UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 18-K

For Foreign Governments and Political Subdivisions Thereof

ANNUAL REPORT

of

HYDRO-QUÉBEC

QUÉBEC, CANADA

(Name of Registrant)

Date of end of last fiscal year: December 31, 2007

SECURITIES REGISTERED*

(As of the close of the fiscal year)

| | | | |

| |

| Title of Issue | | Amounts as to Which

Registration is Effective | | Names of Exchanges

on Which Registered |

N/A | | N/A | | N/A |

| |

| |

Name and address of persons authorized to receive notices

and communications from the Securities and Exchange Commission:

MR. ROBERT KEATING

Delegate General

Québec Government House

One Rockefeller Plaza

26th Floor

New York, NY 10020-2102

Copies to:

| | |

MR. ROBERT E. BUCKHOLZ, JR.

Sullivan & Cromwell LLP

125 Broad Street

New York, NY 10004-2498 | | MR. DANIEL GARANT

Chief Financial Officer

Hydro-Québec

75 René-Lévesque Boulevard West

5th Floor

Montréal, Québec, Canada H2Z 1A4 |

| * | The Registrant is filing this annual report on a voluntary basis. |

The information set forth below is to be furnished:

| 1. | In respect of each issue of securities of the registrant registered, a brief statement as to: |

| | (a) | The general effect of any material modifications, not previously reported, of the rights of the holders of such securities. |

Not applicable.

| | (b) | The title and the material provisions of any law, decree or administrative action, not previously reported, by reason of which the security is not being serviced in accordance with the terms thereof. |

Not applicable.

| | (c) | The circumstances of any other failure, not previously reported, to pay principal, interest, or any sinking fund or amortization installment. |

Not applicable.

| 2. | A statement as of the close of the last fiscal year of the registrant giving the total outstanding of: |

| | (a) | Internal funded debt of the registrant. (Total to be stated in the currency of the registrant. If any internal funded debt is payable in foreign currency, it should not be included under this paragraph (a), but under paragraph (b) of this item.) |

Reference is made to pages 66 and 82 of Exhibit (1) hereto.

| | (b) | External funded debt of the registrant. (Totals to be stated in the respective currencies in which payable. No statement need be furnished as to intergovernmental debt.) |

Reference is made to pages 66, 83 and 84 of Exhibit (1) hereto.

| 3. | A statement giving the title, date of issue, date of maturity, interest rate and amount outstanding, together with the currency or currencies in which payable, of each issue of funded debt of the registrant outstanding as of the close of the last fiscal year of the registrant. |

Reference is made to pages 82 to 84 of Exhibit (1) hereto.

| 4. (a) | As to each issue of securities of the registrant which is registered, there should be furnished a break-down of the total amount outstanding, as shown in Item 3, into the following: |

| | (1) | Total amount held by or for the account of the registrant. |

Not applicable.*

| | (2) | Total estimated amount held by nationals of the registrant (or if registrant is other than a national government by the nationals of its national government); this estimate need be furnished only if it is practicable to do so. |

Not applicable.*

| | (3) | Total amount otherwise outstanding. |

Not applicable.*

| * | No securities of the registrant are registered under the U.S. Exchange Act of 1934, as amended. |

i

| | (b) | If a substantial amount is set forth in answer to paragraph (a)(1) above, describe briefly the method employed by the registrant to reacquire such securities. |

Not applicable.

| 5. | A statement as of the close of the last fiscal year of the registrant giving the estimated total of: |

| | (a) | Internal floating indebtedness of the registrant. (Total to be stated in the currency of the registrant.) |

$143.5 million (including $70.5 million to two of our subsidiaries). The item “floating indebtedness” refers to indebtedness with an original maturity of less than one year.

| | (b) | External floating indebtedness of the registrant. (Total to be stated in the respective currencies in which payable.) |

None.

| 6. | Statements of the receipts, classified by source, and of the expenditures, classified by purpose, of the registrant for each fiscal year of the registrant ended since the close of the latest fiscal year for which such information was previously reported. These statements should be so itemized as to be reasonably informative and should cover both ordinary and extraordinary receipts and expenditures; there should be indicated separately, if practicable, the amount of receipts pledged or otherwise specifically allocated to any issue registered, indicating the issue. |

Reference is made to pages 46 to 81 of Exhibit (1) hereto.

| 7. (a) | If any foreign exchange control, not previously reported, has been established by the registrant (or if the registrant is other than a national government, by its national government), briefly describe the effect of any such action, not previously reported. |

None.

| | (b) | If any foreign exchange control previously reported has been discontinued or materially modified, briefly describe the effect of any such action, not previously reported. |

Not applicable.

ii

EXHIBIT

The following exhibits should be filed as part of the annual report:

| (a) | Copies of any amendments or modifications, other than such have been previously filed, to all exhibits previously filed other than annual budgets. |

Not applicable.

| (b) | A copy of any law, decree, or administrative document outlined in answer to Item 1(b). |

Not applicable.

| (c) | A copy of the latest annual budget of the registrant, if not previously filed, as presented to its legislative body. |

Not applicable.

| This | annual report comprises: |

| (a) | The cover page and pages numbered i to iv consecutively. |

| (b) | The following exhibits: |

| | (1) | Description of Hydro-Québec, dated as of May 2, 2008, including audited consolidated financial statements of Hydro-Québec for the year ended December 31, 2007. |

| | (2) | Consent of KPMG LLP and Ernst & Young LLP. |

| This | annual report is filed subject to the Instructions for Form 18-K for Foreign Governments and Political Subdivisions Thereof. |

EXHIBIT INDEX

| | |

Exhibits | | Description |

| |

| (1) | | Description of Hydro-Québec, dated as of May 2, 2008, including audited consolidated financial statements of Hydro-Québec for the year ended December 31, 2007. |

| |

| (2) | | Consent of KPMG LLP and Ernst & Young LLP. |

iii

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this annual report to be signed on its behalf by the undersigned, thereunto duly authorized, in Montréal, Canada, on the 2nd day of May, 2008.

| | |

HYDRO-QUÉBEC (Name of Registrant) |

| |

| By: | | /s/ Daniel Garant |

| | Daniel Garant |

| | Chief Financial Officer |

iv

EXHIBIT (1)

This description of Hydro-Québec is dated as of May 2, 2008 and appears as Exhibit (1) to Hydro-Québec’s annual report on Form 18-K to the U.S. Securities and Exchange Commission for the fiscal year ended December 31, 2007.

This document may be delivered to you at any time but you should assume that the information is accurate only as of May 2, 2008. Hydro-Québec’s business, financial condition, results of operations and prospects may have changed since that date.

This document does not constitute an offer to sell or the solicitation of an offer to buy any securities of Hydro-Québec, unless it is included in a registration statement filed under the Securities Act of 1933, as amended.

TABLE OF CONTENTS

| | |

| | | Page |

Where You Can Find More Information | | 3 |

Forward-Looking Statements | | 3 |

Foreign Exchange | | 3 |

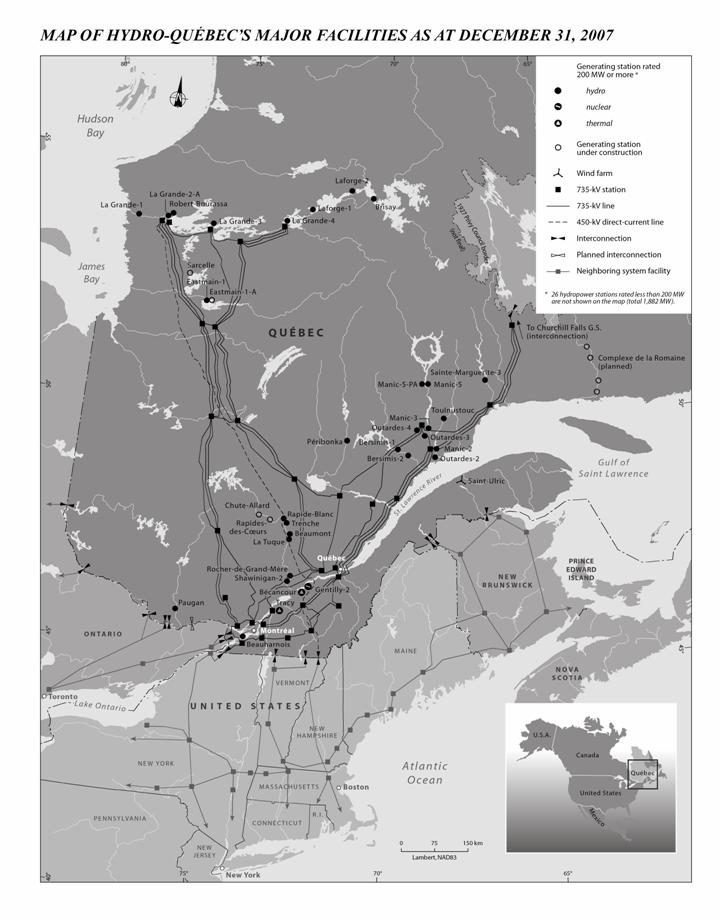

Map of Hydro-Québec’s Major Facilities | | 4 |

Five-Year Review | | 5 |

Hydro-Québec | | 8 |

General | | 8 |

Generation | | 8 |

Generation Operations | | 9 |

Wholesale and Trading Operations | | 11 |

Transmission | | 13 |

Transmission System | | 13 |

Distribution | | 14 |

Electricity Rates | | 15 |

Electricity Sales and Revenue | | 15 |

Construction | | 16 |

Corporate and Other Activities | | 16 |

Corporate Outlook | | 17 |

Development Strategy | | 17 |

Generations Fund | | 18 |

Capital Investment Program | | 19 |

Regulatory Framework | | 22 |

Litigation | | 24 |

Employees | | 24 |

Management’s Discussion and Analysis | | 25 |

Overview | | 25 |

Consolidated Results | | 26 |

Financial Position | | 28 |

Segmented Information | | 30 |

Integrated Enterprise Risk Management | | 41 |

Summary of Certain Material Differences between Canadian GAAP and US GAAP | | 43 |

Auditors’ Report | | 45 |

Consolidated Financial Statements | | 46 |

Supplementary Information | | 82 |

2

WHERE YOU CAN FIND MORE INFORMATION

This document appears as an exhibit to Hydro-Québec’s annual report filed with the U.S. Securities and Exchange Commission (the “SEC”) on Form 18-K for the fiscal year ended December 31, 2007. Additional information with respect to Hydro-Québec is available in the annual report or in other exhibits or amendments to the annual report.

