UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-03706 | |||||

| AMERICAN CENTURY CALIFORNIA TAX-FREE AND MUNICIPAL FUNDS | ||||||

| (Exact name of registrant as specified in charter) | ||||||

| 4500 MAIN STREET, KANSAS CITY, MISSOURI | 64111 | |||||

| (Address of principal executive offices) | (Zip Code) | |||||

CHARLES A. ETHERINGTON 4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 | ||||||

| (Name and address of agent for service) | ||||||

| Registrant’s telephone number, including area code: | 816-531-5575 | |||||

| Date of fiscal year end: | 8-31 | |||||

| Date of reporting period: | 8-31-2011 | |||||

ITEM 1. REPORTS TO STOCKHOLDERS.

| ANNUAL REPORT | AUGUST 31, 2011 |

California High-Yield Municipal Fund |

| President’s Letter | 2 |

| Market Perspective | 3 |

| Performance | 4 |

| Portfolio Commentary | 6 |

| Fund Characteristics | 8 |

| Shareholder Fee Example | 9 |

| Schedule of Investments | 11 |

| Statement of Assets and Liabilities | 19 |

| Statement of Operations | 20 |

| Statement of Changes in Net Assets | 21 |

| Notes to Financial Statements | 22 |

| Financial Highlights | 27 |

| Report of Independent Registered Public Accounting Firm | 29 |

| Management | 30 |

| Approval of Management Agreement | 33 |

| Additional Information | 38 |

Any opinions expressed in this report reflect those of the author as of the date of the report, and do not necessarily represent the opinions of American Century Investments® or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for comparative indices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

Thank you for reviewing this annual report for the period ended August 31, 2011. Our report offers investment performance and portfolio information, presented with the expert perspective and commentary of our municipal bond (muni) portfolio management team.

This report remains one of our most important vehicles for conveying information about investment performance, as well as the market factors and strategies that affect fund returns. For additional, updated information on fund performance, portfolio strategy, and the investment markets, we encourage you to visit our website, americancentury.com. Click on the “Fund Performance” and “Insights & News” headings at the top of our Individual Investors site.

Muni Market Performance Climbed from Six-Month Deficit

As described in greater detail on the following pages, muni market performance improved significantly after our last semiannual report (for the six months ended February 28, 2011).

That reporting period—when the Barclays Capital Municipal Bond Index declined 3.51%—included a turbulent two-and-a-half month span (the end of October 2010 to mid-January 2011) when a supply and demand imbalance roiled the market.

Overblown default fears—fueled by highly publicized analyst projections—compounded the market turbulence and helped trigger a wave of withdrawals from muni mutual funds. Though U.S. economic and stock market performance have been disappointing this year, making tax revenues tougher to collect, muni defaults have not approached the projected rates. Increased austerity and budget-balancing measures have helped maintain financial solvency for municipal issuers.

As 2011 and austerity measures unfolded, issuance of municipal debt declined dramatically and demand surged—relatively high yields compared with those of other high-quality bonds drew a surge of buyers. Munis rallied from mid-January through the end of the summer, helped by the rally of other high-quality bonds. This rewarded those who stayed the course and saw the turbulence as a buying opportunity.

Economic risks remain and more volatility is possible, but our muni portfolio management team liked the summer-end values of munis compared with Treasuries as a starting point for the next period. These dedicated experts provide more market and performance details in our enclosed 12-month Market Perspective and Portfolio Commentary. They will continue to diligently apply their knowledge and skills as they make daily investment decisions for you.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

2

Municipal bond (muni) indices advanced for the 12 months ended August 31, 2011 (see the table below). The moderately positive overall returns resulted from two distinct periods of performance characterized by shifting technical factors and dramatic changes in market sentiment.

After a quiet start to the reporting period, the muni market began to decline sharply in November 2010 amid a supply and demand imbalance. The expiration of the Build America Bonds (BABs) program, in which states and municipalities issued long-term taxable securities with federally subsidized interest rates, at the end of 2010 led to expectations that long-term bond issuance would shift back to the muni market, boosting supply. At the same time, demand for munis cratered as credit concerns—sparked by persistent state budget deficits and exaggerated media predictions of widespread muni defaults—led to heavy outflows from muni mutual funds.

Market conditions changed markedly in mid-January 2011, when the muni market bottomed and began a steady rebound that lasted through the end of the reporting period. The recovery began when opportunistic, non-traditional “cross-over” investors gravitated to the muni market to take advantage of relatively attractive muni yields following the market’s tumble in late 2010 and early 2011. Limited new issuance also contributed favorably to muni market performance—new muni issuance fell by 44% in the first half of 2011 compared with the same period in 2010, constrained by issuer austerity measures and the expiration of the BABs program, which accelerated into 2010 many new issues that would otherwise have come to market in 2011.

Although munis have been one of the top-performing segments in the fixed-income market during the first eight months of 2011, the severe decline from November to mid-January caused munis to underperform the returns of Treasury securities and the broad taxable bond market for the full 12-month period. Intermediate-term munis fared best as short-term munis were held in check by a stable interest rate policy from the Federal Reserve, while longer-term munis suffered disproportionately from muni fund outflows. From a credit and sector perspective, higher-quality munis outperformed lower-rated credits, while general obligation bonds outpaced tax revenue bonds.

| U.S. Fixed-Income Total Returns | ||||

| For the 12 months ended August 31, 2011 | ||||

| Barclays Capital Municipal Market Indices | Barclays Capital U.S. Taxable Market Indices | |||

| 7 Year Municipal Bond | 4.06% | Aggregate Bond | 4.62% | |

| Municipal High Yield Bond | 3.45% | Treasury Bond | 4.17% | |

| Municipal Bond | 2.66% | |||

| California Tax-Exempt Bond | 2.62% | |||

| Long-Term Municipal Bond | 1.84% | |||

3

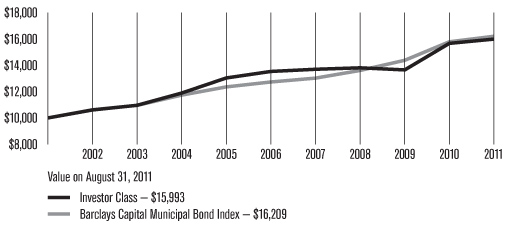

| Total Returns as of August 31, 2011 | ||||||

| Average Annual Returns | ||||||

Ticker Symbol | 1 year | 5 years | 10 years | Since Inception | Inception Date | |

| Investor Class | BCHYX | 2.07% | 3.39% | 4.80% | 5.87% | 12/30/86 |

| Barclays Capital Municipal Bond Index | — | 2.66% | 4.94% | 4.95% | 6.41%(1) | — |

| Institutional Class | BCHIX | 2.27% | — | — | 6.29% | 3/1/10 |

A Class No sales charge* With sales charge* | CAYAX | 1.82% -2.80% | 3.13% 2.19% | — — | 4.43% 3.87% | 1/31/03 |

B Class No sales charge* With sales charge* | CAYBX | 1.06% -2.94% | 2.37% 2.18% | — — | 3.66% 3.66% | 1/31/03 |

| C Class | CAYCX | 1.06% | 2.37% | — | 3.69% | 1/31/03 |

* | Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 4.50% maximum initial sales charge and may be subject to a maximum CDSC of 1.00%. B Class shares redeemed within six years of purchase are subject to a CDSC that declines from 5.00% during the first year after purchase to 0.00% the sixth year after purchase. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied. |

| (1) | Since 12/31/86, the date nearest the Investor Class’s inception for which data are available. |

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. As interest rates rise, bond values will decline. In addition, the lower-rated securities in which the fund invests are subject to greater credit risk, default risk and liquidity risk. Investment income may be subject to certain state and local taxes and, depending on your tax status, the federal alternative minimum tax (AMT). Capital gains are not exempt from state and federal income tax.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

4

| Growth of $10,000 Over 10 Years |

| $10,000 investment made August 31, 2001 |

| Total Annual Fund Operating Expenses | ||||

| Investor Class | Institutional Class | A Class | B Class | C Class |

| 0.51% | 0.31% | 0.76% | 1.51% | 1.51% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. As interest rates rise, bond values will decline. In addition, the lower-rated securities in which the fund invests are subject to greater credit risk, default risk and liquidity risk. Investment income may be subject to certain state and local taxes and, depending on your tax status, the federal alternative minimum tax (AMT). Capital gains are not exempt from state and federal income tax.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

5

Performance Summary

California High-Yield Municipal returned 2.07%* for the fiscal year ended August 31, 2011. By comparison, the Barclays Capital Municipal Bond Index (representing investment-grade municipal bonds) returned 2.66%, while the Barclays Capital Municipal High Yield Bond Index (representing non-investment-grade municipal bonds) returned 3.45%.** In addition, the average return of the California Municipal Debt Funds tracked by Lipper Inc. was 1.30%*** for the 12-month period. (See page 4 and footnotes below for additional performance comparisons.)

The fund’s absolute return for the reporting period reflected the generally positive performance of municipal bond (muni) indices (see page 3). The fund’s performance trailed the return of the broad, investment-grade Municipal Bond Index as lower-quality munis lagged investment-grade munis for the 12 months. However, the fund outpaced its Lipper peer group average, in large part because it held up well during the muni market decline in late 2010 and early 2011.

