UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-03706 | |||||

| AMERICAN CENTURY CALIFORNIA TAX-FREE AND MUNICIPAL FUNDS | ||||||

| (Exact name of registrant as specified in charter) | ||||||

| 4500 MAIN STREET, KANSAS CITY, MISSOURI | 64111 | |||||

| (Address of principal executive offices) | (Zip Code) | |||||

CHARLES A. ETHERINGTON 4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 | ||||||

| (Name and address of agent for service) | ||||||

| Registrant’s telephone number, including area code: | 816-531-5575 | |||||

| Date of fiscal year end: | 08-31 | |||||

| Date of reporting period: | 08-31-2016 | |||||

ITEM 1. REPORTS TO STOCKHOLDERS.

| Annual Report | |

| August 31, 2016 | |

| California Long-Term Tax-Free Fund | |

| Table of Contents |

| President’s Letter | 2 | |

| Performance | 3 | |

| Portfolio Commentary | ||

| Fund Characteristics | ||

| Shareholder Fee Example | ||

| Schedule of Investments | ||

| Statement of Assets and Liabilities | ||

| Statement of Operations | ||

| Statement of Changes in Net Assets | ||

| Notes to Financial Statements | ||

| Financial Highlights | ||

| Report of Independent Registered Public Accounting Firm | ||

| Management | ||

| Approval of Management Agreement | ||

| Proxy Voting Results | ||

| Additional Information | ||

Any opinions expressed in this report reflect those of the author as of the date of the report, and do not necessarily represent the opinions of American Century Investments® or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for comparative indices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

| President’s Letter |

Jonathan Thomas

Jonathan ThomasDear Investor:

Thank you for reviewing this annual report for the period ended August 31, 2016. It provides investment performance and portfolio information for the reporting period, plus longer-term historical performance data.

Annual reports remain important vehicles for conveying information about fund returns, including market factors that affected performance during the reporting period. For additional, updated investment and market insights, we encourage you to visit our website, americancentury.com.

Municipal Bonds (Munis) Generally Extended Their Solid Performance

Key conditions described in our semiannual report letter extended for another six months. Widespread concerns about global economic growth sparked financial market volatility, followed by monetary policy reactions from central banks. The primary catalyst in 2015 was China, where slowing economic growth and currency devaluations sent shock waves through the global markets. These factors re-emerged in January and early February 2016, triggering sell-offs in riskier assets such as stocks and high-yield bonds and encouraging central banks in Japan and Europe to cut interest rates and/or extend their bond-buying (quantitative easing, QE) programs. More QE came after Brexit, the U.K.’s vote to exit the European Union. Monetary policy expansion produced negative interest rates in Japan and Europe, and lowered longer-maturity bond yields globally.

In this bond-friendly environment, munis generally continued to perform well. The broad muni market benefited from its comparatively high overall credit quality, despite defaults in Puerto Rico and financial concerns facing Illinois and New Jersey. We continue to view these as isolated incidents running counter to overall muni credit quality trends. Also, as government bond yields fell globally, after-tax muni yields looked attractive, especially for investors in top tax brackets.

After 12 straight months of positive performance for the broad muni market, we’re positioning muni portfolios for increased volatility (and the possibility of lower returns) after heavy demand compressed the yield differences (spreads) between shorter- and longer-maturity bonds, and higher- and lower-quality bonds. Spreads narrowed to an extent in August 2016 that would indicate a greater chance of widening than narrowing, given the uncertainties ahead, including central bank reviews of their QE programs, the Federal Reserve’s desire to raise interest rates, the fallout from Brexit, and the U.S. presidential election. We appreciate your continued trust in us during this challenging period.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

2

| Performance |

| Total Returns as of August 31, 2016 | ||||||

| Average Annual Returns | ||||||

Ticker Symbol | 1 year | 5 years | 10 years | Since Inception | Inception Date | |

| Investor Class | BCLTX | 7.62% | 5.65% | 4.79% | — | 11/9/83 |

| Bloomberg Barclays Municipal Bond Index | — | 6.88% | 4.80% | 4.87% | — | — |

| Institutional Class | BCLIX | 7.83% | 5.87% | — | 5.82% | 3/1/10 |

| A Class | ALTAX | 9/28/07 | ||||

| No sales charge | 7.35% | 5.39% | — | 4.81% | ||

| With sales charge | 2.53% | 4.42% | — | 4.27% | ||

| C Class | ALTCX | 6.55% | 4.61% | — | 4.03% | 9/28/07 |

Average annual returns since inception are presented when ten years of performance history is not available.

Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 4.50% maximum initial sales charge and may be subject to a maximum CDSC of 1.00%. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Total returns for periods less than one year are not annualized. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. For additional information about the fund, please consult the prospectus.

3

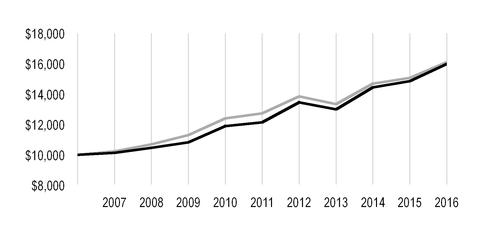

| Growth of $10,000 Over 10 Years |

| $10,000 investment made August 31, 2006 |

| Performance for other share classes will vary due to differences in fee structure. |

| Value on August 31, 2016 | |

| Investor Class — $15,977 | |

| Bloomberg Barclays Municipal Bond Index — $16,093 | |

| Total Annual Fund Operating Expenses | |||

| Investor Class | Institutional Class | A Class | C Class |

| 0.47% | 0.27% | 0.72% | 1.47% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Total returns for periods less than one year are not annualized. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. For additional information about the fund, please consult the prospectus.

4

| Portfolio Commentary |

Portfolio Managers: Joseph Gotelli, Alan Kruss, and Steven Permut

Performance Summary

California Long-Term Tax-Free returned 7.62%* for the 12 months ended August 31, 2016, outperforming the Bloomberg Barclays Municipal Bond Index, which returned 6.88%. Fund returns reflect operating expenses, while index returns do not.

The fund’s absolute return for the reporting period reflected the positive overall performance of municipal bonds (munis) and California and longer-maturity munis in particular. The muni market generally rallied, posting a positive total return in each of the 12 months and outperforming the U.S. Treasury market and the broad taxable investment-grade U.S. fixed-income market for the entire period. In addition to benefiting from a favorable backdrop for U.S. fixed-income securities—which included declining interest rates and muted inflation—munis advanced on stable credit trends, positive flows, and other supportive supply/demand factors.

Favorable Fixed-Income Backdrop, Muni Market Dynamics Fueled Gains

Investor concerns about global growth, commodity prices, and central bank monetary decisions generated volatility during the 12-month period. The U.S. economy continued to exhibit modest growth, particularly compared with the rest of the developed world, but the U.S. Federal Reserve (the Fed) remained focused on the sluggish global landscape and its potential risks to the U.S. economy. This triggered ongoing investor speculation regarding the timing and magnitude of Fed interest rate “normalization” and contributed to the volatile climate. However, the Fed implemented only one rate hike during the period—a 25 basis point increase (1 basis point equals 0.01%) on December 16, 2015, which pushed the range for the federal funds rate target to 0.25%-0.50%.

Despite expectations for additional rate hikes in 2016, the Fed cited concerns about the health of the global economy, the uncertainty triggered by the U.K. vote in late June to exit the European Union (Brexit), and weaker-than-expected U.S. economic growth as reasons to pursue a “lower for longer” rate strategy. Meanwhile, central banks in Europe, Japan, and China continued to implement aggressive stimulus programs in response to weak growth rates and deflation threats in those regions. This action increased the relative attractiveness of the U.S. bond market, where yields were generally higher.

This environment led to positive performance for U.S. Treasuries and other U.S. bond market sectors. Munis generally tracked the U.S. Treasury market, but factors specific to the municipal market helped munis outperform. In particular, supply and demand dynamics remained favorable and supported gains. Overall supply increased only slightly, while demand for munis remained robust due to the tax advantages and perceived “safe-haven” munis offered investors. As of August 31, 2016, muni funds experienced 48 consecutive weeks of positive flows, according to Lipper Inc.

Overall, all major sectors of the muni bond market posted positive returns for the 12-month period, according to Bloomberg Barclays. Reflecting investor demand for yield, longer-maturity and lower-quality munis generally performed better than shorter-maturity and higher-quality securities. In addition, revenue bonds outperformed general obligation (GO) bonds.

* All fund returns referenced in this commentary are for Investor Class shares. Performance for other share classes will vary due to differences in fee structure; when Investor Class performance exceeds that of the fund's benchmark, other share classes may not. See page 3 for returns for all share classes.

5

State and National Fiscal, Credit Backdrops Were Generally Positive

State and local finances in California and across the U.S. remained relatively healthy, even as tax revenue growth slowed due to stock market volatility. Spending restraint enabled most states, including California, to maintain stable credit profiles. Furthermore, California’s job growth outpaced the national average, and the state’s housing market continued to improve. In addition, state officials reported $7.3 billion in reserves at the end of fiscal year 2016 and projected reserves would climb to $8.5 billion by the end of fiscal year 2017. Also, in August 2016, Fitch Ratings upgraded California’s bond credit rating from “A+” to “AA-.”

