UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-03735

The New Economy Fund

(Exact Name of Registrant as Specified in Charter)

333 South Hope Street

Los Angeles, California 90071

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (213) 486-9200

Date of fiscal year end: November 30

Date of reporting period: May 31, 2013

Vincent P. Corti

The New Economy Fund

333 South Hope Street

Los Angeles, California 90071

(Name and Address of Agent for Service)

Copies to:

Kathryn A. Sanders

O’Melveny & Myers LLP

400 South Hope Street, 10th Floor

Los Angeles, California 90071

(Counsel for the Registrant)

ITEM 1 – Reports to Stockholders

The New Economy Fund®

Semi-annual report for the six months ended May 31, 2013

The New Economy Fund seeks long-term growth of capital by investing in securities of companies that can benefit from innovation, exploit new technologies or provide products and services that meet the demands of an evolving global economy.

This fund is one of more than 40 offered by one of the nation’s largest mutual fund families, American Funds, from Capital Group. For more than 80 years, Capital has invested with a long-term focus based on thorough research and attention to risk.

Fund results shown in this report, unless otherwise indicated, are for Class A shares at net asset value. If a sales charge (maximum 5.75%) had been deducted, the results would have been lower. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. For current information and month-end results, visit americanfunds.com.

Here are the average annual total returns on a $1,000 investment with all distributions reinvested for periods ended June 30, 2013 (the most recent calendar quarter-end):

| Class A shares | | | 1 year | | | | 5 years | | | | 10 years | |

| | | | | | | | | | | | | |

| Reflecting 5.75% maximum sales charge | | | 18.78% | | | | 7.46% | | | | 8.72% | |

For other share class results, see americanfunds.com and americanfundsretirement.com.

The total annual fund operating expense ratio was 0.87% for Class A shares as of the prospectus dated February 1, 2013 (unaudited).

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, investment results reflect fee waivers, without which results would have been lower. Visit americanfunds.com for more information.

Investing outside the United States may be subject to risks, such as currency fluctuations, periods of illiquidity and price volatility. These risks may be heightened in connection with investments in developing countries. Global diversification can help reduce these risks. Refer to the fund prospectus and the Risk Factors section of this report for more information on these and other risks associated with investing in the fund.

Fellow investors:

The New Economy Fund returned 19.6% for the six months ended May 31, 2013. This exceeded the 16.4% return of the unmanaged Standard & Poor’s 500 Composite Index, a broad measure of the U.S. stock market, and the 15.1% return (not including expenses) of the Global Service and Information Index, an unmanaged index that tracks companies in the services and information sectors around the world. That figure also compares with the 16.4% return of the Lipper Growth Funds Index, which measures a number of growth funds, and the 10.5% return of the Lipper International Funds Index, which measures funds invested in securities whose primary trading markets are outside the U.S.

For the 10-year period ending May 31, 2013, The New Economy Fund had an average annual total return of 9.7%, compared with 7.6% for the S&P 500 and 7.1% for the Global Service and Information Index. That figure also compares with the 6.7% return of the Lipper Growth Funds Index and the 8.8% return for the Lipper International Funds Index.

Results at a glance

(for periods ended May 31, 2013, with all distributions reinvested)

| | | | | | | | | Average annual total returns |

| | | | | | | | | | | | | | | Lifetime |

| | | Total returns | | | | | | | | | | (since |

| | | 6 months | | 1 year | | 5 years | | 10 years | | 12/1/83) |

| The New Economy Fund (Class A shares) | | | 19.6 | % | | | 33.7 | % | | | 7.0 | % | | | 9.7 | % | | | 11.1 | % |

| Lipper Growth Funds Index | | | 16.4 | | | | 27.0 | | | | 4.3 | | | | 6.7 | | | | 8.9 | |

| Lipper International Funds Index | | | 10.5 | | | | 28.7 | | | | –1.0 | | | | 8.8 | | | | N/A | |

| Global Service and Information Index*† | | | 15.1 | | | | 28.8 | | | | 3.6 | | | | 7.1 | | | | N/A | |

| Standard & Poor’s 500 Composite Index† | | | 16.4 | | | | 27.3 | | | | 5.4 | | | | 7.6 | | | | 10.7 | |

*The index is compiled by Capital Research and Management Company, the investment adviser to the fund.

†This index is unmanaged and, therefore, has no expenses.

Changing dynamics

In many regions around the world, market dynamics are shifting. In the U.S., as the Federal Reserve begins to consider unwinding its quantitative easing programs, stock and bond markets are reacting poorly in anticipation of these potential moves. In the long term, reliance on market forces to determine the level of interest rates should prove healthier and is indicative of continuing, though slow, progress in the economic expansion. In many emerging markets, slower growth and concern over government policies as well as currency moves have added to volatility. In Japan, new political leadership has caused excitement over new measures intended to stimulate investment and demand. In Europe, while the European Central Bank (ECB) and other regional entities continue to work to lift Southern Europe out of its recession, fiscal austerity measures have proved to be difficult to digest in the near term.

Signs of optimism are ongoing — namely, the nascent housing and auto resurgence in the U.S., some growth in the manufacturing sector and the strength of many global corporations’ earnings. While much of

| Where the fund’s assets are invested | | (percent of net assets) |

| | | | | | | | | |

| | | As of 5/31/13 | | As of 11/30/12 |

| United States | | | 56.2 | % | | | 58.6 | % |

| | | | | | | | | |

| Europe | | | | | | | | |

| Euro zone* | | | 6.8 | | | | 6.1 | |

| United Kingdom | | | 4.5 | | | | 3.7 | |

| Other Europe | | | 2.7 | | | | 2.7 | |

| | | | 14.0 | | | | 12.5 | |

| | | | | | | | | |

| Asia & Pacific Basin | | | | | | | | |

| Hong Kong | | | 7.1 | | | | 8.0 | |

| China | | | 4.4 | | | | 5.4 | |

| Japan | | | 2.4 | | | | 1.3 | |

| South Korea | | | 1.3 | | | | 1.5 | |

| Indonesia | | | 1.1 | | | | 1.1 | |

| Philippines | | | 0.8 | | | | 0.9 | |

| Other Asia & Pacific Basin | | | 2.6 | | | | 2.4 | |

| | | | 19.7 | | | | 20.6 | |

| | | | | | | | | |

| Other (including Latin America) | | | | | | | | |

| South Africa | | | 0.3 | | | | 0.2 | |

| Israel | | | 0.1 | | | | 0.2 | |

| | | | 0.4 | | | | 0.4 | |

| | | | | | | | | |

| Short-term securities & other assets less liabilities | | | 9.7 | | | | 7.9 | |

| | | | 100.0 | % | | | 100.0 | % |

| * | Countries using the common currency, the euro, are Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia and Spain. |

Europe continues to struggle for growth, there have been some very positive fundamental improvements in tax and spending policies, which should help in the long run. On a longer term view, the increase in wealth and purchasing power of the growing consumer class in emerging markets should continue to stimulate global demand.

The fund’s portfolio in review

All of The New Economy Fund’s top-10 holdings yielded positive absolute results for the six months, and many of the fund’s largest holdings had very good returns compared to the broader stock market. In particular, many of our holdings in the health care sector did well. The fund’s largest holding by percent of total assets, Gilead Sciences, rose 45.3%. Alexion Pharmaceuticals, the portfolio’s sixth-largest holding, was up 1.6% absolute, but it lagged the broader markets; and Thermo Fisher Scientific, a U.S.-based laboratory equipment company and the fund’s ninth-largest holding, was up 39.0%.

The holding that had the greatest impact to the portfolio’s results for the six months was the fund’s third-largest holding, Netflix, which gained 176.9%. Google, the fund’s fourth-largest holding, was up 24.6%. SOFTBANK, a Japan-based telecommunications and internet company that is the fund’s fifth-largest holding, rose 33.4%. Finally, two of the fund’s top holdings were up, though not as much as the market during the period — Samsung Electronics and Amazon returned 3.9% and 6.7%, respectively.

Looking ahead

While the U.S. recovery continues to slowly move forward, and Europe shows modest signs of improvement (though with a good deal of volatility) a number of crosscurrents remain. Among these, China’s banking system in particular bears watching. Also, as many countries begin to wean themselves from the unusually strong dependence on fiscal policy to maintain economic stability, there are likely to be increased volatility and perhaps temporary disruptions. In this environment, we continue to focus on individual companies, and strive to take advantage of volatility to add or initiate positions in well-managed companies that we believe have growth potential and are attractively priced.

We thank you for your long-term commitment and investment in The New Economy Fund.

Sincerely,

Timothy D. Armour

Vice Chairman of the Board

Claudia P. Huntington

President

July 15, 2013

For current information about the fund,

visit americanfunds.com.

| Summary investment portfolio May 31, 2013 | unaudited |

The following summary investment portfolio is designed to streamline the report and help investors better focus on the fund’s principal holdings. See the inside back cover for details on how to obtain a complete schedule of portfolio holdings.

