Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04236

| JPMorgan Trust II |

(Exact name of registrant as specified in charter)

270 Park Avenue New York, NY 10017 |

(Address of principal executive offices) (Zip code)

Frank J. Nasta 270 Park Avenue New York, NY 10017 |

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (800) 480-4111

Date of fiscal year end: December 31

Date of reporting period: January 1, 2011 through December 31, 2011

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

Table of Contents

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

Table of Contents

Annual Report

J.P. Morgan Specialty Funds

December 31, 2011

Security Capital U.S. Core Real Estate Securities Fund

JPMorgan U.S. Real Estate Fund

Table of Contents

| CEO’s Letter | 1 | |||

Fund Commentaries: | ||||

| 2 | ||||

| 5 | ||||

| Schedules of Portfolio Investments | 8 | |||

| Financial Statements | 12 | |||

| Financial Highlights | 18 | |||

| Notes to Financial Statements | 22 | |||

| Report of Independent Registered Public Accounting Firm | 28 | |||

| Trustees | 29 | |||

| Officers | 31 | |||

| Schedule of Shareholder Expenses | 32 | |||

| Board Approval of Investment Advisory Agreements | 34 | |||

| Tax Letter | 39 | |||

Privacy Policy — Located at the back of this Annual Report | ||||

Investments in a Fund are not bank deposits or obligations of, or guaranteed or endorsed by, any bank and are not insured or guaranteed by the FDIC, the Federal Reserve Board or any other government agency. You could lose money if you sell when the Fund’s share price is lower than when you invested.

Past performance is no guarantee of future performance. The general market views expressed in this report are opinions based on conditions through the end of the reporting period and are subject to change without notice based on market and other conditions. These views are not intended to predict the future performance of a Fund or the securities markets. References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Such views are not meant as investment advice and may not be relied on as an indication of trading intent on behalf of any Fund.

Prospective investors should refer to the Funds’ prospectus for a discussion of the Funds’ investment objectives, strategies and risks. Call J.P. Morgan Funds Service Center at 1-800-480-4111 for a prospectus containing more complete information about a Fund including management fees and other expenses. Please read it carefully before investing.

Table of Contents

JANUARY 25, 2012 (Unaudited)

Dear Shareholder:

Investors greeted 2011 in much the same way they welcomed 2010: with high hopes that an improving U.S. economy would finally get us back on course to recovery.

This optimism quickly faded as the European debt crisis and a host of other economic and geopolitical concerns cast a dark shadow on the prospects for future growth. The combination of weak global economic data, credit downgrades in the U.S. and in Europe, and escalating fears of contagion all resulted in a level of market volatility not seen since the financial crisis three years ago.

|

“Investors greeted 2011 in much the same way they welcomed 2010: With high hopes that an improving U.S. economy would finally get us back on course to recovery.” |

Nonetheless, stocks have regained some of their footing, as positive fourth-quarter economic data on auto sales, payroll employment and manufacturing activity all appear to indicate that consumer confidence is improving and economic growth may be accelerating.

We remain cautious, however, since many of the same challenges that we experienced in 2011 — European debt concerns, uncertainty over monetary and fiscal stimulus, and soft economic data — will likely remain in place this year, laying the groundwork for continued market volatility.

Strong fourth quarter surge caps volatile year

The European debt crisis and other geopolitical and economic events created a generally volatile year for equities, culminating in major sell off in the third quarter. A strong fourth quarter comeback did little to reverse the losses, as the Standard & Poor’s 500 Index (“S&P 500 Index”) ended the year with only slight gains. As of December 31, 2011, the Index had reached a level of 1,258, an increase of 2.1% from one year prior.

Large cap growth stocks lead style categories

Large cap stocks outpaced mid- and small-cap stocks over the 12-month period ended December 31, 2011 (the Russell 1000 Index returned 1.5% and the Russell Mid Cap Index returned -1.6%, compared to a return of -4.2% for the Russell 2000 Index). Overall, large-cap growth stocks fared better than large-cap value stocks as the Russell 1000 Growth Index returned 2.6% for the 12-month reporting period, compared to 0.4% for the Russell 1000 Value Index.

Euro zone uncertainty drives flight-to-quality sentiment

Investors’ lack of confidence in global economic growth prompted them to seek safe havens in U.S. Treasury securities, and high-quality corporate bonds. The Barclays Capital U.S. Aggregate Bond Index returned 7.8%. High yield bonds and emerging market debt securities also performed well, as the Barclays Capital High Yield Index returned 5.0%, and the Barclays Capital Emerging Markets Index returned 7.0% for the 12-month period ended December 31, 2011.

Similar economic concerns pushed yields of U.S. Treasury securities maturing in 10 years or more to historic lows throughout the year. As of the end of the 12-month period ended December 31, 2011, the yields on the benchmark 10-year U.S. Treasury bond dropped from 3.3% to 1.9%. In addition, yields on the 30-year U.S. Treasury bond declined from 4.3% to 2.9%, as did the two-year U.S. Treasury note, from 0.6% to 0.3%.

Lesson for 2012: Keep balance in mind in economic uncertainty

Last year offered its share of shocks to investors: geopolitical upheaval, natural disasters, sovereign-debt crises, and credit-rating downgrades were all among the events competing for the market’s attention. Against the backdrop of an election year, it’s likely that we will face continued global surprises — both on the upside and the downside.

As you reassess your investment strategy for the year ahead, it’s important to stick with a plan that focuses on diversification as well as long-term allocation. Trying to “time” market fluctuations can be risky business, especially given the ongoing uncertainty surrounding the direction of economic growth and the euro zone crisis in the months ahead.

On behalf of everyone at J.P. Morgan Asset Management, thank you for your continued confidence. We look forward to managing your investment needs for years to come. Should you have any questions, please visit www.jpmorganfunds.com or contact the J.P. Morgan Funds Service Center at 1-800-480-4111.

Sincerely yours,

George C.W. Gatch

CEO-Investment Management Americas

J.P. Morgan Asset Management

| DECEMBER 31, 2011 | J.P. MORGAN SPECIALTY FUNDS | 1 | ||||||

Table of Contents

Security Capital U.S. Core Real Estate Securities Fund

FUND COMMENTARY

FOR THE PERIOD AUGUST 31, 2011 (Fund inception date) through DECEMBER 31, 2011 (Unaudited)

| REPORTING PERIOD RETURN: | ||||

| Fund (Select Class Shares)* | 0.97% | |||

| Wilshire US Real Estate Securities Index | 2.45% | |||

| Barclays Capital Investment Grade REIT Index | 2.46% | |||

| U.S. Core Real Estate Securities Composite Benchmark | 2.91% | |||

| Net Assets as of 12/31/2011 (In Thousands) | $9,948 | |||

INVESTMENT OBJECTIVE**

The Security Capital U.S. Core Real Estate Securities Fund (the “Fund”) seeks a risk-adjusted total return over the long-term by investing primarily in real estate securities.

HOW DID THE MARKET PERFORM?

Real estate investment trust (“REIT”) common stocks rebounded strongly in the fourth quarter to end 2011 with attractive total returns amidst highly volatile equity markets buffeted by continued signs of stress in U.S. and global economies and the ongoing potential for contagion associated with a crisis in European financial markets. Returns for REIT senior fixed income securities were strong in 2011 aided, among other things, by a historic swoon in U.S. Treasury yields.

There were distinctive performance differences by property type for common equity investors during 2011, with the underlying themes and influences reflecting company-specific factors, earlier performance differentials as well as shifting investor expectations colored by macro-economic trends. But there was an alternative underlying reality driving company performance during the year that appeared to transcend property type. For much of 2011, REIT stock performance highlighted a bifurcated world of haves and have-nots, generally favoring larger capitalization REITs with high-quality infill (supply constrained) or gateway market portfolios and flexible balance sheets. This mirrored asset-level valuation trends in the larger private-direct market, and is consistent with the broader financial market’s perspective on risk in a year where a 30-year U.S. Treasury Bond generated a 34% total return to investors.

By major property type, self-storage, mall and multifamily companies were the relative outperformers during the reporting period, while the lodging, industrial and shopping center companies lagged.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

This was the initial reporting period for the Fund based on an inception date of August 31, 2011, and considers the fractional period from inception through December 31, 2011. As the Fund invests in equity and fixed income securities, its performance is compared to multiple benchmarks, including broad-based equity and fixed income benchmarks as well as a blended composite benchmark.

