UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-03732

MFS VARIABLE INSURANCE TRUST II

(Exact name of registrant as specified in charter)

500 Boylston Street, Boston, Massachusetts 02116

(Address of principal executive offices) (Zip code)

Susan S. Newton

Massachusetts Financial Services Company

500 Boylston Street

Boston, Massachusetts 02116

(Name and address of agents for service)

Registrant’s telephone number, including area code: (617) 954-5000

Date of fiscal year end: December 31

Date of reporting period: December 31, 2010

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

MFS® INTERNATIONAL GROWTH PORTFOLIO

The report is prepared for the general information of contract owners. It is authorized for distribution to prospective investors only when preceded or accompanied by a current prospectus.

NOT FDIC INSURED Ÿ MAY LOSE VALUE Ÿ NO BANK GUARANTEE Ÿ NOT A DEPOSIT Ÿ NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY OR NCUA/NCUSIF

MFS International Growth Portfolio

LETTER FROM THE CEO

Dear Contract Owners:

After an extended rebound in the financial markets, uncertainty returned in 2010 as investors began to question the durability of the recovery for global economies and markets. That uncertainty led to increased risk aversion, especially as investors saw the eurozone struggle with the debt woes of many of its members. In September, the U.S. Federal Reserve Board’s promises to further loosen monetary policy helped assuage market fears and drive asset prices off their recent lows. A combination of solid earnings and improving economic data gave an additional boost to investor sentiment. As we enter 2011, we are cautiously optimistic that economic growth will continue to improve and that the global economies will recover from the shocks of the past few years. We expect the pace of recovery worldwide will be uneven and volatile.

As always, we continue to be mindful of the many economic challenges faced at the local, national, and international levels. It is in times such as these that we want to remind investors of the merits of maintaining a long-term view, adhering to basic investing principles such as asset allocation and diversification, and working closely with their advisors to research and identify appropriate investment opportunities.

Respectfully,

Robert J. Manning

Chairman and Chief Executive Officer

MFS Investment Management®

February 14, 2011

The opinions expressed in this letter are subject to change, may not be relied upon for investment advice, and no forecasts can be guaranteed.

1

MFS International Growth Portfolio

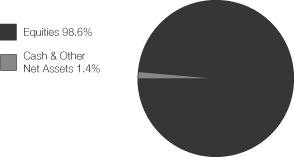

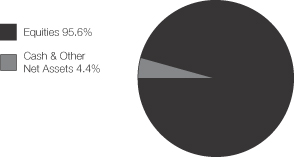

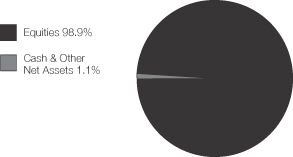

PORTFOLIO COMPOSITION

Portfolio structure

| | | | |

| Top ten holdings | | | | |

| BHP Billiton Ltd. | | | 3.8% | |

| LVMH Moet Hennessy Louis Vuitton S.A. | | | 2.8% | |

| Teck Resources Ltd., “B” | | | 2.3% | |

| Taiwan Semiconductor Manufacturing Co. Ltd., ADR | | | 2.1% | |

| Schneider Electric S.A. | | | 2.1% | |

| Groupe Danone | | | 1.9% | |

| Nestle S.A. | | | 1.8% | |

| Accenture Ltd., “A” | | | 1.7% | |

| Saipem S.p.A. | | | 1.6% | |

| Linde AG | | | 1.6% | |

| | | | |

| Equity sectors | | | | |

| Financial Services | | | 15.4% | |

| Basic Materials | | | 14.3% | |

| Consumer Staples | | | 12.9% | |

| Technology | | | 10.9% | |

| Health Care | | | 10.5% | |

| Retailing | | | 10.3% | |

| Special Products & Services | | | 6.8% | |

| Industrial Goods & Services | | | 5.4% | |

| Energy | | | 5.2% | |

| Utilities & Communications | | | 3.6% | |

| Leisure | | | 2.4% | |

| Transportation | | | 0.9% | |

| | | | |

| Issuer country weightings | | | | |

| United Kingdom | | | 11.7% | |

| France | | | 11.2% | |

| Japan | | | 10.4% | |

| Switzerland | | | 10.1% | |

| Germany | | | 9.6% | |

| Australia | | | 5.7% | |

| Brazil | | | 5.6% | |

| Taiwan | | | 3.7% | |

| Canada | | | 3.4% | |

| Other Countries | | | 28.6% | |

Percentages are based on net assets as of 12/31/10.

The portfolio is actively managed and current holdings may be different.

2

MFS International Growth Portfolio

MANAGEMENT REVIEW

Summary of Results

For the twelve months ended December 31, 2010, Initial Class shares of the MFS International Growth Portfolio (the “fund”) provided a total return of 15.16%, while Service Class shares of the fund provided a total return of 14.86%. These compare with a return of 14.79% for the fund’s benchmark, the Morgan Stanley Capital International (MSCI) All Country World (ex-US) Growth Index.

Market Environment

The first quarter of the reporting period witnessed a continuation of the financial market and macroeconomic rebounds that had begun in early 2009. These recoveries in global activity and asset valuations were generally synchronized around the world, led importantly by emerging Asian economies, but broadening to include most of the global economy to varying degrees. Primary drivers of the recoveries included an unwinding of the inventory destocking that took place earlier, the production of manufacturing and capital goods, as well as massive fiscal and monetary stimulus.

During most of the remainder of the period, heightened risk surrounding the public-debt profiles of several of the peripheral European countries impaired market sentiment. At the same time, the improving trend in global macroeconomic data began to weaken somewhat. These two dynamics caused many asset prices to retrench significantly, as many questioned the durability of the global recovery.

Towards the end of the period, the U.S. Federal Reserve led markets to believe that further monetary loosening would be forthcoming if macroeconomic activity did not show signs of improvement. The prospects for more easing by the Fed improved market sentiment and drove risk-asset prices markedly higher. However, in a text-book case of “buy the rumor, sell the fact,” the weeks following the early November announcement of further quantitative easing saw a sell-off in U.S. Treasury bonds. This rise in Treasury yields occurred despite risk-off behavior in equities and credit markets (which would normally result in Treasury yield compression), and appears to have been the result of a few factors: signs of improved U.S. and global economic activity; opposition to quantitative easing from some quarters; and crowded long positions in U.S. Treasuries. The December agreement on an expansionary U.S. fiscal package also boosted sentiment, leading markets to reach near-term highs in risky asset valuations toward year end.

Contributors to Performance

Stock selection in the retailing sector was a primary factor driving relative performance. The fund’s overweight positions in luxury goods maker LVMH Moët Hennessy Louis Vuitton (France), watch maker Swatch Group (Switzerland), and export trading company Li & Fung (Hong Kong) were among the fund’s top relative contributors. Shares of LVMH rose during the reporting period as the company reported better-than-expected sales and earnings results. Strength was evident across all of LVMH’s business segments, as the company benefited from robust demand for luxury goods, as well as the replenishing of inventories at U.S. and European retailers following the recession.

Stock selection in the financial services and special products & services sectors also positively contributed to relative performance. In the financial services sector, holdings of commercial banking firm Credicorp (b) (Peru) was among the fund’s top contributors. In the special products & services sector, product safety testing company Intertek Group (United Kingdom) was another positive factor.

Stocks in other sectors that contributed to relative results included zircon producer Iluka Resources (b) (Australia), brewery company Companhia de Bebidas das Americas (Brazil), and oil and gas turnkey contractor Saipem S.p.A. (Italy). Shares of Iluka Resources soared as the company’s management announced significantly higher-than-expected earnings in the second half of 2010, following a partial recovery in global demand earlier in the year. The fund’s timing of ownership in shares of diversified mining company Teck Resources (Canada) and digital products manufacturer ARM Holdings (h) (United Kingdom) also helped.

Detractors from Performance

Stock selection in the energy sector held back relative performance. The fund’s investment in shares of oil and gas explorer INPEX (Japan), and timing of ownership in shares of integrated oil and gas company TOTAL (b)(h) (France), negatively impacted relative results. The share price of INPEX fell as the company announced plans to raise capital via a stock issue to finance the development of the Ichthys natural gas project in Australia.

Elsewhere, holdings of securities broker Nomura Holdings (b) (Japan), apparel retailer Esprit Holdings (Hong Kong), stock exchange Deutsche Boerse (Germany), copy machine maker Konica Minolta Holdings (Japan), skin and beauty care products company Beiersdorf (Germany), paint and specialty chemical maker Akzo Nobel (b) (Netherlands), specialty chemical manufacturer Shin-Etsu Chemical (Japan), and oil and gas exploration and production company Petroleo Brasileiro (Brazil) detracted from relative performance.

