(Exact name of registrant as specified in charter)

225 W. Wacker Drive, Suite 1200

Chicago, IL 60606

(Address of principal executive offices)

Mark D. Nerud, President

225 W. Wacker Drive, Suite 1200

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 338-5801

Date of fiscal year end: December 31

Date of reporting period: December 31, 2010

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. §3507.

Montgomery Street Income Securities, Inc. (the “Fund”) had a total return based on net asset value (“NAV”) of 9.12% for the twelve-month period ended December 31, 2010. The total return of the Fund, based on the market price of its New York Stock Exchange traded shares, was 12.50% for the same period.1,3 The Fund’s NAV total return outperformed the Barclay’s Capital U.S. Aggregate Bond Index2, the Fund’s benchmark, which posted a total return of 6.54% for the twelve-month period.3

Pacific Investment Management Company (“PIMCO”) replaced Hartford Investment Management Company (“HIMCO”) as the Fund’s investment adviser on March 15, 2010.

At the start of 2010, investors sought the relative safety of U.S. bonds amid concern about sovereign debt risk, especially in Greece and other peripheral eurozone economies as growing budget shortfalls in Greece, Spain and Portugal raised fears that the region might derail the global economy’s recovery from the crisis that began in 2008. Policymakers wrestled with how long to sustain stimulus programs designed to mitigate the global recession but which threatened to undermine public finances or stoke inflation. While the U.S. Federal Reserve (the “Fed”) kept its main policy rate unchanged, it concluded its $1.25 trillion agency mortgage purchase program in March and also ended the subscription period for purchasing consumer asset-backed securities.

Volatility spiked across the global financial markets during the second quarter as investors’ confidence was shaken by a range of macroeconomic events, including signs that the U.S. and Chinese economies might be slowing. In May, the European Union established a 750 billion euro bailout fund that soothed sovereign debt contagion fears.

U.S. interest rates continued to fall during the third quarter as the tepid economic recovery showed few signs of gathering steam and inflation remained low. At the August Federal Open Market Committee meeting, Federal Reserve Chairman Bernanke strongly signaled the likelihood of another round of quantitative easing in addition to keeping interest rates on hold for a prolonged period of time, which combined with modest but consistently improving economic indicators, prompted a return of risk appetite among investors.

Policy initiatives that aimed to speed up the U.S. recovery and lower the persistently high unemployment rate were the major market drivers during the final quarter. On the monetary front, the Fed continued its unconventional efforts to spur faster growth with the second round of quantitative easing in November. On the fiscal policy front, in December the Obama Administration and Congress reached a major compromise on tax policy that included a cut in payroll taxes, an extension of unemployment benefits and a tax credit for business capital expenditures. Despite their limited duration, these provisions gave another boost to riskier asset markets.

In the final months of 2010, most fixed income markets gave back some of their gains from earlier in 2010 as interest rates rose sharply and investors began to shift toward riskier assets. Signs of economic strength as well as market reaction to expanded fiscal and monetary stimulus drove the yield on the benchmark 10-year Treasury up 78 basis points during the fourth quarter to close the year at 3.30%. Additionally, the treasury yield curve steepened during the year as the Fed kept short term yields anchored at low levels.

1

Total return based on NAV reflects changes in the Fund’s net asset value during the period. Total return based on market value reflects changes in market value. Each figure assumes that dividend and capital gain distributions, if any, were reinvested. These figures will differ depending upon the level of any discount from or premium to NAV at which the Fund’s shares traded during the period.

2

The Barclays Capital U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, mortgage backed securities (agency fixed-rate and hybrid adjustable rate mortgage pass-throughs), asset backed securities and commercial mortgage backed securities. The Index dose not include exposure to high yield or non-dollar securities or cash. Index returns assume reinvestment of dividends, and unlike Fund returns, do not reflect fees or expenses. It is not possible to invest directly in an index.

3

Past results are not necessarily indicative of the future performance of the Fund. Investment return and principal value will fluctuate.

Performance is historical and does not guarantee future results.

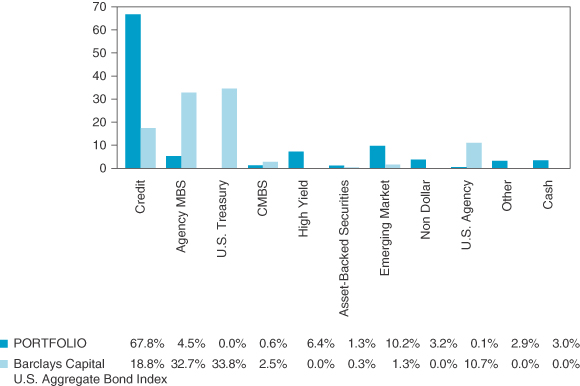

Given the Fund’s primary focus on income generation, the Fund remained overweight in investment grade corporate bonds during the year. The Fund emphasized well-capitalized banks and insurance companies that offered value versus the broader market. These holdings provided the opportunity to take advantage of the steep yield curve as well as the improved asset quality of money center financial institutions. The overweight to credit, specifically within financials, contributed to returns as the overall credit sector rebounded from earlier lows brought about by worries over sovereign credit risk in Greece and elsewhere in Europe that had pressured credit markets across the board.

After underperforming on the heels of a flight to quality and a lagging credit market during the second quarter, the Fund’s position in high yield bonds contributed to performance for the year. Security selection within the sector also contributed positively to performance.

The Fund’s emerging markets exposure also exceeded the benchmark during the year, which contributed to returns from increased risk appetites as well as currency appreciation against the U.S. dollar.

The Fund’s interest rate strategies yielded neutral returns to the benchmark, as tactical duration positioning implemented through Eurodollar futures and a positive yield curve contributed and detracted at various times during the volatile year.

Portfolio percentages are based on total value of the investment portfolio, including net cash equivalents and derivatives.

The quality ratings represent the higher of Moody’s Investors Service, Inc. (“Moody’s”) or Standard & Poor’s Corporation (“S&P”) credit ratings. The ratings of Moody’s and S&P represent these companies’ opinions as to the quality of the securities they rate. Ratings are relative and subjective and are not absolute standards of quality. A bond’s credit quality does not remove the risk of an increase in interest rates or illiquidity in the market.

The Fund maintained an underweight to agency mortgage backed securities (“MBS”) during the period, which slightly detracted from returns, as the sector outperformed. Limited agency MBS issuance combined with demand from non-U.S. buyers supported mortgage valuations, particularly in the fourth quarter.

An underweight to commercial mortgage backed securities (“CMBS”) detracted from returns during the first quarter. Despite a challenging environment for the underlying collateral, CMBS were pricing in a far more draconian outlook than likely at the beginning of the year. Moreover, as both the economy and financial markets improved, so did the fundamental health of the CMBS market.

Percentages are based on total value of the investment portfolio.

PIMCO’s global forecast calls for differentiated growth and inflation across regions in 2011. Key elements of this cyclical outlook include:

•

Policy Stimulus Boosts U.S. Growth — The compromise on tax policy between the Obama Administration and Congress, especially the payroll tax cut and business tax credit, should boost growth over a cyclical time frame by pushing future consumption and investment forward into 2011. The U.S. private sector has also been lifted by the Fed’s second round of quantitative easing. In addition to the U.S., Canada and Australia are expected to grow relatively quickly, supported by their healthy fiscal positions. Australia in particular will benefit from its thriving resource-based industries with strong ties to emerging markets.

