UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2008

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 1-13283

PENN VIRGINIA CORPORATION

(Exact name of registrant as specified in its charter)

| | |

| Virginia | | 23-1184320 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

|

THREE RADNOR CORPORATE CENTER, SUITE 300 100 MATSONFORD ROAD RADNOR, PA 19087 |

| (Address of principal executive offices) (Zip Code) |

(610) 687-8900

(Registrant’s telephone number, including area code)

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by a check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | |

| Large accelerated filer x | | Accelerated filer ¨ |

| Non-accelerated filer ¨ | | (Do not check if a smaller reporting company) Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

As of November 5, 2008, 41,841,263 shares of common stock of the registrant were outstanding.

PENN VIRGINIA CORPORATION AND SUBSIDIARIES

INDEX

PART I. FINANCIAL INFORMATION

Item 1 Financial Statements

PENN VIRGINIA CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF INCOME — unaudited

(in thousands, except per share data)

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2008 | | | 2007 | | | 2008 | | | 2007 | |

Revenues | | | | | | | | | | | | | | | | |

Natural gas | | $ | 101,911 | | | $ | 65,310 | | | $ | 295,636 | | | $ | 193,961 | |

Crude oil | | | 13,764 | | | | 6,299 | | | | 37,442 | | | | 14,985 | |

Natural gas liquids | | | 10,481 | | | | 1,290 | | | | 18,887 | | | | 3,458 | |

Natural gas midstream | | | 184,914 | | | | 100,370 | | | | 494,260 | | | | 310,095 | |

Coal royalties | | | 33,308 | | | | 24,426 | | | | 88,911 | | | | 73,455 | |

Gain on the sale of property and equipment | | | 31,279 | | | | 12,312 | | | | 31,335 | | | | 12,436 | |

Other | | | 9,955 | | | | 5,751 | | | | 28,690 | | | | 16,036 | |

| | | | | | | | | | | | | | | | |

Total revenues | | | 385,612 | | | | 215,758 | | | | 995,161 | | | | 624,426 | |

| | | | | | | | | | | | | | | | |

Expenses | | | | | | | | | | | | | | | | |

Cost of midstream gas purchased | | | 155,564 | | | | 76,192 | | | | 408,247 | | | | 251,000 | |

Operating | | | 23,437 | | | | 17,602 | | | | 66,653 | | | | 47,557 | |

Exploration | | | 8,346 | | | | 12,873 | | | | 19,765 | | | | 23,610 | |

Taxes other than income | | | 7,671 | | | | 5,156 | | | | 23,325 | | | | 15,995 | |

General and administrative | | | 18,289 | | | | 16,439 | | | | 55,006 | | | | 46,539 | |

Impairment of oil and gas properties | | | — | | | | 2,405 | | | | — | | | | 2,405 | |

Depreciation, depletion and amortization | | | 49,978 | | | | 33,207 | | | | 133,481 | | | | 89,823 | |

| | | | | | | | | | | | | | | | |

Total expenses | | | 263,285 | | | | 163,874 | | | | 706,477 | | | | 476,929 | |

| | | | | | | | | | | | | | | | |

Operating income | | | 122,327 | | | | 51,884 | | | | 288,684 | | | | 147,497 | |

| | | | |

Other income (expense) | | | | | | | | | | | | | | | | |

Interest expense | | | (11,938 | ) | | | (10,843 | ) | | | (31,600 | ) | | | (25,878 | ) |

Other | | | (4,088 | ) | | | 576 | | | | (782 | ) | | | 2,536 | |

Derivatives | | | 125,132 | | | | (4,455 | ) | | | (4,387 | ) | | | (22,068 | ) |

| | | | | | | | | | | | | | | | |

Income before minority interest and income taxes | | | 231,433 | | | | 37,162 | | | | 251,915 | | | | 102,087 | |

Minority interest | | | 28,276 | | | | 9,135 | | | | 52,252 | | | | 27,659 | |

Income tax expense | | | 79,419 | | | | 10,913 | | | | 75,792 | | | | 29,033 | |

| | | | | | | | | | | | | | | | |

Net income | | $ | 123,738 | | | $ | 17,114 | | | $ | 123,871 | | | $ | 45,395 | |

| | | | | | | | | | | | | | | | |

Net income per share, basic | | $ | 2.95 | | | $ | 0.45 | | | $ | 2.96 | | | $ | 1.20 | |

| | | | |

Net income per share, diluted | | $ | 2.90 | | | $ | 0.45 | | | $ | 2.94 | | | $ | 1.19 | |

| | | | |

Weighted average shares outstanding, basic | | | 41,881 | | | | 37,898 | | | | 41,715 | | | | 37,748 | |

Weighted average shares outstanding, diluted | | | 42,544 | | | | 38,213 | | | | 42,028 | | | | 38,045 | |

The accompanying notes are an integral part of these consolidated financial statements.

1

PENN VIRGINIA CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS — unaudited

(in thousands, except share data)

| | | | | | | | |

| | | September 30,

2008 | | | December 31,

2007 | |

Assets | | | | | | | | |

Current assets | | | | | | | | |

Cash and cash equivalents | | $ | 19,007 | | | $ | 34,527 | |

Accounts receivable | | | 191,729 | | | | 179,120 | |

Deferred income taxes | | | 2,002 | | | | 16,273 | |

Derivative assets | | | 18,197 | | | | 5,683 | |

Other | | | 20,238 | | | | 8,469 | |

| | | | | | | | |

Total current assets | | | 251,173 | | | | 244,072 | |

| | | | | | | | |

Property and equipment | | | | | | | | |

Oil and gas properties (successful efforts method) | | | 1,963,136 | | | | 1,525,728 | |

Other property and equipment | | | 1,051,126 | | | | 859,380 | |

| | | | | | | | |

| | | 3,014,262 | | | | 2,385,108 | |

Accumulated depreciation, depletion and amortization | | | (614,808 | ) | | | (486,094 | ) |

| | | | | | | | |

Net property and equipment | | | 2,399,454 | | | | 1,899,014 | |

Equity investments | | | 78,634 | | | | 25,640 | |

Goodwill | | | 31,768 | | | | 7,718 | |

Intangibles, net | | | 94,623 | | | | 28,938 | |

Derivative assets | | | 6,019 | | | | 310 | |

Other assets | | | 48,950 | | | | 47,769 | |

| | | | | | | | |

Total assets | | $ | 2,910,621 | | | $ | 2,253,461 | |

| | | | | | | | |

Liabilities and Shareholders’ Equity | | | | | | | | |

Current liabilities | | | | | | | | |

Short-term borrowings | | $ | 46,431 | | | $ | 12,561 | |

Accounts payable and accrued liabilities | | | 209,674 | | | | 205,127 | |

Derivative liabilities | | | 17,959 | | | | 43,048 | |

Income taxes payable | | | 11,426 | | | | 1,163 | |

| | | | | | | | |

Total current liabilities | | | 285,490 | | | | 261,899 | |

| | | | | | | | |

Other liabilities | | | 55,761 | | | | 54,169 | |

Derivative liabilities | | | 4,127 | | | | 3,030 | |

Deferred income taxes | | | 267,187 | | | | 193,950 | |

Long-term debt of the Company | | | 410,000 | | | | 352,000 | |

Long-term debt of PVR | | | 558,100 | | | | 399,153 | |

Minority interests of subsidiaries | | | 309,191 | | | | 179,162 | |

Shareholders’ equity | | | | | | | | |

Preferred stock of $100 par value — 100,000 shares authorized; none issued | | | — | | | | — | |

Common stock of $0.01 par value — 64,000,000 shares authorized; 41,870,477 and 41,408,497 shares issued and outstanding at September 30, 2008 and December 31, 2007 | | | 230 | | | | 225 | |

Paid-in capital | | | 579,327 | | | | 487,606 | |

Retained earnings | | | 449,057 | | | | 332,223 | |

Accumulated other comprehensive loss | | | (5,220 | ) | | | (7,936 | ) |

Treasury stock — 90,308 and 77,924 shares common stock, at cost, on September 30, 2008 and December 31, 2007 | | | (2,629 | ) | | | (2,020 | ) |

| | | | | | | | |

Total shareholders’ equity | | | 1,020,765 | | | | 810,098 | |

| | | | | | | | |

Total liabilities and shareholders’ equity | | $ | 2,910,621 | | | $ | 2,253,461 | |

| | | | | | | | |

The accompanying notes are an integral part of these consolidated financial statements.

