| | |

OMB APPROVAL |

OMB Number: | | 3235-0570 |

Expires: | | September 30, 2007 |

Estimated average burden |

hours per response: | | 19.4 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-04088

Excelsior Funds, Inc.

(Exact name of registrant as specified in charter)

United States Trust Company of New York

114 West 47th Street

New York, New York 10036

(Address of principal executive offices) (Zip code)

BISYS Fund Services

3435 Stelzer Road

Columbus, Ohio 43219

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-212-852-1000

Date of fiscal year end: March 31, 2006

Date of reporting period: March 31, 2006

| Item 1. | Reports to Stockholders. |

EQUITY FUNDS

ANNUAL REPORT

March 31, 2006

TABLE OF CONTENTS

For shareholder account information, current price and yield quotations, or to make an initial purchase or obtain a prospectus, call 1-800-446-1012, from overseas, call 617-483-7297.

| · | | Internet Address: http://www.excelsiorfunds.com |

This report must be preceded or accompanied by a current prospectus.

A description of the policies and procedures that Excelsior Funds use to determine how to vote proxies relating to portfolio securities, as well as information relating to how a Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-800-446-1012, or (ii) by accessing the Excelsior Funds’ internet address and (iii) on the Commission’s website at http://www.sec.gov.

Excelsior Funds file their June 30 and December 31 schedule of portfolio holdings with the Securities and Exchange Commission, on Form N-Q, within sixty days after the applicable reporting period. Excelsior Funds Form N-Q is available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A schedule of each Fund’s portfolio holdings, as of the end of the prior month, is also available on the Funds’ website. This schedule is updated monthly, typically by the 15th calendar day, after the end of each month. The Funds may terminate or modify this policy at anytime.

You should consider the Funds’ investment objectives, risks and expenses carefully before you invest. Information about these and other important subjects is in the Funds’ prospectus, which you should read carefully before investing.

Excelsior Funds, Inc. and Excelsior Funds Trust are distributed by BISYS Fund Services Limited Partnership.

You may write to Excelsior Funds, Inc. and Excelsior Funds Trust at the following address:

Excelsior Funds

P.O. Box 8529

Boston, MA 02266-8529

SHARES IN THE FUNDS ARE NOT DEPOSITS OR OBLIGATIONS OF, OR GUARANTEED OR ENDORSED BY, UNITED STATES TRUST COMPANY OF NEW YORK, U.S. TRUST COMPANY, N.A. THEIR PARENT OR AFFILIATES AND SHARES ARE NOT INSURED BY THE FEDERAL DEPOSIT INSURANCE CORPORATION, THE FEDERAL RESERVE BOARD, OR ANY OTHER AGENCY. INVESTMENTS IN THE FUNDS INVOLVE INVESTMENT RISKS, INCLUDING POSSIBLE LOSS OF PRINCIPAL. FUND SHARES ARE NOT INSURED OR GUARANTEED BY THE U.S. GOVERNMENT.

LETTER TO SHAREHOLDERS

March 31, 2006

Dear Valued Excelsior Fund Shareholder,

I am pleased to bring you the annual report for the year ended March 31, 2006 for the Excelsior Funds. The funds in this report are part of the Excelsior Fund family which had over $18 billion in assets as of the end of the report period and includes a wide array of asset classes and investment strategies designed to meet the individual investor’s needs for performance and tax sensitivity.

By now, you would have received information about changes to the administrative and non-advisory services provided to the Excelsior Funds. As a result, the Excelsior Funds and the Laudus Funds, an affiliated fund family, now share certain complex-wide administrative, compliance, marketing and other functions.

We are pleased with the transition, and remain optimistic that shareholders will approve the board of directors’ recommendation to elect members to jointly oversee the two fund families. It is anticipated that the new unified board will strengthen the oversight provided on behalf of fund shareholders and may result in certain long-term cost and operating efficiencies. All votes are important, so I encourage you to vote your shares as soon as possible if you haven’t already done so.

Given these changes, I want to assure you that the most important aspects of the Excelsior Funds will remain the same. Specifically, the fund management and investment process provided by U.S. Trust, as advisor to the Funds, as well as the funds’ emphasis on enduring performance, will not change.

In closing, we at Excelsior Funds remain committed to helping you reach your long-term investment goals. Thank you for investing with us.

Sincerely,

Evelyn Dilsaver

President

1

We had expected that the financial markets would come into alignment with the financial environment being shaped by the Fed, and that finally came to pass as the fiscal year ending March 31, 2006 drew to a close. The markets improved as uncertainties about the Fed’s intentions, energy costs and Iraq were resolved to a degree—though the latter name was replaced by Iran as a geopolitical issue. Importantly, inflation is contained while growth has moderated to what we believe to be sustainable levels. We think the Fed’s economic shock effect has been temperate on growth overall. While GDP dipped in the fourth quarter of 2005, in response to hurricane after effects, it recovered to a 4.8% rate for the first quarter of 2006. Meanwhile, corporate profits, as reported for the first quarter, were strong indeed. Our confidence that a self-reinforcing expansion is underway continues firm.

Major equity indexes and averages posted new multi-year highs as the fiscal year came to an end. The financial markets reacted well to the Fed’s fifteenth sequential rate increase, to a federal funds rate target of 4.75%. Investors saw moderate economic growth ahead, with the potential for earnings growth, all within a context of well-contained inflation. Stocks, as measured by the Standard & Poor’s 500 Index, began to rally in the middle of the 2005 fourth-quarter, and that rally continued into the first quarter of 2006, making new five-year highs.

We think many of the equity investment themes that worked over the fiscal year should continue to prove successful. Overall, our themes are: (1) pricing power, (2) globalization, (3) secular reflation, (4) M&A, and (5) business versus the domestic consumer. In equities, we favor large-cap stocks over small caps, since small caps have had a long run that we believe is nearing an end. Our preference is for growth over value, when it comes to investment style—since we expect investors will target stable earnings growth, along with companies able to raise dividends and/or buyback shares. In sectors, we see housing slowing, and we continue to think the old economy, meaning industrials and commodity raw materials, especially metals, should outpace consumer sectors. We strongly favor global equities, and particularly those of emerging market nations aiming at developed world status, including China, India and Mexico, along with Russia and Australia as important sources of raw materials.

The Treasury yield curve inverted in the final months of 2005 and into January of 2006, with short-term rates higher than long-term interest rates. Recession fears were sparked, but were countered by no less than new Fed chairman, Ben Bernanke, who emphasized that yield curve inversion, rather than sending a signal of incipient recession, was, instead, a reflection of the global savings glut. We too believe that the yield-curve indicator will fail to reflect a downturn this time, and we are looking for GDP growth of at least 2.5% for full-year 2006. Nevertheless, the beginning of a slower U.S. consumer spending growth trend seems to be in place, and normally, the direct and indirect effects of a percentage point drop in real consumption growth would translate into an almost equal-size drop in GDP growth. But we don’t expect that because business and government spending is accelerating, and the global economy is picking up steam even as U.S. consumers moderate their spending habits.

2

EXCELSIOR FUNDS, INC. | BLENDED EQUITY FUND |

Annual Fiscal Year Review

Concerns over the economic backdrop were raised by the Fed continuing to tighten over the entire fiscal year, leaving the fed funds target rate at 4.75%. Tighter money was seen in clear signs of a slowing domestic housing market. This in turn is generating a strong headwind for the U.S. consumer. But business spending is beginning to ramp up, and strong overseas growth are providing offset, which should result in earnings growth for those companies with market share and pricing power. With the Fed presumably near the end of its monetary tightening cycle, we remain optimistic overall.

Performance Attribution

The Fund modestly under performed the benchmark. The Materials sector was the best-performing sector, benefiting from continued strong demand and pricing. Strong auction house results helped one of our holdings turn in a strong gain, while a number of our consumer stocks rebounded nicely from last year’s weakness. Our Canadian energy holding showed particular strength. We also had good performance among our technology, industrial and financial stocks. The portfolio’s holdings in power transmission underperformed. We initiated purchases in the rail transport sector, emphasizing leading companies that stress efficiency and optimization of rail networks. We also added in steel, emphasizing low-cost producers. Following the recent wave of industry consolidation, industry fundamentals and profitability are currently very strong. We also added in sports and fitness centers, which we expect to benefit from U.S. demographics. We also purchased in financial services, targeting a capital provider to middle market companies. We sold in electronic connectors and in food service distributors.

Outlook

We will continue to emphasize thorough portfolio diversification and those companies that possess favorable corporate cultures and effective employee incentives. We see continued moderate growth in the economy and corporate profits. Growth in the consumer sector should moderate while business spending and net exports strengthen. We believe the portfolio’s mix of stocks should benefit as the economic expansion matures and as growth makes progress over the next few years. We expect to continue our underweight exposure to technology as well as our overweights in materials and in the utility sector, where restructuring should support good returns.

3

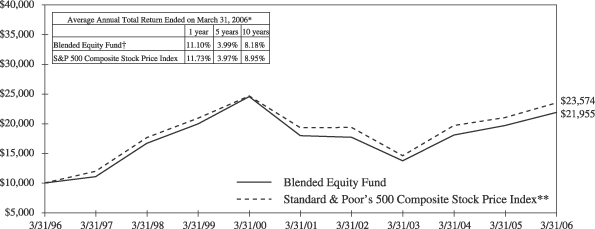

EXCELSIOR FUNDS, INC. | BLENDED EQUITY FUND |

Past performance is not predictive of future performance. Investment returns and principal values will vary and shares may be worth more or less at redemption than their original cost.

