UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04323

Natixis Funds Trust I

(Exact name of Registrant as specified in charter)

888 Boylston Street, Suite 800, Boston, Massachusetts 02199-8197

(Address of principal executive offices) (Zip code)

Natalie Wagner, Esq.

Natixis Distribution, LLC

888 Boylston Street, Suite 800

Boston, Massachusetts 02199-8197

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 449-2810

Date of fiscal year end: December 31

Date of reporting period: December 31, 2021

Item 1. Reports to Stockholders.

| (a) | The Registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows: |

Annual Report

December 31, 2021

Loomis Sayles International Growth Fund

Natixis Oakmark Fund

Natixis Oakmark International Fund

Natixis U.S. Equity Opportunities Fund

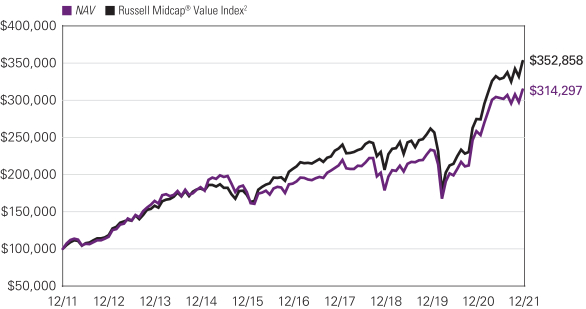

Vaughan Nelson Mid Cap Fund

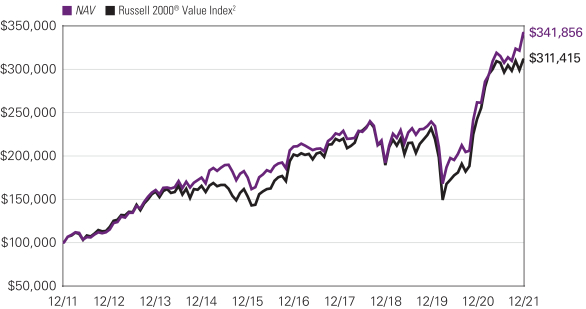

Vaughan Nelson Small Cap Value Fund

Table of Contents

LOOMIS SAYLES INTERNATIONAL GROWTH FUND

| | | | |

| | |

| Manager | | Symbols | | |

| | |

| Aziz V. Hamzaogullari, CFA® | | Class A | | LIGGX |

| | |

| Loomis, Sayles & Company, L.P. | | Class C | | LIGCX |

| | |

| | Class N | | LIGNX |

| | |

| | Class Y | | LIGYX |

Investment Goal

The Fund’s investment goal is long-term growth of capital.

Market Conditions

International equities posted mixed results in 2021. The developed markets performed reasonably well, as investors reacted positively to rising vaccination rates and improving economic growth. In addition, world central banks maintained highly stimulative monetary policies for the majority of the year. Europe led the way, with notable strength for Switzerland, the UK and the oil-sensitive Nordic countries. Canada, which also has an above-average weighting in energy stocks, was another top performer for the year. However, Japan and other Asian markets lagged on a relative basis.

International equities trailed the US market for the fourth consecutive year, largely as a result of the lower representation of technology stocks outside of the US. The weakness in foreign currencies relative to the US dollar also took a sizable bite out of the developed markets’ returns for US-based investors in 2021.

Despite the positive showing for stocks elsewhere in the world, the emerging markets experienced a challenging year and finished with a loss. Improving global growth and higher commodity prices were tailwinds for the asset class, but these factors were outweighed by the prospect of rising US interest rates and strength in the US dollar. The slower vaccination rollout in many emerging countries was a further impediment to returns. China, which lagged considerably due to the combination of slowing growth, increased regulation and disruptions in the nation’s property market, was a key driver of the category’s underperformance.

Portfolio Results

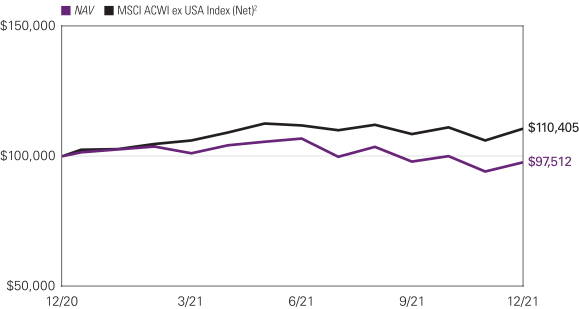

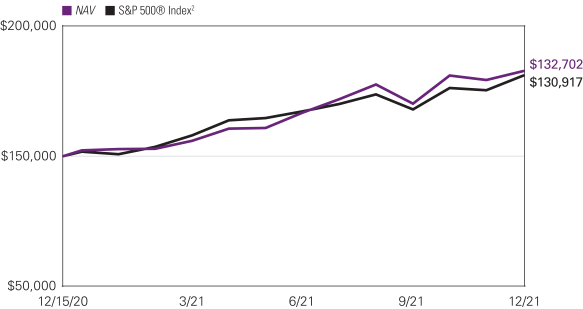

For the 12 months ended December 31, 2021, Class Y shares of the Loomis Sayles International Growth Fund returned -3.81% at net asset value. The Fund underperformed its benchmark, the MSCI All Country World Index ex USA Index (Net), which returned 7.82%.

Explanation of Fund Performance

We are an active manager with a long-term, private equity approach to investing. Through our proprietary bottom-up research framework, we look to invest in those few high-quality businesses with sustainable competitive advantages and profitable growth when they trade at a significant discount to intrinsic value. Given the rare confluence of quality, growth, and valuation, we may study dozens of companies but may only invest in a select few businesses each year. We believe identifying those few businesses with these characteristics is an art, not a science. As a result of this rigorous approach, ours is a selective, high-conviction portfolio of typically 30–45 names.

The Fund’s positions in Alibaba, Vipshop, and Tencent detracted the most from performance. Stock selection in the consumer discretionary, communication services, consumer staples, and energy sectors, as well as our allocations in the consumer discretionary, energy, communication services, consumer staples, industrials, and healthcare sectors detracted from relative performance.

A Fund holding since inception, Alibaba Group is a leading China e-commerce and consumer-engagement platform provider. With approximately 60% of China’s e-commerce transactions estimated to take place through its marketplaces, Alibaba is the world’s largest retail platform, and we believe Alibaba’s scale and interconnected sites create an unparalleled and difficult-to-replicate business ecosystem. Shares have been under pressure since late 2020 due to investor concern regarding increasing regulatory intervention by the Chinese government. In April, China’s State Administration for Market Regulation (SAMR) concluded that Alibaba’s practices had violated antitrust law. The company was fined approximately $2.8 billion and ordered to carry out “comprehensive” self-inspections to standardize business practices and ensure compliance with anti-monopoly laws. Alibaba cooperated fully with the investigation and has changed certain business practices. In August, China passed the Personal Information Protection Law (PIPL), which is focused on protecting personal information rights and interests by standardizing the handling and usage of personal information by businesses. We believe the focus of PIPL is similar to the General Data Protection Regulation (GDPR), which went into effect in the European Union in 2018. The GDPR impacted companies we own in other portfolios such as Alphabet and Facebook, which incurred increased compliance costs and other disruptions as they adjusted certain business practices to comply with the new regulations. However, both companies continued to generate strong growth in revenue and free cash flow due to their competitive advantages and strong value

