

| 3,200,000 | U.S. Treasury Bill (d) | 2.14 | 07/16/19 | 3,197,252 | |||||||||

| 2,000,000 | U.S. Treasury Bill (d) | 1.98 | 07/30/19 | 1,996,639 | |||||||||

| Total U.S. Government & Agency Obligations (Cost $7,193,003) | 7,193,013 | ||||||||||||

| Total Fixed Income Securities (Cost $9,008,435) | 8,984,139 | ||||||||||||

| Investments, at value - 99.0% (Cost $125,685,851) | $ | 229,312,387 | |||||||||||

| Other Assets & Liabilities, Net - 1.0% | 2,304,611 | ||||||||||||

| Net Assets - 100.0% | $ | 231,616,998 | |||||||||||

| ADR | American Depositary Receipt |

| PLC | Public Limited Company |

| (a) | Non-income producing security. |

| (b) | Variable rate security, the interest rate of which adjusts periodically based on changes in current interest rates. Rate represented is as of June 30, 2019. |

| (c) | Perpetual maturity security. |

| (d) | Zero coupon bond. Interest rate presented is yield to maturity. |

The following is a summary of the inputs used to value the Fund's investments as of June 30, 2019.

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used in the table below, please refer to the Security Valuation section in Note 2 of the accompanying Notes to Financial Statements.

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Investments at Value | ||||||||||||||||

| Common Stock | ||||||||||||||||

| Communication Services | $ | 4,518,507 | $ | – | $ | – | $ | 4,518,507 | ||||||||

| Consumer Cyclicals | 2,916,318 | – | – | 2,916,318 | ||||||||||||

| Consumer Discretionary | 15,467,974 | – | – | 15,467,974 | ||||||||||||

| Consumer Staples | 38,683,930 | – | – | 38,683,930 | ||||||||||||

| Energy | 9,756,446 | – | – | 9,756,446 | ||||||||||||

| Financials | 54,146,405 | – | – | 54,146,405 | ||||||||||||

| Health Care | 57,142,012 | – | – | 57,142,012 | ||||||||||||

| Industrials | 9,815,623 | – | – | 9,815,623 | ||||||||||||

| Information Technology | 18,628,697 | – | – | 18,628,697 | ||||||||||||

| Materials | 8,322,089 | – | – | 8,322,089 | ||||||||||||

| Telecommunications | 259,602 | – | – | 259,602 | ||||||||||||

| Transportation | 670,645 | – | – | 670,645 | ||||||||||||

| Corporate Non-Convertible Bonds | – | 1,791,126 | – | 1,791,126 | ||||||||||||

| U.S. Government & Agency Obligations | – | 7,193,013 | – | 7,193,013 | ||||||||||||

| Investments at Value | $ | 220,328,248 | $ | 8,984,139 | $ | – | $ | 229,312,387 | ||||||||

| PORTFOLIO HOLDINGS (Unaudited) | |||

| % of Total Net Assets | |||

| Communication Services | 1.9% | ||

| Consumer Cyclicals | 1.3% | ||

| Consumer Discretionary | 6.7% | ||

| Consumer Staples | 16.7% | ||

| Energy | 4.2% | ||

| Financials | 23.4% | ||

| Health Care | 24.7% | ||

| Industrials | 4.2% | ||

| Information Technology | 8.0% | ||

| Materials | 3.6% | ||

| Telecommunications | 0.1% | ||

| Transportation | 0.3% | ||

| Corporate Non-Convertible Bonds | 0.8% | ||

| U.S. Government & Agency Obligations | 3.1% | ||

| Other Assets & Liabilities, Net | 1.0% | ||

| 100.0% | |||

See Notes to Financial Statements.

