United States

Securities and Exchange Commission

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-03541

| | Asset Management Fund | |

| | (Exact name of registrant as specified in charter) | |

| | 1000 Brickell Avenue, Suite 500, Miami, FL 33131 | |

| | (Address of principal executive offices) | (Zip code) | |

| Beacon Hill Fund Services, Inc., 4041 North High Street, Suite 402, Columbus, Ohio 43214 |

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (800) 247-9780

Date of fiscal year end: 10/31

Date of reporting period: 10/31/12

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Managed By:

Shay Assets Management, Inc.

ANNUAL REPORT

October 31, 2012

CHAIRMAN’S LETTER

The Asset Management Fund (“AMF” and each series, a “Fund”) family of no-load institutional mutual funds is pleased to present to shareholders the 2012 Annual Report.

Politics tend to dominate the news cycle during Presidential election years, forcing fundamentally important issues to the sideline. This year was somewhat different; the confluence of political grandstanding and acute fiscal and economic imbalances have created a somewhat toxic mix for an already polarized Washington to sort out. It will be difficult for each side to come down off their election soap boxes and achieve a meaningful and balanced solution. For example, as we write this letter, the “Fiscal Cliff” debate has begun; we expect that Washington will let this process devolve into a crisis situation before a band-aid solution is achieved (recall the 500 point stock market decline after Congress initially rejected TARP in October 2008).

To repeat what we wrote last year: “we need leadership out of Washington to put policies in place to spur economic growth”. To clarify that statement, we’re not looking for industrial policy from D.C.; instead, our political leaders need to reform the tax code, stabilize discretionary spending and entitlements, and rationalize defense spending. In other words, put into place policies that put the federal budget deficit on a glide path to long-term stability while protecting the “life, liberty, and happiness” of its citizens. This level of policy clarity provides consumers, investors, businesspeople and corporations the confidence to spend and invest. For example, in the 1950’s, decisive political leadership helped to build the interstate highway system; government knew that their job was to build the roads, not drive the car. We fear that today’s politicians prefer the latter, but don’t know when to use the brakes.

That said, consumers and corporations are trying to rebound. An improving employment picture and low interest rates have reduced consumer debt service burdens to 30 year lows and new homes sales are showing signs of life. Corporate profitability is slowing, but cashflow is strong so balance sheets are well-positioned for an upswing in economic activity. The U.S. is in the midst of an energy boom that could bring self-sufficiency in the next ten years; and the agricultural heartland of the country has benefitted from rising food and farmland prices. While the Chinese economy shows signs of bottoming, Europe and Japan remain difficult stories. The U.S. will have to lead the global economy out of its doldrums.

But missteps in fiscal policy are a risk; monetary policy, however, remains highly accommodative. With negative real rates in the U.S., the Fed is pushing on a string and the asset bubble in long-maturity bond prices will not end well. That said, our philosophy continues to focus on investment strategies that offer safety and transparency to our shareholders. With the Fed Quantitative Easing strategies focusing on longer duration securities, shorter duration government mortgage-backed securities are still the right place to preserve capital. We thank you for your support, and continue to focus on maximizing long-term shareholder value within the appropriate risk management framework.

Rodger D. Shay

Chairman

Asset Management Fund

The report has been prepared to provide information to the shareholders of the Funds and must be proceeded or accompanied by a prospectus. It is not to be construed as an offering to sell or buy any shares of the Funds. Such an offering is made only by the prospectus. You may obtain a current copy of the Prospectus by calling 1-800-247-9780 or at AMF’s website (www.amffunds.com). Investors should consider the investment objectives, risks, and expenses of the Funds before investing. Read the prospectus carefully before you invest. Like all Mutual Funds, the Funds are not FDIC insured, may lose value and have no bank guarantee.

MARKET OVERVIEW

October 31, 2012

As investors know, markets tend to have a memory, meaning that the recent behavior of markets tends to influence investors assumptions regarding future prices. Undoubtedly, the housing market exhibited this kind of mindset in the middle of the previous decade. So with a third consecutive year of roughly 2% real GDP growth under our belt, what is the risk that investor complacency assumes another “slow go” year?

Reviewing the key drivers (and deterrents) of growth over the past few years, and their relationship to the investment strategies we manage for our clients, may shed some light on what to expect over the next few years. Given the ongoing discussions regarding the “Fiscal Cliff”, it is noteworthy that these negotiations (and those that follow) may put a brake on federal government spending. Undoubtedly, the short-term impact on GDP will be negative, although if Washington actually comes up with a long-term, sophisticated financial plan for the budget (unlikely, in our view), improved confidence from consumers and investors could certainly add to long term growth prospects. Regardless, we don’t think that will have much impact on interest rates in 2013; if Washington drops the ball, rates will decline somewhat as economic activity weakens. But the problem with the economy isn’t interest rates, its Washington. If the economy stumbles, the Fed’s Quantitative Easing programs already provide a non-economic bid to bond prices, and more QE will be on the way.

Investors should be wary of this “Interest Rate Gap”, i.e., the difference between the price the Fed will pay for fixed income securities and the price that brings in real economic buyers. The Interest Rate Gap is one of the reasons our Funds have maintained their interest rate exposure towards the lower end of our targets; from a risk/reward perspective, investors simply aren’t getting paid to take interest rate risk. The only substantial risk to interest rates we foresee in 2013 is a sharp steepening in the yield curve; “Operation Twist” has succeeded in flattening the yield curve to a level that is historically unsustainable (given the level of real interest rates), so any unanticipated increase in real GDP should initially cause long term interest rates to rise. QE III has also pushed down mortgage rates somewhat; at the margin, this will support faster prepayments, but the impact will mainly be felt by loans originated between 2009 and 2011, which are origination years that our funds have limited exposure.

Non-durable spending has also led the growth in GDP, but this sector has been dominated by healthcare, education, energy, and core services. These sectors tend to fall more into the category of necessities as opposed to luxury items. They have also recently experienced above average price increases, and with real disposable income in the U.S. essentially flat over the past five years, these expenses are likely “crowding out” other consumer expenditures. But the relentless decline in interest rates (particularly mortgage rates) and mortgage debt outstanding means that consumer’s debt servicing burdens are at a thirty year low. We believe debt service is more important than debt to income ratios, which still look high by historical standards. Given that today’s stock of debt is mainly long-term, fixed rate debt, households have greater certainty as to their disposable income. If the economy improves at all and drives down the unemployment rate, the consumer portion of the economy could be surprisingly supportive of GDP in the next few years.

The government’s HARP (“Home Affordable Refinance Program”) programs have certainly been supportive of this trend. Given that our fixed income funds focus exclusively on government and government agency securities, we pay particular attention to housing policy emanating from Washington. In particular, HARP 2.0 – the second iteration of the government’s program to assist underwater homeowners – has been quite beneficial to homeowners this year. HARP-driven refinancings have surged in 2012, achieving a pace of modification that is three times faster than in 2011. We expected this would be the case, and in the first quarter of 2012 sold securities from our funds which we believed to be the most vulnerable to HARP-induced refinancings.

One surprising statistic for 2012 has been the rebound in home prices. While this was inevitable – population growth absorbs excess housing when new construction is dormant – most market participants felt higher prices would occur in 2014-16. But the economic variable that the market fails to predict is macro-shifts in consumer attitudes and how those attitudes drive expenditures. With employment improving, and the “own vs. rent” equation in favor of home ownership, consumers are wading back into the housing markets. Additionally, the inventory of new housing is at a multi-decade low, so any demand will generate real economic activity (not just inventory draw-downs). This is the “Big Kahuna” of the economic recovery; the multiplier effect on housing is large and the impact on household psyche is meaningful. Economists are forecasting that housing can yield anywhere from 0.50% to 2.0% in 2013; if the higher end is achieved, there will be some unanticipated positive results for the economy.

Portfolio composition is subject to change.

Past performance does not guarantee future results. Investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

MARKET OVERVIEW

October 31, 2012

Besides the impact on GDP and interest rates, improving home prices slowly reduces homeowners’ loan-to-values (“LTV”), a key metric that computes the outstanding loan amount relative to the value of the home and determines whether or not a mortgage is refinanceable. Of course, the national decline in home prices since 2007 – at the trough, home prices were down over 30% - means that it will take several years of consistent home price appreciation to get those ratios back to a level that will allow the homeowner to refinance; so while we track home prices closely, we do not expect higher home prices to demonstrably impact prepayment risk for most of our fund’s holdings.

All that said, the likely outcome for 2013 is, in fact, another year of soft economic growth. While our optimism that the U.S. economy will always surprise the naysayers over the long haul, many roadblocks remain to achieving optimal economic growth. In the meantime, we thank all of our shareholders for allowing us to assist them in their investment needs, and look forward to a prosperous 2013.

The report has been prepared to provide information to the shareholders of the Funds and must be proceeded or accompanied by a prospectus. It is not to be construed as an offering to sell or buy any shares of the Funds. Such an offering is made only by the prospectus. You may obtain a current copy of the prospectus by calling 1-800-247-9780 or at AMF’s website (www.amffunds.com). Investors should consider the investment objectives, risks, and expenses of the Funds before investing. Read the prospectus carefully before you invest. Like all mutual funds, the Funds are not FDIC insured, may lose value and have no bank guarantee.

Portfolio composition is subject to change.

