Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04236

JPMorgan Trust II

(Exact name of registrant as specified in charter)

270 Park Avenue

New York, NY 10017

(Address of principal executive offices) (Zip code)

Frank J. Nasta

270 Park Avenue

New York, NY 10017

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (800) 480-4111

Date of fiscal year end: October 31

Date of reporting period: November 1, 2011 through October 31, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

Table of Contents

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

Table of Contents

Annual Report

J.P. Morgan International Equity Funds

October 31, 2012

JPMorgan Emerging Economies Fund

JPMorgan Emerging Markets Equity Fund

JPMorgan Global Equity Income Fund

JPMorgan Global Opportunities Fund

(formerly JPMorgan Global Focus Fund)

JPMorgan International Equity Fund

JPMorgan International Equity Index Fund

JPMorgan International Opportunities Fund

JPMorgan International Value Fund

JPMorgan Intrepid International Fund

Table of Contents

| CEO’s Letter | 1 | |||

| Market Overview | 2 | |||

| 3 | ||||

| 6 | ||||

| 9 | ||||

| 12 | ||||

| 15 | ||||

| 18 | ||||

| 20 | ||||

| 24 | ||||

| 28 | ||||

| Schedules of Portfolio Investments | 31 | |||

| Financial Statements | 76 | |||

| Financial Highlights | 100 | |||

| Notes to Financial Statements | 118 | |||

| Report of Independent Registered Public Accounting Firm | 139 | |||

| Trustees | 140 | |||

| Officers | 143 | |||

| Schedule of Shareholder Expenses | 144 | |||

| Board Approval of Investment Advisory Agreement | 148 | |||

| Tax Letter | 152 | |||

Investments in a Fund are not bank deposits or obligations of, or guaranteed or endorsed by, any bank and are not insured or guaranteed by the FDIC, the Federal Reserve Board or any other government agency. You could lose money if you sell when the Fund’s share price is lower than when you invested.

Past performance is no guarantee of future performance. The general market views expressed in this report are opinions based on market and other conditions through the end of the reporting period and are subject to change without notice. These views are not intended to predict the future performance of a Fund or the securities markets. References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Such views are not meant as investment advice and may not be relied on as an indication of trading intent on behalf of any Fund.

Prospective investors should refer to the Funds’ prospectus for a discussion of the Funds’ investment objectives, strategies and risks. Call J.P. Morgan Funds Service Center at 1-800-480-4111 for a prospectus containing more complete information about a Fund, including management fees and other expenses. Please read it carefully before investing.

Table of Contents

NOVEMBER 26, 2012 (Unaudited)

Dear Shareholder:

Global equity markets continued to seesaw against an uncertain macroeconomic and geopolitical backdrop. In the U.S., improving economic data has been overshadowed by the pending “fiscal cliff.” Concerns about a potential economic “hard landing” in China remain, while escalating tension in the Middle East recently resulted in a conflict between Israel and Hamas, exacerbating fears about the stability of the region. Europe’s debt crisis continues and global equity prices have fluctuated with investors’ changing perception about the viability of corrective actions taken by the European Central Bank.

|

“The constant change in emerging markets economies creates market volatility that we believe can be dampened by holding a range of emerging market equities and fixed income securities representing different regions and sectors.” |

Despite these sharp swings in market momentum, stocks in most parts of the world posted positive returns for the twelve months ended October 31, 2012. Accommodative monetary policies have been a significant catalyst for the positive returns for stocks during the past year and continue to keep yields at historically low levels. As the low interest rate environment persists, an increasing amount of fixed income investors are turning to asset classes like high yield bonds and emerging markets debt in search of higher yielding securities. Higher demand for these securities as well as positive fundamentals led to positive returns for high yield bonds and emerging markets debt during the 12 months ended October 31, 2012.

U.S. Treasury yields remain low while U.S. stocks outperform

Real yields are negative on many parts of the yield curve, meaning that the payment that investors will receive from these bonds is less than the expected rate of inflation. Holders of these securities are willing to see the purchasing power of their money decline in order to access the perceived safety of U.S. Treasury securities, likely a reflection of the elevated level of uncertainty among investors. The yield for 10-year U.S. Treasury securities ended October 2012 at 1.7%, while the yields for 2- and 30-year U.S. Treasury securities finished the reporting period at 0.3% and 2.9%, respectively.

Stock returns across market capitalizations, countries and investment styles varied during the twelve months ended

October 31, 2012. Buoyed by stronger-than-expected economic data, U.S. stocks finished the twelve-month reporting period ahead of international and emerging markets stocks, which were weighed down by Europe’s ongoing debt crisis and concerns about an economic “hard landing” in China.

Emerging markets: An evolving asset class

While the Chinese economy rightfully commands a large amount of attention from emerging markets investors, the asset class encompasses a wide range of countries with diverse cultural and political standards and evolving industries. Changes to local political administrations and economic policies can alter the investment landscape of an emerging market. For example, recently elected Mexican president Pena Nieto has pledged to focus on energy, labor and tax reforms, which has attracted more foreign investors who welcome the proposed business-friendly changes. On the other side of the spectrum, Russia’s recent presidential election has elevated geopolitical risk and therefore lowered the willingness of investors to invest in local Russian companies.

The constant change in emerging markets economies creates market volatility that we believe can be dampened by holding a range of emerging market equities and fixed income securities representing different regions and sectors. The volatility and differences in emerging markets can also create attractive investment opportunities for active managers with the resources in place to monitor disparate emerging economies and the companies that operate in them.

Emerging markets securities can be a valuable tool for investors as they construct their portfolios. As always, we encourage investors to maintain exposure to a variety of asset classes within fixed income, equity and alternative investments.

On behalf of everyone at J.P. Morgan Asset Management, thank you for your continued support. We look forward to managing your investment needs for years to come. Should you have any questions, please visit www.jpmorganfunds.com or contact the J.P. Morgan Funds Service Center at 1-800-480-4111.

Sincerely yours,

George C.W. Gatch

CEO, Global Funds Management

J.P. Morgan Asset Management

| OCTOBER 31, 2012 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | 1 | ||||||

Table of Contents

J.P. Morgan International Equity Funds

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited)

Developed Markets

The debt crisis in Europe continued to be a major source of uncertainty in capital markets. Global equity prices rose and fell with investors’ changing perception about the viability of actions taken by the European Central Bank to curb the crisis. Escalating political and social unrest in the Middle East also weighed on investor sentiment during the reporting period. Despite these concerns, stocks in most parts of the world posted positive returns during the twelve months ended October 31, 2012, bolstered by the accommodative policies of central banks as they continued their efforts to stoke economic growth. International developed stocks underperformed U.S. stocks during the reporting period, as the MSCI Europe, Australasia and Far East (“EAFE”) Index (net of foreign withholding taxes) gained 4.61%.

Emerging Markets

Emerging markets stocks underperformed international developed stocks during the reporting period as the MSCI Emerging Markets Index (net of foreign withholding taxes) gained 2.63%. Fears of an economic “hard landing” in China weighed on the asset class, as did concerns about weaker demand for commodities as a result of slowing global economic growth.

| 2 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | OCTOBER 31, 2012 | ||||

Table of Contents

JPMorgan Emerging Economies Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited)

| REPORTING PERIOD RETURN: | ||||

| Fund (Select Class Shares)* | 3.34% | |||

| Morgan Stanley Capital International (“MSCI”) Emerging Markets Index (net of foreign withholding taxes) | 2.63% | |||

| Net Assets as of 10/31/2012 (In Thousands) | $ | 445,933 | ||

INVESTMENT OBJECTIVE**

The JPMorgan Emerging Economies Fund (the “Fund”) seeks long-term capital growth.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund (Select Class Shares) outperformed the MSCI Emerging Markets Index (net of foreign withholding taxes) (the “Benchmark”) for the twelve months ended October 31, 2012. The Fund’s stock selection in the energy and consumer discretionary sectors contributed to relative performance. The Fund’s stock selection in the consumer staples sector and underweight versus the Benchmark and stock selection in the telecommunications services sector detracted from relative performance.