1 |

propositions. While we expected that Alibaba would experience short-term disruptions as it modified its practices to fully comply with new regulatory changes, we did not believe the changes would ultimately impair the company’s difficult-to-replicate competitive advantages. More recently, we have observed increasing competitive pressure in two of the company’s smaller but faster-growing contributors: video streaming and penetration in lower-tier cities. Through the company’s Taobao Live, Alibaba offers a leading live-streaming social commercial platform, enabling merchants to interact with consumers. The relatively new medium has become a fast-growing vehicle for e-commerce sales, growing from less than 5% of China e-commerce two years earlier to almost 10% in 2020. While Alibaba continues to have a leadership position in live streaming and short video production, we have seen increased competition and market share gains from companies such as Douyin (China’s version of TikTok, owned by ByteDance) and Kuaishou. We expect this newer format will grow to represent approximately 25% of e-commerce sales over time. And while we expect Alibaba to remain a leader, we expect growing competition to take an increasing share of this fast-growing market over time. Growing competitive intensity has also impacted our assessment of Alibaba’s ongoing penetration of lower-tier cities. As internet access in lower-tier cities approaches that of higher-tier cities, we expect growth in e-commerce to be approximately twice that of overall China e-commerce growth. We believe Alibaba maintains leading market share in lower-tier cities, but is likely to face heightened competition from companies such as Pinduoduo, JD.com, and Meituan. We have long assumed that Alibaba’s disproportionate share of China e-commerce would decline, from over 80% at the time of our initial analysis in 2013, to a level closer to 50% of a still-growing market. While the company remains the dominant e-commerce platform in China, we estimate that a meaningful percentage of the company’s incremental growth in the most-recently reported quarter was from these markets where we are seeing signs of heightened competitive intensity. As a function of newer market entrants, faster growth from newer formats of e-commerce and lower-tier cities, and recent regulatory changes, we now expect the company’s market share to normalize at a lower level than we previously expected. While our ongoing analysis has lowered our assessment of intrinsic value for the company, it has not changed our assessment that Alibaba is a high-quality company that remains well positioned to benefit from secular growth in China e-commerce over our long-term investment horizon. We continue to believe that Alibaba trades at a discount to intrinsic value and offers asymmetric reward-to-risk. However, given our most recent analysis, it no longer justified the same degree of capital allocation relative to other opportunities, and we decreased our position size during the period.

Vipshop is a specialty internet retailer focused on off-season, off-price apparel and fashion items which it sells via flash sales. Founded in 2008 with the vision of introducing high-quality, branded fashion merchandise to the China market at value prices, the company is by far the largest flash retailer in China, and the largest player in the off-season, off-price category. In 2020, the company generated over $15 billion in net revenues across its core categories, and today the company is the 5th largest overall retailer in China. We believe that Vipshop creates a strong value proposition for both end customers and vendors alike, which in turn creates a strong network effect that has been difficult to replicate even by the largest e-commerce companies in China. A holding in the strategy since inception, Vipshop’s revenue growth decelerated throughout 2021, but still grew 27% year-over-year through the first three quarters, compared with an estimated 18.5% for total China e-commerce and 21% for the apparel and accessories category, indicating that the company continued to grow market share. The company provided guidance for lower-than-expected revenue growth in the fourth quarter, driven by a deterioration in China’s economic environment and weakening consumer sentiment. Shares have been under pressure throughout the year, first from the forced liquidation of Archegos Capital Management, which had Vipshop among its holdings, then from investor concern regarding increasing regulatory intervention by the Chinese government, and most recently from a slowdown in consumer demand in China. We believe that Vipshop remains a high-quality business benefiting from competitive advantages of brand, scale, and a positive network effect that should enable it to expand its market share as the leading discount branded apparel retailer in China. Further, management believes that the new regulatory restrictions on anti-competitive actions, such as merchant exclusivity provisions, will now enable merchants who were previously unable to sell through Vipshop to use its platform — further expanding its network. While the Covid-19 outbreak and resulting economic weakness have pressured growth over the past year, especially in the company’s smaller physical retail footprint, we believe the company’s reported growth rates reflect the resilience of the business, and that Vipshop will continue to benefit from structural growth in China e-commerce where it has a strong and defensible position in the off-season, off-price niche in which it competes. We believe the current market price embeds expectations for free cash flow growth that are well below our long-term assumptions. With its shares trading at a significant discount to our estimate of intrinsic value, we believe Vipshop offers a compelling reward-to-risk opportunity. We added to our position during the period.

Tencent Holdings is one of the largest internet services companies in China and globally, offering a wide array of value-added services that span social networking and communication, gaming, media and entertainment, and e-commerce and local services. The company also offers online advertising, cloud services, fintech solutions that include payment and wealth management offerings, and has investments in other related businesses. Founded in 1998, the company’s mission is to improve the quality of human life through internet services, and through its platform and ecosystem the company has become a leader in most segments of the internet industry in China. A Fund holding since inception, Tencent reported financial results during the period that were fundamentally solid but mixed with respect to consensus expectations, and growth decelerated due in part to macro and regulatory headwinds. Shares have been under pressure throughout the year due to investor concern regarding increased regulatory intervention by the Chinese government in a growing number of industries, including the internet, fintech, education, and gaming. In July, China’s SAMR fined

| 2

LOOMIS SAYLES INTERNATIONAL GROWTH FUND

the company $1.5 billion for practices within its streaming music business. The fine represented a small portion of the approximately $40 billion of cash on Tencent’s balance sheet. In fintech, we believe regulatory changes are likely to result in increased licensing requirements and guidelines around consumer and micro lending, information sharing, and disclosures, all of which are focused on reducing systematic risk and promoting healthy market development. We believe Tencent is generally compliant with most of the proposed changes, and we do not expect these developments to impact its competitive position. Most recently, China implemented restrictions on the amount of time minors can spend playing online games. Tencent management has embraced the new regulatory framework and highlighted the tools and restrictions it has introduced over the past several years to enable parents to manage minors’ gaming activity and limit both time spent and spending levels – in addition to announcing further restrictions. While gaming represents the company’s single largest source of revenue, approximately 40% of revenue in 2020, we believe the potential impact to the company is small as children under 16 accounted for less than 3% of the company’s gaming revenues. We do not believe that the fine or any of the proposed regulations materially impact Tencent’s strong and sustainable competitive advantages, which include its massive network and ecosystem, distribution, scale, and brand. We believe Tencent is one of the best-positioned companies in the China internet services industry. We believe the near-term uncertainty regarding the regulatory environment does not change the long-term fundamentals; as a leading consumer platform provider, we believe the structural expansion of internet users in China will position Tencent to benefit from multiple growth drivers including gaming, media, advertising, payments, and cloud-computing growth. We believe Tencent’s strong growth prospects are not currently reflected in its share price. As a result, we believe the company’s shares are trading at a significant discount to our estimate of intrinsic value, offering a compelling reward-to-risk opportunity.

The Fund’s positions in Wisetech Global, Novo Nordisk, and Roche contributed the most to performance. Stock selection in the information technology, healthcare, and industrials sectors, along with our allocation in the information technology sector, contributed positively to relative performance.

Wisetech Global is the leading software solutions provider to the global logistics industry. Founded in 1994 to provide freight-forwarding and customs software to the Australian logistics industry, Wisetech solutions are used in whole or in part by over 85% of the world’s 50 largest third-party logistics providers (3PLs) and all of the 25 largest freight forwarders, led by the company’s primary SAAS (software-as-a-service) platform, CargoWise One (CW1). From a single unified platform the company offers function-specific and enterprise-wide modules that support the complex international movement of goods and create substantial efficiencies for its logistics clients. The company’s vision is to become the world’s operating system for global logistics. A holding since Fund inception, Wisetech’s most-recently reported financial results, for its fiscal year ending June 2021, exceeded consensus expectations for revenue, EBITDA (earnings before interest, taxes, depreciation, and amortization), and EPS, and the company provided strong revenue and margin guidance for the current fiscal year. Total revenues increased 18% over the prior-year period and included 12% year-over-year revenue growth from the company’s existing customers, with every calendar-year cohort of new clients showing growth over the prior year, continuing a multi-year trend. The company also had a very successful year signing large new forwarders to its CW1 platform with six wins during the period, and now has 10 of the top 25 that have rolled out CW1 as their global platform or are in the process of doing so. We believe Wisetech benefits from strong and sustainable competitive advantages that include an installed client base with high switching costs, its freight-forwarding industry expertise, significant investments in research and development (R&D), its brand, and network. We believe Wisetech will benefit from secular growth in logistics software and services as companies increasingly move towards outsourcing and away from less effective in-house solutions. With virtually no comparable off-the-shelf competition to its unified global platform, Wisetech is the dominant market share leader in its legacy freight-forwarding market, which still represents only a mid-single-digit share of the overall global logistics and transportation market spending on supply chain management solutions. Through underlying industry growth, continued market share gains in its legacy freight-forwarding market, and ongoing penetration of other parts of the logistics industry performed by 3PLs, including warehouse management, land transportation, and cargo handling, we believe the company can generate compounded annual revenue growth in the high teens over our long-term investment horizon, with faster growth in operating profits and free cash flow as the company benefits from scale and operating leverage. We believe the expectations embedded in Wisetech’s share price continue to underestimate the company’s superior positioning and the sustainability of its growth. As a result, we believe the shares trade at a meaningful discount to our estimate of intrinsic value and represent an attractive reward-to-risk opportunity.