You may read and copy any document we file with the SEC at the SEC’s public reference rooms in Washington, DC. Please call the SEC’s toll free number at 1-800-SEC-0330 for further information on the public reference room. These filings are also available from the Electronic Document Gathering and Retrieval System, which is commonly known by the acronym EDGAR, through the SEC’s website at http://www.sec.gov.

You may request a copy of these filings at no cost by telephoning Hydro-Québec at (514) 289-2519. This document is also available on our website at www.hydroquebec.com; however, any other information available on our website (such website listed in the 18-K is an inactive textual reference only) shall not be deemed to form a part of this document or the annual report to which it appears as an exhibit.

FORWARD-LOOKING STATEMENTS

Various statements made throughout this document are forward looking and contain information about financial results, economic conditions and trends, including, without limitation, the statements under the captions Corporate Outlook and Management’s Discussion and Analysis. The words “estimate”, “believe”, “expect”, “forecast”, “anticipate”, “intend” and “plan” and similar expressions identify forward-looking statements. You are cautioned that any such forward-looking statements are not guarantees of future performance. Forward-looking statements involve risks and uncertainties, and actual results may differ materially from those in the forward-looking statements as a result of various factors. Such factors may include, among others, business risks, such as variations in runoff that affect hydroelectric plant performance, and general levels of economic activity which affect demand for electricity, and risks related to economic parameters, such as changes in interest and exchange rates. You are cautioned not to place undue reliance on these forward-looking statements which speak only as of the date of this document. We undertake no obligation to publicly release the result of any revisions to these forward-looking statements which may be made to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

FOREIGN EXCHANGE

Canada maintains a floating exchange rate for the Canadian dollar in order to permit the rate to be determined by fundamental forces without intervention except as required to maintain orderly conditions. Annual average noon spot exchange rates for major foreign currencies in which the debt of Hydro-Québec is denominated, expressed in Canadian dollars, are shown below.

| | | | | | | | | | | | | | | | | | |

Foreign Currency | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 | | 2008 (1) |

United States Dollar | | $ | 1.4015 | | $ | 1.3015 | | $ | 1.2116 | | $ | 1.1341 | | $ | 1.0748 | | $ | 1.0065 |

Euro | | | 1.5826 | | | 1.6169 | | | 1.5090 | | | 1.4237 | | | 1.4691 | | | 1.5286 |

Swiss Franc | | | 1.0418 | | | 1.0473 | | | 0.9746 | | | 0.9050 | | | 0.8946 | | | 0.9563 |

Pound Sterling | | | 2.2883 | | | 2.3842 | | | 2.2067 | | | 2.0886 | | | 2.1487 | | | 1.9920 |

100 Japanese Yen | | | 1.2088 | | | 1.2035 | | | 1.1035 | | | 0.9753 | | | 0.9121 | | | 0.9633 |

| (1) | Monthly average through the end of April 2008. |

In this document, unless otherwise specified or the context otherwise requires, all dollar amounts are expressed in Canadian dollars.

3

4

FIVE-YEAR REVIEW

Consolidated and Selected Financial Information

| | | | | | | | | | | | | | | | | | | | |

| | | Years ended December 31 | |

| | | 2003 | | | 2004 | | | 2005 | | | 2006 | | | 2007 | |

| | | (in millions of dollars) | |

OPERATIONS | | | | | | | | | | | | | | | | | | | | |

Revenue | | $ | 10,197 | | | $ | 10,341 | | | $ | 10,887 | | | $ | 11,161 | | | $ | 12,330 | |

Expenditure | | | | | | | | | | | | | | | | | | | | |

Operations | | | 2,070 | | | | 2,158 | | | | 2,248 | | | | 2,394 | | | | 2,545 | |

Electricity and fuel purchases | | | 1,380 | | | | 1,464 | | | | 1,496 | | | | 1,315 | | | | 1,555 | |

Depreciation and amortization | | | 1,768 | | | | 1,862 | | | | 2,023 | | | | 2,007 | | | | 1,991 | |

Taxes | | | 567 | | | | 606 | | | | 594 | | | | 529 | | | | 816 | |

Regulatory deferrals | | | — | | | | — | | | | (11 | ) | | | (93 | ) | | | 29 | |

| | | | | | | | | | | | | | | | | | | | |

| | | 5,785 | | | | 6,090 | | | | 6,350 | | | | 6,152 | | | | 6,936 | |

| | | | | | | | | | | | | | | | | | | | |

Operating Income | | | 4,412 | | | | 4,251 | | | | 4,537 | | | | 5,009 | | | | 5,394 | |

Financial expenses | | | 2,492 | | | | 2,083 | | | | 2,186 | | | | 2,212 | | | | 2,512 | |

| | | | | | | | | | | | | | | | | | | | |

Income from continuing operations | | | 1,920 | | | | 2,168 | | | | 2,351 | | | | 2,797 | | | | 2,882 | |

Income (loss) from discontinued operations | | | 18 | | | | 267 | | | | (99 | ) | | | 944 | | | | 25 | |

| | | | | | | | | | | | | | | | | | | | |

Net Income | | $ | 1,938 | | | $ | 2,435 | | | $ | 2,252 | | | $ | 3,741 | | | $ | 2,907 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

DIVIDENDS DECLARED | | $ | 965 | | | $ | 1,350 | | | $ | 1,126 | | | $ | 2,342 | | | $ | 2,095 | |

| | | | | |

BALANCE SHEET SUMMARY | | | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 57,823 | | | $ | 58,072 | | | $ | 60,431 | | | $ | 63,254 | | | $ | 64,852 | |

Long-term debt, including current portion and perpetual debt | | $ | 35,550 | | | $ | 33,401 | | | $ | 33,007 | | | $ | 34,427 | | | $ | 34,534 | |

Equity | | $ | 15,128 | | | $ | 16,220 | | | $ | 17,376 | | | $ | 18,840 | | | $ | 20,892 | |

| | | | | |

INVESTMENTS FOR CONTINUING OPERATIONS AFFECTING CASH | | | | | | | | | | | | | | | | | | | | |

Property, plant and equipment and intangible assets | | $ | 2,739 | | | $ | 3,071 | | | $ | 3,293 | | | $ | 3,348 | | | $ | 3,464 | |

Costs related to Energy Efficiency Plan | | | 10 | | | | 41 | | | | 91 | | | | 149 | | | | 172 | |

| | | | | | | | | | | | | | | | | | | | |

Total investments | | $ | 2,749 | | | $ | 3,112 | | | $ | 3,384 | | | $ | 3,497 | | | $ | 3,636 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

FINANCIAL RATIOS | | | | | | | | | | | | | | | | | | | | |

Interest coverage a | | | 1.73 | | | | 1.79 | | | | 2.00 | | | | 2.06 | | | | 2.13 | |

Capitalization b | | | 29.9 | % | | | 32.7 | % | | | 34.1 | % | | | 36.1 | % | | | 37.5 | % |

Self-financing c | | | 56.3 | % | | | 78.4 | % | | | 58.6 | % | | | 86.5 | % | | | 61.9 | % |

Return on equity d | | | 13.1 | % | | | 15.4 | % | | | 13.3 | % | | | 20.6 | % | | | 15.0 | % |

Profit margin from continuing operations e | | | 18.8 | % | | | 21.0 | % | | | 21.6 | % | | | 25.1 | % | | | 23.4 | % |

| (a) | Sum of operating income and net investment income divided by gross interest expense. |

| (b) | Equity divided by the sum of equity, long-term debt, perpetual debt, short-term borrowings, current portion of long-term debt and derivative instrument liabilities, less derivative instrument assets. |

| (c) | Cash flows from continuing operations less dividends paid, divided by the sum of investments, long-term debt maturities and sinking fund redemptions. |

| (d) | Net income divided by average equity less average accumulated other comprehensive income. |

| (e) | Net income from continuing operations divided by revenue. |

| Note: | Throughout the Five-Year Review, certain comparative figures have been reclassified to reflect the presentation adopted for 2007. |

5

FIVE-YEAR REVIEW (CONTINUED)

Operating Statistics

| | | | | | | | | | | | | | | |

| | | Years ended December 31 |

| | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 |

| | | (in GWh) |

Electricity Sales | | | | | | | | | | | | | | | |

In Québec, by category | | | | | | | | | | | | | | | |

Residential and farm | | | 57,217 | | | 58,002 | | | 57,269 | | | 56,722 | | | 60,046 |

General and institutional | | | 32,314 | | | 33,137 | | | 33,463 | | | 32,440 | | | 34,751 |

