UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-3732

MFS VARIABLE INSURANCE TRUST II

(Exact name of registrant as specified in charter)

500 Boylston Street, Boston, Massachusetts 02116

(Address of principal executive offices) (Zip code)

Susan S. Newton

Massachusetts Financial Services Company

500 Boylston Street

Boston, Massachusetts 02116

(Name and address of agents for service)

Registrant’s telephone number, including area code: (617) 954-5000

Date of fiscal year end: December 31*

Date of reporting period: December 31, 2007

| * | The Strategic Growth Series was reorganized into the MFS Massachusetts Investors Growth Stock Portfolio, and Capital Opportunities Series was reorganized into MFS Core Equity Portfolio, all series of the Registrant, as of June 22, 2007. |

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

Reports for the Capital Opportunities Series and the Strategic Growth Series are not included because the Funds did not have any shareholders at period end. Please see note above.

MFS® Variable Insurance Trust IISM

Annual report

MFS® Value Portfolio

(formerly Value Series)

12/31/07

EIS-ANN

MFS® VALUE PORTFOLIO

(formerly Value Series)

The report is prepared for the general information of contract owners. It is authorized for distribution to prospective investors only when preceded or accompanied by a current prospectus.

NOT FDIC INSURED MAY LOSE VALUE NO BANK OR CREDIT UNION GUARANTEE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY OR NCUA/NCUSIF

LETTER FROM THE CEO

Dear Contract Owners:

The past year has been a great example of why investors should keep their eyes on the long term.

In 2006 the Dow Jones Industrial Average returned 19% and was fairly stable. This year we have seen a greater level of volatility than has been experienced in recent years. The Dow hit several new highs but also experienced swift drops as a global credit crisis swept through markets, spurred by defaults on U.S. subprime loans and a liquidity crunch. Still, even with this volatility, the Dow ended the first three quarters of 2007 with a return near 13%.

U.S. Treasury bonds gained ground, especially in the third quarter as investors sought less risky asset classes. The spreads of many lower-quality debt investments widened.

In 2007 the U.S. dollar fell against the euro, oil prices hit their highest levels yet, and gold spiked to its steepest price in 28 years. Around the globe, stocks sold off as risk aversion mounted. As we have said before, markets can be volatile, and investors should make sure they have an investment plan that can carry them through the peaks and troughs.

If you are focused on a long-term investment strategy, the short-term ups and downs of the markets should not necessarily dictate portfolio action on your part. In our view, investors who remain committed to a long-term plan are more likely to achieve their financial goals.

In any market environment, we believe individual investors are best served by following a three-pronged investment strategy of allocating their holdings across the major asset classes, diversifying within each class, and regularly rebalancing their portfolios to maintain their desired allocations. Of course, these strategies cannot guarantee a profit or protect against a loss. Investing and planning for the long term require diligence and patience, two traits that in our experience are essential to capitalizing on the many opportunities the financial markets can offer — through both up and down economic cycles.

Respectfully,

Robert J. Manning

Chief Executive Officer and Chief Investment Officer

MFS Investment Management®

February 15, 2008

The opinions expressed in this letter are subject to change, may not be relied upon for investment advice, and no forecasts can be guaranteed.

1

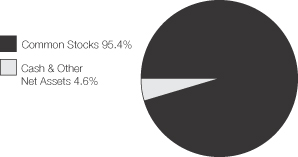

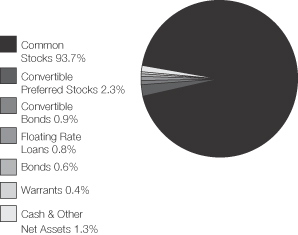

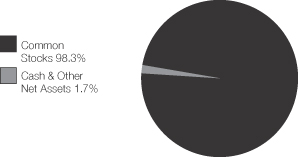

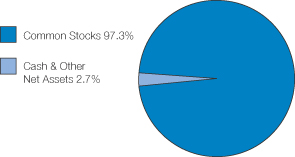

PORTFOLIO COMPOSITION

Portfolio structure

| | |

| Top Ten holdings | | |

| Lockheed Martin Corp. | | 4.2% |

| Altria Group, Inc. | | 3.8% |

| Allstate Corp. | | 3.1% |

| Exxon Mobil Corp. | | 2.9% |

| TOTAL S.A., ADR | | 2.7% |

| Johnson & Johnson | | 2.6% |

| MetLife, Inc. | | 2.5% |

| Bank of America Corp. | | 2.3% |

| Bank of New York Mellon Corp. | | 2.1% |

| Procter & Gamble Co. | | 2.0% |

| | |

| Equity sectors | | |

| Financial Services | | 25.7% |

| Energy | | 14.1% |

| Consumer Staples | | 10.5% |

| Industrial Goods & Services | | 10.0% |

| Health Care | | 9.7% |

| Utilities & Communications | | 8.3% |

| Technology | | 5.3% |

| Retailing | | 4.5% |

| Basic Materials | | 3.6% |

| Leisure | | 3.3% |

| Autos & Housing | | 2.9% |

| Special Products & Services | | 1.2% |

| Transportation | | 0.9% |

Percentages are based on net assets as of 12/31/07.

The portfolio is actively managed and current holdings may be different.

2

MANAGEMENT REVIEW

Summary of Results

For the twelve months ended December 31, 2007, Initial Class shares of the MFS Value Portfolio (the “fund”) provided a total return of 7.92%, while Service Class shares provided a total return of 7.67%. These compare with a return of -0.17% for the fund’s benchmark, the Russell 1000 Value Index.

Market Environment

Despite seemingly robust growth rates during the second and third quarters of 2007, underlying economic activity in the U.S. remained muted relative to other major economies. Overall, global economies witnessed moderate to strong growth during the reporting period as domestic demand improved and world trade accelerated.

With the strong global growth, however, concerns emerged about rising global inflation, especially as capacity became more constrained, wages rose, and energy and food prices advanced. During the reporting period, global central banks (with the exception of the U.S. Federal Reserve Board) tightened monetary conditions, which in turn pushed global bond yields to their highest levels during this economic expansion.

However, financial markets – particularly in the mortgage and structured-products areas – experienced substantial volatility in recent months. Beginning in late July, heightened uncertainty and distress concerning the subprime mortgage market caused several global credit markets to tighten up, forcing central banks to inject liquidity and to reassess their tightening biases as sovereign bond yields declined and credit spreads widened. While credit conditions improved somewhat by late October as the Federal Reserve Board cut interest rates, the level of market turbulence remained significant through year end. Increased market turmoil was also exacerbated by U.S. home foreclosures and uncertainties surrounding falling housing prices. Despite increased volatility across all asset classes and the widening in credit spreads, U.S. labor markets were resilient and wages rose modestly. More broadly, global equity markets rebounded following summer losses and generally held those gains through the end of the reporting period.

Contributors to performance

The combination of strong stock selection and an underweighted position in the financial services sector boosted performance relative to the Russell 1000 Value Index. Not holding poor-performing financial services firm Wachovia and consumer and commercial banking firm Washington Mutual had a positive impact on results.

Stock selection and, to a lesser extent, an overweighted position in the industrial goods and services sector contributed to relative returns. Defense contractor Lockheed Martin(aa) and agricultural equipment manufacturer Deere & Co. were among the fund’s top contributors. Deere’s stock price gain was driven by strong capital management and better-than-expected results throughout the period which pushed its shares up in excess of the market.

Aided by stock selection, the technology sector was another positive area of relative performance. The fund’s holdings of enterprise software company Oracle(aa) and semiconductor chips maker Intel(aa) helped results.

Stock selection and overweighting in the consumer staples sector bolstered relative returns. Tobacco company Altria Group was one of the fund’s top relative performers over the reporting period.

Top contributors in other sectors included integrated oil and gas company Hess, integrated oil company TOTAL(aa) (France), and athletic shoes and apparel manufacturer NIKE(aa). Shares of Hess surged in recent months due largely to hopes that an oil field discovery off the coast of Brazil could nearly double the company’s reserves.

Detractors from performance

The fund’s underweighted positions in strong-performing integrated oil companies, Exxon Mobil and Chevron, held back relative results. Our positioning in telecommunications company AT&T also hurt as the stock turned in strong performance over the reporting period. Holdings of insurance company Allstate, department stores operator Macy’s, financial services firm UBS(aa), and home improvement products maker Masco also dampened results. Shares of Allstate were negatively affected by investor concerns regarding potential subprime mortgage market exposure in its investment portfolio and slowing trends in its core insurance operations.

