Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| ¨ | Registration Statement pursuant to Section 12(b) or (g) of the Securities Exchange Act of 1934. |

| x | Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. |

for the fiscal year ended December 31, 2005

| ¨ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. |

| ¨ | Shell company report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. |

Date of event requiring this shell company report

for the transition period from to

Commission File Number: 0-13355

ASM INTERNATIONAL N.V.

(Exact name of Registrant as specified in its charter)

The Netherlands

(jurisdiction of incorporation or organization)

Jan van Eycklaan 10, 3723 BC Bilthoven, the Netherlands

(Address of principal executive offices)

Securities registered or to be registered pursuant to

Section 12(b) of the Act: None

Securities registered or to be registered pursuant to

Section 12(g) of the Act: Common Shares, par value€ 0.04

Securities for which there is a reporting obligation pursuant to

Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 52,678,952 common shares; no preferred shares.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

If this annual report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨

Indicate by check mark which financial statement item the registrant has elected to follow:

| Item 17 ¨ Item 18 x |

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes ¨ No x

Table of Contents

EX-8.1

EX-12.1

EX-12.2

EX-13.1

EX-15.1

Table of Contents

As used in this report, the terms “we,” “us,” “our,” “ASMI,” and “ASM International” mean ASM International N.V. and its subsidiaries, unless the context indicates another meaning, and the term “common shares” means our common shares, par value€ 0.04 per share. Since we are a Netherlands company, the par value of our common shares is expressed in euros (“€”). The terms “United States” and “U.S.” refer to the United States of America.

Item 1.Identity of Directors, Senior Management and Advisors

Not applicable.

Item 2.Offer Statistics and Expected Timetable

Not applicable.

A. Selected consolidated financial data.

You should read the following selected financial data in conjunction with Item 5 “Operating and Financial Review and Prospects” and Item 18 “Financial Statements.” The selected consolidated financial data presented below as of and for the years ended December 31, 2004 and 2005 have been derived from our audited Consolidated Financial Statements included in Item 18. The selected consolidated financial data presented below as of and for the years ended December 31, 2001, 2002 and 2003 have been derived from our audited Consolidated Financial Statements which are not included in this report.

| 2001 | 20021 | 20031 | 2004 | 2005 | ||||||||||||||||

| (€ in thousands, except per share data) | ||||||||||||||||||||

Consolidated Statements of Operations Data: | ||||||||||||||||||||

Net sales | € | 561,064 | € | 518,802 | € | 581,868 | € | 754,245 | € | 726,418 | ||||||||||

Cost of sales | (337,743 | ) | (328,077 | ) | (380,597 | ) | (472,501 | ) | (473,411 | ) | ||||||||||

Gross profit | 223,321 | 190,725 | 201,271 | 281,744 | 253,007 | |||||||||||||||

Operating expenses: | ||||||||||||||||||||

Selling, general and administrative | (111,851 | ) | (108,393 | ) | (108,019 | ) | (107,040 | ) | (101,185 | ) | ||||||||||

Research and development, net | (79,661 | ) | (88,334 | ) | (79,053 | ) | (84,874 | ) | (100,668 | ) | ||||||||||

Amortization of goodwill | (7,558 | ) | — | — | — | — | ||||||||||||||

Amortization of purchased technology and other intangible assets | — | — | — | (1,389 | ) | (1,748 | ) | |||||||||||||

Impairment of goodwill | — | — | — | — | (30,994 | ) | ||||||||||||||

Total operating expenses | (199,070 | ) | (196,727 | ) | (187,072 | ) | (193,303 | ) | (234,595 | ) | ||||||||||

Earnings (loss) from operations | 24,251 | (6,002 | ) | 14,199 | 88,441 | 18,412 | ||||||||||||||

Loss on equity investments | — | (2,372 | ) | (2,770 | ) | (417 | ) | — | ||||||||||||

Interest income | 3,690 | 1,336 | 1,393 | 2,223 | 5,746 | |||||||||||||||

Interest expense | (5,031 | ) | (9,627 | ) | (11,692 | ) | (12,570 | ) | (16,163 | ) | ||||||||||

Foreign currency transaction gains (losses) | 357 | (2,125 | ) | (2,479 | ) | (111 | ) | (128 | ) | |||||||||||

Income tax benefit (expense) | (4,711 | ) | 1,165 | (7,112 | ) | (10,575 | ) | (7,307 | ) | |||||||||||

Minority interest | (13,373 | ) | (15,890 | ) | (24,570 | ) | (45,608 | ) | (43,558 | ) | ||||||||||

Gain on dilution of investment in subsidiary | 915 | 1,281 | 941 | 2,656 | 2,781 | |||||||||||||||

Net earnings (loss) | € | 6,098 | € | (32,234 | ) | € | (32,090 | ) | € | 24,039 | € | (40,217 | ) | |||||||

Basic net earnings (loss) per share from operations | € | 0.50 | € | (0.12 | ) | € | 0.29 | € | 1.72 | € | 0.35 | |||||||||

Diluted net earnings (loss) per share from operations | € | 0.49 | € | (0.12 | ) | € | 0.29 | € | 1.71 | € | 0.35 | |||||||||

Basic net earnings (loss) per share: | € | 0.12 | € | (0.66 | ) | € | (0.65 | ) | € | 0.47 | € | (0,76 | ) | |||||||

Diluted net earnings (loss) per share: | € | 0.12 | € | (0.66 | ) | € | (0.65 | ) | € | 0.46 | € | (0,76 | ) | |||||||

Basic weighted average number of shares | 48,944 | 49,170 | 49,642 | 51,540 | 52,638 | |||||||||||||||

Diluted weighted average number of shares | 49,958 | 49,170 | 49,642 | 51,858 | 52,638 | |||||||||||||||

| 2001 | 20021 | 20031 | 2004 | 2005 | ||||||||||||||||

Ratios and other data: | ||||||||||||||||||||

Ratio of earnings to fixed charges 2 | 5.6x | —3 | —3 | 7.8x | 1.5x | |||||||||||||||

Number of common shares outstanding (in thousands) | 49,070 | 49,370 | 50,062 | 52,618 | 52,679 | |||||||||||||||

Dividends declared | — | — | — | — | — | |||||||||||||||

3

Table of Contents

| December 31, | |||||||||||||||

| 2001 | 20021 | 20031 | 2004 | 2005 | |||||||||||

| (€ in thousands) | |||||||||||||||

Consolidated Balance Sheet Data: | |||||||||||||||

Cash and cash equivalents | € | 107,577 | € | 70,991 | € | 154,857 | € | 218,614 | € | 134,996 | |||||

Total assets | 757,065 | 648,695 | 661,978 | 823,834 | 812,308 | ||||||||||

Total debt | 160,858 | 147,057 | 207,623 | 297,253 | 257,400 | ||||||||||

Total shareholders’ equity | 320,910 | 260,396 | 204,609 | 256,716 | 238,594 | ||||||||||

| (1) | As previously reflected in the December 31, 2004 Consolidated Financial Statements, we retroactively amended our Consolidated Financial Statements, as required under US GAAP, to account for NuTool, Inc. (“NuTool”) using the equity method of accounting as a result of our acquisition of the remaining interest in NuTool on June 2, 2004. |

| (2) | The ratio of earnings to fixed charges is computed by dividing: |

| • | earnings (loss) before income taxes and minority interest plus fixed charges; by |

| • | fixed charges. |

Fixed charges consist of interest expense, not including interest expense related to operational leases. Also not included in fixed charges are the losses for the early extinguishment of convertible subordinated notes of€ 1.2 million and€ 0.3 million which have been recorded as interest expense in the Consolidated Statements of Operations for the years 2004 and 2005 respectively.

| (3) | Earnings, as calculated for purposes of the ratios, were not sufficient to cover fixed charges. The coverage deficiency was€ 18.8 million for the year 2002 and€ 1.3 million for the year 2003. |

4

Table of Contents

Exchange Rate Information

The following table sets forth, for each period indicated, specified information regarding the United States dollar per euro exchange rates based on the noon buying rate in New York City for cable transfers payable in euros as certified for customs purposes by the Federal Reserve Bank of New York, which is often referred to as the “noon buying rate.” On March 10 , 2006, the noon buying rate was 1.1886 United States dollars per euro.

