|

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| WASHINGTON, D.C. 20549 |

| -------- |

| |

| FORM N-CSR |

| -------- |

| |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT |

| INVESTMENT COMPANIES |

| |

| INVESTMENT COMPANY ACT FILE NUMBER 811-3967 |

| |

| FIRST INVESTORS INCOME FUNDS |

| (Exact name of registrant as specified in charter) |

| |

| 110 Wall Street |

| New York, NY 10005 |

| (Address of principal executive offices) (Zip code) |

| |

| Joseph I. Benedek |

| First Investors Management Company, Inc. |

| Raritan Plaza I |

| Edison, NJ 08837-3620 |

| (Name and address of agent for service) |

| |

| REGISTRANT'S TELEPHONE NUMBER, INCLUDING AREA CODE: |

| 1-212-858-8000 |

| |

| DATE OF FISCAL YEAR END: SEPTEMBER 30, 2010 |

| |

| DATE OF REPORTING PERIOD: SEPTEMBER 30, 2010 |

|

| Item 1. Reports to Stockholders |

| |

| The annual report to stockholders follows |

This report is for the information of the shareholders of the Funds. It is the Funds’ practice to mail only one copy of their annual and semi-annual reports to all family members who reside at the same address and share the same last name. Additional copies of the reports will be mailed if requested by any shareholder in writing or by calling 1-800-423-4026. The Funds will ensure that separate reports are sent to any shareholder who subsequently changes his or her mailing address.

The views expressed in the portfolio manager letters reflect those views of the portfolio managers only through the end of the period covered. Any such views are subject to change at any time based upon market or other conditions and we disclaim any responsibility to update such views. These views may not be relied on as investment advice.

You may obtain a free prospectus for any of the Funds by contacting your representative, calling 1-800-423-4026, writing to us at the following address: First Investors Corporation, 110 Wall Street, New York, NY 10005, or by visiting our website at www.firstinvestors.com. You should consider the investment objectives, risks, charges and expenses of a Fund carefully before investing. The prospectus contains this and other information about the Fund, and should be read carefully before investing.

An investment in a Fund is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. Although the Cash Management Fund seeks to preserve a net asset value at $1.00 per share, it is possible to lose money by investing in it, just as it is possible to lose money by investing in any of the other Funds. Past performance is no guarantee of future results.

A Statement of Additional Information (“SAI”) for any of the Funds may also be obtained, without charge, upon request by calling 1-800-423-4026, writing to us at our address or by visiting our website listed above. The SAI contains more detailed information about the Funds, including information about its Trustees.

Portfolio Manager’s Letter

CASH MANAGEMENT FUND

Dear Investor:

This is the annual report for the First Investors Cash Management Fund for the fiscal year ended September 30, 2010. During the period, the Fund’s return on a net asset value basis was 0.0% for Class A shares and 0.0% for Class B shares. The Fund maintained a $1.00 net asset value per share for each class of shares throughout the year.

While the financial markets showed signs of recovery during the review period, the Federal Reserve (the “Fed”) kept short-term interest rates at record lows, near zero, through the entire reporting period. This effectively determined the Fund’s zero return.

Indeed, First Investors Management Company, Inc. (“FIMCO”), the investment adviser for the Fund, had to waive all of its management fees for the Fund, as well as assume a significant amount of the Fund’s expenses, to avoid a negative yield to the Fund’s shareholders. FIMCO expects the situation to continue and consequently, the yield to shareholders should be at or near zero for the foreseeable future.

Thank you for placing your trust in First Investors. As always, we appreciate the opportunity to serve your investment needs.

Understanding Your Fund’s Expenses (unaudited)

FIRST INVESTORS INCOME FUNDS

FIRST INVESTORS EQUITY FUNDS

As a mutual fund shareholder, you incur two types of costs: (1) transaction costs, including a sales charge (load) on purchase payments (on Class A shares only), a contingent deferred sales charge on redemptions (on Class B shares only); and (2) ongoing costs, including advisory fees; distribution and service fees (12b-1); and other expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 in each Fund at the beginning of the period, April 1, 2010, and held for the entire six-month period ended September 30, 2010. The calculations assume that no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

Actual Expenses Example:

These amounts help you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the “Expenses Paid During Period” shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To estimate the expenses you paid on your account during this period, simply divide your ending account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60), then multiply the result by the number given for your Fund under the heading “Expenses Paid During Period”.

Hypothetical Expenses Example:

These amounts provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio for Class A and Class B shares, and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight and help you compare your ongoing costs only and do not reflect any transaction costs, such as front-end or contingent deferred sales charges (loads). Therefore, the hypothetical expenses example is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Fund Expenses (unaudited)

CASH MANAGEMENT FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 3 for a detailed explanation of the information presented in these examples.

| | | |

| |

| | Beginning | Ending | |

| | Account | Account | Expenses Paid |

| | Value | Value | During Period |

| | (4/1/10) | (9/30/10) | (4/1/10–9/30/10)* |

| Expense Example – Class A Shares | | | |

| Actual | $1,000.00 | $1,000.00 | $1.25 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,023.82 | $1.27 |

| |

| Expense Example – Class B Shares | | | |

| Actual | $1,000.00 | $1,000.00 | $1.25 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,023.82 | $1.27 |

* Expenses are equal to the annualized expense ratio of .25% for Class A shares and .25% for Class B shares, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). Expenses paid during the period are net of expenses waived or assumed.

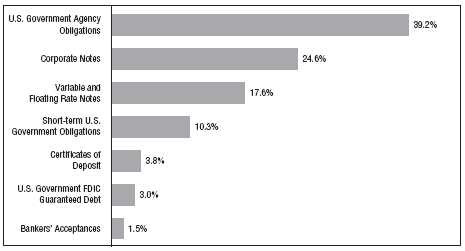

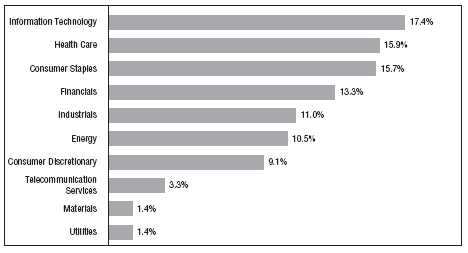

Portfolio Composition

BY SECTOR

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2010, and are based on the total value of investments.

Portfolio of Investments

CASH MANAGEMENT FUND

September 30, 2010

| | | | | | | |

| |

| Principal | | | | Interest | | |

| Amount | | | Security | Rate | * | Value |

| |

| | | | U.S. GOVERNMENT AGENCY | | | | |

| | | | OBLIGATIONS—38.3% | | | | |

| | | | Fannie Mae: | | | | |

| $ 8,500 | M | | 10/4/10 | | 0.17 | % | $ 8,499,879 |

| 5,325 | M | | 11/10/10 | | 0.20 | | 5,323,816 |

| 3,700 | M | | 11/22/10 | | 0.18 | | 3,699,064 |

| 3,049 | M | | 12/1/10 | | 0.17 | | 3,048,122 |

| 3,000 | M | | 12/1/10 | | 0.18 | | 2,999,110 |

| 10,000 | M | | 12/22/10 | | 0.18 | | 9,996,014 |

| 5,000 | M | | 12/30/10 | | 0.17 | | 4,997,875 |

| | | | Federal Home Loan Bank: | | | | |

| 3,000 | M | | 10/15/10 | | 0.18 | | 2,999,790 |

| 1,000 | M | | 10/22/10 | | 0.16 | | 999,907 |

| 2,753 | M | | 10/29/10 | | 0.17 | | 2,752,636 |

| 2,500 | M | | 12/1/10 | | 0.19 | | 2,499,216 |

| 4,200 | M | | Freddie Mac, 11/29/10 | | 0.18 | | 4,198,761 |

| |

| Total Value of U.S. Government Agency Obligations (cost $52,014,190) | | 52,014,190 |

| |

| | | | CORPORATE NOTES—24.0% | | | | |

| 1,500 | M | | Abbott Laboratories, 5/15/11 | | 0.69 | | 1,545,518 |

| | | | Coca-Cola Co.: | | | | |

| 1,500 | M | | 10/25/10 (a) | | 0.25 | | 1,499,750 |

| 3,000 | M | | 1/19/11 (a) | | 0.22 | | 2,997,983 |

| 2,900 | M | | General Electric Capital Corp., 2/1/11 | | 0.73 | | 2,943,071 |

| 1,000 | M | | Johnson & Johnson, 2/10/11 (a) | | 0.25 | | 999,084 |

| 3,000 | M | | Medtronic, Inc., 12/1/10 (a) | | 0.21 | | 2,998,932 |

| 5,000 | M | | Merck & Co., Inc., 10/21/10 (a) | | 0.21 | | 4,999,417 |

| 5,000 | M | | PepsiCo, Inc., 10/26/10 (a) | | 0.18 | | 4,999,375 |

| 4,600 | M | | Procter & Gamble International Finance, 11/3/10 (a) | | 0.26 | | 4,598,903 |

| 5,000 | M | | Walmart Stores, Inc., 10/19/10 (a) | | 0.21 | | 4,999,475 |

| |

| Total Value of Corporate Notes (cost $32,581,508) | | | | 32,581,508 |

| | | | | | | | | |

| |

| Principal | | | | | | Interest | | |

| Amount | | | Security | | | Rate | * | Value |

| |

| | | | VARIABLE AND FLOATING RATE NOTES—17.1% | | |

| $ 5,000 | M | | Federal Farm Credit Bank, 9/20/11 | | | | 0.24 | % | $ 5,000,000 |

| 5,700 | M | | Mississippi Business Finance Corp. | | | | | | |

| | | | (Chevron USA, Inc.), 12/1/30 | | | | 0.25 | | 5,700,000 |

| 3,925 | M | | Monongallia Health Systems, 7/1/40 (LOC: JP Morgan) | | | 0.32 | | 3,925,000 |

| 2,830 | M | | University of Oklahoma Hospital Rev. Series “B” | | | | | |

| | | | 8/15/21(LOC: Bank of Americ12.a) | | | | 0.35 | | 2,830,000 |

| 5,835 | M | | Valdez, Alaska Marine Terminal Rev. | | | | | | |

| | | | (Exxon Pipeline Co., Project B), 12/1/33 | | | | 0.23 | | 5,835,000 |

| |

| Total Value of Variable and Floating Rate Notes (cost $23,290,000) | | | | | 23,290,000 |