Individual contributors to relative performance included the Fund’s overweight positions versus the Benchmark in Great Wall Motor Company Ltd., a Chinese auto maker, and Cielo S.A., a Brazilian credit and debit card-payment processor. Both stocks rose after the companies reported better-than-expected first-quarter earnings. The Fund’s overweight position versus the Benchmark in Samsung Electronics Co., Ltd. also contributed to relative performance. Shares of the communications equipment provider benefited from the company’s strong sales for its smart phones.

Individual detractors from relative performance included the Fund’s overweight positions versus the Benchmark in Vale S.A.,

E Ink Holdings, Inc. and Banco do Brasil S.A. Shares of Vale, a Brazilian iron-ore producer, declined due to a dispute over the company’s unpaid tax claims. Shares of E Ink Holdings, Inc., which provides TFT LCD panels for e-reader devices, declined after the company reported a quarterly loss due to excess inventory at Amazon Inc., one of its major clients. Shares of Brazilian bank Banco do Brasil S.A. declined on concerns about the impact that increasing loan defaults would have on the company’s earnings.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers used a combination of top-down and bottom-up research, seeking attractively priced countries, sectors and stocks with positive catalysts. As a result of this process, the Fund’s largest overweight versus the Benchmark was in the consumer discretionary sector and the Fund’s largest underweight versus the Benchmark was in the financials sector.

| * | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | The advisor seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| OCTOBER 31, 2012 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | 3 | ||||||

Table of Contents

JPMorgan Emerging Economies Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited) (continued)

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO* | ||||||||

| 1. | Samsung Electronics Co., Ltd. (South Korea) | 5.3 | % | |||||

| 2. | Taiwan Semiconductor Manufacturing Co., Ltd., ADR (Taiwan) | 3.1 | ||||||

| 3. | China Construction Bank Corp., Class H (China) | 2.3 | ||||||

| 4. | Industrial & Commercial Bank of China Ltd., Class H (China) | 2.1 | ||||||

| 5. | CNOOC Ltd. (China) | 2.1 | ||||||

| 6. | Vale S.A., ADR (Brazil) | 2.0 | ||||||

| 7. | Hyundai Motor Co. (South Korea) | 2.0 | ||||||

| 8. | Lukoil OAO, ADR (Russia) | 1.9 | ||||||

| 9. | PetroChina Co., Ltd., Class H (China) | 1.9 | ||||||

| 10. | Cia de Bebidas das Americas, ADR (Preferred Stock) (Brazil) | 1.8 | ||||||

PORTFOLIO COMPOSITION BY COUNTRY* | ||||

| China | 18.9 | % | ||

| South Korea | 14.5 | |||

| Brazil | 10.4 | |||

| Taiwan | 9.5 | |||

| Russia | 7.1 | |||

| South Africa | 6.7 | |||

| Turkey | 6.3 | |||

| Thailand | 5.4 | |||

| Hong Kong | 5.2 | |||

| India | 5.1 | |||

| United Kingdom | 1.5 | |||

| Poland | 1.2 | |||

| Hungary | 1.0 | |||

| Others (each less than 1.0%) | 4.8 | |||

| Short-Term Investment | 2.4 | |||

| * | Percentages indicated are based upon total investments as of October 31, 2012. The Fund’s portfolio composition is subject to change. |

| 4 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | OCTOBER 31, 2012 | ||||

Table of Contents

AVERAGE ANNUAL TOTAL RETURNS AS OF OCTOBER 31, 2012 | ||||||||||||||||

| INCEPTION DATE OF CLASS | 1 YEAR | 3 YEAR | SINCE INCEPTION | |||||||||||||

CLASS A SHARES | 2/28/08 | |||||||||||||||

Without Sales Charge | 3.15 | % | 8.54 | % | (1.57 | )% | ||||||||||

With Sales Charge* | (2.26 | ) | 6.61 | (2.70 | ) | |||||||||||

CLASS C SHARES | 2/28/08 | |||||||||||||||

Without CDSC | 2.54 | 7.97 | (2.07 | ) | ||||||||||||

With CDSC** | 1.54 | 7.97 | (2.07 | ) | ||||||||||||

CLASS R5 SHARES | 2/28/08 | 3.53 | 9.01 | (1.14 | ) | |||||||||||

SELECT CLASS SHARES | 2/28/08 | 3.34 | 8.81 | (1.33 | ) | |||||||||||

| * | Sales Charge for Class A Shares is 5.25%. |

| ** | Assumes a 1% CDSC (contingent deferred sales charge) for the one year period and 0% CDSC thereafter. |

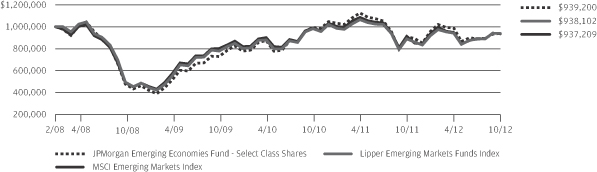

LIFE OF FUND PERFORMANCE (2/28/08 TO 10/31/12)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

The Fund commenced operations on February 28, 2008.

The graph illustrates comparative performance for $1,000,000 invested in Select Class Shares of the JPMorgan Emerging Economies Fund, the MSCI Emerging Markets Index and the Lipper Emerging Markets Funds Index from February 28, 2008 to October 31, 2012. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the MSCI Emerging Markets Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and approximates the minimum possible dividend reinvestment of the securities included in the benchmark. The dividend is reinvested after deduction of withholding tax, applying the maximum rate to nonresident individual investors who do not benefit from double taxation treaties. The performance of the Lipper Emerging Markets Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The MSCI

Emerging Markets Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of emerging markets. The Lipper Emerging Markets Funds Index is an index based on total returns of certain mutual funds within the Fund’s designated category as determined by Lipper, Inc. Investors cannot invest directly in an index.

Select Class Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

International investing involves a greater degree of risk and increased volatility. Changes in currency exchange rates and differences in accounting and taxation policies outside the United States can raise or lower returns. Also, some overseas markets may not be as politically and economically stable as the U.S. and other nations. The Fund is also subject to the additional risk of non-diversified “regional” fund investing.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| OCTOBER 31, 2012 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | 5 | ||||||

Table of Contents

JPMorgan Emerging Markets Equity Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited)

| REPORTING PERIOD RETURN: | ||||

| Fund (Institutional Class Shares)* | 4.80% | |||

| Morgan Stanley Capital International (“MSCI”) Emerging Markets Index (net of foreign withholding taxes) | 2.63% | |||

| Net Assets as of 10/31/2012 (In Thousands) | $ | 2,252,486 | ||

INVESTMENT OBJECTIVE**

The JPMorgan Emerging Markets Equity Fund (the “Fund”) seeks to provide high total return from a portfolio of equity securities from emerging markets issuers.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund (Institutional Class Shares) outperformed the MSCI Emerging Markets Index (net of foreign withholding taxes) (the “Benchmark”) for the twelve months ended October 31, 2012. The Fund’s stock selection in the industrials, information technology and financials sectors contributed to relative performance. The Fund’s stock selection in the telecommunications services and consumer discretionary sectors and underweight versus the Benchmark in the healthcare sector detracted from relative performance.

Individual contributors to relative performance included the Fund’s overweight positions versus the Benchmark in Grupo Financiero Banorte S.A.B. de C.V., Turkiye Garanti Bankasi A.S. and Samsung Electronics Co., Ltd. Shares of Mexican bank Grupo Financiero Banorte S.A.B. de C.V. benefited from the company’s strong first-quarter earnings, which were boosted by robust growth in bank deposits and loans. Shares of Turkiye Garanti Bankasi A.S. rose after the Turkish bank reported better-than-expected third-quarter earnings. Shares of

communications equipment provider Samsung Electronics Co., Ltd. benefited from the company’s strong sales for its smart phones.