3

MFS International Growth Portfolio

Management Review – continued

During the reporting period, the fund’s currency exposure was also a detractor from relative performance. All of MFS’ investment decisions are driven by the fundamentals of each individual opportunity and as such, it is common for our portfolios to have different currency exposure than the benchmark.

Respectfully,

David Antonelli

Portfolio Manager

| (b) | Security is not a benchmark constituent. |

| (h) | Security was not held in the portfolio at period end. |

The views expressed in this report are those of the portfolio manager only through the end of the period of the report as stated on the cover and do not necessarily reflect the views of MFS or any other person in the MFS organization. These views are subject to change at any time based on market or other conditions, and MFS disclaims any responsibility to update such views. These views may not be relied upon as investment advice or an indication of trading intent on behalf of any MFS portfolio. References to specific securities are not recommendations of such securities, and may not be representative of any MFS portfolio’s current or future investments.

4

MFS International Growth Portfolio

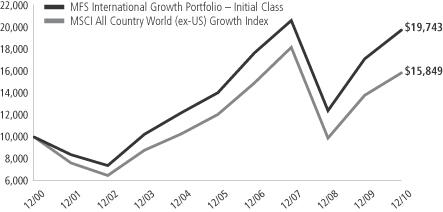

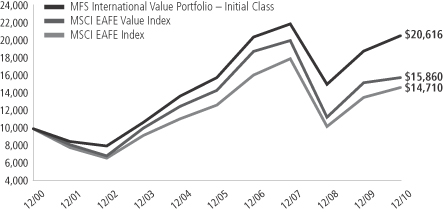

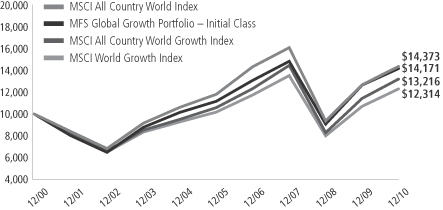

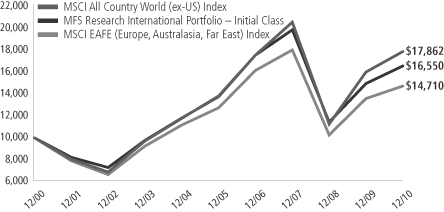

PERFORMANCE SUMMARY THROUGH 12/31/10

The following chart illustrates the historical performance of the fund in comparison to its benchmark(s). Benchmarks are unmanaged and may not be invested in directly. Benchmark returns do not reflect any fees or expenses. The performance of other share classes will be greater than or less than that of the class depicted below. (See Notes to Performance Summary.)

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your units, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. The performance shown does not reflect the deduction of taxes, if any, that a contract holder would pay on fund distributions or the redemption of contract units. The returns for the fund shown also do not reflect the deduction of expenses associated with variable products, such as mortality and expense risk charges, separate account charges, and sales charges imposed by the insurance company separate accounts. Such expenses would reduce the overall returns shown.

Growth of a Hypothetical $10,000 Investment

Total Returns through 12/31/10

Average annual total returns

| | | | | | | | | | | | | | |

| | | Share class | | Class inception date | | 1-yr | | 5-yr | | 10-yr | | Life (t) | | |

| | | Initial Class | | 6/03/96 | | 15.16% | | 7.05% | | 7.04% | | N/A | | |

| | | Service Class | | 8/24/01 | | 14.86% | | 6.78% | | N/A | | 8.84% | | |

| | | | | |

| Comparative benchmark | | | | | | | | | | |

| | | MSCI All Country World (ex-US) Growth Index (f) | | 14.79% | | 5.59% | | 4.71% | | N/A | | |

| (f) | Source: FactSet Research Systems Inc. |

| (t) | For the period from the class inception date through the stated period (for those share classes with less than 10 years of performance history). No comparative benchmark performance information is provided for “life” periods. (See Notes to Performance Summary). |

Benchmark Definition

MSCI All Country World (ex-US) Growth Index – a market capitalization-weighted index that is designed to measure equity market performance for growth securities in the global developed and emerging markets, excluding the U.S.

It is not possible to invest directly in an index.

Notes to Performance Summary

Average annual total return represents the average annual change in value for each share class for the periods presented. Life returns are presented where the share class has less than 10 years of performance history and represent the average annual total return from the class inception date to the stated period end date. As the fund’s share classes may have different inception dates, the life returns may represent different time periods and may not be comparable. As a result, no comparative benchmark performance information is provided for life periods.

Performance results reflect any applicable expense subsidies and waivers in effect during the periods shown. Without such subsidies and waivers the fund’s performance results would be less favorable. Please see the prospectus and financial statements for complete details. All results are historical and assume the reinvestment of any dividends and capital gains distributions.

From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower.

5

MFS International Growth Portfolio

EXPENSE TABLE

Fund Expenses Borne by the Contract Holders During the Period,

July 1, 2010 through December 31, 2010

As a contract holder of the fund, you incur ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period July 1, 2010 through December 31, 2010.

Actual Expenses

The first line for each share class in the following table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each share class in the following table provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight the fund’s ongoing costs only and do not take into account the fees and expenses imposed under the variable contracts through which your investment in the fund is made. Therefore, the second line for each share class in the table is useful in comparing ongoing costs associated with an investment in vehicles (such as the fund) which fund benefits under variable annuity and variable life insurance contracts and to qualified pension and retirement plans only, and will not help you determine the relative total costs of investing in the fund through variable annuity and variable life insurance contracts. If the fees and expenses imposed under the variable contracts were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | |

| Share Class | | | | Annualized Expense Ratio | | | Beginning Account Value 7/01/10 | | | Ending Account Value 12/31/10 | | | Expenses Paid During Period (p) 7/01/10-12/31/10 | |

| Initial Class | | Actual | | | 1.07% | | | | $1,000.00 | | | | $1,264.84 | | | | $6.11 | |

| | Hypothetical (h) | | | 1.07% | | | | $1,000.00 | | | | $1,019.81 | | | | $5.45 | |

| Service Class | | Actual | | | 1.32% | | | | $1,000.00 | | | | $1,263.55 | | | | $7.53 | |

| | Hypothetical (h) | | | 1.32% | | | | $1,000.00 | | | | $1,018.55 | | | | $6.72 | |

| (h) | 5% class return per year before expenses. |

| (p) | Expenses paid is equal to each class’ annualized expense ratio, as shown above, multiplied by the average account value over the period, multiplied by the number of days in the period, divided by the number of days in the year. |

6

MFS International Growth Portfolio

PORTFOLIO OF INVESTMENTS – 12/31/10

The Portfolio of Investments is a complete list of all securities owned by your fund. It is categorized by broad-based asset classes.

