|

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| WASHINGTON, D.C. 20549 |

| -------- |

| |

| FORM N-CSR |

| -------- |

| |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT |

| INVESTMENT COMPANIES |

| |

| INVESTMENT COMPANY ACT FILE NUMBER 811-3967 |

| |

| FIRST INVESTORS INCOME FUNDS |

| (Exact name of registrant as specified in charter) |

| |

| 110 Wall Street |

| New York, NY 10005 |

| (Address of principal executive offices) (Zip code) |

| |

| Joseph I. Benedek |

| First Investors Management Company, Inc. |

| Raritan Plaza I |

| Edison, NJ 08837-3620 |

| (Name and address of agent for service) |

| |

| REGISTRANT'S TELEPHONE NUMBER, INCLUDING AREA CODE: |

| 1-212-858-8000 |

| |

| DATE OF FISCAL YEAR END: SEPTEMBER 30, 2011 |

| |

| DATE OF REPORTING PERIOD: SEPTEMBER 30, 2011 |

| |

| Item 1. | Reports to Stockholders |

| |

| | The annual report to stockholders follows |

This report is for the information of the shareholders of the Funds. It is the policy of each Fund described in this report to mail only one copy of a Fund’s prospectus, annual report, semi-annual report and proxy statements to all shareholders who share the same address and share the same last name and have invested in a Fund covered by the same document. You are deemed to consent to this policy unless you specifi-cally revoke this policy and request that separate copies of such documents be mailed to you. In such case, you will begin to receive your own copies within 30 days after our receipt of the revocation. You may request that separate copies of these disclosure documents be mailed to you by writing to us at: Administrative Data Management Corp., Raritan Plaza I, Edison, NJ 08837-3620 or calling us at 1-800-423-4026.

The views expressed in the portfolio manager letters reflect those views of the portfolio managers only through the end of the period covered. Any such views are subject to change at any time based upon market or other conditions and we disclaim any responsibility to update such views. These views may not be relied on as investment advice.

You may obtain a free prospectus for any of the Funds by contacting your representative, calling 1-800-423-4026, writing to us at the following address: First Investors Corporation, 110 Wall Street, New York, NY 10005, or by visiting our website at www.firstinvestors.com. You should consider the investment objectives, risks, charges and expenses of a Fund carefully before investing. The prospectus contains this and other information about the Fund, and should be read carefully before investing.

An investment in a Fund is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. Although the Cash Management Fund seeks to preserve a net asset value at $1.00 per share, it is possible to lose money by investing in it, just as it is possible to lose money by investing in any of the other Funds. Past performance is no guarantee of future results.

A Statement of Additional Information (“SAI”) for any of the Funds may also be obtained, without charge, upon request by calling 1-800-423-4026, writing to us at our address or by visiting our website listed above. The SAI contains more detailed information about the Funds, including information about its Trustees.

Portfolio Manager’s Letter

CASH MANAGEMENT FUND

Dear Investor:

This is the annual report for the First Investors Cash Management Fund for the fiscal year ended September 30, 2011. During the period, the Fund’s return on a net asset value basis was 0% for Class A shares and 0% for Class B shares. The Fund maintained a $1.00 net asset value per share for each class of shares throughout the year.

In response to continued subpar economic growth, the Federal Reserve (the “Fed”) maintained short-term interest rates at record lows, near zero, throughout the review period. In addition, in August the Fed committed to maintain interest rates at their current exceptionally low levels through at least mid-2013. These were the major factors that determined the Fund’s return.

Last year the Securities and Exchange Commission amended the rules for money market funds. These amendments were aimed at further reducing the risk for money market fund shareholders by increasing a fund’s credit quality and diversification. In addition, the new rules also improved the overall liquidity of a fund’s assets.

To meet these new requirements and to respond to overall conditions in the market, the Fund continued to invest conservatively throughout the review period. It maintained elevated exposure to U.S. Treasury and government obligations, which have very high credit ratings and exceptional liquidity, although a lower return. The Fund has not sought the additional yield that has been available from investments in foreign bank and sovereign obligations as the Fund has historically been conservative relative to its peers. In the current interest rate environment, we have found the risk/reward relationship those obligations offer to be unattractive.

First Investors Management Company, Inc. (“FIMCO”), the Fund’s investment adviser, continued to absorb expenses of the Fund and waived management fees in an effort to avoid a negative yield to its shareholders. In addition, to mitigate expenses, certain shareholder privileges remained limited. FIMCO expects this situation to continue and consequently, the yield to shareholders should remain at or near zero for the foreseeable future.

Thank you for placing your trust in First Investors. As always, we appreciate the opportunity to serve your investment needs.

Understanding Your Fund’s Expenses (unaudited)

FIRST INVESTORS INCOME FUNDS

FIRST INVESTORS EQUITY FUNDS

As a mutual fund shareholder, you incur two types of costs: (1) transaction costs, including a sales charge (load) on purchase payments (on Class A shares only) and a contingent deferred sales charge on redemptions (on Class B shares only); and (2) ongoing costs, including advisory fees; distribution and service fees (12b-1); and other expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 in each Fund at the beginning of the period, April 1, 2011, and held for the entire six-month period ended September 30, 2011. The calculations assume that no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

Actual Expenses Example:

These amounts help you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the “Expenses Paid During Period” shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To estimate the expenses you paid on your account during this period, simply divide your ending account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60), then multiply the result by the number given for your Fund under the heading “Expenses Paid During Period”.

Hypothetical Expenses Example:

These amounts provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio for Class A and Class B shares, and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight and help you compare your ongoing costs only and do not reflect any transaction costs, such as front-end or contingent deferred sales charges (loads). Therefore, the hypothetical expenses example is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Fund Expenses (unaudited)

CASH MANAGEMENT FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 2 for a detailed explanation of the information presented in these examples.

| | | |

| | Beginning | Ending | |

| | Account | Account | Expenses Paid |

| | Value | Value | During Period |

| | (4/1/11) | (9/30/11) | (4/1/11–9/30/11)* |

| Expense Example – Class A Shares | | | |

| Actual | $1,000.00 | $1,000.00 | $0.55 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,024.52 | $0.56 |

| Expense Example – Class B Shares | | | |

| Actual | $1,000.00 | $1,000.00 | $0.55 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,024.52 | $0.56 |

| |

| * | Expenses are equal to the annualized expense ratio of .11% for Class A shares and .11% for Class B |

| shares, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the |

| one-half year period). Expenses paid during the period are net of expenses waived or assumed. |

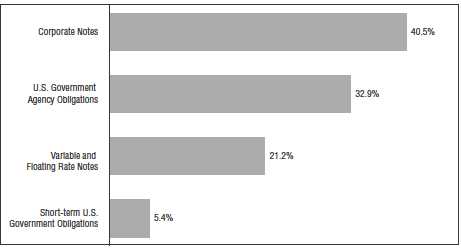

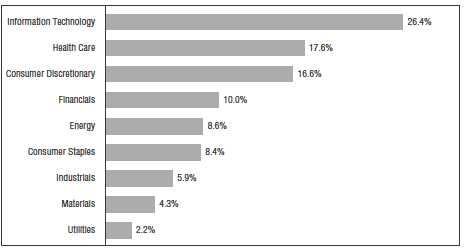

Portfolio Composition

BY SECTOR

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2011, and are based on the total value of investments.

Portfolio of Investments (continued)

CASH MANAGEMENT FUND

September 30, 2011

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | Interest | | | | |

| Amount | | Security | Rate* | | | | Value |

| | | CORPORATE NOTES—40.1% | | | | | |

| $ 4,050M | | 3M Co., 11/1/11 | 0.20 | % | | | $ 4,064,613 |

| | | Coca-Cola Co.: | | | | | |

| 1,000M | | 11/8/11 (a) | 0.19 | | | | 999,799 |

| 5,000M | | 12/6/11 (a) | 0.13 | | | | 4,998,808 |

| 4,000M | | Dupont (E.I.) de Nemours & Co., 11/21/11 (a) | 0.15 | | | | 3,999,150 |

| 4,000M | | General Electric Capital Corp., 11/15/11 | 0.34 | | | | 4,022,829 |

| 6,000M | | Johnson & Johnson, 12/19/11 (a) | 0.08 | | | | 5,998,947 |

| 5,000M | | McDonald’s Corp., 10/14/11 (a) | 0.10 | | | | 4,999,819 |

| 4,000M | | Medtronic, Inc., 10/12/11 (a) | 0.13 | | | | 3,999,841 |

| 5,000M | | Novartis Securities Investment, Ltd., 10/11/11 (a) | 0.17 | | | | 4,999,764 |

| 3,500M | | PepsiCo, Inc., 11/1/11 (a) | 0.10 | | | | 3,499,699 |

| | | Procter & Gamble Co.: | | | | | |

| 3,500M | | 12/2/11 (a) | 0.16 | | | | 3,499,035 |

| 2,000M | | 12/12/11 (a) | 0.15 | | | | 1,999,400 |

| 1,000M | | 1/9/12 (a) | 0.15 | | | | 999,582 |

| 7,000M | | Wal-Mart Stores, Inc., 10/28/11 (a) | 0.08 | | | | 6,999,580 |

| 5,000M | | Walt Disney Co., 10/17/11 (a) | 0.11 | | | | 4,999,755 |

| Total Value of Corporate Notes (cost $60,080,621) | | | | | 60,080,621 |

| | | U.S. GOVERNMENT AGENCY | | | | | |

| | | OBLIGATIONS—32.6% | | | | | |

| | | Fannie Mae: | | | | | |

| 3,396M | | 10/3/11 | 0.10 | | | | 3,395,981 |

| 7,000M | | 12/28/11 | 0.02 | | | | 6,999,658 |

| 4,000M | | Federal Home Loan Bank 12/30/11 | 0.16 | | | | 4,010,770 |

| | | Freddie Mac: | | | | | |

| 11,000M | | 10/6/11 | 0.04 | | | | 10,999,947 |

| 540M | | 10/12/11 | 0.11 | | | | 539,982 |

| 4,925M | | 10/31/11 | 0.08 | | | | 4,924,672 |

| 3,700M | | 11/2/11 | 0.07 | | | | 3,699,770 |

| 4,340M | | 11/9/11 | 0.04 | | | | 4,339,812 |

| 7,524M | | 11/28/11 | 0.03 | | | | 7,523,636 |

| 2,300M | | 12/12/11 | 0.08 | | | | 2,299,632 |

| Total Value of U.S. Government Agency Obligations (cost $48,733,860) | | | | 48,733,860 |