| |

| | | | CERTIFICATES OF DEPOSIT—3.7% | | | | | | |

| 5,000 | M | | Citibank, NA, 12/3/10 (cost $5,000,000) | | | | 0.26 | | 5,000,000 |

| |

| | | | U.S. GOVERNMENT FDIC GUARANTEED | | | | | |

| | | | DEBT—2.9% | | | | | | |

| 3,950 | M | | Morgan Stanley, 12/1/10 (cost $3,967,042) | | | | 0.30 | | 3,967,042 |

| |

| | | | BANKERS’ ACCEPTANCES—1.5% | | | | | | |

| 2,037 | M | | Bank of America, NA, 11/17/10 (cost $2,035,322) | | | 0.63 | | 2,035,322 |

| |

| | | | SHORT-TERM U.S. GOVERNMENT | | | | | | |

| | | | OBLIGATIONS—10.0% | | | | | | |

| | | | U.S. Treasury Bills: | | | | | | |

| 6,600 | M | | 12/9/10 | | | | 0.14 | | 6,598,229 |

| 7,000 | M | | 12/16/10 | | | | 0.16 | | 6,997,694 |

| |

| Total Value of Short-Term U.S. Government Obligations (cost $13,595,923) | | 13,595,923 |

| |

| Total Value of Investments (cost $132,483,985)** | 97.5 | % | | | | 132,483,985 |

| Other Assets, Less Liabilities | 2.5 | | | | | 3,358,161 |

| |

| Net Assets | | | | 100.0 | % | | | | $135,842,146 |

Portfolio of Investments (continued))

CASH MANAGEMENT FUND

September 30, 2010

* The interest rates shown are the effective rates at the time of purchase by the Fund. The interest rates shown on floating rate notes are adjusted periodically; the rates shown are the rates in effect at September 30, 2010.

** Aggregate cost for federal income tax purposes is the same.

(a) Security exempt from registration under Section 4(2) of the Securities Act of 1933 (see Note 4).

Summary of Abbreviations:

LOC Letters of Credit

Accounting Standards Codification (“ASC”) 820 established a three-tier hierarchy of inputs to establish a classification of fair value measurements for disclosure purposes. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below:

Level 1 — quoted prices in active markets for identical securities

Level 2 — other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

Level 3 — significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments)

The inputs methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary, by category of Level, of inputs used to value the Fund’s investments as of September 30, 2010:

| | | | | | | | | | | | |

| | | | | | | Level 2 | | | | | | |

| | | | | | | Other | | | Level 3 | | | |

| | | | Level 1 | | | Significant | | | Significant | | | |

| | | | Quoted | | | Observable | | Unobservable | | | |

| | | | Prices | | | Inputs | | | Inputs | | | Total |

| U.S. Government Agency | | | | | | | | | | | | |

| Obligations | | $ | — | | $ | 52,014,190 | | $ | — | | $ | 52,014,190 |

| Corporate Notes | | | — | | | 32,581,508 | | | — | | | 32,581,508 |

| Variable and Floating Rate Notes: | | | | | | | | | | | | |

| Corporate Notes | | | — | | | 18,290,000 | | | — | | | 18,290,000 |

| U.S. Government Agency | | | | | | | | | | | | |

| Obligations | | | — | | | 5,000,000 | | | — | | | 5,000,000 |

| Certificates of Deposit | | | — | | | 5,000,000 | | | — | | | 5,000,000 |

| U.S. Government FDIC | | | | | | | | | | | | |

| Guaranteed Debt | | | — | | | 3,967,042 | | | — | | | 3,967,042 |

| Bankers’ Acceptances | | | — | | | 2,035,322 | | | — | | | 2,035,322 |

| Short-Term U.S. Government | | | | | | | | | | | | |

| Obligations | | | — | | | 13,595,923 | | | — | | | 13,595,923 |

| Total Investments in Securities | | $ | — | | $ | 132,483,985 | | $ | — | | $ | 132,483,985 |

There were no transfers into or from Level 1 or Level 2 by the Fund during the year ended September 30, 2010.

| |

| 6 | See notes to financial statements |

Portfolio Manager’s Letter

GOVERNMENT FUND

Dear Investor:

This is the annual report for the First Investors Government Fund for the fiscal year ended September 30, 2010. During the period, the Fund’s return on a net asset value basis was 5.4% for Class A shares and 4.7% for Class B shares, including dividends of 43.5 cents per share on Class A shares and 35.9 cents per share on Class B shares.

The Fund invests primarily in Ginnie Maes, which are mortgage-backed bonds issued by the Government National Mortgage Association (GNMA). These bonds are backed by the full faith and credit of the U.S. government and have the highest possible credit rating (AAA).

The review period began with the economy growing at a 5% rate, the best quarter of what has become a disappointing recovery from the Great Recession of 2008-2009. By the second quarter of 2010, growth had slowed to an anemic 1.7% rate, and the unemployment rate had stalled at an uncomfortably high 9.6%. With below trend growth and high unemployment, investors began to worry about the possibility of deflation, as the Consumer Price Index (excluding the volatile food and energy components) was up only 0.9% for the twelve months ending in August, the smallest increase in over 40 years.

With this economic background, the Federal Reserve remained focused on stimulating the economy by keeping interest rates at historically low levels. Consequently, the two-year U.S. Treasury note yield fell to an all-time low, ending the review period at 0.4%. Longer term interest rates also fell, with the ten-year Treasury note yield dropping to 2.5%, a level only seen during the past 40 years in late 2008 when Lehman Brothers failed. The mortgage-backed market generally benefited from falling interest rates until the last two months of the review period, when fear of an increase in prepayments on mortgages due to record low mortgage rates caused the sector to underperform relative to other fixed income investments.

Because of the decline in interest rates, the Fund’s underweight in lower coupon mortgage-backed bonds (which are more sensitive to changes in interest rates) detracted from performance. The Fund’s holdings of mortgage-backed bonds backed by Fannie Mae and Freddie Mac (approximately 14% of assets) also negatively impacted performance. These holdings underperformed GNMA mortgage-backed bonds due to higher prepayments and investor preference for the government guarantee on GNMAs. Lastly, although the Fund held very low cash balances during the review period, even a small amount of cash affected performance because of the extremely low interest rates available on money market investments.

Portfolio Manager’s Letter (continued)

GOVERNMENT FUND

Thank you for placing your trust in First Investors. As always, we appreciate the opportunity to serve your investment needs.

Sincerely,

Fund Expenses (unaudited)

GOVERNMENT FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 3 for a detailed explanation of the information presented in these examples.

| | | |

| |

| | Beginning | Ending | |

| | Account | Account | Expenses Paid |

| | Value | Value | During Period |

| | (4/1/10) | (9/30/10) | (4/1/10–9/30/10)* |

| Expense Example – Class A Shares | | | |

| Actual | $1,000.00 | $1,032.58 | $5.76 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,019.40 | $5.72 |

| Expense Example – Class B Shares | | | |

| Actual | $1,000.00 | $1,029.20 | $9.31 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,015.89 | $9.25 |

* Expenses are equal to the annualized expense ratio of 1.13% for Class A shares and 1.83% for Class B shares, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). Expenses paid during the period are net of expenses waived.

Portfolio Composition

BY SECTOR

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2010, and are based on the total value of investments.

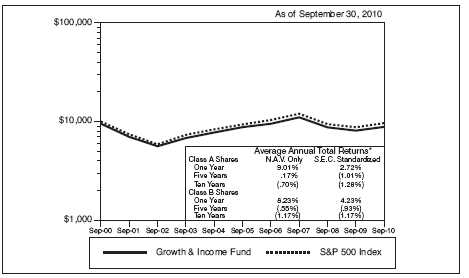

Cumulative Performance Information (unaudited)

GOVERNMENT FUND

Comparison of change in value of $10,000 investment in the First Investors Government Fund (Class A shares) and the Bank of America (“BofA”) Merrill Lynch GNMA Master Index.

The graph compares a $10,000 investment in the First Investors Government Fund (Class A shares) beginning 9/30/00 with a theoretical investment in the BofA Merrill Lynch GNMA Master Index (the “Index”). The Index is a market capitalization-weighted index of securities backed by mortgage pools of the Government National Mortgage Association (GNMA). It is not possible to invest directly in this Index. In addition, the Index does not reflect fees and expenses associated with the active management of a mutual fund portfolio. For purposes of the graph and the accompanying table, unless otherwise indicated, it has been assumed that the maximum sales charge was deducted from the initial $10,000 investment in the Fund and all dividends and distributions were reinvested. Class B shares performance may be greater than or less than that shown in the line graph above for Class A shares based on differences in sales loads and fees paid by shareholders investing in the different classes.

* Average Annual Total Return figures (for the periods ended 9/30/10) include the reinvestment of all dividends and distributions. “N.A.V. Only” returns are calculated without sales charges. The Class A “S.E.C. Standardized” returns shown are based on the maximum sales charge of 5.75% (prior to 6/17/02, the maximum sales charge was 6.25%). The Class B “S.E.C. Standardized” returns are adjusted for the applicable deferred sales charge (maximum of 4% in the first year). During the periods shown, some of the expenses of the Fund were waived or assumed. If such expenses had been paid by the Fund, the Class A “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been (.75%), 3.96% and 4.26%, respectively, and the S.E.C. 30-Day Yield for September 2010 would have been 3.04%. The Class B “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and T en Years would have been .59%, 4.11% and 4.25%, respectively, and the S.E.C. 30-Day Yield for September 2010 would have been 2.54%. Results represent past performance and do not indicate future results. The graph and the returns shown do not reflect the deduction of taxes that a shareholder would pay on distributions or the redemption of fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Index figures are from Bank of America Merrill Lynch & Co. and all other figures are from First Investors Management Company, Inc.

