We have audited the accompanying statement of assets and liabilities, including the portfolio of investments, of Seligman High-Yield Fund, one of the funds constituting Seligman High Income Fund Series, (the “Fund”) as of December 31, 2008, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the periods presented. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2008, by correspondence with the custodian and brokers; where replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Seligman High-Yield Fund of Seligman High Income Fund Series as of December 31, 2008, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for the respective stated periods, in conformity with accounting principles generally accepted in the United States of America.

Matters Relating to the Trustees’

Consideration of the Approval of the

Investment Management Services Agreement

Background

On July 7, 2008, RiverSource Investments, LLC (“RiverSource”), a wholly owned subsidiary of Ameriprise Financial, Inc. (“Ameriprise”), entered into a stock purchase agreement with the shareholders of J. & W. Seligman & Co. Incorporated (“Seligman”) under which RiverSource would acquire all of the outstanding capital stock of Seligman (the “Transaction”). The consummation of the Transaction resulted in the automatic termination of the Fund’s management agreement with Seligman (the “Seligman Management Agreement”). In anticipation of the termination of the Seligman Management Agreement, at a meeting held on July 29, 2008, the trustees of Seligman High Income Fund Series then serving, of which the Fund is a separate series, unanimously approved an investment management agreement between the Fund and RiverSource (the “Proposed Advisory Agreement”). At the special meeting of shareholders of the Fund held on November 3, 2008, the shareholders approved the Proposed Advisory Agreement. The Transaction closed on November 7, 2008, and upon the closing, RiverSource became the investment advisor to the Fund.

Board Considerations

Prior to their approval of the Proposed Advisory Agreement, the trustees requested and evaluated extensive materials from, and were provided materials and information about the Transaction and matters related to the proposed approval by, Seligman, RiverSource and Ameriprise.

In consultation with experienced counsel, who advised on the legal standards for consideration by the trustees, the trustees reviewed the Proposed Advisory Agreement with RiverSource. The independent trustees also discussed the proposed approval with counsel in private sessions.

At their meetings on June 12, 2008, July 17, 2008 and July 29, 2008, the trustees discussed the Transaction with Seligman, and the Transaction and RiverSource’s plans and intentions regarding the Fund with representatives of Ameriprise and RiverSource.

The trustees considered all factors they believed relevant, including the specific matters discussed below. In their deliberations, the trustees did not identify any particular information that was all-important or controlling, and trustees may have attributed different weights to the various factors. The trustees determined that the selection of RiverSource to advise the Fund, and the overall arrangements between the Fund and RiverSource as provided in the Proposed Advisory Agreement, including the proposed advisory fee and the related administration arrangements between the Fund and Ameriprise, were fair and reasonable in light of the services to be performed, expenses incurred and such other matters as the trustees considered relevant. The material factors and conclusions that formed the basis for the trustees’ determination included, in addition, the factors discussed in further detail below:

| |

(i) | the reputation, financial strength and resources of RiverSource, and its parent, Ameriprise; |

| |

(ii) | the capabilities of RiverSource with respect to compliance and its regulatory histories; |

| |

(iii) | an assessment of RiverSource’s compliance system by the Fund’s Chief Compliance Officer; |

| |

(iv) | that RiverSource and Ameriprise assured the trustees that following the Transaction there will not be any diminution in the nature, quality and extent of services provided to the Fund or its shareholders; |

| |

(v) | that within the past year the trustees had performed a full annual review of the Seligman Management Agreement, as required by the Investment Company Act of 1940 (“1940 Act”), for the Fund and had determined that they were satisfied with the nature, extent and quality of services provided thereunder and that the management fee rate for the Fund was satisfactory; |

| |

(vi) | the potential benefits to the Fund of the combination of RiverSource and Seligman to the Fund, including: greater resources to attract and retain high quality investment personnel; greater depth and breadth of investment management capabilities, including a new team of portfolio managers for the Fund; a continued high level of service to the Fund; and the potential for realization of economies of scale over time since the Fund will be part of a much larger fund complex; |

32

Matters Relating to the Trustees’

Consideration of the Approval of the

Investment Management Services Agreement

| |

(vii) | the fact that the Fund’s total advisory and administrative fees would not increase by virtue of the Proposed Advisory Agreement, but would remain the same; |

| |

(viii) | that RiverSource, and not the Fund, would bear the costs of obtaining all approvals of the Proposed Advisory Agreement; |

| |

(ix) | the qualifications of the personnel of RiverSource and Ameriprise that would provide advisory and administrative services to the Fund; |

| |

(x) | the terms and conditions of the Proposed Advisory Agreement, including the trustees’ review of differences from the Seligman Management Agreement; |

| |

(xi) | that RiverSource and Ameriprise have agreed to refrain from imposing or seeking to impose, for a period of two years after the closing of the Transaction, any “unfair burden” (within the meaning of Section 15(f) of 1940 Act) on the Fund; and |

| |

(xii) | that certain members of RiverSource’s management have a significant amount of experience integrating other fund families. |

Nature, Extent and Quality of Services Provided

In considering the nature, extent and quality of the services to be provided under the Proposed Advisory Agreement, the trustees of the Fund considered, among other things, the expected impact of the Transaction on the operations of the Fund, the information provided by RiverSource with respect to the nature, extent and quality of services to be provided by it, RiverSource’s compliance programs and compliance records, and presentations provided on the quality of RiverSource’s investment research capabilities and the other resources it and Ameriprise have indicated that they would dedicate to performing services for the Fund.

The trustees noted the professional experience and qualifications of the new portfolio management team proposed for the Fund and other senior personnel of RiverSource. The trustees considered a report by, the Fund’s Chief Compliance Officer, assessing RiverSource’s compliance system, which was followed by a private session with the Fund’s Chief Compliance Officer. They also discussed RiverSource’s compliance system with the Chief Compliance Officer for the funds managed by RiverSource. The trustees also considered RiverSource’s presentation on the selection of brokers and dealers for portfolio transactions. As administrative services (provided under the Seligman Management Agreement) would be provided to the Fund by Ameriprise at no additional cost under a new administrative services agreement rather than pursuant to the Proposed Advisory Agreement, the trustees considered Ameriprise’s capability to provide such administrative services as well as RiverSource’s and Ameriprise’s roles in coordinating the activities of the Fund’s other service providers. The trustees noted that Ameriprise intended to continue Seligman’s practice of sub-contracting administrative services provided by Seligman for the Fund to State Street Bank and Trust Company for the foreseeable future. The trustees concluded that, overall, they were satisfied with assurances from RiverSource and Ameriprise as to the expected nature, extent and quality of the services to be provided to the Fund under the Proposed Advisory Agreement and the new administrative services agreement.

Costs of Services Provided and Profitability

In considering the costs of services to be provided by RiverSource under the Proposed Advisory Agreement, the trustees considered, among other things, the projected pre-tax, pre-distribution expense profitability of RiverSource’s proposed relationship with the Fund and discussed the assumptions of RiverSource and the limitations of the information provided. The trustees noted that RiverSource had undertaken to provide profitability information in connection with future contract continuances. The trustees also considered RiverSource’s financial condition based on information provided by it.

The trustees noted that the proposed fee under the Proposed Advisory Agreement was the same as provided under the Seligman Management Agreement. The trustees recognized that it is difficult to make comparisons of profitability from fund advisory contracts because comparative information is not generally publicly available

33

Matters Relating to the Trustees’

Consideration of the Approval of the

Investment Management Services Agreement

and is affected by numerous factors. In reviewing the projected profitability information, the trustees considered the effect of fall-out benefits on RiverSource’s expenses. The trustees concluded that they were satisfied that RiverSource’s estimated future profitability from its relationship with the Fund was not excessive.

