As filed with the Securities and Exchange Commission on March 4, 2015

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-3489

THE WRIGHT MANAGED EQUITY TRUST

177 West Putnam Ave.

Greenwich, Connecticut 06830

Vicki Horwitz

Three Canal Plaza, Suite 600

Portland, ME 04101

207-347-2000

Date of fiscal year end: December 31

Date of reporting period: January 1, 2014 – December 31, 2014

ITEM 1. REPORT TO STOCKHOLDERS.

The Wright Managed Blue Chip Investment Funds

The Wright Managed Blue Chip Investment Funds consist of three equity funds from The Wright Managed Equity Trust and one fixed-income fund from The Wright Managed Income Trust. Each of the four funds have distinct investment objectives and policies. They can be used individually or in combination to achieve virtually any objective. Further, as they are all “no-load” funds (no commissions or sales charges), portfolio allocation strategies can be altered as desired to meet changing market conditions or changing requirements without incurring any sales charges.

Approved Wright Investment List

Securities selected for investment in these funds are chosen mainly from a list of “investment grade” companies maintained by Wright Investors’ Service (“Wright”, “WIS” or the “Adviser”). Over 37,000 global companies (covering 69 countries) in Wright’s database are screened as new data becomes available to determine any eligible additions or deletions to the list. The qualifications for inclusion as “investment grade” are companies that meet Wright’s Quality Rating criteria. This rating includes fundamental criteria for investment acceptance, financial strength, profitability & stability and growth. In addition, securities, which are not included in Wright’s “investment grade” list, may also be selected from companies in the fund’s specific benchmark (up to 20% of the market value of the portfolio) in order to achieve broad diversification.

Three Equity Funds

Wright Selected Blue Chip Equities Fund (WSBC) (the “Fund”) seeks to enhance total investment return through price appreciation plus income. The Fund’s portfolio is characterized as a blend of growth and value stocks. The market capitalization of the companies is typically between $1-$10 billion at the time of the Fund’s investment. The Adviser seeks to outperform the Standard & Poor’s MidCap 400 Index (“S&P MidCap 400”) by selecting stocks using fundamental company analysis and company specific criteria such as valuation and earnings trends. The portfolio is then diversified across industries and sectors.

Wright Major Blue Chip Equities Fund (WMBC) (the “Fund”) seeks to enhance total investment return through price appreciation plus income by providing a broadly diversified portfolio of equities of larger well-established companies with market values of $5-$10 billion or more. The Adviser seeks to outperform the Standard & Poor’s 500 Index (“S&P 500”) by selecting stocks, using fundamental company analysis and company specific criteria such as valuation and earnings trends. The portfolio is then diversified across industries and sectors.

Wright International Blue Chip Equities Fund (WIBC) (the “Fund”) seeks total return consisting of price appreciation plus income by investing in a broadly diversified portfolio of equities of well-established, non-U.S. companies. The Fund may buy common stocks traded on the securities exchange of the country in which the company is based or it may purchase American Depositary Receipts (“ADR’s”) traded in the United States. The portfolio is denominated in U.S. dollars and investors should understand that fluctuations in foreign exchange rates may impact the value of their investment. The Adviser seeks to outperform the MSCI World ex U.S. Index (“MSCI World ex U.S.”) by selecting stocks using fundamental company analysis and company-specific criteria such as valuation and earnings trends. The portfolio is then diversified across industries, sectors and countries.

(continued on inside back cover)

| Investment Objectives | | Inside front |

| Letter to Shareholders (Unaudited) | | 2 |

| Performance Summaries (Unaudited) | | 9 |

| Fund Expenses (Unaudited) | | 17 |

| Management and Organization (Unaudited) | | 57 |

| Important Notices Regarding Delivery of Shareholder Documents, Portfolio Holdings and Proxy Voting (Unaudited) | | 59 |

| | | |

| | | | | |

| The Wright Managed Equity Trust | | | The Wright Managed Income Trust | |

| Wright Selected Blue Chip Equities Fund | | | Wright Current Income Fund | |

| Portfolio of Investments | 19 | | Portfolio of Investments | 42 |

| Statement of Assets and Liabilities | 21 | | Statement of Assets and Liabilities | 46 |

| Statement of Operations | 21 | | Statement of Operations | 46 |

| Statements of Changes in Net Assets | 22 | | Statement of Changes in Net Assets | 47 |

| Financial Highlights | 23 | | Financial Highlights | 48 |

| | | | | |

| Wright Major Blue Chip Equities Fund | | | Notes to Financial Statements | 49 |

| Portfolio of Investments | 24 | | Report of Independent Registered Public Accounting Firm | 55 |

| Statement of Assets and Liabilities | 25 | | Federal Tax Information (Unaudited) | 56 |

| Statement of Operations | 25 | | | |

| Statements of Changes in Net Assets | 26 | | | |

| Financial Highlights | 27 | | | |

| | | | | |

| Wright International Blue Chip Equities Fund | | | | |

| Portfolio of Investments | 28 | | | |

| Statement of Assets and Liabilities | 30 | | | |

| Statement of Operations | 30 | | | |

| Statements of Changes in Net Assets | 31 | | | |

| Financial Highlights | 32 | | | |

| | | | | |

| Notes to Financial Statements | 33 | | | |

| Report of Independent Registered Public Accounting Firm | 40 | | | |

| Federal Tax Information (Unaudited) | 41 | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| Letter to Shareholders (Unaudited) |

Dear Shareholder:

SUMMARY: With a strong performance in the fourth quarter capping off a good year, the major U.S. stock indexes traded at record highs as December was ending. Stocks withstood the end of the Fed’s quantitative easing program in Q4, as well as steep drops in crude oil prices, to finish the year near their highs. In the first few trading sessions of 2015, there appears to be some rethinking of the significance of collapsing energy prices. Likewise, the dollar’s big gains in 2014 appear to be more problematic as they continue into 2015. The U.S. economy put in a solid fourth quarter – indeed, a solid final nine months of 2014 after the weather-related stumble in the first quarter – one of the few economies to do so. Based on market action in the first weeks of 2015, higher market volatility appears to be our lot in 2015. Investment-grade bonds enjoyed above-average returns in 2014.

U.S. stocks finished 2014 with a strong performance, as returns across the S&P 1500 all-cap spectrum ranged from 13.7% for the S&P 500 (big caps) to 9.8% for the S&P 400 Midcaps to 5.7% for the S&P 600 SmallCaps. This was a reversal from 2013’s performance rankings, when smaller stocks performed better. The generally strong stock market showing in 2014 is impressive, following as it does a 2013 in which returns ranged from 30% to 40%. In the fourth quarter of 2014, the market averages also had to overcome marked weakness in energy stocks, which declined along with crude oil prices. And that they did, as investors concluded that most sectors will benefit from lower energy costs and rising end-user demand. This is not to say that falling oil prices will not cause disruptions outside of the oil patch, only that on a net basis the effects should be constructive for investors.

If there was a theme that defined global stock market action during the second half of 2014, it was cascading oil prices. Crude oil futures prices fell roughly 40% in the final three months of 2014, more than 25% coming after OPEC’s November 27 decision not to defend higher prices – i.e., not to cut production from the 30-million-barrel-per-day level it has maintained since 2011. In the past, when OPEC has reduced its production quotas, it has been Saudi Arabia that has typically absorbed most of the cuts. That is to say, the Saudi’s were one of the few producers not to cheat on quotas. In 2014, the Saudi’s may have been motivated by a desire to enforce more discipline on the other 11 members of OPEC or possibly to impose some pain on enemies such as Iran and Russia or oil shale producers in North America. Then there is also the possibility that, like other cartels before them, OPEC simply lost control of the market as new production ramps up in the United States and elsewhere.

Another important theme of 2014, particularly in the second half, was the strengthening in U.S. employment, which increased more in 2014 than in any year since 1999. Three million net new jobs were created in the non-farm economy during 2014, nearly 900,000 in the fourth quarter. In terms of net new jobs created, the fourth quarter was the best quarter since 2006 – in other words, since before the financial crisis. From December’s household employment survey, we also learned that the civilian unemployment rate declined to a cycle low of 5.6% in December. Less positive were the decline in average hourly earnings and the retreat to a 37-year low in the labor participation rate. On balance, the latest Bureau of Labor Statistics report on employment conditions is a net positive for GDP in the fourth quarter of 2014 but somewhat of a disappointment to those looking for an increasing share of GDP going to labor.

A third theme driving financial markets in 2014 was the muscular performance of the U.S. dollar. The dollar’s strong performance this past year mostly reflected the fact that U.S. economic performance was once again far better than that of most other developed nations. Based on actual results for the first three quarters of 2014 and the Bureau of Economic Analysis advance estimate for Q4, U.S. GDP grew 2.5% in real terms during 2014,

| Letter to Shareholders (Unaudited) |

measured Q4 2014 over Q4 2013. Compare that with economic growth estimates running under 1% for Japan and the Euro area. Even China’s economic performance is in some sense inferior to the U.S.’s in that its greater growth rate represents a disappointment relative to higher expectations. What’s more, Chinese economic data are somewhat spurious to begin with. In any event, the Japanese yen and the euro depreciated by 12% in 2014 against the dollar and, more broadly, the value of the dollar increased 13% vis-à-vis a trade-weighted basket of major foreign currencies. This brings the dollar’s appreciation since April 2011 to nearly 25%. The euro/dollar exchange rate at the end of 2014 ($1.21), though close to a nine-year low, was actually a bit stronger than its initial $/€ setting of $1.18.

The dollar’s strong showing in 2014 hurt the returns on foreign stocks and bonds to dollar-based investors. So while the local currency prices of foreign stocks and sovereign bonds had gains last year, for the most part those gains translated into losses in terms of U.S. dollars. Yields on sovereign bonds fell sharply throughout 2014, with German bond yields well on their way to the levels of Japanese Government bonds (JGBs). This spiraling down in German rates to all-time lows carried with it most rates in Europe – Greece being an obvious exception – and was assuredly an important factor in the 100+ basis-point decline in 10-year U.S. Treasury yields from December 2013 through early January 2015. What we admit does not make a lot of sense to us is how yields on Spanish and Italian sovereign debt have fallen to levels up to 50 bps below U.S. Treasurys.

The Dow Jones Industrial Average broke through another historical milestone (18000) in December of 2014, while the S&P 500 fell just short of hitting 2100 for the first time ever. In the volatile first few trading days of 2015, the Dow lost its foothold above 18000 and the S&P 500 slipped back almost to 2000. But as has been the case for much of the past three years, stock prices came roaring back from their mini-correction. Typically, since 2012, it was the easier monetary policies from the Fed that snapped investors out of their foul mood. But in early 2015, it was the prospect of significant bond buying by the European Central Bank – which heretofore has only talked up that possibility without delivering on it – that reversed the downward drift in global stock prices.

