OMB APPROVAL

OMB Number: 3235-0570

Expires: July 31, 2022

Estimated average burden hours per response...20.6

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4815

Ultra Series Fund

(Exact name of registrant as specified in charter)

550 Science Drive, Madison, WI 53711

(Address of principal executive offices)(Zip code)

Steven J. Fredricks

Chief Legal Officer & Chief Compliance Officer

550 Science Drive

Madison, WI 53711

(Name and address of agent for service)

Registrant's telephone number, including area code: 608-274-0300

Date of fiscal year end: December 31

Date of reporting period: December 31, 2019

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Certified Financial Statement

Annual Report

December 31, 2019

ULTRA SERIES FUND

Conservative Allocation Fund

Moderate Allocation Fund

Aggressive Allocation Fund

Core Bond Fund

High Income Fund

Diversified Income Fund

Large Cap Value Fund

Large Cap Growth Fund

Mid Cap Fund

International Stock Fund

Madison Target Retirement 2020 Fund

Madison Target Retirement 2030 Fund

Madison Target Retirement 2040 Fund

Madison Target Retirement 2050 Fund

Beginning January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, the insurance company that offers your contract may determine that it will no longer send you paper copies of the fund’s shareholder reports like this one, unless you specifically request paper copies from the insurance company or your financial intermediary. Instead, the shareholder reports will be made available on a website and the insurance company will notify you by mail each time a report is posted and provide you with a website link to access the report. Instructions for requesting paper copies will be provided by your insurance company or financial intermediary.

If you have already elected to receive shareholder reports electronically, you will not be affected by this change and do not need to take any action. If your insurance company or financial intermediary offers electronic delivery, you may elect to receive shareholder reports and other communications from the insurance company or financial intermediary by following the instructions provided by the insurance company or financial intermediary.

You may elect to receive paper copies of all future reports free of charge from the insurance company or financial intermediary. You can inform the insurance company or financial intermediary that you wish to continue receiving paper copies of your shareholder reports by contacting your insurance company or financial intermediary. Your election to receive reports in paper will apply to all funds held in your account with your insurance company or financial intermediary.

Ultra Series Fund | December 31, 2019

| Table of Contents |

| Page | |

| Management’s Discussion of Fund Performance | |

| Period in Review | 2 |

| Allocation Funds | 3 |

| Conservative Allocation Fund | 3 |

| Moderate Allocation Fund | 4 |

| Aggressive Allocation Fund | 5 |

| Core Bond Fund | 6 |

| High Income Fund | 7 |

| Diversified Income Fund | 8 |

| Large Cap Value Fund | 10 |

| Large Cap Growth Fund | 11 |

| Mid Cap Fund | 12 |

| International Stock Fund | 13 |

| Madison Target Retirement 2020 Fund | 15 |

| Madison Target Retirement 2030 Fund | 16 |

| Madison Target Retirement 2040 Fund | 17 |

| Madison Target Retirement 2050 Fund | 18 |

| Notes to Management’s Discussion of Fund Performance | 20 |

| Portfolios of Investments | |

| Conservative Allocation Fund | 23 |

| Moderate Allocation Fund | 24 |

| Aggressive Allocation Fund | 25 |

| Core Bond Fund | 26 |

| High Income Fund | 30 |

| Diversified Income Fund | 32 |

| Large Cap Value Fund | 37 |

| Large Cap Growth Fund | 38 |

| Mid Cap Fund | 39 |

| International Stock Fund | 40 |

| Madison Target Retirement 2020 Fund | 42 |

| Madison Target Retirement 2030 Fund | 42 |

| Madison Target Retirement 2040 Fund | 43 |

| Madison Target Retirement 2050 Fund | 43 |

| Financial Statements | |

| Statements of Assets and Liabilities | 44 |

| Statements of Operations | 46 |

| Statements of Changes in Net Assets | 49 |

| Financial Highlights for a Share of Beneficial Interest Outstanding | 56 |

| Notes to Financial Statements | 70 |

| Report of Independent Registered Public Accounting Firm | 86 |

| Other Information | 87 |

| Trustees and Officers | 93 |

Nondeposit investment products are not federally insured, involve investment risk, may lose value and are not obligations of or guaranteed by any financial institution. For more complete information about Ultra Series Fund, including charges and expenses, request a prospectus from your financial advisor or from CMFG Life Insurance Company, 2000 Heritage Way, Waverly, IA 50677. Consider the investment objectives, risks, and charges and expenses of any fund carefully before investing. The prospectus contains this and other information about the investment company. For more current Ultra Series Fund performance information, please call 1-800-SEC-0330. Current performance may be lower or higher than the performance data quoted within this report. Past performance does not guarantee future results. Nothing in this report represents a recommendation of a security by the investment adviser. Portfolio holdings may have changed since the date of this report.

| 1 |

Ultra Series Fund | December 31, 2019

Management’s Discussion of Fund Performance (unaudited)

PERIOD IN REVIEW

It’s said that people love surprises, although this adage clearly didn’t emerge from surveys of stock market investors. That said, this past year has proved to be the exception, having produced little but positive surprises for investors. This in the face of the wide conviction that the days of rampant stock market advances were behind us, or at least not in our immediate future. We ended 2018 with a falling market. Even as the market recovered in the first half of 2019, the gains appeared fragile. When the yield curve inverted for a short period this past summer (short-term bonds yielding more than long-term bonds) talk of recession was rampant. Stocks ignored the warning behind a reversal in Federal Reserve (Fed) tightening and went on to make another steady move upwards through the end of the year.

All of which is to say that one result that was not predicted for 2019 was a stunning S&P 500® return of 31.49%. If you went back ten years to the fading memory of the Great Recession, the prospect of 13%-plus annualized returns over the ensuing decade would have sounded Pollyanish. But that’s exactly what we have booked, with the S&P 500 rising more than 400% from its 2009 lows. And let’s not leave bond investors out of discussion: the Barclays Aggregate Bond Index was up 8.7% for the year, a result that would have seemed unlikely given Fed policy and the historically low interest rate environment in January when the 10-year Treasury yield was hovering around 2.7%.

U.S. stock market returns were strong across the board, with growth outperforming value and large and mid-cap stocks outperforming smaller stocks. Sector returns were dispersed, but above 20% for the year for all but the single-digit trailing Energy Sector, while the Technology Sector led the way with more than a 40% return. Diversified portfolios were destined for solid results.

As much fun as it is to recap 2019, it’s likely that the more pressing concern for investors in general, and readers of this letter specifically, is what to expect going forward and how to prepare for it. When we look back to those terrifying days on the brink of financial collapse in 2008 and 2009, we are oddly enough spanning what is the longest bull market in U.S. history. By standard measures, stock valuations are generally stretched, and the prospects of any significant acceleration in the earnings denominator of P/E ratios seems dim.

Yet the market advance has been supported by data and Fed policy, with three rate cuts in 2019. Traditional employment measures look as strong as ever and consumer confidence has remained high. Pushing in the opposite direction are the dampening effects of the international trade war. Internationally, central banks continue to have the pedal to the metal, with negative rates now standard.

It seems trite to predict that next year will be different than the last, but we know that when we write this letter a year from now an election will be behind us. That in itself will engender an added layer of uncertainty to 2020, and we know that the markets hate uncertainty. In short, we encourage investors to be prepared for some volatility and considerably more modest stock and bond returns. These are conditions which we believe will increase risk awareness among investors in general, an attitude which we retain in all seasons. Stressed markets generally inspire investors to look for companies with strong fundamentals and stability of earnings, qualities which are already criteria for the stocks held in your portfolio. A steady hand will likely be needed by all – a lesson exemplified by the trying times that began this trailing ten years of capital expansion.

| 2 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

ALLOCATION FUNDS

The Ultra Series Conservative Allocation, Moderate Allocation and Aggressive Allocation Funds (collectively, the “Target Allocation Funds”) invest primarily in shares of registered investment companies (the “Underlying Funds”). The Target Allocation Funds are diversified among a number of asset classes and their allocation among Underlying Funds is based on an asset allocation model developed by Madison Asset Management, LLC (“Madison”), the Funds’ investment adviser. The team may use multiple analytical approaches to determine the appropriate asset allocation, including:

| • | Asset allocation optimization analysis – considers the degree to which returns in different asset classes do or do not move together, and the Funds’ aim to achieve a favorable overall risk profile for any targeted portfolio return. |

| • | Scenario analysis– historical and expected return data is analyzed to model how individual asset classes and combinations of asset classes would affect the Funds under different economic and market conditions. |

| • | Fundamental analysis– draws upon Madison’s investment teams to judge each asset class against current and forecasted market conditions. Economic, industry and security analysis is used to develop return and risk expectations that may influence asset class selection. In addition, Madison has a flexible mandate which permits the Funds, at the sole discretion of Madison, to materially reduce equity risk exposures when and if conditions are deemed to warrant such an action. |

CONSERVATIVE ALLOCATION FUND

INVESTMENT STRATEGY HIGHLIGHTS

Under normal circumstances, the Ultra Series Conservative Allocation Fund’s total net assets will be allocated among various asset classes and Underlying Funds, including those whose shares trade on a stock exchange (exchange traded funds or “ETFs”), with target allocations over time of approximately 35% equity investments and 65% fixed income investments. Underlying Funds in which the Fund invests may include funds advised by Madison and/or its affiliates, including the Madison Funds (the “Affiliated Underlying Funds”). Generally, Madison will not invest more than 75% of the Fund’s net assets, at the time of purchase, in Affiliated Underlying Funds.

