| |

UNITED STATES |

SECURITIES AND EXCHANGE COMMISSION |

Washington, D.C. 20549 |

| |

FORM 10-Q |

| |

(Mark One) |

[X] | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE |

SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2007 |

OR |

[ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE |

SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from | | to |

Commission File Number: 001-07791 |

| |

|

| |

McMoRan Exploration Co. |

| (Exact name of registrant as specified in its charter) |

| |

Delaware | 72-1424200 |

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) |

| | |

1615 Poydras Street | |

New Orleans, Louisiana* | 70112 |

| (Address of principal executive offices) | (Zip Code) |

| |

| |

(504) 582-4000 |

| (Registrant's telephone number, including area code) |

| |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. xYes ÿo No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act (Check one): Large accelerated filer oÿ Accelerated filer x Non-accelerated filer o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities and Exchange Act of 1934). oYes x No

On March 31, 2007, there were issued and outstanding 28,465,630 shares of the registrant’s Common Stock, par value $0.01 per share.

| |

McMoRan Exploration Co. |

|

| |

| | Page |

| | |

| |

| | |

| Financial Statements: | |

| | |

| 3 |

| | |

| 4 |

| | |

| 5 |

| | |

| 6 |

| | |

| 12 |

| | |

| |

| 13 |

| | |

| 24 |

| | |

| 24 |

| | |

| 24 |

| | |

| 25 |

| | |

| E-1 |

McMoRan Exploration Co.

Item 1. Consolidated Financial Statements.

McMoRan EXPLORATION CO.

| | | March 31, | | December 31, | |

| | | 2007 | | 2006 | |

| | | (In Thousands) | |

| ASSETS | | | | | | | |

| Cash and cash equivalents: | | | | | | | |

| Continuing operations | | $ | 57,683 | | $ | 17,830 | |

| Discontinued operations, all restricted | | | 447 | | | 441 | |

Restricted investments | | | 5,984 | | | 5,930 | |

| Accounts receivable | | | 44,836 | | | 45,636 | |

| Inventories | | | 24,066 | | | 25,034 | |

| Prepaid expenses | | | 7,020 | | | 16,190 | |

| Current assets from discontinued operations, excluding cash | | | 6,311 | | | 6,051 | |

| Total current assets | | | 146,347 | | | 117,112 | |

| Property, plant and equipment, net | | | 288,641 | | | 282,538 | |

| Discontinued sulphur business assets | | | 359 | | | 362 | |

| Restricted investments and cash | | | 3,288 | | | 3,288 | |

| Other assets | | | 7,144 | | | 5,377 | |

| Total assets | | $ | 445,779 | | $ | 408,677 | |

| | | | | | | | |

| LIABILITIES AND STOCKHOLDERS’ DEFICIT | | | | | | | |

| Accounts payable | | $ | 61,806 | | $ | 85,504 | |

| Accrued liabilities | | | 29,212 | | | 32,844 | |

| Accrued interest and dividends payable | | | 5,425 | | | 5,479 | |

| Current portion of accrued oil and gas reclamation costs | | | 3,824 | | | 2,604 | |

| Current portion of accrued sulphur reclamation cost | | | 12,506 | | | 12,909 | |

| Current liabilities from discontinued operations | | | 2,259 | | | 3,678 | |

| Total current liabilities | | | 115,032 | | | 143,018 | |

| 6% convertible senior notes | | | 100,870 | | | 100,870 | |

| 5¼% convertible senior notes | | | 115,000 | | | 115,000 | |

| Senior secured term loan | | | 100,000 | | | - | |

| Senior secured revolving credit facility | | | - | | | 28,750 | |

| Accrued oil and gas reclamation costs | | | 23,729 | | | 23,272 | |

| Accrued sulphur reclamation costs | | | 10,620 | | | 10,185 | |

| Contractual postretirement obligation related to discontinued operations | | | 10,235 | | | 9,831 | |

| Other long-term liabilities | | | 16,952 | | | 17,151 | |

| 5% mandatorily redeemable convertible preferred stock | | | 29,074 | | | 29,043 | |

| Stockholders' deficit | | | (75,733 | ) | | (68,443 | ) |

| Total liabilities and stockholders' deficit | | $ | 445,779 | | $ | 408,677 | |

| | | | | | | | |

The accompanying notes are an integral part of these consolidated financial statements.

TABLE OF CONTENTSMcMoRan EXPLORATION CO.

| | | Three Months Ended March 31, | |

| | | 2007 | | 2006 | |

| | | (In Thousands, Except Per Share Amounts) | |

| Revenues: | | | | | | | |

| Oil & Gas | | $ | 51,375 | | $ | 35,441 | |

| Service | | | 322 | | | 4,305 | |

| Total revenues | | | 51,697 | | | 39,746 | |

| Costs and expenses: | | | | | | | |

| Production and delivery costs | | | 17,728 | | | 10,759 | |

| Depletion, depreciation and amortization | | | 27,035 | | | 5,844 | |

| Exploration expenses | | | 9,755 | | | 20,620 | |

| General and administrative expenses | | | 6,397 | | | 8,224 | |

| Start-up costs for Main Pass Energy Hub™ | | | 2,705 | | | 1,846 | |

| Insurance recovery | | | - | | | (1,169 | ) |

| Total costs and expenses | | | 63,620 | | | 46,124 | |

| Operating loss | | | (11,923 | ) | | (6,378 | ) |

| Interest expense, net | | | (5,654 | ) | | (1,833 | ) |

| Other income (expense), net | | | 748 | | | (3,194 | ) |

| Loss from continuing operations | | | (16,829 | ) | | (11,405 | ) |

| Income (loss) from discontinued operations | | | 2,331 | | | (1,677 | ) |

| Net loss | | | (14,498 | ) | | (13,082 | ) |

| Preferred dividends and amortization of convertible preferred stock | | | | | | | |

| issuance costs | | | (405 | ) | | (403 | ) |

| Net loss applicable to common stock | | $ | (14,903 | ) | $ | (13,485 | ) |

| | | | | | | | |

| Basic and diluted net loss per share of common stock: | | | | | | | |

| Continuing operations | | | $(0.61 | ) | | $ (0.44 | ) |

| Discontinued operations | | | 0.08 | | | (0.06 | ) |

| Net loss per share of common stock | | | $(0.53 | ) | | $ (0.50 | ) |

| | | | | | | | |

| Basic and diluted average shares outstanding | | | 28,358 | | | 26,832 | |

The accompanying notes are an integral part of these consolidated financial statements.

McMoRan EXPLORATION CO.

| | | Three Months Ended | |

| | | March 31, | |

| | | 2007 | | 2006 | |

| | | (In Thousands) | |

Cash flow from operating activities: | | | | | | | |

| Net loss | | $ | (14,498 | ) | $ | (13,082 | ) |

| Adjustments to reconcile net loss to net cash provided by (used in) | | | | | | | |

| operating activities: | | | | | | | |

| (Income) loss from discontinued operations | | | (2,331 | ) | | 1,677 | |

| Depreciation and amortization | | | 27,035 | | | 5,844 | |

| Exploration drilling and related expenditures | | | 1,124 | | | 12,342 | |

| Compensation expense associated with stock-based awards | | | 6,507 | | | 9,675 | |

| Amortization of deferred financing costs | | | 604 | | | 481 | |

| Loss on induced conversion of convertible senior notes | | | - | | | 4,301 | |

| Reclamation expenditures | | | (721 | ) | | - | |

| Other | | | (524 | ) | | 470 | |

| (Increase) decrease in working capital: | | | | | | | |

| Accounts receivable | | | (7,613 | ) | | 506 | |

| Accounts payable and accrued liabilities | | | (8,810 | ) | | (17,237 | ) |

| Prepaid expenses and inventories | | | 10,140 | | | (10,892 | ) |

| Increase in working capital | | | (6,283 | ) | | (27,623 | ) |

| Net cash provided by (used in) continuing operations | | | 10,913 | | | (5,915 | ) |

| Net cash used in discontinued operations | | | (2,429 | ) | | (3,490 | ) |

| Net cash provided (used in) by operating activities | | | 8,484 | | | (9,405 | ) |

| | | | | | | | |

Cash flow from investing activities: | | | | | | | |

| Exploration, development and other capital expenditures | | | (38,379 | ) | | (68,847 | ) |

| Proceeds from restricted investments | | | - | | | 7,400 | |

| (Increase) decrease in restricted investments | | | (54 | ) | | 69 | |

| Net cash used in continuing operations | | | (38,433 | ) | | (61,378 | ) |

| Net cash used in discontinued operations | | | - | | | - | |

| Net cash used in investing activities | | | (38,433 | ) | | (61,378 | ) |

| | | | | | | | |

Cash flow from financing activities: | | | | | | | |

| Proceeds from senior secured term loan | | | 100,000 | | | - | |

| Payments under senior secured revolving credit facility, net | | | (28,750 | ) | | - | |

