United States

Securities and Exchange Commission

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-03541

Asset Management Fund

(Exact name of registrant as specified in charter)

690 Taylor Road, Suite 210 Gahanna, OH 43230

(Address of principal executive offices) (Zip code)

Foreside Management Services, LLC, 690 Taylor Road, Suite 210 Gahanna, OH 43230

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 247-9780

Date of fiscal year end: 10/31

Date of reporting period: 10/31/17

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

ANNUAL REPORT

October 31, 2017

2017 SHAREHOLDER LETTER

The Asset Management Fund (“AMF” and each series, a “Fund”) family of no load institutional mutual funds is pleased to present to shareholders the 2017 Annual Report for the Funds advised by Austin Atlantic Asset Management Company.

In 2017, financial markets focused on the potential for faster economic growth and higher corporate profits driven by a more markets-focused government administration. Less regulation and lower taxes should benefit corporate earnings in the future, so forward-looking, equity markets rewarded investors with the 21st Century’s second best 12 month (October/October) performance: a total return of 23.6%, second only to 2013’s 27.2%. While last year’s letter suggested that this economy would respond positively to these policies, we did not expect to see such a buoyant equity market. However, our bearish interest rate forecast was on the mark: in October of 2016, the money market was expecting only one or two 25 basis point rate hikes in 2017, but we felt four was more appropriate. To date, we’ve had three, and the market is expecting the fourth at the December 2017 meeting.

Since our interest rate crystal ball appears to be more transparent than our equity crystal ball, let’s stay there for a moment. For the past several years, we’ve viewed the Fed’s deliberate process of gradual rate hikes as the removal of easy money as opposed to as true monetary tightening. Framing Fed policy in this manner is important; as long as short term rates remain below inflation, monetary policy is historically viewed as accommodative and should be supportive of asset prices. In the 37 years leading up to the 2008-09 financial crisis (i.e., the post-Bretton Woods period), the Fed Funds rate averaged 100 basis points above the Consumer Price Index (ex-food and energy). Currently, Fed Funds is roughly 50 basis points below inflation. Consensus for 2018 is that the Fed will raise the Fed Funds rate to approximately 1.75%, which would put it right on top of current inflation. We’d consider that to be an appropriate place to pause, assuming that inflation remains benign.

Assuming that neutrality is a reasonable place for monetary policy to pause, it’s instructive to look at some key economic indicators today relative to late 2006, when the Fed Funds rate was 5.25%, which was more than 200 basis points above trailing inflation:

| | October | October | |

| | 2006 | 2017 | Comment |

| | | | |

| Unemployment Rate: | 4.4% | 4.1% | [Close to 17 year low of 3.8%] |

| Underemployment Rate: | 8.2% | 7.9% | [11 year low] |

| 4 Quarter Trailing GDP: | 2.2% | 2.4% | [Annual Average since 2000 is 2.1%] |

| GDP Deflator: | 3.1% | 1.8% | [since 2000, peak was 3.4%, average is 2.0%] |

| ISM Manufacturing Index: | 52.2% | 58.7% | [Close to 13 year peak of 60.8%] |

| Fed Funds Rate: | 5.25% | 1.25% | |

Many of the major economic indicators describe an economy that is on firm footing and provide the Fed with a solid rationale for raising rates to the 1.75% - 2.25% range. Inflation scares remain the key, and the wildcards here are wages and cost of goods. The U.S. economy has had a long run of soft labor costs, so the elasticity of labor costs has not been tested in a full employment environment in a long time. Likewise, U.S. consumers have experienced flat or declining costs for many consumer products such as clothing, electronics, and automobiles. Weakness in these markets has largely offset the acceleration in housing and medical services. So any reversal in the former categories – which are mainly imports – could lead to a spike in inflation. Another wild-card will be the reversal of the quantitative easing policies of the Fed (and potentially the other major central banks). The Fed has been absorbing a substantial percentage of the net supply in U.S. Treasuries and agency mortgage-backed securities for the past few years. As their longer maturity bond balances run off, and the housing market continues to improve, we expect longer interest rates to underperform short rates – not the typical scenario when the Fed is hiking rates.

This report has been prepared to provide information to the shareholders of the Funds and must be preceded or accompanied by the Prospectus. It should not be construed as an offering to sell or buy any shares of the Funds. Such an offering is made only by the Prospectus. You may obtain a current copy of the Prospectus by calling 1-800-247-9780 or at the Funds’ website (www.amffunds.com). Investors should consider the investment objectives, risks and expenses of the Funds before investing. Read the Prospectus carefully before you invest. Like all mutual funds, the Funds are not FDIC insured, may lose value and have no bank guarantee.

In the meantime, our equity fund had another strong year. The Fund provides an attractive vehicle for investors that believe a steady improvement in corporate earnings will support equity prices but seek to provide downside protection as well. The new (as of 2016) portfolio management team’s investment process – a blend of fundamental analysis with quantitative models – helps the fund to broaden the investable universe while still maintaining a bias to large cap securities. The fund has been achieving attractive nominal returns but taking less risk than the average equity fund – an admirable combination and one that is in the tradition of this fund.

At the other end of the spectrum, our new fixed income offering, the AAAMCO Ultrashort Financing Fund, is an appropriate vehicle to express the view that the Fed is behind the curve and will need to raise rates faster than the market is assuming. In that scenario, equity valuations may suffer, but the Ultrashort Financing Fund is designed to minimize capital losses while still outperforming short term interest rates.

Regardless, of your desired risk exposure, we are grateful for your continuing support and continue to seek the best investment strategies for achieving our shareholders’ investment objectives.

|  |

| Sean Kelleher | David Holland |

| President | Chairman |

| Austin Atlantic Asset Management Company | Asset Management Fund |

This report has been prepared to provide information to the shareholders of the Funds and must be preceded or accompanied by the Prospectus. It should not be construed as an offering to sell or buy any shares of the Funds. Such an offering is made only by the Prospectus. You may obtain a current copy of the Prospectus by calling 1-800-247-9780 or at the Funds’ website (www.amffunds.com). Investors should consider the investment objectives, risks and expenses of the Funds before investing. Read the Prospectus carefully before you invest. Like all mutual funds, the Funds are not FDIC insured, may lose value and have no bank guarantee.

AAAMCO ULTRA SHORT FINANCING FUND REVIEW

October 31, 2017

One of the key factors that has slowed the economic recovery from the financial crisis is regulatory-driven, de-risking of the financial system. While much of this was certainly necessary, there are always unintended consequences. We’ve observed numerous examples of global banks reducing their exposures to creditworthy clients simply because the services required by these clients no longer met the bank’s required return on capital. So banks have rejected these clients not because of changes in credit quality but simply due to regulatory shifts. When we see regulatory-driven capital re-allocations, our job as money managers is to determine if we can create a pool of capital that provides an attractive risk-adjusted return for an investor base with a return target more consistent with the financial asset in question. Our newest fixed income fund, the Ultrashort Financing Fund, is a good example of this process. The Fund commenced operations on June 6, 2017 and focuses on investments in repurchase agreements (“repos”) backed by government and government agency securities. Repos are short term borrowings over-collateralized by a variety of securities. While repos have been around for many years, particularly as a core asset for money market funds, we are not aware of any bond funds that use repos as a core asset. While the borrowers for most funds are the large, well-known global investment banks, the borrowers in our Fund are the counterparties that can no longer access financing from the global banks. These are the borrowers that have been disintermediated by the global banks as a result of the new bank capital rules. Since the inception of the Fund (June 6, 2017), the Fund has earned an annualized, weighted average yield of 1.42%, which is 0.49% higher than one month T-bills. The Fund’s net asset value has been $10.00 since inception even though short interest rates increased approximately 0.30%, reflecting the short maturities of the repurchase agreements.

We believe this strategy has an exciting future, and thank all of our shareholders for allowing us to assist them with their investment needs, and look forward to serving them in the future.

This report has been prepared to provide information to the shareholders of the Funds and must be preceded or accompanied by the Prospectus. It should not be construed as an offering to sell or buy any shares of the Funds. Such an offering is made only by the Prospectus. You may obtain a current copy of the Prospectus by calling 1-800-247-9780 or at the Funds’ website (www.amffunds.com). Investors should consider the investment objectives, risks and expenses of the Funds before investing. Read the Prospectus carefully before you invest. Like all mutual funds, the Funds are not FDIC insured, may lose value and have no bank guarantee.

Portfolio composition is subject to change.

Past performance does not guarantee future results. Investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

ULTRA SHORT MORTGAGE FUND REVIEW

October 31, 2017

For the year ending October 31, 2017, the Ultra Short Mortgage Fund’s return was -0.61% as compared to the Bloomberg Barclays 6 Month T-Bill Bellwethers Index return of 0.85%. Faster than expected principal prepayments on our mortgage-backed securities positions and low interest rates relative to the expense load of the Fund contributed to most of the underperformance for the year.

