UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2009

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 1-13283

PENN VIRGINIA CORPORATION

(Exact name of registrant as specified in its charter)

| Virginia | 23-1184320 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

THREE RADNOR CORPORATE CENTER, SUITE 300

100 MATSONFORD ROAD

RADNOR, PA 19087

(Address of principal executive offices) (Zip Code)

(610) 687-8900

(Registrant’s telephone number, including area code)

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 (“Exchange Act”) during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by a check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | x | Accelerated filer | ¨ |

| | | | |

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

As of October 31, 2009, 45,385,352 shares of common stock of the registrant were outstanding.

PENN VIRGINIA CORPORATION AND SUBSIDIARIES

INDEX

| | | | Page |

| PART I. | Financial Information | | 1 |

| | | | |

| Item 1. | Financial Statements | | 1 |

| | | | |

| | Consolidated Statements of Income for the Three and Nine Months Ended September 30, 2009 and 2008 | | 1 |

| | | | |

| | Consolidated Balance Sheets as of September 30, 2009 and December 31, 2008 | | 2 |

| | | | |

| | Consolidated Statements of Cash Flows for the Three and Nine Months Ended September 30, 2009 and 2008 | | 3 |

| | | | |

| | Notes to Consolidated Financial Statements | | 4 |

| | | | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | | 25 |

| | | | |

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | | 45 |

| | | | |

| Item 4. | Controls and Procedures | | 48 |

| | | | |

| PART II. | Other Information | | 49 |

| | | | |

| Item 6. | Exhibits | | 49 |

PART I. FINANCIAL INFORMATION

Item 1 Financial Statements

PENN VIRGINIA CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF INCOME – unaudited

(in thousands, except per share data)

| | | Three Months Ended | | | Nine Months Ended | |

| | | September 30, | | | September 30, | |

| | | 2009 | | | 2008 | | | 2009 | | | 2008 | |

| Revenues | | | | | | | | | | | | |

| Natural gas | | $ | 36,654 | | | $ | 101,911 | | | $ | 129,305 | | | $ | 295,636 | |

| Crude oil | | | 13,259 | | | | 13,764 | | | | 31,412 | | | | 37,442 | |

| Natural gas liquids (NGLs) | | | 2,847 | | | | 10,481 | | | | 10,553 | | | | 18,887 | |

| Natural gas midstream | | | 102,262 | | | | 184,914 | | | | 289,123 | | | | 494,260 | |

| Coal royalties | | | 29,821 | | | | 33,308 | | | | 90,448 | | | | 88,911 | |

| Gain on sale of property and equipment | | | 1,945 | | | | 31,279 | | | | 1,918 | | | | 31,335 | |

| Other | | | 8,375 | | | | 9,955 | | | | 25,481 | | | | 28,690 | |

| Total revenues | | | 195,163 | | | | 385,612 | | | | 578,240 | | | | 995,161 | |

| | | | | | | | | | | | | | | | | |

| Expenses | | | | | | | | | | | | | | | | |

| Cost of midstream gas purchased | | | 77,248 | | | | 155,564 | | | | 228,579 | | | | 408,247 | |

| Operating | | | 21,167 | | | | 23,437 | | | | 66,517 | | | | 66,653 | |

| Exploration | | | 16,117 | | | | 8,346 | | | | 54,901 | | | | 19,765 | |

| Taxes other than income | | | 5,294 | | | | 7,671 | | | | 16,656 | | | | 23,325 | |

| General and administrative | | | 19,946 | | | | 18,289 | | | | 58,787 | | | | 55,006 | |

| Depreciation, depletion and amortization | | | 57,869 | | | | 49,978 | | | | 173,160 | | | | 133,481 | |

| Impairments on assets held for sale | | | 87,900 | | | | - | | | | 87,900 | | | | - | |

| Other impairments | | | 4,453 | | | | - | | | | 8,928 | | | | - | |

| Loss on sale of assets | | | - | | | | - | | | | 1,599 | | | | - | |

| Total expenses | | | 289,994 | | | | 263,285 | | | | 697,027 | | | | 706,477 | |

| | | | | | | | | | | | | | | | | |

| Operating income (loss) | | | (94,831 | ) | | | 122,327 | | | | (118,787 | ) | | | 288,684 | |

| | | | | | | | | | | | | | | | | |

| Other income (expense) | | | | | | | | | | | | | | | | |

| Interest expense | | | (22,784 | ) | | | (13,221 | ) | | | (50,332 | ) | | | (35,313 | ) |

| Derivatives | | | (2,529 | ) | | | 125,132 | | | | 8,478 | | | | (4,387 | ) |

| Other | | | 348 | | | | (4,088 | ) | | | 2,274 | | | | (782 | ) |

| | | | | | | | | | | | | | | | | |

| Income (loss) before income taxes and noncontrolling interests | | | (119,796 | ) | | | 230,150 | | | | (158,367 | ) | | | 248,202 | |

| Income tax benefit (expense) | | | 50,405 | | | | (78,921 | ) | | | 69,587 | | | | (74,352 | ) |

| | | | | | | | | | | | | | | | | |

| Net income (loss) | | | (69,391 | ) | | | 151,229 | | | | (88,780 | ) | | | 173,850 | |

| Less net income attributable to noncontrolling interests | | | (10,509 | ) | | | (28,276 | ) | | | (20,512 | ) | | | (52,252 | ) |

| | | | | | | | | | | | | | | | | |

| Income (loss) attributable to Penn Virginia Corporation | | $ | (79,900 | ) | | $ | 122,953 | | | $ | (109,292 | ) | | $ | 121,598 | |

| | | | | | | | | | | | | | | | | |

| Earnings (loss) per share - basic and diluted: | | | | | | | | | | | | | | | | |

| Earnings (loss) per share attributable to Penn Virginia Corporation | | | | | | | | | | | | | | | | |

| Basic | | $ | (1.76 | ) | | $ | 2.94 | | | $ | (2.52 | ) | | $ | 2.91 | |

| Diluted | | $ | (1.76 | ) | | $ | 2.88 | | | $ | (2.52 | ) | | $ | 2.88 | |

| | | | | | | | | | | | | | | | | |

| Weighted average shares outstanding, basic | | | 45,427 | | | | 41,881 | | | | 43,324 | | | | 41,715 | |

| Weighted average shares outstanding, diluted | | | 45,427 | | | | 42,544 | | | | 43,324 | | | | 42,028 | |

The accompanying notes are an integral part of these consolidated financial statements.

PENN VIRGINIA CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS – unaudited

(in thousands, except share data)

| | | September 30, | | | December 31, | |

| | | 2009 | | | 2008 | |

| Assets | | | | | | |

| Current assets | | | | | | |

| Cash and cash equivalents | | $ | 105,034 | | | $ | 18,338 | |

| Accounts receivable, net of allowance for doubtful accounts | | | 100,454 | | | | 149,241 | |

| Derivative assets | | | 25,675 | | | | 67,569 | |

| Inventory | | | 12,134 | | | | 18,468 | |

| Assets held for sale | | | 47,107 | | | | - | |

| Other current assets | | | 3,079 | | | | 9,902 | |

| Total current assets | | | 293,483 | | | | 263,518 | |

| | | | | | | | | |

| Property and equipment | | | | | | | | |

| Oil and gas properties (successful efforts method) | | | 1,939,442 | | | | 2,107,128 | |

| Other property and equipment | | | 1,139,449 | | | | 1,076,471 | |

| Total property and equipment | | | 3,078,891 | | | | 3,183,599 | |

| Accumulated depreciation, depletion and amortization | | | (706,568 | ) | | | (671,422 | ) |

| Net property and equipment | | | 2,372,323 | | | | 2,512,177 | |

| | | | | | | | | |

| Equity investments | | | 87,520 | | | | 78,443 | |

| Intangibles, net | | | 87,108 | | | | 92,672 | |

| Derivative assets | | | 1,950 | | | | 4,070 | |

| Other assets | | | 58,885 | | | | 45,685 | |

| Total assets | | $ | 2,901,269 | | | $ | 2,996,565 | |

| | | | | | | | | |

| Liabilities and shareholders’ equity | | | | | | | | |

| Current liabilities | | | | | | | | |

| Short-term borrowings | | $ | - | | | $ | 7,542 | |

| Accounts payable and accrued liabilities | | | 120,180 | | | | 206,902 | |

| Derivative liabilities | | | 16,261 | | | | 15,534 | |

| Deferred taxes | | | 1,776 | | | | 17,598 | |

| Income taxes payable | | | 7,139 | | | | 18 | |

| Total current liabilities | | | 145,356 | | | | 247,594 | |

| | | | | | | | | |

| Other liabilities | | | 43,797 | | | | 45,887 | |

| Derivative liabilities | | | 7,217 | | | | 8,721 | |

| Deferred income taxes | | | 217,820 | | | | 258,037 | |

| Long-term debt of PVR | | | 628,100 | | | | 568,100 | |

| Revolving credit facility | | | - | | | | 332,000 | |

| Senior notes | | | 291,432 | | | | - | |

| Convertible notes | | | 204,935 | | | | 199,896 | |

| | | | | | | | | |

| Shareholders’ equity: | | | | | | | | |

| Common stock of $0.01 par value – 64,000,000 shares authorized; shares issued and | | | | | | | | |

| outstanding of 45,385,258 and 41,870,893 at September 30, 2009 and December 31, 2008 | | | 265 | | | | 230 | |

| Paid-in capital | | | 704,147 | | | | 599,855 | |

| Retained earnings | | | 327,076 | | | | 443,646 | |

| Deferred compensation obligation | | | 2,282 | | | | 2,237 | |

| Accumulated other comprehensive loss | | | (1,598 | ) | | | (4,182 | ) |

| Treasury stock – 106,558 and 85,227 shares common stock, at cost, on | | | | | | | | |

| September 30, 2009 and December 31, 2008 | | | (2,791 | ) | | | (2,683 | ) |

| Total Penn Virginia Corporation shareholders’ equity | | | 1,029,381 | | | | 1,039,103 | |

| Noncontrolling interests of subsidiaries | | | 333,231 | | | | 297,227 | |

| Total shareholders’ equity | | | 1,362,612 | | | | 1,336,330 | |

| Total liabilities and shareholders’ equity | | $ | 2,901,269 | | | $ | 2,996,565 | |

The accompanying notes are an integral part of these consolidated financial statements.