2

PENN VIRGINIA CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS — unaudited

(in thousands)

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2008 | | | 2007 | | | 2008 | | | 2007 | |

Cash flows from operating activities | | | | | | | | | | | | | | | | |

Net income | | $ | 123,738 | | | $ | 17,114 | | | $ | 123,871 | | | $ | 45,395 | |

Adjustments to reconcile net income to net cash provided by operating activities: | | | | | | | | | | | | | | | | |

Depreciation, depletion and amortization | | | 49,978 | | | | 33,207 | | | | 133,481 | | | | 89,823 | |

Derivative contracts: | | | | | | | | | | | | | | | | |

Total derivative losses (gains) | | | (123,628 | ) | | | 6,053 | | | | 8,516 | | | | 25,569 | |

Cash received (paid) to settle derivatives | | | (19,755 | ) | | | 586 | | | | (46,740 | ) | | | 2,281 | |

Deferred income taxes | | | 62,050 | | | | 9,218 | | | | 61,545 | | | | 21,902 | |

Minority interest | | | 28,276 | | | | 9,135 | | | | 52,252 | | | | 27,659 | |

Gain on the sale of property and equipment | | | (31,279 | ) | | | (12,312 | ) | | | (31,335 | ) | | | (12,436 | ) |

Impairment of oil and gas properties | | | — | | | | 2,405 | | | | — | | | | 2,405 | |

Dry hole and unproved leasehold expense | | | 5,520 | | | | 11,991 | | | | 14,992 | | | | 20,707 | |

Other | | | 2,622 | | | | 1,523 | | | | 1,504 | | | | 2,918 | |

Changes in operating assets and liabilities | | | (5,727 | ) | | | (2,736 | ) | | | (41,399 | ) | | | (17,242 | ) |

| | | | | | | | | | | | | | | | |

Net cash provided by operating activities | | | 91,795 | | | | 76,184 | | | | 276,687 | | | | 208,981 | |

| | | | | | | | | | | | | | | | |

Cash flows from investing activities | | | | | | | | | | | | | | | | |

Acquisitions | | | (162,078 | ) | | | (162,794 | ) | | | (278,185 | ) | | | (239,018 | ) |

Additions to property and equipment | | | (162,857 | ) | | | (109,685 | ) | | | (392,031 | ) | | | (308,987 | ) |

Other | | | 33,215 | | | | 29,142 | | | | 33,954 | | | | 29,385 | |

| | | | | | | | | | | | | | | | |

Net cash used in investing activities | | | (291,720 | ) | | | (243,337 | ) | | | (636,262 | ) | | | (518,620 | ) |

| | | | | | | | | | | | | | | | |

Cash flows from financing activities | | | | | | | | | | | | | | | | |

Dividends paid | | | (2,351 | ) | | | (2,130 | ) | | | (7,037 | ) | | | (6,370 | ) |

Distributions paid to minority interest holders | | | (17,917 | ) | | | (12,937 | ) | | | (45,829 | ) | | | (36,402 | ) |

Borrowings from bank indebtedness | | | 46,431 | | | | — | | | | 46,431 | | | | — | |

Proceeds from Company borrowings | | | 38,000 | | | | 113,000 | | | | 121,000 | | | | 220,500 | |

Repayments of Company borrowings | | | (63,000 | ) | | | (27,000 | ) | | | (63,000 | ) | | | (27,000 | ) |

Proceeds from PVR borrowings | | | 242,000 | | | | 107,000 | | | | 366,800 | | | | 169,000 | |

Repayments of PVR borrowings | | | (65,400 | ) | | | (18,000 | ) | | | (220,800 | ) | | | (23,000 | ) |

Net proceeds from issuance of PVR partners’ capital | | | — | | | | — | | | | 138,015 | | | | — | |

Other | | | (2,311 | ) | | | (188 | ) | | | 8,475 | | | | 7,376 | |

| | | | | | | | | | | | | | | | |

Net cash provided by financing activities | | | 175,452 | | | | 159,745 | | | | 344,055 | | | | 304,104 | |

| | | | | | | | | | | | | | | | |

Net decrease in cash and cash equivalents | | | (24,473 | ) | | | (7,408 | ) | | | (15,520 | ) | | | (5,535 | ) |

Cash and cash equivalents — beginning of period | | | 43,480 | | | | 22,211 | | | | 34,527 | | | | 20,338 | |

| | | | | | | | | | | | | | | | |

Cash and cash equivalents — end of period | | $ | 19,007 | | | $ | 14,803 | | | $ | 19,007 | | | $ | 14,803 | |

| | | | | | | | | | | | | | | | |

Supplemental disclosures: | | | | | | | | | | | | | | | | |

Cash paid for: | | | | | | | | | | | | | | | | |

Interest (net of amounts capitalized) | | $ | 8,599 | | | $ | 13,630 | | | $ | 26,490 | | | $ | 28,397 | |

Income taxes | | $ | 2,791 | | | $ | 162 | | | $ | 4,970 | | | $ | 464 | |

Noncash investing activities: (see Note 4) | | | | | | | | | | | | | | | | |

Issuance of PVR units for acquisition | | $ | 15,171 | | | $ | — | | | $ | 15,171 | | | $ | — | |

PVG units given as consideration for acquisition | | $ | 68,021 | | | $ | — | | | $ | 68,021 | | | $ | — | |

Other liabilities | | $ | 4,673 | | | $ | — | | | $ | 4,673 | | | $ | — | |

The accompanying notes are an integral part of these consolidated financial statements.

3

PENN VIRGINIA CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — unaudited

September 30, 2008

1. Nature of Operations

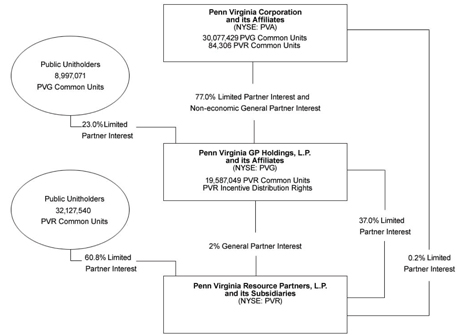

Penn Virginia Corporation (“Penn Virginia,” the “Company,” “we,” “us” or “our”) is an independent oil and gas company primarily engaged in the exploration, development and production of natural gas and oil in various onshore U.S. regions including East Texas, the Mid-Continent, Appalachia, Mississippi and the Gulf Coast. We also indirectly own partner interests in Penn Virginia Resource Partners, L.P. (“PVR”), a publicly traded limited partnership formed by us in 2001. Our ownership interests in PVR are held principally through our general partner and 77% limited partner interests in Penn Virginia GP Holdings, L.P. (“PVG”), a publicly traded limited partnership formed by us in 2006. As of September 30, 2008, PVG owned an approximately 37% limited partner interest in PVR and 100% of the general partner of PVR, which holds a 2% general partner interest in PVR.

We are engaged in three primary business segments: (i) oil and gas, (ii) coal and natural resource management and (iii) natural gas midstream. We directly operate our oil and gas segment. PVR operates our coal and natural resource management and natural gas midstream segments. Because we control the general partner of PVG, the financial results of PVG are included in our consolidated financial statements. Because PVG controls the general partner of PVR, the financial results of PVR are included in PVG’s condensed consolidated financial statements. However, PVG and PVR function with capital structures that are independent of each other and us, with each having publicly traded common units and PVR having its own debt instruments. PVG does not currently have any debt instruments.

2. Penn Virginia Resource Partners, L.P. and Penn Virginia GP Holdings, L.P.

PVR is principally engaged in the management of coal and natural resource properties and the gathering and processing of natural gas in the United States. PVR completed its initial public offering in October 2001. PVG derives its cash flow solely from cash distributions received from PVR. PVG completed its initial public offering in December 2006. PVG’s general partner is an indirect wholly owned subsidiary of ours.

PVR’s coal and natural resource management segment primarily involves the management and leasing of coal properties and the subsequent collection of royalties. PVR also earns revenues from other land management activities, such as selling standing timber, leasing fee-based coal-related infrastructure facilities to certain lessees and end-user industrial plants, collecting oil and gas royalties and from coal transportation, or wheelage, fees.

PVR’s natural gas midstream segment is engaged in providing natural gas processing, gathering and other related services. PVR owns and operates natural gas midstream assets located in Oklahoma and Texas. PVR’s natural gas midstream business derives revenues primarily from gas processing contracts with natural gas producers and from fees charged for gathering natural gas volumes and providing other related services. PVR also owns a natural gas marketing business, which aggregates third-party volumes and sells those volumes into intrastate pipeline systems and at market hubs accessed by various interstate pipelines.

3. Summary of Significant Accounting Policies

Our accounting policies are consistent with those described in our Annual Report on Form 10-K for the year ended December 31, 2007. Please refer to such Form 10-K for a further discussion of those policies.

Basis of Presentation

Our consolidated financial statements include the accounts of Penn Virginia, all of our wholly owned subsidiaries and PVG, of which we indirectly owned the sole general partner and an approximately 77% limited partner interest as of September 30, 2008. PVG GP, LLC, our indirect wholly owned subsidiary, serves as PVG’s sole general partner and controls PVG. Because PVG controls the general partner of PVR, the financial results of PVR are included in PVG’s condensed consolidated financial statements.

4

Intercompany balances and transactions have been eliminated in consolidation. Our consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America for interim financial reporting and Securities and Exchange Commission (“SEC”) regulations. These statements involve the use of estimates and judgments where appropriate. In the opinion of management, all adjustments, consisting of normal recurring accruals, considered necessary for a fair presentation of our consolidated financial statements have been included. These financial statements should be read in conjunction with our consolidated financial statements and footnotes included in our Annual Report on Form 10-K for the year ended December 31, 2007. Operating results for the three and nine months ended September 30, 2008 are not necessarily indicative of the results that may be expected for the year ending December 31, 2008.

