OMB APPROVAL OMB Number: 3235-0570 Expires: August 31, 2020 Estimated average burden hours per response...20.6

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4815

Ultra Series Fund (Exact name of registrant as specified in charter)

550 Science Drive, Madison, WI 53711 (Address of principal executive offices)(Zip code)

Kevin S. Thompson Madison Funds Legal and Compliance Department 550 Science Drive Madison, WI 53711 (Name and address of agent for service)

Registrant’s telephone number, including area code: 608-274-0300

Date of fiscal year end: December 31

Date of reporting period: December 31, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. s 3507.

Item 1. Certified Financial Statement

Ultra Series Fund | December 31, 2017

Table of Contents

Page

Management’s Discussion of Fund Performance

Period in Review

2

Allocation Funds

3

Conservative Allocation Fund

3

Moderate Allocation Fund

4

Aggressive Allocation Fund

6

Core Bond Fund

7

High Income Fund

9

Diversified Income Fund

10

Large Cap Value Fund

11

Large Cap Growth Fund

12

Mid Cap Fund

13

International Stock Fund

14

Notes to Management’s Discussion of Fund Performance

17

Portfolios of Investments

Conservative Allocation Fund

19

Moderate Allocation Fund

20

Aggressive Allocation Fund

21

Core Bond Fund

22

High Income Fund

26

Diversified Income Fund

28

Large Cap Value Fund

33

Large Cap Growth Fund

34

Mid Cap Fund

35

International Stock Fund

36

Financial Statements

Statements of Assets and Liabilities

38

Statements of Operations

40

Statements of Changes in Net Assets

42

Financial Highlights for a Share of Beneficial Interest Outstanding

46

Notes to Financial Statements

56

Report of Independent Registered Public Accounting Firm

72

Other Information

73

Trustees and Officers

81

Nondeposit investment products are not federally insured, involve investment risk, may lose value and are not obligations of or guaranteed by any financial institution. For more complete information about Ultra Series Fund, including charges and expenses, request a prospectus from your financial advisor or from CMFG Life Insurance Company, 2000 Heritage Way, Waverly, IA 50677. Consider the investment objectives, risks, and charges and expenses of any fund carefully before investing. The prospectus contains this and other information about the investment company. For more current Ultra Series Fund performance information, please call 1-800-670-3600. Current performance may be lower or higher than the performance data quoted within. Past performance does not guarantee future results. Nothing in this report represents a recommendation of a security by the investment adviser. Portfolio holdings may have changed since the date of this report.

1

Ultra Series Fund | December 31, 2017

Management’s Discussion of Fund Performance (unaudited)

PERIOD IN REVIEW

The fourth quarter capped a perfect year for stock investors as the S&P 500® Index delivered positive returns every month in 2017, a first based on data going back to 1928. Although bond returns were mixed during the quarter, results were positive for the year despite the Federal Reserve (Fed) increasing short-term interest rates three times over the last twelve months. During the fourth quarter, the S&P 500® gained 6.64%, the Russell Midcap® Index rose 6.07% and the MSCI EAFE® (net) Index advanced 4.23% (3.66% excluding currency effect). The Bloomberg Barclays Intermediate Government/Credit Index declined 0.20% while the Bloomberg Barclays Aggregate Index gained 0.39% during the quarter. Equity market returns for 2017 were outstanding as the S&P 500® Index returned 21.83%, the Russell Midcap® Index advanced 18.52% and the MSCI EAFE® (net) Index gained 25.03% (15.23% excluding currency effect). Bond performance was also positive during 2017 as the Bloomberg Barclays Intermediate Government/ Credit Index gained 2.14% and the Bloomberg Barclays Aggregate Index advanced 3.54% for the year.

A year ago we opined that, with asset values stretched, economic and earnings growth would likely be necessary to support continued gains in the equity markets. This occurred during 2017 as both global economic activity and company earnings not only grew but accelerated into year-end. All 35 OECD (Organization for Economic Cooperation and Development) countries reported positive economic growth during 2017 for the first time since 2007. S&P 500® company earnings reached all-time highs and, with the recent tax cut, expectations are that earnings will grow another 16% in 2018.

Concerns over an unpredictable government administration caused little concern for the markets as the administration’s business-friendly reduction in regulations and tax cuts spawned optimism that long-missing business spending may soon materialize. The resilience of the equity market was impressive as it surged in the face of geopolitical turmoil, dysfunction in Washington and natural disasters. In fact, the largest pull-back in the market during the year was just 3%.

During the fourth quarter, real U.S. Gross Domestic Product (GDP) growth for the third quarter was revised to 3.2%, marking the second consecutive quarter of 3%+ growth. The unemployment rate fell again in the fourth quarter to 4.1%, the lowest rate since December of 2000, and manufacturing continued to grow, driven by renewed strength in the global economy and a weak U.S. dollar. The United States has now added jobs for 86 straight months, the longest streak on record. While wage increases have been modest, household income – which includes not only hourly wages but also hours worked – has shown strong gains. Companies are now reveling in the best opportunities they have seen in years. Strong profit growth was reported in all sectors, although Energy, Materials and Technology companies recorded the strongest gains. Overall earnings growth of the S&P 500® companies was near 10% for the year, with top-line sales growth of over 6%. Although 10% earnings growth was impressive, it didn’t keep pace with the 20% advance of the S&P 500® Index, implying that rich stock valuations got even richer during the period.

As the second longest bull market on record continues to push ahead, it’s likely that a few factors may change in 2018 – inflation, interest rates and monetary policy. In December, the Fed boosted its target Federal Funds rate range by 0.25% (up to 1.25% to 1.5%) and projected three additional hikes in 2018. While rising short-term rates didn’t deter the stock market in 2017, it’s likely that some level of interest rates may entice investors back to a “guaranteed” rate of return. With the S&P 500® trading at approximately 20 times earnings, the earnings yield is 5% (the inverse of P/E or 1/20) and we suspect that the closer to this level interest rates rise, the closer we may be to a “tipping point” for investors favoring bonds over stocks. As we’ve highlighted in previous letters, timing the market is nearly impossible to do with any degree of accuracy, as a slight mistiming can wreak havoc on investor returns. With this in mind, we continue to believe that stocks of lower-risk, higher-quality companies, along with shorter-duration, higher-quality bonds, will allow investors to participate in the market and provide some shelter should volatility return to more typical levels.

2

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

ALLOCATION FUNDS

The Ultra Series Conservative Allocation, Moderate Allocation and Aggressive Allocation Funds (the “Funds”) invest primarily in shares of registered investment companies (the “Underlying Funds”). The Funds will be diversified among a number of asset classes and their allocation among Underlying Funds will be based on an asset allocation model developed by Madison Asset Management, LLC (“Madison”), the Funds’ investment adviser. The team may use multiple analytical approaches to determine the appropriate asset allocation, including:

•

Asset allocation optimization analysis – considers the degree to which returns in different asset classes do or do not move together, and the Funds’ aim to achieve a favorable overall risk profile for any targeted portfolio return.

•

Scenario analysis – historical and expected return data is analyzed to model how individual asset classes and combinations of asset classes would affect the Funds under different economic and market conditions.

•

Fundamental analysis – draws upon Madison’s investment teams to judge each asset class against current and forecasted market conditions. Economic, industry and security analysis is used to develop return and risk expectations that may influence asset class selection. In addition, Madison has a flexible mandate which permits the Funds, at the sole discretion of Madison, to materially reduce equity risk exposures when and if conditions are deemed to warrant such an action.