PENN VIRGINIA CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS – unaudited

(in thousands)

| | | Three Months Ended | | | Nine Months Ended | |

| | | September 30, | | | September 30, | |

| | | 2009 | | | 2008 | | | 2009 | | | 2008 | |

| | | | | | | | | | | | | |

| Cash flows from operating activities | | | | | | | | | | | | |

| Net income (loss) | | $ | (69,391 | ) | | $ | 151,229 | | | $ | (88,780 | ) | | $ | 173,850 | |

| Adjustments to reconcile net income (loss) to net | | | | | | | | | | | | | | | | |

| cash provided by operating activities: | | | | | | | | | | | | | | | | |

| Depreciation, depletion and amortization | | | 57,869 | | | | 49,978 | | | | 173,160 | | | | 133,481 | |

| Impairments | | | 92,353 | | | | - | | | | 96,828 | | | | - | |

| Commodity derivative contracts: | | | | | | | | | | | | | | | | |

| Total derivative losses (gains) | | | 6,312 | | | | (123,628 | ) | | | (2,821 | ) | | | 8,516 | |

| Cash settlements of derivatives | | | 15,507 | | | | (19,755 | ) | | | 51,936 | | | | (46,740 | ) |

| Deferred income taxes | | | (51,928 | ) | | | 61,552 | | | | (70,728 | ) | | | 60,105 | |

| Dry hole and unproved leasehold expense | | | 10,593 | | | | 5,520 | | | | 30,476 | | | | 14,992 | |

| Other | | | 2,685 | | | | (27,374 | ) | | | 16,064 | | | | (26,118 | ) |

| Changes in operating assets and liabilities | | | 20,046 | | | | (5,727 | ) | | | 15,888 | | | | (41,399 | ) |

| Net cash provided by operating activities | | | 84,046 | | | | 91,795 | | | | 222,023 | | | | 276,687 | |

| | | | | | | | | | | | | | | | | |

| Cash flows from investing activities | | | | | | | | | | | | | | | | |

| Acquisitions | | | (32,068 | ) | | | (162,078 | ) | | | (38,261 | ) | | | (278,185 | ) |

| Additions to property, plant and equipment | | | (25,363 | ) | | | (162,857 | ) | | | (218,558 | ) | | | (392,031 | ) |

| Other | | | 2,876 | | | | 33,215 | | | | 8,698 | | | | 33,954 | |

| Net cash used in investing activities | | | (54,555 | ) | | | (291,720 | ) | | | (248,121 | ) | | | (636,262 | ) |

| | | | | | | | | | | | | | | | | |

| Cash flows from financing activities | | | | | | | | | | | | | | | | |

| Dividends paid | | | (2,559 | ) | | | (2,351 | ) | | | (7,278 | ) | | | (7,037 | ) |

| Distributions paid to noncontrolling interest holders | | | (18,455 | ) | | | (17,917 | ) | | | (55,365 | ) | | | (45,829 | ) |

| Proceeds from (repayments of) bank borrowings | | | - | | | | 46,431 | | | | (7,542 | ) | | | 46,431 | |

| Net proceeds from PVR borrowings | | | 31,000 | | | | 176,600 | | | | 60,000 | | | | 146,000 | |

| Net proceeds from (repayments of) Company borrowings | | | (70,000 | ) | | | (25,000 | ) | | | (332,000 | ) | | | 58,000 | |

| Net proceeds from issuance of senior notes | | | - | | | | - | | | | 291,009 | | | | - | |

| Net proceeds from issuance of PVR partners' capital | | | - | | | | - | | | | - | | | | 138,015 | |

| Net proceeds from the sale of PVG units | | | 118,080 | | | | - | | | | 118,080 | | | | - | |

| Net proceeds from issuance of equity | | | - | | | | - | | | | 64,835 | | | | - | |

| Other | | | (860 | ) | | | (2,311 | ) | | | (18,945 | ) | | | 8,475 | |

| Net cash provided by financing activities | | | 57,206 | | | | 175,452 | | | | 112,794 | | | | 344,055 | |

| | | | | | | | | | | | | | | | | |

| Net increase (decrease) in cash and cash equivalents | | | 86,697 | | | | (24,473 | ) | | | 86,696 | | | | (15,520 | ) |

| Cash and cash equivalents – beginning of period | | | 18,337 | | | | 43,480 | | | | 18,338 | | | | 34,527 | |

| Cash and cash equivalents – end of period | | $ | 105,034 | | | $ | 19,007 | | | $ | 105,034 | | | $ | 19,007 | |

| | | | | | | | | | | | | | | | | |

| Supplemental disclosure: | | | | | | | | | | | | | | | | |

| Cash paid (received) during the periods for: | | | | | | | | | | | | | | | | |

| Interest | | $ | 6,055 | | | $ | 8,599 | | | $ | 31,309 | | | $ | 26,490 | |

| Income taxes | | $ | (1,047 | ) | | $ | 2,791 | | | $ | 1,906 | | | $ | 4,970 | |

The accompanying notes are an integral part of these consolidated financial statements.

PENN VIRGINIA CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – unaudited

September 30, 2009

1. Organization

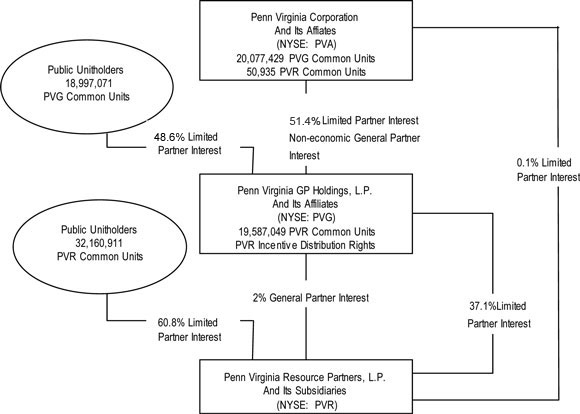

Penn Virginia Corporation (“Penn Virginia,” the “Company,” “we,” “us” or “our”) is an independent oil and gas company primarily engaged in the development, exploration and production of natural gas and oil in various domestic onshore regions including East Texas, the Mid-Continent, Appalachia, Mississippi and the Gulf Coast. We also indirectly own partner interests in Penn Virginia Resource Partners, L.P. (“PVR”), a publicly traded limited partnership formed by us in 2001. Our ownership interests in PVR are held principally through our general partner interest and 51.4% limited partner interest in Penn Virginia GP Holdings, L.P. (“PVG”), a publicly traded limited partnership formed by us in 2006. As of September 30, 2009, PVG owned an approximately 37% limited partner interest in PVR and 100% of the general partner of PVR, which holds a 2% general partner interest in PVR and all of the incentive distribution rights.

We are engaged in three primary business segments: (i) oil and gas, (ii) coal and natural resource management and (iii) natural gas midstream. We directly operate our oil and gas segment and PVR operates our coal and natural resource management and natural gas midstream segments.

2. Basis of Presentation

Our consolidated financial statements include the accounts of Penn Virginia and all of its subsidiaries, including PVG and PVR. Investments in non-controlled entities over which we exercise significant influence are accounted for using the equity method. Intercompany balances and transactions have been eliminated in consolidation. Our consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America. These statements involve the use of estimates and judgments where appropriate. In the opinion of management, all adjustments, consisting of normal recurring accruals, considered necessary for a fair presentation of our consolidated financial statements have been included. Our consolidated financial statements should be read in conjunction with our consolidated financial statements and footnotes included in our Annual Report on Form 10-K for the year ended December 31, 2008. Operating results for the three and nine months ended September 30, 2009 are not necessarily indicative of the results that may be expected for the year ending December 31, 2009. Certain reclassifications have been made to conform to the current period’s presentation. In preparing the accompanying consolidated financial statements, we have evaluated subsequent events through November 5, 2009.

3. Noncontrolling Interests

Effective January 1, 2009, we adopted the new accounting standard on noncontrolling interests in consolidated financial statements. This standard requires that the noncontrolling interests in PVG and PVR be reported on our consolidated balance sheets as a separate item within shareholders’ equity. Net income attributable to the noncontrolling interests in PVG and PVR is separately presented on the face of our consolidated statements of income. Our consolidated financial statements have been retroactively adjusted to reflect the adoption of this standard. Comprehensive income attributable to the noncontrolling interests in PVG and PVR is separately presented in our schedule of comprehensive income. The standard also requires that gains from the sales of subsidiary units be recorded directly to shareholders’ equity. If we sell sufficient controlling interests in our subsidiaries to require deconsolidation of those subsidiaries, then we expect to record a gain or loss on our consolidated statements of income.

The following is a reconciliation of the carrying amount of shareholders’ equity attributable to us, shareholders’ equity attributable to the noncontrolling interests in PVG and PVR and total shareholders’ equity:

| | | Penn Virginia | | | | | | Total | | | | |

| | | Corporation | | | Noncontrolling | | | Shareholders' | | | Comprehensive | |

| | | Shareholders | | | Interests | | | Equity | | | Income (Loss) | |

| | | (in thousands) | |

| Balance at December 31, 2008 | | $ | 1,039,103 | | | $ | 297,227 | | | $ | 1,336,330 | | | | |

| Dividends paid ($0.05625 per share) | | | (7,276 | ) | | | - | | | | (7,276 | ) | | | |

| Distributions to noncontrolling interests holders | | | - | | | | (55,365 | ) | | | (55,365 | ) | | | |

| Issuance of equity | | | 64,835 | | | | - | | | | 64,835 | | | | |

| Sale of PVG units | | | 32,739 | | | | 67,713 | | | | 100,452 | | | | |

| Other changes to shareholders' equity | | | 6,688 | | | | 2,416 | | | | 9,104 | | | | |

| Comprehensive income: | | | | | | | | | | | | | | | |

| Net income (loss) | | | (109,292 | ) | | | 20,512 | | | | (88,780 | ) | | $ | (88,780 | ) |

| Hedging unrealized gain (loss), net of tax | | | 291 | | | | (353 | ) | | | (62 | ) | | | (62 | ) |

| Hedging reclassification adjustment, net of tax | | | 2,293 | | | | 1,081 | | | | 3,374 | | | | 3,374 | |

| Balance at September 30, 2009 | | $ | 1,029,381 | | | $ | 333,231 | | | $ | 1,362,612 | | | $ | (85,468 | ) |