PERFORMANCE

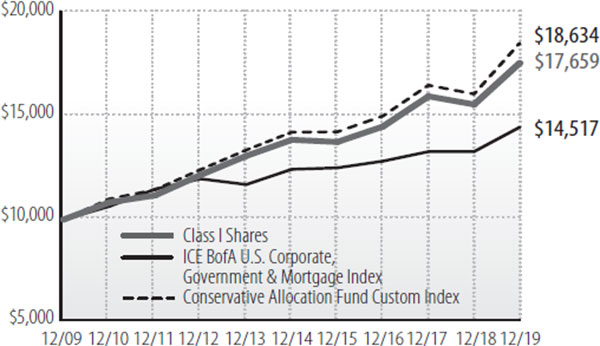

Cumulative Performance of $10,000 Investment1,2

The Ultra Series Conservative Allocation Fund (Class I) returned 12.97% for the year, compared to its Custom Blended Index of 15.44%. The Fund’s Morningstar Allocation 30% to 50% Equity peer group returned 15.26%.

In absolute terms, the Fund had a very good year, though it lagged the stated benchmark. Our concerns over deteriorating market fundamentals and slowing economic data led us to position the Fund defensively. Accordingly, the Fund’s underweight to equities proved to be the biggest detractor to relative performance in 2019’s liquidity driven market. The Fund benefited from a couple key positive asset allocation decisions, notably our overweight allocation to U.S. technology stocks and our bias for larger capitalization stocks versus smaller companies. Positions in longer-duration fixed income investments also contributed positively as interest rates declined.

Returns across nearly all asset classes soared in 2019. U.S. stocks (S&P 500® Index) returned 31.5%, foreign developed markets stocks (MSCI EAFE Index) advanced 22.0%, emerging markets equities (MSCI EM Index) jumped 18.4%, and even bonds (Bloomberg Barclays U.S. Aggregate Bond Index) produced an outsized 8.7% return for the year. The year’s strength was surprising given the backdrop of a global manufacturing recession, flat U.S. earnings growth and generally slowing economic data across the world. However, economic concerns were pushed aside, aided by a massive change in monetary policy provided by the Fed. At year-end 2018 the Fed believed they would need to continue hiking interest rates throughout 2019 but wound up cutting rates three times and expanded their balance sheet by roughly

| 3 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

$400 billion instead. Investors celebrated the Fed’s policy U-turn by pushing market valuations higher and higher.

Moving forward, we continue to be concerned by the disconnect between eroding fundamentals and a combination of overly bullish sentiment and elevated valuations. Risk assets appear to be discounting a very positive future despite an abundance of global policy uncertainty and meager economic growth prospects. Given this environment, we intend to remain cautiously positioned until we see a more favorable risk/reward trade-off for risk assets.

| Average Annual Total Return (%) through December 31, 20191,2 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Year | ||||||

| Ultra Series Conservative Allocation, Class I | 12.97 | 6.67 | 4.90 | 5.85 | |||||

| Ultra Series Conservative Allocation, Class II | 12.69 | 6.40 | 4.64 | 5.59 | |||||

| ICE BofA US Corp, Govt & Mortg Index | 8.96 | 4.14 | 3.11 | 3.80 | |||||

| Conservative Allocation Fund Custom Index | 15.44 | 7.34 | 5.47 | 6.42 | |||||

See accompanying Notes to Management’s Discussion of Fund Performance.

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||

| Bond Funds | 66.7 | % |

| Foreign Stock Funds | 5.1 | % |

| Short-Term Investments | 6.4 | % |

| Stock Funds | 24.8 | % |

| Net Other Assets and Liabilities | (3.0) | % |

MODERATE ALLOCATION FUND

INVESTMENT STRATEGY HIGHLIGHTS

Under normal circumstances, the Ultra Series Moderate Allocation Fund’s total net assets will be allocated among various asset classes and Underlying Funds, including those whose shares trade on a stock exchange (exchange traded funds or “ETFs”), with target allocations over time of approximately 60% equity investments and 40% fixed income investments. Underlying Funds in which the Fund invests may include Affiliated Underlying Funds. Generally, Madison will not invest more than 75% of the Fund’s net assets, at the time of purchase, in Affiliated Underlying Funds.

PERFORMANCE

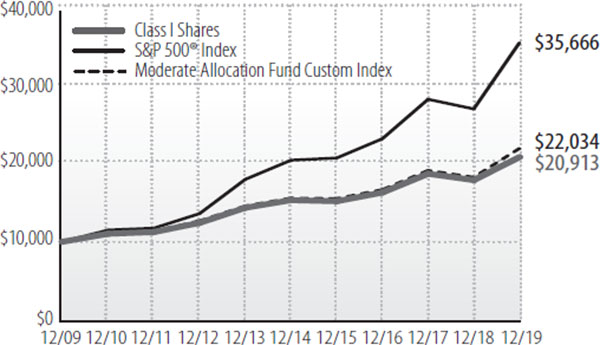

Cumulative Performance of $10,000 Investment1,2

The Ultra Series Moderate Allocation Fund (Class I) returned 16.56% for the year, compared to its Custom Blended Index of 20.29%. The Fund’s Morningstar Allocation 50% to 70% Equity peer group returned 19.04%.

In absolute terms, the Fund had a very good year, though it lagged the stated benchmark. Our concerns over deteriorating market fundamentals and slowing economic data led us to position the Fund defensively. Accordingly, the Fund’s underweight to equities proved to be the biggest detractor to relative performance in 2019’s liquidity driven market. Weak relative performance within the Fund’s core U.S. large cap holdings also weighed on the Fund’s return. The Fund benefited from a couple key positive asset allocation decisions, notably our overweight allocation to U.S technology stocks and our bias for larger capitalization stocks versus smaller companies.

Returns across nearly all asset classes soared in 2019. U.S. stocks (S&P 500® Index) returned 31.5%, foreign developed markets stocks (MSCI EAFE Index) advanced 22.0%, emerging markets equities (MSCI EM Index) jumped 18.4%, and even bonds (Bloomberg Barclays U.S. Aggregate Bond Index) produced an outsized 8.7% return for the year. The year’s strength was surprising given the backdrop of a global manufacturing recession, flat U.S. earnings growth and generally slowing economic data across the world. However, economic concerns were pushed aside, aided by a massive change in monetary policy provided by the Fed. At year-end 2018 the Fed believed they would need to continue hiking interest rates throughout 2019 but wound up cutting rates three times and expanded their balance sheet by roughly $400 billion instead. Investors celebrated the Fed’s policy U-turn by pushing market valuations higher and higher.

| 4 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

Moving forward, we continue to be concerned by the disconnect between eroding fundamentals and a combination of overly bullish sentiment and elevated valuations. Risk assets appear to be discounting a very positive future despite an abundance of global policy uncertainty and meager economic growth prospects. Given this environment, we intend to remain cautiously positioned until we see a more favorable risk/reward trade-off for risk assets.

| Average Annual Total Return (%) through December 31, 20191,2 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||

| Ultra Series Moderate Allocation, Class I | 16.56 | 8.57 | 6.36 | 7.66 | |||||

| Ultra Series Moderate Allocation, Class II | 16.27 | 8.30 | 6.10 | 7.39 | |||||

| S&P 500® Index | 31.49 | 15.27 | 11.70 | 13.56 | |||||

| Moderate Allocation Fund Custom Index | 20.29 | 9.65 | 7.11 | 8.22 | |||||

See accompanying Notes to Management’s Discussion of Fund Performance.

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||

| Bond Funds | 41.0 | % |

| Foreign Stock Funds | 9.5 | % |

| Short-Term Investments | 11.1 | % |

| Stock Funds | 41.8 | % |

| Net Other Assets and Liabilities | (3.4) | % |

AGGRESSIVE ALLOCATION FUND

INVESTMENT STRATEGY HIGHLIGHTS

Under normal circumstances, the Ultra Series Aggressive Allocation Fund’s total net assets will be allocated among various asset classes and Underlying Funds, including ETFs, with target allocations over time of approximately 80% equity investments and 20% fixed income investments. Underlying Funds in which the Fund invests may include Affiliated Underlying Funds. Generally, Madison will not invest more than 75% of Fund’s net assets, at the time of purchase, in Affiliated Underlying Funds.