The above illustration compares a $10,000 investment made in the Fund and a broad-based index over the past ten fiscal years. The chart assumes all dividends and capital gain distributions are reinvested. The Fund’s performance takes into account fees and expenses. The index does not take into account charges, fees and other expenses. Further information relating to Fund performance is contained in the Financial Highlights section of the Prospectus and elsewhere in this report.

| * | | Total return represents the change during the period in a hypothetical account with dividends reinvested. |

| ** | | Source: Standard & Poor’s Corporation—Reflects the reinvestment of income dividends and, where applicable, capital gain distributions. The Standard & Poor’s 500 Composite Stock Price Index is a widely accepted unmanaged index of U.S. stock market performance. |

| † | | Currently certain fees are waived. Had certain fees not been waived, returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. |

4

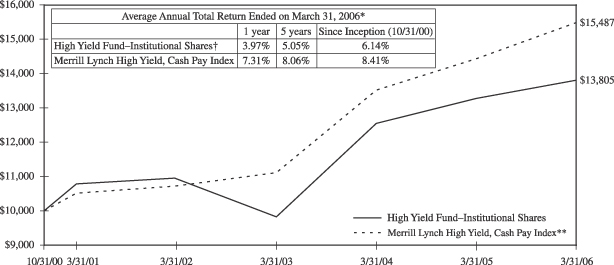

EXCELSIOR FUNDS, INC. | ENERGY AND NATURAL RESOURCES FUND |

Fiscal Year Annual Review

Over the twelve-month reporting period, oil, gas and metal prices moved higher. In the short-run, political pressure on supplies from Iraq, Iran, Nigeria and Venezuela helped lift prices. Hurricanes Katrina and Rita reduced the source of U.S. oil and gas by 20% and 10% respectively, at the end of the reporting period, also drove price spikes. And a cyclical increase in global demand, from China and India in particular, also contributed to prices reaching $70 per barrel by the end of the period. The only factor working to reduce demand was unseasonably warm winter weather in the U.S. Prices moved higher as we entered the new fiscal year.

Performance Attribution

The Fund more than doubled the return of the Standard & Poor’s 500 Index in the first quarter of 2006. The top performers were concentrated in the oil service sector and natural resource sectors. Oil services benefited from higher remediation activity in the Gulf of Mexico following hurricanes Rita and Katrina. On the resource side, higher pulp prices benefited our suppliers to paper producers. We have over-weighted the oil service sector, which is enjoying strong pricing leverage due to capacity constraints and rising drilling expenditures by the producers. Secondly, we have doubled our exposure to the independent refiners. We believe that refining margins should remain strong well into the second half of 2006, a function of a shrinking gasoline pool, as MTBE (a gasoline additive which accounts for 7% of supply), is withdrawn from gasoline under a federal mandate. On the resources side we added in steel, silver and coal. Coal demand is rising as utilities re-stock depleted inventories.

Outlook

The energy sector macro-drivers remain in place. Tight supply/demand fundamentals for North American natural gas and crude oil (with OPEC spare production capacity at a historic low of 1%-2% of global demand) continue. Strong prices for base metals such as copper are supported by ongoing industrialization in China. Barring a global recession, our resource sectors could remain structurally tight through the end of this decade.

5

EXCELSIOR FUNDS, INC. | ENERGY AND NATURAL RESOURCES FUND |

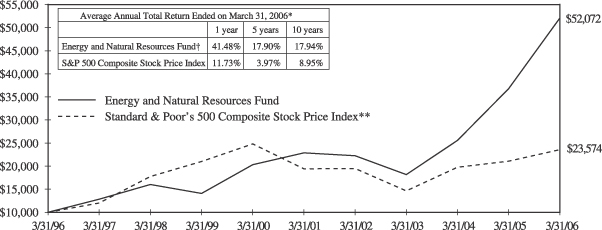

Past performance is not predictive of future performance. Investment returns and principal values will vary and shares may be worth more or less at redemption than their original cost. Concentration in one economic sector may subject an investor to greater volatility.

The above illustration compares a $10,000 investment made in the Fund and a broad-based index over the past ten fiscal years. The chart assumes all dividends and capital gain distributions are reinvested. The Fund’s performance takes into account fees and expenses. The index does not take into account charges, fees and other expenses. Further information relating to Fund performance is contained in the Financial Highlights section of the Prospectus and elsewhere in this report.

| * | | Total return represents the change during the period in a hypothetical account with dividends reinvested. |

| ** | | Source: Standard & Poor’s Corporation—Reflects the reinvestment of income dividends and, where applicable, capital gain distributions. The Standard & Poor’s 500 Composite Stock Price Index is a widely accepted unmanaged index of U.S. stock market performance. |

| † | | Currently certain fees are waived. Had certain fees not been waived, returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. One year returns presented in the table differs from the return presented in the Financial Highlights. This is a result of the calculation of the Financial Highlights return adhering to GAAP presentation. |

6

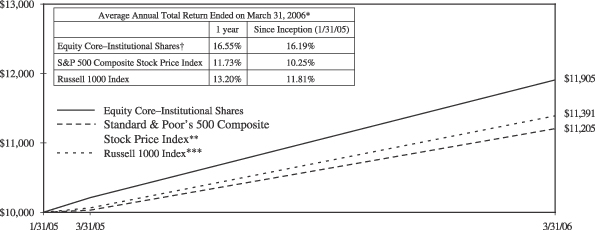

EXCELSIOR FUNDS TRUST | EQUITY CORE FUND |

Fiscal Year Annual Review

The economic backdrop during the fiscal year reflected strong global economic activity. Tightening interest rates in the U.S. clearly slowed the pace of growth, but not, we believe, to levels that will impact earnings growth for select companies with solid market share and pricing power. Both short and long-term interest rates continue to rise, but the Fed presumably is near the end of its monetary tightening cycle. We see clear signs of a slowing domestic housing market, which should lead to a strong headwind for the U.S. consumer. The stock market posted a solid return, with a rally in the last-calendar quarter, which accelerated through the first quarter of 2006, and our portfolio exhibited strong relative performance, which we expect to continue.

Performance Attribution

The Fund’s strong performance was spread across several market sectors. Materials was the best-performing sector, led by steel, pulp for paper, and construction materials. These companies benefited from continued strong demand and pricing in their respective markets. Our consumer holdings, saw gains from strong art auction results, as well as from increased spending on home furnishings, as the boomers continue to improve their retirement homes. We also recorded gains in our energy holdings, in selected technology stocks, financial services and in pharmaceuticals. We experienced moderate negative returns in land and medical devices. We initiated purchases in the rail transport sector, emphasizing leading companies that stress efficiency and optimization of rail networks. We also added in steel, emphasizing low-cost producers. We sold in electronic connectors and in food service distributors.

Outlook

We think the Fed is nearing the end of its monetary tightening cycle, and we still see continued moderate growth in the economy and corporate profits. Growth in the consumer sector should moderate while business spending and net exports strengthen. We believe the portfolio’s mix of stocks should benefit as the economic expansion matures and as growth makes progress over the next few years. We expect to continue our limited exposure to technology as well as our overweights in materials and in the utility sector, where restructuring should support good returns. We will continue to emphasize thorough portfolio diversification and those companies that possess favorable corporate cultures and effective employee incentives.

7

EXCELSIOR FUNDS TRUST | EQUITY CORE FUND |

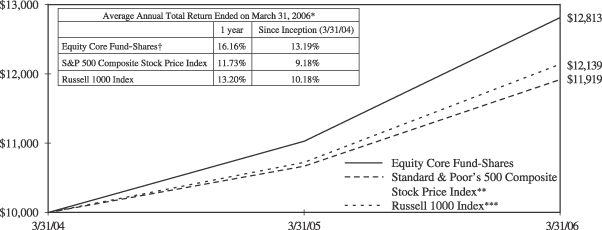

Past performance is not predictive of future performance. Investment returns and principal values will vary and shares may be worth more or less at redemption than their original cost.

The above illustration compares a $10,000 investment made in the Fund and a broad-based index since 3/31/04 (inception date). The chart assumes all dividends and capital gain distributions are reinvested. The Fund’s performance takes into account fees and expenses. The index does not take into account charges, fees and other expenses. Further information relating to Fund performance is contained in the Financial Highlights section of the Prospectus and elsewhere in this report.

| * | | Total return represents the change during the period in a hypothetical account with dividends reinvested. |

| ** | | Source: Standard & Poor’s Corporation—Reflects the reinvestment of income dividends and, where applicable, capital gain distributions. The Standard & Poor’s 500 Composite Stock Price Index is a widely accepted unmanaged index of U.S. stock market performance. |

| *** | | Source: Frank Russell Company—The Russell 1000 Index measures the performance of the 1,000 largest companies in the Russell 3000 Index, which represents approximately 92% of the total market capitalization of the Russell 3000 Index. The Index includes dividends reinvested. |

| † | | Currently certain fees are waived. Had such fees not been waived, returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. |

8

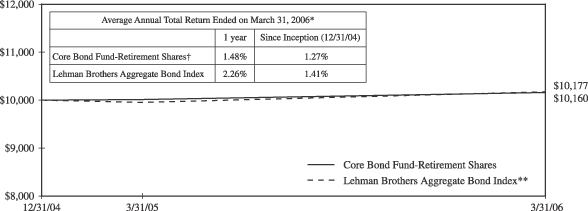

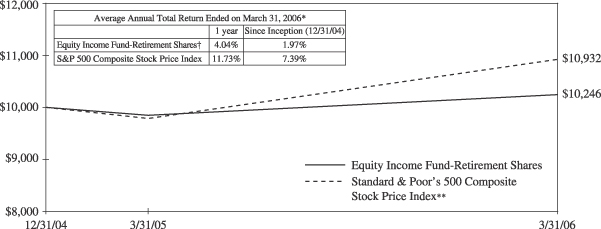

EXCELSIOR FUNDS TRUST | EQUITY INCOME FUND |

Fiscal Year Annual Review

The Equity Income Fund concentrates on investing in stocks that either pay above-average dividends or have the potential to grow their dividends. We are pleased that the trend of new first-time dividend initiation remains strong. Our efforts to grow our income stream by purchasing stocks with above-average dividend payouts from companies with progressive dividend growth policies continued to bear fruit over the fiscal year, ending March 31, 2006. Responding to a perceived need to improve shareholder return, corporate management is intiating new dividends, increasing dividends, and extending long histories of dividend payment.

