|

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| WASHINGTON, D.C. 20549 |

| -------- |

| |

| FORM N-CSR |

| -------- |

| |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT |

| INVESTMENT COMPANIES |

| |

| INVESTMENT COMPANY ACT FILE NUMBER 811-3967 |

FIRST INVESTORS INCOME FUNDS

(Exact name of registrant as specified in charter)

40 Wall Street

New York, NY 10005

(Address of principal executive offices) (Zip code)

Joseph I. Benedek

First Investors Management Company, Inc.

Raritan Plaza I

Edison, NJ 08837-3620

(Name and address of agent for service)

REGISTRANT'S TELEPHONE NUMBER, INCLUDING AREA CODE:

1-212-858-8000

DATE OF FISCAL YEAR END: SEPTEMBER 30

DATE OF REPORTING PERIOD: SEPTEMBER 30, 2014

Item 1. Reports to Stockholders

| |

| The annual report to stockholders follows |

This report is for the information of the shareholders of the Funds. It is the policy of each Fund described in this report to mail only one copy of a Fund’s prospectus, annual report, semi-annual report and proxy statements to all shareholders who share the same mailing address and share the same last name and have invested in a Fund covered by the same document. You are deemed to consent to this policy unless you specifically revoke this policy and request that separate copies of such documents be mailed to you. In such case, you will begin to receive your own copies within 30 days after our receipt of the revocation. You may request that separate copies of these disclosure documents be mailed to you by writing to us at: Administrative Data Management Corp., Raritan Plaza I, Edison, NJ 08837-3620 or calling us at 1-800-423-4026.

The views expressed in the portfolio manager letters reflect those views of the portfolio managers only through the end of the period covered. Any such views are subject to change at any time based upon market or other conditions and we disclaim any responsibility to update such views. These views may not be relied on as investment advice.

You may obtain a free prospectus for any of the Funds by contacting your representative, calling 1-800-423-4026, writing to us at the following address: First Investors Corporation, 40 Wall Street, New York, NY 10005, or by visiting our website at www.firstinvestors.com. You should consider the investment objectives, risks, charges and expenses of a Fund carefully before investing. The prospectus contains this and other information about the Fund, and should be read carefully before investing.

An investment in a Fund is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. Although the Cash Management Fund seeks to preserve a net asset value at $1.00 per share, it is possible to lose money by investing in it, just as it is possible to lose money by investing in any of the other Funds. Past performance is no guarantee of future results.

A Statement of Additional Information (“SAI”) for any of the Funds may also be obtained, without charge, upon request by calling 1-800-423-4026, writing to us at our address or by visiting our website listed above. The SAI contains more detailed information about the Funds, including information about its Trustees.

Portfolio Manager’s Letter

CASH MANAGEMENT FUND

Dear Investor:

I’m pleased to send you the First Investors Cash Management Fund annual report for the fiscal year ended September 30, 2014. During the period, the Fund’s return on a net-asset value basis was 0.0% for Class A shares, Class B shares and Institutional Class shares. The Fund maintained a $1.00 net asset value per share for each class of shares throughout the year.

The U.S. economy, as measured by gross domestic product (“GDP”), grew slightly faster than 2% during the review period, albeit in an unsteady manner, with quarterly growth ranging from –2.1% to 4.6%. This pace of economic growth was sufficient to reduce the unemployment rate from 7.2% to 5.9%, its lowest level since 2008. While a positive development, the employment picture was somewhat tempered by a continued decline in the labor force participation rate and anemic wage growth. Inflation remained subdued, with consumer prices, excluding the volatile food and energy components, increasing only 1.7%, below the Federal Reserve’s (the “Fed’s”) targeted 2% rate. The Fed remained on course to taper its bond buying program, scheduled to conclude in October, and to raise the federal funds rate in the second half of next year.

Interest rates were mixed during the review period. Short- and intermediate-term interest rates moved slightly higher in anticipation of an eventual tightening of monetary policy by the Fed. In particular, two-year and five-year Treasury note yields increased from 0.32% and 1.38% to 0.57% and 1.76%, respectively. In contrast, the benchmark ten-year Treasury note yield ended the review period lower, moving from 2.61% to 2.49%. After touching two-and-a-half year highs at the end of 2013, ten-year yields moved steadily lower for the next three quarters, confounding consensus expectations for higher interest rates in 2014. The move down in long-term yields reflected a number of factors, including slower than expected global economic growth (particularly in Europe), geopolitical events (Ukraine, Gaza, ISIS), which supported “flight-to-safety” flows into the U.S. bond market, and investors’ belief that this Fed tightening cycle would be more benign than in the past.

Yields on money market funds and the instruments that they invest in have remained at record lows, essentially where they have been for the last few years. The Fed has had an extremely accommodative interest rate policy since late 2008 and has indicated a willingness to maintain extraordinarily low short-term interest rates until certain economic conditions improve. While market expectations have varied on when this may occur, the consensus is that the current policy will remain through at least the middle of 2015. Despite the very low returns that money market funds currently offer, they remain an important part of many investment strategies, as evidenced by the approximately $2.5 trillion dollars invested in the category industrywide.

Portfolio Manager’s Letter (continued)

CASH MANAGEMENT FUND

On July 23, 2014, the U.S. Securities and Exchange Commission (“SEC”) adopted amendments to certain rules under the Investment Company Act of 1940 that govern money market funds. There is a transition period extending until October 2016 for the most significant changes, with shorter transition periods for other changes. These changes will impact all SEC-registered money market funds, including the Fund, although they will impact different types of funds in different ways. First Investors Management Company, Inc. (“FIMCO”), the Fund’s investment adviser, is analyzing the impact of these changes and we will communicate to shareholders as the Fund transitions into compliance with the new laws over the next two years.

FIMCO expects the yield to shareholders to be at or near zero for the foreseeable future based on the outlook for money market rates. To avoid a negative yield to its shareholders, FIMCO has absorbed expenses to the Fund and has waived its management fee.

There can be no assurance that the Fund will be able to maintain a stable net-asset value of $1.00 per share. Money market mutual funds are neither insured nor guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency.

Thank you for placing your trust in First Investors. As always, we appreciate the opportunity to serve your investment needs.

Understanding Your Fund’s Expenses (unaudited)

FIRST INVESTORS INCOME FUNDS

FIRST INVESTORS EQUITY FUNDS

As a mutual fund shareholder, you incur two types of costs: (1) transaction costs, including a sales charge (load) on purchase payments (on Class A shares only) and a contingent deferred sales charge on redemptions (on Class B shares only); and (2) ongoing costs, including advisory fees; distribution and service fees (12b-1); and other expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 in each Fund at the beginning of the period, April 1, 2014, and held for the entire six-month period ended September 30, 2014. The calculations assume that no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

Actual Expenses Example:

These amounts help you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the “Expenses Paid During Period” shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To estimate the expenses you paid on your account during this period, simply divide your ending account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60), then multiply the result by the number given for your Fund under the heading “Expenses Paid During Period”.

Hypothetical Expenses Example:

These amounts provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio for each class of shares of a Fund, and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight and help you compare your ongoing costs only and do not reflect any transaction costs, such as front-end or contingent deferred sales charges (loads or account fees that are charged to certain types of accounts, such as an annual custodial fee of $15 for certain IRA accounts and certain other retirement accounts or an annual custodial fee of $30 for 403(b) custodial accounts (subject to exceptions and certain waivers as described in the Funds’ Statement of Additional Information). Therefore, the hypothetical expenses example is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these costs were included, your costs would have been higher.

Fund Expenses (unaudited)

CASH MANAGEMENT FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 3 for a detailed explanation of the information presented in these examples.

| | | | |

| |

| | Annualized | Beginning | Ending | Expenses Paid |

| | Expense | Account Value | Account Value | During Period |

| Expense Example | Ratio | (4/1/14) | (9/30/14) | (4/1/14–9/30/14)* |

| Class A Shares | 0.08% | | | |

| Actual | | $1,000.00 | $1,000.00 | $0.40 |

| Hypothetical** | | $1,000.00 | $1,024.67 | $0.41 |

| Class B Shares | 0.08% | | | |

| Actual | | $1,000.00 | $1,000.00 | $0.40 |

| Hypothetical** | | $1,000.00 | $1,024.67 | $0.41 |

| Institutional Class Shares | 0.08% | | | |

| Actual | | $1,000.00 | $1,000.00 | $0.40 |

| Hypothetical** | | $1,000.00 | $1,024.67 | $0.41 |

| |

| * | Expenses are equal to the annualized expense ratio, multiplied by the average account value over |

| the period, multiplied by 183/365 (to reflect the one-half year period). Expenses paid during the |

| period are net of expenses waived and/or assumed. |

| |

| ** | Assumed rate of return of 5% before expenses |

Portfolio Composition

BY SECTOR

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2014, and are based on the total market value of investments.