U.S. Dollar per Euro Exchange Rate

| September 2005 | October 2005 | November 2005 | December 2005 | January 2006 | February 2006 | March 2006 1 | ||||||||

High | 1.2538 | 1.2148 | 1.2067 | 1.2041 | 1.2287 | 1.2100 | 1.2028 | |||||||

Low | 1.2011 | 1.1914 | 1.1667 | 1.1699 | 1.1980 | 1.1860 | 1.1886 |

| Years Ended December 31, | ||||||||||

| 2001 | 2002 | 2003 | 2004 | 2005 | ||||||

Average exchange rate 2 | 0.8909 | 0.9453 | 1.1411 | 1.2464 | 1.2400 | |||||

| (1) | Through March 10, 2006. |

| (2) | Average of the exchange rate on the last day of each month during the period presented. |

B. Capitalization and indebtedness.

Not applicable.

C. Reasons for the offer and use of proceeds.

Not applicable.

D. Risk factors.

Some of the information in this report constitutes forward-looking statements within the meaning of the United States federal securities laws, including the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These statements include, among others, statements regarding future expenditures, sufficiency of cash generated from operations, maintenance of majority interest in ASM Pacific Technology Ltd. (“ASM Pacific Technology” or “ASMPT”), business strategy, product development, product acceptance, market penetration, market demand, return on investment in new products, product shipment dates and outlooks. These statements may be found under Item 5 “Operating and Financial Review and Prospects,” and elsewhere in this report. Forward-looking statements typically are identified by use of terms such as “may,” “will,” “could,” “should,” “project,” “believe,” “anticipate,” “expect,” “plan,” “estimate,” “forecast,” “potential,” “intend,” “continue” and similar words, although some forward-looking statements are expressed differently. You should be aware that these statements involve risks and uncertainties and our actual results could differ materially from those contained in the forward-looking statements due to a number of factors, including the matters discussed in Item 4 “Information on the Company” and the following discussion of risks. The risks described are not the only ones facing ASMI. Some risks are not yet known and some that we do not currently believe to be material could later become material. Each of these risks could materially affect our business, revenues, income, assets and liquidity and capital resources. All statements are made as of the date of this report and we assume no obligation nor intend to update or revise any forward-looking statements to reflect future developments or circumstances.

RISKS RELATED TO OUR INDUSTRY

Our business could be adversely affected by the cyclical nature of the semiconductor industry.

We sell our products to the semiconductor industry, which is subject to sudden, extreme, cyclical variations in product supply and demand. The timing, length and severity of these cycles are difficult to predict. In the period 2001—2003, the semiconductor industry experienced a cyclical downturn characterized by reduced demand for products, lower average selling prices, reduced investment in semiconductor capital equipment and other factors all of which resulted in lower sales and earnings for our business. This downturn lasted longer than past cycles and, although conditions in the semiconductor equipment market improved, the market remains volatile and hard to predict. Semiconductor manufacturers may contribute to the severity of these cycles by misinterpreting the conditions in the industry and over-investing or under-investing in semiconductor manufacturing capacity and equipment. In any event, the lag

5

Table of Contents

between changes in demand for semiconductor devices and changes in demand for our products by semiconductor manufacturers accentuates the intensity of these cycles in both expansion and contraction phases. We may not be able to respond effectively to these industry cycles.

Downturns in the semiconductor industry often occur in connection with, or anticipation of, maturing product cycles and declines in general economic conditions. Industry downturns have been characterized by reduced demand for semiconductor devices and equipment, production over-capacity and a decline in average selling prices. During a period of declining demand, we must be able to quickly and effectively reduce expenses and motivate and retain key employees. Our ability to reduce expenses in response to any downturn in the semiconductor industry is limited by our need for continued investment in engineering and research and development and extensive ongoing customer service and support requirements. In addition, the long lead time for production and delivery of some of our products creates a risk that we may incur expenditures or purchase inventories for products that we cannot sell. During periods of extended downturn, a portion of our inventory may have to be written down if it is not sold in a timely manner.

Industry upturns have been characterized by fairly abrupt increases in demand for semiconductor devices and equipment and insufficient production capacity. During a period of increasing demand and rapid growth, we must be able to quickly increase manufacturing capacity to meet customer demand and hire and assimilate a sufficient number of additional qualified personnel. Our inability to quickly respond in times of increased demand could harm our reputation and cause some of our existing or potential customers to place orders with our competitors rather than us.

Our industry is subject to rapid technological change and we may not be able to forecast or respond to commercial and technological trends in time to avoid competitive harm.

Our growth strategy and future success depend upon commercial acceptance of products incorporating technologies we are developing, such as plasma enhanced atomic layer deposition processes, rapid thermal processing, low-k dielectrics, copper deposition and silicon or silicon-germanium epitaxy. The semiconductor industry and the semiconductor equipment industry are subject to rapid technological change and frequent introductions of enhancements to existing products as well as significant write-downs and impairment charges and costs that can result from such changes. Technological changes have had and will continue to have a significant impact on our business. Our operating results and our ability to remain competitive are affected by our ability to accurately anticipate customer and market requirements and develop technologies and products to meet these requirements. Our success in developing, introducing and selling new and enhanced products depends upon a variety of factors, including, without limitation:

| • | successful innovation of processes and equipment; |

| • | accurate technology and product selection; |

| • | timely and efficient completion of product design, development and qualification; |

| • | timely and efficient implementation of manufacturing and assembly processes; |

| • | successful product performance in the field; |

| • | effective and timely product support and service; and |

| • | effective product sales and marketing. |

We may not be able to accurately forecast or respond to commercial and technical trends in the semiconductor industry or to the development of new technologies and products by our competitors. Our competitors may develop technologies and products that are more effective than ours or that may be more widely accepted. In addition, we may incur substantial unanticipated costs to ensure the functionality and reliability of our current and future products. If our products are unreliable or do not meet our customers’ expectations, then we may experience reduced orders, higher manufacturing costs, delays in collecting accounts receivable, and/or additional service and warranty expense. We have experienced delays from time to time in the introduction of, and some technical and manufacturing difficulties with, some of our systems and enhancements. We may also experience delays and technical and manufacturing difficulties in future introductions or volume production of new systems or enhancements. Significant delays can occur between a product’s introduction and the commencement of volume production of that product. Any of these events could negatively impact our ability to generate the return we intend to achieve on our investments in new products.

If we fail to adequately invest in research and development, we may be unable to compete effectively.

We have limited resources to allocate to research and development, and must allocate our resources among a wide variety of projects in our front-end and back-end businesses. In 2005, we invested€ 100.7 million in research and development, or 13.9% of our net sales. Because of intense competition in our industry, the cost of failing to invest in strategic developments is high. In order to enhance the benefits

6

Table of Contents

obtained from our research and development expenditures, we have contractual and other relationships with independent research institutes. If we fail to adequately invest in research and development or lose our ability to collaborate with these independent research entities, we may be unable to compete effectively in the front-end and back-end markets in which we operate.

