UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-03599

Name of Registrant: The Royce Fund

Address of Registrant: 745 Fifth Avenue

New York, NY 10151

Name and address of agent for service: John E. Denneen, Esq. 745 Fifth Avenue New York, NY 10151 |

Registrant's telephone number, including area code: (212) 508-4500

Date of fiscal year end: December 31, 2023

Date of reporting period: January 1, 2023 – June 30, 2023

Item 1. Reports to Shareholders.

royceinvest.com

The Royce Funds 2023 Semiannual

Review and Report to Shareholders

June 30, 2023

Royce Dividend Value Fund

Royce Global Financial Services Fund

Royce International Premier Fund

Royce Micro-Cap Fund

Royce Pennsylvania Mutual Fund

Royce Premier Fund

Royce Small-Cap Opportunity Fund

Royce Small-Cap Special Equity Fund

Royce Small-Cap Total Return Fund

Royce Small-Cap Value Fund

Royce Smaller-Companies Growth Fund

Table of Contents

This page is not part of the The Royce Funds 2023 Semiannual Report to Shareholders | 1

Letter to Our Shareholders

THE BIGGER THE BETTER?

U.S. stocks finished the first six months of 2023 in strong shape, with all the major domestic indexes squarely in the black at the end of June. Several factors seemed to play a role in fostering a more optimistic mindset: returns in April and May were low for the large-cap Russell 1000 Index and negative for the small-cap Russell 2000 Index, which likely encouraged some investors to give equities a fresh look. Investors may also have begun looking past concerns about inflation and recession toward a more stable, perhaps even vibrant period of economic growth. Employment stayed strong while recession talk moderated in terms of both coverage and volume. Both were encouraging developments, though the Fed’s decision to skip an interest rate hike in June, even as the central bank all but promised increases in July and September, was almost certainly an even bigger factor.

How well stocks performed during 2023’s first half varied considerably depending on where one looked along the market capitalization spectrum. In general, the farther upward one traveled, the higher the returns ran. Interestingly (and somewhat frustratingly), 2023 began with an advantage for

small-cap stocks. It was short-lived, however, lasting only until this year’s high for the Russell 2000 on Groundhog Day (2/2/23) before giving way to a rather dramatic reversal. As of 1/31/23, the small-cap index was 300 basis points ahead of the Russell 1000 for the year-to-date period (+9.7% versus +6.7%). At the end of June, however, the Russell 2000 was running 859 basis points behind the Russell 1000 for the year-to-date period ended 6/30/23.

Returns for the Russell Microcap, Russell 2000, Russell 1000, and Russell Top 50

Year-to-Date through 6/30/23

Past performance is no guarantee of future results.

2 | This page is not part of the The Royce Funds 2023 Semiannual Report to Shareholders

LETTER TO OUR SHAREHOLDERS

And although returns were lower, large-cap outperformance was also the pattern among non-U.S. stocks, with the difference being that the year-to-date spread was much narrower: the MSCI ACWI ex USA Small Cap Index rose 6.8% in 2023’s first half while the MSCI ACWI ex USA Large Cap Index increased 9.8%.

ARTIFICIAL INTELLIGENCE: A MARKET-SHAPING FORCE?

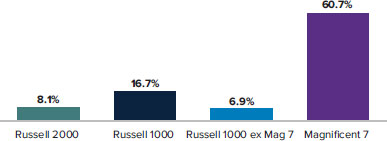

We think a couple of related observations are relevant from the standpoint of small-cap specialists like us: first, two factors affected the shift in leadership between U.S. small- and large-cap stocks, one that disproportionately hurt small caps and another that disproportionately helped a few mega-cap names. Small caps bore the brunt of the damage from the banking crisis, which had its most adverse effects on the share prices of smaller regional players. (It came as no surprise to us that banks were the top-detracting industry in the Russell 2000 for 2023’s first half.) The factor that helped large cap, and in our view the primary driver of that asset class’s higher returns in the first half of the year, was the promise of artificial intelligence (“AI”), a major secular trend whose impacts have just begun to register.

Widespread positive performance masked how top heavy and tightly concentrated returns have become since stocks began rallying near the end of 2022. Looking closer at first-half results reveals the degree to which the prospects for AI drove large-cap performance, which was dominated by impressive results for “The Magnificent Seven,” a handful of mostly familiar behemoths: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla. The combined market capitalizations of these seven companies accounted for 25.1% of the Russell 1000’s total market capitalization at the end of June. To get an additional sense of how enormous they are: Apple, the largest of them as of June 30, had a market cap of $3.05 trillion—which was more than the market cap of the entire Russell 2000 as of that

same date. Considering there are more than 4,000 publicly traded companies in the U.S., this is an almost absurd level of concentration, one that appears unsustainable to us. It is a level of concentration the market has not seen since the ‘Nifty Fifty’ market of the early to mid 1970s. Each of “The Magnificent Seven” is considered one of the primary beneficiaries of AI’s vast untapped potential. Without them, the Russell 2000 would have beaten the Russell 1000 in the first half of 2023. (We feel it’s also worth mentioning that the fall of the Nifty Fifty, all of them established large-cap stocks at the time, precipitated a long run of small-cap outperformance.)

The Russell 2000 Beat the Russell 1000, Excluding the “Magnificent Seven”

Year-to Date Performance for the Russell 2000, Russell 1000, Russell 1000 ex. the Magnificent 7, and the Magnificent 7

Past performance is no guarantee of future results.

ARE SMALL CAPS MOVING FROM BEAR TO BULL?

Unlike their bigger siblings, small caps remained in a bear market at the end of June. The Russell 2000 was down -20.8% from its last peak on 11/8/21, though a positive 7/31/23 brought it out of bear territory—a decline of at least -20.0% from its prior peak. By way of contrast, the Russell 1000 was down only -6.2% from its last peak on 1/3/22, and the tech-heavy Nasdaq fell just -12.9% from its most recent high on 11/19/21, through 6/30/23. Yet we are optimistic both in spite of the relative disadvantage of small-caps and, in some ways, because of it.

The average stock in the Russell 2000 was -28% off its 52-week high at the end of June, which gives

some sense of the opportunity set that exists within small cap—and with it, the potential for improved

performance going forward. Our expectation is that this potential will be realized over the next few years.

This page is not part of the The Royce Funds 2023 Semiannual Report to Shareholders | 3

LETTER TO OUR SHAREHOLDERS

First, significant multiple compression has occurred over the last several months among small caps, particularly small-cap value stocks. The result is that valuations looked highly favorable for the Russell 2000, on both an absolute basis and relative to the Russell 1000, where they remain close to a 20-year low, based on our preferred valuation metric, enterprise value over earnings before interest & taxes (“EV/EBIT”). Unsurprisingly in light of how it has recently lagged growth, the Russell 2000 Value Index finished June much more attractively valued than the Russell 2000 Growth Index, based on that same EV/EBIT metric. It is also worth noting that concerns about elevated valuations in the overall market have played out in an inflationary climate with rising interest rates and widespread anxiety that the economy is about to slip into a recession. We suspect that these concerns will continue to recede as economic news continues to skew more positively. Of course, we are more focused on the absolute valuations of individual companies, which in many instances look appealingly inexpensive to us. The average stock in the Russell 2000 was -28% off its 52-week high at the end of June, which gives some sense of the opportunity set that exists within small cap—and with it, the potential for improved performance going forward. Our expectation is that this potential will be realized over the next few years.

LISTENING TO CLIO, OR A SMALL-CAP HISTORY IN 3 CHARTS

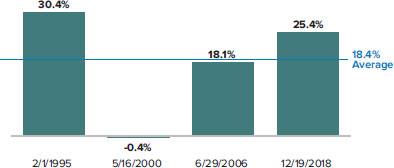

We also see history (and Clio is the Muse of that discipline) showing several reasons why small-cap investors may currently have reasons to be cheerful. We are of course mindful of the fact that history seldom repeats itself. But it often rhymes—and always offers valuable lessons for those of us who take the time to examine previous performance patterns. We began with an analysis of what has happened at the end of past rate hike cycles. While our current era has seen the fastest pace of interest rate hikes on record, there have been other interest rate increase cycles. We looked at the subsequent one-year returns for small cap over four previous rate hike cycles, going back to 1993. The Russell 2000 had positive performance in three of the four periods, and in each of those three, returns were in the double digits. Over all four periods, the small-cap index averaged an impressive 18.4% gain.