Portfolio of Investments

CASH MANAGEMENT FUND

September 30, 2014

| | | | | | | |

| |

| Principal | | | | | Interest | | |

| Amount | | Security | | | Rate | * | Value |

| | | CORPORATE NOTES—39.6% | | | | | |

| $ 5,000M | | 3M Co., 11/3/2014 (a) | | | 0.070 | % | $ 4,999,679 |

| 5,000M | | Abbott Laboratories, 11/6/2014 (a) | | | 0.100 | | 4,999,500 |

| 5,000M | | Apple, Inc., 11/5/2014 (a) | | | 0.090 | | 4,999,562 |

| | | Coca-Cola Co.: | | | | | |

| 2,000M | | 11/3/2014 (a) | | | 0.120 | | 1,999,780 |

| 3,000M | | 12/8/2014 (a) | | | 0.110 | | 2,999,377 |

| 2,000M | | Emerson Electric Co., 11/28/2014 (a) | | | 0.100 | | 1,999,678 |

| 5,000M | | General Electric Capital Corp., 12/29/2014 | | | 0.120 | | 4,998,517 |

| 2,000M | | Honeywell International, Inc., 12/19/2014 (a) | | | 0.110 | | 1,999,517 |

| 5,000M | | IBM Corp., 12/4/2014 (a) | | | 0.100 | | 4,999,111 |

| 5,000M | | PepsiCo, Inc., 11/10/2014 (a) | | | 0.080 | | 4,999,555 |

| | | Procter & Gamble Co.: | | | | | |

| 2,500M | | 12/10/2014 (a) | | | 0.120 | | 2,499,417 |

| 2,500M | | 1/13/2015 (a) | | | 0.140 | | 2,498,989 |

| Total Value of Corporate Notes (cost $43,992,682) | | | | | 43,992,682 |

| | | U.S. GOVERNMENT AGENCY | | | | | |

| | | OBLIGATIONS—39.3% | | | | | |

| | | Fannie Mae: | | | | | |

| 4,465M | | 11/3/2014 | | | 0.090 | | 4,464,632 |

| 6,000M | | 11/5/2014 | | | 0.070 | | 5,999,592 |

| 4,000M | | 12/1/2014 | | | 0.070 | | 3,999,525 |

| 3,000M | | 1/12/2015 | | | 0.090 | | 2,999,227 |

| 3,410M | | 2/11/2015 | | | 0.060 | | 3,409,244 |

| | | Federal Home Loan Bank: | | | | | |

| 3,547M | | 10/15/2014 | | | 0.075 | | 3,546,896 |

| 3,700M | | 10/22/2014 | | | 0.075 | | 3,699,838 |

| 2,300M | | 10/22/2014 | | | 0.080 | | 2,299,893 |

| 4,450M | | 10/29/2014 | | | 0.080 | | 4,449,723 |

| 1,600M | | 11/5/2014 | | | 0.075 | | 1,599,883 |

| 1,250M | | 11/14/2014 | | | 0.075 | | 1,249,885 |

| | | Freddie Mac: | | | | | |

| 5,000M | | 11/24/2014 | | | 0.080 | | 4,999,400 |

| 1,000M | | 11/24/2014 | | | 0.090 | | 999,865 |

| Total Value of U.S. Government Agency Obligations (cost $43,717,603) | | 43,717,603 |

Portfolio of Investments (continued)

CASH MANAGEMENT FUND

September 30, 2014

| | | | | | | |

| |

| Principal | | | | | Interest | | |

| Amount | | Security | | | Rate | * | Value |

| | | VARIABLE AND FLOATING RATE NOTES—14.9% | | |

| $5,000M | | Federal Home Loan Bank, 4/16/2015 | | | 0.114 | % | $ 5,000,434 |

| 5,700M | | Mississippi Business Finance Corp. | | | | | |

| | | (Chevron USA, Inc.), 12/1/2030 | | | 0.030 | | 5,700,000 |

| 5,835M | | Valdez, Alaska Marine Terminal Rev. | | | | | |

| | | (Exxon Pipeline Co., Project B), 12/1/2033 | | 0.030 | | 5,835,000 |

| Total Value of Variable and Floating Rate Notes (cost $16,535,434) | | | | 16,535,434 |

| | | SHORT-TERM U.S. GOVERNMENT | | | | | |

| | | OBLIGATIONS—4.5% | | | | | |

| 5,000M | | U.S. Treasury Bills, 12/11/2014 (cost $4,999,670) | | 0.034 | | 4,999,670 |

| Total Value of Investments (cost $109,245,389)** | 98.3 | % | | | 109,245,389 |

| Other Assets, Less Liabilities | 1.7 | | | | 1,841,709 |

| Net Assets | | | 100.0 | % | $ 111,087,098 |

| |

| * | The interest rates shown are the effective rates at the time of purchase by the Fund. The interest |

| rates shown on floating rate notes are adjusted periodically; the rates shownare the rates in effect |

| at September 30, 2014. |

| |

| ** | Aggregate cost for federal income tax purposes is the same. |

| |

| (a) | Security exempt from registration under Section 4(2) of the Securities Act of 1933 (see Note 4). |

Accounting Standards Codification established a three-tier hierarchy of inputs to establish a classification of fair value measurements for disclosure purposes. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below:

| | |

| Level 1 — | Unadjusted quoted prices in active markets for identical securities that the Fund has |

| | the ability to access. |

| | |

| Level 2 — | Observable inputs other than quoted prices included in Level 1 that are observable |

| | for the asset or liability, either directly or indirectly. These inputs may include quoted |

| | prices for the identical instrument on an inactive market, prices for similar instru- |

| | ments, interest rates, prepayment speeds, credit risk, yield curves, default rates and |

| | similar data. |

| | |

| Level 3 — | Unobservable inputs for the asset or liability, to the extent relevant observable inputs |

| | are not available, representing the Fund’s own assumption about the assumptions a |

| | market participant would use in valuing the asset or liability, and would be based on |

| | the best information available. |

The inputs methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. For example, amortized cost approximates the current fair value of a security, but since the value is not obtained from a quoted price in an active market, such securities are reflected as Level 2.

The following is a summary, by category of Level, of inputs used to value the Fund’s investments as of September 30, 2014:

| | | | | | | | | | | | |

| | | | Level 1 | | | Level 2 | | | Level 3 | | | Total |

| Corporate Notes | | $ | — | | $ | 43,992,682 | | $ | — | | $ | 43,992,682 |

| U.S. Government Agency | | | | | | | | | | | | |

| Obligations | | | — | | | 43,717,603 | | | — | | | 43,717,603 |

| Variable and Floating Rate Notes: | | | | | | | | | | | | |

| Municipal Bonds | | | — | | | 11,535,000 | | | — | | | 11,535,000 |

| U.S. Government Agency | | | | | | | | | | | | |

| Obligations | | | — | | | 5,000,434 | | | — | | | 5,000,434 |

| Short-Term U.S. Government | | | | | | | | | | | | |

| Obligations | | | — | | | 4,999,670 | | | — | | | 4,999,670 |

| Total Investments in Securities | | $ | — | | $ | 109,245,389 | | $ | — | | $ | 109,245,389 |

There were no transfers into or from Level 1 or Level 2 by the Fund for the year ended September 30, 2014. Transfers, if any, between Levels are recognized at the end of the reporting period.

| |

| See notes to financial statements | 7 |

Portfolio Managers’ Letter

LIMITED DURATION HIGH QUALITY BOND FUND

Dear Investor:

This is the annual report for the First Investors Limited Duration High Quality Bond Fund for the fiscal year ended September 30, 20141. During the period, the Fund’s return on a net asset value basis was –0.50% for Class A shares, –0.28% for Advisor Class shares and –0.14% for Institutional Class shares, including dividends of 6.0 cents per share on Class A shares, 6.2 cents per share on Advisor Class shares and 6.6 cents per share on Institutional Class shares.

Economic Overview and Market Summary

The U.S. economy, as measured by gross domestic product (“GDP”), grew slightly faster than 2% during the review period, albeit in an unsteady manner, with quarterly growth ranging from –2.1% to 4.6%. This pace of economic growth was sufficient to reduce the unemployment rate from 7.2% to 5.9%, its lowest level since 2008. While a positive development, the employment picture was somewhat tempered by a continued decline in the labor force participation rate and anemic wage growth. Inflation remained subdued, with consumer prices, excluding the volatile food and energy components, increasing only 1.7%, below the Federal Reserve’s (the “Fed’s”) targeted 2% rate. The Fed remained on course to taper its bond buying program, scheduled to conclude in October, and to raise the federal funds rate in the second half of next year.

Interest rates were mixed during the review period. Short- and intermediate-term interest rates moved slightly higher in anticipation of an eventual tightening of monetary policy by the Fed. In particular, two-year and five-year Treasury note yields increased from 0.32% and 1.38% to 0.57% and 1.76%, respectively. In contrast, the benchmark ten-year Treasury note yield ended the review period lower, moving from 2.61% to 2.49%. After touching two-and-a-half year highs at the end of 2013, ten-year yields moved steadily lower for the next three quarters, confounding consensus expectations for higher interest rates in 2014. The move down in long-term yields reflected a number of factors, including slower than expected global economic growth (particularly in Europe), geopolitical events (Ukraine, Gaza, ISIS), which supported “flight-to-safety” flows into the U.S. bond market, and investors’ belief that this Fed tightening cycle would be more benign than in the past.

Fund Overview and Fiscal Year Performance Attribution

The Fund invests in investment grade fixed income securities. The majority of the Fund’s assets were invested in investment grade corporate bonds, mortgage-backed securities, and U.S. Government securities. The Fund seeks to maintain an average duration of between two and six years.

Since the Fund commenced operations on May 19, 2014, it did not have a full fiscal year of performance to compare with its benchmark, the Bank of America Merrill Lynch 1-5 Year Broad Market Index, for the entire review period. The Fund under-performed the Index when compared over the period since the Fund’s commencement of operations. Relative performance was predominantly a function of asset allocation and Treasury yield curve movements. Specifically, the Fund’s overweight in shorter duration corporate bonds negatively impacted performance as the market rewarded longer-dated securities in the period. This was partially offset by the Fund’s overweight in mortgage backed securities, which had the highest returns relative to other fixed income sectors the Fund invests in during the review period.

Thank you for placing your trust in First Investors. As always, we appreciate the opportunity to serve your investment needs.

1 The Fund’s performance and the performance of its benchmark index are since May 19, 2014, the date the Fund commenced operations.

