| | |

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| |

| FORM N-CSR |

| |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED |

| MANAGEMENT INVESTMENT COMPANIES |

| | |

| Investment Company Act file number: (811- 03630) | |

| |

| Exact name of registrant as specified in charter: Putnam California Tax Exempt Income Fund |

| |

| Address of principal executive offices: One Post Office Square, Boston, Massachusetts 02109 |

| | |

| Name and address of agent for service: | Beth S. Mazor, Vice President |

| | One Post Office Square |

| | Boston, Massachusetts 02109 |

| | |

| Copy to: | John W. Gerstmayr, Esq. |

| | Ropes & Gray LLP |

| | One International Place |

| | Boston, Massachusetts 02110 |

| | |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| | |

| Date of fiscal year end: September 30, 2008 | |

| |

| Date of reporting period: October 1, 2007— September 30, 2008 |

Item 1. Report to Stockholders:

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940:

What makes

Putnam different?

A time-honored tradition in money management

Since 1937, our values have been rooted in a profound sense of responsibility for the money entrusted to us.

A prudent approach to investing

We use a research-driven team approach to seek superior investment results over time.

Funds for every investment goal

We offer a broad range of mutual funds and other financial products so investors and their financial representatives can build diversified portfolios.

A commitment to doing what’s right for investors

With a focus on investment performance, below-average expenses, and in-depth information about our funds, we put the interests of investors first and seek to set the standard for integrity and service.

Industry-leading service

We help investors, along with their financial representatives, make informed investment decisions with confidence.

In 1830, Massachusetts Supreme Judicial Court Justice Samuel Putnam established The Prudent Man Rule, a legal foundation for responsible money management.

THE PRUDENT MAN RULE

All that can be required of a trustee to invest is that he shall conduct himself faithfully and exercise a sound discretion. He is to observe how men of prudence, discretion, and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent disposition of their funds, considering the probable income, as well as the probable safety of the capital to be invested.

Putnam

California

Tax Exempt

Income Fund

9 | 30 | 08

Annual Report

| |

| Message from the Trustees | 1 |

| About the fund | 2 |

| Performance and portfolio snapshots | 4 |

| Interview with your fund’s Portfolio Leader | 5 |

| Performance in depth. | 8 |

| Expenses | 10 |

| Portfolio turnover | 12 |

| Risk | 12 |

| Your fund’s management. | 13 |

| Terms and definitions | 14 |

| Trustee approval of management contract | 15 |

| Other information for shareholders. | 18 |

| Financial statements | 19 |

| Federal tax information | 37 |

| About the Trustees | 38 |

| Officers | 41 |

Cover photograph: © Richard H. Johnson

Message from the Trustees

Dear Fellow Shareholder:

The financial markets have been experiencing the kind of upheaval not seen in decades. Investor confidence has been shaken by losses across a range of sectors and by the collapse of several financial industry companies. Coordinated responses by a full array of economic and financial authorities both in the United States and overseas should restore stability in due course, but investors should not expect a reduction in volatility in the near term. The likelihood of a U.S. recession, in particular, now makes the situation more challenging. History has shown that markets are extremely resilient over the long term, and we expect that, in time, they will recover from this crisis.

As a shareholder of this fund, you should feel confident about the financial standing of Putnam Investments. Our parent companies, Great-West Lifeco and Power Financial Corporation, are among the largest and most successful organizations in the financial services industry. All three companies are well capitalized with strong cash flows.

We are pleased to announce that Robert L. Reynolds, a well-known leader and visionary in the mutual fund industry, has joined the Putnam leadership team as President and Chief Executive Officer of Putnam Investments, effective July 1, 2008. Charles E. Haldeman, Jr., former President and CEO, has taken on the role of Chairman of Putnam Investment Management, LLC, the firm’s fund management company. He continues to serve as President of the Funds and as a Trustee.

Mr. Reynolds brings to Putnam Investments substantial industry experience and an outstanding record of success, including serving as Vice Chairman and Chief Operating Officer at Fidelity Investments from 2000 to 2007. We look forward to working with Mr. Reynolds as we continue our efforts to position Putnam Investments to exceed our shareholders’ expectations.

We would also like to take this opportunity to welcome new shareholders to the fund and to thank all of our investors for your continued confidence in Putnam during these challenging times.

About the fund

Potential for tax-advantaged high current income

When investing in tax-exempt bonds, opportunities come in all shapes and sizes. This is especially true with Putnam California Tax Exempt Income Fund. The fund explores the vast California municipal bond market, seeking to deliver high current income and tax advantages.

Municipal bonds are typically issued by states and local municipalities to raise funds for building and maintaining public facilities. They are backed by either the issuing state, city, or town, or by revenues collected from usage fees. As a result, they have varying degrees of credit risk — that is, the risk that the issuer will not be able to repay the bond.

A municipal bond’s greatest benefit is that its income is generally exempt from federal income tax, and from state income tax for residents of the state in which the bond is issued. In California, this tax exemption is an especially powerful advantage because the state’s maximum income-tax rate is among the highest in the United States. And the sheer size of the California municipal bond market — it is one of the largest and most diverse in the country, encompassing virtually every sector of the municipal bond market — enables it to establish trends and shape demand in municipal bond markets across the country.

The fund seeks to capitalize on the opportunities available in California by investing in a range of bonds —primarily investment grade — across various sectors. When deciding whether to invest in a bond, the fund’s management team primarily considers credit risk and interest-rate risk, as well as the risk that the bond will be prepaid. Once a bond has been purchased, the management team continues to monitor developments that affect the bond market, the specific sector, and the bond issuer.

The goal of the management team’s research and active management is to stay a step ahead of the industry and pinpoint opportunities to adjust the fund’s holdings for the benefit of the fund and its shareholders.

The fund concentrates its investments by region and involves more risk than a fund that invests more broadly. Capital gains, if any, are taxable for federal and, in most cases, state purposes. For some investors, investment income may be subject to the federal alternative minimum tax. Income from federally exempt funds may be subject to state and local taxes. Tax-free funds may not be suitable for IRAs and other non-taxable accounts. Consult your tax advisor for more information. Funds that invest in bonds are subject to certain risks, including interest-rate risk, credit risk, and inflation risk. As interest rates rise, the prices of bonds fall. Long-term bonds are more exposed to interest-rate risk than short-term bonds. Unlike bonds, bond funds have ongoing fees and expenses.

Understanding tax-equivalent yield

To understand the value of tax-free income, it is helpful to compare a municipal bond’s yield with the “tax-equivalent yield” — the before-tax yield that must be offered by a taxable bond in order to equal the municipal bond’s yield after taxes.

How to calculate tax-equivalent yield:

The tax-equivalent yield equals the municipal bond’s yield divided by “one minus the tax rate.” For example, if a municipal bond’s yield is 5%, then its tax-equivalent yield is 7.7%, assuming the maximum 35% federal tax rate for 2008.

Results for investors subject to lower tax rates would not be as advantageous.

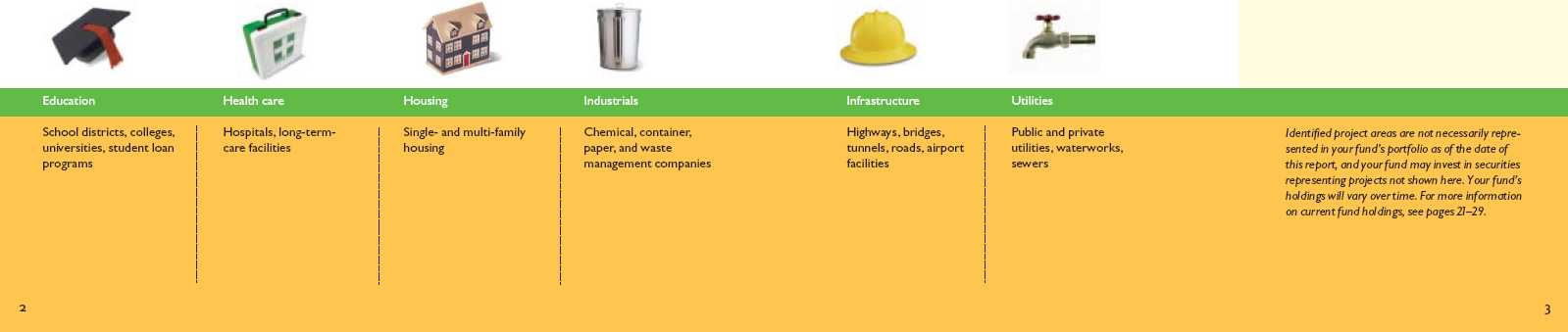

Municipal bonds may finance a range of projects in your community and thus play a key role in its development.

