As filed with the Securities and Exchange Commission on January 5, 2023

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-03802

NEUBERGER BERMAN INCOME FUNDS

(Exact Name of Registrant as specified in charter)

c/o Neuberger Berman Investment Advisers LLC

1290 Avenue of the Americas

New York, New York 10104-0002

(Address of Principal Executive Offices – Zip Code)

Joseph V. Amato

Chief Executive Officer and President

Neuberger Berman Income Funds

c/o Neuberger Berman Investment Advisers LLC

1290 Avenue of the Americas

New York, New York 10104-0002

Lori L. Schneider, Esq.

K&L Gates LLP

1601 K Street, N.W.

Washington, D.C. 20006-1600

(Names and Addresses of agents for service)

Registrant's telephone number, including area code: (212) 476-8800

Date of fiscal year end: October 31

Date of reporting period: October 31, 2022

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940, as amended (“Act”) (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-1090. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Report to Shareholders.

(a) Following is a copy of the annual report transmitted to shareholders pursuant to Rule 30e-1 under the Act.

Neuberger Berman

Income Funds

| |

| |

Institutional Class Shares | |

| |

|

Emerging Markets Debt Fund |

Floating Rate Income Fund |

|

Municipal High Income Fund |

|

Municipal Intermediate Bond Fund |

|

|

Annual Report

October 31, 2022

The "Neuberger Berman" name and logo and "Neuberger Berman Investment Advisers LLC" name are registered service marks of Neuberger Berman Group LLC. The individual Fund names in this piece are either service marks or registered service marks of Neuberger Berman Investment Advisers LLC, an affiliate of Neuberger Berman BD LLC, distributor, member FINRA. ©2022 Neuberger Berman BD LLC, distributor. All rights reserved.

President’s Letter

Dear Shareholder,

I am pleased to present this annual shareholder report for the Neuberger Berman Income Funds covering the fiscal year ended October 31, 2022 (the reporting period).

It was an extremely challenging period in the fixed income market during the reporting period. Sharply rising and persistent inflation was a major factor impacting the market. The U.S. Federal Reserve Board (Fed) initially thought rising prices were transitory and they would come down as COVID-driven supply chain bottlenecks eased. However, these issues continued, labor markets and consumer demand remained robust, and the impact from the war in Ukraine created a "perfect storm," pushing inflation in the U.S. to a new 40-year high.

This caused the Fed to pivot from its highly accommodative monetary policy that was in place to support the economy during the pandemic, to an aggressively tightening policy in an attempt to rein in inflation. The Fed first raised interest rates in March 2022 from a range between 0.00% to 0.25% to a range between 0.25% to 0.50%. With inflation moving steadily higher, the central bank increased the magnitude of its rate hikes at its meetings in May and June and maintained its aggressive 0.75% (75 basis point) hikes in July, September and early November (after the reporting period ended). With the last increase, the Fed funds rate moved to a range between 3.75% and 4.00% and the Fed expects to continue raising rates "until the job is done."

Turning to the fixed income market, with short- and long-term U.S. Treasury yields moving sharply higher, bond prices declined (yields and bond prices move in the opposite direction). Meanwhile, credit spreads significantly widened due to increased investor risk aversion and the Fed’s rate hikes. All told, the broad taxable investment-grade bond market, as measured by the Bloomberg U.S. Aggregate Bond Index, returned -15.68% during the reporting period. The high yield and tax-free bond markets were also negatively impacted by rising rates.

Looking ahead, we believe inflation will moderate in 2023. That said, this will require the Fed to remain vigilant. In particular, we anticipate the central bank to continue to raise rates and leave them higher for longer to ensure inflation remains under control. While we anticipate volatility in fixed income and interest rates markets for some time to come, we believe yields are beginning to look attractive across a growing swath of the fixed income markets as a potential source of both income and diversification. That said, we believe active portfolio management can be valuable to help navigate the factors impacting the markets, and to seek out attractive relative-value opportunities.

Thank you for your support and trust. We look forward to continue serving your investment needs in the years to come.

Sincerely,

Joseph V. Amato

President and CEO

Neuberger Berman Income Funds

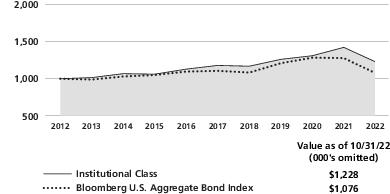

Core Bond Fund Commentary (Unaudited)

Neuberger Berman Core Bond Fund Institutional Class delivered a -16.37% total return for the fiscal year ended October 31, 2022 (the reporting period) and underperformed its benchmark, the Bloomberg U.S. Aggregate Bond Index (the Index), which returned -15.68% for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The fixed income market generated weak results during the reporting period. Whereas the U.S. Federal Reserve Board (Fed) initially characterized rising inflation as being "transitory," this was not the case. Monetary and fiscal policy support provided in earlier periods in response to COVID-19, robust labor markets and consumer spending, supply chain bottlenecks, repercussions from the war in Ukraine, and other factors pushed U.S. inflation to a 40-year high. Against this backdrop, the Fed began an aggressive rate hike campaign in March 2022 to subdue rapidly rising inflation, even if to the detriment of economic growth. Rising yields dragged down fixed income market performance, as yields and bond prices moved in the opposite direction. Meanwhile, U.S. credit spreads significantly widened due to periods of risk aversion and the Fed’s monetary tightening campaign.

In terms of relative performance, sector allocations to non-agency mortgage-backed securities (MBS), commercial mortgage-backed securities (CMBS), U.S. Treasuries and U.S. Treasury Inflation-Protected Securities as well as security selection in investment-grade credit were notable detractors from the Fund’s results. This was partly offset by positive contributions from an underweight exposure to investment-grade credit and security selection within non-agency MBS. In a period of heightened interest rate volatility, the Fund’s interest rate positioning contributed to relative performance, particularly an underweight duration exposure and positioning for a flatter yield curve at times during the reporting period.