Credit Environment

After several years of widening budget deficits and deteriorating credit, the state of California showed signs of stabilization over the 12-month period. In the first quarter of 2011, the state successfully trimmed about half of its budget deficit through a combination of spending cuts and fund transfers, and a budget agreement for the 2012 fiscal year (which began July 1) was approved on schedule for the first time since 2006. Although the approved budget relies on some speculative revenue sources, it also incorporates some meaningful fiscal austerity measures. In addition, the state’s cash flow situation has improved significantly, as evidenced by the limited issuance of seasonal cash-flow debt in 2011.

Nonetheless, many challenges remain for California going forward. The negative impact of a slowing economy and declining stock market on tax revenues (the wealthiest 1% of Californians are responsible for nearly half of the state’s tax revenues), the end of federal stimulus funding, the possibility of cuts in Medicaid, and long-term pension funding issues are all headwinds for the state’s fiscal situation. In addition, local governments have struggled to close their budget gaps as the state has pushed more financial responsibilities down to the local level. While we expect defaults to be rare, we could see widespread credit downgrades among local issuers in California.

| * | All fund returns referenced in this commentary are for Investor Class shares. |

| ** | The Barclays Capital Municipal High Yield Bond Index’s average returns were 2.41% and 4.96% for the five- and ten-year periods ended August 31, 2011, respectively. |

| *** | The average returns for Lipper California Municipal Debt Funds category were 3.09% and 3.78% for the five- and ten-year periods ended August 31, 2011, respectively. Data provided by Lipper Inc. — A Reuters Company. © 2011 Reuters. All rights reserved. Any copying, republication or redistribution of Lipper content, including by caching, framing or similar means, is expressly prohibited without the prior written consent of Lipper. Lipper shall not be liable for any errors or delays in the content, or for any actions taken in reliance thereon. Lipper fund performance data is total return, and is preliminary and subject to revision. The data contained herein has been obtained from company reports, financial reporting services, periodicals and other resources believed to be reliable. Although carefully verified, data on compilations is not guaranteed by Lipper and may be incomplete. No offer or solicitations to buy or sell any of the securities herein is being made by Lipper. |

6

Portfolio Positioning

The fund’s outperformance of its peer group average during the 12-month period occurred primarily during the muni market decline in late 2010 and early 2011. During this period, the fund’s sector allocation and security selection helped the fund hold up better than many of its peers. For example, the fund’s largest sector weighting was land-secured bonds, which typically finance property development projects and comprised more than a quarter of the portfolio throughout the reporting period. The fund’s land-secured bonds are more seasoned and built-out, so they tend to experience less price volatility, and this attribute proved favorable as the muni market declined.

The fund also had limited exposure to corporate-backed munis, tobacco-related bonds, and industrial development securities. These segments of the muni market tend to be more volatile than other revenue bonds, and as a result, they underperformed during the muni market decline. The fund’s holdings among revenue bonds were focused on less economically sensitive sectors such as hospitals, higher education, and essential services (water, sewer, etc.). Essential services bonds were popular with non-traditional cross-over investors that were drawn to the muni market by attractive yields in early 2011.

Although this positioning contributed favorably to performance early in the reporting period, it detracted during the muni market rally in the latter half of the period. The fund’s benchmark index, as well as many of its peers, hold investment-grade munis, and these securities outperformed lower-quality munis in the market rally. In addition, the fund’s emphasis on land-secured bonds weighed on relative results given their lower price volatility.

Since late 2009, the fund has been positioned for a flatter Treasury yield curve (a narrower gap between short- and long-term Treasury yields). This positioning weighed on performance in late 2010 as the Treasury yield curve grew steeper, but it enhanced fund performance in 2011 as the Treasury curve flattened considerably. By the end of the reporting period, we had less conviction in the possibility of further upside, so we eliminated the position in August.

Outlook

We expect the muni market to remain vulnerable to “headline risk”—that is, the potential for an adverse news headline to have a significant effect on muni market performance. In particular, news that could rattle the muni market includes the potential impact of an economic slowdown on state and local budgets, as well as discussion at the federal level of reducing or eliminating the tax exemption for muni interest. Although we don’t foresee any change in munis’ tax-exempt status, the fact that it has been included in the discussion at all is noteworthy.

That said, the recent Treasury rally has caused the spreads between muni and Treasury yields to widen out, creating what we believe are attractive valuations in the muni market. Over time, we expect the gap to narrow back toward historical averages, leading to the outperformance of munis. Furthermore, we believe the fund’s credit position is as strong as it has been in recent memory, and we think this will benefit the portfolio in the current uncertain economic environment.

7

| AUGUST 31, 2011 | |

| Portfolio at a Glance | |

| Weighted Average Maturity | 19.4 years |

| Average Duration (Modified) | 7.0 years |

| 30-Day SEC Yields | |

| Investor Class | 4.53% |

| Institutional Class | 4.73% |

| A Class | 4.08% |

| B Class | 3.52% |

| C Class | 3.53% |

Investor Class 30-Day Tax-Equivalent Yields(1) | |

| 31.98% Tax Bracket | 6.66% |

| 34.70% Tax Bracket | 6.94% |

| 39.23% Tax Bracket | 7.45% |

| 41.05% Tax Bracket | 7.68% |

| (1) | The tax brackets indicated are for combined state and federal income tax. Actual tax-equivalent yields may be lower, if alternative minimum tax is applicable. |

| Top Five Sectors | % of fund investments |

| Land Based | 28% |

| Hospital Revenue | 10% |

| General Obligation (GO) | 9% |

| Electric Revenue | 9% |

| Tax Allocation/Tax Increment Revenue | 6% |

| Types of Investments in Portfolio | % of net assets |

| Municipal Securities | 98.5% |

| Other Assets and Liabilities | 1.5% |

8

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from March 1, 2011 to August 31, 2011.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or Institutional Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not a financial intermediary or retirement plan account), American Century Investments may charge you a $12.50 semiannual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $12.50 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments Brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments Brokerage accounts, you are currently not subject to this fee. We will not charge the fee as long as you choose to manage your accounts exclusively online. If you are subject to the Account Maintenance Fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

9

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Beginning Account Value 3/1/11 | Ending Account Value 8/31/11 | Expenses Paid During Period(1) 3/1/11 - 8/31/11 | Annualized Expense Ratio(1) | |

| Actual | ||||

| Investor Class (after waiver) | $1,000 | $1,071.90 | $2.56 | 0.49% |

| Investor Class (before waiver) | $1,000 | $1,071.90(2) | $2.66 | 0.51% |

| Institutional Class (after waiver) | $1,000 | $1,073.00 | $1.52 | 0.29% |

| Institutional Class (before waiver) | $1,000 | $1,073.00(2) | $1.62 | 0.31% |

| A Class (after waiver) | $1,000 | $1,070.60 | $3.86 | 0.74% |

| A Class (before waiver) | $1,000 | $1,070.60(2) | $3.97 | 0.76% |

| B Class (after waiver) | $1,000 | $1,066.50 | $7.76 | 1.49% |

| B Class (before waiver) | $1,000 | $1,066.50(2) | $7.87 | 1.51% |

| C Class (after waiver) | $1,000 | $1,066.50 | $7.76 | 1.49% |

| C Class (before waiver) | $1,000 | $1,066.50(2) | $7.87 | 1.51% |

| Hypothetical | ||||

| Investor Class (after waiver) | $1,000 | $1,022.74 | $2.50 | 0.49% |

| Investor Class (before waiver) | $1,000 | $1,022.63 | $2.60 | 0.51% |

| Institutional Class (after waiver) | $1,000 | $1,023.74 | $1.48 | 0.29% |

| Institutional Class (before waiver) | $1,000 | $1,023.64 | $1.58 | 0.31% |

| A Class (after waiver) | $1,000 | $1,021.48 | $3.77 | 0.74% |

| A Class (before waiver) | $1,000 | $1,021.37 | $3.87 | 0.76% |

| B Class (after waiver) | $1,000 | $1,017.69 | $7.58 | 1.49% |

| B Class (before waiver) | $1,000 | $1,017.59 | $7.68 | 1.51% |

| C Class (after waiver) | $1,000 | $1,017.69 | $7.58 | 1.49% |

| C Class (before waiver) | $1,000 | $1,017.59 | $7.68 | 1.51% |

| (1) | Expenses are equal to the class’s annualized expense ratio listed in the table above, multiplied by the average account value over the period, multiplied by 184, the number of days in the most recent fiscal half-year, divided by 365, to reflect the one-half year period. |

| (2) | Ending account value assumes the return earned after waiver and would have been lower if a portion of the management fee had not been waived. |

10

Principal Amount | Value | |

| Municipal Securities — 98.5% | ||

| CALIFORNIA — 94.9% | ||

ABC Unified School District GO, Series 2000 B, 0.00%, 8/1/21 (NATL/FGIC)(1)(2) | $1,000,000 | $605,600 |

| Adelanto Public Utility Auth. Rev., Series 2009 A, (Utility System), 6.75%, 7/1/39 | 5,225,000 | 5,417,019 |

| Alhambra Rev., Series 2010 A, (Atherton Baptist Homes), 7.50%, 1/1/30 | 1,640,000 | 1,695,055 |