Performance and portfolio snapshots

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 4.00%; had they, returns would have been lower. See pages 5 and 8–9 for additional performance information. For a portion of the periods, this fund may have limited expenses, without which returns would have been lower. A 1% short-term trading fee may apply. To obtain the most recent month-end performance, visit www.putnam.com.

“We believe that many areas of the municipal bond market have been oversold by panicked investors, creating unique opportunities for the fund to add highly rated bonds paying unusually high yields.”

Thalia Meehan, Portfolio Leader, Putnam California Tax Exempt Income Fund

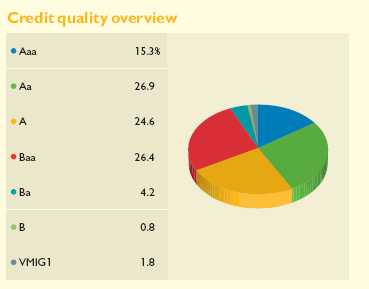

Credit qualities shown as a percentage of portfolio value as of 9/30/08. A bond rated Baa or higher (MIG3/VMIG3 or higher, for short-term debt) is considered investment grade. The chart reflects Moody’s ratings; percentages may include bonds not rated by Moody’s but considered by Putnam Management to be of comparable quality. Ratings will vary over time.

4

Thalia Meehan

Thank you,Thalia, for talking with us today about what has been a tumultuous 12 months for the fixed-income markets. How has this affected the municipal bond market?

The past 12 months have been a historically challenging time for nearly all markets, including municipal bonds. Several factors related to the subprime-lending crisis contributed to an increase in volatility for municipal bonds during the period. Concerns about the credit ratings of municipal bond insurers, which also insure subprime debt, added to the volatility in late 2007 and during the first half of 2008. In addition, forced selling by hedge funds and investment banks put pressure on municipal bonds as these firms needed to raise capital and cover losses. All of this added up to an environment in which all investment-grade asset classes, including municipal bonds, underperformed U.S. Treasuries.

How did Putnam CaliforniaTax Exempt Income Fund fare?

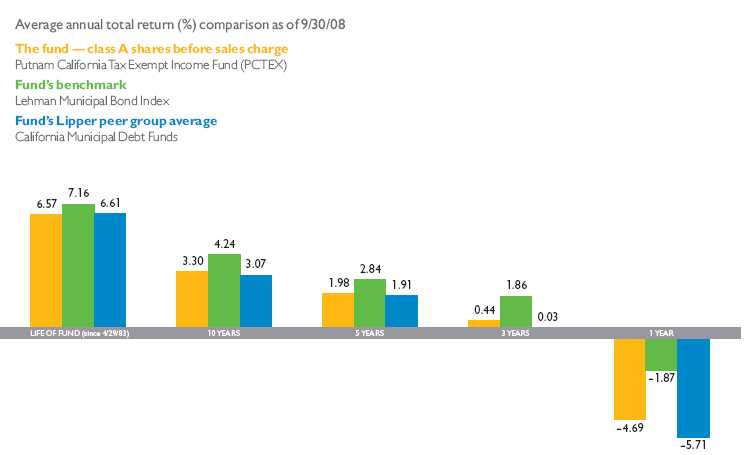

In these rough markets, the fund continued to outperform its peers; however, the fund did post a negative return for the period. For the 12 months ended September 30, 2008, the fund returned –4.69%, outperforming its Lipper class, California Municipal Debt Funds, which returned –5.71%. The fund simultaneously lagged its benchmark, the Lehman Municipal Bond Index, which returned –1.87%. The national benchmark tracks the performance of a broad range of municipal bonds.

The final month of the 12-month period was particularly tumultuous. Can you describe what happened with municipal bonds during that time?

The municipal bond market endured one of its worst months ever in September. As the credit crisis grew to epic proportions, the yield spreads between tax-exempt bonds and Treasury bonds diverged dramatically, as investors eschewed all asset classes with any credit risk.

But three recent factors further compounded the credit concerns. The first was unrelenting downward price pressure on municipal bonds. This pressure was spurred by the forced selling of hedge fund positions and the rumored potential liquidation of AIG’s $50 billion to $60 billion municipal portfolio.

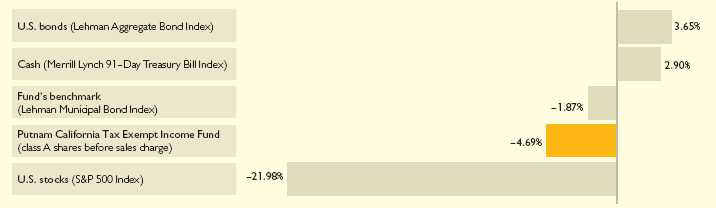

Broad market index and fund performance

This comparison shows your fund’s performance in the context of broad market indexes for the 12 months ended 9/30/08. See the previous page and pages 8–9 for additional fund performance information. Index descriptions can be found on page 14.

5

Second, dealer liquidity became more constrained with the historic bankruptcy of Lehman Brothers, the exit of UBS from the institutional market, and the purchase of Merrill Lynch by Bank of America.

Finally, we saw a temporary lack of primary market supply of municipal bonds due to market conditions. Because new issues typically help provide price discovery in the marketplace, as dealers delayed pricing new issues, secondary market liquidity was negatively affected. All of these issues put downward pressure on municipal bond prices, further hurting the asset class’s performance.

How did you position the portfolio in light of these ongoing issues?

We’ve decided to remain cautious, continuing to focus on keeping the fund’s overall credit quality high. The fund’s shorter-maturity positions helped performance as the yield curve steepened and prices on shorter-term instruments held up better than longer-maturity bonds. Security selection in the insured sector also aided relative performance. At the beginning of the period, nearly all insured bonds traded in a relatively tight range. As concerns rose about monoline insurers (firms that insure issuers of municipal debt), there was growing differentiation in quality among insured issues. Our positioning within insured issues aided performance relative to our peers.

Any notable contributors and detractors?

Puerto Rico Aqueduct and Sewer Authority bonds aided performance for the year. We believed these bonds were being wrongly undervalued due to fears of oversupply in Puerto Rico and general credit market weakness. We were rewarded when the bonds rallied.

Another strong performer was our holding in bonds issued for University of the Pacific, which benefitted from being a short-maturity, high-quality credit bond. This position outperformed on a relative basis as the yield curve steepened and shorter-maturity issues outperformed their longer-maturity counterparts.

Tobacco settlement bond Golden Tobacco was a notable detractor. Tobacco settlement bonds are secured by the income stream from tobacco companies’ lawsuit-settlement obligations to individual states — and generally offer higher yields than bonds of comparable quality. The tobacco sector, however, began underperforming in the fall of 2007 as investors began a flight to quality credit. Because the market for tobacco bonds is large and relatively liquid, investors who wanted to trim credit exposure sold these liquid bonds first, which put pressure on the sector as a whole.

Our exposure to bonds issued by Southern California Public Power Authority also hurt performance. On the whole, prepaid gas bonds help a municipal utility buy

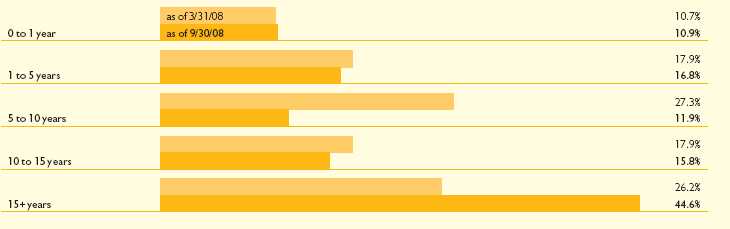

Comparison of maturity composition

This chart illustrates the fund’s composition by maturity, showing the percentage of holdings in different maturity ranges and how the composition has changed over the past six months. Holdings and maturity ranges will vary over time.

6

natural gas at a discounted price. One important feature of a prepaid gas bond, however, is that the bond’s rating is tied to its financial sponsor — in this case, Goldman Sachs. Because Goldman was among the broker/ dealers affected by liquidity problems and concerns about subprime exposure, the performance of these bonds suffered.

What is your outlook for the municipal bond market?

Investors have seen the Federal Reserve [the Fed] dramatically inject liquidity into the markets, and the government take other unprecedented steps to aid the economy and free up credit markets. However, it is important to understand that the effects of many of the changes will take time, and markets are likely, in our view, to remain volatile in the near term — particularly with the lingering concerns over state budgets and monoline insurers.

Despite the current market environment, we see two key reasons why municipal bond funds remain particularly attractive. The first is future tax rates. We believe that income tax rates are unlikely to fall from here and may even rise with a new administration in the White House, given that the Bush tax cuts are scheduled to sunset in 2010. This may cause municipal bonds to become an even more attractive asset class relative to taxable fixed income.