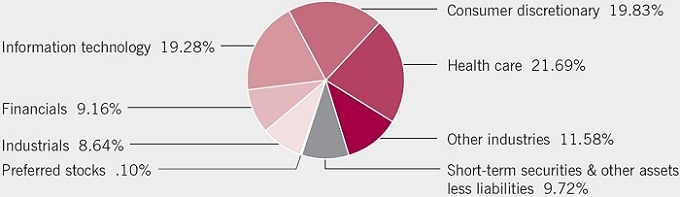

| Industry sector diversification | (percent of net assets) |

| Country diversification | | (percent of net assets) | |

| United States | | | 56.2 | % |

| Hong Kong | | | 7.1 | |

| Euro zone* | | | 6.8 | |

| United Kingdom | | | 4.5 | |

| China | | | 4.4 | |

| Japan | | | 2.4 | |

| Korea | | | 1.3 | |

| Indonesia | | | 1.1 | |

| Russian Federation | | | 0.8 | |

| Sweden | | | 0.8 | |

| Other countries | | | 4.9 | |

| Short-term securities & other assets less liabilities | | | 9.7 | |

| * | Countries using the euro as a common currency; those represented in the fund’s portfolio are Finland, France, Germany, Ireland, the Netherlands and Spain. |

| Common stocks — 90.18% | | Shares | | | Value

(000) | | | Percent of

net assets | |

| Health care — 21.69% | | | | | | | | | |

| Gilead Sciences, Inc.1 | | | 5,413,300 | | | $ | 294,917 | | | | 3.04 | % |

| Alexion Pharmaceuticals, Inc.1 | | | 1,522,600 | | | | 148,514 | | | | 1.53 | |

| Hologic, Inc.1 | | | 7,054,550 | | | | 146,382 | | | | 1.51 | |

| Thermo Fisher Scientific Inc. | | | 1,416,000 | | | | 125,033 | | | | 1.29 | |

| Forest Laboratories, Inc.1 | | | 2,400,000 | | | | 95,400 | | | | .98 | |

| Illumina, Inc.1 | | | 1,271,376 | | | | 89,403 | | | | .92 | |

| BioMarin Pharmaceutical Inc.1 | | | 1,355,730 | | | | 85,004 | | | | .87 | |

| Biogen Idec Inc.1 | | | 335,600 | | | | 79,702 | | | | .82 | |

| Allergan, Inc. | | | 724,700 | | | | 72,100 | | | | .74 | |

| William Demant Holding A/S1,2 | | | 873,000 | | | | 69,669 | | | | .72 | |

| Common stocks | | Shares | | | Value

(000) | | | Percent of

net assets | |

| McKesson Corp. | | | 600,000 | | | $ | 68,316 | | | | .70 | % |

| Celesio AG2 | | | 3,167,000 | | | | 65,463 | | | | .67 | |

| Stryker Corp. | | | 984,000 | | | | 65,328 | | | | .67 | |

| Other securities | | | | | | | 702,161 | | | | 7.23 | |

| | | | | | | | 2,107,392 | | | | 21.69 | |

| | | | | | | | | | | | | |

| Consumer discretionary — 19.83% | | | | | | | | | | | | |

| Galaxy Entertainment Group Ltd.1,2 | | | 49,909,000 | | | | 259,859 | | | | 2.67 | |

| Netflix, Inc.1 | | | 1,098,000 | | | | 248,422 | | | | 2.56 | |

| lululemon athletica inc.1 | | | 1,714,100 | | | | 133,374 | | | | 1.37 | |

| Sky Deutschland AG1,2 | | | 16,303,088 | | | | 109,090 | | | | 1.12 | |

| MGM China Holdings Ltd.2 | | | 36,772,000 | | | | 98,028 | | | | 1.01 | |

| Daily Mail and General Trust PLC, Class A, nonvoting2 | | | 8,020,821 | | | | 93,014 | | | | .96 | |

| Amazon.com, Inc.1 | | | 333,200 | | | | 89,641 | | | | .92 | |

| News Corp., Class A | | | 2,679,164 | | | | 86,028 | | | | .89 | |

| Sands China Ltd.2 | | | 15,342,800 | | | | 81,396 | | | | .84 | |

| Melco Crown Entertainment Ltd. (ADR)1 | | | 2,881,000 | | | | 68,510 | | | | .71 | |

| DIRECTV1 | | | 1,012,100 | | | | 61,870 | | | | .64 | |

| Other securities | | | | | | | 596,929 | | | | 6.14 | |

| | | | | | | | 1,926,161 | | | | 19.83 | |

| | | | | | | | | | | | | |

| Information technology — 19.28% | | | | | | | | | | | | |

| Google Inc., Class A1 | | | 240,700 | | | | 209,508 | | | | 2.16 | |

| Samsung Electronics Co. Ltd.2 | | | 90,437 | | | | 121,961 | | | | 1.26 | |

| Accenture PLC, Class A | | | 1,230,000 | | | | 100,995 | | | | 1.04 | |

| Texas Instruments Inc. | | | 2,555,000 | | | | 91,699 | | | | .94 | |

| NetEase, Inc. (ADR) | | | 1,398,000 | | | | 89,374 | | | | .92 | |

| Intuit Inc. | | | 1,520,000 | | | | 88,829 | | | | .91 | |

| Microsoft Corp. | | | 2,129,400 | | | | 74,273 | | | | .76 | |

| Baidu, Inc., Class A (ADR)1 | | | 749,000 | | | | 72,383 | | | | .75 | |

| Youku Inc., Class A (ADR)1 | | | 3,240,000 | | | | 66,258 | | | | .68 | |

| Other securities | | | | | | | 957,724 | | | | 9.86 | |

| | | | | | | | 1,873,004 | | | | 19.28 | |

| | | | | | | | | | | | | |

| Financials — 9.16% | | | | | | | | | | | | |

| AIA Group Ltd.2 | | | 18,542,200 | | | | 81,828 | | | | .84 | |

| SVB Financial Group1 | | | 835,000 | | | | 64,621 | | | | .66 | |

| State Street Corp. | | | 932,700 | | | | 61,726 | | | | .64 | |

| Other securities | | | | | | | 681,702 | | | | 7.02 | |

| | | | | | | | 889,877 | | | | 9.16 | |

| | | | | | | | | | | | | |

| Industrials — 8.64% | | | | | | | | | | | | |

| Nielsen Holdings NV | | | 3,704,000 | | | | 125,603 | | | | 1.29 | |

| Ryanair Holdings PLC (ADR) | | | 2,274,700 | | | | 111,096 | | | | 1.14 | |

| PT AKR Corporindo Tbk1,2 | | | 173,899,680 | | | | 94,776 | | | | .97 | |

| Common stocks | | Shares | | | Value

(000) | | | Percent of

net assets | |

| Industrials (continued) | | | | | | | | | |

| Union Pacific Corp. | | | 437,977 | | | $ | 67,720 | | | | .70 | % |

| CSX Corp. | | | 2,654,722 | | | | 66,926 | | | | .69 | |

| AirAsia Bhd.2 | | | 62,860,000 | | | | 64,752 | | | | .67 | |

| Other securities | | | | | | | 308,921 | | | | 3.18 | |

| | | | | | | | 839,794 | | | | 8.64 | |

| | | | | | | | | | | | | |

| Telecommunication services — 4.53% | | | | | | | | | | | | |

| SOFTBANK CORP.2 | | | 3,463,000 | | | | 173,210 | | | | 1.78 | |

| Crown Castle International Corp.1 | | | 1,191,300 | | | | 84,880 | | | | .87 | |

| Other securities | | | | | | | 182,361 | | | | 1.88 | |

| | | | | | | | 440,451 | | | | 4.53 | |

| | | | | | | | | | | | | |

| Energy — 1.28% | | | | | | | | | | | | |

| Schlumberger Ltd. | | | 1,122,400 | | | | 81,969 | | | | .85 | |

| Other securities | | | | | | | 41,878 | | | | .43 | |

| | | | | | | | 123,847 | | | | 1.28 | |

| | | | | | | | | | | | | |

| Consumer staples — 0.73% | | | | | | | | | | | | |

| Costco Wholesale Corp. | | | 650,000 | | | | 71,286 | | | | .73 | |

| | | | | | | | | | | | | |

| Utilities — 0.27% | | | | | | | | | | | | |

| Other securities | | | | | | | 26,389 | | | | .27 | |

| | | | | | | | | | | | | |

| Miscellaneous — 4.77% | | | | | | | | | | | | |

| Other common stocks in initial period of acquisition | | | | | | | 463,357 | | | | 4.77 | |

| | | | | | | | | | | | | |

| Total common stocks (cost: $6,124,165,000) | | | | | | | 8,761,558 | | | | 90.18 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Preferred stocks — 0.10% | | | | | | | | | | | | |

| Financials — 0.10% | | | | | | | | | | | | |

| Other securities | | | | | | | 10,114 | | | | .10 | |

| | | | | | | | | | | | | |

| Total preferred stocks (cost: $9,215,000) | | | | | | | 10,114 | | | | .10 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

Short-term securities — 9.42% | | | Principal

amount

(000) | | | |

| | | |

| |

| Freddie Mac 0.097%–0.16% due 6/24/2013–4/21/2014 | | $ | 153,580 | | | | 153,523 | | | | 1.58 | |

| Fannie Mae 0.10%–0.18% due 6/25–8/19/2013 | | | 141,600 | | | | 141,592 | | | | 1.46 | |

| Coca-Cola Co. 0.09%–0.18% due 6/18–12/5/20133 | | | 128,100 | | | | 128,086 | | | | 1.32 | |

| Federal Home Loan Bank 0.11%–0.125% due 7/2–7/24/2013 | | | 79,100 | | | | 79,095 | | | | .81 | |

| Other securities | | | | | | | 412,572 | | | | 4.25 | |

| | | | | | | | | | | | | |

| Total short-term securities (cost: $914,816,000) | | | | | | | 914,868 | | | | 9.42 | |

| | | Value

(000) | | | Percent of

net assets | |

| Total investment securities (cost: $7,048,196,000) | | $ | 9,686,540 | | | | 99.70 | % |

| Other assets less liabilities | | | 28,692 | | | | .30 | |

| | | | | | | | | |

| Net assets | | $ | 9,715,232 | | | | 100.00 | % |

As permitted by U.S. Securities and Exchange Commission regulations, “Miscellaneous” securities include holdings in their first year of acquisition that have not previously been publicly disclosed.

“Other securities” includes all issues that are not disclosed separately in the summary investment portfolio. One of these securities (with a value of $6,608,000, a cost of $31,574,000, and which represented .07% of the net assets of the fund) was acquired from 9/6/2000 to 4/18/2002 through a private placement transaction exempt from registration under the Securities Act of 1933, which may subject it to legal or contractual restrictions on resale.