Fund Expenses (unaudited)

LIMITED DURATION HIGH QUALITY BOND FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 3 for a detailed explanation of the information presented in these examples.

| | | | |

| |

| | Annualized | Beginning | Ending | Expenses Paid |

| | Expense | Account Value | Account Value | During Period |

| Expense Example | Ratio | (4/1/14) | (9/30/14) | (4/1/14–9/30/14)* |

| Class A Shares | 1.05% | | | |

| Actual | | $1,000.00 | $ 994.99 | $3.87 |

| Hypothetical** | | $1,000.00 | $1,014.61 | $3.91 |

| Advisor Class Shares | 0.75% | | | |

| Actual | | $1,000.00 | $ 997.18 | $2.77 |

| Hypothetical** | | $1,000.00 | $1,015.72 | $2.80 |

| Institutional Class Shares | 0.60% | | | |

| Actual | | $1,000.00 | $ 998.60 | $2.22 |

| Hypothetical** | | $1,000.00 | $1,016.27 | $2.24 |

| |

| * | Actual expenses reflect only from the commencement of operations to the end of the period cov- |

| ered (May 19, 2014 through September 30, 2014). Therefore expenses shown are lower than would |

| be expected for a six-month period. Actual expenses for the six-month period will be reflected in |

| future reports. Expenses are equal to the annualized expense ratio multiplied by the average ac- |

| count value over the period, multiplied by 135/365 (to reflect the inception period). Expenses paid |

| during the period are net of expenses waived and/or assumed. |

| |

| ** | Assumed rate of return of 5% before expenses. |

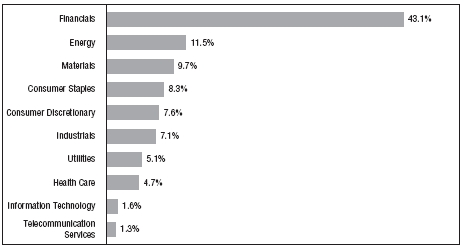

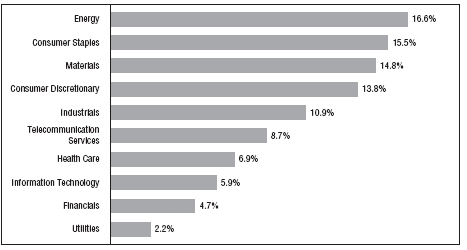

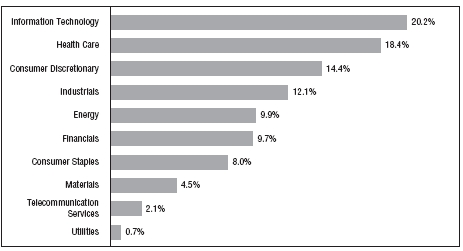

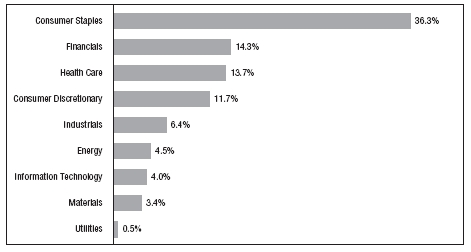

Portfolio Composition

TOP TEN SECTORS

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2014, and are based on the total market value of investments.

Portfolio of Investments

LIMITED DURATION HIGH QUALITY BOND FUND

September 30, 2014

| | | | | | | |

| |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | CORPORATE BONDS—43.1% | | | | | |

| | | Energy—3.2% | | | | | |

| $500M | | BP Capital Markets, PLC, 3.875%, 3/10/2015 | | | | | $ 507,793 |

| 250M | | CNOOC Nexen Finance 2014 ULC, 1.625%, 4/30/2017 | | | | | 250,227 |

| 500M | | DCP Midstream Operating, LP, 2.5%, 12/1/2017 | | | | | 510,566 |

| | | | | | | | 1,268,586 |

| | | Financial Services—7.2% | | | | | |

| 500M | | American Express Co., 7%, 3/19/2018 | | | | | 582,593 |

| 500M | | American International Group, Inc., 8.25%, 8/15/2018 | | | | | 611,248 |

| 500M | | ERAC USA Finance, LLC, 6.375%, 10/15/2017 (a) | | | | | 569,201 |

| 500M | | Ford Motor Credit Co., LLC, 5%, 5/15/2018 | | | | | 546,528 |

| 500M | | General Electric Capital Corp., 5.625%, 5/1/2018 | | | | | 565,548 |

| | | | | | | | 2,875,118 |

| | | Financials—12.1% | | | | | |

| 500M | | Bank of America Corp., 5.65%, 5/1/2018 | | | | | 556,604 |

| 500M | | Barclays Bank, PLC, 6.75%, 5/22/2019 | | | | | 594,880 |

| 500M | | Citigroup, Inc., 6.125%, 11/21/2017 | | | | | 564,460 |

| 500M | | Goldman Sachs Group, Inc., 6.15%, 4/1/2018 | | | | | 564,049 |

| 500M | | JPMorgan Chase & Co., 6%, 1/15/2018 | | | | | 563,014 |

| 500M | | Morgan Stanley, 5.95%, 12/28/2017 | | | | | 560,423 |

| 250M | | SunTrust Banks, Inc., 6%, 9/11/2017 | | | | | 280,964 |

| 500M | | UBS AG, 5.875%, 12/20/2017 | | | | | 563,353 |

| 500M | | Wachovia Corp., 5.75%, 2/1/2018 | | | | | 564,042 |

| | | | | | | | 4,811,789 |

| | | Food/Beverage/Tobacco—2.9% | | | | | |

| 500M | | Anheuser-Busch InBev Worldwide, Inc., 6.875%, 11/15/2019 | | | | | 600,630 |

| 500M | | Diageo Capital, PLC, 5.75%, 10/23/2017 | | | | | 562,129 |

| | | | | | | | 1,162,759 |

| | | Health Care—3.4% | | | | | |

| 250M | | Laboratory Corp. of America Holdings, 2.2%, 8/23/2017 | | | | | 253,303 |

| 500M | | Novartis Securities Investments, Ltd., 5.125%, 2/10/2019 | | | | | 562,082 |

| | | Quest Diagnostics, Inc.: | | | | | |

| 250M | | 6.4%, 7/1/2017 | | | | | 282,529 |

| 250M | | 2.7%, 4/1/2019 | | | | | 251,511 |

| | | | | | | | 1,349,425 |

Portfolio of Investments (continued)

LIMITED DURATION HIGH QUALITY BOND FUND

September 30, 2014

| | | | |

| |

| | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | Manufacturing—3.0% | | |

| $250M | | CRH America, Inc., 8.125%, 7/15/2018 | | $ 302,077 |

| 500M | | Ingersoll-Rand Global Holdings Co., Ltd., 6.875%, 8/15/2018 | | 586,095 |

| 250M | | Tyco Electronics Group SA, 6.55%, 10/1/2017 | | 284,869 |

| | | | | 1,173,041 |

| | | Media-Broadcasting—1.5% | | |

| 500M | | DirecTV Holdings, LLC, 5.875%, 10/1/2019 | | 573,636 |

| | | Media-Diversified—.7% | | |

| 250M | | McGraw-Hill Financial, Inc., 5.9%, 11/15/2017 | | 274,804 |

| | | Metals/Mining—2.6% | | |

| 500M | | Newmont Mining Corp., 5.125%, 10/1/2019 | | 543,550 |

| 500M | | Rio Tinto Finance USA, PLC, 1.625%, 8/21/2017 | | 503,042 |

| | | | | 1,046,592 |

| | | Real Estate Investment Trusts—1.5% | | |

| 500M | | Boston Properties, LP, 5.875%, 10/15/2019 | | 576,648 |

| | | Telecommunications—3.0% | | |

| 500M | | AT&T, Inc., 5.8%, 2/15/2019 | | 573,530 |

| 600M | | Verizon Communications, Inc., 3.65%, 9/14/2018 | | 632,531 |

| | | | | 1,206,061 |

| | | Utilities—2.0% | | |

| 250M | | Electricite de France SA, 6.5%, 1/26/2019 (a) | | 293,388 |

| 500M | | Public Service Electric & Gas Co., 1.8%, 6/1/2019 | | 493,872 |

| | | | | 787,260 |

| Total Value of Corporate Bonds (cost $17,184,351) | | 17,105,719 |

| | | RESIDENTIAL MORTGAGE-BACKED | | |

| | | SECURITIES—19.2% | | |

| | | Fannie Mae—17.4% | | |

| 1,958M | | 2.5%, 1/1/2023 – 2/1/2023 | | 2,008,330 |

| 2,441M | | 3%, 5/1/2021 – 5/1/2023 | | 2,542,526 |

| 823M | | 3.5%, 1/1/2021 – 3/1/2022 (b) | | 866,875 |

| 1,403M | | 4%, 1/1/2021 – 2/1/2024 | | 1,491,088 |

| | | | | 6,908,819 |

| | | | |

| |

| | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | Freddie Mac—1.8% | | |

| $ 669M | | 3.5%, 12/1/2020 | | $ 703,379 |

| Total Value of Residential Mortgage-Backed Securities (cost $7,618,093) | | 7,612,198 |

| | | U.S. GOVERNMENT OBLIGATIONS—11.5% | | |

| | | U.S. Treasury Notes: | | |

| 1,680M | | 0.375%, 5/31/2016 | | 1,678,458 |

| 1,200M | | 0.5%, 6/15/2016 | | 1,201,242 |

| 1,700M | | 0.875%, 5/15/2017 | | 1,697,941 |

| Total Value of U.S. Government Obligations (cost $4,579,655) | | 4,577,641 |

| | | ASSET BACKED SECURITIES—8.1% | | |

| | | Financial Services—4.9% | | |

| 950M | | Ford Credit Auto Owner Trust, 1%, 9/15/2017 | | 953,526 |

| 1,000M | | Nissan Auto Receivables Owner Trust, 1%, 7/16/2018 | | 1,004,759 |

| | | | | 1,958,285 |

| | | Financials—3.2% | | |

| 610M | | Chase Issuance Trust, 1.3%, 2/18/2020 | | 602,155 |

| 630M | | Citibank Credit Card Issuance Trust, 4.55%, 6/20/2017 | | 648,863 |

| | | | | 1,251,018 |

| Total Value of Asset Backed Securities (cost $3,212,761) | | 3,209,303 |

| | | U.S. GOVERNMENT AGENCY | | |

| | | OBLIGATIONS—7.5% | | |

| | | Federal Home Loan Bank: | | |

| 500M | | 0.5%, 9/28/2016 | | 498,782 |

| 1,425M | | 0.7%, 9/29/2016 | | 1,424,390 |

| 300M | | 1.04%, 5/19/2017 | | 299,366 |

| 750M | | 0.875%, 5/24/2017 | | 748,506 |

| Total Value of U.S. Government Agency Obligations (cost $2,973,312) | | 2,971,044 |

| | | SUPRANATIONALS—3.3% | | |

| | | Financials | | |

| 800M | | European Investment Bank, 4.875%, 1/17/2017 | | 872,712 |

| 400M | | International Finance Corp., 2.125%, 11/17/2017 | | 410,557 |

| Total Value of Supranationals (cost $1,285,206) | | 1,283,269 |

Portfolio of Investments (continued)

