UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-04014

Meridian Fund, Inc.®

(Exact name of registrant as specified in charter)

100 Fillmore St., Suite 325

Denver, CO 80206

(Address of principal executive offices) (Zip code)

David J. Corkins

100 Fillmore St., Suite 325

Denver, CO 80206

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-398-2929

Date of fiscal year end: June 30

Date of reporting period: June 30, 2022

| Item 1. | Reports to Stockholders. |

| | (a) | Include a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1). |

The Report to Shareholders is attached herewith.

Annual Report

June 30, 2022

Meridian Fund, Inc.

Meridian Growth Fund

Meridian Contrarian Fund

Meridian Enhanced Equity Fund

Meridian Small Cap Growth Fund

MERIDIAN FUND, INC.

Table of Contents

| 4 |

| 24 |

| 29 |

| 30 |

| 48 |

| 50 |

| 51 |

| 53 |

| 71 |

| 91 |

| 92 |

| 93 |

| 94 |

| 96 |

| Meridian Funds | 3 | www.meridianfund.com |

Meridian Growth Fund

Portfolio Performance and Composition (Unaudited)

Market Overview

U.S. equity markets were volatile during the 12-month period as new COVID-19 variants, global supply-chain issues, the war in Ukraine, and a rapid rise in inflation kept investors on edge. An acceleration in inflation, which climbed to a 40-year high, prompted the U.S. Federal Reserve (Fed) to end its ultra-easy monetary policy and raise interest rates 25 basis points in March, the first rate hike in more than three years. Policymakers continued their campaign against inflation in May and June, raising rates 50 basis points and 75 basis points, respectively. June’s rate hike was the largest in 28 years. In the final weeks of the period, heightened fears that rising interest rates and inflation may lead to an economic recession and weaken corporate profits continued to push equity markets lower.

Against this backdrop, large cap stocks outperformed small caps, according to the Russell indices. From a style perspective, value stocks outperformed growth stocks across capitalization categories.

Fund Performance

The Meridian Growth Fund (the “Fund”) Legacy Class Shares returned -29.20% (net) for the 12-month period ended June 30, 2022, outperforming its benchmark, the Russell 2500® Growth Index, which returned -31.81%.

The index decline was broad-based with all sectors except for energy declining during the period. Notable underperformers included the communication services, information technology, healthcare, and consumer discretionary sectors, which were all down in excess of 25%.

Our investment process prioritizes the management of risk over the opportunity for return. We look to build an “enduring” portfolio that can mitigate capital losses during turbulent bear market environments and, secondarily, participate in the upside during strong market environments. This strategy proved effective during the 12-month period, which was exceptionally volatile and included 39 days of 2% or greater declines in Index performance. The Fund outperformed on all but five of these days.

During the period, the Fund benefitted from positive stock selection in the information technology and healthcare sectors. In addition, an overweight position in the industrials sector aided performance, as industrials as a sector outperformed. We maintained the Fund’s overweight to industrials given our focus on commercial and professional service companies, which tend to exhibit strong competitive advantages and generally less macro sensitivity than the broader sector. Conversely, the Fund’s consumer discretionary holdings detracted from relative performance, as several names declined materially. Market factors were generally positive, although larger cap names within the index continued to outperform smaller cap names, creating a headwind to performance.

Market volatility provided us with the opportunity to establish positions in several high-quality growth companies that we believe had declined to attractive levels during the period. In particular, we took advantage of lower valuation multiples for select information technology and healthcare companies. While we are excited about the significant decline in valuations in both of these sectors, we are seeking to be prudent with position sizes in the event multiples contract even further from here. We believe the types of companies we invest in (strong balance sheets, recurring revenue streams, large and growing addressable markets) will create shareholder value over longer periods of time.

The three largest contributors to the Fund’s relative performance during the period were ON Semiconductor Corp., Matson, Inc., and LPL Financial Holdings, Inc.

ON Semiconductor Corp. is a semiconductor manufacturer with a diverse product portfolio and high exposure to the attractive automotive and industrials end markets. We believe ON Semi’s exposure to the auto end market is particularly attractive as advanced driver assistance systems, self-driving features, and the increasing penetration of electric vehicles have led to strong demand for the semiconductors that power these technologies. We believe the company is also well-positioned in the industrials end market, where it benefits from low pricing pressure due to the longer lifecycle of industrials products relative to consumer products. In the most recent period, the company grew revenues 31%, expanded operating margins by over 500 basis points, and grew adjusted EPS in excess of 200%. We were pleased with ON’s execution and are optimistic that it will hit the long-term financial goals set out by management. Although we trimmed the stock, exiting the period the Fund continued to hold a meaningful position.

Matson, Inc. is a provider of ocean transportation and logistics services. The company transports freight between the continental U.S. and ports in Alaska, Hawaii, and China. One of the things that attracted us to Matson is its position as one of

| Meridian Funds | 4 | www.meridianfund.com |

Meridian Growth Fund

Portfolio Performance and Composition (Unaudited) (continued)

the leading shipping companies operating under the Jones Act, a federal statute that allows only American-owned and-built vessels crewed by Americans to transport goods between U.S. ports. We also like Matson’s expedited China service, which has a large time advantage over traditional steamship lines. In addition, the company has its own terminal operations in West Coast ports, which provides a further transit advantage due to the current backlog of ships waiting to be unloaded. Tailwinds for the stock during the reporting period included a strong pricing environment and pandemic-related shutdowns in China, which further disrupted global supply chains. We believe the company’s express service from China and cheaper-than-air freight costs will appeal to shippers even after supply-chain disruptions resolve. We maintain a positive long-term outlook for Matson and trimmed the Fund’s position as the stock appreciated during the trailing 12-months.

LPL Financial Holdings, Inc. is a leading broker/dealer to independent advisors and RIAs. The company is seeing a powerful shift away from its brokerage platform and towards its advisory platform where returns on assets are notably higher. The company continues to attract new advisors to its platform owning partly to its high payout ratios. LPL is able to pay out a higher percentage of revenues to its advisors owing to the company’s sizeable investment in a self-clearing platform that generates a material cost advantage. In the near term, LPL’s results and share price performance have been driven by increasing interest rates which have a powerful impact on margins. We trimmed the Fund’s position in the stock during the period as the risk-reward profile became less favorable due to the market correction and its impact on assets under management.

The three largest detractors from the Fund's relative performance during the period were 2U, Inc., 8x8, Inc., and Vroom, Inc.

2U, Inc. is an educational technology firm that partners with leading nonprofit colleges and universities to offer online degree programs. The company possesses many of the qualities that we believe define a good business, including long-term contracts and recurring revenue; attractive unit economics that should deliver strong EBITDA margins at scale; and strong brand recognition with marquee university partners to drive continued growth. Unfortunately, headwinds from 2U’s recent acquisition of online course provider edX and incremental losses associated with the merger have resulted in a reduced outlook for the company’s 2022 profits. Further pressuring the stock during the past 12 months was weaker demand for higher education degrees due to a tight labor market and high marketing and sales costs to attract new students. We are closely monitoring the Fund’s holding in 2U and trimmed the Fund’s position in the stock during the period.

8x8, Inc. is a cloud communications provider that offers businesses a unified voice, contact center, video, and chat platform. The company hired a new CEO in late 2020 who has since refocused the company on areas of the market where 8x8 has competitive advantages and the potential to earn higher margins. In conjunction with this change in strategy, the company exited low-growth and low-margin product lines, which has led to what we believe is a temporary slowdown in revenue growth. A recent acquisition that depleted 8x8’s cash position also weighed on investor sentiment. We believe the company will overcome these short-term issues and that, at its current price, the stock is attractively valued. We are willing to be patient as the company works through these setbacks and added to the Fund’s position in the stock during the period.