Respectfully,

| | |

| Nevin Chitkara | | Steven Gorham |

| Portfolio Manager | | Portfolio Manager |

| (aa) | Security is not a benchmark constituent. |

The views expressed in this report are those of the portfolio managers only through the end of the period of the report as stated on the cover and do not necessarily reflect the views of MFS or any other person in the MFS organization. These views are subject to change at any time based on market and other conditions, and MFS disclaims any responsibility to update such views. These views may not be relied upon as investment advice or an indication of trading intent on behalf of any MFS portfolio. References to specific securities are not recommendations of such securities, and may not be representative of any MFS portfolio’s current or future investments.

3

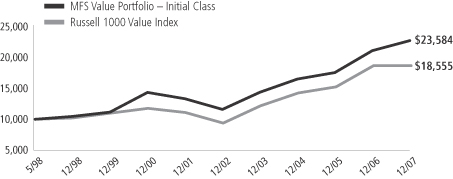

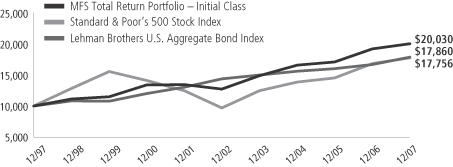

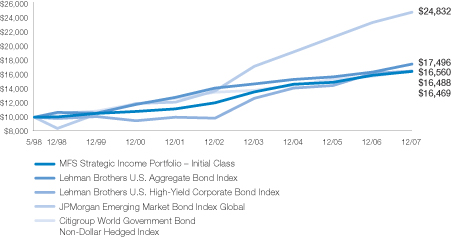

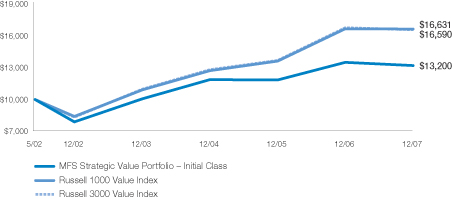

PERFORMANCE SUMMARY THROUGH 12/31/07

The following chart illustrates the historical performance of the fund in comparison to its benchmark index. Index comparisons are unmanaged; do not reflect any fees or expenses; and cannot be invested in directly. The performance of other share classes will be greater than or less than that of the class depicted below. (See Notes to Performance Summary.)

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your units, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. The performance shown does not reflect the deduction of taxes, if any, that a contract holder would pay on fund distributions or the redemption of contract units. The returns for the fund shown also do not reflect the deduction of expenses associated with variable products, such as mortality and expense risk charges, separate account charges, and sales charges imposed by the insurance company separate accounts. Such expenses would reduce the overall returns shown.

Growth of a hypothetical $10,000 investment (t)

Total rates of return through 12/31/07

Average Annual Total Returns

| | | | | | | | | | | | |

| | | Share class | | Class inception date | | 1-yr | | 5-yr | | Life (t) | | |

| | | Initial Class | | 5/06/98 | | 7.92% | | 15.04% | | 9.29% | | |

| | | Service Class | | 8/24/01 | | 7.67% | | 14.76% | | 9.12% | | |

Comparative Index

| | | | | | | | | | | | |

| | | Russell 1000 Value Index (f) | | (0.17)% | | 14.63% | | 6.59% | | |

| (f) | Source: FactSet Research Systems Inc. |

| (t) | For the period from the commencement of the fund’s investment operations, May 6, 1998, through the stated period end. |

Index Definition

Russell 1000 Value Index – constructed to provide a comprehensive barometer for the value securities in the large-cap segment of the U.S. equity universe. Companies in this index generally have lower price-to-book ratios and lower forecasted growth values.

It is not possible to invest directly in an index.

Notes to Performance Summary

Service Class share performance includes the performance of Initial Class shares for periods prior to the inception of Service Class shares (blended performance). This blended performance figure has not been adjusted to take into account differences in the class-specific operating expenses (such as Rule 12b-1 fees). Because operating expenses of Service Class shares are generally higher than those of Initial Class shares, the blended Service Class shares performance shown is higher than it would have been had Service Class shares been offered for the entire period.

Performance results reflect any applicable expense subsidies and waivers in effect during the periods shown. Without such subsidies and waivers the fund’s performance results would be less favorable. Please see the prospectus and financial statements for complete details.

From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower.

4

EXPENSE TABLE

Fund Expenses Borne by the Contract Holders During the Period,

July 1, 2007 through December 31, 2007

As a contract holder of the fund, you incur ongoing costs, including management fees; distribution (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period July 1, 2007 through December 31, 2007.

Actual expenses

The first line for each share class in the following table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

The second line for each share class in the following table provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight the fund’s ongoing costs only and do not take into account the fees and expenses imposed under the variable contracts through which your investment in the fund is made. Therefore, the second line for each share class in the table is useful in comparing ongoing costs associated with an investment in vehicles (such as the fund) which fund benefits under variable annuity and variable life insurance contracts and to qualified pension and retirement plans only, and will not help you determine the relative total costs of investing in the fund through variable annuity and variable life insurance contracts. If the fees and expenses imposed under the variable contracts were included, your costs would have been higher.

| | | | | | | | | | |

Share Class | | | | Annualized

Expense Ratio | | Beginning

Account Value

7/01/07 | | Ending

Account Value

12/31/07 | | Expenses Paid

During Period (p)

7/01/07-12/31/07 |

| Initial Class | | Actual | | 0.82% | | $1,000.00 | | $997.30 | | $4.13 |

| | Hypothetical (h) | | 0.82% | | $1,000.00 | | $1,021.07 | | $4.18 |

| Service Class | | Actual | | 1.07% | | $1,000.00 | | $996.30 | | $5.38 |

| | Hypothetical (h) | | 1.07% | | $1,000.00 | | $1,019.81 | | $5.45 |

| (h) | 5% class return per year before expenses. |

| (p) | Expenses paid is equal to each class’ annualized expense ratio, as shown above, multiplied by the average account value over the period, multiplied by the number of days in the period, divided by the number of days in the year. |

5

PORTFOLIO OF INVESTMENTS – 12/31/07

The Portfolio of Investments is a complete list of all securities owned by your fund.

It is categorized by broad-based asset classes.