Gain on Sale of Subsidiary Units

We account for PVR equity issuances as sales of minority interest. For each PVR equity issuance, we have calculated a gain under SEC Staff Accounting Bulletin No. 51 (or Topic 5-H),Accounting for Sales of Stock by a Subsidiary(“SAB 51”). SAB 51 provides guidance on accounting for the effect of issuances of a subsidiary’s stock on the parent’s investment in that subsidiary. In some situations, SAB 51 allows registrants to elect an accounting policy of recording gains or losses on issuances of stock by a subsidiary either in income or as a capital transaction. Accordingly, we adopted a policy of recording SAB 51 gains and losses directly to shareholders’ equity. As a result of PVR’s unit offering in May 2008, we recognized gains in consolidated shareholders’ equity totaling $39.7 million. See Note 6 – PVR Unit Offering. In addition, we recognized a $36.8 million gain in consolidated shareholders’ equity, net of the related income taxes of $23.2 million, on the sale of PVG units to PVR. PVR subsequently delivered these units as consideration in its acquisition of Lone Star Gathering L.P. See Note 4 — Acquisitions.

New Accounting Standards

In December 2007, the Financial Accounting Standards Board (“FASB”) issued Statement of Financial Accounting Standards (“SFAS”) No. 160,Noncontrolling Interests in Consolidated Financial Statements, an amendment of ARB No. 51, which mandates that a noncontrolling (minority) interest shall be reported in the consolidated statement of financial position within equity, separately from the parent company’s equity. This statement amends ARB No. 51 and clarifies that a noncontrolling interest in a subsidiary is an ownership interest in the consolidated entity. SFAS No. 160 also requires consolidated net income to include amounts attributable to both the parent and noncontrolling interest and requires disclosure, on the face of the consolidated statement of income, of the amounts of consolidated net income attributable to the parent and to the noncontrolling interest. SFAS No. 160 is effective for fiscal years and interim periods beginning after December 15, 2008. We are currently assessing the impact on our consolidated financial statements of adopting SFAS No. 160 effective January 1, 2009.

In April 2008, the FASB issued Staff Position No. FAS 142-3,Determination of the Useful Life of Intangible Assets (“FSP FAS 142-3”), which amends SFAS No. 142,Goodwill and Other Intangible Assets. The pronouncement requires that companies estimating the useful life of a recognized intangible asset consider their historical experience in renewing or extending similar arrangements or, in the absence of historical experience, consider assumptions that market participants would use about renewal or extension. FSP FAS 142-3 is effective for financial statements issued for fiscal years and interim periods beginning after December 15, 2008 and must be applied prospectively to intangible assets acquired after the effective date. Effective January 1, 2009, we will prospectively apply FSP FAS 142-3 to all intangible assets purchased.

In May 2008, the FASB issued Staff Position No. APB 14-1, Accounting for Convertible Debt Instruments That May Be Settled in Cash upon Conversion (Including Partial Cash Settlement) (“FSP APB 14-1”). This standard requires issuers of convertible debt that may be settled wholly or partly in cash to account for the debt and equity components separately. FSP APB 14-1 requires that issuers of convertible debt separately account for the liability and equity components in a manner that will reflect the entity’s nonconvertible debt borrowing rate when interest cost is recognized in subsequent periods. FSP APB 14-1 is effective for financial statements issued for fiscal years beginning after December 15, 2008 and interim periods within those years, and must be applied retrospectively to all periods presented. Early adoption is prohibited. Effective January 1, 2009, the adoption of FSP APB 14-1 would include increased interest expense on a retroactive basis.

In June 2008, the FASB’s Emerging Issues Task Force (“EITF”) reached a consensus with regard to Issue Number 07-5,Determining Whether an Instrument (or Embedded Feature) is Indexed to an Entity’s Own Stock

5

(“EITF 07-5”). Derivative contracts on a company’s own stock may be accounted for as equity instruments, rather than as assets and liabilities, only if the derivative contracts are indexed solely to the company’s stock and can be settled in shares. EITF 07-5 addresses whether provisions that introduce adjustment features (including contingent adjustment features) would preclude treating a derivative contract or an embedded derivative on a company’s own stock as indexed solely to the company’s stock. The EITF reached a consensus that contingent and other adjustment features are consistent with equity indexation if they are based on variables that would be inputs to a “plain vanilla” option or forward pricing model and they do not increase the contract’s exposure to those variables. EITF 07-5 is effective for fiscal years beginning after December 15, 2008. It must initially be applied by recording a cumulative-effect adjustment to opening retained earnings at the date of adoption for the effect of EITF 07-5 on outstanding instruments. We expect no effect on retained earnings as a result of adopting EITF 07-5.

4. Acquisitions

In July 2008, PVR completed the acquisition of substantially all of the assets of Lone Star Gathering, L.P. (“Lone Star Acquisition”). Lone Star’s assets are located in the southern portion of the Fort Worth Basin of North Texas, and include approximately 129 miles of gas gathering pipelines and approximately 240,000 acres dedicated by active producers. The Lone Star Acquisition expands the geographic scope of the PVR natural gas midstream segment into the Barnett Shale play in the Fort Worth Basin. PVR acquired this business for approximately $164.3 million and a liability of $4.7 million, which represents the fair value of a $5.0 million guaranteed payment, plus contingent payments of $30.0 million and $25.0 million. Funding for the acquisition was provided by $80.7 million of borrowings under PVR’s revolving credit facility (the “PVR Revolver”), 2,009,995 PVG common units (which PVR purchased from two of our subsidiaries for $61.8 million) and 542,610 newly issued PVR common units. The contingent payments will be triggered if revenues from certain assets located in a defined geographic area reach certain targets by or before June 30, 2013 and will be funded in cash or PVR common units, at PVR’s election.

In April 2008, PVR acquired a 25% member interest in Thunder Creek Gas Services, LLC (“Thunder Creek”), a joint venture that gathers and transports coalbed methane in Wyoming’s Powder River Basin for $51.6 million in cash, after customary closing adjustments. PVR funded the acquisition with borrowings under the PVR Revolver. The entire member interest is recorded in equity investments on the consolidated balance sheet. This investment includes $37.3 million of fair value for the net assets acquired and $14.3 million of fair value paid in excess of PVR’s portion of the underlying equity in the net assets acquired related to customer contracts and related customer relations. This excess is being amortized to equity earnings over the life of the underlying contracts. The earnings are recorded in other revenues on our consolidated statements of income.

Based on our analysis of the fair value of these acquisitions, we did not deem either of these acquisitions to be material business combinations to our consolidated financial statements and, therefore, are not disclosing pro forma financial information in accordance with SFAS No. 141.

5. Sale of Oil and Gas Properties

In July 2008, we completed the sale of certain unproved oil and gas acreage in Louisiana for cash proceeds of $32.0 million and recognized a $30.5 million gain on that sale in the third quarter of 2008.

6. PVR Unit Offering

In May 2008, PVR issued to the public 5.15 million common units representing limited partner interests in PVR and received $138.0 million in net proceeds. PVG made contributions to PVR of $2.9 million to maintain its 2% general partner interest. PVR used the net proceeds to repay a portion of its borrowings under the PVR Revolver.

7. Fair Value Measurement of Financial Instruments

We adopted SFAS No. 157,Fair Value Measurements, effective January 1, 2008, for financial assets and liabilities measured on a recurring basis. SFAS No. 157 applies to all financial assets and financial liabilities that are being measured and reported on a fair value basis. SFAS No. 157 defines fair value, establishes a framework for measuring fair value and requires enhanced disclosures about fair value measurements. FASB Staff Position FAS 157-2,Effective Date of FASB Statement No. 157 (“FSP SFAS 157-2”), delays the application of SFAS No. 157 for

6

nonfinancial assets and nonfinancial liabilities to fiscal years and interim periods beginning after November 15, 2008. Examples of nonfinancial assets for which this FASB Staff Position delays application of SFAS No. 157 include business combinations, impairment and initial recognition of asset retirement obligations. We are currently assessing the impact on the financial statements of adopting FSP SFAS 157-2 effective January 1, 2009.