| Financing costs | | | (2,177 | ) | | - | |

| Payments for induced conversion of convertible senior notes | | | - | | | (4,301 | ) |

| Dividends paid on convertible preferred stock | | | (374 | ) | | (747 | ) |

| Proceeds from exercise of stock options and other | | | 1,109 | | | 39 | |

| Net cash provided by (used in) continuing operations | | | 69,808 | | | (5,009 | ) |

| Net cash from discontinued operations | | | - | | | - | |

| Net cash provided by (used in) financing activities | | | 69,808 | | | (5,009 | ) |

| Net increase (decrease) in cash and cash equivalents | | | 39,859 | | | (75,792 | ) |

| Cash and cash equivalents at beginning of year | | | 18,271 | | | 132,184 | |

| Cash and cash equivalents at end of period | | | 58,130 | | | 56,392 | |

| Less restricted cash from continuing operations | | | - | | | (1 | ) |

| Less restricted cash from discontinued operations | | | (447 | ) | | (548 | ) |

| Unrestricted cash and cash equivalents at end of period | | $ | 57,683 | | $ | 55,843 | |

The accompanying notes are an integral part of these consolidated financial statements.

TABLE OF CONTENTSMcMoRan EXPLORATION CO.

The consolidated financial statements of McMoRan Exploration Co. (McMoRan), a Delaware Corporation, are prepared in accordance with U.S. generally accepted accounting principles. The consolidated financial statements of McMoRan include the accounts of those subsidiaries where McMoRan directly or indirectly has more than 50 percent of the voting rights and for which the right to participate in significant management decisions is not shared with other shareholders. McMoRan consolidates its wholly owned McMoRan Oil & Gas LLC (MOXY) and Freeport-McMoRan Energy LLC (Freeport Energy) subsidiaries. MOXY conducts all of McMoRan’s oil and gas operations while Freeport Energy is pursuing plans for the development of liquefied natural gas (LNG) facilities and natural gas storage capabilities at the Main Pass Energy Hub (MPEH™) project. As a result of McMoRan’s exit from the sulphur business in 2002, its sulphur results are presented as discontinued operations and the major classes of assets and liabilities related to the sulphur business are separately shown for the periods presented.

The accompanying unaudited consolidated financial statements should be read in conjunction with the McMoRan consolidated financial statements and notes contained in its 2006 Annual Report on Form 10-K. The information furnished herein reflects all adjustments which are, in the opinion of management, necessary for a fair presentation of the results for the periods presented. All such adjustments are, in the opinion of management, of a normal recurring nature. Certain reclassifications of prior year amounts have been made to conform to the current year presentation.

2. STOCK-BASED COMPENSATION

Accounting for Stock-Based Compensation. As of March 31, 2007, McMoRan has eight stock-based employee compensation plans and director compensation plans, all of which have been approved by McMoRan’s shareholders (see Note 8 of McMoRan’s 2006 Form 10-K). On January 1, 2006, McMoRan adopted the fair value recognition provisions of SFAS No. 123 (revised 2004), “Share-Based Payment” (SFAS No. 123R), using the modified prospective transition method. For more information regarding McMoRan’s accounting for stock-based awards see Note 1 of McMoRan’s 2006 Form 10-K.

Stock-Based Compensation Cost. Compensation cost charged to expense for stock-based awards is shown below (in thousands).

| | | | | | Three Months Ended | |

| | | | | | March 31, | |

| | | | | | 2007 | | 2006 | |

| Stock options awarded to employees (including directors) | | | | | $ | 6,281 | | $ | 9,364 | |

| Stock options awarded to non-employees and advisory directors | | | | | | 220 | | | 259 | |

| Restricted stock units | | | | | | 6 | | | 52 | |

| Total compensation cost | | | | | $ | 6,507 | | $ | 9,675 | |

Stock-Based Compensation Plans. In January 2007, McMoRan granted 1,323,500 stock options under its employee compensation plans and consequently, it currently has less than 50,000 options available for grant under its employee compensation plans.

Awards granted under all of the plans generally expire 10 years after the date of grant and vest in 25 percent annual increments beginning one year from the date of grant. The plans provide for employees to be eligible for the following year’s vesting upon retirement and provide for accelerated vesting if there is a change in control (as defined in the plans). Restricted stock unit grants vest over three years and are valued on the date of grant. The remaining restricted stock units outstanding at December 31, 2006, vested in February 2007.

Stock Options. A summary of stock options outstanding as of March 31, 2007 and changes during the three months ended March 31, 2007 follows:

TABLE OF CONTENTS

| | | | | | Weighted | | | |

| | | | Weighted | | Average | | Aggregate | |

| | Number | | Average | | Remaining | | Intrinsic | |

| | Of | | Option | | Contractual | | Value | |

| | Options | | Price | | Term (years) | | ($000) | |

| Balance at January 1 | 7,095,991 | | $ | 15.50 | | | | | | |

| Granted | 1,325,250 | | | 12.23 | | | | | | |

| Exercised | (155,995 | ) | | 7.11 | | | | | | |

| Expired/Forfeited | (12,832 | ) | | 18.55 | | | | | | |

| Balance at March 31 | 8,252,414 | | | 15.06 | | 6.6 | | $ | 124,872 | |

| Vested and exercisable at | | | | | | | | | | |

| March 31 | 6,111,322 | | | 14.90 | | 5.8 | | $ | 91,078 | |

| | | | | | | | | | | |

The fair value of each option award is estimated on the date of grant using a Black-Scholes-Merton option valuation model. Expected volatility is based on implied volatilities from the historical volatility of McMoRan’s stock and to a lesser extent on traded options on McMoRan stock. McMoRan uses historical data to estimate option exercise, forfeitures and expected life of the options. When appropriate, employees who have similar historical exercise behavior are grouped for valuation purposes. The risk-free interest rate is based on Federal Reserve rates in effect for bonds with maturity dates equal to the expected term of the option at the date of grant. McMoRan has not paid, and has no current plan to pay, cash dividends on its common stock. The assumptions used to value stock option awards during the three months ended March 31, 2007 and 2006 are noted in the following table.

| | | | 2007 | | | | 2006 | |

| Fair value (per share) of stock option on grant date | | $ | 6.89 | a | | $ | 11.91 | b |

| Expected and weighted average volatility | | | 52.23 | % | | | 55.5 | % |

| Expected life of options (in years) | | | 6.29 | a | | | 7 | |

| Risk-free interest rate | | | 4.75 | % | | | 4.5 | % |

| a. | Excludes stock options that were granted with immediate vesting (445,000 shares, including 400,000 shares granted to the Co-Chairmen in lieu of cash compensation for 2007) with an expected life of 6.56 years and fair value of stock options on grant date of $7.02 per share. |

| b. | Excludes stock options representing 500,000 shares granted with immediate vesting to the Co-Chairmen in lieu of cash compensation for 2006 with an expected life of six years and fair value of the options on grant date of $11.52 per share. |

As of March 31, 2007, McMoRan had approximately $16.8 million of total unrecognized compensation costs related to unvested stock options, which is expected to be recognized over a weighted average period of approximately 1.1 years.

3. SENIOR SECURED TERM LOAN

Effective January 19, 2007, MOXY entered into a Senior Term Loan Agreement (Term Loan). The loan agreement provides for a five-year, $100 million second lien senior secured term loan facility. Proceeds at closing, net of related fees and discounts, totaled approximately $98.0 million. McMoRan used the net proceeds to repay borrowings under the revolving credit facility ($46.4 million on January 20, 2007), and the remainder will be used to finance MOXY’s future exploration and development activities, working capital requirements and for general corporate purposes. The obligations under the term loan are guaranteed by McMoRan and each of MOXY’s wholly owned subsidiaries.

The term loan contains customary financial covenants and other restrictions. An annual mandatory $10 million repayment of principal is due each December 31 commencing on December 31, 2008. Amounts borrowed under the term loan agreement bear interest, at MOXY’s option, at an annual rate equal to either (1) the higher of the lenders’ prime rate or the federal funds effective rate plus 0.5 percent, plus the applicable margin of 6.0 percent or (2) the rate at which eurodollar deposits in the London interbank market plus 7.0 percent. Interest expense on the term loan in the first quarter of 2007 totaled $2.6 million.

