Exhibit 99.7 Slides of Presentation by Christel Bories, Senior Vice President, Alcan Inc., President and Chief Executive Officer, Alcan Packaging.

![]()

| Forward Looking Statements |

| ||

| Statements made in the course of this presentation which describe the Company's intentions, expectations or predictions may be "forward-looking statements" within the meaning of securities laws. The Company cautions that, by their nature, forward-looking statements involve risk and uncertainty, and actual actions or results could differ materially. Reference should be made to the most recent Form 10-Q and Form 10-K for a summary of major risk factors. In addition, certain non-GAAP measures are used which are reconciled to the comparable GAAP measures herein or on the Company’s website at www.alcan.com in the “Investors” section.

References to "markets" or "market shares" as used in this document do not necessarily reflect regulatory market definitions.

| |||

| © 2005 ALCAN INC. | Slide 2 | ||

| Agenda |

| ||

| |||

| © 2005 ALCAN INC. | Slide 3 | ||

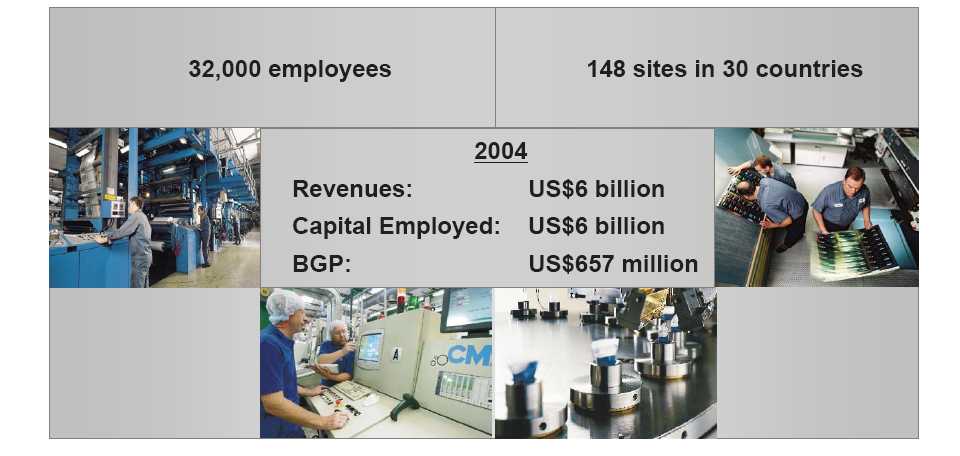

| Alcan Packaging |

| ||

A global leader | |||

|

| |||

| © 2005 ALCAN INC. | Slide 4 | ||

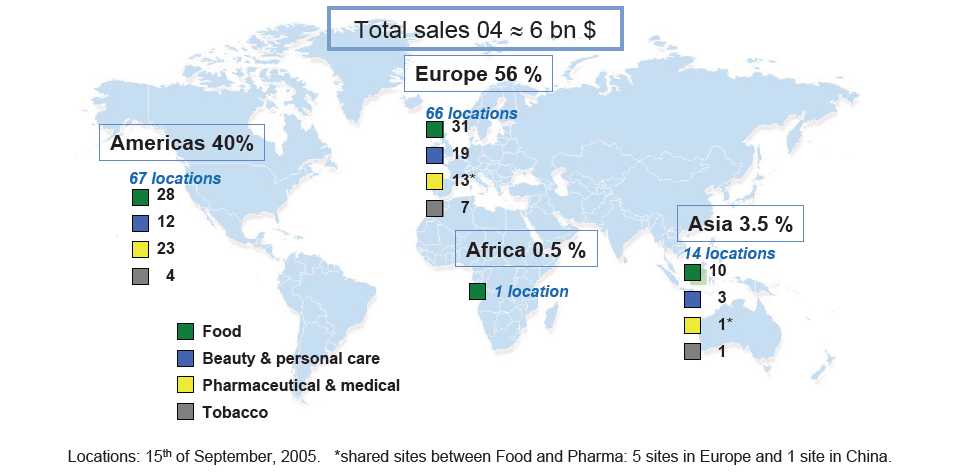

Sales by Region |

| ||

Global reach in all our segments | |||

| |||

© 2005 ALCAN INC. | Slide 5 | ||

| Competitive Landscape |

| |

N°8 overall, but N°2 in high value-added specialty packaging | ||

The World’s Largest Packaging Companies (2004 figures)