For the first time since 2006, the Fed engaged in a steady but slow program of interest rate hikes. The Fed Funds rate was increased from 0.50% to 1.25%, and the market consensus is that several more rate hikes are baked into Fed policy for 2018. These rate hikes allowed for a steady increase in the coupons on the Fund’s portfolio of adjustable rate mortgages. At the other end of the yield curve, interest rates on thirty year fixed rate mortgages did not increase as much, reflecting the continued benign inflation environment. The result was that mortgage prepayments stayed unusually high for a rising mortgage rate environment, reflecting the willingness of adjustable rate mortgagors to lock in historically low fixed rates. Combine this fact with rising home prices and improving borrower credit and the result is the unlocking of many borrowers that were unable to refinance over the past decade. Some factors offset this propensity for faster prepayments, such as increased government insurance fees on GNMA loans. So while the yield on the Fund’s assets increased, principal payoffs due to faster than expected prepayments negatively impacted performance. While our investment strategy remains consistent - we invest in higher coupon government and government agency MBS that we believe will prepay more slowly than market consensus – we’ve further reduced the Fund’s exposure to interest rate risk and have lowered the Fund’s average dollar price investment.

We thank all of our shareholders for allowing us to assist them with their investment needs, and look forward to serving them in the future.

This report has been prepared to provide information to the shareholders of the Funds and must be preceded or accompanied by the Prospectus. It should not be construed as an offering to sell or buy any shares of the Funds. Such an offering is made only by the Prospectus. You may obtain a current copy of the Prospectus by calling 1-800-247-9780 or at the Funds’ website (www.amffunds.com). Investors should consider the investment objectives, risks and expenses of the Funds before investing. Read the Prospectus carefully before you invest. Like all mutual funds, the Funds are not FDIC insured, may lose value and have no bank guarantee.

Portfolio composition is subject to change.

Past performance does not guarantee future results. Investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

ULTRA SHORT MORTGAGE FUND REVIEW

October 31, 2017

Ultra Short Mortgage Fund

Gross Expense Ratio

1.26%

The gross expense ratio above is from the Fund’s prospectus dated March 1, 2017. Additional information pertaining to the Fund’s expense ratios as of October 31, 2017, can be found in the Financial Highlights.

Average Annual Total Return

Periods Ending October 31, 2017*

| | | One

Year | Five

Year | Ten

Year |

| Ultra Short Mortgage Fund(1) | | -0.61% | 0.53% | -0.76% |

| Bloomberg Barclays 6 Month T-Bill Bellwethers Index | | 0.85% | 0.41% | 0.80% |

| * | Assumes reinvestment of all dividends and distributions and the deduction of all applicable fees and expenses. Average annual returns are stated for periods greater than one year. The Bloomberg Barclays 6 Month T-Bill Bellwethers Index does not include a reduction in total return for expenses. |

| (1) | During the fiscal year ended October, 31, 2013, the Ultra Short Mortgage Fund received monies related to certain nonrecurring litigation settlements. If these monies were not received, the Five Year and Ten Year returns would have been lower. |

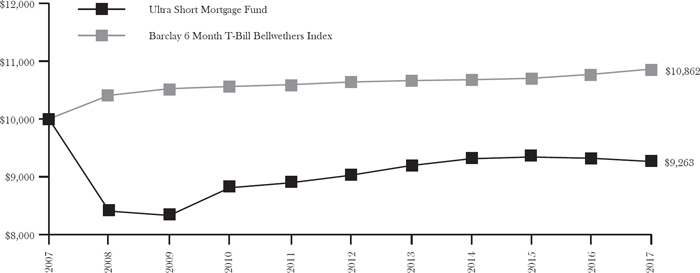

Comparison of change in value of a hypothetical $10,000 investment for the years ended October 31

The following graph shows that an investment of $10,000 in the Fund on October 31, 2007, would have been worth $9,263 on October 31, 2017, assuming all dividends and distributions had been reinvested. A similar investment in the Bloomberg Barclays 6 Month T-Bill Bellwethers Index, over the same period, would have been worth $10,862.

Past performance does not guarantee future results. Investments returns and net asset values will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than original cost. The performance data quoted represents past performance and current returns may be lower or higher. Performance figures in the table and graph do not reflect the deduction of taxes that a shareholder would pay on the Fund distributions or the redemption of Fund shares. The Bloomberg Barclays 6 Month T-Bill Bellwethers Index is an unmanaged index comprised of U.S. Government Treasury Bonds with an average maturity of six months. The index represents unmanaged groups of bonds that differ from the composition of the Fund. The index does not include a reduction in return for expenses. Investors cannot invest directly in an index, although they can invest in its underlying securities. To obtain current month-end performance information for the Fund, please call 1-800-247-9780.

LARGE CAP EQUITY FUND REVIEW

October 31, 2017

For the year ending October 31, 2017, Class AMF of the Large Cap Equity Fund earned 24.63% return for shareholders. Total returns for the Morningstar Large Cap Blend Fund Category and the Fund’s benchmark index (the S&P 500) were 22.34% and 23.63%, respectively. Total return assumes the reinvestment of all capital gains and dividends and the deduction of all applicable fund expenses and fees. While the Large Cap Equity Fund is one of the oldest mutual funds in the country, tracing its track record back to 1953, it’s investment process (implemented in 2016) represents some of the latest thinking and research in equity investment management techniques. While our 2016 results were terrific, we believe the performance in 2017 has been outstanding. The Fund has always been managed with a focus on megacap stocks, which tends to limit volatility relative to the overall market. One way to measure the risk of the Fund relative to the index is known as “Beta”, and is defined as the quotient of the historical price risk of the Fund relative to the historical risk of the S&P 500 Index. For example, the Fund’s Beta is historically in the range of 80%-90% of the market, meaning it tends to be 10%-20% less volatile than the S&P 500. While this protects investors in years like 2008 (S&P 500 was down 38.42% while the Fund was only down 28.57%), it also limits performance in a rallying market. What we’ve seen from the new investment process is that the Fund is still less volatile than the overall market, but is able to capture more upside performance. For example, the Fund’s Beta this year was 86%, or 14% less volatile than the S&P 500 – right in line with its historical trends. An 86% Beta implies that the Fund should have been up 21.16% (86% of the S&P 500’s 23.63% increase). But the Fund actually increased by 24.63%, 3.47% more than what the Fund’s Beta implies. While there have been periods in time when the Fund outperformed its index in a rallying market, the Fund has never outperformed the index for a rally of this magnitude.

How did we do that? First, the scalability of the process allows the investment team to efficiently analyze the full set of eligible companies. While the Fund still focuses on megacap stocks, the investment process allows the Fund to more readily reach into the secondary issues in the S&P 500 to source attractive returns. Simply having a larger universe from which to source investments provides greater opportunity to outperform. So while the Fund’s holdings are more diversified than historically, our largest holdings are still megacap companies: UnitedHealth Group, Oracle, Alphabet, Broadcom, and Bank of America make up 20.6% of the Fund. In summary, the investment philosophy and investment objectives of the Fund have not changed. The new process allows portfolio management to source a broader opportunity set and more objectively analyze the relevant investment variables that drive performance.

We sincerely thank the shareholders of the Fund for their patience and trust as we re-position the Fund, and look forward to serving your investment needs in the future.

This report has been prepared to provide information to the shareholders of the Funds and must be preceded or accompanied by the Prospectus. It should not be construed as an offering to sell or buy any shares of the Funds. Such an offering is made only by the Prospectus. You may obtain a current copy of the Prospectus by calling 1-800-247-9780 or at the Funds’ website (www.amffunds.com). Investors should consider the investment objectives, risks and expenses of the Funds before investing. Read the Prospectus carefully before you invest. Like all mutual funds, the Funds are not FDIC insured, may lose value and have no bank guarantee.

Portfolio composition is subject to change.

Past performance does not guarantee future results. Investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

LARGE CAP EQUITY FUND REVIEW

October 31, 2017

Large Cap Equity Fund

Gross Expense Ratio

Class AMF 1.46%

Class H 1.21%

The gross expense ratio above is from the Fund’s prospectus dated March 1, 2017. Additional information pertaining to the Fund’s expense ratios as of October 31, 2017, can be found in the Financial Highlights.

Average Annual Total Return

Periods Ending October 31, 2017*

| | | One

Year | Five

Year | Ten

Year | Since

Inception |

| Class AMF(1) | 24.63% | 12.63% | 7.25% | |

| Class H(2) | | 24.76% | 12.80% | — | 14.96% |

| S&P 500 | | 23.63% | 15.18% | 7.51% | 17.34%(3) |

| * | Assumes reinvestment of all dividends and distributions and the deduction of all applicable fees and expenses. Average annual returns are stated for periods greater than one year. The S&P 500 does not include a reduction in total return for expenses. |

| (1) | Class AMF of the Fund commenced operations on June 30, 1953. |

| (2) | Class H of the Fund commenced operations on February 20, 2009. |

| (3) | Return presented is for the period from February 20, 2009 to October 31, 2017. |

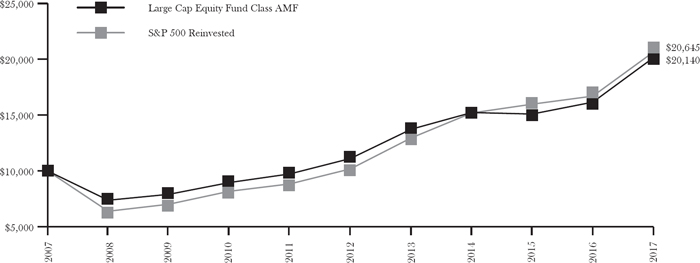

Comparison of change in value of a hypothetical $10,000 investment for the years ended October 31

The following graph shows that an investment of $10,000 in Class AMF of the Fund on October 31, 2007, would have been worth $20,140 on October 31, 2017, assuming all dividends and distributions had been reinvested. A similar investment in the S&P 500, over the same period, would have been worth $20,645.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Performance figures in the table and graph do not reflect the deduction of taxes that a shareholder would pay on the Fund distributions or the redemption of Fund shares. The Standard & Poors 500 Index is an unmanaged index, generally representative of the U.S. stock market as a whole. The index differs from the composition of the Fund. The index does not include a reduction in return for expenses. Investors cannot invest directly in an index, although they can invest in its underlying securities. To obtain current month-end performance information for the Fund, please call 1-800-247-9780.