Headquartered in Denmark, Novo Nordisk is a global healthcare company with nearly 100 years of innovation and leadership in diabetes care. Over this time, Novo has amassed unparalleled experience in the biology of diabetes, expertise in protein science, and developed significant competitive advantages as a result. Its diabetes products have captured approximately one-third of the global branded diabetes care market and account for about 80% of the company’s annual revenues. In its biopharmaceutical business segment, which represents almost 15% of annual revenues, Novo Nordisk has leading positions within hemophilia care, growth hormone therapy, and hormone replacement therapy. We believe Novo’s strong and sustainable advantages include its deep experience in diabetes care and therapeutic proteins, strong infrastructure that took decades to build, efficient manufacturing techniques, a robust pipeline, and economies of scale. A Fund holding since inception, Novo reported solid operating results throughout the period that

3 |

were generally ahead of consensus expectations and reflected a rebound in activity that was depressed in the prior-year period due to Covid-19. In particular, growth was led by the company’s GLP-1 class of therapies — a quickly growing class of non-insulin, anti-diabetic treatments that can postpone the need for insulin for two to four years. Novo’s class-leading Ozempic, a once-weekly therapy with comparable safety and superior efficacy to existing therapies, has contributed to greater penetration of the GLP-1 market as well as share gains from its leading competitor, while Rybelsus, an oral version of Ozempic and the company’s newest GLP-1 innovation, has quickly captured almost 13% of all new prescriptions after its launch in late 2019. In addition to targeting diabetes with its GLP-1s, during the year, Novo received approval for semaglutide (the same molecule behind Ozempic and Rybelsus) in the obesity setting under the brand name Wegovy. While the company is navigating operational challenges that have limited the initial production of Wegovy, the company is seeing robust early demand. Diabetes is a global epidemic with an estimated population of 460 million. The market has been growing annually in the low double digits over the last ten years, driven by aging of the global population and increasing obesity. We believe Novo’s deep experience in diabetes care, differentiated product suite, and leading innovation should enable the company to grow revenues in the high single digits over our long-term investment horizon, with faster growth in free cash flow. We believe the company’s shares continue to sell at a meaningful discount to our estimate of intrinsic value and offer an attractive reward-to-risk opportunity.

Founded in Basel, Switzerland in 1896, Roche is a global biopharmaceutical and diagnostics company. An industry leader in the development and marketing of oncology products, Roche also has a broad product profile with industry-leading therapies and a robust development pipeline across major indications including immunology, infectious disease, ophthalmology, and neuroscience. We believe Roche has substantial and sustainable competitive advantages that include its expertise and reputation within oncology, an integrated diagnostics business, its biologics capability, and its commercialization experience which includes its regulatory experience and scale in manufacturing and distribution. A Fund holding since inception, Roche reported results during the period that were fundamentally solid and generally ahead of consensus expectations. The company benefited from faster growth in its smaller diagnostics division, where its success in rapid development and deployment of Covid-19 testing has highlighted its leadership position in the diagnostics market and has provided a valuable offset to the pandemic-related pressures in the pharmaceuticals division. While we expect pandemic-related demand to wane in the short-to-medium term, we believe the true long-term value of the diagnostics business will persist as it resides in its ability to support and differentiate the innovation within the company’s pharmaceuticals business. In pharmaceuticals, continued strength in the company’s more-recently launched growth products, including Ocrevus for multiple sclerosis and Hemlibra for hemophilia A, more than offset the ongoing decline in its mature oncology products. We believe Roche is successfully managing the inevitable decline for its leading off-patent oncology therapies, advancing its next-generation cancer therapy franchise through innovative follow-on and combination therapies as well as improved administration methods, and products launched since 2012 have collectively grown to reach 52% of sales as of the company’s most-recently reported financial results. In addition to its more-recently launched growth products, we believe Roche’s deep internally developed pipeline, which reflects over $100 billion invested in R&D over the past decade, combined with its ability to identify and capitalize on externally developed technologies such as its acquisition of Spark Therapeutics’ gene therapy platform, provides a significant platform for future growth. We believe Roche continues to execute well operationally, redeploying the cash flows from its mature core franchise to support product extensions and ongoing innovation. The company has a strong lineup of marketed biologic therapies, a growing suite of newly introduced products, and significant and robust pipeline assets that can drive significant long-term value for Roche. While the company now faces biosimilar competition in the US for its mature oncology franchise, we believe the current market price for Roche shares embeds expectations for key revenue and cash flow growth drivers that are well below our long-term assumptions. As a result, we believe the company is selling at a significant discount to our estimate of intrinsic value and offers a compelling reward-to-risk opportunity.

All aspects of our quality-growth-valuation investment thesis must be present simultaneously for us to make an investment. Often our research is completed well in advance of the opportunity to invest. We are patient investors and maintain coverage of high-quality businesses in order to take advantage of meaningful price dislocations if and when they occur. During the period we initiated a new position in CRISPR Therapeutics. We added to our existing holdings in Vipshop. We trimmed our existing positions in Alibaba, Kweichow Moutai, and Yum China. We also trimmed our position in MercadoLibre as it approached our maximum allowable position size. We sold our position in Kuehne + Nagel as it reached our view of intrinsic value.

Outlook

Our investment process is characterized by bottom-up fundamental research and a long-term investment time horizon. The nature of the process leads to a lower-turnover portfolio in which sector positioning is the result of stock selection. The Fund ended the year with overweight positions in the consumer staples, healthcare, consumer discretionary, information technology, and communication services sectors and was underweight in the industrials and energy sectors. We had no exposure to stocks in the financials, materials, utilities, or real estate sectors. From a geographic standpoint we were overweight in Europe and North America, underweight in developed Asia, and approximately equal weight in emerging markets.

| 4

LOOMIS SAYLES INTERNATIONAL GROWTH FUND

Hypothetical Growth of $100,000 Investment in Class Y Shares3

December 15, 2020 (inception) through December 31, 2021

Top Ten Holdings as of December 31, 2021

| | | | | | | | |

| | |

| Security Name | | % of

Net Assets | |

| | 1 | | | Roche Holding AG | | | 6.81 | % |

| | 2 | | | WiseTech Global Ltd. | | | 6.00 | % |

| | 3 | | | MercadoLibre, Inc. | | | 5.97 | % |

| | 4 | | | Adyen NV | | | 5.73 | % |

| | 5 | | | Tencent Holdings Ltd. | | | 5.50 | % |

| | 6 | | | Novartis AG, (Registered) | | | 4.79 | % |

| | 7 | | | Kweichow Moutai Co. Ltd., Class A | | | 4.28 | % |

| | 8 | | | Nestle S.A., (Registered) | | | 4.08 | % |

| | 9 | | | Novo Nordisk A/S, Class B | | | 3.97 | % |

| | 10 | | | Experian PLC | | | 3.76 | % |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced. The holdings listed exclude any temporary cash investments, are presented on an individual security basis and do not represent holdings of the issuer.