Second, the overall credit quality of the municipal asset class remains strong. The fund has benefited from having a bias for higher-quality holdings in the portfolio. We believe that many areas of the municipal bond market have been oversold by panicked investors, creating unique opportunities for the fund to add highly rated bonds paying unusually high yields.

Finally, I’d like to add that in these turbulent credit markets, investors should understand that Putnam’s deep research bench is making a difference for them every day. As confidence in the public ratings agencies is called into question, the in-depth, independent research of a large, integrated team like ours cannot be overemphasized.

Thank you, Thalia, for your time and insights today.

The views expressed in this report are exclusively those of Putnam Management. They are not meant as investment advice.

I N T H E N E W S

In early October, federal lawmakers approved the Emergency Economic Stabilization Act of 2008 (EESA), a $700 billion economic package designed to ease the nation’s worsening credit crisis. Under the law, a Troubled Asset Relief Program (TARP) was originally authorized to purchase failed mortgages and mortgage-related securities at the heart of the credit crisis. However, in mid-November, U.S. Treasury Secretary Henry Paulson redirected TARP’s mission to help relieve pressure in the area of consumer credit. TARP will now focus on offering aid to banks and other firms that issue student, auto, and credit card loans.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future.

Comparison of top sector weightings

This chart shows how the fund’s top weightings have changed over the past six months. Weightings are shown as a percentage of net assets. Holdings will vary over time. Sector concentrations listed after the portfolio schedule in the Financial Statements section of this shareholder report are exclusive of insured or prerefunded status and may differ from the summary information below.

7

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended September 30, 2008, the end of its most recent fiscal year. In accordance with regulatory requirements for mutual funds, we also include expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represents past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section of www.putnam.com or call Putnam at 1-800-225-1581. Class Y shares are generally only available to corporate and institutional clients and clients in other approved programs. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance Total return for periods ended 9/30/08

| | | | | | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

| (inception dates) | (4/29/83) | (1/4/93) | (7/26/99) | (2/14/95) | (1/2/08) |

|

| | NAV | POP | NAV | CDSC | NAV | CDSC | NAV | POP | NAV |

|

| Annual average (life of fund) | 6.57% | 6.40% | 5.78% | 5.78% | 5.72% | 5.72% | 6.16% | 6.02% | 6.59% |

|

| 10 years | 38.38 | 32.88 | 29.79 | 29.79 | 27.89 | 27.89 | 34.20 | 29.78 | 38.80 |

| Annual average | 3.30 | 2.88 | 2.64 | 2.64 | 2.49 | 2.49 | 2.99 | 2.64 | 3.33 |

|

| 5 years | 10.28 | 5.96 | 6.73 | 5.04 | 6.04 | 6.04 | 8.46 | 5.07 | 10.60 |

| Annual average | 1.98 | 1.16 | 1.31 | 0.99 | 1.18 | 1.18 | 1.64 | 0.99 | 2.04 |

|

| 3 years | 1.32 | –2.66 | –0.55 | –3.15 | –1.10 | –1.10 | 0.39 | –2.78 | 1.61 |

| Annual average | 0.44 | –0.89 | –0.18 | –1.06 | –0.37 | –0.37 | 0.13 | –0.94 | 0.53 |

|

| 1 year | –4.69 | –8.55 | –5.45 | –9.98 | –5.40 | –6.31 | –5.11 | –8.20 | –4.41 |

|

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After sales charge returns (public offering price, or POP) for class A and M shares reflect a maximum 4.00% and 3.25% load, respectively, as of 1/2/08. Class B share returns reflect the applicable contingent deferred sales charge (CDSC), which is 5% in the first year, declining to 1% in the sixth year, and is eliminated thereafter. Class C shares reflect a 1% CDSC for the first year that is eliminated thereafter. Class Y shares have no initial sales charge or CDSC. Performance for class B, C, M, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and, except for class Y shares, the higher operating expenses for such shares.

For a portion of the periods, this fund may have limited expenses, without which returns would have been lower.

A 1% short-term trading fee may be applied to shares exchanged or sold within 7 days of purchase.

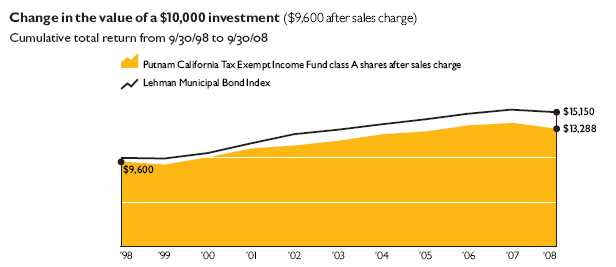

Past performance does not indicate future results. At the end of the same time period, a $10,000 investment in the fund’s class B and class C shares would have been valued at $12,979 and $12,789, respectively, and no contingent deferred sales charges would apply. A $10,000 investment in the fund’s class M shares ($9,675 after sales charge) would have been valued at $12,978 at public offering price. A $10,000 investment in the fund’s class Y share would have been valued at $13,880.

8

Comparative index returns For periods ended 9/30/08

| | |

| | | Lipper California Municipal Debt |

| | Lehman Municipal Bond Index | Funds category average* |

|

| Annual average (life of fund) | 7.16% | 6.61% |

|

| 10 years | 51.50 | 35.51 |

| Annual average | 4.24 | 3.07 |

|

| 5 years | 15.01 | 9.98 |

| Annual average | 2.84 | 1.91 |

|

| 3 years | 5.67 | 0.17 |

| Annual average | 1.86 | 0.03 |

|

| 1 year | –1.87 | –5.71 |

|

Index and Lipper results should be compared to fund performance at net asset value.

* Over the 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 9/30/08, there were 120, 106, 100, 71, and 3 funds, respectively, in this Lipper category.

Fund price and distribution information For the 12-month period ended 9/30/08

| | | | | | | | |

| Distributions | | Class A | | Class B | Class C | Class M | | Class Y |

|

| Number | | 12 | | 12 | 12 | 12 | | 9 |

|

| Income 1 | | $0.341921 | | $0.291046 | $0.280511 | $0.318295 | | $0.268897 |

|

| Capital gains — Long-term 2 | | 0.036700 | | 0.036700 | 0.036700 | 0.036700 | | — |

|

| Capital gains — Short-term 2 | | — | | — | — | — | | — |

|

| Total | | $0.378621 | | $0.327746 | $0.317211 | $0.354995 | | $0.268897 |

|

| Share value | | NAV | POP | NAV | NAV | NAV | POP | NAV |

|

| 9/30/07 | | $8.04 | $8.38* | $8.04 | $8.07 | $8.03 | $8.30 | — |

|

| 1/2/2008† | | — | — | — | — | — | — | $7.96 |

|

| 9/30/08 | | 7.30 | 7.60 | 7.29 | 7.33 | 7.28 | 7.52 | 7.31 |

|

| Current yield (end of period) | | NAV | POP | NAV | NAV | NAV | POP | NAV |

|

| Current dividend rate 3 | | 4.76% | 4.58% | 4.09% | 3.93% | 4.46% | 4.32% | 4.99% |

|

| Taxable equivalent 4 | | 8.16 | 7.86 | 7.02 | 6.74 | 7.65 | 7.41 | 8.56 |

|

| Current 30-day SEC yield 5 | | N/A | 4.29 | 3.80 | 3.64 | N/A | 4.03 | 4.67 |

|

| Taxable equivalent 4 | | N/A | 7.36 | 6.52 | 6.24 | N/A | 6.91 | 8.01 |

|

The classification of distributions, if any, is an estimate. Final distribution information will appear on your year-end tax forms.

* Reflects an increase in sales charges that took effect on 1/2/08.

† Inception date of class Y shares.

1 For some investors, investment income may be subject to the federal alternative minimum tax.

2 Capital gains, if any, are taxable for federal and, in most cases, state purposes.

3 Most recent distribution, excluding capital gains, annualized and divided by NAV or POP at end of period.

4 Assumes maximum 41.70% federal and state combined tax rate for 2008. Results for investors subject to lower tax rates would not be as advantageous.

5 Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

Fund’s annual operating expenses For the fiscal year ended 9/30/07

| | | | | | |

| | | Class A | Class B | Class C | Class M | Class Y |

|

| Total annual fund operating expenses | | 0.76% | 1.40% | 1.55% | 1.05% | 0.55% |

|

Expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown in the next section and in the financial highlights of this report. Expenses are shown as a percentage of average net assets.

