UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-04015

Eaton Vance Mutual Funds Trust

(Exact Name of Registrant as Specified in Charter)

Two International Place, Boston, Massachusetts 02110

(Address of Principal Executive Offices)

Deidre E. Walsh

Two International Place, Boston, Massachusetts 02110

(Name and Address of Agent for Services)

(617) 482-8260

(Registrant’s Telephone Number)

October 31

Date of Fiscal Year End

October 31, 2023

Date of Reporting Period

Item 1. Reports to Stockholders

Eaton Vance

Global Macro Absolute Return Fund

Annual Report

October 31, 2023

Commodity Futures Trading Commission Registration. The Commodity Futures Trading Commission (“CFTC”) has adopted regulations that subject registered investment companies and advisers to regulation by the CFTC if a fund invests more than a prescribed level of its assets in certain CFTC-regulated instruments (including futures, certain options and swap agreements) or markets itself as providing investment exposure to such instruments. The adviser is registered with the CFTC as a commodity pool operator with respect to its management of the Fund. As the commodity pool operator of the Fund, the adviser has claimed relief under the Commodity Exchange Act from certain reporting and recordkeeping requirements. The adviser is also registered as a commodity trading advisor.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

This report must be preceded or accompanied by a current summary prospectus or prospectus. Before investing, investors should consider carefully the investment objective, risks, and charges and expenses of a mutual fund. This and other important information is contained in the summary prospectus and prospectus, which can be obtained from a financial intermediary. Prospective investors should read the prospectus carefully before investing. For further information, please call 1-800-262-1122.

Annual Report October 31, 2023

Eaton Vance

Global Macro Absolute Return Fund

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Management’s Discussion of Fund Performance†

Economic and Market Conditions

The world’s financial markets posted broad gains for the 12-month period ended October 31, 2023. During the period, inflation moderated in many countries, the U.S. economy outperformed expectations, and credit spreads generally tightened. These and other positive dynamics overshadowed concerns about rising global bond yields and heightened geopolitical tensions, including renewed conflict in the Middle East.

The U.S. Federal Reserve (the Fed) raised short-term interest rates during the period, and the cumulative effects of the monetary tightening cycle that began in March 2022 helped reduce U.S. inflation. As a result, the Fed slowed its pace of interest rate increases and signaled that it was nearing the end of its rate hiking campaign. The U.S. economy was resilient in the higher rate environment, posting solid growth as strength in the labor market supported healthy levels of consumer spending.

Inflation also eased in Europe, where the European Central Bank and Bank of England joined the Fed in slowing interest rate increases. However, European economic growth was sluggish amid elevated energy costs, a downturn in global trade, and higher borrowing costs. The prevalence of adjustable-rate mortgages in the U.K. and Southern Europe was particularly challenging for consumers in these regions. While wage gains helped offset the impact of higher household expenses, the U.K. unemployment rate rose and the eurozone labor market showed signs of softening late in the period.

In emerging markets (EM), China ended its zero-COVID policy early in the period, triggering a rebound in economic activity. However, the recovery quickly lost momentum due to several factors, including a drop in consumer confidence and a desire among developed-market (DM) companies to become less dependent on Chinese manufacturing. China’s economy stabilized in the final months of the period, bolstered by various stimulus measures. Nonetheless, the Chinese government seemed more focused on national security interests than economic growth.

During the period, numerous EM countries, including Mexico and several Southeast Asian nations in particular, benefited from DM companies’ efforts to diversify their supply chains beyond China. In addition, because EM central banks were generally ahead of their DM peers in addressing rising inflation risks, many EM central banks were able to cut interest rates during the period -- moves that supported economic growth and asset prices. For the period as a whole, the U.S. dollar broadly weakened, providing another tailwind for EM assets.

Fund Performance

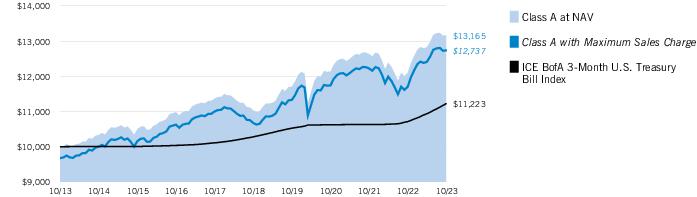

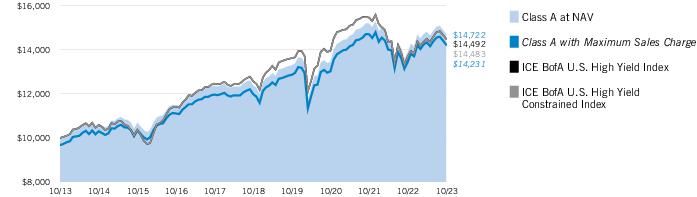

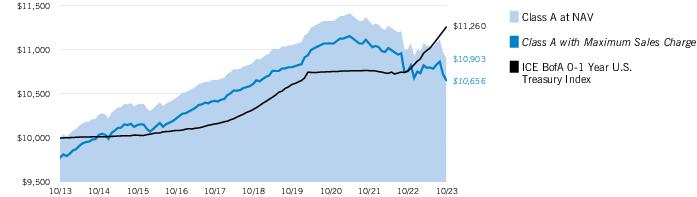

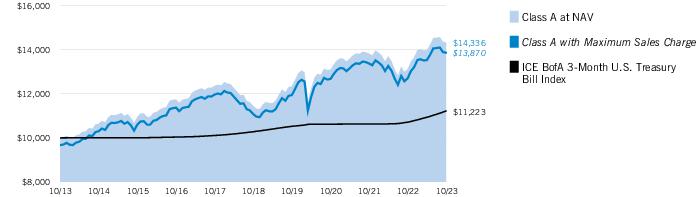

For the 12-month period ended October 31, 2023, Eaton Vance Global Macro Absolute Return Fund (the Fund) returned 8.86% for Class A shares at net asset value (NAV), outperforming its benchmark, the ICE BofA 3-Month U.S. Treasury Bill Index (the Index), which returned 4.77%.

The Fund’s interest rate exposure was the largest contributor to its performance during the period, followed by its currency and sovereign credit exposures. The Fund’s limited allocations to equities and corporate credit also positively impacted returns. Conversely, the Fund’s commodity exposure detracted from performance.

By region, Eastern Europe and Latin America made the largest contributions to returns during the period. In Eastern Europe, the Fund’s long Ukrainian local bond position performed especially well as Western allies provided military aid to the Ukrainian government and liquidity conditions in Ukraine improved. In Latin America, the Fund’s long local bond position in the Dominican Republic was a top contributor to returns, benefiting from solid economic growth and falling inflation in the country.

Investments in Western Europe and the Dollar Bloc -- Canada, New Zealand, and Australia -- also made significant contributions to performance during the period. A long position in Greek equities added significant value in Western Europe, as the Greek stock market surged amid a broad rally in global equities and a market-friendly outcome to the country’s national elections. In the Dollar Bloc, a long position in the Australian dollar versus a short position in the New Zealand dollar was advantageous.

Asia and the Middle East & Africa (MEA) region made solid, yet more modest, contributions to the Fund’s returns, helped by long sovereign credit positions in Sri Lanka and Tanzania alongside the broad tightening in credit spreads during the period. However, gains in Asia and MEA were dampened by other positions that performed poorly, including short sovereign credit positions in Malaysia and South Africa.

The Fund used derivatives extensively to hedge select undesired risk exposures, as well as to gain select desired risk exposures. Some of the notable drivers of performance at the country level involved the use of derivatives. The Fund’s use of derivatives broadly detracted from returns during the period. In particular, currency forwards used to gain long and short exposure to select currencies around the world detracted from returns, as did credit default swaps used to gain long and short exposure to certain sovereign credits, which also acted as hedges to other exposures in certain cases. Additionally, interest rate swaps used to gain select exposures as well as hedge others modestly weighed on Fund performance during the period.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Furthermore, returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the redemption of Fund shares. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Performance

Portfolio Manager(s) Patrick Campbell, CFA, Kyle Lee, CFA, Federico Sequeda, CFA each of Eaton Vance Management and Hussein Khattab, CFA of Eaton Vance Advisers International Ltd.

| % Average Annual Total Returns1,2 | Class

Inception Date | Performance

Inception Date | One Year | Five Years | Ten Years |

| Class A at NAV | 06/27/2007 | 10/31/1997 | 8.86% | 3.60% | 2.79% |

| Class A with 3.25% Maximum Sales Charge | — | — | 5.27 | 2.91 | 2.44 |

| Class C at NAV | 10/01/2009 | 10/31/1997 | 8.06 | 2.87 | 2.21 |

| Class C with 1% Maximum Deferred Sales Charge | — | — | 7.06 | 2.87 | 2.21 |

| Class I at NAV | 06/27/2007 | 10/31/1997 | 9.17 | 3.88 | 3.09 |

| Class R at NAV | 04/08/2010 | 10/31/1997 | 8.62 | 3.36 | 2.57 |

| Class R6 at NAV | 05/31/2017 | 10/31/1997 | 9.27 | 3.98 | 3.14 |

|

| ICE BofA 3-Month U.S. Treasury Bill Index | — | — | 4.77% | 1.77% | 1.16% |

| % Total Annual Operating Expense Ratios3 | Class A | Class C | Class I | Class R | Class R6 |

| | 1.09% | 1.84% | 0.84% | 1.33% | 0.77% |

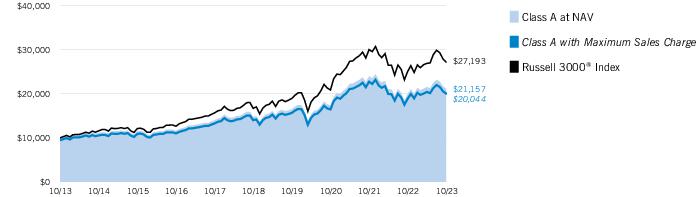

Growth of $10,000

This graph shows the change in value of a hypothetical investment of $10,000 in Class A of the Fund for the period indicated. For comparison, the same investment is shown in the indicated index.

