UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4279

Securian Funds Trust

(Exact name of registrant as specified in charter)

400 Robert Street North

St. Paul, Minnesota 55101-2098

(Address of principal executive offices) (Zip code)

Paul J. Thibodeaux, Esq.

400 Robert Street North

St. Paul, Minnesota 55101-2098

(Name and address of agent for service)

Registrant's telephone number, including area code:

(651) 665-3500

Date of fiscal year end: December 31, 2022

Date of reporting period: December 31, 2022

ITEM 1. REPORT TO STOCKHOLDERS.

Filed herewith.

Offered in Minnesota Life

Insurance Company and

Securian Life Insurance

Company variable products

Annual report

December 31, 2022

SFT Balanced Stabilization Fund

SFT Core Bond Fund

SFT Delaware IvySM Growth Fund

SFT Delaware IvySM Small Cap Growth Fund

SFT Equity Stabilization Fund

SFT Government Money Market Fund

SFT Index 400 Mid-Cap Fund

SFT Index 500 Fund

SFT International Bond Fund

SFT Real Estate Securities Fund

SFT T. Rowe Price Value Fund

SFT Wellington Core Equity Fund

TABLE OF CONTENTS

| | | Page No. | |

Letter from the President | | | 1 | | |

Portfolio Manager Reviews | |

SFT Balanced Stabilization Fund | | | 2 | | |

| SFT Core Bond Fund | | | 7 | | |

SFT Delaware IvySM Growth Fund | | | 12 | | |

SFT Delaware IvySM Small Cap Growth Fund | | | 17 | | |

SFT Equity Stabilization Fund | | | 21 | | |

SFT Government Money Market Fund | | | 26 | | |

SFT Index 400 Mid-Cap Fund | | | 28 | | |

| SFT Index 500 Fund | | | 32 | | |

SFT International Bond Fund | | | 36 | | |

SFT Real Estate Securities Fund | | | 41 | | |

SFT T. Rowe Price Value Fund | | | 45 | | |

SFT Wellington Core Equity Fund | | | 49 | | |

Report of Independent Registered Public Accounting Firm | | | 53 | | |

Investments In Securities | |

SFT Balanced Stabilization Fund | | | 54 | | |

| SFT Core Bond Fund | | | 61 | | |

SFT Delaware IvySM Growth Fund | | | 73 | | |

SFT Delaware IvySM Small Cap Growth Fund | | | 75 | | |

SFT Equity Stabilization Fund | | | 77 | | |

SFT Government Money Market Fund | | | 79 | | |

SFT Index 400 Mid-Cap Fund | | | 80 | | |

| SFT Index 500 Fund | | | 87 | | |

SFT International Bond Fund | | | 95 | | |

SFT Real Estate Securities Fund | | | 98 | | |

SFT T. Rowe Price Value Fund | | | 99 | | |

SFT Wellington Core Equity Fund | | | 102 | | |

Financial Statements | |

Statements of Assets and Liabilities | | | 104 | | |

Statements of Operations | | | 106 | | |

Statements of Changes in Net Assets | | | 108 | | |

Financial Highlights | | | 113 | | |

Notes to Financial Statements | | | 125 | | |

Fund Expense Examples | | | 143 | | |

Proxy Voting and Quarterly Holdings Information | | | 144 | | |

Statement Regarding Liquidity Risk Management Program | | | 145 | | |

Trustees and Executive Officers | | | 146 | | |

Letter from the President

Last year's market performance was one for the record books, but not in a positive way. While fourth quarter returns were generally upbeat, they were not enough to offset the significant losses occurring earlier in the year. Indeed, both equity and fixed income markets recorded sizable losses for the year, a most uncommon outcome.

A driving force in this market weakness was the Federal Reserve's attempt to slow inflation by raising short term interest rates, moving up the target Federal Funds rate to over 4 percent from near zero the year before. The last time rates had risen that aggressively was over forty years ago. Inflation appears to have peaked at 9.1 percent in June, but it still remains at unacceptable levels, so further Federal Reserve tightening is likely.

In 2023, optimistic corporate earnings expectations, continued geopolitical tensions and an inflation-fighting Federal Reserve will likely fuel continued volatility. For now however, the employment picture is strong, and services spending has been enough to offset weakness in manufacturing. But with so much ambiguity in the market, a recession—and higher unemployment—seem to be the base case for many market forecasters. Bond investors appear to be pricing Treasuries to reflect recession concerns, but corporate earnings estimates, and corporate bond spreads don't reflect a downturn. It appears that many risk assets still are not incorporating a generous margin of safety, therefore a level of caution is warranted.

As always, we believe the best investment tactic is to position for the long-term and use diversification to reduce risk of a downside surprise.

Sincerely,

David Kuplic

President, Securian Funds Trust

1

SFT Balanced Stabilization Fund

Jeremy Gogos, Ph.D., CFA, Merlin Erickson Portfolio Managers

Securian Asset Management

Fund Objective

The SFT Balanced Stabilization Fund seeks to maximize risk-adjusted total return relative to its blended benchmark index comprised of 60 percent S&P 500® Index and 40 percent Bloomberg U.S. Aggregate Bond Index (collectively, the "Blended Benchmark Index"). The SFT Balanced Stabilization Fund invests primarily in Class 1 shares of the SFT Index 500 Fund for equity exposure, in a basket of fixed income securities for fixed income exposure and certain derivative instruments. The Fund is subject to risks associated with such investments as described in detail in the Fund's prospectus. The net asset value of the Fund will fluctuate and is not guaranteed. It is possible to lose money by investing in the Fund. There is no assurance that efforts to manage Fund volatility will achieve the desired results.

Performance Update

The Fund generated a total net return of -12.62 percent over the 12 months ending December 31, 2022, outperforming the Blended Benchmark Index which returned -15.79 percent over the same period.

What influenced the Fund's return during the past 12 months?

Equity volatility is what guides the asset allocation of the Fund's strategy. When equity volatility is low, the equity exposure of this strategy will be high. Conversely, when equity volatility is high, the equity exposure of this strategy will be low.

In 2022, markets saw some of the worst risk asset performance in recent memory; essentially every major asset class delivered deeply negative performance. For example, for 2022, the S&P 500® returned -18.11 percent for 2022, and the Bloomberg US Credit Index returned -15.76 percent. Commodities were a lone bright spot in an otherwise challenging year, as the Bloomberg Commodity Index closed out 2022 up 13.75 percent.

In our view, the primary driver of 2022's awful risk asset performance was the monetary policy tightening happening in concert around the globe. We will further discuss this topic shortly. For now, suffice to say that we view the 2022 S&P 500® return of -18.11 percent, and realized volatility of 24.17 percent—an 85th percentile value—as direct consequences of the aggressive monetary tightening the Federal Reserve (the "Fed") pursued in response to the severe inflation backdrop of late 2021 and early 2022.

Elevated volatility wasn't confined to equity. Rates and spreads also saw outsized moves through all of 2022. The 10-year U.S. Treasury yield, investment grade spreads, and high yield spreads all saw volatility in 2022 that ranked in the 82nd to 83rd percentile historically.

Realized 20-day S&P 500® volatility saw a minimum of 13.29 percent, and a maximum of 34.87 percent, over the course of the year. Given this rather elevated volatility, the Fund equity exposure ranged from a minimum of 27.01 percent to a maximum of 50.25 percent, and averaged 36.10 percent for the year. This equity underweight was the primary reason the Fund outperformed its benchmark in 2022.

In absolute terms, the Fund's fixed income holdings modestly outperformed the benchmark's fixed income portion; they saw absolute returns of -12.69 percent and -13.07 percent, respectively. We continued to maintain an overall fixed income underweight relative to the benchmark for essentially all of 2022, and so the overall contributions to return for the Fund and benchmark fixed income were -4.10 percent and -5.19 percent, respectively.

2

What other market conditions or events influenced the Fund's performance during the past 12 months?

In 2022, markets saw the correlation between the S&P 500® and the 10-Year U.S. Treasury go deeply negative again. As we have highlighted previously, the idea of fixed income being a portfolio bulwark against equity losses relies on this correlation being positive. That is, as equity prices decrease, bond yields also decrease and, by extension, bond prices rise, offsetting the equity decline. The prevailing inflation backdrop through all of 2022, and the market expectations for central bank action that that backdrop created, caused equity and fixed income assets to move in tandem for most of 2022. As a result, the canonical 60/40 portfolio saw its second-worst year ever in the available daily history of the S&P 500® Total Return and Bloomberg U.S. Aggregate Bond indexes (1989-present), sorted by worst percent return. For reference, 2008 saw a -20.91 percent return on the same portfolio.

The "growth over value" trade also largely unwound over the course of 2022. The high-flying tech-focused names that powered the absurd COVID-19 equity rally of 2020-2021, and which ended up accounting for a wildly outsized portion of the S&P 500® market capitalization, saw extreme pullbacks in 2022. For example, Meta lost -64.22 percent, Tesla lost -65.03 percent, and Amazon lost -49.62 percent.