Portfolio of Investments

GOVERNMENT FUND

September 30, 2010

| | | | | | | |

| |

| Principal | | | | | | | |

| Amount | | | Security | | | | Value |

| |

| | | | RESIDENTIAL MORTGAGE-BACKED | | | |

| | | | SECURITIES—99.5% | | | | |

| | | | Fannie Mae—13.6% | | | | |

| $ 9,905 | M | | 5%, 8/1/2039 – 12/1/2039 | | | | $ 10,435,144 |

| 23,107 | M | | 5.5%, 7/1/2033 – 10/1/2039 | | | | 24,694,383 |

| 9,744 | M | | 6%, 11/1/2033 – 7/1/2039 | | | | 10,520,413 |

| |

| | | | | | | | 45,649,940 |

| |

| | | | Government National Mortgage Association I | | | |

| | | | Program—85.9% | | | | |

| 43,537 | M | | 4.5%, 6/15/2039 – 9/15/2040 | | | | 45,903,420 |

| 112,849 | M | | 5%, 4/15/2033 – 6/15/2040 | | | | 120,522,266 |

| 54,501 | M | | 5.5%, 3/15/2033 – 10/15/2039 | | | | 58,923,163 |

| 41,604 | M | | 6%, 3/15/2031 – 4/15/2040 | | | | 45,520,572 |

| 12,690 | M | | 6.5%, 10/15/2028 – 3/15/2038 | | | | 14,267,829 |

| 3,689 | M | | 7%, 1/15/2030 – 4/15/2034 | | | | 4,251,039 |

| |

| | | | | | | | 289,388,289 |

| |

| Total Value of Residential Mortgage-Backed Securities (cost $322,876,836) | | | 335,038,229 |

| |

| | | | SHORT-TERM INVESTMENTS—.3% | | | | |

| | | | Money Market Fund | | | | |

| 1,100 | M | | First Investors Cash Reserve Fund, .22% (cost $1,100,000)* | | | 1,100,000 |

| |

| Total Value of Investments (cost $323,976,836) | 99.8 | % | | 336,138,229 |

| Other Assets, Less Liabilities | .2 | | | 700,584 |

| |

| Net Assets | | | | 100.0 | % | | $336,838,813 |

Portfolio of Investments (continued))

GOVERNMENT FUND

September 30, 2010

* Affiliated unregistered money market fund available only to First Investors funds and certain accounts managed by First Investors Management Company, Inc. Rate shown is the 7-day yield at September 30, 2010 (see Note 2).

Accounting Standards Codification (“ASC”) 820 established a three-tier hierarchy of inputs to establish a classification of fair value measurements for disclosure purposes. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below:

Level 1 — quoted prices in active markets for identical securities

Level 2 — other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

Level 3 — significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments)

The inputs methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary, by category of Level, of inputs used to value the Fund’s investments as of September 30, 2010:

| | | | | | | | | | | | |

| | | | | | | Level 2 | | | | | | |

| | | | | | | Other | | | Level 3 | | | |

| | | | Level 1 | | | Significant | | | Significant | | | |

| | | | Quoted | | | Observable | | Unobservable | | | |

| | | | Prices | | | Inputs | | | Inputs | | | Total |

| Residential Mortgage-Backed | | | | | | | | | | | | |

| Securities | | $ | — | | $ | 335,038,229 | | $ | — | | $ | 335,038,229 |

| Money Market Fund | | | 1,100,000 | | | — | | | — | | | 1,100,000 |

| Total Investments in Securities | | $ | 1,100,000 | | | $335,038,229 | | $ | — | | $ | 336,138,229 |

There were no transfers into or from Level 1 or Level 2 by the Fund during the year ended September 30, 2010.

| |

| 12 | See notes to financial statements |

Portfolio Managers’ Letter

INVESTMENT GRADE FUND

Dear Investor:

This is the annual report for the First Investors Investment Grade Fund for the fiscal year ended September 30, 2010. During the period, the Fund’s return on a net asset value basis was 13.1% for Class A shares and 12.2% for Class B shares, including dividends of 45.1 cents per share on Class A shares and 38.7 cents per share on Class B shares.

The review period began with increased optimism for a continued global economic recovery and confidence in the credit markets. However, over the next several months the positive tone was somewhat offset by certain systemic concerns. Weak economic data pointed toward a slower than expected economic recovery. In addition, concern about rising Eurozone deficits and debt levels led to downgrades of European government debt and increased market scrutiny on sovereign risk. Benchmark U.S. Treasury yields moved much lower during the review period as investors flocked to Treasuries for their relative safety. By the end of the review period, some of the sovereign risk concerns were alleviated by the results of the European bank stress test and the financial markets were supported by strong earnings reports. For the corporate bond market, spreads remained range bound during the review period. Sentiments shifted from concerns regarding event risk and regulatory reform risk to confidence in the increased financial strength of corporate issuers. By the end of the review period, the corporate bond market had registered very strong 12-month returns, led by falling interest rates.

The Fund had strong double-digit returns over the period. The majority of the Fund’s assets were invested in investment grade corporate bonds. The Fund increased its corporate bond holdings to over 95% of assets during the review period. In addition, the Fund had a substantial overweight in BBB-rated corporate bonds, which had the highest returns among all investment grade rating classes. Furthermore, the Fund had limited exposure to corporate names associated with the European debt crisis. An additional factor that enhanced performance was the Fund’s underweight in corporate bonds with maturities between one and three years. Shorter maturity bonds had the lowest returns during the review period as falling two-year U.S. Treasury yields reached all-time lows. The Fund’s holdings in high-yield corporate bonds were less than 5% of assets throughout the period.

Portfolio Managers’ Letter (continued)

INVESTMENT GRADE FUND

Thank you for placing your trust in First Investors. As always, we appreciate the opportunity to serve your investment needs.

Fund Expenses (unaudited)

INVESTMENT GRADE FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 3 for a detailed explanation of the information presented in these examples.

| | | |

| |

| | Beginning | Ending | |

| | Account | Account | Expenses Paid |

| | Value | Value | During Period |

| | (4/1/10) | (9/30/10) | (4/1/10–9/30/10)* |

| Expense Example – Class A Shares | | | |

| Actual | $1,000.00 | $1,083.12 | $5.85 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,019.45 | $5.67 |

| |

| Expense Example – Class B Shares | | | |

| Actual | $1,000.00 | $1,079.53 | $9.49 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,015.95 | $9.20 |

* Expenses are equal to the annualized expense ratio of 1.12% for Class A shares and 1.82% for Class B shares, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). Expenses paid during the period are net of expenses waived.

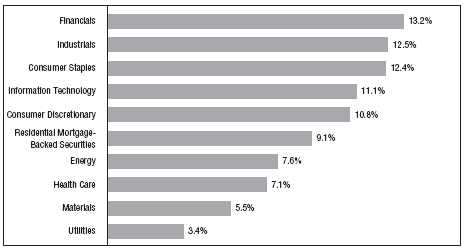

Portfolio Composition

TOP TEN SECTORS

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2010, and are based on the total value of investments.

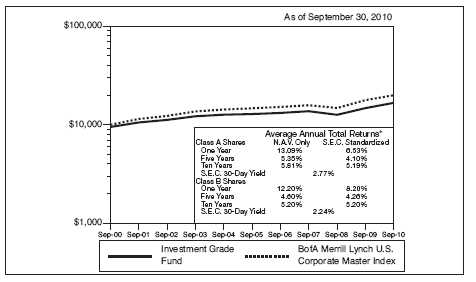

Cumulative Performance Information (unaudited)

INVESTMENT GRADE FUND

Comparison of change in value of $10,000 investment in the First Investors Investment Grade Fund (Class A shares) and the Bank of America (“BofA”) Merrill Lynch U.S. Corporate Master Index.

The graph compares a $10,000 investment in the First Investors Investment Grade Fund (Class A shares) beginning 9/30/00 with a theoretical investment in the BofA Merrill Lynch U.S. Corporate Master Index (the “Index”). The Index tracks the performance of U.S. dollar-denominated investment grade Corporate public debt issued in the U.S. domestic bond market. Qualifying bonds must have at least one year remaining term to maturity, a fixed coupon schedule and a minimum amount outstanding of $150 million. Bonds must be rated investment grade based on a composite of Moody’s and S&P. It is not possible to invest directly in this Index. In addition, the Index does not reflect fees and expenses associated with the active management of a mutual fund portfolio. For purposes of the graph and the accompanying table, unless otherwise indicated, it has been assumed that the maximum sales charge was deducted from the initial $10,000 investment in the Fund and all dividends and distributions were reinvested. Class B shares performance may be greater than or less than that shown in the line graph above for Class A shares based on differences in sales loads and fees paid by shareholders investing in the different classes.

* Average Annual Total Return figures (for the periods ended 9/30/10) include the reinvestment of all dividends and distributions. “N.A.V. Only” returns are calculated without sales charges. The Class A “S.E.C. Standardized” returns shown are based on the maximum sales charge of 5.75% (prior to 6/17/02, the maximum sales charge was 6.25%). The Class B “S.E.C. Standardized” returns are adjusted for the applicable deferred sales charge (maximum of 4% in the first year). During the periods shown, some of the expenses of the Fund were waived or assumed. If such expenses had been paid by the Fund, the Class A “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been 6.42%, 3.97% and 5.03%, respectively, and the S.E.C. 30-Day Yield for September 2010 would have been 2.66%. The Class B “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Te n Years would have been 8.08%, 4.13% and 5.04%, respectively, and the S.E.C. 30-Day Yield for September 2010 would have been 2.14%. Results represent past performance and do not indicate future results. The graph and the returns shown do not reflect the deduction of taxes that a shareholder would pay on distributions or the redemption of fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Index figures are from Bank of America Merrill Lynch & Co. and all other figures are from First Investors Management Company, Inc.