9

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Review your fund’s expenses

The following table shows the expenses you would have paid on a $1,000 investment in Putnam California Tax Exempt Income Fund from April 1, 2008, to September 30, 2008. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

|

| Expenses paid per $1,000* | $3.78 | $6.90 | $7.64 | $5.20 | $2.75 |

|

| Ending value (after expenses) | $963.10 | $958.70 | $959.60 | $960.40 | $964.20 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 9/30/08. The expense ratio may differ for each share class (see the last table in this section). Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended September 30, 2008, use the following calculation method. To find the value of your investment on April 1, 2008, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

|

| Expenses paid per $1,000* | $3.89 | $7.11 | $7.87 | $5.35 | $2.83 |

|

| Ending value (after expenses) | $1,021.15 | $1,017.95 | $1,017.20 | $1,019.70 | $1,022.20 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 9/30/08. The expense ratio may differ for each share class (see the last table in this section). Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

10

Compare expenses using industry averages

You can also compare your fund’s expenses with the average of its peer group, as defined by Lipper, an independent fund-rating agency that ranks funds relative to others that Lipper considers to have similar investment styles or objectives. The expense ratio for each share class shown indicates how much of your fund’s average net assets have been used to pay ongoing expenses during the period.

| | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

|

| Your fund’s annualized expense ratio* | 0.77% | 1.41% | 1.56% | 1.06% | 0.56% |

|

| Average annualized expense ratio for Lipper peer group† | 0.81% | 1.45% | 1.60% | 1.10% | 0.60% |

|

* For the fund’s most recent fiscal half year; may differ from expense ratios based on one-year data in the financial highlights.

† Putnam keeps fund expenses below the Lipper peer group average expense ratio by limiting our fund expenses if they exceed the Lipper average. The Lipper average is a simple average of front-end load funds in the peer group that excludes 12b-1 fees as well as any expense offset and brokerage/service arrangements that may reduce fund expenses. To facilitate the comparison in this presentation, Putnam has adjusted the Lipper average to reflect 12b-1 fees. Investors should note that the other funds in the peer group may be significantly smaller or larger than the fund, and that an asset-weighted average would likely be lower than the simple average. Also, the fund and Lipper report expense data at different times; the fund’s expense ratio shown here is annualized data for the most recent six-month period, while the quarterly updated Lipper average is based on the most recent fiscal year-end data available for the peer group funds as of 9/30/08.

11

Your fund’s portfolio turnover and Morningstar® Risk

Putnam funds are actively managed by teams of experts who buy and sell securities based on intensive analysis of companies, industries, economies, and markets. Portfolio turnover is a measure of how often a fund’s managers buy and sell securities for your fund. A portfolio turnover of 100%, for example, means that the managers sold and replaced securities valued at 100% of a fund’s average portfolio value within a given period. Funds with high turnover may be more likely to generate capital gains that must be distributed to shareholders as taxable income. High turnover may also cause a fund to pay more brokerage commissions and other transaction costs, which may detract from performance.

Funds that invest in bonds or other fixed-income instruments may have higher turnover than funds that invest only in stocks. Short-term bond funds tend to have higher turnover than longer-term bond funds, because shorter-term bonds will mature or be sold more frequently than longer-term bonds. You can use the following table to compare your fund’s turnover with the average turnover for funds in its Lipper category.

Turnover comparisons

Percentage of holdings that change every year

| | | | | | |

| | | 2008 | 2007 | 2006 | 2005 | 2004 |

|

| Putnam California Tax Exempt Income Fund | | 48% | 36% | 12% | 21% | 13% |

|

| Lipper California Municipal Debt Funds category average | | 31% | 23% | 22% | 17% | 24% |

|

Turnover data for the fund is calculated based on the fund’s fiscal-year period, which ends on September 30. Turnover data for the fund’s Lipper category is calculated based on the average of the turnover of each fund in the category for its fiscal year ended during the indicated year. Fiscal years vary across funds in the Lipper category, which may limit the comparability of the fund’s portfolio turnover rate to the Lipper average. Comparative data for 2008 is based on information available as of 9/30/08.

Your fund’s Morningstar® Risk

This risk comparison is designed to help you understand how your fund compares with other funds. The comparison utilizes a risk measure developed by Morningstar, an independent fund-rating agency. This risk measure is referred to as the fund’s Morningstar Risk.

Your fund’s Morningstar Risk is shown alongside that of the average fund in its Morningstar category. The risk bar broadens the comparison by translating the fund’s Morningstar Risk into a percentile, which is based on the fund’s ranking among all funds rated by Morningstar as of September 30, 2008. A higher Morningstar Risk generally indicates that a fund’s monthly returns have varied more widely.

Morningstar determines a fund’s Morningstar Risk by assessing variations in the fund’s monthly returns — with an emphasis on downside variations — over a 3-year period, if available. Those measures are weighted and averaged to produce the fund’s Morningstar Risk. The information shown is provided for the fund’s class A shares only; information for other classes may vary. Morningstar Risk is based on historical data and does not indicate future results. Morningstar does not purport to measure the risk associated with a current investment in a fund, either on an absolute basis or on a relative basis. Low Morningstar Risk does not mean that you cannot lose money on an investment in a fund. Copyright 2008 Morningstar, Inc. All Rights Reserved. The information contained herein (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

12

Your fund’s management

Your fund is managed by the members of the Putnam Tax Exempt Fixed-Income Team. Thalia Meehan is the Portfolio Leader, and Paul Drury, Brad Libby, and Susan McCormack are Portfolio Members, of your fund. The Portfolio Leader and Portfolio Members coordinate the team’s management of the fund.

For a complete listing of the members of the Putnam Tax Exempt Fixed-Income Team, including those who are not Portfolio Leaders or Portfolio Members of your fund, please visit the Individual Investors section of www.putnam.com.

Trustee and Putnam employee fund ownership

As of September 30, 2008, 12 of the 13 Trustees of the Putnam funds owned fund shares. The table below shows the approximate value of investments in the fund and all Putnam funds as of that date by the Trustees and Putnam employees. These amounts include investments by the Trustees’ and employees’ immediate family members and investments through retirement and deferred compensation plans.

| | | |

| | Assets in | Total assets in | |

| | the fund | all Putnam funds | |

| |

| Trustees | $34,000 | $37,000,000 | |

| |

| Putnam employees | $14,000 | $471,000,000 | |

| |

Other Putnam funds managed by the Portfolio Leader and Portfolio Members

Thalia Meehan is the Portfolio Leader, and Paul Drury, Brad Libby, and Susan McCormack are Portfolio Members, of Putnam’s open-end tax-exempt funds for the following states: Arizona, California, Massachusetts, Michigan, Minnesota, New Jersey, New York, Ohio, and Pennsylvania. The same group also manages Putnam Tax Exempt Income Fund, Putnam AMT-Free Insured Municipal Fund, and Putnam Municipal Opportunities Trust.

Paul Drury is the Portfolio Leader, and Brad Libby, Susan McCormack, and Thalia Meehan are Portfolio Members, of Putnam Tax-Free High Yield Fund and Putnam Managed Municipal Income Trust.

Thalia Meehan, Paul Drury, Brad Libby, and Susan McCormack may also manage other accounts and variable trust funds advised by Putnam Management or an affiliate.

Investment team fund ownership

The following table shows how much the fund’s current Portfolio Leader and Portfolio Members have invested in the fund and in all Putnam mutual funds (in dollar ranges). Information shown is as of September 30, 2008, and September 30, 2007.

13

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Net asset value (NAV) is the price, or value, of one share of a mutual fund, without a sales charge. NAVs fluctuate with market conditions. NAV is calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

Public offering price (POP) is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. POP performance figures shown here assume the 4.00% maximum sales charge for class A shares and 3.25% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Current yield is the annual rate of return earned from dividends or interest of an investment. Current yield is expressed as a percentage of the price of a security, fund share, or principal investment.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge. They may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Comparative indexes

Lehman Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

Lehman Municipal Bond Index is an unmanaged index of long-term fixed-rate investment-grade tax-exempt bonds.

Merrill Lynch 91-Day Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflectperformance trends for funds within a category.

14

Trustee approval of management contract

General conclusions

The Board of Trustees of the Putnam funds oversees the management of each fund and, as required by law, determines annually whether to approve the continuance of your fund’s management contract with Putnam Investment Management (“Putnam Management”). In this regard, the Board of Trustees, with the assistance of its Contract Committee consisting solely of Trustees who are not “interested persons” (as such term is defined in the Investment Company Act of 1940, as amended) of the Putnam funds (the “Independent Trustees”), requests and evaluates all information it deems reasonably necessary under the circumstances. Over the course of several months ending in June 2008, the Contract Committee met several times to consider the information provided by Putnam Management and other information developed with the assistance of the Board’s independent counsel and independent staff. The Contract Committee reviewed and discussed key aspects of t his information with all of the Independent Trustees. The Contract Committee recommended, and the Independent Trustees approved, the continuance of your fund’s management contract, effective July 1, 2008.