LIMITED DURATION HIGH QUALITY BOND FUND

September 30, 2014

| | | | | | | |

| |

| | | | | | | | |

| Principal | | | | | | | |

| Amount | | Security | | | | | Value |

| | | VARIABLE AND FLOATING RATE NOTES—1.0% | | | | |

| | | Financials | | | | | |

| $400M | | Bank of America Corp., 1.3031%, 3/22/2018 (cost $406,552) (c) | | | | $ 407,773 |

| | | SHORT-TERM U.S. GOVERNMENT AGENCY | | | | |

| | | OBLIGATIONS—5.4% | | | | | |

| | | Federal Home Loan Bank: | | | | | |

| 650M | | 0.06%, 12/5/2014 | | | | | 649,930 |

| 500M | | 0.065%, 12/24/2014 | | | | | 499,924 |

| | | Freddie Mac: | | | | | |

| 400M | | 0.08%, 11/3/2014 | | | | | 399,971 |

| 600M | | 0.062%, 11/21/2014 | | | | | 599,947 |

| Total Value of Short-Term U.S. Government Agency Obligations (cost $2,149,772) | | | | 2,149,772 |

| | | SHORT-TERM CORPORATE NOTES—1.0% | | | | |

| 400M | | Chevron Corp., 0.09%, 11/25/2014 (cost $399,945) (d) | | | | 399,945 |

| Total Value of Investments (cost $39,809,647) | 100.1 | % | | | 39,716,664 |

| Excess of Liabilities Over Other Assets | (.1 | ) | | | (31,844) |

| Net Assets | | | 100.0 | % | | | $ 39,684,820 |

| |

| (a) | Security exempt from registration under Rule 144A of the Securities Act of 1933 (see Note 4). |

| |

| (b) | A portion or all of the security purchased on a when-issued or delayed delivery basis |

| (see Note 1G). |

| |

| (c) | Interest rates are determined and reset periodically. The interest rates above are the rates in effect |

| at September 30, 2014. |

| |

| (d) | Security exempt from registration under Section 4(2) of the Securities Act of 1933 (see Note 4). |

Accounting Standards Codification established a three-tier hierarchy of inputs to establish a classification of fair value measurements for disclosure purposes. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below:

| | |

| Level 1 — | Unadjusted quoted prices in active markets for identical securities that the Fund has |

| | the ability to access. |

| | |

| Level 2 — | Observable inputs other than quoted prices included in Level 1 that are observable |

| | for the asset or liability, either directly or indirectly. These inputs may include quoted |

| | prices for the identical instrument on an inactive market, prices for similar instru- |

| | ments, interest rates, prepayment speeds, credit risk, yield curves, default rates and |

| | similar data. |

| | |

| Level 3 — | Unobservable inputs for the asset or liability, to the extent relevant observable inputs |

| | are not available, representing the Fund’s own assumption about the assumptions a |

| | market participant would use in valuing the asset or liability, and would be based on |

| | the best information available. |

The inputs methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. For example, amortized cost approximates the current fair value of a security, but since the value is not obtained from a quoted price in an active market, such securities are reflected as Level 2.

The following is a summary, by category of Level, of inputs used to value the Fund’s investments as of September 30, 2014:

| | | | | | | | | | | | |

| | | | Level 1 | | | Level 2 | | | Level 3 | | | Total |

| Corporate Bonds | | $ | — | | $ | 17,105,719 | | $ | — | | $ | 17,105,719 |

| Residential Mortgage-Backed | | | | | | | | | | | | |

| Securities | | | — | | | 7,612,198 | | | — | | | 7,612,198 |

| U.S. Government Obligations | | | — | | | 4,577,641 | | | — | | | 4,577,641 |

| Asset Backed Securities | | | — | | | 3,209,303 | | | — | | | 3,209,303 |

| U.S. Government Agency | | | | | | | | | | | | |

| Obligations | | | — | | | 2,971,044 | | | — | | | 2,971,044 |

| Supranationals | | | — | | | 1,283,269 | | | — | | | 1,283,269 |

| Variable and Floating | | | | | | | | | | | | |

| Rate Notes | | | — | | | 407,773 | | | — | | | 407,773 |

| Short-Term U.S. Government | | | | | | | | | | | | |

| Agency Obligations | | | — | | | 2,149,772 | | | — | | | 2,149,772 |

| Short-Term Corporate Notes | | | — | | | 399,945 | | | — | | | 399,945 |

| Total Investments in Securities* | | $ | — | | $ | 39,716,664 | | $ | — | | $ | 39,716,664 |

| |

| * | The Portfolio of Investments provides information on the industry categorization for |

| corporate bonds, asset backed securities, supranationals and variable and floating rate notes. |

| |

| There were no transfers into or from Level 1 or Level 2 by the Fund for the year ended |

| September 30, 2014. Transfers, if any, between Levels are recognized at the end of the |

| reporting period. |

| |

| See notes to financial statements | 15 |

Portfolio Managers’ Letter

GOVERNMENT FUND

Dear Investor:

This is the annual report for the First Investors Government Fund for the fiscal year ended September 30, 2014. During the period, the Fund’s return on a net asset value basis was 1.71% for Class A shares, 0.86% for Class B shares, 1.73% for Advisor Class shares and 2.08% for Institutional Class shares, including dividends of 25.5 cents per share on Class A shares, 17.3 cents per share on Class B shares, 26.7 cents per share on Advisor Class shares and 28.5 cents per share on Institutional Class shares.

Economic Overview and Market Summary

The U.S. economy, as measured by gross domestic product (“GDP”), grew slightly faster than 2% during the review period, albeit in an unsteady manner, with quarterly growth ranging from –2.1% to 4.6%. This pace of economic growth was sufficient to reduce the unemployment rate from 7.2% to 5.9%, its lowest level since 2008. While a positive development, the employment picture was somewhat tempered by a continued decline in the labor force participation rate and anemic wage growth. Inflation remained subdued, with consumer prices, excluding the volatile food and energy components, increasing only 1.7%, below the Federal Reserve’s (the “Fed’s”) targeted 2% rate. The Fed remained on course to taper its bond buying program, scheduled to conclude in October, and to raise the federal funds rate in the second half of next year.

Interest rates were mixed during the review period. Short- and intermediate-term interest rates moved slightly higher in anticipation of an eventual tightening of monetary policy by the Fed. In particular, two-year and five-year Treasury note yields increased from 0.32% and 1.38% to 0.57% and 1.76%, respectively. In contrast, the benchmark ten-year Treasury note yield ended the review period lower, moving from 2.61% to 2.49%. After touching two-and-a-half year highs at the end of 2013, ten-year yields moved steadily lower for the next three quarters, confounding consensus expectations for higher interest rates in 2014. The move down in long-term yields reflected a number of factors, including slower than expected global economic growth (particularly in Europe), geopolitical events (Ukraine, Gaza, ISIS), which supported “flight-to-safety” flows into the U.S. bond market, and investors’ belief that this Fed tightening cycle would be more benign than in the past.

The broad bond market returned 4.1%, according to Bank of America Merrill Lynch. Both interest rate risk and credit risk were rewarded during the review period, with longer maturity and lower rated bonds seeing the highest returns. Specifically, high yield bonds gained 7.2% as default rates remained historically low. Investment grade corporate bonds benefited primarily from lower interest rates and, secondarily, from tighter credit spreads, gaining 7.1%. Mortgage-backed bonds, whose returns tend to reflect intermediate-term interest rates, gained 3.7%. While the broad Treasury market returned only 2.7%, 10+ year Treasuries were up 11.3% due to the decline in long-term interest rates. Money market returns continued to be essentially flat, reflecting the Fed’s continuation of very easy monetary policy.

The agency mortgage-backed securities (“MBS”) sector outperformed comparable dated Treasury securities as investor demand for agency MBS far outweighed issuance. The Fed remained a large buyer of agency MBS through its Asset Purchase Program, thus contributing to increased demand. Mortgage lenders remained selective, only preferring to lend to borrowers with pristine credit. This resulted in fewer home owners being able to refinance their mortgages, thus reducing both the negative impact that mortgage refinancing would have had on MBS investors and the supply of MBS.

Within the MBS market, 30-year Ginnie Mae (“GNMA”) mortgages returned 3.7% and 30-year Fannie Mae mortgages returned 4.2%. This outperformance of Fannie Mae mortgages over their GNMA counterparts was due to declining relative issuance. Consequently, investors preferred Fannie Mae securities due to their more favorable supply/demand dynamics. Lower-coupon agency MBS outperformed higher-coupon agency MBS. Investors favored lower-coupon agency MBS because they offered higher yields and were less sensitive to prepayments in the falling interest rate environment.

Fund Overview and Fiscal Year Performance Attribution

The Fund underperformed its benchmark, the Citigroup Government and Mortgage Index, during the period under review. Broadly, the Fund’s shorter effective duration had a negative impact on performance as longer-term interest rates decreased during the fiscal year (interest rates and bond prices are inversely related; when rates decrease, prices rise). In particular, the Fund’s underperformance was mainly driven by an underweight in lower-coupon agency MBS and an overweight in higher-coupon agency MBS, and minimal exposure to Treasury maturities 10 years and longer. Lastly, the Fund’s overweight in GNMA agency MBS also contributed to the Fund’s underperformance.

Thank you for placing your trust in First Investors. As always, we appreciate the opportunity to serve your investment needs.

