UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-02340

Montgomery Street Income Securities, Inc.

(Exact name of registrant as specified in charter)

225 W. Wacker Drive, Suite 1200

Chicago, IL 60606

(Address of principal executive offices)

Mark D. Nerud, President

225 W. Wacker Drive, Suite 1200

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 338-5801

Date of fiscal year end: December 31

Date of reporting period: December 31, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. §3507.

Item 1. Report to Stockholders.

Montgomery Street

Income Securities, Inc. (MTS)

Annual Report to Stockholders

December 31, 2012

Portfolio Manager Review (Unaudited)

Portfolio Return

Montgomery Street Income Securities, Inc. (the “Fund”) had a total return based on net asset value (“NAV”) of 12.94% for the twelve-month period ended December 31, 2012. The total return of the Fund, based on the market price of its New York Stock Exchange traded shares, was 15.22% for the same period1. The Fund’s NAV total return outperformed the Barclays Capital U.S. Aggregate Bond Index, the Fund’s benchmark, which posted a total return of 4.22% for the twelve-month period2.

Market Review

In the beginning of 2012, U.S. interest rates reversed their downward trend of 2011 and rose as risk appetites returned to financial markets. U.S. economic data during the first quarter was mostly positive, and markets reflected an improved short term outlook for the economy and optimism over measures taken by policymakers in Europe. Abroad, the European Central Bank (“ECB”) continued its Long Term Refinancing Operations (“LTRO”) and provided Eurozone banks with €529.5 billion in low interest loans in February. Global financial markets took comfort in these short term solutions, leading risky assets to rally through the quarter.

Conversely, the second quarter of the year saw increased concerns of a U.S. cyclical downturn and signs of recession in Europe. Financial markets reflected uncertainty over the outcome of the European debt crisis and U.S. Treasury yields decreased, as did developed market yields around the world. In the U.S., as an effort to support a stronger economic recovery, the U.S. Federal Reserve (“Fed”) renewed “Operation Twist,” a program to extend the average maturity of its holdings of securities, through the end of 2012.

Risk appetite returned again to financial markets during the second half of 2012. The ECB President, Mario Draghi, delivered on his pledge to do “whatever it takes” to support the Euro and the Eurozone by unveiling the ECB’s Outright Monetary Transactions program. The program entails unlimited, but conditional purchases of Eurozone government bonds with maturities of one to three years in the secondary market. In the U.S., weak employment data and below target inflation led to increased anticipation of further central bank action throughout the quarter. During its September meeting, the Federal Open Market Committee (“FOMC”) voted in favor of a third round of quantitative easing (“QE3”), which will be open ended and will continue until there are signs of significant improvement in the labor market. In its new bond buying program, the Fed will purchase an additional $40 billion of agency mortgage-backed securities (“MBS”) per month.

In November, Americans voted President Barack Obama to a second term in office. While the President’s re-election likely cemented the fate of the Affordable Care Act and Dodd Frank reforms, market participants quickly turned their attention to the uncertainty surrounding the impending fiscal cliff. Both political parties recognized that averting the cliff was essential to avoiding a recession in 2013, but negotiations were strained for much of the quarter, with Democrats seeking increased tax revenue from the wealthiest Americans and Republicans asking for spending cuts on entitlement programs. Ultimately, hopes of a grand bargain abated and gave way to a short term deal, thus opening the door to further fiscal negotiations, most notably on a debt ceiling increase and spending cuts (the “sequester”), in 2013.

While U.S. politicians struggled to agree on fiscal policy, the Fed unveiled new monetary policy measures to stimulate the economy. With Operation Twist set to expire at the end of the year, the FOMC announced that they will initiate purchases of $45 billion in treasuries, in addition to the existing purchases of $40 billion in agency MBS, each month. The Fed also took the extraordinary step of linking an increase in the Fed Funds’ rate to specific economic targets. Rates will stay low, between 0% and 0.25%, at least as long as the unemployment rate remains over 6.5% and projected inflation is below 2.5%. These targets replace the Fed’s previous statement that rates would remain low through at least the middle of 2015.

| 1 | Total return based on NAV reflects changes in the Fund’s net asset value during the period. Total return based on market value reflects changes in market value. Each figure assumes that dividend and capital gain distributions, if any, were reinvested. These figures will differ depending upon the level of any discount from or premium to NAV at which the Fund’s shares traded during the year. Past results are not necessarily indicative of the future performance of the Fund. Investment return and principal value will fluctuate. |

| 2 | The Barclays Capital U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, mortgage-backed securities (agency fixed-rate and hybrid adjustable rate mortgage pass-throughs), asset-backed securities and commercial mortgage-backed securities (“CMBS”). The Index does not include exposure to high yield, non-dollar securities or cash. Index returns assume reinvestment of dividends and interest, and unlike Fund returns, do not reflect fees or expenses. It is not possible to invest directly in an index. |

| Montgomery Street Income Securities, Inc. | 1 |

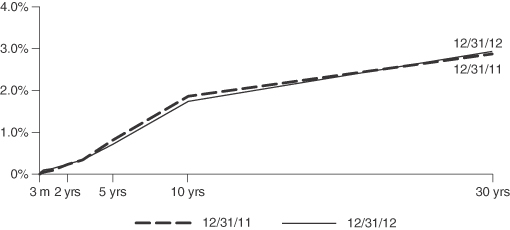

U.S. Treasury Bond Yield Curve

Source: Bloomberg

Performance is historical and does not guarantee future results.

Fund Performance

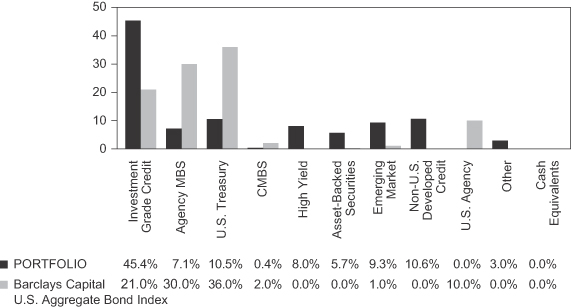

Given the Fund’s primary focus on income generation, the Fund remained overweight to investment grade corporate bonds during the year. The yield to maturity for the Fund at the end of 2012 was 3.30%, versus 1.74% for the benchmark. As seen in the sector distribution table below, the investment concentration differences relative to the benchmark also included an overweight to emerging markets (“EM”) and an underweight to U.S. government securities, which includes U.S. Treasury, U.S. Agency and agency MBS securities. The Fund also had exposure to high yield, asset-backed securities and non-U.S. developed credits, which are not in the index. During the year, the Fund increased exposure to EM, while reducing exposure to U.S. government securities.

Sector Distribution

As of December 31, 2012.

Sector distribution is subject to change.

Percentages are based on total value of the investment portfolio.

| 2 | Montgomery Street Income Securities, Inc. |

The outperformance of the Fund relative to the benchmark resulted from several strategies.

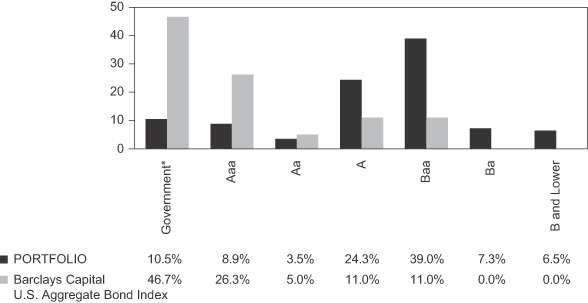

An overweight to investment grade credit relative to the index was positive for performance as this sector outperformed like-duration Treasuries. Within investment grade credit, a focus on the financial sector added to returns as this sector outperformed the broader corporate market amid accommodative monetary policy and improving housing data. Modest out of index exposure to high yield corporate bonds also added to performance as spreads tightened during the fourth quarter. As seen in the quality distribution table below, the Fund focused on Baa rated securities and had an 86% allocation to investment grade securities (those rated Baa or better). An overweight to EM, especially in Brazil, contributed to returns as the Monetary Policy Committee cut its policy rate. Holdings of Russian quasi-sovereign debt also added to performance. An allocation to non-agency MBS, which were supported by positive supply technicals, contributed to performance. Tactical duration exposure to select European countries also contributed to returns as rates declined in this region on renewed confidence in the ECB. An underweight to Build America Bonds was negative for performance as this sector outperformed like-duration Treasuries and investment grade corporate bonds.

Quality Distribution

| * | Government includes U.S. Treasury and U.S. Agency securities. |

As of December 31, 2012.

Quality distribution is subject to change.

Portfolio percentages are based on total value of the investment portfolio.

As specified in the investment guidelines, the quality ratings represent the higher of Moody’s Investors Service, Inc. (“Moody’s”) or Standard & Poor’s Corporation (“S&P”) credit ratings. The ratings of Moody’s and S&P represent these companies’ opinions as to the quality of the securities they rate. Ratings are relative and subjective and are not absolute standards of quality. A bond’s credit quality does not remove the risk of an increase in interest rates or illiquidity in the market.

Derivatives were instrumental in attaining specific exposures targeted to gain from anticipated market developments. The Fund’s underweight to U.S. interest rates, which was slightly negative for returns, was partly facilitated through the use of interest rate swaps. The overweight to EM, which was additive to relative performance, included exposure to local debt in Brazil that was implemented using zero coupon interest rate swaps. Additionally, an overweight to investment grade corporate bonds was positive for performance and was implemented through the use of credit default swaps.

| Montgomery Street Income Securities, Inc. | 3 |

Outlook and Strategy

PIMCO expects the global economy to grow at a real rate of 1.5% to 2.0% in 2013. Real growth will be moderated by efforts to resolve debt overhangs through fiscal restraint as evidenced by the slowing in corporate profits, capital expenditures and global trade. Simultaneously, inflation will likely decrease in the near term. Households should continue to delever their balance sheets while the corporate sector remains reluctant to engage its own. Nominal growth could, however, be bolstered by the continued resolve of central banks. The balance of these forces will determine if gross domestic product growth has slowed to stall speed or if a coordinated global slowdown can be averted.