Historical Performance Post Final Fed Rate Hikes

Subsequent Average Annual 1-Year Returns for the Russell 2000 Following Final Rate Hikes from 3/31/93 through 6/30/23

Past performance is no guarantee of future results.

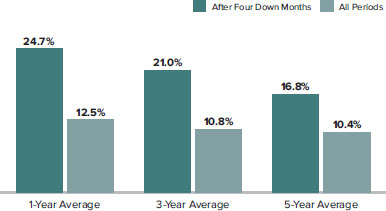

Looking more closely at the present, we find that January and June were the only months so far in 2023 when the Russell 2000 had positive returns. There were four straight down months in between, a rare occurrence that has happened only nine times since the inception of the index on 12/31/78. We wanted to see what shape performance took over the subsequent one-, three-, and five-year spans. What we found was very encouraging, with each period coming in comfortably above the one-, three-, and five-year monthly rolling averages for the Russell 2000 since inception. For the eight periods for which we have data, subsequent one-year returns averaged 24.7%; subsequent three-year returns averaged 21.0%; and subsequent five-year returns averaged 16.8%.

Russell 2000 Average Returns Following Four Consecutive Months with Negative Returns

From Russell 2000 Inception (12/31/78) through 6/30/23

Past performance is no guarantee of future results.

The Russell 2000 has had four consecutive down months in 9 out 534 periods.

4 | This page is not part of the The Royce Funds 2023 Semiannual Report to Shareholders

LETTER TO OUR SHAREHOLDERS

We are all hoping for a robust rebound for the U.S. economy for many reasons, not the

least of which is that small caps, in particular the cyclical industries that mostly populate our

portfolios, tend to do especially well in a thriving economy.

We also looked at data that demonstrates how strong and lasting a rebound small caps have enjoyed after low annualized five-year periods such as we had at the end of June, when the small-cap index’s average annualized 5-year return was a paltry 4.2%. The Russell 2000 had positive annualized five-year returns 100% of the time—in all 81 five-year periods—averaging an impressive 14.9%, which was well above its monthly rolling five-year return since inception of 10.4%.

Why Better Small-Cap Performance May Be Ahead

Subsequent Average Annualized 5-Year Performance for the Russell 2000 Following 5-Year Annualized Return Ranges of Less Than 5% from 12/31/83 through 6/30/23

Past performance is no guarantee of future results.

It appears to us that history is on the side of strong small-cap performance going forward.

THE FUTURE’S SO BRIGHT?

We are all hoping for a robust rebound for the U.S. economy for many reasons, not the least of which is that small caps, in particular the cyclical industries that mostly populate our portfolios, tend to do especially well in a thriving economy. And while some data points remain concerning—most notably higher rates, wobbly industrial production, and a stubbornly inverted yield curve—there are also many signs that the economy is inching closer to recovery. To be sure, a soft landing looks more and more likely to us, while the kind of deep and potentially lengthy recession many have been anticipating since late 2021 looks less and less likely. As Neil

Dutta at Renaissance Macro recently put it, “The statute of limitations has now kicked in” regarding a recession in the U.S.

The U.S. Commerce Department reported a 0.9% seasonally adjusted increase in construction spending for May, which included a significant jump in spending on new manufacturing facilities. There was a 76.3% increase from a year earlier, as well as a 1% advance in May over April. The Commerce Department also showed that spending on manufacturing construction accounted for almost 0.5% of first-quarter GDP, its largest share since 1991. And its second-quarter share of GDP is expected to be even higher. Homebuilding rose by 21.7% in May, a record monthly surge that defied expectations of a slowdown. CapEx has been steady and has shown signs of improving, with the ISM services index re-accelerating in June. Durable goods orders rose for the fourth consecutive month in that same month, hitting a record high for nondefense capital goods (excluding aircraft or core capital goods, a proxy for business equipment investment). Moreover, retail and vehicle sales rose in June while the University of Michigan’s consumer sentiment measure rose in July. Most important, however, was that second-quarter GDP came in higher than expected, thanks to resilient consumers and robust business investment, as inflation continued to moderate, rising at the slowest rate in more than two years. We think investors should also keep in mind that rate hikes and inflation will likely be sunsetting over the next year or so, when the positive impacts of reshoring, the infrastructure bill, and the CHIPs Act will begin to take effect.

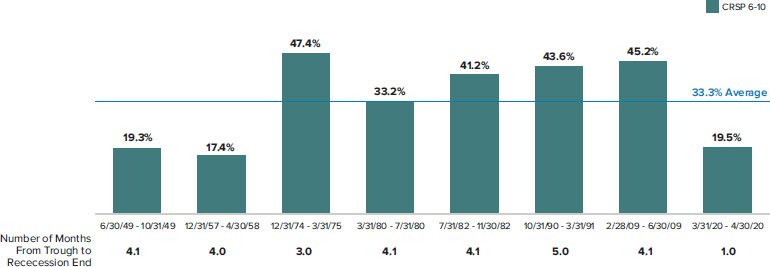

All this encouraging news may be of special relevance to small-cap investors. We looked at data going back to the 1940s, using the Center for Research in Securities Prices data where the CRSP 6-10 is the small-cap proxy, to see what happened to small caps in recessionary periods. The historical pattern is that small caps tend to trough before recessions end, advancing 33.3% on average from the small-cap trough to the end of the recession. As we have said previously, investors typically pay a steep price for waiting, whether for the market to bottom or a recession to end. And a recession remains a possibility, despite recent developments.

This page is not part of the The Royce Funds 2023 Semiannual Report to Shareholders | 5

LETTER TO OUR SHAREHOLDERS

The Price of Waiting for Recessions to End

Average Small-Cap Return from Market Trough to Recession’s End Was 33.3% from 6/30/49 through 4/30/20

Past performance is no guarantee of future results.

Ultimately, of course, we are bottom-up stock pickers. Our knowledge and experience lie in analyzing companies and managing portfolios. So, as important as we think all this data is, we put more trust into what we are hearing from company management teams. In our conversations, there continues to be a sense of cautious optimism—which was reflected in generally solid earnings for many holdings for

the second quarter and few, if any, profit warnings so far for the third. All of this is consistent with our contention that small caps are due—arguably overdue—for a breakout in the coming months. Our confidence in the prospects for disciplined and patient active management within small cap remains high.

Sincerely,

|  |  |

| | | |

| Charles M. Royce | Christopher D. Clark | Francis D. Gannon |

| Chairman, | Chief Executive Officer, and | Co-Chief Investment Officer, |

| Royce Investment Partners | Co-Chief Investment Officer, | Royce Investment Partners |

| | Royce Investment Partners | |

| July 31, 2023 | | |

6 | This page is not part of the The Royce Funds 2023 Semiannual Report to Shareholders

