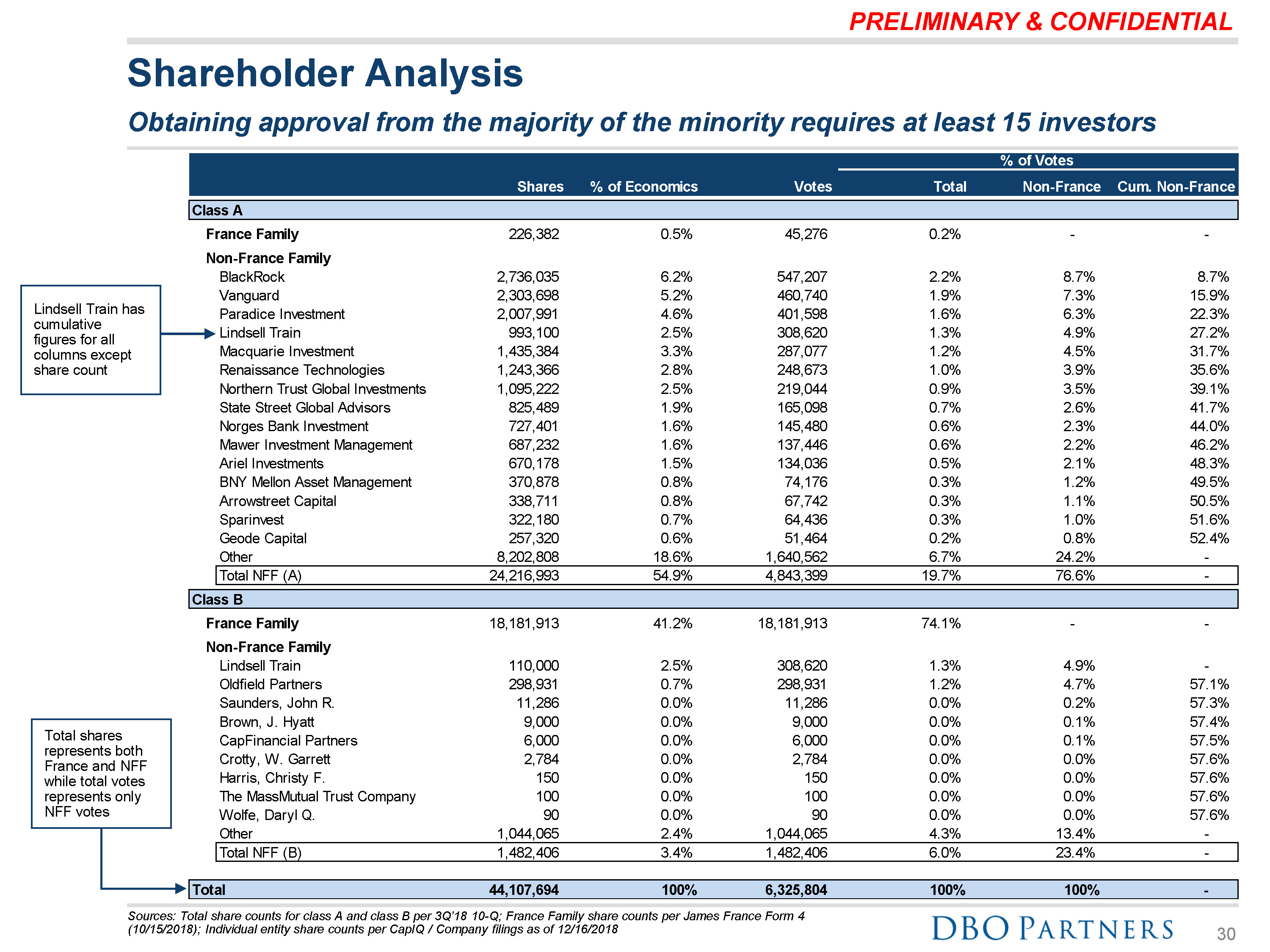

PRELIMINARY & CONFIDENTIAL Shareholder Analysis Obtaining approval from the majority of the minority requires at least 15 investors Sources: Total share counts for class A and class B per 3Q’18 10-Q; France Family share counts per James France Form 4 (10/15/2018); Individual entity share counts per CapIQ / Company filings as of 12/16/2018 30 Shares % of Economics Votes Total % of VotesNon-France Cum. Non-France Class A Total 44,107,694 100% 6,325,804 100% 100% - France FamilyNon-France Family 226,382 0.5% 45,276 0.2% - - BlackRock 2,736,035 6.2% 547,207 2.2% 8.7% 8.7% Vanguard 2,303,698 5.2% 460,740 1.9% 7.3% 15.9% Paradice Investment 2,007,991 4.6% 401,598 1.6% 6.3% 22.3% Lindsell Train 993,100 2.5% 308,620 1.3% 4.9% 27.2% Macquarie Investment 1,435,384 3.3% 287,077 1.2% 4.5% 31.7% Renaissance Technologies 1,243,366 2.8% 248,673 1.0% 3.9% 35.6% Northern Trust Global Investments 1,095,222 2.5% 219,044 0.9% 3.5% 39.1% State Street Global Advisors 825,489 1.9% 165,098 0.7% 2.6% 41.7% Norges Bank Investment 727,401 1.6% 145,480 0.6% 2.3% 44.0% Mawer Investment Management 687,232 1.6% 137,446 0.6% 2.2% 46.2% Ariel Investments 670,178 1.5% 134,036 0.5% 2.1% 48.3% BNY Mellon Asset Management 370,878 0.8% 74,176 0.3% 1.2% 49.5% Arrowstreet Capital 338,711 0.8% 67,742 0.3% 1.1% 50.5% Sparinvest 322,180 0.7% 64,436 0.3% 1.0% 51.6% Geode Capital 257,320 0.6% 51,464 0.2% 0.8% 52.4% Other 8,202,808 18.6% 1,640,562 6.7% 24.2% - Total NFF (A) 24,216,993 54.9% 4,843,399 19.7% 76.6% - Class B France Family 18,181,913 41.2% 18,181,913 74.1% - - Non-France FamilyLindsell Train 110,000 2.5% 308,620 1.3% 4.9% - Oldfield Partners 298,931 0.7% 298,931 1.2% 4.7% 57.1% Saunders, John R. 11,286 0.0% 11,286 0.0% 0.2% 57.3% Brown, J. Hyatt 9,000 0.0% 9,000 0.0% 0.1% 57.4% CapFinancial Partners 6,000 0.0% 6,000 0.0% 0.1% 57.5% Crotty, W. Garrett 2,784 0.0% 2,784 0.0% 0.0% 57.6% Harris, Christy F. 150 0.0% 150 0.0% 0.0% 57.6% The MassMutual Trust Company 100 0.0% 100 0.0% 0.0% 57.6% Wolfe, Daryl Q. 90 0.0% 90 0.0% 0.0% 57.6% Other 1,044,065 2.4% 1,044,065 4.3% 13.4% - Total NFF (B) 1,482,406 3.4% 1,482,406 6.0% 23.4% - Lindsell Train has cumulative figures for all columns except share count Total shares represents both France and NFF while total votes represents only NFF votes