AUXIER FOCUS FUND

STATEMENT OF ASSETS AND LIABILITIES

JUNE 30, 2019

| ASSETS | ||||

| Investments, at value (Cost $125,685,851) | $ | 229,312,387 | ||

| Cash | 3,593,798 | |||

| Receivables: | ||||

| Fund shares sold | 291,214 | |||

| Investment securities sold | 395,144 | |||

| Dividends and interest | 315,739 | |||

| Prepaid expenses | 22,537 | |||

| Total Assets | 233,930,819 | |||

| LIABILITIES | ||||

| Payables: | ||||

| Investment securities purchased | 2,099,770 | |||

| Fund shares redeemed | 17,136 | |||

| Accrued Liabilities: | ||||

| Investment Adviser fees | 124,105 | |||

| Trustees’ fees and expenses | 438 | |||

| Fund services fees | 23,935 | |||

| Other expenses | 48,437 | |||

| Total Liabilities | 2,313,821 | |||

| NET ASSETS | $ | 231,616,998 | ||

| COMPONENTS OF NET ASSETS | ||||

| Paid-in capital | $ | 117,106,618 | ||

| Distributable earnings | 114,510,380 | |||

| NET ASSETS | $ | 231,616,998 | ||

| SHARES OF BENEFICIAL INTEREST AT NO PAR VALUE (UNLIMITED SHARES AUTHORIZED) | ||||

| Investor Shares | 6,177,113 | |||

| A Shares | 117,351 | |||

| Institutional Shares | 3,986,891 | |||

| NET ASSET VALUE, OFFERING AND REDEMPTION PRICE PER SHARE* | ||||

| Investor Shares (based on net assets of $137,994,857) | $ | 22.34 | ||

| A Shares (based on net assets of $2,663,671) | $ | 22.70 | ||

| A Shares Maximum Public Offering Price Per Share (net asset value per share/(100%-5.75%)) | $ | 24.08 | ||

| Institutional Shares (based on net assets of $90,958,470) | $ | 22.81 | ||

| * | Shares redeemed or exchanged within 180 days of purchase are charged a 2.00% redemption fee. |

See Notes to Financial Statements.

AUXIER FOCUS FUND

STATEMENT OF OPERATIONS

YEAR ENDED JUNE 30, 2019

| INVESTMENT INCOME | ||||

| Dividend income (Net of foreign withholding taxes of $37,728) | $ | 4,975,676 | ||

| Interest income | 278,452 | |||

| Total Investment Income | 5,254,128 | |||

| EXPENSES | ||||

| Investment Adviser fees | 1,885,545 | |||

| Fund services fees | 317,267 | |||

| Transfer agent fees: | ||||

| Investor Shares | 57,165 | |||

| A Shares | 1,166 | |||

| Institutional Shares | 8,003 | |||

| Distribution fees: | ||||

| A Shares | 7,041 | |||

| Custodian fees | 24,445 | |||

| Registration fees: | ||||

| Investor Shares | 19,028 | |||

| A Shares | 5,533 | |||

| Institutional Shares | 16,550 | |||

| Professional fees | 67,865 | |||

| Trustees' fees and expenses | 10,412 | |||

| Other expenses | 193,410 | |||

| Total Expenses | 2,613,430 | |||

| Fees waived | (439,910 | ) | ||

| Net Expenses | 2,173,520 | |||

| NET INVESTMENT INCOME | 3,080,608 | |||

| NET REALIZED AND UNREALIZED GAIN (LOSS) | ||||

| Net realized gain (loss) on: | ||||

| Investments | 12,107,729 | |||

| Foreign currency transactions | (3 | ) | ||

| Net realized gain | 12,107,726 | |||

| Net change in unrealized appreciation (depreciation) on investments | 580,575 | |||

| NET REALIZED AND UNREALIZED GAIN | 12,688,301 | |||

| INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 15,768,909 | ||

See Notes to Financial Statements.

AUXIER FOCUS FUND

STATEMENTS OF CHANGES IN NET ASSETS

| For the Year Ended June 30, 2019 | For the Year Ended June 30, 2018 | |||||||||||||||

| OPERATIONS | Shares | Shares | ||||||||||||||

| Net investment income | $ | 3,080,608 | $ | 2,988,968 | ||||||||||||

| Net realized gain | 12,107,726 | 9,308,895 | ||||||||||||||

| Net change in unrealized appreciation (depreciation) | 580,575 | 4,800,356 | ||||||||||||||

| Increase in Net Assets Resulting from Operations | 15,768,909 | 17,098,219 | ||||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||||||||||

| Investor Shares | (9,536,436 | ) | (9,691,375 | )* | ||||||||||||

| A Shares | (161,105 | ) | (145,404 | )** | ||||||||||||

| Institutional Shares | (4,612,293 | ) | (3,576,708 | )*** | ||||||||||||

| Total Distributions Paid | (14,309,834 | ) | (13,413,487 | ) | ||||||||||||

| CAPITAL SHARE TRANSACTIONS | ||||||||||||||||

| Sale of shares: | ||||||||||||||||

| Investor Shares | 8,398,246 | 380,608 | 12,207,193 | 545,032 | ||||||||||||

| A Shares | 303,403 | 13,720 | 76,206 | 3,206 | ||||||||||||

| Institutional Shares | 22,260,504 | 973,396 | 11,795,228 | 510,411 | ||||||||||||

| Reinvestment of distributions: | ||||||||||||||||

| Investor Shares | 9,152,257 | 438,980 | 9,332,848 | 415,331 | ||||||||||||

| A Shares | 156,607 | 7,387 | 140,941 | 6,189 | ||||||||||||

| Institutional Shares | 4,441,627 | 208,820 | 3,423,369 | 149,776 | ||||||||||||