•

Range-Bound U.S. Rates — With U.S. unemployment at 9.4%, PIMCO does not expect the Fed to raise short term rates until 2012 at the earliest. Treasury yields now likely reflect much of the market’s expectations of faster growth and higher long run inflation. With the short end of the yield curve anchored near current low levels, PIMCO expects the 10-year Treasury yield to range between 3.0% and 4.0% over the next year.

•

PIMCO’s New Normal Secular Forecast for Subdued U.S. Growth Remains Intact — While PIMCO’s outlook is for relatively robust U.S. growth over the cyclical, or 9 to 12 month horizon, PIMCO continues to expect a more subdued expansion over a secular, or three to five-year, horizon. Structural imbalances are likely to make it difficult for the U.S. to sustain the 3.0% to 3.5% growth that PIMCO foresees in 2011. The biggest risk for the U.S. concerns the sustainability and effectiveness of its fiscal and monetary policies. The U.S. will remain dependent on the recycling of global savings into its government bond market in an environment where investors are worried about sovereign credit risk. Another risk is that the U.S. private sector may respond to fiscal and monetary stimulus by converting its enhanced liquidity and savings into international as opposed to domestic investment.

Weaker Growth in Europe and the UK — Europe and the UK are expected to attempt significant fiscal policy contraction to stabilize their respective debt burdens. As a result, the growth outlook for Europe and the UK is close to zero, but Europe faces greater challenges. Potential failure of policy coordination in Europe poses significant risks to the entire global economy as one or more sovereign defaults could give rise to a banking crisis with broad systemic consequences.

•

Weak Growth in Japan — Japan faces a shrinking working age population and persistent deflationary pressure, partly mitigated by the success of its high value added industrial base in China and the rest of Asia.

•

Faster Growth in Emerging Markets — China and most other emerging markets should enjoy faster growth than the developed world, as slowing exports are likely to be offset by continued growth in domestic demand. Emerging economies are shifting focus toward tightening fiscal and monetary policies to combat cyclical inflationary pressure. PIMCO expects China will manage this challenge effectively. China’s fiscal flexibility and ongoing infrastructure needs suggest that a policy-induced economic hard landing is a low probability.

With respect to Fund strategy, PIMCO currently expects to employ the following:

•

Maintain a flat to slightly overweight duration position overall consisting predominantly of income producing strategies, though PIMCO will look to adjust duration tactically as rates move within the forecasted range. To mitigate interest rate risk, PIMCO plans to concentrate curve exposure around the longer end of the money market curve, where markets are now pricing in more Fed tightening than PIMCO foresees.

•

Overweight agency mortgages to take advantage of relative value opportunities across mortgage coupons. PIMCO plans on holding non-agency mortgages and CMBS that have senior positions in the capital structure and are another source of attractive yields.

•

Take tactical exposure in several corporate sectors that offer compelling risk-adjusted yields. This may include exposure to major U.S. banks, which should be supported by a steep yield curve, stronger balance sheets and an improved U.S. cyclical outlook.

•

In emerging markets, PIMCO plans to take tactical exposure that favors owning select corporate and quasi-sovereign bonds in countries with strong debt ratings such as Brazil, Mexico and Russia. PIMCO expects to focus on emerging market corporate bonds in the energy, pipeline, metals and mining and banking sectors, which currently offer low leverage, strong asset coverage and attractive valuations compared to comparably rated U.S. corporates. PIMCO also plans to take exposure to local interest rates in Brazil, where yields remain relatively high.

This material contains the current opinions of the investment adviser only through the end of the period of the report as stated on the cover. Such opinions are subject to change without notice and should not be construed as a recommendation.

Investment in the Fund involves risk. The Fund invests in individual bonds whose yields and value fluctuate so that an investment in the Fund may be worth more or less than its original cost. Bond investments are subject to interest rate risk such that when interest rates rise, the price of the bonds, and thus the value of the Fund, can decline and the investor can lose principal value. The Fund’s investments are also subject to credit risk and liquidity risk. Additionally, investing in foreign securities presents certain unique risks not associated with domestic investments, such as currency fluctuation, political and economic changes, and market risks. All of these factors may result in greater share price volatility. Closed-end funds, unlike open-end funds, are not continuously offered or redeemed.

NOT FDIC/NCUA INSURED. NO BANK GUARANTEE. MAY LOSE VALUE. NOT A DEPOSIT.

NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY.

Past performance is no guarantee of future results.

This report is sent to stockholders of Montgomery Street Income Securities, Inc., for their information. It is not a prospectus, circular or representation intended for use in the purchase or sale of shares of the Fund or of any securities mentioned in the report.

The Fund’s market price was $15.78 as of December 31, 2010, compared with $14.68 as of December 31, 2009. The Fund’s shares traded at a 7.8% discount to NAV of $17.12 at December 31, 2010. Shares of closed-end funds frequently trade at a discount to NAV. The price of the Fund’s shares is determined by a number of factors, several of which are beyond the control of Fund management. The Fund, therefore, cannot predict whether its shares will trade at, below or above its NAV.

The Fund’s market price is published daily in The New York Times and on The Wall Street Journal website at www.wsj.com. The Fund’s NAV is available daily on its website at www.montgomerystreetincome.com and published weekly in Barron’s.

Dividends Paid

The Fund paid dividends of $0.17 per share on April 30, 2010, $0.22 per share on July 30, 2010, and $0.17 per share on October 29, 2010 and December 31, 2010, respectively. The decrease in the dividend paid on July 30, 2010 compared to the dividend paid on October 29, 2010 was primarily attributable to a tax election. At its meeting on October 14, 2010, the Fund’s Board of Directors decided to elect, for tax purposes, that the Fund amortize any premiums it pays to purchase the bonds in its portfolio. This election reduced the Fund’s distributable income. The election more closely aligns the distributable income of the Fund with the economics of the portfolio investments.

Dividend Reinvestment and Cash Purchase Option

The Fund maintains an optional Dividend Reinvestment and Cash Purchase Plan (the “Plan”) for the automatic reinvestment of your dividends and capital gain distributions in shares of the Fund. Stockholders who participate in the Plan also can purchase additional shares of the Fund through the Plan’s voluntary cash investment feature. We recommend that you consider enrolling in the Plan to build your investment. The Plan’s features, including the voluntary cash investment feature, are described on page 29 of this report.

Limited Share Repurchases

The Fund is authorized to repurchase a limited number of shares of the Fund’s common stock from time to time when the shares are trading at less than 95% of their NAV. Repurchases are limited to a number of shares each calendar quarter approximately equal to the number of new shares issued under the Plan with respect to income earned for the second preceding calendar quarter. There were 8,000 shares repurchased in the first quarter, 7,000 shares repurchased in the second quarter, 6,000 shares repurchased in the third quarter and 8,000 shares repurchased in the fourth quarter of 2010. There were 6,000 shares repurchased during the first quarter of 2011.

Investment Portfolio

Following the Fund’s first and third quarter ends, a complete portfolio holdings listing is filed with the U.S. Securities and Exchange Commission (“SEC”) on Form N-Q. The form is available in the “Financial Reports” tab on the Fund’s website at www.montgomerystreetincome.com, or on the SEC’s website at www.sec.gov, and it also may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the SEC’s Public Reference Room may be obtained by calling (800) SEC-0330.

Proxy Voting

Information about how the Fund voted any proxies related to its portfolio securities during the twelve-month period ended June 30, 2010 is available in the “Financial Reports” tab on the Fund’s website at www.montgomerystreetincome.com or on the SEC’s website at www.sec.gov. A description of the policies that the Fund uses to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling (877) 437-3938 or on the SEC’s website at www.sec.gov.