AAAMCO ULTRASHORT FINANCING FUND

SCHEDULE OF INVESTMENTS

October 31, 2017

| | | | | | | | | | | | | | |

| | | | Percentage

of Net

Assets | | Maturity

Date | Principal

Amount | | Value | |

| | | | | | | | | | | | | | |

| ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES | | | 13.5 | % | | | | | | | | | |

| 1 Mo. London Interbank Offering Rate (LIBOR) | | | 13.5 | % | | | | | | | | | |

| Freddie Mac | | | | | | | | | | | | | |

| (Floating, LIBOR USD 1M + 0.37%), 1.60%(1) | | | | | | 5/25/24 | | $ | 7,999,316 | | $ | 8,001,803 | |

TOTAL ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES

(Cost $8,011,783) | | | | | | | | | | | | 8,001,803 | |

| | | | | | | | | | | | | | |

| | | | Percentage

of Net

Assets | | | Principal

Amount /

Shares | | Value | |

| | | | | | | | | | | | | | |

| INVESTMENT COMPANIES | | | 0.0 | % | | | | | | | | | |

| Northern Institutional Treasury Portfolio, 0.88%* | | | | | | | | | 35,691 | | $ | 35,691 | |

TOTAL INVESTMENT COMPANIES

(Cost $35,691) | | | | | | | | | | | | 35,691 | |

| | | | | | | | | | | | | | |

| REPURCHASE AGREEMENTS | | | 86.4 | % | | | | | | | | | |

| Amherst Pierpont Securities LLC, 1.15%, (Agreement dated 10/31/17 to be repurchased at $6,000,192 on 11/1/17. Collateralized by Fixed Rate U.S. Government Mortgage-Backed Securities, 3.50% - 6.00%, with a value of $6,120,002, due at 5/1/41 - 5/1/42) | | | | | | | | | 6,000,000 | | | 6,000,000 | |

| Amherst Pierpont Securities LLC, 1.54%, (Agreement dated 10/25/17 to be repurchased at $12,003,593 on 11/1/17. Collateralized by Fixed and Adjustable Rate U.S. Government Mortgage-Backed Securities, 2.00% - 4.50%, with a value of $12,867,883, due at 3/1/44 - 10/15/47) | | | | | | | | | 12,000,000 | | | 12,000,000 | |

| BCM High Income Fund, LP, 1.80%, (Open repurchase agreement which the Fund can initiate closure at any time. Collateralized by SBA Pools 3.50% - 4.84%, with a value of $19,639,824, due at 7/25/42 - 12/25/42, and cash equivalents of $1,298,986) | | | | | | | | | 19,743,218 | | | 19,743,218 | |

| JVB Financial Group, LLC, 2.24%, (Agreement dated 10/11/17 to be repurchased at $8,685,179 on 11/14/17. Collateralized by VIC Master Trust Series 2017-VI Certificates, 4.50%, with a value of $9,184,147 due at 3/20/2042)(2) | | | | | | | | | 8,673,845 | | | 8,673,845 | |

| Vining-Sparks IBG, L.P., 1.89%, (Open repurchase agreement which the Fund can initiate closure at any time. Collateralized by SBA Loans, 4.55% - 5.33% with a value of $5,383,564 due at 9/15/27 - 4/15/42) | | | | | | | | | 4,824,616 | | | 4,824,616 | |

TOTAL REPURCHASE AGREEMENTS

(Cost $51,241,679) | | | | | | | | | | | | 51,241,679 | |

| | | | | | | | | | | | | | |

TOTAL INVESTMENTS

(Cost $59,289,153) | | | 99.9 | % | | | | | | | | 59,279,173 | |

| NET OTHER ASSETS (LIABILITIES) | | | 0.1 | % | | | | | | | | 50,241 | |

| NET ASSETS | | | 100.0 | % | | | | | | | $ | 59,329,414 | |

| | | | | | | | | | | | | | |

| * | The rates presented are the rates in effect at October 31, 2017. |

| (1) | Variable rate security. The rate presented is the rate in effect at October 31, 2017. |

| (2) | Illiquid security, maturity date is greater than 7 days. |

See notes to financial statements.

ULTRA SHORT MORTGAGE FUND

SCHEDULE OF INVESTMENTS

October 31, 2017

| | | Percentage

of Net

Assets | | Maturity

Date | | Principal

Amount | | | Value | |

| | | | | | | | | | |

| ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES | | 54.7 | % | | | | | | | | | |

| 1 Yr. Constant Maturity Treasury Based ARMS | | 28.7 | % | | | | | | | | | |

| Fannie Mae Grantor Trust | | | | | | | | | | | | |

| 4.13%(1) | | | | | 5/25/42 | | $ | 4,949,479 | | $ | 5,172,894 | |

| 3.29%(1) | | | | | 8/25/43 | | | 6,568,517 | | | 6,710,587 | |

| Fannie Mae Whole Loan | | | | | | | | | | | | |

| 3.88%(1) | | | | | 8/25/42 | | | 1,374,826 | | | 1,477,736 | |

| 3.55%(1) | | | | | 8/25/42 | | | 4,272,548 | | | 4,440,387 | |

| 3.21%(1) | | | | | 4/25/45 | | | 7,106,697 | | | 7,319,916 | |

| | | | | | | | | | | | 25,121,520 | |

| 12 Mo. London Interbank Offering Rate (LIBOR) | | 21.4 | % | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | |

| (Floating, ICE LIBOR USD 1Y + 1.72%), 3.45%(2), (3) | | | | | 9/1/36 | | | 156,435 | | | 164,512 | |

| (Floating, ICE LIBOR USD 1Y + 1.73%), 3.53%(2), (3) | | | | | 6/1/37 | | | 6,572,566 | | | 6,882,752 | |

| (Floating, ICE LIBOR USD 1Y + 1.57%), 3.32%(2), (3) | | | | | 9/1/38 | | | 11,162,479 | | | 11,632,743 | |

| | | | | | | | | | | | 18,680,007 | |

| 6 Mo. Certificate of Deposit Based ARMS | | 0.9 | % | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | |

| (Floating, ICE LIBOR USD 6M + 1.00%), 2.40%(2), (3) | | | | | 6/1/21 | | | 66,062 | | | 66,264 | |

| (Floating, ICE LIBOR USD 6M + 1.48%), 2.87%(2), (3) | | | | | 12/1/24 | | | 466,204 | | | 480,561 | |

| Freddie Mac | | | | | | | | | | | | |

| (Floating, ICE LIBOR USD 6M + 1.85%), 3.23%(2), (3) | | | | | 1/1/26 | | | 190,153 | | | 194,203 | |

| | | | | | | | | | | | 741,028 | |

| SBA Pool Floaters | | 3.7 | % | | | | | | | | | |

| Small Business Administration Pool | | | | | | | | | | | | |

| (Variable, Prime Rate U.S. + 0.09%), 4.34%(2) | | | | | 10/25/38 | | | 2,943,288 | | | 3,256,012 | |

| TOTAL ADJUSTABLE RATE MORTGAGE-RELATED SECURITIES | | | | | | | | | | | | |

| (Cost $47,250,750) | | | | | | | | | | | 47,798,567 | |

| FIXED RATE MORTGAGE-RELATED SECURITIES | | 32.2 | % | | | | | | | | | |

| 30 Yr. Securities | | 7.8 | % | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | |

| 5.00% | | | | | 6/1/41 | | | 487,524 | | | 536,886 | |

| 5.00% | | | | | 6/1/41 | | | 898,260 | | | 989,209 | |

| 5.00% | | | | | 6/1/41 | | | 3,478,002 | | | 3,830,150 | |

| Freddie Mac | | | | | | | | | | | | |

| 6.00% | | | | | 6/16/37 | | | 1,352,230 | | | 1,479,279 | |

| | | | | | | | | | | | 6,835,524 | |

| Collateralized Mortgage Obligations | | 24.4 | % | | | | | | | | | |

| Fannie Mae | | | | | | | | | | | | |

| 5.00% | | | | | 2/25/18 | | | 27,117 | | | 27,178 | |

| Freddie Mac | | | | | | | | | | | | |

| 2.00% | | | | | 9/15/44 | | | 14,848,527 | | | 14,829,027 | |

| Government National Mortgage Association | | | | | | | | | | | | |

| 1.35% | | | | | 6/16/37 | | | 6,657,266 | | | 6,506,512 | |

| | | | | | | | | | | | 21,362,717 | |

| TOTAL FIXED RATE MORTGAGE-RELATED SECURITIES | | | | | | | | | | | | |

| (Cost $28,451,757) | | | | | | | | | | | 28,198,241 | |

See notes to financial statements.