Vroom, Inc. operates an end-to-end e-commerce platform for the used car industry. The company is capitalizing on a growing trend in which used car customers are choosing the online shopping experience over the traditional car lot experience. We believe only a few e-commerce platforms will be able to take significant market share from traditional used car dealers due to inventory, sourcing, and operational challenges that most online sellers will be unable to overcome. During the period, increased reconditioning costs due to labor shortages and strong demand at third-party reconditioning partners pressured Vroom’s margins. The company also suffered from higher shipping expenses incurred as a result of needing to transport cars greater distances to refurbishing facilities. Also pressuring the stock during the past 12 months was news that one of Vroom’s refurbishing partners had agreed to be acquired by competitor Carvana. Due to these and other factors negatively impacting the company, we decided to exit the Fund’s position in Vroom during the period.

Outlook

After raising interest rates 150 basis points in the first half of 2022 and indicating that additional rate increases may be needed, it is clear that Federal Reserve policymakers have become increasingly certain that aggressive action is necessary to tame inflation. They also appear more willing to accept the risk of an economic slowdown in exchange for aggressive monetary tightening and lower inflationary pressures. As a result, investors are wary of potential demand destruction and other consequences the broader economy may suffer in the coming months.

As the Federal Reserve embarks on its tightening path, we expect volatility to increase which we believe will create opportunities for capital deployment and portfolio re-positioning. Following the unprecedented monetary and fiscal stimulus introduced as a response to the pandemic, many growth names in the information technology and healthcare

| Meridian Funds | 5 | www.meridianfund.com |

Meridian Growth Fund

Portfolio Performance and Composition (Unaudited) (continued)

sectors experienced meteoric increases in valuation multiples that have finally begun to reset. Our focus going forward remains on companies that can not only weather the current market downturn, but also participate when the market ultimately rebounds. We believe the current correction continues to present us with opportunities to upgrade the quality of the portfolio while seeking to maintain our strict valuation discipline.

Thank you for your continued partnership with ArrowMark.

Brian Schaub & Chad Meade

Co-Portfolio Managers

The views of the author and information discussed in this commentary are as of June 30, 2022, are subject to change, and may not reflect the writer’s current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the fund or any securities or any sectors mentioned in this letter. The subject matter contained in this letter had been derived from several sources believed to be reliable and accurate at the time of compilation. To the extent permitted by federal securities laws, ArrowMark Colorado Holdings, LLC, Meridian Fund, Inc., nor the Fund accept any liability for losses either direct or consequential caused by the use of this third party information. Diversification cannot guarantee gain or prevent losses.

| Meridian Funds | 6 | www.meridianfund.com |

Meridian Growth Fund

Portfolio Performance and Composition (Unaudited) (continued)

Total Return Based on a $10,000 investment for the Period Ended June 30, 2022

This graph shows the change in value of a hypothetical investment of $10,000 in Legacy Class Shares of the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. For comparison, the same investment is shown in the indicated index.

Average Annual Total Return as of 6.30.22

| | Inception | 1 Year | 5 Year | 10 Year | Since

Inception |

| Legacy Class (MERDX) | 8/1/84 | (29.20)% | 6.16% | 9.37% | 11.69% |

| Institutional Class (MRRGX) | 12/24/14 | (29.17)% | 6.19% | — | 7.13% |

| Class A (MRAGX) w/o sales charge | 11/15/13 | (29.43)% | 5.82% | — | 7.41% |

| Class A (MRAGX) with sales charge1 | 11/15/13 | (33.49)% | 4.58% | — | 6.68% |

| Class C (MRCGX) | 7/1/15 | (29.91)% | 5.08% | — | 6.00% |

| Investor Class (MRIGX) | 11/15/13 | (29.25)% | 6.11% | — | 7.74% |

| Russell 2500® Growth Index | 8/1/84 2 | (31.81)% | 7.53% | 10.88% | N/A 3 |

| 1 | Assuming maximum sales charge, if any. Class A Shares are subject to a maximum initial sales charge of 5.75%. |

| 2 | Inception date of Legacy Class Shares. |

| 3 | Inception date of Legacy Class precedes the inception date of Russell 2500® Growth Index. |

See “Disclosures Regarding Fund Performance” on page 29 for important information regarding reported performance.

Past performance is not predictive of future performance. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares and do not reflect the imposition of a 2% redemption fee on shares held 60 days or less to deter market timers. If reflected, the taxes and fees would reduce the performance quoted. Net asset value, investment return and principal value will fluctuate, so shares, when redeemed, may be worth more or less than their original cost.

| Meridian Funds | 7 | www.meridianfund.com |

Meridian Growth Fund

Portfolio Composition (Unaudited)

Top 10 Holdings as of 6.30.22

| Ritchie Bros. Auctioneers, Inc. (Canada) | 3.3% |

| Skechers U.S.A., Inc. Class A | 3.0% |

| Frontdoor, Inc. | 3.0% |

| STERIS Plc | 3.0% |

| Ziff Davis, Inc. | 2.8% |

| ON Semiconductor Corp. | 2.6% |

| Sensata Technologies Holding Plc | 2.4% |

| Generac Holdings, Inc. | 2.1% |

| Sally Beauty Holdings, Inc. | 2.1% |

| QuidelOrtho Corp. | 2.0% |

Portfolio holdings are subject to change and may not reflect the current or future position of the portfolio. Top ten holdings excluding short-term investments are reported as a percentage of net assets.

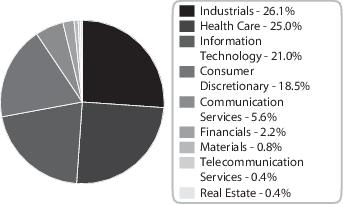

Sector Allocation as of 6.30.22

Sector allocations are subject to change and may not reflect the current or future position of the portfolio. Sector allocations are reported as a percentage of equity investments excluding cash or cash equivalents. As of period end, the Fund invested a significant portion of their assets in securities in the Industrials, Health Care and Information Technology sectors. Changes in economic conditions affecting such sectors would have a greater impact on the Fund and could affect the value, income and/or liquidity of positions in such securities.

For compliance purposes, the Fund’s industry classifications may refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine sub-classifications for reporting ease.

| Meridian Funds | 8 | www.meridianfund.com |

Meridian Contrarian Fund

Portfolio Performance and Composition (Unaudited)

Market Overview

U.S. equity markets were volatile during the 12-month period as new COVID-19 variants, global supply-chain issues, the war in Ukraine, and a rapid rise in inflation kept investors on edge. An acceleration in inflation, which climbed to a 40-year high, prompted the U.S. Federal Reserve (Fed) to end its ultra-easy monetary policy and raise interest rates 25 basis points in March, the first rate hike in more than three years. Policymakers continued their campaign against inflation in May and June, raising rates 50 basis points and 75 basis points, respectively. June’s rate hike was the largest in 28 years. In the final weeks of the period, heightened fears that rising interest rates and inflation may lead to an economic recession and weaken corporate profits continued to push equity markets lower. Although market declines were broad-based, high-growth stocks tumbled the hardest as investors shifted into stocks perceived as having more defensive qualities.

Fund Performance

The Meridian Contrarian Fund (the “Fund”) Legacy Class Shares returned -17.18% (net) for the 12-month period ended June 30, 2022, outperforming its benchmark, the Russell 2500® Index, which returned -21.00%. The Fund underperformed its secondary benchmark, the Russell 2500® Value Index, which returned -13.19%.

Our investment process seeks to identify out-of-favor companies that we believe have depressed valuations and visible catalysts for sustainable improvement. Experience has taught us that businesses with the potential for earnings growth and multiple expansion can be a powerful source of outperformance. As such, we employ a fundamental research-driven process that includes screening for companies that have multiple quarters of year-over-year earnings declines, understanding the reason for the declines, then singling out the companies we believe are poised for an earnings rebound via a cohesive turnaround plan, a new management team, or through improvements or changes to the business. The outcome of this process is a concentrated portfolio of 50-75 of our best ideas.

With a process that prioritizes the management of risk over the opportunity for return, we scrutinize the quality of each prospective investment’s business model and its valuation. Our high standards for quality require that a company have what we believe to be a durable competitive advantage, improving return on invested capital and free cash flow, as well as sustainable future earnings growth.

