Exhibit 99.5 Slides of Presentation by Cynthia Carroll, Senior Vice President, Alcan Inc., President and Chief Executive Officer, Alcan Primary Metal.

![]()

| Forward Looking Statements |

| ||

| Statements made in the course of this presentation which describe the Company's intentions, expectations or predictions may be "forward-looking statements" within the meaning of securities laws. The Company cautions that, by their nature, forward-looking statements involve risk and uncertainty, and actual actions or results could differ materially. Reference should be made to the most recent Form 10-Q and Form 10-K for a summary of major risk factors. In addition, certain non-GAAP measures are used which are reconciled to the comparable GAAP measures herein or on the Company’s website at www.alcan.com in the “Investors” section.

| |||

| © 2005 ALCAN INC. | Slide 2 | ||

| Agenda |

| ||

| |||

| © 2005 ALCAN INC. | Slide 3 | ||

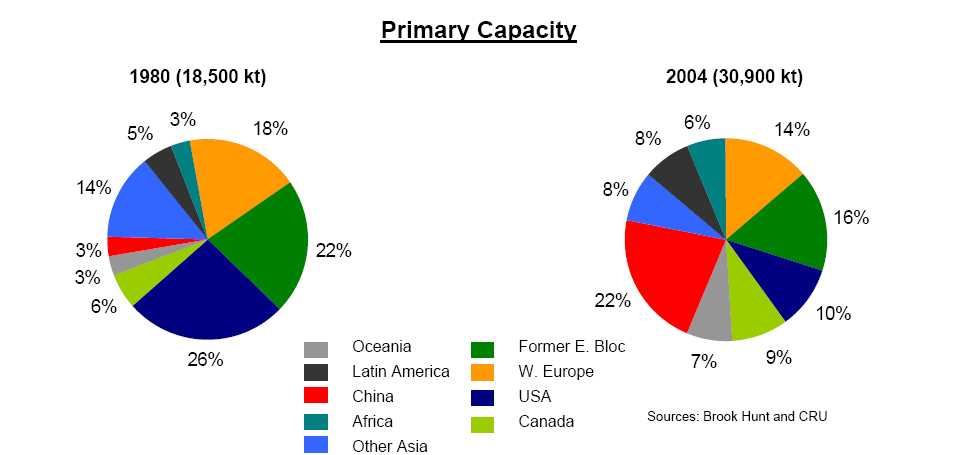

| Primary Aluminum Growth Evolution |

| ||

Growth occurring in regions with available energy at competitive costs and mass market consumers | |||