CONSERVATIVE ALLOCATION FUND

INVESTMENT STRATEGY HIGHLIGHTS

Under normal circumstances, the Ultra Series Conservative Allocation Fund’s total net assets will be allocated among various asset classes and Underlying Funds, including those whose shares trade on a stock exchange (exchange traded funds or “ETFs”), with target allocations over time of approximately 35% equity investments and 65% fixed income investments. Underlying Funds in which the Fund invests may include funds advised by Madison and/or its affiliates, including the Madison Funds (the “Affiliated Underlying Funds”). Generally, Madison will not invest more than 75% of the Fund’s net assets, at the time of purchase, in Affiliated Underlying Funds. Although actual allocations may vary, as of December 31, 2017, the Fund’s asset allocation was:

PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/17

Alternative Funds

2.0%

Money Market Funds

2.3%

Bond Funds

57.9%

Stock Funds

24.1%

Foreign Stock Funds

13.5%

Net Other Assets and Liabilities

0.2%

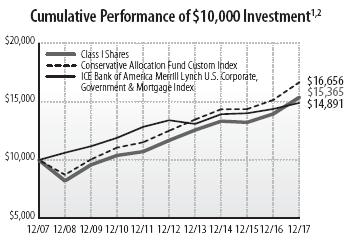

PERFORMANCE

The Ultra Series Conservative Allocation Fund (Class I) returned 10.17% over the 12-month period, slightly outperforming the Conservative Allocation Fund Custom Index return of 10.00%. The Fund lagged the Morningstar Conservative Allocation Category peer group, which returned 10.86%.

For the first time in history, the S&P 500® Index produced a positive return in all 12 calendar months for 2017. Overall, the streak stands at 14 consecutive positive months as of 12/31/2017. Just as noteworthy, if not more so, has been the vanishing of market volatility. The trailing one-year standard deviation of the Index stood at 4% versus the long-term average of roughly 14.5%. Given our conservative DNA, we are quite pleased with how well the Fund kept pace over what has been a remarkable run in the global equity markets. Overall, the Fund captured 102% of the benchmark’s return for the year. A timely move toward international equities late in 2016 was the most notable contributor to 2017 performance as foreign stocks outperformed. Other positives included relative overweight allocations to U.S. growth stocks, European equities, corporate bonds and long-term Treasuries. A modest

3

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

underweight to equities overall, and overweight allocations to U.S. mid cap stocks and hedged Japanese equities were the largest detractors from performance.

Years of consistently low U.S. inflation have provided our U.S. central bank the Fed with the justification and conviction to provide massive levels of monetary stimulus. Importantly, this has been true in terms of both scale and longevity. The Fed’s primary goal since the 2007-09 global financial crisis has been to “reflate” and stimulate the real economy. In reality, the Fed has instead been more successful at “inflating” the value of virtually all investment asset classes. The median U.S. stock, for example, is now trading near all-time record high valuation levels relative to both current and (normalized) long-term earnings. In our view, this level of valuation extreme is not justified given the elevated levels of uncertainty that both global economies (unprecedented debt levels) and established companies (pervasive disruption risk) are facing. Our perspective, then, is that today’s “concocted” increase in asset class valuations is not primarily based on prospects for improving economic fundamentals but rather the cumulative influence of pervasive liquidity and historically low interest rates on investor confidence and financial leverage.

It may sound like a broken record, but our portfolio strategies remain primarily focused on capital preservation. Incremental allocations continue to focus on international equities. In our view, the best investment values continue to be found in high quality U.S. and international large-cap equities, equities with links to commodities (especially oil) and high quality bonds. We believe that lower-quality, higher-risk asset classes are overpriced; our expectation is that the gradual removal of global central bank accommodation, currently scheduled to accelerate in 2018 (led by the Fed), could very well begin to normalize at least some of these extraordinary valuations.

Finally, global debt levels remain elevated and are also near record amounts relative to GDP. Inflationary pressures are slowly building, which could put some modest upward pressure on interest rates. Accordingly, we are making greater use of Treasury Inflation-Protected Securities (TIPS).

However, we believe that any upward trajectory in interest rates will be constrained due to the extraordinary levels of global debt.

We are confident the Fund remains well-positioned for a growth-challenged global economy. We also understand and embrace our ongoing responsibility to insightfully differentiate between attractive and less attractive asset classes as we strive to deliver superior risk-adjusted returns. As always, we sincerely appreciate your support.

Average Annual Total Return (%) through December 31, 20171,2

1 Year

3 Years

5 Years

10 Years

Since 5/1/09 Inception

Ultra Series Conservative Allocation, Class I

10.17

4.87

5.64

4.39

-

Ultra Series Conservative Allocation, Class II

9.90

4.60

5.38

-

7.05

Conservative Allocation Fund Custom Index

10.00

5.10

5.90

5.23

7.66

ICE BofAML US Corp, Govt & Mortg Index

3.63

2.27

2.13

4.06

3.95

See accompanying Notes to Management’s Discussion of Fund Performance.

MODERATE ALLOCATION FUND

INVESTMENT STRATEGY HIGHLIGHTS

Under normal circumstances, the Ultra Series Moderate Allocation Fund’s total net assets will be allocated among various asset classes and Underlying Funds, including ETFs, with target allocations over time of approximately 60% equity investments and 40% fixed income investments. Underlying Funds in which the Fund invests may include Affiliated Underlying Funds. Generally, Madison will not invest more than 75% of the Fund’s net assets, at the time of purchase, in Affiliated Underlying Funds. Although actual allocations may vary, as of December 31, 2017, the Fund’s asset allocation was:

PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/17

Alternative Funds

2.0%

Money Market Funds

1.2%

Bond Funds

33.7%

Stock Funds

39.7%

Foreign Stock Funds

23.3%

Net Other Assets and Liabilities

0.1%

4

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

PERFORMANCE

The Ultra Series Moderate Allocation Fund (Class I) returned 14.80% over the 12-month period, roughly matching the Moderate Allocation Fund Custom Index return of 14.84%. The Fund slightly outperformed the Morningstar Moderate Allocation Category peer group, which returned 14.76%.

For the first time in history, the S&P 500® Index produced a positive return in all 12 calendar months for 2017. Overall, the streak stands at 14 consecutive positive months as of 12/31/2017. Just as noteworthy, if not more so, has been the vanishing of market volatility. The trailing one-year standard deviation of the Index stood at 4% versus the long-term average of roughly 14.5%. Given our conservative DNA, we are quite pleased with how well the Fund kept pace over what has been a remarkable run in the global equity markets. Overall, the Fund captured 100% of the benchmark’s return for the year. A timely move toward international equities late in 2016 was the most notable contributor to 2017 performance as foreign stocks outperformed. Other positives included relative overweight allocations to U.S. growth stocks, European equities, corporate bonds and long-term Treasuries. A modest underweight to equities overall, and overweight allocations to U.S. mid cap stocks and hedged Japanese equities were the largest detractors from performance.

Years of consistently low U.S. inflation have provided our U.S. central bank the Fed with the justification and conviction to provide massive levels of monetary stimulus. Importantly, this has been true in terms of both scale and longevity. The Fed’s primary goal since the 2007-09 global financial crisis has been to “reflate” and stimulate the real economy. In reality, the Fed has instead been more successful at “inflating” the value of virtually all investment asset classes. The median U.S. stock, for example, is now trading near all-time record high valuation levels relative to both current and (normalized) long-term earnings. In our view, this level of valuation extreme is not justified given the elevated levels of uncertainty that both global economies (unprecedented debt levels) and established companies (pervasive disruption risk) are facing. Our perspective, then, is that today’s “concocted” increase in asset class valuations is not primarily based on prospects for improving economic fundamentals but rather the cumulative influence of pervasive liquidity and historically low interest rates on investor confidence and financial leverage.

It may sound like a broken record, but our portfolio strategies remain primarily focused on capital preservation. Incremental allocations continue to focus on international equities. In our view, the best investment values continue to be found in high quality U.S. and international large-cap equities, equities with links to commodities (especially oil) and high quality bonds. We believe that lower-quality, higher-risk asset classes are overpriced; our expectation is that the gradual removal of global central bank accommodation, currently scheduled to accelerate in 2018 (led by the Fed), could very well begin to normalize at least some of these extraordinary valuations.

Finally, global debt levels remain elevated and are also near record amounts relative to GDP. Inflationary pressures are slowly building, which could put some modest upward pressure on interest rates. Accordingly, we are making greater use of TIPS. However, we believe that any upward trajectory in interest rates will be constrained due to the extraordinary levels of global debt.