While the Fund (Select Shares) posted a positive total return for the reporting period, it underperformed each of its multiple benchmarks. This underperformance reflected the selection and weightings of securities within the common equity portion of the Fund. In particular, the Fund responded to market momentum driving valuations among the highest quality REITs by introducing select investments where the Fund’s portfolio managers’ research highlighted value that they believed was overlooked by the market. The Fund’s portfolio managers believe that, as is often the case, these value investments take some time to season and bear fruit. Among the fixed income investments, the Fund successfully offset the drag on performance from a defensive shorter maturity stance among bonds with strong performance from its perpetual preferred investments.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers utilize a bottom-up process to inform both security selection and security type (common equity, preferred equity or debt). They rely on proprietary cash flow models, extensive field work and internal real estate market research to target attractive long-term investment opportunities, emphasizing quality real estate portfolios, flexible balance sheets and transparent business models.

| 2 | J.P. MORGAN SPECIALTY FUNDS | DECEMBER 31, 2011 | ||||

Table of Contents

| TOP TEN HOLDINGS OF THE PORTFOLIO*** | ||||||||

| 1. | Simon Property Group, Inc. | 5.2 | % | |||||

| 2. | Equity Residential | 4.2 | ||||||

| 3. | ProLogis, Inc. | 3.8 | ||||||

| 4. | HCP, Inc. | 3.8 | ||||||

| 5. | Ventas, Inc. | 3.4 | ||||||

| 6. | Rouse Co. LP / TRC Co-Issuer, Inc., 6.750%, 05/01/13 | 3.1 | ||||||

| 7. | General Growth Properties, Inc. | 3.1 | ||||||

| 8. | CubeSmart, Series A, 7.750%, 11/02/16 | 2.9 | ||||||

| 9. | SL Green Realty Corp. | 2.9 | ||||||

| 10. | Ashford Hospitality Trust, Inc., Series D, 8.450%, 07/18/12 | 2.8 | ||||||

PORTFOLIO COMPOSITION BY SECTOR*** | ||||

| Common Stocks | 60.7 | % | ||

| Preferred Stocks | 19.7 | |||

| Corporate Bonds | 12.9 | |||

| Convertible Bonds | 2.3 | |||

| Short-Term Investment | 4.4 | |||

| * | The return shown is based on net asset value calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset value in accordance with accounting principles generally accepted in the United States of America. |

| ** | The advisor seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | Percentages indicated are based upon total investments as of December 31, 2011. The Fund’s composition is subject to change. |

GEOGRAPHIC DIVERSIFICATION | ||||||||

Security Capital Real Estate | NCREIF (b) | |||||||

East | 36.6 | % | 32.9 | % | ||||

Northeast | 22.8 | 19.0 | % | |||||

Mideast | 13.8 | 13.9 | % | |||||

West | 25.4 | % | 34.6 | % | ||||

Pacific | 18.2 | 28.8 | % | |||||

Mountain | 7.2 | 5.8 | % | |||||

South | 21.4 | % | 22.0 | % | ||||

Southeast | 14.2 | 11.6 | % | |||||

Southwest | 7.2 | 10.4 | % | |||||

Midwest | 11.8 | % | 10.5 | % | ||||

East North Central | 7.5 | 8.6 | % | |||||

West North Central | 4.3 | 1.9 | % | |||||

Non-U.S. | 4.8 | % | 0.0 | % | ||||

| (a) | Percentages indicated are based upon total investments as of December 31, 2011. The Fund’s composition is subject to change. |

| (b) | Reflects the industry average of institutions belonging to the National Council of Real Estate Investment Fiduciaries. |

| DECEMBER 31, 2011 | J.P. MORGAN SPECIALTY FUNDS | 3 | ||||||

Table of Contents

Security Capital U.S. Core Real Estate Securities Fund

FUND COMMENTARY

FOR THE PERIOD AUGUST 31, 2011 (Fund Inception Date) through DECEMBER 31, 2011 (Unaudited) (continued)

TOTAL RETURNS AS OF DECEMBER 31, 2011 | ||||||||

| INCEPTION DATE OF CLASS | SINCE INCEPTION*** | |||||||

CLASS A SHARES | 8/31/11 | |||||||

Without Sales Charge | 0.83 | % | ||||||

With Sales Charge* | (4.46 | ) | ||||||

CLASS C SHARES | 8/31/11 | |||||||

Without CDSC | 0.69 | |||||||

With CDSC** | (0.31 | ) | ||||||

CLASS R5 SHARES | 8/31/11 | 1.01 | ||||||

CLASS R6 SHARES | 8/31/11 | 1.02 | ||||||

SELECT CLASS SHARES | 8/31/11 | 0.97 | ||||||

| * | Sales Charge for Class A Shares is 5.25%. |

| ** | Assumes a 1% CDSC (contingent deferred sales charge) for the one year period and 0% CDSC thereafter. |

| *** | Not annualized. |

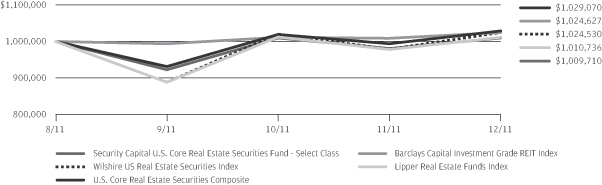

TEN YEAR PERFORMANCE (8/31/11 TO 12/31/11)

Source: Lipper, Inc. The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

The Fund commenced operations on August 31, 2011.

The graph illustrates comparative performance for $1,000,000 invested in Select Class Shares of the Security Capital U.S. Core Real Estate Securities Fund, the Wilshire US Real Estate Securities Index, Barclays Capital Investment Grade REIT Index, U.S. Core Real Estate Securities Composite and the Lipper Real Estate Funds Index from August 31, 2011 to December 31, 2011. The performance of the Fund assumes reinvestment of all dividends and capital gains, if any, and does not include a sales charge. The performance of the indices does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gains of the securities included in the benchmark. The performance of the Lipper Real Estate Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses charged by the Fund. The Wilshire US Real Estate Securities Index is an unmanaged, broad based, float weighted index comprised of publicly traded REITs and real estate operating companies, not including special purpose REITs. It is comprised of major companies engaged in the equity owner-

ship and operation of commercial real estate. The Barclays Capital Investment Grade REIT Index includes publicly issued U.S. corporate and secured notes that meet specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered or 144A securities with registration rights. The Barclays Capital Investment Grade REIT Index only includes the portion of the Barclays Capital U.S. Corporate Index deemed to be a Real Estate Investment Trust. The U.S. Core Real Estate Securities Composite Benchmark is a composite benchmark comprised of unmanaged indexes that includes 60% Wilshire US Real Estate Securities Index, 10% Wells Fargo Hybrid and Preferred Securities REIT Index and 30% Barclays Capital Investment Grade REIT Index. The Lipper Real Estate Funds Index represents the total returns of the funds in the indicated category as defined by Lipper, Inc. Investors cannot invest directly in an index.

Select Class Shares have a $1,000,000 minimum initial investment and carry no sales charge.

Performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| 4 | J.P. MORGAN SPECIALTY FUNDS | DECEMBER 31, 2011 | ||||

Table of Contents

JPMorgan U.S. Real Estate Fund

FUND COMMENTARY

TWELVE MONTHS ENDED DECEMBER 31, 2011 (Unaudited)

| REPORTING PERIOD RETURN: | ||||

| Fund (Class A Shares, without a sales charge)* | 6.02% | |||

| Wilshire US Real Estate Securities Index | 8.56% | |||

| Net Assets as of 12/31/2011 (In Thousands) | $ | 1,410,918 | ||

INVESTMENT OBJECTIVE**

The JPMorgan U.S. Real Estate Fund (the “Fund”) seeks a high level of current income and long-term capital appreciation primarily through investments in real estate securities.

HOW DID THE MARKET PERFORM?

Real estate investment trust (REIT) common stocks rebounded strongly in the fourth quarter to end 2011 with attractive total returns amidst highly volatile equity markets buffeted by continued signs of stress in U.S. and global economies and the ongoing potential for contagion associated with a crisis in European financial markets.

There were distinctive performance differences by property type for common equity investors during 2011, with the underlying themes and influences reflecting company-specific factors, earlier performance differentials as well as shifting investor expectations colored by macro-economic trends. But there was an alternative underlying reality driving company performance during the year that appeared to transcend property type. For much of 2011, REIT stock performance highlighted a bifurcated world of haves and have-nots, generally favoring larger capitalization REITs with high-quality infill (supply constrained) or gateway market portfolios and flexible balance sheets. This mirrored asset-level valuation trends in the larger private-direct market, and is consistent with the broader financial market’s perspective on risk in a year where a 30-year U.S. Treasury Bond generated a 34% total return to investors.

By major property type, self-storage, mall and multifamily companies were the relative outperformers during the reporting period, while lodging, industrial and shopping center companies lagged.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s overall level of return was driven by investors’ continued interest in real estate investments as a source of attractive current income. While the Fund (Class A Shares, without a sales charge) posted an attractive absolute return, it underperformed the Wilshire US Real Estate Securities Index during the reporting period.

The Fund’s underperformance was driven by stock selection and weighting among its office investments, with a notable investment in Commonwealth REIT (CWH). While the Fund’s portfolio managers’ research and investments highlighted value in suburban office companies, including Commonwealth, the stock market favored larger capitalization office companies with portfolios located in high-quality infill markets.