Fall-Out Benefits

The trustees reviewed information about RiverSource’s practices with respect to allocating portfolio brokerage for brokerage and research services. The trustees also considered that broker-dealer affiliates of RiverSource, including a broker-dealer affiliate of Seligman (which became an affiliate of RiverSource following the closing of the Transaction) will receive 12b-1 fees from the Fund in respect of shares held in certain accounts, and that the Fund’s distributor (which also became a subsidiary of RiverSource following the closing of the Transaction) retains a portion of the 12b-1 fees from the Fund and receives a portion of the sales charges on sales or redemptions of certain classes of shares of the Fund. The trustees recognized that RiverSource’s profitability would be somewhat lower without these benefits. The trustees noted that RiverSource may derive reputational and other benefits from its association with the Fund.

Investment Results

The trustees received and reviewed detailed performance information on the Fund at each regular Board meeting during the year in addition to the information received for the meeting regarding approval of the Proposed Advisory Agreement. The trustees noted that a new portfolio manager was being proposed by RiverSource for the Fund and that such manager would use an investment process derived from that used by RiverSource High Yield Bond Fund, modified to comply with the Fund’s investment strategies as disclosed in its prospectus. The trustees discussed the portfolio management team, its investment strategy and process and historical performance record with representatives of RiverSource.

The trustees reviewed performance information of the Fund covering a wide range of periods, including the first six months of the calendar year, the preceding seven calendar years and annualized one-, three- and five-year rolling periods ending June 30, 2008. The trustees reviewed information comparing the Fund to the Lehman Brothers US Corporate High-Yield Index 2% Cap and the Lipper High Current Yield Fund Average, as well as performance relative to the other funds in the Lipper High Current Yield Fund Average and to a group of competitor funds selected by Seligman. The trustees noted that the results of RiverSource High Yield Bond Fund were generally better than that of the Fund for the comparable periods presented, although they lagged its JP Morgan Global High Yield Index benchmark in most periods.

The trustees recognized that it is not possible to predict what effect, if any, consummation of the Transaction would have on the future performance of the Fund.

Management Fee and Other Expenses

The trustees considered the proposed advisory fee rate to be paid by the Fund to RiverSource, which is the same as the management fee rate paid by the Fund under the Seligman Management Agreement. In addition to the materials provided by Seligman, RiverSource provided information regarding the fees for each of the RiverSource funds and managed accounts. The trustees noted that the effective advisory fee rates for the RiverSource funds in the same Lipper category as the Fund were lower than the proposed advisory fee rate for the Fund. The trustees recognized that it is difficult to make comparisons of advisory and management fees because there are variations in the services that are included in the fees paid by other funds.

In considering the proposed advisory fee rate, the trustees noted that the management fee rate under the Seligman Management Agreement covers administrative services provided by Seligman, whereas the Proposed Advisory Agreement does not include such services, but that Ameriprise will provide such services to the Fund pursuant to a separate administrative services agreement initially without a fee. The trustees further considered that the administrative fees, since they are not included in an advisory agreement, could be increased without stockholder approval, although RiverSource noted that, at that time, it did not have an intention to seek an

34

Matters Relating to the Trustees’

Consideration of the Approval of the

Investment Management Services Agreement

increase, and that any such administrative fee increase would require board approval. The trustees also noted RiverSource’s and Ameriprise’s covenants in the Transaction’s stock purchase agreement regarding compliance with Section 15(f) of the 1940 Act.

The trustees compared the Fund’s proposed advisory fee rate to the rate paid by other funds in the Fund’s Lipper category. The Fund’s peer group consisted of the funds in the Lipper High Current Yield Funds Average category having net assets in a range that more closely corresponds to the net assets of the Fund (the “peer group”). The information showed that the Fund’s current effective management fee rate was somewhat higher than the average and the median for the funds in the peer group. The trustees noted that the Fund’s fee rate schedule includes breakpoints although, at the Fund’s current asset levels, it was unlikely to benefit from them in the next year.

The trustees also reviewed the Fund’s total expense ratio as compared to the fees and expenses of funds within its peer group. In considering the expense ratios of the Fund, the trustees noted that the Fund has elected to have shareholder services provided at cost by Seligman Data Corp. (“SDC”). SDC provides services exclusively to the Seligman Group of Funds, and the trustees believed that the arrangement with SDC has provided the Fund and its shareholders with a consistently high level of service. The trustees noted that RiverSource had previously indicated that no changes to the arrangements with SDC were being proposed at the time by RiverSource.

The trustees noted that the Fund’s expense ratio was nearly the highest in its peer group and considerably higher than the median and the average for the peer group. Seligman explained that the Fund’s relatively high expenses were attributable in part to the Fund’s small size relative to the funds in its peer group and high shareholder purchase and redemption activity levels, all of which adversely affected its expense ratio. The trustees concluded that the Fund’s expense ratio was acceptable in the Fund’s particular circumstances.

Economies of Scale

The trustees noted that the management fee schedule for the Fund contains breakpoints that reduce the fee rate on assets above specified levels. The trustees recognized that there is no direct relationship between the economies of scale realized by funds and those realized by their investment advisers as assets increase. The trustees do not believe that there is a uniform methodology for establishing breakpoints that give effect to fund-specific economies of scale with respect to services provided by fund advisers. The trustees also observed that in the investment company industry as a whole, as well as among funds similar to the Fund, there is no uniformity or pattern in the fees and asset levels at which breakpoints (if any) apply, and that the advisory agreements for many competitor funds do not have breakpoints at all. The trustees noted that RiverSource had indicated that no changes to the Fund’s breakpoint arrangements were proposed to be made at the time. Having taken these factors into account, the trustees concluded that the Fund’s breakpoint arrangements were acceptable under the Fund’s circumstances. The trustees also recognized that the Fund may benefit from certain economies of scale over time from becoming a part of the larger RiverSource fund complex, based on potential future synergies of operations.

35

Proxy Results

Shareholders of Seligman High-Yield Fund voted on two proposals at a Special Meeting of Shareholders held on November 3, 2008. Shareholders voted in favor of each of the proposals. The description of each proposal and number of shares voted are as follows:

Proposal 1

To consider and vote upon the proposed Investment Management Services Agreement with RiverSource Investments, LLC:

| | | | | | |

For | | Against | | Abstain |

|

|

|

|

|

35,151,212.467 | | | 1,628,616.196 | | | 1,480,787.304 |

|

|

|

|

|

Proposal 2 (combined votes of both Funds in the Series)

To elect ten trustees to the Board:

| | | | |

| | For | | Withheld |

|

|

|

|

|

Kathleen Blatz | | 51,198,749.236 | | 2,437,544.928 |

|

|

|

|

|

Arne H. Carlson | | 51,131,650.856 | | 2,504,643.308 |

|

|

|

|

|

Pamela G. Carlton | | 51,203,587.404 | | 2,432,706.760 |

|

|

|

|

|

Patricia M. Flynn | | 51,212,005.780 | | 2,424,288.384 |

|

|

|

|

|

Anne P. Jones | | 51,129,788.135 | | 2,506,506.029 |

|

|

|

|

|

Jeffrey Laikind | | 51,183,153.004 | | 2,453,141.160 |

|

|

|

|

|

Stephen R. Lewis, Jr. | | 51,247,061.722 | | 2,389,232.442 |

|

|

|

|

|

Catherine James Paglia | | 51,200,482.648 | | 2,435,811.516 |

|

|

|

|

|

Alison Taunton-Rigby | | 51,166,054.471 | | 2,470,239.693 |

|

|

|

|

|

William F. Truscott | | 51,230,947.413 | | 2,405,346.751 |

|

|

|

|

|

36

Trustees and Officers

Shareholders elect a Board of Trustees that oversees the Fund’s operations. In connection with the acquisition of the Fund’s prior investment manager, J. & W. Seligman & Co. Incorporated, by RiverSource Investments, LLC, shareholders of the Fund voted at a Special Meeting of Shareholders held on November 3, 2008 to elect 10 members to the Fund’s Board. Messrs. Maher and Richie served on the Fund’s Board prior to the acquisition and will continue to do so.

