UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-04010

OCM Mutual Fund

(Exact name of registrant as specified in charter)

2600 Kitty Hawk Road

Suite 119

Livermore, CA 94551

(Address of principal executive offices) (Zip code)

Gregory M. Orrell

Orrell Capital Management, Inc

2600 Kitty Hawk Road

Suite 119

Livermore, CA 94551

(Name and address of agent for service)

Registrant's telephone number, including area code: (925) 455-0802

Date of fiscal year end: November 30

Date of reporting period: November 30, 2022

Item 1. Report to Stockholders.

Annual Report

November 30, 2022

OCM GOLD FUND Shareholder Letter – November 30, 2022

(Unaudited) |

Dear Fellow Shareholders:

Amongst a backdrop of accelerating inflation and rising interest rates, investors aggressively moved to liquidity across most asset classes, particularly in small-cap stocks. For the fiscal year ending November 30, 2022, the OCM Gold Fund’s Advisor Class declined 18.80%. Meanwhile, the OCM Gold Fund’s Investor Class returned -19.25% (-22.87% after maximum sales load). The broader market also suffered, as the S&P 500 Index (the “S&P 500”)1 returned -9.21%. The Philadelphia Gold and Silver Index (“XAU”)2 declined by 5.34%. The Fund’s underperformance versus the XAU over the past fiscal year is tied to its investment strategy of allocation across the precious metals mining industry of large-cap major gold producers to micro-cap exploration companies. The investment strategy over time has allowed the OCM Gold Fund to outperform the XAU over longer reporting periods. Gold priced in U.S. Dollars (“USD”) returned -2.00% with a price of $1,753.50 per ounce. Gold witnessed a volatile year as it peaked at $2,039.10 per ounce on March 9, 2022 while also falling over $350 to a fiscal year low of $1,643.60 on September 23, 2022. Overall, gold proved to be one of the top-performing assets in 2022.

Market Commentary

The Russian invasion of Ukraine was the most significant event over the past year, in our opinion. It was an inflection point not only for the geopolitical landscape but also global monetary order – the end of dollar hegemony. Issues that have been festering just under the surface breached for all to see. After years of extraordinary monetary policies to counter the Covid Pandemic and prior liquidity crises, the war provided the catalyst to unleash inflation. The Federal Reserve’s (the “Fed”)3 aggressive interest rate response after initially believing inflation was ‘transitory” pulled the plug on the bull market in both equities and bonds. Removing the opportunity cost associated with bull markets in financial assets, gold prices posted positive returns in almost every currency globally in 2022.

The tectonic shift in the geopolitical landscape was summarized by Credit Suisse strategist, Zoltan Pozsar,

“Since the end of WWII, the only Great Power conflict investors really had to deal with was the Cold War, and since the conclusion of the Cold War, the world enjoyed a unipolar “moment” – the U.S. was the undisputed hegemon, globalization was the economic order, and the U.S. dollar was the currency of choice. But today, geopolitics has reared its ugly head again: for the first time since WWII, there is a formidable challenger to the existing world order, and for the first time in its young history, the U.S. is facing off against an economically equal or, by some measures, superior adversary.”

China and Russia are leading a group of commodities-producing and manufacturing countries looking to de-dollarize and forge a new monetary order not aligned with U.S. interests. Writing in the People’s Daily back in 2008, Chinese economist Shi Jianxun lamented: “The world urgently needs to create a diversified currency and financial system and fair and just financial order that is not dependent on the United States.”

– 1 –

OCM GOLD FUND Shareholder Letter – November 30, 2022 (Continued)

(Unaudited) |

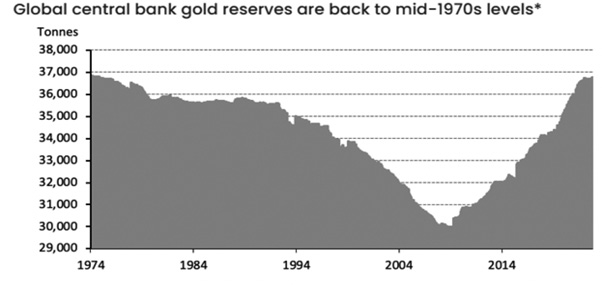

The freezing of Russia’s foreign exchange reserves appears to have hastened the move to de-dollarize. Saudi Arabia has agreed to abandon the petrodollar and accept other currencies for oil settlement. The petrodollar allowed the U.S. a privileged position to run deficits at a favorable exchange and interest rates since the early 70’s that the rest of the world didn’t enjoy. Central bank’s buying of gold in 2022 reached its highest level since 1968, the year the London Gold Pool protecting the gold price at $35 had to be abandoned. Non-U.S. aligned foreign central banks see a future where they no longer need to hold the same level of dollar assets for trade and are selling U.S. Treasury securities and beefing up holdings of gold as a neutral reserve asset.

*Data to 31 October 2022 based on available data and WGC calculations.

Source: IMF IFS, Respective Central Banks, World Gold Council

Moreover, Secretary Jack Lew warned about dollar sanction overreach in 2016 as pointed out by Zoltan Pozsar, “the more we condition the use of the dollar and our financial system on adherence to U.S. foreign policy, the more the risk of migration to other currencies and other financial systems grows”. With $32 trillion in debt and rising interest expense compounding the issue, the need to finance U.S. government debt is growing at a pace the rest of the world may be unwilling to absorb near current interest rates, considering the weaponization of the dollar and the move to a multi-polar world, in our opinion. The Fed may find itself needing to practice extensive yield curve control operations through balance sheet expansion to finance the U.S. government at interest rates low enough to avoid economic contraction if foreign buyers are no longer there. Should inflation remain elevated above the Fed’s 2% target rate, monetizing U.S. debt on the Fed’s balance sheet may lead to a steep markdown of the U.S. dollar versus gold, in our opinion.

– 2 –

OCM GOLD FUND Shareholder Letter – November 30, 2022 (Continued)

(Unaudited) |

The prospect for a period of stagflation over the next 12-18 months is more likely than a “soft landing”, in our view. The yield curve inversion of short-term rates higher than longer-term rates has historically forecast an economic contraction. The yield curve in 2022 was the most inverted it has been since September 1981. If history is a guide, the bond market is pointing to a recession over the next year. The prospect for inflation to remain elevated is related to several factors, in our opinion, namely: labor pressing for cost-of-living increases; de-dollarization increasing the cost of commodities in dollars; manufacturing moving away from low-cost labor centers; and wars are inflationary. In the stagflation period of the 1970’s, gold assets proved to be the best-performing asset class.

Shares of Gold Mining Companies

In review, shares of gold mining companies experienced a challenging year as inflation and lingering supply chain issues led to uneven performance across the sector. The industry suffered from three consecutive quarters of increased average all-in-sustaining costs mostly from inflated fuel and cyanide costs. While these increases impacted sentiment toward the precious metals sector in the short-term, costs have since subsided and are estimated to fall further over the next two years. We foresee inflationary pressures trailing gold price increases in the intermediate term, leading to the gold mining sector seeing the benefits of added cash flow at a time when other sectors are experiencing declining earnings.

Historically, shares of Junior Gold Producers, such as Jaguar Mining, Inc. and Wesdome Gold Mines Ltd. have provided strong relative performance for the Fund. In the cases of Jaguar and Wesdome, both remain poised to deliver production growth over the next two years despite challenges that set production timetables back by twelve months. The Fund has historically had a low turnover signifying our long view of letting our investment thesis on individual companies play out.

Precious metals exploration over the past decade has not kept pace with ore body depletion from mining, punctuating the scarcity value of gold. The bulk of what has been discovered is extremely low grade with unattractive rates of return on capital or in unfavorable operating jurisdictions. Combined with the long lead time from discovery to production of seven to twenty years due to the development and regulatory hurdles to bring a new mine onstream, the trend is for shrinking or flat production by the major gold producers going forward with an emphasis on higher-margin ounces rather than gross production numbers. With major gold producers seeing flat production over the next three to five years along with challenges discovering new ounces, a period of mergers and acquisitions in the precious metals sector seems likely, in our opinion.