We face intense competition from companies which have greater resources than we do, and potential competition from new companies entering the market in which we compete. If we are unable to compete effectively with these companies, our market share may decline and our business could be harmed.

We face intense competition in both the front-end and back-end segments of the semiconductor equipment industry from other established companies. Our primary competitors in the front-end business include Applied Materials, Novellus Systems, Tokyo Electron, Kokusai, and Aviza. Our primary competitors in the back-end business include Kulicke & Soffa, ESEC, Shinkawa, Apic Yamada, BE Semiconductor Industries, Towa, Shinko and Mitsui. A number of our competitors have significantly greater financial, technological, engineering, manufacturing, marketing and distribution resources than we do. Their greater capabilities in these areas may enable them to:

| • | better withstand periodic downturns in the semiconductor industry; |

| • | compete more effectively on the basis of price, technology, service and support; |

| • | more quickly develop enhancements to, and new generations of products; and |

| • | more effectively retain existing customers and attract new customers. |

In addition, new companies may enter the markets in which we compete, further increasing competition in the semiconductor equipment industry.

We believe that our ability to compete successfully depends on a number of factors, including, without limitation:

| • | our success in developing new products and enhancements; |

| • | performance of our products; |

| • | quality of our products; |

| • | ease of use of our products; |

| • | reliability of our products; |

| • | cost of ownership of our products; |

| • | our ability to ship products in a timely manner; |

| • | quality of the technical service we provide; |

| • | timeliness of the services we provide; |

| • | responses to changing market and economic conditions; and |

| • | price of our products and our competitors’ products. |

Some of these factors are outside our control. We may not be able to compete successfully in the future, and increased competition may result in price reductions, reduced profit margins, loss of market share, and inability to generate cash flows that are sufficient to maintain or expand our development of new products.

RISKS RELATED TO OUR BUSINESS

Our quarterly revenues and operating results fluctuate due to a variety of factors, which may result in volatility or a decrease in the price of our common shares.

Our quarterly revenues and operating results have varied significantly in the past and may vary in the future due to a number of factors, including, without limitation:

| • | cyclicality and other economic conditions in the semiconductor industry; |

| • | production capacity constraints; |

| • | the timing of customer orders, cancellations and shipments; |

| • | the length and variability of the sales cycle for our products; |

7

Table of Contents

| • | the introduction of new products and enhancements by us and our competitors; |

| • | the emergence of new industry standards; |

| • | product obsolescence; |

| • | disruptions in sources of supply; |

| • | our ability to time our expenditures in anticipation of future orders; |

| • | our ability to fund our capital requirements; |

| • | changes in our pricing and pricing by our suppliers and competitors; |

| • | our product and revenue mix; |

| • | seasonal fluctuations in demand for our products; |

| • | exchange rate fluctuations; e.g. appreciation of the euro versus the U.S. dollar, which would negatively affect the competitiveness of our manufacturing activities that are domiciled in countries whose currency is the euro; and |

| • | economic conditions generally or in various geographic areas where we or our customers do business. |

In addition, we derive a substantial portion of our net sales from products that have a high average selling price and significant lead times between the initial order and delivery of the product. The timing and recognition of net sales from customer orders can cause significant fluctuations in our operating results from quarter to quarter. Gross margins realized on product sales vary depending upon a variety of factors, including the mix of products sold during a particular period, negotiated selling prices, the timing of new product introductions and enhancements and manufacturing costs. A delay in a shipment near the end of a fiscal quarter or year, due, for example, to rescheduling or cancellations by customers or to unexpected manufacturing difficulties experienced by us, may cause sales in a particular period to fall significantly below our expectations and may materially adversely affect our operating results for that period. Further, our need to continue expenditures for research and development and engineering make it difficult for us to reduce expenses in a particular quarter even if our sales goals for that quarter are not met. Our inability to adjust spending quickly enough to compensate for any sales shortfall would magnify the adverse impact of a sales shortfall on our operating results. In addition, announcements by us or our competitors of new products and technologies could cause customers to defer purchases of our existing systems, which could negatively impact our earnings and our financial position.

As a result of these factors, our operating results may vary significantly from quarter to quarter. Any shortfall in revenues or net income from levels expected by securities analysts and investors could cause a decrease in the trading price of our common shares.

Our products generally have long sales cycles and implementation periods, which increase our costs in obtaining orders and reduce the predictability of our earnings.

Our products are technologically complex. Prospective customers generally must commit significant resources to test and evaluate our products and to install and integrate them into larger systems. In addition, customers often require a significant number of product presentations and demonstrations, in some instances evaluating equipment on site, before reaching a sufficient level of confidence in the product’s performance and compatibility with the customer’s requirements to place an order. As a result, our sales process is often subject to delays associated with lengthy approval processes that typically accompany the design and testing of new products. The sales cycles of our products often last for many months or even years. Longer sales cycles require us to invest significant resources in attempting to make sales and delay the generation of revenue.

Long sales cycles also subject us to other risks, including customer’s budgetary constraints, internal acceptance reviews and cancellations. In addition, orders expected in one quarter could shift to another because of the timing of customer’s purchase decisions. The time required for our customers to incorporate our products into their systems can vary significantly with the needs of our customers and generally exceeds several months, which further complicates our planning processes and reduces the predictability of our operating results.

Our recent acquisitions and any acquisitions or investments we may make in the future could disrupt our business and harm our financial condition.

In June 2004 we acquired the remaining 84.3% interest in NuTool, Inc. (“NuTool”) that we did not already own and in August 2004 we acquired Genitech, Inc. (“Genitech”). For additional information regarding this matter, see Notes 2 and 9 to our Consolidated Financial Statements. In addition, we intend to

8

Table of Contents

consider additional investments in complementary businesses, products or technologies. We may not be able to successfully integrate these businesses and any businesses, products, technologies or personnel that we might acquire in the future, and we may not realize the anticipated benefits from such acquisitions. In particular, our operation of acquired businesses involves numerous risks, including, without limitation:

| • | problems integrating the purchased operations, technologies or products; |

| • | unanticipated costs and liabilities for which we are not able to obtain indemnification from the sellers; |

| • | diversion of management’s attention from our core business; |

| • | adverse effects on existing business relationships with customers; |

| • | risks associated with entering markets in which we have no, or limited, prior experience; |

| • | risks associated with installation, service and maintenance of equipment of which we have limited or no prior experience; |

| • | limited technical documentation of the equipment developed in the acquired company; and |

| • | potential loss of key employees, particularly those of the acquired organizations. |

In addition, in the event of any future acquisitions of such businesses, products or technologies, we could:

| • | issue shares that would dilute our current shareholders’ percentage ownership; |

| • | incur debt; |

| • | assume liabilities; |

| • | incur impairment expenses related to goodwill and other intangible assets; or |

| • | incur large and immediate accounting write-offs. |

Substantially all of our equipment orders are subject to operating, performance, safety, economic specifications and other contractual obligations. We occasionally experience unforeseen difficulties in compliance with these criteria, which can result in increased design, installation and other costs and expenses.