We plan to remain overweight to select energy credits and select diversified U.S. banking credits. We will also continue to favor other credits that could benefit from the ongoing recovery in the U.S. housing market. Outside the U.S., we intend to emphasize a tactical allocation to emerging market credits as opportunities may materialize given easier monetary policy and supporting emerging market demand. On interest rate strategies, we plan to maintain an overall underweight to U.S interest rate duration, as the Fed continues to pursue ‘reflationary’ policies. We will target a tactical overweight to interest rate duration in select emerging market countries where interest rate cuts could materialize should global growth concerns resurface.

This material contains the current opinions and Fund holdings of the investment adviser only through the end of the period of the report as stated on the cover. Such opinions are subject to change without notice and should not be construed as a recommendation.

The Fund may not be suitable for all investors and investment in the Fund involves risk. The Fund may be affected by risks that include specific issuer credit risk, sector concentration risk, market capitalization risk and international investing risk. The Fund invests in individual bonds whose yields and value fluctuate so that an investment in the Fund may be worth more or less than its original cost. Bond investments are subject to interest rate risk such that when interest rates rise, the price of the bonds, and thus the value of the Fund, can decline and the investor can lose principal value. The Fund’s investments are also subject to credit risk and liquidity risk. High-yield bonds, lower-rated bonds and unrated securities are typically more sensitive due to adverse economic or political changes or individual developments specific to the issuer, which may result in higher default risk, volatility, lower interest income and market values. Derivative investments are subject to a number of risks such as liquidity risk, regulatory risk, interest rate risk, market risk, leverage risk, counterparty risk, valuation risk, correlation or basis risk, credit risk and management risk. Mortgage-related and other asset-backed securities include interest rate risk, legal and documentation risk, extension or contraction/prepayment risk making them more sensitive to change in interest rates. Investing in foreign securities presents certain unique risks not associated with domestic investments, such as currency fluctuation, political and economic changes, and market risks. Emerging markets investments may involve greater risk resulting from; less developed and stable economic and political systems, restrictions on investment by foreigners, liquidity and price volatility, exchange controls, confiscations of private property and other government restrictions, security registration, settlement and custody issues. All of these factors may result in greater share price volatility. Closed-end funds, unlike open-end funds, are not continuously offered or redeemed and often trade at a discount to their net asset value.

NOT FDIC/NCUA INSURED. NO BANK GUARANTEE. MAY LOSE VALUE. NOT A DEPOSIT.

NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY.

Past performance is no guarantee of future results.

This report is sent to stockholders of Montgomery Street Income Securities, Inc., for their information. It is not a prospectus, circular or representation intended for use in the purchase or sale of shares of the Fund or of any securities mentioned in the report.

| 4 | Montgomery Street Income Securities, Inc. |

Other Information (Unaudited)

Market Price and Net Asset Value

The Fund’s market price was $16.90 as of December 31, 2012, compared with $15.43 as of December 31, 2011. The Fund’s shares traded at an 8.0% discount to NAV of $18.37 at December 31, 2012, compared to a 9.8% discount to NAV of $17.11 at December 31, 2011. Shares of closed-end funds frequently trade at a discount to NAV. The price of the Fund’s shares is determined by a number of factors, several of which are beyond the control of Fund management. The Fund, therefore, cannot predict whether its shares will trade at, below or above its NAV.

The Fund’s market price is published daily in The New York Times and on The Wall Street Journal’s website at www.wsj.com. The Fund’s NAV is available daily on its website at www.montgomerystreetincome.com and published weekly in Barron’s.

Dividends Paid

The Fund paid dividends of $0.15 per share on May 4, 2012, $0.19 per share on August 3, 2012, $0.22 per share on November 2, 2012 and $0.29 per share on December 31, 2012.

Dividend Reinvestment and Cash Purchase Option

The Fund maintains an optional Dividend Reinvestment and Cash Purchase Plan (the “Plan”) for the automatic reinvestment of your dividends and capital gain distributions in shares of the Fund. Stockholders who participate in the Plan also can purchase additional shares of the Fund through the Plan’s voluntary cash investment feature. We recommend that you consider enrolling in the Plan to build your investment. The Plan’s features, including the voluntary cash investment feature, are described on page 38 of this report.

Limited Share Repurchases

The Fund is authorized to repurchase a limited number of shares of the Fund’s common stock from time to time when the shares are trading at less than 95% of their NAV. Repurchases are limited to a number of shares each calendar quarter approximately equal to the number of new shares issued under the Plan with respect to income distributed for the second preceding calendar quarter. There were 5,000 shares repurchased in each of the first, second and third quarters of 2012 and 6,000 shares in the fourth quarter of 2012. During the first quarter of 2013, 6,000 shares will be repurchased.

Investment Portfolio

Following the Fund’s first and third quarter ends, a complete Investment Portfolio is filed with the U.S. Securities and Exchange Commission (“SEC”) on Form N-Q. The form is available in the “Financial Reports” tab on the Fund’s website at www.montgomerystreetincome.com, or on the SEC’s website at www.sec.gov, and it also may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the SEC’s Public Reference Room may be obtained by calling (800) SEC-0330.

Proxy Voting

Information about how the Fund voted any proxies related to its portfolio securities during the twelve-month period ended June 30, 2012 is available in the “Financial Reports” tab on the Fund’s website at www.montgomerystreetincome.com or on the SEC’s website at www.sec.gov. A description of the policies that the Fund uses to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling (877) 437-3938 or on the SEC’s website at www.sec.gov.

Under the Fund’s current policy, it is the intention of the Fund to invest exclusively in non-voting securities. Under normal circumstances, the Fund does not intend to hold voting securities. In the event that the Fund does come into possession of any voting securities, the Fund intends to dispose of such securities as soon as it is reasonably practicable and prudent to do so. The Fund’s Board of Directors (the “Board”) may change this policy at any time.

Reports to Stockholders

The Fund’s annual and semiannual reports to stockholders will be mailed to stockholders, and also are available in the “Financial Reports” tab on the Fund’s website at www.montgomerystreetincome.com or by calling (877) 437-3938. Those stockholders who wish to view the Fund’s complete Investment Portfolio for the first and third quarters may view the Fund’s Form N-Q, as described above in “Investment Portfolio.”

| Montgomery Street Income Securities, Inc. | 5 |

Change in Officers

Effective January 25, 2013, Diana Gonzalez was appointed Chief Legal Officer, Emily Eibergen as Secretary and Danielle Bergandine as Assistant Secretary of the Fund.

Investment Objectives

The primary investment objective of the Fund is to seek as high a level of current income as is consistent with prudent investment risks, from a diversified portfolio primarily of debt securities. Capital appreciation is a secondary objective. The investment objectives of the Fund may be changed by the Board without stockholder approval. There can be no assurance that the investment objectives of the Fund will be attained. More information on the Fund’s Investment Objectives, Policies, Restrictions and Strategies is available at http://www.montgomerystreetincome.com.

| 6 | Montgomery Street Income Securities, Inc. |

| Investment Portfolio | as of December 31, 2012 |

| Principal Amount ($) | Value ($) | |||||||

Corporate Bonds (58.5%) | ||||||||

| Consumer Discretionary 1.8% | ||||||||

COX Communications Inc., 6.25%, 06/01/18 (a) | 263,000 | 321,318 | ||||||

CSC Holdings LLC, 8.63%, 02/15/19 | 2,000,000 | 2,390,000 | ||||||

NBCUniversal Media LLC, 2.88%, 04/01/16 | 300,000 | 316,274 | ||||||

TCI Communications Inc., 8.75%, 08/01/15 | 35,000 | 41,765 | ||||||

Time Warner Cable Inc., 8.25%, 04/01/19 | 290,000 | 385,914 | ||||||

|

| |||||||

| 3,455,271 | ||||||||

| Consumer Staples 2.2% | ||||||||

Altria Group Inc., 9.70%, 11/10/18 (b) | 1,014,000 | 1,419,527 | ||||||

Altria Group Inc., 9.25%, 08/06/19 (b) | 169,000 | 235,103 | ||||||

Constellation Brands Inc., 4.63%, 03/01/23 | 900,000 | 940,500 | ||||||

Kraft Foods Group Inc., 2.25%, 06/05/17 (a) | 600,000 | 620,589 | ||||||

Kraft Foods Group Inc., 5.38%, 02/10/20 (c) | 268,000 | 321,790 | ||||||

Mondelez International Inc., 5.38%, 02/10/20 | 244,000 | 294,572 | ||||||

Reynolds Group Issuer Inc., 7.13%, 04/15/19 | 300,000 | 322,500 | ||||||

|

| |||||||

| 4,154,581 | ||||||||

| Energy 12.7% | ||||||||

AK Transneft OJSC Via TransCapitalInvest Ltd., 8.70%, 08/07/18 | 2,250,000 | 2,914,312 | ||||||

Anadarko Petroleum Corp., 6.45%, 09/15/36 | 800,000 | 1,002,214 | ||||||

BP Capital Markets Plc, 3.75%, 06/17/13 | 24,000 | 24,336 | ||||||

BP Capital Markets Plc, 3.63%, 05/08/14 | 521,000 | 542,321 | ||||||

Canadian Oil Sands Ltd., 7.75%, 05/15/19 (a) | 1,000,000 | 1,274,309 | ||||||

Canadian Oil Sands Ltd., 4.50%, 04/01/22 (a) | 1,000,000 | 1,091,064 | ||||||

Dolphin Energy Ltd., 5.50%, 12/15/21 (a) | 800,000 | 933,000 | ||||||

El Paso Pipeline Partners Operating Co. LLC, 6.50%, 04/01/20 | 1,000,000 | 1,219,329 | ||||||

Energy Transfer Partners LP, 8.50%, 04/15/14 | 161,000 | 175,068 | ||||||

Gazprom OAO Via Gaz Capital SA, 9.25%, 04/23/19 (a) | 300,000 | 397,125 | ||||||

Midcontinent Express Pipeline LLC, 6.70%, 09/15/19 (a) | 400,000 | 422,293 | ||||||

Novatek OAO via Novatek Finance Ltd., 6.60%, 02/03/21 (a) | 800,000 | 938,000 | ||||||

Odebrecht Drilling Norbe VIII/IX Ltd., 6.35%, 06/30/21 (a) | 291,000 | 326,648 | ||||||