Your Fund’s investment strategy remains a disciplined approach to searching out value and growth opportunities across all segments of the precious metals industry on a global basis. We believe companies that possess strong management, large reserves in the ground in stable jurisdictions and exhibit capital discipline while holding equity dear, will be the companies that outperform over time as they deliver higher levels of free cash flow to maintain a sustainable business model to create shareholder value. We are specifically targeting companies with existing

– 3 –

OCM GOLD FUND Shareholder Letter – November 30, 2022 (Continued)

(Unaudited) |

production that possesses large reserve expansion potential where shareholder value can be created through the drill bit. Your Fund has the flexibility to maneuver within the precious metals sector to invest in opportunities that larger funds and exchange-traded funds cannot; from major gold producers with over one million ounces of annual production, to junior producers with less than 100,000 ounces of annual production, to small exploration and development companies with micro capitalizations.

Conclusion

Wars are historically inflationary. The Russian invasion of Ukraine and the U.S. participation by proxy has proven to be no exception. The origins of the current inflation can be traced back to the Fed’s extraordinary monetary policies enacted to counter liquidity crises in the banking system, such as the 9/11 – dot-com bubble bust, the 2008 Global Financial Crisis and the Covid Pandemic. The Russian-Ukraine war also hastened the move from a unipolar world to a multipolar world that is looking to de-dollarize. A tectonic geopolitical shift, in our opinion, has taken place with profound implications for the USD and demand for Treasury securities going forward. The accelerated buying of gold and selling of U.S. Treasury securities by foreign central banks is no doubt part of the move to de-dollarize, in our opinion. Further, we believe investors should take note that inflation has broken the back of the financial asset bull market in both equities and bonds. The ratio of the S&P 500 to gold rising is a signal a major investment cycle change is in progress from financial assets to real assets, in our opinion. Shares of precious metals mining companies from the 2001 to 2011 period of rising S&P 500 ratio to gold delivered a strong relative performance to the S&P 500.

Relying on gold’s 5,000-year monetary history, we expect gold to continue to retain its purchasing power as the USD is faced with further debasement to meet its growing U.S. debt obligations. Horizon Kinetics notes the familiar pattern of the USD:

“Over the past 73 years, the USD also lost over 91% purchasing power through persistent debasement. Currency devaluation is hardly a new phenomenon. During the 73 years between Marcus Aurelius’s reign ending in 180 CE and the beginning of the reign of Emperor Gallienus, the denarius silver coin was periodically debased – by mixing in a cheaper base metal, like lead – from 75% silver to only 5%.”

– 4 –

OCM GOLD FUND Shareholder Letter – November 30, 2022 (Continued)

(Unaudited) |

We appreciate your shareholding and confidence in the OCM Gold Fund, and we look forward to meeting the investment objective of preserving your purchasing power. Should you have any questions regarding the Fund or gold, please contact your financial adviser or you may contact us directly at 1-800-779-4681. For questions regarding your account, please contact Shareholder Service at 1-800-628-9403.

Sincerely,

Gregory M. Orrell

Portfolio Manager

January 23, 2023

The S&P 500 Index1, a registered trademark of McGraw-Hill Co., Inc. is a market capitalization-weighted index of 500 widely held common stocks. You cannot invest directly in an index.

The Philadelphia Gold and Silver Index (XAU)2 is an unmanaged capitalization-weighted index composed of 16 companies listed on U.S. exchanges involved in the gold and silver mining industry. The index is generally considered as representative of the gold and silver share market. You cannot invest directly in an index.

Federal Reserve3 is the central bank of the United States and arguably the most powerful financial institution in the world. The Federal Reserve System was founded by the U.S. Congress in 1913 to provide the nation with a safe, flexible, and stable monetary and financial system.

– 5 –

OCM GOLD FUND Shareholder Letter – November 30, 2022 (Continued)

(Unaudited) |

Investing in the Fund involves risks including the loss of principal. Many of the companies in which the Fund invests are smaller capitalization companies, which may subject the Fund to greater risk than securities of larger, more-established companies, as smaller companies often have limited product lines, markets or financial resources, and may be subject to more-abrupt market movements. The Fund also invests in securities of gold and precious metals companies which may be subject to greater price fluctuations over short periods of time. The Fund is a non-diversified investment company meaning it will invest in fewer securities than diversified investment companies and its performance may be more volatile. The Fund contains international securities that may provide the opportunity for greater return but also have special risks associated with foreign investing including fluctuations in currency, government regulation, differences in accounting standards and liquidity.

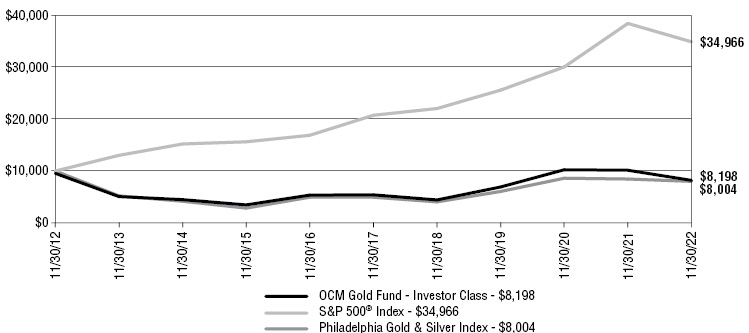

Investor Class Performance as of November 30, 2022

| | OCMGX

(without load) | OCMGX

(with load) | Philadelphia

Gold and Silver

Index (XAU)1 | S&P 5002 | |

Six Months | -14.06% | -17.91% | -5.09% | -0.40% | |

One Year | -19.25% | -22.87% | -5.34% | -9.21% | |

3 Year Annualized | 5.82% | 4.19% | 9.75% | 10.91% | |

5 Year Annualized | 8.70% | 7.70% | 10.13% | 10.98% | |

10 Year Annualized | -1.52% | -1.97% | -2.20% | 13.34% | |

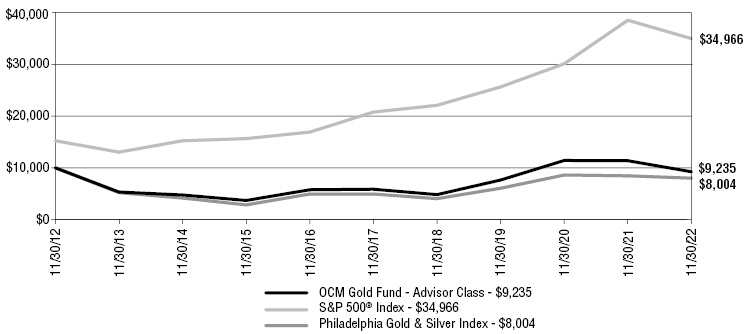

Advisor Class Performance as of November 30, 2022

| | OCMAX | Philadelphia

Gold and Silver

Index (XAU)1 | S&P 5002 | |

Six Months | -13.80% | -5.09% | -0.40% | |

One Year | -18.80% | -5.34% | -9.21% | |

3 Year Annualized | 6.50% | 9.75% | 10.91% | |

5 Year Annualized | 9.50% | 10.13% | 10.98% | |

10 Year Annualized | -0.79% | -2.20% | 13.34% | |

The performance data quoted above represents past performance. Current performance may be lower or higher than the performance data quoted above. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that investor’s shares, when redeemed, may be worth more or less than their original cost. The Fund’s Total Annual Operating Expenses for the Fund’s Investor Class and Advisor

– 6 –

OCM GOLD FUND Shareholder Letter – November 30, 2022 (Continued)

(Unaudited) |

Class are 2.19% and 1.69% respectively. Please review the Fund’s prospectus for more information regarding the Fund’s fees and expenses. For performance information current to the most recent month-end, please call toll-free 800-628-9403. The returns shown include the reinvestment of all dividends but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

1 | The Philadelphia Gold and Silver Index (XAU) is an unmanaged capitalization-weighted index composed of 16 companies listed on U.S. exchanges involved in the gold and silver mining industry. The index is generally considered as representative of the gold and silver share market. You cannot invest directly in an index. The index is used herein for comparative purposes in accordance with SEC regulation. |

2 | The S&P 500 Index, a registered trademark of McGraw-Hill Co., Inc. is a market capitalization-weighted index of 500 widely held common stocks. You cannot invest directly in an index. The index is used herein for comparative purposes in accordance with SEC regulation. |