While we manage the Fund from the bottom up based on individual company fundamentals, we augment this by monitoring overall portfolio characteristics as part of our risk-management process. Two of our primary risk measures are beta-adjusted weight and downside capture, both of which we measure on portfolio, sector, and individual company levels. We analyze the beta-adjusted weights of portfolio holdings against the Russell 2500® Index to determine how sensitive each holding is to movement in the broader market and identify where the Fund’s risk exposure lies within the portfolio. Depending on the degree to which a stock correlates closely with market movement (high beta) or inversely to the market (low beta) we may increase or decrease the Fund’s weighting to align with the Fund’s risk parameters, as we prioritize risk before reward. Downside capture measures how much a stock goes down relative to an overall market decline, with lower capture representing lower risk. For both these measures we focus on absolute levels and changes over time. This is part of our ongoing process of recycling capital.

The three largest contributors to the Fund’s relative performance were First Horizon Corp., ON Semiconductor Corp., and APA Corp.

First Horizon Corp. is a Southeastern U.S. regional bank with significant exposure to five of the fastest-growing metro areas in the nation. It also operates one of the leading mortgage broker lending businesses. The Fund initially invested in First Horizon during the third quarter of 2020 following its merger with IBERIABANK. We believed the merger positioned First Horizon to grow earnings faster on recovery due to a combination of defensive qualities (i.e., cost reductions) and more diverse and durable lending growth and commercial fee income opportunities across the Southern U.S. At the time of the Fund’s investment, the company’s historic valuation and valuation relative to its peers was near a 10-year low, suggesting that expectations for a turnaround story had significantly diminished. However, we believed that, as a quality banking franchise located in the fastest growing U.S. region, the outlook for First Horizon was promising. The stock rallied during the first quarter of 2022 following news that First Horizon would be acquired by Canadian bank Toronto-Dominion Bank Group at a 40% premium to its stock price on February 28. In 2021 and early 2022, even before the acquisition announcement, First Horizon’s stock had been strong, with gains in line with its regional bank peers and above the Russell 2500® Index’s gains. We liquidated the Fund’s position in the stock shortly after the acquisition announcement to harvest gains from the takeout

| Meridian Funds | 9 | www.meridianfund.com |

Meridian Contrarian Fund

Portfolio Performance and Composition (Unaudited) (continued)

premium.

ON Semiconductor Corp. is a semiconductor manufacturer with a diverse product portfolio and high exposure to the attractive automotive and industrials end markets. We believe ON Semi’s exposure to the auto end market is particularly attractive, as advanced driver assistance systems and self-driving features have led to strong demand for the semiconductors that power these technologies. We believe the company is also well positioned in the industrials end market, where it benefits from low pricing pressure due to the longer lifecycle of industrials products relative to consumer products. ON continued to benefit from a global chip shortage driven by a combination of strong demand across a wide range of industries and supply chain disruptions. For the quarter ended March 31, 2022, the company reported year-over-year revenue growth of 31%, driven by the solid performance of its intelligent power and sensing solutions in the automotive and industrial end markets. We were pleased with ON’s execution during the period and are optimistic about its longer-term performance goals, however, we reduced our position in the company based on valuation.

APA Corp. is a global energy exploration and production company with operations in Egypt, the U.K., the North Sea, the U.S. Permian Basin, and Suriname, where it has made a significant oil discovery and sizeable additional discoveries are expected. We believe APA’s core global production profile is underappreciated and we view the business as defensive given the low cost to maintain and grow production. APA’s Suriname project – which is moving closer to development with partner TotalEnergies – will provide differentiated low-cost production growth in two to three years, as TotalEnergies carries the majority of the future development cost. This mix allows APA to aggressively allocate capital to pay down debt and buy back stock as opposed to allocating it to capital-intensive production growth. From June 2021 to June 2022, the stock rallied on APA’s announcement of an aggressive stock buyback plan, its increasing production growth profile, and a spike in oil prices. APA outpaced its oil exploration and production peers and the Russell 2500® Index over the period. Late in the second quarter of 2022, we reduced the Fund’s position in APA as we believe the company had largely achieved its operational improvement and financial leverage reduction goals. Exiting the period, the Fund continued to hold a smaller position in APA based on near-term low-cost production growth, aggressive capital return goals, and the differentiated future production growth potential of Suriname.

The three largest detractors from the Fund’s relative performance during the period were Heron Therapeutics, Inc., SMART Global Holdings, Inc., and Micron Technology, Inc.

Heron Therapeutics, Inc. is a biotechnology company. Its product portfolio includes two treatments for cancer patients suffering from nausea as a result of chemotherapy, both of which currently are on the market. The Fund invested in Heron due to the large market opportunity for the company’s investigational post-operative pain-management drug Zynrelef. Since the Fund’s initial investment, the FDA has approved Zynrelef for pain associated with bunion surgery, open inguinal herniorrhaphy (hernia), total knee arthroplasty, foot or ankle surgery, small-to-medium open abdominal surgery and lower extremity total joint arthroplasty surgery. Investors sent shares lower during the period after management announced a restructuring and cost-reduction plan aimed at reducing headcount by 34%. We are optimistic there is opportunity for Zynrelef to grow market share and added to the Fund’s position in the stock during the past 12 months. Notably, because Zynrelef is a non-opioid drug, it could help to stem opioid abuse.

SMART Global Holdings, Inc. is a diversified technology company with leading market positions in memory controllers, LEDs, high-performance computing (HPC), and the internet of things (IoT). The company hit a rough patch in 2019 and early 2020 when earnings declined due to a combination of volatility in its memory business caused by weakness in Brazil and inventory corrections, growth investments the company had made in new products ahead of revenue, and order delays in its HPC business. While none of these developments is particularly unusual, it is uncommon for all three to turn negative at the same time. Our investment thesis was that the company’s impressive new management team could not only smooth out some of the volatility in the business but also drive growth through superior capital allocation and organic investment. We also believed that strong secular trends were in place for memory controllers, driven by the increased importance of memory for computing speeds and increased memory content in devices, and for HPC, driven by artificial intelligence and machine learning. Smart Global’s stock traded lower during the period due to macro concerns and weakness in its Brazil segment, which is highly exposed to a slowdown in consumer demand for mobile devices and PCs. We took advantage of the downturn and increased the Fund’s position. We are comfortable with the volatility of the Brazil business as, over cycles, this segment has been a solid cash generator that helps fund investments in the strong secular growth prospects for memory controllers and HPC.

Micron Technology, Inc. is a leader in the production of DRAM and NAND memory. The Fund invested in the stock in the third quarter of 2019 during a cyclical downturn in the memory industry. Our rationale was that, while the memory industry is cyclical, we believed there are strong secular drivers in place that will lead to higher peaks and long-term growth. Our secular thesis is based on our conviction that the quest for faster computing speeds will increasingly rely on memory to solve bottlenecks and that increased memory content in nearly everything from mobile phones to automobiles will drive

| Meridian Funds | 10 | www.meridianfund.com |

Meridian Contrarian Fund

Portfolio Performance and Composition (Unaudited) (continued)

demand. Micron’s stock traded lower during the period due to macroeconomic concerns that led to lower earnings expectations. We increased the Fund’s stake in the company during the past 12 months, as we believe our secular thesis remains intact. We wanted to take advantage of what we view as temporary cyclical concerns that caused the stock to trade at less than 10x reasonable trough earnings per share (EPS) estimates and less than 7x recent peak EPS.

Outlook

Macroeconomic concerns are front and center for the markets with inflation, interest rate hikes, and recession risk overshadowing long-term company fundamentals. Although we are encouraged by some early signs suggesting that inflation may be decelerating, indications are that second-quarter earnings could be very disappointing. Against this backdrop, we will continue to look for high-quality companies at valuations that offer us an asymmetric risk/reward opportunity and prudently exploit current market conditions in seeking to make attractive long-term investments.

Thank you for your continued partnership with ArrowMark.