The Independent Trustees’ approval was based on the following conclusions:

• That the fee schedule in effect for your fund represented reasonable compensation in light of the nature and quality of the services being provided to the fund, the fees paid by competitive funds and the costs incurred by Putnam Management in providing such services, and

• That this fee schedule represented an appropriate sharing between fund shareholders and Putnam Management of such economies of scale as may exist in the management of the fund at current asset levels.

These conclusions were based on a comprehensive consideration of all information provided to the Trustees, were subject to the continued application of certain expense reductions and waivers and other considerations noted below, and were not the result of any single factor. Some of the factors that figured particularly in the Trustees’ deliberations and how the Trustees considered these factors are described below, although individual Trustees may have evaluated the information presented differently, giving different weights to various factors. It is also important to recognize that the fee arrangements for your fund and the other Putnam funds are the result of many years of review and discussion between the Independent Trustees and Putnam Management, that certain aspects of such arrangements may receive greater scrutiny in some years than others, and that the Trustees’ conclusions may be based, in part, on their consideration of these same arrangements in prior years.

Management fee schedules and categories; total expenses

The Trustees reviewed the management fee schedules in effect for all Putnam funds, including fee levels and breakpoints, and the assignment of funds to particular fee categories. In reviewing fees and expenses, the Trustees generally focused their attention on material changes in circumstances — for example, changes in a fund’s size or investment style, changes in Putnam Management’s operating costs or responsibilities, or changes in competitive practices in the mutual fund industry — that suggest that consideration of fee changes might be warranted. The Trustees concluded that the circumstances did not warrant changes to the management fee structure of your fund, which had been carefully developed over the years, re-examined on many occasions and adjusted where appropriate. In this regard, the Trustees also noted that shareholders of your fund voted in 2007 to approve new management contracts containing an identical fee structure. The Trustees focuse d on two areas of particular interest, as discussed further below:

• Competitiveness. The Trustees reviewed comparative fee and expense information for competitive funds, which indicated that, in a custom peer group of competitive funds selected by Lipper Inc., your fund ranked in the 58th percentile in management fees and in the 29th percentile in total expenses (less any applicable 12b-1 fees) as of December 31, 2007 (the first percentile being the least expensive funds and the 100th percentile being the most expensive funds). (Because the fund’s custom peer group is smaller than the fund’s broad Lipper Inc. peer group, this expense information may differ from the Lipper peer expense information found elsewhere in this report.) The Trustees noted that expense ratios for a number of Putnam funds, which show the percentage of fund assets used to pay for management and administrative services, distribution (12b-1) fees and other expenses, had been increasing recently as a result of declining net assets and the natural operation of fee breakpoints.

The Trustees noted that the expense ratio increases described above were currently being controlled by expense limitations initially implemented in January 2004. The Trustees have received a commitment from Putnam Management and its parent company to continue this program through at least June 30, 2009. These expense limitations give effect to a commitment by Putnam Management that the expense ratio of each open-end fund would be no higher than the average expense ratio of the competitive funds included in the fund’s relevant Lipper universe (exclusive of any applicable 12b-1 charges in each case). The Trustees observed that this commitment to limit fund expenses has served shareholders well since its inception.

In order to ensure that the expenses of the Putnam funds continue to meet evolving competitive standards, the Trustees requested, and Putnam Management agreed, to extend for the twelve months beginning July 1, 2008, an additional expense limitation for certain funds at an amount equal to the average expense ratio (exclusive of 12b-1 charges) of a custom

15

peer group of competitive funds selected by Lipper to correspond to the size of the fund. This additional expense limitation will be applied to those open-end funds that had above-average expense ratios (exclusive of 12b-1 charges) based on the custom peer group data for the period ended December 31, 2007. This additional expense limitation will not be applied to your fund because it had a below-average expense ratio relative to its custom peer group.

In addition, the Trustees devoted particular attention to analyzing the Putnam funds’ fees and expenses relative to those of competitors in fund complexes of comparable size and with a comparable mix of asset categories. The Trustees concluded that this analysis did not reveal any mattersrequiring further attention at the current time.

• Economies of scale. Your fund currently has the benefit of breakpoints in its management fee that provide shareholders with significant economies of scale, which means that the effective management fee rate of the fund (as a percentage of fund assets) declines as the fund grows in size and crosses specified asset thresholds.

Conversely, if the fund shrinks in size — as has been the case for many Putnam funds in recent years — these breakpoints result in increasing fee levels. In recent years, the Trustees have examined the operation of the existing breakpoint structure during periods of both growth and decline in asset levels. The Trustees concluded that the fee schedule in effect for your fund represented an appropriate sharing of economies of scale at current asset levels.

In connection with their review of the management fees and total expenses of the Putnam funds, the Trustees also reviewed the costs of the services to be provided and profits to be realized by Putnam Management and its affiliates from the relationship with the funds. This information included trends in revenues, expenses and profitability of Putnam Management and its affiliates relating to the investment management and distribution services provided to the funds. In this regard, the Trustees also reviewed an analysis of Putnam Management’s revenues, expenses and profitability with respect to the funds’ management contracts, allocated on a fund-by-fund basis.

Investment performance

The quality of the investment process provided by Putnam Management represented a major factor in the Trustees’ evaluation of the quality of services provided by Putnam Management under your fund’s management contract. The Trustees were assisted in their review of the Putnam funds’ investment process and performance by the work of the Investment Oversight Coordinating Committee of the Trustees and the Investment Oversight Committees of the Trustees, which had met on a regular monthly basis with the funds’ portfolio teams throughout the year. The Trustees concluded that Putnam Management generally provides a high-quality investment process — as measured by the experience and skills of the individuals assigned to the management of fund portfolios, the resources made available to such personnel, and in general the ability of Putnam Management to attract and retain high-quality personnel — but also recognized that this does not guarantee favorab le investment results for every fund in every time period. The Trustees considered the investment performance of each fund over multiple time periods and considered information comparing each fund’s performance with various benchmarks and with the performance of competitive funds.

While the Trustees noted the satisfactory investment performance of certain Putnam funds, they considered the disappointing investment performance of many funds in recent periods, particularly over periods in 2007 and 2008. They discussed with senior management of Putnam Management the factors contributing to such underperformance and actions being taken to improve performance. The Trustees recognized that, in recent years, Putnam Management has taken steps to strengthen its investment personnel and processes to address areas of underperformance, including recent efforts to further centralize Putnam Management’s equity research function. In this regard, the Trustees took into consideration efforts by Putnam Management to improve its ability to assess and mitigate investment risk in individual funds, across asset classes, and across the complex as a whole. The Trustees indicated their intention to continue to monitor performance trends to assess the effectiveness of these efforts and to evaluate whether additional changes to address areas of underperformance are warranted.

In the case of your fund, the Trustees considered that your fund’s class A share cumulative total return performance at net asset value was in the following percentiles of its Lipper Inc. peer group (Lipper California Municipal Debt Funds) (compared using tax-adjusted performance to recognize the different federal income tax treatment for capital gains distributions and exempt-interest distributions) for the one-year, three-year and five-year periods ended December 31, 2007 (the first percentile being the best-performing funds and the 100th percentile being the worst-performing funds):

| | |

| One-year period | 33rd | |

| |

| Three-year period | 45th | |

| |

| Five-year period | 43rd | |

| |

(Because of the passage of time, these performance results may differ from the performance results for more recent periods shown elsewhere in this report.) Over the one-year, three-year and five-year periods ended December 31, 2007, there were 117, 107 and 99 funds, respectively, in your fund’s Lipper peer group.* Past performance is no guarantee of future returns.

* The percentile rankings for your fund’s class A share annualized total return performance in the Lipper California Municipal Debt Funds category for the one-year, five-year, and ten-year periods ended September 30, 2008, were 50%, 55%, and 38%, respectively. Over the one-year, five-year, and ten-year periods ended September 30, 2008, your fund ranked 60th out of 120, 55th out of 100, and 27th out of 71 funds, respectively. Unlike the information above, these rankings reflect performance before taxes. Note that this more recent information was not available when the Trustees approved the continuance of your fund’s management contract.