OGX Austria GmbH, 8.38%, 04/01/22 (a) | 800,000 | 668,000 | ||||||

Petrobras International Finance Co., 5.38%, 01/27/21 | 1,100,000 | 1,238,402 | ||||||

Pioneer Natural Resources Co., 6.88%, 05/01/18 | 2,000,000 | 2,433,172 | ||||||

Pioneer Natural Resources Co., 7.20%, 01/15/28 | 200,000 | 254,869 | ||||||

Plains All American Pipeline LP, 8.75%, 05/01/19 | 1,000,000 | 1,360,412 | ||||||

Pride International Inc., 6.88%, 08/15/20 | 621,000 | 785,385 | ||||||

Ras Laffan Liquefied Natural Gas Co. Ltd. III, 4.00%, 09/30/20 | 797,500 | 895,194 | ||||||

Rockies Express Pipeline LLC, 3.90%, 04/15/15 (c) | 1,800,000 | 1,791,000 | ||||||

SandRidge Energy Inc., 7.50%, 03/15/21 | 900,000 | 963,000 | ||||||

TNK-BP Finance SA, 7.50%, 03/13/13 | 1,600,000 | 1,617,600 | ||||||

TNK-BP Finance SA, 7.88%, 03/13/18 | 500,000 | 606,950 | ||||||

Transcontinental Gas Pipe Line Co. LLC, 6.40%, 04/15/16 | 250,000 | 289,393 | ||||||

|

| |||||||

| 24,163,396 | ||||||||

| Financials 32.7% | ||||||||

Abbey National Treasury Services Plc, 1.89%, 04/25/14 (d) | 800,000 | 798,170 | ||||||

ABN Amro North American Holding Preferred Capital Repackage Trust I, | 1,000,000 | 1,000,000 | ||||||

Ally Financial Inc., 4.63%, 06/26/15 | 900,000 | 938,228 | ||||||

American Express Co., 6.15%, 08/28/17 | 500,000 | 602,486 | ||||||

American Express Credit Corp., 7.30%, 08/20/13 | 700,000 | 730,071 | ||||||

American International Group Inc., 8.25%, 08/15/18 | 500,000 | 656,943 | ||||||

The accompanying notes are an integral part of the financial statements.

| Montgomery Street Income Securities, Inc. | 7 |

| Principal Amount ($) | Value ($) | |||||||

Banco Bradesco SA, 2.41%, 05/16/14 (a) (d) | 500,000 | 503,680 | ||||||

Banco do Brasil SA, 6.00%, 01/22/20 (a) | 500,000 | 581,250 | ||||||

Banco Santander Brasil SA, 4.50%, 04/06/15 (a) | 100,000 | 103,500 | ||||||

Banco Santander Brasil SA, 4.50%, 04/06/15 | 300,000 | 310,500 | ||||||

Banco Santander Chile, 3.75%, 09/22/15 (a) | 500,000 | 525,058 | ||||||

Banco Votorantim SA, 5.25%, 02/11/16 (a) | 400,000 | 421,000 | ||||||

Bank of America Corp., 6.00%, 09/01/17 | 115,000 | 134,667 | ||||||

Banque PSA Finance SA, 2.25%, 04/04/14 (c) (d) | 300,000 | 296,258 | ||||||

Banque PSA Finance SA, 3.88%, 01/14/15, EUR | 100,000 | 134,629 | ||||||

Barclays Bank Plc, 10.18%, 06/12/21 (c) | 1,400,000 | 1,905,988 | ||||||

BBVA Bancomer SA, 4.50%, 03/10/16 (a) | 500,000 | 531,250 | ||||||

BBVA Bancomer SA, 6.50%, 03/10/21 (a) | 400,000 | 444,000 | ||||||

BNP Paribas, 7.78% (callable at 100 beginning 07/02/18) (e) (f), EUR | 500,000 | 732,453 | ||||||

BPCE SA, 2.06%, 02/07/14 (c) (d) | 700,000 | 707,761 | ||||||

Capital One Capital V, 10.25% (callable at 100 beginning 01/02/13) | 1,000,000 | 1,000,000 | ||||||

CBA Capital Trust II, 6.02% (callable at 100 beginning 03/15/16) (a) (e) (f) | 200,000 | 204,215 | ||||||

Citigroup Inc., 6.01%, 01/15/15 | 2,200,000 | 2,403,973 | ||||||

Citigroup Inc., 8.50%, 05/22/19 | 1,235,000 | 1,660,627 | ||||||

Commonwealth Bank of Australia, 1.04%, 03/17/14 (a) (d) | 200,000 | 201,263 | ||||||

Cooperatieve Centrale Raiffeisen-Boerenleenbank BA, 11.00% (callable at 100 beginning 06/30/19) (c) (e) (f) | 1,000,000 | 1,352,500 | ||||||

Credit Agricole SA, 1.77%, 01/21/14 (c) (d) | 400,000 | 403,340 | ||||||

DNB Bank ASA, 3.20%, 04/03/17 (a) | 400,000 | 426,024 | ||||||

Export-Import Bank of Korea, 4.00%, 01/11/17 | 2,700,000 | 2,927,721 | ||||||

Export-Import Bank of Korea, 4.00%, 01/29/21 | 200,000 | 215,043 | ||||||

Ford Motor Credit Co. LLC, 5.63%, 09/15/15 | 2,000,000 | 2,190,068 | ||||||

Ford Motor Credit Co. LLC, 2.50%, 01/15/16 | 200,000 | 202,465 | ||||||

Goldman Sachs Group Inc., 5.95%, 01/18/18 | 650,000 | 756,400 | ||||||

Goldman Sachs Group Inc., 6.15%, 04/01/18 | 600,000 | 704,861 | ||||||

Goldman Sachs Group Inc., 6.00%, 06/15/20 | 2,000,000 | 2,376,424 | ||||||

HBOS Plc, 6.75%, 05/21/18 (c) | 700,000 | 753,375 | ||||||

HSBC Bank Plc, 5.00%, 03/20/23 (d), GBP | 500,000 | 865,271 | ||||||

HSBC Finance Corp., 6.68%, 01/15/21 | 300,000 | 355,911 | ||||||

International Lease Finance Corp., 7.13%, 09/01/18 (a) | 1,700,000 | 1,972,000 | ||||||

Intesa Sanpaolo SpA, 2.71%, 02/24/14 (c) (d) | 800,000 | 799,106 | ||||||

IPIC GMTN Ltd., 4.00%, 03/14/21, EUR | 200,000 | 321,135 | ||||||

JPMorgan Chase & Co., 6.30%, 04/23/19 | 2,500,000 | 3,084,405 | ||||||

JPMorgan Chase Bank NA, 6.00%, 10/01/17 | 600,000 | 710,304 | ||||||

Korea Exchange Bank, 3.13%, 06/26/17 (a) | 400,000 | 416,374 | ||||||

Lazard Group LLC, 6.85%, 06/15/17 | 500,000 | 577,908 | ||||||

LBG Capital No.1 Plc, 7.87%, 08/25/20, GBP | 1,000,000 | 1,721,925 | ||||||

LBG Capital No.1 Plc, 7.88%, 11/01/20 (c) | 450,000 | 484,108 | ||||||

Merrill Lynch & Co. Inc., 6.88%, 04/25/18 | 2,400,000 | 2,893,090 | ||||||

Metropolitan Life Global Funding I, 1.10%, 01/10/14 (c) (d) | 300,000 | 301,493 | ||||||

Morgan Stanley, 6.63%, 04/01/18 | 1,000,000 | 1,178,575 | ||||||

Morgan Stanley, 7.30%, 05/13/19 | 800,000 | 972,176 | ||||||

Morgan Stanley, 5.50%, 01/26/20 | 2,850,000 | 3,197,110 | ||||||

Rabobank Capital Funding Trust III, 5.25% (callable at 100 beginning 10/21/16) (c) (e) (f) | 800,000 | 809,228 | ||||||

RCI Banque SA, 2.22%, 04/11/14 (c) (d) | 600,000 | 599,771 | ||||||

Regions Financial Corp., 4.88%, 04/26/13 | 375,000 | 378,750 | ||||||

Royal Bank of Scotland Plc, 5.38%, 09/30/19, EUR | 1,600,000 | 2,519,831 | ||||||

Russian Agricultural Bank OJSC Via RSHB Capital SA, 6.30%, 05/15/17 | 300,000 | 332,250 | ||||||

Sberbank of Russia Via SB Capital SA, 5.50%, 07/07/15 | 700,000 | 756,700 | ||||||

Sberbank Via SB Capital SA, 5.40%, 03/24/17 | 1,200,000 | 1,311,780 | ||||||

Shinhan Bank, 4.13%, 10/04/16 (a) | 200,000 | 215,919 | ||||||

The accompanying notes are an integral part of the financial statements.

| 8 | Montgomery Street Income Securities, Inc. |

| Principal Amount ($) | Value ($) | |||||||

SLM Corp., 5.38%, 01/15/13 | 1,200,000 | 1,200,985 | ||||||

Sydney Airport Finance Co. Pty Ltd., 5.13%, 02/22/21 (a) (b) | 2,100,000 | 2,335,620 | ||||||

UBS AG Stamford, 5.88%, 12/20/17 | 300,000 | 357,078 | ||||||

USB Capital IX, 3.50% (callable at 100 beginning 02/07/13) (e) (f) | 625,000 | 564,950 | ||||||