Anaheim Public Financing Auth. Lease Rev., Series 1997 A, (Public Improvements), 6.00%, 9/1/24 (AGM)(1) | 1,200,000 | 1,391,784 |

| Beaumont Financing Auth. Local Agency Special Tax Rev., Series 2004 D, 5.80%, 9/1/35 | 2,875,000 | 2,674,871 |

| Beaumont Financing Auth. Local Agency Special Tax Rev., Series 2005 B, 5.40%, 9/1/35 | 1,390,000 | 1,230,303 |

| Beaumont Financing Auth. Local Agency Special Tax Rev., Series 2005 C, 5.50%, 9/1/29 | 855,000 | 797,647 |

| Beaumont Financing Auth. Local Agency Special Tax Rev., Series 2005 C, 5.50%, 9/1/35 | 4,000,000 | 3,593,040 |

| Beaumont Financing Auth. Local Agency Special Tax Rev., Series 2006 A, (Improvement Area No. 19C), 5.35%, 9/1/36 | 2,700,000 | 2,348,136 |

| Beaumont Financing Auth. Local Agency Special Tax Rev., Series 2008 A, (Improvement Area No. 19C), 6.875%, 9/1/36 | 1,050,000 | 1,071,956 |

Berryessa Union School District GO, Series 2000 A, 0.00%, 8/1/21 (AGM)(1)(2) | 1,190,000 | 736,170 |

Berryessa Union School District GO, Series 2000 A, 0.00%, 8/1/22 (AGM)(1)(2) | 1,220,000 | 686,945 |

Berryessa Union School District GO, Series 2000 A, 0.00%, 8/1/23 (AGM)(1)(2) | 1,000,000 | 522,570 |

California Department of Water Resources Power Supply Rev., Series 2008 H, 5.00%, 5/1/22(1) | 4,500,000 | 5,089,905 |

California Department of Water Resources Power Supply Rev. Series 2010 L, 5.00%, 5/1/21(1) | 4,725,000 | 5,588,446 |

California Department of Water Resources Power Supply Rev. Series 2010 L, 5.00%, 5/1/22(1) | 4,200,000 | 4,896,654 |

California Department of Water Resources Water System Rev., Series 2008 AE (Central Valley), 5.00%, 12/1/23(1) | 2,500,000 | 2,846,100 |

California Economic Recovery GO, Series 2004 C5, VRDN, 0.09%, 9/1/11 (LOC: Bank of America N.A.)(1) | 8,600,000 | 8,600,000 |

California Economic Recovery GO, Series 2004 A, 5.25%, 7/1/14 (NATL/FGIC)(1) | 6,000,000 | 6,778,080 |

California Educational Facilities Auth. Rev., (Western University Health Sciences), 6.00%, 10/1/12, Prerefunded at 100% of Par(1)(3) | 1,505,000 | 1,584,434 |

California Educational Facilities Auth. Rev., Series 2009 A, (Pomona College), 5.00%, 1/1/24(1) | 1,400,000 | 1,593,410 |

California GO, 5.25%, 10/1/29(1) | 5,000,000 | 5,284,550 |

California GO, 6.00%, 4/1/38(1) | 5,000,000 | 5,458,700 |

California Health Facilities Financing Auth. Rev., Series 1989 A, (Kaiser Permanente), 0.00%, 10/1/12 (Ambac-TCRS)(1)(2) | 4,000,000 | 3,947,200 |

California Health Facilities Financing Auth. Rev., Series 2008 A, (Scripps Health), 5.50%, 10/1/20(1) | 1,500,000 | 1,709,415 |

California Health Facilities Financing Auth. Rev., Series 2008 A, (Sutter Health), 5.50%, 8/15/16(1) | 5,000,000 | 5,859,050 |

California Health Facilities Financing Auth. Rev., Series 2008 C, (Providence Health & Services), 6.50%, 10/1/33(1) | 1,000,000 | 1,132,420 |

11

Principal Amount | Value |

California Health Facilities Financing Auth. Rev., Series 2008 G, (Catholic Healthcare West), 5.50%, 7/1/25(1) | $2,000,000 | $2,107,980 |

California Health Facilities Financing Auth. Rev., Series 2009 A, (Catholic Healthcare West), 6.00%, 7/1/39(1) | 4,300,000 | 4,558,387 |

California Health Facilities Financing Auth. Rev., Series 2009 A, (Children’s Hospital of Orange County), 6.50%, 11/1/38(1) | 3,000,000 | 3,217,380 |

California Health Facilities Financing Auth. Rev., Series 2010 B, (Stanford Hospital), 5.25%, 11/15/31(1) | 4,000,000 | 4,162,600 |

| California Mobilehome Park Financing Auth. Rev., Series 2001 B, (Rancho Vallecitos - San Marcos), 6.75%, 11/15/36 | 1,905,000 | 1,892,198 |

California Mobilehome Park Financing Auth. Rev., Series 2003 B, (Palomar Estates E&W), 7.00%, 9/15/36(1) | 6,345,000 | 6,384,085 |

| California Mobilehome Park Financing Auth. Rev., Series 2006 B, (Union City Tropics), 5.50%, 12/15/41 | 2,000,000 | 1,676,760 |

| California Municipal Finance Auth. Rev., (Biola University), 5.875%, 10/1/34 | 1,000,000 | 1,004,540 |

| California Municipal Finance Auth. Rev., Series 2011 B, (Azusa Pacific University), 8.00%, 4/1/41 | 3,335,000 | 3,424,311 |

California Public Works Board Lease Rev., Series 1993 D, (Department of Corrections), 5.25%, 6/1/15 (AGM)(1) | 2,000,000 | 2,167,400 |

California Public Works Board Lease Rev., Series 2009 G1, (Various Capital Projects), 5.75%, 10/1/30(1) | 2,000,000 | 2,100,680 |

California Public Works Board Lease Rev., Series 2010 A1, (Various Capital Projects), 6.00%, 3/1/35(1) | 1,250,000 | 1,324,600 |

California State University Fresno Association, Inc. Rev., (Auxiliary Organization Event Center), 7.00%, 7/1/12, Prerefunded at 101% of Par(1)(3) | 2,455,000 | 2,608,855 |

California State University Systemwide Rev., Series 2005 C, (Systemwide Financing Program), 5.00%, 11/1/30 (NATL)(1) | $5,000,000 | $5,171,450 |

California State University Systemwide Rev., Series 2009 A, (Systemwide Financing Program), 5.25%, 11/1/38(1) | 3,000,000 | 3,086,880 |

California Statewide Communities Development Auth. COP, (Sonoma County Indian Health), 6.40%, 9/1/29(1) | 2,085,000 | 2,085,104 |

California Statewide Communities Development Auth. Pollution Control, Rev., Series 2010 A, (Southern California Education), 4.50%, 9/1/29(1) | 4,000,000 | 3,913,040 |

California Statewide Communities Development Auth. Rev., (Cottage Health Obligation Group), 5.25%, 11/1/30(1) | 1,250,000 | 1,273,588 |

| California Statewide Communities Development Auth. Rev., (Lancer Educational Student Housing), 5.625%, 6/1/33 | 2,500,000 | 2,145,875 |

California Statewide Communities Development Auth. Rev., (Southern California Presbyterian Homes), 7.25%, 11/15/41(1) | 2,500,000 | 2,686,450 |

California Statewide Communities Development Auth. Rev., (Thomas Jefferson School of Law), 7.75%, 10/1/11, Prerefunded at 101% of Par(1)(3) | 1,855,000 | 1,884,086 |

California Statewide Communities Development Auth. Rev., Series 2001 C, (Kaiser Permanente), 5.25%, 8/1/31(1) | 4,000,000 | 4,051,640 |

California Statewide Communities Development Auth. Rev., Series 2004 D, (Sutter Health), 5.05%, 8/15/38 (AGM)(1) | 2,000,000 | 2,006,340 |

| California Statewide Communities Development Auth. Rev., Series 2007 A, (California Baptist University), 5.50%, 11/1/38 | 7,000,000 | 5,939,430 |

12

Principal Amount | Value |

California Statewide Communities Development Auth. Rev., Series 2007 A, (Front Porch Communities and Services), 5.125%, 4/1/37(1)(4) | $3,400,000 | $2,798,710 |

| California Statewide Communities Development Auth. Rev., Series 2007 A, (Valleycare Health System), 5.125%, 7/15/31 | 2,000,000 | 1,717,360 |

| Capistrano Unified School District Special Tax Rev., (Community Facilities District No. 90-2), 6.00%, 9/1/33 | 6,250,000 | 6,268,625 |

Carson Redevelopment Agency Tax Allocation Rev., Series 2009 A, (Project Area No. 1), 7.00%, 10/1/36(1) | 2,000,000 | 2,190,800 |

| Chula Vista Community Facilities District No. 06-1 Area A Special Tax Rev., (Eastlake Woods), 6.20%, 9/1/33 | 3,600,000 | 3,600,684 |

Chula Vista Industrial Development Rev., Series 2004 D, (San Diego Gas), 5.875%, 1/1/34(1) | 1,000,000 | 1,096,930 |