Jamie England

Portfolio Manager

The views of the author and information discussed in this commentary are as of June 30, 2022, are subject to change, and may not reflect the writer’s current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the fund or any securities or any sectors mentioned in this letter. The subject matter contained in this letter had been derived from several sources believed to be reliable and accurate at the time of compilation. To the extent permitted by federal securities laws, ArrowMark Colorado Holdings, LLC, Meridian Fund, Inc., nor the Fund accept any liability for losses either direct or consequential caused by the use of this third party information. Diversification cannot guarantee gain or prevent losses.

| Meridian Funds | 11 | www.meridianfund.com |

Meridian Contrarian Fund

Portfolio Performance and Composition (Unaudited) (continued)

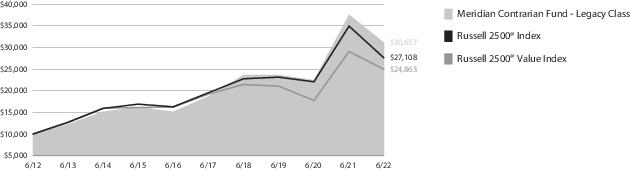

Total Return Based on a $10,000 investment for the Period Ended June 30, 2022

This graph shows the change in value of a hypothetical investment of $10,000 in Legacy Class Shares of the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. For comparison, the same investment is shown in the indicated index.

Average Annual Total Return as of 6.30.22

| | Inception | 1 Year | 5 Year | 10 Year | Since

Inception |

| Legacy Class (MVALX) | 2/10/94 | (17.18)% | 10.55% | 11.85% | 12.33% |

| Class A (MFCAX) w/o sales charge | 11/15/13 | (17.40)% | 10.16% | — | 9.06% |

| Class A (MFCAX) with sales charge1 | 11/15/13 | (22.15)% | 8.86% | — | 8.31% |

| Class C (MFCCX) | 7/1/15 | (18.01)% | 9.42% | — | 8.51% |

| Investor Class (MFCIX) | 11/15/13 | (17.21)% | 10.44% | — | 9.34% |

| Russell 2500® Index | 2/10/94 2 | (21.00)% | 7.04% | 10.49% | 9.68% |

| Russell 2500® Value Index | 2/10/94 2 | (13.19)% | 5.54% | 9.54% | 9.82% |

| 1 | Assuming maximum sales charge, if any. Class A Shares are subject to a maximum initial sales charge of 5.75%. |

| 2 | Inception date of Legacy Class Shares. |

See “Disclosures Regarding Fund Performance” on page 29 for important information regarding reported performance.

Past performance is not predictive of future performance. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares and do not reflect the imposition of a 2% redemption fee on shares held 60 days or less to deter market timers. If reflected, the taxes and fees would reduce the performance quoted. Net asset value, investment return and principal value will fluctuate, so shares, when redeemed, may be worth more or less than their original cost.

| Meridian Funds | 12 | www.meridianfund.com |

Meridian Contrarian Fund

Portfolio Composition (Unaudited)

Top 10 Holdings as of 6.30.22

| Axis Capital Holdings Ltd. | 3.8% |

| Acadia Healthcare Co., Inc. | 3.5% |

| CACI International, Inc. Class A | 3.4% |

| VICI Properties, Inc. | 3.0% |

| Change Healthcare, Inc. | 2.8% |

| First Citizens BancShares, Inc. Class A | 2.7% |

| SMART Global Holdings, Inc. | 2.6% |

| Photronics, Inc. | 2.4% |

| Molson Coors Beverage Co. Class B | 2.4% |

| Driven Brands Holdings, Inc. | 2.3% |

Portfolio holdings are subject to change and may not reflect the current or future position of the portfolio. Top ten holdings excluding short-term investments are reported as a percentage of net assets.

Sector Allocation as of 6.30.22

Sector allocations are subject to change and may not reflect the current or future position of the portfolio. Sector allocations are reported as a percentage of equity investments excluding cash or cash equivalents.

For compliance purposes, the Fund’s industry classifications may refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine sub-classifications for reporting ease.

| Meridian Funds | 13 | www.meridianfund.com |

Meridian Enhanced Equity Fund

Portfolio Performance and Composition (Unaudited)

Market Overview

Investor sentiment soured considerably during the 12-month period ended June 30, 2022, amid sustained generational highs in inflation and a boldly hawkish turn by the U.S. Federal Reserve (the “Fed”). Ongoing supply chain challenges, rising interest rates, Russia’s invasion of Ukraine, and solid wage growth all propelled prices higher, which sparked recession concerns. Many stocks absorbed double-digit losses as interest rates jumped and the U.S. Treasury yield curve flattened.

During the period, the Fed fully transformed its strategy from the accommodative approach implemented in response to the pandemic to an aggressive tightening campaign focused on taming inflation. In addition to wrapping up its pandemic-era bond-buying program, policymakers started reducing the Fed’s balance sheet and implemented the first 50-basis-point hike since 2000, followed by the first 75-basis-point increase in 28 years.

Buoyed by enduring strength in the U.S. labor market, where the unemployment rate lingered at five-decade lows, consumers kept spending through much of the period, although consumer confidence waned in its closing months. Business spending also proved relatively durable, although soaring costs and dimmed economic outlooks ultimately contributed to lowered future corporate profit expectations.

Against this backdrop, value stocks generally outperformed interest rate-sensitive growth stocks, as measured by the Russell family of U.S. indices. Stocks of all market capitalizations endured sizeable setbacks, although large cap names tended to perform better than midcap holdings, which largely outperformed small cap positions.

Fund Performance

The Meridian Enhanced Equity Fund (the “Fund”) Legacy Class Shares declined 13.52% (net) for the 12-month period ended June 30, 2022, underperforming its benchmark, the S&P 500® Index, which retreated 10.62%.

Our investment process prioritizes the management of risk over the opportunity for return. We look to build an “enduring” portfolio that can mitigate capital losses during turbulent bear market environments and offer upside participation during strong bull market environments as well. To achieve that, we seek out quality businesses maintaining considerable competitive advantages and healthy balance sheets that offer robust cash flow characteristics and muted volatility traits.

At any given time, roughly half of the Fund is invested in what we believe to be high quality, larger capitalization companies with promising growth prospects. The balance of the portfolio is invested in equities hedged in a risk-managed approach where more predictable stocks are married with options in an effort to reduce downside risks. Underlying this approach is our commitment to deep fundamental research.

Within the volatile 12-month period, leading detractors included Walt Disney Co. (The), QUALCOMM, Inc., and Liberty Broadband Corp.

Disney’s performance suffered as investor uncertainty remained around the long-term profitability of its streaming business. The sentiment overshadowed recent results featuring ongoing market share gains within the direct-to-consumer streaming offerings and a healthy rebound in park visits and revenue. While disappointed with the stock’s downturn, we intend to stay patient as we believe the company’s broad reservoir of iconic brands and related franchises provide multiple avenues for long-term value creation. In our view, the broader market continues to underestimate Disney’s franchise value and its earnings power.

A leader in the cellular communications technology industry, Qualcomm operates through a hybrid model that combines a high-margin intellectual property (“IP”) licensing business and a “fabless” semiconductor design capability. Its offerings are essential to reliable connectivity for most mobile communication networks, and we remain attracted to Qualcomm’s extensive and defensible IP portfolio, strong financial profile, and continued market share gains in a growing market. Concerns that leading smartphone producer Apple may look to replace Qualcomm’s chips with an in-house design hindered performance during the period. We, however, believe the stock price more than discounts this risk, especially given recent press reports that suggest Apple is struggling to develop an alternative. Given the stock’s seemingly forgiving valuation and the potential for an expansion of the company’s addressable market, Qualcomm remained in the Fund at period-end.