Among the Fund’s largest individual contributor to relative performance was its underweight position in the underperforming shopping center companies sector, although the Fund’s targeted investment in Federal Realty Investment Trust (FRT) contributed to relative performance. Among shopping center companies, investors preferred higher quality REITs due to concerns about the margins and health of retailers as well as shifting formats and business models. This preference benefited FRT, which is generally viewed by investors as owning a higher quality niche real estate portfolio, with properties located in markets that have strong demographics, such as population density and income levels.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers utilize a bottom-up process to inform security selection. They rely on proprietary cash flow models, extensive field work and internal real estate market research to target attractive long-term investment opportunities, emphasizing quality real estate portfolios, flexible balance sheets and transparent business models.

| DECEMBER 31, 2011 | J.P. MORGAN SPECIALTY FUNDS | 5 | ||||||

Table of Contents

JPMorgan U.S. Real Estate Fund

FUND COMMENTARY

TWELVE MONTHS ENDED DECEMBER 31, 2011 (Unaudited) (continued)

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | ||||||||

| 1. | Equity Residential | 8.4 | % | |||||

| 2. | HCP, Inc. | 7.7 | ||||||

| 3. | Simon Property Group, Inc. | 7.5 | ||||||

| 4. | ProLogis, Inc. | 6.6 | ||||||

| 5. | AvalonBay Communities, Inc. | 5.7 | ||||||

| 6. | Ventas, Inc. | 5.4 | ||||||

| 7. | General Growth Properties, Inc. | 5.3 | ||||||

| 8. | Host Hotels & Resorts, Inc. | 4.4 | ||||||

| 9. | Apartment Investment & Management Co., Class A | 4.4 | ||||||

| 10. | Boston Properties, Inc. | 4.0 | ||||||

PORTFOLIO COMPOSITION BY SECTOR*** | ||||

| Common Stocks | 98.9 | % | ||

| Short-Term Investment | 1.1 | |||

| * | The return shown is based on net asset value calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset value in accordance with accounting principles generally accepted in the United States of America. |

| ** | The advisor seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | Percentages indicated are based upon total investments as of December 31, 2011. The Fund’s composition is subject to change. |

GEOGRAPHIC DIVERSIFICATION | ||||||||

| JPMorgan U.S. Real Estate Fund (a) | NCREIF (b) | |||||||

East | 36.9 | % | 32.9 | % | ||||

Northeast | 24.4 | 19.0 | % | |||||

Mideast | 12.5 | 13.9 | % | |||||

West | 30.7 | % | 34.6 | % | ||||

Pacific | 22.4 | 28.8 | % | |||||

Mountain | 8.3 | 5.8 | % | |||||

South | 20.2 | % | 22.0 | % | ||||

Southeast | 12.7 | 11.6 | % | |||||

Southwest | 7.5 | 10.4 | % | |||||

Midwest | 8.3 | % | 10.5 | % | ||||

East North Central | 6.1 | 8.6 | % | |||||

West North Central | 2.2 | 1.9 | % | |||||

Non-U.S. | 3.9 | % | 0.0 | % | ||||

| (a) | Percentages indicated are based upon total investments as of December 31, 2011. The Fund’s composition is subject to change. |

| (b) | Reflects the industry average of institutions belonging to the National Council of Real Estate Investment Fiduciaries. |

| 6 | J.P. MORGAN SPECIALTY FUNDS | DECEMBER 31, 2011 | ||||

Table of Contents

AVERAGE ANNUAL TOTAL RETURNS AS OF DECEMBER 31, 2011 | ||||||||||||||||

| INCEPTION DATE OF CLASS | 1 YEAR | 5 YEAR | 10 YEAR | |||||||||||||

CLASS A SHARES | 4/23/97 | |||||||||||||||

Without Sales Charge | 6.02 | % | (3.06 | )% | 9.52 | % | ||||||||||

With Sales Charge* | 0.46 | (4.10 | ) | 8.94 | ||||||||||||

CLASS C SHARES | 2/19/05 | |||||||||||||||

Without CDSC | 5.50 | (3.54 | ) | 9.15 | ||||||||||||

With CDSC** | 4.50 | (3.54 | ) | 9.15 | ||||||||||||

CLASS R2 SHARES | 11/3/08 | 5.81 | (3.21 | ) | 9.44 | |||||||||||

CLASS R5 SHARES | 5/15/06 | 6.46 | (2.63 | ) | 9.84 | |||||||||||

SELECT CLASS SHARES | 1/19/05 | 6.27 | (2.81 | ) | 9.71 | |||||||||||

| * | Sales Charge for Class A Shares is 5.25%. |

| ** | Assumes a 1% CDSC (contingent deferred sales charge) for the one year period and 0% CDSC thereafter. |

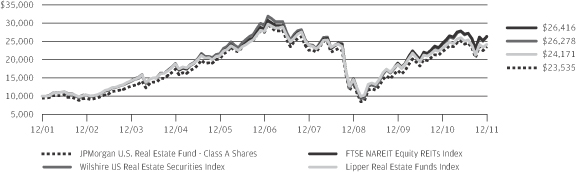

TEN YEAR PERFORMANCE (12/31/01 TO 12/31/11)

Source: Lipper, Inc. The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for the Select Class Shares prior to their inception are based on the performance of the Class A Shares. The actual returns of Select Class Shares would have been different than shown because Select Class Shares have different expenses than Class A Shares.

Returns for the Class C Shares prior to their inception are based on the performance of the Class A Shares. The actual returns of Class C Shares would have been lower than shown because Class C Shares have higher expenses than Class A Shares.

Returns for the Class R5 Shares prior to their inception are based on the performance of the Select Class Shares. The actual returns of Class R5 Shares would have been different than shown because Class R5 Shares have different expenses than Select Class Shares.

Returns for the Class R2 Shares prior to their inception are based on the performance of the Class A Shares. The actual returns of Class R2 Shares would have been lower than shown because Class R2 Shares have higher expenses than Class A Shares.

The graph illustrates comparative performance for $10,000 invested in Class A Shares of the JPMorgan U.S. Real Estate Fund, the Wilshire US Real Estate Securities Index, the FTSE NAREIT Equity REITs Index and the Lipper Real Estate Funds Index from December 31, 2001 to December 31, 2011. The performance of

the Fund assumes reinvestment of all dividends and capital gains, if any, and includes a sales charge. The performance of the indices does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gains of the securities included in the benchmark. The performance of the Lipper Real Estate Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses charged by the Fund. The Wilshire US Real Estate Securities Index is an unmanaged, broad based, float weighted index comprised of publicly traded REITs and real estate operating companies, not including special purpose REITs. It is comprised of major companies in the companies engaged in the equity ownership and operation of commercial real estate. The FTSE NAREIT Equity REITs Index is a free float adjusted market capitalization weighted index that includes all tax qualified REITs listed in the NYSE, AMEX, and NASDAQ National Market. The Lipper Real Estate Funds Index represents the total returns of the funds in the indicated category as defined by Lipper, Inc. Investors cannot invest directly in an index.

Class A Shares have a $1,000 minimum initial investment and carry a 5.25% sales charge.

Performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| DECEMBER 31, 2011 | J.P. MORGAN SPECIALTY FUNDS | 7 | ||||||

Table of Contents

Security Capital U.S. Core Real Estate Securities Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2011

(Amounts in thousands)