There were several adjustments made to the Fund during the reporting period. We increased the Fund’s exposure to investment-grade credit, collateralized loan obligations (CLOs) and asset-backed securities (ABS), and we reduced exposure to U.S. Treasuries and CMBS. At the end of the reporting period, the Fund was overweight in a diversified mix of securitized sectors—including ABS, CMBS, non-agency residential MBS, CLOs, and agency MBS—balanced by underweight exposure in U.S. Treasuries.

The Fund’s use of futures contracts contributed positively to performance during the reporting period.

Looking ahead, while we have conviction that U.S. inflation will head lower for much of next year, we believe it will take continued effort by the Fed. In our view, the central bank is likely to be conservative in leaving rates higher for longer in order to avoid a "double-dip" rise in inflation, as occurred in the 1970s; we believe it will likely look for a convincing decline in inflation before starting to cut rates. We believe inflation and central bank policy should continue to drive market behavior. We anticipate further tightening by developed market central banks, counterbalanced by the potential for slower tightening by emerging markets, which began their tightening cycles much earlier. In our view, this, in turn, is likely to result in a general upward trend in yields. We believe this environment is well suited to active management given the array of macro events and the opportunities that can arise during periods of elevated volatility.

Sincerely,

Thanos Bardas, David M. Brown, Nathan Kush and Brad Tank

Portfolio Managers

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund’s portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

Core Bond Fund (Unaudited)

PORTFOLIO BY INVESTMENT TYPE |

(as a % of Total Net Assets) |

| |

| |

Foreign Government Securities | |

Mortgage-Backed Securities | |

U.S. Government Agency Securities | |

U.S. Treasury Obligations | |

| |

Liabilities Less Other Assets | |

| |

| Includes the impact of the Fund's open positions in derivatives, if any. |

PERFORMANCE HIGHLIGHTS1,2 | | | |

| | Average Annual Total Return

Ended 10/31/2022 |

| | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | |

| | | | | |

| | | | | |

| | | | | |

Bloomberg U.S. Aggregate Bond Index5,6 | | | | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For current performance data, including current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("NBIA") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by NBIA) will decrease the class’s returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2022, the 30-day SEC yields were 4.28%, 4.69%, 4.28%, 3.52% and 4.79% for Investor Class, Institutional Class, Class A, Class C and Class R6 shares, respectively. Absent expense reimbursements and/or fee waivers, the 30-day SEC yields would have been 4.09%, 4.62%, 4.24%, 3.47% and 4.72% for Investor Class, Institutional Class, Class A, Class C and Class R6 shares, respectively.

As stated in the Fund’s most recent prospectus, the total annual operating expense ratios for fiscal year 2021 were 0.88%, 0.43%, 0.80%, 1.57% and 0.33% for Investor Class, Institutional Class, Class A, Class C and Class R6 shares, respectively (before expense reimbursements and/or fee waivers, if any, and after restatement). The expense ratios were 0.79%, 0.39%, 0.79%, 1.54% and 0.29% for Investor Class, Institutional Class, Class A, Class C and Class R6 shares, respectively, after expense reimbursements and/or fee waivers and restatement. The expense ratios for the annual period ended October 31, 2022, can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

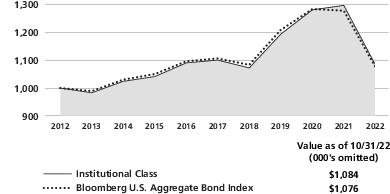

Core Bond Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund’s inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

Emerging Markets Debt Fund Commentary (Unaudited)

Neuberger Berman Emerging Markets Debt Fund Institutional Class generated a -21.48% total return for the fiscal year ended October 31, 2022 (the reporting period), and underperformed its benchmark, a blend consisting of 50% J.P. Morgan Government Bond Index—Emerging Markets (GBI-EM) Global Diversified, 25% J.P. Morgan Emerging Markets Bond Index (EMBI®)—Global Diversified, and 25% J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI)—Diversified (collectively, the Index), which delivered a -20.89% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

For the reporting period, emerging markets (EM) debt experienced a negative shock from Russia’s invasion of Ukraine and then the subsequent rate hiking cycle initiated by the U.S. Federal Reserve Board (Fed) ultimately leading to negative performance across the asset class. The hard currency sovereign debt index (J.P. Morgan EMBI Global Diversified) delivered a -24.19% total return, the corporate debt index (J.P. Morgan CEMBI Diversified) delivered -18.89%, and the local currency index (J.P. Morgan GBI-EM Global Diversified) returned -20.27%.

This was an extremely turbulent period for EM which experienced the resurgence of COVID-19, Russia’s invasion of Ukraine, persistently high inflation, the specter of rising interest rates, and the strengthening dollar. The more transmissible Omicron variant of COVID-19 led to renewed restrictions in multiple countries over the winter and carried into the spring. The largest impact to growth was seen in China where its zero-Covid policy remained in place. In February 2022, Russia’s invasion of Ukraine and consequent sanctions isolated significant parts of Russia’s economy and its financial markets. As a result, EM saw a major risk-off move. Throughout the reporting period, fixed income markets saw continued headwinds from high inflation, with the U.S. consumer price index peaking at 9.1% in June 2022. In late 2021, the Fed announced that it would be tapering asset purchases while also considering rate hikes, which came to fruition in March 2022. With inflation prints persistently higher, the hiking cycle is expected to continue through the year end which the Fed reiterated at Jackson Hole in August, and, at the end of the reporting period, our Fed funds rate expectations were as high as 4.6% for the year ending 2023. The European Central Bank (ECB) also raised rates and signaled it will continue hiking as inflation has soared in the region. As such we saw a sharp rise in core rates, as well as a new multi-decade high for the U.S. dollar index.

