As filed with the Securities and Exchange Commission on March 6, 2012

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-3489

THE WRIGHT MANAGED EQUITY TRUST

440 Wheelers Farms Road

Milford, Connecticut 06461

Christopher A. Madden

Three Canal Plaza, Suite 600

Portland, ME 04101

207-347-2000

Date of fiscal year end: December 31

Date of reporting period: January 1, 2011 – December 31, 2011

ITEM 1. REPORT TO STOCKHOLDERS.

Table of Contents

| Investment Objectives | inside front cover | |||

| Letter to Shareholders (Unaudited) | 2 | |||

| Management Discussion (Unaudited) | 4 | |||

| Performance Summaries (Unaudited) | 10 | |||

| Fund Expenses (Unaudited) | 20 | |||

| Management and Organization (Unaudited) | 71 | |||

| Board of Trustees Annual Approval of the Investment Advisory Agreement (Unaudited) | 72 | |||

| Important Notices Regarding Privacy, Delivery of Shareholder Documents, Portfolio Holdings and Proxy Voting (Unaudited) | 73 | |||

| FINANCIAL STATEMENTS | ||||

| The Wright Managed Equity Trust | The Wright Managed Income Trust | |||

| Wright Selected Blue Chip Equities Fund | Wright Total Return Bond Fund | |||

| Portfolio of Investments | 22 | Portfolio of Investments | 47 | |

| Statement of Assets and Liabilities | 24 | Statement of Assets and Liabilities | 52 | |

| Statement of Operations | 24 | Statement of Operations | 52 | |

| Statements of Changes in Net Assets | 25 | Statements of Changes in Net Assets | 53 | |

| Financial Highlights | 26 | Financial Highlights | 54 | |

| Wright Major Blue Chip Equities Fund | Wright Current Income Fund | |||

| Portfolio of Investments | 27 | Portfolio of Investments | 55 | |

| Statement of Assets and Liabilities | 28 | Statement of Assets and Liabilities | 59 | |

| Statement of Operations | 28 | Statement of Operations | 59 | |

| Statements of Changes in Net Assets | 29 | Statements of Changes in Net Assets | 60 | |

| Financial Highlights | 30 | Financial Highlights | 61 | |

| Wright International Blue Chip Equities Fund | Notes to Financial Statements | 62 | ||

| Portfolio of Investments | 31 | |||

| Statement of Assets and Liabilities | 33 | Report of Independent Registered Public Accounting Firm | 69 | |

| Statement of Operations | 33 | |||

| Statements of Changes in Net Assets | 34 | Federal Tax Information (Unaudited) | 70 | |

| Financial Highlights | 35 | |||

| Notes to Financial Statements | 36 | |||

| Report of Independent Registered Public Accounting Firm | 45 | |||

| Federal Tax Information (Unaudited) | 46 | |||

Letter to Shareholders (Unaudited)

Dear Shareholder:

U.S. stock prices were either up modestly (Dow Jones Industrials), flat (S&P 500) or down slightly (NASDAQ) in 2011, as Europe’s debt crisis dominated financial headlines, more or less offsetting the generally strong corporate profits showing. After double-digit percentage declines in the stock market averages during the third quarter, the fourth quarter rally rescued the year 2011 from the bear market that looked to be developing in September. The year saw a strong move to quality stocks as investors shied away from risk; the dollar and U.S. Treasury bonds were also sought as safe havens, and gold glittered as an alternative bet on economic calamity. 2011 was remarkable for the Arab Spring, which unseated long-entrenched rulers, and for an intensification of pressures on Europe’s bourses and on the euro itself, which also ended up costing a number of European leaders their jobs. As 2012 begins, difficult elections lie ahead for three G-7 leaders, U.S. President Barack Obama, French President Nicolas Sarkozy and German Chancellor Angela Merkel. The incumbents will no doubt do all they can to promote a stronger economic climate; the question is: given today’s many obstacles to growth and countervailing forces in government, how much will they be able to do to jump-start the most sluggish economic recovery in modern times?

After three downbeat quarters, U.S. economic data generally exceeded expectations during the fourth quarter, with Q4 GDP growth shaping up to be the best quarterly showing for the U.S. economy – on the order of 3% – since 2010’s second quarter. Considering that a good portion of the year-end improvement in economic activity represents a favorable swing in business inventories (Q3 GDP growth was reduced around 1.3% by inventory liquidation), sustainable growth in the 3% range does not yet look to be anywhere on the horizon. Instead, about the best one can realistically project is a muddling along in the 1%-2% growth range, and even that will become problematic in the event recession in Europe were to combine with more slowing in China than the soft landing now anticipated. The long-awaited reduction in inflation pressures finally began to show up as 2011 was coming to a close, perhaps a little later than the Federal Reserve had been projecting. Commodities prices mostly went lower in 2011 with the notable exceptions of crude oil and gold, but the core rate of consumer price inflation was stubbornly above 2% as the year was ending.

This past year was also notable for the Occupy Wall Street protest movement, a product of the nation’s high unemployment and a widespread sense that financial industry leaders and government policy makers were conspiring in markets against ordinary investors and wage earners. As we have noted previously, this dissatisfaction and cynicism may be a logical result of the worst recession in the postwar period and what to date has been the shallowest recovery. Congress has drawn the scorn of constituents who believe partisanship has increased to such a degree that compromise is all but impossible, crippling the ability of government to respond to swiftly changing economic conditions. That has led to the nation’s many “kicking-the-can-down-the-road” fiscal policies, ranging from TARP to the acrimonious two-month extension of payroll tax cuts that closed out this past legislative year. Happily, while Washington does not seem to be able to kick its spending/debt habit, the private sector (i.e., households and businesses) continued to repair their balance sheets in 2011, although much more needs to be done.

Corporate profits have been the redeeming feature of our otherwise sub-par economic expansion. The U.S. economy returned to its peak 2007 fourth quarter output level in Q3 2011, 15 quarters after the recession began. That is roughly twice as long as the recoveries following the deep recessions of 1957-58, 1973-75, and 1981-82. In real terms, personal incomes have yet to return to their previous peak level. What stands out about the current recovery is the return of corporate profits to record levels; corporate profits before taxes surpassed the previous peak in the second quarter of 2010, and by this measure Q3 2011 profits were more than 120% higher than at the cycle low in Q4 2008. By contrast, at its December 2011 close, the S&P 500 stock price level was 86% above its 2009 low (but

2

| Letter to Shareholders (Unaudited) | |||

still 20% below its all-time high hit in October 2007). Where the U.S. had a stock market bubble in 2000 and was about to experience the bursting of the real estate bubble at the market peak in 2007, today stock prices are priced at attractive levels relative to earnings. On the basis of forecast year-ahead earnings, the S&P 500’s year-end 2011 price/earnings multiple of 12.3 is three P/E points below its average over the past quarter century.

While the Federal Reserve has had some “success” in reflating the U.S. economy, there remain downward pressures on product prices and interest rates. We continue to believe that interest rates will gradually move higher in 2012. The Fed has effectively anchored rates at the short end of the yield curve by indicating it will keep the fed funds rates close to zero through at least mid-2013. Economic activity continues to run well below the world’s productive capacity, undermining pricing power for businesses to the benefit of consumers. But consumers, still shaken by the economic and financial vicissitudes of 2008-09, have been somewhat more cautious in their spending, boosting the personal savings rate since 2007 by a factor of two relative to the 2005-07 average rate (5% vs 2.2%). That is for the good; indeed, the debt and dissaving excesses of the 1990s and 2000s probably require an extended period of more prudent financial behavior before the imbalances of the bubble years are completely washed out of the nation’s economic system. As this is occurring, we should be prepared for economic growth to remain somewhat constrained compared with long-term growth norms.

The financial turmoil of the past five years has reduced stock prices to comparatively cheap levels, as will become clear once financial conditions begin to normalize. For the most part, U.S. stock returns failed to keep pace with inflation in 2011, and outside the U.S., equities fared far worse. But the growth of corporate fundamentals (sales, assets, earnings, dividends and equity) has continued to create value for stockholders in a way that real estate and fixed-income investments are unlikely to match. Volatility may be elevated from time to time in the near term, but we retain our confidence in the longer-term ability of equities to produce significant positive real rates of return. If you have any questions or suggestions on how we can better serve your investment and wealth management needs, please let me know.

| Sincerely, | ||

| Peter M. Donovan | ||

| Chairman & CEO | ||

3

Management Discussion (Unaudited)

WRIGHT EQUITY FUNDS

In the fourth quarter of 2011, the S&P 500 gained enough to offset its loss for the first nine months of the year. Stocks were up in the first half of the year, but gave it all back and then some in the third quarter as the European debt crisis reemerged as a major risk to the global economy. While news about the European debt crisis was a major mover of the stock market for most of 2011, the protracted wrangling in Washington last summer over the U.S. government’s debt ceiling also contributed to reduced confidence on the part of investors, as well as to a downgrade of U.S. government debt to AA+ by Standard & Poor’s. The stock market’s positive fourth quarter was largely due to a strong October as investors anticipated the announcement, which finally came on October 27, of a tentative plan to resolve Europe’s debt crisis and recapitalize its banks. After the first rush of enthusiasm for the new plan, however, the markets were again besieged with doubts that Europe’s key players France and Germany would have the political will to implement any plan that would be able to keep countries such as Greece and Italy from defaulting and hold the euro together. There was also more political gridlock in Washington. In November, the Congressional Super Committee appointed as part of the debt ceiling deal couldn’t come up with an agreement on tax increases and spending cuts to reduce the budget deficits; in December, Congress could not reach an agreement on extension of supplemental unemployment benefits and 2011’s payroll tax cut for a year – even though both sides wanted to accomplish this. Instead a two-month fix once again kicked the can down the road. Given the uncertainty permeating the investment environment in the last two months of the year, it may be surprising that the market managed to hang on to most of October’s gains; the credit for this goes to steady growth in corporate profits, which have been healthy throughout 2011, and some better-than-expected U.S. economic reports suggesting that the domestic economy picked up late in the year.