Optional prepayments of the term loan are subject to a prepayment premium of 3.0 percent through January 19, 2008, 2.0 percent through January 19, 2009, and 1.0 percent through January 19, 2010. Optional prepayments made after January 19, 2010 are not subject to prepayment premiums. Repayments under the term loan can be accelerated by the lenders upon the occurrence of customary events of default. The term loan will mature on January 19, 2012.

4. EARNINGS PER SHARE

Basic and diluted net loss per share of common stock were calculated by dividing the net loss applicable to continuing operations, net income (loss) from discontinued operations and net loss applicable to common stock by the weighted-average number of common shares outstanding during the periods presented. For purposes of the earnings per share computations, the net loss applicable to continuing operations includes preferred stock dividends and related amortization of the issuance costs.

McMoRan had a net loss from continuing operations in both the first quarter of 2007 and 2006. Accordingly, the assumed exercise of stock options and stock warrants, as well as the assumed conversion of McMoRan’s 5% convertible preferred stock, 6% convertible senior notes and 5¼% convertible senior notes, were excluded from the diluted net loss per share calculations. These instruments were excluded because they are considered to be anti-dilutive, meaning their inclusion would have decreased the reported net loss per share from continuing operations for both periods presented. The excluded share amounts are summarized below:

| | | First Quarter | |

| | | 2007 | | | 2006 | |

| | | (in thousands) | |

In-the-money stock options a ,b | | | 608 | | | | 1,402 | |

Stock warrants a,c | | | 1,511 | | | | 1,810 | |

5% convertible preferred stock d | | | 6,205 | | | | 6,214 | |

6% convertible senior notes e | | | 7,079 | | | | 7,080 | |

5¼% convertible senior notes f | | | 6,938 | | | | 6,938 | |

| | | | | | | | | |

| a. | McMoRan uses the treasury stock method to determine total shares relating to in-the-money stock options and stock warrants to include in its diluted earning per share calculation. |

| b. | Represents stock options with an exercise price less than the average market price for McMoRan’s common stock for the periods presented. |

| c. | Includes stock warrants issued to K1 USA Energy Production Corporation in December 2002 (1.74 million shares) and September 2003 (0.76 million shares). The warrants are exercisable for McMoRan common stock at any time over their respective five-year terms at an exercise price of $5.25 per share. See Note 4 of McMoRan’s 2006 Form 10-K for additional information regarding the warrants. |

| d. | At the election of the holder, and before the shares mature on June 30, 2012, each outstanding share of 5% mandatorily redeemable convertible preferred stock is convertible into 5.1975 shares of McMoRan common stock. See Note 6 of McMoRan’s 2006 Form 10-K, for additional information regarding McMoRan’s convertible preferred stock, including McMoRan’s ability to redeem the shares for cash after June 30, 2007. |

| e. | The notes, issued in July 2003, are convertible at the option of the holder at any time prior to their maturity on July 2, 2008 into shares of McMoRan common stock at a conversion price of $14.25 per share. Net interest expense on the 6% convertible senior notes totaled $1.5 million during the first quarter of 2007 and $1.0 million during the first quarter of 2006. Additional information regarding McMoRan’s 6% convertible senior notes is disclosed in Note 5 of its 2006 Form 10-K. |

| f. | The notes, issued in October 2004, are convertible at the option of the holder at any time prior to their maturity on October 6, 2011 into shares of McMoRan common stock at a conversion price of $16.575 per share. Net interest expense on the 5¼% convertible senior notes totaled $1.4 million during the first quarter of 2007 and $0.8 million during the first quarter of 2006. Additional information regarding McMoRan’s 5¼% convertible senior notes is disclosed in Note 5 of its 2006 Form 10-K. |

Outstanding stock options excluded from the computation of diluted net loss per share of common stock because their exercise prices were greater than the average market price of the common stock during the periods presented are as follows:

| | | First Quarter | |

| | | 2007 | | | 2006 | |

| Outstanding options (in thousands) | | | 5,730 | | | | 1,751 | |

| Average exercise price per share | | $ | 17.44 | | | $ | 20.30 | |

5. OTHER MATTERS

Oil and Gas Activities

Since 2004, McMoRan has participated in 15 discoveries on 29 prospects that have been drilled and fully evaluated, including the positive results announced during the first quarter of 2007 at the Laphroaig well located within the inland waters of St. Mary Parish, Louisiana and the Hurricane Deep well at South Marsh Island Block 217. McMoRan has investments in six prospects that are either in progress or not fully evaluated totaling $57.9 million at March 31, 2007, including $21.3 million for the Blueberry Hill well at Louisiana State Lease 340 and $29.5 million at JB Mountain Deep at South Marsh Island Block 224. McMoRan expects to complete testing of the Blueberry Hill well by mid-year 2007 and information obtained from the testing of this well coupled with the results from the Hurricane Deep well will be incorporated into the future plans for the JB Mountain Deep well, as all three areas demonstrate similar geologic settings and are targeting deep Miocene sands equivalent in age.

Spending commitments under a multi-year exploration program were reached in 2006, concluding the program. During the first quarter of 2006, McMoRan’s management fees associated with its services to the multi-year exploration program totaled $3.0 million, which are reflected as service revenues in the accompanying consolidated statement of operations. McMoRan is currently participating in the drilling of specific exploration wells under another exploration agreement. For more information regarding McMoRan’s exploration agreements see Note 2 of its 2006 Form 10-K.

The determination of oil and gas reserve estimates is a subjective process, and the accuracy of any reserve estimate depends on the quality of available data and the application of engineering and geological interpretation and judgment. Estimates of economically recoverable reserves and future net cash flows depend on a number of variable factors and assumptions that are difficult to predict and may vary considerably from actual results. In particular, reserve estimates for wells with limited or no production history are less reliable than those based on actual production. Subsequent evaluation of the same reserves may result in variations, which may be substantial, in estimated reserves and related estimates of future cash flows. If the capitalized costs of an individual oil and gas property exceed the related estimated future net cash flows, an impairment charge to reduce the capitalized costs to the property’s estimated fair value is required. For more information regarding the risks associated with the reserve estimation process see Item 1A. “Risk Factors” located in McMoRan’s 2006 Form 10-K.

The Cane Ridge well at Louisiana State Lease 18055, located onshore in Vermilion Parish, commenced production in April 2006 at initial rates approximating 9 MMcfe/d. These initial rates decreased significantly and in July 2006 the well was shut-in. The operator was unsuccessful in initial attempts to reestablish production from the well. In December 2006, the operator assigned certain ownership interests in the well to McMoRan. McMoRan is performing remedial operations in an attempt to restore production from the well. At March 31, 2007, McMoRan’s investment in the Cane Ridge well totaled $13.6 million.

The Pecos well located at West Pecan Island in Vermilion Parish, Louisiana commenced production in August 2006. Production rates subsequently decreased and in the first quarter of 2007 McMoRan,initiated remedial operations in an attempt to stimulate the well’s production. These efforts were unsuccessful and McMoRan subsequently recompleted the well to the upper productive interval. After producing and depleting the reserves from the upper productive zone, McMoRan will consider drilling a sidetrack well to recover additional identified potential reserves. McMoRan’s investment in the Pecos well totaled $10.5 million at March 31, 2007.

TABLE OF CONTENTSInterest Cost

Interest expense excludes capitalized interest of $1.1 million in the first quarter of 2007 and $1.4 million in the first quarter of 2006.

Inventories.

Product inventories totaled $1.2 million at March 31, 2007 and $1.1 million at December 31, 2006, consisting entirely of oil associated with operations at Main Pass Block 299. Materials and supplies inventory totaled $22.9 million at March 31, 2007 and $23.9 million at December 31, 2006, reflecting McMoRan’s purchase of certain drilling supplies to be used in its drilling activities, primarily tubulars. The materials and supplies inventory will be partially reimbursed by third party participants in wells supplied with these materials. McMoRan’s inventories are stated at the lower of average cost or market. There have been no required reductions in the carrying value of McMoRan’s inventories for any of the periods presented.