| Redemption of shares: | ||||||||||||||||

| Investor Shares | (41,202,344 | ) | (1,879,232 | ) | (48,745,464 | ) | (2,169,226 | ) | ||||||||

| A Shares | (598,448 | ) | (27,043 | ) | (283,039 | ) | (11,944 | ) | ||||||||

| Institutional Shares | (8,219,687 | ) | (357,162 | ) | (3,857,324 | ) | (168,252 | ) | ||||||||

| Redemption fees: | ||||||||||||||||

| Investor Shares | 5,173 | – | 3,662 | – | ||||||||||||

| A Shares | 93 | – | 55 | – | ||||||||||||

| Institutional Shares | 2,637 | – | 1,208 | – | ||||||||||||

| Decrease in Net Assets from Capital Share Transactions | (5,299,932 | ) | (240,526 | ) | (15,905,117 | ) | (719,477 | ) | ||||||||

| Decrease in Net Assets | (3,840,857 | ) | (12,220,385 | ) | ||||||||||||

| NET ASSETS | ||||||||||||||||

| Beginning of Year | 235,457,855 | 247,678,240 | ||||||||||||||

| End of Year | $ | 231,616,998 | $ | 235,457,855 | **** | |||||||||||

| * | Distribution was the result of net investment income and net realized gain of $1,989,916 and $7,701,459, respectively, at June 30, 2018. |

| ** | Distribution was the result of net investment income and net realized gain of $22,503 and $122,901, respectively, at June 30, 2018. |

| *** | Distribution was the result of net investment income and net realized gain of $741,116 and $2,835,592, respectively, at June 30, 2018. |

| **** | Includes undistributed net investment income of $1,556,427 at June 30, 2018. The requirement to disclose the corresponding amount was eliminated as of June 30, 2019. |

See Notes to Financial Statements.

AUXIER FOCUS FUND

FINANCIAL HIGHLIGHTS

These financial highlights reflect selected data for a share outstanding throughout each year.

| For the Years Ended June 30, | ||||||||||||||||||||

| 2019 | 2018 | 2017 | 2016 | 2015 | ||||||||||||||||

| INVESTOR SHARES | ||||||||||||||||||||

| NET ASSET VALUE, Beginning of Year | $ | 22.25 | $ | 21.95 | $ | 19.69 | $ | 20.50 | $ | 20.75 | ||||||||||

| INVESTMENT OPERATIONS | ||||||||||||||||||||

| Net investment income (a) | 0.28 | 0.26 | 0.23 | 0.21 | 0.17 | |||||||||||||||

| Net realized and unrealized gain | 1.18 | 1.28 | 2.59 | 0.08 | 0.38 | |||||||||||||||

| Total from Investment Operations | 1.46 | 1.54 | 2.82 | 0.29 | 0.55 | |||||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM | ||||||||||||||||||||

| Net investment income | (0.30 | ) | (0.25 | ) | (0.23 | ) | (0.20 | ) | (0.20 | ) | ||||||||||

| Net realized gain | (1.07 | ) | (0.99 | ) | (0.33 | ) | (0.90 | ) | (0.60 | ) | ||||||||||

| Total Distributions to Shareholders | (1.37 | ) | (1.24 | ) | (0.56 | ) | (1.10 | ) | (0.80 | ) | ||||||||||

| REDEMPTION FEES(a)(b) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |||||||||||||||

| NET ASSET VALUE, End of Year | $ | 22.34 | $ | 22.25 | $ | 21.95 | $ | 19.69 | $ | 20.50 | ||||||||||

| TOTAL RETURN | 7.08 | % | 6.97 | % | 14.55 | % | 1.58 | % | 2.69 | % | ||||||||||

| RATIOS/SUPPLEMENTARY DATA | ||||||||||||||||||||

| Net Assets at End of Year (000s omitted) | $ | 137,995 | $ | 161,032 | $ | 185,363 | $ | 203,921 | $ | 231,911 | ||||||||||

| Ratios to Average Net Assets: | ||||||||||||||||||||

| Net investment income | 1.25 | % | 1.14 | % | 1.11 | % | 1.10 | % | 0.83 | % | ||||||||||

| Net expenses | 0.98 | % | 0.98 | % | 1.03 | % | 1.14 | % | 1.24 | % | ||||||||||

| Gross expenses (c) | 1.11 | % | 1.10 | % | 1.16 | % | 1.30 | % | 1.27 | % | ||||||||||

| PORTFOLIO TURNOVER RATE | 3 | % | 3 | % | 5 | % | 6 | % | 4 | % | ||||||||||

| (a) | Calculated based on average shares outstanding during each year. |

| (b) | Less than $0.01 per share. |

| (c) | Reflects the expense ratio excluding any waivers and/or reimbursements. |

See Notes to Financial Statements.