Performance Attribution

During the reporting period, our performance was governed by a strong sell disciple, which enabled us to take profits as our price targets were attained. Our exposure to infrastructure-orientated industrials provided strong contributions. Furthermore, our decision to maintain positions in the telecommunications sector, while eliminating our exposure to power utilities, proved to be very rewarding. Improving sentiment toward telecommunication stocks has been the catalyst for their out-performance while higher interest rates have resulted in negative returns for utilities. Our holding in medical technology contributed only modest under performance. But our heavy underweight in energy and commodities resulted in under performance versus the benchmark. We added a number of new positions over the course of the fiscal year, emphasizing technology, pharmaceuticals and insurers. We targeted what we believe is an exceptional analog semiconductor company, with higher margins and returns on capital than their competitors. We also added a global pharmaceutical firm, with what we see as an attractive new drug pipeline and a drug portfolio that is not heavily exposed to off-patent runoffs. In insurance, we swapped from one re-insurer to another, to capitalize on a distinct valuation advantage. On the sale side, we trimmed in consumer electronics.

Outlook

We remain enthusiastic as many of the companies in our portfolio are growing their business values and increasing their dividends; however, in many cases this progress is not yet fully reflected in their share prices. By our way of thinking, these companies are more attractive today than at this time last year, and we believe we will be rewarded for our patience. Finally, payout ratios and dividend rates continue to rise, underscoring the dynamics that we are acutely focused on. While the Federal Reserves continues to implement tighter monetary policy, we see a soft landing for the economy, which should preserve corporate profit growth.

9

EXCELSIOR FUNDS TRUST | EQUITY INCOME FUND |

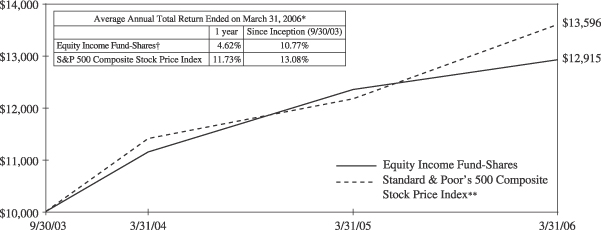

Past performance is not predictive of future performance. Investment returns and principal values will vary and shares may be worth more or less at redemption than their original cost.

The above illustration compares a $10,000 investment made in the Fund and a broad-based index since 9/30/03 (inception date). The chart assumes all dividends and capital gain distributions are reinvested. The Fund’s performance takes into account fees and expenses. The index does not take into account charges, fees and other expenses. Further information relating to Fund performance is contained in the Financial Highlights section of the Prospectus and elsewhere in this report.

| * | | Total return represents the change during the period in a hypothetical account with dividends reinvested. |

| ** | | Source: Standard & Poor’s Corporation—Reflects the reinvestment of income dividends and, where applicable, capital gain distributions. The Standard & Poor’s 500 Composite Stock Price Index is a widely accepted unmanaged index of U.S. stock market performance. |

| † | | Currently certain fees are waived. Had such fees not been waived, returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. |

10

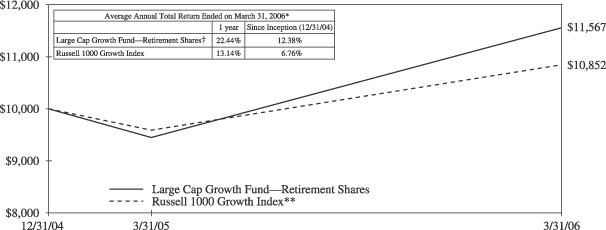

EXCELSIOR FUNDS, INC. | LARGE CAP GROWTH FUND |

Annual Fiscal Year Review

The market built on a strong 2005 post Thanksgiving rally, with one of the strongest first quarters since 1999, which saw the Standard & Poor’s 500 Index for the first quarter of 2006 better its full-year 2005 price gain. This solid performance in spite of continued Fed tightening, a long-awaited slow-down in housing activity, continued global geo-political angst, and higher oil and gas prices, suggests that consumers and investors remain optimistic. The U.S. economy continues to grow at a moderate pace while inflation remains a tame worry. Growth stocks appear relatively attractive on a price earnings basis versus Treasuries and real estate.

Performance Attribution

The Excelsior Large-Cap Growth Fund outpaced our large-cap growth benchmark over the reporting period. This outperformance can be attributed to successful stock selection, particularly within the telecom, financial, technology and consumer discretionary sectors. We favored what we saw as the beginning of a shift back to growth, from the prevailing value orientation of the markets. This strategy helped us capitalize with holdings in the Financial and Internet Industries, that were strong performers year-long. Our health care overweighting injured our relative performance as did our underweight in the energy and materials sectors. Normally, growth stocks would have outperformed value stocks at this stage of the business cycle. However, equity investors took their cues from the bond market and preferred to hold on to interest-rate-sensitive and low-multiple stocks until clear signs of a sustained rebound emerged.

Outlook

Our outlook remains optimistic, as we continue to find evidence that investors are returning to the growth style. Since profits grew at more than double the rate of stocks last year, we may have some more catching up to do. The comparative profit gap between the growth and value styles is beginning to expand in favor of growth. In summary, the earnings, valuation, and sentiment data support our view that the return of growth stock investing is just beginning. We expect the Federal Reserve to end its tightening process in the new fiscal year, and we look for a slow down in commodity and energy price gains. Significant post-hurricane rebuilding should also provide stimulus, and the Congressional elections should have positive impact. Overall, profit growth is likely to sustain the equity markets.

11

EXCELSIOR FUNDS, INC. | LARGE CAP GROWTH FUND |

Past performance is not predictive of future performance. Investment returns and principal values will vary and shares may be worth more or less at redemption than their original cost.

The above illustration compares a $10,000 investment made in the Fund and a broad-based index since 10/1/97 (inception date). The chart assumes all dividends and capital gain distributions are reinvested. The Fund’s performance takes into account fees and expenses. The index does not take into account charges, fees and other expenses. Further information relating to Fund performance is contained in the Financial Highlights section of the Prospectus and elsewhere in this report.

| * | | Total return represents the change during the period in a hypothetical account with dividends reinvested. |

| ** | | Source: Frank Russell Company—The Russell 1000 Growth Index is an unmanaged index composed of those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 1000 Index is composed of the 1000 largest companies in The Russell 3000 Index which is composed of 3,000 of the largest U.S. companies by market capitalization. The Index includes dividends reinvested. |

| † | | Currently certain fees are waived. Had certain fees not been waived, returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. |

12

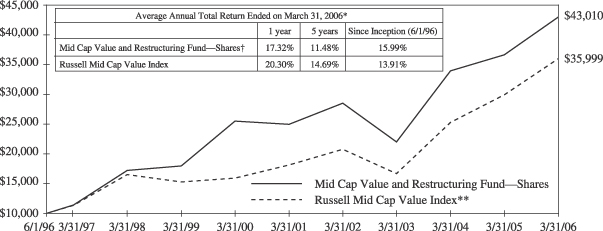

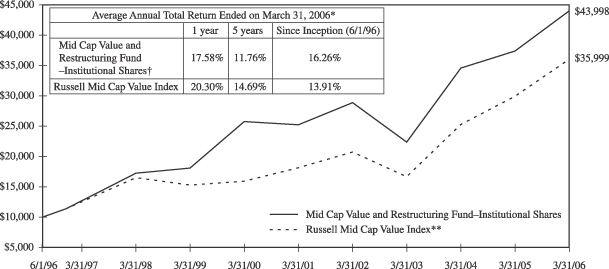

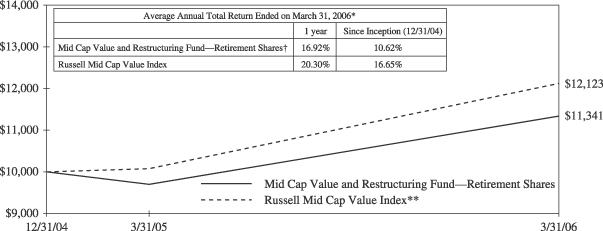

EXCELSIOR FUNDS TRUST | MID CAP VALUE AND RESTRUCTURING FUND |

Fiscal Year Annual Review

The Federal Reserve will eventually conclude its interest rate hikes and at sixteen times earnings, we believe stocks have room to advance. Over the course of the fiscal year, superb growth in corporate earnings and continued low inflation pushed stocks higher. We expect additional gains going forward despite the presence of several shorter-term negatives, including, high oil prices and rising short term interest rates. To our way of thinking, a moderate economic slow down should prove a sustainable source of earnings growth, especially for mid-cap companies poised to challenge their larger rivals.

Performance Attribution

We continue to target highly selective additions to the Fund. We added in consumer products, particularly in home furnishing, where we established a position with a leader in the specialty mattress category. As utilities restock, coal demand is increasing, and we added in this raw materials sector. We expect operating performance in this area to improve as capital expenditures are undertaken. We also opportunistically added to an existing position, which suffered a setback that we saw as temporary. Proceeds for these purchases came from selling in housewares and utilities. Merger and acquisition activity provided benefits, a trend we expect to continue. Mid-cap stocks were outperformers, with mid-cap indexes rising almost double what broad market measures returned. Our energy holdings continued to do well all year long, but non-energy related stocks also shone. Some of our star performers in prior years struggled, but these holdings continue to represent excellent long-term value in our estimation.

Outlook

Operating results of companies owned in the Fund were strong this year, marked by above average profitability and earnings growth. Continued merger and acquisition activity suggests a continuation of the favorable environment for our investment preference for restructuring companies. A few of the Fund’s troubled children, meaning its poor performing stocks, have recently shown signs of improved management. On the whole, the Fund’s investments sell at attractive discounts to market benchmarks on an earnings, cash flow and book value basis. While our expectations are therefore positive, we continue to keep the Fund well diversified, to mitigate risks, and remain true to our mission of purchasing stocks with improving fundamentals and low valuations.

13

EXCELSIOR FUNDS, INC. | MID CAP VALUE AND RESTRUCTURING FUND |

Past performance is not predictive of future performance. Investment returns and principal values will vary and shares may be worth more or less at redemption than their original cost.