ULTRA SHORT MORTGAGE FUND (concluded)

SCHEDULE OF INVESTMENTS

October 31, 2017

| | | Percentage

of Net

Assets | | | | Shares | | Principal

Amount/

Value | |

| | | | | | | | | | | |

| INVESTMENT COMPANIES | | 13.0 | % | | | | | | | | | |

| Northern Institutional Treasury Portfolio, 0.88%* | | | | | | | | 7,321,671 | | $ | 7,321,671 | |

| AAAMCO Ultrashort Financing Fund (4) | | | | | | | | 401,312 | | | 4,013,121 | |

| | | | | | | | | | | | | |

| TOTAL INVESTMENT COMPANIES | | | | | | | | | | | | |

| (Cost $11,334,792) | | | | | | | | | | | 11,334,792 | |

| | | | | | | | | | | | | |

| TOTAL INVESTMENTS | | | | | | | | | | | | |

| (Cost $87,037,299) | | 99.9 | % | | | | | | | | 87,331,600 | |

| NET OTHER ASSETS (LIABILITIES) | | 0.1 | % | | | | | | | | 54,818 | |

| NET ASSETS | | 100.0 | % | | | | | | | $ | 87,386,418 | |

| | | | | | | | | | | | | |

| * | The rates presented are the rates in effect at October 31, 2017. |

| (1) | Variable or floating rate security, the interest rate of which adjusts periodically based on changes in current interest rates and prepayments on the underlying pool of assets. |

| (2) | Variable rate security. The rate presented is the rate in effect at October 31, 2017. |

| (3) | ICE LIBOR is a benchmark rate produced from the average of interest rates that some of the world’s leading banks charge each other for short-term loans. |

| (4) | Affiliated fund, see Note E. |

See notes to financial statements.

LARGE CAP EQUITY FUND

SCHEDULE OF INVESTMENTS

October 31, 2017

| | | Percentage

of Net

Assets | | | | Shares | | Value | |

| | | | | | | | | | |

| COMMON STOCKS | | 98.0 | % | | | | | | | | | |

| Automobiles & Components | | 1.3 | % | | | | | | | | | |

| General Motors Co. | | | | | | | | 14,000 | | $ | 601,720 | |

| | | | | | | | | | | | | |

| Banks | | 5.9 | % | | | | | | | | | |

| Bank of America Corp. | | | | | | | | 66,975 | | | 1,834,445 | |

| PNC Financial Services Group | | | | | | | | | | | | |

| (The), Inc. | | | | | | | | 6,500 | | | 889,135 | |

| | | | | | | | | | | | 2,723,580 | |

| Capital Goods | | 9.9 | % | | | | | | | | | |

| Caterpillar, Inc. | | | | | | | | 3,500 | | | 475,300 | |

| Cummins, Inc. | | | | | | | | 10,000 | | | 1,768,800 | |

| Eaton Corp. PLC | | | | | | | | 20,678 | | | 1,654,654 | |

| Ingersoll-Rand PLC | | | | | | | | 7,689 | | | 681,245 | |

| | | | | | | | | | | | 4,579,999 | |

| Consumer Services | | 8.1 | % | | | | | | | | | |

| Carnival Corp. | | | | | | | | 8,396 | | | 557,411 | |

| McDonald’s Corp. | | | | | | | | 10,365 | | | 1,730,022 | |

| Starbucks Corp. | | | | | | | | 27,000 | | | 1,480,680 | |

| | | | | | | | | | | | 3,768,113 | |

| Diversified Financials | | 1.9 | % | | | | | | | | | |

| Discover Financial Services | | | | | | | | 12,942 | | | 861,031 | |

| Energy | | 3.6 | % | | | | | | | | | |

| Valero Energy Corp. | | | | | | | | 21,335 | | | 1,683,118 | |

| Energy Equipment & Services | | 1.7 | % | | | | | | | | | |

| Schlumberger Ltd. | | | | | | | | 12,000 | | | 768,000 | |

| Food Beverage & Tobacco | | 4.4 | % | | | | | | | | | |

| PepsiCo, Inc. | | | | | | | | 14,154 | | | 1,560,196 | |

| Philip Morris International, Inc. | | | | | | | | 4,500 | | | 470,880 | |

| | | | | | | | | | | | 2,031,076 | |

| Health Care Equipment & Services | | 7.0 | % | | | | | | | | | |

| Aetna, Inc. | | | | | | | | 6,642 | | | 1,129,340 | |

| UnitedHealth Group, Inc. | | | | | | | | 10,060 | | | 2,114,813 | |

| | | | | | | | | | | | 3,244,153 | |

| Household & Personal Products | | 1.7 | % | | | | | | | | | |

| Kimberly-Clark Corp. | | | | | | | | 6,900 | | | 776,319 | |

| Insurance | | 8.0 | % | | | | | | | | | |

| Aflac, Inc. | | | | | | | | 17,975 | | | 1,507,923 | |

| Progressive (The) Corp. | | | | | | | | 24,000 | | | 1,167,600 | |

| Prudential Financial, Inc. | | | | | | | | 9,188 | | | 1,014,906 | |

| | | | | | | | | | | | 3,690,429 | |

| Materials | | 6.2 | % | | | | | | | | | |

| LyondellBasell Industries NV | | | | | | | | 15,753 | | | 1,630,908 | |

| Sherwin-Williams (The) Co. | | | | | | | | 3,125 | | | 1,234,844 | |

| | | | | | | | | | | | 2,865,752 | |

| Pharmaceuticals & Biotechnology | | 7.8 | % | | | | | | | | | |

| AbbVie, Inc. | | | | | | | | 15,000 | | | 1,353,750 | |

| Amgen, Inc. | | | | | | | | 6,570 | | | 1,151,195 | |

| Bristol-Myers Squibb Co. | | | | | | | | 9,700 | | | 598,102 | |

| Eli Lilly & Co. | | | | | | | | 6,400 | | | 524,416 | |

| | | | | | | | | | | | 3,627,463 | |

See notes to financial statements.

LARGE CAP EQUITY FUND (concluded)

SCHEDULE OF INVESTMENTS

October 31, 2017

| | | Percentage

of Net

Assets | | | | | Shares | | Value | |

| Real Estate | | 2.1 | % | | | | | | | | | |

| Simon Property Group, Inc. | | | | | | | | 6,137 | | $ | 953,260 | |

| Retailing | | 3.5 | % | | | | | | | | | |

| Home Depot (The), Inc. | | | | | | | | 5,176 | | | 858,078 | |

| Lowe’s Cos., Inc. | | | | | | | | 9,576 | | | 765,601 | |

| | | | | | | | | | | | 1,623,679 | |

| Semiconductors & Semiconductor | | 4.0 | % | | | | | | | | | |

| Broadcom Ltd. | | | | | | | | 7,000 | | | 1,847,370 | |

| Software & Services | | 14.1 | % | | | | | | | | | |

| Alphabet, Inc.(a) | | | | | | | | 1,800 | | | 1,859,472 | |

| Facebook, Inc.(a) | | | | | | | | 10,200 | | | 1,836,612 | |

| Intuit, Inc. | | | | | | | | 6,250 | | | 943,875 | |

| Oracle Corp. | | | | | | | | 37,237 | | | 1,895,363 | |

| | | | | | | | | | | | 6,535,322 | |

| Technology Hardware & Equipment | | 1.9 | % | | | | | | | | | |

| Western Digital Corp. | | | | | | | | 10,000 | | | 892,700 | |

| Utilities | | 4.9 | % | | | | | | | | | |

| American Electric Power Co., Inc. | | | | | | | | 18,000 | | | 1,339,380 | |

| Edison International | | | | | | | | 11,762 | | | 940,372 | |

| | | | | | | | | | | | 2,279,752 | |

| TOTAL COMMON STOCKS | | | | | | | | | | | | |

| (Cost $35,091,683) | | | | | | | | | | | 45,352,836 | |

| | | Percentage

of Net

Assets | | | | | Shares | | | Value | |

| INVESTMENT COMPANIES | | 2.2 | % | | | | | | | | | |

| Northern Institutional Treasury Portfolio, 0.88%* | | | | | | | | 1,023,416 | | $ | 1,023,416 | |

| TOTAL INVESTMENT COMPANIES | | | | | | | | | | | | |

| (Cost $1,023,416) | | | | | | | | | | | 1,023,416 | |

| | | | | | | | | | | | | |

| TOTAL INVESTMENTS | | | | | | | | | | | | |

| (Cost $36,115,099) | | 100.2 | % | | | | | | | | 46,376,252 | |

| NET OTHER ASSETS (LIABILITIES) | | (0.2 | )% | | | | | | | | (76,687 | ) |

| NET ASSETS | | 100.0 | % | | | | | | | $ | 46,299,565 | |

| | | | | | | | | | | | | |

| * | The rates presented are the rates in effect at October 31, 2017. |

| (a) | Non-income producing security. |

See notes to financial statements.