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | Interest | | | | |

| Amount | | Security | Rate* | | | | Value |

| | | VARIABLE AND FLOATING RATE NOTES—21.0% | | | | |

| $ 3,000M | | Federal Farm Credit Bank, 9/24/12 | 0.12 | % | | | $ 2,998,236 |

| 5,000M | | Federal Home Loan Bank, 6/22/12 | 0.11 | | | | 4,998,530 |

| 5,500M | | Freddie Mac, 11/9/11 | 0.07 | | | | 5,499,707 |

| 5,700M | | Mississippi Business Finance Corp. | | | | | |

| | | (Chevron USA, Inc.), 12/1/30 | 0.09 | | | | 5,700,000 |

| 3,820M | | Monongallia Health Systems,, 7/1/40 (LOC: JP Morgan) 0.40 | | | | 3,820,000 |

| 2,595M | | University of Oklahoma Hospital Rev. Series “B”, | | | | |

| | | 8/15/21 (LOC: Bank of America) | 0.35 | | | | 2,595,000 |

| 5,835M | | Valdez, Alaska Marine Terminal Rev. | | | | | |

| | | (Exxon Pipeline Co., Project B), 12/1/33 | 0.09 | | | | 5,835,000 |

| Total Value of Variable and Floating Rate Notes (cost $31,446,473) | | | | 31,446,473 |

| | | SHORT-TERM U.S. GOVERNMENT | | | | | |

| | | OBLIGATIONS—5.3% | | | | | |

| | | U.S. Treasury Bills: | | | | | |

| 4,000M | | 10/27/11 | 0.01 | | | | 3,999,971 |

| 4,000M | | 12/15/11 | 0.04 | | | | 3,999,708 |

| Total Value of Short-Term U.S. Government Obligations (cost $7,999,679) | | | | 7,999,679 |

| Total Value of Investments (cost $148,260,633)** | 99.0 | % | | | 148,260,633 |

| Other Assets, Less Liabilities | 1.0 | | | | 1,429,397 |

| Net Assets | | | 100.0 | % | | | $149,690,030 |

| |

| * | The interest rates shown are the effective rates at the time of purchase by the Fund. The interest |

| rates shown on floating rate notes are adjusted periodically; the rates shown are the rates in effect |

| at September 30, 2011. |

| ** | Aggregate cost for federal income tax purposes is the same. |

| (a) | Security exempt from registration under Section 4(2) of the Securities Act of 1933 (see Note 4). |

| |

Summary of Abbreviations: |

| LOC | Letters of Credit |

Portfolio of Investments (continued))

CASH MANAGEMENT FUND

September 30, 2011

Accounting Standards Codification (“ASC”) 820 established a three-tier hierarchy of inputs to establish a classification of fair value measurements for disclosure purposes. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below:

| Level 1 — Unadjusted quoted prices in active markets for identical securities that the Fund has the ability to access. |

| Level 2 — Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

| Level 3 — Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumption about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

The inputs methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary, by category of Level, of inputs used to value the Fund’s investments as of September 30, 2011:

| | | | | | | | | | | | |

| | | | Level 1 | | | Level 2 | | | Level 3 | | | Total |

| Corporate Notes | | $ | — | | $ | 60,080,621 | | $ | — | | $ | 60,080,621 |

| U.S. Government Agency | | | | | | | | | | | | |

| Obligations | | | — | | | 48,733,860 | | | — | | | 48,733,860 |

| Variable and Floating Rate Notes: | | | | | | | | | | | | |

| Municipal Bonds | | | — | | | 14,130,000 | | | — | | | 14,130,000 |

| U.S. Government Agency | | | | | | | | | | | | |

| Obligations | | | — | | | 13,496,473 | | | — | | | 13,496,473 |

| Corporate Notes | | | — | | | 3,820,000 | | | — | | | 3,820,000 |

| Short-Term U.S. Government | | | | | | | | | | | | |

| Obligations | | | — | | | 7,999,679 | | | — | | | 7,999,679 |

| Total Investments in Securities | | $ | — | | $ | 148,260,633 | | $ | — | | $ | 148,260,633 |

There were no transfers into or from Level 1 or Level 2 by the Fund during the year ended September 30, 2011.

| | |

| 6 | See notes to financial statements | |

Portfolio Manager’s Letter

GOVERNMENT FUND

Dear Investor:

This is the annual report for the First Investors Government Fund for the fiscal year ended September 30, 2011. During the period, the Fund’s return on a net asset value basis was 5.7% for Class A shares and 4.9% for Class B shares, including dividends of 40.8 cents per share on Class A shares and 33.2 cents per share on Class B shares.

The Fund invests primarily in Ginnie Maes, which are mortgage-backed bonds issued by the Government National Mortgage Association (GNMA). These bonds are backed by the full faith and credit of the U.S. government.

The review period was characterized by significant volatility in the financial markets against a background of disappointing economic growth and fiscal concerns in the United States and Europe. Economic growth fell short of expectations in the first half of 2011 due to higher oil prices as a result of unrest in the Middle East and supply chain disruptions stemming from the earthquake in Japan.

While growth bounced back in the final quarter of the review period, by that time consumer and business sentiment had become notably depressed, reflecting uncertainty about U.S. fiscal policy and concern that the ongoing European sovereign debt crisis would — if unresolved — lead to a financial crisis that could tip the United States back into recession. The unemployment rate remained elevated during the review period at 9.1%. Inflation, as measured by the consumer price index and excluding the volatile food and energy components, moved higher but remained benign at 2% year-over-year.

Interest rates moved lower (and bond prices rose) during the review period. The benchmark two-year U.S. Treasury note yield fell to an all-time low of 0.16%, ending the review period at 0.25%. The ten-year U.S. Treasury yield fell to 1.7% from 2.5%, the lowest level in over 50 years, closing the period at 1.9%. The decline in Treasury rates reflected slower-than-expected economic growth, preference for safe investments due to the uncertainty in Europe (despite the downgrade of the U.S. government’s credit rating by Standard and Poor’s in August), and aggressive actions by the Federal Reserve to stimulate the economy.

The broad bond market returned 5.2% during the review period, according to Bank of America Merrill Lynch. In general, less risky sectors of the market had higher returns. The GNMA mortgage-backed market, in particular, returned 6.8%. The sector benefited from the positive impact of falling interest rates and its high credit quality. Within the GNMA sector, lower coupon mortgage-backed bonds had better returns than higher coupons due to the former’s greater sensitivity to changes in interest rates

Portfolio Manager’s Letter (continued)

GOVERNMENT FUND

and higher prepayments on the latter as homeowners took advantage of record low mortgage rates to refinance outstanding mortgages.

An underweight in lower coupon mortgage-backed bonds detracted from the Fund’s performance versus the Bank of America Merrill Lynch GNMA Master Index. The Fund’s average of 10% of assets in Fannie Mae and Freddie Mac mortgage-backed bonds also had a negative impact on performance as they underperformed GNMAs due to higher prepayments and investor preference for the government guarantee on GNMAs. The Fund benefited from security selection through its focus on mortgage-backed pools with low loan balances. Because mortgages in these pools are less likely to be refinanced, the value of the pools increased during the review period as investors sought securities that provided protection from rising prepayments.

Thank you for placing your trust in First Investors. As always, we appreciate the opportunity to serve your investment needs.

Fund Expenses (unaudited)

GOVERNMENT FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 2 for a detailed explanation of the information presented in these examples.

| | | |

| | Beginning | Ending | |

| | Account | Account | Expenses Paid |

| | Value | Value | During Period |

| | (4/1/11) | (9/30/11) | (4/1/11–9/30/11)* |

| Expense Example – Class A Shares | | | |

| Actual | $1,000.00 | $1,044.91 | $5.74 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,019.45 | $5.67 |

| Expense Example – Class B Shares | | | |

| Actual | $1,000.00 | $1,040.65 | $9.31 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,015.95 | $9.20 |

| |

| * | Expenses are equal to the annualized expense ratio of 1.12% for Class A shares and 1.82% for |

| Class B shares, multiplied by the average account value over the period, multiplied by 183/365 |

| (to reflect the one-half year period). Expenses paid during the period are net of expenses waived. |

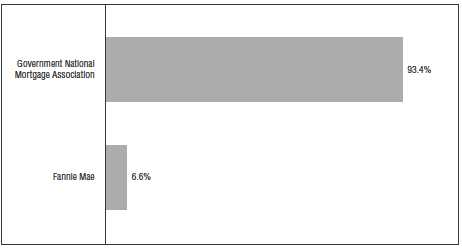

Portfolio Composition

BY SECTOR

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2011, and are based on the total value of investments.

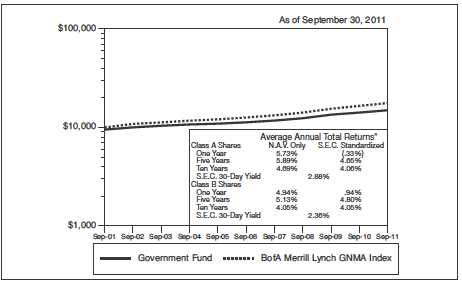

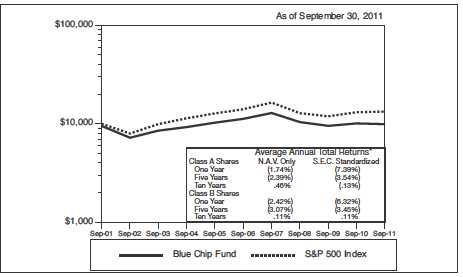

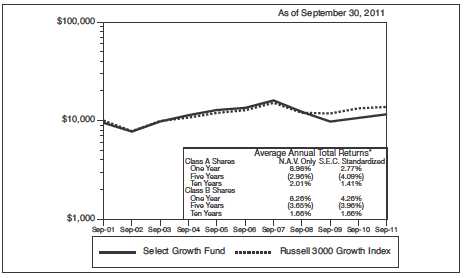

Cumulative Performance Information (unaudited)

GOVERNMENT FUND

Comparison of change in value of $10,000 investment in the First Investors Government Fund (Class A shares) and the Bank of America (“BofA”) Merrill Lynch GNMA Master Index.