16

As a general matter, the Trustees believe that cooperative efforts between the Trustees and Putnam Management represent the most effective way to address investment performance problems. The Trustees noted that investors in the Putnam funds have, in effect, placed their trust in the Putnam organization, under the oversight of the funds’ Trustees, to make appropriate decisions regarding the management of the funds. Based on the responsiveness of Putnam Management in the recent past to Trustee concerns about investment performance, the Trustees concluded that it is preferable to seek change within Putnam Management to address performance shortcomings. In the Trustees’ view, the alternative of engaging a new investment adviser for an underperforming fund would entail significant disruptions and would not provide any greater assurance of improved investment performance.

Brokerage and soft-dollar

allocations; other benefits

The Trustees considered various potential benefits that Putnam Management may receive in connection with the services it provides under the management contract with your fund. These include benefits related to brokerage and soft-dollar allocations, whereby a portion of the commissions paid by a fund for brokerage may be used to acquire research services that may be useful to Putnam Management in managing the assets of the fund and of other clients.

The Trustees considered changes made in 2008, at Putnam Management’s request, to the Putnam funds’ brokerage allocation policy, which expanded the permitted categories of brokerage and research services payable with soft dollars and increased the permitted soft dollar allocation to third-party services over what had been authorized in previous years. The Trustees indicated their continued intent to monitor the potential benefits associated with the allocation of fund brokerage and trends in industry practice to ensure that the principle of seeking “best price and execution” remains paramount in the portfolio trading process.

The Trustees’ annual review of your fund’s management contract arrangements also included the review of its distributor’s contract and distribution plan with Putnam Retail Management Limited Partnership and the investor servicing agreement with Putnam Fiduciary Trust Company (“PFTC”), each of which provides benefits to affiliates of Putnam Management. In the case of the investor servicing agreement, the Trustees considered that certain shareholder servicing functions were shifted to a third-party service provider by PFTC in 2007.

Comparison of retail and

institutional fee schedules

The information examined by the Trustees as part of their annual contract review has included for many years information regarding fees charged by Putnam Management and its affiliates to institutional clients such as defined benefit pension plans, college endowments, etc. This information included comparisons of such fees with fees charged to the funds, as well as a detailed assessment of the differences in the services provided to these two types of clients. The Trustees observed, in this regard, that the differences in fee rates between institutional clients and mutual funds are by no means uniform when examined by individual asset sectors, suggesting that differences in the pricing of investment management services to these types of clients reflect to a substantial degree historical competitive forces operating in separate market places. The Trustees considered the fact that fee rates across different asset classes are typically higher o n average for mutual funds than for institutional clients, as well as the differences between the services that Put-nam Management provides to the Putnam funds and those that it provides to institutional clients of the firm, but did not rely on such comparisons to any significant extent in concluding that the management fees paid by your fund are reasonable.

17

Other information for shareholders

Putnam’s policy on confidentiality

In order to conduct business with our shareholders, we must obtain certain personal information such as account holders’ addresses, telephone numbers, Social Security numbers, and the names of their financial representatives. We use this information to assign an account number and to help us maintain accurate records of transactions and account balances. It is our policy to protect the confidentiality of your information, whether or not you currently own shares of our funds, and, in particular, not to sell information about you or your accounts to outside marketing firms. We have safeguards in place designed to prevent unauthorized access to our computer systems and procedures to protect personal information from unauthorized use. Under certain circumstances, we share this information with outside vendors who provide services to us, such as mailing and proxy solicitation. In those cases, the service providers enter into confidentiality agreements with us, and we provide only the information necessary to process transactions and perform other services related to your account. We may also share this information with our Putnam affiliates to service your account or provide you with information about other Putnam products or services. It is also our policy to share account information with your financial representative, if you’ve listed one on your Putnam account. If you would like clarification about our confidentiality policies or have any questions or concerns, please don’t hesitate to contact us at 1-800-225-1581, Monday through Friday, 8:30 a.m. to 8:00 p.m., or Saturdays from 9:00 a.m. to 5:00 p.m. Eastern Time.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2008, are available in the Individual Investors section of www.putnam.com, and on the SEC’s Web site, www.sec.gov. If you have questions about finding forms on the SEC’s Web site, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Forms N-Q on the SEC’s Web site at www.sec.gov. In addition, the fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s Web site or the operation of the Public Reference Room.

18

Financial statements

These sections of the report, as well as the accompanying Notes, preceded by the Report of Independent Registered Public Accounting Firm, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and noninvestment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal year.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semi-annual report, the highlight table also includes the current reporting period.

19

Report of Independent Registered Public Accounting Firm

The Board of Trustees and Shareholders of

Putnam California Tax Exempt Income Fund:

We have audited the accompanying statement of assets and liabilities of Putnam California Tax Exempt Income Fund, including the fund’s portfolio, as of September 30, 2008, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended and the financial highlights for each of the five years or periods in the period then ended. These financial statements and financial highlights are the responsibility of the fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform our audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2008 by correspondence with the custodian and brokers or by other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Putnam California Tax Exempt Income Fund as of September 30, 2008, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years or periods in the period then ended, in conformity with U.S. generally accepted accounting principles.

Boston, Massachusetts

November 13, 2008

20

The fund’s portfolio 9/30/08

| |

| Key to abbreviations | |

| | |

| AGO Assured Guaranty, Ltd. | IF COP Inverse Floating Rate Certificates of Participation |

| AMBAC AMBAC Indemnity Corporation | MBIA MBIA Insurance Company |

| COP Certificate of Participation | Radian Insd. Radian Group Insured |

| FGIC Financial Guaranty Insurance Company | U.S. Govt. Coll. U.S. Government Collateralized |

| FRN Floating Rate Notes | VRDN Variable Rate Demand Notes |

| FSA Financial Security Assurance | XLCA XL Capital Assurance |

| G.O. Bonds General Obligation Bonds | |

| | |

| | | |

| MUNICIPAL BONDS AND NOTES (97.6%)* | Rating** | Principal amount | Value |

|

| California (93.3%) | | | |

| ABAG Fin. Auth. COP (Odd Fellows Home), 6s, 8/15/24 | A+ | $1,000,000�� | $1,006,690 |

|

| Acalanes, Unified High School Dist. G.O. Bonds (Election of 2002), Ser. A, FGIC, zero %, | | | |

| 8/1/21 (Prerefunded) | Aa2 | 5,815,000 | 3,106,780 |

|

| Alameda Cnty., Unified School Dist. G.O. Bonds, Ser. A, FSA, zero %, 8/1/15 | Aaa | 1,000,000 | 742,920 |

|

| Alameda, Corridor Trans. Auth. Rev. Bonds, Ser. A | | | |

| MBIA, 5 1/4s, 10/1/21 | AA | 9,500,000 | 9,628,440 |

| AMBAC, zero %, 10/1/19 | AA | 48,270,000 | 25,207,559 |

|

| Alhambra, Unified School Dist. G.O. Bonds (Election of 2004), Ser. A, FGIC, 5s, 8/1/24 | A2 | 1,825,000 | 1,697,706 |

|

| Anaheim, COP, MBIA, 6.2s, 7/16/23 # | AA | 32,000,000 | 32,693,760 |

|

| Anaheim, Pub. Fin. Auth. Rev. Bonds (Distr. Syst.), MBIA | | | |

| 5 1/4s, 10/1/23 | AA | 8,675,000 | 8,559,882 |

| 5 1/4s, 10/1/22 | AA | 6,700,000 | 6,667,170 |

| 5s, 10/1/29 | AA | 1,945,000 | 1,820,189 |

|

| Anaheim, Pub. Fin. Auth. Lease Rev. Bonds | | | |

| (Cap. Appn. Sub. Impt.), Ser. C, FSA, zero %, 9/1/30 | Aaa | 1,290,000 | 344,314 |

| (Pub. Impt.), Ser. C, FSA, zero %, 9/1/19 | Aaa | 1,770,000 | 1,007,696 |

|

| Arcadia, Unified School Dist. G.O. Bonds (Election of 2006), Ser. A, FSA, zero %, 8/1/18 | Aaa | 1,500,000 | 868,050 |

|

| Aromas-San Juan, Unified School Dist. G.O. Bonds, Ser. A, FGIC, zero %, 8/1/26 | A- | 1,475,000 | 419,682 |

|

| Azusa, Pub. Fin. Auth. Rev. Bonds (Parity Wtr. Syst. Cap. Impt.), FSA, 5s, 7/1/21 | Aaa | 1,215,000 | 1,214,903 |

|

| Bay Area Toll Auth. of CA Rev Bonds, Ser. F, 5s, 4/1/31 T | AA | 13,600,000 | 12,748,368 |