PERFORMANCE

Cumulative Performance of $10,000 Investment1,2

The Ultra Series Aggressive Allocation Fund (Class I) returned 19.69% for the year, compared to its Custom Blended Index of 24.20%. The Fund’s Morningstar Allocation 70% to 85% Equity peer group returned 21.50%.

In absolute terms, the Fund had a very good year, though it lagged the stated benchmark. Our concerns over deteriorating market fundamentals and slowing economic data led us to position the Fund defensively. Accordingly, the Fund’s underweight to equities proved to be the biggest detractor to relative performance in 2019’s liquidity driven market. Weak relative performance within the Fund’s core U.S. large cap holdings and minimum volatility international position also weighed on the Fund’s return. The Fund benefited from a couple key positive asset allocation decisions, notably our overweight allocation to U.S technology stocks and our bias for larger capitalization stocks versus smaller companies.

Returns across nearly all asset classes soared in 2019. U.S. stocks (S&P 500® Index) returned 31.5%, foreign developed markets stocks (MSCI EAFE Index) advanced 22.0%, emerging markets equities (MSCI EM Index) jumped 18.4%, and even bonds (Bloomberg Barclays U.S. Aggregate Bond Index) produced an outsized 8.7% return for the year. The year’s strength was surprising given the backdrop of a global manufacturing recession, flat U.S. earnings growth and generally slowing economic data across the world. However, economic concerns were pushed aside, aided by a massive change in monetary policy provided by the Fed. At year-end 2018 the Fed believed they would need to continue hiking interest rates throughout 2019 but wound up cutting rates three times and expanded their balance sheet by roughly $400 billion instead. Investors celebrated the Fed’s policy U-turn by pushing market valuations higher and higher.

| 5 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

Moving forward, we continue to be concerned by the disconnect between eroding fundamentals and a combination of overly bullish sentiment and elevated valuations. Risk assets appear to be discounting a very positive future despite an abundance of global policy uncertainty and meager economic growth prospects. Given this environment, we intend to remain cautiously positioned until we see a more favorable risk/reward trade-off for risk assets.

| Average Annual Total Return (%) through December 31, 20191,2 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||

| Ultra Series Aggressive Allocation, Class I | 19.69 | 10.00 | 7.46 | 8.88 | |||||

| Ultra Series Aggressive Allocation, Class II | 19.39 | 9.73 | 7.19 | 8.61 | |||||

| S&P 500® Index | 31.49 | 15.27 | 11.70 | 13.56 | |||||

| Aggressive Allocation Fund Custom Index | 24.20 | 11.44 | 8.36 | 9.59 | |||||

See accompanying Notes to Management’s Discussion of Fund Performance.

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||

| Bond Funds | 21.4 | % |

| Foreign Stock Funds | 13.2 | % |

| Short-Term Investments | 13.8 | % |

| Stock Funds | 55.3 | % |

| Net Other Assets and Liabilities | (3.7) | % |

CORE BOND FUND

INVESTMENT STRATEGY HIGHLIGHTS

Under normal circumstances, the Ultra Series Core Bond Fund invests at least 80% of its net assets in bonds. To keep current income relatively stable and to limit share price volatility, the Fund emphasizes investment grade securities and maintains an intermediate (typically 3-7 year) average portfolio duration, with the goal of being between 85-115% of the market benchmark duration. The Fund also strives to add incremental return in the portfolio by making strategic decisions relating to credit risk, sector exposure and yield curve positioning. The Fund may invest in corporate debt securities, U.S. Government debt securities, foreign government debt securities, non-rated debt securities, and asset-backed, mortgage-backed and commercial mortgage-backed securities.

PERFORMANCE

Cumulative Performance of $10,000 Investment1

The Ultra Core Bond Fund (Class I) returned 8.36% for the one-year period, slightly trailing its benchmark Bloomberg Barclays U.S. Aggregate Bond Index, which returned 8.72%. The Fund’s benchmark Morningstar Intermediate Core Bond returned 8.68%.

The difference between an unmanaged, fee-free index and that of a managed fund, which has management and trading costs, is enough to explain this small performance gap with the Fund’s Index. However, the Fund varied from the index, and most likely many of its peers, in other important ways. The Fund’s overweight to securitized product relative to corporate bonds negatively impacted performance given the large performance difference between asset classes. Additionally, the Fund owned certain high-yield energy bonds which had sub-par performance during the year.

Both investment grade and high yield corporate bonds had strong performances in 2019. For the year, the Bloomberg Barclay’s U.S. Corporate Index had an excess return versus Treasuries of 6.76% (14.54% total return) while the Bloomberg Barclay’s U.S. High Yield Index had an excess return of 9.34% (14.32% total return). Strong fund flows, marginally better economic data and easing trade tensions all contributed to the strong performance of corporate bonds. Current corporate bond spreads over Treasuries are only 10 bps from the tights in early 2018. Given the strong performance in 2019, credit spreads have a limited path to move significantly tighter. Corporate fundamentals are also weak and at the rate corporations issue debt and buyback stock, they are unlikely to improve in the near-term.

With the strong rally in rates, securities have embedded prepayment risk, such as mortgages backed securities

| 6 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

(MBS), lagged other risk assets. For 2019, the Bloomberg Barclay’s U.S. MBS Fixed Rate Index had a total return 6.35% and an excess return versus Treasuries of 0.61%. The Fund has been slowly increasing its allocation to MBS as the relative value to corporate bonds becomes increasingly attractive. The movement of interest rates during 2019 was in sharp contrast to the experience in 2018. From November 2018 through year-end 2019, Treasury rates fell by a large amount. The two-year, ten-year and thirty-year Treasury yields fell 140, 132 and 104 basis points (1 basis point equals 0.01%), respectively. Lower inflation and trade tensions caused the Fed to fully reverse course during 2019 and cut the Federal Funds Rate three times.

The Fund was able to minimize the impact of sharply lower rates by keeping duration between 95% and 105% of the benchmark’s during 2019. The Fund was overweight long Treasury bonds, such as twenty and thirty-year Treasury bonds, which performed well over the last year.

As we look towards 2020, the Fund is currently neutral duration versus the index and plans to keep this positioning for the foreseeable future. The credit allocation was reduced in 2019 and replaced with agency MBS given relative value between the asset classes. The trend of selling credit to swap into a securitized product will continue into 2020. Finally, the Fund will continue to participate in the new issue corporate bond market where bonds offer value relative to existing bonds.

| Average Annual Total Return (%) through December 31, 20191 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||

| Ultra Series Core Bond, Class I | 8.36 | 3.55 | 2.62 | 3.16 | |||||

| Ultra Series Core Bond, Class II | 8.09 | 3.29 | 2.37 | 2.90 | |||||

| Bloomberg Barclays U.S. Aggregate Bond Index | 8.72 | 4.03 | 3.05 | 3.75 |

See accompanying Notes to Management’s Discussion of Fund Performance.

| SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||

| Asset Backed Securities | 4.1 | % |

| Collateralized Mortgage Obligations | 4.2 | % |

| Commercial Mortgage-Backed Securities | 1.8 | % |

| Corporate Notes and Bonds | 30.5 | % |

| Long Term Municipal Bonds | 2.2 | % |

| Mortgage Backed Securities | 25.9 | % |

| Short-Term Investments | 2.5 | % |

| U.S. Government and Agency Obligations | 28.1 | % |

| Net Other Assets and Liabilities | 0.7 | % |

HIGH INCOME FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series High Income Fund invests primarily in lower-rated, higher-yielding income bearing securities, such as “junk” bonds. Because the performance of these securities has historically been strongly influenced by economic conditions, the Fund may rotate securities selection by business sector according to the economic outlook. Under normal market conditions, the Fund invests at least 80% of its net assets in bonds rated lower than investment grade (BBB/Baa) and their unrated equivalents or other high-yielding securities.

PERFORMANCE

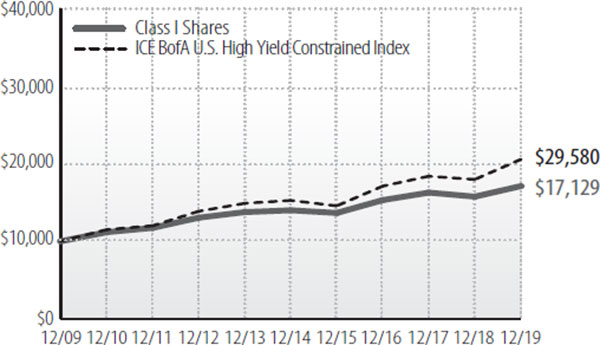

Cumulative Performance of $10,000 Investment1

The Ultra Series High Income Fund (Class I) returned 8.64% during the period, lagging its benchmark ICE BofA U.S. High Yield Constrained® Index’s 14.41% return. The Fund also trailed its Morningstar High Yield Bond peer group, which returned 14.27%.