– 7 –

OCM GOLD FUND Schedule of Investments – November 30, 2022

|

| Shares | | | | | Value |

| COMMON STOCKS 97.3% | | |

Major Gold Producers 33.4% | | | |

| | 85,000 | | | Agnico Eagle Mines Ltd. | | $ | 4,281,450 |

| | 155,000 | | | AngloGold Ashanti Ltd. ADR | | | 2,841,150 |

| | 100,000 | | | B2Gold Corp. | | | 348,000 |

| | 300,000 | | | B2Gold Corp.^ | | | 1,045,941 |

| | 200,000 | | | Barrick Gold Corp. | | | 3,264,000 |

| | 140,000 | | | Endeavour Mining PLC | | | 2,971,305 |

| | 65,000 | | | Newmont Corp. | | | 3,085,550 |

| | | | | | | | 17,837,396 |

| Intermediate/Mid-Tier Gold Producers 23.9% |

| | 325,000 | | | Alamos Gold, Inc. | | | 3,152,500 |

| | 250,000 | | | Dundee Precious Metals, Inc. | | | 1,180,122 |

| | 225,000 | | | Fortuna Silver Mines, Inc.* | | | 839,652 |

| | 130,000 | | | Lundin Gold, Inc. | | | 1,282,412 |

| | 700,000 | | | OceanaGold Corp.* | | | 1,191,644 |

| | 75,000 | | | Pan American Silver Corp. | | | 1,229,250 |

| | 1,000,000 | | | Perseus Mining Ltd. | | | 1,513,609 |

| | 937,500 | | | Resolute Mining Ltd.* | | | 101,812 |

| | 150,000 | | | SSR Mining, Inc. | | | 2,274,000 |

| | | | | | | | 12,765,001 |

Junior Gold Producers 20.7% | | | |

| | 200,000 | | | Argonaut Gold, Inc.* | | | 56,497 |

| | 400,489 | | | Calibre Mining Corp.* | | | 267,945 |

| | 1,375,000 | | | Emerald Resources N.L.* | | | 1,054,605 |

| | 150,000 | | | i-80 Gold Corp.* | | | 425,959 |

| | 1,449,950 | | | Jaguar Mining, Inc. | | | 2,899,469 |

| | 175,000 | | | K92 Mining, Inc.* | | | 1,005,613 |

| | 1,000,000 | | | Minera Alamos, Inc.* | | | 330,806 |

| | 450,000 | | | Mineros S.A. | | | 260,928 |

| | 500,000 | | | Orezone Gold Corp.* | | | 472,049 |

| | 4,100,000 | | | Superior Gold, Inc.* | | | 746,729 |

| | 1,595,000 | | | Thor Explorations Ltd.* | | | 308,281 |

| | 475,000 | | | Wesdome Gold Mines Ltd.* | | | 3,206,215 |

| | | | | | | | 11,035,096 |

| Exploration and Development Companies 4.4% |

| | 400,000 | | | Benchmark Metals, Inc.* | | | 114,481 |

| | 450,000 | | | Black Cat Syndicate Ltd.* | | | 93,158 |

| | 250,000 | | | G Mining Ventures Corp.* | | | 122,658 |

| | 500,000 | | | Galway Metals, Inc.* | | | 98,498 |

| | 123,880 | | | Integra Resources Corp.* | | | 80,119 |

| | 500,000 | | | Lahontan Gold Corp.* | | | 26,018 |

| | 1,000,000 | | | Liberty Gold Corp.* | | | 304,787 |

| | 1,000,000 | | | Maritime Resources Corp.* | | | 37,169 |

| | 616,500 | | | Montage Gold Corp.* | | | 302,476 |

| | 257,945 | | | Paramount Gold Nevada Corp.* | | | 94,305 |

| | 975,000 | | | Rio2 Ltd.* | | | 105,096 |

| | 3,000,000 | | | Royal Road Minerals Ltd.* | | | 289,920 |

| | 4,578,755 | | | RTG Mining, Inc.* | | | 155,391 |

| | 2,512,040 | | | Sutter Gold Mining, Inc.* # | | | — |

| | 1,210,500 | | | Tajiri Resources Corp.* | | | 29,246 |

| | 530,000 | | | West Vault Mining, Inc.* | | | 374,294 |

| | 450,000 | | | Westhaven Gold Corp.* | | | 130,464 |

| | | | | | | | 2,358,080 |

| Royalty/Streaming Companies 7.3% |

| | 100,000 | | | Wheaton Precious Metals Corp. | | | 3,902,765 |

| | | | | | | | |

Primary Silver Producers 7.6% | | | |

| | 625,000 | | | Andean Precious Metals Corp.* | | | 371,692 |

| | 600,000 | | | Aya Gold & Silver, Inc.* | | | 3,693,131 |

| | | | | | | | 4,064,823 |

Total Common Stocks | | | |

| | | | | (Cost $31,015,194) | | | 51,963,161 |

See notes to financial statements.

– 8 –

OCM GOLD FUND Schedule of Investments – November 30, 2022 (Continued)

|

| Shares | | | | | Value |

| WARRANTS 2.4% |

| Exploration and Development Companies 0.0% |

| | 641,000 | | | Euro Sun Mining, Inc. Exercise Price 0.55 CAD, Exp. 6/5/2023* | | $ | — |

| | 225,000 | | | Westhaven Gold Corp. Exercise Price 1.00 CAD, Exp. 3/3/2023* | | | 10,036 |

| | 400,000 | | | Apollo Silver Corp. Exercise Price 1.25 CAD, Exp. 6/25/2023* | | | — |

| | | | | | | | 10,036 |

| Primary Silver Producers 2.4% |

| | 350,000 | | | Aya Gold & Silver, Inc. Exercise Price 3.30 CAD, Exp. 9/3/2023* | | | 1,295,718 |

| | | | | | | | 1,295,718 |

Total Warrants | | | | | | |

| | | | | (Cost $0) | | | 1,305,754 |

| SHORT-TERM INVESTMENT 0.0% |

| | 20,175 | | | UMB Money Market Fiduciary, 0.01% | | $ | 20,175 |

Total Short-Term Investment | | | |

| | | | | (Cost $20,175) | | | 20,175 |

| | | | | | | | |

Total Investments | | | | | | | |

| | | | | (Cost $31,035,369) | | | 99.7 | % | | | 53,289,090 |

Assets less Other Liabilities | | | 0.3 | % | | | 136,684 |

TOTAL NET ASSETS | | | 100.0 | % | | $ | 53,425,774 |

ADR – American Depository Receipt

PLC – Public Limited Company

CAD – Canadian Dollars

^ | Denoted investment is a Canadian security traded on U.S. stock exchange. |

* | Non-income producing security. |

# | Level 3 security fair valued under procedures established by the Board of Trustees, represents 0.00% of Net Assets. The total value of this security is $0. |

See notes to financial statements.

– 9 –

OCM GOLD FUND Schedule of Investments – November 30, 2022 (Continued)

|

SUMMARY OF INVESTMENTS BY COUNTRY

Country | | Value | | | Percent of

Investment Securities | |

Australia | | $ | 2,763,185 | | | | 5.2% | |

Canada | | | 40,807,182 | | | | 76.6 | |

Colombia | | | 260,928 | | | | 0.5 | |

Jersey | | | 289,920 | | | | 0.5 | |

South Africa | | | 2,841,150 | | | | 5.3 | |

United Kingdom | | | 2,971,305 | | | | 5.6 | |

United States1 | | | 3,200,029 | | | | 6.0 | |

Virgin Islands (British) | | | 155,391 | | | | 0.3 | |

Total | | $ | 53,289,090 | | | | 100.0% | |

1 | Includes short-term investments. |

See notes to financial statements.