The primary driver of relative performance early during the reporting period was the underweight exposure to Russia leading up to its invasion of Ukraine across the portfolio. During the reporting period, the underlying hard currency sovereign sleeves detracted from performance, while corporates and local currency contributed to performance. In hard currency country selection, our overweight allocations to frontier and high yielding countries, including positioning in distressed and defaulted countries such as Ghana, Sri Lanka, Ukraine, and Ecuador detracted the most. The absence from Pakistan and Belarus was positive. In instrument selection, our positioning in euro-denominated Romanian sovereign debt was the negative driver. Within corporates, country allocation, and the overweight exposure to Mexico, Brazil and Peru versus the Index was positive while underweight exposure to investment grade Asian countries detracted. Security selection in China detracted due to exposure to the property sector, which faced significant stress resulting in ongoing defaults. The Fund’s local currency sleeve outperformed the Index over the reporting period, driven mainly by rates positioning, though foreign currency (FX) positioning was also positive. The main contributors in rates, in addition to the underweight exposure to Russia, included underweight duration exposure in Poland and Turkey and a long duration exposure in Egypt. Detractors in rates included the underweight in Hungary and exposure to front-end Brazil and Mexico duration given upward pressures on yields amid Fed hawkishness. On the FX side, active positioning throughout the reporting period was additive. The primary contributors were underweights to the Chinese renminbi and an overweight to the Egyptian pound until the devaluation in October when we moved to take off the overweight. Detractors included frontier exposures in Kazakhstan and Ghana.

The contribution from tactical allocation was neutral over the reporting period. The short U.S. interest rate duration position and a credit default swap index (CDX) position that we held to potentially mitigate against the higher risk profile of the strategy were additive. However, the overweight exposure to hard currency sovereigns

relative to the Index was negative even though the neutral position in corporates and the underweight to local currency in favor of cash which were positive.

The Fund’s aggregate use of futures, forward foreign currency, and swap contracts detracted from performance during the reporting period.

Over the reporting period there were a number of changes across the Fund’s portfolio within the tactical asset allocation as well as the underlying sub-asset classes. The Fund partially exited its Russian positions across the portfolio as market conditions permitted.

Within the tactical asset allocation, the Fund started the reporting period with an underweight to hard and local currency while holding a 4% cash position. We deployed cash to move to an overweight position in hard currency in November 2021 and moved back to a neutral position in September 2022. We shifted to a neutral allocation to corporates in March which we have since maintained. The underweight to local currency has been steady throughout. We have also actively traded a basket of currencies and a CDX position in the tactical asset allocation overlay. Finally, we had an interest rate duration underweight through July when we moved to a neutral position.

Within hard currency sovereigns, as of the end of the reporting period we maintained an overweight in the high yield (HY) segment of the market, biased toward BBs, as we believe that the spread widening in the EM HY space has been excessive and exacerbated by a trend of strong outflows from the asset class coupled with below-average levels of trading liquidity. In terms of changes over the reporting period, we increased exposure to Egypt as it remains under an International Monetary Fund (IMF) agreement. We also increased exposure to the Dominican Republic and Panama. We reduced exposure to countries where we have seen valuations tighten, including Costa Rica and Croatia. We also reduced exposure to countries where we believe the fundamentals continue to deteriorate, such as Turkey and Colombia.

In corporate positioning, we actively participated in the new issuance market, though activity was much more limited during the reporting period as issuers adapted to the rising rate environment. Aside from partially exiting Russia, the largest shift in the space was to reduce exposure in China property as the sector faced a series of defaults and limited policy support for offshore issuance. Ancillary to this, we reduced gaming exposure in Macau as China’s zero-Covid policy continued to weigh on tourism and gaming activity. We also reduced exposure in Turkey as the country’s fundamentals have created headwinds for the corporates operating in the country. We added to the Middle East and Latin America. By sector we increased exposure to the utilities and financials sectors while reducing exposure to real estate and metals & mining.

On the local currency side, we maintained a cautious risk stance over the reporting period. Our key overweights in rates include Mexico and Brazil, where we see inflation peaking and central banks that have finished or are near finishing their hiking cycles. Meanwhile, we are underweight in predominately lower yielding countries that have lagged with tightening cycles, particularly in Asia. We stay cautious on EM currencies though given growth pressures and vulnerability to deteriorating current accounts. The FX beta1 exposure is hovering near neutral in the Fund, as it has most of the reporting period, as we focus primarily on relative value positioning across currencies.

EM economies continue to face significant risks from slowing global growth, tighter financial conditions, the zero-Covid policy in China and the fallout of the war in Ukraine. Mitigating these risks, many EM central banks have been proactively raising rates, creating buffers for some time ahead, while IMF engagement by different EM countries support funding needs and reform agendas. While rising U.S. rates have been a major headwind for EM debt returns over the past year, we believe that this factor should pose a more limited downside risk going forward given the sizable rate hikes that are now behind us, and the further rises priced in for the next year.

Sincerely,

Rob Drijkoningen, Gorky Urquieta, Bart Van der Made, Raoul Luttik,

Jennifer Gorgoll, Vera Kartseva and Nish Popat

Portfolio Co-Managers

1 Beta is a measure of the systematic risk of a portfolio. It is the covariance of the portfolio and a market index divided by the variance of the market index. Beta measures the historical sensitivity of a portfolio's returns to movements in the market index. The beta of the market index will always be one. A portfolio with a beta above the market index (i.e., ˃1) means that the portfolio has greater volatility than the market index. If the beta of the portfolio is 1.2, a market increase in return of 1% implies a 1.2% increase in the portfolio's return. If the beta of the portfolio is 0.8, a market decrease in return of 1% implies a 0.8% decrease in the portfolio's return.

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund’s portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

Emerging Markets Debt Fund (Unaudited)

| | |

| | Average Annual Total Return

Ended 10/31/2022 |

| | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | |

| | | | |

| | | | |

| | | | |

| | | |

*

Blended Benchmark is composed of 50% J.P. Morgan Government Bond Index—Emerging Markets (GBI-EM) Global Diversified, 25% J.P. Morgan Emerging Markets Bond Index (EMBI)—Global Diversified, and 25% J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI)—Diversified, and is rebalanced monthly.

