| | |

| UNITED STATES

SECURITIES AND EXCHANGE COMMISSION |

| | |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

| | |

| Investment Company Act file number: | (811-03630) |

| | |

| Exact name of registrant as specified in charter: | Putnam California Tax Exempt Income Fund |

| | |

| Address of principal executive offices: | One Post Office Square, Boston, Massachusetts 02109 |

| | |

| Name and address of agent for service: | Beth S. Mazor, Vice President

One Post Office Square

Boston, Massachusetts 02109 |

| | |

| Copy to: | John W. Gerstmayr, Esq.

Ropes & Gray LLP

800 Boylston Street

Boston, Massachusetts 02199-3600 |

| | |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| | |

| Date of fiscal year end: | September 30, 2011 |

| | |

| Date of reporting period: | October 1, 2010 — September 30, 2011 |

| | |

|

Item 1. Report to Stockholders: | |

| | |

| The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940: | |

Putnam

California Tax Exempt

Income Fund

Annual report

9 | 30 | 11

| | | |

| Message from the Trustees | 1 | | |

| | |

| About the fund | 2 | | |

| | |

| Performance snapshot | 4 | | |

| | |

| Interview with your fund’s portfolio manager | 5 | | |

| | |

| Your fund’s performance | 11 | | |

| | |

| Your fund’s expenses | 14 | | |

| | |

| Terms and definitions | 16 | | |

| | |

| Trustee approval of management contract | 17 | | |

| | |

| Other information for shareholders | 21 | | |

| | |

| Financial statements | 22 | | |

| | |

| Federal tax information | 49 | | |

| | |

| About the Trustees | 50 | | |

| | |

| Officers | 52 | | |

| | |

Message from the Trustees

Dear Fellow Shareholder:

Markets have reflected a heightened state of investor anxiety in recent weeks and months. The deepening European sovereign debt crisis, the potential for an economic slowdown in the United States, and the deceleration of growth by economic powerhouse China have all diminished investors’ appetite for risk.

While volatility may linger for some time, it is important to note that Putnam’s active portfolio managers continue to pursue investment opportunities around the world. In fact, during times when emotion drives market movements, nimble investors have historically had the best opportunities to take advantage of market inefficiencies.

We believe that in volatile markets, it is important to consult your financial advisor to help determine whether your portfolio reflects an appropriate degree of diversification. We also note that Putnam continues to bolster its lineup of funds that seek to limit volatility or guard against downside risk.

We would like to thank John A. Hill, who has served as Chairman of the Trustees since 2000 and who continues on as a Trustee, for his service. We are pleased to announce that Jameson A. Baxter is the new Chair, having served as Vice Chair since 2005 and a Trustee since 1994. Ms. Baxter is President of Baxter Associates, Inc., a private investment firm, and Chair of the Mutual Fund Directors Forum. In addition, she serves as Chair Emeritus of the Board of Trustees of Mount Holyoke College, Director of the Adirondack Land Trust, and Trustee of the Nature Conservancy’s Adirondack Chapter.

Lastly, we would like to take this opportunity to welcome new shareholders to the fund and to thank all of our investors for your continued confidence in Putnam.

About the fund

Potential for tax-advantaged high current income

When investing in tax-exempt bonds, opportunities come in all shapes and sizes. This is especially true for Putnam California Tax Exempt Income Fund, which explores the vast California municipal bond market, investing across a range of market sectors.

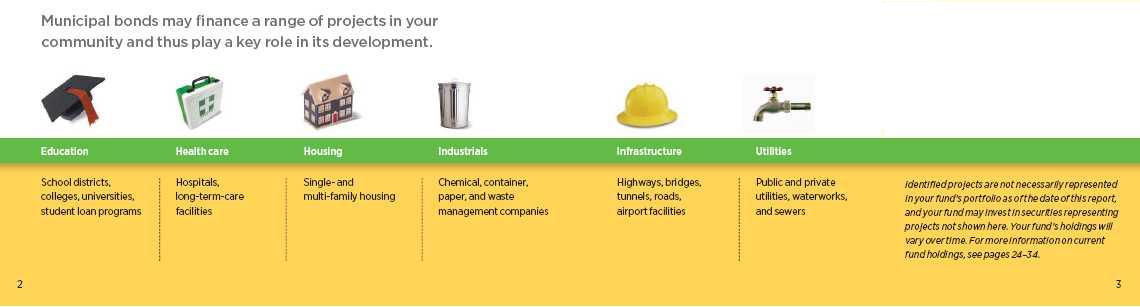

Municipal bonds can help investors keep more of their investment income while also financing important public projects such as schools, roads, and hospitals. Municipal bonds are typically issued by states and local municipalities, and they offer income that is generally exempt from federal income tax.

For residents of the state where the bond is issued, income is typically exempt from state and local income taxes as well. While the stated yields on municipal bonds are usually lower than those on taxable bonds, state tax exemption is a powerful advantage because state income tax can erode investment income significantly.

The fund combines bonds of differing credit quality to increase income potential. In addition to investing in high-quality bonds, the fund’s managers allocate a smaller portion of the portfolio to lower-rated bonds, which may offer higher income in return for more risk. When deciding whether to invest in a bond, the managers carefully consider the risks involved, including credit risk, interest-rate risk, and the risk that the bond will be prepaid.

The fund is backed by the resources of Putnam’s fixed-income organization, in which bond analysts conduct ongoing, rigorous research. Once a bond has been purchased, the managers continue to monitor developments that may affect the bond market, the sector, and the issuer of the bond.

The goal of their in-depth research and active management is to stay a step ahead of the industry and pinpoint opportunities for investors.

Consider these risks before investing: Investments in a single state carry risks of vulnerability to common economic forces and other factors affecting the state’s tax-exempt investments, which may result in greater losses and volatility. Capital gains, if any, are taxable for federal and, in most cases, state purposes. For some investors, investment income may be subject to the federal alternative minimum tax. Funds that invest in bonds are subject to certain risks including interest-rate risk, credit risk, and inflation risk. As interest rates rise, the prices of bonds fall. Long-term bonds are more exposed to interest-rate risk than short-term bonds. Unlike bonds, bond funds have ongoing fees and expenses. The fund may invest significantly in particular segments of the tax-exempt debt market, making it more vulnerable to fluctuations in the values of the securities it holds than a fund that invests more broadly.

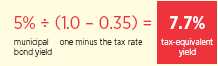

Understanding tax-equivalent yield

To understand the value of tax-free income, it is helpful to compare a municipal bond’s yield with the “tax-equivalent yield” — the before-tax yield that must be offered by a taxable bond in order to equal the municipal bond’s yield after taxes.

How to calculate tax-equivalent yield:

The tax-equivalent yield equals the municipal bond’s yield divided by “one minus the tax rate.” For example, if a municipal bond’s yield is 5%, then its tax-equivalent yield is 7.7%, assuming the maximum 35% federal tax rate for 2011.

Results for investors subject to lower tax rates would not be as advantageous.

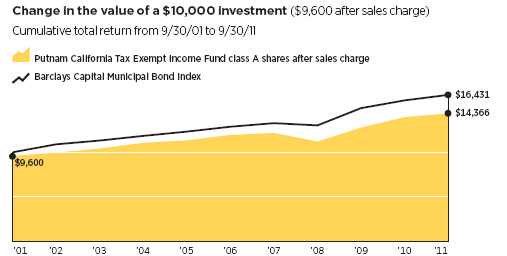

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 4.00%; had they, returns would have been lower. See pages 5 and 11–13 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. To obtain the most recent month-end performance, visit putnam.com.

4

Interview with your fund’s portfolio manager

Thalia Meehan, CFA

Municipal bonds were frequently in the news during the past 12 months. How would you describe the investment environment?

Although the end result for shareholders was positive, the past year has been one of the more volatile periods for municipal bonds in recent memory, beginning in November 2010, when a number of factors combined to create significant headwinds for the market.

First, the Federal Reserve announced it would purchase $600 billion in Treasury bonds over a period of several months in a second round of quantitative easing measures, known as “QE2,” designed in part to keep yields low and encourage investor risk-taking. In theory, this move should have caused government bond yields to fall. But, in fact, the widely anticipated QE2 announcement had already been priced in and investors responded by selling their positions in Treasuries. This sent yields higher and, in turn, put pressure on interest rates in the municipal bond market.

Second, as the end of 2010 approached, investor uncertainty grew over the possibility of pending tax-rate increases and the expiration of the Build America Bonds, or “BABs,” program, which for the past two years had played a key role in lending stability to the municipal bond market. This uncertainty, coupled with dire media coverage of state budget challenges and predictions of widespread defaults, led to a broad sell-off in municipal bonds as investors pulled money out of the asset class.