The fact that the S&P 500 started and ended the year at essentially the same price belies the market volatility over the course of 2011. From its starting point in 2011, the S&P 500 had gained more than 8% by its April high, and then plunged almost 20% over the next five months before clawing its way back to even. In addition to these major swings, what is striking about 2011 is the way that good days followed bad (and vice versa) and sector performance vacillated with little conviction or staying power. In the fourth quarter, the good days outweighed the bad, with the S&P 500 returning close to 12%; the S&P 500’s 2.1% return for the year was entirely due to dividend income. The Dow Jones Industrials edged out the S&P 500 for the quarter with a 13% return; for the year, the Dow returned 8.4%. Nasdaq lagged the S&P 500 for both the quarter (8.2%) and the year (-0.8%). The better tone to news about the U.S. economy led to relatively strong showings by cyclical groups – consumer discretionary, industrials, materials – in the fourth quarter; for the year, defensive sectors such as consumer staples, health care and utilities outperformed. Financial stocks lagged for both periods as worries about Europe’s debt crisis focused attention on banks’ financial health. The S&P MidCap 400 and SmallCap 600 both outperformed the S&P 500 for the fourth quarter but lagged for the year.

In the aggregate, both developed and developing international stock markets lagged the U.S. market for the quarter and the year. The MSCI World ex U.S. index of developed markets returned 3.5% for the fourth quarter and lost 12.2% for all of 2011 in dollar terms. Dollar appreciation cut into the returns, particularly in the fourth quarter and particularly compared to the euro. (For the year, the dollar lost ground compared to the Japanese yen.) In the fourth quarter, the euro currency markets returned 2.2%. The Japanese market lost 3.9% in dollars in the fourth quarter, while the rest of the Pacific region returned 6.0%. For all of 2011, markets in the EMU lost nearly 18% while the Pacific region lost 14%. Emerging markets returned 4.4% in dollar terms in the fourth quarter, led by healthy gains in Latin America. For the year, however, the MSCI Emerging Markets index lost more than 18%.

4

Management Discussion (Unaudited)

SELECTED BLUE CHIP FUND

The S&P MidCap 400 lagged the S&P 500 in 2011 with a loss of 1.7%, despite a good showing compared to the S&P 500 in the fourth quarter with a return of 13%. The Wright Selected Blue Chip Fund (WSBC), which is a mid-cap blend fund, lost 1.2% in 2011, outperforming the MidCap benchmark by 0.5%. For fourth quarter, WSBC also outperformed with a 13.3% return.

In the first quarter, strong stock selection, particularly in the financial sector, accounting for essentially all of the Fund’s outperformance compared to the S&P MidCap 400, while in the second quarter, stock selection accounted for the Fund’s underperformance, mostly due to lagging results in the technology and energy sectors. In the third quarter, when investors showed a preference for larger stocks, the Fund had a smaller loss than the benchmark as its larger median and weighted-average market cap compared to the S&P 400 worked in its favor. Underweight positions in the lagging energy and industrial sectors also helped in Q3. In the fourth quarter, strong stock selection in consumer staples, consumer discretionary and financial sectors were key to the Fund’s strong relative showing. Looking at the year as a whole, sector weighting decisions overall had little impact on relative performance, with superior stock selection within the sectors accounting for the Fund’s outperformance compared to the S&P Midcap 400. Relative performance was particularly strong in the consumer discretionary, utility, financial and materials sectors. Among the issues that made positive contributions for the year were retailer Ross Stores, which contributed a positive 1.1%; Kinetic Concepts +0.6% and Lubrizol +0.6%, both of which were acquired; REIT Rayonier +0.6%; and software company Alliance Data Systems +0.6%. Detracting from relative performance were energy companies Arch Coal -0.9% and HollyFrontier -0.7%; technology companies Lam Research and Vishay Intertechnologies, each -0.9%; and real estate developer Jones Lang LaSalle, also with a negative contribution of 0.9%.

In the face of an uncertain economic environment, WSBC is positioned in the mid-cap universe to take advantage of a preference for quality. WSBC continues to be biased to the larger companies in the S&P MidCap 400 index with larger median and weighted-average market caps compared to the S&P 400; its holdings have better historic earnings growth than the index constituents. In the aggregate, WSBC companies had lower current and forward P/E multiples than those in the MidCap 400. WIS continues to advise diversity in investment portfolios as the best way to navigate difficult economic times.

MAJOR BLUE CHIP FUND

The Wright Major Blue Chip Fund (WMBC) is managed as a blend of the large-cap growth and value stocks in the S&P 500 Composite, selected with a bias toward the higher-quality issues in the index. The WMBC Fund returned 0.1% in 2011 compared to 2.1% for the S&P 500. WMBC outperformed its benchmark in the first quarter of the year, lagged in the middle two quarters, and once again outperformed in Q4 with a 12.9% return compared to 11.8% for the S&P 500.

In the first quarter of 2011, investors favored the smaller stocks in the S&P 500. WMBC was able to overcome its higher median market cap relative to the benchmark by favorable sector allocation and stock selection. In the second and third quarters, a major factor in the Fund’s underperformance compared to the benchmark was its underweight positions in consumer staples and utility stocks, two of the S&P 500’s strongest sectors for both quarters; in the fourth quarter this underweight was a positive for performance as investors favored more cyclical groups. The fourth

5

Management Discussion (Unaudited)

quarter also benefited from strong showings by some of the Fund’s energy holdings (Helmerich & Payne, which contributed +1.0% to performance, National-Oilwell +0.8%, Murphy Oil +0.8) bouncing back from declines that detracted from third quarter performance. For the year as a whole, the underweights in defensive groups, particularly utilities and consumer staples, hurt Fund performance compared to the benchmark, as did the lagging performance of the Fund’s energy, health care and technology holdings relative to those sectors of the S&P 500. Partially offsetting these negatives were relatively strong showings by the Fund’s holdings in the financial and consumer discretionary sectors compared to the S&P 500. Among the issues that made the most positive contributions to the Fund’s performance for the year were consumer discretionary issues Fossil +1.2%; Ralph Lauren +1.0%; and Tiffany +0.6%. Also contributing were marine shipper Kirby Corp. +1.2% and insurer Arch Capital +0.7%. Among the detractors from full-year performance were miner Freeport McMoRan, Murphy Oil and electronics retailer Best Buy, each -0.9%; engineering company Fluor -0.7%; and financial company CME Group -0.8%.

Going into 2012, the economic environment is uncertain. WIS expects that corporate profits will continue to grow, but at a slower pace than in 2011. WMBC is well positioned for such an environment, with its bias toward the higher-quality and more substantial issues in the S&P 500. At year end, WMBC had a higher median market cap and a substantially better earnings growth record over the previous five years than the S&P 500, while offering an attractive valuation with its P/E multiples based on current and forward earnings lower than the S&P 500’s comparable multiples.

INTERNATIONAL BLUE CHIP FUND

In the aggregate, international stocks lagged U.S. stocks in the 2011. The Wright International Blue Chip Fund (WIBC) lost 13.7% in 2011 compared to the MSCI World ex U.S index’s 12.2% loss. In the first quarter of 2011, WIBC was ahead of the benchmark, but lagged in the middle two quarters of the year, particularly the third. In the fourth quarter of 2011, WIBC returned to outperformance with a 5.6% return, ahead of the benchmark’s 3.5%.

Both sector allocation and stock selection contributed positively to WIBC’s performance in the first quarter, with an underweight in the lagging consumer staples group having the most significant effect on relative performance. In the second quarter, stock selection was a negative contributor to performance, particularly in materials and industrials. The Fund’s performance was negatively affected by its position in Sino-Forest, a Canadian company with lumber interests in China, which fell sharply when its accounting practices came into question. The position was sold before the end of the second quarter. In the third quarter, the biggest factor in underperformance was a sell-off in some high-quality companies in the materials sector on concerns about an economic slowdown in China, one of their most important customers. Among the biggest decliners in Q3 were miners Rio Tinto, Teck Resources and BHP Billiton, all of which made positive contributions to performance in the fourth quarter, when stock selection in the materials sector was a major contributor to the Fund’s outperformance compared to its benchmark. For the year as a whole, the Fund’s relative performance benefited from its underweight position in the financial sector, one of the laggard sectors in the MSCI World ex U.S index last year because of growing concerns about the European debt crisis. In addition, the Fund’s financial stock selection also contributed positively. The biggest detractor from WIBC’s relative performance was the aforementioned weakness in materials stocks. Looking at individual issues, for the year positive contributions came from consumer discretionary company Jardine Cycle & Carriage, with a positive contribution of 0.4%; and real estate company Daito Trust Construction, telecom company Vodaphone, and oil company Royal Dutch Shell, which each contributed +0.2%. The list of detractors is laden with materials stocks: Sino Forest -1.0%; Rio Tinto -0.7%; Eurasian Natural Resources -0.6%. Also detracting were European banks BNP

6

Management Discussion (Unaudited)

Paribas -0.8% and Société Generale -0.5%.

Moving into 2012, WIBC remains overweight in Asia, which reflects our view that emerging markets such as China will be the global growth engines going forward. WIBC is underweight in financial stocks and overweight in the consumer discretionary and industrial sectors. In the aggregate, WIBC holdings are priced at significant discounts to the MSCI World ex U.S. index in terms of current price/earnings ratio. We continue to see the inclusion of international stocks as likely to enhance returns in diversified investment portfolios.