The graph compares a $10,000 investment in the First Investors Government Fund (Class A shares) beginning 9/30/01 with a theoretical investment in the BofA Merrill Lynch GNMA Master Index (the “Index”). The Index is a market capitalization-weighted index of securities backed by mortgage pools of the Government National Mortgage Association (GNMA). It is not possible to invest directly in this Index. In addition, the Index does not reflect fees and expenses associated with the active management of a mutual fund portfolio. For purposes of the graph and the accompanying table, unless otherwise indicated, it has been assumed that the maximum sales charge was deducted from the initial $10,000 investment in the Fund and all dividends and distributions were reinvested. Class B shares performance may be greater than or less than that shown in the line graph above for Class A shares based on differences in sales loads and fees paid by shareholders investing in the different classes.

* Average Annual Total Return figures (for the periods ended 9/30/11) include the reinvestment of all dividends and distributions. “N.A.V. Only” returns are calculated without sales charges. The Class A “S.E.C. Standardized” returns shown are based on the maximum sales charge of 5.75% (prior to 6/17/02, the maximum sales charge was 6.25%). The Class B “S.E.C. Standardized” returns are adjusted for the applicable deferred sales charge (maximum of 4% in the first year). During the periods shown, some of the expenses of the Fund were waived or assumed. If such expenses had been paid by the Fund, the Class A “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been (.44%), 4.53% and 3.82%, respectively, and the S.E.C. 30-Day Yield for September 2011 would have been 2.77%. The Class B “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been .83%, 4.68% and 3.80%, respectively, and the S.E.C. 30-Day Yield for September 2011 would have been 2.25%. Results represent past performance and do not indicate future results. The graph and the returns shown do not reflect the deduction of taxes that a shareholder would pay on distributions or the redemption of fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Index figures are from Bank of America Merrill Lynch & Co. and all other figures are from First Investors Management Company, Inc.

Portfolio of Investments

GOVERNMENT FUND

September 30, 2011

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | RESIDENTIAL MORTGAGE-BACKED | | | | |

| | | SECURITIES—99.0% | | | | | |

| | | Fannie Mae—6.5% | | | | | |

| $ 8,433M | | 5%, 8/1/2039 – 11/1/2039 | | | | | $ 9,121,642 |

| 12,651M | | 5.5%, 7/1/2033 – 10/1/2039 | | | | | 13,900,134 |

| | | | | | | | 23,021,776 |

| | | Government National Mortgage Association I | | | | |

| | | Program—92.5% | | | | | |

| 112,873M | | 4.5%, 9/15/2033 – 8/15/2041 | | | | | 122,941,289 |

| 84,039M | | 5%, 6/15/2033 – 6/15/2040 | | | | | 92,752,801 |

| 47,927M | | 5.5%, 3/15/2033 – 10/15/2039 | | | | | 53,320,025 |

| 37,570M | | 6%, 3/15/2031 – 5/15/2040 | | | | | 42,267,941 |

| 10,702M | | 6.5%, 10/15/2028 – 3/15/2038 | | | | | 12,327,434 |

| 3,341M | | 7%, 1/15/2030 – 4/15/2034 | | | | | 3,943,285 |

| | | | | | | | 327,552,775 |

| Total Value of Residential Mortgage-Backed Securities | | | | | |

| (cost $331,702,737) | 99.0 | % | | | 350,574,551 |

| Other Assets, Less Liabilities | 1.0 | | | | 3,537,359 |

| Net Assets | | | 100.0 | % | | | $354,111,910 |

Portfolio of Investments (continued))

GOVERNMENT FUND

September 30, 2011

Accounting Standards Codification (“ASC”) 820 established a three-tier hierarchy of inputs to establish a classification of fair value measurements for disclosure purposes. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below:

| Level 1 — Unadjusted quoted prices in active markets for identical securities that the Fund has the ability to access. |

| Level 2 — Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

| Level 3 — Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumption about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

The inputs methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary, by category of Level, of inputs used to value the Fund’s investments as of September 30, 2011:

| | | | | | | | | | | | |

| | | | Level 1 | | | Level 2 | | | Level 3 | | | Total |

| Residential Mortgage-Backed | | | | | | | | | | | | |

| Securities | | $ | — | | $ | 350,574,551 | | $ | — | | $ | 350,574,551 |

There were no transfers into or from Level 1 or Level 2 by the Fund during the year ended September 30, 2011.

| | |

| 12 | See notes to financial statements | |

Portfolio Managers’ Letter

INVESTMENT GRADE FUND

Dear Investor:

This is the annual report for the First Investors Investment Grade Fund for the fis-cal year ended September 30, 2011. During the period, the Fund’s return on a net asset value basis was 2.5% for Class A shares and 1.8% for Class B shares, including dividends of 42.6 cents per share on Class A shares and 36.2 cents per share on Class B shares.

The Fund invests in investment grade fixed income securities. The majority of the Fund’s assets were in investment grade corporate bonds. The Fund also had as much as 5% of its assets in mortgage-backed securities and 2% in high yield corporate bonds.

The review period began with confidence in the increased financial strength of corporate issuers. However, over the next several months the positive tone was offset by certain systemic concerns. Weak economic data pointed toward an increased likelihood that the U.S. economy was moving in the direction of recession. Concern about rising eurozone deficits and debt levels led to multiple notch downgrades of European government debt and increased market scrutiny on sovereign risk. While the Fund did not have any direct exposure to European government debt, concerns about it had an impact on the Fund’s investments in U.S. corporate bonds due to the possibility that problems in Europe could result in a recession in the United States.

Interest rates moved lower (and bond prices rose) during the review period. The benchmark two-year U.S. Treasury note yield fell to an all-time low of 0.16%, ending the review period at 0.25%. The ten-year U.S. Treasury yield fell to 1.7% from 2.5%, the lowest level in over 50 years, closing the period at 1.9%. The decline in Treasury rates reflected slower-than-expected economic growth, preference for safe investments due to the uncertainty in Europe, and aggressive actions by the Federal Reserve (the “Fed”) to stimulate the economy.

Even after the downgrade of U.S. Government debt by Standard & Poor’s from AAA to AA+ in August, benchmark U.S. Treasury yields moved to record lows in anticipation of action by the Fed to lower long-term interest rates. By the end of the review period, corporate bond spreads had widened year-over-year as European sovereign risk concerns continued to weigh on the market. Nonetheless, the corporate bond market had a positive return of 4% for the period, according to Bank of America Merrill Lynch, due to the general decline in interest rates.

Portfolio Managers’ Letter (continued)

INVESTMENT GRADE FUND

The Fund underperformed the Bank of America Merrill Lynch U.S. Corporate Master Index during the review period. The relative performance was predominantly the result of the Fund’s underweight in corporate bonds with maturities greater than 10 years. Long maturity bonds had the highest returns during the review period, as falling 30-year U.S. Treasury yields reached all-time lows. This was somewhat offset by the Fund’s underweight in corporate bonds in the banking sector, which had negative returns for the review period.

Thank you for placing your trust in First Investors. As always, we appreciate the opportunity to serve your investment needs.

Fund Expenses (unaudited)

INVESTMENT GRADE FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 2 for a detailed explanation of the information presented in these examples.

| | | |

| | Beginning | Ending | |

| | Account | Account | Expenses Paid |

| | Value | Value | During Period |

| | (4/1/11) | (9/30/11) | (4/1/11–9/30/11)* |

| Expense Example – Class A Shares | | | |

| Actual | $1,000.00 | $1,033.99 | $5.61 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,019.55 | $5.57 |

| Expense Example – Class B Shares | | | |

| Actual | $1,000.00 | $1,030.65 | $9.16 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,016.05 | $9.10 |

| |

| * | Expenses are equal to the annualized expense ratio of 1.10% for Class A shares and 1.80% for |

| Class B shares, multiplied by the average account value over the period, multiplied by 183/365 |

| (to reflect the one-half year period). Expenses paid during the period are net of expenses waived. |

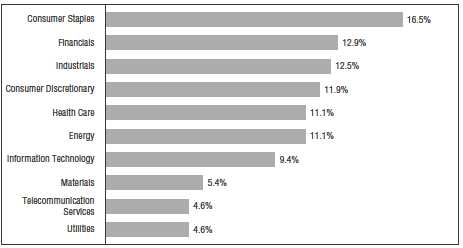

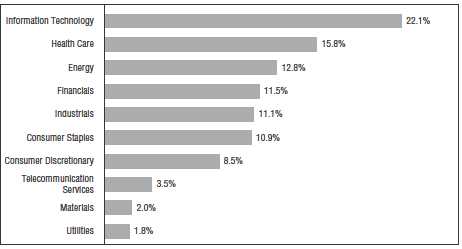

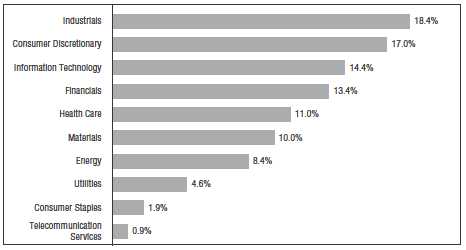

Portfolio Composition

TOP TEN SECTORS

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2011, and are based on the total value of investments.

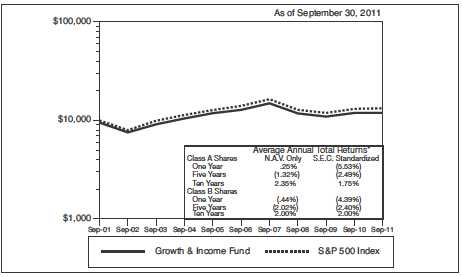

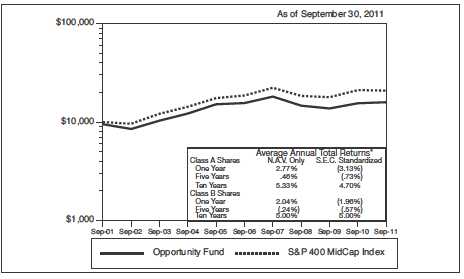

Cumulative Performance Information (unaudited)

INVESTMENT GRADE FUND

Comparison of change in value of $10,000 investment in the First Investors Investment Grade Fund (Class A shares) and the Bank of America (“BofA”) Merrill Lynch U.S. Corporate Master Index.