5 |

Average Annual Total Returns — December 31, 20213

| | | | | | | | | | | | | | | | |

| | | | |

| | | 1 Year | | | Life of Fund | | | Expense Ratios4 | |

| | Gross | | | Net | |

| | | | | |

| Class Y (Inception 12/15/20) | | | | | | | | | | | | | | | | |

| NAV | | | -3.81 | % | | | -2.38 | % | | | 1.35 | % | | | 0.95 | % |

| | | | | |

| Class A (Inception 12/15/20) | | | | | | | | | | | | | | | | |

| NAV | | | -4.07 | | | | -2.64 | | | | 1.60 | | | | 1.20 | |

| With 5.75% Maximum Sales Charge | | | -9.60 | | | | -8.01 | | | | | | | | | |

| | | | | |

| Class C (Inception 12/15/20) | | | | | | | | | | | | | | | | |

| NAV | | | -4.79 | | | | -3.37 | | | | 2.35 | | | | 1.95 | |

| With CDSC1 | | | -5.72 | | | | -3.37 | | | | | | | | | |

| | | | | |

| Class N (Inception 12/15/20) | | | | | | | | | | | | | | | | |

| NAV | | | -3.77 | | | | -2.34 | | | | 1.26 | | | | 0.90 | |

| | | | | |

| Comparative Performance | | | | | | | | | | | | | | | | |

| MSCI ACWI ex USA Index (Net)2 | | | 7.82 | | | | 9.89 | | | | | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| 1 | Performance for Class C shares assumes a 1% contingent deferred sales charge (“CDSC”) applied when you sell shares within one year of purchase and includes automatic conversion to Class A shares after eight years. |

| 2 | The MSCI ACWI ex USA Index (Net) captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding the US) and 27 Emerging Markets (EM) countries. With 2,361 constituents, the index covers approximately 85% of the global equity opportunity set outside the US. |

| 3 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 4 | Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 4/30/22. When a Fund’s expenses are below the limitation, gross and net expense ratios will be the same. See Note 6 of the Notes to Financial Statements for more information about the Fund’s expense limitations. |

| 6

NATIXIS OAKMARK FUND

| | |

| |

| Managers | | Symbols |

| |

| William C. Nygren, CFA® | | Class A NEFOX |

| |

| Kevin G. Grant, CFA®* | | Class C NECOX |

| |

| M. Colin Hudson, CFA® | | Class N NOANX |

| |

| Michael J. Mangan, CFA® | | Class Y NEOYX |

| |

| Michael A. Nicolas, CFA® | | |

| |

| Harris Associates L.P. | | |

| * | Effective January 1, 2022 Kevin G. Grant no longer serves as portfolio manager of the Fund. |

Investment Goal

The Fund seeks long-term capital appreciation.

Market Conditions

Global markets moved higher in the first quarter of 2021 as vaccines reached more and more people. In the United States, newly elected US President Joe Biden signed off on his economic stimulus plan in March. The $1.9 trillion relief package sent $1,400 payments to qualifying Americans and extended unemployment benefits. In response, the Dow Jones Industrial Average and S&P 500® Index soared to record highs. By the end of the second quarter, global cases surpassed 180 million and global deaths approached 4 million. However, more than 800 million people reached full vaccination, representing about 10% of the global population.

That said, a new wave of Covid-19 cases brought on by the Delta variant resulted in a slowdown in economic reopenings around the world as well as new economic restrictions in Asia and Australia. Simultaneously, the Chinese government implemented increased regulations on a range of businesses, including technology companies, prompting unease across global markets. Later, energy suppliers rushed to ramp up production to meet growing demand. However, a supply shortage and bottlenecks at major US ports sent US oil prices in excess of $85 per barrel for the first time since 2014. Natural gas prices also spiked around the world, forcing the suspension of operations at factories in Europe and China. A shortage of semiconductors, in particular, significantly impaired worldwide automobile production. Simultaneously, the new and highly contagious Omicron variant of Covid-19 spread in the fourth quarter as countries across Europe implemented restrictions once again to combat the spread of the disease.

As previously announced, the Federal Reserve slowed its pace of asset purchases in November. The tapering came as the rate of inflation in the US quickened to 6.8% versus the year-ago period. The Fed’s dot plot now calls for three rate hikes each in 2022 and 2023. The Bank of Japan and European Central Bank echoed similar sentiments as they also left interest rates unchanged, while the Bank of England raised its main interest rate from 0.1% to 0.25% following a surge in UK inflation to a 10-year high of 5.1% annual growth in November. All things considered, the International Monetary Fund (IMF) slightly lowered its expectations for global economic growth from 6.0% to 5.9%, with a 4.9% growth rate expected in 2022. The IMF also lowered its outlook for economic growth in the US, Japan and China by 1.0%, 0.4% and 0.1% in October, but raised its estimates for growth in the euro zone by 0.4%.

Performance Results

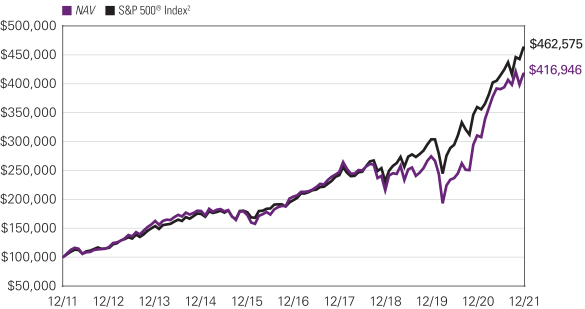

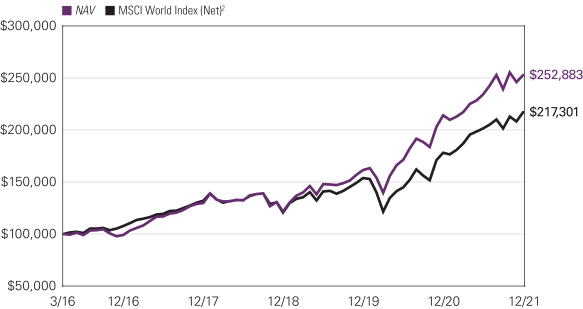

For the 12 months ended December 31, 2021, Class Y shares of the Natixis Oakmark Fund returned 34.35% at net asset value. The Fund outperformed its benchmark, the S&P 500® Index, which returned 28.71%.

Explanation of Fund Performance

As value investors with an emphasis on individual stock selection, our sector weights are a byproduct of our bottom-up process. On an absolute-return basis, the energy sector gained the most value, while holdings in the consumer staples sector delivered the smallest positive collective return.

The leading contributors to fund performance for the year were Alphabet and Gartner. Toward the beginning of 2021, Alphabet’s fourth-quarter results showed faster than expected revenue growth across the board. Total revenue grew 23% year-over-year and reached $56.9 billion, which led to earnings per share of $22.30, and both exceeded market expectations. Revenue in the key search segment grew 17%, owing to “broad-based re-engagement” among advertisers following the Covid-19-related pullback. Importantly, for the first time Alphabet disclosed cloud segment profitability and revealed that the company made massive upfront investments in its go-to-market strategy and engineering resources, implying that the remaining segments are even more profitable than most analysts expected. Later, Alphabet’s results continued to positively surprise the market as the company’s first-quarter total revenue, operating income and earnings per share outpaced expectations by 7%, 39% and 67%, respectively. By segment, search revenue grew 30%,

7 |

YouTube advertising revenue rose 49% and cloud revenue increased 46%. Furthermore, margin trends improved across all segments as underlying operational expenses appear progressively well controlled relative to history. In July, Alphabet’s second-quarter earnings report showed that revenue grew by 62%, again surpassing consensus expectations, and search revenue saw significant growth with a 67% increase year-over-year. Alphabet’s third-quarter earnings release resulted in the company’s share price moving higher into the end of the year. Reported revenue growth amounted to 41% and operating margins (ex-other bets) expanded 670 basis points. In addition, search and YouTube advertising revenue both grew over 40%. Management bought back $12.6 billion worth of stock in the third quarter, which puts the company on pace to meet our expectations for the full-year period. Although Alphabet’s share price declined on news that YouTube TV subscribers lost access to Disney-owned entertainment options, the issue resolved itself shortly thereafter. We believe Alphabet remains an attractive holding with upside potential despite its recent share price appreciation.

In February 2021, Gartner released positive fourth-quarter results, in our view. Revenue modestly surpassed consensus estimates; however, adjusted earnings of $245 million far exceeded expectations of $170 million. Significant margin improvement drove the company’s outperformance despite the disappearance of much of its conferences business, with underlying margins adjusted for conferences expanding by roughly 600 basis points. In May, Gartner reported first-quarter results that were solid, in our assessment. Reported revenue rose 8.4%, adjusted earnings advanced 50% and earnings per share grew nearly 67% from the prior year. We were most impressed that the earnings margin expanded to 29% in the quarter, a solid jump up from the previous typical level in the high teens. We also liked that revenue in both segments, global business sales and global technology sales, increased by 12% and 5%, respectively, despite reduced growth of investment spending and continued challenges from legacy product shutdowns in the global business sales segment. Later, following a strong second-quarter earnings report, Gartner’s share price advanced and finished the third quarter higher. Revenue ($1.17 billion versus $1.12 billion), adjusted earnings ($355 million versus $273.9 million) and earnings per share ($2.24 versus $1.73) all bested consensus estimates. Importantly, we appreciate that top line results are accelerating with improving sales force productivity driving growth. The company also increased its share repurchase authorization by $800 million in the second quarter. Prior to the report, we met with CEO Gene Hall and CFO Craig Safian. We came away impressed with the management team’s enthusiasm and conviction in their vision for the company’s future. We particularly like that Hall is a multi-faceted operator with a history of both consistently enhancing products to drive incremental customer demand and tightly managing the sales organization through significant growth. Strong performance continued toward the end of the year when Gartner released its third-quarter results that showed further organic growth as well as increased sales force productivity, which we believe has promising implications for underlying profitability. In addition, third quarter adjusted earnings of $305 million beat consensus expectations by $50 million. Even accounting for its recent price increase, we believe Gartner still offers a healthy amount of upside potential.