WRIGHT FIXED INCOME FUNDS

Treasury bonds yields declined over the course of 2011. Good news on the economy sent investors out of bonds and into stocks in the first quarter. For most of the rest of 2011, however, Treasury bonds rallied as investors looked for safety amidst concerns about the European debt crisis and political gridlock in the U.S. Standard & Poor’s decision to downgrade U. S. government debt to AA+ seemed to contribute to stock market anxiety but had little effect on Treasury bonds, which rallied after the downgrade. Early in the fourth quarter the rally reversed for a while as investors anticipated the announcement, which finally came on October 27, of a tentative plan to resolve Europe’s debt crisis and recapitalize its banks. After the first rush of enthusiasm for the new plan, however, the markets were again besieged with doubts that Europe’s key players France and Germany would have the political will to implement any plan that would be able to keep countries such as Greece and Italy from defaulting and hold the euro-region together. Before year end, Treasury bonds had resumed their rally. Treasury bond yields at the shortest maturities held at extremely low levels, pegged by the Fed’s stated intention to keep the fed funds rate near zero well into 2013. The Fed’s “operation twist,” whereby it is swapping out of short-term Treasuries into longer-dated issues probably put downward pressure on longer Treasury yields in Q4. Additionally, the inflation fears that popped up early in 2011 appear to have subsided for the time being. The 10-year T-bond yield closed 2011 at 1.88%, down from 3.30% at the beginning of the year and from 1.92% at the end of September (which was up from a record low of 1.72% reached earlier that month). The two-year Treasury yield closed the year at about 0.25%, down from near 0.60% at the end of 2010.

The Barclays U.S. Aggregate bond index’s 7.8% return compared favorably with the S&P 500’s 2.1% return for 2011. Bonds lagged stocks in the fourth quarter with a 1.1% return. All major sectors of the Barclays U.S. Aggregate had positive returns for the year and for the fourth quarter. In keeping with the rally in stocks, spreads on corporate bonds tightened a bit in the fourth quarter of 2011. Over the full year, however, spreads on corporate bonds widened, especially in the financial sector, as investors worried about problems in Europe, U.S. budget deficits and, at times, the risk of recession. Investment-grade corporate bonds returned 1.9% in the fourth quarter, more than doubling the 0.9% return on Treasury bonds. For the year, Treasury bonds were the best-performing sector in the Barclay’s Aggregate with a 9.8% return, followed by corporate bonds, which returned 8.2%. Mortgage-backed securities returned 6.2% for the year, commercial mortgage-backed issues 6.0%, asset-backed 5.1% and Agency bonds 4.9%. High-yield bonds outperformed investment grade corporate bonds in the fourth quarter, but for the year they lagged with a 5.0% return. International investment grade bonds had a loss for the fourth quarter and lagged U.S. bonds for the year with a 4.4% return in dollars, with appreciation of the dollar having a negative effect on dollar-based returns.

7

Management Discussion (Unaudited)

TOTAL RETURN BOND FUND

The Wright Total Return Bond Fund (WTRB), a diversified bond fund, returned 6.7% in 2011 compared to 7.8% for the Barclays U.S. Aggregate Bond index. WTRB outperformed the benchmark in the first quarter with a 0.8% return which doubled the 0.4% return for the Barclays Aggregate. In subsequent quarters, however, it lagged its benchmark, closing the year with a 1.0% return in the fourth quarter compared to 1.1% for the Barclays Aggregate. WTRB had a yield of 2.5% for December 2011 calculated according to SEC guidelines. Dividends paid by this Fund may be more or less than implied by this yield.

WTRB started the year with essentially a neutral duration compared to the Barclays U.S. Aggregate. In the first quarter, the duration position was shortened by a quarter-year compared to the benchmark, reflecting WIS’s expectation that interest rates would move higher. Late in August, with yields near record lows, duration was further shortened to about half a year short compared to the benchmark. Duration positioning had little effect on first-quarter performance but being short compared to the benchmark detracted from the Fund’s relative performance for the rest of 2011 as interest rates declined. The Fund’s duration position was maintained at almost half a year shorter than the benchmark as 2012 began. This positioning reflects our view that, given the uncertainty in the current economic environment, limiting potential losses from rising interest rates is an appropriate strategy even if it would dampen returns should interest rates fall further.

For all of 2011, sector allocation detracted from WTRB’s performance relative to the Barclays U.S. Aggregate benchmark. Throughout the year, WIS maintained overweight positions in corporate bonds, commercial mortgages and asset-backed securities compared to the Barclays Aggregate benchmark, while being significantly underweight in Treasury bonds. Spread tightening accounted for the Fund’s outperformance relative to the benchmark in the first quarter and made a positive contribution in the fourth quarter, but for all of 2011, spreads on non-Treasury sectors widened and Treasury bonds, which were underweighted in WTRB, was the best-performing sector of the Barclays Aggregate. At the end of 2011, the Fund’s sector weightings were: Treasury bonds 14% vs. 36% for the benchmark; agency bonds 0% vs. 6%; corporate 47% vs. 26%; mortgages 28% vs. 31%; asset-backed securities 2% vs. 0%; and commercial mortgages 8% vs. 2%, with 1% in cash.

CURRENT INCOME FUND

For 2011, the mortgage-backed sector of the bond market returned 6.2%, lagging both Treasury bonds, which returned 9.8%, and the Barclays U.S. Aggregate Bond index, which returned 7.8%. The Wright Current Income Fund (WCIF) is managed to be invested in GNMA issues (mortgage-based securities, known as Ginnie Maes, guaranteed by the full faith and credit of the U.S. government) and other mortgage-based securities. WCIF is actively managed to maximize income and minimize principal fluctuation. WCIF returned 6.2% in 2011 compared to 7.9% for the Barclays GNMA Bond index, coming in ahead of the index in the first quarter, but lagging for the rest of the year. In the fourth quarter of 2011, WCIF returned 0.9% compared to 1.3% for the Barclays GNMA benchmark. WCIF had a yield of 2.4% for December calculated according to SEC guidelines. Dividends paid by this Fund may be more or less than implied by this yield.

In addition to its holdings in GNMA-backed mortgage issues, WCIF also held issues backed by Fannie Mae (FNMA), and Freddie Mac (FHLMC), which returned less than GNMA-backed bonds in the 2011 and the fourth quarter. The Fund was 100% in Agency-backed mortgages at the end of 2011. Throughout the year the Fund had a higher average coupon than the GNMA benchmark,

8

Management Discussion (Unaudited)

reflecting the Fund’s mandate to maximize income. At the end of 2011, WCIF’s average coupon was 6.0%, compared to 4.7% for the GNMA benchmark. The emphasis on well-seasoned higher-coupon issues contributes to the Fund’s lower negative convexity compared to the GNMA benchmark, which results in a more stable performance when interest rates are volatile. However, in 2011, the overweight in high-coupon bonds detracted from the Fund’s relative performance. The low level of mortgage rates in the quarter raised prepayment concerns that limited high-coupon issues’ price performance compared to low-coupon issues. WCIF had a longer duration than the GNMA benchmark, but the favorable impact of the duration positioning was not enough to offset the factors that detracted from relative performance.

9

Performance Summaries (Unaudited)

Important

The Total Investment Return is the percent return of an initial $10,000 investment made at the beginning of the period to the ending redeemable value assuming all dividends and distributions are reinvested. After-tax returns are calculated using the historical highest individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Actual after-tax returns depend on the investor's tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. Past performance is not predictive of future performance.

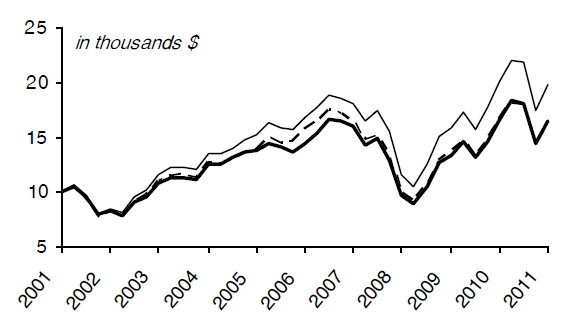

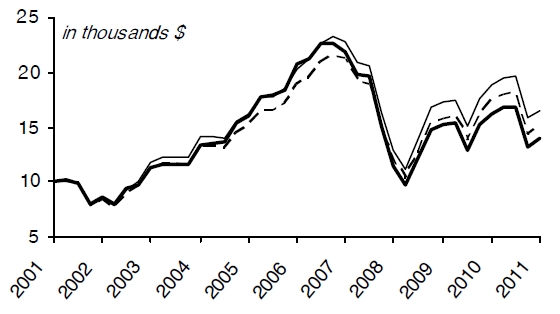

| WRIGHT SELECTED BLUE CHIP EQUITIES FUND | ||||||||||||||||||

| Growth of $10,000 Invested 1/1/02 Through 12/31/11 | ||||||||||||||||||

| Average Annual Total Return | ||||||||||||||||||

| Last 1 Yr | Last 5 Yrs | Last 10 Yrs | ||||||||||||||||

| — WSBC | ||||||||||||||||||

| - Return before taxes | -1.15 | % | 2.66 | % | 5.09 | % | ||||||||||||

| - Return after taxes on distributions | -1.15 | % | 1.76 | % | 4.13 | % | ||||||||||||

| - Return after taxes on distributions and sales of fund shares | -0.75 | % | 2.22 | % | 4.31 | % | ||||||||||||

| — S&P MidCap 400* | -1.73 | % | 3.31 | % | 7.03 | % | ||||||||||||

| ----Average of Morningstar Mid Cap Value/Blend Funds** | -4.12 | % | 0.38 | % | 4.82 | % | ||||||||||||

| Investment Value as of 12/31/11 (in thousands $) | ||||||||||||||||||

| — WSBC | $ | 16.43 | ||||||||||||||||

| — S&P MidCap 400* | $ | 19.74 | ||||||||||||||||

| ----Average of Morningstar Mid Cap Value/Blend Funds** | $ | 16.01 | ||||||||||||||||

* The Fund’s average annual return is compared with that of the S&P MidCap 400, an unmanaged index of stocks in a broad range of industries with market capitalizations of a few billion or less. The performance of the S&P MidCap 400, unlike that of the Fund, reflects no deductions for fees, expense or taxes. As stated in the current prospectus, the Fund’s annual operating expense ratio (gross) is 1.79%. However, Wright and WISDI have contractually agreed to waive a portion of its fees and/or reimburse certain expenses to limit total operating expense to 1.40%, which is in effect until April 30, 2012. During the period, certain fees were waived and/or expenses reimbursed; otherwise, returns would have been lower. Returns greater than one year are annualized.