Industrial | | | 72,546 | | | 69,722 | | | 73,447 | | | 73,297 | | | 73,005 |

Other | | | 5,014 | | | 5,026 | | | 4,998 | | | 4,878 | | | 5,353 |

| | | | | | | | | | | | | | | |

| | | 167,091 | | | 165,887 | | | 169,177 | | | 167,337 | | | 173,155 |

| | | | | | | | | | | | | | | |

Outside Québec | | | | | | | | | | | | | | | |

Long-term | | | 2,047 | | | 1,930 | | | 2,068 | | | 2,384 | | | 2,384 |

Short-term | | | 13,739 | | | 12,462 | | | 13,274 | | | 12,074 | | | 17,240 |

| | | | | | | | | | | | | | | |

| | | 15,786 | | | 14,392 | | | 15,342 | | | 14,458 | | | 19,624 |

| | | | | | | | | | | | | | | |

Total Electricity Sales | | | 182,877 | | | 180,279 | | | 184,519 | | | 181,795 | | | 192,779 |

| | | | | | | | | | | | | | | |

| |

| | | (in millions of dollars) |

Revenue from Electricity Sales | | | | | | | | | | | | | | | |

In Québec, by category | | | | | | | | | | | | | | | |

Residential and farm | | $ | 3,504 | | $ | 3,690 | | $ | 3,690 | | $ | 3,775 | | $ | 4,144 |

General and institutional | | | 2,096 | | | 2,234 | | | 2,284 | | | 2,356 | | | 2,602 |

Industrial | | | 2,742 | | | 2,751 | | | 2,892 | | | 3,022 | | | 3,336 |

Other | | | 236 | | | 247 | | | 255 | | | 249 | | | 286 |

| | | | | | | | | | | | | | | |

| | | 8,578 | | | 8,922 | | | 9,121 | | | 9,402 | | | 10,368 |

| | | | | | | | | | | | | | | |

Outside Québec | | | | | | | | | | | | | | | |

Long-term | | | 207 | | | 179 | | | 174 | | | 198 | | | 225 |

Short-term | | | 1,138 | | | 905 | | | 1,290 | | | 951 | | | 1,392 |

| | | | | | | | | | | | | | | |

| | | 1,345 | | | 1,084 | | | 1,464 | | | 1,149 | | | 1,617 |

| | | | | | | | | | | | | | | |

Total Revenue from Electricity Sales | | $ | 9,923 | | $ | 10,006 | | $ | 10,585 | | $ | 10,551 | | $ | 11,985 |

| | | | | | | | | | | | | | | |

| |

| | | (as at December 31) |

Number of Customer Accounts in Québec, by Category | | | | | | | | | | | | | | | |

Residential and farm | | | 3,343,271 | | | 3,399,776 | | | 3,450,455 | | | 3,501,709 | | | 3,554,443 |

General and institutional | | | 281,997 | | | 282,748 | | | 283,616 | | | 295,618 | | | 299,524 |

Industrial | | | 13,383 | | | 13,117 | | | 12,796 | | | 12,032 | | | 11,565 |

Other | | | 5,812 | | | 5,634 | | | 5,643 | | | 5,767 | | | 3,440 |

| | | �� | | | | | | | | | | | | |

Total Number of Customer Accounts | | | 3,644,463 | | | 3,701,275 | | | 3,752,510 | | | 3,815,126 | | | 3,868,972 |

| | | | | | | | | | | | | | | |

| |

| | | (kWh/customer account) |

Average Annual Consumption in Québec, by Category | | | | | | | | | | | | | | | |

Residential and farm | | | 17,237 | | | 17,203 | | | 16,720 | | | 16,318 | | | 17,019 |

General and institutional | | | 114,651 | | | 117,352 | | | 118,168 | | | 112,010 | | | 116,782 |

Industrial | | | 5,395,359 | | | 5,262,038 | | | 5,668,738 | | | 5,904,382 | | | 6,187,651 |

Other | | | 864,110 | | | 878,211 | | | 886,406 | | | 855,039 | | | 1,162,811 |

6

FIVE-YEAR REVIEW (CONTINUED)

Operating Statistics (continued)

| | | | | | | | | | |

| | | Years ended December 31 |

| | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 |

| | | (in MW) |

Installed Capacity a | | | | | | | | | | |

Hydroelectric | | 31,347 | | 31,622 | | 32,299 | | 32,973 | | 33,305 |

Nuclear | | 675 | | 675 | | 675 | | 675 | | 675 |

Conventional thermal | | 1,592 | | 1,593 | | 1,595 | | 1,665 | | 1,665 |

Wind | | 2 | | 2 | | 2 | | 2 | | 2 |

| | | | | | | | | | |

Total Installed Capacity | | 33,616 | | 33,892 | | 34,571 | | 35,315 | | 35,647 |

| | | | | | | | | | |

| |

| | | (in GWh) |

Total Energy Requirements b | | 194,792 | | 193,025 | | 200,179 | | 199,447 | | 209,818 |

| |

| | | (in MW) |

Peak Power Demand in Québec c | | 36,268 | | 34,956 | | 33,636 | | 36,251 | | 35,352 |

| |

| | | (in km *) |

Lines (overhead and underground) | | | | | | | | | | |

Transmission | | 32,434 | | 32,487 | | 32,544 | | 32,826 | | 33,008 |

Distribution d | | 106,568 | | 107,423 | | 108,344 | | 108,883 | | 109,618 |

| | | | | | | | | | |

| | 139,002 | | 139,910 | | 140,888 | | 141,709 | | 142,626 |

| | | | | | | | | | |

| (a) | In addition, we have access to 4,765 MW of the generation of the Churchill Falls power plant and purchase all the output from seven privately-owned wind farms with a total installed capacity of 420 MW. Moreover, 1,222 MW are available under agreements with other independent suppliers. |

| (b) | Total energy requirements consist of kilowatthours delivered within Québec and to neighboring systems. |

| (c) | Total power demand at the annual domestic peak for the winter beginning in December, including interruptible power. The 2007-2008 winter peak for Québec occurred at 8 a.m. on January 21, 2008. |

| (d) | These figures include off-grid systems but exclude private systems, lines under construction and 44-kV lines (transmission). |

Other Information

| | | | | | | | | | | | | | | |

| | | Years ended December 31 | |

| | | 2003 | | | 2004 | | | 2005 | | | 2006 | | | 2007 | |

Rate Increases | | | | | | | | | | | | | | | |

Average increase from January 1 to December 31 | | — | | | 4.1 | % | | 1.3 | % | | 4.3 | % | | 2.8 | % |

Inflation rate | | 2.8 | % | | 1.8 | % | | 2.2 | % | | 2.0 | % | | 2.2 | % |

Number of Employees (1) | | | | | | | | | | | | | | | |

Permanent as at December 31 | | 18,317 | | | 18,835 | | | 19,009 | | | 19,116 | | | 19,459 | |

Temporary (year’s average) | | 3,596 | | | 3,567 | | | 3,577 | | | 3,799 | | | 3,910 | |

Women | | 28.9 | % | | 29.4 | % | | 29.8 | % | | 30.6 | % | | 31.3 | % |

| (1) | Excludes employees of subsidiaries and joint ventures. |

UNITS OF MEASUREMENT

| | | | | | |

| kV: kilovolt, or 1 thousand volts |

kW: | | kilowatt, or 1 thousand watts | | kWh: | | kilowatthour, or 1 thousand watthours |

MW: | | megawatt, or 1 million watts | | MWh: | | megawatthour, or 1 million watthour |

GW: | | gigawatt, or 1 million kilowatts | | GWh: | | gigawatthour, or 1 million kilowatthours |

| | | | TWh: | | terawatthour, or 1 billion kilowatthours |

7

HYDRO-QUÉBEC

GENERAL

We operate one of the two largest systems in Canada for the generation and distribution of electric power. We supply virtually all electric power distributed in Québec, the largest province in Canada in land area and the second largest in population.

Hydro-Québec was created in 1944 by the Hydro-Québec Act of the Parliament of Québec and is an agent of Québec. All capital stock of Hydro-Québec is held by the Minister of Finance on behalf of the government of Québec (the “Government”).

Our head office is located at 75 René-Lévesque Boulevard West, Montréal, Québec, Canada H2Z 1A4.

Our operations are allocated among five business segments:

| | • | | Generation: Hydro-Québec Production operates and develops our generation facilities in Québec. It also sells electricity in markets outside Québec and engages in energy trading. Hydro-Québec Production is required to provide Hydro-Québec Distribution with up to 165 TWh a year of heritage pool electricity, at an average price of 2.79 ¢/kWh (“Heritage Pool Electricity”). In excess of this volume, it may participate in Hydro-Québec Distribution’s calls for tenders in a context of free market competition; |

| | • | | Transmission: Hydro-Québec TransÉnergie operates and develops our power transmission system in Québec and manages power flows on the transmission grid; |

| | • | | Distribution: Hydro-Québec Distribution operates and develops our distribution system and is responsible for sales and services to Québec customers. It also promotes energy efficiency and ensures the security of the supply of electricity to the Québec market; |

| | • | | Construction: Hydro-Québec Équipement carries out engineering and construction work related to hydroelectric development projects throughout Québec, except in the territory governed by the James Bay and Northern Québec Agreement, where our wholly-owned subsidiary, Société d’énergie de la Baie James (“SEBJ”), assumes this responsibility. Hydro-Québec Équipement also carries out projects for the construction of power transmission lines and substations throughout Québec; and |

| | • | | Corporate and Other Activities: Our corporate units support our divisions to achieve their business objectives. Our corporate units include the Technology Group, the Finance Group, Corporate Affairs and General Secretariat, as well as the Human Resources and Shared Services Group. The Shared Services Centre brings together internal services including goods and services procurement, real estate management, and material and transportation service management. |

GENERATION

Hydro-Québec Production generates electricity to supply the Québec market and sells its excess output on wholesale markets. Hydro-Québec Production also offers balancing and firming capacity services to Hydro-Québec Distribution to offset fluctuations in wind farm output and thereby facilitate the integration of this energy source.