| | | | | | | | | | | | | | | | | |

| Balance at December 31, 2007 | | $ | 835,793 | | | $ | 174,420 | | | $ | 1,010,213 | | | | | |

| Dividends paid ($0.05625 per share) | | | (7,039 | ) | | | - | | | | (7,039 | ) | | | | |

| Distributions to noncontrolling interests holders | | | - | | | | (45,829 | ) | | | (45,829 | ) | | | | |

| Issuance of PVR units | | | - | | | | 138,015 | | | | 138,015 | | | | | |

| Recognition of SAB 51 gain | | | 39,723 | | | | (39,723 | ) | | | - | | | | | |

| Sale of PVG units | | | 36,429 | | | | - | | | | 36,429 | | | | | |

| Change related to acquisition | | | - | | | | 23,469 | | | | 23,469 | | | | | |

| Other changes to shareholders' equity | | | 14,967 | | | | 1,845 | | | | 16,812 | | | | | |

| Comprehensive income: | | | | | | | | | | | | | | | | |

| Net income | | | 121,598 | | | | 52,252 | | | | 173,850 | | | $ | 173,850 | |

| Hedging unrealized loss, net of tax | | | (408 | ) | | | (1,657 | ) | | | (2,065 | ) | | | (2,065 | ) |

| Hedging reclassification adjustment, net of tax | | | 220 | | | | 4,561 | | | | 4,781 | | | | 4,781 | |

| Balance at September 30, 2008 | | $ | 1,041,283 | | | $ | 307,353 | | | $ | 1,348,636 | | | $ | 176,566 | |

In September 2009, we sold 10,000,000 common units of PVG owned by us for $118.1 million, which increased noncontrolling interests by $67.7 million and additional paid-in capital by $50.4 million less $17.7 million in taxes. Prior to the sale, we owned 30,077,429 PVG common units, representing a 77.0% limited partner interest in PVG. After the sale, we owned 20,077,429 PVG common units, representing a 51.4% limited partner interest in PVG.

The following table discloses the effects of changes in our ownership interest in PVG on our equity:

| | | Three Months Ended | | | Nine Months Ended | |

| | | September 30, 2009 | | | September 30, 2009 | |

| | | (in thousands) | |

| Loss attributable to PennVirginia Corporation | | $ | (79,900 | ) | | $ | (109,292 | ) |

| Transfer to noncontrolling interests | | | | | | | | |

| Increase in PennVirginia Corporation's paid-in capital | | | | | | | | |

| for sale of PVG units, net of $17,629 in taxes | | | 32,739 | | | | 32,739 | |

| Changes from loss attributable to PennVirginia Corporation and transfer to noncontrolling interests | | $ | (47,161 | ) | | $ | (76,553 | ) |

4. Fair Value Measurements

Effective January 1, 2009, we adopted the new accounting standard on fair value measurements and disclosures applicable to both our financial and nonfinancial assets and liabilities that are measured and reported on a fair value basis. Our financial instruments that are subject to fair value disclosures consist of cash and cash equivalents, accounts receivable, assets held for sale, accounts payable, derivative instruments and long-term debt. We have followed consistent methods and assumptions to estimate the fair values as more fully described in our Annual Report on Form 10-K for the year ended December 31, 2008. In addition to those methods, the fair value of assets held for sale was derived using a market approach based on indications of interest from potential third-party purchasers of the assets. At September 30, 2009, the carrying values of all of these financial instruments, except the portion of long-term debt attributable to our 4.50% Convertible Senior Subordinated Notes due 2012 (the “Convertible Notes”), approximated fair value. The fair value of the portion of our long-term debt attributable to the Convertible Notes at September 30, 2009 was $206.9 million, which was derived from quoted market prices.

The following table summarizes the valuation of certain assets and liabilities by category as of September 30, 2009:

| | | | | | Fair Value Measurement at September 30, 2009, Using | |

| Description | | Fair Value

Measurements at

September 30, 2009 | | | Quoted Prices in Active

Markets for Identical

Assets (Level 1) | | | Significant Other

Observable Inputs

(Level 2) | | | Significant

Unobservable

Inputs (Level 3) | |

| | | | | | (in thousands) | |

| Publicly traded equities | | $ | 5,257 | | | $ | 5,257 | | | $ | - | | | $ | - | |

| Deferred compensation - noncurrent liability | | | (5,955 | ) | | | (5,955 | ) | | | - | | | | - | |

| Interest rate swap assets - noncurrent | | | 1,138 | | | | - | | | | 1,138 | | | | - | |

| Interest rate swap liabilities - current | | | (10,629 | ) | | | - | | | | (10,629 | ) | | | - | |

| Interest rate swap liabilities - noncurrent | | | (4,548 | ) | | | - | | | | (4,548 | ) | | | - | |

| Commodity derivative assets - current | | | 25,674 | | | | - | | | | 25,674 | | | | - | |

| Commodity derivative assets - noncurrent | | | 813 | | | | - | | | | 813 | | | | - | |

| Commodity derivative liabilities - current | | | (5,631 | ) | | | - | | | | (5,631 | ) | | | - | |

| Commodity derivative liabilities - noncurrent | | | (2,670 | ) | | | - | | | | (2,670 | ) | | | - | |

| Assets held for sale | | | 47,107 | | | | - | | | | 47,107 | | | | - | |

| Total | | $ | 50,556 | | | $ | (698 | ) | | $ | 51,254 | | | $ | - | |

See Note 5, “Derivative Instruments,” for the effects of derivative instruments on our consolidated financial statements.

5. Derivative Instruments

Commodity Derivatives

Oil and Gas Segment

We determine the fair values of our oil and gas derivative agreements using third-party quoted forward prices for NYMEX Henry Hub gas and West Texas Intermediate crude oil as of the end of the reporting period and discount rates adjusted for the credit risk of our counterparties if the derivative in an asset position and our own credit risk if the derivative is in a liability position. ��The following table sets forth our oil and gas commodity derivative positions as of September 30, 2009:

| | | Average | | | Weighted Average Price | | | Fair Value at | |

| | | Volume | | | Additional | | | | | | | | | September 30, | |

| | | Per Day | | | Put Option | | | Floor | | | Ceiling | | | 2009 | |

| | | | | | | | | | | (in thousands) | |

| Natural Gas Costless Collars | | (MMBtu) | | | ($ per MMBtu) | | | | |

| Fourth Quarter 2009 | | 15,000 | | | | | | | 4.25 | | | | 5.70 | | | $ | 64 | |

| First Quarter 2010 | | 35,000 | | | | | | | 4.96 | | | | 7.41 | | | | (325 | ) |

| Second Quarter 2010 | | 30,000 | | | | | | | 5.33 | | | | 8.02 | | | | 539 | |

| Third Quarter 2010 | | 30,000 | | | | | | | 5.33 | | | | 8.02 | | | | 204 | |

| Fourth Quarter 2010 | | 50,000 | | | | | | | 5.65 | | | | 8.77 | | | | 201 | |

| First Quarter 2011 | | 50,000 | | | | | | | 5.65 | | | | 8.77 | | | | (1,266 | ) |

| Second Quarter 2011 | | 30,000 | | | | | | | 5.67 | | | | 7.58 | | | | (188 | ) |

| Third Quarter 2011 | | 30,000 | | | | | | | 5.67 | | | | 7.58 | | | | (498 | ) |

| | | | | | | | | | | | | | | |

| Natural Gas Three-Way Collars | | (MMBtu) | | | ($ per MMBtu) | | | | | |

| Fourth Quarter 2009 | | 30,000 | | | | 6.83 | | | | 9.50 | | | | 13.60 | | | | 7,084 | |

| First Quarter 2010 | | 30,000 | | | | 6.83 | | | | 9.50 | | | | 13.60 | | | | 6,055 | |

| | | | | | | | | | | | | | | | | | | | |

| Natural Gas Swaps | | (MMBtu) | | | ($ per MMBtu) | | | | | |

| Fourth Quarter 2009 | | 40,000 | | | | | | | | 4.91 | | | | | | | | 579 | |

| First Quarter 2010 | | 15,000 | | | | | | | | 6.19 | | | | | | | | 297 | |

| Second Quarter 2010 | | 30,000 | | | | | | | | 6.17 | | | | | | | | 554 | |

| Third Quarter 2010 | | 30,000 | | | | | | | | 6.17 | | | | | | | | (31 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Crude Oil Three-Way Collars | | (barrels) | | | ($ per barrel) | | | | | |

| Fourth Quarter 2009 | | 500 | | | | 80.00 | | | | 110.00 | | | | 179.00 | | | | 1,315 | |

| | | | | | | | | | | | | | | | | | | | | |

| Crude Oil Swaps | | (barrels) | | | ($ per barrel) | | | | | |

| Fourth Quarter 2009 | | 500 | | | | | | | | 59.25 | | | | | | | | (541 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Crude Oil Costless Collars | | (barrels) | | | ($ per barrel) | | | | | |

| First Quarter 2010 | | 500 | | | | | | | | 60.00 | | | | 74.75 | | | | (159 | ) |

| Second Quarter 2010 | | 500 | | | | | | | | 60.00 | | | | 74.75 | | | | (227 | ) |

| Third Quarter 2010 | | 500 | | | | | | | | 60.00 | | | | 74.75 | | | | (271 | ) |

| Fourth Quarter 2010 | | 500 | | | | | | | | 60.00 | | | | 74.75 | | | | (317 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Settlements to be paid in subsequent period | | | | | | | | | | | | | | | | | | | 297 | |

| | | | | | | | | | | | | | | | | | | | | |

| Oil and gas segment commodity derivatives - net asset | | | | | | | $ | 13,366 | |

See the “Financial Statement Impact of Derivatives” section below for the impact of our oil and gas commodity derivatives on our consolidated financial statements.