Past performance does not guarantee future results. Investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

ASSET MANAGEMENT FUND REVIEW

October 31, 2012

Ultra Short Mortgage Fund

With nearly zero interest rate volatility on the front part of the yield curve, the Fund focused on securities that offer stable, prepayment protected yields. The Fund’s holdings are mainly seasoned government agency hybrid ARMs; many of the loans backing these pools provide the borrower with a monthly mortgage payment that cannot be replicated even with fixed mortgage rates at all-time lows. This is because many of the loans in our pools are still in their interest-only period, and interest-only loans are generally not available today given the tight credit terms in the current mortgage market. While the Fund did purchase several securities backed by recently issued mortgages, our focus continues to be on seasoned loans which have a variety of impediments to refinancing. This strategy – focusing on higher coupon, seasoned securities – has allowed the Fund to maintain a relatively attractive yield compared to newly issued securities. The Fund was ranked in the 16th percentile and the 55th percentile of the Morningstar Ultra Short Bond category for the one-year periods ended October 31, 2011 and October 31, 2012, respectively.* The recent outperformance relative to its U.S. Treasury T-bills is mainly due to the Federal Reserve’s policy of keeping short-term interest rates unusually low and thereby limiting their total return while short-term mortgage-backed securities have not been subject to these large scale acquisitions.

Portfolio composition is subject to change.

Past performance does not guarantee future results. Investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

| | * | The Morningstar category is assigned based on the underlying securities in each portfolio. Morningstar places funds in a given category based on their portfolio statistics and compositions over the past three years. When necessary, Morningstar may change a category assignment based on recent changes to the portfolio. Morningstar has classified the Ultra Short Mortgage Fund in the Ultra Short Bond category. The Morningstar percentile rankings were based on 105 funds and 111 funds on 10/31/11 and 10/31/12, respectively. The one, three, five and ten-year percentile rankings for the Ultra Short Fund in the Morningstar Ultra Short Bond category as of 10/31/11 and 10/31/12 were as follows: |

| | | | | | | | | | |

| | | One-year Percentile | | Three-year Percentile | | Five-year Percentile | | Ten-year Percentile | |

| 10/31/11 | | 16th | | | | 92nd | | 100th | |

| 10/31/12 | | 55th | | 16th | | 98th | | 96th | |

The percentile rankings shown reflect any expenses that were voluntarily reduced during the periods presented. In such instances, and without this activity, the percentile rankings may have been less favorable.

ASSET MANAGEMENT FUND REVIEW

October 31, 2012

Ultra Short Fund

With nearly zero interest rate volatility on the front part of the yield curve, the Fund focused on securities that offer stable, prepayment protected yields. The Fund’s holdings are mainly seasoned government agency hybrid ARMs; many of the loans backing these pools provide the borrower with a monthly mortgage payment that cannot be replicated even with fixed mortgage rates at all-time lows. This is because many of the loans backing the funds’ pools are still in their interest-only period, and interest-only loans are generally not available today given the tight credit terms in the current mortgage market. The Fund was ranked in the 60th percentile and the 46th percentile of the Morningstar Ultra Short Bond category for the one-year periods ended October 31, 2011 and October 31, 2012, respectively.* The recent outperformance relative to U.S. Treasury T-bills is mainly due to the Federal Reserve’s policy of keeping short-term interest rates unusually low and thereby limiting their total return while short-term mortgage-backed securities have not been subject to these large scale acquisitions.

Portfolio composition is subject to change.

Past performance does not guarantee future results. Investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

| | * | The Morningstar category is assigned based on the underlying securities in each portfolio. Morningstar places funds in a given category based on their portfolio statistics and compositions over the past three years. When necessary, Morningstar may change a category assignment based on recent changes to the portfolio. Morningstar has classified the Ultra Short Fund in the Ultra Short Bond category. The Morningstar percentile rankings were based on 105 funds and 111 funds on 10/31/11 and 10/31/12, respectively. The one, three, five and ten-year percentile rankings for the Ultra Short Fund in the Morningstar Ultra Short Bond category as of 10/31/11 and 10/31/12 were as follows: |

| | | | | | | | | | |

| | | One-year Percentile | | Three-year Percentile | | Five-year Percentile | | Ten-year Percentile | |

| 10/31/11 | | 60th | | 100th | | 100th | | 100th | |

| 10/31/12 | | 46th | | 97th | | 100th | | 100th | |

The percentile rankings shown reflect any expenses that were voluntarily reduced during the periods presented. In such instances, and without this activity, the percentile rankings may have been less favorable.

ASSET MANAGEMENT FUND REVIEW

October 31, 2012

Short U.S. Government Fund

With historically low interest rate volatility on the short to intermediate portion of the yield curve, the Fund focused on securities that offer stable, prepayment protected yields and fixed rate government agency mortgage-backed securities. This strategy – focusing on higher coupon, seasoned securities – has allowed the fund to maintain a relatively attractive yield compared to newly issued securities. The Fund also used fixed rate MBS to manage interest rate exposure, and the fund was generally positioned toward the lower end of its targeted duration range. The Fed’s Quantitative Easing strategies generally reduced the yield advantage of extending duration during a period when the Federal Reserve was holding short interest rates stable. The Fund was ranked in the 77th percentile and the 33rd percentile of the Morningstar Short Government Bond category for the one year periods ended October 31, 2011 and October 31, 2012, respectively.* The recent outperformance relative to short-term U.S. Treasuries is mainly due to the Federal Reserve’s policy of keeping short term interest rates unusually low and thereby limiting their total return while short-term mortgage-backed securities have not been subject to these large scale acquisitions.

Portfolio composition is subject to change.

Past performance does not guarantee future results. Investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

| | * | The Morningstar category is assigned based on the underlying securities in each portfolio. Morningstar places funds in a given category based on their portfolio statistics and compositions over the past three years. When necessary, Morningstar may change a category assignment based on recent changes to the portfolio. Morningstar has classified the Short U.S. Government Fund in the Short Government Bond category. The Morningstar percentile rankings were based on 161 funds and 145 funds on 10/31/11 and 10/31/12, respectively. The one, three, five and ten-year percentile rankings for the Short U.S. Government Fund in the Morningstar Short Government Bond category as of 10/31/11 and 10/31/12 were as follows: |

| | | | | | | | | | |

| | | One-year Percentile | | Three-year Percentile | | Five-year Percentile | | Ten-year Percentile | |

| 10/31/11 | | 77th | | 62nd | | 99th | | 91st | |

| 10/31/12 | | 33rd | | 63rd | | 97th | | 91st | |

The percentile rankings shown reflect any expenses that were voluntarily reduced during the periods presented. In such instances, and without this activity, the percentile rankings may have been less favorable.

ASSET MANAGEMENT FUND REVIEW

October 31, 2012

Intermediate Mortgage Fund

With historically low interest rate volatility on the intermediate portion of the yield curve, the Fund focused on securities that allowed it to benefit from the various Federal Reserve Quantitative Easing programs. The Fund’s holdings are mainly higher coupon, fixed rate securities and this strategy has allowed the fund to maintain a relatively attractive yield compared to newly issued securities. The Fund also used fixed rate MBS to add yield and manage interest rate exposure, and the fund was generally positioned toward the lower end of its targeted duration range. The Fund was ranked in the 42nd percentile and the 42nd percentile of the Morningstar Short-Term Bond category for the one year periods ended October 31, 2011 and October 31, 2012, respectively.* The recent outperformance relative to short and intermediate term U.S. Treasuries is mainly due to the Federal Reserve’s policy of keeping short-term Treasury rates unusually low and thereby limiting their total return potential while intermediate term mortgage-backed securities have recently benefitted from large scale Fed acquisitions.

Portfolio composition is subject to change.

Past performance does not guarantee future results. Investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

| | * | The Morningstar category is assigned based on the underlying securities in each portfolio. Morningstar places funds in a given category based on their portfolio statistics and compositions over the past three years. When necessary, Morningstar may change a category assignment based on recent changes to the portfolio. Morningstar has classified the Intermediate Mortgage Fund in the Short Term Bond category. The Morningstar percentile rankings were based on 440 funds and 436 funds on 10/31/11 and 10/31/12, respectively. The one, three, five and ten-year percentile rankings for the Intermediate Mortgage Fund in the Morningstar Short Term Bond category as of 10/31/11 and 10/31/12 were as follows: |

| | | | | | | | | | |

| | | One-year Percentile | | Three-year Percentile | | Five-year Percentile | | Ten-year Percentile | |

| 10/31/11 | | 42nd | | 100th | | 100th | | 100th | |

| 10/31/12 | | 42nd | | 98th | | 100th | | 100th | |

The percentile rankings shown reflect any expenses that were voluntarily reduced during the periods presented. In such instances, and without this activity, the percentile rankings may have been less favorable.

ASSET MANAGEMENT FUND REVIEW

October 31, 2012

U.S. Government Mortgage Fund

With historically low interest rate volatility on the intermediate portion of the yield curve, the Fund focused on securities that allowed it to benefit from the various Federal Reserve Quantitative Easing programs. The Fund’s holdings are mainly higher coupon, fixed rate securities and this strategy has allowed the fund to maintain a relatively attractive yield compared to newly issued securities. The Fund also used fixed rate MBS to manage interest rate exposure, and the fund was generally positioned toward the lower end of its targeted duration range. The Fund was ranked in the 98th percentile and the 44th percentile of the Morningstar Intermediate Government Bond category for the one year periods ended October 31, 2011 and October 31, 2012, respectively.* The recent outperformance relative to intermediate term U.S. Treasuries is mainly due to the Federal Reserve’s policy of keeping short-term Treasury rates unusually low and thereby limiting their total return potential while intermediate term mortgage-backed securities have recently benefitted from large scale Fed acquisitions.