The graph compares a $10,000 investment in the First Investors Investment Grade Fund (Class A shares) beginning 9/30/01 with a theoretical investment in the BofA Merrill Lynch U.S. Corporate Master Index (the “Index”). The Index tracks the performance of U.S. dollar-denominated investment grade corporate public debt issued in the U.S. domestic bond market. Qualifying bonds must have at least one year remaining term to maturity, a fixed coupon schedule and a minimum amount outstanding of $250 million. Bonds must be rated investment grade based on a composite of Moody’s and S&P. It is not possible to invest directly in this Index. In addition, the Index does not reflect fees and expenses associated with the active management of a mutual fund portfolio. For purposes of the graph and the accompanying table, unless otherwise indicated, it has been assumed that the maximum sales charge was deducted from the initial $10,000 investment in the Fund and all dividends and distributions were reinvested. Class B shares performance may be greater than or less than that shown in the line graph above for Class A shares based on differences in sales loads and fees paid by shareholders investing in the different classes.

* Average Annual Total Return figures (for the periods ended 9/30/11) include the reinvestment of all dividends and distributions. “N.A.V. Only” returns are calculated without sales charges. The Class A “S.E.C. Standardized” returns shown are based on the maximum sales charge of 5.75% (prior to 6/17/02, the maximum sales charge was 6.25%). The Class B “S.E.C. Standardized” returns are adjusted for the applicable deferred sales charge (maximum of 4% in the first year). During the periods shown, some of the expenses of the Fund were waived or assumed. If such expenses had been paid by the Fund, the Class A “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been (3.53%), 3.96% and 4.21%, respectively, and the S.E.C. 30-Day Yield for September 2011 would have been 2.68%. The Class B “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been (2.22%), 4.12% and 4.16%, respectively, and the S.E.C. 30-Day Yield for September 2011 would have been 2.13%. Results represent past performance and do not indicate future results. The graph and the returns shown do not reflect the deduction of taxes that a shareholder would pay on distributions or the redemption of fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Index figures are from Bank of America Merrill Lynch & Co. and all other figures are from First Investors Management Company, Inc.

Portfolio of Investments (continued)

INVESTMENT GRADE FUND

September 30, 2011

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | CORPORATE BONDS—93.1% | | | | | |

| | | Aerospace/Defense—.4% | | | | | |

| $ 1,800M | | BAE Systems Holdings, Inc., 4.95%, 2014 (a) | | | | | $ 1,932,329 |

| | | Agriculture—.7% | | | | | |

| 2,725M | | Cargill, Inc., 6%, 2017 (a) | | | | | 3,224,547 |

| | | Chemicals—1.7% | | | | | |

| 3,000M | | Chevron Phillips Chemicals Co., LLC, 8.25%, 2019 (a) | | | | | 3,790,851 |

| 4,000M | | Dow Chemical Co., 4.25%, 2020 | | | | | 4,036,596 |

| | | | | | | | 7,827,447 |

| | | Consumer Durables—1.7% | | | | | |

| 2,100M | | Black & Decker Corp., 5.75%, 2016 | | | | | 2,455,927 |

| 1,600M | | Newell Rubbermaid, Inc., 6.75%, 2012 | | | | | 1,639,283 |

| 3,000M | | Stanley Black & Decker, 5.2%, 2040 | | | | | 3,361,170 |

| | | | | | | | 7,456,380 |

| | | Energy—11.7% | | | | | |

| 3,900M | | Canadian Oil Sands, Ltd., 7.75%, 2019 (a) | | | | | 4,778,612 |

| 4,800M | | DCP Midstream, LLC, 9.75%, 2019 (a) | | | | | 6,395,851 |

| 4,000M | | Enbridge Energy Partners, LP, 4.2%, 2021 | | | | | 3,963,672 |

| 3,675M | | Maritime & Northeast Pipeline, LLC, 7.5%, 2014 (a) | | | | | 3,975,071 |

| 4,000M | | Nabors Industries, Inc., 6.15%, 2018 | | | | | 4,465,964 |

| 5,000M | | Petrobras International Finance Co., 5.375%, 2021 | | | | | 5,105,000 |

| 4,100M | | Reliance Holdings USA, Inc., 4.5%, 2020 (a) | | | | | 3,768,905 |

| 5,800M | | Spectra Energy Capital, LLC, 6.2%, 2018 | | | | | 6,561,128 |

| 4,400M | | Suncor Energy, Inc., 6.85%, 2039 | | | | | 5,365,092 |

| 2,700M | | Valero Energy Corp., 9.375%, 2019 | | | | | 3,464,870 |

| 4,000M | | Weatherford International, Inc., 6.35%, 2017 | | | | | 4,523,512 |

| | | | | | | | 52,367,677 |

| | | Financial Services—13.3% | | | | | |

| 2,250M | | Aflac, Inc., 8.5%, 2019 | | | | | 2,742,786 |

| 6,000M | | American Express Co., 7%, 2018 | | | | | 7,107,600 |

| 2,000M | | American International Group, Inc., 4.875%, 2016 | | | | | 1,919,466 |

| 2,800M | | Amvescap, PLC, 5.375%, 2013 | | | | | 2,937,617 |

| 4,000M | | BlackRock, Inc., 5%, 2019 | | | | | 4,392,680 |

| 3,260M | | CoBank, ACB, 7.875%, 2018 (a) | | | | | 3,927,087 |

| 1,800M | | Compass Bank, 6.4%, 2017 | | | | | 1,926,819 |

| 2,950M | | ERAC USA Finance Co., 6.375%, 2017 (a) | | | | | 3,424,136 |

Portfolio of Investments (continued)

INVESTMENT GRADE FUND

September 30, 2011

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | Financial Services (continued) | | | | | |

| $ 4,000M | | FUEL Trust, 4.207%, 2016 (a) | | | | | $ 3,989,188 |

| | | General Electric Capital Corp.: | | | | | |

| 4,000M | | 5.625%, 2017 | | | | | 4,393,324 |

| 2,700M | | 5.5%, 2020 | | | | | 2,949,907 |

| 4,000M | | Glencore Funding, LLC, 6%, 2014 (a) | | | | | 4,118,916 |

| | | Harley-Davidson Funding Corp.: | | | | | |

| 3,800M | | 5.75%, 2014 (a) | | | | | 4,147,031 |

| 2,100M | | 6.8%, 2018 (a) | | | | | 2,448,495 |

| 4,000M | | Protective Life Corp., 7.375%, 2019 | | | | | 4,372,072 |

| 4,600M | | Prudential Financial Corp., 4.75%, 2015 | | | | | 4,806,351 |

| | | | | | | | 59,603,475 |

| | | Financials—16.8% | | | | | |

| | | Bank of America Corp.: | | | | | |

| 1,900M | | 5.65%, 2018 | | | | | 1,806,537 |

| 1,800M | | 5%, 2021 | | | | | 1,608,842 |

| 2,700M | | Barclays Bank, PLC, 5.125%, 2020 | | | | | 2,650,293 |

| 2,500M | | Bear Stearns Cos., Inc., 7.25%, 2018 | | | | | 2,950,797 |

| | | Citigroup, Inc.: | | | | | |

| 5,200M | | 6.375%, 2014 | | | | | 5,508,927 |

| 5,000M | | 6.125%, 2017 | | | | | 5,349,700 |

| | | Goldman Sachs Group, Inc.: | | | | | |

| 6,000M | | 6.15%, 2018 | | | | | 6,225,942 |

| 1,600M | | 6.125%, 2033 | | | | | 1,611,264 |

| 2,750M | | 6.75%, 2037 | | | | | 2,522,847 |

| 6,000M | | JPMorgan Chase & Co., 6%, 2018 | | | | | 6,690,618 |

| | | Merrill Lynch & Co., Inc.: | | | | | |

| 4,000M | | 5%, 2015 | | | | | 3,871,860 |

| 3,600M | | 6.4%, 2017 | | | | | 3,494,570 |

| 5,000M | | MF Global Holdings, Ltd., 6.25%, 2016 | | | | | 4,727,265 |

| | | Morgan Stanley: | | | | | |

| 5,800M | | 5.95%, 2017 | | | | | 5,631,365 |

| 5,000M | | 6.625%, 2018 | | | | | 4,966,760 |

| 6,000M | | SunTrust Banks, Inc., 6%, 2017 | | | | | 6,637,068 |

| 2,200M | | UBS AG, 5.875%, 2017 | | | | | 2,266,801 |

| | | Wells Fargo & Co.: | | | | | |

| 4,000M | | 5.625%, 2017 | | | | | 4,529,756 |

| 1,800M | | 4.6%, 2021 | | | | | 1,927,748 |

| | | | | | | | 74,978,960 |

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | Food/Beverage/Tobacco—7.8% | | | | | |

| $ 4,000M | | Altria Group, Inc., 9.7%, 2018 | | | | | $ 5,307,980 |

| 5,000M | | Anheuser-Busch InBev Worldwide, Inc., 5.375%, 2020 | | | | | 5,835,370 |

| 2,700M | | Bottling Group, LLC, 5.125%, 2019 | | | | | 3,158,457 |

| 1,980M | | Bunge Limited Finance Corp., 5.35%, 2014 | | | | | 2,090,805 |

| 4,000M | | Corn Products International, Inc., 4.625%, 2020 | | | | | 4,218,756 |

| 4,000M | | Dr. Pepper Snapple Group, Inc., 6.82%, 2018 | | | | | 4,944,712 |

| 4,000M | | Lorillard Tobacco Co., 6.875%, 2020 | | | | | 4,442,992 |

| 4,000M | | Philip Morris International, Inc., 5.65%, 2018 | | | | | 4,733,352 |

| | | | | | | | 34,732,424 |

| | | Forest Products/Container—.6% | | | | | |

| 2,200M | | International Paper Co., 9.375%, 2019 | | | | | 2,692,954 |

| | | Health Care—2.0% | | | | | |

| 4,000M | | Biogen IDEC, Inc., 6.875%, 2018 | | | | | 4,906,724 |

| 2,400M | | Novartis, 5.125%, 2019 | | | | | 2,837,520 |

| 1,000M | | Roche Holdings, Inc., 6%, 2019 (a) | | | | | 1,223,664 |

| | | | | | | | 8,967,908 |

| | | Information Technology—6.3% | | | | | |

| 3,000M | | Cisco Systems, Inc., 4.95%, 2019 | | | | | 3,419,208 |

| 2,700M | | Computer Sciences Corp., 6.5%, 2018 | | | | | 2,920,225 |

| 3,000M | | Dell, Inc., 5.875%, 2019 | | | | | 3,421,848 |

| 4,000M | | Harris Corp., 4.4%, 2020 | | | | | 4,263,584 |

| 8,000M | | Motorola, Inc., 6%, 2017 | | | | | 8,867,232 |

| | | Pitney Bowes, Inc.: | | | | | |

| 900M | | 5%, 2015 | | | | | 953,236 |

| 4,000M | | 5.75%, 2017 | | | | | 4,106,396 |

| | | | | | | | 27,951,729 |

| | | Manufacturing—4.0% | | | | | |

| 2,700M | | General Electric Co., 5.25%, 2017 | | | | | 3,003,861 |

| 6,700M | | Ingersoll-Rand Global Holdings Co., 6.875%, 2018 | | | | | 8,227,446 |

| 3,200M | | Johnson Controls, Inc., 5%, 2020 | | | | | 3,536,659 |

| 2,725M | | Tyco Electronics Group SA, 6.55%, 2017 | | | | | 3,207,069 |

| | | | | | | | 17,975,035 |

Portfolio of Investments (continued)