In short, 2022 exemplified the type of market regime we have repeatedly cautioned against, namely one in which investors need portfolio protection approaches beyond a fixed income allocation to mitigate losses.

What strategies and techniques did you employ that specifically affected Fund performance?

Throughout the year, the Fund held a core long position in cash equity that tracks the S&P 500®. In addition, the Fund had short positions in S&P 500® futures, long and short S&P 500® put options, long and short Chicago Board Options Exchange (CBOE) Volatility Index (VIX) call options, and long and short VIX put options. These derivative positions were held either as expressions of the target equity allocation of the Fund given prevailing volatility, or as supplemental hedges for managing the Fund's risk.

What will affect the Fund going forward?

By multiple measures, inflation continued to be a serious economic and political problem through all of 2022. Consumer Price Index (CPI) peaked at 9.1 percent year-over-year on June 30, 2022, and Personal Consumption Expenditures (PCE) printed a 5.20 percent year-over-year change on September 30, 2022. While these inflation metrics, along with market inflation expectations, have been on a downward trajectory to close out the year, every inflation metric is still well above the Fed's stated 2.0 percent target. As a result, 2022 saw the Fed embark on a very aggressive monetary tightening campaign. Its policy rate was at zero to begin 2022; it ended 2022 at 4.25 percent. The Fed Funds rate hasn't increased by more than 4 percent in a one-year period since 1981, when the Fed was contending with inflation of nearly 15 percent year-over-year, and its policy rate was north of 10 percent.

For numerous years, we have been bearish on equities. We viewed easy monetary policy as having distorted valuations across multiple asset classes, and we felt that investors were often foolheartedly latching onto growth narratives to rationalize buying indefensibly overpriced stock. Perhaps ironically, in a year where we view a recession as likely, we are more bullish on equity than we have been for quite some time.

First, let us address the notion of a potential recession. The 10-year to 3-month yield curve was inverted from November 8, 2022 through year-end, and hit a minimum of -85 basis points on December 7, 2022. As many market commentators note, this yield curve anomaly highlights overly aggressive monetary policy moves, and it has happened leading up to every recession in modern history. Based on this data point alone, we would expect a recession within the next 12-24 months. Further, it is worth reiterating that gross domestic product (GDP) printed negative growth in Q1 and Q2 of 2022.

We think signals from the consumer sector also suggest a slowing economy. Consumers have been saving a smaller fraction of their disposable income than ever, and credit card utilization has now reached pre-pandemic levels. Both trajectories are unsustainable. We interpret both of these data points as suggesting a material decrease in consumer demand as 2023 unfolds. When you combine these consumer metrics with rates market data that suggests the Fed has hiked its policy rate to an unsustainable level, we see a 2023 recession as a strong possibility.

3

Perhaps ironically, we view the somewhat grim macroeconomic picture as a potential tailwind for equities. Recent equity market responses to "easier" monetary policy suggest that any pivot in Fed policy will be enthusiastically received by risk markets. Further, in the asset rout of 2022, fundamental equity valuation metrics have reverted to more reasonable levels.

We also view recent geopolitical developments as supportive of a bullish equity view. First, while the response of Western nations has not been perfectly harmonious, our European allies have largely found ways to survive without Russian natural gas, and the Ukrainian resistance has proved a very formidable adversary for Russia's bumbling invasion force. As such, the potential impacts of Russian natural gas and oil supply shortages likely have fewer global economic knock-on effects than originally anticipated. Another key geopolitical development in late 2022 is that China abandoned its zero-COVID policy. The implementation of this policy change is taking an enormous human toll on the Chinese population, and we do not want to marginalize that tragedy. But, if we endeavor to keep our focus on economic issues, we anticipate that supply chain disruption will decrease materially once China's working population weathers this current COVID-19 wave that their government left them woefully unprepared for.

To summarize, we anticipate that the Fed is very close to the end of its tightening campaign. By extension, we think volatility will come down modestly from 2022 levels as 2023 unfolds. And, perhaps most importantly, we anticipate that a 2023 recession will give the Fed the justification it needs to pivot to monetary easing. Should this pivot come to pass, we think a broad risk asset rally is likely.

In a tactical sense, we will continue to use our volatility metrics to inform the equity allocation of the Fund. We will increase equity exposure if we believe volatility will decrease, and decrease equity exposure if we believe volatility will increase. Given our more bullish view of equity returns for the near future, we will maintain the Fund's equity exposure toward the upper end of its allowed range while keeping downside hedge positions in place.

4

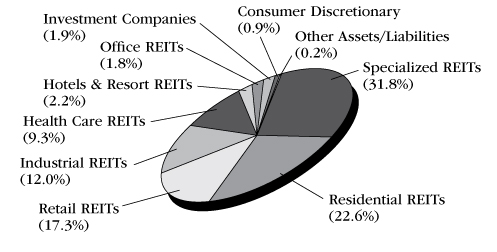

Ten Largest Holdings^

| Security description | | Market

value | | % of net

assets | |

iShares Core S&P 500 ETF | | $ | 40,511,102 | | | | 6.5 | % | |

U.S. Treasury Note 1.000%, 12/15/24 | | | 14,509,453 | | | | 2.3 | % | |

SPDR S&P 500 ETF Trust | | | 13,832,493 | | | | 2.2 | % | |

U.S. Treasury Note 3.875%, 12/31/27 | | | 9,312,015 | | | | 1.5 | % | |

Vanguard S&P 500 ETF | | | 7,088,284 | | | | 1.1 | % | |

U.S. Treasury Bond 4.000%, 11/15/42 | | | 5,452,234 | | | | 0.9 | % | |

CenterPoint Energy Houston Electric LLC, Series AJ 4.850%, 10/01/52 | | | 2,979,109 | | | | 0.5 | % | |

Intercontinental Exchange, Inc. 4.350%, 06/15/29 | | | 2,907,195 | | | | 0.5 | % | |

M&T Bank Corp. 4.553%, 08/16/28 | | | 2,903,016 | | | | 0.5 | % | |

KeyBank NA 4.390%, 12/14/27 | | | 2,890,011 | | | | 0.4 | % | |

| | $ | 102,384,912 | | | | 16.4 | % | |

^Does not include short-term investments or investments in Class 1 shares of the SFT Index 500 Fund, an affiliated Fund in Securian Funds Trust, which provides the SFT Balanced Stabilization Fund with its primary equity exposure.

Sector Diversification (shown as a percentage of net assets)

Asset Quality (shown as a percentage of fixed income investments)

5

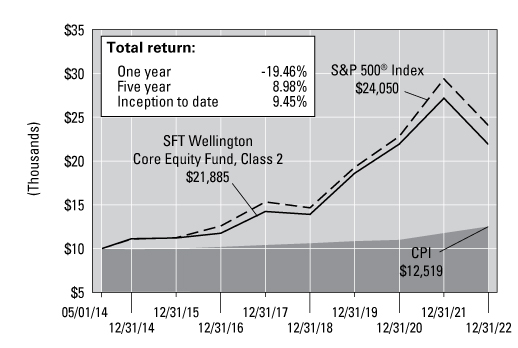

Comparison of Change in Investment Value*

A Hypothetical $10,000 Investment in SFT Balanced Stabilization Fund,

the Blended Benchmark Index and Consumer Price Index (CPI)

On the chart above you can see how the SFT Balanced Stabilization Fund's shares total return compared to its Blended Benchmark Index, comprised of 60 percent of the S&P 500® Index and 40 percent of the Bloomberg U.S. Aggregate Bond Index, and the Consumer Price Index. The three lines represent the total return of a hypothetical $10,000 investment made on May 1, 2013 through December 31, 2022, assuming reinvestment of distributions, if any.

* The results shown are past performance and are not an indication of future performance. Current performance may be lower or higher. The investment returns and principal value of an investment will fluctuate so that shares upon redemption may be worth more or less than their original cost. Performance figures of the Fund do not reflect charges pursuant to the terms of the variable life insurance policies and variable annuity contracts funded by separate accounts that invest in the Fund's shares. When such charges are deducted, actual investment performance in a variable policy or contract will be lower.

Securian Asset Management, Inc. ("Securian AM") and Securian Funds Trust, on behalf of the SFT Balanced Stabilization Fund (the "Fund"), have entered into an Expense Limitation Agreement, dated May 1, 2013, which limits the operating expenses of the Fund, excluding certain expenses (such as interest expense, acquired fund fees, cash overdraft fees, taxes, brokerage commissions, other expenditures which are capitalized in accordance with the generally accepted accounting principles, and other extraordinary expenses not incurred in the ordinary course of the Fund's business), to 0.80% of the Fund's average daily net assets through April 30, 2021. The Expense Limitation Agreement was terminated on May 1, 2021. The Fund is authorized to reimburse Securian AM for management fees previously waived and/or for the cost of expenses previously paid by Securian AM pursuant to this agreement, provided that such reimbursement will not cause the Fund to exceed any limits in effect at the time of such reimbursement. The Fund's ability to reimburse Securian AM in this manner only applies to fees waived or reimbursements made by Securian AM within the three fiscal years prior to the date of such reimbursement. To the extent that the Fund makes such reimbursements to Securian AM, the amount of the reimbursements will be reflected in the financial statements in the Fund's shareholder reports and in Other Expenses under Fees and Expenses of the Fund.