AUXIER FOCUS FUND

FINANCIAL HIGHLIGHTS

These financial highlights reflect selected data for a share outstanding throughout each year.

| For the Years Ended June 30, | ||||||||||||||||||||

| 2019 | 2018 | 2017 | 2016 | 2015 | ||||||||||||||||

| A SHARES SHARES | ||||||||||||||||||||

| NET ASSET VALUE, Beginning of Year | $ | 22.56 | $ | 22.23 | $ | 19.90 | $ | 20.64 | $ | 20.85 | ||||||||||

| INVESTMENT OPERATIONS | ||||||||||||||||||||

| Net investment income (a) | 0.22 | 0.20 | 0.19 | 0.19 | 0.18 | |||||||||||||||

| Net realized and unrealized gain | 1.21 | 1.29 | 2.61 | 0.09 | 0.36 | |||||||||||||||

| Total from Investment Operations | 1.43 | 1.49 | 2.80 | 0.28 | 0.54 | |||||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM | ||||||||||||||||||||

| Net investment income | (0.22 | ) | (0.17 | ) | (0.14 | ) | (0.12 | ) | (0.15 | ) | ||||||||||

| Net realized gain | (1.07 | ) | (0.99 | ) | (0.33 | ) | (0.90 | ) | (0.60 | ) | ||||||||||

| Total Distributions to Shareholders | (1.29 | ) | (1.16 | ) | (0.47 | ) | (1.02 | ) | (0.75 | ) | ||||||||||

| REDEMPTION FEES(a)(b) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |||||||||||||||

| NET ASSET VALUE, End of Year | $ | 22.70 | $ | 22.56 | $ | 22.23 | $ | 19.90 | $ | 20.64 | ||||||||||

| TOTAL RETURN(c) | 6.80 | % | 6.68 | % | 14.28 | % | 1.49 | % | 2.63 | % | ||||||||||

| RATIOS/SUPPLEMENTARY DATA | ||||||||||||||||||||

| Net Assets at End of Year (000s omitted) | $ | 2,664 | $ | 2,782 | $ | 2,797 | $ | 2,698 | $ | 5,541 | ||||||||||

| Ratios to Average Net Assets: | ||||||||||||||||||||

| Net investment income | 0.98 | % | 0.87 | % | 0.91 | % | 0.94 | % | 0.84 | % | ||||||||||

| Net expenses | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | ||||||||||

| Gross expenses (d) | 1.53 | % | 1.44 | % | 1.54 | % | 1.61 | % | 1.56 | % | ||||||||||

| PORTFOLIO TURNOVER RATE | 3 | % | 3 | % | 5 | % | 6 | % | 4 | % | ||||||||||

| (a) | Calculated based on average shares outstanding during each year. |

| (b) | Less than $0.01 per share. |

| (c) | Total Return does not include the effect of front end sales charge or contingent deferred sales charge. |

| (d) | Reflects the expense ratio excluding any waivers and/or reimbursements. |

See Notes to Financial Statements.

AUXIER FOCUS FUND

FINANCIAL HIGHLIGHTS

These financial highlights reflect selected data for a share outstanding throughout each year.

| For the Years Ended June 30, | ||||||||||||||||||||

| 2019 | 2018 | 2017 | 2016 | 2015 | ||||||||||||||||

| INSTITUTIONAL SHARES | ||||||||||||||||||||

| NET ASSET VALUE, Beginning of Year | $ | 22.66 | $ | 22.29 | $ | 19.96 | $ | 20.74 | $ | 20.91 | ||||||||||

| INVESTMENT OPERATIONS | ||||||||||||||||||||

| Net investment income (a) | 0.33 | 0.31 | 0.28 | 0.25 | 0.24 | |||||||||||||||

| Net realized and unrealized gain | 1.19 | 1.30 | 2.61 | 0.08 | 0.36 | |||||||||||||||

| Total from Investment Operations | 1.52 | 1.61 | 2.89 | 0.33 | 0.60 | |||||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM | ||||||||||||||||||||

| Net investment income | (0.30 | ) | (0.25 | ) | (0.23 | ) | (0.21 | ) | (0.17 | ) | ||||||||||

| Net realized gain | (1.07 | ) | (0.99 | ) | (0.33 | ) | (0.90 | ) | (0.60 | ) | ||||||||||

| Total Distributions to Shareholders | (1.37 | ) | (1.24 | ) | (0.56 | ) | (1.11 | ) | (0.77 | ) | ||||||||||

| REDEMPTION FEES(a)(b) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |||||||||||||||