PVR Natural Gas Midstream Segment

PVR determines the fair values of its derivative agreements using quoted forward prices for the respective commodities as of the end of the reporting period and discount rates adjusted for the credit risk of PVR’s counterparties if the derivative is in an asset position and PVR’s own credit risk if the derivative is in a liability position. The following table sets forth PVR’s positions as of September 30, 2009 for commodities related to natural gas midstream revenues and cost of midstream gas purchased:

| | | Average | | | | | | Weighted Average Price | | | Fair Value at | |

| | | Volume | | | Swap | | | Additional | | | | | | | | | September 30, | |

| | | Per Day | | | Price | | | Put Option | | | Put | | | Call | | | 2009 | |

| | | | | | | | | | | | | | | | | | (in thousands) | |

| Crude Oil Three-Way Collar | | (barrels) | | | | | | | | | ($ per barrel) | | | | |

| Fourth Quarter 2009 | | 1,000 | | | | | | | 70.00 | | | | 90.00 | | | | 119.25 | | | $ | 1,433 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| Frac Spread Collar | | (MMBtu) | | | | | | | | | | ($ per MMBtu) | | | | | |

| Fourth Quarter 2009 | | 6,000 | | | | | | | | | | | 9.09 | | | | 13.94 | | | | 864 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| Crude Oil Collar | | (barrels) | | | | | | | | | | ($ per barrel) | | | | | |

| First Quarter 2010 through Fourth Quarter 2010 | | 750 | | | | | | | | | | | 70.00 | | | | 81.25 | | | | 228 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| Crude Oil Collar | | (barrels) | | | | | | | | | | ($ per barrel) | | | | | |

| First Quarter 2010 through Fourth Quarter 2010 | | 1,000 | | | | | | | | | | | 68.00 | | | | 80.00 | | | | (155 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| Natural Gas Purchase Swap | | (MMBtu) | | | ($ per MMbtu) | | | | | | | | | | | | |

| First Quarter 2010 through Fourth Quarter 2010 | | 5,000 | | | | 5.815 | | | | | | | | | | | | | | | | 709 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Settlements to be received in subsequent period | | | | | | | | | | | | | | | | | | | | | | | 1,742 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Natural gas midstream segment commodity derivatives - net asset | | | | | | | | | | | | | | | | | | | $ | 4,821 | |

See the “Financial Statement Impact of Derivatives” section below for the impact of PVR’s natural gas midstream commodity derivatives on our consolidated financial statements.

Interest Rate Swaps

In 2006, we entered into interest rate swaps (the “Interest Rate Swaps”) with notional amounts of $50.0 million to establish fixed interest rates on a portion of the then outstanding borrowings under our revolving credit facility (the “Revolver”) through December 2010. During the first quarter of 2009, we discontinued hedge accounting for all of the Interest Rate Swaps. Accordingly, subsequent fair value gains and losses for the Interest Rate Swaps were recognized in the derivative line item on our consolidated statements of income.

We reported a net derivative liability of $2.9 million at September 30, 2009 related to the Interest Rate Swaps. In September 2009, we paid off all amounts outstanding under the Revolver and, as a result, we reclassified the net hedging losses remaining in accumulated other comprehensive income (“AOCI”) related to the Interest Rate Swaps from AOCI to interest expense. In connection with periodic settlements and the pay down of the Revolver, we reclassified a total of $3.4 million of net hedging losses on the Interest Rate Swaps from AOCI to interest expense during the nine months ended September 30, 2009. See the “Financial Statement Impact of Derivatives” section below for the impact of the Interest Rate Swaps on our consolidated financial statements.

PVR Interest Rate Swaps

PVR has entered into interest rate swaps (the “PVR Interest Rate Swaps”) to establish fixed interest rates on a portion of the outstanding borrowings under its revolving credit facility (the “PVR Revolver”). The following table sets forth the PVR Interest Rate Swap positions at September 30, 2009:

| Dates | | Notional Amounts | | | Weighted-Average Fixed Rate | |

| | | (in millions) | | | | |

| Until March 2010 | | $ | 310.0 | | | | 3.54 | % |

| March 2010 - December 2011 | | $ | 250.0 | | | | 3.37 | % |

| December 2011 - December 2012 | | $ | 100.0 | | | | 2.09 | % |

During the first quarter of 2009, PVR discontinued hedge accounting for all of the PVR Interest Rate Swaps. Accordingly, subsequent fair value gains and losses for the PVR Interest Rate Swaps are recognized in the derivatives line item on our consolidated statements of income. At September 30, 2009, a $2.2 million loss remained in AOCI related to the PVR Interest Rate Swaps. The $2.2 million loss will be recognized in interest expense as the PVR Interest Rate Swaps settle.

PVR reported a (i) net derivative liability of $11.2 million at September 30, 2009 and (ii) loss in AOCI of $2.2 million at September 30, 2009 related to the PVR Interest Rate Swaps. In connection with periodic settlements, PVR reclassified a total of $2.6 million of net hedging losses on the PVR Interest Rate Swaps from AOCI to interest expense during the nine months ended September 30, 2009. See the “Financial Statement Impact of Derivatives” section below for the impact of the PVR Interest Rate Swaps on our consolidated financial statements.

Financial Statement Impact of Derivatives

The following table summarizes the effects of our and PVR’s derivative activities, as well as the location of the gains and losses, on our consolidated statements of income for the three and nine months ended September 30, 2009 and 2008:

| | | Location of gain (loss) | | Three Months Ended | | | Nine Months Ended | |

| | | on derivatives recognized | | September 30, | | | September 30, | |

| | | in income | | 2009 | | | 2008 | | | 2009 | | | 2008 | |

| | | | | (in thousands) | |

| Derivatives de-designated as hedging instruments: | | | | | | | | | | | | | | |

| Interest rate contracts (1) | | Interest expense | | $ | (3,781 | ) | | $ | (1,179 | ) | | $ | (6,464 | ) | | $ | (1,891 | ) |

Increase (decrease) in net income resulting from derivatives de-designated as hedging instruments | | | | | (3,781 | ) | | | (1,179 | ) | | | (6,464 | ) | | | (1,891 | ) |

| | | | | | | | | | | | | | | | | | | |

| Derivatives not designated as hedging instruments: | | | | | | | | | | | | | | | | | | |

| Interest rate contracts | | Derivatives | | | (4,368 | ) | | | (1,333 | ) | | | (3,849 | ) | | | (1,333 | ) |

| Commodity contracts (1) | | Natural gas midstream revenues | | | - | | | | (1,987 | ) | | | - | | | | (6,235 | ) |

| Commodity contracts (1) | | Cost of midstream gas purchased | | | - | | | | 484 | | | | - | | | | 2,107 | |

| Commodity contracts | | Derivatives | | | 1,839 | | | | 126,464 | | | | 12,327 | | | | (3,055 | ) |

Increase (decrease) in net income resulting from derivatives not designated as hedging instruments | | | | | (2,529 | ) | | | 123,628 | | | | 8,478 | | | | (8,516 | ) |

| | | | | | | | | | | | | | | | | | | |

| Total increase (decrease) in net income resulting from derivatives | | | | $ | (6,310 | ) | | $ | 122,449 | | | $ | 2,014 | | | $ | (10,407 | ) |

| | | | | | | | | | | | | | | | | | | |

| Realized and unrealized derivative impact: | | | | | | | | | | | | | | | | | | |

| Cash received (paid) for commodity and interest rate settlements | | Derivatives | | $ | 15,507 | | | $ | (19,755 | ) | | $ | 51,936 | | | $ | (46,740 | ) |

| Cash paid for interest rate contract settlements | | Interest expense | | | - | | | | (1,179 | ) | | | (808 | ) | | | (1,891 | ) |

| Unrealized derivative gain (loss) (2) | | | | | (21,817 | ) | | | 143,383 | | | | (49,114 | ) | | | 38,224 | |

| Total increase (decrease) in net income resulting from derivatives | | | | $ | (6,310 | ) | | $ | 122,449 | | | $ | 2,014 | | | $ | (10,407 | ) |

| (1) | Represents amounts reclassified out of AOCI and into interest expense. At September 30, 2009, a $2.2 million loss remained in AOCI related to the PVR Interest Rate Swaps on which PVR discontinued hedge accounting. |

| (2) | Represents net unrealized gains (losses) in the natural gas midstream, cost of midstream gas purchased, interest expense and derivatives line items on our consolidated statements of income. |

The following table summarizes the fair value of our and PVR’s derivative instruments, as well as the locations of these instruments, on our consolidated balance sheets as of September 30, 2009 and December 31, 2008:

| | | | Fair Values at | | | Fair Values at | |

| | | | September 30, 2009 | | | December 31, 2008 | |

| | | | Derivative | | | Derivative | | | Derivative | | | Derivative | |

| | Balance Sheet Location | | Assets | | | Liabilities | | | Assets | | | Liabilities | |

| | | | (in thousands) | |

| Derivatives de-designated as hedging instruments: | | | | | | | | | | | | | |

| Interest rate contracts | Derivative liabilities - current | | $ | xx | | | $ | - | | | $ | - | | | $ | 3,177 | |

| Interest rate contracts | Derivative liabilities - noncurrent | | | - | | | | - | | | | - | | | | 3,648 | |

| Total derivatives de-designated as hedging instruments | | | - | | | | - | | | | - | | | | 6,825 | |

| | | | | | | | | | | | | | | | | | |

| Derivatives not designated as hedging instruments: | | | | | | | | | | | | | | | | | |

| Interest rate contracts | Derivative assets/liabilities - current | | | - | | | | 10,629 | | | | - | | | | 4,663 | |

| Interest rate contracts | Derivative assets/liabilities - noncurrent | | | 1,138 | | | | 4,548 | | | | - | | | | 5,073 | |

| Commodity contracts | Derivative assets/liabilities - current | | | 25,674 | | | | 5,631 | | | | 67,569 | | | | 7,694 | |

| Commodity contracts | Derivative assets/liabilities - noncurrent | | | 813 | | | | 2,670 | | | | 4,070 | | | | - | |

| Total derivatives not designated as hedging instruments | | | 27,625 | | | | 23,478 | | | | 71,639 | | | | 17,430 | |

| | | | | | | | | | | | | | | | | | |

| Total fair value of derivative instruments | | | $ | 27,625 | | | $ | 23,478 | | | $ | 71,639 | | | $ | 24,255 | |

See Note 4, “Fair Value Measurements,” for a description of how the above-described financial instruments are valued.