The Blended Benchmark Index is comprised of 60 percent of the S&P 500® Index and 40 percent of the Bloomberg U.S. Aggregate Bond Index.

The S&P 500® Index is a broad, unmanaged index of 500 common stocks which are representative of the U.S. stock market overall. The Bloomberg U.S. Aggregate Bond Index is an unmanaged benchmark composite representing the average market-weighted performance of U.S. Treasury and agency securities, investment grade corporate bonds and mortgage-backed securities with maturities greater than one year.

6

Stephen M. Kane, CFA, Laird R. Landmann, Bryan T. Whalen, CFA

Portfolio Managers

TCW

Fund Objective

The SFT Core Bond Fund seeks as high a level of long-term total return as is consistent with prudent investment risk. Preservation of capital is a secondary objective. The SFT Core Bond Fund invests in long-term, fixed income, high quality debt instruments. The investment adviser for the Fund is Securian Asset Management, Inc. Metropolitan West Asset Management, LLC ("Met West") serves as the investment sub-adviser to the Fund and provides investment advice under a sub-advisory agreement. The risks incurred by investing in debt instruments include, but are not limited to, reinvestment of prepaid debt obligations at lower rates of return, and the inability to reinvest at higher interest rates when debt obligations are prepaid more slowly than expected. In addition, the net asset value of the SFT Core Bond Fund may fluctuate in response to changes in interest rates and is not guaranteed.

Performance Update

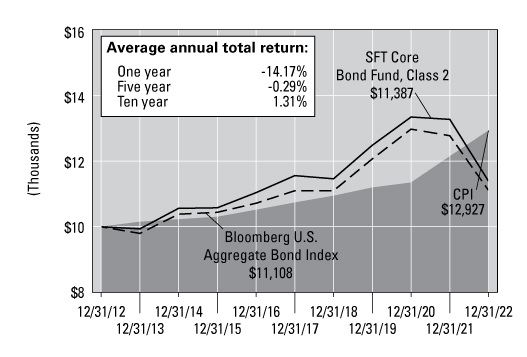

The Fund's Class 2 shares generated a total net return of -14.17 percent over the 12 months ending December 31, 2022, underperforming the Bloomberg U.S. Aggregate Bond Index which returned -13.01 percent over the same period.

What influenced the Fund's return during the past 12 months?

While the challenging effects from the Federal Open Market Committee's shift in policy—from near-zero interest rates to one of the most aggressive hiking cycles in decades—was felt throughout nearly all segments of the market, perhaps no sector bore the brunt of this regime change more than residential Mortgage-Backed Securities ("MBS"). The mortgage market, spurred by pandemic-era stimulus and the Federal Reserve's (the "Fed") sizeable footprint in the agency MBS space, saw record low mortgage rates throughout 2020 and 2021, setting the stage for the downward repricing of the sector in 2022 as the surge in U.S. Treasury rates quickly moved a large segment of the mortgage universe "out of the money" (i.e., no incentive to refinance). As a result, durations extended across the coupon stack as prepayment expectations essentially fell to zero, and, when coupled with elevated volatility, increased hedging costs and heightened selling in the sector to meet outflows, the agency MBS sector posted the worst year of total returns on record, negatively impacting the Fund's sizeable allocation to the space. Similarly, spreads widened across non-agency backed issues amid broader macro uncertainty and elevated rate environment, resulting in falling prices across the sector and a headwind for performance.

What other market conditions or events influenced the Fund's performance during the past 12 months?

Much as any year brings its share of the unexpected, possibly the biggest surprise of 2022 was the Fed finding a long-lost resolve in the face of a capital markets-wide selloff precipitated by a rooted and flowered inflation, germinated in the pandemic (and seeded decades prior). As for the markets, the tumult of the year would be hard to overstate. Pricing weakness was felt across asset classes with broad stock and bond measures dropping more than 15 percent, a first for the record books and a nemesis to diversification. Compounding the deleterious effect of one of the most hawkish and synchronized central bank tightening campaigns in history, low bond yields and relatively lofty stock valuations to start the year set the stage for such disappointing results. What periodic relief there was in 2022 manifested itself as a pattern of sporadic bear market rallies and a near obsession with the word "pivot", though optimism proved unsustainable. "Pivot" now follows "transitory" in the Fed lexicon...will it too be forgotten as Chair Powell stays a steady course?

7

Although late to take action to combat inflation, the Fed initiated its aggressive tightening measures in March to eventually get through four consecutive 75 basis point (bps) increases to the Fed Funds rate, followed by an additional 50 bps bump in December, bringing the target range to 4.25 percent to 4.50 percent by the end of the year. Resilient labor markets—sub 4 percent unemployment—provide continuing cover for an expected 50 bps of further tightening early in 2023 and peak short rates near 5 percent. Fed action has historically worked with a lag, though the first effects of slowing economic activity thus far have already shown up in the interest-rate sensitive housing market. Existing home sales fell for ten consecutive months in 2022, and are now down over 35 percent on a year-over-year basis as mortgage rates rose off historically low levels and affordability sharply deteriorated for new homebuyers on the higher financing costs and still high prices, at least for now.

Finding 4 percent for the first time since 2010 in early October and reaching a high of 4.24 percent later in the month, the 10-Year yield stabilized somewhat lower to close 2022 at 3.89 percent, though still nearly 240 bps above where it started the year. Fixed income remediated into the fourth quarter on reduced rate volatility, with the Bloomberg U.S. Aggregate Index actually gaining 1.9 percent, but year-to-date losses were too steep to overcome, falling a crushing 13 percent. Credit markets lagged in 2022 as spreads widened in both the investment grade and high yield markets. Despite widening, investment grade spreads around 130 bps are still moderately tighter than their long-term averages and substantially narrower than they have been in recessions, suggesting there is room for them to widen further in 2023 if the economy endures a more significant downturn. For leveraged finance, despite a 4Q rally of 4.2 percent, high yield bonds were down 11.2 percent for the year and the amount of distressed debt in the U.S. alone jumped more than 300 percent in 12 months.

Even more affected than the corporate market, agency MBS spreads reached levels similar to where they were in 2008, and delivered an 11.8 percent loss for 2022 despite clawing back 2.1 percent in the fourth quarter. Similarly, non-agency MBS spreads reflected weaker economic expectations than those priced by credit markets, resulting in deeply negative year-to-date returns (though better than the agency MBS market). Meanwhile, commercial real estate remains vulnerable as the work from home dynamic has weighed on office properties, adding to stress in brick-and-mortar retailers and translating to lagging results and an increasing percentage of Commercial Mortgage-Backed Securities ("CMBS") collateral loans going to special servicing. Both agency and non-agency CMBS tumbled approximately 11 percent on the year, with the agency market dragged down mostly on duration while non-agency CMBS experienced more pronounced spread widening. On the Asset-Backed Securities ("ABS") front, early signs of stress are emerging despite a modest current annual loss of 4.3 percent, with delinquencies and writeoffs picking up, especially among the highest risk borrowers.

What strategies and techniques did you employ that specifically affected Fund performance?

Though repositioning into weakness generally produces challenges to immediate performance, improved valuations resulting from spread widening and increased volatility provided attractive opportunities to add exposure to high-quality corporate sectors and issuers, especially more defensive sectors that traditionally withstand prolonged bouts of volatility. As such, positions were added among consumer non-cyclicals, communications, and banking within financials. The resultant overweight to non-cyclicals contributed positively to relative performance as the sector outpaced the broader Index, though communications and financials lagged. Banking was among the largest additions to the corporate basis during the year given strong balance sheets and well-regulated emphasis of liquidity and capital across the sector, though the liquidity needs for many banks led to programmatic issuance and a concomitant widening of spreads past the rest of the investment grade corporate universe. Consistent with the team's relative value discipline, exposure was added to the sector in a disciplined, dollar-cost averaging manner on these increased spread levels.

Similarly, wide spreads and discount dollar pricing provided opportunity to increase the Fund's allocation to residential MBS, which weighed on returns given the significant underperformance of both agency and non-agency backed issues. The immediate performance drag notwithstanding, the team remains constructive on both the relative value and outlook for the sector. Agency MBS, largely "priced to worst" amid fully extended durations, presents upside optionality should rate volatility level off or drop in the coming year, while the relatively high liquidity and government guarantee further underpin constructive sentiment. Among non-agency deals, despite current low prices, collateral backing the deals benefits from record levels of home price appreciation, decreasing

8

loan to value ratios, improved lending standards, and structural supply and demand imbalances, all of which should help to cushion the sector, even in a recessionary environment.