Country | Packaging | Principle Products | |

| 1 Tetrapak | Swe | 9.2 | Liquid Packaging & Packaging Machinery |

| 2 Smurfit Stone Container | USA | 8.3 | Containerboard & Corrugated |

| 3 Amcor | Aus | 8.1 | PET Containers, Closures, Flexibles, Corrugated, Cartons, Metal Cans |

| 4 International Paper | USA | 7.4 | Paperboard, Cartonboard, Folding Cartons |

| 5 Crown Cork & Seal | USA | 7.2 | Metal Cans |

| 6 Toyo Seikan | Jap | 6.6 | Metal Cans, and Plastics & Glass Containers |

| 7 Owens Illinois | USA | 6.3 | Glass and Plastic Containers |

| 8 Alcan Packaging | Can | 6.1 | Flexible Packaging, Rigid Plastics, Cartons, Glass Tubing |

| 9 Rexam | UK | 5.6 | Metal Cans, Rigid Plastics |

| 10 Ball | USA | 5.4 | Metal Cans |

| 11 Avery Dennison | USA | 5.3 | Flexible Packaging and Labels |

| 12 St Gobain | Fra | 4.6 | Glass Containers |

| 13 Weyerhaeuser | USA | 4.5 | Containerboard, Packaging and Recycling |

| 14 Sealed Air | USA | 3.8 | Flexible Packaging and Protective Packaging |

| 15 Jefferson Smurfit | Ire | 3.8 | Containerboard, Packaging and Recycling |

| 16 Pactiv | USA | 3.4 | Flexible and Protective Packaging, Food Service |

| 17 Alcoa | USA | 3.2 | Consumer Products, Food Service, Closures, Flexible Packaging |

| 18 Sonoco | USA | 3.2 | Paper and Plastic Flexibles, Paperboard |

| 19 Bemis | USA | 2.8 | Flexible Packaging and Labels |

| 20 Huhtamaki | Fin | 2.6 | Rigid Thin-Walled Plastic & Paper, Molded Fiber and Flexible Packaging |

107.6 |

The world’s top 20 packaging companies represent less than 25% of the total supply