Ventas Realty LP, 3.13%, 11/30/15 | 100,000 | 105,423 | ||||||

Weyerhaeuser Co., 7.38%, 10/01/19 | 1,000,000 | 1,235,936 | ||||||

|

| |||||||

| 62,411,303 | ||||||||

| Health Care 1.9% | ||||||||

Boston Scientific Corp., 6.40%, 06/15/16 | 1,200,000 | 1,379,364 | ||||||

HCA Inc., 6.50%, 02/15/20 | 2,000,000 | 2,250,000 | ||||||

|

| |||||||

| 3,629,364 | ||||||||

| Industrials 0.9% | ||||||||

Asciano Finance Ltd., 5.00%, 04/07/18 (a) | 300,000 | 324,191 | ||||||

Aviation Capital Group Corp., 7.13%, 10/15/20 (a) | 600,000 | 631,890 | ||||||

AWAS Aviation Capital Ltd., 7.00%, 10/17/16 (a) | 808,000 | 852,440 | ||||||

|

| |||||||

| 1,808,521 | ||||||||

| Materials 2.9% | ||||||||

Anglo American Capital Plc, 9.38%, 04/08/14 (a) | 543,000 | 596,931 | ||||||

Cliffs Natural Resources Inc., 5.90%, 03/15/20 | 1,000,000 | 1,063,339 | ||||||

Dow Chemical Co., 8.55%, 05/15/19 (b) | 990,000 | 1,336,575 | ||||||

Fibria Overseas Finance Ltd., 7.50%, 05/04/20 | 100,000 | 111,000 | ||||||

Fibria Overseas Finance Ltd., 6.75%, 03/03/21 (a) | 200,000 | 221,500 | ||||||

Georgia-Pacific LLC, 5.40%, 11/01/20 (a) | 1,600,000 | 1,903,414 | ||||||

Rio Tinto Finance USA Ltd., 9.00%, 05/01/19 (b) | 200,000 | 274,706 | ||||||

|

| |||||||

| 5,507,465 | ||||||||

| Telecommunication Services 1.3% | ||||||||

British Telecommunications Plc, 1.43%, 12/20/13 (d) | 400,000 | 403,315 | ||||||

Qtel International Finance Ltd., 4.75%, 02/16/21 (a) | 300,000 | 339,000 | ||||||

Rogers Communications Inc., 7.50%, 03/15/15 | 179,000 | 203,867 | ||||||

Telefonica Emisiones SAU, 3.73%, 04/27/15 | 1,400,000 | 1,438,360 | ||||||

|

| |||||||

| 2,384,542 | ||||||||

| Utilities 2.1% | ||||||||

Centrais Eletricas Brasileiras SA, 6.88%, 07/30/19 | 400,000 | 455,000 | ||||||

Duquesne Light Holdings Inc., 6.40%, 09/15/20 (a) | 400,000 | 483,806 | ||||||

Energy Future Holdings Corp., 10.00%, 01/15/20 | 1,000,000 | 1,117,500 | ||||||

Florida Power Corp., 5.80%, 09/15/17 | 195,000 | 233,243 | ||||||

Korea Electric Power Corp., 3.00%, 10/05/15 (a) | 1,400,000 | 1,460,285 | ||||||

NRG Energy Inc. Term Loan, 2.51%, 05/05/18 (d) | 112,500 | 113,599 | ||||||

NRG Energy Inc. Term Loan, 4.00%, 05/05/18 (d) | 85,000 | 85,831 | ||||||

|

| |||||||

| 3,949,264 | ||||||||

| ||||||||

Total Corporate Bonds (cost $102,502,836) | 111,463,707 | |||||||

Non-U.S. Government Agency Asset-Backed Securities 8.6% | ||||||||

Aircraft Certificate Owner Trust (insured by MBIA Assurance Corp.), | 38,020 | 38,685 | ||||||

American Airlines Pass-Through Trust, (2009, 1A), 10.38%, 07/02/19 | 557,594 | 593,838 | ||||||

American Airlines Pass-Through Trust, (2011, 2A), 8.63%, 10/15/21 | 1,880,263 | 1,974,276 | ||||||

Banc of America Funding Corp. REMIC, (2004, A, 1A3), 5.54%, 09/20/34 (d) | 557,863 | 574,230 | ||||||

Banc of America Mortgage Securities Inc. REMIC, (2005, H, 2A5), 3.11%, 09/25/35 (d) | 1,020,368 | 935,085 | ||||||

The accompanying notes are an integral part of the financial statements.

| Montgomery Street Income Securities, Inc. | 9 |

| Principal Amount ($) | Value ($) | |||||||

Bayview Commercial Asset Trust, Interest Only REMIC, (2007, 2A, IO), 4.29%, 07/25/37 (a) (d) | 4,067,675 | 219,883 | ||||||

Bayview Commercial Asset Trust, Interest Only REMIC, (2007, 4A, IO), 3.89%, 09/25/37 (a) (d) | 4,493,386 | 408,296 | ||||||

Bear Stearns Adjustable Rate Mortgage Trust REMIC, (2004, 6, 2A1), 3.13%, 09/25/34 (d) | 672,942 | 615,086 | ||||||

Citigroup Mortgage Loan Trust Inc. REMIC, (2004, NCM2, 1CB2), 6.75%, 08/25/34 | 157,598 | 167,858 | ||||||

Continental Airlines Inc. Pass-Through Trust Class A, 9.00%, 07/08/16 | 1,714,875 | 1,976,394 | ||||||

Countrywide Alternative Loan Trust REMIC, (2004, 35T2, A4), 6.00%, 02/25/35 | 39,266 | 39,286 | ||||||

Countrywide Alternative Loan Trust REMIC (2006, 0A10, 4A1), 0.40%, 08/25/46 (d) | 43,948 | 28,181 | ||||||

Credit Suisse First Boston Mortgage Securities Corp. REMIC, (2004, AR8, 2A1), 2.87%, 09/25/34 (d) | 1,094,163 | 1,111,733 | ||||||

Credit-Based Asset Servicing and Securitization LLC REMIC, (2006, SC1, A), 0.48%, 05/25/36 (a) (d) | 85,302 | 74,934 | ||||||

Galaxy CLO Ltd., (2005, 4A, A1VB), 0.61%, 04/17/17 (a) (d) | 313,818 | 312,005 | ||||||

GMAC Mortgage Corp. Loan Trust (insured by Financial Guaranty Insurance Co.) REMIC, | 203,742 | 181,381 | ||||||

Holmes Master Issuer Plc, (2011, 1A, A3), 1.56%, 10/15/54 (a) (d), EUR | 700,000 | 933,999 | ||||||

Indymac Index Mortgage Loan Trust REMIC, 0.51%, 07/25/35 (d) | 58,526 | 46,379 | ||||||

Nationstar NIM Ltd. Trust, (2007, A, A), 9.79%, 03/25/37 (h) (i) | 22,008 | — | ||||||

Residential Asset Securitization Trust REMIC, (2005, A1, A3), 5.50%, 04/25/35 | 2,075,392 | 2,085,628 | ||||||

Truman Capital Mortgage Loan Trust REMIC, (2006, 1, A), 0.47%, 03/25/36 (a) (d) | 1,471,402 | 1,083,452 | ||||||

United Air Lines Inc. 2009-1 Pass-Through Trust, 10.40%, 11/01/16 | 1,271,527 | 1,462,256 | ||||||

Washington Mutual Mortgage Pass-Through Certificates REMIC, (2005, AR16, 1A3), 2.49%, 12/25/35 (d) | 1,320,000 | 1,202,020 | ||||||

Wells Fargo Mortgage Backed Securities Trust REMIC, (2006, 1, A3), 5.00%, 03/25/21 | 295,098 | 302,945 | ||||||

| ||||||||

Total Non-U.S. Government Agency Asset-Backed Securities (cost $16,579,790) | 16,367,830 | |||||||

Government and Agency Obligations 36.6% | ||||||||

| Government Securities 15.8% | ||||||||

| Sovereign 6.1% | ||||||||

Banco Nacional de Desenvolvimento Economico e Social, 5.50%, 07/12/20 (a) | 400,000 | 471,000 | ||||||

Italy Buoni Poliennali Del Tesoro, 4.50%, 06/01/17, EUR | 4,500,000 | 6,322,013 | ||||||

Spain Government Bond, 4.25%, 10/31/16, EUR | 3,600,000 | 4,820,275 | ||||||

|

| |||||||

| 11,613,288 | ||||||||

| Treasury Inflation Index Securities 0.3% | ||||||||

Australian Government Treasury Inflation Indexed Bond, 4.00%, 08/20/20, AUD (j) | 300,000 | 600,246 | ||||||

| U.S. Treasury Securities 9.4% | ||||||||

U.S. Treasury Bond, 5.50%, 08/15/28 (k) | 1,700,000 | 2,402,578 | ||||||

U.S. Treasury Bond, 4.25%, 11/15/40 | 2,850,000 | 3,639,094 | ||||||

U.S. Treasury Bond, 4.38%, 05/15/41 (k) | 100,000 | 130,281 | ||||||

U.S. Treasury Bond, 3.13%, 02/15/42 (k) | 1,700,000 | 1,777,562 | ||||||

U.S. Treasury Note, 2.00%, 02/15/22 (l) | 5,200,000 | 5,377,533 | ||||||

U.S. Treasury Note, 1.63%, 08/15/22 (l) | 4,500,000 | 4,470,471 | ||||||

|

| |||||||

| 17,797,519 | ||||||||

| U.S. Government Agency Mortgage-Backed Securities 20.8% | ||||||||

| Federal Home Loan Mortgage Corp. 0.0% | ||||||||

Federal Home Loan Mortgage Corp. REMIC, 7.00%, 08/15/21 | 12,429 | 14,477 | ||||||

| Federal National Mortgage Association 20.8% | ||||||||

Federal National Mortgage Association, 5.50%, 01/01/37 | 19,917,027 | 21,764,915 | ||||||

Federal National Mortgage Association, 5.50%, 08/01/37 | 16,333,272 | 17,950,745 | ||||||

|

| |||||||

| 39,715,660 | ||||||||

| ||||||||

Total Government and Agency Obligations (cost $69,432,532) | 69,741,190 | |||||||

The accompanying notes are an integral part of the financial statements.

| 10 | Montgomery Street Income Securities, Inc. |

Contracts/ Principal | Value ($) | |||||||

Purchased Options 0.1% |

| |||||||

Interest Rate Put Swaption, 3 month LIBOR versus 3.45% fixed, Expiration 09/21/15, BBP | 22 | 160,984 | ||||||

| ||||||||

Total Purchased Options (cost $174,446) | 160,984 | |||||||

| ||||||||

Total Investments — 103.8% (cost $188,689,604) | 197,733,711 | |||||||

Total Forward Sales Commitments — (14.5%) (proceeds $27,707,344) | (27,703,358 | ) | ||||||