| SHARES | SECURITY DESCRIPTION | VALUE($) | ||||||

| Common Stocks — 59.7% | |||||||

Diversified — 2.7% |

| |||||||

| 6 | Colonial Properties Trust | 125 | ||||||

| 2 | Vornado Realty Trust | 148 | ||||||

|

| |||||||

| 273 | ||||||||

|

| |||||||

Health Care — 8.8% |

| |||||||

| 9 | HCP, Inc. | 374 | ||||||

| 3 | Health Care REIT, Inc. | 175 | ||||||

| 6 | Ventas, Inc. | 331 | ||||||

|

| |||||||

| 880 | ||||||||

|

| |||||||

Hotels — 3.5% |

| |||||||

| 15 | Host Hotels & Resorts, Inc. | 218 | ||||||

| 3 | Hyatt Hotels Corp., Class A (a) | 131 | ||||||

|

| |||||||

| 349 | ||||||||

|

| |||||||

Industrial — 3.8% |

| |||||||

| 13 | ProLogis, Inc. | 375 | ||||||

|

| |||||||

Multifamily — 11.2% |

| |||||||

| 7 | Apartment Investment & Management Co., Class A | 167 | ||||||

| 2 | AvalonBay Communities, Inc. | 201 | ||||||

| 2 | BRE Properties, Inc. | 114 | ||||||

| 2 | Camden Property Trust | 96 | ||||||

| 7 | Equity Residential | 413 | ||||||

| 5 | UDR, Inc. | 119 | ||||||

|

| |||||||

| 1,110 | ||||||||

|

| |||||||

Office — 12.7% |

| |||||||

| 6 | BioMed Realty Trust, Inc. | 112 | ||||||

| 2 | Boston Properties, Inc. | 191 | ||||||

| 13 | Brandywine Realty Trust | 119 | ||||||

| 6 | CommonWealth REIT | 100 | ||||||

| 6 | Corporate Office Properties Trust | 133 | ||||||

| 6 | Mack-Cali Realty Corp. | 160 | ||||||

| 10 | Piedmont Office Realty Trust, Inc., Class A | 169 | ||||||

| 4 | SL Green Realty Corp. | 282 | ||||||

|

| |||||||

| 1,266 | ||||||||

|

| |||||||

Regional Malls — 9.8% |

| |||||||

| 20 | General Growth Properties, Inc. | 300 | ||||||

| 3 | Macerich Co. (The) | 170 | ||||||

| 4 | Simon Property Group, Inc. | 507 | ||||||

|

| |||||||

| 977 | ||||||||

|

| |||||||

Shopping Centers — 3.4% |

| |||||||

| 1 | Federal Realty Investment Trust | 113 | ||||||

| SHARES | SECURITY DESCRIPTION | VALUE($) | ||||||

Shopping Centers — Continued |

| |||||||

| 7 | Kimco Realty Corp. | 117 | ||||||

| 3 | Regency Centers Corp. | 105 | ||||||

|

| |||||||

| 335 | ||||||||

|

| |||||||

Storage — 3.8% |

| |||||||

| 7 | Extra Space Storage, Inc. | 171 | ||||||

| 2 | Public Storage | 206 | ||||||

|

| |||||||

| 377 | ||||||||

|

| |||||||

Total Common Stocks | 5,942 | |||||||

|

| |||||||

| PRINCIPAL AMOUNT($) | ||||||||

| Convertible Bond — 2.3% | |||||||

Financials — 2.3% |

| |||||||

Office — 2.3% |

| |||||||

| 249 | Corporate Office Properties LP, 4.250%, | 229 | ||||||

|

| |||||||

| Corporate Bonds — 12.7% | |||||||

Financials — 12.7% |

| |||||||

Health Care — 1.4% |

| |||||||

| 58 | Health Care REIT, Inc., 6.200%, 06/01/16 | 62 | ||||||

| 80 | Senior Housing Properties Trust, 4.300%, 01/15/16 | 79 | ||||||

|

| |||||||

| 141 | ||||||||

|

| |||||||

Industrial — 1.4% |

| |||||||

ProLogis LP, | ||||||||

| 78 | 4.500%, 08/15/17 | 78 | ||||||

| 60 | 6.625%, 05/15/18 | 65 | ||||||

|

| |||||||

| 143 | ||||||||

|

| |||||||

Office — 3.1% |

| |||||||

CommonWealth REIT, | ||||||||

| 100 | 6.250%, 08/15/16 | 106 | ||||||

| 100 | 6.500%, 01/15/13 | 101 | ||||||

| 100 | Reckson Operating Partnership LP, 6.000%, 03/31/16 | 104 | ||||||

|

| |||||||

| 311 | ||||||||

|

| |||||||

Diversified — 0.8% |

| |||||||

| 71 | Colonial Realty LP, 6.250%, 06/15/14 | 74 | ||||||

|

| |||||||

Regional Malls — 3.1% |

| |||||||

| 300 | Rouse Co. LP/TRC Co-Issuer, Inc., 6.750%, 05/01/13 (e) | 302 | ||||||

|

| |||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| 8 | J.P. MORGAN SPECIALTY FUNDS | DECEMBER 31, 2011 | ||||

Table of Contents

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Corporate Bonds — Continued | |||||||

Shopping Centers — 2.9% |

| |||||||

| 200 | DDR Corp., 7.500%, 04/01/17 | 216 | ||||||

| 70 | Equity One, Inc., 6.000%, 09/15/16 | 73 | ||||||

|

| |||||||

| 289 | ||||||||

|

| |||||||

Total Corporate Bonds | 1,260 | |||||||

|

| |||||||

| SHARES | ||||||||

| Preferred Stocks ($25 par value) — 19.3% | |||||||

Financials — 19.3% |

| |||||||

Hotels — 4.7% |

| |||||||

| 12 | Ashford Hospitality Trust, Inc., Series D, 8.450%, 07/18/12 (x) | 269 | ||||||

| 9 | Sunstone Hotel Investors, Inc., Series D, 8.000%, 04/06/16 (x) | 195 | ||||||

|

| |||||||

| 464 | ||||||||

|

| |||||||

Multifamily — 1.6% |

| |||||||

| 4 | Apartment Investment & Management Co., Series U, 7.750%, 02/03/12 (x) | 100 | ||||||

| 3 | Equity Lifestyle Properties, Inc., Series A, 8.034%, 02/03/12 (x) | 63 | ||||||

|

| |||||||

| 163 | ||||||||

|

| |||||||

Office — 6.2% |

| |||||||

| 4 | Corporate Office Properties Trust, Series G, 8.000%, 02/03/12 (x) | 104 | ||||||

| 3 | Hudson Pacific Properties, Inc., Series B, 8.375%, 12/10/15 (x) | 84 | ||||||

| 3 | Kilroy Realty Corp., Series E, 7.800%, 02/03/12 (x) | 64 | ||||||

| 7 | Parkway Properties, Inc., Series D, 8.000%, 02/03/12 (x) | 160 | ||||||

| SHARES | SECURITY DESCRIPTION | VALUE($) | ||||||

Office — Continued |

| |||||||

| 3 | SL Green Realty Corp., Series C, 7.625%, 02/03/12 (x) | 62 | ||||||

| 6 | SL Green Realty Corp., Series D, 7.875%, 02/03/12 (x) | 145 | ||||||

|

| |||||||

| 619 | ||||||||

|

| |||||||

Regional Malls — 3.9% | ||||||||

| 8 | CBL & Associates Properties, Inc., Series C, 7.750%, 02/03/12 (x) | 198 | ||||||

| 8 | Glimcher Realty Trust, Series G, 8.125%, 02/03/12 (x) | 191 | ||||||

|

| |||||||

| 389 | ||||||||

|

| |||||||

Storage — 2.9% |

| |||||||

| 12 | CubeSmart, Series A, 7.750%, 11/02/16 (x) | 288 | ||||||

|

| |||||||

Total Preferred Stocks | 1,923 | |||||||

|

| |||||||

| Short-Term Investment — 4.4% | |||||||

Investment Company — 4.4% |

| |||||||

| 435 | JPMorgan Prime Money Market Fund, Institutional Class Shares, 0.090% (b) (l) | 435 | ||||||

|

| |||||||

Total Investments — 98.4% | 9,789 | |||||||

Other Assets in Excess of | 159 | |||||||

|

| |||||||

NET ASSETS — 100.0% | $ | 9,948 | ||||||

|

| |||||||

Percentages indicated are based on net assets.

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2011 | J.P. MORGAN SPECIALTY FUNDS | 9 | ||||||

Table of Contents

JPMorgan U.S. Real Estate Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2011

(Amounts in thousands)

| SHARES | SECURITY DESCRIPTION | VALUE($) | ||||||

| Common Stocks — 98.8% | |||||||

Diversified — 6.7% |

| |||||||

| 2,258 | Colonial Properties Trust | 47,106 | ||||||

| 625 | Vornado Realty Trust | 48,037 | ||||||

|

| |||||||

| 95,143 | ||||||||

|

| |||||||

Health Care — 16.5% |

| |||||||

| 2,631 | HCP, Inc. | 108,998 | ||||||

| 869 | Health Care REIT, Inc. | 47,395 | ||||||

| 1,383 | Ventas, Inc. | 76,217 | ||||||

|

| |||||||

| 232,610 | ||||||||

|

| |||||||

Hotels — 6.2% |

| |||||||

| 4,226 | Host Hotels & Resorts, Inc. | 62,423 | ||||||

| 658 | Hyatt Hotels Corp., Class A (a) | 24,759 | ||||||

|

| |||||||

| 87,182 | ||||||||

|

| |||||||

Industrial — 6.6% |

| |||||||

| 3,249 | ProLogis, Inc. | 92,884 | ||||||

|

| |||||||

Multifamily — 20.4% |

| |||||||

| 2,688 | Apartment Investment & Management Co., Class A | 61,590 | ||||||

| 613 | AvalonBay Communities, Inc. | 80,090 | ||||||

| 583 | BRE Properties, Inc. | 29,445 | ||||||

| 2,065 | Equity Residential | 117,761 | ||||||

|

| |||||||

| 288,886 | ||||||||

|

| |||||||

Office — 16.2% |

| |||||||

| 570 | Boston Properties, Inc. | 56,767 | ||||||

| 2,195 | Brandywine Realty Trust | 20,855 | ||||||

| 1,739 | Corporate Office Properties Trust | 36,979 | ||||||

| 1,442 | Mack-Cali Realty Corp. | 38,484 | ||||||

| 1,589 | Piedmont Office Realty Trust, Inc., Class A | 27,082 | ||||||

| 731 | SL Green Realty Corp. | 48,714 | ||||||

|

| |||||||

| 228,881 | ||||||||

|

| |||||||

Regional Malls — 16.1% |

| |||||||

| 4,976 | General Growth Properties, Inc. | 74,744 | ||||||

| 939 | Macerich Co. (The) | 47,488 | ||||||

| 817 | Simon Property Group, Inc. | 105,309 | ||||||

|

| |||||||

| 227,541 | ||||||||

|

| |||||||

Shopping Centers — 3.8% |

| |||||||

| 196 | Federal Realty Investment Trust | 17,813 | ||||||

| 930 | Regency Centers Corp. | 34,992 | ||||||

|

| |||||||

| 52,805 | ||||||||

|

| |||||||

Storage — 6.3% |

| |||||||

| 1,480 | Extra Space Storage, Inc. | 35,867 | ||||||

| SHARES | SECURITY DESCRIPTION | VALUE($) | ||||||

Storage — Continued | ||||||||

| 394 | Public Storage | 52,956 | ||||||

|

| |||||||

| 88,823 | ||||||||

|

| |||||||

Total Common Stocks | 1,394,755 | |||||||

|

| |||||||

| Short-Term Investment — 1.1% | |||||||

Investment Company — 1.1% | ||||||||

| 15,018 | JPMorgan Prime Money Market Fund, Institutional Class Shares, 0.090% (b) (l) | 15,018 | ||||||

|

| |||||||

Total Investments — 99.9% | 1,409,773 | |||||||

Other Assets in Excess of | 1,145 | |||||||

|

| |||||||

NET ASSETS — 100.0% | $ | 1,410,918 | ||||||

|

| |||||||

Percentages indicated are based on net assets.