| NET ASSET VALUE, End of Year | $ | 22.81 | $ | 22.66 | $ | 22.29 | $ | 19.96 | $ | 20.74 | ||||||||||

| TOTAL RETURN | 7.24 | % | 7.20 | % | 14.72 | % | 1.74 | % | 2.93 | % | ||||||||||

| RATIOS/SUPPLEMENTARY DATA | ||||||||||||||||||||

| Net Assets at End of Year (000s omitted) | $ | 90,958 | $ | 71,644 | $ | 59,518 | $ | 42,969 | $ | 29,366 | ||||||||||

| Ratios to Average Net Assets: | ||||||||||||||||||||

| Net investment income | 1.43 | % | 1.34 | % | 1.32 | % | 1.27 | % | 1.13 | % | ||||||||||

| Net expenses | 0.80 | % | 0.80 | % | 0.86 | % | 1.00 | % | 1.00 | % | ||||||||||

| Gross expenses (c) | 1.10 | % | 1.10 | % | 1.16 | % | 1.31 | % | 1.36 | % | ||||||||||

| PORTFOLIO TURNOVER RATE | 3 | % | 3 | % | 5 | % | 6 | % | 4 | % | ||||||||||

| (a) | Calculated based on average shares outstanding during each year. |

| (b) | Less than $0.01 per share. |

| (c) | Reflects the expense ratio excluding any waivers and/or reimbursements. |

See Notes to Financial Statements.

AUXIER FOCUS FUND

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2019

Note 1. Organization

The Auxier Focus Fund (the “Fund”) is a diversified portfolio of Forum Funds (the “Trust”). The Trust is a Delaware statutory trust that is registered as an open-end, management investment company under the Investment Company Act of 1940, as amended (the “Act”). Under its Trust Instrument, the Trust is authorized to issue an unlimited number of the Fund’s shares of beneficial interest without par value.

The Fund currently offers three classes of shares: Investor Shares, A Shares and Institutional Shares. A Shares are offered at net asset value plus a maximum sales charge of 5.75%. A Shares are also subject to contingent deferred sales charge (“CDSC”) of 1.00% on purchases without an initial sales charge and redeemed less than one year after they are purchased. Investor Shares and Institutional Shares are not subject to a sales charge. Investor Shares, A Shares and Institutional Shares commenced operations on July 9, 1999, July 8, 2005 and May 9, 2012, respectively. The Fund’s investment objective is to provide long-term capital appreciation.

Note 2. Summary of Significant Accounting Policies

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, “Financial Services – Investment Companies.” These financial statements are prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”), which require management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent liabilities at the date of the financial statements, and the reported amounts of increases and decreases in net assets from operations during the fiscal year. Actual amounts could differ from those estimates. The following summarizes the significant accounting policies of the Fund:

Security Valuation – Securities are valued at market prices using the last quoted trade or official closing price from the principal exchange where the security is traded, as provided by independent pricing services on each Fund business day. In the absence of a last trade, securities are valued at the mean of the last bid and ask price provided by the pricing service. Debt securities may be valued at prices supplied by a fund’s pricing agent based on broker or dealer supplied valuations or matrix pricing, a method of valuing securities by reference to the value of other securities with similar characteristics such as rating, interest rate and maturity. Shares of non-exchange traded open-end mutual funds are valued at net asset value (“NAV”). Short-term investments that mature in sixty days or less may be valued at amortized cost.

The Fund values its investments at fair value pursuant to procedures adopted by the Trust’s Board of Trustees (the “Board”) if (1) market quotations are not readily available or (2) the Adviser, as defined in Note 4, believes that the values available are unreliable. The Trust’s Valuation Committee, as defined in the Fund’s registration statement, performs certain functions as they relate to the administration and oversight of the Fund’s valuation procedures. Under these procedures, the Valuation Committee convenes on a regular and ad hoc basis to review such investments and considers a number of factors, including valuation methodologies and significant unobservable inputs, when arriving at fair value.

The Valuation Committee may work with the Adviser to provide valuation inputs. In determining fair valuations, inputs may include market-based analytics that may consider related or comparable assets or liabilities, recent transactions, market multiples, book values and other relevant investment information. Adviser inputs may include an income-based approach in which the anticipated future cash flows of the investment are discounted in determining fair value. Discounts may also be applied based on the nature or duration of any restrictions on the disposition of the investments. The Valuation Committee performs regular reviews of valuation methodologies, key inputs and assumptions, disposition analysis and market activity.

Fair valuation is based on subjective factors and, as a result, the fair value price of an investment may differ from the security’s market price and may not be the price at which the asset may be sold. Fair valuation could result in a different NAV than a NAV determined by using market quotes.

GAAP has a three-tier fair value hierarchy. The basis of the tiers is dependent upon the various “inputs” used to determine the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

Level 1 - Quoted prices in active markets for identical assets and liabilities.