** Morningstar Mid Cap Funds represent the average return of 44 funds with a Mid Cap Value equity style prior to 12/31/99 and 177 current funds ex multi-share classes in the Mid Cap Blend category since 12/31/99 reported in the Morningstar, Inc. database. © 2012 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

10

Performance Summaries (Unaudited)

| WRIGHT SELECTED BLUE CHIP EQUITIES FUND | |||||||||||||

| Industry Weightings | Ten Largest Stock Holdings | ||||||||||||

| % of net assets @ 12/31/11 | % of net assets @ 12/31/11 | ||||||||||||

| Retailing | 13.4 | % | Food, Beverage & Tobacco | 4.1 | % | Ross Stores, Inc. | 3.5 | % | |||||

| Capital Goods | 12.1 | % | Consumer Services | 4.0 | % | Corn Products International, Inc. | 3.4 | % | |||||

| Technology Hardware & Equipment | 7.7 | % | Utilities | 3.8 | % | Rayonier, Inc. | 3.0 | % | |||||

| Insurance | 7.2 | % | Semiconductors & Semiconductor Equipment | 3.7 | % | Endo Pharmaceutical Holdings, Inc. | 3.0 | % | |||||

| Health Care Equipment & Services | 6.9 | % | Transportation | 1.8 | % | Advance Auto Parts, Inc. | 3.0 | % | |||||

| Real Estate | 6.2 | % | Commercial & Professional Services | 1.0 | % | Alliance Data Systems Corp. | 2.9 | % | |||||

| Banks | 5.3 | % | Diversified Financials | 0.8 | % | AGCO Corp. | 2.6 | % | |||||

| Software & Services | 5.0 | % | Household & Personal Products | 0.7 | % | Jones Lang LaSalle, Inc. | 2.5 | % | |||||

| Energy | 4.9 | % | Media | 0.5 | % | KBR, Inc. | 2.5 | % | |||||

| Pharmaceuticals & Biotechnology | 4.7 | % | Telecommunication Services | 0.4 | % | East West Bancorp, Inc. | 2.2 | % | |||||

| Materials | 4.6 | % | Automobiles & Components | 0.4 | % | ||||||||

11

Performance Summaries (Unaudited)

| WRIGHT MAJOR BLUE CHIP EQUITIES FUND | ||||||||||||||||||

| Growth of $10,000 Invested 1/1/02 Through 12/31/11 | ||||||||||||||||||

| Average Annual Total Return | ||||||||||||||||||

| Last 1 Yr | Last 5 Yrs | Last 10 Yrs | ||||||||||||||||

| — WMBC | ||||||||||||||||||

| - Return before taxes | 0.08 | % | -1.62 | % | 1.33 | % | ||||||||||||

| - Return after taxes on distributions | 0.08 | % | -1.73 | % | 1.21 | % | ||||||||||||

| - Return after taxes on distributions and sales of fund shares | 0.05 | % | -1.38 | % | 1.09 | % | ||||||||||||

| — S&P 500* | 2.11 | % | -0.25 | % | 2.92 | % | ||||||||||||

| ----Average of Morningstar Large Cap Value/Blend Funds** | -1.40 | % | -1.02 | % | 2.06 | % | ||||||||||||

| Investment Value on 12/31/11 (in thousands $) | ||||||||||||||||||

| — WMBC | $ | 11.41 | ||||||||||||||||

| — S&P 500* | $ | 13.34 | ||||||||||||||||

| ----Average of Morningstar Large Cap Value/Blend Funds** | $ | 12.27 | ||||||||||||||||

* The Fund’s average annual return is compared with that of the S&P 500, an unmanaged index of 500 widely held common stocks that generally indicates the performance of the market. The performance of the S&P 500, unlike that of the Fund, reflects no deductions for fees, expenses or taxes. As stated in the current prospectus, the Fund’s annual operating expense ratio (gross) is 1.68%. However, Wright and WISDI have contractually agreed to waive a portion of its fees and/or reimburse certain expenses to limit total operating expense to 1.40%, which is in effect until April 30, 2012. During the period, certain fees were waived and/or expenses reimbursed; otherwise, returns would have been lower. Returns greater than one year are annualized.

** Morningstar Large Cap Funds represent the average return of 229 funds with a Large Cap Value equity style prior to 12/31/99 and 650 current funds ex multi-share classes in the Large Cap Blend category since 12/31/99 reported in the Morningstar, Inc. database. © 2012 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

12

Performance Summaries (Unaudited)

| WRIGHT MAJOR BLUE CHIP EQUITIES FUND | |||||||||||||

| Industry Weightings | Ten Largest Stock Holdings | ||||||||||||

| % of net assets @ 12/31/11 | % of net assets @ 12/31/11 | ||||||||||||

| Energy | 16.3 | % | Materials | 3.8 | % | Microsoft Corp. | 4.4 | % | |||||

| Capital Goods | 11.7 | % | Retailing | 3.8 | % | Johnson & Johnson | 4.1 | % | |||||

| Software & Services | 11.7 | % | Food & Staples Retailing | 3.2 | % | Google, Inc., Class A | 4.0 | % | |||||

| Pharmaceuticals & Biotechnology | 11.2 | % | Transportation | 3.0 | % | Cisco Systems, Inc. | 3.9 | % | |||||

| Insurance | 10.8 | % | Semiconductors & Semiconductor Equipment | 2.5 | % | Amgen, Inc. | 3.7 | % | |||||

| Technology Hardware & Equipment | 7.9 | % | Food, Beverage & Tobacco | 2.0 | % | Walgreen Co. | 3.2 | % | |||||

| Health Care Equipment & Services | 5.2 | % | Consumer Durables & Apparel | 0.8 | % | General Dynamics Corp. | 3.2 | % | |||||

| Diversified Financials | 4.0 | % | Consumer Services | 0.5 | % | Humana, Inc. | 3.2 | % | |||||

| National Oilwell Varco, Inc. | 3.1 | % | |||||||||||

| Aflac, Inc. | 3.1 | % | |||||||||||

13

Performance Summaries (Unaudited)

| WRIGHT INTERNATIONAL BLUE CHIP EQUITIES FUND | ||||||||||||||||||

| Growth of $10,000 Invested 1/1/02 Through 12/31/11 | ||||||||||||||||||

| Average Annual Total Return | ||||||||||||||||||

| Last 1 Yr | Last 5 Yrs | Last 10 Yrs | ||||||||||||||||

| — WIBC | ||||||||||||||||||

| - Return before taxes | -13.65 | % | -7.60 | % | 3.36 | % | ||||||||||||

| - Return after taxes on distributions | -13.56 | % | -8.17 | % | 2.94 | % | ||||||||||||

| - Return after taxes on distributions and sales of fund shares | -8.20 | % | -6.22 | % | 2.93 | % | ||||||||||||

| — MSCI World ex U.S. Index* | -12.21 | % | -4.09 | % | 5.14 | % | ||||||||||||

| ----Average of Morningstar Foreign Large Blend Funds** | -13.91 | % | -4.50 | % | 4.10 | % | ||||||||||||

| Investment Value as of 12/31/11 (in thousands $) | ||||||||||||||||||

| — WIBC | $ | 13.92 | ||||||||||||||||

| — MSCI World ex U.S. Index* | $ | 16.50 | ||||||||||||||||

| ----Average of Morningstar Foreign Large Blend Funds** | $ | 14.95 | ||||||||||||||||

* The Fund’s average annual return is compared with that of the MSCI World ex U.S. Index. While the Fund does not seek to match the returns of this index, this unmanaged index generally indicates foreign stock market performance. The performance of the MSCI World ex U.S. Index, unlike that of the Fund, reflects no deductions for fees, expenses or taxes. As stated in the current prospectus, the Fund’s annual operating expense ratio (gross) is 1.77%. However, Wright and WISDI have contractually agreed to waive a portion of its fees and/or reimburse certain expenses to limit total operating expense to 1.85%, which is in effect until April 30, 2012. Returns greater than one year are annualized. Shares held less than 90 days will be subject to a 2.00% redemption fee.

** Morningstar International Equity Funds represent the average of 205 current funds ex multi-share classes in the Foreign Large Blend category reported in the Morningstar, Inc. database. © 2012 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

14

Performance Summaries (Unaudited)

| WRIGHT INTERNATIONAL BLUE CHIP EQUITIES FUND | |||||||||||||

| Country Weightings | Ten Largest Stock Holdings | ||||||||||||

| % of net assets @ 12/31/11 | % of net assets @ 12/31/11 | ||||||||||||

| United Kingdom | 21.3 | % | Spain | 3.0 | % | Nestle SA | 4.9 | % | |||||

| Japan | 15.1 | % | Netherlands | 2.2 | % | AstraZeneca PLC | 3.1 | % | |||||

| Switzerland | 8.7 | % | Norway | 1.7 | % | BASF SE | 2.9 | % | |||||

| France | 8.6 | % | Sweden | 1.7 | % | Toronto-Dominion Bank | 2.6 | % | |||||

| Canada | 8.4 | % | Belgium | 1.4 | % | Sumitomo Corp. | 2.6 | % | |||||

| Germany | 7.7 | % | Brazil | 1.0 | % | Sanofi | 2.5 | % | |||||

| Australia | 5.2 | % | Singapore | 1.0 | % | Yamada Denki Co., Ltd. | 2.4 | % | |||||

| Hong Kong | 4.1 | % | Finland | 0.7 | % | Legal & General Group PLC | 2.2 | % | |||||

| China | 3.7 | % | United States | 0.7 | % | Vodafone Group PLC | 2.2 | % | |||||

| Italy | 3.0 | % | Denmark | 0.5 | % | Rio Tinto, Ltd. | 2.1 | % | |||||

15

Performance Summaries (Unaudited)