– 10 –

OCM GOLD FUND Statement of Assets and Liabilities – November 30, 2022

|

Assets: | | | | |

Investments in unaffiliated issuers, at value (cost $31,035,369) | | $ | 53,289,090 | |

Foreign currency, at value (cost $79,545) | | | 80,331 | |

Receivable for fund shares sold | | | 103,179 | |

Interest and dividends receivable | | | 129,125 | |

Reclaims receivable | | | 342 | |

Prepaid expenses and other assets | | | 35,657 | |

Total assets | | | 53,637,724 | |

| | | | | |

Liabilities: | | | | |

Payable for fund shares redeemed | | | 87,463 | |

Accrued distribution fees | | | 16,171 | |

Investment adviser fees | | | 41,198 | |

Accrued transfer agent fees and expenses | | | 15,560 | |

Accrued fund administration and accounting fees | | | 17,633 | |

Accrued Trustees’ fees | | | 3,400 | |

Accrued audit fees | | | 16,000 | |

Accrued report to shareholders | | | 5,152 | |

Accrued expenses and other liabilities | | | 9,373 | |

Total liabilities | | | 211,950 | |

Net Assets | | $ | 53,425,774 | |

| | | | | |

Net Assets Consist of: | | | | |

Shares of beneficial interest, no par value: unlimited shares authorized | | $ | 32,468,621 | |

Total distributable earnings | | | 20,957,153 | |

Net Assets | | $ | 53,425,774 | |

| | | | | |

Calculation of Maximum Offering Price: | | | | |

Investor Class: | | | | |

Net asset value and redemption price per share | | $ | 9.35 | |

Maximum sales charge (4.50% of offering price) | | | 0.44 | |

Offering price to public | | | 9.79 | |

Net assets applicable to shares outstanding | | $ | 11,747,142 | |

Shares outstanding | | | 1,256,372 | |

Advisor Class: | | | | |

Net asset value and redemption price per share | | $ | 10.62 | |

Net assets applicable to shares outstanding | | $ | 41,678,632 | |

Shares outstanding | | | 3,925,384 | |

Total Shares Outstanding | | | 5,181,756 | |

See notes to financial statements.

– 11 –

OCM GOLD FUND Statement of Operations – Year Ended November 30, 2022

|

Investment Income | | | | |

Interest | | $ | 143 | |

Dividend (net of foreign withholding taxes of $108,546) | | | 924,467 | |

Total investment income | | | 924,610 | |

| | | | | |

Expenses | | | | |

Investment advisory fees | | | 576,715 | |

Transfer agent fees and expenses | | | 118,538 | |

Fund administration and accounting fees | | | 116,348 | |

Distribution fees - Investor Class | | | 96,454 | |

Distribution fees - Advisor Class | | | 68,802 | |

Legal fees | | | 44,771 | |

Federal and state registration fees | | | 43,319 | |

Chief Compliance Officer fees | | | 30,450 | |

Custody fees | | | 23,399 | |

Audit fees | | | 16,000 | |

Reports to shareholders | | | 15,683 | |

Trustees’ fees | | | 11,346 | |

Other expenses | | | 17,502 | |

Total expenses | | | 1,179,327 | |

Net investment loss | | | (254,717 | ) |

| | | | | |

Realized and Unrealized Gain (Loss) on Investments: | | | | |

Net realized loss on investments and foreign currency transactions | | | (263,176 | ) |

Net change in unrealized appreciation/depreciation on investments and foreign currency translations | | | (13,018,336 | ) |

Net loss on investments | | | (13,281,512 | ) |

| | | | | |

Net decrease in net assets from operations | | $ | (13,536,229 | ) |

See notes to financial statements.

– 12 –

OCM GOLD FUND Statements of Changes in Net Assets

|

| | | Year Ended

November 30,

2022 | | Year Ended

November 30,

2021 |

Operations: | | | | | | |

Net investment loss | | $ | (254,717) | | $ | (388,294) |

Net realized gain (loss) on investments and foreign currency transactions | | | (263,176) | | | 1,149,554 |

Net change in unrealized appreciation/depreciation on investments and foreign currency transactions | | | (13,018,336) | | | (1,295,766) |

Net decrease in net assets from operations | | | (13,536,229) | | | (534,506) |

| | | | | | | |

Distributions Paid to Shareholders | | | | | | |

Distributions: | | | | | | |

Investor Class | | | (179,695) | | | (192,546) |

Advisor Class | | | (481,166) | | | (884,171 |

Total | | | (660,861) | | | (1,076,717) |

| | | | | | | |

Fund Share Transactions | | | | | | |

Investor Class: | | | | | | |

Net proceeds from shares sold | | | 594,078 | | | 1,034,437 |

Distributions reinvested | | | 155,297 | | | 171,134 |

Payment of shares redeemed1 | | | (2,698,963) | | | (2,238,684) |

Net decrease in net assets from Investor Class share transactions | | | (1,949,588) | | | (1,033,113) |

| | | | | | | |

Advisor Class: | | | | | | |

Net proceeds from shares sold | | | 16,975,338 | | | 18,796,257 |

Distributions reinvested | | | 458,060 | | | 839,586 |

Payment of shares redeemed2 | | | (16,275,498) | | | (22,522,613) |

Net increase (decrease) in net assets from Advisor Class share transactions | | | 1,157,900 | | | (2,886,770) |

Net decrease in net assets from Fund share transactions | | | (791,688) | | | (3,919,883) |

| | | | | | | |

Total decrease in net assets | | | (14,988,778) | | | (5,531,106) |

| | | | | | | |

Net Assets, Beginning of Period | | | 68,414,552 | | | 73,945,658 |

Net Assets, End of Period | | $ | 53,425,774 | | $ | 68,414,552 |

See notes to financial statements.

– 13 –

OCM GOLD FUND Statements of Changes in Net Assets (Continued)

|

| | | Year Ended

November 30,

2022 | | Year Ended

November 30,

2021 |

Transactions in shares | | |

Investor Class: | | |

Shares sold | | | 52,125 | | | 83,147 |

Shares issued on reinvestment of distributions | | | 14,131 | | | 13,454 |

Shares redeemed | | | (264,004) | | | (178,692) |

Net decrease in Investor Class shares outstanding | | | (197,748) | | | (82,091) |

| | | | | | | |

Advisor Class: | | | | | | |

Shares sold | | | 1,387,111 | | | 1,328,775 |

Shares issued on reinvestment of distributions | | | 36,911 | | | 58,836 |

Shares redeemed | | | (1,389,952) | | | (1,628,111) |

Net increase (decrease) in Advisor Class shares outstanding | | | 34,070 | | | (240,500) |

Net Decrease in Fund Shares Outstanding | | | (163,678) | | | (322,591) |

1 | Net of redemption fees of $2,776 for the year ended November 30, 2022 and $2,178 for the year ended November 30, 2021, respectively. |

2 | Net of redemption fees of $25,166 for the year ended November 30, 2022 and $43,151 for the year ended November 30, 2021, respectively. |

See notes to financial statements.

– 14 –

OCM GOLD FUND Notes to Financial Statements – November 30, 2022

|

Note 1. Organization

OCM Mutual Fund (the “Trust”) is registered under the Investment Company Act of 1940, as amended (“1940 Act”), as an open-end management investment company. The Trust was organized as a Massachusetts business trust on January 6, 1984 and consists of the OCM Gold Fund (the “Fund”). The Fund is a non-diversified fund. The investment objective for the Fund is long-term growth of capital through investing primarily in equity securities of domestic and foreign companies engaged in activities related to gold and precious metals.

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946 “Financial Services—Investment Companies.”

Note 2. Significant Accounting Policies

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements.

Security Valuation – Portfolio securities that are listed on national securities exchanges, other than the NASDAQ Stock Market LLC, are valued at the last sale price as of the close of business of such securities exchanges, or, in the absence of recorded sales, at the average of readily available closing bid and ask prices on such exchanges. NASDAQ Global Select Market, Global Market and Capital Market securities are valued at the NASDAQ Official Closing Price (“NOCP”). If a NOCP is not issued for a given day, these securities are valued at the average of readily available closing bid and ask prices. Unlisted securities are valued at the average of the quoted bid and ask prices in the over-the-counter market. Short-term investments which mature in less than 60 days are valued at amortized cost (unless the Fund’s investment adviser determines that this method does not represent fair value). Short-term investments which mature after 60 days are valued at market. Securities and other assets for which market quotations are not readily available are valued at fair value as determined in good faith by the Fund’s investment adviser. In compliance with Rule 2a-5 under the 1940Act, the Fund’s Board of Trustees has designated the investment adviser as the valuation designee, and the investment adviser performs the fair value determinations relating to Fund investments. For each investment that is fair valued, the investment adviser considers, to the extent applicable, various factors including, but not limited to, the type of security, the financial condition of the company, comparable companies in the public market, the nature and duration of the cause for a quotation not being readily available and other relevant factors.

Fair Value Measurements and Disclosures defines fair value, establishes a framework for measuring fair value in accordance with GAAP, and expands disclosure about fair value measurements. It also provides guidance on determining when there has been a significant decrease in the volume and level of activity for an asset or a liability, when a transaction is not orderly, and how that information must be incorporated into a fair value measurement.