Each member of the Board oversees 163 portfolios in the fund complex managed by RiverSource Investments, which includes 59 Seligman Funds and 104 RiverSource Funds. The address of each Director is 901 S. Marquette Ave., Minneapolis, MN 55402.

Independent Trustees

| | |

Name, (Age), Position(s)

held with Fund | | Principal Occupation(s) During Past Five Years, Directorships

and Other Information |

|

|

|

Kathleen Blatz (54)1,2,6,7

• Trustee: From

November 7, 2008 | | Attorney. Formerly, Chief Justice, Minnesota Supreme Court, 1998-2006. |

|

|

|

Arne H. Carlson (74)1,2,3,5,6

• Trustee: From

November 7, 2008 | | Formerly, Chairman, RiverSource Funds, 1999-2006; Governor of Minnesota. |

|

|

|

Pamela G. Carlton (54)4,6,7

• Trustee: From

November 7, 2008 | | President, Springboard — Partners in Cross Cultural Leadership (consulting company). |

|

|

|

Patricia M. Flynn (58)1,3,6

• Trustee: From

November 7, 2008 | | Trustee Professor of Economics and Management, Bentley College. Formerly, Dean, McCallum Graduate School of Business, Bentley College. |

|

|

|

Anne P. Jones (73)1,2,6,7

• Trustee: From

November 7, 2008 | | Attorney and Consultant. |

|

|

|

Jeffrey Laikind, CFA (73)4,6,7

• Trustee: From

November 7, 2008 | | Director, American Progressive Insurance. Formerly, Managing Director, Shikiar Asset Management. |

|

|

|

Stephen R. Lewis, Jr. (69)1,2,3,4,6

• Trustee and Chairman

of the Board: From

November 7, 2008 | | President Emeritus and Professor of Economics, Carleton College; Director, Valmont Industries, Inc. (manufactures irrigation systems). |

|

|

|

John F. Maher (64)4,6,7

• Trustee: December 2006

to Date | | Retired President and Chief Executive Officer, and former Director, Great Western Financial Corporation (bank holding company) and its principal subsidiary, Great Western Bank (a federal savings bank). |

|

|

|

| |

| |

See footnotes on page 38. |

37

Trustees and Officers

Independent Trustees (continued)

| | |

Name, (Age), Position(s)

held with Fund | | Principal Occupation(s) During Past Five Years, Directorships

and Other Information |

|

|

|

Catherine James Paglia (56)2,3,4,5,6

• Trustee: From

November 7, 2008 | | Director, Enterprise Asset Management, Inc. (private real estate and asset management company). |

|

|

|

Leroy C. Richie (66)3,4,6

• Trustee: 2000 to Date | | Counsel, Lewis & Munday, P.C. (law firm); Director, Vibration Control Technologies, LLC (auto vibration technology); Lead Outside Director, Digital Ally Inc. (digital imaging) and Infinity, Inc. (oil and gas exploration and production); Director and Chairman, Highland Park Michigan Economic Development Corp.; and Chairman, Detroit Public Schools Foundation; Director, OGE Energy Corp. (energy and energy services provider). Formerly, Chairman and Chief Executive Officer, Q Standards Worldwide, Inc. (library of technical standards); Director, Kerr-McGee Corporation (diversified energy and chemical company); Trustee, New York University Law Center Foundation; and Vice Chairman, Detroit Medical Center and Detroit Economic Growth Corp. |

|

|

|

Alison Taunton-Rigby (64)3,4,5,6

• Trustee: From

November 7, 2008 | | Chief Executive Officer and Director, RiboNovix, Inc. since 2003 (biotechnology); Director, Idera Pharmaceutical, Inc. (biotechnology); Healthways, Inc. (health management programs). Formerly, President, Forester Biotech. |

|

|

|

| | |

Interested Trustee* | | |

|

|

|

William F. Truscott (48)*6

• Trustee and Vice

President:

From November 7, 2008 | | President – US Asset Management and Chief Investment Officer, Ameriprise Financial, Inc. and President, Chairman of the Board, and Chief Investment Officer, RiverSource Investments, LLC; Director, President and Chief Executive Officer, Ameriprise Certificate Company; and Chairman of the Board, Chief Executive Officer, and President, RiverSource Distributors, Inc. Formerly, Senior Vice President — Chief Investment Officer, Ameriprise Financial, Inc.; and Chairman of the Board and Chief Investment Officer, RiverSource Investments, LLC, 2001-2005. |

|

|

|

| | |

| |

* | Mr. Truscott is considered an “interested person” of the Fund, as defined in the Investment Company Act of 1940, as amended, by virtue of his position with Ameriprise Financial, Inc. and its affiliates. |

| |

Member: | 1 Board Governance Committee |

| 2 Compliance Committee |

| 3 Contracts Committee |

| 4 Distribution Committee |

| 5 Executive Committee |

| 6 Investment Review Committee |

| 7 Joint Audit Committee |

38

Trustees and Officers

Fund Officers

The Board appoints officers who are responsible for day-to-day business decisions based on policies it has established. The officers serve at the pleasure of the Board. In addition to Mr. Truscott, who is a Trustee and Vice President of the Fund, the Fund’s other officers are:

| | |

Name, (Age), Position(s)

held with Fund, Address | | Principal Occupation(s) During Past Five Years |

|

|

|

Patrick T. Bannigan (43)

• President: From

November 7, 2008

• 172 Ameriprise Financial

Center

Minneapolis, MN 55474 | | Director and Senior Vice President — Asset Management, Products and Marketing, RiverSource Investments, LLC; Director and Vice President — Asset Management, Products and Marketing, RiverSource Distributors, Inc. Formerly, Managing Director and Global Head of Product, Morgan Stanley Investment Management, 2004-2006; President, Touchstone Investments, 2002-2004. |

|

|

|

Michelle M. Keeley (44)

• Vice President: From

November 7, 2008

• 172 Ameriprise Financial

Center

Minneapolis, MN 55474 | | Executive Vice President — Equity and Fixed Income, Ameriprise Financial, Inc. and RiverSource Investments, LLC; Vice President — Investments, Ameriprise Certificate Company. Formerly, Senior Vice President — Fixed Income, Ameriprise Financial, Inc., 2002-2006 and RiverSource Investments, LLC, 2004-2006. |

|

|

|

Amy K. Johnson (43)

• Vice President: From

November 7, 2008

• 5228 Ameriprise

Financial Center

Minneapolis, MN 55474 | | Vice President — Asset Management and Trust Company Services, RiverSource Investments, LLC. Formerly, Vice President — Operations and Compliance, RiverSource Investments, LLC, 2004-2006; Director of Product Development — Mutual Funds, Ameriprise Financial, Inc., 2001-2004. |

|

|

|

Scott R. Plummer (49)

• Vice President, General

Counsel and Secretary:

From November 7, 2008

• 5228 Ameriprise

Financial Center

Minneapolis, MN 55474 | | Vice President and Chief Counsel — Asset Management, Ameriprise Financial, Inc.; Chief Counsel, RiverSource Distributors, Inc. and Chief Legal Officer and Assistant Secretary, RiverSource Investments, LLC; Vice President, General Counsel, and Secretary, Ameriprise Certificate Company. Formerly, Vice President — Asset Management Compliance, Ameriprise Financial, Inc., 2004-2005; Senior Vice President and Chief Compliance Officer, USBancorp Asset Management, 2002-2004. |

|

|

|

Lawrence P. Vogel (52)