|

| Bay Area Toll Auth. of CA Rev. Bonds | | | |

| (San Francisco Bay Area), Ser. F1, 5s, 4/1/34 | AA | 5,000,000 | 4,637,900 |

| Ser. F, 5s, 4/1/31 | AA | 3,100,000 | 2,905,878 |

| (San Francisco Bay Area), Ser. F, 5s, 4/1/26 | AA | 15,500,000 | 14,784,364 |

| (San Francisco Bay Area), Ser. F, 5s, 4/1/24 | AA | 10,245,000 | 9,901,895 |

|

| Burbank, Pub. Fin. Auth. Rev. Bonds (West Olive Redev.), AMBAC, 5s, 12/1/26 | AA | 3,390,000 | 3,093,070 |

|

| Burbank, Unified School Dist. G.O. Bonds (Election of 1997), Ser. C, FGIC, zero %, 8/1/18 | A+ | 2,345,000 | 1,386,387 |

|

| CA Edl. Fac. Auth. Rev. Bonds | | | |

| (Claremont Graduate U.), Ser. A, 6s, 3/1/38 | A3 | 1,045,000 | 1,048,658 |

| (CA Lutheran U.), 5 3/4s, 10/1/38 | Baa1 | 5,000,000 | 4,519,900 |

| (Stanford U.), Ser. Q, 5 1/4s, 12/1/32 | Aaa | 22,360,000 | 22,722,678 |

| (U. Redlands), Ser. A, 5 1/8s, 8/1/38 | A3 | 6,430,000 | 5,659,107 |

| (Claremont Graduate U.), Ser. A, 5 1/8s, 3/1/28 | A3 | 1,270,000 | 1,147,394 |

| (Claremont Graduate U.), Ser. A, 5s, 3/1/31 | A3 | 2,465,000 | 2,189,733 |

| (CA College of Arts), 5s, 6/1/30 | Baa3 | 1,825,000 | 1,518,291 |

| (Lutheran U.), Ser. C, 5s, 10/1/29 | Baa1 | 1,500,000 | 1,270,005 |

| (Claremont Graduate U.), Ser. A, 5s, 3/1/26 | A3 | 1,200,000 | 1,089,804 |

| (Lutheran U.), Ser. C, 5s, 10/1/24 | Baa1 | 1,250,000 | 1,113,150 |

| (U. of the Pacific), 5s, 11/1/16 | A2 | 1,095,000 | 1,128,507 |

| (U. of the Pacific), 5s, 11/1/14 | A2 | 295,000 | 309,470 |

| (U. of the Pacific), 5s, 11/1/13 | A2 | 525,000 | 551,602 |

| (U. of the Pacific), 5s, 11/1/11 | A2 | 625,000 | 656,025 |

| (Lutheran U.), Ser. C, 4 1/2s, 10/1/19 | Baa1 | 2,830,000 | 2,587,865 |

|

| CA Hlth. Fac. Fin. Auth. Rev. Bonds | | | |

| (Catholic Hlth. Care West), Ser. J, 5 5/8s, 7/1/32 | A2 | 5,000,000 | 4,532,450 |

| (Sutter Hlth.), Ser. A, MBIA, 5 3/8s, 8/15/30 | AA | 1,600,000 | 1,616,928 |

| (Kaiser Permanente), Ser. A, 5 1/4s, 4/1/39 | A+ | 1,000,000 | 878,620 |

| (Kaiser Permanente), Ser. A, 5s, 4/1/37 | A+ | 10,000,000 | 8,472,300 |

| (Cedars-Sinai Med. Ctr.), 5s, 11/15/34 | A2 | 6,750,000 | 5,831,258 |

| (CA-NV Methodist), 5s, 7/1/26 | A+ | 1,745,000 | 1,604,074 |

21

| | | |

| MUNICIPAL BONDS AND NOTES (97.6%)* cont. | Rating** | Principal amount | Value |

|

| California cont. | | | |

| CA Hlth. Fac. Fin. Auth. Rev. Bonds | | | |

| (Lucile Salter Packard Hosp.), Ser. C, AMBAC, 5s, 8/15/24 | Aa2 | $6,390,000 | $6,056,378 |

| (Stanford Hosp. & Clinics), Ser. A, 5s, 11/15/23 | A1 | 7,250,000 | 6,698,493 |

| Ser. B, AMBAC, 5s, 7/1/21 | AA | 3,500,000 | 3,431,890 |

| (Cedars Sinai Med. Ctr.), 5s, 11/15/15 | A2 | 2,900,000 | 2,950,199 |

|

| CA Hsg. Fin. Agcy. Rev. Bonds | | | |

| (Home Mtge.), Ser. H, FGIC, 5 3/4s, 8/1/30 | Aa2 | 15,000 | 15,008 |

| (Multi-Fam. Hsg. III), Ser. B, MBIA, 5 1/2s, 8/1/39 | AA | 1,650,000 | 1,467,923 |

| (Home Mtge.), Ser. L, 5.2s, 8/1/28 | Aa2 | 4,500,000 | 4,188,645 |

| (Home Mtge.), Ser. M, 4 3/4s, 8/1/42 | Aa2 | 8,050,000 | 6,069,700 |

| (Home Mtge.), Ser. K, 4 5/8s, 8/1/26 | Aa2 | 2,500,000 | 2,041,175 |

| (Home Mtge.), Ser. I, 4.6s, 8/1/21 | Aa2 | 5,000,000 | 4,408,100 |

|

| CA Infrastructure & Econ. Dev. Bank Rev. Bonds | | | |

| (Bay Area Toll Bridges), Ser. A, FGIC, 5s, 7/1/29 (Prerefunded) | Aaa | 5,000,000 | 4,905,150 |

| (Oakland Unified School Dist. Fin.), 5s, 8/15/22 | A+ | 4,985,000 | 4,697,615 |

| Ser. B, 4s, 6/1/10 | B/P | 1,000,000 | 526,510 |

| Ser. A, zero %, 12/1/20 | B/P | 2,445,000 | 726,018 |

| Ser. A, zero %, 12/1/19 | B/P | 3,445,000 | 1,093,546 |

| Ser. A, zero %, 12/1/18 | B/P | 4,890,000 | 1,606,561 |

| Ser. A, zero %, 12/1/17 | B/P | 2,445,000 | 830,762 |

| Ser. A, zero %, 12/1/16 | B/P | 2,445,000 | 858,537 |

| Ser. A, zero %, 12/1/15 | B/P | 2,440,000 | 884,915 |

|

| CA Muni. Fin. Auth. COP | | | |

| (Cmnty. Hosp. Central CA), 5 1/4s, 2/1/46 | Baa2 | 11,000,000 | 8,553,710 |

| (Cmnty. Hosp. Central CA), 5 1/4s, 2/1/27 | Baa2 | 8,000,000 | 6,837,920 |

| (Cmnty. Hosp. of Central CA), 5s, 2/1/22 | Baa2 | 2,400,000 | 2,113,320 |

|

| CA Muni. Fin. Auth. Rev. Bonds | | | |

| (Biola U.), 5 7/8s, 10/1/34 | Baa1 | 5,000,000 | 4,617,050 |

| (Biola U.), 5.8s, 10/1/28 | Baa1 | 220,000 | 206,404 |

| (Loma Linda U.), 5s, 4/1/28 | A2 | 2,000,000 | 1,805,060 |

| (U. Students Coop Assn.), 5s, 4/1/22 | BBB– | 790,000 | 726,547 |

|

| CA Poll. Control Fin. Auth. VRDN (Pacific Gas & Electric Corp.) | | | |

| Ser. F, 3.9s, 11/1/26 | A–1+ | 3,600,000 | 3,600,000 |

| Class C, 3.65s, 11/1/26 | A–1+ | 13,800,000 | 13,800,000 |

| Ser. E, 3.9s, 11/1/26 | A–1+ | 7,800,000 | 7,800,000 |

|

| CA Poll. Control Fin. Auth. Solid Waste Disp. Rev. Bonds | | | |

| (Keller Canyon Landfill Co.), 6 7/8s, 11/1/27 | BB– | 1,000,000 | 939,920 |

| (Waste Management, Inc.), Ser. A-2, 5.4s, 4/1/25 | BBB | 7,500,000 | 6,112,500 |