As 2011 progressed, however, the municipal bond market gained back a good deal of what it lost in the fourth quarter. Widespread defaults did not materialize, and in fact remained quite low relative to their historical average. States continued to face challenges in balancing their budgets, but by the end

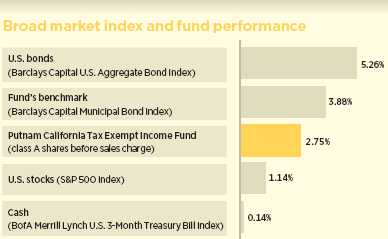

This comparison shows your fund’s performance in the context of broad market indexes for the 12 months ended 9/30/11. See pages 4 and 11–13 for additional fund performance information. Index descriptions can be found on page 16.

5

of the period all state legislatures that were slated to enact budgets had done so, including California, which passed its budget on time for the first time in years. Income tax receipts also generally have begun to modestly improve versus last year. As investors ultimately realized that municipal credit conditions were not nearly as bleak as some feared, they re-entered the municipal market.

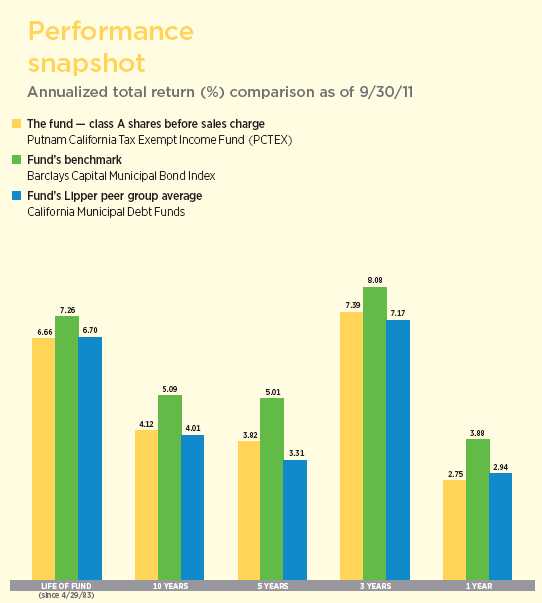

The fund’s returns during its fiscal year trailed those of its benchmark, although the fund’s performance generally was in line with its Lipper peer group average.

What effect did recent policy debates have on the tax-exempt bond market?

It was a very eventful period from a policy perspective. First, the popular BABs program expired at the end of 2010. BABs are taxable municipal bonds that carry special tax credits and federal subsidies for the states and local governments that issue them, which resulted in substantial savings on borrowing costs. Issuers in all 50 states participated in the BABs program, and, despite some speculation that the program might be extended, it was allowed to expire on December 31, 2010.

The expiration of the BABs program caused a significant spike in municipal bond supply at the end of 2010. To lock in the federal subsidy BABs offered, many states pushed up issuance originally slated for the first quarter of 2011 into the fourth quarter of 2010. Because excess supply can lead to lower prices when demand fails to keep pace, some investors worried that the unusually high issuance at the end of 2010 would continue in the tax-free market in 2011, undermining price stability. However, tax-free issuance year to date in 2011 has been even lower than expected, which helped to provide price stability to the market.

Speculation about changes to tax policy also affected the market. At the end of 2010, the Bush-era tax cuts were slated to expire, and

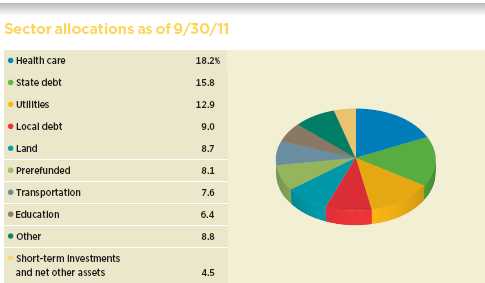

Allocations are represented as a percentage of the fund’s net assets. Summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities and the exclusion of as-of trades, if any. Holdings and allocations may vary over time.

6

it was unclear for several weeks whether Congress would pass legislation to extend current federal income tax rates. Eventually, a bill was passed in December to preserve current tax rates through the end of 2012, but taxes have remained a part of political discussions all year.

More recently, the 12-member “super committee,” created through August’s debt ceiling legislation, has been tasked with reducing the deficit by at least $1.2 trillion. Recommendations from this committee are due to Congress by November 23, and a vote by lawmakers is scheduled to take place by December 23. If legislators fail to cut spending by $1.2 trillion over the next 10 years, automatic across-the-board cuts would be implemented to make up the difference. Expenditure cuts, whether negotiated or automatic, could have an impact on the municipal bond market.

On the revenue side, there have been proposals for the deficit reduction plan that also could impact the municipal bond market. Simplification of the tax code is one possibility, with potential changes to a number of the existing marginal rates, which would affect the relative attractiveness of municipal bonds. While it is difficult to determine the eventual outcome of the super committee’s deliberations, the future tax treatment of municipal bonds will likely be a “tax expenditure” that will receive a significant amount of scrutiny. We believe the likelihood of eliminating municipal bonds’ tax-exempt status is low. It is possible that some types

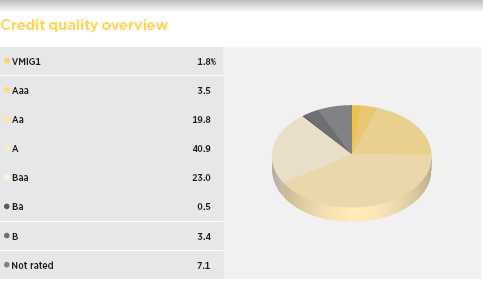

Credit qualities are shown as a percentage of net assets as of 9/30/11. A bond rated Baa or higher (MIG3/VMIG3 or higher, for short-term debt) is considered investment grade. The chart reflects Moody’s ratings; percentages may include bonds or derivatives not rated by Moody’s but rated by Standard & Poor’s or, if unrated by S&P, by Fitch, and then included in the closest equivalent Moody’s rating. Ratings will vary over time. Credit qualities are included for portfolio securities and are not included for derivative instruments and cash. The fund itself has not been rated by an independent rating agency.

7

of bonds, such as so-called “private activity” bonds, might lose their ability to issue in the tax-exempt market in the future. In any case, it appears highly likely that state and local governments will face continued pressure as debate over the deficit reduction continues, and this increases the possibility of headline-driven price volatility.

In August, Standard & Poor’s downgraded its credit rating for U.S. Treasuries and a number of municipal bonds. What impact did that have on the market?

On the heels of its August 5 downgrade of U.S. sovereign debt, Standard & Poor’s [S&P] lowered its ratings from AAA to AA+ for more than 11,000 municipal securities, including taxable and tax-exempt securities. While this number does seem large, it covers less than 1% of the $3 trillion municipal bond market. These securities all had links to the federal government, and, according to S&P, the affected issues fall into four broad categories: municipal housing bonds backed by the federal government or invested in U.S. government securities; bonds of certain government-related entities in the housing and public power sectors; bonds backed by federal leases; and defeased bonds secured by U.S. Treasury and agency securities in escrow.

The downgrade was not surprising given the interdependence of state and federal finances, and S&P had been suggesting such a move was imminent for some time. To date, state general-obligation, or “G.O.,” bond ratings were unchanged; 13 states continue to hold AAA ratings. Nonetheless, we believe S&P’s downgrades underscore the importance of performing intensive fundamental research when investing in the municipal bond market. At Putnam, we independently research every bond we hold and assess the

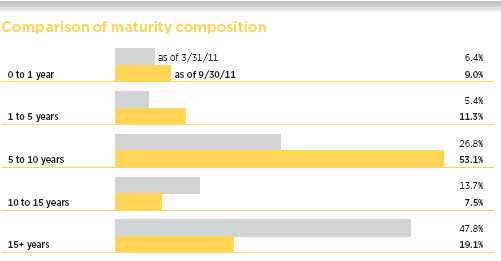

This chart illustrates the fund’s composition by maturity, showing the percentage of holdings in different maturity ranges and how the composition has changed over the past six months. Holdings and maturity ranges will vary over time. The effective maturity dates of bonds with call features may change as a result of market conditions.

8

credit risk it represents before we add it to the portfolio.

How did you position the portfolio during the fund’s fiscal year?

For much of the period, our strategy was to position the portfolio for improving fundamentals in the municipal bond market. While we felt that the budget challenges faced by many states were significant, we were confident that conditions would improve as long as the broad economy did not stall.

Against this backdrop, we believed that essential service revenue bonds remained attractive, while we continued to limit the fund’s exposure to local G.O.s, which are securities issued at the city or county level. We believe that as the federal government looks to reduce transfer payments to the states — and as states, in turn, seek to close their deficits by reducing spending — these types of bonds are at risk for downgrades or other headline-driven price volatility. And unlike state general obligation bonds, local G.O.s rely more on property tax revenue than on income or sales taxes. With real estate prices still under pressure in many markets, property taxes have been slower to recover than other tax sources.

From a credit perspective, we held an overweight position in A- and Baa-rated securities versus the fund’s benchmark, which contributed positively to relative returns. In terms of sectors, we positioned the fund in California state G.O.s, higher education, power, and health care, specifically hospitals.

What is your outlook?