|

| |||

| © 2005 ALCAN INC. | Slide 4 | ||

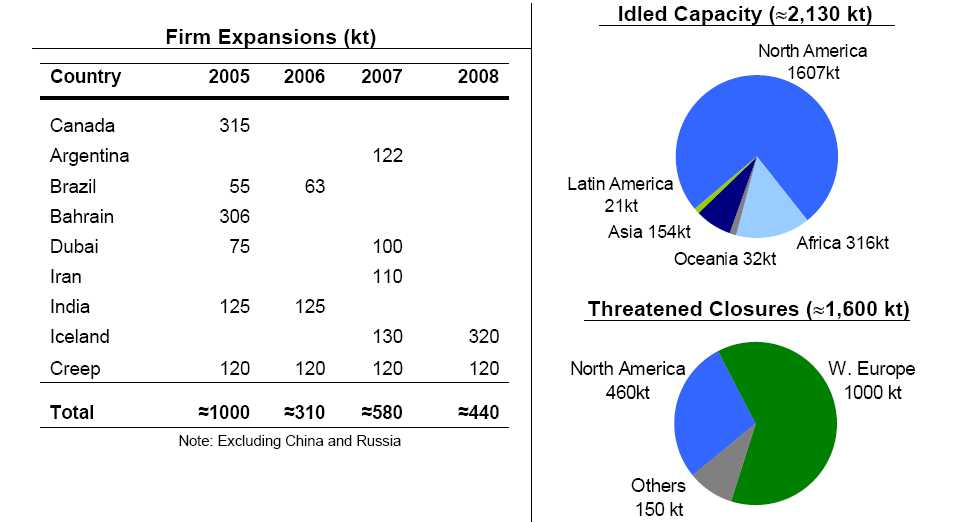

| World Primary Aluminum Balance |

| ||

| |||

| © 2005 ALCAN INC. | Slide 5 | ||

| World Primary Aluminum Balance |

| ||

|

| |||

| © 2005 ALCAN INC. | Slide 6 | ||

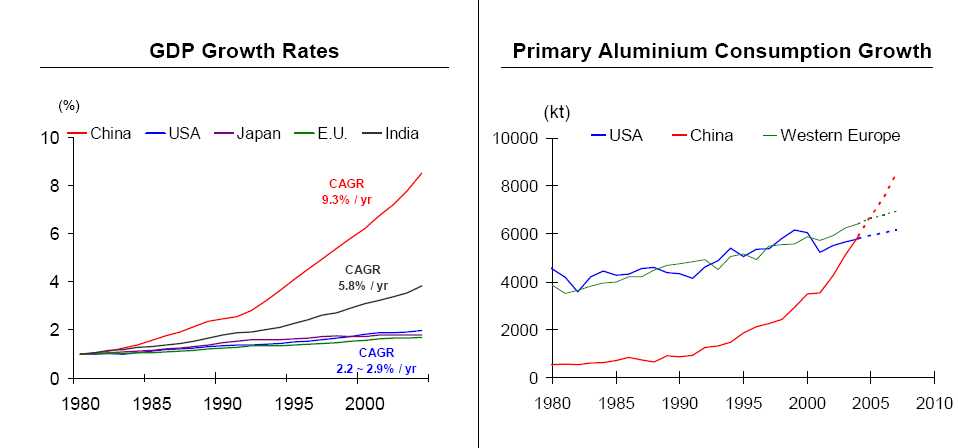

| Primary Aluminum Growth |

| ||

China has been responsible for almost 50% of the growth in world primary | |||

| |||

| © 2005 ALCAN INC. | Slide 7 | ||

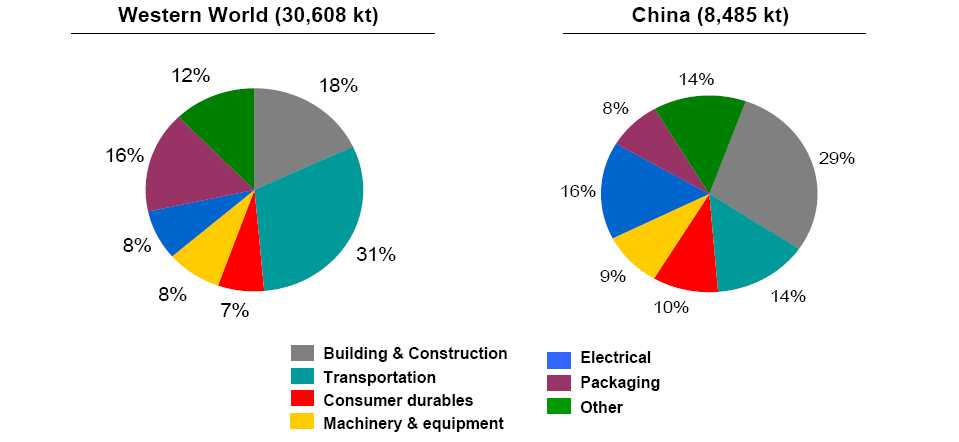

| 2004 Total Consumption by End-use China vs. Western World |

| ||

China’s aluminum consumption has been driven by growth in its overall economic activity and by higher penetration ratios in its main end-use markets | |||