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For current performance data, including current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("NBIA") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by NBIA) will decrease the class’s returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2022, the 30-day SEC yields were 8.47%, 8.10% and 7.33% for Institutional Class, Class A and Class C shares, respectively. Absent expense reimbursements and/or fee waivers, the 30-day SEC yields would have been 8.18%, 7.66% and 7.01% for Institutional Class, Class A and Class C shares, respectively.

As stated in the Fund’s most recent prospectus, the total annual operating expense ratios for fiscal year 2021 were 0.96%, 1.39% and 2.12% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.79%, 1.16% and 1.91% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended October 31, 2022, can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

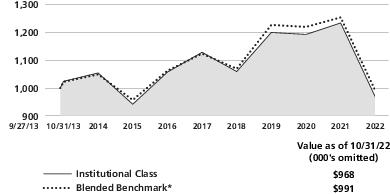

Emerging Markets Debt Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund’s inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

*

Blended benchmark is composed of 50% J.P. Morgan Government Bond Index (GBI)—Emerging Markets Global Diversified, 25% J.P. Morgan Emerging Markets Bond Index (EMBI)—Global Diversified, and 25% J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI)—Diversified, and is rebalanced monthly.

Floating Rate Income Fund Commentary (Unaudited)

Neuberger Berman Floating Rate Income Fund Institutional Class generated a -2.96% total return for the fiscal year ended October 31, 2022 (the reporting period) and underperformed its benchmark, the Morningstar LSTA US Leveraged Loan Index* (the Index), which provided a -1.78% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

While the senior floating rate bank loan market saw negative returns during the reporting period, the drawdowns were much less pronounced than other fixed income categories given the short duration and floating rate nature of the asset class, which acts as an inflation hedge. Whereas the U.S. Federal Reserve Board (Fed) initially characterized rising inflation as being "transitory," this was not the case. Higher inflation cut into real growth as robust consumer spending, supply chain bottlenecks, a tight labor market, repercussions from the war in Ukraine, and other factors combined to push U.S. inflation to a 40-year high. Against this backdrop, the Fed began an aggressive rate hike campaign in March 2022, which is expected to continue until inflation is under control. Weighted average bid prices on the loan market declined over the period due to risk aversion and concerns over rising recession odds.

The Fund tactically adjusted its position in non-floating rate securities during the reporting period. We have the flexibility to allocate up to 20% of the portfolio to these securities, usually fixed-rate senior bonds. Relative value between floating rate loans and fixed-rate bonds fluctuated given the heightened volatility and wider high yield bond credit spreads. Against this backdrop, the Fund's non-floating rate allocation ended the reporting period at approximately 7.3% of net assets compared to 5.4% of net assets at the beginning of the reporting period.

In terms of the Fund's portfolio credit quality, security selection within B and CCC and below rated issuers were the best performers. Conversely, an underweight to and security selection within BB, an underweight to and security selection within BBB, and an overweight to CCC and below and B rated issuers versus the Index were the worst performers.

The Fund’s use of swap contracts detracted from performance during the reporting period.

From a sector perspective, security selection within and an underweight to software, security selection within entertainment, and security selection within and an underweight to retailers were the best performers. In contrast, security selection within information technology services, security selection within and an overweight to health care, and security selection within and an underweight to electronics (technology) versus the Index were the worst performers.

Looking ahead, we believe current floating rate loan valuations offer investors an attractive opportunity, especially given our below average default outlook. While the tightening of financial conditions, still-elevated inflation and challenging news out of Europe have been creating incremental volatility, real growth is slowing but still positive with supply chains returning back to normal. We see these factors acting to mitigate inflationary pressures, which could eventually lead to a less aggressive path for Fed policy. In our view, healthy consumer and business balance sheets, growing nominal gross domestic product and solid job growth should remain supportive for issuer fundamentals. While inventories are building as a result of slowing demand, we remain focused on sector dynamics and idiosyncratic risks to individual issuers. Despite short-term volatility resulting from heightened uncertainty in commodity prices, central bank tightening and negative news flow out of Europe, we believe our bottom-up, fundamental credit research that focuses on security selection, avoiding credit deterioration, and putting only our "best ideas" into portfolios, will position us well to take advantage of the increased volatility.

Sincerely,

Joseph P. Lynch and Stephen J. Casey

Portfolio Managers

*Neuberger Berman Floating Rate Income Fund’s benchmark was renamed from S&P/LSTA Leveraged Loan Index to Morningstar LSTA US Leveraged Loan Index effective 8/29/2022.

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund’s portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

The loan ratings noted above represent segments of the Morningstar LSTA US Leveraged Loan Index, which are determined based on the ratings issued by S&P Global.

Floating Rate Income Fund (Unaudited)

PORTFOLIO BY MATURITY DISTRIBUTION |

(as a % of Total Investments*) |

| |

One to less than Five Years | |

Five to less than Ten Years | |

| |

| |

| |

| Does not include Short-Term Investments or the impact of the Fund’s open positions in derivatives, if any. |

| |

| | | |

| | Average Annual Total Return

Ended 10/31/2022 |

| | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | |

| | | | | |

| | | | | |

| | | | | |

Morningstar LSTA US Leveraged Loan Index*5 ,6 | | | | |

*

Effective August 29, 2022, the S&P/LSTA Leveraged Loan Index changed its name to Morningstar LSTA US Leveraged Loan Index.

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For current performance data, including current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("NBIA") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by NBIA) will decrease the class’s returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2022, the 30-day SEC yields were 7.50%, 7.12% and 6.36% for Institutional Class, Class A and Class C shares, respectively. Absent expense reimbursements and/or fee waivers, the 30-day SEC yields would have been 7.37%, 6.97% and 6.23% for Institutional Class, Class A and Class C shares, respectively.

As stated in the Fund’s most recent prospectus, the total annual operating expense ratios for fiscal year 2021 were 0.79%, 1.19% and 1.93% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any, and after restatement). The expense ratios were 0.61%, 0.98% and 1.73% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers and restatement. The expense ratios for the annual period ended October 31, 2022, can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

Floating Rate Income Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund’s inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

*

Effective August 29, 2022, the S&P/LSTA Leveraged Loan Index changed its name to Morningstar LSTA US Leveraged Loan Index.