Under the Fund’s current policy, it is the intention of the Fund to invest exclusively in non-voting securities. Under normal circumstances, the Fund does not intend to hold voting securities. In the event that the Fund does come into possession of any voting securities, the Fund intends to dispose of such securities as soon as it is reasonably practicable and prudent to do so. The Board may change this policy at any time.

The Fund’s annual and semiannual reports to stockholders will be mailed to stockholders, and also are available in the “Financial Reports” tab on the Fund’s website at www.montgomerystreetincome.com or by calling (877) 437-3938. Those stockholders who wish to view the Fund’s complete portfolio holdings listing for the first and third quarters may view the Fund’s Form N-Q, as described above in “Investment Portfolio”.

Change in Portfolio Managers

Effective March 15, 2010, when the Fund transitioned advisory services to PIMCO, Mark R. Kiesel and Saumil H. Parikh became the portfolio managers of the Fund. Mr. Kiesel and Mr. Parikh are managing directors of PIMCO. Mr. Kiesel joined PIMCO in 1996 and previously served as PIMCO’s head of equity derivatives and as a senior credit analyst. He has 16 years of investment experience. Prior to joining PIMCO in 2000, Mr. Parikh was a financial economist and market strategist at UBS Warburg. He has 11 years of investment experience.

Investment Objectives, Policies, Restrictions and Strategies

At the Annual Meeting of Stockholders held on July 8, 2010, the stockholders voted to revise or eliminate certain of the Fund’s prior investment policies. The Fund’s Board of Directors approved certain additional changes to the Fund’s investment policies and restrictions that were effective September 15, 2010. The restated investment objectives, policies and restrictions of the Fund, and its associated investment strategies, risks, instruments and practices, are set forth beginning on page 34 of this report.

Total Non-U.S. Government Agency Asset-Backed Securities (cost $24,202,403)

23,538,103

Government and Agency Obligations 0.3%

Government Securities 0.2%

Sovereign 0.2%

Banco Nacional de Desenvolvimento Economico e Social, 5.50%, 07/12/20 (a)

400,000

411,000

U.S. Government Agency Mortgage-Backed Securities 0.1%

Federal Home Loan Mortgage Corp. 0.0%

Federal Home Loan Mortgage Corp. REMIC, 7.00%, 08/15/21

17,021

19,708

Federal National Mortgage Association 0.1%

Federal National Mortgage Association REMIC, 5.00%, 06/25/34

202,781

213,174

Total Government and Agency Obligations (cost $618,375)

643,882

Short Term Investments 0.4%

U.S. Treasury Securities 0.2%

U.S. Treasury Bill, 0.13%, 01/13/11 (f)

260,000

259,988

Repurchase Agreements 0.2%

Repurchase Agreement with Credit Suisse Securities (USA) LLC., 0.24% (Collateralized by $98,000 U.S. Treasury Note, 3.63%, due 08/15/19, value $102,471) acquired on 12/31/2010, due 01/03/2011 at $100,002

100,000

100,000

Repurchase Agreement with Deutsche Bank Securities Inc., 0.20% (Collateralized by $227,000 U.S. Treasury Bond, 6.75%, due 08/15/26, value $301,484) acquired on 12/31/2010, due 01/04/2011 at $300,002

300,000

300,000

Total Short Term Investments (cost $659,989)

659,988

Total Investments — 99.4% (cost $174,631,611)

176,533,638

Other Assets and Liabilities, Net 0.6% (f)

1,063,593

Total Net Assets — 100%

$

177,597,231

The accompanying notes are an integral part of the financial statements.

Rule 144A liquid or Section 4(2) liquid security. The Fund’s investment adviser has deemed this security to be liquid based on procedures approved by the Fund’s Board of Directors. As of December 31, 2010, the aggregate value of Rule 144A liquid or Section 4(2) liquid securities was $41,667,489 (23.7% of net assets).

(b)

Perpetual maturity security.

(c)

Interest rate is fixed until stated call date and variable thereafter.

(d)

Restricted Rule 144A or Section 4(2) security. Rule 144A or Section 4(2) of the Securities Act of 1933, as amended, provides an exemption from the registration requirements for resale of this security to institutional buyers.

(e)

Floating rate note. Floating rate notes are securities whose yields vary with a designated market index or market rate, such as the coupon-equivalent of the U.S. Treasury bill rate. These securities are shown at their current rate as of December 31, 2010.

(f)

All or a portion of the security or cash pledged as collateral for open futures contracts or swap agreements. Total value of securities or cash pledged as of December 31, 2010 was $285,988.

Abbreviations:

EUR – European Currency Unit (Euro)

GBP – British Pound

GSC – Goldman Sachs & Co.

GSI – Goldman Sachs International

MBIA – Municipal Bond Investors Assurance

NIM – Net Interest Margin

REMIC – Real Estate Mortgage Investment Conduit

Restricted Securities

Restricted securities are purchased in private placement transactions and cannot be sold without prior registration unless the sale is pursuant to an exemption under the Securities Act of 1933, as amended. The following table consists of Rule 144A securities held by the Fund at December 31, 2010 that have not been deemed liquid by the Fund’s investment adviser.

Initial Acquisition Date

Cost

Value at End of Period

Percent of Net Assets

Banco Santander Brasil SA, 4.50%, 04/06/15

12/01/2010

$

498,586

$

102,007

0.1

%

IPIC GMTN Ltd., 5.00%, 11/15/20

11/09/2010

297,351

293,971

0.2

$

795,937

$

395,978

0.3

%

Summary of Written Options

Contracts

Premiums

Options outstanding at December 31, 2009

228

$

119,409

Options expired during the year

(228

)

(119,409

)

Options outstanding at December 31, 2010

—

$

—

Schedule of Open Futures Contracts

Contracts Long

Unrealized Appreciation

90-Day Sterling Future, Expiration December 2011

29

$

10,136

$

10,136

Schedule of Open Forward Foreign Currency Contracts

Counterparty

Currency Purchased/Sold

Settlement Date

Notional Amount

Currency Value

Unrealized Gain

GSC

USD/EUR

01/25/2011

EUR (855,000)

$

(1,142,501

)

$

51,894

GSC

USD/EUR

01/25/2011

EUR (548,000)

(732,270

)

29,344

GSC

USD/EUR

01/06/2011

EUR (1,347,000)

(1,800,002

)

33,568

GSC

USD/GBP

03/21/2011

GBP (1,405,000)

(2,189,205

)

2,524

$

(5,863,978

)

$

117,330

The accompanying notes are an integral part of the financial statements.

GSI Canadian Natural Resources Ltd., 6.25%, 03/15/38

0.73

%

1.00

%

12/20/2015

$

(500,000

)

$

6,428

$

4,882

1

When the Fund is a seller of protection and a credit event occurs, as defined under the terms of that particular swap agreement, the Fund will either (i) pay the buyer of protection an amount equal to the notional amount of the referenced obligation and take delivery of the referenced obligation or underlying security comprising the referenced index or (ii) pay a net settlement amount in the form of cash or securities equal to the notional amount of the swap agreement less the recovery value of the referenced obligation or underlying security comprising the referenced index.

2

Implied credit spreads, represented in absolute terms, utilized in determining the market value of credit default swap agreements on corporate issues, sovereign issues of an emerging market country, credit indices or U.S. municipal issues serve as an indicator of the current status of the payment/performance risk and represent the likelihood or risk of default for the credit derivative. The implied credit spread of a particular referenced entity reflects the cost of buying/selling protection and may include upfront payments required to be made to enter into the agreement. Wider credit spreads represent a deterioration of the referenced entity’s credit soundness and a greater likelihood or risk of default or other credit event occurring as defined under the terms of the agreement.