| |||

| © 2005 ALCAN INC. | Slide 8 | ||

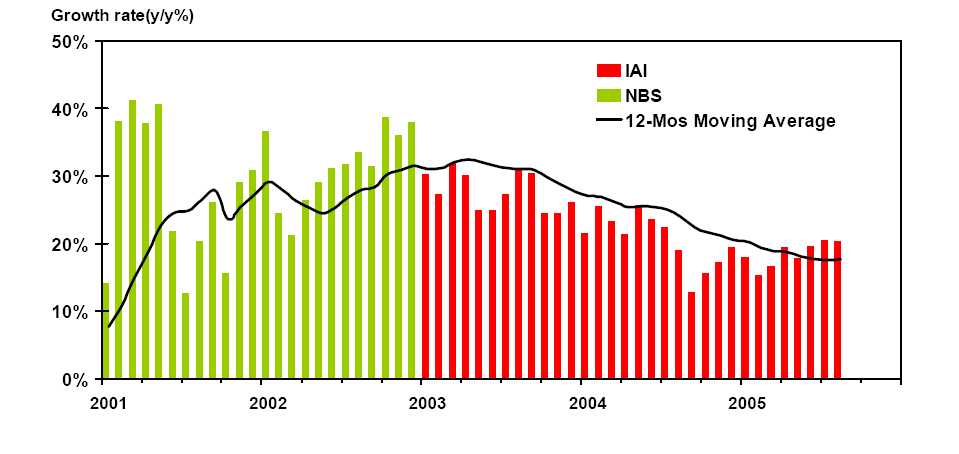

| China Primary Production Growth |

| ||

Growth rate of primary metal production in China is slowing down | |||

|

| |||

| © 2005 ALCAN INC. | Slide 9 | ||

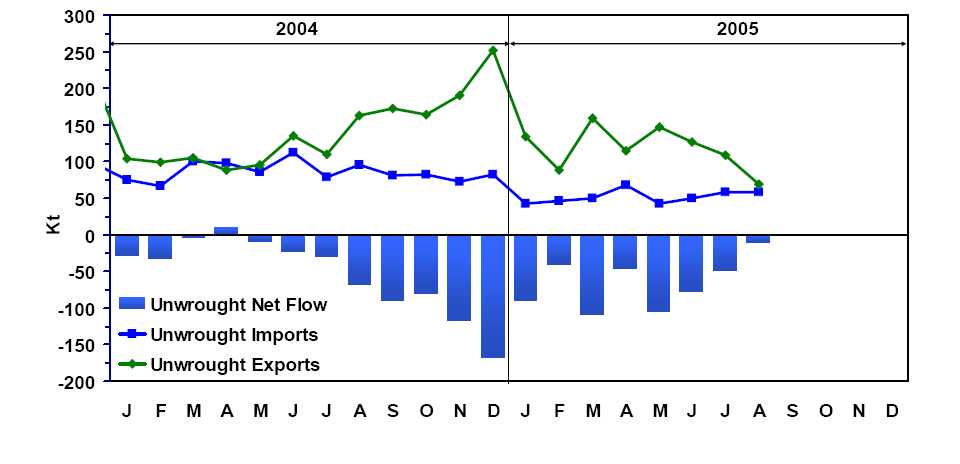

| China Unwrought Aluminum Imports and Exports |

| ||

China imports are relatively stable but exports are dropping | |||

|

| |||

| © 2005 ALCAN INC. | Slide 10 | ||

| Alcan Primary Metal |

| ||

Close to 50% of Alcan’s primary production is based on self-generated power | |||