We are confident the Fund remains well-positioned for a growth-challenged global economy. We also understand and embrace our ongoing responsibility to insightfully differentiate between attractive and less attractive asset classes as we strive to deliver superior risk-adjusted returns. As always, we sincerely appreciate your support.

5

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

Average Annual Total Return (%) through December 31, 20171,2

1 Year

3 Years

5 Years

10 Years

Since 5/1/09 Inception

Ultra Series Moderate Allocation, Class I

14.80

6.89

8.58

4.67

–

Ultra Series Moderate Allocation, Class II

14.52

6.62

8.31

–

9.44

Moderate Allocation Fund Custom Index

14.84

7.09

8.61

5.91

10.22

S&P 500® Index

21.83

11.41

15.79

8.50

16.15

See accompanying Notes to Management’s Discussion of Fund Performance.

AGGRESSIVE ALLOCATION FUND

INVESTMENT STRATEGY HIGHLIGHTS

Under normal circumstances, the Ultra Series Aggressive Allocation Fund’s total net assets will be allocated among various asset classes and Underlying Funds, including ETFs, with target allocations over time of approximately 80% equity investments and 20% fixed income investments. Underlying Funds in which the Fund invests may include Affiliated Underlying Funds. Generally, Madison will not invest more than 75% of Fund’s net assets, at the time of purchase, in Affiliated Underlying Funds. Although actual allocations may vary, as of December 31, 2017, the Fund’s asset allocation was:

PORTFOLIO ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/17

Alternative Funds

2.0%

Money Market Funds

1.4%

Bond Funds

13.7%

Stock Funds

51.5%

Foreign Stock Funds

31.2%

Net Other Assets and Liabilities

0.2%

PERFORMANCE

The Ultra Series Aggressive Allocation Fund (Class I) returned 18.52% over the 12-month period, modestly underperforming the Aggressive Allocation Fund Custom Index return of 18.83%. The Fund outperformed the Morningstar Aggressive Allocation Category peer group, which returned 17.44%.

For the first time in history, the S&P 500® Index produced a positive return in all 12 calendar months for 2017. Overall, the streak stands at 14 consecutive positive months as of 12/31/2017. Just as noteworthy, if not more so, has been the vanishing of market volatility. The trailing one-year standard deviation of the Index stood at 4% versus the long-term average of roughly 14.5%. Given our conservative DNA, we are quite pleased with how well the Fund kept pace over what has been a remarkable run in the global equity markets. Overall, the Fund captured 98% of the benchmark’s return for the year. A timely move toward international equities late in 2016 was the most notable contributor to 2017 performance as foreign stocks outperformed. Other positives included relative overweight allocations to U.S. growth stocks, European equities and long-term Treasuries. A modest underweight to equities overall, and overweight allocations to U.S. mid cap stocks and hedged Japanese equities were the largest detractors from performance.

Years of consistently low U.S. inflation have provided our U.S. central bank the Fed with the justification and conviction to provide massive levels of monetary stimulus. Importantly, this has been true in terms of both scale and longevity. The Fed’s primary goal since the 2007-09 global financial crisis has been to “reflate” and stimulate the real economy. In reality, the Fed has instead been more successful at “inflating” the value of virtually all investment asset classes. The median U.S. stock, for example, is now trading near all-time record high valuation levels relative to both current and (normalized) long-term earnings. In our view, this level of valuation extreme is not justified given the elevated levels of uncertainty that both global economies (unprecedented debt levels) and established companies (pervasive disruption risk) are facing. Our perspective, then, is that today’s “concocted” increase in asset class valuations is not primarily based on prospects for improving economic fundamentals but rather the cumulative influence of pervasive liquidity and historically low interest rates on investor confidence and financial leverage.

6

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

It may sound like a broken record, but our portfolio strategies remain primarily focused on capital preservation. Incremental allocations continue to focus on international equities. In our view, the best investment values continue to be found in high quality U.S. and international large-cap equities, equities with links to commodities (especially oil) and high quality bonds. We believe that lower-quality, higher-risk asset classes are overpriced; our expectation is that the gradual removal of global central bank accommodation, currently scheduled to accelerate in 2018 (led by the Fed), could very well begin to normalize at least some of these extraordinary valuations.

Finally, global debt levels remain elevated and are also near record amounts relative to GDP. Inflationary pressures are slowly building, which could put some modest upward pressure on interest rates. Accordingly, we are making greater use of TIPS. However, we believe that any upward trajectory in interest rates will be constrained due to the extraordinary levels of global debt.

We are confident the Fund remains well-positioned for a growth-challenged global economy. We also understand and embrace our ongoing responsibility to insightfully differentiate between attractive and less attractive asset classes as we strive to deliver superior risk-adjusted returns. As always, we sincerely appreciate your support.

Average Annual Total Return (%) through December 31, 20171,2

1 Year

3 Years

5 Years

10 Years

Since 5/1/09 Inception

Ultra Series Aggressive Allocation, Class I

18.52

8.45

10.90

4.62

-

Ultra Series Aggressive Allocation, Class II

18.22

8.18

10.62

-

11.44

Aggressive Allocation Fund Custom Index

18.83

8.65

10.78

6.32

12.23

S&P 500® Index

21.83

11.41

15.79

8.50

16.15

See accompanying Notes to Management’s Discussion of Fund Performance.

CORE BOND FUND

INVESTMENT STRATEGY HIGHLIGHTS

Under normal circumstances, the Ultra Series Core Bond Fund invests at least 80% of its net assets in bonds. To keep current income relatively stable and to limit share price volatility, the Fund emphasizes investment grade securities and maintains an intermediate (typically 3-7 year) average portfolio duration, with the goal of being between 85- 115% of the market benchmark duration. The Fund also strives to add incremental return in the portfolio by making strategic decisions relating to credit risk, sector exposure and yield curve positioning. The Fund may invest in corporate debt securities, U.S. Government debt securities, foreign government debt securities, non-rated debt securities, and asset-backed, mortgage-backed and commercial mortgage-backed securities.

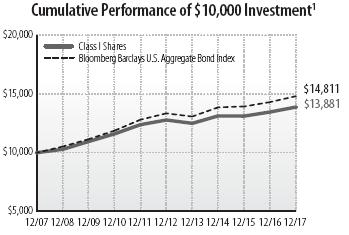

PERFORMANCE

The Ultra Series Core Bond Fund (Class I) returned 3.11% over the 12-month period, underperforming the Fund’s benchmark, the Bloomberg Barclays U.S. Aggregate® Bond Index, which returned 3.54%. The Morningstar Intermediate-Term Bond peer group returned 3.88% for the period.

An old adage states “may you live in interesting times.” There is debate about where the saying originated and whether it is a curse or blessing. However, if you view this adage through the market’s lens, the financial markets are acting as if nothing interesting at all will happen in comings years. Equity valuations are at elevated levels and risk premiums (“spreads”) on investment grade and high yield corporate bonds are at or near historical lows. Movements in nearly all asset classes, be they currencies, fixed income or equities, exhibited very subdued levels of volatility throughout 2017.

7

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

The probability of 2018 experiencing as little volatility as 2017 is very low when looking at the markets from a historical perspective. Few things hold true in financial markets, but one that does is that they are mean reverting and another is that trends last until they don’t. If the markets do become more “interesting” in 2018, investors will have to decide if the old adage is a blessing or a curse.

A theme that persisted all year was the flattening of the Treasury yield curve. The yield on the 10-year U.S. Treasury Bond less the 2-year U.S. Treasury Bond ended the year at 52 basis points (bps) after starting the year at 125 bps. The flattening of the yield curve was mostly a function of the Fed raising interest rates three times during the year while longer maturity bond yields didn’t move much due to low inflation. The two-year U.S. Treasury Bond ended the year near the high for the year at 1.88% versus starting 2017 at 1.20%. The curve shifts drove large differences among performance across the yield curve. During the year the Bloomberg Barclay’s U.S. Intermediate Treasury® Index returned 1.14% versus the Bloomberg Barclay’s U.S. Long Treasury Index® gaining 8.53%.