– 15 –

OCM GOLD FUND Notes to Financial Statements – November 30, 2022 (Continued)

|

Under Fair Value Measurements and Disclosures, various inputs are used in determining the value of the Fund’s investments. These inputs are summarized into three broad levels as described below:

| | ● | Level 1 – Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access. |

| | ● | Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

| | ● | Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs to measure fair value may fall into different Levels of the fair value hierarchy. In such cases, for disclosure purposes, the Level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest Level input that is significant to the fair value measurement in its entirety.

– 16 –

OCM GOLD FUND Notes to Financial Statements – November 30, 2022 (Continued)

|

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities. The following is a summary of the inputs used, as of November 30, 2022, in valuing the Fund’s assets carried at fair value:

Sector | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Common Stocks | | | | | | | | | | | | | | | | |

Major Gold Producers | | $ | 17,837,396 | | | $ | — | | | $ | — | | | $ | 17,837,396 | |

Intermediate/Mid-Tier Gold Producers | | | 12,765,001 | | | | — | | | | — | | | | 12,765,001 | |

Junior Gold Producers | | | 11,035,096 | | | | — | | | | — | | | | 11,035,096 | |

Exploration and Development Companies | | | 2,358,080 | | | | — | | | | — | | | | 2,358,080 | |

Royalty/Streaming Companies | | | 3,902,765 | | | | — | | | | — | | | | 3,902,765 | |

Primary Silver Producers | | | 4,064,823 | | | | — | | | | — | | | | 4,064,823 | |

Warrants | | | 10,036 | | | | 1,295,718 | | | | — | | | | 1,305,754 | |

Short-Term Investment | | | 20,175 | | | | — | | | | — | | | | 20,175 | |

Total | | $ | 51,993,372 | | | $ | 1,295,718 | | | $ | — | | | $ | 53,289,090 | |

The Fund held three Level 2 securities at November 30, 2022. Euro Sun Mining, Inc., Apollo Gold & Silver Corp. and Aya Gold & Silver, Inc., all Warrants, are being valued at intrinsic value, in accordance the Fund’s fair value methodologies. The Fund held one Level 3 security at November 30, 2022. Sutter Gold Mining, Inc. (“SGM CN”) has ceased operations and a receiver for the company’s assets has been appointed. The common shares of SGM CN will be valued at zero, in accordance with the Fund’s fair value methodologies until such time as the receiver has finalized the sale of the company’s assets.

There was no Level 3 activity during the year ended November 30, 2022 and did not warrant a Level 3 rollforward disclosure.

The Level 3 investments for the Fund represented 0.00% of net assets and did not warrant a disclosure of significant unobservable valuation inputs.

– 17 –

OCM GOLD FUND Notes to Financial Statements – November 30, 2022 (Continued)

|

Foreign Currency – Investment securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollar amounts at the date of valuation. Purchases and sales of investment securities and income and expense items denominated in foreign currencies are translated into U.S. dollar amounts on the respective dates of such transactions. The Fund does not isolate that portion of the results of operations resulting from changes in foreign exchange rates on investments from the fluctuations arising from changes in market prices of securities held. Such fluctuations for the year ended November 30, 2022 are included within the realized and unrealized gain/loss on investments section of the Statement of Operations.

Reported net realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions, and the difference between the amounts of dividends, interest and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in the fair value of assets and liabilities, other than investments in securities at fiscal period end, resulting from changes in exchange rates. Such fluctuations for the year ended November 30, 2022 are included within the realized and unrealized gain/loss on investments section of the Statement of Operations.

Federal Income Taxes – The Fund intends to comply with the requirements of the Internal Revenue Code of 1986, as amended (“Code”), necessary to qualify as a regulated investment company and to make the requisite distributions of income to its shareholders to relieve it from all or substantially all federal income taxes. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding on the applicable country’s tax rules and rate.

Accounting for Uncertainty in Income Taxes (“Income Tax Statement”) requires an evaluation of tax positions taken (or expected to be taken) in the course of preparing the Fund’s tax returns to determine whether these positions meet a “more-likely-than-not” standard that, based on the technical merits, have a more than fifty percent likelihood of being sustained by a taxing authority upon examination. A tax position that meets the “more-likely-than-not” recognition threshold is measured to determine the amount of benefit to recognize in the financial statements. The Fund’s policy is to classify interest and penalties associated with underpayment of federal and state income taxes, if any, as income tax expense on the Statement of Operations. As of November 30, 2022, the Fund did not have any interest or penalties associated with the underpayment of any income taxes.

The Income Tax Statement requires management of the Fund to analyze all open tax years, fiscal years 2019-2022 as defined by the Internal Revenue Service statute of limitations for all major jurisdictions, including federal tax authorities and certain state tax authorities. As of and during the year ended November 30, 2022, the Fund did not have a liability for any unrecognized tax benefits. The Fund has no examinations in progress and is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

– 18 –

OCM GOLD FUND Notes to Financial Statements – November 30, 2022 (Continued)

|

Share Classes – The Fund offers two classes of shares, Investor Class and Advisor Class. The outstanding shares of the Fund on April 1, 2010 were renamed “Investor Class shares.” The Advisor Class shares commenced operations on April 1, 2010. The two classes represent interests in the same portfolio of investments and have the same rights. Income, expenses (other than expenses attributable to a specific class) and realized and unrealized gains and losses on investments are allocated to each class of shares in proportion to their relative net assets.

Securities Transactions and Investment Income – Securities transactions are accounted for on a trade date basis. Realized gains and losses on sales of securities are calculated on the identified cost basis. Dividend income is recorded on the ex-dividend date and interest income is recorded on an accrual basis. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

Distributions to Shareholders – The character of distributions made during the year from net investment income or net realized gains may differ from the characterization for federal income tax purposes due to differences in the recognition of income, expense or gain items for financial statement and tax purposes. To the extent that these differences are attributable to permanent book and tax accounting differences, the components of net assets have been adjusted.

Redemption Fee – A 1.50% redemption fee is retained by the Fund to offset transaction costs and other expenses associated with short-term investing. The fee is imposed on redemptions or exchanges of shares held less than three months from their purchase date. The Fund records the fee as a reduction of shares redeemed and as a credit to shares of beneficial interest. For the year ended November 30, 2022, the Investor Class and the Advisor Class received $2,776 and $25,166 in redemption fees, respectively.

Guarantees and Indemnifications – In the normal course of business, the Fund enters into contracts with service providers that contain general indemnification clauses. Also, under the Fund’s organizational documents, its officers and Trustees are indemnified by the Fund against certain liabilities arising out of the performance of their duties to the Fund. The Fund notes that insofar as indemnification for liabilities arising under the Securities Act of 1933 may be permitted to trustees and officers, the Fund has been advised that in the opinion of the Securities and Exchange Commission (the “SEC”) such indemnification is against public policy as expressed in that Act and is, therefore, unenforceable. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims against the Fund that have not yet occurred. Based on experience, the Fund expects the risk of loss to be remote.

Use of Estimates – The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

– 19 –

OCM GOLD FUND Notes to Financial Statements – November 30, 2022 (Continued)

|

Derivative Instruments – Equity securities in the gold mining industry, particularly the smaller companies, may occasionally issue warrants as part of their capital structure. A warrant gives the holder the right to purchase the underlying equity at the exercise price until the expiration date of the warrant. The Fund may hold such warrants for exposure to smaller companies in the portfolio or other reasons associated with the Fund’s overall objective of long-term growth, though warrants will typically not be a significant part of the Fund’s portfolio. The Fund’s maximum risk in holding warrants is the loss of the entire amount paid for the warrants. At November 30, 2022, the Fund held warrants as listed on the Schedule of Investments.

Note 3. Investment Advisory Agreement and Affiliated Parties

The Fund has an investment advisory agreement with Orrell Capital Management, Inc. (“OCM” or the “Adviser”). Under the agreement, the Fund pays OCM a fee computed daily and payable monthly, at the following annual rates based upon average daily net assets:

Assets | Fee Rate |

$0 to $250 million | 0.950% |

$250 million to $500 million | 0.800% |

$500 million to $1 billion | 0.700% |

Over $1 billion | 0.600% |

Under the investment advisory agreement, the Adviser is responsible for reimbursing the Fund to maintain a voluntary ratio of expenses to average daily net assets for the Investor Class shares and Advisor Class shares at 2.99% and 2.49%, respectively.