While technical factors in the market have been positive — specifically, light supply and stable demand — uncertainty remains. We believe that states will continue to face financial challenges as the economy struggles to find its footing. For the most part, however, we believe that the fiscal conditions of states and municipalities are showing signs of improvement. Tax receipts are beginning to improve, albeit slowly, and we believe defaults will remain relatively low.

Our concerns remain focused on the economy and Congress’s plans to reduce the deficit. Higher federal income tax rates, a change in the tax status of municipal bonds, or significant cuts in state funding all would have consequences for the municipal bond market. But for investors with longer time horizons, we believe that our actively managed approach remains a prudent way to diversify holdings and generate tax-exempt income in the municipal bond market.

Thank you, Thalia, for bringing us up to date.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

Portfolio Manager Thalia Meehan holds a B.A. from Williams College. A CFA charterholder, Thalia joined Putnam in 1989 and has been in the investment industry since 1983.

In addition to Thalia, your fund’s portfolio managers are Paul Drury and Susan McCormack.

9

IN THE NEWS

U.S. corporations are holding more cash on their books than at any time in nearly 50 years. At the end of June, non-financial companies held more than $2 trillion in cash and other liquid assets, according to the Federal Reserve (the Fed). This marks an increase of more than $88 billion since the end of March. Cash accounted for 7.1% of all company assets, according to the Fed, the highest level since 1963. The Fed’s analysis does not include the substantial amount of cash that U.S. companies hold overseas. While critics are putting pressure on companies to use the cash to invest or create more jobs, others say the sizeable cash holdings could provide an important buffer for U.S. companies if European bank woes should spark a global financial crisis.

10

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended September 30, 2011, the end of its most recent fiscal year. In accordance with regulatory requirements for mutual funds, we also include expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class Y shares are not available to all investors. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance Total return for periods ended 9/30/11

| | | | | | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

| (inception dates) | (4/29/83) | (1/4/93) | (7/26/99) | (2/14/95) | (1/2/08) |

|

| | Before | After | | | | | Before | After | Net |

| | sales | sales | Before | After | Before | After | sales | sales | asset |

| | charge | charge | CDSC | CDSC | CDSC | CDSC | charge | charge | value |

|

| Annual average | | | | | | | | | |

| (life of fund) | 6.66% | 6.51% | 5.89% | 5.89% | 5.81% | 5.81% | 6.26% | 6.13% | 6.70% |

|

| 10 years | 49.74 | 43.66 | 40.56 | 40.56 | 38.40 | 38.40 | 45.38 | 40.58 | 51.33 |

| Annual average | 4.12 | 3.69 | 3.46 | 3.46 | 3.30 | 3.30 | 3.81 | 3.46 | 4.23 |

|

| 5 years | 20.60 | 15.77 | 16.96 | 15.05 | 16.06 | 16.06 | 18.87 | 14.89 | 21.88 |

| Annual average | 3.82 | 2.97 | 3.18 | 2.84 | 3.02 | 3.02 | 3.52 | 2.81 | 4.04 |

|

| 3 years | 23.86 | 18.98 | 21.67 | 18.67 | 21.11 | 21.11 | 22.85 | 18.92 | 24.80 |

| Annual average | 7.39 | 5.96 | 6.76 | 5.87 | 6.59 | 6.59 | 7.10 | 5.95 | 7.66 |

|

| 1 year | 2.75 | –1.32 | 2.24 | –2.66 | 1.95 | 0.97 | 2.45 | –0.88 | 2.99 |

|

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns for class A and M shares reflect the deduction of the maximum 4.00% and 3.25% sales charge, respectively, levied at the time of purchase. Class B share returns after contingent deferred sales charge (CDSC) reflect the applicable CDSC, which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns after CDSC reflect a 1% CDSC for the first year that is eliminated thereafter. Class Y shares have no initial sales charge or CDSC. Performance for class B, C, M, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and the higher operating expenses for such shares, except for class Y shares, for which 12b-1 fees are not applicable.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

Class B share performance does not reflect conversion to class A shares.

11

Comparative index returns For periods ended 9/30/11

| | |

| | Barclays Capital | Lipper California Municipal Debt Funds |

| | Municipal Bond Index | category average* |

|

| Annual average (life of fund) | 7.26% | 6.70% |

|

| 10 years | 64.31 | 48.42 |

| Annual average | 5.09 | 4.01 |

|

| 5 years | 27.71 | 17.87 |

| Annual average | 5.01 | 3.31 |

|

| 3 years | 26.24 | 23.10 |

| Annual average | 8.08 | 7.17 |

|

| 1 year | 3.88 | 2.94 |

|

Index and Lipper results should be compared with fund performance before sales charge, before CDSC, or at net asset value.

* Over the 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 9/30/11, there were 115, 111, 98, 78, and 3 funds, respectively, in this Lipper category.

Past performance does not indicate future results. At the end of the same time period, a $10,000 investment in the fund’s class B and class C shares would have been valued at $14,056 and $13,840 respectively, and no contingent deferred sales charges would apply. A $10,000 investment in the fund’s class M shares ($9,675 after sales charge) would have been valued at $14,058. A $10,000 investment in the fund’s class Y shares would have been valued at $15,133.

12

Fund price and distribution information For the 12-month period ended 9/30/11

| | | | | | | |

| Distributions | Class A | Class B | Class C | Class M | Class Y |

|

| Number | 12 | 12 | 12 | 12 | 12 |

|

| Income 1 | $0.358774 | $0.310545 | $0.299858 | $0.336981 | $0.375557 |

|

| Capital gains 2 | —�� | — | — | — | — |

|

| Total | $0.358774 | $0.310545 | $0.299858 | $0.336981 | $0.375557 |

|

| | Before | After | Net | Net | Before | After | Net |

| | sales | sales | asset | asset | sales | sales | asset |

| Share value | charge | charge | value | value | charge | charge | value |

|

| 9/30/10 | $7.99 | $8.32 | $7.98 | $8.03 | $7.97 | $8.24 | $8.01 |

|

| 9/30/11 | 7.83 | 8.16 | 7.83 | 7.87 | 7.81 | 8.07 | 7.85 |

|

| | Before | After | Net | Net | Before | After | Net |

| | sales | sales | asset | asset | sales | sales | asset |

| Current yield (end of period) | charge | charge | value | value | charge | charge | value |

|

| Current dividend rate 3 | 4.56% | 4.37% | 3.93% | 3.75% | 4.29% | 4.15% | 4.76% |

|

| Taxable equivalent 4 | 7.82% | 7.50% | 6.74% | 6.43% | 7.36% | 7.12% | 8.16% |

|

| Current 30-day SEC yield 5 | N/A | 3.83% | 3.36% | 3.22% | N/A | 3.60% | 4.21% |

|

| Taxable equivalent 4 | N/A | 6.57% | 5.76% | 5.52% | N/A | 6.17% | 7.22% |

|

The classification of distributions, if any, is an estimate. Before-sales-charge share value and current dividend rate for class A and M shares, if applicable, do not take into account any sales charge levied at the time of purchase. After-sales-charge share value, current dividend rate, and current 30-day SEC yield, if applicable, are calculated assuming that the maximum sales charge (4.00% for class A shares and 3.25% for class M shares) was levied at the time of purchase. Final distribution information will appear on your year-end tax forms.

1 For some investors, investment income may be subject to the federal alternative minimum tax.

2 Capital gains, if any, are taxable for federal and, in most cases, state purposes.

3 Most recent distribution, excluding capital gains, annualized and divided by share price before or after sales charge at period-end.

4 Assumes maximum 41.70% federal and state combined tax rate for 2011. Results for investors subject to lower tax rates would not be as advantageous.

5 Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

13

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

| | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

|

| Total annual operating expenses for the fiscal year | | | | | |

| ended 9/30/10* | 0.75% | 1.38% | 1.53% | 1.03% | 0.53% |

|

| Annualized expense ratio for the six-month period | | | | | |

| ended 9/30/11† | 0.75% | 1.38% | 1.53% | 1.03% | 0.53% |

|

Fiscal-year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report. Expenses are shown as a percentage of average net assets.* Restated to reflect projected expenses under a management contract effective 1/1/10.

† For the fund’s most recent fiscal half year; may differ from expense ratios based on one-year data in the financial highlights.

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in the fund from April 1, 2011, to September 30, 2011. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

|

| Expenses paid per $1,000*† | $3.94 | $7.25 | $8.03 | $5.41 | $2.79 |

|

| Ending value (after expenses) | $1,098.20 | $1,096.20 | $1,094.80 | $1,096.80 | $1,100.60 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 9/30/11. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

14

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended September 30, 2011, use the following calculation method. To find the value of your investment on April 1, 2011, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | |

| | Class A | Class B | Class C | Class M | Class Y |

|

| Expenses paid per $1,000*† | $3.80 | $6.98 | $7.74 | $5.22 | $2.69 |

|

| Ending value (after expenses) | $1,021.31 | $1,018.15 | $1,017.40 | $1,019.90 | $1,022.41 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 9/30/11. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

15

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Before sales charge, or net asset value, is the price, or value, of one share of a mutual fund, without a sales charge. Before-sales-charge figures fluctuate with market conditions, and are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

After sales charge is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. After-sales-charge performance figures shown here assume the 4.00% maximum sales charge for class A shares and 3.25% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Current yield is the annual rate of return earned from dividends or interest of an investment. Current yield is expressed as a percentage of the price of a security, fund share, or principal investment.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge. They may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Comparative indexes

Barclays Capital U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

Barclays Capital Municipal Bond Index is an unmanaged index of long-term fixed-rate investment-grade tax-exempt bonds.