|

| |||

| © 2005 ALCAN INC. | Slide 11 | ||

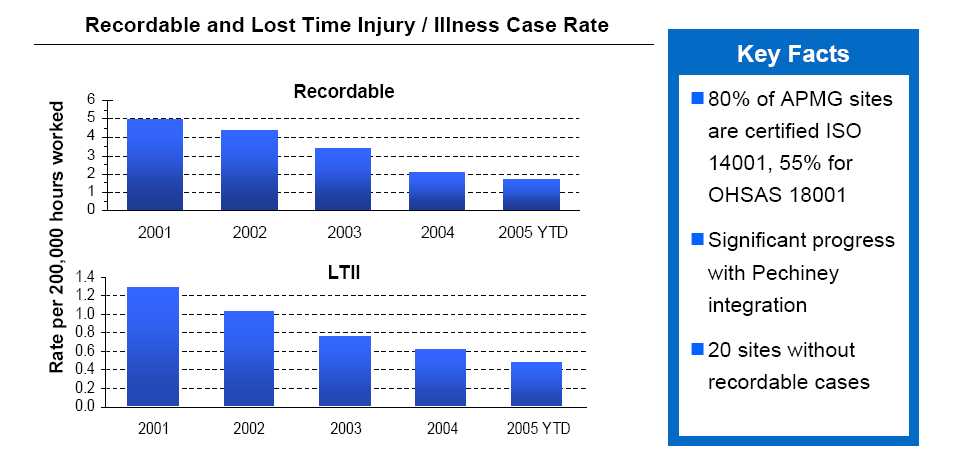

| EHS Performance -Safety |

| ||

Safety results improving continuously | |||

| |||

| © 2005 ALCAN INC. | Slide 12 | ||

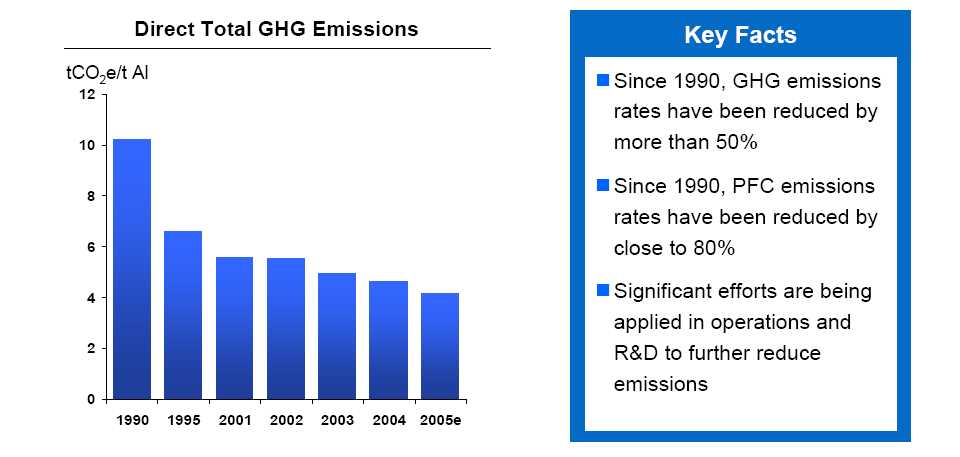

| EHS Performance - Environment |

| ||

Successfully addressing GHG emissions while increasing production | |||

| |||

| © 2005 ALCAN INC. | Slide 13 | ||

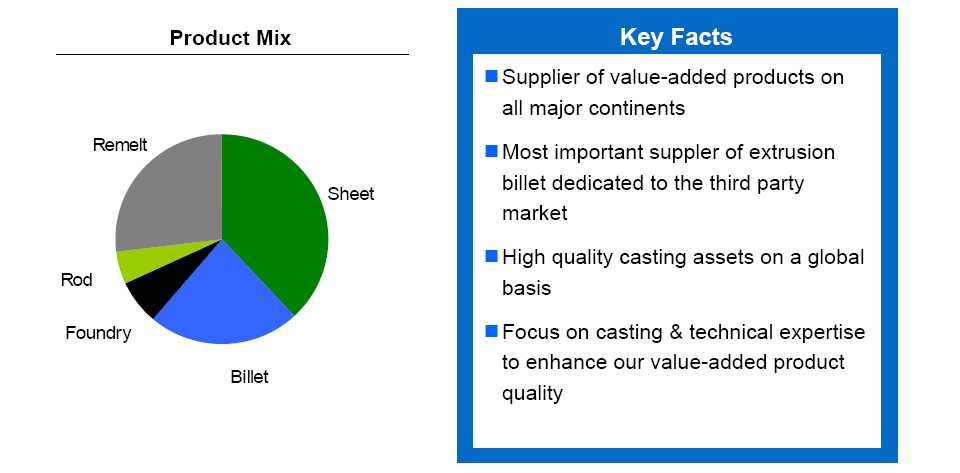

| Value-Added Products |

| ||

In 2005, APMG will have records sales in billet, small form and remeltingot | |||