Portfolio composition is subject to change.

Past performance does not guarantee future results. Investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

| | * | The Morningstar category is assigned based on the underlying securities in each portfolio. Morningstar places funds in a given category based on their portfolio statistics and compositions over the past three years. When necessary, Morningstar may change a category assignment based on recent changes to the portfolio. Morningstar has classified the U.S. Government Mortgage Fund in the Intermediate Government Bond category. The Morningstar percentile rankings were based on 359 funds and 351 funds on 10/31/11 and 10/31/12, respectively. The one, three, five and ten-year percentile rankings for the U.S. Government Mortgage Fund in the Morningstar Intermediate Government Bond category as of 10/31/11 and 10/31/12 were as follow |

| | | | | | | | | | |

| | | One-year Percentile | | Three-year Percentile | | Five-year Percentile | | Ten-year Percentile | |

| 10/31/11 | | 98th | | 99th | | 100th | | 100th | |

| 10/31/12 | | 44th | | 97th | | 100th | | 100th | |

The percentile rankings shown reflect any expenses that were voluntarily reduced during the periods presented. In such instances, and without this activity, the percentile rankings may have been less favorable.

AMF LARGE CAP EQUITY FUND REVIEW

October 31, 2012

Large Cap Equity Fund Review

During the one-year period ending October 31, 2012, the AMF Large Cap Equity Fund (“Class AMF”) produced a total return of 14.16%. Total return figures for the Fund’s peer group and benchmark index were 12.55% for the Morningstar Large Blend Category and 15.20% for the Standard & Poor’s 500 Index for the same period. Total return assumes the reinvestment of all dividends and capital gains and the deduction of all applicable fees and expenses. The AMF Large Cap Equity Fund contains approximately 30 high quality, large capitalization common stock investments. Stemming from its focus on companies that have demonstrated an ability to achieve long-term sustainable earnings and dividend growth, the Fund is more heavily weighted toward sectors of the market that are less cyclical in nature. The Fund’s largest sector weighting is in consumer staples, approximately twice the market weighting. Individual security performance, relative market sector performance and fund expense ratio are the primary drivers of the Fund’s investment return relative to its peer group and index benchmarks. For the one-year period ending October 31, 2012, the AMF Large Cap Equity Fund outperformed its peer group, the Morningstar Large Blend Category, by 161 basis points and underperformed the S&P 500 Index by 104 basis points. Net of the Fund’s 120 basis point expense ratio, the Fund outperformed the S&P 500 index by 16 basis points.

During the past year, the domestic economy has produced positive growth although the pace has been slow. Gross Domestic Product (GDP) growth has hovered around the 2% mark throughout the 12-month period. The employment picture has also improved somewhat, but here again the rate of improvement is tepid. The unemployment rate has just recently dipped below the 8% level, however, that leaves a sizeable portion of the U.S. working population still looking for employment. The level of underemployment, people with jobs but not earning at their full capacity, also remains quite high. The Federal Reserve has been actively trying to address these matters with an extremely accommodative monetary policy. The result of which has further reduced interest rates from this time last year. Short-term interest rates are near zero, while the benchmark 10-year Treasury note yields approximately 1.69%.

There are rays of light emanating from recent economic reports. The housing market is showing steady signs of improvement, as distressed sales have become a smaller part of the resale market, and new home sales volume has increased. Home prices are making positive headway as historically low mortgage rates help affordability and the employment picture slowly improves. Consumer confidence has also been steadily improving as consumers continue the deleveraging process and personal balance sheets improve. Higher consumer confidence has also led to strong retail sales figures.

Looking at the year from a business perspective, profit margins have remained elevated after efficiencies were implemented during and after the “Great Recession” of 2008-2009, which has translated into continued earnings and cash flow growth. However, the slow rate of economic growth in the U.S., coupled with a slowdown in global economic growth, has tempered revenue growth. Concerns over the 2012 Presidential election outcome and uncertainly regarding a resolution to the year-end “fiscal cliff” have put the brakes on business investment. However, dividend paying companies continued to expand their payouts and many companies also repurchased shares during the year as cash continued to mount on their balance sheets. As interest rates continued their decline, reducing the attractiveness of investment alternatives, price-earnings (p/e) ratios expanded (and earnings yields contracted) over the course of the year. The total return of the stock market during the 12-month period can be summarized as a combination of expanding p/e ratios, nominal earnings growth and higher dividend payouts.

The AMF Large Cap Equity Fund’s investment philosophy focuses on investing in high quality, large capitalization common stocks. More specifically, we seek to acquire equity stakes in established companies that we believe have the ability to produce long-term sustainable earnings and dividend growth at favorable valuations for long-term ownership. We believe that this is a prudent way for investors to accumulate wealth over the long-term and benefit from the merits of compounding. As of October 31, 2012, the portfolio’s 30 holdings had a weighted average earnings yield of 7.19% (12-month trailing earnings divided by the closing stock price on 10/31/12). The weighted average 5-year historical earnings growth rate for these holdings was 6.49%. This period includes the recession of 2008-2009 as well as the subsequent economic recovery, which has been slower than normal. The weighted average dividend yield of our current portfolio holdings as of October 31, 2012 is 2.61%. Over the previous 5-year period, the growth rate of these dividends has been 9.02% on a weighted average basis. The current earnings and dividend yields available in the equity market today are very attractive relative to the “risk-free” alternative in the U.S. Treasury market.

Our long-term approach to investing in high quality companies once again resulted in low portfolio turnover of 8% during the year. Two additions were made to the portfolio during the period, namely Walt Disney and DuPont. We believe that each company provides us with a favorable combination of earnings and dividend growth and were available at attractive valuations.

Portfolio composition is subject to change.

Past performance does not guarantee future results. Investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

AMF LARGE CAP EQUITY FUND REVIEW

October 31, 2012

Disney’s television broadcasting network, led by ESPN, theme parks, filmed entertainment and merchandising products have generated steady growth over its history, which we feel will continue well into the future. DuPont’s agricultural seed and crop protection products, performance chemical, coatings and materials, and electronic, safety and protection products provide for a diversified revenue mix capable of producing attractive long-term earnings growth in our opinion. DuPont also pays out a handsome dividend. Valuation is a significant factor in our investment process, which prompted our two recent additions, as well as led to reductions in a number of existing positions after significant price appreciation. Some of the more notable reductions included Home Depot, TJX Companies, Wal-Mart Stores and Abbott Labs.

As we look forward into the next twelve months, investors have plenty of things to worry about – the “fiscal cliff,” slow economic growth, high unemployment, the government deficit to name a few. However, each and every year it seems there is a laundry list of things to worry about, and next year you can be sure that investors will have new worries on their minds. At the AMF Large Cap Equity Fund, your portfolio management team prefers to focus on company specific fundamentals and valuation. By identifying investments that offer the opportunity for long-term sustainable earnings and dividend growth and making acquisitions when valuations are attractive, we feel that long-term wealth creation can be achieved even as investor sentiment ebbs and flows over the course of time. In fact pessimism is often our friend, as it is during those times that valuations are often most attractive.

Portfolio composition is subject to change.

Past performance does not guarantee future results. Investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

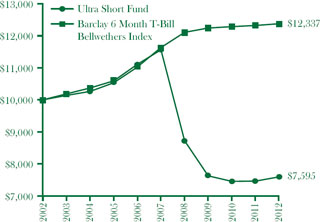

Investment Comparison (Unaudited)

Comparison of change in value of a hypothetical $10,000 investment for the years ended October 31

| | | | | |

| Ultra Short Mortgage Fund | | | | |

| | | | | |

| Gross Expense Ratio 0.97% |

| |

| The above expense ratio is from the Funds’ prospectus dated March 1, 2012. Additional information pertaining to the Funds’ expense ratios as of October 31, 2012 can be found in the Financial Highlights. |

| | | | |

Average Annual Total Return Periods Ending October 31, 2012 |

| | | | |

| | One Year | Five Year | Ten Year |

| Ultra Short Mortgage Fund | 1.46% | –2.03% | 0.38% |

| Barclay 6 Month T-Bill | | | |

| Bellwethers Index | 0.12% | 0.92% | 1.96% |

| | | | |

| | | | |

| | | | | |

| | | | | |

| Ultra Short Fund | | | | |

| | | | | |

| Gross Expense Ratio 1.09% |

| | | | |

| The above expense ratio is from the Funds’ prospectus dated March 1, 2012. Additional information pertaining to the Funds’ expense ratios as of October 31, 2012 can be found in the Financial Highlights. |

| | | | |

Average Annual Total ReturnPeriods Ending October 31, 2012 |

| |

| | One Year | Five Year | Ten Year |

| Ultra Short Fund | | | |

| Barclay 6 Month T-Bill | | | |

| Bellwethers Index | 0.12% | 0.92% | 1.96% |

| | | | | |

| |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Performance figures in the table and graph do not reflect the deduction of taxes that a shareholder would pay on the Fund distributions or the redemption of Fund shares. The Barclay 6 Month T-Bill Bellwethers Index is an unmanaged index comprised of U.S. Government Treasury Bonds with an average maturity of six months. The index represents unmanaged groups of bonds that differ from the composition of each AMF Fund. The index does not include a reduction in return for expenses. Investors cannot invest directly in an index, although they can invest in its underlying securities. To obtain current month-end performance information for any of the AMF Funds, please call 1-800-247-9780. |