T-Mobile US and Fiserv were the largest detractors from Fund performance for the calendar year. T-Mobile US reported fourth-quarter revenue, adjusted earnings and earnings per share that were better than the market had expected. We were pleased that the company continued to outgrow its industry and achieved significant merger benefits faster than had been expected, realizing $1.3 billion of savings in 2020. We found it very important that the company continued to make headway in this buildout as we believe a large amount of T-Mobile’s growth potential rests on the expansion of its new network. We were further impressed that despite the company’s rapid network development, full-year 2020 free cash flow reached $3 billion, which far exceeded our estimates. In May, the company’s first-quarter earnings report showed above-consensus estimate numbers for customer additions and adjusted earnings, while also leading the industry across all customer metrics. We also appreciated the low brand churn the company boasted in comparison to competitors. Later in the year, T-Mobile’s second-quarter earnings report included results that aligned with our expectations. Post-paid net additions bested consensus estimates, service revenue growth of almost 6% led the industry and adjusted earnings exceeded analysts’ estimates. We thought the company’s third-quarter earnings results were impressive given that T-Mobile is at a peak point in its integration with Sprint and is operating in an elevated competitive environment. We appreciated that accounts grew 3.9% and organic service revenue grew 4.5%, both of which led the industry. In addition, management raised its guidance across the board, and the company’s adjusted earnings guidance now aligns with our estimates. We believe the valuation for T-Mobile remains attractive, offering a compelling reason to own.

Even though Fiserv’s first-quarter earnings disappointed investors, we saw the results as respectable considering the challenging operating environment. Importantly, organic revenue grew 4% from the prior year, earnings rose 15% and earnings per share advanced 18%. In merchant acquiring organic growth amounted to 8% and margins improved 650 basis points, while gross payment volume in Clover (Fiserv’s cloud-based point-of-sale product) grew 36%, ecommerce transactions grew 24% and the company won a record number of new customers during the period. In addition, we were pleased that Fiserv executed $612 million worth of share repurchases in the quarter (or about 0.8% of it share base). Later, Fiserv delivered strong second-quarter earnings results as exhibited by revenue, earnings and earnings per share that increased 18%, 41% and 47%, respectively. In addition, margins expanded 510 basis points to 33.9%. However, news that Amazon was reportedly developing a point-of-sale solution pressured Fiserv’s share price in September as investors feared increased competition. Fiserv’s third quarter earnings results were in line with market estimates, with organic revenue growth of 10%, operating margins increasing 130 basis points and adjusted earnings per share growing 23%. However, investors reacted poorly to the release, focusing on a client (speculated to be Stripe) that was part of a joint venture with Wells Fargo, which is serviced by Fiserv, deciding to leave. This likely stoked fears that other companies may decide to insource their payment

| 8

NATIXIS OAKMARK FUND

processing in the future. The departure is not expected to impact Fiserv’s financial results due to its minimal contribution and management anticipating the move. Despite the client loss, we appreciate that Fiserv still posted strong segment results and growth in customers, independent software vendors, and capabilities on its platform. We continue to believe the company is undervalued and find the investment attractive on a risk-to-reward basis.

Outlook

With seemingly constant uncertainty in politics, economics and market sentiment, we focus on finding undervalued and well-managed companies that will benefit from economic tailwinds while proving capable of weathering difficult environments. We believe this approach best services our goal of growing and protecting our investors’ capital over the long term.

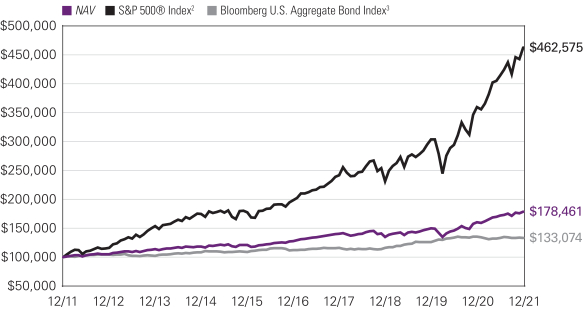

Hypothetical Growth of $100,000 Investment in Class Y Shares3

December 31, 2011 through December 31, 2021

Top Ten Holdings as of December 31, 2021

| | | | | | | | |

| | |

| Security Name | | % of

Net Assets | |

| | 1 | | | Alphabet, Inc., Class A | | | 3.53 | % |

| | 2 | | | Ally Financial, Inc. | | | 3.33 | % |

| | 3 | | | EOG Resources, Inc. | | | 2.89 | % |

| | 4 | | | Capital One Financial Corp. | | | 2.86 | % |

| | 5 | | | Charles Schwab Corp. (The) | | | 2.80 | % |

| | 6 | | | Gartner, Inc. | | | 2.51 | % |

| | 7 | | | Meta Platforms, Inc., Class A | | | 2.45 | % |

| | 8 | | | Citigroup, Inc. | | | 2.43 | % |

| | 9 | | | Goldman Sachs Group, Inc. (The) | | | 2.32 | % |

| | 10 | | | Humana, Inc. | | | 2.29 | % |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced. The holdings listed exclude any temporary cash investments, are presented on an individual security basis and do not represent holdings of the issuer.

9 |

Average Annual Total Returns —December 31, 20213

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | Life of

Class N | | | Expense Ratios4 | |

| | Gross | | | Net | |

| | | | | | | |

| Class Y | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 34.35 | % | | | 15.35 | % | | | 15.35 | % | | | — | % | | | 0.95 | % | | | 0.80 | % |

| | | | | | | |

| Class A | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 33.97 | | | | 15.05 | | | | 15.05 | | | | — | | | | 1.20 | | | | 1.05 | |

| With 5.75% Maximum Sales Charge | | | 26.25 | | | | 13.70 | | | | 14.37 | | | | — | | | | | | | | | |

| | | | | | | |

| Class C | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 32.99 | | | | 14.20 | | | | 14.37 | | | | — | | | | 1.95 | | | | 1.80 | |

| With CDSC1 | | | 31.99 | | | | 14.20 | | | | 14.37 | | | | — | | | | | | | | | |

| | | | | | | |

| Class N (Inception 5/1/17) | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 34.54 | | | | — | | | | — | | | | 15.48 | | | | 1.05 | | | | 0.75 | |

| | | | | | | |

| Comparative Performance | | | | | | | | | | | | | | | | | | | | | | | | |

| S&P 500® Index2 | | | 28.71 | | | | 18.47 | | | | 16.55 | | | | 18.02 | | | | | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com/performance. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| 1 | Performance for Class C shares assumes a 1.00% contingent deferred sales charge (“CDSC”) applied when you sell shares within one year of purchase and includes automatic conversion to Class A shares after eight years. |

| 2 | S&P 500® Index is a widely recognized measure of U.S. stock market performance. It is an unmanaged index of 500 common stocks chosen for market size, liquidity, and industry group representation, among other factors. It also measures the performance of the large cap segment of the U.S. equities market. |

| 3 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 4 | Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 4/30/23. When a Fund’s expenses are below the limitations, gross and net expense ratios will be the same. See Note 6 of the Notes to Financial Statements for more information about the Fund’s expense limitations. |

| 10

NATIXIS OAKMARK INTERNATIONAL FUND

| | |

| |

| Managers | | Symbols |

| |

| David G. Herro, CFA® | | Class A NOIAX |

| |

| Michael L. Manelli, CFA® | | Class C NOICX |

| |

| Harris Associates L.P. | | Class N NIONX |

| |

| | Class Y NOIYX |

Investment Goal

The Fund seeks long-term capital appreciation.