Investments in affiliates

A company is considered to be an affiliate of the fund under the Investment Company Act of 1940 if the fund’s holdings in that company represent 5% or more of the outstanding voting shares. The value of the fund’s holdings in affiliated companies is included in “Other securities” under the respective industry sectors in the summary investment portfolio. Further details on these holdings and related transactions during the six months ended May 31, 2013, appear below.

| | | Beginning

shares | | | Additions | | | Reductions | | | Ending

shares | | | Dividend

income

(000) | | | Value of

affiliates at

5/31/2013

(000) | |

| Exelixis, Inc.1 | | | 10,950,900 | | | | 980,000 | | | | — | | | | 11,930,900 | | | $ | — | | | $ | 57,746 | |

| NuVasive, Inc.1 | | | 2,205,286 | | | | 45,000 | | | | — | | | | 2,250,286 | | | | — | | | | 48,876 | |

| Avanti Communications Group PLC1,2 | | | 6,933,372 | | | | — | | | | — | | | | 6,933,372 | | | | — | | | | 28,170 | |

| | | | | | | | | | | | | | | | | | | $ | — | | | $ | 134,792 | |

The following footnotes apply to either the individual securities noted or one or more of the securities aggregated and listed as a single line item.

| 1 | Security did not produce income during the last 12 months. |

| 2 | Valued under fair value procedures adopted by authority of the board of trustees. The total value of all such securities, including those in “Miscellaneous” and “Other securities,” was $2,888,440,000, which represented 29.73% of the net assets of the fund. This amount includes $2,881,832,000 related to certain securities trading outside the U.S. whose values were adjusted as a result of significant market movements following the close of local trading. |

| 3 | Acquired in a transaction exempt from registration under section 4(2) of the Securities Act of 1933. May be resold in the U.S. in transactions exempt from registration, normally to qualified institutional buyers. The total value of all such securities, including those in “Other securities,” was $426,478,000, which represented 4.39% of the net assets of the fund. |

Key to abbreviation

ADR = American Depositary Receipts

See Notes to Financial Statements

Financial statements

Statement of assets and liabilities

at May 31, 2013 | | unaudited

(dollars in thousands) |

| | | | | |

| Assets: | | | | | | | | |

| Investment securities, at value: | | | | | | | | |

| Unaffiliated issuers (cost: $6,894,896) | | $ | 9,551,748 | | | | | |

| Affiliated issuers (cost: $153,300) | | | 134,792 | | | $ | 9,686,540 | |

| Cash | | | | | | | 110 | |

| Receivables for: | | | | | | | | |

| Sales of investments | | | 14,116 | | | | | |

| Sales of fund’s shares | | | 21,758 | | | | | |

| Dividends and interest | | | 13,740 | | | | 49,614 | |

| | | | | | | | 9,736,264 | |

| Liabilities: | | | | | | | | |

| Payables for: | | | | | | | | |

| Purchases of investments | | | 2,991 | | | | | |

| Repurchases of fund’s shares | | | 7,545 | | | | | |

| Investment advisory services | | | 3,284 | | | | | |

| Services provided by related parties | | | 5,175 | | | | | |

| Trustees’ deferred compensation | | | 1,849 | | | | | |

| Other | | | 188 | | | | 21,032 | |

| Net assets at May 31, 2013 | | | | | | $ | 9,715,232 | |

| | | | | | | | | |

| Net assets consist of: | | | | | | | | |

| Capital paid in on shares of beneficial interest | | | | | | $ | 6,553,699 | |

| Undistributed net investment income | | | | | | | 20,760 | |

| Undistributed net realized gain | | | | | | | 502,614 | |

| Net unrealized appreciation | | | | | | | 2,638,159 | |

| Net assets at May 31, 2013 | | | | | | $ | 9,715,232 | |

(dollars and shares in thousands, except per-share amounts)

Shares of beneficial interest issued and outstanding (no stated par value) —

unlimited shares authorized (293,277 total shares outstanding)

| | | Net assets | | Shares

outstanding | | Net asset

value per share |

| Class A | | $ | 7,194,538 | | | | 216,465 | | | $ | 33.24 | |

| Class B | | | 51,081 | | | | 1,613 | | | | 31.66 | |

| Class C | | | 245,884 | | | | 7,855 | | | | 31.30 | |

| Class F-1 | | | 235,350 | | | | 7,069 | | | | 33.29 | |

| Class F-2 | | | 162,482 | | | | 4,889 | | | | 33.23 | |

| Class 529-A | | | 255,510 | | | | 7,739 | | | | 33.02 | |

| Class 529-B | | | 7,732 | | | | 243 | | | | 31.75 | |

| Class 529-C | | | 75,281 | | | | 2,375 | | | | 31.70 | |

| Class 529-E | | | 13,042 | | | | 399 | | | | 32.71 | |

| Class 529-F-1 | | | 17,006 | | | | 516 | | | | 32.98 | |

| Class R-1 | | | 26,663 | | | | 833 | | | | 32.00 | |

| Class R-2 | | | 145,933 | | | | 4,541 | | | | 32.14 | |

| Class R-3 | | | 206,679 | | | | 6,309 | | | | 32.76 | |

| Class R-4 | | | 191,687 | | | | 5,805 | | | | 33.02 | |

| Class R-5 | | | 170,646 | | | | 5,118 | | | | 33.34 | |

| Class R-6 | | | 715,718 | | | | 21,508 | | | | 33.28 | |

See Notes to Financial Statements

Statement of operations

for the six months ended May 31, 2013 | | unaudited

(dollars in thousands) |

| | | | | |

| Investment income: | | | | | | | | |

| Income: | | | | | | | | |

| Dividends (net of non-U.S. taxes of $1,609) | | $ | 64,245 | | | | | |

| Interest (net of non-U.S. taxes of $17) | | | 656 | | | $ | 64,901 | |

| | | | | | | | | |

| Fees and expenses*: | | | | | | | | |

| Investment advisory services | | | 17,524 | | | | | |

| Distribution services | | | 11,286 | | | | | |

| Transfer agent services | | | 6,727 | | | | | |

| Administrative services | | | 857 | | | | | |

| Reports to shareholders | | | 379 | | | | | |

| Registration statement and prospectus | | | 189 | | | | | |

| Trustees’ compensation | | | 462 | | | | | |

| Auditing and legal | | | 46 | | | | | |

| Custodian | | | 453 | | | | | |

| State and local taxes | | | 31 | | | | | |

| Other | | | 245 | | | | 38,199 | |

| Net investment income | | | | | | | 26,702 | |

| | | | | | | | | |

| Net realized gain and unrealized appreciation on investments and currency: | | | | | | | | |

| Net realized gain (loss) on: | | | | | | | | |

| Investments | | | 527,141 | | | | | |

| Currency transactions | | | (380 | ) | | | 526,761 | |

| Net unrealized appreciation on: | | | | | | | | |

| Investments (net of non-U.S. taxes of $81) | | | 987,196 | | | | | |

| Currency translations | | | 66 | | | | 987,262 | |

| Net realized gain and unrealized appreciation on investments and currency | | | | | | | 1,514,023 | |

| Net increase in net assets resulting from operations | | | | | | $ | 1,540,725 | |

*Additional information related to class-specific fees and expenses is included in the Notes to Financial Statements.

See Notes to Financial Statements

| Statements of changes in net assets | (dollars in thousands) |

| | | Six months

ended May 31,

2013 * | | Year ended

November 30,

2012 |

| | | | | | | | | |

| Operations: | | | | | | | | |

| Net investment income | | $ | 26,702 | | | $ | 41,858 | |

| Net realized gain on investments and currency transactions | | | 526,761 | | | | 302,895 | |

| Net unrealized appreciation on investments and currency translations | | | 987,262 | | | | 987,990 | |

| Net increase in net assets resulting from operations | | | 1,540,725 | | | | 1,332,743 | |

| | | | | | | | | |

| Dividends and distributions paid to shareholders: | | | | | | | | |

| Dividends from net investment income | | | (46,579 | ) | | | (32,433 | ) |

| Distributions from net realized gain on investments | | | (236,050 | ) | | | — | |

| Total dividends and distributions paid to shareholders | | | (282,629 | ) | | | (32,433 | ) |

| | | | | | | | | |

| Net capital share transactions | | | 656,836 | | | | (348,396 | ) |

| | | | | | | | | |

| Total increase in net assets | | | 1,914,932 | | | | 951,914 | |

| | | | | | | | | |

| Net assets: | | | | | | | | |

| Beginning of period | | | 7,800,300 | | | | 6,848,386 | |

| End of period (including undistributed net investment income: | | | | | | | | |

| $20,760 and $40,637, respectively) | | $ | 9,715,232 | | | $ | 7,800,300 | |

*Unaudited.

See Notes to Financial Statements

| Notes to financial statements | unaudited |

1. Organization

The New Economy Fund (the “fund”) is registered under the Investment Company Act of 1940 as an open-end, diversified management investment company. The fund seeks long-term growth of capital by investing in securities of companies that can benefit from innovation, exploit new technologies or provide products and services that meet the demands of an evolving global economy. Shareholders approved a proposal to reorganize the fund from a Massachusetts business trust to a Delaware statutory trust. The reorganization may be completed in 2013; however, the fund reserves the right to delay the implementation.

The fund has 16 share classes consisting of five retail share classes (Classes A, B and C, as well as two F share classes, F-1 and F-2), five 529 college savings plan share classes (Classes 529-A, 529-B, 529-C, 529-E and 529-F-1) and six retirement plan share classes (Classes R-1, R-2, R-3, R-4, R-5 and R-6). The 529 college savings plan share classes can be used to save for college education. The retirement plan share classes are generally offered only through eligible employer-sponsored retirement plans. The fund’s share classes are further described below:

| Share class | | Initial sales charge | | Contingent deferred sales

charge upon redemption | | Conversion feature |

| Classes A and 529-A | | Up to 5.75% | | None (except 1% for certain redemptions within one year of purchase without an initial sales charge) | | None |

| Classes B and 529-B* | | None | | Declines from 5% to 0% for redemptions within six years of purchase | | Classes B and 529-B convert to Classes A and 529-A, respectively, after eight years |

| Class C | | None | | 1% for redemptions within one year of purchase | | Class C converts to Class F-1 after 10 years |

| Class 529-C | | None | | 1% for redemptions within one year of purchase | | None |

| Class 529-E | | None | | None | | None |

| Classes F-1, F-2 and 529-F-1 | | None | | None | | None |

| Classes R-1, R-2, R-3, R-4, R-5 and R-6 | | None | | None | | None |

*Class B and 529-B shares of the fund are not available for purchase.

Holders of all share classes have equal pro rata rights to assets, dividends and liquidation proceeds. Each share class has identical voting rights, except for the exclusive right to vote on matters affecting only its class. Share classes have different fees and expenses (“class-specific fees and expenses”), primarily due to different arrangements for distribution, administrative and shareholder services. Differences in class-specific fees and expenses will result in differences in net investment income and, therefore, the payment of different per-share dividends by each share class.