Stock prices in the U.S. are not cheap, but neither is the S&P 500’s 17-18 price/earnings multiple on trailing 12-month earnings excessive. Investment-grade fixed-income securities offer little competition to stocks today – the 10-year Treasury note yield has fallen below 2% in January – and outside of the energy sector, corporate fundamentals are on the mend, in Wright’s view. Barring severe market weakness, we believe that the Fed will raise interest rates sometime this summer – if only to get a start on what we believe will be a glacially slow transition to more normal interest rates. This backdrop of moderate growth, low inflation and modestly rising interest rates should prove to be favorable for stocks and not terribly unfavorable for corporate bonds in 2015. One should probably expect the S&P 500’s three-year hiatus from an old-style market correction of 10% or more to end in 2015. Still, the balance sheet of the U.S. stock market appears to have far more going for it than agents working against it, which may extend the bull market that began in March 2009 into a seventh “fat year” in March 2015. If you have any questions on Wright’s views on these matters or on other wealth management issues, please contact me.

Sincerely,

Peter M. Donovan

Chairman & CEO

| Management Discussion (Unaudited) |

WRIGHT EQUITY FUNDS

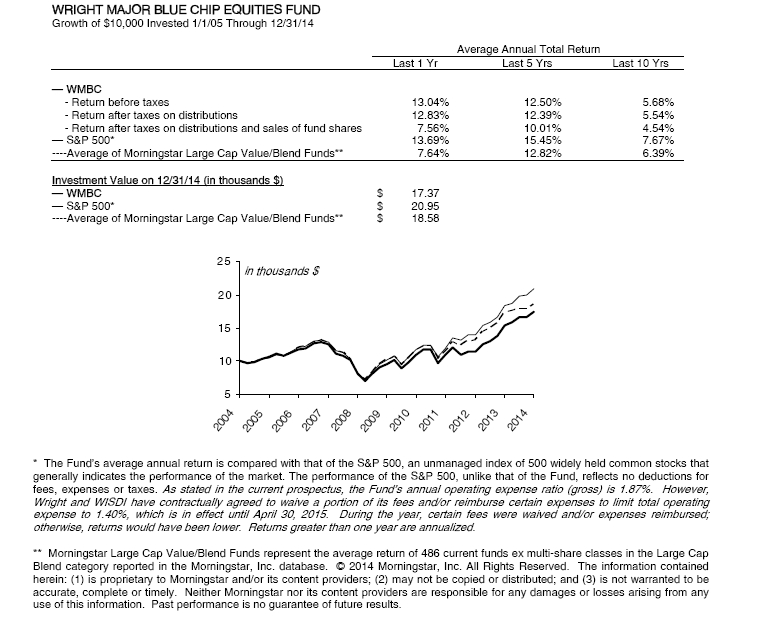

MAJOR BLUE CHIP FUND

The Wright Major Blue Chip Fund (WMBC) is managed as a blend of the large-cap growth and value stocks in the S&P 500 Composite, selected with a focus on the higher-quality issues in the index. The WMBC Fund had a total return of 13.0% in 2014, as compared with a 13.7% return for the S&P 500, the Fund’s benchmark.

The main positive contributors to the Fund’s performance in 2014 were health care stocks, which contributed to its relative performance; roughly two-thirds of this positive contribution was the result of stock selection and roughly one-third came from the Fund’s overweight position in the sector compared with its benchmark (average 2014 portfolio weight of 18% vs 14% for the S&P 500). The Fund also got a positive contribution to its relative performance from stocks in the industrial sector, strictly on stock selection, as the Fund had close to a market weight (11%) in this sector. Technology stocks, which constituted 24% of Fund holdings on average during 2014 as compared to the sector’s 23% weight in the S&P 500, also chipped in with a positive contribution to 2014’s relative performance. Detracting from the Fund’s 2014 relative performance were stocks in the financial sector, where the Fund averaged a slight underweight position during 2014 (15% vs 16%); adverse stock selection accounted for most of the negative contribution to WMBC Fund performance. At December 31, 2014, the WMBC Fund was slightly overweight financial stocks (18% vs 17% at year-end 2014).

Three of the five biggest individual contributors to the Fund’s performance in 2014 were information technology stocks – Intel, Microsoft and Apple – each of which made a healthy contribution to the Fund’s relative performance this past year. Amgen and General Dynamics round out the top five contributors for the year. The biggest individual detractors from the Fund’s performance in 2014 tended to be energy stocks, such as Halliburton, Chevron and Schlumberger, and financial stocks, such as Aflac, Intercontinental Exchange and Mastercard. The Fund was slightly underweight energy stocks and slightly overweight financials at year-end 2014.

The major U.S. stock market indexes hit record highs as 2014 ended, outdoing foreign markets, most of which retreated slightly for the year. The U.S. economy was also one of the few economies to post solid growth this past year, and it did so despite a weather-related stumble in the first quarter. Over the course of 2014, equity investors brushed aside a series of attempts to “correct” lower, including one in the fourth quarter around the time the Fed was ending its QE-3 bond-buying program. Steep drops in crude oil prices hurt stocks in the energy sector, but for the most part the rest of market saw lower energy costs as a good thing, a factor that propelled smaller stocks to a near-10% return in the fourth quarter. In early 2015, there appears to be some rethinking of the significance of collapsing energy prices; might it signal a recessionary drop in global demand? Likewise, the dollar’s strength in 2014 looks more problematic in 2015, threatening export businesses and the profits of multinational corporations.

With its focus on stocks that are, on average, of higher quality than those that populate the S&P 500, the WMBC Fund is believed to be well positioned for what we believe may be a more challenging investment environment in 2015. The WMBC Fund has a higher average weighted market cap than the S&P 500 ($150 billion vs $130 billion) and a five-year earnings growth record nearly as good as that of the S&P 500 (13.3% vs 14.1%). Stocks in the WMBC were judged to be comparatively attractive values relative to the S&P 500 at

| Management Discussion (Unaudited) |

the beginning of 2015: based on current earnings, the WMBC’s average P/E multiple was 18.5x at 12/31/2014 as compared with 18.8x for the S&P 500; based on forecast forward 12 months’ earnings, the WMBC’s P/E was 15.5x vs 16.6x for the S&P 500 benchmark.

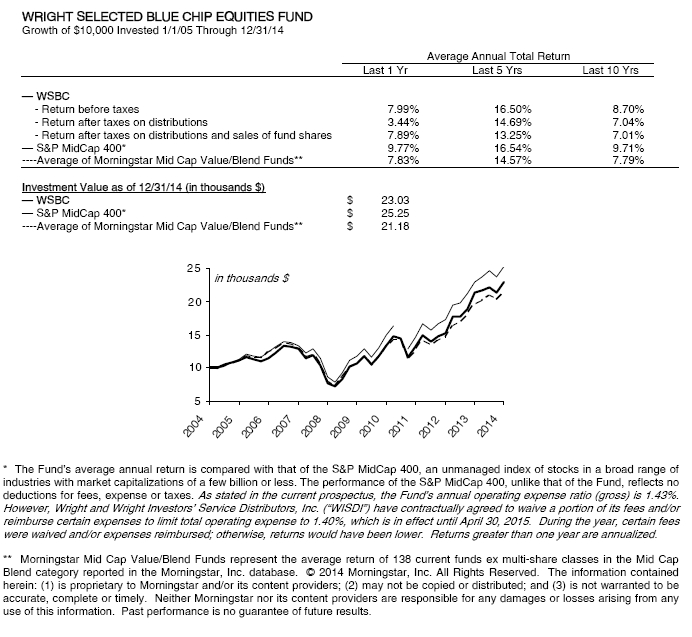

SELECTED BLUE CHIP FUND

The Wright Selected Blue Chip Fund (WSBC), a mid-cap blend fund, had a total return of 8.0% in 2014, as compared with its benchmark, the S&P MidCap Index, which returned 9.8%. Over the three years 2012-14, the WSBC Fund has averaged a 0.9% premium over the S&P400 MidCap Index’s 20.0% average annual rate of total return.

The main positive contributors to the Fund’s performance in 2014 were consumer discretionary stocks and, to a lesser degree, industrials and utilities, in each case due mainly to stock selection. Over the course of 2014, the WSBC Fund was slightly overweight all three of these sectors relative to the S&P MidCap index: consumer discretionary, 16% vs 13%; industrials, 19% vs 17%; and utilities, 5.1% vs 4.7%. Financial stocks (average portfolio weight 22% vs 23%) were the main detractors from Fund performance in 2014 on adverse stock selection.

Among individual stocks, the biggest positive contributors to Fund performance for the full year 2014 were Hanesbrands, Alaska Airgoup, Skyworks Solutions, Universal Health and Foot Locker. Detracting from this past year’s relative performance were Waddell & Reed Financial, Bancorpsouth, Hollyfrontier, Neustar, and Acxiom.

With the U.S. economy still growing at a sub-par pace as 2014 was ending, we believe that the WSBC Fund’s focus on quality securities should serve it well in 2015. WSBC continues to be slightly tilted toward the larger companies in the S&P MidCap 400 index, those with larger median ($4.7 billion vs $3.8 billion) and weighted-average market caps ($6.2 billion vs $5.4 billion) compared to the S&P 400. WSBC’s holdings have shown better historical earnings growth than the MidCap index constituents (15% vs 13% for the trailing five years). The WSBC Fund’s year-end 2014 P/E multiples were at a discount to comparable multiples for the S&P 400 MidCaps: 18.2x vs 21.3x on a trailing 12-month earnings basis, and 15.0x vs 18.4x on a forward 12-month basis.

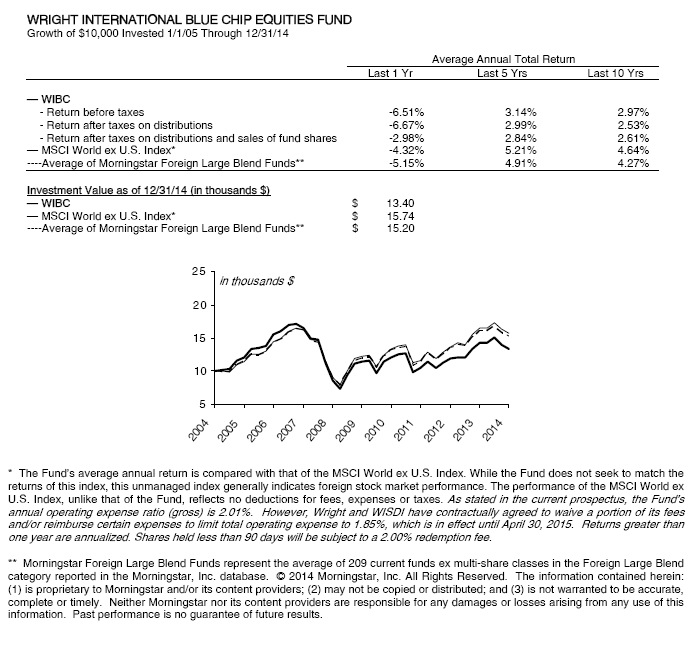

INTERNATIONAL BLUE CHIP FUND

In total return terms, the Wright International Blue Chip Fund (WIBC) had a loss of 6.5% in 2014, about 2.2% more than the MSCI World ex U.S. index, which lost 4.3%. Foreign stocks generally underperformed U.S. stocks during 2014, with much of the underperformance the result of declining foreign currencies.