From a national credit rating perspective, downgrades outpaced upgrades in the second calendar quarter of 2016, largely due to troubled credits in Illinois and Michigan. Overall, the national muni default rate remained low. We continue to believe it is unlikely any states will default, but special circumstances may continue to pressure isolated state, local, and commonwealth credit ratings, such as those in Puerto Rico, Illinois, New Jersey, and Michigan.

Longer Maturity, Longer Duration Drove Outperformance

Our maturity strategy primarily accounted for the portfolio’s outperformance versus the Bloomberg Barclays index. In particular, we maintained a slight flattening bias with respect to the portfolio’s yield-curve positioning, holding more exposure to longer-maturity munis than the index. This strategy aided relative performance as yields on longer-maturity securities declined more than yields on shorter-maturity munis, causing the muni yield curve to flatten. The portfolio’s duration (price sensitivity to interest rate changes), which was slightly longer than the index’s, also lifted performance in this yield environment.

Elsewhere, sector and security selection produced mixed results relative to the index. Overall, our preference for revenue bonds over GO bonds aided results. Within the revenue sector, an overweight position relative to the index in lease revenue bonds aided results, while an underweight position in industrial development revenue bonds detracted. Meanwhile, security selection among special tax and water and sewer bonds aided relative results, while our selections among lease revenue and local GO bonds detracted.

Focus on Yield in Range-Bound Market

We believe U.S. economic fundamentals support slightly higher interest rates. But low inflation, weaker global economic fundamentals, low interest rates in Europe and Japan, weak commodity prices, a strong U.S. dollar, and geopolitical uncertainty (particularly in the wake of the Brexit vote) will, in our view, likely keep Fed action slow and data dependent, and keep rates range-bound in the near term. For this reason, we are comfortable maintaining a slightly longer-than-average duration and a slight bias toward lower-quality credits—two strategies that have helped enhance the portfolio’s yield. We also believe volatility may escalate ahead of the November U.S. presidential election, and such volatility may cause credit spreads (the yield differential between high-quality and low-quality munis of similar maturity) to widen. This potential backdrop may present compelling buying opportunities among lower-quality credits. In this environment, we believe fundamental credit research, active management, and security selection will become increasingly important.

6

| Fund Characteristics |

| AUGUST 31, 2016 | |

| Portfolio at a Glance | |

| Weighted Average Maturity | 17.7 years |

| Average Duration (Modified) | 5.6 years |

| Top Five Sectors | % of fund investments |

| General Obligation (GO) - Local | 16% |

| Hospital | 13% |

| General Obligation (GO) - State | 11% |

| Lease Revenue | 9% |

| Prerefunded | 8% |

| Types of Investments in Portfolio | % of net assets |

| Municipal Securities | 101.9% |

| Other Assets and Liabilities | (1.9)% |

7

| Shareholder Fee Example |

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from March 1, 2016 to August 31, 2016.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or Institutional Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not a financial intermediary or retirement plan account), American Century Investments may charge you a $12.50 semiannual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $12.50 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments Brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments Brokerage accounts, you are currently not subject to this fee. If you are subject to the Account Maintenance Fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

8

| Beginning Account Value 3/1/16 | Ending Account Value 8/31/16 | Expenses Paid During Period(1) 3/1/16 - 8/31/16 | Annualized Expense Ratio(1) | |

| Actual | ||||

| Investor Class | $1,000 | $1,039.60 | $2.41 | 0.47% |

| Institutional Class | $1,000 | $1,040.60 | $1.38 | 0.27% |

| A Class | $1,000 | $1,038.30 | $3.69 | 0.72% |

| C Class | $1,000 | $1,034.40 | $7.52 | 1.47% |

| Hypothetical | ||||

| Investor Class | $1,000 | $1,022.77 | $2.39 | 0.47% |

| Institutional Class | $1,000 | $1,023.78 | $1.37 | 0.27% |

| A Class | $1,000 | $1,021.52 | $3.66 | 0.72% |

| C Class | $1,000 | $1,017.75 | $7.46 | 1.47% |

| (1) | Expenses are equal to the class's annualized expense ratio listed in the table above, multiplied by the average account value over the period, multiplied by 184, the number of days in the most recent fiscal half-year, divided by 366, to reflect the one-half year period. |

9

| Schedule of Investments |

AUGUST 31, 2016

| Principal Amount | Value | |||||

| MUNICIPAL SECURITIES — 101.9% | ||||||

| California — 101.2% | ||||||

| ABAG Finance Authority for Nonprofit Corps. Rev., (Sharp Healthcare Obligated Group), 6.00%, 8/1/30 | $ | 1,000,000 | $ | 1,220,470 | ||

| ABAG Finance Authority for Nonprofit Corps. Rev., (Sharp Healthcare Obligated Group), 6.25%, 8/1/39 | 1,200,000 | 1,387,404 | ||||

| ABAG Finance Authority for Nonprofit Corps. Rev., (Sharp Healthcare Obligated Group), 5.00%, 8/1/43 | 500,000 | 595,015 | ||||

| Alameda Corridor Transportation Authority Rev., 5.00%, 10/1/37 | 1,000,000 | 1,217,600 | ||||

Alameda Corridor Transportation Authority Rev., Capital Appreciation, 0.00%, 10/1/32 (NATL)(1) | 1,000,000 | 623,890 | ||||

Alameda Corridor Transportation Authority Rev., Capital Appreciation, 0.00%, 10/1/35 (NATL)(1) | 3,750,000 | 2,059,575 | ||||

| Alum Rock Union Elementary School District GO, 6.00%, 8/1/39 | 1,000,000 | 1,296,370 | ||||

| Anaheim Public Financing Authority Rev., 5.375%, 10/1/36 | 300,000 | 354,369 | ||||

| Anaheim Public Financing Authority Rev., 5.25%, 10/1/39 | 2,500,000 | 2,769,450 | ||||

| Anaheim Public Financing Authority Rev., 5.00%, 5/1/46 | 2,200,000 | 2,646,094 | ||||

| Bay Area Toll Authority Rev., 5.00%, 4/1/43 | 2,655,000 | 3,207,665 | ||||

| Bay Area Toll Authority Rev., 5.00%, 10/1/54 | 1,500,000 | 1,800,525 | ||||

| Bay Area Toll Authority Rev., VRDN, 1.26%, 9/1/16 | 550,000 | 550,171 | ||||

| Bay Area Toll Authority Rev., VRDN, 1.66%, 9/1/16 | 1,250,000 | 1,263,075 | ||||

| Bay Area Toll Authority Rev., VRDN, 1.81%, 9/1/16 | 500,000 | 509,175 | ||||

| California Educational Facilities Authority Rev., (Chapman University), 5.00%, 4/1/25 | 285,000 | 360,665 | ||||

| California Educational Facilities Authority Rev., (Claremont Mckenna College), 5.00%, 1/1/32 | 750,000 | 947,970 | ||||

| California Educational Facilities Authority Rev., (Harvey Mudd College), 5.25%, 12/1/41 | 2,000,000 | 2,376,500 | ||||

California Educational Facilities Authority Rev., (Santa Clara University), 5.625%, 4/1/18, Prerefunded at 100% of Par(2) | 4,675,000 | 5,044,605 | ||||

| California Educational Facilities Authority Rev., (Santa Clara University), 5.625%, 4/1/37 | 325,000 | 350,308 | ||||

| California Educational Facilities Authority Rev., (University of Redlands), 5.00%, 10/1/36 | 500,000 | 607,350 | ||||

| California Educational Facilities Authority Rev., (University of Redlands), 5.00%, 10/1/37 | 500,000 | 606,875 | ||||

| California Educational Facilities Authority Rev., (University of Redlands), 5.00%, 10/1/38 | 500,000 | 606,400 | ||||

| California Educational Facilities Authority Rev., (University of Southern California), 5.00%, 10/1/39 | 2,000,000 | 2,175,040 | ||||

| California Educational Facilities Authority Rev., (University of the Pacific), 5.00%, 11/1/33 | 500,000 | 616,565 | ||||

California Health Facilities Financing Authority Rev., (Adventist Health System/West Obligated Group), 4.00%, 3/1/22(3) | 1,200,000 | 1,382,220 | ||||

California Health Facilities Financing Authority Rev., (Adventist Health System/West Obligated Group), 4.00%, 3/1/39(3) | 1,385,000 | 1,528,001 | ||||

| California Health Facilities Financing Authority Rev., (Cedars-Sinai Medical Center), 5.00%, 11/15/32 | 400,000 | 500,044 | ||||

| California Health Facilities Financing Authority Rev., (Children's Hospital of Orange County), 6.50%, 11/1/38 (GA: Children's Healthcare of California) | 4,500,000 | 5,299,650 | ||||

10

| Principal Amount | Value | |||||

| California Health Facilities Financing Authority Rev., (Dignity Health Obligated Group), 6.00%, 7/1/39 | $ | 3,400,000 | $ | 3,880,862 | ||

| California Health Facilities Financing Authority Rev., (Lucile Salter Packard Children's Hospital at Stanford Obligated Group), 5.00%, 8/15/43 | 1,000,000 | 1,190,460 | ||||

California Health Facilities Financing Authority Rev., (Lucile Salter Packard Children's Hospital at Stanford Obligated Group), VRDN, 1.45%, 3/15/17, Prerefunded at 100% of Par(2) | 150,000 | 150,744 | ||||