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | |

| COMMON STOCKS – 98.6% | | | | | | | | |

| Airlines – 0.9% | | | | | | | | |

| Copa Holdings S.A., “A” | | | 36,320 | | | $ | 2,137,069 | |

| | | | | | | | |

| Alcoholic Beverages – 4.2% | | | | | | | | |

| Companhia de Bebidas das Americas, ADR | | | 109,790 | | | $ | 3,406,784 | |

| Diageo PLC | | | 171,422 | | | | 3,167,077 | |

| Heineken N.V. | | | 28,163 | | | | 1,380,799 | |

| Pernod Ricard S.A. | | | 27,898 | | | | 2,623,027 | |

| | | | | | | | |

| | | | | | $ | 10,577,687 | |

| | | | | | | | |

| Apparel Manufacturers – 6.3% | | | | | | | | |

| Compagnie Financiere Richemont S.A. | | | 46,276 | | | $ | 2,722,118 | |

| Li & Fung Ltd. | | | 566,600 | | | | 3,287,575 | |

| LVMH Moet Hennessy Louis Vuitton S.A. | | | 42,882 | | | | 7,054,026 | |

| Swatch Group Ltd. | | | 6,443 | | | | 2,872,131 | |

| | | | | | | | |

| | | | | | $ | 15,935,850 | |

| | | | | | | | |

| Broadcasting – 1.5% | | | | | | | | |

| Grupo Televisa S.A., ADR (a) | | | 57,100 | | | $ | 1,480,603 | |

| Publicis Groupe S.A. | | | 46,500 | | | | 2,423,380 | |

| | | | | | | | |

| | | | | | $ | 3,903,983 | |

| | | | | | | | |

| Brokerage & Asset Managers – 4.4% | | | | | | | | |

| Aberdeen Asset Management PLC | | | 744,394 | | | $ | 2,354,825 | |

| BM&F Bovespa S.A. | | | 380,000 | | | | 3,005,663 | |

| Deutsche Boerse AG | | | 36,501 | | | | 2,526,611 | |

| ICAP PLC | | | 163,496 | | | | 1,363,750 | |

| Nomura Holdings, Inc. | �� | | 273,600 | | | | 1,735,485 | |

| | | | | | | | |

| | | | | | $ | 10,986,334 | |

| | | | | | | | |

| Business Services – 6.8% | | | | | | | | |

| Accenture Ltd., “A” (s) | | | 86,090 | | | $ | 4,174,504 | |

| Amadeus IT Holding S.A. (a) | | | 93,523 | | | | 1,959,604 | |

| Capita Group PLC | | | 193,116 | | | | 2,097,071 | |

| Hays PLC | | | 1,111,086 | | | | 2,232,926 | |

| Infosys Technologies Ltd., ADR | | | 24,780 | | | | 1,885,262 | |

| Intertek Group PLC | | | 79,670 | | | | 2,204,788 | |

| Michael Page International | | | 317,870 | | | | 2,750,529 | |

| | | | | | | | |

| | | | | | $ | 17,304,684 | |

| | | | | | | | |

| Computer Software – 1.4% | | | | | | | | |

| Dassault Systems S.A. | | | 21,802 | | | $ | 1,643,741 | |

| SAP AG | | | 39,392 | | | | 2,005,566 | |

| | | | | | | | |

| | | | | | $ | 3,649,307 | |

| | | | | | | | |

| Computer Software – Systems – 3.4% | | | | | | | | |

| Acer, Inc. | | | 1,239,750 | | | $ | 3,831,100 | |

| Konica Minolta Holdings, Inc. | | | 256,000 | | | | 2,661,214 | |

| NICE Systems Ltd., ADR (a) | | | 56,960 | | | | 1,987,904 | |

| | | | | | | | |

| | | | | | $ | 8,480,218 | |

| | | | | | | | |

| Consumer Products – 4.6% | | | | | | | | |

| AmorePacific Corp. (a) | | | 1,665 | | | $ | 1,671,015 | |

| Beiersdorf AG | | | 40,376 | | | | 2,240,458 | |

| Henkel KGaA, IPS | | | 32,310 | | | | 2,009,188 | |

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| COMMON STOCKS – continued | | | | | |

| Consumer Products – continued | | | | | | | | |

| Reckitt Benckiser Group PLC | | | 59,082 | | | $ | 3,247,043 | |

| Uni-Charm Corp. | | | 59,700 | | | | 2,371,479 | |

| | | | | | | | |

| | | | | | $ | 11,539,183 | |

| | | | | | | | |

| Electrical Equipment – 2.6% | | | | | | | | |

| Keyence Corp. | | | 4,300 | | | $ | 1,243,163 | |

| Schneider Electric S.A. | | | 36,008 | | | | 5,389,159 | |

| | | | | | | | |

| | | | | | $ | 6,632,322 | |

| | | | | | | | |

| Electronics – 5.5% | | | | | | | | |

| Hoya Corp. | | | 77,700 | | | $ | 1,887,232 | |

| Infineon Technologies AG (a) | | | 202,496 | | | | 1,884,156 | |

| Samsung Electronics Co. Ltd. | | | 3,353 | | | | 2,803,769 | |

| Taiwan Semiconductor Manufacturing Co. Ltd., ADR | | | 431,040 | | | | 5,405,242 | |

| Tokyo Electron Ltd. | | | 32,100 | | | | 2,032,196 | |

| | | | | | | | |

| | | | | | $ | 14,012,595 | |

| | | | | | | | |

| Energy – Independent – 0.7% | | | | | | | | |

| INPEX Corp. | | | 319 | | | $ | 1,868,266 | |

| | | | | | | | |

| Energy – Integrated – 2.9% | | | | | | | | |

| OAO Gazprom, ADR | | | 106,260 | | | $ | 2,683,065 | |

| Petroleo Brasileiro S.A., ADR | | | 48,060 | | | | 1,818,590 | |

| Suncor Energy, Inc. | | | 74,722 | | | | 2,876,756 | |

| | | | | | | | |

| | | | | | $ | 7,378,411 | |

| | | | | | | | |

| Engineering – Construction – 0.8% | | | | | | | | |

| JGC Corp. | | | 90,000 | | | $ | 1,954,038 | |

| | | | | | | | |

| Food & Beverages – 4.1% | | | | | | | | |

| Coca-Cola Hellenic Bottling Co. S.A. | | | 44,654 | | | $ | 1,155,233 | |

| Groupe Danone | | | 75,158 | | | | 4,722,389 | |

| Nestle S.A. | | | 75,873 | | | | 4,442,831 | |

| | | | | | | | |

| | | | | | $ | 10,320,453 | |

| | | | | | | | |

| Food & Drug Stores – 2.4% | | | | | | | | |

| Dairy Farm International Holdings Ltd. | | | 214,200 | | | $ | 1,989,918 | |

| Lawson, Inc. | | | 27,500 | | | | 1,359,927 | |

| Tesco PLC | | | 420,151 | | | | 2,783,993 | |

| | | | | | | | |

| | | | | | $ | 6,133,838 | |

| | | | | | | | |

| Internet – 0.6% | | | | | | | | |

| Yahoo Japan Corp. | | | 4,113 | | | $ | 1,595,757 | |

| | | | | | | | |

| Leisure & Toys – 0.9% | | | | | | | | |

| Shimano, Inc. | | | 44,000 | | | $ | 2,238,207 | |

| | | | | | | | |

| Machinery & Tools – 2.0% | | | | | | | | |

| KONE Oyj “B” | | | 44,737 | | | $ | 2,486,933 | |

| Schindler Holding AG | | | 20,608 | | | | 2,437,695 | |

| | | | | | | | |

| | | | | | $ | 4,924,628 | |

| | | | | | | | |

| Major Banks – 6.1% | | | | | | | | |

| Credit Suisse Group AG | | | 68,357 | | | $ | 2,754,019 | |

| Erste Group Bank AG | | | 56,679 | | | | 2,661,509 | |

7

MFS International Growth Portfolio

Portfolio of Investments – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| COMMON STOCKS – continued | |

| Major Banks – continued | | | | | | | | |

| HSBC Holdings PLC | | | 347,524 | | | $ | 3,527,819 | |

| Julius Baer Group Ltd. | | | 55,670 | | | | 2,607,857 | |

| Standard Chartered PLC | | | 140,550 | | | | 3,781,112 | |

| | | | | | | | |

| | | | | | $ | 15,332,316 | |

| | | | | | | | |

| Medical & Health Technology & Services – 1.9% | |

| Diagnosticos da America S.A. | | | 90,400 | | | $ | 1,225,301 | |

| Fleury S.A. | | | 63,600 | | | | 1,021,048 | |

| Fresenius Medical Care AG & Co. KGaA | | | 41,957 | | | | 2,423,782 | |

| | | | | | | | |

| | | | | | $ | 4,670,131 | |

| | | | | | | | |

| Medical Equipment – 3.1% | | | | | | | | |

| Essilor International S.A. | | | 31,511 | | | $ | 2,028,560 | |

| Sonova Holding AG | | | 25,726 | | | | 3,320,993 | |

| Synthes, Inc. | | | 19,130 | | | | 2,584,084 | |

| | | | | | | | |

| | | | | | $ | 7,933,637 | |

| | | | | | | | |

| Metals & Mining – 7.5% | | | | | | | | |

| BHP Billiton Ltd. | | | 208,972 | | | $ | 9,671,582 | |

| Iluka Resources Ltd. (a) | | | 381,247 | | | | 3,564,047 | |

| Teck Resources Ltd., “B” | | | 93,395 | | | | 5,803,960 | |

| | | | | | | | |

| | | | | | $ | 19,039,589 | |

| | | | | | | | |

| Oil Services – 1.6% | | | | | | | | |

| Saipem S.p.A. | | | 81,532 | | | $ | 4,013,762 | |

| | | | | | | | |

| Other Banks & Diversified Financials – 4.9% | |

| Akbank T.A.S. | | | 453,200 | | | $ | 2,518,430 | |

| Banco Santander Brasil S.A., ADR | | | 279,220 | | | | 3,797,392 | |

| Bank Rakyat Indonesia | | | 1,436,500 | | | | 1,674,057 | |

| China Construction Bank (a) | | | 1,421,410 | | | | 1,274,602 | |

| Credicorp Ltd. | | | 8,320 | | | | 989,331 | |

| HDFC Bank Ltd. | | | 38,773 | | | | 2,034,553 | |

| | | | | | | | |

| | | | | | $ | 12,288,365 | |

| | | | | | | | |

| Pharmaceuticals – 5.5% | | | | | | | | |

| Bayer AG | | | 44,085 | | | $ | 3,257,766 | |

| Merck KGaA | | | 17,104 | | | | 1,367,936 | |

| Novo Nordisk A/S, “B” | | | 22,471 | | | | 2,533,907 | |

| Roche Holding AG | | | 13,145 | | | | 1,926,059 | |

| Santen, Inc. | | | 53,800 | | | | 1,868,654 | |

| Teva Pharmaceutical Industries Ltd., ADR | | | 57,200 | | | | 2,981,836 | |

| | | | | | | | |

| | | | | | $ | 13,936,158 | |

| | | | | | | | |

| Precious Metals & Minerals – 0.5% | | | | | | | | |

| Newcrest Mining Ltd. | | | 30,150 | | | $ | 1,247,066 | |

| | | | | | | | |

| Specialty Chemicals – 6.3% | | | | | | | | |

| Akzo Nobel N.V. | | | 55,731 | | | $ | 3,461,893 | |

| L’Air Liquide S.A. | | | 19,431 | | | | 2,457,388 | |

| Linde AG | | | 26,316 | | | | 3,993,107 | |

| Shin-Etsu Chemical Co. Ltd. | | | 64,900 | | | | 3,517,182 | |

| Symrise AG | | | 90,647 | | | | 2,486,226 | |

| | | | | | | | |

| | | | | | $ | 15,915,796 | |

| | | | | | | | |

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| COMMON STOCKS – continued | |