INVESTMENT GRADE FUND

September 30, 2011

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | Media-Broadcasting—4.7% | | | | | |

| $ 3,950M | | British Sky Broadcasting Group, PLC, 9.5%, 2018 (a) | | | | | $ 5,083,697 |

| | | Comcast Corp.: | | | | | |

| 4,000M | | 5.15%, 2020 | | | | | 4,522,600 |

| 3,100M | | 6.95%, 2037 | | | | | 3,728,274 |

| 4,000M | | DirecTV Holdings, LLC, 7.625%, 2016 | | | | | 4,304,184 |

| 3,000M | | Time Warner Cable, Inc., 6.75%, 2018 | | | | | 3,495,789 |

| | | | | | | | 21,134,544 |

| | | Media-Diversified—1.0% | | | | | |

| | | McGraw-Hill Cos., Inc.: | | | | | |

| 1,800M | | 5.9%, 2017 | | | | | 1,949,049 |

| 2,300M | | 6.55%, 2037 | | | | | 2,505,802 |

| | | | | | | | 4,454,851 |

| | | Metals/Mining—4.6% | | | | | |

| 4,000M | | Alcoa, Inc., 6.15%, 2020 | | | | | 4,058,796 |

| 5,000M | | ArcelorMittal, 6.125%, 2018 | | | | | 4,833,330 |

| 3,800M | | Newmont Mining Corp., 5.125%, 2019 | | | | | 4,143,292 |

| 2,595M | | Rio Tinto Finance USA, Ltd., 6.5%, 2018 | | | | | 3,118,123 |

| 4,000M | | Vale Overseas, Ltd., 5.625%, 2019 | | | | | 4,228,000 |

| | | | | | | | 20,381,541 |

| | | Real Estate Investment Trusts—5.8% | | | | | |

| 5,000M | | Boston Properties, LP, 5.875%, 2019 | | | | | 5,496,665 |

| 3,000M | | Digital Realty Trust, LP, 5.25%, 2021 | | | | | 2,975,031 |

| 5,000M | | HCP, Inc., 5.375%, 2021 | | | | | 5,025,810 |

| 4,000M | | ProLogis, LP, 6.625%, 2018 | | | | | 4,153,452 |

| 4,000M | | Simon Property Group, LP, 5.75%, 2015 | | | | | 4,417,856 |

| 4,000M | | Ventas Realty, LP, 4.75%, 2021 | | | | | 3,848,816 |

| | | | | | | | 25,917,630 |

| | | Retail-General Merchandise—1.6% | | | | | |

| 2,500M | | GAP, Inc., 5.95%, 2021 | | | | | 2,355,635 |

| 4,000M | | Home Depot, Inc., 5.875%, 2036 | | | | | 4,673,084 |

| | | | | | | | 7,028,719 |

| | | Telecommunications—.9% | | | | | |

| 3,300M | | GTE Corp., 6.84%, 2018 | | | | | 3,980,318 |

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | Transportation—1.8% | | | | | |

| $ 3,000M | | Con-way, Inc., 7.25%, 2018 | | | | | $ 3,369,123 |

| 4,000M | | GATX Corp., 8.75%, 2014 | | | | | 4,628,720 |

| | | | | | | | 7,997,843 |

| | | Utilities—4.8% | | | | | |

| 3,000M | | E. ON International Finance BV, 5.8%, 2018 (a) | | | | 3,445,404 |

| 1,900M | | Electricite de France SA, 6.5%, 2019 (a) | | | | | 2,224,157 |

| 4,000M | | Exelon Generation Co., LLC, 6.2%, 2017 | | | | | 4,516,044 |

| | | Great River Energy Co.: | | | | | |

| 602M | | 5.829%, 2017 (a) | | | | | 672,830 |

| 3,700M | | 4.478%, 2030 (a) | | | | | 3,890,746 |

| 3,000M | | Ohio Power Co., 5.375%, 2021 | | | | | 3,362,388 |

| 2,561M | | Sempra Energy, 9.8%, 2019 | | | | | 3,589,070 |

| | | | | | | | 21,700,639 |

| | | Waste Management—.9% | | | | | |

| 3,755M | | Republic Services, Inc., 3.8%, 2018 | | | | | 3,910,247 |

| Total Value of Corporate Bonds (cost $390,309,702) | | | | | 416,217,197 |

| | | RESIDENTIAL MORTGAGE-BACKED | | | | |

| | | SECURITIES—4.9% | | | | | |

| | | Fannie Mae | | | | | |

| 20,001M | | 5%, 12/1/2039 – 10/1/2040 (cost $20,901,762) | | | | 21,741,736 |

| Total Value of Investments (cost $411,211,464) | 98.0 | % | | | 437,958,933 |

| Other Assets, Less Liabilities | 2.0 | | | | 9,111,014 |

| Net Assets | | | 100.0 | % | | | $447,069,947 |

| |

| (a) | Security exempt from registration under Rule 144A of Securities Act of 1933 (see Note 4). |

Portfolio of Investments (continued)

INVESTMENT GRADE FUND

September 30, 2011

Accounting Standards Codification (“ASC”) 820 established a three-tier hierarchy of inputs to establish a classification of fair value measurements for disclosure purposes. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below:

| Level 1 — Unadjusted quoted prices in active markets for identical securities that the Fund has the ability to access. |

| Level 2 — Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

| Level 3 — Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumption about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

The inputs methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary, by category of Level, of inputs used to value the Fund’s investments as of September 30, 2011:

| | | | | | | | | | | | |

| | | | Level 1 | | | Level 2 | | | Level 3 | | | Total |

| Corporate Bonds | | $ | — | | $ | 416,217,197 | | $ | — | | $ | 416,217,197 |

| Residential Mortgage-Backed | | | | | | | | | | | | |

| Securities | | | — | | | 21,741,736 | | | — | | | 21,741,736 |

| Total Investments in Securities* | | $ | — | | $ | 437,958,933 | | $ | — | | $ | 437,958,933 |

| |

| * | The Portfolio of Investments provides information on the industry categorization for corporate bonds. |

| |

| | There were no transfers into or from Level 1 or Level 2 by the Fund during the year ended |

| September 30, 2011. |

| | |

| 22 | See notes to financial statements | |

Portfolio Manager’s Letter

FUND FOR INCOME

Dear Investor:

This is the annual report for the First Investors Fund For Income for the fiscal year ended September 30, 2011. During the period, the Fund’s return on a net asset value basis was 1.0% for Class A shares and 0.4% for Class B shares, including dividends of 17.1 cents per share on Class A shares and 15.5 cents per share on Class B shares.

In the bond market, the first half of the reporting period was one of generally poor returns, at least for higher-quality paper. The Bank of America Merrill Lynch U.S. Broad Market Index returned –0.9%. Investment grade corporate bonds fell 0.6%, U.S. Treasury bonds declined by 2.8% and municipal bonds lost 4.2%.

High yield bonds, however, which are rated below investment grade and which are the most speculative sector, produced strong equity-like returns of 6.1%, according to the Bank of America Merrill Lynch BB-B U.S. Cash Pay High Yield Constrained Index (the “Index”).

The second half of the year was a mirror image of the first half. Investors who had been hungry for yield in what they believed was a modestly improving economic environment became fearful on the back of negative headlines out of Europe and weakening U.S. economic data. Fear of potential global recession replaced fear of inflation as the primary motivator for investors. A continuing European sovereign debt crisis, concerns about the European banks, the downgrade of the U.S. credit rating and fears of a double dip recession whipsawed investors. As in previous times of financial stress, markets generally became more correlated, with the exception of the highest quality and most liquid government securities such as U.S. Treasuries, which rallied thanks to their perceived safe haven status.

Credit markets, including high yield bonds, have also been subject to these sharp pricing swings. The unwinding of “double decker” funds, primarily in Asia, caused further technical pressure in high yield markets. (Double decker funds seek to increase yields by pairing junk bonds with foreign currency swaps.) By the end of the review period, high yield markets had given back much of what they gained in the first half of the year, with the Index finishing with a modest gain of just 1.9%.

In this environment, the Fund also produced a modest gain, outperforming the Index on a gross of fees basis, but underperforming fully net of fees. The Fund holds a higher percentage of large, liquid issues than the Index and those issues were the quickest to decline in price when the markets seized up near the end of the review period. Lower-quality, less liquid issues appeared to be more price-resilient because they could not be sold at all. We have already seen many portfolio names bounce back and believe that the portfolio is well positioned with creditworthy companies that should continue to produce highly attractive yields.

Portfolio Manager’s Letter (continued)

FUND FOR INCOME

Thank you for placing your trust in First Investors. As always, we appreciate the opportunity to serve your investment needs.

Fund Expenses (unaudited)

FUND FOR INCOME

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 2 for a detailed explanation of the information presented in these examples.

| | | |

| | Beginning | Ending | |

| | Account | Account | Expenses Paid |

| | Value | Value | During Period |

| | (4/1/11) | (9/30/11) | (4/1/11–9/30/11)* |

| Expense Example – Class A Shares | | | |

| Actual | $1,000.00 | $952.97 | $6.27 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,018.65 | $6.48 |

| Expense Example – Class B Shares | | | |

| Actual | $1,000.00 | $950.01 | $9.68 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,015.14 | $10.00 |

| |

| * | Expenses are equal to the annualized expense ratio of 1.28% for Class A shares and 1.98% for |

| Class B shares, multiplied by the average account value over the period, multiplied by 183/365 |

| (to reflect the one-half year period). Expenses paid during the period are net of expenses waived. |

Portfolio Composition

TOP TEN SECTORS

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2011, and are based on the total value of investments.

Cumulative Performance Information (unaudited)

FUND FOR INCOME

Comparison of change in value of $10,000 investment in the First Investors Fund For Income (Class A shares), the Bank of America (“BofA”) Merrill Lynch BB-B U.S. Cash Pay High Yield Constrained Index.

The graph compares a $10,000 investment in the First Investors Fund For Income (Class A shares) beginning 9/30/01 with a theoretical investment in the BofA Merrill Lynch BB-B U.S. Cash Pay High Yield Constrained Index (the “Index”). The Index contains all securities in the BofA Merrill Lynch U.S. Cash Pay High Yield Index rated BB1 through B3, based on an average of Moody’s, S&P and Fitch, but caps issuer exposure at 2%. Index constituents are capitalization-weighted, based on their current amount outstanding, provided the total allocation to an individual issuer does not exceed 2%. It is not possible to invest directly in this Index. In addition, the Index does not reflect fees and expenses associated with the active management of a mutual fund portfolio. For purposes of the graph and the accompanying table it is assumed that all dividends and distributions were reinvested. Class B shares performance may be greater than or less than that shown in the line graph above for Class A shares based on differences in sales loads and fees paid by shareholders investing in the different classes.

* Average Annual Total Return figures (for the periods ended 9/30/11) include the reinvestment of all dividends and distributions. “N.A.V. Only” returns are calculated without sales charges. The Class A “S.E.C. Standardized” returns shown are based on the maximum sales charge of 5.75% (prior to 6/17/02, the maximum sales charge was 6.25%). The Class B “S.E.C. Standardized” returns are adjusted for the applicable deferred sales charge (maximum of 4% in the first year). During the periods shown, some of the expenses of the Fund were waived or assumed. If such expenses had been paid by the Fund, the Class A “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been (4.77%), 1.55% and 5.06%, respectively, and the S.E.C. 30-Day Yield for September 2011 would have been 6.60%. The Class B “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been (3.43%), 1.77% and 5.11%, respectively, and the S.E.C. 30-Day Yield for September 2011 would have been 6.26%. Results represent past performance and do not indicate future results. The graph and the returns shown do not reflect the deduction of taxes that a shareholder would pay on distributions or the redemption of fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. The issuers of high yield bonds, in which the Fund primarily invests, pay higher interest rates because they have a greater likelihood of financial difficulty, which could result in their inability to repay the bonds fully when due. Prices of high yield bonds are also subject to greater fluctuations. Index figures are from Bank of America Merrill Lynch and all other figures are from First Investors Management Company, Inc.

Portfolio of Investments

FUND FOR INCOME

September 30, 2011

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | CORPORATE BONDS—96.2% | | | | | |

| | | Automotive—4.6% | | | | | |

| $ 5,225M | | Chrysler Group LLC/CG Co – Issuer, Inc., 8.25%, 2021 (a) | | | | | $ 4,049,375 |

| 3,300M | | Cooper Tire & Rubber Co., 8%, 2019 | | | | | 3,217,500 |

| 2,825M | | Cooper-Standard Automotive, Inc., 8.5%, 2018 | | | | | 2,895,625 |

| 3,950M | | Exide Technologies, 8.625%, 2018 | | | | | 3,693,250 |

| 2,525M | | Ford Motor Co., 6.625%, 2028 | | | | | 2,518,556 |

| 2,575M | | Hertz Corp., 6.75%, 2019 | | | | | 2,349,687 |

| 3,325M | | Jaguar Land Rover, PLC, 7.75%, 2018 (a) | | | | | 2,975,875 |

| 2,100M | | Oshkosh Corp., 8.5%, 2020 | | | | | 2,047,500 |

| | | | | | | | 23,747,368 |

| | | Building Materials—3.1% | | | | | |

| 3,875M | | Associated Materials, LLC, 9.125%, 2017 | | | | | 3,158,125 |

| | | Building Materials Corp.: | | | | | |

| 3,625M | | 6.875%, 2018 (a) | | | | | 3,534,375 |

| 4,175M | | 7.5%, 2020 (a) | | | | | 4,195,875 |

| 2,475M | | Griffon Corp., 7.125%, 2018 | | | | | 2,196,562 |

| 3,700M | | Texas Industries, Inc., 9.25%, 2020 | | | | | 2,895,250 |

| | | | | | | | 15,980,187 |

| | | Capital Goods—.6% | | | | | |

| 2,650M | | Belden CDT, Inc., 9.25%, 2019 | | | | | 2,875,250 |

| | | Chemicals—3.7% | | | | | |

| 2,950M | | Ferro Corp., 7.875%, 2018 | | | | | 2,964,750 |

| 1,325M | | Huntsman International, LLC, 8.625%, 2021 | | | | | 1,275,313 |

| 1,750M | | Kinove German Bondco GmbH, 9.625%, 2018 (a) | | | | | 1,592,500 |

| 3,325M | | Lyondell Chemical Co., 11%, 2018 | | | | | 3,607,625 |

| 2,575M | | Polymer Group, Inc., 7.75%, 2019 (a) | | | | | 2,581,438 |

| 1,200M | | PolyOne Corp., 7.375%, 2020 | | | | | 1,209,000 |

| | | Solutia, Inc.: | | | | | |

| 3,925M | | 8.75%, 2017 | | | | | 4,199,750 |

| 1,275M | | 7.875%, 2020 | | | | | 1,348,313 |

| | | | | | | | 18,778,689 |

| | | Consumer Durables—.5% | | | | | |

| 2,975M | | Sealy Mattress Co., 8.25%, 2014 | | | | | 2,818,813 |

Portfolio of Investments (continued)

FUND FOR INCOME

September 30, 2011

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | Consumer Non-Durables—1.3% | | | | | |

| $ 3,200M | | Easton-Bell Sports, Inc., 9.75%, 2016 | | | | | $ 3,360,000 |

| 375M | | Levi Strauss & Co., 7.625%, 2020 | | | | | 350,625 |

| 3,025M | | Phillips Van-Heusen Corp., 7.375%, 2020 | | | | | 3,168,688 |

| | | | | | | | 6,879,313 |

| | | Energy—14.0% | | | | | |

| 1,600M | | Antero Resources Finance Corp., 7.25%, 2019 (a) | | | | | 1,528,000 |

| | | Basic Energy Services, Inc.: | | | | | |

| 450M | | 7.125%, 2016 | | | | | 418,500 |

| 2,600M | | 7.75%, 2019 (a) | | | | | 2,483,000 |

| 2,925M | | Berry Petroleum Co., 8.25%, 2016 | | | | | 2,998,125 |

| 1,850M | | Chesapeake Energy Corp., 7.25%, 2018 | | | | | 1,979,500 |

| | | Concho Resources, Inc.: | | | | | |

| 2,300M | | 8.625%, 2017 | | | | | 2,449,500 |

| 625M | | 7%, 2021 | | | | | 625,000 |

| 1,225M | | 6.5%, 2022 | | | | | 1,212,750 |

| | | Consol Energy, Inc.: | | | | | |

| 1,875M | | 8%, 2017 | | | | | 1,968,750 |

| 3,700M | | 8.25%, 2020 | | | | | 3,912,750 |

| | | Copano Energy, LLC: | | | | | |

| 550M | | 7.75%, 2018 | | | | | 565,125 |

| 1,025M | | 7.125%, 2021 | | | | | 1,007,062 |

| 4,750M | | Crosstex Energy, LP, 8.875%, 2018 | | | | | 4,892,500 |

| 2,000M | | Denbury Resources, Inc., 8.25%, 2020 | | | | | 2,110,000 |

| 2,750M | | El Paso Corp., 6.5%, 2020 | | | | | 2,950,469 |

| 1,575M | | El Paso Pipeline Partners Operating Co., LLC, 5%, 2021 | | | | | 1,585,631 |

| 750M | | Encore Acquisition Co., 9.5%, 2016 | | | | | 813,750 |

| 2,500M | | Expro Finance Luxembourg SCA, 8.5%, 2016 (a) | | | | | 2,187,500 |

| | | Ferrellgas Partners, LP: | | | | | |

| 3,450M | | 9.125%, 2017 | | | | | 3,501,750 |

| 1,663M | | 8.625%, 2020 | | | | | 1,621,425 |

| 3,975M | | Forest Oil Corp., 7.25%, 2019 | | | | | 3,895,500 |

| 3,375M | | Genesis Energy, LP, 7.875%, 2018 (a) | | | | | 3,223,125 |

| 850M | | Helix Energy Solutions Group, Inc., 9.5%, 2016 (a) | | | | | 867,000 |

| | | Hilcorp Energy I, LP: | | | | | |

| 175M | | 7.75%, 2015 (a) | | | | | 177,187 |

| 3,875M | | 8%, 2020 (a) | | | | | 3,962,188 |

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | Energy (continued) | | | | | |