| Growth of Investment2 | Amount Invested | Period Beginning | At NAV | With Maximum Sales Charge |

| Class C | $10,000 | 10/31/2013 | $12,446 | N.A. |

| Class I, at minimum investment | $1,000,000 | 10/31/2013 | $1,356,310 | N.A. |

| Class R | $10,000 | 10/31/2013 | $12,896 | N.A. |

| Class R6, at minimum investment | $5,000,000 | 10/31/2013 | $6,811,219 | N.A. |

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Furthermore, returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the redemption of Fund shares. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

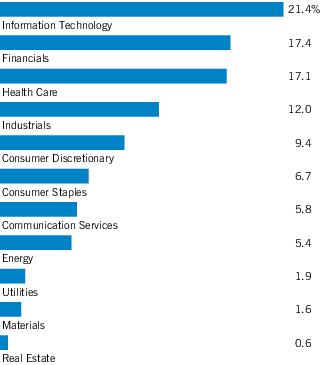

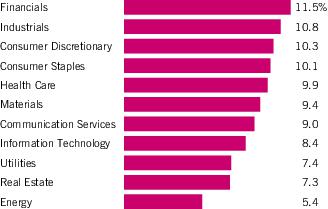

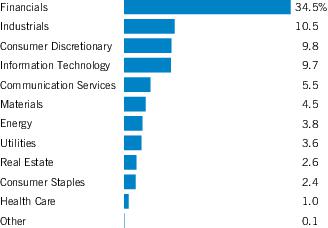

| Asset Allocation (% of net assets)1 |

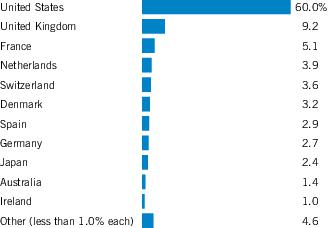

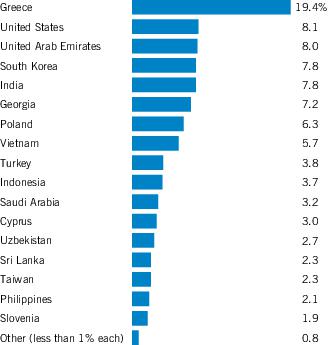

| Foreign Currency Exposures (% of net assets)2 |

| Iceland | 2.6% |

| Dominican Republic | 2.5 |

| Australia | 2.4 |

| Uzbekistan | 2.2 |

| Hungary | 1.9 |

| Serbia | 1.9 |

| Canada | 1.6 |

| India | 1.5 |

| Korea, South | 1.4 |

| Uruguay | 1.2 |

| Armenia | 1.1 |

| Mexico | 1.0 |

| Other | 0.6 4 |

| Saudi Arabia | -1.0 |

| Oman | -1.2 |

| Bahrain | -1.5 |

| Philippines | -2.1 |

| New Zealand | -2.3 |

| China | -3.7 |

| Euro | -6.7 |

| Total Long | 26.2% |

| Total Short | -22.8% |

| Total Net | 3.4% |

Fund invests in an affiliated investment company (Portfolio) with the same objective(s) and policies as the Fund. References to investments are to the Portfolio’s holdings.

Footnotes:

| 1 | Other Net Assets represents other assets less liabilities and includes any investment type that represents less than 1% of net assets. |

2 Currency exposures include all foreign exchange denominated assets, currency derivatives and commodities (including commodity derivatives). Total exposures may exceed 100% due to implicit leverage created by derivatives.

3 Net of securities sold short.

4 Includes amounts each less than 1.0% or –1.0%, as applicable.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Endnotes and Additional Disclosures

| † | The views expressed in this report are those of the portfolio manager(s) and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance and the Fund(s) disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. This commentary may contain statements that are not historical facts, referred to as “forward-looking statements.” The Fund’s actual future results may differ significantly from those stated in any forward-looking statement, depending on factors such as changes in securities or financial markets or general economic conditions, the volume of sales and purchases of Fund shares, the continuation of investment advisory, administrative and service contracts, and other risks discussed from time to time in the Fund’s filings with the Securities and Exchange Commission. |

| | |

| 1 | ICE BofA 3-Month U.S. Treasury Bill Index is an unmanaged index of U.S. Treasury securities maturing in 90 days. ICE® BofA® indices are not for redistribution or other uses; provided “as is”, without warranties, and with no liability. Eaton Vance has prepared this report and ICE Data Indices, LLC does not endorse it, or guarantee, review, or endorse Eaton Vance’s products. BofA® is a licensed registered trademark of Bank of America Corporation in the United States and other countries. Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. |

| 2 | Total Returns at NAV do not include applicable sales charges. If sales charges were deducted, the returns would be lower. Total Returns shown with maximum sales charge reflect the stated maximum sales charge. Unless otherwise stated, performance does not reflect the deduction of taxes on Fund distributions or redemptions of Fund shares.Performance prior to the inception date of a class may be linked to the performance of an older class of the Fund. This linked performance is adjusted for any applicable sales charge, but is not adjusted for class expense differences. If adjusted for such differences, the performance would be different. The performance of Class R6 is linked to Class I. Performance presented in the Financial Highlights included in the financial statements is not linked.Effective November 5, 2020, Class C shares automatically convert to Class A shares eight years after purchase. The average annual total returns listed for Class C reflect conversion to Class A shares after eight years. Prior to November 5, 2020, Class C shares automatically converted to Class A shares ten years after purchase. |

| 3 | Source: Fund prospectus. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report. Performance reflects expenses waived and/or reimbursed, if applicable. Without such waivers and/or reimbursements, performance would have been lower. |

| | Fund profile subject to change due to active management. |

| | Additional Information |

| | A long position is the purchase of an investment with the expectation that it will rise in value. |

| | A short position is the sale of a borrowed investment with the expectation that it will decline in value. |

| | Spread is the difference in yield between a U.S. Treasury bond and another debt security of the same maturity but different credit quality. |

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Example

As a Fund shareholder, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchases; and (2) ongoing costs, including management fees; distribution and/or service fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of Fund investing and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (May 1, 2023 to October 31, 2023).

Actual Expenses

The first section of the table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the actual Fund expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual Fund return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would be higher.

| | Beginning

Account Value

(5/1/23) | Ending

Account Value

(10/31/23) | Expenses Paid

During Period*

(5/1/23 – 10/31/23) | Annualized

Expense

Ratio |

| Actual | | | | |

| Class A | $1,000.00 | $1,026.60 | $ 7.61 | 1.49% |

| Class C | $1,000.00 | $1,021.60 | $11.31 | 2.22% |

| Class I | $1,000.00 | $1,026.70 | $ 6.23 | 1.22% |

| Class R | $1,000.00 | $1,024.10 | $ 8.78 | 1.72% |

| Class R6 | $1,000.00 | $1,028.40 | $ 5.88 | 1.15% |

| |

| Hypothetical | | | | |

| (5% return per year before expenses) | | | | |

| Class A | $1,000.00 | $1,017.69 | $ 7.58 | 1.49% |

| Class C | $1,000.00 | $1,014.01 | $11.27 | 2.22% |

| Class I | $1,000.00 | $1,019.06 | $ 6.21 | 1.22% |

| Class R | $1,000.00 | $1,016.54 | $ 8.74 | 1.72% |

| Class R6 | $1,000.00 | $1,019.41 | $ 5.85 | 1.15% |

| * | Expenses are equal to the Fund's annualized expense ratio for the indicated Class, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on April 30, 2023. The Example reflects the expenses of both the Fund and the Portfolio. |

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Statement of Assets and Liabilities

| | October 31, 2023 |

| Assets | |

| Investment in Global Macro Portfolio, at value (identified cost $1,896,357,131) | $ 1,792,136,435 |

| Receivable for Fund shares sold | 11,409,971 |

| Total assets | $1,803,546,406 |

| Liabilities | |

| Payable for Fund shares redeemed | $ 2,873,759 |

| Payable to affiliates: | |

| Distribution and service fees | 50,365 |

| Trustees' fees | 42 |

| Accrued expenses | 478,095 |

| Total liabilities | $ 3,402,261 |

| Net Assets | $1,800,144,145 |

| Sources of Net Assets | |

| Paid-in capital | $ 2,462,941,986 |

| Accumulated loss | (662,797,841) |

| Net Assets | $1,800,144,145 |

| Class A Shares | |

| Net Assets | $ 148,688,732 |

| Shares Outstanding | 18,228,236 |

Net Asset Value and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | $ 8.16 |

Maximum Offering Price Per Share

(100 ÷ 96.75 of net asset value per share) | $ 8.43 |

| Class C Shares | |

| Net Assets | $ 21,089,315 |

| Shares Outstanding | 2,574,870 |

Net Asset Value and Offering Price Per Share*

(net assets ÷ shares of beneficial interest outstanding) | $ 8.19 |

| Class I Shares | |

| Net Assets | $ 1,401,232,898 |

| Shares Outstanding | 172,137,853 |

Net Asset Value, Offering Price and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | $ 8.14 |

| Class R Shares | |

| Net Assets | $ 1,171,353 |

| Shares Outstanding | 143,334 |

Net Asset Value, Offering Price and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | $ 8.17 |