STATEMENTS OF ASSETS & LIABILITIES

October 31, 2017

| | | AAAMCO Ultrashort Financing Fund | | | Ultra Short Mortgage Fund | | | Large Cap Equity Fund | |

| Assets: | | | | | | | | | | | | |

| Investments, at cost | | $ | 8,047,474 | | | $ | 83,024,178 | | | $ | 36,115,099 | |

| Investments, at value | | | 8,037,494 | | | | 83,318,479 | | | | 46,376,252 | |

| Investments in affiliates, at value (Cost $0, $4,013,121 and $0, respectively) | | | — | | | | 4,013,121 | | | | — | |

| Repurchase agreements, cost equals fair value | | | 51,241,679 | | | | — | | | | — | |

| Receivable for dividends and interest | | | 53,352 | | | | 208,671 | | | | 31,363 | |

| Receivable for paydowns on mortgage-backed securities | | | — | | | | 9,719 | | | | — | |

| Receivable from Adviser/Distributor | | | 36,090 | | | | 20,378 | | | | 3,375 | |

| Total Assets | | | 59,368,615 | | | | 87,570,368 | | | | 46,410,990 | |

| | | | | | | | | | | | | |

| Liabilities: | | | | | | | | | | | | |

| Income distribution payable | | | — | | | | 82,252 | | | | — | |

| Investment advisory fees payable | | | 15,099 | | | | 33,501 | | | | 25,357 | |

| Distribution fees payable | | | 768 | | | | 18,611 | | | | 8,437 | |

| Unitary fees payable | | | 23,334 | | | | 49,586 | | | | 25,830 | |

| Capital shares redeemed payable | | | — | | | | — | | | | 51,801 | |

| Total Liabilities | | | 39,201 | | | | 183,950 | | | | 111,425 | |

| Net Assets | | $ | 59,329,414 | | | $ | 87,386,418 | | | $ | 46,299,565 | |

| | | | | | | | | | | | | |

| Class I | | | | | | | | | | | | |

| Net assets | | $ | 9,048,793 | | | $ | 87,386,418 | | | $ | — | |

| Shares of common stock outstanding | | | 905,078 | | | | 12,481,525 | | | | — | |

| Net asset value per share | | $ | 10.00 | | | $ | 7.00 | | | $ | — | |

| | | | | | | | | | | | | |

| Class Y | | | | | | | | | | | | |

| Net assets | | $ | 50,280,621 | | | $ | — | | | $ | — | |

| Shares of common stock outstanding | | | 5,029,607 | | | | — | | | | — | |

| Net asset value per share | | $ | 10.00 | | | $ | — | | | $ | — | |

| | | | | | | | | | | | | |

| Class AMF | | | | | | | | | | | | |

| Net assets | | $ | — | | | $ | — | | | $ | 40,103,888 | |

| Shares of common stock outstanding | | | — | | | | — | | | | 4,074,026 | |

| Net asset value per share | | $ | — | | | $ | — | | | $ | 9.84 | |

| | | | | | | | | | | | | |

| Class H | | | | | | | | | | | | |

| Net assets | | $ | — | | | $ | — | | | $ | 6,195,677 | |

| Shares of common stock outstanding | | | — | | | | — | | | | 630,679 | |

| Net asset value per share | | $ | — | | | $ | — | | | $ | 9.82 | |

| | | | | | | | | | | | | |

| Net Assets | | | | | | | | | | | | |

| Paid in capital | | $ | 59,359,352 | | | $ | 382,120,332 | | | $ | 27,911,066 | |

| Accumulated undistributed net investment income (loss) | | | 999 | | | | 85,505 | | | | (1 | ) |

| Accumulated undistributed net realized gains (losses) | | | (20,957 | ) | | | (295,113,720 | ) | | | 8,127,347 | |

| Unrealized appreciation (depreciation) on investments | | | (9,980 | ) | | | 294,301 | | | | 10,261,153 | |

| Net assets | | $ | 59,329,414 | | | $ | 87,386,418 | | | $ | 46,299,565 | |

| | | | | | | | | | | | | |

See notes to financial statements.

STATEMENTS OF OPERATIONS

For the Year or Period Ended October 31, 2017

| | | AAAMCO Ultrashort Financing Fund* | | | Ultra Short Mortgage Fund | | | Large Cap Equity Fund | |

| INVESTMENT INCOME: | | | | | | | | | | | | |

| Interest income | | $ | 377,300 | | | $ | 1,637,675 | | | $ | — | |

| Dividend income | | | 5,166 | | | | 29,001 | | | | 1,099,503 | |

| Dividend income from investment in affiliates | | | — | | | | 13,127 | | | | — | |

| Total investment income | | | 382,466 | | | | 1,679,803 | | | | 1,099,503 | |

| | | | | | | | | | | | | |

| Operating expenses: | | | | | | | | | | | | |

| Investment advisory | | | 68,953 | | | | 483,200 | | | | 286,487 | |

| Distribution — Class AMF Shares | | | — | | | | — | | | | 95,728 | |

| Distribution — Class I Shares | | | 2,940 | | | | 268,444 | | | | — | |

| Unitary | | | 151,219 | | | | 642,090 | | | | 262,910 | |

| Total expenses before reductions | | | 223,112 | | | | 1,393,734 | | | | 645,125 | |

| Expenses reduced by Investment Adviser | | | (117,397 | ) | | | (174,636 | ) | | | — | |

| Expenses reduced by Distributor | | | — | | | | (107,376 | ) | | | (38,291 | ) |

| Unitary Fee Waiver | | | (39,794 | ) | | | — | | | | — | |

| Net expenses | | | 65,921 | | | | 1,111,722 | | | | 606,834 | |

| Net investment income | | | 316,545 | | | | 568,081 | | | | 492,669 | |

| | | | | | | | | | | | | |

| REALIZED AND UNREALIZED GAINS (LOSSES) | | | | | | | | | | | | |

| FROM INVESTMENT ACTIVITIES: | | | | | | | | | | | | |

| Net realized gains (loss) from investment transactions | | | (9,652 | ) | | | (572,466 | ) | | | 9,094,101 | |

| Net increase from payment by affiliates | | | 12,500 | | | | — | | | | — | |

| Change in unrealized appreciation (depreciation) on investments | | | (9,980 | ) | | | (578,941 | ) | | | 86,114 | |

| Net realized and unrealized gains (losses) from investment activities | | | (7,132 | ) | | | (1,151,407 | ) | | | 9,180,215 | |

| CHANGE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 309,413 | | | $ | (583,326 | ) | | $ | 9,672,884 | |

| | | | | | | | | | | | | |

| * | For the period from June 6, 2017, commencement of operations, to October 31, 2017. |

See notes to financial statements.

STATEMENTS OF CHANGES IN NET ASSETS

| | | AAAMCO

Ultrashort

Financing Fund |

| | | Since Inception to

October 31, 2017* |

| | | | | |

| Increase (decrease) in net assets: | | | | |

| Operations: | | | | |

| Net investment income | | $ | 316,545 | |

| Net realized losses from investment transactions | | | (9,652 | ) |

| Net increase from payment by affiliates | | | 12,500 | |

| Change in unrealized depreciation on investments | | | (9,980 | ) |

| Change in net assets resulting from operations | | | 309,413 | |

| Dividends paid to shareholders: | | | | |

| From net investment income: | | | | |

| Class I Stockholders | | | (40,777 | ) |

| Class Y Stockholders | | | (286,074 | ) |

| Total dividends paid to stockholders | | | (326,851 | ) |

| Capital Transactions: | | | | |

| Class I Shares: | | | | |

| Proceeds from sale of shares | | | 9,010,000 | |

| Value of shares issued to shareholders in reinvestment of dividends | | | 40,777 | |

| Class Y Shares: | | | | |

| Proceeds from sale of shares | | | 50,010,000 | |

| Value of shares issued to shareholders in reinvestment of dividends | | | 286,075 | |

| Change in net assets from capital transactions | | | 59,346,852 | |

| Change in net assets | | | 59,329,414 | |

| Net Assets: | | | | |

| Beginning of period | | | — | |

| End of period | | $ | 59,329,414 | |

| Accumulated undistributed net investment income | | $ | 999 | |

| * | For the period from June 6, 2017, commencement of operations, to October 31, 2017. |

See notes to financial statements.

STATEMENTS OF CHANGES IN NET ASSETS (continued)

| | | Ultra Short Mortgage Fund | |

| | | Year Ended

October 31,

2017 | | | Year Ended

October 31,

2016 | |

| Increase (decrease) in net assets: | | | | | | | | |

| Operations: | | | | | | | | |

| Net investment income | | $ | 568,081 | | | $ | 1,087,396 | |

| Net realized gains (losses) from investment transactions | | | (572,466 | ) | | | 531,340 | |

| Change in unrealized depreciation on investments | | | (578,941 | ) | | | (2,138,000 | ) |

| Change in net assets resulting from operations | | | (583,326 | ) | | | (519,264 | ) |

| Dividends paid to stockholders: | | | | | | | | |

| From net investment income | | | (1,780,575 | ) | | | (2,263,353 | ) |

| Total dividends paid to stockholders | | | (1,780,575 | ) | | | (2,263,353 | ) |

| Capital Transactions: | | | | | | | | |

| Proceeds from sale of shares | | | 2,000,059 | | | | 19,481,854 | |

| Value of shares issued to shareholders in reinvestment of dividends | | | 432,767 | | | | 500,577 | |

| Cost of shares redeemed | | | (32,577,526 | ) | | | (71,682,538 | ) |

| Change in net assets from capital transactions | | | (30,144,700 | ) | | | (51,700,107 | ) |

| Change in net assets | | | (32,508,601 | ) | | | (54,482,724 | ) |

| Net Assets: | | | | | | | | |

| Beginning of year | | | 119,895,019 | | | | 174,377,743 | |

| End of year | | $ | 87,386,418 | | | $ | 119,895,019 | |

| Accumulated undistributed net investment income | | $ | 85,505 | | | $ | 36,479 | |

See notes to financial statements.