SFAS No. 157 requires fair value measurements to be classified and disclosed in one of the following three categories:

| | • | | Level 1: Unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets or liabilities. Level 1 inputs generally provide the most reliable evidence of fair value. |

| | • | | Level 2: Quoted prices in markets that are not active or inputs, which are observable, either directly or indirectly, for substantially the full term of the asset or liability. |

| | • | | Level 3: Prices or valuation techniques that require inputs that are both significant to the fair value measurement and unobservable (i.e., supported by little or no market activity). |

The following table summarizes the valuation of our financial instruments by the above SFAS No. 157 categories as of September 30, 2008 (in thousands):

| | | | | | | | | | | | | | |

Description | | Fair Value

Measurements,

September 30,

2008 | | | Fair Value Measurement at September 30, 2008, Using |

| | | Quoted Prices in

Active Markets for

Identical Assets

(Level 1) | | Significant Other

Observable

Inputs (Level 2) | | | Significant

Unobservable

Inputs (Level 3) |

Trading securities | | $ | 5,463 | | | $ | 5,463 | | $ | — | | | $ | — |

Interest rate swap liability - current | | | (2,370 | ) | | | — | | | (2,370 | ) | | | — |

Interest rate swap liability - noncurrent | | | (3,105 | ) | | | — | | | (3,105 | ) | | | — |

Commodity derivative assets - current | | | 18,197 | | | | — | | | 18,197 | | | | — |

Commodity derivative assets - noncurrent | | | 6,019 | | | | — | | | 6,019 | | | | — |

Commodity derivative liability - current | | | (15,589 | ) | | | — | | | (15,589 | ) | | | — |

Commodity derivative liability - noncurrent | | | (1,022 | ) | | | — | | | (1,022 | ) | | | — |

| | | | | | | | | | | | | | |

Total | | $ | 7,593 | | | $ | 5,463 | | $ | 2,130 | | | $ | — |

| | | | | | | | | | | | | | |

See Note 8 — Derivative Instruments, for the effects of these instruments on our consolidated statements of income.

We use the following methods and assumptions to estimate the fair values in the above table:

| | • | | Trading securities: Our trading securities consist of various publicly traded equities. The fair values are based on quoted market prices, which are level 1 inputs. |

| | • | | Commodity derivative instruments: Our oil and gas commodity derivatives consist of costless collars, swaps and three-way option derivative contracts, while PVR utilizes costless collars, three-way collars and swap derivative contracts in its natural gas midstream segment. We determine the fair values of our oil and gas commodity derivative agreements based on third-party forward price quotes for NYMEX Henry Hub gas and West Texas Intermediate crude oil closing prices. PVR determines the fair values of its commodity derivative agreements based on forward price quotes for the respective commodities. We generally use the income approach, using valuation techniques that convert future cash flows to a single discounted value. The discount rates used in the discounted cash flow projections include a measure of nonperformance risk. Each of these is a level 2 input. See Note 8 — Derivative Instruments. |

| | • | | Interest rate swaps: We have entered into interest rate swap agreements (the “Revolver Swaps”) to establish fixed rates on a portion of the outstanding borrowings under our revolving credit facility (the |

7

“Revolver”). PVR has entered into interest rate swap agreements (the “PVR Revolver Swaps”) to establish fixed rates on a portion of the outstanding borrowings under the PVR Revolver. We estimate the fair value of the swaps based on published interest rate yield curves as of the date of the estimate. The discount rates used in the discounted cash flow projections include a measure of nonperformance risk. Each of these is a level 2 input. See Note 8 — Derivative Instruments.

8. Derivative Instruments

For commodity derivative instruments, we recognize changes in fair values in earnings currently, rather than deferring such amounts in accumulated other comprehensive income (shareholders’ equity).

Oil and Gas Segment Commodity Derivatives

We utilize costless collars, swaps and three-way option derivative contracts to hedge against the variability in cash flows associated with forecasted sales of our future oil and gas production. While the use of derivative instruments limits the risk of adverse price movements, such use may also limit future revenues from favorable price movements.

The counterparty to a costless collar contract is required to make a payment to us if the settlement price for any settlement period is below the floor price for such contract. We are required to make a payment to the counterparty if the settlement price for any settlement period is above the ceiling price for such contract. Neither party is required to make a payment to the other party if the settlement price for any settlement period is equal to or greater than the floor price and equal to or less than the ceiling price for such contract. The counterparty to a swap contract is required to make a payment to us if the settlement price for any settlement period is less than the swap price for such contract, and we are required to make a payment to the counterparty if the settlement price for any settlement period is greater than the swap price for such contract.

A three-way collar contract is a combination of options: a sold call, a purchased put and a sold put. The sold call establishes the maximum price that we will receive for the contracted commodity volumes. The purchased put establishes the minimum price that we will receive for the contracted volumes unless the market price for the commodity falls below the sold put strike price, at which point the minimum price equals the reference price (i.e., NYMEX) plus the excess of the purchased put strike price over the sold put strike price.

8

We determined the fair values of our oil and gas derivative agreements based on third-party forward price quotes for NYMEX Henry Hub gas and West Texas Intermediate crude oil closing prices as of September 30, 2008, the credit risk of our counterparties and our own credit risk in accordance with SFAS No. 157. The following table sets forth our positions as of September 30, 2008:

| | | | | | | | | | | | | | | |

| | | Average Volume

Per Day | | Weighted Average Price | | Estimated

Fair Value | |

| | | Additional Put

Option | | Floor | | Ceiling | |

| | | (in MMBtus) | | (per MMBtu) | | (in thousands) | |

Natural Gas Costless Collars | | | | | | | | | | | | | | | |

Fourth Quarter 2008 (1) | | 10,000 | | | | | $ | 7.50 | | $ | 9.10 | | $ | (2,220 | ) |

| | | |

| | | (in MMBtus) | | (per MMBtu) | | | |

Natural Gas Three-Way Collars | | | | | | | | | | | | | | | |

Fourth Quarter 2008 | | 67,500 | | $ | 5.89 | | $ | 8.55 | | $ | 11.26 | | | 3,050 | |

First Quarter 2009 | | 65,000 | | $ | 6.00 | | $ | 8.67 | | $ | 11.68 | | | 5,830 | |

Second Quarter 2009 | | 40,000 | | $ | 6.38 | | $ | 8.75 | | $ | 10.79 | | | 3,039 | |

Third Quarter 2009 | | 40,000 | | $ | 6.38 | | $ | 8.75 | | $ | 10.79 | | | 2,303 | |

Fourth Quarter 2009 | | 30,000 | | $ | 6.83 | | $ | 9.50 | | $ | 13.60 | | | 2,625 | |

First Quarter 2010 | | 30,000 | | $ | 6.83 | | $ | 9.50 | | $ | 13.60 | | | 1,862 | |

| | | |

| | | (in MMBtus) | | (per MMBtu) | | | |

Natural Gas Basis Swaps | | | | | | | | | | | | | | | |

Fourth Quarter 2008 | | 15,000 | | | | | $ | 0.39 | | | | | | 179 | |

| | | |

| | | (in barrels) | | (per barrel) | | | |

Crude Oil Three-Way Collars | | | | | | | | | | | | | | | |

Fourth Quarter 2008 | | 500 | | $ | 80.00 | | $ | 110.00 | | $ | 179.00 | | | 547 | |

First Quarter 2009 | | 500 | | $ | 80.00 | | $ | 110.00 | | $ | 179.00 | | | 576 | |

Second Quarter 2009 | | 500 | | $ | 80.00 | | $ | 110.00 | | $ | 179.00 | | | 551 | |

Third Quarter 2009 | | 500 | | $ | 80.00 | | $ | 110.00 | | $ | 179.00 | | | 517 | |

Fourth Quarter 2009 | | 500 | | $ | 80.00 | | $ | 110.00 | | $ | 179.00 | | | 481 | |

| | | | | | | | | | | | | | | |

Oil and gas segment commodity derivatives - net asset | | | | | | | | | | | | | $ | 19,340 | |

| | | | | | | | | | | | | | | |

| | (1) | This position expires in October 2008. |

At September 30, 2008, we reported a net derivative asset related to the oil and gas commodity derivatives of $19.3 million. See theAdoption of SFAS No. 161 section below for the impact of the oil and gas commodity derivatives on our consolidated statements of income.

PVR Natural Gas Midstream Segment Commodity Derivatives

PVR utilizes costless collars, three-way collars and swap derivative contracts to hedge against the variability in cash flows associated with forecasted natural gas midstream revenues and cost of midstream gas purchased. PVR also utilizes swap derivative contracts to hedge against the variability in its “frac spread.” PVR’s frac spread is the spread between the purchase price for the natural gas PVR purchases from producers and the sale price for the NGLs that PVR sells after processing. PVR hedges against the variability in its frac spread by entering into swap derivative contracts to sell NGLs forward at a predetermined swap price and to purchase an equivalent volume of natural gas forward on an MMBtu basis. While the use of derivative instruments limits the risk of adverse price movements, such use may also limit future revenues or cost savings from favorable price movements.

The counterparty to a costless collar contract is required to make a payment to PVR if the settlement price for any settlement period is below the floor price for such contract. PVR is required to make a payment to the counterparty if the settlement price for any settlement period is above the ceiling price for such contract. Neither party is required to make a payment to the other party if the settlement price for any settlement period is equal to or greater than the floor price and equal to or less than the ceiling price for such contract. The counterparty to a swap contract is required to make a payment to PVR if the settlement price for any settlement period is less than the swap price for such contract, and PVR is required to make a payment to the counterparty if the settlement price for any settlement period is greater than the swap price for such contract.

A three-way collar contract consists of a collar contract as described above plus a put option contract sold by PVR with a price below the floor price of the collar. This additional put requires PVR to make a payment to the counterparty if the settlement price for any settlement period is below the put option price. By combining the collar

9

contract with the additional put option, PVR is entitled to a net payment equal to the difference between the floor price of the collar contract and the additional put option price if the settlement price is equal to or less than the additional put option price. If the settlement price is greater than the additional put option price, the result is the same as it would have been with a collar contract only. This strategy enables PVR to increase the floor and the ceiling prices of the collar beyond the range of a traditional collar contract while defraying the associated cost with the sale of the additional put option.