Overall, the high-yield market experienced strong performance in 2019. We believe the result was due to several factors, including: 1) the potential for improved trade negotiations with China; 2) a strong new issue market for high-yield bonds, which allowed companies to refinance debt at very attractive coupons; 3) several interest rate cuts, which supported a rally in treasury bond prices and, thus, higher prices for high-yield bonds; and 4) solid company-specific fundamentals. As a result, the average spread-over-treasuries (or the additional yield investors receive from assets that carry greater risk than government bonds) ended the year at 372 basis points (1 basis point equals 0.01%), or 165 bps tighter than at the start of the year. This spread tightening continues to keep us cautious when adding new bonds to the portfolio given overall valuations.

| 7 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

Within the high-yield rating categories, higher-quality bonds outperformed during the year. BB-rated bonds (49% of the total market) outperformed with a 15.74% total return, while B-rated bonds (39.0% of the total market) were essentially in-line posting a total return of 14.26%. CCC-rated corporate bonds (12% of the total market) lagged the overall market with a total return of 9.56%. Importantly, however, we note that longer-dated bonds with 7-10 year maturities significantly outperformed similarly-rated 1-5 year maturities.

The Fund underperformed, in part, due to a conservatively high cash balance in a rising market and an overweight in short-duration bonds. On a sector level, the Fund had underexposure to the volatile Basic Industry and Energy Sectors, as well as to the Telecommunications Sector. The Fund was also negatively impacted by its bond selection within the Healthcare, Basic Industry, Energy and Services Sectors. Partially offsetting these negatives, the Fund had a positive contribution to performance from an overweight in the Capital Goods and Real Estate sectors. The Fund also benefited from bond selection in the Telecommunications Sector. As of December 31, 2019, the yield-to-worst of the Fund was 4.76% and the average rating within the Fund was B2.

The Fund will continue to emphasize BB-rated and B-rated corporate bonds. With the substantial spread tightening last year, we see little on the near-term horizon to drive further material price appreciation in the year ahead. Thus, we initially anticipate high yield’s total return to be in the low-single-digits in 2020. Our targeted total return factors in a fairly conservative fundamental view, as well as continued support by the Fed as it pertains to interest rate policy (we view the Fed’s decisions as a wildcard to the annual performance). Therefore, we anticipate a potential decline in bond prices will partially offset the positive return generated by coupon income. We intend to maintain our bias towards higher-quality credit and a relatively higher cash position.

| Average Annual Total Return (%) through December 31, 20191 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||

| Ultra Series High Income, Class I | 8.64 | 3.79 | 4.11 | 5.53 | |||||

| Ultra Series High Income, Class II | 8.36 | 3.53 | 3.85 | 5.27 | |||||

| ICE BofA U.S. High Yield Constrained Index | 14.41 | 6.32 | 6.14 | 7.48 |

See accompanying Notes to Management’s Discussion of Fund Performance.

| SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||||

| Bond Funds | 2.6 | % | ||

| Communication Services | 5.4 | % | ||

| Consumer Discretionary | 18.2 | % | ||

| Consumer Staples | 6.1 | % | ||

| Energy | 10.2 | % | ||

| Financials | 9.6 | % | ||

| Health Care | 7.6 | % | ||

| Industrials | 17.7 | % | ||

| Information Technology | 2.5 | % | ||

| Materials | 3.5 | % | ||

| Real Estate | 2.8 | % | ||

| Short-Term Investments | 6.2 | % | ||

| U.S. Treasury Bills | 5.4 | % | ||

| Utilities | 4.0 | % | ||

| Net Other Assets and Liabilities | (1.8) | % | ||

DIVERSIFIED INCOME FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Diversified Income Fund seeks income by investing in a broadly diversified array of securities including bonds, common stocks, real estate securities, foreign market bonds and stocks and money market instruments. Bonds, stock and cash components will vary, reflecting the portfolio managers’ judgments of the relative availability of attractively yielding and priced stocks and bonds; however, under normal market conditions, the Fund’s portfolio managers generally attempt to target a 40% bond and 60% stock investment allocation. Nevertheless, bonds (including investment grade, high yield and mortgage- or asset-backed) may constitute up to 80% of the Fund’s assets, stocks (including common stocks, preferred stocks and convertible bonds) may constitute up to 70% of the Fund’s assets, real estate securities may constitute up to 25% of the Fund’s assets, foreign (including American Depositary Receipts (“ADRs”) and emerging market) stocks and bonds may constitute up to 25% of the Fund’s assets, and money market instruments may constitute up to 25% of the Fund’s

| 8 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

assets. Although the Fund is permitted to invest up to 80% of its assets in lower credit quality bonds, under normal circumstances, the Fund intends to limit the investment in lower credit quality bonds to less than 50% of the Fund’s assets. The balance between the two strategies of the Fund (fixed income and equity investing) is determined after reviewing the risks associated with each type of investment, with the goal of meaningful risk reduction as market conditions demand.

PERFORMANCE

Cumulative Performance of $10,000 Investment1

The Ultra Series Diversified Income Fund had strong absolute gains from both the equity side and bond side of the portfolio. The Fund was up 19.68% (Class I) for the annual period. This slightly trailed the Fund’s customized index (50% stock index, 50% bond index) which returned 20.03%. Stocks, represented by the S&P 500® Index, were up 31.49%, while the broad bond market, represented by the ICE BofA U.S. Corporate, Government and Mortgage Index was up 8.96%. The Fund’s peer group, the Morningstar Allocation 50-70% Equity, was up 19.04%.

For the year the equity side of the Fund had solid returns, although did not keep pace with the S&P 500’s soaring return of 31.49%. Sector allocation and stock selection both detracted from performance. For sector allocation, an underweight position in Technology and overweight positions in Energy and Industrials negatively impacted results. In terms of stock selection, there were overall positive contributions from Consumer Staples, Materials and Utilities, which were more than offset by weakness in Technology, Financials, Communication Services and Industrials. Some of the best performing individual stocks were in Technology including software firm Microsoft (MSFT) which was the best performing stock in the portfolio, and management consulting company Accenture (ACN). Both firms reported earnings that exceeded expectations. The Fund reduced its position in Microsoft during the year as it no longer has an above-market yield. Within Industrials, other notable outperforming stocks were industrial distributor Fastenal (FAST) and diversified conglomerate United Technologies (UTX). Both companies reported better than expected sales and earnings. In Utilities, renewable power utility NextEra (NEE) was additive to results. The company generated solid growth from its investments in clean energy including wind and solar power. On the negative side, within Financials, exchange operator CME Group (CME) was the worst performing stock in the portfolio. Regional bank PNC Financial Services Group (PNC) also negatively impacted performance. The Fund sold both stocks. In Health Care, pharmaceutical firm Pfizer (PFE) detracted from results. It is in the process of making a transformational acquisition that will temporarily slow down its growth. We believe the thesis remains intact and that Pfizer remains well positioned long-term. Within Industrials, global conglomerate 3M (MMM) was a notable underperforming stock. It struggled with slower than expected growth and deteriorating margins. The Fund sold 3M as we believe the thesis was invalidated. Another notable underperforming stock was alcohol manufacturer Diageo (DEO). The Fund sold the stock to move proceeds into other areas of the market. The Fund continues to hold all stocks mentioned except for CME, Diageo, 3M and PNC.

The fixed income side of the portfolio was also positive for the past year. Over the past year, treasury yields fell sharply before rising again during the fourth quarter. The 10-year Treasury note which began the year at 2.68%, traded as low as 1.46% in early September before closing the year at 1.91%. Similarly, the 2-year Treasury note began the year at 2.49%, traded as low as 1.43% in early September and closed the year at 1.57%. Lower yields translated into positive returns for bond holders over the trailing 12 months. The Bloomberg/Barclays Aggregate Bond Index generated an 8.73% return for the year. For the annual period the fixed portion of the Madison Diversified income Fund outperformed before fees, returning 9.17% versus the ICE BofA U.S. Corporate, Government and Mortgage Index’s return of 8.96%. The Fund’s overweight to longer maturity Treasuries helped performance while the Fund’s allocation to securitized products was a detractor to performance given the relative underperformance versus corporate bonds. The

| 9 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

sharp move down in interest rates increased prepayment risks and widened spreads on mortgage backed securities (MBS).