The Fund does not compensate Trustees and Officers affiliated with OCM. For the year ended November 30, 2022, the expenses accrued for Trustees who are not affiliated with OCM are reported on the Statement of Operations. The Fund pays fees and related expenses for the services of the Fund’s Chief Compliance Officer. The expenses incurred for the Chief Compliance Officer are reported on the Statement of Operations.

Note 4. Distribution Agreement and Plan

The Trust has adopted a Distribution Plan (the “Plan”) pursuant to Rule 12b-1 under the 1940 Act. The Plan authorizes the Fund to reimburse the distributor for marketing expenses incurred in distributing shares of the Fund, including the cost of printing sales material and making payments to dealers of the Fund’s Investor Class and

– 20 –

OCM GOLD FUND Notes to Financial Statements – November 30, 2022 (Continued)

|

Advisor Class, in any fiscal year, subject to limits of 0.99% and 0.25%, respectively, of the average daily net assets of each respective class. For the year ended November 30, 2022, the Investor Class and the Advisor Class incurred $96,454 and $68,802, respectively, in expenses under the Plan.

Note 5. Purchases and Sales of Securities

Purchases and sales of investment securities (excluding short-term securities and U.S. government obligations) for the year ended November 30, 2022 were $5,057,058 and $7,183,456, respectively. There were no purchases or sales of U.S. government obligations.

Note 6. Federal Income Tax Information

At November 30, 2022, gross unrealized appreciation and depreciation of investments owned by the Fund, based on cost for federal income tax purposes were as follows:

Cost of investments | | $ | 31,385,315 |

Unrealized appreciation on investments | | $ | 28,661,487 |

Unrealized depreciation on investments | | | (6,757,712) |

Unrealized depreciation on foreign currency | | | (662) |

Net unrealized appreciation on investments... | | $ | 21,903,113 |

The difference between cost amounts for financial statement and federal income tax purposes is due primarily to investments in passive foreign investment companies.

GAAP requires that certain components of net assets be reclassified between financial and tax reporting. These reclassifications have no effect on net asset value per share. For the year ended November 30, 2022, permanent differences in book and tax accounting have been reclassified to paid in capital and total distributable earnings/(deficits) as follows:

Increase (Decrease) |

Paid in Capital | Total Distributable

Earnings |

$ (1,770,859) | $ 1,770,859 |

– 21 –

OCM GOLD FUND Notes to Financial Statements – November 30, 2022 (Continued)

|

The tax character of distributions paid during the fiscal years ended November 30, 2022 and 2021 was as follows:

| | | 2022 | | | 2021 |

Ordinary income | | $ | — | | | $ | 216,984 |

Net long-term capital gains | | | 660,861 | | | | 859,733 |

Total distributions | | $ | 660,861 | | | $ | 1,076,717 |

As of November 30, 2022, the components of accumulated earnings on a tax basis were as follows:

Undistributed ordinary income | | $ | — |

Undistributed long-term gains | | | — |

Tax accumulated earnings | | | — |

Accumulated capital and other losses | | | (945,960) |

Unrealized appreciation on investments. | | | 21,903,775 |

Unrealized depreciation on foreign currency | | | (662) |

Total accumulated earnings | | $ | 20,957,153 |

The Fund has $203,672 in qualified late-year losses, which are deferred until fiscal year 2023 for tax purposes. Net late-year ordinary losses incurred after December 31 and within the taxable year and net late-year specified losses incurred after October 31 and within the taxable year are deemed to arise on the first day of the Fund’s next taxable year.

As of November 30, 2022, the Fund had a short-term capital loss carryforward of $109,443 and a long-term capital loss carryforward of $632,845. To the extent that the fund may realize future net capital gains, those gains will be offset by any of its unused capital loss carryforward. Future capital loss carryover utilization in any given year may be subject to Internal Revenue Code limitations.

Note 7. Concentration of Risk

Investing in foreign securities involves certain risks not necessarily found in U.S. markets. These include risks associated with adverse changes in economic, political, regulatory and other conditions, changes in currency exchange rates, exchange control regulations, expropriation of assets or nationalization, imposition of withholding

– 22 –

OCM GOLD FUND Notes to Financial Statements – November 30, 2022 (Continued)

|

taxes on dividend or interest payments or capital gains, and possible difficulty in obtaining and enforcing judgments against foreign entities. Further, issuers of foreign securities are subject to different, and often less comprehensive, accounting, reporting, and disclosure requirements than domestic issuers.

As the Fund concentrates its investments in the gold mining industry, a development adversely affecting the industry (for example, changes in the mining laws which increases production costs or a significant decrease in the market price of gold) would have a greater adverse effect on the Fund than it would if the Fund invested in a number of different industries.

Note 8. Illiquid Securities

Pursuant to Rule 22e-4 under the 1940 Act, the Fund has adopted a Liquidity Risk Management Program (“LRMP”) that requires, among other things, that the Fund limits its illiquid investments that are assets to no more than 15% of net assets. An illiquid investment is any security which may not reasonably be expected to be sold or disposed of in current market conditions in seven calendar days or less without the sale or disposition significantly changing the market value of the investment. If the Adviser, at any time, determines that the value of illiquid securities held by the Fund exceeds 15% of its net asset value, the Adviser will take such steps as it considers appropriate to reduce them as soon as reasonably practicable in accordance with the Fund’s written LRMP.

Note 9. Market Disruption and Geopolitical Risks

Certain local, regional or global events such as war, acts of terrorism, the spread of infectious illness or other public health issues, or other events could have a significant impact on a security or instrument. Since 2020, the novel strain of coronavirus (COVID-19) has negatively affected the worldwide economy, as well as the economies of individual countries, the financial health of individual companies and the market in general in significant and unforeseen ways. Following Russia’s large-scale invasion of Ukraine, the President of the United States signed an Executive Order in February 2022 prohibiting U.S. persons from entering transactions with the Central Bank of Russia and Executive Orders in March 2022 prohibiting U.S. persons from importing oil and gas from Russia as well as other popular Russian exports, such as diamonds, seafood and vodka. There may also be restrictions on investments in Chinese companies. For example, the President of the United States of America signed an Executive Order in June 2021 affirming and expanding the U.S. policy prohibiting U.S. persons from purchasing or investing in publicly-traded securities of companies identified by the U.S. Government as “Chinese Military-Industrial Complex Companies.” The list of such companies can change from time to time, and as a result of forced selling or an inability to participate in an investment the Advisor otherwise believes is attractive, the Fund may incur losses. The duration of the coronavirus outbreak and the Russian-Ukraine conflict could adversely affect the Fund’s performance, the

– 23 –

OCM GOLD FUND Notes to Financial Statements – November 30, 2022 (Continued)

|

performance of the securities in which the Fund invests and may lead to losses on your investment. The ultimate impact of COVID-19 and Russia Invasion on the financial performance of the Fund’s investments is not reasonably estimable at this time. Management is actively monitoring these events.

Note 10. New Accounting Pronouncements

In October 2020, the SEC adopted new regulations governing the use of derivatives by registered investment companies (“Rule 18f-4”). Rule 18f-4 will impose limits on the amount of derivatives a fund can enter into, eliminate the asset segregation framework currently used by funds to comply with Section 18 of the 1940 Act, and require funds whose use of derivatives is greater than a limited specified amount to establish and maintain a comprehensive derivatives risk management program and appoint a derivatives risk manager. The Fund has adopted procedures in accordance with Rule 18f-4.

In December 2020, the SEC adopted a new rule providing a framework for fund valuation practices (“Rule 2a-5”). Rule 2a-5 establishes requirements for determining fair value in good faith for purposes of the 1940 Act. Rule 2a-5 will permit fund boards to designate certain parties to perform fair value determinations, subject to board oversight and certain other conditions. Rule 2a-5 also defines when market quotations are “readily available” for purposes of the 1940 Act and the threshold for determining whether a fund must fair value a security. In connection with Rule 2a-5, the SEC also adopted related recordkeeping requirements and is rescinding previously issued guidance, including with respect to the role of a board in determining fair value and the accounting and auditing of fund investments. The Fund has adopted procedures in accordance with Rule 2a-5 and has designated the Fund’s investment adviser as its valuation designee.