PVR determines the fair values of its derivative agreements based on forward price quotes for the respective commodities as of September 30, 2008, the credit risks of the counterparties and PVR’s own credit risk. The following table sets forth PVR’s positions as of September 30, 2008 for commodities related to natural gas midstream revenues and cost of midstream gas purchased:

| | | | | | | | | | | | | | | | | | |

| | | Average Volume

Per Day | | Weighted

Average Price | | Weighted Average Price

Collars | | Fair Value

(in thousands) | |

| | | | Additional Put

Option | | Put | | Call | |

| | | (in MMBtu) | | (per MMBtu) | | | | | | | | | |

Frac Spread | | | | | | | | | | | | | | | | | | |

Fourth Quarter 2008 | | 7,824 | | $ | 5.02 | | | | | | | | | | | $ | (2,805 | ) |

| | | | | | |

| | | (in gallons) | | (per gallon) | | | | | | | | | |

Ethane Sale Swap | | | | | | | | | | | | | | | | | | |

Fourth Quarter 2008 | | 34,440 | | $ | 0.4700 | | | | | | | | | | | | (706 | ) |

| | | | | | |

| | | (in gallons) | | (per gallon) | | | | | | | | | |

Propane Sale Swaps | | | | | | | | | | | | | | | | | | |

Fourth Quarter 2008 | | 26,040 | | $ | 0.7175 | | | | | | | | | | | | (1,751 | ) |

| | | | | | |

| | | (in barrels) | | (per barrel) | | | | | | | | | |

Crude Oil Sale Swaps | | | | | | | | | | | | | | | | | | |

Fourth Quarter 2008 | | 560 | | $ | 49.27 | | | | | | | | | | | | (2,611 | ) |

| | | | | |

| | | (in gallons) | | | | | | (per gallon) | | | |

Natural Gasoline Collar | | | | | | | | | | | | | | | | | | |

Fourth Quarter 2008 | | 6,300 | | | | | | | | $ | 1.4800 | | $ | 1.6465 | | | (266 | ) |

| | | | | |

| | | (in barrels) | | | | | | (per barrel) | | | |

Crude Oil Collar | | | | | | | | | | | | | | | | | | |

Fourth Quarter 2008 | | 400 | | | | | | | | $ | 65.00 | | $ | 75.25 | | | (936 | ) |

| | | | | | |

| | | (in MMBtu) | | (per MMBtu) | | | | | | | | | |

Natural Gas Sale Swaps | | | | | | | | | | | | | | | | | | |

Fourth Quarter 2008 | | 4,000 | | $ | 6.97 | | | | | | | | | | | | 219 | |

| | | | | |

| | | (in barrels) | | | | | | (per barrel) | | | |

Crude Oil Three-Way Collar | | | | | | | | | | | | | | | | | | |

First Quarter 2009 through Fourth Quarter 2009 | | 1,000 | | | | | $ | 70.00 | | $ | 90.00 | | $ | 119.25 | | | (1,128 | ) |

| | | | | |

| | | (in MMBtu) | | | | | | (per MMBtu) | | | |

Frac Spread Collar | | | | | | | | | | | | | | | | | | |

First Quarter 2009 through Fourth Quarter 2009 | | 6,000 | | | | | | | | $ | 9.09 | | $ | 13.94 | | | 1,435 | |

| | | | | | |

Settlements to be paid in subsequent period | | | | | | | | | | | | | | | | | (3,186 | ) |

| | | | | | | | | | | | | | | | | | |

Natural gas midstream segment commodity derivatives - net liability | | | | | | | | | | | | | | | | $ | (11,735 | ) |

| | | | | | | | | | | | | | | | | | |

At September 30, 2008, PVR reported a (i) net derivative liability related to the natural gas midstream segment of $11.7 million and (ii) loss in accumulated other comprehensive income (“AOCI”) of $0.9 million related to derivatives in the natural gas midstream segment, net of the related income tax benefit of $0.5 million, for which PVR discontinued hedge accounting in 2006. The $0.9 million loss, net of the related income tax benefit of $0.5 million, will be recorded in earnings through the end of 2008 as the hedged transactions settle. See theAdoption of SFAS No. 161 section below for the impact of the natural gas midstream commodity derivatives on our consolidated statements of income.

Interest Rate Swaps

We have entered into the Revolver Swaps to establish fixed rates on a portion of the outstanding borrowings under the Revolver until December 2010. The notional amounts of the Revolver Swaps total $50.0 million. We will pay a weighted average fixed rate of 5.34% on the notional amount, and the counterparties will pay a variable rate equal to the three-month London Interbank Offered Rate (“LIBOR”). Settlements on the Revolver Swaps are

10

recorded as interest expense. The Revolver Swaps are designated as cash flow hedges. Accordingly, the effective portion of the change in the fair value of the swap transactions is recorded each period in other comprehensive income. The ineffective portion of the change in fair value, if any, is recorded to current period earnings as interest expense. We reported a (i) derivative liability of $2.1 million at September 30, 2008 and (ii) loss in AOCI of $1.4 million, net of the related income tax expense of $0.7 million, at September 30, 2008 related to the Revolver Swaps. In connection with periodic settlements, we recognized $0.3 million and $0.7 million in net hedging losses on the Revolver Swaps in interest expense for the three and nine months ended September 30, 2008.

Interest Rate Swaps—PVR

PVR has entered into the PVR Revolver Swaps to establish fixed rates on a portion of the outstanding borrowings under the PVR Revolver. Until March 2010, the notional amounts of the PVR Revolver Swaps total $210.0 million, or approximately 38% of PVR’s total long term debt outstanding as of September 30, 2008, with PVR paying a weighted average fixed rate of 4.23% on the notional amount, and the counterparties paying a variable rate equal to the three-month LIBOR. From March 2010 to December 2011, the notional amounts of the Revolver Swaps total $150.0 million with PVR paying a weighted average fixed rate of 4.23% on the notional amount, and the counterparties paying a variable rate equal to the three-month LIBOR. Settlements on the PVR Revolver Swaps are recorded as interest expense. Certain of the PVR Revolver Swaps are designated as cash flow hedges. Accordingly, the effective portion of the change in the fair value of the transactions for the swaps that are designated as cash flow hedges are recorded each period in AOCI. PVR reported a (i) derivative liability of $3.4 million at September 30, 2008 and (ii) loss in AOCI of $1.3 million, net of the related income tax expense of $0.7 million, at September 30, 2008 related to the PVR Revolver Swaps. In connection with periodic settlements, PVR recognized $0.8 million and $1.2 million in net hedging losses in interest expense for the three and nine months ended September 30, 2008.

Adoption of SFAS No. 161

In March 2008, the FASB issued SFAS No. 161,Disclosures about Derivative Instruments and Hedging Activities,an Amendment of FASB Statement No. 133, which amends and expands SFAS No. 133,Accounting for Derivative Instruments and Hedging Activities. We elected to adopt SFAS No. 161 early, effective June 30, 2008. SFAS No. 161 requires companies to disclose how and why an entity uses derivative instruments, how derivative instruments and related hedged items are accounted for and how derivative instruments and related hedged items affect an entity’s financial position, financial performance and cash flows.

11

The following table summarizes the effects of our consolidated derivative activities, as well as the location of the gains and losses, on our consolidated statements of income for the three and nine months ended September 30, 2008 (in thousands):

| | | | | | | | | | |

| | | Location of gain (loss) on

derivatives recognized in income | | Three Months

Ended September 30, | | | Nine Months

Ended September 30, | |

| | | | 2008 | | | 2008 | |

Derivatives designated as hedging instruments under SFAS No. 133: | | | | | | | | | | |

Interest rate contracts | | Interest expense | | $ | (1,179 | ) | | $ | (1,891 | ) |

| | | | | | | | | | |

Decrease in net income resulting from derivatives designated as hedging instruments under SFAS No. 133 | | | | $ | (1,179 | ) | | $ | (1,891 | ) |

| | | | | | | | | | |

Derivatives not designated as hedging instruments under SFAS No. 133: | | | | | | | | | | |

Interest rate contracts | | Derivatives | | $ | (1,333 | ) | | $ | (1,333 | ) |

Commodity contracts (1) | | Natural gas midstream revenues | | | (1,987 | ) | | | (6,235 | ) |

Commodity contracts (1) | | Cost of midstream gas purchased | | | 484 | | | | 2,107 | |

Commodity contracts | | Derivatives | | | 126,464 | | | | (3,055 | ) |

| | | | | | | | | | |

Increase (decrease) in net income resulting from derivatives not designated as hedging instruments under SFAS No. 133 | | | | $ | 123,628 | | | $ | (8,516 | ) |

| | | | | | | | | | |

Total increase (decrease) in net income resulting from derivatives | | | | $ | 122,449 | | | $ | (10,407 | ) |

| | | | | | | | | | |

Realized and unrealized derivative impact: | | | | | | | | | | |

Cash paid for commodity contract settlements | | Derivatives | | $ | (19,755 | ) | | $ | (46,740 | ) |

Cash paid for interest rate contract settlements | | Interest expense | | | (1,179 | ) | | | (1,891 | ) |

Unrealized derivative gain | | (2) | | | 143,383 | | | | 38,224 | |

| | | | | | | | | | |

Increase (decrease) in net income | | | | $ | 122,449 | | | $ | (10,407 | ) |

| | | | | | | | | | |

| | (1) | These amounts represent reclassifications from AOCI. Subsequent to the discontinuation of hedge accounting for commodity derivatives in 2006, amounts remaining in AOCI have been reclassified into earnings in the same period or periods during which the original hedge forecasted transaction affects earnings. The amount remaining in AOCI that will be reclassified to earnings in future periods is $0.9 million, net of related income taxes of $0.5 million. |

| | (2) | This activity represents unrealized gains in the natural gas midstream, cost of midstream gas purchased and derivatives lines on our consolidated statements of income. |

Cash paid for commodity derivatives is included on the Derivatives line on our consolidated statement of income, and cash paid for interest rate swaps is included on the Interest expense line on our consolidated statement of income.