The Fund ended the year positioned slightly below benchmark duration and maintaining its overweight to corporate bonds. However, the Fund continues to execute swaps selling credit holdings and moving the proceeds into higher quality Treasury and securitized holdings. We view this as actively raising the overall Fund quality and expect to execute more transactions in the months ahead.

| Average Annual Total Return (%) through December 31, 20191 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||

| Ultra Series Diversified Income, Class I | 19.68 | 10.41 | 7.99 | 9.08 | |||||

| Ultra Series Diversified Income, Class II | 19.38 | 10.13 | 7.72 | 8.81 | |||||

| S&P 500® Index | 31.49 | 15.27 | 11.70 | 13.56 | |||||

| ICE BofA US Corp, Govt & Mortgage Index | 8.96 | 4.14 | 3.11 | 3.80 | |||||

| Custom Blended Index (50% Fixed, 50% Equity) | 20.03 | 9.80 | 7.55 | 8.82 | |||||

See accompanying Notes to Management’s Discussion of Fund Performance.

| SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||||

| Asset Backed Securities | 1.5 | % | ||

| Collateralized Mortgage Obligations | 1.5 | % | ||

| Commercial Mortgage-Backed Securities | 0.4 | % | ||

| Common Stocks | 68.9 | % | ||

| Corporate Notes and Bonds | 8.4 | % | ||

| Long Term Municipal Bonds | 1.0 | % | ||

| Mortgage Backed Securities | 7.3 | % | ||

| Short-Term Investments | 2.4 | % | ||

| U.S. Government and Agency Obligations | 8.5 | % | ||

| Net Other Assets and Liabilities | 0.1 | % | ||

LARGE CAP VALUE FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Large Cap Value Fund will, under normal market conditions, maintain at least 80% of its net assets in large cap stocks. The Fund follows a “value” approach, meaning the portfolio managers seek to invest in stocks at prices below their perceived intrinsic value as estimated based on fundamental analysis of the issuing company and its prospects. By investing in value stocks, the Fund attempts to limit the downside risk over time but may also produce smaller gains than other stock funds if their intrinsic values are not realized by the market or if growth-oriented investments are favored by investors. The Fund will diversify its holdings among various industries and among companies within those industries.

PERFORMANCE

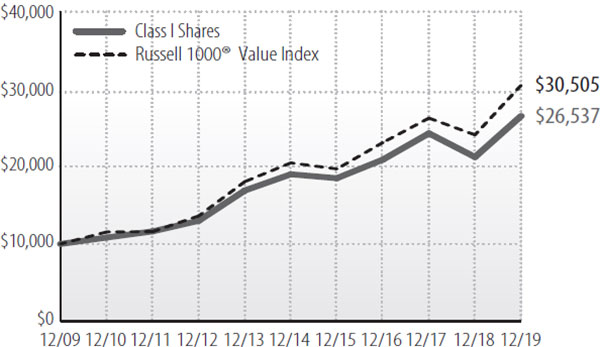

Cumulative Performance of $10,000 Investment1

For the full year, the Ultra Series Large Cap Value Fund (Class I) returned 24.93% for the annual period, compared to its benchmark Russell 1000® Value Index’s return of 26.54%.

Sector allocation was detractive while stock selection was additive to results. For sector allocation, underweight positions in the Health Care, Technology and Industrials Sectors negatively impacted performance. In terms of stock selection, there were positive contributions from Financials, Real Estate, Materials, Energy, Industrials and Technology, which was partially offset by weakness in Communication Services and Health Care. In Technology, payment solutions provider First Data (FDC) was the best performing stock in the portfolio. It was acquired by rival Fiserv (FISV) during the year, which the Fund subsequently sold. Within Real Estate, industrial real estate firm Prologis (PLD) contributed nicely to results. The company continues to expand its global portfolio of industrial buildings and warehouses. Within Industrials, engineering and construction firm Jacobs Engineering (J) performed well following a series of strong earnings reports that featured a higher backlog. In Financials, global money center banks J.P. Morgan (JPM) and Bank of America (BAC) were notable outperforming stocks. Both banks benefited from higher interest rates and a positively sloping yield curve. We believe each bank is well managed and attractively valued. On the negative side, within Industrials, mining and construction equipment manufacturer Caterpillar (CAT) was the worst performing stock in the portfolio. In Materials, iron ore producer Vale (VALE) was detractive. It had one of its tailings dams in Brazil collapse, which resulted in a human and environmental tragedy. The

| 10 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

Fund sold the stock immediately after this incident occurred. Within Utilities, independent power producer NRG Energy (NRG) negatively impacted results and was sold following two strong years of returns. Within Financials, life insurance provider Met Life (MET) was another underperforming stock. The Fund sold MET due to concerns about the impact of low interest rates on its underlying business. Another notable underperforming stock was airline carrier Delta (DAL). We believe our thesis on DAL remains intact and that the stock’s valuation is cheap. The Fund continues to hold all stocks mentioned above except for CAT, FDC, FISV, MET, NRG and VALE.

| Average Annual Total Return (%) through December 31, 20191 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||

| Ultra Series Large Cap Value, Class I | 24.93 | 8.27 | 6.90 | 10.25 | |||||

| Ultra Series Large Cap Value, Class II | 24.61 | 8.00 | 6.63 | 9.98 | |||||

| Russell 1000® Value Index | 26.54 | 9.68 | 8.29 | 11.80 | |||||

See accompanying Notes to Management’s Discussion of Fund Performance.

| SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||||

| Communication Services | 5.6 | % | ||

| Consumer Discretionary | 4.9 | % | ||

| Consumer Staples | 2.1 | % | ||

| Energy | 12.5 | % | ||

| Financials | 27.3 | % | ||

| Health Care | 11.1 | % | ||

| Industrials | 7.6 | % | ||

| Information Technology | 3.4 | % | ||

| Materials | 13.6 | % | ||

| Real Estate | 2.6 | % | ||

| Short-Term Investments | 2.2 | % | ||

| Utilities | 7.0 | % | ||

| Net Other Assets and Liabilities | 0.1 | % | ||

LARGE CAP GROWTH FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Large Cap Growth Fund invests primarily in common stocks of larger companies and will, under normal market conditions, maintain at least 80% of its net assets in large cap stocks. The Fund invests in well-established companies with competitive advantages that have demonstrated patterns of consistent growth. To a lesser extent, the Fund may invest in the stocks of less established companies that may offer more rapid growth potential. The Fund invests when a stock trades at a good price in relation to underlying value and the Fund looks to sell or trim a stock when the portfolio manager deems a stock to be overpriced compared to underlying value.

PERFORMANCE

Cumulative Performance of $10,000 Investment1

The Ultra Series Large Cap Growth Fund (Class I) returned 31.13% for the annual period, compared to its benchmark Russell 1000® Growth Index return of 36.39%. The Fund underperformed its peer group, the U.S. Large Growth category, which returned 33.02%.

The types of stocks that led the market returns for the year varied by period. For the first nine months of the year, the market was more conducive to defensive growth stocks. During that time period, the Russell 1000® Defensive Growth Index generated a 26.62% return compared to the 22.37% return for the Russell 1000® Dynamic Growth Index. However, during the fourth quarter 2019, the trend reversed and the Dynamic Growth Index outperformed the Defensive Growth Index 13.41% to 7.94%. This fourth quarter rally for the stocks of less stable businesses led to the Dynamic Growth Index outperforming the Defensive Growth Index for the year. Stylistically, the Fund’s holdings more closely resemble the stocks that constitute the Defensive as opposed to the Dynamic Index, and we believe it is likely that the Fund will underperform the broader Russell 1000 Growth Index over time periods when dynamic growth stocks outperform defensive growth stocks. The Fund’s high active share (its differentiation to the benchmark) will cause it to experience year-to-year variability in returns when compared to the benchmark returns, although we believe this differentiation provides the Fund the opportunity to outperform over time.

Throughout 2019, the Fund’s portfolio managers sold stocks and trimmed weight in names where competitive positions were deemed to be threatened, where growth

| 11 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

was decelerating, or where the stocks were assessed to be expensive per the team’s valuation criteria. Conversely, stocks were purchased when the team believed competitive positions to be strong and when it believed the growth or value of a business was underappreciated. The Fund purchased three new stocks in 2019 in the Energy, Communications Services and Financials sectors. For the year, portfolio turnover was below long-term averages.

For 2019, the Fund enjoyed strong relative performance from its Industrial, Health Care, and Real Estate sector holdings, which enjoyed better returns than the benchmark constituents in these sectors. The Fund’s industrial holdings rebounded strongly after 2018’s sell-off. The Fund’s health care holdings also performed above the benchmark’s Health Care sector holdings, although the sector itself underperformed the broader benchmark. The Fund’s Real Estate sector holding also outperformed its sector for the year.