SEE NOTES TO FINANCIAL STATEMENTS.

| 10 | J.P. MORGAN SPECIALTY FUNDS | DECEMBER 31, 2011 | ||||

Table of Contents

J.P. Morgan Specialty Funds

NOTES TO SCHEDULES OF PORTFOLIO INVESTMENTS:

AS OF DECEMBER 31, 2011

| REIT | — Real Estate Investment Trust | |

| (a) | — Non-income producing security. | |

| (b) | — Investment in affiliate. Money market fund registered under the Investment Company Act of 1940, as amended, and advised by J.P. Morgan Investment Management Inc. | |

| (e) | — Security is exempt from registration under Rule 144A of the Securities Act of 1933, as amended. Unless otherwise indicated, this security has been determined to be liquid under procedures established by the Board of Trustees and may be resold in transactions exempt from registration, normally to qualified institutional buyers. | |

| (l) | — The rate shown is the current yield as of December 31, 2011. | |

| (x) | — The date shown reflects the first date on which the issuer may redeem the security at par value. The coupon rate for this security is based on par value and is the rate currently in effect as of December 31, 2011. |

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2011 | J.P. MORGAN SPECIALTY FUNDS | �� | 11 | |||||

Table of Contents

STATEMENTS OF ASSETS AND LIABILITIES

AS OF DECEMBER 31, 2011

(Amounts in thousands, except per share amounts)

| U.S. Core Real Estate Securities Fund | U.S. Real Estate Fund | |||||||

ASSETS: | ||||||||

Investments in non-affiliates, at value | $ | 9,354 | $ | 1,394,755 | ||||

Investments in affiliates, at value | 435 | 15,018 | ||||||

|

|

|

| |||||

Total investment securities, at value | 9,789 | 1,409,773 | ||||||

Receivables: | ||||||||

Fund shares sold | — | (a) | 2,431 | |||||

Dividends from non-affiliates | 67 | 3,777 | ||||||

Dividends from affiliates | — | (a) | 1 | |||||

Due from Advisor | 62 | — | ||||||

Prepaid expenses and other assets | 100 | — | ||||||

|

|

|

| |||||

Total Assets | 10,018 | 1,415,982 | ||||||

|

|

|

| |||||

LIABILITIES: | ||||||||

Payables: | ||||||||

Dividends | — | (a) | — | |||||

Fund shares redeemed | — | 3,555 | ||||||

Accrued liabilities: | ||||||||

Investment advisory fees | — | 398 | ||||||

Shareholder servicing fees | 2 | 231 | ||||||

Distribution fees | — | (a) | 50 | |||||

Custodian and accounting fees | 9 | 20 | ||||||

Trustees’ and Chief Compliance Officer’s fees | — | (a) | 2 | |||||

Transfer agent fees | 2 | 666 | ||||||

Audit fees | 53 | 35 | ||||||

Other | 4 | 107 | ||||||

|

|

|

| |||||

Total Liabilities | 70 | 5,064 | ||||||

|

|

|

| |||||

Net Assets | $ | 9,948 | $ | 1,410,918 | ||||

|

|

|

| |||||

| (a) | Amount rounds to less than $1,000. |

SEE NOTES TO FINANCIAL STATEMENTS.

| 12 | J.P. MORGAN SPECIALTY FUNDS | DECEMBER 31, 2011 | ||||

Table of Contents

| U.S. Core Real Estate Securities Fund | U.S. Real Estate Fund | |||||||

NET ASSETS: | ||||||||

Paid in capital | $ | 9,718 | $ | 1,111,892 | ||||

Accumulated undistributed net investment income | — | (a) | 199 | |||||

Accumulated net realized gains (losses) | (12 | ) | (100,855 | ) | ||||

Net unrealized appreciation (depreciation) | 242 | 399,682 | ||||||

|

|

|

| |||||

Total Net Assets | $ | 9,948 | $ | 1,410,918 | ||||

|

|

|

| |||||

Net Assets: | ||||||||

Class A | $ | 2,548 | $ | 186,958 | ||||

Class C | 50 | 13,763 | ||||||

Class R2 | — | 5,524 | ||||||

Class R5 | 50 | 15,816 | ||||||

Class R6 | 51 | — | ||||||

Select Class | 7,249 | 1,188,857 | ||||||

|

|

|

| |||||

Total | $ | 9,948 | $ | 1,410,918 | ||||

|

|

|

| |||||

Outstanding units of beneficial interest (shares) ($0.0001 per value; unlimited number of shares authorized): | ||||||||

Class A | 170 | 11,571 | ||||||

Class C | 3 | 861 | ||||||

Class R2 | — | 343 | ||||||

Class R5 | 3 | 975 | ||||||

Class R6 | 3 | — | ||||||

Select Class | 483 | 73,429 | ||||||

Net Asset Value: (b) | ||||||||

Class A — Redemption price per share | $ | 14.98 | $ | 16.16 | ||||

Class C — Offering price per share (c) | 15.00 | 15.99 | ||||||

Class R2 — Offering and redemption price per share | — | 16.10 | ||||||

Class R5 — Offering and redemption price per share | 15.00 | 16.22 | ||||||

Class R6 — Offering and redemption price per share | 15.00 | — | ||||||

Select Class — Offering and redemption price per share | 15.00 | 16.19 | ||||||

Class A maximum sales charge | 5.25 | % | 5.25 | % | ||||

Class A maximum public offering price per share | $ | 15.81 | $ | 17.06 | ||||

|

|

|

| |||||

Cost of investments in non-affiliates | $ | 9,112 | $ | 995,073 | ||||

Cost of investments in affiliates | 435 | 15,018 | ||||||

| (a) | Amount rounds to less than $1,000. |

| (b) | Per share amounts may not recalculate due to rounding of net assets and/or shares outstanding. |

| (c) | Redemption price for Class C Shares varies based upon length of time the shares are held. |

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2011 | J.P. MORGAN SPECIALTY FUNDS | 13 | ||||||

Table of Contents

STATEMENTS OF OPERATIONS

FOR THE PERIODS INDICATED

(Amounts in thousands)

| U.S. Core Real Estate Securities Fund Period Ended 12/31/2011 (a) | U.S. Real Estate Fund Year Ended 12/31/2011 | |||||||

INVESTMENT INCOME: | ||||||||

Interest income from non-affiliates | $ | 9 | $ | — | ||||

Dividend income from non-affiliates | 61 | 29,175 | ||||||

Dividend income from affiliates | — | (b) | 35 | |||||

|

|

|

| |||||

Total investment income | 70 | 29,210 | ||||||

|

|

|

| |||||

EXPENSES: | ||||||||

Investment advisory fees | 8 | 9,249 | ||||||

Administration fees | 1 | 1,364 | ||||||

Distribution fees: | ||||||||

Class A | — | (b) | 518 | |||||

Class C | — | (b) | 110 | |||||

Class R2 | — | 17 | ||||||

Shareholder servicing fees: | ||||||||

Class A | — | (b) | 518 | |||||

Class C | — | (b) | 37 | |||||

Class R2 | — | 9 | ||||||

Class R5 | — | (b) | 8 | |||||

Select Class | 3 | 3,248 | ||||||

Custodian and accounting fees | 11 | 83 | ||||||

Interest expense to affiliates | — | — | (b) | |||||

Professional fees | 53 | 77 | ||||||

Trustees’ and Chief Compliance Officer’s fees | — | (b) | 15 | |||||

Printing and mailing costs | 1 | 340 | ||||||

Registration and filing fees | 4 | 118 | ||||||

Transfer agent fees | 3 | 2,132 | ||||||

Offering costs | 50 | — | ||||||

Other | 6 | 22 | ||||||

|

|

|

| |||||

Total expenses | 140 | 17,865 | ||||||

|

|

|

| |||||

Less amounts waived | (1 | ) | (2,069 | ) | ||||

Less earnings credits | — | (b) | — | (b) | ||||

Less expense reimbursements | (126 | ) | (939 | ) | ||||

|

|

|

| |||||

Net expenses | 13 | 14,857 | ||||||

|

|

|

| |||||

Net investment income (loss) | 57 | 14,353 | ||||||

|

|

|

| |||||

REALIZED/UNREALIZED GAINS (LOSSES): | ||||||||

Net realized gain (loss) on transactions from: | ||||||||

Investments in non-affiliates | 1 | 123,924 | ||||||

Change in net unrealized appreciation (depreciation) of: | ||||||||

Investments in non-affiliates | 242 | (36,766 | ) | |||||

|

|

|

| |||||

Net realized/unrealized gains (losses) | 243 | 87,158 | ||||||

|

|

|

| |||||

Change in net assets resulting from operations | $ | 300 | $ | 101,511 | ||||

|

|

|

| |||||

| (a) | Commencement of operations was August 31, 2011. |

| (b) | Amount rounds to less than $1,000. |

SEE NOTES TO FINANCIAL STATEMENTS.

| 14 | J.P. MORGAN SPECIALTY FUNDS | DECEMBER 31, 2011 | ||||

Table of Contents

STATEMENTS OF CHANGES IN NET ASSETS

FOR THE PERIODS INDICATED

(Amounts in thousands)

| U.S. Core Real Estate Securities Fund | U.S. Real Estate Fund | |||||||||||

| Period Ended 12/31/2011 (a) | Year Ended 12/31/2011 | Year Ended 12/31/2010 | ||||||||||