High Income Bond Fund Commentary (Unaudited)

Neuberger Berman High Income Bond Fund Investor Class generated a -11.62% total return for the fiscal year ended October 31, 2022 (the reporting period), underperforming its benchmark, the ICE BofA U.S. High Yield Constrained Index (the Index), which provided a -11.45% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The overall high yield market, as measured by the Index, generated weak results during the reporting period. Whereas the U.S. Federal Reserve Board (Fed) initially characterized rising inflation as being "transitory," this was not the case. Robust consumer spending, supply chain bottlenecks, a tight labor market, repercussions from the war in Ukraine, and other factors combined to push U.S. inflation to a 40-year high. Against this backdrop, the Fed began an aggressive rate hike campaign in March 2022, which is expected to continue until inflation is under control, even if it potentially leads to a recession. U.S. credit spreads significantly widened due to periods of risk aversion and the Fed’s monetary tightening campaign.

From a sector perspective, security selection within and an overweight versus the Index to gas distribution, security selection within and an underweight to health care, and security selection within diversified financial services were the top performers. In contrast, security selection within technology & electronics and real estate & homebuilders, and security selection within and an underweight to energy were the worst performers.

In terms of the Fund's portfolio credit quality, security selection within BB and an overweight to non-rated and B rated issuers were the best performers. Conversely, an overweight to CCC and below, security selection within B, and security selection within and an underweight to BBB and above rated issuers versus the Index were the worst performers.

The Fund’s use of swap contracts detracted from performance during the reporting period.

As it became increasingly clear that the Fed would have to become more aggressive with tightening monetary policy, we selectively increased the Fund’s exposure to shorter duration BB and B rated issuers, while reducing exposure to CCC and below rated issuers. As credit spreads widened over the reporting period, we subsequently looked to decrease the Fund’s exposure to higher beta1 (risk) issuers, particularly in the CCC and below credit tier.

Looking ahead, we believe current high yield valuations offer investors an attractive opportunity, especially given our below average default outlook. While the tightening of financial conditions, still-elevated inflation and challenging news out of Europe have been creating incremental volatility, real growth is slowing but still positive, with supply chains returning back to normal. We see these factors acting to mitigate inflationary pressures, which could eventually lead to a less aggressive path for Fed policy. In our view, healthy consumer and business balance sheets, growing nominal gross domestic product and solid job growth should remain supportive for issuer fundamentals. While inventories are building as a result of slowing demand, we remain focused on sector dynamics and idiosyncratic risks to individual issuers. Despite short-term volatility resulting from heightened uncertainty in commodity prices, central bank tightening and negative news flow out of Europe, we believe our bottom-up, fundamental credit research that focuses on security selection, avoiding credit deterioration, and putting only our "best ideas" into portfolios, will position us well to take advantage of the increased volatility.

Sincerely,

Joe Lind and Christopher Kocinski

Portfolio Co-Managers

1 Beta is a measure of the systematic risk of a portfolio. It is the covariance of the portfolio and a market index divided by the variance of the market index. Beta measures the historical sensitivity of a portfolio's returns to movements in the market index. The beta of the market index will always be one. A portfolio with a beta above the market index (i.e. ˃1) means that the portfolio has greater volatility than the market index. If the beta of the portfolio is 1.2, a market increase in return of 1% implies a 1.2% increase in the portfolio's return. If the beta of the portfolio is 0.8, a market decrease in return of 1% implies a 0.8% decrease in the portfolio's return.

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund’s portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

The performance of certain rated bonds within the benchmark, as noted above, represent issues that are rated Ba1/BB+ through Ba3/BB-, B1/B+ through B3/B- and Caa1/CCC+ or lower, based on an average of Moody’s, S&P and Fitch, as calculated by ICE BofA. Issues rated Baa3/BBB- and higher are not in the Index.

High Income Bond Fund (Unaudited)

PORTFOLIO BY MATURITY DISTRIBUTION |

(as a % of Total Investments*) |

| |

One to less than Five Years | |

Five to less than Ten Years | |

| |

| |

| Does not include Short-Term Investments or the impact of the Fund’s open positions in derivatives, if any. |

PERFORMANCE HIGHLIGHTS8,9 | | | |

| | Average Annual Total Return

Ended 10/31/2022 |

| | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | |

| | | | | |

| | | | | |

| | | | | |

ICE BofA U.S. High Yield Constrained Index5,6 | | | | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For current performance data, including current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("NBIA") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by NBIA) will decrease the class’s returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2022, the 30-day SEC yields were 8.10%, 8.26%, 7.93%, 7.10%, 7.60%, 8.36% and 8.76% for Investor Class, Institutional Class, Class A, Class C, Class R3, Class R6 and Class E shares, respectively. Absent repayments, the 30-day SEC yield would have been 7.86% for Class A shares.

As stated in the Fund’s most recent prospectus, the total annual operating expense ratios for fiscal year 2021 were 0.85%, 0.69%, 1.13%, 1.83%, 1.33% and 0.59% for Investor Class, Institutional Class, Class A, Class C, Class R3 and Class R6 shares, respectively, and the estimated total annual operating expense ratio for fiscal year 2022 is 0.55% for Class E (before expense reimbursements and/or fee waivers, if any). The total annual operating expense ratio for Class A includes the class’s repayment of expenses previously reimbursed and/or fees previously waived under the contractual expense limitation by NBIA. The estimated expense ratio for fiscal year 2022 is 0.07% for Class E after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended October 31, 2022, can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

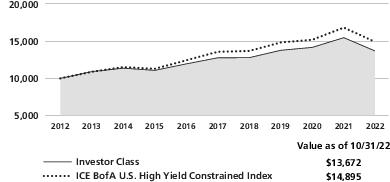

High Income Bond Fund (Unaudited)

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund’s inception if it has not operated for 10 years. The graph is based on the Investor Class shares only; the performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

Municipal High Income Fund Commentary (Unaudited)