|

| |||

| © 2005 ALCAN INC. | Slide 14 | ||

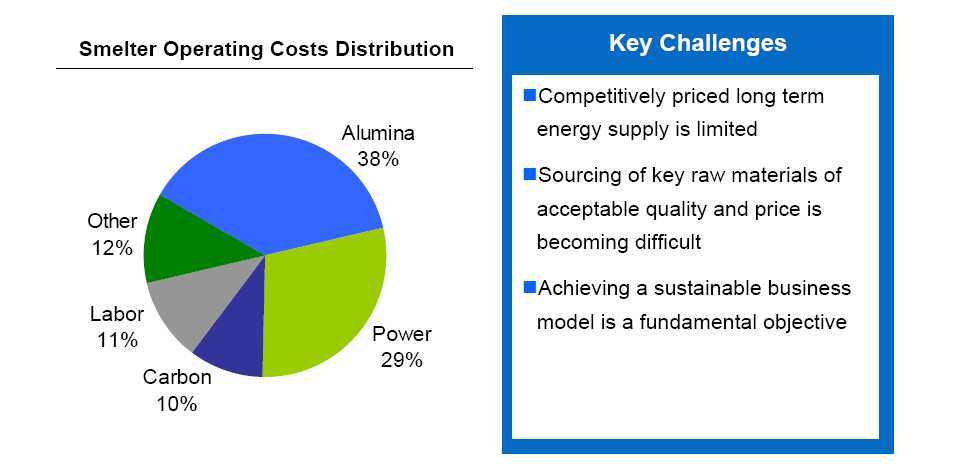

| Cost Drivers and Key Challenges |

| ||

Primary aluminiumindustry must address several challenges | |||

| |||

| © 2005 ALCAN INC. | Slide 15 | ||

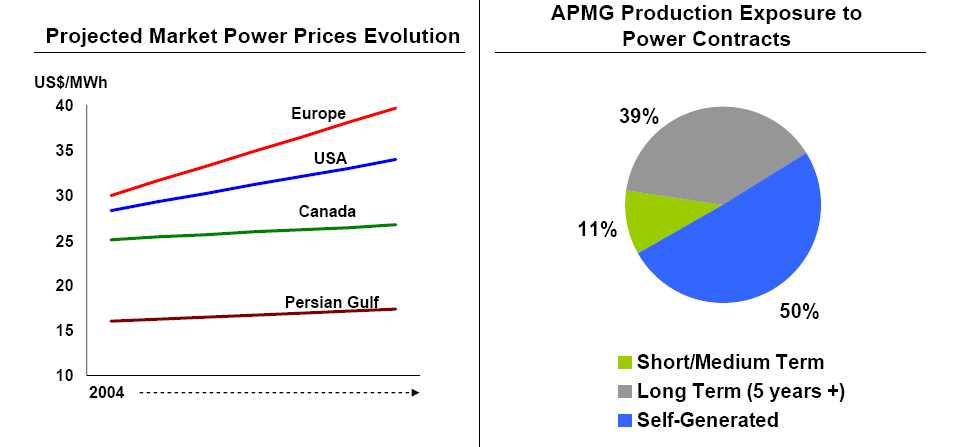

| Competitive Position |

| ||

Close to 90% of Alcan’sproduction is based on self-generated power and long | |||

|

| |||

| © 2005 ALCAN INC. | Slide 16 | ||

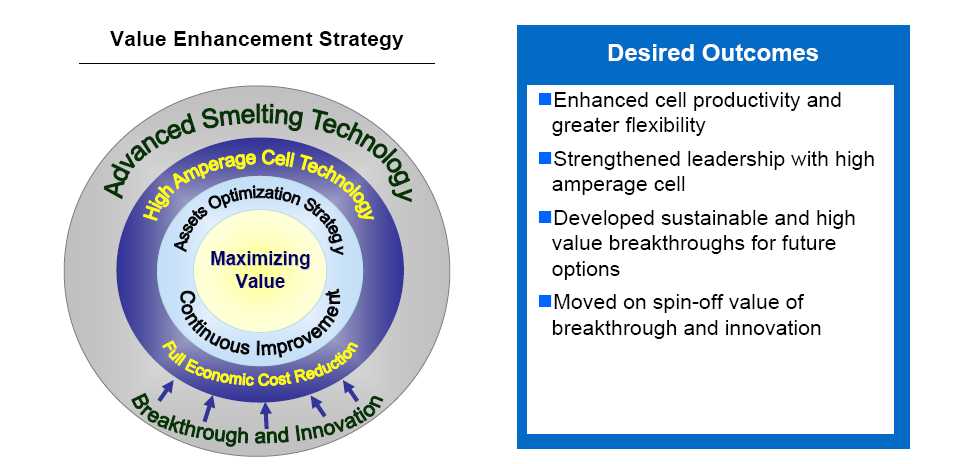

| Drivers for Value Creation |

| ||

Moving simultaneously on all value drivers, through our asset optimization initiatives | |||