7

See Notes to Financial Statements.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Statement of Assets and Liabilities — continued

| | October 31, 2023 |

| Class R6 Shares | |

| Net Assets | $227,961,847 |

| Shares Outstanding | 28,024,098 |

Net Asset Value, Offering Price and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | $ 8.13 |

| On sales of $100,000 or more, the offering price of Class A shares is reduced. |

| * | Redemption price per share is equal to the net asset value less any applicable contingent deferred sales charge. |

8

See Notes to Financial Statements.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

| | Year Ended |

| | October 31, 2023 |

| Investment Income | |

| Dividend income allocated from Portfolio (net of foreign taxes withheld of $104,156) | $ 10,355,839 |

| Interest and other income allocated from Portfolio (net of foreign taxes withheld of $1,217,757) | 121,389,075 |

| Expenses, excluding interest and dividend expense, allocated from Portfolio | (11,652,370) |

| Interest and dividend expense allocated from Portfolio | (6,652,668) |

| Total investment income from Portfolio | $ 113,439,876 |

| Expenses | |

| Distribution and service fees: | |

| Class A | $ 442,832 |

| Class C | 246,373 |

| Class R | 6,492 |

| Trustees’ fees and expenses | 500 |

| Custodian fee | 63,000 |

| Transfer and dividend disbursing agent fees | 1,435,964 |

| Legal and accounting services | 83,800 |

| Printing and postage | 167,215 |

| Registration fees | 115,836 |

| Miscellaneous | 36,510 |

| Total expenses | $ 2,598,522 |

| Net investment income | $ 110,841,354 |

| Realized and Unrealized Gain (Loss) from Portfolio | |

| Net realized gain (loss): | |

| Investment transactions (net of foreign capital gains taxes of $267,910) | $ (187,450,530) |

| Written options | 920 |

| Securities sold short | (769,825) |

| Futures contracts | 17,099,665 |

| Swap contracts | (12,239,645) |

| Foreign currency transactions | (7,268,536) |

| Forward foreign currency exchange contracts | 3,519,479 |

| Non-deliverable bond forward contracts | 6,414,099 |

| Net realized loss | $(180,694,373) |

| Change in unrealized appreciation (depreciation): | |

| Investments (including net increase in accrued foreign capital gains taxes of $3,047) | $ 285,303,491 |

| Written options | 58,487 |

| Securities sold short | 2,271,798 |

| Futures contracts | (19,741,273) |

| Swap contracts | (18,489,493) |

| Foreign currency | 2,248,951 |

| Forward foreign currency exchange contracts | (20,545,732) |

| Non-deliverable bond forward contracts | (972,046) |

| Net change in unrealized appreciation (depreciation) | $ 230,134,183 |

| Net realized and unrealized gain | $ 49,439,810 |

| Net increase in net assets from operations | $ 160,281,164 |

9

See Notes to Financial Statements.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Statements of Changes in Net Assets

| | Year Ended October 31, |

| | 2023 | 2022 |

| Increase (Decrease) in Net Assets | | |

| From operations: | | |

| Net investment income | $ 110,841,354 | $ 115,574,082 |

| Net realized gain (loss) | (180,694,373) | 110,827,016 |

| Net change in unrealized appreciation (depreciation) | 230,134,183 | (319,960,670) |

| Net increase (decrease) in net assets from operations | $ 160,281,164 | $ (93,559,572) |

| Distributions to shareholders: | | |

| Class A | $ (7,161,278) | $ (8,063,152) |

| Class C | (976,813) | (1,034,667) |

| Class I | (67,278,432) | (66,924,119) |

| Class R | (58,071) | (49,057) |

| Class R6 | (11,553,886) | (13,033,990) |

| Total distributions to shareholders | $ (87,028,480) | $ (89,104,985) |

| Tax return of capital to shareholders: | | |

| Class A | $ (1,392,886) | $ (1,174,555) |

| Class C | (187,468) | (156,590) |

| Class I | (13,198,515) | (10,455,314) |

| Class R | (11,216) | (7,965) |

| Class R6 | (2,239,903) | (1,997,959) |

| Total tax return of capital to shareholders | $ (17,029,988) | $ (13,792,383) |

| Transactions in shares of beneficial interest: | | |

| Class A | $ (19,774,332) | $ (95,399,484) |

| Class C | (6,429,832) | (7,095,253) |

| Class I | (54,773,375) | (290,445,028) |

| Class R | (134,355) | 114,208 |

| Class R6 | (31,965,995) | (96,685,321) |

| Net decrease in net assets from Fund share transactions | $ (113,077,889) | $ (489,510,878) |

| Net decrease in net assets | $ (56,855,193) | $ (685,967,818) |

| Net Assets | | |

| At beginning of year | $ 1,856,999,338 | $ 2,542,967,156 |

| At end of year | $1,800,144,145 | $1,856,999,338 |

10

See Notes to Financial Statements.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

| | Class A |

| | Year Ended October 31, |

| | 2023 | 2022 | 2021 | 2020 | 2019 |

| Net asset value — Beginning of year | $ 7.910 | $ 8.660 | $ 8.640 | $ 8.740 | $ 8.590 |

| Income (Loss) From Operations | | | | | |

| Net investment income(1) | $ 0.483 | $ 0.418 | $ 0.368 | $ 0.356 | $ 0.438 |

| Net realized and unrealized gain (loss) | 0.220 | (0.792) | (0.016) | (0.046) | 0.078 |

| Total income (loss) from operations | $ 0.703 | $ (0.374) | $ 0.352 | $ 0.310 | $ 0.516 |

| Less Distributions | | | | | |

| From net investment income | $ (0.378) | $ (0.325) | $ (0.332) | $ (0.410) | $ (0.366) |

| Tax return of capital | (0.075) | (0.051) | — | — | — |

| Total distributions | $ (0.453) | $ (0.376) | $ (0.332) | $ (0.410) | $ (0.366) |

| Net asset value — End of year | $ 8.160 | $ 7.910 | $ 8.660 | $ 8.640 | $ 8.740 |

| Total Return(2) | 8.86% | (4.27)% | 4.11% | 3.63% | 6.14% |

| Ratios/Supplemental Data | | | | | |

| Net assets, end of year (000’s omitted) | $148,689 | $163,369 | $276,486 | $398,174 | $366,740 |

| Ratios (as a percentage of average daily net assets):(3) | | | | | |

| Expenses (4) | 1.41% (5) | 1.14% (5) | 1.10% | 1.05% | 1.04% |

| Net investment income | 5.88% | 5.03% | 4.20% | 4.11% | 5.06% |

| Portfolio Turnover of the Portfolio | 96% | 81% | 88% | 81% | 61% |

| (1) | Computed using average shares outstanding. |

| (2) | Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested and do not reflect the effect of sales charges. |

| (3) | Includes the Fund’s share of the Portfolio's allocated expenses. |

| (4) | Includes interest and/or dividend expense, including on securities sold short and/or reverse repurchase agreements if applicable, of 0.37%, 0.08%, 0.06%, 0.01% and 0.01% of average daily net assets for the years ended October 31, 2023, 2022, 2021, 2020 and 2019, respectively. |

| (5) | Includes a reduction by the investment adviser of a portion of the Portfolio’s adviser fee due to the Portfolio’s investment in the Liquidity Fund (equal to 0.01% and less than 0.01% of average daily net assets for the years ended October 31, 2023 and 2022, respectively). |

11

See Notes to Financial Statements.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Financial Highlights — continued

| | Class C |

| | Year Ended October 31, |

| | 2023 | 2022 | 2021 | 2020 | 2019 |

| Net asset value — Beginning of year | $ 7.950 | $ 8.690 | $ 8.680 | $ 8.770 | $ 8.620 |

| Income (Loss) From Operations | | | | | |

| Net investment income(1) | $ 0.427 | $ 0.365 | $ 0.307 | $ 0.305 | $ 0.374 |

| Net realized and unrealized gain (loss) | 0.208 | (0.786) | (0.026) | (0.044) | 0.082 |

| Total income (loss) from operations | $ 0.635 | $ (0.421) | $ 0.281 | $ 0.261 | $ 0.456 |

| Less Distributions | | | | | |

| From net investment income | $ (0.330) | $ (0.276) | $ (0.271) | $ (0.351) | $ (0.306) |

| Tax return of capital | (0.065) | (0.043) | — | — | — |

| Total distributions | $ (0.395) | $ (0.319) | $ (0.271) | $ (0.351) | $ (0.306) |

| Net asset value — End of year | $ 8.190 | $ 7.950 | $ 8.690 | $ 8.680 | $ 8.770 |

| Total Return(2) | 8.06% | (4.91)% | 3.37% | 2.91% | 5.39% |

| Ratios/Supplemental Data | | | | | |

| Net assets, end of year (000’s omitted) | $21,089 | $26,640 | $36,557 | $54,464 | $106,291 |

| Ratios (as a percentage of average daily net assets):(3) | | | | | |

| Expenses (4) | 2.12% (5) | 1.84% (5) | 1.80% | 1.75% | 1.76% |

| Net investment income | 5.18% | 4.38% | 3.49% | 3.51% | 4.31% |

| Portfolio Turnover of the Portfolio | 96% | 81% | 88% | 81% | 61% |

| (1) | Computed using average shares outstanding. |

| (2) | Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested and do not reflect the effect of sales charges. |

| (3) | Includes the Fund’s share of the Portfolio's allocated expenses. |

| (4) | Includes interest and/or dividend expense, including on securities sold short and/or reverse repurchase agreements if applicable, of 0.37%, 0.08%, 0.06%, 0.01% and 0.01% of average daily net assets for the years ended October 31, 2023, 2022, 2021, 2020 and 2019, respectively. |

| (5) | Includes a reduction by the investment adviser of a portion of the Portfolio’s adviser fee due to the Portfolio’s investment in the Liquidity Fund (equal to 0.01% and less than 0.01% of average daily net assets for the years ended October 31, 2023 and 2022, respectively). |