California Health Facilities Financing Authority Rev., (Providence Health & Services Obligated Group), 6.50%, 10/1/18, Prerefunded at 100% of Par(2) | 1,000,000 | 1,123,080 | ||||

| California Health Facilities Financing Authority Rev., (Providence Health & Services Obligated Group), 5.50%, 10/1/39 | 1,000,000 | 1,139,240 | ||||

California Health Facilities Financing Authority Rev., (Providence St. Joseph Health Obligated Group), 5.00%, 10/1/28(3) | 1,180,000 | 1,532,560 | ||||

| California Health Facilities Financing Authority Rev., (Scripps Health Obligated Group), 5.00%, 11/15/19 | 1,000,000 | 1,131,030 | ||||

| California Health Facilities Financing Authority Rev., (St. Joseph Health System Obligated Group), 5.00%, 7/1/37 | 180,000 | 214,072 | ||||

| California Health Facilities Financing Authority Rev., (St. Joseph Health System Obligated Group), 5.75%, 7/1/39 | 1,000,000 | 1,135,060 | ||||

| California Health Facilities Financing Authority Rev., (St. Joseph Health System), VRDN, 0.62%, 9/1/16 (LOC: U.S. Bank N.A.) | 2,500,000 | 2,500,000 | ||||

| California Health Facilities Financing Authority Rev., (Stanford Health Care Obligated Group), 5.00%, 8/15/51 | 500,000 | 588,115 | ||||

| California Health Facilities Financing Authority Rev., (Sutter Health Obligated Group), 6.00%, 8/15/42 | 1,500,000 | 1,795,965 | ||||

| California Health Facilities Financing Authority Rev., (Sutter Health Obligated Group), 5.00%, 8/15/43 | 720,000 | 870,041 | ||||

| California Health Facilities Financing Authority Rev., (Sutter Health Obligated Group), 5.00%, 11/15/46 | 2,000,000 | 2,454,940 | ||||

| California Health Facilities Financing Authority Rev., (Sutter Health Obligated Group), 5.25%, 11/15/46 | 1,500,000 | 1,513,995 | ||||

| California Health Facilities Financing Authority Rev., (Sutter Health Obligated Group), 5.00%, 8/15/52 | 1,500,000 | 1,774,755 | ||||

| California Infrastructure & Economic Development Bank Rev., (Academy of Motion Picture Arts and Sciences Obligated Group), 5.00%, 11/1/41 | 740,000 | 889,709 | ||||

| California Infrastructure & Economic Development Bank Rev., (Colburn School), VRDN, 1.56%, 9/1/16 | 935,000 | 941,461 | ||||

| California Infrastructure & Economic Development Bank Rev., (Museum Associates), VRDN, 2.11%, 9/1/16 | 1,000,000 | 1,020,460 | ||||

| California Infrastructure & Economic Development Bank Rev., (Pacific Gas & Electric Co.), VRDN, 0.63%, 9/1/16 (LOC: Union Bank N.A.) | 1,800,000 | 1,800,000 | ||||

| California Infrastructure & Economic Development Bank Rev., (Walt Disney Family Museum LLC), 5.00%, 2/1/30 (GA: Walt & Lilly Disney Foundation) | 550,000 | 694,204 | ||||

| California Infrastructure & Economic Development Bank Rev., (Walt Disney Family Museum LLC), 4.00%, 2/1/32 (GA: Walt & Lilly Disney Foundation) | 900,000 | 1,025,595 | ||||

California Municipal Finance Authority Rev., (Azusa Pacific University), 8.00%, 4/1/21, Prerefunded at 100% of Par(2) | 665,000 | 873,378 | ||||

| California Municipal Finance Authority Rev., (Azusa Pacific University), 5.00%, 4/1/41 | 500,000 | 580,680 | ||||

| California Municipal Finance Authority Rev., (Community Hospitals of Central California Obligated Group), 5.00%, 2/1/40 | 1,420,000 | 1,667,307 | ||||

| California Municipal Finance Authority Rev., (Community Hospitals of Central California Obligated Group), 5.00%, 2/1/46 | 1,000,000 | 1,164,330 | ||||

11

| Principal Amount | Value | |||||

| California Municipal Finance Authority Rev., (Emerson College), 6.00%, 1/1/42 | $ | 2,000,000 | $ | 2,416,240 | ||

| California Municipal Finance Authority Rev., (Northbay Healthcare Group Obligated Group), 5.00%, 11/1/26 | 790,000 | 978,044 | ||||

| California Municipal Finance Authority Rev., (Terwilliger Plaza, Inc.), 5.00%, 6/1/46 | 500,000 | 574,880 | ||||

| California Municipal Finance Authority Rev., (Touro College and University System Obligated Group), 5.25%, 1/1/34 | 300,000 | 341,778 | ||||

| California Municipal Finance Authority Rev., (Touro College and University System Obligated Group), 5.25%, 1/1/40 | 1,000,000 | 1,131,860 | ||||

| California Municipal Finance Authority Rev., (University of La Verne), 6.25%, 6/1/40 | 1,000,000 | 1,161,690 | ||||

California Pollution Control Financing Authority Rev., 5.00%, 11/21/45(4) | 1,000,000 | 1,028,590 | ||||

California School Finance Authority Rev., (Aspire Public Schools Obligated Group), 5.00%, 8/1/46(4) | 250,000 | 287,030 | ||||

California State Public Works Board Rev., 5.00%, 9/1/22, Prerefunded at 100% of Par(2) | 500,000 | 615,260 | ||||

California State Public Works Board Rev., 5.00%, 9/1/23, Prerefunded at 100% of Par(2) | 1,865,000 | 2,356,838 | ||||

| California State Public Works Board Rev., 5.25%, 12/1/26 | 1,000,000 | 1,204,460 | ||||

| California State Public Works Board Rev., 5.75%, 11/1/29 | 1,685,000 | 1,938,879 | ||||

| California State Public Works Board Rev., 5.75%, 10/1/30 | 2,000,000 | 2,289,860 | ||||

| California State Public Works Board Rev., 5.00%, 4/1/37 | 2,170,000 | 2,553,656 | ||||

| California State Public Works Board Rev., 5.00%, 11/1/38 | 1,500,000 | 1,823,595 | ||||

California State University Rev., 5.25%, 5/1/19, Prerefunded at 100% of Par(2) | 2,230,000 | 2,509,486 | ||||

| California State University Rev., 5.00%, 11/1/19 | 1,000,000 | 1,135,880 | ||||

| California State University Rev., 4.00%, 11/1/45 | 1,005,000 | 1,134,635 | ||||

| California Statewide Communities Development Authority Rev., (Adventist Health System/West Obligated Group), 5.00%, 3/1/35 | 715,000 | 879,243 | ||||

| California Statewide Communities Development Authority Rev., (American Baptist Homes of the West Obligated Group), 5.00%, 10/1/45 | 600,000 | 703,896 | ||||

| California Statewide Communities Development Authority Rev., (CHF-Irvine LLC), 5.00%, 5/15/40 | 1,200,000 | 1,457,076 | ||||

| California Statewide Communities Development Authority Rev., (Collis P and Howard Huntington Memorial Hospital Obligated Group), 5.00%, 7/1/34 | 500,000 | 594,475 | ||||

| California Statewide Communities Development Authority Rev., (Collis P and Howard Huntington Memorial Hospital Obligated Group), 5.00%, 7/1/44 | 1,300,000 | 1,534,429 | ||||

| California Statewide Communities Development Authority Rev., (Cottage Health System Obligated Group), 5.25%, 11/1/30 | 1,000,000 | 1,151,120 | ||||

| California Statewide Communities Development Authority Rev., (Henry Mayo Newhall Memorial Hospital), 5.25%, 10/1/43 (AGM) | 750,000 | 901,612 | ||||

| California Statewide Communities Development Authority Rev., (Kaiser Credit Group), 5.00%, 4/1/42 | 2,780,000 | 3,242,453 | ||||

| California Statewide Communities Development Authority Rev., (Trinity Health Corp. Obligated Group), 5.00%, 12/1/41 | 500,000 | 589,405 | ||||

| Carson Redevelopment Agency Successor Agency Tax Allocation, 5.00%, 10/1/19 (AGM) | 485,000 | 545,407 | ||||

| Carson Redevelopment Agency Successor Agency Tax Allocation, 5.00%, 10/1/20 (AGM) | 785,000 | 901,141 | ||||

| Cathedral City Redevelopment Agency Successor Agency Tax Allocation, 5.00%, 8/1/28 (AGM) | 1,190,000 | 1,451,217 | ||||

| City & County of San Francisco COP, 5.00%, 4/1/29 | 1,170,000 | 1,291,504 | ||||

12

| Principal Amount | Value | |||||

Contra Costa Water District Rev., 3.00%, 10/1/21(3) | $ | 1,750,000 | $ | 1,925,350 | ||

| Del Mar Race Track Authority Rev., 5.00%, 10/1/35 | 660,000 | 749,595 | ||||

Foothill-Eastern Transportation Corridor Agency Rev., Capital Appreciation, 0.00%, 1/15/24(5) | 700,000 | 626,780 | ||||

Foothill-Eastern Transportation Corridor Agency Rev., Capital Appreciation, 0.00%, 1/15/33(1) | 750,000 | 415,838 | ||||