Pension Plan and Other Benefits

During 2000, McMoRan elected to terminate its defined benefit plan. The plan’s termination is still pending approval from the Internal Revenue Service and the Pension Benefit Guaranty Corporation. McMoRan also provides certain health care and life insurance benefits (Other Benefits) to retired employees. For more information regarding these Pension and Other Benefit plans see Note 8 of McMoRan’s 2006 Form 10-K. The components of net periodic Pension and Other Benefit costs for the three months ended March 31, 2007 and 2006 for this plan follows (in thousands):

| | Pension Benefits | | Other Benefits | |

| | 2007 | | 2006 | | 2007 | | 2007 | |

| Service cost | $ | - | | $ | - | | $ | 5 | | $ | 5 | |

| Interest cost | | 58 | | | 84 | | | 86 | | | 85 | |

| Return on plan assets | | (18 | ) | | (8 | ) | | - | | | - | |

| Amortization of prior service costs | | | | | | | | | | | | |

| and actuarial gains | | - | | | - | | | 14 | | | 22 | |

| Net periodic benefit expense | $ | 40 | | $ | 76 | | $ | 105 | | $ | 112 | |

Accrued Reclamation Obligations

McMoRan follows SFAS No. 143 “Accounting for Asset Retirement Obligations” in determining amounts to record for the fair value of obligations associated with the removal of long-lived assets in the period they are incurred. For more information regarding McMoRan’s accounting for asset retirement obligations see Notes 1 and 11 of McMoRan’s 2006 Form 10-K). A summary of changes in McMoRan’s consolidated discounted asset retirement obligations (including both current and long-term obligations) since December 31, 2006 follows (in thousands):

Oil and Natural Gas | | | |

| Asset retirement obligation at beginning of year | $ | 25,876 | |

| Liabilities settled | | (1,944 | )a |

| Accretion expense | | 428 | |

| Incurred liabilities | | - | |

| Revision for changes in estimates | | 3,193 | b |

| Asset retirement obligations at March 31, 2007 | $ | 27,553 | |

| | | | |

Sulphur | | | |

| Asset retirement obligations at beginning of year: | $ | 23,094 | |

| Liabilities settled | | (402 | ) |

| Accretion expense | | 434 | |

| Revision for changes in estimates | | - | |

| Asset retirement obligation at March 31, 2007 | $ | 23,126 | |

a. Includes $1.2 million of costs included in accounts payable at March 31, 2007 for completed work.

b. Reflects increases in the estimated reclamation costs at two fields. The work associated with the increase at one field has been completed

($0.7 million) and McMoRan expects all of the work at the other field to be completed over the next 12 months.

6. COMPREHENSIVE LOSS

McMoRan did not have any other comprehensive income (loss) items until it adopted SFAS 158 “Accounting for Defined Benefit and Other Postretirement Plans” on December 31, 2006 (see Note 8 of McMoRan’s 2006 Form 10-K). McMoRan’s comprehensive loss for the three months ended March 31, 2007 is shown below (in thousands).

| Net loss | $ | (14,498 | ) |

| Other comprehensive income (loss): | | | |

| Amortization of minimum pension liability adjustment | | 14 | |

| Total accumulated comprehensive loss | $ | (14,484 | ) |

| | | | |

7. NEW ACCOUNTING STANDARDS

Accounting for Uncertainty in Income Taxes.

Effective January 1, 2007, McMoRan adopted Financial Accounting Standards Board (FASB) Interpretation No. 48 “Accounting for Uncertainty in Income Taxes” (FIN 48). FIN 48 clarifies the accounting for income taxes by prescribing the minimum recognition threshold a tax position is required to meet before being recognized in the financial statements. FIN 48 also provides guidance on derecognition, measurement, classification, interest and penalties, accounting in interim periods, disclosure and transition. The adoption of FIN 48 had no effect on McMoRan’s financial statements.

As of January 1, 2007 and March 31, 2007, McMoRan had approximately $232.1 million and $237.2 million, respectively, of unrecognized tax benefits relating to its reported net losses and other temporary differences from operations. McMoRan has recorded a full valuation allowance on these deferred tax assets (see Note 9 of McMoRan’s 2006 Form 10-K). McMoRan’s effective tax rate would be reduced in future periods to the extent these deferred tax assets are recognized; however, there is no current expectation that these unrecognized tax benefits will significantly decrease within the next twelve months. Interest or penalties associated with income taxes are recorded as components of the provision for income taxes, although no such amounts have been recognized in the accompanying financial statements. McMoRan’s major taxing jurisdictions are the United States (federal) and Louisiana. Tax periods open to audit for McMoRan include federal income tax returns and Louisiana income tax returns for calendar years subsequent to 2002.

Fair Value Measurements.

In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements.” SFAS No. 157 establishes a framework for measuring fair value in generally accepted accounting principles (GAAP), clarifies the definition of fair value within that framework, and expands disclosures about the use of fair value measurements. In many of its pronouncements, the FASB has previously concluded that fair value information is relevant to the users of financial statements and has required (or permitted) fair value as a measurement objective. However, prior to the issuance of this statement, there was limited guidance for applying the fair value measurement objective in GAAP. This statement does not require any new fair value measurements in GAAP. SFAS No. 157 is effective for fiscal years beginning after November 15, 2007, with early adoption allowed. McMoRan is still reviewing the provisions of SFAS No. 157 and has not determined the impact of adoption.

In February 2007, the FASB issued SFAS No. 159 “The Fair Value Option for Financial Assets and Liabilities - Including an amendment of FASB No. 115.” SFAS No. 159 permits entities to choose to measure many financial instruments and certain other items at fair value. This statement is effective for fiscal years beginning after November 15, 2007, with early adoption allowed. McMoRan has not yet determined the impact, if any, that adopting this standard might have on its financial statements.

8. RATIO OF EARNINGS TO FIXED CHARGES

McMoRan sustained losses from continuing operations totaling $16.8 million for the first quarter of 2007 and $11.4 million for the first quarter of 2006, which were inadequate to cover its fixed charges of $6.8 million and $3.2 million for each of the respective first-quarter periods. For this calculation, earnings consist of loss from continuing operations and fixed charges. Fixed charges include interest and that portion of rent deemed representative of interest.

To the Board of Directors and Stockholders of McMoRan Exploration Co.:

We have reviewed the condensed consolidated balance sheet of McMoRan Exploration Co. (a Delaware corporation) as of March 31, 2007, and the related consolidated statements of operations and cash flow for the three-month periods ended March 31, 2007 and 2006. These financial statements are the responsibility of the Company’s management.

We conducted our review in accordance with the standards of the Public Company Accounting Oversight Board (United States). A review of interim financial information consists principally of applying analytical procedures and making inquiries of persons responsible for financial and accounting matters. It is substantially less in scope than an audit conducted in accordance with the standards of the Public Company Accounting Oversight Board, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Accordingly, we do not express such an opinion.

Based on our review, we are not aware of any material modifications that should be made to the condensed consolidated interim financial statements referred to above for them to be in conformity with U.S. generally accepted accounting principles.

We have previously audited in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of McMoRan Exploration Co. as of December 31, 2006, and the related consolidated statements of operations, cash flow and changes in stockholders’ deficit for the year then ended (not presented herein), and in our report dated March 12, 2007, we expressed an unqualified opinion on those consolidated financial statements. In our opinion, the information set forth in the accompanying condensed consolidated balance sheet as of December 31, 2006, is fairly stated, in all material respects, in relation to the consolidated balance sheet from which it has been derived.

/s/ ERNST & YOUNG LLP

New Orleans, Louisiana

April 30, 2007

TABLE OF CONTENTS

OVERVIEW

In management’s discussion and analysis “we,” “us,” and “our” refer to McMoRan Exploration Co. and its wholly owned consolidated subsidiaries, McMoRan Oil & Gas LLC (MOXY) and Freeport-McMoRan Energy LLC (Freeport Energy). You should read the following discussions in conjunction with our consolidated financial statements, the related discussion and analysis of financial condition and results of operations and our discussion of “Business and Properties” in our Form 10-K for the year ended December 31, 2006 (2006 Form 10-K), filed with the Securities and Exchange Commission. The results of operations reported and summarized below are not necessarily indicative of future operating results. Unless otherwise specified, all references to Notes refers to Notes to Consolidated Financial Statements included elsewhere in this Form 10-Q.

We engage in the exploration, development and production of oil and natural gas offshore in the Gulf of Mexico and onshore in the Gulf Coast region, with a focus on potentially significant hydrocarbons which we believe are contained in large, deep geologic structures often located beneath shallow reservoirs where significant reserves have been produced. We are also pursuing plans for the development of liquefied natural gas (LNG) facilities at the Main Pass Energy Hub™ (MPEH™) using our former sulphur mining facilities at Main Pass Block 299 (Main Pass) in the Gulf of Mexico. This proposed project includes the conversion of our former Main Pass sulphur facilities into a hub for the receipt and processing of LNG and the storage and distribution of natural gas. We were previously engaged in mining of sulphur at Main Pass until August 2000 and discontinued other sulphur business activities in June 2002.