| © 2005 ALCAN INC. | Slide 6 |

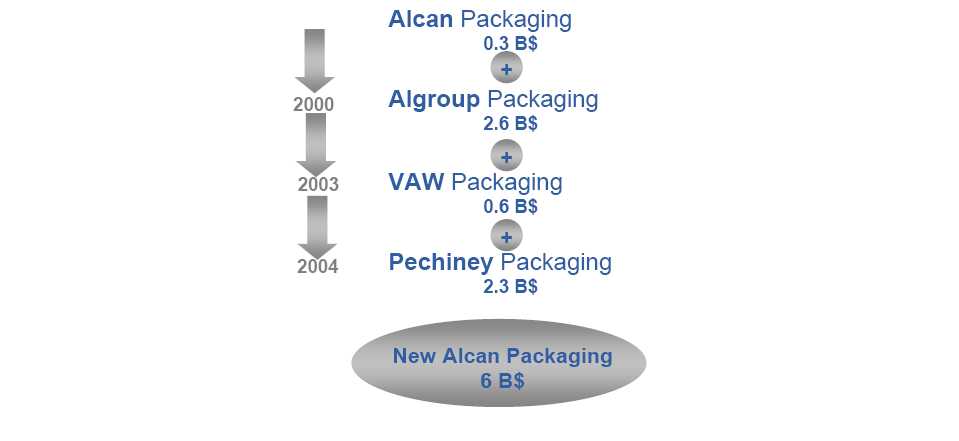

| Milestones |

| ||

Leadership through major acquisitions | |||

|

| |||

| © 2005 ALCAN INC. | Slide 7 | ||

| Market Position |

| ||

Leading Positions in Key Segments | |||

|

| |||

| © 2005 ALCAN INC. | Slide 8 | ||

| Market Participation |

| ||

Focused on attractive markets where we can differentiate | |||

| |||

| © 2005 ALCAN INC. | Slide 9 | ||

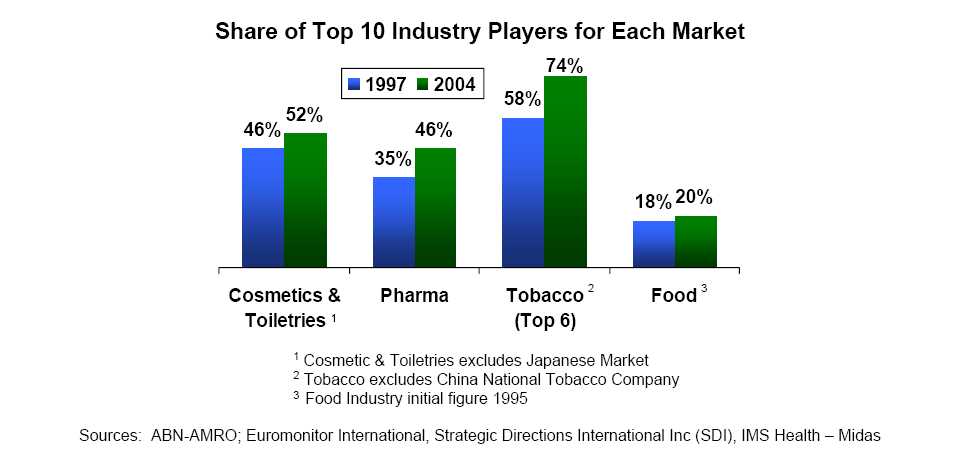

Market Participation |

| ||

Trends have not changed but …are accelerating | |||

| ■The footprints of our largest customers are changing, as they are investing heavily ■Globalization and consolidation of our customer base create pressure on bothprice ■Consumer needs are changing with life cycles and demographics (aging population) in ■More demand for service innovationand supply chain integration ■Regulatory requirementsare increasing. | |||

…and two new trends may continue | |||

■Softness in Western Europe consumer demand is creating a highly competitive | |||

■Oil prices are likely to remain high, which will continue todrive higher resin prices | |||