| Specialty Stores – 1.6% | | | | | | | | |

| Esprit Holdings Ltd. | | | 414,169 | | | $ | 1,971,523 | |

| Industria de Diseno Textil S.A. | | | 28,741 | | | | 2,151,922 | |

| | | | | | | | |

| | | | | | $ | 4,123,445 | |

| | | | | | | | |

| Telecommunications – Wireless – 1.9% | |

| MTN Group Ltd. | | | 120,819 | | | $ | 2,465,350 | |

| Philippine Long Distance Telephone Co. | | | 39,970 | | | | 2,330,139 | |

| | | | | | | | |

| | | | | | $ | 4,795,489 | |

| | | | | | | | |

| Telephone Services – 1.7% | | | | | | | | |

| China Unicom Ltd. | | | 2,148,000 | | | $ | 3,072,993 | |

| Telefonica S.A. | | | 55,739 | | | | 1,263,621 | |

| | | | | | | | |

| | | | | | $ | 4,336,614 | |

| | | | | | | | |

Total Common Stocks

(Identified Cost, $216,172,332) | | | | | | $ | 249,205,198 | |

| | | | | | | | |

|

| MONEY MARKET FUNDS (v) – 0.8% | |

| MFS Institutional Money Market Portfolio, 0.18%, at Cost and Net Asset Value | | | 2,123,761 | | | $ | 2,123,761 | |

| | | | | | | | |

Total Investments

(Identified Cost, $218,296,093) | | | $ | 251,328,959 | |

OTHER ASSETS, LESS

LIABILITIES – 0.6% | | | | 1,475,234 | |

| | | | | | | | |

| Net Assets – 100.0% | | | $ | 252,804,193 | |

| | | | | | | | |

| (a) | Non-income producing security. |

| (s) | Security or a portion of the security was pledged to cover collateral requirements for securities sold short and written options. At December 31, 2010, the value of securities pledged amounted to $166,321. At December 31, 2010, the fund had no short sales outstanding. |

| (v) | Underlying fund that is available only to investment companies managed by MFS. The rate quoted is the annualized seven-day yield of the fund at period end. |

The following abbreviations are used in this report and are defined:

| ADR | | American Depository Receipt |

| IPS | | International Preference Stock |

| PLC | | Public Limited Company |

See Notes to Financial Statements

8

MFS International Growth Portfolio

FINANCIAL STATEMENTS | STATEMENT OF ASSETS AND LIABILITIES

This statement represents your fund’s balance sheet, which details the assets and liabilities comprising the total value of the fund.

| | | | | | | | |

At 12/31/10 | | | | | | | | |

Assets | | | | | | | | |

Investments – | | | | | | | | |

Non-affiliated issuers, at value (identified cost, $216,172,332) | | | $249,205,198 | | | | | |

Underlying funds, at cost and value | | | 2,123,761 | | | | | |

Total investments, at value (identified cost, $218,296,093) | | | $251,328,959 | | | | | |

Foreign currency, at value (identified cost, $48,565) | | | 48,613 | | | | | |

Receivables for | | | | | | | | |

Investments sold | | | 1,429,793 | | | | | |

Fund shares sold | | | 109,722 | | | | | |

Interest and dividends | | | 427,032 | | | | | |

Other assets | | | 8,567 | | | | | |

Total assets | | | | | | | $253,352,686 | |

Liabilities | | | | | | | | |

Payables for | | | | | | | | |

Investments purchased | | | $299,726 | | | | | |

Fund shares reacquired | | | 86,655 | | | | | |

Payable to affiliates | | | | | | | | |

Investment adviser | | | 12,459 | | | | | |

Shareholder servicing costs | | | 132 | �� | | | | |

Distribution and/or service fees | | | 428 | | | | | |

Administrative services fee | | | 495 | | | | | |

Payable for Trustees’ compensation | | | 78 | | | | | |

Deferred country tax expense payable | | | 43,806 | | | | | |

Accrued expenses and other liabilities | | | 104,714 | | | | | |

Total liabilities | | | | | | | $548,493 | |

Net assets | | | | | | | $252,804,193 | |

Net assets consist of | | | | | | | | |

Paid-in capital | | | $197,544,320 | | | | | |

Unrealized appreciation (depreciation) on investments and translation of assets and liabilities in foreign currencies

(net of $43,806 deferred country tax) | | | 33,007,396 | | | | | |

Accumulated net realized gain (loss) on investments and foreign currency transactions | | | 19,674,240 | | | | | |

Undistributed net investment income | | | 2,578,237 | | | | | |

Net assets | | | | | | | $252,804,193 | |

Shares of beneficial interest outstanding | | | | | | | 18,270,880 | |

| | | | | | | | | | | | |

| | | Net assets | | | Shares

outstanding | | | Net asset value

per share | |

Initial Class | | | $221,456,475 | | | | 15,992,589 | | | | $13.85 | |

Service Class | | | 31,347,718 | | | | 2,278,291 | | | | 13.76 | |

See Notes to Financial Statements

9

MFS International Growth Portfolio

FINANCIAL STATEMENTS | STATEMENT OF OPERATIONS

This statement describes how much your fund earned in investment income and accrued in expenses. It also describes any gains and/or losses generated by fund operations.

| | | | | | | | |

| Year ended 12/31/10 | | | | | | | | |

| Net investment income | | | | | | | | |

Income | | | | | | | | |

Dividends | | | $5,950,128 | | | | | |

Interest | | | 80,737 | | | | | |

Dividends from underlying funds | | | 8,172 | | | | | |

Foreign taxes withheld | | | (581,755 | ) | | | | |

Total investment income | | | | | | | $5,457,282 | |

Expenses | | | | | | | | |

Management fee | | | $2,131,103 | | | | | |

Distribution and/or service fees | | | 68,993 | | | | | |

Shareholder servicing costs | | | 27,351 | | | | | |

Administrative services fee | | | 84,613 | | | | | |

Trustees’ compensation | | | 27,727 | | | | | |

Custodian fee | | | 209,211 | | | | | |

Shareholder communications | | | 18,417 | | | | | |

Auditing fees | | | 55,958 | | | | | |

Legal fees | | | 7,157 | | | | | |

Miscellaneous | | | 29,313 | | | | | |

Total expenses | | | | | | | $2,659,843 | |

Fees paid indirectly | | | (10 | ) | | | | |

Net expenses | | | | | | | $2,659,833 | |

Net investment income | | | | | | | $2,797,449 | |

Realized and unrealized gain (loss) on investments and foreign currency transactions | | | | | | | | |

Realized gain (loss) (identified cost basis) | | | | | | | | |

Investment transactions (net of $7,813 country tax) | | | $28,087,937 | | | | | |

Foreign currency transactions | | | (206,902 | ) | | | | |

Net realized gain (loss) on investments and foreign currency transactions | | | | | | | $27,881,035 | |

Change in unrealized appreciation (depreciation) | | | | | | | | |

Investments (net of $2,032 increase in deferred country tax) | | | $7,195,481 | | | | | |

Translation of assets and liabilities in foreign currencies | | | 10,342 | | | | | |

Net unrealized gain (loss) on investments and foreign currency translation | | | | | | | $7,205,823 | |

Net realized and unrealized gain (loss) on investments and foreign currency | | | | | | | $35,086,858 | |

Change in net assets from operations | | | | | | | $37,884,307 | |

See Notes to Financial Statements

10

MFS International Growth Portfolio

FINANCIAL STATEMENTS | STATEMENTS OF CHANGES IN NET ASSETS

These statements describe the increases and/or decreases in net assets resulting from operations, any distributions, and any shareholder transactions.