Portfolio of Investments

INVESTMENT GRADE FUND

September 30, 2010

| | | | | |

| |

| Principal | | | | | |

| Amount | | | Security | | Value |

| |

| | | | CORPORATE BONDS—96.8% | | |

| | | | Aerospace/Defense—1.5% | | |

| $ 1,800 | M | | BAE Systems Holdings, Inc., 4.95%, 2014 (a) | $ 1,988,010 |

| 4,000 | M | | Lockheed Martin Corp., 4.25%, 2019 | | 4,368,808 |

| |

| | | | | | 6,356,818 |

| |

| | | | Agriculture—1.3% | | |

| 2,725 | M | | Cargill, Inc., 6%, 2017 (a) | | 3,226,397 |

| 1,900 | M | | Potash Corp. of Saskatchewan, Inc., 4.875%, 2020 | | 2,023,671 |

| |

| | | | | | 5,250,068 |

| |

| | | | Automotive—1.1% | | |

| 4,000 | M | | Daimler Chrysler NA, LLC, 6.5%, 2013 | | 4,578,580 |

| |

| | | | Chemicals—.9% | | |

| 3,000 | M | | Chevron Phillips Chemicals Co., LLC, 8.25%, 2019 (a) | | 3,803,037 |

| |

| | | | Consumer Durables—2.0% | | |

| 2,100 | M | | Black & Decker Corp., 5.75%, 2016 | | 2,432,653 |

| | | | Newell Rubbermaid, Inc.: | | |

| 1,600 | M | | 6.75%, 2012 | | 1,713,029 |

| 1,900 | M | | 4.7%, 2020 | | 1,993,168 |

| 2,400 | M | | Stanley Black & Decker, Inc., 5.2%, 2040 | | 2,412,617 |

| |

| | | | | | 8,551,467 |

| |

| | | | Energy—13.2% | | |

| 3,900 | M | | Canadian Oil Sands, Ltd., 7.75%, 2019 (a) | | 4,846,179 |

| 4,800 | M | | DCP Midstream, LLC, 9.75%, 2019 (a) | | 6,397,061 |

| 1,800 | M | | Energy Transfer Partners, LP, 8.5%, 2014 | | 2,138,834 |

| 850 | M | | Kinder Morgan Finance Co., 5.35%, 2011 | | 864,875 |

| 1,275 | M | | Marathon Oil Corp., 7.5%, 2019 | | 1,635,291 |

| 3,842 | M | | Maritime & Northeast Pipeline, LLC, 7.5%, 2014 (a) | | 4,197,394 |

| 4,000 | M | | Nabors Industries, Inc., 6.15%, 2018 | | 4,458,576 |

| | | | Nexen, Inc.: | | |

| 2,000 | M | | 5.05%, 2013 | | 2,179,852 |

| 4,000 | M | | 6.4%, 2037 | | 4,373,260 |

| 2,000 | M | | Northern Border Partners, LP, 7.1%, 2011 | | 2,050,860 |

| 900 | M | | Plains All American Pipeline, LP, 8.75%, 2019 | | 1,144,105 |

| 5,800 | M | | Spectra Energy Capital, LLC, 6.2%, 2018 | | 6,793,412 |

| 4,400 | M | | Suncor Energy, Inc., 6.85%, 2039 | | 5,292,844 |

| 2,700 | M | | Valero Energy Corp., 9.375%, 2019 | | 3,453,373 |

Portfolio of Investments (continued)

INVESTMENT GRADE FUND

September 30, 2010

| | | | |

| |

| Principal | | | | |

| Amount | | | Security | Value |

| |

| | | | Energy (continued) | |

| | | | Weatherford International, Inc., 6.35%, 2017 | |

| $ 4,000 | M | | 6.35%, 2017 | $ 4,489,548 |

| 1,000 | M | | 5.125%, 2020 | 1,024,264 |

| |

| | | | | 55,339,728 |

| |

| | | | Financial Services—11.2% | |

| 6,000 | M | | American Express Co., 7%, 2018 | 7,237,110 |

| 5,040 | M | | Amvescap, PLC, 5.375%, 2013 | 5,377,272 |

| 4,000 | M | | BlackRock, Inc., 5%, 2019 | 4,417,664 |

| 3,260 | M | | CoBank, ACB, 7.875%, 2018 (a) | 3,789,091 |

| 1,800 | M | | Compass Bank, 6.4%, 2017 | 1,909,258 |

| | | | ERAC USA Finance Co.: | |

| 1,170 | M | | 8%, 2011 (a) | 1,192,154 |

| 2,200 | M | | 6.375%, 2017 (a) | 2,561,293 |

| 4,000 | M | | General Electric Capital Corp., 5.625%, 2017 | 4,474,916 |

| | | | Harley-Davidson Funding Corp.: | |

| 1,800 | M | | 5.75%, 2014 (a) | 1,921,700 |

| 2,100 | M | | 6.8%, 2018 (a) | 2,286,753 |

| 2,000 | M | | MetLife, Inc., 4.75%, 2021 | 2,126,162 |

| 4,000 | M | | Protective Life Corp., 7.375%, 2019 | 4,510,188 |

| 4,600 | M | | Prudential Financial Corp., 4.75%, 2015 | 4,980,264 |

| |

| | | | | 46,783,825 |

| |

| | | | Financials—16.9% | |

| 1,900 | M | | Bank of America Corp., 5.65%, 2018 | 2,016,166 |

| 5,400 | M | | Barclays Bank, PLC, 5.125%, 2020 | 5,849,058 |

| 1,500 | M | | Bear Stearns Cos., Inc., 7.25%, 2018 | 1,829,883 |

| | | | Citigroup, Inc.: | |

| 5,200 | M | | 6.375%, 2014 | 5,779,446 |

| 4,400 | M | | 6.125%, 2017 | 4,813,327 |

| | | | Goldman Sachs Group, Inc.: | |

| 3,400 | M | | 6.15%, 2018 | 3,777,036 |

| 1,600 | M | | 6.45%, 2036 | 1,609,731 |

| 2,750 | M | | 6.75%, 2037 | 2,867,450 |

| 5,000 | M | | JPMorgan Chase & Co., 6%, 2018 | 5,718,455 |

| 7,600 | M | | Merrill Lynch & Co., Inc., 5%, 2015 | 8,101,592 |

| | | | Morgan Stanley: | |

| 5,800 | M | | 5.95%, 2017 | 6,239,414 |

| 5,000 | M | | 6.625%, 2018 | 5,551,545 |

| 5,000 | M | | SunTrust Banks, Inc., 6%, 2017 | 5,423,080 |

| | | | |

| |

| Principal | | | | |

| Amount | | | Security | Value |

| |

| | | | Financials (continued) | |

| | | | UBS AG: | |

| $ 2,200 | M | | 5.875%, 2017 | $ 2,492,976 |

| 4,000 | M | | 4.875%, 2020 | 4,225,940 |

| 4,000 | M | | Wells Fargo & Co., 5.625%, 2017 | 4,562,780 |

| |

| | | | | 70,857,879 |

| |

| | | | Food/Beverage/Tobacco—8.9% | |

| 4,600 | M | | Altria Group, Inc., 9.7%, 2018 | 6,235,944 |

| 5,000 | M | | Anheuser-Busch InBev Worldwide, Inc., 5.375%, 2020 | 5,654,430 |

| 2,700 | M | | Bottling Group, LLC, 5.125%, 2019 | 3,103,804 |

| 1,980 | M | | Bunge Limited Finance Corp., 5.35%, 2014 | 2,115,454 |

| 4,500 | M | | Corn Products International, Inc., 4.625%, 2020 | 4,612,554 |

| 4,000 | M | | Dr. Pepper Snapple Group, Inc., 6.82%, 2018 | 4,956,560 |

| 5,000 | M | | Lorillard Tobacco Co., 6.875%, 2020 | 5,297,905 |

| 4,600 | M | | Philip Morris International, Inc., 5.65%, 2018 | 5,394,218 |

| |

| | | | | 37,370,869 |

| |

| | | | Forest Products/Container—.7% | |

| 2,200 | M | | International Paper Co., 9.375%, 2019 | 2,858,511 |

| |

| | | | Health Care—3.5% | |

| 5,300 | M | | Biogen IDEC, Inc., 6.875%, 2018 | 6,228,433 |

| 2,400 | M | | Novartis, 5.125%, 2019 | 2,760,264 |

| 1,000 | M | | Pfizer, Inc., 6.2%, 2019 | 1,233,349 |

| 1,000 | M | | Roche Holdings, Inc., 6%, 2019 (a) | 1,213,525 |

| 3,000 | M | | Watson Pharmaceuticals, Inc., 5%, 2014 | 3,271,245 |

| |

| | | | | 14,706,816 |

| |

| | | | Information Technology—2.7% | |

| 3,000 | M | | Adobe Systems, Inc., 4.75%, 2020 | 3,235,260 |

| 3,000 | M | | Dell, Inc., 5.875%, 2019 | 3,487,209 |

| 3,208 | M | | Dun & Bradstreet Corp., 6%, 2013 | 3,521,688 |

| 900 | M | | Pitney Bowes, Inc., 5%, 2015 | 972,996 |

| |

| | | | | 11,217,153 |

Portfolio of Investments (continued)

INVESTMENT GRADE FUND

September 30, 2010

| | | | |

| |

| Principal | | | | |

| Amount | | | Security | Value |

| |

| | | | Manufacturing—3.1% | |

| $ 1,750 | M | | Briggs & Stratton Corp., 8.875%, 2011 | $ 1,811,250 |

| 2,700 | M | | General Electric Co., 5.25%, 2017 | 3,043,445 |

| 2,100 | M | | Ingersoll-Rand Global Holdings Co., 6.875%, 2018 | 2,553,965 |

| 3,200 | M | | Johnson Controls, Inc., 5%, 2020 | 3,523,520 |

| 1,725 | M | | Tyco Electronics Group SA, 6.55%, 2017 | 2,020,458 |

| |

| | | | | 12,952,638 |

| |

| | | | Media-Broadcasting—6.0% | |

| 3,950 | M | | British Sky Broadcasting Group, PLC, 9.5%, 2018 (a) | 5,401,708 |