Market Conditions

Global markets moved higher in the first quarter of 2021 as vaccines reached more and more people. In the United States, newly elected US President Joe Biden signed off on his economic stimulus plan in March. The $1.9 trillion relief package sent $1,400 payments to qualifying Americans and extended unemployment benefits. In response, the Dow Jones Industrial Average and S&P 500® Index soared to record highs. By the end of the second quarter, global cases surpassed 180 million and global deaths approached 4 million. However, more than 800 million people reached full vaccination, representing about 10% of the global population.

That said, a new wave of Covid-19 cases brought on by the Delta variant resulted in a slowdown in economic reopenings around the world as well as new economic restrictions in Asia and Australia. Simultaneously, the Chinese government implemented increased regulations on a range of businesses, including technology companies, prompting unease across global markets. Later, energy suppliers rushed to ramp up production to meet growing demand. However, a supply shortage and bottlenecks at major US ports sent US oil prices in excess of $85 per barrel for the first time since 2014. Natural gas prices also spiked around the world, forcing the suspension of operations at factories in Europe and China. A shortage of semiconductors in particular significantly impaired worldwide automobile production. Simultaneously, the new and highly contagious Omicron variant of Covid-19 spread in the fourth quarter and countries across Europe implemented restrictions once again to combat the spread of the disease.

As previously announced, the Federal Reserve slowed its pace of asset purchases in November. The tapering came as the rate of inflation in the United States quickened to 6.8% versus the year-ago period. The Fed’s dot plot now calls for three rate hikes each in 2022 and 2023, and two in 2024. The Bank of Japan and European Central Bank echoed similar sentiments as they also left interest rates unchanged, while the Bank of England raised its main interest rate from 0.1% to 0.25% following a surge in UK inflation to a 10-year high of 5.1% annual growth in November. All things considered, the International Monetary Fund (IMF) slightly lowered its expectations for 2021 global economic growth from 6.0% to 5.9%, with a 4.9% growth rate expected in 2022. The IMF also lowered its outlook for 2021 economic growth in the United States, Japan and China by 1.0%, 0.4% and 0.1% respectively in October, but raised its estimates for growth in the euro zone by 0.4%.

Performance Results

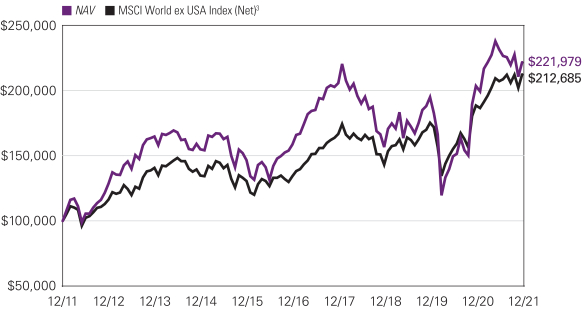

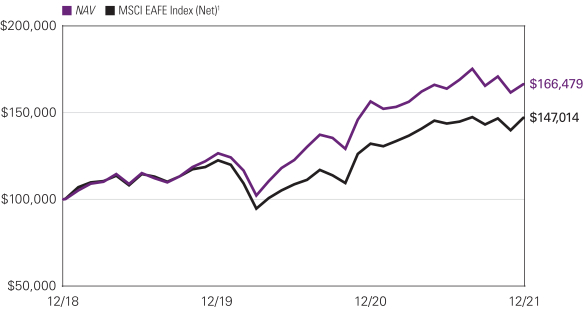

For the 12 months ended December 31, 2021, Class Y shares of the Natixis Oakmark International Fund returned 8.97% at net asset value. The Fund underperformed its benchmark, the MSCI World ex USA Index (Net), which returned 12.62%.

Explanation of Fund Performance

Geographically, the Fund’s average weightings for the year were 83% in Europe, 3% in Canada and 3% in Australia. The remaining positions were in Japan, China, South Africa, South Korea, India, Mexico and Indonesia.

On an absolute-return basis, shares in the energy sector produced the largest positive collective return, while the consumer staples sector lost the most value.

The top contributors to the yearly return were Glencore and Lloyds Banking Group. Early in the year, Glencore’s full-year results showed that adjusted earnings in both the industrials and marketing segments exceeded our expectations by 10% and 4%, respectively. Full-year total adjusted earnings of $11.56 billion were also better than market estimates of $10.69 billion. The industrials segment benefited from both a recovery in commodities prices from Covid-19 lows and higher production. Management also proposed a $0.12 per share dividend, which surpassed analysts’ estimates for $0.0625 per share. Later, Glencore’s share price increased after the company released its first-quarter production report late in April, which showed that copper production increased 2.7% year-over-year. Glencore continued to outperform expectations in the third quarter, benefiting from rising commodity prices and a disciplined cost program. Copper, the company’s most important commodity, is benefiting from rising production and lower costs. Glencore held its annual investor day in December, where the company reinforced its plan to emphasize low-cost, large-scale assets in future-facing commodities, while responsibly running down its coal business over time. We appreciate management’s focus on increasing

11 |

risk-adjusted returns by exiting assets that require a lot of management’s time, are in high-risk jurisdictions, have limited mine-life or face other constraints while not being material financial contributors. Prior to the company’s investor day, we spoke with Chairman Kalidas Madhavpeddi who possesses a solid background within the industry, in our view. He emphasized his appreciation for Glencore’s anti-bureaucratic culture, which leads to innovative ideas from younger talent, and the focus on financial returns in decision making. We are optimistic about Madhavpeddi’s abilities and the company’s future.

Lloyds Banking Group delivered strong fourth-quarter results largely driven by lower-than-expected impairment charges, which reached GBP 128 million compared with market forecasts for GBP 586 million. Profit before tax and net income both surpassed market projections by 5%, while pre-provision profit was 7% better than market estimates. In addition, the company’s common equity Tier 1 ratio grew to 16.2% and management announced plans to resume capital distributions. Later, Lloyds’ share price soared upon the release of solid first-quarter earnings, which were driven by a reserve release of GBP 459 million for credit losses that resulted in a GBP 323 million net impairment credit and pointed to management’s view of an improving economic outlook in the UK. Lloyds’ first-quarter revenues reached GBP 3.6 billion, and the company’s common equity Tier 1 ratio expanded by 54 basis points to 16.7%, despite funding half of its full-year pension contribution in the first quarter. In addition, Lloyds saw strong inflows of low-cost deposits, while higher-than-expected mortgage underwriting margins led to the company increasing its net interest margin target to more than 245 basis points, which exceeded our estimate of 240 basis points. Operating expenditure trends were also positive, in our view. Following a conversation with new CEO Charlie Nunn, our confidence in the company’s leadership was solidified as he emphasized a desire to grow the firm in both a profitable and responsible manner in order to create shareholder value. With a higher interest rate environment approaching, we believe financial services companies that are well managed and fundamentally sound, such as Lloyds Banking Group, are positioned to recognize upside potential.

The largest detractors from return were Alibaba Group and Credit Suisse Group. In February, Alibaba Group reported fiscal third-quarter revenue of CNY 221.08 billion and adjusted earnings of CNY 68.38 billion, both of which outpaced market forecasts by slightly more than 3%. Soon after, news outlets reported that officials in China asked Alibaba to dispose of its media assets over concern about the company’s influence over public opinion. In addition, China’s State Administration introduced new regulations for e-commerce platforms. Subsequently, internet companies in China removed Alibaba’s popular UC internet browser from its application stores. In the second quarter of 2021, China’s State Administration for Market Regulation fined Alibaba $2.8 billion, which was the largest antitrust penalty issued in the country’s history. The fine (which represents 4% of the company’s 2019 annual domestic revenue) was imposed because the regulatory body found that Alibaba’s practice of requiring merchants to remain exclusive on its platforms hindered competition. The company stated it does not expect a material impact on its business as a result of the new regulations. Later, the company’s share price plunged upon the release of fiscal full-year earnings, even though results were largely in line with our full-year estimates on an organic basis. Along with the earnings release, management announced it would reinvest all incremental profits in the next fiscal year, which disappointed investors. While this strategy will likely produce low or no near-term profit growth, management believes these investments will help grow its user base over the long term. Most recently, Alibaba’s second-quarter earnings report disappointed investors as growth meaningfully decelerated during the quarter and management lowered its full-year revenue growth guidance. Factors causing the slowdown in growth include a decrease in the retail spending environment in China, increased competition in e-commerce and Alibaba’s reinvestments into its merchant base, which coincided with recent increased regulation from the Chinese government. At the company’s investor day, we were impressed by Alibaba’s presentation on its growing cloud business, where the company believes its technology lead is at least two years ahead of its peers. Despite the current headwinds facing the company, we remain shareholders of Alibaba as we believe it is an important driver of innovation in China and several of its businesses have yet to fully scale.