| | | | | |

| Issuer | | Shares/Par | | Value ($) |

| COMMON STOCKS – 100.0% | | | | | |

| Aerospace – 7.9% | | | | | |

| Lockheed Martin Corp. | | 163,140 | | $ | 17,172,116 |

| Northrop Grumman Corp. | | 87,550 | | | 6,884,932 |

| Raytheon Co. | | 16,750 | | | 1,016,725 |

| United Technologies Corp. | | 93,260 | | | 7,138,120 |

| | | | | |

| | | | $ | 32,211,893 |

| | | | | |

| Alcoholic Beverages – 1.1% | | | | | |

| Diageo PLC | | 211,009 | | $ | 4,516,745 |

| | | | | |

| Apparel Manufacturers – 1.5% | | | | | |

| NIKE, Inc., “B” | | 96,260 | | $ | 6,183,742 |

| | | | | |

| Automotive – 0.5% | | | | | |

| Johnson Controls, Inc. | | 54,790 | | $ | 1,974,632 |

| | | | | |

| Broadcasting – 2.0% | | | | | |

| Citadel Broadcasting Corp. (l) | | 4,905 | | $ | 10,104 |

| E.W. Scripps Co., “A” (l) | | 24,880 | | | 1,119,849 |

| Omnicom Group, Inc. | | 42,940 | | | 2,040,938 |

| Walt Disney Co. | | 96,940 | | | 3,129,223 |

| WPP Group PLC | | 134,160 | | | 1,717,611 |

| | | | | |

| | | | $ | 8,017,725 |

| | | | | |

| Brokerage & Asset Managers – 4.0% | | | | | |

| Franklin Resources, Inc. | | 31,480 | | $ | 3,602,256 |

| Goldman Sachs Group, Inc. | | 34,270 | | | 7,369,764 |

| Lehman Brothers Holdings, Inc. (l) | | 38,470 | | | 2,517,477 |

| Merrill Lynch & Co., Inc. | | 56,470 | | | 3,031,310 |

| | | | | |

| | | | $ | 16,520,807 |

| | | | | |

| Business Services – 1.2% | | | | | |

| Accenture Ltd., “A” | | 132,980 | | $ | 4,791,269 |

| | | | | |

| Chemicals – 2.1% | | | | | |

| Dow Chemical Co. | | 35,350 | | $ | 1,393,497 |

| PPG Industries, Inc. | | 87,530 | | | 6,147,232 |

| Syngenta AG | | 4,680 | | | 1,187,435 |

| | | | | |

| | | | $ | 8,728,164 |

| | | | | |

| Computer Software – 1.7% | | | | | |

| Oracle Corp. (a) | | 310,330 | | $ | 7,007,251 |

| | | | | |

| Computer Software – Systems – 2.0% | | | | | |

| Hewlett - Packard Co. | | 73,570 | | $ | 3,713,814 |

| International Business Machines Corp. | | 42,740 | | | 4,620,194 |

| | | | | |

| | | | $ | 8,334,008 |

| | | | | |

| Construction – 2.4% | | | | | |

| Masco Corp. (l) | | 230,940 | | $ | 4,990,613 |

| Sherwin - Williams Co. (l) | | 31,130 | | | 1,806,785 |

| Toll Brothers, Inc. (a)(l) | | 141,380 | | | 2,836,083 |

| | | | | |

| | | | $ | 9,633,481 |

| | | | | |

| Consumer Goods & Services – 2.0% | | | | | |

| Procter & Gamble Co. | | 111,870 | | $ | 8,213,495 |

| | | | | |

| Containers – 0.2% | | | | | |

| Smurfit - Stone Container Corp. (a)(l) | | 65,550 | | $ | 692,208 |

| | | | | |

| | | | | |

| Issuer | | Shares/Par | | Value ($) |

| COMMON STOCKS – continued | | | | | |

| Electrical Equipment – 1.4% | | | | | |

| Rockwell Automation, Inc. | | 39,410 | | $ | 2,717,714 |

| W.W. Grainger, Inc. (l) | | 36,220 | | | 3,169,974 |

| | | | | |

| | | | $ | 5,887,688 |

| | | | | |

| Electronics – 1.6% | | | | | |

| Intel Corp. | | 243,270 | | $ | 6,485,578 |

| | | | | |

| Energy – Independent – 3.2% | | | | | |

| Apache Corp. | | 41,950 | | $ | 4,511,303 |

| Devon Energy Corp. | | 60,310 | | | 5,362,162 |

| EOG Resources, Inc. | | 36,240 | | | 3,234,420 |

| | | | | |

| | | | $ | 13,107,885 |

| | | | | |

| Energy – Integrated – 10.9% | | | | | |

| Chevron Corp. | | 38,135 | | $ | 3,559,140 |

| ConocoPhillips | | 65,190 | | | 5,756,277 |

| Exxon Mobil Corp. | | 128,232 | | | 12,014,056 |

| Hess Corp. | | 74,300 | | | 7,493,898 |

| Marathon Oil Corp. | | 42,120 | | | 2,563,423 |

| Royal Dutch Shell PLC, ADR | | 27,300 | | | 2,298,660 |

| TOTAL S.A., ADR | | 133,690 | | | 11,042,794 |

| | | | | |

| | | | $ | 44,728,248 |

| | | | | |

| Food & Beverages – 3.6% | | | | | |

| General Mills, Inc. | | 42,230 | | $ | 2,407,110 |

| Kellogg Co. | | 85,950 | | | 4,506,359 |

| Nestle S.A. | | 10,805 | | | 4,950,998 |

| PepsiCo, Inc. | | 38,638 | | | 2,932,624 |

| | | | | |

| | | | $ | 14,797,091 |

| | | | | |

| Food & Drug Stores – 0.9% | | | | | |

| CVS Caremark Corp. | | 90,308 | | $ | 3,589,743 |

| | | | | |

| Gaming & Lodging – 1.3% | | | | | |

| Royal Caribbean Cruises Ltd. (l) | | 124,610 | | $ | 5,288,448 |

| | | | | |

| General Merchandise – 1.2% | | | | | |

| Macy’s, Inc. | | 188,970 | | $ | 4,888,654 |

| | | | | |

| Health Maintenance Organizations – 2.2% | | | | | |

| UnitedHealth Group, Inc. | | 52,820 | | $ | 3,074,124 |

| WellPoint, Inc. (a) | | 68,680 | | | 6,025,296 |

| | | | | |

| | | | $ | 9,099,420 |

| | | | | |

| Insurance – 8.7% | | | | | |

| Allstate Corp. | | 244,330 | | $ | 12,761,356 |

| Chubb Corp. | | 46,850 | | | 2,557,073 |

| Genworth Financial, Inc., “A” | | 128,530 | | | 3,271,088 |

| Hartford Financial Services Group, Inc. | | 45,200 | | | 3,940,988 |

| MetLife, Inc. | | 165,100 | | | 10,173,462 |

| Prudential Financial, Inc. | | 32,820 | | | 3,053,573 |

| | | | | |

| | | | $ | 35,757,540 |

| | | | | |

| Machinery & Tools – 0.7% | | | | | |

| Deere & Co. | | 7,380 | | $ | 687,226 |

| Eaton Corp. | | 14,200 | | | 1,376,690 |

| Timken Co. | | 29,520 | | | 969,732 |

| | | | | |

| | | | $ | 3,033,648 |

| | | | | |

6

Portfolio of Investments – continued

| | | | | |

| Issuer | | Shares/Par | | Value ($) |

| COMMON STOCKS – continued | | | | | |

| Major Banks – 7.4% | | | | | |

| Bank of America Corp. | | 224,184 | | $ | 9,249,832 |

| Bank of New York Mellon Corp. | | 173,075 | | | 8,439,137 |

| PNC Financial Services Group, Inc. | | 60,900 | | | 3,998,085 |

| State Street Corp. | | 47,040 | | | 3,819,648 |

| SunTrust Banks, Inc. | | 75,660 | | | 4,727,993 |

| | | | | |

| | | | $ | 30,234,695 |

| | | | | |

| Other Banks & Diversified Financials – 5.6% | | | | | |

| American Express Co. | | 50,070 | | $ | 2,604,641 |

| Citigroup, Inc. | | 218,380 | | | 6,429,107 |

| Fannie Mae | | 149,070 | | | 5,959,819 |

| Freddie Mac | | 34,380 | | | 1,171,327 |

| UBS AG | | 142,120 | | | 6,599,969 |

| | | | | |

| | | | $ | 22,764,863 |

| | | | | |

| Pharmaceuticals – 7.5% | | | | | |

| Abbott Laboratories | | 46,160 | | $ | 2,591,884 |

| GlaxoSmithKline PLC | | 82,970 | | | 2,105,516 |

| Johnson & Johnson | | 156,580 | | | 10,443,886 |

| Merck & Co., Inc. | | 120,940 | | | 7,027,823 |

| Pfizer, Inc. | | 84,850 | | | 1,928,641 |

| Wyeth | | 152,280 | | | 6,729,253 |

| | | | | |

| | | | $ | 30,827,003 |

| | | | | |

| Railroad & Shipping – 0.9% | | | | | |

| Burlington Northern Santa Fe Corp. | | 38,460 | | $ | 3,201,026 |

| Norfolk Southern Corp. | | 9,410 | | | 474,640 |

| | | | | |

| | | | $ | 3,675,666 |

| | | | | |

| Specialty Chemicals – 1.3% | | | | | |

| Air Products & Chemicals, Inc. | | 29,477 | | $ | 2,907,317 |

| Praxair, Inc. | | 24,570 | | | 2,179,605 |

| | | | | |

| | | | $ | 5,086,922 |

| | | | | |

| Specialty Stores – 0.9% | | | | | |

| Advance Auto Parts, Inc. | | 22,530 | | $ | 855,915 |

| Lowe’s Cos., Inc. | | 26,110 | | | 590,608 |

| Staples, Inc. | | 98,500 | | | 2,272,395 |

| | | | | |

| | | | $ | 3,718,918 |

| | | | | |

| Telecommunications – Wireless – 1.7% | | | | | |

| Sprint Nextel Corp. | | 192,810 | | $ | 2,531,595 |

| Vodafone Group PLC | | 1,178,567 | | | 4,392,535 |

| | | | | |

| | | | $ | 6,924,130 |

| | | | | |

| Telephone Services – 2.5% | | | | | |

| AT&T, Inc. | | 109,400 | | $ | 4,546,664 |

| Embarq Corp. | | 58,594 | | | 2,902,161 |

| TELUS Corp. (non - voting shares) | | 16,274 | | | 791,646 |

| Verizon Communications, Inc. | | 47,980 | | | 2,096,246 |

| | | | | |

| | | | $ | 10,336,717 |

| | | | | |

| Tobacco – 3.8% | | | | | |

| Altria Group, Inc. | | 206,890 | | $ | 15,636,746 |

| | | | | |

| | | | | | | |

| Issuer | | Shares/Par | | Value ($) | |

| COMMON STOCKS – continued | | | | | | | |

| Utilities – Electric Power – 4.1% | | | | | | | |

| Dominion Resources, Inc. (l) | | | 110,958 | | $ | 5,264,957 | |

| Entergy Corp. | | | 27,740 | | | 3,315,485 | |

| FPL Group, Inc. | | | 57,770 | | | 3,915,651 | |

| PG&E Corp. | | | 31,210 | | | 1,344,839 | |

| PPL Corp. | | | 26,920 | | | 1,402,263 | |

| Public Service Enterprise Group, Inc. | | | 16,410 | | $ | 1,612,118 | |

| | | | | | | |

| | | | | $ | 16,855,313 | |

| | | | | | | |

Total Common Stocks

(Identified Cost, $307,890,314) | | | | | $ | 409,550,336 | |

| | | | | | | |

| | |

| SHORT-TERM OBLIGATIONS – 0.1% | | | | | | | |

| American Express Credit Corp., 4.12%, due 1/02/08, at Amortized Cost and Value (y) | | $ | 219,000 | | $ | 218,975 | |