The following subsidiaries, affiliates and interests are also part of this segment:

| | • | | Bucksport Energy LLC (69.44% interest; cogeneration plant in Maine); |

| | • | | Churchill Falls (Labrador) Corporation Limited (“CF(L)Co”) (34.2% interest; hydroelectric generation activities); |

| | • | | Société en commandite Betsiamites (86.31% interest; ownership of assets related to the partial diversion of the Portneuf, Sault aux Cochons and Manouane rivers); |

| | • | | Gestion Production HQ inc. (wholly-owned; investment in local generation businesses); |

| | • | | HQ Energy Marketing Inc. (“HQEM”) (wholly-owned; conducts energy transactions in other Canadian provinces and holds shares in energy trading companies in Canada and the United States); and |

| | • | | H.Q. Energy Services (U.S.) Inc. (“HQUS”) (wholly-owned subsidiary of HQEM; power marketer in the United States). |

8

GENERATION OPERATIONS

Facilities

In Québec, our electric generation system comprises 87 power stations currently in service, of which 57 are hydroelectric, 28 are thermal, one is nuclear and one is a wind farm, with a total installed capacity of 35,647 MW as of December 31, 2007.

The following table lists the generation facilities in service as of such date.

GENERATION FACILITIES IN SERVICE IN QUÉBEC (1)

| | | | |

Name of Facility | | Years Commissioned (2) | | Capacity |

| | | | | (MW) |

Hydroelectric | | | | |

Robert-Bourassa | | 1979-1981 | | 5,616 |

La Grande-4 | | 1984-1986 | | 2,779 |

La Grande-3 | | 1982-1984 | | 2,417 |

La Grande-2-A | | 1991-1992 | | 2,106 |

Beauharnois | | 1932-1961 | | 1,755 |

Manic-5 | | 1970-1971 | | 1,528 |

La Grande-1 | | 1994-1995 | | 1,436 |

Manic-3 | | 1975-1976 | | 1,244 |

Bersimis-1 | | 1956-1959 | | 1,125 |

Manic-5-PA | | 1989-1990 | | 1,064 |

Manic-2 | | 1965-1967 | | 1,041 |

Outardes-3 | | 1969 | | 1,026 |

Sainte-Marguerite-3 | | 2003 | | 884 |

Laforge-1 | | 1993-1994 | | 878 |

Bersimis-2 | | 1959-1960 | | 845 |

Carillon | | 1962-1964 | | 752 |

Outardes-4 | | 1969 | | 746 |

Toulnustouc | | 2005 | | 553 |

Eastmain-1 | | 2006 | | 507 |

Outardes-2 | | 1978 | | 472 |

Brisay | | 1993 | | 469 |

Laforge-2 | | 1996 | | 319 |

Trenche | | 1950-1955 | | 303 |

Beaumont | | 1958-1959 | | 270 |

La Tuque | | 1940-1955 | | 263 |

Rocher-de-Grand-Mère | | 2004 | | 230 |

Rapide-Blanc | | 1934-1955 | | 204 |

Paugan | | 1928-1956 | | 202 |

Shawinigan-2 | | 1911-1929 | | 200 |

Manic-1 | | 1966-1967 | | 184 |

Shawinigan-3 | | 1948-1949 | | 184 |

Rapides-des-Ïles | | 1966-1973 | | 176 |

Chelsea | | 1927-1939 | | 153 |

Péribonka | | 2007-2008 | | 135 |

Première-Chute | | 1968-1975 | | 130 |

La Gabelle | | 1924-1931 | | 129 |

Les Cèdres | | 1914-1924 | | 126 |

Grand-Mère | | 1915-1930 | | 105 |

Others (19 facilities - less than 100 MW)(3) | | 1910-2007 | | 749 |

| | | | |

Total | | | | 33,305 |

| | | | |

Thermal | | | | |

Tracy (oil) | | 1964-1968 | | 660 |

Bécancour, La Citière and Cadillac (gas turbine) | | 1976-1993 | | 881 |

Others (24 diesel plants) (3) | | 1946-2001 | | 124 |

| | | | |

Total | | | | 1,665 |

| | | | |

Nuclear | | | | |

| | | | |

Gentilly-2 (4) | | 1983 | | 675 |

| | | | |

Wind Farm | | | | |

| | | | |

Saint-Ulric (3 wind turbines) | | 2001 | | 2 |

| | | | |

| (1) | Installed capacity shown for the generation stations reflects the capacity of alternators operating in winter conditions at a water temperature of 41°F. |

| (2) | Indicates years when facilities began commercial operation. |

| (3) | Some facilities are owned by Hydro-Québec Distribution. |

| (4) | The Gentilly-2 plant has a Canada-Deuterium-Uranium heavy water moderated reactor, using heavy water as a moderator and coolant, and uranium dioxide as fuel. |

9

Power Purchases

We purchase power and energy from the Churchill Falls generation station in Labrador through agreements with CF(L)Co and Newfoundland and Labrador Hydro (“N&LH”). Under an initial power contract with CF(L)Co, we have agreed to purchase annually, through the year 2041, 4,083 MW of power. In June 1999, we signed another agreement with CF(L)Co to guarantee us the availability of 682 MW of additional power until 2041 for each November 1 to March 31 period. In February 2001, we agreed to purchase approximately 1.5 TWh annually from N&LH until March 2004. In 2004, this contract was renewed for the purchase of approximately 1.4 TWh annually for a five-year period. In 2007, purchases under the CF(L)Co and N&LH agreements totaled 30.0 TWh at a cost of $161 million as compared to 31.2 TWh at a cost of $159 million in 2006.

We have a capacity agreement with New Brunswick Power Generation Corporation (formerly known as New Brunswick Power Corporation) for the purchase of 200 MW annually until October 31, 2011. We also have an agreement with Alcan Inc. (“Alcan”), which was amended in 2006, for the purchase of 365 MW of peak power and 375 MW of additional peak power until December 31, 2045. Under this 2006 amendment, we agreed to purchase from Alcan 150 MW of additional peak power until January 1, 2013 which, if certain conditions are met, will be extended until December 31, 2045.

In addition, we purchase power under 83 long-term contracts with independent producers located in Québec. During 2007, 3.9 TWh were purchased under these contracts, at a total cost of $252 million. For 2008, we expect to purchase approximately 4.2 TWh under these contracts.

We also purchase power in connection with our trading operations (see “Wholesale and Trading Operations”).

Peak

We use energy purchased from our neighboring systems, which experience different demand patterns, to meet a portion of our peak power needs in Québec (see “Wholesale and Trading Operations”). The following table summarizes our peak power demand in Québec and installed capacity as at December 31 for the years 2003 through 2007.

| | | | | | |

| | | Peak Power

Demand (1) | | Installed

Capacity (2)(3) | | Total

Average Load (4) |

| | | | | (MW) | | |

2003 | | 36,268 | | 33,616 | | 22,237 |

2004 | | 34,956 | | 33,892 | | 21,975 |

2005 | | 33,636 | | 34,571 | | 22,851 |

2006 | | 36,251 | | 35,315 | | 22,768 |

2007 | | 35,352 | | 35,647 | | 23,952 |

| (1) | Total power demand at the annual domestic peak for the winter beginning in the preceding December, including interruptible power. The 2007-2008 winter peak occurred at 8:00 a.m. on January 21, 2008. |

| (2) | In addition, we have access to 4,765 MW of the generation of the Churchill Falls power plant and purchase all the output from seven privately-owned wind farms with a total installed capacity of 420 MW. Moreover, 1,222 MW are available under various agreements with other independent suppliers. |

| (3) | Installed capacity shown for the generation stations reflects the capacity of alternators operating in winter conditions at a water temperature of 41°F. |

| (4) | Annual energy demand, including sales outside Québec, divided by the number of hours in the year. |

Investment Outside Québec

We hold an indirect interest in Bucksport Energy LLC, a thermal energy plant located in Maine, U.S. The plant, which started its commercial operations in January 2001, produces approximately 1.3 TWh of electricity per year. HQUS supplies the plant with natural gas and receives most of the electricity under fifteen-year contracts through January 2016.

10

WHOLESALEAND TRADING OPERATIONS

Québec Wholesale Market

The Québec wholesale electricity market has been open since May 1, 1997. This market is comprised of 11 distributors: Hydro-Québec Distribution, nine distributors operating municipal systems and one regional electricity cooperative. As a result of the opening of the wholesale market, the municipal systems can, subject to the Government’s authorization, purchase electricity from suppliers other than Hydro-Québec Distribution, and independent generators in Québec can sell their electricity on the wholesale market using Hydro-Québec TransÉnergie’s transmission facilities.

Under a call for tenders issued by Hydro-Québec Distribution in 2002, Hydro-Québec Production signed an agreement with Hydro-Québec Distribution for the supply of 600 MW over a 20-year period starting in March 2007, which is in addition to the Heritage Pool Electricity.

Markets Outside Québec

Currently, our main markets outside Québec consist of neighboring networks located in Canada and the northeastern United States.

In 2007, electricity sales outside Québec accounted for 10.2% of our total electricity sales, up from 8.0% in 2006 (see “Management’s Discussion and Analysis - Segmented Information - Generation”). Additional sales commitments were met using electricity purchases and our surplus Québec generation capacity.