• Treasurer: 2000 to Date

• 100 Park Avenue

New York, NY 10017 | | Treasurer of each of the investment companies of the Seligman Group of Funds since 2000; and Treasurer, Seligman Data Corp. since 2000. Formerly, Senior Vice President, J. & W. Seligman & Co. Incorporated and Vice President of each of the investment companies of the Seligman Group of Funds, 1992-2008. |

|

|

|

39

Trustees and Officers

Fund Officers (continued)

| | |

Name, (Age), Position(s)

held with Fund, Address | | Principal Occupation(s) During Past Five Years |

|

|

|

Eleanor T.M. Hoagland (56)

• Chief Compliance

Officer: 2004 to Date

• Money Laundering

Prevention Officer

and Identity Theft

Prevention Officer: From

November 7, 2008

• 100 Park Avenue

New York, NY 10017 | | Chief Compliance Officer, RiverSource Investments, LLC (J. & W. Seligman & Co. Incorporated prior to November 7, 2008), of each of the investment companies of the Seligman Group of Funds since 2004; Money Laundering Prevention Officer and Identity Theft Prevention Officer, RiverSource Investments, LLC for each of the investment companies of the Seligman Group of Funds since November 7, 2008. Formerly, Managing Director, J. & W. Seligman & Co. Incorporated and Vice President of each of the investment companies of the Seligman Group of Funds, 2004-2008. |

|

|

|

The Fund’s Statement of Additional Information (SAI) includes additional information about Fund trustees and is available, without charge, upon request. You may call toll-free (800) 221-2450 in the US or call collect (212) 682-7600 outside the US to request a copy of the SAI, to request other information about the Fund, or to make shareholder inquiries.

40

Required Federal Income Tax Information

(unaudited)

Dividends paid for the year ended December 31, 2008, other than qualified dividend income, are subject to federal income tax as “ordinary income.” In order to claim the dividends received deduction for these distributions, corporate shareholders must have held their shares for 46 days or more during the 90-day period beginning 45 days before each ex-dividend date. Under the Internal Revenue Code, the dividends paid to corporate shareholders that qualify for the dividends received deduction were as follows:

| | | | |

| | Dividends Received

Deduction Percent | |

|

|

|

|

Class A | | 1.26 | % | |

|

|

|

|

|

Class B | | 1.44 | | |

|

|

|

|

|

Class C | | 1.15 | | |

|

|

|

|

|

Class D | | 1.90 | | |

|

|

|

|

|

Class I | | 1.18 | | |

|

|

|

|

|

Class R | | 1.23 | | |

|

|

|

|

|

For the year ended December 31, 2008, the Fund designates the following as qualified dividends to individual shareholders:

| | | | |

| | | | |

| | Qualified Dividends

Percent | |

|

|

|

|

|

Class A | | 0.97 | % | |

|

|

|

|

|

Class B | | 1.11 | | |

|

|

|

|

|

Class C | | 0.89 | | |

|

|

|

|

|

Class D | | 1.46 | | |

|

|

|

|

|

Class I | | 0.91 | | |

|

|

|

|

|

Class R | | 0.94 | | |

|

|

|

|

|

In order for an individual to claim dividends received as qualified dividends, individual shareholders must have held their shares for more than 60 days during the 121-day period beginning 60 days before each ex-dividend date.

41

Additional Fund Information

Fund Symbols

Class A: SHYBX

Class B: SBBHX

Class C: SHCCX

Class R: SHYRX

Manager

From November 7, 2008

RiverSource Investments, LLC

200 Ameriprise Financial Center

Minneapolis, MN 55474

Until November 6, 2008

J. & W. Seligman & Co.

Incorporated

100 Park Avenue

New York, NY 10017

General Distributor

RiverSource Fund Distributors, Inc.

(formerly Seligman Advisors, Inc.)

100 Park Avenue

New York, NY 10017

Shareholder Service Agent

Seligman Data Corp.

100 Park Avenue

New York, NY 10017

Mail Inquiries to:

P.O. Box 9759

Providence, RI o2940-9759

Independent Registered Public Accounting Firm

Deloitte & Touche LLP

Important Telephone Numbers

| |

(800) 221-2450 | Shareholder Services |

(800) 445-1777 | Retirement Plan

Services |

(212) 682-7600 | Outside the

United States |

(800) 622-4597 | 24-Hour Automated

Telephone Access

Service |

| |

|

Quarterly Schedule of Investments

A complete schedule of portfolio holdings owned by the Fund will be filed with the SEC for the first and third quarter of each fiscal year on Form N-Q, and will be available to shareholders (i) without charge, upon request, by calling toll-free (800) 221-2450 in the US or collect (212) 682-7600 outside the US or (ii) on the SEC’s website at www.sec.gov.1 In addition, the Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330. Certain of the information contained in the Fund’s Form N-Q is also made available to shareholders on Seligman’s website at www.seligman.com.1

Proxy Voting

A description of the policies and procedures used by the Fund to determine how to vote proxies relating to portfolio securities as well as information regarding how the Fund voted proxies relating to portfolio securities during the 12-month period ended June 30 of each year will be available (i) without charge, upon request, by calling toll-free (800) 221-2450 in the US or collect (212) 682-7600 outside the US and (ii) on the SEC’s website at www.sec.gov.1 Information for each new 12-month period ending June 30 will be available no later than August 31 of that year.

| |

1 | These website references are inactive textual references and information contained in or otherwise accessible through these websites does not form a part of this report or the Fund’s prospectuses or statement of additional information. |

42

This report is intended only for the information of shareholders or those who have received the offering prospectus covering shares of Beneficial Interest of Seligman High-Yield Fund, which contains information about the investment objectives, risks, charges, and expenses of the Fund, each of which should be considered carefully before investing or sending money.

TXHY2 12/08

Seligman

U.S. Government

Securities Fund

Annual Report

December 31, 2008

Seeking High Current

Income by Investing in

US Government Securities

Table of Contents

1

Interview With Your Portfolio Manager

Note: In conjunction with the acquisition of the Fund’s previous investment manager by RiverSource Investments, LLC, the Seligman Investment Grade Team is no longer responsible for the portfolio management of the Fund. The Fund is now managed by RiverSource Investments.

| |

Q. | How did Seligman U.S. Government Securities Fund perform during the year ended December 31, 2008? |

| |

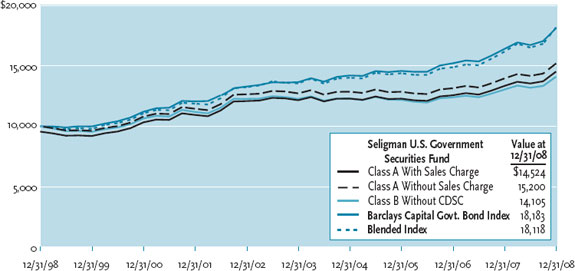

A. | For the year ended December 31, 2008, Seligman U.S. Government Securities Fund posted a total return of 8.8%, based on the net asset value of Class A shares. In comparison, the Fund’s peers, as measured by the Lipper General US Government Funds Average returned 7.3%. The Barclays Capital Government Bond Index returned 12.4%. The Blended Index, which is comprised of an equal 50% weighting in the Barclays Capital Government Bond Index and the Barclays Capital Fixed-Rate Mortgage Backed Securities Index, returned 10.5%. |

| |

Q. | How did market conditions and economic events impact the performance of the Fund during the year? |

| |

A. | The economic landscape during the year ended can be characterized by several major themes: further erosion in the housing market as prices remained on a downward trend, significant selling pressure as a result of deflating consumer confidence, continued large bank and brokerage firm write-offs which accelerated an ongoing flight to quality and credit contraction, and the significant widening of spreads. |