| | | | | | | |

| |

| COLLATERAL FOR SECURITIES LOANED – 4.6% | | | | |

| Navigator Securities Lending Prime Portfolio, at Cost and Net Asset Value | | | 18,904,997 | | $ | 18,904,997 | |

| | | | | | | |

Total Investments

(Identified Cost, $327,014,286) | | | | | $ | 428,674,308 | |

| | | | | | | |

OTHER ASSETS, LESS

LIABILITIES – (4.7)% | | | (19,122,777 | ) |

| | | | | | | |

| Net Assets – 100.0% | | | | | $ | 409,551,531 | |

| | | | | | | |

| (a) | Non-income producing security. |

| (l) | All or a portion of this security is on loan. |

| (y) | The rate shown represents an annualized yield at time of purchase. |

The following abbreviations are used in this report and are defined:

| ADR | American Depository Receipt |

See Notes to Financial Statements

7

FINANCIAL STATEMENTS | STATEMENT OF ASSETS AND LIABILITIES

This statement represents your fund’s’ balance sheet, which details the assets and liabilities comprising the total value of the fund.

| | | | |

| At 12/31/07 | | | | |

| Assets: | | | | |

| Investments, at value including $18,435,674 of securities on loan (identified cost $327,014,286) | | $428,674,308 | | |

| Receivable for investments sold | | 719,454 | | |

| Receivable for fund shares sold | | 391 | | |

| Interest and dividends receivable | | 640,696 | | |

| Other assets | | 13,551 | | |

| Total assets | | | | $430,048,400 |

| Liabilities: | | | | |

| Payable to custodian | | $2,168 | | |

| Payable for investments purchased | | 703,723 | | |

| Payable for fund shares reacquired | | 709,317 | | |

| Collateral for securities loaned, at value | | 18,904,997 | | |

| Payable to affiliates | | | | |

Management fee | | 33,933 | | |

Distribution fees | | 3,907 | | |

Administrative services fee | | 1,064 | | |

| Payable for independent trustees’ compensation | | 1,395 | | |

| Accrued expenses and other liabilities | | 136,365 | | |

| Total liabilities | | | | $20,496,869 |

| Net assets | | | | $409,551,531 |

| Net assets consist of: | | | | |

| Paid-in capital | | $249,898,334 | | |

| Unrealized appreciation (depreciation) on investments and translation of assets and liabilities in foreign currencies | | 101,657,103 | | |

| Accumulated net realized gain (loss) on investments and foreign currency transactions | | 52,006,102 | | |

| Undistributed net investment income | | 5,989,992 | | |

Net assets | | | | $409,551,531 |

| Shares of beneficial interest outstanding | | | | 21,857,822 |

| Initial Class shares | | | | |

Net Assets | | $267,967,441 | | |

Shares outstanding | | 14,268,722 | | |

Net asset value per share | | | | $18.78 |

| Service Class shares | | | | |

Net Assets | | $141,584,090 | | |

Shares outstanding | | 7,589,100 | | |

Net asset value per share | | | | $18.66 |

See Notes to Financial Statements

8

FINANCIAL STATEMENTS | STATEMENT OF OPERATIONS

This statement describes how much your fund earned in investment income and accrued in expenses. It also describes any gains and/or losses generated by fund operations.

| | | | | | |

| Year ended 12/31/07 | | | | | | |

| Net Investment income | | | | | | |

| Income | | | | | | |

Dividends | | $10,073,688 | | | | |

Interest | | 193,663 | | | | |

Foreign taxes withheld | | (133,224 | ) | | | |

| Total investment income | | | | | $10,134,127 | |

| Expenses | | | | | | |

Management fee | | $3,401,119 | | | | |

Distribution fees | | 363,590 | | | | |

Administrative services fee | | 118,991 | | | | |

Independent trustees’ compensation | | 43,260 | | | | |

Custodian fee | | 101,035 | | | | |

Shareholder communications | | 25,833 | | | | |

Auditing fees | | 41,993 | | | | |

Legal fees | | 5,949 | | | | |

Miscellaneous | | 38,901 | | | | |

| Total expenses | | | | | $4,140,671 | |

Fees paid indirectly | | (1,527 | ) | | | |

| Net expenses | | | | | $4,139,144 | |

| Net investment income | | | | | $5,994,983 | |

| Realized and unrealized gain (loss) on investments and foreign currency transactions | | | | | | |

| Realized gain (loss) (identified cost basis) | | | | | | |

Investment transactions | | $53,104,359 | | | | |

Foreign currency transactions | | 27 | | | | |

| Net realized gain (loss) on investments and foreign currency transactions | | | | | $53,104,386 | |

| Change in unrealized appreciation (depreciation) | | | | | | |

Investments | | $(23,649,280 | ) | | | |

Translation of assets and liabilities in foreign currencies | | (4,690 | ) | | | |

| Net unrealized gain (loss) on investments and foreign currency translation | | | | | $(23,653,970 | ) |

| Net realized and unrealized gain (loss) on investments and foreign currency | | | | | $29,450,416 | |

| Change in net assets from operations | | | | | $35,445,399 | |

See Notes to Financial Statements

9

FINANCIAL STATEMENTS | STATEMENTS OF CHANGES IN NET ASSETS

These statements describe the increases and/or decreases in net assets resulting from operations, any distributions, and any shareholder transactions.

| | | | | | |

| For years ended 12/31 | | 2007 | | | 2006 | |

| Change in net assets | | | | | | |

| From operations | | | | | | |

| Net investment income | | $5,994,983 | | | $6,900,070 | |

| Net realized gain (loss) on investments and foreign currency transactions | | 53,104,386 | | | 25,849,450 | |

| Net unrealized gain (loss) on investments and foreign currency translation | | (23,653,970 | ) | | 52,348,771 | |

| Change in net assets from operations | | $35,445,399 | | | $85,098,291 | |

| Distributions declared to shareholders | | | | | | |

| From net investment income | | | | | | |

| Initial Class | | $(4,956,730 | ) | | $(4,852,928 | ) |

| Service Class | | (1,958,742 | ) | | (1,683,628 | ) |

| From net realized gain on investments | | | | | | |

| Initial Class | | (18,004,251 | ) | | (11,895,426 | ) |

| Service Class | | (8,308,499 | ) | | (4,878,814 | ) |

| Total distributions declared to shareholders | | $(33,228,222 | ) | | $(23,310,796 | ) |

| Change in net assets from fund share transactions | | $(57,093,670 | ) | | $(44,120,463 | ) |

| Total change in net assets | | $(54,876,493 | ) | | $17,667,032 | |

| Net assets | | | | | | |

| At beginning of period | | 464,428,024 | | | 446,760,992 | |

| At the end of period (including undistributed net investment income of $5,989,992 and $6,910,454, respectively) | | $409,551,531 | | | $464,428,024 | |

See Notes to Financial Statements

10

FINANCIAL STATEMENTS | FINANCIAL HIGHLIGHTS

The financial highlights table is intended to help you understand the fund’s financial performance for the past 5 years. Certain information reflects financial results for a single fund share. The total returns in the table represent the rate by which an investor would have earned (or lost) on an investment in the fund share class (assuming reinvestment of all distributions) held for the entire period.