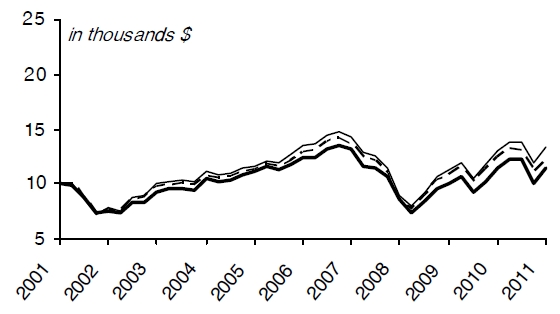

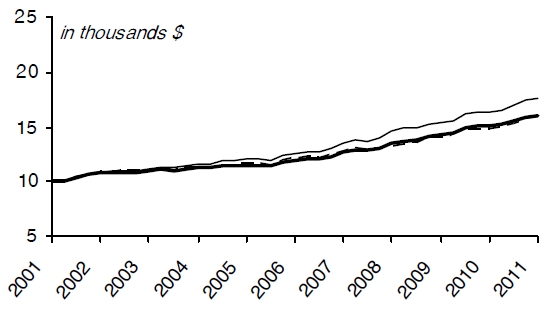

| WRIGHT TOTAL RETURN BOND FUND | ||||||||||||||||||

| Growth of $10,000 Invested 1/1/02 Through 12/31/11 | ||||||||||||||||||

| Average Annual Total Return | ||||||||||||||||||

| Last 1 Yr | Last 5 Yrs | Last 10 Yrs | ||||||||||||||||

| — WTRB | ||||||||||||||||||

| - Return before taxes | 6.68 | % | 6.11 | % | 5.10 | % | ||||||||||||

| - Return after taxes on distributions | 5.22 | % | 4.46 | % | 3.46 | % | ||||||||||||

| - Return after taxes on distributions and sales of fund shares | 4.31 | % | 4.24 | % | 3.38 | % | ||||||||||||

| — Barclays Capital U.S. Aggregate Bond Index* | 7.84 | % | 6.50 | % | 5.78 | % | ||||||||||||

| ----Average of Morningstar Intermediate Term Bond Funds** | 5.77 | % | 5.09 | % | 4.71 | % | ||||||||||||

| Investment Value as of 12/31/11 (in thousands $) | ||||||||||||||||||

| — WTRB | $ | 16.45 | ||||||||||||||||

| — Barclays Capital U.S. Aggregate Bond Index* | $ | 17.54 | ||||||||||||||||

| ----Average of Morningstar Intermediate Term Bond Funds** | $ | 15.85 | ||||||||||||||||

* The Fund’s average annual return is compared with that of the Barclays Capital U.S. Aggregate Bond Index, an unmanaged index that is a broad representation of the investment-grade fixed income market in the U.S. The Barclays Capital U.S. Aggregate Bond Index, unlike the Fund, reflects no deductions for fees, expenses or taxes. As stated in the current prospectus, the Fund’s annual operating expense ratio (gross) is 1.43%. However, Wright and WISDI have contractually agreed to waive a portion of its fees and/or reimburse certain expenses to limit total operating expense to 0.95%, which is in effect until April 30, 2012. During the period, certain fees were waived and/or expenses reimbursed; otherwise, returns would have been lower. Returns greater than one year are annualized.

** Morningstar average represents the return of 334 current funds ex multi-share classes in the Intermediate Term Bond category in the Morningstar, Inc. database. © 2012 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

16

Performance Summaries (Unaudited)

| WRIGHT TOTAL RETURN BOND FUND | ||||||||||||||||||

| Holdings by Security Type | Five Largest Bond Holdings | |||||||||||||||||

| % of net assets @ 12/31/11 | % of net assets @ 12/31/11 | |||||||||||||||||

| Asset-Backed Securities | 2.3 | % | GNMA, Series 2010-44, Class NK | 4.00% | 10/20/37 | 3.2 | % | |||||||||||

| Corporate Bonds | 46.8 | % | U.S. Treasury Note | 3.25% | 06/30/16 | 2.7 | % | |||||||||||

| Mortgage-Backed Securities | 36.2 | % | U.S. Treasury Bond | 6.13% | 11/15/27 | 2.7 | % | |||||||||||

| U.S. Treasuries | 13.6 | % | U.S. Treasury Note | 4.50% | 05/15/17 | 2.7 | % | |||||||||||

| FNMA Pool #888366 | 7.00% | 04/01/37 | 2.3 | % | ||||||||||||||

| Holdings by Credit Quality | ||||||||||||||||||

| % of net assets @ 12/31/11 | ||||||||||||||||||

| A | 21 | % | ||||||||||||||||

| Aa | 5 | % | ||||||||||||||||

| Aaa | 52 | % | ||||||||||||||||

| Baa | 20 | % | ||||||||||||||||

| <Baa | 2 | % | ||||||||||||||||

| U.S. Government Agencies | 0 | % | ||||||||||||||||

| U.S. Treasuries | 0 | % | ||||||||||||||||

17

Performance Summaries (Unaudited)

| WRIGHT CURRENT INCOME FUND | ||||||||||||||||||

| Growth of $10,000 Invested 1/1/02 Through 12/31/11 | ||||||||||||||||||

| Average Annual Total Return | ||||||||||||||||||

| Last 1 Yr | Last 5 Yrs | Last 10 Yrs | ||||||||||||||||

| — WCIF | ||||||||||||||||||

| - Return before taxes | 6.22 | % | 6.00 | % | 4.82 | % | ||||||||||||

| - Return after taxes on distributions | 4.69 | % | 4.30 | % | 3.03 | % | ||||||||||||

| - Return after taxes on distributions and sales of fund shares | 4.01 | % | 4.13 | % | 3.07 | % | ||||||||||||

| — Barclays Capital GNMA Backed Bond Index* | 7.89 | % | 6.96 | % | 5.84 | % | ||||||||||||

| ----Average of Morningstar Government Mortgage Funds** | 6.51 | % | 5.58 | % | 4.68 | % | ||||||||||||

| Investment Value as of 12/31/11 (in thousands $) | ||||||||||||||||||

| — WCIF | $ | 16.02 | ||||||||||||||||

| — Barclays Capital GNMA Backed Bond Index* | $ | 17.64 | ||||||||||||||||

| ----Average of Morningstar Government Mortgage Funds** | $ | 15.80 | ||||||||||||||||

* The Fund’s average annual return is compared with that of the Barclays Capital GNMA Backed Bond Index. While the Fund does not seek to match the returns of the Barclays Capital GNMA Backed Bond Index, Wright believes that this unmanaged index generally indicates the performance of government and corporate mortgage-backed bond markets. The Barclays Capital GNMA Backed Bond Index, unlike the Fund, reflects no deductions for fees, expenses or taxes. As stated in the current prospectus, the Fund’s annual operating expense ratio (gross) is 1.33%. However, Wright and WISDI have contractually agreed to waive a portion of its fees and/or reimburse certain expenses to limit total operating expense to 1.00%, which is in effect until April 30, 2012. During the period, certain fees were waived and/or expenses reimbursed; otherwise, returns would have been lower. Returns greater than one year are annualized.

** The Morningstar Government Mortgage Fund Average represents the average return of all 107 current funds ex multi-share classes with a government mortgage investment objective reported in the Morningstar, Inc. database. © 2012 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

18

Performance Summaries (Unaudited)

| WRIGHT CURRENT INCOME FUND | ||||||||||||

| Holdings by Security Type | Five Largest Bond Holdings | |||||||||||

| % of net assets @ 12/31/11 | % of net assets @ 12/31/11 | |||||||||||

| FNMA Pool #995149 | 6.50% | 10/01/38 | 3.7 | % | ||||||||

| Agency Mortgage-Backed Securities | 98.1 | % | GNMA, Series 2010-116, Class PB | 5.00% | 06/16/40 | 3.7 | % | |||||

| FNMA Pool #889307 | 5.00% | 07/01/37 | 2.7 | % | ||||||||

| FHLMC Gold Pool #G08081 | 6.00% | 09/01/35 | 2.5 | % | ||||||||

| FNMA Pool #256182 | 6.00% | 03/01/36 | 2.5 | % | ||||||||

| Weighted Average Maturity | ||||||||||||

| @ 12/31/11 | 5.4 | Years | ||||||||||

19

Fund Expenses (Unaudited)

Example:

As a shareholder of a fund, you incur two types of costs: (1) transaction costs, including redemption fees (if applicable); and (2) ongoing costs including management fees; distribution or service fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in a fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2011 – December 31, 2011).

Actual Expenses:

The first line of the tables shown on the following page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes:

The second line of the tables provides information about hypothetical account values and hypothetical expenses based on the actual Fund expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual return of the Fund. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees (if applicable). Therefore, the second line of the tables is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