| 4,000 | M | | Comcast Corp., 5.15%, 2020 | 4,379,820 |

| | | | Cox Communications, Inc.: | |

| 2,000 | M | | 4.625%, 2013 | 2,158,692 |

| 3,100 | M | | 8.375%, 2039 (a) | 4,174,950 |

| 4,000 | M | | DirecTV Holdings, LLC, 7.625%, 2016 | 4,465,140 |

| 3,700 | M | | Time Warner Cable, Inc., 6.75%, 2018 | 4,419,594 |

| |

| | | | | 24,999,904 |

| |

| | | | Media-Diversified—2.2% | |

| | | | McGraw-Hill Cos., Inc.: | |

| 1,800 | M | | 5.9%, 2017 | 2,036,223 |

| 2,300 | M | | 6.55%, 2037 | 2,661,415 |

| 4,000 | M | | News America, Inc., 5.3%, 2014 | 4,518,656 |

| |

| | | | | 9,216,294 |

| |

| | | | Metals/Mining—6.1% | |

| 4,000 | M | | Alcoa, Inc., 6.15%, 2020 | 4,120,160 |

| 4,000 | M | | AngloGold Ashanti Holdings, PLC, 5.375%, 2020 | 4,239,448 |

| 4,000 | M | | ArcelorMittal, 6.125%, 2018 | 4,332,712 |

| 3,800 | M | | Newmont Mining Corp., 5.125%, 2019 | 4,258,687 |

| 2,595 | M | | Rio Tinto Finance USA, Ltd., 6.5%, 2018 | 3,134,262 |

| | | | Vale Overseas, Ltd.: | |

| 4,000 | M | | 5.625%, 2019 | 4,429,664 |

| 900 | M | | 4.625%, 2020 | 934,055 |

| |

| | | | | 25,448,988 |

| | | | |

| |

| Principal | | | | |

| Amount | | | Security | Value |

| |

| | | | Real Estate Investment Trusts—3.2% | |

| $ 4,000 | M | | Boston Properties, LP, 5.875%, 2019 | $ 4,477,156 |

| 4,000 | M | | ProLogis, 7.625%, 2014 | 4,326,484 |

| 4,000 | M | | Simon Property Group, LP, 5.75%, 2015 | 4,560,088 |

| |

| | | | | 13,363,728 |

| |

| | | | Retail-General Merchandise—1.0% | |

| 4,000 | M | | Home Depot, Inc., 5.875%, 2036 | 4,278,996 |

| |

| | | | Telecommunications—3.8% | |

| 4,000 | M | | AT&T, Inc., 5.8%, 2019 | 4,776,272 |

| 4,000 | M | | Deutsche Telekom Intl. Finance BV, 5.875%, 2013 | 4,470,984 |

| 3,300 | M | | GTE Corp., 6.84%, 2018 | 3,917,651 |

| 2,400 | M | | Verizon Wireless Capital, LLC, 5.55%, 2014 | 2,716,140 |

| |

| | | | | 15,881,047 |

| |

| | | | Transportation—1.1% | |

| 4,000 | M | | GATX Corp., 8.75%, 2014 | 4,728,312 |

| |

| | | | Utilities—5.6% | |

| 4,000 | M | | E. ON International Finance BV, 5.8%, 2018 (a) | 4,740,788 |

| | | | Electricite de France SA: | |

| 1,900 | M | | 6.5%, 2019 (a) | 2,324,321 |

| 2,100 | M | | 6.95%, 2039 (a) | 2,750,112 |

| 1,193 | M | | Entergy Gulf States, Inc., 5.25%, 2015 | 1,194,905 |

| 4,000 | M | | Exelon Generation Co., LLC, 6.2%, 2017 | 4,696,380 |

| 714 | M | | Great River Energy Co., 5.829%, 2017 (a) | 802,314 |

| 3,000 | M | | Ohio Power Co., 5.375%, 2021 | 3,429,345 |

| 2,561 | M | | Sempra Energy, 9.8%, 2019 | 3,575,981 |

| |

| | | | | 23,514,146 |

| |

| | | | Waste Management—.8% | |

| 3,300 | M | | Allied Waste NA, Inc., 7.125%, 2016 | 3,539,220 |

| |

| Total Value of Corporate Bonds (cost $365,391,377) | 405,598,024 |

Portfolio of Investments (continued)

INVESTMENT GRADE FUND

September 30, 2010

| | | | | | |

| |

| Principal | | | | | | |

| Amount | | | Security | | | Value |

| |

| | | | SHORT-TERM INVESTMENTS—.9% | | | |

| | | | Money Market Fund | | | |

| $ 3,650 | M | | First Investors Cash Reserve Fund, .22% | | | |

| | | | (cost $3,650,000) (b) | | | $ 3,650,000 |

| |

| Total Value of Investments (cost $369,041,377) | 97.7 | % | 409,248,024 |

| Other Assets, Less Liabilities | 2.3 | | 9,448,766 |

| |

| Net Assets | | | | 100.0 | % | $418,696,790 |

(a) Security exempt from registration under Rule 144A of Securities Act of 1933 (see Note 4).

(b) Affiliated unregistered money market fund available only to First Investors funds and certain accounts managed by First Investors Management Company, Inc. Rate shown is the 7-day yield at September 30, 2010 (see Note 2).

Accounting Standards Codification (“ASC”) 820 established a three-tier hierarchy of inputs to establish a classification of fair value measurements for disclosure purposes. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below:

Level 1 — quoted prices in active markets for identical securities

Level 2 — other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

Level 3 — significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments)

The inputs methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary, by category of Level, of inputs used to value the Fund’s investments as of September 30, 2010:

| | | | | | | | | | | | |

| | | | | | | Level 2 | | | | | | |

| | | | | | | Other | | | Level 3 | | | |

| | | | Level 1 | | | Significant | | | Significant | | | |

| | | | Quoted | | | Observable | | Unobservable | | | |

| | | | Prices | | | Inputs | | | Inputs | | | Total |

| Corporate Bonds | | $ | — | | $ | 405,598,024 | | $ | — | | $ | 405,598,024 |

| Money Market Fund | | | 3,650,000 | | | — | | | — | | | 3,650,000 |

| Total Investments in Securities* | | $ | 3,650,000 | | $ | 405,598,024 | | $ | — | | $ | 409,248,024 |

* The Portfolio of Investments provides information on the industry categorization for corporate bonds.

There were no transfers into or from Level 1 or Level 2 by the Fund during the year ended September 30, 2010.

| |

| 22 | See notes to financial statements |

Portfolio Manager’s Letter

FUND FOR INCOME

Dear Investor:

This is the annual report for the First Investors Fund For Income for the fiscal year ended September 30, 2010. During the period, the Fund’s return on a net asset value basis was 15.7% for Class A shares and 14.4% for Class B shares, including dividends of 18.0 cents per share on Class A shares and 16.5 cents per share on Class B shares.

The review period proved to be very positive for the Fund, encompassing three very strong quarters of performance, as well as one very challenging quarter. In the first, second and last quarters, the U.S. high yield market generated very attractive returns, with the riskier segments of the market turning in the best returns. Despite record new U.S. issuance, both primary and secondary bonds were well bid and spreads continued to tighten throughout the period. Yield-seeking assets continued to flow into the high yield market, which still offered an above-average spread, easily absorbing the debt being issued by high yield companies looking to secure fixed rate financing largely for the purposes of refinancing and extending near-term debt obligations, thereby improving their balance sheets. In short, the review period overall offered a “win” for all of the high yield market’s participants. As in 2009, the distressed portion of the market genera ted outsized gains, followed by CCC credits. The insurance, financials and banking sectors — where a high degree of distressed or formerly distressed paper is concentrated — continued to be outsized earners.

In the third quarter of the review period, however, market sentiment turned sharply on the back of a variety of headline news that refocused investors on risk; such as Greece’s sovereign debt crisis, tension in the Korean peninsula, and the blow-out of BP’s deep-water well in the Gulf of Mexico. Investors interested in reducing equity risk sent stock markets deep into the red during the quarter. U.S. Treasuries outperformed, as investors pushed down yields to record lows in search of safety. Weak employment and housing data released in June made investors question the prospect of strong growth going forward. U.S. high yield bonds, although not as firm as Treasuries, impressed by delivering a flat return. Investors continued to appear confident that corporations would be able to repay borrowed money, even if they would not expand earnings quickly enough to justify appreciation of the stock market. Within the high yield market itself, the theme was similar during the quarter. Riskier CCC credits, mirroring weak equity markets, underperformed at this moment of stress. Dispersion of returns by industry during the third quarter was much lower than that experienced in 2009, or during the rest of 2010.

In summary, the high yield market during the period provided the investment community with plenty of positive news to satisfy its greed, and just enough fear to remind us of the key importance of careful credit analysis and prudent risk control in the

Portfolio Manager’s Letter (continued)

FUND FOR INCOME

longer term. System shocks are, by definition, unpredictable, and investments in bond portfolios should target resiliency. In this environment, the Fund performed admirably. Our carefully selected credit mix preserved capital better than the market during its most challenging month (May) and largely kept pace with the market’s positive performance, even while underweighted in the more speculative insurance and banking sectors. During the second half of the review period, the fund performed particularly well by taking advantage of smaller, analyzable market opportunities and dislocations. For example, strong performance in the energy sector, and in particular the oil sector, followed from our analysis that the market had mispriced a number of securities in the wake of the explosion of BP’s oil well in the Gulf of Mexico. Against a market backdrop that continues to offer strong fundamental advantages and technical support by market participants, we will continue to work to i dentify incremental opportunities for attractive returns with reasonable risk.

Thank you for placing your trust in First Investors. As always, we appreciate the opportunity to serve your investment needs.

Sincerely,

* Mr. Comeaux is part of a portfolio management team that began managing the Fund on April 24, 2009.

Fund Expenses (unaudited)

FUND FOR INCOME

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 3 for a detailed explanation of the information presented in these examples.

| | | |

| |

| | Beginning | Ending | |

| | Account | Account | Expenses Paid |

| | Value | Value | During Period |

| | (4/1/10) | (9/30/10) | (4/1/10–9/30/10)* |

| Expense Example – Class A Shares | | | |

| Actual | $1,000.00 | $1,071.52 | $6.65 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,018.65 | $6.48 |

| |

| Expense Example – Class B Shares | | | |

| Actual | $1,000.00 | $1,063.67 | $10.24 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,015.14 | $10.00 |

* Expenses are equal to the annualized expense ratio of 1.28% for Class A shares and 1.98% for Class B shares, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). Expenses paid during the period are net of expenses waived.

Portfolio Composition

TOP TEN SECTORS

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2010, and are based on the total value of investments.

Cumulative Performance Information (unaudited)

FUND FOR INCOME

Comparison of change in value of $10,000 investment in the First Investors Fund For Income (Class A shares), the Bank of America (“BofA”) Merrill Lynch BB-B US Cash Pay High Yield Constrained Index† and the Credit Suisse High Yield Index II.