Our energy-trading subsidiary, HQUS, is a member of New York ISO, ISO New England, Midwest ISO (which includes all or parts of Illinois, Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Missouri, Montana, Nebraska, North Dakota, Ohio, Pennsylvania, South Dakota, Wisconsin and Manitoba) and PJM Interconnection (which includes all or parts of Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia and the District of Columbia). ISOs, or Independent Systems Operators, and RTOs, or Regional Transmission Organizations, enable participants to buy and sell energy, schedule bilateral transactions and reserve transmission service. HQUS holds a permit from the U.S. Federal Energy Regulatory Commission to sell at market-based rates.

HQEM, our wholly-owned energy-trading subsidiary operating in Canada, trades in the Ontario and New Brunswick wholesale markets. HQEM is a member of the Independent Electricity System Operator (the Ontario ISO).

We have two long-term export contracts for the sale of energy or power. The following table summarizes our principal energy export agreements.

PRINCIPAL ENERGY EXPORT AGREEMENTS

| | | | | | | |

| | | Expiry

Date | | Power | | | Maximum

Annual

Deliveries |

| | | | | (MW) | | | (TWh) |

Long-Term Sales - Power and Energy (not interruptible) | | | | | | | |

Cornwall Electric - Canada | | 2019 | | 45 | | | 0.2 |

Vermont Joint Owners (“VJO”) | | 2020 | | 335 | (1) | | 2.2 |

| (1) | By separate agreement with a VJO Member, 25 MW (0.2 TWh) are being repurchased annually until April 30, 2012. |

11

Electricity Sales and Revenue

The following table summarizes electricity sales and revenue outside Québec, by category, for the years 2003 through 2007.

ELECTRICITY SALES AND REVENUE OUTSIDE QUÉBEC

| | | | | | | | | | | | | | | |

| | | Years ended December 31 |

| | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 |

| | | (in GWh) |

Electricity Sales | | | | | | | | | | | | | | | |

Long-term | | | 2,047 | | | 1,930 | | | 2,068 | | | 2,384 | | | 2,384 |

Short-term | | | 13,739 | | | 12,462 | | | 13,274 | | | 12,074 | | | 17,240 |

| | | | | | | | | | | | | | | |

Total Electricity Sales | | | 15,786 | | | 14,392 | | | 15,342 | | | 14,458 | | | 19,624 |

| | | | | | | | | | | | | | | |

| |

| | | (in millions of dollars) |

Revenue from Electricity Sales | | | | | | | | | | | | | | | |

Long-term | | $ | 207 | | $ | 179 | | $ | 174 | | $ | 198 | | $ | 225 |

Short-term | | | 1,138 | | | 905 | | | 1,290 | | | 951 | | | 1,392 |

| | | | | | | | | | | | | | | |

Total Revenue from Electricity Sales | | $ | 1,345 | | $ | 1,084 | | $ | 1,464 | | $ | 1,149 | | $ | 1,617 |

| | | | | | | | | | | | | | | |

12

TRANSMISSION

Hydro-Québec TransÉnergie provides the following services:

| | • | | transmission of electricity to supply native load. The native load is made up of the total transmission requirements of the Québec wholesale market (see “Generation – Québec Wholesale Market”) but excludes customers in remote communities; Hydro-Québec Distribution is Hydro-Québec TransÉnergie’s largest customer; |

| | • | | point-to-point transmission service; as at the end of 2007, Hydro-Québec TransÉnergie had signed transmission service agreements with 34 customers, including Hydro-Québec Production which is the largest customer for this service; and |

| | • | | connections of privately-owned generation facilities to Hydro-Québec TransÉnergie’s transmission system; Hydro-Québec TransÉnergie currently serves 29 private producers. |

This segment includes our holding in Cedars Rapids Transmission Company Limited, which is a transmission provider that owns and operates a 325 MW interconnection line that links Hydro-Québec TransÉnergie’s grid at the Les Cèdres substation with the Cornwall Electric system in Ontario and the National Grid system in New York.

TRANSMISSION SYSTEM

Some generation stations in Québec are located at substantial distances from consumer centers. As a result, Hydro-Québec TransÉnergie’s power transmission system is one of the most extensive and comprehensive in North America, comprising more than 20,000 miles of lines.

This system includes the following facilities as at December 31, 2007.

| | | | |

Voltage | | Substations | | Lines (miles) (1) |

765 kV and 735 kV | | 38 | | 7,097 |

450 kV DC | | 2 | | 757 |

315 kV | | 63 | | 3,186 |

230 kV | | 50 | | 1,887 |

161 kV | | 41 | | 1,251 |

120 kV | | 212 | | 4,091 |

69 kV or less | | 103 | | 2,241 |

| | | | |

TOTAL | | 509 | | 20,510 |

| | | | |

| (1) | Miles covered by the transmission system. Many facilities carry two lines on the same infrastructure. |

In May 1997, Hydro-Québec TransÉnergie opened access to its transmission grid in accordance with the Hydro-Québec Open Access Transmission Tariff. Consequently, electricity distributors, producers and marketers in and outside Québec have the option to enter into transactions with distributors and producers located outside Québec to buy or sell electricity and to wheel in, wheel out or wheel through Hydro-Québec TransÉnergie’s transmission lines at specified rates. The capacity available on the system is posted on the OASIS (Open Access Same-Time Information System) website.

Hydro-Québec TransÉnergie’s Direction – Contrôle des mouvements d’énergie (System Control unit) in Montréal and regional telecontrol centers are designed to optimize energy resources, supervise power flow and monitor system security. The transmission system is linked through interconnections with other major power systems in Canada and the northeastern United States.

The following table shows existing interconnections with neighboring systems outside Québec, excluding the lines to Churchill Falls, as at December 31, 2007.

INTERCONNECTIONS WITH NEIGHBORING SYSTEMS OUTSIDE QUÉBEC

| | | | | | | | |

| | | | | Maximum Carrying

Capacity | | Hydro-Québec TransÉnergie’s

Current Reception Capacity | | Voltage |

| | | | | (MW) | | (MW) | | (kV) |

CANADA | | Ontario | | 1,295 (1) | | 720 | | 120 and 230 |

| | New Brunswick | | 1,200 | | 785 | | 230, 315 and 345 |

UNITED STATES | | New York | | 2,125 (1) | | 1,000 | | 120 and 765 |

| | New England | | 2,275 | | 1,870 | | 120 and 450 |

| (1) | Ontario and New York State are partially served by the same installations, limiting the simultaneous export capacity to these two systems to 3,100 MW. |

13

DISTRIBUTION

The primary responsibility of Hydro-Québec Distribution is to deliver electricity to Québec customers. To fulfill this responsibility, Hydro-Québec Distribution purchases Heritage Pool Electricity from Hydro-Québec Production and, to meet demand beyond that volume, purchases additional electricity under market conditions by issuing calls for tenders from suppliers in the market (see “Regulatory Framework – Energy Board Act”).

Our distribution system is comprised of 68,100 miles of medium voltage lines (almost exclusively 25 kV), as well as 38,100 miles of low voltage lines. Approximately 10% of all such lines are underground.

We sell to a wide range of customers, from industrial users, which accounted for 42.2% of sales volume in 2007, to residential customers and farms, which represented 34.7% of sales volume in the same period. Revenues are also derived from sales to commercial and institutional customers as well as municipalities.

Through marketing efforts, we have developed some flexibility in the management of our system. We currently have 1,600 MW of interruptible power and 810 MW of concurrent peak-saving capacity in our residential dual-energy market.

We have entered into nine special agreements with various industrial customers for whom electricity costs represent a substantial proportion of total production costs. Some of these agreements provide for the sale, on a long-term basis, of firm energy at prices that vary in accordance with a formula based on the market price of aluminum produced by those customers. We manage the exposure to fluctuations in aluminum prices resulting from these contracts by entering into financial transactions, such as futures or swaps (see “Note 16 to the 2007 Consolidated Financial Statements”). In 2007, deliveries under these agreements accounted for approximately 38% of the total energy deliveries to industrial users.

Hydro-Québec Distribution relies on various sources to supply the Québec market. To meet requirements in excess of the Heritage Pool Electricity reserved for it by Hydro-Québec Production, Hydro-Québec Distribution issues short- and long-term calls for tender. For requirements of less than three months, it may also buy electricity directly on the market, without a call for tender, under an exemption granted by the Energy Board. For unforeseen needs that cannot be met otherwise, it relies on a framework agreement with Hydro-Québec Production covering the period from January 1, 2007 to December 31, 2008.

Further to calls for tenders issued since 2002, Hydro-Québec Distribution signed contracts with Hydro-Québec Production for the supply of 600 MW over a 20-year period beginning in March 2007 and with six independent producers for the supply of more than 1,500 MW (including 990 MW of wind-generated electricity) for deliveries beginning between July 2006 and December 2012.

The following table summarizes these contracts.

LONG-TERM CONTRACTS AWARDED BY TENDER

| | | | | | | | |

Producers | | Type of power | | Capacity

(MW) | | Starting Date | | Expiry Date |

Hydro-Québec Production | | Hydroelectric | | 600 | | 2007 | | 2027 |

Trans-Canada Energy Ltd | | Cogeneration | | 507 | | 2006 | | 2026 |

Cartier Wind Energy Inc. | | Wind | | 740 | | 2006 to 2012 | | 2026 to 2032 |

Northland Power Inc. | | Wind | | 250 | | 2009 and 2010 | | 2029 to 2030 |

Bowater Canadian Forest Products Inc. | | Forest biomass cogeneration | | 17 | | 2006 | | 2026 |

Kruger Inc. | | Forest biomass cogeneration | | 16 | | 2007 | | 2027 |

Tembec inc. | | Forest biomass cogeneration | | 8 | | 2008 | | 2028 |

In 2005, Hydro-Québec Distribution issued a call for tenders for an additional 2,000 MW of wind-generated electricity, with deliveries starting no later than December 2010. The retained bids will be announced in Spring 2008.