Individual detractors from relative performance included the Fund’s overweight positions versus the Benchmark in Bharti Airtel Ltd., OGX Petroleo e Gas Participacoes S.A. and Infosys Ltd., ADR. Shares of Indian telecommunication provider Bharti Airtel Ltd. declined amid concerns about increasing market competition in India’s telecommunications industry. Shares of Brazilian energy company OGX Petroleo e Gas Participacoes S.A. declined due to investors’ concerns about the company’s announced management change. Shares of Infosys Ltd., ADR decreased after the Indian software and programming company reported disappointing fiscal year-end earnings.

HOW WAS THE FUND POSITIONED?

The Fund employed an active strategy in which portfolio construction was focused on the highest-conviction ideas found at the stock level. The Fund’s portfolio managers used bottom-up fundamental research to determine the Fund’s security weightings against the Benchmark, rigorously researching companies in an attempt to determine their underlying value and potential for future earnings growth. As a result of this process, the Fund’s largest overweight versus the Benchmark was in the consumer staples sector and the Fund’s largest underweight versus the Benchmark was in the materials sector.

| 6 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | OCTOBER 31, 2012 | ||||

Table of Contents

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | ||||||||

| 1. | Samsung Electronics Co., Ltd. (South Korea) | 5.1 | % | |||||

| 2. | Taiwan Semiconductor Manufacturing Co., Ltd., ADR (Taiwan) | 4.2 | ||||||

| 3. | Housing Development Finance Corp., Ltd. (India) | 4.1 | ||||||

| 4. | China Mobile Ltd. (Hong Kong) | 3.2 | ||||||

| 5. | Cia de Bebidas das Americas, ADR (Preferred Stock) (Brazil) | 3.1 | ||||||

| 6. | Turkiye Garanti Bankasi AS (Turkey) | 2.9 | ||||||

| 7. | Hyundai Motor Co. (South Korea) | 2.6 | ||||||

| 8. | CNOOC Ltd. (China) | 2.6 | ||||||

| 9. | Petroleo Brasileiro S.A., ADR (Brazil) | 2.5 | ||||||

| 10. | AIA Group Ltd. (Hong Kong) | 2.4 | ||||||

PORTFOLIO COMPOSITION BY COUNTRY*** | ||||

| Brazil | 14.5 | % | ||

| China | 11.8 | |||

| South Korea | 11.3 | |||

| India | 10.3 | |||

| South Africa | 10.1 | |||

| Hong Kong | 10.0 | |||

| Taiwan | 7.2 | |||

| Indonesia | 4.3 | |||

| Turkey | 3.8 | |||

| Mexico | 3.1 | |||

| Russia | 3.0 | |||

| United Kingdom | 2.6 | |||

| Luxembourg | 1.9 | |||

| Chile | 1.8 | |||

| Malaysia | 1.1 | |||

| Others (each less than 1.0%) | 0.8 | |||

Short-Term Investment | 2.4 | |||

| * | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | The advisor seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | Percentages indicated are based upon total investments as of October 31, 2012. The Fund’s portfolio composition is subject to change. |

| OCTOBER 31, 2012 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | 7 | ||||||

Table of Contents

JPMorgan Emerging Markets Equity Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited) (continued)

AVERAGE ANNUAL TOTAL RETURNS AS OF OCTOBER 31, 2012 | ||||||||||||||||

| INCEPTION DATE OF CLASS | 1 YEAR | 5 YEAR | 10 YEAR | |||||||||||||

CLASS A SHARES | 9/28/01 | |||||||||||||||

Without Sales Charge | 4.36 | % | (2.89 | )% | 16.15 | % | ||||||||||

With Sales Charge* | (1.12 | ) | (3.93 | ) | 15.52 | |||||||||||

CLASS B SHARES | 9/28/01 | |||||||||||||||

Without CDSC | 3.80 | (3.37 | ) | 15.69 | ||||||||||||

With CDSC** | (1.20 | ) | (3.83 | ) | 15.69 | |||||||||||

CLASS C SHARES | 2/28/06 | |||||||||||||||

Without CDSC | 3.83 | (3.37 | ) | 15.57 | ||||||||||||

With CDSC*** | 2.83 | (3.37 | ) | 15.57 | ||||||||||||

INSTITUTIONAL CLASS SHARES | 11/15/93 | 4.80 | (2.49 | ) | 16.67 | |||||||||||

SELECT CLASS SHARES | 9/10/01 | 4.65 | (2.64 | ) | 16.42 | |||||||||||

| * | Sales Charge for Class A Shares is 5.25%. |

| ** | Assumes a 5% CDSC (contingent deferred sales charge) for the one year period, 2% CDSC for the five year period and 0% CDSC thereafter. |

| *** | Assumes a 1% CDSC for the one year period and 0% CDSC thereafter. |

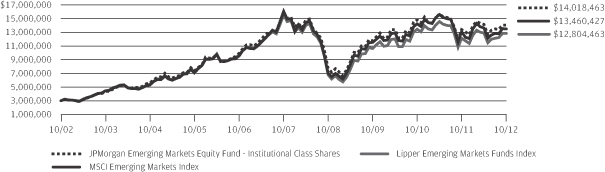

TEN YEAR PERFORMANCE (10/31/02 TO 10/31/12)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for Class C Shares prior to its inception date were based on the performance of Class B Shares. The actual returns of Class C Shares would have been similar to those shown because Class C Shares have expenses similar to those of Class B Shares.

The graph illustrates comparative performance for $3,000,000 invested in Institutional Class Shares of the JPMorgan Emerging Markets Equity Fund, the MSCI Emerging Markets Index and the Lipper Emerging Markets Funds Index from October 31, 2002 to October 31, 2012. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the MSCI Emerging Markets Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and approximates the maximum possible dividend reinvestment of the securities included in the benchmark. The dividend is reinvested after deduction of withholding tax, applying the maximum rate to nonresident individual investors who do not benefit from double taxation treaties. The performance of the Lipper Emerging Markets Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The MSCI Emerging Markets Index is a free float-adjusted market capitalization

weighted index that is designed to measure the equity market performance of emerging markets. The Lipper Emerging Markets Funds Index is an index based on the total returns of the funds in the indicated category, as defined by Lipper, Inc. Investors cannot invest directly in an index.

Institutional Class Shares have a $3,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

International investing involves a greater degree of risk and increased volatility. Changes in currency exchange rates and differences in accounting and taxation policies outside the U.S. can raise or lower returns. Also, some overseas markets may not be as politically and economically stable as the United States and other nations.

Because Class B shares automatically convert to Class A shares after 8 years, the 10 Year average annual total return shown above for Class B reflects Class A performance for the period after conversion.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| 8 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | OCTOBER 31, 2012 | ||||

Table of Contents

JPMorgan Global Equity Income Fund

FUND SUMMARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited)

| REPORTING PERIOD RETURN: | ||||

| Fund (Select Class Shares)* | 9.43% | |||

| Morgan Stanley Capital International (“MSCI”) World Index (net of foreign withholding taxes) | 9.45% | |||

| Net Assets as of 10/31/2012 (In Thousands) | $ | 37,867 | ||

INVESTMENT OBJECTIVE**

The JPMorgan Global Equity Income Fund (the “Fund”) seeks to provide both current income and long-term capital appreciation.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund (Select Class Shares) underperformed the MSCI World Index (net of foreign withholding taxes) (the “Benchmark”) for the twelve months ended October 31, 2012. The Fund’s stock selection and underweight position versus the Benchmark in the consumer non-durable sector detracted from relative performance. Stock selection in the insurance sector also detracted. The Fund’s stock selection in the banks and finance sector and stock selection and underweight versus the Benchmark in the basic industries sector contributed to relative performance.