20

| EQUITY FUNDS | FIXED INCOME FUNDS | |||||||

| Wright Selected Blue Chip Equities Fund | Wright Total Return Bond Fund | |||||||

| Beginning | Ending | Expenses Paid | Beginning | Ending | Expenses Paid | |||

| Account Value (7/1/11) | Account Value (12/31/11) | During Period* | Account Value (7/1/11) | Account Value (12/31/11) | During Period* | |||

| (7/1/11-12/31/11) | (7/1/11-12/31/11) | |||||||

| Actual Fund Shares | $1,000.00 | $912.15 | $6.75 | Actual Fund Shares | $1,000.00 | $1,038.11 | $4.88 | |

| Hypothetical (5% return per year before expenses) | Hypothetical (5% return per year before expenses) | |||||||

| Fund Shares | $1,000.00 | $1,018.15 | $7.12 | Fund Shares | $1,000.00 | $1,020.42 | $4.84 | |

| *Expenses are equal to the Fund’s annualized expense ratio of 1.40% multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on June 30, 2011. | *Expenses are equal to the Fund’s annualized expense ratio of 0.95% multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on June 30, 2011. | |||||||

| Wright Major Blue Chip Equities Fund | Wright Current Income Fund | |||||||

| Beginning | Ending | Expenses Paid | Beginning | Ending | Expenses Paid | |||

| Account Value (7/1/11) | Account Value (12/31/11) | During Period* | Account Value (7/1/11) | Account Value (12/31/11) | During Period* | |||

| (7/1/11-12/31/11) | (7/1/11-12/31/11) | |||||||

| Actual Fund Shares | $1,000.00 | $ 932.32 | $6.82 | Actual Fund Shares | $1,000.00 | $1,031.31 | $4.61 | |

| Hypothetical (5% return per year before expenses) | Hypothetical (5% return per year before expenses) | |||||||

| Fund Shares | $1,000.00 | $1,018.15 | $7.12 | Fund Shares | $1,000.00 | $1,020.67 | $4.58 | |

| *Expenses are equal to the Fund’s annualized expense ratio of 1.40% multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on June 30, 2011. | *Expenses are equal to the Fund’s annualized expense ratio of 0.90% multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on June 30, 2011. | |||||||

| Wright International Blue Chip Equities Fund | ||||||||

| Beginning | Ending | Expenses Paid | ||||||

| Account Value (7/1/11) | Account Value (12/31/11) | During Period* | ||||||

| (7/1/11-12/31/11) | ||||||||

| Actual Fund Shares | $1,000.00 | $ 825.41 | $8.24 | |||||

| Hypothetical (5% return per year before expenses) | ||||||||

| Fund Shares | $1,000.00 | $1,016.18 | $9.10 | |||||

| *Expenses are equal to the Fund’s annualized expense ratio of 1.79% multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on June 30, 2011. | ||||||||

21

Wright Selected Blue Chip Equities Fund (WSBC)

Portfolio of Investments – As of December 31, 2011

| Shares | Value | Shares | Value | |||||||||

| HOUSEHOLD & PERSONAL PRODUCTS - 0.7% | ||||||||||||

| Energizer Holdings, Inc.* | 2,925 | $ | 226,629 | |||||||||

| AUTOMOBILES & COMPONENTS - 0.4% | ||||||||||||

| BorgWarner, Inc.* | 2,225 | $ | 141,821 | INSURANCE - 7.2% | ||||||||

| American Financial Group, Inc. | 11,445 | $ | 422,206 | |||||||||

| BANKS - 5.3% | Arthur J. Gallagher & Co. | 5,650 | 188,936 | |||||||||

| Commerce Bancshares, Inc. | 8,175 | $ | 311,631 | Everest Re Group, Ltd. | 2,625 | 220,736 | ||||||

| East West Bancorp, Inc. | 35,930 | 709,618 | HCC Insurance Holdings, Inc. | 21,495 | 591,113 | |||||||

| Fulton Financial Corp. | 69,640 | 683,168 | Reinsurance Group of America, Inc. | 5,855 | 305,924 | |||||||

| $ | 1,704,417 | WR Berkley Corp. | 17,257 | 593,468 | ||||||||

| $ | 2,322,383 | |||||||||||

| CAPITAL GOODS - 12.1% | ||||||||||||

| AGCO Corp.* | 19,880 | $ | 854,244 | MATERIALS - 4.6% | ||||||||

| BE Aerospace, Inc.* | 14,230 | 550,843 | Albemarle Corp. | 3,030 | $ | 156,075 | ||||||

| Hubbell, Inc. - Class B | 4,035 | 269,780 | Ashland, Inc. | 5,250 | 300,090 | |||||||

| KBR, Inc. | 28,965 | 807,255 | Rock-Tenn Co. - Class A | 11,405 | 658,069 | |||||||

| SPX Corp. | 5,045 | 304,062 | Valspar Corp. | 9,285 | 361,836 | |||||||

| Thomas & Betts Corp.* | 9,590 | 523,614 | $ | 1,476,070 | ||||||||

| Timken Co. | 5,350 | 207,098 | ||||||||||

| URS Corp.* | 11,405 | 400,544 | MEDIA - 0.5% | |||||||||

| $ | 3,917,440 | John Wiley & Sons, Inc. - Class A | 3,330 | $ | 147,852 | |||||||

| COMMERCIAL AND PROFESSIONAL SERVICES - 1.0% | PHARMACEUTICALS & BIOTECHNOLOGY - 4.7% | |||||||||||

| Towers Watson & Co. - Class A | 5,550 | $ | 332,611 | Endo Pharmaceuticals Holdings, Inc.* | 28,055 | $ | 968,739 | |||||

| Medicis Pharmaceutical Corp. - Class A | 16,250 | 540,313 | ||||||||||

| CONSUMER SERVICES - 4.0% | $ | 1,509,052 | ||||||||||

| Brinker International, Inc. | 26,245 | $ | 702,316 | |||||||||

| Cheesecake Factory, Inc. (The)* | 10,705 | 314,192 | REAL ESTATE - 6.2% | |||||||||

| ITT Educational Services, Inc.* | 4,745 | 269,943 | Hospitality Properties Trust (REIT) | 10,395 | $ | 238,877 | ||||||

| $ | 1,286,451 | Jones Lang LaSalle, Inc. | 13,220 | 809,857 | ||||||||

| Rayonier, Inc. (REIT) | 21,737 | 970,123 | ||||||||||

| DIVERSIFIED FINANCIALS - 0.8% | $ | 2,018,857 | ||||||||||

| Affiliated Managers Group, Inc.* | 805 | $ | 77,240 | |||||||||

| Raymond James Financial, Inc. | 6,255 | 193,655 | RETAILING - 13.4% | |||||||||

| $ | 270,895 | Advance Auto Parts, Inc. | 13,830 | $ | 962,983 | |||||||

| Ascena Retail Group, Inc.* | 4,245 | 126,161 | ||||||||||

| ENERGY - 4.9% | Dick's Sporting Goods, Inc. | 2,930 | 108,058 | |||||||||

| Arch Coal, Inc. | 28,665 | $ | 415,929 | Dollar Tree, Inc.* | 7,172 | 596,065 | ||||||

| HollyFrontier Corp. | 13,789 | 322,663 | Foot Locker, Inc. | 8,280 | 197,395 | |||||||

| Oceaneering International, Inc. | 8,680 | 400,408 | PetSmart, Inc. | 4,340 | 222,599 | |||||||

| Southern Union Co. | 8,480 | 357,093 | PVH Corp. | 7,270 | 512,462 | |||||||

| Superior Energy Services, Inc.* | 3,030 | 86,173 | Rent-A-Center, Inc. | 10,295 | 380,915 | |||||||

| $ | 1,582,266 | Ross Stores, Inc. | 23,820 | 1,132,165 | ||||||||

| Williams-Sonoma, Inc. | 2,725 | 104,913 | ||||||||||

| FOOD, BEVERAGE & TOBACCO - 4.1% | $ | 4,343,716 | ||||||||||

| Corn Products International, Inc. | 20,890 | $ | 1,098,605 | |||||||||

| Ralcorp Holdings, Inc.* | 2,525 | �� | 215,888 | SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 3.7% | ||||||||

| $ | 1,314,493 | Atmel Corp.* | 13,425 | $ | 108,743 | |||||||

| Fairchild Semiconductor International, Inc.* | 22,710 | 273,428 | ||||||||||

| HEALTH CARE EQUIPMENT & SERVICES - 6.9% | Lam Research Corp.* | 18,370 | 680,057 | |||||||||

| Health Management Associates, Inc. - Class A* | 41,480 | $ | 305,708 | RF Micro Devices, Inc.* | 12,920 | 69,768 | ||||||

| LifePoint Hospitals, Inc.* | 10,395 | 386,174 | Skyworks Solutions, Inc.* | 3,530 | 57,257 | |||||||

| Lincare Holdings, Inc. | 10,595 | 272,397 | $ | 1,189,253 | ||||||||

| Mednax, Inc.* | 1,715 | 123,497 | ||||||||||

| Omnicare, Inc. | 6,965 | 239,944 | SOFTWARE & SERVICES - 5.0% | |||||||||

| Universal Health Services, Inc. - Class B | 16,045 | 623,509 | Alliance Data Systems Corp.* | 8,980 | $ | 932,483 | ||||||

| WellCare Health Plans, Inc.* | 5,145 | 270,113 | Synopsys, Inc.* | 7,470 | 203,184 | |||||||

| $ | 2,221,342 | ValueClick, Inc.* | 30,580 | 498,148 | ||||||||

| $ | 1,633,815 | |||||||||||

| See Notes to Financial Statements. | 22 | |

Wright Selected Blue Chip Equities Fund (WSBC)

Portfolio of Investments – As of December 31, 2011

| Shares | Value | |||||||||||

| TECHNOLOGY HARDWARE & EQUIPMENT - 7.7% | ||||||||||||

| Arrow Electronics, Inc.* | 10,195 | $ | 381,395 | |||||||||

| Avnet, Inc.* | 19,175 | 596,151 | ||||||||||

| DST Systems, Inc. | 5,855 | 266,519 | ||||||||||

| Ingram Micro, Inc. - Class A* | 7,670 | 139,517 | ||||||||||

| Jack Henry & Associates, Inc. | 10,195 | 342,654 | ||||||||||

| MICROS Systems, Inc.* | 1,920 | 89,434 | ||||||||||

| QLogic Corp.* | 11,810 | 177,150 | ||||||||||

| Tech Data Corp.* | 5,650 | 279,166 | ||||||||||

| Vishay Intertechnology, Inc.* | 25,030 | 225,020 | ||||||||||

| $ | 2,497,006 | |||||||||||

| TELECOMMUNICATION SERVICES - 0.4% | ||||||||||||

| Telephone & Data Systems, Inc. | 5,650 | $ | 146,278 | |||||||||

| TRANSPORTATION - 1.8% | ||||||||||||

| Kansas City Southern* | 8,780 | $ | 597,128 | |||||||||

| UTILITIES - 3.8% | ||||||||||||

| NV Energy, Inc. | 20,790 | $ | 339,916 | |||||||||

| ONEOK, Inc. | 5,755 | 498,901 | ||||||||||

| UGI Corp. | 12,920 | 379,848 | ||||||||||

| $ | 1,218,665 | |||||||||||

| TOTAL EQUITY INTERESTS - 99.2% | ||||||||||||

| (identified cost, $29,259,854) | $ | 32,098,440 | ||||||||||

| SHORT-TERM INVESTMENTS - 2.0% | ||||||||||||

| Fidelity Government Money Market Fund, 0.01% (1) | $ | 665,583 | ||||||||||

| TOTAL SHORT-TERM INVESTMENTS - 2.0% | ||||||||||||

| (identified cost, $665,583) | $ | 665,583 | ||||||||||

| TOTAL INVESTMENTS — 101.2% | ||||||||||||

| (identified cost, $29,925,437) | $ | 32,764,023 | ||||||||||

| LIABILITIES, IN EXCESS OF OTHER ASSETS — (1.2)% | (402,264 | ) | ||||||||||

| NET ASSETS — 100.0% | $ | 32,361,759 | ||||||||||

REIT — Real Estate Investment Trust

| * | Non-income producing security. |

| (1) | Variable rate security. Rate presented is as of December 31, 2011. |

| See Notes to Financial Statements. | 23 | |

Wright Selected Blue Chip Equities Fund (WSBC)