BofA (Bank of America) Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

16

Trustee approval of management contract

General conclusions

The Board of Trustees of the Putnam funds oversees the management of each fund and, as required by law, determines annually whether to approve the continuance of your fund’s management contract with Putnam Investment Management (“Putnam Management”) and the sub-management contract with respect to your fund between Putnam Management and its affiliate, Putnam Investments Limited (“PIL”).

The Board of Trustees, with the assistance of its Contract Committee, which consists solely of Trustees who are not “interested persons” (as this term is defined in the Investment Company Act of 1940, as amended) of the Putnam funds (“Independent Trustees”), requests and evaluates all information it deems reasonably necessary under the circumstances in connection with its annual contract review. Over the course of several months ending in June 2011, the Contract Committee met on a number of occasions with representatives of Putnam Management, and separately in executive session, to consider the information that Putnam Management provided and other information developed with the assistance of the Board’s independent counsel and independent staff. The Contract Committee reviewed and discussed key aspects of this information with all of the Independent Trustees on a number of occasions. At the Trustees’ June 17, 2011 meeting, the Contract Committee recommended, and the Independent Trustees approved, the continuance of your fund’s management and sub-management contracts, effective July 1, 2011. (Because PIL is an affiliate of Putnam Management and Putnam Management remains fully responsible for all services provided by PIL, the Trustees have not evaluated PIL as a separate entity, and all subsequent references to Putnam Management below should be deemed to include reference to PIL as necessary or appropriate in the context.)

The Independent Trustees’ approval was based on the following conclusions:

• That the fee schedule in effect for your fund represented reasonable compensation in light of the nature and quality of the services being provided to the fund, the fees paid by competitive funds, and the costs incurred by Putnam Management in providing services, and

• That the fee schedule represented an appropriate sharing between fund shareholders and Putnam Management of such economies of scale as may exist in the management of the fund at current asset levels.

These conclusions were based on a comprehensive consideration of all information provided to the Trustees and were not the result of any single factor. Some of the factors that figured particularly in the Trustees’ deliberations and how the Trustees considered these factors are described below, although individual Trustees may have evaluated the information presented differently, giving different weights to various factors. It is also important to recognize that the management arrangements for your fund and the other Putnam funds are the result of many years of review and discussion between the Independent Trustees and Putnam Management, that some aspects of the arrangements may receive greater scrutiny in some years than others, and that the Trustees’ conclusions may be based, in part, on their consideration of fee arrangements in previous years.

Management fee schedules and total expenses

The Trustees reviewed the management fee schedules in effect for all Putnam funds, including fee levels and breakpoints. In reviewing management fees, the Trustees

17

generally focus their attention on material changes in circumstances — for example, changes in assets under management or investment style, changes in Putnam Management’s operating costs, or changes in competitive practices in the mutual fund industry — that suggest that consideration of fee changes might be warranted. The Trustees concluded that the circumstances did not warrant changes to the management fee structure of your fund.

Most of the open-end Putnam funds have new management contracts, with new fee schedules reflecting the implementation of more competitive fee levels for many funds, complex-wide breakpoints for the open-end funds, and performance fees for some funds. These new management contracts have been in effect for a little over a year — since January or, for a few funds, February, 2010. The Trustees approved the new management contracts on July 10, 2009, and fund shareholders subsequently approved the contracts by overwhelming majorities of the shares voted.

Because these management contracts had been implemented only recently, the Contract Committee had limited practical experience with the operation of the new fee structures. Under its new management contract, your fund has the benefit of breakpoints in its management fee that provide shareholders with significant economies of scale in the form of reduced fee levels as assets under management in the Putnam family of funds increase. The Contract Committee observed that the complex-wide breakpoints of the open-end funds had only been in place for a short while, and the Trustees will examine the operation of this new breakpoint structure in future years in light of further experience.

As in the past, the Trustees also focused on the competitiveness of each fund’s total expense ratio. In order to ensure that expenses of the Putnam funds continue to meet evolving competitive standards, the Trustees and Putnam Management agreed in 2009 to implement certain expense limitations. These expense limitations serve in particular to maintain competitive expense levels for funds with large numbers of small shareholder accounts and funds with relatively small net assets. Most funds, including your fund, had sufficiently low expenses that these expense limitations did not apply. The expense limitations were: (i) a contractual expense limitation applicable to all retail open-end funds of 37.5 basis points on investor servicing fees and expenses and (ii) a contractual expense limitation applicable to all open-end funds of 20 basis points on so-called “other expenses” (i.e., all expenses exclusive of management fees, investor servicing fees, distribution fees, investment-related expenses, interest, taxes, brokerage commissions and extraordinary expenses). Putnam Management’s support for these expense limitations was an important factor in the Trustees’ decision to approve the continuance of your fund’s management and sub-management contracts.

The Trustees reviewed comparative fee and expense information for a custom group of competitive funds selected by Lipper Inc. This comparative information included your fund’s percentile ranking for effective management fees and total expenses (excluding any applicable 12b-1 fee), which provides a general indication of your fund’s relative standing. In the custom peer group, your fund ranked in the 2nd quintile in effective management fees (determined for your fund and the other funds in the custom peer group based on fund asset size and the applicable contractual management fee schedule) and in the 2nd quintile in total expenses (excluding any applicable 12b-1 fees) as of December 31, 2010 (the first quintile representing the least expensive funds and the fifth quintile the most expensive funds). The fee and expense data reported by Lipper as of December 31, 2010 reflected the most

18

recent fiscal year-end data available in Lipper’s database at that time.

In connection with their review of the management fees and total expenses of the Putnam funds, the Trustees also reviewed the costs of the services provided and the profits realized by Putnam Management and its affiliates from their contractual relationships with the funds. This information included trends in revenues, expenses and profitability of Putnam Management and its affiliates relating to the investment management, investor servicing and distribution services provided to the funds. In this regard, the Trustees also reviewed an analysis of Putnam Management’s revenues, expenses and profitability, allocated on a fund-by-fund basis, with respect to the funds’ management, distribution, and investor servicing contracts. For each fund, the analysis presented information about revenues, expenses and profitability for each of the agreements separately and for the agreements taken together on a combined basis. The Trustees concluded that, at current asset levels, the fee schedules in place represented reasonable compensation for the services being provided and represented an appropriate sharing of such economies of scale as may exist in the management of the funds at that time.

The information examined by the Trustees as part of their annual contract review for the Putnam funds has included for many years information regarding fees charged by Putnam Management and its affiliates to institutional clients such as defined benefit pension plans, college endowments, and the like. This information included comparisons of those fees with fees charged to the funds, as well as an assessment of the differences in the services provided to these different types of clients. The Trustees observed that the differences in fee rates between institutional clients and mutual funds are by no means uniform when examined by individual asset sectors, suggesting that differences in the pricing of investment management services to these types of clients may reflect historical competitive forces operating in separate markets. The Trustees considered the fact that in many cases fee rates across different asset classes are higher on average for mutual funds than for institutional clients, as well as the differences between the services that Putnam Management provides to the Putnam funds and those that it provides to its institutional clients. The Trustees did not rely on these comparisons to any significant extent in concluding that the management fees paid by your fund are reasonable.

Investment performance

The quality of the investment process provided by Putnam Management represented a major factor in the Trustees’ evaluation of the quality of services provided by Putnam Management under your fund’s management contract. The Trustees were assisted in their review of the Putnam funds’ investment process and performance by the work of several investment oversight committees of the Trustees, which met on a regular basis with the funds’ portfolio teams and with the Chief Investment Officer and other members of Putnam Management’s Investment Division throughout the year. The Trustees concluded that Putnam Management generally provides a high-quality investment process — based on the experience and skills of the individuals assigned to the management of fund portfolios, the resources made available to them, and in general Putnam Management’s ability to attract and retain high-quality personnel — but also recognized that this does not guarantee favorable investment results for every fund in every time period. The Trustees considered the investment performance of each fund over multiple time periods and considered information comparing each fund’s performance with various benchmarks and with the performance of competitive funds.

19

The Committee noted the substantial improvement in the performance of most Putnam funds during the 2009–2010 period and Putnam Management’s ongoing efforts to strengthen its investment personnel and processes. The Committee also noted the disappointing investment performance of some funds for periods ended December 31, 2010 and considered information provided by Putnam Management regarding the factors contributing to the underperformance and actions being taken to improve the performance of these particular funds. The Trustees indicated their intention to continue to monitor performance trends to assess the effectiveness of these efforts and to evaluate whether additional actions to address areas of underperformance are warranted.