| |

| Weak economic data points released in January in manufacturing, employment, and retail sales fueled fears of global recession and sparked a sharp sell-off in equities. The credit freeze continued as growth slowed and banks and brokers reined in capital as the financial system continued to absorb losses related to subprime debt. The combined crises in housing, the credit market, and the economy spurred an activist Federal Reserve Board (the Fed) and the Administration to take unprecedented steps to shore up the economy. |

| |

| As the year unfolded, concerns regarding the housing market spread to other asset classes. Fears of spreading credit problems led to an overwhelming unwillingness by banks and other financial institutions to lend. Ongoing declines in asset values at financial institutions effectively resulted in a dysfunctional lending market in the US. The collapse of credit growth, along with the continued erosion of household net worth due to weakening housing and equity markets severely hampered consumer spending. |

| |

| In September we witnessed the unfolding of several unprecedented events that affected markets on a global scale. Fannie Mae and Freddie Mac were put into conservatorship. On September 15, Lehman Brothers filed for bankruptcy. The ripple effects of the failing of this 158-year old investment bank were wide-spread. Several cash management funds with exposure to Lehman debt suffered, with the net asset value of the Reserve Primary Fund falling below $1 per share — “breaking the buck.” Credit markets across the globe froze up, which had a significant implication on markets as a whole. Investors started focusing more on higher quality stocks. |

| |

| The downgrading of AIG’s credit rating led to a liquidity crisis (its stock price suffered a 95% decline on September 16, 2008) that ended in the largest government bailout of a company in US history. Merrill Lynch quickly sold itself to Bank of America, and commercial banks WAMU and Wachovia were quickly sold to JPMorgan Chase and Wells Fargo, respectively. |

2

Interview With Your Portfolio Manager

| |

| Interest rates fell significantly during the period as investors fled riskier assets for the relative safety of Treasuries, pushing prices higher and yields lower. Away from Treasuries, however, other fixed income sectors posted less-strong results. Securities with credit risk — especially those with mortgage-related credit risk — faced significant selling pressure during the July and August “credit panic.” Although the market stabilized temporarily in the fall, November brought a fresh round of panic as the market was spooked by increasing talk of an impending recession — a conversation that continued through the end of the year. |

| |

Q. | What investment strategies and techniques materially impacted the Fund’s performance during the year? |

| |

A. | One of the Fund’s principal strategies during the year, and one that benefitted the Fund’s performance during the year, was to maintain a duration that exceeded that of the benchmark. This strategy was employed to enable the portfolio to participate in the ongoing rally in US Treasuries as investors broadly sought higher quality instruments, as well as in anticipation of continued sluggish growth. |

| |

| Though its allocation to mortgage-backed securities was decreased in the second half of the year, the Fund’s exposure to this asset class detracted from the Fund’s results, as mortgage-backed securities posted positive returns but underperformed both agency securities and Treasuries during the annual period. That said, issue selection within mortgage-backed securities boosted returns, particularly the Fund’s emphasis on premium coupon securities. Higher coupon mortgage-backed securities outperformed lower coupon mortgage-backed securities for the period. |

| |

| At the end of December, we believed that fixed income market fundamentals had taken a back seat in investors’ minds to technical factors and to overly-pessimistic fears regarding both liquidity and the U.S. economy, causing rates to decline more than was warranted. Thus, we intend to position the Fund to take advantage of the compelling valuations that we saw in the last months of the period and to participate in the recovery of high quality spread sectors, or non-Treasury sectors, that we anticipate for 2009 when fears have hopefully subsided and liquidity returns to the markets. We expect economic growth prospects and the potential for higher inflation to ultimately recapture investors’ attention. |

|

|

The views and opinions expressed are those of the Portfolio Managers, are provided for general information only, and do not constitute specific tax, legal, or investment advice to, or recommendation for, and person. There can be no guarantee as to the accuracy of market forecasts. Opinions, estimates, and forecasts may be changed without notice. |

3

Performance and Portfolio Overview

This section of the report is intended to help you understand the performance of Seligman U.S. Government Securities Fund and to provide a summary of the Fund’s portfolio characteristics.

Performance data quoted in this report represents past performance and does not guarantee or indicate future investment results. The rates of return will vary and the principal value of an investment will fluctuate. Shares, if redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Total returns of the Fund as of the most recent month-end will be available at www.seligman.com1 by the seventh business day following that month-end. Calculations assume reinvestment of distributions, if any. Performance data quoted does not reflect the deduction of taxes that an investor may pay on distributions or the redemption of shares.

The chart on page 5 compares $10,000 hypothetical investments made in Class A shares, with and without the initial 4.5% maximum sales charge, and in Class B shares, without contingent deferred sales charge (“CDSC”), to $10,000 investments made in the Barclays Capital Government Bond Index and the Blended Index for the ten-year period ended December 31, 2008. The ten-year return for Class B shares reflects automatic conversion to Class A shares approximately eight years after their date of purchase. The performance of Class C and Class R shares, which commenced on later dates, and of Class A and Class B shares for other periods, with and without applicable sales charges and CDSCs, is not shown in the chart but is included in the total returns table that follows the chart. The performance of Class C and Class R shares will differ from the performance shown for Class A and Class B shares, based on the differences in sales charges and fees paid by shareholders.

Returns for Class A shares are calculated with and without the effect of the initial 4.5% maximum sales charge that became effective on January 7, 2008. Although for all periods presented the Fund’s Class A shares reflect the 4.5% maximum sales charge, the actual returns for periods prior to January 7, 2008 would have been lower if the 4.75% maximum sales charge then in effect was incurred. Returns for Class B shares are calculated with and without the effect of the maximum 5% CDSC, charged on redemptions made within one year of the date of purchase, declining to 1% in the sixth year and 0% thereafter. Returns for Class C and Class R shares are calculated with and without the effect of the 1% CDSC, charged on redemptions made within one year of purchase. Returns for Class C shares would have been lower for periods prior to June 4, 2007 if the 1% initial sales charge then in effect was incurred. On May 16, 2008, Class D shares of the Fund were converted to Class C shares at their respective net asset values. Effective at the close of business on May 16, 2008, Class D shares are no longer offered by the Fund.

An investment in the Fund is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

| |

|

1 | The website reference is an inactive textual reference and information contained in or otherwise accessible through the website does not form a part of this report or the Fund’s prospectus or statement of additional information. |

4

Performance and Portfolio Overview

Investment Results

|

Total Returns |

For Periods Ended December 31, 2008 |

|

| | | | | | | | | | | | | | | | | | | |

| | | | Average Annual | |

| | | |

|

|

| | Six

Months* | | One

Year | | Five

Years | | Ten

Years | | Class C

Since

Inception

5/27/99 | | Class R

Since

Inception

4/30/03 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class A | | | | | | | | | | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

With Sales Charge | | 2.26 | % | | 3.82 | % | | 2.66 | % | | 3.80 | % | | n/a | | | n/a | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Without Sales Charge | | 7.12 | | | 8.76 | | | 3.61 | | | 4.28 | | | n/a | | | n/a | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class B | | | | | | | | | | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

With CDSC† | | 1.86 | | | 3.08 | | | 2.47 | | | n/a | | | n/a | | | n/a | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Without CDSC | | 6.86 | | | 8.08 | | | 2.83 | | | 3.66 | ‡ | | n/a | | | n/a | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class C | | | | | | | | | | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

With 1% CDSC | | 5.71 | | | 6.94 | | | n/a | | | n/a | | | n/a | | | n/a | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Without CDSC | | 6.71 | | | 7.94 | | | 2.83 | | | n/a | | | 3.98 | % | | n/a | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class R | | | | | | | | | | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