Fund Expenses (unaudited)

GOVERNMENT FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 3 for a detailed explanation of the information presented in these examples.

| | | | |

| |

| | Annualized | Beginning | Ending | Expenses Paid |

| | Expense | Account Value | Account Value | During Period |

| Expense Example | Ratio | (4/1/14) | (9/30/14) | (4/1/14–9/30/14)* |

| Class A Shares | 1.07% | | | |

| Actual | | $1,000.00 | $1,012.28 | $5.40 |

| Hypothetical** | | $1,000.00 | $1,019.71 | $5.42 |

| Class B Shares | 1.90% | | | |

| Actual | | $1,000.00 | $1,008.29 | $9.57 |

| Hypothetical** | | $1,000.00 | $1,015.54 | $9.60 |

| Advisor Class Shares | 0.70% | | | |

| Actual | | $1,000.00 | $1,013.76 | $3.53 |

| Hypothetical** | | $1,000.00 | $1,021.56 | $3.55 |

| Institutional Class Shares | 0.65% | | | |

| Actual | | $1,000.00 | $1,014.54 | $3.28 |

| Hypothetical** | | $1,000.00 | $1,021.81 | $3.29 |

| |

| * | Expenses are equal to the annualized expense ratio, multiplied by the average account value over |

| the period, multiplied by 183/365 (to reflect the one-half year period). Expenses paid during the |

| period are net of expenses waived. |

| |

| ** | Assumed rate of return of 5% before expenses. |

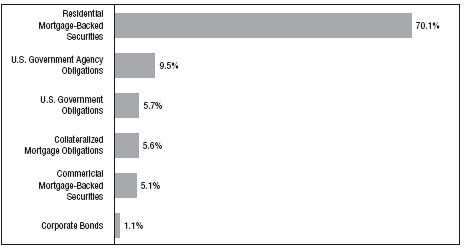

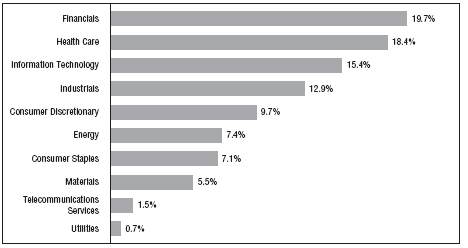

Portfolio Composition

BY SECTOR

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2014, and are based on the total value of investments.

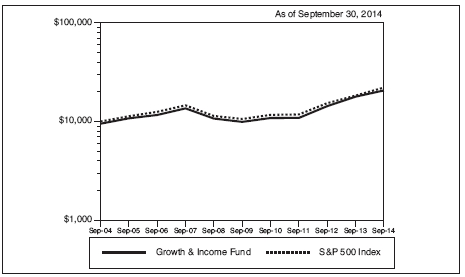

Cumulative Performance Information (unaudited)

GOVERNMENT FUND

Comparison of change in value of $10,000 investment in the First Investors Government Fund (Class A shares) and the Citigroup U.S. Government/Mortgage Index.

| | | | |

| | | Average Annual Total Returns* | |

| | | | Advisor | Institutional |

| N.A.V. Only | Class A | Class B | Class | Class |

| One Year | 1.71% | 0.86% | 1.73% | 2.08% |

| Five Years | 2.61% | 1.87% | N/A | N/A |

| Ten Years, Since Inception** | 3.65% | 3.07% | (0.04%) | 0.34% |

| | | | Advisor | Institutional |

| S.E.C. Standardized | Class A | Class B | Class | Class |

| One Year | (4.16%) | (3.12%) | 1.73% | 2.08% |

| Five Years | 1.40% | 1.51% | N/A | N/A |

| Ten Years, Since Inception** | 3.04% | 3.07% | (0.04%) | 0.34% |

| S.E.C. 30-Day Yield*** | 1.68% | 0.98% | 2.19% | 2.21% |

The graph compares a $10,000 investment in the First Investors Government Fund (Class A shares) beginning 9/30/04 with a theoretical investment in the Citigroup U.S. Government/Mortgage Index (the “Index”). The Index is an unmanaged index that is a combination of the Citigroup Government Index and the Citigroup Mortgage Index. The Citigroup U.S. Government Index tracks the performance of the U.S. Treasury and U.S. Government-sponsored indices within the Citigroup U.S. Broad Investment Grade Bond Index. The Citigroup Mortgage Index tracks the performance of the mortgage component of the Citigroup U.S. Broad Investment Grade Bond Index, which is comprised of 30- and 15-year GNMA, FNMA and FHLMC pass-throughs and FNMA and FHLMC balloon mortgages. It is not possible to invest directly in this Index. In addition, the Index does not reflect fees and expenses

Cumulative Performance Information (unaudited) (continued)

GOVERNMENT FUND

associated with the active management of a mutual fund portfolio. For purposes of the graph and the accompanying table, unless otherwise indicated, it has been assumed that the maximum sales charge was deducted from the initial $10,000 investment in the Fund and all dividends and distributions were reinvested. Class B shares, Advisor Class shares and Institutional Class shares performance may be greater than or less than that shown in the line graph above for Class A shares based on differences in sales loads and fees paid by shareholders investing in the different classes.

*Average Annual Total Return figures (for the periods ended 9/30/14) include the reinvestment of all dividends and distributions. “N.A.V. Only” returns are calculated without sales charges. The Class A “S.E.C. Standardized” returns shown are based on the maximum sales charge of 5.75%. The Class B “S.E.C. Standardized” returns are adjusted for the applicable deferred sales charge (maximum of 4% in the first year). The Advisor Class and Institutional Class “S.E.C. Standardized” returns shown are the same as the N.A.V. Only returns since these classes are sold without sales charges. During the periods shown, some of the expenses of the Fund were waived or assumed. If such expenses had been paid by the Fund, the Class A “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been (4.28%), 1.29% and 2.89%, respectively, and the S.E.C. 30-Day Yield for September 2014 would have been 1.57%. The Class B “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been (3.23%), 1.40% and 2.92%, respectively, and the S.E.C. 30-Day Yield for September 2014 would have been 0.86%. The Advisor Class “S.E.C. Standardized” Average Annual Total Return for One Year and Since Inception would have been 1.62% and (2.95%), respectively, and the S.E.C. 30-Day Yield for September 2014 would have been 2.07%. The Institutional Class “S.E.C. Standardized” Average Annual Total Return for One Year and Since Inception would have been 1.96% and 0.19%, respectively, and the S.E.C. 30-Day Yield for September 2014 would have been 2.09%. Results represent past performance and do not indicate future results. The graph and the returns shown do not reflect the deduction of taxes that a shareholder would pay on distributions or the redemption of fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Index figures are from Citigroup and all other figures are from First Investors Management Company, Inc.

**The Since Inception returns for Advisor Class shares and Institutional Class shares are for the periods beginning 4/1/13 (commencement of operations for those classes).

*** The S.E.C. 30-Day Yield shown is for September 2014.

Portfolio of Investments

GOVERNMENT FUND

September 30, 2014

| | | | |

| |

| | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | RESIDENTIAL MORTGAGE-BACKED | | |

| | | SECURITIES—70.7% | | |

| | | Fannie Mae—37.1% | | |

| $ 6,182M | | 2.5%, 9/1/2023 – 11/1/2023 | | $ 6,323,016 |

| 12,229M | | 3%, 8/1/2022 – 7/1/2023 | | 12,734,266 |

| 29,055M | | 3.5%, 10/1/2025 – 5/1/2044 | | 30,173,173 |

| 49,443M | | 4%, 2/1/2024 – 10/14/2044 (a) | | 52,466,188 |

| 10,738M | | 4.5%, 11/1/2040 – 1/1/2042 | | 11,720,381 |

| 7,155M | | 5%, 8/1/2039 – 4/1/2040 | | 7,947,227 |

| 3,463M | | 5.5%, 7/1/2033 – 10/1/2039 | | 3,894,893 |

| | | | | 125,259,144 |

| | | Freddie Mac—5.3% | | |

| 746M | | 3%, 6/1/2021 | | 774,311 |

| 8,629M | | 3.5%, 9/1/2032 – 8/1/2044 (a) | | 8,861,465 |

| 5,565M | | 4%, 11/1/2040 | | 5,937,773 |

| 2,099M | | 5%, 8/1/2039 | | 2,351,333 |

| | | | | 17,924,882 |

| | | Government National Mortgage Association I | | |

| | | Program—28.3% | | |

| 6,087M | | 4%, 11/15/2025 – 6/15/2042 | | 6,546,238 |

| 20,039M | | 4.5%, 9/15/2033 – 6/15/2040 | | 21,999,496 |

| 23,949M | | 5%, 6/15/2033 – 4/15/2040 | | 26,710,373 |

| 17,196M | | 5.5%, 3/15/2033 – 10/15/2039 | | 19,377,137 |

| 14,877M | | 6%, 2/15/2032 – 4/15/2040 | | 17,089,968 |

| 1,502M | | 6.5%, 6/15/2034 – 3/15/2038 | | 1,710,494 |

| 1,931M | | 7%, 6/15/2023 – 4/15/2034 | | 2,135,138 |

| | | | | 95,568,844 |

| Total Value of Residential Mortgage-Backed Securities (cost $232,445,585) | | 238,752,870 |

| | | U.S. GOVERNMENT AGENCY | | |

| | | OBLIGATIONS—9.6% | | |

| | | Fannie Mae: | | |

| 12,800M | | 0.875%, 8/28/2017 | | 12,719,411 |

| 4,300M | | 1.875%, 9/18/2018 | | 4,345,614 |

| 3,025M | | 2.625%, 9/6/2024 | | 2,982,075 |

| 7,000M | | Federal Farm Credit Bank, 2.79%, 11/12/2020 | | 7,012,572 |

| 5,000M | | Freddie Mac, 3.75%, 3/27/2019 | | 5,416,435 |

| Total Value of U.S. Government Agency Obligations (cost $32,515,904) | | 32,476,107 |

Portfolio of Investments (continued)