12

The following table summarizes the fair value of our derivative instruments, as well as the locations of these instruments on our consolidated balance sheets as of September 30, 2008 (in thousands):

| | | | | | | | |

| | | | | Derivative Assets | | Derivative Liabilities |

| | | Balance Sheet Location | | Estimated fair values as of September 30, 2008 |

Derivatives designated as hedging instruments under SFAS No. 133: | | | | | | | | |

Interest rate contracts | | Derivative liabilities - current | | $ | — | | $ | 1,063 |

Interest rate contracts | | Derivative liabilities - noncurrent | | | — | | | 1,351 |

| | | | | | | | |

Total derivatives designated as hedging instruments under SFAS No. 133 | | | | $ | — | | $ | 2,414 |

| | | | | | | | |

Derivatives not designated as hedging instruments under SFAS No. 133: | | | | | | | | |

Interest rate contracts | | Derivative liabilities - current | | $ | — | | $ | 1,307 |

Interest rate contracts | | Derivative liabilities - noncurrent | | | — | | | 1,754 |

Commodity contracts | | Derivative assets/liabilities - current | | | 18,197 | | | 15,589 |

Commodity contracts | | Derivative assets/liabilities - noncurrent | | | 6,019 | | | 1,022 |

| | | | | | | | |

Total derivatives not designated as hedging instruments under SFAS No. 133 | | | | $ | 24,216 | | $ | 19,672 |

| | | | | | | | |

Total estimated fair value of derivative instruments | | | | $ | 24,216 | | $ | 22,086 |

| | | | | | | | |

The following table summarizes the effect of the Revolver Swaps and the PVR Revolver Swaps on our total interest expense for the three and nine months ended September 30, 2008 (in thousands):

| | | | | | | | |

| | | Three Months

Ended | | | Nine Months

Ended | |

Source | | September 30, 2008 | |

Interest on borrowings | | $ | (11,251 | ) | | $ | (31,939 | ) |

Capitalized interest (1) | | | 492 | | | | 2,230 | |

Interest rate swaps | | | (1,179 | ) | | | (1,891 | ) |

| | | | | | | | |

Total interest expense | | $ | (11,938 | ) | | $ | (31,600 | ) |

| | | | | | | | |

| | (1) | Capitalized interest for the nine months ended September 30, 2008 was primarily related to the construction of PVR’s natural gas gathering facilities. PVR had no capitalized interest in the three months ended September 30, 2008. |

The above derivative activity represents cash flow hedges. As of September 30, 2008, neither PVR nor we owned derivative instruments that were classified as fair value hedges or trading securities. In addition, as of September 30, 2008, neither PVR nor we owned derivative instruments containing credit risk contingencies.

9. PVR Senior Notes Repayment and PVR Revolver Amendment

In July 2008, PVR paid an aggregate of $63.3 million to the holders of its Senior Unsecured Notes due 2013 (the “PVR Notes”) to repay 100% of the aggregate principal amount of the PVR Notes as provided in the Note Purchase Agreements governing the PVR Notes. This amount consisted of approximately $58.4 million aggregate principal amount outstanding on the PVR Notes, $1.1 million in accrued and unpaid interest on the PVR Notes through the prepayment date and $3.8 million in make-whole amounts due in connection with the prepayment of the PVR Notes. PVR repaid the PVR Notes with borrowings under the PVR Revolver.

In August 2008, PVR amended and restated the PVR Revolver to increase its available borrowings under the PVR Revolver from $600.0 million to $700.0 million and to make it a secured facility. The PVR Revolver is secured by substantially all of PVR’s assets.

13

10. Income Taxes

The total liability for unrecognized tax benefits at September 30, 2008 was $5.5 million, including $4.1 million of tax positions which would change the effective tax rate if recognized. During the three and nine months ended September 30, 2008, the liability for unrecognized tax benefits decreased by $0.4 and $4.9 million relating to settlements with taxing authorities.

We are currently evaluating the filing status of a subsidiary in two states. If management and the states’ taxing authority determine that the subsidiary’s income is taxable in those states, we may be requested to pay taxes of approximately $2.8 million will be made within the next 12 months. We classified $2.8 million of the total liability for unrecognized tax benefits as a current liability on our consolidated balance sheet at September 30, 2008. This current liability represents our best estimate of the change in unrecognized tax benefits that we expect to incur within the next 12 months.

The 2008 effective income tax rates include the effects of settlements of liabilities for unrecognized tax benefits for the three and nine months ended September 30, 2008.

11. Earnings per Share

The following is a reconciliation of the numerators and denominators used in the calculation of basic and diluted earnings per share for the three and nine months ended September 30, 2008 and 2007:

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2008 | | | 2007 | | | 2008 | | | 2007 | |

| | | (in thousands, except per

share data) | | | (in thousands, except per

share data) | |

Net income | | $ | 123,738 | | | $ | 17,114 | | | $ | 123,871 | | | $ | 45,395 | |

| Less: Portion of subsidiary net income allocated to undistributed share-based compensation awards | | | (219 | ) | | | (60 | ) | | | (418 | ) | | | (170 | ) |

| | | | | | | | | | | | | | | | |

| | $ | 123,519 | | | $ | 17,054 | | | $ | 123,453 | | | $ | 45,225 | |

Weighted average shares, basic | | | 41,881 | | | | 37,898 | | | | 41,715 | | | | 37,748 | |

Effect of dilutive securities: | | | | | | | | | | | | | | | | |

Convertible notes | | | 279 | | | | — | | | | — | | | | — | |

Stock options | | | 384 | | | | 315 | | | | 313 | | | | 297 | |

| | | | | | | | | | | | | | | | |

Weighted average shares, diluted | | | 42,544 | | | | 38,213 | | | | 42,028 | | | | 38,045 | |

| | | | | | | | | | | | | | | | |

Net income per share, basic | | $ | 2.95 | | | $ | 0.45 | | | $ | 2.96 | | | $ | 1.20 | |

| | | | | | | | | | | | | | | | |

Net income per share, diluted | | $ | 2.90 | | | $ | 0.45 | | | $ | 2.94 | | | $ | 1.19 | |

| | | | | | | | | | | | | | | | |

12. Share-Based Compensation

Stock Compensation Plans

We recognized a total of $1.6 million and $1.0 million for the three months ended September 30, 2008 and 2007 and $4.3 million and $3.0 million for the nine months ended September 30, 2008 and 2007 of compensation expense related to the granting of common stock and deferred common stock units and the vesting of stock options and restricted stock granted under our stock compensations plans. The total income tax benefit recognized in our consolidated statements of income for our stock compensation plans was $0.6 million and $0.4 million for the three months ended September 30, 2008 and 2007 and $1.7 million and $1.2 million for the nine months ended September 30, 2008 and 2007.

Stock Options. In February 2008, we granted 446,458 stock options with a weighted average exercise price of $42.27 and a weighted average grant date fair value of $12.83 per option. The options granted vest over a three-year period, with one-third vesting in each year. We recognize compensation expense on a straight-line basis over the vesting period.

14

Restricted Stock. In February 2008, we also granted 39,354 shares of restricted stock with a weighted average grant date fair value of $42.27 per share. The restricted stock granted vests over a three-year period, with one-third vesting in each year. We recognize compensation expense on a straight-line basis over the vesting period.

PVR Long-Term Incentive Plan

PVR recognized a total of $0.8 million and $0.7 million for the three months ended September 30, 2008 and 2007 and $2.4 million and $1.8 million for the nine months ended September 30, 2008 and 2007 of compensation expense related to the granting of common units and deferred common units and the vesting of restricted units granted under its long-term incentive plan. During the nine months ended September 30, 2008, PVR’s general partner granted 134,551 restricted units with a weighted average grant date fair value of $26.87 per unit to employees of Penn Virginia and its affiliates. During the same period, 70,007 restricted units with a weighted average grant date fair value of $27.27 per unit vested. The restricted units granted in 2008 vest over a three-year period, with one-third vesting in each year. PVR recognizes compensation expense on a straight-line basis over the vesting period.