| |||

| © 2005 ALCAN INC. | Slide 17 | ||

| Continuous Improvement System |

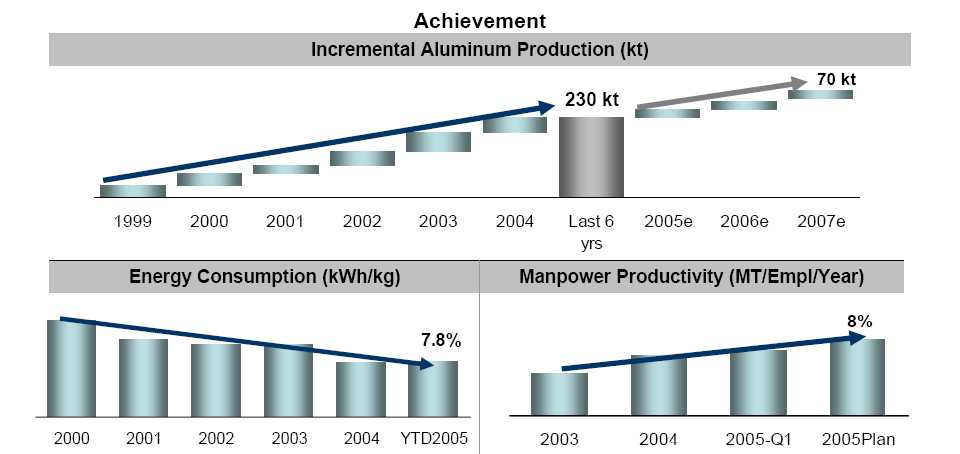

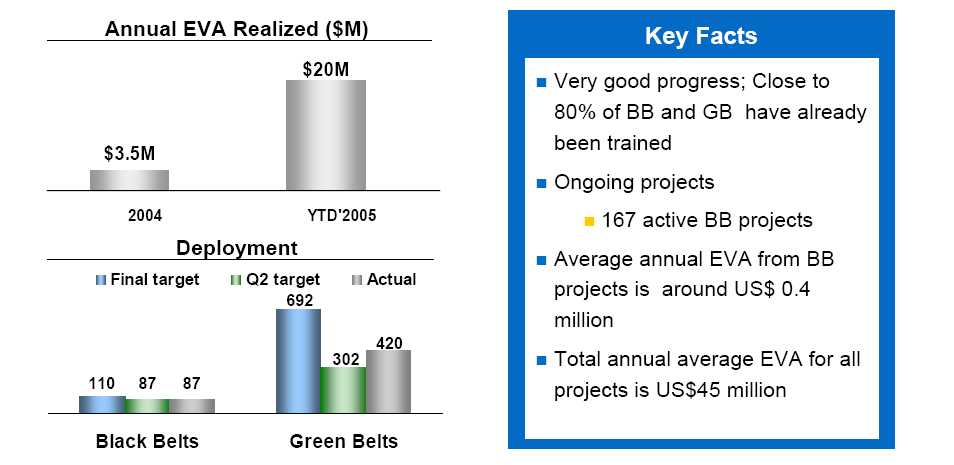

| ||

CI deployment delivered substantial value across all Primary Metal Group sectors | |||

|

| |||

| © 2005 ALCAN INC. | Slide 18 | ||

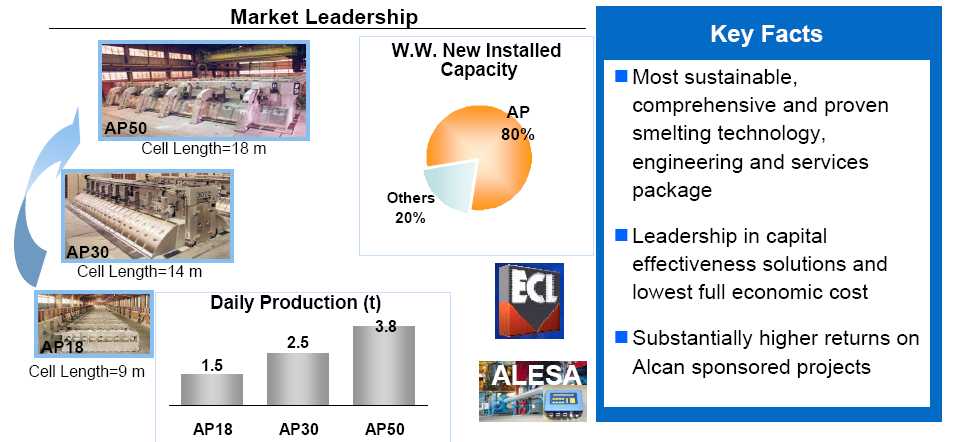

| Alcan’sSmelting Technology Unsurpassed Offer |

| ||

Alcan’sglobal leading edge smelting technology package is an unparalleled competitive advantage | |||

|

| |||

| © 2005 ALCAN INC. | Slide 19 | ||

| Growth Through Strategic Initiatives |

| |

New Strategic Model for Maximizing Value | ||

| InitiativesCompleted AlouetteExpansion ■Smelting Technology: AP30 OthersInitiatives ■Closure of ArvidaSoderberg Ningxia JVInvestment ■Smelting Technology: GAMI -Prebake | Sohar JVProject, Oman ■Smelting Technology: AP35 ■Capacity: 330 kt/line ■Start-up year: Line 1-2008 and Line 2-2010 ■Alcan ownership: 20% of Line 1 and 60% of Line2 ■Power: Long-term dedicated gas-fired power plant CoegaJV Project, South Africa ■Smelting Technology: AP35