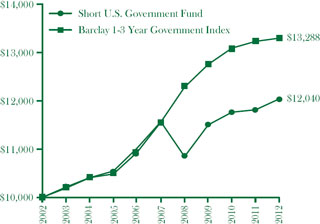

Investment Comparison (Unaudited)

Comparison of change in value of a hypothetical $10,000 investment for the years ended October 31

| | | | | |

| Short U.S. Government Fund | | | | |

| | | | | |

| Gross Expense Ratio 0.73% |

| |

| The above expense ratio is from the Funds’ prospectus dated March 1, 2012. Additional information pertaining to the Funds’ expense ratios as of October 31, 2012 can be found in the Financial Highlights. |

| | | | |

Average Annual Total Return Periods Ending October 31, 2012 |

| | | | |

| | One Year | Five Year | Ten Year |

| Short U.S. Government Fund | 1.91% | 0.81% | 1.87% |

| Barclay 1-3 Year Government Index | 0.42% | 2.73% | 2.78% |

| | | | |

| | | | | |

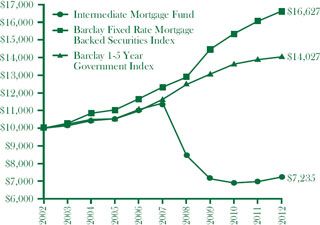

| | | | | |

| Intermediate Mortgage Fund | | | | |

| | | | | |

| Gross Expense Ratio 0.82% | Net Expense Ratio 0.75% |

| | | | |

| The above expense ratios are from the Funds’ prospectus dated March 1, 2012. As indicated in the difference between the gross and net expense ratio, contractual fee waivers are in effect from March 1, 2012 through February 28th, 2013. Additional information pertaining to the Funds’ expense ratios as of October 31, 2012 can be found in the Financial Highlights. |

| | | | |

Average Annual Total Return Periods Ending October 31, 2012 |

| | | | |

| | One Year | Five Year | Ten Year |

| Intermediate Mortgage Fund | 3.72% | –8.72% | –3.18% |

| Barclay Fixed Rate Mortgage | | | |

| Backed Securities Index | 3.56% | 6.17% | 5.22% |

| Barclay 1-5 Year Government Index | 1.05% | 3.83% | 2.29% |

| |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Performance figures in the table and graph do not reflect the deduction of taxes that a shareholder would pay on the Fund distributions or the redemption of Fund shares. The Barclay 1-3 Year Government Index is an unmanaged index generally representative of government securities with maturities of one to three years. The Barclay Fixed Rate Mortgage Backed Securities Index is a broad-based unmanaged index that represents the general performance of fixed rate mortgage bonds. The Barclay 1-5 Year Government Index is an unmanaged index generally representative of government securities with maturities of one to five years. The indices represent unmanaged groups of bonds that differ from the composition of each AMF Fund. The indices do not include a reduction in return for expenses. Investors cannot invest directly in an index, although they can invest in its underlying securities. To obtain current month-end performance information for any of the AMF Funds, please call 1-800-247-9780. |

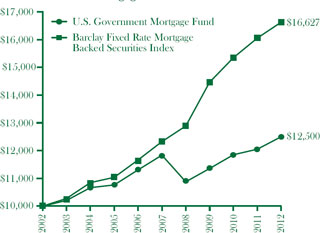

Investment Comparison (Unaudited)

Comparison of change in value of a hypothetical $10,000 investment for the years ended October 31

| | | | | |

| U.S. Government Mortgage Fund | | | | |

| | | | | |

| Gross Expense Ratio 0.73% |

| |

| The above expense ratio is from the Funds’ prospectus dated March 1, 2012. Additional information pertaining to the Funds’ expense ratios as of October 31, 2012 can be found in the Financial Highlights. |

| | | | |

Average Annual Total Return Periods Ending October 31, 2012 |

| | | | |

| | One Year | Five Year | Ten Year |

| U.S. Government Mortgage Fund | 3.73% | 1.10% | 2.26% |

| Barclay Fixed Rate Mortgage | | | |

| Backed Securities Index | 3.56% | 6.17% | 5.22% |

| | | | |

| |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Performance figures in the table and graph do not reflect the deduction of taxes that a shareholder would pay on the Fund distributions or the redemption of Fund shares. The Barclay Fixed Rate Mortgage Backed Securities Index is a broad-based unmanaged index that represents the general performance of fixed rate mortgage bonds. The index represents unmanaged groups of bonds that differ from the composition of each AMF Fund. The index does not include a reduction in return for expenses. Investors cannot invest directly in an index, although they can invest in its underlying securities. To obtain current month-end performance information for any of the AMF Funds, please call 1-800-247-9780. |

Investment Comparison (Unaudited)

Comparison of change in value of a hypothetical $10,000 investment for the years ended October 31

| | | | | | |

| Large Cap Equity Fund | | | | |

| | | | | |

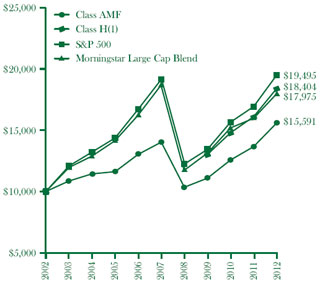

| The following graph shows that an investment of $10,000 in the Class AMF of the Fund on October 31, 2002 would have been worth $15,591 on October 31, 2012, assuming all dividends and distributions had been reinvested. A similar investment in the S&P 500, over the same period, would have been to $19,495. A similar investment in the Morningstar Large Cap Blend, over the same period, would have worth to $17,975. | Gross Expense Ratio Class AMF 1.24% Class H 0.99% The above expense ratios are from the Funds’ prospectus dated March 1, 2012. Additional information pertaining to the Funds’ expense ratios as of October 31, 2012 can be found in the Financial Highlights. |

| | |

| Average Annual Total Return Periods Ending October 31, 2012* |

| |

| | One Year | Five Year | Ten Year | Since Inception |

| Class AMF | 14.16% | 2.13% | 4.54% | |

| Class H(1) | 14.33% | N/A | N/A | 17.96% |

| Morningstar Large Cap Blend | 12.55% | –0.79% | 6.04% | |

| S&P 500 | 15.20% | 0.36% | 6.91% | |

| | | | | | |

| * Assumes reinvestment of all dividends and distributions and the deduction of all applicable fees and expenses. Average annual returns are stated for periods greater than one year. The S&P 500 does not include a reduction in total return for expenses. |

| |

| |

| |

| |

| | |

| (1) Class H of the Fund commenced operations on February 20, 2009. An investment of $10,000 in Class H on February 20, 2009 would have been worth $18,405 on October 31, 2012. |

| |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Performance figures in the table and graph do not reflect the deduction of taxes that a shareholder would pay on the Fund distributions or the redemption of Fund shares. The Morningstar Large Cap Blend Average consists of funds that, by portfolio practice, invest at least 70% of assets in domestic stocks in the top 70% of the capitalization of the U.S. equity market. These portfolios tend to invest across the spectrum of U.S. industries, and owing to their broad exposure, the portfolios’ returns are often similar to those of the S&P 500 Index. The Standard & Poors 500 Index is an unmanaged index, generally representative of the U.S. stock market as a whole. Each of these indices represents an unmanaged group of securities that differ from the composition of each AMF Fund. Investors cannot invest directly in an index, although they can invest in its underlying securities. To obtain current month-end performance information for any of the AMF Funds, please call 1-800-247-9780. |

ASSET MANAGEMENT FUND

ULTRA SHORT MORTGAGE FUND

SCHEDULE OF INVESTMENTS

October 31, 2012

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | Maturity Date | | Principal Amount | | Value | |

| ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES* | | | 58.3% | | | | | | | | | | |

| 1 Yr. Constant Maturity Treasury Based ARMS | | | 38.7% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 2.49% | | | | | | 7/1/28 | | $ | 1,893,423 | | $ | 1,998,895 | |

| 2.11% | | | | | | 8/1/29 | | | 1,517,285 | | | 1,581,777 | |

| 2.27% | | | | | | 3/1/30 | | | 220,749 | | | 232,086 | |

| 2.34% | | | | | | 5/1/33 | | | 748,165 | | | 795,217 | |

| 2.48% | | | | | | 9/1/33 | | | 2,398,371 | | | 2,526,396 | |

| 2.32% | | | | | | 1/1/35 | | | 6,258,596 | | | 6,669,698 | |

| 2.38% | | | | | | 1/1/35 | | | 4,998,513 | | | 5,342,411 | |

| 2.80% | | | | | | 9/1/36 | | | 13,026,474 | | | 14,009,686 | |

| 2.83% | | | | | | 6/1/37 | | | 18,719,299 | | | 20,114,954 | |

| 2.32% | | | | | | 9/1/38 | | | 8,579,177 | | | 9,222,135 | |

| 2.71% | | | | | | 9/1/38 | | | 21,067,058 | | | 22,562,188 | |

| 2.85% | | | | | | 5/25/42 | | | 5,594,986 | | | 5,886,188 | |

| Fannie Mae Grantor Trust | | | | | | | | | | | | | |

| 3.48% | | | | | | 5/25/42 | | | 7,448,843 | | | 7,612,003 | |

| 2.80% | | | | | | 8/25/43 | | | 8,991,682 | | | 9,282,563 | |

| Fannie Mae Whole Loan | | | | | | | | | | | | | |

| 3.05% | | | | | | 8/25/42 | | | 8,509,696 | | | 9,191,757 | |

| 3.63% | | | | | | 8/25/42 | | | 3,202,853 | | | 3,427,885 | |

| 2.73% | | | | | | 4/25/45 | | | 15,667,392 | | | 16,790,153 | |

| Freddie Mac | | | | | | | | | | | | | |

| 2.32% | | | | | | 10/1/22 | | | 552,434 | | | 569,991 | |

| 2.28% | | | | | | 9/1/27 | | | 979,798 | | | 1,018,453 | |

| 2.24% | | | | | | 9/1/28 | | | 6,761,104 | | | 7,076,037 | |

| 2.25% | | | | | | 9/1/30 | | | 557,565 | | | 575,341 | |

| 2.36% | | | | | | 7/1/31 | | | 3,475,747 | | | 3,610,679 | |

| | | | | | | | | | | | | 150,096,493 | |

| 12 Mo. London Interbank Offering Rate (LIBOR) | | | 7.7% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 2.74% | | | | | | 8/1/37 | | | 28,219,765 | | | 30,336,247 | |