Competitive concerns and a push for investments in riskier technology upgrades dampened returns across the telecommunication services industry during the period, which weighed on Liberty Broadband. The company holds a considerable investment in Charter Communications, a leading broadband provider with dominant share across its markets. Given the resiliency of Liberty Broadband’s subscription-based broadband businesses, its robust free cash flow profile, and

| Meridian Funds | 14 | www.meridianfund.com |

Meridian Enhanced Equity Fund

Portfolio Performance and Composition (Unaudited) (continued)

the mission-critical nature of its fiber-based communications backbone, we believe the potential upside continues to outweigh any further downside. Additionally, we believe Liberty Broadband’s significantly discounted exposure to Charter provides a margin of safety.

Top individual contributors during the period included Duolingo, Inc., On Holding AG, and Ginkgo Bioworks Holdings, Inc., all of which we exited after their stock prices exceeded fundamentals. We reinvested the proceeds in an assortment of mission-critical goods and services providers who are category leaders but sustained what we believed to be overdone declines in sentiment.

With more than 500 million downloads of its software worldwide, Duolingo is a leading language learning platform. It offers courses in 40 different languages, and we were attracted to the company’s success at reducing barriers to access and learning, the efficiency and affordability facilitated by its mobile app, and the fun inherent in its gamification of content. A digital native company, Duolingo fit well within our strategy of finding companies that are successfully using emerging technology to change legacy systems and industries. Early in the 12-month period, the company went public and reported impressive quarterly results, but in the wake of the stock’s subsequent sharp rise and implications for valuation, the Fund sold out of the position.

Similarly, the stock of Switzerland-based On Holding jumped as it went public early in the period and the Fund was rewarded for its participation in the IPO. Our interest in this developer of high-performance athletic shoes was rooted in a deep appreciation for the brand, which is highly regarded in the running community, and a founder-led culture that prioritizes innovation, which tends to lead to technically superior products. Yet, when its valuation exceeded our target, we liquidated the Fund’s stake.

Ginkgo Bioworks rallied after merging with a special purpose acquisition company in the fall of 2021 and the Fund similarly exited the holding when we believed the price was no longer justified by the fundamentals. Ginkgo is a leader in the emerging field of synthetic biology, in which cells are programmed to design, test, and build better products. Synthetic biology applications already drive innovation across the food, fragrance, and pharmaceutical markets, and since we believe Ginkgo will continue to be a key partner in the space, we are monitoring its progress.

Outlook

Looking ahead, we don’t anticipate the path will get any smoother in the coming quarters. Inflation is poised to remain elevated across a broad swath of the economy, which will likely prompt further monetary tightening by the Fed. Geopolitical risks, particularly in Ukraine, remain front of mind, especially in energy markets, which are further hamstrung by structural challenges due to years of underinvestment, and in food supplies, which are seeing material shifts on the supply side. The likelihood of a recession or stagflation has expanded as consumers contend with the competing pressures of the tightening money supply and higher prices on services and goods, especially staples.

Admittedly, our outlook is relatively uninspiring, but we believe that out of volatility, opportunity is born. We typically look to capitalize on market disruptions by buying high-quality businesses that we believe will compound value over the long-term. Regardless of whether conditions are good or poor, we stick to our playbook and prudently work to manage risk by leveraging deep fundamental company-level research rather than macroeconomic assessments. Meanwhile, our charge remains to prioritize risk over return, even if that means trading some incremental market upside for downside protection. Through the combination of stock selection and our covered call strategy, we believe our disciplined and conservative approach to deploying capital is ideal for a market that still appears to have gotten ahead of economic realities.

Thank you for your continued partnership with ArrowMark.

Clay Freeman

Portfolio Manager

The views of the author and information discussed in this commentary are as of June 30, 2022, are subject to change, and may not reflect the writer’s current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the fund or any securities or any sectors mentioned in this letter. The subject matter contained in this letter had been derived from several sources believed to be reliable and accurate at the time of compilation. To the extent permitted by federal securities laws,

| Meridian Funds | 15 | www.meridianfund.com |

Meridian Enhanced Equity Fund

Portfolio Performance and Composition (Unaudited) (continued)

ArrowMark Colorado Holdings, LLC, Meridian Fund, Inc., nor the Fund accept any liability for losses either direct or consequential caused by the use of this third party information. Diversification cannot guarantee gain or prevent losses.

| Meridian Funds | 16 | www.meridianfund.com |

Meridian Enhanced Equity Fund

Portfolio Performance and Composition (Unaudited) (continued)

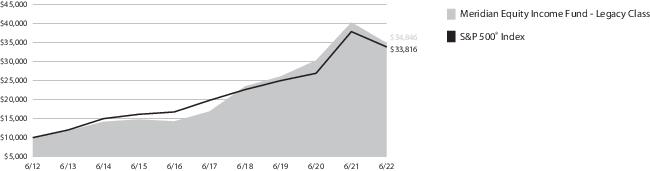

Total Return Based on a $10,000 investment for the Period Ended June 30, 2022

This graph shows the change in value of a hypothetical investment of $10,000 in Legacy Class Shares of the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. For comparison, the same investment is shown in the indicated index.

Average Annual Total Return as of 6.30.22

| | Inception | 1 Year | 5 Year | 10 Year | Since

Inception |

| Legacy Class (MEIFX) | 1/31/05 | (13.52)% | 15.54% | 13.30% | 9.49% |

| Class A (MRAEX) w/o sales charge | 11/15/13 | (13.80)% | 15.15% | — | 11.47% |

| Class A (MRAEX) with sales charge1 | 11/15/13 | (18.77)% | 13.80% | — | 10.70% |

| Class C (MRCEX) | 7/1/15 | (14.23)% | 14.66% | — | 12.05% |

| Investor Class (MRIEX) | 11/15/13 | (13.55)% | 15.46% | — | 11.75% |

| S&P 500® Index | 1/31/05 2 | (10.62)% | 11.31% | 12.96% | 9.10% |

| 1 | Assuming maximum sales charge, if any. Class A Shares are subject to a maximum initial sales charge of 5.75%. |

| 2 | Inception date of Legacy Class Shares. |

See “Disclosures Regarding Fund Performance” on page 29 for important information regarding reported performance.

Past performance is not predictive of future performance. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares and do not reflect the imposition of a 2% redemption fee on shares held 60 days or less to deter market timers. If reflected, the taxes and fees would reduce the performance quoted. Net asset value, investment return and principal value will fluctuate, so shares, when redeemed, may be worth more or less than their original cost.

| Meridian Funds | 17 | www.meridianfund.com |

Meridian Enhanced Equity Fund

Portfolio Composition (Unaudited)

Top 10 Holdings as of 6.30.22

| Lamb Weston Holdings, Inc. | 8.2% |

| ON Semiconductor Corp. | 6.4% |

| Zoom Video Communications, Inc. Class A | 5.2% |

| Wells Fargo & Co. | 4.9% |

| Coty, Inc. Class A | 4.9% |

| CoStar Group, Inc. | 4.7% |

| Maxar Technologies, Inc. | 4.0% |

| Sally Beauty Holdings, Inc. | 4.0% |

| Spectrum Brands Holdings, Inc. | 3.2% |

| Dole Plc | 3.1% |

Portfolio holdings are subject to change and may not reflect the current or future position of the portfolio. Top ten holdings excluding short-term investments and options written are reported as a percentage of net assets.

Sector Allocation as of 6.30.22

Sector allocations are subject to change and may not reflect the current or future position of the portfolio. Sector allocations are reported as a percentage of equity investments excluding cash or cash equivalents. As of period end, the Fund invested a significant portion of their assets in securities in the Information Technology sector. Changes in economic conditions affecting such sector would have a greater impact on the Fund and could affect the value, income and/or liquidity of positions in such securities.

For compliance purposes, the Fund’s industry classifications may refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine sub-classifications for reporting ease.

| Meridian Funds | 18 | www.meridianfund.com |

Meridian Small Cap Growth Fund

Portfolio Performance and Composition (Unaudited)

Market Overview

U.S. equity markets were volatile during the 12-month period as new COVID-19 variants, global supply-chain issues, the war in Ukraine, and a rapid rise in inflation kept investors on edge. An acceleration in inflation, which climbed to a 40-year high, prompted the U.S. Federal Reserve (Fed) to end its ultra-easy monetary policy and raise interest rates 25 basis points in March, the first rate hike in more than three years. Policymakers continued their campaign against inflation in May and June, raising rates 50 basis points and 75 basis points, respectively. June’s rate hike was the largest in 28 years. In the final weeks of the period, heightened fears that rising interest rates and inflation may lead to an economic recession and weaken corporate profits continued to push equity markets lower.