| | | Inergy, LP: | | | | | |

| $ 2,475M | | 7%, 2018 | | | | | $ 2,338,875 |

| 975M | | 6.875%, 2021 | | | | | 892,125 |

| 1,500M | | Linn Energy, LLC, 6.5%, 2019 (a) | | | | | 1,387,500 |

| 2,450M | | Murray Energy Corp., 10.25%, 2015 (a) | | | | | 2,352,000 |

| | | Penn Virginia Corp.: | | | | | |

| 1,025M | | 10.375%, 2016 | | | | | 1,078,813 |

| 800M | | 7.25%, 2019 | | | | | 744,000 |

| | | Quicksilver Resources, Inc.: | | | | | |

| 1,075M | | 8.25%, 2015 | | | | | 1,026,625 |

| 2,100M | | 11.75%, 2016 | | | | | 2,278,500 |

| 2,550M | | 9.125%, 2019 | | | | | 2,511,750 |

| 1,975M | | Sandridge Energy, Inc., 7.5%, 2021 (a) | | | | | 1,826,875 |

| 1,600M | | SESI, LLC, 6.375%, 2019 (a) | | | | | 1,552,000 |

| 600M | | SM Energy Co., 6.625%, 2019 (a) | | | | | 600,000 |

| | | | | | | | 71,525,150 |

| | | Financials—5.0% | | | | | |

| | | Ally Financial, Inc.: | | | | | |

| 3,700M | | 6.25%, 2017 | | | | | 3,236,982 |

| 5,525M | | 8%, 2020 | | | | | 5,127,863 |

| | | Ford Motor Credit Co., LLC: | | | | | |

| 3,100M | | 6.625%, 2017 | | | | | 3,231,961 |

| 4,600M | | 5.875%, 2021 | | | | | 4,583,992 |

| 800M | | General Motors Financial Co., 6.75%, 2018 (a) | | | | | 788,000 |

| | | International Lease Finance Corp.: | | | | | |

| 500M | | 5.875%, 2013 | | | | | 485,000 |

| 5,450M | | 8.625%, 2015 | | | | | 5,429,563 |

| 1,900M | | 8.75%, 2017 | | | | | 1,914,250 |

| 775M | | 8.25%, 2020 | | | | | 761,438 |

| | | | | | | | 25,559,049 |

| | | Food/Beverage/Tobacco—1.0% | | | | | |

| | | CF Industries, Inc.: | | | | | |

| 2,000M | | 6.875%, 2018 | | | | | 2,237,500 |

| 725M | | 7.125%, 2020 | | | | | 827,406 |

| 2,700M | | JBS USA, LLC, 7.25%, 2021 (a) | | | | | 2,254,500 |

| | | | | | | | 5,319,406 |

Portfolio of Investments (continued)

FUND FOR INCOME

September 30, 2011

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | Food/Drug—1.9% | | | | | |

| $ 5,175M | | McJunkin Red Man Corp., 9.5%, 2016 | | | | | $ 4,761,000 |

| 3,600M | | NBTY, Inc., 9%, 2018 | | | | | 3,703,500 |

| 1,525M | | Tops Holding Corp./Tops Markets, LLC, 10.125%, 2015 | | | | | 1,532,625 |

| | | | | | | | 9,997,125 |

| | | Forest Products/Containers—3.0% | | | | | |

| 2,375M | | Clearwater Paper Corp., 7.125%, 2018 | | | | | 2,369,062 |

| 1,750M | | Exopack Holding Corp., 10%, 2018 (a) | | | | | 1,645,000 |

| 1,400M | | JSG Funding, PLC (Smurfit Kappa Funding, PLC), 7.75%, 2015 | | | | | 1,351,000 |

| 2,675M | | Mercer International, Inc., 9.5%, 2017 | | | | | 2,641,563 |

| 3,050M | | Reynolds Group Escrow, LLC, 7.75%, 2016 (a) | | | | | 3,072,875 |

| 1,725M | | Reynolds Group Issuer, Inc., 9%, 2019 (a) | | | | | 1,474,875 |

| | | Sealed Air Corp.: | | | | | |

| 1,750M | | 8.125%, 2019 (a)(b) | | | | | 1,771,875 |

| 925M | | 8.375%, 2021 (a)(b) | | | | | 936,563 |

| | | | | | | | 15,262,813 |

| | | Gaming/Leisure—1.4% | | | | | |

| 1,775M | | Ameristar Casinos, Inc., 7.5%, 2021 (a) | | | | | 1,726,187 |

| 2,300M | | MCE Finance, Ltd., 10.25%, 2018 | | | | | 2,449,500 |

| 1,550M | | National CineMedia, LLC, 7.875%, 2021 | | | | | 1,542,250 |

| 675M | | NCL Corp., Ltd., 11.75%, 2016 | | | | | 762,750 |

| 769M | | Yonkers Racing Corp., 11.375%, 2016 (a) | | | | | 788,225 |

| | | | | | | | 7,268,912 |

| | | Health Care—6.4% | | | | | |

| 4,375M | | Aviv Healthcare Properties, LP, 7.75%, 2019 | | | | | 4,145,312 |

| 1,250M | | Capella Healthcare, 9.25%, 2017 (a) | | | | | 1,193,750 |

| 4,750M | | Community Health Systems, Inc., 8.875%, 2015 | | | | | 4,678,750 |

| 2,475M | | ConvaTec Healthcare, 10.5%, 2018 (a) | | | | | 2,190,375 |

| 1,425M | | DaVita, Inc., 6.375%, 2018 | | | | | 1,371,563 |

| 4,400M | | Genesis Health Ventures, Inc., 9.75%, 2015 (c)(d) | | | | | 2,750 |

| | | HCA, Inc.: | | | | | |

| 1,675M | | 6.5%, 2020 | | | | | 1,641,500 |

| 4,800M | | 7.5%, 2022 | | | | | 4,440,000 |

| 1,950M | | 7.75%, 2021 (a) | | | | | 1,837,875 |

| | | Healthsouth Corp.: | | | | | |

| 2,275M | | 7.25%, 2018 | | | | | 2,172,625 |

| 1,175M | | 7.75%, 2022 | | | | | 1,072,187 |

| 4,000M | | IASIS Healthcare, LLC, 8.375%, 2019 (a) | | | | | 3,260,000 |

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | Health Care (continued) | | | | | |

| $ 265M | | Select Medical Corp., 7.625%, 2015 | | | | | $ 230,881 |

| 1,600M | | Universal Hospital Services, Inc., 8.5%, 2015 (a) | | | | | 1,566,000 |

| | | Vanguard Health Holding Co. II, LLC: | | | | | |

| 1,925M | | 8%, 2018 | | | | | 1,775,813 |

| 1,075M | | 7.75%, 2019 | | | | | 963,469 |

| | | | | | | | 32,542,850 |

| | | Information Technology—2.8% | | | | | |

| | | Equinix, Inc.: | | | | | |

| 1,875M | | 8.125%, 2018 | | | | | 1,982,812 |

| 1,250M | | 7%, 2021 | | | | | 1,248,437 |

| | | Fidelity National Information Services, Inc.: | | | | | |

| 1,200M | | 7.625%, 2017 | | | | | 1,254,000 |

| 2,400M | | 7.875%, 2020 | | | | | 2,508,000 |

| 725M | | iGATE Corp., 9%, 2016 (a) | | | | | 677,875 |

| | | Jabil Circuit, Inc.: | | | | | |

| 350M | | 7.75%, 2016 | | | | | 387,625 |

| 3,825M | | 8.25%, 2018 | | | | | 4,350,938 |

| 2,100M | | MEMC Electronic Materials, Inc., 7.75%, 2019 | | | | | 1,821,750 |

| | | | | | | | 14,231,437 |

| | | Manufacturing—2.8% | | | | | |

| 2,400M | | Amsted Industries, 8.125%, 2018 (a) | | | | | 2,496,000 |

| 3,850M | | Case New Holland, Inc., 7.875%, 2017 | | | | | 4,119,500 |

| 4,825M | | Manitowoc Co., Inc., 8.5%, 2020 | | | | | 4,390,750 |

| 2,325M | | Park-Ohio Industries, Inc., 8.125%, 2021 | | | | | 2,185,500 |

| 1,275M | | Terex Corp., 10.875%, 2016 | | | | | 1,357,875 |

| | | | | | | | 14,549,625 |

| | | Media-Broadcasting—4.5% | | | | | |

| 2,800M | | Allbritton Communication Co., 8%, 2018 | | | | | 2,646,000 |

| | | Belo Corp.: | | | | | |

| 4,000M | | 7.25%, 2027 | | | | | 3,330,000 |

| 725M | | 7.75%, 2027 | | | | | 619,875 |

| 4,225M | | Cumulus Media, Inc., 7.75%, 2019 (a) | | | | | 3,580,687 |

| 2,475M | | Nexstar/Mission Broadcasting, Inc., 8.875%, 2017 | | | | | 2,456,438 |

| | | Sinclair Television Group, Inc.: | | | | | |

| 4,000M | | 9.25%, 2017 (a) | | | | | 4,220,000 |

| 1,000M | | 8.375%, 2018 | | | | | 990,000 |

| 5,250M | | XM Satellite Radio, Inc., 7.625%, 2018 (a) | | | | | 5,328,750 |

| | | | | | | | 23,171,750 |

Portfolio of Investments (continued)

FUND FOR INCOME

September 30, 2011

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| |

| | | Media-Cable TV—6.9% | | | | | |

| $ 3,525M | | Cablevision Systems Corp., 8.625%, 2017 | | | | | $ 3,688,031 |

| | | CCO Holdings, LLC: | | | | | |

| 350M | | 7%, 2019 (a) | | | | | 340,375 |

| 2,500M | | 7%, 2019 | | | | | 2,437,500 |

| 2,975M | | Cequel Communications Holdings I, Inc., 8.625%, 2017 (a) | | | | | 2,960,125 |

| | | Clear Channel Worldwide: | | | | | |

| 2,500M | | 9.25%, 2017 Series “A” | | | | | 2,550,000 |

| 5,450M | | 9.25%, 2017 Series “B” | | | | | 5,599,875 |

| 4,900M | | DISH DBS Corp., 7.875%, 2019 | | | | | 5,022,500 |

| 1,525M | | Echostar DBS Corp., 7.125%, 2016 | | | | | 1,551,687 |

| 3,525M | | Quebecor Media, Inc., 7.75%, 2016 | | | | | 3,536,313 |

| 4,850M | | UPC Germany GmbH, 8.125%, 2017 (a) | | | | | 4,874,250 |

| 2,800M | | UPC Holding BV, 9.875%, 2018 (a) | | | | | 2,814,000 |

| | | | | | | | 35,374,656 |

| | | Media-Diversified—1.5% | | | | | |

| 3,400M | | Entravision Communications Corp., 8.75%, 2017 | | | | | 3,204,500 |

| 3,200M | | Lamar Media Corp., 7.875%, 2018 | | | | | 3,216,000 |

| 1,000M | | NAI Entertainment Holdings, LLC, 8.25%, 2017 (a) | | | | | 1,035,000 |