AUXIER FOCUS FUND

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2019

Level 2 - Prices determined using significant other observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.). Short-term securities with maturities of sixty days or less are valued at amortized cost, which approximates market value, and are categorized as Level 2 in the hierarchy. Municipal securities, long-term U.S. government obligations and corporate debt securities are valued in accordance with the evaluated price supplied by a pricing service and generally categorized as Level 2 in the hierarchy. Other securities that are categorized as Level 2 in the hierarchy include, but are not limited to, warrants that do not trade on an exchange, securities valued at the mean between the last reported bid and ask quotation and international equity securities valued by an independent third party with adjustments for changes in value between the time of the securities’ respective local market closes and the close of the U.S. market.

Level 3 - Significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments).

The aggregate value by input level, as of June 30, 2019, for the Fund’s investments is included at the end of the Fund’s Schedule of Investments.

Security Transactions, Investment Income and Realized Gain and Loss – Investment transactions are accounted for on the trade date. Dividend income is recorded on the ex-dividend date. Foreign dividend income is recorded on the ex-dividend date or as soon as possible after determining the existence of a dividend declaration after exercising reasonable due diligence. Income and capital gains on some foreign securities may be subject to foreign withholding taxes, which are accrued as applicable. Interest income is recorded on an accrual basis. Premium is amortized and discount is accreted using the effective interest method. Identified cost of investments sold is used to determine the gain and loss for both financial statement and federal income tax purposes.

Foreign Currency Translations – Foreign currency amounts are translated into U.S. dollars as follows: (1) assets and liabilities at the rate of exchange at the end of the respective period; and (2) purchases and sales of securities and income and expenses at the rate of exchange prevailing on the dates of such transactions. The portion of the results of operations arising from changes in the exchange rates and the portion due to fluctuations arising from changes in the market prices of securities are not isolated. Such fluctuations are included with the net realized and unrealized gain or loss on investments.

Distributions to Shareholders – The Fund declares any dividends from net investment income and pays them annually. Any net capital gains realized by the Fund are distributed at least annually. Distributions to shareholders are recorded on the ex-dividend date. Distributions are based on amounts calculated in accordance with applicable federal income tax regulations, which may differ from GAAP. These differences are due primarily to differing treatments of income and gain on various investment securities held by the Fund, timing differences and differing characterizations of distributions made by the Fund.

Federal Taxes – The Fund intends to continue to qualify each year as a regulated investment company under Subchapter M of Chapter 1, Subtitle A, of the Internal Revenue Code of 1986, as amended (“Code”), and to distribute all of its taxable income to shareholders. In addition, by distributing in each calendar year substantially all of its net investment income and capital gains, if any, the Fund will not be subject to a federal excise tax. Therefore, no federal income or excise tax provision is required. The Fund files a U.S. federal income and excise tax return as required. The Fund’s federal income tax returns are subject to examination by the Internal Revenue Service for a period of three fiscal years after they are filed. As of June 30, 2019, there are no uncertain tax positions that would require financial statement recognition, de-recognition or disclosure.

Income and Expense Allocation – The Trust accounts separately for the assets, liabilities and operations of each of its investment portfolios. Expenses that are directly attributable to more than one investment portfolio are allocated among the respective investment portfolios in an equitable manner.

The Fund's class-specific expenses are charged to the operations of that class of shares. Income and expenses (other than expenses attributable to a specific class) and realized and unrealized gains or losses on investments are allocated to each class of shares based on the class’ respective net assets to the total net assets of the Fund.

Redemption Fees – A shareholder who redeems or exchanges shares within 180 days of purchase will incur a redemption fee of 2.00% of the current NAV of shares redeemed or exchanged, subject to certain limitations. The fee is charged for the benefit of the remaining shareholders and will be paid to the Fund to help offset transaction costs. The fee is accounted for as an addition to paid-in capital. The Fund reserves the right to modify the terms of or terminate the fee at any time. There are limited exceptions to

AUXIER FOCUS FUND

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2019

the imposition of the redemption fee. Redemption fees incurred for the Fund, if any, are reflected on the Statements of Changes in Net Assets.

Commitments and Contingencies – In the normal course of business, the Fund enters into contracts that provide general indemnifications by the Fund to the counterparty to the contract. The Fund’s maximum exposure under these arrangements is dependent on future claims that may be made against the Fund and, therefore, cannot be estimated; however, based on experience, the risk of loss from such claims is considered remote. The Fund has determined that none of these arrangements requires disclosure on the Fund’s balance sheet.