Clovis Public Financing Auth. Lease Rev., (Corporate Yard), 5.375%, 3/1/20 (Ambac)(1) | 1,780,000 | 1,804,208 |

Corcoran COP 8.75%, 6/1/16(4) | 345,000 | 411,268 |

Duarte Unified School District GO, Series 1999 B, 0.00%, 11/1/23 (AGM)(1)(2) | 1,150,000 | 591,629 |

Eastern Municipal Water District Water and Sewer COP, Series 2008 H, 5.00%, 7/1/33(1) | 4,000,000 | 4,112,720 |

| El Dorado County Community Facilities District No. 2001-1 Special Tax Rev., (Promontory Specific), 6.30%, 9/1/31 | 2,500,000 | 2,441,750 |

| Folsom Community Facilities District No. 7 Special Tax Rev., 5.75%, 9/1/14 | 1,885,000 | 1,885,000 |

Foothill-De Anza Community College District GO, 0.00%, 8/1/21 (NATL)(1)(2) | 3,000,000 | 1,984,290 |

Foothill/Eastern Transportation Corridor Agency Toll Road Rev., 5.875%, 1/15/27(1)(2) | 5,000,000 | 4,922,150 |

| Fullerton Community Facilities District No. 1 Special Tax Rev., (Amerige Heights), 6.20%, 9/1/32 | 3,000,000 | 3,043,170 |

| Fullerton Unified School District Special Tax Rev., (Community Facilities District No. 2001-1), 6.375%, 9/1/31 | 5,000,000 | 5,078,000 |

Golden State Tobacco Securitization Corp. Settlement Rev., Series 2007 A1, 5.125%, 6/1/47(1) | 8,500,000 | 5,484,880 |

Golden State Tobacco Securitization Corp. Settlement Rev., Series 2007 A1, 5.75%, 6/1/47(1) | 9,500,000 | 6,731,320 |

| Hemet Unified School District Special Tax Rev., (Community Facilities District No. 2005-2), 5.25%, 9/1/30 | 2,670,000 | 2,394,616 |

| Hemet Unified School District Special Tax Rev., (Community Facilities District No. 2005-2), 5.25%, 9/1/35 | 1,510,000 | 1,298,494 |

Hesperia Public Financing Auth. Tax Allocation Rev., Series 2007 A, (Redevelopment and Housing), 5.50%, 9/1/32 (XLCA)(1) | 3,000,000 | 2,243,040 |

Hesperia Public Financing Auth. Tax Allocation Rev., Series 2007 A, (Redevelopment and Housing), 5.50%, 9/1/37 (XLCA)(1) | 2,025,000 | 1,452,431 |

| Highland Community Facilities District No. 2001-1 Special Tax Rev., 6.45%, 9/1/28 | 2,000,000 | 2,000,000 |

Independent Cities Finance Auth. Mobile Home Park Rev., Series 2011 A, (Castle Mobile Estates), 6.75%, 8/15/46(1) | 2,500,000 | 2,554,375 |

| Independent Cities Lease Finance Auth. Rev., Series 2004 A, (Morgan Hill - Hacienda Valley Mobile Estates), 5.90%, 11/15/34 | 2,235,000 | 2,129,106 |

| Independent Cities Lease Finance Auth. Rev., Series 2006 B, (San Juan Mobile Estates), 5.55%, 5/15/31 | 500,000 | 447,590 |

13

Principal Amount | Value |

| Independent Cities Lease Finance Auth. Rev., Series 2006 B, (San Juan Mobile Estates), 5.85%, 5/15/41 | $1,150,000 | $1,016,543 |

| Independent Cities Lease Finance Auth. Rev., Series 2007 A, (Santa Rosa Leisure Mobilehome Park), 5.70%, 11/15/47 | 3,430,000 | 3,090,361 |

| Irvine Unified School District Special Tax Rev., (Community Facilities District No. 06-1), 6.70%, 9/1/35 | 1,000,000 | 1,061,700 |

| Jurupa Community Services District Special Tax Rev., Series 2008 A, (Community Facilities District No. 25), 8.875%, 9/1/38 | 2,000,000 | 2,223,420 |

| Lake Elsinore Community Facilities District No. 2004-3 Special Tax Rev., Series 2005 A, (Rosetta Canyon Improvement Area No. 1), 5.25%, 9/1/35 | 1,225,000 | 1,045,440 |

| Lake Elsinore Community Facilities District No. 2004-3 Special Tax Rev., Series 2006 A, (Rosetta Canyon Improvement Area No. 2), 5.25%, 9/1/37 | 5,000,000 | 4,198,850 |

| Lake Elsinore Community Facilities District No. 2005-1 Special Tax Rev., Series 2006 A, 5.35%, 9/1/36 | 1,100,000 | 962,819 |

| Lake Elsinore Community Facilities District No. 2005-2 Special Tax Rev., Series 2005 A, (Alverhill Ranch Improvement Area A), 5.45%, 9/1/36 | 4,000,000 | 3,478,200 |

| Lake Elsinore Unified School District Special Tax Rev., (Community Facilities District No. 2005-1, Improvement Area A), 5.40%, 9/1/35 | 2,245,000 | 1,987,072 |

Lincoln Community Facilities District No. 2003-1 Special Tax Rev., (Lincoln Crossing), 6.00%, 9/1/13, Prerefunded at 102% of Par(3) | 1,775,000 | 1,996,059 |

Los Angeles Community College District GO, Series 2008 F1, (Election of 2003), 5.00%, 8/1/27(1) | 2,000,000 | 2,149,120 |

| Los Angeles Community Facilities District No. 3 Special Tax Rev., (Cascades Business Park & Golf Course), 6.40%, 9/1/22 | 1,310,000 | 1,317,402 |

Los Angeles Department of Airports Rev., Series 2008 C, (Los Angeles International Airport), 5.25%, 5/15/25(1) | 2,000,000 | 2,163,360 |

| Milpitas Improvement Bond Act of 1915 Special Assessment Rev., Series 1996 A, (Local Improvement District No 18), 6.75%, 9/2/16 | 1,120,000 | 1,132,723 |

Modesto Irrigation District COP, Series 2009 A, (Capital Improvements), 6.00%, 10/1/39(1) | 3,000,000 | 3,193,110 |

Montebello Community Redevelopment Agency Tax Allocation Rev., Series 2009 A, (Montebello Hills Redevelopment), 8.10%, 3/1/27(1) | 2,000,000 | 2,200,040 |

Moorpark Mobile Home Park Rev., Series 2011 A, (Villa Delaware Arroyo), 6.50%, 5/15/41(1) | 4,000,000 | 4,033,840 |

| Moreno Valley Unified School District Special Tax Rev., (Community Facilities District No. 2002-1), 6.20%, 9/1/32 | 4,000,000 | 4,021,680 |

| Murrieta Community Facilities District No. 2002-2 Special Tax Rev., Series 2004 A, (The Oaks Improvement Area), 6.00%, 9/1/34 | 1,920,000 | 1,797,542 |

| Murrieta Improvement Bond Act of 1915 Special Tax Rev., (Community Facilities District No. 2000-1), 6.375%, 9/1/30 | 4,060,000 | 4,061,137 |

Oakland Unified School District Alameda County GO, Series 2009 A, (Election of 2006), 6.125%, 8/1/29(1) | 2,500,000 | 2,683,575 |

Oceanside Community Development Commission Tax Allocation Rev., (Downtown Redevelopment), 5.70%, 9/1/25(1) | 3,500,000 | 3,401,475 |

14

Principal Amount | Value |

| Oceanside Community Facilities District No. 2001-1 Special Tax Rev., Series 2002 A, (Morrow Hills Development), 6.20%, 9/1/32 | $2,435,000 | $2,280,645 |

| Orange County Community Facilities District Special Tax Rev., (No. 06-1-Delaware Rio Public Improvements), 6.00%, 10/1/40 | 1,375,000 | 1,363,698 |

Oxnard School District GO, Series 2001 A, 5.75%, 8/1/30 (NATL)(1) | 3,000,000 | 3,235,920 |

| Palomar Pomerado Health Care District COP, 6.75%, 11/1/39 | 4,000,000 | 4,080,360 |

| Palomar Pomerado Health Care District COP, 6.00%, 11/1/41 | 1,145,000 | 1,073,884 |

Palomar Pomerado Health Care District COP, (Indian Health Council, Inc.), 6.25%, 10/1/29(1) | 2,345,000 | 2,356,022 |

| Perris Public Financing Auth. Special Tax Rev., Series 2003 A, 6.25%, 9/1/33 | 2,955,000 | 2,961,205 |

| Perris Public Financing Auth. Special Tax Rev., Series 2004 A, 6.125%, 9/1/34 | 2,995,000 | 2,960,438 |

| Perris Public Financing Auth. Special Tax Rev., Series 2008 A, (Community Facilities District No. 2005-4), 6.60%, 9/1/38 | 2,210,000 | 2,100,848 |