Neuberger Berman Municipal High Income Fund Institutional Class generated a -16.80% total return for the fiscal year ended October 31, 2022 (the reporting period) and underperformed its benchmark, a blend consisting of 65% Bloomberg Municipal Bond Index and 35% Bloomberg Municipal High Yield Index (collectively, the Index), which provided a -13.56% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The investment-grade municipal bond market generated weak results but outperformed the taxable bond market during the reporting period. All told, the Bloomberg Municipal Bond Index returned -11.98% for the reporting period, whereas the overall taxable investment-grade bond market, as measured by the Bloomberg U.S. Aggregate Bond Index, returned -15.68%. Whereas the U.S. Federal Reserve Board (Fed) initially characterized rising inflation as being "transitory," this was not the case. Robust consumer spending, supply chain bottlenecks, repercussions from the war in Ukraine, and other factors combined to push U.S. inflation to a 40-year high. Against this backdrop, the Fed began an aggressive rate hike campaign in March 2022, which is expected to continue until inflation is under control, even if it potentially leads to a recession. Rising yields dragged down fixed income market performance, as yields and bond prices moved in the opposite direction.

In terms of the Fund’s performance, having a slightly longer duration than the Index detracted from returns as interest rates moved sharply higher. An overweight to lower coupon/longer duration bonds versus the Index was also a headwind for results. A significant overweight to bonds rated BBB was also detrimental, as these higher yielding securities underperformed. On the upside, security selection in the housing sector contributed to returns.

In terms of portfolio changes during the reporting period, the Fund’s exposure to securities rated AAA was decreased, whereas its allocation to securities rated A was increased. Meanwhile, we increased the Fund’s duration over the reporting period.

Looking ahead, we anticipate market volatility to remain elevated until there is more clarity on the economic outlook. From a supply/demand perspective, municipal mutual fund outflows reached record highs during the reporting period, as the Fed raises rates in an attempt to rein in inflation. Meanwhile, municipal supply remains lower than in 2021 and new issuance tends to be lighter as we near the end of the year. While municipal credit fundamentals have generally peaked in our view, for the most part, we believe issuers are cushioned with solid balance sheets. In addition, we believe stronger cash positions should help mitigate losses as economic growth moderates. We continue to be cautious in terms of our duration positioning but believe higher yields and volatility create a favorable backdrop to deploy cash and capitalize on attractively valued securities.

Sincerely,

James L. Iselin, S. Blake Miller and Eric J. Pelio

Portfolio Managers

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund’s portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

The bond ratings noted above represent segments of the Bloomberg Municipal Bond Index and Bloomberg Municipal High Yield Index, which are determined based on the average ratings issued by S&P Global, Moody’s and Fitch.

Municipal High Income Fund (Unaudited)

PORTFOLIO BY STATE AND TERRITORY |

(as a % of Total Net Assets) |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

Other Assets Less Liabilities | |

| |

| Includes the impact of the Fund's open positions in derivatives, if any. |

| | |

| | Average Annual Total Return

Ended 10/31/2022 |

| | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | |

| | | | |

| | | | |

| | | | |

| | | |

*

Blended benchmark is composed of 65% Bloomberg Municipal Bond Index and 35% Bloomberg Municipal High Yield Index and is rebalanced monthly.

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For current performance data, including current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("NBIA") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by NBIA) will decrease the class’s returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2022, the 30-day SEC yields were 4.03%, 3.66% and 2.89% for Institutional Class, Class A and Class C shares, respectively. The tax-equivalent yields were 6.81%, 6.18% and 4.88% for Institutional Class, Class A and Class C shares, respectively, for a shareholder in the highest federal income tax bracket (37% plus 3.8% Medicare contribution tax).13 Absent expense reimbursements and/or fee waivers, the 30-day SEC yields would have been 3.69%, 1.25% and -16.38% for Institutional Class, Class A and Class C shares, respectively. A negative 30-day SEC yield results when a fund’s accrued expenses exceed its income for the relevant period. Please note, in such instances the 30-day SEC yield may not equal the Fund’s actual rate of income earned and distributed by the Fund and, therefore, a per share distribution may still be paid to shareholders.

As stated in the Fund’s most recent prospectus, the total annual operating expense ratios for fiscal year 2021 were 0.79%, 1.21% and 2.02% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.52%, 0.89% and 1.64% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended October 31, 2022, can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

Municipal High Income Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund’s inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

*

Blended benchmark is composed of 65% Bloomberg Municipal Bond Index and 35% Bloomberg Municipal High Yield Index and is rebalanced monthly.

Municipal Impact Fund Commentary (Unaudited)

Neuberger Berman Municipal Impact Fund Institutional Class generated a -10.88% total return for the fiscal year ended October 31, 2022 (the reporting period) and outperformed its benchmark, the Bloomberg Municipal Bond Index (the Index), which provided a -11.98% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The investment-grade municipal bond market generated weak results but outperformed the taxable bond market during the reporting period. All told, the Index returned -11.98% for the reporting period, whereas the overall taxable investment-grade bond market, as measured by the Bloomberg U.S. Aggregate Bond Index, returned -15.68%. Whereas the U.S. Federal Reserve Board (Fed) initially characterized rising inflation as being "transitory," this was not the case. Robust consumer spending, supply chain bottlenecks, repercussions from the war in Ukraine, and other factors combined to push U.S. inflation to a 40-year high. Against this backdrop, the Fed began an aggressive rate hike campaign in March 2022, which is expected to continue until inflation is under control, even if it potentially leads to a recession. Rising yields dragged down fixed income market performance, as yields and bond prices moved in the opposite direction.

Looking at the Fund’s performance, having a shorter duration than the Index contributed to relative returns as interest rates moved sharply higher during the reporting period.

An underweight to securities rated BBB versus the Index was additive for performance, as was security selection of these bonds that we did own. On the downside, security selection of revenue bonds detracted from results. An overweight to securities issued by the state of Michigan was also a headwind for performance.