The share price of Credit Suisse Group suffered upon revelations about the company’s exposure to Greensill Capital followed by its association with Archegos Capital Management. Investors sold shares over concerns that an investment fund run by its asset management division had exposure to the now-insolvent Greensill Capital, which specialized in supply chain finance. The lost market cap far surpassed Credit Suisse’s direct exposure to Greensill and ignored the fact that a large portion of its clients’ exposure was in cash, highly rated securities or insured investments. At the end of March, Credit Suisse’s share price dropped again as New York-based hedge fund client Archegos Capital defaulted on its margin calls to the company’s prime brokerage business. Credit Suisse announced it incurred a CHF 4.4 billion charge related to the Archegos Capital incident in the first quarter. While the amount exceeded both our initial expectations and consensus estimates, first quarter pre-tax profit of about CHF 3.6 billion, excluding the charge, exceeded analysts’ estimates for about CHF 1.2–1.5 billion in pre-tax profit driven by strong underlying performance across all three business segments. That being said, the company guided for an additional CHF 600 million charge in the second quarter to cover further Archegos-related losses. The company ultimately executed a small capital raise in an effort to boost its CET1 ratio to 13.0%. Credit Suisse’s third-quarter earnings results tracked ahead of our fiscal year estimates. Importantly, net new money inflected positively following second-quarter outflows related to the Archegos Capital and Greensill Capital incidents, suggesting that the potential reputational damage is less than feared. Following the company’s capital markets day and subsequent conversations with management, we learned that Credit Suisse planned to take additional capital from the lower return / higher risk investment bank and

| 12

NATIXIS OAKMARK INTERNATIONAL FUND

allocate capital toward the higher return / lower risk wealth management segment, a strategy we fully support. The company is also looking to generate CHF 1 billion — CHF 1.5 billion in savings from procurement initiatives, along with a new organizational structure that will serve to simplify the organization, reduce costs and enhance risk functions. Given the addition of David Wildermuth (formerly at Goldman Sachs with more than 30 years of banking experience) as chief risk officer in January and the arrival of new Chairman António Horta-Osório, the former CEO of Lloyds Banking Group, we expect better governance and risk management going forward.

Outlook

With seemingly constant uncertainty in politics, economics and market sentiment, we focus on finding undervalued and well-managed companies that will benefit from economic tailwinds while proving capable of weathering difficult environments. We believe this approach best services our goal of growing and protecting our investors’ capital over the long term.

Hypothetical Growth of $100,000 Investment in Class Y Shares1,4

December 31, 2011 through December 31, 2021

13 |

Top Ten Holdings as of December 31, 2021

| | | | | | | | |

| | |

| Security Name | | % of

Net Assets | |

| | 1 | | | Lloyds Banking Group PLC | | | 3.70 | % |

| | 2 | | | Bayer AG, (Registered) | | | 3.70 | % |

| | 3 | | | BNP Paribas S.A. | | | 3.48 | % |

| | 4 | | | Allianz SE, (Registered) | | | 3.38 | % |

| | 5 | | | Intesa Sanpaolo SpA | | | 3.21 | % |

| | 6 | | | Credit Suisse Group AG, (Registered) | | | 3.20 | % |

| | 7 | | | Bayerische Motoren Werke AG | | | 3.13 | % |

| | 8 | | | Glencore PLC | | | 2.92 | % |

| | 9 | | | Continental AG | | | 2.74 | % |

| | 10 | | | CNH Industrial NV | | | 2.58 | % |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced. The holdings listed exclude any temporary cash investments, are presented on an individual security basis and do not represent holdings of the issuer.

Average Annual Total Returns — December 31, 20214

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | Life of

Class N | | | Expense Ratios5 | |

| | Gross | | | Net | |

| | | | | | | |

| Class Y (Inception 5/1/17) | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV1 | | | 8.97 | % | | | 6.94 | % | | | 8.30 | % | | | — | % | | | 1.11 | % | | | 0.90 | % |

| | | | | | | |

| Class A | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 8.73 | | | | 6.69 | | | | 8.18 | | | | — | | | | 1.36 | | | | 1.15 | |

| With 5.75% Maximum Sales Charge | | | 2.50 | | | | 5.44 | | | | 7.54 | | | | — | | | | | | | | | |

| | | | | | | |

| Class C | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 7.92 | | | | 5.89 | | | | 7.54 | | | | — | | | | 2.11 | | | | 1.90 | |

| With CDSC2 | | | 6.92 | | | | 5.89 | | | | 7.54 | | | | — | | | | | | | | | |

| | | | | | | |

| Class N (Inception 5/1/17) | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 9.01 | | | | — | | | | — | | | | 4.36 | | | | 1.17 | | | | 0.85 | |

| | | | | | | |

| Comparative Performance | | | | | | | | | | | | | | | | | | | | | | | | |

| MSCI World ex USA Index (Net)3 | | | 12.62 | | | | 9.63 | | | | 7.84 | | | | 8.22 | | | | | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com/performance. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| 1 | Prior to the inception of Class Y shares (5/1/2017), performance is that of Class A shares and reflects the higher net expenses of that share class. |

| 2 | Performance for Class C shares assumes a 1.00% contingent deferred sales charge (“CDSC”) applied when you sell shares within one year of purchase, and includes automatic conversion to Class A shares after eight years. |

| 3 | MSCI World ex USA Index (Net) is an unmanaged index that is designed to measure the equity market performance of developed markets, excluding the United States. |

| 4 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 5 | Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 4/30/23. When a Funds expenses are below the limitation, gross and net expense ratios will be the same. See Note 6 of the Notes to Financial Statements for more information about the Funds expense limitations. |

| 14

NATIXIS U.S. EQUITY OPPORTUNITIES FUND

| | | | |

| |

| Managers | | Symbols |

| | |

William C. Nygren, CFA® | | Class A | | NEFSX |

| | |

| Kevin G. Grant, CFA®* | | Class C | | NECCX |

| | |

M. Colin Hudson, CFA® | | Class N | | NESNX |

| | |

Michael J. Mangan, CFA®, CPA | | Class Y | | NESYX |

| | |

| Michael A. Nicolas, CFA® | | | | |

| | |

| Harris Associates L.P. | | | | |

| |

| | |

| | |

| Aziz V. Hamzaogullari, CFA® | | | | |

| | |

| Loomis, Sayles & Company, L.P. | | | | |

| * | Effective January 1, 2022 Kevin G. Grant no longer serves as portfolio manager of the Fund. |

Investment Goal

The Fund seeks long-term growth of capital.

Market Conditions

U.S. equities produced strong returns in 2021, marking the eighth year of the past ten in which the major large-cap indexes posted a double-digit gain. The gradual lifting of virus-related restrictions led to a substantial improvement in economic growth and corporate earnings compared to their levels of the previous year, contributing to the gains for stocks. While rising inflation prompted the Federal Reserve (Fed) to adopt a more hawkish tone in the fourth quarter, leading to increased market volatility, the major large-cap indexes closed the year at or near their all-time highs. In the continuation of a long-standing trend, mega-cap technology and communication services stocks were the key drivers of U.S. market performance in 2021.

Performance Results

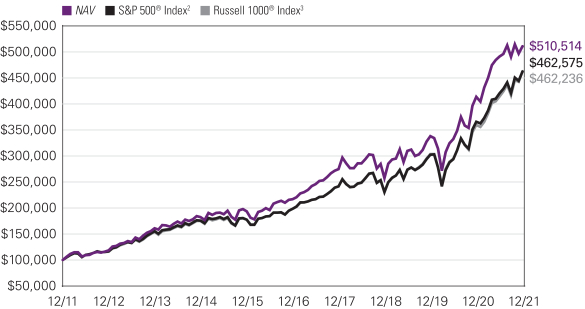

For the 12 months ended December 31, 2021, Class Y shares of the Natixis U.S. Equity Opportunities Fund returned 23.48% at net asset value. The Fund underperformed its primary benchmark, the S&P 500® Index, which returned 28.71%, and also underperformed its secondary benchmark, the Russell 1000® Index, which returned 26.45%.