12

See Notes to Financial Statements.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Financial Highlights — continued

| | Class I |

| | Year Ended October 31, |

| | 2023 | 2022 | 2021 | 2020 | 2019 |

| Net asset value — Beginning of year | $ 7.900 | $ 8.640 | $ 8.630 | $ 8.720 | $ 8.580 |

| Income (Loss) From Operations | | | | | |

| Net investment income(1) | $ 0.504 | $ 0.446 | $ 0.393 | $ 0.385 | $ 0.458 |

| Net realized and unrealized gain (loss) | 0.211 | (0.786) | (0.024) | (0.039) | 0.074 |

| Total income (loss) from operations | $ 0.715 | $ (0.340) | $ 0.369 | $ 0.346 | $ 0.532 |

| Less Distributions | | | | | |

| From net investment income | $ (0.397) | $ (0.345) | $ (0.359) | $ (0.436) | $ (0.392) |

| Tax return of capital | (0.078) | (0.055) | — | — | — |

| Total distributions | $ (0.475) | $ (0.400) | $ (0.359) | $ (0.436) | $ (0.392) |

| Net asset value — End of year | $ 8.140 | $ 7.900 | $ 8.640 | $ 8.630 | $ 8.720 |

| Total Return(2) | 9.17% | (4.00)% | 4.31% | 4.07% | 6.34% |

| Ratios/Supplemental Data | | | | | |

| Net assets, end of year (000’s omitted) | $1,401,233 | $1,413,454 | $1,851,665 | $2,323,831 | $2,859,484 |

| Ratios (as a percentage of average daily net assets):(3) | | | | | |

| Expenses (4) | 1.13% (5) | 0.84% (5) | 0.80% | 0.75% | 0.75% |

| Net investment income | 6.14% | 5.39% | 4.50% | 4.45% | 5.31% |

| Portfolio Turnover of the Portfolio | 96% | 81% | 88% | 81% | 61% |

| (1) | Computed using average shares outstanding. |

| (2) | Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. |

| (3) | Includes the Fund’s share of the Portfolio's allocated expenses. |

| (4) | Includes interest and/or dividend expense, including on securities sold short and/or reverse repurchase agreements if applicable, of 0.37%, 0.08%, 0.06%, 0.01% and 0.01% of average daily net assets for the years ended October 31, 2023, 2022, 2021, 2020 and 2019, respectively. |

| (5) | Includes a reduction by the investment adviser of a portion of the Portfolio’s adviser fee due to the Portfolio’s investment in the Liquidity Fund (equal to 0.01% and less than 0.01% of average daily net assets for the years ended October 31, 2023 and 2022, respectively). |

13

See Notes to Financial Statements.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Financial Highlights — continued

| | Class R |

| | Year Ended October 31, |

| | 2023 | 2022 | 2021 | 2020 | 2019 |

| Net asset value — Beginning of year | $ 7.930 | $ 8.670 | $ 8.660 | $ 8.750 | $ 8.610 |

| Income (Loss) From Operations | | | | | |

| Net investment income(1) | $ 0.465 | $ 0.410 | $ 0.352 | $ 0.338 | $ 0.417 |

| Net realized and unrealized gain (loss) | 0.211 | (0.790) | (0.027) | (0.034) | 0.073 |

| Total income (loss) from operations | $ 0.676 | $(0.380) | $ 0.325 | $ 0.304 | $ 0.490 |

| Less Distributions | | | | | |

| From net investment income | $ (0.364) | $ (0.311) | $ (0.315) | $ (0.394) | $ (0.350) |

| Tax return of capital | (0.072) | (0.049) | — | — | — |

| Total distributions | $(0.436) | $(0.360) | $(0.315) | $(0.394) | $(0.350) |

| Net asset value — End of year | $ 8.170 | $ 7.930 | $ 8.670 | $ 8.660 | $ 8.750 |

| Total Return(2) | 8.62% | (4.45)% | 3.78% | 3.55% | 5.80% |

| Ratios/Supplemental Data | | | | | |

| Net assets, end of year (000’s omitted) | $ 1,171 | $ 1,267 | $ 1,274 | $ 968 | $ 861 |

| Ratios (as a percentage of average daily net assets):(3) | | | | | |

| Expenses (4) | 1.63% (5) | 1.33% (5) | 1.29% | 1.25% | 1.26% |

| Net investment income | 5.65% | 4.95% | 4.02% | 3.89% | 4.82% |

| Portfolio Turnover of the Portfolio | 96% | 81% | 88% | 81% | 61% |

| (1) | Computed using average shares outstanding. |

| (2) | Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. |

| (3) | Includes the Fund’s share of the Portfolio's allocated expenses. |

| (4) | Includes interest and/or dividend expense, including on securities sold short and/or reverse repurchase agreements if applicable, of 0.37%, 0.08%, 0.06%, 0.01% and 0.01% of average daily net assets for the years ended October 31, 2023, 2022, 2021, 2020 and 2019, respectively. |

| (5) | Includes a reduction by the investment adviser of a portion of the Portfolio’s adviser fee due to the Portfolio’s investment in the Liquidity Fund (equal to 0.01% and less than 0.01% of average daily net assets for the years ended October 31, 2023 and 2022, respectively). |

14

See Notes to Financial Statements.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Financial Highlights — continued

| | Class R6 |

| | Year Ended October 31, |

| | 2023 | 2022 | 2021 | 2020 | 2019 |

| Net asset value — Beginning of year | $ 7.890 | $ 8.630 | $ 8.620 | $ 8.710 | $ 8.570 |

| Income (Loss) From Operations | | | | | |

| Net investment income(1) | $ 0.510 | $ 0.450 | $ 0.398 | $ 0.391 | $ 0.464 |

| Net realized and unrealized gain (loss) | 0.212 | (0.783) | (0.024) | (0.040) | 0.073 |

| Total income (loss) from operations | $ 0.722 | $ (0.333) | $ 0.374 | $ 0.351 | $ 0.537 |

| Less Distributions | | | | | |

| From net investment income | $ (0.403) | $ (0.351) | $ (0.364) | $ (0.441) | $ (0.397) |

| Tax return of capital | (0.079) | (0.056) | — | — | — |

| Total distributions | $ (0.482) | $ (0.407) | $ (0.364) | $ (0.441) | $ (0.397) |

| Net asset value — End of year | $ 8.130 | $ 7.890 | $ 8.630 | $ 8.620 | $ 8.710 |

| Total Return(2) | 9.27% | (3.80)% | 4.37% | 4.01% | 6.53% |

| Ratios/Supplemental Data | | | | | |

| Net assets, end of year (000’s omitted) | $227,962 | $252,269 | $376,984 | $390,210 | $224,436 |

| Ratios (as a percentage of average daily net assets):(3) | | | | | |

| Expenses (4) | 1.05% (5) | 0.77% (5) | 0.73% | 0.68% | 0.69% |

| Net investment income | 6.23% | 5.44% | 4.56% | 4.51% | 5.37% |

| Portfolio Turnover of the Portfolio | 96% | 81% | 88% | 81% | 61% |

| (1) | Computed using average shares outstanding. |

| (2) | Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. |

| (3) | Includes the Fund’s share of the Portfolio's allocated expenses. |

| (4) | Includes interest and/or dividend expense, including on securities sold short and/or reverse repurchase agreements if applicable, of 0.37%, 0.08%, 0.06%, 0.01% and 0.01% of average daily net assets for the years ended October 31, 2023, 2022, 2021, 2020 and 2019, respectively. |

| (5) | Includes a reduction by the investment adviser of a portion of the Portfolio’s adviser fee due to the Portfolio’s investment in the Liquidity Fund (equal to 0.01% and less than 0.01% of average daily net assets for the years ended October 31, 2023 and 2022, respectively). |

15

See Notes to Financial Statements.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Notes to Financial Statements

1 Significant Accounting Policies

Eaton Vance Global Macro Absolute Return Fund (the Fund) is a non-diversified series of Eaton Vance Mutual Funds Trust (the Trust). The Trust is a Massachusetts business trust registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company. The Fund offers five classes of shares. Class A shares are generally sold subject to a sales charge imposed at time of purchase. Class C shares are sold at net asset value and are generally subject to a contingent deferred sales charge (see Note 5). Effective November 5, 2020, Class C shares automatically convert to Class A shares eight years after their purchase as described in the Fund’s prospectus. Class I, Class R and Class R6 shares are sold at net asset value and are not subject to a sales charge. Each class represents a pro rata interest in the Fund, but votes separately on class-specific matters and (as noted below) is subject to different expenses. Realized and unrealized gains and losses and net investment income and losses, other than class-specific expenses, are allocated daily to each class of shares based on the relative net assets of each class to the total net assets of the Fund. Sub-accounting, recordkeeping and similar administrative fees payable to financial intermediaries, which are a component of transfer and dividend disbursing agent fees on the Statement of Operations, are not allocated to Class R6 shares. Each class of shares differs in its distribution plan and certain other class-specific expenses. The Fund invests its assets in interests in Global Macro Portfolio (the Portfolio), a Massachusetts business trust, having the same investment objective and policies as the Fund. The value of the Fund’s investment in the Portfolio reflects the Fund’s proportionate interest in the net assets of the Portfolio (approximately 100% at October 31, 2023). The performance of the Fund is directly affected by the performance of the Portfolio. The consolidated financial statements of the Portfolio, including the consolidated portfolio of investments, are included elsewhere in this report and should be read in conjunction with the Fund’s financial statements.