CHANGE IN NET ASSETS RESULTING FROM OPERATIONS: | ||||||||||||

Net investment income (loss) | $ | 57 | $ | 14,353 | $ | 15,791 | ||||||

Net realized gain (loss) | 1 | 123,924 | 69,713 | |||||||||

Change in net unrealized appreciation (depreciation) | 242 | (36,766 | ) | 241,490 | ||||||||

|

|

|

|

|

| |||||||

Change in net assets resulting from operations | 300 | 101,511 | 326,994 | |||||||||

|

|

|

|

|

| |||||||

DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||||||

Class A | ||||||||||||

From net investment income | (16 | ) | (3,957 | ) | (2,301 | ) | ||||||

Return of capital | (2 | ) | — | (3,462 | ) | |||||||

From net realized gains | (1 | ) | — | — | ||||||||

Class C | ||||||||||||

From net investment income | — | (b) | (217 | ) | (61 | ) | ||||||

Return of capital | — | (b) | — | (164 | ) | |||||||

From net realized gains | — | (b) | — | — | ||||||||

Class R2 | ||||||||||||

From net investment income | — | (68 | ) | (6 | ) | |||||||

Return of capital | — | — | (4 | ) | ||||||||

Class R5 | ||||||||||||

From net investment income | (1 | ) | (382 | ) | (202 | ) | ||||||

Return of capital | — | (b) | — | (278 | ) | |||||||

From net realized gains | — | (b) | — | — | ||||||||

Class R6 | ||||||||||||

From net investment income | (1 | ) | — | — | ||||||||

Return of capital | — | (b) | — | — | ||||||||

From net realized gains | — | (b) | — | — | ||||||||

Select Class | ||||||||||||

From net investment income | (49 | ) | (28,779 | ) | (11,619 | ) | ||||||

Return of capital | (8 | ) | — | (12,513 | ) | |||||||

From net realized gains | (2 | ) | — | — | ||||||||

|

|

|

|

|

| |||||||

Total distributions to shareholders | (80 | ) | (33,403 | ) | (30,610 | ) | ||||||

|

|

|

|

|

| |||||||

CAPITAL TRANSACTIONS: | ||||||||||||

Change in net assets from capital transactions | 9,728 | (118,706 | ) | 176,393 | ||||||||

|

|

|

|

|

| |||||||

NET ASSETS: | ||||||||||||

Change in net assets | 9,948 | (50,598 | ) | 472,777 | ||||||||

Beginning of period | — | 1,461,516 | 988,739 | |||||||||

|

|

|

|

|

| |||||||

End of period | $ | 9,948 | $ | 1,410,918 | $ | 1,461,516 | ||||||

|

|

|

|

|

| |||||||

Accumulated undistributed net investment income | $ | — | (b) | $ | 199 | $ | 1,716 | |||||

|

|

|

|

|

| |||||||

| (a) | Commencement of operations was August 31, 2011. |

| (b) | Amount rounds to less than 1,000 |

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2011 | J.P. MORGAN SPECIALTY FUNDS | 15 | ||||||

Table of Contents

STATEMENTS OF CHANGES IN NET ASSETS

FOR THE PERIODS INDICATED (continued)

(Amounts in thousands)

| U.S. Core Real Estate Securities Fund | U.S. Real Estate Fund | |||||||||||

| Period Ended 12/31/2011 (a) | Year Ended 12/31/2011 | Year Ended 12/31/2010 | ||||||||||

CAPITAL TRANSACTIONS: | ||||||||||||

Class A | ||||||||||||

Proceeds from shares issued | $ | 2,452 | $ | 56,334 | $ | 213,840 | ||||||

Dividends and distributions reinvested | 19 | 3,672 | 5,422 | |||||||||

Cost of shares redeemed | — | (95,446 | ) | (257,650 | ) | |||||||

|

|

|

|

|

| |||||||

Change in net assets from Class A capital transactions | $ | 2,471 | $ | (35,440 | ) | $ | (38,388 | ) | ||||

|

|

|

|

|

| |||||||

Class C | ||||||||||||

Proceeds from shares issued | $ | 50 | $ | 3,544 | $ | 4,247 | ||||||

Dividends and distributions reinvested | — | (b) | 193 | 197 | ||||||||

Cost of shares redeemed | — | (4,706 | ) | (3,938 | ) | |||||||

|

|

|

|

|

| |||||||

Change in net assets from Class C capital transactions | $ | 50 | $ | (969 | ) | $ | 506 | |||||

|

|

|

|

|

| |||||||

Class R2 | ||||||||||||

Proceeds from shares issued | $ | — | $ | 6,064 | $ | 956 | ||||||

Dividends and distributions reinvested | — | 62 | 9 | |||||||||

Cost of shares redeemed | — | (1,595 | ) | (169 | ) | |||||||

|

|

|

|

|

| |||||||

Change in net assets from Class R2 capital transactions | $ | — | $ | 4,531 | $ | 796 | ||||||

|

|

|

|

|

| |||||||

Class R5 | ||||||||||||

Proceeds from shares issued | $ | 50 | $ | 7,380 | $ | 8,903 | ||||||

Dividends and distributions reinvested | — | (b) | 371 | 403 | ||||||||

Cost of shares redeemed | — | (12,736 | ) | (45,090 | ) | |||||||

|

|

|

|

|

| |||||||

Change in net assets from Class R5 capital transactions | $ | 50 | $ | (4,985 | ) | $ | (35,784 | ) | ||||

|

|

|

|

|

| |||||||

Class R6 | ||||||||||||

Proceeds from shares issued | $ | 50 | $ | — | $ | — | ||||||

Dividends and distributions reinvested | — | (b) | — | — | ||||||||

|

|

|

|

|

| |||||||

Change in net assets from Class R6 capital transactions | $ | 50 | $ | — | $ | — | ||||||

|

|

|

|

|

| |||||||

Select | ||||||||||||

Proceeds from shares issued | $ | 7,048 | $ | 515,242 | $ | 695,732 | ||||||

Dividends and distributions reinvested | 59 | 8,133 | 2,553 | |||||||||

Cost of shares redeemed | — | (605,218 | ) | (449,022 | ) | |||||||

|

|

|

|

|

| |||||||

Change in net assets from Select capital transactions | $ | 7,107 | $ | (81,843 | ) | $ | 249,263 | |||||

|

|

|

|

|

| |||||||

Total change in net assets from capital transactions | $ | 9,728 | $ | (118,706 | ) | $ | 176,393 | |||||

|

|

|

|

|

| |||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| 16 | J.P. MORGAN SPECIALTY FUNDS | DECEMBER 31, 2011 | ||||

Table of Contents

| U.S. Core Real Estate Securities Fund | U.S. Real Estate Fund | |||||||||||

| Period Ended 12/31/2011 (a) | Year Ended 12/31/2011 | Year Ended 12/31/2010 | ||||||||||

SHARE TRANSACTIONS: | ||||||||||||

Class A | ||||||||||||

Issued | 169 | 3,508 | 15,080 | |||||||||

Reinvested | 1 | 234 | 390 | |||||||||

Redeemed | — | (5,985 | ) | (17,830 | ) | |||||||

|

|

|

|

|

| |||||||

Change in Class A Shares | 170 | (2,243 | ) | (2,360 | ) | |||||||

|

|

|

|

|

| |||||||

Class C |

| |||||||||||

Issued | 3 | 221 | 306 | |||||||||

Reinvested | — | (b) | 13 | 14 | ||||||||

Redeemed | — | (298 | ) | (286 | ) | |||||||

|

|

|

|

|

| |||||||

Change in Class C Shares | 3 | (64 | ) | 34 | ||||||||

|

|

|

|

|

| |||||||

Class R2 |

| |||||||||||

Issued | — | 377 | 67 | |||||||||

Reinvested | — | 4 | 1 | |||||||||

Redeemed | — | (99 | ) | (12 | ) | |||||||

|

|

|

|

|

| |||||||

Change in Class R2 Shares | — | 282 | 56 | |||||||||

|

|

|

|

|

| |||||||

Class R5 |

| |||||||||||

Issued | 3 | 454 | 667 | |||||||||

Reinvested | — | (b) | 24 | 28 | ||||||||

Redeemed | — | (784 | ) | (3,839 | ) | |||||||

|

|

|

|

|

| |||||||

Change in Class R5 Shares | 3 | (306 | ) | (3,144 | ) | |||||||

|

|

|

|

|

| |||||||

Class R6 |

| |||||||||||

Issued | 3 | — | — | |||||||||

Reinvested | — | (b) | — | — | ||||||||

|

|

|

|

|

| |||||||

Change in Class R6 Shares | 3 | — | — | |||||||||

|

|

|

|

|

| |||||||

Select |

| |||||||||||

Issued | 479 | 31,954 | 49,314 | |||||||||

Reinvested | 4 | 537 | 182 | |||||||||

Redeemed | — | (36,834 | ) | (31,251 | ) | |||||||

|

|

|

|

|

| |||||||

Change in Select Shares | 483 | (4,343 | ) | 18,245 | ||||||||

|

|

|

|

|

| |||||||

| (a) | Commencement of operations was August 31, 2011. |

| (b) | Amount rounds to less than 1,000. |

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2011 | J.P. MORGAN SPECIALTY FUNDS | 17 | ||||||

Table of Contents

FOR THE PERIODS INDICATED

| Per share operating performance | |||||||||||||||||||||||||||||||

| Investment operations | Distributions | |||||||||||||||||||||||||||||||

| Net asset value, beginning of period | Net investment income (loss) | Net realized and unrealized gains (losses) on investments | Total from investment operations | Net investment income | Net realized gain | Return of capital | Total distributions | |||||||||||||||||||||||||

U.S. Core Real Estate Securities Fund |

| |||||||||||||||||||||||||||||||

Class A |

| |||||||||||||||||||||||||||||||

August 31, 2011 (e) through December 31, 2011 | $ | 15.00 | $ | 0.35 | (f) | $ | (0.23 | ) | $ | 0.12 | $ | (0.10 | ) | $ | — | (g) | $ | (0.04 | ) | $ | (0.14 | ) | ||||||||||