| 6 Mo. Certificate of Deposit Based ARMS | | | 0.7% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 1.48% | | | | | | 6/1/21 | | | 809,029 | | | 817,483 | |

| 1.96% | | | | | | 12/1/24 | | | 1,388,749 | | | 1,429,324 | |

| Freddie Mac | | | | | | | | | | | | | |

| 2.19% | | | | | | 1/1/26 | | | 557,748 | | | 578,117 | |

| | | | | | | | | | | | | 2,824,924 | |

| 6 Mo. London Interbank Offering Rate (LIBOR) | | | 3.4% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 2.02% | | | | | | 9/1/27 | | | 2,851,739 | | | 2,964,759 | |

| 1.97% | | | | | | 3/1/28 | | | 2,847,098 | | | 2,951,316 | |

| 2.46% | | | | | | 6/1/28 | | | 404,608 | | | 428,149 | |

| 1.95% | | | | | | 9/1/33 | | | 1,329,532 | | | 1,378,994 | |

| 2.00% | | | | | | 11/1/33 | | | 2,222,830 | | | 2,308,011 | |

| 2.02% | | | | | | 11/1/33 | | | 968,573 | | | 1,003,987 | |

| Freddie Mac | | | | | | | | | | | | | |

| 2.86% | | | | | | 9/1/30 | | | 2,311,591 | | | 2,470,892 | |

| | | | | | | | | | | | | 13,506,108 | |

| | | | | | | | | �� | | | | | |

| | | | | | | | | | | | | | |

| See notes to financial statements. | | | | | | | | | | | | | |

ASSET MANAGEMENT FUND

ULTRA SHORT MORTGAGE FUND

SCHEDULE OF INVESTMENTS

October 31, 2012

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | Maturity Date | | Principal Amount | | Value | |

| Cost of Funds Index Based ARMS | | | 8.4% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 3.31% | | | | | | 2/1/28 | | $ | 11,021,619 | | $ | 11,690,863 | |

| 2.37% | | | | | | 8/1/33 | | | 6,913,874 | | | 7,216,771 | |

| 2.96% | | | | | | 11/1/36 | | | 7,374,342 | | | 7,891,438 | |

| 2.35% | | | | | | 6/1/38 | | | 6,010,522 | | | 6,278,392 | |

| | | | | | | | | | | | | 33,077,464 | |

| TOTAL ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES | | | | | | | | | | | | 232,089,349 | |

| FIXED RATE MORTGAGE-RELATED SECURITIES | | | 35.3% | | | | | | | | | | |

| 15 Yr. Securities | | | 7.6% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 3.00% | | | | | | 9/1/22 | | | 19,648,586 | | | 20,775,310 | |

| 2.50% | | | | | | 10/1/27 | | | 6,109,485 | | | 6,412,656 | |

| 2.50% | | | | | | 10/1/27 | | | 2,744,294 | | | 2,880,474 | |

| | | | | | | | | | | | | 30,068,440 | |

| 30 Yr. Securities | | | 9.9% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 4.00% | | | | | | 5/1/42 | | | 17,252,323 | | | 18,115,733 | |

| 4.00% | | | | | | 8/1/42 | | | 4,854,914 | | | 5,428,624 | |

| Freddie Mac | | | | | | | | | | | | | |

| 4.00% | | | | | | 3/1/42 | | | 11,719,342 | | | 12,288,000 | |

| Government National Mortgage Association | | | | | | | | | | | | | |

| 4.00% | | | | | | 12/15/41 | | | 2,969,117 | | | 3,255,387 | |

| | | | | | | | | | | | | 39,087,744 | |

| Collateralized Mortgage Obligations | | | 17.8% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 5.00% | | | | | | 2/25/18 | | | 3,314,635 | | | 3,534,124 | |

| 4.00% | | | | | | 10/25/23 | | | 2,034,977 | | | 2,109,342 | |

| 5.00% | | | | | | 3/25/24 | | | 4,391,403 | | | 4,734,468 | |

| 4.50% | | | | | | 6/25/36 | | | 11,168,063 | | | 11,654,433 | |

| 4.00% | | | | | | 8/25/37 | | | 3,704,149 | | | 3,905,311 | |

| Freddie Mac | | | | | | | | | | | | | |

| 4.00% | | | | | | 6/15/36 | | | 13,124,235 | | | 13,602,075 | |

| Government National Mortgage Association | | | | | | | | | | | | | |

| 4.77% | | | | | | 8/16/27 | | | 1,984,982 | | | 1,989,271 | |

| 5.00% | | | | | | 8/20/35 | | | 6,267,481 | | | 6,335,043 | |

| 4.50% | | | | | | 11/20/36 | | | 2,445,694 | | | 2,470,177 | |

| 4.00% | | | | | | 6/20/39 | | | 18,367,148 | | | 19,728,337 | |

| | | | | | | | | | | | | 70,062,581 | |

| TOTAL FIXED RATE MORTGAGE-RELATED SECURITIES | | | | | | | | | | | | 139,218,765 | |

| U.S. GOVERNMENT OBLIGATIONS | | | 0.6% | | | | | | | | | | |

| FHLMC Structured Pass-Through Securities | | | | | | | | | | | | | |

| 3.31% | | | | | | 3/25/44 | | | 2,158,211 | | | 2,248,113 | |

| TOTAL U.S. GOVERNMENT OBLIGATIONS | | | | | | | | | | | | 2,248,113 | |

| U.S. GOVERNMENT AGENCIES | | | 1.0% | | | | | | | | | | |

| FDIC Structured Sale Guaranteed Notes | | | | | | | | | | | | | |

| 1.68%(a)(b) | | | | | | 1/7/13 | | | 2,500,000 | | | 2,499,825 | |

| 3.00%(b) | | | | | | 9/30/19 | | | 1,580,961 | | | 1,618,508 | |

| TOTAL U.S. GOVERNMENT AGENCIES | | | | | | | | | | | | 4,118,333 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| See notes to financial statements. | | | | | | | | | | | | | |

ASSET MANAGEMENT FUND

ULTRA SHORT MORTGAGE FUND

SCHEDULE OF INVESTMENTS

October 31, 2012

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | | | Shares | | Value | |

| INVESTMENT COMPANIES | | | 0.0% | | | | | | | | | | |

| Northern Institutional Treasury Portfolio, 0.04% | | | | | | | | | 917 | | $ | 917 | |

| TOTAL INVESTMENT COMPANIES | | | | | | | | | | | | 917 | |

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | | | Principal Amount | | Value | |

| REPURCHASE AGREEMENTS | | | 4.7% | | | | | | | | | | |

Bank of America, 0.23%, (Agreement dated 10/31/12

to be repurchased at $18,722,120 on 11/1/12.

Collateralized by Fixed Rate U.S. Government

Mortgage-Backed Securities, 2.50% - 3.00%, with a

value of $19,096,441, due at 12/20/40 - 4/20/42) | | | | | | | | $ | 18,722,000 | | $ | 18,722,000 | |

| TOTAL REPURCHASE AGREEMENTS | | | | | | | | | | | | 18,722,000 | |

TOTAL INVESTMENTS

(Cost $385,828,628)(c) | | | 99.9% | | | | | | | | | 394,149,364 | |

| NET OTHER ASSETS (LIABILITIES) | | | 0.1% | | | | | | | | | 240,290 | |

| NET ASSETS | | | 100.0% | | | | | | | | $ | 394,389,654 | |

| | | | | | | | | | | | | | |

| | |

| * | The rates presented are the rates in effect at October 31, 2012. |

| (a) | Zero coupon bond reflects effective yield on the date of purchase. |

| (b) | Securities purchased in a transaction exempt from registration under Rule 144A of the Securities Act of 1933. These securities may not be publicly traded without registration under the Securities Act of 1933. The value of these securities is determined by valuations supplied by a pricing service or brokers. |

| (c) | Represents cost for financial reporting purposes. |

| | FDIC - Federal Deposit Insurance Corporation. |

| | FHLMC - Federal Home Loan Mortgage Corporation. |

See notes to financial statements.