Foothill-Eastern Transportation Corridor Agency Rev., Capital Appreciation, 0.00%, 1/15/42(1) | 1,250,000 | 478,138 | ||||

| Foothill-Eastern Transportation Corridor Agency Rev., 6.50%, 1/15/43 | 500,000 | 611,620 | ||||

| Foothill-Eastern Transportation Corridor Agency Rev., 5.75%, 1/15/46 | 1,000,000 | 1,198,180 | ||||

| Foothill-Eastern Transportation Corridor Agency Rev., 6.00%, 1/15/49 | 3,250,000 | 3,940,722 | ||||

| Foothill-Eastern Transportation Corridor Agency Rev., VRDN, 5.50%, 1/15/23 | 1,000,000 | 1,195,010 | ||||

Golden State Tobacco Securitization Corp. Rev., Capital Appreciation, 0.00%, 6/1/25 (AGM)(1) | 1,000,000 | 852,850 | ||||

| Golden State Tobacco Securitization Corp. Rev., 4.50%, 6/1/27 | 445,000 | 452,116 | ||||

| Golden State Tobacco Securitization Corp. Rev., 5.00%, 6/1/33 | 750,000 | 757,387 | ||||

| Grossmont Union High School District GO, 5.00%, 8/1/43 | 1,000,000 | 1,212,290 | ||||

| Hayward Area Recreation and Park District COP, 5.125%, 1/1/39 | 1,000,000 | 1,184,050 | ||||

| Inland Valley Development Agency Tax Allocation, 5.25%, 9/1/37 | 555,000 | 664,241 | ||||

| Inland Valley Development Agency Tax Allocation, 5.00%, 9/1/44 | 590,000 | 687,675 | ||||

| Irvine Rev., VRDN, 0.58%, 9/1/16 (LOC: State Street Bank & Trust Co.) | 800,000 | 800,000 | ||||

| Irvine Special Assessment, 4.00%, 9/2/17 | 365,000 | 376,702 | ||||

| Irvine Special Assessment, 4.00%, 9/2/18 | 375,000 | 398,070 | ||||

| Irvine Special Assessment, 4.00%, 9/2/19 | 600,000 | 653,664 | ||||

| Irvine Special Assessment, 5.00%, 9/2/26 | 1,000,000 | 1,279,070 | ||||

| Irvine Special Assessment, VRDN, 0.58%, 9/1/16 (LOC: U.S. Bank N.A.) | 900,000 | 900,000 | ||||

| Irvine Special Tax, 5.00%, 9/1/49 | 1,000,000 | 1,146,760 | ||||

| Kaweah Delta Health Care District Rev., 4.00%, 6/1/45 | 1,250,000 | 1,339,062 | ||||

| La Verne COP, (Brethren Hillcrest Homes), 5.00%, 5/15/29 | 635,000 | 723,925 | ||||

| Live Oak Elementary School District/Santa Cruz County COP, 5.00%, 8/1/39 (AGM) | 1,850,000 | 2,246,695 | ||||

| Long Beach Bond Finance Authority Rev., 5.00%, 11/15/35 (GA: Merrill Lynch & Co.) | 330,000 | 432,062 | ||||

| Long Beach Bond Finance Authority Rev., 5.50%, 11/15/37 (GA: Merrill Lynch & Co.) | 695,000 | 954,110 | ||||

| Long Beach Marina System Rev., 5.00%, 5/15/40 | 1,250,000 | 1,452,712 | ||||

Los Alamitos Unified School District COP, Capital Appreciation, 0.00%, 8/1/24(5) | 1,100,000 | 1,002,551 | ||||

Los Angeles Community College District GO, 5.00%, 8/1/17, Prerefunded at 100% of Par (NATL)(2) | 1,425,000 | 1,484,280 | ||||

| Los Angeles Community College District GO, 2.00%, 8/1/22 | 450,000 | 476,591 | ||||

| Los Angeles County Regional Financing Authority Rev., (MonteCedro, Inc.), 3.00%, 11/15/21 (California Mortgage Insurance) | 245,000 | 245,480 | ||||

| Los Angeles County Sanitation Districts Financing Authority Rev., 5.00%, 10/1/35 | 1,500,000 | 1,852,410 | ||||

Los Angeles Department of Airports Rev., 5.25%, 5/15/18, Prerefunded at 100% of Par(2) | 2,120,000 | 2,288,434 | ||||

13

| Principal Amount | Value | |||||

| Los Angeles Department of Airports Rev., 5.00%, 5/15/40 | $ | 1,000,000 | $ | 1,136,890 | ||

| Los Angeles Department of Airports Rev., 5.00%, 5/15/40 | 2,000,000 | 2,270,660 | ||||

| Los Angeles Department of Water & Power Rev., 5.00%, 7/1/19 | 1,000,000 | 1,122,520 | ||||

| Los Angeles Department of Water & Power Rev., 5.25%, 7/1/38 | 4,000,000 | 4,324,440 | ||||

| Los Angeles Department of Water & Power Rev., VRDN, 0.54%, 9/1/16 (SBBPA: Citibank N.A.) | 2,900,000 | 2,900,000 | ||||

| Los Angeles Department of Water & Power Rev., VRDN, 0.54%, 9/1/16 (SBBPA: Citibank N.A.) | 5,000,000 | 5,000,000 | ||||

| Los Angeles Unified School District GO, 4.00%, 7/1/17 | 1,000,000 | 1,029,570 | ||||

Los Angeles Unified School District GO, 5.00%, 7/1/17, Prerefunded at 100% of Par (AGM)(2) | 1,020,000 | 1,058,597 | ||||

| Los Angeles Unified School District GO, 5.00%, 7/1/18 | 1,280,000 | 1,384,243 | ||||

| Los Angeles Unified School District GO, 5.00%, 7/1/18 | 2,000,000 | 2,162,880 | ||||

| Los Angeles Unified School District GO, 5.25%, 7/1/26 | 1,000,000 | 1,156,980 | ||||

| Los Angeles Unified School District GO, 5.00%, 7/1/29 | 2,000,000 | 2,238,740 | ||||

| Los Angeles Unified School District GO, 5.00%, 7/1/30 | 690,000 | 861,486 | ||||

| M-S-R Energy Authority Rev., 7.00%, 11/1/34 (GA: Citigroup, Inc.) | 1,000,000 | 1,533,080 | ||||

| M-S-R Energy Authority Rev., 7.00%, 11/1/34 (GA: Citigroup, Inc.) | 880,000 | 1,349,110 | ||||

| M-S-R Energy Authority Rev., 6.50%, 11/1/39 (GA: Citigroup, Inc.) | 425,000 | 634,138 | ||||

Manhattan Beach Unified School District GO, Capital Appreciation, 0.00%, 9/1/29(1) | 5,905,000 | 4,251,423 | ||||

| Modesto Irrigation District COP, 5.75%, 10/1/34 | 2,500,000 | 2,795,100 | ||||

| Mount San Antonio Community College District GO, 5.00%, 8/1/34 | 1,000,000 | 1,220,310 | ||||

| Municipal Improvement Corp. of Los Angeles Rev., 4.00%, 11/1/34 | 600,000 | 677,466 | ||||

| Municipal Improvement Corp. of Los Angeles Rev., 4.00%, 11/1/35 | 750,000 | 841,117 | ||||

| New Haven Unified School District GO, 12.00%, 8/1/18 (AGM) | 880,000 | 1,069,077 | ||||

| New Haven Unified School District GO, 5.00%, 8/1/45 | 1,500,000 | 1,831,560 | ||||

Newport Beach Rev., (Hoag Memorial Hospital/Newport Healthcare Obligated Group), 6.00%, 12/1/21, Prerefunded at 100% of Par(2) | 1,000,000 | 1,259,850 | ||||

| North Lake Tahoe Public Financing Authority Rev., 5.00%, 12/1/21 | 500,000 | 601,795 | ||||

| Oakland Unified School District/Alameda County GO, 5.50%, 8/1/32 | 1,000,000 | 1,219,270 | ||||

| Oakland Unified School District/Alameda County GO, 6.625%, 8/1/38 | 460,000 | 579,968 | ||||

| Oakland Unified School District/Alameda County GO, 5.00%, 8/1/40 | 450,000 | 548,249 | ||||

| Ontario Public Financing Authority Rev., 5.00%, 7/1/43 | 1,000,000 | 1,209,870 | ||||

| Orange County Community Facilities District Special Tax, 5.00%, 8/15/35 | 1,000,000 | 1,186,150 | ||||

| Orange County Sanitation District Rev., 4.00%, 11/15/16 | 2,000,000 | 2,012,000 | ||||

| Orange County Transportation Authority Rev., 5.00%, 8/15/25 | 1,000,000 | 1,238,570 | ||||

| Oxnard Financing Authority Rev., 5.00%, 6/1/32 (AGM) | 1,500,000 | 1,810,770 | ||||

| Oxnard Financing Authority Rev., 5.00%, 6/1/33 (AGM) | 1,000,000 | 1,203,210 | ||||

Oxnard School District GO, 3.00%, 8/1/40 (AGM)(5) | 700,000 | 749,616 | ||||

| Palomar Health COP, 6.75%, 11/1/39 | 500,000 | 558,780 | ||||

| Palomar Health COP, 6.00%, 11/1/41 | 750,000 | 807,150 | ||||

Palomar Health GO, Capital Appreciation, 0.00%, 8/1/19 (AGC)(5) | 1,670,000 | 2,059,310 | ||||