The following is a summary of significant accounting policies of the Fund. The policies are in conformity with accounting principles generally accepted in the United States of America (U.S. GAAP). The Fund is an investment company and follows accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946.

A Investment Valuation—Valuation of securities by the Portfolio is discussed in Note 1A of the Portfolio's Notes to Consolidated Financial Statements, which are included elsewhere in this report.

B Income—The Fund's net investment income or loss consists of the Fund's pro rata share of the net investment income or loss of the Portfolio, less all actual and accrued expenses of the Fund.

C Federal and Other Taxes—The Fund’s policy is to comply with the provisions of the Internal Revenue Code applicable to regulated investment companies and to distribute to shareholders each year substantially all of its net investment income, and all or substantially all of its net realized capital gains. Accordingly, no provision for federal income or excise tax is necessary.

In addition to the requirements of the Internal Revenue Code, the Fund may also be required to recognize its pro rata share of the capital gains taxes incurred by the Portfolio. In doing so, the daily net asset value would reflect the Fund’s pro rata share of the estimated reserve for such taxes incurred by the Portfolio.

As of October 31, 2023, the Fund had no uncertain tax positions that would require financial statement recognition, de-recognition, or disclosure. The Fund files a U.S. federal income tax return annually after its fiscal year-end, which is subject to examination by the Internal Revenue Service for a period of three years from the date of filing.

D Expenses—The majority of expenses of the Trust are directly identifiable to an individual fund. Expenses which are not readily identifiable to a specific fund are allocated taking into consideration, among other things, the nature and type of expense and the relative size of the funds.

E Use of Estimates—The preparation of the financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expense during the reporting period. Actual results could differ from those estimates.

F Indemnifications—Under the Trust’s organizational documents, its officers and Trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the Fund. Under Massachusetts law, if certain conditions prevail, shareholders of a Massachusetts business trust (such as the Trust) could be deemed to have personal liability for the obligations of the Trust. However, the Trust’s Declaration of Trust contains an express disclaimer of liability on the part of Fund shareholders and the By-laws provide that the Trust shall assume, upon request by the shareholder, the defense on behalf of any Fund shareholders. Moreover, the By-laws also provide for indemnification out of Fund property of any shareholder held personally liable solely by reason of being or having been a shareholder for all loss or expense arising from such liability. Additionally, in the normal course of business, the Fund enters into agreements with service providers that may contain indemnification clauses. The Fund's maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred.

G Other—Investment transactions are accounted for on a trade date basis.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Notes to Financial Statements — continued

2 Distributions to Shareholders and Income Tax Information

The Fund expects to pay any required income distributions monthly and intends to distribute annually all or substantially all of its net realized capital gains. The Fund may include in its distributions amounts attributable to the imputed interest on foreign currency exposures and certain other derivative positions which, in certain circumstances, may result in a return of capital for federal income tax purposes. Distributions to shareholders are recorded on the ex-dividend date. Distributions are declared separately for each class of shares. Shareholders may reinvest income and capital gain distributions in additional shares of the same class of the Fund at the net asset value as of the ex-dividend date or, at the election of the shareholder, receive distributions in cash. Distributions to shareholders are determined in accordance with income tax regulations, which may differ from U.S. GAAP. As required by U.S. GAAP, only distributions in excess of tax basis earnings and profits are reported in the financial statements as a return of capital. Permanent differences between book and tax accounting relating to distributions are reclassified to paid-in capital. For tax purposes, distributions from short-term capital gains are considered to be from ordinary income.

The tax character of distributions declared for the years ended October 31, 2023 and October 31, 2022 was as follows:

| | Year Ended October 31, |

| | 2023 | 2022 |

| Ordinary income | $87,028,480 | $89,104,985 |

| Tax return of capital | $17,029,988 | $13,792,383 |

As of October 31, 2023, the components of distributable earnings (accumulated loss) on a tax basis were as follows:

| Deferred capital losses | $ (401,170,448) |

| Net unrealized depreciation | (261,627,393) |

| Accumulated loss | $(662,797,841) |

At October 31, 2023, the Fund, for federal income tax purposes, had deferred capital losses of $401,170,448 which would reduce its taxable income arising from future net realized gains on investment transactions, if any, to the extent permitted by the Internal Revenue Code, and thus would reduce the amount of distributions to shareholders, which would otherwise be necessary to relieve the Fund of any liability for federal income or excise tax. The deferred capital losses are treated as arising on the first day of the Fund’s next taxable year and retain the same short-term or long-term character as when originally deferred. Of the deferred capital losses at October 31, 2023, $27,231,590 are short-term and $373,938,858 are long-term.

3 Investment Adviser Fee and Other Transactions with Affiliates

The investment adviser fee is earned by Eaton Vance Management (EVM), an indirect, wholly-owned subsidiary of Morgan Stanley, as compensation for investment advisory services rendered to the Fund. The investment adviser fee is computed at an annual rate as a percentage of the Fund’s average daily net assets that are not invested in other investment companies for which EVM or its affiliates serve as investment adviser or administrator as follows and is payable monthly:

| Average Daily Net Assets | Annual Fee Rate |

| Up to $500 million | 0.615% |

| $500 million but less than $1 billion | 0.595% |

| $1 billion but less than $1.5 billion | 0.575% |

| $1.5 billion but less than $2 billion | 0.555% |

| $2 billion but less than $3 billion | 0.520% |

| $3 billion but less than $5 billion | 0.490% |

| $5 billion but less than $10 billion | 0.475% |

| $10 billion and over | 0.465% |

For the year ended October 31, 2023, the Fund incurred no investment adviser fee on such assets. Pursuant to an investment sub-advisory agreement, EVM has delegated a portion of the investment management of the Fund to Eaton Vance Advisers International Ltd. (EVAIL), an affiliate of EVM and an indirect, wholly-owned subsidiary of Morgan Stanley. EVM pays EVAIL a portion of its investment adviser fee for sub-advisory services provided to the

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Notes to Financial Statements — continued

Fund. To the extent the Fund’s assets are invested in the Portfolio, the Fund is allocated its share of the Portfolio’s investment adviser fee. The Portfolio has engaged Boston Management and Research (BMR) to render investment advisory services. See Note 2 of the Portfolio’s Notes to Consolidated Financial Statements which are included elsewhere in this report. EVM also serves as the administrator of the Fund, but receives no compensation.

EVM provides sub-transfer agency and related services to the Fund pursuant to a Sub-Transfer Agency Support Services Agreement. For the year ended October 31, 2023, EVM earned $78,275 from the Fund pursuant to such agreement, which is included in transfer and dividend disbursing agent fees on the Statement of Operations. The Fund was informed that Eaton Vance Distributors, Inc. (EVD), an affiliate of EVM and the Fund's principal underwriter, received $1,396 as its portion of the sales charge on sales of Class A shares for the year ended October 31, 2023. The Fund was informed that Morgan Stanley affiliated broker-dealers, which may be deemed to be affiliates of EVM, BMR and EVD, also received a portion of the sales charge on sales of Class A shares for the year ended October 31, 2023 in the amount of $762. EVD also received distribution and service fees from Class A, Class C and Class R shares (see Note 4) and contingent deferred sales charges (see Note 5).

Trustees and officers of the Fund who are members of EVM’s or BMR's organizations receive remuneration for their services to the Fund out of the investment adviser fee. Certain officers and Trustees of the Fund and the Portfolio are officers of the above organizations.

4 Distribution Plans

The Fund has in effect a distribution plan for Class A shares (Class A Plan) pursuant to Rule 12b-1 under the 1940 Act. Pursuant to the Class A Plan, the Fund pays EVD a distribution and service fee of 0.25% (0.30% prior to July 1, 2023) per annum of its average daily net assets attributable to Class A shares for distribution services and facilities provided to the Fund by EVD, as well as for personal services and/or the maintenance of shareholder accounts. Distribution and service fees paid or accrued to EVD for the year ended October 31, 2023 amounted to $442,832 for Class A shares.

The Fund also has in effect distribution plans for Class C shares (Class C Plan) and Class R shares (Class R Plan) pursuant to Rule 12b-1 under the 1940 Act. Pursuant to the Class C Plan, the Fund pays EVD amounts equal to 0.75% per annum of its average daily net assets attributable to Class C shares for providing ongoing distribution services and facilities to the Fund. For the year ended October 31, 2023, the Fund paid or accrued to EVD $184,780 for Class C shares. The Class R Plan requires the Fund to pay EVD an amount up to 0.50% per annum of its average daily net assets attributable to Class R shares for providing ongoing distribution services and facilities to the Fund. The Trustees of the Trust have currently limited Class R distribution payments to 0.25% per annum of the average daily net assets attributable to Class R shares. For the year ended October 31, 2023, the Fund paid or accrued to EVD $3,246 for Class R shares.

Pursuant to the Class C and Class R Plans, the Fund also makes payments of service fees to EVD, financial intermediaries and other persons in amounts equal to 0.25% per annum of its average daily net assets attributable to that class. Service fees paid or accrued are for personal services and/or the maintenance of shareholder accounts. They are separate and distinct from the sales commissions and distribution fees payable to EVD. Service fees paid or accrued for the year ended October 31, 2023 amounted to $61,593 and $3,246 for Class C and Class R shares, respectively.