Stocks in the consumer staples, health care and information technology sectors made positive contributions to the WIBC Fund’s relative performance in 2014, with stock selection (as opposed to big overweight or underweight bets) the main factor. Hurting the Fund’s performance this past year were the financials, industrials and energy sectors. At year-end 2014, financials remained the Fund’s biggest position at 25%, but that was slightly below MSCI World ex U.S. index’s 27% weight; other sector weights were closer to benchmark weights.

| Management Discussion (Unaudited) |

The biggest individual positive contributors to the WIBC Fund’s performance for 2014 were Alimentation Couche-Tard, Astrazeneca, Actelion Limited, Asahi Kasei and Daito Trust Construction. Detractors included Norwegian energy stock Statoil, British maker of power systems Rolls Royce Holdings, German chemical producer BASF, French bank BNP Paribas, and Canadian methanol supplier/distributor Methanex. In the aggregate, WIBC Fund holdings are priced at a significant discount to the MSCI World ex U.S. index in terms of current price/earnings ratios (13.5 vs 15.8 at December 31, 2014). Over the past five years, WIBC holdings have averaged superior earnings growth rates (16% vs 9%). Average weighted market cap is not significantly different from the MSCI World ex U.S.’s ($56.5 billion vs $55.4 billion).

In their final Open Market Committee of 2014, Fed officials cited economic turmoil abroad as an “important source of downside risks��� to U.S. economic activity and employment. The Fed nonetheless went ahead with indications to the market that it expected interest rates to go higher in 2015. This expectation was premised on foreign policy makers taking appropriate actions to foster greater economic growth and to forestall deflationary pressures, which were judged to be building in several markets around the world. Indeed, one week into 2015, Eurostat reported that consumer prices in the Euro area swung to deflation in the 12 months ended December (-0.2% year-over-year). Oil prices cascading lower were obviously a big factor in the decline in the Eurozone CPI, but prices for any number of goods outside of energy were heading lower as well. What falling oil prices says about slow growth in global demand generally and whether to expect oil prices to remain low for the duration are uncertainties that should make economic policy makers want to err on the side of growth in 2015… |

| • Japan’s GDP contracted for two successive quarters, prompting the Abe government to postpone the next phase of sales tax increases scheduled for October 2015 for 18 months and call for new elections. The December 2014 elections strengthened Prime Minister Shinzo Abe’s position, allowing BOJ bond buying to continue at a heavy rate and perhaps enabling Abe to gain headway on market reforms, the unused arrow in his policy quiver. |

• The European Central Bank met on January 22, 2015, and as expected the ECB announced plans to purchase 1.1 trillion euros of sovereign bonds and other longer-term securities. The ECB’s foray into quantitative easing is expected to 1) keep long-term interest rates low, 2) force investors out the risk curve, and 3) through the “wealth effect,” increase consumer spending and business investment, resulting in faster economic growth and a firming of prices. • China appears to be targeting 7% economic growth for 2015, down from the official target of 7.5% GDP growth established in 2012. Judging by purchasing managers’ survey readings, though, even 7% growth, which would be the lowest since its brief sojourn in the 6%-7% range in 2008-09, might be a big challenge. The strong showing of Chinese stocks in the second half of 2014 may be one of the few leading indicators pointing toward a sanguine 2015 GDP outlook. • U.S. GDP growth, which was in the 4.5%-5% (annual rate) range during the middle two quarters of 2014, will be hard pressed to achieve anything approaching 4% growth in 2015. Indeed, while there is an outside chance for 3% growth, the impact of falling oil prices on the oil patch – where a fair chunk of recent growth has originated – has made us ease back on our economic growth and inflation projections for the coming year. Compared with other developed economies, the U.S. should be able to continue its above-average showing. • World GDP growth in 2014 is estimated to have inched up from the 2%-2.25% rates of 2012-13 to just shy of 2.5%. Per Bloomberg, consensus forecasts are for gradual improvement to a 3% growth rate by 2016, which presumes that recessions in Europe and Japan will be short-lived. Lower energy prices stand to benefit the oil-importing world but not without disruptions. The debt bubble that kicked off the financial crisis in 2007 has not been deflated – public debt has replaced private debt – suggesting that |

| Management Discussion (Unaudited) |

| headwinds will limit global growth for some time to come. Global recession looks to be avoidable, but slower growth does not. |

We continue to see the inclusion of international stocks as likely to enhance risk-adjusted returns in diversified investment portfolios.

CURRENT INCOME FUND

The Wright Current Income Fund (WCIF) had a total return of 4.4% in 2014, 1.6% shy of the total return on the Barclays GNMA bond index, the Fund’s benchmark, which gained 6.0%, and the Barclays U.S. Aggregate bond index, which also had a 6.0% total return this past year. The WCIF Fund is managed to be invested in GNMA issues (mortgage-based securities, known as Ginnie Maes, guaranteed by the full faith and credit of the U.S. government) and other mortgage-based securities. The WCIF Fund is actively managed to maximize income and minimize principal fluctuation. WCIF had a yield of 2.8% at December 31, 2014, calculated according to SEC guidelines. Dividends paid by this Fund may be more or less than implied by this yield.

In addition to its holdings in GNMA-backed mortgage issues, WCIF also holds issues backed by Fannie Mae (FNMA) and Freddie Mac (FHLMC), both of which are under the conservatorship of the U.S. Treasury through the Federal Housing Finance Agency (FHFA). At the end of 2014, the WCIF Fund was 95% invested in agency-backed mortgages, versus 100% for the index, with 5% in cash, cash equivalents or agency securities.

The Fund continues to have a higher average coupon than the GNMA benchmark, reflecting the Fund’s mandate to maximize income. At December 31, 2014, WCIF’s average coupon was 5.1%, compared to 3.9% for the GNMA benchmark. The Fund remains substantially overweight in higher coupon mortgages relative to its benchmark. At the end of the year, the Fund held 69% of its assets in mortgages with 5% or greater coupons, compared to only 14% for the benchmark. The Fund’s biggest positions were in mortgages with 5%-6% coupons (36%, versus 11% for the index) and 6%-7% coupons (28% of the portfolio, compared to 2% for the index). By comparison, 24% of the Fund’s assets were held in mortgages with 3%-5% coupons, compared to 85% for the GNMA benchmark. The emphasis on well-seasoned higher-coupon issues contributes to the Fund’s lesser negative convexity compared to the GNMA benchmark, which tends to result in a more stable performance when interest rates are volatile.

At year-end 2014, the average duration of the mortgages held by the Fund, at 3.8 years, was slightly longer than the GNMA index’s 3.5 year duration. As interest rates fell during 2014, the average duration of the Fund declined to 3.8 from 4.4 years one year earlier; the average duration in the GNMA index shortened to 3.5 years from 5.6 years at the end of 2013. At year-end, 67% of securities held in the Fund had a duration of five years or less, compared to 41% for the benchmark. By contrast, 33% of the Fund’s assets had durations of five years or more, as compared to 59% for the GNMA index.

Yields on sovereign bonds fell sharply in 2014. German bond yields appear to be well on their way to the levels of Japanese Government bonds (JGBs); from a spread of as much as 300 basis points during 2008, German 10-year bund yields ended 2014 within 20 bps of JGBs. That represents a 50 basis-point narrowing in the bund/JGB spread since the beginning of 2014. This spiraling down in German rates has carried with it most rates in Europe and has even been an important factor in the 100+ basis-point decline in 10-year |

| Management Discussion (Unaudited) |

| Treasury yields from December 2013 through December 2014.

TOTAL RETURN BOND FUND

The Wright Total Return Bond Fund (WTRB), a diversified bond fund, was closed at the end of December 2014. |

| Performance Summaries (Unaudited) |

Important The Total Investment Return is the percent return of an initial $10,000 investment made at the beginning of the period to the ending redeemable value assuming all dividends and distributions are reinvested. After-tax returns are calculated using the historical highest individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Actual after-tax returns depend on the investor's tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. Past performance is not predictive of future performance. |

| Performance Summaries (Unaudited) |

| WRIGHT SELECTED BLUE CHIP EQUITIES FUND | |

| | |

| Industry Weightings | | Ten Largest Stock Holdings |

| % of net assets @ 12/31/14 | | % of net assets @ 12/31/14 |

| | | | | | | | | | | | | | |

Capital Goods Health Care Equipment & Services | | 8.6 7.5 | % % | | Semiconductors & Semiconductor Equipment | | 3.2 | % | | Hanesbrands, Inc. Skyworks Solutions, Inc. | | 3.4 3.2 | % % |

| Commercial & Professional Services | | 6.9 | % | | Diversified Financials | | 3.0 | % | | UGI Corp. | | 3.0 | % |

| Technology Hardware & Equipment | | 6.7 | % | | Energy | | 2.4 | % | | Foot Locker, Inc. | | 2.8 | % |

| Materials | | 6.5 | % | | Consumer Services | | 2.2 | % | | Brinker International, Inc. | | 2.7 | % |

| Real Estate | | 6.3 | % | | Household & Personal Products | | 2.2 | % | | Omega Healthcare Investors, Inc. REIT | | 2.7 | % |

| Utilities | | 6.3 | % | | Pharmaceuticals & Biotechnology | | 2.0 | % | | Packaging Corp. of America | | 2.5 | % |

| Insurance | | 5.5 | % | | Transportation | | 1.9 | % | | Carlisle Cos., Inc. | | 2.5 | % |

| Banks | | 5.4 | % | | Media | | 1.7 | % | | Deluxe Corp. | | 2.4 | % |

| Retailing | | 5.1 | % | | Automobiles & Components | | 1.4 | % | | Centene Corp. | | 2.4 | % |

| Software & Services | | 4.6 | % | | Industrial | | 1.3 | % | | | | | |

| Consumer Discretionary | | 3.8 | % | | Food, Beverage & Tobacco | | 1.1 | % | | | | | |