2. Significant accounting policies

The financial statements have been prepared to comply with accounting principles generally accepted in the United States of America. These principles require management to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates. The fund follows the significant accounting policies described below, as well as the valuation policies described in the next section on valuation.

Security transactions and related investment income — Security transactions are recorded by the fund as of the date the trades are executed with brokers. Realized gains and losses from security transactions are determined based on the specific identified cost of the securities. Dividend income is recognized on the ex-dividend date and interest income is recognized on an accrual basis. Market discounts, premiums and original issue discounts on fixed-income securities are amortized daily over the expected life of the security.

Class allocations — Income, fees and expenses (other than class-specific fees and expenses) and realized and unrealized gains and losses are allocated daily among the various share classes based on their relative net assets. Class-specific fees and expenses, such as distribution, administrative and shareholder services, are charged directly to the respective share class.

Dividends and distributions to shareholders — Dividends and distributions to shareholders are recorded on the ex-dividend date.

Currency translation — Assets and liabilities, including investment securities, denominated in currencies other than U.S. dollars are translated into U.S. dollars at the exchange rates supplied by one or more pricing vendors on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the exchange rates on the dates of such transactions. On the accompanying financial statements, the effects of changes in exchange rates on investment securities are included with the net realized gain or loss and net unrealized appreciation or depreciation on investments. The realized gain or loss and unrealized appreciation or depreciation resulting from all other transactions denominated in currencies other than U.S. dollars are disclosed separately.

3. Valuation

Capital Research and Management Company (“CRMC”), the fund’s investment adviser, values the fund’s investments at fair value as defined by accounting principles generally accepted in the United States of America. The net asset value of each share class of the fund is generally determined as of approximately 4:00 p.m. New York time each day the New York Stock Exchange is open.

Methods and inputs — The fund’s investment adviser uses the following methods and inputs to establish the fair value of the fund’s assets and liabilities. Use of particular methods and inputs may vary over time based on availability and relevance as market and economic conditions evolve.

Equity securities are generally valued at the official closing price of, or the last reported sale price on, the exchange or market on which such securities are traded, as of the close of business on the day the securities are being valued or, lacking any sales, at the last available bid price. Prices for each security are taken from the principal exchange or market on which the security trades.

Fixed-income securities, including short-term securities purchased with more than 60 days left to maturity, are generally valued at prices obtained from one or more pricing vendors. Vendors value such securities based on one or more of the inputs described in the following table. The table provides examples of inputs that are commonly relevant for valuing particular classes of fixed-income securities in which the fund is authorized to invest. However, these classifications are not exclusive, and any of the inputs may be used to value any other class of fixed-income security.

| Fixed-income class | | Examples of standard inputs |

| All | | Benchmark yields, transactions, bids, offers, quotations from dealers and trading systems, new issues, spreads and other relationships observed in the markets among comparable securities; and proprietary pricing models such as yield measures calculated using factors such as cash flows, financial or collateral performance and other reference data (collectively referred to as “standard inputs”) |

| Corporate bonds & notes; convertible securities | | Standard inputs and underlying equity of the issuer |

| Bonds & notes of governments & government agencies | | Standard inputs and interest rate volatilities |

When the fund’s investment adviser deems it appropriate to do so (such as when vendor prices are unavailable or not deemed to be representative), fixed-income securities will be valued in good faith at the mean quoted bid and ask prices that are reasonably and timely available (or bid prices, if ask prices are not available) or at prices for securities of comparable maturity, quality and type.

Securities with both fixed-income and equity characteristics, or equity securities traded principally among fixed-income dealers, are generally valued in the manner described above for either equity or fixed-income securities, depending on which method is deemed most appropriate by the fund’s investment adviser. Short-term securities purchased within 60 days to maturity are valued at amortized cost, which approximates fair value. The value of short-term securities originally purchased with maturities greater than 60 days is determined based on an amortized value to par when they reach 60 days.

Securities and other assets for which representative market quotations are not readily available or are considered unreliable by the fund’s investment adviser are fair valued as determined in good faith under fair valuation guidelines adopted by authority of the fund’s board of trustees as further described below. The investment adviser follows fair valuation guidelines, consistent with U.S. Securities and Exchange Commission rules and guidance, to consider relevant principles and factors when making fair value determinations. The investment adviser considers relevant indications of value that are reasonably and timely available to it in determining the fair value to be assigned to a particular security, such as the type and cost of the security; contractual or legal restrictions on resale of the security; relevant financial or business developments of the issuer; actively traded similar or related securities; conversion or exchange rights on the security; related corporate actions; significant events occurring after the close of trading in the security; and changes in overall market conditions. In addition, the closing prices of equity securities that trade in markets outside U.S. time zones may be adjusted to reflect significant events that occur after the close of local trading but before the net asset value of each share class of the fund is determined. Fair valuations and valuations of investments that are not actively trading involve judgment and may differ materially from valuations that would have been used had greater market activity occurred.

Processes and structure — The fund’s board of trustees has delegated authority to the fund’s investment adviser to make fair value determinations, subject to board oversight. The investment adviser has established a Joint Fair Valuation Committee (the “Fair Valuation Committee”) to administer, implement and oversee the fair valuation process, and to make fair value decisions. The Fair Valuation Committee regularly reviews its own fair value decisions, as well as decisions made under its standing instructions to the investment adviser’s valuation teams. The Fair Valuation Committee reviews changes in fair value measurements from period to period and may, as deemed appropriate, update the fair valuation guidelines to better reflect the results of back testing and address new or evolving issues. The Fair Valuation Committee reports any changes to the fair valuation guidelines to the board of trustees with supplemental information to support the changes. The fund’s board and audit committee also regularly review reports that describe fair value determinations and methods.

The fund’s investment adviser has also established a Fixed-Income Pricing Review Group to administer and oversee the fixed-income valuation process, including the use of fixed-income pricing vendors. This group regularly reviews pricing vendor information and market data. Pricing decisions, processes and controls over security valuation are also subject to additional internal reviews, including an annual control self-evaluation program facilitated by the investment adviser’s compliance group.

Classifications — The fund’s investment adviser classifies the fund’s assets and liabilities into three levels based on the inputs used to value the assets or liabilities. Level 1 values are based on quoted prices in active markets for identical securities.

Level 2 values are based on significant observable market inputs, such as quoted prices for similar securities and quoted prices in inactive markets. Certain securities trading outside the U.S. may transfer between Level 1 and Level 2 due to valuation adjustments resulting from significant market movements following the close of local trading. Level 3 values are based on significant unobservable inputs that reflect the investment adviser’s determination of assumptions that market participants might reasonably use in valuing the securities. The valuation levels are not necessarily an indication of the risk or liquidity associated with the underlying investment. For example, U.S. government securities are reflected as Level 2 because the inputs used to determine fair value may not always be quoted prices in an active market. The following table presents the fund’s valuation levels as of May 31, 2013 (dollars in thousands):

| | | Investment securities | |

| | | Level 1 | | | Level 2* | | | Level 3 | | | Total | |

| Assets: | | | | | | | | | | | | | | | | |

| Common stocks: | | | | | | | | | | | | | | | | |

| Health care | | $ | 1,758,709 | | | $ | 348,683 | | | $ | — | | | $ | 2,107,392 | |

| Consumer discretionary | | | 1,030,531 | | | | 889,022 | | | | 6,608 | | | | 1,926,161 | |

| Information technology | | | 1,416,085 | | | | 456,919 | | | | — | | | | 1,873,004 | |

| Financials | | | 428,372 | | | | 461,505 | | | | — | | | | 889,877 | |

| Industrials | | | 604,481 | | | | 235,313 | | | | — | | | | 839,794 | |

| Telecommunication services | | | 130,357 | | | | 310,094 | | | | — | | | | 440,451 | |

| Energy | | | 123,847 | | | | — | | | | — | | | | 123,847 | |

| Consumer staples | | | 71,286 | | | | — | | | | — | | | | 71,286 | |

| Utilities | | | — | | | | 26,389 | | | | — | | | | 26,389 | |

| Miscellaneous | | | 309,450 | | | | 153,907 | | | | — | | | | 463,357 | |

| Preferred stocks | | | — | | | | 10,114 | | | | — | | | | 10,114 | |

| Short-term securities | | | — | | | | 914,868 | | | | — | | | | 914,868 | |

| Total | | $ | 5,873,118 | | | $ | 3,806,814 | | | $ | 6,608 | | | $ | 9,686,540 | |

| * | Securities with a market value of $2,591,263,000, which represented 26.67% of the net assets of the fund, transferred from Level 1 to Level 2 since the prior fiscal year-end, primarily due to significant market movements following the close of local trading. |

4. Risk factors

Investing in the fund may involve certain risks including, but not limited to, those described below.

Market conditions — The prices of, and the income generated by, the common stocks and other securities held by the fund may decline due to market conditions and other factors, including those directly involving the issuers of securities held by the fund. The fund may be subject to additional risks because it invests in a more limited group of sectors and industries than the broad market.

Investing in growth-oriented stocks — Growth-oriented stocks may involve larger price swings and greater potential for loss than other types of investments.

Investing in small companies — Investing in smaller companies may pose additional risks. For example, it is often more difficult to value or dispose of small company stocks and more difficult to obtain information about smaller companies than about larger companies. In addition, the prices of these stocks may be more volatile than stocks of larger, more established companies.

Investing outside the U.S. — Securities of issuers domiciled outside the U.S., or with significant operations outside the U.S., may lose value because of adverse political, social, economic or market developments in the countries or regions in which the issuer operates. These securities may also lose value due to changes in foreign currency exchange rates against the U.S. dollar and/or currencies of other countries. Securities markets in certain countries may be more volatile and/or less liquid than those in the U.S. Investments outside the U.S. may also be subject to different settlement and accounting practices and different regulatory, legal and reporting standards, and may be more difficult to value, than those in the U.S. The risks of investing outside the U.S. may be heightened in connection with investments in emerging markets.

Investing in emerging markets — Investing in emerging markets may involve risks in addition to and greater than those generally associated with investing in developed countries. For instance, developing countries may have less developed legal and accounting systems than those in developed countries. The governments of these countries may be less stable and more likely to impose capital controls, nationalize a company or industry, place restrictions on foreign ownership and on withdrawing sale proceeds of securities from the country, and/or impose punitive taxes that could adversely affect the prices of securities. In addition, the economies of these countries may be dependent on relatively few industries that are more susceptible to local and global changes. Securities markets in these countries can also be relatively small and have substantially lower trading volumes. As a result, securities issued in these countries may be more volatile and less liquid, and may be more difficult to value, than securities issued in countries with more developed economies and/or markets. Additionally, there may be increased settlement risks for transactions in local securities.