With 1% CDSC | | 5.99 | | | 7.50 | | | n/a | | | n/a | | | n/a | | | n/a | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Without CDSC | | 6.99 | | | 8.50 | | | 3.33 | | | n/a | | | n/a | | | 2.92 | % | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Benchmarks** | | | | | | | | | | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Barclays Capital Government Bond Index | | 10.13 | | | 12.39 | | | 6.06 | | | 6.16 | | | 6.67 | | | 5.48 | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Blended Index | | 8.36 | | | 10.46 | | | 5.83 | | | 6.12 | | | 6.46 | | | 5.36 | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lipper General US Government Funds Average | | 6.51 | | | 7.27 | | | 4.18 | | | 4.68 | | | 5.12 | | | 3.63 | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5

Performance and Portfolio Overview

Investment Results

Net Asset Value Per Share

| | | | | | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| | 12/31/08 | | 6/30/08 | | 12/31/07 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class A | | | $ | 7.34 | | | | $ | 6.94 | | | | $ | 6.95 | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class B | | | | 7.36 | | | | | 6.95 | | | | | 6.96 | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class C | | | | 7.35 | | | | | 6.95 | | | | | 6.96 | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class R | | | | 7.34 | | | | | 6.94 | | | | | 6.95 | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Durationøøø | | | | | | | | | | | | | | | | |

December 31, 2008 | | | | | | | | | | | | | | 4.1 years | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| | | | | |

Dividend Per Share and Yield Information

For Periods Ended December 31, 2008 | | | | |

|

|

|

|

|

|

Dividends Paidø | | SEC 30-Day Yieldsøø | |

| |

|

|

$ | 0.208 | | 1.55 | % | |

|

| |

|

|

|

| 0.156 | | 0.85 | | |

|

| |

|

|

|

| 0.156 | | 0.85 | | |

|

| |

|

|

|

| 0.192 | | 1.34 | | |

|

| |

|

|

|

| | |

|

* | | Returns for periods of less than one year are not annualized. |

| | |

** | | The Barclays Capital Government Bond Index (the “Barclays Capital Index”), the Blended Index, and the Lipper General US Government Funds Average (the “Lipper Average”) are unmanaged benchmarks that assume reinvestment of dividends and exclude the effect of fees, taxes and sales charges. The Barclays Capital Index and the Blended Index also exclude the effect of expenses. The Lipper Average includes funds that invest at least 65% of their assets in US government and government agency issues. The Barclays Capital Index is a benchmark index made up of the Treasury Bond Index and the Agency Bond Index as well as the 1-3 Year Government Index and 20+ Year Treasury Index. The Blended Index is an index created by J.W. Seligman & Co. Incorporated (“JWS”), the Fund’s former investment manager. The Blended Index consists of a fifty percent equal weighting in the Barclays Capital Index and the Barclays Capital Fixed-Rate Mortgage Backed Securities Index (the “Barclays Capital MBS Index”), which covers the fixed-rate agency mortgage-backed pass-through securities of the Government National Mortgage Association (Ginnie Mae), the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac). In JWS’s view, the Blended Index better represents the securities in which the Fund expects to invest since Fund shareholders approved amendments to the Fund’s principal investment strategies in October 2005. The Fund’s holdings, however, may not be evenly weighted among the securities covered by the Barclays Capital Index and Barclays Capital MBS Index, and the weighting of the Fund’s holdings may vary significantly among such securities. The Fund is actively managed and its holdings are subject to change. Investors cannot invest directly in an average or an index. |

| | |

† | | The CDSC is 5% if you sell your shares within one year of purchase, and 2% for the five-year period. |

| | |

‡ | | The ten-year return for Class B shares reflects automatic conversion to Class A shares approximately eight years after their date of purchase. |

| | |

ø | | Represents per share amount paid or declared for the year ended December 31, 2008. |

| | |

øø | | Current yield, representing the annualized yield for the 30-day period ended December 31, 2008, has been computed in accordance with SEC regulations and will vary. |

| | |

øøø | | Duration is the average amount of time that it takes to receive the interest and principal of a bond or portfolio of bonds. The duration formula is based on a formula that calculates the weighted average of the cash flows (interest and principal payments) of the bond, discounted to present time. |

| | | | | | | |

Composition of Net Assets | | | | | | | |

|

|

|

|

|

|

|

|

|

| | Percentage of Net Assets | |

| |

|

|

| | 12/31/08 | | 12/31/07 | |

|

|

|

|

|

|

US Treasury Securities | | 27.3 | | | 21.2 | | |

|

|

|

|

|

|

|

|

Other US Full Faith and Credit Obligations | | 1.6 | | | 3.1 | | |

|

|

|

|

|

|

|

|

US Government Agency Obligations | | 18.3 | | | 14.0 | | |

|

|

|

|

|

|

|

|

Mortgage-Backed Securities | | 45.7 | | | 61.7 | | |

|

|

|

|

|

|

|

|

Short-Term Holdings and Other Assets Less Liabilities | | 7.1 | | | — | | |

|

|

|

|

|

|

|

|

Total | | 100.0 | | | 100.0 | | |

|

|

|

|

|

|

|

|

6

Understanding and Comparing Your Fund’s Expenses

As a shareholder of the Fund, you incur ongoing expenses, such as management fees, distribution and/or service (12b-1) fees, and other Fund expenses. The information below is intended to help you understand your ongoing expenses (in dollars) of investing in the Fund and to compare them with the ongoing expenses of investing in other mutual funds. Please note that the expenses shown in the table are meant to highlight your ongoing expenses only and do not reflect any transactional costs, such as sales charges (also known as loads) on certain purchases or redemptions. Therefore, the table is useful in comparing ongoing expenses only, and will not help you to determine the relative total expenses of owning different funds. In addition, if transactional costs were included, your total expenses would have been higher.

The table is based on an investment of $1,000 invested at the beginning of July 1, 2008 and held for the entire six-month period ended December 31, 2008.

Actual Expenses

The table below provides information about actual expenses and actual account values. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value at the beginning of the period by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During Period” for the Fund’s share class that you own to estimate the expenses that you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The table below also provides information about hypothetical expenses and hypothetical account values based on the actual expense ratio of each class and an assumed rate of return of 5% per year before expenses, which is not the actual return of any class of the Fund. The hypothetical expenses and account values may not be used to estimate the ending account value or the actual expenses you paid for the period. You may use this information to compare the ongoing expenses of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | Actual | | Hypothetical | |

| | | | | | | |

| |

|

|

| | Beginning

Account

Value

7/1/08 | | Annualized

Expense

Ratio* | | Ending

Account

Value

12/31/08 | | Expenses Paid

During Period

7/1/08 to 12/31/08** | | Ending

Account

Value

12/31/08 | | Expenses Paid

During Period

7/1/08 to 12/31/08** | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class A | | $ | 1,000.00 | | 1.41 | % | | $ | 1,071.20 | | | $ | 7.34 | | | $ | 1,018.05 | | | $ | 7.15 | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class B | | | 1,000.00 | | 2.18 | | | | 1,068.60 | | | | 11.34 | | | | 1,014.18 | | | | 11.04 | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class C | | | 1,000.00 | | 2.19 | | | | 1,067.10 | | | | 11.38 | | | | 1,014.13 | | | | 11.09 | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class R | | | 1,000.00 | | 1.68 | | | | 1,069.90 | | | | 8.74 | | | | 1,016.69 | | | | 8.52 | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