What will affect the Fund going forward?

The path towards economic stability will be challenging as uncertainty over the trajectory of monetary policy, inflation, and geopolitical tensions renders the market susceptible to continued volatility. Without question, the effects of higher rates and tighter financial conditions will continue to be felt into 2023, with a recession the most likely outcome. However, unlike the last two recessions, we believe this one is not likely to be crisis-driven (i.e., subprime meltdown or pandemic), but rather by the Fed, suggesting a different look than recent versions. As such, the team's approach is to remain disciplined and opportunistic. Specific to the inflation picture in the U.S., prices appear to have peaked, with expectations for further deceleration as economic activity slows. As a corollary to that, it is anticipated that the yield curve will steepen significantly, with the two-year rate dropping quickly to reflect an easing Fed (by year-end 2022, the curve has steepened more than 30 bps from the cycle low). Positioning reflects this, under a belief that disciplined active managers will be well-situated to take advantage of market volatility and thus set the stage for strong prospective returns.

With the bellwether Treasury yield above the team's estimate of sustainable levels, the duration of the strategy was extended throughout 2022 to approximately 0.5 years long versus the Index. On sector positioning, allocations dictate caution given that corporate spread levels remain insufficient. As such, the strategy emphasizes more resilient sectors and issues subject to less would-be volatility, with the expectation that as recession unfolds, the non-linear move in spreads will allow for de-risking as valuations improve, while maintaining room to increase exposure during larger corrections. Unlike credit markets, both agency and non-agency MBS prices reflect economic pressure, and represent what we view as attractive value at this point. Expectations are that agency MBS could be used as buy liquidity for other opportunities in market volatility. As for non-agency holdings, especially long-seasoned legacy issues, these continue to exhibit good collateral performance, i.e., low delinquencies and improving loan-to-value ratios, though some volatility is possible, particularly if unemployment rises. The team remains selective in these sectors and, similar to credit, will look to reduce higher quality holdings, using proceeds to migrate down the quality spectrum as valuations cheapen to improve the return outlook. Finally, exposure to other securitized issues is higher quality, particularly in the CMBS market, which faces stress in 2023 as rising delinquencies ultimately filter through to defaults and losses. ABS at the top of the capital structure provides what we believe to be fair compensation given robust structures, with an ongoing focus on off-the-run sectors that offer more attractive yields than more traditional credit cards and auto receivables.

9

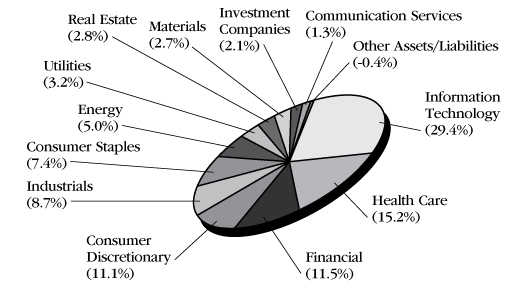

Ten Largest Holdings^

| Security description | | Market

value | | % of net

assets | |

U.S. Treasury Bond 2.000%, 11/15/41 | | $ | 34,735,371 | | | | 7.9 | % | |

Federal National Mortgage Association 2.500%, 12/25/51, TBA | | | 25,285,488 | | | | 5.8 | % | |

Federal National Mortgage Association 5.000%, 01/12/53, TBA | | | 21,151,711 | | | | 4.8 | % | |

Federal National Mortgage Association 2.000%, 01/12/53, TBA | | | 16,481,938 | | | | 3.8 | % | |

Federal National Mortgage Association 3.000%, 02/25/52, TBA | | | 15,498,984 | | | | 3.5 | % | |

U.S. Treasury Bond 4.000%, 11/15/52 | | | 15,343,659 | | | | 3.5 | % | |

U.S. Treasury Note 3.750%, 12/31/27 | | | 9,122,788 | | | | 2.1 | % | |

Federal National Mortgage Association 2.000%, 11/01/51 | | | 8,401,492 | | | | 1.9 | % | |

Federal National Mortgage Association 4.500%, 01/12/53, TBA | | | 6,296,625 | | | | 1.4 | % | |

U.S. Treasury Note 3.875%, 11/30/27 | | | 5,920,849 | | | | 1.3 | % | |

| | $ | 158,238,905 | | | | 36.0 | % | |

^Excludes short-term investments.

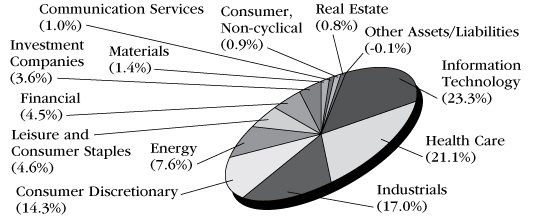

Sector Diversification (shown as a percentage of net assets)

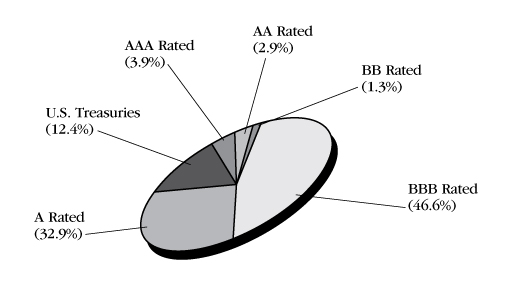

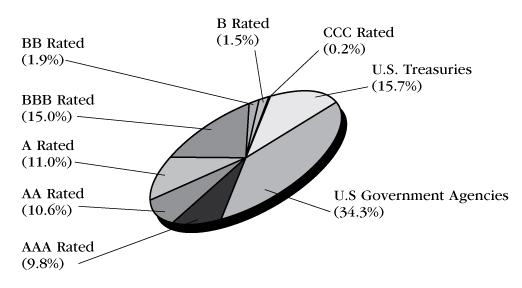

Asset Quality (shown as a percentage of investments)

10

Comparison of Change in Investment Value*

A Hypothetical $10,000 Investment in SFT Core Bond Fund,

Bloomberg U.S. Aggregate Bond Index and Consumer Price Index (CPI)

On the chart above you can see how the SFT Core Bond Fund's Class 2 shares total return compared to the Bloomberg U.S. Aggregate Bond Index and the Consumer Price Index. The three lines represent the total return of a hypothetical $10,000 investment made on December 31, 2012 through December 31, 2022, assuming reinvestment of distributions, if any.

* The results shown are past performance and are not an indication of future performance. Current performance may be lower or higher. The investment returns and principal value of an investment will fluctuate so that shares upon redemption may be worth more or less than their original cost. Performance figures of the Fund do not reflect charges pursuant to the terms of the variable life insurance policies and variable annuity contracts funded by separate accounts that invest in the Fund's shares. When such charges are deducted, actual investment performance in a variable policy or contract will be lower.

The Bloomberg U.S. Aggregate Bond Index is an unmanaged benchmark composite representing average market-weighted performance of U.S. Treasury and agency securities, investment-grade corporate bonds and mortgage-backed securities with maturities greater than one year.

11

SFT Delaware IvySM Growth Fund

Bradley M. Klapmeyer, CFA, Brad Angermeier, CFA Portfolio Managers

Delaware Investments Fund Advisers

Fund Objective

The SFT Delaware IvySM Growth Fund seeks to provide growth of capital. The Fund pursues its objective by investing primarily in a diversified portfolio of common stocks issued by large capitalization companies. The investment adviser for the Fund is Securian Asset Management, Inc. Delaware Investments Fund Advisers serves as investment sub-adviser to the Fund and provides investment advice under a sub-advisory agreement. The risks incurred by investing in the Fund include, but are not limited to, the risk of declines in the market for large cap stocks or in the equity markets generally.

Performance Update

The Fund generated a total net return of -27.15 percent over the 12 months ending December 31, 2022, outperforming the Russell 1000 Growth® Index which returned -29.14 percent over the same period.

What influenced the Fund's return during the past 12 months?

After solid gains of 38.5 percent and 27.6 percent respectively for 2020 and 2021, the Russell 1000 Growth® Index posted a sizeable drawdown of 29.1 percent for calendar year 2022. Despite this decline, it is important to keep things in perspective. Excluding a slight drop of 1.5 percent in 2018, this marks the first year of a significant negative return for the Fund's benchmark since the recession of 2008-2009.

While value styles shined during 2022, there were also moments of clarity wherein investors were drawn back to business quality—profitability, cash flow, and competitive advantage—as a necessary consideration. The market's hunt for the next "thematic" trade, whether that be a peak interest rates, lower inflation, or a Federal Reserve (the "Fed") policy pivot, was not a sustainable and repeatable investment strategy. It is not surprising that in a period when the relative growth of many "hyper-growth" companies disappointed, investors returned to a theme with lasting power—business quality.