Palos Verdes Peninsula Unified School District GO, 0.00%, 8/1/33(1) | 2,600,000 | 1,685,138 | ||||

Paramount Unified School District GO, Capital Appreciation, 0.00%, 8/1/51 (BAM)(1) | 7,500,000 | 870,225 | ||||

Pomona Public Financing Authority Rev., 4.00%, 6/1/36 (AGM)(3) | 1,045,000 | 1,170,985 | ||||

| Pomona Unified School District GO, 6.55%, 8/1/29 (NATL) | 1,000,000 | 1,370,660 | ||||

14

| Principal Amount | Value | |||||

| Pomona Unified School District GO, 6.15%, 8/1/30 (NATL) | $ | 855,000 | $ | 1,065,963 | ||

| Port of Los Angeles Rev., 5.00%, 8/1/27 | 500,000 | 560,125 | ||||

| Porterville Public Financing Authority Rev., 5.625%, 10/1/36 | 1,500,000 | 1,800,105 | ||||

Poway Unified School District GO, Capital Appreciation, 0.00%, 8/1/41(1) | 2,110,000 | 982,564 | ||||

| Poway Unified School District Rev., 7.875%, 9/15/39 | 1,010,000 | 1,178,286 | ||||

| Riverside County Asset Leasing Corp. Rev., 5.00%, 11/1/43 | 1,000,000 | 1,168,790 | ||||

| Riverside County Redevelopment Successor Agency Tax Allocation, 6.50%, 10/1/40 | 625,000 | 750,994 | ||||

Riverside County Transportation Commission Rev., Capital Appreciation, 0.00%, 6/1/31(1) | 1,555,000 | 893,114 | ||||

| Riverside Sewer Rev., 5.00%, 8/1/40 | 500,000 | 603,785 | ||||

| Sacramento County Airport System Rev., 5.625%, 7/1/29 | 1,000,000 | 1,086,380 | ||||

| Sacramento County Sanitation Districts Financing Authority Rev., VRN, 0.98%, 9/1/16 (NATL) | 1,500,000 | 1,424,025 | ||||

| Sacramento Municipal Utility District Rev., 5.00%, 8/15/28 | 1,050,000 | 1,413,846 | ||||

| Sacramento Redevelopment Agency Successor Agency Tax Allocation, 5.00%, 12/1/34 (BAM) | 385,000 | 465,450 | ||||

| Saddleback Valley Unified School District Public Financing Authority Special Tax, 6.00%, 9/1/16 (AGM) | 1,000,000 | 1,000,000 | ||||

San Bernardino Community College District GO, Capital Appreciation, 0.00%, 8/1/19(5) | 7,400,000 | 8,276,826 | ||||

| San Buenaventura Rev., (Community Memorial Health System), 7.50%, 12/1/41 | 1,350,000 | 1,680,480 | ||||

| San Diego County Rev., (Sanford Burnham Prebys Medical Discovery Institute), 5.00%, 11/1/25 | 275,000 | 353,018 | ||||

| San Diego County Rev., (Sanford Burnham Prebys Medical Discovery Institute), 5.00%, 11/1/26 | 850,000 | 1,083,682 | ||||

| San Diego County Rev., (Sanford Burnham Prebys Medical Discovery Institute), 5.00%, 11/1/30 | 225,000 | 280,526 | ||||

| San Diego County Regional Airport Authority Rev., 5.00%, 7/1/40 | 1,500,000 | 1,701,735 | ||||

| San Diego County Regional Airport Authority Rev., 5.00%, 7/1/43 | 1,000,000 | 1,168,420 | ||||

| San Diego Public Facilities Financing Authority Rev., 5.00%, 10/15/44 | 1,300,000 | 1,593,306 | ||||

San Diego Public Facilities Financing Authority Sewer Rev., 5.25%, 5/15/19, Prerefunded at 100% of Par(2) | 2,000,000 | 2,249,200 | ||||

| San Diego Public Facilities Financing Authority Water Rev., 5.00%, 8/1/30 | 2,000,000 | 2,427,600 | ||||

| San Diego Unified Port District Rev., 5.00%, 9/1/24 | 500,000 | 613,260 | ||||

San Diego Unified School District GO, Capital Appreciation, 0.00%, 7/1/44(1) | 2,880,000 | 1,188,634 | ||||

San Diego Unified School District GO, Capital Appreciation, 0.00%, 7/1/49(1) | 1,000,000 | 346,410 | ||||

| San Francisco City & County Airport Comm-San Francisco International Airport Rev., 5.25%, 5/1/23 | 3,000,000 | 3,354,330 | ||||

| San Francisco City & County Airport Comm-San Francisco International Airport Rev., 5.00%, 5/1/40 | 2,150,000 | 2,430,897 | ||||

San Francisco City & County Redevelopment Agency Tax Allocation, 6.625%, 2/1/21, Prerefunded at 100% of Par(2) | 500,000 | 625,800 | ||||

| San Francisco City & County Redevelopment Agency Tax Allocation, 5.00%, 8/1/31 | 400,000 | 479,996 | ||||

| San Francisco City & County Redevelopment Agency Tax Allocation, 5.00%, 8/1/43 | 500,000 | 588,875 | ||||

| San Francisco Public Utilities Commission Water Rev., 5.00%, 11/1/41 | 1,000,000 | 1,174,810 | ||||

15

| Principal Amount | Value | |||||

| San Francisco Public Utilities Commission Water Rev., 5.00%, 11/1/45 | $ | 1,000,000 | $ | 1,214,530 | ||

| San Joaquin Hills Transportation Corridor Agency Rev., 5.00%, 1/15/34 | 1,000,000 | 1,175,380 | ||||

| San Joaquin Hills Transportation Corridor Agency Rev., 5.00%, 1/15/44 | 1,000,000 | 1,167,210 | ||||

| San Joaquin Hills Transportation Corridor Agency Rev., 5.25%, 1/15/44 | 1,000,000 | 1,129,110 | ||||

| San Mateo Special Tax, 5.875%, 9/1/32 | 685,000 | 809,923 | ||||

| San Mateo Special Tax, 5.50%, 9/1/44 | 750,000 | 856,380 | ||||

| Santa Clara Electric Rev., 5.00%, 7/1/30 | 500,000 | 583,065 | ||||

| Santa Cruz County Redevelopment Agency Tax Allocation, 5.00%, 9/1/35 (AGM) | 1,500,000 | 1,831,650 | ||||

| Santa Monica Redevelopment Agency Tax Allocation, 5.00%, 7/1/42 | 400,000 | 464,016 | ||||

| Santa Monica Redevelopment Agency Tax Allocation, 5.875%, 7/1/42 | 400,000 | 481,080 | ||||

Santa Rosa Wastewater Rev., Capital Appreciation, 0.00%, 9/1/24 (Ambac)(1) | 2,000,000 | 1,732,180 | ||||

| Silicon Valley Clean Water Rev., 5.00%, 8/1/45 | 1,205,000 | 1,484,488 | ||||

| Sonoma Community Development Agency Successor Agency Tax Allocation, 5.00%, 6/1/33 (NATL) | 1,325,000 | 1,634,520 | ||||

| South Placer Wastewater Authority Rev., VRN, 0.89%, 9/1/16 | 1,650,000 | 1,643,730 | ||||

| Southern California Public Power Authority Rev., 5.00%, 7/1/17 | 1,050,000 | 1,089,322 | ||||

Southwestern Community College District GO, Capital Appreciation, 0.00%, 8/1/46(1) | 5,000,000 | 1,836,550 | ||||

| State of California GO, 5.00%, 2/1/27 | 3,000,000 | 3,678,600 | ||||

| State of California GO, 5.00%, 2/1/28 | 1,000,000 | 1,223,960 | ||||

| State of California GO, 5.00%, 3/1/28 | 2,000,000 | 2,532,980 | ||||

State of California GO, 5.00%, 9/1/30(3) | 2,000,000 | 2,550,100 | ||||

| State of California GO, 5.25%, 9/1/32 | 2,000,000 | 2,399,480 | ||||

| State of California GO, 6.50%, 4/1/33 | 5,000,000 | 5,738,000 | ||||

| State of California GO, 5.00%, 4/1/38 | 2,500,000 | 2,663,625 | ||||

| State of California GO, 6.00%, 4/1/38 | 2,500,000 | 2,833,625 | ||||

| State of California GO, 6.00%, 11/1/39 | 5,000,000 | 5,807,050 | ||||

| State of California GO, 5.50%, 3/1/40 | 3,000,000 | 3,448,650 | ||||

| State of California GO, 5.00%, 10/1/41 | 2,000,000 | 2,373,680 | ||||

| State of California GO, 5.00%, 8/1/45 | 2,795,000 | 3,474,045 | ||||

| State of California GO, VRN, 1.46%, 9/1/16 | 2,000,000 | 2,010,000 | ||||

| State of California GO, VRN, 1.56%, 9/1/16 | 800,000 | 806,024 | ||||

| State of California GO, VRN, 1.71%, 9/1/16 | 960,000 | 973,651 | ||||

| State of California Department of Water Resources Power Supply Rev., 5.00%, 5/1/18 | 2,000,000 | 2,147,220 | ||||

| State of California Department of Water Resources Power Supply Rev., 5.00%, 5/1/21 | 715,000 | 766,845 | ||||

| Stockton Public Financing Authority Rev., 5.00%, 9/1/27 (BAM) | 1,000,000 | 1,242,480 | ||||

| Stockton Public Financing Authority Rev., 6.25%, 10/1/40 | 750,000 | 948,765 | ||||

| Stockton Unified School District GO, 5.00%, 8/1/29 | 3,485,000 | 4,358,167 | ||||

| Stockton Unified School District GO, 5.00%, 8/1/31 | 1,000,000 | 1,235,040 | ||||

| Stockton Unified School District GO, 5.00%, 8/1/42 (AGM) | 430,000 | 511,872 | ||||

| Susanville Public Financing Authority Rev., 6.00%, 6/1/45 | 1,000,000 | 1,107,510 | ||||