Explanation of Fund Performance

Each of the portfolio’s segments uses a distinct investment style, providing shareholders with exposure to a variety of different stocks:

| • | | The Harris Associates L.P. Large Cap Value segment invests primarily in the common stocks of larger-capitalization companies that Harris Associates L.P. (“Harris Associates”) believes are trading at a substantial discount to the company’s “true business value.” |

| • | | The Loomis, Sayles & Company, L.P. All Cap Growth segment invests primarily in equity securities and may invest in companies of any size. The segment employs a growth style of equity management that emphasizes companies with sustainable competitive advantages versus others, long-term structural growth drivers that will lead to above-average future cash flow growth, attractive cash flow returns on invested capital, and management teams focused on creating long-term value for shareholders. The segment aims to invest in companies when they trade at a significant discount to the estimate of intrinsic value. |

Both segments contributed positively to the Fund’s performance.

Harris Associates Large Cap Value Segment

As value investors with an emphasis on individual stock selection, our sector weights are a byproduct of our bottom-up process. On an absolute-return basis, the energy sector gained the most value, while holdings in the industrials sector delivered the smallest positive collective return.

The largest contributors to fund performance for the year were Alphabet and Capital One Financial. Toward the beginning of the year, Alphabet’s fourth-quarter results showed faster than expected revenue growth across the board. Total revenue grew 23% year-over-year and reached $56.9 billion, which led to earnings per share of $22.30, and both exceeded market expectations. Revenue in the key search segment grew 17%, owing to “broad-based re-engagement” among advertisers following the Covid-19-related pullback. Importantly, for the first time Alphabet disclosed cloud segment profitability and revealed that the company made massive upfront

15 |

investments in its go-to-market strategy and engineering resources, implying that the remaining segments are even more profitable than most analysts expected. Later, Alphabet’s results continued to positively surprise the market as the company’s first-quarter total revenue, operating income and earnings per share outpaced expectations by 7%, 39% and 67%, respectively. By segment, search revenue grew 30%, YouTube advertising revenue rose 49% and cloud revenue increased 46%. Furthermore, margin trends improved across all segments as underlying operational expenses appear progressively well controlled relative to history. In July, Alphabet’s second-quarter earnings report showed that revenue grew by 62%, again surpassing consensus expectations, and search revenue saw significant growth with a 67% increase year-over-year. Alphabet’s third-quarter earnings release resulted in the company’s share price moving higher into the end of the year. Reported revenue growth amounted to 41% and operating margins (ex-Other Bets) expanded 670 basis points. In addition, search and YouTube advertising revenue both grew over 40%. Management bought back $12.6 billion worth of stock in the third quarter, which puts the company on pace to meet our expectations for the full-year period. Although Alphabet’s share price declined on news that YouTube TV subscribers lost access to Disney-owned entertainment options, the issue resolved itself shortly thereafter. We believe Alphabet remains an attractive holding with upside potential despite its recent share price appreciation.

Capital One Financial issued first-quarter results that we saw as very good and that built on positive trends from prior quarters. Likewise, the company’s total net revenue and net interest margin exceeded market projections, while earnings per share were about 70% ahead of forecasts. We were pleased that credit quality remained strong, and charge-offs across lending categories fell once again from historically low levels. Credit card purchase volume grew 8% from last year, while deposits grew 15.1% and the average consumer deposit cost ratio reached an all-time low of 0.36%. Impressively, Capital One released loan loss reserves of $1.6 billion in the quarter, which was larger than the reserve release we had estimated for the full year. Capital One delivered another solid set of earnings results for its second quarter, in our view. A $1.7 billion loan reserve release led to earnings per share of $7.62, and the card charge-off rate fell 23 basis points versus the previous quarter’s already historically low rate to 2.29%. In October, investors responded unfavorably to CEO Richard Fairbank’s emphatic commentary surrounding elevated spending, the need to invest defensively in technology and the costliness of doing so given the competition for technology talent. That said, we think the company’s third-quarter earnings report highlighted strong results as charge-offs fell further from already all-time low levels, card purchase volume grew 28% year-over-year, ending loan balance improved 5% sequentially and net interest margins grew 46 basis points. In addition, Capital One executed $2.7 billion in third-quarter share repurchases (equivalent to 3.5% of its share base) and still ended the period with excess capital equal to 13% of its market cap. Our investment thesis for the company remains intact, and we believe it trades at a discount to our perception of its intrinsic value.

The largest detractors to fund performance for the year were Ally Financial and Fiserv. As management had predicted and we had expected, Ally Financial released good fourth-quarter results early in the year. Total net revenue rose 21% from a year earlier while earnings per share advanced 68% and both exceeded market forecasts. In addition, total deposits grew 13% and average total earning assets (including auto loans and mortgages) rose 3% year-over-year. Notably, the company’s provision for credit losses decreased materially from $998 million in the fourth quarter of 2020 to $102 million in the fourth quarter of 2021. Ally announced a new $1.60 billion share repurchase authorization in January following favorable results from the most recent Federal Reserve board stress test. In April, Ally’s first-quarter earnings report included earnings per share ($2.09 ex-items vs. $1.17) that beat analysts’ estimates as well as a reported return on tangible common equity of 24%. In fact, most metrics came in well above increasingly elevated expectations. Net interest margins expanded 26 basis points sequentially to 3.18%, retail deposits grew 21% year-over-year and deposit customers grew 14%. The company’s second-quarter earnings report in July continued to show strength as shown by return on tangible common equity of around 27%. New retail auto originations finished at the highest level in 15 years, while new originated yields maintained above 7%. In addition, net interest margins expanded to nearly 3.6%. In October, Ally reported a positive third-quarter earnings report, in our view. Return on average tangible common equity was assisted by a low credit loss environment and expanding net interest margins. Record retail application flow continued to show strength for a fourth straight year. However, the wholesale business continued to show weakness with loan balances at roughly half pre-pandemic levels. Later in the fourth quarter, Ally announced its decision to acquire digital credit card provider Fair Square Financial (FSF) for $750 million. FSF has been growing balances rapidly, and we believe the deal can add at least 150 basis points to core return on average tangible common equity over the medium term.

Even though Fiserv’s first-quarter earnings disappointed investors, we saw the results as respectable considering the challenging operating environment. Importantly, organic revenue grew 4% from the prior year, earnings rose 15% and earnings per share advanced 18%. In merchant acquiring, organic growth amounted to 8% and margins improved 650 basis points, while gross payment volume in Clover (Fiserv’s cloud-based point-of-sale product) grew 36%, e-commerce transactions grew 24% and the company won a record number of new customers during the period. In addition, we were pleased that Fiserv executed $612 million worth of share repurchases in the quarter (or about 0.8% of its share base). Later, Fiserv delivered strong second-quarter earnings results as exhibited by revenue, earnings and earnings per share that increased 18%, 41% and 47%, respectively. In addition, margins expanded 510 basis points to 33.9%. However, news that Amazon was reportedly developing a point-of-sale solution pressured Fiserv’s share price in

| 16

NATIXIS U.S. EQUITY OPPORTUNITIES FUND

September as investors feared increased competition. Fiserv’s third-quarter earnings results were in line with market estimates, with organic revenue growth of 10%, operating margins increasing 130 basis points and adjusted earnings per share growing 23%. However, investors reacted poorly to the release, focusing on a client (speculated to be Stripe) that was part of a joint venture with Wells Fargo, which is serviced by Fiserv, deciding to leave. This likely stoked fears that other companies may decide to insource their payment processing in the future. The departure is not expected to impact Fiserv’s financial results due to its minimal contribution and management anticipating the move. Despite the client loss, we appreciate that Fiserv still posted strong segment results and growth in customers, independent software vendors, and capabilities on its platform. We continue to believe the company is undervalued and find the investment attractive on a risk-to-reward basis.

Loomis, Sayles & Company All Cap Growth Segment

We are an active manager with a long-term, private equity approach to investing. Through our proprietary bottom-up research framework, we look to invest in those few high-quality businesses with sustainable competitive advantages and profitable growth when they trade at a significant discount to intrinsic value. For the period, the All Cap Growth segment posted a positive absolute return. Our holdings in the information technology, communication services, industrials, healthcare, financials, energy, and consumer staples sectors contributed positively to results. Our holdings in the consumer discretionary sector detracted from the segment’s performance.