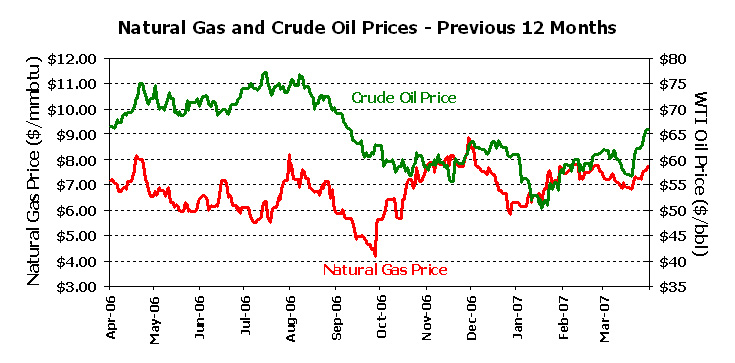

North American natural gas prices increased during the first quarter of 2007 largely because of cold winter weather and resulting drawdowns of natural gas storage levels. Natural gas prices averaged $7.16 per mmbtu in the first quarter of 2007 and currently approximate $7.75 per mmbtu. The market fundamentals for oil continue to be positive. The average price for crude oil approximated $58.30 per barrel in the first quarter of 2007 and currently approximates $61.25 per barrel. Future oil and natural gas prices are subject to change and these changes are not within our control (see Item 1A. “Risk Factors” of our 2006 Form 10-K). Our average realizations during the first quarter of 2007 were $7.59 per thousand cubic feet (Mcf) of natural gas and $54.24 per barrel for oil, including the sale of sour crude oil produced at Main Pass and Garden Banks Block 625 (see “Results of Operations” below).

OIL & GAS ACTIVITIES

Exploration Activities and Development Activities

Since 2004, we have participated in 15 discoveries on 29 prospects that have been drilled and fully evaluated, including the positive results announced during the first quarter of 2007 at the Laphroaig well located within the inland waters of St. Mary Parish, Louisiana and Hurricane Deep well at South Marsh Island Block 217 (discussed below). We have investments in six prospects that are either in progress or not fully evaluated totaling $57.9 million at March 31, 2007, including $21.3 million for the Blueberry Hill well at Louisiana State Lease 340 and $29.5 million at JB Mountain Deep

at South Marsh Island Block 224. We expect to finalize testing of the Blueberry Hill well by mid-year 2007 and information obtained from the testing of this well coupled with the results from the Hurricane Deep well will be incorporated into the future plans for the JB Mountain Deep well, as all three areas demonstrate similar geologic settings and are targeting deep Miocene sands equivalent in age. We currently have rights to approximately 360,000 gross acres and plan to participate in the drilling of 8 to 10 exploratory wells in 2007.

In March 2007, we conducted a successful production test at the Laphroaig discovery, which indicated a gross flow rate of approximately 41 million cubic feet of natural gas per day (MMcf/d), 16 MMcf/d net to us, on a 31/64th choke with flowing tubing pressure of 13,177 pounds per square inch. Infrastructure near this onshore location will allow production to be established quickly with first production currently expected in the third quarter of 2007. As previously reported, the Laphroaig discovery was deepened to a true vertical depth of 19,060 feet in February 2007. Wireline logs indicated the well encountered 56 net feet of hydrocarbon sand over a 75 foot gross interval. We have rights to 2,100 gross acres in this area and our working interest in the well is 50 percent and our net revenue interest is 38.5 percent.

The Hurricane Deep well commenced drilling in October 2006 and reached a total vertical depth of 20,712 feet in March 2007. Logs indicated that a thick Gyrodina (Gyro) sand was encountered totaling 900 gross feet. Based on wireline logs the top of this Gyro sand is credited with a potential 40 feet of hydrocarbons in a 53 foot gross interval. This sand thickness suggests that prospects in the Mound Point, JB Mountain, Hurricane and Blueberry Hill area may have thick sands as potential Gyro reservoirs. The Hurricane Deep well has been temporarily abandoned pending the receipt of special tubulars, which are expected to be received mid-2007. Initial production from the well is expected in the third quarter of 2007. The Hurricane Deep well also has two zones behind pipe in the shallower Rob-L and Operc sections of the well. The Hurricane Deep well is located in 12 feet of water on OCS 310, one mile northeast of the currently producing Hurricane discovery well.

We are currently participating in four exploratory wells and one development well as noted in the table below.

| | Working Interest | Net Revenue Interest | Prospect Acreage a | Water Depth | Proposed Total Depth b | Recent Depth | Spud Date |

| | % | % | | Feet | feet | Feet | |

South Timbalier Block 70 “Cas” d | 15.0 | 12.4 | 5,000 | 65 | 25,000 | 13,400 | January 30, 2007 |

Vermilion Block 31 “Cottonwood Point” c | 15.0 | 11.3 | 5,523 | 15 | 21,000 | 12,300 | March 1, 2007 |

South Marsh Island Block 212 “Flatrock” c,d | 25.0 | 18.8 | 3,805 | 10 | 16,500 | 11,200 | March 27, 2007 |

Louisiana State Lease 340 “Mound Point South” d | 18.3 | 14.5 | 6,400 | 8 | 20,000 | 5,500 | April 12, 2007 |

Louisiana State Lease 18350 “Point Chevreuil #2 Development” | 25.0 | 17.5 | 4,303 | <10 | 14,500 | 12,900 | April 12, 2007 |

Near-Term Exploration Well | | | | | | | |

Matagorda Island Blocks 526/557 “Deep Cavallo” | 40.0 | 29.8 | 6,878 | 70 | 14,000 | n/a | Mid-2007 |

| a. | Gross acres encompassing prospect to which we retain exploration rights. |

| b. | Planned target measured depth, which is subject to change. |

| c. | Prospect will be eligible for deep gas royalty relief under current Minerals Management Service (MMS) guidelines, which could result in an increased net revenue interest for early production. If MMS approves the application for royalty relief, each lease may be exempt from paying MMS royalties on up to the initial 25 Bcf of production. |

| d. | Wells in which we are the operator. |

At March 31, 2007, our total drilling and related leasehold costs associated with in-progress wells totaled $7.1 million, including $3.3 million for Cas, $2.7 million for Cottonwood Point, $1.0 million for Flatrock and $0.1 million for Mound Point South.

The Blueberry Hill well encountered four potentially productive hydrocarbon bearing sands below 22,200 feet in February 2005. Testing of this well commenced in the fourth quarter of 2006 following the receipt of special tubulars and casing for the high pressure well. The well has been perforated but production has not been established because of a blockage above the perforated intervals. Additional operations to clear the blockage and complete testing of the well are expected to be finalized by mid-year 2007. We have a 49.0 percent working interest and a 33.9 percent net revenue interest in the Blueberry Hill well.

The JB Mountain Deep exploration well commenced drilling in July 2005 and was drilled to a measured depth of 24,600 feet (true vertical depth of 24,557 feet). Interpretation of wireline logs indicated 120 gross feet of potential hydrocarbon bearing sands at a depth of approximately 21,900 feet that will require further evaluation. Wireline logs also indicated an additional 115 gross feet of potential hydrocarbons at a depth of approximately 24,250 feet. A liner was set to protect the lower zone and the well has been temporarily abandoned.

Production Update

Our first-quarter 2007 production averaged 70 million cubic feet of natural gas equivalents per day (MMcfe/d) compared with 46 MMcfe/d in the first quarter of 2006. Our first-quarter 2007 rate includes production from Main Pass of approximately 1,750 barrels of oil per day (bbls/d) (10.5 MMcfe/d) compared with rates of 2,400 bbls/d (14.3 MMcfe/d) in the first quarter of 2006. The first-quarter 2007 rates also reflect lower than expected production from the Hurricane No. 1 well at South Marsh Island Block 217 and Eugene Island Block 193 C-1 and C-2 wells, partially offset by higher than anticipated production from the King of the Hill well at High Island Block 131 and the Long Point wells at Louisiana State Lease 18090. Our share of second quarter production is expected to average between 60-70 MMcfe/d. These estimates include the impact of planned downtime associated with maintenance at the Long Point No. 2 well. We expect rates to increase as production from the Laphroaig and Hurricane Deep wells is established.

JB Mountain and Mound Point Area Development Activities

We are a participant in a program that began in 2002 and includes the JB Mountain and Mound Point Offset discoveries in the OCS 310 and Louisiana State Lease 340 areas, respectively. The program currently holds a 55 percent working interest and a 38.8 percent net revenue interest in the JB Mountain prospect and a 30.4 percent working interest and a 21.6 percent net revenue interest in the Mound Point Offset prospect. Under terms of the program, the third party partner is funding all of the costs attributable to our interests in the properties, and will own all of the program’s interests until the program’s aggregate production totals 100 Bcfe attributable to the program’s net revenue interest, at which point 50 percent of the program’s interests would revert to us. All exploration and development costs associated with the program’s interest in any future wells is to be funded by the third party partner during the period prior to when our potential reversion occurs.