Sutter Union High School District GO, Capital Appreciation, 0.00%, 8/1/49 (BAM)(1) | 2,225,000 | 605,534 | ||||

16

| Principal Amount | Value | |||||

| Sweetwater Union High School District GO, 4.00%, 8/1/42 | $ | 1,205,000 | $ | 1,347,214 | ||

| Tobacco Securitization Authority of Southern California Rev., (San Diego County Tobacco Asset Securitization Corp.), 5.00%, 6/1/37 | 500,000 | 500,040 | ||||

| Tuolumne Wind Project Authority Rev., 5.625%, 1/1/29 | 1,200,000 | 1,329,732 | ||||

| Tustin Unified School District Special Tax, 6.00%, 9/1/40 | 2,000,000 | 2,321,660 | ||||

| University of California Rev., 5.00%, 5/15/25 | 1,000,000 | 1,245,570 | ||||

| University of California Rev., VRDN, 5.00%, 5/15/23 | 2,000,000 | 2,499,220 | ||||

Ventura County Community College District GO, 5.50%, 8/1/18, Prerefunded at 100% of Par(2) | 3,000,000 | 3,284,340 | ||||

| Victor Valley Community College District GO, 4.00%, 8/1/44 | 3,350,000 | 3,785,734 | ||||

| West Contra Costa Unified School District GO, 4.00%, 8/1/46 | 1,000,000 | 1,113,290 | ||||

Yosemite Community College District GO, Capital Appreciation, 0.00%, 8/1/38(1) | 3,000,000 | 1,577,310 | ||||

| 359,861,475 | ||||||

| Guam — 0.7% | ||||||

| Guam Government Power Authority Rev., 5.50%, 10/1/40 | 2,150,000 | 2,411,290 | ||||

TOTAL INVESTMENT SECURITIES — 101.9% (Cost $319,111,290) | 362,272,765 | |||||

| OTHER ASSETS AND LIABILITIES — (1.9)% | (6,690,001) | |||||

| TOTAL NET ASSETS — 100.0% | $ | 355,582,764 | ||||

| NOTES TO SCHEDULE OF INVESTMENTS | ||

| AGC | - | Assured Guaranty Corporation |

| AGM | - | Assured Guaranty Municipal Corporation |

| BAM | - | Build America Mutual Assurance Company |

| COP | - | Certificates of Participation |

| GA | - | Guaranty Agreement |

| GO | - | General Obligation |

| LOC | - | Letter of Credit |

| NATL | - | National Public Finance Guarantee Corporation |

| SBBPA | - | Standby Bond Purchase Agreement |

| VRDN | - | Variable Rate Demand Note. Interest reset date is indicated. Rate shown is effective at the period end. |

| VRN | - | Variable Rate Note. Interest reset date is indicated. Rate shown is effective at the period end. |

| (1) | Security is a zero-coupon bond. Zero-coupon securities are issued at a substantial discount from their value at maturity. |

| (2) | Escrowed to maturity in U.S. government securities or state and local government securities. |

| (3) | When-issued security. The issue price and yield are fixed on the date of the commitment, but payment and delivery are scheduled for a future date. |

| (4) | Security was purchased pursuant to Rule 144A under the Securities Act of 1933 and may be sold in transactions exempt from registration, normally to qualified institutional investors. The aggregate value of these securities at the period end was $1,315,620, which represented 0.4% of total net assets. |

| (5) | Coupon rate adjusts periodically based upon a predetermined schedule. Interest reset date is indicated. Rate shown is effective at the period end. |

See Notes to Financial Statements.

17

| Statement of Assets and Liabilities |

| AUGUST 31, 2016 | |||

| Assets | |||

| Investment securities, at value (cost of $319,111,290) | $ | 362,272,765 | |

| Cash | 167,738 | ||

| Receivable for capital shares sold | 60,144 | ||

| Interest receivable | 3,664,894 | ||

| 366,165,541 | |||

| Liabilities | |||

| Payable for investments purchased | 10,067,163 | ||

| Payable for capital shares redeemed | 167,600 | ||

| Accrued management fees | 139,100 | ||

| Distribution and service fees payable | 7,301 | ||

| Dividends payable | 201,613 | ||

| 10,582,777 | |||

| Net Assets | $ | 355,582,764 | |

| Net Assets Consist of: | |||

| Capital paid in | $ | 311,118,908 | |

| Undistributed net investment income | 639 | ||

| Undistributed net realized gain | 1,301,742 | ||

| Net unrealized appreciation | 43,161,475 | ||

| $ | 355,582,764 | ||

| Net Assets | Shares Outstanding | Net Asset Value Per Share | ||||

| Investor Class | $341,176,406 | 28,012,681 | $12.18 | |||

| Institutional Class | $324,613 | 26,653 | $12.18 | |||

| A Class | $7,251,127 | 595,471 | $12.18* | |||

| C Class | $6,830,618 | 560,775 | $12.18 | |||

*Maximum offering price $12.75 (net asset value divided by 0.955).

See Notes to Financial Statements.

18

| Statement of Operations |

| YEAR ENDED AUGUST 31, 2016 | |||

| Investment Income (Loss) | |||

| Income: | |||

| Interest | $ | 13,178,267 | |

| Expenses: | |||

| Management fees | 1,611,144 | ||

| Distribution and service fees: | |||

| A Class | 16,532 | ||

| C Class | 68,813 | ||

| Trustees' fees and expenses | 20,954 | ||

| Other expenses | 3,646 | ||

| 1,721,089 | |||

| Net investment income (loss) | 11,457,178 | ||

| Realized and Unrealized Gain (Loss) | |||

| Net realized gain (loss) on: | |||

| Investment transactions | 2,897,910 | ||

| Futures contract transactions | 20,910 | ||

| 2,918,820 | |||

| Change in net unrealized appreciation (depreciation) on: | |||

| Investments | 11,020,381 | ||

| Futures contracts | (16,875 | ) | |

| 11,003,506 | |||

| Net realized and unrealized gain (loss) | 13,922,326 | ||

| Net Increase (Decrease) in Net Assets Resulting from Operations | $ | 25,379,504 | |

See Notes to Financial Statements.

19

| Statement of Changes in Net Assets |

| YEARS ENDED AUGUST 31, 2016 AND AUGUST 31, 2015 | ||||||

| Increase (Decrease) in Net Assets | August 31, 2016 | August 31, 2015 | ||||

| Operations | ||||||

| Net investment income (loss) | $ | 11,457,178 | $ | 11,665,482 | ||

| Net realized gain (loss) | 2,918,820 | (319,618 | ) | |||

| Change in net unrealized appreciation (depreciation) | 11,003,506 | (1,586,988 | ) | |||

| Net increase (decrease) in net assets resulting from operations | 25,379,504 | 9,758,876 | ||||

| Distributions to Shareholders | ||||||

| From net investment income: | ||||||

| Investor Class | (11,082,052 | ) | (11,274,436 | ) | ||

| Institutional Class | (11,026 | ) | (9,947 | ) | ||

| A Class | (203,292 | ) | (213,905 | ) | ||

| C Class | (160,169 | ) | (167,194 | ) | ||

| Decrease in net assets from distributions | (11,456,539 | ) | (11,665,482 | ) | ||

| Capital Share Transactions | ||||||

| Net increase (decrease) in net assets from capital share transactions (Note 5) | (1,513,704 | ) | (14,190,101 | ) | ||

| Net increase (decrease) in net assets | 12,409,261 | (16,096,707 | ) | |||

| Net Assets | ||||||

| Beginning of period | 343,173,503 | 359,270,210 | ||||

| End of period | $ | 355,582,764 | $ | 343,173,503 | ||

| Undistributed net investment income | $ | 639 | $ | — | ||

See Notes to Financial Statements.

20

| Notes to Financial Statements |

AUGUST 31, 2016

1. Organization

American Century California Tax-Free and Municipal Funds (the trust) is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company and is organized as a Massachusetts business trust. California Long-Term Tax-Free Fund (the fund) is one fund in a series issued by the trust. The fund’s investment objective is to seek safety of principal and high current income that is exempt from federal and California income taxes.

The fund offers the Investor Class, the Institutional Class, the A Class and the C Class. The A Class may incur an initial sales charge. The A Class and C Class may be subject to a contingent deferred sales charge. The share classes differ principally in their respective sales charges and distribution and shareholder servicing expenses and arrangements. The Institutional Class is made available to institutional shareholders or through financial intermediaries whose clients do not require the same level of shareholder and administrative services as shareholders of other classes. As a result, the Institutional Class is charged a lower unified management fee.