Initial Class

| | | | | | | | | | | | | | | |

| | | Years ended 12/31 | |

| | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

| Net asset value, beginning of period | | $18.70 | | | $16.30 | | | $15.51 | | | $13.61 | | | $11.05 | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | |

| Net investment income (d) | | $0.27 | | | $0.28 | | | $0.24 | | | $0.21 | | | $0.19 | |

Net realized and unrealized gain (loss) on investments and

foreign currency | | 1.22 | | | 3.04 | | | 0.77 | | | 1.87 | | | 2.56 | |

| Total from investment operations | | $1.49 | | | $3.32 | | | $1.01 | | | $2.08 | | | $2.75 | |

| Less distributions declared to shareholders | | | | | | | | | | | | | | | |

| From net investment income | | $(0.30 | ) | | $(0.27 | ) | | $(0.22 | ) | | $(0.18 | ) | | $(0.19 | ) |

| From net realized gain on investments | | (1.11 | ) | | (0.65 | ) | | — | | | — | | | — | |

| Total distributions declared to shareholders | | $(1.41 | ) | | $(0.92 | ) | | $(0.22 | ) | | $(0.18 | ) | | $(0.19 | ) |

| Net asset value, end of period | | $18.78 | | | $18.70 | | | $16.30 | | | $15.51 | | | $13.61 | |

| Total return (%) (k)(s) | | 7.92 | | | 20.96 | | | 6.60 | | | 15.52 | (b) | | 25.31 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | |

| Expenses (f) | | 0.83 | | | 0.86 | | | 0.85 | | | 0.83 | | | 0.84 | |

| Net investment income | | 1.40 | | | 1.62 | | | 1.51 | | | 1.53 | | | 1.65 | |

| Portfolio turnover | | 25 | | | 26 | | | 22 | | | 36 | | | 57 | |

| Net assets at end of period (000 Omitted) | | $267,967 | | | $323,094 | | | $319,952 | | | $339,705 | | | $310,818 | |

See Notes to Financial Statements

11

Financial Highlights – continued

Service Class

| | | | | | | | | | | | | | | |

| | | Years ended 12/31 | |

| | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

| Net asset value, beginning of period | | $18.59 | | | $16.21 | | | $15.43 | | | $13.56 | | | $11.01 | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | |

| Net investment income (d) | | $0.22 | | | $0.23 | | | $0.20 | | | $0.18 | | | $0.16 | |

| Net realized and unrealized gain (loss) on investments and foreign currency | | 1.22 | | | 3.02 | | | 0.77 | | | 1.85 | | | 2.56 | |

| Total from investment operations | | $1.44 | | | $3.25 | | | $0.97 | | | $2.03 | | | $2.72 | |

| Less distributions declared to shareholders | | | | | | | | | | | | | | | |

| From net investment income | | $(0.26 | ) | | $(0.22 | ) | | $(0.19 | ) | | $(0.16 | ) | | $(0.17 | ) |

| From net realized gain on investments | | (1.11 | ) | | (0.65 | ) | | — | | | — | | | — | |

| Total distributions declared to shareholders | | $(1.37 | ) | | $(0.87 | ) | | $(0.19 | ) | | $(0.16 | ) | | $(0.17 | ) |

| Net asset value, end of period | | $18.66 | | | $18.59 | | | $16.21 | | | $15.43 | | | $13.56 | |

| Total return (%) (k)(s) | | 7.67 | | | 20.66 | | | 6.34 | | | 15.18 | (b) | | 25.09 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | |

| Expenses (f) | | 1.08 | | | 1.11 | | | 1.10 | | | 1.08 | | | 1.09 | |

| Net investment income | | 1.16 | | | 1.37 | | | 1.27 | | | 1.28 | | | 1.39 | |

| Portfolio turnover | | 25 | | | 26 | | | 22 | | | 36 | | | 57 | |

| Net assets at end of period (000 Omitted) | | $141,584 | | | $141,334 | | | $126,809 | | | $119,496 | | | $83,780 | |

| (b) | The fund’s net asset value and total return calculation include a non-recurring accrual recorded as a result of an administrative proceeding regarding disclosure of brokerage allocation practices in connection with fund sales. The non-recurring accrual did not have a material impact on the net asset value per share based on the shares outstanding on the day the proceeds were recorded. |

| (d) | Per share data are based on average shares outstanding. |

| (f) | Ratios do not reflect reductions from fees paid indirectly, if applicable. |

| (k) | The total return does not reflect expenses that apply to separate accounts. Inclusion of these charges would reduce the total return figures for all periods shown. |

| (s) | From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower. |

See Notes to Financial Statements

12

NOTES TO FINANCIAL STATEMENTS

| (1) | | Business and Organization |

MFS Value Portfolio (formerly Value Series) (the fund) is a series of MFS Variable Insurance Trust II (formerly known as MFS/Sun Life Series Trust) (the trust). The trust is organized as a Massachusetts business trust and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company. The shares of the fund are sold to variable accounts established by insurance companies to fund benefits under variable contracts issued by such companies, and qualified retirement and pension plans.

| (2) | | Significant Accounting Policies |

General – The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. The fund can invest in foreign securities. Investments in foreign securities are vulnerable to the effects of changes in the relative values of the local currency and the U.S. dollar and to the effects of changes in each country’s legal, political, and economic environment.

Investment Valuations – Equity securities, including restricted equity securities, are generally valued at the last sale or official closing price as reported by an independent pricing service on the market or exchange on which they are primarily traded. For securities for which there were no sales reported that day, equity securities are generally valued at the last quoted daily bid quotation as reported by an independent pricing service on the market or exchange on which they are primarily traded. For securities held short for which there were no sales reported for the day, the position is generally valued at the last quoted daily ask quotation as reported by an independent pricing service on the market or exchange on which such securities are primarily traded. Short-term instruments with a maturity at issuance of 60 days or less may be valued at amortized cost, which approximates market value. Open-end investment companies are generally valued at their net asset value per share. Securities and other assets generally valued on the basis of information from an independent pricing service may also be valued at a broker-dealer bid quotation. The values of foreign securities and other assets and liabilities expressed in foreign currencies are converted to U.S. dollars using the mean of bid and asked prices for rates reported by an independent pricing service.

The Board of Trustees has delegated primary responsibility for determining or causing to be determined the value of the fund’s investments (including any fair valuation) to the adviser pursuant to valuation policies and procedures approved by the Board. If the adviser determines that reliable market quotations are not readily available, investments are valued at fair value as determined in good faith by the adviser in accordance with such procedures under the oversight of the Board of Trustees. Under the fund’s valuation policies and procedures, market quotations are not considered to be readily available for many types of debt instruments and certain types of derivatives. These investments are generally valued at fair value based on information from independent pricing services. In addition, investments may be valued at fair value if the adviser determines that an investment’s value has been materially affected by events occurring after the close of the exchange or market on which the investment is principally traded (such as foreign exchange or market) and prior to the determination of the fund’s net asset value, or after the halting of trading of a specific security where trading does not resume prior to the close of the exchange or market on which the security is principally traded. Events that occur on a frequent basis after foreign markets close (such as developments in foreign markets and significant movements in the U.S. markets) and prior to the determination of the fund’s net asset value may be deemed to have a material affect on the value of securities traded in foreign markets. Accordingly, the fund’s foreign equity securities may often be valued at fair value. The adviser may rely on independent pricing services or other information (such as the correlation with price movements of similar securities in the same or other markets; the type, cost and investment characteristics of the security; the business and financial condition of the issuer; and trading and other market data) to assist in determining whether to fair value and at what value to fair value an investment. The value of an investment for purposes of calculating the fund’s net asset value can differ depending on the source and method used to determine value. When fair valuation is used, the value of investments used to determine the fund’s net asset value may differ from quoted or published prices for the same investments.

In September 2006, FASB Statement No. 157, Fair Value Measurements (the “Statement”) was issued, and is effective for fiscal years beginning after November 15, 2007 and for all interim periods within those fiscal years. This Statement provides a single definition of fair value, a hierarchy for measuring fair value and expanded disclosures about fair value measurements. Management is evaluating the application of the Statement to the fund, and believes the impact will be limited to expanded disclosures resulting from the adoption of this Statement in the fund’s financial statements.

Foreign Currency Translation – Purchases and sales of foreign investments, income, and expenses are converted into U.S. dollars based upon currency exchange rates prevailing on the respective dates of such transactions. Gains and losses attributable to foreign currency exchange rates on sales of securities are recorded for financial statement purposes as net realized gains and losses on investments. Gains and losses attributable to foreign exchange rate movements on income and

13

Notes to Financial Statements – continued

expenses are recorded for financial statement purposes as foreign currency transaction gains and losses. That portion of both realized and unrealized gains and losses on investments that results from fluctuations in foreign currency exchange rates is not separately disclosed.

Security Loans – State Street Bank and Trust Company (“State Street”), as lending agent, may loan the securities of the fund to certain qualified institutions (the “Borrowers”) approved by the fund. The loans are collateralized at all times by cash and/or U.S. Treasury securities in an amount at least equal to the market value of the securities loaned. State Street provides the fund with indemnification against Borrower default. The fund bears the risk of loss with respect to the investment of cash collateral. On loans collateralized by cash, the cash collateral is invested in a money market fund or short-term securities. A portion of the income generated upon investment of the collateral is remitted to the Borrowers, and the remainder is allocated between the fund and the lending agent. On loans collateralized by U.S. Treasury securities, a fee is received from the Borrower, and is allocated between the fund and the lending agent. Net income from securities lending is included in interest income on the Statement of Operations. The dividend and interest income earned on the securities loaned is accounted for in the same manner as other dividend and interest income.

Indemnifications – Under the fund’s organizational documents, its officers and trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the fund. Additionally, in the normal course of business, the fund enters into agreements with service providers that may contain indemnification clauses. The fund’s maximum exposure under these agreements is unknown as this would involve future claims that may be made against the fund that have not yet occurred.