There are three producing wells and approximately 13,000 gross acres on Louisiana State Lease 340 and OCS 310 that are subject to the 100 Bcfe arrangement. The three producing wells in the program averaged an aggregate gross rate of approximately 22 MMcfe/d during the first quarter of 2007. The recompletion of the JB Mountain No. 1 well was completed in March 2007. Recent aggregated gross production rates for the three wells have approximated 35 MMcfe/d. We believe there are further exploration and development opportunities associated with this acreage.

MAIN PASS ENERGY HUB™ PROJECT

We are pursuing plans for the development of the MPEH™ Project. As of March 31, 2007, we have incurred approximately $38.8 million of cash costs associated with our pursuit of the establishment of the MPEH™, including $2.5 million during the first quarter of 2007. All of the these costs have been and will continue to be charged to expense until permits are received and commercial feasibility is established, at which point, we will begin to capitalize certain subsequent expenditures related to the development of

the project. We expect to spend approximately $9 million to advance the licensing process and to pursue commercial arrangements for the project over the remainder of 2007.

The Maritime Administration (MARAD) approved our license application for the MPEH™ project in January 2007. We are continuing discussions with potential LNG suppliers as well as gas marketers and consumers in the United States to develop commercial arrangements for the facilities.

The project’s location near large and liquid U.S. gas markets and the significant potential of the onsite cavern storage provide attractive commercial opportunities for LNG suppliers, and natural gas consumers and marketers. The MPEH™ facility, as approved, will be capable of regasifying LNG at a peak rate of 1.6 billion cubic feet (Bcf) per day, storing 28 Bcf of natural gas in salt caverns and delivering 3.1 Bcf per day, including gas from storage, of natural gas to the U.S. market.

Unique advantages of the MPEH™ project include use of existing offshore structures, onsite natural gas cavern storage capabilities, significant logistical savings associated with the offshore location and premium markets available from its eastern Gulf of Mexico location. These advantages would provide LNG suppliers with a highly attractive netback price and offer U.S. natural gas consumers a reliable source of supply.

Prior to commencing construction of the facility, we expect to enter into commercial arrangements that would enable us to finance the construction costs of the project, projected to cost approximately $800 million and a potential additional investment of up to $600 million for pipelines and cavern storage, based on preliminary engineering estimates and for the capacities allowable under our permits.

We currently own 100 percent of the MPEH™ project. However two entities have separate options to participate as passive equity investors for up to an aggregate 25 percent of our equity interest in the project (see Notes 4 and 11 of our 2006 Form 10-K). Future financing arrangements may also reduce our equity interest in the project.

For additional information regarding our MPEH™ Project see Items 1. and 2. “Business and Properties - Main Pass Energy Hub™ Project” in our 2006 Form 10-K.

RESULTS OF OPERATIONS

Our only segment is “Oil and Gas.” We are pursuing a new business segment, “Energy Services,” whose start-up activities are reflected as a single expense line item within the accompanying consolidated statements of operations. See “Discontinued Operations” below for information regarding our former sulphur segment.

We use the successful efforts accounting method for our oil and gas operations, which requires exploration costs, other than costs of successful drilling and in-progress exploratory wells, to be charged to expense as incurred. We anticipate that we may experience operating losses during the near-term, primarily because of our significant planned exploration activities and the start-up costs associated with establishing the MPEH™, which include permitting fees and costs associated with the pursuit of commercial arrangements for the project. Additionally, energy insurance market conditions negatively affected the mid-year 2006 renewal of our well control, offshore property and business interruption insurance coverage, significantly increasing our premium costs and reducing our coverage limits from prior year levels.

Our operating loss for the first quarter of 2007 totaled $11.9 million, which includes $3.2 million of charges to depreciation, depletion and amortization expense to increase the estimates for the accrued reclamation costs for the Vermilion Block 160 and Ship Shoal Block 296 fields, $9.8 million of exploration expenses including $1.3 million of nonproductive drilling and related costs, $6.5 million of non-cash compensation costs associated with stock-based awards (see “Stock-Based Compensation” below), and $2.7 million of start-up costs associated with MPEH™.

In the first quarter of 2006, we had an operating loss of $6.4 million, reflecting $20.6 million of exploration expenses, including nonproductive well drilling and related costs of $12.3 million, and $1.8

million of MPEH™ start-up costs. Our operating losses during the first quarter of 2006 were partially offset by insurance recoveries totaling $1.2 million primarily reflecting recoveries associated with our Main Pass oil operations. Summarized operating data is as follows:

| | Three Months Ended |

| | March 31, |

| OPERATING DATA: | 2007 | | 2006 |

| Sales Volumes | | | |

| Gas (thousand cubic feet, or Mcf) | 3,849,100 | | 2,159,400 |

Oil (barrels) a | 344,400 | | 296,900 |

Plant products (equivalent barrels) b | 72,600 | | 14,300 |

| Average Realization | | | |

| Gas (per Mcf) | $ 7.59 | | $ 8.12 |

| Oil (per barrel) | 54.24 | | 57.15 |

| a. | Sales volumes from Main Pass totaled approximately 160,200 barrels in the first quarter of 2007 compared with 199,300 barrels in the first quarter of 2006. Main Pass produces sour crude oil, which sells at a discount to other crude oils. |

| b. | We received approximately $3.4 million and $0.8 million of revenues associated with plant products (ethane, propane, butane, etc.) during the first quarters of 2007 and 2006, respectively (see “Oil and Gas Operations” below). |

Oil and Gas Operations

A summary of increases (decreases) in our oil and gas revenues between the periods follows (in thousands):

| | First | |

| | Quarter | |

| Oil and natural gas revenues - prior year period | $ | 35,441 | |

| Increase (decrease) | | | |

| Sales volumes: | | | |

| Oil and condensate | | 3,280 | |

| Natural gas | | 13,726 | |

| Price realizations: | | | |

| Oil and condensate | | (1,571 | ) |

| Natural gas | | (2,038 | ) |

| Plant products revenues | | 2,589 | |

| Other | | (52 | ) |

| Oil and gas revenues - current year period | $ | 51,375 | |

Our first-quarter 2007 oil and natural gas revenues reflect a significant increase in volumes sold of natural gas (78 percent) and smaller increases in the volumes sold of oil and condensate (16 percent). These increases were partially offset by reduced average realizations received on our sales volumes for both natural gas (7 percent) and oil and condensate (5 percent). The increase in sales volumes primarily reflects the establishment of production from new fields during 2006. For information regarding new producing fields commencing operations during 2006 see Items 1. and 2. “Business and Properties” in our 2006 Form 10-K.

Our service revenues totaled $0.3 million for the first quarter of 2007 compared with $4.3 million for the first quarter of 2006. The decrease primarily reflects the conclusion of our multi-year exploration venture with a private partner (Note 5) and the termination of the third party oil and gas processing fees at Main Pass. Our service revenues for 2007 will be substantially reduced from amounts realized in 2006.

Production and delivery costs totaled $17.7 million in the first quarter of 2007 compared to $10.8 million in the first quarter of 2006. This increase primarily reflects additional costs from the establishment of production from new fields for the first quarter of 2007 as compared with the first quarter of 2006. Additionally, our insurance costs have increased significantly from prior year amounts following the mid-year 2006 renewal of our property well control and business interruption insurance policies reflecting

effects of the 2005 hurricanes on the insurance industry as well as the increased number of our producing fields during 2006. The amount of insurance charged to production costs totaled $2.3 million in the first quarter of 2007 compared with $0.4 million in the first quarter of 2006. The increase in our production costs also reflects increased well workover costs, which totaled $3.1 million in the first quarter of 2007 compared with $2.6 million in the first quarter of 2006. Our current period workover costs were primarily related to operations that restored production to the Eugene Island Block 97 No. 3 well and the Eugene Island Block 193 C-1 and C-2 wells and the ongoing efforts to restore production to the Cane Ridge well at Louisiana State Lease 18055 (see below and Note 5).

Depletion, depreciation and amortization expense totaled $27.0 million compared with $5.8 million in the first quarter of 2006. The increase primarily reflects additional production from fields that commenced production in 2006, as well as changes in capital costs and/or estimated proved reserves on certain of these fields compared to when they initially commenced production during 2006. As indicated in Note 1 of our 2006 Form 10-K, we record depletion, depreciation and amortization expense on a field-by-field basis using the units-of-production method. Our depletion, depreciation and amortization rates are directly affected by estimates of proved reserve quantities, which are subject to a significant level of uncertainty, especially for fields with little or no production history. Subsequent revisions to reserve estimates for the same fields can yield significantly different results.