What other market conditions or events influenced the Fund's performance during the past 12 months?

There were some key events that occurred in 2022 that will shape the outlook for the coming year. Particularly notable was the aggressive increase of interest rates by the Fed. The Fed raised rates 4.25 percent, starting at near zero in March 2022 and ending the year at 4.375 percent. Additionally, starting in June 2022 the Fed initiated quantitative tightening by reducing its balance sheet by $80 to $90 billion per month. The inversion of the yield curve provided support for those arguing a recession is on the horizon.

This aggressive policy response was necessary as inflation hit a four-decade high. While a portion of the sharp move higher in inflation was attributable to unique circumstances associated with the pandemic, such as supply disruptions and continued China COVID-19 lockdowns, the services component continued to remain elevated. Exiting the year, the Fed made it clear that it wants to address the "stable prices" portion of its dual mandate and that it, too, believes some amount of economic pain is required to get there.

Labor markets remained strong throughout the year. The unemployment rate remained at a 50-year low despite the Fed's tightening and clear signals of economic slowing. One clear signal of slowing was the move lower in manufacturing data with headline data hovering around contraction territory. Housing data weakened as activity was directly affected by the higher rates, which more than doubled from their lows, cratering affordability. The ripple effects from a slowdown in housing can easily turn into waves given its importance to the overall economy.

12

What strategies and techniques did you employ that specifically affected Fund performance?

From a sector perspective, strong stock selection in the consumer discretionary, information technology (IT) and communication services sectors were the largest contributors to the Fund's outperformance. Stock selection in the industrials and financials sectors, along with underweight positions in the energy and healthcare sectors, were the largest detractors to the Fund's performance.

The consumer discretionary sector was the largest contributor to the Fund's outperformance. Lack of exposure to Tesla Inc., accounted for most of the Fund's consumer discretionary contribution. We remain convicted in our view that economics in the auto industry will be competed away over time and Tesla is overpriced relative to its realizable future earnings. Additional positive contributors, but of lesser magnitude, included LVMH Moet Hennessy Louis Vuitton SE Unsponsored ADR and Ferrari NV.

Positive relative performance in the IT sector was helped by outperformance from the Funds overweight positions in Motorola Solutions Inc., Visa Inc., and VeriSign Inc. Each of these names provide critical components or services to their customers such that their businesses should be able to outperform in periods of economic weakness. These positive contributions were able to overwhelm negative stock contributions from PayPal Holdings Inc., Salesforce Inc., and NVIDIA Corp.

Within communications services sector, relative outperformance was driven by Electronic Arts Inc. Despite benefiting from the pandemic, Electronic Arts has been able to sustain growth due to subscription-like video game franchises. Lack of exposure to Netflix, Inc. and an underweight exposure to Meta Platforms, Inc. also drove the Fund's outperformance.

The relative underperformance within the industrials sector was driven by weakness in TransUnion and Stanley, Black & Decker Inc., along with a lack of exposure to a machinery stocks. TransUnion's weakness was related to the company's exposure to both mortgage activity and to fintech health. Stanley, Black & Decker struggled to forecast end-market demand and was also hit with input prices. Machinery stocks, such a Caterpillar Inc. (not owned), saw strong relative performance as investors favored relative value. Notable positive offsets to this industrials' headwind were relative strength from the Fund's overweight positions in CoStar Group Inc. and J.B. Hunt Transport Services Inc.

The energy sector was a negative contributor during the year as the Fund lacked exposure. Energy was driven by rising commodity prices related to unfortunate geopolitical events. We remain comfortable with our lack of exposure to these transitory trends.

What will affect the Fund going forward?

We are full of optimism that the current environment, while volatile, is extremely ripe for active stock picking to generate significant value. It is unlikely that we will return to a zero-rate environment and with that regime change comes a different set of standards. Higher valuation levels and access to capital will have to be earned through consistent growth, strong cash generation, strong profitability, and disciplined capital management. The days of free money and an "everyone wins" mentality is likely behind us.

We believe this regime change will highlight the importance of high-quality stock selection and the minimization, through a disciplined process, of behavioral mistakes. The likelihood of false positives, or mistakes, has already dramatically increased in the post-pandemic reopening euphoria and we believe this will likely continue to increase over the coming years. The tendency to favor growth as a way to validate quality will be exposed as a poor investment strategy resulting in a high degree of what we call "growth flame-outs" that can be associated with material disappointment.

Inflationary pressures are cooling, but they may prove to be more resilient. This is important because the persistence of inflation could keep the Fed involved longer, which we believe has negative ramifications on economic activity both for 2023 and likely for 2024. Risk assets (cyclicals and high growth) will periodically react

13

positively to the concept of a "Fed Pivot" wherein the central bank would slow or pause its rate hikes, thereby creating a bullish narrative. We believe these "risk-on" events will be difficult to sustain until expectations are reset materially lower and overly optimistic outlooks are extinguished.

Investors should favor these high-quality stocks through cycles, and especially in periods of downside volatility, as we believe quality-first investing is a superior long-term strategy for durable compounding. If downside volatility does not surface, we believe our portfolio of high-quality growth stocks will likewise shine as their "growthy" attributes will prove to be more sustainable, remain underappreciated and allow for strong upside participation.

Our conviction is high as we believe business quality is more persistent than growth, and through-the-cycle outperformance can be achieved through a disciplined stock selection process that prioritizes high-quality business models first and growth second.

14

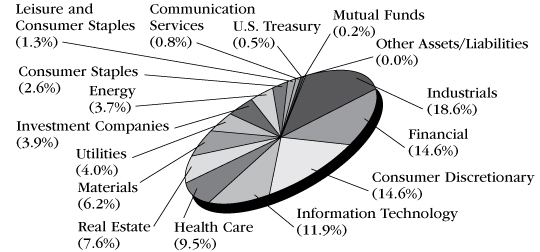

Ten Largest Holdings^

| Security description | | Market

value | | % of net

assets | |

Microsoft Corp. | | $ | 59,118,508 | | | | 12.4 | % | |

Apple, Inc. | | | 37,856,924 | | | | 7.9 | % | |

Visa, Inc. Class A | | | 28,353,423 | | | | 5.9 | % | |

Alphabet, Inc. Class A | | | 24,128,611 | | | | 5.0 | % | |

Motorola Solutions, Inc. | | | 23,366,050 | | | | 4.9 | % | |

VeriSign, Inc. | | | 22,922,584 | | | | 4.8 | % | |

Amazon.com, Inc. | | | 22,425,060 | | | | 4.7 | % | |

UnitedHealth Group, Inc. | | | 20,417,232 | | | | 4.3 | % | |

CoStar Group, Inc. | | | 20,280,745 | | | | 4.2 | % | |

Coca-Cola Co. | | | 16,081,499 | | | | 3.4 | % | |

| | $ | 274,950,636 | | | | 57.5 | % | |

^Excludes short-term investments.

Sector Diversification (shown as a percentage of net assets)

15

Comparison of Change in Investment Value*

A Hypothetical $10,000 Investment in SFT Delaware IvySM Growth Fund,

the Russell 1000 Growth® Index and Consumer Price Index (CPI)

On the chart above you can see how the SFT Delaware IvySM Growth Fund's shares total return compared to the Russell 1000 Growth® Index and the Consumer Price Index. The three lines represent the total return of a hypothetical $10,000 investment made on May 1, 2014 through December 31, 2022, assuming reinvestment of distributions, if any.

* The results shown are past performance and are not an indication of future performance. Current performance may be lower or higher. The investment returns and principal value of an investment will fluctuate so that shares upon redemption may be worth more or less than their original cost. Performance figures of the Fund do not reflect charges pursuant to the terms of the variable life insurance policies and variable annuity contracts funded by separate accounts that invest in the Fund's shares. When such charges are deducted, actual investment performance in a variable policy or contract will be lower.

The Russell 1000 Growth® Index is an unmanaged index that measures the performance of those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values. The index measures the performance of the 1,000 largest companies in the Russell 3000 Index, which measures the performance of the 3,000 largest U.S. companies based on total market capitalization.

'Ivy' is the registered service mark of Ivy Distributors, Inc., an affiliate of the Delaware Investments Fund Advisers, the Fund's sub-adviser.

16

SFT Delaware IvySM Small Cap Growth Fund

Timothy J. Miller, CFA, Kenneth G. McQuade, CFA Portfolio Managers

Delaware Investments Fund Advisers

Fund Objective

The SFT Delaware IvySM Small Cap Growth Fund seeks to provide growth of capital. The Fund pursues its objective by investing primarily in a diversified portfolio of common stocks issued by small capitalization companies. The investment adviser for the Fund is Securian Asset Management, Inc. Delaware Investments Fund Advisers serves as investment sub-adviser to the Fund and provides investment advice under a sub-advisory agreement. The risks incurred by investing in the Fund include, but are not limited to, the risk of declines in the market for small cap stocks or in the equity markets generally.