Investment Transactions and Income – Investment transactions are recorded on the trade date. Interest income is recorded on the accrual basis. All premium and discount is amortized or accreted for financial statement purposes in accordance with U.S. generally accepted accounting principles. All discount is accreted for tax reporting purposes as required by federal income tax regulations. Dividends received in cash are recorded on the ex-dividend date. Certain dividends from foreign securities will be recorded when the fund is informed of the dividend if such information is obtained subsequent to the ex-dividend date. Dividend and interest payments received in additional securities are recorded on the ex-dividend or ex-interest date in an amount equal to the value of the security on such date.

The fund may receive proceeds from litigation settlements. Any proceeds received from litigation involving portfolio holdings are reflected in the Statement of Operations in realized gain/loss if the security has been disposed of by the fund or in unrealized gain/loss if the security is still held by the fund. Any other proceeds from litigation not related to portfolio holdings are reflected as other income in the Statement of Operations.

Fees Paid Indirectly – The fund’s custody fee may be reduced according to an arrangement that measures the value of cash deposited with the custodian by the fund. This amount, for the year ended December 31, 2007, is shown as a reduction of total expenses on the Statement of Operations.

Tax Matters and Distributions – The fund intends to qualify as a regulated investment company, as defined under Subchapter M of the Internal Revenue Code, and to distribute all of its taxable income, including realized capital gains. As a result, no provision for federal income tax is required. The fund adopted the provisions of FASB Interpretation No. 48, Accounting for Uncertainty in Income Taxes (“the Interpretation”) on January 1, 2007. The Interpretation prescribes a minimum threshold for financial statement recognition of the benefit of a tax position taken or expected to be taken in a tax return. There was no impact resulting from the adoption of this Interpretation on the fund’s financial statements. Each of the fund’s federal tax returns for the prior three fiscal years remains subject to examination by the Internal Revenue Service. It is the fund’s policy to record interest and penalty charges on underpaid taxes associated with its tax positions as interest expense and other expense, respectively. No such charges were recorded in the current financial statements. Foreign taxes, if any, have been accrued by the fund in the accompanying financial statements.

Distributions to shareholders are recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from U.S. generally accepted accounting principles. Certain capital accounts in the financial statements are periodically adjusted for permanent differences in order to reflect their tax character. These adjustments have no impact on net assets or net asset value per share. Temporary differences which arise from recognizing certain items of income, expense, gain or loss in different periods for financial statement and tax purposes will reverse at some time in the future. Distributions in excess of net investment income or net realized gains are temporary overdistributions for financial statement purposes resulting from differences in the recognition or classification of income or distributions for financial statement and tax purposes.

Book/tax differences primarily relate to wash sale loss deferrals.

14

Notes to Financial Statements – continued

The tax character of distributions declared to shareholders is as follows:

| | | | |

| | | 12/31/07 | | 12/31/06 |

| Ordinary income (including any short-term capital gains) | | $7,811,648 | | $6,536,556 |

| Long-term capital gain | | 25,416,574 | | 16,774,240 |

| Total distributions | | $33,228,222 | | $23,310,796 |

The federal tax cost and the tax basis components of distributable earnings were as follows:

| | | |

| As of 12/31/07 | | | |

| Cost of investments | | $328,266,156 | |

| Gross appreciation | | 115,562,583 | |

| Gross depreciation | | (15,154,431 | ) |

| Net unrealized appreciation (depreciation) | | $100,408,152 | |

| Undistributed ordinary income | | 8,683,703 | |

| Undistributed long-term capital gain | | 50,591,730 | |

| Other temporary differences | | (30,388 | ) |

Multiple Classes of Shares of Beneficial Interest – The fund offers multiple classes of shares, which differ in their respective distribution fees. All shareholders bear the common expenses of the fund based on daily net assets of each class, without distinction between share classes. Dividends are declared separately for each class. Differences in per share dividend rates are generally due to differences in separate class expenses.

| (3) | | Transactions with Affiliates |

Investment Adviser – The fund has an investment advisory agreement with Massachusetts Financial Services Company (MFS) to provide overall investment management and related administrative services and facilities to the fund. The management fee is computed daily and paid monthly at the following annual rates:

| | |

| First $1 billion of average daily net assets | | 0.75% |

| Average daily net assets in excess of $1 billion | | 0.65% |

The management fee incurred for the year ended December 31, 2007 was equivalent to an annual effective rate of 0.75% of the fund’s average daily net assets.

The investment adviser has agreed to pay a portion of the fund’s operating expenses, exclusive of certain other fees and expenses, such that the operating expenses of the fund do not exceed 0.90% for the Initial Class shares and 1.15% for the Service Class shares, based on the average daily net assets of the fund. This written agreement will continue through August 31, 2008 unless changed or rescinded by the fund’s Board of Trustees. For the year ended December 31, 2007, the fund’s actual operating expenses did not exceed the limit and therefore, the investment adviser did not pay any portion of the fund’s expenses.

Distributor – MFS Fund Distributors, Inc. (MFD), a wholly-owned subsidiary of MFS, is the distributor of shares of the fund. The Trustees have adopted a distribution plan for the Service Class shares pursuant to Rule 12b-1 under the Investment Company Act of 1940.

The fund’s distribution plan provides that the fund will pay MFD distribution fees equal to 0.25% per annum of its average daily net assets attributable to Service Class shares as partial consideration for services performed and expenses incurred by MFD and financial intermediaries in connection with the sale and distribution of the fund’s Service Class shares and the sale and distribution of the variable annuity or variable life insurance contracts investing indirectly in Service Class shares. MFD may subsequently pay all, or a portion, of the distribution fees to financial intermediaries.

Shareholder Servicing Agent – MFS Service Center, Inc. (MFSC), a wholly-owned subsidiary of MFS, has contracted to provide transfer agent and recordkeeping functions in connection with the issuance, transfer, and redemption of each class of shares of the fund under a Shareholder Servicing Agent Agreement. During the year ended December 31, 2007, MFSC did not receive a fee for this service.

Administrator – MFS provides certain financial, legal, shareholder communications, compliance, and other administrative services to the fund. Under an administrative services agreement, the fund partially reimburses MFS the costs incurred to provide these services. The fund is charged an annual fixed amount of $10,000 plus a fee based on average daily net assets.

The administrative services fee incurred for the year ended December 31, 2007 was equivalent to an annual effective rate of 0.0263% of the fund’s average daily net assets.

15

Notes to Financial Statements – continued

Trustees’ and Officers’ Compensation – The fund pays compensation to trustees in the form of a retainer, attendance fees, and additional compensation to the Board chairperson. The fund does not pay compensation directly to officers of the fund who are also officers of the investment adviser, all of whom receive remuneration for their services to the fund from MFS. Certain officers of the fund are officers or directors of MFS, MFD, and MFSC.

Other – This fund and certain other MFS funds (the funds) have entered into a services agreement (the Agreement) which provides for payment of fees by the funds to Tarantino LLC in return for the provision of services of an Independent Chief Compliance Officer (ICCO) for the funds. The ICCO is an officer of the funds and the sole member of Tarantino LLC. The funds can terminate the Agreement with Tarantino LLC at any time under the terms of the Agreement. MFS has agreed to bear all expenses associated with office space, other administrative support, and supplies provided to the ICCO. For the year ended December 31, 2007, the fee paid to Tarantino LLC was $2,217.

Purchases and sales of investments, other than U.S. government securities, purchased option transactions, and short-term obligations, aggregated $110,841,270 and $192,579,893, respectively.

| (5) | | Shares of Beneficial Interest |

The fund’s Declaration of Trust permits the Trustees to issue an unlimited number of full and fractional shares of beneficial interest. Transactions in fund shares were as follows:

| | | | | | | | | | | | |

| | | Year ended 12/31/07 | | | Year ended 12/31/06 | |

| | | Shares | | | Amount | | | Shares | | | Amount | |

| Shares sold | | | | | | | | | | | | |

Initial Class | | 230,880 | | | $4,385,870 | | | 353,749 | | | $6,188,916 | |

Service Class | | 441,487 | | | 8,316,726 | | | 474,451 | | | 8,113,573 | |

| | 672,367 | | | $12,702,596 | | | 828,200 | | | $14,302,489 | |

| Shares issued to shareholders in reinvestment of distributions | | | | | | | | | | | | |

Initial Class | | 1,215,510 | | | $22,960,981 | | | 992,201 | | | $16,748,354 | |

Service Class | | 546,130 | | | 10,267,241 | | | 390,389 | | | 6,562,442 | |

| | 1,761,640 | | | $33,228,222 | | | 1,382,590 | | | $23,310,796 | |

| Shares reacquired | | | | | | | | | | | | |

Initial Class | | (4,454,852 | ) | | $(84,197,974 | ) | | (3,701,196 | ) | | $(63,174,279 | ) |