Other Assets and Liabilities, Net 10.8% | 20,546,281 | |||||||

| ||||||||

Total Net Assets — 100% | $ | 190,576,634 | ||||||

Forward Sales Commitments (14.5%) | ||||||||

| U.S. Government Agency Mortgage-Backed Securities (14.5%) | ||||||||

Federal National Mortgage Association, 5.50%, 01/15/41 | (25,500,000 | ) | (27,703,358 | ) | ||||

| ||||||||

Total Forward Sales Commitments (cost $27,707,344) | (27,703,358 | ) | ||||||

Notes to the Investment Portfolio

| (a) | Rule 144A, Section 4(2) of the Securities Act of 1933 or other security which is restricted to resale to institutional investors. The Fund’s investment adviser has deemed these securities to be liquid based on procedures approved by the Fund’s Board of Directors. As of December 31, 2012, the aggregate value of Rule 144A or Section 4(2) liquid securities was $26,229,214 (13.8% of net assets). |

| (b) | The interest rate for this security is inversely affected by upgrades or downgrades to the credit rating of the issuer. |

| (c) | Rule 144A, Section 4(2) of the Securities Act of 1933 or other security which is restricted to resale to institutional investors. The Fund’s investment adviser has deemed these securities to be illiquid based on procedures approved by the Fund’s Board of Directors. See Restricted Securities in the Notes to Investment Portfolio. |

| (d) | Floating rate note. Floating rate notes are securities whose yields vary with a designated market index or market rate. Rate stated was in effect as of December 31, 2012. |

| (e) | Perpetual maturity security. |

| (f) | Interest rate is fixed until stated call date and variable thereafter. |

| (g) | Security fair valued in good faith in accordance with the procedures approved by the Fund’s Board of Directors. Good faith fair valued securities may be classified as Level 2 or Level 3 for Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 820 “Fair Value Measurements and Disclosures” based on the applicable valuation inputs. See FASB ASC Topic 820 “Fair Value Measurements and Disclosures” in the Notes to the Financial Statements. |

| (h) | Security is in default relating to principal and/or interest. |

| (i) | Non-income producing security. |

| (j) | Treasury inflation indexed note. Par amount is not adjusted for inflation. |

| (k) | All or a portion of the security is pledged or segregated as collateral. See the Notes to the Financial Statements. |

| (l) | All or a portion of the security was purchased on a delayed delivery basis. As of December 31, 2012, the total cost of investments purchased on a delayed delivery basis was $7,636,498. |

| Abbreviations: | ||

| AUD – Australian Dollar | JPY – Japanese Yen | |

| BBP – Barclays Bank PLC | KRW – Korean Won | |

| BCL – Barclays Capital Inc. | LIBOR – London Interbank Offered Rate | |

| BOA – Bancamerica Securities/Bank of America NA | MBIA – Municipal Bond Investors Assurance | |

| BRL – Brazilian Real | MXN – Mexican Peso | |

| CAD – Canadian Dollar | NIM – Net Interest Margin | |

| CDX – Credit Default Swap Index | NOK – Norwegian Krone | |

| CNY – Chinese Yuan | REMIC – Real Estate Mortgage Investment Conduit | |

| EUR – European Currency Unit (Euro) | SGD – Singapore Dollar | |

| EURIBOR – Europe Interbank Offered Rate | USD – United States Dollar | |

| GBP – British Pound | ZAR – South African Bond | |

| GSC – Goldman Sachs & Co. | ||

| GSI – Goldman Sachs International | ||

The accompanying notes are an integral part of the financial statements.

| Montgomery Street Income Securities, Inc. | 11 |

Restricted Securities

Restricted securities are purchased in private placement transactions and cannot be sold without prior registration unless the sale is pursuant to an exemption under the Securities Exchange Act of 1933, as amended. The following table consists of Rule 144A securities held by the Fund at December 31, 2012 that have been deemed illiquid by the Fund’s investment adviser.

Initial Acquisition | Cost | Ending Value | Percent of Net Assets | |||||||||||||

| ABN Amro North American Holding Preferred Capital Repackage Trust I , 3.41% (callable at 100 beginning 12/07/13) | 03/31/2010 | $ | 861,712 | $ | 1,000,000 | 0.5 | % | |||||||||

| BPCE SA , 2.06%, 02/07/14 | 02/01/2011 | 699,604 | 707,761 | 0.4 | ||||||||||||

| Banque PSA Finance SA , 2.25%, 04/04/14 | 03/29/2011 | 300,000 | 296,258 | 0.2 | ||||||||||||

| Barclays Bank Plc , 10.18%, 06/12/21 | 03/22/2010 | 1,743,555 | 1,905,988 | 1.0 | ||||||||||||

| Cooperatieve Centrale Raiffeisen-Boerenleenbank BA, 11.00% (callable at 100 beginning 06/30/19) | 03/30/2010 | 1,185,942 | 1,352,500 | 0.7 | ||||||||||||

| Credit Agricole SA , 1.77%, 01/21/14 | 01/14/2011 | 400,000 | 403,340 | 0.2 | ||||||||||||

| HBOS Plc , 6.75%, 05/21/18 | 10/11/2010 | 712,686 | 753,375 | 0.4 | ||||||||||||

| Intesa Sanpaolo SpA , 2.71%, 02/24/14 | 02/16/2011 | 800,000 | 799,106 | 0.4 | ||||||||||||

| Kraft Foods Group Inc. , 5.38%, 02/10/20 | 07/25/2012 | 319,905 | 321,790 | 0.2 | ||||||||||||

| LBG Capital No.1 Plc , 7.88%, 11/01/20 | 03/25/2010 | 413,760 | 484,108 | 0.2 | ||||||||||||

| Metropolitan Life Global Funding I , 1.10%, 01/10/14 | 01/05/2011 | 300,000 | 301,493 | 0.2 | ||||||||||||

| RCI Banque SA , 2.22%, 04/11/14 | 04/06/2011 | 600,000 | 599,771 | 0.3 | ||||||||||||

| Rabobank Capital Funding Trust III, 5.25% (callable at 100 beginning 10/21/16) | 03/25/2010 | 727,436 | 809,228 | 0.4 | ||||||||||||

| Rockies Express Pipeline LLC , 3.90%, 04/15/15 | 04/20/2012 | 1,708,229 | 1,791,000 | 0.9 | ||||||||||||

| $ | 10,772,829 | $ | 11,525,718 | 6.0 | % | |||||||||||

| Schedule of Written Options | Expiration Date | Exercise Price | Contracts | Value | ||||||||||||

| Interest Rate Put Swaption, 3 Month LIBOR versus 2.50% fixed, BCL | 09/21/2015 | N/A | 92 | $ | (141,746 | ) | ||||||||||

| $ | (141,746 | ) | ||||||||||||||

| Summary of Written Options | Contracts | Premiums | ||||||

| Options outstanding at December 31, 2011 | 133 | $ | 61,614 | |||||

| Options written during the period | 279 | 304,205 | ||||||

| Options closed during the period | (185 | ) | (142,135 | ) | ||||

| Options expired during the period | (135 | ) | (56,149 | ) | ||||

| Options outstanding at December 31, 2012 | 92 | $ | 167,535 | |||||

| Schedule of Open Futures Contracts | Contracts Long | Unrealized Appreciation | ||||||

| 3-Month Euro Euribor Interest Rate Future, Expiration September 2014 | 1 | $5,062 | ||||||

| 3-Month Euro Euribor Interest Rate Future, Expiration December 2014 | 1 | 1,446 | ||||||

| 3-Month Euro Euribor Interest Rate Future, Expiration March 2015 | 1 | 1,605 | ||||||

| 3-Month Euro Euribor Interest Rate Future, Expiration June 2015 | 1 | 1,704 | ||||||

| $9,817 | ||||||||

The accompanying notes are an integral part of the financial statements.

| 12 | Montgomery Street Income Securities, Inc. |

Schedule of Open Forward Foreign Currency Contracts

| Counterparty | Currency Purchased/Sold | Settlement Date | Notional Amount | Currency Value | Unrealized Gain/(Loss) | |||||||||||||

| BCL | BRL/USD | 02/04/2013 | BRL | 3,819,909 | $ | 1,857,385 | $ | (2,673 | ) | |||||||||

| BCL | CAD/USD | 03/21/2013 | CAD | 488,000 | 489,798 | (4,457 | ) | |||||||||||

| BCL | CNY/USD | 02/01/2013 | CNY | 9,363,750 | 1,499,476 | (524 | ) | |||||||||||

| BCL | CNY/USD | 02/01/2013 | CNY | 3,781,800 | 605,603 | 5,603 | ||||||||||||

| BCL | CNY/USD | 08/05/2013 | CNY | 1,741,964 | 275,932 | (4,533 | ) | |||||||||||

| BCL | EUR/USD | 03/18/2013 | EUR | 149,000 | 196,802 | 1,901 | ||||||||||||

| BCL | KRW/USD | 02/28/2013 | KRW | 511,260,000 | 475,924 | 6,577 | ||||||||||||

| BCL | MXN/USD | 04/03/2013 | MXN | 7,081,189 | 543,232 | 6,981 | ||||||||||||

| BCL | NOK/USD | 02/14/2013 | NOK | 2,906,000 | 522,044 | 21,773 | ||||||||||||

| BCL | SGD/USD | 01/25/2013 | SGD | 1,128,477 | 923,758 | (2,845 | ) | |||||||||||

| BCL | USD/AUD | 01/31/2013 | AUD | (2,069,000 | ) | (2,143,804 | ) | 15,074 | ||||||||||

| BCL | USD/CNY | 02/01/2013 | CNY | (13,847,499 | ) | (2,217,486 | ) | (47,916 | ) | |||||||||

| BCL | USD/CNY | 08/05/2013 | CNY | (96,440 | ) | (15,276 | ) | (292 | ) | |||||||||

| BCL | USD/CNY | 08/05/2013 | CNY | (943,575 | ) | (149,465 | ) | (2,856 | ) | |||||||||

| BCL | USD/EUR | 03/18/2013 | EUR | (12,890,000 | ) | (17,025,328 | ) | (195,602 | ) | |||||||||

| GSC | USD/EUR | 03/18/2013 | EUR | (400,000 | ) | (528,327 | ) | 1,872 | ||||||||||

| BCL | USD/GBP | 03/12/2013 | GBP | (1,370,000 | ) | (2,225,042 | ) | (23,793 | ) | |||||||||

| GSC | USD/JPY | 01/17/2013 | JPY | (79,438,000 | ) | (917,037 | ) | 47,310 | ||||||||||

| $ | (17,831,811 | ) | $ | (178,400 | ) | |||||||||||||

Schedule of Interest Rate Swap Agreements

| Counterparty | Floating Rate Index | Fund Paying/Receiving | Fixed Rate | Expiration Date | Notional Amount1 | Unrealized Appreciation/ (Depreciation) | ||||||||||||||||||||