The Information Technology sector was a strong sector for the Russell 1000 Growth Index during 2019, returning 51.8%. The Fund’s holdings in the sector underperformed their benchmark comparison in aggregate, and the Fund’s underweight in the sector also was a relative performance drag. The Fund’s holdings also underperformed the comparable benchmark sectors in the Communications Services, Materials, Consumer Discretionary, Energy, and Financial sectors. We believe this primarily reflects the outperformance of dynamic growth names during the period. Finally, the Fund’s cash holdings were a performance drag during the year.

Our goal is to provide superior long-term returns while assuming less risk to do so. We continue to believe in the merit of thinking independently, investing for the long-term, and emphasizing risk management. We remain confident that the strategy will outperform over a full market cycle.

| Average Annual Total Return (%) through December 31, 20191 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||

| Ultra Series Large Cap Growth, Class I | 31.13 | 16.94 | 11.79 | 12.15 | |||||

| Ultra Series Large Cap Growth, Class II | 30.80 | 16.65 | 11.51 | 11.87 | |||||

| Russell 1000® Growth Index | 36.39 | 20.49 | 14.63 | 15.22 | |||||

See accompanying Notes to Management’s Discussion of Fund Performance.

| SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||||

| Communication Services | 10.3 | % | ||

| Consumer Discretionary | 19.3 | % | ||

| Energy | 2.3 | % | ||

| Financials | 17.9 | % | ||

| Health Care | 11.3 | % | ||

| Industrials | 10.6 | % | ||

| Information Technology | 14.5 | % | ||

| Materials | 7.9 | % | ||

| Real Estate | 1.5 | % | ||

| Short-Term Investments | 4.3 | % | ||

| Net Other Assets and Liabilities | 0.1 | % | ||

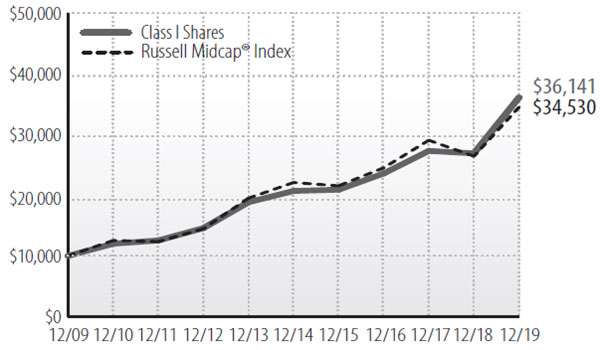

MID CAP FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Mid Cap Fund generally invests in common stocks of midsize companies and will, under normal market conditions, maintain at least 80% of its net assets in mid cap securities. The Fund seeks attractive long-term returns through bottom-up security selection based on fundamental analysis in a diversified portfolio of high-quality companies with attractive valuations. These will typically be industry leading companies in niches with strong growth prospects. The Fund’s portfolio managers believe in selecting stocks for the Fund that show steady, sustainable growth and reasonable valuations. As a result, stocks of issuers that are believed to have a blend of both value and growth potential will be selected for investment.

PERFORMANCE

Cumulative Performance of $10,000 Investment1

The Ultra Series Mid Cap Fund returned 34.27% (Class I) for the annual period, outperforming its benchmark Russell Midcap® Index’s 30.54% return. The Fund slightly underperformed its peer group, the Morningstar Mid-Cap Growth category, which returned 34.37%.

| 12 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

Sector allocation was slightly detractive over the full year. This was primarily due to our underweight in the Information Technology Sector, which was the strongest sector in the Russell Midcap® Index, advancing 43%. The next largest detractors from a sector allocation perspective were Consumer Discretionary and Communication Services, where we were overweight in these underperforming sectors. Not being exposed to the underperforming Energy and Utility Sectors resulted in these areas being the biggest positive contributor to our sector allocation. Being underweight in Consumer Staples proved beneficial as well.

Strong stock selection drove all of our outperformance during the year. Our top individual contributors were Liberty Broadband, Arch Capital Group, Copart, CDW, and IHS Markit. Our largest detractors were Dollar Tree, Markel, Henry Schein, Alliance Data Systems and Progressive. Liberty Broadband owns approximately 22% of Charter Communications, its main asset. Liberty Broadband benefitted from strong results from Charter throughout the year, highlighted by robust internet subscription additions and accelerating free cash flow growth. Arch Capital Group bounced back from choppy performance in 2018 with consistently strong results in 2019. The industry backdrops for both its mortgage insurance and property and casualty (P&C) insurance businesses were much more favorable during the year. Copart continued to defy predictions of slowing growth, posting 20% revenue growth and 30% earnings per share growth in the latest 12-month period. The company is executing very well and is winning market share and increasing its global bidder base, which sets up the company well for further success.

Our bottom contributors were Progressive Corp, Alliance Data Systems, Kemper, Covetrus, and Henry Schein. The negative impact from these five was minimal – in aggregate they detracted less than a percentage point from our annual return. Auto insurers Progressive and Kemper were purchased mid-year. The auto insurance industry is in transition from a “hard” market to either a “neutral” or “soft” market, which has soured investor sentiment on the stocks. Our investment in private label credit company provider Alliance Data was a mistake. While part of our investment thesis came to fruition, it wasn’t to the extent we had hoped. Given its small position and our lower conviction, we sold the remaining stake late in 2019.

| Average Annual Total Return (%) through December 31, 20191 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||

| Ultra Series Mid Cap, Class I | 34.27 | 15.24 | 11.78 | 13.71 | |||||

| Ultra Series Mid Cap, Class II | 33.93 | 14.96 | 11.50 | 13.43 | |||||

| Russell Midcap® Index | 30.54 | 12.06 | 9.33 | 13.19 | |||||

See accompanying Notes to Management’s Discussion of Fund Performance.

| SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||||

| Communication Services | 5.9 | % | ||

| Consumer Discretionary | 19.8 | % | ||

| Consumer Staples | 1.3 | % | ||

| Financials | 29.9 | % | ||

| Health Care | 4.6 | % | ||

| Industrials | 16.3 | % | ||

| Information Technology | 10.3 | % | ||

| Materials | 5.8 | % | ||

| Short-Term Investments | 6.2 | % | ||

| Net Other Assets and Liabilities | (0.1) | % | ||

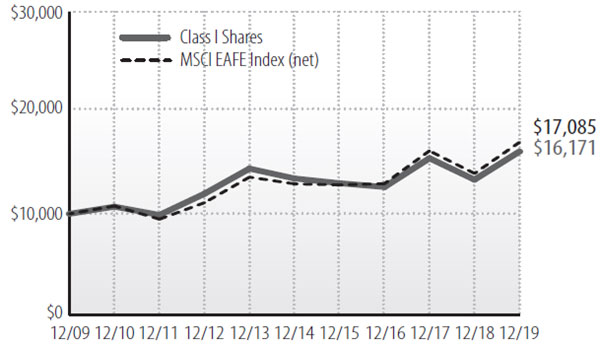

INTERNATIONAL STOCK FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series International Stock Fund will invest, under normal market conditions, at least 80% of its net assets in the stock of foreign companies. Typically, a majority of the Fund’s assets are invested in relatively large cap stocks of companies located or operating in developed countries. The Fund may also invest up to 30% of its assets in securities of companies whose principal business activities are located in emerging market countries. The portfolio managers typically maintain this segment of the Fund’s portfolio in such stocks which it believes have a low market price relative to their perceived value based on fundamental analysis of the issuing company and its prospects. The Fund may also invest in foreign debt and other income bearing securities at times when it believes that income bearing securities have greater capital appreciation potential than equity securities.

| 13 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

PERFORMANCE

Cumulative Performance of $10,000 Investment1

The Ultra Series International Equity portfolio had strong absolute performance in 2019 but trailed the MSCI EAFE Index for the year with a return of 20.81% (Class I). The Index was up 22.01%. The Fund also underperformed its Morningstar Foreign Large Blend Index which returned 21.61%.

Stock selection in the Financials sector helped relative returns as Aon, the global insurance broker domiciled in the United Kingdom, continued to drive positive performance during the period, rising almost 45%. This long-term holding has demonstrated the ability to generate strong free cash flow from operating leverage derived from continued strong organic revenue growth and disciplined spending and capital allocation. Results continue to show momentum on new client wins and growth in newer products.

Stock selection in the Materials sector has also driven positive relative returns as shares of DSM rose more than 60%. DSM is a global specialty chemical company and operates within health, nutrition, and materials. DSM is a much more stable business than in the past when the company was more focused on commodity chemicals. It also is now a higher quality company with improving margins, higher growth, and little-to-no financial leverage. The structural growth of the nutrition segment should provide more resilience in earnings than was experienced during the last cyclical downturn. Unlike a pharmaceutical company, investors typically ascribe little to no value for a chemical company’s “pipeline.”