Service Class | | (1,001,443 | ) | | (18,826,514 | ) | | (1,086,414 | ) | | (18,559,469 | ) |

| | (5,456,295 | ) | | $(103,024,488 | ) | | (4,787,610 | ) | | $(81,733,748 | ) |

| Net change | | | | | | | | | | | | |

Initial Class | | (3,008,462 | ) | | $(56,851,123 | ) | | (2,355,246 | ) | | $(40,237,009 | ) |

Service Class | | (13,826 | ) | | (242,547 | ) | | (221,574 | ) | | (3,883,454 | ) |

| | (3,022,288 | ) | | $(57,093,670 | ) | | (2,576,820 | ) | | $(44,120,463 | ) |

The fund and other funds managed by MFS participate in a $1 billion unsecured committed line of credit provided by a syndication of banks under a credit agreement. In addition, the fund and other funds managed by MFS have established uncommitted borrowing arrangements with certain banks. Borrowings may be made for temporary financing needs. Interest is charged to each fund, based on its borrowings, generally at a rate equal to the Federal Reserve funds rate plus 0.30%. In addition, a commitment fee, based on the average daily, unused portion of the committed line of credit, is allocated among the participating funds at the end of each calendar quarter. For the year ended December 31, 2007, the fund’s commitment fee and interest expense were $2,162 and $255, respectively, and are included in miscellaneous expense on the Statement of Operations.

16

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees of MFS Variable Insurance Trust II, (formerly known as MFS/Sun Life Series Trust) and the Shareholders of MFS Value Portfolio (formerly known as Value Series):

We have audited the accompanying statement of assets and liabilities, including the portfolio of investments, of MFS Value Portfolio (one of the portfolios comprising MFS Variable Insurance Trust II) (the “Trust”) as of December 31, 2007, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Trust’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Trust is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Trust’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2007, by correspondence with the custodian and brokers; where replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, such financial statements and financial highlights present fairly, in all material respects, the financial position of MFS Value Portfolio as of December 31, 2007, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and its financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

DELOITTE & TOUCHE LLP

Boston, Massachusetts

February 15, 2008

17

TRUSTEES AND OFFICERS – IDENTIFICATION AND BACKGROUND

The Trustees and officers of the Trust, as of February 1, 2008, are listed below, together with their principal occupations during the past five years. (Their titles may have varied during that period.) The address of each Trustee and officer is 500 Boylston Street, Boston, Massachusetts 02116.

| | | | | | |

Name, Date of Birth | | Position(s) Held

with Fund | | Trustee/Officer

Since(1) | | Principal Occupations During the Past Five Years &

Other Directorships(2) |

| INTERESTED TRUSTEE | | | | | | |

David D. Horn(3) (born 06/07/41) | | Trustee | | April 1986 | | Private investor; Retired; Sun Life Assurance Company of Canada, Former Senior Vice President and General Manager for the United States (until 1997); Retired: Sun Life Assurance Company of Canada, Director (until March 2004) |

| | |

| INDEPENDENT TRUSTEES | | | | |

J. Kermit Birchfield (born 01/08/40) | | Chairman | | May 1997 | | Consultant; Century Partners, Inc. (investments), Director (1988 to present); Displaytech, Inc. (technology), Director (1995 to present); Dessin Fournir LLC (furniture manufacturer), Director (2005 to present); Intermountain Gas Company, Inc. & Intermountain Industries, Inc. (oil & gas exploration and production) (1988 to present); Site Watch LLC (software to monitor oil tanks) Managing Director (2006 to present); Juridica Investments (fund investing in judicial matters) Director (2007 to present); Dairy Mart Convenience Stores, Inc. (convenience stores), Chairman (1997 to 2003) |

| | | |

Robert C. Bishop (born 01/13/43) | | Trustee | | May 2001 | | Autolmmune Inc. (pharmaceutical product licensing), Chairman, President and Chief Executive Officer (1992 to present); Caliper Life Sciences Corp. (laboratory analytical instruments), Director (2002 to present); Millipore Corporation (biopharmaceutical/research laboratory products), Director (1997 to present); Optobionics Corporation (ophthalmic devices), Director (2002 to 2007); Quintiles Transnational Corp. (contract research services), Director (until 2003) |

| | | |

Frederick H. Dulles (born 03/12/42) | | Trustee | | May 2001 | | Ten State International Law PLLC (law firm), Of Counsel (since 2006); Prudential Carolina Real Estate, (real estate), Broker (since 2006); Free Enterprise Foundation, Inc. (research institute), Director & Secretary (until 2008); Disher, Hamrick & Myers Residential, Inc. (real estate) Broker (until 2006); Frederick H. Dulles law practice (until 2006); Ten State Street LLP (law firm), Member (until 2005); McFadden, Pilkington & Ward LLP (solicitors and registered foreign lawyers), Member & Of Counsel (until 2003) |

| | | |

Marcia A. Kean (born 06/30/48) | | Trustee | | April 2005 | | Feinstein Kean Healthcare (consulting), Chief Executive Officer (since December 2002), Managing Director (prior to May 2001); Ardais Corporation (biotech products), Senior Vice President – Commercialization (February 2002 until November 2002) |

| | | |

Ronald G. Steinhart (born 06/15/40) | | Trustee | | May 2001 | | Private investor; Penske Automotive Group (automotive retailer), Director (2001 to present); Penson Worldwide, Inc. (securities clearance), Director (2006 to present); Animal Health International, Inc. (animal health products), Director (2007 to present); Texas Industries (concrete/aggregates/cement), Director (2007 to present); Carreker Corporation (technology consulting) Director (until 2005); Prentiss Properties Trust (real estate investment trust), Director (until 2006) |

| | | |

Haviland Wright (born 07/21/48) | | Trustee | | May 2001 | | Elixir Technologies Corporation (software) Director (2005 to present); Nano Loa Inc. (liquid crystal displays), Director (2003 to present); Silk Displays, Inc. (smart polymers) Director (2007 to present); Displaytech, Inc. (technology) Chairman and CEO (1995 – 2002) |

| | | |

| TRUSTEE EMERITUS | | | | | | |

Samuel Adams (born 10/19/25) | | Trustee Emeritus | | | | Retired; Kirkpatrick & Lockhart Preston Gates Ellis LLP (law firm), Of Counsel |

| | | |

| OFFICERS | | | | | | |

Maria F. Dwyer(4) (born 12/01/58) | | President | | November 2005 | | Massachusetts Financial Services Company, Executive Vice President and Chief Regulatory Officer (since March 2004); Fidelity Management & Research Company, Vice President (prior to March 2004); Fidelity Group of Funds, President and Treasurer (prior to March 2004) |

| | | |

Tracy Atkinson(4) (born 12/30/64) | | Treasurer | | September 2005 | | Massachusetts Financial Services Company, Senior Vice President (since September 2004); PricewaterhouseCoopers LLP, Partner (prior to September 2004) |

| | | |

Christopher R. Bohane(4) (born 01/18/74) | | Assistant Secretary and Assistant Clerk | | July 2005 | | Massachusetts Financial Services Company, Vice President and Senior Counsel (since April 2003); Kirkpatrick & Lockhart LLP (law firm), Associate (prior to April 2003) |

18

Trustees and Officers – continued

| | | | | | |

Name, Date of Birth | | Position(s) Held

with Fund | | Trustee/Officer

Since(1) | | Principal Occupations During the Past Five Years &

Other Directorships(2) |

Ethan D. Corey(4) (born 11/21/63) | | Assistant Secretary and Assistant Clerk | | July 2005 | | Massachusetts Financial Services Company, Senior Vice President and Associate General Counsel (since April 2006); Special Counsel (prior to April 2006); Dechert LLP (law firm), Counsel (prior to December 2004) |

| | | |

David L. DiLorenzo(4) (born 08/10/68) | | Assistant Treasurer | | July 2005 | | Massachusetts Financial Services Company, Vice President (since June 2005); JP Morgan Investor Services, Vice President (January 2001 to June 2005) |

| | | |

Timothy M. Fagan(4) (born 07/10/68) | | Assistant Secretary and Assistant Clerk | | September 2005 | | Massachusetts Financial Services Company, Vice President and Senior Counsel (since September 2005); John Hancock Advisers, LLC, Vice President and Chief Compliance Officer (September 2004 to August 2005) Senior Attorney (prior to September 2004); John Hancock Group of Funds, Vice President and Chief Compliance Officer (September 2004 to December 2004) |

| | | |

Mark D. Fischer(4) (born 10/27/70) | | Assistant Treasurer | | July 2005 | | Massachusetts Financial Services Company, Vice President (since May 2005); JP Morgan Investment Management Company, Vice President (prior to May 2005) |