GOVERNMENT FUND

September 30, 2014

| | | | |

| |

| | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | U.S. GOVERNMENT OBLIGATIONS—5.8% | | |

| | | U.S. Treasury Notes: | | |

| $ 5,550M | | 1.5%, 5/31/2019 | | $ 5,492,768 |

| 5,400M | | 2.25%, 7/31/2021 | | 5,419,197 |

| 8,720M | | 2.375%, 8/15/2024 | | 8,619,860 |

| Total Value of U.S. Government Obligations (cost $19,737,928) | | 19,531,825 |

| | | COLLATERALIZED MORTGAGE | | |

| | | OBLIGATIONS—5.6% | | |

| | | Fannie Mae—4.4% | | |

| 7,048M | | 3%, 2/25/2024 | | 7,243,176 |

| 6,998M | | 4%, 2/25/2025 | | 7,552,155 |

| | | | | 14,795,331 |

| | | Freddie Mac—1.2% | | |

| 4,077M | | 3%, 8/15/2039 | | 4,170,850 |

| Total Value of Collateralized Mortgage Obligations (cost $19,317,822) | | 18,966,181 |

| | | COMMERCIAL MORTGAGE-BACKED | | |

| | | SECURITIES—5.1% | | |

| | | Fannie Mae—3.6% | | |

| 2,911M | | 2.27%, 1/1/2023 | | 2,825,651 |

| 1,300M | | 2.96%, 11/1/2018 | | 1,348,416 |

| 2,947M | | 3.76%, 4/1/2018 | | 3,138,664 |

| 4,500M | | 3.84%, 5/1/2018 | | 4,809,938 |

| | | | | 12,122,669 |

| | | Federal Home Loan Mortgage Corporation—1.5% | | |

| 5,000M | | Multi Family Structured Pass Through 2.13%, 1/25/2019 | | 5,041,810 |

| Total Value of Commercial Mortgage-Backed Securities (cost $17,574,636) | | 17,164,479 |

| | | CORPORATE BONDS—1.1% | | |

| | | Financials | | |

| 3,932M | | Excalibur One 77B, LLC, 1.492%, 1/1/2025 (cost $3,913,601) | | 3,758,393 |

| | | | | | |

| |

| | | | | | | |

| Principal | | | | | | |

| Amount | | Security | | | | Value |

| | | SHORT-TERM U.S. GOVERNMENT AGENCY | | | |

| | | OBLIGATIONS—3.0% | | | | |

| $10,000M | | Freddie Mac, 0.01%, 11/5/2014 (cost $9,999,903) | | | $ 9,999,903 |

| Total Value of Investments (cost $335,505,379) | 100.9 | % | | 340,649,758 |

| Excess of Liabilities Over Other Assets | (.9 | ) | | (3,014,314) |

| Net Assets | | | 100.0 | % | | $ 337,635,444 |

| |

| (a) | A portion or all of the security purchased on a when-issued or delayed delivery basis |

| (see Note 1G). |

Portfolio of Investments (continued)

GOVERNMENT FUND

September 30, 2014

Accounting Standards Codification established a three-tier hierarchy of inputs to establish a classification of fair value measurements for disclosure purposes. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below:

| | |

| Level 1 — | Unadjusted quoted prices in active markets for identical securities that the Fund has |

| | the ability to access. |

| | |

| Level 2 — | Observable inputs other than quoted prices included in Level 1 that are observable |

| | for the asset or liability, either directly or indirectly. These inputs may include quoted |

| | prices for the identical instrument on an inactive market, prices for similar instru- |

| | ments, interest rates, prepayment speeds, credit risk, yield curves, default rates and |

| | similar data. |

| | |

| Level 3 — | Unobservable inputs for the asset or liability, to the extent relevant observable inputs |

| | are not available, representing the Fund’s own assumption about the assumptions a |

| | market participant would use in valuing the asset or liability, and would be based on |

| | the best information available. |

The inputs methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. For example, amortized cost approximates the current fair value of a security, but since the value is not obtained from a quoted price in an active market, such securities are reflected as Level 2.

The following is a summary, by category of Level, of inputs used to value the Fund’s investments as of September 30, 2014:

| | | | | | | | | | | | |

| | | | Level 1 | | | Level 2 | | | Level 3 | | | Total |

| Residential Mortgage-Backed | | | | | | | | | | | | |

| Securities | | $ | — | | $ | 238,752,870 | | $ | — | | $ | 238,752,870 |

| U.S. Government Agency | | | | | | | | | | | | |

| Obligations | | | — | | | 32,476,107 | | | — | | | 32,476,107 |

| U.S. Government Obligations | | | — | | | 19,531,825 | | | — | | | 19,531,825 |

| Collateralized Mortgage | | | | | | | | | | | | |

| Obligations | | | — | | | 18,966,181 | | | — | | | 18,966,181 |

| Commercial Mortgage-Backed | | | | | | | | | | | | |

| Securities | | | — | | | 17,164,479 | | | — | | | 17,164,479 |

| Corporate Bonds | | | — | | | 3,758,393 | | | — | | | 3,758,393 |

| Short-Term U.S. Government | | | | | | | | | | | | |

| Agency Obligations | | | — | | | 9,999,903 | | | — | | | 9,999,903 |

| Total Investments in Securities | | $ | — | | $ | 340,649,758 | | $ | — | | $ | 340,649,758 |

There were no transfers into or from Level 1 or Level 2 by the Fund for the year ended September 30, 2014. Transfers, if any, between Levels are recognized at the end of the reporting period.

| |

| 24 | See notes to financial statements |

Portfolio Managers’ Letter

INVESTMENT GRADE FUND

Dear Investor:

This is the annual report for the First Investors Investment Grade Fund for the fiscal year ended September 30, 2014. During the period, the Fund’s return on a net asset value basis was 5.50% for Class A shares, 4.53% for Class B shares, 5.61% for Advisor Class shares and 5.98% for Institutional Class shares, including dividends of 39.2 cents per share on Class A shares, 32.9 cents on Class B shares, 40.2 cents on Advisor Class shares and 42.8 cents on Institutional Class shares.

Economic Overview and Market Summary

The U.S. economy, as measured by gross domestic product (“GDP”), grew slightly faster than 2% during the review period, albeit in an unsteady manner, with quarterly growth ranging from –2.1% to 4.6%. This pace of economic growth was sufficient to reduce the unemployment rate from 7.2% to 5.9%, its lowest level since 2008. While a positive development, the employment picture was somewhat tempered by a continued decline in the labor force participation rate and anemic wage growth. Inflation remained subdued, with consumer prices, excluding the volatile food and energy components, increasing only 1.7%, below the Federal Reserve’s (the “Fed’s”) targeted 2% rate. The Fed remained on course to taper its bond buying program, scheduled to conclude in October, and to raise the federal funds rate in the second half of next year.

Interest rates were mixed during the review period. Short- and intermediate-term interest rates moved slightly higher in anticipation of an eventual tightening of monetary policy by the Fed. In particular, two-year and five-year Treasury note yields increased from 0.32% and 1.38% to 0.57% and 1.76%, respectively. In contrast, the benchmark ten-year Treasury note yield ended the review period lower, moving from 2.61% to 2.49%. After touching two-and-a-half year highs at the end of 2013, ten-year yields moved steadily lower for the next three quarters, confounding consensus expectations for higher interest rates in 2014. The move down in long-term yields reflected a number of factors, including slower than expected global economic growth (particularly in Europe), geopolitical events (Ukraine, Gaza, ISIS), which supported “flight-to-safety” flows into the U.S. bond market, and investors’ belief that this Fed tightening cycle would be more benign than in the past.

The broad bond market returned 4.1%, according to Bank of America Merrill Lynch. Both interest rate risk and credit risk were rewarded during the review period, with longer maturity and lower rated bonds seeing the highest returns. Specifically, high yield bonds gained 7.2% as default rates remained historically low. Investment grade corporate bonds benefited primarily from lower interest rates and, secondarily, from tighter credit spreads, gaining 7.1%. Mortgage-backed bonds, whose returns tend to reflect intermediate-term interest rates, gained 3.7%. While the broad Treasury market returned only 2.7%, 10+ year Treasuries were up 11.3% due to the decline in long-term interest rates. Money market returns continued to be essentially flat, reflecting the Fed’s continuation of very easy monetary policy.

Portfolio Managers’ Letter (continued)

INVESTMENT GRADE FUND

The corporate bond market began the review period on a firm note with corporate spreads tightening amongst a backdrop of rising Treasury yields. Very strong technical factors helped support the market, and a wave of new issue supply met an upsurge in demand for investment grade corporate debt. Even as benchmark Treasury yields reversed course and fell during the first half of 2014, positive technicals continued to help corporate bond spreads narrow. Corporate bond spreads began to widen only towards the end of the review period as volatility increased in the market. Lower beta sectors became safe havens for corporate bond investors as riskier assets traded with greater volatility.

The positive returns of the corporate bond market during the review period were predominantly a result of duration and Treasury curve movement. Of note, corporate bonds with maturities greater than 10 years outperformed shorter maturity debt, reflecting the substantial move lower in long-term bond yields (bond prices and yields have an inverse relationship; when prices rise, yields fall).

Fund Overview and Fiscal Year Performance Attribution

The Fund invests in investment grade fixed income securities. Over the course of the review period, the majority of the Fund’s assets were invested in investment grade corporate bonds. The Fund also had as much as 3% of its assets invested in high yield securities.

The Fund underperformed its benchmark, the Bank of America Merrill Lynch Corporate Index, during the review period. The relative performance was predominantly a function of the Fund’s positioning for expected higher interest rates. Specifically, the Fund was negatively impacted by its underweight in corporate bonds with maturities greater than 10 years, which significantly outperformed shorter-dated corporate bonds. This underweight was partially offset by the Fund’s overweight in BBB-rated corporate bonds, which had the highest returns of any rating tier during the review period.

Thank you for placing your trust in First Investors. As always, we appreciate the opportunity to serve your investment needs.

Fund Expenses (unaudited)

INVESTMENT GRADE FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 3 for a detailed explanation of the information presented in these examples.

| | | | |

| |

| | Annualized | Beginning | Ending | Expenses Paid |

| | Expense | Account Value | Account Value | During Period |

| Expense Example | Ratio | (4/1/14) | (9/30/14) | (4/1/14-9/30/14)* |

| Class A Shares | 1.05% | | | |

| Actual | | $1,000.00 | $1,021.90 | $5.32 |

| Hypothetical** | | $1,000.00 | $1,019.81 | $5.32 |

| Class B Shares | 1.90% | | | |

| Actual | | $1,000.00 | $1,017.71 | $9.61 |

| Hypothetical** | | $1,000.00 | $1,015.54 | $9.60 |

| Advisor Class Shares | 0.67% | | | |

| Actual | | $1,000.00 | $1,023.42 | $3.40 |

| Hypothetical** | | $1,000.00 | $1,021.71 | $3.40 |

| Institutional Class Shares | 0.64% | | | |

| Actual | | $1,000.00 | $1,024.71 | $3.25 |

| Hypothetical** | | $1,000.00 | $1,021.86 | $3.24 |

| |

| * | Expenses are equal to the annualized expense ratio, multiplied by the average account value over |

| the period, multiplied by 183/365 (to reflect the one-half year period). Expenses paid during the |

| period are net of expenses waived. |

| |

| ** | Assumed rate of return of 5% before expenses. |

Portfolio Composition

BY SECTOR

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2014, and are based on the total value of investments.