Individual detractors from relative performance included the Fund’s overweight positions versus the Benchmark in QBE Insurance Group Ltd., and Canon, Inc. Shares of Australian insurance company QBE Insurance Group Ltd. declined as the company warned that its insurance profit margin might decline in the second half of the year. Shares of the Japanese imaging company Canon, Inc. underperformed, weighed down by concerns about a strong yen, sluggish demand for office equipment, slowing demand in China and a territorial dispute with that same country, which resulted in the Chinese boycotting Japanese goods.

Individual contributors to relative performance included the Fund’s overweight positions versus the Benchmark in Telecom

Corp. of New Zealand Ltd. and Wells Fargo & Co. Shares of Telecom Corp. of New Zealand Ltd., a communications services company, rose as investors were attracted to the stock’s dividend yield. The company has been returning capital to shareholders following the spin off of its Chorus network unit. Shares of U.S. bank Wells Fargo & Co. benefited from investors’ optimism surrounding the bank’s competitive positioning and resulting market share gains.

HOW THE FUND WAS MANAGED

The Fund’s portfolio managers employed a bottom-up fundamental approach to stock selection, rigorously researching companies in an attempt to determine their underlying value and potential for future growth. The Fund’s portfolio managers looked for dividend yielding equity securities that they believed were undervalued and possessed the long-term earnings power and strong cash flow generation that would enable them to grow their dividends.

In addition, the Fund employed futures and currency forwards to help manage cash flows and attempt to keep the Fund’s currency exposure in line with the Benchmark.

| * | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | The advisor seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| OCTOBER 31, 2012 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | 9 | ||||||

Table of Contents

JPMorgan Global Equity Income Fund

FUND SUMMARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited) (continued)

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO* | ||||||||

| 1. | Time Warner, Inc. | 2.8 | % | |||||

| 2. | Royal Dutch Shell plc, Class A (Netherlands) | 2.8 | ||||||

| 3. | Merck & Co., Inc. | 2.7 | ||||||

| 4. | Australia & New Zealand Banking Group Ltd. (Australia) | 2.5 | ||||||

| 5. | Pfizer, Inc. | 2.1 | ||||||

| 6. | Vodafone Group plc (United Kingdom) | 2.1 | ||||||

| 7. | Eni S.p.A. (Italy) | 2.0 | ||||||

| 8. | Telecom Corp. of New Zealand Ltd. (New Zealand) | 2.0 | ||||||

| 9. | Roche Holding AG (Switzerland) | 1.9 | ||||||

| 10. | Verizon Communications, Inc. | 1.9 | ||||||

PORTFOLIO COMPOSITION BY COUNTRY* | ||||

| United States | 30.4 | % | ||

| United Kingdom | 12.1 | |||

| France | 8.3 | |||

| Japan | 8.1 | |||

| Australia | 6.8 | |||

| Germany | 6.2 | |||

| Netherlands | 5.4 | |||

| Switzerland | 5.1 | |||

| China | 2.9 | |||

| Italy | 2.0 | |||

| Sweden | 2.0 | |||

| New Zealand | 2.0 | |||

| Singapore | 1.8 | |||

| Hong Kong | 1.4 | |||

| Indonesia | 1.0 | |||

| Others (each less than 1.0%) | 1.8 | |||

| Short-Term Investment | 2.7 | |||

| * | Percentages indicated are based upon total investments as of October 31, 2012. The Fund’s portfolio composition is subject to change. |

| 10 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | OCTOBER 31, 2012 | ||||

Table of Contents

AVERAGE ANNUAL TOTAL RETURNS AS OF OCTOBER 31, 2012 | ||||||||||||

| INCEPTION DATE OF CLASS | 1 YEAR | SINCE INCEPTION | ||||||||||

CLASS A SHARES | 2/28/11 | |||||||||||

Without Sales Charge | 9.17 | % | (0.29 | )% | ||||||||

With Sales Charge* | 3.44 | (3.45 | ) | |||||||||

CLASS C SHARES | 2/28/11 | |||||||||||

Without CDSC | 8.74 | (0.75 | ) | |||||||||

With CDSC** | 7.74 | (0.75 | ) | |||||||||

CLASS R2 SHARES | 2/28/11 | 8.96 | (0.53 | ) | ||||||||

CLASS R5 SHARES | 2/28/11 | 9.70 | 0.17 | |||||||||

SELECT CLASS SHARES | 2/28/11 | 9.43 | (0.04 | ) | ||||||||

| * | Sales Charge for Class A Shares is 5.25%. |

| ** | Assumes a 1% CDSC (contingent deferred sales charge) for the one year period and 0% CDSC thereafter. |

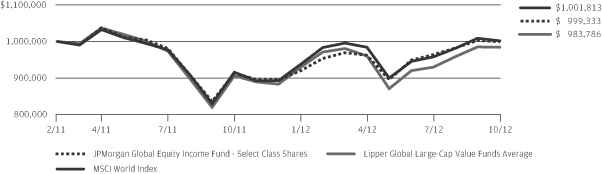

LIFE OF FUND PERFORMANCE (2/28/11 TO 10/31/12)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date, month-end performance information please call 1-800-480-4111.

The Fund commenced operations on February 28, 2011.

The graph illustrates comparative performance for $1,000,000 invested in Select Class Shares of the JPMorgan Global Equity Income Fund, the MSCI World Index and the Lipper Global Large-Cap Value Funds Average, from February 28, 2011 to October 31, 2012. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the MSCI World Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and approximates the minimum possible dividend reinvestment of the securities included in the benchmark. The dividend is reinvested after deduction of withholding tax, applying the maximum rate to non-resident institutional investors who do not benefit from double taxation treaties. These expenses are not identical to the expenses incurred by the Fund. The performance of the Lipper Global Large-Cap Value Funds Average includes expenses associated with a mutual fund, such as investment management fees. The MSCI World Index is a free float-adjusted market capitalization weighted index that is

designed to measure the equity market performance of developed markets. Investors cannot invest directly in an index. The Lipper Global Large-Cap Value Funds Average is an average based on the total returns of all mutual funds within the Fund’s designated category as determined by Lipper, Inc.

Select Class Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

International investing involves a greater degree of risk and increased volatility. Changes in currency exchange rates and differences in accounting and taxation policies outside the U.S. can raise or lower returns. Also, some overseas markets may not be as politically and economically stable as the United States and other nations.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| OCTOBER 31, 2012 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | 11 | ||||||

Table of Contents

JPMorgan Global Opportunities Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited)

| REPORTING PERIOD RETURN: | ||||

| Fund (Select Class Shares)* | 8.88% | |||

| Morgan Stanley Capital International (“MSCI”) World Index (net of foreign withholding taxes) | 9.45% | |||

| Net Assets as of 10/31/2012 (In Thousands) | $4,623 | |||

INVESTMENT OBJECTIVE**

The JPMorgan Global Opportunities Fund (the “Fund”), previously known as the JPMorgan Global Focus Fund1, seeks to provide long-term capital growth.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund (Select Class Shares) underperformed the MSCI World Index (net of foreign withholding taxes) (the “Benchmark”) for the twelve months ended October 31, 2012. The Fund’s stock selection in the energy sector detracted from relative performance. The Fund’s stock selection in the transportation services & consumer cyclicals sectors contributed to relative performance.

Individual detractors from the Fund’s relative performance included the Fund’s overweight positions versus the Benchmark in Humana, Inc., Shire plc. and Kinross Gold Corp. Shares of Humana, Inc. declined after the healthcare company warned of rising cost pressures and lowered its guidance for fiscal 2012 earnings. Shares of Shire plc., an Irish drug company, fell after the FDA approved a generic version of one of its best-selling drugs and the company’s CEO announced he would retire in 2013. Shares of Kinross Gold Corp. declined after the Canadian gold miner took a large goodwill write-down on its Tasiast mine in Africa and warned of project delays. Like many of its peers, the company also struggled with rising cost pressures.