In the case of your fund, the Trustees considered that its class A share cumulative total return performance at net asset value was in the following quartiles of its Lipper Inc. peer group (Lipper California Municipal Debt Funds) for the one-year, three-year and five-year periods ended December 31, 2010 (the first quartile representing the best-performing funds and the fourth quartile the worst-performing funds):

| | | |

| One-year period | 1st | | |

| | |

| Three-year period | 2nd | | |

| | |

| Five-year period | 2nd | | |

| | |

Over the one-year, three-year and five-year periods ended December 31, 2010, there were 120, 115 and 101 funds, respectively, in your fund’s Lipper peer group. (When considering performance information, shareholders should be mindful that past performance is not a guarantee of future results.)

Brokerage and soft-dollar allocations; investor servicing

The Trustees considered various potential benefits that Putnam Management may receive in connection with the services it provides under the management contract with your fund. These include benefits related to brokerage allocation and the use of soft dollars, whereby a portion of the commissions paid by a fund for brokerage may be used to acquire research services that are expected to be useful to Putnam Management in managing the assets of the fund and of other clients. Subject to policies established by the Trustees, soft-dollar credits acquired through these means are used primarily to supplement Putnam Management’s internal research efforts. However, the Trustees noted that a portion of available soft-dollar credits continues to be allocated to the payment of fund expenses. The Trustees indicated their continued intent to monitor regulatory developments in this area with the assistance of their Brokerage Committee and also indicated their continued intent to monitor the potential benefits associated with fund brokerage and soft-dollar allocations and trends in industry practices to ensure that the principle of seeking best price and execution remains paramount in the portfolio trading process.

Putnam Management may also receive benefits from payments that the funds make to Putnam Management’s affiliates for investor or distribution services. In conjunction with the annual review of your fund’s management contract, the Trustees reviewed your fund’s investor servicing agreement with Putnam Investor Services, Inc. (“PSERV”) and its distributor’s contracts and distribution plans with Putnam Retail Management Limited Partnership (“PRM”), both of which are affiliates of Putnam Management. The Trustees concluded that the fees payable by the funds to PSERV and PRM, as applicable, for such services are reasonable in relation to the nature and quality of such services.

20

Other information for shareholders

Important notice regarding Putnam’s privacy policy

In order to conduct business with our shareholders, we must obtain certain personal information such as account holders’ names, addresses, Social Security numbers, and dates of birth. Using this information, we are able to maintain accurate records of accounts and transactions.

It is our policy to protect the confidentiality of our shareholder information, whether or not a shareholder currently owns shares of our funds. In particular, it is our policy not to sell information about you or your accounts to outside marketing firms. We have safeguards in place designed to prevent unauthorized access to our computer systems and procedures to protect personal information from unauthorized use.

Under certain circumstances, we must share account information with outside vendors who provide services to us, such as mailings and proxy solicitations. In these cases, the service providers enter into confidentiality agreements with us, and we provide only the information necessary to process transactions and perform other services related to your account. Finally, it is our policy to share account information with your financial representative, if you’ve listed one on your Putnam account.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2011, are available in the Individual Investors section at putnam.com, and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Forms N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of September 30, 2011, Putnam employees had approximately $298,000,000 and the Trustees had approximately $65,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

21

Financial statements

These sections of the report, as well as the accompanying Notes, preceded by the Report of Independent Registered Public Accounting Firm, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal year.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

22

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of

Putnam California Tax Exempt Income Fund:

We have audited the accompanying statement of assets and liabilities of Putnam California Tax Exempt Income Fund (the fund), including the fund’s portfolio, as of September 30, 2011, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended and the financial highlights for each of the years or periods in the five-year period then ended. These financial statements and financial highlights are the responsibility of the fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform our audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2011 by correspondence with the custodian and brokers or by other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Putnam California Tax Exempt Income Fund as of September 30, 2011 the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years or periods in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

Boston, Massachusetts

November 14, 2011

23

| |

| The fund’s portfolio 9/30/11 | |

| | |

| Key to holding’s abbreviations | |

| ABAG Association Of Bay Area Governments | G.O. Bonds General Obligation Bonds |

| AGM Assured Guaranty Municipal Corporation | NATL National Public Finance Guarantee Corp. |

| AGO Assured Guaranty, Ltd. | Radian Insd. Radian Group Insured |

| AMBAC AMBAC Indemnity Corporation | SGI Syncora Guarantee, Inc. |

| Cmnwlth. of PR Gtd. Commonwealth of | TAN Tax Anticipation Notes |

| Puerto Rico Guaranteed | U.S. Govt. Coll. U.S. Government Collateralized |

| COP Certificates of Participation | VRDN Variable Rate Demand Notes |

| FGIC Financial Guaranty Insurance Company | |

| | | |

| MUNICIPAL BONDS AND NOTES (99.2%)* | Rating** | Principal amount | Value |

|

| California (92.4%) | | | |

| ABAG Fin. Auth. for Nonprofit Corps. Rev. Bonds | | | |

| (Sharp Hlth. Care), 6 1/4s, 8/1/39 | A2 | $20,750,000 | $22,424,318 |

| (St. Rose Hosp.), Ser. A, 6s, 5/15/29 | A– | 5,625,000 | 6,080,569 |

|

| Alameda, Corridor Trans. Auth. Rev. Bonds, | | | |

| Ser. A, AMBAC, zero %, 10/1/19 | A– | 29,270,000 | 19,122,969 |

|

| Anaheim, Pub. Fin. Auth. Rev. Bonds | | | |

| (Elec. Syst. Distr. Fac.), Ser. A, 5 3/8s, 10/1/36 | AA– | 3,000,000 | 3,244,230 |

| (Distr. Syst.), NATL, 5s, 10/1/29 | A+ | 1,945,000 | 1,976,801 |

|

| Arcadia, Unified School Dist. G.O. Bonds | | | |

| (Election of 2006), Ser. A, AGM, zero %, 8/1/18 | AA+ | 1,500,000 | 1,131,720 |

|

| Bay Area Toll Auth. of CA Rev Bonds, Ser. F, | | | |

| 5s, 4/1/31 T | AA | 13,600,000 | 14,190,858 |

|

| Burbank, Pub. Fin. Auth. Rev. Bonds (West Olive | | | |

| Redev.), AMBAC, 5s, 12/1/26 | BBB+ | 3,390,000 | 3,060,899 |

|

| CA Rev. Bonds | | | |

| (Catholic Hlth. Care West), Ser. A, 6s, 7/1/39 | A2 | 10,500,000 | 11,242,560 |

| (Adventist Hlth. Syst.-West), Ser. A, | | | |

| 5 3/4s, 9/1/39 | A | 10,500,000 | 10,980,585 |

|

| CA Edl. Fac. Auth. Rev. Bonds | | | |

| (Claremont Graduate U.), Ser. A, 6s, 3/1/38 | A3 | 1,045,000 | 1,109,842 |

| (CA Lutheran U.), 5 3/4s, 10/1/38 | Baa1 | 5,000,000 | 5,106,550 |

| (U. of the Pacific), 5 1/2s, 11/1/39 | A2 | 1,250,000 | 1,310,500 |

| (U. of the Pacific), 5 1/4s, 11/1/29 | A2 | 1,265,000 | 1,334,714 |

| (Loyola-Marymount U.), Ser. A, 5 1/8s, 10/1/40 | A2 | 2,955,000 | 3,071,752 |

| (U. Redlands), Ser. A, 5 1/8s, 8/1/38 | A3 | 6,430,000 | 6,287,383 |

| (Claremont Graduate U.), Ser. A, 5 1/8s, 3/1/28 | A3 | 1,270,000 | 1,321,575 |

| (U. of The Pacific), 5s, 11/1/36 | A2 | 10,735,000 | 10,844,818 |

| (U. of La Verne), Ser. A, 5s, 6/1/31 | Baa2 | 1,970,000 | 1,810,253 |

| (Chapman U.), 5s, 4/1/31 | A2 | 2,000,000 | 2,048,580 |

| (Claremont Graduate U.), Ser. A, 5s, 3/1/31 | A3 | 2,465,000 | 2,505,722 |

| (U. of the Pacific), 5s, 11/1/30 | A2 | 2,500,000 | 2,536,675 |

| (CA College of Arts), 5s, 6/1/30 | Baa3 | 1,825,000 | 1,638,648 |

| (Lutheran U.), Ser. C, 5s, 10/1/29 | Baa1 | 1,500,000 | 1,492,950 |

| (U. of The Pacific), 5s, 11/1/25 | A2 | 4,000,000 | 4,142,760 |

| (Lutheran U.), Ser. C, 5s, 10/1/24 | Baa1 | 1,250,000 | 1,260,688 |

| (Lutheran U.), Ser. C, 4 1/2s, 10/1/19 | Baa1 | 2,830,000 | 2,863,111 |

|

24

| | | |

| MUNICIPAL BONDS AND NOTES (99.2%)* cont. | Rating** | Principal amount | Value |

|

| California cont. | | | |

| CA Hlth. Fac. Fin. Auth. Rev. Bonds | | | |

| (Providence Hlth. & Svcs.), Ser. C, | | | |

| 6 1/2s, 10/1/38 | Aa2 | $5,400,000 | $6,110,586 |

| (Providence Hlth. & Svcs.), Ser. C, 6 1/2s, | | | |

| 10/1/38 (Prerefunded 10/1/18) | Aa2 | 100,000 | 133,371 |

| (Providence Hlth. & Svcs.), Class C, | | | |

| 6 1/4s, 10/1/28 | Aa2 | 3,350,000 | 3,805,600 |

| (Catholic Hlth. Care West), Ser. J, 5 5/8s, 7/1/32 | A2 | 2,750,000 | 2,833,215 |

| (Sutter Hlth.), Ser. A, 5 1/4s, 11/15/46 | Aa3 | 10,000,000 | 10,120,000 |

| (Stanford Hosp.), Ser. A-2, 5 1/4s, 11/15/40 | Aa3 | 1,000,000 | 1,034,850 |

| (Cedars Sinai Med. Ctr.), 5s, 8/15/39 | A2 | 14,170,000 | 14,105,810 |

| (Cedars-Sinai Med. Ctr.), 5s, 11/15/34 | AAA | 6,250,000 | 6,249,688 |

| (CA-NV Methodist), 5s, 7/1/26 | A– | 1,745,000 | 1,782,483 |

|

| CA Hsg. Fin. Agcy. Rev. Bonds | | | |

| Ser. J, 5 3/4s, 8/1/47 | A | 3,275,000 | 3,272,577 |

| (Home Mtge.), Ser. H, FGIC, 5 3/4s, 8/1/30 | A | 10,000 | 10,017 |

| (Multi-Fam. Hsg. III), Ser. B, NATL, 5 1/2s, 8/1/39 | A3 | 1,650,000 | 1,504,404 |

| (Home Mtge.), Ser. L, 5.2s, 8/1/28 | A | 2,525,000 | 2,453,139 |

| (Home Mtge.), Ser. I, 4 7/8s, 8/1/41 | A | 5,000,000 | 4,204,950 |

| (Home Mtge.), Ser. M, 4 3/4s, 8/1/42 | A | 8,050,000 | 6,479,606 |

| (Home Mtge.), Ser. K, 4 5/8s, 8/1/26 | Baa2 | 2,500,000 | 2,237,700 |

| (Home Mtge.), Ser. I, 4.6s, 8/1/21 | A | 3,310,000 | 3,133,279 |

|

| CA Infrastructure & Econ. Dev. Bank Rev. Bonds | | | |

| (CA Indpt. Syst. Operator), Ser. A, 6 1/4s, 2/1/39 | A1 | 12,000,000 | 12,986,640 |

| (Oakland Unified School Dist. Fin.), 5s, 8/15/22 | A2 | 4,985,000 | 4,993,275 |

|

| CA Muni. Fin. Auth. COP (Cmnty. Hosp. Central CA) | | | |

| 5 1/4s, 2/1/46 | Baa2 | 11,000,000 | 9,276,410 |

| 5 1/4s, 2/1/37 | Baa2 | 14,650,000 | 12,831,642 |

|

| CA Muni. Fin. Auth. Rev. Bonds | | | |

| (U. of La Verne), Ser. A, 6 1/4s, 6/1/40 | Baa2 | 4,000,000 | 4,137,240 |

| (Biola U.), 5 7/8s, 10/1/34 | Baa1 | 11,000,000 | 11,264,660 |

| (Biola U.), 5.8s, 10/1/28 | Baa1 | 220,000 | 228,785 |

| (Eisenhower Med. Ctr.), Ser. A, 5 3/4s, 7/1/40 F52 | Baa1 | 10,500,000 | 10,584,945 |

| (Loma Linda U.), 5s, 4/1/28 | A | 2,000,000 | 2,036,460 |

| (U. Students Coop Assn.), 5s, 4/1/22 | BBB– | 790,000 | 790,743 |

|

| CA Muni. Fin. Auth. Sr. Living Rev. Bonds | | | |

| (Pilgrim Place Claremont), Ser. A, 6 1/8s, 5/15/39 | A– | 4,000,000 | 4,273,880 |

|

| CA Poll. Control Fin. Auth. Rev. Bonds (San Jose | | | |

| Wtr. Co.), 5.1s, 6/1/40 | A | 4,500,000 | 4,610,430 |

|

| CA Poll. Control Fin. Auth. VRDN (Pacific Gas & | | | |

| Electric Corp.) | | | |

| Ser. F, 0.1s, 11/1/26 | A–1+ | 23,800,000 | 23,800,000 |

| Class C, 0.12s, 11/1/26 | A–1+ | 10,600,000 | 10,600,000 |

| Ser. E, 0.1s, 11/1/26 | VMIG1 | 18,900,000 | 18,900,000 |

|

| CA Poll. Control Fin. Auth. Solid Waste Disp. | | | |

| Rev. Bonds (Waste Management, Inc.) | | | |

| Ser. A-2, 5.4s, 4/1/25 | BBB | 7,500,000 | 7,676,700 |

| Ser. B, 5s, 7/1/27 | BBB | 4,500,000 | 4,480,245 |

|

| CA Poll. Control Fin. Auth. Wtr. Fac. Rev. Bonds | | | |

| (American Wtr. Cap. Corp.), 5 1/4s, 8/1/40 | BBB+ | 4,000,000 | 3,929,680 |

|

25

| | | |

| MUNICIPAL BONDS AND NOTES (99.2%)* cont. | Rating** | Principal amount | Value |

|

| California cont. | | | |

| CA State G.O. Bonds | | | |

| 6 1/2s, 4/1/33 | A1 | $43,000,000 | $50,352,570 |

| 5 3/4s, 4/1/31 | A1 | 40,620,000 | 44,329,825 |

|

| CA State Enterprise Auth. Swr. Fac. Rev. Bonds | | | |

| (Anheuser-Busch), 5.3s, 9/1/47 | A– | 2,000,000 | 2,001,820 |

|

| CA State Pub. Wks. Board Rev. Bonds | | | |

| Ser. I-1, 6 1/8s, 11/1/29 | A2 | 3,000,000 | 3,311,850 |

| (Dept. of Ed. — Riverside Campus), Ser. B, | | | |

| 6 1/8s, 4/1/29 | A2 | 490,000 | 537,863 |

| (Dept. of Dev. Svcs. — Porterville), Ser. C, | | | |

| 6s, 4/1/27 | A2 | 575,000 | 637,411 |

| (Dept. of Ed. — Riverside Campus), Ser. B, | | | |

| 6s, 4/1/26 | A2 | 2,625,000 | 2,927,689 |

| (Trustees CA State U.), Ser. D, 6s, 4/1/26 | Aa3 | 1,365,000 | 1,552,455 |

| (Riverside Campus), Ser. B, 6s, 4/1/25 | A2 | 1,755,000 | 1,968,145 |

| (Dept. of Dev. Svcs. — Porterville), Ser. C, | | | |

| 6s, 4/1/24 | A2 | 3,615,000 | 4,049,089 |

| (Dept. of Ed. — Riverside Campus), Ser. B, | | | |

| 6s, 4/1/24 | A2 | 4,485,000 | 5,023,559 |

| Ser. G-1, 5 3/4s, 10/1/30 | A2 | 11,500,000 | 12,077,760 |

| Ser. A-1, 5 1/2s, 3/1/25 | A2 | 2,500,000 | 2,696,850 |

| (Regents U.), Ser. E, 5s, 4/1/29 | Aa2 | 7,015,000 | 7,358,595 |

| (Regents U.), Ser. E, 5s, 4/1/28 | Aa2 | 8,290,000 | 8,766,924 |

|

| CA State Pub. Wks. Board Lease Rev. Bonds | | | |

| Ser. A, NATL, 6 1/2s, 9/1/17 | A2 | 24,580,000 | 27,039,966 |

| (Dept. of Corrections-State Prisons), Ser. A, | | | |

| AMBAC, 5s, 12/1/19 | A2 | 17,250,000 | 18,310,875 |

|

| CA State U. Rev. Bonds (Systemwide), Ser. A, | | | |

| 5 3/4s, 11/1/28 | Aa2 | 5,000,000 | 5,597,800 |

|

| CA Statewide Cmnty. Dev. Auth. COP (The Internext | | | |

| Group), 5 3/8s, 4/1/30 | BBB | 15,300,000 | 13,953,753 |

|

| CA Statewide Cmnty. Dev. Auth. Rev. Bonds | | | |

| (Thomas Jefferson School of Law), Ser. A, | | | |

| 7 1/4s, 10/1/38 | BB+ | 2,415,000 | 2,453,205 |

| (American Baptist Homes West), 6 1/4s, 10/1/39 | BBB | 4,500,000 | 4,508,370 |

| (Sutter Hlth.), Ser. A, 6s, 8/15/42 | Aa3 | 5,000,000 | 5,458,750 |

| (Irvine LLC-UCI East Campus), 6s, 5/15/40 | Baa2 | 11,000,000 | 10,924,760 |

| (American Baptist Homes West), 5 3/4s, 10/1/25 | BBB | 950,000 | 950,589 |

| (Sutter Hlth.), Ser. B, 5 1/4s, 11/15/48 | Aa3 | 2,000,000 | 2,012,080 |

| (Huntington Memorial Hosp.), 5s, 7/1/35 | A+ | 11,175,000 | 10,975,973 |

| (Sr. Living-Presbyterian Homes), Ser. A, | | | |

| 4 7/8s, 11/15/36 | BBB | 1,000,000 | 859,550 |

|

| CA Statewide Cmnty. Dev. Auth. 144A Rev. Bonds | | | |

| (Front Porch Cmntys. & Svcs.), Ser. A, | | | |

| 5 1/8s, 4/1/37 | BBB | 9,500,000 | 7,924,995 |

|

| CA Statewide Cmnty. Dev. Auth. Special | | | |

| Tax Rev. Bonds | | | |

| (Cmnty. Fac. Dist. No. 1-Zone 1C), 7 1/4s, 9/1/30 | BB/P | 2,270,000 | 2,289,295 |

| (Citrus Garden Apt. Project - D1), 5 1/4s, 7/1/22 | BBB | 1,630,000 | 1,616,015 |

| (Cmnty. Fac. Dist. No. 1-Zone 1B), zero %, 9/1/20 | BB/P | 1,110,000 | 536,208 |

|

26

| | | |

| MUNICIPAL BONDS AND NOTES (99.2%)* cont. | Rating** | Principal amount | Value |

|

| California cont. | | | |

| CA Statewide Cmnty., Dev. Auth. Rev. Bonds | | | |

| (Sr. Living — Presbyterian Homes), 7 1/4s, 11/15/41 | BBB | $6,000,000 | $6,463,620 |

| (Enloe Med. Ctr.), 6 1/4s, 8/15/33 | A– | 7,500,000 | 8,110,650 |

| (Enloe Med. Ctr.), 6 1/4s, 8/15/28 | A– | 5,000,000 | 5,542,350 |

| (Catholic Hlth. Care West), Ser. A, 5 1/2s, 7/1/30 | A2 | 9,940,000 | 10,214,443 |

| (Kaiser Permanente), Ser. B, 5 1/4s, 3/1/45 | A+ | 19,000,000 | 19,117,610 |

| Ser. C, 5 1/4s, 8/1/31 | A+ | 7,600,000 | 7,751,696 |

| (Kaiser Permanente), Ser. B, 5s, 3/1/41 | A+ | 1,815,000 | 1,815,617 |

| (Henry Mayo Newhall Memorial Hosp.), 5s, 10/1/27 | A– | 3,685,000 | 3,802,662 |

| (Henry Mayo Newhall Memorial Hosp.), 5s, 10/1/20 | A– | 1,055,000 | 1,138,957 |

|

| CA Statewide Fin. Auth. Tobacco Settlement Rev. | | | |

| Bonds, Class B, 5 5/8s, 5/1/29 | B2 | 2,990,000 | 2,738,601 |

|

| CA Tobacco Securitization Agcy. Rev. Bonds | | | |

| (Sonoma Cnty. Corp.), Ser. B, 5 1/2s, 6/1/30 | | | |

| (Prerefunded 6/1/12) | AAA/F | 3,145,000 | 3,224,348 |

|

| Carlsbad, Unified School Dist. G.O. Bonds, FGIC, | | | |

| NATL, zero %, 11/1/21 | Aa2 | 2,250,000 | 1,418,940 |

|

| Castaic Lake, Wtr. Agcy. COP (Water Syst. Impt.), | | | |

| AMBAC, zero %, 8/1/27 | AA | 10,000,000 | 4,199,100 |

|

| Chino Basin, Desalter Auth. Rev. Bonds, Ser. A, | | | |

| AGO, 5s, 6/1/30 | AA+ | 3,540,000 | 3,740,647 |

|

| Chula Vista, Cmnty. Fac. Dist. Special Tax | | | |

| Rev. Bonds | | | |

| (No. 06-1 Eastlake Woods Area), 6.2s, 9/1/33 | BBB/P | 3,750,000 | 3,771,750 |

| (No. 06-1 Eastlake Woods Area), 6.15s, 9/1/26 | BBB/P | 2,000,000 | 2,040,480 |

| (No. 07-1 Otay Ranch Village Eleven), | | | |

| 5 7/8s, 9/1/34 | BB+/P | 2,335,000 | 2,284,541 |

| (No. 07-I Otay Ranch Village Eleven), 5.1s, 9/1/26 | BB+/P | 340,000 | 322,293 |

|

| Chula Vista, Indl. Dev. Rev. Bonds (San Diego Gas) | | | |

| Ser. C, 5 7/8s, 2/15/34 | Aa3 | 2,600,000 | 2,886,026 |

| Ser. D, 5 7/8s, 1/1/34 | Aa3 | 5,000,000 | 5,550,050 |

|

| Coast, Cmnty. College Dist. G.O. Bonds, NATL | | | |

| zero %, 8/1/22 | Aa1 | 1,280,000 | 745,331 |

| zero %, 8/1/21 | Aa1 | 4,500,000 | 2,794,455 |

|

| Commerce, Redev. Agcy. Rev. Bonds (Project 1), | | | |

| zero %, 8/1/21 (Escrowed to maturity) | AAA/P | 58,200,000 | 34,624,926 |

|

| Compton, Unified School Dist. G.O. Bonds | | | |

| (Election of 2002), Ser. D, AMBAC | | | |

| zero %, 6/1/18 | Aa3 | 7,295,000 | 5,521,221 |

| zero %, 6/1/17 | Aa3 | 7,145,000 | 5,733,362 |

|

| Contra Costa, Home Mtge. Fin. Auth. Rev. Bonds, | | | |

| Ser. G, NATL, zero %, 9/1/17 (Escrowed | | | |

| to maturity) | Aaa | 23,705,000 | 15,425,792 |

|

| Corona, Cmnty. Fac. Dist. Special Tax (No. 97-2 | | | |

| Eagle Glen), Ser. 97-2, 5 3/4s, 9/1/16 | BBB+/P | 2,395,000 | 2,411,813 |

|

| Delano, COP (Delano Regl. Med. Ctr.), 5.6s, 1/1/26 | BBB– | 20,200,000 | 19,581,880 |

|

| Duarte, COP, Ser. A | | | |

| 5 1/4s, 4/1/31 | A1 | 7,000,000 | 6,999,860 |

| 5 1/4s, 4/1/24 | A1 | 7,500,000 | 7,505,400 |

|

27

| | | |

| MUNICIPAL BONDS AND NOTES (99.2%)* cont. | Rating** | Principal amount | Value |

|

| California cont. | | | |

| El Camino, Hosp. Dist. Rev. Bonds, Ser. A, AMBAC, | | | |

| 6 1/4s, 8/15/17 (Escrowed to maturity) | AA/F | $8,510,000 | $9,743,695 |

|

| Folsom Cordova, Unified School Dist. G.O. Bonds | | | |

| (School Fac. Impt. Dist. No. 1), Ser. A, NATL, | | | |

| zero %, 10/1/25 | Aa3 | 1,505,000 | 673,608 |

|

| Foothill-De Anza, Cmnty. College Dist. G.O. | | | |

| Bonds, Ser. C, 5s, 8/1/40 | Aaa | 6,750,000 | 7,270,695 |

|

| Foothill/Eastern Corridor Agcy. Rev. Bonds (CA | | | |

| Toll Roads) | | | |

| 5 3/4s, 1/15/40 | Baa3 | 19,000,000 | 17,439,340 |

| NATL, 5 3/8s, 1/15/14 | Baa1 | 5,000,000 | 5,027,750 |

| Ser. A, 5s, 1/1/35 | Baa3 | 2,000,000 | 1,684,740 |

|

| Golden State Tobacco Securitization Corp. Rev. | | | |

| Bonds | | | |

| Ser. A-4, 7.8s, 6/1/42 (Prerefunded 6/1/13) | Aaa | 6,075,000 | 6,807,341 |

| Ser. 03 A-1, 6 1/4s, 6/1/33 (Prerefunded 6/1/12) | Aaa | 8,760,000 | 9,429,352 |

| Ser. A-1, 5s, 6/1/33 | BB+ | 12,340,000 | 8,654,906 |

| Ser. A, 4.55s, 6/1/22 | AA+ | 4,085,000 | 4,143,375 |

| Ser. A-1, 4 1/2s, 6/1/27 | BBB– | 10,675,000 | 8,339,630 |

| Ser. S-B, zero %, 6/1/47 | B | 24,000,000 | 797,280 |

| Ser. A, AMBAC, zero %, 6/1/24 | A2 | 15,500,000 | 7,789,060 |

|

| Golden West, School Fin. Auth. Rev. Bonds, | | | |

| Ser. A, NATL | | | |

| zero %, 8/1/20 | Baa1 | 2,000,000 | 1,272,660 |

| zero %, 2/1/20 | Baa1 | 2,480,000 | 1,619,068 |

|

| Huntington Beach, Cmnty. Fac. Dist. Special Tax | | | |

| (No. 2003-1 Huntington Ctr.) | | | |

| 5.85s, 9/1/33 | BB+/P | 2,845,000 | 2,793,164 |

| 5.8s, 9/1/23 | BB+/P | 1,000,000 | 1,010,030 |

|

| Imperial Irrigation Elec. Dist. Rev. Bonds | | | |

| Ser. A, 6 1/4s, 11/1/31 | AA– | 1,000,000 | 1,172,240 |

| Ser. A, 5 1/2s, 11/1/41 | AA– | 9,000,000 | 9,825,120 |

| 5 1/8s, 11/1/38 | AA– | 7,000,000 | 7,326,970 |

|

| Irvine Ranch, Wtr. Dist. VRDN, 0.69s, 4/1/33 | VMIG1 | 7,900,000 | 7,900,000 |

|

| Irvine, Impt. Board Act of 1915 G.O. Bonds | | | |

| (Assmt. Dist. No. 03-19-Group 2), 5.45s, 9/2/23 | BBB/P | 935,000 | 943,696 |

|

| Irvine, Impt. Board Act of 1915 Special | | | |

| Assmt. Bonds | | | |

| (Dist. No. 00-18 Group 3), 5.55s, 9/2/26 | BBB+/P | 1,825,000 | 1,828,486 |

| (Dist. No. 04-20), 5s, 9/2/25 | BB–/P | 2,000,000 | 1,960,640 |

| (Dist. No. 04-20), 5s, 9/2/21 | BB–/P | 1,000,000 | 1,020,450 |

| (Dist. No. 04-20), 5s, 9/2/20 | BB–/P | 1,000,000 | 1,029,830 |

| (Dist. No. 04-20), 5s, 9/2/19 | BB–/P | 1,000,000 | 1,032,500 |

| (Dist. No. 04-20), 4 7/8s, 9/2/18 | BB–/P | 1,000,000 | 1,032,540 |

|

| Irvine, Impt. Board Act of 1915 Ltd. Oblig. | | | |

| Special Assmt. Bonds (No. 03-19 Group 4), | | | |

| 5s, 9/2/29 | BB–/P | 665,000 | 595,268 |

|

| Las Virgenes, Unified School Dist. G.O. Bonds | | | |

| Ser. A, AGM, 5s, 8/1/28 | AA+ | 5,245,000 | 5,514,960 |

| AGM, zero %, 11/1/23 | AA+ | 1,395,000 | 763,107 |

|

28

| | | |

| MUNICIPAL BONDS AND NOTES (99.2%)* cont. | Rating** | Principal amount | Value |

|

| California cont. | | | |

| Long Beach, Bond Fin. Auth. Rev. Bonds | | | |

| (Natural Gas), Ser. A, 5 1/2s, 11/15/28 | A | $5,000,000 | $4,950,500 |

|

| Los Angeles, Cmnty. College Dist. G.O. Bonds | | | |

| (Election of 2008), Ser. A, 6s, 8/1/33 | Aa1 | 10,000,000 | 11,556,600 |

|

| Los Angeles, Cmnty. Redev. Agcy. Fin. Auth. Rev. | | | |

| Bonds (Bunker Hill), Ser. A, AGM, 5s, 12/1/27 | AA+ | 16,000,000 | 16,734,720 |

|

| Los Angeles, Dept. Arpt. Rev. Bonds (Los Angeles | | | |

| Intl. Arpt.), Ser. D, 5s, 5/15/40 | AA | 11,500,000 | 12,295,685 |

|

| Los Angeles, Harbor Dept. Rev. Bonds, U.S. Govt. | | | |

| Coll., 7.6s, 10/1/18 (Escrowed to maturity) | AA+ | 14,970,000 | 18,527,770 |

|

| Los Angeles, Unified School Dist. G.O. Bonds | | | |

| Ser. D, 5s, 1/1/34 | Aa2 | 3,865,000 | 4,036,065 |

| Ser. F, 5s, 7/1/29 | Aa2 | 2,000,000 | 2,138,740 |

|

| M-S-R Energy Auth. Rev. Bonds, Ser. A, | | | |

| 6 1/2s, 11/1/39 | A | 5,000,000 | 5,504,200 |

|

| Metro. Wtr. Dist. Rev. Bonds (Southern CA Wtr. | | | |

| Wks.), 5 3/4s, 8/10/18 | AAA | 20,000,000 | 23,865,400 |

|

| Murrieta Valley, Unified School Dist. G.O. Bonds, | | | |

| AGM, zero %, 9/1/31 | AA+ | 6,445,000 | 1,937,560 |

|

| Napa Valley, Cmnty. College Dist. G.O. Bonds | | | |

| (Election of 2002), Ser. C, NATL | | | |

| zero %, 8/1/22 | Aa2 | 5,000 | 2,992 |

| zero %, 8/1/21 | Aa2 | 8,575,000 | 5,448,298 |

|

| North Natomas, Cmnty. Fac. Special Tax Bonds | | | |

| Ser. B, 6 3/8s, 9/1/31 | BBB–/P | 6,150,000 | 6,160,455 |

| (Dist. No. 4), Ser. D, 5s, 9/1/33 | BBB–/P | 3,770,000 | 3,259,994 |

| Ser. D, 5s, 9/1/26 | BBB–/P | 1,710,000 | 1,576,244 |

|

| Oakland, Joint Powers Fin. Auth. VRDN (Fruitvale | | | |

| Transit Village), Ser. B, 0.16s, 7/1/33 | VMIG1 | 1,275,000 | 1,275,000 |

|

| Oakland, Swr. Rev. Bonds, Ser. A, AGM, 5s, 6/15/26 | AA+ | 3,690,000 | 3,836,751 |

|

| Oakland, Unified School Dist. Alameda Cnty., G.O. | | | |

| Bonds (Election of 2006), Ser. A, 6 1/8s, 8/1/29 | A2 | 4,000,000 | 4,331,080 |

|

| Orange Cnty., Cmnty. Fac. Dist. Special | | | |

| Tax Rev. Bonds | | | |

| (Ladera Ranch — No. 03-1), Ser. A, 5 5/8s, 8/15/34 | BBB–/P | 2,750,000 | 2,750,990 |

| (Ladera Ranch No. 02-1), Ser. A, 5.55s, 8/15/33 | BBB–/P | 3,725,000 | 3,637,202 |

| (Ladera Ranch — No. 03-1), Ser. A, 5 1/2s, 8/15/23 | BBB–/P | 1,000,000 | 1,001,850 |

|

| Palomar Pomerado, Hlth. G.O. Bonds (Election | | | |

| of 2004), Ser. A, AGO | | | |

| zero %, 8/1/27 | AA+ | 3,395,000 | 1,369,713 |

| zero %, 8/1/26 | AA+ | 5,000,000 | 2,164,250 |

| zero %, 8/1/24 | AA+ | 5,130,000 | 2,555,253 |

|

| Pico Rivera, Pub. Fin. Auth. Lease Rev. Bonds | | | |

| 5 3/4s, 9/1/39 | A+ | 6,000,000 | 6,258,720 |

| 5 1/2s, 9/1/31 | A+ | 1,000,000 | 1,048,900 |

|

| Placentia, Redev. Auth. Tax Alloc. Rev. Bonds, | | | |

| Ser. B, 5 3/4s, 8/1/32 | BBB+ | 3,000,000 | 2,748,690 |

|

| Poway, Unified School Dist. G.O. Bonds (Election | | | |

| of 2008), zero %, 8/1/29 | Aa2 | 11,350,000 | 4,197,457 |

|

29

| | | |

| MUNICIPAL BONDS AND NOTES (99.2%)* cont. | Rating** | Principal amount | Value |

|

| California cont. | | | |

| Rancho Cordova, Cmnty. Fac. Dist. Special Tax | | | |

| (No. 2003-1 Sunridge Anatolia), 6.1s, 9/1/37 | BB+/P | $1,485,000 | $1,398,558 |

|

| Rancho Mirage, Joint Powers Fin. Auth. Rev. Bonds | | | |

| (Eisenhower Med. Ctr.), Ser. A, 5s, 7/1/47 | Baa1 | 6,000,000 | 5,311,860 |

|

| Redding, Elec. Syst. COP, NATL, 6.368s, 7/1/22 | | | |

| (Escrowed to maturity) | Baa1 | 18,465,000 | 22,446,239 |

|

| Redwood City, Redev. Agcy., TAN (Redev. Area | | | |