Pleasant Valley School District/Ventura County GO, Series 2002 A, 5.85%, 8/1/31 (NATL)(1) | 4,835,000 | 5,224,846 |

| Poway Unified School District Public Financing Auth. Rev., 7.875%, 9/15/39 | 4,000,000 | 4,284,480 |

| Rancho Cordova Community Facilities District No. 2003-1 Special Tax Rev., (Sunridge Anatolia), 5.375%, 9/1/37 | 3,000,000 | 2,536,290 |

| Rancho Cordova Community Facilities District No. 2004-1 Special Tax Rev., (Sunridge Park Area), 6.125%, 9/1/37 | 5,000,000 | 4,677,300 |

Riverside County COP, 5.75%, 11/1/31 (NATL)(1) | 2,365,000 | 2,427,696 |

| Riverside County Improvement Bond Act of 1915 Special Assessment Rev., (District No. 168-Rivercrest), 6.70%, 9/2/26 | 1,875,000 | 1,882,688 |

Riverside County Redevelopment Agency Tax Allocation Rev., Series 2010 E, (Interstate 215 Corridor), 6.25%, 10/1/30(1) | 2,200,000 | 2,283,160 |

| Riverside Unified School District Special Tax Rev., (Community Facilities District No. 13, Improvement Area 1), 5.375%, 9/1/34 | 2,000,000 | 1,697,560 |

| Riverside Unified School District Special Tax Rev., Series 2005 A, (Community Facilities School District No. 15, Improvement Area 2), 5.25%, 9/1/30 | 1,000,000 | 917,770 |

| Rohnert Park Finance Auth. Rev., Series 2001 A, (Las Casitas de Sonoma), 6.40%, 4/15/36 | 4,315,000 | 4,316,424 |

| Romoland School District Special Tax Rev., (Community Facilities District No. 1, Improvement Area 1), 5.40%, 9/1/36 | 4,000,000 | 3,505,280 |

| Roseville Community Facilities District No. 1 Special Tax Rev., (The Fountains), 6.125%, 9/1/38 | 2,600,000 | 2,544,620 |

Roseville Finance Auth. Electric System Rev., 5.00%, 2/1/37(1) | 1,295,000 | 1,323,050 |

Sacramento Airport System Rev., Series 2009 D, (Grant Revenue Bonds), 6.00%, 7/1/35(1) | 4,000,000 | 4,262,160 |

Sacramento County COP, 5.75%, 2/1/30(1) | 3,000,000 | 3,136,110 |

Sacramento Municipal Utility District Electric Rev., Series 1997 K, 5.25%, 7/1/24 (Ambac)(1) | 4,000,000 | 4,498,720 |

| Sacramento Special Tax Rev. (North Natomas Community Facilities District No.1), 6.30%, 9/1/26 | 3,840,000 | 3,848,218 |

San Buenaventura Rev., (Community Memorial Health System), 7.50%, 12/1/41(1) | 3,850,000 | 3,822,010 |

15

Principal Amount | Value |

San Buenaventura City COP, (Wastewater Revenue), 5.00%, 3/1/29 (NATL)(1) | $1,975,000 | $2,018,944 |

San Diego Redevelopment Agency Tax Allocation Rev., Series 2009 A, (North Park Redevelopment), 7.00%, 11/1/39(1) | 3,000,000 | 3,189,150 |

San Francisco City and County Airports Commission Rev., Series 2008 34D, (San Francisco International Airport), 5.25%, 5/1/26(1) | 3,000,000 | 3,205,620 |

San Francisco City and County Airports Commission Rev., Series 2011 D, 5.00%, 5/1/31(1) | 5,390,000 | 5,644,246 |

San Francisco City and County Redevelopment Agency Lease Rev., (George R. Mascone), 0.00%, 7/1/13(1)(2) | 1,250,000 | 1,221,763 |

San Francisco City and County Redevelopment Financing Auth. Tax Allocation Rev., Series 2009 D, (Mission Bay South Redevelopment), 6.625%, 8/1/39(1) | 2,000,000 | 2,037,900 |

San Francisco City and County Redevelopment Financing Auth. Tax Allocation Rev., Series 2011 C, (Mission Bay South Redevelopment), 6.75%, 8/1/41(1) | 1,000,000 | 1,060,230 |

San Francisco City and County Redevelopment Financing Auth. Tax Allocation Rev., Series 2011 D, (Mission Bay South Redevelopment), 7.00%, 8/1/41(1) | 1,250,000 | 1,311,350 |

San Jose Airport Rev., Series 2011 A2, 5.25%, 3/1/34(1) | 2,605,000 | 2,643,945 |

| San Marcos Public Facilities Auth. Special Tax Rev., Series 2004 A, 5.45%, 9/1/24 | 2,790,000 | 2,718,074 |

Santa Barbara County Water COP, 5.50%, 9/1/22 (Ambac)(1) | 3,005,000 | 3,143,951 |

Santa Cruz County Redevelopment Agency Tax Allocation Rev., Series 2009 A, (Live Oak/Soquel Community Improvement), 7.00%, 9/1/36(1) | 3,000,000 | 3,327,000 |

| Santa Margarita Water District Special Tax Rev., Series 2011 A, (Community Facilities District No. 99-1), 5.25%, 9/1/29 | 1,000,000 | 1,008,520 |

| Santa Margarita Water District Special Tax Rev., Series 2011 B, (Community Facilities District No. 99-1), 5.875%, 9/1/38 | 650,000 | 656,604 |

Shasta Lake Public Finance Auth. Rev., (Electrical Enterprise), 6.25%, 4/1/13, Prerefunded at 102% of Par(1)(3) | 7,755,000 | 8,643,645 |

| Soledad Improvement Bond Act of 1915 District No. 2002-01 Special Assessment Rev., (Diamond Ridge), 6.75%, 9/2/33 | 2,160,000 | 2,173,586 |

Southern California Public Power Auth. Rev., (Southern Transmission), 0.00%, 7/1/14 (NATL-IBC)(1)(5) | 2,400,000 | 2,267,136 |

Southern California Public Power Auth. Rev., (Southern Transmission), 0.00%, 7/1/15 (NATL-IBC)(1)(5) | 1,250,000 | 1,144,875 |

Southern California Public Power Auth. Rev., Series 2008 A, (Southern Transmission), 5.00%, 7/1/22(1) | 5,750,000 | 6,485,827 |

Stockton Community Facilities District Special Tax Rev., (Spanos Park West No. 2001-1), 6.375%, 9/1/12, Prerefunded at 102% of Par(1)(3) | 4,195,000 | 4,529,258 |

| Sunnyvale Community Facilities District No. 1 Special Tax Rev., 7.75%, 8/1/32 | 6,500,000 | 6,499,610 |

Susanville Public Financing Auth. Rev., Series 2010 B, (Utility Enterprises), 6.00%, 6/1/45(1) | 3,000,000 | 2,944,320 |

Tahoe-Truckee Unified School District GO, Series 1999 A, (Improvement District No. 2), 0.00%, 8/1/22 (NATL/FGIC)(1)(2) | 2,690,000 | 1,514,658 |

Tahoe-Truckee Unified School District GO, Series 1999 A, (Improvement District No. 2), 0.00%, 8/1/23 (NATL/FGIC)(1)(2) | 2,220,000 | 1,160,105 |

16

Principal Amount | Value |

| Tracy Community Facilities District No. 2006-1 Special Tax Rev., (NEI Phase II), 5.75%, 9/1/36 | $3,105,000 | $2,702,281 |

| Tri-Dam Power Auth. Rev., 4.00%, 5/1/16 | 2,165,000 | 2,273,683 |

| Tri-Dam Power Auth. Rev., 4.00%, 11/1/16 | 2,165,000 | 2,275,891 |

Tuolumne Wind Project Auth. Rev., Series 2009 A, 5.875%, 1/1/29(1) | 2,000,000 | 2,217,420 |

Turlock Health Facility COP, Series 2007 B, (Emanuel Medical Center, Inc.), 5.50%, 10/15/37(1) | 1,000,000 | 857,200 |

Turlock Public Financing Auth. Tax Allocation Rev., 7.50%, 9/1/39(1) | 2,770,000 | 2,916,533 |

| Tustin Community Facilities District No. 06-1 Special Tax Rev., Series 2007 A, (Tustin Legacy/Columbus Villages), 6.00%, 9/1/36 | 5,000,000 | 4,861,400 |

| Tustin Community Facilities District No. 07-1 Special Tax Rev., (Tustin Legacy/Retail Center), 6.00%, 9/1/37 | 1,300,000 | 1,261,741 |

Tustin Unified School District Special Tax Rev., (Community Facilities District No. 06-1), 5.75%, 9/1/30(1) | 1,000,000 | 1,009,790 |

Tustin Unified School District Special Tax Rev., (Community Facilities District No. 06-1), 6.00%, 9/1/40(1) | 1,500,000 | 1,511,400 |

Twin Rivers Unified School District COP, (Facility Bridge Program), VRDN, 3.50%, 5/31/13 (AGM)(1) | 4,000,000 | 4,003,240 |

| Val Verde Unified School District Special Tax Rev., (Community Facilities District No. 1, Improvement Area A), 5.40%, 9/1/30 | 2,500,000 | 2,193,025 |

| Val Verde Unified School District Special Tax Rev., (Community Facilities District No. 1, Improvement Area A), 5.45%, 9/1/36 | 2,600,000 | 2,190,656 |