In 2007, pursuant to calls for tenders for the sale of excess energy, Hydro-Québec Distribution signed 73 contracts for a maximum of 600 MW/month for the period from April through September 2007. Also in 2007, Hydro-Québec Distribution and TransCanada Energy Ltd. agreed to the suspension of a long-term contract of 507 MW for the year 2008, with another possible suspension for 2009.

Calls for tenders could be made in the coming years in order to balance energy supply and demand in Québec (see “Regulatory Framework – Energy Board Act”).

14

ELECTRICITY RATES

Under the applicable provisions of the Energy Board Act, rates are fixed or modified by the Energy Board (see “Regulatory Framework – Energy Board Act”). Rates are fixed to allow recovery of authorized service costs, including estimated supply costs, and a reasonable rate of return on shareholder’s equity. In February 2008, the Energy Board approved an average rate increase of 2.90% effective April 1, 2008.

The following table shows rate increases applicable for each year, from 2003 to 2008, as well as annual inflation rates:

| | | | | | | | | | | | | | | | | | |

| | | 2003 | | | 2004 | | | 2005 | | | 2006 | | | 2007 | | | 2008 | |

Rate increase as of April 1 | | nil | | | 4.45 | % (1) | | 1.2 | % | | 5.33 | % | | 1.92 | % | | 2.90 | % |

Inflation Rate (2) | | 2.8 | % | | 1.8 | % | | 2.2 | % | | 2.0 | % | | 2.2 | % | | 2.0 | % (3) |

| (1) | For 2004: 3% effective January 1 and 1.41% effective April 1. |

| (2) | Canadian Consumer Price Index for the calendar year. |

ELECTRICITY SALESAND REVENUE

The following table summarizes electricity sales and revenue in Québec, by category of customers, for the years 2003 through 2007.

ELECTRICITY SALES AND REVENUE IN QUÉBEC

| | | | | | | | | | | | | | | |

| | | Years ended December 31 |

| | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 |

| | | (in GWh) |

Electricity Sales, by Category | | | | | | | | | | | | | | | |

Residential and farm | | | 57,217 | | | 58,002 | | | 57,269 | | | 56,722 | | | 60,046 |

General and institutional | | | 32,314 | | | 33,137 | | | 33,463 | | | 32,440 | | | 34,751 |

Industrial | | | 72,546 | | | 69,722 | | | 73,447 | | | 73,297 | | | 73,005 |

Other | | | 5,014 | | | 5,026 | | | 4,998 | | | 4,878 | | | 5,353 |

| | | | | | | | | | | | | | | |

Total Electricity Sales | | | 167,091 | | | 165,887 | | | 169,177 | | | 167,337 | | | 173,155 |

| | | | | | | | | | | | | | | |

| |

| | | (in millions of dollars) |

Revenue from Electricity Sales, by Category | | | | | | | | | | | | | | | |

Residential and farm | | $ | 3,504 | | $ | 3,690 | | $ | 3,690 | | $ | 3,775 | | $ | 4,144 |

General and institutional | | | 2,096 | | | 2,234 | | | 2,284 | | | 2,356 | | | 2,602 |

Industrial | | | 2,742 | | | 2,751 | | | 2,892 | | | 3,022 | | | 3,336 |

Other | | | 236 | | | 247 | | | 255 | | | 249 | | | 286 |

| | | | | | | | | | | | | | | |

Total Revenue from Electricity Sales | | $ | 8,578 | | $ | 8,922 | | $ | 9,121 | | $ | 9,402 | | $ | 10,368 |

| | | | | | | | | | | | | | | |

| |

| | | (as at December 31) |

Number of Customer Accounts, by Category | | | | | | | | | | | | | | | |

Residential and farm | | | 3,343,271 | | | 3,399,776 | | | 3,450,455 | | | 3,501,709 | | | 3,554,443 |

General and institutional | | | 281,997 | | | 282,748 | | | 283,616 | | | 295,618 | | | 299,524 |

Industrial | | | 13,383 | | | 13,117 | | | 12,796 | | | 12,032 | | | 11,565 |

Other | | | 5,812 | | | 5,634 | | | 5,643 | | | 5,767 | | | 3,440 |

| | | | | | | | | | | | | | | |

Total Number of Customer Accounts | | | 3,644,463 | | | 3,701,275 | | | 3,752,510 | | | 3,815,126 | | | 3,868,972 |

| | | | | | | | | | | | | | | |

15

CONSTRUCTION

Hydro-Québec Équipement carries out engineering and construction services for hydroelectric development projects throughout Québec, except in the territory governed by the James Bay and Northern Québec Agreement, where such work is handled by the SEBJ. Hydro-Québec Équipement also builds power transmission lines and substations throughout Québec.

CORPORATE AND OTHER ACTIVITIES

This segment encompasses our Technology Group, which was created in February 2006, and corporate services such as the procurement of goods and services, finance and human resources. The following are under the supervision of the Technology Group:

| | • | | Hydro-Québec CapiTech inc. (“HQ CapiTech”) (wholly-owned; a venture capital company investing in businesses that provide energy-related high-technology products and services); |

| | • | | Hydro-Québec IndusTech inc. (“HQ IndusTech”) (wholly-owned; it holds a 64.82% interest in TM4 inc., a joint venture with Groupe Industriel Marcel Dassault, which is pursuing the development of an electrical motor for automobiles); and |

| | • | | Institut de recherche d’Hydro-Québec (“IREQ”) (our energy-technology research and development division). |

In 2006, we sold our interests in foreign holdings previously held through Hydro-Québec International inc. (“HQI”) and TransÉnergie HQ Inc. for a gain of approximately $917 million (see “Management’s Discussion and Analysis – Segmented Information – Corporate and Other Activities”). In 2007, we completed the sale of HQI’s foreign holdings by concluding the sale of DirectLink, in Australia, for a gain of approximately $18 million.

16

CORPORATE OUTLOOK

DEVELOPMENT STRATEGY

In September 2006, we presented our five-year Strategic Plan (the “Strategic Plan”) for the 2006-2010 period. This Strategic Plan was discussed in a parliamentary commission in 2006.

The Strategic Plan sets forth three main priorities: energy efficiency; complementary development of hydroelectric and wind power, the two main renewable energy sources in Québec; and technological innovation. More specifically, we plan:

| | • | | to promote conservation of energy by investing in energy saving programs; |

| | • | | to increase our hydroelectric generating capacity by accelerating project development and by creating a portfolio of projects with a total generating capacity of 4,500 MW; |

| | • | | the complementary development of our hydroelectric capacity and of up to 4,000 MW of wind power by 2015; |

| | • | | to increase, with technological innovations, the productivity of our generating facilities, reduce losses on our transmission and distribution systems and make buildings more energy-efficient; and |

| | • | | the development of innovative energy efficiency technologies. |

In 2008, Hydro-Québec expects to earn net income of $2.6 billion, which is $100 million more than the amount indicated in the financial outlook of the Strategic Plan 2006–2010. This projection takes into account the fact that water-power royalties paid to the Government by Hydro-Québec Production will increase by approximately $300 million, primarily because in 2007, a transition year, the half-rate rule applied.

Hydro-Québec plans to invest $4.4 billion in 2008. A substantial portion of these investments, 60%, will be devoted to development and growth activities, while 40% will be used to finance work to ensure the long-term operability of facilities.

Hydro-Québec Production will continue to increase hydroelectric production capacity in Québec. In 2008, it will continue work on the Eastmain-1-A/Sarcelle/Rupert project (construction began in 2007) and permitting for the Romaine complex. It will also complete the commissioning of Péribonka generating station and will gradually begin commissioning Chute-Allard and Rapides-des-Coeurs generating stations. In addition, Hydro-Québec Production will continue to facilitate the integration of wind power by compensating for fluctuations in wind farm output.

Hydro-Québec TransÉnergie will continue its efforts to enhance service quality and the reliability and security of the power transmission system. To meet the growing demand in Québec, Hydro-Québec TransÉnergie will carry out several major projects to bring new hydroelectric and wind power facilities onto the grid, in particular Eastmain-1-A and Sarcelle powerhouses and the wind farms built in response to Hydro-Québec Distribution’s first call for tenders. As well, Hydro-Québec TransÉnergie will work to ensure the long-term operability of its transmission assets, including interconnections with neighboring systems. It will also complete the connection of Péribonka, Chute-Allard and Rapides-des-Coeurs generating stations while continuing work related to the new interconnection with Ontario.

Hydro-Québec Distribution will continue to deliver reliable electricity and quality services to its Québec customers. At the beginning of 2008, it completed the final step in implementing the Customer Information System. It will pursue its investments to automate the distribution grid and ensure the long-term operability of its facilities while analyzing various solutions to improve its operating efficiency, such as remote meter reading using radio technology. During the year, Hydro-Québec Distribution will also disclose the bidders selected in its tender call for a second block of wind power. Finally, it will continue to implement the Energy Efficiency Plan (which includes measures for low-income households) to achieve the objective of 4.7 TWh in energy savings set for 2010.

Finally, we expect to present our 2009-2013 Strategic Plan in Fall 2008.

17

GENERATIONS FUND

As stipulated in the Watercourses Act (Québec), Hydro-Québec Production will pay the same statutory royalties as those paid by private producers of hydro-electricity in Québec. These water-power royalties, which will be paid to the Government, consist of a statutory royalty for the electricity delivered during the year and a contractual royalty payable pursuant to the contract awarded for the operation of a generation station.