Market participants are currently pricing only two increases in Fed Funds rate while the Fed has stated an expectation of three rate hikes. If market expectations move towards the Fed’s, there is a real possibility of a flat or inverted yield curve by year-end unless inflation expectations move meaningfully higher. We expect that inflation will pick-up and that there will be a term premium in the Treasury market by next year-end. This should steepen the yield curve and provide opportunities to extend duration in the Fund.

Another theme throughout 2017 was the strong performance of corporate bonds. The Bloomberg Barclay’s U.S. Corporate Bond® Index had an excess return of 3.46% in 2017. Similar to Treasuries, there was a bifurcation in performance between intermediate corporate bonds, which returned 2.56% more than Treasuries, and long corporates, which had an excess return of 5.54%.

As mentioned above, spreads are at or near historically tight levels across the corporate bond market. With very low interest rates and narrow spreads, corporations are likely to issue a substantial amount of debt in 2018. Much of this debt will be from mergers and acquisitions activity and many market strategists believe this will be a near-record year for that type of activity. This type of behavior is classic late credit cycle activity and provides a source of risk going into 2018.

Positioning

As we enter 2018, the Fund will still be positioned in an overweight of spread product (non-Treasury issues) while having a more conservative duration (interest rate risk) position. If longer-term interest rates were to rise by a further 15 to 20 bps, we would look to become more neutral versus the benchmark within the 20- and 30-year bond segment. We still believe that the credit sectors remain expensive and, even though the Fund is currently overweight corporate bonds, we are actively looking to take advantage of swap opportunities to move up in quality.

Average Annual Total Return (%) through December 31, 20171

Since

5/1/09

1 Year

3 Years

5 Years

10 Years

Inception

Ultra Series Core Bond,

Class I

3.11

1.87

1.66

3.33

–

Ultra Series Core Bond,

Class II

2.85

1.61

1.41

–

3.17

Bloomberg Barclays U.S.

Aggregate Bond Index

3.54

2.24

2.10

4.01

3.96

See accompanying Notes to Management’s Discussion of Fund Performance.

SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/17

Asset Backed Securities

2.2

%

Collateralized Mortgage Obligations

2.1

%

Commercial Mortgage-Backed Securities

2.0

%

Corporate Notes and Bonds

34.0

%

Long Term Municipal Bonds

4.3

%

Mortgage Backed Securities

26.5

%

U.S. Government and Agency Obligations

26.2

%

Money Market Funds

1.5

%

Net Other Assets and Liabilities

1.2

%

8

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

HIGH INCOME FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series High Income Fund invests primarily in lower-rated, higher-yielding income bearing securities, such as “junk” bonds. Because the performance of these securities has historically been strongly influenced by economic conditions, the Fund may rotate securities selection by business sector according to the economic outlook. Under normal market conditions, the Fund invests at least 80% of its net assets in bonds rated lower than investment grade (BBB/Baa) and their unrated equivalents or other high-yielding securities.

PERFORMANCE

The Ultra Series High Income Fund (Class I) returned 6.32% during the period, lagging the ICE Bank of America Merrill Lynch U.S. High Yield Constrained® Index’s 7.48% return. The Fund also trailed its Morningstar High Yield Bond Category peer group, which returned 7.07%.

Overall, the high yield market experienced its second consecutive full-year of positive total returns. We believe the gains have been supported by positive fundamental and economic data, along with a favorable political backdrop. For the full-year 2017, high yield corporate bonds returned 7.47%, or about 181 bps below the average annual total return since 1987.

Within the high yield rating categories, CCC-rated bonds had the best annual total return at +10.59%, while BB-rated bonds trailed at +7.15% and B-rated bonds experienced a +6.74% total return. The outperformance by the CCC category had a negative impact on the Fund, as we were underweight lower quality bonds and more volatile sectors. We intend to maintain our bias towards higher quality credit and a relatively higher cash position, particularly given the current valuations of high yield bonds.

On a sector level, the Fund had underexposure to Healthcare (+8.52%), Metals & Mining (+9.85%) and Steel (+10.09%), all of which outpaced the overall market return. The Fund also underperformed in its bond selection within the Telecom and Media sectors. Partially offsetting these negatives, the Fund had a positive contribution to performance from an overweight in the Services (+9.00%) and Utilities (+11.59%) sectors, both of which outperformed the overall market. The Fund also benefited from bond selection in Consumer-related sectors. The largest single factor related to the Fund’s underperformance relative to the benchmark was a high-single-digit cash balance. As of December 29, 2017, the yield-to-worst of the Fund was 4.83% and the average rating within the Fund was Ba3.

For 2018, the Fund will continue to emphasize BB-rated and B-rated corporate bonds. Given unattractive high yield bond valuations, we believe conservative positioning is prudent. We highlight that, as of December 29, 2017, the average spread-over-Treasuries in the high yield bond market is just modestly above the current cycle’s lowest level, which likely leaves little room for further spread tightening. Thus, we anticipate the high yield market’s total return to be relatively flat in 2018 with the positive return generated by the bond’s coupons offset by the potential decline in the market prices of the underlying bonds.

Average Annual Total Return (%) through December 31, 20171

Since

5/1/09

1 Year

3 Years

5 Years

10 Years

Inception

Ultra Series High Income,

Class I

6.32

5.16

4.53

6.43

–

Ultra Series High Income,

Class II

6.06

4.90

4.27

–

7.53

ICE BofAmerica Merrill

Lynch US High Yield

Constrained Index

7.48

6.40

5.81

7.96

10.99

See accompanying Notes to Management’s Discussion of Fund Performance.

9

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/17

Consumer Discretionary

22.6

%

Consumer Staples

7.8

%

Energy

7.6

%

Financials

10.6

%

Health Care

7.9

%

Industrials

15.7

%

Information Technology

4.3

%

Materials

4.7

%

Money Market Funds

7.8

%

Real Estate

1.5

%

Telecommunication Services

3.2

%

Utilities

5.1

%

Net Other Assets and Liabilities

1.2

%

DIVERSIFIED INCOME FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Diversified Income Fund seeks income by investing in a broadly diversified array of securities including bonds, common stocks, real estate securities, foreign market bonds and stocks and money market instruments. Bonds, stock and cash components will vary, reflecting the portfolio managers’ judgments of the relative availability of attractively yielding and priced stocks and bonds; however, under normal market conditions, the Fund’s portfolio managers generally attempt to target a 40% bond and 60% stock investment allocation. Nevertheless, bonds (including investment grade, high yield and mortgage- or asset-backed) may constitute up to 80% of the Fund’s assets, stocks (including common stocks, preferred stocks and convertible bonds) may constitute up to 70% of the Fund’s assets, real estate securities may constitute up to 25% of the Fund’s assets, foreign (including American Depositary Receipts (“ADRs”) and emerging market) stocks and bonds may constitute up to 25% of the Fund’s assets, and money market instruments may constitute up to 25% of the Fund’s assets. Although the Fund is permitted to invest up to 80% of its assets in lower credit quality bonds, under normal circumstances, the Fund intends to limit the investment in lower credit quality bonds to less than 50% of the Fund’s assets. The balance between the two strategies of the Fund (fixed income and equity investing) is determined after reviewing the risks associated with each type of investment, with the goal of meaningful risk reduction as market conditions demand.

PERFORMANCE

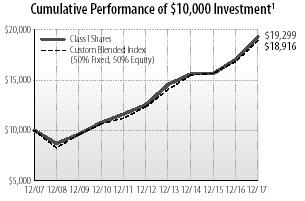

For the twelve month period, the Ultra Series Diversified Income Fund (Class I) returned 13.31% compared to its Custom Blended Index (50% S&P 500® Index and 50% ICE Bank of America Merrill Lynch U.S. Corporate Government and Mortgage Index) return of 12.42%. The Fund’s Morningstar peer group, the Moderate Allocation Category, returned 14.76% over the same period.