The above illustration compares a $10,000 investment made in the Fund and a broad-based index since 6/1/96 (inception date). The chart assumes all dividends and capital gain distributions are reinvested. The Fund’s performance takes into account fees and expenses. The index does not take into account charges, fees and other expenses. Further information relating to Fund performance is contained in the Financial Highlights section of the Prospectus and elsewhere in this report.

| * | | Total return represents the change during the period in a hypothetical account with dividends reinvested. |

| ** | | Source: Frank Russell Company—The Russell Mid Cap Value Index measures the performance of medium-sized value-oriented securities. |

| † | | Currently certain fees are waived. Had certain fees not been waived, returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. |

14

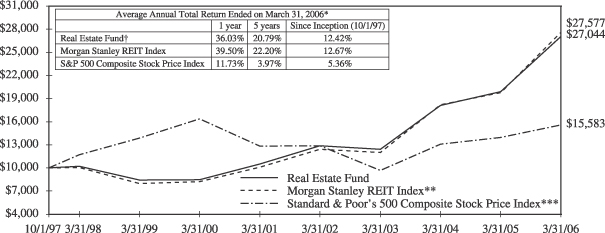

EXCELSIOR FUNDS, INC. | REAL ESTATE FUND |

Fiscal Year Annual Review

Three major themes were reflected in the Fund throughout the twelve-month reporting period: industry consolidation, index inclusion and healthy dividend growth. There were several acquisitions which saw larger REITs expand through acquisition; additionally, private buyers, intent on filling out real estate allocations and searching for income streams, also acquired individual REITs. Most of this capital flowed back into the sector during first quarter 2006; we think that these cash-recycled effects have now been absorbed into the market. By the end of the reporting period, the number of REITs in the Standard & Poor’s 500 Index stood at 12, for an annual increase in number greater than 25%. When it comes to dividends, of approximately 150 equity REITs, more than 50 increased their dividend rate in the reporting period, and we continue to think the overall economic picture will support continued REIT dividend growth.

Performance Attribution

Over the reporting period, the performance of REIT securities significantly exceeded that of most market indices. With the continued growth in the economy, investors are more confident of higher occupancy rates and future rental rates in the commercial sector. Among the major property sectors, the office sector was the best performer during the year. The health care properties and regional malls were the worst performers of the group. We initiated positions in two specialized mid-cap companies where we expect that the growth in cash flow and dividends should outpace that of their larger brethren over time. In addition, in sectors where fundamentals currently appear compelling, we initiated positions in a large-cap name in the apartment sector, a small-cap company in the lodging industry and a small-cap stock in the health care sector.

Outlook

In the first quarter of 2006, the last of the annual fiscal reporting period, we saw a flurry of merger and acquisitions transactions, specifically, with private buyers conducting multiple REIT acquisitions. With these major transactions now behind us, we expect a slowdown in M&A activity going forward. On the other hand, we have seen some of the major REITs paring back on their properties for very attractive returns, and we expect this trend to continue. Still, with the Fed increasing interest rates overall, negative pressure on equities, and REITs in particular, is increasing. Other income plays may become more attractive to investors as real estate financing becomes more expensive.

15

EXCELSIOR FUNDS, INC. | REAL ESTATE FUND |

Past performance is not predictive of future performance. Investment returns and principal values will vary and shares may be worth more or less at redemption than their original cost. Concentration in one economic sector may subject an investor to greater volatility.

The above illustration compares a $10,000 investment made in the Fund and broad-based indices since 10/1/97 (inception date). The chart assumes all dividends and capital gain distributions are reinvested. The Fund’s performance takes into account fees and expenses. The indices do not take into account charges, fees and other expenses. Further information relating to Fund performance is contained in the Financial Highlights section of the Prospectus and elsewhere in this report.

| * | | Total return represents the change during the period in a hypothetical account with dividends reinvested. |

| ** | | Source: Morgan Stanley & Co., Incorporated—Reflects the reinvestment of income dividends and, where applicable, capital gain distributions. The Morgan Stanley REIT Index is an unmanaged capitalization-weighted index composed of the largest and most actively traded REITs designed to provide a broad measure of real estate equity performance. |

| *** | | Source: Standard & Poor’s Corporation—Reflects the reinvestment of income dividends and, where applicable, capital gain distributions. The Standard & Poor’s 500 Composite Stock Price Index is a widely accepted unmanaged index of U.S. stock market performance. |

| † | | Currently certain fees are waived. Had certain fees not been waived, returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. |

16

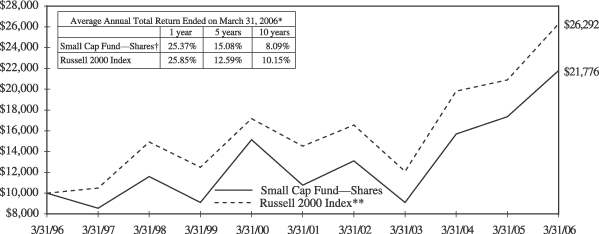

EXCELSIOR FUNDS, INC. | SMALL CAP FUND |

Annual Fiscal Year Review

The small cap trend seems to have confounded many experts who had concluded that the asset class was due for a bout of underperformance, given the strong multi-year run for small-caps in previous years. The simple fact is, in addition to still many very reasonable valuations, a vast liquidity shift in favor of hedge funds has occurred. These managers may find small and mid-cap issues far more appealing for rapid appreciation. It is very difficult for a hedge fund manager to influence the likes of large-cap industry leaders, but their ownership impact can be significant further down the food chain. Throughout the reporting period, an otherwise attractive environment for small-cap stocks, including positive macroeconomic trends and strong corporate fundamentals, the markets were overshadowed by the triple threat of rising market interest rates, surging oil prices, hurricane devastation and ongoing violence in the Middle East.

Performance Attribution

The portfolio’s positive return in the quarter was driven by several factors. Our long-term investors recall that our disciplines lead us to issues that have heretofore underperformed and carry low valuations relative to their own history. Technology has been a favored area for us. Very noticeably, for the first time in a long time, this sector has begun to contribute to performance. After almost six years of a tech bear market, we are seeing the confluence of many factors, which have led us to add new positions in this sector, and to increase existing holdings. The tech companies that survived the downturn have dramatically improved their balance sheets, utilization rates, and margin structure. At the same time, many firms are shrinking their share base through share repurchase programs. Hence, our activity focus continues on highly selective technology additions to the Fund’s portfolio.

Outlook

If we are correct in our assessment of hedge fund capital inflows as a prime motivator of small cap stock prices, we would look for a continuance of the current trend. Moreover, given our commitment to the technology sector, as capital spending by business ramps higher, we see expanded revenues leading to improved margins and with a smaller share count—a perfect formula for earnings leverage. We think technology is the likely beneficiary of a greater need for productivity, particular as global competition continues.

17

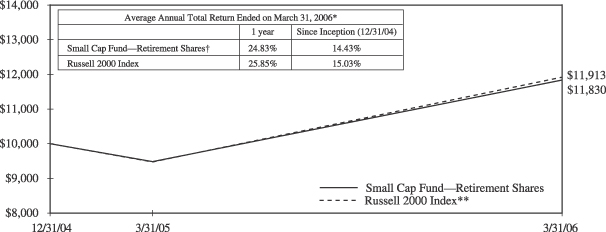

EXCELSIOR FUNDS, INC. | SMALL CAP FUND |

Past performance is not predictive of future performance. Investment returns and principal values will vary and shares may be worth more or less at redemption than their original cost. There is greater volatility associated with an investment in the Small Cap Market.

The above illustration compares a $10,000 investment made in the Fund and a broad-based index over the past ten fiscal years. The chart assumes all dividends and capital gain distributions are reinvested. The Fund’s performance takes into account fees and expenses. The index does not take into account charges, fees and other expenses. Further information relating to Fund performance is contained in the Financial Highlights section of the Prospectus and elsewhere in this report.

| * | | Total return represents the change during the period in a hypothetical account with dividends reinvested. |

| ** | | Source: Frank Russell Company—The Russell 2000 Index is an unmanaged index and is composed of the 2,000 smallest companies in the Russell 3000 Index. The Russell 3000 Index is composed of 3,000 of the largest U.S. companies by market capitalization. The index includes dividends reinvested. |

| † | | Currently certain fees are waived. Had certain fees not been waived, returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. |

18

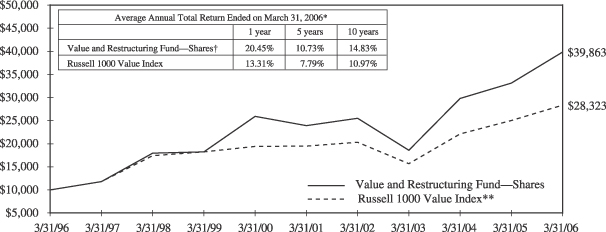

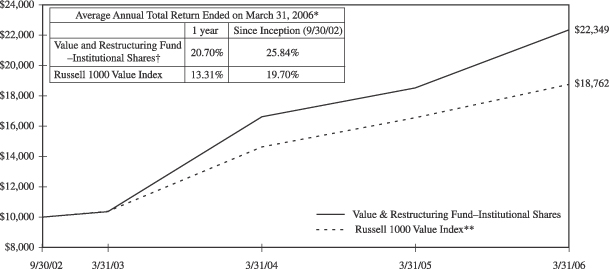

EXCELSIOR FUNDS, INC. | VALUE AND RESTRUCTURING FUND |

Annual Fiscal Year Review

Long-term equity fundamentals pointed toward higher stock prices in our estimation at the start of the twelve-month period ending March 31. Superb growth in corporate earnings and continued low inflation pushed stocks higher. Stocks mounted a major rally in the last quarter of 2005 and continued to make new five-year highs in the first quarter of 2006. The Federal Reserve will eventually conclude its interest rate hikes while stocks still have room, at sixteen times earnings, to advance.