| | | | | | | | |

For years ended 12/31 | | | 2010 | | | | 2009 | |

Change in net assets | | | | | | | | |

From operations | | | | | | | | |

Net investment income | | | $2,797,449 | | | | $1,964,427 | |

Net realized gain (loss) on investments and foreign currency transactions | | | 27,881,035 | | | | 4,026,805 | |

Net unrealized gain (loss) on investments and foreign currency translation | | | 7,205,823 | | | | 44,703,242 | |

Change in net assets from operations | | | $37,884,307 | | | | $50,694,474 | |

Distributions declared to shareholders | | | | | | | | |

From net investment income | | | $(1,936,143 | ) | | | $(1,417,238 | ) |

Change in net assets from fund share transactions | | | $9,593,366 | | | | $52,895,067 | |

Total change in net assets | | | $45,541,530 | | | | $102,172,303 | |

Net assets | | | | | | | | |

At beginning of period | | | 207,262,663 | | | | 105,090,360 | |

At end of period (including undistributed net investment income of $2,578,237 and

$1,931,646, respectively) | | | $252,804,193 | | | | $207,262,663 | |

See Notes to Financial Statements

11

MFS International Growth Portfolio

FINANCIAL STATEMENTS | FINANCIAL HIGHLIGHTS

The financial highlights table is intended to help you understand the fund’s financial performance for the past 5 years. Certain information reflects financial results for a single fund share. The total returns in the table represent the rate by which an investor would have earned (or lost) on an investment in the fund share class (assuming reinvestment of all distributions) held for the entire period.

| | | | | | | | | | | | | | | | | | | | |

| Initial Class | | Years ended 12/31 | |

| | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net asset value, beginning of period | | | $12.13 | | | | $8.90 | | | | $17.63 | | | | $17.93 | | | | $15.42 | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | | $0.15 | | | | $0.14 | | | | $0.16 | | | | $0.21 | | | | $0.23 | |

Net realized and unrealized gain (loss) on investments and foreign currency | | | 1.68 | | | | 3.20 | | | | (6.04 | ) | | | 2.57 | | | | 3.70 | |

Total from investment operations | | | $1.83 | | | | $3.34 | | | | $(5.88 | ) | | | $2.78 | | | | $3.93 | |

| Less distributions declared to shareholders | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | $(0.11 | ) | | | $(0.11 | ) | | | $(0.19 | ) | | | $(0.27 | ) | | | $(0.11 | ) |

From net realized gain on investments | | | — | | | | — | | | | (2.66 | ) | | | (2.81 | ) | | | (1.31 | ) |

Total distributions declared to shareholders | | | $(0.11 | ) | | | $(0.11 | ) | | | $(2.85 | ) | | | $(3.08 | ) | | | $(1.42 | ) |

Net asset value, end of period | | | $13.85 | | | | $12.13 | | | | $8.90 | | | | $17.63 | | | | $17.93 | |

Total return (%) (k)(s) | | | 15.16 | | | | 38.06 | | | | (39.82 | ) | | | 16.58 | | | | 26.04 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | | | | | |

Expenses (f) | | | 1.09 | | | | 1.25 | | | | 1.22 | | | | 1.11 | | | | 1.12 | |

Net investment income | | | 1.21 | | | | 1.39 | | | | 1.25 | | | | 1.16 | | | | 1.40 | |

Portfolio turnover | | | 66 | | | | 56 | | | | 73 | | | | 56 | | | | 86 | |

Net assets at end of period (000 omitted) | | | $221,456 | | | | $179,925 | | | | $87,034 | | | | $139,633 | | | | $140,242 | |

| |

| Service Class | | Years ended 12/31 | |

| | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net asset value, beginning of period | | | $12.06 | | | | $8.84 | | | | $17.53 | | | | $17.85 | | | | $15.36 | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | | $0.11 | | | | $0.12 | | | | $0.13 | | | | $0.15 | | | | $0.19 | |

Net realized and unrealized gain (loss) on investments and foreign currency | | | 1.67 | | | | 3.18 | | | | (6.00 | ) | | | 2.56 | | | | 3.69 | |

Total from investment operations | | | $1.78 | | | | $3.30 | | | | $(5.87 | ) | | | $2.71 | | | | $3.88 | |

| Less distributions declared to shareholders | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | $(0.08 | ) | | | $(0.08 | ) | | | $(0.16 | ) | | | $(0.22 | ) | | | $(0.08 | ) |

From net realized gain on investments | | | — | | | | — | | | | (2.66 | ) | | | (2.81 | ) | | | (1.31 | ) |

Total distributions declared to shareholders | | | $(0.08 | ) | | | $(0.08 | ) | | | $(2.82 | ) | | | $(3.03 | ) | | | $(1.39 | ) |

Net asset value, end of period | | | $13.76 | | | | $12.06 | | | | $8.84 | | | | $17.53 | | | | $17.85 | |

Total return (%) (k)(s) | | | 14.86 | | | | 37.69 | | | | (39.96 | ) | | | 16.26 | | | | 25.75 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | | | | | |

Expenses (f) | | | 1.34 | | | | 1.50 | | | | 1.46 | | | | 1.37 | | | | 1.37 | |

Net investment income | | | 0.94 | | | | 1.17 | | | | 1.04 | | | | 0.85 | | | | 1.15 | |

Portfolio turnover | | | 66 | | | | 56 | | | | 73 | | | | 56 | | | | 86 | |

Net assets at end of period (000 omitted) | | | $31,348 | | | | $27,338 | | | | $18,056 | | | | $28,689 | | | | $22,979 | |

| (d) | Per share data is based on average shares outstanding. |

| (f) | Ratios do not reflect reductions from fees paid indirectly, if applicable. |

| (k) | The total return does not reflect expenses that apply to separate accounts. Inclusion of these charges would reduce the total return figures for all periods shown. |

| (s) | From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower. |

See Notes to Financial Statements

12

MFS International Growth Portfolio

NOTES TO FINANCIAL STATEMENTS

| (1) | | Business and Organization |

MFS International Growth Portfolio (the fund) is a series of MFS Variable Insurance Trust II (the trust). The trust is organized as a Massachusetts business trust and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company. The shareholders of each series of the trust are separate accounts of insurance companies, which offer variable annuity and/or life insurance products, and qualified retirement and pension plans.

| (2) | | Significant Accounting Policies |

General – The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. In the preparation of these financial statements, management has evaluated subsequent events occurring after the date of the fund’s Statement of Assets and Liabilities through the date that the financial statements were issued. The fund invests in foreign securities, including securities of emerging market issuers. Investments in foreign securities are vulnerable to the effects of changes in the relative values of the local currency and the U.S. dollar and to the effects of changes in each country’s legal, political, and economic environment. The markets of emerging markets countries are generally more volatile than the markets of developed countries with more mature economies. All of the risks of investing in foreign securities previously described are heightened when investing in emerging markets countries.

Investment Valuations – Equity securities, including restricted equity securities, are generally valued at the last sale or official closing price as provided by a third-party pricing service on the market or exchange on which they are primarily traded. Equity securities, for which there were no sales reported that day, are generally valued at the last quoted daily bid quotation as provided by a third-party pricing service on the market or exchange on which such securities are primarily traded. Equity securities held short, for which there were no sales reported for that day, are generally valued at the last quoted daily ask quotation as provided by a third-party pricing service on the market or exchange on which such securities are primarily traded. Short-term instruments with a maturity at issuance of 60 days or less generally are valued at amortized cost, which approximates market value. Open-end investment companies are generally valued at net asset value per share. Securities and other assets generally valued on the basis of information from a third-party pricing service may also be valued at a broker/dealer bid quotation. Values obtained from third-party pricing services can utilize both transaction data and market information such as yield, quality, coupon rate, maturity, type of issue, trading characteristics, and other market data. The values of foreign securities and other assets and liabilities expressed in foreign currencies are converted to U.S. dollars using the mean of bid and asked prices for rates provided by a third-party pricing service.