Performance and Expenses

Performance and Expenses

As of June 30, 2023

| | | | | AVERAGE ANNUAL TOTAL RETURNS (%) | | | ANNUAL OPERATING

EXPENSES (%) |

| | YTD 1 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | SINCE

INCEPTION | INCEPTION

DATE | GROSS | NET |

| Royce Dividend Value Fund | 11.92 | 22.44 | 12.85 | 6.12 | 7.34 | 8.14 | N/A | 8.15 | 5/3/04 | 1.623 | 1.343 |

| Royce Global Financial Services Fund | 3.51 | 6.04 | 7.11 | 3.67 | 7.18 | 7.53 | N/A | 7.31 | 12/31/03 | 1.983 | 1.573 |

| Royce International Premier Fund | 4.45 | 4.16 | 0.18 | 2.38 | 6.17 | N/A | N/A | 5.51 | 12/31/10 | 1.59 3 | 1.44 3 |

| Royce Micro-Cap Fund | 9.41 | 17.63 | 16.07 | 6.71 | 6.53 | 5.91 | 8.15 | 10.33 | 12/31/91 | 1.24 | 1.24 |

| Royce Pennsylvania Mutual Fund | 15.37 | 21.50 | 15.51 | 7.58 | 9.09 | 8.47 | 9.69 | 12.892 | N/A | 0.96 | 0.96 |

| Royce Premier Fund | 14.31 | 19.60 | 13.07 | 7.99 | 9.27 | 8.41 | 10.62 | 11.19 | 12/31/91 | 1.18 | 1.18 |

| Royce Small-Cap Opportunity Fund | 13.16 | 20.42 | 23.76 | 8.91 | 10.14 | 10.39 | 10.83 | 11.91 | 11/19/96 | 1.23 | 1.23 |

| Royce Small-Cap Special Equity Fund | 7.85 | 15.89 | 13.89 | 6.25 | 6.98 | 8.52 | 8.40 | 8.60 | 5/1/98 | 1.21 | 1.21 |

| Royce Small-Cap Total Return Fund | 8.95 | 9.42 | 14.29 | 5.81 | 7.76 | 7.73 | 8.40 | 9.97 | 12/15/93 | 1.26 | 1.26 |

| Royce Small-Cap Value Fund | 8.40 | 20.91 | 17.60 | 3.68 | 5.48 | 4.96 | 8.53 | 8.33 | 6/14/01 | 1.593 | 1.493 |

| Royce Smaller-Companies Growth Fund | 15.33 | 22.28 | 7.10 | 4.76 | 8.00 | 6.91 | 9.45 | 10.11 | 6/14/01 | 1.553 | 1.493 |

| INDEX | | | | | | | | | | | |

| Russell 2000 Index | 8.09 | 12.31 | 10.82 | 4.21 | 8.26 | 8.43 | 8.89 | N/A | N/A | N/A | N/A |

| Russell Microcap Index | 2.32 | 6.63 | 9.09 | 2.07 | 7.29 | 7.70 | 7.55 | N/A | N/A | N/A | N/A |

| Russell 2000 Value Index | 2.50 | 6.01 | 15.43 | 3.54 | 7.29 | 7.72 | 8.29 | N/A | N/A | N/A | N/A |

| Russell 2000 Growth Index | 13.55 | 18.53 | 6.10 | 4.22 | 8.83 | 8.85 | 9.23 | N/A | N/A | N/A | N/A |

| Russell 2500 Index | 8.79 | 13.58 | 12.29 | 6.55 | 9.38 | 9.32 | 9.86 | N/A | N/A | N/A | N/A |

| MSCI ACWI ex USA Small Cap Index | 6.84 | 10.93 | 8.15 | 2.62 | 5.75 | 4.71 | 8.49 | N/A | N/A | N/A | N/A |

| MSCI ACWI Small Cap Index | 8.02 | 13.02 | 10.83 | 4.53 | 7.62 | 7.20 | 9.35 | N/A | N/A | N/A | N/A |

1 Not annualized.

2 For Royce Pennsylvania Mutual Fund, the average annual total return shown is for the 50-year period ended 6/30/23.

3 Reflects Service Class expenses which include a 25bps distribution and/or service fee.

Important Performance, Expense, and Risk Information

All performance information in this Review and Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Investment and Service Class shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund (2% for Royce International Premier Fund). Redemption fees are not reflected in the performance shown above; if they were, performance would be lower. Current performance may be higher or lower than performance quoted. Current month-end performance may be obtained at www.royceinvest.com. All performance and expense information reflects results of the Funds’ oldest share Class (Investment Class or Service Class, as the case may be). Price and total return information is based on net asset values calculated for shareholder transactions. Annual gross operating expenses reflect the Fund’s gross total annual operating expenses and include management fees, any 12b-1 distribution and/or service fees, other expenses, and any applicable acquired fund fees and expenses. Annual net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse operating expenses, excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business, to the extent necessary to maintain net operating expenses at or below: 1.34% for Royce Dividend Value Fund; 1.44% for Royce International Premier Fund; and 1.49% for each the Royce Global Financial Services, Small-Cap Value, and Smaller-Companies Growth Funds through April 30, 2024. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds and other investment companies.

Service Class shares bear an annual distribution expense that is not borne by the Funds’ Investment Class. If such distribution expenses had been reflected for Funds showing Investment Class performance, returns would have been lower. Each series of The Royce Fund is subject to market risk–the possibility that common stock prices will decline, sometimes sharply and unpredictably, over short or extended periods of time. Such declines may be caused by various factors, including market, financial, and economic conditions, governmental or central bank actions, and other factors, such as the recent Covid pandemic, that may not be directly related to the issuer of a security held by a Fund. This pandemic could adversely affect global market, financial, and economic conditions in ways that cannot necessarily be foreseen. Investments in securities of micro-cap, small-cap, and/or mid-cap companies may involve considerably more risk than investments in securities of larger-cap companies. Certain Funds invest a significant portion of their respective assets in foreign companies that may be subject to different risks than investments in securities of U.S. companies, including adverse political, social, economic, or other developments that are unique to a particular country or region. Therefore, the prices of securities of foreign companies in particular countries or regions may, at times, move in a different direction than those of securities of U.S. companies. Because such investments are usually denominated in foreign currencies and such Funds do not intend to hedge their foreign currency exposures, the U.S. dollar value of such investments may be harmed by declines in the value of foreign currencies in relation to the U.S. dollar. Certain Funds invest a significant portion of their assets in a limited number of stocks or focus their investments in a particular sector or industry, which may involve considerably more risk than a more broadly diversified portfolio because they may be more susceptible to any single corporate, economic, political, regulatory, or market event. A broadly diversified portfolio, however, does not ensure a profit or guarantee against loss. (Please see “Primary Risks for Fund Investors” and “Investing in Foreign Securities” in the prospectus.) This Review and Report must be preceded or accompanied by a prospectus. Please read the prospectus carefully before investing or sending money. Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. The Russell Microcap Index includes 1,000 of the smallest securities in the small-cap Russell 2000 Index along with the next smallest eligible securities as determined by Russell. The Russell 2000 Value and Growth Indexes consist of the respective value and growth stocks within the Russell 2000 as determined by Russell Investments. The Russell 2500 is an unmanaged, capitalization-weighted index of the 2,500 smallest publicly traded U.S. companies in the Russell 3000 index. The MSCI ACWI ex USA Small Cap Index is an unmanaged, capitalization-weighted index of global small-cap stocks, excluding the United States. The MSCI ACWI Small Cap Index is an unmanaged, capitalization-weighted index of global small-cap stocks. Index returns include net reinvested dividends and/or interest income. The performance of an index does not represent exactly any particular investment as you cannot invest directly in an index. Distributor: Royce Fund Services, LLC.

This page is not part of the The Royce Funds 2023 Semiannual Report to Shareholders | 7

MANAGER’S DISCUSSION (UNAUDITED)

Royce Dividend Value Fund (RDV)

Chuck Royce

FUND PERFORMANCE

Royce Dividend Value Fund was up 11.9% for the year-to-date period ended 6/30/23, outperforming its benchmark, the Russell 2500 Index, which rose 8.8% for the same period. The Fund also outpaced its benchmark for the 1- and 3-year periods ended 6/30/23.

WHAT WORKED… AND WHAT DIDN’T

Six of the portfolio’s eight equity sectors made a positive impact on performance for the year-to-date period ended 6/30/23. The sectors making the largest positive contributions were Industrials, Financials, and Materials, while the only negative impacts came from Real Estate and Energy. Health Care made the smallest contribution. At the industry level, metals & mining (Materials), capital markets, and banks (both from Financials) made the biggest positive contributions while the biggest detractors were real estate management & development (Real Estate), insurance (Financials), and oil, gas & consumable fuels (Energy).