Ventura County Community College District GO, Series 2008 C, (Election of 2002), 5.50%, 8/1/33(1) | 1,600,000 | 1,729,152 |

Vernon Electric System Rev., Series 2009 A, 5.125%, 8/1/21(1) | 5,000,000 | 4,843,050 |

| West Sacramento Community Facilities District No. 20 Special Tax Rev., 5.30%, 9/1/35 | 1,740,000 | 1,496,243 |

Yosemite Community College District GO, (Election of 2004), 0.00%, 8/1/16 (AGM)(1)(2) | 3,545,000 | 3,068,304 |

| Yuba City Redevelopment Agency Tax Allocation Rev., 5.70%, 9/1/24 | 2,270,000 | 2,103,995 |

Yuba City Unified School District GO, 0.00%, 3/1/25 (NATL/FGIC)(1)(2) | 1,500,000 | 624,045 |

| 472,202,501 | ||

| GUAM — 0.7% | ||

Guam Government GO, Series 2009 A, 7.00%, 11/15/39(1) | 3,300,000 | 3,407,250 |

| PUERTO RICO — 2.2% | ||

Puerto Rico GO, Series 2006 A, (Public Improvement), 5.25%, 7/1/30(1) | 1,145,000 | 1,109,642 |

Puerto Rico GO, Series 2008 A, 6.00%, 7/1/38(1) | 2,500,000 | 2,523,425 |

Puerto Rico GO, Series 2009 B, (Public Improvement), 6.00%, 7/1/39(1) | 2,000,000 | 2,020,940 |

Puerto Rico Sales Tax Financing Corp. Rev., Series 2007 A, VRN, 1.10%, 11/1/11(1) | 10,000,000 | 5,374,800 |

| 11,028,807 | ||

| U.S. VIRGIN ISLANDS — 0.7% | ||

| Virgin Islands Public Finance Auth. Rev., Series 2009 A, (Diageo Matching Fund Bonds), 6.75%, 10/1/37 | 2,000,000 | 2,123,740 |

Virgin Islands Public Finance Auth. Rev., Series 2010 B, (Subordinated Lien), 5.25%, 10/1/29(1) | 1,500,000 | 1,492,140 |

| 3,615,880 | ||

TOTAL INVESTMENT SECURITIES — 98.5%(Cost $488,953,321) | 490,254,438 | |

| OTHER ASSETS AND LIABILITIES — 1.5% | 7,421,074 | |

| TOTAL NET ASSETS — 100.0% | $497,675,512 | |

17

| Futures Contracts | ||||

| Contracts Purchased | Expiration Date | Underlying Face Amount at Value | Unrealized Gain (Loss) | |

| 29 | U.S. Long Bond | December 2011 | $3,944,906 | $(18,870) |

| Contracts Sold | Expiration Date | Underlying Face Amount at Value | Unrealized Gain (Loss) | |

| 92 | U.S. Treasury 2-Year Notes | December 2011 | $20,286,000 | $1,230 |

Notes to Schedule of Investments

AGM = Assured Guaranty Municipal Corporation

Ambac = Ambac Assurance Corporation

Ambac-TCRS = Ambac Assurance Corporation - Transferrable Custodial Receipts

COP = Certificates of Participation

FGIC = Financial Guaranty Insurance Company

GO = General Obligation

NATL = National Public Finance Guarantee Corporation

NATL-IBC = National Public Finance Guarantee Corporation - Insured Bond Certificates

VRDN = Variable Rate Demand Note. Interest reset date is indicated. Rate shown is effective at the period end.

VRN = Variable Rate Note. Interest reset date is indicated. Rate shown is effective at the period end.

XLCA = XL Capital Ltd.

| (1) | Security, or a portion thereof, has been segregated for futures contracts. At the period end, the aggregate value of securities pledged was $24,231,000. |

| (2) | Convertible capital appreciation bond. These securities are issued with a zero-coupon and become interest bearing at a predetermined rate and date and are issued at a substantial discount from their value at maturity. Interest reset or final maturity date is indicated, as applicable. Rate shown is effective at the period end. |

| (3) | Escrowed to maturity in U.S. government securities or state and local government securities. |

| (4) | Security was purchased under Rule 144A of the Securities Act of 1933 or is a private placement and, unless registered under the Act or exempted from registration, may only be sold to qualified institutional investors. The aggregate value of these securities at the period end was $3,209,978, which represented 0.6% of total net assets. |

| (5) | Security is a zero-coupon municipal bond. Zero-coupon securities are issued at a substantial discount from their value at maturity. |

See Notes to Financial Statements.

18

| AUGUST 31, 2011 | ||||

| Assets | ||||

| Investment securities, at value (cost of $488,953,321) | $490,254,438 | |||

| Cash | 504,981 | |||

| Receivable for investments sold | 896,550 | |||

| Receivable for capital shares sold | 687,907 | |||

| Interest receivable | 9,353,474 | |||

| 501,697,350 | ||||

| Liabilities | ||||

| Payable for investments purchased | 2,485,846 | |||

| Payable for capital shares redeemed | 723,702 | |||

| Payable for variation margin on futures contracts | 37,156 | |||

| Accrued management fees | 210,457 | |||

| Distribution and service fees payable | 39,898 | |||

| Dividends payable | 524,779 | |||

| 4,021,838 | ||||

| Net Assets | $497,675,512 | |||

| Net Assets Consist of: | ||||

| Capital paid in | $535,773,022 | |||

| Accumulated net realized loss | (39,380,987 | ) | ||

| Net unrealized appreciation | 1,283,477 | |||

| $497,675,512 | ||||

| Net assets | Shares outstanding | Net asset value per share | ||||||

| Investor Class | $374,466,726 | 39,836,377 | $9.40 | |||||

| Institutional Class | $9,784,296 | 1,041,092 | $9.40 | |||||

| A Class | $89,027,893 | 9,470,508 | $9.40 | * | ||||

| B Class | $479,232 | 50,977 | $9.40 | |||||

| C Class | $23,917,365 | 2,544,027 | $9.40 | |||||

| * | Maximum offering price $9.84 (net asset value divided by 0.955) |

See Notes to Financial Statements.

19

| YEAR ENDED AUGUST 31, 2011 | ||||

| Investment Income (Loss) | ||||

| Income: | ||||

| Interest | $28,463,245 | |||

| Expenses: | ||||

| Management fees | 2,537,831 | |||

| Distribution and service fees: | ||||

| A Class | 239,351 | |||

| B Class | 7,209 | |||

| C Class | 254,137 | |||

| Trustees’ fees and expenses | 27,929 | |||

| Other expenses | 2,162 | |||

| 3,068,619 | ||||

| Fees waived | (93,432 | ) | ||

| 2,975,187 | ||||

| Net investment income (loss) | 25,488,058 | |||

| Realized and Unrealized Gain (Loss) | ||||

| Net realized gain (loss) on: | ||||

| Investment transactions | (5,982,536 | ) | ||

| Futures contract transactions | (1,952,320 | ) | ||

| (7,934,856 | ) | |||

| Change in net unrealized appreciation (depreciation) on: | ||||

| Investments | (9,827,929 | ) | ||

| Futures contracts | (148,880 | ) | ||

| (9,976,809 | ) | |||

| Net realized and unrealized gain (loss) | (17,911,665 | ) | ||

| Net Increase (Decrease) in Net Assets Resulting from Operations | $7,576,393 | |||

See Notes to Financial Statements.

20

| YEARS ENDED AUGUST 31, 2011 AND AUGUST 31, 2010 | ||||||||

| Increase (Decrease) in Net Assets | 2011 | 2010 | ||||||

| Operations | ||||||||

| Net investment income (loss) | $25,488,058 | $26,407,392 | ||||||

| Net realized gain (loss) | (7,934,856 | ) | (4,867,527 | ) | ||||

| Change in net unrealized appreciation (depreciation) | (9,976,809 | ) | 50,932,301 | |||||

| Net increase (decrease) in net assets resulting from operations | 7,576,393 | 72,472,166 | ||||||

| Distributions to Shareholders | ||||||||

| From net investment income: | ||||||||

| Investor Class | (19,320,213 | ) | (20,168,524 | ) | ||||

| Institutional Class | (413,005 | ) | (668 | ) | ||||

| A Class | (4,626,144 | ) | (4,958,395 | ) | ||||

| B Class | (29,339 | ) | (40,637 | ) | ||||

| C Class | (1,036,820 | ) | (1,241,451 | ) | ||||

| Decrease in net assets from distributions | (25,425,521 | ) | (26,409,675 | ) | ||||

| Capital Share Transactions | ||||||||

| Net increase (decrease) in net assets from capital share transactions | (39,890,836 | ) | 3,228,416 | |||||

| Net increase (decrease) in net assets | (57,739,964 | ) | 49,290,907 | |||||

| Net Assets | ||||||||

| Beginning of period | 555,415,476 | 506,124,569 | ||||||

| End of period | $497,675,512 | $555,415,476 | ||||||

| Accumulated net investment loss | — | $(50,885 | ) | |||||

See Notes to Financial Statements.