Substantially all of our equipment sales have specific commercial terms and are conditioned on our demonstration, and our customer’s acceptance, that the equipment meets specified operating and performance criteria, either before shipment or after installation in a customer’s facility. We occasionally experience difficulties in adhering to and demonstrating compliance with these terms and criteria, which can lead to unanticipated expenses for the performance of the contract or the redesign, modification and testing of the equipment and related software. To the extent this occurs in the future, our cost of goods sold and operating income will be adversely affected. If we are not able to demonstrate compliance with the particular contract or the performance and operating specifications in respect of specific equipment, we may have to pay penalties to the customer, issue credit notes to the customer and/or take other remedial action, including payment of damages, any one of which could negatively affect our operating income.

We derive a significant percentage of our revenue from sales to a small number of large customers, and if we are not able to retain these customers, or they reschedule, reduce or cancel orders, our revenues would be reduced and our financial results would suffer.

Our largest customers account for a significant percentage of our revenues. Our largest customer accounted for 17.2% and our ten largest customers accounted for 43.7% of our net sales in 2005. Sales to and the relative importance of these large customers have varied significantly from year to year and will continue to fluctuate in the future. These sales also may fluctuate significantly from quarter to quarter. We may not be able to retain our key customers or they may cancel purchase orders or reschedule or decrease their level of purchases from us, which would reduce our revenues and negatively affect our financial results. In addition, any difficulty in collecting amounts due from one or more key customers could harm our financial results.

We may need additional funds to finance our future growth and ongoing research and development activities. If we are unable to obtain such funds, we may not be able to expand our business as planned.

In the past, we have experienced severe capital constraints that adversely affected our operations and ability to compete. We may require additional capital to finance our future growth and fund our ongoing research and development activities beyond 2006. Our capital requirements depend on many factors, including acceptance of and demand for our products, and the extent to which we invest in new technology and research and development projects.

9

Table of Contents

If we raise additional funds through the issuance of equity securities, the percentage ownership of our existing shareholders would be diluted. If we finance our capital requirements with debt, we may incur significant interest costs. Additional financing may not be available to us when needed or, if available, may not be available on terms acceptable to us.

If we are unable to raise needed additional funds, we may have to reduce the amount we spend on research and development, slow down our introduction of new products, reduce capital expenditures necessary to support future growth and/or take other measures to reduce expenses which could limit our growth and ability to compete.

We could be harmed by the loss of key management.

The success of our operations depends in significant part upon the experience of our management team, particularly our founder and CEO. We do not have employment agreements with some members of our management team and we do not maintain “key man” life insurance policies. The loss of services from our key executives and the transition process with new management could harm or cause difficulties in our business, prospects, financial condition and results of operations.

We may not be able to recruit or retain qualified personnel or integrate qualified personnel into our organization. Consequently, we could experience reduced sales, delayed product development and diversion of management resources.

Our business and future operating results depend in part upon our ability to attract and retain qualified management, technical, sales and support personnel for our operations on a worldwide basis. Competition for qualified personnel is intense, and we cannot guarantee that we will be able to continue to attract and retain qualified personnel particularly during sustained economic upturns in the industry. Availability of qualified technical personnel varies from country to country, and may affect the operations of our subsidiaries in some parts of the world. Our operations could be negatively affected if we lose key executives or employees or are unable to attract and retain skilled executives and employees as needed. In particular, if our growth strategies are successful, we may not have sufficient personnel to manage that growth and may not be able to attract the personnel needed. Although we have agreements with some, but not all, employees restricting their ability to compete with us after their employment terminates, we do not maintain insurance to protect against the loss of key executives or employees. Our future growth and operating results will depend on:

| • | our ability to continue to broaden our senior management group; |

| • | our ability to attract, hire and retain skilled employees; and |

| • | the ability of our officers and key employees to continue to expand, train and manage our employee base. |

We have in the past experienced intense competition for skilled personnel during market expansions and believe competition will again be intense if the semiconductor market experiences a sustained expansion. Consequently, we generally attempt to minimize reductions in skilled personnel in reaction to industry downturns, which reduces our ability to lower costs by payroll reduction.

Although we currently are a majority shareholder of ASM Pacific Technology, we may not be able to maintain our majority interest, which, if other circumstances are such that we do not control ASM Pacific Technology, would prevent us from consolidating its results of operations with ours. This event would have a significant negative effect on our consolidated net earnings from operations.

We derive a significant portion of our net sales, earnings from operations and net earnings from the consolidation of the results of operations of ASM Pacific Technology with our results. If we do not maintain our majority interest in ASM Pacific Technology, and if other circumstances are such that we do not control it through other means, we would no longer be able to consolidate its results of operations with ours. Any such determination of whether we could continue to consolidate would be based on whether we still have a “controlling financial interest” within the meaning of United States generally accepted accounting principles. If we were to become unable to consolidate the results of operations of ASM Pacific Technology with our results, the results of operations of ASM Pacific Technology would no longer be included in our earnings from operations. Instead, our proportionate share of ASM Pacific Technology’s earnings would be reflected as a separate line-item called “share of results from investments” in our Consolidated Statements of Operations. We would no longer be able to consolidate the assets and liabilities of ASM Pacific Technology and would have to reflect the net investment in ASM Pacific Technology in the line-item “investments” in our Consolidated Balance Sheet. This event would have a significant negative effect on our consolidated earnings from operations, although our net earnings would be reduced only to the extent of the reduction of our ownership interest in ASM Pacific Technology.

10

Table of Contents

ASM Pacific Technology has an employee share incentive program pursuant to which it can issue up to an aggregate of 5.0% of its total issued shares, excluding shares subscribed for or purchased under the program, to directors and employees. When ASM Pacific Technology issues shares pursuant to this program, our ownership interest is diluted. If the current maximum amount of shares is issued under this program, our ownership interest would continue to be above 50.0%. However, our interest could further be diluted if ASM Pacific Technology issues additional equity. Any such decision by ASM Pacific Technology to issue additional shares requires the approval of a majority of shareholders, which means that, at present, our approval would be required. Although we could purchase shares of ASM Pacific Technology if necessary to maintain our majority interest, we may be unable to do so if we do not have sufficient financial resources at that time.

Although we are a majority shareholder, ASM Pacific Technology is not obligated to pay dividends to us and may take actions or enter into transactions that are detrimental to us.

ASM Pacific Technology is a Cayman Islands limited liability company that is based in Hong Kong and listed on the Hong Kong Stock Exchange. As of December 31, 2005, we owned 53.59% of ASM Pacific Technology through our wholly-owned subsidiary, Advanced Semiconductor Materials (Netherlands Antilles) N.V., a Netherlands Antilles company, and the remaining 46.41% was owned by the public.

Two of the six directors of ASM Pacific Technology are affiliates of ASM International. However, they are under no obligation to take any actions that are beneficial to us. Issues and conflicts of interest therefore may arise which might not be resolved in our best interests.

In addition, the directors of ASM Pacific Technology are under no obligation to declare a payment of dividends to shareholders. As a shareholder of ASM Pacific Technology, we cannot compel the payment or amount of dividends. With respect to the payment of dividends, the directors must consider the financial position of ASM Pacific Technology after the dividend. Since a portion of our cash flows available for our front-end segment is derived from the dividends we receive from ASM Pacific Technology, its failure to declare dividends in any year would negatively impact the cash position of our front-end segment for that year and reduce cash available to service our indebtedness. Cash dividends received from ASM Pacific Technology totaled€ 24.1 million,€ 40.4 million and€ 37.0 million, in 2003, 2004 and 2005, respectively.