Note 11. Subsequent Events

Management has evaluated events and transactions for potential recognition or disclosure through the date the financial statements were issued. The Fund declared the following distributions:

| | Record

Date | | | Payable

Date | | | Share

Class | | | Long Term

Capital Gain | | | Short Term

Capital Gain | | | Ordinary

Income | |

| | | 12/15/2022 | | | | 12/16/2022 | | | | Advisor | | | $ | 0.00478 | | | $ | 0.00000 | | | $ | 0.0000 | |

| | | 12/15/2022 | | | | 12/16/2022 | | | | Investor | | | | 0.00478 | | | | 0.00000 | | | | 0.0000 | |

Management has determined there are no other material events that would require disclosure in the Fund’s financial statements through this date.

– 24 –

OCM GOLD FUND Financial Highlights Investor Class

|

| | | Year

Ended

Nov. 30,

2022 | | | Year

Ended

Nov. 30,

2021 | | | Year

Ended

Nov. 30,

2020 | | | Year

Ended

Nov. 30,

2019 | | | Year

Ended

Nov. 30,

2018 | |

| | | | | | | | | | | | | | | | | | | | | |

Per Share Operating Performance | | | | | | | | | | | | | | | | | | | | |

(For a share outstanding throughout each period) | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 11.71 | | | $ | 11.94 | | | $ | 8.62 | | | $ | 7.05 | | | $ | 9.26 | |

| | | | | | | | | | | | | | | | | | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment loss1 | | | (0.08 | ) | | | (0.11 | ) | | | (0.16 | ) | | | (0.14 | ) | | | (0.19 | ) |

Net realized and unrealized gain (loss) on investments and foreign currency transactions | | | (2.16 | ) | | | 0.01 | | | | 4.05 | | | | 3.37 | | | | (1.36 | ) |

Net increase from payments by affiliates (Note 3) | | | — | | | | — | | | | — | 2 | | | — | | | | — | |

Total from investment operations | | | (2.24 | ) | | | (0.10 | ) | | | 3.89 | | | | 3.23 | | | | (1.55 | ) |

| | | | | | | | | | | | | | | | | | | | | |

Less Distributions: | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | — | | | | (0.08 | ) | | | — | | | | — | | | | — | |

Distribution from net realized gains | | | (0.12 | ) | | | (0.05 | ) | | | (0.57 | ) | | | (1.66 | ) | | | (0.66 | ) |

Total distributions | | | (0.12 | ) | | | (0.13 | ) | | | (0.57 | ) | | | (1.66 | ) | | | (0.66 | ) |

| | | | | | | | | | | | | | | | | | | | | |

Redemption fee proceeds | | | — | 2 | | | — | 2 | | | — | 2 | | | — | 2 | | | — | 2 |

| | | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 9.35 | | | $ | 11.71 | | | $ | 11.94 | | | $ | 8.62 | | | $ | 7.05 | |

| | | | | | | | | | | | | | | | | | | | | |

Total return* | | | (19.25 | )% | | | (0.95 | )% | | | 48.15 | % | | | 56.65 | % | | | (18.24 | )% |

| | | | | | | | | | | | | | | | | | | | | |

Ratios/Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

Net assets, end of year (in 000’s) | | $ | 11,747 | | | $ | 17,024 | | | $ | 18,343 | | | $ | 22,467 | | | $ | 17,146 | |

Ratio of expenses to average net assets | | | 2.32 | % | | | 2.19 | % | | | 2.29 | % | | | 2.91 | % | | | 2.93 | % |

Ratio of net investment loss to average net assets | | | (0.80 | )% | | | (0.89 | )% | | | (1.53 | )% | | | (1.89 | )% | | | (2.27 | )% |

Portfolio turnover rate | | | 9 | % | | | 11 | % | | | 1 | % | | | 18 | % | | | 6 | % |

1 | Based on average shares method. |

2 | Amount represents less than $0.01 per share. |

See notes to financial statements.

– 25 –

OCM GOLD FUND Financial Highlights Advisor Class

|

| | | Year

Ended

Nov. 30,

2022 | | | Year

Ended

Nov. 30,

2021 | | | Year

Ended

Nov. 30,

2020 | | | Year

Ended

Nov. 30,

2019 | | | Year

Ended

Nov. 30,

2018 | |

| | | | | | | | | | | | | | | | | | | | | |

Per Share Operating Performance | | | | | | | | | | | | | | | | | | | | |

(For a share outstanding throughout each period) | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 13.21 | | | $ | 13.46 | | | $ | 9.57 | | | $ | 7.58 | | | $ | 9.86 | |

| | | | | | | | | | | | | | | | | | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment loss1 | | | (0.04 | ) | | | (0.05 | ) | | | (0.13 | ) | | | (0.11 | ) | | | (0.15 | ) |

Net realized and unrealized gain (loss) on investments and foreign currency transactions | | | (2.44 | ) | | | — | | | | 4.54 | | | | 3.71 | | | | (1.47 | ) |

Net increase from payments by affiliates (Note 3) | | | — | | | | — | | | | — | 2 | | | — | | | | — | |

Total from investment operations | | | (2.48 | ) | | | (0.05 | ) | | | 4.41 | | | | 3.60 | | | | (1.62 | ) |

| | | | | | | | | | | | | | | | | | | | | |

Less Distributions: | | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | — | | | | (0.16 | ) | | | — | | | | — | | | | — | |

Distribution from net realized gains | | | (0.12 | ) | | | (0.05 | ) | | | (0.57 | ) | | | (1.66 | ) | | | (0.66 | ) |

Total distributions | | | (0.12 | ) | | | (0.21 | ) | | | (0.57 | ) | | | (1.66 | ) | | | (0.66 | ) |

| | | | | | | | | | | | | | | | | | | | | |

Redemption fee proceeds | | | 0.01 | | | | 0.01 | | | | 0.05 | | | | 0.05 | | | | — | 2 |

| | | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 10.62 | | | $ | 13.21 | | | $ | 13.46 | | | $ | 9.57 | | | $ | 7.58 | |

| | | | | | | | | | | | | | | | | | | | | |

Total return | | | (18.80 | )% | | | (0.42 | )% | | | 49.40 | % | | | 58.54 | %3 | | | (17.81 | )%3 |

| | | | | | | | | | | | | | | | | | | | | |

Ratios/Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

Net assets, end of year (in 000’s) | | $ | 41,679 | | | $ | 51,390 | | | $ | 55,603 | | | $ | 12,507 | | | $ | 6,624 | |

Ratio of expenses to average net assets | | | 1.82 | % | | | 1.69 | % | | | 1.79 | % | | | 2.38 | % | | | 2.31 | % |

Ratio of net investment loss to average net assets | | | (0.30 | )% | | | (0.39 | )% | | | (1.03 | )% | | | (1.36 | )% | | | (1.65 | )% |

Portfolio turnover rate | | | 9 | % | | | 11 | % | | | 1 | % | | | 18 | % | | | 6 | % |

1 | Based on average shares method. |

2 | Amount represents less than $0.01 per share. |

3 | Total returns would have been higher/lower had expenses not been waived/recovered by the Adviser. |

See notes to financial statements.

– 26 –

OCM GOLD FUND Report of Independent Registered Public Accounting Firm

|

To the Board of Trustees of OCM Mutual Fund and

Shareholders of OCM Gold Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of OCM Gold Fund (the “Fund”), a series of OCM Mutual Fund (the “Trust”), including the schedule of investments, as of November 30, 2022, the related statement of operations for the year then ended, and the statements of changes in net assets for each of the two years in the period then ended, the financial highlights for each of the five years in the period then ended, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of November 30, 2022, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB. We have served as the auditor of the fund since 2018.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of the Fund’s internal control over financial reporting. As part of our audit we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as

– 27 –

OCM GOLD FUND Report of Independent Registered Public Accounting Firm (Continued) |

evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of November 30, 2022 by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

| |

TAIT, WELLER & BAKER LLP |

Philadelphia, Pennsylvania

January 25, 2023

– 28 –

OCM GOLD FUND Expense Example – For the Period Ended November 30, 2022

(Unaudited) |

As a shareholder of the OCM Gold Fund (the “Fund”), you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption fees on certain redemptions; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from June 1, 2022 to November 30, 2022 (the “period”).