Actively pursuing brownfield expansion |

| © 2005 ALCAN INC. | Slide 20 |

| Competitive Position |

| ||

2009 target: 55% of production in first quartile; 80% in lower half | |||

| |||

| © 2005 ALCAN INC. | Slide 21 | ||

| Summary |

| |

Competitive Strengths | Key Priorities |

| ■APMG’s distinctive position due to significant self generated power | ■EHS - meet / exceed requirements |

| ■APMG’smarket leading position with its AP technology | ■Continuous Improvement full deployment |

| ■APMG’s world-class low-cost smelting operations with further AOS opportunities | ■Achievement of AOS and other operating initiatives |

| ■APMG’s diversified operational position both from a geographic and market standpoint | ■Full Economic Cost Reduction to improve APMG’s returns on major projects and maintain global leadership in technology sales |

| ■APMG’s growth through low-cost capital initiatives | ■Strong customer focus in line with VAP strategy |

| ■A balanced portfolio of R&D activities supporting current assets and developing future options | ■Growth through selective capital deployment |

| ■Technology leverage by selling technology licenses, equipment, and services | ■Business model in major projects that is aimed at maximizing value |

| ■Synergy and business opportunities resulting from Pechiney integration | |

■Discipline to apply Alcan Integrated Management Systems | |

| © 2005 ALCAN INC. | Slide 22 |

| © 2005 ALCAN INC. | Slide 23 |

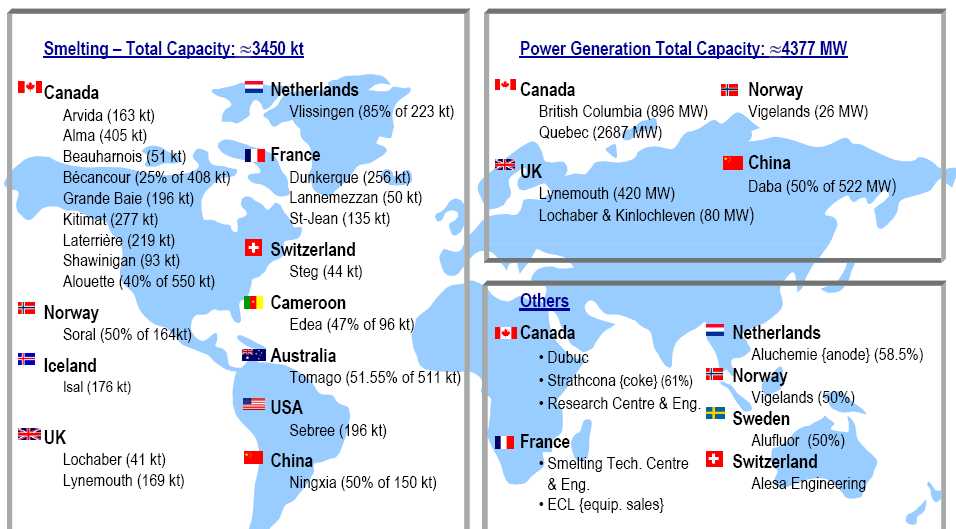

| Primary Metal Group Global Presence |

| ||

|

| |||

| © 2005 ALCAN INC. | Slide 24 | ||

| Innovation and Growth Platform |

| ||

APMG leads the most innovative strategic R&D program in the industry | |||

|

| |||

| © 2005 ALCAN INC. | Slide 25 | ||

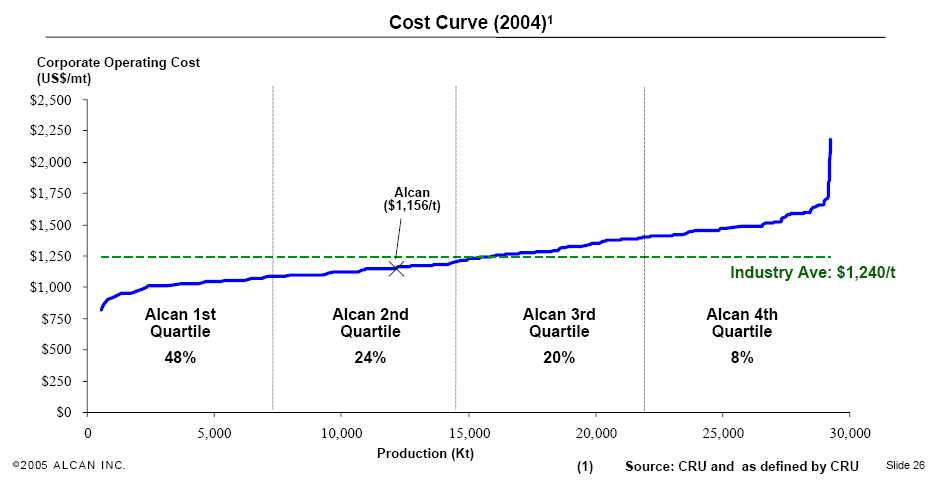

| APMG on the Cost Curve |

| ||

Alcan’scompetitive cost position is driven by favourable power contract and self-generated energy supply as well as efficient low-cost facilities | |||