Against this backdrop, large cap stocks outperformed small caps, according to the Russell indices. From a style perspective, value stocks outperformed growth stocks across capitalization categories.

Fund Performance

The Meridian Small Cap Growth Fund (the “Fund”) Legacy Class Shares returned -32.39% (net) for the 12-month period ended June 30, 2022, outperforming its benchmark, the Russell 2000® Growth Index, which returned -33.43%.

The index decline was broad-based with all sectors except for energy and utilities declining during the period. Notable underperformers included the communication services, information technology, and consumer discretionary sectors, which were all down in excess of 30%.

Our investment process prioritizes the management of risk over the opportunity for return. We look to build an “enduring” portfolio that can mitigate capital losses during turbulent bear market environments and, secondarily, participate in the upside during strong market environments. This strategy proved effective during the 12-month period, which was exceptionally volatile and included 40 days of 2% or greater declines in Index performance. The Fund outperformed on all but two of these days.

During the period, the Fund benefitted from positive stock selection in the information technology and materials sectors. In addition, an overweight position in the industrials sector aided performance, as industrials was one of the top performing sectors in the index. We maintained the Fund’s overweight to industrials given our focus on commercial and professional service companies, which tend to exhibit strong competitive advantages and generally less macro sensitivity than the broader sector. Conversely, select healthcare holdings detracted from relative performance, as several names declined materially. Market factors were generally mixed, although larger cap names within the index continued to outperform smaller cap names, creating a headwind for performance.

Market volatility provided us with the opportunity to establish positions in several high-quality growth companies that we believe had declined to attractive levels during the period. In particular, we took advantage of lower valuation multiples for select information technology and healthcare companies. While we are excited about the significant decline in valuations in both of these sectors, we are seeking to be prudent with position sizes in the event multiples contract even further from here. We believe the types of companies we invest in (strong balance sheets, recurring revenue streams, large and growing addressable markets), will create shareholder value over longer periods of time.

The three largest contributors to the Fund's relative performance during the period were Hudson Technologies, Inc., Echo Global Logistics, Inc., and Mimecast Ltd.

Hudson Technologies, Inc. is the market leader in recycled and reclaimed refrigerants with proprietary reclamation technology and a national distribution network. We have owned shares of the company for several years due to our belief that its leading position would allow the company to capitalize on improving supply-demand dynamics from the Environmental Protection Agency’s (EPA’s) phaseout of R-22 (refrigerant used in air conditioners). The phaseout concluded in 2020 and virgin R-22 is no longer being produced. This has resulted in strong refrigerant pricing given stable demand and more limited supply. As a result, overall fundamentals have accelerated which resulted in 150% revenue growth and 45% operating margins in its most recent quarter. We are optimistic that another catalyst for growth is the AIM Act to reduce the production of hydrofluorocarbons (HFCs). Similar to the phaseout of R-22, we believe this will result in strong supply-demand dynamics for reclaimed HFC refrigerants and allow Hudson to capitalize on its market-leading position. During the period, we trimmed our position in the stock.

Echo Global Logistics, Inc. is an asset-light transportation company providing technology-enabled transportation and

| Meridian Funds | 19 | www.meridianfund.com |

Meridian Small Cap Growth Fund

Portfolio Performance and Composition (Unaudited) (continued)

supply chain management solutions. We believe Echo’s proprietary technology platforms for truckload quoting and transit times fulfill a growing need within the commercial trucking industry. By helping link supply and demand between smaller shippers and carriers, Echo’s solutions enable both parties to increase productivity and efficiency. As a result, smaller carriers can reduce the number of empty miles and improve profitability while shippers can gain access to a significant amount of trucking capacity among smaller carriers. The company’s stock soared during the period after The Jordan Company, a private equity firm, offered to buy Echo at more than a 50% premium to its stock price. The acquisition was completed in November, and we were pleased to see our investment thesis validated.

Mimecast Ltd. is a cybersecurity firm focused primarily on email security. One of the things that initially attracted us to Mimecast was its email threat intelligence, which we believe is more robust than that of many of its competitors. This intelligence enables the company to capture and quarantine a higher number of harmful emails while avoiding capturing and quarantining emails that are benevolent. Demand for cybersecurity solutions, particularly among large enterprises, continues to rise, adding to our excitement for cybersecurity firms in general and Mimecast in particular. We took advantage of an opportunity to build a position in the stock after concerns about a security breach temporarily depressed Mimecast’s share price. Our research indicated the breach impacted a limited number of existing customers and that demand from new customers remained robust. During the period, the stock rallied after Mimecast announced that private equity firm Permira had made an offer to buy it at a premium to its stock price. The deal closed in the first half of 2022.

The three largest detractors from the Fund’s relative performance during the period were 2U, Inc., 8x8, Inc., and Momentive Global, Inc.

2U, Inc. is an educational technology firm that partners with leading nonprofit colleges and universities to offer online degree programs. The company possesses many of the qualities that we believe define a good business, including long-term contracts and recurring revenue; attractive unit economics that should deliver strong EBITDA margins at scale; and strong brand recognition with marquee university partners to drive continued growth. Unfortunately, headwinds from 2U’s recent acquisition of online course provider edX and incremental losses associated with the merger have resulted in a reduced outlook for the company’s 2022 profits. Further pressuring the stock during the past 12 months was weaker demand for higher education degrees due to a tight labor market and high marketing and sales costs to attract new students. We are closely monitoring the Fund’s holding in 2U and trimmed the Fund’s position in the stock during the period.

8x8, Inc. is a cloud communications provider that offers businesses a unified voice, contact center, video, and chat platform. The company hired a new CEO in late 2020 who has since refocused the company on areas of the market where 8x8 has competitive advantages and the potential to earn higher margins. In conjunction with this change in strategy, the company exited low-growth and low-margin product lines, which has led to what we believe is a temporary slowdown in revenue growth. A recent acquisition that depleted 8x8’s cash position also weighed on investor sentiment. We believe the company will overcome these short-term issues and that, at its current price, the stock is attractively valued. We are willing to be patient as the company works through these setbacks and added to the Fund’s position in the stock during the period.

Momentive Global, Inc. develops survey software that enables organizations to collect and analyze feedback and insights. Its most recognized brand is the online survey tool SurveyMonkey. Momentive offers customers a free, self-service software solution and then applies an upsell strategy to convert customers to a more robust, paid version of the product. By investing profits from this self-service business into its enterprise-grade product, Momentive has been able to build an enterprise business that now makes up 35% of total revenues. During the period, the stock declined due mostly to continued disappointment that the Zendesk acquisition was voted down, and that no other potential suitors have subsequently expressed interest. Additionally, there is some level of concern that a slower pace of investment spending will negatively impact revenue growth in future quarters, and that an economic downturn could impact spending on surveys to a larger degree than it will on other segments of software. We believe Momentive will continue to generate a healthy combination of growth and profitability going forward, even during a potential downturn. We also believe the company’s relatively nascent enterprise business can take share in a downturn owing to its position as the low-cost survey solution. During the period, we trimmed the Fund’s position in Momentive Global.

Outlook

After raising interest rates 150 basis points in the first half of 2022 and indicating that additional rate increases may be needed, it is clear that Federal Reserve policymakers have become increasingly certain that aggressive action is necessary to tame inflation. They also appear more willing to accept the risk of an economic slowdown in exchange for aggressive monetary tightening and lower inflationary pressures. As a result, investors are wary of potential demand destruction and other consequences the broader economy may suffer in the coming months.

| Meridian Funds | 20 | www.meridianfund.com |

Meridian Small Cap Growth Fund

Portfolio Performance and Composition (Unaudited) (continued)

As the Federal Reserve embarks on its tightening path, we expect volatility to increase which we believe will create opportunities for capital deployment and portfolio re-positioning. Following the unprecedented monetary and fiscal stimulus introduced as a response to the pandemic, many growth names in the information technology and healthcare sectors experienced meteoric increases in valuation multiples that have finally begun to reset. Our focus going forward remains on companies that can not only weather the current market downturn, but also participate when the market ultimately rebounds. We believe the current correction continues to present us with opportunities to upgrade the quality of the portfolio while seeking to maintain our strict valuation discipline.

Thank you for your continued partnership with ArrowMark.

Brian Schaub & Chad Meade

Co-Portfolio Managers

The views of the author and information discussed in this commentary are as of June 30, 2022, are subject to change, and may not reflect the writer’s current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the fund or any securities or any sectors mentioned in this letter. The subject matter contained in this letter had been derived from several sources believed to be reliable and accurate at the time of compilation. To the extent permitted by federal securities laws, ArrowMark Colorado Holdings, LLC, Meridian Fund, Inc., nor the Fund accept any liability for losses either direct or consequential caused by the use of this third party information. Diversification cannot guarantee gain or prevent losses.

| Meridian Funds | 21 | www.meridianfund.com |

Meridian Small Cap Growth Fund

Portfolio Performance and Composition (Unaudited) (continued)

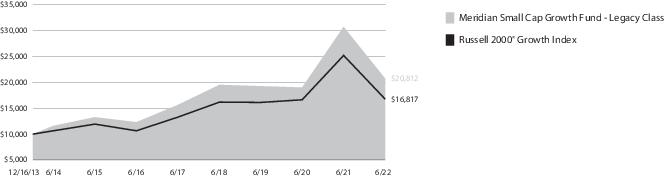

Total Return Based on a $10,000 investment for the Period Ended June 30, 2022

This graph shows the change in value of a hypothetical investment of $10,000 in Legacy Class Shares of the Fund over the past 10 years (or for the life of the Fund if shorter). Performance calculations are as of the end of June each year. For comparison, the same investment is shown in the indicated index.

Average Annual Total Return as of 6.30.22

| | Inception | 1 Year | 5 Year | Since

Inception |

| Legacy Class (MSGGX) | 12/16/13 | (32.39)% | 5.80% | 8.96% |

| Institutional Class (MSGRX) | 12/24/14 | (32.36)% | 5.86% | 7.05% |

| Class A (MSGAX) w/o sales charge | 12/16/13 | (32.63)% | 5.44% | 8.60% |

| Class A (MSGAX) with sales charge1 | 12/16/13 | (36.51)% | 4.20% | 7.85% |

| Class C (MSGCX) | 7/1/15 | (33.10)% | 4.71% | 5.51% |

| Investor Class (MISGX) | 12/16/13 | (32.44)% | 5.70% | 8.89% |

| Russell 2000® Growth Index | 12/16/13 2 | (33.43)% | 4.80% | 6.28% |

| 1 | Assuming maximum sales charge, if any. Class A Shares are subject to a maximum initial sales charge of 5.75%. |

| 2 | Inception date of Legacy Class Shares. |

See “Disclosures Regarding Fund Performance” on page 29 for important information regarding reported performance.

Past performance is not predictive of future performance. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares and do not reflect the imposition of a 2% redemption fee on shares held 60 days or less to deter market timers. If reflected, the taxes and fees would reduce the performance quoted. Net asset value, investment return and principal value will fluctuate, so shares, when redeemed, may be worth more or less than their original cost.

| Meridian Funds | 22 | www.meridianfund.com |

Meridian Small Cap Growth Fund

Portfolio Composition (Unaudited)

Top 10 Holdings as of 6.30.22

| Heritage-Crystal Clean, Inc. | 3.4% |

| Ritchie Bros. Auctioneers, Inc. (Canada) | 3.3% |

| Frontdoor, Inc. | 3.1% |

| Skechers U.S.A., Inc. Class A | 2.9% |

| QuidelOrtho Corp. | 2.1% |

| Sally Beauty Holdings, Inc. | 2.1% |

| Matson, Inc. | 1.8% |

| Merit Medical Systems, Inc. | 1.8% |

| Forward Air Corp. | 1.7% |

| Hudson Technologies, Inc. | 1.5% |

Portfolio holdings are subject to change and may not reflect the current or future position of the portfolio. Top ten holdings excluding short-term investments are reported as a percentage of net assets.

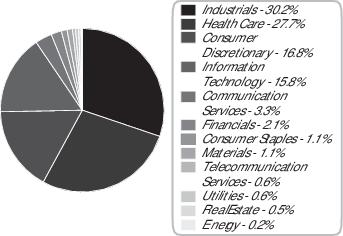

Sector Allocation as of 6.30.22

Sector allocations are subject to change and may not reflect the current or future position of the portfolio. Sector allocations are reported as a percentage of equity investments excluding cash or cash equivalents. As of period end, the Fund invested a significant portion of their assets in securities in the Industrials and Health Care sectors. Changes in economic conditions affecting such sectors would have a greater impact on the Fund and could affect the value, income and/or liquidity of positions in such securities.

For compliance purposes, the Fund’s industry classifications may refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine sub-classifications for reporting ease.

| Meridian Funds | 23 | www.meridianfund.com |

Meridian Fund, Inc.

Expense Disclosure

June 30, 2022 (Unaudited)

Disclosures Regarding Fund Expenses

Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and (2) ongoing costs, including management fees; service and distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period of January 1, 2022 through June 30, 2022.

Actual Expenses

The first table below provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (e.g., an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number reported under “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption fees. Therefore, the second table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Meridian Funds | 24 | www.meridianfund.com |

Meridian Growth Fund

Fund Expenses

June 30, 2022 (Unaudited)

Expense Example

| Actual | Annualized

Expense Ratio | Beginning Account

Value January 1, 2022 | Ending Account Value

June 30, 2022 | Expenses Paid During

the Period 1 |

| Legacy Class (MERDX) | 0.87% | $1,000.00 | $710.70 | $3.69 |

| Institutional Class (MRRGX) | 0.83% | $1,000.00 | $710.70 | $3.52 |

| Class A (MRAGX) | 1.17% | $1,000.00 | $709.40 | $4.96 |

| Class C (MRCGX) | 1.87% | $1,000.00 | $707.10 | $7.92 |

| Investor Class (MRIGX) | 0.92% | $1,000.00 | $710.40 | $3.90 |

| Hypothetical 2 | Annualized

Expense Ratio | Beginning Account

Value January 1, 2022 | Ending Account Value

June 30, 2022 | Expenses Paid During

the Period 1 |

| Legacy Class (MERDX) | 0.87% | $1,000.00 | $1,020.48 | $4.36 |

| Institutional Class (MRRGX) | 0.83% | $1,000.00 | $1,020.68 | $4.16 |

| Class A (MRAGX) | 1.17% | $1,000.00 | $1,018.99 | $5.86 |

| Class C (MRCGX) | 1.87% | $1,000.00 | $1,015.52 | $9.35 |

| Investor Class (MRIGX) | 0.92% | $1,000.00 | $1,020.23 | $4.61 |

| 1 | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by 181 days, the number of days in the most recent fiscal half-year, then divided by 365. |

| 2 | Hypothetical 5% return before expenses. |

The above “Annualized Expense Ratios” reflect waivers and/or reimbursements of expenses by the Fund’s Adviser. Such waivers and/or reimbursements may not be withdrawn earlier than one year after the date of the current prospectus. The “Financial Highlights” included within the Fund’s financial statements shows the gross expense ratios for each share class.