| (Waste Management, Inc.), Ser. B, 5s, 7/1/27 | BBB | 4,500,000 | 3,334,275 |

|

| CA State G.O. Bonds | | | |

| 5 1/2s, 3/1/27 | A1 | 5,000,000 | 4,999,750 |

| 5 1/2s, 3/1/26 | A1 | 6,000,000 | 6,008,400 |

| AMBAC, 5 1/2s, 4/1/11 | AA | 16,545,000 | 17,552,425 |

| 5 1/4s, 3/1/30 | A1 | 2,155,000 | 2,069,274 |

| 5 1/4s, 12/1/24 | A1 | 12,135,000 | 11,913,779 |

| 5 1/4s, 12/1/23 | A1 | 11,000,000 | 10,852,160 |

| 5 1/4s, 2/1/20 | A1 | 5,000,000 | 5,119,800 |

| 5 1/8s, 3/1/25 | A1 | 2,060,000 | 1,998,756 |

| 5 1/8s, 3/1/24 | A1 | 2,435,000 | 2,372,883 |

| 5 1/8s, 4/1/23 | A1 | 2,250,000 | 2,192,760 |

| 5s, 2/1/29 (Prerefunded) | AAA | 400,000 | 425,532 |

| AMBAC, 4 1/4s, 12/1/35 | AA | 6,000,000 | 4,621,620 |

|

| CA State Dept. of Wtr. Resources Rev. Bonds | | | |

| FSA, 5 1/8s, 12/1/29 | Aaa | 4,885,000 | 4,892,425 |

| FSA, 5 1/8s, 12/1/29 (Prerefunded) | Aaa | 115,000 | 123,103 |

| (Central Valley), Ser. AE, 5s, 12/1/29 | Aaa | 3,000,000 | 2,860,440 |

| (Pwr. Supply), Ser. H, 5s, 5/1/21 | Aa3 | 6,000,000 | 5,944,560 |

|

| CA State Pub. Wks. Board Rev. Bonds (Dept. of Gen. Svcs. Butterfield), Ser. ST-A | | | |

| 5 1/4s, 6/1/25 | A2 | 2,500,000 | 2,360,675 |

| 5s, 6/1/23 | A2 | 2,900,000 | 2,718,141 |

|

22

| | | |

| MUNICIPAL BONDS AND NOTES (97.6%)* cont. | Rating** | Principal amount | Value |

|

| California cont. | | | |

| CA State Pub. Wks. Board Lease Rev. Bonds | | | |

| Ser. A, MBIA, 6 1/2s, 9/1/17 | AA | $28,000,000 | $31,742,480 |

| (Dept. of Corrections-State Prisons), Ser. A, AMBAC, 5s, 12/1/19 | AA | 33,500,000 | 33,237,695 |

|

| CA Statewide Cmnty. Dev. Mandatory Put Bonds (Hsg. Equity Res.), Ser. B, 5.2s, 6/15/09 | Baa1 | 5,850,000 | 5,943,542 |

|

| CA Statewide Cmnty. Dev. Auth. COP (The Internext Group), 5 3/8s, 4/1/30 | BBB | 15,300,000 | 12,688,596 |

|

| CA Statewide Cmnty. Dev. Auth. Rev. Bonds (Henry Mayo Newhall Memorial Hosp.) | | | |

| 5s, 10/1/27 | A+ | 3,685,000 | 3,234,251 |

| 5s, 10/1/20 | A+ | 1,055,000 | 1,008,633 |

|

| CA Statewide Cmnty. Dev. Auth. 144A Rev. Bonds (Front Porch Cmntys. & Svcs.), Ser. A, | | | |

| 5 1/8s, 4/1/37 | BBB | 5,000,000 | 3,935,950 |

|

| CA Statewide Cmnty. Dev. Auth. Special Tax Mandatory Put Bonds (Hsg. Equity Res. — C), | | | |

| Ser. C, 5.2s, 6/15/09 | Baa1 | 4,000,000 | 4,063,960 |

|

| CA Statewide Cmnty. Dev. Auth. Special Tax Rev. Bonds | | | |

| (Cmnty. Fac. Dist. No. 1-Zone 1C), 7 1/4s, 9/1/30 | BB/P | 2,270,000 | 2,301,281 |

| (Citrus Garden Apt. Project – D1), 5 1/4s, 7/1/22 | A | 1,630,000 | 1,521,507 |

| (Cmnty. Fac. Dist. No. 1-Zone 1B), zero %, 9/1/20 | BB/P | 1,435,000 | 516,830 |

|

| CA Statewide Cmnty., Dev. Auth. Rev. Bonds | | | |

| (Irvine LLC-UCI East Campus), 6s, 5/15/40 | Baa2 | 10,000,000 | 9,281,400 |

| (Kaiser Permanente), Ser. B, 5s, 3/1/41 | A+ | 7,500,000 | 6,287,250 |

| (Huntington Memorial Hosp.), 5s, 7/1/21 | A+ | 2,205,000 | 2,067,254 |

| (Kaiser Permanente), Ser. A, 4 3/4s, 4/1/33 | A+ | 1,600,000 | 1,316,848 |

|

| CA Statewide Cmntys., Dev. Auth. Rev. Bonds | | | |

| (Thomas Jefferson School of Law), Ser. A, 7 1/4s, 10/1/38 | BB+ | 2,415,000 | 2,197,481 |

| (Enloe Med. Ctr.), 6 1/4s, 8/15/33 | A+ | 7,500,000 | 7,537,650 |

| (Enloe Med. Ctr.), 6 1/4s, 8/15/28 | A+ | 5,000,000 | 5,058,250 |

| (Catholic Hlth. Care West), Ser. A, 5 1/2s, 7/1/30 | A2 | 12,000,000 | 10,865,880 |

| (Kaiser Permanente), Ser. B, 5 1/4s, 3/1/45 | A+ | 14,000,000 | 12,121,480 |

| (Sr. Living-Presbyterian Homes), Ser. A, 4 7/8s, 11/15/36 | BBB+ | 1,000,000 | 769,210 |

|

| CA Statewide Fin. Auth. Tobacco Settlement Rev. Bonds, Class B, 5 5/8s, 5/1/29 | Baa3 | 3,355,000 | 2,855,742 |

|

| CA Tobacco Securitization Agcy. Rev. Bonds (Sonoma Cnty. Corp.), Ser. B, 5 1/2s, 6/1/30 (Prerefunded) | AAA/F | 5,000,000 | 5,417,500 |

|

| CA Tobacco Securitization Agcy. stepped coupon Rev. Bonds zero %,(5.25s, 12/1/10) 6/1/21 †† | Baa3 | 10,000,000 | 7,621,600 |

|

| Cabrillo, Cmnty. College Dist. G.O. Bonds, Ser. C, AMBAC, zero %, 5/1/26 | AA | 10,095,000 | 3,827,015 |

|

| Carlsbad, Unified School Dist. G.O. Bonds, FGIC, zero %, 11/1/21 | Aa3 | 2,250,000 | 1,063,890 |

|

| Center, Unified School Dist. G.O. Bonds (Election of 1991), Ser. D, MBIA, zero %, 8/1/23 | AA | 5,855,000 | 2,267,524 |

|

| Central CA Joint Pwr. Hlth. Fin. Auth. COP (Cmnty. Hosp. of Central CA), 6s, 2/1/30 (Prerefunded) | AAA | 9,000,000 | 9,505,350 |

|

| Chabot-Las Positas, Cmnty. College Dist. G.O. Bonds (Election of 2004), Ser. B, AMBAC, zero %, 8/1/17 | Aa2 | 3,785,000 | 2,360,667 |

|

| Chino Basin, Desalter Auth. Rev. Bonds, Ser. A, AGO, 5s, 6/1/30 | Aaa | 5,865,000 | 5,374,217 |

|

| Chino Basin, Regl. Fin. Auth. Rev. Bonds, AMBAC, 5 3/4s, 8/1/22 | AA | 32,000,000 | 32,043,200 |

|

| Chino Valley, Unified School Dist. G.O. Bonds (Election of 2002), Ser. D, FGIC | | | |

| zero %, 8/1/26 | A1 | 4,415,000 | 1,352,491 |

| zero %, 8/1/25 | A1 | 3,945,000 | 1,281,967 |

|

| Chula Vista, Cmnty. Fac. Dist. Special Tax Rev. Bonds | | | |

| (No. 06-1 Eastlake Woods Area), 6.2s, 9/1/33 | BBB/P | 3,750,000 | 3,440,063 |

| (No. 06-1 Eastlake Woods Area), 6.15s, 9/1/26 | BBB/P | 2,000,000 | 1,868,220 |

| (No. 97-3), 6.05s, 9/1/29 (Prerefunded) | BB+/P | 4,420,000 | 4,657,133 |

| (No. 07-1 Otay Ranch Village Eleven), 5 7/8s, 9/1/34 | BB/P | 2,500,000 | 2,188,150 |

| (No. 07-I Otay Ranch Village Eleven), 5.1s, 9/1/26 | BB/P | 360,000 | 296,176 |

|

| Chula Vista, Indl. Dev. Rev. Bonds (San Diego Gas), Ser. B, 5s, 12/1/27 | A1 | 5,000,000 | 4,180,400 |

|