| | | | | | | | 7,455,500 |

| | | Metals/Mining—6.5% | | | | | |

| 3,400M | | AK Steel Corp., 7.625%, 2020 | | | | | 2,996,250 |

| | | Arch Coal, Inc.: | | | | | |

| 2,375M | | 7.25%, 2020 | | | | | 2,291,875 |

| 975M | | 7.25%, 2021 (a) | | | | | 943,312 |

| | | FMG Resources (August 2006) Property, Ltd.: | | | | | |

| 1,250M | | 6.375%, 2016 (a) | | | | | 1,131,250 |

| 1,550M | | 6.875%, 2018 (a) | | | | | 1,371,750 |

| 2,600M | | JMC Steel Group, 8.25%, 2018 (a) | | | | | 2,457,000 |

| 2,750M | | Metals USA, Inc., 11.125%, 2015 | | | | | 2,811,875 |

| 5,025M | | Novelis, Inc., 8.375%, 2017 | | | | | 4,999,875 |

| 1,225M | | Thompson Creek Metals Co., Inc., 7.375%, 2018 (a) | | | | | 1,108,625 |

| | | United States Steel Corp.: | | | | | |

| 850M | | 7%, 2018 | | | | | 769,250 |

| 5,675M | | 7.375%, 2020 | | | | | 5,135,875 |

| 2,425M | | Vedanta Resources, PLC, 9.5%, 2018 (a) | | | | | 2,134,000 |

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | Metals/Mining (continued) | | | | | |

| | | Vulcan Materials Co.: | | | | | |

| $ 1,875M | | 6.5%, 2016 | | | | | $ 1,730,149 |

| 800M | | 6.4%, 2017 | | | | | 752,000 |

| 1,275M | | 7%, 2018 | | | | | 1,224,000 |

| 1,750M | | 7.5%, 2021 | | | | | 1,635,323 |

| | | | | | | | 33,492,409 |

| | | Real Estate Investment Trusts—.8% | | | | | |

| 800M | | CB Richard Ellis Service, 6.625%, 2020 | | | | | 772,000 |

| | | Developers Diversified Realty Corp.: | | | | | |

| 675M | | 9.625%, 2016 | | | | | 765,166 |

| 550M | | 7.875%, 2020 | | | | | 583,570 |

| | | Omega Healthcare Investors, Inc.: | | | | | |

| 950M | | 6.75%, 2022 | | | | | 910,813 |

| 975M | | 7.5%, 2020 | | | | | 989,625 |

| | | | | | | | 4,021,174 |

| | | Retail-General Merchandise—5.3% | | | | | |

| 3,825M | | DineEquity, Inc., 9.5%, 2018 | | | | | 3,815,437 |

| 2,050M | | J.C. Penney Corp., Inc., 7.95%, 2017 | | | | | 2,193,500 |

| | | Limited Brands, Inc.: | | | | | |

| 2,050M | | 8.5%, 2019 | | | | | 2,326,750 |

| 600M | | 6.625%, 2021 | | | | | 607,500 |

| 2,325M | | Needle Merger Sub Corp., 8.125%, 2019 (a) | | | | | 2,034,375 |

| | | QVC, Inc.: | | | | | |

| 2,025M | | 7.5%, 2019 (a) | | | | | 2,166,750 |

| 375M | | 7.375%, 2020 (a) | | | | | 401,250 |

| 2,300M | | Sears Holding Corp., 6.625%, 2018 | | | | | 1,909,000 |

| 4,900M | | Toys R Us Property Co. I, Inc., 10.75%, 2017 | | | | | 5,206,250 |

| 1,400M | | Toys R Us Property Co. II, Inc., 8.5%, 2017 | | | | | 1,372,000 |

| 3,150M | | Wendy’s/Arby’s Restaurants, LLC, 10%, 2016 | | | | | 3,331,125 |

| 475M | | Yankee Acquisition Corp., 8.5%, 2015 | | | | | 458,375 |

| 1,675M | | YCC Holdings, LLC/Yankee Finance, Inc., 10.25%, 2016 | | | | | 1,432,125 |

| | | | | | | | 27,254,437 |

Portfolio of Investments (continued)

FUND FOR INCOME

September 30, 2011

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | Services—2.3% | | | | | |

| $ 2,050M | | CoreLogic, Inc., 7.25%, 2021 (a) | | | | | $ 1,850,125 |

| 850M | | FTI Consulting, Inc., 6.75%, 2020 | | | | | 824,500 |

| | | Iron Mountain, Inc.: | | | | | |

| 1,525M | | 7.75%, 2019 | | | | | 1,521,188 |

| 2,300M | | 8.375%, 2021 | | | | | 2,357,500 |

| 2,500M | | PHH Corp., 9.25%, 2016 | | | | | 2,581,250 |

| 2,375M | | Reliance Intermediate Holdings, LP, 9.5%, 2019 (a) | | | | | 2,505,625 |

| | | | | | | | 11,640,188 |

| | | Telecommunications—7.9% | | | | | |

| | | Citizens Communications Co.: | | | | | |

| 5,500M | | 7.125%, 2019 | | | | | 5,266,250 |

| 775M | | 9%, 2031 | | | | | 664,562 |

| 2,900M | | Clearwire Communications, LLC, 12%, 2015 (a) | | | | | 2,472,250 |

| | | Frontier Communications Corp.: | | | | | |

| 1,875M | | 8.125%, 2018 | | | | | 1,846,875 |

| 1,250M | | 8.5%, 2020 | | | | | 1,218,750 |

| 2,125M | | GCI, Inc., 8.625%, 2019 | | | | | 2,225,937 |

| 5,575M | | Inmarsat Finance, PLC, 7.375%, 2017 (a) | | | | | 5,616,813 |

| | | Intelsat Jackson Holdings, Ltd.: | | | | | |

| 1,125M | | 7.25%, 2019 (a) | | | | | 1,046,250 |

| 1,175M | | 7.5%, 2021 (a) | | | | | 1,095,688 |

| 2,875M | | 8.5%, 2019 | | | | | 2,817,500 |

| | | Sprint Capital Corp.: | | | | | |

| 4,675M | | 6.9%, 2019 | | | | | 4,020,500 |

| 3,825M | | 6.875%, 2028 | | | | | 2,878,313 |

| 6,850M | | Wind Acquisition Finance SA, 11.75%, 2017 (a) | | | | | 5,856,750 |

| | | Windstream Corp.: | | | | | |

| 1,725M | | 7.875%, 2017 | | | | | 1,755,188 |

| 1,775M | | 7.75%, 2020 | | | | | 1,739,500 |

| | | | | | | | 40,521,126 |

| | | Transportation—2.8% | | | | | |

| 4,200M | | Aguila 3 SA, 7.875%, 2018 (a) | | | | | 3,843,000 |

| 4,575M | | CHC Helicopter SA, 9.25%, 2020 (a) | | | | | 3,911,625 |

| | | Navios Maritime Holdings: | | | | | |

| 2,025M | | 8.875%, 2017 | | | | | 1,984,500 |

| 2,700M | | 8.125%, 2019 | | | | | 2,268,000 |

| 2,700M | | Swift Services Holdings, Inc., 10%, 2018 | | | | | 2,416,500 |

| | | | | | | | 14,423,625 |

| | | | | | | |

| | | | | | | | |

| | | | | | | |

| | | | | | | |

| Principal | | | | | | | |

| Amount | | | | | | | |

| or Shares | | Security | | | | | Value |

| | | Utilities—5.2% | | | | | |

| | | AES Corp.: | | | | | |

| $ 875M | | 9.75%, 2016 | | | | | $ 945,000 |

| 800M | | 8%, 2017 | | | | | 808,000 |

| 1,275M | | 7.375%, 2021 (a) | | | | | 1,211,250 |

| 2,600M | | Calpine Construction Finance Co., LP, 8%, 2016 (a) | | | | 2,678,000 |

| 2,775M | | Calpine Corp., 7.5%, 2021 (a) | | | | | 2,664,000 |

| 3,750M | | Energy Future Holdings Corp., 10%, 2020 | | | | | 3,656,250 |

| 1,522M | | Indiantown Cogeneration Utilities, LP, 9.77%, 2020 | | | | 1,600,634 |

| 2,750M | | Intergen NV, 9%, 2017 (a) | | | | | 2,811,875 |

| | | NRG Energy, Inc.: | | | | | |

| 4,625M | | 7.375%, 2017 | | | | | 4,792,656 |

| 2,350M | | 7.625%, 2019 (a) | | | | | 2,150,250 |

| 1,375M | | 8.5%, 2019 | | | | | 1,333,750 |

| 1,935M | | NSG Holdings, LLC, 7.75%, 2025 (a) | | | | | 1,886,625 |

| | | | | | | | 26,538,290 |

| | | Wireless Communications—.4% | | | | | |

| | | MetroPCS Wireless, Inc.: | | | | | |

| 1,025M | | 7.875%, 2018 | | | | | 999,375 |

| 1,050M | | 6.625%, 2020 | | | | | 926,625 |

| | | | | | | | 1,926,000 |

| Total Value of Corporate Bonds (cost $517,518,604) | | | | | 493,155,142 |

| | | COMMON STOCKS—.0% | | | | | |

| | | Automotive—.0% | | | | | |

| 37,387 | * | Safelite Glass Corporation – Class “B” (c) | | | | | 4,767 |

| 2,523 | * | Safelite Realty Corporation (c) | | | | | 25 |

| | | | | | | | 4,792 |

| | | Telecommunications—.0% | | | | | |

| 8 | * | Viatel Holding (Bermuda), Ltd. (c) | | | | | — |

| 18,224 | * | World Access, Inc. | | | | | 9 |

| | | | | | | | 9 |

| Total Value of Common Stocks (cost $385,770) | | | | | 4,801 |

| Total Value of Investments (cost $517,904,374) | 96.2 | % | | | 493,159,943 |

| Other Assets, Less Liabilities | 3.8 | | | | 19,258,706 |

| Net Assets | | | 100.0 | % | | | $512,418,649 |

Portfolio of Investments (continued)

FUND FOR INCOME

September 30, 2011

| |

| * | Non-income producing |