The Cane Ridge well at Louisiana State Lease 18055, located onshore in Vermilion Parish, commenced production in April 2006 at initial rates approximating 9 MMcfe/d. These initial rates decreased significantly and in July 2006 the well was shut-in. The operator was unsuccessful in initial attempts to reestablish production from the well. In December 2006, the operator assigned its certain ownership interests in the well to us. We are performing remedial operations in an attempt to restore production from the well. At March 31, 2007, our investment in the Cane Ridge well totaled $13.6 million.

The Pecos well located at West Pecan Island in Vermilion Parish, Louisiana commenced production in August 2006. Production rates subsequently decreased and we initiated remedial operations in the first quarter of 2007 in an attempt to stimulate the well’s production. These efforts were unsuccessful and we subsequently recompleted the well to the upper productive interval. After producing and depleting the reserves from the upper productive zone, we will consider drilling a sidetrack well to recover additional identified potential reserves. Our investment in the Pecos well totaled $10.5 million at March 31, 2007.

As further explained in Note 5, accounting rules require that the carrying value of proved oil and gas property costs be assessed for possible impairment under certain circumstances, and reduced to fair value by a charge to earnings if impairment is deemed to have occurred. Conditions affecting current and estimated future cash flows that could require impairment charges include, but are not limited to, lower anticipated oil and natural gas prices, increased production, development and reclamation costs and downward revisions of reserve estimates. As more fully explained in Item 1A. “Risk Factors” in our 2006 Form 10-K, a combination of any or all of these conditions could require impairment charges to be recorded in future periods.

The determination of oil and natural gas reserve estimates is a subjective process, and the accuracy of any reserve estimate depends on the quality of available data and the application of engineering and geological interpretation and judgment. Estimates of economically recoverable reserves and future net cash flows depend on a number of variable factors and assumptions that are difficult to predict and may vary considerably from actual results. In particular, reserve estimates for wells with limited or no production history are less reliable than those based on actual production. Subsequent evaluation of the same reserves may result in variations, which may be substantial, in estimated reserves and related estimates of future cash flows. If the capitalized costs of an individual oil and gas property exceed the related estimated future net cash flows, an impairment charge to reduce the capitalized costs to the property’s estimated fair value is required. For more information regarding the risks associated with the reserve estimation process see Item 1A. “Risk Factors” in our 2006 Form 10-K.

Our exploration expenses fluctuate based on the outcome of drilling exploratory wells, the structure of our drilling arrangements and the incurrence of geological and geophysical costs, including the cost of seismic data. Summarized exploration expenses are as follows (in millions):

TABLE OF CONTENTS

| | Three Months Ended | |

| | March 31, | |

| | 2007 | | 2006 | |

| Geological and geophysical, | | | | | | |

including 3-D seismic purchases a | $ | 6.9 | | $ | 7.0 | |

| Non productive exploratory costs, including | | | | | | |

| related lease costs | | 1.1 | b | | 12.3 | c |

| Other | | 1.8 | | | 1.3 | |

| | $ | 9.8 | | $ | 20.6 | |

| a. | Includes compensation costs associated with outstanding stock-based awards totaling $3.2 million in the first quarter of 2007 and $5.0 million in the first quarter of 2006 (see “Stock-Based Compensation” below and Note 2). |

| b. | Primarily reflects the nonproductive exploratory well drilling and related costs associated with the “Marlin” well at Grand Isle Block 18 evaluated to be nonproductive in January 2007. |

| c. | Includes nonproductive exploratory well drilling and related costs primarily associated with a well at South Pass Block 26 ($8.1 million) and wells West Cameron Block 95 ($2.5 million) and South Marsh Island Block 230 ($1.7 million), which were evaluated as being non-productive in January 2006. |

Other Financial Results

General and administrative expense totaled $6.4 million in the first quarter of 2007 and $8.2 million in the first quarter of 2006. The total amount of stock based compensation costs decreased from $4.7 million in the first quarter of 2006 to $3.1 million in the first quarter of 2007 (see “Stock-Based Compensation” below).

Interest expense, net of capitalized interest, totaled $5.7 million in the first quarter of 2007 and $1.8 million in the first quarter of 2006. Capitalized interest totaled $1.1 million in the first quarter of 2007 and $1.4 million in the first quarter of 2006. The higher interest expense during 2007 reflects borrowings under secured debt agreements (see “Capital Resources and Liquidity” below). First-quarter 2006 conversions of our senior notes resulted in a reduction in interest expense of $0.6 million for previously accrued amounts (including $0.3 million accrued and outstanding at December 31, 2005) that were reclassified to losses on conversions of debt in other non-operating expense in the accompanying consolidated statements of operations. For more information regarding these conversion transactions see Note 5 of our 2006 Form 10-K.

CAPITAL RESOURCES AND LIQUIDITY

The table below summarizes our cash flow information by categorizing the information as cash provided by or (used in) operating activities, investing activities and financing activities and distinguishing between our continuing operations and the discontinued operations (in millions):

| | Three Months Ended | |

| | March 31, | |

| | 2007 | | | 2006 | |

Continuing operations | | | | | | | |

| Operating | $ | 10.9 | | | $ | (5.9 | ) |

| Investing | | (38.4 | ) | | | (61.4 | ) |

| Financing | | 69.8 | | | | (5.0 | ) |

Discontinued operations | | | | | | | |

| Operating | | (2.4 | ) | | | (3.5 | ) |

| Investing | | - | | | | - | |

| Financing | | - | | | | - | |

| | | | | | | | |

Total cash flow | | | | | | | |

| Operating | | 8.5 | | | | (9.4 | ) |

| Investing | | (38.4 | ) | | | (61.4 | ) |

| Financing | | 69.8 | | | | (5.0 | ) |

First-Quarter 2007 Cash Flows Compared with First-Quarter 2006

Operating cash flow from our continuing operations in 2007 increased from prior year levels reflecting lower working capital requirements and increased oil and natural gas revenues. Our operating cash flows during the first quarter of 2006 include the $15.3 million net payment to settle litigation (see Item 3. “Legal Proceedings” in our 2006 Form 10-K) and higher cash used for working capital purposes including significant payments of accounts payable and increased materials and supply inventory purchases.

Cash used in our discontinued operations decreased from first-quarter 2006 amounts primarily reflecting receipt of $5.2 million of insurance proceeds related to our Port Sulphur property loss claims. We expect to collect the remaining $2.5 million of insurance proceeds related to our Port Sulphur property loss claims by mid-2007. We are performing significant reclamation activities as part of a modified reclamation plan for the Port Sulphur facilities in the second half of 2007 and in 2008 (see “Discontinued Operations” below). Cash used in discontinued operations reflects the caretaking and other costs required to maintain these and other non-operating sulphur facilities. Reclamation costs associated with our discontinued operations totaled $0.4 million in the first quarter of 2007.

Our investing cash flows reflect exploration, development and other capital expenditures associated with our oil and gas activities (see “Oil and Gas Activities” above). Our exploration, development and other capital expenditures for 2007 are expected to approximate $150 million, including $100 million for exploration costs and approximately $50 million for currently identified development costs. These planned capital expenditures may increase as additional exploration opportunities are presented to us or to fund development costs associated with additional successful wells. We plan to fund our exploration and development activities with our available unrestricted cash (approximately $58 million at March 31, 2007), our revolving credit facility (see "Senior Secured Debt Financings" below) and operating cash flows. We will require commercial arrangements to obtain financing for the MPEH™ project. We may also pursue additional funding through potential debt or equity financing for our oil and gas and MPEH™ activities.

Our financing activities during the first quarter of 2007 reflect net borrowings under our senior secured financing arrangements of approximately $69.1 million (see “Senior Secured Debt Financings below). Investing cash flows in the first quarter of 2006 include the liquidation of $7.4 million of previously escrowed U.S. government notes, which was used to pay the $3.9 million semi-annual interest payment due on January 2, 2006 for our 6% convertible senior notes. The remaining $3.5 million was used to fund a portion of our debt conversion transactions (see “Debt Conversion Transactions below and Note 5 of our 2006 Form 10-K).

Our continuing operations’ financing activities also included payments of dividends on our mandatorily redeemable preferred stock totaling $0.4 million in the first quarter of 2007 compared with $0.7 million in the first quarter of 2006, including approximately $0.4 million associated with the dividend

payment from the fourth quarter of 2005 that was paid on January 3, 2006. Proceeds received from the exercise of stock options totaled $1.1 million in the first quarter of 2007.