Performance Attribution

The apparent abatement of corporate defensiveness and increased emphasis on improving businesses favored our type of investing throughout the year, and the fund saw two of its holdings acquired at a premium. Energy holdings continued to do well over the reporting period, and our holdings reflected higher oil and gas prices reflecting increased global demand and shortages from Hurricanes Rita and Katrina. Our non-energy related stocks also fared well, as commercial construction picked up for the first time since 2000 and rental equipment rates soared, boosting our holdings in the sector. Negative impact was recorded in real estate and mortgages; sectors that declined on rising interest rate concerns, as the Fed boosted the fed funds target rate to 4.75% by the end of the reporting period. But we think our holdings in this sector continue to represent excellent long-term value.

Outlook

On the whole, the Fund’s investments sell at an attractive discount to market benchmarks on an earnings, cash flow, and book value basis. Continued merger and acquisition activity suggests a continuation of the favorable environment for our investment preference for restructuring companies. While our expectations are therefore positive, we continue to keep the Fund well diversified to mitigate potential risks, and remain true to our mission of purchasing stocks with improving fundamentals and low valuations. We continue to look for improvement in the energy and commodity sectors, given global demand trends, and health care may prove an important source of positive performance in the coming year. Solid business growth should counteract the Fed’s tightening and higher energy costs, allowing for earnings acceleration for carefully selected stocks.

19

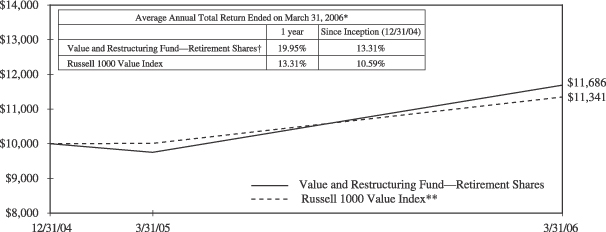

EXCELSIOR FUNDS, INC. | VALUE AND RESTRUCTURING FUND |

Past performance is not predictive of future performance. Investment returns and principal values will vary and shares may be worth more or less at redemption than their original cost.

The above illustration compares a $10,000 investment made in the Fund and a broad-based index over the past ten fiscal years. The chart assumes all dividends and capital gain distributions are reinvested. The Fund’s performance takes into account fees and expenses. The index does not take into account charges, fees and other expenses. Further information relating to Fund performance is contained in the Financial Highlights section of the Prospectus and elsewhere in this report.

| * | | Total return represents the change during the period in a hypothetical account with dividends reinvested. |

| ** | | Source: Frank Russell Company—The Russell 1000 Value Index is an unmanaged index composed of those Russell 1000 Index companies with lower price-to-book ratios and lower forecasted growth values. The Russell 1000 Index is composed of the 1000 largest companies in The Russell 3000 Index which is composed of 3,000 of the largest U.S. companies by market capitalization. The Index includes dividends reinvested. |

| † | | Currently certain fees are waived. Had certain fees not been waived, returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. |

20

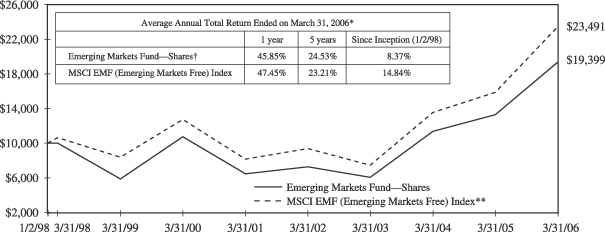

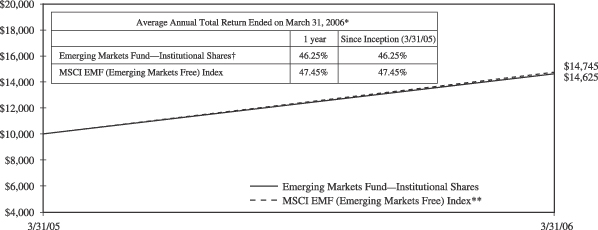

EXCELSIOR FUNDS, INC. | EMERGING MARKETS FUND |

Fiscal Year Annual Review

Emerging markets chalked up positive returns for the Fund’s fiscal year, continuing their longest streak of out performance since 1998. Larger-cap equities that are index constituents tended to lead the way. The BRIC countries (Brazil, Russia, India, and China) are becoming a focal point for emerging market investors. These four countries generated some of the best returns for the asset class, with Russia leading the way, followed by India, Brazil, and China in that order.

Performance Attribution

Strategically, from a sector perspective, the Fund has long believed that some of the best stock opportunities are in domestic related companies, as opposed to export oriented companies. We expressed this view by over weighting sectors like telecommunications, consumer stocks, and banks. Telecommunications has long been the largest sector over weight in the Fund. We hold cellular companies listed in Mexico, which are continuing to gain market share throughout Latin America. We also hold Russian long distance providers, where we see continued opportunity. On the consumer side, we targeted household equipment in Turkey and Mexico, where consumers are getting a boost from continued economic growth and moderating inflation. We also remain focused on banking stocks in Latin America, where reduced interest rates and declining inflation are benefiting banks and adding strong loan growth. From a pure country perspective, BRIC exposure also helped the Emerging Markets Fund. The Fund had over weights in Brazil, Russia, and China. We believe that country assessment is critical to the investment process, which led us to over weight these countries some time ago. Our relative under performance against the benchmark reflects greater caution in our investments in Latin America.

Outlook

Going forward, we continue to believe that domestic oriented stocks, as opposed to export driven stocks, will perform best in emerging markets. Many emerging market countries are benefiting from financial strength that is allowing them to withstand upward pressure on interest rates. This development could make for a very robust environment for domestic oriented emerging market stocks. Given these strong financial conditions and promising growth prospects, especially for the BRIC countries, we believe emerging markets can close the valuation gap with developed world equities. And we expect investors will come to terms with higher valuation levels for emerging market equities, and if the growth impetus for emerging markets shifts to domestic drivers, the valuation gap could be narrowed further.

21

EXCELSIOR FUNDS, INC. | EMERGING MARKETS FUND |

Past performance is not predictive of future performance. Investment returns and principal values will vary and shares may be worth more or less at redemption than their original cost. International investing is subject to special risks such as currency fluctuations and differences in accounting and taxation standards.

The above illustration compares a $10,000 investment made in the Fund and a broad-based index since 1/2/98 (inception date). For comparative purposes, the value of the index on 12/31/97 is used as the beginning value on 1/2/98. The chart assumes all dividends and capital gain distributions are reinvested. The Fund’s performance takes into account fees and expenses. The index does not take into account charges, fees and other expenses. Further information relating to Fund performance is contained in the Financial Highlights section of the Prospectus and elsewhere in this report.

| * | | Total return represents the change during the period in a hypothetical account with dividends reinvested. |

| ** | | Source: Morgan Stanley & Co., Incorporated—Morgan Stanley Capital International EMF (Emerging Markets Free) Index is a widely-accepted, unmanaged index composed of a sample of companies representative of the market structure of 26 global emerging market countries. The Index includes dividends reinvested. |

| † | | Currently certain fees are waived. Had such fees not been waived, returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. Returns do not reflect the 2% fee imposed on shares redeemed 30 days or less after their date of purchase. |

22

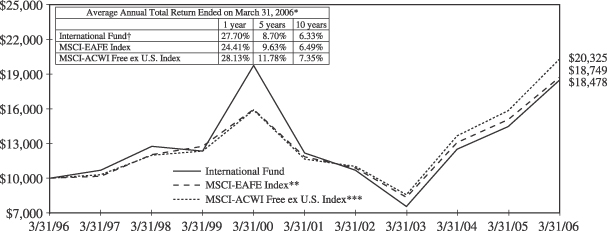

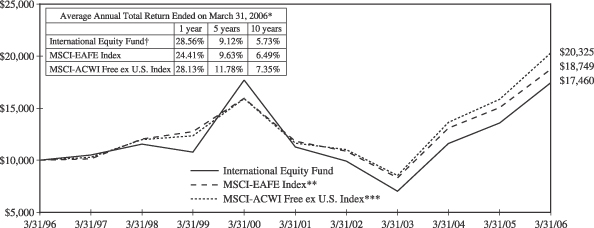

EXCELSIOR FUNDS, INC. | INTERNATIONAL FUND |

Annual Fiscal Year Review

International markets continued to strongly outperform the U.S. market for the twelve-month reporting period ending March 31, 2006. The performance differential was impressive with the global indexes approximately doubling the return for U.S. equities. Investors perceived overseas growth and relatively cheaper valuation as reasons for buying foreign stocks while the U.S. Federal Reserve continued to tighten monetary policy, raising the federal funds target rate to 4.75% by the end of the reporting period. The Fed’s action helped support the dollar, and exchange rate fluctuations added only marginally to the return of international equities during the quarter. Finally, the long-awaited turnaround of the Japanese economy has finally arrived, also contributing to strength for international equities.

Performance Attribution

The main contributor to the strong performance of the international equity benchmarks was the exceptional regional performance of the Continental European markets. Emerging markets continued to outperform the developed markets of the world based on strong investment flows. The BRIC markets (Brazil, Russia, India and China) continued to drive overall emerging markets performance, which is consistent with recent performance patterns. Strong earnings growth, attractive valuations and strongly improved quality characteristics of the emerging markets asset class are attracting heavy fund flows. Our sector weights, specifically, our underweight position in financials, continued to be detrimental to overall performance as the sector benefited from increased merger and acquisition (M&A) activity in Europe. The portfolio remains overweight in the information technology and health care sectors. This is largely offset by an underweight position in financial services. In Asia, consistent with our pursuit of eliminating internal portfolio inefficiencies, we eliminated smaller positions in consumer products and services.

Outlook

Our continued positive stance toward international investing is based on attractive relative valuations compared to U.S. equities. The U.S. profit cycle appears to be near a peak, whereas profits in most international markets have ample room to expand. We continue to favor the Japanese equity market, since stock valuations are not remotely reflecting the surprising strength of the Japanese economic recovery. Solid earnings growth acceleration and continued M&A activity continue to make Europe an attractive investment destination. Our exposure to Emerging Markets is approaching a benchmark-neutral position. Our expectations relative to domestic positions remain considerably higher.