Management — The investment adviser to the fund actively manages the fund’s investments. Consequently, the fund is subject to the risk that the methods and analyses employed by the investment adviser in this process may not produce the desired results. This could cause the fund to lose value or its investment results to lag relevant benchmarks or other funds with similar objectives.

5. Taxation and distributions

Federal income taxation — The fund complies with the requirements under Subchapter M of the Internal Revenue Code applicable to mutual funds and intends to distribute substantially all of its net taxable income and net capital gains each year. The fund is not subject to income taxes to the extent such distributions are made. Therefore, no federal income tax provision is required.

As of and during the period ended May 31, 2013, the fund did not have a liability for any unrecognized tax benefits. The fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the period, the fund did not incur any interest or penalties.

The fund is not subject to examination by U.S. federal tax authorities for tax years before 2008, by state tax authorities for tax years before 2007 and by tax authorities outside the U.S. for tax years before 2006.

Non-U.S. taxation — Dividend and interest income are recorded net of non-U.S. taxes paid. Gains realized by the fund on the sale of securities in certain countries are subject to non-U.S. taxes. The fund records a liability based on unrealized gains to provide for potential non-U.S. taxes payable upon the sale of these securities.

Distributions — Distributions paid to shareholders are based on net investment income and net realized gains determined on a tax basis, which may differ from net investment income and net realized gains for financial reporting purposes. These differences are due primarily to different treatment for items such as currency gains and losses; short-term capital gains and losses; and deferred expenses. The fiscal year in which amounts are distributed may differ from the year in which the net investment income and net realized gains are recorded by the fund for financial reporting purposes.

The components of distributable earnings on a tax basis are reported as of the fund’s most recent year-end. As of November 30, 2012, the fund had tax basis undistributed ordinary income of $42,294,000, capital loss deferral of $23,361,000, and undistributed long-term capital gains of $235,263,000.

As of May 31, 2013, the tax basis unrealized appreciation (depreciation) and cost of investment securities were as follows (dollars in thousands):

| Gross unrealized appreciation on investment securities | | $ | 2,885,548 | |

| Gross unrealized depreciation on investment securities | | | (247,204 | ) |

| Net unrealized appreciation on investment securities | | | 2,638,344 | |

| Cost of investment securities | | | 7,048,196 | |

The tax character of distributions paid to shareholders was as follows (dollars in thousands):

| | | Six months ended May 31, 2013 | | | Year ended November 30, 2012 | |

| | | | | | Long-term | | | Total | | | | | | Long-term | | | Total | |

| | | Ordinary | | | capital | | | distributions | | | Ordinary | | | capital | | | distributions | |

| Share class | | income | | | gains | | | paid | | | income | | | gains | | | paid | |

| Class A | | $ | 35,632 | | | $ | 178,162 | | | $ | 213,794 | | | $ | 25,493 | | | $ | — | | | $ | 25,493 | |

| Class B | | | — | | | | 1,543 | | | | 1,543 | | | | — | | | | — | | | | — | |

| Class C | | | — | | | | 5,991 | | | | 5,991 | | | | — | * | | | — | | | | — | |

| Class F-1 | | | 786 | | | | 4,288 | | | | 5,074 | | | | 624 | | | | — | | | | 624 | |

| Class F-2 | | | 998 | | | | 3,248 | | | | 4,246 | | | | 552 | | | | — | | | | 552 | |

| Class 529-A | | | 1,139 | | | | 6,060 | | | | 7,199 | | | | 767 | | | | — | | | | 767 | |

| Class 529-B | | | — | | | | 234 | | | | 234 | | | | — | | | | — | | | | — | |

| Class 529-C | | | — | | | | 1,911 | | | | 1,911 | | | | — | * | | | — | | | | — | |

| Class 529-E | | | 33 | | | | 309 | | | | 342 | | | | 15 | | | | — | | | | 15 | |

| Class 529-F-1 | | | 101 | | | | 391 | | | | 492 | | | | 66 | | | | — | | | | 66 | |

| Class R-1 | | | — | | | | 701 | | | | 701 | | | | — | | | | — | | | | — | |

| Class R-2 | | | — | | | | 3,844 | | | | 3,844 | | | | — | | | | — | | | | — | |

| Class R-3 | | | 491 | | | | 5,174 | | | | 5,665 | | | | 274 | | | | — | | | | 274 | |

| Class R-4 | | | 1,047 | | | | 4,799 | | | | 5,846 | | | | 712 | | | | — | | | | 712 | |

| Class R-5 | | | 1,192 | | | | 3,825 | | | | 5,017 | | | | 892 | | | | — | | | | 892 | |

| Class R-6 | | | 5,160 | | | | 15,570 | | | | 20,730 | | | | 3,038 | | | | — | | | | 3,038 | |

| Total | | $ | 46,579 | | | $ | 236,050 | | | $ | 282,629 | | | $ | 32,433 | | | $ | — | | | $ | 32,433 | |

*Amount less than one thousand.

6. Fees and transactions with related parties

CRMC, the fund’s investment adviser, is the parent company of American Funds Distributors,® Inc. (“AFD”), the principal underwriter of the fund’s shares, and American Funds Service Company® (“AFS”), the fund’s transfer agent. CRMC, AFD and AFS are considered related parties to the fund.

Investment advisory services — The fund has an investment advisory and service agreement with CRMC that provides for monthly fees accrued daily. These fees are based on a series of decreasing annual rates beginning with 0.580% on the first $500 million of daily net assets and decreasing to 0.345% on such assets in excess of $27 billion. For the six months ended May 31, 2013, the investment advisory services fee was $17,524,000, which was equivalent to an annualized rate of 0.403% of average daily net assets.

Class-specific fees and expenses — Expenses that are specific to individual share classes are accrued directly to the respective share class. The principal class-specific fees and expenses are described on the following page:

Distribution services — The fund has plans of distribution for all share classes, except Class F-2, R-5 and R-6 shares. Under the plans, the board of trustees approves certain categories of expenses that are used to finance activities primarily intended to sell fund shares and service existing accounts. The plans provide for payments, based on an annualized percentage of average daily net assets, ranging from 0.25% to 1.00% as noted below. In some cases, the board of trustees has limited the amounts that may be paid to less than the maximum allowed by the plans. All share classes with a plan may use up to 0.25% of average daily net assets to pay service fees, or to compensate AFD for paying service fees, to firms that have entered into agreements with AFD to provide certain shareholder services. The remaining amounts available to be paid under each plan are paid to dealers to compensate them for their sales activities.

For Class A and 529-A shares, distribution-related expenses include the reimbursement of dealer and wholesaler commissions paid by AFD for certain shares sold without a sales charge. These share classes reimburse AFD for amounts billed within the prior 15 months but only to the extent that the overall annual expense limit of 0.25% is not exceeded. As of May 31, 2013, there were no unreimbursed expenses subject to reimbursement for Class A or 529-A shares.

| | Share class | | Currently approved limits | | Plan limits |

| | Class A | | | 0.25 | % | | | 0.25 | % | |

| | Class 529-A | | | 0.25 | | | | 0.50 | | |

| | Classes B and 529-B | | | 1.00 | | | | 1.00 | | |

| | Classes C, 529-C and R-1 | | | 1.00 | | | | 1.00 | | |

| | Class R-2 | | | 0.75 | | | | 1.00 | | |

| | Classes 529-E and R-3 | | | 0.50 | | | | 0.75 | | |

| | Classes F-1, 529-F-1 and R-4 | | | 0.25 | | | | 0.50 | | |

| | Transfer agent services — The fund has a shareholder services agreement with AFS under which the fund compensates AFS for providing transfer agent services to each of the fund’s share classes. These services include recordkeeping, shareholder communications and transaction processing. In addition, the fund reimburses AFS for amounts paid to third parties for performing transfer agent services on behalf of fund shareholders. |

| | |

| | Administrative services — The fund has an administrative services agreement with CRMC under which the fund compensates CRMC for providing administrative services to Class A, C, F, 529 and R shares. These services include, but are not limited to, coordinating, monitoring, assisting and overseeing third parties that provide services to fund shareholders. Under the agreement, Class A shares pay an annual fee of 0.01% and Class C, F, 529 and R shares pay an annual fee of 0.05% of their respective average daily net assets. |

| | 529 plan services — Each 529 share class is subject to service fees to compensate the Commonwealth of Virginia for the maintenance of the 529 college savings plan. The quarterly fee is based on a series of decreasing annual rates beginning with 0.10% on the first $30 billion of the net assets invested in Class 529 shares of the American Funds and decreasing to 0.06% on such assets between $120 billion and $150 billion. The fee for any given calendar quarter is accrued and calculated on the basis of the average net assets of Class 529 shares of the American Funds for the last month of the prior calendar quarter. The fee is included in other expenses on the accompanying financial statements. The Commonwealth of Virginia is not considered a related party. |

| | Class-specific expenses under the agreements described on the previous page for the six months ended May 31, 2013, were as follows (dollars in thousands): |

| | Share class | | Distribution

services | | Transfer agent

services | | Administrative

services | | 529 plan

services |

| | Class A | | $7,821 | | $5,563 | | $326 | | Not applicable |

| | Class B | | 251 | | 47 | | Not applicable | | Not applicable |

| | Class C | | 1,059 | | 182 | | 53 | | Not applicable |

| | Class F-1 | | 224 | | 118 | | 45 | | Not applicable |

| | Class F-2 | | Not applicable | | 58 | | 32 | | Not applicable |

| | Class 529-A | | 236 | | 154 | | 56 | | $111 |

| | Class 529-B | | 37 | | 6 | | 2 | | 4 |

| | Class 529-C | | 335 | | 50 | | 17 | | 33 |

| | Class 529-E | | 29 | | 5 | | 3 | | 6 |

| | Class 529-F-1 | | — | | 10 | | 4 | | 7 |

| | Class R-1 | | 117 | | 14 | | 6 | | Not applicable |

| | Class R-2 | | 498 | | 235 | | 34 | | Not applicable |

| | Class R-3 | | 461 | | 159 | | 46 | | Not applicable |

| | Class R-4 | | 218 | | 89 | | 44 | | Not applicable |

| | Class R-5 | | Not applicable | | 36 | | 37 | | Not applicable |

| | Class R-6 | | Not applicable | | 1 | | 152 | | Not applicable |

| | Total class-specific expenses | | $11,286 | | $6,727 | | $857 | | $161 |

Trustees’ deferred compensation — Trustees who are unaffiliated with CRMC may elect to defer the cash payment of part or all of their compensation. These deferred amounts, which remain as liabilities of the fund, are treated as if invested in shares of the fund or other American Funds. These amounts represent general, unsecured liabilities of the fund and vary according to the total returns of the selected funds. Trustees’ compensation of $462,000, shown on the accompanying financial statements, includes $205,000 in current fees (either paid in cash or deferred) and a net increase of $257,000 in the value of the deferred amounts.