Individual contributors to the Fund’s relative performance included the Fund’s overweight positions versus the Benchmark in Samsung Electronics Co., Ltd., Comcast Corp. and Wells

Fargo & Co. Shares of semiconductor, electronics and communications-equipment provider Samsung Electronics Co., Ltd. benefited as the company’s earnings were bolstered by robust sales for its smart phones and a turnaround in its display business. Shares of Comcast Corp., the U.S. cable TV, phone and internet provider, benefited as the company added more subscribers than expected, returned more capital to shareholders and saw ratings gains at recently-acquired NBC. Shares of U.S. bank Wells Fargo & Co. benefited from investors’ optimism surrounding the bank’s competitive positioning and resulting market share gains.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers employed a bottom-up fundamental approach to stock selection, seeking to identify what they believed to be the most attractive investment opportunities within each sector. The Fund’s portfolio managers sought stocks that they believed possessed an attractive valuation signal (as measured by a proprietary dividend discount model) and a timely catalyst that would enable the stock to realize its inherent value.

In addition, the Fund employed futures and currency forwards to help manage cash flows and attempt to keep the Fund’s currency exposure in line with the Benchmark.

| 1 | The advisor seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. Effective November 1, 2011, the Fund modified some of its investment strategies and lowered its advisory fee and expense cap. |

| 12 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | OCTOBER 31, 2012 | ||||

Table of Contents

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | ||||||||

| 1. | Apple, Inc. | 2.7 | % | |||||

| 2. | Wells Fargo & Co. | 2.2 | ||||||

| 3. | Royal Dutch Shell plc, Class A (Netherlands) | 2.0 | ||||||

| 4. | Unilever N.V., CVA (Netherlands) | 1.8 | ||||||

| 5. | Merck & Co., Inc. | 1.7 | ||||||

| 6. | Microsoft Corp. | 1.6 | ||||||

| 7. | Citigroup, Inc. | 1.6 | ||||||

| 8. | British American Tobacco plc (United Kingdom) | 1.5 | ||||||

| 9. | Vodafone Group plc (United Kingdom) | 1.5 | ||||||

| 10. | Union Pacific Corp. | 1.5 | ||||||

PORTFOLIO COMPOSITION BY COUNTRY*** | ||||

| United States | 46.5 | % | ||

| United Kingdom | 13.4 | |||

| Japan | 8.6 | |||

| Netherlands | 5.4 | |||

| Germany | 4.9 | |||

| Switzerland | 4.4 | |||

| France | 4.3 | |||

| Ireland | 3.1 | |||

| Hong Kong | 2.4 | |||

| South Korea | 1.0 | |||

| Belgium | 1.0 | |||

| Others (each less than 1.0%) | 5.0 | |||

| * | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | The advisor seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. Effective November 1, 2011, the Fund changed its investment strategy and lowered its advisory fee and expense cap. |

| *** | Percentages indicated are based upon total investments as of October 31, 2012. The Fund’s portfolio composition is subject to change. |

| OCTOBER 31, 2012 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | 13 | ||||||

Table of Contents

JPMorgan Global Opportunities Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited) (continued)

AVERAGE ANNUAL TOTAL RETURNS AS OF OCTOBER 31, 2012 | ||||||||||||||||

| INCEPTION DATE OF CLASS | 1 YEAR | 5 YEAR | SINCE INCEPTION | |||||||||||||

CLASS A SHARES | 3/30/07 | |||||||||||||||

Without Sales Charge | 8.70 | % | (2.44 | )% | (0.44 | )% | ||||||||||

With Sales Charge* | 2.97 | (3.49 | ) | (1.39 | ) | |||||||||||

CLASS C SHARES | 3/30/07 | |||||||||||||||

Without CDSC | 8.11 | (2.95 | ) | (0.95 | ) | |||||||||||

With CDSC** | 7.11 | (2.95 | ) | (0.95 | ) | |||||||||||

CLASS R2 SHARES | 11/1/11 | 8.42 | (2.49 | ) | (0.48 | ) | ||||||||||

CLASS R5 SHARES | 3/30/07 | 9.15 | (2.01 | ) | 0.01 | |||||||||||

CLASS R6 SHARES | 11/1/11 | 9.16 | (2.01 | ) | 0.01 | |||||||||||

SELECT CLASS SHARES | 3/30/07 | 8.88 | (2.21 | ) | (0.20 | ) | ||||||||||

| * | Sales Charge for Class A Shares is 5.25%. |

| ** | Assumes a 1% CDSC (contingent deferred sales charge) for the one year period and 0% CDSC thereafter. |

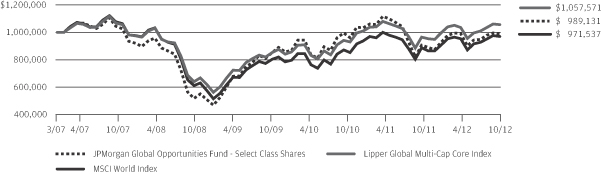

LIFE OF FUND PERFORMANCE (3/30/07 TO 10/31/12)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date, month-end performance information please call 1-800-480-4111.

The Fund commenced operations on March 30, 2007.

Effective November 1, 2011, some of the Fund’s investment strategies were modified and performance would have been different if the Fund was managed using its current strategies.

Returns for Class R2 Shares prior to its inception date were based on the performance of Class A Shares. The actual returns of R2 Shares would have been lower than shown because R2 Shares have higher expenses than Class A Shares.

Returns for Class R6 Shares prior to its inception date were based on the performance of Class R5 Shares. The actual returns of Class R6 Shares would have been different than those shown because Class R5 Shares have different expenses than Class R6 Shares.

The graph illustrates comparative performance for $1,000,000 invested in Select Class Shares of the JPMorgan Global Opportunities Fund, the MSCI World Index and the Lipper Global Multi-Cap Core Index from March 30, 2007 to October 31, 2012. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the MSCI World Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and approximates the minimum possible dividend reinvestment of the securities included in the benchmark. The dividend is reinvested after deduction of

withholding tax, applying the maximum rate to non-resident institutional investors who do not benefit from double taxation treaties. The performance of the Lipper Global Multi-Cap Core Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The Lipper Global Multi-Cap Core Index is an index based on total returns of certain mutual funds within the Fund’s designated category as determined by Lipper, Inc. Investors cannot invest directly in an index.

From the inception of the Fund through October 31, 2010, the Fund did not experience any shareholder purchase and sale activity. If such shareholder activity had occurred, the Fund’s performance may have been impacted.

Select Class Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

International investing involves a greater degree of risk and increased volatility. Changes in currency exchange rates and differences in accounting and taxation policies outside the U.S. can raise or lower returns. Also, some overseas markets may not be as politically and economically stable as the United States and other nations.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| 14 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | OCTOBER 31, 2012 | ||||

Table of Contents

JPMorgan International Equity Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited)

| REPORTING PERIOD RETURN: | ||||

| Fund (Select Class Shares)* | 7.91% | |||

| Morgan Stanley Capital International (“MSCI”) Europe, Australasia and Far East (“EAFE”) Index (net of foreign withholding taxes) | 4.61% | |||

| Net Assets as of 10/31/2012 (In Thousands) | $ | 1,076,035 | ||

INVESTMENT OBJECTIVE**

The JPMorgan International Equity Fund (the “Fund”) seeks total return from long-term capital growth and income. Total return consists of capital growth and current income.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund (Select Class Shares) outperformed the MSCI EAFE Index (net of foreign withholding taxes) (the “Benchmark”) for the twelve months ended October 31, 2012. The Fund’s stock selection, most notably in the information technology sector, contributed to the Fund’s relative performance. The Fund’s stock selection in the financials sector detracted from the Fund’s relative performance.