Senior Secured Debt Financings

Senior Secured Revolving Credit Facility. In April 2006, we established a four-year, $100 million Senior Secured Revolving Credit Facility (the facility) for MOXY’s oil and natural gas operations with a group of banks. The facility may be increased to $150 million with additional lender commitments. The facility provides borrowing capacity based on estimates of MOXY’s oil and natural gas reserves and is re-determined on a semi-annual basis on April 1 and October 1 of each year. The borrowing base under this facility is currently $50 million. Our borrowings under the facility totaled $28.8 million at December 31, 2006. As discussed below, we repaid all borrowings under the credit facility following the closing of a term loan. We expect to use the facility for working capital and other general corporate purposes.

The variable-rate facility is secured by (1) substantially all the oil and gas properties (including related oil and natural gas proved reserves) of MOXY and (2) the pledge by McMoRan of its ownership interest in MOXY and by MOXY of its ownership interest in each of its wholly owned subsidiaries. The facility is guaranteed by McMoRan and each of MOXY’s wholly owned subsidiaries and contains customary financial covenants and other restrictions.

Senior Term Loan Agreement. In January 2007, we entered into a Senior Term Loan Agreement (Term Loan) (Note 3). The loan agreement provides for a five-year, $100 million second lien senior secured term loan facility, which matures in January 2012. Proceeds at closing, net of related fees and discounts totaled approximately $98 million. We used the net proceeds to repay borrowings outstanding under the revolving credit facility ($46.4 million), and will use the remainder to finance our future oil and gas exploration and development activities, working capital requirements and for general corporate purposes.

The term loan contains customary financial covenants and other restrictions. An annual mandatory $10 million repayment of principal is due each year commencing on December 31, 2008. The variable-rate loan is subject to certain prepayment premiums over the initial three years and is guaranteed by McMoRan and each of MOXY’s wholly owned subsidiaries. The term loan is secured with a second lien on our oil and gas properties, including Main Pass. In connection with the closing of the term loan, our revolving credit facility was amended to reduce its borrowing base from $70 million to $50 million.

Debt Conversion Transactions

In the first quarter of 2006, we privately negotiated transactions to induce conversion of $29.1 million of our 6% convertible senior notes and $25.0 million of our 5¼% convertible senior notes, into approximately 3.6 million shares of our common stock based on the respective conversion price for each set of convertible notes (Note 4). We paid an aggregate $4.3 million in the transactions and recorded an approximate $4.0 million net charge to expense in the first quarter of 2006. The net charge reflects the $4.3 million inducement payment, reflected in the accompanying consolidated statement of operations as other non-operating expense, less $0.3 million of previously accrued interest expense recorded during 2005. We funded approximately $3.5 million of the cash payments from restricted cash held in escrow for funding interest payments on the convertible notes and paid the remaining portion with available unrestricted cash. The annual interest cost savings as a result of these transactions approximates $3.1 million. We intend to consider opportunities to negotiate additional conversion transactions in the future.

STOCK-BASED COMPENSATON

Effective January 1, 2006, we adopted the fair value recognition provisions of Statement of Financial Accounting Standards No. 123 (revised 2004), “Share-Based Payment” or (SFAS No. 123R), using the modified prospective transition method. For more information regarding our accounting for stock-based awards see Note 1 of our 2006 Form 10-K

Compensation cost charged against earnings for stock-based awards is shown below (in thousands).

| | | Three Months Ended | |

| | | March 31, | |

| | | 2007 | | 2006 | |

| General and administrative expenses | | $ | 3,056 | | $ | 4,651 | |

| Exploration expenses | | | 3,214 | | | 4,999 | |

| Main Pass Energy Hub start-up costs | | | 237 | | | 25 | |

| Total stock-based compensation cost | | $ | 6,507 | | $ | 9,675 | |

| | | | | | | | |

Our stock based compensation for the first quarter of 2007 was reduced from amounts charged to expense in the comparable period last year, reflecting the reduction in the amount of stock options awarded as well as the decrease in the fair value of our options on the respective dates of grant (Note 2). As of March 31, 2007, total compensation cost related to nonvested stock option awards not yet recognized in earnings was approximately $16.8 million, which is expected to be recognized over a weighted average period of approximately 1.1 years. Compensation expense related to currently outstanding and unvested stock-based awards is expected to approximate $2.0 million per quarter for the remainder of 2007.

DISCONTINUED OPERATIONS

Our discontinued operations resulted in income of $2.3 million in the first quarter of 2007 and a loss of $1.7 million in the first quarter of 2006. The aggregate estimated closure costs for Port Sulphur approximates $12.7 million. We are accelerating the closure of the Port Sulphur facilities and are considering several different alternatives under our reclamation plans. We incurred approximately $0.4 million of these costs in the first quarter of 2007. We estimate that we may incur up to an additional $10.0 million of these costs over the next twelve months under our currently anticipated closure plan, which is subject to change pending regulatory approval of the final plans. We received $5.2 million of insurance proceeds associated with our Port Sulphur property loss claims resulting from the damages incurred during the 2005 hurricanes. We expect to receive the remaining $2.5 million of insurance proceeds under these claims by mid-year 2007. The summarized results of the discontinued operations are as follows (in thousands):

| | | First Quarter | |

| | | 2007 | | 2006 | |

| Sulphur retiree costs | | $ | 435 | | $ | 460 | |

| Legal expenses | | | 31 | | | 50 | |

| Caretaking costs | | | 184 | | | 430 | |

| Accretion expense - sulphur | | | | | | | |

| reclamation obligations | | | 434 | | | 348 | |

| Insurance | | | 388 | | | 418 | |

| General and administrative | | | 28 | | | 31 | |

| Other | | | (3,831 | )a | | (60 | ) |

| (Income) loss from discontinued operations | | $ | (2,331 | ) | $ | 1,677 | |

a. Primarily reflects $4.2 million of finalized insurance recoveries associated with the Port Sulphur property damage claims resulting from the 2005 hurricanes.

NEW ACCOUNTING STANDARDS

Accounting for Uncertainty in Income Taxes.

Effective January 1, 2007, we adopted Financial Accounting Standards Board (FASB) Interpretation No. 48 “Accounting for Uncertainty in Income Taxes” (FIN 48). FIN 48 clarifies the accounting for income taxes by prescribing the minimum recognition threshold a tax position is required to meet before being recognized in the financial statements. FIN 48 also provides guidance on derecognition, measurement,

classification, interest and penalties, accounting in interim periods, disclosure and transition. The adoption of FIN 48 had no effect on our financial statements.

As of January 1, 2007 and March 31, 2007, we had approximately $232.1 million and $237.2 million, respectively, of unrecognized tax benefits relating to our reported net losses and other temporary differences from operations. We have recorded a full valuation allowance on these deferred tax assets (see Note 9 of our 2006 Form 10-K). Our effective tax rate would be reduced in future periods to the extent these deferred tax assets are recognized; however, there is no current expectation that these unrecognized tax benefits will significantly decrease within the next twelve months. Interest or penalties associated with income taxes are recorded as components of the provision for income taxes, although no such amounts have been recognized in the accompanying financial statements. Our major taxing jurisdictions are the United States (federal) and Louisiana. Tax periods open to audit include our federal income tax returns and Louisiana income tax returns for calendar years subsequent to 2002.

Fair Value Measurements.

In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements.” SFAS No. 157 establishes a framework for measuring fair value in generally accepted accounting principles (GAAP), clarifies the definition of fair value within that framework, and expands disclosures about the use of fair value measurements. In many of its pronouncements, the FASB has previously concluded that fair value information is relevant to the users of financial statements and has required (or permitted) fair value as a measurement objective. However, prior to the issuance of this statement, there was limited guidance for applying the fair value measurement objective in GAAP. This statement does not require any new fair value measurements in GAAP. SFAS No. 157 is effective for fiscal years beginning after November 15, 2007, with early adoption allowed. We are still reviewing the provisions of SFAS No. 157 and have not determined the impact of adoption.

In February 2007, the FASB issued SFAS No. 159 “The Fair Value Option for Financial Assets and Liabilities - Including an amendment of FASB No. 115.” SFAS No. 159 permits entities to choose to measure many financial instruments and certain other items at fair value. This statement is effective for fiscal years beginning after November 15, 2007, with early adoption allowed. We have not yet determined the impact, if any, that adopting this standard might have on our financial statements.

CAUTIONARY STATEMENT

Management’s Discussion and Analysis of Financial Condition and Results of Operations contain forward-looking statements. All statements other than statements of historical fact included in this report, including, without limitation, statements regarding plans and objectives of our management for future operations and our exploration and development activities are forward-looking statements.