Class C | ||||||||||||||||||||||||||||||||

August 31, 2011 (e) through December 31, 2011 | 15.00 | 0.11 | (f) | (0.01 | ) | 0.10 | (0.06 | ) | — | (g) | (0.04 | ) | (0.10 | ) | ||||||||||||||||||

Class R5 | ||||||||||||||||||||||||||||||||

August 31, 2011 (e) through December 31, 2011 | 15.00 | 0.16 | (f) | (0.02 | ) | 0.14 | (0.10 | ) | — | (g) | (0.04 | ) | (0.14 | ) | ||||||||||||||||||

Class R6 | ||||||||||||||||||||||||||||||||

August 31, 2011 (e) through December 31, 2011 | 15.00 | 0.16 | (f) | (0.02 | ) | 0.14 | (0.10 | ) | — | (g) | (0.04 | ) | (0.14 | ) | ||||||||||||||||||

Select Class | ||||||||||||||||||||||||||||||||

August 31, 2011 (e) through December 31, 2011 | 15.00 | 0.19 | (f) | (0.05 | ) | 0.14 | (0.10 | ) | — | (g) | (0.04 | ) | (0.14 | ) | ||||||||||||||||||

| (a) | Annualized for periods less than one year. |

| (b) | Not annualized for periods less than one year. |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions. |

| (d) | Includes earnings credits and interest expense, each of which is less than 0.01%, if applicable or unless otherwise noted. |

| (e) | Commencement of operations. |

| (f) | Calculated based upon average shares outstanding. |

| (g) | Amount rounds to less than $0.01. |

| (h) | Certain non-recurring expenses incurred by the Fund were not annualized for the period ended December 31, 2011. |

| (i) | The net investment income ratios for Class A and Select Class are disproportionate due to the timing of shareholder capital transactions and when the Fund earned income over the period. |

| (j) | Ratios are disproportionate between classes due to the size of net assets and fixed expenses. |

SEE NOTES TO FINANCIAL STATEMENTS.

| 18 | J.P. MORGAN SPECIALTY FUNDS | DECEMBER 31, 2011 | ||||

Table of Contents

| Ratios/Supplemental data | |||||||||||||||||||||||||

| Ratios to average net assets (a) | ||||||||||||||||||||||||||

| Net asset value, end of period | Total return (excludes sales charge) (b)(c) | Net assets, end of period (000’s) | Net expenses (d) | Net investment income (loss) | Expenses without waivers, reimbursements and earnings credits | Portfolio turnover rate (b) | ||||||||||||||||||||

| $ | 14.98 | 0.83 | % | $ | 2,548 | 1.18 | %(h) | 7.03 | %(h)(i) | 5.74 | % (h)(j) | 8 | % | |||||||||||||

| 15.00 | 0.69 | 50 | 1.68 | (h) | 2.29 | (h) | 11.12 | (h)(j) | 8 | |||||||||||||||||

| 15.00 | 1.01 | 50 | 0.73 | (h) | 3.24 | (h) | 10.27 | (h)(j) | 8 | |||||||||||||||||

| 15.00 | 1.02 | 51 | 0.68 | (h) | 3.29 | (h) | 10.22 | (h)(j) | 8 | |||||||||||||||||

| 15.00 | 0.97 | 7,249 | 0.93 | (h) | 3.82 | (h)(i) | 9.39 | (h)(j) | 8 | |||||||||||||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2011 | J.P. MORGAN SPECIALTY FUNDS | 19 | ||||||

Table of Contents

FINANCIAL HIGHLIGHTS

FOR THE PERIODS INDICATED (continued)

| Per share operating performance | |||||||||||||||||||||||||||||||

| Investment operations | Distributions | |||||||||||||||||||||||||||||||

| Net asset value, beginning of period | Net investment income (loss) | Net realized and unrealized gains (losses) on investments | Total from investment operations | Net investment income | Net realized gain | Return of capital | Total distributions | |||||||||||||||||||||||||

U.S. Real Estate Fund |

| |||||||||||||||||||||||||||||||

Class A |

| |||||||||||||||||||||||||||||||

Year Ended December 31, 2011 | $ | 15.55 | $ | 0.12 | (e) | $ | 0.80 | $ | 0.92 | $ | (0.31 | ) | $ | — | $ | — | $ | (0.31 | ) | |||||||||||||

Year Ended December 31, 2010 | 12.19 | 0.15 | (e) | 3.51 | 3.66 | (0.12 | ) | — | (0.18 | ) | (0.30 | ) | ||||||||||||||||||||

Year Ended December 31, 2009 | 10.12 | 0.22 | (e) | 2.11 | 2.33 | (0.22 | ) | — | (0.04 | ) | (0.26 | ) | ||||||||||||||||||||

Year Ended December 31, 2008 | 17.09 | 0.30 | (6.92 | ) | (6.62 | ) | (0.32 | ) | — | (0.03 | ) | (0.35 | ) | |||||||||||||||||||

Year Ended December 31, 2007 | 22.62 | 0.22 | (e) | (4.23 | ) | (4.01 | ) | (0.25 | ) | (1.27 | ) | — | (1.52 | ) | ||||||||||||||||||

Class C | ||||||||||||||||||||||||||||||||

Year Ended December 31, 2011 | 15.39 | 0.04 | (e) | 0.80 | 0.84 | (0.24 | ) | — | — | (0.24 | ) | |||||||||||||||||||||

Year Ended December 31, 2010 | 12.08 | 0.08 | (e) | 3.48 | 3.56 | (0.07 | ) | — | (0.18 | ) | (0.25 | ) | ||||||||||||||||||||

Year Ended December 31, 2009 | 10.04 | 0.17 | (e) | 2.10 | 2.27 | (0.19 | ) | — | (0.04 | ) | (0.23 | ) | ||||||||||||||||||||

Year Ended December 31, 2008 | 16.99 | 0.26 | (6.91 | ) | (6.65 | ) | (0.27 | ) | — | (0.03 | ) | (0.30 | ) | |||||||||||||||||||

Year Ended December 31, 2007 | 22.49 | 0.12 | (e) | (4.21 | ) | (4.09 | ) | (0.14 | ) | (1.27 | ) | — | (1.41 | ) | ||||||||||||||||||

Class R2 | ||||||||||||||||||||||||||||||||

Year Ended December 31, 2011 | 15.50 | 0.09 | (e) | 0.80 | 0.89 | (0.29 | ) | — | — | (0.29 | ) | |||||||||||||||||||||

Year Ended December 31, 2010 | 12.18 | 0.14 | (e) | 3.47 | 3.61 | (0.11 | ) | — | (0.18 | ) | (0.29 | ) | ||||||||||||||||||||

Year Ended December 31, 2009 | 10.12 | 0.20 | (e) | 2.11 | 2.31 | (0.21 | ) | — | (0.04 | ) | (0.25 | ) | ||||||||||||||||||||

November 3, 2008 (g) through December 31, 2008 | 11.11 | 0.13 | (1.12 | ) | (0.99 | ) | — | — | — | — | ||||||||||||||||||||||

Class R5 | ||||||||||||||||||||||||||||||||

Year Ended December 31, 2011 | 15.61 | 0.19 | (e) | 0.80 | 0.99 | (0.38 | ) | — | — | (0.38 | ) | |||||||||||||||||||||

Year Ended December 31, 2010 | 12.23 | 0.18 | (e) | 3.56 | 3.74 | (0.18 | ) | — | (0.18 | ) | (0.36 | ) | ||||||||||||||||||||

Year Ended December 31, 2009 | 10.14 | 0.27 | (e) | 2.11 | 2.38 | (0.25 | ) | — | (0.04 | ) | (0.29 | ) | ||||||||||||||||||||

Year Ended December 31, 2008 | 17.11 | 0.43 | (6.99 | ) | (6.56 | ) | (0.38 | ) | — | (0.03 | ) | (0.41 | ) | |||||||||||||||||||

Year Ended December 31, 2007 | 22.65 | 0.35 | (e) | (4.27 | ) | (3.92 | ) | (0.35 | ) | (1.27 | ) | — | (1.62 | ) | ||||||||||||||||||

Select Class | ||||||||||||||||||||||||||||||||

Year Ended December 31, 2011 | 15.58 | 0.16 | (e) | 0.80 | 0.96 | (0.35 | ) | — | — | (0.35 | ) | |||||||||||||||||||||

Year Ended December 31, 2010 | 12.21 | 0.19 | (e) | 3.52 | 3.71 | (0.16 | ) | — | (0.18 | ) | (0.34 | ) | ||||||||||||||||||||

Year Ended December 31, 2009 | 10.13 | 0.25 | (e) | 2.11 | 2.36 | (0.24 | ) | — | (0.04 | ) | (0.28 | ) | ||||||||||||||||||||

Year Ended December 31, 2008 | 17.10 | 0.38 | (6.97 | ) | (6.59 | ) | (0.35 | ) | — | (0.03 | ) | (0.38 | ) | |||||||||||||||||||

Year Ended December 31, 2007 | 22.64 | 0.28 | (e) | (4.24 | ) | (3.96 | ) | (0.31 | ) | (1.27 | ) | — | (1.58 | ) | ||||||||||||||||||

| (a) | Annualized for periods less than one year. |

| (b) | Not annualized for periods less than one year. |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions. |

| (d) | Includes earnings credits and interest expense, each of which is less than 0.01%, if applicable or unless otherwise noted. |

| (e) | Calculated based upon average shares outstanding. |

| (f) | Due to ratio being annualized, the ratio may appear disproportionate to other share classes. |

| (g) | Commencement of offering of class of shares. |

SEE NOTES TO FINANCIAL STATEMENTS.