Affiliated officers and trustees — Officers and certain trustees of the fund are or may be considered to be affiliated with CRMC, AFD and AFS. No affiliated officers or trustees received any compensation directly from the fund.

7. Capital share transactions

Capital share transactions in the fund were as follows (dollars and shares in thousands):

| | | Sales* | | | Reinvestments of dividends

and distributions | | | Repurchases* | | | Net increase

(decrease) | |

| Share class | | Amount | | | Shares | | | Amount | | | Shares | | | Amount | | | Shares | | | Amount | | | Shares | |

| | | | | | | | | | | | | | | |

| Six months ended May 31, 2013 | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Class A | | $ | 605,881 | | | | 19,596 | | | $ | 208,058 | | | | 7,397 | | | $ | (481,955 | ) | | | (15,806 | ) | | $ | 331,984 | | | | 11,187 | |

| Class B | | | 3,416 | | | | 115 | | | | 1,531 | | | | 57 | | | | (10,924 | ) | | | (372 | ) | | | (5,977 | ) | | | (200 | ) |

| Class C | | | 47,045 | | | | 1,604 | | | | 5,896 | | | | 222 | | | | (23,749 | ) | | | (818 | ) | | | 29,192 | | | | 1,008 | |

| Class F-1 | | | 88,509 | | | | 2,828 | | | | 4,991 | | | | 177 | | | | (27,367 | ) | | | (892 | ) | | | 66,133 | | | | 2,113 | |

| Class F-2 | | | 49,849 | | | | 1,612 | | | | 3,851 | | | | 137 | | | | (16,271 | ) | | | (541 | ) | | | 37,429 | | | | 1,208 | |

| Class 529-A | | | 31,488 | | | | 1,032 | | | | 7,189 | | | | 257 | | | | (13,482 | ) | | | (445 | ) | | | 25,195 | | | | 844 | |

| Class 529-B | | | 377 | | | | 13 | | | | 234 | | | | 8 | | | | (1,637 | ) | | | (56 | ) | | | (1,026 | ) | | | (35 | ) |

| Class 529-C | | | 8,303 | | | | 284 | | | | 1,909 | | | | 71 | | | | (4,883 | ) | | | (168 | ) | | | 5,329 | | | | 187 | |

| Class 529-E | | | 1,628 | | | | 54 | | | | 342 | | | | 13 | | | | (594 | ) | | | (20 | ) | | | 1,376 | | | | 47 | |

| Class 529-F-1 | | | 2,968 | | | | 96 | | | | 491 | | | | 18 | | | | (1,126 | ) | | | (37 | ) | | | 2,333 | | | | 77 | |

| Class R-1 | | | 4,845 | | | | 160 | | | | 701 | | | | 26 | | | | (5,035 | ) | | | (172 | ) | | | 511 | | | | 14 | |

| Class R-2 | | | 23,847 | | | | 800 | | | | 3,839 | | | | 141 | | | | (25,117 | ) | | | (849 | ) | | | 2,569 | | | | 92 | |

| Class R-3 | | | 39,323 | | | | 1,295 | | | | 5,659 | | | | 204 | | | | (33,303 | ) | | | (1,114 | ) | | | 11,679 | | | | 385 | |

| Class R-4 | | | 35,898 | | | | 1,187 | | | | 5,845 | | | | 209 | | | | (25,823 | ) | | | (840 | ) | | | 15,920 | | | | 556 | |

| Class R-5 | | | 29,247 | | | | 949 | | | | 5,009 | | | | 178 | | | | (16,026 | ) | | | (528 | ) | | | 18,230 | | | | 599 | |

| Class R-6 | | | 125,517 | | | | 4,056 | | | | 20,730 | | | | 737 | | | | (30,288 | ) | | | (986 | ) | | | 115,959 | | | | 3,807 | |

| Total net increase (decrease) | | $ | 1,098,141 | | | | 35,681 | | | $ | 276,275 | | | | 9,852 | | | $ | (717,580 | ) | | | (23,644 | ) | | $ | 656,836 | | | | 21,889 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year ended November 30, 2012 | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Class A | | $ | 520,447 | | | | 19,362 | | | $ | 24,629 | | | | 1,044 | $ | | | (921,314 | ) | | | (34,589 | ) | | $ | (376,238 | ) | | | (14,183 | ) |

| Class B | | | 3,885 | | | | 151 | | | | — | | | | — | | | | (26,445) | | | | (1,046 | ) | | | (22,560 | ) | | | (895 | ) |

| Class C | | | 31,070 | | | | 1,223 | | | | — | | | | — | | | | (48,106 | ) | | | (1,914 | ) | | | (17,036 | ) | | | (691 | ) |

| Class F-1 | | | 56,584 | | | | 2,092 | | | | 611 | | | | 26 | | | | (82,817 | ) | | | (3,076 | ) | | | (25,622 | ) | | | (958 | ) |

| Class F-2 | | | 47,810 | | | | 1,740 | | | | 440 | | | | 19 | | | | (27,751 | ) | | | (1,031 | ) | | | 20,499 | | | | 728 | |

| Class 529-A | | | 34,535 | | | | 1,305 | | | | 766 | | | | 33 | | | | (25,062 | ) | | | (945 | ) | | | 10,239 | | | | 393 | |

| Class 529-B | | | 350 | | | | 14 | | | | — | | | | — | | | | (4,094 | ) | | | (163 | ) | | | (3,744 | ) | | | (149 | ) |

| Class 529-C | | | 10,843 | | | | 426 | | | | — | | | | — | | | | (9,543 | ) | | | (374 | ) | | | 1,300 | | | | 52 | |

| Class 529-E | | | 1,704 | | | | 65 | | | | 15 | | | | — | † | | | (1,465 | ) | | | (57 | ) | | | 254 | | | | 8 | |

| Class 529-F-1 | | | 3,231 | | | | 120 | | | | 66 | | | | 3 | | | | (2,377 | ) | | | (91 | ) | | | 920 | | | | 32 | |

| Class R-1 | | | 6,015 | | | | 232 | | | | — | | | | — | | | | (9,901 | ) | | | (380 | ) | | | (3,886 | ) | | | (148 | ) |

| Class R-2 | | | 35,868 | | | | 1,386 | | | | — | | | | — | | | | (45,105 | ) | | | (1,751 | ) | | | (9,237 | ) | | | (365 | ) |

| Class R-3 | | | 49,626 | | | | 1,885 | | | | 274 | | | | 12 | | | | (60,409 | ) | | | (2,299 | ) | | | (10,509 | ) | | | (402 | ) |

| Class R-4 | | | 52,920 | | | | 1,994 | | | | 711 | | | | 30 | | | | (60,124 | ) | | | (2,279 | ) | | | (6,493 | ) | | | (255 | ) |

| Class R-5 | | | 25,996 | | | | 956 | | | | 890 | | | | 38 | | | | (28,021 | ) | | | (1,033 | ) | | | (1,135 | ) | | | (39 | ) |

| Class R-6 | | | 135,693 | | | | 5,159 | | | | 3,038 | | | | 128 | | | | (43,879 | ) | | | (1,623 | ) | | | 94,852 | | | | 3,664 | |

| Total net increase (decrease) | | $ | 1,016,577 | | | | 38,110 | | | $ | 31,440 | | | | 1,333 | | | $ | (1,396,413 | ) | | | (52,651 | ) | | $ | (348,396 | ) | | | (13,208 | ) |

*Includes exchanges between share classes of the fund.

†Amount less than one thousand.

8. Investment transactions

The fund made purchases and sales of investment securities, excluding short-term securities and U.S. government obligations, if any, of $1,473,641,000 and $1,398,002,000, respectively, during the six months ended May 31, 2013.

Financial highlights

| | | | | | | | | | | Income (loss) from investment operations1 | |

| | | | | | | Net asset

value,

beginning

of period | | | Net

investment

income

(loss) | | | Net gains

(losses) on

securities

(both realized

and unrealized) | | | Total from

investment

operations | |

| Class A: | | | Six months ended 5/31/20134,5 | | | $ | 28.83 | | | $ | .10 | | | $ | 5.37 | | | $ | 5.47 | |

| | | | Year ended 11/30/2012 | | | | 24.14 | | | | .16 | | | | 4.65 | | | | 4.81 | |

| | | | Year ended 11/30/2011 | | | | 24.22 | | | | .11 | | | | (.02 | ) | | | .09 | |

| | | | Year ended 11/30/2010 | | | | 21.87 | | | | .18 | | | | 2.28 | | | | 2.46 | |

| | | | Year ended 11/30/2009 | | | | 15.22 | | | | .12 | | | | 6.76 | | | | 6.88 | |

| | | | Year ended 11/30/2008 | | | | 30.09 | | | | .29 | | | | (12.57 | ) | | | (12.28 | ) |

| Class B: | | | Six months ended 5/31/20134,5 | | | | 27.45 | | | | (.02 | ) | | | 5.11 | | | | 5.09 | |

| | | | Year ended 11/30/2012 | | | | 23.04 | | | | (.05 | ) | | | 4.46 | | | | 4.41 | |

| | | | Year ended 11/30/2011 | | | | 23.14 | | | | (.08 | ) | | | (.02 | ) | | | (.10 | ) |

| | | | Year ended 11/30/2010 | | | | 20.95 | | | | — | 7 | | | 2.19 | | | | 2.19 | |