The graph compares a $10,000 investment in the First Investors Fund For Income (Class A shares) beginning 9/30/00 with theoretical investments in the BofA Merrill Lynch BB-B US Cash Pay High Yield Constrained Index and the Credit Suisse High Yield Index II (the “Indices”). The BofA Merrill Lynch BB-B US Cash Pay High Yield Constrained Index contains all securities in the BofA Merrill Lynch US Cash Pay High Yield Index rated BB1 through B3, based on an average of Moody’s, S&P and Fitch, but caps issuer exposure at 2%. Index constituents are capitalization-weighted, based on their current amount outstanding, provided the total allocation to an individual issuer does not exceed 2%. The Credit Suisse High Yield Index II is designed to measure the performance of the high yield bond market. As of 9/30/10, the Index consisted of 1,243 different issues, most of which are cash-pay; also included in the Index are zero-coupon bonds, step bonds, payment-in-kind bonds a nd bonds which are in default. As of 9/30/10, approximately 0.71% of the market value of the Index was in default. The bonds included in the Index have an average maturity of 6.58 years, an average duration of 3.72 years and an average coupon of 8.54%. It is not possible to invest directly in these Indices. In addition, the Indices do not reflect fees and expenses associated with the active management of a mutual fund portfolio. For purposes of the graph and the accompanying table it is assumed that all dividends and distributions were reinvested. Class B shares performance may be greater than or less than that shown in the line graph above for Class A shares based on differences in sales loads and fees paid by shareholders investing in the different classes.

* Average Annual Total Return figures (for the periods ended 9/30/10) include the reinvestment of all dividends and distributions. “N.A.V. Only” returns are calculated without sales charges. The Class A “S.E.C. Standardized” returns shown are based on the maximum sales charge of 5.75% (prior to 6/17/02, the maximum sales charge was 6.25%). The Class B “S.E.C. Standardized” returns are adjusted for the applicable deferred sales charge (maximum of 4% in the first year). During the periods shown, some of the expenses of the Fund were waived or assumed. If such expenses had been paid by the Fund, the Class A “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been 9.05%, 2.39% and 3.84%, respectively, and the S.E.C. 30-Day Yield for September 2010 would have been 5.37%. The Class B “S.E.C. Standardized” Average Annual Total Return for One Year, Five Years and Ten Years would have been 10 .39%, 2.62% and 3.93%, respectively, and the S.E.C. 30-Day Yield for September 2010 would have been 5.00%. Results represent past performance and do not indicate future results. The graph and the returns shown do not reflect the deduction of taxes that a shareholder would pay on distributions or the redemption of fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. The issuers of the high yield bonds, in which the Fund primarily invests, pay higher interest rates because they have a greater likelihood of financial difficulty, which could result in their inability to repay the bonds fully when due. Prices of high yield bonds are also subject to greater fluctuations. BofA Merrill Lynch BB-B US Cash Pay High Yield Constrained Index figures from Bank of America Merrill Lynch, Credit Suisse High Yiel d Index II figures are from Credit Suisse Corporation and all other figures are from First Investors Management Company, Inc.

† We have added a comparison to the BofA Merrill Lynch BB-B US Cash Pay High Yield Constrained Index this year since it more closely reflects the performance of the securities in which the Fund invests. After this year we will not show a comparison to the Credit Suisse High Yield Index II.

Portfolio of Investments

FUND FOR INCOME

September 30, 2010

| | | | | |

| |

| Principal | | | | | |

| Amount | | | Security | | Value |

| |

| | | | CORPORATE BONDS—97.0% | | |

| | | | Automotive—3.2% | | |

| $ 2,200 | M | | Cooper Tire & Rubber Co., 8%, 2019 | | $ 2,279,750 |

| 2,825 | M | | Cooper-Standard Automotive, 8.5%, 2018 (a) | | 2,945,062 |

| | | | Goodyear Tire & Rubber Co.: | | |

| 2,500 | M | | 10.5%, 2016 | | 2,843,750 |

| 1,575 | M | | 8.25%, 2020 | | 1,665,562 |

| 1,750 | M | | Navistar International Corp., 8.25%, 2021 | | 1,876,875 |

| 2,100 | M | | Oshkosh Corp., 8.5%, 2020 | | 2,283,750 |

| 2,325 | M | | TRW Automotive, Inc., 7.25%, 2017 (a) | | 2,481,938 |

| |

| | | | | | 16,376,687 |

| |

| | | | Building Materials—2.4% | | |

| | | | Building Materials Corp.: | | |

| 1,475 | M | | 6.875%, 2018 (a) | | 1,456,562 |

| 4,175 | M | | 7.5%, 2020 (a) | | 4,216,750 |

| 1,375 | M | | Interface, Inc., 11.375%, 2013 | | 1,567,500 |

| 1,725 | M | | Mohawk Industries, Inc., 6.875%, 2016 | | 1,804,781 |

| 3,450 | M | | Texas Industries, Inc., 9.25%, 2020 (a) | | 3,596,625 |

| |

| | | | | | 12,642,218 |

| |

| | | | Capital Goods—.6% | | |

| 2,650 | M | | Belden CDT, Inc., 9.25%, 2019 (a) | | 2,875,250 |

| |

| | | | Chemicals—4.3% | | |

| 1,475 | M | | Chemtura Corp., 7.875%, 2018 (a) | | 1,545,062 |

| 2,175 | M | | Ferro Corp., 7.875%, 2018 | | 2,267,437 |

| 7,075 | M | | Georgia Gulf Corp., 9%, 2017 (a) | | 7,446,437 |

| 3,125 | M | | Lyondell Chemical Co., 11%, 2018 | | 3,472,656 |

| 1,600 | M | | PolyOne Corp., 7.375%, 2020 | | 1,654,000 |

| | | | Solutia, Inc.: | | |

| 3,925 | M | | 8.75%, 2017 | | 4,307,688 |

| 1,275 | M | | 7.875%, 2020 | | 1,369,031 |

| |

| | | | | | 22,062,311 |

| |

| | | | Consumer Durables—1.0% | | |

| | | | Sealy Mattress Co.: | | |

| 3,500 | M | | 8.25%, 2014 | | 3,543,750 |

| 1,392 | M | | 10.875%, 2016 (a) | | 1,583,400 |

| |

| | | | | | 5,127,150 |

Portfolio of Investments (continued)