Distribution and service fees are subject to the limitations contained in the Financial Industry Regulatory Authority Rule 2341(d).

5 Contingent Deferred Sales Charges

A contingent deferred sales charge (CDSC) of 1% generally is imposed on redemptions of Class C shares made within 12 months of purchase. Class A shares may be subject to a 0.75% CDSC if redeemed within 12 months of purchase (depending on the circumstances of purchase). Generally, the CDSC is based upon the lower of the net asset value at date of redemption or date of purchase. No charge is levied on shares acquired by reinvestment of dividends or capital gain distributions. For the year ended October 31, 2023, the Fund was informed that EVD received $1,782 of CDSCs paid by Class C shareholders and no CDSCs paid by Class A shareholders.

6 Investment Transactions

For the year ended October 31, 2023, increases and decreases in the Fund's investment in the Portfolio aggregated $98,428,362 and $324,965,141, respectively.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Notes to Financial Statements — continued

7 Shares of Beneficial Interest

The Fund’s Declaration of Trust permits the Trustees to issue an unlimited number of full and fractional shares of beneficial interest (without par value). Such shares may be issued in a number of different series (such as the Fund) and classes. Transactions in Fund shares, including direct exchanges

pursuant to share class conversions, were as follows:

| | Year Ended

October 31, 2023 | | Year Ended

October 31, 2022 |

| | Shares | Amount | | Shares | Amount |

| Class A | | | | | |

| Sales | 2,582,682 | $ 21,176,228 | | 4,592,167 | $ 38,339,067 |

| Issued to shareholders electing to receive payments of distributions in Fund shares | 961,393 | 7,894,152 | | 1,048,566 | 8,652,844 |

| Redemptions | (5,962,136) | (48,844,712) | | (16,937,765) | (142,391,395) |

| Net decrease | (2,418,061) | $ (19,774,332) | | (11,297,032) | $ (95,399,484) |

| Class C | | | | | |

| Sales | 251,217 | $ 2,070,905 | | 332,112 | $ 2,778,239 |

| Issued to shareholders electing to receive payments of distributions in Fund shares | 137,435 | 1,132,928 | | 142,074 | 1,173,583 |

| Redemptions | (1,166,680) | (9,633,665) | | (1,328,038) | (11,047,075) |

| Net decrease | (778,028) | $ (6,429,832) | | (853,852) | $ (7,095,253) |

| Class I | | | | | |

| Sales | 56,538,440 | $ 462,831,949 | | 71,497,227 | $ 591,643,634 |

| Issued to shareholders electing to receive payments of distributions in Fund shares | 8,312,329 | 68,104,954 | | 8,239,895 | 67,606,194 |

| Redemptions | (71,703,485) | (585,710,278) | | (115,115,585) | (949,694,856) |

| Net decrease | (6,852,716) | $ (54,773,375) | | (35,378,463) | $(290,445,028) |

| Class R | | | | | |

| Sales | 55,567 | $ 454,739 | | 45,748 | $ 382,213 |

| Issued to shareholders electing to receive payments of distributions in Fund shares | 8,421 | 69,287 | | 6,942 | 57,022 |

| Redemptions | (80,439) | (658,381) | | (39,849) | (325,027) |

| Net increase (decrease) | (16,451) | $ (134,355) | | 12,841 | $ 114,208 |

| Class R6 | | | | | |

| Sales | 4,150,302 | $ 34,107,676 | | 3,247,581 | $ 27,190,898 |

| Issued to shareholders electing to receive payments of distributions in Fund shares | 297,034 | 2,432,730 | | 295,011 | 2,422,349 |

| Redemptions | (8,387,320) | (68,506,401) | | (15,238,556) | (126,298,568) |

| Net decrease | (3,939,984) | $ (31,965,995) | | (11,695,964) | $ (96,685,321) |

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Report of Independent Registered Public Accounting Firm

To the Trustees of Eaton Vance Mutual Funds Trust and Shareholders of Eaton Vance Global Macro Absolute Return Fund:

Opinion on the Financial Statements and Financial Highlights

We have audited the accompanying statement of assets and liabilities of Eaton Vance Global Macro Absolute Return Fund (the “Fund") (one of the funds constituting Eaton Vance Mutual Funds Trust), as of October 31, 2023, the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, the financial highlights for each of the five years in the period then ended, and the related notes. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Fund as of October 31, 2023, and the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Fund's management. Our responsibility is to express an opinion on the Fund's financial statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. We believe that our audits provide a reasonable basis for our opinion.

/s/ Deloitte & Touche LLP

Boston, Massachusetts

December 22, 2023

We have served as the auditor of one or more Eaton Vance investment companies since 1959.

Eaton Vance

Global Macro Absolute Return Fund

October 31, 2023

Federal Tax Information (Unaudited)

The Form 1099-DIV you receive in February 2024 will show the tax status of all distributions paid to your account in calendar year 2023. Shareholders are advised to consult their own tax adviser with respect to the tax consequences of their investment in the Fund. As required by the Internal Revenue Code and/or regulations, shareholders must be notified regarding the status of qualified dividend income for individuals and 163(j) interest dividends.

Qualified Dividend Income. For the fiscal year ended October 31, 2023, the Fund designates approximately $1,562,190, or up to the maximum amount of such dividends allowable pursuant to the Internal Revenue Code, as qualified dividend income eligible for the reduced tax rate of 15%.

163(j) Interest Dividends. For the fiscal year ended October 31, 2023, the Fund designates 100% of distributions from net investment income as a 163(j) interest dividend.

Global Macro Portfolio

October 31, 2023

Consolidated Portfolio of Investments

| Collateralized Mortgage Obligations — 3.7% |

| Security | Principal

Amount

(000's omitted) | Value |

| Federal Home Loan Mortgage Corp.: | | | |

| Series 1650, Class K, 6.50%, 1/15/24 | $ | 3 | $ 3,493 |

| Series 1817, Class Z, 6.50%, 2/15/26 | | 4 | 4,142 |

| Series 1927, Class ZA, 6.50%, 1/15/27 | | 25 | 24,370 |

| Series 2344, Class ZD, 6.50%, 8/15/31 | | 150 | 149,983 |

| Series 2458, Class ZB, 7.00%, 6/15/32 | | 324 | 328,371 |

Interest Only:(1)

Series 4791, Class JI, 4.00%, 5/15/48 | | 4,024 | 844,753 |

| Federal Home Loan Mortgage Corp. Structured Agency Credit Risk Debt Notes: | | | |

| Series 2020-DNA4, Class B1, 11.435%, (30-day average SOFR + 6.114%), 8/25/50(2)(3) | | 3,671 | 4,089,292 |

| Series 2020-HQA4, Class B1, 10.685%, (30-day average SOFR + 5.364%), 9/25/50(2)(3) | | 1,854 | 2,008,076 |

| Series 2022-HQA1, Class M1B, 8.821%, (30-day average SOFR + 3.50%), 3/25/42(2)(3) | | 1,479 | 1,527,024 |

| Series 2022-HQA1, Class M2, 10.571%, (30-day average SOFR + 5.25%), 3/25/42(2)(3) | | 2,957 | 3,120,484 |

| Federal National Mortgage Association: | | | |

| Series G94-7, Class PJ, 7.50%, 5/17/24 | | 2 | 2,375 |

| Series 1994-42, Class ZQ, 7.00%, 4/25/24 | | 21 | 21,287 |

| Series 1994-79, Class Z, 7.00%, 4/25/24 | | 3 | 2,549 |

| Series 1994-89, Class ZQ, 8.00%, 7/25/24 | | 11 | 11,180 |

| Series 1996-35, Class Z, 7.00%, 7/25/26 | | 7 | 6,819 |

| Series 1998-16, Class H, 7.00%, 4/18/28 | | 61 | 61,733 |

| Series 1998-44, Class ZA, 6.50%, 7/20/28 | | 95 | 95,082 |

| Series 1999-25, Class Z, 6.00%, 6/25/29 | | 100 | 99,029 |

| Series 2000-2, Class ZE, 7.50%, 2/25/30 | | 20 | 20,799 |

| Series 2000-49, Class A, 8.00%, 3/18/27 | | 32 | 32,775 |

| Series 2001-31, Class ZA, 6.00%, 7/25/31 | | 787 | 777,568 |

| Series 2001-74, Class QE, 6.00%, 12/25/31 | | 240 | 240,767 |

| Series 2009-48, Class WA, 5.794%, 7/25/39(4) | | 1,145 | 1,140,461 |

| Series 2011-38, Class SA, 0.00%, (13.157% - 30-day average SOFR x 3, Floor 0.00%), 5/25/41(5) | | 648 | 396,333 |

| Series 2023-54, Class C, 6.50%, 11/25/53 | | 2,610 | 2,558,604 |

| Interest Only:(1) | | | |

| Series 424, Class C8, 3.50%, 2/25/48 | | 5,111 | 945,850 |

| Series 2018-21, Class IO, 3.00%, 4/25/48 | | 4,528 | 805,082 |

| Series 2018-58, Class BI, 4.00%, 8/25/48 | | 700 | 140,780 |

| Government National Mortgage Association: | | | |

| Series 2023-148, Class HL, 6.50%, 10/20/53 | | 2,610 | 2,605,702 |

| Sereis 2023-151, Class GL, 6.50%, 10/20/53 | | 1,890 | 1,886,530 |

| Series 2023-155, Class CH, 6.50%, 10/20/53 | | 7,140 | 7,119,529 |

| PNMAC GMSR Issuer Trust: | | | |

| Series 2018-GT1, Class A, 9.289%, (1 mo. SOFR + 3.85%), 2/25/25(2)(3) | | 9,000 | 9,000,381 |

| Security | Principal

Amount

(000's omitted) | Value |

| PNMAC GMSR Issuer Trust: (continued) | | | |

| Series 2018-GT2, Class A, 8.089%, (1 mo. USD LIBOR + 2.65%), 8/25/25(2)(3) | $ | 8,064 | $ 8,063,082 |

| Unison Trust, Series 2021-1, Class A, 4.50%, 4/25/50(2)(4) | | 22,480 | 17,541,715 |