Performance Update

The Fund generated a total net return of -26.87 percent over the 12 months ending December 31, 2022, underperforming the Russell 2000 Growth® Index which returned -26.36 percent over the same period.

What influenced the Fund's return during the past 12 months?

For small-cap growth stocks, 2022 was the third-worst year of the past 25, eclipsed only by the global financial crisis of 2008-2009 and the 2002 "tech bubble." The double-whammy of rising interest rates, which hurt valuations, and the lingering pandemic-induced economic disruption, which dampened earnings estimates, was largely responsible. The 10-year Treasury yield, which had been in a downtrend since 2008, bottomed near zero and remained there for almost a year following the onset of the pandemic. In 2021, growth stocks thrived as the economy responded to significant fiscal and monetary stimulus. Earnings growth surged for most major sectors of the market. But that surprisingly strong growth led to significant shortages and supply-chain disruptions that fueled inflation and led to the conditions that stifled equity markets in 2022.

What other market conditions or events influenced the Fund's performance during the past 12 months?

Small-cap growth stocks had been a major beneficiary of the low interest rate, healthy economic environment and were thus vulnerable to rising rates. During 2022, the 10-year Treasury yield rose from 1.5 percent to 3.9 percent and the yield curve inverted midway through the year. High yield spreads rose more than 250 basis points by midyear signaling increased concern about a potential recession (a basis point equals one-hundredth of a percentage point). The combination crushed small-cap growth stocks by the end of the second quarter. A brief attempt at a late summer rally was thwarted over the balance of the year. The Russell 2000® Growth Index declined more than 26 percent for the year and lagged the Russell 2000® Value Index, which declined 16 percent. High-valuation, non-earning growth stocks were punished the most during the year. Energy was the only sector to generate a positive return. The worst-performing sectors were communication services, consumer discretionary, real estate, and information technology (IT).

What strategies and techniques did you employ that specifically affected Fund performance?

Throughout the fiscal year, the Fund consistently maintained its strategy of diversifying across sectors while emphasizing quality growth companies. The Fund performed ahead of the benchmark for most of the year before it succumbed to the relentless pressure on growth stocks. Those stocks that had outperformed most during the year were the last targets of the selloff. Energy stocks were a prime example. Although energy companies dramatically outperformed for the first 10 months of the year, beginning in mid-November, energy stocks sold off significantly in spite of a fundamental outlook that remains healthy. BJ's Wholesale Club Holdings Inc. was another example. A large position in the Fund, BJ's had been a strong performer throughout the year but fell under the pressure of the

17

market selloff—again, despite consistently good sales and earnings results. The Fund's attribution for the year shows that stock selection contributed positively in all sectors of the Fund except healthcare.

Sector allocation, or weighting, detracted in the IT sector, which was consistently overweight the benchmark during the fiscal period. The Fund's small underweight in the energy sector also detracted. The benchmark energy sector was up 41.9 percent for the year while the Fund gained 39.4 percent. A weighting of one percentage point below the benchmark was to blame.

The Fund's allocation to the healthcare sector detracted, primarily the result of poor stock selection. Several holdings that previously were strong performers drastically reversed course due to high valuations, underwhelming profitability, weakness in procedure volumes, and disappointing sales as potential customers were constrained by rising prices. The overall healthcare sector underperformed the broader index, a departure from typical down years. More specifically, small-cap healthcare did not perform like a defensive sector. The repercussions of COVID-19 on the healthcare system lasted well beyond expectations. Many companies with new products or services faced challenges getting in front of decision-makers, obtaining budget sign offs, or hiring personnel to accept, install, and implement new product platforms.

In many cases we felt the new product or service was superior and would gain traction in the marketplace, but that scenario was rarely realized. For example, Omnicell Inc. has a best-in-class solution for medication management that has successfully gained share in past years but hit a significant wall this period due to budget constraints and facilities' inability to implement new platforms while labor is scarce. As a result, previously consistent revenues and bookings dried up for several quarters and visibility was lost.

For the healthcare sector as a whole, we decided to maintain our positions in some companies where we felt sufficiently confident that competitive advantages remained compelling. In other instances, we exited our positions and moved on. We may renew those positions if and when sales visibility better matches our investment horizon. Through this environment, we maintained our long-term philosophy of owning names with novel offerings that make healthcare more efficient and value based.

The industrials sector contributed on both an absolute and relative basis during the period, benefiting from advantageous stock selection. Our neutral allocation also contributed slightly as the industrial sector outperformed the market as a whole. We had exposure to alternative energy, resource management, and electrification, which we think have plenty of demand and visibility going forward. Lesser exposure to housing-related names, such as building supplies, and areas only growing via cyclical inflation also aided performance. We maintained our process of searching for areas of the economy that have long-term growth potential rather than attempting to time cyclical stocks.

The consumer discretionary sector was the largest positive contributor for the year while the IT sector was a modest drag. Stock selection led the way in the consumer discretionary sector. Monarch Casino & Resort Inc., Texas Roadhouse Inc., and Visteon Corp. were all significant contributors. Other relative contributors (declining less than the Russell 2000 Growth® Index) included Churchill Downs Inc. and Marriott Vacations Worldwide Corp. Pent-up demand for experiences, both travel and dining, helped drive success for these companies.

The IT sector has historically been a large driver of outperformance for the Fund and we expect it will continue to be the most-favored sector from a fundamental growth perspective. That said, the sector corrected last year, reflecting the macro factors mentioned above. We reduced our large overweight versus the index throughout the year as we exited less-seasoned companies in favor of a higher quality, profitable group of stocks. The result was performance for the year that essentially matched the benchmark, with the drag from an overweight offset by modestly positive stock selection. The Fund also benefited from several take-outs as private equity firms took advantage of lower stock prices to make strategic acquisitions. Sailpoint Technologies Holdings Inc., ForgeRock Inc., and Switch Inc. were among the companies acquired.

What will affect the Fund going forward?

At the end of the Fund's fiscal year, we see no need to change its strategic positioning as we navigate through the headwind of interest rate hikes and their impact on the economy. Clearly a lot of damage has been done to small-cap stock valuations, obviating the need to be overly defensive. The Fund's emphasis on high-quality, sustainable-growth businesses across all major sectors of the market has worked well in the small-cap growth asset class and remains the focus of the Fund.

18

Ten Largest Holdings^

| Security description | | Market

value | | % of stock

portfolio | |

BJ's Wholesale Club Holdings, Inc. | | $ | 3,992,756 | | | | 2.8 | % | |

Allegro MicroSystems, Inc. | | | 3,852,917 | | | | 2.7 | % | |

Visteon Corp. | | | 3,284,618 | | | | 2.3 | % | |

Red Rock Resorts, Inc. Class A | | | 3,243,291 | | | | 2.3 | % | |

Marriott Vacations Worldwide Corp. | | | 3,145,637 | | | | 2.2 | % | |

Kinsale Capital Group, Inc. | | | 2,988,912 | | | | 2.1 | % | |

Cactus, Inc. Class A | | | 2,977,503 | | | | 2.1 | % | |

Paycor HCM, Inc. | | | 2,829,270 | | | | 2.0 | % | |

Inmode Ltd. | | | 2,754,077 | | | | 2.0 | % | |

Texas Roadhouse, Inc. | | | 2,748,509 | | | | 2.0 | % | |

| | $ | 31,817,490 | | | | 22.5 | % | |

^Excludes short-term investments.

Sector Diversification (shown as a percentage of net assets)

19

Comparison of Change in Investment Value*

A Hypothetical $10,000 Investment in SFT Delaware IvySM Small Cap Growth Fund,

the Russell 2000 Growth® Index and Consumer Price Index (CPI)

On the chart above you can see how the SFT Delaware IvySM Small Cap Growth Fund's shares total return compared to the Russell 2000 Growth® Index and the Consumer Price Index. The three lines represent the total return of a hypothetical $10,000 investment made on May 1, 2014 through December 31, 2022, assuming reinvestment of distributions, if any.

* The results shown are past performance and are not an indication of future performance. Current performance may be lower or higher. The investment returns and principal value of an investment will fluctuate so that shares upon redemption may be worth more or less than their original cost. Performance figures of the Fund do not reflect charges pursuant to the terms of the variable life insurance policies and variable annuity contracts funded by separate accounts that invest in the Fund's shares. When such charges are deducted, actual investment performance in a variable policy or contract will be lower.

The Russell 2000 Growth® Index is an unmanaged index of those Russell 2000 Index growth companies with higher price-to-book ratios and higher forecasted growth values. The index is broad-based, comprised of 2,000 of the smallest U.S.-domiciled company common stocks based on total market capitalization.