STATEMENTS OF CHANGES IN NET ASSETS (concluded)

| | | Large Cap Equity Fund | |

| | | Year Ended

October 31,

2017 | | | Year Ended

October 31,

2016 | |

| Increase (decrease) in net assets: | | | | | | | | |

| Operations: | | | | | | | | |

| Net investment income | | $ | 492,669 | | | $ | 505,894 | |

| Net realized gains from investment transactions | | | 9,094,101 | | | | 10,417,303 | |

| Change in unrealized appreciation (depreciation) on investments | | | 86,114 | | | | (8,053,698 | ) |

| Change in net assets resulting from operations | | | 9,672,884 | | | | 2,869,499 | |

| Dividends paid to shareholders: | | | | | | | | |

| From net investment income: | | | | | | | | |

| Class AMF Stockholders | | | (449,507 | ) | | | (446,355 | ) |

| Class H Stockholders | | | (82,031 | ) | | | (71,839 | ) |

| From net realized gains: | | | | | | | | |

| Class AMF Shares | | | (8,615,460 | ) | | | (2,362,365 | ) |

| Class H Shares | | | (1,243,999 | ) | | | (349,126 | ) |

| Total dividends paid to stockholders | | | (10,390,997 | ) | | | (3,229,685 | ) |

| Capital Transactions: | | | | | | | | |

| Class AMF Shares: | | | | | | | | |

| Proceeds from sale of shares | | | 815,172 | | | | 598,431 | |

| Value of shares issued to shareholders in reinvestment of dividends | | | 8,349,483 | | | | 2,511,047 | |

| Cost of shares redeemed | | | (5,056,728 | ) | | | (5,182,189 | ) |

| Class H Shares: | | | | | | | | |

| Proceeds from sale of shares | | | 1,446,466 | | | | 611,561 | |

| Value of shares issued to shareholders in reinvestment of dividends | | | 23,809 | | | | 6,596 | |

| Cost of shares redeemed | | | (541,444 | ) | | | (1,781,351 | ) |

| Change in net assets from capital transactions | | | 5,036,758 | | | | (3,235,905 | ) |

| Change in net assets | | | 4,318,645 | | | | (3,596,091 | ) |

| Net Assets: | | | | | | | | |

| Beginning of year | | | 41,980,920 | | | | 45,577,011 | |

| End of year | | $ | 46,299,565 | | | $ | 41,980,920 | |

| Accumulated net investment loss | | $ | (1 | ) | | $ | (1 | ) |

See notes to financial statements.

AAAMCO ULTRASHORT FINANCING FUND — CLASS I SHARES

FINANCIAL HIGHLIGHTS

Selected data for a share outstanding throughout the period indicated.

| | | Period ended

October 31,

2017* | |

| Net asset value, beginning of period | | $ | 10.00 | |

| Income from investment operations: | | | | |

| Net investment income | | | 0.0533 | |

| Net realized and unrealized gains from investments | | | 0.0018 | (a) |

| Total from investment operations | | | 0.0551 | |

| Less distributions: | | | | |

| Dividends paid to stockholders: | | | | |

| From net investment income | | | (0.0551 | ) |

| Change in net asset value | | | — | |

| Net asset value, end of period | | $ | 10.00 | |

| Total return | | | 0.55 | %(b) |

| Ratios/Supplemental data: | | | | |

| Net assets, end of period (in 000’s) | | $ | 9,049 | |

| Ratio of net expenses to average net assets | | | 0.34 | %(c) |

| Ratio of net investment income to average net assets | | | 1.32 | %(c) |

| Ratio of gross expenses to average net assets | | | 1.05 | %(c) |

| Portfolio turnover rate | | | 389 | %(b) |

| * | For the period from June 6, 2017, commencement of operations, to October 31, 2017. |

| (a) | Realized and unrealized gains and losses per share in this caption are balancing amounts necessary to reconcile the change in net asset value per share for the period, and may not reconcile with the aggregate gains and losses in the Statement of Operations due to share transactions for the period. |

| (b) | Not annualized for periods less than one year. |

| (c) | Annualized for periods less than one year. |

See notes to financial statements.

AAAMCO ULTRASHORT FINANCING FUND — CLASS Y SHARES

FINANCIAL HIGHLIGHTS

Selected data for a share outstanding throughout the period indicated.

| | | Period ended

October 31,

2017* | |

| Net asset value, beginning of period | | $ | 10.00 | |

| Income from investment operations: | | | | |

| Net investment income | | | 0.0553 | |

| Net realized and unrealized gains from investments | | | 0.0018 | (a) |

| Total from investment operations | | | 0.0571 | |

| Less distributions: | | | | |

| Dividends paid to stockholders: | | | | |

| From net investment income | | | (0.0571 | ) |

| Change in net asset value | | | — | |

| Net asset value, end of period | | $ | 10.00 | |

| Total return | | | 0.57 | %(b),(c) |

| Ratios/Supplemental data: | | | | |

| Net assets, end of period (in 000’s) | | $ | 50,281 | |

| Ratio of net expenses to average net assets | | | 0.29 | %(d) |

| Ratio of net investment income to average net assets | | | 1.37 | %(d) |

| Ratio of gross expenses to average net assets | | | 0.96 | %(d) |

| Portfolio turnover rate | | | 389 | %(c) |

| * | For the period from June 6, 2017, commencement of operations, to October 31, 2017. |

| | |

| (a) | Realized and unrealized gains and losses per share in this caption are balancing amounts necessary to reconcile the change in net asset value per share for the period, and may not reconcile with the aggregate gains and losses in the Statement of Operations due to share transactions for the period. |

| | |

| (b) | During the period ended October 31, 2017, the AAAMCO UltraShort Financing Fund received monies from the Adviser. |

If these monies were not received, the return for the period would have been 0.47%.

| (c) | Not annualized for periods less than one year. |

| | |

| (d) | Annualized for periods less than one year. |

See notes to financial statements.

ULTRA SHORT MORTGAGE FUND

FINANCIAL HIGHLIGHTS

Selected data for a share outstanding throughout the period indicated. |

| |

| | | Year Ended October 31, |

| | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 | |

| Net asset value, beginning of year | | $ | 7.16 | | | $ | 7.29 | | | $ | 7.36 | | | $ | 7.37 | | | $ | 7.36 | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.0205 | | | | 0.0439 | | | | 0.0575 | | | | 0.0722 | | | | 0.0626 | |

| Net realized and unrealized gains (losses) from investments | | | (0.0636 | ) | | | (0.0603 | ) | | | (0.0339 | ) | | | 0.0225 | | | | 0.0725 | |

| Total from investment operations | | | (0.0431 | ) | | | (0.0164 | ) | | | 0.0236 | | | | 0.0947 | | | | 0.1351 | |

| | | | | | | | | | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends paid to stockholders: | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.1169 | ) | | | (0.1136 | ) | | | (0.0936 | ) | | | (0.1047 | ) | | | (0.1251 | ) |

| Change in net asset value | | | (0.16 | ) | | | (0.13 | ) | | | (0.07 | ) | | | (0.01 | ) | | | 0.01 | |

| Net asset value, end of year | | $ | 7.00 | | | $ | 7.16 | | | $ | 7.29 | | | $ | 7.36 | | | $ | 7.37 | |

| Total return | | | (0.61) % | | | | (0.22) % | | | | 0.32% | | | | 1.30% | | | | 1.86%* | |

| Ratios/Supplemental data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (in 000’s) | | $ | 87,386 | | | $ | 119,895 | | | $ | 174,378 | | | $ | 197,512 | | | $ | 274,862 | |

| Ratio of net expenses to average net assets | | | 1.03% | | | | 0.96% | | | | 0.92% | | | | 0.80% | | | | 0.79% | |

| Ratio of net investment income to average net assets | | | 0.53% | | | | 0.75% | | | | 0.85% | | | | 1.08% | | | | 0.99% | |

| Ratio of gross expenses to average net assets** | | | 1.30% | | | | 1.22% | | | | 1.18% | | | | 1.09% | | | | 1.12% | |

| Portfolio turnover rate | | | 26% | | | | 26% | | | | 22% | | | | 3% | | | | 30% | |

| * | During the fiscal year ended October 31, 2013, the Ultra Short Mortgage Fund received monies related to certain nonrecurring litigation settlements. If these monies were not received, the One Year return would have been (0.20)%. |

| ** | During the periods shown, certain fees were voluntarily reduced. If such voluntary fee reductions had not occurred, the ratios would have been as indicated. |

See notes to financial statements.