| |

| ASSET MANAGEMENT FUND |

| ULTRA SHORT FUND |

| SCHEDULE OF INVESTMENTS |

| October 31, 2012 |

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | Maturity Date | | Principal Amount | | Value | |

| ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES* | | | 79.3% | | | | | | | | | | |

| 1 Yr. Constant Maturity Treasury Based ARMS | | | 57.3% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 2.30% | | | | | | 10/1/28 | | $ | 135,458 | | $ | 142,714 | |

| 2.66% | | | | | | 12/1/30 | | | 372,175 | | | 397,045 | |

| 2.26% | | | | | | 7/1/33 | | | 531,605 | | | 556,206 | |

| 2.71% | | | | | | 9/1/38 | | | 916,065 | | | 981,078 | |

| Freddie Mac | | | | | | | | | | | | | |

| 2.37% | | | | | | 11/1/28 | | | 111,818 | | | 117,225 | |

| 2.86% | | | | | | 1/1/29 | | | 514,081 | | | 550,582 | |

| 2.28% | | | | | | 7/1/30 | | | 362,956 | | | 380,594 | |

| 2.32% | | | | | | 9/1/30 | | | 76,008 | | | 80,780 | |

| 2.54% | | | | | | 8/1/31 | | | 820,279 | | | 864,322 | |

| | | | | | | | | | | | | 4,070,546 | |

| 12 Mo. London Interbank Offering Rate (LIBOR) | | | 22.0% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 2.74% | | | | | | 8/1/37 | | | 1,452,101 | | | 1,561,008 | |

| TOTAL ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES | | | | | | | | | | | | 5,631,554 | |

| FIXED RATE MORTGAGE-RELATED SECURITIES | | | 14.7% | | | | | | | | | | |

| 15 Yr. Securities | | | 14.7% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 2.50% | | | | | | 10/1/27 | | | 994,601 | | | 1,043,956 | |

| TOTAL FIXED RATE MORTGAGE-RELATED SECURITIES | | | | | | | | | | | | 1,043,956 | |

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | | | Shares | | Value | |

| INVESTMENT COMPANIES | | | 5.1% | | | | | | | | | | |

| Northern Institutional Treasury Portfolio, 0.04% | | | | | | | | | 359,804 | | $ | 359,804 | |

| TOTAL INVESTMENT COMPANIES | | | | | | | | | | | | 359,804 | |

TOTAL INVESTMENTS

(Cost $6,899,257)(a) | | | 99.1% | | | | | | | | | 7,035,314 | |

| OTHER NET ASSETS (LIABILITIES) | | | 0.9% | | | | | | | | | 60,404 | |

| NET ASSETS | | | 100.0% | | | | | | | | $ | 7,095,718 | |

| | | | | | | | | | | | | | |

| | |

| * | The rates presented are the rates in effect at October 31, 2012. |

| (a) | Represents cost for financial reporting purposes. |

See notes to financial statements.

| |

| ASSET MANAGEMENT FUND |

| SHORT U.S. GOVERNMENT FUND |

| SCHEDULE OF INVESTMENTS |

| October 31, 2012 |

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | Maturity Date | | Principal Amount | | Value | |

| ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES* | | | 32.5% | | | | | | | | | | |

| 1 Yr. Constant Maturity Treasury Based ARMS | | | 32.5% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 2.55% | | | | | | 5/1/31 | | $ | 549,400 | | $ | 586,431 | |

| 2.38% | | | | | | 1/1/35 | | | 427,513 | | | 456,926 | |

| 2.80% | | | | | | 9/1/36 | | | 605,883 | | | 651,613 | |

| 2.71% | | | | | | 9/1/38 | | | 1,641,283 | | | 1,757,765 | |

| Fannie Mae Grantor Trust | | | | | | | | | | | | | |

| 3.48% | | | | | | 5/25/42 | | | 843,190 | | | 861,659 | |

| 2.80% | | | | | | 8/25/43 | | | 1,755,914 | | | 1,812,718 | |

| Freddie Mac | | | | | | | | | | | | | |

| 2.34% | | | | | | 3/1/27 | | | 276,063 | | | 289,478 | |

| 2.54% | | | | | | 8/1/31 | | | 1,196,380 | | | 1,260,618 | |

| | | | | | | | | | | | | 7,677,208 | |

| TOTAL ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES | | | | | | | | | | | | 7,677,208 | |

| FIXED RATE MORTGAGE-RELATED SECURITIES | | | 60.6% | | | | | | | | | | |

| 15 Yr. Securities | | | 37.5% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 3.50% | | | | | | 7/1/21 | | | 1,825,270 | | | 1,937,420 | |

| 2.50% | | | | | | 2/1/26 | | | 419,014 | | | 438,890 | |

| 3.00% | | | | | | 1/1/27 | | | 4,145,984 | | | 4,378,279 | |

| 2.50% | | | | | | 10/1/27 | | | 1,989,202 | | | 2,087,913 | |

| Freddie Mac | | | | | | | | | | | | | |

| 8.00% | | | | | | 12/17/15 | | | 12,370 | | | 12,942 | |

| | | | | | | | | | | | | 8,855,444 | |

| 30 Yr. Securities | | | 4.0% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 4.00% | | | | | | 5/1/42 | | | 905,437 | | | 950,750 | |

| Collateralized Mortgage Obligations | | | 19.1% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 4.00% | | | | | | 8/25/37 | | | 926,037 | | | 976,328 | |

| Freddie Mac | | | | | | | | | | | | | |

| 4.50% | | | | | | 4/15/19 | | | 2,834,387 | | | 3,001,673 | |

| | | | | | | | | | | | | | |

See notes to financial statements.

| |

| ASSET MANAGEMENT FUND |

| SHORT U.S. GOVERNMENT FUND |

| SCHEDULE OF INVESTMENTS |

| October 31, 2012 |

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | Maturity Date | | Principal Amount | | Value | |

| Government National Mortgage Association | | | | | | | | | | | | | |

| 4.77% | | | | | | 8/16/27 | | $ | 86,304 | | $ | 86,490 | |

| 3.96% | | | | | | 6/16/31 | | | 142,385 | | | 145,470 | |

| 4.50% | | | | | | 11/20/36 | | | 284,686 | | | 287,536 | |

| | | | | | | | | | | | | 4,497,497 | |

| TOTAL FIXED RATE MORTGAGE-RELATED SECURITIES | | | | | | | | | | | | 14,303,691 | |

| U.S. GOVERNMENT AGENCIES | | | 2.1% | | | | | | | | | | |

| FDIC Structured Sale Guaranteed Notes | | | | | | | | | | | | | |

| 1.68%(a)(b) | | | | | | 1/7/13 | | | 500,000 | | | 499,965 | |

| TOTAL U.S. GOVERNMENT AGENCIES | | | | | | | | | | | | 499,965 | |

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | | | Shares | | Value | |

| INVESTMENT COMPANIES | | | 0.0% | | | | | | | | | | |

| Northern Institutional Treasury Portfolio 0.04% | | | | | | | | | 381 | | $ | 381 | |

| TOTAL INVESTMENT COMPANIES | | | | | | | | | | | | 381 | |

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | | | Principal Amount | | Value | |

| REPURCHASE AGREEMENTS | | | 4.7% | | | | | | | | | | |

Bank of America, 0.23%, (Agreement dated 10/31/12

to be repurchased at $1,103,007 on 11/1/12

Collateralized by Fixed Rate U.S. Government

Mortgage-Backed Security, 3.00%, with a value of

$1,125,060, due at 12/20/40) | | | | | | | | $ | 1,103,000 | | $ | 1,103,000 | |

| TOTAL REPURCHASE AGREEMENTS | | | | | | | | | | | | 1,103,000 | |

TOTAL INVESTMENTS

(Cost $23,076,526)(c) | | | 99.9% | | | | | | | | | 23,584,245 | |

| NET OTHER ASSETS (LIABILITIES) | | | 0.1% | | | | | | | | | 22,887 | |

| NET ASSETS | | | 100.0% | | | | | | | | $ | 23,607,132 | |

| | | | | | | | | | | | | | |

| | |

| * | The rates presented are the rates in effect at October 31, 2012. |

| (a) | Securities purchased in a transaction exempt from registration under Rule 144A of the Securities Act of 1933. These securities may not be publicly traded without registration under the Securities Act of 1933. The value of these securities is determined by valuations supplied by a pricing service or brokers. |

| (b) | Zero coupon bond reflects effective yield on the date of purchase. |

| (c) | Represents cost for financial reporting purposes. |

| | FDIC - Federal Deposit Insurance Corporation. |

See notes to financial statements.