| 20 | J.P. MORGAN SPECIALTY FUNDS | DECEMBER 31, 2011 | ||||

Table of Contents

| Ratios/Supplemental data | |||||||||||||||||||||||||

| Ratios to average net assets (a) | ||||||||||||||||||||||||||

| Net asset value, end of period | Total return (excludes sales charge) (b)(c) | Net assets, end of period (000’s) | Net expenses (d) | Net investment income (loss) | Expenses without waivers, reimbursements and earnings credits | Portfolio turnover rate (b) | ||||||||||||||||||||

| $ | 16.16 | 6.02 | % | $ | 186,958 | 1.17 | % | 0.72 | 1.37 | % | 67 | % | ||||||||||||||

| 15.55 | 30.36 | 214,760 | 1.17 | 1.05 | 1.29 | 71 | ||||||||||||||||||||

| 12.19 | 24.47 | 197,111 | 1.18 | 2.37 | 1.40 | 81 | ||||||||||||||||||||

| 10.12 | (39.55 | ) | 190,173 | 1.18 | 1.91 | 1.29 | 50 | |||||||||||||||||||

| 17.09 | (17.68 | ) | 261,293 | 1.18 | 1.03 | 1.27 | 64 | |||||||||||||||||||

| 15.99 | 5.50 | 13,763 | 1.67 | 0.23 | 1.87 | 67 | ||||||||||||||||||||

| 15.39 | 29.68 | 14,244 | 1.67 | 0.56 | 1.79 | 71 | ||||||||||||||||||||

| 12.08 | 23.90 | 10,763 | 1.68 | 1.86 | 1.89 | 81 | ||||||||||||||||||||

| 10.04 | (39.86 | ) | 8,477 | 1.68 | 1.58 | 1.79 | 50 | |||||||||||||||||||

| 16.99 | (18.08 | ) | 8,161 | 1.68 | 0.55 | 1.77 | 64 | |||||||||||||||||||

| 16.10 | 5.81 | 5,524 | 1.42 | 0.55 | 1.65 | 67 | ||||||||||||||||||||

| 15.50 | 29.95 | 947 | 1.42 | 0.97 | 1.54 | 71 | ||||||||||||||||||||

| 12.18 | 24.16 | 65 | 1.43 | 2.12 | 1.64 | 81 | ||||||||||||||||||||

| 10.12 | (8.91 | ) | 45 | 1.43 | 8.82 | (f) | 1.58 | 50 | ||||||||||||||||||

| 16.22 | 6.46 | 15,816 | 0.72 | 1.17 | 0.92 | 67 | ||||||||||||||||||||

| 15.61 | 30.94 | 19,999 | 0.72 | 1.34 | 0.84 | 71 | ||||||||||||||||||||

| 12.23 | 25.06 | 54,102 | 0.73 | 2.84 | 0.94 | 81 | ||||||||||||||||||||

| 10.14 | (39.30 | ) | 30,576 | 0.73 | 2.75 | 0.84 | 50 | |||||||||||||||||||

| 17.11 | (17.31 | ) | 24,218 | 0.73 | 1.61 | 0.82 | 64 | |||||||||||||||||||

| 16.19 | 6.27 | 1,188,857 | 0.92 | 0.97 | 1.12 | 67 | ||||||||||||||||||||

| 15.58 | 30.69 | 1,211,566 | 0.92 | 1.33 | 1.04 | 71 | ||||||||||||||||||||

| 12.21 | 24.81 | 726,698 | 0.93 | 2.58 | 1.14 | 81 | ||||||||||||||||||||

| 10.13 | (39.41 | ) | 314,364 | 0.93 | 2.40 | 1.04 | 50 | |||||||||||||||||||

| 17.10 | (17.49 | ) | 334,791 | 0.93 | 1.32 | 1.02 | 64 | |||||||||||||||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2011 | J.P. MORGAN SPECIALTY FUNDS | 21 | ||||||

Table of Contents

AS OF DECEMBER 31, 2011

1. Organization

JPMorgan Trust I (“JPM I”) and JPMorgan Trust II (“JPM II”) (the “Trusts”) were formed on November 12, 2004, as Delaware statutory trusts, pursuant to Declarations of Trust dated November 5, 2004 and are registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as open-end management investment companies.

The following are 2 separate funds of the Trusts, (collectively, the “Funds”) covered by this report:

| Fund | Classes Offered | Trust | Diversified/Non-Diversified | |||

| Security Capital U.S. Core Real Estate Securities Fund | Class A, Class C, Class R5, Class R6 and Select Class | JPM I | Non-Diversified | |||

| JPMorgan U.S. Real Estate Fund | Class A, Class C, Class R2, Class R5 and Select Class | JPM II | Non-Diversified |

Security Capital U.S. Core Real Estate Securities Fund (“U.S. Core Real Estate Securities Fund”) commenced operations on August 31, 2011.

The investment objective of the U.S. Core Real Estate Securities Fund is to seek to provide a risk-adjusted total return over the long term by investing primarily in real estate securities.

The investment objective of the JPMorgan U.S. Real Estate Fund (“U.S. Real Estate Fund”) is to seek to provide a high level of current income and long term capital appreciation primarily through investments in real estate securities.

Class A Shares generally provide for a front-end sales charge while Class C Shares provide for a contingent deferred sales charge (“CDSC”). No sales charges are assessed with respect to the Class R2, Class R5, Class R6 and Select Class Shares. All classes of shares have equal rights as to earnings, assets and voting privileges except that each class may bear different distribution and shareholder servicing fees and each class has exclusive voting rights with respect to its distribution plan and shareholder servicing agreements. Certain Class A Shares, for which front-end sales charges have been waived, may be subject to a CDSC as described in the Funds’ prospectus.

2. Significant Accounting Policies

The following is a summary of significant accounting policies followed by the Trusts in the preparation of their financial statements. The policies are in accordance with accounting principles generally accepted in the United States of America. The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expenses for the period. Actual results could differ from those estimates.

A. Valuation of Investments — Equity securities listed on a North American, Central American, South American or Caribbean securities exchange shall generally be valued at the last sale price on the exchange on which the security is principally traded that is reported before the time when the net assets of the Fund are valued. The value of securities listed on The NASDAQ Stock Market LLC shall generally be the NASDAQ Official Closing Price. Fixed income securities (other than certain short-term investments maturing in less than 61 days) are valued each day based on prices received from independent or affiliated pricing services approved by the Board of Trustees or third party broker-dealers. The broker-dealers or pricing services use multiple valuation techniques to determine fair value. In instances where sufficient market activity exists, the broker-dealers or pricing services may utilize a market-based approach through which quotes from market makers are used to determine fair value. In instances where sufficient market activity may not exist or is limited, the broker-dealers or pricing services also utilize proprietary valuation models which may consider market transactions in comparable securities and the various relationships between securities in determining value and/or market characteristics such as benchmark yield curves, option-adjusted spreads, credit spreads, estimated default rates, coupon rates, anticipated timing of principal repayments, underlying collateral, and other unique security features in order to estimate the relevant cash flows, which are then discounted to calculate the fair values. Generally, short-term investments of sufficient credit quality maturing in less than 61 days are valued at amortized cost, which approximates market value. Certain investments of the Funds may, depending upon market conditions, trade in relatively thin markets and/or in markets that experience significant volatility. As a result of these conditions, the prices used by the Funds to value securities may differ from the value that would be realized if these securities were sold, and the differences could be material. Futures and options shall generally be valued on the basis of available market quotations. Swaps and other derivatives are valued daily, primarily using independent or affiliated pricing services approved by the Board of Trustees. If valuations are not available from such services or values received are deemed not representative of market value, values will be obtained from a third party broker-dealer or counterparty. Investments in other open-end investment companies are valued at such investment company’s net asset value per share as of the report date.

Securities or other assets for which market quotations are not readily available or for which market quotations do not represent the value at the time of pricing (including certain illiquid securities) are fair valued in accordance with procedures established by and under the supervision and responsibility of the Board of Trustees. Under these procedures, the Funds primarily employ a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information for the investment to determine the fair value of the investment. The Funds may also use an income-based valuation approach in which the anticipated future cash flows of the investment are discounted to calculate fair value. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. Valuations may be based upon current market prices of securities that are comparable in coupon, rating, maturity and industry. It is possible that the estimated values may differ significantly from the values that would have been used had a ready market for the investments existed, and such differences could be material. Trading in securities on most foreign exchanges and over-the-counter markets is normally completed before the close of the domestic market and may also take place on days when the domestic market is closed. In accordance with procedures

| 22 | J.P. MORGAN SPECIALTY FUNDS | DECEMBER 31, 2011 | ||||

Table of Contents

adopted by the Board of Trustees, the Funds apply fair value pricing on equity securities on a daily basis except for North American, Central American, South American and Caribbean equity securities held in their portfolios by utilizing the quotations of an independent pricing service, unless the Funds’ advisor determines that use of another valuation methodology is appropriate. The pricing service uses statistical analyses and quantitative models to adjust local market prices using factors such as subsequent movement and changes in the prices of indices, securities and exchange rates in other markets, in determining fair value as of the time a Fund calculates its net asset values.

Valuations reflected in this report are as of the report date. As a result, changes in valuation due to market events and/or issuer related events after the report date and prior to issuance of the report are not reflected herein.

The various inputs that are used in determining the fair value of the Funds’ investments are summarized into the three broad levels listed below.