21

1. Organization

American Century California Tax-Free and Municipal Funds (the trust) is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company and is organized as a Massachusetts business trust. California High-Yield Municipal Fund (the fund) is one fund in a series issued by the trust. The fund is nondiversified as defined under the 1940 Act. The fund’s investment objective is to seek high current income that is exempt from federal and California income taxes. The fund pursues its objective by investing a portion of its assets in lower-rated and unrated municipal securities.

The fund is authorized to issue the Investor Class, the Institutional Class, the A Class, the B Class and the C Class. The A Class may incur an initial sales charge. The A Class, B Class and C Class may be subject to a contingent deferred sales charge. The share classes differ principally in their respective sales charges and distribution and shareholder servicing expenses and arrangements. The Institutional Class is made available to institutional shareholders or through financial intermediaries whose clients do not require the same level of shareholder and administrative services as shareholders of other classes. As a result, the Institutional Class is charged a lower unified management fee. Sale of the Institutional Class commenced on March 1, 2010. On October 21, 2011, all outstanding B Class shares were converted to A Class shares and the fund discontinued issuance of the B Class.

2. Significant Accounting Policies

The following is a summary of significant accounting policies consistently followed by the fund in preparation of its financial statements. The financial statements are prepared in conformity with accounting principles generally accepted in the United States of America, which may require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from these estimates.

Investment Valuations — The fund determines the fair value of its investments and computes its net asset value per share as of the close of regular trading (usually 4 p.m. Eastern time) on the New York Stock Exchange (NYSE) on each day the NYSE is open.

Debt securities maturing in greater than 60 days at the time of purchase are valued at the evaluated mean as provided by independent pricing services or at the mean of the most recent bid and asked prices as provided by investment dealers. Debt securities maturing within 60 days at the time of purchase may be valued at cost, plus or minus any amortized discount or premium or at the evaluated mean as provided by an independent pricing service. Evaluated mean prices are commonly derived through utilization of market models, which may consider, among other factors, trade data, quotations from dealers and active market makers, relevant yield curve and spread data, related sector levels, creditworthiness, and other relevant market information on the same or comparable securities.

Exchange-traded futures contracts are valued at the settlement price as provided by the appropriate clearing corporation.

If the fund determines that the market price for a portfolio security is not readily available or the valuation methods mentioned above do not reflect a security’s fair value, such security is valued as determined in good faith by the Board of Trustees or its designee, in accordance with procedures adopted by the Board of Trustees. Circumstances that may cause the fund to use these procedures to value a security include, but are not limited to: a security has been declared in default; trading in a security has been halted during the trading day; there is a foreign market holiday and no trading occurred; or an event occurred between the close of a foreign exchange and the NYSE that may affect the value of a security.

Security Transactions — Security transactions are accounted for as of the trade date. Net realized gains and losses are determined on the identified cost basis, which is also used for federal income tax purposes.

Investment Income — Interest income is recorded on the accrual basis and includes accretion of discounts and amortization of premiums.

22

Income Tax Status — It is the fund’s policy to distribute substantially all net investment income and net realized gains to shareholders and to otherwise qualify as a regulated investment company under provisions of the Internal Revenue Code. The fund is no longer subject to examination by tax authorities for years prior to 2008. At this time, management believes there are no uncertain tax positions which, based on their technical merit, would not be sustained upon examination and for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months. Accordingly, no provision has been made for federal or state income taxes.

When-Issued — The fund may engage in securities transactions on a when-issued basis. Under these arrangements, the securities’ prices and yields are fixed on the date of the commitment, but payment and delivery are scheduled for a future date. During this period, securities are subject to market fluctuations. The fund will segregate cash, cash equivalents or other appropriate liquid securities on its records in amounts sufficient to meet the purchase price.

Multiple Class — All shares of the fund represent an equal pro rata interest in the net assets of the class to which such shares belong, and have identical voting, dividend, liquidation and other rights and the same terms and conditions, except for class specific expenses and exclusive rights to vote on matters affecting only individual classes. Income, non-class specific expenses, and realized and unrealized capital gains and losses of the fund are allocated to each class of shares based on their relative net assets.

Distributions to Shareholders — Distributions from net investment income are declared daily and paid monthly. Distributions from net realized gains, if any, are generally declared and paid annually.

Indemnifications — Under the trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the fund. In addition, in the normal course of business, the fund enters into contracts that provide general indemnifications. The maximum exposure under these arrangements is unknown as this would involve future claims that may be made against a fund. The risk of material loss from such claims is considered by management to be remote.

3. Fees and Transactions with Related Parties

Management Fees — The trust has entered into a management agreement with American Century Investment Management, Inc. (ACIM) (the investment advisor), under which ACIM provides the fund with investment advisory and management services in exchange for a single, unified management fee (the fee) per class. The agreement provides that all expenses of managing and operating the fund, except distribution and service fees, brokerage expenses, taxes, interest, fees and expenses of the independent trustees (including legal counsel fees), and extraordinary expenses, will be paid by ACIM. The fee is computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The fee consists of (1) an Investment Category Fee based on the daily net assets of the fund and certain other accounts managed by the investment advisor that are in the same broad investment category as the fund and (2) a Complex Fee based on the assets of all the funds in the American Century Investments family of funds. The rates for the Investment Category Fee range from 0.1925% to 0.3100%. The rates for the Complex Fee range from 0.2500% to 0.3100% for the Investor Class, A Class, B Class and C Class. The Institutional Class is 0.2000% less at each point within the Complex Fee range. From September 1, 2010 through July 31, 2011, the investment advisor voluntarily agreed to waive 0.020% of its management fee. The total amount of the waiver for each class for the year ended August 31, 2011 was $69,628, $1,366, $17,629, $136 and $4,673 for the Investor Class, Institutional Class, A Class, B Class and C Class, respectively. The effective annual management fee before waiver for each class for the year ended August 31, 2011 was 0.50% for the Investor Class, A Class, B Class and C Class and 0.30% for the Institutional Class. The effective annual management fee after waiver for each class for the year ended August 31, 2011 was 0.48% for the Investor Class, A Class, B Class and C Class and 0.28% for the Institutional Class.

Distribution and Service Fees — The Board of Trustees has adopted a separate Master Distribution and Individual Shareholder Services Plan for each of the A Class, B Class and C Class (collectively the plans), pursuant to Rule 12b-1 of the 1940 Act. The plans provide that the A Class will pay American Century Investment Services, Inc. (ACIS) an annual distribution and service fee of 0.25%. The plans provide that the B Class and C Class will

23

each pay ACIS an annual distribution and service fee of 1.00%, of which 0.25% is paid for individual shareholder services and 0.75% is paid for distribution services. The fees are computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The fees are used to pay financial intermediaries for distribution and individual shareholder services. Fees incurred under the plans during the year ended August 31, 2011 are detailed in the Statement of Operations.

Related Parties — Certain officers and trustees of the trust are also officers and/or directors of American Century Companies, Inc. (ACC), the parent of the trust’s investment advisor, ACIM, the distributor of the trust, ACIS, and the trust’s transfer agent, American Century Services, LLC.

The fund had a mutual funds services agreement with J.P. Morgan Investor Services Co. (JPMIS). JPMorgan Chase Bank (JPMCB) was a custodian of the fund. JPMIS and JPMCB are wholly owned subsidiaries of JPMorgan Chase & Co. (JPM). Prior to August 31, 2011, JPM was an equity investor in ACC. The services provided to the fund by JPMIS and JPMCB terminated on July 31, 2011.

4. Investment Transactions

Purchases and sales of investment securities, excluding short-term investments, for the year ended August 31, 2011 were $184,695,959 and $231,765,455 respectively.

5. Capital Share Transactions

Transactions in shares of the fund were as follows (unlimited number of shares authorized):

| Year ended August 31, 2011 | Year ended August 31, 2010(1) | |||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||

| Investor Class | ||||||||||||||||

| Sold | 8,511,978 | $79,214,553 | 8,560,326 | $79,770,530 | ||||||||||||

| Issued in reinvestment of distributions | 1,577,617 | 14,566,298 | 1,630,497 | 15,236,776 | ||||||||||||

| Redeemed | (13,359,965 | ) | (123,867,707 | ) | (9,144,211 | ) | (85,139,104 | ) | ||||||||

| (3,270,370 | ) | (30,086,856 | ) | 1,046,612 | 9,868,202 | |||||||||||

| Institutional Class | ||||||||||||||||

| Sold | 1,331,279 | 12,513,170 | 2,694 | 25,000 | ||||||||||||

| Issued in reinvestment of distributions | 45,139 | 412,959 | 71 | 668 | ||||||||||||

| Redeemed | (338,091 | ) | (3,045,420 | ) | — | — | ||||||||||

| 1,038,327 | 9,880,709 | 2,765 | 25,668 | |||||||||||||

| A Class | ||||||||||||||||

| Sold | 2,586,970 | 24,073,713 | 2,306,535 | 21,540,276 | ||||||||||||

| Issued in reinvestment of distributions | 360,424 | 3,326,466 | 370,535 | 3,462,892 | ||||||||||||

| Redeemed | (4,480,944 | ) | (41,206,399 | ) | (3,064,884 | ) | (28,530,752 | ) | ||||||||

| (1,533,550 | ) | (13,806,220 | ) | (387,814 | ) | (3,527,584 | ) | |||||||||

| B Class | ||||||||||||||||

| Sold | 63 | 589 | 191 | 1,776 | ||||||||||||

| Issued in reinvestment of distributions | 2,275 | 21,041 | 2,614 | 24,493 | ||||||||||||

| Redeemed | (56,890 | ) | (523,069 | ) | (4,748 | ) | (44,265 | ) | ||||||||

| (54,552 | ) | (501,439 | ) | (1,943 | ) | (17,996 | ) | |||||||||

| C Class | ||||||||||||||||

| Sold | 316,280 | 2,938,770 | 304,086 | 2,826,002 | ||||||||||||

| Issued in reinvestment of distributions | 52,701 | 486,787 | 61,306 | 572,964 | ||||||||||||

| Redeemed | (951,568 | ) | (8,802,587 | ) | (702,493 | ) | (6,518,840 | ) | ||||||||

| (582,587 | ) | (5,377,030 | ) | (337,101 | ) | (3,119,874 | ) | |||||||||

| Net increase (decrease) | (4,402,732 | ) | $(39,890,836 | ) | 322,519 | $3,228,416 | ||||||||||

| (1) | March 1, 2010 (commencement of sale) through August 31, 2010 for the Institutional Class. |