The following table summarizes our interest expense for the three and nine months ended September 30, 2009 and 2008, including the effect of the Interest Rate Swaps and the PVR Interest Rate Swaps:

| | | Three Months Ended September 30, | | | Nine Months Ended September 30, | |

| Source | | 2009 | | | 2008 | | | 2009 | | | 2008 | |

| | | (in thousands) | |

| Interest on borrowings | | $ | 19,567 | | | $ | 12,534 | | | $ | 45,565 | | | $ | 35,652 | |

| Capitalized interest | | | (566 | ) | | | (492 | ) | | | (1,697 | ) | | | (2,230 | ) |

| Interest rate swaps | | | 3,783 | | | | 1,179 | | | | 6,464 | | | | 1,891 | |

| Total interest expense | | $ | 22,784 | | | $ | 13,221 | | | $ | 50,332 | | | $ | 35,313 | |

At September 30, 2009, we reported a commodity derivative asset related to our oil and gas segment of $13.4 million. At September 30, 2009, we reported a commodity derivative asset related to the PVR natural gas midstream segment of $4.8 million. The contracts underlying such commodity derivative asset are with four counterparties, all of which are investment grade financial institutions, and such commodity derivative asset is substantially concentrated with one of those counterparties. This concentration may impact our overall credit risk, either positively or negatively, in that these counterparties may be similarly affected by changes in economic or other conditions. Neither we nor PVR paid or received collateral with respect to our or PVR’s derivative positions. The maximum amount of loss due to credit risk if counterparties to our or PVR’s derivative asset positions fail to perform according to the terms of the contracts would be equal to the fair value of the contracts as of September 30, 2009. No significant uncertainties related to the collectability of amounts owed to us or PVR exist with regard to these counterparties.

The above-described hedging activity represents cash flow hedges. As of September 30, 2009, neither we nor PVR owned any derivative instruments that were classified as fair value hedges or trading securities or that contained credit risk contingencies.

6. Common Stock Offering

On May 22, 2009, we completed the sale of 3.5 million shares of our common stock in a registered public offering. The net sales proceeds of $64.8 million were used to repay borrowings under the Revolver.

7. Long-Term Debt

The long-term debt on our consolidated balance sheet as of September 30, 2009 consisted of our 10.375% Senior Notes due 2016 (the “Senior Notes”), the Convertible Notes and PVR’s outstanding debt under the PVR Revolver. There was no debt outstanding under the Revolver as of September 30, 2009.

In June 2009, we issued and sold $300.0 million of Senior Notes. The Senior Notes mature on June 15, 2016 and bear interest at an annual rate of 10.375%. The Senior Notes were sold at 97% of par, equating to an effective yield to maturity of approximately 11%. The net proceeds from the sale of the Senior Notes of $281.6 million were used to repay borrowings under the Revolver. The obligations under the Senior Notes are fully and unconditionally guaranteed by our oil and gas subsidiaries, which are also guarantors under the Revolver. See Note 8, “Guarantor Subsidiaries.”

In December 2007, we issued and sold $230.0 million of Convertible Notes. The Convertible Notes mature on November 15, 2012 and bear interest at an annual rate of 4.50%. See Note 9, “Convertible Notes.”

In June 2009, the borrowing base under the Revolver was revised from $450.0 million to $367.0 million due to the issuance of the Senior Notes. The Revolver, which matures in December 2010, is secured by a portion of our proved reserves. As of December 31, 2008, the weighted average interest rate on borrowings outstanding under the Revolver was approximately 2.6%. As of September 30, 2009, we had no debt outstanding under the Revolver. Interest is payable at a base rate plus an applicable margin of ranging from 1.125% to 2.125% if we select the base rate borrowing option under the Revolver, or at a rate derived from the London Interbank Offered Rate (“LIBOR”) plus an applicable margin ranging from 2.00% to 3.00% if we select the LIBOR-based borrowing option.

In March 2009, PVR increased the size of the PVR Revolver from $700.0 million to $800.0 million, which resulted in $9.3 million of debt issuance costs that will be amortized over the remaining life of the PVR Revolver. The PVR Revolver is secured with substantially all of PVR’s assets. The December 2011 maturity date for the PVR Revolver did not change. As of September 30, 2009, all of PVR’s long-term debt was indebtedness outstanding under the PVR Revolver. PVR’s debt is non-recourse to us and PVG. Interest is payable at a base rate plus an applicable margin of up to 1.25% if PVR selects the base rate borrowing option under the PVR Revolver, or at a rate derived from the LIBOR plus an applicable margin ranging from 1.75% to 2.75% if PVR selects the LIBOR-based borrowing option. As of September 30, 2009 and December 31, 2008, the weighted average interest rate on borrowings outstanding under the PVR Revolver was approximately 2.5% and 3.2%.

The following table summarizes our and PVR’s long-term debt as of September 30, 2009 and December 31, 2008:

| | | September 30, | | | December 31, | |

| | | 2009 | | | 2008 | |

| | | (in thousands) | |

| Short-term borrowings | | $ | - | | | $ | 7,542 | |

| Revolving credit facility | | | - | | | | 332,000 | |

| Senior notes, net of discount (1) | | | 291,432 | | | | - | |

| Convertible notes, net of discount | | | 204,935 | | | | 199,896 | |

| Total recourse debt of the Company | | $ | 496,367 | | | $ | 539,438 | |

| Long-term debt of PVR | | | 628,100 | | | | 568,100 | |

| | | | | | | | | |

| Total consolidated debt | | | 1,124,467 | | | | 1,107,538 | |

| Less: Short-term borrowings | | | - | | | | (7,542 | ) |

| Total consolidated long-term debt | | $ | 1,124,467 | | | $ | 1,099,996 | |

| (1) | Includes original issue discount of $9.0 million, which is amortizable through June 15, 2016. |

8. Guarantors Subsidiaries

The Senior Notes are fully and unconditionally and joint and severally guaranteed by our oil and gas subsidiaries (collectively, the “Guarantor Subsidiaries”). The primary non-guarantor subsidiaries are PVG and PVR (collectively, the “Non-guarantor Subsidiaries”). As such, the Company is subject to the requirements Rule 3-10(f) of Regulation S-X of the Securities and Exchange Commission regarding financial statements of guarantors and issuers of registered guaranteed securities.

The condensed consolidating financial information below present the financial position, results of operations and cash flows of the Company, the Guarantor Subsidiaries and Non-guarantor Subsidiaries:

| Balance Sheets | | September 30, 2009 | |

| | | Penn Virginia | | | Guarantor | | | Non-guarantor | | | | | | | |

| | | Corporation | | | Subsidiaries | | | Subsidiaries | | | Eliminations | | | Consolidated | |

| | | (in thousands) | |

| Assets | | | |

| Cash and cash equivalents | | $ | 83,336 | | | $ | - | | | $ | 21,698 | | | $ | - | | | $ | 105,034 | |

| Accounts receivable | | | - | | | | 40,449 | | | | 60,005 | | | | - | | | | 100,454 | |

| Inventory | | | - | | | | 10,314 | | | | 1,820 | | | | - | | | | 12,134 | |

| Assets held for sale | | | - | | | | 47,107 | | | | - | | | | - | | | | 47,107 | |

| Other current assets | | | 16,794 | | | | 341 | | | | 12,525 | | | | (906 | ) | | | 28,754 | |

| Total current assets | | | 100,130 | | | | 98,211 | | | | 96,048 | | | | (906 | ) | | | 293,483 | |

| Property and equipment, net | | | 7,074 | | | | 1,483,397 | | | | 910,103 | | | | (28,251 | ) | | | 2,372,323 | |

| Investments in affiliates (equity method) | | | 1,492,547 | | | | 183,762 | | | | - | | | | (1,676,309 | ) | | | - | |

| Other assets | | | 19,476 | | | | 48 | | | | 237,809 | | | | (21,870 | ) | | | 235,463 | |

| Total assets | | $ | 1,619,227 | | | $ | 1,765,418 | | | $ | 1,243,960 | | | $ | (1,727,336 | ) | | $ | 2,901,269 | |

| | | | | | | | | | | | | | | | | | | | | |

| Liabilities and shareholders’ equity | | | | | | | | | | | | | | | | | | | | |

| Accounts payable and accrued liabilities | | $ | 16,831 | | | $ | 45,615 | | | $ | 57,734 | | | $ | - | | | $ | 120,180 | |

| Other current liabilities | | | 16,960 | | | | - | | | | 10,900 | | | | (2,684 | ) | | | 25,176 | |

| Total current liabilities | | | 33,791 | | | | 45,615 | | | | 68,634 | | | | (2,684 | ) | | | 145,356 | |

| Deferred income taxes | | | 19,137 | | | | 220,552 | | | | - | | | | (21,869 | ) | | | 217,820 | |

| Long-term debt of PVR | | | - | | | | - | | | | 628,100 | | | | - | | | | 628,100 | |

| Long-term debt of the Company | | | 496,367 | | | | - | | | | - | | | | - | | | | 496,367 | |

| Other long-term liabilities | | | 14,077 | | | | 6,704 | | | | 30,233 | | | | - | | | | 51,014 | |

| Shareholders’ equity | | | 1,055,855 | | | | 1,492,547 | | | | 183,762 | | | | (1,702,783 | ) | | | 1,029,381 | |

| Noncontrolling interests in subsidiaries | | | - | | | | - | | | | 333,231 | | | | - | | | | 333,231 | |

| Total liabilities and shareholders’ equity | | $ | 1,619,227 | | | $ | 1,765,418 | | | $ | 1,243,960 | | | $ | (1,727,336 | ) | | $ | 2,901,269 | |

| Balance Sheets | | December 31, 2008 | |

| | | Penn Virginia | | | Guarantor | | | Non-guarantor | | | | | | | |

| | | Corporation | | | Subsidiaries | | | Subsidiaries | | | Eliminations | | | Consolidated | |

| | | (in thousands) | |

| Assets | | | |

| Cash and cash equivalents | | $ | - | | | $ | - | | | $ | 18,338 | | | $ | - | | | $ | 18,338 | |

| Accounts receivable | | | - | | | | 75,962 | | | | 73,279 | | | | - | | | | 149,241 | |

| Inventory | | | - | | | | 16,595 | | | | 1,873 | | | | - | | | | 18,468 | |

| Other current assets | | | 37,455 | | | | 7,241 | | | | 32,823 | | | | (48 | ) | | | 77,471 | |

| Total current assets | | | 37,455 | | | | 99,798 | | | | 126,313 | | | | (48 | ) | | | 263,518 | |

| Property and equipment, net | | | 8,255 | | | | 1,637,832 | | | | 895,247 | | | | (29,157 | ) | | | 2,512,177 | |