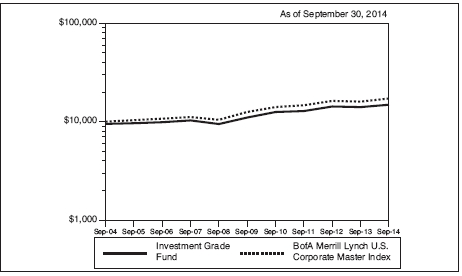

Cumulative Performance Information (unaudited)

INVESTMENT GRADE FUND

Comparison of change in value of $10,000 investment in the First Investors Investment Grade Fund (Class A shares) and the Bank of America (“BofA”) Merrill Lynch U.S. Corporate Master Index.

| | | | |

| | | Average Annual Total Returns* | |

| | | | Advisor | Institutional |

| N.A.V. Only | Class A | Class B | Class | Class |

| One Year | 5.50% | 4.53% | 5.61% | 5.98% |

| Five Years | 6.11% | 5.30% | N/A | N/A |

| Ten Years, Since Inception** | 4.61% | 4.00% | 1.95% | 2.30% |

| | | | Advisor | Institutional |

| S.E.C. Standardized | Class A | Class B | Class | Class |

| One Year | (0.59%) | 0.53% | 5.61% | 5.98% |

| Five Years | 4.85% | 4.97% | N/A | N/A |

| Ten Years, Since Inception** | 3.99% | 4.00% | 1.95% | 2.30% |

| S.E.C. 30-Day Yield*** | 1.94% | 1.23% | 2.42% | 2.47% |

The graph compares a $10,000 investment in the First Investors Investment Grade Fund (Class A shares) beginning 9/30/04 with a theoretical investment in the BofA Merrill Lynch U.S. Corporate Master Index (the “Index”). The Index includes publicly-issued, fixed rate, non-convertible investment grade dollar-denominated, S.E.C.-registered corporate debt having at least one year to maturity and an outstanding par value of at least $250 million. Bonds must be rated investment grade based on a composite of Moody’s and S&P. It is not possible to invest directly in this Index. In addition, the Index does not reflect fees and expenses associated with the active management of a mutual fund portfolio. For purposes of the graph and the accompanying table, unless otherwise indicated, it has been assumed that the maximum sales charge was deducted from the initial $10,000 investment in the Fund and all dividends and distributions were reinvested. Class B shares, Advisor Class shares

and Institutional Class shares performance may be greater than or less than that shown in the line graph above for Class A shares based on differences in sales loads and fees paid by shareholders investing in the different classes.

*Average Annual Total Return figures (for the periods ended 9/30/14) include the reinvestment of all dividends and distributions. “N.A.V. Only” returns are calculated without sales charges. The Class A “S.E.C. Standardized” returns shown are based on the maximum sales charge of 5.75%. The Class B “S.E.C. Standardized” returns are adjusted for the applicable deferred sales charge (maximum of 4% in the first year). The Advisor Class and Institutional Class “S.E.C. Standardized” returns shown are the same as the N.A.V. Only returns since these classes are sold without sales charges. During the periods shown, some of the expenses of the Fund were waived or assumed. If such expenses had been paid by the Fund, the Class A “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been (0.70%), 4.74% and 3.88%, respectively, and the S.E.C. 30-Day Yield for September 2014 would have been 1.84%. The Class B “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been 0.42%, 4.87% and 3.89%, respectively, and the S.E.C. 30-Day Yield for September 2014 would have been 1.11%. The Advisor Class “S.E.C. Standardized” Average Annual Total Return for One Year and Since Inception would have been 5.49% and (0.97%), respectively, and the S.E.C. 30-Day Yield for September 2014 would have been 2.30%. The Institutional Class “S.E.C. Standardized” Average Annual Total Return for One Year and Since Inception would have been 5.87% and 2.16%, respectively, and the S.E.C. 30-Day Yield for September 2014 would have been 2.35%. Results represent past performance and do not indicate future results. The graph and the returns shown do not reflect the deduction of taxes that a shareholder would pay on distributions or the redemption of fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Index figures are from Bank of America Merrill Lynch & Co. and all other figures are from First Investors Management Company, Inc.

**The Since Inception returns for Advisor Class shares and Institutional Class share are for the periods beginning 4/1/13 (commencement of operations for those classes).

*** The S.E.C. 30-day yield shown is for September 2014.

Portfolio of Investments

INVESTMENT GRADE FUND

September 30, 2014

| | | | |

| |

| | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | CORPORATE BONDS—97.8% | | |

| | | Agriculture—.6% | | |

| $ 2,725M | | Cargill, Inc., 6%, 11/27/2017 (a) | | $ 3,080,261 |

| | | Automotive—1.4% | | |

| 2,000M | | Daimler Finance NA, LLC, 2.95%, 1/11/2017 (a) | | 2,070,984 |

| 5,000M | | Johnson Controls, Inc., 5%, 3/30/2020 | | 5,530,605 |

| | | | | 7,601,589 |

| | | Chemicals—2.7% | | |

| 5,000M | | CF Industries, Inc., 3.45%, 6/1/2023 | | 4,910,540 |

| 4,000M | | Dow Chemical Co., 4.25%, 11/15/2020 | | 4,273,280 |

| 5,000M | | LyondellBasell Industries NV, 6%, 11/15/2021 | | 5,838,530 |

| | | | | 15,022,350 |

| | | Consumer Durables—.5% | | |

| 2,300M | | Newell Rubbermaid, Inc., 4.7%, 8/15/2020 | | 2,468,965 |

| | | Energy—11.2% | | |

| 5,000M | | Canadian Oil Sands, Ltd., 7.75%, 5/15/2019 (a) | | 6,051,885 |

| 5,000M | | Continental Resources, Inc., 5%, 9/15/2022 | | 5,281,250 |

| 4,800M | | DCP Midstream, LLC, 9.75%, 3/15/2019 (a) | | 6,152,208 |

| 3,000M | | DCP Midstream Operating, LP, 2.5%, 12/1/2017 | | 3,063,396 |

| 5,000M | | Enbridge Energy Partners, LP, 4.2%, 9/15/2021 | | 5,285,280 |

| 5,000M | | Kinder Morgan Energy Partners, LP, 3.45%, 2/15/2023 | | 4,786,055 |

| 5,000M | | Nabors Industries, Inc., 6.15%, 2/15/2018 | | 5,647,105 |

| 4,000M | | ONEOK Partners, LP, 3.375%, 10/1/2022 | | 3,907,268 |

| 5,000M | | Petrobras International Finance Co., 5.375%, 1/27/2021 | | 5,079,100 |

| 5,800M | | Spectra Energy Capital, LLC, 6.2%, 4/15/2018 | | 6,560,374 |

| 4,000M | | Valero Energy Corp., 9.375%, 3/15/2019 | | 5,148,640 |

| 4,000M | | Weatherford International, Inc., 6.35%, 6/15/2017 | | 4,488,204 |

| | | | | 61,450,765 |

| | | Financial Services—16.8% | | |

| 1,250M | | Aflac, Inc., 8.5%, 5/15/2019 | | 1,583,611 |

| | | American Express Co.: | | |

| 4,000M | | 7%, 3/19/2018 | | 4,660,748 |

| 2,000M | | 4.05%, 12/3/2042 | | 1,900,162 |

| | | American International Group, Inc.: | | |

| 1,200M | | 8.25%, 8/15/2018 | | 1,466,994 |

| 3,100M | | 6.4%, 12/15/2020 | | 3,692,953 |

| 4,000M | | Ameriprise Financial, Inc., 5.3%, 3/15/2020 | | 4,536,116 |

| | | | |

| |

| | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | Financial Services (continued) | | |

| $ 6,400M | | Assured Guaranty US Holding, Inc., 5%, 7/1/2024 | | $ 6,474,355 |

| 4,300M | | Berkshire Hathaway, Inc., 3.4%, 1/31/2022 | | 4,431,442 |

| 1,000M | | BlackRock, Inc., 5%, 12/10/2019 | | 1,131,364 |

| 4,000M | | CoBank ACB, 7.875%, 4/16/2018 (a) | | 4,739,452 |

| 2,400M | | Compass Bank, 6.4%, 10/1/2017 | | 2,644,752 |

| | | ERAC USA Finance, LLC: | | |

| 3,750M | | 4.5%, 8/16/2021 (a) | | 4,066,965 |

| 3,000M | | 7%, 10/15/2037 (a) | | 3,975,141 |

| 6,200M | | Ford Motor Credit Co., LLC, 8.125%, 1/15/2020 | | 7,757,614 |

| | | General Electric Capital Corp.: | | |

| 9,400M | | 5.3%, 2/11/2021 | | 10,602,899 |

| 6,800M | | 6.75%, 3/15/2032 | | 8,990,566 |

| 2,700M | | Harley-Davidson Financial Services, Inc., 2.4%, 9/15/2019 (a) | | 2,702,130 |

| | | Harley-Davidson Funding Corp.: | | |

| 2,000M | | 5.75%, 12/15/2014 (a) | | 2,021,296 |

| 1,800M | | 6.8%, 6/15/2018 (a) | | 2,103,523 |

| 4,000M | | Liberty Mutual Group, Inc., 4.95%, 5/1/2022 (a) | | 4,313,200 |

| 4,550M | | Protective Life Corp., 7.375%, 10/15/2019 | | 5,570,051 |

| 2,000M | | Prudential Financial, Inc., 7.375%, 6/15/2019 | | 2,438,216 |

| | | | | 91,803,550 |

| | | Financials—19.5% | | |

| | | Bank of America Corp.: | | |

| 3,250M | | 5.65%, 5/1/2018 | | 3,617,926 |

| 5,925M | | 5%, 5/13/2021 | | 6,515,811 |

| 4,625M | | 5.875%, 2/7/2042 | | 5,562,182 |

| | | Barclays Bank, PLC: | | |

| 2,000M | | 5.125%, 1/8/2020 | | 2,246,792 |

| 3,800M | | 3.75%, 5/15/2024 | | 3,783,850 |

| | | Citigroup, Inc.: | | |

| 4,200M | | 6.125%, 11/21/2017 | | 4,741,464 |

| 2,000M | | 4.5%, 1/14/2022 | | 2,147,712 |

| 3,000M | | Deutsche Bank AG London, 3.7%, 5/30/2024 | | 2,979,951 |

| | | Goldman Sachs Group, Inc.: | | |

| 2,000M | | 5.375%, 3/15/2020 | | 2,228,330 |

| 5,900M | | 5.75%, 1/24/2022 | | 6,715,427 |

| 3,000M | | 3.625%, 1/22/2023 | | 2,983,332 |

| 5,250M | | 6.125%, 2/15/2033 | | 6,301,533 |

| | | JPMorgan Chase & Co.: | | |

| 9,200M | | 6%, 1/15/2018 | | 10,359,458 |

| 4,000M | | 4.5%, 1/24/2022 | | 4,292,404 |

Portfolio of Investments (continued)