* | Expenses of Class B, Class C and Class R shares differ from the expenses of Class A shares due to the differences in 12b-1 fees paid by each share class. See the Fund’s prospectus for a description of each share class and its expenses and sales charges. |

| |

** | Expenses are equal to the annualized expense ratio based on actual expenses for the period July 1, 2008 to December 31, 2008, multiplied by the average account value over the period, multiplied by 184/366 (number of days in the period). |

7

|

Portfolio of Investments |

December 31, 2008 |

| | | | | | | |

| | Principal

Amount | | Value | |

US Full Faith and Credit Obligations 28.9% | | | | | | | |

|

|

|

|

|

|

|

|

US Treasury Bonds: | | | | | | | |

|

|

|

|

|

|

|

|

1.75%, 1/15/2028 | | $ | 517,060 | | $ | 477,877 | |

|

|

|

|

|

|

|

|

5.375%, 2/15/2031 | | | 375,000 | | | 515,391 | |

|

|

|

|

|

|

|

|

4.5%, 2/15/2036 | | | 585,000 | | | 777,411 | |

|

|

|

|

|

|

|

|

US Treasury Inflation-Protected Security: | | | | | | | |

|

|

|

|

|

|

|

|

2%, 1/15/2014 | | | 363,469 | | | 344,500 | |

|

|

|

|

|

|

|

|

2%, 1/15/2016 | | | 283,798 | | | 271,870 | |

|

|

|

|

|

|

|

|

US Treasury Notes: | | | | | | | |

|

|

|

|

|

|

|

|

2.125%, 4/30/2010 | | | 260,000 | | | 266,297 | |

|

|

|

|

|

|

|

|

4.5%, 2/28/2011 | | | 175,000 | † | | 189,274 | |

|

|

|

|

|

|

|

|

4.875%, 6/30/2012 | | | 735,000 | | | 826,358 | |

|

|

|

|

|

|

|

|

4.125%, 8/31/2012 | | | 2,830,000 | † | | 3,130,690 | |

|

|

|

|

|

|

|

|

2%, 11/30/2013 | | | 3,415,000 | | | 3,504,647 | |

|

|

|

|

|

|

|

|

1.5%, 12/31/2013 | | | 3,950,000 | | | 3,942,285 | |

|

|

|

|

|

|

|

|

4%, 2/15/2014 | | | 405,000 | | | 459,169 | |

|

|

|

|

|

|

|

|

4.625%, 11/15/2016 | | | 1,000,000 | | | 1,180,938 | |

|

|

|

|

|

|

|

|

4.25%, 11/15/2017 | | | 3,315,000 | | | 3,862,754 | |

|

|

|

|

|

|

|

|

1.375%, 7/15/2018 | | | 251,165 | | | 234,977 | |

|

|

|

|

|

|

|

|

3.75%, 11/15/2018 | | | 2,672,000 | † | | 3,025,620 | |

|

|

|

|

|

|

|

|

US Treasury STRIPS Principal 6.5%, 11/15/2026* | | | 2,400,000 | | | 1,383,754 | |

|

|

|

|

|

|

|

|

Total US Full Faith and Credit Obligations (Cost $22,581,796) | | | | | | 24,393,812 | |

|

|

|

|

|

|

|

|

|

US Government Agency ObligationsØ 18.3% | | | | | | | |

|

|

|

|

|

|

|

|

Fannie Mae: | | | | | | | |

|

|

|

|

|

|

|

|

3.255%, 6/9/2010 | | | 580,000 | | | 598,379 | |

|

|

|

|

|

|

|

|

3.25%, 8/12/2010 | | | 870,000 | | | 901,421 | |

|

|

|

|

|

|

|

|

4.75%, 11/19/2012 | | | 730,000 | † | | 804,027 | |

|

|

|

|

|

|

|

|

5%, 2/13/2017 | | | 2,500,000 | † | | 2,841,022 | |

|

|

|

|

|

|

|

|

5%, 7/9/2018 | | | 500,000 | † | | 487,855 | |

|

|

|

|

|

|

|

|

Federal Home Loan Bank: | | | | | | | |

|

|

|

|

|

|

|

|

2.625%, 5/20/2011 | | | 2,565,000 | † | | 2,624,988 | |

|

|

|

|

|

|

|

|

3.625%, 10/18/2013 | | | 2,000,000 | | | 2,106,294 | |

|

|

|

|

|

|

|

|

5%, 11/17/2017 | | | 500,000 | | | 574,295 | |

|

|

|

|

|

|

|

|

Freddie Mac: | | | | | | | |

|

|

|

|

|

|

|

|

6%, 6/15/2011 | | | 500,000 | | | 554,465 | |

|

|

|

|

|

|

|

|

5.5%, 8/20/2012 | | | 2,610,000 | † | | 2,915,370 | |

|

|

|

|

|

|

|

|

5%, 7/15/2014 | | | 900,000 | | | 1,015,163 | |

|

|

|

|

|

|

|

|

Total US Government Agency Obligations (Cost $14,393,850) | | | | | | 15,423,279 | |