Lastly, positioning in emerging markets was additive to relative returns. In contrast, a lower-than-benchmark weight and stock selection in the Consumer Discretionary Sector detracted from relative returns as shares of Japanese auto manufacturer Suzuki declined 16% during the year. In India, Suzuki’s largely important Maruti division released a negative June sales report, and was further hurt by the government’s new budget, which included a fuel tax increase.

However, the stock recovered slightly following the announcement that the Indian government is reconsidering the planned hike in auto registration charges. We continue to believe the slowdown in auto demand in India is temporary and the medium to long-term story remains unchanged. Also in the sector, shares of Japanese discount retailer Pan Pacific, formerly Don Quijote, lagged the overall market during the period, despite rising almost 8%. Elsewhere, strategy returns were hurt by stock selection in the Real Estate sector. Lastly, cash was the largest detractor from performance. Cash is a residual of our process, not a strategic asset in the portfolio. Corporate fundamentals weakened throughout the year, while increasingly positive sentiment drove valuations higher. As a result, stocks in our portfolio reached target valuations faster than we could find high-quality relative value investments to replace them with. This resulted in slightly elevated cash levels, which weighed down performance relative to benchmark.

| Average Annual Total Return through December 31, 20191 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||

| Ultra Series International Stock, Class I | 20.81 | 8.51 | 3.67 | 4.92 | |||||

| Ultra Series International Stock, Class II | 20.51 | 8.24 | 3.41 | 4.66 | |||||

| MSCI EAFE Index (net) | 22.01 | 9.56 | 5.67 | 5.50 | |||||

See accompanying Notes to Management’s Discussion of Fund Performance.

| SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||||

| Communication Services | 4.0 | % | ||

| Consumer Discretionary | 11.4 | % | ||

| Consumer Staples | 8.5 | % | ||

| Energy | 6.1 | % | ||

| Financials | 17.6 | % | ||

| Health Care | 10.3 | % | ||

| Industrials | 15.3 | % | ||

| Information Technology | 11.6 | % | ||

| Materials | 6.7 | % | ||

| Real Estate | 2.9 | % | ||

| Short-Term Investments | 2.5 | % | ||

| Utilities | 3.0 | % | ||

| Net Other Assets and Liabilities | 0.1 | % | ||

| 14 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

| GEOGRAPHICAL ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||||

| Japan | 16.2 | % | ||

| United Kingdom | 15.6 | % | ||

| France | 13.2 | % | ||

| Germany | 7.9 | % | ||

| Netherlands | 6.6 | % | ||

| Canada | 5.4 | % | ||

| Switzerland | 5.2 | % | ||

| Ireland | 4.5 | % | ||

| Sweden | 3.7 | % | ||

| Norway | 3.6 | % | ||

| Singapore | 2.6 | % | ||

| South Korea | 2.6 | % | ||

| United States | 2.5 | % | ||

| Finland | 2.4 | % | ||

| China | 1.6 | % | ||

| Denmark | 1.5 | % | ||

| Australia | 1.3 | % | ||

| Israel | 1.1 | % | ||

| Spain | 0.9 | % | ||

| Luxembourg | 0.7 | % | ||

| Hong Kong | 0.4 | % | ||

| Mexico | 0.4 | % | ||

| Other Net Assets | 0.1 | % | ||

MADISON TARGET RETIREMENT 2020 FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Madison Target Retirement 2020 Fund invests primarily in shares of registered investment companies according to an asset allocation strategy developed by the Fund’s investment adviser for investors planning to retire in or within a few years of 2020. Over time, the Fund’s asset allocation will gradually shift until it reaches the more conservative allocation target of approximately 10-30% in stock funds and 70-90% in bond funds. The asset allocation strategy is designed to reduce the volatility of investment returns in the later years while still providing the potential for higher total returns over the target period.

PERFORMANCE

Cumulative Performance of $10,000 Investment1,3

The Ultra Series Target Retirement 2020 Fund (Class I) returned 11.76% for the year, compared to the S&P Target Date to 2020® Index’s return of 14.16%. The Fund’s Morningstar Target-Date 2020 peer group returned 16.92%.

In absolute terms, the Fund had a very good year, though it lagged the stated benchmark. Our concerns over deteriorating market fundamentals and slowing economic data led us to position the Fund defensively. Accordingly, the Fund’s underweight to equities proved to be the biggest detractor to relative performance in 2019’s liquidity driven market. Positions in commodities and international minimum volatility holdings also detracted from the Fund’s return. The Fund benefited from a couple key positive asset allocation decisions, notably our overweight allocation to U.S technology stocks and our bias for larger capitalization stocks versus smaller companies.

Returns across nearly all asset classes soared in 2019. U.S. stocks (S&P 500® Index) returned 31.5%, foreign developed markets stocks (MSCI EAFE Index) advanced 22.0%, emerging markets equities (MSCI EM Index) jumped 18.4%, and even bonds (Bloomberg Barclays U.S. Aggregate Bond Index) produced an outsized 8.7% return for the year. The year’s strength was surprising given the backdrop of a global manufacturing recession, flat U.S. earnings growth and generally slowing economic data across the world. However, economic concerns were pushed aside, aided by a massive change in monetary policy provided by the Fed. At year-end 2018 the Fed believed they would need to continue hiking interest rates throughout 2019 but wound up cutting rates three times and expanded their balance sheet by roughly $400 billion instead. Investors celebrated the Fed’s policy U-turn by pushing market valuations higher and higher.

Moving forward, we continue to be concerned by the disconnect between eroding fundamentals and a combination of overly bullish sentiment and elevated valuations. Risk assets appear to be discounting a very positive future despite an abundance of global policy uncertainty and meager economic growth prospects. Given this environment, we intend to remain cautiously positioned until we see a more favorable risk/reward trade-off for risk assets.

| 15 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

| Average Annual Total Return (%) through December 31, 20191,3 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||

| Ultra Series Madison Target Retirement 2020, Class I | 11.76 | 5.83 | 4.53 | 6.15 | |||||

| S&P Target Date® To 2020 Index | 14.16 | 7.09 | 5.49 | 6.65 | |||||

See accompanying Notes to Management’s Discussion of Fund Performance.

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||||

| Alternative Funds | 3.0 | % | ||

| Bond Funds | 71.9 | % | ||

| Foreign Stock Funds | 6.0 | % | ||

| Stock Funds | 14.0 | % | ||

| Net Other Assets and Liabilities | 5.1 | % | ||

MADISON TARGET RETIREMENT 2030 FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Madison Target Retirement 2030 Fund invests primarily in shares of registered investment companies according to an asset allocation strategy developed by the Fund’s investment adviser for investors planning to retire in or within a few years of 2030. Over time, the Fund’s asset allocation will gradually shift until it reaches the more conservative allocation target of approximately 10-30% in stock funds and 70-90% in bond funds. The asset allocation strategy is designed to reduce the volatility of investment returns in the later years while still providing the potential for higher total returns over the target period.

PERFORMANCE

Cumulative Performance of $10,000 Investment1,3

The Ultra Series Target Retirement 2030 Fund (Class I) returned 17.10% for the year, compared to the S&P Target Date to 2030® Index’s return of 18.58%. The Fund’s Morningstar Target-Date 2030 peer group returned 21.18%.

In absolute terms, the Fund had a very good year, though it lagged the stated benchmark. Our concerns over deteriorating market fundamentals and slowing economic data led us to position the Fund defensively. Accordingly, the Fund’s underweight to equities proved to be the biggest detractor to relative performance in 2019’s liquidity driven market. Positions in commodities and international minimum volatility holdings also detracted from the Fund’s return. The Fund benefited from a couple key positive asset allocation decisions, notably our overweight allocation to U.S technology stocks and our bias for larger capitalization stocks versus smaller companies. Also, the Fund’s holdings in longer duration fixed income investments contributed positively as interest rates declined.

Returns across nearly all asset classes soared in 2019. U.S. stocks (S&P 500® Index) returned 31.5%, foreign developed markets stocks (MSCI EAFE Index) advanced 22.0%, emerging markets equities (MSCI EM Index) jumped 18.4%, and even bonds (Bloomberg Barclays U.S. Aggregate Bond Index) produced an outsized 8.7% return for the year. The year’s strength was surprising given the backdrop of a global manufacturing recession, flat U.S. earnings growth and generally slowing economic data across the world. However, economic concerns were pushed aside, aided by a massive change in monetary policy provided by the Fed. At year-end 2018 the Fed believed they would need to continue hiking interest rates throughout 2019 but wound up cutting rates three times and expanded their balance sheet by roughly $400 billion instead. Investors celebrated the Fed’s policy U-turn by pushing market valuations higher and higher.