FUND FOR INCOME

September 30, 2010

| | | | |

| |

| Principal | | | | |

| Amount | | | Security | Value |

| |

| | | | Consumer Non-Durables—2.0% | |

| $ 2,575 | M | | Acco Brands Corp., 10.625%, 2015 | $ 2,890,437 |

| 2,450 | M | | Jarden Corp., 7.5%, 2020 | 2,560,250 |

| 3,025 | M | | Phillips Van-Heusen Corp., 7.375%, 2020 | 3,202,719 |

| 1,525 | M | | Spectrum Brands, Inc., 9.5%, 2018 (a) | 1,637,469 |

| |

| | | | | 10,290,875 |

| |

| | | | Energy—15.4% | |

| | | | Anadarko Petroleum Corp.: | |

| 2,42 | M | | 6.375%, 2017 | 2,676,026 |

| 1,350 | M | | 6.95%, 2019 | 1,508,922 |

| | | | Berry Petroleum Co.: | |

| 2,600 | M | | 10.25%, 2014 | 2,944,500 |

| 2,925 | M | | 8.25%, 2016 | 3,012,750 |

| | | | Chesapeake Energy Corp.: | |

| 1,750 | M | | 9.5%, 2015 | 2,034,375 |

| 1,850 | M | | 7.25%, 2018 | 2,002,625 |

| 2,300 | M | | Concho Resources, Inc., 8.625%, 2017 | 2,449,500 |

| | | | Consol Energy, Inc.: | |

| 1,875 | M | | 8%, 2017 (a) | 2,039,062 |

| 4,425 | M | | 8.25%, 2020 (a) | 4,856,437 |

| 1,325 | M | | Continental Resources, 7.125%, 2021 (a) | 1,384,625 |

| 3,500 | M | | Copano Energy, LLC, 7.75%, 2018 | 3,552,500 |

| 4,750 | M | | Crosstex Energy, LP, 8.875%, 2018 | 4,999,375 |

| | | | El Paso Corp.: | |

| 1,050 | M | | 8.25%, 2016 | 1,173,375 |

| 4,325 | M | | 7%, 2017 | 4,614,195 |

| 350 | M | | 7.25%, 2018 | 378,986 |

| 275 | M | | 7.75%, 2032 | 286,924 |

| 750 | M | | Encore Acquisition Co., 9.5%, 2016 | 840,937 |

| 3,975 | M | | Expro Finance Luxembourg SCA, 8.5%, 2016 (a) | 3,806,062 |

| | | | Ferrellgas Partners, LP: | |

| 3,450 | M | | 9.125%, 2017 | 3,756,187 |

| 2,475 | M | | 8.625%, 2020 | 2,666,812 |

| 1,900 | M | | Helix Energy Solutions Group, Inc., 9.5%, 2016 (a) | 1,933,250 |

| | | | Hilcorp Energy I, LP: | |

| 175 | M | | 7.75%, 2015 (a) | 177,625 |

| 3,100 | M | | 9%, 2016 (a) | 3,231,750 |

| 3,875 | M | | 8%, 2020 (a) | 4,000,938 |

| | | | | |

| |

| Principal | | | | | |

| Amount | | | Security | | Value |

| |

| | | | Energy (continued) | | |

| $ 2,475 | M | | Inergy, LP, 7%, 2018 (a) | | $ 2,549,250 |

| 1,600 | M | | Linn Energy, LLC, 9.875%, 2018 | | 1,764,000 |

| 1,025 | M | | Penn Virginia Corp., 10.375%, 2016 | | 1,127,500 |

| | | | Pioneer Natural Resource Co.: | | |

| 375 | M | | 6.65%, 2017 | | 401,731 |

| 2,925 | M | | 7.5%, 2020 | | 3,233,289 |

| 1,275 | M | | QEP Resources, Inc., 6.875%, 2021 | | 1,386,563 |

| | | | Quicksilver Resources, Inc.: | | |

| 575 | M | | 8.25%, 2015 | | 609,500 |

| 1,175 | M | | 7.125%, 2016 | | 1,166,188 |

| 2,100 | M | | 11.75%, 2016 | | 2,472,750 |

| 1,775 | M | | 9.125%, 2019 | | 1,954,719 |

| 1,100 | M | | Southwestern Energy Co., 7.5%, 2018 | | 1,248,500 |

| 1,150 | M | | Whiting Petroleum Corp., 6.5%, 2018 | | 1,181,625 |

| |

| | | | | | 79,423,353 |

| |

| | | | Financials—3.4% | | |

| | | | Ford Motor Credit Co., LLC: | | |

| 1,800 | M | | 7.5%, 2012 | | 1,911,623 |

| 2,725 | M | | 8.7%, 2014 | | 3,059,706 |

| 1,075 | M | | 5.625%, 2015 | | 1,106,629 |

| 925 | M | | 6.625%, 2017 | | 986,890 |

| | | | International Lease Finance Corp.: | | |

| 1,550 | M | | 5.55%, 2012 | | 1,559,688 |

| 1,400 | M | | 6.375%, 2013 | | 1,414,000 |

| 750 | M | | 6.625%, 2013 | | 755,625 |

| 1,275 | M | | 8.625%, 2015 (a) | | 1,367,438 |

| 1,900 | M | | 8.75%, 2017 (a) | | 2,042,500 |

| 3,125 | M | | Pinafore, LLC, 9%, 2018 (a) | | 3,296,875 |

| |

| | | | | | 17,500,974 |

| |

| | | | Food/Beverage/Tobacco—4.2% | | |

| 3,333 | M | | Bumble Bee Foods, LLC, 7.75%, 2015 | | 3,582,975 |

| 2,675 | M | | CF Industries, Inc., 7.125%, 2020 | | 2,932,469 |

| 7,625 | M | | JBS USA, LLC, 8.25%, 2018 | | 7,901,406 |

| 3,900 | M | | Michael Foods, Inc., 9.75%, 2018 (a) | | 4,192,500 |

| 2,700 | M | | Smithfield Foods, Inc., 10%, 2014 (a) | | 3,118,500 |

| |

| | | | | | 21,727,850 |

Portfolio of Investments (continued)

FUND FOR INCOME

September 30, 2010

| | | | |

| |

| Principal | | | | |

| Amount | | | Security | Value |

| |

| | | | Food/Drug—1.1% | |

| $ 925 | M | | McJunkin Red Man Corp., 9.5%, 2016 (a) | $ 818,625 |

| 1,700 | M | | NBTY, Inc., 9%, 2018 (a) | 1,793,500 |

| 950 | M | | Rite Aid Corp., 9.75%, 2016 | 1,020,063 |

| 1,775 | M | | Tops Markets, LLC, 10.125%, 2015 (a) | 1,914,781 |

| |

| | | | | 5,546,969 |

| |

| | | | Forest Products/Containers—1.0% | |

| 1,450 | M | | Graham Packaging Co., LP, 8.25%, 2018 (a) | 1,480,812 |

| 3,775 | M | | Reynolds Group Escrow, LLC, 7.75%, 2016 (a) | 3,859,938 |

| |

| | | | | 5,340,750 |

| |

| | | | Gaming/Leisure—4.0% | |

| 2,300 | M | | Equinox Holdings, Inc., 9.5%, 2016 (a) | 2,363,250 |

| 2,550 | M | | Las Vegas Sands Corp., 6.375%, 2015 | 2,585,063 |

| 2,610 | M | | Mandalay Resort Group, 6.375%, 2011 | 2,551,275 |

| 2,300 | M | | MCE Finance, Ltd., 10.25%, 2018 (a) | 2,570,250 |

| 1,950 | M | | MGM Mirage, Inc., 9%, 2020 (a) | 2,062,125 |

| 3,000 | M | | NCL Corp., Ltd., 11.75%, 2016 | 3,375,000 |

| 2,425 | M | | Wynn Las Vegas, LLC, 7.75%, 2020 (a) | 2,570,500 |

| 2,326 | M | | Yonkers Racing Corp., 11.375%, 2016 (a) | 2,535,340 |

| |

| | | | | 20,612,803 |

| |

| | | | Health Care—5.4% | |

| 1,250 | M | | Capella Healthcare, 9.25%, 2017 (a) | 1,340,625 |

| 6,375 | M | | Community Health Systems, Inc., 8.875%, 2015 | 6,789,375 |

| 4,400 | M | | Genesis Health Ventures, Inc., 9.75%, 2011 (b)(c) | 2,750 |

| | | | HCA, Inc.: | |

| 5,700 | M | | 6.75%, 2013 | 5,842,500 |

| 2,800 | M | | 6.375%, 2015 | 2,807,000 |

| | | | Healthsouth Corp.: | |

| 1,650 | M | | 7.25%, 2018 | 1,687,125 |

| 950 | M | | 7.75%, 2022 | 959,500 |

| | | | LVB Acquisition Holding, LLC (Biomet, Inc.): | |

| 625 | M | | 10%, 2017 | 692,969 |

| 2,000 | M | | 11.625%, 2017 | 2,237,500 |

| 2,475 | M | | Talecris Biotherapeutics Holdings Corp., 7.75%, 2016 | 2,734,875 |

| 2,450 | M | | Valeant Pharmaceuticals International, 6.75%, 2017 (a) | 2,505,125 |

| |

| | | | | 27,599,344 |

| | | | |

| |

| Principal | | | | |

| Amount | | | Security | Value |

| |

| | | | Information Technology—2.3% | |

| | | | Brocade Communications Systems, Inc.: | |

| $ 750 | M | | 6.625%, 2018 (a) | $ 783,750 |

| 850 | M | | 6.875%, 2020 (a) | 896,750 |

| 2,425 | M | | Equinix, Inc., 8.125%, 2018 | 2,600,812 |

| | | | Fidelity National Information Services, Inc.: | |

| 700 | M | | 7.625%, 2017 (a) | 750,750 |

| 450 | M | | 7.875%, 2020 (a) | 487,125 |

| | | | Jabil Circuit, Inc.: | |

| 350 | M | | 7.75%, 2016 | 385,438 |

| 3,825 | M | | 8.25%, 2018 | 4,293,563 |

| 1,500 | M | | JDA Software Group, Inc., 8%, 2014 (a) | 1,597,500 |

| |

| | | | | 11,795,688 |

| |

| | | | Manufacturing—4.3% | |

| 2,400 | M | | Amsted Industries, 8.125%, 2018 (a) | 2,511,000 |

| | | | Case New Holland, Inc.: | |

| 2,200 | M | | 7.75%, 2013 | 2,400,750 |

| 2,075 | M | | 7.875%, 2017 (a) | 2,264,344 |

| 2,850 | M | | Coleman Cable, Inc., 9%, 2018 | 2,928,375 |

| 1,325 | M | | CPM Holdings, Inc,, 10.625%, 2014 (a) | 1,434,312 |

| 2,000 | M | | ESCO Corp., 8.625%, 2013 (a) | 2,060,000 |

| | | | Terex Corp.: | |

| 3,100 | M | | 10.875%, 2016 | 3,553,375 |

| 5,100 | M | | 8%, 2017 | 5,131,875 |

| |

| | | | | 22,284,031 |

| |

| | | | Media-Broadcasting—3.6% | |

| 2,800 | M | | Allbritton Communication Co., 8%, 2018 | 2,821,000 |

| | | | Belo Corp.: | |

| 4,000 | M | | 7.25%, 2027 | 3,430,000 |

| 725 | M | | 7.75%, 2027 | 643,437 |

| | | | Lin Television Corp.: | |

| 1,900 | M | | 6.5%, 2013 | 1,895,250 |

| 675 | M | | 6.5%, 2013 | 678,375 |

| 875 | M | | 8.375%, 2018 (a) | 928,594 |

| 2,475 | M | | Nexstar/Mission Broadcasting, Inc., 8.875%, 2017 (a) | 2,592,563 |

| | | | Sinclair Television Group: | |

| 4,000 | M | | 9.25%, 2017 (a) | 4,310,000 |

| 1,000 | M | | 8.375%, 2018 (a) | 1,012,500 |

| |

| | | | | 18,311,719 |

Portfolio of Investments (continued)

FUND FOR INCOME

September 30, 2010

| | | | |

| |

| Principal | | | | |

| Amount | | | Security | Value |

| |

| | | | Media-Cable TV—8.3% | |

| $ 6,250 | M | | Atlantic Broadband Finance, LLC, 9.375%, 2014 | $ 6,367,187 |

| 3,025 | M | | Cablevision Systems Corp., 8.625%, 2017 | 3,342,625 |

| 1,000 | M | | CCH II, LLC, 13.5%, 2016 | 1,192,500 |

| 1,900 | M | | Cequel Communications Holdings I, Inc., 8.625%, 2017 (a) | 2,014,000 |

| | | | Clear Channel Worldwide: | |

| 2,500 | M | | 9.25%, 2017 | 2,662,500 |

| 4,925 | M | | 9.25%, 2017 – Series “B” | 5,282,062 |

| | | | Echostar DBS Corp.: | |

| 2,250 | M | | 6.625%, 2014 | 2,356,875 |

| 2,525 | M | | 7.75%, 2015 | 2,704,906 |

| 2,225 | M | | Insight Communications Co., Inc., 9.375%, 2018 (a) | 2,375,187 |

| | | | Quebecor Media, Inc.: | |

| 1,300 | M | | 7.75%, 2016 | 1,347,125 |

| 1,000 | M | | 7.75%, 2016 | 1,036,250 |

| 4,850 | M | | UPC Germany GmbH, 8.125%, 2017 (a) | 5,068,250 |

| 1,575 | M | | Videotron LTEE, 6.375%, 2015 | 1,618,313 |

| 4,650 | M | | Virgin Media Finance, PLC, 9.5%, 2016 | 5,277,750 |

| |

| | | | | 42,645,530 |

| |

| | | | Media-Diversified—1.1% | |

| 2,475 | M | | Entravision Communications Corp., 8.75%, 2017 (a) | 2,536,875 |

| 1,225 | M | | Interpublic Group of Cos., Inc., 10%, 2017 | 1,436,313 |

| 1,700 | M | | Lamar Media Corp., 7.875%, 2018 | 1,793,500 |

| | | | MediaNews Group, Inc.: | |

| 2,625 | M | | 6.875%, 2013 (b)(c) | 1,641 |

| 3,100 | M | | 6.375%, 2014 (b)(c) | 1,938 |

| |

| | | | | 5,770,267 |

| |

| | | | Metals/Mining—2.3% | |

| 2,750 | M | | Metals USA, Inc., 11.125%, 2015 | 2,928,750 |

| | | | Novelis, Inc.: | |

| 2,075 | M | | 7.25%, 2015 | 2,121,688 |

| 1,600 | M | | 11.5%, 2015 | 1,836,000 |

| 1,175 | M | | Steel Dynamics, Inc., 7.625%, 2020 (a) | 1,224,938 |

| 1,011 | M | | Teck Resources, Ltd., 10.75%, 2019 | 1,275,050 |

| 2,425 | M | | Vedanta Resources, PLC, 9.5%, 2018 (a) | 2,631,125 |

| |

| | | | | 12,017,551 |

| | | | |

| |

| Principal | | | | |

| Amount | | | Security | Value |

| |

| | | | Real Estate Investment Trusts—2.4% | |

| $ 1,375 | M | | Brandywine Operating Partnership, LP, 5.7%, 2017 | $ 1,394,313 |