The top-contributing position in 2023’s first half was First Citizens BancShares, which we’ve owned for many years, due mostly to its strong liquidity position and stellar deposit franchise. Its valuation looked attractive to us in late 2022, when we began adding shares that were trading at roughly 5x earnings per share. More recently, First Citizens was chosen by the FDIC to acquire Silicon Valley Bank, most likely owing to its long history of buying failed banks. Silicon Valley’s travails notwithstanding, the purchase was accretive to First Citizens’ tangible book value and earnings, helping to spur a sharp rise in its stock. Hubbell Incorporated manufactures plugs, receptacles, connectors, lighting fixtures, high voltage test and measurement equipment, and voice and data signal processing components. During 2023’s first half, growing demand for grid modernization and electrification drove earnings and revenue growth, trends that the company expects to continue.

The Fund’s top detractor in 2023’s first half was Lindsay Corporation, which provides center pivot irrigation systems for commercial agriculture. Lindsay’s stock retreated as corn and wheat prices came off highs and farm income was forecasted to decline from peak levels. The company also faces difficult year-over-year comparisons later this year because several severe storms in 2022 drove higher pivot-replacement demand. Internationally, Lindsay has faced irrigation order delays in the high growth Brazilian market due to a political transition that pushed out implementation of a government financing program for agricultural products growers. BOK Financial is an Oklahoma-based bank holding company. Its shares were caught up in the widespread declines that affected many smaller regional banks in the wake of Silicon Valley and Signature Banks failing as well as fiscal first-quarter results that saw declines in net income from the same quarter in 2022 and declines in average deposits. Confident in its long-term prospects, we held our shares at the end of June.

| | Top Contributors to Performance | | Top Detractors from Performance | |

| | Year-to-Date Through 6/30/23 (%)1 | | Year-to-Date Through 6/30/23 (%)2 | |

| | First Citizens BancShares Cl. A | 1.83 | | Lindsay Corporation | -0.97 | |

| | Hubbell Incorporated | 1.16 | | BOK Financial | -0.61 | |

| | Worthington Industries | 1.06 | | RMR Group (The) Cl. A | -0.30 | |

| | Lincoln Electric Holdings | 0.89 | | Assured Guaranty | -0.11 | |

| | Graco | 0.86 | | State Street | -0.09 | |

| | 1 Includes dividends | | | 2 Net of dividends | | |

The Fund’s advantage over the Russell 2500 was attributable to stock selection in 2023’s first half. This was most impactful in the Financials sector, where First Citizens BancShares, Artisan Partners Asset Management, and Brazilian stock exchange B3-Brasil, Bolsa, Balcao drove our relative edge. Stock picks were also additive in Materials, as was our much lower weighting in Energy. Conversely, our much lower exposures to resurgent Information Technology and Consumer Discretionary stocks, as well as our lack of exposure to Communication Services, detracted from relative results.

CURRENT POSITIONING AND OUTLOOK

We see an array of potential triggers that could possibly jumpstart small- and mid-cap performance in the coming months. First, a soft landing looks more and more likely to us, and a recession—specifically the kind of deep and potentially lengthy contraction many have been anticipating since late 2021—looks less and less likely. We have already seen promising developments that seem to suggest a nascently robust economy: durable goods orders rose for the fourth consecutive month in June—and hit a record high for nondefense capital goods (excluding aircraft or core capital goods, a proxy for business equipment investment)—while homebuilding rose by 21.7% in May, a record monthly surge that also defied expectations for a slowdown. Even more important, in our view, is the ongoing sense of cautious optimism we have been hearing from many management teams—which was reflected by generally solid earnings for many holdings for the second quarter. Amid the difficulties of bear markets and periods of economic uncertainty, we think it’s crucial to remind investors of the opportunity to build their small- and/or mid-cap allocation at attractively low prices. History shows that investors who had the necessary patience and discipline to stay invested during periods of sluggish or negative performance have been rewarded. We continue to see the currently unsettled period as an opportune time to invest in select small- and mid-caps for the long run.

8 | The Royce Funds 2023 Semiannual Report to Shareholders

| PERFORMANCE AND PORTFOLIO REVIEW (UNAUDITED) | TICKER SYMBOLS RYDVX RDVIX |

Performance and Expenses

Average Annual Total Return (%) Through 6/30/23

| | JAN-JUN 20231 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | SINCE INCEPTION (5/3/04) |

| RDV | 11.92 | 22.44 | 12.85 | 6.12 | 7.34 | 8.14 | 8.15 |

| Annual Gross Operating Expenses: 1.62% Annual Net Operating Expenses: 1.34% | |

| 1 Not annualized | | | | | | | |

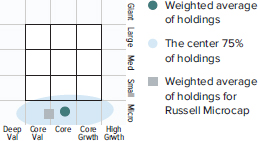

Morningstar Style Map™ As of 6/30/23

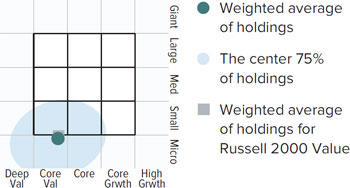

The Morningstar Style Map is the Morningstar Style Box™ with the center 75% of fund holdings plotted as the Morningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 89 for additional information.

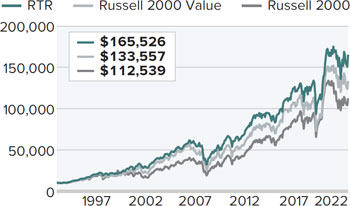

Value of $10,000

Invested on 5/3/04 as of 6/30/23 ($)

Top 10 Positions

% of Net Assets

| KBR | 4.5 |

| HEICO Corporation Cl. A | 4.2 |

| Carlyle Group | 3.9 |

| AptarGroup | 3.8 |

| Franco-Nevada | 3.8 |

| Hubbell Incorporated | 3.7 |

| SEI Investments | 3.6 |

| Graco | 3.5 |

| Worthington Industries | 3.3 |

| Royal Gold | 3.2 |

Portfolio Sector Breakdown

% of Net Assets

| Industrials | 35.6 |

| Financials | 30.0 |

| Materials | 19.2 |

| Consumer Discretionary | 4.3 |

| Health Care | 3.3 |

| Information Technology | 2.7 |

| Real Estate | 2.1 |

| Energy | 1.3 |

| Cash and Cash Equivalents | 1.5 |

| Calendar Year Total Returns (%) | |

| YEAR | RDV |

| 2022 | -13.6 |

| 2021 | 20.1 |

| 2020 | 4.5 |

| 2019 | 29.8 |

| 2018 | -16.2 |

| 2017 | 21.7 |

| 2016 | 16.4 |

| 2015 | -5.7 |

| 2014 | -2.1 |

| 2013 | 30.7 |

| 2012 | 16.9 |

| 2011 | -4.5 |

| 2010 | 30.1 |

| 2009 | 37.7 |

| 2008 | -31.5 |

| Upside/Downside Capture Ratios | |

| Periods Ended 6/30/23 (%) | | |

| | UPSIDE | DOWNSIDE |

| 10-Year | 92 | 104 |

| From 6/30/04 (Start of Fund’s First Full Quarter) | 92 | 92 |

| Portfolio Diagnostics | |

| Fund Net Assets | $63 million |

| Number of Holdings | 50 |

| Turnover Rate | 13% |

| Average Market Capitalization 1 | $6,433 million |

| Weighted Average P/E Ratio 2,3 | 14.6x |

| Weighted Average P/B Ratio 2 | 2.7x |

| Active Share 4 | 97% |

| U.S. Investments (% of Net Assets) | 75.1% |

| Non-U.S. Investments (% of Net Assets) | 23.4% |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E Ratio calculation excludes companies with zero or negative earnings (7% of portfolio holdings as of 6/30/23). |

| 4 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

Important Performance and Expense Information

All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.royceinvest.com. All performance and risk information reflects results of the Service Class (its oldest class). Annual gross operating expenses reflect the total gross operating expenses for the Fund’s Service Class and include management fees, 12b-1 distribution and/or service fees, and other expenses. Annual net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed, without right of termination, to waive fees and/or reimburse expenses to the extent necessary to maintain the Service Class’s annual net operating expenses (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business) at or below 1.34% through April 30, 2024. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2023. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s benchmark. It is calculated by measuring the Fund’s performance in quarters when the primary benchmark went up and dividing it by such benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s primary benchmark. It is calculated by measuring the Fund’s performance in quarters when the primary benchmark goes down and dividing it by such benchmark’s return in those quarters.