24

6. Fair Value Measurements

The fund’s securities valuation process is based on several considerations and may use multiple inputs to determine the fair value of the positions held by the fund. In conformity with accounting principles generally accepted in the United States of America, the inputs used to determine a valuation are classified into three broad levels as follows:

| • | Level 1 valuation inputs consist of unadjusted quoted prices in an active market for identical securities; |

| • | Level 2 valuation inputs consist of direct or indirect observable market data (including quoted prices for similar securities, evaluations of subsequent market events, interest rates, prepayment speeds, credit risk, etc.); or |

| • | Level 3 valuation inputs consist of unobservable data (including a fund’s own assumptions). |

The level classification is based on the lowest level input that is significant to the fair valuation measurement. The valuation inputs are not necessarily an indication of the risks associated with investing in these securities or other financial instruments.

As of period end, the fund’s municipal securities and unrealized gain (loss) on futures contracts were classified as Level 2 and Level 1, respectively. The Schedule of Investments provides additional information on the fund’s portfolio holdings.

7. Derivative Instruments

Interest Rate Risk — The fund is subject to interest rate risk in the normal course of pursuing its investment objectives. The value of bonds generally declines as interest rates rise. A fund may enter into futures contracts based on a bond index or a specific underlying security. A fund may purchase futures contracts to gain exposure to increases in market value or sell futures contracts to protect against a decline in market value. Upon entering into a futures contract, a fund will segregate cash, cash equivalents or other appropriate liquid securities on its records in amounts sufficient to meet requirements. Subsequent payments (variation margin) are made or received daily, in cash, by a fund. The variation margin is equal to the daily change in the contract value and is recorded as unrealized gains and losses. A fund recognizes a realized gain or loss when the futures contract is closed or expires. Net realized and unrealized gains or losses occurring during the holding period of futures contracts are a component of net realized gain (loss) on futures contract transactions and change in net unrealized appreciation (depreciation) on futures contracts, respectively. One of the risks of entering into futures contracts is the possibility that the change in value of the contract may not correlate with the changes in value of the underlying securities. The fund frequently utilized interest rate risk derivative instruments throughout the reporting period, though the amounts held at period end as disclosed on the Schedule of Investments were lower than the fund’s typical volume during the period.

The value of interest rate risk derivative instruments as of August 31, 2011, is disclosed on the Statement of Assets and Liabilities as a liability of $37,156 in payable for variation margin on futures contracts. For the year ended August 31, 2011, the effect of interest rate risk derivative instruments on the Statement of Operations was $(1,952,320) in net realized gain (loss) on futures contract transactions and $(148,880) in change in net unrealized appreciation (depreciation) on futures contracts.

8. Risk Factors

The fund concentrates its investments in a single state and therefore may have more exposure to credit risk related to the state of California than a fund with a broader geographical diversification. The fund invests a portion of its assets in lower-rated debt securities, which are subject to substantial risks including price volatility, liquidity risk, and default risk.

25

9. Federal Tax Information

The tax character of distributions paid during the years ended August 31, 2011 and August 31, 2010 were as follows:

| 2011 | 2010 | |||||||

| Distributions Paid From | ||||||||

| Exempt income | $25,425,521 | $26,409,675 | ||||||

| Taxable ordinary income | — | — | ||||||

| Long-term capital gains | — | — | ||||||

The book-basis character of distributions made during the year from net investment income or net realized gains may differ from their ultimate characterization for federal income tax purposes. These differences reflect the differing character of certain income items and net realized gains and losses for financial statement and tax purposes, and may result in reclassification among certain capital accounts on the financial statements.

As of August 31, 2011, the federal tax cost of investments and the components of distributable earnings on a tax-basis were as follows:

| Federal tax cost of investments | $488,941,712 | |||

| Gross tax appreciation of investments | $18,630,691 | |||

| Gross tax depreciation of investments | (17,317,965 | ) | ||

| Net tax appreciation (depreciation) of investments | $1,312,726 | |||

| Net tax appreciation (depreciation) on derivatives | — | |||

| Other book-to-tax adjustments | $(215,547 | ) | ||

| Net tax appreciation (depreciation) | $1,097,179 | |||

| Accumulated capital losses | $(32,789,723 | ) | ||

| Capital loss deferral | $(6,404,966 | ) |

The difference between book-basis and tax-basis cost and unrealized appreciation (depreciation) is attributable primarily to the tax deferral on book-to-tax amortization policies and the realization for tax purposes of unrealized gains (losses) on futures contracts. Other book-to-tax adjustments are attributable primarily to the tax deferral of losses on straddle positions.

The accumulated capital losses represent net capital loss carryovers that may be used to offset future realized capital gains for federal income tax purposes. Future capital loss carryover utilization in any given year may be subject to Internal Revenue Code limitations. Capital loss carryovers expire as follows:

| 2015 | 2016 | 2017 | 2018 | 2019 |

| $(1,856,959) | $(59,454) | $(11,784,441) | $(12,885,340) | $(6,203,529) |

The capital loss deferral represents net capital losses incurred in the ten-month period ended August 31, 2011. The fund has elected to treat such losses as having been incurred in the following fiscal year for federal income tax purposes.

On December 22, 2010, the Regulated Investment Company Modernization Act of 2010 (the “Act”) was enacted, which changed various technical rules governing the tax treatment of regulated investment companies. The changes are generally effective for taxable years beginning after the date of enactment. Under the Act, the fund will be permitted to carry forward capital losses incurred in taxable years beginning after the date of enactment for an unlimited period. However, any losses incurred during those future taxable years will be required to be utilized prior to the losses incurred in pre-enactment taxable years, which carry an expiration date. As a result of this ordering rule, pre-enactment capital loss carryforwards may be more likely to expire unused.

26

| For a Share Outstanding Throughout the Years Ended August 31 (except as noted) | |||||||||||||

| Per-Share Data | Ratios and Supplemental Data | ||||||||||||

| Income From Investment Operations: | Distributions From: | Ratio to Average Net Assets of: | |||||||||||

Net Asset Value, Beginning of Period | Net Investment Income (Loss) | Net Realized and Unrealized Gain (Loss) | Total From Investment Operations | Net Investment Income | Net Asset Value, End of Period | Total Return(1) | Operating Expenses | Operating Expenses (before expense waiver) | Net Investment Income (Loss) | Net Investment Income (Loss) (before expense waiver) | Portfolio Turnover Rate | Net Assets, End of Period (in thousands) | |

| Investor Class | |||||||||||||

| 2011 | $9.69 | 0.47(2) | (0.29) | 0.18 | (0.47) | $9.40 | 2.07% | 0.49% | 0.51% | 5.10% | 5.08% | 37% | $374,467 |

| 2010 | $8.88 | 0.47(2) | 0.81 | 1.28 | (0.47) | $9.69 | 14.78% | 0.49% | 0.51% | 5.08% | 5.06% | 17% | $417,503 |

| 2009 | $9.50 | 0.48 | (0.62) | (0.14) | (0.48) | $8.88 | (1.16)% | 0.52% | 0.52% | 5.56% | 5.56% | 26% | $373,313 |

| 2008 | $9.90 | 0.48 | (0.40) | 0.08 | (0.48) | $9.50 | 0.81% | 0.52% | 0.52% | 4.91% | 4.91% | 31% | $455,741 |

| 2007 | $10.25 | 0.48 | (0.35) | 0.13 | (0.48) | $9.90 | 1.22% | 0.52% | 0.52% | 4.70% | 4.70% | 17% | $467,477 |

| Institutional Class | |||||||||||||

| 2011 | $9.69 | 0.49(2) | (0.29) | 0.20 | (0.49) | $9.40 | 2.27% | 0.29% | 0.31% | 5.30% | 5.28% | 37% | $9,784 |

2010(3) | $9.28 | 0.25(2) | 0.41 | 0.66 | (0.25) | $9.69 | 7.16% | 0.29%(4) | 0.31%(4) | 5.24%(4) | 5.22%(4) | 17%(5) | $27 |

| A Class | |||||||||||||