For 2008, these royalties, indexed annually to the Consumer Price Index, consist of:

| | • | | a statutory royalty of $2.77 ($2.72 in 2007) per thousand kilowatt-hours of electricity produced; and |

| | • | | a contractual royalty of $0.651 ($0.639 in 2007) per thousand kilowatt-hours of electricity produced. |

Under the Generations Fund Act, payment of these royalties is being phased in over two years, beginning January 1, 2007. These royalties totaled $263 million for 2007 (for this transition year, the half-rate rule applied) and are expected to total $565 million for 2008.

18

CAPITAL INVESTMENT PROGRAM

Our capital investment program includes capital expenditures for fixed and intangible assets and investments in energy efficiency programs. The following table is a summary of our projected capital investments affecting cash for the years 2003 through 2007. The table also includes estimates for 2008 and the two-year period 2009 and 2010; these estimates are based on, among other things, a projected growth in demand for electricity in Québec of 0.5% yearly for the next three years. In 2007, capital investments in fixed and intangible assets, excluding energy efficiency programs, totaled $3,464 million.

CAPITAL INVESTMENTS AFFECTING CASH

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | Estimated |

| | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 | | 2008 | | 2009 and 2010 |

| | | (millions of dollars) |

Fixed and Intangible Assets | | | | | | | | | | | | | | | | | | | | | |

Generation | | $ | 1,428 | | $ | 1,820 | | $ | 1,780 | | $ | 1,615 | | $ | 1,807 | | $ | 1,909 | | $ | 4,704 |

Transmission (1) | | | 609 | | | 541 | | | 733 | | | 882 | | | 778 | | | 1,330 | | | 2,604 |

Distribution | | | 540 | | | 601 | | | 645 | | | 690 | | | 721 | | | 754 | | | 1,758 |

Construction | | | 4 | | | 11 | | | 6 | | | 4 | | | 3 | | | 6 | | | 14 |

Corporate and Other Activities | | | 158 | | | 98 | | | 129 | | | 157 | | | 155 | | | 144 | | | 220 |

| | | | | | | | | | | | | | | | | | | | | |

| | | 2,739 | | | 3,071 | | | 3,293 | | | 3,348 | | | 3,464 | | | 4,143 | | | 9,300 |

Energy Efficiency Programs | | | 10 | | | 41 | | | 91 | | | 149 | | | 172 | | | 251 | | | 508 |

| | | | | | | | | | | | | | | | | | | | | |

Total Investments | | $ | 2,749 | | $ | 3,112 | | $ | 3,384 | | $ | 3,497 | | $ | 3,636 | | $ | 4,394 | | $ | 9,808 |

| | | | | | | | | | | | | | | | | | | | | |

| (1) | Includes sub-transmission. |

The Sainte-Marguerite-3 and Rocher-de-Grand-Mère generating stations were completed in 2004, Toulnustouc in 2005 and

Eastmain-1 in 2006.

In 2007, the commissioning of the $176 million Mercier generation station in the Outaouais region was completed and added 51 MW to our installed capacity and 0.3 TWh to our annual output. The first generating unit at Péribonka, in the Saguenay-Lac-St-Jean region, also came on stream in November 2007 and the remaining two units came into operation in the first quarter of 2008. The Péribonka plant has an installed capacity of 385 MW and an annual output of 2.2 TWh. The total cost of the project is approximately $1.4 billion. Moreover, Sainte-Marguerite-3 reached its full 884-MW capacity following the recommissioning of its second unit in 2007.

The Chute-Allard and Rapides-des-Coeurs developments on the Saint-Maurice River are close to completion. Commissioning will begin in Spring 2008 and will continue over the next year. The two generating stations will have a combined installed capacity of 139 MW and annual output of 0.9 TWh, at an expected total cost of $960 million.

After obtaining the necessary governmental approvals, we began construction of the Eastmain-1-A/Sarcelle/Rupert project in the James Bay Region in 2007. The cost of work is estimated at $5.0 billion, making it Québec’s largest hydroelectric project of the decade. This project consists of building two generating stations and diverting part of the Rupert River into the Eastmain-1 reservoir and from there to the lower Grande Rivière. This partial diversion will increase the output of three existing powerhouses. Once completed, this project will add 893 MW to our installed capacity and will have annual output of 8.5 TWh. The project’s various components will come into operation in stages from the end of 2009 until 2012.

The environmental impact assessment for the Romaine hydroelectric complex was tabled with the relevant authorities in January 2008. The estimated $6.5-billion project calls for four generation stations with a total installed capacity of 1,550 MW and annual output of 8.0 TWh to be developed on the Romaine River in the Mingan Region. Should construction commence in Summer 2009, commissioning of the facilities should begin by late 2014 and be completed by the end of 2020.

We are continuing preliminary studies related to the construction of a 1,550 MW complex on the Petit Mécatina River, about 186 miles east of the Romaine River. This initial phase, scheduled to end in Spring 2008, will allow us to determine the development’s configuration and cost.

19

Allocation of Capital Expenditures for our Generation, Transmission and Distribution Business Segments

The following tables summarize the allocation of estimated capital expenditures for 2008 and for the two-year period 2009 and 2010 among our three major business segments:

GENERATION BUSINESS SEGMENT

| | | | | | | | | | | | |

| | | Available

Power | | Planned Date

of Operation | | Estimated Capital

Expenditures | |

| | | | | 2008 | | | 2009 and 2010 | |

| | | (MW) | | | | (millions of dollars) | |

MAIN REHABILITATION PROJECTS | | | | | | | | | | | | |

Improvement and rebuilding of facilities | | — | | Continuous

program | | $ | 497 | | | $ | 1,730 | |

| | | | |

ONGOING GENERATION PROJECTS | | | | | | | | | | | | |

Péribonka | | 385 | | 2008 | | | 58 | | | | 4 | |

Chute-Allard and Rapides-des-cœurs | | 139 | | 2008-2009 | | | 163 | | | | 31 | |

Eastmain-1-A/Sarcelle/Rupert powerhouse | | 893 | | 2009-2012 | | | 1,042 | | | | 2,281 | |

| | | | |

PROJECTSALREADYCOMMISSIONED | | — | | 2008 and

prior years | | | 57 | | | | 49 | |

| | | | |

GENERATION PROJECTSUNDER STUDY | | | | | | | | | | | | |

Complexe La Romaine | | 1,550 | | 2014-2020 | | | 43 | | | | 517 | |

| | | | | | | | | | | | |

OTHER | | — | | — | | | 49 | (1) | | | 92 | (2) |

| | | | | | | | | | | | |

| | | | | | $ | 1,909 | | | $ | 4,704 | |

| | | | | | | | | | | | |

| (1) | Includes 81.7% in equipment and 18.3% in buildings. |

| (2) | Includes 80.5% in equipment and 19.5% in buildings. |

TRANSMISSION BUSINESS SEGMENT

| | | | | | | | | | |

| | | Planned Date

of Operation | | Estimated Capital

Expenditures | |

| | | | | 2008 | | | 2009 and 2010 | |

| | | | | (millions of dollars) | |

TRANSMISSIONFACILITIES (1) | | | | | | | | | | |

Equipment improvement (2) | | Continuous

program | | $ | 646 | | | $ | 1,505 | |

System improvement program | | | | | | | | | | |

Rapides-des-Coeurs and Chute-Allard integration | | 2007-2008 | | | 5 | | | | — | |

Péribonka integration | | 2007-2008 | | | 11 | | | | 1 | |

Wind Power interconnection – 990 MW | | 2007-2012 | | | 116 | | | | 228 | |

Saraguay substation | | 2008 | | | 25 | | | | — | |

Saint-Lin substation | | 2008 | | | 30 | | | | 5 | |

Ontario interconnection | | 2008-2009 | | | 255 | | | | 72 | |

Saint-Maxime substation | | 2008-2010 | | | 14 | | | | 25 | |

315 kV Chenier – Outaouais line | | 2010 | | | 12 | | | | 197 | |

Sorel substation | | 2010 | | | 13 | | | | 35 | |

Soulanges substation | | 2010 | | | 8 | | | | 18 | |

Eastmain-1-A and Sarcelle integration | | 2010-2011 | | | 8 | | | | 153 | |

Hauterive substation (Alcoa) | | 2012-2013 | | | 16 | | | | 26 | |

La Romaine integration | | 2014-2017 | | | 6 | | | | 25 | |

OTHER | | | | | 165 | (3) | | | 314 | (4) |

| | | | | | | | | | |

| | | | $ | 1,330 | | | $ | 2,604 | |

| | | | �� | | | | | | |

| (1) | Includes sub-transmission facilities. |

| (2) | Includes system maintenance and demand growth. |

| (3) | Includes 16.0% in equipment, 3.6% in buildings, 57.0% in telecommunications and 23.4% in technology. |

| (4) | Includes 16.7% in equipment, 3.9% in buildings, 70.9% in telecommunications and 8.6% in technology. |

20

DISTRIBUTION BUSINESS SEGMENT

| | | | | | | | |

| | | Estimated Capital Expenditures | |

| | | 2008 | | | 2009 and 2010 | |

| | | (millions of dollars) | |

DISTRIBUTIONSYSTEM (1) | | | | | | | | |

System maintenance | | $ | 212 | | | $ | 653 | |

System improvements and demand growth | | | 400 | | | | 818 | |

OTHER | | | 142 | (2) | | | 287 | (3) |

| | | | | | | | |

| | $ | 754 | | | $ | 1,758 | |

| | | | | | | | |

| (1) | Includes investments in distribution facilities and investments in generation and transmission facilities of our off-grid systems. |

| (2) | Includes 59.2% in equipment, 24.9% in buildings and 15.9% in telecommunications and technology. |

| (3) | Includes 64.4% in equipment, 22.8% in buildings and 12.8% in telecommunications and technology. |

Cash Requirements

The total estimated cash requirements for 2008 are approximately $7.5 billion, and include approximately $4.4 billion in capital investments, approximately $1.0 billion for long-term debt repayment and sinking fund redemption and approximately $2.1 billion for the payment of dividends declared for 2007. Our self-financing ratio (defined as cash from operations less dividends paid, divided by the sum of investments (excluding net changes in short-term investments), long-term debt maturities and sinking fund redemption) is expected to be 49.9% in 2008, compared to 61.9% in 2007.

We estimate that cash requirements for capital investments, long-term debt repayment and sinking fund redemption will amount to approximately $11.3 billion in aggregate for the two-year period 2009 and 2010.

21

REGULATORY FRAMEWORK

Hydro-Québec Act

Under the provisions of the Hydro-Québec Act, we are mandated to supply power and to pursue endeavors in energy-related research and promotion, energy conversion and conservation, and any field connected with or related to power or energy.

Under the Hydro-Québec Act, the Government is entitled to declare a dividend from Hydro-Québec when certain financial criteria are met (see “Note 18 to the 2007 Consolidated Financial Statements”). In its latest budget tabled in March 2008, the Government announced that Hydro-Québec’s dividend policy was revised and raised to its distributable surplus which is close to 75% of net income. This change of policy began with the dividend payable for our fiscal year ending December 31, 2007.

Energy Board Act

The Act respecting the Régie de l’énergie (the “Energy Board Act”), enacted in 1996, grants the Energy Board exclusive authority to determine or modify our rates and conditions under which electricity is transmitted and distributed by us. Hydro-Québec TransÉnergie and Hydro-Québec Distribution’s activities in Québec are therefore regulated. Under this legislation, rates are set by reasoned decision of three commissioners after public hearings. Moreover, the Act stipulates that rates are determined on a basis that allows for recovery of the cost of service plus a reasonable return on the rate base.

The Energy Board consists of seven full-time members appointed by the Government and, in the exercise of its functions, is charged with reconciling the public interest, consumer protection and the fair treatment of the electric power carrier and of distributors. The Energy Board Act was amended in December 2006 to grant the Energy Board new powers regarding energy efficiency programs and actions as well as mandatory reliability standards.

Under the Energy Board Act, we have been granted exclusive rights for the distribution of electric power throughout Québec, excluding the territories served by distributors operating a municipal or private electric system as of May 13, 1997.

The Energy Board has the authority to:

| | • | | fix, or modify, after holding public hearings, our rates and conditions for the transmission and distribution of electric power; |

| | • | | approve our electric power supply plan; |

| | • | | designate a reliability coordinator for Québec and adopt the standards of reliability proposed by the designated reliability coordinator; |

| | • | | authorize our transmission and distribution investment projects; |

| | • | | approve our distribution commercial programs; and |

| | • | | rule upon complaints from customers concerning rates or services. |

Generation

The Energy Board’s jurisdiction does not extend to generation.

Transmission

Transmission rates and service terms and conditions are subject to approval by the Energy Board. On February 29, 2008, the Energy Board approved an annual rate of $70.82/kW/year for firm point-to-point service with a rate rider (a rate rider is a temporary credit or charge approved by a regulator) for 2008 of minus $1.16/kW/year and an hourly rate of $8.08/MWh, applicable retroactively as of January 1, 2008, and set the amount payable for transmission of the native load supply at $2,528,628,100 per year with a rate rider for 2008 of minus $41,417,800. The Energy Board also approved the proposed terms and conditions for its Open Access Transmission Tariff.

22

On August 14, 2007, the Direction – Contrôle des mouvements d’énergie (System Control unit) of Hydro-Québec TransÉnergie was designated the reliability coordinator for Québec by the Energy Board.

Distribution

Electricity required to meet Québec’s needs in excess of the Heritage Pool Electricity must be purchased through a competitive bidding process. The Energy Board approved our Electricity Supply Plan 2005-2014, as well as our Call for Tenders and Contract Awarding Procedure and Code of Ethics on Conducting Calls for Tenders. Purchase contracts for electricity in excess of the Heritage Pool Electricity are subject to the approval of the Energy Board.

In August 2007, Hydro-Québec Distribution filed with the Energy Board an application to modify its rates and certain conditions regarding the distribution of electricity in Québec for the rate year beginning April 1, 2008. On February 26, 2008, the Energy Board granted an average rate increase of 2.9% to Hydro-Québec Distribution.

National Energy Board Act

Our exports of electric power are subject to the National Energy Board Act which provides that a permit or license must be obtained from the National Energy Board of Canada (the “National Board”) for such exports. We hold the following four permits for short-term exports (contracts of five years or less):

| | • | | two permits expiring on December 31, 2010 authorizing us to export annually, for a continuous period of no more than five years for any single contract, up to 30 TWh of interruptible energy and up to 20 TWh of firm energy to the United States; |

| | • | | two permits granted to our subsidiary, HQEM, expiring on April 7, 2009. These permits allow HQEM, as a power marketer outside Québec, to export annually to the United States up to 30 TWh of firm and interruptible energy from interconnections located in other provinces, under contracts with a term of five years or less. |

Each of these permits allows us to take advantage of the spot market in the United States; however, long-term export contracts (more than five years) require prior issuance of specific permits or licenses by the National Board.

On March 5, 2007, HQEM’s permit to export natural gas to the United States was renewed for a two-year period.

The National Board also regulates international power lines and we operate our interconnections with the United States in accordance with the terms and conditions of Certificates of Public Convenience and Necessity issued by the National Board.

Environmental Regulation

Our activities are subject to federal and provincial environmental laws and regulations, and, to some extent, municipal by-laws.

Before beginning new construction, our projects are subject to environmental impact assessment studies as well as information and consultation processes. The studies are submitted for review and approval by government departments and agencies responsible for issuing governmental authorizations. In some instances, the approval process includes public hearings by an independent body.

Environmental protection is a central concern of Hydro-Québec. Most activities that have an impact on the environment are governed by ISO 14001—certified environmental management system. ISO 14001 is the environmental management standard of the International Organization for Standardization. In addition, every year, we review our management of environmental issues and publish a Sustainability Report.

23

LITIGATION

Innus of Takuikan Uashat Mak Mani-Utenam

On December 30, 2003, representatives of the Innus of Takuikan Uashat Mak Mani-Utenam instituted an action against the Attorney-General of Canada, the Attorney-General of Québec and us seeking judicial recognition of their aboriginal rights and of their unextinguished Indian title over certain areas of land in Québec. Plaintiffs who claim not to be parties to the 1975 James Bay and Northern Québec Agreement (the “Agreement”) allege that the Agreement and certain federal and provincial laws are illegal, inoperative, unconstitutional and not binding upon the plaintiffs. The plaintiffs seek various orders, including rendering of accounts and revenue sharing for the unlawful use and management of the lands, notably in respect of hydroelectric facilities on these lands, and awarding damages from Canada, Québec and us, jointly and severally, in an amount of up to $1.5 billion (subject to further increase by the plaintiffs). In June 2005, as requested by the parties, the Québec Superior Court suspended the legal action for five years. Negotiations are ongoing between the governments and the Innus.

Innus of Pessamit

In November 2006, the Innus of Pessamit re-activated an action which was filed in 1998 against the Attorney-General of Canada, the Attorney-General of Québec and us seeking judicial recognition of their aboriginal rights and title over certain areas of land in Québec where our Manicouagan-Outardes hydroelectric facilities are located. The Innus intend to seek various orders including an award of damages against Canada, Québec and us, jointly and severally, in an amount of $11 billion. With Québec, we intend to contest this claim.

EMPLOYEES

We had 19,459 permanent employees as at December 31, 2007, and an average of 3,910 temporary employees during 2007. These numbers do not include employees of our subsidiaries and joint ventures. Unionized employees represent approximately 85% of our work force.

Eight collective agreements govern the working conditions of our unionized employees. These collective agreements provide for a profit-sharing plan tied to the attainment of our business objectives and for annual salary increases of 2% through 2008, except for our 3,300 specialists who have already agreed to a further 2% increase in 2009.

24

MANAGEMENT’S DISCUSSIONAND ANALYSIS

OVERVIEW

Income from continuing operations totaled $2,882 million, compared to $2,797 million last year, when a $234-million non-recurring foreign exchange gain was recognized. This result is primarily due to a $290-million increase in net electricity exports.

Income from discontinued operations totaled $25 million in 2007, mainly as a result of a gain on the sale of our interest in DirectLink, in Australia. This transaction, which was concluded on February 28, 2007, marked the completion of our plan to dispose of HQI’s foreign holdings.

Net income declined by $834 million from 2006 to $2,907 million, mainly as a result of gains of $917 million on the sale of assets in 2006, including $813 million for the sale of our interest in HQI Transelec Chile S.A. (“Transelec”), in Chile.

Revenue totaled $12,330 million, an increase of $1,169 million (11%) from 2006. Revenue from electricity sales reached $11,985 million, compared to $10,551 million in 2006, an increase of $1,434 million due to higher electricity sales in Québec ($966 million) and outside Québec ($468 million). Other revenue decreased by $265 million, primarily due to the recognition in the second quarter of 2006 of a non-recurring foreign exchange gain in the amount of $234 million on debts and swaps denominated in U.S. dollars.

Total expenditure reached $6,936 million, an increase of $784 million from 2006. This was mainly due to a $240-million increase in electricity and fuel purchases and the payment of water-power royalties to the Government since January 2007 for $263 million.