3

The maximum potential amount the Fund could be required to pay as a seller of credit protection or receive as a buyer of credit protection if a credit event occurs is limited to the total notional amount which is defined under the terms of the swap agreement.

FASB Topic 815, “Derivatives and Hedging”*

The following is a summary of the fair valuations of the Fund’s derivative instruments categorized by risk exposure.

Fair values of derivative instruments on the Statement of Assets and Liabilities as of December 31, 2010:

Assets

Credit Contracts

Interest Rate Contracts

Foreign Currency Exchange Rate Contracts

Forward foreign currency contracts

$—

$—

$

117,330

Variation margin**

—

2,826

—

Unrealized appreciation on swap agreements

4,882

—

—

Swap premiums paid

1,640

—

—

$6,522

$2,826

$

117,330

The effect of derivative instruments on the Statement of Operations for the year ended December 31, 2010:

Net realized gain (loss) from:

Credit Contracts

Interest Rate Contracts

Foreign Currency Exchange Rate Contracts

Total

Forward foreign currency contracts***

$—

$—

$

(17,721

)

$

(17,721

)

Futures contracts

—

785,331

—

785,331

Options contracts

—

(28,438

)

—

(28,438

)

Swap agreements

1,264

—

—

1,264

$1,264

$756,893

$

(17,721

)

$

740,436

Net change in unrealized appreciation (depreciation) on:

Credit Contracts

Interest Rate Contracts

Foreign Currency Exchange Rate Contracts

Total

Forward foreign currency contracts***

$—

$—

$

117,330

$

117,330

Futures contracts

—

(64,486

)

—

(64,486

)

Options contracts****

—

51,505

—

51,505

Swap agreements

4,882

—

—

4,882

$4,882

$(12,981

)

$

117,330

$

109,231

The accompanying notes are an integral part of the financial statements.

See Note C in the Notes to Financial Statements for additional information.

**

The fair value of derivative instruments may include cumulative appreciation (depreciation) of futures contracts as reported in the Notes to the Investment Portfolio. Only current day’s variation margin is reported within the Statement of Assets and Liabilities.

***

Net realized gain on forward foreign currency contracts is included in net realized gain from foreign currency related items in the Statement of Operations. Net change in unrealized appreciation (depreciation) on forward foreign currency contracts is included in net change in unrealized appreciation (depreciation) in foreign currency related items.

****

Includes change in unrealized appreciation (depreciation) on purchased and written options. Unrealized appreciation (depreciation) on purchased options is located in net change in unrealized appreciation (depreciation) on investments in the Statement of Operations. Unrealized appreciation (depreciation) on written options is located in net change in unrealized appreciation (depreciation) on written options contracts in the Statement of Operations.

Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 820, “Fair Value Measurements and Disclosure”

This standard establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires additional disclosures about fair value measurements. Various inputs are used in determining the value of the Fund’s investments under FASB ASC Topic 820 guidance. The inputs are summarized into three broad categories. Level 1 includes exchange-listed prices. Level 2 includes valuations determined from significant direct or indirect observable inputs. Direct observable inputs include broker quotes, closing prices of similar securities in active markets, closing prices for identical or similar securities in non-active markets or corporate action or reorganization entitlement values. Indirect observable inputs include factors such as interest rates, yield curves, prepayment speeds or credit ratings. Level 2 includes valuations of vendor evaluated debt instruments, broker quotes in active markets, securities valued at amortized cost, modeled over-the-counter derivatives contracts and swap agreements valued by pricing services. Level 3 includes valuations determined from significant unobservable inputs including management’s own assumptions in determining the fair value of the investment. Inputs used to determine the fair value of Level 3 securities include security specific inputs such as: credit quality, credit rating spreads, issuer news, trading characteristics, call features or maturity; or industry specific inputs such as trading activity of similar markets or securities, changes in the security’s underlying index or comparable securities’ models. Level 3 valuations include certain single source quotes received from brokers (either directly or through a vendor), securities restricted to resale due to market events, newly issued securities or securities for which reliable quotes are not available. There were no significant transfers between the three category levels during the year. The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. See “Security Valuation” in the Notes to the Financial Statements for security valuation accounting policies.

The following table summarizes the Fund’s investments in securities and other financial instruments as of December 31, 2010 by valuation level.

Assets - Securities

Level 1

Level 2

Level 3

Total

Corporate Bonds

$

—

$

151,691,665

$

—

$

151,691,665

Non-U.S. Government Agency Asset Backed Securities

—

23,538,103

—

23,538,103

Government and Agency Obligations

—

643,882

—

643,882

Short Term Investments

—

659,988

—

659,988

Fund Total

$

—

$

176,533,638

$

—

$

176,533,638

Assets - Other Financial Instruments†

Level 1

Level 2

Level 3

Total

Futures Contracts

$

10,136

$

—

$

—

$

10,136

Forward Foreign Currency Contracts

—

117,330

—

117,330

Credit Default Swap Agreement

—

4,882

—

4,882

Fund Total

$

10,136

$

122,212

$

—

$

132,348

†

Investments in other financial instruments are derivative instruments not reflected in the Investment Portfolio and include forward foreign currency contracts, futures contracts, and swap agreements. All derivatives are reflected at the unrealized appreciation/(depreciation) on the instrument.

The accompanying notes are an integral part of the financial statements.

The following table is a rollforward of Level 3 investments by category for which significant unobservable inputs were used to determine fair value for the year ended December 31, 2010:

Balance at Beginning of Period

Transfers Out of Level 3 During the Period

Sales

Total Realized and Unrealized Gain/(Loss)

Balance at End of Period

Non-U.S. Government Agency Asset Backed Securities

$

1,552,377

$

(1,081,086

)

$

(563,520

)

$

92,229

$

—

The accompanying notes are an integral part of the financial statements.

Net realized and unrealized gain (loss) on investment transactions

0.71

1.33

(2.84

)

(0.67

)

(0.03

)

Total from investment operations

1.43

2.06

(1.89

)

0.38

0.87

Less distributions from:

Net investment income

(0.73

)

(0.77

)

(1.05

)

(1.12

)

(1.05

)

Net asset value, end of year

$

17.12

$

16.42

$

15.13

$

18.07

$

18.81

Per share market value, end of year

$

15.78

$

14.68

$

13.82

$

16.13

$

17.28

Closing price on New York Stock Exchange for each share of Common Stock outstanding:

High ($)

16.78

15.10

17.27

17.80

17.57

Low ($)

14.67

13.19

11.25

15.77

16.30

Total Return

Based on market price (%) b

12.50

12.04

(7.94

)

(0.23

)

8.70

Based on net asset value (%) b

9.12

14.47

(10.04

)

2.68

5.37

Ratios to Average Net Assets and Supplemental Data

Net assets, end of year ($ millions)

178

170

157

188

195

Ratio of expenses (%)

0.82

0.76

0.73

0.67

0.70

Ratio of net investment income (%)

4.28

4.64

5.57

5.64

4.78

Portfolio turnover rate (%)

132

175

170

122

199

a

Based on average shares outstanding during the year.

b

Total return based on net asset value reflects changes in the Fund’s net asset value during the year. Total return based on market price reflects changes in market price. Each figure includes reinvestment of dividends. These figures will differ depending upon the level of any discount or premium between market price and net asset value.

c

The Fund changed investment adviser effective March 15, 2010.

d

The Fund changed investment adviser effective June 9, 2006.

The accompanying notes are an integral part of the financial statements.

Montgomery Street Income Securities Inc. (the “Fund”) is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a closed-end, diversified management investment company.