INVESTMENT GRADE FUND

September 30, 2014

| | | | |

| |

| | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | Financials (continued) | | |

| | | Morgan Stanley: | | |

| $4,050M | | 5.95%, 12/28/2017 | | $ 4,539,426 |

| 5,500M | | 6.625%, 4/1/2018 | | 6,303,715 |

| 6,000M | | 5.5%, 7/28/2021 | | 6,767,556 |

| 4,000M | | SunTrust Banks, Inc., 6%, 9/11/2017 | | 4,495,424 |

| 4,000M | | UBS AG, 4.875%, 8/4/2020 | | 4,458,492 |

| 4,000M | | U.S. Bancorp., 3.6%, 9/11/2024 | | 3,961,080 |

| | | Wells Fargo & Co.: | | |

| 2,900M | | 4.6%, 4/1/2021 | | 3,180,424 |

| 8,600M | | 3.45%, 2/13/2023 | | 8,459,820 |

| | | | | 106,642,109 |

| | | Food/Beverage/Tobacco—8.2% | | |

| 4,000M | | Altria Group, Inc., 9.7%, 11/10/2018 | | 5,157,352 |

| 5,000M | | Anheuser-Busch InBev SA/NV, 4.625%, 2/1/2044 | | 5,085,235 |

| | | Anheuser-Busch InBev Worldwide, Inc.: | | |

| 1,000M | | 6.875%, 11/15/2019 | | 1,201,260 |

| 4,000M | | 5.375%, 1/15/2020 | | 4,518,000 |

| 5,225M | | Bunge Ltd. Finance Corp., 8.5%, 6/15/2019 | | 6,501,833 |

| 4,200M | | Dr. Pepper Snapple Group, Inc., 6.82%, 5/1/2018 | | 4,889,434 |

| 4,165M | | Ingredion, Inc., 4.625%, 11/1/2020 | | 4,467,446 |

| 4,000M | | Philip Morris International, Inc., 5.65%, 5/16/2018 | | 4,527,544 |

| | | SABMiller Holdings, Inc.: | | |

| 4,000M | | 3.75%, 1/15/2022 (a) | | 4,083,588 |

| 4,000M | | 4.95%, 1/15/2042 (a) | | 4,178,348 |

| | | | | 44,610,040 |

| | | Forest Products/Container—1.0% | | |

| 5,000M | | Rock-Tenn Co., 4.9%, 3/1/2022 | | 5,367,960 |

| | | Health Care—4.6% | | |

| 4,000M | | Biogen IDEC, Inc., 6.875%, 3/1/2018 | | 4,645,756 |

| | | Express Scripts Holding Co.: | | |

| 4,050M | | 4.75%, 11/15/2021 | | 4,429,639 |

| 1,800M | | 3.5%, 6/15/2024 | | 1,766,079 |

| 4,000M | | Laboratory Corp. of America Holdings, 3.75%, 8/23/2022 | | 4,052,384 |

| 4,000M | | Mylan, Inc., 3.125%, 1/15/2023 (a) | | 3,828,000 |

| 4,000M | | Novartis Capital Corp., 4.4%, 5/6/2044 | | 4,176,948 |

| 1,400M | | Novartis Securities Investments, Ltd., 5.125%, 2/10/2019 | | 1,573,828 |

| 580M | | Roche Holdings, Inc., 6%, 3/1/2019 (a) | | 672,826 |

| | | | | 25,145,460 |

| | | | |

| |

| | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | Information Technology—1.5% | | |

| $4,000M | | Harris Corp., 4.4%, 12/15/2020 | | $ 4,259,408 |

| 4,000M | | Symantec Corp., 3.95%, 6/15/2022 | | 4,054,720 |

| | | | | 8,314,128 |

| | | Manufacturing—2.9% | | |

| 5,000M | | CRH America, Inc., 8.125%, 7/15/2018 | | 6,041,550 |

| 4,000M | | Ingersoll-Rand Global Holdings Co., Ltd., 6.875%, 8/15/2018 | | 4,688,760 |

| 4,550M | | Tyco Electronics Group SA, 6.55%, 10/1/2017 | | 5,184,611 |

| | | | | 15,914,921 |

| | | Media-Broadcasting—4.2% | | |

| 1,800M | | ABC, Inc., 8.75%, 8/15/2021 | | 2,403,112 |

| 3,950M | | British Sky Broadcasting Group, PLC, 9.5%, 11/15/2018 (a) | | 5,029,879 |

| 2,000M | | CBS Corp., 3.375%, 3/1/2022 | | 2,005,988 |

| 4,000M | | Comcast Corp., 4.25%, 1/15/2033 | | 4,061,400 |

| 3,000M | | DirecTV Holdings, LLC, 3.8%, 3/15/2022 | | 3,054,033 |

| 2,000M | | Sirius XM Radio, Inc., 5.25%, 8/15/2022 (a) | | 2,095,000 |

| 4,000M | | Time Warner Cable, Inc., 5%, 2/1/2020 | | 4,450,228 |

| | | | | 23,099,640 |

| | | Media-Diversified—1.1% | | |

| | | McGraw-Hill Financial, Inc.: | | |

| 3,350M | | 5.9%, 11/15/2017 | | 3,682,374 |

| 2,300M | | 6.55%, 11/15/2037 | | 2,398,224 |

| | | | | 6,080,598 |

| | | Metals/Mining—5.2% | | |

| 5,000M | | Alcoa, Inc., 6.15%, 8/15/2020 | | 5,517,635 |

| 4,000M | | ArcelorMittal, 6.125%, 6/1/2018 | | 4,250,000 |

| 4,000M | | Glencore Finance Canada, Ltd., 4.95%, 11/15/2021 (a) | | 4,263,060 |

| 4,200M | | Newmont Mining Corp., 5.125%, 10/1/2019 | | 4,565,824 |

| 5,000M | | Rio Tinto Finance USA, Ltd., 3.75%, 9/20/2021 | | 5,194,870 |

| 4,000M | | Vale Overseas, Ltd., 5.625%, 9/15/2019 | | 4,486,692 |

| | | | | 28,278,081 |

Portfolio of Investments (continued)

INVESTMENT GRADE FUND

September 30, 2014

| | | | |

| |

| | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | Real Estate Investment Trusts—4.7% | | |

| $4,000M | | Boston Properties, LP, 5.875%, 10/15/2019 | | $ 4,613,188 |

| 4,000M | | Digital Realty Trust, LP, 5.25%, 3/15/2021 | | 4,347,348 |

| 4,000M | | HCP, Inc., 5.375%, 2/1/2021 | | 4,469,384 |

| | | ProLogis, LP: | | |

| 3,000M | | 4.5%, 8/15/2017 | | 3,215,571 |

| 2,000M | | 3.35%, 2/1/2021 | | 1,998,586 |

| 2,700M | | Simon Property Group, LP, 3.375%, 10/1/2024 | | 2,675,519 |

| 4,000M | | Ventas Realty, LP, 4.75%, 6/1/2021 | | 4,360,960 |

| | | | | 25,680,556 |

| | | Retail-General Merchandise—2.3% | | |

| 6,000M | | GAP, Inc., 5.95%, 4/12/2021 | | 6,832,926 |

| 2,000M | | Home Depot, Inc., 5.875%, 12/16/2036 | | 2,470,844 |

| 3,600M | | Lowe’s Cos., Inc., 4.25%, 9/15/2044 | | 3,522,719 |

| | | | | 12,826,489 |

| | | Telecommunications—1.3% | | |

| 2,000M | | AT&T, Inc., 6.5%, 9/1/2037 | | 2,437,798 |

| 4,000M | | Verizon Communications, Inc., 5.15%, 9/15/2023 | | 4,432,688 |

| | | | | 6,870,486 |

| | | Transportation—3.1% | | |

| 4,000M | | Burlington North Santa Fe, LLC, 5.15%, 9/1/2043 | | 4,408,164 |

| 4,000M | | Con-way, Inc., 7.25%, 1/15/2018 | | 4,606,308 |

| 4,125M | | GATX Corp., 4.75%, 6/15/2022 | | 4,466,496 |

| 3,000M | | Penske Truck Leasing Co., LP, 4.875%, 7/11/2022 (a) | | 3,229,167 |

| | | | | 16,710,135 |

| | | Utilities—5.0% | | |

| 3,000M | | E.ON International Finance BV, 5.8%, 4/30/2018 (a) | | 3,390,573 |

| 1,900M | | Electricite de France SA, 6.5%, 1/26/2019 (a) | | 2,229,747 |

| 4,000M | | Exelon Generation Co., LLC, 5.2%, 10/1/2019 | | 4,440,044 |

| | | Great River Energy Co.: | | |

| 291M | | 5.829%, 7/1/2017 (a) | | 313,959 |

| 3,424M | | 4.478%, 7/1/2030 (a) | | 3,627,762 |

| 4,200M | | National Fuel Gas Co., 8.75%, 5/1/2019 | | 5,223,809 |

| | | | | | |

| |

| | | | | | | |

| Principal | | | | | | |

| Amount | | Security | | | | Value |

| | | Utilities (continued) | | | | |

| $ 900M | | Northern States Power Co., 4.125%, 5/15/2044 | | | $ 908,571 |

| 3,000M | | Ohio Power Co., 5.375%, 10/1/2021 | | | | 3,480,840 |

| 2,881M | | Sempra Energy, 9.8%, 2/15/2019 | | | | 3,757,853 |

| | | | | | | 27,373,158 |