LARGE CAP EQUITY FUND — CLASS AMF SHARES

FINANCIAL HIGHLIGHTS

Selected data for a share outstanding throughout the period indicated. |

| |

| | | Year Ended October 31, | |

| | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 | |

| Net asset value, beginning of year | | $ | 10.34 | | | $ | 10.43 | | | $ | 11.37 | | | $ | 11.10 | | | $ | 9.41 | |

| | | | | | | | | | | | | | | | | | | | | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.11 | | | | 0.12 | | | | 0.13 | | | | 0.13 | | | | 0.11 | |

| Net realized and unrealized gains (losses) from investments | | | 2.02 | | | | 0.57 | | | | (0.20 | ) | | | 1.03 | | | | 2.02 | |

| Total from investment operations | | | 2.13 | | | | 0.69 | | | | (0.07 | ) | | | 1.16 | | | | 2.13 | |

| | | | | | | | | | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends paid to stockholders: | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.11 | ) | | | (0.12 | ) | | | (0.14 | ) | | | (0.14 | ) | | | (0.12 | ) |

| From net realized gains | | | (2.52 | ) | | | (0.66 | ) | | | (0.73 | ) | | | (0.75 | ) | | | (0.32 | ) |

| Total distributions | | | (2.63 | ) | | | (0.78 | ) | | | (0.87 | ) | | | (0.89 | ) | | | (0.44 | ) |

| Change in net asset value | | | (0.50 | ) | | | (0.09 | ) | | | (0.94 | ) | | | 0.27 | | | | 1.69 | |

| Net asset value, end of year | | $ | 9.84 | | | $ | 10.34 | | | $ | 10.43 | | | $ | 11.37 | | | $ | 11.10 | |

| Total return | | | 24.63% | | | | 7.06% | | | | (0.87)% | | | | 10.90% | | | | 23.55 | % |

| Ratios/Supplemental data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (in 000’s) | | $ | 40,104 | | | $ | 36,668 | | | $ | 39,017 | | | $ | 54,780 | | | $ | 89,562 | |

| Ratio of net expenses to average net assets | | | 1.40% | | | | 1.32% | | | | 1.28% | | | | 1.24% | | | | 1.22% | |

| Ratio of net investment income to average net assets | | | 1.09% | | | | 1.18% | | | | 1.22% | | | | 1.13% | | | | 1.11% | |

| Ratio of gross expenses to average net assets** | | | 1.50% | | | | 1.42% | | | | 1.38% | | | | 1.34% | | | | 1.32% | |

| Portfolio turnover rate | | | 112% | | | | 76% | | | | 9% | | | | 7% | | | | 5% | |

| ** | During the periods shown, certain fees were voluntarily reduced. If such voluntary fee reductions had not occurred, the ratios would have been as indicated. |

See notes to financial statements.

LARGE CAP EQUITY FUND — CLASS H SHARES

FINANCIAL HIGHLIGHTS

Selected data for a share outstanding throughout the period indicated. |

| |

| | | Year Ended October 31, | |

| | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 | |

| Net asset value, beginning of year | | $ | 10.34 | | | $ | 10.43 | | | $ | 11.36 | | | $ | 11.10 | | | $ | 9.41 | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.12 | | | | 0.15 | | | | 0.14 | | | | 0.13 | | | | 0.13 | |

| Net realized and unrealized gains (losses) from investments | | | 2.02 | | | | 0.56 | | | | (0.19 | ) | | | 1.04 | | | | 2.01 | |

| Total from investment operations | | | 2.14 | | | | 0.71 | | | | (0.05 | ) | | | 1.17 | | | | 2.14 | |

| | | | | | | | | | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends paid to stockholders: | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.14 | ) | | | (0.14 | ) | | | (0.15 | ) | | | (0.16 | ) | | | (0.13 | ) |

| From net realized gains | | | (2.52 | ) | | | (0.66 | ) | | | (0.73 | ) | | | (0.75 | ) | | | (0.32 | ) |

| Total distributions | | | (2.66 | ) | | | (0.80 | ) | | | (0.88 | ) | | | (0.91 | ) | | | (0.45 | ) |

| Change in net asset value | | | (0.52 | ) | | | (0.09 | ) | | | (0.93 | ) | | | 0.26 | | | | 1.69 | |

| Net asset value, end of year | | $ | 9.82 | | | $ | 10.34 | | | $ | 10.43 | | | $ | 11.36 | | | $ | 11.10 | |

| Total return | | | 24.76 | % | | | 7.23 | % | | | (0.62 | )% | | | 10.99 | % | | | 23.74 | % |

| Ratios/Supplemental data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (in 000’s) | | $ | 6,196 | | | $ | 5,313 | | | $ | 6,560 | | | $ | 6,864 | | | $ | 5,755 | |

| Ratio of net expenses to average net assets | | | 1.25 | % | | | 1.16 | % | | | 1.13 | % | | | 1.09 | % | | | 1.07 | % |

| Ratio of net investment income to average net assets | | | 1.24 | % | | | 1.38 | % | | | 1.33 | % | | | 1.15 | % | | | 1.24 | % |

| Ratio of gross expenses to average net assets | | | 1.25 | % | | | 1.16 | % | | | 1.13 | % | | | 1.09 | % | | | 1.07 | % |

| Portfolio turnover rate | | | 112 | % | | | 76 | % | | | 9 | % | | | 7 | % | | | 5 | % |

See notes to financial statements.

NOTES TO FINANCIAL STATEMENTS

October 31, 2017

Asset Management Fund (the “Trust”) was reorganized as a Delaware statutory trust on September 30, 1999, and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a diversified open-end management company. As an investment company, as defined in Financial Accounting Standards Board (“FASB”) Accounting Standards Update 2013-08, the Trust follows accounting and reporting guidance under FASB Accounting Standards Codification Topic 946, “Financial Services-Investment Companies.” As of October 31, 2017, the Trust is authorized to issue an unlimited number of shares, at no par value, in three separate series: the AAAMCO Ultrashort Financing Fund, the Ultra Short Mortgage Fund and the Large Cap Equity Fund (referred to individually as a “Fund” and collectively as the “Funds”). The AAAMCO Ultrashort Financing Fund is authorized to issue two classes of shares: Class I Shares and Class Y Shares. Class I and Class Y Shares of the AAAMCO Ultrashort Financing Fund have the same rights and obligations except: (i) Class I Shares bear a distribution fee, while Class Y Shares do not have any distribution fee, which will cause Class I Shares to have a higher expense ratio and to pay lower dividends than those related to Class Y Shares; (ii) other expenses, which are determined to properly apply to one class of shares upon approval by the Board of Trustees of the Trust (“Board”), will be borne solely by the class to which such expenses are attributable; and (iii) each class will have exclusive voting rights with respect to the matters relating to its own distribution arrangements. The AAAMCO Ultrashort Financing Fund commenced operations on June 6, 2017. The Ultra Short Mortgage Fund offers a single class of shares. The Large Cap Equity Fund is authorized to issue two classes of shares: Class AMF Shares and Class H Shares. Class AMF and Class H Shares of the Large Cap Equity Fund have the same rights and obligations except: (i) Class AMF Shares bear a distribution fee, while Class H Shares do not have any distribution fee, which will cause Class AMF Shares to have a higher expense ratio and to pay lower dividend rates than those related to Class H Shares; (ii) other expenses, which are determined to properly apply to one class of shares upon approval by the Board of Trustees of the Trust (“Board”), will be borne solely by the class to which such expenses are attributable; and (iii) each class will have exclusive voting rights with respect to the matters relating to its own distribution arrangements.

The Trust maintains an insurance policy that insures its officers and trustees against certain liabilities. Under the Trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust. In addition, in the normal course of business, the Trust enters into contracts with its vendors and others that provide general indemnification. Each Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against a Fund.

A. Significant accounting policies are as follows:

SECURITY VALUATION

Investments are recorded at fair value. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The valuation techniques employed by the Funds, as described below, maximize the use of observable inputs and minimize the use of unobservable inputs in determining fair value. These inputs are summarized in the following three broad levels:

| ● | Level 1 — quoted prices in active markets for identical assets |

| ● | Level 2 — other significant observable inputs (including quoted prices of similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| ● | Level 3 — significant unobservable inputs (including a Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. For example, certain short-term debt securities may be valued using amortized cost. Generally, amortized cost approximates the fair value of a security, but since this valuation is not obtained from a quoted price in an active market, such securities would be reflected as Level 2 in the fair value hierarchy.

The Funds’ prices for equity securities are generally provided by an independent third party pricing service approved by the Board as of the close of the regular trading session of the New York Stock Exchange, normally at 4:00 pm EST, each business day on which the share price of each Fund is calculated. Equity securities listed or traded on a primary exchange are valued at the closing price, if available, or the last sales price on the primary exchange. If no sale occurred on the valuation date, the securities will be valued at the mean of the latest bid and ask quotations as of the close of the primary exchange. Investments in other open-end registered investment companies are valued at their respective net asset value (“NAV”) as reported by such companies. In these types of situations, valuations are typically categorized as Level 1 in the fair value hierarchy.

The Funds’ debt and other fixed income securities are generally valued at an evaluated bid price provided by an independent pricing source approved by the Board. To value debt securities, pricing services may use various pricing techniques which take into account appropriate factors such as market activity, yield, quality, coupon rate, maturity, type of issue, trading characteristics, call features, credit ratings and other data, as well as broker quotes. Short-term debt securities of sufficient credit quality that mature within sixty days may be valued at amortized cost, which may approximate fair value. Repurchase agreements are valued at par daily, as long as the

NOTES TO FINANCIAL STATEMENTS (continued)

October 31, 2017

market value of collateral is sufficient to support this valuation. In each of these situations, valuations are typically categorized as Level 2 in the fair value hierarchy. If a pricing service is unable to provide valuations for a particular security or securities, or the Trust’s Pricing Committee has determined that such valuations are unreliable, the Board has approved the use of a fair valuation methodology implemented by the Trust’s Pricing Committee to fair value the security or securities.