| |||

| © 2005 ALCAN INC. | Slide 26 | ||

| World Primary Aluminum Market |

| ||

|

| |||

| © 2005 ALCAN INC. | Slide 27 | ||

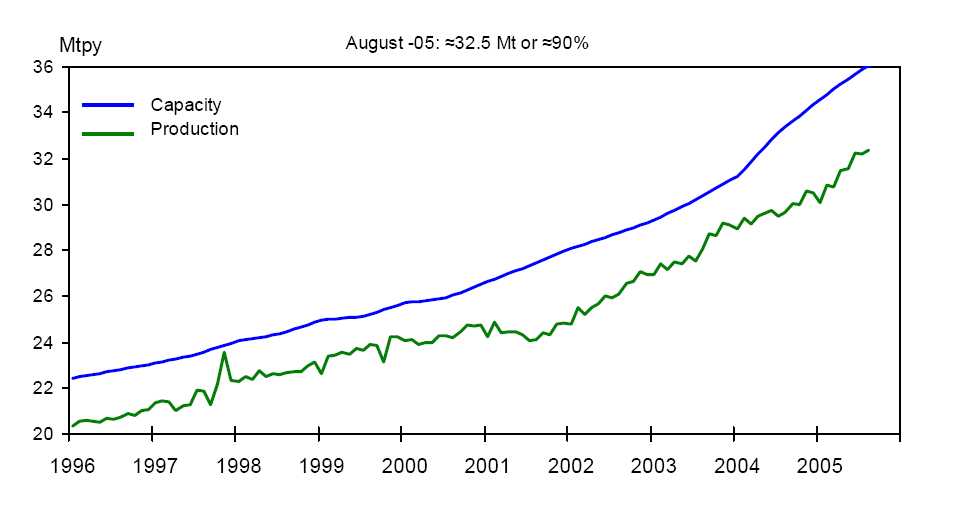

| World Primary Aluminum Operating Rate |

| ||

|

| |||

| © 2005 ALCAN INC. | Slide 28 | ||

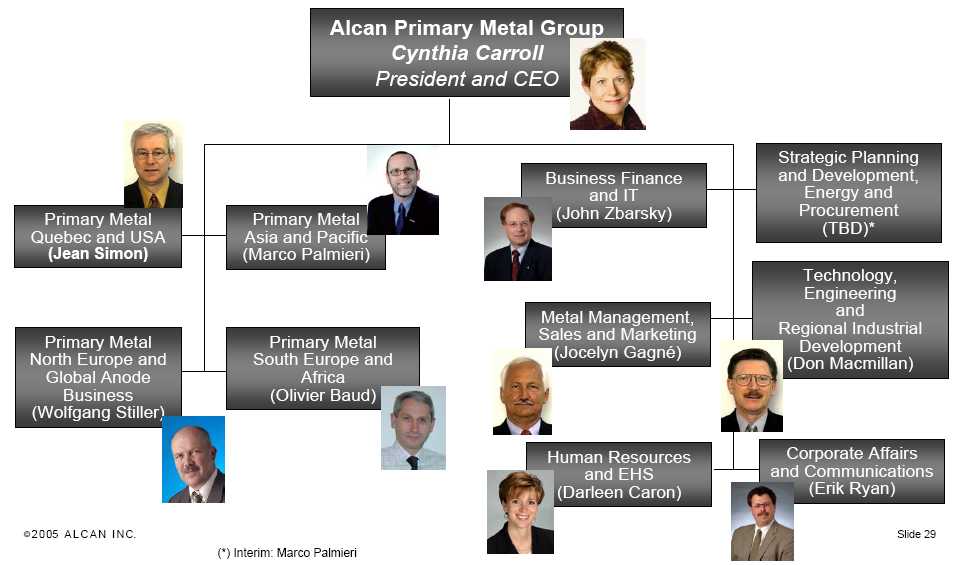

| AlcanPrimary Metal Organization |

| |

|

| ||