The directors of ASM Pacific Technology owe their fiduciary duties to ASM Pacific Technology, and may approve transactions to which we are a party only if the transactions are commercially beneficial to ASM Pacific Technology. Further, under the listing rules of the Hong Kong Stock Exchange, directors who are on the boards of both ASM Pacific Technology and ASM International are not permitted to vote on a transaction involving both entities. This would disqualify both of the two affiliates of ASM International who currently serve on the board of ASM Pacific Technology from voting on any such transaction.

As a shareholder of ASM Pacific Technology, we can vote our shares in accordance with our own interests. However, we may not be entitled to vote on transactions involving both us and ASM Pacific Technology under the listing rules of the Hong Kong Stock Exchange and the Hong Kong Takeover Code. In particular, under the Hong Kong Takeover Code we would be excluded from voting if we were directly involved in a takeover of ASM Pacific Technology in a transaction requiring a shareholder vote.

Our reliance on a limited number of suppliers could result in disruption of our operations.

We outsource a substantial portion of the manufacturing of our front-end business to a limited number of suppliers. We are in the process of developing additional internal and external sources of supply for these manufacturing processes in the future, including an additional front-end supply source in Singapore. If our suppliers were unable or unwilling to deliver products to us in the quantities we require for any reason, including natural disaster, labor unrest, capacity constraints, supply chain management problems or contractual disputes, we may be unable to fill customer orders on a timely basis, which could negatively affect our financial performance and customer relationships.

Because the costs to semiconductor manufacturers of switching from one semiconductor equipment supplier to another can be high, it may be more difficult to sell our products to customers having a competing installed base, which could limit our growth in sales and market share.

We believe that once a semiconductor manufacturer has selected a supplier’s equipment for a particular product line, that manufacturer generally continues to rely on that supplier for future equipment requirements, including new generations of similar products. Changing from one equipment supplier to another is expensive and requires a substantial investment of resources by the customer. Accordingly, it is difficult to achieve significant sales to a customer using another supplier’s equipment. Our inability to sell our products to potential customers who use another supplier’s equipment could adversely affect our ability to increase revenue and market share.

11

Table of Contents

Our ability to compete could be jeopardized if we are unable to protect our intellectual property rights from challenges by third parties; claims or litigation regarding intellectual property rights could require us to incur significant costs.

Our success and ability to compete depend in large part upon protecting our proprietary technology. We rely on a combination of patent, trade secret, copyright and trademark laws, nondisclosure and other contractual agreements and technical measures to protect our proprietary rights. These agreements and measures may not be sufficient to protect our technology from third party infringements, or to protect us from the claims of others. In addition, patents issued to us may be challenged, invalidated or circumvented, rights granted to us under patents may not provide competitive advantages to us, and third parties may assert that our products infringe their patents, copyrights or trade secrets. Third parties could also independently develop similar products or duplicate our products.

In addition, monitoring unauthorized use of our products is difficult and we cannot be certain that the steps we have taken will prevent unauthorized use of our technology. The laws of some countries in which our products are or may be developed, manufactured or sold, including various countries in Asia, may not protect our products or intellectual property rights to the same extent as do the laws of the Netherlands and the United States and thus make the possibility of piracy of our technology and products more likely in these countries. If competitors are able to use our technology as their own, our ability to compete effectively could be harmed.

In recent years, there has been substantial litigation regarding patent and other intellectual property rights in semiconductor-related industries. Unrelated to our 1997 settlement with Applied Materials, discussed below, we entered into a settlement agreement with Applied Materials in August 2004 dismissing all claims and counter-claims over certain patent infringement proceedings in the United States without prejudice and without payment of any kind by any party and without licensing any patents. In addition, in April 2003, we and our subsidiary, ASM America entered into a binding memorandum of understanding regarding the settlement of mutual patent infringement claims between ASM America and Genus. In the future, additional litigation may be necessary to enforce patents issued to us, to protect trade secrets or know-how owned by us or to defend us against claimed infringement of the rights of others and to determine the scope and validity of the proprietary rights of others.

Claims that our products infringe the proprietary rights of others would force us to defend ourselves and possibly our customers or suppliers against the alleged infringement. Such claims, if successful, could subject us to significant liability for damages and invalidate our proprietary rights. Regardless of the outcome, patent infringement litigation is time-consuming and expensive to resolve and diverts management time and attention.

Intellectual property litigation could force us to do one or more of the following, any one of which could severely harm our business:

| • | forfeit our proprietary rights; |

| • | stop manufacturing or selling our products that incorporate the challenged intellectual property; |

| • | obtain from the owner of the infringed intellectual property right a license to sell, produce, use, have produced, have sold or have used the relevant technology, which license may not be available on reasonable terms or at all or may involve significant royalty payments; |

| • | pay damages, including treble damages and attorney’s fees in some circumstances; or |

| • | redesign those products that use the challenged intellectual property. |

We license the use of some patents from a competitor pursuant to a settlement agreement; if the agreement is terminated, our business could be adversely affected.

In October 1997, we entered into an agreement to settle mutual patent infringement litigation with Applied Materials, which was amended and restated in 1998, pursuant to which Applied Materials agreed to grant us a worldwide, non-exclusive and royalty-bearing license to use all of the litigated patents and certain additional patents that were not part of the litigation. In return we agreed to pay Applied Materials a settlement fee and to grant it a worldwide, non-exclusive and royalty-free license to use a number of our patents including but not limited to those patents which we were enforcing in the litigation. All licenses expire at the end of the life of the underlying patents. Our obligation to pay certain royalties to Applied Materials continues until the expiration of the corresponding underlying patent. In addition, the settlement agreement included covenants for limited periods during which the parties would not litigate the issue of whether certain of our products infringe any of Applied Materials’ patents that were not licensed to us under the settlement agreement. The covenants, which lasted for different periods of time for different products, have expired. Upon the occurrence of an event of default or other specified events, including, among other things, our failure to pay royalties, a change of control of ASM International, and improper use of the licenses, Applied Materials may terminate the settlement agreement, including the licenses included in the agreement.

12

Table of Contents

Additional litigation with Applied Materials regarding other matters or the operation of the settlement agreement itself could occur. Litigation with Applied Materials, which has greater financial resources than we do, could negatively impact our earnings and financial position.

We must offer a possible change of control transaction to Applied Materials first.

Pursuant to our 1997 settlement agreement with Applied Materials, one of our competitors, as amended and restated in 1998, if we desire to effect a change of control transaction, as defined in the settlement agreement, with a competitor of Applied Materials, we must first offer the change of control transaction to Applied Materials on the same terms as we would be willing to accept from that competitor pursuant to a bona fide arm’s-length offer made by that competitor.

We operate worldwide; economic, political, military or other events in a country where we make significant sales or have significant operations could interfere with our success or operations there and harm our business.

We market and sell our products and services throughout the world. A substantial portion of our manufacturing employees and operations are in the People’s Republic of China and the success of our business depends on our operations there. In addition, we have facilities in the Netherlands, the United States, Japan, Hong Kong, Singapore, Malaysia and South Korea. Our operations are subject to risks inherent in doing business internationally, including, without limitation:

| • | unexpected changes in regulatory or legal requirements or changes in one country in which we do business which are inconsistent with regulations in another country in which we do business; |

| • | fluctuations in exchange rates and currency controls; |

| • | political conditions and instability, particularly in the countries in which our manufacturing facilities are located; |

| • | economic conditions and instability; |

| • | terrorist activities; |

| • | human health emergencies, such as the outbreak of infectious diseases or viruses, particularly in the countries in which our manufacturing facilities are located; |

| • | tariffs and other trade barriers, including current and future import and export restrictions, and freight rates; |

| • | difficulty in staffing, coordinating and managing international operations; |

| • | burden of complying with a wide variety of foreign laws and licensing requirements; |

| • | difficulty in protecting intellectual property rights in some foreign countries; |

| • | limited ability to enforce agreements and other rights in some foreign countries; |

| • | longer accounts receivable payment cycles in some countries; and |

| • | business interruption and damage from natural disasters. |

To the extent that such disruptions slow the global economy or, more particularly, result in delays or cancellations of purchase orders, our business and results of operations could be materially and adversely affected.