| Over the Counter Interest Rate Swap Agreements | ||||||||||||||||||||||||||

| BBP | 3-Month South African Johannesburg Interbank Rate | Paying | 6.00% | 03/20/2018 | ZAR | 8,700,000 | $ | 10,093 | ||||||||||||||||||

| BBP | Mexican Interbank Rate | Paying | 5.60% | 09/06/2016 | MXN | 6,000,000 | 3,490 | |||||||||||||||||||

| BBP | Mexican Interbank Rate | Paying | 5.60% | 09/06/2016 | MXN | 12,900,000 | 8,142 | |||||||||||||||||||

| BBP | Mexican Interbank Rate | Paying | 5.60% | 09/06/2016 | MXN | 22,000,000 | 7,940 | |||||||||||||||||||

| BBP | Mexican Interbank Rate | Paying | 6.65% | 06/02/2021 | MXN | 2,000,000 | 8,122 | |||||||||||||||||||

| BBP | Mexican Interbank Rate | Paying | 6.65% | 06/02/2021 | MXN | 3,000,000 | 12,657 | |||||||||||||||||||

| GSC | 3-Month South African Johannesburg Interbank Rate | Paying | 6.00% | 09/19/2017 | ZAR | 9,000,000 | 6,909 | |||||||||||||||||||

| GSC | Brazil Interbank Rate | Paying | 9.93% | 01/02/2015 | BRL | 1,400,000 | 31,731 | |||||||||||||||||||

| GSC | Brazil Interbank Rate | Paying | 8.26% | 01/02/2015 | BRL | 17,000,000 | 104,588 | |||||||||||||||||||

| GSC | Brazil Interbank Rate | Paying | 8.26% | 01/02/2015 | BRL | 6,000,000 | 33,635 | |||||||||||||||||||

| GSC | Brazil Interbank Rate | Paying | 8.26% | 01/02/2015 | BRL | 4,000,000 | 22,732 | |||||||||||||||||||

| GSC | Mexican Interbank Rate | Paying | 5.60% | 09/06/2016 | MXN | 118,000,000 | 139,039 | |||||||||||||||||||

| GSC | Mexican Interbank Rate | Paying | 5.60% | 09/06/2016 | MXN | 3,600,000 | 4,145 | |||||||||||||||||||

| GSC | Mexican Interbank Rate | Paying | 5.25% | 09/06/2019 | MXN | 18,800,000 | (8,805 | ) | ||||||||||||||||||

| $ | 384,418 | |||||||||||||||||||||||||

| Centrally Cleared Interest Rate Swap Agreements | ||||||||||||||||||||||||||

| N/A | 3-Month LIBOR | Paying | 1.50% | 01/04/2018 | 3,000,000 | $ | (6,344 | ) | ||||||||||||||||||

| 1 | Notional amount is stated in USD unless otherwise noted. |

The accompanying notes are an integral part of the financial statements.

| Montgomery Street Income Securities, Inc. | 13 |

Schedule of Credit Default Swap Agreements

| Counterparty | Reference Obligation | Implied Credit Spread3 | Fixed Received/ Pay Rate6 | Expiration Date | Notional Amount1,5 | Value4 | Unrealized Appreciation/ (Depreciation) | |||||||||||||||||||

| Over the Counter Credit Default Swap Agreements | ||||||||||||||||||||||||||

| Credit default swap agreements — sell protection2 | ||||||||||||||||||||||||||

| BBP | Anadarko Petroleum Corp., 1.00%, 06/20/17 | 1.37% | 1.00% | 06/20/2017 | $ | (100,000 | ) | $ | (1,581 | ) | $ | 1,789 | ||||||||||||||

| GSI | Arcelormittal, 6.13%, 06/01/18 | 2.82% | 1.00% | 03/20/2016 | (900,000 | ) | (50,288 | ) | (21,534 | ) | ||||||||||||||||

| GSI | Canadian Natural Resources Ltd., 6.25%, 03/15/38 | 0.69% | 1.00% | 12/20/2015 | (500,000 | ) | 4,642 | 3,499 | ||||||||||||||||||

| BBP | CDX.NA.IG.17 | N/A | 1.00% | 12/20/2016 | (300,000 | ) | 3,026 | 1,876 | ||||||||||||||||||

| GSI | CDX.NA.IG.17 | N/A | 1.00% | 12/20/2016 | (300,000 | ) | 3,027 | 2,202 | ||||||||||||||||||

| BBP | CDX.NA.IG.18 | N/A | 1.00% | 06/20/2017 | (1,400,000 | ) | 9,415 | 4,529 | ||||||||||||||||||

| BOA | CDX.NA.IG.18 | N/A | 1.00% | 06/20/2017 | (1,600,000 | ) | 10,760 | 858 | ||||||||||||||||||

| GSI | CDX.NA.IG.18 | N/A | 1.00% | 06/20/2017 | (4,100,000 | ) | 27,573 | 45,935 | ||||||||||||||||||

| BBP | Federative Republic of Brazil, 12.25%, 03/06/30 | 0.77% | 1.00% | 06/20/2016 | (2,400,000 | ) | 18,943 | 26,483 | ||||||||||||||||||

| GSI | Federative Republic of Brazil, 12.25%, 03/06/30 | 1.00% | 1.00% | 09/20/2017 | (1,400,000 | ) | (230 | ) | 30,707 | |||||||||||||||||

| GSI | Forest Oil Corp., 7.25%, 06/15/19 | 5.53% | 5.00% | 06/20/2017 | (1,000,000 | ) | (20,434 | ) | 7,482 | |||||||||||||||||

| GSI | Gazprom International BV, 5.63%, 07/22/13 | 1.54% | 1.00% | 03/20/2017 | (2,000,000 | ) | (44,516 | ) | 122,416 | |||||||||||||||||

| BBP | Metlife Inc., 4.75%, 02/08/21 | 1.56% | 1.00% | 12/20/2017 | (300,000 | ) | (7,889 | ) | 3,997 | |||||||||||||||||

| GSI | MGM Resorts International, 7.63%, 01/15/17 | 0.63% | 5.00% | 03/20/2014 | (1,000,000 | ) | 53,315 | 26,232 | ||||||||||||||||||

| GSI | NRG Energy Inc., 5.00%, 06/20/17 | 3.07% | 5.00% | 06/20/2017 | (600,000 | ) | 48,284 | 83,784 | ||||||||||||||||||

| GSI | NRG Energy Inc., 8.50%, 06/15/19 | 2.83% | 5.00% | 03/20/2017 | (200,000 | ) | 17,231 | 31,869 | ||||||||||||||||||

| GSI | NRG Energy Inc., 8.50%, 06/15/19 | 3.07% | 5.00% | 06/20/2017 | (1,000,000 | ) | 80,474 | 153,391 | ||||||||||||||||||

| BBP | Prudential Financial Inc., 4.50%, 07/15/13 | 1.44% | 1.00% | 12/20/2017 | (400,000 | ) | (8,310 | ) | 3,528 | |||||||||||||||||

| GSI | Russian Federation, 7.50%, 03/31/30 | 1.23% | 1.00% | 09/20/2017 | (700,000 | ) | (7,484 | ) | 32,528 | |||||||||||||||||

| GSI | United Mexican States, 5.95%, 03/19/19 | 0.89% | 1.00% | 09/20/2017 | (1,600,000 | ) | 8,023 | 33,738 | ||||||||||||||||||

| BBP | United Mexican States, 7.50%, 04/08/33 | 0.67% | 1.00% | 06/20/2016 | (1,200,000 | ) | 13,686 | 13,160 | ||||||||||||||||||

| $ | (23,000,000 | ) | $ | 157,667 | $ | 608,469 | ||||||||||||||||||||

| Centrally Cleared Credit Default Swap Agreements | ||||||||||||||||||||||||||

| Credit default swap agreements — sell protection2 | ||||||||||||||||||||||||||

| N/A | CDX.NA.IG.19 | N/A | 1.00% | 12/20/2017 | $ | (72,100,000 | ) | $ | (158,536 | ) | $ | 46,871 | ||||||||||||||

| 1 | Notional amount is stated in USD. |

| 2 | If the Fund is a seller of protection and a credit event occurs, as defined under the terms of that particular swap agreement, the Fund will either (i) pay the buyer of protection an amount equal to the notional amount of the referenced obligation and take delivery of the referenced obligation or underlying securities comprising the referenced index or (ii) pay a net settlement amount in the form of cash or securities equal to the notional amount of the swap agreement less the recovery value of the reference obligation or underlying securities comprising the referenced index. |

| 3 | Implied credit spreads, represented in absolute terms, utilized in determining the value of credit default swap agreements on corporate issues and sovereign issues serve as an indicator of the current status of the payment/performance risk and represent the likelihood or risk of default for the credit derivative. The implied credit spread of a particular referenced entity reflects the cost of buying/selling protection and may include upfront payments required to be made to enter into the agreement. Wider credit spreads represent a deterioration of the referenced entity’s credit soundness and a greater likelihood or risk of default or other credit event occurring as defined under the terms of the applicable agreement. |

| 4 | The prices and resulting values for credit default swap agreements on credit indices serve as an indicator of the current status of the payment/performance risk and represent the likelihood or risk of default for the credit derivative. Increasing market values, in absolute terms when compared to the notional amount of the swap, represent a deterioration of the referenced entity’s credit soundness and a greater likelihood or risk of default or other credit event occurring as defined under the terms of the agreement. |

| 5 | The maximum potential amount the Fund could be required to pay as a seller of credit protection if a credit event occurs is limited to the total notional amount which is defined under the terms of each swap agreement. |

| 6 | If the Fund is a seller of protection, the Fund receives the fixed rate. |

The accompanying notes are an integral part of the financial statements.

| 14 | Montgomery Street Income Securities, Inc. |

Financial Statements

Statement of Assets and Liabilities as of December 31, 2012

| Assets | ||||

| Investments in securities, at value (cost $188,689,604) | $ | 197,733,711 | ||

| Cash | 228,708 | |||

| Foreign currency (cost $105,829) | 107,110 | |||

| Receivables: | ||||

Investments sold | 27,848,803 | |||

Forward foreign currency contracts | 107,091 | |||

Interest | 1,987,941 | |||

Variation margin on financial derivative instruments | 49,929 | |||

Dividend reinvestment | 140,552 | |||

| Deposits with brokers | 310,000 | |||

| Unrealized appreciation on OTC swap agreements | 1,023,226 | |||

| OTC swap premiums paid | 97,018 | |||

| Other assets | 16,861 | |||

| Total assets | 229,650,950 | |||

| Liabilities | ||||

| Accrued management and investment advisory fee | 120,511 | |||

| Accrued administrative fee | 36,725 | |||

| Written options, at value (premiums $167,535) | 141,746 | |||

| Payables: | ||||

Investment securities purchased | 57,241 | |||

Treasury roll transactions | 7,636,498 | |||

Reverse repurchase agreements | 2,205,500 | |||

Interest | 322 | |||

Investment forward sales commitments, at value (cost $27,707,344) | 27,703,358 | |||

Forward foreign currency contracts | 285,491 | |||

| Deposits from counterparties | 246,000 | |||

| Unrealized depreciation on OTC swap agreements | 30,339 | |||

| OTC swap premiums received | 511,371 | |||

| Other liabilities | 99,214 | |||

| Total liabilities | 39,074,316 | |||

| Net Asset Value | $ | 190,576,634 | ||

| Net assets consist of: | ||||

| Paid-in capital | 202,607,373 | |||

| Undistributed (excess of distributions over) net investment income | (616,927 | ) | ||

| Net unrealized appreciation on investments and foreign currency related items | 9,955,580 | |||

| Accumulated net realized loss | (21,369,392 | ) | ||

| Net Asset Value | $ | 190,576,634 | ||

| Net Asset Value per share ($190,576,634/10,375,675 shares of common stock outstanding, $.01 par value, 30,000,000 shares authorized) | $ | 18.37 | ||

The accompanying notes are an integral part of the financial statements.

| Montgomery Street Income Securities, Inc. | 15 |

Statement of Operations for the year ended December 31, 2012

| Investment Income | ||||

| Income: | ||||

| Interest | $ | 7,581,208 | ||

| Total income | 7,581,208 | |||

| Expenses: | ||||

| Management and investment advisory fee | 464,870 | |||

| Administrative fee | 421,897 | |||

| Directors’ fees and expenses | 107,954 | |||

| Legal | 104,269 | |||

| Audit fees | 56,098 | |||

| Insurance | 48,503 | |||

| Stockholder reporting | 47,399 | |||

| Stockholder services | 29,325 | |||

| NYSE listing fee | 24,222 | |||

| Interest expense | 7,478 | |||

| Custodian fees | 7,016 | |||

| Other | 26,224 | |||

| Total expenses | 1,345,255 | |||

| Net investment income | 6,235,953 | |||

| Realized and Unrealized Gain (Loss) on Investment Transactions and Foreign Currency Related Items | ||||

| Net realized gain from: | ||||

| Investment transactions | 4,056,913 | |||

| Futures contracts | 173,839 | |||

| Swap agreements | 1,532,508 | |||

| Written options contracts | 163,524 | |||

| Foreign currency related items | 293,600 | |||

| Net change in unrealized appreciation (depreciation) on: | ||||

| Investments | 8,627,102 | |||

| Futures contracts and centrally cleared swap agreements | (63,082 | ) | ||

| OTC swap agreements | 1,300,206 | |||

| Written options contracts | 7,531 | |||

| Foreign currency related items | (497,833 | ) | ||

| Net gain on investment transactions and foreign currency related Items | 15,594,308 | |||

| Net increase in net assets resulting from operations | $ | 21,830,261 | ||

The accompanying notes are an integral part of the financial statements.

| 16 | Montgomery Street Income Securities, Inc. |

Statements of Changes in Net Assets

| Year Ended December 31, | ||||||||

| Increase (Decrease) in Net Assets | 2012 | 2011 | ||||||

| Operations: | ||||||||

| Net investment income | $ | 6,235,953 | $ | 7,623,277 | ||||

| Net realized gain on investment transactions and foreign currency related items | 6,220,384 | 1,079,427 | ||||||

| Net change in unrealized appreciation (depreciation) during the year on investment transactions and foreign currency related items | 9,373,924 | (1,450,451 | ) | |||||

| Net increase in net assets resulting from operations | 21,830,261 | 7,252,253 | ||||||

| Distributions to stockholders from net investment income | (8,811,954 | ) | (7,360,210 | ) | ||||

| Fund share transactions: | ||||||||

| Reinvestment of distributions | 413,770 | 374,855 | ||||||

| Cost of shares repurchased | (343,385 | ) | (376,187 | ) | ||||

| Net increase (decrease) in net assets from Fund share transactions | 70,385 | (1,332 | ) | |||||

| Net increase (decrease) in net assets | 13,088,692 | (109,289 | ) | |||||

| Net assets at beginning of year | 177,487,942 | 177,597,231 | ||||||

| Net assets at end of year (including undistributed (excess of distributions over) net investment income of $(616,927) and $(44,744), respectively) | $ | 190,576,634 | $ | 177,487,942 | ||||

| Other Information | ||||||||

| Shares outstanding at beginning of year | 10,371,852 | 10,371,952 | ||||||

| Shares issued to stockholders in reinvestment of distributions | 24,823 | 23,900 | ||||||

| Shares repurchased | (21,000 | ) | (24,000 | ) | ||||

| Net increase/(decrease) in fund shares outstanding | 3,823 | (100 | ) | |||||

| Shares outstanding at end of year | 10,375,675 | 10,371,852 | ||||||

The accompanying notes are an integral part of the financial statements.

| Montgomery Street Income Securities, Inc. | 17 |

Financial Highlights

| Years Ended December 31, | 2012 | 2011 | 2010c | 2009 | 2008 | |||||||||||||||

| Selected Per Share Data | ||||||||||||||||||||

| Net asset value, beginning of year | $ | 17.11 | $ | 17.12 | $ | 16.42 | $ | 15.13 | $ | 18.07 | ||||||||||

| Income from investment operations: | ||||||||||||||||||||

Incomea | 0.73 | 0.86 | 0.86 | 0.85 | 1.07 | |||||||||||||||

Operating expensesa | (0.13 | ) | (0.12 | ) | (0.14 | ) | (0.12 | ) | (0.12 | ) | ||||||||||

Net investment incomea | 0.60 | 0.74 | 0.72 | 0.73 | 0.95 | |||||||||||||||

Net realized and unrealized gain (loss) on investment transactions | 1.51 | (0.04 | ) | 0.71 | 1.33 | (2.84 | ) | |||||||||||||

| Total from investment operations | 2.11 | 0.70 | 1.43 | 2.06 | (1.89 | ) | ||||||||||||||

| Less distributions from: | ||||||||||||||||||||

Net investment income | (0.85 | ) | (0.71 | ) | (0.73 | ) | (0.77 | ) | (1.05 | ) | ||||||||||

| Net asset value, end of year | $ | 18.37 | $ | 17.11 | $ | 17.12 | $ | 16.42 | $ | 15.13 | ||||||||||

| Per share market value, end of year | $ | 16.90 | $ | 15.43 | $ | 15.78 | $ | 14.68 | $ | 13.82 | ||||||||||

| Closing price range on New York Stock Exchange for each share of Common Stock outstanding: | ||||||||||||||||||||

High ($) | 17.30 | 16.03 | 16.78 | 15.10 | 17.27 | |||||||||||||||

Low ($) | 15.38 | 15.05 | 14.67 | 13.19 | 11.25 | |||||||||||||||

| Total Return | ||||||||||||||||||||

| Based on market value (%)b | 15.22 | 2.28 | 12.50 | 12.04 | (7.94 | ) | ||||||||||||||

| Based on net asset value (%)b | 12.94 | 4.54 | 9.12 | 14.47 | (10.04 | ) | ||||||||||||||

| Ratio to Average Net Assets and Supplemental Data | ||||||||||||||||||||

| Net assets, end of year ($ millions) | 191 | 177 | 178 | 170 | 157 | |||||||||||||||

| Ratio of net expenses (%) | 0.72 | 0.71 | 0.82 | 0.76 | 0.73 | |||||||||||||||

| Ratio of net investment income (%) | 3.35 | 4.24 | 4.28 | 4.64 | 5.57 | |||||||||||||||

| Portfolio turnover rate (%) | 246 | 49 | 132 | 175 | 170 | |||||||||||||||

| a | Based on average shares outstanding during the year. |

| b | Total return based on net asset value reflects changes in the Fund’s net asset value during the year. Total return based on market value reflects changes in market price. Each figure includes reinvestment of dividends. These figures will differ depending upon the level of any discount or premium between market price and net asset value. |

| c | The Fund changed investment adviser effective March 15, 2010. |

The accompanying notes are an integral part of the financial statements.

| 18 | Montgomery Street Income Securities, Inc. |

Notes to Financial Statements

A. Significant Accounting Policies

Montgomery Street Income Securities Inc. (the “Fund”) is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a closed-end, diversified management investment company. Pacific Investment Management Company LLC (“PIMCO” or “Adviser”) serves as the investment adviser to the Fund.

The Fund’s financial statements are prepared in accordance with U.S. generally accepted accounting principles (“GAAP”), which requires the use of management estimates. Actual results could differ from those estimates. The policies described below are followed consistently by the Fund in the preparation of its financial statements.