Individual contributors to the Fund’s relative performance included the Fund’s overweight positions in Samsung Electronics Co., Ltd., WPP plc and Anheuser-Busch InBev N.V. Shares of semiconductor, electronics and communications-equipment provider Samsung Electronics Co., Ltd. benefited as the company’s earnings were bolstered by robust sales for its smart phones and turnaround in its display business. Shares of U.K. advertising company WPP plc advanced due to the company’s better-than-expected 2011 results and expectations that events such as the London Olympics, the European Soccer Championships and the U.S. Presidential elections would support further revenue growth in 2012. Shares of Anheuser-Busch InBev N.V. increased after the beverages company reported strong revenue, boosted by continued growth in emerging markets and a recovery in its U.S. operations.

Individual detractors from the Fund’s relative performance included the Fund’s overweight positions versus the Benchmark in Canon, Inc., Tesco plc, and BG Group plc. Shares of Canon, Inc., the Japanese imaging company, underperformed, weighed down by concerns about a strong yen, sluggish demand for office equipment, slowing demand in China and a territorial dispute with China, which resulted in the Chinese boycotting Japanese goods. Shares of U.K. grocery store operator Tesco plc declined as competitive pressures and a challenging domestic economic environment prompted the company to issue its first profit warning in 20 years. Shares of BG Group plc, which is engaged in the exploration, development and production of natural gas and oil, declined following the company’s announcement that project delays would hold back output growth next year.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers continued to focus on stock selection to build a portfolio of international equities. They

used bottom-up fundamental research to identify what they believed were attractively priced stocks of well-managed companies with the potential to grow their earnings faster than their industry peers.

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | ||||||||

| 1. | Royal Dutch Shell plc, Class A (Netherlands) | 2.8 | % | |||||

| 2. | Nestle S.A. (Switzerland) | 2.4 | ||||||

| 3. | HSBC Holdings plc (United Kingdom) | 2.3 | ||||||

| 4. | Total S.A. (France) | 2.2 | ||||||

| 5. | Vodafone Group plc (United Kingdom) | 2.1 | ||||||

| 6. | Standard Chartered plc (United Kingdom) | 2.0 | ||||||

| 7. | BG Group plc (United Kingdom) | 1.9 | ||||||

| 8. | Roche Holding AG (Switzerland) | 1.9 | ||||||

| 9. | SAP AG (Germany) | 1.8 | ||||||

| 10. | Anheuser-Busch InBev N.V. (Belgium) | 1.7 | ||||||

PORTFOLIO COMPOSITION BY COUNTRY*** | ||||

| United Kingdom | 24.1 | % | ||

| Japan | 14.4 | |||

| France | 13.2 | |||

| Switzerland | 12.1 | |||

| Germany | 10.1 | |||

| Netherlands | 4.6 | |||

| China | 4.3 | |||

| Hong Kong | 2.6 | |||

| Australia | 2.1 | |||

| Belgium | 1.7 | |||

| South Korea | 1.4 | |||

| Israel | 1.2 | |||

| Ireland | 1.1 | |||

| Taiwan | 1.1 | |||

| Others (each less than 1.0%) | 2.5 | |||

| Short-Term Investment | 3.5 | |||

| * | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | The advisor seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | Percentages indicated are based upon total investments as of October 31, 2012. The Fund’s portfolio composition is subject to change. |

| OCTOBER 31, 2012 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | 15 | ||||||

Table of Contents

JPMorgan International Equity Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited) (continued)

AVERAGE ANNUAL TOTAL RETURNS AS OF OCTOBER 31, 2012 | ||||||||||||||||

| INCEPTION DATE OF CLASS | 1 YEAR | 5 YEAR | 10 YEAR | |||||||||||||

CLASS A SHARES | 2/28/02 | |||||||||||||||

Without Sales Charge | 7.70 | % | (4.10 | )% | 7.13 | % | ||||||||||

With Sales Charge* | 2.04 | (5.13 | ) | 6.56 | ||||||||||||

CLASS B SHARES | 2/28/02 | |||||||||||||||

Without CDSC | 7.15 | (4.62 | ) | 6.66 | ||||||||||||

With CDSC** | 2.15 | (5.10 | ) | 6.66 | ||||||||||||

CLASS C SHARES | 1/31/03 | |||||||||||||||

Without CDSC | 7.16 | (4.61 | ) | 6.56 | ||||||||||||

With CDSC*** | 6.16 | (4.61 | ) | 6.56 | ||||||||||||

CLASS R2 SHARES | 11/3/08 | 7.45 | (4.31 | ) | 7.02 | |||||||||||

CLASS R5 SHARES | 5/15/06 | 8.19 | (3.69 | ) | 7.57 | |||||||||||

CLASS R6 SHARES | 11/30/10 | 8.23 | (3.67 | ) | 7.58 | |||||||||||

SELECT CLASS SHARES | 1/1/97 | 7.91 | (3.87 | ) | 7.43 | |||||||||||

| * | Sales Charge for Class A Shares is 5.25%. |

| ** | Assumes a 5% CDSC (contingent deferred sales charge) for the one year period, 2% CDSC for the five year period and 0% CDSC thereafter. |

| *** | Assumes a 1% CDSC for the one year period and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE (10/31/02 TO 10/31/12)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for Class C Shares prior to its inception date were based on the performance of Class B Shares. The actual returns of Class C Shares would have been similar to those shown because Class C Shares have expenses similar to those of Class B Shares.

Returns for Class R5 Shares prior to its inception date were based on the performance of the Select Class Shares. The actual returns of Class R5 Shares would have been different than those shown because Class R5 Shares have different expenses than Select Class Shares.

Returns for Class R2 Shares prior to its inception date were based on the performance of Class A Shares. The actual returns of R2 Shares would have been lower than shown because R2 Shares have higher expenses than Class A Shares.

Returns for Class R6 Shares prior to its inception date were based on the performance of Class R5 Shares. The actual returns of Class R6 Shares would have

been different than those shown because Class R5 Shares have different expenses than Class R6 Shares.

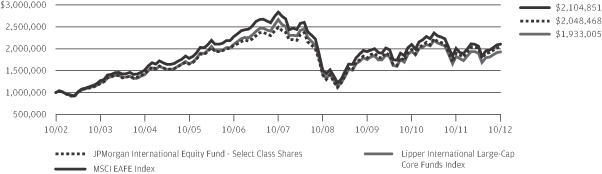

The graph illustrates comparative performance for $1,000,000 invested in Select Class Shares of the JPMorgan International Equity Fund, the MSCI EAFE Index and the Lipper International Large-Cap Core Funds Index from October 31, 2002 to October 31, 2012. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the MSCI EAFE Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and approximates the minimum possible dividend reinvestment of the securities included in the benchmark. The dividend is reinvested after deduction of withholding tax, applying the maximum rate to non-resident institutional investors who do not benefit from double taxation treaties. The performance of the Lipper International Large-Cap Core Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The MSCI EAFE Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The Lipper International Large-Cap Core Funds Index is based on the total returns of certain mutual funds within the Fund’s designated category, as defined by Lipper, Inc. Investors cannot invest directly in an index.

| 16 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | OCTOBER 31, 2012 | ||||

Table of Contents

Select Class Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

International investing involves a greater degree of risk and increased volatility. Changes in currency exchange rates and differences in accounting and taxation policies outside the U.S. can raise or lower returns. Also, some overseas markets may not be as politically and economically stable as the United States and other nations.

Because Class B Shares automatically convert to Class A Shares after 8 years, the 10 year average annual total return shown above for Class B reflects Class A performance for the period after conversion.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| OCTOBER 31, 2012 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | 17 | ||||||

Table of Contents

JPMorgan International Equity Index Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited)

| REPORTING PERIOD RETURN: | ||||

| Fund (Select Class Shares)* | 5.40% | |||

| Morgan Stanley Capital International (“MSCI”) Europe, Australasia and Far East (“EAFE”) GDP Index | 3.49% | |||

| Net Assets as of 10/31/2012 (In Thousands) | $ | 585,393 | ||

INVESTMENT OBJECTIVE**

The JPMorgan International Equity Index Fund (the “Fund”) seeks to provide investment results that correspond to the aggregate price and dividend performance of the securities in the MSCI EAFE Gross Domestic Product (“GDP”) Index (the “Benchmark”).