Our operational results could be negatively impacted by currency fluctuations.

Our assets, liabilities and operating expenses and those of our subsidiaries are to a large extent denominated in the currency of the country where each entity is established. Our financial statements, including our Consolidated Financial Statements, are expressed in euros. The translation exposures that result from the inclusion of financial statements of our subsidiaries that are expressed in the currencies of the countries where the subsidiaries are located are not hedged. As a result, our operational results are exposed to fluctuations of various exchange rates. These net translation exposures are taken into account in determining Shareholders’ Equity.

In addition, foreign currency fluctuations may affect the prices of our products. Prices for our products for sales to our customers throughout the world are currently denominated in various foreign currencies including, but not limited to, United States dollars, euros, Japanese yen and Chinese yuan. If there is a significant devaluation of the currency in a specific country, the prices of our products will increase relative to that country’s currency and our products may be less competitive in that country. Also, we cannot be sure that our international customers will continue to be willing to place orders denominated in these currencies. If they do not, our revenue and operating results will be subject to additional foreign exchange rate fluctuations.

13

Table of Contents

Although we monitor our exposure to currency fluctuations, these fluctuations could negatively impact our earnings, cash flow and financial position.

If our products are found to be defective, we may be required to recall and/or replace them, which could be costly and result in a material adverse effect on our business, financial condition and results of operations.

One or more of our products may be found to be defective after we have already shipped the products in volume, requiring a product replacement or recall. We may also be subject to product returns and product liability claims that could impose substantial costs and have a material and adverse effect on our business, financial condition and results of operations.

Environmental laws and regulations may expose us to liability and increase our costs.

Our operations are subject to many environmental laws and regulations wherever we operate governing, among other things, air emissions, wastewater discharges, the use and handling of hazardous substances, waste disposal and the investigation and remediation of soil and groundwater contamination. In February 2003, the European Commission published a directive on waste electrical and electronic equipment (“WEEE”) (Directive 2002/96/EC, which was amended in December 2003 by Directive 2003/108/EC), and which has been implemented in the Netherlands. In principle, the rules result in “take-back” obligations of manufacturers and/or the responsibility of manufacturers for the financing of the collection, recovery and disposal of electrical and electronic equipment by requiring that European Union Member States adopt appropriate measures to minimize WEEE disposal and achieve high levels of collection and separation of WEEE. As of August 13, 2005 producers of WEEE will have to provide for the financing of the collection, treatment, recovery and environmentally sound disposal of WEEE. Another directive of the European Commission (Directive 2002/95/EC) provides for a ban on the use of lead and some flame retardants in manufacturing electronic components. To the extent these and other regulations apply to our business in Europe and elsewhere throughout the world, these measures could adversely affect our manufacturing costs or product sales by forcing us or our suppliers to change production processes or use more costly materials.

As with other companies engaged in similar activities, we face inherent risks of environmental liability in our current and historical manufacturing activities. Costs associated with future environmental compliance or remediation obligations could adversely affect our business.

Members of our Supervisory Board and Management Board and our executive officers control approximately 23.2% of our voting power which gives them significant influence over matters voted on by our shareholders, including the election of members of our Supervisory Board and Management Board and makes it substantially more difficult for a shareholder group to remove or elect such members without the support of management.

Our Chairman and Chief Executive Officer controlled approximately 21.8% of the voting power of our outstanding common shares as of December 31, 2005, and the members of our Supervisory Board and Management Board and all our executive officers as a group controlled approximately 23.2% of the voting power of our outstanding common shares as of that date. Accordingly, these persons have significant influence on the outcome of matters submitted to a shareholder vote, such as the election of the members of our Supervisory Board and Management Board. Persons nominated in a non-binding nomination by the Supervisory Board for appointment by the shareholders to the Supervisory Board or Management Board at the annual general meeting of shareholders will be elected if the number of affirmative votes exceeds the number of negative votes cast by holders of the outstanding shares present or represented at the meeting and entitled to vote. Persons nominated in a binding nomination by the Supervisory Board for appointment by shareholders to the Supervisory Board and Management Board at the annual general meeting of shareholders are so appointed unless shareholders reject such nomination by a vote of at least two-thirds of the votes cast, provided that the votes to reject represent at least 50% of all issued and outstanding shares eligible to vote. This makes it difficult for a group of shareholders to remove or elect members of our Supervisory Board or Management Board without the support of management.

Our anti-takeover provisions may prevent a beneficial change of control.

Our shareholders have granted to Stichting Continuïteit ASM International, or Stichting, a non-membership organization with a board composed of our President and Chief Executive Officer, the Chairman of our Supervisory Board and three independent members, the right to acquire and vote our preferred shares to maintain the continuity of our company. Toward that objective, Stichting will evaluate, when called for, whether a takeover offer is in our best interest, and may, if it determines that such action is

14

Table of Contents

appropriate, acquire preferred shares with voting power equal to 50.0% of the voting power of the outstanding common shares. This is likely to be sufficient to enable it to prevent a change of control from occurring. For additional information regarding Stichting, see Item 7. “Major Shareholders and Related Party Transactions.”

These provisions may prevent us from entering into a change of control transaction that may otherwise offer our shareholders an opportunity to sell shares at a premium over the market price.

Our stock price has fluctuated and may continue to fluctuate widely.

The market price of our common shares has fluctuated substantially in the past. Between January 1, 2005 and December 31, 2005, the sales price of our common shares, as reported on the NASDAQ Stock Market, ranged from a low of US$ 12.83 to a high of US$ 19.15. The market price of our common shares will continue to be subject to significant fluctuations in the future in response to a variety of factors, including the risk factors discussed in this report and the following, without limitation:

| • | future announcements concerning our business or that of our competitors or customers; |

| • | the introduction of new products or changes in product pricing policies by us or our competitors; |

| • | litigation regarding proprietary rights or other matters; |

| • | changes in analysts’ earnings estimates; |

| • | developments in the financial markets; |

| • | quarterly fluctuations in operating results; |

| • | general economic, political and market conditions, such as recessions or international currency fluctuations; or |

| • | general conditions in the semiconductor and semiconductor equipment industries. |

In addition, public stock markets frequently experience substantial price and trading volume volatility, particularly in the high technology sectors of the market. This volatility has significantly affected the market prices of securities of many technology companies for reasons frequently unrelated to or disproportionately impacted by the operating performance of these companies. These broad market fluctuations may adversely affect the market price of our common shares.

Compliance with Internal Controls Evaluations and Attestation Requirements.

We are subject to United States securities laws, including the Sarbanes-Oxley Act of 2002 and the rules and regulations adopted by the U.S. Securities and Exchange Commission pursuant to the Act. Under section 404 of the Sarbanes-Oxley Act and the related regulations, we are required to perform an evaluation of our internal controls over financial reporting and have our independent auditor publicly attest to this evaluation beginning with the year ended December 31, 2006. We have commenced the evaluation and expect to complete it in the course of 2006. Internal control evaluations and attestation requirements are time-consuming and expensive. If we would fail to complete the evaluation of our internal controls over financial reporting in time, if we would identify material weaknesses in these internal controls, or if our independent accountant could not timely attest to our evaluation, we could be subject to regulatory scrutiny and decreased public confidence in our internal controls, which may adversely affect the market price of our common shares.