2. Significant Accounting Policies

The following is a summary of significant accounting policies consistently followed by the fund in preparation of its financial statements. The fund is an investment company and follows accounting and reporting guidance in accordance with accounting principles generally accepted in the United States of America. This may require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from these estimates. Management evaluated the impact of events or transactions occurring through the date the financial statements were issued that would merit recognition or disclosure.

Investment Valuations — The fund determines the fair value of its investments and computes its net asset value per share at the close of regular trading (usually 4 p.m. Eastern time) on the New York Stock Exchange (NYSE) on each day the NYSE is open. The Board of Trustees has adopted valuation policies and procedures to guide the investment advisor in the fund’s investment valuation process and to provide methodologies for the oversight of the fund’s pricing function.

Fixed income securities are valued at the evaluated mean as provided by independent pricing services or at the mean of the most recent bid and asked prices as provided by investment dealers. Municipal securities are valued using market models that consider trade data, quotations from dealers and active market makers, relevant yield curve and spread data, creditworthiness, trade data or market information on comparable securities, and other relevant security specific information.

Open-end management investment companies are valued at the reported net asset value per share. Exchange-traded futures contracts are valued at the settlement price as provided by the appropriate clearing corporation.

If the fund determines that the market price for an investment is not readily available or the valuation methods mentioned above do not reflect an investment’s fair value, such investment is valued as determined in good faith by the Board of Trustees or its delegate, in accordance with policies and procedures adopted by the Board of Trustees. In its determination of fair value, the fund may review several factors including, but not limited to, market information regarding the specific investment or comparable investments and correlation with other investment types, futures indices or general market indicators. Circumstances that may cause the fund to use these procedures to value an investment include, but are not limited to: an investment has been declared in default or is distressed; trading in a security has been suspended during the trading day or a security is not actively trading on its principal exchange; prices received from a regular pricing source are deemed unreliable; or there is a foreign market holiday and no trading occurred.

The fund monitors for significant events occurring after the close of an investment’s primary exchange but before the fund’s net asset value per share is determined. Significant events may include, but are not limited to: corporate announcements and transactions; governmental action and political unrest that could impact a specific investment or an investment sector; or armed conflicts, natural disasters and similar events that could affect investments in a specific country or region.

21

Security Transactions — Security transactions are accounted for as of the trade date. Net realized gains and losses are determined on the identified cost basis, which is also used for federal income tax purposes.

Investment Income — Interest income is recorded on the accrual basis and includes accretion of discounts and amortization of premiums.

Segregated Assets — In accordance with the 1940 Act, the fund segregates assets on its books and records to cover certain types of investments, including, but not limited to, futures contracts and when-issued securities. American Century Investment Management, Inc. (ACIM) (the investment advisor) monitors, on a daily basis, the securities segregated to ensure the fund designates a sufficient amount of liquid assets, marked-to-market daily. The fund may also receive assets or be required to pledge assets at the custodian bank or with a broker for margin requirements on futures contracts.

Income Tax Status — It is the fund’s policy to distribute substantially all net investment income and net realized gains to shareholders and to otherwise qualify as a regulated investment company under provisions of the Internal Revenue Code. Accordingly, no provision has been made for income taxes. The fund files U.S. federal, state, local and non-U.S. tax returns as applicable. The fund's tax returns are subject to examination by the relevant taxing authority until expiration of the applicable statute of limitations, which is generally three years from the date of filing but can be longer in certain jurisdictions. At this time, management believes there are no uncertain tax positions which, based on their technical merit, would not be sustained upon examination and for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

Multiple Class — All shares of the fund represent an equal pro rata interest in the net assets of the class to which such shares belong, and have identical voting, dividend, liquidation and other rights and the same terms and conditions, except for class specific expenses and exclusive rights to vote on matters affecting only individual classes. Income, non-class specific expenses, and realized and unrealized capital gains and losses of the fund are allocated to each class of shares based on their relative net assets.

Distributions to Shareholders — Distributions from net investment income, if any, are declared daily and paid monthly. Distributions from net realized gains, if any, are generally declared and paid annually.

Indemnifications — Under the trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the fund. In addition, in the normal course of business, the fund enters into contracts that provide general indemnifications. The maximum exposure under these arrangements is unknown as this would involve future claims that may be made against a fund. The risk of material loss from such claims is considered by management to be remote.

3. Fees and Transactions with Related Parties

Certain officers and trustees of the trust are also officers and/or directors of American Century Companies, Inc. (ACC). The trust's investment advisor, ACIM, the trust's distributor, American Century Investment Services, Inc. (ACIS), and the trust's transfer agent, American Century Services, LLC, are wholly owned, directly or indirectly, by ACC.

Management Fees — The trust has entered into a management agreement with ACIM, under which ACIM provides the fund with investment advisory and management services in exchange for a single, unified management fee (the fee) per class. The agreement provides that all expenses of managing and operating the fund, except distribution and service fees, brokerage expenses, taxes, interest, fees and expenses of the independent trustees (including legal counsel fees), and extraordinary expenses, will be paid by ACIM. The fee is computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The fee consists of (1) an Investment Category Fee based on the daily net assets of the fund and certain other accounts managed by the investment advisor that are in the same broad investment category as the fund and (2) a Complex Fee based on the assets of all the funds in the American Century Investments family of funds. The rates for the Investment Category Fee range from 0.1625% to 0.2800%. The rates for the Complex Fee range from 0.2500% to 0.3100% for the Investor Class, A Class and C Class. The rates for the Complex Fee range from 0.0500% to 0.1100% for the Institutional Class. The effective annual management fee for each class for the year ended August 31, 2016 was 0.46% for the Investor Class, A Class and C Class and 0.26% for the Institutional Class.

Distribution and Service Fees — The Board of Trustees has adopted a separate Master Distribution and Individual Shareholder Services Plan for each of the A Class and C Class (collectively the plans), pursuant to Rule 12b-1 of the 1940 Act. The plans provide that the A Class will pay ACIS an annual distribution and

22

service fee of 0.25%. The plans provide that the C Class will pay ACIS an annual distribution and service fee of 1.00%, of which 0.25% is paid for individual shareholder services and 0.75% is paid for distribution services. The fees are computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The fees are used to pay financial intermediaries for distribution and individual shareholder services. Fees incurred under the plans during the year ended August 31, 2016 are detailed in the Statement of Operations.

Trustees’ Fees and Expenses — The Board of Trustees is responsible for overseeing the investment advisor’s management and operations of the fund. The trustees receive detailed information about the fund and its investment advisor regularly throughout the year, and meet at least quarterly with management of the investment advisor to review reports about fund operations. The fund’s officers do not receive compensation from the fund.

Interfund Transactions — The fund may enter into security transactions with other American Century Investments funds and other client accounts of the investment advisor, in accordance with the 1940 Act rules and procedures adopted by the Board of Trustees. The rules and procedures require, among other things, that these transactions be effected at the independent current market price of the security. During the period, the interfund purchases and sales were $23,180,438 and $1,700,000, respectively. The interfund transactions had no effect on the Statement of Operations in net realized gain (loss) on investment transactions.

4. Investment Transactions

Purchases and sales of investment securities, excluding short-term investments, for the year ended August 31, 2016 were $93,309,637 and $83,244,571, respectively.

5. Capital Share Transactions

Transactions in shares of the fund were as follows (unlimited number of shares authorized):

| Year ended August 31, 2016 | Year ended August 31, 2015 | |||||||||

| Shares | Amount | Shares | Amount | |||||||

| Investor Class | ||||||||||

| Sold | 1,404,677 | $ | 16,819,809 | 1,043,154 | $ | 12,296,446 | ||||

| Issued in reinvestment of distributions | 714,860 | 8,550,951 | 721,400 | 8,508,080 | ||||||

| Redeemed | (2,240,396 | ) | (26,719,080 | ) | (2,905,163 | ) | (34,174,882 | ) | ||

| (120,859 | ) | (1,348,320 | ) | (1,140,609 | ) | (13,370,356 | ) | |||

| Institutional Class | ||||||||||

| Sold | — | — | 22,124 | 259,950 | ||||||

| Issued in reinvestment of distributions | 922 | 11,026 | 843 | 9,947 | ||||||

| 922 | 11,026 | 22,967 | 269,897 | |||||||

| A Class | ||||||||||

| Sold | 87,084 | 1,046,515 | 51,183 | 601,935 | ||||||

| Issued in reinvestment of distributions | 16,840 | 201,493 | 17,971 | 211,962 | ||||||

| Redeemed | (77,356 | ) | (916,499 | ) | (161,544 | ) | (1,910,307 | ) | ||

| 26,568 | 331,509 | (92,390 | ) | (1,096,410 | ) | |||||

| C Class | ||||||||||

| Sold | 92,752 | 1,109,415 | 44,530 | 529,113 | ||||||

| Issued in reinvestment of distributions | 7,849 | 93,842 | 8,302 | 97,919 | ||||||

| Redeemed | (143,704 | ) | (1,711,176 | ) | (52,774 | ) | (620,264 | ) | ||

| (43,103 | ) | (507,919 | ) | 58 | 6,768 | |||||

| Net increase (decrease) | (136,472 | ) | $ | (1,513,704 | ) | (1,209,974 | ) | $ | (14,190,101 | ) |

6. Fair Value Measurements

The fund’s investments valuation process is based on several considerations and may use multiple inputs to determine the fair value of the investments held by the fund. In conformity with accounting principles generally

23

accepted in the United States of America, the inputs used to determine a valuation are classified into three broad levels.

| • | Level 1 valuation inputs consist of unadjusted quoted prices in an active market for identical investments. |

| • | Level 2 valuation inputs consist of direct or indirect observable market data (including quoted prices for comparable investments, evaluations of subsequent market events, interest rates, prepayment speeds, credit risk, etc.). These inputs also consist of quoted prices for identical investments initially expressed in local currencies that are adjusted through translation into U.S. dollars. |

| • | Level 3 valuation inputs consist of unobservable data (including a fund’s own assumptions). |

The level classification is based on the lowest level input that is significant to the fair valuation measurement. The valuation inputs are not necessarily an indication of the risks associated with investing in these securities or other financial instruments. There were no significant transfers between levels during the period.