| Consumer Durables & Apparel | | 3.4 | % | | Communications Equipment | | 0.6 | % | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| Performance Summaries (Unaudited) |

| Performance Summaries (Unaudited) |

| WRIGHT MAJOR BLUE CHIP EQUITIES FUND | |

| | |

| Industry Weightings | | Ten Largest Stock Holdings |

| % of net assets @ 12/31/14 | | % of net assets @ 12/31/14 |

| | | | | | | | | | | | | | |

Software & Services Pharmaceuticals & Biotechnology | | 11.7 10.4 | % % | | Semiconductor Equipment & Products | | 4.2 | % | | Johnson & Johnson Microsoft Corp. | | 4.8 4.8 | % % |

| Capital Goods | | 10.1 | % | | Retailing | | 3.7 | % | | JPMorgan Chase & Co. | | 4.5 | % |

| Banks | | 8.9 | % | | Utilities | | 3.6 | % | | Bank of America Corp. | | 4.4 | % |

| Health Care Equipment & Services | | 8.5 | % | | Insurance | | 3.5 | % | | Intel Corp. | | 4.2 | % |

| Technology Hardware & Equipment | | 8.5 | % | | Telecommunication Services | | 3.3 | % | | QUALCOMM, Inc. | | 4.1 | % |

| Energy | | 7.6 | % | | Consumer Durables & Apparel | | 1.4 | % | | Coca-Cola Co. (The) | | 4.0 | % |

| Diversified Financials | | 5.8 | % | | Materials | | 1.0 | % | | Oracle Corp. | | 4.0 | % |

| Food, Beverage & Tobacco | | 5.3 | % | | Industrial | | 0.7 | % | | 3M Co. | | 3.9 | % |

| | | | | | Media | | 0.2 | % | | Amgen, Inc. | | 3.8 | % |

| Performance Summaries (Unaudited) |

| Performance Summaries (Unaudited) |

| WRIGHT INTERNATIONAL BLUE CHIP EQUITIES FUND | |

| | |

| Country Weightings | | Ten Largest Stock Holdings |

| % of net assets @ 12/31/14 | | % of net assets @ 12/31/14 |

| | | | | | | | | | | | | | |

| Japan | | 24.3 | % | | Ireland | | 1.2 | % | | Nestle SA | | 3.2 | % |

| United Kingdom | | 15.9 | % | | Denmark | | 1.0 | % | | Legal & General Group PLC | | 2.8 | % |

| Switzerland | | 11.2 | % | | Norway | | 0.7 | % | | KDDI Corp. | | 2.8 | % |

| Germany | | 11.1 | % | | Israel | | 0.6 | % | | Swiss Re AG | | 2.8 | % |

Canada France | | 9.9 7.9 | % % | | Netherlands Finland | | 0.6 0.5 | % % | | Alimentation Couche-Tard, Inc.- Class B | | 2.7 | % |

| Spain | | 7.1 | % | | Austria | | 0.4 | % | | BASF SE | | 2.5 | % |

| Australia | | 2.4 | % | | Sweden | | 0.3 | % | | Actelion, Ltd. | | 2.2 | % |

| Italy | | 2.0 | % | | Greece | | 0.2 | % | | Asahi Kasei Corp. | | 2.1 | % |

| Hong Kong | | 1.4 | % | | | | | | | BNP Paribas SA | | 2.0 | % |

| | | | | | | | | | | Muenchener Rueckversicherungs-Gesellschaft AG – Class R | | 2.0 | % |

| | | | | | | | | | | | | | |

| Performance Summaries (Unaudited) |

| Performance Summaries (Unaudited) |

| WRIGHT CURRENT INCOME FUND | |

| | |

| Holdings by Security Type | Five Largest Bond Holdings |

| % of net assets @ 12/31/14 | % of net assets @ 12/31/14 |

| | | | | | | | | | | | | |

| Agency Mortgage-Backed Securities | | 94.9 | % | | | | | GNMA, Series 2010-116, Class PB | 5.00% | 06/16/40 | 3.6 | % |

| Other U.S. Government Guaranteed | | 2.8 | % | | | | | FNMA Pool #821082 | 6.00% | 03/01/35 | 3.5 | % |

| | | | | | | | | Vessel Management Services, Inc. | 5.13% | 04/16/35 | 2.8 | % |

| | | | | | | | | FHLMC, Series 4142, Class PN | 2.50% | 12/15/32 | 2.7 | % |

| | | | | | | | | FHLMC Gold Pool #Q11280 | 4.00% | 09/01/42 | 2.7 | % |

| Weighted Average Maturity | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| @ 12/31/14 | | 11.2 | Years | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Fund Expenses (Unaudited) |

Example:

As a shareholder of a fund, you incur two types of costs: (1) transaction costs, including redemption fees (if applicable); and (2) ongoing costs including management fees; distribution or service fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in a fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2014 – December 31, 2014).

Actual Expenses:

The first line of the tables shown on the following page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes:

The second line of the tables provides information about hypothetical account values and hypothetical expenses based on the actual Fund expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual return of the Fund. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees (if applicable). Therefore, the second line of the tables is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Fund Expenses (Unaudited) |

EQUITY FUNDS

Wright Selected Blue Chip Equities Fund

| | Beginning Account Value (7/1/14) | Ending Account Value (12/31/14) | Expenses Paid During Period* (7/1/14-12/31/14) |

| Actual Fund Shares | $1,000.00 | $ 1,039.81 | $7.20 |

| Hypothetical (5% return per year before expenses) |

| Fund Shares | $1,000.00 | $ 1,018.15 | $7.12 |

*Expenses are equal to the Fund’s annualized expense ratio of 1.40% multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). The example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on June 30, 2014.

Wright Major Blue Chip Equities Fund

| | Beginning Account Value (7/1/14) | Ending Account Value (12/31/14) | Expenses Paid During Period* (7/1/14-12/31/14) |

| Actual Fund Shares | $1,000.00 | $1,043.15 | $7.21 |

| Hypothetical (5% return per year before expenses) |

| Fund Shares | $1,000.00 | $1,018.15 | $7.12 |

*Expenses are equal to the Fund’s annualized expense ratio of 1.40% multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). The example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on June 30, 2014.

Wright International Blue Chip Equities Fund

| | Beginning Account Value (7/1/14) | Ending Account Value (12/31/14) | Expenses Paid During Period* (7/1/14-12/31/14) |

| Actual Fund Shares | $1,000.00 | $888.90 | $8.81 |

| Hypothetical (5% return per year before expenses) |

| Fund Shares | $1,000.00 | $1,015.88 | $9.40 |

*Expenses are equal to the Fund’s annualized expense ratio of 1.85% multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). The example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on June 30, 2014.

FIXED-INCOME FUNDS

Wright Current Income Fund

| | Beginning Account Value (7/1/14) | Ending Account Value (12/31/14) | Expenses Paid During Period* (7/1/14-12/31/14) |

| Actual Fund Shares | $1,000.00 | $1,019.15 | $4.58 |

| Hypothetical (5% return per year before expenses) |

| Fund Shares | $1,000.00 | $1,020.67 | $4.58 |

*Expenses are equal to the Fund’s annualized expense ratio of 0.90% multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). The example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on June 30, 2014.

Wright Selected Blue Chip Equities Fund (WSBC) Portfolio of Investments - As of December 31, 2014 |

EQUITY INTERESTS - 99.6% |

AUTOMOBILES & COMPONENTS - 1.4% |

| Gentex Corp. | 14,510 | | $ | 524,246 | |

BANKS - 5.4% |

| BancorpSouth, Inc. | 5,810 | | $ | 130,783 | |

| Commerce Bancshares, Inc. | 3,722 | | | 161,870 | |

| East West Bancorp, Inc. | 10,400 | | | 402,584 | |

| Fulton Financial Corp. | 67,355 | | | 832,508 | |

| New York Community Bancorp, Inc. | 23,115 | | | 369,840 | |

| Valley National Bancorp | 12,190 | | | 118,365 | |

| | | | $ | 2,015,950 | |

CAPITAL GOODS - 8.6% |

| AECOM Technology Corp.* | 23,245 | | $ | 705,951 | |

| Alliant Techsystems, Inc. | 4,685 | | | 544,631 | |

| Carlisle Cos., Inc. | 10,210 | | | 921,350 | |

| Esterline Technologies Corp.* | 1,990 | | | 218,263 | |

| Exelis, Inc. | 18,620 | | | 326,409 | |

| Huntington Ingalls Industries, Inc. | 3,660 | | | 411,604 | |

| Vectrus, Inc.* | 3,885 | | | 106,449 | |

| | | | $ | 3,234,657 | |

COMMERCIAL & PROFESSIONAL SERVICES - 6.9% |

| Deluxe Corp. | 14,320 | | $ | 891,420 | |

| Global Payments, Inc. | 9,950 | | | 803,263 | |

| RR Donnelley & Sons Co. | 37,435 | | | 629,095 | |

| Towers Watson & Co. - Class A | 2,375 | | | 268,779 | |

| | | | $ | 2,592,557 | |

COMMUNICATIONS EQUIPMENT - 0.6% |

| ARRIS Group, Inc.* | 7,125 | | $ | 215,104 | |

CONSUMER DISCRETIONARY - 3.8% |

| Brinker International, Inc. | 17,595 | | $ | 1,032,651 | |

| Signet Jewelers, Ltd. | 2,890 | | | 380,237 | |

| | | | $ | 1,412,888 | |

CONSUMER DURABLES & APPAREL - 3.4% |

| Hanesbrands, Inc. | 11,365 | | $ | 1,268,561 | |

CONSUMER SERVICES - 2.2% |

| Apollo Education Group, Inc.* | 9,950 | | $ | 339,395 | |

| DeVry Education Group, Inc. | 10,015 | | | 475,412 | |

| | | | $ | 814,807 | |

DIVERSIFIED FINANCIALS - 3.0% |

| MSCI, Inc. | 7,770 | | $ | 368,609 | |

| Raymond James Financial, Inc. | 6,935 | | | 397,306 | |

| Signature Bank* | 1,340 | | | 168,786 | |

| Waddell & Reed Financial, Inc. - Class A | 4,085 | | | 203,515 | |

| | | | $ | 1,138,216 | |

ENERGY - 2.4% |

| Cimarex Energy Co. | 1,275 | | $ | 135,150 | |

| HollyFrontier Corp. | 17,119 | | | 641,620 | |

| Superior Energy Services, Inc. | 3,285 | | | 66,193 | |

| Western Refining, Inc. | 1,790 | | | 67,626 | |

| | | | $ | 910,589 | |

FOOD, BEVERAGE & TOBACCO - 1.1% |

| Ingredion, Inc. | 3,465 | | $ | 293,971 | |

| Keurig Green Mountain, Inc. | 1,005 | | | 133,057 | |

| | | | $ | 427,028 | |

HEALTH CARE EQUIPMENT & SERVICES - 7.5% |

| Align Technology, Inc.* | 2,010 | | $ | 112,379 | |

| Centene Corp.* | 8,540 | | | 886,879 | |

| Health Net, Inc.* | 8,475 | | | 453,667 | |

| MEDNAX, Inc.* | 2,480 | | | 163,953 | |

| Omnicare, Inc. | 5,265 | | | 383,976 | |

| Universal Health Services, Inc. - Class B | 5,715 | | | 635,851 | |

| VCA, Inc.* | 3,850 | | | 187,765 | |

| | | | $ | 2,824,470 | |

HOUSEHOLD & PERSONAL PRODUCTS - 2.2% |

| Energizer Holdings, Inc. | 6,550 | | $ | 842,068 | |

INDUSTRIAL - 1.3% |

| Con-way, Inc. | 2,315 | | $ | 113,852 | |

| JetBlue Airways Corp.* | 12,920 | | | 204,911 | |

| Kirby Corp.* | 1,945 | | | 157,039 | |

| | | | $ | 475,802 | |

INSURANCE - 5.5% |

| American Financial Group, Inc. | 6,320 | | $ | 383,750 | |

| Everest Re Group, Ltd. | 1,025 | | | 174,558 | |

| HCC Insurance Holdings, Inc. | 16,115 | | | 862,475 | |

| Reinsurance Group of America, Inc. | 3,275 | | | 286,955 | |

| WR Berkley Corp. | 7,127 | | | 365,330 | |

| | | | $ | 2,073,068 | |

MATERIALS - 6.5% |

| Albemarle Corp. | 5,200 | | $ | 312,676 | |

| Olin Corp. | 10,850 | | | 247,055 | |

| Packaging Corp. of America | 11,945 | | | 932,307 | |

| Rock-Tenn Co. - Class A | 7,320 | | | 446,374 | |

| Steel Dynamics, Inc. | 11,405 | | | 225,135 | |

| Worthington Industries, Inc. | 9,505 | | | 286,005 | |

| | | | $ | 2,449,552 | |

MEDIA - 1.7% |

| John Wiley & Sons, Inc. - Class A | 3,280 | | $ | 194,307 | |

| Meredith Corp. | 8,410 | | | 456,831 | |

| | | | $ | 651,138 | |

PHARMACEUTICALS & BIOTECHNOLOGY - 2.0% |

| Charles River Laboratories International, Inc.* | 3,210 | | $ | 204,284 | |

| United Therapeutics Corp.* | 4,175 | | | 540,621 | |

| | | | $ | 744,905 | |

REAL ESTATE - 6.3% |

| American Campus Communities, Inc. REIT | 5,395 | | $ | 223,137 | |

| Corrections Corp. of America REIT | 9,695 | | | 352,317 | |

| Jones Lang LaSalle, Inc. | 5,200 | | | 779,636 | |

| Omega Healthcare Investors, Inc. REIT | 26,260 | | | 1,025,978 | |

| | | | $ | 2,381,068 | |

| See Notes to Financial Statements. | 19 | |

Wright Selected Blue Chip Equities Fund (WSBC) Portfolio of Investments - As of December 31, 2014 |

RETAILING - 5.1% |

| Advance Auto Parts, Inc. | 3,460 | | $ | 551,109 | |

| Big Lots, Inc. | 8,220 | | | 328,964 | |

| Foot Locker, Inc. | 18,490 | | | 1,038,768 | |

| | | | $ | 1,918,841 | |

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 3.2% |

| Skyworks Solutions, Inc. | 16,630 | | $ | 1,209,167 | |

SOFTWARE & SERVICES - 4.6% |

| Alliance Data Systems Corp.* | 2,275 | | $ | 650,764 | |

| Cadence Design Systems, Inc.* | 35,765 | | | 678,462 | |

| NeuStar, Inc. - Class A* | 14,770 | | | 410,606 | |

| | | | $ | 1,739,832 | |

TECHNOLOGY HARDWARE & EQUIPMENT - 6.7% |

| Arrow Electronics, Inc.* | 10,530 | | $ | 609,582 | |

| Avnet, Inc. | 12,520 | | | 538,610 | |

| Broadridge Financial Solutions, Inc. | 8,475 | | | 391,375 | |

| Ingram Micro, Inc.* | 6,740 | | | 186,294 | |

| PTC, Inc.* | 4,955 | | | 181,601 | |

| Tech Data Corp.* | 5,650 | | | 357,249 | |

| Zebra Technologies Corp.* | 3,080 | | | 238,423 | |

| | | | $ | 2,503,134 | |

TRANSPORTATION - 1.9% |

| Alaska Air Group, Inc. | 11,945 | | $ | 713,833 | |

UTILITIES - 6.3% |

| Great Plains Energy, Inc. | 15,090 | | $ | 428,707 | |

| IDACORP, Inc. | 6,230 | | | 412,363 | |

| ONE Gas, Inc. | 9,786 | | | 403,379 | |

| UGI Corp. | 29,857 | | | 1,133,969 | |

| | | | $ | 2,378,418 | |

TOTAL EQUITY INTERESTS - 99.6% (identified cost, $28,229,183) | | $ | 37,459,899 | |

SHORT-TERM INVESTMENTS - 0.3% |

| Fidelity Government Money Market Fund, 0.01% (1) | 121,978 | | $ | 121,978 | |

TOTAL SHORT-TERM INVESTMENTS - 0.3% (identified cost, $121,978) | | $ | 121,978 | |

TOTAL INVESTMENTS — 99.9% (identified cost, $28,351,161) | | $ | 37,581,877 | |

| OTHER ASSETS, IN EXCESS OF LIABILITIES — 0.1% | | | 27,995 | |

| NET ASSETS — 100.0% | | $ | 37,609,872 | |

REIT — Real Estate Investment Trust

| * | Non-income producing security. |

(1) Variable rate security. Rate presented is as of December 31, 2014.

| See Notes to Financial Statements. | 20 | |

| Wright Selected Blue Chip Equities Fund (WSBC) |

| STATEMENT OF ASSETS AND LIABILITIES |

| As of December 31, 2014 |

| | | | | | | |

| ASSETS: | | | TRUE | |

| | Investments, at value | | | | |

| | (identified cost $28,351,161) (Note 1A) | | $ | 37,581,877 | ###### |

| | Dividends receivable | | | 40,001 | |

| | Prepaid expenses and other assets | | | 9,800 | |

| | Total assets | | $ | 37,631,678 | |

| | | | | | | |

| LIABILITIES: | | | | |

| | Payable for fund shares reacquired | | $ | 5,095 | |

| | Accrued expenses and other liabilities | | | 16,711 | |

| | Total liabilities | | $ | 21,806 | |

| NET ASSETS | | $ | 37,609,872 | |

| | | | | | | |

| NET ASSETS CONSIST OF: | | | | |

| | Paid-in capital | | $ | 26,651,724 | |

| | Accumulated net realized gain on investments | | | 1,727,432 | |

| | Unrealized appreciation on investments | | | 9,230,716 | |

| | Net assets applicable to outstanding shares | | $ | 37,609,872 | |

| | | | | | | |

| SHARES OF BENEFICIAL INTEREST OUTSTANDING AT $0.000 PAR VALUE (UNLIMITED SHARES AUTHORIZED) | | | 2,952,997 | |

| | | | | | | |

| NET ASSET VALUE, OFFERING PRICE, AND REDEMPTION PRICE PER SHARE OF BENEFICIAL INTEREST | | $ | 12.74 | |

| | | | | | | |

| STATEMENT OF OPERATIONS |

| For the Year Ended December 31, 2014 |

| | | | | | | |

| INVESTMENT INCOME (Note 1C) | | | TRUE | |

| 3E+07 | Dividend income | | $ | 646,415 | |

| | Total investment income | | $ | 646,415 | |

| | | | | | | |

| Expenses – | | | | |

| | Investment adviser fee (Note 3) | | $ | 234,545 | |

| | Administrator fee (Note 3) | | | 46,909 | |

| | Trustee expense (Note 3) | | | 14,403 | |

| | Custodian fee | | | 5,007 | |

| | Accountant fee | | | 39,175 | |

| | Distribution expenses (Note 4) | | | 97,726 | |

| | Transfer agent fee | | | 28,628 | |

| | Printing | | | 165 | |

| | Shareholder communications | | | 5,466 | |

| | Audit services | | | 17,000 | |

| | Legal services | | | 49,744 | |

| | Compliance services | | | 6,221 | |

| | Registration costs | | | 19,600 | |

| | Interest expense (Note 8) | | | 1,795 | |

| | Miscellaneous | | | 23,412 | |

| | Total expenses | | $ | 589,796 | |

| | | | | | | |

| Deduct – | | | | |

| | Waiver and/or reimbursement by the principal underwriter and/or investment adviser (Note 4) | | $ | (19,420 | ) |

| | Net expenses | | $ | 570,376 | |

| | Net investment income | | $ | 76,039 | |

| | | | | | | |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS: | |

| | Net realized gain on investment transactions | | $ | 6,165,711 | |

| | Net change in unrealized appreciation (depreciation) on investments | | | (3,334,464 | ) |

| | Net realized and unrealized gain on investments | | $ | 2,831,247 | |

| | Net increase in net assets from operations | | $ | 2,907,286 | |

| | | | | | | |

| See Notes to Financial Statements. | 21 | |

| Wright Selected Blue Chip Equities Fund (WSBC) |

| | | | Years Ended | |

| STATEMENTS OF CHANGES IN NET ASSETS | | December 31, 2014 | | December 31, 2013 | |

| | | | | | | | | | | |

| INCREASE (DECREASE) IN NET ASSETS: | | | | | | | | | |

From operations – | | | | | | | | | |

| | Net investment income (loss) | | $ | 76,039 | | | $ | (20,491 | ) | |

| 0 | Net realized gain on investment transactions | | | 6,165,711 | | | | 5,721,464 | | |

| | Net change in unrealized appreciation (depreciation) on investments | | | (3,334,464 | ) | | | 6,436,418 | | |

| | Net increase in net assets from operations | | $ | 2,907,286 | | | $ | 12,137,391 | | |

| Distributions to shareholders (Note 2) | | | | | | | | | |

| | From net investment income | | $ | (97,816 | ) | | $ | (7,466 | ) | |

| | From net realized capital gains | | | (6,795,055 | ) | | | (4,709,210 | ) | |

| | Total distributions | | $ | (6,892,871 | ) | | $ | (4,716,676 | ) | |

| Net increase in net assets resulting from fund share transactions (Note 6) | | $ | 1,391,495 | | | $ | 2,860,851 | | |

| Net increase (decrease) in net assets | | $ | (2,594,090 | ) | | $ | 10,281,566 | | |

| ## | | | | | | | | | | |

| NET ASSETS: | | | | | | | | | |

| | At beginning of year | | | 40,203,962 | | | | 29,922,396 | | |

| | At end of year | | $ | 37,609,872 | | | $ | 40,203,962 | | |

| | | | | | | | | | | |

| See Notes to Financial Statements. | 22 | |

| Wright Selected Blue Chip Equities Fund (WSBC) |

| These financial highlights reflect selected data for a share outstanding throughout each year. | | | | |

| | | Years Ended December 31, |

| FINANCIAL HIGHLIGHTS | | 2014 | 2013 | 2012 | 2011 | 2010 |

| | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of year | | $ | 14.160 | | $ | 11.530 | | $ | 10.280 | | $ | 10.400 | | $ | 8.400 | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | |

Net investment income (loss) (1) | | | 0.027 | | | (0.007 | ) | | 0.028 | | | (0.018 | ) | | (0.022 | ) |

| Net realized and unrealized gain (loss) | | | 1.043 | | | 4.412 | | | 1.616 | | | (0.102 | ) | | 2.030 | |

| | Total income (loss) from investment operations | | 1.070 | | | 4.405 | | | 1.644 | | | (0.120 | ) | | 2.008 | |

| | | | | | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.036 | ) | | — | (2) | (0.025 | ) | | — | | | (0.008 | ) |

| From net realized gains | | | (2.454 | ) | | (1.775 | ) | (0.369 | ) | | — | | | — | |

| | Total distributions | | | (2.490 | ) | | (1.775 | ) | | (0.394 | ) | | — | | | (0.008 | ) |

| Net asset value, end of year | | $ | 12.740 | | $ | 14.160 | | $ | 11.530 | | $ | 10.280 | | $ | 10.400 | |

Total Return(3) | | | 7.99 | % | | 39.82 | % | | 16.02 | % | | (1.15 | )% | | 23.93 | % |

Ratios/Supplemental Data(4): | | | | | | | | | | | | | | | | |

| Net assets, end of year (000 omitted) | | $37,610 | | $40,204 | | $29,922 | | $32,362 | | $28,370 | |

| Ratios (As a percentage of average daily net assets): |

| Net expenses | | | 1.45 | % | 1.40 | % | 1.40 | % | 1.40 | % | 1.40 | % |

| Net investment income (loss) | | | 0.19 | % | (0.06 | )% | 0.25 | % | (0.17 | )% | (0.24 | )% |

| Portfolio turnover rate | | | 66 | % | 76 | % | 54 | % | 82 | % | 60 | % |

| | | | | | | | | | | | | | | | | |

| | | | | For the years ended December 31, 2014, 2013, 2012, 2011 and 2010 | For the years ended December 31, 2014, 2013, 2012, 2011 and 2010 | | | | | | | |

| (1) | Computed using average shares outstanding. |

| (2) | Less than $0.001 per share. |

| (3) | Total return is calculated assuming a purchase at the net asset value on the first day and a sale at the net asset value on the last day of each year reported. Dividends and distributions, if any, are assumed to be reinvested at the net asset value on the reinvestment date. |

| (4) | For each of the years presented, the operating expenses of the Fund were reduced by a waiver of fees and/or allocation of expenses to the principal underwriter and/or investment adviser. Had such action not been undertaken, expenses and net investment income (loss) ratios would have been as follows: |

| | | | 2014 | 2013 | 2012 | 2011 | 2010 |

| | |

| Ratios (As a percentage of average daily net assets): |

| Expenses | | | 1.51 | % | | 1.43 | % | | 1.48 | % | | 1.46 | % | | 1.79 | % |

| Net investment income (loss) | | | 0.13 | % | | (0.09 | )% | | 0.17 | % | | (0.23 | )% | | (0.63 | )% |

| | | | | | | | | | | | | | | | | | |

| See Notes to Financial Statements. | 23 | |

Wright Major Blue Chip Equities Fund (WMBC) Portfolio of Investments - As of December 31, 2014 |

BANKS - 8.9% |

| Bank of America Corp. | 39,110 | | $ | 699,678 | |

| JPMorgan Chase & Co. | 11,455 | | | 716,854 | |

| | | | $ | 1,416,532 | |

CAPITAL GOODS - 10.1% |

| 3M Co. | 3,825 | | $ | 628,524 | |

| General Dynamics Corp. | 3,915 | | | 538,782 | |

| Rockwell Automation, Inc. | 4,040 | | | 449,248 | |

| | | | $ | 1,616,554 | |

CONSUMER DURABLES & APPAREL - 1.4% |

| Garmin, Ltd. | 2,335 | | $ | 123,358 | |

| Polaris Industries, Inc. | 465 | | | 70,327 | |

| Walgreens Boots Alliance, Inc. | 395 | | | 30,099 | |

| | | | $ | 223,784 | |

DIVERSIFIED FINANCIALS - 5.8% |

| Affiliated Managers Group, Inc.* | 1,055 | | $ | 223,913 | |

| CBRE Group, Inc. - Class A* | 1,535 | | | 52,574 | |

| Franklin Resources, Inc. | 1,525 | | | 84,439 | |

| T. Rowe Price Group, Inc. | 6,465 | | | 555,085 | |

| | | | $ | 916,011 | |

ENERGY - 7.6% |

| California Resources Corp.* | 378 | | $ | 2,083 | |

| Chevron Corp. | 3,720 | | | 417,310 | |

| Halliburton Co. | 6,045 | | | 237,750 | |

| Occidental Petroleum Corp. | 945 | | | 76,176 | |

| Schlumberger, Ltd. | 5,530 | | | 472,317 | |

| | | | $ | 1,205,636 | |

FOOD, BEVERAGE & TOBACCO - 5.3% |

| Coca-Cola Co. (The) | 15,090 | | $ | 637,100 | |

| Monster Beverage Corp.* | 1,945 | | | 210,741 | |

| | | | $ | 847,841 | |

HEALTH CARE EQUIPMENT & SERVICES - 8.5% |

| Abbott Laboratories | 9,175 | | $ | 413,059 | |

| Humana, Inc. | 3,370 | | | 484,033 | |

| Stryker Corp. | 4,895 | | | 461,745 | |

| | | | $ | 1,358,837 | |

INDUSTRIAL - 0.7% |

| Cummins, Inc. | 770 | | $ | 111,011 | |

INSURANCE - 3.5% |

| MetLife, Inc. | 10,250 | | $ | 554,422 | |

MATERIALS - 1.0% |

| CF Industries Holdings, Inc. | 575 | | $ | 156,710 | |

MEDIA - 0.2% |

| Scripps Networks Interactive, Inc. - Class A | 395 | | $ | 29,732 | |

PHARMACEUTICALS & BIOTECHNOLOGY - 10.4% |

| Amgen, Inc. | 3,830 | | $ | 610,081 | |

| Gilead Sciences, Inc.* | 3,005 | | | 283,251 | |

| Johnson & Johnson | 7,265 | | | 759,701 | |

| | | | $ | 1,653,033 | |

RETAILING - 3.7% |

| TJX Cos., Inc. (The) | 8,605 | | $ | 590,131 | |

SEMICONDUCTOR EQUIPMENT & PRODUCTS - 4.2% |

| Intel Corp. | 18,295 | | $ | 663,926 | |

SOFTWARE & SERVICES - 11.7% |

| Google, Inc. - Class A* | 175 | | $ | 92,866 | |

| Google, Inc. - Class C* | 175 | | | 92,120 | |

| Intuit, Inc. | 795 | | | 73,291 | |

| MasterCard, Inc. - Class A | 1,190 | | | 102,530 | |

| Microsoft Corp. | 16,290 | | | 756,670 | |

| Oracle Corp. | 14,030 | | | 630,929 | |

| Visa, Inc. - Class A | 445 | | | 116,679 | |

| | | | $ | 1,865,085 | |

TECHNOLOGY HARDWARE & EQUIPMENT - 8.5% |

| Apple, Inc. | 5,030 | | $ | 555,211 | |

| QUALCOMM, Inc. | 8,715 | | | 647,786 | |

| Western Digital Corp. | 1,355 | | | 149,999 | |

| | | | $ | 1,352,996 | |

TELECOMMUNICATION SERVICES - 3.3% |

| AT&T, Inc. | 15,865 | | $ | 532,905 | |

UTILITIES - 3.6% |

| NextEra Energy, Inc. | 5,370 | | $ | 570,777 | |

TOTAL EQUITY INTERESTS - 98.4% (identified cost, $13,250,928) | | $ | 15,665,923 | |

SHORT-TERM INVESTMENTS - 1.4% |

| Fidelity Government Money Market Fund, 0.01% (1) | 219,716 | | $ | 219,716 | |

TOTAL SHORT-TERM INVESTMENTS - 1.4% (identified cost, $219,716) | | $ | 219,716 | |

TOTAL INVESTMENTS — 99.8% (identified cost, $13,470,644) | | $ | 15,885,639 | |

| OTHER ASSETS, IN EXCESS OF LIABILITIES — 0.2% | | | 39,271 | |

| NET ASSETS — 100.0% | | $ | 15,924,910 | |

* — Non-income producing security.

| (1) | Variable rate security. Rate presented is as of December 31, 2014. |

| See Notes to Financial Statements. | 24 | |

| Wright Major Blue Chip Equities Fund (WMBC) |

| STATEMENT OF ASSETS AND LIABILITIES |

| As of December 31, 2014 |

| | | | | | | |

| ASSETS: | | | TRUE | |

| | Investments, at value | | | | |

| | (identified cost $13,470,644) (Note 1A) | | $ | 15,885,639 | ###### |

| | Receivable for fund shares sold | | | 34,128 | |

| | Dividends receivable | | | 7,142 | |

| | Prepaid expenses and other assets | | | 8,068 | |

| | Total assets | | $ | 15,934,977 | |

| | | | | | | |

| LIABILITIES: | | | | |

| | Accrued expenses and other liabilities | | | 10,067 | |

| | Total liabilities | | $ | 10,067 | |

| NET ASSETS | | $ | 15,924,910 | |

| | | | | | | |

| NET ASSETS CONSIST OF: | | | | |

| | Paid-in capital | | $ | 14,542,718 | |

| | Accumulated net realized loss on investments | | | (1,035,111 | ) |

| | Undistributed net investment income | | | 2,308 | |

| | Unrealized appreciation on investments | | | 2,414,995 | |

| | Net assets applicable to outstanding shares | | $ | 15,924,910 | |

| | | | | | | |

| SHARES OF BENEFICIAL INTEREST OUTSTANDING AT $0.000 PAR VALUE (UNLIMITED SHARES AUTHORIZED) | | | 833,780 | |

| | | | | | | |

| NET ASSET VALUE, OFFERING PRICE, AND REDEMPTION PRICE PER SHARE OF BENEFICIAL INTEREST | | $ | 19.10 | |

| | | | | | | |

| STATEMENT OF OPERATIONS |

| For the Year Ended December 31, 2014 |

| | | | | | | |

| INVESTMENT INCOME (Note 1C) | | | TRUE | |

| 1E+07 | Dividend income | | $ | 369,107 | |

| | Total investment income | | $ | 369,107 | |

| | | | | | | |

| Expenses – | | | | |

| | Investment adviser fee (Note 3) | | $ | 104,798 | |

| | Administrator fee (Note 3) | | | 20,960 | |

| | Trustee expense (Note 3) | | | 14,403 | |

| | Custodian fee | | | 5,000 | |

| | Accountant fee | | | 37,419 | |

| | Distribution expenses (Note 4) | | | 43,666 | |

| | Transfer agent fee | | | 25,082 | |

| | Printing | | | 73 | |

| | Shareholder communications | | | 4,559 | |

| | Audit services | | | 17,000 | |

| | Legal services | | | 11,068 | |

| | Compliance services | | | 5,545 | |

| | Registration costs | | | 19,129 | |

| | Interest expense (Note 8) | | | 766 | |

| | Miscellaneous | | | 15,670 | |

| | Total expenses | | $ | 325,138 | |

| | | | | | | |

| Deduct – | | | | |

| | Waiver and/or reimbursement by the principal underwriter and/or investment adviser (Note 4) | | $ | (79,843 | ) |

| | Net expenses | | $ | 245,295 | |

| | Net investment income | | $ | 123,812 | |

| | | | | | | |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS: | |

| | Net realized gain on investment transactions | | $ | 2,701,317 | |

| | Net change in unrealized appreciation (depreciation) on investments | | | (677,283 | ) |

| | Net realized and unrealized gain on investments | | $ | 2,024,034 | |

| | Net increase in net assets from operations | | $ | 2,147,846 | |

| | | | | | | |

| See Notes to Financial Statements. | 25 | |

| Wright Major Blue Chip Equities Fund (WMBC) |

| | | | Years Ended | |

| STATEMENTS OF CHANGES IN NET ASSETS | | December 31, 2014 | | December 31, 2013 | |

| | | | | | | | | | | |

| INCREASE (DECREASE) IN NET ASSETS: | | | | | | | | | |

From operations – | | | | | | | | | |

| | Net investment income | | $ | 123,812 | | | $ | 105,865 | | |

| 0 | Net realized gain on investment transactions | | | 2,701,317 | | | | 1,526,891 | | |

| | Net change in unrealized appreciation (depreciation) on investments | | | (677,283 | ) | | | 3,279,155 | | |

| | Net increase in net assets from operations | | $ | 2,147,846 | | | $ | 4,911,911 | | |

| Distributions to shareholders (Note 2) | | | | | | | | | |

| | From net investment income | | $ | (126,109 | ) | | $ | (103,923 | ) | |

| | Total distributions | | $ | (126,109 | ) | | $ | (103,923 | ) | |

| Net decrease in net assets resulting from fund share transactions (Note 6) | | $ | (3,788,496 | ) | | $ | (2,675,499 | ) | |

| Net increase (decrease) in net assets | | $ | (1,766,759 | ) | | $ | 2,132,489 | | |

| ## | | | | | | | | | | |

| NET ASSETS: | | | | | | | | | |

| | At beginning of year | | | 17,691,669 | | | | 15,559,180 | | |

| | At end of year | | $ | 15,924,910 | | | $ | 17,691,669 | | |

| | | | | | | | | | | |

| UNDISTRIBUTED NET INVESTMENT INCOME INCLUDED IN NET ASSETS AT END OF YEAR | | $ | 2,308 | | | $ | 4,605 | | |

| | | | | | | | | | | |

| See Notes to Financial Statements. | 26 | |

| Wright Major Blue Chip Equities Fund (WMBC) |

| These financial highlights reflect selected data for a share outstanding throughout each year. | | | | |

| | | Years Ended December 31, |

| FINANCIAL HIGHLIGHTS | | 2014 | 2013 | 2012 | 2011 | 2010 |

| | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of year | | $ | 17.030 | | $ | 12.690 | | $ | 12.260 | | $ | 12.250 | | $ | 10.870 | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | |

Net investment income (loss)(1) | | | 0.127 | | | 0.096 | | | 0.082 | | | (0.012 | ) | | 0.044 | |

| Net realized and unrealized gain (loss) | | | 2.095 | | | 4.344 | | | 0.437 | | | 0.022 | | | 1.389 | |

| | Total income (loss) from investment operations | | 2.222 | | | 4.440 | | | 0.519 | | | 0.010 | | | 1.433 | |

| | | | | | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.152 | ) | | (0.100 | ) | | (0.089 | ) | | — | | | (0.053 | ) |

| Net asset value, end of year | | $ | 19.100 | | $ | 17.030 | | $ | 12.690 | | $ | 12.260 | | $ | 12.250 | |

Total Return(2) | | | 13.04 | % | | 35.03 | % | | 4.23 | % | | 0.08 | % | | 13.19 | % |

Ratios/Supplemental Data(3): | | | | | | | | | | | | | | | | |

| Net assets, end of year (000 omitted) | | $15,925 | | $17,692 | | $15,559 | | $18,921 | | $21,676 | |

| Ratios (As a percentage of average daily net assets): |

| Net expenses | | | 1.40 | % | 1.40 | % | 1.40 | % | 1.40 | % | 1.41 | % |

| Net investment income (loss) | | | 0.71 | % | 0.65 | % | 0.64 | % | (0.09 | )% | 0.39 | % |

| Portfolio turnover rate | | | 62 | % | 64 | % | 76 | % | 154 | % | 68 | % |

| | | | | | | | | | | | | | | | | |

| | | | | For the years ended December 31, 2014, 2013, 2012, 2011 and 2010 | For the years ended December 31, 2014, 2013, 2012, 2011 and 2010 | | | | | | | |

| (1) | Computed using average shares outstanding. |

| (2) | Total return is calculated assuming a purchase at the net asset value on the first day and a sale at the net asset value on the last day of each year reported. Dividends and distributions, if any, are assumed to be reinvested at the net asset value on the reinvestment date. |

| (3) | For each of the years presented, the operating expenses of the Fund were reduced by a waiver of fees and/or allocation of expenses to the principal underwriter and/or investment adviser. Had such action not been undertaken, expenses and net investment income (loss) ratios would have been as follows: |

| | | | 2014 | 2013 | 2012 | 2011 | 2010 |

| | |

| Ratios (As a percentage of average daily net assets): |

| Expenses | | | 1.86 | % | | 1.87 | % | | 1.84 | % | | 1.70 | % | | 1.68 | % |

| Net investment income (loss) | | | 0.25 | % | | 0.17 | % | | 0.20 | % | | (0.39 | )% | | 0.13 | % |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| See Notes to Financial Statements. | 27 | |

Wright International Blue Chip Equities Fund (WIBC) Portfolio of Investments - As of December 31, 2014 |

AUSTRALIA - 2.4% |

| Australia & New Zealand Banking Group, Ltd. | 7,270 | | $ | 190,916 | |

| Commonwealth Bank of Australia | 3,850 | | | 269,853 | |

| CSL, Ltd. | 842 | | | 59,727 | |

| Seek, Ltd. | 9,824 | | | 138,842 | |

| | | | $ | 659,338 | |

AUSTRIA - 0.4% |

| Voestalpine AG | 2,807 | | $ | 111,392 | |

CANADA - 9.9% |

| Alimentation Couche-Tard, Inc. - Class B | 17,911 | | $ | 752,935 | |

| Catamaran Corp.* | 6,348 | | | 329,498 | |

| CGI Group, Inc. - Class A* | 10,245 | | | 391,756 | |

| Magna International, Inc. | 1,490 | | | 161,948 | |

| Manulife Financial Corp. | 22,660 | | | 433,929 | |

| Methanex Corp. | 3,489 | | | 160,767 | |

| Toronto-Dominion Bank (The) | 11,420 | | | 547,312 | |

| | | | $ | 2,778,145 | |

DENMARK - 1.0% |

| AP Moeller - Maersk A/S - Class B | 134 | | $ | 269,361 | |

FINLAND - 0.5% |

| Nokia OYJ | 18,061 | | $ | 143,367 | |

FRANCE - 7.9% |

| AXA SA | 12,548 | | $ | 291,603 | |

| BNP Paribas SA | 9,454 | | | 563,525 | |

| Cie Generale des Etablissements Michelin | 2,510 | | | 228,612 | |

| Orange SA | 10,771 | | | 184,423 | |

| Societe Generale SA | 4,307 | | | 182,357 | |

| Total SA | 10,092 | | | 519,247 | |

| Vivendi SA | 6,976 | | | 174,651 | |

| Zodiac Aerospace | 2,107 | | | 71,159 | |

| | | | $ | 2,215,577 | |

GERMANY - 11.1% |

| Allianz SE | 1,424 | | $ | 236,669 | |

| BASF SE | 8,289 | | | 700,904 | |

| Bayer AG | 2,222 | | | 303,827 | |

| Bayerische Motoren Werke AG | 2,199 | | | 238,869 | |

| Continental AG | 900 | | | 191,182 | |

| Daimler AG | 3,906 | | | 325,984 | |

| Muenchener Rueckversicherungs-Gesellschaft AG - Class R | 2,778 | | | 557,172 | |