| 4,650 | M | | CB Richard Ellis Service, 11.625%, 2017 | 5,405,625 |

| | | | Developers Diversified Realty Corp.: | |

| 675 | M | | 9.625%, 2016 | 753,868 |

| 625 | M | | 7.875%, 2020 | 648,711 |

| 2,675 | M | | Dupont Fabros Tech, LP, 8.5%, 2017 | 2,882,312 |

| 1,000 | M | | HRPT Properties Trust, 6.25%, 2017 | 1,050,548 |

| |

| | | | | 12,135,377 |

| |

| | | | Retail-General Merchandise—6.7% | |

| 3,075 | M | | Federated Retail Holdings, Inc., 5.9%, 2016 | 3,290,250 |

| 2,900 | M | | HSN, Inc., 11.25%, 2016 | 3,320,500 |

| 2,050 | M | | J.C. Penney Corp., Inc., 7.95%, 2017 | 2,311,375 |

| | | | Limited Brands, Inc.: | |

| 1,700 | M | | 8.5%, 2019 | 1,984,750 |

| 475 | M | | 7%, 2020 | 515,375 |

| | | | Macys Retail Holdings, Inc.: | |

| 2,875 | M | | 7.45%, 2017 | 3,227,188 |

| 1,050 | M | | 6.65%, 2024 | 1,073,625 |

| 3,525 | M | | QVC, Inc., 7.5%, 2019 (a) | 3,701,250 |

| 3,000 | M | | Sears Holding Corp., 6.625%, 2018 (a) | 3,022,500 |

| 2,050 | M | | Susser Holdings & Finance, 8.5%, 2016 | 2,142,250 |

| 4,900 | M | | Toys R Us Property Co. I, Inc., 10.75%, 2017 | 5,561,500 |

| 1,400 | M | | Toys R Us Property Co. II, Inc., 8.5%, 2017 (a) | 1,487,500 |

| 3,025 | M | | Yankee Acquisition Corp., 8.5%, 2015 | 3,138,438 |

| |

| | | | | 34,776,501 |

| |

| | | | Services—2.3% | |

| 2,200 | M | | Hertz Corp., 10.5%, 2016 | 2,348,500 |

| | | | Iron Mountain, Inc.: | |

| 225 | M | | 8.75%, 2018 | 239,906 |

| 1,450 | M | | 8%, 2020 | 1,538,813 |

| 2,275 | M | | Kar Holdings, Inc., 8.75%, 2014 | 2,380,219 |

| 2,500 | M | | PHH Corp., 9.25%, 2016 (a) | 2,612,500 |

| 2,375 | M | | Reliance Intermediate Holdings, LP, 9.5%, 2019 (a) | 2,529,375 |

| |

| | | | | 11,649,313 |

Portfolio of Investments (continued)

FUND FOR INCOME

September 30, 2010

| | | | |

| |

| Principal | | | | |

| Amount | | | Security | Value |

| |

| | | | Telecommunications—9.0% | |

| | | | Citizens Communications Co.: | |

| $ 5,500 | M | | 7.125%, 2019 | $ 5,665,000 |

| 775 | M | | 9%, 2031 | 830,219 |

| | | | Frontier Communications Corp.: | |

| 50 | M | | 7.875%, 2015 | 54,250 |

| 1,875 | M | | 8.125%, 2018 | 2,057,812 |

| 1,250 | M | | 8.5%, 2020 | 1,385,937 |

| 2,125 | M | | GCI, Inc., 8.625%, 2019 | 2,279,062 |

| 5,575 | M | | Inmarsat Finance, PLC, 7.375%, 2017 (a) | 5,853,750 |

| | | | Intelsat Jackson Holdings, Ltd.: | |

| 750 | M | | 9.5%, 2016 | 803,438 |

| 725 | M | | 8.5%, 2019 (a) | 790,250 |

| | | | Nextel Communications, Inc.: | |

| 3,550 | M | | 5.95%, 2014 | 3,550,000 |

| 5,725 | M | | 7.375%, 2015 | 5,782,250 |

| | | | Qwest Communications International, Inc.: | |

| 3,500 | M | | 7.5%, 2014 | 3,587,500 |

| 2,125 | M | | 8%, 2015 | 2,310,938 |

| 1,275 | M | | Sprint Capital Corp., 6.875%, 2028 | 1,173,000 |

| 3,850 | | | Wind Acquisition Finance SA, 11.75%, 2017 (a) | 4,333,656 |

| | M | | Windstream Corp.: | |

| 3,100 | M | | 8.625%, 2016 | 3,293,750 |

| 1,550 | M | | 7.875%, 2017 | 1,623,625 |

| 1,025 | M | | 7.75%, 2020 (a) | 1,037,813 |

| |

| | | | | 46,412,250 |

| |

| | | | Transportation—2.3% | |

| 2,475 | M | | Aircastle, Ltd., 9.75%, 2018 (a) | 2,539,969 |

| 3,350 | M | | CHC Helicopter SA, 9.25%, 2020 (a) | 3,400,250 |

| | | | Navios Maritime Holdings: | |

| 4,175 | M | | 9.5%, 2014 | 4,279,375 |

| 775 | M | | 8.875%, 2017 (a) | 821,500 |

| 925 | M | | Teekay Corp., 8.5%, 2020 | 1,011,719 |

| |

| | | | | 12,052,813 |

| |

| | | | Utilities—4.4% | |

| 875 | M | | AES Corp., 9.75%, 2016 | 1,010,625 |

| 2,600 | M | | Calpine Construction Finance Co., LP, 8%, 2016 (a) | 2,795,000 |

| 225 | M | | Calpine Corp., 7.875%, 2020 (a) | 232,312 |

| 875 | M | | CMS Energy Corp., 8.75%, 2019 | 1,049,142 |

| | | | | | |

| |

| Principal | | | | | | |

| Amount | | | | | | |

| or Shares | | | Security | | | Value |

| |

| | | | Utilities (continued) | | | |

| $ 5,250 | M | | Dynegy Holdings, Inc., 7.75%, 2019 | | | $ 3,622,500 |

| 1,700 | M | | Energy Future Holdings Corp., 10%, 2020 (a) | | 1,696,192 |

| 3,475 | M | | Intergen NV, 9%, 2017 (a) | | | 3,692,188 |

| | | | NRG Energy, Inc.: | | | |

| 4,625 | M | | 7.375%, 2017 | | | 4,752,188 |

| 1,375 | M | | 8.5%, 2019 | | | 1,455,781 |

| 2,600 | M | | NSG Holdings, LLC, 7.75%, 2025 (a) | | | 2,379,000 |

| |

| | | | | | | 22,684,928 |

| |

| Total Value of Corporate Bonds (cost $476,114,050) | | | 499,662,502 |

| |

| | | | COMMON STOCKS—.0% | | | |

| | | | Automotive—.0% | | | |

| 37,387 | | * | Safelite Glass Corporation – Class “B” (b) | | | 7,290 |

| 2,523 | | * | Safelite Realty Corporation (b) | | | 25 |

| |

| | | | | | | 7,315 |

| |

| | | | Telecommunications—.0% | | | |

| 8 | | * | Viatel Holding (Bermuda), Ltd. (b) | | | — |

| 18,224 | | * | World Access, In c. | | | 15 |

| |

| | | | | | | 15 |

| |

| Total Value of Common Stocks (cost $385,770) | | | 7,330 |

| |

| | | | SHORT-TERM INVESTMENTS—3.4% | | |

| | | | Money Market Fund | | | |

| $ 17,660M | | | First Investors Cash Reserve Fund, .22% | | | |

| | | | (cost $17,660,000) (d) | | | 17,660,000 |

| |

| Total Value of Investments (cost $494,159,820) | 100.4 | % | 517,329,832 |

| Excess of Liabilities Over Other Assets | (.4 | ) | (1,931,829) |

| |

| Net Assets | | | | 100.0 | % | $515,398,003 |

* Non-income producing

(a) Security exempt from registration under Rule 144A of Securities Act of 1933 (see Note 4).

(b) Securities valued at fair value (see Note 1A)

(c) In default as to principal and/or interest payment

(d) Affiliated unregistered money market fund available only to First Investors funds and certain accounts managed by First Investors Management Company, Inc. Rate shown is the 7-day yield at September 30, 2010 (see Note 2).

Portfolio of Investments (continued)

FUND FOR INCOME

September 30, 2010

Accounting Standards Codification (“ASC”) 820 established a three-tier hierarchy of inputs to establish a classification of fair value measurements for disclosure purposes (see Note 1A). The three-tier hierarchy of inputs is summarized in the three broad Levels listed below:

Level 1 — quoted prices in active markets for identical securities

Level 2 — other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

Level 3 — significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments)

The inputs methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary, by category of Level, of inputs used to value the Fund’s investments as of September 30, 2010:

| | | | | | | | | | | | |

| | | | | | | Level 2 | | | | | | |

| | | | | | | Other | | | Level 3 | | | |

| | | | Level 1 | | | Significant | | | Significant | | | |

| | | | Quoted | | | Observable | | Unobservable | | | |

| | | | Prices | | | Inputs | | | Inputs | | | Total |

| Corporate Bonds | | $ | — | | $ | 499,656,173 | | $ | 6,329 | | $ | 499,662,502 |

| Common Stocks | | | 15 | | | — | | | 7,315 | | | 7,330 |

| Money Market Fund | | | 17,660,000 | | | — | | | — | | | 17,660,000 |

| Total Investments in Securities* | | $ | 17,660,015 | | $ | 499,656,173 | | $ | 13,644 | | $ | 517,329,832 |

* The Portfolio of Investments provides information on the industry categorization for the portfolio.