The Fund’s financial statements are prepared, as of the close of the New York Stock Exchange (“NYSE”) on December 31, 2010, in accordance with accounting principles generally accepted in the United States of America (“GAAP”) which requires the use of management estimates. Actual results could differ from those estimates. The policies described below are followed consistently by the Fund in the preparation of its financial statements.

Security Valuation. Investments are stated at value determined as of the close of regular trading (generally, 4:00 PM Eastern Time) on the NYSE on each day the exchange is open for trading. Debt securities are valued by independent pricing services approved by, or at the direction of, the Fund’s Board of Directors (the “Board”). If the pricing services are unable to provide valuations, debt securities are valued at the most recent bid quotation or evaluated price, as applicable, obtained from a broker/dealer or widely used quotation system. Fixed income securities with a remaining maturity of sixty days or less, maturing at par, are valued at amortized cost, unless it is determined that such price does not approximate market value. Forward foreign currency contracts are valued at the forward foreign currency exchange rate as of the close of the NYSE. Exchange traded derivatives, including futures and option contracts, are valued based upon their quoted daily settlement prices. In the event that the settlement price is unavailable, the closing price will be used for valuation. Non-exchange traded derivatives, including swap agreements, are generally valued by approved pricing services. If the pricing services are unable to provide valuations, non-exchange traded derivatives are valued at the most recent bid quotation or evaluated price, as applicable, obtained from a broker/dealer or by pricing models using observable inputs. Pricing services used to value debt and derivative securities may use various pricing techniques which take into account appropriate factors such as yield, quality, coupon rate, maturity, type of issue, trading characteristics, call features, credit ratings and other data, as well as broker quotes.

Market quotations may not be readily available for certain debt and derivative investments. If market quotations are not readily available or if it is determined that a quotation of an investment does not represent market value, then the investment is valued at a “fair value” as determined in good faith using procedures approved by the Board. Although there can be no assurance, in general, the fair value of a security is the amount the owner of such security might reasonably expect to receive upon its current sale. Situations that may require a security to be fair valued may include instances where a security is thinly traded or restricted as to resale. In addition, securities may be fair valued based on the occurrence of a significant event. Significant events may be specific to a particular issuer, such as mergers, restructurings or defaults. Alternatively, significant events may affect an entire market, such as natural disasters or government actions. Securities are fair valued based on observable and unobservable inputs including Jackson Fund Services’ (“JFS” or the “Administrator”) own assumptions in determining fair value. Under the procedures adopted by the Board, the Administrator may rely on independent pricing services or other sources to assist in determining the fair value of a security. Factors considered to determine fair value include the correlation with price movement of similar securities in the same or other markets; the type, cost and investment characteristics of the security; the business and financial condition of the issuer; and trading or other market data. The value of an investment for purposes of calculating the Fund’s net asset value (“NAV”) can differ depending on the source and method used to determine the value.

In January 2010, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2010-06 “Improving Disclosures about Fair Value Measurements”. ASU 2010-06 clarifies existing disclosure requirements and mandates additional disclosure regarding fair value measurements. Effective for interim and annual reporting periods beginning after December 15, 2009, entities are required to disclose significant transfers into and out of Level 1 and 2 measurements in the fair value hierarchy and the reasons for those transfers. Effective for fiscal years beginning after December 15, 2010, and for interim periods within those fiscal years, entities will need to disclose information about purchases, sales, issuances and settlements of Level 3 securities on a gross basis, rather than as a net number. See the Notes to the Investment Portfolio, FASB Accounting Standards Codification (“ASC”) Topic 820, “Fair Value Measurements and Disclosure”, for expanded disclosure of fair value measurements.

Security Transactions and Investment Income. Investment transactions are accounted for on a trade date plus one basis for daily NAV calculations. However, for financial reporting purposes, investment transactions are reported on trade date. Interest income is recorded on the accrual basis. All premiums and discounts are amortized/accreted for financial reporting purposes. Dividend income is recorded on the ex-dividend date.

Foreign Currency Translations. The accounting records of the Fund are maintained in U.S. dollars. Investment securities and other assets and liabilities denominated in a foreign currency are translated into U.S. dollars generally using exchange

rates in effect as of 4:00 PM Eastern Time. Purchases and sales of investment securities, income receipts, and expense payments are translated into U.S. dollars at the exchange rates prevailing on the respective dates of such transactions. The Fund does not isolate that portion of the results of operations resulting from changes in foreign exchange rates on investments from the fluctuations arising from changes in market prices of foreign securities. Such fluctuations are included in net realized gain (loss) on investment transactions and net change in unrealized appreciation (depreciation) on investments, respectively.

Net realized gains and losses on foreign currency related items are considered ordinary income for tax purposes and arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions, the difference between the amounts of dividends, interest, and foreign withholding taxes recorded and the U.S. dollar equivalent of the amounts actually received or paid, and the realized gains or losses resulting from portfolio and transaction hedges. Net change in unrealized appreciation (depreciation) on foreign currency related items arises from changes in the fair value of assets and liabilities, other than investments in securities, at period end resulting from changes in exchange rates.

Federal Income Taxes. The Fund intends to qualify as a “regulated investment company” and to distribute substantially all net investment income and net capital gains, if any, to its stockholders and otherwise comply with Subchapter M of the Internal Revenue Code applicable to regulated investment companies. Therefore, no federal income tax provision is required.

Distribution of Income and Capital Gains. The amount and timing of distributions are determined in accordance with federal income tax regulations, which may differ from GAAP. Distributions of net investment income are paid quarterly. Net realized gains from investment transactions will be distributed to stockholders at least annually to the extent they exceed available capital loss carryforwards. The Fund uses the specific identification method for determining realized gain or loss on investments sold for both financial and federal income tax reporting purposes.

Contingencies. In the normal course of business, the Fund may enter into contracts with service providers that contain general indemnification clauses. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet been made. However, based on experience to date, the Fund expects any risk of loss to be remote.

B. Investments and Risks

When-Issued/Delayed Delivery Securities. The Fund may purchase securities with delivery or payment to occur at a date beyond the normal settlement period. At the time the Fund enters into a commitment to purchase a security, the transaction is recorded and the value of the security is reflected in the NAV. The price of such security and the date when the security will be delivered and paid for are fixed at the time the transaction is negotiated. The value of the security may vary with market fluctuations. No interest accrues to the Fund until settlement of the trade. Certain risks may arise upon entering into when-issued or delayed delivery securities from the potential inability of counterparties to meet the terms of their contracts or if the issuer does not issue the securities due to political, economic, or other factors. Additionally, losses may arise due to changes in the value of the underlying securities.

Illiquid Investments and Restricted Securities. Illiquid securities and other investments are those that may not be sold or disposed of in the ordinary course of business within seven days, at approximately the price used to determine the Fund’s NAV per share. The Fund may not be able to sell illiquid investments when Pacific Investment Management Company (“PIMCO” or the “Adviser”) considers it desirable to do so or may have to sell such investments at a price that is lower than the price that could be obtained if the investments were liquid. A sale of illiquid investments may require more time and may result in higher dealer discounts and other selling expenses than would the sale of those that are liquid. Illiquid investments also may be more difficult to value, due to the unavailability of reliable market quotations for such investments, and investment in them may have an adverse impact on NAV. The Fund may also purchase certain restricted securities, commonly known as Rule 144A and Section 4(2) paper securities, which may be determined to be liquid pursuant to policies and guidelines established by the Board.

Securities Loaned. The Fund entered into a securities lending arrangement with The Bank of New York Mellon (the “Custodian”). Under the terms of the agreement, the Fund received a fee equal to a percentage of the net income generated by the collateral held and each lending transaction. The Custodian was authorized to loan securities on behalf of the Fund to approved borrowers and was required to maintain collateral at least equal to the value of the securities loaned. On February 17, 2010, the Fund terminated its securities lending arrangement with the Custodian.