In terms of adjustments to the portfolio during the reporting period, we extended the Fund’s duration, but remained shorter than the Index. We also increased the Fund’s allocation to securities rated BBB during the reporting period. As always, the Fund maintained its exposure to what we believed were projects that were impactful for their communities. We also continued to focus on sustainable issuers with what we view as having best-in-class operations, with managements that make sound financial decisions.

Looking ahead, we anticipate market volatility to remain elevated until there is more clarity on the economic outlook. From a supply/demand perspective, municipal mutual fund outflows reached record highs during the reporting period, as the Fed raises rates in an attempt to rein in inflation. Meanwhile, municipal supply remains lower than in 2021 and new issuance tends to be lighter as we near the end of the year. While municipal credit fundamentals have generally peaked in our view, for the most part, we believe issuers are cushioned with solid balance sheets. In addition, we believe stronger cash positions should help mitigate losses as economic growth moderates. We continue to be cautious in terms of our duration positioning but believe higher yields and volatility create a favorable backdrop to deploy cash and capitalize on attractively valued securities.

Sincerely,

James L. Iselin, S. Blake Miller, James Lyman and Jeffrey Hunn

Portfolio Managers

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund’s portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

The bond ratings noted above represent segments of the Bloomberg Municipal Bond Index, which are determined based on the average ratings issued by S&P Global, Moody’s and Fitch.

Municipal Impact Fund (Unaudited)

PORTFOLIO BY STATE AND TERRITORY |

(as a % of Total Net Assets) |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

Other Assets Less Liabilities | |

| |

| Includes the impact of the Fund’s open positions in derivatives, if any. |

PERFORMANCE HIGHLIGHTS12,14 | | |

| | Average Annual Total Return

Ended 10/31/2022 |

| | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | |

| | | | |

| | | | |

| | | | |

Bloomberg Municipal Bond Index5,6 | | | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For current performance data, including current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("NBIA") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by NBIA) will decrease the class’s returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2022, the 30-day SEC yields were 2.84%, 2.47% and 1.72% for Institutional Class, Class A and Class C shares, respectively. The tax-equivalent yields were 4.80%, 4.17% and 2.91% for Institutional Class, Class A and Class C shares, respectively, for a shareholder in the highest federal income tax bracket (37% plus 3.8% Medicare contribution tax).13 Absent expense reimbursements and/or fee waivers, the 30-day SEC yields would have been 2.37%, -11.88% and -13.54% for Institutional Class, Class A and Class C shares, respectively. A negative 30-day SEC yield results when a fund’s accrued expenses exceed its income for the relevant period. Please note, in such instances the 30-day SEC yield may not equal the Fund’s actual rate of income earned and distributed by the Fund and, therefore, a per share distribution may still be paid to shareholders.

As stated in the Fund’s most recent prospectus, the total annual operating expense ratios for fiscal year 2021 were 0.84%, 1.43%, and 2.22% for Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.43%, 0.80% and 1.55% for Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended October 31, 2022, can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

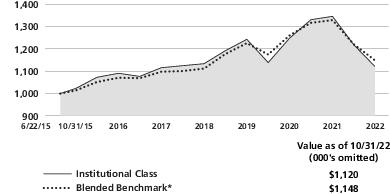

Municipal Impact Fund (Unaudited)

COMPARISON OF A $1,000,000 INVESTMENT

(000's omitted)

This graph shows the change in value of a hypothetical $1,000,000 investment in the Fund over the past 10 fiscal years, or since the Fund’s inception if it has not operated for 10 years. The graph is based on the Institutional Class shares only; the performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

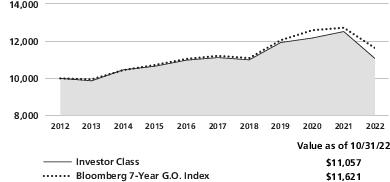

Municipal Intermediate Bond Fund Commentary (Unaudited)

Neuberger Berman Municipal Intermediate Bond Fund Investor Class generated a -11.66% total return for the fiscal year ended October 31, 2022 (the reporting period) and underperformed its benchmark, the Bloomberg 7-Year General Obligation (G.O.) Index (the Index), which provided a -8.64% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The investment-grade municipal bond market generated weak results but outperformed the taxable bond market during the reporting period. All told, the Bloomberg Municipal Bond Index returned -11.98% for the reporting period, whereas the overall taxable investment-grade bond market, as measured by the Bloomberg U.S. Aggregate Bond Index, returned -15.68%. Whereas the U.S. Federal Reserve Board (Fed) initially characterized rising inflation as being "transitory," this was not the case. Robust consumer spending, supply chain bottlenecks, repercussions from the war in Ukraine, and other factors combined to push U.S. inflation to a 40-year high. Against this backdrop, the Fed began an aggressive rate hike campaign in March 2022, which is expected to continue until inflation is under control, even if it potentially leads to a recession. Rising yields dragged down fixed income market performance, as yields and bond prices moved in the opposite direction.

In terms of the Fund’s performance, having a slightly longer duration than the Index detracted from returns as interest rates moved sharply higher. An overweight to lower coupon/longer duration bonds versus the Index was also a headwind for results. An out-of-benchmark allocation to certain revenue bonds was not rewarded, as they underperformed their general obligation bond counterparts. However, allocations to the electric and industrial revenue sectors were additive for returns. An overweight exposure to bonds rated BBB was also detrimental, as these higher yielding securities underperformed. Finally, an overweight to securities issued by the state of New York contributed to performance.

In terms of portfolio changes during the reporting period, the Fund’s exposure to securities rated AAA was decreased, whereas its allocation to securities rated A was increased. Duration was managed in a fairly tight band during the reporting period.

Looking ahead, we anticipate market volatility to remain elevated until there is more clarity on the economic outlook. From a supply/demand perspective, municipal mutual fund outflows reached record highs during the reporting period, as the Fed raises rates in an attempt to rein in inflation. Meanwhile, municipal supply remains lower than in 2021 and new issuance tends to be lighter as we near the end of the year. While municipal credit fundamentals have generally peaked in our view, for the most part, we believe issuers are cushioned with solid balance sheets. In addition, we believe stronger cash positions should help mitigate losses as economic growth moderates. We continue to be cautious in terms of our duration positioning but believe higher yields and volatility create a favorable backdrop to deploy cash and capitalize on attractively valued securities.