23

EXCELSIOR FUNDS, INC. | INTERNATIONAL FUND |

Past performance is not predictive of future performance. Investment returns and principal values will vary and shares may be worth more or less at redemption than their original cost. International investing is subject to special risks such as currency fluctuations and differences in accounting and taxation standards.

The above illustration compares a $10,000 investment made in the Fund and broad-based indices over the past ten fiscal years. The chart assumes all dividends and capital gain distributions are reinvested. The Fund’s performance takes into account fees and expenses. The indices do not take into account charges, fees and other expenses. Further information relating to Fund performance is contained in the Financial Highlights section of the Prospectus and elsewhere in this report.

| * | | Total return represents the change during the period in a hypothetical account with dividends reinvested. |

| ** | | Source: Morgan Stanley & Co., Incorporated—Morgan Stanley Capital International EAFE (Europe, Australia, Asia, Far East) Index is a widely accepted, unmanaged index composed of a sample of companies from 21 countries representing the developed stock markets outside North America. |

| *** | | Source: Morgan Stanley & Co., Incorporated—Morgan Stanley Capital International All Country World Index Free ex U.S. is a widely accepted, unmanaged index of global stock market performance comprising 47 countries with developed and emerging markets excluding the United States. |

| † | | Currently certain fees are waived. Had such fees not been waived returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. Returns do not reflect the 2% fee imposed on shares redeemed 30 days or less after their date of purchase. |

24

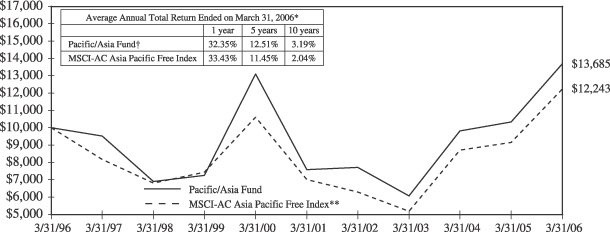

EXCELSIOR FUNDS, INC. | PACIFIC/ASIA FUND |

Fiscal Year Annual Review

The evidence continues to mount that the Japanese economy is indeed in a turnaround mode. This was the major change in the financial environment throughout the twelve-month reporting period, ending March 31. Discussions by the Bank of Japan regarding the end to their Quantitative Easing program of lower interest rates lend strong support to this viewpoint. Even oil prices, which were up thirty percent in the period, failed to hold back the emerging Japanese economic transformation. Currency has had little effect on the Fund’s performance in the first quarter. The Yen was essentially flat with only the Korean Won having any measurable effect. We expect further strengthening of Asian currencies as the year progresses, and relative to the U.S. dollar, so the Yen could add to the Fund’s performance.

Performance Attribution

Overall, looking back twelve-months, performance was quite disparate on a country basis. Japan, as noted, provided positive impetus for the Fund. Elsewhere around the region, much stronger performance was to be had from Indonesia, India and Thailand. These markets have been strong on the back of domestic strong consumption trends. Sector performance saw gains in food and chemicals. Negative performance came from Thai-based financials. The Fund continues to raise its exposure to the Japanese market, in particular in the area of financials and consumer products and services. Although we sold one Japanese position, we added four others in: financials (several), real estate and ceramics for technology. We sold our positions in a number of stocks that had produced strong returns for the Fund and had reached valuation targets, particularly in the energy sector.

Outlook

We expect that the primary drivers of performance for the year ahead will be economic growth in China and Japan. China must continue on a single-digit, managed path of economic development, to avoid inflation problems. The infrastructure build-out for the 2008 Olympics in China should continue to fuel Beijing’s needs for global commodities. Japan, must not derail the growth that the economy has exhibited for the past year, and it must continue to lead its economy out of a deflationary episode of many years duration. But we see strong growth engines in the Fund’s region continuing to contribute to future performance.

25

EXCELSIOR FUNDS, INC. | PACIFIC/ASIA FUND |

Past performance is not predictive of future performance. Investment returns and principal values will vary and shares may be worth more or less at redemption than their original cost. International investing is subject to special risks such as currency fluctuations and differences in accounting and taxation standards.

The above illustration compares a $10,000 investment made in the Fund and a broad-based index over the past ten fiscal years. The chart assumes all dividends and capital gain distributions are reinvested. The Fund’s performance takes into account fees and expenses. The index does not take into account charges, fees and other expenses. Further information relating to Fund performance is contained in the Financial Highlights section of the Prospectus and elsewhere in this report.

| * | | Total return represents the change during the period in a hypothetical account with dividends reinvested. |

| ** | | Source: Morgan Stanley & Co., Incorporated—The Morgan Stanley Capital International All Country Asia Pacific Free Index is a widely-accepted, unmanaged index composed of a sample of companies representative of the market structure of 10 developed and emerging market countries: China Free, Hong Kong, Japan, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand. The Index aims to capture 85% of the free float adjusted market capitalization in each industry group, in each country, for those securities not subject to foreign ownership restrictions. The Index includes dividends reinvested. |

| † | | Currently certain fees are waived. Had such fees not been waived, returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. Returns do not reflect the 2% fee imposed on shares redeemed 30 days or less after their date of purchase. |

26

Excelsior Funds, Inc.

Portfolio of Investments — March 31, 2006

Blended Equity Fund

| | | | | |

Shares

| | | | Value

|

| COMMON STOCKS — 97.09% |

| | | CONSUMER DISCRETIONARY — 13.58% |

| 57,093 | | Autozone, Inc.(a) | | $ | 5,691,601 |

| 89,443 | | Coach, Inc.(a) | | | 3,092,939 |

| 38,124 | | Dillards, Inc., Class A | | | 992,749 |

| 195,565 | | Eastman Kodak Co. | | | 5,561,869 |

| 98,800 | | eBay(a) | | | 3,859,128 |

| 304,540 | | Furniture Brands International, Inc. | | | 7,464,275 |

| 1,155 | | Interpublic Group of Companies, Inc.(a) | | | 11,042 |

| 255,940 | | John Wiley & Sons, Class A | | | 9,687,329 |

| 126,466 | | Life Time Fitness, Inc.(a) | | | 5,924,932 |

| 189,096 | | Sotheby’s Holdings, Inc., Class A(a) | | | 5,491,348 |

| 176,400 | | Target Corp. | | | 9,174,564 |

| 163,030 | | Timberland Co., Class A(a) | | | 5,580,517 |

| | | | |

|

|

| | | | | | 62,532,293 |

| | | | |

|

|

| | | CONSUMER STAPLES — 6.50% |

| 88,200 | | Altria Group, Inc. | | | 6,249,852 |

| 158,542 | | Anheuser Busch Cos., Inc. | | | 6,780,841 |

| 51,200 | | Kellogg Co. | | | 2,254,848 |

| 156,100 | | Wal-Mart Stores, Inc. | | | 7,374,164 |

| 50,000 | | Walgreen Co. | | | 2,156,500 |

| 79,899 | | Wm. Wrigley Jr. Co. | | | 5,113,536 |

| | | | |

|

|

| | | | | | 29,929,741 |

| | | | |

|

|

| | | ENERGY — 8.51% |

| 129,044 | | Apache Corp. | | | 8,453,672 |

| 37,100 | | Chevron Corp. | | | 2,150,687 |

| 258,697 | | Exxon Mobil Corp. | | | 15,744,300 |

| 13,200 | | Royal Dutch Shell plc ADR | | | 821,832 |

| 155,608 | | Suncor Energy, Inc. | | | 11,984,928 |

| | | | |

|

|

| | | | | | 39,155,419 |

| | | | |

|

|

| | | FINANCIAL — 17.63% |

| 154,000 | | American Capital Strategies Ltd. | | | 5,414,640 |

| 92,600 | | American Express Co. | | | 4,866,130 |

| 56,591 | | American International Group, Inc. | | | 3,740,099 |

| 18,520 | | Ameriprise Financial, Inc. | | | 834,511 |

| 168,520 | | Bank of America Corp. | | | 7,674,401 |

| 74 | | Berkshire Hathaway, Inc., Class A(a) | | | 6,685,900 |

| 48,387 | | Goldman Sachs Group, Inc. | | | 7,594,824 |

| 23,350 | | HSBC Holdings plc ADR | | | 1,956,263 |

| | | | | |

Shares

| | | | Value

|

| COMMON STOCKS — (continued) |

| | | FINANCIAL — (continued) |

| 177,321 | | Leucadia National Corp. | | $ | 10,578,971 |

| 49,088 | | Mellon Financial Corp. | | | 1,747,533 |

| 55,600 | | Merrill Lynch & Co., Inc. | | | 4,379,056 |

| 119,588 | | RenaissanceRe Holdings Ltd. | | | 5,216,429 |

| 213,100 | | State Street Corp. | | | 12,877,633 |

| 177,300 | | Washington Mutual, Inc. | | | 7,556,526 |

| | | | |

|

|

| | | | | | 81,122,916 |

| | | | |

|

|

| | | HEALTH CARE — 11.11% | | | |

| 180,800 | | Abbott Laboratories | | | 7,678,576 |

| 22,100 | | Genzyme Corp.- General Division(a) | | | 1,485,562 |

| 28,000 | | HCA, Inc. | | | 1,282,120 |

| 18,100 | | Hospira, Inc.(a) | | | 714,226 |

| 235,270 | | Johnson & Johnson | | | 13,932,690 |

| 107,195 | | Medtronic, Inc. | | | 5,440,146 |

| 107,252 | | Novo-Nordisk A/S ADR | | | 6,659,277 |

| 301,300 | | Pfizer, Inc. | | | 7,508,396 |

| 59,100 | | Schering Plough Corp. | | | 1,122,309 |

| 68,715 | | WellPoint, Inc.(a) | | | 5,320,602 |

| | | | |

|

|

| | | | | | 51,143,904 |

| | | | |

|

|

| | | INDUSTRIALS — 10.36% | | | |

| 3,000,000 | | Bombardier, Inc., Class B(a) | | | 8,736,000 |

| 115,826 | | Canadian National Railway Co. | | | 5,244,601 |

| 52,100 | | Dover Corp. | | | 2,529,976 |

| 631,184 | | General Electric Co. | | | 21,952,579 |

| 46,850 | | Illinois Tool Works, Inc. | | | 4,512,124 |

| 63,291 | | Quanta Services, Inc.(a) | | | 1,013,922 |

| 35,000 | | Tyco International Ltd. | | | 940,800 |

| 78,500 | | Waste Management, Inc. | | | 2,771,050 |

| | | | |

|

|

| | | | | | 47,701,052 |

| | | | |

|

|

| | | INFORMATION TECHNOLOGY — 11.48% |

| 694,444 | | 3com Corp.(a) | | | 3,555,553 |

| 152,352 | | Analog Devices, Inc. | | | 5,833,558 |

| 21,000 | | Broadcom Corp., Class A(a) | | | 906,360 |

| 432,065 | | Cisco Systems, Inc.(a) | | | 9,362,849 |

| 65,239 | | International Business Machines Corp. | | | 5,380,260 |

| 316,700 | | Microsoft Corp. | | | 8,617,407 |

| 234,468 | | National Instruments Corp. | | | 7,648,346 |

| 141,200 | | NCR Corp.(a) | | | 5,900,748 |

| 26,000 | | Nvidia Corp.(a) | | | 1,488,760 |

| 75,022 | | SAP AG ADR | | | 4,075,195 |

See Notes to Financial Statements.