Repurchase Agreements. The Fund may enter into repurchase agreements with certain banks and broker/dealers whereby the Fund agrees to purchase a security with a simultaneous agreement by the seller to repurchase the security back from the Fund at a specified price and date or upon demand. The Fund, through the Custodian or sub-custodian bank, receives delivery of underlying securities used as collateral, the amount of which, at the time of purchase and each subsequent business day, is required to be maintained at such a level that the collateral’s value is at least equal to the principal amount of the repurchase price plus accrued interest. The Custodian holds the collateral in a separate account until the agreement matures. If the counterparty defaults and the value of the collateral declines or if bankruptcy proceedings are commenced with respect to the counterparty, realization of the collateral by the Fund may be delayed or limited.

U.S. Government Agencies or Government Sponsored Enterprises. The Fund may invest in U.S. government agencies or government sponsored enterprises. U.S. government securities are obligations of and, in certain cases, guaranteed by, the U.S. government, its agencies or instrumentalities. Some U.S. government securities, such as Treasury bills, notes and bonds, and securities guaranteed by the Government National Mortgage Association, are supported by the full faith and credit of the U.S. government; others, such as those of the Federal Home Loan Bank, are supported by the right of the issuer to borrow from the U.S. Department of the Treasury (the “U.S. Treasury”); others, such as those of the Federal National Mortgage Association (“FNMA”) are supported by the discretionary authority of the U.S. government to purchase the agency’s obligations. U.S. government securities may include zero coupon securities, which do not distribute interest on a current basis and tend to be subject to greater risk than interest-paying securities of similar maturities.

Government-related guarantors (i.e., guarantors who are not backed by the full faith and credit of the U.S. government) include FNMA and the Federal Home Loan Mortgage Corporation (“FHLMC”). FNMA purchases conventional (i.e., not insured or guaranteed by any government agency) residential mortgages from a list of approved seller/servicers which include state and federally chartered savings and loan associations, mutual savings banks, commercial banks and credit unions and mortgage bankers. Pass-through securities issued by FNMA are guaranteed as to timely payment of principal and interest by FNMA, but are not backed by the full faith and credit of the U.S. government. FHLMC issues Participation Certificates (“PCs”), which are pass-through securities, each representing an undivided interest in a pool of residential mortgages. FHLMC guarantees the timely payment of interest and ultimate collection of principal, but PCs are not backed by the full faith and credit of the U.S. government.

In September 2008, the Federal Housing Finance Agency (“FHFA”) placed FNMA and FHMLC into conservatorship. As the conservator, FHFA succeeded to all rights, titles, powers and privileges of FNMA and FHLMC and of any stockholder, officer or director of FNMA and FHLMC with respect to FNMA and FHLMC and each enterprise’s assets. In connection with the conservatorship, the U.S. Treasury entered into a Senior Preferred Stock Purchase Agreement with FNMA and FHLMC. This agreement contains various covenants that severely limit each enterprise’s operations. In exchange for entering into these agreements, the U.S. Treasury received senior preferred stock in each enterprise and warrants to purchase each enterprise’s common stock. The U.S. Treasury announced the creation of a new secured lending facility, which is available to FNMA and FHLMC as a liquidity backstop and the creation of a temporary program to purchase mortgage-backed securities issued by FNMA and FHLMC. FNMA and FHLMC are continuing to operate as going concerns while in conservatorship and each remains liable for all of its obligations, including its guaranty obligations, associated with its mortgage-backed securities.

Market, Credit and Counterparty Risk. In the normal course of business the Fund trades and holds financial instruments and enters into financial transactions where risk of potential loss exists due to changes in the market including rates and liquidity (“market risk”) or failure of the issuer to perform (“credit risk”). Similar to credit risk, the Fund may be exposed to counterparty risk, or the risk that an institution or other entity with which the Fund has unsettled or open transactions will default. Financial assets, which potentially expose the Fund to market, credit and counterparty risk, consist principally of cash due from counterparties and investments. The extent of the Fund’s exposure to market, credit and counterparty risks with respect to these financial assets is reflected in their carrying value as recorded in the Fund’s Statement of Assets and Liabilities.

C. Financial Derivative Instruments

FASB ASC Topic 815, “Derivatives and Hedging”. This standard includes the requirement for enhanced qualitative disclosures about objectives and strategies for using derivative instruments and disclosures regarding credit-related contingent features in derivative instruments, as well as quantitative disclosures in the semi-annual and annual financial statements about fair value, gains and losses and volume of activity for derivative instruments. Information about these instruments is disclosed in the context of each instrument’s primary underlying risk exposure that is categorized as credit,

equity price, interest rate, and foreign currency exchange rate risk. The objectives, strategies and underlying risks for each instrument are discussed in the following paragraphs.

A tabular disclosure for each derivative investment by risk category is presented in the Notes to the Investment Portfolio which references the location on the Statement of Assets and Liabilities and the realized and unrealized gain (loss) in the Statement of Operations for each derivative investment. The derivative instruments outstanding as of the year ended December 31, 2010 as disclosed in the Notes to the Investment Portfolio and the amounts of realized and changes in unrealized gains and losses on derivative instruments during the year as disclosed in the Statement of Operations serve as indicators of the volume of derivative activity for the Fund. The Fund closed options positions held at December 31, 2009 and did not enter into new options transactions during the year. The Fund began initiating transactions in credit default swap agreements during the year.

Options Contracts. The Fund may be subject to interest rate risk in the normal course of pursuing its investment objective. The Fund bought call and put options on futures and sold (“wrote”) call options on futures to manage its exposure to and hedge against changes in interest rates. An option contract on an interest rate futures contract is an option, for which a negotiated premium is paid, with an exchange-specified expiration date, to enter into an interest rate futures contract that is exchange-specified in terms of the financial instrument, settlement date, and exercise price. A “put” on an interest rate futures contract requires a writer of the contract to enter into the buy side of the specified interest rate futures contract if a buyer of the put exercises the put before the expiration date. A “call” on an interest rate futures contract requires a writer of the contract to enter into the sell side of the specified interest rate futures contract if a buyer of the call exercises the call before the expiration date. Exercise of the option requires that the writer immediately deposit initial margin on the interest rate futures contract and immediately mark any loss position to the market. Upon exercise of the option, the Fund may immediately enter into an offsetting futures contract with respect to the futures contract that was exercised.

When the Fund purchases an option, the premium paid by the Fund is recorded as an asset and is subsequently marked-to-market to reflect the current value of the option. Premiums paid for purchasing options which expire are treated as realized losses. Premiums paid for purchasing options which are exercised or closed are added to the cost basis of the underlying investment or offset against the proceeds of the underlying investment transaction to determine realized gain or loss. When the Fund writes a call or put option, the premium received by the Fund is recorded as a liability and is subsequently marked to market to reflect the current value of the option. Premiums received from writing options which expire are treated as realized gains. Premiums received from writing options which are exercised or closed are added to the proceeds of the underlying investment transaction or reduce the cost basis of the underlying investment to determine the realized gain or loss.

Options contracts involve, to varying degrees, risk of loss in excess of the premium paid or received recorded by the Fund. The primary risks associated with the use of option contracts on futures contracts involve similar risks to trading in the underlying futures contracts, including the imperfect correlation between the change in value of the securities held by the Fund and the prices of the underlying futures contracts and the possibility the Fund may not be able to enter into a closing transaction because of an illiquid market. Option contracts entered into by the Fund during the year were traded on public markets that are regulated by the Commodities Futures Trading Commission. Similar to futures contracts, there is minimal counterparty risk to the Fund since the options on futures contracts traded by the Fund were exchange traded and the exchange’s clearing house, as counterparty to all exchange traded options, guarantees the options contracts against default. The Fund held no option contracts at December 31, 2010.