Sincerely,

James L. Iselin and S. Blake Miller

Portfolio Managers

Information about principal risks of investing in the Fund is set forth in the prospectus and statement of additional information.

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund’s portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

The bond ratings noted above represent segments of the Bloomberg 7-Year General Obligation (G.O.) Index, which are determined based on the average ratings issued by S&P Global, Moody’s and Fitch.

Municipal Intermediate Bond Fund (Unaudited)

PORTFOLIO BY STATE AND TERRITORY |

(as a % of Total Net Assets) |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

Other Assets Less Liabilities | |

| |

| Includes the impact of the Fund's open positions in derivatives, if any. |

| | | |

| | Average Annual Total Return

Ended 10/31/2022 |

| | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | |

| | | | | |

| | | | | |

| | | | | |

Bloomberg 7-Year G.O. Index5,6 | | | | |

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For current performance data, including current to the most recent month-end, please visit www.nb.com/performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares.

The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("NBIA") had not reimbursed certain expenses and/or waived a portion of the investment management fees during certain of the periods shown. Repayment by a class (of expenses previously reimbursed and/or fees previously waived by NBIA) will decrease the class’s returns. Please see Note B in the Notes to Financial Statements for specific information regarding expense reimbursement and/or fee waiver arrangements.

For the period ended October 31, 2022, the 30-day SEC yields were 3.10%, 3.25%, 2.88% and 2.12% for Investor Class, Institutional Class, Class A and Class C shares, respectively. The tax-equivalent yields were 5.24%, 5.49%, 4.86% and 3.58% for Investor Class, Institutional Class, Class A and Class C shares, respectively, for a shareholder in the highest federal income tax bracket (37% plus 3.8% Medicare contribution tax).13 Absent expense reimbursements and/or fee waivers, the 30-day SEC yields would have been 2.73%, 3.09%, 1.84% and -1.74% for Investor Class, Institutional Class, Class A and Class C shares, respectively. A negative 30-day SEC yield results when a fund’s accrued expenses exceed its income for the relevant period. Please note, in such instances the 30-day SEC yield may not equal the Fund’s actual rate of income earned and distributed by the Fund and, therefore, a per share distribution may still be paid to shareholders.

As stated in the Fund’s most recent prospectus, the total annual operating expense ratios for fiscal year 2021 were 0.60%, 0.44%, 0.82% and 1.58% for Investor Class, Institutional Class, Class A and Class C shares, respectively (before expense reimbursements and/or fee waivers, if any). The expense ratios were 0.45%, 0.30%, 0.67% and 1.42% for Investor Class, Institutional Class, Class A and Class C shares, respectively, after expense reimbursements and/or fee waivers. The expense ratios for the annual period ended October 31, 2022, can be found in the Financial Highlights section of this report.

Returns shown with a sales charge reflect the deduction of the current maximum initial sales charge of 4.25% for Class A shares and the contingent deferred sales charge (CDSC) for Class C shares. The CDSC for Class C shares is 1.00%, which is reduced to 0% after 1 year. The performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses. Please see the prospectus for more information about sales charge structures, if any, and class expenses for your share class.

Municipal Intermediate Bond Fund (Unaudited)

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years, or since the Fund’s inception if it has not operated for 10 years. The graph is based on the Investor Class shares only; the performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses (see Performance Highlights chart on previous page). The result is compared with benchmarks, which include a broad-based market index and may include a more narrowly based index. Market indices have not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a shareholder would pay on Fund distributions or on the redemption of Fund shares. Results represent past performance and do not indicate future results.

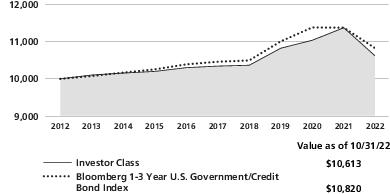

Short Duration Bond Fund Commentary (Unaudited)

Neuberger Berman Short Duration Bond Fund Investor Class generated a -6.70% total return for the fiscal year ended October 31, 2022 (the reporting period) and underperformed its benchmark, the Bloomberg 1-3 Year U.S. Government/Credit Bond Index (the Index), which provided a -4.88% total return for the same period. (Performance for all share classes is provided in the table immediately following this letter.)

The fixed income market generated weak results during the reporting period. The U.S. Federal Reserve Board (Fed) initially characterized rising inflation as being "transitory," however this was not the case. Robust consumer spending, supply chain bottlenecks, repercussions from the war in Ukraine, and other factors combined to push U.S. inflation to a 40-year high. Against this backdrop, the Fed began an aggressive rate hike campaign in March 2022, which is expected to continue until inflation is under control, even if it potentially leads to a recession. Rising yields dragged down fixed income market performance, as yields and bond prices moved in the opposite direction. Meanwhile, U.S. credit spreads significantly widened due to periods of risk aversion and the Fed’s monetary tightening campaign.

The largest detractor from the Fund’s performance during the reporting period was its exposure to corporate bonds. Their spreads widened due to their duration, interest rate sensitivity and periods of investor risk aversion, not because of significantly weakening corporate fundamentals, in our view. Elsewhere, the allocation to structured products, including commercial mortgage-backed securities (CMBS), mortgage credit and collateralized loan obligations (CLO), were headwinds for results. Futures contracts were used to manage the Fund’s overall duration positioning. On the upside, having a modestly short duration versus the Index was a small contributor to relative performance as interest rates moved sharply higher.

The Fund’s use of futures and swap contracts detracted from performance during the reporting period.

We maintained the Fund’s overall positioning over the reporting period, focusing on a diversified mix of non-Treasury spread sectors. During the second half of the reporting period, we trimmed our allocations to CMBS and credit risk transfer securities. The proceeds were then largely redeployed into CLOs, agency pass-through securities and asset-backed securities.