'Ivy' is the registered service mark of Ivy Distributors, Inc., an affiliate of the Delaware Investments Fund Advisers, the Fund's sub-adviser.

20

SFT Equity Stabilization Fund

Jeremy Gogos, Ph.D., CFA, Merlin Erickson

Portfolio Managers

Securian Asset Management

Fund Objective

The SFT Equity Stabilization Fund seeks to maximize risk-adjusted total return relative to its blended benchmark index comprised of 60 percent S&P 500® Low Volatility Index, 20 percent S&P 500® BMI International Developed Low Volatility Index and 20 percent Bloomberg U.S. 3-Month Treasury Bellwether Index (collectively, the "Blended Benchmark Index"). The SFT Equity Stabilization Fund invests at least 80 percent of its assets in equity securities. Equity securities include those that are equity based, such as ETFs that invest primarily in U.S. and foreign equity securities. The Fund is subject to risks associated with such investments as described in detail in the Fund's prospectus. The net asset value of the Fund will fluctuate and is not guaranteed. It is possible to lose money by investing in the Fund. There is no assurance that efforts to manage Fund volatility will achieve the desired results.

Performance Update

The Fund generated a total net return of -9.71 percent over the 12 months ending December 31, 2022, underperforming the Blended Benchmark Index which returned -4.59 percent over the same period.

What influenced the Fund's return during the past 12 months?

Equity volatility is what guides the asset allocation of the Fund's strategy. When equity volatility is low, the equity exposure of the Fund's strategy will be high. Conversely, when equity volatility is high, the equity exposure of the Fund's strategy will be low.

In 2022, the markets saw some of the worst risk asset performance in recent memory, and the losses were not concentrated in a single asset class; essentially every major asset class delivered deeply negative performance in 2022. For example, the S&P 500® returned -18.11 percent for 2022, and the Bloomberg US Credit Index returned -15.76 percent. Commodities were a lone bright spot in an otherwise challenging year, as the Bloomberg Commodity Index closed out 2022 up 13.75 percent.

In our view, the primary driver of 2022's awful risk asset performance was the monetary policy tightening happening in concert around the globe. We will further discuss this topic shortly. For now, suffice to say that we view the 2022 S&P 500® return of -18.11 percent, and realized volatility of 24.17 percent—an 85th percentile value—as direct consequences of the aggressive monetary tightening the Federal Reserve (the "Fed") pursued in response to the severe inflation backdrop of late 2021 and early 2022.

Elevated volatility wasn't confined to equity. Rates and spreads also saw outsized moves through all of 2022. The 10-year U.S. Treasury yield, investment grade spreads, and high yield spreads all saw volatility in 2022 that ranked in the 82nd to 83rd percentile historically.

Realized 20-day S&P 500® volatility saw a minimum of 13.29 percent, and a maximum of 34.87 percent, over the course of the year. Similarly, the Chicago Board Options Exchange (CBOE) Volatility Index (VIX) varied from a minimum of 16.60, to a maximum of 36.45, over the course of 2022. Its average value for the year was 25.62. Given this rather elevated volatility, the Fund equity exposure ranged from a minimum of 51.01 percent to a maximum of 92.92 percent, and averaged 70.78 percent for the year. This equity underweight was a key driver of performance for the Fund this past year. Style allocation within equity also drove performance through the Fund's low volatility and dividend-focused equity.

21

What other market conditions or events influenced the Fund's performance during the past 12 months?

In 2022, the markets saw the correlation between the S&P 500® and the 10-year U.S. Treasury go deeply negative again. This correlation closed out 2022 at -0.45. As we have highlighted previously, the idea of fixed income being a portfolio bulwark against equity losses relies on this correlation being positive. That is, as equity prices decrease, bond prices rise, offsetting the equity decline. The prevailing inflation backdrop through all of 2022, and the market expectations for central bank action that that backdrop created, caused equity and fixed income assts to move in tandem for most of 2022. Thus, the canonical 60/40 portfolio saw its second-worst year ever (-15.56 percent) in the available daily history of the S&P Total Return and Bloomberg Aggregate indexes. For reference, 2008 saw a -20.91 percent return on the same portfolio.

The "growth over value" trade largely unwound over the course of 2022. The high-flying tech-focused names that powered the absurd COVID-19 equity rally of 2020-2021, and which ended up accounting for a wildly outsized portion of the S&P 500® market capitalization, saw extreme pullbacks in 2022. For example, Meta lost -64.22 percent, Tesla lost -65.03 percent, and Amazon lost -49.62 percent.

In short, 2022 exemplified the type of market regime we have repeatedly cautioned against, namely one in which investors need portfolio protection approaches beyond a fixed income allocation to mitigate losses.

What strategies and techniques did you employ that specifically affected Fund performance?

Throughout the year, the Fund held a core long position in domestic and international minimum volatility and dividend-focused cash equity. In addition, the Fund had long and short positions in S&P 500® futures, long and short S&P 500® put options, long and short S&P 500® call options, long and short Chicago Board Options Exchange (CBOE) Volatility Index (VIX) call options, and long and short VIX put options. These derivative positions were held either as expressions of the target equity allocation of the Fund given prevailing volatility, or as supplemental hedges for managing the Fund's risk.

What will affect the Fund going forward?

By multiple measures, inflation continued to be a serious economic and political problem through all of 2022. Consumer Price Index (CPI) peaked at 9.1 percent year-over-year on June 30, 2022, and Personal Consumption Expenditures (PCE) printed a 5.20 percent year-over-year change on September 30, 2022. While these inflation metrics, along with market inflation expectations, have been on a downward trajectory to close out the year, every inflation metric is still well above the Fed's stated 2.0 percent target. As a result, the Fed hiked its policy rate from zero to begin 2022, to 4.25 percent at the end of the year. The Fed Funds rate hasn't increased by more than 4 percent in a one-year period since 1981, when the Fed was contending with inflation of nearly 15 percent year-over-year, and its policy rate was north of 10 percent.

For numerous years, we have been bearish on equities. We viewed easy monetary policy as having distorted valuations across multiple asset classes, and we felt that investors were often foolheartedly latching onto growth narratives to rationalize buying indefensibly overpriced stock. Perhaps ironically, in a year where we view a recession as likely, we are more bullish on equity than we have been for quite some time.

First, let us address the notion of a potential recession. The 10-year to 3-month yield curve was inverted from November 8, 2022 through year-end, and hit a minimum of -85 basis points on December 7, 2022. As many market commentators note, this yield curve anomaly highlights overly aggressive monetary policy moves, and it has happened leading up to every recession in modern history. Based on this data point alone, we would expect a recession within the next 12-24 months. Further, it is worth reiterating that gross domestic product (GDP) printed negative growth in Q1 and Q2 of 2022.

We think signals from the consumer sector also suggest a slowing economy. Consumers have been saving a smaller fraction of their disposable income than ever, and credit card utilization has now reached pre-pandemic levels. Both trajectories are unsustainable. We interpret both of these data points as suggesting a material decrease in consumer demand as 2023 unfolds. When you combine these consumer metrics with rates market data that suggests the Fed has hiked its policy rate to an unsustainable level, we see a 2023 recession as a strong possibility.

22

Perhaps ironically, we view the somewhat grim macroeconomic picture as a potential tailwind for equities. Recent equity market responses to "easier" monetary policy suggest that any pivot in Fed policy will be enthusiastically received by risk markets. Further, in the asset rout of 2022, fundamental equity valuation metrics have reverted to more reasonable levels.

We also view recent geopolitical developments as supportive of a bullish equity view. First, while the response of Western nations has not been perfectly harmonious, our European allies have largely found ways to survive without Russian natural gas, and the Ukrainian resistance has proved a very formidable adversary for Russia's bumbling invasion force. As such, the potential impacts of Russian natural gas and oil supply shortages likely have fewer global economic knock-on effects than originally anticipated. Another key geopolitical development in late 2022 is that China abandoned its zero-COVID policy. The implementation of this policy change is taking an enormous human toll on the Chinese population, and we do not want to marginalize that tragedy. But, if we endeavor to keep our focus on economic issues, we anticipate that supply chain disruption will decrease materially once China's working population weathers this current COVID-19 wave that their government left them woefully unprepared for.

To summarize, we anticipate that the Fed is very close to the end of its tightening campaign. By extension, we think volatility will come down modestly from 2022 levels as 2023 unfolds. And, perhaps most importantly, we anticipate that a 2023 recession will give the Fed the justification it needs to pivot to monetary easing. Should this pivot come to pass, we think a broad risk asset rally is likely.

In a tactical sense, we will continue to use our volatility metrics to inform the equity allocation of the Fund. We will increase equity exposure if we believe volatility will decrease, and decrease equity exposure if we believe volatility will increase. Given our more bullish view of equity returns for the near future, we will maintain the Fund's equity exposure toward the upper end of its allowed range while keeping downside hedge positions in place.