As of period end, the fund’s investment securities were classified as Level 2. The Schedule of Investments provides additional information on the fund’s portfolio holdings.

7. Derivative Instruments

Interest Rate Risk — The fund is subject to interest rate risk in the normal course of pursuing its investment objectives. The value of bonds generally declines as interest rates rise. A fund may enter into futures contracts based on a bond index or a specific underlying security. A fund may purchase futures contracts to gain exposure to increases in market value or sell futures contracts to protect against a decline in market value. Upon entering into a futures contract, a fund will segregate cash, cash equivalents or other appropriate liquid securities on its records in amounts sufficient to meet requirements. Subsequent payments (variation margin) are made or received daily, in cash, by a fund. The variation margin is equal to the daily change in the contract value and is recorded as unrealized gains and losses. A fund recognizes a realized gain or loss when the futures contract is closed or expires. Net realized and unrealized gains or losses occurring during the holding period of futures contracts are a component of net realized gain (loss) on futures contract transactions and change in net unrealized appreciation (depreciation) on futures contracts, respectively. One of the risks of entering into futures contracts is the possibility that the change in value of the contract may not correlate with the changes in value of the underlying securities. During the period, the fund participated in interest rate risk derivative instruments.

At period end, the fund did not have any derivative instruments disclosed on the Statement of Assets and Liabilities. For the year ended August 31, 2016, the effect of interest rate risk derivative instruments on the Statement of Operations was $20,910 in net realized gain (loss) on futures contract transactions and $(16,875) in change in net unrealized appreciation (depreciation) on futures contracts.

8. Risk Factors

The fund focuses its investments in a single state and therefore may have more exposure to credit risk related to the state of California than a fund with a broader geographical diversification.

9. Federal Tax Information

The tax character of distributions paid during the years ended August 31, 2016 and August 31, 2015 were as follows:

| 2016 | 2015 | |||||

| Distributions Paid From | ||||||

| Exempt income | $ | 11,456,539 | $ | 11,664,699 | ||

| Taxable ordinary income | — | $ | 783 | |||

| Long-term capital gains | — | — | ||||

The book-basis character of distributions made during the year from net investment income or net realized gains may differ from their ultimate characterization for federal income tax purposes. These differences reflect the differing character of certain income items and net realized gains and losses for financial statement and tax purposes, and may result in reclassification among certain capital accounts on the financial statements.

24

As of August 31, 2016, the federal tax cost of investments and the components of distributable earnings on a tax-basis were as follows:

| Federal tax cost of investments | $ | 319,111,290 | |

| Gross tax appreciation of investments | $ | 43,168,366 | |

| Gross tax depreciation of investments | (6,891 | ) | |

| Net tax appreciation (depreciation) of investments | $ | 43,161,475 | |

| Undistributed exempt income | $ | 639 | |

| Accumulated long-term gains | $ | 1,301,742 | |

The cost of investments for federal income tax purposes was the same as the cost for financial reporting purposes.

25

| Financial Highlights |

| For a Share Outstanding Throughout the Years Ended August 31 (except as noted) | |||||||||||||

| Per-Share Data | Ratios and Supplemental Data | ||||||||||||

| Income From Investment Operations: | Ratio to Average Net Assets of: | ||||||||||||

Net Asset Value, Beginning of Period | Net Investment Income (Loss)(1) | Net Realized and Unrealized Gain (Loss) | Total From Investment Operations | Distributions From Net Investment Income | Net Asset Value, End of Period | Total Return(2) | Operating Expenses | Net Investment Income (Loss) | Portfolio Turnover Rate | Net Assets, End of Period (in thousands) | |||

| Investor Class | |||||||||||||

| 2016 | $11.70 | 0.40 | 0.48 | 0.88 | (0.40) | $12.18 | 7.62% | 0.47% | 3.33% | 24% | $341,176 | ||

| 2015 | $11.76 | 0.39 | (0.06) | 0.33 | (0.39) | $11.70 | 2.86% | 0.47% | 3.33% | 31% | $329,152 | ||

| 2014 | $10.94 | 0.38 | 0.82 | 1.20 | (0.38) | $11.76 | 11.10% | 0.47% | 3.32% | 46% | $344,356 | ||

| 2013 | $11.70 | 0.37 | (0.76) | (0.39) | (0.37) | $10.94 | (3.45)% | 0.47% | 3.19% | 44% | $346,396 | ||

| 2012 | $10.94 | 0.41 | 0.77 | 1.18 | (0.42) | $11.70 | 10.92% | 0.47% | 3.65% | 76% | $412,713 | ||

| Institutional Class | |||||||||||||

| 2016 | $11.70 | 0.42 | 0.48 | 0.90 | (0.42) | $12.18 | 7.83% | 0.27% | 3.53% | 24% | $325 | ||

| 2015 | $11.77 | 0.42 | (0.07) | 0.35 | (0.42) | $11.70 | 2.97% | 0.27% | 3.53% | 31% | $301 | ||

| 2014 | $10.94 | 0.40 | 0.83 | 1.23 | (0.40) | $11.77 | 11.42% | 0.27% | 3.52% | 46% | $33 | ||

| 2013 | $11.70 | 0.40 | (0.76) | (0.36) | (0.40) | $10.94 | (3.26)% | 0.27% | 3.39% | 44% | $29 | ||

| 2012 | $10.94 | 0.44 | 0.76 | 1.20 | (0.44) | $11.70 | 11.14% | 0.27% | 3.85% | 76% | $30 | ||

| A Class | |||||||||||||

| 2016 | $11.70 | 0.37 | 0.48 | 0.85 | (0.37) | $12.18 | 7.35% | 0.72% | 3.08% | 24% | $7,251 | ||

| 2015 | $11.76 | 0.36 | (0.06) | 0.30 | (0.36) | $11.70 | 2.60% | 0.72% | 3.08% | 31% | $6,655 | ||

| 2014 | $10.94 | 0.35 | 0.82 | 1.17 | (0.35) | $11.76 | 10.83% | 0.72% | 3.07% | 46% | $7,778 | ||

| 2013 | $11.70 | 0.34 | (0.76) | (0.42) | (0.34) | $10.94 | (3.70)% | 0.72% | 2.94% | 44% | $8,572 | ||

| 2012 | $10.94 | 0.38 | 0.77 | 1.15 | (0.39) | $11.70 | 10.64% | 0.72% | 3.40% | 76% | $16,214 | ||

| For a Share Outstanding Throughout the Years Ended August 31 (except as noted) | |||||||||||||

| Per-Share Data | Ratios and Supplemental Data | ||||||||||||

| Income From Investment Operations: | Ratio to Average Net Assets of: | ||||||||||||

Net Asset Value, Beginning of Period | Net Investment Income (Loss)(1) | Net Realized and Unrealized Gain (Loss) | Total From Investment Operations | Distributions From Net Investment Income | Net Asset Value, End of Period | Total Return(2) | Operating Expenses | Net Investment Income (Loss) | Portfolio Turnover Rate | Net Assets, End of Period (in thousands) | |||

| C Class | |||||||||||||

| 2016 | $11.70 | 0.28 | 0.48 | 0.76 | (0.28) | $12.18 | 6.55% | 1.47% | 2.33% | 24% | $6,831 | ||

| 2015 | $11.76 | 0.28 | (0.06) | 0.22 | (0.28) | $11.70 | 1.83% | 1.47% | 2.33% | 31% | $7,066 | ||

| 2014 | $10.94 | 0.26 | 0.82 | 1.08 | (0.26) | $11.76 | 10.00% | 1.47% | 2.32% | 46% | $7,104 | ||

| 2013 | $11.70 | 0.26 | (0.76) | (0.50) | (0.26) | $10.94 | (4.41)% | 1.47% | 2.19% | 44% | $7,471 | ||

| 2012 | $10.94 | 0.30 | 0.76 | 1.06 | (0.30) | $11.70 | 9.82% | 1.47% | 2.65% | 76% | $11,321 | ||

| Notes to Financial Highlights |

(2) Total returns are calculated based on the net asset value of the last business day and do not reflect applicable sales charges, if any. Total returns for periods less than one year are not annualized.

See Notes to Financial Statements.

| Report of Independent Registered Public Accounting Firm |

To the Board of Trustees of the American Century California Tax-Free and Municipal Funds and Shareholders of the California Long-Term Tax-Free Fund: