UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-04087

Manning & Napier Fund, Inc.

(Exact name of registrant as specified in charter)

| | |

| 290 Woodcliff Drive, Fairport, NY | | 14450 |

| (Address of principal executive offices) | | (Zip Code) |

B. Reuben Auspitz 290 Woodcliff Drive, Fairport, NY 14450

(Name and address of agent for service)

Registrant’s telephone number, including area code: 585-325-6880

Date of fiscal year end: December 31, 2007

Date of reporting period: January 1, 2007 through December 31, 2007

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

| ITEM 1: | REPORTS TO STOCKHOLDERS |

Manning & Napier Fund, Inc.

| | | | |

| CORE BOND SERIES | | | | | Annual Report - December 31, 2007 |

Management Discussion and Analysis (unaudited)

Dear Shareholders:

It would be a bit of an understatement to describe 2007 as an “eventful” year; it was a wild ride during which fixed income investors were buffeted by a number of factors. “Subprime”, a relatively obscure term, entered the everyday vernacular. Securities that were thought to be rated “AAA” turned out not to be. There were high profile disasters as well as conservative success stories. And, as always seems to be the case, the Federal Reserve (the “Fed”) once again played a prominent role.

Given the added risk associated with corporate bonds and mortgage-backed bonds, they traditionally carry higher yields when compared to similar maturity U.S. Treasury securities. That difference is called the “credit spread” when referring to corporate bonds, and the “pre-payment spread” when referring to pass-through securities such as mortgage-backed bonds. Over the long-term, those spreads have allowed corporate bonds and mortgage-backed bonds to generate higher total returns than U.S. Treasuries. That tendency led to the activation of the Core Bond Series back in April of 2005.

Unfortunately in 2007, the credit/pre-payment spreads associated with those securities widened; U.S. Treasury yields moved sharply lower last year while yields in the mortgage-backed sector were only slightly lower and corporate yields were slightly higher. As a result mortgage-backed and corporate bond investors did earn their coupons, plus in many instances a modest capital gain, but those returns failed to keep up with the returns of the U.S. Treasury market. The fact that the Core Bond Series concentrates its investments in spread investments worked against the Series last year, so it underperformed relative to its benchmark, which includes a significant U.S. Treasury and Agency component.

As for specifics, the yield on the market-weighted U.S. Treasury index dropped from 4.87% to 3.66%. The biggest declines were on the short-end of the yield curve where yields on bonds with 2-year maturities fell 176 basis points (1.76%), starting the year at 4.81% and finishing it at 3.05%; long-term U.S. Treasury rates dropped from 4.81% to 4.45%, a 36 basis point (0.36%) decline. As for the mortgage-backed market, the yield on that index fell 34 basis points (0.34%), from 5.66% to 5.32%; the yield on the corporate index moved higher, rising from 5.70% to 5.81%.

The first quarter of the year was relatively quiet since the economic releases were relatively mixed. On the good side, unemployment was down to 4.4% in March, payroll growth was still relatively robust, and the 4-week average of initial claims for unemployment insurance was drifting lower. Unfortunately, the good news in the labor markets was offset by the bad news in the housing sector; it remained under duress, and it started to become apparent that the hoped for bottom of the housing market was still quite a ways off.

During the second quarter of the year, rates on short- and long-term bonds began to move in opposite directions, reflecting two distinct factors. On the short-end of the yield curve, a significant change in the market’s supply/demand dynamics pushed rates lower. A shrinking Federal deficit mitigates the Treasury’s borrowing needs, which in turn shrinks the supply of U.S. Treasury Bills, while foreign central banks began paring back their longer-term U.S. Treasury purchases, focusing instead on U.S. Treasury Bills. The combination of a shrinking supply and increased demand pushed short-term U.S. Treasury rates lower. On the intermediate-to-long end of the yield curve, rates rose due to a marked change in the market’s expectations about monetary policy and the rate of economic growth. As we moved into the summer, a number of the economic releases suggested that the rate of economic growth was picking back up. At the same time, the Fed started to hedge when it came to defining what it considered to be an acceptable rate of inflation. The markets responded by re-adjusting intermediate-to-longer term interest rates higher.

Market psychology definitely changed during the third quarter of the year and the precipitous drop in interest rates began, triggered by a flight to quality and a reassessment of the trajectory of Fed policy. While the problems in the market for subprime mortgage loans were well known prior to the third quarter, the collapse of two high profile hedge funds at Bear Stearns along with a couple of European bank announcements revealed the first set of identifiable

Management Discussion and Analysis (unaudited)

victims. That caused investors to exit and/or avoid anything remotely tied to the subprime sector. The proceeds were parked in the perceived safest, most liquid alternative, specifically short-term U.S. Treasury instruments.

Given the financial dislocations caused by this flight to quality, both the Fed and European central banks responded by injecting liquidity into the financial system. The Fed began by cutting the discount rate (the rate charged to banks to borrow reserves directly from the Fed), and followed that initial move with a cut in the Fed Funds target (the rate charged by banks to borrow reserves from each other). Cutting the targeted Fed Funds rate was not only a response to the liquidity concerns associated with a flight to quality, but also a response to a weakening labor market.

During the fourth quarter there were two additional policy moves enacted by the Fed. It followed up its 50 basis point cut in September with 25 basis point cuts in October and December. The Fed and the markets were both responding to the headwinds that continued to buffet the U.S. economy. The housing sector continued to sink with new home sales dropping 50% from their highs, existing home sales down one-third, and home prices posting year-over-year declines, a decidedly rare occurrence. What was more troubling was the fact that the problems in the housing sector appeared to have spilled over into other sectors of the economy. Job growth had slowed and the unemployment rate had risen to 5.0%, a level not seen since the end of 2005. At some point that should affect income growth, which had been remarkably robust. It was not just the consumer sector that troubled the market; the manufacturing sector appeared to be weakening as well.

Given the economic headwinds, credit concerns rose. In addition, the corporate bond market is dominated by financial issuers, one of the sectors most impacted by the subprime mess. As was mentioned, credit spreads widened quite dramatically. As for the mortgage-backed sector, its spreads typically widen when interest rate volatility picks up; that was definitely the case in 2007, and pre-payment spreads widened.

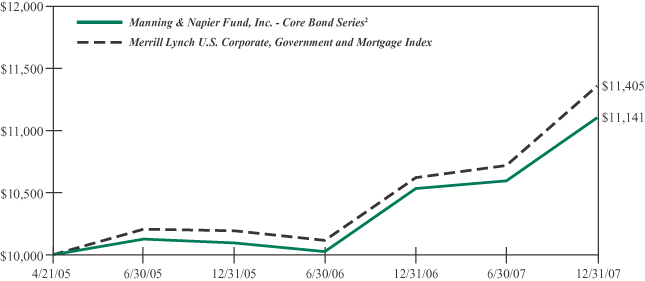

As for the performance of the Core Bond Series in 2007, its total return was 5.58%. That lagged the Merrill Lynch U.S. Corporate, Government & Mortgage Index (which includes all U.S. Treasury, U.S. Agency, investment-grade corporate bonds, and plain vanilla mortgage-backed securities with maturities of more than one year), which returned 7.17% in 2007. The underperformance can be traced primarily to the strong performance of U.S. Treasury market, which we believe to be a short-term phenomenon.

We appreciate your business and wish you all the very best in the coming year.

Sincerely,

Manning & Napier Advisors, Inc.

Performance Update as of December 31, 2007 (unaudited)

| | | | | | |

| | | Average Annual Total Returns

As of December 31, 2007 | | |

| | | One

Year | | Since

Inception1 | | |

Manning & Napier Fund, Inc. - Core Bond Series2 | | 5.58% | | 4.09% | | |

Merrill Lynch U.S. Corporate, Government & Mortgage Index3 | | 7.17% | | 4.99% | | |

The following graph compares the value of a $10,000 investment in the Manning & Napier Fund, Inc. - Core Bond Series from its inception1 (4/21/05) to present (12/31/07) to the Merrill Lynch U.S. Corporate, Government & Mortgage Index.

1Performance numbers for the Series and Index are calculated from April 21, 2005, the Series’ inception date.

2The Series’ performance does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. The Series’ performance is historical and may not be indicative of future results. The performance returns shown are inclusive of the net expense ratio of the Series. For the year ended December 31, 2007, this net expense ratio was 0.80%. The gross expense ratio, which does not account for any voluntary or contractual waivers currently in effect, was 0.84% for the year ended December 31, 2007.

3The unmanaged Merrill Lynch U.S. Corporate, Government & Mortgage Index (formerly Merrill Lynch U.S. Domestic Master Index) is a market value weighted measure that represents U.S. government, corporate, and pass-through securities issued by entities within the United States, by supranational entities, or by entities headquartered outside of the United States but who have issued dollar-denominated securities within the United States. The Index only includes investment-grade securities with maturities of greater than one year. The Index returns assume reinvestment of coupons and, unlike Series returns, do not reflect any fees or expenses.

Shareholder Expense Example (unaudited)

As a shareholder of the Series, you may incur two types of costs: (1) transaction costs, including potential wire charges on redemptions and (2) ongoing costs, including management fees and other Series expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Series and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2007 to December 31, 2007).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Series’ actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Series’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid during the period. You may use this information to compare the ongoing costs of investing in the Series and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as potential wire charges on redemptions. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | |

| | | Beginning

Account Value

7/1/07 | | Ending

Account Value

12/31/07 | | Expenses Paid

During Period*

7/1/07-12/31/07 |

Actual | | $ | 1,000.00 | | $ | 1,049.40 | | $ | 4.13 |

Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | $ | 1,021.17 | | $ | 4.08 |

*Expenses are equal to the Series’ annualized expense ratio (for the six-month period) of 0.80%, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). Expenses are based on the most recent fiscal half year; therefore, the expense ratio stated above may differ from the expense ratio stated in the financial highlights, which is based on one-year data. The Series’ total return would have been lower had certain expenses not been waived during the period.

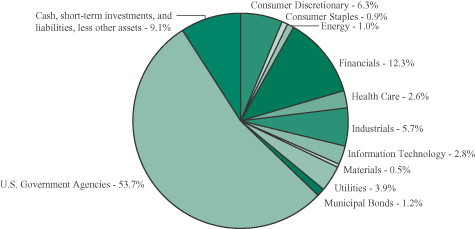

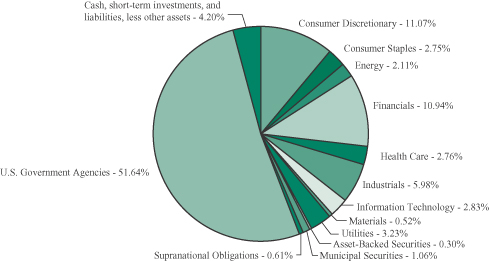

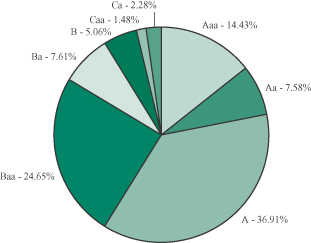

Portfolio Composition as of December 31, 2007 (unaudited)

Sector Allocation1

1As a percentage of net assets.

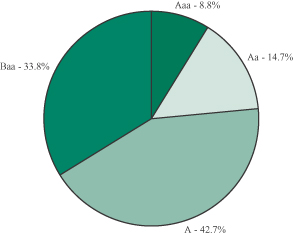

Credit Quality Ratings2,3

2As a percentage of total corporate bonds and municipal bonds.

3Based on ratings from Moody’s, or the S&P equivalent. The Series may use different ratings provided by other rating agencies for purposes of determining compliance with the Series’ investment policies.

Investment Portfolio - December 31, 2007

| | | | | | | | |

| | | Credit

Rating1

(unaudited) | | Principal

Amount | | Value

(Note 2) |

| | | | | | | | |

| | | |

CORPORATE BONDS - 36.0% | | | | | | | | |

| | | |

Convertible Corporate Bonds - 2.8% | | | | | | | | |

Consumer Discretionary - 0.7% | | | | | | | | |

Hotels, Restaurants & Leisure - 0.7% | | | | | | | | |

Carnival Corp., 2.00%, 4/15/2021 | | A3 | | $ | 305,000 | | $ | 356,469 |

| | | | | | | | |

Health Care - 1.2% | | | | | | | | |

Biotechnology - 0.9% | | | | | | | | |

Amgen, Inc., 0.375%, 2/1/2013 | | A2 | | | 515,000 | | | 452,556 |

| | | | | | | | |

Health Care Equipment & Supplies - 0.3% | | | | | | | | |

Medtronic, Inc., 1.625%, 4/15/2013 | | A1 | | | 120,000 | | | 128,100 |

| | | | | | | | |

Total Health Care | | | | | | | | 580,656 |

| | | | | | | | |

Information Technology - 0.9% | | | | | | | | |

Software - 0.9% | | | | | | | | |

Amdocs Ltd., 0.50%, 3/15/2024 (Guernsey) (Note 7) | | Baa3 | | | 465,000 | | | 472,556 |

| | | | | | | | |

Total Convertible Corporate Bonds

(Identified Cost $1,455,261) | | | | | | | | 1,409,681 |

| | | | | | | | |

Non-Convertible Corporate Bonds - 33.2% | | | | | | | | |

Consumer Discretionary - 5.6% | | | | | | | | |

Hotels, Restaurants & Leisure - 1.0% | | | | | | | | |

McDonald’s Corp., 5.80%, 10/15/2017 | | A3 | | | 480,000 | | | 496,981 |

| | | | | | | | |

Media - 2.9% | | | | | | | | |

AOL Time Warner (now known as Time Warner, Inc.), 7.625%, 4/15/2031 | | Baa2 | | | 510,000 | | | 564,376 |

Comcast Corp., 6.50%, 11/15/2035 | | Baa2 | | | 570,000 | | | 581,650 |

The Walt Disney Co., 7.00%, 3/1/2032 | | A2 | | | 280,000 | | | 321,742 |

| | | | | | | | |

| | | | | | | | 1,467,768 |

| | | | | | | | |

Multiline Retail - 1.0% | | | | | | | | |

Target Corp., 5.875%, 3/1/2012 | | A2 | | | 485,000 | | | 502,097 |

| | | | | | | | |

Specialty Retail - 0.7% | | | | | | | | |

Lowe’s Companies, Inc., 8.25%, 6/1/2010 | | A1 | | | 300,000 | | | 327,765 |

| | | | | | | | |

Total Consumer Discretionary | | | | | | | | 2,794,611 |

| | | | | | | | |

Consumer Staples - 0.9% | | | | | | | | |

Food & Staples Retailing - 0.9% | | | | | | | | |

The Kroger Co., 7.25%, 6/1/2009 | | Baa2 | | | 215,000 | | | 221,167 |

The Kroger Co., 5.50%, 2/1/2013 | | Baa2 | | | 230,000 | | | 230,604 |

| | | | | | | | |

Total Consumer Staples | | | | | | | | 451,771 |

| | | | | | | | |

Energy - 1.0% | | | | | | | | |

Oil, Gas & Consumable Fuels - 1.0% | | | | | | | | |

Anadarko Petroleum Corp., 5.95%, 9/15/2016 | | Baa3 | | | 455,000 | | | 463,295 |

| | | | | | | | |

| | |

| 6 | | The accompanying notes are an integral part of the financial statements. |

Investment Portfolio - December 31, 2007

| | | | | | | | |

| | | Credit

Rating1

(unaudited) | | Principal

Amount | | Value

(Note 2) |

| | | | | | | | |

| | | |

CORPORATE BONDS (continued) | | | | | | | | |

| | | |

Non-Convertible Corporate Bonds (continued) | | | | | | | | |

Financials - 12.3% | | | | | | | | |

Capital Markets - 3.0% | | | | | | | | |

The Goldman Sachs Group, Inc., 6.345%, 2/15/2034 | | A1 | | $ | 640,000 | | $ | 577,997 |

Lehman Brothers Holdings, Inc., 4.9775%,11/16/20095 | | A1 | | | 240,000 | | | 233,804 |

Lehman Brothers Holdings, Inc., 6.50%, 7/19/2017 | | A2 | | | 235,000 | | | 237,786 |

Merrill Lynch & Co., Inc., 6.00%, 2/15/2017 | | A1 | | | 235,000 | | | 229,872 |

Merrill Lynch & Co., Inc., 6.11%, 1/29/2037 | | A2 | | | 230,000 | | | 203,134 |

| | | | | | | | |

| | | | | | | | 1,482,593 |

| | | | | | | | |

Commercial Banks - 5.2% | | | | | | | | |

Commonwealth Bank of Australia3, 4/30/2010 (Australia) (Note 7) | | Aa1 | | | 400,000 | | | 415,520 |

Manufacturers & Traders Trust Co., 6.625%, 12/4/2017 | | A2 | | | 495,000 | | | 494,862 |

PNC Bank National Association, 5.25%, 1/15/2017 | | A1 | | | 510,000 | | | 484,284 |

U.S. Bank National Association, 6.375%, 8/1/2011 | | Aa2 | | | 625,000 | | | 655,491 |

Wachovia Corp., 5.25%, 8/1/2014 | | A1 | | | 590,000 | | | 576,864 |

| | | | | | | | |

| | | | | | | | 2,627,021 |

| | | | | | | | |

Consumer Finance - 0.8% | | | | | | | | |

Toyota Motor Credit Corp., 10.00%, 5/4/2022 | | Aaa | | | 400,000 | | | 384,000 |

| | | | | | | | |

Diversified Financial Services - 0.8% | | | | | | | | |

Bank of America Corp. Capital Trust VI, 5.625%, 3/8/2035 | | Aa2 | | | 455,000 | | | 388,605 |

| | | | | | | | |

Insurance - 2.5% | | | | | | | | |

Ambac Financial Group, Inc., 5.95%, 12/5/2035 | | Aa2 | | | 820,000 | | | 640,046 |

American International Group, Inc., 4.25%, 5/15/2013 | | Aa2 | | | 660,000 | | | 627,838 |

| | | | | | | | |

| | | | | | | | 1,267,884 |

| | | | | | | | |

Total Financials | | | | | | | | 6,150,103 |

| | | | | | | | |

Health Care - 1.4% | | | | | | | | |

Pharmaceuticals - 1.4% | | | | | | | | |

Abbott Laboratories, 3.50%, 2/17/2009 | | A1 | | | 265,000 | | | 261,525 |

Wyeth, 6.50%, 2/1/2034 | | A3 | | | 420,000 | | | 445,756 |

| | | | | | | | |

Total Health Care | | | | | | | | 707,281 |

| | | | | | | | |

Industrials - 5.7% | | | | | | | | |

Aerospace & Defense - 0.7% | | | | | | | | |

Boeing Capital Corp., 6.50%, 2/15/2012 | | A2 | | | 310,000 | | | 332,803 |

| | | | | | | | |

Air Freight & Logistics - 0.4% | | | | | | | | |

FedEx Corp., 3.50%, 4/1/2009 | | Baa2 | | | 210,000 | | | 206,607 |

| | | | | | | | |

| | |

| The accompanying notes are an integral part of the financial statements. | | 7 |

Investment Portfolio - December 31, 2007

| | | | | | | | |

| | | Credit

Rating1

(unaudited) | | Principal

Amount | | Value

(Note 2) |

| | | | | | | | |

| | | |

CORPORATE BONDS (continued) | | | | | | | | |

| | | |

Non-Convertible Corporate Bonds (continued) | | | | | | | | |

Industrials (continued) | | | | | | | | |

Airlines - 0.9% | | | | | | | | |

Southwest Airlines Co., 5.25%, 10/1/2014 | | Baa1 | | $ | 475,000 | | $ | 462,924 |

| | | | | | | | |

Industrial Conglomerates - 1.3% | | | | | | | | |

General Electric Capital Corp., 6.75%, 3/15/2032 | | Aaa | | | 570,000 | | | 647,168 |

| | | | | | | | |

Machinery - 0.4% | | | | | | | | |

John Deere Capital Corp., 5.50%, 4/13/2017 | | A2 | | | 225,000 | | | 226,770 |

| | | | | | | | |

Road & Rail - 2.0% | | | | | | | | |

CSX Corp., 6.00%, 10/1/2036 | | Baa3 | | | 705,000 | | | 639,851 |

Union Pacific Corp., 5.65%, 5/1/2017 | | Baa2 | | | 340,000 | | | 335,614 |

| | | | | | | | |

| | | | | | | | 975,465 |

| | | | | | | | |

Total Industrials | | | | | | | | 2,851,737 |

| | | | | | | | |

Information Technology - 1.9% | | | | | | | | |

Communications Equipment - 1.9% | | | | | | | | |

Cisco Systems, Inc., 5.25%, 2/22/2011 | | A1 | | | 205,000 | | | 210,178 |

Cisco Systems, Inc., 5.50%, 2/22/2016 | | A1 | | | 250,000 | | | 254,242 |

Corning, Inc., 6.20%, 3/15/2016 | | Baa1 | | | 475,000 | | | 489,392 |

| | | | | | | | |

Total Information Technology | | | | | | | | 953,812 |

| | | | | | | | |

Materials - 0.5% | | | | | | | | |

Metals & Mining - 0.5% | | | | | | | | |

Alcoa, Inc., 5.87%, 2/23/2022 | | Baa1 | | | 250,000 | | | 241,600 |

| | | | | | | | |

Utilities - 3.9% | | | | | | | | |

Electric Utilities - 2.1% | | | | | | | | |

American Electric Power Co., Inc., 5.375%, 3/15/2010 | | Baa2 | | | 465,000 | | | 471,659 |

Exelon Generation Co. LLC, 5.35%, 1/15/2014 | | A3 | | | 580,000 | | | 564,453 |

| | | | | | | | |

| | | | | | | | 1,036,112 |

| | | | | | | | |

Multi-Utilities - 1.8% | | | | | | | | |

CenterPoint Energy Resources Corp., 7.875%, 4/1/2013 | | Baa3 | | | 335,000 | | | 367,826 |

Duke Energy Field Services LLC (now known as DCP Midstream LLC), 7.875%, 8/16/2010 | | Baa2 | | | 280,000 | | | 300,359 |

Sempra Energy, 7.95%, 3/1/2010 | | Baa1 | | | 210,000 | | | 224,376 |

| | | | | | | | |

| | | | | | | | 892,561 |

| | | | | | | | |

Total Utilities | | | | | | | | 1,928,673 |

| | | | | | | | |

Total Non-Convertible Corporate Bonds

(Identified Cost $16,752,969) | | | | | | | | 16,542,883 |

| | | | | | | | |

TOTAL CORPORATE BONDS

(Identified Cost $18,208,230) | | | | | | | | 17,952,564 |

| | | | | | | | |

| | |

| 8 | | The accompanying notes are an integral part of the financial statements. |

Investment Portfolio - December 31, 2007

| | | | | | | | | |

| | | Credit

Rating1

(unaudited) | | | Principal

Amount | | Value

(Note 2) |

| | | | | | | | | |

| | | |

MUNICIPAL BONDS - 1.2% | | | | | | | | | |

Canyon Independent School District, G.O. Bond, 4.50%, 2/15/2030 | | AAA | 2 | | $ | 100,000 | | $ | 98,072 |

Chapel Hill Independent School District, School Building, G.O. Bond, 4.50%, 8/15/2032 | | Aaa | | | | 100,000 | | | 97,666 |

Commerce Independent School District, School Building, G.O. Bond, 4.50%, 8/15/2037 | | Aaa | | | | 100,000 | | | 96,504 |

Harlandale Independent School District, School Building, G.O. Bond, 4.75%, 8/15/2036 | | Aaa | | | | 100,000 | | | 100,065 |

Katy Texas Independent School District, School Building, G.O. Bond, 4.50%, 2/15/2031 | | Aaa | | | | 100,000 | | | 97,773 |

Keller Independent School District, School Building, G.O. Bond, 4.75%, 8/15/2032 | | Aaa | | | | 100,000 | | | 100,532 |

| | | | | | | | | |

TOTAL MUNICIPAL BONDS

(Identified Cost $576,813) | | | | | | | | | 590,612 |

| | | | | | | | | |

| | | |

U.S. GOVERNMENT AGENCIES - 53.7% | | | | | | | | | |

Mortgage-Backed Securities - 50.6% | | | | | | | | | |

Fannie Mae, Pool #762352, 5.00%, 4/1/2019 | | | | | | 16,255 | | | 16,284 |

Fannie Mae, Pool #255274, 5.00%, 6/1/2019 | | | | | | 16,666 | | | 16,697 |

Fannie Mae, Pool #795855, 5.50%, 9/1/2019 | | | | | | 283,352 | | | 287,319 |

Fannie Mae, Pool #840165, 4.50%, 11/1/2020 | | | | | | 153,025 | | | 150,464 |

Fannie Mae, Pool #813938, 4.50%, 12/1/2020 | | | | | | 189,609 | | | 186,435 |

Fannie Mae, Pool #256114, 4.50%, 1/1/2021 | | | | | | 391,745 | | | 385,189 |

Fannie Mae, Pool #881624, 4.50%, 1/1/2021 | | | | | | 390,255 | | | 383,724 |

Fannie Mae, Pool #902047, 5.00%, 11/1/2021 | | | | | | 922,364 | | | 923,357 |

Fannie Mae, Pool #912409, 5.00%, 2/1/2022 | | | | | | 173,342 | | | 173,529 |

Fannie Mae, Pool #254375, 6.50%, 7/1/2022 | | | | | | 4,026 | | | 4,165 |

Fannie Mae, Pool #786281, 6.50%, 7/1/2034 | | | | | | 287,231 | | | 296,046 |

Fannie Mae, Pool #815409, 4.50%, 2/1/2035 | | | | | | 227,332 | | | 215,276 |

Fannie Mae, Pool #745147, 4.50%, 12/1/2035 | | | | | | 3,493,014 | | | 3,307,774 |

Fannie Mae, Pool #872535, 6.50%, 6/1/2036 | | | | | | 727,172 | | | 747,564 |

Fannie Mae, Pool #898299, 6.50%, 10/1/2036 | | | | | | 844,886 | | | 868,579 |

Fannie Mae, TBA4, 4.50%, 1/15/2038 | | | | | | 1,688,000 | | | 1,597,270 |

Fannie Mae, TBA4, 6.00%, 1/15/2038 | | | | | | 2,190,000 | | | 2,223,533 |

Federal Home Loan Mortgage Corp., Pool #M90974, 4.50%, 3/1/2010 | | | | | | 69,196 | | | 68,900 |

Federal Home Loan Mortgage Corp., Pool #B16835, 5.50%, 10/1/2019 | | | | | | 257,001 | | | 260,349 |

Federal Home Loan Mortgage Corp., Pool #G11896, 4.50%, 1/1/2021 | | | | | | 1,090,910 | | | 1,072,033 |

Federal Home Loan Mortgage Corp., Pool #G12419, 5.00%, 10/1/2021 | | | | | | 194,387 | | | 194,597 |

Federal Home Loan Mortgage Corp., Pool #G18168, 5.00%, 2/1/2022 | | | | | | 898,174 | | | 899,160 |

| | |

| The accompanying notes are an integral part of the financial statements. | | 9 |

Investment Portfolio - December 31, 2007

| | | | | | | | | |

| | | | | Principal

Amount/

Shares | | Value

(Note 2) | |

| | | | | | | | | |

| | | |

U.S. GOVERNMENT AGENCIES (continued) | | | | | | | | | |

Mortgage-Backed Securities (continued) | | | | | | | | | |

Federal Home Loan Mortgage Corp., Pool #G18182, 5.50%, 5/1/2022 | | | | $ | 749,868 | | $ | 758,894 | |

Federal Home Loan Mortgage Corp., Pool #A27705, 6.50%, 10/1/2034 | | | | | 96,982 | | | 99,955 | |

Federal Home Loan Mortgage Corp., Pool #G01782, 6.50%, 2/1/2035 | | | | | 69,422 | | | 71,681 | |

Federal Home Loan Mortgage Corp., Pool #A52716, 6.50%, 10/1/2036 | | | | | 1,604,118 | | | 1,649,224 | |

Federal Home Loan Mortgage Corp., TBA4, 4.50%, 1/15/2023 | | | | | 1,527,000 | | | 1,501,710 | |

Federal Home Loan Mortgage Corp., TBA4, 5.00%, 1/15/2023 | | | | | 1,749,000 | | | 1,750,640 | |

Federal Home Loan Mortgage Corp., TBA4, 5.50%, 1/15/2023 | | | | | 985,000 | | | 996,697 | |

Federal Home Loan Mortgage Corp., TBA4, 5.00%, 1/15/2038 | | | | | 3,025,000 | | | 2,951,266 | |

Federal Home Loan Mortgage Corp., TBA4, 5.50%, 1/15/2038 | | | | | 989,000 | | | 986,836 | |

GNMA, Pool #487193, 5.00%, 4/15/2020 | | | | | 86,450 | | | 86,671 | |

GNMA, Pool #563559, 6.50%, 4/15/2032 | | | | | 51,202 | | | 53,085 | |

GNMA, Pool #631703, 6.50%, 9/15/2034 | | | | | 76,424 | | | 79,117 | |

| | | | | | | | | |

Total Mortgage-Backed Securities

(Identified Cost $25,072,693) | | | | | | | | 25,264,020 | |

| | | | | | | | | |

| | | |

Other Agencies - 3.1% | | | | | | | | | |

Federal Home Loan Mortgage Corp., 6.25%, 7/15/2032

(Identified Cost $1,405,919) | | | | | 1,275,000 | | | 1,519,140 | |

| | | | | | | | | |

TOTAL U.S. GOVERNMENT AGENCIES

(Identified Cost $26,478,612) | | | | | | | | 26,783,160 | |

| | | | | | | | | |

| | | |

SHORT-TERM INVESTMENTS - 32.4% | | | | | | | | | |

Dreyfus Treasury Cash Management - Institutional Shares | | | | | 1,224,474 | | | 1,224,474 | |

Fannie Mae Discount Note, 1/14/2008 | | | | $ | 8,500,000 | | | 8,486,050 | |

Fannie Mae Discount Note, 1/31/2008 | | | | | 4,500,000 | | | 4,483,376 | |

Federal Home Loan Bank Discount Note, 1/18/2008 | | | | | 2,000,000 | | | 1,995,680 | |

| | | | | | | | | |

TOTAL SHORT-TERM INVESTMENTS

(Identified Cost $16,191,353) | | | | | | | | 16,189,580 | |

| | | | | | | | | |

TOTAL INVESTMENTS - 123.3%

(Identified Cost $61,455,008) | | | | | | | | 61,515,916 | |

| | | |

LIABILITIES, LESS OTHER ASSETS - (23.3%) | | | | | | | | (11,607,165 | ) |

| | | | | | | | | |

NET ASSETS - 100% | | | | | | | $ | 49,908,751 | |

| | | | | | | | | |

| | |

| 10 | | The accompanying notes are an integral part of the financial statements. |

Investment Portfolio - December 31, 2007

Key:

G.O. Bond - General Obligation Bond

TBA - to be announced

1Credit ratings from Moody’s (unaudited).

2Credit ratings from S&P (unaudited).

3Restricted securities - Investment in securities that are restricted as to public resale under the Securities Act of 1933, as amended. This security was aquired on April 13, 2007 at a cost of $400,000 ($100.00 per share) and has been determined to be illiquid under guidelines established by the Board of Directors. This security amounts to $415,520, or 0.8%, of the Series’ net assets as of December 31, 2007 (see Note 2 to the financial statements).

4Securities purchased on a forward commitment or when-issued basis (see Note 2 to the financial statements).

5The coupon rate is a floating rate and is subject to change quarterly. The coupon rate stated is the rate as of December 31, 2007.

| | |

| The accompanying notes are an integral part of the financial statements. | | 11 |

Statement of Assets and Liabilities

December 31, 2007

| | | |

ASSETS: | | | |

| | | |

| |

Investments, at value (identified cost, $61,455,008) (Note 2) | | $ | 61,515,916 |

Interest receivable | | | 407,714 |

Dividends receivable | | | 3,183 |

| | | |

TOTAL ASSETS | | | 61,926,813 |

| | | |

| LIABILITIES: | | | |

| |

Accrued management fees (Note 3) | | | 19,895 |

Accrued fund accounting and transfer agent fees (Note 3) | | | 3,016 |

Accrued Chief Compliance Officer service fees (Note 3) | | | 721 |

Payable for purchases of delayed delivery securities (Note 2) | | | 11,953,282 |

Audit fees payable | | | 29,477 |

Payable for fund shares repurchased | | | 6,773 |

Other payables and accrued expenses | | | 4,898 |

| | | |

TOTAL LIABILITIES | | | 12,018,062 |

| | | |

TOTAL NET ASSETS | | $ | 49,908,751 |

| | | |

NET ASSETS CONSIST OF: | | | |

| |

Capital stock | | $ | 49,659 |

Additional paid-in-capital | | | 49,487,703 |

Undistributed net investment income | | | 4,622 |

Accumulated net realized gain on investments | | | 305,859 |

Net unrealized appreciation on investments | | | 60,908 |

| | | |

TOTAL NET ASSETS | | $ | 49,908,751 |

| | | |

NET ASSET VALUE, OFFERING PRICE AND REDEMPTION PRICE PER SHARE ($49,908,751/4,965,938 shares) | | $ | 10.05 |

| | | |

| | |

| 12 | | The accompanying notes are an integral part of the financial statements. |

Statement of Operations

For the Year Ended December 31, 2007

| | | | |

INVESTMENT INCOME: | | | | |

| | | | |

| | | | |

| |

Interest | | $ | 2,282,645 | |

Dividends | | | 67,912 | |

| | | | |

Total Investment Income | | | 2,350,557 | |

| | | | |

| EXPENSES: | | | | |

| |

Management fees (Note 3) | | | 281,238 | |

Fund accounting and transfer agent fees (Note 3) | | | 34,595 | |

Directors’ fees (Note 3) | | | 7,844 | |

Chief Compliance Officer service fees (Note 3) | | | 6,100 | |

Audit fees | | | 29,499 | |

Custodian fees | | | 6,299 | |

Miscellaneous | | | 28,289 | |

| | | | |

Total Expenses | | | 393,864 | |

Less reduction of expenses (Note 3) | | | (18,694 | ) |

| | | | |

Net Expenses | | | 375,170 | |

| | | | |

NET INVESTMENT INCOME | | | 1,975,387 | |

| | | | |

| REALIZED AND UNREALIZED GAIN ON INVESTMENTS: | | | | |

| |

Net realized gain on investments | | | 580,680 | |

Net change in unrealized appreciation (depreciation) on investments | | | 87,790 | |

| | | | |

| |

NET REALIZED AND UNREALIZED GAIN ON

INVESTMENTS | | | 668,470 | |

| | | | |

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 2,643,857 | |

| | | | |

| | |

| The accompanying notes are an integral part of the financial statements. | | 13 |

Statements of Changes in Net Assets

| | | | | | | | |

| | | For the

Year Ended

12/31/07 | | | For the

Year Ended

12/31/06 | |

| | | | | | | | |

| INCREASE (DECREASE) IN NET ASSETS: | | | | | | | | |

| | |

| OPERATIONS: | | | | | | | | |

| | |

Net investment income | | $ | 1,975,387 | | | $ | 1,329,985 | |

Net realized gain on investments | | | 580,680 | | | | 225,664 | |

Net change in unrealized appreciation (depreciation) on investments | | | 87,790 | | | | 123,352 | |

| | | | | | | | |

Net increase from operations | | | 2,643,857 | | | | 1,679,001 | |

| | | | | | | | |

DISTRIBUTIONS TO SHAREHOLDERS (Note 8): | | | | | | | | |

| | |

From net investment income | | | (1,978,671 | ) | | | (1,327,178 | ) |

From net realized gain on investments | | | (300,431 | ) | | | — | |

| | | | | | | | |

Total distributions to shareholders | | | (2,279,102 | ) | | | (1,327,178 | ) |

| | | | | | | | |

CAPITAL STOCK ISSUED AND REPURCHASED: | | | | | | | | |

| | |

Net increase from capital share transactions

(Note 5) | | | 3,847,920 | | | | 16,766,575 | |

| | | | | | | | |

Net increase in net assets | | | 4,212,675 | | | | 17,118,398 | |

| | |

| NET ASSETS: | | | | | | | | |

| | |

Beginning of year | | | 45,696,076 | | | | 28,577,678 | |

| | | | | | | | |

End of year (including undistributed net investment income of $4,622 and $7,906, respectively) | | $ | 49,908,751 | | | $ | 45,696,076 | |

| | | | | | | | |

| | |

| 14 | | The accompanying notes are an integral part of the financial statements. |

Financial Highlights

| | | | | | |

| | | For the

Year Ended

12/31/07 | | For the

Year Ended

12/31/06 | | For the

Period 4/21/051

to 12/31/05 |

| | | | | | |

| | | | | | |

| Per share data (for a share outstanding throughout each period): | | | | | | |

Net asset value - Beginning of period | | $9.98 | | $9.89 | | $10.00 |

| | | | | | |

Income (loss) from investment operations: | | | | | | |

Net investment income | | 0.42 | | 0.36 | | 0.21 |

Net realized and unrealized gain (loss) on investments | | 0.13 | | 0.09 | | (0.11) |

| | | | | | |

Total from investment operations | | 0.55 | | 0.45 | | 0.10 |

| | | | | | |

Less distributions to shareholders: | | | | | | |

From net investment income | | (0.42) | | (0.36) | | (0.21) |

From net realized gain on investments | | (0.06) | | — | | — |

| | | | | | |

Total distributions to shareholders | | (0.48) | | (0.36) | | (0.21) |

| | | | | | |

Net asset value - End of period | | $10.05 | | $9.98 | | $9.89 |

| | | | | | |

Total return2 | | 5.58% | | 4.51% | | 0.98% |

| Ratios (to average net assets)/Supplemental Data: | | | | | | |

Expenses* | | 0.80% | | 0.80% | | 0.80%3 |

Net investment income | | 4.21% | | 3.87% | | 3.08%3 |

Portfolio turnover | | 346% | | 313% | | 293% |

Net assets - End of period (000’s omitted) | | $49,909 | | $45,696 | | $28,578 |

| | | | | | |

|

*The investment advisor did not impose all of its management fee. If these expenses had been incurred by the Series, the expense ratio (to average net assets) would have been increased as follows: |

| | 0.04% | | 0.08% | | 0.20%3 |

1Commencement of operations.

2Represents aggregate total return for the period indicated, and assumes reinvestment of all distributions. Total return would have been lower had certain expenses not been waived during the period. Periods less than one year are not annualized.

3Annualized.

| | |

| The accompanying notes are an integral part of the financial statements. | | 15 |

Notes to Financial Statements

Core Bond Series (the “Series”) is a no-load non-diversified series of Manning & Napier Fund, Inc. (the “Fund”). The Fund is organized in Maryland and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company.

The Series’ investment objective is to provide long-term total return by investing primarily in investment grade bonds and other financial instruments, including derivatives, with economic characteristics similar to bonds.

The Fund’s Advisor is Manning & Napier Advisors, Inc. (the “Advisor”). Shares of the Series are offered to investors, clients and employees of the Advisor and its affiliates. The total authorized capital stock of the Fund consists of 5.0 billion shares of common stock each having a par value of $0.01. As of December 31, 2007, 3.33 billion shares have been designated in total among 27 series, of which 125 million have been designated as Core Bond Series Class A common stock.

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

Security Valuation

Debt securities, including government bonds, sovereign bonds, corporate bonds and mortgage-backed securities, will normally be valued on the basis of evaluated bid prices provided by an independent pricing service. Certain investments in securities held by the Series were valued on a basis of a price provided by a principal market maker. These prices may differ from the value that would have been used had a broader market for securities existed.

Municipal securities will normally be valued on the basis of market valuations provided by an independent pricing service that utilizes the latest price quotations and a matrix system (which considers such factors as security prices of similar securities, yields, maturities and ratings).

Securities for which representative valuations or prices are not available from the Fund’s pricing service may be valued at fair value. Due to the inherent uncertainty of valuations of such securities, the fair value may differ significantly from the values that would have been used had a ready market for such securities existed. If trading or events occurring after the close of the principal market in which securities are traded are expected to materially affect the value of those securities, then they may be valued at their fair value, taking this trading or these events into account. Fair value is determined in good faith by the Advisor under procedures approved by and under the general supervision and responsibility of the Fund’s Board of Directors (the “Board”).

Short-term investments that mature in sixty days or less are valued at amortized cost, which approximates market value. Investments in open-end investment companies are valued at their net asset value per share on valuation date.

Security Transactions, Investment Income and Expenses

Security transactions are accounted for on trade date. Interest income, including amortization of premium and accretion of discounts using the effective interest method, is earned from settlement date and accrued daily. Dividend income is recorded on an accrual basis on ex-dividend date.

Expenses are recorded on an accrual basis. Most expenses of the Fund can be attributed to a specific series. Expenses which cannot be directly attributed are apportioned among the series in the Fund in such a manner as deemed equitable by the Fund’s Board, taking into consideration, among other things, the nature and type of expense.

Notes to Financial Statements

| 2. | SIGNIFICANT ACCOUNTING POLICIES (continued) |

Security Transactions, Investment Income and Expenses (continued)

The Series uses the identified cost method for determining realized gain or loss on investments for both financial statement and federal income tax reporting purposes.

Securities Purchased on a When-Issued Basis or Forward Commitment

The Series may purchase securities on a when-issued basis or forward commitment. These transactions involve a commitment by the Series to purchase securities for a predetermined price with payment and delivery taking place beyond the customary settlement period. When such purchases are outstanding, the Series will designate liquid assets in an amount sufficient to meet the purchase price. When purchasing a security on a delayed delivery basis, the Series assumes the rights and risks of ownership of the security, including the risk of price and yield fluctuations, and takes such fluctuations into account when determining its net asset value. The Series may sell the when-issued securities before they are delivered, which may result in a capital gain or loss.

In connection with its ability to purchase or sell securities on a forward commitment basis, the Series may enter into forward roll transactions principally using To Be Announced (TBA) securities. Forward roll transactions require the sale of securities for delivery in the current month, and a simultaneous agreement to repurchase substantially similar (same type, coupon and maturity) securities on a specified future date. Risks of entering into forward roll transactions include the potential inability of the counterparty to meet the terms of the agreement; the potential of the Series to receive inferior securities at redelivery as compared to the securities sold to the counterparty; counterparty credit risk; and the potential pay down speed variance between the mortgage-backed pools. During the roll period, the Series forgoes principal and interest paid on the securities. The Series accounts for such dollar rolls as purchases and sales. The Series had TBA dollar rolls outstanding as of December 31, 2007, which are included in Payable for Purchases of Delayed Delivery Securities on the Statement of Assets and Liabilities.

Restricted Securities

Restricted securities are purchased in private placement transactions, are not registered under the Securities Act of 1933, as amended, and may have contractual restrictions on resale. Information regarding restricted securities is included at the end of the Series’ Investment Portfolio.

Illiquid Securities

A security may be considered illiquid if so deemed in good faith by the Advisor under procedures approved by and under the general supervision and responsibility of the Fund’s Board. Securities that are illiquid are marked with the applicable footnote on the Investment Portfolio.

Federal Taxes

The Series’ policy is to comply with the provisions of the Internal Revenue Code applicable to regulated investment companies. The Series is not subject to federal income tax or excise tax to the extent that the Series distributes to shareholders each year its taxable income, including any net realized gains on investments, in accordance with requirements of the Internal Revenue Code. Accordingly, no provision for federal income tax or excise tax has been made in the financial statements.

On June 29, 2007, the Series adopted Financial Accounting Standards Board Interpretation No. 48 - Accounting for Uncertainty in Income Taxes (“FIN 48”). FIN 48 prescribes the minimum recognition threshold a tax position must meet in connection with accounting for

Notes to Financial Statements

| 2. | SIGNIFICANT ACCOUNTING POLICIES (continued) |

Federal Taxes (continued)

uncertainties in income tax positions taken or expected to be taken by an entity before being measured and recognized in the financial statements. Management has determined that FIN 48 did not have a material impact on the Series’ financial statements. The Series files income tax returns in the U.S. federal jurisdiction, various states and foreign jurisdictions, as required. No income tax returns are currently under investigation. The statute of limitations on the Series’ tax returns remains open for the years ended December 31, 2005 through December 31, 2007.

Additionally, based on the Fund’s understanding of the tax rules and rates related to income, gains and transactions for foreign jurisdictions in which it invests, the Series will provide for foreign taxes, and where appropriate, deferred foreign tax.

Distributions of Income and Gains

Distributions to shareholders of net investment income and net realized gains are made annually. An additional distribution may be necessary to avoid taxation of the Series. Distributions are recorded on the ex-dividend date.

Indemnifications

The Fund’s organizational documents provide former and current directors and officers with a limited indemnification against liabilities arising in connection with the performance of their duties to the Fund. In the normal course of business, the Fund may also enter into contracts that provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown as this would be dependent on future claims that may be made against the Fund. The risk of material loss from such claims is considered remote.

Other

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

| 3. | TRANSACTIONS WITH AFFILIATES |

The Fund has an Investment Advisory Agreement (the “Agreement”) with the Advisor, for which the Series pays a fee, computed daily and payable monthly, at an annual rate of 0.60% of the Series’ average daily net assets.

Under the Agreement, personnel of the Advisor provide the Series with advice and assistance in the choice of investments and the execution of securities transactions, and otherwise maintain the Series’ organization. The Advisor also provides the Fund with necessary office space and fund administration and support services. The salaries of all officers of the Fund (except a percentage of the Fund’s Chief Compliance Officer’s salary, which is paid by the Fund), and of all Directors who are “affiliated persons” of the Fund, or of the Advisor, and all personnel of the Fund, or of the Advisor, performing services relating to research, statistical and investment activities, are paid by the Advisor. Each “non-affiliated” Director receives an annual stipend, which is allocated among all the active series of the Fund. In addition, these Directors also receive a fee per Board meeting attended for each active series of the Fund plus a fee for each committee meeting attended.

Notes to Financial Statements

| 3. | TRANSACTIONS WITH AFFILIATES (continued) |

The Advisor has contractually agreed, until at least April 30, 2009, to waive its fee and, if necessary, pay other operating expenses of the Series in order to maintain total direct annual fund operating expenses for the Series at no more than 0.80% of average daily net assets each year. Accordingly, the Advisor waived fees of $18,694 for the year ended December 31, 2007, which is reflected as a reduction of expenses on the Statement of Operations. The Advisor is not eligible to recoup any expenses that have been waived or reimbursed in prior years.

Manning & Napier Investor Services, Inc., a registered broker-dealer affiliate of the Advisor, acts as distributor for the Fund’s shares. The services of Manning & Napier Investor Services, Inc. are provided at no additional cost to the Series.

For fund accounting and transfer agent services, the Fund pays the Advisor an annual fee of 0.11% of the Fund’s average daily net assets up to $900 million, 0.07% of the Fund’s average daily net assets between $900 million and $1.5 billion, and 0.04% of the Fund’s average daily net assets over $1.5 billion. Additionally, certain transaction and account-based fees and out-of-pocket expenses, including charges for reporting relating to the Fund’s compliance program, are charged. Expenses not directly attributable to a series are allocated based on each series’ relative net assets or number of accounts, depending on the expense. The Advisor has an agreement with Citi Fund Services Ohio, Inc. (“Citi”) (formerly BISYS Fund Services Ohio, Inc.) under which Citi serves as sub-accountant and sub-transfer agent.

| 4. | PURCHASES AND SALES OF SECURITIES |

For the year ended December 31, 2007, purchases and sales of securities, other than United States Government securities and short-term securities, were $9,674,855 and $4,872,989, respectively. Purchases and sales of United States Government securities, other than short-term securities, were $146,888,741 and $141,153,698, respectively.

| 5. | CAPITAL STOCK TRANSACTIONS |

Transactions in shares of Core Bond Series were:

| | | | | | | | | | | | | |

| | | For the Year

Ended 12/31/07 | | | For the Year

Ended 12/31/06 | |

| | | Shares | | | Amount | | | Shares | | | Amount | |

Sold | | 587,661 | | | $ 5,932,540 | | | 1,637,576 | | | $ | 16,250,398 | |

Reinvested | | 225,784 | | | 2,243,435 | | | 130,284 | | | | 1,304,357 | |

Repurchased | | (426,400 | ) | | (4,328,055 | ) | | (79,452 | ) | | | (788,180 | ) |

| | | | | | | | | | | | | |

Total | | 387,045 | | | $ 3,847,920 | | | 1,688,408 | | | $ | 16,766,575 | |

| | | | | | | | | | | | | |

Substantially all of the Series’ shares represent investments by fiduciary accounts over which the Advisor has sole investment discretion.

The Series may trade in financial instruments with off-balance sheet risk in the normal course of its investing activities to assist in managing exposure to various market risks. These financial instruments include written options, forward foreign currency exchange contracts and futures contracts and may involve, to a varying degree, elements of risk in excess of the amounts recognized for financial statement purposes. No such investments were held by the Series on December 31, 2007.

Notes to Financial Statements

Investing in securities of foreign companies and foreign governments involves special risks and considerations not typically associated with investing in securities of domestic companies and the United States Government. These risks include revaluation of currencies and future adverse political and economic developments. Moreover, securities of foreign companies and foreign governments and their markets may be less liquid and their prices more volatile than those of comparable domestic companies and the United States Government.

| 8. | FEDERAL INCOME TAX INFORMATION |

The amount and characterization of certain income and capital gains to be distributed are determined in accordance with federal income tax regulations, which may differ from accounting principles generally accepted in the United States of America. These differences are primarily due to differing book and tax treatments in the timing of the recognition of net investment income or gains and losses, including Post-October losses. The Series may periodically make reclassifications among its capital accounts to reflect income and gains available for distribution (or available capital loss carryovers) under income tax regulations, without impacting the Series’ net asset value. Any such reclassifications are not reflected in the financial highlights.

The tax character of distributions paid were as follows:

| | | | | | |

| | | For the Year

Ended 12/31/07 | | For the Year

Ended 12/31/06 |

Ordinary income | | $ | 2,029,563 | | $ | 1,327,178 |

Long-term capital gains | | | 249,539 | | | — |

At December 31, 2007, the tax basis components of distributable earnings and the net unrealized appreciation based on identified cost for federal income tax purposes were as follows:

| | | | |

Cost for federal income tax purposes | | $ | 61,455,008 | |

| |

Unrealized appreciation | | $ | 476,360 | |

Unrealized depreciation | | | (415,452 | ) |

| | | | |

Net unrealized appreciation | | $ | 60,908 | |

Undistributed ordinary income | | | 161,029 | |

Undistributed long-term capital gains | | | 149,452 | |

| 9. | RECENT ACCOUNTING PRONOUNCEMENTS |

In September 2006, FASB Statement of Financial Accounting Standards No. 157, Fair Value Measurements (“FAS 157”) was issued, and is effective for fiscal years beginning after November 15, 2007. FAS 157 defines fair value, establishes a framework for measuring fair value, and expands disclosure about fair value measurements. The standard does not expand the use of fair value in any new circumstances, but provides clarification on acceptable fair value methods and applications. At this time, management is evaluating the implications of FAS 157, but it is not expected to materially impact the Series’ financial statements.

Report of Independent Registered Public Accounting Firm

To the Board of Directors of Manning & Napier Fund, Inc. and Shareholders of Core Bond Series:

In our opinion, the accompanying statement of assets and liabilities, including the investment portfolio, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of the Core Bond Series (a series of Manning & Napier Fund, Inc., hereafter referred to as the “Series”) at December 31, 2007, and the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the periods indicated, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Series’ management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at December 31, 2007 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

Columbus, Ohio

February 20, 2008

Supplemental Tax Information (unaudited)

Pursuant to Section 852 of the Internal Revenue Code, as amended, the Series hereby designates $249,539 as capital gains for its taxable year ended December 31, 2007.

Renewal of Investment Advisory Agreements (unaudited)

During the period covered by this shareholder report, the Board of Directors (the “Board”) of Manning & Napier Fund, Inc. (the “Fund”) considered approval of two separate investment advisory agreements with Manning & Napier Advisors, Inc. (the “Advisor”):

| | • | | At a meeting held on August 30, 2007, the Board approved a new investment advisory agreement between the Fund and the Advisor (the “New Investment Advisory Agreement”) and recommended that the New Investment Advisory Agreement be submitted to shareholders for approval. Shareholders approved the New Investment Advisory Agreement at a meeting held on December 17, 2007. |

| | • | | At a meeting held on November 12, 2007, the Board approved the continuation of the then-current investment advisory agreement between the Fund and the Advisor (the “Current Investment Advisory Agreement”), which was to be superseded by the New Investment Advisory Agreement upon its approval by the Fund’s shareholders. The continuation of the Current Investment Advisory Agreement was necessary as a result of the delay in obtaining the number of votes necessary to convene the shareholder meeting and approve the New Investment Advisory Agreement with respect to all investment portfolios of the Fund (the “Series”). |

Consideration of New Investment Advisory Agreement:

In response to recent regulatory and compliance initiatives promulgated by the SEC over the past year, the Fund engaged in a comprehensive review of all material aspects of the Fund’s operations, including the Fund’s Current Investment Advisory Agreement. As a result of its review, the Board determined that the Current Investment Advisory Agreement should be amended for the purpose of modernizing the form of the agreement and to include additional provisions in the agreement that are customarily included in investment advisory agreements between registered investment companies and their investment advisors, but which are not included in the Current Investment Advisory Agreement. Accordingly, at the Board meeting on November 16, 2006, representatives of the Advisor presented to the Board proposed changes to the Current Investment Advisory Agreement in order to address the Board’s request to update and modernize the Current Investment Advisory Agreement. As a result of the discussions between the Board and representatives of the Advisor at the November 2006 Board meeting, the Board determined to formally consider the approval of a new investment advisory agreement between the Fund and the Advisor, which would incorporate the changes proposed at the November 2006 Board meeting, at its in-person Board meeting in August 2007.

At an in-person meeting held on August 30, 2007, the Board considered the approval of the New Investment Advisory Agreement between the Fund and the Advisor. Based on the information it received at the meeting and the November 16, 2006 Board meeting, the Board approved the New Investment Advisory Agreement subject to its further approval by the Fund’s shareholders. Representatives of the Advisor attended the meeting and presented additional oral and written information to the Board to assist the Board in its considerations. At the meeting, the Board concluded it was reasonable to take into account the conclusions the Board made when considering and evaluating the renewal of the Current Investment Advisory Agreement (the “2006 Annual Review”), which occurred at the November 16, 2006 in-person Board meeting, as part of its considerations to approve the New Investment Advisory Agreement. The discussion immediately below outlines the materials and information presented to the Board in connection with the Board’s 2006 Annual Review of the Current Investment Advisory Agreement and the conclusions made by the Directors when determining to continue the Current Investment Advisory Agreement for an additional one-year period.

Renewal of Investment Advisory Agreements (unaudited)

In connection with its review and deliberations, the Board considered the following factors and reached a conclusion with respect to such factors.

| | • | | The Board considered the services provided by the Advisor under the Current Investment Advisory Agreement including, among others: deciding what securities to purchase and sell for each Series; arranging for the purchase and sale of such securities by placing orders with broker-dealers; administering the affairs of the Fund (including the books and records of the Fund not maintained by third party service providers such as the custodian or sub-transfer agent); arranging for the insurance coverage for the Fund; and supervising the preparation of tax returns, SEC filings (including registration statements) and reports to shareholders for the Fund. The Board also considered the nature and quality of such services provided under the Current Investment Advisory Agreement in light of the Advisor’s services provided to the Fund for 21 years. The Board discussed the quality of these services with representatives from the Advisor and concluded that the Advisor was performing its services to the Fund required under the Current Investment Advisory Agreement in a reasonable manner. |

| | • | | The Board considered the investment performance of the various Series of the Fund. The investment performance for each Series was reviewed on a cumulative basis since inception and on a one year basis. In addition, annualized performance for the following time periods was considered: inception, three year, five year, ten year, and current market cycle. A market cycle includes periods of both rising and falling markets. Returns for established benchmark indices for each Series were provided for each time period. The Board noted that all the Series were competitive against their respective benchmark indices over all time periods noted above through September 30, 2006. In addition, the Board considered at the meeting (and considers on a quarterly basis) a peer group performance analysis consisting of Morningstar universes of mutual funds with similar investment objectives. The Board discussed the performance with representatives from the Advisor and concluded that the investment performance of each of the Fund’s Series was reasonable based on the Fund’s actual performance and comparative performance, especially performance over the current market cycle. |

| | • | | The Board considered the costs of the Advisor’s services and the profits of the Advisor as they relate to the Advisor’s services to the Fund under the Current Investment Advisory Agreement. In reviewing the Advisor’s costs and profits, the Board discussed the Advisor’s revenues generated from the Fund (on both an actual and adjusted basis) and its expenses associated with providing the services under the Current Investment Advisory Agreement. In addition, the Board reviewed the Advisor’s expenses associated with Fund activities outside of the Current Investment Advisory Agreement (such as expense reimbursements pursuant to expense caps and payments made by the Advisor to third party platforms on which shares of the Fund are available for purchase). It was noted by representatives of the Advisor that 6 of the 18 active Series of the Fund are currently experiencing expenses above the capped expense ratios. After discussing the above costs and profits, the Board concluded that the Advisor’s profitability relating to its services provided under the Current Investment Advisory Agreement was reasonable. |

| | • | | The Board considered the fees and expenses of the various Series of the Fund. The Advisor presented the advisory fees and total expenses for each Series, including the |

Renewal of Investment Advisory Agreements (unaudited)

| | advisory fee adjusted for any expense waivers or reimbursements (either contractual or voluntary) paid by the Advisor. The advisory fees and expense ratios of each Series were compared to an average (on both a mean and median basis) of similar funds as disclosed on the Morningstar database. Representatives of the Advisor discussed with the Board the levels of its advisory fee for each Series of the Fund and as compared to the median and mean advisory fees for similar funds as listed on Morningstar. Expense ratios for every Series, except the High Yield Bond Series, are currently below the median and mean for similar funds as listed on Morningstar. Based on their review of the information provided, the Board concluded that the fees and expenses of each Series of the Fund were reasonable on a comparative basis. |

| | • | | The Board also considered the other benefits the Advisor derives from its relationship with the Fund. Such other benefits include certain research products provided by soft dollars. Given the level of soft dollar transactions involving the Fund, the Board concluded that these additional benefits to the Advisor were reasonable. |

| | • | | In addition to the factors described above, the Board considered the Advisor’s personnel, investment strategies, policies and procedures relating to compliance with personal securities transactions, and reputation, expertise and resources in domestic and foreign financial markets. The Board concluded that these factors support the conclusion that the Advisor performs its services in a reasonable manner. |

| | • | | The Board did not consider economies of scale at this time because of the multiple uses of the Fund (for the Advisor’s discretionary investment account clients in addition to direct investors), the current profitability of the Advisor’s services to the Fund under the Current Investment Advisory Agreement, and the overall size of the Fund complex. |

Based on the Board’s deliberations and their evaluation of the information described above, the Board, including a majority of Directors that are “not interested” as defined in the Investment Company Act of 1940 (the “1940 Act”), concluded that the compensation under the Current Investment Advisory Agreement was fair and reasonable in light of the services and expenses and such other matters as the Directors considered to be relevant in the exercise of their reasonable judgment. Accordingly, the Board approved the renewal of the Current Investment Advisory Agreement for another year. In the course of their deliberations, the Directors did not identify any particular information that was all important or controlling.

As stated above, at the August 30, 2007 Board meeting, the Board concluded it was reasonable to take into account the conclusions set forth above when determining whether to approve the New Investment Advisory Agreement. The Board’s conclusion in this regard was based on the fact that the New Investment Advisory Agreement is identical to the Current Investment Advisory Agreement except for certain provisions of the Agreement which have been updated and modernized in response to the Board’s specific request. Further, the Board’s conclusion in this regard was based on the fact that the New Investment Advisory Agreement does not change either the investment advisory fees payable by the Fund to the Advisor or the day-to-day investment management services the Advisor provides to the Fund.

In addition to the conclusions formed with respect to the 2006 Annual Review, the Directors considered specific information at the August 30, 2007 Board meeting concerning the additional provisions included in the New Investment Advisory Agreement. The Directors considered the fact that these additional provisions are designed to (i) address and memorialize certain standard practices and regulatory requirements of mutual funds and their investment advisors; (ii) further

Renewal of Investment Advisory Agreements (unaudited)

delineate the duties and obligations of the Fund and the Advisor; (iii) modernize the agreement to reflect current industry practice and applicable law; and (iv) generally improve the overall quality of the agreement. The Board further considered the fact that the New Investment Advisory Agreement does not alter the actual day-to-day investment management services provided by the Advisor to each Series of the Fund, and the investment advisory fee rate paid to the Advisor under the New Investment Advisory Agreement for a Series is the same as the fee rate paid by the Series under the Current Investment Advisory Agreement.

Based on its evaluation of the information and the conclusions with respect thereto at its meetings on November 16, 2006 and August 30, 2007, the Board unanimously concluded that: (a) the terms of the New Investment Advisory Agreement were fair and reasonable; (b) the approval of the New Investment Advisory Agreement would be in the best interests of the shareholders and the Fund; and (c) it would recommend the approval of the New Investment Advisory Agreement to shareholders. In the course of their deliberations, the Board did not identify any particular information or factor that was all-important or controlling.

Consideration of Current Investment Advisory Agreement

At a meeting held on November 12, 2007, the Board considered the continuation of the Current Investment Advisory Agreement and simultaneously conducted its annual review of the services provided to the Fund by the Adviser (the “2007 Annual Review”). Representatives of the Advisor attended the meeting and presented additional oral and written information to the Board to assist the Board in its considerations. The discussion immediately below outlines the materials and information presented to the Board in connection with the Board’s 2007 Annual Review of the Current Investment Advisory Agreement and the conclusions made by the Directors when determining to continue the Current Investment Advisory Agreement.

In connection with its review and deliberations, the Board considered the following factors and reached a conclusion with respect to such factors.

| | • | | The Board considered the services provided by the Advisor under the Current Investment Advisory Agreement including, among others: deciding what securities to purchase and sell for each Series; arranging for the purchase and sale of such securities by placing orders with broker-dealers; administering the affairs of the Fund (including the books and records of the Fund not maintained by third party service providers such as the custodian or sub-transfer agent); arranging for the insurance coverage for the Fund; and supervising the preparation of tax returns, SEC filings (including registration statements) and reports to shareholders for the Fund. The Board also considered the nature and quality of such services provided under the Current Investment Advisory Agreement in light of the Advisor’s services provided to the Fund for 21 years. The Board discussed the quality of these services with representatives from the Advisor and concluded that the Advisor was performing its services to the Fund required under the Current Investment Advisory Agreement in a reasonable manner. |

| | • | | The Board considered the investment performance of the various Series of the Fund. The investment performance for each Series was reviewed on a cumulative basis since inception and on a one year basis. In addition, annualized performance for the following time periods was considered: inception, three year, five year, ten year, and current market cycle. A market cycle includes periods of both rising and falling markets. Returns for established benchmark indices for each Series were provided for |

Renewal of Investment Advisory Agreements (unaudited)

| | each time period. The Board noted that all the Series were competitive against their respective benchmark indices over all time periods noted above through September 30, 2007. In addition, the Board considered at the meeting (and considers on a quarterly basis) a peer group performance analysis consisting of Morningstar universes of mutual funds with similar investment objectives. The Board discussed the performance with representatives from the Advisor and concluded that the investment performance of each of the Fund’s Series was reasonable based on the Fund’s actual performance and comparative performance, especially performance over the current market cycle. |

| | • | | The Board considered the costs of the Advisor’s services and the profits of the Advisor as they relate to the Advisor’s services to the Fund under the Current Investment Advisory Agreement. In reviewing the Advisor’s costs and profits, the Board discussed the Advisor’s revenues generated from the Fund (on both an actual and adjusted basis) and its expenses associated with providing the services under the Current Investment Advisory Agreement. In addition, the Board reviewed the Advisor’s expenses associated with Fund activities outside of the Current Investment Advisory Agreement (such as expense reimbursements pursuant to expense caps and payments made by the Advisor to third party platforms on which shares of the Fund are available for purchase). It was noted by representatives of the Advisor that 4 of the 18 active Series of the Fund are currently experiencing expenses above the capped expense ratios. After discussing the above costs and profits, the Board concluded that the Advisor’s profitability relating to its services provided under the Current Investment Advisory Agreement was reasonable. |

| | • | | The Board considered the fees and expenses of the various Series of the Fund. The Advisor presented the advisory fees and total expenses for each Series, including the advisory fee adjusted for any expense waivers or reimbursements (either contractual or voluntary) paid by the Advisor. The advisory fees and expense ratios of each Series were compared to an average (on both a mean and median basis) of similar funds as disclosed on the Morningstar database. Representatives of the Advisor discussed with the Board the levels of its advisory fee for each Series of the Fund and as compared to the median and mean advisory fees for similar funds as listed on Morningstar. Expense ratios for every Series, except the High Yield Bond Series and Global Fixed Income Series, are currently below the median and mean for similar funds as listed on Morningstar. Based on their review of the information provided, the Board concluded that the fees and expenses of each Series of the Fund were reasonable on a comparative basis. |

| | • | | The Board also considered the other benefits the Advisor derives from its relationship with the Fund. Such other benefits include certain research products provided by soft dollars. Given the level of soft dollar transactions involving the Fund, the Board concluded that these additional benefits to the Advisor were reasonable. |

| | • | | In addition to the factors described above, the Board considered the Advisor’s personnel, investment strategies, policies and procedures relating to compliance with personal securities transactions, and reputation, expertise and resources in domestic and foreign financial markets. The Board concluded that these factors support the conclusion that the Advisor performs its services in a reasonable manner. |

Renewal of Investment Advisory Agreements (unaudited)

| | • | | The Board did not consider economies of scale at this time because of the multiple uses of the Fund (for the Advisor’s discretionary investment account clients in addition to direct investors), the current profitability of the Advisor’s services to the Fund under the Current Investment Advisory Agreement, and the overall size of the Fund complex. |

Based on the Board’s deliberations and their evaluation of the information described above, the Board, including a majority of Directors that are not “interested persons” as defined in the 1940 Act, concluded that the compensation under the Current Investment Advisory Agreement was fair and reasonable in light of the services and expenses and such other matters as the Directors considered to be relevant in the exercise of their reasonable judgment. Accordingly, the Board approved the renewal of the Current Investment Advisory Agreement. In the course of their deliberations, the Directors did not identify any particular information that was all important or controlling.

Proxy Voting Results (unaudited)

A special meeting of the shareholders of Manning & Napier Fund, Inc. was held on November 12, 2007. The number of votes necessary to conduct the meeting and approve each proposal was obtained, and the results of the votes of shareholders on proposals before them are listed below:

Election of Directors.

| | | | |

| | | Number of Shares

voted for | | Number of Shares

withheld |

B. Reuben Auspitz | | 215,932,354.541 | | 15,898,685.154 |

Stephen B. Ashley | | 215,960,751.214 | | 15,870,288.481 |

Peter L. Faber | | 217,504,725.208 | | 14,326,314.487 |

Harris H. Rusitzky | | 215,924,013.609 | | 15,907,026.086 |

To approve the investment advisory agreement between Manning & Napier Advisors, Inc. and Manning & Napier Fund, Inc.

| | |

| | | Number of shares voted |

For | | 3,191,080.260 |

Against | | 0 |

Abstain (includes broker non-votes) | | 0 |

Eliminating, amending, or reclassifying certain fundamental investment policies or restrictions.

Proposal 3.A.i. To approve changes to the fundamental policy regarding borrowing money.

| | |

| | | Number of shares voted |

For | | 3,191,080.260 |

Against | | 0 |

Abstain (includes broker non-votes) | | 0 |