Actual Expenses

The row titled “Actual” in the table below provides information about actual account values and actual expenses. You may use this information, together with the amount you invested, to estimate the expenses you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 equals 8.6), then multiply the result by the number in the appropriate line for your share class under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during the periods.

Hypothetical Example for Comparison Purposes

The row titled “Hypothetical” in the table below provides information about hypothetical account values and hypothetical expenses based on each class’ actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not each class’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the classes of the Fund and other funds. To do so, compare these 5% hypothetical examples with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) and redemption fees. Therefore, the hypothetical lines of the table are useful in comparing the ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

– 29 –

OCM GOLD FUND Expense Example – For the Period Ended November 30, 2022 (Continued)

(Unaudited) |

Expenses Paid During the Period

| | Beginning

Account Value

June 1, 2022 | Ending

Account Value

November 30, 2022 | Expenses Paid

During the

Period Ended

November 30, 2022* |

Investor Class | | | |

Actual | $ 1,000.00 | $ 859.40 | $ 11.35 |

Hypothetical (5% return before expenses) | 1,000.00 | 1,012.87 | 12.28 |

Advisor Class | | | |

Actual | 1,000.00 | 862.00 | 8.98 |

Hypothetical (5% return before expenses) | 1,000.00 | 1,015.42 | 9.72 |

* | Expenses are equal to the Investor Class’ and Advisor Class’ annualized expense ratios of 2.43% and 1.93%, respectively, for the period, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

– 30 –

OCM GOLD FUND Other Information

(Unaudited) |

Investments by Sector – As of November 30, 2022

As a Percentage of Total Investments

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. Shareholders may obtain the Fund’s Form N-PORT on the SEC’s website at http://www.sec.gov.

A description of the Fund’s proxy voting policies and procedures and a record of the Fund’s proxy votes for the year ended June 30, 2022 are available without charge, upon request by calling toll free 1-800-779-4681 and on the SEC’s website at http://www.sec.gov. The Fund’s proxy voting policies and procedures are also available on the Fund’s website at http://www.ocmgoldfund.com.

– 31 –

OCM GOLD FUND - INVESTOR CLASS Performance Results – Year Ended November 30, 2022

(Unaudited) |

Average Annual Total Returns

| | Investor Class | S&P 500® Index | Philadelphia

Gold & Silver Index |

1 year | -22.87% | -9.21% | -5.34% |

5 year | 7.70% | 10.98% | 10.13% |

10 year | -1.97% | 13.34% | -2.20% |

– 32 –

OCM GOLD FUND - ADVISOR CLASS Performance Results – Year Ended November 30, 2022

(Unaudited) |

Average Annual Total Returns

| | Advisor Class | S&P 500® Index | Philadelphia

Gold & Silver Index |

1 year | -18.80% | -9.21% | -5.34% |

5 year | 9.50% | 10.98% | 10.13% |

10 year | -0.79% | 13.34% | -2.20% |

– 33 –

OCM GOLD FUND Annual Renewal of Investment Advisory Agreement

(Unaudited) |

On October 19, 2022, the Board of Trustees of OCM Mutual Fund approved the continuation of the Fund’s investment advisory agreement with Orrell Capital Management, Inc. (the “Adviser”). Prior to approving the continuation of the agreement, the Board considered:

| | ● | the nature, extent and quality of the services provided by the Adviser |

| | ● | the investment performance of the Fund |

| | ● | the costs of the services to be provided and profits to be realized by the Adviser from its relationship with the Fund |

| | ● | the extent to which economies of scale would be realized as the Fund grows and whether fee levels reflect those economies of scale |

| | ● | the expense ratio of the Fund |

All of the factors discussed by the Trustees were considered as a whole and were considered separately by the Trustees who are not “interested persons” of the Trust (the “Independent Trustees”), meeting in executive session. The factors were viewed in their totality by the Trustees, with no single factor being the principal or determinative factor in the Trustees’ determination of whether to approve the continuation of the investment advisory agreement. The Trustees recognized that the management and fee arrangements for the Fund are the result of years of review and discussion between the Independent Trustees and the Adviser, that certain aspects of such arrangements may receive greater scrutiny in some years than in others and that the Trustees’ conclusions may be based, in part, on their consideration of these same arrangements and information received during the course of the year and in prior years.

The material considerations and determinations of the Board, including all of the Independent Trustees, are provided below.

In considering the nature, extent and quality of the services provided by the Adviser, the Board considered an oral presentation by the Adviser describing the portfolio management, shareholder communication, and regulatory compliance services provided by the Adviser to the Fund. Based on their review and discussions with management, the Trustees believe that the Adviser provides high quality services to the Fund, and they noted that their overall confidence in the Adviser is high. The Trustees also concluded that they were satisfied with the nature, extent and quality of the investment advisory services provided to the Fund by the Adviser, as the Adviser has worked to obtain good performance for the Fund, and performance has remained strong in recent periods, and that the nature and extent of the services provided by the Adviser are appropriate to ensure that the Fund’s operations are conducted in compliance with applicable laws, rules and regulations, as there have been no material compliance violations.

– 34 –

OCM GOLD FUND Annual Renewal of Investment Advisory Agreement (Continued)

(Unaudited) |

The Trustees compared the performance of the Fund to benchmark indices over various periods of time. The Adviser provided information regarding and led discussions of factors impacting the performance of the Fund, outlining current market conditions and explaining the Adviser’s expectations and strategies for the future. Based on this information and discussions with Mr. Orrell, the Fund’s portfolio manager, the Trustees concluded, within the context of their full deliberations, that the investment results that the Adviser had been able to achieve for the Fund were reasonable and support renewal of the investment advisory agreement, noting that the Adviser has historically been able to achieve positive performance for shareholders. The Trustees noted that the Fund adhered to its investment style.

In concluding that the advisory fees payable by the Fund were reasonable, the Trustees reviewed the profits realized by the Adviser, from its relationship with the Fund. They discussed in detail the profitability of the Adviser as it relates to the Fund, and they discussed the impact of the intermediary service fees on the profitability. The Trustees also considered the resources and revenues that the Adviser has put into managing and distributing the Fund and concluded that the level of profitability realized by the Adviser from its provision of services to the Fund is reasonable, and that the overall expense ratio and investment advisory fee were fair and within a reasonable range of industry averages. The Trustees determined that the Adviser has spent significant resources and time to maintain and improve the Fund, and that the Adviser has not recognized unreasonable profits.

As part of its analysis the Board considered the value of the research the Adviser received from broker-dealers executing securities transactions for the Fund. The Trustees concluded that the research obtained by the Adviser is beneficial to the Fund and that the Adviser had executed the Fund’s portfolio transactions in a manner designed to obtain best execution for the Fund. The Trustees determined such research has been used for legitimate purposes relating to the Fund by aiding in the investment decision-making process. The Trustees concluded that the other benefits realized by the Adviser from its relationship with the Fund were minimal and reasonable.

The Trustees also reviewed reports comparing the expense ratios of each class and advisory fees paid by the Fund to those paid by other comparable mutual funds in the same category and concluded that the advisory fees paid by the Fund and the expense ratios of each class of the Fund were within a reasonable range of comparable mutual funds. In making this conclusion, the Trustees also noted the unique expertise of the Adviser and that the Adviser does not currently engage any sub-advisers for the Fund. The Trustees also discussed the advisory fees payable by the Fund in relation to other advisory clients of the Adviser. The Trustees determined that they did not find anything to suggest that the fees charged to the Fund are unreasonable in comparison to other fees charged by the Adviser.

– 35 –

OCM GOLD FUND Annual Renewal of Investment Advisory Agreement (Continued)

(Unaudited) |

The Trustees concluded that the Fund has the right structure in place to continue to realize lower fees and expenses as asset levels continue to increase. The Trustees also considered whether the investment advisory agreement fee schedule should be adjusted for an increase in assets under management. They concluded that the existing “breakpoints” embodied in the investment advisory agreement would result in substantially lower fee rates than those of comparable mutual funds.

After reviewing the materials provided at the meeting, management’s presentation, as well as other information regularly provided at the Board’s quarterly meetings throughout the year regarding the quality of services provided by the Adviser, the performance of the Fund, expense information, regulatory compliance issues, trading information and related matters and other factors deemed relevant by the Board, the Trustees, including all of the Independent Trustees, determined to continue the investment advisory agreement.

– 36 –

OCM GOLD FUND Additional Fund Information

(Unaudited) |