| Investments in affiliates (equity method) | | | 1,574,758 | | | | 268,314 | | | | - | | | | (1,843,072 | ) | | | - | |

| Other assets | | | 32,857 | | | | 49 | | | | 237,065 | | | | (49,101 | ) | | | 220,870 | |

| Total assets | | $ | 1,653,325 | | | $ | 2,005,993 | | | $ | 1,258,625 | | | $ | (1,921,378 | ) | | $ | 2,996,565 | |

| | | | | | | | | | | | | | | | | | | | | |

Liabilities and shareholders’ equity | | | | | | | | | | | | | | | | | | | | |

| Current maturities of long-term debt | | $ | 7,542 | | | $ | - | | | $ | - | | | $ | - | | | $ | 7,542 | |

| Accounts payable and accrued liabilities | | | 8,294 | | | | 129,190 | | | | 69,418 | | | | - | | | | 206,902 | |

| Other current liabilities | | | 15,032 | | | | - | | | | 18,166 | | | | (48 | ) | | | 33,150 | |

| Total current liabilities | | | 30,868 | | | | 129,190 | | | | 87,584 | | | | (48 | ) | | | 247,594 | |

| Deferred income taxes | | | 11,868 | | | | 295,270 | | | | - | | | | (49,101 | ) | | | 258,037 | |

| Long-term debt of PVR | | | - | | | | - | | | | 568,100 | | | | - | | | | 568,100 | |

| Long-term debt of the Company | | | 531,896 | | | | - | | | | - | | | | - | | | | 531,896 | |

| Other long-term liabilities | | | 10,433 | | | | 6,775 | | | | 37,400 | | | | - | | | | 54,608 | |

| Shareholders’ equity | | | 1,068,260 | | | | 1,574,758 | | | | 268,314 | | | | (1,872,229 | ) | | | 1,039,103 | |

| Noncontrolling interests in subsidiaries | | | - | | | | - | | | | 297,227 | | | | - | | | | 297,227 | |

| Total liabilities and shareholders’ equity | | $ | 1,653,325 | | | $ | 2,005,993 | | | $ | 1,258,625 | | | $ | (1,921,378 | ) | | $ | 2,996,565 | |

| Income Statements | | Three Months Ended September 30, 2009 | |

| | | Penn Virginia | | | Guarantor | | | Non-guarantor | | | | | | | |

| | | Corporation | | | Subsidiaries | | | Subsidiaries | | | Eliminations | | | Consolidated | |

| | | (in thousands) | |

| Revenues | | $ | - | | | $ | 55,748 | | | $ | 155,596 | | | $ | (16,181 | ) | | $ | 195,163 | |

| Cost of midstream gas purchased | | | - | | | | - | | | | 92,355 | | | | (15,107 | ) | | | 77,248 | |

| Operating | | | - | | | | 13,277 | | | | 8,964 | | | | (1,074 | ) | | | 21,167 | |

| Exploration | | | - | | | | 16,117 | | | | - | | | | - | | | | 16,117 | |

| Taxes other than income | | | 103 | | | | 4,186 | | | | 1,005 | | | | - | | | | 5,294 | |

| General and administrative | | | 6,359 | | | | 5,133 | | | | 8,454 | | | | - | | | | 19,946 | |

| Depreciation, depletion and amortization | | | 987 | | | | 39,326 | | | | 17,857 | | | | (301 | ) | | | 57,869 | |

| Impairments on assets held for sale | | | - | | | | 87,900 | | | | - | | | | - | | | | 87,900 | |

| Impairments | | | - | | | | 4,453 | | | | - | | | | - | | | | 4,453 | |

| Loss on sale of assets | | | - | | | | - | | | | - | | | | - | | | | - | |

| Operating expenses | | | 7,449 | | | | 170,392 | | | | 128,635 | | | | (16,482 | ) | | | 289,994 | |

| Operating income | | | (7,449 | ) | | | (114,644 | ) | | | 26,961 | | | | 301 | | | | (94,831 | ) |

| Equity in earnings of subsidiaries | | | (65,354 | ) | | | 4,462 | | | | - | | | | 60,892 | | | | - | |

| Interest expense and other | | | (16,841 | ) | | | 566 | | | | (6,161 | ) | | | - | | | | (22,436 | ) |

| Derivatives | | | 281 | | | | - | | | | (2,810 | ) | | | - | | | | (2,529 | ) |

| Income (loss) before income taxes and noncontrolling interests | | | (89,363 | ) | | | (109,616 | ) | | | 17,990 | | | | 61,193 | | | | (119,796 | ) |

| Income tax benefit (expense) | | | 9,162 | | | | 44,262 | | | | (3,019 | ) | | | - | | | | 50,405 | |

| Net income (loss) | | | (80,201 | ) | | | (65,354 | ) | | | 14,971 | | | | 61,193 | | | | (69,391 | ) |

| Less net income attributable to noncontrolling interests | | | - | | | | - | | | | (10,509 | ) | | | - | | | | (10,509 | ) |

| Net income (loss) attributable to Penn Virginia Corporation | | $ | (80,201 | ) | | $ | (65,354 | ) | | $ | 4,462 | | | $ | 61,193 | | | $ | (79,900 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Income Statements | | Three Months Ended September 30, 2008 | |

| | | Penn Virginia | | | Guarantor | | | Non-guarantor | | | | | | | | | |

| | | Corporation | | | Subsidiaries | | | Subsidiaries | | | Eliminations | | | Consolidated | |

| | | (in thousands) | |

| Revenues | | $ | - | | | $ | 156,725 | | | $ | 285,453 | | | $ | (56,566 | ) | | $ | 385,612 | |

| Cost of midstream gas purchased | | | - | | | | - | | | | 211,262 | | | | (55,698 | ) | | | 155,564 | |

| Operating | | | - | | | | 15,067 | | | | 9,238 | | | | (868 | ) | | | 23,437 | |

| Exploration | | | - | | | | 8,346 | | | | - | | | | - | | | | 8,346 | |

| Taxes other than income | | | 145 | | | | 6,537 | | | | 989 | | | | - | | | | 7,671 | |

| General and administrative | | | 5,542 | | | | 5,122 | | | | 7,625 | | | | - | | | | 18,289 | |

| Depreciation, depletion and amortization | | | 867 | | | | 32,665 | | | | 16,907 | | | | (461 | ) | | | 49,978 | |

| Impairments | | | - | | | | - | | | | - | | | | - | | | | - | |

| Operating expenses | | | 6,554 | | | | 67,737 | | | | 246,021 | | | | (57,027 | ) | | | 263,285 | |

| Operating income | | | (6,554 | ) | | | 88,988 | | | | 39,432 | | | | 461 | | | | 122,327 | |

| Equity in earnings of subsidiaries | | | 63,757 | | | | 9,504 | | | | - | | | | (73,261 | ) | | | - | |

| Interest expense and other | | | (6,604 | ) | | | 493 | | | | (11,198 | ) | | | - | | | | (17,309 | ) |

| Derivatives | | | 109,390 | | | | - | | | | 15,742 | | | | - | | | | 125,132 | |

| Income (loss) before income taxes and noncontrolling interests | | | 159,989 | | | | 98,985 | | | | 43,976 | | | | (72,800 | ) | | | 230,150 | |

| Income tax benefit (expense) | | | (37,497 | ) | | | (35,229 | ) | | | (6,195 | ) | | | - | | | | (78,921 | ) |

| Net income (loss) | | | 122,492 | | | | 63,756 | | | | 37,781 | | | | (72,800 | ) | | | 151,229 | |

| Less net income attributable to noncontrolling interests | | | - | | | | - | | | | (28,276 | ) | | | - | | | | (28,276 | ) |

| Net income (loss) attributable to Penn Virginia Corporation | | $ | 122,492 | | | $ | 63,756 | | | $ | 9,505 | | | $ | (72,800 | ) | | $ | 122,953 | |

| Income Statements | | Nine Months Ended September 30, 2009 | |

| | | Penn Virginia | | | Guarantor | | | Non-guarantor | | | | | | | |

| | | Corporation | | | Subsidiaries | | | Subsidiaries | | | Eliminations | | | Consolidated | |

| | | (in thousands) | |

| Revenues | | $ | - | | | $ | 176,092 | | | $ | 461,907 | | | $ | (59,759 | ) | | $ | 578,240 | |

| Cost of midstream gas purchased | | | - | | | | - | | | | 285,129 | | | | (56,550 | ) | | | 228,579 | |

| Operating | | | - | | | | 42,788 | | | | 26,938 | | | | (3,209 | ) | | | 66,517 | |

| Exploration | | | - | | | | 54,901 | | | | - | | | | - | | | | 54,901 | |

| Taxes other than income | | | 692 | | | | 12,756 | | | | 3,208 | | | | - | | | | 16,656 | |

| General and administrative | | | 17,384 | | | | 15,970 | | | | 25,433 | | | | - | | | | 58,787 | |

| Depreciation, depletion and amortization | | | 2,836 | | | | 119,242 | | | | 51,988 | | | | (906 | ) | | | 173,160 | |

| Impairments on assets held for sale | | | - | | | | 87,900 | | | | - | | | | - | | | | 87,900 | |

| Impairments | | | - | | | | 8,928 | | | | - | | | | - | | | | 8,928 | |

| Loss on sale of assets | | | - | | | | 1,599 | | | | - | | | | - | | | | 1,599 | |

| Operating expenses | | | 20,912 | | | | 344,084 | | | | 392,696 | | | | (60,665 | ) | | | 697,027 | |

| Operating income | | | (20,912 | ) | | | (167,992 | ) | | | 69,211 | | | | 906 | | | | (118,787 | ) |

| Equity in earnings of subsidiaries | | | (90,132 | ) | | | 11,790 | | | | - | | | | 78,342 | | | | - | |

| Interest expense and other | | | (32,045 | ) | | | 1,453 | | | | (17,466 | ) | | | - | | | | (48,058 | ) |

| Derivatives | | | 20,483 | | | | - | | | | (12,005 | ) | | | - | | | | 8,478 | |

| Income (loss) before income taxes and noncontrolling interests | | | (122,606 | ) | | | (154,749 | ) | | | 39,740 | | | | 79,248 | | | | (158,367 | ) |

| Income tax benefit (expense) | | | 12,408 | | | | 64,617 | | | | (7,438 | ) | | | - | | | | 69,587 | |

| Net income (loss) | | | (110,198 | ) | | | (90,132 | ) | | | 32,302 | | | | 79,248 | | | | (88,780 | ) |

| Less net income attributable to noncontrolling interests | | | - | | | | - | | | | (20,512 | ) | | | - | | | | (20,512 | ) |

| Net income (loss) attributable to Penn Virginia Corporation | | $ | (110,198 | ) | | $ | (90,132 | ) | | $ | 11,790 | | | $ | 79,248 | | | $ | (109,292 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Income Statements | | Nine Months Ended September 30, 2008 | |

| | | Penn Virginia | | | Guarantor | | | Non-guarantor | | | | | | | | | |

| | | Corporation | | | Subsidiaries | | | Subsidiaries | | | Eliminations | | | Consolidated | |

| | | (in thousands) | |

| Revenues | | $ | 3 | | | $ | 383,391 | | | $ | 719,228 | | | $ | (107,461 | ) | | $ | 995,161 | |

| Cost of midstream gas purchased | | | - | | | | - | | | | 513,778 | | | | (105,531 | ) | | | 408,247 | |

| Operating | | | - | | | | 43,370 | | | | 25,213 | | | | (1,930 | ) | | | 66,653 | |

| Exploration | | | - | | | | 19,765 | | | | - | | | | - | | | | 19,765 | |

| Taxes other than income | | | 821 | | | | 19,480 | | | | 3,024 | | | | - | | | | 23,325 | |

| General and administrative | | | 18,063 | | | | 14,869 | | | | 22,074 | | | | - | | | | 55,006 | |

| Depreciation, depletion and amortization | | | 2,516 | | | | 90,849 | | | | 41,337 | | | | (1,221 | ) | | | 133,481 | |

| Impairments | | | - | | | | - | | | | - | | | | - | | | | - | |

| Operating expenses | | | 21,400 | | | | 188,333 | | | | 605,426 | | | | (108,682 | ) | | | 706,477 | |

| Operating income | | | (21,397 | ) | | | 195,058 | | | | 113,802 | | | | 1,221 | | | | 288,684 | |

| Equity in earnings of subsidiaries | | | 142,925 | | | | 23,668 | | | | - | | | | (166,593 | ) | | | - | |

| Interest expense and other | | | (17,609 | ) | | | 1,555 | | | | (20,041 | ) | | | - | | | | (36,095 | ) |

| Derivatives | | | 2,037 | | | | - | | | | (6,424 | ) | | | - | | | | (4,387 | ) |

| Income (loss) before income taxes and noncontrolling interests | | | 105,956 | | | | 220,281 | | | | 87,337 | | | | (165,372 | ) | | | 248,202 | |

| Income tax benefit (expense) | | | 14,421 | | | | (77,355 | ) | | | (11,418 | ) | | | - | | | | (74,352 | ) |

| Net income (loss) | | | 120,377 | | | | 142,926 | | | | 75,919 | | | | (165,372 | ) | | | 173,850 | |

| Less net income attributable to noncontrolling interests | | | - | | | | - | | | | (52,252 | ) | | | - | | | | (52,252 | ) |

| Net income (loss) attributable to Penn Virginia Corporation | | $ | 120,377 | | | $ | 142,926 | | | $ | 23,667 | | | $ | (165,372 | ) | | $ | 121,598 | |

| Statements of Cash Flows | | Three Months Ended September 30, 2009 | |

| | | Penn Virginia | | | Guarantor | | | Non-guarantor | | | | | | | |

| | | Corporation | | | Subsidiaries | | | Subsidiaries | | | Eliminations | | | Consolidated | |

| | | (in thousands) | |

| Net cash provided by (used in) operating activitities | | $ | (32,443 | ) | | $ | 73,615 | | | $ | 42,874 | | | $ | - | | | $ | 84,046 | |

| Cash flows provided by (used in) investing activities: | | | | | | | | | | | | | | | | | | | | |

| Investment in (distributions from) affiliates | | | 188,080 | | | | 129,948 | | | | - | | | | (318,028 | ) | | | - | |

| Additions to property and equipment | | | (201 | ) | | | (18,059 | ) | | | (39,171 | ) | | | - | | | | (57,431 | ) |

| Proceeds from the sale of assets and other | | | - | | | | 2,576 | | | | 300 | | | | - | | | | 2,876 | |

| Cash flows provided by (used in) investing activities | | | 187,879 | | | | 114,465 | | | | (38,871 | ) | | | (318,028 | ) | | | (54,555 | ) |

| Cash flows provided by (used in) financing activities: | | | | | | | | | | | | | | | | | | | | |

| Distributions paid to noncontrolling interest holders | | | - | | | | - | | | | (18,455 | ) | | | - | | | | (18,455 | ) |

| Net proceeds from (repayments of) borrowings | | | (70,000 | ) | | | - | | | | 31,000 | | | | - | | | | (39,000 | ) |

| Net proceeds from issuance of senior notes | | | - | | | | - | | | | - | | | | - | | | | - | |

| Net proceeds from the sale of PVG units | | | - | | | | - | | | | 118,080 | | | | - | | | | 118,080 | |

| Net proceeds from issuance of equity | | | - | | | | - | | | | - | | | | - | | | | - | |

| Capital contributions from (distributions to) affiliates | | | - | | | | (188,080 | ) | | | (129,948 | ) | | | 318,028 | | | | - | |

| Other | | | (3,419 | ) | | | - | | | | - | | | | - | | | | (3,419 | ) |

| Cash flows provided by (used in) financing activities | | | (73,419 | ) | | | (188,080 | ) | | | 677 | | | | 318,028 | | | | 57,206 | |

| Net decrease in cash and cash equivalents | | | 82,017 | | | | - | | | | 4,680 | | | | - | | | | 86,697 | |

| Cash and cash equivalents - beginning of period | | | 1,319 | | | | - | | | | 17,018 | | | | - | | | | 18,337 | |

| Cash and cash equivalents - end of period | | $ | 83,336 | | | $ | - | | | $ | 21,698 | | | $ | - | | | $ | 105,034 | |

| | | | | | | | | | | | | | | | | | | | | |

| Statements of Cash Flows | | Three Months Ended September 30, 2008 | |

| | | Penn Virginia | | | Guarantor | | | Non-guarantor | | | | | | | | | |

| | | Corporation | | | Subsidiaries | | | Subsidiaries | | | Eliminations | | | Consolidated | |

| | | (in thousands) | |

| Net cash provided by operating activitities | | $ | (15,949 | ) | | $ | 87,190 | | | $ | 20,554 | | | $ | - | | | $ | 91,795 | |

| Cash flows provided by (used in) investing activities: | | | | | | | | | | | | | | | | | | | | |

| Investment in (distributions from) affiliates | | | (21,431 | ) | | | 72,718 | | | | - | | | | (51,287 | ) | | | - | |

| Additions to property and equipment | | | (260 | ) | | | (213,572 | ) | | | (111,103 | ) | | | - | | | | (324,935 | ) |

| Proceeds from the sale of assets and other | | | - | | | | 32,233 | | | | 982 | | | | - | | | | 33,215 | |

| Cash flows provided by (used in) investing activities | | | (21,691 | ) | | | (108,621 | ) | | | (110,121 | ) | | | (51,287 | ) | | | (291,720 | ) |

| Cash flows provided by (used in) financing activities: | | | | | | | | | | | | | | | | | | | | |

| Distributions paid to noncontrolling interest holders | | | - | | | | - | | | | (17,917 | ) | | | - | | | | (17,917 | ) |

| Net proceeds from (repayments of) borrowings | | | 21,431 | | | | - | | | | 176,600 | | | | - | | | | 198,031 | |

| Net proceeds from equity issuance | | | | | | | | | | | - | | | | - | | | | - | |

| Capital contributions from (distributions to) affiliates | | | - | | | | 21,431 | | | | (72,718 | ) | | | 51,287 | | | | - | |

| Other | | | (1,208 | ) | | | - | | | | (3,454 | ) | | | - | | | | (4,662 | ) |

| Cash flows provided by (used in) financing activities | | | 20,223 | | | | 21,431 | | | | 82,511 | | | | 51,287 | | | | 175,452 | |

| Net increase in cash and cash equivalents | | | (17,417 | ) | | | - | | | | (7,056 | ) | | | - | | | | (24,473 | ) |

| Cash and cash equivalents - beginning of period | | | 17,465 | | | | - | | | | 26,015 | | | | - | | | | 43,480 | |

| Cash and cash equivalents - end of period | | $ | 48 | | | $ | - | | | $ | 18,959 | | | $ | - | | | $ | 19,007 | |

| Statements of Cash Flows | | Nine Months Ended September 30, 2009 | |

| | | Penn Virginia | | | Guarantor | | | Non-guarantor | | | | | | | |

| | | Corporation | | | Subsidiaries | | | Subsidiaries | | | Eliminations | | | Consolidated | |

| | | (in thousands) | |

| Net cash provided by operating activitities | | $ | (16,124 | ) | | $ | 122,813 | | | $ | 115,334 | | | $ | - | | | $ | 222,023 | |

| Cash flows provided by (used in) investing activities: | | | | | | | | | | | | | | | | | | | | |

| Investment in (distributions from) affiliates | | | 101,778 | | | | 153,012 | | | | - | | | | (254,790 | ) | | | - | |

| Additions to property and equipment | | | (1,655 | ) | | | (181,873 | ) | | | (73,291 | ) | | | - | | | | (256,819 | ) |

| Proceeds from the sale of assets and other | | | - | | | | 7,826 | | | | 872 | | | | - | | | | 8,698 | |

| Cash flows provided by (used in) investing activities | | | 100,123 | | | | (21,035 | ) | | | (72,419 | ) | | | (254,790 | ) | | | (248,121 | ) |

| Cash flows provided by (used in) financing activities: | | | | | | | | | | | | | | | | | | | | |

| Distributions paid to noncontrolling interest holders | | | - | | | | - | | | | (55,365 | ) | | | - | | | | (55,365 | ) |

| Net proceeds from (repayments of) borrowings | | | (339,542 | ) | | | - | | | | 60,000 | | | | - | | | | (279,542 | ) |

| Net proceeds from issuance of senior notes | | | 291,009 | | | | - | | | | - | | | | - | | | | 291,009 | |

| Net proceeds from the sale of PVG units | | | - | | | | - | | | | 118,080 | | | | | | | | 118,080 | |