© 2005 ALCAN INC. | Slide 10 | ||

| Market Growth |

| |

Our customersare growing fast in new geographies | ||

| ||

| Market Trends -Illustration |

| ||

Consolidation …both on the customer and supplier side | |||

| |||

| © 2005 ALCAN INC. | Slide 12 | ||

| Raw Material Impact |

| ||

Plastic-basedproducts impacted by increased oil prices | |||

| |||

| © 2005 ALCAN INC. | Slide 13 | ||

| Integration and Synergies |

| ||

| |||

| © 2005 ALCAN INC. | Slide 14 | ||

| Strategy Summary |

| ||

| |||

| © 2005 ALCAN INC. | Slide 15 | ||

| Operating Excellence |

| ||

Laying the foundation for future success | |||

| |||

| © 2005 ALCAN INC. | Slide 16 | ||

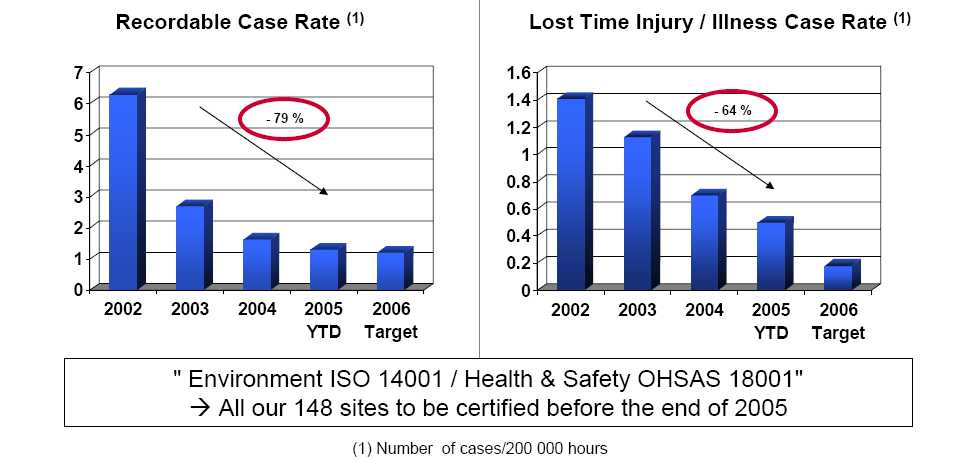

| Operating Excellence - EHS |

| ||

Significant improvement over the last 3 years | |||

|

| |||

| © 2005 ALCAN INC. | Slide 17 | ||

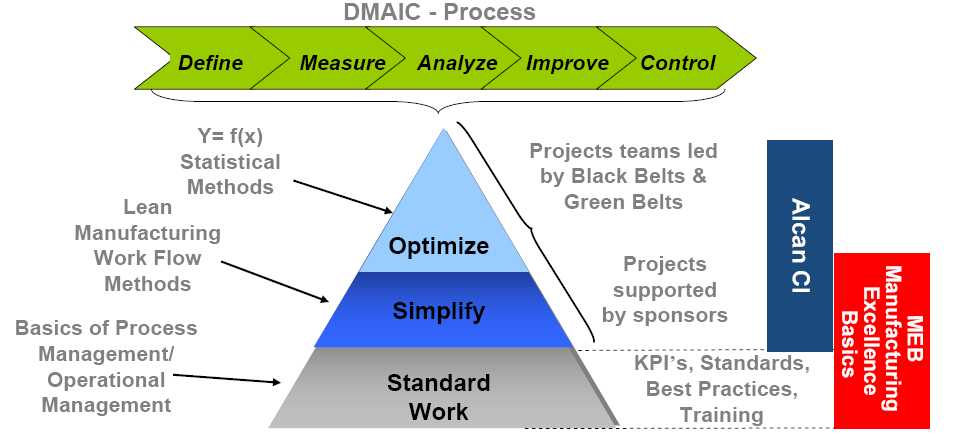

| Operating Excellence -CI |

| ||

Lean 6 sigma supported by manufacturing excellence basics to accelerate deployment and exchange of best practices | |||