27

Excelsior Funds, Inc.

Portfolio of Investments — March 31, 2006

Blended Equity Fund — (continued)

| | | | | |

Shares

| | | | Value

|

| COMMON STOCKS — (continued) |

| | | INFORMATION TECHNOLOGY — (continued) |

| 6,220 | | Symbol Technologies, Inc. | | $ | 65,808 |

| | | | |

|

|

| | | | | | 52,834,844 |

| | | | |

|

|

| | | RAW/INTERMEDIATE MATERIALS — 7.98% |

| 255,093 | | Aracruz Cellulose S.A. ADR | | | 13,504,623 |

| 128,846 | | E.I. Du Pont de Nemours & Co. | | | 5,438,590 |

| 100,147 | | Nucor Corp. | | | 10,494,404 |

| 84,424 | | Vulcan Materials Co. | | | 7,315,340 |

| | | | |

|

|

| | | | | | 36,752,957 |

| | | | |

|

|

| | | REAL ESTATE — 2.39% | | | |

| 175,018 | | St. Joe Co. | | | 10,998,131 |

| | | | |

|

|

| | | UTILITIES — 7.55% | | | |

| 384,715 | | AES Corp.(a) | | | 6,563,238 |

| 482,621 | | Centerpoint Energy, Inc. | | | 5,757,669 |

| 597,681 | | EL Paso Corp. | | | 7,202,056 |

| 301,471 | | Sierra Pacific Resources(a) | | | 4,163,315 |

| 247,000 | | TXU Corp. | | | 11,055,719 |

| | | | |

|

|

| | | | | | 34,741,997 |

| | | | |

|

|

| | | TOTAL COMMON STOCKS

(Cost $256,592,210) | | | 446,913,254 |

| FOREIGN COMMON STOCKS — 1.91% |

| | | GERMANY — 1.91% | | | |

| 160,000 | | Bayerische Motoren Werke AG | | | 8,811,879 |

| | | | |

|

|

| | | TOTAL FOREIGN COMMON STOCKS

(Cost $6,879,108) | | | 8,811,879 |

| | | | |

|

|

| | | | | |

Principal

Amount

| | | | Value

|

| REPURCHASE AGREEMENT — 2.62% |

| $12,058,000 | | JP Morgan Chase Securities, Inc., 3.40%, dated 03/31/06, to be repurchased 04/03/06, repurchase price $12,061,416 (collateralized by U.S. Treasury Note, par value $9,032,000, 8.125%, maturing 08/15/21; total market value $12,147,188) | | $ | 12,058,000 |

| | | | |

|

|

| | | TOTAL REPURCHASE AGREEMENT

(Cost $12,058,000) | | | 12,058,000 |

| | | | |

|

|

| | | | | | | |

TOTAL INVESTMENTS

(Cost $275,529,318)(b) | | 101.62 | % | | $ | 467,783,133 | |

LIABILITIES IN EXCESS OF

OTHER ASSETS | | (1.62 | ) | | | (7,473,923 | ) |

| | |

|

| |

|

|

|

NET ASSETS | | 100.00 | % | | $ | 460,309,210 | |

| | |

|

| |

|

|

|

| (a) | Non-income producing security. |

| (b) | Unrealized appreciation (depreciation) of securities: |

| | | | |

Unrealized

Appreciation

| | Unrealized

(Depreciation)

| | Net Unrealized

Appreciation/

(Depreciation)

|

| $194,361,643 | | $(2,107,828) | | $192,253,815 |

ADR—American Depository Receipt

Ltd.—Limited

plc—Public Limited Company

See Notes to Financial Statements.

28

Excelsior Funds, Inc.

Portfolio of Investments — March 31, 2006

Blended Equity Fund — (continued)

The summary of the Fund’s investments as of March 31, 2006 is as follows: (Unaudited)

| | | | | | | |

Sector Diversification

| | % of

Net

Assets

| | | Value

| |

Financial | | 17.63 | % | | $ | 81,122,916 | |

Consumer Discretionary | | 15.49 | | | | 71,344,172 | |

Information Technology | | 11.48 | | | | 52,834,844 | |

Health Care | | 11.11 | | | | 51,143,904 | |

Industrials | | 10.36 | | | | 47,701,052 | |

Energy | | 8.51 | | | | 39,155,419 | |

Raw/Intermediate Materials | | 7.98 | | | | 36,752,957 | |

Utilities | | 7.55 | | | | 34,741,997 | |

Consumer Staples | | 6.50 | | | | 29,929,741 | |

Repurchase Agreement | | 2.62 | | | | 12,058,000 | |

Real Estate | | 2.39 | | | | 10,998,131 | |

| | |

|

| |

|

|

|

Total Investments | | 101.62 | % | | $ | 467,783,133 | |

Liabilities in Excess of Other Assets | | (1.62 | ) | | | (7,473,923 | ) |

| | |

|

| |

|

|

|

Net Assets | | 100.00 | % | | $ | 460,309,210 | |

| | |

|

| |

|

|

|

See Notes to Financial Statements.

29

Excelsior Funds, Inc.