The Royce Funds 2023 Semiannual Report to Shareholders | 9

MANAGER’S DISCUSSION (UNAUDITED)

Royce Global Financial Services Fund (RFS)

Chuck Royce

FUND PERFORMANCE

Royce Global Financial Services Fund increased 3.5% for the year-to-date period ended 6/30/23, lagging its broad-based global benchmark, the MSCI ACWI Small Cap Index, which was up 8.0% for the same period.

WHAT WORKED… AND WHAT DIDN’T

During the first half of 2023, the Fund had investments in five equity sectors, four of which made positive contributions to performance. Financials led by a wide margin, followed by Real Estate and Industrials. Information Technology was the only detractor while Materials made the smallest contribution. At the industry level, capital markets (Financials), real estate management & development (Real Estate), and financial services (Financials) contributed most for the year-to-date period. Banks (Financials) and software (Information Technology) were the only detractors while professional services (Industrials) was flat for the year-to-date period ended 6/30/23. At the country level, Canada, the U.S., and the United Kingdom contributed most for the year-to-date period, while Israel, Bermuda, and South Africa were the largest detractors.

The top-contributing position in 2023’s first half was First Citizens BancShares, which we’ve owned for many years, due mostly to its strong liquidity position and stellar deposit franchise. Its valuation looked attractive to us in late 2022, when we began adding shares that were trading at roughly 5x earnings per share. More recently, First Citizens was chosen by the FDIC to acquire Silicon Valley Bank, most likely owing to its long history of buying failed banks. Silicon Valley’s travails notwithstanding, the purchase was accretive to First Citizens’ tangible book value and earnings, and helped spur a sharp rise in its stock. Ares Management is an alternative asset manager which also has a business development company that lends money to companies for long-term growth initiatives. It raises capital of its own at attractive rates before lending it at higher ones. With most of its loans in variable rate arrangements, it can generate more interest income as rates rise. Ares’s first-quarter results included a more than 35% year-over-year increase in core earnings per share.

| | | | | |

| | Top Contributors to Performance | | Top Detractors from Performance | |

| | Year-to-Date Through 6/30/23 (%)1 | | Year-to-Date Through 6/30/23 (%)2 | |

| | First Citizens BancShares Cl. A | 2.68 | | First Republic Bank | -1.73 | |

| | Ares Management Cl. A | 1.02 | | Charles Schwab | -1.49 | |

| | FirstService Corporation | 0.98 | | BOK Financial | -0.87 | |

| | Canaccord Genuity Group | 0.87 | | Tel Aviv Stock Exchange | -0.79 | |

| | Intermediate Capital Group | 0.63 | | Altus Group | -0.67 | |

| | 1 Includes dividends | | | 2 Net of dividends | | |

| | | | | | | |

The top-detracting position was San Francisco-based regional bank, First Republic Bank. It was the third bank to declare insolvency in 2023 (following Silicon Valley and Signature Banks) and the second-largest failure since the fall of Washington Mutual in the 2008 Financial Crisis. It was hurt by having too many uninsured deposits and too many reserves in long-term debt instruments, which began losing value when interest rates began to rise. The result was a bailout by JPMorgan Chase in May. The banking crisis helped drive down the shares of financial services specialist, Charles Schwab, which has a banking business in addition to its discount brokerage.

The portfolio’s relative performance will often hinge not just on the performance of financial stocks—which were once more underwater within the MSCI ACWI Small Cap in the first half of 2023—but also on those sectors where we have little or no exposure relative to our broad-based global benchmark. The Fund’s much greater exposure to Financials hurt relative results, even as stock selection in the sector was additive, as was our much lower weighting in resurgent Information Technology and Industrials. Conversely, stock selection was additive in Real Estate, as was our lack of exposure to Energy and Utilities.

CURRENT POSITIONING AND OUTLOOK

Fears of a global recession receded somewhat in June, led by positive economic data in the U.S. and a pause of interest rate increases by the Federal Reserve. Of course, economic data out of Europe, as well as geopolitical tensions and a sluggish Chinese economy, all continued to weigh on the global economic outlook at the end of June. In this context, the near-term forecast for equities remains as unclear as any we can recall, though over the long term we also still see better weather on the horizon, especially for global small-cap stocks. Indeed, throughout 2022 and into 2023, we have been struck by the contrast between the more confident—albeit cautious—outlooks from the many management teams we met with, and the fatalistic headlines seen almost every day. Of course, the Fund’s companies boast generally strong long-term growth prospects, low debt, positive free cash flows, high returns on invested capital, and/or proven management expertise. Overall, we believe they appear well positioned for a market that is more focused on fundamentals and/or from a reaccelerating global economy. And while recession remains a reality or possibility (depending on geography), none of us knows how long it will last or how deep it will go. What we do know is that history shows us that any recession—like any bear market—is ultimately finite and will be followed by a recovery. It’s worth keeping in mind that history also shows that small caps will likely begin an upward move before many of us know for sure that the economy is rebounding in earnest. For this and other reasons, we would welcome any degree of increased scrutiny of company fundamentals.

10 | The Royce Funds 2023 Semiannual Report to Shareholders

| PERFORMANCE AND PORTFOLIO REVIEW (UNAUDITED) | TICKER SYMBOLS RYFSX RGFIX |

Performance and Expenses

Average Annual Total Return (%) Through 6/30/23

| | JAN-JUN 20231 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | SINCE INCEPTION (12/31/03) |

| RFS | 3.51 | 6.04 | 7.11 | 3.67 | 7.18 | 7.53 | 7.31 |

| Annual Gross Operating Expenses: 1.98% Annual Net Operating Expenses: 1.57% |

| 1 Not annualized | | | | | | |

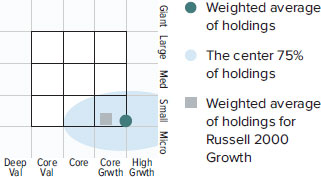

Morningstar Style Map™ As of 6/30/23

The Morningstar Style Map is the Morningstar Style Box™ with the center 75% of fund holdings plotted as the Morningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 89 for additional information.

Portfolio Country Breakdown 1,2

% of Net Assets

| United States | 46.6 |

| Canada | 25.1 |

| Bermuda | 5.5 |

| Israel | 4.6 |

| India | 2.7 |

| France | 2.7 |

| United Kingdom | 2.6 |

| Panama | 2.2 |

| Brazil | 2.1 |

| New Zealand | 1.6 |

¹ Represents countries that are 1.5% or more of net assets.

² Securities are categorized by the country of their headquarters.