13. Comprehensive Income

Comprehensive income represents changes in shareholders’ equity during the reporting period, including net income and charges directly to shareholders’ equity which are excluded from net income. The following table sets forth the components of comprehensive income for the three and nine months ended September 30, 2008 and 2007:

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2008 | | | 2007 | | | 2008 | | | 2007 | |

| | | (in thousands) | | | (in thousands) | |

Net income | | $ | 123,738 | | | $ | 17,114 | | | $ | 123,871 | | | $ | 45,395 | |

Unrealized holding losses on derivative activities, net of tax | | | (1,468 | ) | | | (1,215 | ) | | | (2,187 | ) | | | (505 | ) |

Reclassification adjustment for derivative activities, net of tax | | | 2,610 | | | | 925 | | | | 4,781 | | | | 1,938 | |

Pension plan adjustment | | | 41 | | | | (35 | ) | | | 122 | | | | (106 | ) |

| | | | | | | | | | | | | | | | |

Comprehensive income | | $ | 124,921 | | | $ | 16,789 | | | $ | 126,587 | | | $ | 46,722 | |

| | | | | | | | | | | | | | | | |

14. Suspended Well Costs

Two exploratory wells that were pending determination of proved reserves as of December 31, 2007 were subsequently determined to be successful. Accordingly, we reclassified $2.6 million of capitalized exploratory drilling costs related to these wells to wells, equipment and facilities during the nine months ended September 30, 2008.

Two exploratory wells that were pending determination of proved reserves as of December 31, 2007 were subsequently determined to be unsuccessful. Accordingly, we charged $1.8 million to expense related to these wells during the nine months ended September 30, 2008.

15

15. Commitments and Contingencies

Legal

We are involved, from time to time, in various legal proceedings arising in the ordinary course of business. While the ultimate results of these proceedings cannot be predicted with certainty, our management believes that these claims will not have a material effect on our financial position, liquidity or operations.

Drilling Commitments

In July 2008, we entered into two agreements to purchase oil and gas well drilling services from a third party, which is scheduled to commence in the second quarter of 2009. The agreements include early termination provisions that would require us to pay a penalty if we terminate the agreements after their execution but prior to the end of their three-year terms, unless certain events occur. The amount of the penalty is based on the number of days remaining in the three-year terms for both contracts. As of September 30, 2008, the total penalty amount would have been approximately $41.6 million if we had terminated both agreements on that date. Management intends to utilize drilling services under these agreements for the full three-year term and has no plans to terminate the agreements early.

Environmental Compliance

Extensive federal, state and local laws govern oil and natural gas operations, regulate the discharge of materials into the environment or otherwise relate to the protection of the environment. Numerous governmental departments issue rules and regulations to implement and enforce such laws that are often difficult and costly to comply with and which carry substantial administrative, civil and even criminal penalties for failure to comply. Some laws, rules and regulations relating to protection of the environment may, in certain circumstances, impose “strict liability” for environmental contamination, rendering a person liable for environmental and natural resource damages and cleanup costs without regard to negligence or fault on the part of such person. Other laws, rules and regulations may restrict the rate of oil and natural gas production below the rate that would otherwise exist or even prohibit exploration or production activities in sensitive areas. In addition, state laws often require some form of remedial action to prevent pollution from former operations, such as closure of inactive pits and plugging of abandoned wells. The regulatory burden on the oil and natural gas industry increases its cost of doing business and consequently affects its profitability. These laws, rules and regulations affect our operations, as well as the oil and gas exploration and production industry in general. We believe that we are in substantial compliance with current applicable environmental laws, rules and regulations and that continued compliance with existing requirements will not have a material adverse impact on our financial condition or results of operations. Nevertheless, changes in existing environmental laws or the adoption of new environmental laws have the potential to adversely affect our operations.

PVR’s operations and those of its lessees are subject to environmental laws and regulations adopted by various governmental authorities in the jurisdictions in which these operations are conducted. The terms of PVR’s coal property leases impose liability on the relevant lessees for all environmental and reclamation liabilities arising under those laws and regulations. The lessees are bonded and have indemnified PVR against any and all future environmental liabilities. PVR regularly visits its coal properties to monitor lessee compliance with environmental laws and regulations and to review mining activities. PVR’s management believes that its operations and those of its lessees comply with existing laws and regulations and does not expect any material impact on its financial condition or results of operations.

As of September 30, 2008 and December 31, 2007, PVR’s environmental liabilities included $1.2 million and $1.5 million, which represents PVR’s best estimate of the liabilities as of those dates related to its coal and natural resource management and natural gas midstream businesses. PVR has reclamation bonding requirements with respect to certain unleased and inactive properties. Given the uncertainty of when a reclamation area will meet regulatory standards, a change in this estimate could occur in the future.

16

Mine Health and Safety Laws

There are numerous mine health and safety laws and regulations applicable to the coal mining industry. However, since PVR does not operate any mines and does not employ any coal miners, PVR is not subject to such laws and regulations. Accordingly, we have not accrued any related liabilities.

16. Segment Information

Segment information has been prepared in accordance with SFAS No. 131,Disclosure about Segments of an Enterprise and Related Information.Under SFAS No. 131, operating segments are defined as components of an enterprise about which separate financial information is available and is evaluated regularly by the chief operating decision maker, or decision-making group, in assessing performance. Our decision-making group consists of our Chief Executive Officer and other senior officers. This group routinely reviews and makes operating and resource allocation decisions among our oil and gas operations and PVR’s coal and natural resource management operations and PVR’s natural gas midstream operations. Accordingly, our reportable segments are as follows:

| | • | | Oil and Gas—crude oil and natural gas exploration, development and production. |

| | • | | PVR Coal and Natural Resource Management—management and leasing of coal properties and subsequent collection of royalties; other land management activities such as selling standing timber; leasing of fee-based coal-related infrastructure facilities to certain lessees and end-user industrial plants; collection of oil and gas royalties; and coal transportation, or wheelage fees. |

| | • | | PVR Natural Gas Midstream—natural gas processing, gathering and other related services. |

17

The following tables present a summary of certain financial information relating to our segments as of and for the three and nine months ended September 30, 2008 and 2007:

| | | | | | | | | | | | | | | | | | | |

| | | Oil and Gas | | | PVR Coal and

Natural Resource

Management | | | PVR Natural

Gas

Midstream | | Eliminations

and Other | | | Consolidated | |

| | | (in thousands) | |

For the Three Months Ended September 30, 2008: | | | | | | | | | | | | | | | | | | | |

Revenues | | $ | 157,364 | | | $ | 41,858 | | | $ | 186,609 | | $ | (219 | ) | | $ | 385,612 | |

Intersegment revenues (1) | | | (639 | ) | | | (198 | ) | | | 57,007 | | | (56,170 | ) | | | — | |

Operating costs and expenses | | | 35,072 | | | | 6,571 | | | | 221,779 | | | (50,115 | ) | | | 213,307 | |

Depreciation, depletion and amortization | | | 32,665 | | | | 8,794 | | | | 8,109 | | | 410 | | | | 49,978 | |

| | | | | | | | | | | | | | | | | | | |

Operating income (loss) | | $ | 88,988 | | | $ | 26,295 | | | $ | 13,728 | | $ | (6,684 | ) | | | 122,327 | |

| | | | | | | | | | | | | | | | | | | |

Interest expense | | | | | | | | | | | | | | | | | | (11,938 | ) |

Other | | | | | | | | | | | | | | | | | | (4,088 | ) |

Derivatives | | | | | | | | | | | | | | | | | | 125,132 | |

| | | | | | | | | | | | | | | | | | | |

Income before minority interest and taxes | | | | | | | | | | | | | | | | | $ | 231,433 | |

| | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 1,595,691 | | | $ | 588,430 | | | $ | 619,652 | | $ | 106,848 | | | $ | 2,910,621 | |

Equity investments (2) | | $ | — | | | $ | 25,459 | | | $ | 53,175 | | $ | — | | | $ | 78,634 | |

Goodwill | | $ | — | | | $ | — | | | $ | 31,768 | | $ | — | | | $ | 31,768 | |

Additions to property and equipment and acquisitions | | $ | 213,573 | | | $ | 497 | | | $ | 110,606 | | $ | 259 | | | $ | 324,935 | |

| | | | | |

For the Three Months Ended September 30, 2007: | | | | | | | | | | | | | | | | | | | |

Revenues | | $ | 85,745 | | | $ | 28,218 | | | $ | 101,374 | | $ | 421 | | | $ | 215,758 | |

Intersegment revenues (1) | | | (414 | ) | | | 198 | | | | 414 | | | (198 | ) | | | — | |

Operating costs and expenses | | | 36,029 | | | | 4,871 | | | | 82,917 | | | 6,850 | | | | 130,667 | |