| Net proceeds from issuance of equity | | | 64,835 | | | | - | | | | - | | | | - | | | | 64,835 | |

| Capital contributions from (distributions to) affiliates | | | - | | | | (101,778 | ) | | | (153,012 | ) | | | 254,790 | | | | - | |

| Other | | | (16,965 | ) | | | - | | | | (9,258 | ) | | | - | | | | (26,223 | ) |

| Cash flows provided by (used in) financing activities | | | (663 | ) | | | (101,778 | ) | | | (39,555 | ) | | | 254,790 | | | | 112,794 | |

| Net increase (decrease) in cash and cash equivalents | | | 83,336 | | | | - | | | | 3,360 | | | | - | | | | 86,696 | |

| Cash and cash equivalents - beginning of period | | | - | | | | - | | | | 18,338 | | | | - | | | | 18,338 | |

| Cash and cash equivalents - end of period | | $ | 83,336 | | | $ | - | | | $ | 21,698 | | | $ | - | | | $ | 105,034 | |

| | | | | | | | | | | | | | | | | | | | | |

| Statements of Cash Flows | | Nine Months Ended September 30, 2008 | |

| | | Penn Virginia | | | Guarantor | | | Non-guarantor | | | | | | | | | |

| | | Corporation | | | Subsidiaries | | | Subsidiaries | | | Eliminations | | | Consolidated | |

| | | (in thousands) | |

| Net cash provided by operating activitities | | $ | (8,440 | ) | | $ | 192,049 | | | $ | 93,078 | | | $ | - | | | $ | 276,687 | |

| Cash flows provided by (used in) investing activities: | | | | | | | | | | | | | | | | | | | | |

| Investment in (distributions from) affiliates | | | (104,431 | ) | | | 94,197 | | | | - | | | | 10,234 | | | | - | |

| Additions to property and equipment | | | (1,059 | ) | | | (422,974 | ) | | | (246,183 | ) | | | - | | | | (670,216 | ) |

| Proceeds from the sale of assets and other | | | - | | | | 32,297 | | | | 1,657 | | | | - | | | | 33,954 | |

| Cash flows provided by (used in) investing activities | | | (105,490 | ) | | | (296,480 | ) | | | (244,526 | ) | | | 10,234 | | | | (636,262 | ) |

| Cash flows provided by (used in) financing activities: | | | | | | | | | | | | | | | | | | | | |

| Distributions paid to noncontrolling interest holders | | | - | | | | - | | | | (45,829 | ) | | | - | | | | (45,829 | ) |

| Net proceeds from (repayments of) borrowings | | | 104,431 | | | | - | | | | 146,000 | | | | - | | | | 250,431 | |

| Net proceeds from equity issuance | | | - | | | | - | | | | 138,015 | | | | - | | | | 138,015 | |

| Capital contributions from (distributions to) affiliates | | | - | | | | 104,431 | | | | (94,197 | ) | | | (10,234 | ) | | | - | |

| Other | | | 5,512 | | | | - | | | | (4,074 | ) | | | - | | | | 1,438 | |

| Cash flows provided by (used in) financing activities | | | 109,943 | | | | 104,431 | | | | 139,915 | | | | (10,234 | ) | | | 344,055 | |

| Net increase (decrease) in cash and cash equivalents | | | (3,987 | ) | | | - | | | | (11,533 | ) | | | - | | | | (15,520 | ) |

| Cash and cash equivalents - beginning of period | | | 4,035 | | | | - | | | | 30,492 | | | | - | | | | 34,527 | |

| Cash and cash equivalents - end of period | | $ | 48 | | | $ | - | | | $ | 18,959 | | | $ | - | | | $ | 19,007 | |

9. Convertible Notes

Effective January 1, 2009, we adopted the new accounting standard regarding convertible debt instruments that may be settled in cash upon conversion, including partial cash settlement, and accounted for the adoption of this standard as a change in accounting principle. This standard therefore been applied retroactively to all periods presented.

Because the Convertible Notes can be settled wholly or partly in cash upon conversion into our common stock, this standard requires us to account separately for the liability and equity components in a manner that reflects our nonconvertible debt borrowing rate when measuring interest cost of the Convertible Notes. The value assigned to the liability component was the estimated value of a similar debt issuance without the conversion feature as of the issuance date in December 2007. Transaction costs associated with issuing the instrument were allocated to the liability and equity components in proportion to the allocation of the original proceeds and were accounted for as debt issuance costs and equity issuance costs. In addition, recognizing the Convertible Notes as two separate components resulted in a tax basis difference associated with the liability component that represents a temporary difference. Because the liability component was valued exclusive of the conversion feature, the Convertible Notes were recorded at a discount reflecting the below-market coupon interest rate. This discount is accreted through additional interest expense to par value over the remaining expected life of the debt of approximately four years.

The following tables reflect the effects of adopting the standard on our consolidated statements of income for the three and nine months ended September 30, 2008:

| | | Three Months Ended September 30, 2008 | |

| | | As originally | | | | | | Effects of | |

| Consolidated Statement of Income | | reported | | | As adjusted | | | change | |

| | | (in thousands) | |

| Interest expense - (1) | | $ | (11,938 | ) | | $ | (13,221 | ) | | $ | (1,283 | ) |

| Income tax benefit (expense) - (2) | | | 79,419 | | | | 78,921 | | | | (498 | ) |

| Net income (loss) - (3) | | | 152,014 | | | | 151,229 | | | | (785 | ) |

| Net loss attributable to Penn Virginia Corporation | | | 123,738 | | | | 122,953 | | | | (785 | ) |

| | | | | | | | | | | | | |

| Income per share attributable to Penn Virginia Corporation: | | | | | | | | | | | | |

| Basic | | $ | 2.95 | | | $ | 2.94 | | | $ | (0.01 | ) |

| Diluted | | $ | 2.90 | | | $ | 2.88 | | | $ | (0.02 | ) |

| | | | | | | | | | | | | |

| | | Nine Months Ended September 30, 2008 | |

| | | As originally | | | | | | | Effects of | |

| Consolidated Statement of Income | | reported | | | As adjusted | | | change | |

| | | (in thousands) | |

| Interest expense - (1) | | $ | (31,600 | ) | | $ | (35,313 | ) | | $ | (3,713 | ) |

| Income tax benefit (expense) - (2) | | | 75,792 | | | | 74,352 | | | | (1,440 | ) |

| Net income (loss) - (3) | | | 176,123 | | | | 173,850 | | | | (2,273 | ) |

| Net income (loss) attributable to Penn Virginia Corporation | | | 123,871 | | | | 121,598 | | | | (2,273 | ) |

| | | | | | | | | | | | | |

| Income per share attributable to Penn Virginia Corporation: | | | | | | | | | | | | |

| Basic | | $ | 2.96 | | | $ | 2.91 | | | $ | (0.05 | ) |

| Diluted | | $ | 2.94 | | | $ | 2.88 | | | $ | (0.06 | ) |

| (1) | Represents additional interest expense that would have been recorded related to the debt discount had the standard been in place when the Convertible Notes were issued. This increase is partially offset by variances in capitalized interest and the amortization of debt issuance costs, which resulted from the separation of the debt and equity components of the Convertible Notes. |

| (2) | The adjustment to income tax benefit (expense) is based on our effective tax rates. |

| (3) | Net income (loss) includes noncontrolling interests. |

The following tables reflect the effects of adopting the standard on our consolidated balance sheet at December 31, 2008:

| | | December 31, 2008 | |

| | | As originally | | | | | | Effects of | |

| Consolidated Balance Sheet | | reported | | | As adjusted | | | change | |

| | | (in thousands) | |

| Oil and gas properties (1) | | $ | 2,106,126 | | | $ | 2,107,128 | | | $ | 1,002 | |

| Other assets (2) | | | 46,674 | | | | 45,685 | | | | (989 | ) |

| Deferred income taxes (3) | | | 245,789 | | | | 258,037 | | | | 12,248 | |

| Convertible notes (4) | | | 230,000 | | | | 199,896 | | | | (30,104 | ) |

| Paid-in capital (5) | | | 578,639 | | | | 599,855 | | | | 21,216 | |

| Retained earnings (6) | | | 446,993 | | | | 443,646 | | | | (3,347 | ) |

| (1) | The impact on oil and gas properties is due to capitalized interest. |

| (2) | The adjustment to other assets reflects a decrease in debt issuance costs. |

| (3) | The impact on deferred income taxes is due to the change in the tax basis of the liability component. |

| (4) | The impact on the Convertible Notes balance is due to the unamortized discount balance. |

| (5) | The impact on the paid-in capital balance is due to the equity component and related issue costs as well as the change in deferred income taxes. |

| (6) | The impact on retained earnings is due to the additional interest expense, net of tax, that would have been incurred had the standard been in place when the Convertible Notes were issued. |

The following tables reflect the effects of adopting the standard on our consolidated statements of cash flows for the three and nine months ended September 30, 2008:

| | | Three Months Ended September 30, 2008 | |

| | | As originally | | | | | | Effects of | |

| Consolidated Statement of Cash Flows | | reported | | | As adjusted | | | change | |

| | | (in thousands) | |

| Cash flows from operating activities | | | | | | | | | |

| Net income (loss) | | $ | 152,014 | | | $ | 151,229 | | | $ | (785 | ) |

| Deferred income taxes | | | 62,050 | | | | 61,552 | | | | (498 | ) |

| Other | | | (28,657 | ) | | | (27,374 | ) | | | 1,283 | |

| Total impact on the statement of cash flows | | $ | 185,407 | | | $ | 185,407 | | | $ | - | |

| | | | | | | | | | | | | |

| | | Nine Months Ended September 30, 2008 | |

| | | As originally | | | | | | | Effects of | |

| Consolidated Statement of Cash Flows | | reported | | | As adjusted | | | change | |

| | | (in thousands) | |

| Cash flows from operating activities | | | | | | | | | | | | |

| Net income | | $ | 176,123 | | | $ | 173,850 | | | $ | (2,273 | ) |

| Deferred income taxes | | | 61,545 | | | | 60,105 | | | | (1,440 | ) |

| Other | | | (29,831 | ) | | | (26,118 | ) | | | 3,713 | |

| Total impact on the statement of cash flows | | $ | 207,837 | | | $ | 207,837 | | | $ | - | |