|

|

|

|

|

|

|

|

Mortgage-Backed SecuritiesØØ 45.7% | | | | | | | |

|

|

|

|

|

|

|

|

Fannie MaeØ: | | | | | | | |

|

|

|

|

|

|

|

|

4.5%, 12/1/2020 | | | 984,015 | | | 1,009,978 | |

|

|

|

|

|

|

|

|

5%, 6/25/2025 | | | 2,000,000 | † | | 1,996,232 | |

|

|

|

|

|

|

|

|

4.841%, 11/1/2034# | | | 1,075,007 | | | 1,074,852 | |

|

|

|

|

|

|

|

|

4.737%, 8/1/2035# | | | 1,298,779 | | | 1,296,274 | |

|

|

|

|

|

|

|

|

8

|

Portfolio of Investments |

December 31, 2008 |

| | | | | | | |

| | Principal

Amount

or Shares | | Value | |

Fannie Mae: (continued) | | | | | | | |

|

|

|

|

|

|

|

|

5.5%, 2/1/2036 | | $ | 1,983,750 | | $ | 2,036,217 | |

|

|

|

|

|

|

|

|

5.356%, 4/1/2036# | | | 814,154 | | | 830,420 | |

|

|

|

|

|

|

|

|

6.047%, 4/1/2036# | | | 1,296,704 | | | 1,328,454 | |

|

|

|

|

|

|

|

|

5.959%, 8/1/2036# | | | 668,034 | | | 683,885 | |

|

|

|

|

|

|

|

|

5.82%, 9/1/2037# | | | 972,667 | | | 999,044 | |

|

|

|

|

|

|

|

|

6.5%, 9/1/2037 | | | 2,022,594 | | | 2,071,945 | |

|

|

|

|

|

|

|

|

6.5%, 12/1/2037 | | | 3,570,489 | † | | 3,713,108 | |

|

|

|

|

|

|

|

|

6.5%, TBA 1/2009 | | | 3,000,000 | | | 3,115,782 | |

|

|

|

|

|

|

|

|

Freddie MacØ: | | | | | | | |

|

|

|

|

|

|

|

|

6.161%, 8/1/2036# | | | 779,970 | | | 791,849 | |

|

|

|

|

|

|

|

|

6.109%, 12/1/2036# | | | 1,521,409 | | | 1,566,099 | |

|

|

|

|

|

|

|

|

Freddie Mac GoldØ: | | | | | | | |

|

|

|

|

|

|

|

|

5%, 5/1/2018 | | | 1,377,928 | | | 1,422,680 | |

|

|

|

|

|

|

|

|

5.5%, 10/1/2018 | | | 1,196,107 | | | 1,237,400 | |

|

|

|

|

|

|

|

|

7%, 4/1/2038 | | | 386,101 | | | 400,985 | |

|

|

|

|

|

|

|

|

6%, TBA 1/2009 | | | 1,000,000 | | | 1,030,156 | |

|

|

|

|

|

|

|

|

4.5%, TBA 1/2009 | | | 3,000,000 | | | 3,067,500 | |

|

|

|

|

|

|

|

|

5.5%, TBA 1/2009 | | | 3,250,000 | | | 3,326,680 | |

|

|

|

|

|

|

|

|

5.5%, TBA 1/2009 | | | 2,800,000 | | | 2,882,687 | |

|

|

|

|

|

|

|

|

Ginnie Mae: | | | | | | | |

|

|

|

|

|

|

|

|

5%, 5/20/2029 | | | 440,232 | | | 444,248 | |

|

|

|

|

|

|

|

|

5.5%, 10/15/2035 | | | 1,597,777 | | | 1,650,071 | |

|

|

|

|

|

|

|

|

Small Business Administration 5.199%, 8/10/2012 | | | 493,280 | | | 501,515 | |

|

|

|

|

|

|

|

|

Total Mortgage-Backed Securities (Cost $37,834,163) | | | | | | 38,478,061 | |

|

|

|

|

|

|

|

|

|

Short Term Holdings 22.2% | | | | | | | |

|

|

|

|

|

|

|

|

Federal Home Loan Bank 0.28%, 3/25/2009 | | | 2,500,000 | † | | 2,499,745 | |

|

|

|

|

|

|

|

|

US Treasury Bill 0.50%, 10/22/2009 | | | 2,000,000 | | | 1,994,742 | |

|

|

|

|

|

|

|

|

US Treasury Note 3.5%, 8/15/2009 | | | 1,500,000 | | | 1,529,825 | |

|

|

|

|

|

|

|

|

SSgA U.S. Treasury Money Market Fund | | | 12,673,821 | shs. | | 12,673,821 | |

|

|

|

|

|

|

|

|

Total Short-Term Holdings (Cost $18,645,168) | | | | | | 18,698,133 | |

|

|

|

|

|

|

|

|

Total Investments (Cost $93,454,977) 115.1% | | | | | | 96,993,285 | |

|

|

|

|

|

|

|

|

Other Assets Less Liabilities (15.1)% | | | | | | (12,732,996 | ) |

|

|

|

|

|

|

|

|

Net Assets 100.0% | | | | | $ | 84,260,289 | |

|

|

|

|

|

|

|

|

| | |

|

* | | STRIPS (Separate Trading of Registered Interest and Principal of Securities) Principal is purchased at a discount, receives no interest and receives a single payment at maturity. |

|

Ø | | Securities issued by these agencies are neither guaranteed nor issued by the United States Government. |

|

ØØ | | Investments in mortgage-backed securities are subject to principal paydowns. As a result of prepayments from refinancing or satisfaction of the underlying mortgage instruments, the average life may be less than the original maturity. This in turn may impact the ultimate yield realized from these investments. |

|

# | | Floating rate security, the interest rate is reset periodically. The interest rate disclosed reflects the rate in effect at December 31, 2008. |

|

† | | At December 31, 2008, these securities with a total value of $24,007,650 were held as collateral for the TBA securities. |

TBA—To be announced.

See Notes to Financial Statements.

9

Statement of Assets and Liabilities

December 31, 2008

| | | | |

Assets: | | | | |

|

|

|

|

|

Investments, at value: | | | | |

|

|

|

|

|

US Full Faith and Credit Obligations (cost $22,581,796) | | $ | 24,393,812 | |

|

|

|

|

|

US Government Agency Obligations (cost $14,393,850) | | | 15,423,279 | |

|

|

|

|

|

Mortgage-Backed Securities (cost $37,834,163) | | | 38,478,061 | |

|

|

|

|

|

Short-Term Holdings (cost $18,645,168) | | | 18,698,133 | |

|

|

|

|

|

Total investments (cost $93,454,977) | | | 96,993,285 | |

|

|

|

|

|

Cash (including restricted cash of $10,000) | | | 27,916 | |

|

|

|

|

|

Receivable for shares of Beneficial Interest sold | | | 936,132 | |

|

|

|

|

|

Dividends and interest receivable | | | 477,354 | |

|

|

|

|

|

Paydown receivable | | | 39,511 | |

|

|

|

|

|

Expenses prepaid to shareholder service agent | | | 4,816 | |

|

|

|

|

|

Other | | | 2,674 | |

|

|

|

|

|

Total Assets | | | 98,481,688 | |

|

|

|

|

|

Liabilities: | | | | |

|

|

|

|

|

Payable for securities purchased | | | 13,260,070 | |

|

|

|

|

|

Payable for shares of Beneficial Interest repurchased | | | 781,272 | |

|

|

|

|

|

Dividends payable | | | 62,173 | |

|

|

|

|

|

Distribution and service fees (12b-1) payable | | | 37,937 | |

|

|

|

|

|

Management fees payable | | | 35,224 | |

|

|

|

|

|

Accrued expenses and other | | | 44,723 | |

|

|

|

|

|

Total Liabilities | | | 14,221,399 | |

|

|

|

|

|

Net Assets | | $ | 84,260,289 | |

|

|

|

|

|

Composition of Net Assets: | | | | |

|

|

|

|

|

Shares of Beneficial Interest, at par ($0.001 par value; unlimited shares authorized; 11,470,030 shares outstanding): | | | | |

|

|

|

|

|

Class A | | $ | 6,702 | |

|

|

|

|

|

Class B | | | 1,215 | |

|

|

|

|

|

Class C | | | 2,944 | |

|

|

|

|

|

Class R | | | 609 | |

|

|

|

|

|

Additional paid-in capital | | | 87,269,498 | |

|

|

|

|

|

Dividends in excess of net investment income (Note 7) | | | (21,148 | ) |

|

|

|

|

|

Accumulated net realized loss (Note 7) | | | (6,537,839 | ) |

|

|

|

|

|

Net unrealized appreciation of investments | | | 3,538,308 | |

|

|

|

|

|

Net Assets | | $ | 84,260,289 | |

|

|

|

|

|

Net Asset Value Per Share: | | | | |

|

|

|

|

|

Class A ($49,207,829 ÷ 6,702,682 shares) | | $ | 7.34 | |

|

|

|

|

|

Class B ($8,941,291 ÷ 1,215,366 shares) | | $ | 7.36 | |

|

|

|

|

|

Class C ($21,645,636 ÷ 2,943,964 shares) | | $ | 7.35 | |

|

|

|

|

|

Class R ($4,465,533 ÷ 608,018 shares) | | $ | 7.34 | |

|

|

|

|

|

|

|

See Notes to Financial Statements. |

10

Statement of Operations

For the Year Ended December 31, 2008

| | | | |

Investment Income: | | | | |

|

|

|

|

|

Interest | | $ | 2,934,730 | |

|

|

|

|

|

Dividends | | | 332 | |

|

|

|

|

|

Other | | | 244 | |

|

|

|

|

|

Total Investment Income | | | 2,935,306 | |

|

|

|

|

|

| | | | |

Expenses: | | | | |

|

|

|

|

|

Distribution and service (12b-1) fees | | | 371,653 | |

|

|

|

|

|

Management fee | | | 355,918 | |

|

|

|

|

|

Shareholder account services | | | 334,511 | |

|

|

|

|

|

Registration | | | 65,833 | |

|

|

|

|

|

Auditing and legal fees | | | 39,360 | |

|

|

|

|

|

Custody and related services | | | 31,533 | |

|

|

|

|

|

Shareholder reports and communications | | | 23,939 | |

|

|

|

|

|

Trustees’ fees and expenses | | | 5,509 | |

|

|

|

|

|

Miscellaneous | | | 8,624 | |

|

|

|

|

|

Total Expenses | | �� | 1,236,880 | |

|

|

|

|

|