Portfolio of Investments — March 31, 2006

Energy and Natural Resources Fund

| | | | | |

Shares

| | | | Value

|

| COMMON STOCKS — 98.31% | | |

| | | ENERGY — 73.78% | | | |

| 570,400 | | Allis-Chalmers Energy, Inc.(a) | | $ | 7,774,552 |

| 100,000 | | Anadarko Petroleum Corp. | | | 10,101,000 |

| 138,000 | | Apache Corp. | | | 9,040,380 |

| 100,000 | | Arena Resources, Inc.(a) | | | 3,490,000 |

| 115,000 | | Atwood Oceanics, Inc.(a) | | | 11,616,150 |

| 400,000 | | Bill Barrett Corp. (a) | | | 13,036,000 |

| 180,600 | | BJ Services Co. | | | 6,248,760 |

| 62,740 | | BP plc ADR | | | 4,325,296 |

| 200,000 | | Bronco Drilling Co., Inc.(a) | | | 5,260,000 |

| 225,000 | | Cheniere Energy, Inc.(a) | | | 9,128,250 |

| 144,500 | | Chesapeake Energy Corp. | | | 4,538,745 |

| 106,388 | | Devon Energy Corp. | | | 6,507,754 |

| 63,000 | | Diamond Offshore Drilling | | | 5,638,500 |

| 1,038,000 | | Endeavor International Corp.(a) | | | 3,020,580 |

| 250,000 | | ENSCO International, Inc. | | | 12,862,500 |

| 1,100,000 | | Gasco Energy, Inc.(a) | | | 6,160,000 |

| 210,000 | | GlobalSantaFe Corp. | | | 12,757,500 |

| 250,000 | | GMX Resources, Inc.(a) | | | 9,362,500 |

| 250,000 | | Grant Prideco, Inc.(a) | | | 10,710,000 |

| 500,000 | | Hanover Compressor Co.(a) | | | 9,310,000 |

| 2,500,000 | | Kodiak Oil & Gas Corp.(a) | | | 6,037,500 |

| 92,300 | | Nabors Industries Ltd.(a) | | | 6,606,834 |

| 210,000 | | National-Oilwell, Inc.(a) | | | 13,465,200 |

| 221,600 | | Newfield Exploration Co.(a) | | | 9,285,040 |

| 147,800 | | Noble Corp. | | | 11,986,580 |

| 700,000 | | Parallel Petroleum Corp.(a) | | | 12,915,000 |

| 200,000 | | Patterson-UTI Energy, Inc. | | | 6,392,000 |

| 500,000 | | Petrohawk Energy Corp.(a) | | | 6,850,000 |

| 640,000 | | Petroquest Energy, Inc.(a) | | | 6,457,600 |

| 334,500 | | Range Resources Corp. | | | 9,135,195 |

| 115,500 | | Schlumberger Ltd. | | | 14,618,835 |

| 177,600 | | Southwestern Energy Co.(a) | | | 5,716,944 |

| 147,800 | | Suncor Energy, Inc. | | | 11,383,556 |

| 200,000 | | Talisman Energy, Inc. | | | 10,636,000 |

| 150,000 | | Tesoro Corp. | | | 10,251,000 |

| 181,200 | | TETRA Technologies, Inc.(a) | | | 8,523,648 |

| 400,000 | | Todco, Class A | | | 15,764,000 |

| 152,400 | | Transocean Sedco Forex, Inc.(a) | | | 12,237,720 |

| 113,400 | | Ultra Petroleum Corp.(a) | | | 7,065,954 |

| 350,000 | | Valero Energy | | | 20,922,999 |

| 544,500 | | Willbros Group, Inc.(a) | | | 11,075,130 |

| 166,666 | | XTO Energy, Inc. | | | 7,261,638 |

| | | | |

|

|

| | | | | | 385,476,840 |

| | | | |

|

|

| | | | | |

Shares

| | | | Value

|

| COMMON STOCKS — (continued) | | |

| | | RAW/INTERMEDIATE MATERIALS — 23.17% |

| 150,000 | | 3M Co. | | $ | 11,353,500 |

| 97,500 | | Aracruz Cellulose S.A. ADR | | | 5,161,650 |

| 160,000 | | Arch Coal, Inc. | | | 12,150,400 |

| 200,000 | | Canadian Natural Resources Ltd. | | | 11,078,000 |

| 202,100 | | Freeport-McMoRan Copper & Gold, Inc., Class B | | | 12,079,517 |

| 1,500,000 | | Hecla Mining Co.(a) | | | 9,915,000 |

| 175,000 | | Holly Corp. | | | 12,971,000 |

| 700,000 | | Kinross Gold Corp.(a) | | | 7,651,000 |

| 75,000 | | Newmont Mining Corp. | | | 3,891,750 |

| 196,000 | | Peabody Energy Corp. | | | 9,880,360 |

| 158,800 | | Phelps Dodge Corp. | | | 12,788,164 |

| 200,000 | | United States Steel Corp. | | | 12,136,000 |

| | | | |

|

|

| | | | | | 121,056,341 |

| | | | |

|

|

| | | UTILITIES — 1.36% | | |

| 332,000 | | Williams Cos., Inc. | | | 7,101,480 |

| | | | |

|

|

| | | TOTAL COMMON STOCKS

(Cost $455,466,737) | | | 513,634,661 |

| | | | |

|

|

| | |

Principal

Amount

| | | | |

| REPURCHASE AGREEMENT — 4.08% | | |

| $21,335,000 | | JP Morgan Chase Securities, Inc., 3.40%, dated 03/31/06, to be repurchased 04/03/06, repurchase price $21,341,045 (collateralized by U.S. Treasury Note, par value $15,981,000, 8.125%, maturing 08/15/21; total market value $21,492,778) | | | 21,335,000 |

| | | | |

|

|

| | | TOTAL REPURCHASE AGREEMENT

(Cost $21,335,000) | | | 21,335,000 |

| | | | |

|

|

| | | | | | | |

TOTAL INVESTMENTS

(Cost $476,801,737)(b) | | 102.39 | % | | $ | 534,969,661 | |

LIABILITIES IN EXCESS OF

OTHER ASSETS | | (2.39 | ) | | | (12,463,721 | ) |

| | |

|

| |

|

|

|

NET ASSETS | | 100.00 | % | | $ | 522,505,940 | |

| | |

|

| |

|

|

|

See Notes to Financial Statements.

30

Excelsior Funds, Inc.

Portfolio of Investments — March 31, 2006

Energy and Natural Resources Fund — (continued)

| (a) | Non-income producing security. |

| (b) | Unrealized appreciation (depreciation) of securities: |

| | | | |

Unrealized

Appreciation

| | Unrealized

(Depreciation)

| | Net Unrealized

Appreciation/

(Depreciation)

|

| $63,953,948 | | $(5,786,024) | | $58,167,924 |

ADR—American Depository Receipt

Ltd.—Limited

plc—public limited company

The summary of the Fund’s investments as of March 31, 2006 is as follows: (Unaudited)

| | | | | | | |

Sector Diversification

| | % of

Net

Assets

| | | Value

| |

Energy | | 73.78 | % | | $ | 385,476,840 | |

Raw/Intermediate Materials | | 23.17 | | | | 121,056,341 | |

Repurchase Agreement | | 4.08 | | | | 21,335,000 | |

Utilities | | 1.36 | | | | 7,101,480 | |

| | |

|

| |

|

|

|

Total Investments | | 102.39 | % | | $ | 534,969,661 | |

Liabilities in Excess of Other Assets | | (2.39 | ) | | | (12,463,721 | ) |

| | |

|

| |

|

|

|

Net Assets | | 100.00 | % | | $ | 522,505,940 | |

| | |

|

| |

|

|

|

See Notes to Financial Statements.

31

Excelsior Funds, Inc.

Portfolio of Investments — March 31, 2006

Equity Core Fund

| | | | | |

| | | | | | |

Shares

| | | | Value

|

| COMMON STOCKS — 92.23% | | |

| | | CONSUMER DISCRETIONARY — 16.87% |

| 41,105 | | Autozone, Inc.(a) | | $ | 4,097,758 |

| 132,499 | | Dillards, Inc., Class A | | | 3,450,274 |

| 132,143 | | Eastman Kodak Co. | | | 3,758,147 |

| 162,500 | | Furniture Brands International, Inc. | | | 3,982,875 |

| 104,164 | | John Wiley & Sons, Class A | | | 3,942,607 |

| 80,000 | | Life Time Fitness, Inc.(a) | | | 3,748,000 |

| 166,000 | | Sotheby’s Holdings, Inc., Class A(a) | | | 4,820,641 |

| 108,770 | | Timberland Co., Class A(a) | | | 3,723,197 |

| | | | |

|

|

| | | | | | 31,523,499 |

| | | | |

|

|

| | | CONSUMER STAPLES — 4.31% |

| 93,806 | | Anheuser Busch Cos., Inc. | | | 4,012,083 |

| 63,278 | | Wm. Wrigley Jr. Co. | | | 4,049,792 |

| | | | |

|

|

| | | | | | 8,061,875 |

| | | | |

|

|

| | | ENERGY — 7.41% |

| 57,100 | | Apache Corp. | | | 3,740,621 |

| 72,294 | | Exxon Mobil Corp. | | | 4,399,813 |

| 74,032 | | Suncor Energy, Inc. | | | 5,701,944 |

| | | | |

|

|

| | | | | | 13,842,378 |

| | | | |

|

|

| | | FINANCIAL — 13.10% |

| 117,427 | | American Capital Strategies Ltd. | | | 4,128,733 |

| 48 | | Berkshire Hathaway, Inc., Class A(a) | | | 4,336,800 |

| 26,184 | | Lehman Brothers Holding, Inc. | | | 3,784,374 |

| 84,659 | | Leucadia National Corp. | | | 5,050,756 |

| 110,713 | | North Fork Bancorporation, Inc. | | | 3,191,856 |

| 91,354 | | RenaissanceRe Holdings Ltd. | | | 3,984,861 |

| | | | |

|

|

| | | | | | 24,477,380 |

| | | | |

|

|

| | | HEALTH CARE — 9.33% |

| 68,353 | | Johnson & Johnson | | | 4,047,865 |

| 75,331 | | Medtronic, Inc. | | | 3,823,048 |

| 77,325 | | Novo-Nordisk A/S ADR | | | 4,801,109 |

| 64,099 | | Roche Holdings Ltd. ADR | | | 4,760,152 |

| | | | |

|

|

| | | | | | 17,432,174 |

| | | | |

|

|

| | | | | |

| | | | | | |

Shares

| | | | Value

|

| COMMON STOCKS — (continued) | | |

| | | INDUSTRIALS — 9.83% |

| 1,930,962 | | Bombardier, Inc., Class B(a) | | $ | 5,622,961 |

| 82,500 | | Canadian National Railway Co. | | | 3,735,600 |

| 115,682 | | General Electric Co. | | | 4,023,420 |

| 310,700 | | Quanta Services, Inc.(a) | | | 4,977,414 |

| | | | |

|

|

| | | | | | 18,359,395 |

| | | | |

|

|

| | | INFORMATION TECHNOLOGY — 7.51% |

| 933,293 | | 3com Corp.(a) | | | 4,778,460 |

| 112,577 | | Analog Devices, Inc. | | | 4,310,573 |

| 151,407 | | National Instruments Corp. | | | 4,938,897 |

| | | | |

|

|

| | | | | | 14,027,930 |

| | | | |

|

|

| | | RAW/INTERMEDIATE MATERIALS — 13.22% |

| 97,537 | | Aracruz Cellulose S.A. ADR | | | 5,163,609 |

| 94,404 | | E.I. Du Pont de Nemours & Co. | | | 3,984,793 |

| 55,801 | | Monsanto Co. | | | 4,729,135 |

| 52,850 | | Nucor Corp. | | | 5,538,151 |

| 61,000 | | Vulcan Materials Co. | | | 5,285,650 |

| | | | |

|

|

| | | | | | 24,701,338 |

| | | | |

|

|

| | | REAL ESTATE — 2.27% |

| 67,592 | | St. Joe Co. | | | 4,247,481 |

| | | | |

|

|

| | | UTILITIES — 8.38% |

| 274,996 | | AES Corp.(a) | | | 4,691,432 |

| 224,593 | | Centerpoint Energy, Inc. | | | 2,679,394 |

| 395,821 | | EL Paso Corp. | | | 4,769,643 |

| 255,200 | | Sierra Pacific Resources(a) | | | 3,524,312 |

| | | | |

|

|

| | | | | | 15,664,781 |

| | | | |

|

|

| | | TOTAL COMMON STOCKS

(Cost $148,821,548) | | | 172,338,231 |

| | | | |

|

|

| FOREIGN COMMON STOCKS — 2.43% | | |

| | | GERMANY — 2.43% | | | |

| 82,507 | | Bayerische Motoren Werke AG | | | 4,544,011 |

| | | | |

|

|

| | | TOTAL FOREIGN COMMON STOCKS

(Cost $3,702,066) | | | 4,544,011 |

| | | | |

|

|

See Notes to Financial Statements.

32

Excelsior Funds, Inc.

Portfolio of Investments — March 31, 2006

Equity Core Fund — (continued)

| | | | | |

Principal Amount

| | | | Value

|

| REPURCHASE AGREEMENT — 5.79% | | |

| $10,818,000 | | JP Morgan Chase Securities, Inc., 3.40%, dated 03/31/06, to be repurchased 04/03/06, repurchase price $10,821,065 (collateralized by U.S. Treasury Note, par value $8,103,000, 8.125%, maturing 08/15/21; total market value $10,898,014) | | $ | 10,818,000 |

| | | | |

|

|