| |

| ASSET MANAGEMENT FUND |

| INTERMEDIATE MORTGAGE FUND |

| SCHEDULE OF INVESTMENTS |

| October 31, 2012 |

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | Maturity Date | | Principal Amount | | Value | |

| ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES* | | | 11.6% | | | | | | | | | | |

| 1 Yr. Constant Maturity Treasury Based ARMS | | | 11.6% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 2.52% | | | | | | 7/1/37 | | $ | 1,509,745 | | $ | 1,628,091 | |

| 2.71% | | | | | | 9/1/38 | | | 1,259,589 | | | 1,348,982 | |

| | | | | | | | | | | | | 2,977,073 | |

| TOTAL ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES | | | | | | | | | | | | 2,977,073 | |

| FIXED RATE MORTGAGE-RELATED SECURITIES | | | 83.7% | | | | | | | | | | |

| 15 Yr. Securities | | | 41.6% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 7.00% | | | | | | 3/1/15 | | | 19,295 | | | 20,160 | |

| 7.00% | | | | | | 3/1/15 | | | 21,192 | | | 22,142 | |

| 7.00% | | | | | | 3/1/15 | | | 38,459 | | | 40,123 | |

| 7.50% | | | | | | 11/1/15 | | | 38,669 | | | 40,879 | |

| 6.50% | | | | | | 1/1/16 | | | 30,369 | | | 31,930 | |

| 6.00% | | | | | | 6/1/16 | | | 120,158 | | | 128,418 | |

| 6.00% | | | | | | 7/1/17 | | | 97,472 | | | 106,025 | |

| 6.00% | | | | | | 7/1/17 | | | 152,182 | | | 164,642 | |

| 3.50% | | | | | | 7/1/21 | | | 1,460,216 | | | 1,549,936 | |

| 2.50% | | | | | | 2/1/26 | | | 628,521 | | | 658,335 | |

| 3.00% | | | | | | 9/1/26 | | | 4,829,899 | | | 5,100,513 | |

| 2.50% | | | | | | 10/1/27 | | | 2,486,503 | | | 2,609,891 | |

| Freddie Mac | | | | | | | | | | | | | |

| 6.00% | | | | | | 6/1/17 | | | 167,034 | | | 180,956 | |

| | | | | | | | | | | | | 10,653,950 | |

| 30 Yr. Securities | | | 38.6% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 4.00% | | | | | | 5/1/42 | | | 1,358,155 | | | 1,426,125 | |

| Freddie Mac | | | | | | | | | | | | | |

| 3.50% | | | | | | 11/1/41 | | | 2,934,848 | | | 3,122,672 | |

| 4.00% | | | | | | 3/1/42 | | | 1,598,092 | | | 1,675,637 | |

| 3.00% | | | | | | 8/1/42 | | | 3,481,120 | | | 3,648,019 | |

| | | | | | | | | | | | | 9,872,453 | |

| Collateralized Mortgage Obligations | | | 3.5% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 4.00% | | | | | | 10/25/32 | | | 471,013 | | | 487,310 | |

| Government National Mortgage Association | | | | | | | | | | | | | |

| 4.77% | | | | | | 8/16/27 | | | 86,304 | | | 86,490 | |

| 4.50% | | | | | | 11/20/36 | | | 323,486 | | | 326,724 | |

| | | | | | | | | | | | | 900,524 | |

| TOTAL FIXED RATE MORTGAGE-RELATED SECURITIES | | | | | | | | | | | | 21,426,927 | |

| | | | | | | | | | | | | | |

| U.S. GOVERNMENT AGENCIES | | | 0.8% | | | | | | | | | | |

| FDIC Structured Sale Guaranteed Notes | | | | | | | | | | | | | |

| 3.00%(a) | | | | | | 9/30/19 | | | 197,620 | | | 202,314 | |

| TOTAL U.S. GOVERNMENT AGENCIES | | | | | | | | | | | | 202,314 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| See notes to financial statements. | | | | | | | | | | | | | |

| |

| ASSET MANAGEMENT FUND |

| INTERMEDIATE MORTGAGE FUND |

| SCHEDULE OF INVESTMENTS |

| October 31, 2012 |

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | | | | Shares | | Value | |

| INVESTMENT COMPANIES | | | 3.9% | | | | | | | | | | |

| Northern Institutional Treasury Portfolio, 0.04% | | | | | | | | | 998,495 | | $ | 998,495 | |

| TOTAL INVESTMENT COMPANIES | | | | | | | | | | | | 998,495 | |

TOTAL INVESTMENTS

(Cost $24,966,443)(b) | | | 100.0% | | | | | | | | | 25,604,809 | |

| NET OTHER ASSETS (LIABILITIES) | | | 0.0% | | | | | | | | | (3,214 | ) |

| NET ASSETS | | | 100.0% | | | | | | | | $ | 25,601,595 | |

| | |

| * | The rates presented are the rates in effect at October 31, 2012. |

| (a) | Securities purchased in a transaction exempt from registration under Rule 144A of the Securities Act of 1933. These securities may not be publicly traded without registration under the Securities Act of 1933. The value of these securities is determined by valuations supplied by a pricing service or brokers. |

| (b) | Represents cost for financial reporting purposes. |

| | FDIC - Federal Deposit Insurance Corporation. |

See notes to financial statements.

| |

| ASSET MANAGEMENT FUND |

| U.S. GOVERNMENT MORTGAGE FUND |

| SCHEDULE OF INVESTMENTS |

| October 31, 2012 |

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | Maturity Date | | Principal Amount | | Value | |

| ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES* | | | 22.3% | | | | | | | | | | |

| 1 Yr. Constant Maturity Treasury Based ARMS | | | 19.5% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 2.52% | | | | | | 7/1/37 | | $ | 2,357,456 | | $ | 2,542,252 | |

| 2.71% | | | | | | 9/1/38 | | | 1,832,130 | | | 1,962,156 | |

| | | | | | | | | | | | | 4,504,408 | |

| HYBRID ARMS | | | 2.8% | | | | | | | | | | |

| Freddie Mac | | | | | | | | | | | | | |

| 2.46% | | | | | | 11/1/36 | | | 630,065 | | | 661,015 | |

| TOTAL ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES | | | | | | | | | | | | 5,165,423 | |

| FIXED RATE MORTGAGE-RELATED SECURITIES | | | 74.6% | | | | | | | | | | |

| 10 Yr. Securities | | | 1.7% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 3.50% | | | | | | 7/1/21 | | | 365,054 | | | 387,484 | |

| | | | | | | | | | | | | | |

| 15 Yr. Securities | | | 17.4% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 7.00% | | | | | | 3/1/15 | | | 26,541 | | | 27,731 | |

| 2.50% | | | | | | 2/1/26 | | | 628,521 | | | 658,335 | |

| 3.00% | | | | | | 9/1/26 | | | 2,414,949 | | | 2,550,257 | |

| 2.50% | | | | | | 10/1/27 | | | 745,951 | | | 782,967 | |

| | | | | | | | | | | | | 4,019,290 | |

| 30 Yr. Securities | | | 41.5% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 5.00% | | | | | | 3/1/38 | | | 271,618 | | | 295,819 | |

| 4.00% | | | | | | 5/1/42 | | | 679,077 | | | 713,062 | |

| Freddie Mac | | | | | | | | | | | | | |

| 3.50% | | | | | | 11/1/41 | | | 782,626 | | | 832,713 | |

| 4.00% | | | | | | 3/1/42 | | | 676,556 | | | 709,384 | |

| 3.00% | | | | | | 8/1/42 | | | 6,464,938 | | | 6,774,893 | |

| Government National Mortgage Association | | | | | | | | | | | | | |

| 7.50% | | | | | | 2/15/24 | | | 62,420 | | | 72,113 | |

| 7.00% | | | | | | 4/15/27 | | | 85,448 | | | 98,657 | |

| 6.00% | | | | | | 1/15/29 | | | 96,083 | | | 108,721 | |

| | | | | | | | | | | | | 9,605,362 | |

| Collateralized Mortgage Obligations | | | 14.0% | | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | | |

| 4.00% | | | | | | 1/25/33 | | | 44,331 | | | 45,433 | |

| Freddie Mac | | | | | | | | | | | | | |

| 4.50% | | | | | | 4/15/19 | | | 2,843,911 | | | 3,011,760 | |

| 4.00% | | | | | | 3/15/33 | | | 95,315 | | | 102,978 | |

| Government National Mortgage Association | | | | | | | | | | | | | |

| 4.77% | | | | | | 8/16/27 | | | 86,304 | | | 86,490 | |

| | | | | | | | | | | | | 3,246,661 | |

| TOTAL FIXED RATE MORTGAGE-RELATED SECURITIES | | | | | | | | | | | | 17,258,797 | |

| |

| ASSET MANAGEMENT FUND |

| U.S. GOVERNMENT MORTGAGE FUND |

| SCHEDULE OF INVESTMENTS |

| October 31, 2012 |

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | Maturity Date | | Principal Amount | | Value | |

| U.S. GOVERNMENT AGENCIES | | | 0.8% | | | | | | | | | | |

FDIC Structured Sale Guaranteed Notes

3.00%(a) | | | | | | 9/30/19 | | $ | 197,620 | | $ | 202,314 | |

| TOTAL U.S. GOVERNMENT AGENCIES | | | | | | | | | | | | 202,314 | |

| | | | | | | | | | | | | | |

| | | Percentage of Net Assets | | | | | Shares | | Value | |

| INVESTMENT COMPANIES | | | 2.2% | | | | | | | | | | |

| Northern Institutional Treasury Portfolio, 0.04% | | | | | | | | | 503,445 | | $ | 503,445 | |

| TOTAL INVESTMENT COMPANIES | | | | | | | | | | | | 503,445 | |

TOTAL INVESTMENTS

(Cost $ 22,487,239)(b) | | | 99.9% | | | | | | | | | 23,129,979 | |

| NET OTHER ASSETS (LIABILITIES) | | | 0.1% | | | | | | | | | 13,042 | |

| NET ASSETS | | | 100.0% | | | | | | | | $ | 23,143,021 | |

| | |

| * | The rates presented are the rates in effect at October 31, 2012. |

| (a) | Securities purchased in a transaction exempt from registration under Rule 144A of the Securities Act of 1933. These securities may not be publicly traded without registration under the Securities Act of 1933. The value of these securities is determined by valuations supplied by a pricing service or brokers. |

| (b) | Represents cost for financial reporting purposes. |

| | FDIC - Federal Deposit Insurance Corporation. |

See notes to financial statements.