The Board of Trustees has delegated primary responsibility for determining or causing to be determined the value of the fund’s investments (including any fair valuation) to the adviser pursuant to valuation policies and procedures approved by the Board. If the adviser determines that reliable market quotations are not readily available, investments are valued at fair value as determined in good faith by the adviser in accordance with such procedures under the oversight of the Board of Trustees. Under the fund’s valuation policies and procedures, market quotations are not considered to be readily available for most types of debt instruments and floating rate loans and many types of derivatives. These investments are generally valued at fair value based on information from third-party pricing services. In addition, investments may be valued at fair value if the adviser determines that an investment’s value has been materially effected by events occurring after the close of the exchange or market on which the investment is principally traded (such as foreign exchange or market) and prior to the determination of the fund’s net asset value, or after the halting of trading of a specific security where trading does not resume prior to the close of the exchange or market on which the security is principally traded. Events that occur on a frequent basis after foreign markets close (such as developments in foreign markets and significant movements in the U.S. markets) and prior to the determination of the fund’s net asset value may be deemed to have a material effect on the value of securities traded in foreign markets. Accordingly, the fund’s foreign equity securities may often be valued at fair value. The adviser generally relies on third-party pricing services or other information (such as the correlation with price movements of similar securities in the same or other markets; the type, cost and investment characteristics of the security; the business and financial condition of the issuer; and trading and other market data) to assist in determining whether to fair value and at what value to fair value an investment. The value of an investment for purposes of calculating the fund’s net asset value can differ depending on the source and method used to determine value. When fair valuation is used, the value of an investment used to determine the fund’s net asset value may differ from quoted or published prices for the same investment. There can be no assurance that the fund could obtain the fair value assigned to an investment if it were to sell the investment at the same time at which the fund determines its net asset value per share.

13

MFS International Growth Portfolio

Notes to Financial Statements – continued

Various inputs are used in determining the value of the fund’s assets or liabilities. These inputs are categorized into three broad levels. In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, an investment’s level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement. The fund’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment, and considers factors specific to the investment. Level 1 includes unadjusted quoted prices in active markets for identical assets or liabilities. Level 2 includes other significant observable market-based inputs (including quoted prices for similar securities, interest rates, prepayment speed, and credit risk). Level 3 includes unobservable inputs, which may include the adviser’s own assumptions in determining the fair value of investments. The following is a summary of the levels used as of December 31, 2010 in valuing the fund’s assets or liabilities:

| | | | | | | | | | | | | | | | |

| Investments at Value | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Equity Securities: | | | | | | | | | | | | | | | | |

United Kingdom | | | $29,510,934 | | | | $— | | | | $— | | | | $29,510,934 | |

France | | | 28,341,670 | | | | — | | | | — | | | | 28,341,670 | |

Japan | | | 20,764,120 | | | | 5,568,680 | | | | — | | | | 26,332,800 | |

Switzerland | | | 25,667,786 | | | | — | | | | — | | | | 25,667,786 | |

Germany | | | 24,194,797 | | | | — | | | | — | | | | 24,194,797 | |

Australia | | | 14,482,695 | | | | — | | | | — | | | | 14,482,695 | |

Brazil | | | 14,274,778 | | | | — | | | | — | | | | 14,274,778 | |

Taiwan | | | 9,236,342 | | | | — | | | | — | | | | 9,236,342 | |

Canada | | | 8,680,715 | | | | — | | | | — | | | | 8,680,715 | |

Other Countries | | | 68,482,681 | | | | — | | | | — | | | | 68,482,681 | |

| Mutual Funds | | | 2,123,761 | | | | — | | | | — | | | | 2,123,761 | |

| Total Investments | | | $245,760,279 | | | | $5,568,680 | | | | $— | | | | $251,328,959 | |

For further information regarding security characteristics, see the Portfolio of Investments.

Of the level 2 investments presented above, equity investments amounting to $1,243,163 were considered level 1 investments at the beginning of the period. Of the level 1 investments presented above, equity investments amounting to $116,545,699 were considered level 2 investments at the beginning of the period. The primary reason for changes in the classifications between levels 1 and 2 occurs when foreign equity securities are fair valued using other observable market-based inputs in place of the closing exchange price due to events occurring after the close of the exchange or market on which the investment is principally traded. The fund’s foreign equity securities may often be valued at fair value.

Foreign Currency Translation – Purchases and sales of foreign investments, income, and expenses are converted into U.S. dollars based upon currency exchange rates prevailing on the respective dates of such transactions or on the reporting date for foreign denominated receivables and payables. Gains and losses attributable to foreign currency exchange rates on sales of securities are recorded for financial statement purposes as net realized gains and losses on investments. Gains and losses attributable to foreign exchange rate movements on receivables, payables, income and expenses are recorded for financial statement purposes as foreign currency transaction gains and losses. That portion of both realized and unrealized gains and losses on investments that results from fluctuations in foreign currency exchange rates is not separately disclosed.

Short Sales – The fund may enter into short sales whereby it sells a security it does not own in anticipation of a decline in the value of that security. The fund will realize a gain if the security price decreases and a loss if the security price increases between the date of the short sale and the date on which the fund replaces the borrowed security. Losses from short sales can exceed the proceeds of the security sold; and they can also exceed the potential loss from an ordinary buy and sell transaction. The amount of any premium, dividends, or interest the fund may be required to pay in connection with a short sale will be recognized as a fund expense. The fund segregates cash or marketable securities in an amount that, when combined with the amount of proceeds from the short sale deposited with the broker, at least equals the current market value of the security sold short. At December 31, 2010, the fund has yet to enter into such transactions.

Security Loans – State Street Bank and Trust Company (“State Street”), as lending agent, loans the securities of the fund to certain qualified institutions (the “Borrowers”) approved by the fund. The loans are collateralized by cash and/or U.S. Treasury and federal agency obligations in an amount typically at least equal to the market value of the securities loaned. The market value of the loaned securities is determined at the close of business of the fund and any additional required collateral is delivered to the fund on the next business day. State Street provides the fund with indemnification against Borrower default. The fund bears the risk of loss with respect to the investment of cash collateral. On loans collateralized by cash, the cash collateral is invested in a money market fund or short-term securities. A portion of the income generated upon investment of the collateral is remitted to the Borrowers, and the remainder is allocated between the fund and the lending agent. On loans

14

MFS International Growth Portfolio

Notes to Financial Statements – continued

collateralized by U.S. Treasury and/or federal agency obligations, a fee is received from the Borrower, and is allocated between the fund and the lending agent. Income from securities lending is included in interest income on the Statement of Operations. The dividend and interest income earned on the securities loaned is accounted for in the same manner as other dividend and interest income.

Indemnifications – Under the fund’s organizational documents, its officers and Trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the fund. Additionally, in the normal course of business, the fund enters into agreements with service providers that may contain indemnification clauses. The fund’s maximum exposure under these agreements is unknown as this would involve future claims that may be made against the fund that have not yet occurred.

Investment Transactions and Income – Investment transactions are recorded on the trade date. Interest income is recorded on the accrual basis. Dividends received in cash are recorded on the ex-dividend date. Certain dividends from foreign securities will be recorded when the fund is informed of the dividend if such information is obtained subsequent to the ex-dividend date. Dividend and interest payments received in additional securities are recorded on the ex-dividend or ex-interest date in an amount equal to the value of the security on such date.

The fund may receive proceeds from litigation settlements. Any proceeds received from litigation involving portfolio holdings are reflected in the Statement of Operations in realized gain/loss if the security has been disposed of by the fund or in unrealized gain/loss if the security is still held by the fund. Any other proceeds from litigation not related to portfolio holdings are reflected as other income in the Statement of Operations.

Fees Paid Indirectly – The fund’s custody fee may be reduced according to an arrangement that measures the value of cash deposited with the custodian by the fund. This amount, for the year ended December 31, 2010, is shown as a reduction of total expenses on the Statement of Operations.

Tax Matters and Distributions – The fund intends to qualify as a regulated investment company, as defined under Subchapter M of the Internal Revenue Code, and to distribute all of its taxable income, including realized capital gains. As a result, no provision for federal income tax is required. The fund’s federal tax returns for the prior three fiscal years remain subject to examination by the Internal Revenue Service. Foreign taxes, if any, have been accrued by the fund in the accompanying financial statements.

Distributions to shareholders are recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from U.S. generally accepted accounting principles. Certain capital accounts in the financial statements are periodically adjusted for permanent differences in order to reflect their tax character. These adjustments have no impact on net assets or net asset value per share. Temporary differences which arise from recognizing certain items of income, expense, gain or loss in different periods for financial statement and tax purposes will reverse at some time in the future. Distributions in excess of net investment income or net realized gains are temporary overdistributions for financial statement purposes resulting from differences in the recognition or classification of income or distributions for financial statement and tax purposes.

Book/tax differences primarily relate to wash sale loss deferrals.