23

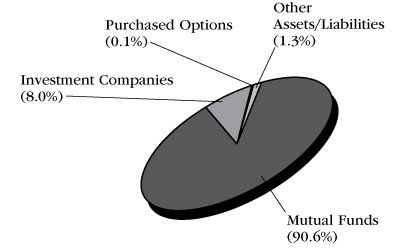

Ten Largest Holdings^

| Security description | | Market

value | | % of market

value | |

iShares Edge MSCI Minimum Volatility USA ETF | | $ | 105,101,035 | | | | 32.0 | % | |

iShares Edge MSCI Minimum Volatility EAFE ETF | | | 79,735,463 | | | | 24.3 | % | |

iShares Core High Dividend ETF | | | 59,510,825 | | | | 18.1 | % | |

iShares Edge MSCI Minimum Volatility Emerging Markets ETF | | | 21,385,516 | | | | 6.5 | % | |

iShares MSCI Germany ETF | | | 16,326,301 | | | | 5.0 | % | |

BlackRock Short Maturity Bond ETF | | | 15,698,407 | | | | 4.7 | % | |

| | $ | 297,757,547 | | | | 90.6 | % | |

^Excludes short-term investments.

Sector Diversification (shown as a percentage of net assets)

24

Comparison of Change in Investment Value*

A Hypothetical $10,000 Investment in SFT Equity Stabilization Fund,

the Blended Benchmark Index and Consumer Price Index (CPI)

On the chart above you can see how the SFT Equity Stabilization Fund's shares total return compared to its Blended Benchmark Index, comprised of 60 percent of the S&P 500® Low Volatility Index, 20% S&P 500® BMI International Developed Low Volatility Index and 20% Bloomberg U.S. 3-Month Treasury Bellwether Index and the Consumer Price Index. The three lines represent the total return of a hypothetical $10,000 investment made on November 18, 2015 through December 31, 2022, assuming reinvestment of distributions, if any.

* The results shown are past performance and are not an indication of future performance. Current performance may be lower or higher. The investment returns and principal value of an investment will fluctuate so that shares upon redemption may be worth more or less than their original cost. Performance figures of the Fund do not reflect charges pursuant to the terms of the variable life insurance policies and variable annuity contracts funded by separate accounts that invest in the Fund's shares. When such charges are deducted, actual investment performance in a variable policy or contract will be lower.

Securian Asset Management, Inc. ("Securian AM") and Securian Funds Trust, on behalf of the SFT Equity Stabilization Fund (the "Fund"), have entered into an Expense Limitation Agreement, dated November 18, 2015, which limits the operating expenses of the Fund, excluding certain expenses (such as interest expense, acquired fund fees, cash overdraft fees, taxes, brokerage commissions, other expenditures which are capitalized in accordance with the generally accepted accounting principles, and other extraordinary expenses not incurred in the ordinary course of the Fund's business), to 0.80% of the Fund's average daily net assets through April 30, 2021. The Expense Limitation Agreement was terminated on May 1, 2021. The Fund is authorized to reimburse Securian AM for management fees previously waived and/or for the cost of expenses previously paid by Securian AM pursuant to this agreement, provided that such reimbursement will not cause the Fund to exceed any limits in effect at the time of such reimbursement. The Fund's ability to reimburse Securian AM in this manner only applies to fees waived or reimbursements made by Securian AM within the three fiscal years prior to the date of such reimbursement. To the extent that the Fund makes such reimbursements to Securian AM, the amount of the reimbursements will be reflected in the financial statements in the Fund's shareholder reports and in Other Expenses under Fees and Expenses of the Fund.

The Blended Benchmark Index is comprised of 60 percent of the S&P 500® Low Volatility Index, 20% S&P 500® BMI International Developed Low Volatility Index and 20% Bloomberg U.S. 3-Month Treasury Bellwether Index.

The S&P 500® Low Volatility Index measures performance of the 100 least volatile stocks in the S&P 500®. The S&P 500® BMI International Developed Low Volatility Index measures the performance of the 200 least volatile stocks in the S&P Developed Market large/midcap universe. Constituents are weighted relative to the inverse of their corresponding volatility, with the least volatile stocks receiving the highest weights. The Bloomberg U.S. 3-Month Treasury Bellwether Index tracks the market for the on-the-run 3-month Treasury bill issued by the U.S. government.

25

SFT Government Money Market Fund

Lena Harhaj, CFA, Katie Brisson

Portfolio Managers

Securian Asset Management

Fund Objective

The SFT Government Money Market Fund seeks maximum current income to the extent consistent with liquidity and the preservation of capital. The Fund invests at least 99.5 percent of its total assets in cash, government securities, and/or repurchase agreements that are collateralized fully (i.e., collateralized by cash or government securities). Investment in the SFT Government Money Market Fund is neither insured nor guaranteed by the U.S. Government, and there can be no assurance that the Fund will be able to maintain a stable net asset value of $1.00 per share. It is possible to lose money by investing in the Fund.

Performance Update

The Fund generated a total net return of 1.12 percent over the 12 months ending December 31, 2022; the 3-month U.S. Treasury Bill returned 1.51 percent over the same period.

What influenced the Fund's return during the past 12 months?

Money market funds in general outperformed stock and bond investments during the last year. Rates increased across the entire U.S. Treasury curve during an active Federal Reserve (the "Fed") hiking cycle. The Federal Open Market Committee voted to increase rates in 7 of the 8 meetings for a total of 425 basis points.

What other market conditions or events influenced the Fund's performance during the past 12 months?

Rates on the short end of the U.S. Treasury curve increased approximately 400-450 basis points, while the longer dated tenors ranged 200-325 basis points.

What strategies and techniques did you employ that specifically affected Fund performance?

The Fund continues to pick up incremental yield versus U.S. Treasury Bills by purchasing short-dated Agency Discount Notes.

What will affect the Fund going forward?

As the Fed finishes it's hiking cycle, short term rates will have settled to levels not seen since 2007. The yield curve remains inverted from 6-months to 10-year tenors and is therefore not incentivizing any duration extension in the broad fixed income market. The supply and demand of money market instruments, and in particular the gap, will impact yields in short-dated U.S. Treasury bills to the extent that they trade through reverse repo rates.

26

The results shown are past performance and are not an indication of future performance. Current performance may be lower or higher. The investment returns and principal value of an investment will fluctuate so that shares upon redemption may be worth more or less than their original cost. Investment in the SFT Government Money Market Fund is neither insured nor guaranteed by the U.S. Government or any other agency, and there can be no assurance that the Fund will be able to maintain a stable net asset value of $1.00 per share. Shares upon redemption may be worth more or less than their original cost.

Performance figures of the Fund do not reflect charges pursuant to the terms of the variable life insurance policies and variable annuity contracts funded by separate accounts that invest in the Fund's shares. When such charges are deducted, actual investment performance in a variable policy or contract will be lower.

The Bloomberg U.S. Treasury Bill 1-3 Month Index is a market value-weighted index of investment-grade fixed-rate public obligations of the U.S. Treasury with maturities of three months, excluding zero coupons.

Effective May 1, 2012, the Board of Trustees of Securian Funds Trust (the "Trust") approved a Restated Net Investment Income Maintenance Agreement among the Trust (on behalf of the Fund), Securian Asset Management, Inc. ("Securian AM") and Securian Financial Services, Inc. ("Securian Financial"). A similar agreement was previously approved by the Board of Directors of Advantus Series Fund, Inc., the Trust's predecessor, effective October 29, 2009. Under such Agreement, Securian AM agrees to waive, reimburse or pay the Fund's expenses so that the Fund's daily net investment income does not fall below zero. Securian Financial may also waive its Rule 12b-1 fees. Securian AM and Securian Financial each has the option under the Agreement to recover the full amount waived, reimbursed or paid (the "Expense Waiver") on any day on which the Fund's net investment income exceeds zero. On any day, however, the Expense Waiver does not constitute an obligation of the Fund unless Securian AM or Securian Financial has expressly exercised its right to recover a specified portion of the Expense Waiver on that day, in which case such specified portion is then due and payable by the Fund. In addition, the right of Securian AM and/or Securian Financial to recover the Expense Waiver is subject to the following limitations: (1) if a repayment of the Expense Waiver by the Fund would cause the Fund's net investment income to fall below zero, such repayment is deferred until a date when repayment would not cause the Fund's net investment income to fall below zero; (2) the right to recover any portion of the Expense Waiver expires three years after the effective date of that portion of the Expense Waiver; and (3) any repayment of the Expense Waiver by the Fund cannot cause the Fund's expense ratio to exceed 1.25%. If Securian AM and Securian Financial exercise their rights to be paid such waived amounts, the Fund's future yield will be negatively affected for an indefinite period. The Agreement is effective through April 30, 2023, and shall continue in effect thereafter, provided such continuance is specifically approved by Securian AM, Securian Financial, and a majority of the Trust's independent Trustees.