Within the fair value pricing methodology implemented by the Pricing Committee, among the more specific factors that are considered in determining the fair value of investments in debt instruments are: (1) information obtained with respect to market transactions in such securities or comparable securities; (2) the price and extent of public trading in similar securities of the issuer or comparable securities; (3) the fundamental analytical data relating to the investment; (4) quotations from broker/ dealers, yields, maturities, ratings and various relationships between securities; and (5) evaluation of the forces which influence the market in which these securities are purchased and sold. The fair valuation process also takes into consideration factors such as interest rate changes, movements in credit spreads, default rate assumptions, repayment assumptions, type and quality of collateral, and security seasoning. Imprecision in estimating fair value can impact the

amount of unrealized appreciation or depreciation recorded for a particular security, and differences in the assumptions used could result in a different determination of fair value, and those differences could be material. Depending on the source and relative significance of the valuation inputs in these instances, the instruments may be classified as Level 2 or Level 3 in the fair value hierarchy.

Fair value pricing, including evaluated prices obtained from pricing services, is inherently a process of estimates and judgments. Fair value prices may fluctuate less than market prices due to technical issues which may impact the prices at which the Funds can purchase or sell securities. Market prices can be impacted by technical factors such as short term changes in market liquidity and volatility which may not directly impact fair value prices. In addition, changes in the value of portfolio investments priced at fair value may be less frequent and of greater magnitude than changes in the price of securities that trade frequently in the marketplace, resulting in potentially greater NAV volatility.

While the Trust’s policy is intended to result in a calculation of a Fund’s NAV that fairly reflects security values at the time of pricing, the Trust cannot ensure that fair value prices would accurately reflect the price that a Fund could obtain for a security if it were to dispose of that security, particularly in a forced or distressed sale.

The following is a summary of the inputs used to value the Funds’ investments as of October 31, 2017:

| Portfolio | | Level 1-

Quoted Prices | | | Level 2 -

Other Significant

Observable Inputs | | | Level 3 -

Significant

Unobservable Inputs | | | Total | |

| AAAMCO Ultrashort Financing Fund | | | | | | | | | | | | | | | | |

| Adjustable Rate Mortgage-Related Securities | | $ | — | | | $ | 8,001,803 | | | $ | — | | | $ | 8,001,803 | |

| Investment Companies | | | 35,691 | | | | — | | | | — | | | | 35,691 | |

| Repurchase Agreements | | | — | | | | 51,241,679 | | | | — | | | | 51,241,679 | |

| Total Investments | | | 35,691 | | | | 59,243,482 | | | | — | | | | 59,279,173 | |

| Ultra Short Mortgage Fund | | | | | | | | | | | | | | | | |

| Adjustable Rate Mortgage-Related Securities | | | — | | | | 47,798,567 | | | | — | | | | 47,798,567 | |

| Fixed Rate Mortgage-Related Securities | | | — | | | | 28,198,241 | | | | — | | | | 28,198,241 | |

| Investment Companies | | | 11,334,792 | | | | — | | | | — | | | | 11,334,792 | |

| Total Investments | | | 11,334,792 | | | | 75,996,808 | | | | — | | | | 87,331,600 | |

| Large Cap Equity Fund | | | | | | | | | | | | | | | | |

| Common Stocks | | | 45,352,836 | | | | — | | | | — | | | | 45,352,836 | |

| Investment Companies | | | 1,023,416 | | | | — | | | | — | | | | 1,023,416 | |

| Total Investments | | | 46,376,252 | | | | — | | | | — | | | | 46,376,252 | |

| | | | | | | | | | | | | | | | | |

As of October 31, 2017, there were no Level 3 securities held by the Funds. The Trust’s policy is to disclose transfers between levels based on valuations at the end of the reporting period. There were no transfers between Level 1, 2 or 3 as of October 31, 2017, based on levels assigned to securities as of October 31, 2016.

REPURCHASE AGREEMENTS

The AAAMCO Ultrashort Financing Fund and the Ultra Short Mortgage Fund may invest in obligations of the U.S. Government or other obligations that are not subject to any investment limitation on the part of national banks that may

NOTES TO FINANCIAL STATEMENTS (continued)

October 31, 2017

be purchased from government securities dealers or the custodian bank, subject to the seller’s agreement to repurchase them at an agreed upon date and price. The Funds, through the custodian, receives delivery of the underlying collateral for each repurchase agreement. The Funds require the custodian to take possession of all collateral for repurchase agreements. The Fund’s require the fair value of collateral underlying the repurchase agreement to be at least 102% of the repurchase price, including any accrued interest earned on the repurchase agreement. If the counterparty defaults, and the fair value of the collateral declines, realization of the collateral by a Fund may be delayed or limited. There were no repurchase agreements held by the Ultra Short Mortgage Fund as of October 31, 2017.

The Funds may enter into transactions subject to enforceable netting arrangements (“netting arrangements”) under a repurchase agreement. Generally, netting arrangements allow the Funds to offset any exposure to a specific counterparty with any collateral received or delivered to that counterparty. In addition, netting arrangements provide the right for the non-defaulting party to liquidate the collateral and calculate the net exposure to the defaulting party or request additional collateral. Generally, the Funds manage their cash collateral and securities collateral on a counterparty basis. As of October 31, 2017, the AAAMCO Ultrashort Financing Fund has invested in the repurchase agreements described below, with gross exposures on the Statement of Assets and Liabilities, that could be netted subject to netting agreements.

The following table presents the repurchase agreements, which are subject to netting arrangements, as well as the collateral received related to those repurchase agreements.

| | | | | | | | Gross Amounts Not Offset in the

Statement of Assets and Liabilities |

| Fund Name | | Counterparty | | Gross Amounts of Assets

Presented in Statement of

Assets and Liabilities | Financial

Instruments | | Net

Amount |

| AAAMCO Ultrashort Financing Fund | | Amherst Pierpont Securities LLC | | | $ | 18,000,000 | | | | $ | (18,000,000 | ) | | | $ | — |

| | | BCM High Income Fund, LP | | | | 19,743,218 | | | | | (19,743,218 | ) | | | | — |

| | | JVB Financial Group, LLC | | | | 8,673,845 | | | | | (8,673,845 | ) | | | | — |

| | | Vining-Sparks IBG, L.P. | | | | 4,824,616 | | | | | (4,824,616 | ) | | | | — |

| | | Total | | | $ | 51,241,679 | | | | $ | (51,241,679 | ) | | | $ | — |

SECURITIES PURCHASED OR SOLD ON A WHEN-ISSUED OR DELAYED DELIVERY BASIS

Each Fund may purchase or sell securities on a when-issued basis or delayed-delivery basis. With when-issued transactions, securities are bought or sold during the periods between the announcement of an offering and the issuance and payment date of the securities. When securities are purchased or sold on a delayed-delivery basis, the price of the securities is fixed at the time of the commitment to purchase or sell is made, but settlement may take place at a future date. By the time of delivery, securities purchased or sold on a when-issued or delayed-delivery basis may be valued at less than the purchase or sell price. At the time when-issued or delayed-delivery securities are purchased or sold, a Fund must set aside funds or securities in a segregated account to pay for the purchase or as collateral for the sale. There were no securities purchased or sold on a when-issued or delayed-delivery basis held by the Funds as of October 31, 2017.

MORTGAGE-BACKED TO-BE-ANNOUNCED TRANSACTIONS

A Mortgage-Backed To-Be-Announced (“TBA”) trade represents a forward contract for the purchase or sale of single-

family mortgage-related securities to be delivered on a specified future date. In a typical TBA trade, the specific pool of mortgages that will be delivered to fulfill the forward contract are unknown at the time of the trade. The parties to a TBA trade agree upon the issuer, coupon, price, product type, amount of securities and settlement date for delivery. Settlement for TBA trades is standardized to occur on one specific day each month. The mortgage-related securities that ultimately will be delivered, and the loans backing those mortgage-related securities, frequently have not been created or originated at the time of the TBA trade, even though a price for the securities is agreed to at that time.

The Ultra Short Mortgage Fund may engage in TBA transactions to manage cash positions as well as to manage interest rate and prepayment risks. The Fund may engage in forward sales of TBA trades only when the Fund has identified the actual mortgage pool held in position to be delivered in fulfillment of the TBA trade obligation(specifying the pool or CUSIP number). These pools must be deliverable into the sold TBA position. At October 31, 2017, there were no mortgage-backed TBA positions held in the Ultra Short Mortgage Fund.

NOTES TO FINANCIAL STATEMENTS (continued)

October 31, 2017

DIVIDENDS TO SHAREHOLDERS

AAAMCO Ultrashort Financing Fund and Ultra Short Mortgage Fund:

Dividends from net investment income are declared daily and paid monthly. Net short-term and long-term capital gains, if any, are declared and paid annually.

Large Cap Equity Fund:

Dividends from net investment income are declared and paid at least quarterly. Net short-term and long-term capital gains, if any, are declared and paid annually.

For all Funds, distributions from net investment income and from net realized capital gains are determined in accordance with Federal income tax regulations, which may differ from accounting principles generally accepted in the United States of America. These “book/tax” differences are either considered temporary or permanent in nature. To the extent these differences are permanent in nature (e.g. reclass of dividend distribution and return of capital), such amounts are reclassified within the composition of net assets based on their federal tax-basis treatment; temporary differences do not require reclassification. Distributions to shareholders that exceed net investment income and net realized capital gains for tax purposes are reported as distributions of capital.

FEDERAL TAXES

No provision is made for Federal income taxes as it is the policy of each Fund to continue to qualify as a regulated investment company by complying with the provisions available to certain investment companies, as defined in applicable sections of the Internal Revenue Code, and to make distributions of net investment income and net realized capital gains sufficient to relieve it from all, or substantially all, federal income taxes.