Top 10 Positions

% of Net Assets

| First Citizens BancShares Cl. A | 5.2 |

| Franco-Nevada | 4.7 |

| Tel Aviv Stock Exchange | 4.6 |

| Sprott | 4.5 |

| FirstService Corporation | 4.4 |

| E-L Financial | 3.5 |

| Popular | 3.4 |

| KKR & Co. | 3.1 |

| Altus Group | 3.0 |

| BOK Financial | 2.9 |

Portfolio Industry Breakdown

% of Net Assets

| Capital Markets | 50.5 |

| Banks | 15.3 |

| Real Estate Management & Development | 9.2 |

| Insurance | 8.5 |

| Financial Services | 4.8 |

| Metals & Mining | 4.6 |

| Machinery | 1.4 |

| Software | 1.4 |

| Trading Companies & Distributors | 1.2 |

| Closed-End Funds | 1.0 |

| Professional Services | 0.2 |

| Cash and Cash Equivalents | 1.9 |

Value of $10,000

Invested on 12/31/03 as of 6/30/23 ($)

| Calendar Year Total Returns (%) | |

| YEAR | RFS |

| 2022 | -20.3 |

| 2021 | 20.3 |

| 2020 | 15.3 |

| 2019 | 24.2 |

| 2018 | -13.4 |

| 2017 | 22.5 |

| 2016 | 12.9 |

| 2015 | -4.7 |

| 2014 | 3.5 |

| 2013 | 42.0 |

| 2012 | 20.7 |

| 2011 | -11.3 |

| 2010 | 18.5 |

| 2009 | 32.1 |

| 2008 | -35.4 |

| | |

| Portfolio Diagnostics | |

| Fund Net Assets | $26 million |

| Number of Holdings | 56 |

| Turnover Rate | 9% |

| Average Market Capitalization 1 | $3,242 million |

| Weighted Average P/E Ratio 2,3 | 10.2x |

| Weighted Average P/B Ratio 2 | 1.6x |

| Active Share 4 | 99% |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E Ratio calculation excludes companies with zero or negative earnings (10% of portfolio holdings as of 6/30/23). |

| 4 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

Upside/Downside Capture Ratios

Periods Ended 6/30/23 (%)

| | UPSIDE | DOWNSIDE |

| 10-Year | 91 | 90 |

| Fund’s First Full Quarter (12/31/03) | 87 | 86 |

Important Performance and Expense Information

All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.royceinvest.com. Annual gross operating expenses reflect the total gross operating expenses for the Fund’s Service Class and include management fees, 12b-1 distribution and/or service fees, other expenses and acquired fund fees and expenses. Annual net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive fees and/or reimburse expenses to the extent necessary to maintain the Fund’s annual net operating expenses, (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business), at or below 1.49% through April 30, 2024. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through its investments in mutual funds and other investment companies. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2023. Certain Funds invest a significant portion of their respective assets in foreign companies that may be subject to different risks than investments in securities of U.S. companies, including adverse political, social, economic, or other developments that are unique to a particular country or region. Therefore, the prices of securities of foreign companies in particular countries or regions may, at times, move in a different direction than those of securities of U.S. companies. Because such investments are usually denominated in foreign currencies and such Funds do not intend to hedge their foreign currency exposures, the U.S. dollar value of such investments may be harmed by declines in the value of foreign currencies in relation to the U.S. dollar. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s primary benchmark. It is calculated by measuring the Fund’s performance in quarters when the primary benchmark went up and dividing it by such benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s primary benchmark. It is calculated by measuring the Fund’s performance in quarters when the primary benchmark goes down and dividing it by such benchmark’s return in those quarters.

The Royce Funds 2023 Semiannual Report to Shareholders | 11

MANAGERS’ DISCUSSION (UNAUDITED)

Royce International Premier Fund (RIP)

Mark Rayner, CA, Mark Fischer

FUND PERFORMANCE

Royce International Premier Fund advanced 4.5% for the year-to-date period ended 6/30/23, trailing its benchmark, the MSCI ACWI ex USA Small Cap Index, which was up 6.8% for the same period. The Fund beat its benchmark, however, for the 10-year and since inception (12/31/10) periods ended 6/30/23.

WHAT WORKED… AND WHAT DIDN’T

Five of the Fund’s eight equity sectors made positive contributions to performance in 2023’s first half, led by Information Technology, Industrials (its two largest sectors), and Financials, while Communication Services, Health Care, and Real Estate detracted.

The Fund’s biggest contributor at the position level was Odontoprev, Brazil’s largest provider of corporate dental care plans. We like Odontoprev’s high margin yet asset-light business model, which enables it to generate strong cash flows and returns on invested capital, as well as structural growth prospects supported by Brazil’s expanding middle class. Compared to almost 80% in the U.S., we estimate that only 14% of Brazilians have private dental coverage today. Its stock appeared to benefit earlier in the year from its perception as a quality stock, as Brazilian investors flocked to more defensive companies. Given the expectations for sustained high interest rates in Brazil, the market has been gravitating to companies with lower debt, making Odontoprev’s strong net cash position particularly appealing to local investors. In mid-May, the company’s share price also rose on first-quarter 2023 results, which saw an 11% year-on-year growth in revenues, with demand especially strong among small- to mid-sized businesses. Along with the lower-than-expected costs of providing dental services, adjusted earnings before interest, taxes, depreciation & amortization jumped by 22%.

Canada’s Open Text is the global market leader in enterprise content management software that collects, cleans, and analyzes unstructured data, including emails, PDFs, and human resources records. Its rising share price was mostly driven by better-than-expected results for 2023’s fiscal third quarter, released in May. Management also confirmed that a recent acquisition was progressing ahead of schedule, with cost synergies already bearing fruit and deleveraging underway, resulting in management raising full-year guidance.

| | | | | |

| | Top Contributors to Performance | | Top Detractors from Performance | |

| | Year-to-Date Through 6/30/23 (%)1 | | Year-to-Date Through 6/30/23 (%)2 | |

| | Odontoprev | 1.01 | | Restore | -0.75 | |

| | Open Text | 0.69 | | BML | -0.57 | |

| | Alimak Group | 0.65 | | Learning Technologies Group | -0.48 | |

| | SimCorp | 0.54 | | Norva24 Group | -0.43 | |

| | Marlowe | 0.54 | | NICE Information Service | -0.42 | |

| | 1 Includes dividends | | | 2 Net of dividends | | |

| | | | | | | |

Restore, the Fund’s biggest detractor, is a UK-based support services company, with roughly 70% of group operating profit coming from its Records Management segment, which provides storage and retrieval solutions to around 6,000 clients. Restore’s share price came under pressure in mid-May when it released a trading statement that showed 4% revenue growth year over year while also reducing full-year 2023 profit before tax guidance, primarily as a result of weakness in its office IT recycling business. In mid-June, the company’s CFO announced his intention to step down. Despite these headwinds, we remain confident in Restore’s long-term prospects. BML is Japan’s leading diagnostics testing service provider, with a diversified ‘B2B’ customer-base of 30,000 clinics and 1,000 hospitals. BML’s share price fell due to negative short-term earnings growth momentum associated with the phase-out of COVID-related testing revenues as well as cost inflation in testing consumables. We believe these pressures are transitory. With net cash equal to roughly 80% of its market capitalization, BML trades at what we think is a very attractive valuation. We also believe that this discount will narrow over time as earnings momentum recovers.

The Fund’s relative disadvantage versus the MSCI ACWI ex USA Small Cap came from stock selection. Stock picks in Industrials, Communication Services, and Health Care hurt most. In addition, each of the Fund’s five biggest detractors hampered both absolute and relative results. Conversely, our much lower exposure to Real Estate, stock selection in Financials, and lack of exposure to Energy were all additive relative to the benchmark.

CURRENT POSITIONING AND OUTLOOK

In 2023’s second quarter, we observed what we think was a meaningful operational stress test for many of our holdings. Companies across various regions and industries have been experiencing more cautious customer demand in the face of an uncertain macroeconomic climate, while inflation continues to be a persistent issue in many market segments. While near-term growth expectations may have slowed, we have found that our companies have solidly passed this operational stress test. Their customers remain loyal while their balance sheets are robust, they continue to create shareholder value, and our conviction in their ability to create value over the long run is unchanged. Many less steadfast market participants, however, have penalized businesses for even just a small miss on growth or margin expectations. This volatility offered us a window of opportunity to deploy cash at an accelerated rate during the quarter by building positions in existing holdings that are out-of-favor and by initiating four new positions. Economic uncertainty may well linger for the next several quarters, with share prices possibly behaving erratically as a result. But we are as optimistic about the future of our strategy as ever and believe we are well-positioned to capitalize on the inevitable dislocations between value creation and valuation. By investing in businesses with above-average returns trading at reasonable valuations, we believe the Fund should also achieve above-average performance over time.

12 | The Royce Funds 2023 Semiannual Report to Shareholders

| PERFORMANCE AND PORTFOLIO REVIEW (UNAUDITED) | TICKER SYMBOLS RYIPX RIPNX RIPIX |

Performance and Expenses

Average Annual Total Return (%) Through 6/30/23

| | JAN-JUN 20231 | 1-YR | 3-YR | 5-YR | 10-YR | SINCE INCEPTION (12/31/10) |

| RIP | 4.45 | 4.16 | 0.18 | 2.38 | 6.17 | 5.51 |

| Annual Gross Operating Expenses: 1.59% Annual Net Operating Expenses: 1.44% |

| 1 Not annualized | | |

Relative Returns: Monthly Rolling Average Annual Return Periods

Since Inception Through 6/30/23

On a monthly rolling basis, The Fund outperformed the MSCI ACWI x USA SC in 100% of all 10-year periods; 99% of all 5-year periods; and 60% of all 1-year periods.

| | PERIODS BEATING THE INDEX | | FUND AVG (%) 1 | INDEX AVG (%) 1 |

| 10-year | 31/31 | 100% | 8.4 | 6.6 |

| 5-year | 90/91 | 99% | 8.7 | 5.8 |

| 1-year | 83/139 | 60% | 7.2 | 6.0 |

1Average of monthly rolling average annual total returns over the specified periods.

Morningstar Style Map™ As of 6/30/23

The Morningstar Style Map is the Morningstar Style Box™ with the center 75% of fund holdings plotted as the Morningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 89 for additional information.

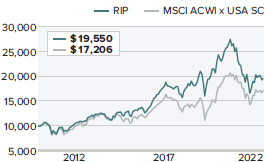

Value of $10,000

Invested on 12/31/10 as of 6/30/23 ($)

Top 10 Positions

% of Net Assets

| Hansen Technologies | 3.3 |

| IPH | 2.8 |

| TKC Corporation | 2.8 |

| Restore | 2.6 |

| BML | 2.5 |

| Marlowe | 2.3 |

| Intertek Group | 2.2 |

| Loomis | 2.1 |

| Odontoprev | 2.1 |

| Riken Keiki | 2.1 |

Portfolio Sector Breakdown

% of Net Assets

| Industrials | 39.9 |

| Information Technology | 24.4 |

| Health Care | 9.6 |

| Financials | 6.0 |

| Materials | 5.0 |

| Communication Services | 3.5 |

| Consumer Discretionary | 2.7 |

| Real Estate | 0.5 |

| Preferred Stock | 1.8 |

| Cash and Cash Equivalents | 6.6 |

Upside/Downside Capture Ratios

Periods Ended 6/30/23 (%)

| | UPSIDE | DOWNSIDE |

| 10-Year | 99 | 95 |

| Fund’s First Full Quarter (12/31/10) | 99 | 90 |

| Calendar Year Total Returns (%) | |

| YEAR | RIP |

| 2022 | -27.2 |

| 2021 | 5.8 |

| 2020 | 15.7 |

| 2019 | 34.2 |

| 2018 | -12.8 |

| 2017 | 39.8 |

| 2016 | -1.1 |

| 2015 | 16.2 |

| 2014 | -8.2 |

| 2013 | 18.3 |

| 2012 | 23.4 |

| 2011 | -16.8 |

| Portfolio Country Breakdown 1,2 | |

| % of Net Assets | |

| | |

| Japan | 23.9 |

| United Kingdom | 20.9 |

| Sweden | 6.6 |

| Australia | 6.2 |

| Switzerland | 5.0 |

| Germany | 5.0 |

| Canada | 4.4 |

| Brazil | 3.6 |

| Italy | 3.5 |

¹ Represents countries that are 3% or more of net assets.

² Securities are categorized by the country of their headquarters.

Portfolio Diagnostics

| Fund Net Assets | $815 million |

| Number of Holdings | 59 |

| Turnover Rate | 18% |

| Average Market Capitalization 1 | $1,562 million |

| Weighted Average P/E Ratio 2,3 | 21.5x |

| Weighted Average P/B Ratio 2 | 2.4x |

| Active Share 4 | 99% |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E Ratio calculation excludes companies with zero or negative earnings (6% of portfolio holdings as of 6/30/23). |

| 4 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

Important Performance and Expense Information

All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 2% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.royceinvest.com. All performance and risk information reflects results of the Service Class (its oldest class). Price and total return information is based on net asset values for shareholder transactions. Certain immaterial adjustments were made to the net assets of Royce International Premier Fund at 12/31/19 and 12/31/20 for financial reporting purposes, and as a result the calendar year total returns based on those net asset values differ from the adjusted net asset values and calendar year total returns reported in the Financial Highlights. Annual gross operating expenses reflect the total gross operating expenses for the Fund’s Service Class and include management fees, 12b-1 distribution and/or service fees, and other expenses. Annual net operating expenses reflect contractual fee waivers and/or expense reimbursements. All expense information is reported as of the Fund’s most current prospectus. Royce & Associates has contractually agreed to waive its fees and/or reimburse operating expenses to the extent necessary to maintain the Fund’s annual net operating expenses, (excluding brokerage commissions, taxes, interest, litigation expenses, acquired fund fees and expenses, and other expenses not borne in the ordinary course of business), at or below 1.44% through April 30, 2024. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2023. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s primary benchmark. It is calculated by measuring the Fund’s performance in quarters when the primary benchmark went up and dividing it by such benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s primary benchmark. It is calculated by measuring the Fund’s performance in quarters when the primary benchmark goes down and dividing it by such benchmark’s return in those quarters.

The Royce Funds 2023 Semiannual Report to Shareholders | 13

MANAGERS’ DISCUSSION (UNAUDITED)

Royce Micro-Cap Fund (RMC)

Jim Stoeffel, Brendan Hartman

FUND PERFORMANCE

Royce Micro-Cap Fund beat its primary benchmark, the Russell Microcap Index, and its secondary benchmark, the Russell 2000 Index, for the 1-, 3-, and 5-year periods ended 6/30/23. The Fund also outperformed the Russell 2000 for the 25-, 30-year, and since inception (12/31/91) periods ended 6/30/23 (data for the Russell Microcap only goes back to 2000). For the year-to-date period ended 6/30/23, the Fund advanced 9.4%, outpacing both the Russell Microcap, which was up 2.3%, and the Russell 2000, which gained 8.1%, for the same period.

WHAT WORKED… AND WHAT DIDN’T

Seven of the Fund’s 10 equity sectors made a positive contribution to performance in the first half of 2023, led by Information Technology, Industrials, and Health Care. Financials and Communications Services detracted while Real Estate made the smallest contribution. The top-contributing industries were semiconductors & semiconductor equipment (Information Technology), machinery (Industrials), and electronic equipment, instruments & components (Information Technology), while banks (Financials), specialty retail (Consumer Discretionary), and professional services (Industrials) were the biggest detractors.

The Fund’s two top contributing positions in 2023’s first half are benefiting from the growing significance of silicon carbide semiconductors in electric vehicles. While we have been selling shares of each, we continue to hold solid positions because we believe this is a secular trend in its early stages. Axcelis Technologies makes and services ion implantation, dry strip, thermal processing, and curing equipment used in semiconductor chip fabrication. Axcelis is a predominant player in providing ion implantation systems for the semiconductor industry, which is becoming increasingly important as power management devices become critical in numerous industries. Aehr Test Systems has unique semiconductor testing systems that address processes where the cost of chip failure is especially high. Arlo Technologies provides home security cameras and related security monitoring services. For the past year or so, Arlo has been transforming its business from a legacy, low margin hardware focus to a subscription model with recurring revenues and high margins. We believe the stock hit an inflection point in this transition during the second quarter of 2023 when the superior economics of the subscription model and its impact on growth and margins became evident to investors.

| | | | | |

| | Top Contributors to Performance | | Top Detractors from Performance | |

| | Year-to-Date Through 6/30/23 (%)1 | | Year-to-Date Through 6/30/23 (%)2 | |

| | Axcelis Technologies | 1.16 | | Cutera | -0.65 | |

| | Aehr Test Systems | 0.94 | | Investar Holding Corporation | -0.61 | |

| | Arlo Technologies | 0.80 | | DZS | -0.60 | |

| | CIRCOR International | 0.80 | | Western New England Bancorp | -0.55 | |

| | Universal Stainless & Alloy Products | 0.79 | | Territorial Bancorp | -0.53 | |

| | 1 Includes dividends | | | 2 Net of dividends | | |

| | | | | | | |

The top detractor was aesthetic medical device maker, Cutera, which suffered through an earnings guidance cut as its core business slowed. An ensuing boardroom battle resulted in the firing of the well regarded CEO and Chair, creating more uncertainty. This individual has since rejoined the company as an advisor while the Board looks for a permanent CEO. We held shares as we believe there is significant asset value in the business that, once stabilized by new management, should make it an appealing part of a larger company. Regional bank Investar Holding Corporation was hurt by the recent banking crisis and concerns about increased credit losses in a slowing economy. However, we think these risks are outweighed by its longer-term prospects in a growing economy. DZS manufactures communications network equipment that helps deliver high speed fiber access. DZS lowered earnings guidance and was also in non-compliance with loan covenants that it is working with lenders to renegotiate while also dealing with a revenue recognition issue that DZS described as a one-off discovered during the collection process. We held a small position at the end of June.