Item 4. Information on the Company

The information in this Item 4 should be read in conjunction with the risks discussed under Item 3.D “Risk Factors.”

A. History and development of the Company.

ASM International N.V. was incorporated on March 4, 1968 as a Netherlandsnaamloze vennootschap, or public limited liability company, and was previously known as Advanced Semiconductor Materials International N.V. Our principal executive offices are located at Jan van Eycklaan 10, 3723 BC Bilthoven, the Netherlands. Our telephone number at that location is +31 30 229 84 11. Our authorized agent in the United States is our subsidiary, ASM America Inc,, a Delaware corporation, located at 3440 East University Drive, Phoenix, Arizona 85034, United States of America.

15

Table of Contents

B. Business overview.

Introduction

Our Business

As a semiconductor capital equipment supplier, we design, manufacture and sell production systems and services to our customers for the production of semiconductor devices, or integrated circuits. The semiconductor capital equipment market is composed of three major market segments: wafer processing equipment, assembly and packaging equipment, and test equipment. ASMI is mainly active in the wafer processing and assembly and packaging market segments. The wafer processing segment is referred to as “front-end.” Assembly and packaging is referred to as “back-end.”

Front-end production systems perform processes on round slices of silicon, called a wafer. During these processes, thin films, or layers, of various materials are grown or deposited onto the wafer, or an existing thin film on a wafer undergoes modification, such as a temperature treatment, or local etching. These films form numerous individual and separable circuits on the wafer, called “dies” or “chips.” After probing and selecting these individual circuits for correct performance, the dies on the processed wafer are separated, with each die of the same wafer containing the same circuitry. Back-end production systems then assemble and connect one or more of these known good dies—or sometimes several different known good dies from different wafers, each supplying a different functionality—in a single package, to form a complex semiconductor device that will perform calculations, store data and interface with its environment.

Our front-end operations are conducted through wholly-owned subsidiaries, the three most significant being ASM Europe B.V. (“ASM Europe”), located in the Netherlands, ASM America, Inc. (“ASM America”), located in the United States, and ASM Japan K.K. (“ASM Japan”), located in Japan.

Our back-end operations are conducted through our majority-owned subsidiary, ASM Pacific Technology Ltd. (“ASM Pacific Technology” or “ASMPT”), with principal operations in Hong Kong, the People’s Republic of China, Singapore, and Malaysia. At December 31, 2005, we owned 53.59% of the outstanding equity of ASM Pacific Technology.

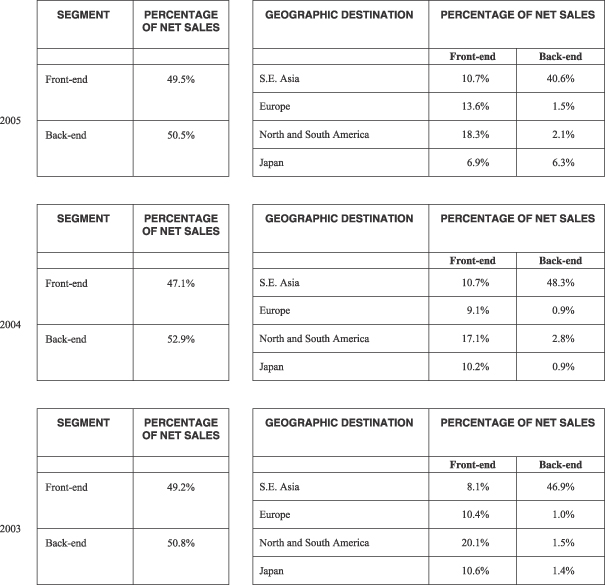

The location of our front-end facilities allows us to interact closely with customers in the world’s major front-end geographic market segments: Europe, North America, and Asia. We address a part of the “deposition and related tools” market segment, defined by VLSI Research1. Our front-end segment accounted for 47.1% of our net sales in 2004 and 49.5% of our net sales in 2005.

Our back-end facilities are in close proximity to where most customer assembly and packaging operations are located. We address parts of the “bonding equipment” and “packaging equipment” segments, defined by VLSI Research2. We also manufacture and sell lead-frames. Our back-end segment accounted for 52.9% of our net sales in 2004 and 50.5% of our net sales in 2005.

Through our majority-owned subsidiary, NanoPhotonics AG (“NanoPhotonics”), located in Germany, we participate in the “process diagnostic equipment” market segment, defined by VLSI Research3, which is part of the test equipment market. The metrology subassemblies produced by NanoPhotonics are also sold as an integrated subassembly on our wafer processing systems for “integrated metrology” purposes. At December 31, 2005, we owned 69.1% of the outstanding equity of NanoPhotonics.

Industry Background and Major Business Trends

Semiconductor devices are the key enablers of the electronic age. Each semiconductor device can hold many individual components, most of which are transistors. For over 30 years now, the average number of components per integrated semiconductor device, at the optimum cost-per-component, has been increased by a factor of two, every 18 to 24 months. This trend is generally referred to as Moore’s law, after Gordon Moore, one of the founders of Intel. Increases in complexity, along with simultaneous reductions in the cost-per-component, have mainly been achieved by reducing the size of individual transistors, so that a larger number of transistors fit within a given size die. Today, transistors less than 100nm (one billionth of a meter) long are manufactured in high volume, while over several billion transistors can be manufactured on a single die.

| 1 | www.vlsiresearch.com, VIC code 460.00000, accessed December 2004. |

| 2 | www.vlsiresearch.com, VIC codes 540.00000 and 550.00000, accessed December 2004. |

| 3 | www.vlsiresearch.com, VIC code 350.00000, accessed December 2004. |

16

Table of Contents

A second development decreases the cost per device by increasing the size of the wafer (the silicon substrate upon which semiconductors are built), so that more devices can be produced within one production cycle. Today, most of the newly installed semiconductor device fabrication capacity employs 300mm wafers, with each wafer typically holding between a few dozen to several thousand individual circuits. The simultaneous increase in the complexity of devices, and the substantial decrease in cost-per-component has supported an approximately US$ 1.1 trillion electronics industry, and behind that, a semiconductor industry of approximately US$ 235 billion (Gartner, Dec 9, 2005 4). The semiconductor industry in turn, is supported by the US$ 34 billion (Gartner, Oct 6, 2005 5) semiconductor capital equipment industry which supplies the needed production systems and services needed.

The yield, or the fraction of chips (known good dies) on a wafer that operate according to specifications, is usually one of the most important variables that influences the performance of the integrated device manufacturers. Large initial investments are needed to build an automated production line in an ultra-clean environment in order to achieve high yield. The capital equipment in this production line is increasingly becoming an important determinant for the yield of the factory.

Parallel to the above-mentioned trends of transistor scaling and larger wafer size, another trend is beginning to emerge on the die level: heterogeneous integration. While the components on a chip that perform calculation and storage can undergo scaling, other components, such as inductors, capacitors, sensors, micromechanical, photonic, or micro-fluidic devices, do not scale as easily as do transistors and some capacitors. Yet, in order to make devices with these components small and cost-effective enough, they will eventually also have to be integrated into the same semiconductor device. Although several functions can be integrated on a single die, as in a system on a chip (“SoC”), for economical reasons this is usually limited to the components that scale with Moore’s law (“more Moore”), and use the same base material (silicon). For components that do not scale, or components that use a different base material (GaAs, for example) it is not always practical or economically feasible to place them on the same die. In that case, integration of several dies, sometimes coming from different supply lines, in a single package to form a system in a package (“SiP”) is the alternative solution that provides the desired functionality. This trend is sometimes referred to as “more than Moore.”