| |

| ASSET MANAGEMENT FUND |

| LARGE CAP EQUITY FUND |

| SCHEDULE OF INVESTMENTS |

| October 31, 2012 |

| | | | | | | | | | | |

| | | Percentage of Net Assets | | Shares | | Value | |

| COMMON STOCKS | | | 96.6% | | | | | | | |

| Aerospace & Defense | | | 6.1% | | | | | | | |

| General Dynamics Corp. | | | | | | 30,000 | | $ | 2,042,400 | |

| United Technologies Corp. | | | | | | 42,000 | | | 3,282,720 | |

| | | | | | | | | | 5,325,120 | |

| Air Freight & Logistics | | | 3.4% | | | | | | | |

| United Parcel Service, Inc. | | | | | | 40,000 | | | 2,930,000 | |

| Beverages | | | 8.3% | | | | | | | |

| Coca-Cola Co. | | | | | | 100,000 | | | 3,718,000 | |

| PepsiCo, Inc. | | | | | | 50,000 | | | 3,462,000 | |

| | | | | | | | | | 7,180,000 | |

| Chemicals | | | 3.4% | | | | | | | |

| Du Pont (E.I.) De Nemours | | | | | | 38,000 | | | 1,691,760 | |

| Praxair, Inc. | | | | | | 12,000 | | | 1,274,520 | |

| | | | | | | | | | 2,966,280 | |

| Commercial Banks | | | 4.3% | | | | | | | |

| Wells Fargo & Co. | | | | | | 110,000 | | | 3,705,900 | |

| Communications Equipment | | | 1.0% | | | | | | | |

| Cisco Systems, Inc. | | | | | | 50,000 | | | 857,000 | |

| Diversified Financial Services | | | 3.2% | | | | | | | |

| American Express Co. | | | | | | 50,000 | | | 2,798,500 | |

| Food & Staples Retailing | | | 6.1% | | | | | | | |

| Sysco Corp. | | | | | | 50,000 | | | 1,553,500 | |

| Wal-Mart Stores, Inc. | | | | | | 50,000 | | | 3,751,000 | |

| | | | | | | | | | 5,304,500 | |

| Food Products | | | 2.8% | | | | | | | |

| General Mills, Inc. | | | | | | 60,000 | | | 2,404,800 | |

| Health Care Equipment & Supplies | | | 5.0% | | | | | | | |

| Becton, Dickinson & Co. | | | | | | 30,000 | | | 2,270,400 | |

| Medtronic, Inc. | | | | | | 50,000 | | | 2,079,000 | |

| | | | | | | | | | 4,349,400 | |

| Hotels, Restaurants & Leisure | | | 4.0% | | | | | | | |

| McDonald’s Corp. | | | | | | 40,000 | | | 3,472,000 | |

| Household Products | | | 4.0% | | | | | | | |

| Procter & Gamble | | | | | | 50,000 | | | 3,462,000 | |

| Industrial Conglomerates | | | 7.2% | | | | | | | |

| 3M Company | | | | | | 35,000 | | | 3,066,000 | |

| General Electric Co. | | | | | | 150,000 | | | 3,159,000 | |

| | | | | | | | | | 6,225,000 | |

| Insurance | | | 4.5% | | | | | | | |

| Berkshire Hathaway, Inc.(a) | | | | | | 30 | | | 3,885,150 | |

| IT Services | | | 6.0% | | | | | | | |

| Automatic Data Processing | | | | | | 30,000 | | | 1,733,700 | |

| International Business Machines Corp. | | | | | | 18,000 | | | 3,501,540 | |

| | | | | | | | | | 5,235,240 | |

| Media | | | 3.4% | | | | | | | |

| The Walt Disney Company | | | | | | 60,000 | | | 2,944,200 | |

| | | | | | | | | | | |

See notes to financial statements.

| |

| ASSET MANAGEMENT FUND |

| LARGE CAP EQUITY FUND |

| SCHEDULE OF INVESTMENTS |

| October 31, 2012 |

| | | | | | | | | | | |

| | | Percentage of Net Assets | | Shares | | Value | |

| Oil & Gas Consumable Fuels | | | 8.3% | | | | | | | |

| Chevron Corp. | | | | | | 32,000 | | $ | 3,526,720 | |

| Exxon Mobil Corp. | | | | | | 40,000 | | | 3,646,800 | |

| | | | | | | | | | 7,173,520 | |

| Pharmaceuticals | | | 8.0% | | | | | | | |

| Abbott Laboratories | | | | | | 50,000 | | | 3,276,000 | |

| Johnson & Johnson | | | | | | 52,000 | | | 3,682,640 | |

| | | | | | | | | | 6,958,640 | |

| Software | | | 3.9% | | | | | | | |

| Microsoft Corp. | | | | | | 120,000 | | | 3,424,200 | |

| Specialty Retail | | | 3.7% | | | | | | | |

| Home Depot | | | | | | 25,000 | | | 1,534,500 | |

| TJX Companies | | | | | | 40,000 | | | 1,665,200 | |

| | | | | | | | | | 3,199,700 | |

| TOTAL COMMON STOCKS | | | | | | | | | 83,801,150 | |

| INVESTMENT COMPANIES | | | 3.4% | | | | | | | |

| Northern Institutional Treasury Portfolio 0.04% | | | | | | 3,000,224 | | | 3,000,224 | |

| TOTAL INVESTMENT COMPANIES | | | | | | | | | 3,000,224 | |

TOTAL INVESTMENTS

(Cost $57,734,803)(b) | | | 100.0% | | | | | | 86,801,374 | |

| NET OTHER ASSETS (LIABILITIES) | | | 0.0% | | | | | | (15,416 | ) |

| NET ASSETS | | | 100.0% | | | | | $ | 86,785,958 | |

| | | | | | | | | | | |

| | |

| (a) | Non-income producing security. |

| (b) | Represents cost for financial reporting purposes. |

| |

ASSET MANAGEMENT FUND STATEMENTS OF ASSETS & LIABILITIES October 31, 2012 |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Ultra Short Mortgage Fund | | | Ultra Short Fund | | | Short U.S. Government Fund | | | Intermediate Mortgage Fund | | | U.S. Government Mortgage Fund | | | Large Cap Equity Fund | |

| Assets | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments, at cost | | $ | 385,828,628 | | | $ | 6,899,257 | | | $ | 23,076,526 | | | $ | 24,966,443 | | | $ | 22,487,239 | | | $ | 57,734,803 | |

| Investments, at value | | $ | 394,149,364 | | | $ | 7,035,314 | | | $ | 23,584,245 | | | $ | 25,604,809 | | | $ | 23,129,979 | | | $ | 86,801,374 | |

| Receivable for dividends and interest | | | 958,155 | | | | 17,696 | | | | 59,254 | | | | 63,137 | | | | 59,273 | | | | 99,933 | |

| Receivable for investments sold | | | 274,385 | | | | 56,065 | | | | 20,816 | | | | — | | | | 15,784 | | | | — | |

| Receivable for capital shares sold | | | — | | | | — | | | | — | | | | — | | | | — | | | | 9,733 | |

| Receivable from Adviser / Distributor | | | 171,911 | | | | 3,058 | | | | 2,383 | | | | 5,590 | | | | 2,309 | | | | 7,226 | |

| Total Assets | | $ | 395,553,815 | | | $ | 7,112,133 | | | $ | 23,666,698 | | | $ | 25,673,536 | | | $ | 23,207,345 | | | $ | 86,918,266 | |

| Liabilities | | | | | | | | | | | | | | | | | | | | | | | | |

| Income distribution payable | | $ | 542,664 | | | $ | 5,650 | | | $ | 35,437 | | | $ | 43,381 | | | $ | 40,526 | | | $ | — | |

| Investment advisory fees payable | | | 149,580 | | | | 2,706 | | | | 5,005 | | | | 7,603 | | | | 4,907 | | | | 49,445 | |

| Administration fees payable | | | 39,405 | | | | 707 | | | | 2,370 | | | | 2,579 | | | | 2,317 | | | | 9,288 | |

| Distribution fees payable | | | 83,100 | | | | 1,503 | | | | 3,003 | | | | 3,258 | | | | 2,944 | | | | 18,066 | |

| Capital shares redeemed payable | | | 53,997 | | | | — | | | | — | | | | 10 | | | | — | | | | 43 | |

| Accrued expenses and other payable | | | 295,415 | | | | 5,849 | | | | 13,751 | | | | 15,110 | | | | 13,630 | | | | 55,466 | |

| Total Liabilities | | | 1,164,161 | | | | 16,415 | | | | 59,566 | | | | 71,941 | | | | 64,324 | | | | 132,308 | |

| Net Assets | | $ | 394,389,654 | | | $ | 7,095,718 | | | $ | 23,607,132 | | | $ | 25,601,595 | | | $ | 23,143,021 | | | $ | 86,785,958 | |

| Class I | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets | | $ | 394,389,654 | | | $ | 7,095,718 | | | $ | 23,607,132 | | | $ | 25,601,595 | | | $ | 23,143,021 | | | $ | — | |

| Share of common stock outstanding | | | 53,564,658 | | | | 1,387,040 | | | | 2,542,007 | | | | 5,651,433 | | | | 2,588,805 | | | | — | |

| Net asset value per share | | $ | 7.36 | | | $ | 5.12 | | | $ | 9.29 | | | $ | 4.53 | | | $ | 8.94 | | | $ | — | |

| Class AMF | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | 82,372,767 | |

| Share of common stock outstanding | | | — | | | | — | | | | — | | | | — | | | | — | | | | 8,754,350 | |

| Net asset value per share | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | 9.41 | |