| |||

| © 2005 ALCAN INC. | Slide 18 | ||

| © 2005 ALCAN INC. | Slide 19 |

Manufacturing Footprint |

| ||

A strong base for low-cost export | |||

|

| |||

| © 2005 ALCAN INC. | Slide 20 | ||

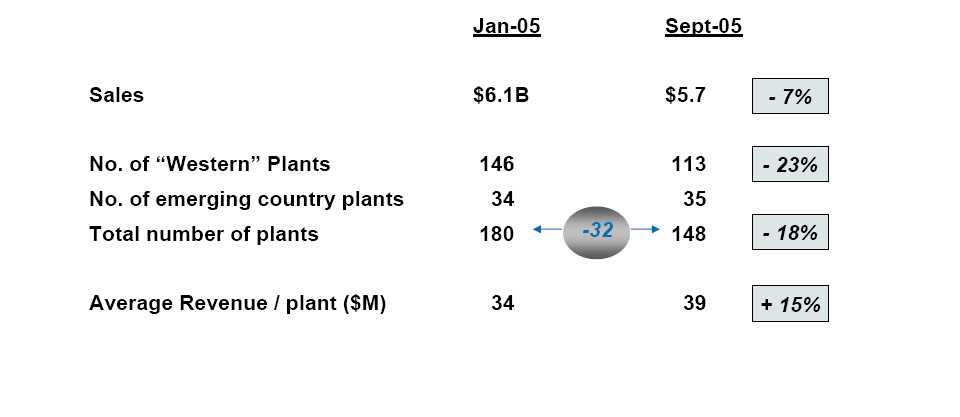

| Manufacturing Footprint |

| ||

Reinforcing our Western businesses | |||

| |||

| © 2005 ALCAN INC. | Slide 21 | ||

| Manufacturing Footprint |

| ||

|

| |||

| © 2005 ALCAN INC. | Slide 22 | ||

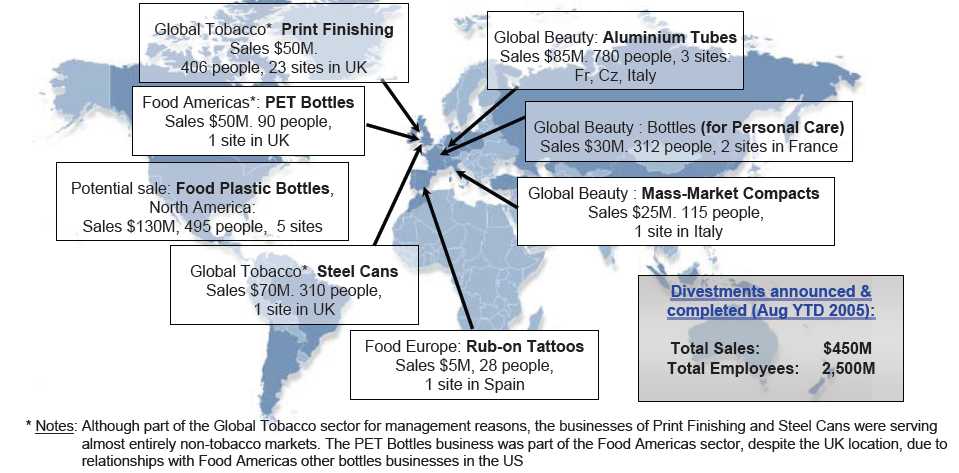

| Portfolio Rationalization |

| ||

Exiting Mature and Unprofitable Segments … | |||

|

| |||

| © 2005 ALCAN INC. | Slide 23 | ||

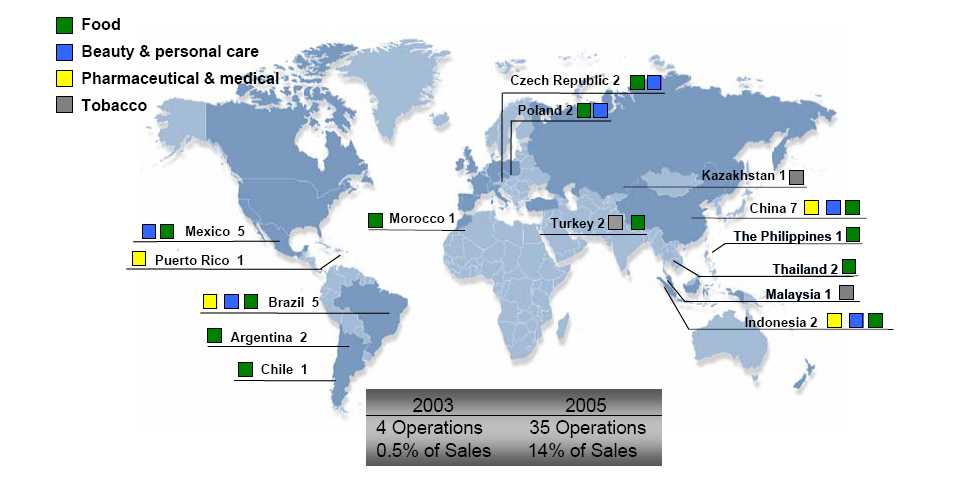

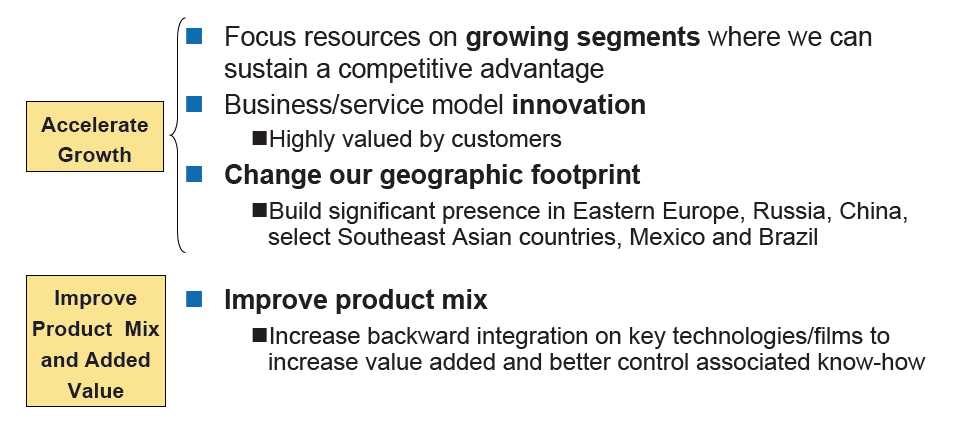

| Growth |

| ||

Focusing on growing, attractive market segments | |||

| |||

| © 2005 ALCAN INC. | Slide 24 | ||

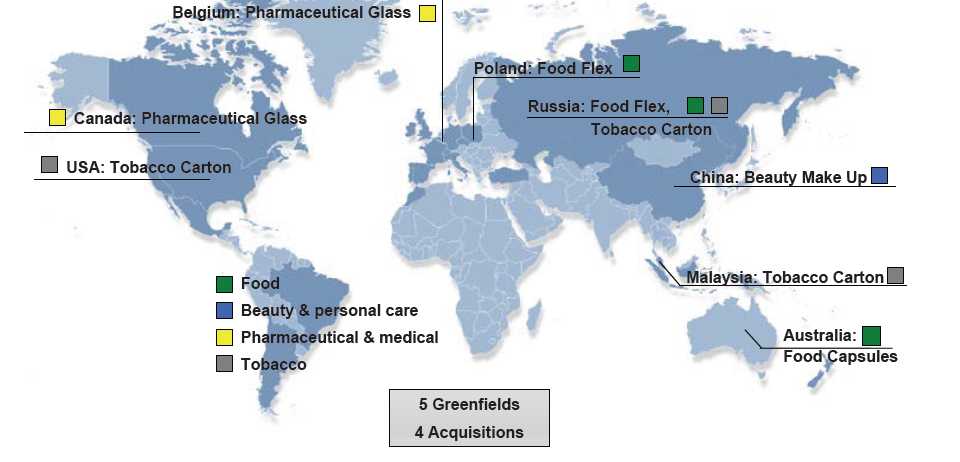

| Growth –Portfolio Realignment |

| ||