The trends outlined above are the drivers of the broad semiconductor roadmap which semiconductor equipment companies track in developing new production systems and process technologies. These new systems and technologies must be developed well ahead of volume demand for the semiconductor devices they make. As a result, there is a large lead time between the investment in a new technology, and its commercial success. With the combination of a long lead time and the short product life-cycles comes the inherent difficulty of matching supply and demand, which results in the high volatility associated with the semiconductor industry. In this highly cyclical industry, the front-end and back-end market segments have historically reacted differently to market forces. We believe, therefore, that operating in both segments works in our favor to reduce the impact of business cycles on our operations.

Our Strategy

Our strategic objective is to realize profitable, sustainable growth by capitalizing on our technological innovations, manufacturing infrastructure and sales and support offices located close to our global customers. We intend to enhance our market position by providing customers with the advanced, cost-effective, and reliable products they need, along with excellence in customer service and support. The key elements of our strategy include:

| 1. | Realizing profitable growth for our front-end segment, by systematically increasing our operating efficiency and reducing manufacturing costs through vertical integration of our supply chain, and the location of significant parts of our manufacturing capability in lower labor rate countries, building upon experiences gained in our back-end segment. |

| 2. | Maintaining our global reach through our operating, sales and customer service facilities in key parts of the world in order to establish and maintain long-term customer relationships. |

| 3. | Strengthening our relationships with independent research institutes, universities, customers and suppliers and entering into strategic alliances to enhance the scope and depth of our research and development activities. |

| 4. | Advancing our existing technology base by developing new materials and processes which can increase performance of semiconductor devices and reduce customer cost of ownership. |

| 4 | http://www.gartner.com/press_releases/pr2005.html, accessed January 2006. |

| 5 | http://www.gartner.com/press_releases/pr2005.html, accessed January 2006. |

17

Table of Contents

| 5. | Leveraging our strong technology and manufacturing capabilities to capture market share early in the lifecycle of significant technology advancements, such as the shift to 300mm wafers, the move to copper-low k, or to transistor engineering. |

| 6. | Capitalizing on our technology leadership in both back-end and front-end major market segments to become a leader in the coming revolution that takes us beyond the confines of “Moore’s law” to the heterogeneous integration environment of “more than Moore” technology. |

| 7. | Expanding our intellectual property portfolio, by filing patent applications for key developments in equipment, software, materials and processes, and simultaneously increasing our royalty related revenue by exploiting our intellectual property portfolio through licensing programs. |

Background of Semiconductor Manufacturing Processes

Overview

The process of manufacturing an integrated semiconductor, from raw material to finished device, includes two major segments: the front-end and back-end manufacturing processes. We participate in both segments.

Front-end Manufacturing Process

The front-end manufacturing process, or wafer processing, can be divided in three distinct manufacturing processes: wafer manufacturing, transistor formation, known as front-end of the line (“FEOL”) processing, and interconnect formation, known as back-end of the line (“BEOL”). We develop and sell technology, develop and manufacture equipment, and provide services used by semiconductor device manufacturers in each of these sections of front-end manufacturing.

In the wafer manufacturing process a large single crystal of very pure silicon is grown from molten silicon. The crystal is then sliced into a large number of thin slices, or wafers, of single crystalline silicon. These slices are polished to an atomic level flatness before the next steps are executed. For advanced applications, some layers are deposited on the wafer for later use, by either epitaxy or diffusion/oxidation (described below). Epitaxial wafers are even flatter and contain fewer defects at the surface than polished wafers. Some wafers are made with an embedded electrically insulating layer, such as silicon oxide, just below a very thin top layer of pure silicon. These special wafers are called Silicon-on Insulator or SOI wafers and are used for some of the most advanced microprocessors. The finished wafers, still without pattern on them, are shipped to the integrated device manufacturers and foundries for further processing.

During FEOL and BEOL wafer processing, multiple thin films of either electrically insulating material, also called dielectrics, or conductive material are modified, grown, or deposited on a silicon wafer. First, several material processing cycles are used in the FEOL to build the basic transistor and other components such as capacitors and resistors. Second, several processing cycles are used in the BEOL to build additional components such as capacitors, inductors and resistors, and to electrically connect the large amount of transistors and components. Patterning of deposited layers with lithography and etching (described below) creates the transistors, other components and connecting wires, which together make up the integrated circuit. Each integrated circuit is on a single “chip” or a “die” on the wafer. A finished wafer may contain a few dozen to several thousand individual dies. Front-end processes are performed either one wafer at a time in single wafer processing systems or many wafers at a time in batch processing systems. Multiple processes are repeated on each layer as the wafer is processed.

The number and precise order of the process steps vary depending upon the complexity and design of the integrated circuit. The performance of the circuit is determined in part by the various electrical characteristics of the materials used in the layers of the circuit and the wafer. Simple circuits may have as few as ten layers, while complex circuits may have more than one hundred layers. The front-end manufacturing process is capital intensive, requiring multiple units of several different production systems. Many different but complementary methods are used to modify, grow, or deposit materials on the wafers. ASMI is most active in developing and manufacturing the equipment used by semiconductor device manufacturers in the deposition processes, i.e., those steps that involve the creation of insulating, conducting and semi-conducting layers on the wafer surface.

The front-end manufacturing process is complete when all of the layers have been deposited and patterned on the wafer. As a last step, the correct electrical functioning of the integrated circuits on each die is confirmed by probing. Non-functioning circuits are marked so they can be eliminated before the back-end processing. The introduction of even trace levels of foreign particles or material can make a circuit, or even an entire wafer, unusable. To reduce the level of foreign particles or material, front-end processing is performed in clean rooms with ultra low particle and contamination levels. Once the front-end processing is complete, the entire wafer with multiple, functioning, integrated circuits is shipped to the back-end facility

18

Table of Contents

where it is separated into dies, which are then bonded, packaged, and tested before final shipment of the semiconductor device to the end customer. Back-end processes do not require the same level of contaminant control. These processes are performed in facilities that differ from facilities in which front-end processes are performed.

The following is an alphabetical list of the principal front-end process technologies used by semiconductor device manufacturers:

| • | Atomic Layer Deposition (“ALD”) is an advanced technology that deposits single atomic layers on wafers one at a time, and at low temperatures. This process is used to create ultra-thin films of exceptional quality and flatness. Plasma is sometimes used to enhance the process further (Plasma Enhanced ALD, PEALD) |

| • | Chemical Mechanical Polishing (“CMP”) is a technology that planarizes, or levels, layers deposited on wafers by polishing them with a chemical solution called slurry. Planarization reduces the vertical height differences of the various layers. This increases the number of layers that can be processed without introducing reliability problems. Electrochemical Mechanical Polishing (“ECMP”) is comparable to CMP aided with an electric current. |

| • | Chemical Vapor Deposition (“CVD”) is a technique in which one or more gaseous reactants are used to form a solid insulating or conducting layer on the surface of a wafer. Low pressure (Low Pressure CVD, LPCVD) or plasma is sometimes used to enhance the process further (Plasma Enhanced CVD, PECVD). |

| • | Clean removes undesirable contaminants from the wafer’s surface. |