The tax character of distributions declared to shareholders for the last two fiscal years is as follows:

| | | | | | | | |

| | | 12/31/10 | | | 12/31/09 | |

| Ordinary income (including any short-term capital gains) | | | $1,936,143 | | | | $1,417,238 | |

The federal tax cost and the tax basis components of distributable earnings were as follows:

| | | | |

| As of 12/31/10 | | | | |

| Cost of investments | | | $218,951,945 | |

| Gross appreciation | | | 39,401,120 | |

| Gross depreciation | | | (7,024,106 | ) |

| Net unrealized appreciation (depreciation) | | | $32,377,014 | |

| Undistributed ordinary income | | | 4,590,472 | |

| Undistributed long-term capital gain | | | 18,333,928 | |

| Other temporary differences | | | (41,541 | ) |

Multiple Classes of Shares of Beneficial Interest – The fund offers multiple classes of shares, which differ in their respective distribution and/or service fees. The fund’s income, realized and unrealized gain (loss), and common expenses are allocated to shareholders based on the daily net assets of each class. Dividends are declared separately for each class. Differences in per

15

MFS International Growth Portfolio

Notes to Financial Statements – continued

share dividend rates are generally due to differences in separate class expenses. The fund’s distributions declared to shareholders as reported on the Statements of Changes in Net Assets are presented by class as follows:

| | | | | | | | |

| | | From net investment

income | |

| | | Year ended

12/31/10 | | | Year ended

12/31/09 | |

| Initial Class | | | $1,752,956 | | | | $1,263,603 | |

| Service Class | | | 183,187 | | | | 153,635 | |

| Total | | | $1,936,143 | | | | $1,417,238 | |

| (3) | | Transactions with Affiliates |

Investment Adviser – The fund has an investment advisory agreement with MFS to provide overall investment management and related administrative services and facilities to the fund. The management fee is computed daily and paid monthly at the following annual rates:

| | | | |

| First $1 billion of average daily net assets | | | 0.90% | |

| Next $1 billion of average daily net assets | | | 0.80% | |

| Average daily net assets in excess of $2 billion | | | 0.70% | |

The management fee incurred for the year ended December 31, 2010 was equivalent to an annual effective rate of 0.90% of the fund’s average daily net assets.

The investment adviser has agreed to pay a portion of the fund’s total annual operating expenses, exclusive of interest, taxes, extraordinary expenses, brokerage and transaction costs and investment-related expenses, such that total annual operating expenses do not exceed 1.35% of average daily net assets for the Initial Class shares and 1.60% of average daily net assets for the Service Class shares. This written agreement will continue until April 30, 2012. For the year ended December 31, 2010, the fund’s actual operating expenses did not exceed the limit and therefore, the investment adviser did not pay any portion of the fund’s expenses related to this agreement.

Distributor – MFS Fund Distributors, Inc. (MFD), a wholly-owned subsidiary of MFS, is the distributor of shares of the fund. The Trustees have adopted a distribution plan for the Service Class shares pursuant to Rule 12b-1 under the Investment Company Act of 1940.

The fund’s distribution plan provides that the fund will pay MFD distribution and/or service fees equal to 0.25% per annum of its average daily net assets attributable to Service Class shares as partial consideration for services performed and expenses incurred by MFD and financial intermediaries (including participating insurance companies that invest in the fund to fund variable annuity and variable life insurance contracts, sponsors of qualified retirement and pension plans that invest in the fund, and affiliates of these participating insurance companies and plan sponsors) in connection with the sale and distribution of the Service Class shares. MFD may subsequently pay all, or a portion, of the distribution and/or service fees to financial intermediaries.

Shareholder Servicing Agent – MFS Service Center, Inc. (MFSC), a wholly-owned subsidiary of MFS, receives a fee from the fund for its services as shareholder servicing agent. For the year ended December 31, 2010, the fee was $27,323, which equated to 0.0115% annually of the fund’s average daily net assets. MFSC also receives payment from the fund for out-of-pocket expenses paid by MFSC on behalf of the fund. For the year ended December 31, 2010, these costs amounted to $28.

Administrator – MFS provides certain financial, legal, shareholder communications, compliance, and other administrative services to the fund. Under an administrative services agreement, the fund partially reimburses MFS the costs incurred to provide these services. The fund is charged an annual fixed amount of $10,000 plus a fee based on average daily net assets. The administrative services fee incurred for the year ended December 31, 2010 was equivalent to an annual effective rate of 0.0357% of the fund’s average daily net assets.

Trustees’ and Officers’ Compensation – The fund pays compensation to Trustees in the form of a retainer, attendance fees, and additional compensation to the Board chairperson. The fund does not pay compensation directly to officers of the fund who are also officers of the investment adviser, all of whom receive remuneration for their services to the fund from MFS. Certain officers of the fund are officers or directors of MFS, MFD, and MFSC.

Other – This fund and certain other funds managed by MFS (the funds) have entered into services agreements (the Agreements) which provide for payment of fees by the funds to Tarantino LLC and Griffin Compliance LLC in return for the provision of services of an Independent Chief Compliance Officer (ICCO) and Assistant ICCO, respectively, for the funds. The ICCO and Assistant ICCO are officers of the funds and the sole members of Tarantino LLC and Griffin Compliance LLC, respectively. The funds can terminate the Agreements with Tarantino LLC and Griffin Compliance LLC at any time under the

16

MFS International Growth Portfolio

Notes to Financial Statements – continued

terms of the Agreements. MFS has agreed to bear all expenses associated with office space, other administrative support, and supplies provided to the ICCO and Assistant ICCO. For the year ended December 31, 2010, the aggregate fees paid by the fund to Tarantino LLC and Griffin Compliance LLC were $4,065 and are included in miscellaneous expense on the Statement of Operations.

The fund invests in the MFS Institutional Money Market Portfolio which is managed by MFS and seeks a high level of current income consistent with preservation of capital and liquidity. Income earned on this investment is included in dividends from underlying funds on the Statement of Operations. This money market fund does not pay a management fee to MFS.

Purchases and sales of investments, other than U.S. Government securities, purchased option transactions, and short-term obligations, aggregated $163,081,395 and $151,266,931, respectively.

| (5) | | Shares of Beneficial Interest |

The fund’s Declaration of Trust permits the Trustees to issue an unlimited number of full and fractional shares of beneficial interest. Transactions in fund shares were as follows:

| | | | | | | | | | | | | | | | |

| | | Year ended 12/31/10 | | | Year ended 12/31/09 | |

| | | Shares | | | Amount | | | Shares | | | Amount | |

| Shares sold | | | | | | | | | | | | | | | | |

Initial Class | | | 5,318,787 | | | | $62,995,452 | | | | 6,779,227 | | | | $67,075,450 | |

Service Class | | | 529,150 | | | | 6,406,687 | | | | 615,094 | | | | 6,459,951 | |

| | | 5,847,937 | | | | $69,402,139 | | | | 7,394,321 | | | | $73,535,401 | |

| Shares issued to shareholders in reinvestment of distributions | | | | | | | | | | | | | | | | |

Initial Class | | | 142,981 | | | | $1,752,956 | | | | 148,834 | | | | $1,263,603 | |

Service Class | | | 15,004 | | | | 183,187 | | | | 18,182 | | | | 153,635 | |

| | | 157,985 | | | | $1,936,143 | | | | 167,016 | | | | $1,417,238 | |

| Shares reacquired | | | | | | | | | | | | | | | | |

Initial Class | | | (4,301,835 | ) | | | $(55,307,266 | ) | | | (1,869,251 | ) | | | $(18,228,127 | ) |

Service Class | | | (532,563 | ) | | | (6,437,650 | ) | | | (408,327 | ) | | | (3,829,445 | ) |

| | | (4,834,398 | ) | | | $(61,744,916 | ) | | | (2,277,578 | ) | | | $(22,057,572 | ) |

| Net change | | | | | | | | | | | | | | | | |

Initial Class | | | 1,159,933 | | | | $9,441,142 | | | | 5,058,810 | | | | $50,110,926 | |

Service Class | | | 11,591 | | | | 152,224 | | | | 224,949 | | | | 2,784,141 | |

| | | 1,171,524 | | | | $9,593,366 | | | | 5,283,759 | | | | $52,895,067 | |

The fund and certain other funds managed by MFS participate in a $1.1 billion unsecured committed line of credit, subject to a $1 billion sublimit, provided by a syndication of banks under a credit agreement. Borrowings may be made for temporary financing needs. Interest is charged to each fund, based on its borrowings, generally at a rate equal to the higher of the Federal Reserve funds rate or one month LIBOR plus an agreed upon spread. A commitment fee, based on the average daily, unused portion of the committed line of credit, is allocated among the participating funds at the end of each calendar quarter. In addition, the fund and other funds managed by MFS have established unsecured uncommitted borrowing arrangements with certain banks for temporary financing needs. Interest is charged to each fund, based on its borrowings, at a rate equal to the Federal Reserve funds rate plus an agreed upon spread. For the year ended December 31, 2010, the fund’s commitment fee and interest expense were $2,642 and $1,959, respectively, and are included in miscellaneous expense on the Statement of Operations.