Security Valuation. Under the Fund’s valuation policy and procedures, the Fund’s Board of Directors (the “Board”) has delegated the daily operational oversight of the securities valuation function to Jackson Fund Services (“JFS” or “Administrator”), a division of Jackson National Asset Management, LLC. The Board has delegated to the Pricing Committee of JFS (“Pricing Committee”), the authority to approve determinations of fair valuations of securities for which market quotations are not readily available as well as to supervise JFS in the performance of its responsibilities pursuant to the valuation policy and procedures. The Pricing Committee consists of the Fund’s Chief Executive Officer, Chief Financial Officer and Chief Compliance Officer. For those securities fair valued under procedures adopted by the Board, the Pricing Committee reviews and affirms the reasonableness of the fair valuation determinations after considering all relevant information that is reasonably available. The Pricing Committee’s fair valuation determinations are subject to review by the Chair of the Fund’s Valuation Committee on a monthly basis and the Board at its next regularly scheduled meeting covering the calendar quarter in which the fair valuation was determined.

Investments are stated at value determined as of the close of regular trading (generally, 4:00 PM Eastern Time) on the New York Stock Exchange (“NYSE”) on each day the exchange is open for trading. Debt securities are valued by independent pricing services approved by, or at the direction of, the Board. If the pricing services are unable to provide valuations, debt securities are valued at the most recent bid quotation or evaluated price, as applicable, obtained from a broker/dealer or widely used quotation system. Fixed income securities with a remaining maturity of sixty days or less, maturing at par, are valued at amortized cost, unless it is determined that such price does not approximate market value. Forward foreign currency contracts are generally valued at the forward foreign currency exchange rate as of the close of the NYSE. Futures contracts traded on a liquid exchange are valued at the settlement price. If the settlement price is not available, exchange traded futures are valued at the last sales price as of the close of business on the local exchange. Options traded on an exchange are valued at the last traded price as of the close of business on the local exchange. If the last trade is determined to not be representative of fair value, exchange traded options are valued at the last bid. Centrally cleared swap agreements, listed on a multilateral or trade facility platform, such as a registered exchange, are valued by the respective exchange. The exchange determines a daily settlement price via pricing models which use, as appropriate, its members’ actionable levels across complete term structures along with external third party prices for centrally cleared credit default swaps and underlying rates including overnight index swap rates and forward interest rates for centrally cleared interest rate swaps. Over the counter (“OTC”) derivatives, including options and swap agreements, are generally valued by approved pricing services. If the pricing services are unable to provide valuations, OTC derivatives are valued at the most recent bid quotation or evaluated price, as applicable, obtained from a broker/dealer or by pricing models using observable inputs. Pricing services used to value debt and derivative securities may use various pricing techniques which take into account appropriate factors such as yield, credit quality, coupon rate, maturity, type of issue, trading characteristics, call features, credit ratings, broker quotes and other relevant data.

Market quotations may not be readily available for certain debt and derivative investments. If market quotations are not readily available or if it is determined that a quotation of an investment does not represent market value, then the investment is valued at a “fair value” as determined in good faith using procedures approved by the Board. Although there can be no assurance, in general, the fair value of a security is the amount the owner of such security might reasonably expect to receive upon its current sale. Situations that may require a security to be fair valued may include instances where a security is thinly traded or restricted as to resale. In addition, securities may be fair valued based on the occurrence of a significant event. Significant events may be specific to a particular issuer, such as mergers, restructurings or defaults. Alternatively, significant events may affect an entire market, such as natural disasters or government actions. Securities are fair valued based on observable and unobservable inputs including the Administrator‘s own assumptions in determining fair value. Under the procedures adopted by the Board, the Administrator may rely on independent pricing services or other sources, including the Fund’s Adviser, to assist in determining the fair value of a security. Factors considered to determine fair value include the correlation with price movement of similar securities in the same or other markets; the type, cost and investment characteristics of the security; the business and financial condition of the issuer; and trading or other market data. The value of an investment for purposes of calculating the Fund’s net asset value (“NAV”) can differ depending on the source and method used to determine the value.

| Montgomery Street Income Securities, Inc. | 19 |

Recent Accounting Pronouncements — In December 2011, Financial Accounting Standards Board (“FASB”) released Accounting Standards Update (“ASU”) 2011-11 “Disclosures about Offsetting Assets and Liabilities”. ASU 2011-11 requires an entity to disclose information about offsetting and related arrangements to enable users of its financial statements to understand the effect of those arrangements on its financial position. ASU 2011-11 will enhance disclosures by requiring improved information about financial instruments and derivative instruments that meet the criteria for offsetting amounts in the balance sheet or are subject to a master netting arrangement. The information will enable users of an entity’s financial statements to evaluate the effect or potential effect of netting arrangements on an entity’s financial positions, including the effect or potential effect of rights of setoff associated with certain financial instruments and derivative instruments. ASU 2011-11 is effective for the annual periods beginning on or after January 1, 2013 and the interim periods within those annual periods. Management is currently evaluating the impact ASU 2011-11 will have on the Fund’s financial statements.

Security Transactions, Investment Income and Expenses. Investment transactions are reported on trade date for financial reporting purposes. Interest income including level-yield amortization of discounts and premiums is accrued daily. The Fund may place a debt obligation on non-accrual status and reduce related interest income by ceasing accruals and writing off interest receivable when the collection of all or a portion of interest has become doubtful. A debt obligation is removed from non-accrual status when the issuer resumes interest payments or when collectability of interest is reasonably assured. Dividend income is recorded on the ex-dividend date. Expenses are recorded on an accrual basis.

Federal Income Taxes. The Fund intends to qualify as a “regulated investment company” and to distribute substantially all net investment income and net capital gains, if any, to its stockholders and otherwise comply with Subchapter M of the Internal Revenue Code applicable to regulated investment companies. Therefore, no federal income tax provision is required.

Distribution of Income and Capital Gains. The amount and timing of distributions are determined in accordance with federal income tax regulations, which may differ from GAAP. Distributions of net investment income are paid quarterly. Net realized gains from investment transactions will be distributed to stockholders at least annually to the extent they exceed available capital loss carryforwards. The Fund uses the specific identification method for determining realized gain or loss on investments sold for both financial and federal income tax reporting purposes.

Contingencies. In the normal course of business, the Fund may enter into contracts with service providers that contain general indemnification clauses. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet been made. However, based on experience to date, the Fund expects any risk of loss to be remote.

B. FASB Accounting Standards Update (“ASC”) Topic 820, “Fair Value Measurements and Disclosure”

This standard establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires additional disclosures about fair value measurements. Various inputs are used in determining the value of the Fund’s investments under FASB ASC Topic 820 guidance. The inputs are summarized into three broad categories.

Level 1 includes valuations based on unadjusted quoted prices of identical securities in active markets, including valuations for securities listed on an exchange.

Level 2 includes valuations determined from significant direct or indirect observable inputs. Direct observable inputs include broker quotes, closing prices of similar securities in active markets, closing prices for identical or similar securities in non-active markets. Indirect significant observable inputs include factors such as interest rates, yield curves, prepayment speeds or credit ratings. Level 2 includes valuations of vendor evaluated debt instruments, broker quotes in active markets, securities valued at amortized cost, centrally cleared swap agreements, modeled OTC derivatives contracts and swap agreements valued by pricing services.

Level 3 includes valuations determined from significant unobservable inputs including the Administrator’s own assumptions in determining the fair value of the investment. Inputs used to determine the fair value of Level 3 securities include security specific inputs such as: credit quality, credit rating spreads, issuer news, trading characteristics, call features or maturity; or industry specific inputs such as trading activity of similar markets or securities, changes in the security’s underlying index or comparable securities’ models. Level 3 valuations include certain single source quotes received from brokers (either directly or through a vendor), securities restricted to resale due to market events, newly issued or investments for which reliable quotes are not available.

To assess the continuing appropriateness of security valuation, the Administrator regularly compares prior day prices with current day prices, transaction prices and alternative vendor prices. When the comparison results exceed pre-defined

| 20 | Montgomery Street Income Securities, Inc. |

thresholds, the Administrator challenges the prices exceeding tolerance levels with the pricing service or broker. To verify Level 3 unobservable inputs, the Administrator uses a variety of techniques as appropriate to substantiate these valuation approaches including a regular review of key inputs and assumptions, transaction back-testing or disposition analysis and review of related market activity.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following table summarizes the Fund’s investments in securities and other financial instruments as of December 31, 2012 by valuation level.

| Assets — Investments in Securities | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Corporate Bonds | $— | $ | 111,463,707 | $ | — | $111,463,707 | ||||||||||

| Non-U.S. Government Agency Asset-Backed Securities | — | 16,367,830 | — | 16,367,830 | ||||||||||||

| Government and Agency Obligations | — | 69,741,190 | — | 69,741,190 | ||||||||||||

| Purchased Options | — | 160,984 | — | 160,984 | ||||||||||||

| Fund Total | $— | $ | 197,733,711 | $ | — | $197,733,711 | ||||||||||

| Liabilities — Investments in Securities | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| U.S. Government Agency Mortgage-Backed Securities | $— | $ | (27,703,358 | ) | $ | — | $(27,703,358 | ) | ||||||||

| Fund Total | $— | $ | (27,703,358 | ) | $ | — | $(27,703,358 | ) | ||||||||

| Assets — Other Financial Instruments* | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Futures Contracts | $ | 9,817 | $— | $ | — | $9,817 | ||||||||||

| Forward Foreign Currency Contracts | — | 107,091 | — | 107,091 | ||||||||||||

| Interest Rate Swap Agreements | — | 393,223 | — | 393,223 | ||||||||||||

| Credit Default Swap Agreements | — | 630,003 | — | 630,003 | ||||||||||||

| Centrally Cleared Credit Default Swap Agreements | — | 46,871 | — | 46,871 | ||||||||||||

| Fund Total | $ | 9,817 | $1,177,188 | $ | — | $1,187,005 | ||||||||||

| Liabilities — Other Financial Instruments* | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Written Options | $— | $(141,746 | ) | $ | — | $(141,746 | ) | |||||||||

| Forward Foreign Currency Contracts | — | (285,491 | ) | — | (285,491 | ) | ||||||||||

| Interest Rate Swap Agreements | — | (8,805 | ) | — | (8,805 | ) | ||||||||||

| Centrally Cleared Interest Rate Swap Agreements | — | (6,344 | ) | — | (6,344 | ) | ||||||||||

| Credit Default Swap Agreements | — | (21,534 | ) | — | (21,534 | ) | ||||||||||

| Fund Total | $— | $(463,920 | ) | $ | — | $(463,920 | ) | |||||||||