Relative to the Russell Microcap, both sector allocation and stock selection were additive to Fund performance. The combination of our larger weighting and stock picks in Information Technology and Industrials helped most, along with our lower exposure to Financials. Offsetting our relative edge somewhat were lower exposure to Health Care, stock selection and our higher weight in Communication Services, and stock picks in Consumer Discretionary.

CURRENT POSITIONING AND OUTLOOK

While Artificial Intelligence (“AI”) has seen ample hype, we see it as one more secular trend that is driving demand for semiconductors and processing bandwidth. This plays into our portfolio positioning as select smaller technology names are providing critical components in this value chain. We view our technology companies as “picks and shovel” providers into a myriad of long-term technology trends while many of our industrial companies appear to possess similar characteristics. We also expect many industrial companies to benefit from the increasing use of AI to drive efficiencies in their operations. More significantly, however, we believe many of these large macro trends require substantial infrastructure investments and have underlying government support, one example being the shift to green energy, which requires significant investments in electrical transmission capabilities. While we are excited about our positioning in the intermediate term, we are also cognizant of short-term market pressures, most notably the unprecedented pace of Fed rate hikes. Although inflationary pressures have meaningfully moderated, the Fed remains in a hawkish mode. These pressures are likely to be exacerbated by commercial banks tightening lending standards. Likewise, the attempted coup in Russia highlighted the ever present black swan risks that are hard to underwrite. That said, we believe the intermediate-term opportunities outweigh the short-term risks, and our outlook remains constructive.

14 | The Royce Funds 2023 Semiannual Report to Shareholders

| PERFORMANCE AND PORTFOLIO REVIEW (UNAUDITED) | TICKER SYMBOLS RYOTX RMCFX RYMCX |

Performance and Expenses

Average Annual Total Return (%) Through 6/30/23

| | JAN-JUN 20231 | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | 25-YR | 30-YR | SINCE INCEPTION (12/31/91) |

| RMC | 9.41 | 17.63 | 16.07 | 6.71 | 6.53 | 5.91 | 8.15 | 8.28 | 9.58 | 10.33 |

| Annual Operating Expenses: 1.24% | | | | |

| 1 Not annualized | | | | | | | |

Morningstar Style Map™ As of 6/30/23

The Morningstar Style Map is the Morningstar Style Box™ with the center 75% of fund holdings plotted as the Morningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 89 for additional information.

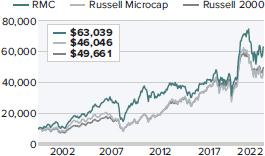

Value of $10,000

Invested on 6/30/00 (Russell Microcap Index Inception) as of 6/30/23 ($)

Top 10 Positions

% of Net Assets

| Photronics | 1.5 |

| Universal Stainless & Alloy Products | 1.4 |

| Newpark Resources | 1.4 |

| Modine Manufacturing | 1.4 |

| Distribution Solutions Group | 1.3 |

| Axcelis Technologies | 1.3 |

| Aehr Test Systems | 1.2 |

| Quanex Building Products | 1.2 |

| Cohu | 1.2 |

| PDF Solutions | 1.2 |

Portfolio Sector Breakdown

% of Net Assets

| Information Technology | 27.8 |

| Industrials | 25.1 |

| Consumer Discretionary | 12.5 |

| Financials | 11.5 |

| Health Care | 8.1 |

| Materials | 5.0 |

| Communication Services | 4.1 |

| Energy | 3.0 |

| Real Estate | 0.6 |

| Cash and Cash Equivalents | 2.3 |

| Calendar Year Total Returns (%) |

| YEAR | RMC |

| 2022 | -22.6 |

| 2021 | 31.0 |

| 2020 | 24.5 |

| 2019 | 21.2 |

| 2018 | -8.9 |

| 2017 | 5.4 |

| 2016 | 19.7 |

| 2015 | -13.3 |

| 2014 | -4.1 |

| 2013 | 21.3 |

| 2012 | 8.0 |

| 2011 | -12.1 |

| 2010 | 30.1 |

| 2009 | 55.7 |

| 2008 | -40.9 |

| Upside/Downside Capture Ratios |

| Periods Ended 6/30/23 (%) | | |

| | UPSIDE | DOWNSIDE |

| 10-Year | 87 | 86 |

| From 6/30/00 (Russell Microcap Index Inception) | 93 | 82 |

| Portfolio Diagnostics | |

| Fund Net Assets | $305 million |

| Number of Holdings | 125 |

| Turnover Rate | 9% |

| Average Market Capitalization 1 | $547 million |

| Weighted Average P/B Ratio 2 | 1.7x |

| Active Share 3 | 90% |

| U.S. Investments (% of Net Assets) | 87.0% |

| Non-U.S. Investments (% of Net Assets) | 10.7% |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

Important Performance and Expense Information

All performance information in this Report reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed within 30 days of purchase may be subject to a 1% redemption fee payable to the Fund, which is not reflected in the performance shown above; if it were, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained at www.royceinvest.com. All performance and risk information reflects results of the Investment Class (its oldest class). Price and total return information is based on net asset values calculated for shareholder transactions. Annual operating expenses reflect the total gross operating expenses for the Fund’s Investment Class as of the Fund’s most current prospectus and include management fees and other expenses. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2023. Upside Capture Ratio measures a manager’s performance in up markets relative to the Fund’s primary benchmark. It is calculated by measuring the Fund’s performance in quarters when the primary benchmark went up and dividing it by such benchmark’s return in those quarters. Downside Capture Ratio measures a manager’s performance in down markets relative to the Fund’s primary benchmark. It is calculated by measuring the Fund’s performance in quarters when the primary benchmark goes down and dividing it by such benchmark’s return in those quarters.

The Royce Funds 2023 Semiannual Report to Shareholders | 15

MANAGERS’ DISCUSSION (UNAUDITED)

Royce Pennsylvania Mutual Fund® (PMF)

Steven McBoyle, Jay Kaplan, CFA®, Chuck Royce, Miles Lewis, CFA®, Andrew Palen, Lauren Romeo, CFA®

FUND PERFORMANCE

Royce Pennsylvania Mutual Fund beat its small-cap benchmark, the Russell 2000 Index, for the 1-, 3-, 5-, 10-, 15-, 20-, 25-, 30-, 35-, and 40-year periods ended 6/30/23. The Fund’s average annual total return for the 50 years through the end of June was 12.9%. The Fund also gained 15.4% for the year-to-date period ended 6/30/23, well ahead of the Russell 2000, which was up 8.1% for the same period.

WHAT WORKED… AND WHAT DIDN’T

Nine of the Fund’s 10 equity sectors contributed to 2023’s first-half results, led by Industrials, Information Technology, and Consumer Discretionary. Communication Services detracted while Energy and Health Care contributed least. The top-contributing industries were semiconductors & semiconductor equipment (Information Technology), followed by machinery and building products (both in Industrials). Interactive media & services (Communication Services) detracted most, followed by biotechnology and pharmaceuticals (both in Health Care).