Futures Contracts. The Fund may be subject to interest rate risk in the normal course of pursuing its investment objective. The Fund used futures contracts to manage its exposure to or hedge against changes in interest rates and as an efficient means of adjusting exposure to certain markets as part of its overall investment strategy. Upon entering into a futures contract, the Fund is required to deposit with the broker an amount of cash or cash equivalents equal to a certain percentage of the contract amount known as the “initial margin”. The Fund receives from or pays to the counterparty an amount of cash equal to the daily fluctuation in the value of the contracts. Such receipts or payments, known as the “variation margin”, are recorded by the Fund until the contracts are terminated at which time realized gains and losses are recognized. Futures contracts involve, to varying degrees, risk of loss in excess of the variation margin recorded by the Fund. The primary risks associated with the use of futures contracts are the imperfect correlation between the change in value of the securities held by the Fund and the prices of the futures contracts and the possibility the Fund may not be able to enter into a closing transaction because of an illiquid market. With futures, there is minimal counterparty risk to the Fund since future contracts are exchange traded and the exchange’s clearinghouse, as counterparty to all exchange traded futures, guarantees the futures contracts against default.

The Fund has claimed an exclusion from the definition of the term “commodity pool operator” under the Commodity Exchange Act and, therefore, it is not subject to registration or regulation as a commodity pool operator under that Act.

Forward Foreign Currency Contracts. The Fund may be subject to foreign currency exchange rate risk in the normal course of pursuing its investment objective. The Fund entered into forward foreign currency contracts to minimize foreign currency risk on portfolio securities denominated in foreign currencies and as part of its overall investment strategy. A forward foreign currency contract is an agreement between two parties to buy and sell a currency at a set price on a future date. The use of forward foreign currency contracts does not eliminate fluctuations in the underlying prices of the Fund’s portfolio securities, but it does establish a rate of foreign exchange that can be achieved in the future. The market value of a forward foreign currency contact fluctuates with changes in foreign currency exchange rates. Forward foreign currency contracts are marked-to-market daily and the change in value is recorded by the Fund as an unrealized gain or loss and as a receivable or payable from forward foreign currency contracts. Upon delivery or receipt of the currency, a realized gain or loss which is equal to the difference between the value of the contract at the time it was opened and the value at the time it was closed is recorded. Forward foreign currency contracts involve market risk in excess of the receivable or payable related to forward foreign currency contracts recorded by the Fund. Although contracts limit the risk of loss due to a decline in the value of the hedged currency, they also limit any potential gain that might result should the value of the currency increase. Additionally, the Fund could be exposed to the risk of a previously hedged position becoming unhedged if the counterparty to a contract is unable to meet the terms of the contract or if the value of the currency changes unfavorably to the U.S. dollar.

Swap Agreements. Swap agreements are privately negotiated agreements between the Fund and a counterparty to exchange the return generated by one instrument for the return generated by another instrument. Swap agreements are illiquid investments. If the Fund transacts in swap agreements, they are a party to International Swaps and Derivatives Association, Inc. (“ISDA”) Master Agreements (“ISDA Master Agreements”) with select counterparties. The ISDA Master Agreements govern transactions in over-the-counter derivative and forward foreign currency contracts and maintain provisions for general obligations, representations, agreements, collateral and events of default or termination. Events of termination include conditions that may entitle counterparties to elect to terminate early and cause settlement of all outstanding transactions under the applicable ISDA Master Agreement. Any election of early termination could be material to the financial statements. The amount of collateral exchanged is based on provisions within the ISDA Master Agreements and is determined by the net exposure with the counterparty and is not identified for a specific swap agreement.

Swap agreements are marked-to-market daily and change in value is recorded by the Fund as an unrealized gain or loss. Swap premiums paid or received at the beginning of the measurement period which are recorded by the Fund represent payments made or received upon entering into the swap agreement to compensate for differences between the stated terms of the swap agreement and prevailing market conditions relating to credit spreads, interest rates, currency exchange rates, and other relevant factors as appropriate. These upfront payments are amortized over the life of the swap agreement and recorded as a realized gain or loss upon termination or maturity of the swap agreement. A liquidation payment received or made at the termination of the swap agreement is recorded as realized gain or loss. Net periodic payments received or paid by the Fund are included as part of realized gain or loss.

Entering into swap agreements involves, to varying degrees, elements of credit and market risk in excess of the unrealized gain or loss recorded by the Fund. Such risks involve the possibility that there will be no liquid market for these agreements, that there may be unfavorable changes the value of underlying securities and that the counterparty to the agreements may default on its obligation to perform. In addition, entering into swap agreements involves documentation risk resulting from the possibility that the parties to the swap agreements may disagree as to the meaning of contractual terms in the agreements. The credit risk associated with contracts is reduced by master netting arrangements to the extent that if an event of default occurs, all amounts with the counterparty are terminated and settled on a net basis. The Fund’s overall exposure to credit risk subject to master netting arrangements can change substantially within a short period, as it is affected by each transaction subject to the arrangement.

Credit Default Swap Agreements. The Fund may be subject to credit rate risk in the normal course of pursuing its investment objective. The Fund used credit default swap agreements on corporate issues to manage the Fund’s credit exposure. Credit default swap agreements involve one party making a stream of payments (referred to as the buyer of protection) to another party (the seller of protection) in exchange for the right to receive a specified return if a credit event occurs for the referenced entity. A credit event is defined under the terms of each swap agreement and may include, but is not limited to, underlying entity default, bankruptcy, write-down, principal shortfall or interest shortfall. If a credit event occurs and cash settlement is not elected, a variety of other deliverable obligations may be delivered in lieu of the specific

referenced obligation. The ability to deliver other obligations may result in a cheapest-to-deliver option (the buyer of protection’s right to choose the deliverable obligation with the lowest value following a credit event).

The Fund can be either a seller or buyer of protection when entering into a credit default swap agreement. As a seller of protection, the Fund will generally receive from the buyer of protection a fixed rate of income throughout the term of the swap if there is no credit event. As a seller, the Fund adds leverage to its portfolio because, in addition to its total net assets, the Fund is subject to investment exposure on the notional amount of the swap. If the Fund is a seller of protection and a credit event occurs, as defined under the terms of that particular swap agreement, the Fund will either pay to the buyer of protection an amount equal to the notional amount of the swap and take delivery of the referenced obligation or other deliverable obligations or pay a net settlement amount in the form of cash or securities equal to the notional amount of the swap less the recovery value of the referenced obligation. If the Fund is a buyer of protection and a credit event occurs, as defined under the terms of that particular swap agreement, the Fund will either receive from the seller of protection an amount equal to the notional amount of the swap and deliver the referenced obligation or other deliverable obligations or receive a net settlement amount in the form of cash or securities equal to the notional amount of the swap less the recovery value of the referenced obligation. Until a credit event occurs, recovery values are determined by market makers considering either industry standard recovery rates or entity specific factors and considerations. When a credit event occurs, the recovery value is determined by a facilitated auction, administered by ISDA, whereby a minimum number of allowable broker bids, together with a specified valuation method, are used to calculate the settlement value.