Equity returns in the Fund compared favorably to the S&P 500® for the year. Sector allocation was negative versus the Index while stock selection was positive. For sector allocation, an overweight position in Energy along with an underweight position in Technology negatively impacted results. In terms of stock selection, there were favorable results in Industrials, Consumer Discretionary, Utilities, Consumer Staples and Materials, partially offset by weakness in Financials, Technology, and Health Care.

The fixed income portion of the Fund modestly outperformed its benchmark for the year before fees and expenses. In the final quarter of 2017, the Fund benefited from an overall move higher in interest rates but lost performance due to the flattening yield curve as the Fund is underweight 20- and 30-year bonds. The Fund’s mortgage positions outperformed the Index as did corporate and municipal bond positions. The Fund’s corporate bond performance was driven by an overweight in triple-B rated corporate bonds and an allocation to high yield while the mortgage positions benefited from owning less 30-year mortgages than the Index.

10

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

We continue to favor stocks of lower-risk, higher-quality companies, along with shorter-duration, higher-quality bonds in the Fund given the environment of rising interest rates, rising volatility and stretched equity valuations that we see ahead.

Average Annual Total Return (%) through December 31, 20171

Since

5/1/09

1 Year

3 Years

5 Years

10 Years

Inception

Ultra Series Diversified

Income, Class I

13.31

7.33

8.98

6.80

–

Ultra Series Diversified

Income, Class II

13.03

7.06

8.71

–

9.82

Custom Blended Index

(50% Fixed, 50% Equity)

12.42

6.91

8.90

6.58

10.11

ICE BofAML US Corp, Govt

& Mortgage Index

3.63

2.27

2.13

4.06

3.95

S&P 500® Index

21.83

11.41

15.79

8.50

16.15

See accompanying Notes to Management’s Discussion of Fund Performance.

SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/17

Asset Backed Securities

0.3

%

Collateralized Mortgage Obligations

1.2

%

Commercial Mortgage-Backed Securities

0.6

%

Common Stocks

62.4

%

Corporate Notes and Bonds

13.1

%

Long Term Municipal Bonds

2.5

%

Mortgage Backed Securities

9.1

%

U.S. Government and Agency Obligations

8.9

%

Money Market Funds

1.6

%

Net Other Assets and Liabilities

0.3

%

LARGE CAP VALUE FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Large Cap Value Fund will, under normal market conditions, maintain at least 80% of its net assets in large cap stocks. The Fund follows a “value” approach, meaning the portfolio managers seek to invest in stocks at prices below their perceived intrinsic value as estimated based on fundamental analysis of the issuing company and its prospects. By investing in value stocks, the Fund attempts to limit the downside risk over time but may also produce smaller gains than other stock funds if their intrinsic values are not realized by the market or if growth-oriented investments are favored by investors. The Fund will diversify its holdings among various industries and among companies within those industries.

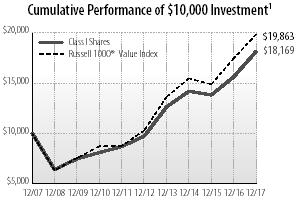

PERFORMANCE

For the full year, the Ultra Series Large Cap Value Fund (Class I) returned 16.23%, outperforming the Russell 1000® Value Index return of 13.66%. The Fund also outperformed its Morningstar peer group, the Morningstar Large Value Category, which returned 15.51% for the period.

Sector allocation detracted from performance, but stock selection was strong. In terms of sector allocation, underweight positions in Health Care and Technology, along with an overweight position in Industrials negatively impacted results. For stock selection, there were positive contributions from Utilities, Industrials, Health Care, Real Estate, and Technology, while there were negative results in Financials, Consumer Discretionary, and Materials. In Utilities, NRG Energy (NRG) was the best performing stock in the portfolio, while FedEx Corp. (FDX) was significantly additive to results within Industrials. In Health Care, medical device manufacturer Baxter (BAX) contributed nicely to performance as it had solid sales and earnings growth due to new product launches. Within Real Estate, data center real estate investment trust (REIT) Digital Realty (DLR) was a top performer as there was strong demand for its data center solutions. The Fund sold the stock as it reached what we believe was a full valuation. Another notable outperforming stock was mobile phone operator T-Mobile (TMUS) within Telecom. It continues to take subscriber market share with its innovative pricing plans and improved cellular network. On the negative side, within Financials, insurance conglomerate American International Group (AIG) hurt results as it reported weak underwriting profits on business it wrote as recently as 2016, which we believe impaired the thesis and the stock was sold. Within Consumer Discretionary, home furnishing retailer Lowe’s Companies (LOW) negatively impacted the portfolio. It had

11

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

a disappointing earnings report with weaker than expected same-store sales and the stock was sold we believe its thesis was impaired. In Materials, Nucor (NUE) was detractive to results and was sold. In Energy, exploration and production company Apache (APA) was the worst performing stock in the portfolio as it was hurt by low oil and natural gas prices. APA was sold to move the proceeds into other stocks where we have higher conviction levels. The Fund continues to hold all stocks mentioned above except for APA, AIG, DLR, LOW and NUE.

Average Annual Total Return (%) through December 31, 20171

Since

5/1/09

1 Year

3 Years

5 Years

10 Years

Inception

Ultra Series Large Cap

Value, Class I

16.23

8.53

13.32

6.15

–

Ultra Series Large Cap

Value, Class II

15.94

8.26

13.04

–

13.53

Russell 1000® Value Index

13.66

8.65

14.04

7.10

15.15

See accompanying Notes to Management’s Discussion of Fund Performance.

SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/17

Consumer Discretionary

3.3

%

Consumer Staples

2.2

%

Energy

15.4

%

Financials†

27.6

%

Health Care

6.7

%

Industrials

12.1

%

Information Technology

6.9

%

Materials

12.4

%

Money Market Funds

1.1

%

Real Estate

4.1

%

Telecommunication Services

4.1

%

Utilities

3.9

%

Net Other Assets and Liabilities

0.2

%

†Financials includes securities in the following industries: Capital Markets; Commercial Banks; Diversified Financial Services; and Insurance.

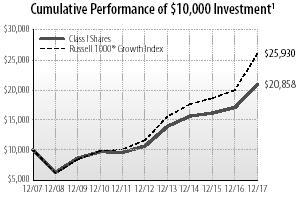

LARGE CAP GROWTH FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Large Cap Growth Fund invests primarily in common stocks of larger companies and will, under normal market conditions, maintain at least 80% of its net assets in large cap stocks. Stocks selected for the Fund will represent primarily well-established companies that have a demonstrated pattern of consistent growth. To a lesser extent, the Fund may invest in less established companies that may offer more rapid growth potential. The Fund has an active trading strategy which will lead to more portfolio turnover than a more passively-managed Fund.

PERFORMANCE

The Ultra Series Large Cap Growth Fund (Class I) returned 22.28% for the period, underperforming its benchmark, the Russell 1000® Growth Index, which returned 30.21%. The Fund underperformed its peer group, the Morningstar Large Growth category, which averaged a return of 30.01% over the same period.

The stock market, as measured by the Russell 1000 Growth® Index (RLG), produced a very strong year in 2017. During the year, market leadership was somewhat narrow as the Information Technology sector was dominant and accounted for nearly half of the total return of the RLG for the period. The next best sector, Consumer Discretionary (which includes Amazon), accounted for just 17% of the RLG’s return. The top ten individual company contributors to the RLG accounted for over 40% of the total return during the year. Our underweighting to these top ten performers resulted in approximately a 1.7% drag (before fees) on relative performance.

This current environment has favored high growth companies regardless of their valuation levels, which has created a near-term headwind for portfolio managers such as us that follow a discipline where valuation metrics are an integral part of their process (sometimes called GARP or Growth At a Reasonable Price). To demonstrate this challenge, just compare the 2017 return of 30.2% for the RLG versus a total return of just 13.6% for the Russell 1000® Value Index (RLV). Fortunately, this trend was showing signs of reversing itself late in the year.

12

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

During the year, our sector allocation decisions were slightly negative. For example, our under-weighting in Technology companies hampered our relative returns. In addition, although we held less than 3% cash on average during the year, it was still a slight drag on relative results given the strong market. We did benefit from a less than market weighting in Materials, Telecom and Utilities.