Depreciation, depletion and amortization | | | 22,152 | | | | 5,833 | | | | 4,812 | | | 410 | | | | 33,207 | |

| | | | | | | | | | | | | | | | | | | |

Operating income (loss) | | $ | 27,150 | | | $ | 17,712 | | | $ | 14,059 | | $ | (7,037 | ) | | | 51,884 | |

| | | | | | | | | | | | | | | | | | | |

Interest expense | | | | | | | | | | | | | | | | | | (10,843 | ) |

Other | | | | | | | | | | | | | | | | | | 576 | |

Derivatives | | | | | | | | | | | | | | | | | | (4,455 | ) |

| | | | | | | | | | | | | | | | | | | |

Income before minority interest and taxes | | | | | | | | | | | | | | | | | $ | 37,162 | |

| | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 1,151,331 | | | $ | 561,169 | | | $ | 287,769 | | $ | 46,287 | | | $ | 2,046,556 | |

Equity investments | | $ | — | | | $ | 26,428 | | | $ | 60 | | $ | — | | | $ | 26,488 | |

Goodwill | | $ | — | | | $ | — | | | $ | 7,718 | | $ | — | | | $ | 7,718 | |

Additions to property and equipment and acquisitions | | $ | 166,500 | | | $ | 93,449 | | | $ | 10,755 | | $ | 1,775 | | | $ | 272,479 | |

| | (1) | Intersegment revenues represent gas gathering and processing transactions for the three months ended September 30, 2008 between the PVR natural gas midstream segment and the oil and gas segment. The PVR natural gas midstream segment gathered and processed the natural gas delivered by the oil and gas segment and then purchased the processed gas and NGLs from the oil and gas segment for $55.7 million to sell to third parties. Intersegment revenues also represent agent fees paid by the oil and gas segment to the PVR natural gas midstream segment for marketing certain natural gas production and rail car rental fees paid by a corporate affiliate to the PVR coal and natural resource management segment. |

| | (2) | The increase in equity investments is due to the 25% member interest in Thunder Creek that PVR acquired in 2008 for $51.6 million. See Note 4 — Acquisitions. |

18

| | | | | | | | | | | | | | | | | | | |

| | | Oil and

Gas | | | PVR Coal and

Natural

Resource

Management | | | PVR Natural

Gas Midstream | | Eliminations

and Other | | | Consolidated | |

| | | (in thousands) | |

For the Nine Months Ended September 30, 2008: | | | | | | | | | | | | | | | | | | | |

Revenues | | $ | 385,100 | | | $ | 111,604 | | | $ | 499,009 | | $ | (552 | ) | | $ | 995,161 | |

Intersegment revenues (1) | | | (1,709 | ) | | | (594 | ) | | | 108,576 | | | (106,273 | ) | | | — | |

Operating costs and expenses | | | 97,484 | | | | 20,417 | | | | 541,270 | | | (86,175 | ) | | | 572,996 | |

Depreciation, depletion and amortization | | | 90,849 | | | | 22,733 | | | | 18,589 | | | 1,310 | | | | 133,481 | |

| | | | | | | | | | | | | | | | | | | |

Operating income (loss) | | $ | 195,058 | | | $ | 67,860 | | | $ | 47,726 | | $ | (21,960 | ) | | | 288,684 | |

| | | | | | | | | | | | | | | | | | | |

Interest expense | | | | | | | | | | | | | | | | | | (31,600 | ) |

Other | | | | | | | | | | | | | | | | | | (782 | ) |

Derivatives | | | | | | | | | | | | | | | | | | (4,387 | ) |

| | | | | | | | | | | | | | | | | | | |

Income before minority interest and taxes | | | | | | | | | | | | | | | | | $ | 251,915 | |

| | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 1,595,691 | | | $ | 588,430 | | | $ | 619,652 | | $ | 106,848 | | | $ | 2,910,621 | |

Equity investments (2) | | $ | — | | | $ | 25,459 | | | $ | 53,175 | | $ | — | | | $ | 78,634 | |

Goodwill | | $ | — | | | $ | — | | | $ | 31,768 | | $ | — | | | $ | 31,768 | |

Additions to property and equipment and acquisitions | | $ | 422,975 | | | $ | 25,186 | | | $ | 220,997 | | $ | 1,058 | | | $ | 670,216 | |

| | | | | |

For the Nine Months Ended September 30, 2007: | | | | | | | | | | | | | | | | | | | |

Revenues | | $ | 226,665 | | | $ | 84,716 | | | $ | 312,084 | | $ | 961 | | | $ | 624,426 | |

Intersegment revenues (1) | | | (1,154 | ) | | | 594 | | | | 1,154 | | | (594 | ) | | | — | |

Operating costs and expenses | | | 81,480 | | | | 15,489 | | | | 270,966 | | | 19,171 | | | | 387,106 | |

Depreciation, depletion and amortization | | | 58,628 | | | | 16,643 | | | | 13,957 | | | 595 | | | | 89,823 | |

| | | | | | | | | | | | | | | | | | | |

Operating income (loss) | | $ | 85,403 | | | $ | 53,178 | | | $ | 28,315 | | $ | (19,399 | ) | | | 147,497 | |

| | | | | | | | | | | | | | | | | | | |

Interest expense | | | | | | | | | | | | | | | | | | (25,878 | ) |

Other | | | | | | | | | | | | | | | | | | 2,536 | |

Derivatives | | | | | | | | | | | | | | | | | | (22,068 | ) |

| | | | | | | | | | | | | | | | | | | |

Income before minority interest and taxes | | | | | | | | | | | | | | | | | $ | 102,087 | |

| | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 1,151,331 | | | $ | 561,169 | | | $ | 287,769 | | $ | 46,287 | | | $ | 2,046,556 | |

Equity investments | | $ | — | | | $ | 26,428 | | | $ | 60 | | $ | — | | | $ | 26,488 | |

Goodwill | | $ | — | | | $ | — | | | $ | 7,718 | | $ | — | | | $ | 7,718 | |

Additions to property and equipment and acquisitions | | $ | 367,558 | | | $ | 146,915 | | | $ | 28,619 | | $ | 4,913 | | | $ | 548,005 | |

| | (1) | Intersegment revenues represent gas gathering and processing transactions for the nine months ended September 30, 2008 between the PVR natural gas midstream segment and the oil and gas segment. The PVR natural gas midstream segment gathered and processed the natural gas delivered by the oil and gas segment and then purchased the processed gas and NGLs from the oil and gas segment for $105.5 million to sell to third parties. Intersegment revenues also represent agent fees paid by the oil and gas segment to the PVR natural gas midstream segment for marketing certain natural gas production and rail car rental fees paid by a corporate affiliate to the PVR coal and natural resource management segment. |

| | (2) | The increase in equity investments is due to the 25% member interest in Thunder Creek that PVR acquired in 2008 for $51.6 million. See Note 4 — Acquisitions. |

19

| Item 2 | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following discussion and analysis of the financial condition and results of operations of Penn Virginia Corporation and its subsidiaries should be read in conjunction with our consolidated financial statements and the accompanying notes in Item 1, “Financial Statements.”

Overview of Business

We are an independent oil and gas company primarily engaged in the exploration, development and production of natural gas and oil in various onshore U.S. regions including East Texas, the Mid-Continent, Appalachia, Mississippi and the Gulf Coast. We also indirectly own partner interests in PVR, which is engaged in the coal and natural resource management and natural gas midstream businesses. Our ownership interests in PVR are held principally through our ownership of the general partner and 77% limited partner interests in PVG. At September 30, 2008, PVG owned an approximately 37% limited partner interest in PVR and 100% of the general partner of PVR, which held a 2% general partner interest in PVR.

We are engaged in three primary business segments: (i) oil and gas, (ii) coal and natural resource management and (iii) natural gas midstream. We operate our oil and gas segment. PVR operates our coal and natural resource management and natural gas midstream segments and is consolidated by PVG because PVG controls PVR’s general partner. We consolidate PVG’s results into our financial statements because we control the general partner of PVG. Our operating income was $288.7 million in the nine months ended September 30, 2008, compared to $147.5 million in the same period of 2007. In the nine months ended September 30, 2008, the oil and gas segment contributed $195.1 million, or 68%, to operating income, the PVR coal and natural resource management segment contributed $67.9 million, or 24%, to operating income and the PVR natural gas midstream segment contributed $47.7 million, or 17%, to operating income.

The following table presents a summary of certain financial information relating to our segments for the nine months ended September 30, 2008 and 2007 (in thousands):

| | | | | | | | | | | | | | | | |

| | | Oil and

Gas | | PVR Coal and

Natural Resource

Management | | PVR

Natural Gas

Midstream | | Eliminations

and Other | | | Consolidated |

For the Nine Months Ended September 30, 2008: | | | | | | | | | | | | | | | | |

Revenues | | $ | 383,391 | | $ | 111,010 | | $ | 607,585 | | $ | (106,825 | ) | | $ | 995,161 |

Operating costs and expenses | | | 97,484 | | | 20,417 | | | 541,270 | | | (86,175 | ) | | | 572,996 |

Depreciation, depletion and amortization | | | 90,849 | | | 22,733 | | | 18,589 | | | 1,310 | | | | 133,481 |

| | | | | | | | | | | | | | | | |

Operating income (loss) | | $ | 195,058 | | $ | 67,860 | | $ | 47,726 | | $ | (21,960 | ) | | $ | 288,684 |

| | | | | | | | | | | | | | | | |

For the Nine Months Ended September 30, 2007: | | | | | | | | | | | | | | | | |