17

MFS International Growth Portfolio

Notes to Financial Statements – continued

| (7) | | Transactions in Underlying Funds – Affiliated Issuers |

An affiliated issuer may be considered one in which the fund owns 5% or more of the outstanding voting securities, or a company which is under common control. For the purposes of this report, the fund assumes the following to be affiliated issuers:

| | | | | | | | | | | | | | |

| Underlying Funds | | Beginning

Shares/Par

Amount | | Acquisitions

Shares/Par

Amount | | | Dispositions

Shares/Par

Amount | | | Ending

Shares/Par

Amount | |

| MFS Institutional Money Market Portfolio | | 4,001,551 | | | 67,229,368 | | | | (69,107,158 | ) | | | 2,123,761 | |

| | | | |

| Underlying Funds | | Realized

Gain (Loss) | | Capital Gain

Distributions | | | Dividend

Income | | | Ending

Value | |

| MFS Institutional Money Market Portfolio | | $— | | | $— | | | | $8,172 | | | | $2,123,761 | |

18

MFS International Growth Portfolio

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees of MFS Variable Insurance Trust II and the Shareholders of

MFS International Growth Portfolio:

We have audited the accompanying statement of assets and liabilities, including the portfolio of investments, of MFS International Growth Portfolio (the “Fund”) (one of the portfolios comprising MFS Variable Insurance Trust II) as of December 31, 2010, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2010, by correspondence with the custodian and brokers; where replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of MFS International Growth Portfolio as of December 31, 2010, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

DELOITTE & TOUCHE LLP

Boston, Massachusetts

February 14, 2011

19

MFS International Growth Portfolio

TRUSTEES AND OFFICERS – IDENTIFICATION AND BACKGROUND

The Trustees and officers of the Trust, as of February 1, 2011, are listed below, together with their principal occupations during the past five years. (Their titles may have varied during that period.) The address of each Trustee and officer is 500 Boylston Street, Boston, Massachusetts 02116.

| | | | | | |

Name, Date of Birth | | Position(s) Held

with Fund | | Trustee/Officer

Since (1) | | Principal Occupations During the Past Five Years and

Other Directorships (2) |

| INTERESTED TRUSTEE | | | | |

David D. Horn (3) (born 6/07/41) | | Trustee | | April 1986 | | Private investor; Sun Life Assurance Company of Canada, Senior Vice President and General Manager for the United States (until 1997); Director (until March 2004) |

| | |

| INDEPENDENT TRUSTEES | | | | |

J. Kermit Birchfield (born 1/08/40) | | Chairman | | May 1997 | | Consultant; Century Partners, Inc. (investments), Director; Displaytech, Inc. (technology), Chairman; Dessin Fournir LLC (furniture manufacturer), Director; Site Watch LLC (software to monitor oil tanks), Managing Director (2006 to present); Juridica Investments (fund investing in judicial matters), Director (2007 to present), Immuno Science, Inc. (medical research), Independent Director (2009 to present), Intermountain Industries, Inc. (oil & gas exploration and production), Director (until February 2009) |

| | | |

Robert C. Bishop (born 1/13/43) | | Trustee | | May 2001 | | AutoImmune, Inc. (pharmaceutical product development), Chairman, President and Chief Executive Officer; Caliper Life Sciences Corp. (laboratory analytical instruments), Chairman; Optobionics Corporation (ophthalmic devices), Director (until 2007); Millipore Corporation (purification/filtration products), Director (until July 2010); Waterstreet Capital (leverage buyouts), Advisory Board (until August 2010) |

| | | |

Frederick H. Dulles (born 3/12/42) | | Trustee | | May 2001 | | Dulles International Law LLC (law firm), Senior Lawyer (since 2009); Juridica Capital Management (US) Inc. (litigation financing), Vice President and General Counsel (since 2009); Dulles Properties LLC (real estate), Broker (since 2008); The Citadel School of Business Administration (education), Adjunct Professor (since 2003); Disher, Hamrick & Myers Residential, Inc. (real estate), Broker (until 2006); Frederick H. Dulles Law Practice (law firm), (until 2006); Charlestown School of Law (education), Adjunct Professor (until 2007); Prudential Carolina Real Estate, (real estate), Broker (until 2008); Free Enterprise Foundation Inc. (research institute), Director & Secretary (until 2008); Ten State International Law PLLP (law firm), Of Counsel (until 2009) |

| | | |

Marcia A. Kean (born 6/30/48) | | Trustee | | April 2005 | | Feinstein Kean Healthcare (consulting), Chief Executive Officer |

| | | |

Ronald G. Steinhart (born 6/15/40) | | Trustee | | May 2001 | | Private investor; Penske Automotive Group (automotive retailer), Director; Animal Health International, Inc. (animal health products), Director (since 2007); Texas Industries (concrete/aggregates/cement), Director (since 2007); Susser Holdings Corporation (retail convenience stores and distributor of wholesale motor fuel), Director (since 2009); Prentiss Properties Trust (real estate investment trust), Director (until 2006); Penson Worldwide, Inc. (securities clearance), Director (until 2008) |

| | | |

Haviland Wright (born 7/21/48) | | Trustee | | May 2001 | | X-Change Corp. (multi-media web services), Director (since 2010); Nano Loa Inc. (liquid crystal displays), Director (until 2009); Profitability of Hawaii (software), Chief Development Officer (until 2010); Elixir Technologies Corporation (software), Director (until 2010) |

| | | |

| OFFICERS | | | | | | |

Maria F. DiOrioDwyer (4)

(born 12/01/58) | | President | | November 2005 | | Massachusetts Financial Services Company, Executive Vice President and Chief Regulatory Officer; Chief Compliance Officer (since December 2006) |

| | | |

| Christopher R. Bohane (4) (born 1/18/74) | | Assistant Secretary and Assistant Clerk | | July 2005 | | Massachusetts Financial Services Company, Vice President and Senior Counsel |

| | | |

John M. Corcoran (4) (born 4/13/65) | | Treasurer | | October 2008 | | Massachusetts Financial Services Company, Senior Vice President (since October 2008); State Street Bank and Trust (financial services provider), Senior Vice President, (until September 2008) |

| | | |

Ethan D. Corey (4) (born 11/21/63) | | Assistant Secretary and Assistant Clerk | | July 2005 | | Massachusetts Financial Services Company, Senior Vice President and Associate General Counsel |

| | | |

David L. DiLorenzo (4) (born 8/10/68) | | Assistant Treasurer | | July 2005 | | Massachusetts Financial Services Company, Vice President |

| | | |

Timothy M. Fagan (4) (born 7/10/68) | | Assistant Secretary and Assistant Clerk | | September 2005 | | Massachusetts Financial Services Company, Vice President and Senior Counsel |

| | | |

Mark D. Fischer (4) (born 10/27/70) | | Assistant Treasurer | | July 2005 | | Massachusetts Financial Services Company, Vice President |

20

MFS International Growth Portfolio

Trustees and Officers – continued

| | | | | | |

Name, Date of Birth | | Position(s) Held

with Fund | | Trustee/Officer

Since (1) | | Principal Occupations During the Past Five Years and

Other Directorships (2) |

Robyn L. Griffin (born 7/04/75) | | Assistant Independent Chief Compliance Officer | | August 2008 | | Griffin Compliance LLC (provider of compliance services), Principal (since August 2008); State Street Corporation (financial services provider), Mutual Fund Administration Assistant Vice President (October 2006 – July 2008); Liberty Mutual Group (insurance), Personal Market Assistant Controller (April 2006 – October 2006); Deloitte & Touche LLP (professional services firm), Senior Manager (prior to April 2006) |

| | | |

Brian E. Langenfeld (4) (born 3/07/73) | | Assistant Secretary and Assistant Clerk | | May 2006 | | Massachusetts Financial Services Company, Vice President and Senior Counsel (since May 2006); John Hancock Advisers, LLC, Assistant Vice President and Counsel (until April 2006) |

| | | |

Ellen Moynihan (4) (born 11/13/57) | | Assistant Treasurer | | May 1997 | | Massachusetts Financial Services Company, Senior Vice President |

| | | |

Susan S. Newton (4) (born 3/07/50) | | Assistant Secretary and Assistant Clerk | | May 2005 | | Massachusetts Financial Services Company, Senior Vice President and Associate General Counsel |

| | | |

Susan A. Pereira (4)

(born 11/05/70) | | Assistant Secretary and Assistant Clerk | | July 2005 | | Massachusetts Financial Services Company, Vice President and Senior Counsel |

| | | |

Mark N. Polebaum (4) (born 5/01/52) | | Secretary and Clerk | | February 2006 | | Massachusetts Financial Services Company, Executive Vice President, General Counsel and Secretary (since January 2006); Wilmer Cutler Pickering Hale and Dorr LLP (law firm), Partner (until January 2006) |

| | | |

Frank L. Tarantino (born 3/07/44) | | Independent Chief Compliance Officer | | September 2004 | | Tarantino LLC (provider of compliance services), Principal |

| | | |