See “Disclosure Regarding Fund Expenses” on page 24 for further information on how the above examples were calculated.

| Meridian Funds | 25 | www.meridianfund.com |

Meridian Contrarian Fund

Fund Expenses

June 30, 2022 (Unaudited)

Expense Example

| Actual | Annualized

Expense Ratio | Beginning Account

Value January 1, 2022 | Ending Account Value

June 30, 2022 | Expenses Paid During

the Period 1 |

| Legacy Class (MVALX) | 1.14% | $1,000.00 | $790.90 | $5.06 |

| Class A (MFCAX) | 1.46% | $1,000.00 | $789.90 | $6.48 |

| Class C (MFCCX) | 2.21% | $1,000.00 | $786.90 | $9.79 |

| Investor Class (MFCIX) | 1.19% | $1,000.00 | $790.70 | $5.28 |

| Hypothetical 2 | Annualized

Expense Ratio | Beginning Account

Value January 1, 2022 | Ending Account Value

June 30, 2022 | Expenses Paid During

the Period 1 |

| Legacy Class (MVALX) | 1.14% | $1,000.00 | $1,019.14 | $ 5.71 |

| Class A (MFCAX) | 1.46% | $1,000.00 | $1,017.55 | $ 7.30 |

| Class C (MFCCX) | 2.21% | $1,000.00 | $1,013.84 | $11.04 |

| Investor Class (MFCIX) | 1.19% | $1,000.00 | $1,018.89 | $ 5.96 |

| 1 | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by 181 days, the number of days in the most recent fiscal half-year, then divided by 365. |

| 2 | Hypothetical 5% return before expenses. |

The above “Annualized Expense Ratios” reflect waivers and/or reimbursements of expenses by the Fund’s Adviser. Such waivers and/or reimbursements may not be withdrawn earlier than one year after the date of the current prospectus. The “Financial Highlights” included within the Fund’s financial statements shows the gross expense ratios for each share class.

See “Disclosure Regarding Fund Expenses” on page 24 for further information on how the above examples were calculated.

| Meridian Funds | 26 | www.meridianfund.com |

Meridian Enhanced Equity Fund

Fund Expenses

June 30, 2022 (Unaudited)

Expense Example

| Actual | Annualized

Expense Ratio | Beginning Account

Value January 1, 2022 | Ending Account Value

June 30, 2022 | Expenses Paid During

the Period 1 |

| Legacy Class (MEIFX) | 1.21% | $1,000.00 | $828.90 | $5.49 |

| Class A (MRAEX) | 1.56% | $1,000.00 | $827.40 | $7.07 |

| Class C (MRCEX) | 2.00% | $1,000.00 | $825.80 | $9.05 |

| Investor Class (MRIEX) | 1.20% | $1,000.00 | $828.50 | $5.44 |

| Hypothetical 2 | Annualized

Expense Ratio | Beginning Account

Value January 1, 2022 | Ending Account Value

June 30, 2022 | Expenses Paid During

the Period 1 |

| Legacy Class (MEIFX) | 1.21% | $1,000.00 | $1,018.79 | $6.06 |

| Class A (MRAEX) | 1.56% | $1,000.00 | $1,017.06 | $7.80 |

| Class C (MRCEX) | 2.00% | $1,000.00 | $1,014.88 | $9.99 |

| Investor Class (MRIEX) | 1.20% | $1,000.00 | $1,018.84 | $6.01 |

| 1 | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by 181 days, the number of days in the most recent fiscal half-year, then divided by 365. |

| 2 | Hypothetical 5% return before expenses. |

The above “Annualized Expense Ratios” reflect waivers and/or reimbursements of expenses by the Fund’s Adviser. Such waivers and/or reimbursements may not be withdrawn earlier than one year after the date of the current prospectus. The “Financial Highlights” included within the Fund’s financial statements shows the gross expense ratios for each share class.

See “Disclosure Regarding Fund Expenses” on page 24 for further information on how the above examples were calculated.

| Meridian Funds | 27 | www.meridianfund.com |

Meridian Small Cap Growth Fund

Fund Expenses

June 30, 2022 (Unaudited)

Expense Example

| Actual | Annualized

Expense Ratio | Beginning Account

Value January 1, 2022 | Ending Account Value

June 30, 2022 | Expenses Paid During

the Period 1 |

| Legacy Class (MSGGX) | 1.18% | $1,000.00 | $724.30 | $5.04 |

| Institutional Class (MSGRX) | 1.10% | $1,000.00 | $724.60 | $4.70 |

| Class A (MSGAX) | 1.50% | $1,000.00 | $723.10 | $6.41 |

| Class C (MSGCX) | 2.18% | $1,000.00 | $720.40 | $9.30 |

| Investor Class (MISGX) | 1.25% | $1,000.00 | $723.90 | $5.34 |

| Hypothetical 2 | Annualized

Expense Ratio | Beginning Account

Value January 1, 2022 | Ending Account Value

June 30, 2022 | Expenses Paid During

the Period 1 |

| Legacy Class (MSGGX) | 1.18% | $1,000.00 | $1,018.94 | $ 5.91 |

| Institutional Class (MSGRX) | 1.10% | $1,000.00 | $1,019.34 | $ 5.51 |

| Class A (MSGAX) | 1.50% | $1,000.00 | $1,017.36 | $ 7.50 |

| Class C (MSGCX) | 2.18% | $1,000.00 | $1,013.98 | $10.89 |

| Investor Class (MISGX) | 1.25% | $1,000.00 | $1,018.60 | $ 6.26 |

| 1 | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by 181 days, the number of days in the most recent fiscal half-year, then divided by 365. |

| 2 | Hypothetical 5% return before expenses. |

The above “Annualized Expense Ratios” reflect waivers and/or reimbursements of expenses by the Fund’s Adviser. Such waivers and/or reimbursements may not be withdrawn earlier than one year after the date of the current prospectus. The “Financial Highlights” included within the Fund’s financial statements shows the gross expense ratios for each share class.

See “Disclosure Regarding Fund Expenses” on page 24 for further information on how the above examples were calculated.

| Meridian Funds | 28 | www.meridianfund.com |

Meridian Fund, Inc.

Performance Disclosure

June 30, 2022 (Unaudited)

Disclosures Regarding Fund Performance

Past performance is not predictive of future performance. Current performance may be lower or higher than the quoted past performance. Reported performance assumes reinvestment of Fund distributions. Reported performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares, nor does it reflect the 2% redemption fee on shares sold within 60 days of original purchase date. If reflected, the taxes and fees would reduce the performance quoted. Net asset value, investment return and principal value will fluctuate, so shares, when redeemed, may be worth more or less than their original cost. You can obtain the most current month-end performance at www.meridianfund.com.

Performance prior to September 5, 2013 reflects each Fund’s performance under the management of Aster Investment Management Co.

Legacy class shares are no longer offered to the public effective March 1, 2014, except under certain limited circumstances.

Investor Class, Class A, and Class C Shares of the Meridian Growth Fund are closed to new investors effective June 15, 2017. Existing investors may continue to purchase shares.

Investor Class, Class A, and Class C Shares of the Meridian Small Cap Growth Fund are closed to new investors effective June 29, 2018. Existing investors may continue to purchase shares.

Indices are typically unmanaged, and do not reflect deductions for fees or expenses. You cannot invest directly in an index.

Investors should consider the investment objective and policies, risk considerations, charges and ongoing expenses of an investment carefully before investing. The prospectus contains this and other information relevant to an investment in any of the Meridian Funds. Please read the prospectus carefully before you invest. To obtain a prospectus, please contact your investment representative or the Funds' transfer agent at 800.446.6662 or access our website at www.meridianfund.com.

| Meridian Funds | 29 | www.meridianfund.com |

Meridian Growth Fund

Schedule of Investments

June 30, 2022

| | Shares | Value |

| Common Stocks - 95.0% |

| Communication Services - 4.5% |

| Interactive Media & Services - 4.5% |

| Cargurus, Inc.1 | 329,018 | $ 7,070,597 |

| Ziff Davis, Inc.1,2 | 537,370 | 40,050,186 |

| ZipRecruiter, Inc. Class A1,2 | 1,136,827 | 16,847,776 |

| Total Communication Services | | 63,968,559 |