Note 3. Cash – Concentration in Uninsured Account

For cash management purposes, the Fund may concentrate cash with the Fund’s custodian. This typically results in cash balances exceeding the Federal Deposit Insurance Corporation (“FDIC”) insurance limits. As of June 30, 2019, the Fund had $3,343,798 at MUFG Union Bank, N.A. that exceeded the FDIC insurance limit.

Note 4. Fees and Expenses

Investment Adviser – Auxier Asset Management LLC (the “Adviser”) is the investment Adviser to the Fund. Pursuant to an investment advisory agreement, the Adviser receives an advisory fee, payable monthly, from the Fund at an annual rate of 0.80% of the Fund’s average daily net assets.

Distribution – Foreside Fund Services, LLC serves as the Fund’s distributor (the “Distributor”). The Distributor is not affiliated with the Adviser or Atlantic Fund Administration, LLC, a wholly owned subsidiary of Apex US Holdings, LLC (d/b/a Apex Fund Services) (“Apex”) or their affiliates. The Fund has adopted a Distribution Plan (the “Plan”) for A Shares of the Fund in accordance with Rule 12b-1 of the Act. Under the Plan, the Fund pays the Distributor and/or any other entity as authorized by the Board a fee of up to 0.25% of the average daily net assets of A Shares. The Distributor has no role in determining the investment policies or which securities are to be purchased or sold by the Trust or its Funds.

For the year ended June 30, 2019, there were $11,242 front-end sales charges assessed on the sale of A Shares and no contingent deferred sales charges were assessed on the sale of A Shares. The Distributor received $1,711 of the total front-end sales charges.

Other Service Providers – Apex provides fund accounting, fund administration, compliance and transfer agency services to the Fund. The fees related to these services are included in Fund services fees within the Statement of Operations. Apex also provides certain shareholder report production and EDGAR conversion and filing services. Apex provides a Principal Executive Officer, a Principal Financial Officer, a Chief Compliance Officer and an Anti-Money Laundering Officer to the Fund, as well as certain additional compliance support functions.

Trustees and Officers – Each Independent Trustee’s annual retainer is $31,000 ($41,000 for the Chairman), and the Audit Committee Chairman receives an additional $2,000 annually. The Trustees and Chairman may receive additional fees for special Board meetings. Each Trustee is also reimbursed for all reasonable out-of-pocket expenses incurred in connection with his or her duties as a Trustee, including travel and related expenses incurred in attending Board meetings. The amount of Trustees’ fees attributable to the Fund is disclosed in the Statement of Operations. Certain officers of the Trust are also officers or employees of the above named service providers, and during their terms of office received no compensation from the Fund.

Note 5. Expense Reimbursement and Fees Waived

The Adviser has contractually agreed to waive its fee and/or reimburse Fund expenses to limit Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement (excluding all taxes, interest, portfolio transaction expenses, dividend expenses on short sales, and extraordinary expenses) to 0.98%, 1.25% and 0.80% of the Investor Shares, A Shares and Institutional Shares, respectively, through at least October 31, 2019. These contractual waivers may only be raised or eliminated with consent of the Board. Other fund service providers have voluntarily agreed to waive a portion of their fees. These voluntary reductions may be reduced or eliminated at any time. For the year ended June 30, 2019, the fees waived and expenses reimbursed were as follows:

AUXIER FOCUS FUND

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2019

| Investment Adviser Fees Waived | Investment Adviser Expenses Reimbursed | Other Waivers | Total Fees Waived and Expenses Reimbursed | |||||||||||

| $ | 207,601 | $ | 144,024 | $ | 88,285 | $ | 439,910 | |||||||

The Adviser may be reimbursed by the Fund for fees waived and expenses reimbursed by the Adviser pursuant to the Expense Cap if such payment is made within three years of the fee waiver or expense reimbursement, and does not cause the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement to exceed the lesser of (i) the then-current expense cap, or (ii) the expense cap in place at the time the fees/expenses were waived/reimbursed. As of June 30, 2019, $1,032,795 is subject to recapture by the Adviser. Other Waivers are not eligible for recoupment.

Note 6. Security Transactions

The cost of purchases and proceeds from sales of investment securities (including maturities), other than short-term investments, during the year ended June 30, 2019, totaled $6,574,028 and $24,083,059.