Total Collateralized Mortgage Obligations

(identified cost $83,143,549) | | | $ 65,676,000 |

| Security | Shares | Value |

| Belgium — 0.0%(6) |

| Cenergy Holdings S.A. | | 19,171 | $ 128,952 |

| | | | $ 128,952 |

| Bulgaria — 0.3% |

| Eurohold Bulgaria AD(7) | | 5,302,921 | $ 4,876,582 |

| | | | $ 4,876,582 |

| Cyprus — 0.4% |

| Bank of Cyprus Holdings PLC | | 2,032,276 | $ 6,266,037 |

| Galaxy Cosmos Mezz PLC(7) | | 23,855 | 12,878 |

| Optima bank S.A.(7) | | 68,150 | 511,978 |

| Sunrisemezz PLC(7) | | 134,028 | 36,970 |

| | | | $ 6,827,863 |

| Georgia — 0.1% |

| Bank of Georgia Group PLC | | 19,303 | $ 781,525 |

| Georgia Capital PLC(7) | | 68,200 | 764,570 |

| TBC Bank Group PLC | | 22,924 | 749,179 |

| | | | $ 2,295,274 |

| Greece — 1.0% |

| Alpha Services and Holdings S.A.(7) | | 740,700 | $ 1,108,778 |

| Eurobank Ergasias Services and Holdings S.A.(7) | | 1,206,500 | 1,972,053 |

| Hellenic Telecommunications Organization S.A. | | 127,496 | 1,787,033 |

| Ideal Holdings S.A.(7) | | 6,439 | 39,662 |

| JUMBO S.A. | | 79,363 | 2,088,085 |

| Motor Oil (Hellas) Corinth Refineries S.A. | | 41,500 | 988,430 |

| Mytilineos S.A. | | 56,975 | 2,110,605 |

| National Bank of Greece S.A.(7) | | 251,300 | 1,439,283 |

| OPAP S.A. | | 92,863 | 1,572,940 |

| Piraeus Financial Holdings S.A.(7) | | 1,035,900 | 3,070,557 |

22

See Notes to Consolidated Financial Statements.

Global Macro Portfolio

October 31, 2023

Consolidated Portfolio of Investments — continued

| Security | Shares | Value |

| Greece (continued) |

| Public Power Corp. S.A.(7) | | 65,900 | $ 672,645 |

| Titan Cement International S.A. | | 3,416 | 63,976 |

| | | | $ 16,914,047 |

| Iceland — 0.2% |

| Arion Banki HF(2) | | 1,015,472 | $ 934,018 |

| Eik Fasteignafelag HF(7) | | 3,253,209 | 266,568 |

| Eimskipafelag Islands HF | | 220,734 | 744,248 |

| Hagar HF | | 921,987 | 451,359 |

| Islandsbanki HF | | 668,258 | 494,113 |

| Reginn HF(7) | | 1,291,872 | 207,661 |

| Reitir Fasteignafelag HF | | 875,641 | 483,667 |

| Siminn HF | | 1,879,514 | 118,694 |

| | | | $ 3,700,328 |

| Indonesia — 0.2% |

| Bank Central Asia Tbk PT | | 2,370,000 | $ 1,305,682 |

| Bank Mandiri Persero Tbk PT | | 2,570,000 | 918,138 |

| Bank Negara Indonesia Persero Tbk PT | | 540,000 | 162,965 |

| Bank Rakyat Indonesia Persero Tbk PT | | 3,500,000 | 1,094,393 |

| | | | $ 3,481,178 |

| Poland — 0.2% |

| Alior Bank S.A.(7) | | 4,493 | $ 70,732 |

| Allegro.eu S.A.(2)(7) | | 25,328 | 181,685 |

| Asseco Poland S.A. | | 2,879 | 52,714 |

| Bank Millennium S.A.(7) | | 31,797 | 55,326 |

| Bank Polska Kasa Opieki S.A. | | 9,589 | 291,383 |

| Budimex S.A. | | 671 | 75,114 |

| CCC S.A.(7) | | 2,124 | 20,103 |

| CD Projekt S.A. | | 3,509 | 87,608 |

| Cyfrowy Polsat S.A.(7) | | 13,477 | 42,021 |

| Dino Polska S.A.(2)(7) | | 2,655 | 251,575 |

| Enea S.A.(7) | | 14,841 | 25,725 |

| Eurocash S.A. | | 4,498 | 14,964 |

| Grupa Azoty S.A.(7) | | 2,748 | 14,378 |

| Grupa Kety S.A. | | 524 | 88,390 |

| Jastrzebska Spolka Weglowa S.A.(7) | | 2,720 | 32,312 |

| KGHM Polska Miedz S.A. | | 7,219 | 192,641 |

| KRUK S.A. | | 921 | 101,885 |

| LPP S.A. | | 60 | 193,288 |

| mBank S.A.(7) | | 790 | 97,662 |

| Orange Polska S.A. | | 33,830 | 62,751 |

| ORLEN S.A. | | 29,591 | 467,950 |

| PGE S.A.(7) | | 48,920 | 84,960 |

| Powszechna Kasa Oszczednosci Bank Polski S.A.(7) | | 45,365 | 469,925 |

| Security | Shares | Value |

| Poland (continued) |

| Powszechny Zaklad Ubezpieczen S.A. | | 32,554 | $ 368,377 |

| Santander Bank Polska S.A.(7) | | 1,888 | 205,050 |

| Tauron Polska Energia S.A.(7) | | 56,565 | 49,747 |

| Text S.A. | | 908 | 24,463 |

| Warsaw Stock Exchange | | 1,386 | 12,872 |

| XTB S.A.(2) | | 2,593 | 20,159 |

| | | | $ 3,655,760 |

| Spain — 0.0%(6) |

| AmRest Holdings SE(7) | | 3,936 | $ 24,965 |

| | | | $ 24,965 |

| United Kingdom — 0.0%(6) |

| Pepco Group N.V.(7)(8) | | 9,358 | $ 37,929 |

| Tesnik Cuatro, Ltd.(9) | | 409,000 | 572,723 |

| | | | $ 610,652 |

| Vietnam — 0.4% |

| Bank for Foreign Trade of Vietnam JSC(7) | | 99,972 | $ 353,542 |

| Binh Minh Plastics JSC | | 14,820 | 47,414 |

| Coteccons Construction JSC(7) | | 48,000 | 99,367 |

| FPT Corp. | | 662,286 | 2,315,811 |

| Hoa Phat Group JSC(7) | | 475,478 | 446,175 |

| KIDO Group Corp. | | 10,295 | 26,618 |

| Military Commercial Joint Stock Bank | | 914,921 | 681,401 |

| Mobile World Investment Corp. | | 1,082,498 | 1,665,844 |

| Phu Nhuan Jewelry JSC | | 348,840 | 1,023,999 |

| Refrigeration Electrical Engineering Corp. | | 287,788 | 659,297 |

| Vietnam Dairy Products JSC | | 90,281 | 250,044 |

| Vingroup JSC(7) | | 78,738 | 129,869 |

| | | | $ 7,699,381 |

Total Common Stocks

(identified cost $43,842,498) | | | $ 50,214,982 |

| Security | Principal

Amount

(000's omitted) | Value |

| India — 0.1% |

| Indiabulls Housing Finance, Ltd., 4.50%, 9/28/26(8) | USD | 2,970 | $ 2,647,072 |

Total Convertible Bonds

(identified cost $2,970,000) | | | $ 2,647,072 |

23

See Notes to Consolidated Financial Statements.

Global Macro Portfolio

October 31, 2023

Consolidated Portfolio of Investments — continued

| Foreign Corporate Bonds — 2.3% |

| Security | Principal

Amount

(000's omitted) | Value |

| Armenia — 0.0%(6) |

| Ardshinbank CJSC Via Dilijan Finance BV, 6.50%, 1/28/25(8) | USD | 953 | $ 941,087 |

| | | | $ 941,087 |

| Brazil — 0.1% |

| Coruripe Netherlands BV: | | | |

| 10.00%, 2/10/27(2) | USD | 903 | $ 639,216 |

| 10.00%, 2/10/27(8) | USD | 1,989 | 1,407,974 |

| | | | $ 2,047,190 |

| China — 0.1% |

| KWG Group Holdings, Ltd., 7.875%, 8/30/24(10) | USD | 1,571 | $ 122,931 |

| Shimao Group Holdings, Ltd., 5.60%, 7/15/26(8)(10) | USD | 5,100 | 127,500 |

| Sunac China Holdings, Ltd.: | | | |

| 6.50%, 7/9/23(8)(10) | USD | 2,000 | 290,000 |

| 8.35%, 4/19/23(8)(10) | USD | 3,270 | 468,428 |

| Times China Holdings, Ltd.: | | | |

| 5.55%, 6/4/24(8)(10) | USD | 3,999 | 138,365 |

| 6.75%, 7/16/23(8)(10) | USD | 2,966 | 74,150 |

| | | | $ 1,221,374 |

| Hungary — 0.1% |

| MBH Bank Nyrt, 8.625% to 10/19/26, 10/19/27(8)(11) | EUR | 1,243 | $ 1,326,917 |