Either as a seller of protection or a buyer of protection of a credit default swap agreement, the Fund’s maximum risk of loss from counterparty risk is the fair value of the agreement. This risk is mitigated by having a master netting arrangement between the Fund and the counterparty and by posting collateral by the counterparty to the Fund to cover the Fund’s exposure to the counterparty. The maximum potential amount of future payments (undiscounted) that the Fund as a seller of protection could be required to make under a credit default swap agreement would be an amount equal to the notional amount of the agreement. Notional amounts of all credit default swap agreements outstanding as of December 31, 2010, for which the Fund is the seller of protection are disclosed in the Notes to the Portfolio of Investment. These potential amounts would be partially offset by any recovery values of the respective referenced obligations, upfront payments received upon entering into the agreement or net amounts received from the settlement of buy protection credit default swap agreements entered into by the Fund for the same referenced entity or entities.

D. Purchases and Sales of Securities

During the year ended December 31, 2010, purchases and sales of investment securities, excluding U.S. government obligations and short-term investments, aggregated $206,825,576 and $122,782,560, respectively. During the year ended December 31, 2010, purchases and sales of long-term U.S. government obligations aggregated $24,030,786 and $104,120,409, respectively.

Fund Transactions and Brokerage. Subject to compliance with Rule 17a-7 under the 1940 Act, the Adviser is permitted to cause the Fund to purchase securities from or sell securities to another account, including another investment company, advised by the Adviser.

There are occasions when portfolio transactions for the Fund are executed as part of concurrent authorizations to purchase or sell the same security for the Fund and for other accounts served by the Adviser or an affiliated company. They are effected only when the Adviser believes that to do so is in the best interest of the Fund and the other accounts participating. When such concurrent authorizations occur, the executions will be allocated in an equitable manner.

E. Fees and Agreements

Investment Advisory Agreement. Prior to March 15, 2010, the Fund had an Investment Advisory Agreement whereby the Fund paid Hartford Investment Management Company (“HIMCO”) a quarterly fee equal to the product of (a) one quarter of 0.25%, times (b) the average of the net assets of the Fund on the last business day of each calendar month of the then ended calendar quarter. On March 15, 2010 the Fund and PIMCO entered into an Interim Investment Advisory Agreement whereby the Fund paid PIMCO the same fee paid to HIMCO. On July 8, 2010, the Fund and PIMCO entered into a new Investment Advisory Agreement whereby the Fund pays PIMCO a quarterly fee at the annual rate of 0.25% of the average daily net assets of the Fund.

Fund Accounting and Administration Services Agreement. The Fund has entered into a Fund Accounting and Administration Services Agreement (“Administration Agreement”) with JFS. Pursuant to the Administration Agreement, the Fund pays JFS an annual fee, payable monthly, equal to 0.25% of the average daily value of the net assets of the Fund up

to $100 million; 0.20% of the average daily value of the net assets of the Fund from $100 million to $200 million; and 0.15% of the average daily value of the net assets of the Fund over $200 million. JFS makes individuals available to the Fund to serve as its officers. Officers are not directly compensated by the Fund.

Directors’ Fees and Expenses. The Fund pays each Board Director a retainer fee plus specified amounts for each Board and Committee meeting attended.

F. Income Tax Matters

The following information is presented on an income tax basis. The timing and characterization of certain income and capital gains are determined in accordance with federal tax regulations, which may differ from GAAP. These differences primarily relate to timing differences in recognizing certain gains and losses on investment transactions and accounting treatment for notional principal contracts. To the extent that differences arise that are permanent in nature, such amounts are reclassified within the components of net assets on the Statement of Assets and Liabilities based on their federal income tax treatment; timing differences do not require reclassification. Timing and permanent differences do not impact the NAV of the Fund. At December 31, 2010, permanent differences increased undistributed net investment income and accumulated realized loss by $76,792.

At December 31, 2010, the cost of investments and the components of net unrealized depreciation are listed in the following table.

Cost of Investments

Gross Unrealized Depreciation

Gross Unrealized Appreciation

Net Unrealized Appreciation

$174,709,513

$

(3,091,943

)

$

4,916,068

$

1,824,125

At December 31, 2010, the Fund had undistributed net ordinary income of $250,334.

The distributions paid of $7,567,767 and $7,985,367 for the years ended December 31, 2010 and 2009, respectively, were from net ordinary income.

At December 31, 2010, the Fund had unused capital loss carryforwards available for federal income tax purposes which may be applied against any future realized net taxable capital gains or until the respective expiration dates occur as noted below.

Year of Expiration

Amount

2014

$

1,984,761

2015

596,899

2016

12,721,218

2017

11,494,100

Total

$

26,796,978

The Regulated Investment Company Modernization Act of 2010 (“Act”) was enacted on December 22, 2010. In general, the provisions of the Act will be effective for the Fund’s fiscal year ending December 31, 2011. Under the Act, the Fund will be permitted to carry forward capital losses for an unlimited period. However, any losses incurred during those future taxable years will be required to be utilized prior to the losses incurred in pre-enactment taxable years. As a result of this ordering rule, pre-enactment capital loss carry forwards may be more likely to expire unused. Additionally, post-enactment capital losses that are carried forward will retain their character as either short-term or long-term capital losses, and will not be considered exclusively short-term as under previous law. Relevant information regarding the impact of the Act on the Fund will be contained within the Income Tax Matters section of the financial statement notes in the Fund’s Annual Report for the fiscal year ending December 31, 2011.

The Fund had $220,261 of capital losses realized from November 1, 2010 through December 31, 2010, which were deferred for tax purposes to January 1, 2011, the first day of the current fiscal year.

FASB ASC Topic 740, “Income Taxes”, provides guidance for how uncertain tax positions should be recognized, measured, presented and disclosed in the financial statements. FASB ASC Topic 740 requires the evaluation of tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether the tax positions are “more-likely-than-not” of being sustained by the applicable tax authority. Tax positions not deemed to meet the “more-likely-than-not” threshold would result in the Fund recording a tax expense in the current year. FASB ASC Topic 740 requires that management evaluate the tax positions taken in returns for 2007 through 2010 which remain subject to examination, by the

Internal Revenue Service. These returns are not subject to examination by any other tax jurisdictions. Management completed an evaluation of the Fund’s tax positions and based on that evaluation, determined that no provision for federal income tax was required in the Fund’s financial statements during the period ended December 31, 2010.

G. Share Repurchases

The Fund is authorized to effect repurchases of its shares in the open market from time to time when the Fund’s shares trade at a discount to their NAV. During the year ended December 31, 2010, the Fund purchased 29,000 shares of common stock on the open market at a total cost of $457,941. The weighted average discount of these purchases, comparing the purchase price to the NAV at the time of purchase, was 7.42%. During the year ended year ended 2009, the Fund purchased 42,000 shares of common stock on the open market at a total cost of $594,007. The weighted average discount of these purchases, comparing the purchase price to the NAV on the day of purchase, was 10.2%.

H. Subsequent Events

Management has evaluated subsequent events for the Fund through the date the financial statements are issued, and has concluded there are no events that require financial statement disclosure and/or adjustments to the financial statements.

Report of Independent Registered Public Accounting Firm

To the Stockholders and Board of Directors of

Montgomery Street Income Securities, Inc.:

We have audited the accompanying statement of assets and liabilities, including the investment portfolio, of Montgomery Street Income Securities, Inc. (the “Fund”) as of December 31, 2010, and the related statements of operations, changes in net assets and the financial highlights for the year then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. The statement of changes in net assets for the year ended December 31, 2009 and the financial highlights for each of the fiscal years presented in the four-year period ended December 31, 2009 were audited by other auditors, whose report dated February 24, 2010, expressed an unqualified opinion on the statement and financial highlights.