Our stock selection in the Technology, Health Care and Consumer Discretionary sectors negatively impacted our relative performance. While we did benefit from our significant Technology holdings, our underweighting of the select few high growth, mega-cap companies that led the market higher hindered results. In addition, our exposure to certain biotechnology companies in the Health Care sector and to media companies in the Consumer Discretionary sector also held back our relative performance. We did selectively cut back on our holdings in these areas, but many of these companies appear to be very inexpensive such that we have maintained ample exposure.

The basic backdrop for the stock market remains favorable. Interest rates and inflation remain low, the global economy is growing at a very solid pace and consumer confidence is very high. The passage of the business friendly income tax bill also added to this favorable setting. However, we do anticipate a more subdued market in 2018, given relatively high stock valuations and the likelihood of the Federal Reserve continuing to raise interest rates. As such, we remain optimistic but are cognizant of rising market risks and continued investor complacency. We believe investors will be well served by focusing on lower-risk, higher-quality companies for the foreseeable future. We remain diligent and committed to investing in high quality growth companies that can deliver consistent results in a variety of economic environments and also offer a margin of safety from a valuation perspective.

Average Annual Total Return (%) through December 31, 20171

Since

5/1/09

1 Year

3 Years

5 Years

10 Years

Inception

Ultra Series Large Cap

Growth, Class I

22.28

10.11

14.33

7.63

–

Ultra Series Large Cap

Growth, Class II

21.98

9.84

14.05

–

13.42

Russell 1000® Growth

Index

30.21

13.79

17.33

10.00

17.30

See accompanying Notes to Management’s Discussion of Fund Performance.

SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/17

Consumer Discretionary

18.8

%

Consumer Staples

9.9

%

Energy

3.8

%

Financials

8.2

%

Health Care

20.1

%

Industrials

4.5

%

Information Technology†

28.6

%

Materials

1.7

%

Money Market Funds

2.6

%

Real Estate

1.8

%

Net Other Assets and Liabilities

0.0

%

†Information Technology includes securities in the following industries: Computers and Peripherals; Electronic Equipment, Instruments & Components; Internet Software & Services; IT Services and Software.

MID CAP FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series Mid Cap Fund generally invests in common stocks of midsize companies and will, under normal market conditions, maintain at least 80% of its net assets in mid cap securities. The Fund seeks attractive long-term returns through bottom-up security selection based on fundamental analysis in a diversified portfolio of high-quality growth companies with attractive valuations. These will typically be industry leading companies in niches with strong growth prospects. The Fund’s portfolio managers believe in selecting stocks for the Fund that show steady, sustainable growth and reasonable valuations. As a result, stocks of issuers that are believed to have a blend of both value and growth potential will be selected for investment.

13

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

PERFORMANCE

The Ultra Series Mid Cap Fund (Class I) returned 15.74% for the annual period, trailing its benchmark Russell Midcap® Index’s 18.52% return. The Fund lagged its peer group, the Morningstar Mid-Cap Growth category, which returned 25.81%.

Both sector allocation and stock selection were unfavorable over the past 12 months. We were underweight the three weakest sectors of the Index – Telecommunications Services, Energy, and Real Estate – but we were also heavily underweight Information Technology, the best performing sector. The Fund was materially overweight Consumer Discretionary, which lagged the broader market. Our top three individual contributors were Copart, CDW, and Brookfield Asset Management. Our bottom three contributors were Sally Beauty, World Fuel, and Omnicom.

Copart is an auctioneer of salvaged cars. The more expensive components used in cars today and the skyrocketing usage of mobile phones while driving have increased the supply of totaled cars that flow through Copart’s lots. CDW is a value-added distributor selling hardware, software and services from thousands of vendors. The company is benefitting from growth in overall Information Technology spending. Brookfield Asset Management is an alternative asset manager that possesses the global scope, financial wherewithal, and operating acumen needed to invest in hard assets like real estate and infrastructure. Brookfield is currently in a high-growth phase that is benefitting from investors increasing allocations to hard assets.

Sally Beauty and World Fuel Services reported disappointing results for an extended period of time, and both stocks are no longer held in the Fund. Omnicom is an advertising agency that is experiencing a slowdown in ad spending from global consumer firms that have historically been bedrocks of agency business. The valuation of the stock more than reflects the slowdown.

Average Annual Total Return (%) through December 31, 20171

Since

5/1/09

1 Year

3 Years

5 Years

10 Years

Inception

Ultra Series Mid Cap,

Class I

15.74

9.68

13.38

7.89

–

Ultra Series Mid Cap,

Class II

15.45

9.41

13.09

–

15.08

Russell Midcap® Index

18.52

9.58

14.96

9.11

16.95

See accompanying Notes to Management’s Discussion of Fund Performance.

SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/17

Consumer Discretionary

23.4

%

Consumer Staples

1.6

%

Energy

0.9

%

Financials

21.7

%

Health Care

13.5

%

Industrials

16.1

%

Information Technology

6.4

%

Materials

6.6

%

Money Market Funds

5.1

%

Real Estate

4.7

%

Net Other Assets and Liabilities

0.0

%

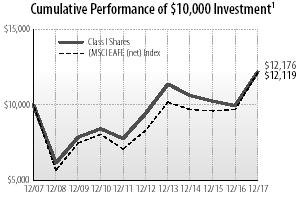

INTERNATIONAL STOCK FUND

INVESTMENT STRATEGY HIGHLIGHTS

The Ultra Series International Stock Fund will invest, under normal market conditions, at least 80% of its net assets in the stock of foreign companies. Typically, a majority of the Fund’s assets are invested in relatively large cap stocks of companies located or operating in developed countries. The Fund may also invest up to 30% of its assets in securities of companies whose principal business activities are located in emerging market countries. The portfolio managers typically maintain this segment of the Fund’s portfolio in such stocks which it believes have a low market price relative to their perceived value based on fundamental analysis of the issuing company and its prospects. The Fund may also invest in foreign debt and other income bearing securities at times when it believes that income bearing securities have greater capital appreciation potential than equity securities.

14

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - continued | December 31, 2017

PERFORMANCE

The Ultra Series International Stock Fund (Class I) returned 22.54% for the year, trailing the MSCI EAFE (net) Index’s 25.03% return. The Fund lagged its peer group, the Morningstar Foreign Large Blend Category, which returned 25.53%.

The strength of the global economy over the past year exceeded expectations, with positive growth occurring in all major regions, albeit off low levels. Outside the United States, earnings growth of over 20% drove stock returns higher in 2017. Sector leadership was dominated by cyclicals, and more specifically by Information Technology (+39% during 2017). More defensive, and some higher quality sectors such as Consumer Staples, Healthcare and Telecommunications, lagged in this market. As with sectors, regions with higher exposure to the global economy outperformed, driven by rising global growth prospects, a weaker U.S. dollar, and the improvement of industrial commodities prices. These factors especially benefited emerging markets, which generated extraordinary returns of 37.3% in 2017. Emerging markets Technology companies were especially favored by investors seeking companies with higher revenue and earnings growth – as well as higher valuations. Among developed markets, Japan generated significant returns in the fourth quarter, nearly matching the EAFE benchmark for the year after lagging in the first three quarters. Continental European equities outperformed the MSCI EAFE Index in U.S. dollar terms in 2017, boosted by stronger currencies. UK equities generated solid absolute returns of 22% in the year but modestly lagged the broader EAFE market amidst a challenging political backdrop and Brexit negotiations, which pushed valuation multiples lower.

Portfolio Review

Stock selection in the Healthcare sector detracted from performance in both the quarter and the year, as our holding in Shire underperformed. While having fallen nearly 10% in 2017 and being one of the largest relative detractors, Shire’s stock appears to be improving, rising in line with the benchmark during the fourth quarter. At 9.5x earnings with a 14% ROE, we expect the fundamentals of this company will drive earnings and cash flows in 2018, which we believe should ultimately rerate its valuation higher.