Moving forward, we continue to be concerned by the disconnect between eroding fundamentals and a combination of overly bullish sentiment and elevated valuations. Risk assets appear to be discounting a very positive future despite an abundance of global policy uncertainty and meager economic growth prospects. Given this environment, we intend to remain cautiously positioned until we see a more favorable risk/reward trade-off for risk assets.

| 16 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

| Average Annual Total Return (%) through December 31, 20191,3 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||

| Ultra Series Madison Target Retirement 2030, Class I | 17.10 | 8.34 | 6.24 | 7.69 | |||||

| S&P Target Date® To 2030 Index | 18.58 | 8.82 | 6.73 | 7.91 | |||||

See accompanying Notes to Management’s Discussion of Fund Performance.

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||||

| Alternative Funds | 9.0 | % | ||

| Bond Funds | 39.8 | % | ||

| Foreign Stock Funds | 13.0 | % | ||

| Stock Funds | 33.0 | % | ||

| Net Other Assets and Liabilities | 5.2 | % | ||

MADISON TARGET RETIREMENT 2040 FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Madison Target Retirement 2040 Fund invests primarily in shares of registered investment companies according to an asset allocation strategy developed by the Fund’s investment adviser for investors planning to retire in or within a few years of 2040. Over time, the Fund’s asset allocation will gradually shift until it reaches the more conservative allocation target of approximately 10-30% in stock funds and 70-90% in bond funds. The asset allocation strategy is designed to reduce the volatility of investment returns in the later years while still providing the potential for higher total returns over the target period.

PERFORMANCE

Cumulative Performance of $10,000 Investment1,3

The Ultra Series Target Retirement 2040 Fund (Class I) returned 18.86% for the year, compared to the S&P Target Date to 2040® Index’s return of 22.10%. The Fund’s Morningstar Target-Date 2040 peer group returned 23.48%.

In absolute terms, the Fund had a very good year, though it lagged the stated benchmark. Our concerns over deteriorating market fundamentals and slowing economic data led us to position the Fund defensively. Accordingly, the Fund’s underweight to equities proved to be the biggest detractor to relative performance in 2019’s liquidity driven market. Positions in commodities and international minimum volatility holdings also detracted from the Fund’s return. The Fund benefited from a couple key positive asset allocation decisions, notably our overweight allocation to U.S technology stocks and our bias for larger capitalization stocks versus smaller companies. Also, the Fund’s holdings in longer duration fixed income investments contributed positively as interest rates declined.

Returns across nearly all asset classes soared in 2019. U.S. stocks (S&P 500® Index) returned 31.5%, foreign developed markets stocks (MSCI EAFE Index) advanced 22.0%, emerging markets equities (MSCI EM Index) jumped 18.4%, and even bonds (Bloomberg Barclays U.S. Aggregate Bond Index) produced an outsized 8.7% return for the year. The year’s strength was surprising given the backdrop of a global manufacturing recession, flat U.S. earnings growth and generally slowing economic data across the world. However, economic concerns were pushed aside, aided by a massive change in monetary policy provided by the Fed. At year-end 2018 the Fed believed they would need to continue hiking interest rates throughout 2019 but wound up cutting rates three times and expanded their balance sheet by roughly $400 billion instead. Investors celebrated the Fed’s policy U-turn by pushing market valuations higher and higher.

Moving forward, we continue to be concerned by the disconnect between eroding fundamentals and a combination of overly bullish sentiment and elevated valuations. Risk assets appear to be discounting a very positive future despite an abundance of global policy uncertainty and meager economic growth prospects. Given this environment, we intend to remain cautiously positioned until we see a more favorable risk/reward trade-off for risk assets.

| 17 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

| Average Annual Total Return (%) through December 31, 20191,3 | |||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||||

| Ultra Series Madison Target Retirement 2040 | 18.86 | 9.20 | 6.90 | 8.33 | |||||

| S&P Target Date® To 2040 Index | 22.10 | 10.18 | 7.67 | 8.90 |

See accompanying Notes to Management’s Discussion of Fund Performance.

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||||

| Alternative Funds | 8.9 | % | ||

| Bond Funds | 30.9 | % | ||

| Foreign Stock Funds | 16.0 | % | ||

| Stock Funds | 38.9 | % | ||

| Net Other Assets and Liabilities | 5.3 | % | ||

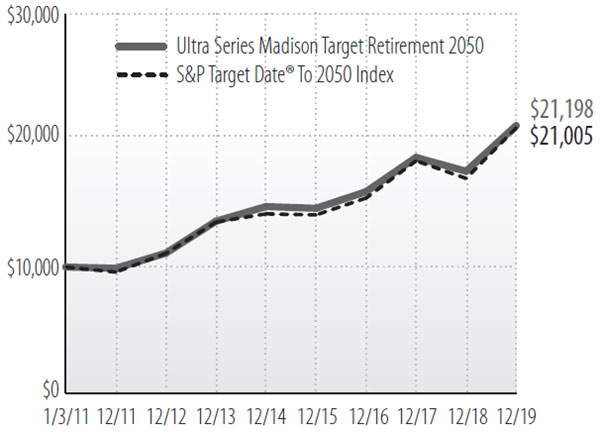

MADISON TARGET RETIREMENT 2050 FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Madison Target Retirement 2050 Fund invests primarily in shares of registered investment companies according to an asset allocation strategy developed by the Fund’s investment adviser for investors planning to retire in or within a few years of 2050. Over time, the Fund’s asset allocation will gradually shift until it reaches the more conservative allocation target of approximately 10-30% in stock funds and 70-90% in bond funds. The asset allocation strategy is designed to reduce the volatility of investment returns in the later years while still providing the potential for higher total returns over the target period.

PERFORMANCE

Cumulative Performance of $10,000 Investment1,3

The Ultra Series Target Retirement 2050 Fund (Class I) returned 20.55% for the year, compared to the S&P Target Date to 2040® Index’s return of 23.44%. The Fund’s Morningstar Target-Date 2050 peer group returned 24.97%.

In absolute terms, the Fund had a very good year, though it lagged the stated benchmark. Our concerns over deteriorating market fundamentals and slowing economic data led us to position the Fund defensively. Accordingly, the Fund’s underweight to equities proved to be the biggest detractor to relative performance in 2019’s liquidity driven market. Positions in commodities and international minimum volatility holdings also detracted from the Fund’s return. The Fund benefited from a couple key positive asset allocation decisions, notably our overweight allocation to U.S technology stocks and our bias for larger capitalization stocks versus smaller companies. Also, the Fund’s holdings in longer duration fixed income investments contributed positively as interest rates declined.

Returns across nearly all asset classes soared in 2019. U.S. stocks (S&P 500® Index) returned 31.5%, foreign developed markets stocks (MSCI EAFE Index) advanced 22.0%, emerging markets equities (MSCI EM Index) jumped 18.4%, and even bonds (Bloomberg Barclays U.S. Aggregate Bond Index) produced an outsized 8.7% return for the year. The year’s strength was surprising given the backdrop of a global manufacturing recession, flat U.S. earnings growth and generally slowing economic data across the world. However, economic concerns were pushed aside, aided by a massive change in monetary policy provided by the Fed. At year-end 2018 the Fed believed they would need to continue hiking interest rates throughout 2019 but wound up cutting rates three times and expanded their balance sheet by roughly $400 billion instead. Investors celebrated the Fed’s policy U-turn by pushing market valuations higher and higher.

Moving forward, we continue to be concerned by the disconnect between eroding fundamentals and a combination of overly bullish sentiment and elevated valuations. Risk assets appear to be discounting a very positive future despite an abundance of global policy uncertainty and meager economic growth prospects. Given this environment, we intend to remain cautiously positioned until we see a more favorable risk/reward trade-off for risk assets.

| 18 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

| Average Annual Total Return (%) through December 31, 20191,3 | |||||||||

| 1 Year | 3 Years | 5 Years | Since 1/3/11 Inception | ||||||

| Ultra Series Madison Target Retirement 2050 | 20.55 | 9.91 | 7.47 | 8.71 | |||||

| S&P Target Date® To 2050 Index | 23.44 | 10.76 | 8.13 | 8.60 | |||||

See accompanying Notes to Management’s Discussion of Fund Performance.

| PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS AS OF 12/31/19 | ||||

| Alternative Funds | 8.9 | % | ||

| Bond Funds | 21.9 | % | ||

| Foreign Stock Funds | 19.0 | % | ||

| Stock Funds | 44.8 | % | ||

| Net Other Assets and Liabilities | 5.4 | % | ||

| 19 |

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2019

Notes to Management’s Discussion of Fund Performance (unaudited)