| As of December 31, 2011 | For the Year Ended December 31, 2011 | |||||||||||||

| ASSETS: | INVESTMENT INCOME (Note 1C) | |||||||||||||

| Investments, at value | 0 | Dividend income | $ | 376,367 | ||||||||||

| (identified cost $29,925,437) (Note 1A) | $ | 32,764,023 | Total investment income | $ | 376,367 | |||||||||

| Receivable for fund shares sold | 86,626 | |||||||||||||

| Dividends receivable | 31,467 | Expenses – | ||||||||||||

| Prepaid expenses and other assets | 15,622 | Investment adviser fee (Note 3) | $ | 182,636 | ||||||||||

| Total assets | $ | 32,897,738 | Administrator fee (Note 3) | 36,527 | ||||||||||

| Trustee expense (Note 3) | 14,523 | |||||||||||||

| LIABILITIES: | Custodian fee | 3,142 | ||||||||||||

| Payable for fund shares reacquired | $ | 20,538 | Accountant fee | 38,408 | ||||||||||

| Payable for investment securities purchased | 501,834 | Distribution expenses (Note 4) | 76,098 | |||||||||||

| Accrued expenses and other liabilities | 13,607 | Transfer agent fee | 33,776 | |||||||||||

| Total liabilities | $ | 535,979 | Printing | 137 | ||||||||||

| NET ASSETS | $ | 32,361,759 | Shareholder communications | 7,045 | ||||||||||

| Audit services | 17,317 | |||||||||||||

| NET ASSETS CONSIST OF: | Legal services | 2,465 | ||||||||||||

| Paid-in capital | $ | 28,737,960 | Compliance services | 870 | ||||||||||

| Accumulated net realized gain on investments | 785,213 | Registration costs | 19,069 | |||||||||||

| Unrealized appreciation on investments | 2,838,586 | Interest expense (Note 8) | 664 | |||||||||||

| Net assets applicable to outstanding shares | $ | 32,361,759 | Miscellaneous | 12,114 | ||||||||||

| Total expenses | $ | 444,791 | ||||||||||||

| SHARES OF BENEFICIAL INTEREST OUTSTANDING AT $0.000 PAR VALUE (UNLIMITED SHARES AUTHORIZED) | 3,148,022 | |||||||||||||

| Deduct – | ||||||||||||||

| NET ASSET VALUE, OFFERING PRICE, AND REDEMPTION PRICE PER SHARE OF BENEFICIAL INTEREST | $ | 10.28 | Waiver and/or reimbursement by the principal underwriter and/or investment adviser (Note 4) | $ | (17,976 | ) | ||||||||

| Net expenses | $ | 426,815 | ||||||||||||

| Net investment loss | $ | (50,448 | ) | |||||||||||

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS: | ||||||||||||||

| Net realized gain on investment transactions | $ | 1,748,539 | ||||||||||||

| Net change in unrealized appreciation (depreciation) on investments | (2,203,596 | ) | ||||||||||||

| Net realized and unrealized loss on investments | $ | (455,057 | ) | |||||||||||

| Net decrease in net assets from operations | $ | (505,505 | ) | |||||||||||

| See Notes to Financial Statements. | 24 | |

Wright Selected Blue Chip Equities Fund (WSBC)

| Years Ended | ||||||||||

| STATEMENTS OF CHANGES IN NET ASSETS | December 31, 2011 | December 31, 2010 | ||||||||

| INCREASE (DECREASE) IN NET ASSETS: | ||||||||||

From operations – | ||||||||||

| Net investment loss | $ | (50,448 | ) | $ | (45,144 | ) | ||||

| 0 | Net realized gain on investment transactions | 1,748,539 | 1,233,621 | |||||||

| Net change in unrealized appreciation (depreciation) on investments | (2,203,596 | ) | 2,909,492 | |||||||

| Net increase (decrease) in net assets from operations | $ | (505,505 | ) | $ | 4,097,969 | |||||

| Distributions to shareholders (Note 2) | ||||||||||

| From net investment income | $ | - | $ | (17,380 | ) | |||||

| Total distributions | $ | - | $ | (17,380 | ) | |||||

| Net increase in net assets resulting from fund share transactions (Note 6) | $ | 4,496,809 | $ | 7,526,879 | ||||||

| Net increase in net assets | $ | 3,991,304 | $ | 11,607,468 | ||||||

| NET ASSETS: | ||||||||||

| At beginning of year | 28,370,455 | 16,762,987 | ||||||||

| At end of year | $ | 32,361,759 | $ | 28,370,455 | ||||||

| See Notes to Financial Statements. | 25 | |

| These financial highlights reflect selected data for a share outstanding throughout each year. | |||||||||||||||||||

| Years Ended December 31, | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||||||

| Net asset value, beginning of year | $ | 10.400 | $ | 8.400 | $ | 6.060 | $ | 11.100 | $ | 12.270 | |||||||||

| Income (loss) from investment operations: | |||||||||||||||||||

Net investment income (loss) (1) | (0.018 | ) | (0.022 | ) | 0.011 | (0.013 | ) | (0.013 | ) | ||||||||||

| Net realized and unrealized gain (loss) | (0.102 | ) | 2.030 | 2.329 | (4.121 | ) | 1.340 | ||||||||||||

| Total income (loss) from investment operations | (0.120 | ) | 2.008 | 2.340 | (4.134 | ) | 1.327 | ||||||||||||

| Less distributions: | |||||||||||||||||||

| From net investment income | — | (0.008 | ) | — | — | (0.016 | ) | ||||||||||||

| From net realized gains | — | — | — | (0.906 | ) | (2.481 | ) | ||||||||||||

| Total distributions | — | (0.008 | ) | — | (0.906 | ) | (2.497 | ) | |||||||||||

| Net asset value, end of year | $ | 10.280 | $ | 10.400 | $ | 8.400 | $ | 6.060 | $ | 11.100 | |||||||||

Total Return(2) | (1.15 | )% | 23.93 | % | 38.61 | % | (39.81 | )% | 11.59 | % | |||||||||

Ratios/Supplemental Data(3): | |||||||||||||||||||

| Net assets, end of year (000 omitted) | $32,362 | $28,370 | $16,763 | $13,364 | $23,923 | ||||||||||||||

| Ratios (As a percentage of average daily net assets): | |||||||||||||||||||

| Net expenses | 1.40 | % | 1.40 | % | 1.36 | % | 1.26 | % | 1.26 | % | |||||||||

| Net expenses after custodian fee reduction | N/A | N/A | 1.36 | % | 1.25 | % | 1.25 | % | |||||||||||

| Net investment income (loss) | (0.17 | )% | (0.24 | )% | 0.15 | % | (0.15 | )% | (0.10 | )% | |||||||||

| Portfolio turnover rate | 82 | % | 60 | % | 41 | % | 72 | % | 67 | % | |||||||||

| (1) | Computed using average shares outstanding. | ||||||||||||||||||

| (2) | Total return is calculated assuming a purchase at the net asset value on the first day and a sale at the net asset value on the last day of each year reported. Dividends and distributions, if any, are assumed to be reinvested at the net asset value on the reinvestment date. | ||||||||||||||||||

| (3) | For each of the years presented, the operating expenses of the Fund were reduced by a waiver of fees and/or allocation of expenses to the principal underwriter and/or investment adviser. Had such action not been undertaken, expenses and net investment loss ratios would have been as follows: | ||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||||||

| Ratios (As a percentage of average daily net assets): | |||||||||||||||||||

| Expenses | 1.46 | % | 1.79 | % | 2.15 | % | 1.90 | % | 1.66 | % | |||||||||

| Expenses after custodian fee reduction | N/A | N/A | 2.15 | % | 1.89 | % | 1.66 | % | |||||||||||

| Net investment loss | (0.23 | )% | (0.63 | )% | (0.64 | )% | (0.79 | )% | (0.51 | )% | |||||||||

| See Notes to Financial Statements. | 26 | |

Wright Major Blue Chip Equities Fund (WMBC)