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund (Select Class Shares) outperformed the Benchmark for the twelve months ended October 31, 2012. The Fund’s exposure to emerging markets stocks, which are not held in the Benchmark, drove the Fund’s relative outperformance as emerging markets stocks outperformed international developed markets stocks during the reporting period.

The Fund’s strategy is not a full replication approach. The Fund seeks to achieve a correlation of 0.90 with the Benchmark, without taking into account the Fund’s expenses. Perfect correlation would be 1.00. The tracking error (a measure of how closely the return of a portfolio follows the return of an index to which it is benchmarked) of this strategy during the reporting period can be attributed to not owning all the names in the Benchmark and the Fund’s exposure to emerging markets stocks.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers constructed the Fund with country weightings based on GDP rather than equity market capitalization. Each country was weighted by GDP, because the Fund’s portfolio managers believed that this measure served as a better indication of each country’s potential earning power than traditional market capitalization. The Fund’s emerging markets exposure at the end of the reporting period was approximately 9.3%.

During the reporting period, the Fund’s portfolio managers used a combination of exchange-traded funds and futures to help manage cash flows. The Fund continued to track the Benchmark, consistent with its investment strategy, and attempted to provide broad international exposure for U.S. investors.

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | ||||||||

| 1. | Eni S.p.A. (Italy) | 2.0 | % | |||||

| 2. | Banco Santander S.A. (Spain) | 1.4 | ||||||

| 3. | Siemens AG (Germany) | 1.2 | ||||||

| 4. | BASF SE (Germany) | 1.1 | ||||||

| 5. | Total S.A. (France) | 1.1 | ||||||

| 6. | Sanofi (France) | 1.1 | ||||||

| 7. | Anheuser-Busch InBev N.V. (Belgium) | 1.1 | ||||||

| 8. | Bayer AG (Germany) | 1.1 | ||||||

| 9. | Telefonica S.A. (Spain) | 1.0 | ||||||

| 10. | SAP AG (Germany) | 1.0 | ||||||

PORTFOLIO COMPOSITION BY COUNTRY*** | ||||

| Japan | 18.3 | % | ||

| Germany | 13.0 | |||

| France | 9.5 | |||

| Italy | 7.9 | |||

| United Kingdom | 7.3 | |||

| Spain | 5.7 | |||

| Australia | 5.5 | |||

| Netherlands | 4.1 | |||

| Switzerland | 2.7 | |||

| Belgium | 1.9 | |||

| Sweden | 1.9 | |||

| Norway | 1.6 | |||

| Austria | 1.5 | |||

| Denmark | 1.1 | |||

| Greece | 1.0 | |||

| Hong Kong | 1.0 | |||

| Others (each less than 1.0%) | 15.4 | |||

| Short-Term Investment | 0.6 | |||

| * | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | The advisor seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | Percentages indicated are based upon total investments as of October 31, 2012. The Fund’s portfolio composition is subject to change. |

| 18 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | OCTOBER 31, 2012 | ||||

Table of Contents

AVERAGE ANNUAL TOTAL RETURNS AS OF OCTOBER 31, 2012 | ||||||||||||||||

| INCEPTION DATE OF CLASS | 1 YEAR | 5 YEAR | 10 YEAR | |||||||||||||

CLASS A SHARES | 4/23/93 | |||||||||||||||

Without Sales Charge | 5.16 | % | (7.14 | )% | 7.72 | % | ||||||||||

With Sales Charge* | (0.35 | ) | (8.13 | ) | 7.15 | |||||||||||

CLASS B SHARES | 1/14/94 | |||||||||||||||

Without CDSC | 4.43 | (7.82 | ) | 7.10 | ||||||||||||

With CDSC** | (0.57 | ) | (8.38 | ) | 7.10 | |||||||||||

CLASS C SHARES | 11/4/97 | |||||||||||||||

Without CDSC | 4.43 | (7.80 | ) | 6.95 | ||||||||||||

With CDSC*** | 3.43 | (7.80 | ) | 6.95 | ||||||||||||

CLASS R2 SHARES | 11/3/08 | 4.94 | (7.38 | ) | 7.45 | |||||||||||

SELECT CLASS SHARES | 10/28/92 | 5.40 | (6.91 | ) | 7.99 | |||||||||||

| * | Sales Charge for Class A Shares is 5.25%. |

| ** | Assumes a 5% CDSC (contingent deferred sales charge) for the one year period, 2% CDSC for the five year period and 0% CDSC thereafter. |

| *** | Assumes a 1% CDSC for the one year period and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE (10/31/02 TO 10/31/12)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for Class R2 Shares prior to its inception date were based on the performance of the Select Class Shares. Class R2 Shares performance has been adjusted to reflect the difference in expenses between classes.

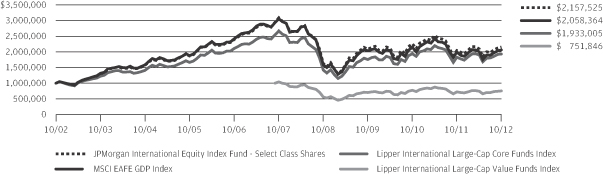

The graph illustrates comparative performance for $1,000,000 invested in Select Class Shares of the JPMorgan International Equity Index Fund, the MSCI EAFE GDP Index and Lipper International Large-Cap Core Funds Index from October 31, 2002 to October 31, 2012 and Lipper International Large-Cap Value Funds Index from September 30, 2007 (inception of the index) to October 31, 2012. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the MSCI EAFE GDP Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and approximates the minimum possible dividend reinvestment of the securities included in the benchmark. The dividend is reinvested after deduction of withholding tax, applying the maximum rate to non-resident institutional investors who do not benefit from double taxation treaties. The performance of the Lipper International Large-Cap Core Funds Index and the Lipper International Large-Cap Value Funds Index include expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The MSCI EAFE GDP Index is a country weighted index that is designed

to measure the size of developed market economies, excluding the U.S. & Canada. The Lipper International Large-Cap Core Funds Index and the Lipper International Large-Cap Value Funds Index are based on the total returns of certain mutual funds within the Fund’s designated category as defined by Lipper, Inc. Investors cannot invest directly in an index.

Select Class Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

International investing involves a greater degree of risk and increased volatility. Changes in currency exchange rates and differences in accounting and taxation policies outside of the U.S. can raise or lower returns. Also, some overseas markets may not be as politically and economically stable as the United States and other nations.

Because Class B Shares automatically convert to Class A Shares after 8 years, the 10 year average annual total return shown above for Class B reflects Class A performance for the period after conversion.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| OCTOBER 31, 2012 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | 19 | ||||||

Table of Contents

JPMorgan International Opportunities Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited)

| REPORTING PERIOD RETURN: | ||||

| Fund (Institutional Class Shares)* | 7.45% | |||

| Morgan Stanley Capital International (“MSCI”) Europe, Australasia and Far East (“EAFE”) Index (net of foreign withholding taxes) | 4.61% | |||

| Net Assets as of 10/31/2012 (In Thousands) | $ | 835,185 | ||

INVESTMENT OBJECTIVE**

The JPMorgan International Opportunities Fund (the “Fund”) seeks to provide high total return from a portfolio of equity securities of foreign companies in developed and, to a lesser extent, emerging markets.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund (Institutional Class Shares) outperformed the MSCI EAFE Index (net of foreign withholding taxes) (the “Benchmark”) for the twelve months ended October 31, 2012. The Fund’s stock selection, most notably in the semiconductors and transportation services & consumer cyclicals sectors, contributed to the Fund’s relative performance. The Fund’s stock selection in the autos and consumer non durable sectors detracted from the Fund’s relative performance.