Our holding in Assa Abloy underperformed. This global leader in locks produces high, stable financial productivity in an industry with high barriers to entry (such as building codes and regulations that differ globally). Despite rising 13% during the year, the stock underperformed during the fourth quarter, falling nearly 9%, the result of a company specific, transitory issues in China, rising materials costs, and the CEO’s retirement announcement. However, we believe the stock will resume strong performance in 2018 due to a bottoming in their China operations coupled with strength in EMEA and North America.

Cash also continued to be a significant drag on relative performance in the quarter and the year. As equity markets continued to rise during the quarter and valuations remain elevated in historical terms, we have trimmed or sold some investments that have reached our target valuations faster than we have been able to replace them. Our cash exposure – which historically averages less than 5% of assets – is a byproduct of our process and is not a managed allocation. Our intention, as always, is to remain fully invested.

In contrast, stock selection in the consumer discretionary sector was additive to relative returns. Shares of Japanese retailer Don Quijote rose after reporting strong results driven by better sales and cost control, leading to operating profit margin expansion, while also increasing guidance. In the Industrials sector, Dutch software company Wolters Kluwer was a strong performer, both during the quarter and throughout the year, rising 13% and 47% respectively. Stock selection in the Real Estate sector was also beneficial to relative returns. Daiwa House was a

15

Ultra Series Fund | Management’s Discussion of Fund Performance (unaudited) - concluded | December 31, 2017

strong performer as it rose 11% during the quarter and 44% for the year. The Japanese diversified real estate company operates in the construction of residential housing (both single family and rental condominiums) as well as commercial facilities, including logistics and medical facilities as well as convenience stores. Positive stock selection in the Telecommunications sector was driven by Nordic telecommunications provider Telenor, which owns additional assets in emerging markets Malaysia and Thailand. Telenor stock rallied nearly 28% in the quarter, mostly because management reported earnings in July that beat expectations.

Average Annual Total Return through December 31, 20171

Since

5/1/09

1 Year

3 Years

5 Years

10 Years

Inception

Ultra Series International

Stock, Class I

22.54

4.73

5.28

1.99

–

Ultra Series International

Stock, Class II

22.24

4.47

5.02

–

8.40

MSCI EAFE Index (net)

25.03

7.80

7.90

1.94

9.54

See accompanying Notes to Management’s Discussion of Fund Performance.

SECTOR ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/17

Consumer Discretionary

16.6

%

Consumer Staples

10.5

%

Energy

7.6

%

Financials

17.4

%

Health Care

7.3

%

Industrials

15.9

%

Information Technology

7.2

%

Materials

5.5

%

Money Market Funds

1.6

%

Real Estate

2.6

%

Telecommunication Services

6.1

%

Utilities

1.5

%

Net Other Assets and Liabilities

0.2

%

GEOGRAPHICAL ALLOCATION AS A PERCENTAGE OF NET ASSETS

AS OF 12/31/17

Japan

18.5

%

United Kingdom

16.6

%

France

10.6

%

Netherlands

6.8

%

Switzerland

6.5

%

Canada

4.4

%

Germany

4.2

%

Sweden

3.4

%

Ireland

3.3

%

Australia

3.2

%

Norway

2.9

%

Belgium

2.5

%

Denmark

2.5

%

Singapore

2.5

%

United States

2.3

%

Spain

1.7

%

Finland

1.5

%

Taiwan

1.5

%

Turkey

1.1

%

Brazil

0.9

%

Italy

0.7

%

Luxembourg

0.6

%

Net Other Assets and Liabilities

0.2

%

16

Ultra Series Fund | December 31, 2017

Notes to Management’s Discussion of Fund Performance (unaudited)

1

Fund returns are calculated after fund level expenses have been subtracted, but do not include any separate account fees, charges or expenses imposed by the variable annuity and variable life insurance contracts that invest in the Fund, as described in the Prospectus. If these fees, charges, or expenses were included, fund returns would have been lower. Fund returns also assume that dividends and capital gains are reinvested in additional shares of the Fund. Investment return and principal value will fluctuate, so an investor’s shares, when redeemed, may be worth more or less than when purchased. Further information relating to the Fund’s performance is contained in the Prospectus and elsewhere in this report. The Fund’s past performance is not indicative of future performance. Current performance may be lower or higher than the performance data cited. For Ultra Series Fund performance data current to the most recent month-end, please call 1-800-670-3600 or visit www.ultraseriesfund.com. Indices are unmanaged and investors cannot invest in them directly. Index returns do not reflect fees or expenses.

2

Effective July 1, 2014 the Investment Adviser contractually agreed to waive a portion of the management fee for the Conservative, Moderate and Aggressive Allocation Funds until at least June 30, 2015. This waiver was renewed through April 30, 2018. If these waivers were not in place, returns would have been lower.

Morningstar Percentile rankings note: 1st percentile is top, 99th percentile is bottom.

BENCHMARK DESCRIPTIONS

Allocation Fund Indexes*

The Conservative Allocation Fund Custom Index consists of 65% Bloomberg Barclays US Aggregate Bond Index, 24.5% Russell 3000® Index and 10.5% MSCI ACWI ex-USA Index (net). See market index descriptions below.

The Moderate Allocation Fund Custom Index consists of 40% Bloomberg Barclays US Aggregate Bond Index, 42% Russell 3000® Index and 18% MSCI ACWI ex-USA Index (net). See market index descriptions below.

The Aggressive Allocation Fund Custom Index consists of 20% Bloomberg Barclays US Aggregate Bond Index, 56% Russell 3000® Index and 24% MSCI ACWI ex-USA Index (net). See market index descriptions below.

Hybrid Fund Custom Indexes*

The Custom Blended Index consists of 50% S&P 500 Index and 50% Bank of America Merrill Lynch U.S. Corporate, Government & Mortgage Index. See market indexes descriptions below.

*The Custom Indexes are calculated using a monthly re-balancing frequency (i.e., rebalanced back to original constituent weight every calendar month-end).

Market Indexes

The ICE Bank of America Merrill Lynch U.S. Corporate, Government & Mortgage Index is a broad-based measure of the total rate of return performance of the U.S. investment-grade bond markets. The index is a capitalization-weighted aggregation of outstanding U.S. treasury, agency and supranational mortgage pass-through, and investment-grade corporate bonds meeting specified selection criteria.

17

Ultra Series Fund | Notes to Management’s Discussion of Fund Performance (unaudited) - concluded | December 31, 2017

The ICE Bank of America Merrill Lynch U.S. High Yield Constrained Index tracks the performance of below investment grade U.S. dollar denominated corporate bonds publicly issued in the U.S. domestic market, but limits any individual issuer to a maximum weighting of 2%.

The Bloomberg Barclays Intermediate Government Credit Index measures the investment grade, U.S. dollar-denominated, fixed-rate, taxable corporate and government related bond markets. It is composed of the U.S. corporate index and a non-corporate component that includes foreign agencies, sovereigns, supranationals and local authorities.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, mortgage backed securities, asset backed securities and commercial mortgage-backed securities.

The MSCI EAFE (Europe, Australasia & Far East) Index (net) is a free float-adjusted market capitalization index that is designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI EAFE Index (net) is calculated on a total return basis with dividends reinvested after the deduction of withholding taxes.

The MSCI ACWI ex USA Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI ex USA (net) is calculated on a total return basis with dividends reinvested after the deduction of withholding taxes.

The Russell 1000® Growth Index is a large-cap market index which measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

The Russell 1000® Value Index is a large-cap market index which measures the performance of those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values.

The Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents 98% of the investable U.S. equity market.

The Russell Midcap® Index is a mid-cap market index which measures the performance of the mid-cap segment of the U.S. equity universe.

The S&P 500® Index is a large-cap market index which measures the performance of a representative sample of 500 leading companies in leading industries in the U.S.

Past performance is no guarantee of future results.

Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

18

Ultra Series Fund | December 31, 2017

Conservative Allocation Fund Portfolio of Investments

Shares

Value (Note 2)

INVESTMENT COMPANIES - 99.8%

Alternative Funds - 2.0%

SPDR Gold Shares*

24,457

$

3,024,108

Bond Funds - 57.9%

Baird Aggregate Bond Fund Institutional Shares

825,819

8,976,647

iShares 20+ Year Treasury Bond ETF

36,340

4,610,092

iShares 7-10 Year Treasury Bond ETF

39,456

4,165,370

iShares TIPS Bond Fund ETF

98,952

11,288,444

Madison Core Bond Fund Class Y (A)

3,370,781

33,640,397

Madison Corporate Bond Fund Class Y (A)

886,851

10,260,871

Vanguard Short-Term Corporate Bond ETF

84,465

6,698,075

Virtus Seix Floating Rate High Income Fund, Class R6

862,511

7,512,473

87,152,369

Foreign Stock Funds - 13.5%

iShares MSCI Eurozone ETF

62,615

2,716,239

iShares MSCI Japan ETF

18,859

1,130,220

Vanguard FTSE All-World ex-U.S. ETF

202,475

11,079,432

Vanguard FTSE Emerging Markets ETF

41,201

1,891,538

Vanguard FTSE Europe ETF

46,631

2,758,223

WisdomTree Japan Hedged Equity Fund

12,782

758,356

20,334,008

Money Market Funds - 2.3%

State Street Institutional U.S. Government

Money Market Fund, 1.21%, Premier Class

3,388,009

3,388,009

Stock Funds - 24.1%

Energy Select Sector SPDR Fund

17,443

1,260,431

iShares Core S&P Mid-Cap ETF

16,403

3,112,961

Madison Dividend Income Fund Class Y (A)

400,874

10,703,348

Madison Investors Fund Class Y (A)

466,612

10,662,079

Madison Mid Cap Fund Class Y (A)

239,672

2,365,565

PowerShares Optimum Yield Diversified

Commodity Strategy No. K-1 Portfolio

209,196

3,650,470

Vanguard Financials ETF

10,612

743,265

Vanguard Growth ETF

23,860

3,355,909

Vanguard Information Technology ETF

2,980

490,895

36,344,923

TOTAL INVESTMENTS - 99.8%

(Cost $139,532,351**)

150,243,417

NET OTHER ASSETS AND LIABILITIES - 0.2%

231,204

TOTAL NET ASSETS - 100.0%

$

150,474,621

*

Non-income producing.

**

Aggregate cost for Federal tax purposes was $139,788,001.

(A)

Affiliated Company (see Note 11).

ETF

Exchange Traded Fund.

See accompanying Notes to Financial Statements.

19

Ultra Series Fund | December 31, 2017

Moderate Allocation Fund Portfolio of Investments

Shares

Value (Note 2)

INVESTMENT COMPANIES - 99.9%

Alternative Funds - 2.0%

SPDR Gold Shares*

39,873

$

4,930,296

Bond Funds - 33.7%

Baird Aggregate Bond Fund Institutional Shares

252,273

2,742,207

iShares 20+ Year Treasury Bond ETF

59,179

7,507,448

iShares 7-10 Year Treasury Bond ETF

45,880

4,843,551

iShares TIPS Bond Fund ETF

107,434

12,256,071

Madison Core Bond Fund Class Y (A)

4,268,407

42,598,706

Madison Corporate Bond Fund Class Y (A)

437,539

5,062,324

Virtus Seix Floating Rate High Income Fund, Class R6

835,576

7,277,868

82,288,175

Foreign Stock Funds - 23.3%

iShares MSCI Eurozone ETF

178,102

7,726,065

iShares MSCI Japan ETF

61,118

3,662,801

Vanguard FTSE All-World ex-U.S. ETF

530,814

29,046,142

Vanguard FTSE Emerging Markets ETF

134,180

6,160,204

Vanguard FTSE Europe ETF

133,472

7,894,869

WisdomTree Japan Hedged Equity Fund

37,064

2,199,007

56,689,088

Money Market Funds - 1.2%

State Street Institutional U.S. Government

Money Market Fund, 1.21%, Premier Class

2,970,572

2,970,572

Stock Funds - 39.7%

Energy Select Sector SPDR Fund

40,991

2,962,010

iShares Core S&P Mid-Cap ETF

42,379

8,042,687

Madison Dividend Income Fund Class Y (A)

1,081,152

28,866,751

Madison Investors Fund Class Y (A)

1,258,199

28,749,850

Madison Large Cap Value Fund Class Y (A)

530,228

7,757,239

Madison Mid Cap Fund Class Y (A)

491,383

4,849,948

PowerShares Optimum Yield Diversified

Commodity Strategy No. K-1 Portfolio

341,225

5,954,376

Vanguard Financials ETF

17,280

1,210,291

Vanguard Growth ETF

51,671

7,267,526

Vanguard Information Technology ETF

7,352

1,211,095

96,871,773

TOTAL INVESTMENTS - 99.9%

(Cost $211,969,758**)

243,749,904

NET OTHER ASSETS AND LIABILITIES - 0.1%

315,029

TOTAL NET ASSETS - 100.0%

$

244,064,933

*

Non-income producing.

**

Aggregate cost for Federal tax purposes was $212,727,572.

(A)

Affiliated Company (see Note 11).

ETF

Exchange Traded Fund.

See accompanying Notes to Financial Statements.

20

Ultra Series Fund | December 31, 2017

Aggressive Allocation Fund Portfolio of Investments

Shares

Value (Note 2)

INVESTMENT COMPANIES - 99.8%

Alternative Funds - 2.0%

SPDR Gold Shares*

13,920

$

1,721,208

Bond Funds - 13.7%

iShares 20+ Year Treasury Bond ETF

12,077

1,532,088

iShares 7-10 Year Treasury Bond ETF

18,205

1,921,902

Madison Core Bond Fund Class Y (A)

841,003

8,393,210

11,847,200

Foreign Stock Funds - 31.2%

iShares MSCI Eurozone ETF

90,342

3,919,036

iShares MSCI Japan ETF

28,738

1,722,268

Vanguard FTSE All-World ex-U.S. ETF

235,650

12,894,768

Vanguard FTSE Emerging Markets ETF

71,574

3,285,962

Vanguard FTSE Europe ETF

67,703

4,004,633

WisdomTree Japan Hedged Equity Fund

20,332

1,206,298

27,032,965

Money Market Funds - 1.4%

State Street Institutional U.S. Government

Money Market Fund, 1.21%, Premier Class

1,215,283

1,215,283

Stock Funds - 51.5%

Energy Select Sector SPDR Fund

20,074

1,450,547

iShares Core S&P Mid-Cap ETF

23,100

4,383,918

Madison Dividend Income Fund Class Y (A)

432,730

11,553,878

Madison Investors Fund Class Y (A)

502,853

11,490,182

Madison Large Cap Value Fund Class Y (A)

291,130

4,259,230

Madison Mid Cap Fund Class Y (A)

428,588

4,230,159

PowerShares Optimum Yield Diversified

Commodity Strategy No. K-1 Portfolio

101,742

1,775,398

Vanguard Financials ETF

9,218

645,629

Vanguard Growth ETF

27,562

3,876,596

Vanguard Information Technology ETF

5,203

857,090

44,522,627

TOTAL INVESTMENTS - 99.8%

(Cost $71,603,748**)

86,339,283

NET OTHER ASSETS AND LIABILITIES - 0.2%

145,177

TOTAL NET ASSETS - 100.0%

$

86,484,460

*

Non-income producing.

**

Aggregate cost for Federal tax purposes was $71,793,660.

(A)

Affiliated Company (see Note 11).

ETF

Exchange Traded Fund.

See accompanying Notes to Financial Statements.

21

Ultra Series Fund | December 31, 2017

Core Bond Fund Portfolio of Investments

Par Value

Value (Note 2)

ASSET BACKED SECURITIES - 2.2%

CarMax Auto Owner Trust, Series 2014-1, Class B, 1.69%, 8/15/19

$

510,000

$

509,788

CarMax Auto Owner Trust, Series 2017-1, Class A2, 1.54%, 2/18/20

673,133

672,244