| | | | Year ended 11/30/2009 | | | | 14.50 | | | | (.02 | ) | | | 6.50 | | | | 6.48 | |

| | | | Year ended 11/30/2008 | | | | 28.80 | | | | .10 | | | | (12.00 | ) | | | (11.90 | ) |

| Class C: | | | Six months ended 5/31/20134,5 | | | | 27.15 | | | | (.02 | ) | | | 5.05 | | | | 5.03 | |

| | | | Year ended 11/30/2012 | | | | 22.80 | | | | (.05 | ) | | | 4.40 | | | | 4.35 | |

| | | | Year ended 11/30/2011 | | | | 22.90 | | | | (.08 | ) | | | (.02 | ) | | | (.10 | ) |

| | | | Year ended 11/30/2010 | | | | 20.75 | | | | — | 7 | | | 2.16 | | | | 2.16 | |

| | | | Year ended 11/30/2009 | | | | 14.39 | | | | (.02 | ) | | | 6.44 | | | | 6.42 | |

| | | | Year ended 11/30/2008 | | | | 28.63 | | | | .10 | | | | (11.91 | ) | | | (11.81 | ) |

| Class F-1: | | | Six months ended 5/31/20134,5 | | | | 28.87 | | | | .10 | | | | 5.36 | | | | 5.46 | |

| | | | Year ended 11/30/2012 | | | | 24.16 | | | | .16 | | | | 4.66 | | | | 4.82 | |

| | | | Year ended 11/30/2011 | | | | 24.23 | | | | .11 | | | | (.01 | ) | | | .10 | |

| | | | Year ended 11/30/2010 | | | | 21.90 | | | | .18 | | | | 2.28 | | | | 2.46 | |

| | | | Year ended 11/30/2009 | | | | 15.11 | | | | .12 | | | | 6.77 | | | | 6.89 | |

| | | | Year ended 11/30/2008 | | | | 29.91 | | | | .28 | | | | (12.48 | ) | | | (12.20 | ) |

| Class F-2: | | | Six months ended 5/31/20134,5 | | | | 28.88 | | | | .14 | | | | 5.36 | | | | 5.50 | |

| | | | Year ended 11/30/2012 | | | | 24.19 | | | | .23 | | | | 4.65 | | | | 4.88 | |

| | | | Year ended 11/30/2011 | | | | 24.27 | | | | .18 | | | | (.02 | ) | | | .16 | |

| | | | Year ended 11/30/2010 | | | | 21.93 | | | | .24 | | | | 2.29 | | | | 2.53 | |

| | | | Year ended 11/30/2009 | | | | 15.24 | | | | .14 | | | | 6.81 | | | | 6.95 | |

| | | | Period from 8/1/2008 to 11/30/20084 | | | | 22.62 | | | | .07 | | | | (7.45 | ) | | | (7.38 | ) |

| Class 529-A: | | | Six months ended 5/31/20134,5 | | | | 28.65 | | | | .09 | | | | 5.32 | | | | 5.41 | |

| | | | Year ended 11/30/2012 | | | | 24.00 | | | | .14 | | | | 4.63 | | | | 4.77 | |

| | | | Year ended 11/30/2011 | | | | 24.10 | | | | .10 | | | | (.02 | ) | | | .08 | |

| | | | Year ended 11/30/2010 | | | | 21.77 | | | | .17 | | | | 2.27 | | | | 2.44 | |

| | | | Year ended 11/30/2009 | | | | 15.16 | | | | .12 | | | | 6.72 | | | | 6.84 | |

| | | | Year ended 11/30/2008 | | | | 29.98 | | | | .28 | | | | (12.52 | ) | | | (12.24 | ) |

| Class 529-B: | | | Six months ended 5/31/20134,5 | | | | 27.54 | | | | (.04 | ) | | | 5.13 | | | | 5.09 | |

| | | | Year ended 11/30/2012 | | | | 23.15 | | | | (.08 | ) | | | 4.47 | | | | 4.39 | |

| | | | Year ended 11/30/2011 | | | | 23.27 | | | | (.11 | ) | | | (.01 | ) | | | (.12 | ) |

| | | | Year ended 11/30/2010 | | | | 21.09 | | | | (.02 | ) | | | 2.20 | | | | 2.18 | |

| | | | Year ended 11/30/2009 | | | | 14.63 | | | | (.03 | ) | | | 6.54 | | | | 6.51 | |

| | | | Year ended 11/30/2008 | | | | 29.05 | | | | .08 | | | | (12.12 | ) | | | (12.04 | ) |

| Class 529-C: | | | Six months ended 5/31/20134,5 | | | | 27.49 | | | | (.03 | ) | | | 5.12 | | | | 5.09 | |

| | | | Year ended 11/30/2012 | | | | 23.11 | | | | (.07 | ) | | | 4.45 | | | | 4.38 | |

| | | | Year ended 11/30/2011 | | | | 23.24 | | | | (.10 | ) | | | (.02 | ) | | | (.12 | ) |

| | | | Year ended 11/30/2010 | | | | 21.06 | | | | (.01 | ) | | | 2.19 | | | | 2.18 | |

| | | | Year ended 11/30/2009 | | | | 14.62 | | | | (.03 | ) | | | 6.53 | | | | 6.50 | |

| | | | Year ended 11/30/2008 | | | | 29.04 | | | | .09 | | | | (12.10 | ) | | | (12.01 | ) |

| Class 529-E: | | | Six months ended 5/31/20134,5 | | | | 28.35 | | | | .05 | | | | 5.28 | | | | 5.33 | |

| | | | Year ended 11/30/2012 | | | | 23.75 | | | | .07 | | | | 4.57 | | | | 4.64 | |

| | | | Year ended 11/30/2011 | | | | 23.85 | | | | .03 | | | | (.01 | ) | | | .02 | |

| | | | Year ended 11/30/2010 | | | | 21.57 | | | | .10 | | | | 2.24 | | | | 2.34 | |

| | | | Year ended 11/30/2009 | | | | 15.01 | | | | .06 | | | | 6.67 | | | | 6.73 | |

| | | | Year ended 11/30/2008 | | | | 29.71 | | | | .20 | | | | (12.39 | ) | | | (12.19 | ) |

| Dividends and distributions | | | | | | | | | | | | |

Dividends

(from net

investment

income) | | Distributions

(from capital

gains) | | Total

dividends

and

distributions | | Net asset

value, end

of period | | Total return2,3 | | Net assets,

end of

period

(in millions) | | Ratio of

expenses to

average net

assets before

waivers | | Ratio of

expenses to average net assets after waivers3 | | Ratio of net income (loss) to average net assets3 |

| $ | (.18 | ) | | $ | (.88 | ) | | $ | (1.06 | ) | | $ | 33.24 | | | | 19.60 | % | | $ | 7,194 | | | | .86 | %6 | | | .86 | %6 | | | .63 | %6 |

| | (.12 | ) | | | — | | | | (.12 | ) | | | 28.83 | | | | 20.02 | | | | 5,919 | | | | .87 | | | | .87 | | | | .59 | |

| | (.17 | ) | | | — | | | | (.17 | ) | | | 24.14 | | | | .31 | | | | 5,298 | | | | .85 | | | | .85 | | | | .45 | |

| | (.11 | ) | | | — | | | | (.11 | ) | | | 24.22 | | | | 11.34 | | | | 5,760 | | | | .86 | | | | .86 | | | | .78 | |

| | (.23 | ) | | | — | | | | (.23 | ) | | | 21.87 | | | | 45.88 | | | | 5,733 | | | | .95 | | | | .94 | | | | .67 | |

| | (.23 | ) | | | (2.36 | ) | | | (2.59 | ) | | | 15.22 | | | | (44.67 | ) | | | 4,237 | | | | .83 | | | | .79 | | | | 1.24 | |

| | — | | | | (.88 | ) | | | (.88 | ) | | | 31.66 | | | | 19.09 | | | | 51 | | | | 1.62 | 6 | | | 1.62 | 6 | | | (.13 | )6 |

| | — | | | | — | | | | — | | | | 27.45 | | | | 19.09 | | | | 50 | | | | 1.63 | | | | 1.63 | | | | (.19 | ) |

| | — | | | | — | | | | — | | | | 23.04 | | | | (.39 | ) | | | 62 | | | | 1.62 | | | | 1.62 | | | | (.34 | ) |

| | — | | | | — | | | | — | | | | 23.14 | | | | 10.45 | | | | 90 | | | | 1.64 | | | | 1.64 | | | | — | 8 |

| | (.03 | ) | | | — | | | | (.03 | ) | | | 20.95 | | | | 44.73 | | | | 117 | | | | 1.72 | | | | 1.71 | | | | (.09 | ) |

| | (.04 | ) | | | (2.36 | ) | | | (2.40 | ) | | | 14.50 | | | | (45.08 | ) | | | 100 | | | | 1.60 | | | | 1.56 | | | | .47 | |

| | — | | | | (.88 | ) | | | (.88 | ) | | | 31.30 | | | | 19.08 | | | | 246 | | | | 1.66 | 6 | | | 1.66 | 6 | | | (.16 | )6 |

| | — | | | | — | | | | — | | | | 27.15 | | | | 19.08 | | | | 186 | | | | 1.67 | | | | 1.67 | | | | (.22 | ) |

| | — | | | | — | | | | — | | | | 22.80 | | | | (.47 | ) | | | 172 | | | | 1.63 | | | | 1.63 | | | | (.33 | ) |

| | (.01 | ) | | | — | | | | (.01 | ) | | | 22.90 | | | | 10.45 | | | | 188 | | | | 1.64 | | | | 1.64 | | | | .01 | |

| | (.06 | ) | | | — | | | | (.06 | ) | | | 20.75 | | | | 44.81 | | | | 182 | | | | 1.69 | | | | 1.68 | | | | (.09 | ) |

| | (.07 | ) | | | (2.36 | ) | | | (2.43 | ) | | | 14.39 | | | | (45.09 | ) | | | 113 | | | | 1.62 | | | | 1.58 | | | | .46 | |

| | (.16 | ) | | | (.88 | ) | | | (1.04 | ) | | | 33.29 | | | | 19.55 | | | | 235 | | | | .87 | 6 | | | .87 | 6 | | | .63 | 6 |