| Siemens AG | 1,227 | | | 139,193 | |

| Volkswagen AG | 1,930 | | | 420,605 | |

| | | | $ | 3,114,405 | |

GREECE - 0.2% |

| Dynagas LNG Partners LP | 3,900 | | $ | 64,038 | |

HONG KONG - 1.4% |

| Cheung Kong Holdings, Ltd. | 16,000 | | $ | 268,838 | |

| Sun Hung Kai Properties, Ltd. | 8,000 | | | 122,040 | |

| | | | $ | 390,878 | |

| | Shares | | | Value | |

IRELAND - 1.2% |

| Ryanair Holdings PLC* | 15,868 | | $ | 187,978 | |

| Shire PLC | 1,984 | | | 140,231 | |

| | | | $ | 328,209 | |

ISRAEL - 0.6% |

| Check Point Software Technologies, Ltd.* | 2,090 | | $ | 164,211 | |

ITALY - 2.0% |

| Enel SpA | 19,668 | | $ | 87,962 | |

| Eni SpA | 11,000 | | | 193,136 | |

| Intesa Sanpaolo SpA | 99,771 | | | 292,403 | |

| | | | $ | 573,501 | |

JAPAN - 24.3% |

| ABC-Mart, Inc. | 1,800 | | $ | 87,527 | |

| Asahi Kasei Corp. | 63,000 | | | 580,896 | |

| Asics Corp. | 4,400 | | | 106,243 | |

| Bandai Namco Holdings, Inc. | 5,700 | | | 121,897 | |

| Bridgestone Corp. | 3,500 | | | 122,578 | |

| Central Japan Railway Co. | 2,191 | | | 331,496 | |

| Daiwa Securities Group, Inc. | 26,000 | | | 205,493 | |

| Fuji Heavy Industries, Ltd. | 5,100 | | | 182,910 | |

| Hitachi Metals, Ltd. | 4,000 | | | 68,794 | |

| Hitachi, Ltd. | 21,000 | | | 157,761 | |

| Hoya Corp. | 6,600 | | | 225,973 | |

| ITOCHU Corp. | 43,400 | | | 467,683 | |

| KDDI Corp. | 12,200 | | | 777,108 | |

| Konica Minolta, Inc. | 5,800 | | | 64,098 | |

| Maeda Road Construction Co., Ltd. | 7,000 | | | 104,625 | |

| Mazda Motor Corp. | 13,600 | | | 332,074 | |

| Mitsubishi Corp. | 7,800 | | | 144,231 | |

| Mitsubishi Electric Corp. | 8,000 | | | 96,484 | |

| Mitsubishi Heavy Industries, Ltd. | 22,000 | | | 122,904 | |

| Murata Manufacturing Co., Ltd. | 1,700 | | | 187,873 | |

| NHK Spring Co., Ltd. | 10,500 | | | 92,481 | |

| Nippon Paint Holdings Co., Ltd. | 6,000 | | | 176,154 | |

| Nippon Telegraph & Telephone Corp. | 5,500 | | | 284,920 | |

| Omron Corp. | 3,600 | | | 163,643 | |

| ORIX Corp. | 16,600 | | | 210,935 | |

| Panasonic Corp. | 7,400 | | | 88,075 | |

| Sekisui Chemical Co., Ltd. | 12,000 | | | 145,627 | |

| Sekisui House, Ltd. | 5,300 | | | 70,154 | |

| Sumitomo Corp. | 16,000 | | | 165,745 | |

| Sumitomo Rubber Industries, Ltd. | 10,400 | | | 156,137 | |

| Suzuki Motor Corp. | 7,000 | | | 212,519 | |

| Tokyo Gas Co., Ltd. | 9,000 | | | 48,950 | |

| Toyota Motor Corp. | 7,700 | | | 485,396 | |

| | | | $ | 6,789,384 | |

NETHERLANDS - 0.6% |

| Boskalis Westminster NV | 3,012 | | $ | 165,650 | |

NORWAY - 0.7% |

| Yara International ASA | 4,500 | | $ | 200,346 | |

SPAIN - 7.1% |

| Banco Bilbao Vizcaya Argentaria SA | 19,684 | | $ | 187,072 | |

| Banco Santander SA | 15,061 | | | 127,499 | |

| See Notes to Financial Statements. | 28 | |

Wright International Blue Chip Equities Fund (WIBC) Portfolio of Investments - As of December 31, 2014 |

| | Shares | | | Value | |

| | | | | | |

| Enagas SA | 7,265 | | | 230,193 | |

| Gas Natural SDG SA | 18,435 | | | 464,214 | |

| Grifols SA | 3,350 | | | 134,257 | |

| Iberdrola SA | 61,812 | | | 418,631 | |

| Red Electrica Corp. SA | 1,555 | | | 137,754 | |

| Telefonica SA | 20,219 | | | 291,635 | |

| | | | $ | 1,991,255 | |

SWEDEN - 0.3% |

| TeliaSonera AB | 12,115 | | $ | 77,999 | |

SWITZERLAND - 11.2% |

| Actelion, Ltd. | 5,338 | | $ | 619,405 | |

| Nestle SA | 12,038 | | | 883,784 | |

| Novartis AG | 4,120 | | | 382,914 | |

| Roche Holding AG | 550 | | | 149,394 | |

| Swiss Re AG | 9,196 | | | 774,161 | |

| UBS AG* | 8,274 | | | 136,977 | |

| Zurich Insurance Group AG (Inhaberktie) | 577 | | | 181,000 | |

| | | | $ | 3,127,635 | |

UNITED KINGDOM - 15.9% |

| Aberdeen Asset Management PLC | 22,394 | | $ | 150,915 | |

| AstraZeneca PLC | 6,491 | | | 461,066 | |

| Aviva PLC | 32,290 | | | 243,937 | |

| BP PLC | 39,545 | | | 253,425 | |

| British American Tobacco PLC | 3,371 | | | 183,968 | |

| GlaxoSmithKline PLC | 25,043 | | | 537,305 | |

| IMI PLC | 5,884 | | | 115,875 | |

| Legal & General Group PLC | 203,073 | | | 787,171 | |

| Rio Tinto PLC | 8,453 | | | 395,410 | |

| Rolls-Royce Holdings PLC | 30,133 | | | 408,768 | |

| Royal Dutch Shell PLC - Class B | 5,504 | | | 191,639 | |

| Vodafone Group PLC | 110,815 | | | 384,713 | |

| WPP PLC | 15,782 | | | 330,979 | |

| | | | $ | 4,445,171 | |

TOTAL EQUITY INTERESTS - 98.7% (identified cost, $22,431,738) | | $ | 27,609,862 | |

SHORT-TERM INVESTMENTS - 0.9% |

| Fidelity Government Money Market Fund, 0.01% (1) | 258,808 | | $ | 258,808 | |

TOTAL SHORT-TERM INVESTMENTS - 0.9% (identified cost, $258,808) | | $ | 258,808 | |

TOTAL INVESTMENTS — 99.6% (identified cost, $22,690,546) | | $ | 27,868,670 | |

| OTHER ASSETS, IN EXCESS OF LIABILITIES — 0.4% | | | 123,712 | |

| NET ASSETS — 100.0% | | $ | 27,992,382 | |

LP — Limited Partnership

PLC — Public Limited Company

| * | Non-income producing security. |

| (1) | Variable rate security. Rate presented is as of December 31, 2014. |

| See Notes to Financial Statements. | 29 | |

| Wright International Blue Chip Equities Fund (WIBC) |

| STATEMENT OF ASSETS AND LIABILITIES |

| As of December 31, 2014 |

| | | | | | | |

| ASSETS: | | | TRUE | |

| | Investments, at value | | | | |

| | (identified cost $22,690,546) (Note 1A) | | $ | 27,868,670 | ###### |

| | Receivable for fund shares sold | | | 2,352 | |

| | Dividends receivable | | | 26,705 | |

| | Tax reclaims receivable | | | 103,285 | |

| | Prepaid expenses and other assets | | | 9,525 | |

| | Total assets | | $ | 28,010,537 | |

| | | | | | | |

| LIABILITIES: | | | | |

| | Payable for fund shares reacquired | | $ | 916 | |

| | Due to broker | | | 204 | |

| | Accrued expenses and other liabilities | | | 17,035 | |

| | Total liabilities | | $ | 18,155 | |

| NET ASSETS | | $ | 27,992,382 | |

| | | | | | | |

| NET ASSETS CONSIST OF: | | | | |

| | Paid-in capital | | $ | 74,197,140 | |

| | Accumulated net realized loss on investments and foreign currency | | | (51,369,270 | ) |

| | Distributions in excess of net investment income | | | (1,499 | ) |

| | Unrealized appreciation on investments and foreign currency | | | 5,166,011 | |

| | Net assets applicable to outstanding shares | | $ | 27,992,382 | |

| | | | | | | |

| SHARES OF BENEFICIAL INTEREST OUTSTANDING AT $0.000 PAR VALUE (UNLIMITED SHARES AUTHORIZED) | | | 1,878,798 | |

| | | | | | | |

| NET ASSET VALUE, OFFERING PRICE, AND REDEMPTION PRICE PER SHARE OF BENEFICIAL INTEREST* | | $ | 14.90 | |

| | | | | | | |

| * | | Shares redeemed or exchanged within three months of purchase are charged a 2.00% redemption fee. |

| STATEMENT OF OPERATIONS |

| For the Year Ended December 31, 2014 |

| | | | | | | |

| INVESTMENT INCOME (Note 1C) | | | TRUE | |

| 2E+07 | Dividend income (net of foreign taxes $146,005) | | $ | 1,328,887 | |

| | Total investment income | | $ | 1,328,887 | |

| | | | | | | |

| Expenses – | | | | |

| | Investment adviser fee (Note 3) | | $ | 252,055 | |

| | Administrator fee (Note 3) | | | 53,561 | |

| | Trustee expense (Note 3) | | | 14,403 | |

| | Custodian fee | | | 32,074 | |

| | Accountant fee | | | 62,559 | |

| | Distribution expenses (Note 4) | | | 78,767 | |

| | Transfer agent fee | | | 44,728 | |

| | Printing | | | 133 | |

| | Shareholder communications | | | 5,364 | |

| | Audit services | | | 17,000 | |

| | Legal services | | | 22,127 | |

| | Compliance services | | | 5,984 | |

| | Registration costs | | | 19,478 | |

| | Interest expense (Note 8) | | | 866 | |

| | Miscellaneous | | | 23,888 | |

| | Total expenses | | $ | 632,987 | |

| | | | | | | |

| Deduct – | | | | |

| | Waiver and/or reimbursement by the principal underwriter and/or investment adviser (Note 4) | | $ | (49,242 | ) |

| | Net expenses | | $ | 583,745 | |

| | Net investment income | | $ | 745,142 | |

| | | | | | | |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND FOREIGN CURRENCY: | |

| Net realized gain (loss) – | | | | |

| | Investment transactions | | $ | 1,059,269 | |

| | Foreign currency transactions | | | (17,463 | ) |

| | Net realized loss | | $ | 1,041,806 | |

| | | | | | | |

| Change in unrealized appreciation (depreciation) – | | | | |

| | Investments | | $ | (3,700,369 | ) |

| | Foreign currency translations | | | (14,933 | ) |

| | Net change in unrealized appreciation (depreciation) on investments | | $ | (3,715,302 | ) |

| | Net realized and unrealized loss on investments and foreign currency translations | | $ | (2,673,496 | ) |

| | Net decrease in net assets from operations | | $ | (1,928,354 | ) |

| | | | | | | |

| See Notes to Financial Statements. | 30 | |

| Wright International Blue Chip Equities Fund (WIBC) |