Portfolio of Investments – As of December 31, 2011

| Shares | Value | Shares | Value | |||||||||

| PHARMACEUTICALS & BIOTECHNOLOGY - 11.2% | ||||||||||||

| Amgen, Inc. | 10,940 | $ | 702,457 | |||||||||

| CAPITAL GOODS - 11.7% | Endo Pharmaceuticals Holdings, Inc.* | 14,020 | 484,111 | |||||||||

| Cummins, Inc. | 5,360 | $ | 471,787 | Forest Laboratories, Inc.* | 4,920 | 148,879 | ||||||

| Fastenal Co. | 2,275 | 99,213 | Johnson & Johnson | 11,890 | 779,746 | |||||||

| Fluor Corp. | 7,635 | 383,659 | $ | 2,115,193 | ||||||||

| General Dynamics Corp. | 9,175 | 609,312 | ||||||||||

| Precision Castparts Corp. | 3,375 | 556,166 | RETAILING - 3.8% | |||||||||

| WW Grainger, Inc. | 515 | 96,403 | Bed Bath & Beyond, Inc.* | 1,835 | $ | 106,375 | ||||||

| $ | 2,216,540 | Best Buy Co., Inc. | 21,875 | 511,219 | ||||||||

| Ross Stores, Inc. | 2,060 | 97,912 | ||||||||||

| CONSUMER DURABLES & APPAREL - 0.8% | $ | 715,506 | ||||||||||

| Garmin, Ltd. | 3,745 | $ | 149,088 | |||||||||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 2.5% | ||||||||||||

| CONSUMER SERVICES - 0.5% | Analog Devices, Inc. | 2,715 | $ | 97,142 | ||||||||

| WMS Industries, Inc.* | 4,700 | $ | 96,444 | Intel Corp. | 15,195 | 368,479 | ||||||

| $ | 465,621 | |||||||||||

| DIVERSIFIED FINANCIALS - 4.0% | ||||||||||||

| CME Group, Inc. | 2,275 | $ | 554,349 | SOFTWARE & SERVICES - 11.7% | ||||||||

| IntercontinentalExchange, Inc.* | 805 | 97,043 | Accenture PLC - Class A | 2,130 | $ | 113,380 | ||||||

| T. Rowe Price Group, Inc. | 1,690 | 96,246 | Akamai Technologies, Inc.* | 3,085 | 99,584 | |||||||

| $ | 747,638 | Google, Inc. - Class A* | 1,175 | 758,932 | ||||||||

| Microsoft Corp. | 31,935 | 829,033 | ||||||||||

| ENERGY - 16.3% | Oracle Corp. | 15,855 | 406,681 | |||||||||

| Atwood Oceanics, Inc.* | 12,480 | $ | 496,579 | $ | 2,207,610 | |||||||

| Cameron International Corp.* | 5,065 | 249,147 | ||||||||||

| Diamond Offshore Drilling, Inc. | 1,395 | 77,088 | TECHNOLOGY HARDWARE & EQUIPMENT - 7.9% | |||||||||

| Helmerich & Payne, Inc. | 8,955 | 522,614 | Apple, Inc.* | 240 | $ | 97,200 | ||||||

| Murphy Oil Corp. | 10,425 | 581,089 | Cisco Systems, Inc. | 40,450 | 731,336 | |||||||

| National Oilwell Varco, Inc. | 8,735 | 593,893 | Cognizant Technology Solutions Corp. - Class A* | 1,395 | 89,712 | |||||||

| Noble Corp.* | 15,930 | 481,405 | Western Digital Corp.* | 18,865 | 583,872 | |||||||

| Schlumberger, Ltd. | 1,250 | 85,387 | $ | 1,502,120 | ||||||||

| $ | 3,087,202 | |||||||||||

| TRANSPORTATION - 3.0% | ||||||||||||

| FOOD & STAPLES RETAILING - 3.2% | Kirby Corp.* | 8,660 | $ | 570,174 | ||||||||

| Walgreen Co. | 18,500 | $ | 611,610 | |||||||||

| TOTAL EQUITY INTERESTS - 98.4% | ||||||||||||

| FOOD, BEVERAGE & TOBACCO - 2.0% | (identified cost, $19,546,427) | $ | 18,612,791 | |||||||||

| Brown-Forman Corp. - Class B | 1,180 | $ | 95,002 | |||||||||

| Coca-Cola Co. (The) | 3,965 | 277,431 | SHORT-TERM INVESTMENTS - 1.5% | |||||||||

| $ | 372,433 | Fidelity Government Money Market Fund, 0.01% (1) | 292,858 | $ | 292,858 | |||||||

| HEALTH CARE EQUIPMENT & SERVICES - 5.2% | TOTAL SHORT-TERM INVESTMENTS - 1.5% | |||||||||||

| Humana, Inc. | 6,825 | $ | 597,938 | (identified cost, $292,858) | $ | 292,858 | ||||||

| Stryker Corp. | 7,930 | 394,201 | ||||||||||

| $ | 992,139 | TOTAL INVESTMENTS — 99.9% | ||||||||||

| (identified cost, $19,839,285) | $ | 18,905,649 | ||||||||||

| INSURANCE - 10.8% | ||||||||||||

| Aflac, Inc. | 13,580 | $ | 587,471 | OTHER ASSETS, IN EXCESS OF LIABILITIES — 0.1% | 15,314 | |||||||

| Arch Capital Group, Ltd.* | 14,975 | 557,519 | ||||||||||

| PartnerRe, Ltd. | 6,825 | 438,233 | NET ASSETS — 100.0% | $ | 18,920,963 | |||||||

| RenaissanceRe Holdings, Ltd. | 6,315 | 469,647 | ||||||||||

| $ | 2,052,870 | PLC — Public Limited Company | ||||||||||

| * Non-income producing security. | ||||||||||||

| MATERIALS - 3.8% | (1) Variable rate security. Rate presented is as of December 31, 2011. | |||||||||||

| CF Industries Holdings, Inc. | 1,400 | $ | 202,972 | |||||||||

| Freeport-McMoRan Copper & Gold, Inc. | 10,865 | 399,723 | ||||||||||

| Monsanto Co. | 1,540 | 107,908 | ||||||||||

| $ | 710,603 | |||||||||||

| See Notes to Financial Statements. | 27 | |

Wright Major Blue Chip Equities Fund (WMBC)

| STATEMENT OF OPERATIONS | ||||||||||||||

| As of December 31, 2011 | For the Year Ended December 31, 2011 | |||||||||||||

| ASSETS: | INVESTMENT INCOME (Note 1C) | |||||||||||||

| Investments, at value | 0 | Dividend income | $ | 258,102 | ||||||||||

| (identified cost $19,839,285) (Note 1A) | $ | 18,905,649 | Total investment income | $ | 258,102 | |||||||||

| Receivable for fund shares sold | 2,334 | |||||||||||||

| Dividends receivable | 10,116 | Expenses – | ||||||||||||

| Prepaid expenses and other assets | 14,815 | Investment adviser fee (Note 3) | $ | 117,907 | ||||||||||

| Total assets | $ | 18,932,914 | Administrator fee (Note 3) | 23,582 | ||||||||||

| Trustee expense (Note 3) | 14,523 | |||||||||||||

| LIABILITIES: | Custodian fee | 5,000 | ||||||||||||

| Accrued expenses and other liabilities | $ | 11,951 | Accountant fee | 37,554 | ||||||||||

| Total liabilities | $ | 11,951 | Distribution expenses (Note 4) | 49,128 | ||||||||||

| NET ASSETS | $ | 18,920,963 | Transfer agent fee | 31,434 | ||||||||||

| Printing | 88 | |||||||||||||

| NET ASSETS CONSIST OF: | Shareholder communications | 6,157 | ||||||||||||

| Paid-in capital | $ | 25,078,622 | Audit services | 17,252 | ||||||||||

| Accumulated net realized loss on investments | (5,224,023 | ) | Legal services | 682 | ||||||||||

| Unrealized depreciation on investments | (933,636 | ) | Compliance services | 812 | ||||||||||

| Net assets applicable to outstanding shares | $ | 18,920,963 | Registration costs | 19,172 | ||||||||||

| Interest expense (Note 8) | 1,164 | |||||||||||||

| SHARES OF BENEFICIAL INTEREST OUTSTANDING AT $0.000 PAR VALUE (UNLIMITED SHARES AUTHORIZED) | 1,543,767 | Miscellaneous | 9,633 | |||||||||||

| Total expenses | $ | 334,088 | ||||||||||||

| NET ASSET VALUE, OFFERING PRICE, AND REDEMPTION PRICE PER SHARE OF BENEFICIAL INTEREST | $ | 12.26 | ||||||||||||

| Deduct – | ||||||||||||||

| Waiver and/or reimbursement by the principal underwriter and/or investment adviser (Note 4) | $ | (57,809 | ) | |||||||||||

| Net expenses | $ | 276,279 | ||||||||||||

| Net investment loss | $ | (18,177 | ) | |||||||||||

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS: | ||||||||||||||

| Net realized gain on investment transactions | $ | 2,830,519 | ||||||||||||

| Net change in unrealized appreciation (depreciation) on investments | (2,666,829 | ) | ||||||||||||

| Net realized and unrealized gain on investments | $ | 163,690 | ||||||||||||

| Net increase in net assets from operations | $ | 145,513 | ||||||||||||

| See Notes to Financial Statements. | 28 | |

Wright Major Blue Chip Equities Fund (WMBC)

| Years Ended | ||||||||||

| STATEMENTS OF CHANGES IN NET ASSETS | December 31, 2011 | December 31, 2010 | ||||||||

| INCREASE (DECREASE) IN NET ASSETS: | ||||||||||

From operations – | ||||||||||

| Net investment income (loss) | $ | (18,177 | ) | $ | 92,781 | |||||

| 0 | Net realized gain on investment transactions | 2,830,519 | 1,024,058 | |||||||

| Net change in unrealized appreciation (depreciation) on investments | (2,666,829 | ) | 1,503,779 | |||||||

| Net increase in net assets from operations | $ | 145,513 | $ | 2,620,618 | ||||||

| Distributions to shareholders (Note 2) | ||||||||||

| From net investment income | $ | - | $ | (94,651 | ) | |||||

| Total distributions | $ | - | $ | (94,651 | ) | |||||

| Net decrease in net assets resulting from fund share transactions (Note 6) | $ | (2,900,561 | ) | $ | (8,187,311 | ) | ||||

| Net decrease in net assets | $ | (2,755,048 | ) | $ | (5,661,344 | ) | ||||

| NET ASSETS: | ||||||||||

| At beginning of year | 21,676,011 | 27,337,355 | ||||||||

| At end of year | $ | 18,920,963 | $ | 21,676,011 | ||||||

| See Notes to Financial Statements. | 29 | |

Wright Major Blue Chip Equities Fund (WMBC)