| | (.11 | ) | | | — | | | | (.11 | ) | | | 28.87 | | | | 20.03 | | | | 143 | | | | .86 | | | | .86 | | | | .61 | |

| | (.17 | ) | | | — | | | | (.17 | ) | | | 24.16 | | | | .33 | | | | 143 | | | | .85 | | | | .85 | | | | .44 | |

| | (.13 | ) | | | — | | | | (.13 | ) | | | 24.23 | | | | 11.32 | | | | 167 | | | | .86 | | | | .86 | | | | .77 | |

| | (.10 | ) | | | — | | | | (.10 | ) | | | 21.90 | | | | 45.93 | | | | 187 | | | | .91 | | | | .91 | | | | .66 | |

| | (.24 | ) | | | (2.36 | ) | | | (2.60 | ) | | | 15.11 | | | | (44.68 | ) | | | 188 | | | | .85 | | | | .81 | | | | 1.22 | |

| | (.27 | ) | | | (.88 | ) | | | (1.15 | ) | | | 33.23 | | | | 19.75 | | | | 162 | | | | .58 | 6 | | | .58 | 6 | | | .92 | 6 |

| | (.19 | ) | | | — | | | | (.19 | ) | | | 28.88 | | | | 20.35 | | | | 106 | | | | .59 | | | | .59 | | | | .87 | |

| | (.24 | ) | | | — | | | | (.24 | ) | | | 24.19 | | | | .58 | | | | 72 | | | | .59 | | | | .59 | | | | .72 | |

| | (.19 | ) | | | — | | | | (.19 | ) | | | 24.27 | | | | 11.63 | | | | 63 | | | | .59 | | | | .59 | | | | 1.06 | |

| | (.26 | ) | | | — | | | | (.26 | ) | | | 21.93 | | | | 46.33 | | | | 54 | | | | .62 | | | | .61 | | | | .69 | |

| | — | | | | — | | | | — | | | | 15.24 | | | | (32.63 | ) | | | 2 | | | | .21 | | | | .19 | | | | .37 | |

| | (.16 | ) | | | (.88 | ) | | | (1.04 | ) | | | 33.02 | | | | 19.54 | | | | 255 | | | | .94 | 6 | | | .94 | 6 | | | .56 | 6 |

| | (.12 | ) | | | — | | | | (.12 | ) | | | 28.65 | | | | 19.92 | | | | 197 | | | | .93 | | | | .93 | | | | .53 | |

| | (.18 | ) | | | — | | | | (.18 | ) | | | 24.00 | | | | .32 | | | | 156 | | | | .90 | | | | .90 | | | | .40 | |

| | (.11 | ) | | | — | | | | (.11 | ) | | | 24.10 | | | | 11.27 | | | | 135 | | | | .91 | | | | .91 | | | | .75 | |

| | (.23 | ) | | | — | | | | (.23 | ) | | | 21.77 | | | | 45.84 | | | | 110 | | | | .97 | | | | .97 | | | | .64 | |

| | (.22 | ) | | | (2.36 | ) | | | (2.58 | ) | | | 15.16 | | | | (44.68 | ) | | | 69 | | | | .87 | | | | .83 | | | | 1.22 | |

| | — | | | | (.88 | ) | | | (.88 | ) | | | 31.75 | | | | 19.03 | | | | 8 | | | | 1.74 | 6 | | | 1.74 | 6 | | | (.25 | )6 |

| | — | | | | — | | | | — | | | | 27.54 | | | | 18.96 | | | | 8 | | | | 1.75 | | | | 1.75 | | | | (.31 | ) |

| | — | | | | — | | | | — | | | | 23.15 | | | | (.52 | ) | | | 10 | | | | 1.72 | | | | 1.72 | | | | (.43 | ) |

| | — | | | | — | | | | — | | | | 23.27 | | | | 10.34 | | | | 13 | | | | 1.74 | | | | 1.74 | | | | (.10 | ) |

| | (.05 | ) | | | — | | | | (.05 | ) | | | 21.09 | | | | 44.65 | | | | 14 | | | | 1.80 | | | | 1.80 | | | | (.18 | ) |

| | (.02 | ) | | | (2.36 | ) | | | (2.38 | ) | | | 14.63 | | | | (45.14 | ) | | | 10 | | | | 1.71 | | | | 1.66 | | | | .38 | |

| | — | | | | (.88 | ) | | | (.88 | ) | | | 31.70 | | | | 19.06 | | | | 75 | | | | 1.73 | 6 | | | 1.73 | 6 | | | (.24 | )6 |

| | — | | | | — | | | | — | | | | 27.49 | | | | 18.95 | | | | 60 | | | | 1.74 | | | | 1.74 | | | | (.28 | ) |

| | (.01 | ) | | | — | | | | (.01 | ) | | | 23.11 | | | | (.53 | ) | | | 49 | | | | 1.71 | | | | 1.71 | | | | (.41 | ) |

| | — | | | | — | | | | — | | | | 23.24 | | | | 10.35 | | | | 44 | | | | 1.72 | | | | 1.72 | | | | (.07 | ) |

| | (.06 | ) | | | — | | | | (.06 | ) | | | 21.06 | | | | 44.71 | | | | 36 | | | | 1.79 | | | | 1.79 | | | | (.18 | ) |

| | (.05 | ) | | | (2.36 | ) | | | (2.41 | ) | | | 14.62 | | | | (45.15 | ) | | | 23 | | | | 1.70 | | | | 1.66 | | | | .39 | |

| | (.09 | ) | | | (.88 | ) | | | (.97 | ) | | | 32.71 | | | | 19.40 | | | | 13 | | | | 1.18 | 6 | | | 1.18 | 6 | | | .31 | %6 |

| | (.04 | ) | | | — | | | | (.04 | ) | | | 28.35 | | | | 19.59 | | | | 10 | | | | 1.20 | | | | 1.20 | | | | .26 | |

| | (.12 | ) | | | — | | | | (.12 | ) | | | 23.75 | | | | — | 8 | | | 8 | | | | 1.19 | | | | 1.19 | | | | .11 | |

| | (.06 | ) | | | — | | | | (.06 | ) | | | 23.85 | | | | 10.93 | | | | 7 | | | | 1.21 | | | | 1.21 | | | | .44 | |

| | (.17 | ) | | | — | | | | (.17 | ) | | | 21.57 | | | | 45.45 | | | | 6 | | | | 1.28 | | | | 1.27 | | | | .34 | |

| | (.15 | ) | | | (2.36 | ) | | | (2.51 | ) | | | 15.01 | | | | (44.86 | ) | | | 4 | | | | 1.19 | | | | 1.15 | | | | .90 | |

| See footnotes on page 25. | The New Economy Fund | 23 |

Financial highlights (continued)

| | | | | Income (loss) from investment operations1 | |

| | | | | Net asset

value,

beginning

of period | | Net

investment

income

(loss) | | Net gains

(losses) on

securities

(both realized

and unrealized) | | Total from

investment

operations |

| Class 529-F-1: | | | Six months ended 5/31/20134,5 | | | $ | 28.65 | | | $ | .12 | | | $ | 5.32 | | | $ | 5.44 | |

| | | | Year ended 11/30/2012 | | | | 24.01 | | | | .19 | | | | 4.62 | | | | 4.81 | |

| | | | Year ended 11/30/2011 | | | | 24.09 | | | | .16 | | | | (.03 | ) | | | .13 | |

| | | | Year ended 11/30/2010 | | | | 21.77 | | | | .21 | | | | 2.27 | | | | 2.48 | |

| | | | Year ended 11/30/2009 | | | | 15.17 | | | | .15 | | | | 6.73 | | | | 6.88 | |

| | | | Year ended 11/30/2008 | | | | 30.00 | | | | .32 | | | | (12.52 | ) | | | (12.20 | ) |

| Class R-1: | | | Six months ended 5/31/20134,5 | | | | 27.72 | | | | (.01 | ) | | | 5.17 | | | | 5.16 | |

| | | | Year ended 11/30/2012 | | | | 23.27 | | | | (.04 | ) | | | 4.49 | | | | 4.45 | |

| | | | Year ended 11/30/2011 | | | | 23.39 | | | | (.08 | ) | | | (.01 | ) | | | (.09 | ) |

| | | | Year ended 11/30/2010 | | | | 21.20 | | | | .01 | | | | 2.21 | | | | 2.22 | |

| | | | Year ended 11/30/2009 | | | | 14.71 | | | | (.01 | ) | | | 6.57 | | | | 6.56 | |

| | | | Year ended 11/30/2008 | | | | 29.22 | | | | .11 | | | | (12.18 | ) | | | (12.07 | ) |

| Class R-2: | | | Six months ended 5/31/20134,5 | | | | 27.84 | | | | (.01 | ) | | | 5.19 | | | | 5.18 | |

| | | | Year ended 11/30/2012 | | | | 23.37 | | | | (.05 | ) | | | 4.52 | | | | 4.47 | |

| | | | Year ended 11/30/2011 | | | | 23.47 | | | | (.08 | ) | | | (.02 | ) | | | (.10 | ) |

| | | | Year ended 11/30/2010 | | | | 21.26 | | | | — | 7 | | | 2.21 | | | | 2.21 | |

| | | | Year ended 11/30/2009 | | | | 14.76 | | | | (.03 | ) | | | 6.59 | | | | 6.56 | |

| | | | Year ended 11/30/2008 | | | | 29.30 | | | | .08 | | | | (12.22 | ) | | | (12.14 | ) |

| Class R-3: | | | Six months ended 5/31/20134,5 | | | | 28.38 | | | | .05 | | | | 5.29 | | | | 5.34 | |

| | | | Year ended 11/30/2012 | | | | 23.77 | | | | .07 | | | | 4.58 | | | | 4.65 | |

| | | | Year ended 11/30/2011 | | | | 23.87 | | | | .03 | | | | (.02 | ) | | | .01 | |

| | | | Year ended 11/30/2010 | | | | 21.58 | | | | .11 | | | | 2.25 | | | | 2.36 | |

| | | | Year ended 11/30/2009 | | | | 15.01 | | | | .07 | | | | 6.67 | | | | 6.74 | |

| | | | Year ended 11/30/2008 | | | | 29.72 | | | | .21 | | | | (12.40 | ) | | | (12.19 | ) |