Extending our footprint in attractive segments and geographies | |||

| |||

| © 2005 ALCAN INC. | Slide 25 | ||

| Innovation Process |

| ||

Driving profitable, sustainable organic growth | |||

|

| |||

| © 2005 ALCAN INC. | Slide 26 | ||

| BGP Margin |

| ||

Target 15% in 2009 | |||

|

| |||

| © 2005 ALCAN INC. | Slide 27 | ||

APPENDIX

| |

|

| |

| © 2005 ALCAN INC. | Slide 29 |

| AlcanPackaging Locations |

| ||

| |||

| © 2005 ALCAN INC. | Slide 30 | ||

| Alcan Packaging Organization |

| ||

| |||

| © 2005 ALCAN INC. | Slide 31 | ||

| Food Flexible Worldwide No. 1 |

| ||

| |||

| © 2005 ALCAN INC. | Slide 32 | ||

| Pharmaceutical Worldwide No. 1 |

| ||

| |||

| © 2005 ALCAN INC. | Slide 33 | ||

| Cosmetics & Personal Care Worldwide No. 1 |

| ||

| |||

| © 2005 ALCAN INC. | Slide 34 | ||

| Tobacco Worldwide No. 2 –Soon No. 1 |

| ||

| |||

| © 2005 ALCAN INC. | Slide 35 | ||

| © 2005 ALCAN INC. | Slide 36 |