| | | | $ 1,326,917 |

| Iceland — 0.6% |

| Arion Banki HF, 6.00%, 4/12/24(8) | ISK | 1,000,000 | $ 7,073,171 |

| Landsbankinn HF, 5.00%, 11/23/23(8) | ISK | 560,000 | 3,983,070 |

| WOW Air HF: | | | |

| 0.00% (9)(10)(12) | EUR | 79 | 0 |

| 0.00%, (3 mo. EURIBOR + 9.00%)(9)(10)(12) | EUR | 3,600 | 0 |

| | | | $ 11,056,241 |

| India — 0.8% |

| Indian Railway Finance Corp., Ltd., 2.80%, 2/10/31(8) | USD | 15,006 | $ 11,913,256 |

| JSW Steel, Ltd., 5.05%, 4/5/32(8) | USD | 1,466 | 1,131,308 |

| Reliance Communications, Ltd., 6.50%, 11/6/20(8)(10) | USD | 1,800 | 40,500 |

| Vedanta Resources Finance II PLC, 13.875%, 1/21/24(8) | USD | 1,481 | 1,319,954 |

| | | | $ 14,405,018 |

| Security | Principal

Amount

(000's omitted) | Value |

| Mexico — 0.1% |

| Alpha Holding S.A. de CV: | | | |

| 9.00%, 2/10/25(8)(10) | USD | 3,667 | $ 68,760 |

| 10.00%, 12/19/22(8)(10) | USD | 1,741 | 26,117 |

| Grupo Kaltex S.A. de CV, 14.50%, (13.00% cash and 1.50% PIK), 9/30/25(2) | USD | 1,124 | 1,011,600 |

| | | | $ 1,106,477 |

| Moldova — 0.1% |

| Aragvi Finance International DAC, 8.45%, 4/29/26(8) | USD | 2,301 | $ 1,584,814 |

| | | | $ 1,584,814 |

| Nigeria — 0.0%(6) |

| IHS Netherlands Holdco BV, 8.00%, 9/18/27(8) | USD | 354 | $ 289,760 |

| SEPLAT Energy PLC, 7.75%, 4/1/26(8) | USD | 439 | 371,745 |

| | | | $ 661,505 |

| Saint Lucia — 0.1% |

| Digicel International Finance, Ltd./Digicel International Holdings, Ltd., 8.75%, 5/25/24(8) | USD | 1,120 | $ 1,028,754 |

| | | | $ 1,028,754 |

| South Africa — 0.0%(6) |

| Petra Diamonds US Treasury PLC, 9.75% PIK, 3/8/26(8) | USD | 562 | $ 480,189 |

| | | | $ 480,189 |

| Turkey — 0.2% |

| Limak Iskenderun Uluslararasi Liman Isletmeciligi AS, 9.50%, 7/10/36(8) | USD | 4,373 | $ 3,839,532 |

| | | | $ 3,839,532 |

| Uzbekistan — 0.1% |

| International Finance Corp., 16.00%, 2/21/25 | UZS | 16,000,000 | $ 1,313,204 |

| | | | $ 1,313,204 |

Total Foreign Corporate Bonds

(identified cost $63,382,847) | | | $ 41,012,302 |

24

See Notes to Consolidated Financial Statements.

Global Macro Portfolio

October 31, 2023

Consolidated Portfolio of Investments — continued

| Loan Participation Notes — 1.2% |

| Security | Principal

Amount

(000's omitted) | Value |

| Uzbekistan — 1.2% |

| Daryo Finance BV (borrower - Uzbek Industrial and Construction Bank ATB), 18.75%, 6/15/25(8)(9)(13) | UZS | 151,973,440 | $ 12,143,756 |

| Europe Asia Investment Finance BV (borrower - Joint Stock Commercial Bank "Asaka"), 18.70%, 7/21/26(8)(9)(13) | UZS | 125,249,130 | 9,544,508 |

Total Loan Participation Notes

(identified cost $24,959,768) | | | $ 21,688,264 |

| Reinsurance Side Cars — 0.9% |

| Security | Shares | Value |

| Eden Re II, Ltd.: | | | |

| Series 2021A, 0.00%, 3/21/25(2)(9)(14)(15) | | 255,989 | $ 116,731 |

| Series 2022A, 0.00%, 3/20/26(2)(9)(14)(15) | | 193,872 | 143,523 |

| Series 2022B, 0.00%, 3/20/26(2)(9)(14)(15) | | 415,091 | 313,394 |

| Series 2023B, 0.00%, 3/19/27(2)(9)(14)(15) | | 2,800,000 | 3,215,800 |

| Mt. Logan Re, Ltd., Series A-1(7)(9)(15)(16) | | 4,400 | 5,206,235 |

| Sussex Capital, Ltd.: | | | |

| Designated Investment Series 16, 12/21(7)(9)(15)(16) | | 817 | 15,233 |

| Designated Investment Series 16, 11/22(7)(9)(15)(16) | | 793 | 439,382 |

| Series 16, Preference Shares(9)(15)(16) | | 5,500 | 6,031,506 |

Total Reinsurance Side Cars

(identified cost $13,564,952) | | | $ 15,481,804 |

| Senior Floating-Rate Loans — 0.9%(17) |

| Borrower/Description | Principal

Amount

(000's omitted) | Value |

| Argentina — 0.0%(6) |

| Desa, LLC, Term Loan, 2.50%, 6/30/24(9)(18) | $ | 788 | $ 278,045 |

| | | | $ 278,045 |

| Mexico — 0.9% |

| Petroleos Mexicanos, Term Loan, 8.447%, (SOFR + 3.00%), 6/28/24 | $ | 15,931 | $ 15,652,203 |

| | | | $ 15,652,203 |

Total Senior Floating-Rate Loans

(identified cost $16,522,231) | | | $ 15,930,248 |

| Sovereign Government Bonds — 38.7% |

| Security | Principal

Amount

(000's omitted) | Value |

| Albania — 1.1% |

| Albania Government International Bond: | | | |

| 3.50%, 10/9/25(8) | EUR | 2,157 | $ 2,188,119 |

| 3.50%, 6/16/27(8) | EUR | 209 | 206,634 |

| 5.90%, 6/9/28(8) | EUR | 16,495 | 16,901,210 |

| | | | $ 19,295,963 |

| Argentina — 0.5% |

| Republic of Argentina: | | | |

| 0.75% to 7/9/27, 7/9/30(19) | USD | 4,552 | $ 1,275,059 |

| 1.00%, 7/9/29 | USD | 1,102 | 298,852 |

| 3.50% to 7/9/29, 7/9/41(19) | USD | 9,543 | 2,524,842 |

| 3.625% to 7/9/24, 7/9/35(19) | USD | 10,421 | 2,601,153 |

| 4.255% to 7/9/24, 1/9/38(19) | USD | 6,269 | 1,908,755 |

| | | | $ 8,608,661 |

| Armenia — 1.1% |

| Republic of Armenia Treasury Bond: | | | |

| 9.00%, 4/29/26 | AMD | 169,160 | $ 409,003 |

| 9.25%, 4/29/28 | AMD | 2,178,230 | 5,188,837 |

| 9.60%, 10/29/33 | AMD | 4,493,125 | 10,679,715 |

| 9.75%, 10/29/50 | AMD | 571,827 | 1,364,103 |

| 9.75%, 10/29/52 | AMD | 621,020 | 1,479,102 |

| | | | $ 19,120,760 |

| Barbados — 0.7% |

| Government of Barbados, 6.50%, 10/1/29(8) | USD | 13,422 | $ 12,649,952 |

| | | | $ 12,649,952 |

| Benin — 1.0% |

| Benin Government International Bond: | | | |

| 4.875%, 1/19/32(8) | EUR | 8,006 | $ 6,355,651 |

| 4.95%, 1/22/35(8) | EUR | 3,809 | 2,742,823 |

| 6.875%, 1/19/52(8) | EUR | 13,654 | 9,497,367 |

| | | | $ 18,595,841 |

| Cyprus — 0.5% |

| Cyprus Government International Bond: | | | |

| 2.75%, 2/26/34(8) | EUR | 812 | $ 753,195 |

| 4.125%, 4/13/33(8) | EUR | 7,242 | 7,731,351 |

| | | | $ 8,484,546 |

25

See Notes to Consolidated Financial Statements.

Global Macro Portfolio

October 31, 2023

Consolidated Portfolio of Investments — continued

| Security | Principal

Amount

(000's omitted) | Value |

| Dominican Republic — 2.4% |

| Dominican Republic: | | | |

| 8.00%, 1/15/27(8) | DOP | 96,000 | $ 1,570,419 |

| 8.00%, 2/12/27(8) | DOP | 490,340 | 8,108,153 |

| 11.25%, 9/15/35(2) | DOP | 106,250 | 1,856,850 |

| 12.00%, 8/8/25(2) | DOP | 332,200 | 5,912,628 |

| 12.75%, 9/23/29(2) | DOP | 368,500 | 7,187,520 |

| 13.00%, 6/10/34(8) | DOP | 232,600 | 4,752,252 |

| 13.625%, 2/3/33(2) | DOP | 206,150 | 4,134,557 |

| Dominican Republic Central Bank Notes: | | | |

| 8.00%, 3/12/27(8) | DOP | 31,580 | 504,933 |

| 12.00%, 10/3/25(2) | DOP | 138,420 | 2,466,310 |

| 13.00%, 12/5/25(2) | DOP | 216,700 | 3,939,317 |