Note 7. Federal Income Tax

As of June 30, 2019, cost for federal income tax purposes is $125,632,409 and net unrealized appreciation consists of:

| Gross Unrealized Appreciation | $ | 111,540,690 | ||

| Gross Unrealized Depreciation | (7,860,712 | ) | ||

| Net Unrealized Appreciation | $ | 103,679,978 |

Distributions paid during the fiscal years ended as noted were characterized for tax purposes as follows:

| 2019 | 2018 | |||||||

| Ordinary Income | $ | 3,201,085 | $ | 2,986,907 | ||||

| Long-Term Capital Gain | 11,108,749 | 10,426,580 | ||||||

| $ | 14,309,834 | $ | 13,413,487 | |||||

As of June 30, 2019, distributable earnings (accumulated loss) on a tax basis were as follows:

| Undistributed Ordinary Income | $ | 1,458,951 | ||

| Undistributed Long-Term Gain | 9,371,451 | |||

| Unrealized Appreciation | 103,679,978 | |||

| Total | $ | 114,510,380 |

The difference between components of distributable earnings on a tax basis and the amounts reflected in the Statement of Assets and Liabilities are primarily due to wash sales and equity return of capital.

Note 8. Recent Accounting Pronouncements

In August 2018, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update No. 2018-13 “Fair Value Measurement (Topic 820): Disclosure Framework – Changes to the Disclosure Requirements for Fair Value Measurement” (“ASU 2018-13”) which includes amendments intended to improve the effectiveness of disclosures in the notes to financial statements. For example, ASU 2018-13 includes additional disclosures regarding the range and weighted average of significant unobservable inputs used to develop Level 3 fair value measurements, and clarifications to the narrative description of measurement uncertainty disclosures. ASU 2018-13 is effective for interim and annual periods beginning after December 15, 2019. Early adoption is permitted and the Fund has adopted ASU 2018-13 within these financial statements.

In September 2018, the Securities and Exchange Commission released Final Rule 33-10532 captioned “Disclosure Update and Simplification,” which includes: (i) an amendment to require presentation of the total, rather than the components, of distributable earnings on the Statement of Assets and Liabilities; and (ii) an amendment to require presentation of the total, rather than the components, of distributions to shareholders, except for tax return of capital distributions, on the Statements of Changes in Net Assets. The amendments also removed the requirement for parenthetical disclosure of undistributed net investment income on the

AUXIER FOCUS FUND

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2019

Statements of Changes in Net Assets. These changes were effective November 5, 2018. These amendments are reflected in the Fund's financial statements for the year ended June 30, 2019.

Note 9. Subsequent Events

Subsequent events occurring after the date of this report through the date these financial statements were issued have been evaluated for potential impact, and the Fund has had no such events.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees of Forum Funds

and the Shareholders of Auxier Focus Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Auxier Focus Fund, a series of shares of beneficial interest in Forum Funds (the “Fund”), including the schedule of investments, as of June 30, 2019, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the five-year period then ended, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of June 30, 2019, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and its financial highlights for each of the years in the five-year period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities law and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risk of material misstatement of those financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of June 30, 2019 by correspondence with the custodian and brokers, or by other appropriate auditing procedures where replies from brokers were not received. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

BBD, LLP

Philadelphia, Pennsylvania

August 26, 2019

AUXIER FOCUS FUND

ADDITIONAL INFORMATION (Unaudited)

JUNE 30, 2019

Proxy Voting Information

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to securities held in the Fund’s portfolio is available, without charge and upon request, by calling (877) 328-9437 and on the SEC’s website at www.sec.gov. The Fund’s proxy voting record for the most recent twelve-month period ended June 30 is available, without charge and upon request, by calling (877) 328-9437 and on the SEC’s website at www.sec.gov.

Availability of Quarterly Portfolio Schedules

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. These filings are available, without charge and upon request on the SEC’s website at www.sec.gov or may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330.

Shareholder Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments on certain classes, redemption fees, exchange fees and CDSC fees, and (2) ongoing costs, including management fees, 12b-1 fees, and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund, and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2019 through June 30, 2019.

Actual Expenses – The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes – The second line under each share class of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) on purchase payments on certain classes, redemption fees, exchange fees, and CDSC fees. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value January 1, 2019 | Ending Account Value June 30, 2019 | Expenses Paid During Period* | Annualized Expense Ratio* | |||||||||||||

| Investor Shares | ||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,112.55 | $ | 5.13 | 0.98 | % | ||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,019.93 | $ | 4.91 | 0.98 | % | ||||||||

| A Shares | ||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,111.12 | $ | 6.54 | 1.25 | % | ||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,018.60 | $ | 6.26 | 1.25 | % | ||||||||

AUXIER FOCUS FUND

ADDITIONAL INFORMATION (Unaudited)

JUNE 30, 2019

| Beginning Account Value January 1, 2019 | Ending Account Value June 30, 2019 | Expenses Paid During Period* | Annualized Expense Ratio* | |||||||||||||

| Institutional Shares | ||||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,113.22 | $ | 4.19 | 0.80 | % | ||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,020.83 | $ | 4.01 | 0.80 | % | ||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (181) divided by 365 to reflect the half-year period. |

Federal Tax Status of Dividends Declared during the Fiscal Year