Individual contributors to the Fund’s relative performance included the Fund’s overweight positions versus the Benchmark in Samsung Electronics Co., Ltd., Intercontinental Hotels Group plc and Hon Hai Precision Industry Co., Ltd. Shares of semiconductor, electronics and communications-equipment provider Samsung Electronics Co., Ltd. benefited as the company’s earnings were bolstered by robust sales for its smart phones and a turnaround in its display business. Shares of hotel operator Intercontinental Hotels Group plc benefited as growth in U.S. and China operations bolstered earnings and the company continued to return capital to shareholders. Shares of Hon Hai Precision Industry Co., Ltd., increased as revenues continued to grow, bolstered by strong sales of Apple products. Apple Inc. is the largest client of the Taiwanese consumer electronics contract manufacturer.

Individual detractors from the Fund’s relative performance included the Fund’s overweight positions versus the Benchmark in Nippon Sheet Glass Co., Ltd., Mitsubishi Electric Corp. and BG Group plc. Shares of Japanese glass maker Nippon Sheet Glass Co., Ltd. declined as the slowdown in European auto and construction activity, increased competition from Chinese manufacturers and the resignation of the company’s U.S. head of operations weighed on the stock. Mitsubishi Electric Corp. is a Japanese electronics maker. The stock declined as orders for factory automation equipment slowed and the company was prohibited from bidding on state contracts after the Japanese government accused the company of overcharging. Shares of BG Group plc, which is engaged in the exploration, development and production of natural gas and oil, declined following the company’s announcement that project delays would hold back output growth next year.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers employed a bottom-up fundamental approach to stock selection, seeking to identify what they believed were the most attractive investment opportunities within each sector. The Fund’s portfolio managers looked for stocks that they believed possessed an attractive valuation signal (as measured by a proprietary dividend discount model) and a timely catalyst that would enable the stock to realize its inherent value.

In addition, the Fund employed futures and currency forwards to help manage cash flows and attempt to keep the Fund’s currency exposure in line with that of its Benchmark.

| 20 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | OCTOBER 31, 2012 | ||||

Table of Contents

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | ||||||||

| 1. | Royal Dutch Shell plc, Class A (Netherlands) | 3.3 | % | |||||

| 2. | HSBC Holdings plc (United Kingdom) | 3.0 | ||||||

| 3. | Rio Tinto plc (United Kingdom) | 2.6 | ||||||

| 4. | Unilever N.V., CVA (Netherlands) | 2.4 | ||||||

| 5. | Vodafone Group plc (United Kingdom) | 2.3 | ||||||

| 6. | GlaxoSmithKline plc (United Kingdom) | 2.3 | ||||||

| 7. | British American Tobacco plc (United Kingdom) | 2.1 | ||||||

| 8. | Nestle S.A. (Switzerland) | 1.9 | ||||||

| 9. | BG Group plc (United Kingdom) | 1.8 | ||||||

| 10. | Bayer AG (Germany) | 1.8 | ||||||

PORTFOLIO COMPOSITION BY COUNTRY*** | ||||

| United Kingdom | 25.7 | % | ||

| Japan | 17.4 | |||

| Germany | 10.1 | |||

| Switzerland | 7.3 | |||

| Netherlands | 7.2 | |||

| France | 6.6 | |||

| Hong Kong | 3.4 | |||

| Sweden | 2.8 | |||

| Australia | 2.5 | |||

| China | 2.4 | |||

| Ireland | 2.4 | |||

| South Korea | 2.0 | |||

| Canada | 1.4 | |||

| Belgium | 1.3 | |||

| Taiwan | 1.0 | |||

| Finland | 1.0 | |||

| Others (each less than 1.0%) | 3.1 | |||

| Short-Term Investment | 2.4 | |||

| * | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | The advisor seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | Percentages indicated are based upon total investments as of October 31, 2012. The Fund’s portfolio composition is subject to change. |

| OCTOBER 31, 2012 | J.P. MORGAN INTERNATIONAL EQUITY FUNDS | 21 | ||||||

Table of Contents

JPMorgan International Opportunities Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2012 (Unaudited) (continued)

AVERAGE ANNUAL TOTAL RETURNS AS OF OCTOBER 31, 2012 | ||||||||||||||||

| INCEPTION DATE OF CLASS | 1 YEAR | 5 YEAR | 10 YEAR | |||||||||||||

CLASS A SHARES | 9/10/01 | |||||||||||||||

Without Sales Charge | 6.95 | % | (5.38 | )% | 7.13 | % | ||||||||||

With Sales Charge* | 1.37 | (6.40 | ) | 6.55 | ||||||||||||

CLASS B SHARES | 9/10/01 | |||||||||||||||

Without CDSC | 6.46 | (5.86 | ) | 6.71 | ||||||||||||

With CDSC** | 1.46 | (6.37 | ) | 6.71 | ||||||||||||

CLASS C SHARES | 7/31/07 | |||||||||||||||

Without CDSC | 6.47 | (5.85 | ) | 6.61 | ||||||||||||

With CDSC*** | 5.47 | (5.85 | ) | 6.61 | ||||||||||||

CLASS R6 SHARES | 11/30/10 | 7.59 | (4.93 | ) | 7.78 | |||||||||||

INSTITUTIONAL CLASS SHARES | 2/26/97 | 7.45 | (4.97 | ) | 7.76 | |||||||||||

SELECT CLASS SHARES | 9/10/01 | 7.28 | (5.15 | ) | 7.53 | |||||||||||

| * | Sales Charge for Class A Shares is 5.25%. |

| ** | Assumes a 5% CDSC (contingent deferred sales charge) for the one year period, 2% CDSC for the five year period and 0% CDSC thereafter. |

| *** | Assumes a 1% CDSC for the one year period and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE (10/31/02 TO 10/31/12)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for Class C Shares prior to its inception date were based on the performance of Class B Shares. The actual returns of Class C Shares would have been similar to those shown because Class C Shares have expenses similar to those of Class B Shares.

Returns for Class R6 Shares prior to its inception date were based on the performance of Institutional Class Shares. The actual returns of Class R6 Shares would have been different than those shown because Institutional Class Shares have different expenses than Class R6 Shares.

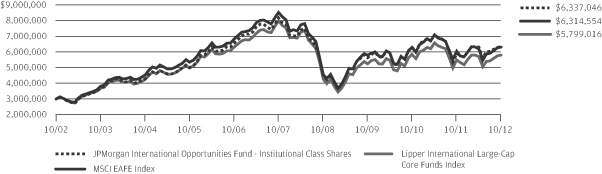

The graph illustrates comparative performance for $3,000,000 invested in Institutional Class Shares of the JPMorgan International Opportunities Fund, the MSCI EAFE Index and the Lipper International Large-Cap Core Funds Index from October 31, 2002 to October 31, 2012. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the MSCI EAFE Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and approximates the minimum possible dividend reinvestment of the

securities included in the benchmark. The dividend is reinvested after deduction of withholding tax, applying the maximum rate to non-resident institutional investors who do not benefit from double taxation treaties. The performance of the Lipper International Large-Cap Core Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The MSCI EAFE Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The Lipper International Large-Cap Core Funds Index is based on the total returns of certain mutual funds within the Fund’s designated category, as defined by Lipper, Inc. Investors cannot invest directly in an index.

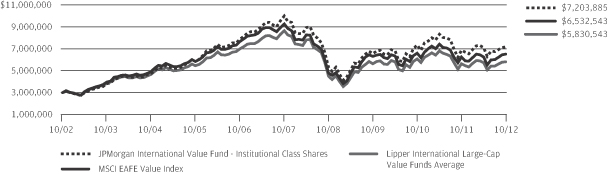

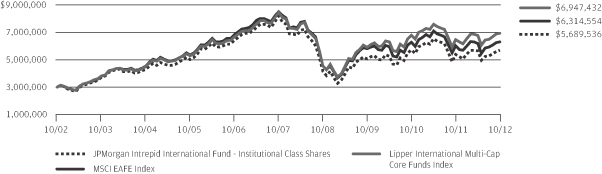

Institutional Class Shares have a $3,000,000 minimum initial investment.