| | | |

Brian E. Langenfeld(4) (born 03/07/73) | | Assistant Secretary and Assistant Clerk | | May 2006 | | Massachusetts Financial Services Company, Assistant Vice President and Counsel (since May 2006); John Hancock Advisers, LLC, Assistant Vice President and Counsel (May 2005 to April 2006); John Hancock Advisers, LLC, Attorney and Assistant Secretary (prior to May 2005) |

| | | |

Ellen Moynihan(4) (born 11/13/57) | | Assistant Treasurer | | May 1997 | | Massachusetts Financial Services Company, Senior Vice President |

| | | |

Susan S. Newton(4) (born 03/07/50) | | Assistant Secretary and Assistant Clerk | | May 2005 | | Massachusetts Financial Services Company, Senior Vice President and Assistant General Counsel (since April 2005); John Hancock Advisers, LLC, Senior Vice President, Secretary and Chief Legal Officer (prior to April 2005); John Hancock Group of Funds, Senior Vice President, Secretary and Chief Legal Officer (prior to April 2005) |

| | | |

Susan A. Pereira(4) (born 11/05/70) | | Assistant Secretary and Assistant Clerk | | July 2005 | | Massachusetts Financial Services Company, Vice President and Senior Counsel (since June 2004); Bingham McCutchen LLP (law firm), Associate (January 2001 to June 2004) |

| | | |

Mark N. Polebaum(4) (born 05/01/52) | | Secretary and Assistant Clerk | | February 2006 | | Massachusetts Financial Services Company, Executive Vice President, General Counsel and Secretary (since January 2006); Wilmer Cutler Pickering Hale and Dorr LLP (law firm), Partner (prior to January 2006) |

| | | |

Frank L. Tarantino (born 03/07/44) | | Independent Chief Compliance Officer | | September 2004 | | Tarantino LLC (provider of compliance services), Principal (since June 2004); CRA Business Strategies Group (consulting services), Executive Vice President (April 2003 to June 2004); David L. Babson & Co. (investment adviser), Managing Director, Chief Administrative Officer and Director (February 1997 to March 2003) |

| | | |

Richard S. Weitzel(4) (born 7/16/70) | | Assistant Secretary and Assistant Clerk | | October 2007 | | Massachusetts Financial Services Company, Vice President and Assistant General Counsel (since 2007); Vice President and Senior Counsel (since May 2004); Massachusetts Department of Business and Technology, General Counsel (February 2003 to April 2004); Massachusetts Office of the Attorney General, Assistant Attorney General ( April 2001 to February 2003); Ropes and Gray, Associate (prior to April 2001) |

| | | |

James O. Yost(4) (born 06/12/60) | | Assistant Treasurer | | April 1992 | | Massachusetts Financial Services Company, Senior Vice President |

| (1) | Date first appointed to serve as Trustee/Officer of an MFS fund or a Compass variable account. Each Trustee has served continuously since appointment. |

| (2) | Directorships or trusteeships of companies required to report to the Securities and Exchange Commission (i.e., “public companies”). |

| (3) | “Interested person” of the Sun Life of Canada (U.S.), within the meaning of the Investment Company Act of 1940 (referred to as the 1940 Act), which is the principal federal law governing investment companies like the Series. The address of Sun Life of Canada (U.S.) is One Sun Life Executive Park, Wellesley Hills, Massachusetts 02481. |

| (4) | “Interested person” of MFS within the meaning of the 1940 Act. The address of MFS is 500 Boylston Street, Boston, Massachusetts 02116. |

The Trust does not hold annual meetings for the purpose of electing Trustees, and Trustees are not elected for fixed terms. Each Trustee and officer holds office until his or her successor is chosen and qualified, or until his or her earlier death, resignation, retirement or removal.

All Trustees currently serve as Trustees of the Trust and have served in that capacity since originally elected or appointed. All of the Trustees are also Managers of the Compass Variable Accounts. The executive officers of the Trust hold similar offices for the Compass Variable Accounts and other funds in the MFS fund complex. As of January 1, 2008, each Trustee serves as a Trustee or Manager of 35 Accounts/Funds.

19

Trustees and Officers – continued

The Statement of Additional Information contains further information about the Trustees and is available without charge upon request by calling 1-800-225-2606.

| | |

Investment Adviser

Massachusetts Financial Services Company 500 Boylston Street, Boston, MA 02116-3741 | | Custodian State Street Bank and Trust Company 225 Franklin Street, Boston, MA 02110 |

Distributor

MFS Fund Distributors, Inc. 500 Boylston Street, Boston, MA 02116-3741 | | Independent Registered Public Accounting Firm Deloitte & Touche LLP 200 Berkeley Street, Boston, MA 02116 |

Portfolio Managers Nevin Chitkara Steven Gorham | | |

20

BOARD REVIEW OF INVESTMENT ADVISORY AGREEMENT

The Investment Company Act of 1940 requires that both the full Board of Trustees and a majority of the non-interested (“independent”) Trustees, voting separately, annually approve the continuation of the investment advisory agreement between MFS Variable Insurance Trust II (the “Trust”) and Massachusetts Financial Services Company (MFS) on behalf of the Fund. The Trustees consider matters bearing on the Fund and the advisory arrangements at their meetings throughout the year, including a review of performance data at each regular meeting. In addition, the independent Trustees met several times over the course of three months beginning in May and ending in July 2007 (“contract review meetings”) for the specific purpose of considering whether to approve the continuation of the investment advisory agreement for the Fund. The independent Trustees were assisted in their evaluation of the investment advisory agreement by independent legal counsel, from whom they received separate legal advice and with whom they met separately from MFS management during various contract review meetings. The independent Trustees were also assisted in this process by the Fund’s Independent Chief Compliance Officer, a full-time senior officer appointed by and reporting to the independent Trustees.

In connection with their deliberations, the Trustees, including the independent Trustees, considered such information and factors as they believed, in light of the legal advice furnished to them and their own business judgment, to be relevant. The investment advisory agreement was considered separately for the Fund, although the Trustees also took into account the common interests of all Funds in the Trust in their review. As described below, the Trustees considered the nature, quality, and extent of the various investment advisory, administrative, and shareholder services performed by MFS under the existing investment advisory agreement and other arrangements with the Trust.

In connection with their contract review meetings, the Trustees received and relied upon materials which included, among other items: (i) information provided by Lipper Inc. on the investment performance of the Fund for various time periods ended December 31, 2006, compared to the investment performance of a group of funds with substantially similar investment classifications/objectives (the “Lipper performance universe”), as well as the investment performance of a group of funds identified by objective criteria suggested by MFS (“peer funds”), (ii) information provided by Lipper Inc. on the Fund’s advisory fees and other expenses compared to the advisory fees and other expenses of comparable funds identified by Lipper (the “Lipper expense group”), as well as the advisory fees and other expenses of peer funds identified by objective criteria suggested by MFS, (iii) information provided by MFS on the advisory fees of comparable portfolios of its other clients, including institutional separate account and other clients, (iv) information as to whether, and to what extent applicable, expense waivers, reimbursements or fee “breakpoints” are observed for the Fund, (v) information regarding MFS’ financial results and financial condition, including MFS’ and certain of its affiliates’ estimated profitability from services performed for the Fund, (vi) MFS’ views regarding the outlook for the mutual fund industry and its strategic business plans, (vii) descriptions of various functions performed by MFS for the Trust, such as compliance monitoring and portfolio trading practices, and (viii) information regarding the overall organization of MFS, including information about MFS’ senior management and other personnel providing investment advisory, administrative and other services to the Fund. The comparative performance, fee and expense information prepared and provided by Lipper Inc. was not independently verified, and the independent Trustees did not independently verify any information provided to them by MFS.

The Trustees’ conclusion as to the continuation of the investment advisory agreement was based on comprehensive consideration of all information provided to the Trustees and not the result of any single factor. Some of the factors that figured particularly in the Trustees’ deliberations are described below for the Fund, while individual Trustees may have given different weight to various factors and evaluated the information presented as a whole differently than another Trustee. The Trustees recognized that the fee arrangements for the Fund reflect years of review and discussion between the independent Trustees and MFS, that certain aspects of such arrangements may receive greater scrutiny in some years than others, and that the Trustees’ conclusions may be based, in part, on their consideration of these same arrangements during the course of the year and in prior years.

Based on information provided by Lipper Inc. and MFS, the Trustees compared the Fund’s total return investment performance to the performance of a peer group of funds over various time periods. The Trustees placed particular emphasis on the total return performance of the Fund’s Initial Class shares in comparison to the performance of funds in its Lipper performance universe over the one-, three- and five-year periods. The Trustees did not rely on performance results for more recent periods, including those shown elsewhere in this report.